Commission, October 18, 2019, No M.9433

EUROPEAN COMMISSION

Judgment

MEIF 6 FIBRE / KCOM GROUP

Subject: Case M.9433 – MEIF 6 Fibre / KCOM Group

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 13 September 2019, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which MEIF 6 Fibre Limited (“MEIF 6 Fibre” or the “Notifying Party”, UK), controlled by Macquarie Group Limited (“Macquarie”, Australia), acquires within the meaning of Article 3(1)(b) of the Merger Regulation sole control of KCOM Group Public Limited Company (“KCOM”, UK) (the “Transaction”). Macquarie and KCOM are collectively referred to as the “Parties”. (3)

1. THE PARTIES

(2) MEIF 6 Fibre is a wholly-owned indirect subsidiary of Macquarie European Infrastructure Fund 6 SCSp (“MEIF 6”), managed, in turn, by Macquarie Infrastructure and Real Assets (“MIRA”). Macquarie is a diversified financial services group that has established leading positions as a global specialist in a wide range of sectors, including as owner and investor in telecommunications infrastructure. One of MIRA’s investments in the European telecommunications sector is a 25% interest in Arqiva Limited (“Arqiva”). Arqiva is a provider of transmission towers and terrestrial TV and radio broadcasting services in the UK. Arqiva jointly controls Freeview, (4) the UK’s main Digital Terrestrial Television (“DTT”) platform.

(3) KCOM is a provider of IT and communications services to consumers and businesses in the UK. It is primarily active in North-East England in the city of Kingston Upon Hull and the surrounding area in the East Riding of Yorkshire (the “Hull area (5)”), where KCOM is the regulated incumbent. Besides its activities in the Hull area, KCOM provides IT, communications and connectivity services to large and/or multi-sided enterprises and public sector organisations across the UK.

2. THE CONCENTRATION

(4) On 3 June 2019, the boards of MEIF 6 Fibre and KCOM announced that they had agreed on the terms of a recommended cash offer, to be made by MEIF 6 Fibre, for the entire issued and to be issued ordinary share capital of KCOM, including all voting rights attached to the shares.

(5) On 4 July 2019, the UK Takeover Panel announced that a public auction in respect of KCOM would be required to take place. The auction commenced on 8 July 2019 in accordance with a timetable and rules mandated by the Takeover Panel.

(6) On 12 July 2019, MEIF 6 Fibre submitted a revised increased offer of approximately EUR 698.3 million, which the directors of KCOM recommended unanimously.

(7) On 26 July 2019, MEIF 6 Fibre’s acquisition of the shares received unconditional approval from the UK’s Financial Conduct Authority, and the scheme of arrangement became effective on 1 August 2019. (6) MEIF 6 Fibre now owns 100% of the share capital in KCOM. (7)

(8) Therefore, the Transaction consists of the acquisition of sole control by MEIF 6 Fibre over KCOM within the meaning of Article 3(1)(b) of the Merger Regulation.

3. UNION DIMENSION

(9) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (Macquarie: EUR […], KCOM: EUR 342 million). (8) Each of them has an EU-wide turnover in excess of EUR 250 million (Macquarie: EUR […], KCOM: EUR 342 million), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an Union dimension pursuant to Article 1(2) of the Merger Regulation.

4. RELEVANT MARKETS

(10) The Parties are active in several telecommunications and TV markets in the UK. KCOM is active, at the retail level, in fixed telephony and in fixed internet access services, while Macquarie, via its shareholding in Arqiva, which in turn holds negative joint control over Freeview, the UK’s main DTT platform, is active in retail TV services. The corresponding relevant markets are examined in sections 4.1 to 4.4 below.

(11) In addition, the Parties are both active in retail business connectivity services. Macquarie, through its shareholding in Arqiva, is active in site sharing services and KCOM is active in colocation services. However, due to the Parties’ limited positions, the Transaction does not give rise to any horizontally (9) or vertically affected markets. (10) Therefore, for the purpose of the present decision, the Commission will not discuss further the Parties’ activities in retail business connectivity, site sharing and colocation services.

4.1. Retail supply of fixed telephony services

(12) Fixed telephony services to end customers comprise the provision of subscriptions enabling access to public telephone networks at a fixed location for the purpose of making and/or receiving calls and related services. (11)

(13) KCOM is the incumbent provider of fixed telephony services to consumers and businesses based on its own copper and fibre networks in the Hull area. In addition, KCOM provides fixed telephony services to business throughout the UK. (12)

(14) Macquarie is not active in the retail supply of fixed telephony services in the UK.

4.1.1. Product market definition

4.1.1.1. Commission precedents

(15) In previous decisions (13), the Commission considered whether a distinction between local/national and international calls as well as between residential and non- residential customers should be drawn, on the basis of the distinctions in the Commission Recommendation 2003/311/EC (14), but ultimately left the exact product market definition open.

(16) More recently, the Commission also considered that managed Voice over Internet Protocol (“VoIP”) services (15) and traditional telephony are interchangeable and therefore belong to the same market. (16) In recent decisions, the Commission considered that an overall retail market for fixed telephony services exists, which includes VoIP services. (17)

4.1.1.2. The Notifying Party’s view

(17) The Notifying Party submits that, in line with previous Commission decisions, the relevant product market is the overall retail market for the provision of fixed telephony services including VoIP services, with no need for further segmentation.

(18) However, the Notifying Party considers that the exact scope of the relevant product market can be left open, as no competition concerns arise on any plausible basis. (18)

4.1.1.3. The Commission’s assessment

(19) The results of the market investigation conducted in the present case generally supported the market definition derived from the Commission’s past decisional practice, and indicated that the retail market for fixed telephony services includes VoIP services. (19) Moreover, the majority of respondents to the market investigation agreed with a segmentation between residential customers (including small business customers) and large business customers. (20)

(20) The Commission considers that, in any event, for the purposes of this decision, the exact product market definition with regard to the retail supply of fixed telephony services can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement under any plausible product market definition.

4.1.2. Geographic market definition

4.1.2.1. Commission precedents

(21) In previous decisions, the Commission concluded that the retail market for the provision of fixed telephony services was national in scope. (21) This is due to the continuing importance of national regulation in the telecommunications sector, the supply of upstream wholesale services that works on a national basis, and the fact that the pricing policies of telecommunications providers are predominantly national. (22)

4.1.2.2. The Notifying Party’s view

(22) The Notifying Party stresses that KCOM’s activities in the retail supply of fixed telephony services focus mainly on the Hull area (23), but ultimately agrees with previous Commission decisions defining a national market. (24)

(23) However, the Notifying Party considers that the exact scope of the relevant geographic market can be left open, as no competition concerns arise on any plausible basis. (25)

4.1.2.3. The Commission’s assessment

(24) A large majority of respondents to the market investigation indicated that the Hull area is a separate geographic market distinct from the rest of the UK for the retail supply of fixed telephony services, since the competitive conditions in said area significantly differ from the rest of the UK. (26)

(25) The Commission also notes that Ofcom, in its most recent market review, has defined the Hull area as a separate geographic market in relation to a number of wholesale markets confirming that competitive conditions within the area are sufficiently homogenous and appreciably different from the surrounding area. (27)

(26) However, for the purposes of this decision, the Commission considers that the exact geographic market definition with regard to the retail supply of fixed telephony services can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement, irrespective of whether the scope of this market is considered national or limited to the Hull area.

4.2. Retail supply of fixed internet access services

(27) Fixed internet access services at the retail level consist of the provision of a fixed telecommunications link enabling customers to access the internet through a fixed telecommunications connection.

(28) KCOM is the incumbent provider of fixed internet access services to consumers and businesses based on its own copper and fibre networks in the Hull area. (28) In addition, KCOM provides connectivity services to business throughout the UK.

(29) Macquarie is not active in the retail supply of fixed internet access services in the UK. However, as of August 2019, Macquarie holds a [Size and nature of Macquarie Capital’s shareholding] stake in operator Voneus Limited (“Voneus”). Voneus specialises in the provision of internet access through “fixed-wireless” networks to homes and businesses in remote rural communities that do not have access to fibre or copper-based networks.

4.2.1. Product market definition

4.2.1.1. Commission precedents

(30) In previous cases, the Commission considered, but ultimately left open, possible segmentations within the supply of retail fixed internet access services according to (i) product type, distinguishing between narrowband, broadband and dedicated access and (ii) distribution mode, distinguishing between xDSL, fibre, cable (fixed- only) and internet provided through the mobile network infrastructure (fixed- wireless). (29) At the same time, the Commission noted that the retail market for fixed internet access services should not be segmented according to download speed. (30)

(31) The Commission also considered distinguishing between residential and small business customers, on the one hand, and larger business customers and public authorities, on the other hand, but ultimately left the question open. (31)

4.2.1.2. The Notifying Party’s view

(32) The Notifying Party argues that fixed-wireless services are not able to compete with fixed-only services and thus these two technologies belong to separate product markets. Consequently, there would be no overlap between KCOM’s fibre and copper-based and Voneus’ fixed-wireless offering. (32)

(33) However, the Notifying Party considers that the exact scope of the relevant product market can be left open, as no competition concerns arise on any possible basis. Even if these two technologies were considered as part of the same product and geographic (national) market, the Notifying Party submits that the Parties’ combined market share and the increment resulting from the Transaction would be marginal. (33)

4.2.1.3. The Commission’s assessment

(34) Responses to the market investigation provided mixed views as to whether the relevant product market should include fixed-wireless internet access or should be limited to fixed-only internet access. Several respondents explained that it ultimately depends on whether the two technologies can deliver the same level of service, which may vary from location to location. (34)

(35) In this respect, the Commission notes that Ofcom, in its most recent market review, concluded “[fixed wireless access] services are not close substitutes to fixed-line broadband” and therefore do not belong to the same product market. (35)

(36) The majority of respondents to the market investigation agreed with a segmentation between residential customers (including small business customers) and large business customers. (36)

(37) In any event, for the purpose of this decision, the Commission considers that the exact product market definition in relation of the retail supply of fixed internet access services can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement under any plausible product market definition.

4.2.2. Geographic market definition

4.2.2.1. Commission precedents

(38) In previous decisions, the Commission concluded that the retail market for the provision of fixed internet services was national in scope. (37) In Liberty Global/BASE Belgium, the Commission considered whether the geographic scope of the market should be defined on a national, regional basis or by reference to the footprint of the operators’ networks, but ultimately left the question open. (38)

4.2.2.2. The Notifying Party’s view

(39) The Notifying Party submits that there is no geographic overlap between KCOM and Voneus since the former primarily provides retail fixed internet access services based on its fixed infrastructure in the Hull area, while the latter specifically targets rural communities that are not yet served by fixed-only internet services. (39)

(40) However, the Notifying Party considers that the exact scope of the relevant geographic market can be left open, as no competition concerns arise on any plausible basis. Even if these two technologies were considered as part of the same product and geographic (national) market, the Notifying Party submits that the Parties’ combined market share and the increment resulting from the Transaction would be marginal. (40)

4.2.2.3. The Commission’s assessment

(41) A large majority of respondents to the market investigation indicated that the Hull area is a separate geographic market from the rest of the UK for the retail supply of fixed internet access services, since the competitive conditions in that area significantly differ from the rest of the UK. (41)

(42) The Commission also notes that Ofcom, in its most recent market review, has defined the Hull area as a separate geographic market in relation to a number of wholesale markets confirming that competitive conditions within the area are sufficiently homogenous and appreciably different from the surrounding area. (42)

(43) However, for the purposes of this decision, the Commission considers that the exact geographic market definition with regard to the retail supply of fixed internet access services can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement irrespective of the relevant geographic market definition.

4.3. Retail supply of TV services

(44) TV distributors either limit themselves to carrying TV channels and making them available to end users, or also act as channel aggregators, which “package” TV channels into “bouquet” retail offers. The TV services supplied by TV distributors to end users consist of: (i) packages of linear TV channels (which they have either acquired or produced themselves); and (ii) content aggregated in non-linear services, such as video on demand (“VOD”), Subscription VOD (“SVOD”), Transactional VOD (“TVOD”) and Pay-Per-View (“PPV”). TV content can be delivered to end users through a number of technical platforms including terrestrial (“DTT”), cable, satellite and IPTV. (43) Over-The-Top (“OTT”) players deliver channels and content in both a linear and non-linear fashion through the use of the internet.

(45) Macquarie is active in the retail supply of TV services via its shareholding in Arqiva, which in turn holds negative joint control over Freeview, the UK’s main DTT platform. (44)

(46) KCOM is not active in the retail supply of TV services. (45)

4.3.1. Product market definition

4.3.1.1. Commission precedents

(47) In previous cases, the Commission distinguished two separate markets for the retail supply of television services: (i) Free-to-Air (“FTA”) TV and (ii) pay-TV. (46) The Commission also considered whether pay-TV can be segmented further according to: (i) linear vs non-linear pay-TV services; (47) (ii) distribution technologies (e.g. cable, satellite, or terrestrial); (48) and (iii) premium vs basic pay-TV services. (49) In certain countries, due to the large penetration of pay-TV services and the fact that such services also carry the main FTA channels, the Commission has identified two separate product markets for: (i) basic pay-TV services (including FTA services) and (ii) premium pay-TV services. In previous cases, the Commission has left open the market definition with regard to each of these potential sub-segments. (50)

4.3.1.2. The Notifying Party’s view

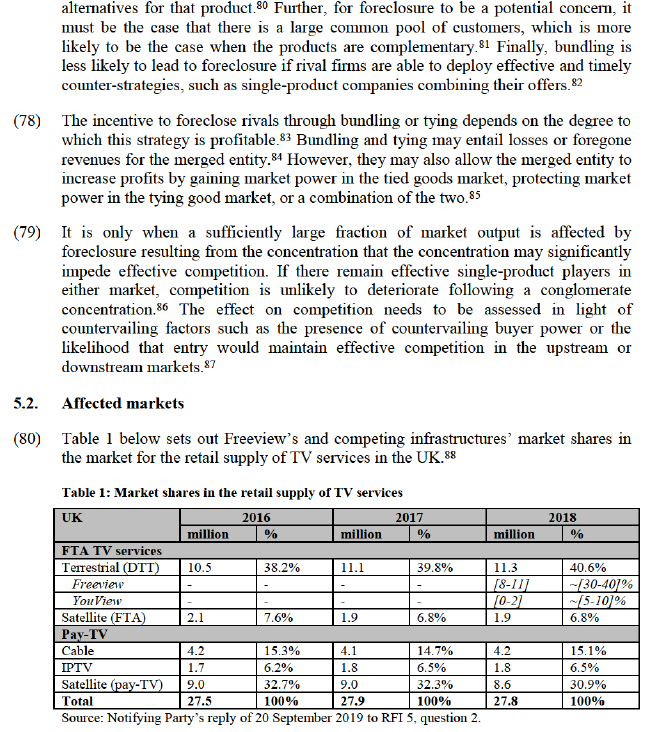

(48) The Notifying Party argues that neither KCOM nor Arqiva are active in the market for the retail provision of TV services. According to the Notifying Party, Arqiva’s role in the sector is limited to the provision of backbone infrastructure services for the broadband and transmission of TV content over the DTT platform.51 The Notifying Party submits that even within the Freeview joint venture, Arqiva’s role is that of an infrastructure provider. (52)

(49) Moreover, the Notifying Party states that there are no material vertical links between Macquarie and KCOM as neither one is engaged in activities upstream or downstream of a market in which the other is active. (53)

(50) Based on the above, the Notifying Party submits that the relevant market definition can be left open, as, regardless of the market definition adopted, the Transaction does not raise competitive concerns. (54)

4.3.1.3. The Commission’s assessment

(51) The market investigation was inconclusive as to whether market segmentations considered in prior Commission decisions in relation to FTA, basic and premium pay-TV services are relevant for the UK retail TV market. Several respondents indicated that past distinctions have become increasingly blurred, mainly due to the emergence of streaming television services, which are offered both by traditional TV platforms and new players (e.g. Netflix, Amazon). (55) Likewise, the majority of respondents indicated that the distinction between linear and non-linear TV services has become blurred and that these are increasingly viewed as substitutes by consumers. (56)

(52) Regarding market segmentations based on the different distribution platforms for the provision of retail TV services (e.g., terrestrial television, cable, IPTV and satellite), the results of the market investigation indicated that those technologies are, in general, substitutable from a consumer perspective. (57)

(53) In any event, for the purpose of this decision, the exact product market definition in relation to the retail supply of TV services can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement under any plausible product market definition.

4.3.2. Geographic market definition

4.3.2.1. Commission precedents

(54) The Commission has previously considered that the market for the retail provision of TV services is either national, or limited to the geographic coverage of a supplier’s cable network. (58)

4.3.2.2. The Notifying Party’s view

(55) The Notifying Party submits that, for the assessment of the Transaction, the precise geographic market definition relating to Arqiva’s activities is likely to be national in scope at the widest. However, the Notifying Party states that, in light of the lack of any affected market, a precise market definition is not required with respect to each of Arqiva’s activities. (59)

4.3.2.3. The Commission’s assessment

(56) The results of the market investigation are consistent with the Commission’s previous findings that the market is either national, or limited to the geographic coverage of a supplier’s cable network. (60)

(57) In any event, for the purpose of this decision, the exact geographic market definition in relation of the retail supply of TV services can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement under any plausible geographic market definition.

4.4. Retail supply of multiple play services

(58) The term “multiple play” relates to offers comprising two or more of the following services provided to retail consumers: fixed telephony, fixed internet access, TV and mobile telecommunications services. Multiple play comprising two, three or four of these services is referred to as dual play (“2P”), triple play (“3P”) and quadruple play (“4P”) respectively.

(59) Three of the four telecommunications services referenced in paragraph (58) above are fixed services, provided over a fixed network such as cable, copper or fibre infrastructure, namely fixed telephony, fixed internet access and TV services. Multiple play comprising any combination of two or more of these fixed services without a mobile component is referred to as “fixed multiple play”.

(60) As explained above, Macquarie, via Arqiva, exercises negative joint control over Freeview, the UK’s main DTT platform, while KCOM is active in the supply of retail fixed telephony and fixed internet access services to consumers in the Hull area. (61)

(61) Therefore, the Transaction could potentially give the Parties the possibility to offer a 3P fixed bundle consisting of fixed telephony, fixed internet access and TV services.

4.4.1. Product market definition

4.4.1.1. Commission precedents

(62) In previous decisions (62), the Commission took into consideration, but ultimately left open, the question as to whether there exists a market for multiple play bundles that is separate from the markets for each of the components of the bundles. In its previous analysis of this market (63), the Commission examined the factors associated to the raise in popularity of multiple play offers. In particular, customers choose multiple play bundles mainly because of the lower price, additional benefits and convenience of having one supplier/point of contact. From the supply-side, operators offer bundled services as a tool to increase customer loyalty and reduce customer churn.

4.4.1.2. The Notifying Party’s view

(63) The Notifying Party considers that there is unlikely to be a separate retail market for the provision of multiple play services due to potential demand-side substitutability between multi-play offerings and their separate component services. (64)

4.4.1.3. The Commission’s assessment

(64) The results of the market investigation on the possible existence of a separate market for the retail provision of multiple play services was inconclusive. (65) A number of respondents have highlighted the increasing penetration of bundled offers in the UK and the competitive strength that such bundles have in attracting consumers and in providing them with discounted mobile services offers. It was noted, at the same time, that the transition to this new business model is by no means completed and that consumers still have and exercise the option to buy unbundled services. (66)

As a result, the market investigation does not allow establishing with the required degree of certainty the existence of a separate market for multiple play bundles in the UK and which combinations of services would be included in such market, if it were to exist.

(66) In any event, for the purposes of this decision, the exact product market definition with regard to the retail supply of multiple play services can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement under any plausible product market definition.

4.4.2. Geographic market definition

4.4.2.1. Commission precedents

(67) In previous decisions, the Commission considered that the geographic scope of any possible retail market for multiple play services would be national since the components of the multiple play offers are offered individually at national level and the bundling of the services would not change the geographic scope of the components. It nevertheless left the exact geographic delineation of the possible multiple play market open. (67) However, in a recent decision, the Commission noted that bundles display their competitive effects on a national basis. (68)

4.4.2.2. The Notifying Party’s view

(68) The Notifying Party has not offered any views on the geographic scope of a possible market for the retail provision of multiple play services.

4.4.2.3. The Commission’s assessment

(69) As explained above, the majority of respondents to the market investigation consider that the market for the provision of retail TV services is either national, or limited to the geographic coverage of a supplier’s cable network (69), and that the markets for retail fixed internet access and retail fixed telephony services is limited to the Hull area. (70)

(70) The exact geographic market definition with regard to the retail supply of multiple play services can be left open for the purpose of this decision, as the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement under any plausible geographic market definition.

5. COMPETITIVE ASSESSMENT

(71) Macquarie will be active in both the retail supply of TV services (via its stake in Arqiva, which jointly controls Freeview) and the retail supply of fixed telephony and fixed internet access services in the Hull area (via KCOM):

(a) Freeview is the UK’s main DTT platform. It is a joint venture owned and operated by five shareholders, namely Arqiva, which provides the transmission services and infrastructure, and the broadcasters Channel 4, ITV, BBC and Sky, each of which has a 20% shareholding. Arqiva exercises a negative joint control over Freeview; (71)

(b) KCOM provides fixed internet access and fixed telephony services to about […] customers in the Hull area.

(72) End customers can procure fixed telephony, fixed internet access and TV services from the same provider. Freeview’s TV services can therefore be considered as complementary or at least closely related to KCOM’s fixed internet access and fixed telephony services within the meaning of paragraph 91 of the Non-Horizontal Merger Guidelines. Accordingly, the Commission will examine whether the Transaction may give rise to conglomerate effects in relation to Freeview’s TV services and KCOM’s fixed telephony and fixed internet access services. (72)

5.1. Legal framework

(73) According to the Non-Horizontal Merger Guidelines, in most circumstances, conglomerate mergers do not lead to competition problems. (73)

(74) However, foreclosure effects may arise when the combination of products in related markets confer on the economic entity resulting from the Transaction (the “merged entity”) the ability and incentive to leverage a strong market position from one market to another closely related market by means of tying or bundling or other exclusionary practices. The Non-Horizontal Merger Guidelines distinguish between bundling, which usually refers to the way products are offered and priced by the merged entity (74) and tying, usually referring to situations where customers that purchase one good (the tying good) are required to also purchase another good from the producer (the tied good).

(75) Tying and bundling as such are common practices that often have no anticompetitive consequences. Nevertheless, in certain circumstances, these practices may lead to a reduction in actual or potential rivals’ ability or incentive to compete. Foreclosure may also take more subtle forms, such as the degradation of the quality of the standalone product. (75) This may reduce the competitive pressure on the merged entity allowing it to increase prices. (76)

(76) In assessing the likelihood of such a scenario, the Commission examines, first, whether the merged firm would have the ability to foreclose its rivals (77), second, whether it would have the economic incentive to do so (78) and, third, whether a foreclosure strategy would have a significant detrimental effect on competition, thus causing harm to consumers. (79) In practice, these factors are often examined together as they are closely intertwined.

(77) In order to be able to foreclose competitors, the merged entity must have a significant degree of market power, which does not necessarily amount to dominance, in one of the markets concerned. The effects of bundling or tying can only be expected to be substantial when at least one of the merging parties’ products is viewed by many customers as particularly important and there are few relevant

(81) Based on this data, Freeview had a market share of approximately [30-40]% in the retail supply of TV services and approximately [70-80]% in FTA TV services in 2018.89

(82) The Parties were not able to provide detailed market share estimates as regards KCOM’s activities in the retail supply of fixed telephony and fixed internet access services. KCOM is the incumbent operator and owner of the only universal fixed network in the Hull area. In its most recent market review of the wholesale local access and wholesale broadband access markets,90 Ofcom concluded that KCOM holds significant market power (“SMP”) in both markets in the Hull Area. As both of these wholesale markets underpin the provision of retail telecommunication services, Ofcom also considered the impact on the retail supply of fixed telephony and fixed internet access services within the Hull Area. Ofcom found that, while other telecommunications providers have started investing in fibre infrastructure in the Hull area, notably Cityfibre and MS3, KCOM holds a near 100% share in the Hull area. (91), (92) As a result of these SMP findings, KCOM is subject to a number of regulatory requirements including general access obligations, non-discrimination and cost/pricing obligations, and transparency and reporting requirements.

(83) Nationwide, KCOM’s market share was below 1% both for the retail supply of fixed telephony services and fixed internet access services in 2016, 2017 and 2018. (93)

(84) In light of Freeview’s market share of over 30% in the market for the retail supply of TV services in the UK and KCOM’s strong position in the Hull area, the Transaction may have a significant impact within the meaning of Section 6.4 of the Form CO in relation to the retail supply of TV services and the retail supply of fixed telephony and fixed internet access services, which will be examined in section 5.3 below.

5.3. Conglomerate effects analysis

(85) Freeview’s TV offering is complementary to the fixed telephony and fixed internet access services supplied by KCOM, because end customers can procure fixed telephony, fixed internet access and TV services from one and the same provider. The Commission therefore examined whether the Transaction could give rise to conglomerate non-coordinated effects consisting of the potential foreclosure of fixed telephony and fixed internet access services that compete with KCOM, and/or the potential foreclosure of suppliers of TV services that compete with Freeview, as a result of a bundling or tying strategy by the merged entity.

5.3.1. The Notifying Party’s view

(86) The Notifying Party considers that there can be no plausible competition concern related to the hypothetical bundling of Freeview’s TV offering with KCOM’s retail fixed telephony and fixed internet access services.

(87) The Notifying Party recalls that Freeview is a not-for-profit, public broadcaster-led DTT service that is offered free of charge across the entire UK. Since the completion of the switchover from analogue to digital television, FTA TV channels in the UK have primarily been provided to consumers in the UK through two platforms: (i) Freeview, as replacement for the analogue network, and (ii) Freesat, delivered by satellite. (94)

(88) As the main provider of DTT services in the UK, Freeview transmits 15 high- definition channels and over 70 standard FTA channels on a subscription-free basis, available via a Freeview-enabled television or set-top box. There is no direct contractual relationship between Freeview and the end users of its platform since it can be accessed automatically, free of charge, by anyone with the necessary equipment. Freeview does not itself manufacture or sell the equipment needed to access the platform. The same considerations apply to Freeview Play, which brings together Freeview’s linear DTT offering with non-linear, on-demand elements, which is also available free of charge. (95), (96)

(89) The Notifying Party considers that the merged entity would not have the ability to bundle Freeview’s and KCOM’s services or to implement any form of foreclosure strategy.

(90) Firstly, Arqiva only exercises negative joint control over Freeview. As a result, although it can block Freeview’s strategic decisions, it cannot positively influence its commercial conduct. In the present case, the public broadcaster shareholders of Freeview are unlikely to agree to any kind of foreclosure strategy because (i) they are incentivised to ensure the widest possible distribution of their FTA TV channels, (ii) they would not benefit from KCOM’s potential gains resulting from such a strategy, and (iii) they would breach their statutory and regulatory obligations (see paragraph (91) below). (97)

(91) Secondly, Freeview’s public service nature is reflected in Freeview’s shareholder agreement and the various statutory and regulatory obligations that apply to its public broadcaster shareholders (i.e. Channel 4, ITV, BBC) under the UK’s Communications Act 2003. These rules include a “must-offer” obligation to ensure that public broadcasters offer high quality programming, free of charge, to viewers across the UK. (98)

(92) In addition, the Notifying Party considers that the merged entity would not have the incentive to bundle the services or to implement any form of foreclosure strategy as such conduct would be implausible from a commercial and practical perspective. Given that Freeview is already available free of charge, there would be no incentive to include Freeview in a bundled offer as it would not offer the customer anything more than that already freely available via their TV aerial. (99)

5.3.2. The Commission’s assessment

(93) The Commission considers that the merged entity will not have the ability and incentive to foreclose non-integrated competitors by bundling or tying KCOM’s fixed telephony and fixed internet access services and Freeview’s TV offering. Even if the merged entity engaged in a strategy to foreclose rivals through bundling or tying, such strategy would not have a significant detrimental effect on competition.

5.3.2.1. Lack of ability to foreclose

(94) The merged entity would not have the ability to foreclose rivals by bundling Freeview’s TV offering with KCOM’s fixed telephony and fixed internet access services. As explained by the Notifying Party and confirmed by the market investigation, Freeview is available free of charge across the entire UK. Customers can access Freeview either via (i) a Freeview-enabled television, or (ii) a set-top box. Since 2010, all TV sets in the UK are automatically Freeview-compatible, which means that customers simply need to connect their TV to a working aerial through an outlet in the wall. According to an Ofcom research from August 2018, 95% of UK households have a DTT-compatible digital TV set and therefore do not even require a set-top box. (100) For the remaining 5% of older, analogue models, Freeview can be accessed through the one-off purchase of a set-top box. For both methods of accessing, the Freeview platform is free to access and does not require any fixed internet access connection. (101)

(95) ITV, one of Freeview’s shareholders, thus indicates that “KCOM is already able to ‘bundle’ its services with Freeview (on a non-exclusive basis) as Freeview is an open standard available to any manufacturers meeting its technical specifications. Such a decision by KCOM would not preclude any other provider from doing the same. The merger does not appear to alter KCOM’s ability to ‘bundle’ nor that of its competitors to do the same were it to go down this route.” (102) Sky, another Freeview shareholder, confirms that any KCOM competitor would have the ability to replicate a bundled offer. (103) Accordingly, there is no scope for the merged entity to implement a foreclosure strategy with regard to a product which is already available free of charge in the market.

(96) One market participant mentioned the possibility that the merged entity could offer subsidised set-top boxes. However, such conduct would not enable the merged entity to foreclose rivals. First, KCOM’s competitors would be able to replicate any (hypothetical) bundling strategy. Second, such strategy would concern only about 5% of UK households without Freeview-compatible TV. Third, for other customers, a potential bundling strategy would require the inclusion of additional channels and/or content to make the bundle commercially attractive. This is illustrated by existing bundled TV and telecommunications offerings of a number of KCOM’s competitors (e.g. BT, TalkTalk, Plusnet). These competitors, while also including the basic Freeview TV offer in their package, offer differentiated pay-TV services with additional channels and/or content not otherwise available on Freeview. (104) However, KCOM will not gain any competitive advantage through the Transaction with respect to the additional TV content, which is the decisive factor in developing a bundled TV and telecommunications product.

(97) Furthermore, the merged entity would not have the ability to change the current nature of Freeview’s FTA TV offering (e.g., by making KCOM Freeview’s exclusive distributor in the Hull area) for the following reasons.

(98) Firstly, a foreclosure strategy would not be in line with Freeview’s role in the UK as replacement of the prior FTA TV analogue offering that it was designed to replace. (105) As the Notifying Party explains, Ofcom has specific responsibilities for the regulation of DTT under the Communications Act 2003 that go beyond its responsibilities for other television platforms, including a requirement to promote competition in the relevant markets. (106)

(99) This is also reflected in Freeview’s shareholder agreement which states, among other things, that Freeview will [Extract of Freeview shareholder agreement]. (107)

(100) Secondly, Arqiva only exercises negative joint control over Freeview and does not have the ability to positively steer the company’s strategic direction. Arqiva could not, therefore, cause Freeview to marginalise any competitor of KCOM without first obtaining unanimous consent of all of its public (FTA TV) broadcaster shareholders (i.e. Channel 4, ITV, BBC) as well as Sky. (108)

(101) The public broadcaster shareholders are not likely to agree to any kind of foreclosure strategy. As pointed out by the Notifying Party, FTA TV broadcasters are generally incentivised to ensure the widest possible distribution of their channels as they are financed by advertising revenues, public funds and licence fees. (109) Furthermore, Freeview's other shareholders would not benefit from a foreclosure strategy aimed at favouring KCOM as they have no structural relationship with the latter. Finally, the public broadcasters would breach their statutory and regulatory obligations (see paragraph (102) below).

(102) Thirdly, Freeview’s public broadcaster shareholders are subject to a “must-offer” obligation, which requires them to allow their digital channels “to be broadcast or distributed by means of every appropriate network” and to ensure that they are “available for reception, by means of appropriate networks, by as many members of its intended audience as practicable”. (110) Applicable rules also prohibit imposing any charge to receive the relevant channels.

(103) In addition, UK telecommunications network operators are under a “must-carry” obligation to carry the public broadcasters on their network. It would therefore be unlawful to prevent them from doing so. (111)

(104) Therefore, in light of (i) Freeview’s FTA TV offering, (ii) the negative nature of Arqiva's joint control over Freeview and (iii) the specific obligations applying to Freeview as well as its public broadcaster shareholders, the merged entity would not have the ability to engage in an exclusionary bundling strategy.

(105) The Commission also notes that the merged entity would not have a sufficient degree of market power to leverage its position in the supply of fixed telephony and fixed internet access services to foreclose competitors active in the supply of retail TV services. KCOM is only active in the Hull area with regard to the provision of retail fixed telephony and fixed internet access services to end customers. Therefore, any potential bundling strategy would be confined to a territory of about [100 000- 200 000] customers. However, all of the Parties’ competitors active in the supply of retail TV services, notably Freesat (112), the main alternative provider of FTA TV services, are active nationwide. (113) Irrespective of whether the Hull area is a distinct market, these competitors have revenue streams from their activities in the rest of the UK and are hence not dependent on their revenues from the Hull area.

5.3.2.2. Lack of incentive to foreclose

(106) Irrespective of the merged entity’s ability to foreclose competitors, the Commission concludes that the merged entity would not have the incentive to bundle Freeview’s TV offering with KCOM’s fixed telephony and fixed internet access services.

(107) Given that Freeview is already available free of charge, there would be no commercial incentive to pursue a foreclosure strategy by including Freeview in a bundled offer as it would not provide customers anything more than services already freely available via their TV aerial. From the demand-side, there would therefore be very little (if any) premium attached to any theoretical bundle whose TV element is based solely on Freeview (or, for the same reasons, Freeview Play). Accordingly, no competing standalone provider of telecommunications services could be disadvantaged by such a bundle.

(108) Moreover, the merged entity would not have an incentive to pursue any foreclosure strategy by changing the nature of the Freeview’s FTA TV offering as this would be in breach of Freeview’s shareholder agreement and public broadcasters’ statutory and regulatory obligations (see paragraphs (97) to (104) above).

5.3.2.3. Lack of effects on competition

(109) Even if the merged entity attempted to pursue a foreclosure strategy, the Commission considers that such strategy would be unlikely to result in a significant increase of sales of the merged entity or a significant reduction of sales prospects by the merged entity’s rivals.

(110) As explained above, Freeview is available free of charge across the entire UK. The merged entity’s competitors would be able to replicate any (hypothetical) bundling strategy. In addition, the merged entity would not be able to change the current nature of Freeview’s FTA TV offering. Therefore, any potential foreclosure strategy would not be likely to have any negative effects on competition.

(111) Moreover, as noted in paragraph (105), KCOM is only active in the Hull area Therefore, even if a potential bundling strategy had negative effects on the sales prospects of competitors, these effects would be confined to a territory of about [100 000-200 000] customers and would not significantly affect competitors’ overall revenue streams.

5.3.3. Conclusion

(112) In light of the above considerations and based on the results of the market investigation, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement with respect to the relationship between the markets for the retail supply of TV services, the retail supply of fixed telephony services and the retail supply of fixed internet access services.

6. CONCLUSION

(113) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the “Merger Regulation”). With effect from 1 December 2009, the Treaty on the Functioning of the European Union (the “TFEU”) has introduced certain changes, such as the replacement of “Community” by “Union” and “common market” by “internal market”. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the “EEA Agreement”).

3 Publication in the Official Journal of the European Union No C 316, 20.9.2019, p. 9.

4 The other four shareholders are public service broadcasters Channel 4, ITV and BBC, as well as the broadcaster Sky. Form CO, paragraph 16.

5 The Hull area, as defined by the Office of communications (“Ofcom”), the UK’s communications regulator, refers to the area where KCOM operates as the incumbent and consists of the Kingston upon Hull City Council area and some parts of the East Riding of Yorkshire Council area.

6 Macquarie is subject to Article 7(2)(b) of the Merger Regulation. While the public offer to acquire KCOM has closed, Macquarie must not exercise its voting rights until the Transaction has been declared compatible with the internal market.

7 KCOM used to be listed on the main market of the London Stock Exchange. KCOM applied for the cancellation of the listing and trading of KCOM shares to take effect from shortly after the scheme becomes effective. Accordingly, KCOM has now been removed from the London Stock Exchange and will be re-registered as a private limited company.

8 Turnover calculated in accordance with Article 5 of the Merger Regulation.

9 Even if the Parties’ fixed-only (KCOM) and fixed-wireless (Macquarie, via its stake in Voneus) activities in retail fixed internet access and business connectivity services were considered as part of the same product and geographic (national) market, the Parties’ combined market share and increment resulting from the Transaction would be negligible in light of the limited scope of Voneus’ activities (i.e. amount to approximately [0-5]% in retail fixed internet access services and [0-5]% in retail business connectivity services). In colocation services, Arqiva no longer actively markets its services since June 2013 although it does provide excess data centre capacity to existing customers on an incidental basis. The only conceivable geographic overlap between KCOM’s and Arqiva’s activities would be in London, where the merged entity would hold a combined market share below [0-5]%.

10 Although Arqiva provides site sharing services to KCOM and KCOM provides fixed telephony services and business connectivity services to a number of non-customer facing business divisions of Arqiva, these services do not give rise to a meaningful vertical relationship between the Parties as they do not constitute important inputs under the meaning of paragraph 34 of the Commission’s Guidelines on the assessment of non-horizontal mergers under the Council Regulation on the control of concentrations between undertakings (“Non-Horizontal Merger Guidelines”), OJ C 265, 18.10.2008. This is because these services (i) do not represent a significant cost factor relative to the price of Parties’ respective services; (ii) are not a critical component without which the Parties’ respective services could not be effectively offered; (iii) do not represent a significant source of product differentiation for the Parties’ respective services; and (iv) the cost of switching to alternative suppliers of these inputs would not be relatively high, given the numerous alternative suppliers. Notifying Party’s reply of 4 October 2019 to RFI 6, questions 4 and 5.

11 Commission decision of 20 September 2013 in case M.6990 – Vodafone/Kabel Deutschland, paragraph 131; Commission decision of 4 February 2016 in case M.7637 – Liberty Global/Base Belgium, recital 69; and Commission decision of 3 August 2016 in case M.7978 – Vodafone/Liberty Global/Dutch JV, paragraph 21.

12 KCOM’s infrastructure in the Hull area and its national long-distance network have been designed as separate segments in order to comply with certain regulatory obligations in the Hull area. In fact, CityFibre Holdings purchased KCOM’s national network in December 2015, and [Details of relationship between KCOM and CityFibre]. Form CO, paragraph 89.

13 Commission decision of 7 September 2005 in case M.3914 – Tele2/Versatel, paragraph 10; Commission decision of 29 June 2009 in case M.5532 – Carphone Warehouse/Tiscali UK, paragraphs 35 and 39; Commission decision of 29 January 2010 in case M.5730 – Telefónica/Hansenet Telekommunikation, paragraphs 16 and 17.

14 Commission Recommendation of 11 February 2003 on relevant product and service markets within the electronic communications sector susceptible to ex ante regulation in accordance with Directive 2002/21/EC of the European Parliament and of the Council on a common regulatory framework for electronic communication networks and services (Text with EEA relevance) (notified under document number C(2003) 497), OJ L 114, 8.5.2003, p. 45–49.

15 VoIP is a technology that allows users to make voice calls using a broadband internet connection instead of a regular (or analogue) phone line.

16 Commission decision of 20 September 2013 in case M.6990 – Vodafone/Kabel Deutschland, paragraph 131.

17 Commission decision of 4 February 2016 in case M.7637 – Liberty Global/BASE Belgium, recital 69; Commission decision of 3 August 2016 in case M.7978 – Vodafone/Liberty Global/Dutch JV, paragraph 26.

18 Form CO, paragraph 151.

19 Replies to questionnaire Q1 to TV and telecommunication operators, questions 6 and 6.1. Throughout this decision, when the Commission refers to the (number of) respondents in relation to a given question of the market investigation, this excludes all respondents that have not provided an answer to that question, unless stated otherwise.

20 Replies to questionnaire Q1 to TV and telecommunication operators, questions 8 and 8.1.

21 Commission decision of 30 May 2018 in case M.7000 – Liberty Global/Ziggo, paragraph 150; Commission decision of 19 May 2015 in case M.7421 – Orange/Jazztel, recital 37; Commission decision of 3 August 2016 in case M.7978 – Vodafone/Liberty Global/ Dutch JV, paragraph 29.

22 Commission decision of 29 June 2009 in case M.5532 – Carphone Warehouse/Tiscali UK, paragraph 47; Commission decision of 7 December 2006 in case M.4442 – Carphone Warehouse Group plc/AOL UK, paragraph 19; Commission decision of 7 September 2005 in case M.3914 – Tele2/Versatel, paragraph 18.

23 Form CO, paragraph 88.

24 Form CO, paragraph 152.

25 Form CO, paragraph 152.

26 Replies to questionnaire Q1 to TV and telecommunication operators, questions 11 and 11.1.

27 Ofcom, “Wholesale Local Access and Wholesale Broadband Access Market Reviews: Review of competition in the Hull Area” (published 31 July 2018), paragraphs 3.40 and 3.107-3.110.

28 In addition, KCOM has [single digit] fixed-wireless customers in the Hull area, which it supplies on an exceptional basis to address the needs of this small number of business customers who needed help in gaining access to broadband and were on the edge of KCOM’s full fibre build plan. These customers generate annual revenues of less than EUR [<10 000], amounting to approximately [0-5]% of KCOM’s latest annual revenue. The Commission considers that, for the purpose of its assessment, such marginal activity in the retail supply of fixed-wireless internet access services can be disregarded. Form CO, paragraphs 103-107.

29 Commission decision of 29 June 2010 in case M.5532 – Carphone Warehouse/Tiscali UK, paragraphs 7- 21; Commission decision of 20 September 2013 in case M.6990 – Vodafone/Kabel Deutschland, paragraphs 192-194; Commission decision of 3 August 2016 in case M.7978 – Vodafone/Liberty Global/Dutch JV, paragraph 38.

30 Commission decision of 29 June 2010 in case M.5532 – Carphone Warehouse/Tiscali UK, paragraphs 7- 21; Commission decision of 20 September 2013 in case M.6990 – Vodafone/Kabel Deutschland, paragraphs 192-194; Commission decision of 3 August 2016 in case M.7978 – Vodafone/Liberty Global/Dutch JV, paragraph 38.

31 Commission decision of 19 May 2015 in case M.7421 – Orange/Jazztel, recital 42; Commission decision of 30 May 2018 in case M.7000 – Liberty Global/Ziggo, paragraph 165; Commission decision of 7 October 2016 in case M.8131 – Tele2 Sverige/TDC Sverige, paragraph 32.

32 Form CO, paragraphs 108 and 112.

33 Form CO, paragraph 113

34 Replies to questionnaire Q1 to TV and telecommunication operators, questions 7 and 7.1.

35 Notifying Party’s reply of 20 September 2019 to RFI 5, question 1; Ofcom, “Wholesale Local Access and Wholesale Broadband Access Market Reviews – Review of competition in the Hull Area” (published 31 July 2018), paragraph 3.33.

36 Replies to questionnaire Q1 to TV and telecommunication operators, questions 8 and 8.1.

37 Commission decision of 29 June 2010 in case M.5532 – Carphone Warehouse/Tiscali UK, paragraph 47; Commission decision of 29 January 2010 in case M.5730 – Telefónica/Hansenet Telekommunikation, paragraph 28; Commission decision of 20 September 2013 in case M.6990 – Vodafone/Kabel Deutschland, paragraph 197; Commission decision of 3 August 2016 in case M.7978 – Vodafone/Liberty Global/Dutch JV, paragraph 40; and Commission decision of 30 May 2018 in case M.7000 – Liberty Global/Ziggo, paragraph 169.

38 Commission decision of 4 February 2016 in case M.7637 – Liberty Global/BASE Belgium, recitals 62-64.

39 Form CO, paragraphs 109-112.

40 Form CO, paragraph 113.

41 Replies to questionnaire Q1 to TV and telecommunication operators, questions 11 and 11.1.

42 Ofcom, “Wholesale Local Access and Wholesale Broadband Access Market Reviews: Review of competition in the Hull Area” (published 31 July 2018), paragraphs 3.40 and 3.107-3.110.

43 IPTV is the abbreviation for Internet Protocol TV; it is a system through which television services are delivered using the internet protocol over a packet-switched network such as the internet, instead of being delivered through traditional terrestrial, satellite signal and cable television formats.

44 Arqiva also has a stake in another DTT platform, YouView, however, Arqiva is one of seven shareholders in YouView (the others being the BBC, ITV, Channel 4, Channel 5, BT and TalkTalk) [Information concerning governance and control of YouView]. Notifying Party’s reply of 4 October 2019 to RFI 6, question 8.

45 Previously, KCOM also offered IPTV services in the Hull area, but it ceased these services in April 2006. During the period 2012 to 2018, KCOM resold a TV product by YouView, but withdrew the offer [Details of KCOM’s former retail TV offering]. In light of this marginal activity, for the purpose of this decision, KCOM will not be considered active in the retail supply of TV services. Form CO, paragraphs 205-207.

46 See for instance the Commission decisions of 18 July 2007 in case M.4504 – SFR/Télé 2 France, recital 40, and of 25 June 2008 in case M.5121 – News Corp /Premiere, paragraph 20. In other cases this question has been left open (see for instance the Commission decisions of 24 February 2015 in case M.7194 – Liberty Global/Corelio/W&W/De Vijver Media, recital119-120, of 25 June 2008 in case M.5121

– News Corp/Premiere, paragraphs 15 and 21, and of 30 May 2018 in case M.7000 – Liberty Global/Ziggo, paragraph 135).

47 Commission decision of 24 February 2015 in case M.7194 – Liberty Global/Corelio/W&W/De Vijver Media, recital 124; Commission decision of 25 June 2008 in case M.5121 – News Corp/Premiere, paragraph 21; Commission decision of 30 May 2018 in case M.7000 – Liberty Global/Ziggo, paragraph 135.

48 Commission decision of 24 February 2015 in case M.7194 – Liberty Global/Corelio/W&W/De Vijver Media, recital127; Commission decision of 25 June 2008 in case M.5121 – News Corp/Premiere, paragraph 22; Commission decision of 21 December 2010 in case M.5932 – News Corp/BskyB, paragraph 105; Commission decision of 30 May 2018 in case M.7000 – Liberty Global/Ziggo, paragraph 136.

49 Commission decision of 24 February 2015 in case M.7194 – Liberty Global/Corelio/W&W/De Vijver Media, recital 119.

50 Commission decision of 15 June 2018 in case M.8861 – Comcast/Sky, paragraphs 57-59; Commission decision of 7 April 2017 in case M.8354 – Fox/Sky, paragraph 101; .

51 Form CO, paragraph 214.

52 Form CO, paragraph 219.

53 Form CO, paragraph 125.

54 Form CO, paragraph 222.

55 Replies to questionnaire Q1 to TV and telecommunication operators, questions 3 and 3.1.

56 Replies to questionnaire Q1 to TV and telecommunication operators, questions 4 and 4.1.

57 Replies to questionnaire Q1 to TV and telecommunication operators, questions 5 and 5.1.

58 Commission decision of 24 February 2015 in case M.7194 – Liberty Global/Corelio/W&W/De Vijver Media.

59 Form CO, paragraphs 96 and 223.

60 Replies to questionnaire Q1 to TV and telecommunication operators, questions 10 and 10.1.

61 KCOM is also [Details of KCOM internal planning].

62 Commission decision of 4 February 2016 in case M.7637 – Liberty Global/BASE Belgium, recital 96; Commission decision of 19 May 2015 in case M.7421 Orange/Jazztel, recitals 86 and 91; Commission decision of 20 September 2013 in case M.6990 – Vodafone/Kabel Deutschland, paragraph 261; Commission decision of 3 July 2012 in case M.6584 – Vodafone/Cable & Wireless, paragraphs 102-104; Commission decision of 16 June 2011 in case M.5900 – LGI/KBW, paragraphs 183-186; Commission decision of 25 January 2010 in case M.5734 – Liberty Global Europe/Unitymedia, paragraphs 43-48; Commission decision of 30 May 2018 in case M.7000 – Liberty Global/Ziggo, paragraph 230.

63 See, for example, Commission decision of 3 August 2016 in case M.7978 – Vodafone/Liberty Global/Dutch JV, paragraphs 93 and 102.

64 Notifying Party’s reply of 14 October 2019 to RFI 7, question 4.

65 Replies to questionnaire Q1 to TV and telecommunication operators, questions 9 and 9.1.

66 Replies to questionnaire Q1 to TV and telecommunication operators, question 9.1.

67 Commission decision of 19 May 2015 in case M.7421 – Orange/Jazztel, recitals 89-90; Commission decision of 20 September 2013 in case M.6990 – Vodafone/Kabel Deutschland, paragraphs 263-265; Commission decision of 16 June 2011 in case M.5900 – LGI/KBW, paragraphs 183-186.

68 Commission decision of 30 May 2018, in case 7000 – Liberty Global/Ziggo, paragraph 232.

69 Replies to questionnaire Q1 to TV and telecommunication operators, questions 10 and 10.1.

70 Replies to questionnaire Q1 to TV and telecommunication operators, questions 11 and 11.1.

71 More precisely, Arqiva holds a 20% shareholding in DTV Services Limited, which trades under the Freeview brand name. Arqiva considers that it exercises negative joint control over Freeview because [Information concerning governance and control of Freeview]. Form CO, paragraph 188.

72 The Commission does not carry out a separate analysis of potential vertical effects arising from the Transaction, i.e. treating retail TV services as an input in the provision of multiple play services. While it is not possible to conclude on the existence of a single multiple play services market in the UK (see section 4.4), in any case, similar considerations would apply in the context of an assessment of vertical effects as those set out in the analysis of conglomerate effects.

73 Non-Horizontal Merger Guidelines, paragraph 92.

74 Within bundling practices, the distinction is also made between pure bundling and mixed bundling. In the case of pure bundling the products are only sold jointly in fixed proportions. With mixed bundling the products are also available separately, but the sum of the stand-alone prices is higher than the bundled price.

75 Non-Horizontal Merger Guidelines, paragraph 33.

76 Non-Horizontal Merger Guidelines, paragraph 93.

77 Non-Horizontal Merger Guidelines, paragraphs 95 to 104.

78 Non-Horizontal Merger Guidelines, paragraphs 105 to 110.

79 Non-Horizontal Merger Guidelines, paragraphs 111 to 118.

80 Non-Horizontal Merger Guidelines, paragraph 99.

81 Non-Horizontal Merger Guidelines, paragraph 100.

82 Non-Horizontal Merger Guidelines, paragraph 103.

83 Non-Horizontal Merger Guidelines, paragraph 105.

84 Non-Horizontal Merger Guidelines, paragraph106.

85 Non-Horizontal Merger Guidelines, paragraph 108.

86 Non-Horizontal Merger Guidelines, paragraph 113.

87 Non-Horizontal Merger Guidelines, paragraph 114.

88 Arquiva’s estimate of approximately (8-11) million Freeviewers households is based on the « UK households by TV platform » tracker by Broadcasters Audience Research Board(« BARB »), which sets out approximate figures for the number of viewers using each if the UK’s main linear TV platforms. Competing infrastructure market shares’ and the market size are based on both BARB and Ofcom’s Communications Market Review 2018. Notifying Party’s reply of 14 October 2019 to RFI 7, question 2.

89 The Parties were not able to provide more detailed market share estimates as regards the possible segmentation between FTA TV and basic pay-TV vs. premium pay-TV as well as by linearity of the content. In any event, Freeview is a FTA TV distributor and is not active in the provision of premium pay- TV and non-linear services. Therefore, Freeview does not hold any market share in any possible premium pay-TV or non-linear services markets (Notifying Party’s reply of 20 September 2019 to RFI 5, question 3). With regard to non-linear services, while Freeview Play allows viewers to access VOD services, it only redirects viewers to broadcasters’ own VOD platforms (e.g. BBC iPlayer). Form CO, paragraph 226.

90 Ofcom, “Wholesale Local Access and Wholesale Broadband Access Market Reviews: Review of competition in the Hull Area” (published 31 July 2018).

91 Notifying Party’s reply of 20 September 2019 to RFI 5, question 1; Notifying Party’s reply of 4 October 2019 to RFI 6, question 1.

92 Nevertheless, Ofcom considered market shares in a hypothetical overall market for the retail supply of broadband services (i.e. including both fixed-wireless and fixed-broadband services). Ofcom found that Connexin, Purebroadband and Quickline would have a combined market share of “less than 10% of retail broadband consumers in the Hull Area” and that KCOM would “still have a greater than 90% share of all connections”. Notifying Party’s reply of 20 September 2019 to RFI 5, question 1.

93 Notifying Party’s reply of 20 September 2019 to RFI 5, question 2; Notifying Party’s reply of 4 October 2019 to RFI 6, question 1.

94 Form CO, paragraphs 229-230.

95 As of 2015, Freeview also offers Freeview Play. Consumers can access the service via a Freeview Play- compatible TV, using a Freeview Play recorder, or by installing the Freeview app (available free of charge) on their phone or tablet. In line with the public-service nature of Freeview, the specification for Freeview Play is entirely open source, meaning the technologies required to design and implement Freeview Play-compatible TVs and boxes are publicly available to broadcasters and manufacturers. Form CO, paragraph 231.

96 Form CO, paragraph 16.

97 Form CO, paragraph 218.

98 Form CO, paragraphs 251-252.

99 Form CO, paragraph 217.

100 Ofcom, "Communications Market Report" (published 2 August 2018), Figure 1.4.

101 Form CO, paragraph 216.

102 ITV’s reply to questionnaire Q1 to TV and telecommunication operators, question 12.1.

103 Sky’s reply to questionnaire Q1 to TV and telecommunication operators, question 14.1.

104 Notifying Party's reply of 4 October 2019 to RFI 6, question 10.

105 Form CO, paragraph 230-233.

106 Ofcom, “The Future of Free to View TV: A discussion document” (published 28 May 2014), pages 8-9. In full, the Ofcom report states: “FTV [free to view] television can be delivered by a variety of TV transmission technologies, but the cornerstone of free to view television in the UK is currently DTT. Under the Communications Act 2003, Ofcom has specific responsibilities for the regulation of DTT that go further than our responsibilities for other television platforms, reflecting the role that DTT has in making PSB [public service broadcasting] available to all. Specifically, our duties under the Act require us to secure both the optimal use of the electromagnetic spectrum, and the availability throughout the UK of a wide range of TV and radio services which (taken as a whole) are both of high quality and calculated to appeal to a variety of tastes and interests. We are also required to have due regard to the desirability of promoting the fulfilment of the purposes of PSB in the UK and promoting competition in relevant markets. And in performing our duties we are required to have regard to, in particular, the interests of consumers in respect of choice, price, quality of service and value for money.”

107 Form CO, paragraph 236.

108 Form CO, paragraph 218.

109 Form CO, paragraph 235.

110 Form CO, paragraph 251.

111 Form CO, paragraphs 253-261.

112 To be noted also that Freesat is a joint venture between two of Freeview’s public service broadcasters shareholders, BBC and ITV. Notifying Party’s reply of 4 October 2019, question 9.

113 Notifying Party’s reply of 4 October 2019 to RFI 6, question 9; Notifying Party’s reply of 14 October 2019 to RFI 7, question 5.