Commission, July 15, 2019, No M.9370

EUROPEAN COMMISSION

Judgment

TELENOR / DNA

Subject: Case M.9370 – Telenor/DNA

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 7 June 2019, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Telenor ASA (“Telenor”, Norway) acquires sole control of the whole of DNA Plc (“DNA”, Finland) within the meaning of Article 3(1)(b) of the Merger Regulation (the “Transaction”) (3). Telenor is designated hereinafter as the “Notifying Party”, while Telenor and DNA are together referred to as the “Parties”.

1. THE PARTIES

(2) Telenor is a telecommunications operator based in Norway. It provides mobile and fixed telecommunications services in Norway, Denmark and Sweden, and limited mobile telecommunications services in Finland. It also provides TV distribution services in Norway, Denmark, Finland and Sweden. Outside the EEA, Telenor provides mobile telecommunications services in Asia.

(3) DNA is a telecommunications operator based in Finland. It provides mobile and fixed telecommunications services, broadband services and TV distribution services in Finland. DNA’s telecommunications activities outside of Finland are limited. DNA is listed on the Helsinki Stock Exchange and is not directly or indirectly controlled by any persons or person. Finda Telecoms Oy, a 100% subsidiary of Finda Oy, is the largest shareholder of DNA, holding a 28.26% shareholding interest. PHP Holding Oy is the second largest shareholder, holding a 25.78% shareholding interest. The remainder of DNA’s shares are widely dispersed.

2. THE CONCENTRATION

(4) Telenor Mobile Holdings AS (a wholly owned subsidiary of Telenor) has signed two separate Share Purchase Agreements on 9 April 2019: one with Finda Telecoms Oy and Finda Oy and the other with PHP Holding Oy (together, the "SPAs"). Pursuant to the SPAs, Telenor will acquire 28.26% and 25.78% of the issued and outstanding shares in DNA from Finda Telecoms Oy and PHP Holding Oy, respectively.

(5) On 6 May 2019, the general meetings of Finda Telecoms Oy and PHP Holding Oy approved the transactions contemplated under the SPAs.

(6) Upon closing of the transactions contemplated under the SPAs, Telenor is obligated to launch a mandatory takeover bid for all remaining issued and outstanding shares in DNA in accordance with the Finnish Securities Markets Act.

(7) Following the Transaction, Telenor will own (at least) 54.04% of the issued and outstanding shares in DNA.

(8) Therefore, the Transaction consists of the acquisition of sole control by Telenor over DNA within the meaning of Article 3(1)(b) of the Merger Regulation.

3. EU DIMENSION

(9) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (4) (Telenor: EUR 11 437 million; DNA: EUR 912 million; combined: EUR 12 349 million; in 2018). Each of them has an EU-wide turnover in excess of EUR 250 million (Telenor: EUR […]; DNA: EUR […]; combined: EUR […]; in 2018), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State.

(10) The Transaction therefore has an EU dimension pursuant to Article 1(2) of the Merger Regulation.

4. RELEVANT MARKETS

4.1. Introduction

(11) The Parties’ activities overlap in the areas of: (i) retail supply of TV services, (ii) wholesale acquisition of TV channels and (iii) machine-to-machine (“M2M”) mobile subscriptions to business customers only in Finland giving rise to a number of affected markets, as described in Section 5.2., paragraph 86 below.

(12) In addition, the Parties are present in the areas of: (i) wholesale international roaming services and (ii) wholesale call termination services on fixed and mobile networks. Those services are vertically linked to the (i) retail supply of mobile telecommunications services and (ii) retail supply of fixed telephony services. This gives rise to a number of vertically affected markets, as described in Section 5.2., paragraph 87 below.

4.2. Market for retail supply of TV services

(13) In the market for the retail supply of TV services, TV distributors provide end users with TV services, which typically consist of: (i) linear TV channels or packages of linear TV channels (the latter either acquired or produced themselves); and (ii) content aggregated in non-linear services, such as Subscription Video on Demand (“SVOD”), Transactional VOD (“TVOD”) and Advertising VOD (“AVOD”). Linear and non-linear TV services can be delivered to end users through several platforms including cable, satellite (“direct-to-home” or “DTH”), mobile, terrestrial (“digital terrestrial television” or “DTT”), IPTV and as an Over-the-Top (“OTT”) service. Finally, TV services can be delivered to end users living in single dwelling units (“SDUs”) or multi dwelling units (“MDUs”).

(14) DNA offers retail TV services in Finland to end consumers via cable, mobile, IPTV, OTT and DTT. Telenor is active in the retail supply of TV services in Finland, via its subsidiary Canal Digital, offering retail TV services to end customers via DTH only.

4.2.1. Product market definition

(15) The Notifying Party submits that the Transaction should be assessed on the basis of an overall market for the retail supply of TV services in Finland. In particular, the Notifying Party considers that it is not appropriate to sub-divide the market for the retail supply of TV services along the lines assessed in previous investigations, including on the basis of distribution technology/platform, nature of TV services (i.e. pay TV and free-to-air (“FTA”) TV, linear and non-linear services), or by type of dwelling unit. The main reasons put forward by the Notifying Party are as follows: (i) all technical forms of TV distribution are substitutable at least to some extent and all customers have access to more than one alternative form of TV distribution, (ii) from the viewpoint of end users there is substitutability among distributors of FTA channels, which traditionally represent over 90% of total viewing in Finland, and pay TV channels, (iii) linear and non-linear services have converged to the extent that it has become increasingly difficult to distinguish between them, and (iv) a segmentation by type of dwelling unit would not be appropriate because there are no significant differences of price, content or technological distribution platforms between MDUs and SDUs.

(16) The Notifying Party concludes that the product market definition can be left open as the Transaction does not give rise to competition concerns on the basis of any plausible market definition of the relevant product market.

(17) In the past, the Commission considered the retail provision of free-to-air (FTA) TV and pay TV services as separate markets, but ultimately left open the product market definition. (5) The Commission also considered whether the provision of pay retail TV can be segmented further according to: (i) linear vs non-linear pay TV services (6); and

(ii) according to distribution technologies (e.g. cable, OTT, satellite, IPTV or terrestrial) (7); and (iii) basic pay TV services vs premium pay TV services (8) but has left open the market definition with regard to each of these potential sub-segments. The Commission has also previously considered whether retail TV services to SDUs and MDUs form part of the same product market but ultimately left the exact product market definition open. (9)

(18) Most of the respondents to the market investigation indicated that the market for retail supply of TV services in Finland should not be segmented into (i) linear and non-linear services (10) or by (ii) distribution technologies. (11)

(19) With regard to a potential segmentation in FTA and pay TV services, the respondents to the market investigation provided mixed responses. While some respondents pointed to the different dynamics of these segments, most respondents did not consider FTA and pay TV services to be different markets, because both FTA and pay TV channels are consumed in bundles and have the same viewer base. (12)

(20) As for a potential segmentation between basic pay TV services and premium pay TV services, the respondents to the market investigation provided mixed responses as well. Some respondents pointed to the fact that a clear distinction between the two would not be possible, while others stated that there is no basic pay TV per se in Finland and that the distinction is rather between FTA and premium pay TV. (13)

(21) Regarding the possible segmentation by type of dwelling unit, the result of the market investigation is mixed as well. Most of the respondents did not consider this segmentation appropriate, while some pointed to the fact that the differentiation might be relevant for FTA channels, while for pay TV, each household enters into individual contracts, regardless of the type of dwelling unit. (14)

(22) The Commission considers that for the purposes of this Decision the question whether (i) FTA services and pay TV services, (ii) linear pay TV services and non- linear pay TV services, (iii) different distribution technologies, (iv) basic pay TV services and premium pay TV services, and (v) SDUs and MDUs belong to the same product market can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market under any of the possible market definitions above.

4.2.2. Geographic market definition

(23) The Notifying Party submits that, in line with the Commission’s previous decisions (15), the market for retail supply of TV services is national in scope, based on the following reasons: (i) suppliers of retail TV services compete on a national basis for end-customers; (ii) the Parties offer their Finnish TV channels for end-customers in Finland only; (iii) regulatory regimes for the retail supply of TV services are national; and (iv) many TV offerings are influenced by national cultural factors and domestic end-customer preferences.

(24) The Notifying Party concludes that the geographic market definition can be left open in this case as the Transaction does not give rise to competition concerns on the basis of any plausible geographic market definition.

(25) In previous decisions, the Commission has considered the geographic scope of the market as national, primarily since suppliers of retail TV services compete on a national basis, or limited to the coverage area of each operator. (16) The market investigation in this case has not provided any indication that the Commission should depart from its previous findings.

(26) Therefore, for the purposes of this Decision, the Commission considers that the relevant market for the retail supply of TV services is national in scope.

4.3. Market for wholesale acquisition of TV channels

(27) In the market for wholesale acquisition of TV channels, TV distributors acquire the right to distribute TV channels from TV broadcasters. Some TV distributors are vertically integrated and distribute their own channels directly to the end-customers. Most broadcasters provide the same or a similar set of TV channels to several TV distributors.

4.3.1. Product market definition

(28) The Notifying Party submits that the Transaction should be assessed on the basis of an overall market for the wholesale acquisition of TV channels. The Notifying Party considers that a further segmentation of the market into FTA and pay TV channels, by genre (e.g. films, sports, news, youth, etc.), or by the type of infrastructure used is not appropriate.

(29) With regard to a possible segmentation into FTA and pay TV channels, the Notifying Party submits as one of its arguments against a distinction into different markets that TV distributors’ negotiations with broadcasters supplying TV channels usually cover all their channels at the same time. With regard to a possible segmentation by genre, the Notifying Party points out that any lack of substitutability between e.g. news and sports channels is compensated by the versatility of the main FTA channels, which account for a substantial portion of total viewing time and which include content from all genres in the same channels and due to the development of OTT services and TV streaming, viewers are able to look for content of a certain genre on the generalist channels, thus increasing the substitutability with the more specialised channels. Finally, with regard to a possible segmentation by infrastructure used, the Notifying Party points out that in Finland, a wholesale purchaser of TV channels broadcasting on several distribution platforms/technologies does not negotiate different contracts for each type of infrastructure, but rather as a whole package.

(30) The Notifying Party concludes that the product market definition can be left open in this case as the Transaction does not give rise to competition concerns on the basis of any plausible product market definition.

(31) In previous decisions, the Commission considered whether the market for wholesale acquisition of TV channels can be segmented further according to: (i) FTA channels and pay TV channels, (ii) genres; (iii) by the type of infrastructure used, or (iv) linear TV channels and non-linear services, but has left open the market definition with regard to each of these potential sub-segments. (17)

(32) Most competitors and most TV broadcasters who participated in the market investigation did not consider that the market for wholesale acquisition of TV channels should be segmented further. (18) Some competitors however considered that the wholesale market should be segmented between FTA channels and premium pay TV channels.(19) Moreover, while most TV broadcasters considered that OTT is increasingly becoming an alternative to other distribution technologies, the Finnish public broadcaster Yle submitted that distribution platforms are not substitutive to each other, because all of them are needed in order to reach all audiences. (20)

(33) The Commission considers that for the purposes of this Decision the exact product market definition can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market under any possible market definition.

4.3.2.Geographic market definition

(34) The Notifying Party submits that the geographic scope of the market is national, because the Finnish-speaking region is limited to Finland itself and most distributors cover the Finnish territory. However, it submits that the market definition can be left open in the present case.

(35) The Commission has previously considered the market for the wholesale acquisition of TV channels to cover either a Member State (21), a linguistic region distributed over several states (22), or a sub-national region defined by the footprint of a certain distribution network (23). In certain cases, all three options were envisaged, and the market definition was left open. (24)

(36) The market investigation indicated that the market could be national and regional (i.e. Nordic). (25) Finnish competitors indicated that they acquire licensing rights to distribute TV channels and/or audiovisual content on a national level, while international competitors acquire licensing rights mainly on a national, but sometimes also on a regional (Nordic) level. (26) The suppliers of TV channels (i.e. TV broadcasters) distribute their channels mainly on a national and regional (Nordic) level, but some also in the linguistic region or on EEA or worldwide level. (27)

(37) The Commission considers that for the purposes of this Decision the exact geographic market definition can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market under any possible market definition.

4.4. Market for retail supply of mobile telecommunication services

(38) Mobile telecommunications services to end customers include services for national and international voice calls, SMS (including MMS and other messages), mobile internet with data services, and retail international roaming services. (28) A possible segment of the market for retail mobile telecommunications services includes machine-to-machine (“M2M”) subscriptions. These allow machines, devices, appliances, etc., to connect wirelessly to the internet via mobile networks, or other technologies, permitting the transmission and receipt of data to a central server.

4.4.1. Product market definition

(39) The Notifying Party submits that M2M subscriptions to business customers are a separate segment of the overall market for retail mobile telecommunications services, but does not take a position on the relevant product market apart from that.

(40) In previous decisions, the Commission has considered that there is an overall retail market for mobile telecommunications services constituting a separate market from retail fixed telecommunication services. (29) The Commission did not further segment the overall retail mobile market based on the type of service (voice calls, SMS, MMS, mobile Internet data services), or the type of network technology. The Commission considered possible segments of the overall retail market for mobile telecommunication services between pre-paid or post-paid services and private customers or business customers, concluding that these did not constitute separate product markets but represent rather market segments within an overall retail market. (30) The Commission also considered whether M2M subscriptions constitute a separate product market or a segment of the market for retail mobile telecommunications services, and concluded that the overall retail mobile market excludes M2M services. (31)

(41) The market investigation in this case did not provide any new elements justifying a departure from Commission's previous decisions. (32)

(42) For the purpose of this Decision, the Commission therefore concludes that M2M subscriptions constitute a separate market.As for the market for the provision of retail mobile telecommunications services, the exact product market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any possible market definition.

4.4.2. Geographic market definition

(43) The Notifying Party does not take a position on the geographic scope of the market for retail mobile telecommunications services. As for the market for M2M subscriptions, the Notifying Party submits that it is national in scope.

(44) In previous decisions, the Commission has found that the markets for mobile telecommunication services to end consumers are national in scope. (33) It has not addressed the geographic scope of M2M subscripitons in previous decisions.

(45) Most respondents to the market investigation did not take a view on the geographic market definition of this market. However, one respondent submitted that the market for mobile telecommunications services as well as the market for M2M subscriptions might be pan-Nordic in scope, i.e. including Finland, Norway, Denmark and Sweden. This is because business customers who are active at a pan-Nordic level seek M2M services at the same level. (34)

(46) For the purpose of this Decision, the Commission concludes that the the market for the provision of retail mobile telecommunications services is national in scope. As for the market for M2M subscriptions, the exact geographic market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any possible market definition.

4.5. Market for retail supply of fixed telephony services

(47) On the market for retail supply of fixed telephony services, operators provide fixed voice services to end customers. In line with previous Commission decisions, fixed voice services include the provision of connection services or access at a fixed location or address to the public telephone network for the purpose of making and receiving calls and related services.

4.5.1. Product market definition

(48) The Notifying Party does not take a position on the relevant product market.

(49) In previous decisions (35), the Commission considered whether a distinction between local/national and international calls as well as between residential and non- residential customers should be drawn on the basis of the distinctions in the Commission Recommendation 2003/311/EC but ultimately left the exact product market definition open.

(50) More recently, the Commission also considered that managed Voice over Internet Protocol ("VoIP") services and traditional telephony are interchangeable and therefore belong to the same market. (36) In Liberty Global/Ziggo (37) the Commission left the exact market definition open (and in particular whether there is a separate market for residential and non-residential customers, as well as whether VoIP and traditional fixed telephony belong to the same market) while in Liberty Global/BASE (38) and in Vodafone/Liberty Global/Dutch JV (39) the Commission considered that an overall retail market for fixed telephony services exists.

(51) The market investigation in this case did not provide any new elements justifying a departure from Commission's previous decisions. (40)

(52) For the purpose of this Decision, the exact product market definition can be left open as the Transaction does not give rise to serious doubts as to its compatibility with the internal market under any possible market definition.

4.5.2. Geographic market definition

(53) The Notifying Party does not take a position on the relevant geographic market.

(54) In its previous decisions, the Commission concluded that the retail market for the provision of fixed telephony services was national in scope. (41)

(55) Most respondents to the market investigation did not take a view on the geographic scope of this market. However, one respondent considered the market to be narrower than national, while another submitted that business customers that operate in more than one Nordic country require pan-Nordic mobile and fixed telecommunication services. (42)

(56) For the purpose of this Decision, the exact geographic market definition in relation to the provision of retail supply of fixed telephony services can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any possible market definition.

4.6. Market for wholesale international roaming services

(57) International roaming services allow mobile telecommunications subscribers to make and receive calls and use other services such as SMS and data services when abroad. To be able to offer this service to their customers, MNOs conclude wholesale agreements with other MNOs providing access and capacity on mobile networks in their respective countries. Demand for wholesale international roaming services comes from MNOs who wish to provide their own customers with mobile services outside their own network. At a downstream level, retail customers demand access to mobile telecommunications services when abroad.

4.6.1. Product market definition

(58) The Notifying Party submits, in accordance with Commission practice, that there is a market for the provision of wholesale international roaming services.

(59) In previous decisions, the Commission has considered a separate product market for wholesale international roaming services comprising both terminating calls and originating calls. (43)

(60) The market investigation in this case did not provide any new elements justifying a departure from Commission's previous decisions. (44)

(61) Therefore, the Commission retains its previous product market definition of a wholesale market for international roaming services comprising both terminating and originating calls.

4.6.2. Geographic market definition

(62) The Notifying Party submits, in accordance with Commission practice, that the market for the provision of wholesale international roaming services is national scope.

(63) In previous decisions, the Commission found that the wholesale market for international roaming services is national in scope, given that wholesale international agreements can be concluded only with companies which have an operating licence in the relevant country and the licences to provide mobile services are restricted to a national territory. (45)

(64) Most respondents to the market investigation did not take a view on the geographic market definition. One respondent however considered that the market might be pan- Nordic, because the demand for such services from both consumers and business customers is pan-Nordic. (46)

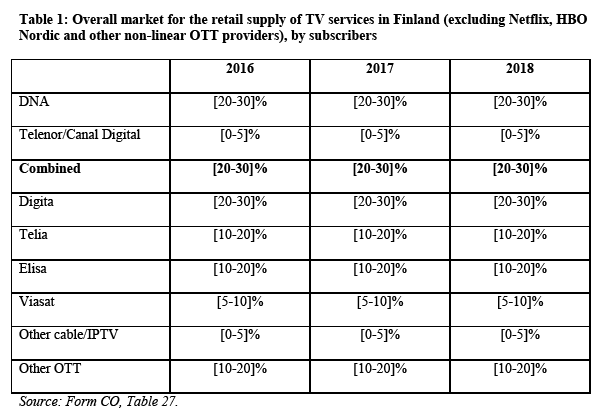

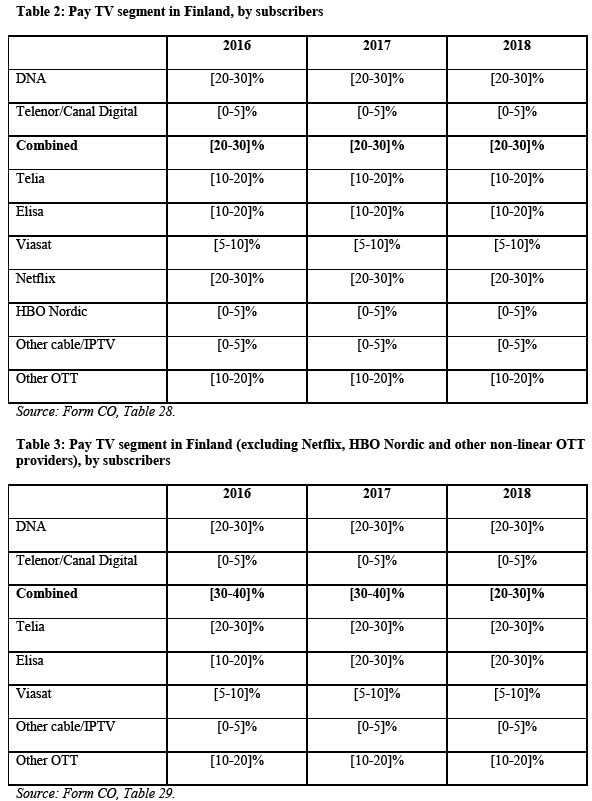

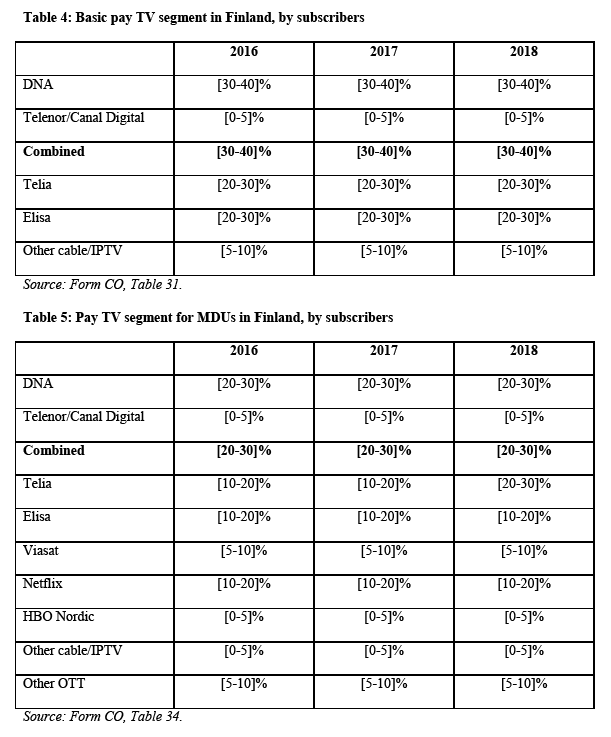

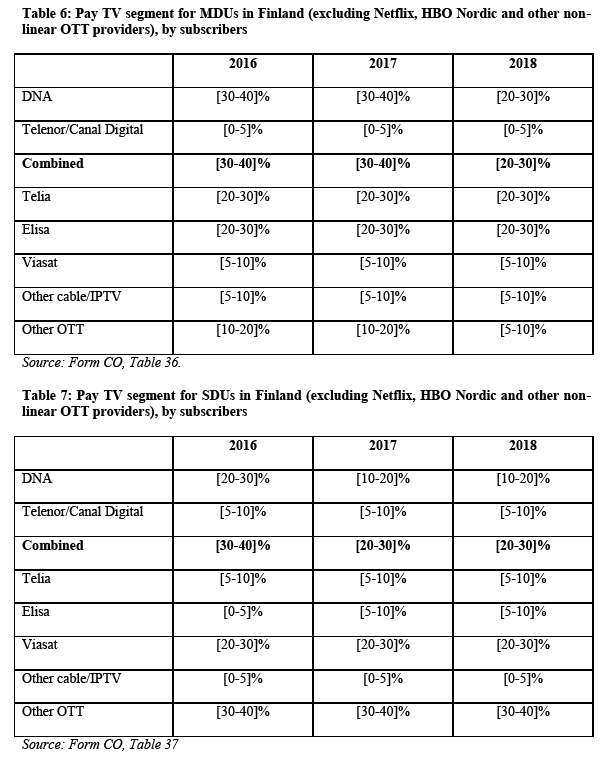

(65) The Commission concludes that the markets for wholesale international roaming services are national.

4.7. Market for wholesale mobile call termination services

(66) Call termination is the service provided by network operator B to network operator A whereby a call originating on operator A's network is delivered to a user on operator B's network. Call termination therefore allows users of different networks to communicate with one another. Call termination is a wholesale service that the various network operators provide to one another on the basis of interconnection agreements, upstream of the provision of communication services to end customers.

4.7.1. Product market definition

(67) The Notifying Party does not take a position on the relevant product market but instead refers to the Commission’s previous decisions where it has defined the relevant market as the provision of wholesale call termination services on mobile networks.

(68) As established in previous Commission decisions (47), there is no substitute for call termination on each individual network since the operator transmitting the outgoing call can reach the intended recipient only through the operator of the network to which the recipient is connected.

(69) The market investigation in this case did not provide any new elements justifying a departure from Commission's previous decisions. (48)

(70) The Commission considers that as regards wholesale call termination services, and in line with previous decisions, termination on each individual mobile network constitutes a separate product market.

4.7.2. Geographic market definition

(71) The Notifying Party does not take a position on the relevant geographic market but instead refers to the Commission’s previous decisions (49) where it defined the relevant market as national.

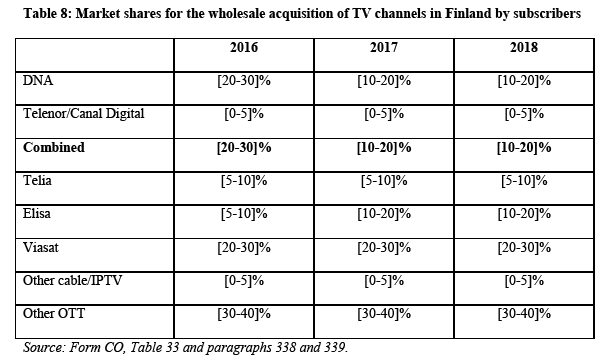

(72) The market investigation in this case did not provide any new elements justifying a departure from Commission's previous decisions. (50)

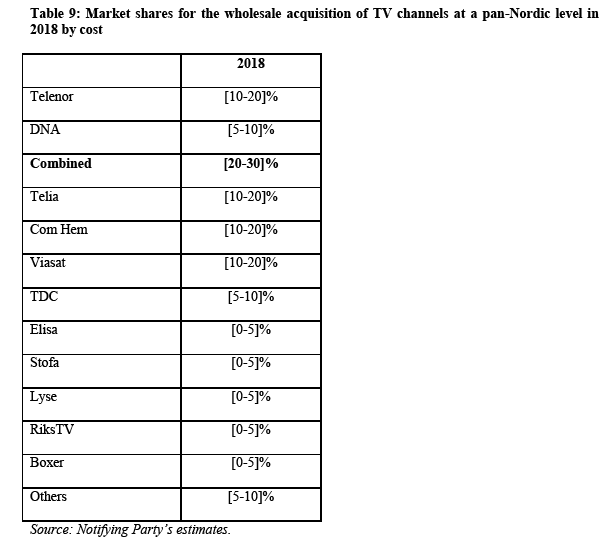

(73) The Commission concludes, in line with previous decisions, that the market for mobile call termination services is national in scope, as each wholesale market for call termination corresponds to the dimensions of the operator’s network and therefore is limited to the national territory of the operator's network. This is primarily due to regulatory barriers as the geographic scope of a network licence is, in principle, limited to areas which do not extend beyond the borders of a Member State.

4.8. Market for wholesale fixed call termination services

(74) As in the case of call termination on mobile networks, call termination on fixed networks is the service provided by network operator B to network operator A whereby a call originating on operator A's network is delivered to a user on operator B's network. Call termination therefore allows users of different networks to communicate with one another. Call termination is a wholesale service that the various network operators provide to one another on the basis of interconnection agreements, upstream of the provision of communication services to end customers.

4.8.1. Product market definition

(75) The Notifying Party does not take a position on the relevant product market but instead refers to the Commission’s previous decisions where it has defined the relevant market as the provision of wholesale fixed call termination services.

(76) As established in previous Commission decisions (51), there is no substitute for call termination on each individual network since the operator transmitting the outgoing call can reach the intended recipient only through the operator of the network to which the recipient is connected.

(77) The market investigation in this case did not provide any new elements justifying a departure from Commission's previous decisions. (52)

(78) The Commission considers that as regards wholesale call termination services, and in line with previous decisions, termination on each individual fixed network constitutes a separate product market.

4.8.2. Geographic market definition

(79) The Notifying Party does not take a position on the relevant geographic market but instead refers to the Commission’s previous decisions (53) where it defined the relevant market as national.

(80) While most respondents to the market investigation did not take a view on the geographic market definition, one respondent submitted that the market might be narrower than national in scope, since the Finnish regulator Traficom defined fixed network termination services as regional geographic markets and concluded that there are several companies having significant market power whithin their respective regional markets.. (54)

(81) The Commission concludes, in line with previous decisions, that the wholesale market for fixed call termination services is national in scope, considering that the geographic scope of each wholesale market for call termination should correspond to the dimensions of the operator’s network, which is limited to national borders due to regulatory barriers.

5. COMPETITIVE ASSESSMENT

5.1. Analytical framework

(82) Under Article 2(2) and (3) of the Merger Regulation, the Commission must assess whether a proposed concentration would significantly impede effective competition in the internal market or in a substantial part of it, in particular through the creation or strengthening of a dominant position.

(83) In this respect, a merger may entail horizontal and/or non-horizontal effects. Horizontal effects are those deriving from a concentration where the undertakings concerned are actual or potential competitors of each other in one or more of the relevant markets concerned. Non-horizontal effects are those deriving from a concentration where the undertakings concerned are active in different relevant markets.

(84) As regards non-horizontal mergers, two broad types of such mergers can be distinguished: vertical mergers and conglomerate mergers. (55) Vertical mergers involve companies operating at different levels of the supply chain. (56) Conglomerate mergers are mergers between firms that are in a relationship which is neither horizontal (as competitors in the same relevant market) nor vertical (as suppliers or customers). (57)

(85) The Commission appraises horizontal effects in accordance with the guidance set out in the relevant notice, that is to say the Horizontal Merger Guidelines. (58) Additionally, the Commission appraises non-horizontal effects in accordance with the guidance set out in the relevant notice, that is to say the Non-Horizontal Merger Guidelines. (59)

5.2. Identification of affected markets

(86) In the present case, the Transaction gives rise to horizontally affected markets in the retail supply of TV services in Finland, in the wholesale acquisition of TV channels in Finland and at pan-Nordic level, and in the supply of M2M mobile subscriptions in Finland and at a possible pan-Nordic level.

(87) The Transaction gives also rise to vertically affected markets in relation to the upstream provision of wholesale international roaming services in Norway and the downstream supply of retail mobile telecommunications services in Finland, as well as the upstream provision of wholesale international roaming services in Finland, and the downstream supply of retail mobile telecommunication services in Norway. In addition, the Transaction gives rise to affected markets in relation to the upstream provision of wholesale mobile and fixed call termination services and the downstream provision of retail mobile telecommunication services and retail fixed telephony services in Norway, Finland, Sweden and Denmark.

5.3. Horizontal unilateral effects

5.3.1. Introduction

(88) The Horizontal Merger Guidelines distinguish between two main ways in which mergers between actual or potential competitors on the same relevant market may significantly impede effective competition, namely non-coordinated and coordinated effects. (60)

(89) Under the substantive test set out in Article 2(2) and (3) of the Merger Regulation, also mergers that do not lead to the creation or the strengthening of the dominant position of a single firm may be incompatible with the internal market. Indeed, the Merger Regulation recognises that in oligopolistic markets, it is all the more necessary to maintain effective competition. This is in view of the more significant consequences that mergers may have on such markets. For this reason, the Merger Regulation provides that "under certain circumstances, concentrations involving the elimination of important competitive constraints that the merging parties had exerted upon each other, as well as a reduction of competitive pressure on the remaining competitors, may, even in the absence of a likelihood of coordination between the members of the oligopoly, result in a significant impediment to effective competition". (61)

(90) The Horizontal Merger Guidelines list a number of factors which may influence whether or not significant horizontal non-coordinated effects are likely to result from a merger, such as the large market shares of the merging firms, the fact that the merging firms are close competitors, the limited possibilities for customers to switch suppliers, or the fact that the merger would eliminate an important competitive force. That list of factors applies equally regardless of whether a merger would create or strengthen a dominant position, or would otherwise significantly impede effective competition due to non-coordinated effects. Furthermore, not all of these factors need to be present to make significant non-coordinated effects likely and it is not an exhaustive list. (62)

(91) Finally, the Horizontal Merger Guidelines describe a number of factors, which could counteract the harmful effects of the merger on competition, including the likelihood of buyer power, entry and efficiencies.

1.1.1. Retail supply of TV services

1.1.1.1. Introduction

(92) The Parties’ activities overlap in the overall market for the retail supply of TV services in Finland, as well as in the following possible segmentations: (i) pay TV, (ii) basic pay TV, (iii) premium pay TV, (iv) pay TV for MDUs, and (v) pay TV for SDUs. The Commission notes that in all of these possible segments, Telenor/Canal Digital is only active via satellite/DTH. The tables bellow illustrate the Parties’ market shares by number of subscribers in the affected markets. (63)

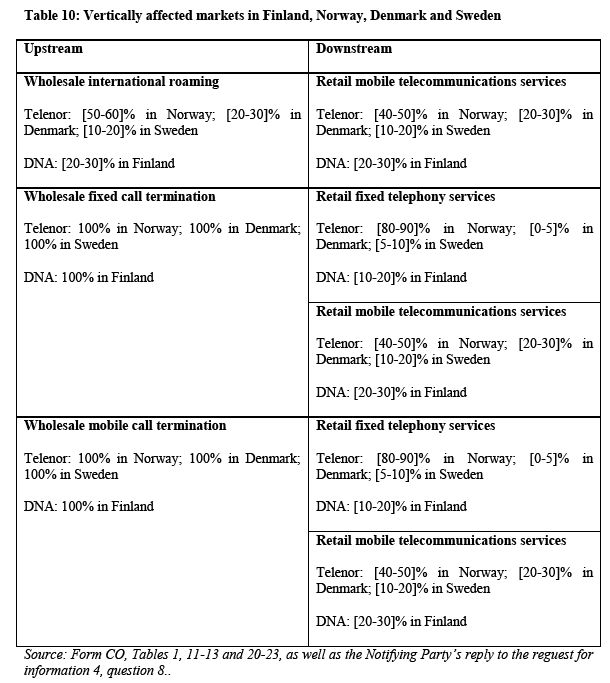

5.3.2.2. Notifying Party’s view

(93) The Notifying Party submits that the Transaction would not give rise to any competitive concerns in relation to the market for the retail supply of TV services or any plausible segment thereof for the following reasons. First, the overlap between the Parties’ activities is de minimis, except in the possible segment of pay TV for SDUs. Second, the merged entity will face fierce competition from a wide range of TV distributors. Finally, the Notifying Party submits that the distribution of pay-TV services over DTT and DTH is in structural decline in Finland, while streaming of TV and video and the corresponding use of mobile data is rapidly growing in Finland.

5.3.2.3. Commission’s assessment

(94) The Commission considers that the Transaction is unlikely to result in any significant horizontal non-coordinated effects on the market for the retail supply of TV services in Finland or any subsegment thereof, for the following reasons.

(95) First, if the overall market for retail supply of TV services (excluding non-linear OTT providers) is considered, the combined market share of the Parties would be below 25%. This could be an indication that the Transaction is not liable to impede effective competition in relation to this market.. (64)

(96) Second, as shown in Tables 1-7, the increment brought about by the Transaction would be less than [0-5]% under any of the possible market segmentations, except the possible segment for pay TV services to SDUs. Such a low increment indicates that the Transaction is unlikely to affect the structure of the market.

(97) Third, a sufficient number of viable alternative distributors of TV channels will remain on the Finnish market post-Transaction, covering also the different technology platforms for distribution, including Digita (who is the primary DTT distributor in Finland), Telia, Elisa (who are both offering retail TV services via cable, IPTV and OTT) and Viasat (who is offering retail TV services via satellite/DTH, as well as cable, IPTV and DTT).

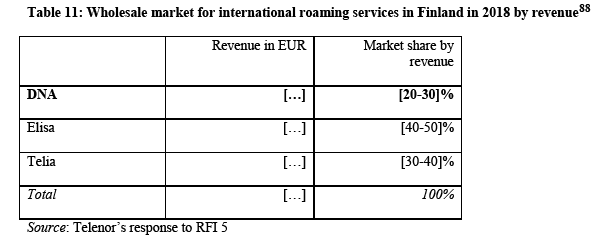

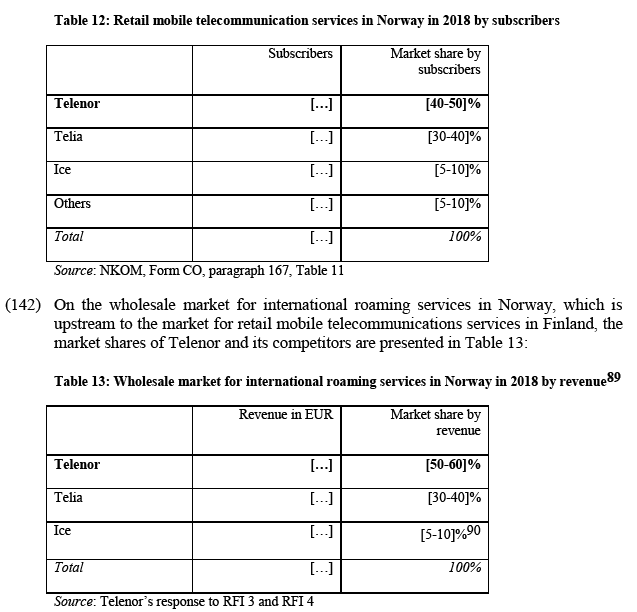

(98) Fourth, there are new players in the distribution of TV channels to end consumers, namely the broadcasters that distribute their channels over-the-top, including Bonnier/MTV, Sanoma/Nelonen, Yle and Discovery.

(99) Fifth, the results of the market investigation confirmed that Telenor/Canal Digital and DNA are not close competitors in the Finnish market for the retail supply of TV services. Telenor/Canal Digital is mainly competing with Viasat, while DNA is mainly competing with Telia and Elisa. (65)

(100) Finally, while the majority of competitors responding to the market investigation considered that competition would likely decrease (66), large customers of TV distribution services considered that the Transaction would have either a positive or no material impact on the intensity of competition. (67)

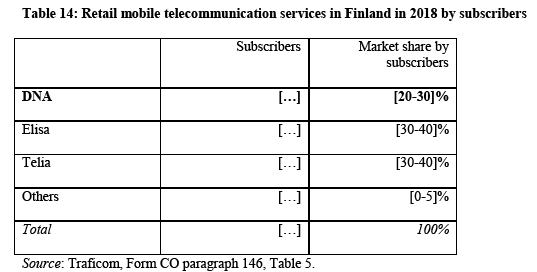

5.3.2.4. Conclusion

(101) In light of the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market as regards the market for the retail supply of TV services or any subsegment thereof in Finland.

5.3.3. Wholesale acquisition of TV channels

5.3.3.1. Introduction

(102) Both Parties (68) are active in the wholesale acquisition of TV channels in Finland. Telenor is also active in the other three Nordic countries, i.e. Norway, Denmark and Sweden. Table 8 below illustrates the Parties’ market shares by number of subscribers in the overall market for wholesale aquisiton of TV channels in Finland. (69)

(103) Table 9 below illustrates the Parties’ estimated market shares by cost in the overall market for wholesale aquisiton of TV channels at a possible pan-Nordic level.

(104) The Parties’ combined estimated market share by subscribers in the overall market for wholesale acquisition of TV channels in Finland is of only [10-20]%. Telenor/Canal Digital has an estimated market share of [0-5]% and DNA an estimated market share of [10-20]%. The Notifying Party confirmed that in relation to a possible segmentation by genre, the market shares would not vary significantly, since the TV channels on offer are similar for most TV distributors in Finland. As for a possible segmentation by type of infrastructure used, the Notifying Party submitted that there is no overlap between the Parties’ activities based on infrastructure.

(105) At a possible pan-Nordic level, i.e. including Finland, Norway, Denmark and Sweden, the merged entity would have an estimated combined market share by cost in the overall market for wholesale acquisition of TV channels of [20-30]%, with Telenor having an estimated share of [10-20]% and DNA an estimated share of [5- 10]%. (70) The merged entity’s main competitors would be Telia with an estimated share of [10-20]%, Com Hem with an estimated share of [10-20]% and Viasat with an estimated share of [10-20]%. The Notifying Party confirmed that the market shares for the overall market for wholesale acquisition of TV channels broadly reflect the market shares in relation to a possible segmentation by genre, type of infrastructure or linear TV channels and non-linear TV services.

(106) Therefore, the overall market for the wholesale acquisition of TV channels, regardless of possible segmentations, is horizontally affected on the demand side in Finland as well as at a possible pan-Nordic level.

5.3.3.2. Notifying Party’s view

(107) The Notifying Party submits that the shares in the market for the wholesale acquisition of TV channels in Finland reflect those of the market for premium pay- TV services (excluding Netflix, HBO Nordic and other non-linear OTT providers). This is because they exclude FTA services (for which TV distributors do not pay for channels) as well as basic pay TV channels (which in Finland account for a relatively small proportion of total cost of wholesale acquisition of TV channels).

(108) The Notifying Party submits that even if the Parties' shares in the market for wholesale acquisition of TV channels reflect a different segmentation of the overall market for the retail supply of TV services in Finland, the Transaction will have no significant impact on competition as Telenor/Canal Digital's limited presence on the market in Finland means that any overlap is de minimis.

(109) The Notifying Party submits that Telenor/Canal Digital has a small customer base and distributes TV services only via one type of distribution platform (satellite/DTH). Hence, the combination of DNA with Telenor/Canal Digital would not significantly enhance the bargaining position of the merged entity vis-à-vis the wholesale suppliers of TV channels (i.e. broadcasters).

5.3.3.3. Commission’s assessment

(110) The Commission considers that the Transaction is unlikely to result in any significant horizontal non-coordinated effects on the market for wholesale acquisition of TV channels (or any subsegment thereof) in Finland or at the pan- Nordic level, for the following reasons.

(111) First, the combined market share of the Parites in any possible market for wholesale acquisition of TV channels in Finland or at a pan-Nordic level would remain below 30%.

(112) Second, the increment brought by the Transaction would only be between [0-5]% and Telenor/Canal Digital is only active as an acquirer and distributor of TV channels via satellite/DTH.

(113) Third, the Parties are not close competitors in Finland or at a pan-Nordic level. At both levels, sufficient alternative suppliers would remain: Viasat, Elisa and Telia in Finland and Telia, Com Hem and Viasat at a pan-Nordic level, as well as a number of smaller suppliers.

(114) Finally, the Commission notes that it has not received any complaints from the respondents to the market investigation regarding the market for wholesale acquisition of TV channels. (71)

(115) The Commission considers that, as a result of the Transaction, there will also be no increase in buyer power vis-à-vis TV channels providers in Finland or at a pan- Nordic level. Telenor’s share in the acquisition of TV channels is minimal in Finland. Therefore, its addition would not bring about a significant change in the balance of bargaining power vis-à-vis TV channels providers. The same is true for DNA at a pan-Nordic level.

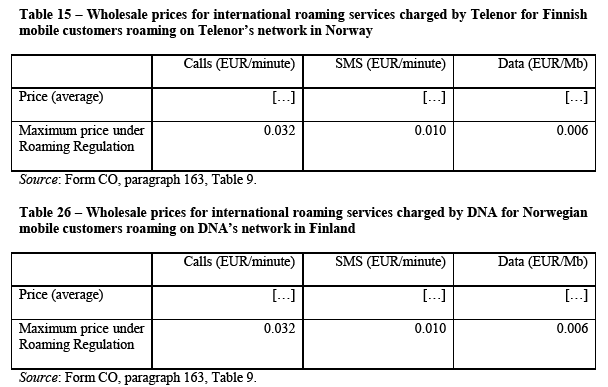

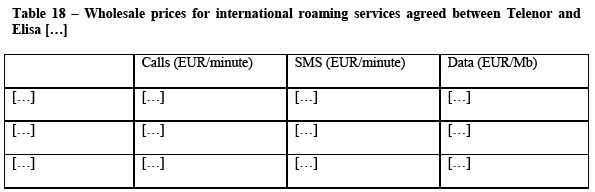

5.3.3.4. Conclusion

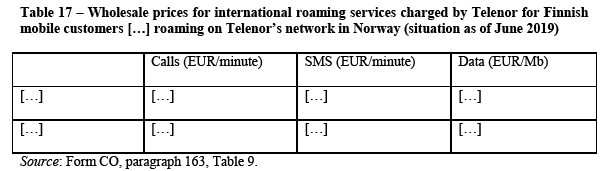

(116) In light of the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market as regards the market for the wholesale acquisition of TV channels or any segementations thereof in Finland or at a possible pan-Nordic level.

5.3.4. Market for M2M subscriptions

5.3.4.1. Introduction

(117) In the market for M2M mobile subscriptions, the Parties’ activities in Finland and at a possible pan-Nordic level. The merged entity would have a combined market share of [20-30]% by revenue (DNA: [20-30]%, Telenor: [0-5]%). At a possible pan- Nordic level, the merged entity would have a combined estimated market share of [60-70]% by revenue (DNA: [0-5]%, Telenor: [50-60]%). (72) Therefore, the market for M2M mobile subscriptions is horizontally affected. (73)

5.3.4.2. Notifying Party’s view

(118) The Notifying Party submits that, since the overlap between the Parties is de minimis and the merged entity will face fierce competition from a wide range of M2M providers including the two other Finnish MNOs, namely Elisa and Telia, the Transaction will not affect competition in this segment.

5.3.4.3. Commission’s assessment

(119) The Commission considers that the Transaction is unlikely to result in any significant horizontal non-coordinated effects on the market for M2M subscriptions in Finland or at the pan-Nordic level, for the following reasons.

(120) First, the combined market share of the Parties in Finland would be below 25% by revenue. Additionally, the Commission notes that the increment brought about by the Transaction would be of [0-5]%. At a possible pan-Nordic level, the increment brought about by the Transaction would be of [0-5]% or less.

(121) Second, the merged entity would continue to face strong competition in Finland from Telia, who has a market share [20-30]% by revenue, and from Elisa, who has a market share of [10-20]% by revenue. At a possible pan-Nordic level, the merged entity would mainly face competition from Telia, who has a market share of [10- 20]% by revenue, and Tele2, who has a market share of [5-10]% by revenue.

(122) Third, the majority of the repondents that took part in the market investigation confirmed that competition in the market for M2M subscriptions will likely stay the same. (74) One competitor pointed to the fact that customers are increasingly looking for pan-Nordic or even global coverage. (75)

(123) Regarding the pan-Nordic level, the Commission notes that pre-Transaction only Telia was truly able to offer M2M subscriptions at a pan-Nordic level, because Telenor had only a de minimis presence in Finland. Post-Transaction, Telenor would become the first undertaking to be able to compete with Telia at a pan-Nordic level. Additionally, while the merged entity would have very large market shares at a pan- Nordic level, the Commission notes that it would likely not have the ability to foreclose competitors in any of the countries, since M2M subscriptions are in principle covered by the EU Roaming Regulation. (76)

5.3.4.4. Conclusion

(124) In light of the above, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market as regards the market for M2M subscriptions in Finland or at a possible pan-Nordic level.

5.4. Vertical effects

5.4.1. Introduction

(125) A merger between companies which operate at different levels of the supply chain may significantly impede effective competition if such merger gives rise to foreclosure. (77) Foreclosure occurs where actual or potential competitors' access to supplies or markets is hampered or eliminated as a result of the merger, thereby reducing those companies' ability and/or incentive to compete. (78) Such foreclosure may discourage entry or expansion of competitors or encourage their exit. (79)

(126) The Non-Horizontal Merger Guidelines distinguish between two forms of foreclosure. Input foreclosure occurs where the merger is likely to raise the costs of downstream competitors by restricting their access to an important input. Customer foreclosure occurs where the merger is likely to foreclose upstream competitors by restricting their access to a sufficient customer base. (80)

(127) Pursuant to the Non-Horizontal Merger Guidelines, input foreclosure arises where, post-merger, the new entity would be likely to restrict access to the products or services that it would have otherwise supplied absent the merger, thereby raising its downstream rivals' costs by making it harder for them to obtain supplies of the input under similar prices and conditions as absent the merger. (81)

(128) For input foreclosure to be a concern, the merged entity should have a significant degree of market power in the upstream market. Only when the merged entity has such a significant degree of market power, can it be expected that it will significantly influence the conditions of competition in the upstream market and thus, possibly, the prices and supply conditions in the downstream market. (82)

(129) In assessing the likelihood of an anticompetitive input foreclosure scenario, the Commission examines, first, whether the merged entity would have, post-merger, the ability to substantially foreclose access to inputs, second, whether it would have the incentive to do so, and third, whether a foreclosure strategy would have a significant detrimental effect on competition downstream. (83)

(130) Pursuant to the Non-Horizontal Merger Guidelines, customer foreclosure may occur when a supplier integrates with an important customer in the downstream market and because of this downstream presence, the merged entity may foreclose access to a sufficient customer base to its actual or potential rivals in the upstream market (the input market) and reduce their ability or incentive to compete, which in turn, may raise downstream rivals' costs by making it harder for them to obtain supplies of the input under similar prices and conditions as absent the merger. This may allow the merged entity profitably to establish higher prices on the downstream market. (84)

(131) For customer foreclosure to be a concern, a vertical merger must involve a company which is an important customer with a significant degree of market power in the downstream market. If, on the contrary, there is a sufficiently large customer base, at present or in the future, that is likely to turn to independent suppliers, the Commission is unlikely to raise competition concerns on that ground. (85)

(132) In assessing the likelihood of an anticompetitive customer foreclosure scenario, the Commission examines, first, whether the merged entity would have the ability to foreclose access to downstream markets by reducing its purchases from its upstream rivals, second, whether it would have the incentive to reduce its purchases upstream, and third, whether a foreclosure strategy would have a significant detrimental effect on consumers in the downstream market. (86)

(133) The Parties’ market shares in the relevant markets are presented in Table 10.

5.4.2. Wholesale markets for call termination services on fixed and on mobile networks – Retail market for fixed telephony services and retail market for mobile telecommunications services

(134) As regards the wholesale markets for call termination on fixed and mobile networks, given that the network operators have a 100% market share on call termination services on their own fixed or mobile network, Telenor has a 100% market share on fixed and mobile call termination services on its own networks in Norway, Denmark and Sweden and DNA has a 100% market share on fixed and mobile call termination services on its own network in Finland. As the Parties are active on separate markets for fixed and mobile call termination services over their respective networks, there is no horizontal overlap between their respective activities in these markets. However, the Transaction gives rise to vertically affected markets since Telenor is a customer of DNA and DNA is a customer of Telenor with regard to wholesale call termination services on fixed and mobile networks on their respective telephony networks.

(135) However, the markets for wholesale call termination on fixed and mobile networks are regulated ex-ante by the Finnish Transport and Communications Agency, the Norwegian Communications Authority, the Danish Business Authority and the Swedish Post and Telecom Authority. These regulators ensure that access to call termination is granted on reasonable conditions and that rates remain reasonable and non-discriminatory. Moreover, the Commission notes that, as established by Article 75 of the European Electronic Communications Code (87), by 31 December 2020 the Commission shall adopt a delegated act setting the Eurorates (a single Union-wide fixed and a single Union-wide mobile termination rate). That means that fixed and mobile termination rates, currently established by the Finnish, Swedish, Danish and Norwegian regulators, will be set by the European Commission through the delegated act.

(136) Therefore, the merged entity would not have the ability to discriminate against Telenor’s competitors in Norway, Denmark and Sweden for access to call termination services in Finland. Similarly, Telenor would not have the ability to discriminate against DNA’s competitors in Finland for access to call termination services in Norway, Denmark and Sweden.

(137) In light of the above, the Commission concludes that the Transaction does not give rise to serious doubts as to the compatibility with the internal market in relation to the vertical link between the upstream markets for the wholesale supply of call termination services on fixed and on mobile networks and the downstream markets for the retail supply of fixed telephony services and retail supply of mobile telecommunications services.

5.4.3. Wholesale market for international roaming services – Retail market for mobile telecommunications services

5.4.3.1. Introduction

(138) Telenor is active on the market for wholesale international roaming services on its own mobile networks in Norway, Denmark and Sweden. DNA is active on this market on its own network in Finland. Telenor is a purchaser of international roaming services in Finland, and DNA is a purchaser of international roaming services in Norway, Denmark and Sweden.

(139) As shown in Table 10 above, the only vertically affected markets are:

(a) the upstream wholeale market for international roaming services in Finland and the downstream retail market for mobile telecommunications services in Norway; and

(b) the upstream wholesale market for international roaming services in Norway and the downstream retail market for mobile telecommunications services in Finland.

(140) On the wholesale market for international roaming services in Finland, which is upstream to the market for retail mobile telecommunications services in Norway, the market shares of DNA and its competitors are presented in Table 11:

(141) On the market for retail mobile telecommunication services in Norway, which is downstream to the market for international roaming services in Finland, the market shares of Telenor and its competitors are presented in Table 12:

(143) On the market for retail mobile telecommunication services in Finland, which is downstream to the market for international roaming services in Norway, the market shares of DNA and its competitors are presented in Table 14:

(144) Both Parties have entered into discount agreements for international roaming (“Discount Agreements”) with a large number of MNOs in the Nordic countries. As result of these Discount Agreements, the average prices for international roaming calls, SMS messages and data services charged by Telenor for Finnish mobile customers roaming on its own network in Norway and the average prices charged by DNA for Norwegian mobile customers roaming on its network in Finland are lower than the price caps foreseen in the Roaming Regulation.

5.4.3.2. Notifying Party’s view

Finland

(145) The Notifying Party submits that the Transaction would not affect competition on the market for the provision of retail mobile telecommunication services in Finland for the following reasons.

(146) First, the Transaction would not have any impact on the cost structures of the merged entity’s competitors. Any attempts to disadvantage competitors in Finland by raising the charges for international roaming would be ineffective considering that the cost of outbound roaming by MNOs in Finland in Telenor countries, including Norway, only represent a fraction of the competing MNOs’ total costs, i.e. less than [0-5]%. (91)

(147) Second, the merged entity’s competitors would continue to have access to alternative providers of wholesale international roaming services in each country in which Telenor operates, including in Norway. (92)

(148) Third, the Roaming Regulation prevents Telenor from charging in excess of prescribed price levels for roaming services. (93)

(149) The Notifying Party also argues that it would lack both the ability and incentive to cease entering into, or deteriorate the conditions of Discount Agreements with competing MNOs in Finland. […]. The Notifying Party refers to the Discount Agreement with […]. (94)

(150) The Notifying Party submits that, on the wholesale market for international roaming services in Finland, the Transaction would also not affect competition in Finland for the following reasons.

(151) First, Telenor accounts for a relatively small share of demand for wholesale international roaming in Finland. (95)

(152) Second, roaming in Finland does not account for a significant portion of Telenor’s outbound roaming. Telenor indicates that demand from Telenor in 2018 accounted for approximately [10-20]% of the total wholesale international roaming costs incurred in Finland. Even if Telenor would, post-Transaction, steer away all international roaming […] to DNA, this would not have a significant impact on the market position of […] in Finland considering that Telenor’s purchasing of wholesale roaming services in Finland in 2018 amounted to only EUR […], which accounts for less than […]% of […] total revenue in 2018. (96)

(153) Third, the Roaming Regulation imposes a price cap on the average wholesale charge that the mobile operator of a visited network may levy from the mobile operators of a roaming customer’s home network for the provision of a regulated roaming call originating on that visited network. (97)

Norway

(154) The Notifying Party submits that the Transaction would not affect competition on the market for the provision of retail mobile telecommunication services in Norway for the following reasons.

(155) First, international roaming in Finland is not a significant factor in the competition for Norwegian retail customers. As an illustration, the Notifying Party refers to the minutes generated by Norwegian customers roaming on DNA’s network in Finland in 2018 accounting for less than [0-5]% of DNA’s total inbound international roaming minutes. (98)

(156) Second, the merged entity’s competitors in Norway would continue to have access to alternative providers of wholesale international roaming services in Finland, namely Telia and Elisa. (99)

(157) Third, the Transaction would not have any impact on the cost structures of the merged entity’s competitors in Norway, namely Telia and Ice, as the roaming costs in Finland of Telia and Ice’s Norwegian customers are estimated at less than [0-5]% of the total costs of these operators. As a result, any attempt by the merged entity to raise Finnish charges for international roaming services would be ineffective and would not impact on competition in the retail mobile telecommunications market in Norway. (100)

(158) The Notifying Party also submits that, on the wholesale market for international roaming services in Norway, the Transaction would also not affect competition in Norway considering the very limited revenue generated by Finnish roaming customers. The Notifying Party estimates that its competitors Telia and Ice generated roaming revenue from DNA of less than [0-5]% of their total revenue and consequently, even if all DNA customers were to be steered to Telenor’s network in Norway, that would not represent a significant revenue loss for Telia or Ice. (101)

5.4.3.3. Commission’s assessment

(159) The Commission considers that the Transaction does not give rise to serious doubts as to its compatibility with the internal market in relation to the vertical link between the upstream markets for wholesale international roaming services and the downstream markets for the retail supply of mobile telecommunication services.

(160) The Commission notes that the markets for wholesale international roaming activities are subject to sector-specific EU regulation, which prevents mobile operators from refusing access to their network and from charging excessive termination fees. Under the Roaming Regulation, (102) MNOs must meet all reasonable requests for wholesale roaming access and MNOs are bound by the price cap imposed by the Roaming Regulation on the wholesale prices that MNOs can charge from their roaming customers. Key obligations under the regulation include an obligation to meet all reasonable requests, an obligation to publish a reference offer, caps on wholesale and retail charges (for calls, SMS messages and data services), and transparency and information requirements. The Roaming Regulation therefore effectively prevents MNOs from refusing access to their respective network and from charging excessive termination fees.

(161) That said, it is to be noted that actual market prices for international roaming services may be significantly lower than the price caps foreseen by the Roaming Regulation. In fact, as part of their wholesale roaming agreements, MNOs can agree on discounted rates for calls, SMS messages and data services, which in some cases can be a fraction of the maximum price foreseen by the Roaming Regulation.

(162) As discussed in paragraph 144, the Parties have entered into Discount Agreements with a large number of MNOs in the Nordic countries. Telenor has entered into Discount Agreements with […]. (103) Neither DNA nor Elisa have own mobile networks in any of the countries in which Telenor has its own networks, namely Norway, Denmark and Sweden, and are therefore fully dependent on international roaming agreements with MNOs in those countries. Telia, […], is present in all four Nordic countries with its own mobile network, including in each of Telenor’s markets, and is therefore less dependent on the mobile networks of competing MNOs in these countries for international roaming services. (104) As for DNA, it has entered into Discount Agreements with […]. (105)

(163) As a result of these Discount Agreements, the average prices for international roaming calls, SMS messages and data services charged by Telenor for Finnish mobile customers roaming on its network in Norway and the average prices charged by DNA for Norwegian mobile customers roaming on its network in Finland are lower than the price caps foreseen in the Roaming Regulation. The average prices are presented in the tables below:

(164) The Discount Agreements that Telenor has in place with […] are lower than the average prices presented in Table 6 above, in particular for […]. The actual discounted wholesale prices […] are presented in the table below:

(165) Absent the Discount Agreements, wholesale prices charged by Telenor to Finnish MNOs, such as Elisa, would therefore be significantly higher.

Market power

(166) In line with the Non-Horizontal Guidelines, for input foreclosure to be a concern, the merged entity should have a significant degree of market power in the upstream market. Only when the merged entity has such a significant degree of market power, can it be expected that it will significantly influence the conditions of competition in the upstream market and thus, possibly, the prices and supply conditions in the downstream market. (106)

(167) On the basis of the market shares provided by the Notifying Party (see Table 3), and the limited number of alternative providers of wholesale international roaming services, Telenor may have a certain degree of market power in the wholesale market for international roaming in Norway. This power is, however, limited by the Roaming Regulation, as explained in paragraph 156 above.

(168) As for DNA, the market share figures provided by the Notifying Party (see Table 2) do not provide any indication of significant market power on the market for wholesale international roaming services in Finland. In any case, any market power held by DNA would be limited by the Roaming Regulation, as explained above in paragraph 156.

(169) Considering the lack of market power of DNA on the wholesale market for international roaming in Finland, the remainder of the assessment in this section will focus on whether the merged entity, through its more significant position in the market for wholesale international roaming services in Norway, could foreclose competing MNOs in the downstream market for mobile telecommunications in Finland.

Ability and Incentive to foreclose

(170) In line with the Non-Horizontal Guidelines, in assessing the likelihood of an anticompetitive input foreclosure scenario, the Commission examines, first, whether the merged entity would have, post-merger, the ability to substantially foreclose access to inputs, second, whether it would have the incentive to do so, and third, whether a foreclosure strategy would have a significant detrimental effect on competition downstream. (107)

(171) In this case, the Commission considers that the merged entity would not have the ability or incentive to foreclose downstream competitors by refusing to enter into Discount Agreements with competing MNOs in Finland.

(172) The Commission considers that any risk of foreclosure would be limited to the Finnish MNO Elisa, with which Telenor today has a Partnership Agreement (108) and Telenor and Elisa are […].

(173) Through the Transaction, Telenor would acquire a mobile network in Finland, and hence the importance for Telenor to have a Discount Agreement with Elisa covering the Finnish market would diminish (109). Telenor has indicated that […]. (110) As explained by the Notifying Party, post-Transaction Telenor expects to […]. (111)

(174) Post-Transaction, Elisa would also be the only MNO in Finland without its own mobile networks in any of the other Nordic countries and would be reliant on its direct competitors in Finland, namely the merged entity and Telia, for wholesale roaming services in Norway (where Telenor and Telia are currently the only MNOs offering international roaming services).

(175) As explained by the Notifying Party, the Finnish market is distinguished by the higher consumption of mobile data than virtually any other country in the world, with MNOs offering unlimited data as a standard package and data transfer speeds exceeding 100 Mbps being commonplace. The Notifying Party refers to figures from Traficom which estimate that approximately 80% of all B2C mobile subscriptions in Finland have unlimited data transfer and all three MNOs, namely DNA, Elisa and Telia offer such subscriptions with unlimited data as standard, with pricing differentiated primarily on the basis of data transfer speed. (112) Apart from unlimited data within Finland, it is also commonplace for Finnish MNOs to offer unlimited data roaming across the Nordic and Baltic countries. (113) Such offers rely (at least partially) on the MNO having access to its own mobile networks in those roaming countries or having roaming agreements with discounted rates for data in place with competing MNOs. Telia can rely on its own mobile networks in all Nordic countries and the Baltics, while Elisa has benefitted pre-Transaction from a Discount Agreement with Telenor […].

(176) Absent such a Discount Agreement, the cost of offering mobile subscribers an unlimited data roaming package in all Nordic countries would be higher for an MNO such as Elisa.

(177) The Commission considers, however, that the Transaction would not affect Elisa’s ability to offer unlimited data packages on its own network to its mobile subscribers in Finland, but could only affect, to a limited degree, Elisa’s ability to offer such packages for use by its mobile subscribers when travelling in other Nordic countries where Elisa currently relies on the Discount Agreement with Telenor.

(178) The Commission furthermore considers that the price caps foreseen by the Roaming Regulation provide a limit on the price increase that could affect Elisa should the Discount Agreement that it has negotiated with Telenor be terminated. (114)

(179) The Commission also considers that several viable alternative providers of wholesale international roaming services remain with which Elisa could seek to negotiate Discount Agreements. In Sweden, in addition to Telenor and Telia, also Tele2 and Hi3G provide wholesale international roaming services. In Denmark, in addition to Telenor and Telia, also TDC and Hi3G provide such services. The number of viable alternatives in Norway today is more limited, with only Telenor, Telia and Ice being active as MNOs. Ice is a pure 4G network operator and is currently not active in the provision of wholesale international roaming services. It is, however, a possible entrant on that market in the near future, in particular once VoLTE roaming is rolled out. (115)

(180) Furthermore, in a situation where neither Telenor nor Telia would agree to enter into a Discount Agreement with Elisa for wholesale international roaming services in Norway, but Elisa would succeed in negotiating a Discount Agreement in Sweden and Denmark, the proportion of roaming traffic that would not be charged at discounted rates would be limited to the traffic generated by Elisa’s mobile subscribers roaming in Norway. In 2018, the data traffic volume of Elisa into Telenor’s networks in Norway represented only [20-30]% (i.e. [… ] Gb out of a total of […] Gb) of Elisa’s total traffic volumes into Telenor’s networks in Nordic countries (i.e. Norway, Sweden, and Denmark). (116)

(181) The Commission also takes note of the agreement reached between Telenor and Elisa on […], by which the two sides agree to extend the Discount Agreement in place between Telenor and Elisa […], at the following rates (117):

(182) By reaching this agreement with Telenor, Elisa will continue to benefit from discounted rates […]. The data roaming rates agreed therein correspond to […].

(183) In light of all the above, the Commission considers that the merged entity has neither the ability nor the incentive to foreclose its competitors, in particular Elisa, on the downstream market for mobile telecommunications in Finland.

5.4.3.4. Conclusion

(184) In light of the analysis above, the Commission concludes that the Transaction does not give rise to serious doubts as to its compatibility with the internal market in relation to the vertical link between the upstream markets for wholesale international roaming services in Norway and Finland and the downstream markets for the retail supply of mobile telecommunication services in Norway and Finland.

6. CONCLUSION

(185) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 Publication in the Official Journal of the European Union No C 203, 17.6.2019, p. 6.

4 Turnover calculated in accordance with Article 5 of the Merger Regulation.

5 Commission decision of 18 July 2007 in case M.4504 – SFR/Télé 2 France, recital 40, and Commission decision of 25 June 2008 in case M.5121 – News Corp/Premiere, recital 20. See also Commission decision of 8 December 2018 in case M.8842 – Tele2/Com Hem Holding, paragraph 35; Commission decision of 7 April 2017 in case M.8354 – Fox/Sky, paragraph 97; Commission decision of 3 August 2016 in case M.7978 – Vodafone/Liberty Global/Dutch JV, paragraph 56; Commission decision of 24 February 2015 in case M.7194 – Liberty Global/Corelio/W&W/De Vijver Media, recital 119-120; Commission decision of 25 June 2008 in case M.5121 – News Corp/Premiere, recitals 15 and 21; and Commission decision of 30 May 2018 in case M.7000 – Liberty Global/Ziggo, paragraph 71.

6 Commission decisions of 8 December 2018 in case M.8842 – Tele2/Com Hem Holding, paragraph 35; Commission decision of 6 February 2018 in case M.8665 – Discovery/Scripps, paragraph 33; Commission decision of 7 April 2017 in case M.8354 – Fox/Sky, paragraphs 98 and 99; Commission decision of 3 August 2016 in case M.7978 – Vodafone/Liberty Global/Dutch JV, paragraph 58; Commission decision of 24 February 2015 in case M.7194 – Liberty Global/Corelio/W&W/De Vijver Media, recital 124; Commission decision of 25 June 2008 in case M.5121 – News Corp/Premiere, recital 21; and Commission decision of 30 May 2018 in case M.7000 – Liberty Global/Ziggo, paragraph 72.

7 Commission decision of 8 December 2018 in case M.8842 – Tele2/Com Hem Holding, paragraph 35; Commission decision of 6 February 2018 in case M.8665 – Discovery/Scripps, paragraph 33; Commission decision of 7 April 2017 in case M.8354 – Fox/Sky, paragraph 100; Commission decision of 3 August 2016 in case M.7978 – Vodafone/Liberty Global/Dutch JV, paragraph 62; Commission decision of 24 February 2015 in case M.7194 – Liberty Global/Corelio/W&W/De Vijver Media, recital 127. Commission decision of 25 June 2008 in case M.5121 – News Corp/Premiere, recital 22; Commission decision of 21 December 2010 in case M.5932 – News Corp/BskyB, recital 105. Commission decision of 30 May 2018 in case M.7000 – Liberty Global/Ziggo, paragraph 137.

8 Commission decision of 24 February 2015 in case M.7194 – Liberty Global/Corelio/W&W/De Vijver Media, recital 119.

9 Commission decision of 8 December 2018 in case M.8842 – Tele2/Com Hem Holding, paragraph 36; Commission decision of 20 September 2013 in case M.6990 – Vodafone/Kabel Deutschland, paragraphs 92-96.

10 See replies to questionnaire Q1 – Questionnaire to competitors, questions 7 and 7.1.

11 See replies to questionnaire Q1 – Questionnaire to competitors, questions 3-4; replies to questionnaire Q3

– Questionnaire to customers of TV distribution services, questions 3 and 3.1.

12 See replies to questionnaire Q1 – Questionnaire to competitors, questions 5 and 5.1.

13 See replies to questionnaire Q1 – Questionnaire to competitors, questions 6 and 6.1.

14 See replies to questionnaire Q1 – Questionnaire to competitors, questions 8 and 8.1; replies to questionnaire Q3 – Questionnaire to customers of TV distribution services, questions 4 and 4.1.

15 Commission decision of 8 December 2018 in case M.8842 – Tele2/Com Hem Holding, paragraph 41; Commission decision of 26 February 2007 in case M.4521 – LGI/Telenet, recital 25; Commission decision of 24 February 2015 in case M.7194 – Liberty Global/Corelio/W&W/De Vijver Media, recital 139; Commission decision of 25 June 2008 in case M.5121 – News Corp/Premiere, recital 24; Commission decision of 25 January 2010 in case M.5734 – Liberty Global Europe/Unitymedia, recitals 40 and 43; Commission decision of 21 December 2010 in case M.5932 – NewsCorp/BSkyB, recital 109; Commission decision of 21 December 2011 in case M.6369 – HBO/Ziggo/HBO Nederland, recital 42; Commission decision of 15 April 2013 in case M.6880 – Liberty Global/Virgin Media, recital 54; Commission decision of 30 May 2018 in case M.7000 – Liberty Global/Ziggo, paragraph 140.

16 See footnote 15.

17 Commission decision of 30 May 2018 in case M.7000 – Liberty Global/Ziggo, paragraph 115; Commission decision of 6 February 2018 in case M.8665 – Discovery/Scripps, paragraph 23; Commission decision of 3 August 2016 in case M.7978 – Vodafone/Liberty Global/Dutch JV, paragraph 180; Commission decision of 24 February 2015 in case M.7194 – Liberty Global/Corelio/W&W/De Vijver Media, recital 101.

18 See replies to questionnaire Q1 – Questionnaire to competitors, questions 9 and 9.1; replies to questionnaire Q2 – Questionnaire to TV broadcasters, questions 5 and 5.1.

19 See replies to questionnaire Q1 – Questionnaire to competitors, question 9.1.

20 See replies to questionnaire Q2 – Questionnaire to TV broadcasters, question 5.1.

21 Commission decision of 30 May 2018 in case M.7000 – Liberty Global/Ziggo, paragraph 121.

22 Commission decision of 6 February 2018 in case M.8665 – Discovery/Scripps, paragraph 27.

23 Commission decision of 24 February 2015 in case M.7194 – Liberty Global/Corelio/W&W/De Vijver Media, paragraph 108.

24 Commission decision of 7 April 2017 in case M.8354 – Fox/Sky, paragraph 89.

25 See replies to questionnaire Q1 – Questionnaire to competitors, questions 10 and 10.1; replies to questionnaire Q2 – Questionnaire to TV broadcasters, questions 6 and 6.1.

26 See replies to questionnaire Q1 – Questionnaire to competitors, question 10.

27 See replies to questionnaire Q2 – Questionnaire to TV broadcasters, questions 6, 7 and 7.1.

28 Commission decision of 30 May 2018 in case M.7000 – Liberty Global/Ziggo, paragraph 199.

29 Commission decision of 11 May 2016 in case M.7612 – Hutchison 3G UK/Telefónica UK, recital 252; Commission decision of 30 May 2018 in case M.7000 – Liberty Global/Ziggo, paragraph 207 and Commission decision of 2 July 2014 in case M.7018 – Telefónica Deutschland/E-Plus, recital 64.

30 Commission decision of 1 September 2016 in case M.7758 – Hutchison 3G Italy/Wind/JV, recital 162; Commission decision of 3 August 2016 in case M.7978 – Vodafone/Liberty Global/Dutch JV, paragraph 74; Commission decision of 11 May 2016 in case M.7612 – Hutchison 3G UK/Telefónica UK, recitals 255, 261, 270, 279, 287; Commission decision of 2 July 2014 in case M.7018 – Telefónica Deutschland/E-Plus, recitals 31 to 55; Commission decision of 30 May 2018 in case M.7000 – Liberty Global/Ziggo, paragraphs 201 and 207; Commission decision of 28 May 2014 in case M.6992 – Hutchison 3G UK/Telefónica Ireland, recital 141; Commission decision of 12 December 2012 in case M.6497 – Hutchison 3G Austria/Orange Austria, recital 58.