Commission, April 16, 2018, No M.8765

EUROPEAN COMMISSION

Judgment

LENOVO / FUJITSU / FCCL

Subject: Case M.8765 - Lenovo/Fujitsu/FCCL

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 7 March 2018, the European Commission received notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 by which Lenovo Group Limited ("Lenovo") and Fujitsu Limited ("Fujitsu") establish a joint venture, (the "JV" or "FCCL") through Lenovo acquiring a majority stake in certain assets relating to Fujitsu’s personal computer business (the "Transaction"). (3) Lenovo and Fujitsu are designated hereinafter as "the Parties".

1. THE PARTIES

(2) Lenovo is a multinational computer technology group that develops, manufactures and markets desktops and notebook, workstations, servers, storage drives, and IT management software. Lenovo also manufactures smart mobile devices, and offers IT services.

(3) Fujitsu is a Japanese information and communication technology company offering a wide range of technology products, solutions and services. Among others, Fujitsu is active in the design, manufacturing, and marketing of desktops, notebooks, and tablets.

(4) The JV, FCCL, will comprise most of Fujitsu’s personal computer business, notably its desktops, notebooks and tablets, as well as various accessories and peripherals, including R&D functions. The JV will, however, not include the following functions of Fujitsu’s personal computer business which will be retained by Fujitsu: (i) the manufacturing of desktops and certain tablets, and (ii) sales and post-sales support/maintenance for business customers. The JV will be fully functional. It will have its own assets, personnel and dedicated management. Its activities will go beyond one specific function for the parents, as FCCL will be active in R&D, manufacturing and sales of Personal Computers (PCs). FCCL will also be market facing: it will continue to procure input for its manufacturing from other third parties than the parents and products designed and manufactured for consumers will be marketed by the JV to third party customers. Only desktops, notebooks and tablets for professional use will be sold exclusively to Fujitsu, however on arm's length basis. The JV will not have any sales/purchase relations with Lenovo.

2. THE OPERATION

(5) The Transaction will be implemented as follows: first, Fujitsu will group the relevant assets under Fujitsu Client Computing Limited (FCCL), a wholly-owned subsidiary of Fujitsu which already holds most of the relevant assets. Second, Fujitsu will transfer a majority stake of 51% of FCCL’s shares to Lenovo International Coöperatief U.A., an entity solely controlled by Lenovo. Fujitsu will retain a shareholding of 44% in FCCL and Development Bank of Japan ("DBJ") will hold 5% of the shares in FCCL. Post-Transaction, FCCL will be jointly controlled by Lenovo and Fujitsu: strategic decisions on the business strategy of the JV, including business plan will have to be agreed by both parents. DBJ will only be a minority shareholder and DBJ will not have control over FCCL.

(6) The Transaction therefore constitutes a concentration within the meaning of Article 3(1)(b) and Article 3(4) of the Merger Regulation.

3. EU DIMENSION

(7) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (4) (Lenovo, EUR 39 217 million, Fujitsu EUR 37 518 million). Each of them has an EU-wide turnover in excess of EUR 250 million (Lenovo,[…], Fujitsu, […]), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State.

(8) The Transaction therefore has an EU dimension pursuant to Article 1(2) of the Merger Regulation.

4. RELEVANT MARKETS

4.1. Relevant product markets

4.1.1. Market for Personal computers

(i) The Parties' views

(9) According to the Parties, PCs are general purpose, single user computer systems, which comprise desktops (5), notebooks (6), and tablets (7).

(10) The Parties submit that the market for PCs can be considered as constituting one single market (with a potential further subdivision according to the type of end- customer category). This is because: (i) there is a chain of demand-side substitutability between desktops and notebooks on the one hand, and between notebooks and tablets on the other hand; (ii) today notebooks and tablets offer equivalent features to those of desktops and (iii) from the supply side, most manufacturers offer all three products.

(11) The Parties also submit that the PC market can be further segmented according to the type of the end-customer category (personal use (8) versus professional use (9)). One argument for such distinction is that customers of both segments may have different needs with respect to their PCs features. (10) In addition, PCs designed for consumers and PCs designed for non-consumers (i.e. business customers) generally are distributed through different distribution channels (distributors/resellers versus direct distribution). (11)

(12) However, the Parties consider that the exact market definition can be left open as the Transaction does not give rise to competitive concerns irrespective of the product market definition retained.

(ii) Commission's assessment

(13) In its most recent decisions M.6196 - Lenovo/Medion, the Commission considered the existence of separate product markets for (i) desktops and (ii) notebooks (or portable PCs). Further, the Commission considered the existence of a distinct product market for tablets (at the time a new type of device) within the portable PCs market. Moreover, the Commission segmented each of these markets according to the type of end-customer category (professional use versus private use). The exact product market definition was ultimately left open.

(14) In its decisions in cases M.7047 Microsoft / Nokia and M.7202 Lenovo / Motorola Mobility, the Commission considered tablets in the context of (smart) mobile (phone) devices. When doing so, the Commission considered tablets either (a) to belong to a single market of smart mobile devices (consisting of smartphones and tablets) or (b) to form a separate product market (tablets only). The Commission also considered a further subdivision of this market according to the type of end- customer category (professional use vs. private use).

(15) In the present case, the market investigation produced mixed results as regards the question whether desktops, notebooks and tablets belong to the same market or each product forms a distinct product market. (12) From a supply side point of view, the large majority of suppliers indicated that they manufacture all three types of products. (13) However, views were mixed as regards the question whether desktops, notebooks and tablets are alternatives to each other. Some respondents pointed out that desktops and notebooks, and notebooks and tablets respectively could be closer alternatives in terms of functionality and price than desktops and tablets. (14)

(16) As regards the question whether desktops, notebooks and tablets should be distinguished by type of use (i.e. personal versus professional use), the results of the market investigation were also mixed. (15) Competitors pointed out that they manufacture desktops, notebooks and tablets for both personal and professional use. (16) Some of the distributors pointed out that they focus only on the professional or the personal segment. About half of the distributors indicated that they sell desktops, notebooks and tablets for both personal and professional use. (17) Views of business customers were also mixed: some business customers indicated that they purchase desktops, notebooks and tablets for both personal and professional use and this distinction might not be warranted, while others indicated that products for professional use are different since they require certain features such as long battery life, webcams or network specifications. (18)

(17) However, for the purpose of the present decision, the exact product market definition can be left open since the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible product market definition.

4.1.2. Market for PC accessories/peripherals

(i) The Parties' views

(18) In relation to the market for accessories and peripherals, the Parties submit that each of these accessories/peripherals constitutes a separate product market, with potential further segmentation e.g. as regards monitors. However, in the light of the limited activities of the Parties, the Parties propose to leave the market definition open.

(ii) Commission's assessment

(19) In recent cases (19), the Commission considered a distinction between (i) accessories for notebooks; (ii) storage devices and (iii) computer peripherals other than monitors, which were considered separately. The Commission also noted that storage devices could be further segmented between external hard disc drives (XHDD), solid state drives (SSD), external CD/DVD writers, and USB sticks. As regards monitors, the Commission has previously considered a segmentation by type of technology (Cathode Ray Tube or Liquid Crystal Display) and a segmentation between branded monitors (manufactured under own brand label) and unbranded (on an OEM basis) monitors. (20)

(20) The market investigation in this case did not produce any indication which could warrant a departure from findings in previous cases.

(21) For the purpose of the present decision, the exact product market definition can be left open since the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible product market definition.

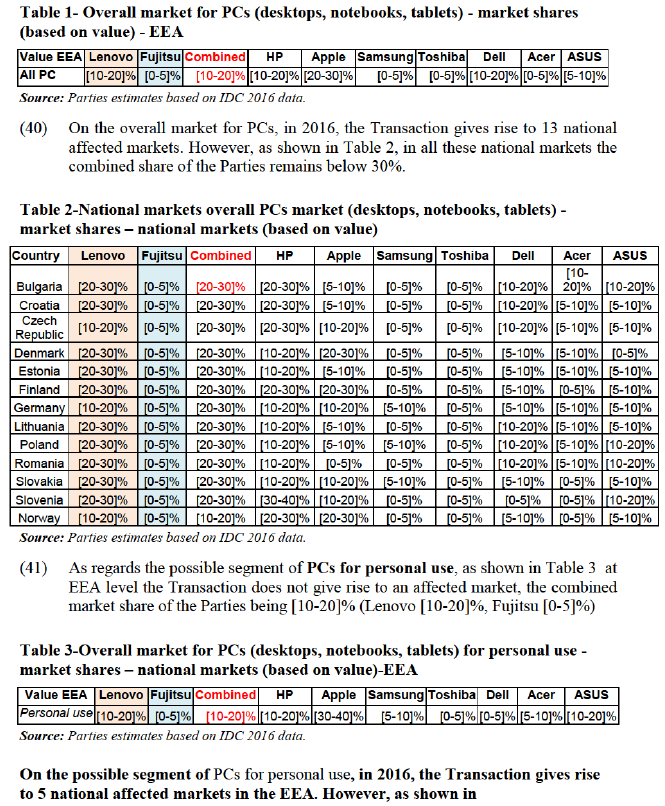

4.1.3. Market for IT services

(i) The Parties' views

(22) The Parties submit that there is one overall product market for IT services. All these business solutions have in common that they relate to IT components (including PCs) and technology and the use thereof.

(ii) Commission's assessment

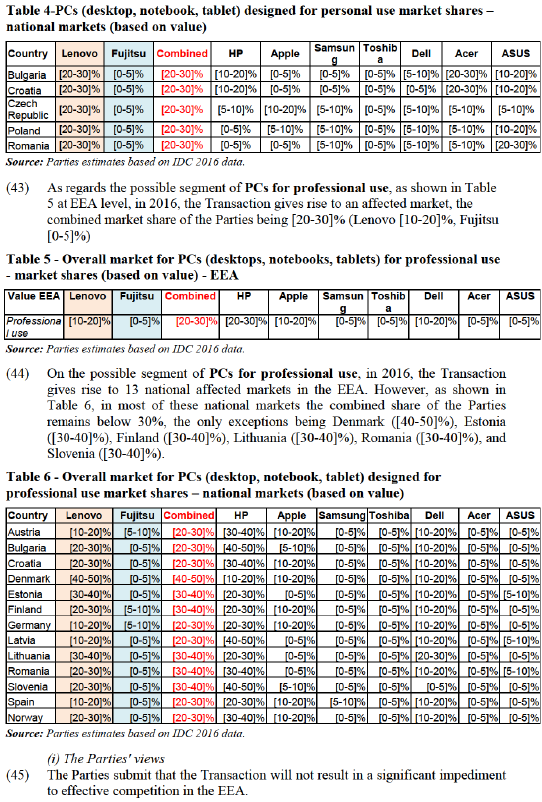

(23) In previous cases such as M.6127 - Atos/Siemens IT Solutions & Services (21), M. 7458 - IBM/INF Business of Deutsche Lufthansa (22), and M. 8180 - Verizon/Yahoo (23), the Commission considered the market for IT services in its potential segments. According to Commission's past practice, IT services may be further segmented by functionality into (i) consulting; (ii) implementation; (iii) IT outsourcing; (iv) business process outsourcing; (v) software support; and (vi) hardware support and by industry sector: (i) banking & securities; (ii) communications, media & services; (iii) education; (iv) government; (v) healthcare providers; (vi) insurance; (vii) manufacturing & natural resources; (viii) retail; (ix) transportation; (x) utilities; and (xi) wholesale trade.

(24) The market investigation in this case did not produce any indication which could warrant a departure from findings in previous cases.

(25) For the purpose of the present decision, the exact product market definition can be left open since the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible product market definition.

4.2. Relevant geographic markets

4.2.1. Market for personal computers

(i) The Parties' views

(26) The Parties submit that the overall market for PCs and all of its possible segments are at least EEA-wide, if not worldwide in scope.

(ii) Commission's assessment

(27) In recent cases the Commission took the view that the geographic scope of the PC market to be either EEA-wide or national (24). As regards tablets, in its decisions Microsoft / Nokia (2013) and Lenovo / Motorola Mobility (2014) the Commission considered the market for smart mobile devises (smartphones and tablets) to be at least EEA-wide, if not worldwide, in scope. (25)

(28) The market investigation in the present case provided mixed results as to the exact scope of the overall market for PCs and its possible segments (that is to say desktops, notebooks and tablets, each of which can be further segmented by type of use – for personal or for professional use). (26) Most competitors explain that they are able to sell desktops, notebooks and tablets in all countries in EEA. (27) Most respondents consider that there are no country specific end-customer requirements as regards desktops, notebooks and tablets throughout the EEA. (28) Those respondents who pointed out specific end-customer requirements mentioned keyboard differences and operating system language differences as regards desktops and notebooks. Many distributors and resellers explained that they source and distribute desktops, notebooks and tablets at national level, rather than at EEA level. (29) The answers of business customers were also mixed as regards the level at which they source desktops, notebooks and tablets. (30) Therefore the market investigation did not provide indications regarding which would justify a departure from the Commission's findings in previous cases.

(29) For the purpose of the present decision, the exact geographic market definition can be left open since the Transaction does not raise serious doubts as regards its compatibility with the internal market irrespective of the geographic market definition.

4.2.2. Market for PC accessories/peripherals

(i) The Parties' views

(30) The Parties submit that the relevant markets for accessories/peripherals are at least EEA-wide in scope. However, in the present case, the exact scope of the geographic market can ultimately be left open given the Parties' very limited activity both in the EEA as well as within each of the EEA countries.

(ii) Commission's assessment

(31) In its decision Lenovo / Medion (31) the Commission considered that the geographic markets for computer accessories and peripherals could be either EEA-wide or national in scope.

(32) The market investigation in this case did not produce any indication which could warrant a departure from the finding in this previous case.

(33) For the purposes of the present decision, the exact geographic market definition can be left open since the Transaction does not raise serious doubts as regards its compatibility with the internal market irrespective of the geographic market definition.

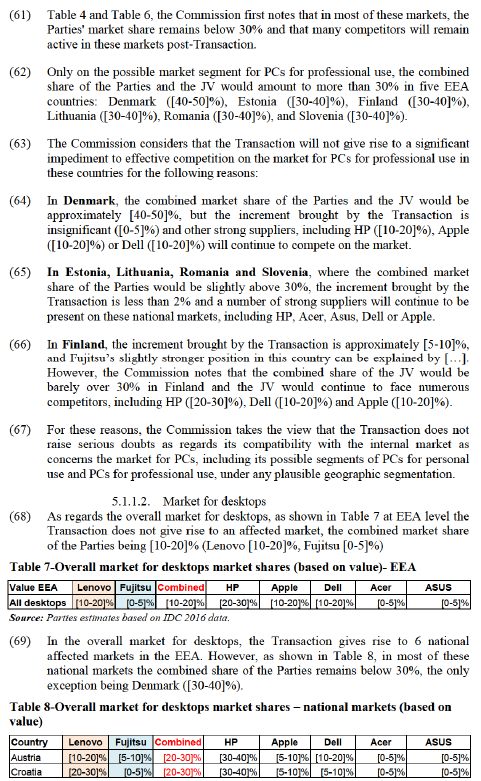

4.2.3. Market for IT services

(i) The Parties' views

(34) The Parties submit that the market for solutions business or IT services is worldwide in scope.

(ii) Commission's assessment

(35) In past decisions, the Commission took the view that the scope of various IT services markets could be either EEA-wide or national in scope, but ultimately left the market definition open. (32) The market investigation in this case did not produce any indication which could warrant a departure from findings in previous cases.

(36) Also for the purposes of the present decision, the exact geographic market definition can be left open since the Transaction does not raise serious doubts as regards its compatibility with the internal market irrespective of the geographic market definition.

5. COMPETITIVE ASSESSMENT

(37) The activities of the Parties and the joint venture horizontally overlap in the manufacture and sale of PCs (desktops, notebooks and tablets) and in the manufacture and sale of peripherals/accessories for their own branded desktops, notebooks and tablets.

(38) Furthermore, as PCs represent an input for the downstream market of IT services where Fujitsu is active, the Transaction gives rise to vertical relationships between the upstream market for PCs and its segments and the downstream market for IT services.

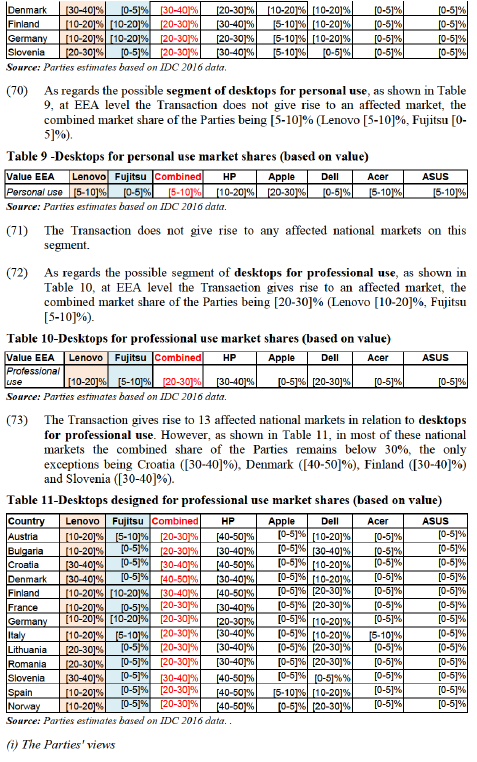

5.1. Horizontal non-coordinated effects

5.1.1. Market for personal computers (comprising desktops, notebooks and tablets)

5.1.1.1. Overall market for PCs (comprising desktops, notebooks and tablets)

(39) On the overall market for PCs the Transaction does not give rise to an affected market at the EEA level. As shown in Table 1, in 2016, at EEA level, the Parties' and JV's combined market share would be [10-20] % based on value (33) (Lenovo [10-20]%, Fujitsu [0-5]%).

(42) Table 4, in all these national markets the combined share of the Parties and the JV remains below 30%.

(46) First, the Parties note that their combined share at EEA level in the overall market for PCs remains below 20% with the single exception of PCs designed for professional use where it amounts to only [20-30]%

(47) Second, their combined share of the market for PCs designed for professional use ([20-30]%) is lower than the market share of the market leader Hewlett Packard "HP" ([20-30]%), and not much higher than the market share of Dell ([10-20]%). Dell is closely followed by Apple ([10-20]%), the company that is the undisputable market leader in the overall PC market and the market for PCs for personal use if market shares are calculated based on value.

(48) Third, the increment in market share that would arise as a result of the Transaction would be less than [0-5]% at EEA level.

(49) In addition, even considering alternative product market definitions (such as a distinction between desktops, notebooks, and tablets), the combined EEA-wide market shares are always less than 25%, and the increment is also always low.

(50) Further, the JV and the Parties will continue to face fierce competition from a large number of powerful personal computer players including, among others, Acer, Apple, Asus, Dell, HP, Samsung and Toshiba.

(51) Lastly, there are low barriers to entry and expansion since there are no critical patents/IP rights for PC manufacturing business itself, and since there are virtually no technological hurdles to overcome and no capacity constraints at the manufacturing level. The Parties submit that there is a real threat of new entry into and/or expansion in the personal computer market by technology giants such as Google and Microsoft if prices on the relevant personal computer markets were to increase.

(ii) Commission's assessment

(52) The Commission considers that the Transaction is unlikely to raise serious doubts as to its compatibility with the internal market in the overall market for PCs for the following reasons:

(53) According to Commission's Guidelines on the assessment of horizontal mergers under the Council Regulation on the control of concentrations between undertakings (the "Horizontal Guidelines") (34), combined market shares below 25% may indicate that the concentration is not likely to impede effective competition.

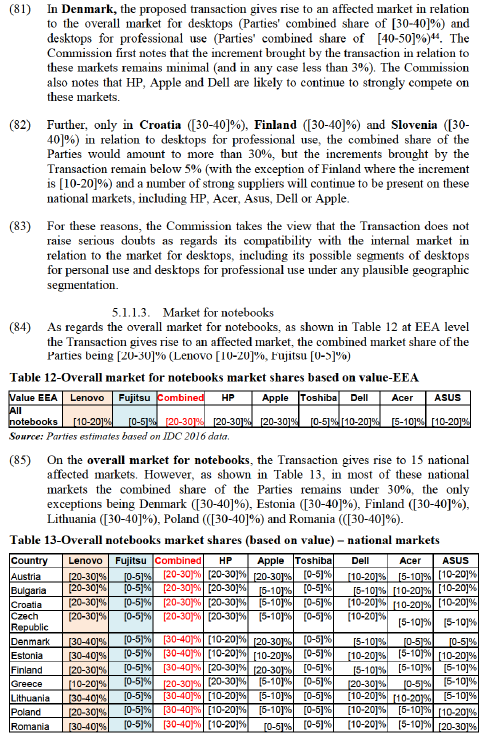

(54) The Commission first notes that at EEA level, the Transaction will not give rise to affected markets in the overall market for PCs, with the exception of the possible market segment of PCs for professional use, where the combined market share of the Parties would be slightly above 20% ([20-30]%). The Commission also notes that the increment brought by the Transaction remains low at EEA level (and in any case below 4%)

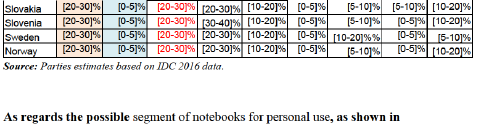

(55) Second, in the overall market for PCs, at EEA level, the Parties and the JV will continue to face strong competition from many established competitors such as HP, Dell, Asus, Apple, Acer, Toshiba and Samsung. These suppliers are active throughout the EEA.

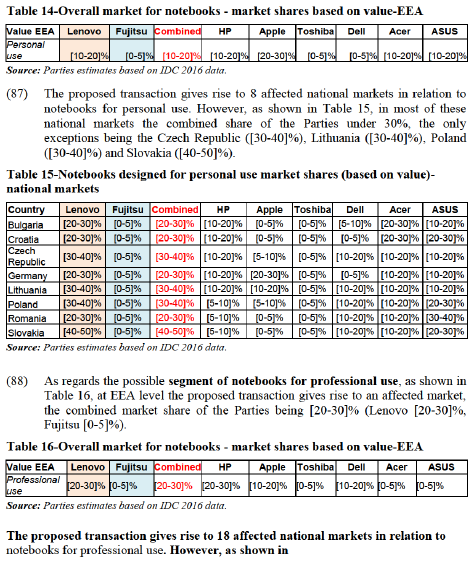

(56) Third, the large majority of respondents to the market investigation do not consider Lenovo and Fujitsu as close competitors in the overall PCs market, irrespective of the possible market segment. Lenovo is perceived as a closer competitor to larger suppliers such as HP (due to portfolio, pricing and business model), Dell or Acer, while Fujitsu is considered one of the more marginal competitors in the EEA, in particular as regards PCs for personal use. (35)

(57) Fourth, the large majority of participants to the market investigation confirmed that a sufficient number of competitors will continue to compete in the overall market for PCs, both for personal use, as well as for professional use at EEA- level.36 The Parties' customers are either distributors/resellers or large business customers which generally source from more than one supplier at a time. (37)

(58) Furthermore, respondents confirmed the entry on the market of new manufacturers such as Google and Microsoft. (38)

(59) Finally, the vast majority of market participants did not consider that the Transaction will have a negative impact on the overall market for PCs, PCs for personal use or PCs for professional use or the prices for PCs. (39)

(60) Furthermore, in relation to the national affected markets identified in Table 2,

(74) In relation to the market for desktops and its possible segments, the Parties reiterate the arguments presented in Section 5.1.1.1.

(ii) The Commission's assessment

(75) The Commission considers that the Proposed Transaction is unlikely to raise serious doubts as to its compatibility with the internal market in the market for desktops for the following reasons:

(76) The Commission first notes that at EEA-level, the Proposed Transaction will not give rise to affected markets in the market for desktops, with the exception of the possible market segment of desktops for professional use, where the combined market share of the Parties and the JV would be slightly above 20% ([20-30]%). The Commission also notes that the increment brought by the Transaction remains rather low at EEA level (and in any case below 7%)

(77) Second, in the market for desktops, at EEA level, the Parties and the JV will continue to face strong competition from many established competitors such as HP, Dell, Asus, Apple and Acer. These suppliers are active throughout the EEA.

(78) Third, the large majority of respondents to the market investigation do not consider Lenovo and Fujitsu close competitors with regard to desktops, irrespective of the possible market segment. Market participants consider Fujitsu to be a minor supplier in the desktops for personal use segment and a slightly stronger player in the professional desktops segment. However, overall, Lenovo is perceived by the respondents as a closer competitor to larger suppliers such as HP (due to portfolio, pricing and business model), Dell or Acer, while Fujitsu is considered one of the more marginal competitors in the EEA. (40)

(79) Furthermore, the large majority of participants to the market investigation confirmed that a sufficient number of competitors will continue to compete in the market for desktops, both for personal use, as well as for professional use at EEA- level. (41) The Parties' customers are either distributors/resellers or large business customers which generally source from more than one supplier at a time. (42) Finally, the vast majority of market participants did not consider that the Proposed Transaction will have a negative impact on the market for desktops, desktops for personal use or desktops for professional use or the prices for desktops. (43)

(80) Furthermore, in relation to the national affected markets identified in Table 8 and Table 11, the Commission first notes that in most of these markets, the Parties' market share remains below 30% and that many competitors will remain active in these markets post-Transaction.

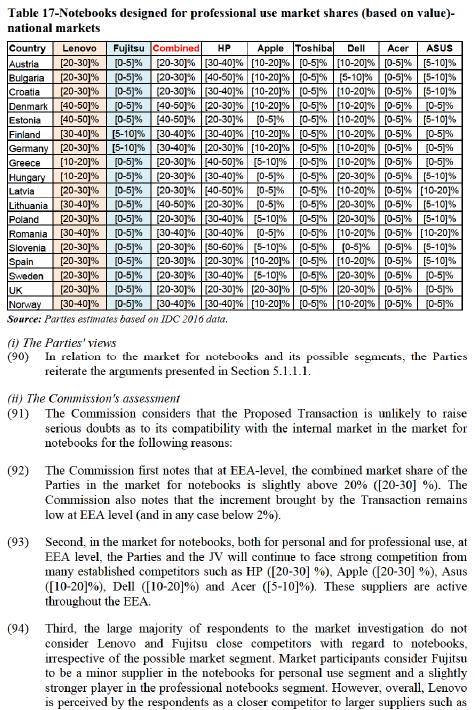

(86) Table 14, at EEA level the proposed transaction does not give rise to an affected market, the combined market share of the Parties being [10-20]% (Lenovo [10- 20]%, Fujitsu [0-5]%).

(89) Table 17, in most of these national markets the combined share of the Parties remains under 30%, the only exceptions being the Denmark ([50-60]%), Estonia ([40-50]%), Finland ([30-40]%), Germany ([30-40]%), Lithuania ([40-50]%), Romania ([30-40]%) and Norway ([30-40]%).

HP (due to portfolio, pricing and business model), Dell or Acer, while Fujitsu is considered one of the more marginal competitors in the EEA. (45)

(95) Furthermore, the large majority of participants to the market investigation confirmed that a sufficient number of competitors will continue to compete in the market for notebooks, both for personal use, as well as for professional use at EEA-level. (46) The Parties' customers are either distributors/resellers or large business customers which generally source from more than one supplier at a time. (47) Finally, the vast majority of market participants did not consider that the Proposed Transaction will have a negative impact on the market for notebooks, notebooks for personal use or notebooks for professional use or the prices for notebooks. (48)

Furthermore, in relation to the national affected markets identified in Table 13, Table 15 and

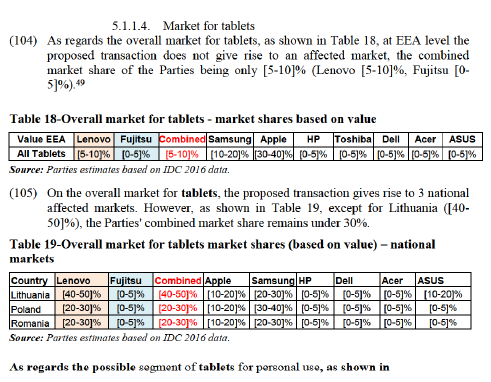

(96) Table 17, the Commission first notes that in most of these markets, the Parties' market share remains below 30% and that many competitors will remain active in these markets post-Transaction.

(97) Thus, as regards the overall market for notebooks, the proposed transaction gives rise to 15 national affected markets but only in 6 countries the combined share of the parties is above 30%: Denmark ([30-40]%), Estonia ([30-40]%), Finland ([30-40]%), Lithuania ([30-40]%), Poland ([30-40]%) and Romania ([30- 40]%). The Commission first notes in relation to these national markets that the increment brought by the transaction is minimal and in any case below 1% in most countries and [0-5]% in Finland. The Commission also notes that HP, Apple, Acer, Asus and Dell are likely to continue to strongly compete on these markets.

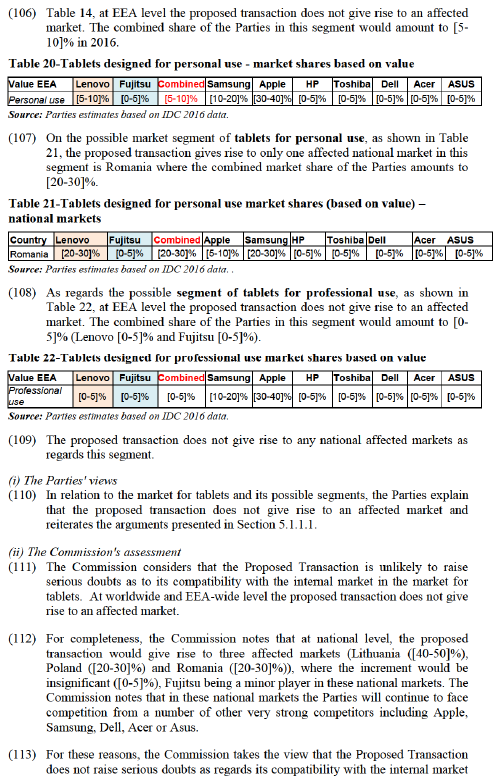

(98) As regards the segment of notebooks for personal use, the proposed transaction gives rise to 8 national affected markets but only in 4 countries the combined share of the parties is above 30%: the Czech Republic ([30-40]%), Lithuania ([30-40]%), Poland ([30-40]%) and Slovakia ([40-50]%). The Commission notes that in these countries the increment brought by the transaction is minimal and in any case below 1%.The Commission also notes that HP, Apple, Acer, Asus and Dell are likely to continue to strongly compete on these markets.

(99) As regards the segment of notebooks for professional use, the proposed transaction gives rise to 18 national affected markets but only in 7 countries the combined share of the Parties is above 30%: Denmark ([50-60]%), Estonia ([40- 50]%), Finland ([30-40]%), Germany ([30-40]%), Lithuania ([40-50]%), Romania ([30-40]%) and Norway ([30-40]%).

(100) In Denmark, in 2016, the combined market share of the Parties would be slightly above 50% ([50-60]%), with Fujitsu contributing an increment of [0-5]%. The Commission notes that between 2014 and 2016, the market share of Fujitsu has dropped from [0-5] % to [0-5] % and that Fujitsu is a minor player in this market, behind HP ([10-20]%), Apple ([10-20]%), Dell ([10-20]%) and Acer ([0-5]%). The Commission notes that two other players, Toshiba and Asus are also present in Denmark.

(101) In Estonia, in 2016, the combined market share of the Parties is close to 50% ([40-50]%), with Fujitsu contributing a small increment of [0-5]%. However, the Commission notes that Fujitsu is a minor player in this market, behind HP ([20- 30]%), Dell ([10-20]%), Asus ([5-10]%), Apple ([0-5]%) and Acer ([0-5]%).

(102) The Commission notes that in Lithuania, Romania and Norway, the increment brought by the transaction is minimal and in any case below 2%. In Finland and Germany the increment brought by the Transaction is slightly higher ([5-10] %). The Commission also notes that a number of strong suppliers, including HP, Acer, Asus, Dell and Apple will continue to compete in this segment in all these countries.

(103) For these reasons, the Commission takes the view that the Proposed Transaction does not raise serious doubts as regards its compatibility with the internal market in relation to the market for notebooks, including its possible segments of notebooks for personal use and notebooks for professional use under any plausible geographic segmentation.

(116) Table 25, at EEA level the proposed transaction does not give rise to an affected market. The combined share of the Parties in this segment would amount to [10- 20]% (Lenovo [10-20]% and Fujitsu [0-5]%).

(119) Table 28. Among these countries, only in 6 countries, the combined market share of the Parties is above 30%: Denmark ([40-50]%), Estonia ([30-40]%), Finland ([30-40]%), Lithuania ([30-40]%), Romania ([30-40]%) and Norway ([30-40]%).

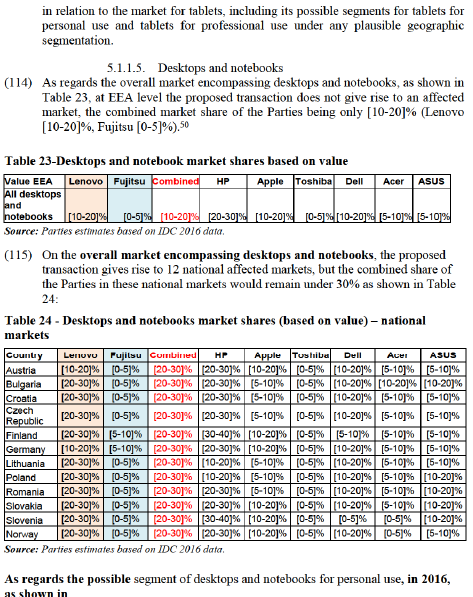

model), Dell or Acer, while Fujitsu is considered one of the more marginal competitors in the EEA.51

(125) Furthermore, the large majority of participants to the market investigation confirmed that a sufficient number of competitors will continue to compete in the market for desktops and notebooks, both for personal use, as well as for professional use at EEA-level.52 The Parties' customers are either distributors/resellers or large business customers which generally source from more than one supplier at a time. (53)

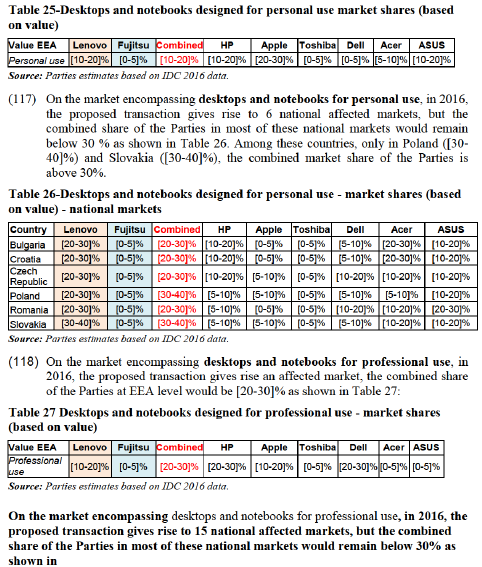

(126) Finally, the vast majority of market participants did not consider that the Proposed Transaction will have a negative impact on the market for desktops and notebooks, desktops and notebooks for personal use or desktops and notebooks for professional use or the prices for desktops and notebooks. (54)

Furthermore, in relation to the national affected markets identified in Table 24, Table 26 and

(127) Table 28, the Commission first notes that in most of these markets, the Parties' market share remains below 30% and that many competitors will remain active in these markets post-Transaction.

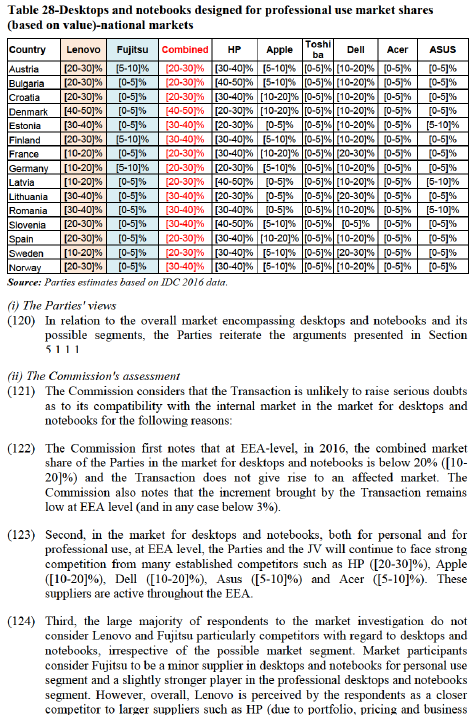

(128) Thus, as regards the overall market for desktops and notebooks, the transaction gives rise to 12 national affected markets, but the combined share of the Parties in these national markets would remain under 30%. The Commission also notes that HP, Apple, Acer, Asus and Dell are likely to continue to strongly compete on these markets.

(129) As regards the segment of desktops and notebooks for personal use, the transaction gives rise to 6 national affected markets but only in 2 countries the combined share of the parties is above 30%: Poland ([30-40]%) and Slovakia ([30-40]%). The Commission notes that in these countries the increment brought by the transaction is minimal and in any case below 1%.The Commission also notes that HP, Apple, Acer, Asus and Dell are likely to continue to strongly compete on these markets.

(130) As regards the segment of desktops and notebooks for professional use, the transaction gives rise to 15 national affected markets but only in 6 countries the combined market share of the Parties is above 30%: Denmark ([40-50]%), Estonia ([30-40]%), Finland ([30-40]%), Lithuania ([30-40]%), Romania ([30- 40]%) and Norway ([30-40]%).

(131) In Denmark, in 2016, the combined market share of the Parties would be [40- 50]%, with Fujitsu contributing an increment of [0-5]%. The Commission notes that between 2014 and 2015, the market share of Fujitsu has dropped from [0-5]% to [0-5]% and that Fujitsu is a minor player in this market, behind HP ([20-30]%), Apple ([10-20]%), Dell ([10-20]%) and Acer ([0-5]%). The Commission notes that two other players, Toshiba and Asus are also present in Denmark.

(132) The Commission notes that in Estonia ([30-40]%), Finland ([30-40]%), Lithuania ([30-40]%), Romania ([30-40]%) and Norway ([30-40]%), the increment brought by the transaction is low and in any case below 2%. In Finland, the increment brought by the Transaction is slightly higher ([5-10]%). However, the Commission also notes that a number of strong suppliers, including HP, Acer, Asus, Dell and Apple will continue to compete in this segment in all these countries.

(133) For these reasons, the Commission concludes that the Transaction does not raise serious doubts as regards its compatibility with the internal market in relation to the market encompassing desktops and notebooks, including its possible segments of desktops and notebooks for personal use and for professional use under any plausible geographic segmentation.

5.1.1.6. Notebooks and tablets

(134) On the market encompassing notebooks and tablets, the proposed transaction does not give rise to an affected market at EEA level, the combined market share of the Parties being only [10-20]% (Lenovo [10-20]%, Fujitsu [0-5]%), as shown in Table 29:

(135) Table 30.

(144) Third, the large majority of respondents to the market investigation do not consider Lenovo and Fujitsu particularly competitors with regard to notebooks and tablets, irrespective of the possible market segment. Market participants consider Fujitsu to be a minor supplier in notebooks and tablets for personal use segment and a slightly stronger player in the professional notebooks and tablets segment. However, overall, Lenovo is perceived by the respondents as a closer competitor to larger suppliers such as HP (due to portfolio, pricing and business model), Dell or Acer, while Fujitsu is considered one of the more marginal competitors in the EEA. (55)

(145) Furthermore, the large majority of participants to the market investigation confirmed that a sufficient number of competitors will continue to compete in the market for notebooks and tablets, both for personal use, as well as for professional use at EEA-level. (56) The Parties' customers are either distributors/resellers or large business customers which generally source from more than one supplier at a time. (57)

(146) Finally, the vast majority of market participants did not consider that the Transaction will have a negative impact on the market for notebooks and tablets, notebooks and tablets for personal use or notebooks and tablets for professional use or the prices for notebooks and tablets. (58)

Furthermore, in relation to the national affected markets identified in

(147) Table 30, Table 32, and Table 34, the Commission first notes that in most of these markets, the Parties' market share remains below 30% and that many competitors will remain active in these markets post-Transaction.

(148) Thus, as regards the overall market for notebooks and tablets, the transaction gives rise to 15 national affected markets, but the combined share of the Parties in these national markets would remain under 30%, with two exceptions Estonia ([30-40]%) and Lithuania ([30-40]%).The Commission first notes that the increment brought by the Transaction in these countries is insignificant (under 1%) and that HP, Apple, Acer, Asus and Dell are likely to continue to strongly compete on these markets.

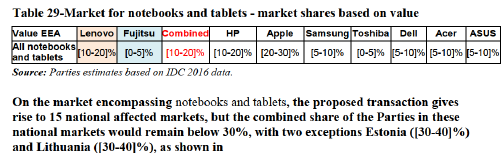

(149) As regards the segment of notebooks and tablets for personal use, the transaction gives rise to 5 national affected markets and in all these national markets the combined share of the parties remains below 30%, with the exception of Poland where it amounts to [30-40]%. The Commission notes that in these countries the increment brought by the transaction is minimal and in any case below 1%. The Commission also notes that HP, Apple, Acer, Asus and Dell are likely to continue to strongly compete on these markets.

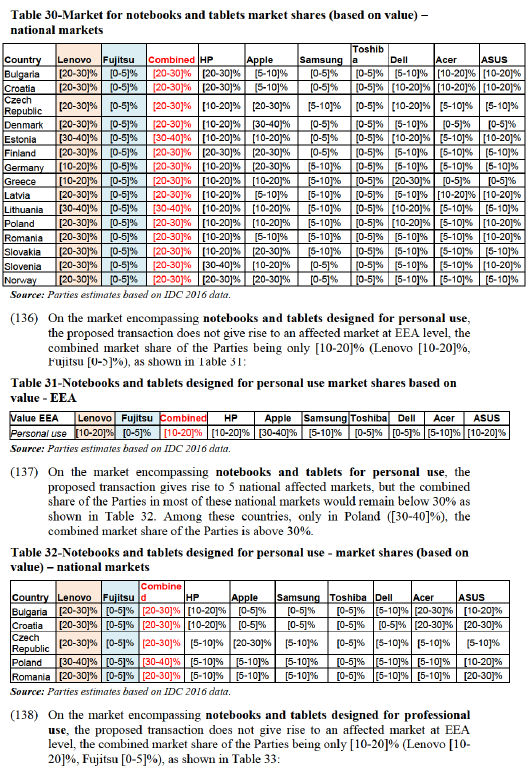

(150) As regards the segment of notebooks and tablets for professional use, the transaction gives rise to 14 national affected markets but only in 5 countries the combined market share of the Parties is above 30%: Denmark ([40-50]%), Estonia ([40-50]%), Finland ([30-40]%), Lithuania ([30-40]%) and Romania ([30- 40]%).

(151) In Denmark, in 2016, the combined market share of the Parties would be [40- 50]%, with Fujitsu contributing an increment of [0-5]%. The Commission notes that between 2014 and 2015, the market share of Fujitsu has dropped from [0-5]% to [0-5]% and that Fujitsu is a minor player in this market, behind Apple ([10- 20]%), HP ([10-20]%), Dell ([10-20]%), Samsung ([0-5]%) and Acer ([0-5]%). The Commission notes that two other players, Toshiba and Asus are also present in Denmark.

(152) In Estonia, in 2016, the combined market share of the Parties would be [40-50]%, with Fujitsu contributing an increment of [0-5]%. The Commission notes that between 2014 and 2015, the market share of Fujitsu has slightly increased from [0-5]% to [0-5]% but that Fujitsu is a minor player in this market, behind HP ([20-30]%), Dell ([10-20]%), Asus ([5-10]%), Apple ([0-5]%) and Acer ([0-5]%).

(153) The Commission notes that in Finland ([30-40]%), Lithuania ([30-40]%) and Romania ([30-40]%), the increment brought by the transaction is low and in any case below 2%. In Finland the increment brought by the Transaction is slightly higher ([5-10]%). The Commission also notes that a number of strong suppliers, including HP, Acer, Asus, Dell and Apple will continue to compete in this segment in all these countries.

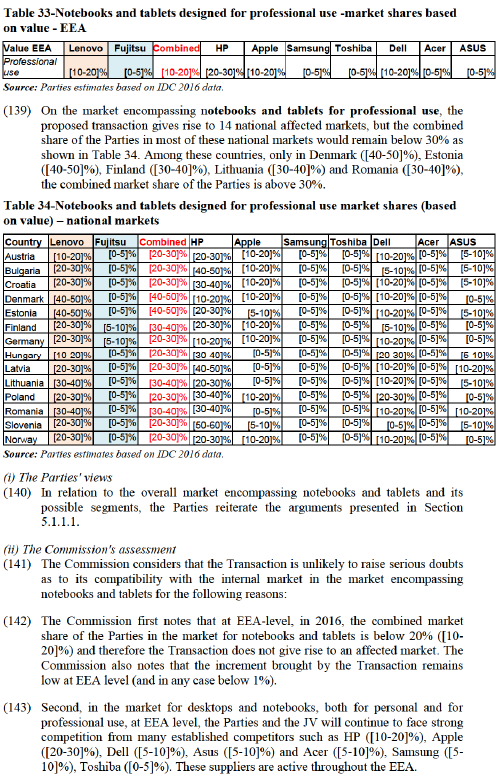

(154) For these reasons, the Commission concludes that the Transaction does not raise serious doubts as regards its compatibility with the internal market in relation to the market encompassing notebook and tablets, including its possible segments of notebooks and tablets for personal use or for professional use under any plausible geographic segmentation.

5.1.2. Market for PC accessories/peripherals

(i) The Parties' views

(155) The Parties submit their activities as regards accessories/peripherals are very limited in all product segments discussed in previous Commission decisions, both at EEA level and at national level and in any case do not give rise to any affected market.

(156) Currently FCCL […].The relevant arrangements in area of accessories/peripherals will remain unchanged after this transaction.

(ii) Commission's assessment

(157) The Commission first notes that the Transaction does not give rise to an affected market with respect to peripherals and accessories neither at EEA-level, nor at national level.

(158) The Commission also notes that respondents to the market investigations explained that Fujitsu is a minor player in the area of peripherals and accessories and did not raise any concerns as regards this market and its possible segmentations. (59)

(159) For these reasons the Commission takes the view that the proposed Transaction does not raise serious doubts as regards its compatibility with the internal market in respect of the markets of computer accessories and peripherals, under any plausible geographic segmentation.

5.2. Coordinated effects

(160) According to the Horizontal Merger Guidelines, coordination is more likely to emerge in markets where it is relatively simple to reach a common understanding on the terms of coordination. In addition, three conditions are necessary for coordination to be sustainable. First, the coordinating firms must be able to monitor to a sufficient degree whether the terms of coordination are being adhered to. Second, discipline requires that there is some form of credible deterrent mechanism that can be activated if deviation is detected. Third, the reactions of outsiders, such as current and future competitors not participating in the coordination, as well as customers, should not be able to jeopardise the results expected from the coordination. (60)

(161) The Commission considers that the Transaction does not affect the structure of the markets discussed in Section 5.1. in such a way that the conditions for coordination would be fulfilled post-Transaction and that therefore the Transaction is unlikely to lead to coordinated effects in the overall market for PCs and its possible segments in the EEA and in the affected national markets for the following reasons:

(162) First, the Commission notes that the Parties' combined share at EEA level remains around 20% or lower in all markets and market segments discussed in Section 5.1., and in most national markets the combined share of the Parties remains under 30%. Furthermore, beside the Parties, a large number of suppliers will continue to compete in these markets, including HP, Apple, Dell, Asus, Acer, Toshiba and Samsung.

(163) Second, the Transaction will not eliminate a significant competitive force from these markets.

(164) Third, the Commission considers that the Transaction will only bring a small change in market symmetry (given Fujitsu’s position as one of the minor competitors and therefore the small increment). There are no indications that any of the merging parties were preventing or disrupting any attempts at coordination in the past.

(165) Finally, the large product portfolios and differentiated products that competitors in these markets have are unlikely to facilitate coordination in this case.

5.3. Vertical effects

(166) The Transaction gives rise to a vertical relationship between the upstream market for PCs - desktops, notebooks and tablets where both Parties are active and the downstream market for IT services where Fujitsu is active, as PCs can be considered an input for the market for IT services.

(i) The Parties' views

(167) The Parties submit that the market for Solutions Business or IT services is potentially vertically related to the market for manufacturing of desktops, notebooks and tablets. Fujitsu is active in this market and its businesses can be grouped into Infrastructure solutions, Industry Solutions and Business and Technology Solutions. (61) Infrastructure Solutions typically consist of various IT components and combine them to serve specific infrastructure related usage scenarios. Industry Solutions consist in the design, building and operation of IT systems and services to improve efficiency, increase productivity and reduce costs for customers. The remaining Business and Technology Solutions can relate to areas such as human centric workplaces, administration, smart mobility, smart grids, technical computing, and security.

(168) The Parties submit that Fujitsu's activities in the IT services market are limited. The Parties explain that Fujitsu has a market share of [0-5]% at EEA level in the IT services market and its possible segmentations, and its market share in each of the EEA countries is not materially different from its market share at EEA level (approximately [0-5]%) with the only exception of Finland (approximately [5- 10]%) (62).

(169) Fujitsu also explains that it currently has no direct sales to the main competitors in the IT services market (IBM, Accenture, Atos, Capgemini), while Lenovo currently sells PCs to three of these companies [details of Lenovo’s business activities].

(ii) Commission's assessment

(170) According to the Non-Horizontal Merger Guidelines, foreclosure occurs when actual or potential rivals’ access to supplies or markets is hampered, thereby reducing those companies’ ability and/or incentive to compete. Such foreclosure may discourage entry or expansion of rivals or encourage their exit. (63)

(171) The Non-Horizontal Merger Guidelines distinguish between two forms of foreclosure: input foreclosure occurs where the merger is likely to raise the costs of downstream rivals by restricting their access to an important input and customer foreclosure occurs where the merger is likely to foreclose upstream rivals by restricting their access to a sufficient customer base. (64)

(172) In order for foreclosure to be a concern, three conditions need to be met post- merger: (i) the merged entity needs to have the ability to foreclose its rivals; (ii) the merged entity needs to have the incentive to foreclose its rivals; and (iii) the foreclosure strategy needs to have a significant detrimental effect on the parameters of competition on the downstream market (input foreclosure) or on consumers (customer foreclosure). In practice, these factors are often examined together since they are closely intertwined.

(173) The Commission has analysed in the present case whether the Transaction could give rise to a possible risk of input foreclosure for the desktops, notebooks and tablets supplied by the Parties to the detriment of the Parties' competitors active in the downstream market for IT services and its possible segments thereof. The Commission takes the view that the Transaction is unlikely to give rise to input or customer foreclosure concerns for the following reasons:

(174) First, the Commission notes that the Parties and the JV would not have the ability to foreclose Fujitsu's rival suppliers on the IT services market, given that the Parties would not hold market power in any of the possible upstream markets for desktops, notebooks and tablets for professional use. (65)

(175) Second, IT services suppliers would have many options to purchase their desktops, notebooks and tablets on the upstream market, such as HP, Dell, Asus, Acer or Apple.

(176) Third, market investigation respondents did not raise concerns with respect to IT services. (66)

(177) Given Fujitsu's very limited position in the downstream market for IT services and its possible segmentations thereof, both at EEA level and at national level, the Commission considers that customer foreclosure concerns can also be excluded.

(178) In light of the above, the Commission concludes that the Transaction does not give rise to serious doubts as to its compatibility with the internal market in relation to the vertical link between the upstream market for PCs - desktops, notebooks and tablets and the downstream market for IT services.

6. CONCLUSION

(179) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 Publication in the Official Journal of the European Union No C 96, 14.03.2018, p. 31.

4 Turnover calculated in accordance with Article 5 of the Merger Regulation.

5 Desktops are stand-alone computers whose use is usually restricted to a fixed place.

6 Notebooks (also referred to as ‘laptops’) are compact computers with an integrated keyboard, a flat screen, a large storage hard disk, and a battery. They are designed for either private or business mobile users, and, as such, are highly transportable.

7 Tablets are mobile devices between a laptop and a smartphone. They are generally operated using a touch screen and run a mobile operating system, which may be proprietary (e.g. iOS on the Apple iPad) or non-proprietary (e.g. Android on the Samsung Galaxy Tab).

8 Also referred to as “consumer”.

9 Also referred to as “non-consumer”.

10 See case M.4979 - Acer / Packard Bell (2008), paragraph 16.

11 See case M.4979 - Acer / Packard Bell (2008), paragraph 16-17.

12 See responses to Questionnaire Q1 to competitors, Questions 3-7, Questionnaire Q2 to distributors and resellers, questions B1 and B2 and Questionnaire Q3 to business customers, question B2.

13 See responses to Questionnaire Q1 to competitors, Questions 3-7.

14 See responses to Questionnaire Q1 to competitors, Questions 3-7, Questionnaire Q2 to distributors and resellers, questions B1 and B2 and Questionnaire Q3 to business customers, question B2.

15 See responses to Questionnaire Q1 to competitors, Questions 9-10, Questionnaire Q2 to distributors and resellers, questions B3 and B4 and Questionnaire Q3 to business customers, question B3.

16 See responses to Questionnaire Q1 to competitors, Question 9 and 10.

17 See responses to Questionnaire Q2 to distributors and resellers, questions B3 and B4.

18 Questionnaire Q3 to business customers, question B3.

19 See Commission's decision of 26 July 2011 in case M. 6196 - Lenovo/Medion, paragraph 26.

20 See Commission decision of 26 March 2009 in Case COMP/M.5455 – TPV/Philips Branded Monitors and Commission's decision of 26 July 2011 in case M. 6196 - Lenovo/Medion, paragraph 20.

21 Commission decision in case M.6127 - Atos/Siemens IT Solutions & Services, of 25 March 2011.

22 Commission decision in case M. 7458 - IBM/INF Business of Deutsche Lufthansa, of 15 December 2014.

23 Commission decision in case M. 8180 - Verizon/Yahoo, of 21 December 2016.

24 Commission Decisions in case M.4979 - Acer / Packard Bell, paragraph 21-23 and M.6196 - Lenovo / Medion, paragraph 17.

25 Commission decisions in M.7047 - Microsoft/ Nokia, paragraphs 70-72 and M.7202 – Lenovo/ Motorola Mobility, paragraphs 27-29.

26 See responses to Questionnaire Q1 to competitors, Questions 11-19, Questionnaire Q2 to distributors and resellers, questions C1 - C9 and Questionnaire Q3 to business customers, questions C1-C6.

27 See responses to Questionnaire Q1 to competitors, Question 14.

28 See responses to Questionnaire Q1 to competitors, Questions 11, Questionnaire Q2 to distributors and resellers, questions C1 – C3 and Questionnaire Q3 to business customers, questions C4-C6. .

29 See responses to Questionnaire Q2 to distributors and resellers, questions C1 – C3.

30 See responses to Questionnaire Q3 to business customers, questions C1-C3.

31 See Commission's decision of 26 July 2011 in case M. 6196 - Lenovo/Medion.

32 Commission decisions in case M. 7458 - IBM/INF Business of Deutsche Lufthansa, of 15 December 2014 and case M. 8180 - Verizon/Yahoo, of 21 December 2016.

33 Figures based on volume are similar to those based on value, according to IDC data.

34 OJ 2004/C 31/03.

35 See responses to Questionnaire Q1 to competitors, Questions 20-23, Questionnaire Q2 to distributors and resellers, questions D1-D5 and Questionnaire Q3 to business customers, questions D1-D5.

36 See responses to Questionnaire Q1 to competitors, Questions 24, Questionnaire Q2 to distributors and resellers, questions D8-D10 and Questionnaire Q3 to business customers, questions D8-D10.

37 See responses Questionnaire Q2 to distributors and resellers, questions D6-D7 and Questionnaire Q3 to business customers, questions D6-D7.

38 See responses to Questionnaire Q1 to competitors, Questions 25, Questionnaire Q2 to distributors and resellers, questions E1-E7 and Questionnaire Q3 to business customers, questions E1-E7.

39 See responses to Questionnaire Q1 to competitors, Questions 27-33, Questionnaire Q2 to distributors and resellers, questions F1-F7 and Questionnaire Q3 to business customers, questions F1-F7.

40 See responses to Questionnaire Q1 to competitors, Questions 20.1, 20.4, 21.1., 21.4, 22.1 and 22.4, Questionnaire Q2 to distributors and resellers, questions D2.1., D2.4., D3.1., D3.4, D4.1. and D4.4. and Questionnaire Q3 to business customers, questions D2.1., D2.4., D3.1., D3.4, D4.1. and D4.4..

41 See responses to Questionnaire Q1 to competitors, Questions 24, Questionnaire Q2 to distributors and resellers, questions D8-D10 and Questionnaire Q3 to business customers, questions D8-D10.

42 See responses Questionnaire Q2 to distributors and resellers, questions D6-D7 and Questionnaire Q3 to business customers, questions D6-D7.

43 See responses to Questionnaire Q1 to competitors, Questions 27-33, Questionnaire Q2 to distributors and resellers, questions F1-F7 and Questionnaire Q3 to business customers, questions F1-F7.

44 The Parties submit that Lenovo’s strong position in Denamark is (…).

45 See responses to Questionnaire Q1 to competitors, Questions 20.1, 20.4, 21.1., 21.4, 22.1 and 22.4, Questionnaire Q2 to distributors and resellers, questions D2.1., D2.4., D3.1., D3.4, D4.1. and D4.4. and Questionnaire Q3 to business customers, questions D2.1., D2.4., D3.1., D3.4, D4.1. and D4.4..

46 See responses to Questionnaire Q1 to competitors, Questions 24, Questionnaire Q2 to distributors and resellers, questions D8-D10 and Questionnaire Q3 to business customers, questions D8-D10.

47 See responses Questionnaire Q2 to distributors and resellers, questions D6-D7 and Questionnaire Q3 to business customers, questions D6-D7.

48 See responses to Questionnaire Q1 to competitors, Questions 27-33, Questionnaire Q2 to distributors and resellers, questions F1-F7 and Questionnaire Q3 to business customers, questions F1-F7.

49 At worldwide level, the Parties combined share remains below (5-10)% in value, irrespective of the market segment.

50 At worldwide level, the Parties combined share remains below (5-10)% in value, irrespective of the market segment.

51 See responses to Questionnaire Q1 to competitors, Questions 20.1, 20.4, 21.1., 21.4, 22.1 and 22.4, Questionnaire Q2 to distributors and resellers, questions D2.1., D2.4., D3.1., D3.4, D4.1. and D4.4. and Questionnaire Q3 to business customers, questions D2.1., D2.4., D3.1., D3.4, D4.1. and D4.4..

52 See responses to Questionnaire Q1 to competitors, Questions 24, Questionnaire Q2 to distributors and resellers, questions D8-D10 and Questionnaire Q3 to business customers, questions D8-D10.

53 See responses Questionnaire Q2 to distributors and resellers, questions D6-D7 and Questionnaire Q3 to business customers, questions D6-D7.

54 See responses to Questionnaire Q1 to competitors, Questions 27-33, Questionnaire Q2 to distributors and resellers, questions F1-F7 and Questionnaire Q3 to business customers, questions F1-F7.

55 See responses to Questionnaire Q1 to competitors, Questions 20.1, 20.4, 21.1., 21.4, 22.1 and 22.4, Questionnaire Q2 to distributors and resellers, questions D2.1., D2.4., D3.1., D3.4, D4.1. and D4.4. and Questionnaire Q3 to business customers, questions D2.1., D2.4., D3.1., D3.4, D4.1. and D4.4..

56 See responses to Questionnaire Q1 to competitors, Questions 24, Questionnaire Q2 to distributors and resellers, questions D8-D10 and Questionnaire Q3 to business customers, questions D8-D10.

57 See responses Questionnaire Q2 to distributors and resellers, questions D6-D7 and Questionnaire Q3 to business customers, questions D6-D7.

58 See responses to Questionnaire Q1 to competitors, Questions 27-33, Questionnaire Q2 to distributors and resellers, questions F1-F7 and Questionnaire Q3 to business customers, questions F1-F7.

59 See responses to Questionnaire Q1 to competitors, Question 34, Questionnaire Q2 to distributors and resellers, question F8 and Questionnaire Q3 to business customers, question F8.

60 Horizontal Merger Guidelines, paragraph 41.

61 The Parties submit that Lenovo has some limited activities in the IT services market which are related to after-sale services.

62 In countries other than Finland, Fujitsu’s market share ranges between [0-5]% and [0-5]%.

63 Guidelines on the assessment of non-horizontal mergers under the Council Regulation on the control of concentration between undertakings (the Non-Horizontal Merger Guidelines) OJ C 265/6, 18.10.2008, paragraphs 29-30.

64 See Non-Horizontal Merger Guidelines, paragraph 30.

65 See sections 5.1.1.2, 5.1.1.3 and 5.1.1.4.

66 See responses to Questionnaire Q1 to competitors, Question F1, Questionnaire Q2 to distributors and resellers, question G1 and Questionnaire Q3 to business customers, question G1.