Commission, May 8, 2018, No M.8770

EUROPEAN COMMISSION

Judgment

PRYSMIAN / GENERAL CABLE

Subject: Case M.8770 – Prysmian/General Cable

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 28 March 2018, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Prysmian S.p.A. ("Prysmian" or "the Notifying Party") acquires control of General Cable Corporation ("General Cable"), by way of purchase of shares (the "Transaction")3. Prysmian and General Cable are collectively referred to as "Parties".

1. THE PARTIES

(2) Prysmian, based in Italy, is the holding company of the Prysmian Group, which is active worldwide in the development, design, production, supply and installation of cables used in the energy and telecommunications industries.

(3) General Cable, based in the United States of America ("United States"), is active worldwide in the development, design, production, supply and distribution of wire and cable products used in a variety of industries, including energy and telecommunications.

2. THE OPERATION

(4) The Transaction concerns the acquisition of sole control by Prysmian over General Cable by way of purchase of shares. Under the Merger Agreement signed on 3 December 2017, Prysmian committed to acquire 100% of the outstanding shares of General Cable for a cash consideration of USD 30 per share, which amounts to total aggregate consideration of approximately USD 1 500 million.

(5) As part of the Transaction, Alisea Corporation ("Alisea"), a newly created United States-based company wholly owned by Prysmian, will be merged with and into General Cable. The separate corporate existence of Alisea will cease and General Cable will be the surviving corporation in the merger and will become a wholly- owned subsidiary of Prysmian.

(6) The Transaction therefore constitutes a concentration pursuant to Article 3(1)(b) of the Merger Regulation.

3. EU DIMENSION

(7) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million4. Each of them has an EU-wide turnover in excess of EUR 250 million, but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension.

4. RELEVANT MARKETS

(8) Both Parties are active in the production and sale of telecommunications cables ("telecom") and energy cables, including cable accessories. While Prysmian is one of the main suppliers of such cables in Europe, General Cable has a stronger presence in North and Latin America. In Europe, General Cable has six manufacturing facilities, located in Germany, France and Spain.

(9) Telecom cables are used to transmit voice, data or other forms of communication signals via electromagnetical or optical (light) signals through a fixed-line connection. A distinction can be made between optical fibre cables and copper cables. Optical fibre cables are typically used for the transmission of electronic communications signals in local area networks (LANs), last-mile access networks, metropolitan area networks, and long-distance networks (including submarine connections). The Parties also identify possible separate markets for optical ground wire (OPGW), optical fibres, cable accessories/connectivity products (such as rack products, rack mounted products, point-of-presence solutions, distribution closures, duct systems), and copper rod.

(10) The Parties' activities overlap in optical fibre cables, copper cables, and optical ground wire. There is no overlap between the Parties' operations in optical fibres and no overlap in the EEA in copper rod. With regard to accessories/connectivity products, General Cable does not sell such products on a stand-alone basis to third parties.

(11) Energy cables include three different types of cables: (i) power cables for the transmission and distribution of electrical power; (ii) general wiring used for electrical systems in buildings and industrial applications including for railways and automotive applications; and (iii) overhead bare conductors for the aerial transmission of energy. Overhead bare conductors are not, however, technically considered as cables as they are not insulated.

(12) The Parties are both active in the manufacture and supply of general wiring and power cables. There is no overlap in overhead bare conductors, which are only supplied by General Cable. Both Parties also supply power cable accessories (cable joints, terminations, and resins), and cable installation and services. General Cable does not sell any cable accessories on a stand-alone basis, and neither Party provide cable installation, services and maintenance on a stand- alone basis, but exclusively as part of the power cable supply.

4.1.Product Market definition

4.1.1.Optical fibre cables

(13) The Notifying Party considers that there is a single market for optical fibre cables, without the need for further segmentations. The Notifying Party submits that it would make little sense to make a distinction based on the type of cable, in particular as regards the distinction between single-mode fibre ("SMF") and cables using multi-mode fibre ("MMF"), because the specifications in this market are made by customers, and that a range of different cables are generally supplied within the same contract.

(14) The Commission has previously considered the market for optical fibre cables and its possible sub-segmentations but ultimately left the exact product market definition open.5 Potential sub-segmentations include terrestrial and submarine optical fibre cables, and cables using SMF and cables using MMF.

(15) The Commission concludes that, in line with its previous decisions, optical fibre cables constitute a relevant product market. For the purpose of the present decision, the question as to whether SMF and MMF6, and terrestrial and submarine optical fibre cables constitute separate product markets can be left open as no competition concern arises under any alternative product market definition.

4.1.2.General wiring cables

(16) The Notifying Party refers to the Commissions previous decisions and does not dispute the Commission's assessment as included therein. It submits that general wiring cables include all cables with a common production process: the reference production process is based on the same manufacturing sequence7. The manufacturing sequence is completed in full or in part according to cable design defined by the final customer, specific for the final use/application. From the demand side, the final customer has the possibility to buy products for different applications through different supply channels and, therefore, it is common in the market to consider general wiring as a single market.

(17) The Commission has previously considered a single market for general wiring cables. It has also considered a further subdivision of the general wiring market based on applications, but left it open whether such subdivisions could constitute separate relevant product markets.

(18) The Commission has noted that general wiring cables are sold through electrical wholesalers and cable distributors or directly to installers and to original equipment manufacturers ("OEMs").

(19) General wiring cables may have many different industrial applications requiring specific features. Substitutability considerations do not apply to the single product but rather to the suppliers’ ability to adapt their cables to customers’ specifications.

(20) Although on the demand side general wiring cables for different applications have different requirements and may not always be used for other applications, on the supply side the design and production of wiring for different types of applications are largely similar, even if some adaptation (including in some instances the purchase of additional machinery) may be required in order to switch to the production of general wiring cables to suit another industrial application. The Commission has previously also noted that, even if smaller suppliers may concentrate on specific types of cables or applications, most mid-sized and large suppliers produce the whole range of general wiring cables for different applications.

(21) The market investigation has confirmed the approach taken by the Commission in its previous decisions, namely that general wiring constitutes a single relevant product market, with a majority of the respondents indicating that the general wiring market should not be further segmented by application. The respondents supporting a further segmentation by application did not, however, indicate the criteria relevant for such further segmentation.8

(22) The Commission concludes that for the purposes of this decision, and in line with its previous decisions, general wiring constitutes a single product market.

4.1.3.Power cables

(23) The Commission has previously segmented power cables by voltage (low and medium voltage and high and extra high voltage) and considered a further segmentation by the insulation technology used (mass impregnation and extruded/XLPE technology), the transmission technology (alternating and direct current), and the installation environment (underground and submarine).

(24) Voltage: In its past decisions, the Commission considered two separate power cable markets based on voltage to be delineated as follows: (i) low voltage ("LV") cables rated up to 1 kilovolt ("kV") and medium voltage ("MV") cables rated from 1 kV to 33/45 kV on the one hand; and (ii) high voltage ("HV") cables rated 33/45 kV to 132 kV and extra high voltage ("EHV") cables rated 275 kV and 400 kV on the other hand9. The Commission has also considered whether the more appropriate threshold to separate the LV/MV and HV/EHV markets would be 66 kV instead of 33/45 kV without reaching a definitive conclusion.10

(25) This alternative voltage range delimitation (i.e. 66 kV) is put forward also by the Notifying Party in the present case. The Notifying Party explains that LV/MV power cables are predominantly used for the distribution of electricity. They are commodity products, which are purchased by national utilities, but also by regional and local utilities as well as the industry (for example, railways, manufacturing enterprises, etc.). LV/MV cables are generally characterized by large standardization, which implies that products from different manufacturers are often very similar as they need to comply with detailed constructional specifications. HV/EHV power cables are, in turn, used for the transmission of power mainly by large national operators, such as Transmission System Operators ("TSOs") and Distribution Network Operators ("DNOs"). The customer usually purchases HV and EHV cables on a project-by-project basis, thereby defining the type of cable required for a specific project. Customers may order complete installation with cable terminations, design and construction, often including accessories, installation, supervision and system integration.

(26) The Notifying Party argues that cables up to and including 66 kV should be considered MV power cables. The main reason to delimit the LV/MV power cable market at 66 kV is due to the technology development relating in particular to submarine inter-array cables used in offshore windfarms. These are short- length cables connecting wind turbines to each other. The Notifying Party argues that such inter-array cables are typically considered as MV cables as their function is one of distribution, while so-called "export cables" that connect the offshore windfarm to the shore are HV/EHV transmission cables.

(27) The responses to the market investigation are mixed in terms of the voltage level which separates MV from HV power cables. Respondents are split between a cut- off point at 33/45 kV and 66 kV, with respondents also indicating alternative cut- off voltages based on e.g. national standards, to separate MV from HV power cables. It was also suggested that the cut-off point may be different for submarine and underground power cables, with the 66 kV cut-off point more suitable for submarine applications.11

(28) Insulation: The two main technologies used for the insulation of power cables are: (i) mass impregnation ("MI"), which is the older technology, where the conductor is wrapped in paper impregnated with dielectric fluid; and (ii) extruded cables/XLPE technology, which is the newer technology, where the conductor is contained within cross-linked polyethylene. With regard to underground applications, XLPE is used almost exclusively. With regard to submarine applications, MI is being replaced with XLPE due to lower production costs, however adoption has been slow.

(29) The Commission has previously considered a segmentation of power cables based on insulation technology, i.e. between MI and XLPE.12 The two technologies were found to be non-substitutable from a supply-side perspective as the equipment used for the production of MI cables cannot be used for XLPE production, and vice versa. However, from the demand-side, the Commission has noted that MI technology is to some extent being replaced by XLPE technology (in particular for LV, MV and HV cables) as it is simpler to install, requires less maintenance and is more environmentally friendly as the risk of leakage is reduced. On that basis, the Commission has concluded that this segmentation was not warranted for either LV/MV cables or HV/EHV cables.

(30) The Notifying Party does not dispute this market segmentation. It notes that such potential segmentation only applies to submarine HV/EHV cables, as MI technology is generally not used for LV/MV power cables nor is it used for underground cables, except for the underground cable sections at the end of MI HVDC insulated submarine cable links. As regards underground HV/EHV cables, the Notifying Party consequently considers that segmentation by insulation is not relevant, as only extruded/XLPE technology has been used in the EEA in recent years.

(31) The market investigation suggests that there is a distinction between the two insulation methods. From the supply side all respondents confirmed that MI and XLPE insulated cables are different so that switching from the production of cables using one insulation technology to cables using another insulation technology would imply significant technical difficulties and/or costs. From the demand side, the majority of respondents took the view that it is impossible or very difficult to use these two insulation technologies interchangeably. Respondents explained that XLPE is mainly used for HV/EHV AC whereas MI is mainly used for EHV DC applications. MI is a more mature and therefore more reliable technology whereas XLPE is cost effective but does not yet have a long reliability feedback.13

(32) Transmission technology: Power cables are either alternating current ("AC") or direct current ("DC").

(33) The Commission has previously considered the AC/DC segmentation and found that AC and DC cables could form different product markets. 14 From a demand side, DC cables systems appear to be more costly as additional AC/DC converters were needed at either end of the DC cable given that both the power production (e.g. in a wind farm) and the national transmission systems are AC. Above a certain distance (approximately 80 to 120km), DC systems become cost effective as the high initial expenditure outweighs the on-going cost associated with energy losses that occur on AC cables. AC appeared to be the preferred choice unless it is technically necessary to use DC. From a supply side, there appeared to be technical barriers to switching related to the development of DC cable technology (in particular for the associated accessories).

(34) The Notifying Party notes that such segmentation between AC and DC only exists for longer length cables with higher voltage and therefore does not apply to LV/MV cables. For HV/EHV, the choice between AC and DC technology is generally dictated by technical factors and economic factors. These factors are applicable to both land cable systems and submarine cable systems. Some well- known technical factors dictating the choice of DC technology are the connection of networks having different frequencies, a decision to keep two asynchronous networks operating at their own set frequencies, and the need to avoid an increase of short circuit currents in the AC networks at both ends of the HVDC link.

(35) The basis for the economic analysis is the "break-even distance" concept. The "break-even distance" is not a fixed value but it varies as a function of technology developments and other technical and economic factors (e.g. the cost of raw materials). The Notifying Party has estimated the "break-even distance" for power cables (both underground and submarine) is in the order of 100-150 km.

(36) According to the Notifying Party, the ease of switching from the manufacturing of AC to DC underground power cables is comparable to the ease of switching from the manufacturing of AC submarine power cables to DC submarine power cables. However, it should be considered that, even though both HVDC underground and HVDC submarine power cables are normally used in long distance projects, HVDC submarine systems require a more sophisticated design, the development of flexible joints, major factory investments in cable handling facilities, know-how, installation, and project management capabilities that are greater than for HVDC land projects.

(37) Both from a demand and a supply side, the market investigation has confirmed that several factors differentiate AC from DC cables, such as the length of the cable, the power to be transmitted, costs, and frequency of networks to be connected.15 The break-even distance has been broadly estimated at 100-150km.16 From the supply side, a strong majority of cable suppliers took the view that AC and DC cables are different so that switching from the production of AC to DC and vice versa would imply significant technical difficulties and/or costs.17

(38) Installation environment: Power cables can be installed either on land (so called underground cables) or on the sea bed (so called submarine cables).

(39) The Commission has previously considered the segmentation between underground and submarine power cables and found that underground and submarine cables could form different product markets.18 A number of factors suggested that submarine and underground cables could belong to different product markets, such as limited or non-existent interchangeability and substitutability as well as possible differences in the manufacturing processes and the know-how needed to manufacture either type of power cables.

(40) The Notifying Party notes that underground and submarine cables should be considered as separate product markets due to the vastly different product characteristics and intended use, which make them not substitutable. From the supply side, the manufacturing process of submarine and land cable is the same except for an extra-step (armouring) required for the former. Therefore, submarine cable capacity can be used for the production of underground cables, if necessary. This results in one-sided supply substitutability of underground with submarine cables. From the demand side, the Notifying Party notes that submarine cables are not standard products: they are usually purchased on a project-by-project basis, and they are bespoke for each project; strong engineering teams are required not only for systems design but also for installation, as well as installation capabilities; submarine power cables are also manufactured and supplied in very long lengths (to limit the amount of joints under water).

(41) The market investigation has confirmed to a large extent the above position. From the supply side, the respondents confirmed that switching from the production of underground power cables to submarine power cables, or vice versa, would imply significant technical difficulties and/or costs.19 Factors that explain this difficulty include the importance of closeness/access to the sea, and need for additional equipment, large investments and significant time for switching. From the demand side, customers agree that submarine and underground cables are completely different and cannot be used interchangeably.20 Certain respondents take the view that the actual cables used in submarine and underground applications are similar but there are certain differences, for example waterproof coating and armouring, which means that a submarine cable can from a technical perspective be used for underground applications but not vice versa. However, it may not be cost-effective to use a submarine cable for underground applications.21

(42) In any event, for the purposes of the present decision, the Commission considers that the exact product market definition for LV/MV and HV/EHV power cables can be left open given that the Transaction does not raise serious doubt as to its compatibility with the internal market, even on the narrowest possible market definition.

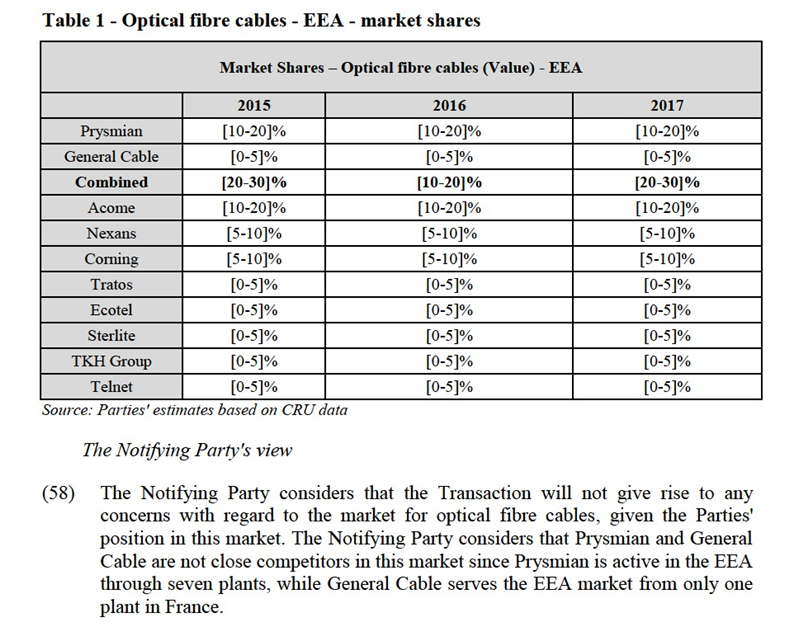

4.2.Geographic market definition

4.2.1.Optical fibre cables

(43) The Commission has previously considered all telecom cables markets, including optical fibre cables and copper cables, to be at least EEA-wide due to their cross- border nature both in terms of supply and demand22.

(44) The Notifying Party considers that for optical fibre cables, the market would be worldwide due to various elements, including the international presence of optical fibre cable suppliers, standardisation of cables, significant trade flows (both exports and imports) in optical fibre cables, […]. The Notifying Party points to the fact that a significant part of optical fibre cables sold in the EEA are imported from outside the EEA, especially from North America and the Asian Pacific areas. Sterlite, an Indian manufacturer, is mentioned as one of the suppliers of optical fibre cables in the EEA which imports all its cables from its plants in India.

(45) The results of the market investigation do not put into question the Commission's previous findings as to the geographic scope of the telecom cables markets being at least EEA wide. Few respondents (in particular a few customers based in France)23 mention the limited number of suppliers that offer optical fibre cables that have been qualified by customers as meeting the specific technical specifications of telecom operator's optical fibre infrastructure in a country.24 However, the market investigation has not revealed anything which would cast a doubt on the ability of customers, in particular large telecom operators, to qualify additional suppliers to take part in their procurement processes. The Commission does not therefore consider appropriate to depart from previous findings that the market in question is at least EEA wide.

(46) For the purpose of the present decision it can thus be concluded that the geographic scope of the market for telecom cables and optical fibre cables in particular, is at least EEA-wide.

4.2.2.General wiring cables

(47) The Commission has previously considered the market for general wiring to be at least EEA wide. First, cable specifications have been harmonised. Second, there are multinational actors on the market operating at European level. Third, customers purchase general wiring from other EEA countries as well as outside of the EEA.

(48) The Notifying Party does not dispute this geographic market definition.

(49) The market investigation confirmed to a large extent the existence of an at least EEA-wide market for general wiring cables. A large majority of respondents, both customers and competitors, indicate that the market is at least EEA wide.25 Only a small number of respondents pointed to factors such as national requirements, logistics and importance of local presences that could lead to a narrower geographic market.26 On this point, the Commission notes that, while very few customers indicated that they would have difficulties in purchasing general wiring cables from suppliers located outside their own country, a third of respondents indicate that they actually purchase from suppliers located in another EEA country.27 Apart from EEA based manufacturers, suppliers with manufacturing in North Africa (Maghreb) are mentioned as active in the EEA.28

(50) Based on the above and in line with the precedents of the Commission and for the purpose of the present decision it can be concluded that the geographic market for general wiring is at least EEA-wide.

4.2.3.Power cables

(51) The Commission has previously considered the market for the supply of power cables to be at least EEA-wide.29 First, product standards are widely harmonised across the EEA. Second, customers purchase EEA-wide. Third, due to the deregulation of electricity markets and low transport costs, trade flows between Member States have significantly increased.

(52) The Notifying Party does not dispute the Commission's findings.

(53) The market investigation broadly confirmed that there are limited differences between the conditions of supply in different EEA Member States, and that customers purchase on an EEA-wide basis. On LV/MV power cables, some customers may tend to purchase more from suppliers present in the same Member State of the customer, than from elsewhere in the EU. Even in such situations, the manufacturing of the power cable itself often occurs outside the borders of that country.30 The majority of customers and competitors responding to the market investigation consider that the market for LV/MV power cables, HV/EHV underground power cables, and HV/EHV submarine power cables to be at least EEA wide.31 A majority of customers also indicate that they are able to purchase different types of power cables equally from all countries in the EEA and that they currently purchase power cables from outside their own home country, either from elsewhere in the EEA or from suppliers located outside of the EEA.32

(54) The Commission considers that in line with its previous decisions, the geographic market for power cables is at least EEA wide.

5. COMPETITIVE ASSESSMENT

5.1.Horizontal non-coordinated effects

(55) The Transaction gives rise to five affected markets (or potential markets) at EEA level, namely: (i) optical fibre cables; (ii) general wiring; (iii) HV/EHV underground power cables; (iv) LV/MV submarine power cables; and (v) HV/EHV submarine power cables. The affected market will be discussed below. In addition, and despite the LV/MV underground power cable market not being an affected market at EEA level, in view of concerns raised by customers for such cables located in particular in France, the Commission will also discuss the LV/MV underground power cable market.

(56) The Transaction does not give rise to any vertical links between the Parties.

5.1.1. Market for optical fibre cables

(57) On the market for optical fibre cables, the Parties would have a combined market share of slightly above 20% based on market share figures for 2015 and 2017, as presented in 1:

with market shares above 10% at EEA level. General Cable is a smaller supplier, with [0-5]% market share in 2017. The increment brought by the Transaction is therefore limited.

(63) Third, the Parties are not very close competitors at EEA level. Prysmian has a wider product portfolio than General Cable34, targets a wide range of customers35, and is active throughout the EEA with seven manufacturing plants located in France, Spain, United Kingdom, Romania and the Netherlands.36 General Cable is only active in the manufacture and sale of optical fibre cables through its French subsidiary Silec, and only supplies customers from Silec's manufacturing plant located in France (Montereau). General Cable's customers are […].37

(64) Fourth, while the results of the market investigation give a mixed view as to the likely impact of the Transaction on the intensity of competition in the market for telecommunication cables and optical fibre cables specifically, a majority of respondents are confident that the Transaction has a neutral or positive impact on their own company38.

(65) Certain customers in France expressed some concerns regarding the impact of the Transaction on the optical cables market, citing the leading role that both Prysmian and General Cable, in addition to Nexans and Acome, play in the supply of optical fibre cables that meet the technical specifications and have been qualified by the telecom operators managing optical fibre infrastructure in France. The concerns are also linked to the current worldwide shortage of optical fibre, which is used for the manufacture of optical fibre cables. However, the Commission notes that this shortage is a result of undercapacity by manufacturers of optical fibre to meet the booming demand; nonetheless capacities are set to increase with the main optical fibre preform suppliers […] investing in such

The Notifying Party's view

(69) The Notifying Party submits that the Transaction will not impede competition in the general wiring market. The Parties' combined share remains under 25% in this market and General Cable is one of the smaller suppliers of general wiring cables accounting for only [0-5]% of the market in 2016.

(70) The Notifying Party points out that the general wiring market is highly fragmented with over 100 suppliers active in this market, including Nexans, Leoni and NKT. Further, the cables and wires in this market are generally standardised and entry on the market is not difficult. There has been continuous entry on this market in particular from extra-EEA countries including China, Egypt, Turkey, Russia, and Korea. Some of these suppliers such as Carslie from the United States, LS Cable from Korea and El Sewedi from Egypt are very active in the EEA.

(71) The Notifying Party further explains that General Cable is not a significant competitive force and that Prysmian and General Cable are not close competitors in this market. General Cable does not have any particular know-how or technology that other competitors in the industry do not have. General Cable has a much smaller footprint than Prysmian in the EU and it is not perceived as one of the main suppliers. There are no specific areas where Prysmian and General Cable compete more closely than any other general wiring suppliers.

(72) Finally, the Notifying Party considers that in light of the high number of manufacturers active in this market and the degree of standardisation of the general wiring products, the Parties' customers incur very low switching costs in changing suppliers. Moreover, the general wiring market suffers from an excess of capacity, enabling competing suppliers to increase supply to counter any hypothetical price increase by the merged entity post-Transaction.

Commission's assessment

(73) The Commission considers that the Transaction will not raise serious doubts as to its compatibility with the internal market in the general wiring market for the following reasons.

(74) According to the Horizontal Guidelines44, combined market shares below 25% may indicate that the concentration is not likely to impede effective competition.

(75) The Commission first notes that at EEA level, the combined share of the Parties remains [20-30]% in 2016, and remained [20-30]% in the previous two years as well. Prysmian has a share of almost [10-20]% in 2016, while General Cable is one of the smaller suppliers, with only [0-5]% market share.

(76) Second the Commission considers that there are many suppliers in the general wiring market, including Nexans ([10-20]%), Leoni ([5-10]%), NKT ([0-5]%), Wilms Cable ([0-5]%) and TF Cable ([0-5]%). Many other smaller suppliers, including local manufacturers, account for almost 50% of the market.

(77) Third, the results of the market investigation confirm the Notifying Party's statements that Prysmian and General Cable are not close competitors in the general wiring market, as most market participants considered Prysmian closer to other suppliers such as Nexans or NKT.45 Further, the large majority of respondents consider that sufficient suppliers will remain active in the market for general wiring cables.46 The market investigation has not provided any indication of suppliers being capacity constrained.

(78) Finally, the Commission notes that most respondents are of the opinion that the Transaction is unlikely to have any negative effects on the market for general wiring, mainly because there are many other suppliers on this market.47

(79) For these reasons, the Commission takes the view that the Transaction will not raise serious doubts as to its compatibility with the internal market in relation to general wiring cables in the EEA.

5.1.3. Market for LV/MV underground power cables

(80) The Transaction does not give rise to an affected market in relation to LV/MV underground power cables at EEA level. The Parties' combined market share remains below 20% between 2014 and 2016, irrespective of the voltage threshold considered (33/45 kV or 66 kV). General Cable is one of the smaller suppliers of LV/MV underground power cables, with a market share of [0-5]% between 2014 and 2016.48

(81) Certain customers of LV/MV underground power cables in France, including EDF/Enedis (which is responsible for the management of the largest part of the electricity distribution network), raised concerns that the Transaction would eliminate General Cable as an independent competitor and therefore would limit the number of viable suppliers of LV/MV cables in France.49 Those customers argued that because of specifications issued for these types of cables in France, logistic difficulties and transport costs, Prysmian and General Cable were their main viable suppliers50. In their view, post-Transaction, the merged entity may raise prices of underground LV/MV power cables in France.

(82) However, after further investigation into these claims, the Commission considers that such concerns are unfounded for the following reasons:

(83) First, the Commission notes that while the market is at least EEA wide (see above paragraphs (51)-(54)), also in France the Parties have limited market shares. In fact, in France, in 2017, the combined market share of the Parties amounted to [20-30]% (Prysmian [10-20]%, General Cable [10-20]%) in the market for underground LV/MV power cables, and that Prysmian's share has been declining since 2014 (when it amounted to [10-20]%), while General Cable's market share has remained relatively stable.

(84) Second, the Commission notes that in France the specifications for underground LV/MV power cables used in the distribution network are issued by EDF/Enedis51 and they do not differ significantly from specifications in other EEA countries, in particular neighbouring countries like Italy and Spain. Furthermore, cable customers are in charge of "qualifying" the suppliers, their plants and specific cable designs/products. The qualification process of a cable product may take up to 18 months52. However, suppliers which are in the process of being qualified by EDF/Enedis can already participate in calls for proposals (which are made public at EU-wide level) and be awarded one lot or more. These suppliers will be able to start supplying the products once the qualification process is over. As framework contracts are generally concluded for 4 years, this allows time for a new supplier to complete the qualification process and start supplying within the time of the framework contract.53

(85) Third, the Commission notes that, apart from the Parties, four other viable suppliers have been qualified by EDF/ENEDIS including Nexans, NKT (with qualified production plants in Germany and Czech Republic), TopCable (with qualified production plants in Spain), and Imacab (with production plant in Morocco in the process of being qualified)54. In the latest tender for medium-voltage cables (2018), EDF/Enedis awarded framework contracts with pre- determined volumes to six suppliers, including Nexans, NKT, TopCable and Imacab.55 Suppliers with plants outside of France are able to win sizeable contracts, including with EDF/Enedis.56 Therefore, customers such as EDF/ENEDIS are able to facilitate the entry on the market of new suppliers.

(86) Further, the Commission notes that transport costs57 and logistic difficulties are limited, with manufacturers relying on third party logistics providers to deliver the products to their customers58. Regular sized trucks are used to transport these products. Transport costs do not prevent suppliers from using plants located outside the borders of France to supply French customers. General Cable supplies part of its qualified medium voltage power cables for the French market from its plant in Spain (Barcelona region), where also TopCable has its manufacturing plant for such cables intended for France. NKT supplies the French market from its manufacturing plants in Cologne and the Czech Republic. Imacab, a newly qualified supplier by EDF/Enedis, will supply its cables from its plant in Morocco.59 This demonstrates that suppliers with plants outside France are able to supply French customers with underground LV/MV power cables without encountering major transport costs and logistic difficulties.

(87) Therefore Commission considers that French customers including EDF/ENEDIS will have a sufficient number of alternative suppliers which would be able to defeat any attempt on the part of the merged entity to raise prices.

(88) For these reasons, the Commission takes the view that the Transaction will not raise serious doubts as to its compatibility with the internal market in relation to underground LV/MV power cables in the EEA or in France.

5.1.4.Market for HV/EHV underground power cables

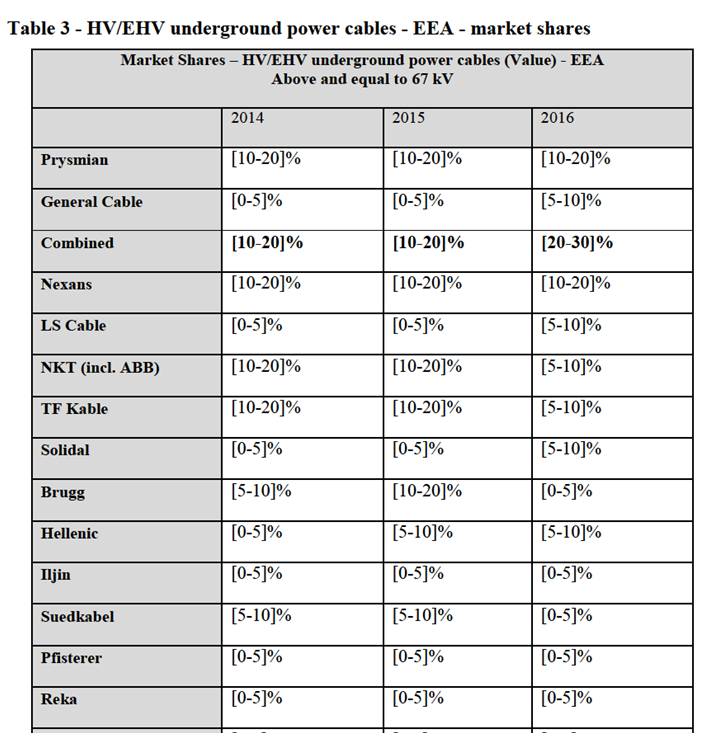

The Transaction gives rise to an affected market in relation to the overall market for underground HV/EHV power cables, where the combined market share of the Parties in 201660 is [20-30]% (Prysmian [10-20]%, General Cable [5-10]%), if the voltage threshold considered is 67 kV and above. If the voltage considered is 33/45 kV and above, the Transaction does not give rise to an affected market (combined market share: [10-20]% (in 2014), [10-20]% (in 2015), and [10-20]% (in 2016)). The Parties' and their competitors' market shares on the overall market for HV/EHV underground power cables are presented in

(89) Table 3 below:

The Notifying Party' views

(91) The Notifying Party considers that the overall market for underground HV/EHV power cables is very competitive, with many operators active from both EEA and non-EEA countries. Such power cables are sold either in the context of projects or in the context of multi-year framework contracts.

(92) The Notifying Party points out that the Parties' combined share will remain under 25% and that General Cable is one of the smaller suppliers in the EEA. The Notifying Party considers that the Transaction will not remove a significant competitive force, as General Cable does not have any particular know-how or technology compared to other suppliers and it has a much smaller footprint than Prysmian in the EEA. As a result, General Cable cannot be considered as a close competitor to Prysmian.

(93) As regards the possible market for underground HV/EHV DC power cables, the Notifying Party considers that this market represents only 1% of the overall HV/EHV power cables market (less than EUR 25 million in 2015-2016) and since this is a bidding market and revenues are generated in relation to large and infrequent interconnector projects, market shares are not representative of market power. Many other suppliers have the technology and capacity to produce underground HV/EHV DC power cables and could win future interconnector projects.

Commission's assessment

(94) The Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market in the overall market for underground HV/EHV power cables for the following reasons:

(95) First the Commission notes that the combined market share of the Parties in this market in 2016 amounted to only [20-30]% (Prysmian [10-20]%, General Cable [5-10]%).

(96) The Commission also notes that the market is extremely fragmented with over 15 players active in this market in the EEA. While Prysmian is the market leader, it is closely followed by other global suppliers such as Nexans, LS Cable and NKT.

(97) Second, the results of the market investigation show that Nexans and NKT are considered closer competitors to Prysmian than General Cable for underground HV/EHG power cables.62 Further, the large majority of respondents, including customers, consider that sufficient suppliers will remain active in the market for underground HV/EHG power cables63. Customers of underground HV/EHV power cables usually qualify several suppliers.64

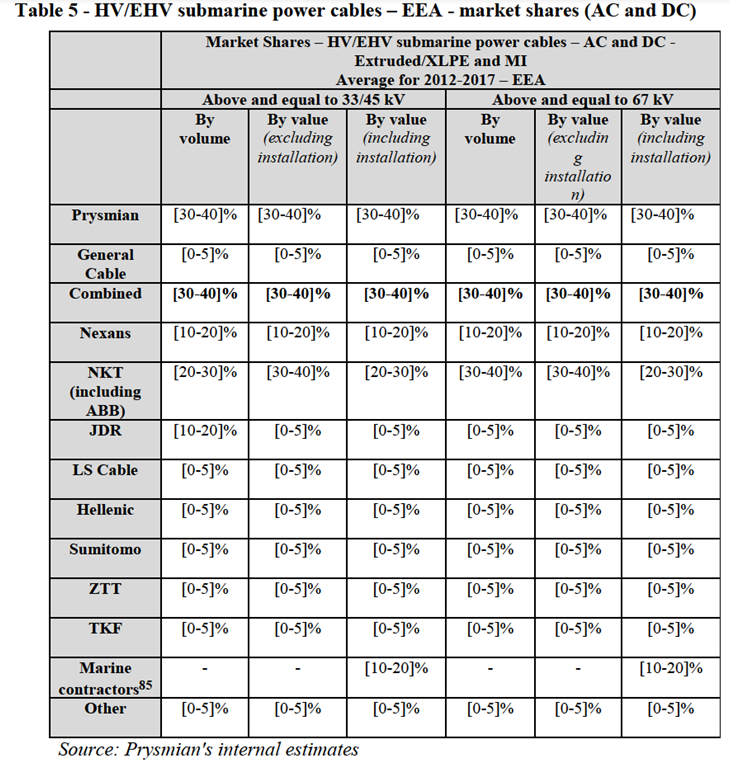

(98) Third, the Commission notes that most respondents are of the opinion that the Transaction is unlikely to have any negative effects on the market for underground HV/EHG power cables.65

(99) Furthermore, in relation to the possible segment for underground HV/EHV DC power cables, the Commission makes the following observations:

(100) Based on the information provided by the Notifying Party, underground HV/EHV DC cables have been rare in the last five years, with only three such tenders for projects being issued in the period 2012-2016:

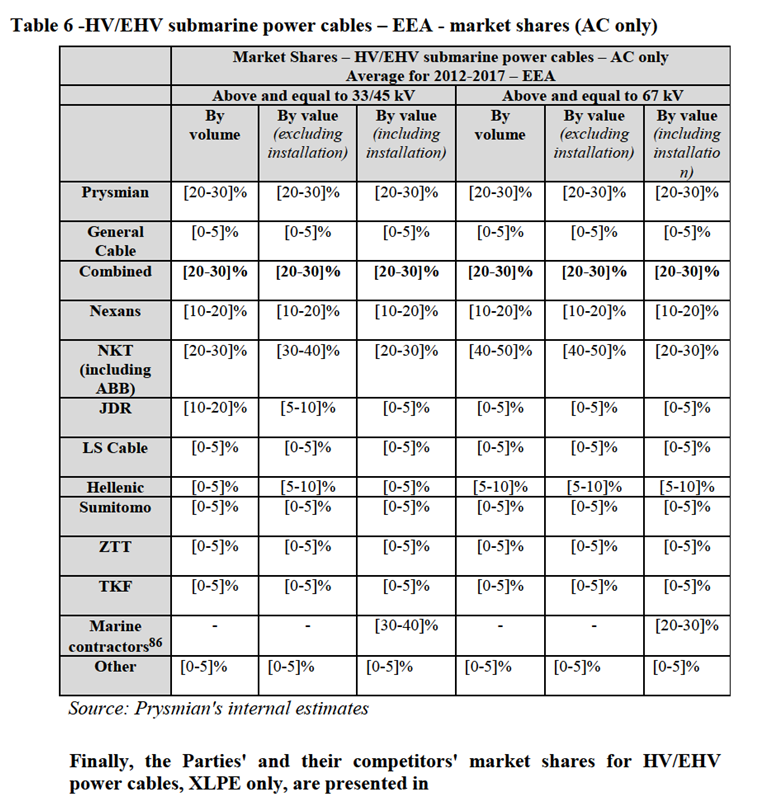

(101) The France-Italy project (project Piossasco-Grande Ile) was awarded to […]. The France-UK project (project Eurotunnel) was awarded to […] and the Germany-Belgium project (Project ALEGrO) was awarded to […].66

(102) The Commission first notes that such projects are infrequent and, because projects are awarded through tenders, market shares may not give an accurate picture of the market or of the strength of the suppliers. For example, in […].67 The most recent tender had taken place in 2011 (the "SydVästlänken" project in Sweden) and it was awarded to ABB (today part of NKT).68 The HVDC land segment also represents a small fraction (20%) of HVDC cables compared to the submarine HVDC segment and also just 1% of the overall HV/EHV market.69

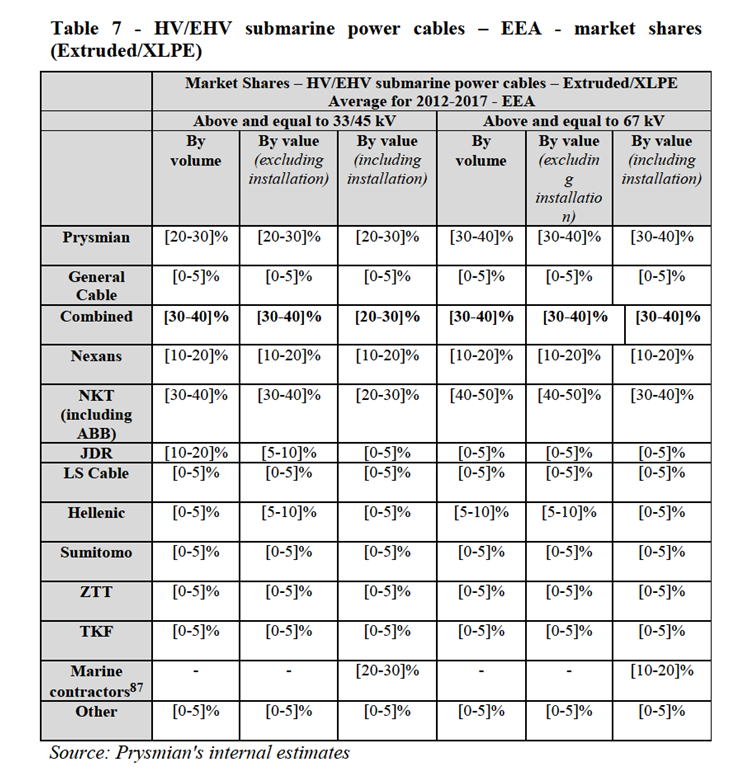

(103) Second, the Commission considers that Prysmian and General Cable are not close competitors in underground HV/EHV DC power cables. This is because on the one hand, in terms of capacity, General Cable has very limited underground HVDC capacity ([…] cable km/year) compared to Prysmian ([…] km/year).70 This means that […]. Prysmian's HVDC capacity is more similar to competitors such as NKT or Nexans. On the other hand, respondents to the market investigation also did not identify General Cable and Prysmian as close competitors, considering that Prysmian was a closer competitor to NKT and Nexans.71

(104) Third, the Commission notes that a number of established players such as Nexans, NKT and Sumitomo took part in the tenders discussed in paragraphs (101) above and (102). Furthermore, the HVDC market is set to develop further due to the EU's Energy 2020 Strategy. Extensive HVDC projects are required to connect EEA countries with resources of renewable energy (wind farms in the North Sea). In the upcoming Suedlink project in Germany, which will require approximately 3000 to 4000 km of HVDC cable, […].72 NKT (through its acquisition of ABB) is considered as the most innovative supplier of HV/EHV DC cables. Other international major players, in particular from Asia, who already have experience in HV/EHV DC cables are Sumitomo (Japan) and LS Cable (Korea). These players could also participate in future tenders.73

(105) Finally, most respondents to the market investigation consider that enough suppliers of underground HV/EHV power cables will remain in the market and did not raise any specific concerns as regards these types of cables.74

(106) For these reasons, the Commission takes the view that the Transaction does not raise serious doubts as to its compatibility with the internal market in relation to underground HV/EHV power cables or the possible market for underground HV/EHV DC power cables in the EEA.

5.1.5. Market for LV/MV submarine power cables

The Parties' and their competitors' market shares in the market for LV/MV submarine power cables are presented in

(107) Table 4 below:

below 67 kV. The combined market share of the Parties would be [10-20]% (for cables below 33/45 kV) and [10-20]% (for cables below 66 kV) respectively. No competition concerns could, therefore, arise as a result of the Transaction.

Commission's assessment

(110) The Commission considers that the LV/MV submarine power cable market is an affected market. Market share calculations, such as those relied upon by the Parties, which include the value of the installation services also provided by marine contractors and allocating them […] ([50-60]% for cables under 67 kV), do not, however, give a good indication of the market power of the various submarine power cable suppliers. Rather than competitors, marine contractor are often direct customers of cable manufacturers.77 Therefore, market shares based on volume (calculated by core kilometre) and value but excluding cable installation, should also be considered. Although the Commission does not question that installation may be included in many contracts tendered, the exclusion of installation from the market share calculations gives better insight into how each of the cable suppliers compares against other cable suppliers, which may or may not have in-house cable laying capabilities.

(111) For the reasons set out below, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to LV/MV submarine power cables78.

(112) First, the Parties' combined market share, calculated based on value and excluding installation, would not be particularly high. Considering a market below 33/45 kV, the combined market share by value would be [20-30]%, with an increment of [5-10]%. Considering a market below 67 kV, the combined market share by value would be [20-30]% with an increment of [5-10]%. According to the Horizontal Guidelines79, combined market shares below 25% may indicate that the concentration is not likely to impede effective competition. By volume, the combined market shares would be higher, namely [40-50]% for a market below 33/45 kV but in such market the increment brought by the Transaction would be limited to [0-5]%. On a market comprising submarine cables below 67 kV, i.e. comprising the inter-array cables used in offshore windfarms, the combined market share by volume would not be particularly high at [30-40]% with an increment of [5-10]%.

(113) Second, several viable alternative suppliers will remain in the market post- Transaction, including in particular Nexans (share by value, excluding installation: [50-60]% for voltages below 33/45 kV or [30-40]% for voltages below 67 kV), and JDR ([0-5]% or [30-40]%), but also smaller players such as NKT ([0-5]% or [0-5]%), Hellenic ([0-5]% or [0-5]%), and Twentsche Kabelfabriek (TKF), the latter recently increasingly successful in the EEA market, securing a large portion ([40-50]%) of the order intake for submarine power cables below 67 kV in 2017.

(114) The market share figures show a large fluctuation from one year to another, which supports the argument presented by the Parties that submarine cables are acquired on a project by project basis and projects are relatively infrequent and often span over a multi-year period. There are also large variations in the market shares of competitors depending on where the cut-off point in voltage between MV and HV is placed, which may be explained by the importance of offshore windfarms for the demand for submarine power cables. Offshore wind farms represent, in fact, a large portion of the total demand for LV/MV submarine power cables in Europe.80 The inter-array cables connecting the individual turbines to each other in an offshore windfarm are usually 33 kV and increasingly 66 kV.81 The importance of the inter-array cables is visible when comparing the size of the LV/MV market, depending if a 33/45 kV or 66 kV cut-off point is chosen. For the period 2012-2017, the total value of the EEA market (order intake) was EUR 94 million when considering only cables with a voltage below 33 kV, while if cables under 67 kV are included the total value of the EEA market increases to EUR 843 million. Post-Transaction, three large players of similar size (namely the merged entity, JDR and Nexans) and some smaller players (including some with increasing success in more recent years, in particular TKF) would compete for the supply of such cables for offshore windfarm projects.

(115) Third, the market investigation confirms that a majority of competitors and customers consider that for LV/MV submarine power cables a sufficient number of suppliers will remain post-Transaction to maintain a similar level of competition and choice to customers as today.82 Most competitors responding to the market investigation expect the intensity of competition to remain the same post-Transaction on the market for LV/MV submarine power cables, while responses from customers are inconclusive on this point, as some customers expect a decrease of competition, but a similar number expect competition to remain the same.83

(116) Fourth, respondents to the market investigation do not identify General Cable as Prysmian's closest competitor. The majority of respondents consider Nexans, NKT and JDR as Prysmian's closest competitors on the market for LV/MV submarine power cables.84

(117) For these reasons, the Commission takes the view that the Transaction does not raise serious doubts in relation to submarine LV/MV power cables in the EEA.

5.1.6. Market for HV/EHV submarine power cables

(118) The Parties overlap with regard to the supply of HV/EHV submarine power cables. While Prysmian is active both with regard to AC and DC cable technology, General Cable is not active in DC technology for submarine cables. Both are active with regard to extruded/XLPE technology, but only Prysmian is active with regard to MI technology and only in relation to its DC cable offering.

(119) To calculate market shares, a weighted average covering the six-year period 2012-2017 is used. This approach has been chosen to reflect the fluctuating market size and market shares from one year to the other, which is explained by the fact that competition occurs on a project by project basis, projects are relatively infrequent and span generally over several years.

The Parties' and their competitors' market shares on the overall market for HV/EHV submarine power cables, including AC and DC, are presented in

(120) Table 5 below:

(121)

Table 6 below. As explained by the Parties, the market share figures presented in

(122) Table 6 below are also applicable for a possible sub-segmentation by insulation, i.e. HV/EHC submarine AC extruded/XLPE cables, in view of the fact that during the 2012-2017 period no AC projects for HV/EHV submarine power cables with MI insulation were recorded.

(123) Table 7:

bidding markets where the customers have strong bargaining power and able to "stimulate competitive offers".

Commission's assessment

(124) For the reasons set out below, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to HV/EHV submarine power cables, irrespective of any possible segmentation.

(125) First, as shown in

(126) Table 5,

(127) Table 6 and

(128) Table 7 above, the combined market share of the Parties would not be very high and the increment would be small.

(129) Considering the overall market of HV/EHV submarine power cables with voltages from 33/45 kV and above

(130) Table 5), the combined market share would be around [30-40]%, with an increment of around [0-5]% (by value) and [0-5]% (by volume). Considering an overall market above 66 kV

(131) Table 5), the combined market share would be approximately [30-40]% with an increment of [0-5]% (by value) and [0-5]% (by volume).

(132) Considering the market for HV/EHV submarine power cables, AC only, with voltages from 33/45 kV and above

(133) Table 6), the combined market share would be around [20-30]% (by value) and [20-30]% (by volume), with an increment of around [0-5]% (by value) and [0- 5]% (by volume). Considering the AC market above 66 kV

(134) Table 6), the combined market share would be approximately [20-30]% (by value) and [20-30]% (by volume) with an increment of [0-5]% (by value) and [0- 5]% (by volume).

(135) Finally, considering the market for HV/EHV submarine power cables, XLPE only, with voltages from 33/45 kV and above

(136) Table 7), the combined market share would be around [30-40]% (by value) and [30-40]% (by volume), with an increment of [0-5]% (by value) and [0-5]% (by volume). Considering the XLPE market above 66 kV

(137) Table 7), the combined market share would be approximately [30-40]% (by value) and [30-40]% (by volume) with an increment of [0-5]% (by value) and [0- 5]% (by volume).

(138) Second, a number of strong competitors will remain in the market, including two large players and several smaller players.

(139) The largest players in the HV/EHV submarine market will be Nexans and NKT alongside the merged entity. In view of the very small increment brought to the market share of Prysmian as a result of the Transaction, the relative strength of the three main players will remain almost unchanged.

(140) Both Nexans and NKT are significant players in the power cable industry. Nexans is a worldwide full range cable provider similar to Prysmian. It supplies LV/MV as well as HV/EHV power cables, both for underground and submarine applications, both AC and DC and XLPE and MI technology. NKT, in particular following its acquisition in 2017 of ABB's HV power cables business, is one of the leading players in the EEA and worldwide supplying the full range of power cables similarly to Prysmian and Nexans.

(141) In addition to Nexans and NKT, there are other existing players on the market that will continue to place a competitive constraint on the merged entity post- Transaction, in addition to the non-EEA players that have recently entered or are in the process of entering the EEA market (see paragraphs (146) - (151)).

(142) These include in particular Hellenic Cables, and JDR Cables. Hellenic Cables offers AC XLPE submarine power cables across all voltage ranges (300 V to 500 kV)88 and while its average market share in the period 2012-2016 is below [5- 10]%, it has been successful in securing the award of several contracts for 150 kV AC XLPE power cables (in 2014 and 2016).89

(143) According to information provided by the Parties, Hellenic Cables has also implemented a EUR 60 million investment plan for the manufacture of high- voltage submarine power cables.90

(144) JDR Cables, which was recently acquired by TF Kable, is a strong player in particular for inter-array cables for offshore windfarm projects. The market shares in

(145) Table 4 illustrate the strength of JDR Cables for such cables. JDR is not, however, active in submarine cables of higher voltages than 72 kV.91

(146) Third, the Parties are not each other's closest competitors. As pointed out by the Parties, the product range offered by Prysmian and General Cable differs in that Prysmian offers the full range of HV/EHV submarine power cables, including both AC and DC, as well as extruded/XLPE and MI insulation. General Cable, on the other hand, has a more focused product range, limited to the lower voltages (up to 220 kV) and exclusively AC and XLPE. The Parties can therefore compete against one another only for a limited range of products. This is also confirmed overall by the market investigation, where in response to the Commission's questionnaire competitors and customers ranked Nexans and NKT as Prysmian's closest competitors, ahead of General Cable.92 On the other hand, while competitors ranked Nexans as the closest competitor to General Cable (followed by Prysmian and NKT), customers indicated that Prysmian would be General Cable's closest competitor, but closely followed by Nexans and NKT.93 This reflects the fact that while Prysmian is active across the whole range of HV/EHV submarine power cables, General Cable is active only in certain segments (AC, XLPE, lower voltages). As explained by Nexans, while General Cable has a more limited presence in the EEA than Prysmian and is not active in each segment, the company is an important player for inter-array cables (33 kV and 66 kV) with its manufacturing plant limited for voltages used in inter-array cables. Thus, General Cable is not a player for EHV cables.94 RTE, the TSO in France, notes that it does not view General Cable as a player in HV submarine power cables.95

(147) Fourth, there has been significant market entry and expansion in recent years from non-EEA (in particular Asian) competitors and power cable suppliers already active in the EEA.

(148) One key competitor, Nexans, explains that the submarine HV/EHV technology was initially developed in Europe and while suppliers in Europe had a technological advantage over Asian competitors in the past, the latter have now caught up with the European manufacturers. The HV/EHV submarine projects in the EEA which have been won in recent years by Asian players are testament to their success.96

(149) As the Commission found in Case M.8239 NKT/ABB High Voltage Cable Business, until 2009 there was an anti-competitive agreement in place in the power cable industry. The cartel had two main configurations, one of which included Japanese and Korean producers refraining from competing for projects in the EEA, thus staying out of the European "home territory". Since this time, a number of Asian players, most importantly LS Cables (Korea), Sumitomo (Japan), and most recently ZTT (China), have successfully entered the market. Other Asian players are also seeking entry and are competing for contracts in the EEA. When considering the historic market shares, the role of the Asian players in the market appears to be minimal with single digit market shares. As concluded by the Commission in the NKT/ABB High Voltage Cable Business case, these market shares seem to under-represent the competitive role Asian players have in the EEA market today with both LS Cables and Sumitomo frequently participating in tenders and both companies having also won recently contracts for large complex HV/EHV submarine power cable projects in the EEA.

(150) The Commission concluded that LS Cables, Sumitomo and ZTT have successfully entered the market in the EEA, […].97

(151) The market investigation in the present case confirmed the successful entry of non-EEA players to the EEA market for HV/EHV submarine cables. A majority of customers responding to the market investigation indicate that non-EEA suppliers are active or very active in the EEA and have awarded or considered awarding such suppliers contracts for HV/EHV submarine cables.98 Similarly, a majority of competitors consider that non-EEA players compete for projects in the EEA and are starting to win contracts.99

(152) Given the success of LS Cables, Sumitomo, and most recently ZTT in the HV/EHV submarine cable market in the EEA, the Commission considers that, despite their low market shares, these Asian players place a significant competitive constraint on the merged entity post-Transaction.

(153) In addition to Asian entry, there has also been entry by existing EEA power cable suppliers. Hellenic Cables is mentioned in this context, […].100

5.2. Horizontal coordinated effects

(154) A merger in a concentrated market may significantly impede effective competition due to horizontal coordinated effects if, through the creation or strengthening of a collective dominant position, it increases the likelihood that firms are able to coordinate their behaviour in this way and raise prices, even without entering into an agreement or resorting to a concerted practice within the meaning of Article 101 TFEU.101 A merger may also make coordination easier, more stable or more effective for firms that were already coordinating before the merger, either by making the coordination more robust or by permitting firms to coordinate on even higher prices.102

The Notifying Party's view

(155) The Notifying Party submits that the affected markets do not have the features typically recognised as conducive to coordination and that the acquisition of sole control over General Cable could not result in a change of incentives for market participants to coordinate in any of the affected markets. It takes the view that it is unlikely that the risk that the remaining players start co-ordinating their competitive behaviour will be enhanced, considering (i) the minor role of General Cable in the EEA, (ii) the fact that it does not play a role as maverick in any of the affected markets, neither in terms of aggressive prices nor in terms of innovation, and (iii) the fact that its acquisition does not increase the symmetry between the remaining market players in the affected markets.

Commission's assessment

(156) Based on the results of the market investigation, the Commission does not consider that the change brought about by the Transaction is likely to make coordination more likely in the industry.

(157) First, the affected markets present characteristics which make coordination difficult (even in the absence of an agreement or a concerted practice within the meaning of Article 101 TFEU).103 In the market for optical fibre cables and in the market for general wiring, supply and demand is highly fragmented. In the various power cable markets, there is limited transparency on the market, especially as regards MV and HV/EHV power cables, as these markets are characterised by infrequent, large volume orders often awarded through sophisticated and complex tendering procedures. As regards the lower voltage cables, especially LV, demand and supply is fragmented. The Transaction does not diminish these market characteristics which make coordination difficult.

(158) Second, the Transaction does not significantly increase symmetry in the market, given General Cable's limited position. Based on the market share figures presented in Tables 1-7, the market will remain relatively asymmetrical post- Transaction.

(159) Third, the Asian players that had under the previous cartel arrangement colluded to stay outside the European market have now effectively entered the EEA market.104 Players such as Sumitomo and LS Cables that were fined for their involvement in the cartel are now participating in tenders and win contracts both for submarine and underground power cables. A number of customers responding to the market investigation indicate that following the Commission's investigation into the cartel, an increase in competition in the EEA market is visible.105 In addition, players from North Africa have also started selling in the EEA (e.g.Imacab, Tunisie Cables).106

(160) Fourth, the market investigation has not indicated that either of the Parties is viewed as a maverick player, the removal of which as a competitive player would increase the likelihood or significance of coordinated effects in other ways.

6. CONCLUSION

(161) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 Publication in the Official Journal of the European Union No C 120, 06.04.2018, p. 22.

4 Turnover calculated in accordance with Article 5 of the Merger Regulation.

5 Commission Decision in Case M.6092 – Prysmian / Draka Holding of 9 February 2011, paragraph 23.

6 The Parties submit that […] MMFs represent […] percentage of the Parties' optical cables sales.

7 Copper drawing - bunching - insulating - laying up - external jacketing - mechanical protection - external sheathing.

8 See responses to Questionnaire Q3 to customers of general wiring cables, question B.1.1.

9 Case COMP/M.1882 Pirelli / BICC, decision of 19 July 2000, paragraphs 15 – 28 and 32.

10 Case COMP/M.8239 NKT/ABB High voltage cable business, decision of 27 February 2017, paragraph 14 and 16.

11 See responses to Questionnaire Q1 to competitors, question B.B.1., responses to Questionnaire Q2 to customers of power cables, question B.A.2 .

12 Case COMP/M.1882 Pirelli / BICC, decision of 19 July 2000, paragraphs 29-32; Case COMP/M.8239 NKT/ABB High voltage cable business, decision of 27 February 2017, paragraphs 18- 21.

13 See responses to Questionnaire Q1 to competitors, questions B.B.7 and B.B.8; responses to Questionnaire Q2 to customers of power cables, questions B.A.5 and B.A.6.

14 Case COMP/M.8239 NKT/ABB High voltage cable business, decision of 27 February 2017, paragraphs 22-26.

15 See responses to Questionnaire Q1 to competitors, questions B.B4-B.B.6; Questionnaire Q2 to customers of power cables, questions B.A.3 and B.A.4.

16 See responses to Questionnaire Q1 to competitors, questions B.B4-B.B.6; Questionnaire Q2 to customers of power cables, questions B.A.3 and B.A.4.

17 See responses to Questionnaire Q1 to competitors, questions B.B4-B.B.6.

18 Case COMP/M.8239 - NKT/ABB High voltage cable business, decision of 27 February 2017, paragraphs 27-31.

19 See responses to Questionnaire Q1 to competitors, question B.B.10.

20 See responses to Questionnaire Q2 to customers of power cables, question B.A.7.

21 See responses to Questionnaire Q2 to customers of power cables, questions B.A.7

22 Commission Decision in Case M.6092 Prysmian/Draka Holding, decision of 9 February 2011, paragraphs 45-48.

23 Both Prysmian and General Cable have optical fibre cable manufacturing plants in the country and have been successful in securing contracts with French customers, including large telecom operators, for the supply of optical fibre cables.

24 See responses to Questionnaire Q4 to customers of telecommunication cables, questions 3-5; Non- confidential minutes of conference call with VINCI Energies of 23 April 2018.

25 See responses to Questionnaire Q3 to customers of general wiring cables, question C.1; responses to Questionnaire Q1 to competitors, question C.1.

26 See responses to Questionnaire Q3 to customers of general wiring cables, questions C.1 and C.2.

27 See responses to Questionnaire Q3 to customers of general wiring cables, questions C.2 and C.3.

28 See responses to Questionnaire Q3 to customers of general wiring cables, question C.1.1.

29 Case COMP/M.1882 – Pirelli / BICC, decision of 19 July 2000, paragraph 55; Case COMP/M.6092 –Prysmian/Draka Holding, decision of 9 February 2011, paragraph 52.

30 See responses to Questionnaire Q2 to customers of power cables, question C.1.

31 See responses to Questionnaire Q2 to customers of power cables, questions C.1, C.2 and C.3; responses to Questionnaire Q1 to competitors, questions C.2, C.3, and C.4.

32 See responses to Questionnaire Q2 to customers of power cables, questions C.4, C.5.

33 OJ 2004/C 31/03.

34 While Prysmian is active in the manufacturing and sale of optical fibre cables used for network applications, infrastructural applications and internal/enterprise applications, General Cable is mainly active in optical fibre cables for network applications, and has a more limited presence for infrastructural applications, and does not offer any optical fibre cables for internal/enterprise applications.

35 Prysmian's customers include incumbent and new telecom operators, cable TV operators, transport operators, power utilities, system integrators, installation contractors, distributors and local authorities.

36 See response by Prysmian of 27 April 2018 to the Commission's request for information of 25 April 2018.

37 See response by Prysmian of 18 April 2018 to the Commission's request for information of 16 April 2018; response by Prysmian of 27 April 2018 to the Commission's request for information of 25 April 2018.

38 See responses to Questionnaire Q4 to customers of telecom cables, questions 3 and 4.

39 See the Notifying Partys’ response of 18 April 2018 to the Request for Information of 16 April 2018, question 5.

40 See the Notifying Partys’ response of 29 April 2018 to the Request for Information of 25 April 2018, question 7.5.

41 According to the Notifying Party, the averge costs of transport for optical fibre cables represents between […] of the total cost. See Notifying Party’s response of 29 April to the Request for Information of 25 April 2018, paint 8.12.

42 See the Notifying Partys’ response of 29 April to the Request for Information of 25 April 2018, question 8.12.

43 The most recent year covered by the CRU dataset used by the Notifying Party to estimate market shares for energy cables is 2016 ; See Form CO, footnote 39 and Form CO, Annex CO 6.

44 OJ 2004/C 31/03.

45 See responses to Questionnaire Q1 to competitors, questions E1 and E2 and Questionnaire Q3 to general wiring customers, questions E1 and E2.

46 See responses to Questionnaire Q1 to competitors, question E3 and Questionnaire Q3 to general wiring customers, question E3.

47 See responses to Questionnaire Q1 to competitors, question F1 and Questionnaire Q3 to general wiring customers, question F1.

48 The most recent year covered by the CRU dataset used by the Notifying Party to estimate market shares for energy cables is 2016; see Form CO, footnote 39 and Form CO, Annex CO 6.

49 See responses to Questionnaire Q2 to customers of underground power cables, question E3; Non- confidential minutes of the conference call with EDF of 23 March 2018.

50 Prysmian and General Cable have each a plant close to Paris from where they supply some of their main customers.

51 One of the most used standards for underground LV/MV power cables in France is the NF C33-226 standard. The French specifications for the various types of underground LV/MV power cables are based on European-wide standards. EDF/ENEDIS complements these standards with technical characteristics required in the calls for tender. Such specifications, except duration and corrosion specifications are the same of other MV cables commercialised in Europe. In recent years, French standards for underground LV/MV power cables have been brought closer to standards in the EU, by removing lead elements that enhanced their specificity in the EU context. See Memorandum of the Notifying Party of 25 April 2018.

52 The lab testing focuses on testing the endurance and resistance to corrosion of the aluminium tape of the cable.

53 See non-confidential minutes of the conference call with EDF of 20 April 2018 and non-confidential minutes of the conference call with Synelva, of 19 April 2018, and Minutes of the conference call with URM of 20 April 2018.

54 See non-confidential minutes of the conference call with EDF of 20 April 2018.

55 See non-confidential minutes of the conference call with EDF of 20 April 2018.

56 See non-confidential minutes of the conference call with EDF of 20 April 2018.

57 According to Notifying Party's data, transport costs for underground LV/MV power cables account for […] of the cost of the cable. See Memorandum of the Notifying Party of 25 April 2018.

58 See non-confidential minutes of the conference call with EDF of 20 April 2018.

59 See non-confidential minutes of the conference call with EDF of 20 April 2018.

60 The most recent year covered by the CRU dataset used by the Notifying Party to estimate market shares for energy cables is 2016; see Form CO, footnote 39 and Form CO, Annex CO 6.

61 See Form CO, Annex PN RFI 1Q31.

62 See responses to Questionnaire Q1 to competitors, questions E1 and E2 and Questionnaire Q2 to customers of power cables, questions E.1.1 and E.2.1.

63 See responses to Questionnaire Q1 to competitors, question E3 and Questionnaire Q2 to customers of power cables, question E3.

64 See non-confidential minutes of the call with RTE, of 23 April 2018.

65 See responses to Questionnaire Q1 to competitors, question F1 and Questionnaire Q2 to customers of power cables, question F1.

66 Annex PN RFI 1, question 31.

67 Form CO, paragraph 254.

68 Annex PN RFI 1, question 31.

69 Form CO, paragraph 253.

70 Annex PN RFI 1, question 31.

71 See responses to Questionnaire Q1 to competitors, question F1 and Questionnaire Q2 to customers of power cables, question E3.

72 Annex PN RFI 1, question 31.

73 See responses to Questionnaire Q1 to competitors, question F.3.1.

74 See responses to Questionnaire Q1 to competitors, question E.3.3 and Questionnaire Q2 to customers of power cables, question E.3.3.

75 The Parties explain that the market share figures attributed to « marine contractors » only represents the estimated value for the laying of the submarine power cable, i.e the cable installation. The market share attributed to cable manufacturers represents the value of all their cable supplies including to marine contractors : See Form CO, paragraph 261.

76 The Parties explain that accessories and accessory installation are included in the cable supply contract for submarine power cables. Cable maintenance can be provided as part of the guaranter to the cable, and therefore as part of the cable supply contract , or separately. For submarine cables, however , such maintenance is rare, considering that access to a cable which is laid on the seabed is very difficult, cable installation therefore refers to the actual laying of the cable, and not to accessories and maintenance.

77 The Notifying Party explains that the award of projects for inter-array cables (which is the predominant usage of LV/MV submarine cables) is either organised in such way that the windfarm developer requests tenders from marine contractors for the supply and installation of the inter-array cables. In such situations the marine contractors are the customers of cable manufacturers. Alternatively, the windfarm developer tenders for the supply of inter-array cables directly from the cable manufacturers and separately from the supply of cables requests quotations from marine contractors for the installation of the inter-array cables. Some manufacturers with cable laying vessels can also offer turnkey solutions to developers, i.e. cable and installation (See paragraphs 322-323, Form CO). In fact, the Notifying Party explains that the installation of inter-array cables is often handled by marine contractors/balance of plant contractors, rather than cable manufacturers themselves (see paragraph 86, Form CO).

78 A further segmentation by transmission and insulation technology is not warranted for LV/MV submarine power cables are they are as a rule AC and insulated using extruded/XLPE technology.

79 OJ 2004/C 31/03.

80 The Notifying Party explains that the MV submarine power cable market is predominantly based on the supply of inter-array cables for offshore windfarms. Apart from inter-array cables, the MV submarine power cable segment includes short connections between islands, which are normally up to a voltage of 20 kV, but represent a minority of LV/MV submarine power cables.

81 See Form CO, paragraphs 82-84.

82 See responses to Questionnaire Q1to competitors of power cables, question E.3.5; responses to Questionnaire Q2 to customers of power cables, question E.3.4

83 See responses to Questionnaire Q1 to competitors of power cables, question G.2.4; responses to Questionnaire Q2 to customers of power cables, question G.2.3.

84 See responses to Questionnaire Q1 to competitors of power cables, questions E.1.3 and E.2.3; responses to Questionnaire Q2 to customers of power cables, questions E.1.2, E.2.2.

85 See footnote 75.

86 See footnote 75.

87 See footnote 75.

88 See response to Questionnaire Q1 to competitors, questions A.1 and A.3.

89 See responses to Questionnaire Q1 to competitors, questions F.2 and F.2.1.

90 See Form CO, paragraph 230.

91 See: http://www.jdrcables.com/oil-gas/subsea-power-cables/

92 See response to Questionnaire Q1 to competitors, question E.1.4; responses to Questionnaire Q2 to customers of power cables, question E.1.3.

93 See response to Questionnaire Q1 to competitors, question E.2.4; responses to Questionnaire Q2 to customers of power cables, question E.2.3.

94 See response by Nexans to Questionnaire Q1 to competitors, question E.1.4.1.

95 See response by RTE to Questionnaire Q2 to customers, question E.2.3.1.

96 See response by Nexans to Questionnaire Q1 to competitors, question D.4.6.

97 See Commission decision of 27.2.2017 in case M.8239 NKT/ABB High Voltage Cable Business, paragraphs 68-70.

98 See responses to Questionnaire Q2 to customers of power cables, question D.7.4.

99 See responses to Questionnaire Q2 to competitors, question D.4.5.

100 See responses to Questionnaire Q1 to competitors, questions F.2 and F.2.1.

101 Horizontal Merger Guidelines, paragraph 39.

102 Horizontal Merger Guidelines, paragraph 39.

103 The fact that in 2014 the Commission found a cartel in the power cables sector (see Commission decision of 2 April 2014 in Case AT.39610 – Power Cables) does not as such undermine this conclusion. In fact, in that case the cartel arrangement was underpinned by periodical meetings and contacts by email, telephone and fax; without such complex monitoring and enforcement mechanisms established through the cartel, it would be more difficult to reach or sustain a collusive outcome on the market.