Commission, March 27, 2019, No M.9276

EUROPEAN COMMISSION

Judgment

SIKA / FINANCIERE DRY MIX SOLUTIONS

Subject: Case M.9276 - Sika/Financière Dry Mix Solutions Commission decision pursuant to Article 6(1)(b) of Council

Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 20 February 2019, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Sika AG (‘Sika’, Switzerland) acquires within the meaning of Article 3(1)(b) of the Merger Regulation sole control of the whole of Financière Dry Mix Solutions SAS (‘Parex’, France) (the ‘Transaction’), by way of purchase of shares (Sika and Parex are designated hereinafter as the ‘Parties’). (3)

1. THE PARTIES

(2) Sika is a developer and producer of high-quality concrete admixtures, mortars, sealants and adhesives, damping and reinforcing materials, structural strengthening systems, industrial flooring as well as roofing and waterproofing systems, which are used in the building sector and by manufacturing industries.

(3) Parex is mainly active in the production and commercialisation of mortar products used in the construction industry. Parex’s products fall into three business lines: (i) façade protection and decoration (comprising façade renders and external thermal insulation composite systems (‘ETICS’)), (ii) ceramic tile- setting materials (such as tile adhesives, self-levelling compounds, or tile grouts), and (iii) concrete repair and waterproofing systems (such as technical products used on existing concrete works).

(4) The Saint-Gobain Group (‘Saint-Gobain’) holds a minority shareholding (10.75%) in Sika. (4) Saint-Gobain attempted a hostile takeover of Sika, which ended on 11 June 2018 through a settlement agreement between Saint-Gobain and the Burkard Family. As a result, Saint-Gobain became a minority shareholder of Sika, but that minority shareholding does not confer any veto rights upon Saint- Gobain and it is subject to a number of lock-up provisions. At the core there is a prohibition to (i) increase its stake beyond the current shareholding (until 11 May 2022) and not beyond 12.875% (until 11 May 2024), and to (ii) reach any vote pooling agreements or similar agreements between Saint-Gobain and other shareholders in Sika. In addition, Saint-Gobain is not represented on the board of Sika and its voting power does not provide any control (not even through a blocking minority) given that typically at least 60% of all votes are being represented at the ordinary general assembly of Sika, and decisions require absolute majority of the votes represented at the general assembly.

2. THE CONCENTRATION

(5) On 7 January 2019, the Parties signed a Put Option Agreement setting out Sika’s irrevocable commitment to purchase 100% of the shares in Parex on the terms and conditions set forth in the Sale and Purchase Agreement (‘SPA’). The Put Option Agreement allows the sellers, upon completion of a works council consultation process in France, to sell to Sika the shares in Parex in accordance with the agreed SPA, which was executed on 12 February 2019.

(6) As a result of the Transaction, Sika will acquire sole control over Parex within the meaning of Article 3(1)(b) of the Merger Regulation.

3. EU DIMENSION

(7) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (5) (Sika: EUR 5 949 million, Parex: EUR 1 023 million). Each of them has an EU-wide turnover in excess of EUR 250 million (Sika: EUR […], Parex: EUR […]), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension.

4. MARKET DEFINITION AND COMPETITIVE ASSESSMENT

(8) The activities of the Parties overlap in different areas giving rise to horizontally affected markets in France in (i) mortars, in particular (a) construction dry premix mortar and (b) tile-fixing dry premix mortar; (ii) chemical-based concrete and mortar admixtures; (iii) concrete works, in particular structural reinforcing/strengthening; (iv) polyurethane (‘PU’) sealants for DIY (6) /consumers and, in Spain in (v) ETICS.

4.1. Mortars

(9) Mortar is a building material, usually made of sand, binders (like cement) and various additives (for example, pigments or waterproof compounds). Mortars are used to bind construction materials together or to fill the gap between them. In particular, construction mortars are used for various building construction purposes (e.g. casting and setting, masonry, plastering, floor levelling, and concrete repair); while tile-fixing mortars are used for fixing tiles, both on substrate (adhesive mortars) and as sealants between tiles (grouts).

4.1.1. Market definition

4.1.1.1. Product market definition

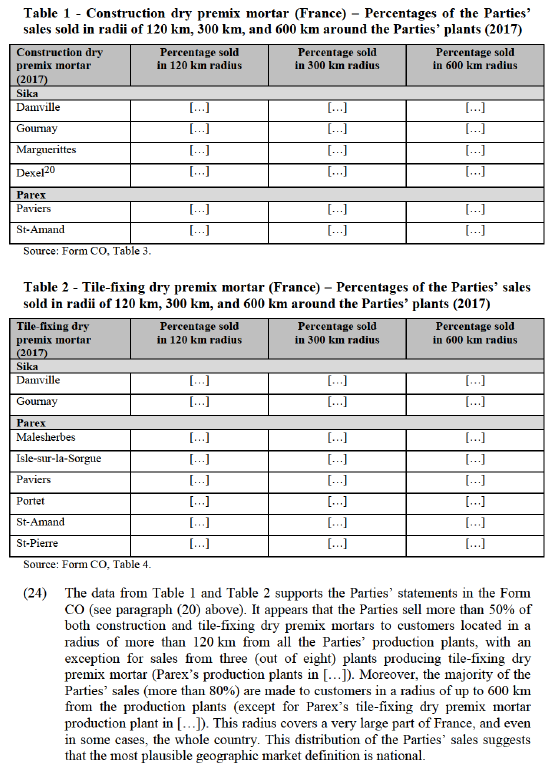

(a) The Commission’s precedents

(10) In previous decisions, the Commission distinguished between premix mortars, which are mixed at the factory and on-site mortars, which are mixed on the construction site. (7)

(11) Within premix mortars, the Commission distinguished between dry mortars (supplied in a dry powder form), wet mortars (ready-mixed with water at the factory), and ready-to-use paste mortars (supplied as paste, including organic compounds as binders). (8)

(12) The Commission also distinguished between mortars based on the application, namely: (i) construction mortars, used for various building construction purposes such as casting and setting, masonry, plastering, floor levelling and concrete repair; (ii) façade mortars, used as an outer layer of buildings for protective or aesthetic purposes, or as part of insulation systems and (iii) tile-fixing mortars, used for fixing tiles, both on substrate (adhesive mortars) and as sealants between tiles (grouts). (9)

(b) The Parties’ views

(13) The Parties agree with the segmentation adopted by the Commission in previous decisions. The Parties thus submit that mortars should be segmented according to (i) the place where the mortar is mixed, (ii) the physical form of the mortar, and (iii) the final application of the mortar. (10)

(c) The Commission’s assessment

(14) The majority of respondents to the market investigation (customers and competitors) confirmed that the market for mortar should be divided according to (i) the place where the mortar is mixed (at factory or on the construction site), (ii) the physical form of the mortar (dry, wet or paste), and (iii) the final application of the mortar (construction, tile-fixing or façade). (11)

(15) In the present case, the overlap between Parties’ activities gives rise to horizontally affected markets in (i) construction dry premix mortar, and (ii) tile- fixing dry premix mortar. With regard to these products, the majority of the respondents (customers and competitors) to the market investigation confirmed that there is a price difference between them; tile-fixing dry premix mortar is more expensive than construction dry premix mortar. (12)

(16) In line with previous Commission decisions and considering the information provided by the Parties and the results of the market investigation, the Commission is of the view that construction dry premix mortar and tile-fixing dry premix mortar should be considered separate product markets for assessing the Transaction.

4.1.1.2. Geographic market definition

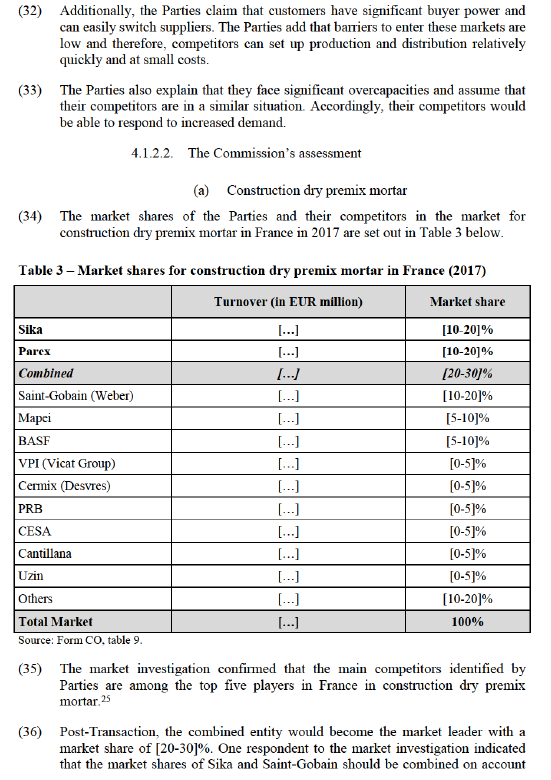

(a) The Commission’s precedents

(17) In previous decisions, the Commission left the geographic market definition open and conducted the competitive assessment both at national and at local/regional levels, assuming a 120 km radius around the production plant. (13) In another decision, the Commission considered that the geographic market corresponded to a radius of 120 km around each of the Parties’ production plants. (14)

(18) In the most recent decision concerning mortars, the Commission carried out its competitive assessment on the basis of (i) national markets and, (ii) with regard to large volume/low value heavy mortars, the Commission also considered narrower hypothetical regional/local markets, assuming a 120 km radius around production plants. (15)

(b) The Parties’ views

(19) The Parties submit that the geographical markets in the area of premix mortars should be national for all sub-segments. (16)

(20) They argue that their supplies of mortars are not limited to a certain geographic area within a country. The Parties explain that they have either only one plant per country or if there are several production plants their supply area would be much larger than a 120 km radius around those plants. Moreover, they submit that even low value/large volume premix mortars (price range up to approximately EUR […] per kg) tend to be distributed in a much larger radius than 120 km around the respective plant and that the price level tends to be homogeneous at a national level. (17)

(21) The Parties add that in certain markets like France, distance plays a less important role for large volume/low value heavy mortars because, compared to building traditions in other countries, large volume/low value heavy mortars are used only to a small extent in France. They are therefore produced in lower quantities and fewer production sites, which makes shipping over longer distances necessary. (18)

(22) The Parties further explain that construction and tile-fixing dry premix mortar products could be partially qualified as low value/large volume premix mortars, and the Parties sell these products to customers that are located more than 120 km from their respective production plants in France. They add that those construction dry premix mortar products are mostly shipped over distances that are even longer than 300 km. (19)

(c) The Commission’s assessment

(23) The Parties’ respective sales of construction and tile-fixing dry premix mortars in France in 2017, sold in radii of 120 km, 300 km, and 600 km around the Parties’ plants, are set out in Table 1 and Table 2 below.

(25) With regard to construction dry premix mortar, the same number of customers indicated that the shipping distance from their supplier to their outlet (s) was 0– 120 km and 120–300 km. (21) Concerning competitors, the competitors that expressed a view indicated that the majority of their sales took place in a radius larger than 120 km around their production plants. (22)

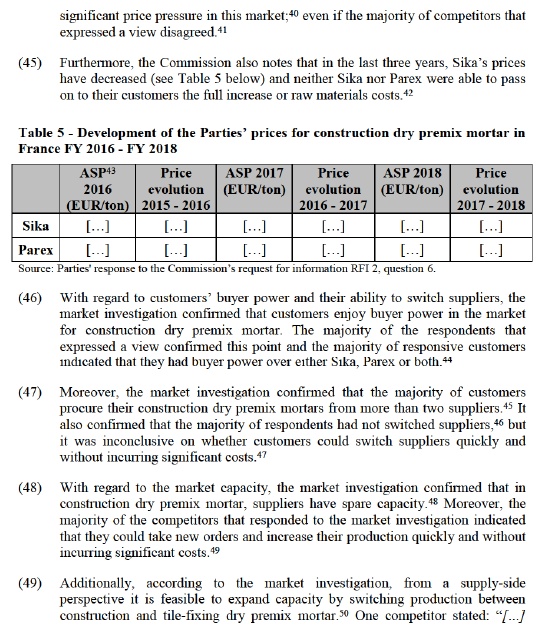

(26) Regarding tile-fixing dry premix mortar, the same number of customers indicated that, for the majority of their sales, the shipping distance from the supplier’s plant to their outlet (s) was 0–120 km and 120–300 km. (23) The majority of competitors that expressed a view respondents indicated the majority of their sales took place in a radius of 120 to 300 km from their plants. (24)

(27) Therefore, in the present case, the sales of the Parties and the results of the market investigation do not seem to support a geographic market definition based on sales done in a radius of less than 120 km around the Parties’ production plants.

(28) In conclusion, in line with previous Commission decisions and considering the information provided by the Parties and the results of the market investigation, the Commission is of the view that, for assessing the Transaction, the relevant geographic market for construction dry premix and tile-fixing dry premix mortars could be national in scope. In any event, the precise geographic market definition can be left open, as the Transaction does not raise competition concerns under any plausible market definition.

4.1.2. Competitive assessment

(29) The Parties’ activities in mortar overlap in the areas of façade dry, façade paste, construction dry, tile-fixing dry and tile-fixing paste premix mortars, giving rise to affected markets for construction dry premix mortar and tile-fixing dry premix mortar at national level (France) and at a local/regional level, assuming 120 km, 300 km and 600 km radii around Parex’s production plants in France.

4.1.2.1. The Parties’ views

(30) With regard to both construction and tile-fixing dry premix mortars, the Parties submit that the Transaction does not raise competition concerns because the Parties’ combined market share will be lower than [20-30]% for construction dry premix mortar and lower than [20-30]% for tile-fixing dry premix mortar. Moreover, the combined entity will continue to face significant competition from both large competitors, including multinational, and smaller local competitors.

(31) With regard to construction dry premix mortar, the Parties also claim that new competitors successfully entered the market for construction dry premix mortar in France. Concerning tile-fixing dry premix mortar, the Parties submit that private labels offered by distributors exercise significant price pressure.

among the three companies that offer most similar products to those of Parex (30) and five customers shared this view. (31)

(40) However, in response to both questions on similarity (see first phrase of paragraph (39) above), the majority of the respondents (customers and competitors) to the market investigation also mentioned Saint-Gobain (Weber) among the three companies that offer most similar products to those of the Parties. (32)

(41) Furthermore, the Commission also took into account in its assessment the difference in price between Sika’s and Parex’s products in this market. (33) Sika’s average sales price is clearly higher than Parex’s prices. According to the Parties, construction dry premix mortars are standardised but not identical. There are different levels of sophistication demanded by customers. High sophistication requires more components/raw materials, hence higher costs and different cost structures. Sika offers more sophisticated products, while Parex offers more basic ones; but while the Parties’ average sales prices for construction dry premix mortar are significantly different, their gross profit margins are closer to each other. (34)

(42) With regard to competitive pressure and based on the information provided by the Parties, the Commission considers that the market for construction dry premix mortars is driven by prices and post-Transaction, Saint-Gobain (Weber), Mapei and BASF are likely to continue exercising significant competitive pressure on the combined entity. All of them have market shares above 5% and have two or more mortar production plants in France. (35)

(43) Moreover, Saint-Gobain (Weber) and Mapei are historical market leaders of the market for construction dry premix mortar. (36) Furthermore, Saint-Gobain has an important distribution network in France, in which it sells under different banners, including Point.P Materiaux de Construction, Point.P Travaux Publics, Décpcéram or La Plateforme du Bâtiment; (37) and according to the Parties, Mapei is known for its aggressive pricing strategy. (38)

(44) Additionally, the Parties claim that small suppliers price very aggressively and exercise significant price pressure on the market. (39) The Parties identified six competitors with market shares between [0-5]% and [0-5]% and other suppliers with a combined market share of [10-20]%. The majority of the customers that responded to the market investigation confirmed that smaller suppliers exercise

little time and cost associated with switching production assuming the right equipment is available.” (51)

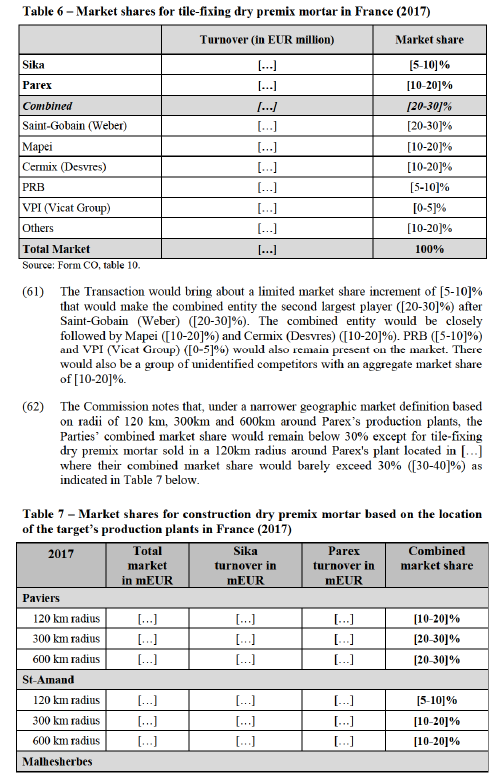

(50) With regard to barriers to entry, the majority of competitors indicated that in the market for construction dry premix mortar, there are barriers that prevent entry such as regulatory requirements at Union and national levels. (52) The Commission notes that the regulatory requirements, as described by the Parties, seem to take less than 1 year and entail investments of less than EUR 100 000. (53)

(51) Moreover, the majority of the customers that responded to the market investigation indicated that entry was possible (54) and two competitors indicated that there have been new entries in the last five years and referred to the following companies: S&P Reinforcement (‘S&P’), Cermix and RUREDIL. (55)

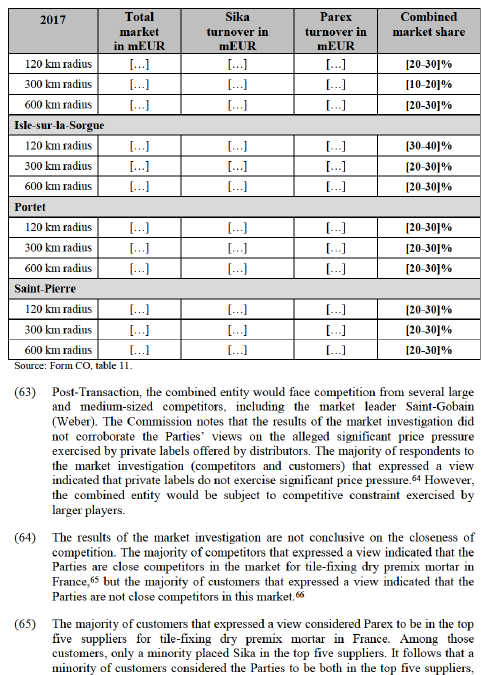

(52) In this regard, the Parties explained that S&P announced a launch of a range of mortar products in 2019;56 Cermix and PRB entered the market for construction dry premix mortar from the markets for tile-fixing and façade dry premix mortars, respectively. (57) Furthermore, the Parties stated that Baumit may also have plans to enter the French market shortly. (58)

(53) With regard to the impact of the Transaction in the market for construction dry premix mortar, the majority of competitors that responded to the market investigation expect a decrease in product choice and price 59 and the majority of customers that expressed a view expect an increase of prices. (60)

(54) Additionally, a competitor indicated that the minority shareholding (10.75%) that Saint-Gobain has in Sika, could give the combined entity a significant competitive advantage and its products could receive a preferential treatment within Saint-Gobain’s distribution network in France at the expense of other suppliers. (61)

(55) Before the Transaction, Sika and Parex already had separate distribution agreements with Saint-Gobain. They sold their products in part through Saint- Gobain’s distribution network in France. Taking this into account, the distribution related issue raised during the market investigation is not merger specific with regard to Sika. With regard to Parex, the Commission considers that based on the information provided by the Parties even if Saint-Gobain could have the ability to provide preferential treatment to the products of the combined entity, it is unlikely that it would have the incentives to do so. Saint-Gobain is not the only available distributor; there are other relevant distributors available in France such as Chausson, Gedimat, CMEM or Leroy Merlin that follow a multi-brand strategy. Only one respondent to the market investigation raised this issue without further substantiation besides the minority shareholding of Saint-Gobain in Sika. However, Saint-Gobain would not be able to recapture the reduction of the sales of its own products, which would derive from providing preferential treatment to the Parties’ products, through the benefits resulting from its minority shareholding in Sika. Moreover, according to public available sources, in February 2019 Saint-Gobain was considering selling part of its distribution network in France, Point.P Travaux Publics. (62)

(56) The Commission notes that, based on the information provided by the Parties and the results of the market investigation, post-Transaction the combined entity would become a market leader in construction dry premix mortar at a national level; however, the Parties’ combined share would remain moderate ([20-30]%) and, under a narrower relevant geographic market based on the location of Parex’s production plants, the Parties’ combined shares would be lower (see Table 4 above).

(57) Moreover, post-Transaction more than 10 competitors would remain in the market and they are likely to continue exercising significant competitive pressure on the combined entity.

(58) The Commission further notes that (i) customers have some degree of buyer power and multisource; (ii) there is spare capacity in the market and it is possible to switch production from tile-fixing to construction dry premix mortar, and (iii) there have been new entrants in the last five years, which have quickly obtained market recognition (e.g. market shares of 3.4%) and more entrants are expected. Additionally, the Parties claim that in this market product choice for customers increases rather than decreases. (63)

(59) In conclusion, in light of the evidence available to it, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with regard to the market for construction dry premix mortar in France.

(b) Tile-fixing dry premix mortar

(60) The market shares of the Parties and their competitors in the market for tile-fixing dry premix mortar in France in 2017 are set out in Table 6 below.

and among them, only one customer ranked the Parties next to each to other, the other customers ranked them more distantly.67

(66) The results of the market investigation confirm that there is spare capacity in the French market for tile-fixing dry premix mortar, and therefore that competitors could respond to increased demand. The Parties indicated that they experience overcapacity in all their respective plants in France. (68) Responses from the competitors that expressed a view suggest that they are in a similar situation. Indeed, the majority of competitors that expressed a view indicated that they have spare capacity for the production of tile-fixing dry premix mortar in France. (69) Consequently, they confirmed that they would be able take on new orders and increase their production quickly and without incurring significant costs. (70)

(67) The results of the market investigation confirm the Parties’ views on customers’ strong buyer power. All the competitors that expressed a view indicated that customers for tile-fixing dry premix mortar have strong buyer power. (71) One competitor notably explained that tile-fixing dry premix mortar is more commoditized compared to construction dry premix mortar and the market is “more mature.” (72) Similarly, the majority of customers that expressed a view indicated that they have negotiating power over one or both Parties in relation to their purchases of tile-fixing dry premix mortar. (73) Several customers explained notably their negotiating power is due to the presence of numerous competitors in the market. (74)

(68) In the same vein, the results of the market investigation suggest that customers can easily switch suppliers. The majority of customers that expressed a view indicated that they have more than two suppliers for tile-fixing dry premix mortar. (75) The majority of customers that expressed a view indicated they have not switched suppliers. (76) However, they also indicated that they could start purchasing from a new supplier quickly and without incurring significant costs. (77)

(69) The results of the market investigation do not confirm the Parties’ views on the ability of suppliers to enter the market due to low barriers to entry. The majority of respondents to the market investigation (customers and competitors) that expressed a view indicated that there has been no entry in the last five years. (78) One competitor identified two suppliers, which allegedly entered the market in the past five years (namely, Kerakoll and Ardex). The Parties subsequently confirmed that those two suppliers have been present in the market but for a longer period (approximately 10 years for Kerakoll and more than 15 years for Ardex). (79) The Commission notes that they are not part of the main competitors identified by the Parties in Table 6 above. Half of the customers that expressed a view indicated that entry would not be possible. (80) The Commission further notes that several customers considered that the presence of numerous competitors in the market would act as a barrier to entry, because the market would be less attractive for new suppliers. (81)

(70) With regard to the impact of the Transaction, the majority of participants to the market investigation (competitors and customers) that expressed a view indicated that they would not expect price increases, losses of quality and choice post- Transaction. (82) Some participants indicated that prices would increase and product choice would decrease. However, those claims were based on the reduction of the number of competitors but they were not further substantiated. (83) One competitor indicated that prices could decrease due to the size of the combined entity that would allow it to pursue an aggressive pricing strategy, but this claim was also not further substantiated. (84)

(71) On balance and in light of the evidence available to it, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with regard to the market for tile-fixing dry premix mortar in France.

4.2. Chemical-based concrete and mortar admixtures

(72) Concrete and mortar admixtures are ingredients that are added to improve the properties of concrete or mortar (e.g. reducing the water content or extending the workability). They can be either chemical-based or mineral-based. Within chemical-based admixtures, so-called performance polymers are one of the most important groups.

4.2.1. Market definition

4.2.1.1. Product market definition

(a) The Commission’s precedents

(73) As regards concrete and mortar admixtures, the Commission found in previous decisions that chemical-based and mineral-based admixtures constitute separate product markets, due to their different product characteristics, the important price differences, the lower performance of mineral-based admixtures and the difference in technology and quality. (85)

(74) Within chemical-based admixtures, the Commission made no further distinction according to the different types of admixtures (such as mortar and concrete admixtures) as it found that customers typically source the entirety of the admixtures they require from a single supplier, which suggested a high degree of supply-side substitutability. (86)

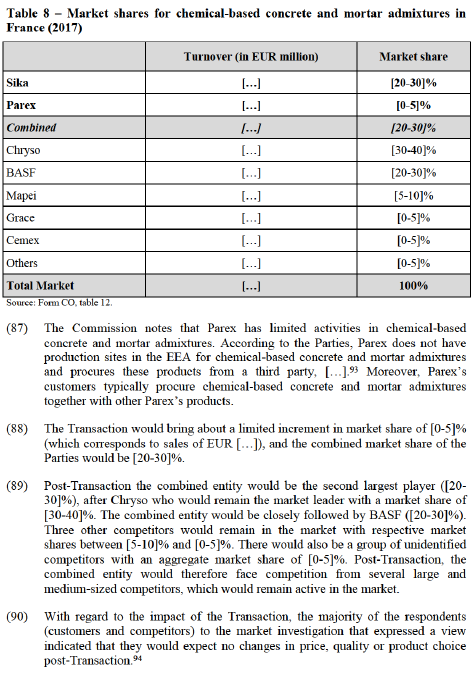

(b) The Parties’ views

(75) The Parties agree with the segmentation adopted by the Commission in previous decisions on concrete and mortar admixtures. They submit that, in the present case, the relevant product market should be the market for chemical-based admixtures where the Parties’ activities overlap. (87)

(c) The Commission’s assessment

(76) In the market investigation, the majority of respondents (customers and competitors) that expressed a view confirmed that the market for concrete and mortar admixtures should be further segmented into chemical-based and mineral- based concrete and mortar admixtures. These are separate product markets due to different characteristics, prices, performance, technology and quality. (88)

(77) In line with previous Commission decisions and considering the information provided by the Parties and the results of the market investigation, the Commission is of the view that chemical-based concrete and mortar admixtures should be considered as a separate product market for assessing the Transaction.

4.2.1.2. Geographic market definition

(a) The Commission’s precedents

(78) In a previous decision, the Commission left open whether the relevant geographic market would be EEA-wide or smaller. (89) In a more recent decision, the Commission conducted the competitive assessment on the basis of national markets as the narrowest plausible market definition. (90)

(b) The Parties’ views

(79) The Parties submit that the precise geographic market definition for concrete and mortar admixtures can be left open. They explain that their activities only overlap in chemical-based concrete and mortar admixtures in France. (91)

(c) The Commission’s assessment

(80) In the market investigation, the majority of customers and the majority of competitors that expressed a view agreed with the Commission’s previous finding that the competition conditions for concrete and mortar admixtures are relatively homogeneous within certain EEA countries and with the Commission’s analysis of competition on a country-by-country basis. (92)

(81) In line with the most recent Commission decisions and considering the information provided by the Parties and the results of the market investigation, the Commission is of the view that, for the purpose of this decision, it will consider the relevant geographic market for chemical-based admixtures national in scope.

4.2.2. Competitive assessment

(82) The overlap between the Parties’ activities in concrete and mortar admixtures gives rise to an affected market in respect of chemical-based concrete and mortar admixtures in France.

4.2.2.1. The Parties’ views

(83) The Parties submit that the Transaction will not raise competition concerns because it will lead to a marginal increment in market shares (around [0-5]%) and the Parties’ combined market share will be lower than 30%. Moreover, the combined entity will continue to face significant competition from numerous competitors.

(84) Additionally, the Parties claim that customers have significant buyer power and can easily switch suppliers. The Parties add that barriers to enter the markets are low and therefore, competitors can set up production and distribution relatively quickly and at small costs.

(85) The Parties also explain that they face significant overcapacities and assume that their competitors are in a similar situation. Accordingly, their competitors would be able to respond to increased demand.

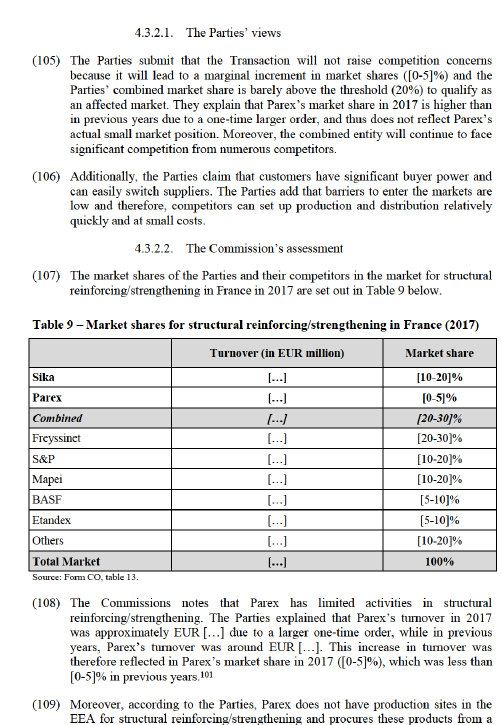

4.2.2.2. The Commission’s assessment

(86) The market shares of the Parties and their competitors in the market for chemical- based concrete and mortar admixtures in France in 2017 are set out in Table 8 below.

(91) Moreover, in the French market for chemical-based concrete and mortar admixtures, customers have some degree of buyer power and, six competitors entered the market in the last 10 years.

(92) In conclusion, in light of the evidence available to it, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with regard to the market for chemical-based concrete and mortar admixtures in France.

4.3. Concrete works

(93) Concrete works encompass a variety of products that are used for concrete surface treatment or to repair concrete structures, in particular to fill cracks and voids, to protect concrete structures against chemicals and corrosion, and to allow the application of coatings.

(94) Within concrete works, the Parties’ activities overlap in the following sub- categories: (i) anchoring resins, (ii) bonding agents, (iii) corrosion protection control and (iv) structural reinforcing/strengthening.

4.3.1. Market definition

4.3.1.1. Product market definition

(a) The Commission’s precedents

(95) In a previous decision, the Commission found that concrete works should be segmented along the following lines: injection resins, polymer concrete, resin- based grouts, anchoring resins, bonding agents, primers, impregnations, corrosion protection/control, structural reinforcing/strengthening, and ancillaries (cleaners, release agents, etc.). Each of those segments constituted a separate product market. (95)

(b) The Parties’ views

(96) The Parties agree with the segmentation adopted by the Commission in its past decision on concrete works. They submit that the relevant product markets should be the markets for anchoring resins, bonding agents, corrosion protection control and structural reinforcing/strengthening. (96)

(c) The Commission’s assessment

(97) In the market investigation, the majority of customers and the majority of competitors that expressed a view confirmed the product market definition as established in the previous Commission decision, namely the market for concrete works should be divided as follows: injection resins, polymer concrete, resin- based grouts, anchoring resins, bonding agents, primers, impregnations, corrosion protection/control, structural reinforcing/strengthening, and ancillaries (cleaners, release agents, etc.). (97)

(98) In line with the Commission’s prior decisional practice and considering the information provided by the Parties and the results of the market investigation, the Commission is of the view that structural reinforcing/strengthening should be considered as a separate product market for assessing the Transaction.

4.3.1.2. Geographic market definition

(a) The Commission’s precedents

(99) In a previous decision, the Commission considered that national markets were the narrowest plausible geographic market definition and carried out its competitive assessment on this basis. (98)

(b) The Parties’ views

(100) The Parties submit that the competitive assessment for concrete works, in particular for structural reinforcing/strengthening, should be conducted on a national basis. They explain that their activities only overlap in some sub- segments of concrete works in France and the United Kingdom. (99)

(c) The Commission’s assessment

(101) In the market investigation, the majority of customers and the majority of competitors that expressed a view agreed with the Commission’s previous finding that the competition conditions for concrete works are relatively homogeneous within certain EEA countries and with the Commission’s analysis of competition on a country-by-country basis. (100)

(102) In line with the Commission’s prior decisional practice and considering the information provided by the Parties and the results of the market investigation, the Commission is of the view that, for the purpose of this decision, it will consider the relevant geographic market for structural reinforcing/strengthening national in scope.

4.3.2. Competitive assessment

(103) The overlap between the Parties’ activities in concrete works gives rise to an affected market in respect of structural reinforcing/strengthening in France.

(104) Structural reinforcing/strengthening consists of strengthening concrete substrates or increasing shear capacity of concrete beams by using prefabricated plates made from carbon fibre reinforced polymer or other materials.

third party, […].102 Furthermore, Parex’s customers typically procure structural reinforcing/strengthening together with other Parex products, in particular with construction dry premix mortar. (103)

(110) The Transaction would bring about a limited increment in market share of [0-5]% (which corresponds to sales of EUR […]), and the combined market share of the Parties would be slightly above 20% ([20-30]%).

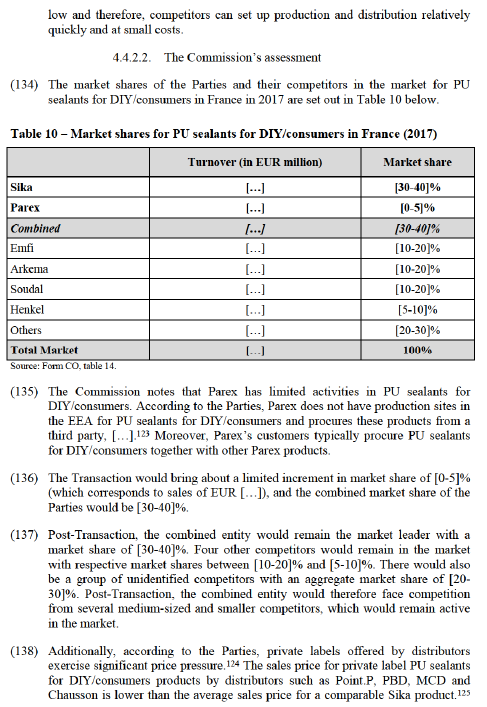

(111) Post-Transaction, the combined entity would be the second largest player ([20- 30]%), after Freyssinet who would remain the market leader with a market share of [20-30]%. The combined entity would be very closely followed by S&P ([10- 20]%). Three other competitors would remain in the market with market shares between [10-20]% and [5-10]%. There would also be a group of unidentified competitors with an aggregate market share of [10-20]%. Post-Transaction, the combined entity would therefore face competition from several large and medium-sized competitors, which would remain active in the market.

(112) Concerning customers’ buyer power, the results of the market investigation confirm the Parties’ views, the majority of competitors that expressed a view indicated that customers have buyer power. (104) Similarly, the majority of customers that expressed a view indicated that they have negotiating power over either or both Party(ies). (105)

(113) With regard to barriers to entry, the results of the market investigation do not support the Parties’ views according to which competitors can quickly enter the market due to low barriers to entry.

(114) None of the competitors that expressed a view considered that new players could quickly establish a market presence without incurring significant investments (106) and the majority of customers that expressed a view indicated that entry is not possible. (107) Participants to the market investigation mentioned several barriers to entry, such as certifications, financial and technical abilities and the presence of numerous competitors in the market. (108) However, according to the Parties, in the last 10 years, there have been two entries in the market, Mapei (c. 10 years ago) and S&P (c. 5-7 years ago), which have market shares of or above [10-20]%. (109)

(115) With regard to the impact of the Transaction, the majority of the respondents (customers and competitors) to the market investigation that expressed a view indicated that they expect price increases post-Transaction. (110) Concerning quality and product choice, one competitor expected a decrease while another one expected no changes. (111) However, these claims were mainly based on the reduction of the number of competitors but they were not further substantiated.

(116) The Commission finds that the Transaction is unlikely to significantly change the market structure. Parex has a market share below [0-5]%. It does not produce these products and procures them from a third party. Post-Transaction, Freyssinet, which would remain the market leader ([20-30]%) and the other competitors in the market (more than five) are likely to continue exercising competitive pressure on the combined entity. In fact, in the last two years, based on the Parties’ data, Sika’s prices decreased by more than [5-10]% each year and Parex’s prices […]. (112)

(117) Moreover, in the French market for structural reinforcing/strengthening, customers have buyer power and, despite the existence of barriers to entry, two competitors entered in the last 10 years. Furthermore, one of the barriers to entry mentioned in the market investigation was the presence of numerous competitors (see paragraph (114) above).

(118) Additionally, the Parties explained that the combined entity would not have incentives to increase prices because the market is very price sensitive and customers will otherwise switch to other suppliers. (113) As regards product choice, the Parties explained that the combined entity would very likely continue to offer Parex’s products post-Transaction. (114) Moreover, concerning decrease of quality, regulatory requirements are likely to be a safeguard against it.

(119) In conclusion, on balance and in light of the evidence available to it, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with regard to the market for structural reinforcing/strengthening in France.

4.4. Sealants

(120) Sealants are substances used to block the passage of fluids through the surface of joints or openings in materials such as sanitary joints, roofing joints, expansion joints and window and door joints.

4.4.1. Market definition

4.4.1.1. Product market definition

(a) The Commission’s precedents

(121) In previous decisions, the Commission considered a possible distinction between adhesives and sealants, but ultimately left the market definition open. The Commission categorised adhesives and sealants into three end-use groups, according to the target customer group, namely adhesives and sealants for consumers and DIY customers, adhesives and sealants for the construction sector, and adhesives and sealants for industrial applications. As regards adhesives and sealants for industrial applications, the Commission considered further segmentations according to the specific application such as automotive, bookbinding, labelling, packaging and according to the adhesive technology, such as water-based technologies, solvent-based technologies, hot melts or reactive adhesives, but ultimately left the market definition open. (115)

(122) In its most recent decision on sealants, the Commission considered that there were likely distinct product markets for adhesives and for sealants. The Commission also considered that the market for sealants should most likely be further segmented into sealants produced for the construction and the consumer sectors respectively. The Commission noted that the lack of true demand- or supply-side substitutability between the different sealant technologies suggested that separate product markets may exist for each type of sealant, i.e. acrylic sealants, polysulfide sealants, polyurethane sealants, silicone sealants and silyl- modified polymers. However, the Commission left ultimately the precise product market definition open. (116)

(b) The Parties’ views

(123) The Parties submit that the precise product market definition can be left open as no competition concerns would arise under the narrowest product market definition based on the target customer group and the sealant technology. (117)

(c) The Commission’s assessment

(124) In the market investigation, the majority of customers and the majority of competitors that expressed a view confirmed the market for sealants should be segmented according to (i) the target consumer group (professional construction or DIY/consumer), and (ii) the technology (silicone, acrylic, polyurethane (PU), silyl-modified polymers). (118)

(125) In line with the most recent Commission decisions concerning sealants and considering the information provided by the Parties and the results of the market investigation, the Commission is of the view that PU sealants for DIY/consumers should be considered as a separate product market for assessing the Transaction.

4.4.1.2. Geographic market definition

(a) The Commission’s precedents

(126) In previous decisions, the Commission considered that the geographic market for industrial sealants and adhesives may vary depending on the application. For some of them, the Commission considered the geographic market to be at least EEA-wide. For other applications, the Commission found evidence that suggested the presence of national markets. (119)

(127) In its most recent decision on sealants, the Commission considered it likely that the geographical scope for the market for sealants for DIY/consumers was national. The geographical market for sealants for the professional construction segment was found to be likely supra-national or at least regional, namely Western Europe, Central and Eastern Europe, as well as Scandinavia. However, the Commission ultimately left the precise geographic market definition open. (120)

(b) The Parties’ views

(128) The Parties submit that the precise definition of the geographic market can be left open, as the Transaction will not raise competition concerns even when considering national markets.121

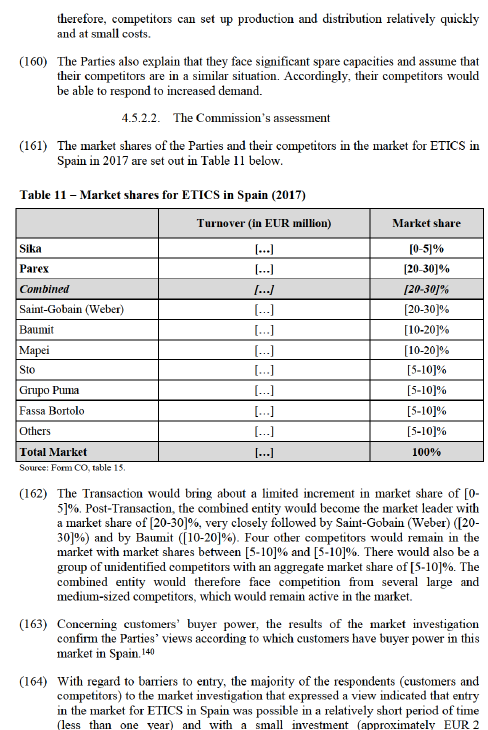

(c) The Commission’s assessment

(129) In the market investigation, the majority of customers and the majority of competitors that expressed a view agreed with the Commission’s previous finding that the competition conditions for sealants are relatively homogeneous within certain EEA countries and with the Commission’s analysis of competition on a country-by-country basis. (122)

(130) In line with the most recent Commission decisions and considering the information provided by the Parties and the results of the market investigation, the Commission is of the view that, for the purpose of this decision, it will consider the relevant geographic market for PU sealants for DIY/consumers national in scope.

4.4.2. Competitive assessment

(131) The overlap between the Parties’ activities in sealants gives rise to an affected market in respect of PU sealants for DIY/consumers in France.

4.4.2.1. The Parties’ views

(132) The Parties submit that the Transaction will not raise competition concerns in the market for PU sealants for DIY/consumers in France because it will lead to a marginal increment in market share (around [0-5]%). The combined entity will continue to face significant competition from numerous competitors, in particular price pressure from private label brands offered by distributors.

(133) Additionally, the Parties claim that customers have significant buyer power and can easily switch suppliers. The Parties add that barriers to enter the market are

However, the market investigation did not fully support this claim. The majority of competitors that expressed a view supported the Parties’ claim; but the majority of responsive customers did not. (126)

(139) Concerning customers’ buyer power, the results of the market investigation confirm the Parties’ views, the majority of competitors that expressed a view indicated that customers have some degree of buyer power. (127) Similarly, the majority of customers that expressed a view indicated that they have negotiating power over either or both Party(ies). (128)

(140) With regard to barriers to entry, the results of the market investigation do not support the Parties’ views according to which competitors can quickly enter the market due to low barriers to entry.

(141) A majority of competitors that expressed a view considered that new players could not establish a market presence without incurring significant investments and the majority of customers that expressed a view indicated that entry is not possible. Several barriers to entry were mentioned by participants to the market investigation, such as certifications, brand awareness and the presence of numerous competitors in the market. (129)

(142) However, according to the Parties, the set-up of production and distribution requires only small investments (approximately EUR 1 000 000) and can be done in a relatively short timeframe (approximately 1-2 years). Furthermore, according to the Parties, manufacturers of construction dry premix mortar such as Saint- Gobain (Weber), Mapei, PRB and Cermix/Desvres could be interested in offering PU sealants for DIY/consumers as an add-on to their product portfolio. (130)

(143) With regard to the impact of the Transaction, the majority of the respondents (customers and competitors) to the market investigation that expressed a view indicated that they would not expect changes in price, quality or product choice post-Transaction. (131)

(144) The Commission notes that the Transaction is unlikely to change significantly the market structure. Parex has a market share below [0-5]%. It does not produce these products and procures them from a third party. Post-Transaction, competitors in the market (more than four) are likely to continue exercising competitive pressure on the combined entity. Moreover, one of the barriers to entry mentioned in the market investigation was the presence of numerous competitors (see paragraph (141) above).

(145) Furthermore, in the French market for PU sealants for DIY/consumers, customers have buyer power.

(146) In conclusion, in light of the evidence available to it, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with regard to the market for PU sealants for DIY/consumers in France.

4.5. ETICS

(147) ETICS are on-site applied systems of prefabricated products for external wall insulation, usually composed of different types of façade mortars, insulation materials and glass fibre mesh fabrics. They enhance the thermal performance of buildings at a competitive cost and also serve an aesthetic function as they cover the external wall.

4.5.1. Market definition

4.5.1.1. Product market definition

(a) The Commission’s precedents

(148) In a previous decision, the Commission noted, as a result of its market investigation, that ETICS did not compete with other insulation systems. Similarly, ETICS could either be sold as separate components (component sales) or as a complete system (system sales). As system sales were most of the time guaranteed by a certification scheme, and thus provide additional advantages for the user, the Commission found that a switch of users would be unlikely and a separate market for ETICS is likely. The Commission, however, left the exact product market definition open. (132)

(b) The Parties’ views

(149) The Parties submit that the relevant product market should be the market for ETICS. They explain that their activities only overlap in Spain where they almost exclusively sell ETIC as systems. (133)

(c) The Commission’s assessment

(150) In the market investigation, the majority of respondents (customers and competitors) that expressed a view confirmed that ETICS are different from other insulation systems (134) and a distinction should be done between component sales and system sales (see paragraph (148) above). (135)

(151) In line with previous Commission decisions and considering the information provided by the Parties and the results of the market investigation, the Commission is of the view that ETICS should be considered as a separate product market for assessing the Transaction.

4.5.1.2. Geographic market definition

(a) The Commission’s precedents

(152) In a previous decision, the Commission considered that the markets for ETICS were national due to specific national building regulations and transportation costs. (136)

(b) The Parties’ views

(153) The Parties submit that the competitive assessment should be conducted on a national basis. They explain that their activities in ETICS only overlap in Spain. (137)

(c) The Commission’s assessment

(154) In the market investigation, the majority of respondents (customers and competitors) that expressed a view agreed with the Commission’s previous analysis of competition on a country-by-country basis. (138)

(155) In line with previous Commission decisions and considering the information provided by the Parties and the results of the market investigation, the Commission is of the view that, for assessing the Transaction, the relevant geographic market for ETICS is national in scope.

4.5.2. Competitive assessment

(156) The overlap between the Parties’ activities in ETICS gives rise to an affected market in Spain.

(157) The Parties also produce and sell in Spain façade dry premix mortar, which is a minor component of ETICS, but they do not produce or sell the main ETICS components i.e. insulation materials and glass fibre mesh. This vertical relationship does not give rise to an affected market since the Parties’ individual and combined market shares in the (upstream) market for façade dry premix mortar in Spain is below [5-10]% and their individual and combined market shares in the (downstream) market for ETICS in Spain are below [20-30]%. (139)

4.5.2.1. The Parties’ views

(158) The Parties submit that the Transaction will not raise competition concerns because the Parties’ combined market will be lower than [20-30]% and the Transaction will lead to a small market share increment ([0-5]%). Moreover, the combined entity will face significant competition from numerous competitors.

(159) The Parties claim that customers have significant buyer power and can easily switch suppliers. The Parties add that barriers to enter the market are low and

million). (141) The Commission notes that, according to the Parties, Sika entered the Spanish market for ETICS in 2015. (142)

(165) Concerning production capacity, the market investigation confirmed the existence of spare capacity in the market for ETICS in Spain. (143)

(166) With regard to the impact of the Transaction, the majority of the respondents (customers and competitors) to the market investigation that expressed a view indicated that post-Transaction they would expect no changes with regard to prices and an increase in quality and product choice. (144)

(167) In conclusion, in light of the evidence available to it, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with regard to the market for ETICS in Spain.

5. CONCLUSION

(168) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement

1 OJ L 24, 29.1.2004, p. 1 (the ‘Merger Regulation’). With effect from 1 December 2009, the Treaty on the Functioning of the European Union (‘TFEU’) has introduced certain changes, such as the replacement of ‘Community’ by ‘Union’ and ‘common market’ by ‘internal market’. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the "EEA Agreement").

3 Publication in the Official Journal of the European Union No C 75, 28.02.2019, p. 6.

4 Form CO, paragraph 31; Parties’ response to the Commission’s request for information RFI 2, questions 1 and 2.

5 Turnover calculated in accordance with Article 5 of the Merger Regulation and the Commission Consolidated Jurisdictional Notice (OJ C 95, 16.4.2008, p. 1).

6 DIY refers to ‘Do-It-Yourself.’

7 Commission Decision in Case M.7498 – Compagnie de Saint-Gobain/Sika (2015), recital 25; Commission Decision in Case M.4898 – Compagnie de Saint-Gobain/Maxit (2008), recitals 16 and 19; Commission Decision in Case M.3572 – Cemex/RMC (2014), recitals 14-17.

8 Commission Decision in Case M.7498 – Compagnie de Saint-Gobain/Sika (2015), recitals 25 and 26; Commission Decision in Case M.4898 – Compagnie de Saint-Gobain/Maxit (2008), recital 20.

9 Commission Decision in Case M.7498 – Compagnie de Saint-Gobain/Sika (2015), recital 27; Commission Decision in Case M.7249 – CVC/Parexgroup (2014), recitals 17 and 18; Commission Decision in Case M.4898 – Compagnie de Saint-Gobain/Maxit (2008), recitals 21 and 22.

10 Form CO, paragraph 63.

11 Questionnaire to Customers (France) - Q2, question 6; Questionnaire to Competitors (France) – Q1, question 5.

12 Questionnaire to Customers (France) - Q2, question 7; Questionnaire to Competitors (France) – Q1, question 6.

13 Commission Decision in Case M.7249 – CVC/Parexgroup (2014), recitals 20-23; Commission Decision in Case M.4898 – Compagnie de Saint-Gobain/Maxit (2008), recitals 27-29; Commission Decision in Case M.4719 – Heidelberg Cement/Hanson (2007), recitals 32 and 35; Commission Decision in Case M.1779 – Anglo American/Tarmac (2000), recital 23.

14 Commission Decision in Case M.7054 – Cemex/Holcim Assets (2014), recital 356.

15 Commission Decision in Case M.7498 – Compagnie de Saint-Gobain/Sika (2015), recital 36.

16 Form CO, paragraph 65.

17 Form CO, paragraph 66.

18 Form CO, paragraph 67.

19 Form CO, paragraph 68.

20 (…)

21 Questionnaire to Customers (France) – Q2, question 8.

22 Questionnaire to Competitors (France) – Q1, question 7.1.

23 Questionnaire to Customers (France) – Q2, question 8.

24 Questionnaire to Competitors (France) – Q1, question 7.2.

25 Questionnaire to Customers (France) – Q2, question 10 ; Questionnaire to Competitors (France) – Q1 question 9.

26 Questionnaire to Competitors (France) – Q1, question 33.1.

27 Questionnaire to Customers (France) – Q2, question 11.1 ; Questionnaire to Competitors (France) – Q1, question 10.1.

28 Questionnaire to Customers (France) – Q2, question 12.

29 Questionnaire to Competitors (France) – Q1, question 11.

30 Questionnaire to Competitors (France) – Q1, question 12.

31 Questionnaire to Customers (France) – Q2, question 13.

32 Questionnaire to Customers (France) – Q2, questions 12 and 13; Questionnaire to Competitors (France) – Q1, questions 11 and 12.

33 Parties’ response to the Commission’s request for information RFI 2, question 6.

34 Parties’ response to the Commission’s follow-up questions to request for information RFI 2, question 2.a.

35 Form CO, paragraph 125.

36 Parties’ response to the Commission’s request for information RFI 2, question 7.

37 Questionnaire to Competitors (France) – Q1, question 35. See also Saint-Gobain’s website at: http://www.sgdb-france.fr/nos-enseignes-XR57.

38 Form CO, paragraph 126.

39 Form CO, paragraph 127.

40 Questionnaire to Customers (France) – Q2, question 14.

41 Questionnaire to Competitors (France) – Q1, question 13.

42 Parties’ response to the Commision’s request for information RFI 2, question 7.

43 ASP refers to ‘Average Sales Prices’

44 Questionnaire to Customers (France) – Q2, question, question 29 ; Questionnaire to Competitors (France) – Q1, question 18.1.

45 Questionnaire to Customers (France) – Q2, question 16.1.

46 Questionnaire to Customers (France) – Q2, question 17.1.

47 Questionnaire to Customers (France) – Q2, question 18.1.

48 Questionnaire to Competitors (France) – Q1, question 15.1 ; see also Form CO, paragraphs 174-182.

49 Questionnaire to Competitors (France) – Q1, question 16.1.

50 Questionnaire to Competitors (France) – Q1, question 17 ; see also, Form CO, paragraph.

51 Questionnaire to Competitors (France) – Q1, question 17.

52 Questionnaire to Competitors (France) – Q1, questions 20.1 and 20.1.1.

53 Parties’ response to the Commission’s request for information RFI 2 and follow-up questions, questions 10 and 3.a, respectively.

54 Questionnaire to Customers (France) – Q2, question 30.

55 Questionnaire to Competitors (France) – Q1, questions 19.1 and 19.1.1.

56 Parties’ response to the Commission’s request for information RFI 2, question 9.

57 Form CO, paragraph 128.

58 Parties’ response to the Commission’s request for information RFI 2, question 11; see also, Form CO, paragraph 237.

59 Questionnaire to Competitors (France) – Q1, question 34.1.

60 Questionnaire to Customers (France) – Q2, question 32.1; Questionnaire to Competitors (France) – Q1, question 34.1.

61 Questionnaire to Competitors (France) – Q1, question 33.1.

62 Press release of 12 February 2019, Point.P TP pourrait être vendu par Saint-Gobain, available at: https://www.lemoniteurmateriels.fr/article/point-p-tp-pourrait-etre-vendu-par-saint-gobain,817230.

63 Parties’ response to the Commission’s request for information RFI 2, question 11.

64 Questionnaire to Competitors (France) – Q1, question, question 14; Questionnaire to customers (France) - Q2, question 15.

65 Questionnaire to Competitors (France) – Q1, question 10.2.

66 Questionnaire to Customers (France) – Q2, question 11.2.

67 Questionnaire to Customers (France) – Q2, question 10.

68 Form CO, paragraphs 174 and 180.

69 Questionnaire to Competitors (France) – Q1, question 15.2.

70 Questionnaire to Competitors (France) – Q1, question 16.2.

71 Questionnaire to Competitors (France) – Q1, question 18.2.

72 Questionnaire to Competitors (France) – Q1, question 18.2.1.

73 Questionnaire to Customers (France) – Q2, question 29.

74 Questionnaire to Customers (France) – Q2, question 29.

75 Questionnaire to Customers (France) – Q2, question 16.2.

76 Questionnaire to Customers (France) – Q2, question 17.2.

77 Questionnaire to Customers (France) – Q2, question 18.2.

78 Questionnaire to Competitors (France) – Q1, question 19.2; Questionnaire to Customers (France) – Q2, question 30.

79 Parties’ response to the Commission’s request for information RFI 2, question 9 (ii).

80 Questionnaire to Customers (France) – Q2, question 30.

81 Questionnaire to Customers (France) – Q2, question 30.

82 Questionnaire to Competitors (France) – Q1, question 34.2; Questionnaire to Customers (France) – Q2, question 32.2.

83 Questionnaire to Competitors (France) – Q1, question 34.2; Questionnaire to Customers (France) – Q2, question 32.2.

84 Questionnaire to Competitors (France) – Q1, question 34.2.

85 Commission Decision in Case M.7498 – Compagnie de Saint-Gobain/Sika (2015), recitals 103 and 105; Commission Decision in Case M.4177 – BASF/Degussa (2006), recital 17.

86 Commission Decision in Case M.7498 – Compagnie de Saint-Gobain/Sika (2015), recital 104.

87 Form CO, paragraph 78.

88 Questionnaire to Competitors (France) – Q1, question 21; Questionnaire to Customers (France) – Q2, question 19.

89 Commission Decision in Case M.4177 – BASF/Degussa (2006), recital 31.

90 Commission Decision in Case M.7498 – Compagnie de Saint-Gobain/Sika (2015), recital. 106.

91 Form CO, paragraph 80.

92 Questionnaire to Competitors (France) – Q1, question 22; Questionnaire to Customers (France) – Q2, question 20.

93 Form CO, paragraph 181.

94 Questionnaire to Customers (France) – Q2, question 32.3; Questionnaire to Competitors (France) - Q1, question 34.3.

95 Commission Decision in Case M.7498 - Compagnie de Saint-Gobain/Sika (2015), recital. 114.

96 Form CO, paragraph 83.

97 Questionnaire to Competitors (France) – Q1, question 24; Questionnaire to Customers (France) – Q2, question 22.

98 Commission Decision in Case M.7498 - Compagnie de Saint-Gobain/Sika (2015), recital 116.

99 Form CO, paragraph 84.

100 Questionnaire to Competitors (France) – Q1, question 25; Questionnaire to Customers (France) – Q2, question 23.

101 Parties’ response to the Commission’s request for information RFI 2, question 22.

102 Form CO, paragraph 181.

103 Parties’ response to the Commission’s request for information RFI 2, question 16.

104 Questionnaire to Competitors (France) – Q1, question 31.2.

105 Questionnaire to Customers (France) – Q2, question 29.

106 Questionnaire to Competitors (France) – Q1, question 32.2

107 Questionnaire to Customers (France) – Q2, question 30.

108 Questionnaire to Competitors (France) – Q1, question 32.2.1; Questionnaire to Customers (France) – Q2, question 30.

109 Parties’ response to the Commission’s request for information RFI 2, questions 10 and 22.

110 Questionnaire to Competitors (France) – Q1, question 34.4; Questionnaire to Customers (France) – Q2, question 32.4.

111 Questionnaire to Competitors (France) – Q1, question 34.4.1.

112 Parties’ response to the Commission’s request for information RFI 2, questions 16 and 22.

113 Parties’ response to the Commission’s request for information RFI 2, question 21.

114 Parties’ response to the Commission’s request for information RFI 2, question 22.

115 Commission Decision in Case M.7465 – Arkema/Bostik (2015), recitals 9-12; Commission Decision in Case M.4941 – Henkel/Adhesives & Electronic Business (2008), recitals 10-15; Commission Decision in Case M.3612 – Henkel/Sovereign (2004), recitals 10-20.

116 Commission Decision in Case M.8152 - Arkema/Den Braven (2016), recitals 15-31.

117 Form CO, paragraph 105.

118 Questionnaire to Competitors (France) – Q1, question 27; Questionnaire to Customers (France) – Q2, question 25.

119 Commission Decision in Case M.7465 – Arkema/Bostik (2015), recital 11; Commission Decision in Case M.4941 – Henkel/Adhesives & Electronic Business (2008), recitals 38-58; Commission Decision in Case M.3612 – Henkel/Sovereign (2004), recitals 36-42.

120 Commission Decision in Case M.8152 – Arkema/Den Braven (2016), recitals 41-43.

121 Form CO, paragraph 107.

122 Questionnaire to Competitors (France) – Q1, question 28; Questionnaire to Customers (France) – Q2, question 26.

123 Form CO, paragraph 181.

124 Form CO, paragraph 154.

125 Parties' response to the Commission's request for information RFI 2, question 25.

126 Questionnaire to Competitors (France) – Q1, question 30; Questionnaire to Customers (France) – Q2, question 28.

127 Questionnaire to Competitors (France) – Q1, question 31.3.

128 Questionnaire to Customers (France) – Q2, question 29.

129 Questionnaire to Competitors (France) – Q1, question 32.3; Questionnaire to Customers (France) – Q2, question 30.

130 Parties’ response to the Commission’s request for information RFI 2, question 26.

131 Questionnaire to Competitors (France) – Q1, question 34.5; Questionnaire to Customers (France) – Q2, question 32.5.

132 Commission Decision in Case M.4898 – Compagnie de Saint-Gobain/Maxit (2008), recital 144.

133 Form CO, paragraph 92.

134 Questionnaire to Competitors and Customers (Spain) – Q3, question 6.

135 Questionnaire to Competitors and Customers (Spain) – Q3, question 7.

136 Commission Decision in Case M.4898 – Compagnie de Saint-Gobain/Maxit (2008), recital 145.

137 Form CO, paragraph 94.

138 Questionnaire to Competitors and Customers (Spain) – Q3, question 8.

139 Form CO, Tables 6 and 15.

140 Questionnaire to Competitors and Customers (Spain) – Q3, question 11.

141 Questionnaire to Competitors and Customers (Spain) – Q3, question 12.

142 Form CO, paragraph 240.

143 Questionnaire to Competitors and Customers (Spain) – Q3, question 13.

144 Questionnaire to Competitors and Customers (Spain) – Q3, question.15.