Commission, May 28, 2020, No M.9447

EUROPEAN COMMISSION

Judgment

HITACHI / ABB (POWER GRID DIVISION

Subject: Case M.9447 – Hitachi/ABB (Power Grid Division)

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 20 April 2020, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Hitachi Ltd (“Hitachi”, Japan) acquires within the meaning of Article 3(1)(b) of the Merger Regulation sole control of ABB Management Holding AG (“ABB (Power Grid Division)” or “Target”, Switzerland), controlled by ABB Ltd (“ABB”) (3). Hitachi is referred to as the “Notifying Party” and Hitachi and ABB (Power Grid Division) collectively are designated hereinafter as the “Parties”.

1. THE PARTIES

(2) Hitachi is a global company, headquartered in Japan and active in a variety of business segments including IT Solution, Energy Solution, Industry Solution, Mobility Solution and SmartLife Solution.

(3) ABB (Power Grid Division)'s activities involve the development, engineering, manufacturing and sale of products, systems and projects relating to: (a) high voltage (“HV”) products; (b) transformers; (c) power grid automation (“GA”); and (d) power grid integration (“GI”).

2. THE CONCENTRATION

(4) The concentration relates to the proposed acquisition from ABB, of 80.1% of the issued share capital of ABB Management Holding AG of Switzerland, by Hitachi. It will result in the acquisition of sole control by Hitachi of the Target within the meaning of Article 3(1)(b) of the EU Merger Regulation (EUMR), following which ABB will retain 19.9% of the Target (“the Proposed Transaction”).

(5) Prior to the Proposed Transaction, ABB will contribute its entire power grids business to the newly created Swiss legal entity ABB Management Holding AG, which will be the holding company for the Target Group. As such, following the SPA signed by Hitachi and ABB on 17 December 2018, Hitachi will acquire 80.1% of the issued share capital of the Target.

(6) ABB will hold a non-controlling minority shareholding in the Target post- transaction (19.9%). ABB will not acquire, or retain, any additional rights, which confer upon it the power to veto decisions which are essential for the strategic commercial venture of the Target.

(7) Accordingly, the Proposed Transaction involves the acquisition of sole control of the Target by Hitachi within the meaning of Article 3(1) (b) of the EUMR.

3. EU DIMENSION

(8) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (4) (Hitachi: EUR 99 647 million; ABB: [confidential details on the Target's worldwide turnover]). Each of them has an EU-wide turnover in excess of EUR 250 million (Hitachi: [confidential details on the Parties' EEA-wide turnover]; ABB: [confidential details on the Parties' EEA-wide turnover]), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension.

4. MARKET DEFINITION

(9) Hitachi and the Target are both active in the supply of electrical equipment for use in the transmission and distribution of electricity within power systems, including (i) HV products, (ii) transformers, (iii) GA products and (iv) GI products. The focus of the assessment is on these four general product groups with several segments. (5) The products are sold as part of turnkey systems or on a stand-alone basis for industries like power generation or transportation. (6)

4.1. High voltage (HV) products

(10) HV products are predominantly used in transmission networks, operating at high voltages (above 52 kV (7)) to transmit electricity over long distances.

(11) HV products are usually installed in HV substations. (8) The main components of HV substations are: (i) HV circuit breakers; (ii) HV disconnectors; (iii) HV instrument transformers; (iv) power transformers; and (v) HV or MV surge arresters. These components in an HV substation must be insulated in order to prevent short circuits. This can either be done by installing the components at a distance from each other, so they are air-insulated (air-insulated switchgear substation, or “AIS substation”). Where less space is available, the switchgear units of the substation are assembled within encapsulated enclosures infused with pressurised sulfur hexafluoride gas, so they are gas-insulated (“GIS substation”). (9)

(12) HV products are also used in a variety of other power-system related applications, such as switching and protection of power transmission and distribution grids or power generation plants, integration of renewables, enhancement of energy efficiency in industrial settings, and improvement of power quality in industry and power grids.

(13) The Notifying Party has only limited activities in HV products, focusing on a few components: HV gas-insulated switchgear (“GIS”), HV circuit breakers, and LV capacitors). The Target is an important producer of most HV products as well as certain MV and LV products and related services. (10)

4.1.1. Product market

(A) The Commission’s decisional practice

(14) In previous cases, the Commission has acknowledged the existence of a HV product market, subdividing electrical products and systems according to their respective voltage levels into three broad product segments:

· Low Voltage (“LV”) products (<1 kV)

· Medium Voltage (“MV”) products for distribution networks operating at voltages between 1kV and 52 kV;

· HV products for transmission networks operating at voltages between 52 kV and 800 kV.

(15) The Commission also considered whether individual HV products might constitute a separate product market. However, the Commission has to date left open whether individual HV products belong to separate markets or whether they all belong to one overall market. (11)

(16) Individual HV products previously considered by the Commission are (i) HV switchgear (both AIS and GIS); (ii) HV circuit breakers; (iii) HV instrument transformers; (iv) HV disconnectors; and (v) HV coils. (12)

(B) The Notifying Party’s view

(17) The Notifying Party considers that the entire HV product area should be treated as one overall product market for all HV products and that it should not be further segmented, insofar as: (i) customers tender on a project-based basis and do not specifically look for suppliers of specific products but rather expect suppliers to offer a comprehensive product range; (ii) from a supply-side perspective, customers will often require and purchase a variety of HV products for one and the same project; (iii) in a previous decision, which concerned a similar product portfolio as the Proposed Transaction, the Notifying Party suggested an overall market for HV products on the basis of similar considerations, (13) and this approach was largely confirmed by the market investigation. (14)

(18) Taking into account the Parties' activities in the HV area, this market would include but not be limited to HV switchgear (incl. GIS and AIS), HV circuit breakers, HV instrument transformers, HV disconnectors, HV surge arresters (incl. accessories), HV circuit breaker components and other HV products, HV cable accessories and HV capacitors, harmonic filters, and other Reactive Power Compensation (“RPC”) (15) products.

(19) In any case, given Hitachi's de minimis position on a global and EEA-wide basis, the Notifying Party submits that the exact product market definition for HV products can be left open since, even if the Commission were to examine the Proposed Transaction on the basis of the narrowest plausible HV product segments, this would not give rise to any competition concerns on a global or EEA-wide basis.

(C) The Commission’s assessment

(20) In the market investigation, a majority of customers and competitors suggested a segmentation of the market for HV products into the following: (16)

- HV Instrument Transformers

- HV Disconnectors

- HV Switchgear, either overall or GIS and AIS separately

- HV Circuit Breakers, either overall or HV disconnecting circuit breakers and generator circuit breakers separately.

- (Competitors in addition also suggest a sub-segmentation for HV live-tank circuit breakers and HV dead-tank circuit breakers separately).

(21) At the same time, the market investigation confirmed the arguments of the Notifying Party regarding supply side substitutability. In particular, the results showed that the same suppliers typically supply all or most HV products in the sub-categories, with the possible exception of smaller suppliers that are more specialised. (17) This would point to an overall market for HV products from a supply-side perspective.

(22) In any event, out of the potential markets for each HV product listed in paragraph (20), the Proposed Transaction only results in horizontally affected markets related to HV circuit breakers and HV generator circuit breakers (a potential sub-segment of this potential market) and vertically affected (18) markets related to HV AIS modules (downstream) and MV switchgear and power transformers (upstream). (19)

(23) As the other HV products do not give rise to any affected market, these will not be further discussed in this Decision.

(24) In conclusion, the Commission will analyse the Proposed Transaction on the basis of all plausible product markets, but will leave the market definition open as the Proposed Transaction does not raise concerns on any plausible market.

4.1.2. Geographic market

(A) The Commission’s decisional practice

(25) In previous decisions the Commission found that the market for HV products is at least EEA-wide. (20)

(B) The Notifying Party’s view

(26) Regarding the geographic market definition, the Notifying Party considers that, for all HV products, competition takes place on a global basis. As such, it agrees with the Commission’s previous findings that the relevant geographic market for HV products is at least EEA-wide. (21)

(C) The Commission’s assessment

(27) The results of the market investigation point towards a worldwide market for all sub-segments of HV products, as a clear majority (22) of customers (23) and of competitors (24) confirmed. According to a majority of competitors, (25) HV products sold in other world regions are generally substitutable for the HV products used in the EEA, as they are produced in line with international (IEC) standards. Nevertheless, some technical requirements are specific to the area of installation, such as special seismic conditions or minimum ambient temperatures. (26)

(28) Within the EEA, HV products do not differ across individual Member States, neither with regard to their technical specifications nor with regard to price, as confirmed by a majority of participants in the market investigation. (27) Geographical proximity to end-customers is not required to be successful in the electrical equipment industry (28) and transport costs only make up a small percentage of the purchase price of individual HV products (less than 5% according to a majority of customers). (29) National markets can thus be excluded for the purpose of the present case.

(29) In conclusion, the exact definition of the market for HV products can be left open between the EEA and worldwide, as the Proposed Transaction does not give rise to serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement on any of the two plausible geographic market definitions.

4.2. Transformers

(30) A transformer is the electromagnetic equipment that transfers electricity from one electrical circuit to another and steps the voltage up or down as required. (30) There are two main types of transformers used within a power grid: power transformers and distribution transformers. Another type of transformers, used in railway rolling stock applications, is traction transformers.

(31) Transformers come in different sizes (large, medium and small), depending on the voltage and power rating covered, but categorisation varies from supplier to supplier. Transformers always consist of two main components: the steel core, and several winding coils. Together, the steel core and the winding coils form the "active part" of a transformer.

(32) Transformers might be further sub-segmented within the three segments indicated above (power transformers, distribution transformers and traction transformers):

- Power transformers: generator step-up transformers; substation and system inertia transformers; HVDC converter transformers; power transformers used in industrial or special applications; and shunt reactors (and other types of reactors).

- Distribution transformers: liquid-filled distribution transformers; and dry-type distribution transformers.

- Traction transformers: used for railway rolling stock applications, and come in different designs in terms of size, weight and power ratings.

(33) The Parties’ activities in transformers:

- The Target is active in the design, manufacture and sale of different types of transformers (such as power transformers, distribution transformers, and traction transformers) as well as specific transformer components (including, e.g., bushings and tap-changers) and related services. (31)

- The Notifying Party has limited activities in transformers on a global basis. Although Hitachi has a transformer portfolio which is similar to that of the Target, its sales of transformers are [outside the EEA] and, in particular, it has no stand-alone sales of transformers in the EEA. (32) In addition, Hitachi does not sell any transformer components externally.

4.2.1. Product market

(A) The Commission’s decisional practice

(34) In previous decisions the Commission has considered whether power and distribution transformers constituted separate relevant product markets or whether they belong to an overall market for transformers, while ultimately leaving the precise product market definition open. (33)

(B) The Notifying Party’s view

(35) The Notifying Party submits that the relevant product market is the overall transformers market since, ultimately, all transformers serve the same purpose, i.e. mainly to increase or decrease the voltage levels of electrical power for its efficient transport on transmission and distribution networks. Hitachi submits that it would be inappropriate to further segment the overall transformers market from a demand or from a supply-side perspective by voltage type, technology used (e.g., dry-type or liquid filled) or end-use application (e.g. utility vs. industrial customers, subsea or railway rolling stock), and that this is in line with the market investigation in Alstom Holdings/Areva T&D, in which a majority of respondents supported an overall transformers market.

(36) In any event, the Notifying Party submitted information for the narrower product segments of (i) power transformers, (ii) distribution transformers overall (as well as (ii.1) oil-filled distribution transformers, and (ii.2) dry-type distribution transformers); and (iii) traction transformers.

(37) In addition, with regard to components used for the manufacture of transformers, the Notifying Party provided data for each of the transformer components that the Target sells externally (bushings, tap changers, measurement and safety devices, and insulation components and materials), even though it submits that the relevant market should be the overall market for transformers (including components), and that it would not be appropriate to define separate markets for transformer components or sub-segment it by specific component products.

(C) The Commission’s assessment

(38) The vast majority of the respondents to the Commission’s market investigation consider that, in light of their characteristics, price and intended use, it is appropriate (both from a supply-side and demand-side substitutability point of view) to segment the market by transformer type into power transformers, distribution transformers and traction transformers, and have not signalled that a further segmentation beyond that is warranted. (34)

(39) In any event the precise product market definition can be left open since the Notifying Party provided market shares for the narrowest plausible segmentations of transformers according to the Commission’s previous assessments, i.e. for power (35) and traction (36) transformers separately, and for overall distribution transformers as well as for oil-filled and dry-type distribution transformers separately, (37) (as well as for each transformer component that the Target sells externally) (38) and no competition concerns arise regardless of the ultimate product market definition.

4.2.2. Geographic market

(A) The Commission’s decisional practice

(40) In previous cases the Commission considered that the relevant geographic market for transformers was at least EEA-wide in scope, possibly even worldwide, although the precise definition was left open. (39)

(B) The Notifying Party’s view

(41) In relation to the geographic scope of the market for transformers (and transformer components), Hitachi argues that it is global and that it can ultimately be left open since Hitachi is not active in the EEA.

(42) In any event, the Notifying Party provided information on both an EEA-wide and global basis and for the narrowest segments within the area of transformers and for each transformer component that the Target sells externally.

(C) The Commission’s assessment

(43) The market investigation is not conclusive on whether the relevant geographic market should be EEA-wide or global. (40) In any event, no horizontal concerns arise under either definition (because Hitachi is not active in the EEA). For the purpose of the assessment of the only material vertical link (that for traction transformers used for railway rolling stock), the market shares at both the EEA and globally are similar and thus the competition analysis is applicable regardless of the precise geographic market definition.

4.3. Railway rolling stock

4.3.1. Product market

(A) The Commission’s decisional practice

(44) In previous decisions the Commission has considered trains reaching speeds equal to or higher than 250 km/h (high and very high-speed trains) as a separate product market, distinct from intercity trains which are incapable of achieving similar speeds. Moreover, the Commission has considered a potential further sub-segmentation between high-speed trains (top speed between 250 and 300 km/h) and very high-speed trains (top speed greater than 300 km/h), while ultimately leaving the precise product market definition open. (41)

(B) The Notifying Party’s view

(45) The Notifying Party submits that the relevant product markets for railway rolling stock are (i) very high-speed trains (top speed above 300 km/h), (ii) high- speed trains (top speed between 250 and 299 km/h), and (iii) mainline railway rolling stock (intercity and regional trains).

(46) In any event, the Notifying Party submitted information for the narrowest plausible product segments of (i) high-speed trains (top speed between 250 and 299 km/h), (ii) very high-speed trains (top speed equal to or above 300 km/h), (iii) intercity/regional trains (top speed between 160 and 249 km/h), and (iv) commuter trains (top speed below 160 km/h), as well as for the broader product markets of (v) all high-speed trains (including high-speed and very high-speed trains) and (vi) combined market for intercity/regional + commuter trains.

(C) The Commission’s assessment

(47) For the purpose of the present case, the Commission considers that the precise product market definition can be left open since, for the purpose of the vertical assessment for traction transformers for railway rolling stock applications, the Proposed Transaction does not raise concerns even on the narrowest segments (in particular, in the segment for intercity/regional trains, where the Notifying Party is present).

4.3.2. Geographic market

(A) The Commission’s decisional practice

(48) In previous decisions the Commission has defined the relevant markets for high and very high-speed rolling stock as at least EEA-wide (including Switzerland) while not excluding the possibility of these markets being worldwide (excluding China, South Korea and Japan) and leaving the precise geographic market definition open. (42)

(49) For regional trains (43) and intercity trains (44), the Commission has previously considered the market to be likely at least EEA-wide.

(B) The Notifying Party’s view

(50) The Notifying Party submits that in its view, and in line with the geographic market definition in Siemens/Alstom, the geographic market for high and very high-speed trains is at least EEA wide, if not worldwide (excluding China, Japan and Korea).

(51) In any event, the Notifying Party also submitted information on a worldwide basis (including China, Japan and Korea) for all plausible segments.

(C) The Commission’s assessment

(52) For the purpose of the present case, the Commission considers that the precise geographic market definition can be left open since, for the purpose of the vertical assessment for traction transformers for railway rolling stock applications, the Proposed Transaction does not raise concerns either in the EEA or globally (in particular, given that both the upstream shares of the Target for traction transformers and the downstream shares of the Notifying Party in the different railway rolling stock segments are relatively similar in the EEA and worldwide).

4.4. Grid automation

(53) GA is the digitalisation and automation of power grids and/or substations, which provide the ability to remotely control and monitor the operating conditions of primary and secondary assets of a transmission or distribution network throughout the entire network. GA solutions consist of hardware and software products, systems and services. (45)

(54) GA systems that digitalize and automatize power grid operations can be summarized under the term "Power System Management Solutions". GA solutions operating at substation level include products and systems that enable the automated monitoring, control and supervision of substation assets - these solutions are referred to as "Substation Automation Systems" (SAS). GA solutions operating at the enterprise level via the control center are used to manage the entire grid network composed of numerous substations, using SCADA software solutions to enable secure, efficient and optimized operation of the electric power system as a whole. They are therefore referred to as "Network Management Systems" (NMS). (46)

(55) GA solutions also exist for Microgrids, i.e. distributed energy resources that can also operate in "islanded" mode (so-called "Microgrid Automation Systems" (MAS)). The automation system architecture is similar to SAS and NMS, but MAS additionally includes battery energy storage solutions (BESS) and a power conversion system (PCS). (47)

(56) GA solutions can also include enterprise application software (“EAS”) solutions which help businesses improve their efficiency, reliability, safety and sustainability. (48) In GA solutions, enterprise software is used in the control center to collect and manage data on the condition and availability of major plant equipment, thus enabling plant operators to plan maintenance schedules more effectively and avoid unnecessary equipment inspections and unexpected breakdowns, which can cause expensive interruptions in production time. Business analytics solutions track, analyze and manage data in support of corporate decision making processes. (49)

(57) The Target's GA business is divided into (i) GA systems and products, including SAS, NMS, microgrid automation systems and communication systems; (ii) standalone GA products, including different GA components and software sold on a standalone basis; and (iii) enterprise application software (EAS). (50) Approximately [confidential details on the Target's breakdown of GA sales]% of the Target’s GA sales are generated with system solutions. (51)

(58) Hitachi has only limited activities in GA on a global basis [mainly focusing outside the EEA], and Hitachi does not offer GA products or systems in Europe. Hitachi's GA solutions are designed and developed [Confidential details on Hitachi's sales strategy for GA products]. [Confidential details on Hitachi's sales strategy for GA products]. (52)

4.4.1. Product market

(A) The Commission’s decisional practice

Energy Automation and Information Systems

(59) The Commission has previously considered an overall market for Energy Automation and Information Systems (‘EAIS’) as a potential segment within the market for Transmission and Distribution. (53)

(60) The Commission has also considered dividing the market for EAIS into two sub-segments: i) power system management and ii) protection relays. (54) Furthermore, the Commission has considered whether a market exists both in the turnkey area and at the level of individual components. (55)

(61) The Commission has also considered a potential sub-segmentation of power system management into i) Substation Automation Systems (‘SAS’) and ii) Network Management Systems (‘NMS’), because they from a demand-side perspective perform different functions. (56)

(62) Additionally, the Commission has considered to do a further sub-segmentation of NMS into i) Energy Management Systems (‘EMS’), ii) Distribution Management Systems (‘DMS’) and iii) Wide Area Monitoring Systems (‘WAMS’). (57) Ultimately, the Commission has left the final definition of the product market open in all its previous decisional practice. (58)

Enterprise Application Software

(63) The Commission has previously considered a market for the provision of enterprise application software (‘EAS’) as a segment within business software (59). Furthermore, the Commission has considered further distinctions, ultimately leaving the market definition open. These possible further distinctions are explained in the three paragraphs below.

(64) The Commission has considered dividing EAS into the following sub-segments: i) Enterprise Resource Planning (‘ERP’), ii) Customer Relationship Management (‘CRM’), iii) Supplier Relationship Management (‘SRM’), iv) Supply Chain Management (‘SCM’), v) Product Lifecycle Management (‘PLM’) and vi) Business Analytics (‘BA’). (60)

(65) Within the ERP segment, sub-segments based on functionality have been considered, namely i) Financial Management Systems (‘FMS’), ii) Human Resources (‘HR’) and iii) Enterprise Project Management (‘EPM’). (61) Furthermore, the Commission has considered whether each of these three segments should be subdivided into two sub-segments, namely i) high-function solutions and ii) mid-market solutions. (62)

(66) Within the BA segment the Commission has in past cases considered a possible distinction between i) Performance Management Tools and Applications (‘PMT’) and ii) Data Warehouse Platforms (‘DWP’). (63) PMT was itself considered as possibly divided between i) business intelligence (‘BI’), ii) Financial performance strategy management (‘FPSM’) applications, iii) CRM analytics, iv) SCM analytics, (v) service operations management applications, vi) workforce analytics, and vii) analytic spatial information management tools. (64) BI has been considered as possibly sub-segmented into i) Query, Reporting and Analysis (‘QRA’) tools on the one hand and ii) Advanced Analytics on the other. (65)

(B) The Notifying Party’s view

EAIS

(67) The Notifying Party submits that the relevant product market is the overall EAIS market. (66) However, the precise market definition can be left open as no concerns will arise under any plausible market definition.

(68) According to the Notifying Party, Automation customers require the set-up of a complete solution and hence issue a call for tenders for an entire EAIS rather than for individual automation products, making it necessary for suppliers to offer a comprehensive range of products in order to be able to compete successfully on the market. Where products are sold on a stand-alone basis, those sales are usually made to other system integrators for a specific project. (67)

(69) Furthermore, the Notifying Party argues that a distinction between SAS and NMS or any further sub-segmentation is not appropriate, as the underlying system remains the same and there is a high degree of supply-side substitutability in relation to the automation products required (both hardware and software). (68) Likewise, after-sale services should not be considered a separate market, as they are inherent to and constitutive of the different products and systems which the Parties offer in the area of transmission and distribution. (69)

(70) The Notifying Party submits that there is no separate market or segment for power network communication solutions, noting that the activities of the Parties in this area predominantly involve the supply of communication solutions in the context and as part of the provision of a SAS or NMS system (i.e. the Parties do not focus on the supply of stand-alone communication systems). (70)

(71) Furthermore, the Notifying Party submits that products, systems and services for energy management solutions should fall within an overall market for EAIS including both power system management and single devices that are sold stand- alone, such as e.g. protective relays, communication equipment and automation software. (71)

EAS

(72) The Notifying Party submits that the relevant product market should be the overall market for EAS. (72) While there is business software with various different functionalities, there is no clear-cut line between those functionalities (73) as often software solutions are tailored to the needs of a respective customer and hence usually include more than just one functionality. In addition, supply-side substitutability between the single functionalities is high. (74) However, given that, in its view, there is an absence of any concerns arising under all plausible market delineations, the Notifying Party submits that the market definition can ultimately be left open. (75)

(C) The Commission’s assessment

EAIS

(73) The Commission considers that the EAIS market can be segmented between power management systems and stand-alone products. Within power system management systems a segmentation between SAS and NMS can be considered, the latter potentially further divided between EMS, DMS and WAMS.

(74) Furthermore, a separate segment for MAS can be considered as well as stand- alone products for communication products or systems, protective relays, automation software and remote terminal units (RTUs).

(75) The results of the market investigation were mixed but generally supported a segmentation of the EAIS product market. (76)

(76) However, in this case the Commission can leave the product market definition open as the Proposed Transaction does not raise competition concerns on any plausible market.

(77) Given the absence of any horizontally or vertically affected markets, the Commission will not further discuss this market.

EAS

(78) The results of the market investigation were mixed but generally supported a segmentation of the EAS market. (77) However, in this case the Commission can leave the product market definition open as the Proposed Transaction does not raise competition concerns on any plausible market.

(79) Given the absence of any horizontally or vertically affected markets, the Commission will not further discuss this market.

4.4.2. Geographic market

(A) The Commission’s decisional practice

EAIS

(80) The Commission has previously considered the plausible EAIS markets to be EEA-wide or world-wide, but has ultimately left the precise geographic market definition open. (78)

EAS

(81) The Commission has considered the relevant geographic market for EAS to be EEA-wide or worldwide. (79) With respect to CRM and BA (including possible sub-segments), the Commission has considered the market to be at least EEA- wide and possibly worldwide. (80)

(82) Concerning high function solutions for HR and FMS, the Commission has concluded that the market is global. (81)

(B) The Notifying Party’s view

EAIS

(83) The Notifying Party submits that the relevant geographic market for EAIS is global and, in any event, far larger than a geographic area including the EEA. All product markets within GA are global in scope, as there are no trade barriers through technical standards, the vast majority of customers and the major suppliers are active at a global level, and transportation costs do not limit the ability of manufacturers to compete effectively in countries where they do not have production. However, the geographic market definition can be left open in this case, as Hitachi is not active in the EEA. (82)

EAS

(84) The Notifying Party submits that the relevant geographic market for EAS (and its segments and sub-segments, if examined separately) is global and, in any event, far larger than a geographic area including the EEA. All product markets within GA are global in scope, as there are no trade barriers through technical standards, the vast majority of customers and the major suppliers are active at a global level, and transportation costs do not limit the ability of manufacturers to compete effectively in countries where they do not have production. However, the geographic market definition can be left open in this case, as Hitachi had no sales in EAS in the past three years (2016-2018). (83)

(C) The Commission’s assessment

EAIS

(85) The Commission has in the past analysed the segments of the EAIS market at EEA and worldwide level. The majority of the respondents to the market investigation considered the plausible EAIS markets worldwide in scope. (84à) However, as the Proposed Transaction does not raise competition concerns on any plausible market the geographic market definition can be left open.

(86) Given the absence of any horizontally or vertically affected markets, the Commission will not further discuss this market.

EAS

(87) The Commission has in the past analysed the segments of the EAS market at EEA and worldwide level. The majority of the respondents to the market investigation considered the plausible EAS markets to be worldwide in scope. (85) However, as the Proposed Transaction does not raise competition concerns on any plausible market the geographic market definition can be left open

(88) Given the absence of any horizontally or vertically affected markets, even for the narrowest plausible combination of product and geographical market definitions, the Commission will not further discuss this market.

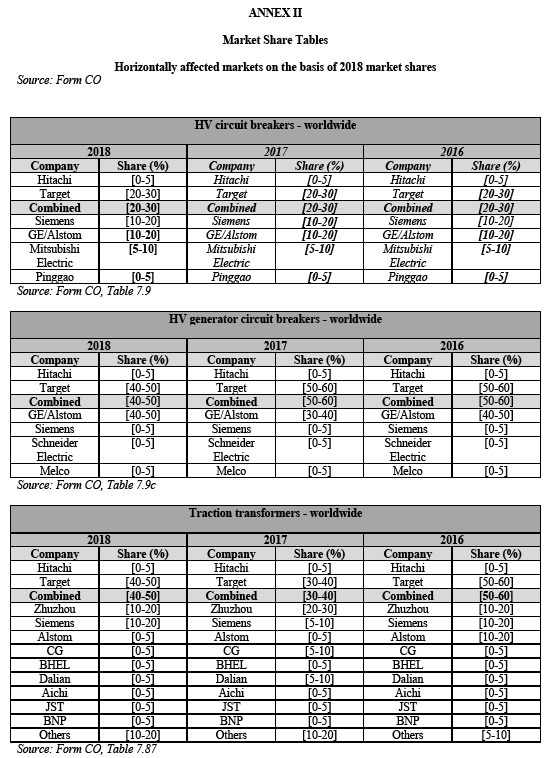

4.5. Grid Integration

(89) The Target’s Grid Integration (“GI”) business line is active in the design, manufacture and sale of HV substations, high voltage direct current (HVDC) stations, flexible alternating current transmission systems (FACTS), and (high) power semiconductors as well as related services. Each of these products could be potentially sub-segmented into several other different markets. This business line also includes charging infrastructure for buses, trams and electric vehicles, and power consulting services. Hitachi has de minimis activities in GI on a global basis. In this business area, Hitachi's focus is on the manufacturing and supply of power semiconductors. (86)

4.5.1. Product market

T&D turnkey systems

(A) The Commission’s decisional practice

(90) In previous decisions relating to the overall market for transmission and distribution and its various components, the Commission has considered the overall market for transmission and distribution and its various components, both when they are supplied individually or integrated into a system. (87)

(91) In one decision, while the market definitions were ultimately left open, the following potential product markets were identified: (i) HV products, (ii) MV products, (iii) power transformers, (iv) transmission systems and distribution systems, (v) energy automation and information systems and (vi) transmission and distribution services. (88)

(92) The Commission has considered in the past that the transmission and distribution systems could constitute a single market comprising the design and installation of turnkey systems, either for transmission networks or for distribution networks, but ultimately left the market definition open. (89) The Commission has previously considered identifying tentative product markets for HV turnkey projects (transmission systems), as distinguished from MV turnkey projects (distribution systems). (90) In another decision, the question whether the transmission and distribution systems together constitute a separate market, or whether the market for transmission systems should be considered as a separate market was left open. (91) Also, the Commission has previously looked into the markets for HVDC and FACTS, (92) but ultimately left the market definition open. (93)

(B) The Notifying Party’s view

(93) The Notifying Party submits that the relevant product market is the overall market for T&D turnkey systems, and that the narrowest plausible segments within this market are HVDC stations/systems, FACTS and substations.

(94) The Notifying Party submits that it would also be inappropriate to further segment the overall market for T&D turnkey systems from a demand or supply- side perspective. This is because from a supply-side perspective, all major EPC companies in the T&D sector have the necessary capabilities to offer all main types of T&D projects (including HVDC, FACTS and substations) and equipment and resources will typically be sourced externally as required. Whereas from a demand-side perspective, customers will set out the required specifications for a project in the tender documents and it is not decisive which type of provider undertakes the project, as long as the specifications are met, and all major providers can do all types of projects. In addition, large-scale T&D projects often include a combination of HVDC, FACTS and substations.

(95) As regards HVDC, the Notifying Party maintains that neither HVDC, nor the following HVDC solutions – HVDC Light and HVDC Classic solutions, belong to separate product markets, for the following reasons.

(96) HVDC Classic is the "traditional" HVDC technology, which operates with a power of more than 100 MW whereas, HVDC Light is a technology developed by ABB in the 1990s. While there are certain differences in the distance and power ranges that can be covered by each of the systems, they are now largely interchangeable and it often depends on the customer's preferences and/or budget whether to choose a "classic" or "light" HVDC solution. Furthermore, from a supply-side perspective most large vendors now offer both types of HVDC solutions.

(97) Moreover, each HVDC station is a tailored solution, depending on the requirements and characteristics of the respective project and the customer. A segmentation on the basis of these two technologies would not reflect the complexity of these systems, and the variety of HVDC station offerings. Such systems are in practice largely customized to meet the needs of customers so that the exact composition and set-up of HVDC stations based on the same technology can differ.

(98) The Notifying Party submits that it would not be appropriate to segment FACTS (into Series compensation FACTS, and the latter into a) fixed (Fixed Series Compensation or Fixed SC), and b) controlled Series compensation FACTS; and (ii) (Dynamic) Shunt compensation FACTS, and the latter into: (i) static compensators (STATCOM), and (ii) static VAR compensators (SVC)) for the reasons explained below.

(99) First, the main intended use of any FACTS, irrespective of the technology used, is to boost transmission capacities without having to build or use new transmission lines or power generation facilities. Both Series Compensation and (Dynamic) Shunt Compensation are used to compensate power quality issues quickly through reactive power, ensuring higher grid stability.

(100) Second, both technologies use similar impedance devices, like capacitors or reactors, which are used to control voltage in the network.

(101) Third, a segmentation by these technologies would not reflect the complexity and variety of FACTS offerings. Such systems are in practice largely customized to meet the needs of customers so that the exact composition and set-up of FACTS based on the same technology can differ. The choice between series or shunt type of compensation is the result of plan optimization based on customer requirements and network characteristics.

(102) Fourth, just as the Target and Hitachi offer these technologies, other players in this space, such as Siemens, also offer different technologies to customers indicating a high degree of supply-side substitutability.

(103) The Notifying Party further submits that it is not appropriate to further differentiate between different types of substations within this segment for the following reasons.

(104) Substations are used in transmission and distribution networks to convert and transfer electricity from the power generation plant to the end-customer. Depending on the terrain, specific project, amount of energy supplied, budget, customer requirements, etc., the supplier will choose a substation setup that is suitable to meet the requirements. However, the basic function of a substation is always the same, namely to convert and to transfer electricity.

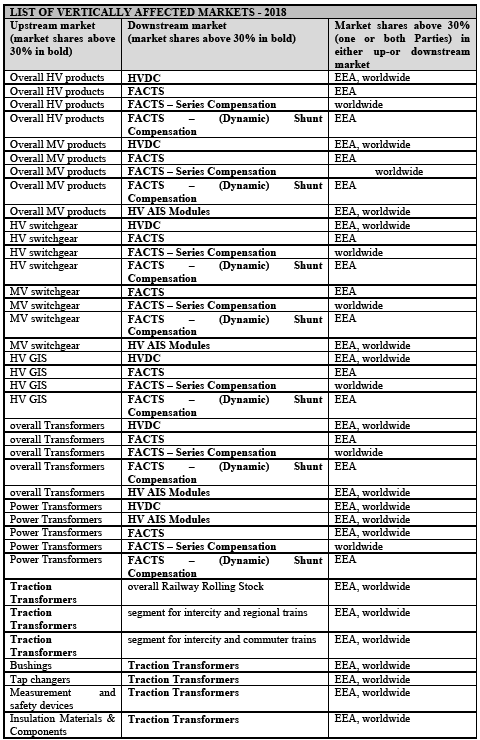

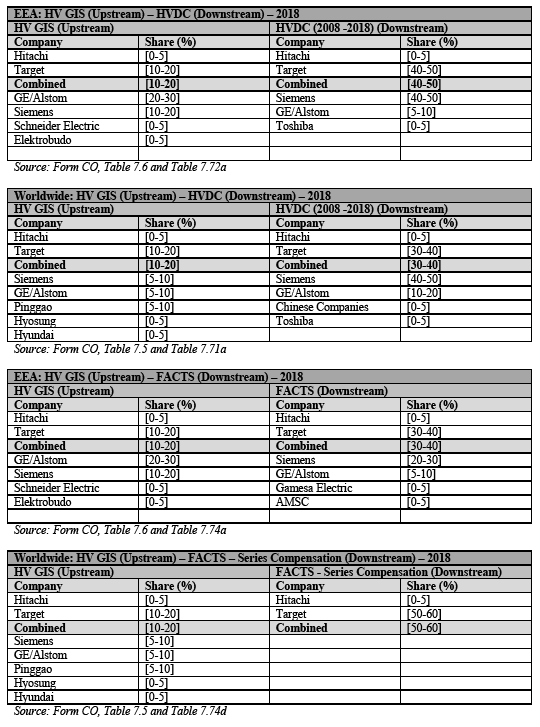

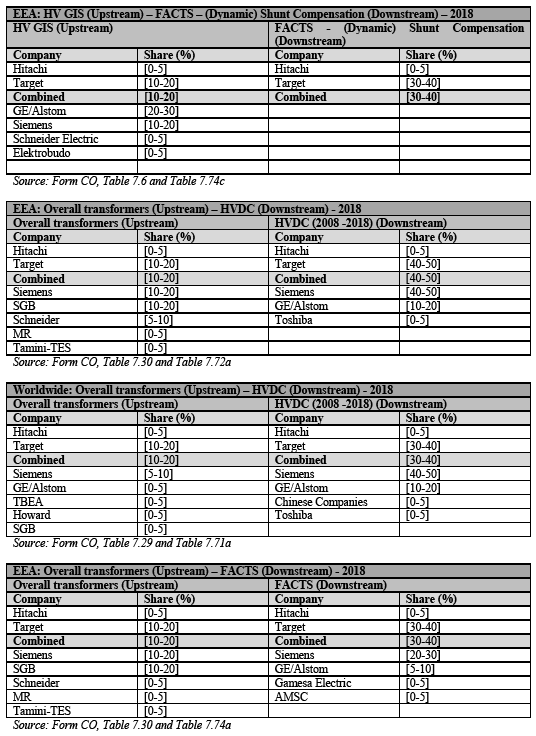

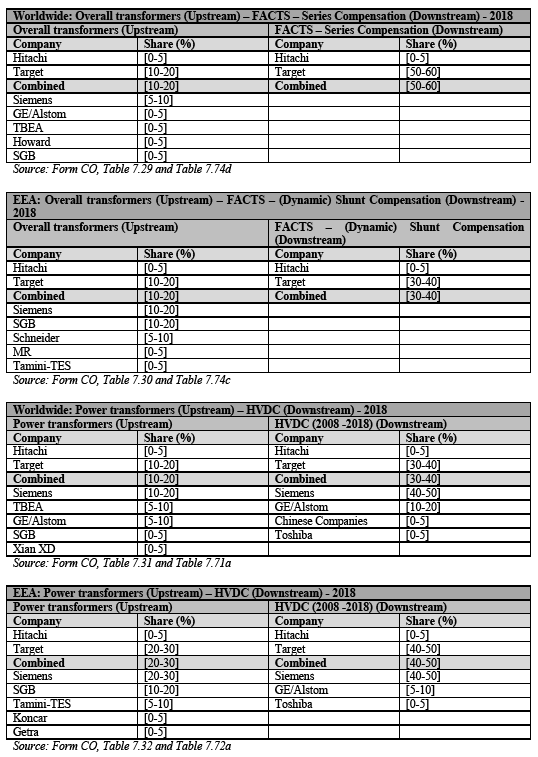

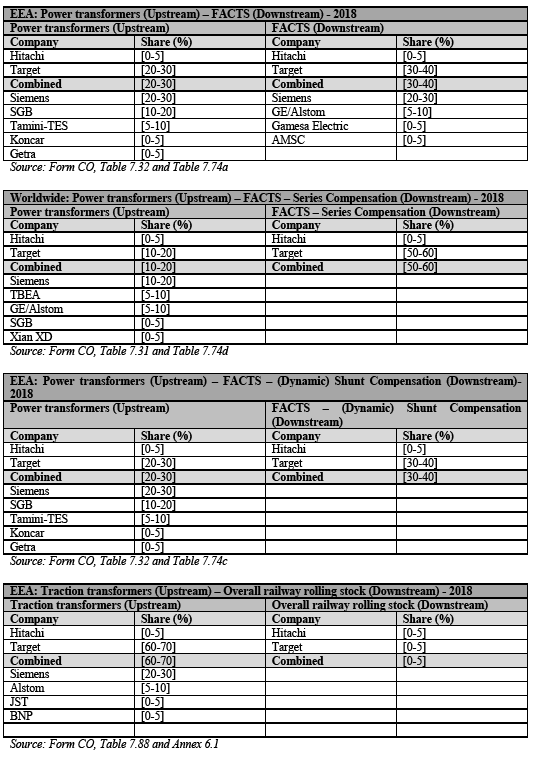

(105) While substation setups can roughly be divided into AIS substations, GIS substations, and mobile substations, the additional existence of Hybrid Substations already shows that the distinction between the different types is blurred. There is no clear-cut distinction between AIS, GIS and Hybrid and there are many different setups that are possible and which use either more air- insulated or more gas-insulated equipment, depending on the respective project.

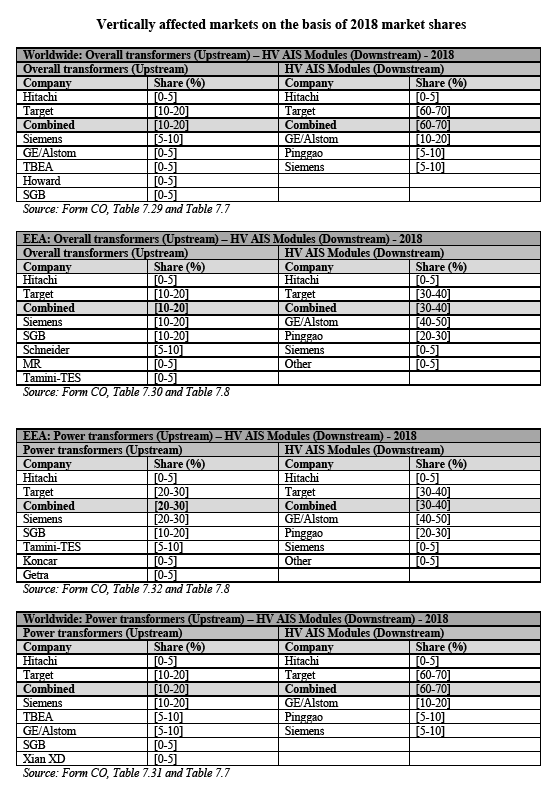

(106) In addition, substation-offerings are tender-based, and the EPC companies will source the required equipment according to the project specifications. From a supply and demand-side point of view, there is no significant difference in supplying either an AIS or GIS (or hybrid) substation.

(C) The Commission’s assessment

(107) The Commission conducted its market investigation on the basis of and in respect of the plausible sub-segments mentioned above. The market investigation examined whether sub-segmentation is warranted for the following products that could be offered within HVDC stations, FACTS and substations: (94)

- segmentation of HVDC stations/systems into: (i) HVDC Classic (the “traditional” HVDC technology, operating with a power of more than 100 MW), and (ii) HVDC Light/Plus (used for undersea cable links and long underground cable links, with range from around 80 kV up to 320 kV)

- segmentation of FACTS into: (i) Series compensation FACTS, and the latter into a) fixed (Fixed Series Compensation or Fixed SC), and b) controlled Series compensation FACTS; and (ii) (Dynamic) Shunt compensation FACTS, and the latter into: (i) static compensators (STATCOM), and (ii) static VAR compensators (SVC);

- segmentation of substations into: (i) AIS substation; (ii) GIS substation; (iii) Hybrid substation; and (iv) Mobile substation.

(108) The market investigation confirmed that T&D turnkey systems could be viewed as a separate market, with the majority of customers and competitors confirming such an understanding. (95) The results of the market investigation on any plausible segmentations within T&D turnkey systems were mixed.

(109) As regards T&D turnkey systems, the majority of customers considered that T&D turnkey systems could be segmented between HVDC stations/systems, FACTS and substations. For example, a customer explained that these segments require different knowledge. Another customer explained that the products require different supply chains. (96) On the other hand, competitors had divergent views whether HVDC stations/systems, FACTS and substations are part of one market for T&D turnkey systems, or can be viewed as belonging to different markets. One competitor that opined that these products belong to different markets explained that there are different electronic engineering standards applicable to these products. (97)

(110) As regards a possible segmentation between HVDC Classic and HVDC Light/Plus, the market investigation also yielded mixed results. While the majority of customers considered that a segmentation between HVDC Classic and HVDC Light/Plus is warranted, (98) the majority of competitors were of the opposite view. (99)

(111) As regards FACTS sub-segmentation into Series compensation FACTS and (Dynamic) Shunt compensation FACTS, the majority of customers considered that such a segmentation is not warranted. (100) One customer explained that there is not a lot of difference between these two products, and another one that it is likely that these products will be supplied by the same manufacturers. (101) Competitors were split in their view as to whether Series compensation FACTS and (Dynamic) Shunt compensation FACTS belong to the same market or not. Those who considered that the products should not be segmented explained that these different technologies have the same basic functionality and suppliers mostly offer several technologies; and that these products are complementary to secure the grid quality. (102)

(112) As regards the possible segmentation of Series compensation FACTS into fixed (Fixed Series Compensation or Fixed SC), and controlled Series compensation FACTS, the majority of customers and competitors considered that such a segmentation is not warranted. (103)

(113) As regards the possible segmentation of (Dynamic) Shunt compensation FACTS into static compensators (STATCOM), and static VAR compensators (SVC), customers and competitors were split in their view as to whether these products should belong to separate markets or not. (104)

(114) Finally, as regards the possible segmentation of substations into: (i) AIS substations; (ii) GIS substations; (iii) Hybrid substations; and (iv) Mobile substations, the majority of customers considered that these products could be part of different markets. For example, customers explained that prices of the products differ; there are different supply chain operating for these products; and not all suppliers can offer the various different designs. (105)

(115) Taking into account the Notifying Party's arguments and the results of the market investigation, the Commission considers that, in any case, the precise scope of the product market definition of T&D Turnkey systems can be left open since the Proposed Transaction does not raise serious doubts on the narrowest plausible segmentation within T&D turnkey systems, which in this case is HVDC stations, FACTS and substations, and the further sub- segmentation for HVDC stations/systems between HVDC Classic and HVDC Light/Plus; for FACTS between Series compensation FACTS (fixed (Fixed Series Compensation or Fixed SC), and controlled Series compensation FACTS) and (Dynamic) Shunt compensation FACTS (static compensators (STATCOM), and static VAR compensators (SVC)); and for substations between AIS substations, GIS substations, hybrid substations, and mobile substations.

Power semiconductors

(116) Semiconductors are materials, such as silicon, which can act as an insulator, but are also capable of conducting electricity. Therefore, they are a good medium for the control of electrical current. Semiconductors are at the heart of many devices which are produced by the Parties and can be found in virtually every electronic device today. They are rarely bought as end-products by consumers. Rather, they are an input product for equipment manufacturers in virtually all sectors within the electronic equipment industry.

(117) The Proposed Transaction relates to power semiconductors (including high power semiconductors), which have a different functionality compared to general semiconductors. (106) Power semiconductors include integrated circuits (ICs), discretes, as well as many other types of power semiconductors and modules. The Proposed Transaction relates to power discretes, such as diodes, rectifiers, transistors or thyristors, and modules (the transaction relates to these products in the sense that one or both of the Parties produces them).

(118) The overlap between the Parties' global offerings mainly relates to high power standard IGBT modules, where both Parties have a limited position at a global level and in the EEA. In addition, both Parties also had minor sales of discretes (more specifically: diodes / rectifiers) both globally and in the EEA. (107)

(A) The Commission’s decisional practice

(119) In previous cases relating to semiconductors, the Commission distinguished between ICs, discretes, and sensors and actuators, respectively (and further sub- segments, as applicable). (108) The Commission also considered within discretes a distinction between the segments for RF and microwave, power transistors and thyristors, rectifiers and power diodes, and small signal and other discretes. (109)

(B) The Notifying Party’s view

(120) The Notifying Party submits that these cases relating to general semiconductors can give a rough indication as to how to further segment the relevant markets based on the relevant types of semiconductors available, as they are not directly applicable to high power semiconductors which differ in functionality and in the relevant sub-types compared to general semiconductors.

(121) The Notifying Party submits that in the area of power semiconductors, a distinction can be made between discretes (including, e.g., thyristors and diodes/rectifiers) and modules. While it would also appear plausible to further segment discretes into thyristors, diodes/rectifiers, IGCTs, GTOs and GCTs as well as IGBTs, the Notifying Party maintains that it would not be appropriate to distinguish between power, high power and extra-high power semiconductors for the following reasons.

(122) First, the basic functionality remains the same regardless of the exact (high) power level. Power semiconductors provide for one switch with high power, as opposed to “general semiconductors” that provide for millions of “low power” switches.

(123) Second, the input material for all power semiconductors is the same (primarily silicon). Producing different power semiconductors therefore does not require any substantive change in the materials used, or the manufacturing facilities.

(124) Third, there is no established standard or defined term as to where to draw the line between power, high power and extra high power - notably, also established industry reports including IHS only provide sales data for power semiconductors overall rather than splitting between power and high power or power, high power, and extra high power. Suppliers such as the Target offer a wide range of product types with voltage ratings ranging (in the case of the Target) from 200 to 8500 V and current ratings from 25 to 13500 A. Whether or not a product would qualify as power, high power or even extra high power would ultimately depend (apart from the definition of these categories) on the required specifications of the customer on these two metrics. Moreover, the IHS reports only distinguish between power levels (powers vs. high power) for two types of semiconductors, i.e., thyristors and diodes/rectifiers.

(125) Fourth, while there is a difference in suppliers for “general” semiconductors and “power semiconductors”, there is no such distinction between power, high power and extra high power. While certain suppliers (such as e.g. Hitachi) may focus on semiconductors that are usually provided at the lower end of the range, in principle, all suppliers are capable of providing power and high-power semiconductors as the underlying basic technology is similar.

(126) Fifth, while there is a difference between the types of semiconductors included in the categories of “general” semiconductors and “power semiconductors”, there is no such difference between the types of devices that are offered in power, high power and extra high power. Furthermore, the types of semiconductors offered by the Parties can be both power and high power (or extra high power).

(127) Lastly, in terms of downstream use, parallel and multilevel connection of lower power semiconductors are increasingly used to better harvest the economy of scale of the lower power components.

(128) In any event, the Notifying Party submits that the market definition can ultimately be left open. (110)

(C) The Commission’s assessment

(129) The Commission conducted its market investigation on the basis of and in respect of the plausible sub-segments of power semiconductors mentioned above.

(130) The majority of customers and competitors considered that power semiconductors could be segmented between thyristors, diodes/rectifiers, integrated gate-commutated thyristors (IGCTs), gate turn-off thyristors (GTOs), gate-commutated thyristors (GCTs), transistors (insulated gate-bipolar transistors (IGBTs), IGBT dies, press-pack IGBTs, bipolar semiconductors, IGBT modules, diode modules, Integrated Circuits (ICs), and modules of thyristors/diodes. (111) Some customers and competitors further explained that there could be also other plausible segments of power semiconductors. (112)

(131) As regards plausible segmentation of power semiconductors as per different power levels (power, high power, extra high power), the market investigation yielded mixed results. The majority of customers considered that such segmentation is not warranted. (113) On the other hand, the majority of competitors considered that power semiconductors could be further segmented into power, high power, extra high power. (114) Some competitors however did not consider such a segmentation appropriate. For example, a competitor explained that the distinction between general semiconductors and power semiconductors is sufficient to classify the use of the semiconductor, and a further distinction of power semiconductors is not needed. This competitor also explained that customers usually can choose between several options of power semiconductors depending on the topology used in the system and the design of the system in terms of building block, and this makes a segmentation into power ranges difficult. (115)

(132) As regards a plausible segmentation of IGBT modules into (i) standard IGBT modules and (ii) other (application-specific) IGBT modules, the majority of customers considered that this is not warranted. (116) Competitors’ view on this question were split. (117) For example, competitors explained that the value of specific modules parameters differ per application, but they are usually not specific for one application; It is not important to segment the IGBT, as specific modules are only for specific cases; the technology for the IGBT modules is the same. (118)

(133) Taking into account the Notifying Party's arguments and the results of the market investigation, the Commission considers that, in any case, the precise scope of the product market definition for power semiconductors can be left open since the Proposed Transaction does not raise serious doubts on the narrowest plausible segmentation within power semiconductors, which in this case are power semiconductor discretes; power semiconductor modules; high- power semiconductors; power diodes/rectifiers (including all power levels); high power diodes/rectifiers; power thyristors (including all power levels); high power thyristors; standard IGBT modules (which are only high power); thyristor/diode modules (& rectifier bridges) (which are only high power); GTOs, IGCTs & GCTs (which are only high power); press-pack IGBT modules (which are only high power); discrete IGBTs (which are only high power); intelligent power modules (IGBT-IPMS) (which are only high power); power integrated modules (PIM/CIB) (which are only high power); bipolar power transistors (which are only lower to medium power, but not high power); power ICs (which are only lower to medium power, but not high power). (119)

EV charging infrastructure

(A) The Notifying Party’s view

(134) The Notifying Party submits that charging infrastructure for electric vehicles could form a distinct product market within the area of Grid Integration, without further distinguishing between the different vehicle types e.g. (a) charging infrastructure for public transportation and (b) charging infrastructure for other vehicles. Nevertheless, the Notifying Party submits that the precise market definition can be left open, as the Proposed Transaction will not raise any competitive concerns in relation to EV charging systems.

(B) The Commission’s assessment

(135) The majority of customers and competitors considered that EV charging infrastructure could be viewed as a separate market within GI products. (120)

(136) Furthermore, the majority of customers considered that EV charging infrastructure could be segmented into (i) charging infrastructure for electric vehicles for the public transport (trams and buses), and (ii) charging infrastructure for other electric vehicles types. (121) Some customers explained that not all suppliers are capable of providing (yet) the whole range of charging infrastructure. However, the majority of competitors were of the opposite view, and considered that such a segmentation is not warranted. (122)

(137) Taking into account the Notifying Party's arguments and the results of the market investigation, the Commission considers that, in any case, the precise scope of the product market definition for charging infrastructure for electric vehicles can be left open since the Proposed Transaction does not raise serious doubts on the narrowest plausible segmentation within charging infrastructure for electric vehicles, which in this case is charging infrastructure for electric buses used for public transportation.

4.5.2. Geographic market

(A) The Commission’s decisional practice

(138) The Commission has considered in a previous case that the scope of the geographic market for transmission & distribution (T&D) equipment is at least EEA-wide. (123) In another case, the Commission left open the question whether the geographic market for transmission and distribution products is EEA-wide or worldwide in scope. (124)

(B) The Notifying Party’s view

(139) The Notifying Party submits that, in particular, HVDC stations and FACTS are tendered globally and all large suppliers are also active globally. The Notifying Party submits that the exact scope of the geographic market for T&D turnkey systems need not be defined in this case, as concerns will neither arise in case of an EEA-wide market definition (in which case there would not be an overlap between the parties, as Hitachi is not active in T&D turnkey systems within the EEA) nor in case of a global market definition.

(140) As regards semiconductors, the market investigation in a recent Commission decision gave strong indications that the markets for semiconductors are worldwide in scope (although the Commission has left open the precise scope of the geographic market). (125)

(141) The Notifying Party submits that the markets for power semiconductors are indeed global in scope and that all the larger providers are also active globally.

(142) The Notifying Party submits that the market segment for charging infrastructure for electric vehicles is global in scope. First, all major suppliers of charging infrastructure for electric vehicles are active globally and sell to customers on a global basis. Second, prices for charging infrastructures for electric vehicles are quoted on a global basis, and do not vary substantially according to geographic region. Third, manufacturers of electric vehicles generally apply a worldwide purchasing policy to most of their input products, including for the charging infrastructures. In any event, the Notifying Party submits that the precise geographic market definition can ultimately be left open in this case as no concerns will arise under any plausible narrower geographic market definition. (126)

(C) The Commission’s assessment

(143) The results of the market investigation point towards a worldwide market for all sub-segments of GI products, as a majority of customers (127) and of competitors (128) confirmed. According to a majority of competitors, GI systems and products sold across different world regions are substitutable (e.g., in terms of product specifications, safety and industry standards). Competitors also explained that standards are similar across the world and suppliers can comply with the diverse standards. (129) Both customers and competitors confirmed that suppliers of GI products participate in tenders across the whole of the world. (130)

(144) Within the EEA, competitors do not supply the same GI systems and/or products at materially different prices (by 5-10%) across individual Member States. (131) Transport costs for GI products across the EEA only make up a small percentage of the purchase price of individual GI products (less than 5% according to a majority of customers (132) and between 5-10% according to a majority of competitors (133)). The majority of competitors explained that they participate in tenders for GI systems and products in the whole of the EEA, (134) and this was also confirmed by customers. (135) National markets can thus be excluded for the purpose of the present case.

(145) In any event, there is no need to close the geographic market definition for GI products between the EEA and worldwide, as the Proposed Transaction does not lead to serious doubts under any plausible market definition.

4.6. Internet of things (IoT) platforms

4.6.1. Product market

(146) Hitachi has an IoT platform called "Lumada" which can be used for the acceleration of digital solutions using field data from customer assets.

(147) Whilst the term “platform” is used for many sorts of platforms, the “real IoT platforms” are so-called IoT Application Enablement Platforms, i.e. IoT platforms to develop and run industrial IoT applications. In that sense, IoT platforms are comparable to operating systems, since, like an operating system, the platforms serve as a basis for the development and operation of software. In the context of industrial IoT, this software consists of industrial IoT applications that meet industrial customers’ growing needs. (136)

(148) The Commission has not yet considered the supply of IoT platforms such as the Lumada Platform in detail. However, the Commission has examined operating systems on several occasions. (137)

(149) The Notifying Party submits that the relevant product market for the purposes of assessing the Lumada Platform should be the market for the supply of IoT platforms, or, alternatively, a broader market for “infrastructure software” (Infrastructure software is typically distinguished from other (secondary) software products such as middleware, application software and office software, and operating/browser software). According to the Notifying Party, IoT platforms constitute comprehensive solutions with many functionalities, as opposed to a specific solution for a particular functionality. In any event, the Notifying Party submits that the exact product market definition can be left open since the Proposed Transaction does not substantially affect the supply of IoT platforms.

(150) The majority of customers and competitors explained that industrial IoT platforms should not be considered separately from other (non-industrial) IoT platforms. (138) Market respondents explained that a platform is rarely segment specific even though it can host apps that could be segment specific; that such platforms can be employed for both industrial and non-industrial use; and that IoT platforms can span across different commercial segments. (139)

(151) The majority of customers and competitors confirmed that IoT platforms are part of a broader market for “infrastructure software” (infrastructure software being the foundation and thus the infrastructure for the development and operation of secondary software). (140)

(152) Finally, majority of customers and competitors considered that IoT platforms are rather a comprehensive solution with many different functionalities, as opposed to a specific solution for a particular functionality. (141)

(153) Taking into account the Notifying Party's arguments and the results of the market investigation, the Commission considers that, in any case, the precise scope of the product market definition can be left open since the Proposed Transaction does not raise serious doubts on the narrowest plausible segmentation, which in this case is IoT platforms.

4.6.2. Geographic market

(154) The Notifying Party submits that the geographic scope of both the market for IoT platforms or the broader market for infrastructure software is global in scope. According to the Notifying Party, licensing agreements for IoT platforms such as the Lumada platform are generally concluded on a global basis and the objective conditions for competition are essentially the same across the world. Neither import restrictions, transport costs nor technical requirements constitute significant limitations. Certain country-specific limitations due to regulations may exist, but, as far as the supply-side is concerned, they do not constitute an obstacle for swift supply on a global basis.

(155) The Commission market investigation gave strong indications that the market for IoT platforms is worldwide in scope, with the vast majority of competitors and customers confirming such scope. (142) Competitors and customers explained that the market conditions are the same worldwide, and that IoT platforms suppliers are active and offer the same platforms on a worldwide basis.

(156) In any event, there is no need to close the geographic market definition for IoT platforms, as the Proposed Transaction does not lead to serious doubts under any plausible market definition (EEA-wide or worldwide).

5. COMPETITIVE ASSESSMENT

(157) In the EEA and/or globally, the activities of the Parties give rise to a number of affected markets in relation to HV products, transformers, and GI products. Specifically, the affected markets relate to: (i) three HV product categories (including a number of plausible sub-segments thereof) (143), (ii) two transformer categories (including a number of plausible sub-segments thereof) (144), and (iii) two GI product categories – HVDC and FACTS (including a number of plausible sub-segments thereof).

(158) The competitive assessment below addresses the potential horizontal, vertical and conglomerate effects derived from the Proposed Transaction in the affected markets.

5.1. The Notifying Party’s view

(159) The Notifying Party argues that the Proposed Transaction will not give rise to any Significant Impediment to Effective Competition (“SIEC”) on any market, for the following reasons:

(i) The activities of the Parties are complementary, both as far as the scope of products are concerned, and in relation to their geographic presence (with Hitachi being active mainly [outside the EEA], where the Target has minor activities at best). (145) In the EEA, overlaps resulting from the activities of the Parties are limited. (146) Even in these markets, the Proposed Transaction will only lead to small market share increments and not give rise to any substantive foreclosure effects. (147)

(ii) Even on a global level, the Parties do not consider each other close competitors and face competitive constraints from major suppliers such as Siemens, GE and Schneider. On the markets for transmission and distribution products as well as turnkey solutions and related services, new Chinese and Korean suppliers are increasingly present. (148)

(iii) On the newer markets for automation software and solutions, the companies face competition both from a large number of established IT companies and their competitors in the "traditional" fields, as well as additional pressure from several new entrants in these markets with low entry barriers. This pressure is exacerbated by the competitive nature of the sector and strong downward pricing pressure from customers.

5.2. Horizontal non-coordinated effects

(160) The Proposed Transaction would, based on the 2018 market share data, give rise to two horizontally affected markets, one in relation to HV circuit breakers, and the other in relation to traction transformers, both in a global market.

(161) Market share data for these affected markets are available in Annex II to this Decision (“Annex II”).

5.2.1. HV products

(162) In the group of HV products, based on 2018 figures an affected market only arises on a global (149) market for HV circuit breakers and, in case of a further sub- segmentation, HV generator circuit breakers.

5.2.1.1. HV circuit breakers and HV generator circuit breakers

(A) The Notifying Party’s view

(163) The Notifying Party argues that one overall market should be defined for HV products, as outlined in paragraph (17). This market would not be affected either at EEA or at worldwide level. The Parties’ combined market shares in an worldwide market for HV products would remain below 20% in the past years ([10-20]% in 2016, [10-20]% […]* and [10-20]% in 2018). In an EEA market for HV products, there would be no overlap as Hitachi is not present.

(164) A further segmentation leads to an affected market for HV circuit breakers and HV generator circuit breakers at worldwide level. However, on an EEA-wide market, there would not be a horizontal overlap between the Parties as Hitachi is not present in the market for HV circuit breakers within the EEA.

(165) The Notifying Party also points out that the market is highly competitive, given the presence of strong global suppliers for HV circuit breakers (and relevant sub-segments), notably GE/Alstom and Siemens, which both have market shares of more than 20%, as well as Meclo and Schneider Electric.

(B) The Commission’s assessment

(166) In a global market for HV circuit breakers, the Parties’ combined share was approximately [20-30]% in 2016-2018. Hitachi's worldwide market share was below [0-5]% in 2016, 2017 and 2018, and the increment would be de minimis. The five year average (2014-2018) was higher, with a combined market share of the Parties of [30-40]% at global level. Given Hitachi’s share of [0-5]% (over the period 2014-18), the increment in market share resulting from the Proposed Transaction would be small even when looking at a longer time frame.

(167) The pre-merger HHI for HV circuit breakers on a worldwide sales basis in 2018 was [2000 – 2500] and the post-merger HHI will be [2000 – 2500] resulting in a delta of [50-60]. As such, the Parties’ activities in HV circuit breakers meet the requirements of the filter contained at paragraph 20 of the Horizontal Merger Guidelines.

(168) A further horizontally affected markets would arise in the potential sub-segment of the market of HV generator circuit breakers. These markets are only horizontally affected in a potential worldwide market, as Hitachi is not present in circuit breakers in the EEA. The Parties’ combined share in a worldwide market for HV generator circuit breakers was [40-50]% in 2018. Hitachi’s worldwide market share was below [0-5]% in 2016, 2017 and 2018, and the increment would be de minimis ([0-5]%) in 2018.

(169) The pre-merger HHI for generator circuit breakers on a worldwide sales basis in 2018 was [4000 – 4500] whereas the post-merger HHI will be [4000 – 4500] resulting in a delta of just [60-70]. As such, the Parties’ activities in generator circuit breakers meet the requirements of the filter contained at paragraph 20 Horizontal Merger Guidelines.

(170) In addition, the arguments of the Parties that Hitachi and the Target do not compete in the EEA and that on a global level strong competitors are present (see paragraph (159)) were confirmed in the market investigation for HV products in general, without exceptions, and are thus also valid for HV circuit breakers and HV generator circuit breakers.

(171) First, the market investigation confirmed the argument of the Notifying Party that it and the Target do not compete in HV products in the EEA. Hitachi is not considered an important supplier of HV products in the EEA, as confirmed by a majority of participants in the market investigation. (150) In particular, Hitachi is not perceived as a key supplier of HV circuit breakers and HV generator circuit breakers by a majority of both customers and competitors, (151) neither in the EEA overall nor in a part of it. (152) Therefore the Proposed Transaction does not materially change the competitive structure of the market for HV circuit breakers and HV generator circuit breakers.

(172) Second, the Target’s main competitors mentioned by most market participants are Siemens, GE/Alstom, Schneider Electric, (153) with no major differences between countries in the EEA. (154) As a customer explained, “[t]here is a sufficiently large number of companies that manufacture HV products so that a selection is possible at any time.” The market investigation also showed that specialised or local suppliers of HV products are generally able to compete with large-scale suppliers such as the Target and Hitachi. (155) There are thus sufficient credible producers of HV circuit breakers and HV generator circuit breakers available throughout the EEA.

(173) Third, switching from one supplier of HV products to another is easy. A very large majority of customers reported that they had switched supplier in the past. (156) A clear majority of customers consider that they would retain sufficient alternative sources of supply and could switch to another supplier than the Target or Hitachi if the merged entity were to supply at worse conditions after the Proposed Transaction is implemented. (157) This would be the case for any subsegment of a HV product market, in any part of the EEA. (158) The possibility to switch suppliers of any HV products, including HV circuit breakers and HV generator circuit breakers, thus constitutes additional competitive constraints.

(174) Finally, none of the customers who participated in the market investigation expect the Proposed Transaction to have a negative impact on the markets for any HV products, including circuit breakers and generator circuit breakers. (159)

(175) Therefore, taking into account the Notifying Party's arguments and the results to the market investigation, the Commission concludes that the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market as a result of horizontal non-coordinated effects with respect to the affected HV product categories HV circuit breakers and its sub-segment, HV generator circuit breakers.

5.2.2. Transformers

(A) The Notifying Party’s view

(176) The Notifying Party submits that the appropriate data with which to assess traction transformers is the order basis, which allows for a more accurate comparison with the order-based railway rolling stock share data. However, if reviewed on a sales basis, the Proposed Transaction would only give rise to one horizontally affected segment in 2018 in the market for traction transformers on a worldwide basis.

(177) The combined share of the Parties would be [40-50]% in 2018 with a de minimis increment from Hitachi of [0-5]%. Hitachi had no sales of traction transformers in the EEA in 2018 and, globally, [Confidential details on Hitachi's position on the worldwide market for traction transformers].

(178) There are no other horizontally affected markets or segments in 2018 within transformers. On this basis, Hitachi submits that the Proposed Transaction will not give rise to any competition concerns.

(B) The Commission’s assessment

(179) The Commission considers that, taking into account the Notifying Party's arguments and in particular the fact that Hitachi had sales of traction transformers [outside the EEA], and the minimal increment of market shares worldwide (below [0-5]%, and with an HHI delta brought by the Proposed Transaction below 150 (160)). As such, the Parties’ activities in traction transformers meet the requirements of the filter contained at paragraph 20 of the Horizontal Merger Guidelines.

(180) Also no respondent to the Commission’s market investigation raised any horizontal concerns with respect to the Parties’ combined activities in traction transformers. The Commission therefore concludes that the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market with regard to horizontal non-coordinated effects in relation to transformer products.

5.3. Vertical non-coordinated effects

(181) The Proposed Transaction gives rise or strengthens various vertical relationships at EEA-wide or worldwide level. Hitachi has a limited presence in most products and, out of these, the relationships in the table below lead to affected markets. All materially vertically affected markets result from one of the Parties’ relatively strong presence in five product markets: HV AIS modules, traction transformers, HVDC and FACTS. Therefore the analysis of vertical non-coordinated affects will focus on the analysis of these product groups. (161)

5.3.1. HV products: vertical links in relation to HV AIS modules

(182) Both in the EEA and at worldwide level, two vertically affected markets arise because of the activities of the Target in HV AIS modules, a market which is downstream of the market for MV products (MV switchgear in particular) and transformers (power transformers in particular) where Hitachi also has some very limited activities.

(183) In the EEA, the Target’s market share in HV AIS modules was [30-40]% in 2018 ([70-80]% in 2016 and [40-50]% in 2017). In a worldwide market, the Target’s market share in HV AIS was [60-70]% in 2018 ([80-90]% in 2016 and [70-80]% in 2017).