Commission, October 8, 2018, No M.8842

EUROPEAN COMMISSION

Judgment

TELE2 / COM HEM HOLDING

Subject: Case M.8842 – Tele2 / Com Hem Holdings

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 3 September 2018, the European Commission received notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/20043 by which Tele2 AB (Sweden) ("Tele2" or the “Notifying Party"), controlled by Kinnevik AB (“Kinnevik”), intends to acquire sole control of Com Hem Holding AB (Sweden) ("Com Hem") by way of a statutory merger (the "Transaction")4. Tele2 and Com Hem are collectively referred to as the "Parties".

1. THE PARTIES AND THE TRANSACTION

(2) Tele2 is a Swedish telecommunications provider mainly offering mobile telecommunications services (voice and data), and to a lesser extent fixed telephony services, fixed internet access services, as well as data communication services and related services, in several European countries. In Sweden, Tele2 operates as a mobile network operator (“MNO”) and also operates a fixed backbone network, partly owned and partly leased, which is connected to Tele2’s mobile networks. Tele2 operates in Sweden through its subsidiary Tele2 Sverige AB. Tele2 is listed on Nasdaq Stockholm.

(3) Tele2 is de facto controlled by Kinnevik which holds about 47.9% of its voting rights, representing between 67 and 70% of the votes at Tele2’s general meetings in 2014-2017. Kinnevik is a Swedish investment company listed on Nasdaq Stockholm. Kinnevik has equity interests in various companies active inter alia in the sectors of telecommunications, e-commerce, entertainment and financial services.

(4) Currently the main shareholders of Kinnevik are Verdere S.a.r.l ("Verdere"), which holds 7% of Kinnevik’s share capital and 30% of the voting rights, and Camshaft S.a.r.l. ("Camshaft"), which holds 2.4% of Kinnevik’s share capital and 10% of the voting rights. […].5

(5) Verdere and Camshaft also hold 1.9% of the share capital in Modern Times Group MTG AB ("MTG"), which, including its subsidiary Viasat AB (“Viasat”), is primarily active in Sweden as a retail TV services distributor, programme company and producer of TV content.6 This participation does not give Verdere and Camshaft any specific right or power over MTG’s commercial strategy other than standard shareholder rights. Verdere and/or Camshaft (and/or Kinnevik) neither have any affiliated member in the MTG board of directors or in the nomination committee appointing the directors nor any specific right to be represented in the board and/or in the nomination committee. Therefore, Verdere and Camshaft have no relevant influence over MTG and this participation will thus not be further considered in this Decision.

(6) Com Hem offers broadband, TV, mobile and telephony services to Swedish households and companies. In the provision of retail TV services, Com Hem’s subscriber base consists of approximately 50% of Sweden’s households. Com Hem is listed on Nasdaq Stockholm. Kinnevik is the largest shareholder in Com Hem, with a share participation of 19%. However, no shareholder has sole or joint control over Com Hem.

(7) On 9 January 2018, Tele2 and Com Hem entered into a merger agreement and a joint merger plan. The Parties have agreed to combine their business operations through a statutory merger in accordance with Swedish Law. The Transaction will be implemented by Tele2 absorbing Com Hem. Post-Transaction, Tele2 will remain listed on Nasdaq Stockholm and de facto controlled by Kinnevik.

(8) The Transaction constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

2. EU DIMENSION

(9) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million7 (Tele2: EUR […] ; Com Hem: EUR 740.6 million; in 2017). Each of them has an EU-wide turnover in excess of EUR 250 million (Tele2: EUR […]; Com Hem 740.6 million; in 2017), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension. 8

3. RELEVANT MARKETS

(10) In Sweden, the Parties' activities mainly overlap in the areas of: (i) retail supply of fixed internet access services; (ii) retail supply of mobile telecommunications services; and (iii) retail supply of multiple play services. Moreover, Tele2 and/or Com Hem are active in Sweden in the areas of (iv) retail supply of fixed telephony services (Tele2 and Com Hem) and (v) retail supply of TV services (Com Hem).

(11) In addition, Tele2 and/or Com Hem are present in the areas of: (i) wholesale access and call origination on mobile networks (Tele2); (ii) wholesale mobile call termination services (Tele2); (iii) wholesale fixed call termination services (Tele2 and Com Hem), and (iv) wholesale international roaming services (Tele2). Those services are vertically linked to (i) retail supply of mobile telecommunications services and (ii) retail supply of fixed telephony services.

3.1. Retail supply of fixed telephony services

(12) Fixed telephony services comprise the provision of connection services at a fixed location or access to the public telephone network, for the purpose of making and/or receiving calls and related services. Both Tele2 and Com Hem offer fixed telephony services at retail level in Sweden.

3.1.1. Product market definition

(13) The Notifying Party submits that the market for retail fixed telephony services constitutes one single market without the need to distinguish between type of call (local, national and international) or type of technology (traditional fixed lines or VoIP).

(14) In previous decisions9, the Commission considered whether a distinction between local/national and international calls as well as between residential and non- residential customers should be drawn on the basis of the distinctions in the Commission Recommendation 2003/311/EC but ultimately left the exact product market definition open.

(15) More recently, the Commission also considered that managed Voice over Internet Protocol ("VoIP") services and traditional telephony are interchangeable and therefore belong to the same market.10 In Liberty Global/Ziggo11 the Commission left the exact market definition open (and in particular whether there is a separate market for residential and non-residential customers, as well as whether VoIP and traditional fixed telephony belong to the same market) while in Liberty Global/BASE12 and in Vodafone/Liberty Global/Dutch JV13 the Commission considered that an overall retail market for fixed telephony services exists.

(16) The market investigation in the present case has not provided any indication that the Commission should depart from its previous findings.

(17) In any event, the Commission considers that for the purposes of this Decision, the exact scope of the product market definition, and specifically, whether fixed line and VoIP telephony services belong to the same product market, and whether there is a separate market for residential and non-residential customers, can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any possible market definition.

3.1.2.Geographic market definition

(18) The Notifying Party submits that, in line with the previous approaches taken by the Commission, the relevant geographic scope of the market is national.

(19) In its previous decisions, the Commission concluded that the retail market for the provision of fixed telephony services was national in scope.14 The market investigation in the present case has not provided any indication that the Commission should depart from its previous findings.15

(20) Therefore the Commission considers that the relevant market for the retail provision of fixed telephony services is national in scope.

3.2.Retail supply of fixed internet services

(21) Fixed internet access services at the retail level consist of the provision of a fixed telecommunications link enabling customers to access the internet. Both Tele2 and Com Hem offer fixed internet access services at retail level in Sweden.

3.2.1.Product market definition

(22) The Notifying Party submits that the relevant product market is the overall market for the retail provision of fixed internet access services, without further segmentations. In particular, the Notifying Party considers that a distinction by customer type is not needed and that the market for the retail supply of fixed internet access services should include both residential and small business customers, as well as large business customers and public authorities. The Notifying Party further considers that there the market should not be further segmented on the basis of the different type of distribution mode (such as fibre, cable xDSL). Finally, the Notifying Party does not consider that a combined fixed and mobile internet retail market exists in Sweden today since, despite significant advances in mobile broadband connectivity, consumers do not view mobile and fixed internet as direct substitutes.

(23) In recent cases, the Commission considered but ultimately left open possible segmentations according to (i) product type (distinguishing narrowband, broadband, and dedicated access), and (ii) distribution mode (distinguishing xDSL, fibre, cable, and mobile broadband), and has acknowledged that the retail market for fixed internet access services should not be divided according to download speed or technology.16 The Commission has also considered distinguishing between residential and small business customers, on the one hand, and larger business and public authorities, on the other hand.17

(24) With regard to a possible segmentation of the market for the retail provision of fixed internet services according to customer type or according to distribution technology (i.e. DSL, cable or fibre), on the one side, mobile and fixed operators provided mixed results on whether this distinction is necessary.18 On the other side, with regard to a possible segmentation by customer type, business customers highlighted the difference between the provision of fixed internet access services targeted at private and at business customers.19

(25) With regards to a potential segmentation in multiple dwelling units ("MDUs") such as housing associations or apartment buildings, and single dwelling units ("SDUs") such as individual households, the market investigation provided mixed results on whether the market for retail fixed internet access services should be split by MDU and SDU.20 While most of the respondents did not express a view, one respondent indicated that fixed internet services delivered over fiber based access networks and cable-TV-networks to SDUs, and fixed internet services delivered over fiber based access networks and cable-TV-networks to MDUs constitute separate product markets.

(26) In any event, the Commission considers that for the purposes of this Decision, the exact scope of the product market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any possible market definition.

3.2.2.Geographic market definition

(27) The Notifying Parties submit that, in line with the previous approaches taken by the Commission and the Swedish Post and Telecom Authority (Post- och telestyrelsen – PTS), the relevant geographic scope of the market is national.

(28) In its previous decisions, the Commission concluded that the retail market for the provision of fixed internet services was national in scope.21 The market investigation in the present case has not provided any indication that the Commission should depart from its previous findings.22 Therefore the Commission considers that the relevant market for the retail provision of fixed internet services is national in scope.

3.3.Retail supply of TV services

(29) In the market for the retail provision of TV services, the suppliers of linear and non-linear (mainly Video-On-Demand, "VOD") TV services serve end customers who wish to purchase such services. The TV services supplied by TV distributors to end users consist of: (i) packages of linear TV channels (which they have either acquired or produced themselves); and (ii) content aggregated in non-linear services, such as Video on Demand ("VOD"), Subscription VOD ("SVOD"), Transaction VOD ("TVOD") and Pay Per View ("PPV"). TV content can be delivered to end users through a number of technical means including cable, satellite and IPTV23. So-called over-the-top (“OTT”)24 players deliver channels and content in both a linear and non-linear fashion through the use of the internet.

(30) Com Hem (but not Tele2) offers retail TV services in Sweden to end consumers.

3.3.1.Product market definition

(31) The Notifying Party submits that it is not relevant to delineate the market for the retail provision of TV services based on the segmentation analysed by the Commission in its previous decisions25, namely: (i) the type of technology used; (ii) the nature of TV services provided in terms of Pay TV and Free-To-Air (“FTA”) TV services; and, (iii) the nature of TV services provided in terms of linear and non-linear services.

(32) According to the Notifying Party, a potential distinction in the Swedish TV market would be between MDUs and SDUs. This distinction has been considered in past decisions of the Swedish Competition Authority ("SCA") in this industry.26 In SDUs the end customer typically chooses its own TV distributor and pays directly for its subscription. In MDUs, on the other hand, it is common to have a collective agreement between the landlord / housing association and a single TV distributor. In such a setup the landlord / housing association chooses the TV distributor and pays for a basic TV package (this cost is covered through a portion of the monthly management fees paid by apartment owners to the housing association).

(33) In its previous decisions the Commission has considered the retail provision of FTA TV and Pay TV services as separate markets but ultimately left open the product market definition 27. The Commission also considered whether retail TV can be segmented further according to: (ii) linear vs non-linear -TV services28; (iii) according to distribution technologies (e.g. cable, OTT, satellite, IPTV or terrestrial)29; and (iv) premium Pay-TV vs basic Pay-TV services30 but, has left open the market definition with regard to each of these potential sub-segments.

(34) The Commission has also previously considered whether retail TV services to SDUs and MDUs form part of the same product market but ultimately left it open.31

(35) Most of the respondents to the market investigation indicated that the market for the provision of retail TV services in Sweden should not be segmented into (i) FTA and Pay-TV services; (ii) linear and non-linear services, or by(iii) distribution technologies.32

(36) With regards to a potential segmentation in SDU and MDU, most of the respondents to the market investigation consider that the market for retail supply of TV services should not be split by MDU and SDU since similar content is distributed through the different technologies and there are not significant pricing differences.33

(37) In any event, given the fact that the assessment of the Transaction would remain the same whether (i) FTA services and Pay TV services, (ii) linear Pay TV services and non-linear Pay TV services, (iii) different distribution technologies, and (iv) SDUs and MDUs are considered to belong to the same product market or to give rise to separate markets, the exact scope of the relevant market for TV services can be left open in this regard.

(38) In any event, the Commission considers that for the purposes of this Decision the exact product market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any possible market definition.

3.3.2.Geographic market definition

(39) The Commission has in the past considered that the geographic scope of the market for the retail provision of TV services could be national since providers of retail TV services compete on a nationwide basis or limited to the coverage area of each cable operator.34

(40) The Notifying Party considers that the question whether the scope of the market for the retail provision of TV services should be either national, since TV distributors compete on a nationwide basis, or limited to the coverage area of each cable operator, could be left open.

(41) Most of the respondents to the market investigation consider that the market for the retail provision of TV services is national in scope.35

(42) In any event, the Commission considers that the exact geographic market definition can be left open in this case as the Transaction does not raise serious doubts as to its compatibility with the internal market under any possible market definition.

3.4.Retail supply of mobile telecommunications services

(43) Mobile telecommunications services to end customers (also referred to as "retail mobile services") include services for national and international voice calls, SMS (including MMS and other messages), mobile internet with data services, access to content via the mobile network and retail international roaming services.36 Both Parties provide mobile telecommunication services at retail level to end- customers in Sweden.37

3.4.1.Product market definition

(44) The Notifying Party submits that, in line with previous Commission decisions, the relevant product market is the overall retail market for mobile telecommunications services. It considers that it is not necessary for the Commission to further segment this market by reference to type of customer (business or private), service type (national or international calls, internet data services, voice and text services), type of tariff (post-paid or pre-paid) or type of network technology.

(45) In previous cases concerning retail mobile telecommunications services, the Commission has considered that there is an overall retail market for mobile telecommunications services constituting a separate market from retail fixed telecommunication services.38 The Commission did not further segment the overall retail mobile market based on the type of service (voice calls, SMS, MMS, mobile Internet data services), or the type of network technology. The Commission considered possible segments of the overall retail market for mobile telecommunication services between pre-paid or post-paid services and private customers or business customers, concluding that these did not constitute separate product markets but represent rather market segments within an overall retail market.39

(46) Most respondents to the market investigation in the present case agreed with the Commission’s previous product market definition and considered that the retail market for mobile telecommunications services should be defined as an overall market, without further segmentations.40

(47) In any event, for the purpose of this Decision, the exact product market definition in relation to the provision of retail mobile telecommunications services can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any possible market definition.

3.4.2.Geographic market definition

(48) The Notifying Party submits that, in line with the Commission's previous decisions,41 the market for mobile telecommunications services to end customers is national in scope and therefore corresponds to the territory of Sweden.

(49) The market investigation in the present case has not provided any indications that the Commission should depart from its previous findings.42 In light of the above, the Commission considers that the retail market for mobile telecommunications services is national in scope.

3.5.Retail supply of multiple play services

(50) The term "multiple play" relates to offers comprising two or more of the following services provided to retail consumers: mobile telecommunication services, fixed telephony, fixed internet access and TV services. Multiple play comprising two, three or four of these services is referred to as dual play ("2P"), triple play ("3P") and quadruple play ("4P") respectively.

(51) Three of the four services referenced in paragraph (50) above, namely fixed telephony, TV services and fixed internet access, are fixed services as they are provided over a fixed network such as cable, copper or fibre infrastructure. Multiple play comprising any combination of two or more of these fixed services without a mobile component is referred to as "fixed multiple play". Multiple play comprising one or more of these fixed services in combination with a mobile component (including either voice or data, or both together) is referred to as"fixed-mobile multiple play" or “fixed-mobile convergence” (“FMC”). Fixed- mobile multiple play may involve a single mobile subscription (SIM card) or more than one mobile subscription combined with the fixed services.

(52) Both Tele2 and Com Hem offer fixed multiple play bundles, Com Hem to a greater extent than Tele2. None of the Parties offers fixed-mobile multiple play services.

3.5.1.Product market definition

(53) The Notifying Party submits that multiple play markets are not relevant in Sweden, due mainly to their limited scope, and that the competitive assessment of the Transaction should be carried out separately in each individual market (fixed telephony, fixed internet, TV services and mobile services).

(54) In previous cases the Commission has considered but ultimately left open the question as to whether there exist one or more multiple play markets which are distinct from each of the underlying individual telecommunication services.43

(55) In previous cases the Commission has also noted that due to different services, delivered over different infrastructures (fixed for dual play and triple play or fixed and mobile for quadruple play), that are included in the different multiple play bundles, instead of one possible market for multiple play, there could be several candidate multiple play markets: a market for fixed bundles (dual play and triple play) and another separate market for FMC bundles. The possibility for several mobile subscriptions to be included in a quadruple play bundle further complicates the picture.44

(56) In Sweden, the uptake of multiple play services remains relatively modest. In 2017, the total number of bundled telecommunication subscriptions amounted to roughly 1.9 million compared to a total of approximately 14.4 million mobile telecommunication services subscriptions, 3.9 million fixed broadband subscriptions and 5.3 million television subscriptions.45

(57) The most common multiple play service in Sweden is the 2P combination of television and fixed internet services (approximately 551 700 subscriptions in 2017). There is a marked ongoing decline in the number of subscriptions of multiple play bundles with a fixed telephony component in tune with the decline of overall standalone fixed telephony subscriptions.46 Moreover, in Sweden, fixed-mobile multiple play bundles are not widespread. In 2017, mobile subscriptions sold in a 4P bundle represented less than 1% of all mobile subscriptions.

(63) Most respondents to the market investigation of the case at hand considered that a possible market for multiple play (irrespective of what type of multiple play bundles are included in such possible market) would be national in scope.50

(64) Therefore, for the purposes of this Decision, the Commission considers that the geographic scope of any possible retail market for multiple play services in Sweden would be national.

3.6.Wholesale access and call origination on mobile networks

(65) MNOs provide wholesale access and call origination services which enable operators without their own network, namely MVNOs and Service Providers, to have access to one or more of the MNOs networks in order to provide retail mobile services to end customers “Full” or “thick” MVNOs maintain their own core infrastructure and use MNOs only for access to a radio network. By contrast, “light” or “thin” MVNOs do not have their own infrastructure and rely entirely on the infrastructure of an MNO.51 As far as the Parties are concerned, only Tele2 is active on this market in Sweden. Three more providers in Sweden offer wholesale access and call origination on mobile networks, namely, Telia, Telenor and Tre.

3.6.1.Product market definition

(66) In line with previous Commission decisions, the Notifying Party submits that there is an overall market for wholesale access and call origination services.

(67) In previous cases,52 the Commission defined a wholesale market for access and call origination on public mobile networks. The services provided by MNOs to non-MNOs were considered as key elements required for non-MNOs to be able to provide retail mobile communication services. Since both services were considered to be generally supplied together they were seen to be part of a single market. The market investigation in the present case has not provided any reasons to depart from this approach.

(68) In view of the above, the Commission concludes that there is a distinct wholesale market for access and call origination on public mobile telephone networks.

3.6.2.Geographic market definition

(69) In line with previous Commission decisions, the Notifying Party submits that the relevant geographic scope of the market for wholesale access and call origination on mobile networks is national, i.e. limited to the territory of Sweden.

(70) In previous cases, the Commission considered the wholesale market for access and call origination to be national in scope due to regulatory barriers stemming from the fact that licenses granted to MNOs are generally national in scope.53 The market investigation in the present case has not provided any reasons to depart from this approach.

(71) Based on the above, the Commission concludes the wholesale market for access and call origination on public mobile networks to be national in scope, that is to say limited to the territory of Sweden.

3.7.Wholesale market for call termination on mobile networks

(72) Call termination services are provided when calls originate from one network and terminate on another network. Call termination thus allows users of different networks to communicate with one another. Call termination is a wholesale service provided by various network operators to one another on the basis of interconnection agreements, upstream of the provision of communication services to end customers.54 Call termination services could be provided either on mobile or fixed networks.

(73) Tele2 is active on the wholesale market for call termination on mobile networks in Sweden.

3.7.1.Product market definition

(74) The Notifying Party submits that each individual network constitutes a separate wholesale market for call termination on mobile networks, in line with previous Commission decisions.

(75) In previous cases, the Commission concluded that each individual mobile network constitutes a separate product market.55 More specifically, the Commission considered that there is no substitute for call termination on each individual network since the operator transmitting the outgoing call can reach the intended recipient only through the operator of the network to which the recipient is connected. Each individual network therefore constitutes a separate market for termination. This applies both to fixed networks and to mobile networks.56

(76) In view of the above, the Commission concludes that each individual mobile network constitutes a separate wholesale market for call termination. More specifically for the purposes of this case, the Commission concludes that the relevant market is the wholesale market for call termination on the mobile network of Tele2.

3.7.2. Geographic market definition

(77) The Notifying Party submits that wholesale market for call termination should correspond to the dimensions of the operator's network and therefore be considered as national in scope.

(78) In line with its previous decisions57, the Commission considers the market to be national in scope. The information available to the Commission does not provide any indication that it would be warranted for the present case to depart from the previous practice for defining the geographic market. For the purposes of this Decision, the Commission therefore concludes that the wholesale markets for call termination on mobile networks are national.

3.8.Wholesale international roaming services

(79) In order for a provider of retail mobile services to be able to provide its end customers with telecommunication services outside their home countries, it must enter into agreements with providers of wholesale international roaming services which are primarily active in other national markets. Only Tele2 is active on this market, both in Sweden and in the Netherlands.

(80) Roaming agreements can be concluded with a preferred foreign operator which offers tailor-made service conditions, as can be seen in particular in the creation of international roaming alliances.

3.8.1. Product market definition

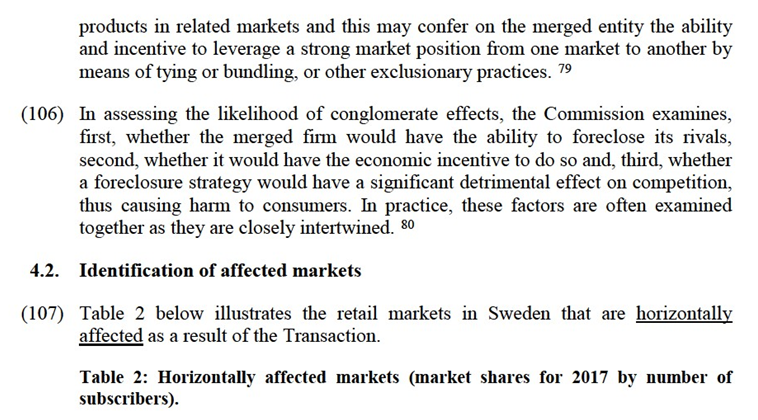

(81) The Notifying Party submits that the Commission has defined a separate wholesale market for international roaming services comprising both terminating calls and originating calls.58

(82) In the case at hand, the Commission retains its previous product market definition of a separate wholesale market for international roaming comprising both terminating calls and originating calls.

3.8.2.Geographic market definition

(83) In line with previous Commission decisions59 the Notifying Party submits that the wholesale market for international roaming services is national in scope, i.e. Sweden, for the case at hand. This is due to the fact that wholesale international agreements can only be concluded with companies which have an operating licence in the relevant country and the licences to provide mobile services are restricted to a national territory.

(84) In line with its past decisions60, the Commission retains its previous geographic market definition and considers that the wholesale market for international roaming services is national in scope.

3.9.Wholesale call termination services on fixed networks

(85) As explained in paragraph (72) above, call termination is the wholesale service provided by network operators that allows users of different networks to communicate with each other.

(86) The market for wholesale termination of calls on fixed networks is therefore vertically related to the retail markets for fixed and mobile telephony services.

(87) Both Tele2 and Com Hem are active in the provision of wholesale call termination services on fixed networks in Sweden.

3.9.1.Product market definition

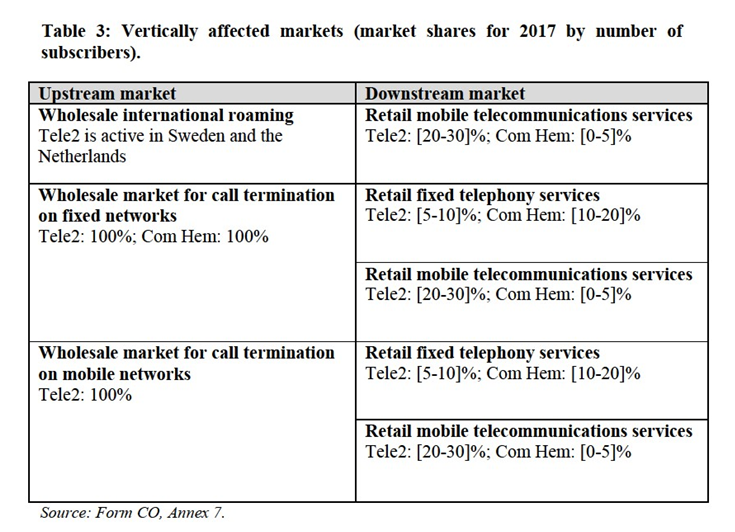

(88) In line with previous Commission decisions61, the Notifying Party submits that the relevant product market is the wholesale market for call termination on each individual fixed network.

(89) In previous decisions the Commission considered an overall wholesale market for call termination on each individual fixed network, without it being necessary to consider further possible segmentations of the market.62

(90) For the purposes of the present Decision, the Commission retains its previous product market definition and considers that the relevant product market is the overall wholesale market for call termination on the fixed network of Tele2 and the wholesale market for call termination on the fixed network to which Com Hem has access.

3.9.2.Geographic market definition

(91) The Notifying Party considers the geographic scope of the wholesale market for call termination on fixed networks to be national. This is primarily due to regulatory barriers as the geographical scope of licenses is in principle limited to areas which do not extend beyond the borders of a Member State.

(92) In line with previous decisions the Commission considers the geographic scope of the wholesale market for call termination on a fixed network to be national.63

4.COMPETITIVE ASSESSMENT

4.1.Analytical framework

(93) Under Article 2(2) and (3) of the Merger Regulation, the Commission must assess whether a proposed concentration would significantly impede effective competition in the internal market or in a substantial part of it, in particular through the creation or strengthening of a dominant position.

(94) In this respect, a merger may entail horizontal and/or non-horizontal effects. Horizontal effects are those deriving from a concentration where the undertakings concerned are actual or potential competitors of each other in one or more of the relevant markets concerned. Non-horizontal effects are those deriving from a concentration where the undertakings concerned are active in different relevant markets.

(95) As regards non-horizontal mergers, two broad types of such mergers can be distinguished: vertical mergers and conglomerate mergers.64 Vertical mergers involve companies operating at different levels of the supply chain.65 Conglomerate mergers are mergers between firms that are in a relationship which is neither horizontal (as competitors in the same relevant market) nor vertical (as suppliers or customers).66

(96) A case where a merger entails both horizontal and non-horizontal effects may for instance be when the merging firms are not only in a vertical or conglomerate relationship, but are also actual or potential competitors of each other in one or more of the relevant markets concerned. In such a case, the Commission will appraise horizontal, vertical and/or conglomerate effects in accordance with the guidance set out in the relevant notices.67

(97) The Commission appraises horizontal effects in accordance with the guidance set out in the relevant notice, that is to say the Horizontal Merger Guidelines.68 Additionally, the Commission appraises non-horizontal effects in accordance with the guidance set out in the relevant notice, that is to say the Non-Horizontal Merger Guidelines.69

4.1.1.Horizontal effects

(98) The Horizontal Merger Guidelines distinguish between two main ways in which mergers between actual or potential competitors on the same relevant market may significantly impede effective competition, namely non-coordinated and coordinated effects.

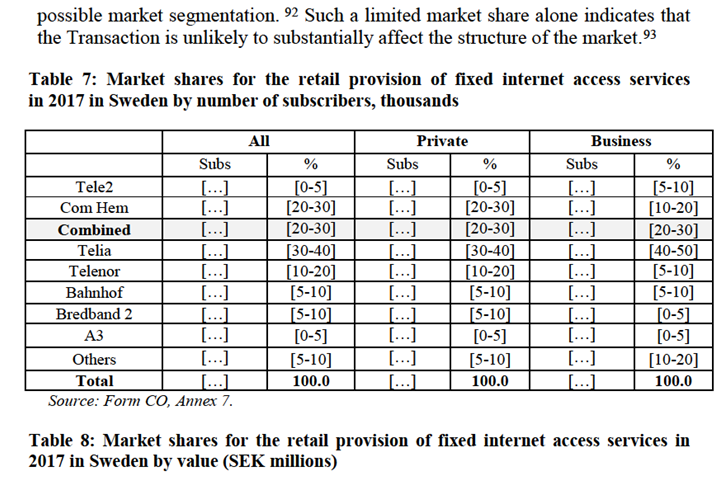

(99) As regards horizontal non-coordinated effects, under the substantive test set out in Article 2(2) and (3) of the Merger Regulation, also mergers that do not lead to the creation or the strengthening of the dominant position of a single firm may be incompatible with the internal market. Indeed, the Merger Regulation recognises that in oligopolistic markets, it is all the more necessary to maintain effective competition.70 This is in view of the more significant consequences that mergers may have on such markets. For this reason, the Merger Regulation provides that "under certain circumstances, concentrations involving the elimination of important competitive constraints that the merging parties had exerted upon each other, as well as a reduction of competitive pressure on the remaining competitors, may, even in the absence of a likelihood of coordination between the members of the oligopoly, result in a significant impediment to effective competition".71

(100) The Horizontal Merger Guidelines list a number of factors which may influence whether or not significant horizontal non-coordinated effects are likely to result from a merger, such as the large market shares of the merging firms, the fact that the merging firms are close competitors, the limited possibilities for customers to switch suppliers, or the fact that the merger would eliminate an important competitive force. That list of factors applies equally regardless of whether a merger would create or strengthen a dominant position, or would otherwise significantly impede effective competition due to non-coordinated effects. Furthermore, not all of these factors need to be present to make significant non- coordinated effects likely and it is not an exhaustive list.72 Finally, the Horizontal Merger Guidelines describe a number of factors, which could counteract the harmful effects of a merger on competition, including the likelihood of buyer power, entry and efficiencies.

(101) A merger in a concentrated market may also significantly impede effective competition due to horizontal coordinated effects where, through the creation or the strengthening of a collective dominant position, it increases the likelihood that firms are able to coordinate their behaviour and raise prices, even without entering into an agreement or resorting to a concerted practice within the meaning of Article 101 TFEU. A merger may also make coordination easier, more stable or more effective for firms that were already coordinating before the merger, either by making the coordination more robust or by permitting firms to coordinate on even higher prices.73

(102) To assess whether a merger gives rise to horizontal coordinated effects, the Commission should examine, first, whether it would be possible to reach terms of coordination and, second, whether the coordination would be likely to be sustainable.74

4.1.2.Vertical effects

(103) A merger is said to result in foreclosure where actual or potential rivals' access to supplies or markets is hampered or eliminated as a result of the merger, thereby reducing these companies' ability and/or incentive to compete.75 Such foreclosure may discourage entry or expansion of rivals or encourage their exit. Such foreclosure is regarded as anti-competitive where the merged entity — and, possibly, some of its competitors as well — are as a result able to profitably increase the price charged to consumers.76

(104) Two forms of vertical foreclosure can be distinguished. The first is where the merger is likely to raise the costs of downstream rivals by restricting their access to an important input (input foreclosure). The second is where the merger is likely to result in foreclosure of upstream rivals by restricting their access to a sufficiently large customer base (customer foreclosure).

4.1.3.Conglomerate effects

(105) In the majority of circumstances, conglomerate mergers do not lead to any competition problems but in certain specific cases there may be harm to competition.77 The main concern in the context of conglomerate effects is that of foreclosure. 78 Conglomerate mergers may allow the merged entity to combine

(112) Therefore, the Commission considers that the Transaction does not give rise to serious doubts as to the compatibility with the internal market as regards the wholesale markets for call termination on Com Hem's and Tele2's fixed networks and this market will, therefore, no longer be discussed in this Decision.

(113) As regards the wholesale market for mobile call termination services, since each MNO's network constitutes a separate market for the provision of wholesale call termination, there is no horizontal overlap between the Parties’ activities on this market, as only Tele2 is active on a its own separate mobile network with a 100% market share over its network. However, the Transaction gives rise to vertically affected markets since Com Hem is a customer of Tele2 with regard to wholesale call termination services on mobile networks in its capacity as provider of fixed telephony and mobile telecommunications services.

(114) However, in Sweden the market for wholesale call termination on mobile networks is regulated ex-ante by the PTS. In its latest decision on call termination on mobile networks, PTS imposed price caps and non-discrimination obligations on both Tele2 ensuring that its call termination services are provided on a fair basis.84

(115) Therefore, the Commission considers that the Transaction does not give rise to serious doubts as to the compatibility with the internal market as regards the wholesale market for mobile call termination services, on Tele2’s mobile network. Therefore, this market will no longer be discussed in this Decision.

(116) As regards the market for wholesale international roaming, the Commission notes that this market is subject to sector-specific EU regulation, which prevents mobile operators from refusing access to their network and from charging excessive termination fees.85 Under the Roaming Regulation, MNOs must meet all reasonable requests for wholesale roaming access86 and MNOs are bound by the price cap imposed by the Roaming Regulation on the wholesale prices that MNOs can charge to their roaming customers. Key obligations under the regulation include an obligation to meet all reasonable access requests, an obligation to publish a reference offer, caps on wholesale and retail charges (for calls, SMS messages and data services), and transparency and information requirements. The Roaming Regulation therefore effectively prevents MNOs from refusing access to their respective network and from charging excessive termination fees.

services to the consumer market in Sweden. Telenor Sweden provides voice and data services to both businesses and consumers, through a range of wireless, fixed and broadband technologies. Tre is the fourth largest MNO offering mobile telephony and mobile broadband to both businesses and consumers in Sweden.

(122) In the retail fixed internet market, the other main players are Bahnhof and Bredband2. Bahnhof was one of the country's first independent internet service providers ("ISP"). Bredband2 is an internet access provider that provides its services based on optical fibre technology. Both companies offer fixed broadband services to private and business customers and mobile services to business customers.

(123) Viasat operates a satellite Pay TV platform in Sweden and is part of the MTG group, primarily active as a retail TV distributor. Viasat is also active in the retail provision of fixed broadband services through open fibre networks.

(124) With respect to multiple play offers, at present Telia and Telenor are the main players, offering different bundles including all services. In particular they offer all types of fixed-only bundles and have recently launched quadruple play offers (including mobile services).

4.4. Assessment of horizontal effects

4.4.1. Retail market for the provision of mobile telecommunications services

4.4.1.1.Notifying Party’s view

(125) The Notifying Party submits that the Transaction would not give rise to any competitive concerns in relation to the retail market for mobile telecommunications services in Sweden for the following reasons. First, the increment brought about by the Transaction is minimal (less than [0-5]%). Second, Com Hem does not have a meaningful standalone presence on this market given that it sells mobile services only to business customers. Third, as suggested by diversion ratios, Com Hem is not a close competitor of Tele2. Fourth, the merged entity will face post-transaction strong competitive pressure from the other MNOs in the market.

4.4.1.2.Commission's assessment

(126) The Parties and their main competitors' market shares by number of subscribers and by value for the overall retail mobile market for the possible segmentation into private customers and business customers are illustrated in Table 5 and Table 6 below. As shown below the increment brought about by the Transaction would be less than 1% under any of these possible market segmentations.87 Such a low increment indicates that the Transaction is unlikely to affect the structure of the market.

operator in the provision of retail mobile services.89 In particular, business customers do not consider Com Hem as a viable competitor to the four MNOs in Sweden.90 Finally, most of the respondents to the market investigation consider that the Transaction would not have a significant impact on the market for the provision of retail mobile telecommunications services in Sweden.91

(129) Finally, with reference to potential coordinated effects, the Commission notes that post-Transaction the market structure in the retail mobile market would remain unchanged with the only exception related to the limited increment of Tele2's position in the business segment brought by Com Hem's position. The market leader Telia will have a market share significantly higher compared to the one of the merged entity and the other two main players Telenor and Tre would remain in the market with a significant market share, respectively [10-20]% and [10-20]% by subscribers. As a result, the Transaction would not bring about any significant changes (either by increasing market symmetry or by removing a potential disruptive player), which would facilitate coordination.

4.4.1.3.Conclusion

(130) In light of the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market as regards the retail market for mobile telecommunications services in Sweden.

4.4.2. Retail market for the provision of fixed internet access services

4.4.2.1. Notifying Party’s view

(131) The Notifying Party submits that the Transaction would not give rise to any competitive concerns in relation to the retail market for fixed internet access services in Sweden for the following reasons. First the increment brought about by the Transaction is not significant (approximately [0-5]% in terms of subscribers). Second, the Parties do not consider themselves to be close competitors and maintain that the internet offerings of Com Hem and Tele2 are largely complementary. Third, several alternative operators would remain active in the market after the Transaction.

4.4.2.2. Commission's assessment

(132) The Parties and their main competitors' market shares by number of subscribers and by value for the overall retail fixed internet access market as well as for the possible segmentation into private customers and business customers are illustrated in Table 7 and Table 8 below. As shown below the combined market share of the merged entity would be around or slightly above 20% under any

(134) The market shares figures would not differ significantly in the possible narrower market for the provision of fixed internet services to private and business customers. With respect to the segment of broadband services to private customers, the merged entity’s share would be [20-30]% by volume and [20-30]% by value, with the increment from Tele2 amounting to [0-5]% and [0-5]% respectively. With respect to the segment of broadband services to business customers, the merged entity’s share would be around [20-30]% by volume and [10-20]% by value. Telia will remain the clear leader with market shares above 30% in all segments while Telenor will be the third largest operator in the market, with a share by subscribers of [10-20]% in the private segment and of [5-10]% in the business one.

(135) Moreover, with regards to the competitive dynamics on the fixed internet market in Sweden, the Commission notes that according to the majority of respondents to the market investigation the level of price competition in the retail market for fixed internet services in Sweden (on the overall market as well as on the residential and business segments of it) is either high or very high pre-Transaction.94

(136) The results of the market investigation also indicate that Tele2 and Com Hem are not close competitors for the provision of fixed internet access services in Sweden with Telia being the closest competitor to both Tele2 and Com Hem.95 In particular, business customers consider Telia and Telenor's offering as closest competitor to Tele2 in terms of parameters such as brand and network quality in Sweden.96 Finally, most of the respondents to the market investigation consider that the Transaction would not have a significant impact on the market for the provision of retail fixed internet access services in Sweden.97

4.4.2.3. Conclusion

(137) In light of the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market as regards the retail market for internet access services in Sweden.

4.4.3.Retail market for the provision of multiple play services

4.4.3.1. Notifying Party’s view

(138) The Notifying Party submits that the Transaction would not give rise to any competitive concerns in relation to the retail market for the provision of multiple

predominantly fixed player, the Commission has also considered the likelihood of each Party, absent the Transaction, becoming a significant player in the FMC segment99 and the effect the Transaction might have on this potential competition between the Parties.

(144) In this respect, the Commission firstly notes that the FMC multiple play segment is nascent in Sweden and has come into existence in earnest only recently through the launch of quadruple play offers from Telia and Telenor. The total number of such subscriptions amounted to just 140 000 at the end of 2017. The Commission has examined, through the review of internal documents, the Parties' respective FMC capabilities and ambitions in the standalone scenario absent the Transaction.

(145) Com Hem has tried to secure an MVNO agreement with a view to couple their fixed services with a mobile component for a number of years. The Commission has reviewed the conditions and parameters set out in Com Hem's latest request for quote as well as the conditions in the single offer received by […] and has concluded that, […].100

(146) […]. In conclusion, absent the Transaction, Tele2's capabilities to offer a FMC product remain uncertain.

(147) Moreover, Tele2's internal documents include […]101 […]102 […]. The Commission considers this as at least an indication that the Transaction may increase competition in the FMC segment compared to the situation that would likely materialize absent the Transaction.

(148) With reference to potential coordinated effects, the Commission notes that post- Transaction the market structure in the multiple play markets, and possible sub- segments, will remain highly asymmetric. In an overall market including all subscriptions of all types of multiple play services, the market leader Telia will have a market share roughly twice that of the merged entity and roughly four times that of the third largest actor, Telenor. With particular regard to fixed- mobile multiple play services, if anything, the entry of a third player on this market would be likely to make any potential coordination more difficult compared to the situation absent the Transaction.

(149) Finally, it is also worth noting that, although Tre does not currently supply multiple play services it would still enjoy a significant presence in the retail mobile telecommunications services markets and thanks to the presence of open fibre networks and third party fixed network operators in Sweden it could potentially enter the multiple play markets based on wholesale fixed network access or partner with remaining fixed operators and could disrupt any possible coordination.

4.4.3.3.Conclusion

(150) In light of the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market as regards any of the potential retail markets for multiple play services in Sweden.

4.5.Assessment of conglomerate effects

(151) Tele2's services in the market(s) for retail mobile telecommunications services and Com Hem's services in the markets for fixed telecommunications and TV services are complementary or at least closely related. Accordingly, the Commission has examined whether the Transaction would give rise to conglomerate effects by foreclosing competitors in the retail market for mobile telecommunications services, the retail market for fixed telephony services, the retail market for internet access services, the retail market for TV services and/or a potential market for multiple-play bundles.

(152) According to the Commission's Guidelines on the assessment of Non-horizontal Merger Guidelines,103 conglomerate effects require (a) the ability to foreclose,(b) the incentives to foreclose and (c) the likelihood that a foreclosure strategy would have a significant detrimental effect on competition and harm consumers. In order to be taken into account, any conglomerate effect must be merger specific. In other words, the conglomerate effect must result from Tele2's acquisition of Com Hem.

4.5.1. Notifying Party's view

(153) The Notifying Party submits that the Transaction would not result in anti- competitive foreclosure of standalone service providers.

(154) First, the Notifying Party points to the Non-horizontal Merger Guidelines in which the Commission recognizes that conglomerate mergers do not normally lead to competition problems and can produce significant procompetitive benefits.

(155) Secondly, the development of FMC services in Sweden is at a nascent stage. The number of fixed mobile bundles is still very limited and significant demand for standalone services will remain. With specific regard to fixed Internet and TV, standalone subscriptions constitute the majority of subscriptions (more than 50% for broadband and around 75%, for TV). Consequently, even if the Transaction would increase FMC uptake in Sweden, it would not result in anti-competitive foreclosure of standalone service providers.

(156) Furthermore, the Parties’ combined shares in mobile services and fixed broadband services range between approximately 15–30%, i.e. at levels that do not confer significant market power. Consequently, according to the Notifying Party the combined entity will lack the market power to unduly leverage its position from mobile services into fixed services or from fixed broadband services into mobile services.

(157) With specific regard to TV services, where the combined entity will hold approx. [50-60]% of TV subscriptions, the Notifying Party submits that this high market share does not result in market power in light of the recent developments and in particular the build-out of fibre: - The rapid build out of fibre allows a majority of customers to subscribe to Pay TV services through IPTV from Com Hem, Telia, Telenor and Viasat. Since the overbuild between the fibre network and coax network is already in excess of 80% and likely to be higher with respect to MDUs, the threat from IPTV is real. The number of Pay TV subscriptions via fibre-based IPTV has nearly doubled from 2014 to 2017 and in this segment Com Hem holds only a [10-20]% share; - The build out of fibre is transforming the competitive dynamics by allowing a greater choice of service providers. This has in turn resulted in high competitive pressure even from smaller market participants in the Pay TV market. Hence, the combined entity will lack any market power to leverage its position in Pay TV services into other services by raising standalone TV prices. Moreover, increasing competition from OTT services further constrains the pricing of all Pay TV distributors as it allows customers to completely bypass traditional Pay TV distributors’ services, in particular for Premium TV.

(158) The Notifying Party further submits that the Swedish telecommunications market is characterized by low switching costs for both fixed and mobile services.

(159) With regard to the mobile segment, the Notifying Party submits that Sweden boasts a larger share of corporate paid mobile subscriptions compared to other European countries (almost one in four in 2016). Corporate customers would in principle not be potential FMC customers and therefore mobile only providers will have continued opportunities to compete for customers even if FMC were to pick up in the Swedish market.

(160) With respect to the FMC-addressable mobile segment, i.e. post-paid subscriptions for private customers, this would account for approx. half of the Swedish market and consequently there would be ample room for a mobile only player. Furthermore, also in this segment customers are currently purchasing mobile separate from fixed and many customers are expected to continuously prefer standalone services.

(161) The Notifying Party concludes that the Transaction is likely to increase rollout of FMC services in Sweden, and that this will benefit consumers. However, there is nothing to suggest that standalone suppliers of fixed and mobile services would risk being marginalised following the Transaction.

4.5.2.Commission's assessment

(162) The Commission has assessed the likely impact of the Transaction on the merged entity's ability and incentive to engage in practices related to multiple play bundles which would likely result in anticompetitive foreclosure of competitors in the retail market for mobile telecommunications services, in the retail market for fixed telephony services, in the retail market for internet access services, in the retail market for TV services and/or in a potential market for multiple-play bundles with mobile and fixed components.

(163) Some respondents to the market investigation have expressed concerns with respect to the possibility for the merged entity to foreclose standalone operators by offering multiple play bundles. According to these respondents, the combination of Tele2 and Com Hem would allow the merged entity to offer FMC services on terms which others would find challenging to match. One respondent considers that the merged entity would be able to enter into exclusivity arrangements with TV channel/content providers, which would seriously weaken the competitors' ability to compete in Sweden.

(164) Another company submitted that the Transaction will give Tele2 access to an extensive fixed infrastructure network in Sweden covering more than 50% of the Swedish households via Com Hem’s cable/fibre footprint and its DTT platform Boxer.104 Tele2’s stated rationale for the merger would be to create a leading integrated operator in Sweden by leveraging Com Hem’s strong presence in residential fixed-line and cross-selling services to the respective customer bases. The merged entity will have the ability and the incentive (i) to offer fixed-mobile bundles in which the mobile component is discounted and subsidised by the fixed component, thus inciting customers to migrate to converged fixed/mobile offerings, and (ii), even where there is no formal bundling, to cross-sell its mobile offerings to Com Hem’s fixed line customers. The merged entity's strategy could be particularly successful for MDU customers, because they would be locked-in by virtue of long term contracts.

(165) The Commission has assessed whether the merged entity would have the ability and incentive to use its market power in one market to foreclose competitors in another market by bundling products after the Transaction.

4.5.3.Ability to foreclose

(166) In order to have the ability to foreclose rivals, the merged entity must have a significant degree of market power in at least one of the markets concerned. That is, at least one of the Parties' products must be viewed by many customers as particularly important and there must be few relevant alternatives for that product.105

(167) With respect to the market for retail mobile telecommunications services in Sweden, the merged entity's market share will be below 30%. Moreover, there are at least two significant competitors with a comparable market position (Telia and Telenor) and a third MNO with a 15% market share. The Commission is therefore of the view that based on its position in the market for retail mobile telecommunications services in Sweden, it is unlikely that after the Transaction the merged entity will have the ability to leverage its position in the market for retail mobile telecommunications services into the retail market for fixed telephony services, the retail market for internet access services, the retail market for TV and/or in a potential market for multiple-play bundles with mobile and fixed components.

(168) Similarly, the merged entity's estimated market shares will not exceed 30% neither in the retail market for fixed telephony services nor in the retail market for internet access services.

(169) The only potential market where Com Hem has a sizable market share is the market for retail supply of TV services, where it had a market share of [50-60]% in terms of subscriptions in 2017.106 However, in terms of revenues Com Hem's market share is more limited, at [30-40]% in 2016.107

(170) In this regards, first it appears that customers in Sweden have relevant alternatives in the TV market: Telia and Telenor have both a market share in TV subscriptions higher than 15%. MTG/Viasat has to be considered as well, taking into account (i) its market share of [5-10]% in subscriptions and [10-20]% in revenues, and (ii) the fact that it is an integrated TV player active both as TV (satellite) retail distributor and as TV channels provider.

(171) Moreover, Com Hem's market share is declining (it was [50-60]% in 2015 and [50-60]% in 2016). This is partially due to the fact that Com Hem distributes its TV services mainly through Digital Terrestrial Television – DTT, that is declining, and through its coax network, that is submitted to the increasing competitive pressure of IPTV via fibre, where Com Hem's presence is more limited, with a [10-20]% market share (Telia is by far the leader with [50-60]% and Telenor has [10-20]%). In this last respect, in 2017, about 70% of Swedish households had access to fibre (75% in urban areas).108 According to Com Hem's estimation, more than […] of its coax network is already overbuilt by fibre.109 Total subscriptions for IPTV via fibre passed from 596 000 in 2014 (11.4% of the market) to more than one million in 2017 (19.5% of the market).

(172) The situation does not change substantially focusing on the MDU segment. In this respect, Com Hem's market share, although slightly higher, is declining (from [50 - 60]% in 2014 to [50 - 60]% in 2017, first half), confronted with the rise of IPTV via fibre: 377 000 total subscriptions in 2014 (13% of the total market), 520 000 in 2017 first half (17.2% of the market). Com Hem has a limited share in IPTV for MDU customers ([10 - 20]%), Telia again having a much higher share of [60 - 70]% . As for the alleged advantage enjoyed by Com Hem because of the long-term contracts concluded with MDU customers, actually about […] of Com Hem MDU subscribers are not bound by any binding period and may terminate their contracts with […] notice. As for the remaining […], […]. 110

(173) Furthermore, the Commission notes that the Swedish FMC market is still at an early stage and most subscriptions in all services are still sold standalone: notably in 2017, according to PTS data, only 25% of TV subscriptions were sold bundled with one or more other telecommunications services. Only (i) 2% of mobile subscriptions, (ii) 8% of broadband subscriptions and (iii) 27% of fixed telephony subscriptions were sold in a bundle including TV services.111 Although, as pointed out by some respondents to the market investigation112, the Transaction may somewhat speed up the uptake of fixed-mobile bundles and notably of bundles including TV, it appears that providers of standalone services (or of bundled services excluding TV) would still have a sizeable share of the market at their disposal. It is in particular worth noting that currently the number of mobile subscriptions sold in bundle with TV services is marginal113.

(174) As mentioned above, mobile services are mainly sold stand-alone in Sweden. Even if the merged entity were to start offering fixed-mobile bundles at discounted prices compared to the price of the standalone components, the possible increase in fixed-mobile bundles in the next years does not seem to allow a radical and rapid change of this situation to such an extent as to marginalise providers of standalone services (or of bundled services excluding TV) reducing their ability and incentive to compete. Moreover, this is all the more true when considering the limited interaction between mobile services and TV services. In this respect one participant to the market investigation pointed to the upcoming developments of the mobile communication services and the increasing possibility to use mobile handsets for digital connectivity as well as for voice and messaging.114 Moreover, bundles including TV services are less relevant for business consumers, who represent a considerable portion of the mobile market in Sweden. In light of that, also in a scenario of increasing relevance of FMC offers in Sweden, it is unlikely that mobile-only operators would be marginalised.

(175) Finally, with respect to the alleged ability of the merged entity to enter into exclusivity arrangements with TV channel/content providers, which would weaken the competitors' ability to compete in Sweden, at present Tele2 is not active in the TV sector and as a consequence the Transaction would not directly increase the presence of the merged entity in the markets for the acquisition of TV content and/or for the acquisition of TV channels. Moreover, considering the limited interaction between mobile telecommunications and TV services in Sweden, it is unlikely that any possible development of FMC offers would substantially increase the market power of the merged entity as to obtain exclusive arrangements with the most important TV rights holders/channel providers.

(176) Based on the above, considering the competitive scenario and the current development of the FMC in Sweden, the Commission considers that customers in Sweden will have relevant alternatives in the TV market and multiple play products including TV services could be easily substituted by the stand-alone components. Therefore, the merged entity will not have the ability to foreclose competitors in the adjacent markets.

4.5.4.Incentive to foreclose

(177) The Commission has also assessed whether the merged entity will have an incentive to engage in bundling of retail supply of mobile telecommunications services and fixed telecommunications, fixed Internet access and TV services, to foreclose rivals from effectively competing for customers who purchase both fixed and mobile services.

(178) After the Transaction, the merged entity might consider introducing a price- discrimination strategy consisting of somewhat increasing the price of the standalone fixed products and/or to lower the price of fixed-mobile bundles.115 As a result of such a price discrimination strategy, customers who buy fixed and mobile products separately could incur an increase in their total cost of ownership while customers who opt into the bundle could be better-off.

(179) As regards the potential increase in the price of standalone fixed products, the Commission considers that the incentive to do so for the merged entity would be mitigated by the existence of alternative fixed offers by Telia, Telenor and other relevant fixed operators (see table 4 at paragraph (119)). Moreover, it is doubtful that this strategy could be viable, considering that most subscriptions in all services, including fixed ones, are still sold standalone.

(180) As regards the sale of bundles at a discount, the Commission considers this to be in the interest of consumers and unlikely to lead to the marginalisation of mobile- only players who will continue to compete to sell mobile services to customers who purchase both fixed and mobile services (as well as to customers who purchase exclusively mobile services). In this respect, the vast majority of consumers in Sweden still subscribes separately to fixed and mobile products.116 The incentives are further mitigated by the fact that the merged entity will have a fixed cable infrastructure that covers only about 60% of the Swedish households and hence cannot rely on this infrastructure to offer fixed and mobile bundles in all parts of Sweden.

4.5.5. Effects on competition

(181) The Commission has also assessed the effects of a possible foreclosure strategy on competition, and thus on consumers.

(182) As for the possible impact on mobile-only operators, it has already been mentioned that only relatively few customers currently use fixed-mobile bundles. In particular, in 2017 fixed/mobile subscriptions represented less than 4% of the total mobile subscriptions.117 This implies that a significant demand for mobile- only products will remain on the market, also in case of a discount strategy by the merged entity and an increasing development of FMC offers, in light of the elements mentioned above, at paragraphs (173) and (180).

(183) The Transaction might accelerate the trend towards fixed-mobile convergence in Sweden. By combining a strong fixed offer with a strong mobile offer, the Transaction could somewhat speed up the uptake of FMC offers. However, the Commission considers that even where customers would be converted more rapidly into fixed-mobile bundles, this does not in itself undermine the ability of mobile-only competitors to effectively compete for customers. Finally, it is also worth noting that, as discussed in paragraph (149) above, mobile-only operators could potentially enter the multiple play markets based on wholesale fixed network access or partner with remaining fixed operators.

(184) In addition, the Commission considers that the Transaction generates a third, fully integrated player owning both a fixed and a mobile network. According to the Parties' internal documents, a major rationale of the Transaction would be to increase the Parties' ability to market fixed-mobile bundles by combining Tele2's mobile assets with Com Hem's fixed assets. As a result, the Commission considers that the Transaction has the potential to stimulate the Notifying Parties' ability to compete in fixed-mobile bundles with Telia and Telenor.

4.5.6.Conclusion on conglomerate effects

(185) Based on the above considerations, the Commission is of the view that the Transaction does not give rise to serious doubts as to its compatibility with the internal market in relation to anti-competitive conglomerate effects.

5. CONCLUSION

(186) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This Decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this Decision

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 OJ L 24, 29.1.2004, p. 1 (the "Merger Regulation").

4 Publication in the Official Journal of the European Union No C 321, 11.9.2018, p. 5.

5 For the purposes of the competitive assessment in the present case, the question whether Verdere and Camshaft control Kinnevik can be left open given that the outcome of the competitive assessment will not change whether or not they control it. For the purposes of the case at hand, the Commission has therefore undertaken the competitive assessment of the Transaction as if, with their combined 40% of voting rights, Verdere and Camshaft exercise de facto control over Kinnevik.

6 This situation is the result of Kinnevik’s decision to distribute all of the shares that it held in MTG to its shareholders. For completeness, it is mentioned that Kinnevik previously had a minority shareholding in MTG. However, following a reclassification of Kinnevik’s MTG class A shares into MTG class B shares on 1 August 2018, and a distribution of Kinnevik’s MTG class B shares to Kinnevik’s shareholders on 14 August 2018, Kinnevik does not own any shares in MTG. See: https://www kinnevik.com/media--contact/press-releases/2018/8/2208838-Kinneviks-Board-of- Directors-has-set-the-record-date-for-the-distribution-of-Kinneviks-shares-in-MTG. MTG’s shareholding structure is currently widely dispersed and MTG is not controlled by any of its shareholders. See: https://www mtg.com/the-share/#ownership.

7 Turnover calculated in accordance with Article 5 of the Merger Regulation.

8 See paragraph 74, Form CO.

9 Commission decision of 7 September 2005 in Case M.3914 – Tele2/Versatel, paragraph 10; Commission decision of 29 June 2010 in Case M.5532 – Carphone Warehouse/Tiscali UK, paragraphs 35 and 39; Commission decision of 9 January 2010 in Case M.5730 – Telefónica/Hansenet Telekommunikation, paragraphs 16 and 17.

10 Commission decision of 20 September 2013 in Case M.6990 - Vodafone/Kabel Deutschland, paragraph 131.

11 Commission decision of 10 October 2014 in Case M.7000 Liberty Global/Ziggo, recital 125.

12 Commission decision of 4 February 2016 in case M.7637 Liberty Global/BASE Belgium, recital 69.

13 Commission decision of 3 August 2016 in case M.7978 – Vodafone/Liberty Global/Dutch JV, paragraph 26.

14 See Commission decision of 10 October 2014 in Case M.7000 Liberty Global/Ziggo, recital 127; Commission decision of 19 May 2015 in Case M.7421 Orange/Jazztel, recital 37. Commission decision of 3 August 2016 in case M.7978 – Vodafone/Liberty Global/Dutch JV, paragraph 29.

15 See replies to Q1 – mobile operators of 4 September 2018, question 18. See also Q2 – fixed operators of 4 September 2018, question 18.

16 See Commission decision of 29 June 2010 in Case M.5532 – Carphone Warehouse/Tiscali UK, recitals 7-21; Case M.6990 Vodafone/Kabel Deutschland, recital s192-194. Commission decision of 3 August 2016 in case M.7978 – Vodafone/Liberty Global/Dutch JV, paragraph 38.

17 See Commission decision of 19 May 2015 in case M.7421 Orange/Jazztel, recital 42; Commission decision of 10 October 2014 in case M.7000 Liberty Global/Ziggo, recital 132; Commission decision of 7 October 2016 in case M.8131 Tele2 Sverige/TDC Sverige, recital 32.

18 See replies to Q1 – mobile operators of 4 September 2018, question 12. See also Q2 – fixed operators of 4 September 2018, question 12.

19 See replies to Q3 – business customers of 4 September 2018, question C.A.4.

20 See replies to Q1 – mobile operators of 4 September 2018, question 13. See also Q2 – fixed operators of 4 September 2018, question 13.

21 See Commission decision of 29 June 2010 in Case M.5532 – Carphone Warehouse/Tiscali UK, recital 47; Case M.5730 Telefonica/Hansenet, recital 28; Case M.6990 Vodafone/Kabel Deutschland, recital 197. Commission decision of 3 August 2016 in case M.7978 – Vodafone/Liberty Global/Dutch JV, paragraph 40.

22 See replies to Q1 – mobile operators of 4 September 2018, question 18. See also Q2 – fixed operators of 4 September 2018, question 18. See replies to Q3 – business customers of 4 September 2018, question C.B.2.

23 IPTV is the abbreviation for Internet Protocol TV; it is a system through which television services are delivered using the Internet protocol over a packet-switched network such as the internet, instead of being delivered through traditional terrestrial, satellite signal and cable television formats.

24 Over-the-top (OTT) is any application or service that provides a product over the Internet and bypasses traditional distribution. Applications and services that are provided as 'over-the-top' are most typically related to media and communication.

25 Commission decision of 21 December 2010 in case M.5932 News Corp/BskyB; Commission decision of 22 September 2006 in case M.4353 Permira/All3Media Group; Commission decision of 15 April 2013 in case M.6880 Liberty Global/Virgin Media; Commission decision of 24 February 2015 in case M.7194 Liberty Global/Corelio/W&W/De Vijver Media.

26 See e.g., SCA decision of 21 September 2016, Dnr 411/2016, Com Hem /Boxer, recitals 50-52.

27 Commission decisions of 18 July 2007 in case M.4504 SFR/Télé 2 France, recital 40, and of 25 June 2008 in case M.5121 News Corp / Premiere, recital 20. See also, Commission decision of 7 April 2017 in case M.8354 – Fox / Sky, paragraph 97; Commission decision of 3 August 2016 in case M.7978 – Vodafone/Liberty Global/Dutch JV, paragraph 56; Commission decisions of 24 February 2015 in case M.7194 Liberty Global / Corelio / W&W / De Vijver Media, recital 119-120, of 25 June 2008 in case M.5121 News Corp/Premiere, recitals 15 and 21, and of 10 October 2014 in case M.7000 Liberty Global/Ziggo, recital 108).

28 Commission decision of 6 February 2018 in case M.8665 – Discovery / Scripps, paragraph 33; Commission decision of 7 April 2017 in case M.8354 – Fox / Sky, paragraph 98 and 99; Commission decision of 3 August 2016 in case M.7978 – Vodafone/Liberty Global/Dutch JV, paragraph 58; Commission decision of 24 February 2015 in case M.7194 Liberty Global / Corelio / W&W / De Vijver Media, recital 124. Commission decision of 25 June 2008 in case M.5121 News Corp/Premiere, recital 21. Commission decision of 10 October 2014 in case M.7000 Liberty Global/Ziggo, recitals 109–110.

29 Commission decision of 6 February 2018 in case M.8665 – Discovery / Scripps, paragraph 33; Commission decision of 7 April 2017 in case M.8354 – Fox / Sky, paragraph 100; Commission decision of 3 August 2016 in case M.7978 – Vodafone/Liberty Global/Dutch JV, paragraph 62; Commission decision of 24 February 2015 in case M.7194 Liberty Global / Corelio / W&W / De Vijver Media, recital 127. Commission decision of 25 June 2008 in case M.5121 News Corp/Premiere, recital 22; Commission decision of 21 December 2010 in case M.5932 News Corp/BskyB, recital 105. Commission decision of 10 October 2014 in case M.7000 Liberty Global/Ziggo, recital 113.

30 Commission decision of 24 February 2015 in case M.7194 Liberty Global / Corelio / W&W / De Vijver Media, recital 119.

31 Commission decision of 20 September 2013 in case M.6990 – Vodafone/Kabel Deutschland, paragraphs 92-96.

32 See replies to Q1 – mobile operators of 4 September 2018, question 20. See also Q2 – fixed operators of 4 September 2018, question 20.