Commission, March 26, 2020, No M.9316

EUROPEAN COMMISSION

Judgment

PEAB / YIT'S PAVING AND MINERAL AGGREGATES BUSINESS

Subject: Case M.9316 – PEAB / YIT’s PAVING AND MINERAL AGGREGATES BUSINESS

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 20 February 2020, the Commission received the notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/20043 by which Peab AB (“Peab” or “Notifying Party”) acquires sole control of the mineral aggregates business of YIT Oyj (“YIT”) in Denmark, Finland, Norway and Sweden (the “Transaction”, as set out in paragraph 5 below). The business targeted by the acquisition is referred to as the “Target”, while Peab and the Target are collectively referred to as the “Parties”. In a post-Transaction context, Peab, all the subsidiaries under its control and the Target may also be collectively referred to as the “merged entity”.

1. THE PARTIES

(2) Peab, the acquirer, is a construction and civil engineering company, active in businesses such as civil engineering; construction and renovations of buildings and infrastructure; paving of roads and other surfaces; as well as the production of mineral aggregates, concrete, asphalt and prefabricated concrete elements. Peab is registered in Sweden.

(3) YIT, the seller, is a construction company active in the construction and renovation of buildings and infrastructure; the paving of roads and other surfaces; and the production of mineral aggregates and asphalt. YIT is registered in Finland.

(4) The Target comprises the following YIT businesses: i) the production and sale of mineral aggregates in Finland, Norway and Sweden; ii) the production and sale of asphalt in Denmark, Finland, Norway and Sweden; iii) the paving of roads in Denmark, Finland, Norway and Sweden; iv) sale of bitumen in Norway, and v) operation of transport sea vessels. Bitumen is a marginal activity as the Target does not produce bitumen but rather buys them from oil companies for its own asphalt production needs. If asphalt production falls below the forecasted production, the Target sells the surplus it does not need. Transport is also a marginal activity as the Target has only one cargo ship and one bulk carrier ship, which carry, inter alia, some mineral aggregates.

2. THE OPERATION

(5) The Transaction is accomplished by way of a share acquisition (Finland, Norway and Denmark) and partly through a business asset acquisition (Sweden). Peab will acquire all shares of the Danish company YIT Danmark A/S, all shares of the Norwegian company YIT Norge AS and all shares of the Finnish company YIT Teollisuus Oy. In addition, Peab will acquire from the Swedish company YIT Sverige AB all assets related to its mineral aggregates, asphalt and paving businesses. The concentration will be implemented by the conclusion of an agreement.

3. THE CONCENTRATION

(6) As a result of the Transaction Peab will acquire sole control within the meaning of Article 3(1)(b) the Merger Regulation over the Target.

4. UNION DIMENSION

(7) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million4 (Peab: EUR 5 471 million; Target: EUR 600 million). Each of them has a Union-wide turnover in excess of EUR 250 million (Peab: EUR 4 815 million; Target: EUR 457 million), but they do not achieve more than two-thirds of their aggregate Union-wide turnover within one and the same Member State. The notified operation therefore has Union dimension.

5. RELEVANT MARKETS AND COMPETITIVE ASSESSMENT.

5.1. Introduction and overview of horizontal and vertical links

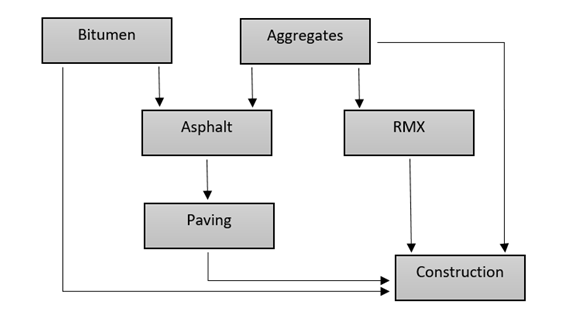

(8) Mineral aggregates (“aggregates”) are different types of grained particulate minerals used as base materials in the construction of buildings, roads and other infrastructure. They are also used as raw material in the production of concrete, asphalt and mortar. Bitumen is a viscous liquid or semi-liquid form of petroleum found in natural deposits and often obtained as a result of oil refining process. It is primarily used as a binding agent in the production of asphalt (road bitumen), in the construction industry and in the production of paper (industrial bitumen). Asphalt is the building material of roads, bicycle lanes, car parks, sidewalks, sport areas and airport runways. It is a mixture of aggregates and bitumen. Ready-mix concrete (“RMX”) is a common construction material made of cement, aggregates and water. It is manufactured at a concrete plant and transported in a semi-wet form in specific mixer truck vehicles to the construction site. Paving, also referred to as contract surfacing, is the application of asphalt and other materials to surface roads, car parks, footpaths, airport runways and other sites. Construction has been defined as the on-site construction or assembly of buildings and other structures, including building engineering. The upstream- downstream relationships of these various products and services are illustrated in figure 1 below.

Figure 1 Upstream - downstream links between the relevant construction materials and services

(9) The Transaction involves a number of horizontal overlaps and vertical relationships. Horizontal overlaps include:

i.) the production and sales of aggregates in Finland, Sweden and Norway. ii.) the production and sales of asphalt in Norway and Sweden; and

iii.) the supply of road paving services in Norway and Sweden.

(10) There is no horizontal overlap in asphalt or paving in Finland or Denmark as Peab is not active in these activities in these Member States. Neither the Target nor Peab is active in aggregates in Denmark. Furthermore, Peab is not active in bitumen, while the Target is not active in RMX and construction. As regards the latter, YIT’s construction business is not part of the Transaction.

(11) Vertical relationships between the Parties include:

i.) Aggregates – asphalt relationship in Norway and Sweden

ii.) Aggregates – RMX relationship in Finland, Norway and Sweden

iii.) Aggregates – construction relationship in Finland, Norway and Sweden

iv.) Bitumen – asphalt relationship in Norway

v.) Transport – aggregates relationship in Norway.

vi.) Asphalt – paving relationship in Norway and Sweden vii.) Paving – construction in Norway and Sweden

(12) The aggregates – asphalt relationship stems from the fact that both Parties are active in aggregates and asphalt in Norway and Sweden. However, there is no such relationship in Finland as Peab is not active in asphalt in Finland. As Peab is active in RMX in Finland, Norway and Sweden and the Target is active in aggregates in all of these EEA Contracting Parties, there is an aggregates – RMX link between the parties in all these EEA Contracting Parties. Likewise, the Target’s aggregates activities are in a vertical relationship with Peab’s construction activities in Finland, Norway and Sweden. The Target’s minor activities in bitumen restricted to Norway, and thus the vertical links to asphalt only occurs in Norway. The same applies to transport as the Target operates a cargo ship and a bulk carrier ship only in Norway and these carry, inter alia, some mineral aggregates. Asphalt is the main input in paving but due to the fact that Peab is not active in asphalt and paving in Denmark and Finland, the asphalt- paving vertical link only arises in Norway and Sweden. Finally, Peab is active in construction, of which road construction is a particular segment, and paving could be regarded as an input service to road construction. This vertical link only arises in Norway and Sweden as Peab is only active in road construction in these EEA Contracting Parties.

(13) There are no bitumen-construction links as the Target only sells bitumen to asphalt producers. Lastly, there are no RMX-construction vertical links because the Target is not active in either activity.

5.2. Market definition

5.2.1. Aggregates

5.2.1.1. Product market definition

(14) Aggregates are used as (i) base materials in the construction of roads, buildings and other infrastructure, and (ii) raw materials to make products such as concrete, asphalt and mortar. They may be quarried from land and dredged from the sea (together, “primary aggregates”); obtained from waste products of other mining or industrial services (“secondary aggregates”); or obtained from recycled sources such as demolition sites and construction waste (“recycled aggregates”). The two types of aggregates are crushed rock (“crushed rock”) on the one hand and gravel and sand (“gravel and sand”) on the other. Finally, “specialist aggregates” such as rail ballast, high polished stone value ('PSV') aggregates, and high-purity limestone aggregates can also be distinguished from primary and secondary/recycled aggregates used in the asphalt, RMX and construction businesses.

(A) The Notifying Party’s view

(15) The Notifying Party submits that the distinction between primary and secondary/recycled aggregates is irrelevant as (i) there is no overlap in secondary aggregates, and (ii) secondary/recycled aggregates make up a very small share of the overall market (less than 4% in Finland and Sweden and less than 1% in Norway).5 Furthermore, in the Notifying Party’s view, secondary aggregates can be substituted by primary aggregates for all purposes, whereas the opposite is not always true.6 Consequently, the total aggregates market essentially corresponds to the primary aggregates market.

(16) The Notifying Party further submits that, within primary aggregates, no distinction should be made between i) gravel and sand on the one hand and ii) crushed rock on the other as the two types of aggregates are substitutable for most uses.7 Customers buying aggregates for construction purposes usually procure all types of aggregates.8 RMX customers traditionally used gravel and sand but due to the scarcity of natural gravel, it is increasingly replaced by crushed rock.9 Generally crushed rock is used for asphalt production and thus asphalt producers seek to buy crushed rock.10 The price differences between the two types of aggregates are minimal.11 When aggregates are purchased in public procurements, gravel/sand and crushed rock is usually purchased together.12

(17) As regards the distinction between specialist and other primary and secondary/recycled aggregates, the Notifying Party submits that Peab only produces specialist aggregates in Sweden, whereas the Target only does so in Finland. There is no vertical link between one party’s specialist aggregates production and the other party’s operations. Absent horizontal and vertical links, the Notifying Party considers that the distinction between specialist aggregates on the one hand and primary and secondary/recycled aggregates on the other can be left open.13

(18) Thus the Notifying Party considers that, for the purposes of the Transaction, the relevant product market covers all aggregates.

(B) Commission precedents

(19) In some past decisions the Commission considered aggregates as a single, separate product market without further distinctions.14

(20) In other cases, the Commission has considered, but ultimately left open, a segmentation between (i) primary aggregates (crushed rock, gravel and sand) and (ii) secondary / recycled aggregates (such as colliery and china clay waste, slate, power station ash, slags and demolition/construction waste).15

(21) Within the primary aggregates category, the Commission has also considered a further distinction between (i) gravel and sand and (ii) crushed rock, but ultimately left the definition open.16

(22) Additionally, the Commission has also carried out a separate assessment of the impact of a merger as regards specialist aggregates despite ultimately leaving open the market definition.17

(C) The Commission’s assessment

(C.i) Primary vs secondary/recycled aggregates

(23) The market investigation has not produced conclusive results on the distinction between primary and secondary/recycled aggregates. Some respondents consider that slag is interchangeable with primary aggregates18 and, in a more general fashion, there is a degree of substitutability between primary and secondary/recycled aggregates.19 Others exclude the possibility of switching between these types of aggregates.20

(24) However, the Parties’ presence in secondary/recycled aggregates is minimal without there being any horizontal and vertical links between their respective operations.21 Considering these aggregates separately would therefore not lead to competition concerns. Furthermore, the responses to the market investigation suggest that secondary and recycled aggregates can always be substituted with primary aggregates and doubts on the substitutability arise in the opposite direction.22 This would imply that there can be no market power separately in secondary/recycled aggregates because producers of primary aggregates exercise a constraint on producers of secondary/recycled aggregates. Thus, the separate investigation of secondary/recycled aggregates is not warranted.

(25) The Commission also notes that secondary/recycled aggregates are a very small part of the overall aggregates market. In line with the Notifying Party’s view, public statistics indicate that the share of secondary/recycled aggregates is less than 4% of total aggregates production in Sweden and Finland and less than 1% of total aggregates production in Norway.23 Thus the competitive assessment of an overall aggregates market and a separate primary aggregates market would essentially be the same.

(26) Consequently, for the purpose of the assessment of the Transaction, the Commission will not distinguish primary and secondary/recycled aggregates.

(C.ii) Specialist aggregates vs. primary and secondary/recycled aggregates

(27) Concerning the possible segmentation between specialist aggregates, on one side, and primary/secondary/recycled aggregates on the other, similar considerations apply as in the case of the potential primary aggregates – secondary/recycled aggregates distinction. First, the Parties’ presence is minimal in specialist aggregates without there being any horizontal and vertical links between their respective operations.24 Thus considering these aggregates separately would not lead to competition concerns. Second, the specialist aggregates segment is a niche market relative to the primary and secondary/recycled aggregates segment, constituting less than 0.5-5% of the two segments combined.25 Consequently, the competitive assessment of an overall aggregates market and a separate primary/secondary/recycled aggregates market would substantially be the same.

(28) Consequently, for the purpose of the assessment of the Transaction, the Commission will not distinguish specialist aggregates and primary, secondary/recycled aggregates.

(C.iii) Crushed rock vs. gravel and sand

(29) The market investigation indicated that crushed rock and gravel/sand can be used interchangeably in construction.26

(30) RMX producers indicated that they use both types of aggregates interchangeably27 or use gravel/sand only in quality products.28 However, if gravel and sand is not available nearby, it will be substituted with crushed rock.29 Thus, while only gravel and sand has been used in RMX production, it is increasingly replaced by crushed rock. For example, according to a report by the Swedish Geological Survey, 2016 was the first year when rock material in Sweden surpassed gravel and sand in the manufacture of concrete. Out of the aggregates used for manufacture of concrete, 51 % consisted of rock material.30 These facts suggest a significant degree of substitutability between the two types of aggregates for the purposes of RMX production.

(31) The market investigation also indicated that mainly crushed rock is used for asphalt and that gravel and sand is not suitable for this purpose.31

(32) Further, construction represents around 80 % of all aggregates use, with asphalt and RMX representing 11% and 5 % of total use respectively (disregarding specialist aggregates).32

(33) Based on the above the Commission considers that gravel and sand can be substituted with crushed rock, even if, in the case of RMX, the substitution is not perfect. However, despite the lack of full substitutability in the case of RMX, it appears difficult to raise the price of gravel and sand as construction customers would readily switch to crushed rock, making such a small but not insignificant price increase unprofitable. Since the market investigation has not yielded any indications that arbitrage could be prevented by aggregate producers, the Commission does not consider that selectively raising the price for RMX customers (i.e. price discrimination) is feasible. On the contrary, there are indications that quarries do not even control the final destination of their deliveries,33 which makes it unlikely that they would be able to control secondary sales. Thus, despite the lack of perfect substitutability, crushed rock can be considered as a demand-side constraint that prevents price increases in gravel and sand.

(34) As regards substitution of crushed rock with gravel and sand, the Commission considers that such substitution is possible in construction and in RMX production but not in asphalt production. However, for the same reasons as discussed above in relation to substitution from gravel and sand to crushed rock, increasing the price of crushed rock appears difficult because the switching of construction customers would defeat such a move and selectively raising the price for asphalt customers does not appear feasible due to the inability of the aggregates suppliers to control arbitrage. Thus, despite the lack of perfect substitutability, gravel and sand can be considered as a demand-side constraint that prevents price increases in crushed rock.

(35) On this basis, the Commission considers that the degree of substitution is at such levels that an overall aggregates market is probable. Consistent with this, the Swedish Competition Authority has concluded (and was upheld by the Swedish Market Court on this point) that sand and gravel belong to the same product market with crushed rock as they are substitutable with each other to more than only a limited extent.34

(36) Thus, while the Commission also received unsubstantiated responses on this issue, the market investigation overall suggests that crushed rock and gravel and sand belong to one market. In any event, the question whether separate markets should be defined for crushed rock, on the one hand, and gravel and sand on the other, can be left open as this would not change the competitive assessment in this case.

(37) Consequently, for the purpose of the assessment of the Transaction, the Commission will take a single aggregates market as a basis without distinguishing between (i) gravel and sand and ii) crushed rock. However, it ultimately leaves this question open as it would not change the competitive assessment.

5.2.1.2. Geographic market definition

(A) The Notifying Party’s view

(38) The Notifying Party submits that the definition of a relevant geographic market for aggregates is dependent on the fact that aggregates are heavy and voluminous products with significant transport costs. Around half of the price of aggregates is made up of transport costs.35 Consequently, the size of the geographic market depends on the distance to which it is economically reasonable to transport aggregates.

(39) In the Notifying Party’s view, this distance varies to a certain extent by country and by region, as it depends on the cost of producing the aggregates (if aggregates can be produced at a lower cost, they can be sold competitively further away from the production site than aggregates produced at a higher cost), and the cost of transport.36 The cost of producing aggregates in turn is tied to a number of variable components (e.g. whether the quarry is on an owned or leased property, the amount of landscaping works necessary for production), while the cost of transport depends on the location of the quarry and the road network available.37 Further, in sparsely populated areas aggregates need to be transported to longer distances despite the higher costs as the place of use are often further away from the source of aggregates than in more densely populated areas. Thus quarries tend to compete in somewhat larger areas in sparsely populated areas than in metropolitan areas.38

(40) Based on the share of the Parties’ aggregates sales to different distances the Notifying Party considers that the most appropriate geographic market is a 50 km radius around the quarry and 80 km radius is the second best alternative.39 For example, based on internal estimates, in Sweden [50-60]% of Peab’s aggregates are used within a radius of 25 km of the quarry, [90-100]% is used within a radius 50 km and [90-100]% were used within 80 km from the quarry. The corresponding figures of the Target are as follows: [20-30]% of aggregates are used within a radius of 25 km, [70-80] % of aggregates are used within a radius of 50 km and [90-100]% are used within a radius of 80 km.40

(41) Further, while in the countries affected by the Transaction aggregates are predominantly transported by road, in certain areas, most notably in northern Norway, they are also transported by boat. In the case of boat transport, aggregates can be transported to distances of 150-250 km.41

(B) Commission precedents

(42) In past decisions, the Commission has considered the aggregates market to be local/regional in scope42 and has retained a radius of 50 to 80 km depending on the particularities of the areas concerned.43 This approach was based on the fact that aggregates are heavy and voluminous products with significant transport costs.

(43) Exceptionally, a national market was also defined but this concerned the Netherlands, which has a relatively small size, very easy geography as well as a dense and good quality road network.44

(44) Most recently, in Holcim /Lafarge, the Commission retained a 50-80 km radius around the production site as the relevant geographic market, in line with the standard practice.45

(C) The Commission’s assessment

(45) It is clear on the basis of the precedents that the appropriate market size depends on how far it is reasonable to transport aggregates, which is confirmed by the fact that customers that the maximum distance from which customers source aggregates is 100 km.46

(46) However, the maximum distance could be an exceptional outlier that does not reflect real competitive conditions. If the vast majority of aggregates are sold within a shorter radius, competition between suppliers mostly takes place within the smaller area determined by that radius and a supplier that is located from 100 km from the customer does not exercise competitive constraints on suppliers closer to the customer in a meaningful way. In this regard, the market investigation indicates that the vast majority of aggregates are sold within a radius of 50 km.47

(47) The Commission also notes that, in line with the Notifying Party’s view, the investigation confirmed that in northern Norway aggregates are also transported by boat.48 For example respondents included a shipping company that operates in Northern Norway and transports aggregates for both Parties.49 The Target also operates boats that transport, inter alia, aggregates.50 This is in line with the fact that northern Norway has a long and fractured coastline, that the population centres are located along the coast and that all inland destinations are relatively close to the coast. In the case of boat transport, aggregates can be transported to longer distances than by road, approximately 200 km.51

(48) Thus, in line with the precedents, the Commission considers that the appropriate geographic market is in general a radius of 50 kms in Finland, Norway and Sweden. However, to the extent necessary, it will also take into account regional variations in the competitive assessment. The most important regional variation is that in northern Norway boat transport is also used and this increases the area within which aggregates suppliers compete.

5.2.2. Bitumen

5.2.2.1. Product market definition

(49) Bitumen is a viscous liquid or semi-liquid form of petroleum found in natural deposits and often obtained as a result of oil refining process. It is primarily used as a binding agent in the production of asphalt (road bitumen), in the construction industry and in the production of paper (industrial bitumen).

(A) The Notifying Party’s view

(50) The Notifying Party considers bitumen to be one product market without further segmentation. However, it submits that the exact product market definition can be left open for the purpose of this case52.

(B) Commission precedents

(51) In previous decisions, the Commission has considered that bitumen should be distinguished from other refined oil products, based on its characteristics and specific use53. In addition, the Commission has considered but ultimately left open, a further segmentation according to the type of bitumen used for a given end-application, such as road/standard bitumen, modified bitumen, bitumen emulsions and industrial bitumen.54

(C) Commi

ssion’s assessment

(52) In line with previous decisions, the Commission considers a distinct market for the supply of bitumen, with a potential further segmentation, depending on the type of bitumen.55 In this case, the Target processes the purchased bitumen predominantly for its own asphalt production in Norway,56 and sells any surplus on an ad-hoc basis to third parties.57 Because of the Target’s minor activity, the competitive assessment would not change under any plausible product market definition. For the purpose of this case, the exact product market definition can therefore be left open, as regardless of the exact product market definition for bitumen, no competition concerns would arise as a result of the transaction.

5.2.2.2. Geographic market definition

(A) The Notifying Party’s view

(53) The Notifying Party submits that, in line with precedents, the market for bitumen should be national. However, the Notifying Party also notes that the exact geographic market definition can be left open as the Transaction will not result in any competition issues due to the vertical relationship between bitumen and asphalt.58

(B) Commission precedents

(54) In its past practice, the Commission has assessed national markets for the supply of bitumen and considered whether the geographical scope of bitumen supply could be narrower than national, without ever concluding on the market definition.59 In addition, the Commission has considered whether the geographic scope of bitumen markets could be radius-based, pointing to radii of 200-300 km and 400-500 km.60

(C) The Commission’s assessment

(55) In the present case, the Target sells bitumen in Norway over a distance of up to 600 km.61 The market investigation has not provided any indications that would speak against defining bitumen markets in this case in line with the Commission's findings in previous cases. In any event, for the purpose of this decision the exact scope of the geographic market can be left open, as the Transaction would not give rise to any competition concerns in this regard, irrespective of the exact market definition.

5.2.3. Asphalt

5.2.3.1. Product market definition

(56) Asphalt is used for surfacing roads, car parks, footpath pavements, airport runways and other sites. As asphalt is produced by heating but it may also be produced at lower temperatures as so-called half-warm mix or cold mix asphalt, which is generally done by heating the asphalt mix with steam or adding chemicals to the asphalt mix. Regardless of the production temperature, all asphalt is used for generally similar paving purposes. Warm asphalt mix is more durable than half-warm mix, which is in turn more durable than cold mix. The vast majority (around 90%) of all asphalt produced and used in paving in the countries affected by the Transaction is warm mix.62 Asphalt is 100% recyclable and because of the increased focus on the circular economy, the share of recycled asphalt has been increasing over the recent years.63 Asphalt can be produced in a fixed plant or in a mobile plant, which can change location several times a year.64 Most suppliers are vertically integrated with in-house paving operations,65 and asphalt is used exclusively for paving.66

(A) The Notifying Party’s view

(57) The Notifying Party submits that, with a single exception, all of the Parties’ and their competitors’ asphalt plants produce warm asphalt in all of the horizontally and vertically affected markets and therefore the distinction between warm, half- warm and cold mix asphalt is irrelevant.67

(58) The Notifying Party further submits that mobile plants are usually sent to a particular location for specific paving projects, for which competition takes place before the plant is moved.68 As mobile plants produce asphalt almost exclusively for captive use, they do not in actuality compete with fixed plants in asphalt production.69

(59) As regards the link between asphalt and paving, the Notifying Party considers that paving has indeed a strong vertical link to the upstream market of production and sale of asphalt. In the countries affected by the Transaction, there is a high degree of vertical integration between the production of asphalt and paving. In addition to the Parties, many notable players in Norway and Sweden such as NCC, Skanska, Svevia, Sandahls and Veidekke operate on both levels and source most or at least a significant amount of their asphalt internally.70 Nonetheless, the Parties and other notable asphalt producers also sell significant amounts of asphalt to external customers such as independent, including some independent paving contractors. As such independent paving operators exist and asphalt is sold to them regularly, the Notifying Party considers that asphalt and paving form two separate markets.71

(B) Commission precedents

(60) In past decisions, the Commission has consistently found that the production and sale of asphalt constitutes a distinct product market without further subdivision into warm, half-warm and cold mix asphalt.72 Likewise, past decisions have consistently found that asphalt constitutes a distinct product market, separate from paving.73

(61) The Commission has not previously assessed the use of mobile plants, since the Commission’s previous cases only related to Member States in which mobile plants are not used.

(C) The Commission’s assessment

(62) Given that the asphalt produced in all but one of the horizontally and vertically affected markets is warm asphalt, there is no need to distinguish between warm, half-warm and cold mix in this case. In other words asphalt in this case means warm asphalt and is the sole focus of the assessment.

(63) As regards the question whether asphalt and paving should constitute one combined market or, on the contrary, asphalt and paving should form separate markets, the market investigation confirmed that there are a number of independent paving operators, mostly small firms in big metropolitan areas.74 The majority of respondents also submitted that although the majority of the asphalt is produced for captive use, some asphalt is sold on the external market.75 Furthermore, detailed catchment area data reveals that significant amounts of asphalt are sold externally.76 As asphalt is sold regularly between buyers and sellers, there is demand for asphalt separate from demand for paving works that include captive asphalt production. Separate demand means that asphalt is a product separate from paving and thus forms a product market distinct from the market for paving.77

(64) The Notifying Party also made the argument that mobile plants should be excluded from the product market definition. In this regard, the market investigation revealed that mobile plants are not always an alternative to fixed plants. Whether or not they are an alternative to customers depends on the actual location even within a country. Therefore the Commission will assess this question in the geographic market definition in Section 5.2.3.2. The Commission notes, however, that the Notifying Party’s argument that asphalt production in mobile plants is purely captive does not justify excluding asphalt produced in mobile plants from the product market. Captive production by a mobile plant is not different from captive production by a fixed plant and the Notifying Party does not argue that captive production should be excluded per se. On the contrary, the Notifying Party considers that market shares based on the combined merchant and captive production are a better indicator of market power than market shares based only on merchant sales, which is not consistent with the view that production by mobile plants should be excluded from the market.78

(65) On the basis of the above, for the purposes of the present decision, the Commission considers that asphalt is a market separate from paving. The Commission does not distinguish between warm, half-warm and cold mix asphalt in this case as practically the only type of asphalt that matters for the competitive assessment is warm asphalt. The issue of mobile plants is taken into account in the geographic market definition as they can only be a viable customer choice in certain areas.

5.2.3.2 Geographic market definition

(A) The Notifying Party’s view

(66) The Notifying Party submits that asphalt is produced by heating and as a result it is perishable because it is best laid before it cools down and hardens. In practice this implies that it has to be laid within 2-3 hours of production, which limits the transport time to 1–2 hours.79

(67) Consequently, the Notifying Party considers that, in line with precedents, the relevant geographic market is local in scope and correspond to the catchment area of each asphalt plant.80

(68) Just like in the case of aggregates, the Notifying Party is of the view that the size of the geographic market varies to a certain extent by country and by region.81 In general, transport distances tend to be shorter in urban areas and longer in sparsely populated areas.82 In suitable regions, namely in Northern Norway, asphalt can also be transported by boat occasionally. Boats can transport larger amounts than trucks because the increased volume makes it easier to keep the asphalt warm, which in turn reduces its perishability. Thus, asphalt can be transported further by boat than by truck.83

(69) Based on the share of the Parties’ asphalt sales to different distances the Notifying Party considers that the most appropriate geographic market is a 50 km radius around the asphalt plants but notes that a wider radius could be more appropriate in sparsely populated areas.84 For example, based on internal estimates, in Sweden [60-70]% of asphalt produced by Peab is used within a radius of 25 km of the asphalt plant, [80-90]% is used within a radius 50 km and [90-100]% is used within 80 km from the plant. The corresponding figures of the Target are as follows: [20-30]% of the asphalt it produced is used within a radius of 25 km, [70-80] % of its production is used within a radius of 50 km and [90-100]% is used within a radius of 80 km.85

(70) The Notifying Party also suggests that radiuses of 40 km and 80 km can also be used as an alternative but considers that radiuses smaller or larger than these are not plausible. 86 Further, in the case of boat transport in Northern Norway, the transport distance can be 250 km.87

(B) Commission precedents

(71) In previous decisions, the radius of catchment areas that comprised the relevant geographic market varied between 25 km and 100 km depending on the circumstances.88 In line with the Notifying Party’s view, these precedents confirm that asphalt is a perishable product which needs to be transported in special heated containers to prevent it from hardening before it can be laid.

(72) In the most recent Holcim/Lafarge case that concerned the United Kingdom, the Commission retained a radius of 40 km around the asphalt facility.89

(C) The Commission’s assessment

(73) In line with the precedents and the Notifying Parties’ view, the market investigation confirmed that asphalt is perishable and needs to be laid within a few hours of production.90 For example, a competitor observed that “The driving distance combined with the driving time determines the maximum distance to transport the asphalt from production facility’s to paving site. Mixed asphalt has a minimum temperature that defines if you can pave the material or not.”91

(74) Given the perishable nature of asphalt, the definition of the relevant geographic market revolves around the appropriate radius of the catchment area within which most of the competition takes place. In this regard customers indicated that they source close to 100 % of their asphalt within a radius of 50 km from their paving projects,92 while 5 out of 7 competitors submitted that they sell 85%-100% of their asphalt within this radius.93 Thus, most of the competitive interactions between competitors with fixed plants in Norway and Sweden take place within a radius of 50 km from the asphalt plant.

(75) However, the Commission notes that two competitors indicated that they sell 25% and 30 % of their asphalt outside the radius of 50 km but within a radius of 80 km.94 Furthermore, another of the Parties’ competitors submitted that there are few asphalt plants in the north of Norway and thus distances can be larger.95 These facts suggest that in sparsely populated rural areas the appropriate size of the geographic market may be larger than a radius of 50km around the plant and rather correspond to a radius of 80 km around the plant.

(76) The market investigation also confirmed that asphalt is transported by boat in northern Norway and therefore in that region the transport distances and the geographic market can be larger.96 Boats can transport larger amounts than trucks and the increased volume allows longer travel distances97 because it is easier to keep larger volumes warm.

(77) Mobile asphalt plants are also relevant in the systematic identification of competitive constraints the Parties face. In this regard the market investigation indicates that, unless there is no alternative, municipalities prefer fixed plants over mobile plants due to environmental concerns. The use of mobile plants leads to noise, dust and other types of pollution. Furthermore, fixed plants can use a much higher share of recycled asphalt than mobile plants. Consequently, in densely populated areas, where there are enough fixed plants and where issues such as dust and noise weigh more, mobile plants are not used. By contrast, mobile plants are used in less densely populated areas since in those areas environmental concerns weigh less and there is not always a fixed plant nearby. More specifically, responses to the market investigation indicated that mobile plants are considered as an alternative in northern Sweden and in the whole of Norway with the exception of metropolitan areas such as, for example, Oslo, Bergen, Stavanger and Trondheim. Within the regions where mobile plants are an alternative, they can be moved to any area within 10 to 30 days.98

(78) Although mobile plants are mainly used captively to support the asphalt supplier’s paving operations, there is nothing to prevent an owner of a mobile asphalt plant to deploy such a plant for merchant asphalt sales. Thus, if there is an opportunity to sell asphalt externally, mobile plants can represent additional constraints in these regions. Further, even when they are used captively, they may constrain other suppliers’ merchant sales indirectly.99

(79) Based on the above, the Commission will retain geographic markets with a radius of 50 km but will take into account regional differences in the competitive assessment as appropriate. These regional differences are as follows:

i.) in sparsely populated areas a radius of 80 km may be more appropriate;

ii.) in northern Norway boat transport is also an alternative that can result in a larger geographic market as boat transport allows larger volumes, which reduces perishability; and

iii.) in northern Sweden and in Norway outside the metropolitan areas, mobile asphalt plants can also be competitive constraints.

5.2.4. Paving (contract surfacing)

5.2.4.1. Product market definition

(A) The Notifying Party’s view

(80) The Notifying Party submits that, in line with the Commission’s previous decisions, paving of roads / contract surfacing constitutes one product market.100

(B) Commission precedents

(81) In previous decisions, the Commission has considered contract surfacing to be a relevant product market in itself, distinct from the materials used (namely aggregates and asphalt).101

(C) The Commission’s assessment

(82) As discussed in Section 5.2.3.1., paving is distinct from asphalt. Within paving, the market investigation indicated that standards and working methods differ on the basis of the surface to be paved (e.g. highways, roads, streets, pavements, parking lots, airport runways etc.) such that paving works paving works to be performed for one type of surface are not suitable to execute paving works for another type of surface.102 However, respondents also considered that most suppliers are capable of performing all kinds of paving works and that all suppliers are capable of performing most of the paving works.103 Consequently, the Commission considers that paving is a single, distinct product market.

5.2.4.2. Geographic market definition

(A) The Notifying Party’s view

(83) The Notifying Party considers that the paving market is national as all the major competitors on the paving market in Sweden and Norway are active on a national basis. The machinery and equipment used in paving can be moved around nationally if needed.

(B) Commission precedents

(84) In Holcim Lafarge, the Commission considered that the market for contract surfacing, i.e. paving, is national in scope.104 This finding was based on the fact that equipment for paving is mobile and can be moved around to the point of demand, that the asphalt input is sourced from the vicinity of the paving project and that the biggest paving players in the United Kingdom are all active nationally.105

(C) The Commission’s assessment

(85) A majority of both customers and competitors considered that paving players bid nationally and not only regionally.106 As bidding has substantial costs, it is unlikely that a firm would bid in a tender if it did not consider that it has a non- negligible chance of success. Consequently, the fact that bidding takes place nationally indicates that suppliers constrain each other in the entire EEA state concerned and not only in the region where they have equipment or employees. This would therefore be indicative of a national market. In the same vein, respondents to the market investigation were of the view that paving suppliers can bid competitively anywhere in the EEA state regardless of having equipment and employees in the area, even if they considered that local presence is an advantage.107 The Commission notes that having an advantage implies differentiation within the same market rather than separate markets.

(86) As regards the possibility of a market larger than national in scope, competitors considered that they would not be able to bid competitively in an EEA State where they are not present.108 Similarly, customers considered that paving companies from neighbouring countries cannot bid competitively without presence in their own Member State, in this case Sweden.109 Barriers include cultural differences, language and lack of contacts.110

(87) On the basis of the above, the Commission considers that, in line with precedents, the market for paving is national.

5.2.5. RMX

5.2.5.1. Product market definition

(A) The Notifying Party’s view

(88) The Notifying Party submits that, in line with the Commission’s precedents,

RMX constitutes a single product market.111

(B) Commission precedents

(89) The Commission has consistently considered RMX to constitute a single, distinct product market.112

(C) The Commission’s assessment

(90) RMX is homogenous and distinct from other types of building materials. Given the consistent past practice, which is in accordance with the Notifying Party’s view, the Commission considers that RMX is a single distinct product market without further subdivisions.

5.2.5.2. Geographic market definition

(A) The Notifying Party’s view

(91) The Notifying Party submits that the definition of a relevant geographic market for RMX is dependent on the fact that RMX is perishable over time, and can therefore only be transported up to a maximum distance.113 A second limiting factor is the question of economic viability of transport distances.114

(92) In the view of the Notifying Party, exact driving distances may vary from location to location. Distances may be larger compared other European states given the size of the countries relevant to the Transaction. Transport distances may also vary depending on the density of population.115 In less populated areas, distances tend to be longer. In urban areas on the other hand, there are more competing plants and traffic congestion, making the costs caused by longer transport distances a bigger disadvantage than in less populated areas. In urban areas, maximum distances for RMX therefore tend to be shorter.

(93) The Notifying Party submits that a clear majority of its RMX products are sold within a radius of 50 km or less. On average, its Finnish plants sell approximately [70-80]% of its products within an area of 25 km from the plant, but [50-60]% of its products outside a radius of 15 km116. Swedish and Norwegian RMX plants would sell close to [90-100]% of its products within a distance of 25 km, and [70-80]% within a radius of 15 km around a plant117. The Notifying Party estimates that maximum transportation distances for RMX are 100 km, and for some plants in Sweden up to 150 km.

(94) Based on this sale shares, the Notifying Party submits that a radius of 50 km around each plant can be used as the relevant geographic area for RMX, with a radius of 25 km as an alternative.118

(B) Commission precedents

(95) In past decisions, the Commission has considered that a relevant geographic market for RMX is a catchment area of a radius of 25 km around each plant119. However, the decision concerned markets located predominantly in France, Germany and the UK, and was partly based on the responses to the market investigation as well as arguments provided by the Notifying Party in the context of the Transaction in the respective countries.

(C) The Commission’s assessment

(96) The Commission considers that a plausible geographic market for RMX would be either 25 km or 50 km around each plant. Based on previous decisions, as well as information provided by the Notifying Party, a narrower catchment area would be the more likely alternative in urban and more densely populated areas. However, the Commission acknowledge the argument by the Notifying Party that in Finland, Norway and Sweden, transport distances depend highly on the specific region in question. In the northern and other rural regions, which are sparsely populated, a catchment area around of 25 km around each plant would likely underestimated the actual sales territory.

(97) However, the ultimate market definition can be left open for the assessment of the case. As the Target is not active in the RMX business120, no horizontal overlaps occur. Vertical relationships are considered in the context of a link with upstream aggregates businesses in all three countries. For the assessment of this specific case, applying a wider catchment area of 50 km is the more prudent approach.

(98) With respect to possible input foreclosure, the market shares on the respective aggregates markets upstream are decisive. However, those would not change under a narrower geographic market definition. On the other hand, the overall number of affected markets would decline, as fewer catchment areas would overlap as a radius of 25 km would be considered as catchment area for RMX.

(99) Downstream market shares would indeed matter for the assessment of possible customer foreclosure. However, customer foreclosure is not a concern in the context of the aggregates – RMX relation, as further explained in the competitive assessment section.

(100) For the purposes of the present decision, a wider catchment area will be used as general assumption, as it would allow for a more prudent analysis. The ultimate geographical market definition can be left open between catchment areas of 25 km and 50 km around each RMX site, as it would not change the outcome of the assessment.

5.2.6. Construction

5.2.6.1. Product market definition

(A) The Notifying Party’s view

(101) The Notifying Party submits that the market definition can be left open as the number of affected markets and the Notifying Party’s market share will remain roughly the same under all plausible market definitions.

(B) Commission precedents

(102) Construction has in the past been defined as the on-site construction or assembly of buildings and other structures and building engineering.

(103) In previous decisions, the Commission has considered the division of the construction market into three sub-segments: the construction of residential buildings (blocks of flats, single household buildings), the construction of non- residential buildings (industrial buildings, offices, shopping centres and hospitals) and the construction of infrastructure/civil engineering (roads, bridges, railroads, sewage systems).121 The Commission has, however, usually left the final market definition open. Within the segments of residential building, non-residential building and infrastructure building, a further segmentation has occasionally been made based on contract value.122

(104) The Commission also considered dividing the infrastructure construction / civil engineering segment into the construction of roads, the construction of bridges, the construction of tunnels and other infrastructure construction.123 However, in this case too, the Commission has left the final product market definition open.

(C) The Commission’s assessment

(105) The Parties do not have any horizontal overlap in construction as the Target is not active in construction. Peab’s share in construction stays below 30 % under any market definition that the Commission considers plausible in all three EEA states involved in the Transaction.124 Thus construction markets are of interest because they are the downstream leg of a vertical link involving aggregates in the upstream market. In these vertical relationships the competitive assessment is the same under any market definition that the Commission considers plausible.

(106) Consequently, for the purpose of the assessment of the Transaction, the exact market definition can be left open.

5.2.6.2. Geographic market definition

(A) The Notifying Party’s view

(107) The Notifying Party considers the market for construction to be national, and considers that the ultimate geographic market definition can be left open.

(B) Commission precedents

(108) In previous cases, the Commission has considered the market for construction works to be national, and potentially EEA-wide for certain types of construction works such as the construction of tunnels or bridges. However, geographic market definitions were ultimately left open.125

(C) The Commission’s assessment

(109) For the present case, the Commission considers the market for construction to be national or wider. Peab itself is active in construction in Finland, Sweden and Norway, which is also the case for Skanska. NCC and Veidekke have a presence in construction in both Norway and Sweden126. However, companies do not compete in all parts of the EEA, and market investigation provided no information on whether presence in the respective country is a perquisite for successfully competing for construction projects.

(110) For the assessment of the case, a geographic market of at least national is considered, as no concerns would occur under the narrower definitions.

5.2.7. Transport

5.2.7.1. Product market definition

(111) The Target owns a general dry cargo ship and a bulk carrier that operate in northern Norway127.

(A) The Notifying Party’s view

(112) The Notifying Party submits that transport business has a vertical relationship with its aggregations operations, as the vessels are to transport, inter alia, aggregates. However, the Notifying Party considers that the relevant product market can be left open as the relationship between aggregates and cargo shipping does not give rise to affected markets under any plausible market definitions or result in any competition issues.128

(B) Commission precedents

(113) In its previous decisions, the Commission defined a separate product market for short-sea container liner shipping, i.e. distinct from deep-sea container shipping, non-liner shipping and non-containerised shipping, such as bulk shipping.129

(114) Additionally, the Commission has recognised the need to consider vessel sizes and contract types when defining the relevant product market for vessels.130

(C) The Commission’s assessment

(115) Given that the Target only has one cargo ship and one bulk carrier ship, which carry, inter alia, some mineral aggregates, the Commission considers that the market definition can be left open as there are no conceivable competition concerns linked to these transport vessels.

5.2.7.2. Geographic market definition

(A) The Notifying Party’s view

(116) The Notifying Party submits information on the basis of a national market, and considers that the exact geographic market definition can be left open.131

(B) Commission precedents

(117) In previous decisions, the Commission has considered that smaller ships tend to focus on coastal/short-range trade, while larger ships tend to go long-range, which may be worldwide.132 Ultimately, the market definition was left open.

(C) The Commission’s assessment

(118) The ships in question are rather small,133 the geographic market is therefore smaller than worldwide. For the assessment of this case, the market definition can be left open. Possible vertical effects would origin from the link between the Target’s cargo ship business in northern Norway and the aggregates production of Peab. Combined market shares in aggregates stay below 30% in all local markets in Norway.134 Markets could therefore only become affected if market shares in cargo shipping would exceed 30%.

(119) On a national level, market shares are negligible below 2%. If markets would be defined regional, no links would occur, as Peab’s two quarries are located in central Norway in Verrabotn135 and in Jessheim near Oslo.136 Therefore, under an even more narrow market definition than national, upstream and downstream market would no longer fall into the same geographic area.

(120) Thus the Commission considers that the exact geographic market definition can be left open.

5.3. Competitive assessment

5.3.1. Market share methodology

(121) In the case of local markets defined as a catchment area around a plant or a quarry, obtaining reliable sales and volume data for each local competitor poses great challenges. Such data is not readily available and reliable data collection may not be possible. Thus, in previous cases,137 the Commission has relied on indirect estimation of market shares and proxies.

(122) Following the methodology used in previous cases, the market shares for catchment areas have been compiled as follows.138

· The size of the market (local demand) is computed as the product of consumption per capita in the relevant country and the population of the catchment area. A NASA population dataset has been used to estimate the size of the local market in terms of population.

· The Parties' combined sales attributed to each catchment area are all sales of the production site in the centre of the catchment area plus a share of the sales of each of the Parties' production sites with an overlapping catchment area, calculated based on the percentage of the overlap from the entire catchment area.

· The Parties’ local market share is calculated as these sales divided by the total estimated consumption for the relevant product in the catchment area.

· Unless otherwise stated, the sales market shares of competitors are estimated by allocating the market volume minus the Parties' volumes to each competitor in proportion to its production capacity shares in the area. The production capacity share of each competitor is calculated in relation to the total capacity of competitors in the area

(123) The Commission considers that this methodology is in line with precedents in this sector139 and provides the best available proxy given the challenges of data gathering. The Commission notes that because the total market size is proxied with per capita consumption and population data whereas the Parties’ sales are concrete sales figures, the market shares can sometimes exceed 100%, especially in more sparsely populated areas.

5.3.2. Overview of affected markets

(124) Table 1 below gives an overview of the product and country combinations in relation to which the Transaction gives rise to affected markets. A cell in a table does not necessarily correspond to a specific market as in many cases the markets are local. Thus one cell can refer to several markets, involving the same product(s) and the same EEA state.

Table 1 - overview of affected markets

Finland | Swe de n | Norway |

Horizontally affe cted marke ts | ||

aggregates | aggregates |

|

| asphalt | asphalt |

| paving |

|

Vertically affe cted marke ts | ||

| aggregates-asphalt | aggregates-asphalt |

aggregates-RMX | aggregates-RMX | aggregates-RMX |

aggregates – construction |

| aggregates – construction |

| asphalt – paving | asphalt – paving |

|

| bitumen – asphalt |

(125) The Commission notes that there are no affected markets in relation to transport, which would only concern Norway. The relationship would be between transport and aggregates as the Target’s boats transport some aggregates from time to time. As discussed in Section 5.2.7., combined market shares in aggregates stay below 30% in all local markets in Norway.140 Markets could therefore only become affected if market shares in cargo shipping would exceed 30%. If the cargo shipping market is national or wider, this would be wholly implausible as the Target has only two boats. If the cargo shipping market is local with a very small radius, the market share is still unlikely to exceed 30% and, in addition, the Target’s boats could not serve the catchment areas of Peab’s quarries. This is because Peab has only two quarries in Norway, one in Jessheim in southern Norway and one in Verrabotn in central Norway, whereas the Target’s boats operate in northern Norway.141

5.3.3. Finland

5.3.3.1. Horizontally affected markets

(A) Aggregates

(A.i) List of affected markets and market shares

(126) Overall, Peab currently has limited presence in the aggregates business in Finland. It operates three aggregates quarries located in the wider Forssa area in south-western Finland and in the wider Lahti area in the southeast.142

(127) The Target, on the other hand, is a well-established supplier of aggregates in Finland. It owns approximately 200 aggregates quarries, around half of which are currently operative.143

(128) Overlaps of catchment areas of the three quarries currently owned by the Notifying Party with a number of catchment areas around the YIT’s quarries give rise to 15 horizontally affected market in the Turku / Forssa / Uusimaa area. In addition, six market become vertically affected in the area of Lahti / Lappeenranta. The affected markets are listed in Tables 2 and Table 3 below.

Table 2 - horizontally affected aggregates markets in the Turku / Forssa / Uusima area

Catchment area | Peab | Target | Combined |

|

|

|

|

Forssa / Forssanporti | [5-10]% | [30-40]% | [40-50]% |

Forssa / Vuori | [5-10]% | [30-40]% | [40-50]% |

Humppila | [5-10]% | [20-30]% | [20-30]% |

Jokioinen, Mylly mäki | [5-10]% | [30-40]% | [30-40]% |

Jokioinen, Ripunkallio | [5-10]% | [30-40]% | [40-50]% |

Murronmaa | [0-5]% | [20-30]% | [30-40]% |

Nummensyrjä | [0-5]% | [20-30]% | [30-40]% |

Salo, Hiekkanummi | [0-5]% | [20-30]% | [30-40]% |

Somero, Matinmäki | [5-10]% | [30-40]% | [30-40]% |

Somero Sora-Heikkilä | [5-10]% | [30-40]% | [30-40]% |

Tammela, Penttilä | [0-5]% | [40-50]% | [40-50]% |

Vahva Sora | [0-5]% | [20-30]% | [20-30]% |

Tehdaspalsta | [0-5]% | [20-30]% | [30-40]% |

Hämeenlinna | [0-5]% | [20-30]% | [20-30]% |

Pusula | [0-5]% | [20-30]% | [20-30]% |

Source: Form CO, table 1, paragraph 80.

Table 3 - horizontally affected aggregates markets in the Lahti/Lappenrata area

Catchment area | Peab | Target | Combined |

|

|

|

|

Hämeenlinna | [0-5]% | [20-30]% | [20-30]% |

Hamina | [0-5]% | [20-30]% | [20-30]% |

Kotka | [0-5]% | [20-30]% | [20-30]% |

Lahti | [0-5]% | [20-30]% | [20-30]% |

Luumäki, Heimala | [0-5]% | [20-30]% | [20-30]% |

Ämmänäyräs | [0-5]% | [20-30]% | [20-30]% |

Source: Form CO, table 1, paragraph 80.

(129) A further segmentation of aggregates into crushed rock and gravel / sand would not substantially change that picture. In the Turku / Forssa / Uusimaa area, three more markets would be horizontally affected in that case (Pori, Söörmarkku, Ulvia), all with moderate market shares of well under 30%. In the Lahti / Lappeenranta area, three additional markets would become horizontally affected (Pernaja, Keltti 1, 2), all three with moderate market shares of below 30%. Also under such distinction, as shown in Table 4 and 5, combined market shares do not exceed [40-50]% in any affected areas, which is also the case for the combined market shares for the overall aggregates market.

Table 4 - market shares in horizontally affected aggregates markets separately for i) crushed rock and ii) gravel and sand

Catchment area | Crushed Rock | Gravel + Sand |

|

|

|

Forssa / Forssanporti144 | - | - |

Forssa / Vuori | [40-50]% | - |

Humppila | - | [30-40]% |

Jokioinen, Mylly mäki | - | [40-50]% |

Jokioinen, Ripunkallio | [30-40]% | - |

Murronmaa | - | [40-50]% |

Nummensyrjä145 | - | - |

Salo, Hiekkanummi | - | [30-40]% |

Somero, Matinmäki | - | [40-50]% |

Somero Sora-Heikkilä | - | [40-50]% |

Tammela, Penttilä | [40-50]% | - |

Vahva Sora | [10-20]% | [20-30]% |

Tehdaspalsta | - | [40-50]% |

Hämeenlinna | [20-30]% | - |

Pulsua | - | [20-30]% |

Pori | [20-30]% | - |

Söörmarkku | [20-30]% | - |

Ulvila | [20-30]% | - |

Source: Form CO, Annex 7, Table 67.

Table 5 - market shares in horizontally affected aggregates markets in the Lahti / Lappeenranta area separately for i) crushed rock and ii) gravel and sand

Catchment area | Crushed Rock | Gravel + Sand |

|

|

|

Hämeenlinna | [20-30]% | - |

Hamina | [40-50]% | [5-10]% |

Kotka | [40-50]% | - |

Lahti | [20-30]% | - |

Luumäki, Heimala | [30-40]% | - |

Ämmänäyräs | - | [10-20]% |

Pernaja | [20-30]% | - |

Kouvola, Keltti 1 | [20-30]% | - |

Kouvola, Keltti 2 | [20-30]% | - |

Source: Form CO, Annex 7, Table 67.

(130) Tables 4 and 5 show that in most quarries, either crushed rock or gravel / sand is produced. In few catchment areas, market shares in segments may be lower than in the overall aggregates market. This is because in Tables 2 and 3, production of all aggregates by both parties within the catchment area is taken into account. In Tables 4 and 5, only all production by the parties of the specific type of aggregates that is produced in the respective quarry is analysed.

(A.ii) The Notifying Party's view

(131) The Notifying Party considers that the Transaction would have no impact on the aggregates markets in question. First, an increase of the Parties’ combined market shares would only be nominal, as the Notifying Party’s production is used fully captively and therefore would not put competitive pressure on the market. Production will remain for internal use only post Transaction.146

(132) Second, the combined market shares in the local areas would still remain moderate, and the Notifying Party would still meet plenty of competition in all markets.147

(A.iii) The Commission’s assessment (A.iii.a) Common characteristics of all markets

(133) Market shares as discussed in this section comprise both captive and non-captive production. As discussed under 5.3.1, also volumes that are not sold on the market, but used internally by companies with an integrated downstream business, are considered. For the purposes of the assessment, no distinction is therefore made between captive and non-captive sales, despite the Notifying Party’s argument that almost the entire production of aggregates in its three quarries would be used internally148. This is because also internally used volumes reflect the market power of a specific company. The Notifying Party also appears to acknowledge that switching between internal and external sales is relatively easy149, and that captively used production would reflect the capability to participate in the market or extent their sales.150

(134) Aggregates are a rather homogeneous product, and as evidenced by the market investigation, costs of switching between suppliers are generally moderate. A majority of customers responding to the investigation indicate that they can easily switch to other companies than the ones they source from151. The only reported barriers to switching pertain to different price levels or lack availability, and only to a minor degree on product differentiation connected to respective specific suppliers152. All undertakings that have responded to the market investigation source from more than one aggregates supplier153. Therefore, the presence of actual or potential alternative aggregates suppliers within a market exert competitive pressure on aggregates companies, as customers can switch when prices are raised unilaterally.

(135) Production of aggregates in Finland is generally limited due to the fact that sourcing aggregates requires a permit, which is not easy to obtain because of environmental requirements. Respondents to the market investigation consistently state that acquiring a permit could take several years, a factor that constrains capacity expansion.154 Therefore, barriers to enter the market or to expand production are not negligible. Even though the costs for opening a new or additional quarry are moderate155, the time required to get a permit makes a timely entry into any market to respond to increased demand in that market unlikely, which may lead to capacity constraints.

(136) Responses from the market investigation indicated that, while there is not a general capacity problem regarding aggregates in Finland, there are regional differences156. This was further developed during calls with aggregates competitors. One of the main competitors of YIT confirmed that there would be significant excess capacities in rural Finland, for example in the Forssa area, where lots of excess capacities exist157. By contrast, access to aggregates would be more difficult in metropolitan areas, such as Helsinki.158

(137) Despite a more limited availability in metropolitan areas, as highlighted by the same competitor, in such areas however aggregates could not only be sourced from quarries, but also as by-product from construction sites, such as construction of roads, metro lines or tunnels. Such aggregates would add another 10% to 40% to the overall market of aggregates159. As these volumes are linked to specific construction projects, the availability of aggregates in metropolitan areas would be subject to significant variations. Therefore, in some years, demand for aggregates would outstrip capacities, including in Helsinki and other metropolitan areas.160

(A.iii.b) Turku / Forssa / Uusimaa area

(138) The Commission considers that there are two main reasons why the Transaction will not lead to higher prices for aggregates in the Turku / Forssa / Uusimaa area. First, the Transaction does not change the competitive structure of the market, as merged entity would not have a significantly stronger position compared to situation pre-transaction. Increments remain close to or below [5-10]% in all of the areas. This was further substantiated by replies to the market investigation. As an illustration, a competitor in aggregates production in Finland expressly confirmed the Transaction would not have material effects on the market structure regarding aggregates in the Forssa / Turku / Uusimaa area161.

(139) The point that the Transaction would not change the market structure was further substantiated in the market investigation. None of the respondents stated that Peab would currently exercise significant or even some competitive pressure on YIT, while customers rather stated that it would not exercise any significant pressure (a majority stated it would not be able to answer this question)162. Therefore, no significant competitive force would leave the market due to the Transaction.

(140) Second, the merged entity would still be constrained by other players. This is illustrated in the first place by the fact its combined market shares remain below 45% in all markets, and well below that figure in most of the regions. As switching costs for aggregates customers are generally moderate, the presence of alternative suppliers leave customers with the option of sourcing from other companies. In the second place, as Table 6 shows, the competitor base consists of both small players as well as larger, integrated competitors, in line with overall market structures within Finland generally.

(141) The fragmentation of the Finnish market for aggregates is illustrated by the fact that, in 2013, there were more than 6000 permits across the country for quarrying various kind of grounds. 4000 of these quarries were producing gravel and sand, 1800 rock, and 200 other types of grounds163. Overall, around one third of all aggregates in the wider Turku / Forssa / Uusimaa area are produced by smaller suppliers.

Table 6 - estimated market shares of aggregates competitors in the Turkuu / Forssa / Uusima area

Competitor | Estimated market shares164 |

|

|

Rudus (CRH) | [10-20]% |

Hämeen Kuljetus | [5-10]% |

Destia | [5-10]% |

NCC | [5-10]% |

TerraWise | [5-10]% |

Palovuoren Kivi | [5-10]% |

Kiertomaa | [5-10]% |

Läänin Kuljetus | [5-10]% |

Hämeen kuljetus | [5-10]% |

Others | approx. [30-40]% |

Source: Form CO, Table 16

(A.iii.c) Lahti / Lappeenranta area

(142) Similar arguments as stated above are valid for the assessment of the Lahti / Lappeenranta area. First, the Transaction would not change the structure of competition in the area compared to the situation pre-transaction. Increments in all markets are close to or below [0-5]%. Therefore, Peab would not gain a stronger position than YIT currently has. As the market investigation confirmed, Peab currently does not form a significant competitive constrain on YIT165. Therefore, no significant competitor would be eliminated due to the Transaction.

(143) Second, the merged entity would still face significant competition, as its modest market shares remain below 30% in the Lathi / Lappeenranta area below 30%. As switching costs for aggregates customers are generally moderate, the presence of alternative suppliers leave customers with the option of sourcing from other companies. As switching costs between aggregates suppliers are generally moderate, the merged entity will not be in a position to raise prices unilaterally.

(144) Also in the Lahti / Lappeenranta area, the merged entity faces competition from a number of competitors. The competitor base consists partly of bigger, integrated companies such as Rudus, Destia or NCC. In addition to this, a large number of small suppliers with a market share below 5% account for around [40-50]% of all aggregates supply in the region, as Table 7 shows.

Table 7 - estimated market shares of aggregates competitors in the Lahti / Lappeenranta area

Competitor | Estimated market shares166 |

|

|

Rudus (CRH) | [20-30]% |

Savon Kuljetus | [10-20]% |

Destia | [5-10]% |

NCC | [5-10]% |

Tykkimäki | [5-10]% |

Turpeinen | [5-10]% |

Others | approx. [40-50]% |

Source: Form CO, Table 17.

(A.iii.d) Conclusion

(145) Based on the above the Commission considers that the Transaction will not lead to a significant impediment of effective competition due to unilateral effects in the markets for aggregates in Finland.

5.3.3.2. Vertically affected markets

(A) Aggregates – RMX

(A.i) List of affected markets and market shares

(146) The Notifying party has a limited presence in the aggregates business in Finland. It operates three aggregates quarries located in the wider Forssa area in south- western Finland and in the wider Lahti area in the southeast.167 However, the Notifying Party is well active in the production of RMX in Finland and operates several RMX plants in the south and the west of the country168.

(147) The Target, on the other hand, has no RMX production169, but is very strong in the aggregates business. It owns approximately 200 aggregates quarries, around half of which are currently operative.170

(148) Potential concerns result therefore from the fact that the merged entity would reach a strong presence both in upstream aggregates and downstream RMX markets. The Transaction gives rise to a number of vertically affected markets, as catchment areas around the YIT’s quarries overlap with the catchment areas of Peab’s RMX plants. In given local markets, combined market shares exceed 30% either or both upstream and / or downstream. Concerns arise therefore in the context of both input foreclosure and customer foreclosure.

(149) Lists with affected markets are presented in the respective sections A.iii.a (input foreclosure) and A.iii.b (customer foreclosure).

(A.ii) The Notifying Party's view

(150) The Notifying Party considers that it would not have the ability to engage in input foreclosure, as RMX competitors would still have the opportunity to source from a large number of other suppliers in all areas. An obvious lack of ability would also eliminate any incentive to engage in such a strategy.171

(151) As for customer foreclosure, the Notifying Party submits that aggregates are a highly versatile product with many end-uses. As aggregates competitors would still be able to sell to other RMX manufacturers, as well as construction, asphalt or mortar companies, there would be no ability for customer foreclosure.172

(A.iii) The Commission’s assessment (A.iii.a) Input foreclosure

(152) The Transaction gives rise to a number of vertically affected markets with a combined upstream market share of more than 30% and an overlap with the catchment area of one of the Notifying Party's RMX plants. All these markets, listed in Table 8, are broadly located in the wider Turku / Forssa / Uusimaa area.

Table 8 - upstreamaggregates markets with combined market shares above 30%

Catchment area | Combinedmarket shares in upstream aggregates | Overlapping RMX plants173 |

|

|

|

Forssa, Forssanportti | [40-50]% | Loimaa, Salo, Ylöjärvi, Tampere, Naantali, Lieto, Lohja, Kirkkonummi, Espoo |

Forssa, Vuori | [40-50]% | Loimaa, Salo, Ylöjarvi, Lieto, Tampere, Naantali, Lohja, Kirkkonummi, Espoo |

Jokioinen, Myllymäki | [30-40]% | Loimaa, Ylöjärvi, Tampere, Lieto, Naantali, Salo, Lohja, Espoo |

Jokioinen, Ripunkallio | [40-50]% | Loimaa, Salo, Ylöjärvi, Lieto, Naantali, Tampere, Lohja, Kirkkonummi, Espoo |

Salo, Hiekkanummi | [30-40]% | Lohja, Salo, Loimaa, Lieto, Naantali, Kirkkonummi, Espoo, Helsinki |

Somero, Matinmäki | [30-40]% | Lohja, Loimaa, Salo, Lieto, Naantali, Kirkkonummi, Espoo, Helsinki |

Somero, Sora-Heikkilä | [30-40]% | Lohja, Loimaa, Salo, Lieto, Naantali, Kirkkonummi, Espoo, Helsinki |

Tammela, Pentt | [40-50]% | Loimaa, Salo, Ylöjärvi, Tampere, Naantali, Lieto, Kirkkonummi, Espoo, Helsinki |

Source: Form CO, Table 169, paragraph 702.

(153) RMX can be generally produced using both types of aggregates, crushed rock or gravel and sand. Whereas gravel / sand is generally the preferred for the production of RMX174, it is more and more replaced by crushed rock175. The market investigation confirmed that it is generally possible to use both crushed rock and gravel / sand for RMX production176.

(154) For the assessment of input foreclosure, the conclusion would remain the same even if a product segmentation between crushed rock and gravel / sand was made. A segmentation would indeed give rise to two additional affected markets in Murronmaa and Humppila. However, as Table 9 shows, also with a segmentation in crushed rock and gravel / sand, combined market shares of the merged entity would remain in similar ranges compared to overall combined markets shares and remain below [40-50]% in all of the markets.

Table 9 - upstream aggregates markets with a combined market share of more than 30% separately for i) crushed rock and ii) gravel and sand

Catchment area | Crushed Rock | Gravel + Sand |

|

|

|

Forssa, Forssanportti177 | - | - |

Forssa, Vuori | [40-50]% | [30-40]% |

Humppila, Kair | - | [30-40]% |

Jokioinen, Myllymäki | - | [40-50]% |

Jokioinen, Ripunkallio | [30-40]% | - |