Commission, August 20, 2019, No M.9332

EUROPEAN COMMISSION

Judgment

ERICSSON / KATHREIN ANTENNA AND FILTER ASSETS

Subject: Case M.9332 - ERICSSON / KATHREIN ANTENNA AND FILTER ASSETS

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 15 July 2019, the European Commission received notification of a proposed concentration pursuant to Article 4 and following a referral pursuant to Article 4(5) of the Merger Regulation by which Telefonaktiebolaget LM Ericsson (publ) (“Ericsson” or “Notifying Party”, Sweden) acquires within the meaning of Article 3(1)(b) of the Merger Regulation sole control of parts of Kathrein SE (“Kathrein Group”, Germany) (the “Transaction”) by way of purchase of assets. The Transaction only concerns Kathrein Group’s business in passive antennas and filters as components for mobile network equipment (“Kathrein” or “Target Business”).3 Ericsson and Kathrein Group are collectively referred to as the “Parties”.

1. THE PARTIES

(2) Ericsson is a public company headquartered in Stockholm, Sweden. It is a global provider of network equipment and software, as well as services for network and business operations. Ericsson’s business is divided into four segments: “Network solutions”, “Digital Services”, “Managed Services”, and “Other”.

(3) Kathrein Group, headquartered in Rosenheim, Germany, is a provider of communication technologies solutions. Kathrein divides its activities in: ”Business Solutions in communication technology”, “Mobile Communication”, ”Satellite Reception”, “Special Communication”, and “Broadcast”.

2.THE TRANSACTION

(4) Under an Umbrella Asset Purchase Agreement entered into on 25 February 2019, Ericsson will acquire Kathrein Group’s antenna and filter assets as components in mobile network equipment, belonging to Kathrein Group’s wider “Mobile Communication” business segment.4 The Transaction will be carried out through the acquisition of various assets (e.g. tangible fixed assets, all inventory, all intangible assets and intangible fixed assets) and the client base representing Kathrein Group’s antenna and filter products business. Therefore, the Transaction consists of the acquisition of sole control by Ericsson over part of Kathrein Group within the meaning of Article 3(1)(b) of the Merger Regulation.

3. EU DIMENSION

(5) The Transaction does not have a Union dimension within the meaning of Article 1(2) or Article 1(3) of the Merger Regulation.

(6) Nonetheless, the Transaction fulfils the two conditions set out in Article 4(5) of the Merger Regulation since it is a concentration within the meaning of Article 3 of the Merger Regulation and it is capable of being reviewed under the national competition laws of at least three Member States, namely Cyprus, Estonia, Germany, the Netherlands and, potentially, Austria.

(7) On 19 March 2019, the Notifying Party informed the Commission by means of a reasoned submission that the Transaction should be examined by the Commission pursuant to Article 4(5) of the Merger Regulation. A copy of that submission was transmitted to the Member States on 19 March 2019.

(8) As none of the Member States competent to review the Transaction expressed its disagreement within 15 working days as regards the request to refer the case to the Commission, the Transaction is deemed to have a Union dimension pursuant to Article 4(5) of the Merger Regulation.

(9) Therefore, on 10 April 2019, the Commission informed the Parties and Member States that the Transaction was deemed to have a Union dimension and would have to be notified to the Commission.

4.RELEVANT MARKETS

4.1.Introduction

(10) Ericsson supplies mobile network equipment, one part of which is Radio Access Network (“RAN”) equipment. RAN equipment establishes a connection between individual mobile devices and the core network through radio connections. Notable components of the RAN equipment are antennas, filters, radio units5, baseband6, and cabling. Ericsson manufactures baseband and radio units which are the key components of the RAN equipment that it supplies to mobile network operators (“MNOs”).

(11) Kathrein manufactures antennas and filters and supplies them directly to MNOs or to RAN equipment suppliers, such as Ericsson, which resell them to MNOs as complementary components of the RAN equipment.

4.2.RAN equipment

4.2.1.Product market definition

4.2.1.1.Commission precedents

(12) In Nokia/Alcatel-Lucent7, Ericsson/Nortel Group8, and Nokia Siemens Networks/Motorola Network Business9, the Commission distinguished between (i) RAN equipment, (ii) Core Network Systems (“CNS”)10 and (iii) network-related services.

(13) With regard to RAN equipment, in Nokia/Alcatel-Lucent, the Commission examined whether a potential market for RAN equipment could be sub-segmented as follows: (i) by technology standards (2G/3G/4G)11, (ii) between macro-cells12 and small cells13 and (iii) Single RAN ("SRAN") equipment14 as a potential separate market segment. Ultimately, the Commission left the precise market definition open.

4.2.1.2. Notifying Party’s views

(14) The Notifying Party refers to the Commission precedents listed at paragraphs (12)- (13).

(15) With regard to the possible sub-segmentation of the market for RAN equipment by technology standards, the Notifying Party submits that current RAN equipment supports multiple technology standards and further segmentation is not justified.15 More generally, with regard to technology standards, the Notifying Party explains that the share of 2G and 3G has been steadily declining in the past few years while 4G is increasing and 5G has been slowly emerging since 2018.16 The Notifying Party explains that, at the present date, 5G has not yet been commercially launched. Nevertheless, the Notifying Party considers that, since 2017 and 2018, 5G mobile network technology is no longer in a pure development phase.17

(16) With regard to the possible sub-segmentation between small cells and macro cells, the Notifying Party considers that such distinction is not justified. In the Notifying Party’s view, the main difference between macro cell RAN equipment and small cell RAN equipment lies in the output power. While small cell RAN equipment can provide output for a smaller radius (normally between 10 m to 100 m), the radius of macro cell RAN equipment is significantly larger (normally up to 20 km or more). The Notifying Party explains that small cells are generally used if the macro cells’ capacity is insufficient and needs to be complemented to deploy a mobile network, for instance during time slots with heavy data traffic. Small cells thus can provide hot spots for users such that users receive a better signal in certain areas.18

(17) With regard to the potential separate segment for SRAN equipment, the Notifying Party submits that such segmentation would no longer be relevant, as currently all RAN equipment supports multiple technology standards (see paragraph (15)).19 Therefore, in the Notifying Party's view, SRAN equipment forms part of the overall market for RAN equipment.

(18) With regard to new solutions emerging in the industry, such as virtualised RAN solutions20, the Notifying Party submits that there are virtually no (or very few)current commercial deployments in which the full RAN equipment is virtualised. Therefore, according to the Notifying Party virtualised RAN equipment does not have any relevance to assess the Transaction.21

(19) In the Notifying Party’s view, the Commission does not have to conclude on the exact product market definition with regard to RAN equipment as the Transaction does not give rise to competitive concerns under any plausible market definition.22

4.2.1.3.Commission’s assessment

(20) The market investigation provides mixed results as to whether segmenting the RAN equipment market is appropriate.23

(21) Several respondents explain that RAN equipment suppliers are generally active across all possible segments. With regard to a possible segmentation by technology standards, respondents explain that the same equipment can be used across different technologies, although several respondents expect 5G technology to require equipment different from legacy technologies. Respondents did not express any firm views as regards as possible segment for SRAN, which the Commission understands may no longer be relevant given that RAN equipment supports multiple technology standards. A number of market participants consider that the segmentation between small cells and macro cells is still relevant.

(22) As regards virtualised RAN solutions, the results of the market investigation strongly suggest that they belong to the same product market as traditional RAN solutions.24 Respondents explain that while virtualised RAN solutions use very different technologies from traditional RAN solutions, they perform the same functions as traditional RAN solutions. Moreover, respondents confirm that virtualised RAN solutions are a new trend in the market which may gain more relevance in the future.

(23) Moreover, as explained in more detail in Section 4.3 and 4.4 below, the results of the market investigation indicate that passive antennas, antenna modules and filters should be considered to belong to markets distinct from the market for other RAN equipment components and that the same finding may potentially apply to active antennas. Accordingly, the notion of 'RAN equipment' used in this section and in the remainder of this decision, unless specified otherwise, excludes passive antennas, active antennas, antenna modules (see Section 4.3.1), and filters (see Section 4.4.1).

(24) With the exception of the segmentation mentioned in the previous paragraph, for the purpose of this decision, the exact product market definition for RAN equipment can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible product market definition.

4.2.2.Geographic market definition

4.2.2.1.Commission precedents

(25) In Nokia/Alcatel-Lucent,25 the Commission considered that the relevant geographic market for RAN equipment is at least EEA-wide, if not global. The Commission ultimately left the exact geographic market definition open.

4.2.2.2.Notifying Party’s views

(26) The Notifying Party submits that the relevant geographic market is at least EEA- wide if not worldwide. In the Notifying Party’s view, this is because (i) mobile network equipment is based on international standards, (ii) there are no regulatory barriers, (iii) transportation costs are low, and consequently (iv) suppliers and customers generally supply and source RAN equipment on a worldwide basis.26

4.2.2.3.Commission’s assessment

(27) A majority of respondents to the market investigation indicate that they supply and/or procure RAN equipment on a global basis, with the main RAN equipment suppliers based in Europe, USA and Asia.27

(28) In any event, for the purpose of this decision, the exact geographic market definition for the supply of filters can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market regardless of whether the market is EEA-wide or global.

4.3.Antennas

(29) Antennas function as a converter between two kinds of electromagnetic waves, cable bounded waves and free space waves. They link the users’ equipment and the base transceiver station in the RAN. An antenna covers a specific area which depends on the antenna's capacity.

(30) There are different types of antennas, depending on the number of ports and on whether the antenna is “passive”, “active” or hybrid.

(31) The number of ports of an antenna determines the number of signals that can be received and transmitted by the antenna, i.e. the number of frequency bands that can be used. A single-band antenna is a 2-port antenna which supports the usage of one frequency band. Multi-band antennas combine various bands and functions in one antenna (e.g. a 4-port antenna supports two frequency bands, a 6-port antenna supports three frequency bands etc.).28

(32) Passive antennas are connected to other components of the RAN equipment (e.g., radio, baseband) via a high frequency coax cable (a “feeder”) which transports the analogue signal. The use of a feeder with passive antennas entails some signal loss from the radio unit to the passive antenna due to the characteristics of radio waves and the transmission of analogue signals.29

(33) Active antennas integrate an antenna module and a radio component in the same physical unit. Antenna modules are a specific kind of passive antenna exclusively designed to be used in an active antenna as they have provisions for mechanical mounting and for an electrical connection of a radio module in order to create an active antenna product.30 In an active antenna, the antenna module and the radio component are thus mechanically and electrically integrated to avoid signal loss. The Notifying Party explains that signal loss is also prevented in active antennas due to the existence of a digital connection between the radio and baseband, irrespective of the distance between them. However, the housing for active antennas is larger and heavier than for passive antennas and therefore its installation is more complex.31

(34) According to the Notifying Party, capacity requirements have changed due to the development from 2G/3G over 4G to 5G mobile networks. While passive antennas will still be used in 5G networks, the Notifying Party expects an increasing demand by MNOs for active antennas in order to increase capacity and improve the performance of 5G networks.32

(35) There are two types of active antennas: (i) semi-active antennas and (ii) advanced antenna systems ("AAS"), also called massive multiple-in multiple-out (“massive MIMO” or “mMIMO”). In a semi-active antenna, conventional radio units are built into an antenna housing. In an AAS antenna, the radio unit is physically integrated with the antenna. The Notifying Party explains that this is necessary due to the large number of antenna branches (16 up to hundreds) used to provide the ability to concentrate a narrow radio beam to individual or multiple users and the requirement of their synchronisation. The Notifying Party submits that AAS active antennas still represent a small proportion of sales but their importance is expected to rapidly increase with the evolution of 5G networks. 33

(36) In addition, there are hybrid antennas that can be described as a mounting solution where the antenna manufacturer has devised a way of mounting an AAS active antenna on top of one of its passive antennas, behind a shroud that has the same profile and looks as the passive antenna.34

(37) In light of the foregoing, three possible segmentations of the antenna market can be considered: (i) single-band and various types of multi-band antennas (e.g. 4-port, 6- port etc. antennas), (ii) passive antennas and antenna modules for active antennas, and (iii) passive antennas and active antennas. Active antennas (and antenna modules integrated therein) may also be segmented between semi-active antennas and AAS (or mMIMO) antennas.

4.3.1.Product market definition

4.3.1.1. Notifying Party’s views

(38) In the Notifying Party’s view, antennas belong to a separate product market, distinct from other RAN equipment components.35

(39) As regards the possible distinction between single- and multiband antennas, the Notifying Party explains that, irrespective of the number of ports, passive antennas fulfil the same function and are thus substitutable.36 In the Notifying Party’s view, MNOs can achieve the same functionality by using two or more antennas with a low number of ports instead of one antenna with a high number of ports. However, as MNOs require compact antennas, the global trend is clearly towards multiband antennas with an increasing number of bands.37 The Notifying Party considers that there is supply-side substitutability as antenna manufacturers generally offer both single-band and different types of multi-band antennas.38

(40) The Notifying Party did not express any firm views as to other possible sub- segmentations of the antenna product market.39 However, the Notifying Party considers that technical and commercial differences between antenna modules, passive and active antennas may indicate that they belong to separate product markets.

(41) First, according to the Notifying Party, an antenna module is specifically designed to be included in a RAN equipment supplier’s final product (i.e. the active antenna) and is supplied to one specific RAN equipment supplier only. In contrast, passive antennas are more standardised products designed to fulfil the needs of multiple MNOs.

(42) Second, in the Notifying Party’s view, while passive and active antennas fulfil the same general technical function, they have different use cases. The demand for active antennas is driven by the need for more capacity, such as in densely populated areas or in the context of the roll-out of 5G networks. Moreover, the price level for an active antenna is significantly higher compared to a passive antenna due to the costs of the additional radio component.

(43) Third, while antenna modules and passive antennas are produced by antenna manufacturers, RAN equipment suppliers are best suited to manufacture active antennas which requires radio capabilities.

(44) With regard to hybrid antennas, the Notifying Party submits that these consists of two separate antenna products, the passive antenna and the active antenna, which are mechanically connected.40

(45) The Notifying Party submits that the Commission does not have to conclude on the exact product market definition as the Transaction does not raise any competition concerns under any plausible product market definition.41

4.3.1.2.Commission’s assessment

(46) The Commission has not previously examined the relevant market for antennas as components for mobile network equipment.42

RAN equipment and passive antennas

(47) The results of the market investigation suggest that passive antennas, as well as antenna modules, belong to a product market distinct from the market for RAN equipment components.

(48) First, a majority of the respondents consider that passive antennas are distinct from other components of the RAN equipment and therefore belong to a separate product market.43

(49) Second, the results of the market investigation confirm that passive antennas have a distinct function in the RAN and are not substitutable with other RAN equipment components. Moreover, MNOs can mix-and-match, purchasing passive antennas on a stand-alone basis, separately from other components of the RAN equipment, or as part of a bundle consisting of a passive antenna and other RAN equipment components (“turnkey solution”).

(50) Third, from the supply side, respondents indicate that passive antennas and other RAN equipment components are generally manufactured by a different set of suppliers, with the exception of Huawei which produces both passive antennas (as well as antenna modules) and other RAN equipment components.44

(51) Therefore, the Commission concludes that passive antennas and antenna modules belong to a product market distinct from other RAN equipment components.

RAN equipment and active antennas

(52) With regard to active antennas, several respondents point to the closer integration of antennas and radio units in active antenna systems. In these, antennas are an integral part of the RAN equipment and cannot be procured separately from other RAN equipment components.45 Therefore, active antennas may not constitute a separate product market distinct from other RAN equipment components.

(53) The Commission considers that, for the purpose of the present decision, the exact product market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market, irrespective of whether active antennas constitute a separate product market distinct from other RAN equipment components.

Single-band and multi-band passive antennas

(54) The results of the market investigation indicate that there is no demand-side substitutability between single- and multi-band antennas, although there may be substitutability from the supply side.

(55) From the demand-side, respondents to the market investigation explain that while the basic function of all antennas is the same, single-band and multi-band antennas are generally used for different purposes and the decision to deploy single- or multi- band antennas is primarily driven by these deployment considerations. Multi-band antennas are designed to support multiple bands of frequencies. They are used to reduce the number of antennas installed on a site given that the same coverage can be achieved with one multi-band antenna as with several single-band antennas. Single-band antennas, on the other hand, are mainly used for special purposes.46

(56) A majority of respondents to the market investigation express the view that multi- band antennas present characteristics (e.g., in terms of functionalities, performance, overall size/weight, price) that cannot be replicated by using single-band antennas, and vice versa.47 In particular, in most cases, multi-band antennas cannot be replaced with several single-band antennas due to size, weight or volume restrictions and visual impact limitations.

(57) Accordingly, demand for single-band and multi-band antennas is not responsive to price changes as confirmed by the results of the market investigation. A majority of respondents, most notably MNOs, responded that they would not switch from procuring multi-band antennas to single-band antennas (or vice versa) in case of a price increase of 5-10%.48

(58) From the supply side, the vast majority of respondents consider that single- and multi-band antennas are fully substitutable.49 While it is easier to design and manufacture single-band antennas, (nearly) all antenna manufacturers have developed and offer both types of antennas without any relevant specialisations.

(59) The Commission considers that, for the purpose of the present decision, the exact product market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market, irrespective of whether the relevant product market is further segmented between single-band and multi-band antennas.

Passive antennas and antenna modules

(60) There are mixed views as to whether a segmentation between passive antennas and antenna modules is appropriate.50 Overall, the results of the market investigation suggest that passive antennas and antenna modules may be substitutes from the supply side, but there does not appear to be any demand-side substitutability.

(61) Respondents to the market investigation explain that antenna modules are specifically developed and supplied to RAN equipment suppliers for the production of active antennas and therefore constitute a separate business for antenna manufacturers in the upstream market.51

(62) In contrast, antenna manufacturers emphasize the fact that antenna modules are built from the same components as passive antennas. Antenna manufacturers confirm that the main difference lies in the procurement process: passive antennas can be sold on a stand-alone basis to end customers, while antenna modules are produced for original equipment manufacturers, i.e., RAN equipment suppliers, which integrate them directly into the RAN equipment and sell them to end customers.52 Importantly, passive antennas are standardised products while antenna modules are customer specific, i.e., manufactured in accordance with customer specifications. Antenna modules for active antennas are developed on the basis of partnership agreements between antenna manufacturers and RAN equipment suppliers.53

(63) From the supply-side, a majority of respondents indicate that it is common for antenna manufacturers to produce both passive antennas and antenna modules.54

(64) Respondents did not express any views as regards a possible distinction between antenna modules for semi-active and AAS antennas.

(65) The Commission considers that, for the purpose of the present decision, it can be left open whether there is a separate product market for antenna modules, distinct from passive antennas, and whether such a market would have to be further segmented depending on the type of active antenna for which antenna modules are used, i.e. semi-active and AAS active antennas. The Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition.

Passive antennas and active antennas

(66) The results of the market investigation suggest that a segmentation between passive and active antennas is appropriate given the limited degree of demand-side substitutability and the lack of supply-side between passive and active antennas.55

(67) First, from the demand-side, the results of the market investigation confirm that passive and active antennas have the same basic function, i.e., providing coverage for mobile communication services. However, there are important differences between passive and active antennas in terms of their technical and commercial characteristics as well as use cases.

(68) The results of the market investigation confirm that active antennas have a better performance than passive antennas stemming from lower signal loss and higher capacity. Therefore, they are used in highly densely populated areas while passive antennas are used for standard sites. Active antennas are needed in the context of the 5G network roll out as they support massive MIMO applications much more efficiently and have better beamforming56 capabilities.57 Respondents to the market investigation also confirm that AAS active antennas are technically more advanced than semi-active antennas and will be more relevant in the long run in the context of the 5G roll-out.58

(69) At the same time, the results of the market investigation also point to some disadvantages that active antennas have in comparison to passive antennas: (i) they are heavier due to integration of the radio unit, (ii) they only support a limited number of frequency bands, (iii) they are less scalable and more maintenance- intensive, and (iv) they contain RAN vendor-proprietary components and interfaces increasing MNOs’ dependence on a specific RAN equipment supplier. By contrast, passive antennas are interoperable with RAN equipment of any RAN vendor due to established standardised physical interfaces.59

(70) Second, in respect of price, respondents indicate that active antennas are more expensive than passive antennas but also explain that the choice for active antennas seems to be driven by their improved performance and not by their price.60 Accordingly, demand for passive and active antennas is not responsive to price changes, as confirmed by the results of the market investigation. A majority of respondents, most notably MNOs, responded that they would not switch from procuring passive antennas to active antennas (or vice versa) in case of a price increase of 5-10%.61

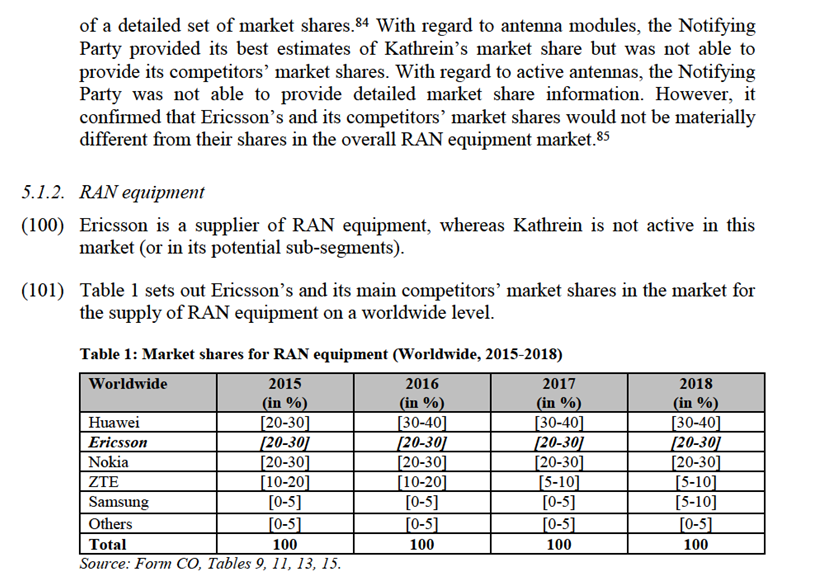

(71) Third, MNOs responding to the market investigation explain that passive and active antennas are complementary and they typically would need to use a mix of active and passive antennas in their networks.62 Currently, the share of active antennas installed in mobile networks is very small and according to some respondents, active antennas are only “used for pilots and still in development”.63 Several MNOs indicate that they already deploy a mix of passive and active antennas. Several MNOs explained that AAS active antennas are necessary for the deployment of 5G network, especially to efficiently employ the 3.5GHz band. As a result, the proportion of active antennas in mobile networks is expected to grow significantly.64

(72) Fourth, a majority of respondents to the market investigation do not consider that there is supply-side substitution between passive and active antennas.65 Passive antennas are produced by dedicated antenna manufacturers and supplied to MNOs on a standalone basis or as part of a turnkey solution. The only exception is Huawei which has end-to-end in-house capabilities. By contrast, active antennas are manufactured by RAN equipment suppliers and antenna manufacturers only supply the antenna module as they generally lack radio capabilities. MNOs procure active antennas as integrated solutions only from RAN equipment suppliers.66

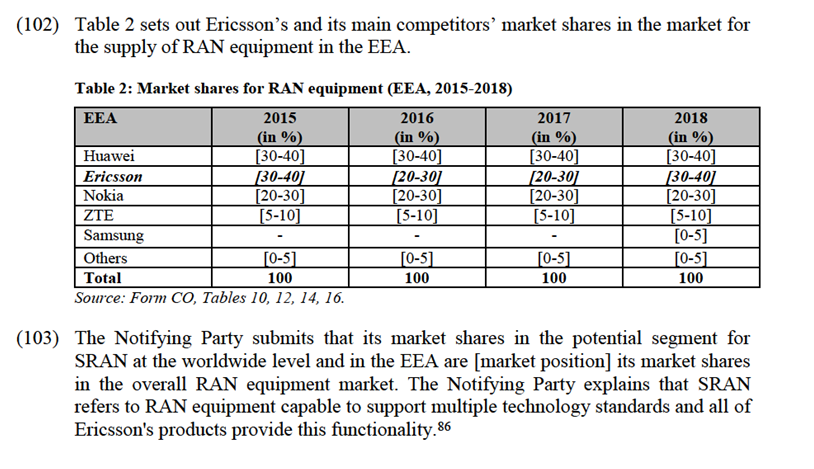

(73) Respondents did not express any views as regards a possible distinction between different types of active antennas, i.e. semi-active and AAS antennas.

(74) Therefore, the Commission concludes that passive antennas and active antennas belong to separate product markets.67 For the purpose of the present decision, it can be left open whether the market for active antennas has to be further segmented between semi-active and AAS active antennas as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition.

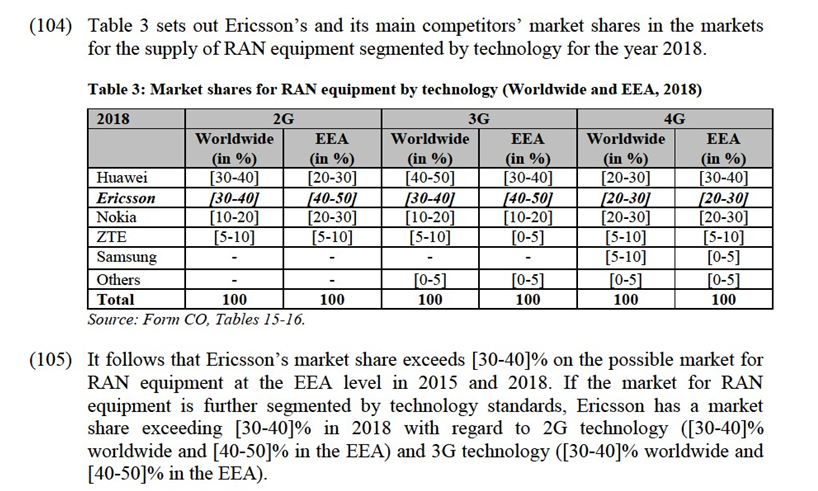

Conclusion

(75) In light of the foregoing, for the purpose of this decision, the Commission concludes that passive antennas belong to a separate product market distinct from other RAN equipment components. In addition, the Commission concludes that passive and active antennas belong to separate product markets.

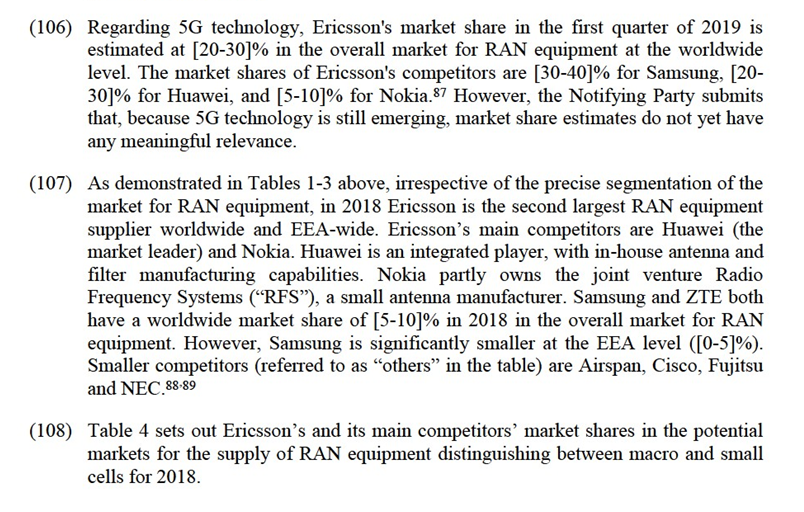

(76) The question whether passive antennas and antenna modules as well as single-band and multi-band antennas belong to distinct product markets can be left open. Likewise, the question whether the potential product market for active antennas would have to be segmented between semi-active and AAS active antennas and whether antenna modules used for semi-active antennas and AAS antennas belong to distinct product markets can be left open. With respect to these questions, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible product market definition.

4.3.2.Geographic market definition

4.3.2.1.Notifying Party’s views

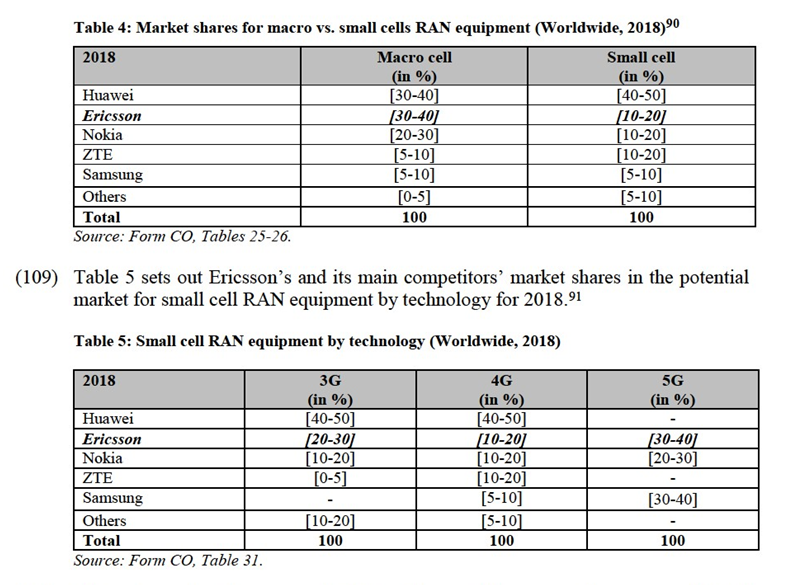

(77) The Notifying Party refers to the Commission decision in Nokia/Alcatel Lucent68 according to which the relevant geographic market for RAN equipment is at least EEA-wide, if not global (as discussed in paragraph (25)). The Notifying Party submits that the same market dynamics apply to antennas, which are RAN equipment components.

(78) The Notifying Party submits that the Commission does not have to conclude on the exact geographic market definition as the Transaction does not raise any competition concerns under any plausible geographic market definition.

4.3.2.2.Commission’s assessment

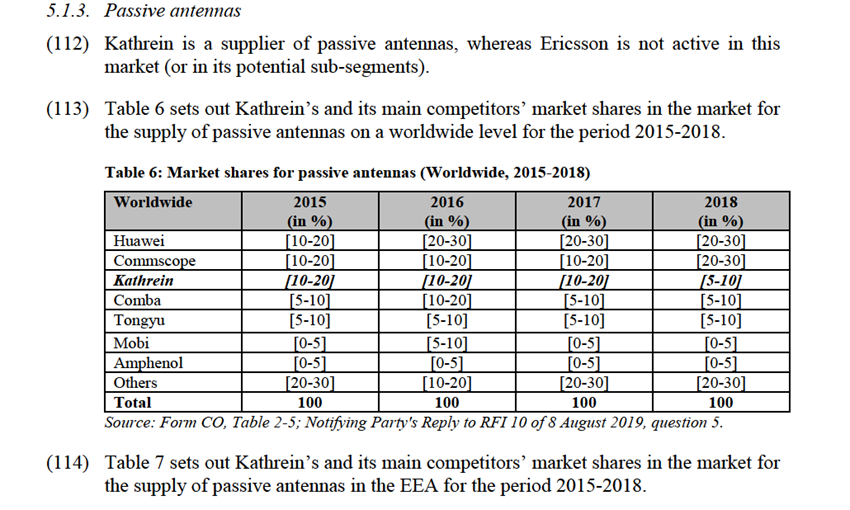

(79) A majority of respondents to the market investigation indicate that they supply and/or procure (all types of) antennas on a global basis, with the main suppliers being based in Europe, USA and Asia.69

(80) In any event, for the purpose of this decision, the exact geographic market definition for the supply of antennas can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market regardless of whether the market is considered to be EEA-wide or global.

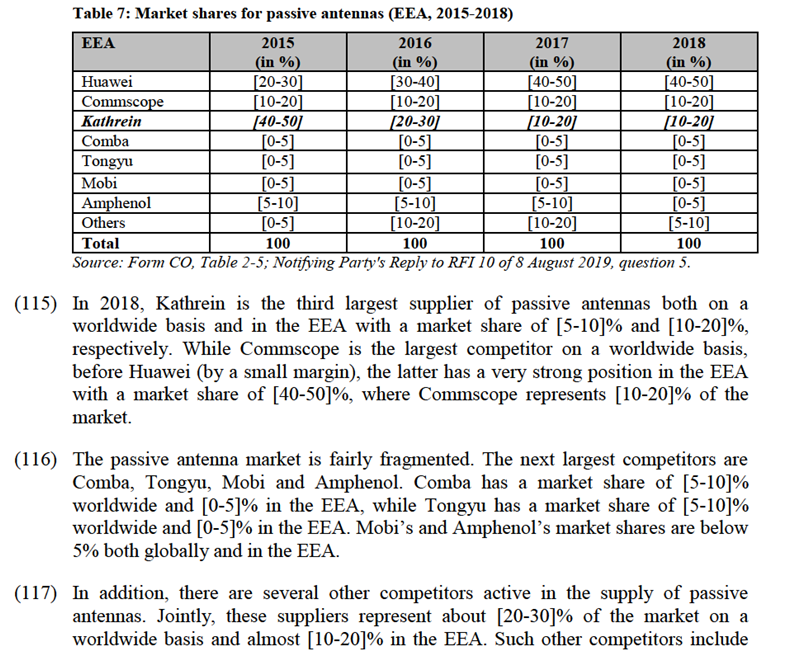

4.4.Filters

(81) Filters perform mainly two functions: they amplify the signal from the transceiver for transmission through the antenna, and connect different passive antennas into one common feeder to minimize both signal loss on the feeder as such as well as to minimize the need for individual feeders to be installed in the mast up to the antenna.

4.4.1.Product market definition

4.4.1.1.Notifying Party’s views

(82) In the Notifying Party’s view, RAN equipment and filters belong to separate product markets.70

(83) According to the Notifying Party, filters are commodity-type products with no significant distinguishing characteristics and no further segmentation of the market for filters is necessary.71

(84) The Notifying Party submits that the Commission does not have to conclude on the exact product market definition as the Transaction does not raise any competition concerns under any plausible product market definition.72

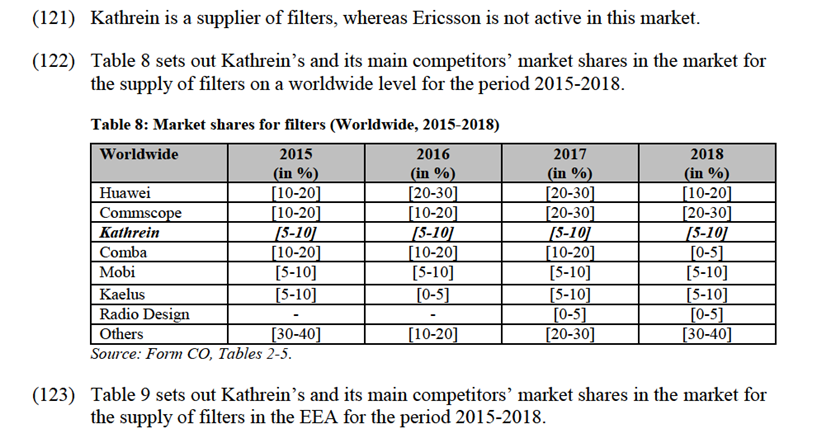

4.4.1.2. Commission’s assessment

(85) The Commission has not previously examined the relevant market for filters as components for mobile network equipment.73

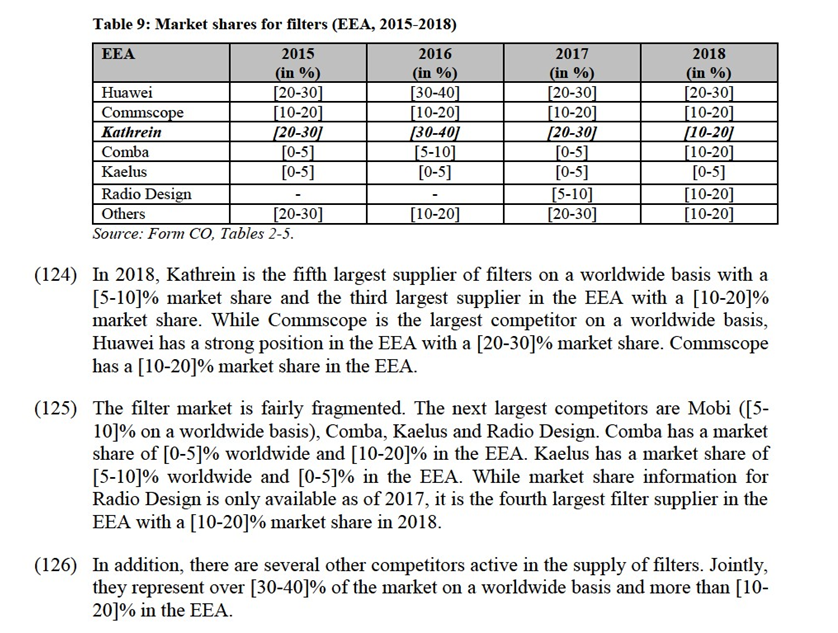

(86) The results of the market investigation suggest that filters constitute a separate product market, distinct from other RAN equipment components.74 A majority of the respondents consider that filters are distinct from other components of the RAN equipment and therefore belong to a separate product market.75

(87) Moreover, the market investigation confirms that no further sub-segmentation of the possible market for filters is necessary. 76

(88) Therefore, the Commission concludes that filters constitute a separate product market distinct from other RAN equipment components.

4.4.2.Geographic market definition

4.4.2.1.Notifying Party’s views

(89) The Notifying Party refers to the Commission decision in Nokia/Alcatel Lucent77 according to which the relevant geographic market for RAN equipment is at least EEA-wide, if not global (as discussed in paragraph (25)). The Notifying Party submits that the same market dynamics apply to filters, which are RAN equipment components.

(90) The Notifying Party submits that the Commission does not have to conclude on the exact geographic market definition as the Transaction does not raise any competition concerns under any plausible market definition.

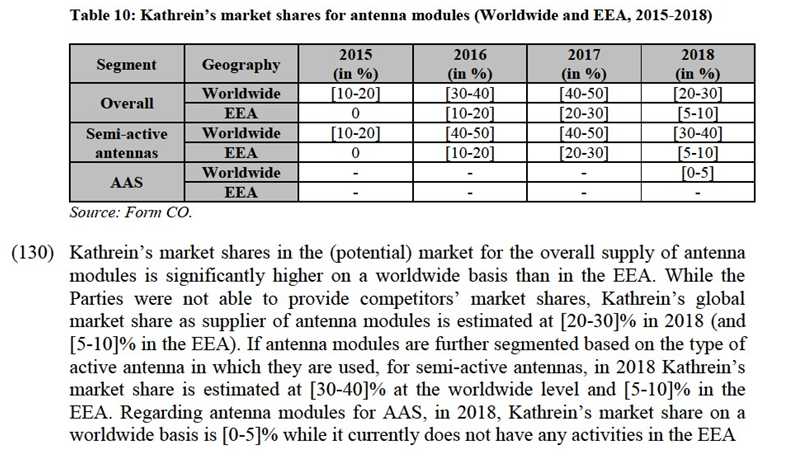

4.4.2.2.Commission’s assessment

(91) A majority of respondents to the market investigation indicate that they supply and/or procure filters on a global basis, with the main suppliers being based in Europe, USA and Asia.78

(92) In any event, for the purpose of this decision, the exact geographic market definition for the supply of filters can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market regardless of whether the market is EEA-wide or global.

5. COMPETITIVE ASSESSMENT

(93) Ericsson and Kathrein’s activities do not lead to any horizontal overlap. The Transaction creates a number of non-horizontal, i.e. conglomerate and vertical relationships. These relationships are examined in Sections 5.2 and 5.3 below, after a presentation of Ericsson and Kathrein’s market shares in Section 5.1.

5.1.Market shares

(94) According to the Non-Horizontal Merger Guidelines, market shares and concentration levels provide useful first indications of the market structure and of the competitive importance of both the merging parties and their competitors.79

5.1.1.Market shares methodology

(95) With regard to RAN equipment, the Notifying Party provided value-based market share estimates based on information from Dell’Oro Group80. According to the Notifying Party, these estimates are based on reported and estimated RAN equipment manufacturers’ revenues.81

(96) With regard to passive antennas and filters, the Notifying Party estimates the size of the respective markets on the basis of MNOs’ purchasing volumes. The Notifying Party thus estimated the market size by using indicators, including capex forecasts by the top MNOs, publications by operators on expansion plans, information on spectrum auctions, analyst data on sold radio units and antenna market forecasts (especially EJL Wireless Report82).

(97) The Notifying Party estimated market shares by value for passive antennas and filters on the basis of the price paid by MNOs for the respective products. Market share estimates correspond to merchant sales, i.e., exclude internal sales within the different branches of integrated companies which have both antenna and radio manufacturing capabilities.

(98) Market share estimates presented in Sections 5.1.3. and 5.1.4. below thus take into account all possible sales channels for passive antennas and filters, namely (i) direct sales to MNOs, (ii) sales to RAN equipment suppliers which then resell these antennas/filters, possibly as part of a turnkey solution, and (iii) sales to other sales partners, such as distributors.83

(99) With regard to antenna modules and active antennas, the Notifying Party submits that there are no publicly available market reports which would allow the estimation

5.2.Conglomerate assessment

5.2.1.Analytical framework

(137) According to the Non-Horizontal Merger Guidelines, in most circumstances, conglomerate mergers do not lead to competition problems.99

(138) However, foreclosure effects may arise when the combination of products in related markets may confer on the merged entity the ability and incentive to leverage a strong market position from one market to another closely related market by means of tying or bundling or other exclusionary practices. The Non-Horizontal Merger Guidelines distinguish between bundling, which usually refers to the way products are offered and priced by the merged entity100 and tying, usually referring to situations where customers that purchase one good (the tying good) are required to also purchase another good from the producer (the tied good).

(139) Tying and bundling as such are common practices that often have no anticompetitive consequences. Nevertheless, in certain circumstances, these practices may lead to a reduction in actual or potential rivals’ ability or incentive to compete. Foreclosure may also take more subtle forms, such as the degradation of the quality of the standalone product.101 This may reduce the competitive pressure on the merged entity allowing it to increase prices.102

(140) In assessing the likelihood of such a scenario, the Commission examines, first, whether the merged firm would have the ability to foreclose its rivals,103 second, whether it would have the economic incentive to do so104 and, third, whether a foreclosure strategy would have a significant detrimental effect on competition, thus causing harm to consumers.105 In practice, these factors are often examined together as they are closely intertwined.

(141) In order to be able to foreclose competitors, the merged entity must have a significant degree of market power, which does not necessarily amount to dominance, in one of the markets concerned. The effects of bundling or tying can only be expected to be substantial when at least one of the merging parties’ products is viewed by many customers as particularly important and there are few relevant alternatives for that product.106 Further, for foreclosure to be a potential concern, it must be the case that there is a large common pool of customers, which is more likely to be the case when the products are complementary.107 Finally, bundling is less likely to lead to foreclosure if rival firms are able to deploy effective and timely counter-strategies, such as single-product companies combining their offers.108

(142) The incentive to foreclose rivals through bundling or tying depends on the degree to which this strategy is profitable.109 Bundling and tying may entail losses or foregone revenues for the merged entity.110 However, they may also allow the merged entity to increase profits by gaining market power in the tied goods market, protecting market power in the tying good market, or a combination of the two.111

(143) It is only when a sufficiently large fraction of market output is affected by foreclosure resulting from the concentration that the concentration may significantly impede effective competition. If there remain effective single-product players in either market, competition is unlikely to deteriorate following a conglomerate concentration.112 The effect on competition needs to be assessed in light of countervailing factors such as the presence of countervailing buyer power or the likelihood that entry would maintain effective competition in the upstream or downstream markets.113

5.2.2.Affected markets

(144) The Transaction may have a significant impact within the meaning of Section 6.4 of the Form CO in relation to the supply of RAN equipment and the supply of both passive antennas (Section 5.2.3) and filters (Section 5.2.4), the latter products being required by MNOs in addition to RAN equipment in order to deploy mobile networks. 114

5.2.3.Passive antennas and RAN equipment

(145) Kathrein's passive antennas are complementary to the RAN equipment supplied by Ericsson, these products consisting in different components necessary to build mobile networks. The Transaction thus creates a conglomerate relationship between the activities of Ericsson and Kathrein.

(146) Passive antennas are procured by MNOs either (i) directly from antenna manufacturers, or (ii) indirectly, via a bundle sold by RAN equipment suppliers consisting of passive antennas and other RAN equipment components. This bundle constitutes what is designated in the industry as a "turnkey solution".

(147) The Commission examined whether the Transaction could give rise to conglomerate non-coordinated effects consisting of the potential foreclosure of suppliers of passive antennas that compete with Kathrein, and/or the potential foreclosure of suppliers of RAN equipment that compete with Ericsson as a result of the implementation of a conglomerate strategy by the merged entity.

(148) A possible practice that could potentially lead to conglomerate effects is mixed bundling.115 Post-Transaction, the merged entity could attempt to reduce its competitors’ ability to compete by offering its bundled sales of passive antennas and RAN equipment to MNOs at a price lower than the sum of the standalone prices for these products.116 In doing so, or even independently thereof, the merged entity may reduce its passive antenna sales to competing non-integrated RAN equipment suppliers. Such practices could potentially lead to the anticompetitive marginalization of rivals selling standalone components (i.e., non-integrated competitors) and to consumer harm, if the bundled offer was not replicable and the bundling strategy diverted sufficient demand from non-integrated rivals so as to make them unable to compete effectively.

5.2.3.1. Notifying Party’s view

(149) The Notifying Party considers that conglomerate effects are unlikely for the following reasons.

(150) First, the Notifying Party submits that the merged entity would not have the technical ability to increase its bundled sales. According to the Notifying Party, the choice between purchasing passive antennas on a standalone basis from antenna suppliers or as part of a (bundled) turnkey solution is made by MNOs, which specify in their tenders whether they prefer being offered bundles (generally for commercial reasons) or standalone components. Suppliers thus offer their products in a bundled or standalone manner depending on the specific requirements set out by MNO customers. MNOs thus have a strong countervailing buyer power and are unlikely to be influenced in their procurement decision in this regard.117

(151) Second, the Notifying Party points out that neither Ericsson nor the Target Business have a significant competitive position in any plausible relevant market. In 2018, Kathrein’s estimated market shares for passive antennas are below 20% on any plausible market segment (down from over [40-50]% in the EEA in 2015) and Ericsson’s estimated market share in RAN equipment is about [30-40]% both on a worldwide basis and in the EEA. Ericsson’s market share is only higher, albeit below [40-50]%, for 2G and 3G technology. According to the Notifying Party, neither Ericsson’s RAN equipment nor Kathrein’s passive antennas are viewed as particularly important and several credible alternative suppliers with a comparable product offering will remain on the market.118

(152) Third, the Notifying Party explains that competing RAN equipment suppliers and antenna manufacturers will continue to effectively compete with the merged entity even in the event that it sold passive antennas as a bundle together with RAN equipment. RAN equipment suppliers will be able to replicate turnkey solutions offered by the merged entity: (i) Huawei and Nokia already have in-house passive antenna capabilities and (ii) other RAN equipment suppliers, such as Samsung and ZTE, already source passive antennas from third parties in order to offer turnkey solutions.119 According to the Notifying Party, there will remain a sufficient number of alternative antenna suppliers after the Transaction. Standalone antenna suppliers will thus continue to sell passive antennas to competing RAN equipment suppliers and directly to MNOs and will therefore continue to have a large enough pool of customers.120

(153) Fourth, the Notifying Party submits that MNOs can easily switch suppliers of RAN equipment and passive antennas and multi-source from various manufacturers.121

(154) The Notifying Party submits that the merged entity will in any case not have the incentive to push for an increase in its bundled sales or to tie its sales of RAN equipment and passive antennas. It submits that passive antennas have a low value compared to other RAN equipment components, in particular the baseband and the radio. Therefore, a bundling strategy risking losing MNO customers would not be profitable.122

(155) Overall, the Notifying Party submits that the Transaction will not result in any significant reduction of sales by competitors that offer products on a stand-alone basis. In the first place, MNOs will continue to determine their own procurement strategy. In the Notifying Party's view, MNOs could not be forced by a bundling strategy to purchase a turnkey solution that they would not believe optimal for their needs. In the second place, passive antenna manufacturers will continue to supply both MNOs and RAN equipment suppliers which will enable the latter to also offer turnkey solution to MNOs.123

5.2.3.2. Commission’s assessment

(156) The Commission considers that the merged entity will not have the ability and incentive to foreclose non-integrated competitors by bundling its sales of passive antennas and other RAN equipment components. Even if the merged entity engaged in a strategy to foreclose rivals though bundling or tying, such strategy would not have a significant detrimental effect on competition.

As regards ability

(157) First, the Commission considers that the merged entity does not have a sufficient degree of market power to leverage its position in the supply of passive antennas or in the supply of RAN equipment to foreclose non-integrated competitors active in these markets.

(158) With regard to RAN equipment, the market shares presented in Section 5.1.2. do not suggest that Ericsson has significant market power. In an overall market for the supply of RAN equipment, Ericsson's market share is about [30-40]% both on a worldwide level and at EEA level in 2018. If the market for RAN equipment is further segmented by technology standards, Ericsson's market share is about [40- 50]% in 2018 in 2G and 3G technology both on a worldwide level and in the EEA. Its market share for the more recent 4G technology remains below 30%. If the market for RAN equipment is further segmented between macro and small cells, Ericsson’s market share is [30-40]% in the possible segment for macro-cell RAN equipment in 2018 and [30-40]% in the possible segment for small cells for 5G technology in 2018; however, more recently its market share decreased to [20-30]% in the latter segment. For all other segments and years, Ericsson’s market share remains below 30%. In addition, Ericsson’s market position has remained stable over the period 2015 to 2018.

(159) Irrespective of the precise segmentation of the market for RAN equipment, in 2018 Ericsson is the [market position] RAN equipment supplier (except for legacy technologies 2G and 3G in the EEA, [market position]). Ericsson’s main competitors are Huawei (the market leader) and Nokia. Samsung and ZTE are also significant competitors. Ericsson also faces smaller competitors, namely Airspan, Cisco, Fujitsu and NEC.

(160) The results of the market investigation confirm that Ericsson is unlikely to have a significant degree of market power. The majority of antenna manufacturers, RAN equipment suppliers and MNOs that responded to the market investigation consider that Ericsson’s RAN equipment product portfolio is comparable to the products of other RAN equipment suppliers in terms of quality, performance and price.124 This result supports the notion that Ericsson faces significant competitors that present credible alternatives to MNOs.

(161) With regard to passive antennas, similarly, market shares presented in Section 5.1.3. do not suggest that Kathrein has market power.125 In 2018, Kathrein is the [market position] supplier of passive antennas both on a worldwide basis and in the EEA with a market share of [5-10]% and [10-20]%, respectively. Notably, Kathrein’s market position has [market position] over the period 2015 to 2018, as explained in Section 5.1.3. Kathrein thus faces significant competitive constraints from suppliers with material market shares like Commscope, Huawei or Comba.

(162) The results of the market investigation confirm that Kathrein is not a particularly important competitor in the supply of passive antennas and that there are several credible alternative suppliers. The majority of antenna manufacturers, RAN equipment suppliers and MNOs that responded to the market investigation consider that Kathrein’s passive antenna offering is comparable with the products of other antenna manufacturers in terms of quality, performance and price.126

(163) MNOs confirm that they procure passive antennas from several different suppliers. Besides Kathrein, MNOs generally list Huawei, Commscope, Comba and Amphenol as their top passive antenna suppliers.127 According to the Notifying Party, Comba was able to improve the quality of its products significantly in the past few years, [supplier information].128 Other antenna manufacturers frequently mentioned by market participants as credible alternatives are CellMax, Mobi, RFS, Rosenberger, Tongyu and Wi-com.129 One MNO summarizes the supply situation as follows: "There are more than 10 main passive antenna manufacturers, and an uncertain number of small manufacturers over the world."130

(164) In the course of the market investigation, only one MNO submitted a different view and considered that Kathrein offers unique products in terms of quality, price and innovation.131,132 This respondent indicated that, even if Huawei's passive antennas are comparable to Kathrein’s products, however, Huawei is not an independent antenna supplier.

(165) However, this view is at odds with Kathrein's current market position and [market position] over the past few years. Moreover, these comments are inconsistent with the majority view expressed by other MNOs and respondents to the market investigation. With respect to Huawei, although the company appears to predominately sell passive antennas to MNOs (on a standalone basis or as part of turnkey solutions), the Commission notes that Huawei also generated sales to RAN equipment suppliers, albeit in more limited volumes. [business relationship].133

(166) Respondents to the market investigation also explain why, in their view, Kathrein has [market position] market shares over the last few years. According to several respondents, the quality of Kathrein's product is on par with that of the other main suppliers, but its prices are generally higher, making Kathrein less competitive.134 [internal documents]. On a quarterly basis, Kathrein receives written feedback from Ericsson on its performance as a supplier. In a 2018 report, Ericsson thus described Kathrein's commercial position as "[supplier information] ".135

(167) Second, the Commission notes that the merged entity is unlikely to be able to significantly increase its (bundled) sales of passive antennas and RAN equipment post-Transaction in light of MNOs’ demand patterns.

(168) In the first place, the results of the market investigation confirm that MNOs procure passive antennas both directly from antenna manufacturers and from RAN equipment suppliers. Based on the responses to the market investigation, the proportion of passive antennas purchased on a standalone basis is estimated to be at least 50% market-wide, however with significant variation across MNOs.136

(169) According to MNOs, the advantages of purchasing turnkey solutions are: (i) bundle discounts, (ii) one-stop-shopping and reduced coordination efforts from an operational perspective, and (iii) RAN equipment suppliers taking the responsibility for the installation and integration of the passive antenna into the RAN equipment and ensuring the compatibility and interoperability of all components used across the mobile network. However, MNOs also indicate that purchasing turnkey solutions entails several disadvantages, namely: (i) higher and/or hidden costs (e.g. service fees), (ii) less freedom and control in the selection of the best components and their network integration, and (iii) increased dependency on a single RAN equipment supplier.137 Overall, it appears that the more price-sensitive MNOs tend to negotiate with antenna manufacturers directly when procuring passive antennas on a standalone basis.138 For other MNOs, the main reason for procuring passive antennas on a standalone basis is to keep a better control of the design and deployment of their mobile networks, including by testing and integrating passive antennas themselves.139

(170) The results indicate that MNOs assess the costs and benefits of both options, i.e. to opt for a standalone or turnkey solution, on a case-by-case basis.140 An MNO explains that it is pro-actively increasing its share of standalone passive antenna purchases after an integrated RAN equipment supplier had increased its share of bundled sales by granting vouchers for passive antennas.141 This MNO thus developed a counter-strategy in order to effectively avoid being dependent on an integrated supplier.

(171) The results of the market investigation also confirm that mixing-and-matching passive antennas and RAN equipment from different vendors presents no interoperability issues to MNOs. This is because the integration of passive antennas in RAN equipment is governed by established, market-wide interoperability standards (i.e., the 3rd Generation Partnership Project ("3GPP") standard).142,143 The combination of passive antennas and RAN equipment takes place by connecting the antenna with a standardized connector via a high frequency coax cable, which transports the analogue signal to the passive antenna. In each case, the standards for the control and monitoring interface between a base station and a variety of tower- top equipment are observed.144

(172) Accordingly, although MNOs recognize that any infrastructure exchange causes some switching costs, for instance in terms of the testing of new components, switching between different passive antenna suppliers is technically and commercially possible.145 MNOs confirm that switching between suppliers is easy as passive antennas are commoditised products that are interoperable with any RAN vendor’s equipment.146

(173) In the second place, MNOs that responded to the market investigation confirm that they multi-source passive antennas and generally work with more than two different suppliers at the same time.147

(174) Besides the advantage of being less dependent on a single supplier, multi-sourcing is required as antenna specifications differ across mobile network sites. Therefore, even an integrated RAN equipment supplier would be unlikely to hold an antenna portfolio covering all types of passive antennas and would need to procure certain types from third-party suppliers.148 Thus, an antenna manufacturer explained in the course of the market investigation that it continues to sell passive antennas to integrated RAN equipment suppliers, such as Nokia or Huawei.149

(175) In the third place, while respondents to the market investigation consider that the merged entity may have the technical ability to respond to a RFQ for a standalone RAN equipment solution with a bundled offer (to the extent that such an offer would be permissible under the relevant tender rules), there are mixed views as to whether the merged entity would be successful in increasing its bundled sales after the Transaction.150 MNOs indicate that they will remain in control of their procurement strategy. For instance, one MNO explains that, when selecting passive antennas and RAN equipment, “it considers all relevant factors such as quality/performance, price and maintaining a balance between different vendors on the market”.151

(176) In contrast to MNOs, most antenna manufacturers and RAN equipment suppliers believe that the merged entity will be able to increase its bundled sales and divert demand away from standalone suppliers.152 However, only few respondents believe that such an increase would have a negative impact on competition and make it more difficult for stand-alone players to compete.153

(177) Third, the Commission notes that non-integrated competitors have effective and timely counter-strategies available in order to be able to effectively compete with the merged entity in the event of a potential foreclosure strategy by the merged entity.

(178) The majority of antenna manufacturers, RAN equipment suppliers and MNOs that responded to the market investigation consider that standalone antenna manufacturers and RAN equipment suppliers will have the ability to replicate turnkey solutions offered by the merged entity.154 Several antenna manufacturers explain that standalone competitors already team up, for instance against the integrated player Huawei, and that RAN equipment suppliers can purchase passive antennas from several sources for their turnkey solutions.155 Overall, the results indicate that the partnership model is how the majority of RAN equipment suppliers currently operates. All RAN equipment suppliers seem to collaborate with antenna manufacturers and offer bundles or could enter into such partnerships.156

(179) Only a few respondents are concerned that while the Parties' competitors may have the technical ability to replicate the merged entity’s turnkey solution through partnerships, non-integrated players would not be as competitive as the merged entity. In particular, they submit that non-integrated players will not be able to replicate the merged entity's bundle discount. Moreover, they are concerned that standalone antenna manufacturers may become less competitive due to the reduced demand post-Transaction.157 However, these concerns are not consistent with the fact that non-integrated players are already competing effectively with integrated players pre-Transaction.

(180) Moreover, MNOs consider that post-Transaction there will remain a sufficient number of alternative antenna manufacturers and RAN equipment suppliers such that MNOs can continue purchasing these components on a standalone basis, even if the merged entity were to tie its passive antenna and RAN equipment sales.158 With regard to RAN equipment suppliers, the results of the market investigation confirm that the Transaction would leave the number of suppliers unaffected and that customers currently purchasing RAN equipment on a standalone basis expect to be able to do so post-Transaction.159

As regards incentives

(181) In light of the foregoing, the merged entity is unlikely to have an incentive to engage in a pure bundling or tying strategy. As explained in paragraph (168), a significant share of MNOs is not interested in buying turnkey solutions, but instead prefers to buy passive antennas and RAN equipment on a standalone basis. If the merged entity were to pursue a pure bundling or tying strategy, it would risk losing the sales from customers who prefer to mix-and-match and purchase only passive antennas or only RAN equipment from the merged entity together with the standalone product of another supplier. A share of these customers may decide to cease purchasing these products from the merged entity.

(182) In this context, it is also relevant to mention that the value of passive antennas is significantly lower than the value of the other RAN equipment components.160 The Notifying Party estimates that passive antennas represent around [5-10]% of the RAN equipment value.161 Respondents to the market investigation unanimously confirm that passive antennas represent only a small portion of the overall value of the RAN equipment, even in case of a complex multi-band antenna. Therefore, it is very unlikely that Ericsson would be willing to forego sales of RAN equipment in order to gain market shares on the market for the supply of passive antennas where turnover and profits are more modest. Vice versa, it is very unlikely that Ericsson would be able to convince MNO customers to buy a bundle consisting of passive antennas and RAN equipment, if such customers were looking to buy passive antennas on a standalone basis.

(183) It also appears unlikely that the merged entity will have the incentive to foreclose rivals though a mixed bundling strategy and/or through the reduction of passive antenna sales to non-integrated competitors.

(184) First, the majority of antenna manufacturers and RAN equipment suppliers that responded to the market investigation considers that the merged entity will have an incentive to increase its bundled sales.162 Respondents indicate that Ericsson will have the option of either selling passive antennas and RAN equipment at market rates, thus gaining the antenna margin as part of the company's profit, or offering a bundle at a reduced price to increase its sales and gain market share. Nevertheless, MNOs cast doubt that the merged entity will have an incentive to expand bundled sales by pointing to the fact that Ericsson already has an agreement with Kathrein to distribute antennas and could already today offer commercial advantages to customers purchasing a turnkey solution as opposed to purchasing components in a standalone form.163

(185) Second, in its assessment of the likely incentives of the merged firm, the Commission may take into account factors such as, inter alia, the type of strategies adopted on the market in the past or the content of internal documents.164

(186) With respect to past strategies adopted on the market, respondents to the market investigation indicate that Huawei, which is already integrated, employs a mixed bundling strategy offering bundles at a reduced price.165 Therefore, a number of respondents are concerned that, assuming that the merged entity would increase bundled sales to MNOs as a result of the Transaction, it may at the same time have an incentive to decrease its passive antenna sales to competing RAN equipment suppliers (for commercial or technical reasons, such as capacity constraints). This would be in line with Huawei’s strategy to only have limited passive antenna sales to competing RAN equipment suppliers.166

(187) [reference to internal documents on post-Transaction business strategy]167

(188) It follows that, on balance, the merged entity is unlikely to have the incentive to foreclose rivals through bundling, tying or other exclusionary strategies.

As regards effects

(189) Even if the merged entity engaged in a mixed bundling strategy or other exclusionary strategy, for all the reasons set out in paragraphs (157)-(180), such strategy would be unlikely to result in a significant reduction of sales prospects by standalone rivals in the market leading to a reduction in rivals’ ability or incentive to compete.

(190) The implementation of a mixed bundling strategy may potentially lead to (i) a reduction of Ericsson's procurement of passive antennas from third parties and (ii) a reduction of Kathrein's passive antenna sales to third parties.

(191) With regard to the first effect, the Commission notes that, before the Transaction, Ericsson’s position as customer for other standalone antenna manufacturers is limited. According to the results of the market investigation, Ericsson represents less than 10% of most antenna manufacturers’ sales of passive antennas. Ericsson represents between 10% and 30% of passive antenna sales of only two antenna manufacturers.168 Moreover, several passive antenna suppliers indicate that they would be able to start selling or increase their sales to customers other than Ericsson.169

(192) In any event, as explained in paragraph (174), an integrated RAN equipment supplier is likely to continue to procure passive antennas from a range of different suppliers. [business strategy].170 [business strategy]. According to Ericsson, this is due to the need to fulfil specific requests from customers who prefer to multi-source and procure passive antennas from a number of different suppliers. [business strategy].171 [business strategy].172

(193) With regard to the second effect, the Commission notes that Kathrein’s position as supplier to standalone RAN equipment manufacturers is fairly limited pre- Transaction. According to the results of the market investigation, Kathrein represents less than 10% of other RAN equipment suppliers’ passive antenna purchases (in order for them to offer turnkey solutions to MNOs).173 Moreover, several RAN equipment suppliers indicate that they would be able to start sourcing or increase their purchases from antenna manufacturers other than Kathrein.174 Consequently, even in the unlikely scenario that Ericsson would reduce its sales of passive antennas to competing RAN equipment suppliers, this would not affect their ability to source passive antennas and, thus, they would continue to compete effectively as suppliers of both stand-alone and turnkey solutions to MNOs.

(194) Moreover, for the reasons set out in paragraphs (167) to (176), the Commission does not expect that the Transaction will divert significant demand from standalone products to bundled sales. In any case, the Parties’ non-integrated competitors are able to replicate the merged entity’s bundled offer as there remains a sufficient number of standalone players in both markets.

5.2.3.3.Conclusion

(195) In light of the above considerations and based on the results of the market investigation, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with respect to the relationship between the market for the supply of passive antennas and the market for the supply of RAN equipment.

5.2.4.Filters and RAN equipment

(196) Kathrein's filters are complementary to the RAN equipment supplied by Ericsson, all these products consisting in components necessary to build mobile networks. The Transaction thus creates a conglomerate relationship between Ericsson and Kathrein.

(197) Like passive antennas, filters are procured by MNOs either (i) directly from filter manufacturers, or (ii) indirectly, via a bundle sold by RAN equipment suppliers consisting of filters and other RAN equipment components as part of a turnkey solution.

(198) The Commission examined whether the Transaction could give rise to conglomerate effects consisting of the potential foreclosure of suppliers of filters that compete with Kathrein, and/or the foreclosure of suppliers of RAN equipment that compete with Ericsson.

5.2.4.1.Notifying Party’s view

(199) The Notifying Party considers that conglomerate effects are unlikely for the following reasons.

(200) First, the Notifying Party submits that the merged entity would not have the technical ability to increase its bundled sales because, as described in relation to passive antennas, suppliers offer their products in a bundled or standalone manner depending on the specific requirements set out by their MNO customers. MNOs thus have a strong countervailing buyer power and are unlikely to be influenced in their procurement decision in this regard.175

(201) Second, the Notifying Party points out that neither Ericsson nor the Target Business have a significant competitive position in any conceivable relevant market. In 2018,Kathrein’s estimated market share for filters remains below 20% (down from over [30-40]% in the EEA in 2016) and Ericsson’s estimated market share in RAN equipment is about [30-40]% both on a worldwide basis and in the EEA.

(202) Third, the Notifying Party explains that other RAN equipment suppliers and filter manufacturers will continue to effectively compete with the merged entity even in the event that it sold filters as a bundle together with RAN equipment. As for passive antennas, RAN equipment suppliers will be able to replicate turnkey solutions offered by the merged entity, either relying on in-house filters capacities or procuring filters from alternative suppliers.176 Standalone filter manufacturers will thus continue to sell filters to competing RAN equipment suppliers and to MNOs directly and will therefore continue to have a large enough pool of customers.

(203) Fourth, the Notifying Party submits that MNOs can easily switch suppliers of RAN equipment and filters and multi-source from various manufacturers.177

(204) The Notifying Party submits that the merged entity will in any case not have the incentive to push for an increase in its bundled sales or to tie its sales of RAN equipment and filters. It submits that filters have a low value compared to other RAN equipment components. Therefore, a bundling strategy risking losing MNO customers would not be profitable.178

5.2.4.2. Commission’s assessment

(205) The Commission considers that the merged entity will not have the ability to foreclose non-integrated competitors by bundling its sales of filters and other RAN equipment components. Even if the merged entity engaged in a strategy to foreclose rivals though bundling or tying, such strategy would not have a significant detrimental effect on competition.

As regards ability

(206) First, the Commission considers that the merged entity does not have a sufficient degree of market power to leverage its position in the supply of filters or in the supply of RAN equipment to foreclose non-integrated competitors active in these markets.

(207) With regard to RAN equipment, the Commission refers to paragraphs (157)-(160) above which set out why Ericsson is unlikely to have a significant degree of market power.

(208) With regard to filters, market shares presented in Section 5.1.4. do not suggest that Kathrein has market power. In 2018, Kathrein is the fifth largest supplier of filters on a worldwide basis with a [5-10]% market share and the third largest supplier in the EEA with a [10-20]% market share. Notably, as explained in detail in Section 5.1.4, Kathrein’s market position has [market position] over the period 2015 to 2018. Kathrein thus faces significant competition from the main market players, namely Commscope, Huawei, Comba, Mobi, Kaelus and Radio Design.

(209) The results of the market investigation confirm that Kathrein is not a particularly important competitor in the supply of filters and that there are many credible alternative suppliers. A majority of filter manufacturers, RAN equipment suppliers and MNOs that responded to the market investigation consider that Kathrein’s filter offering is comparable with the products of other filter manufacturers in terms of quality, performance and price.179

(210) MNOs confirm that they rely on several different filter suppliers. Besides Kathrein, MNOs generally list Huawei, Commscope and Radio Design as their top suppliers of filters.180 MNOs do not identify any relevant differences across filter manufacturers. A respondent thus explains that “most suppliers have a broad range of filters in their portfolios, i.e. there are no types of filters produced by Kathrein which are not also offered by competitors”.181 One filter manufacturer explains that the filter market is characterized by a high level of customization; however, this is not consistent with the majority view of other respondents to the market investigation.182

(211) Second, the Commission notes that the merged entity is unlikely to be able to significantly increase its (bundled) sales of filters and RAN equipment post- Transaction in light of MNOs’ demand patterns, as set out for passive antennas in paragraphs (167)-(174). Compared to passive antennas, the results of the market investigation suggest that MNOs are even less likely to purchase bundles consisting of filters and other RAN equipment components because filters are generally procured separately and represent a limited portion of the cost of the RAN equipment.183 A respondent thus explained that “[t]he filter market has a huge diversity and usually is not involved in the RAN process. Cost is residual comparing with the RAN.”184 Therefore, the filter and RAN equipment markets seem to be less closely related than the passive antenna and RAN equipment markets.

(212) Third, the Commission notes that non-integrated competitors have effective and timely counter-strategies available in order to be able to effectively compete with the merged entity in the event of a potential foreclosure strategy by the merged entity. A majority of respondents consider that standalone filter manufacturers will have the ability to compete with the merged entity, even in the event that it sold filters as a bundle together with RAN equipment.185 As explained in detail for passive antennas in paragraphs (177)-(180), standalone competitors can and do to some extent collaborate already pre-Transaction in order to offer bundled products and compete against integrated players.

As regards incentives

(213) In light of the foregoing, the merged entity is unlikely to have an incentive to engage in a pure bundling or tying strategy. If the merged entity were to pursue a pure bundling or tying strategy, it would risk losing the sales from customers who prefer to mix-and-match filters and RAN equipment from different suppliers. A share of these customers may decide to no longer purchase from the merged entity at all.

(214) In this context, it is also relevant to mention that the value of filters is significantly lower than the value of the other RAN equipment components. The Notifying Party estimates that filters represent around [0-5]% of the RAN equipment value.186 Therefore, it is very unlikely that Ericsson would be willing to forego RAN equipment sales in order to gain market shares in filters where turnover and profits are more modest. Vice versa, it is very unlikely that Ericsson would be able to convince MNO customers to buy a bundle consisting of filters and RAN equipment, if such customers were looking to buy filters on a standalone basis.

(215) With respect to mixed bundling, several market participants indicate that, in their view, the merged entity will pursue a similar bundling strategy as for passive antennas and/or combine its bundling strategy by offering bundles consisting of passive antennas, filters and other RAN equipment components.187

(216) As noted in paragraphs (181)-(188) with regard to passive antennas, it appears unlikely that the merged entity will have the incentive to foreclose rivals though a mixed bundling strategy and/or through the reduction of filter sales to non-integrated competitors. [reference to internal documents on post-Transaction business strategy].

(217) It follows that, on balance, the merged entity is unlikely to have the incentive to foreclose rivals through bundling or tying or other exclusionary practices.

As regards effects

(218) Even if the merged entity engaged in a mixed bundling strategy, for all the reasons set out in paragraphs (206)-(212), the Commission notes that such strategy is unlikely to result in a significant reduction of sales prospects by standalone rivals in the market leading to a reduction in rivals’ ability or incentive to compete.

5.2.4.3. Conclusion

(219) In light of the above considerations and based on the results of the market investigation, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with respect to the relationship between the market for the supply of filters and the market for the supply of RAN equipment.

5.3.Vertical assessment

5.3.1. Analytical framework

(220) According to the Non-Horizontal Merger Guidelines, a vertical merger may significantly impede effective competition as a result of non-coordinated effects if such merger gives rise to foreclosure.

(221) The Non-Horizontal Merger Guidelines distinguish between two forms of foreclosure. Input foreclosure occurs where the merger is likely to raise the costs of downstream competitors by restricting their access to an important input. Customer foreclosure occurs where the merger is likely to foreclose upstream competitors by restricting their access to a sufficient customer base.

(222) In assessing the likelihood of an anticompetitive foreclosure scenario, the Commission examines, first, whether the merged entity would have, post-merger, the ability to substantially foreclose access to inputs or customers, second, whether it would have the incentive to do so, and third, whether a foreclosure strategy would have a significant detrimental effect on competition.188

(223) As regards ability to foreclose, under the Non-Horizontal Merger Guidelines, input foreclosure may lead to competition problems if the upstream input is important for the downstream product.189 For input foreclosure to be a concern, a vertically integrated merged entity must have a significant degree of market power in the upstream market. It is only in those circumstances that the merged entity can be expected to have significant influence on the conditions of competition in the upstream market and thus, possibly, on prices and supply conditions in the downstream market.190