Commission, May 31, 2017, No M.8297

EUROPEAN COMMISSION

Judgment

GE / BAKER HUGHES

Subject: Case M.8297 - GE / Baker Hughes

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 20 April 2017, the Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which General Electric Company ("GE", the United States) intends to acquire within the meaning of Article 3(1)(b) of the Merger Regulation sole control over Baker Hughes Incorporated ("BHI", the United States) by way of purchase of shares ("the proposed Transaction").3 GE is hereinafter referred to as "the Notifying Party". GE and BHI are collectively referred to as the 'Parties', whilst the undertaking resulting from the proposed Transaction is referred to as "the merged entity"

1. THE PARTIES

(2) GE has a broad and diversified range of activities, including GE’s oil and gas manufacturing and technology solutions spanning across subsea & drilling, rotating equipment, imaging and sensing.

(3) BHI is active in the provision of oilfield services (OFS) on a global scale to oil and gas exploration and production companies (E&P) with a focus on the drilling and evaluation of wells as well as on the completion and production of wells.

2. THE OPERATION

(4) The Parties have entered into a Transaction Agreement pursuant to which GE will acquire sole control over BHI by way of purchase of shares. GE will own 62.5% of the voting and economic rights of a newly-formed company that will include BHI and GE’s Oil & Gas business.

3. EUROPEAN UNION DIMENSION

(5) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million4. Each of them has a Union-wide turnover in excess of EUR 250 million, but they do not achieve more than two-thirds of their aggregate Union-wide turnover within one and the same Member State. The notified operation therefore has an Union dimension within the meaning of Article 1(3) of the Merger Regulation

4. MARKET DEFINITION

(6) The Parties activities in the OFS industry overlap in a number of areas. In addition, the Transaction leads to a number of vertical relationships. More precisely5:

· Horizontal overlaps:

o Electrical submersible pumps (ESPs);

o Inline inspection services (ILI);

o Downstream and upstream chemicals;

o Permanent downhole gauges;

o ESP sensors.

· Vertically relationships:

o Sensors (upstream) and wireline and drilling services (downstream);

o Electric motors (upstream) and cementing services (downstream);

o Pressure transmitters (upstream) and surface data logging (SDL, downstream);

o Wireline tools (upstream) and wireline logging services (downstream);

o ESP sensors, ESP bypass systems and autoflow valves (upstream), and ESPs (downstream).

4.1.Electric submersible pumps (ESP)

4.1.1. Product market definition

(7) Artificial lift systems are used to lift the fluids up to the surface of the well by increasing the pressure inside the production tubing. They are needed in wells where the natural pressure in the reservoir is insufficient to lift hydrocarbons. Only a small proportion of wells have enough natural pressure to allow the free flow of fluids to the surface without artificial means. Moreover, this natural energy decreases as wells age and come closer to the end of their production life- span. In wells that do have enough natural pressure, the installation of an artificial lift can also respond to commercial decisions of the oil company wishing to increase the production of the well.

(8) The activities of the Parties in the EEA only overlap in the supply of ESPs, which are a type of artificial lift system. Worldwide, the Parties' activities also overlap in the provision of progressive cavity pumps (PCPs) and gas lifts.6

(9) The Commission has not previously assessed the market(s) for artificial lift systems.

(10) The Notifying Party submits that ESPs should be considered a product market separate from other types of artificial lift systems because each system has its own specific features and cannot be interchangeably used. It argues, however, that horizontal pumping systems should be considered as forming part of the same market as ESPs. Finally, the Notifying Party submits that segmentation between onshore and offshore ESPs is not warranted.7

4.1.1.1. Different types of artificial lift systems

(11) ESPs consist of a downhole pumping system that is electrically driven and comprised of a series of centrifugal pumps which vary according to wellbore characteristics. ESPs force fluids to surface by augmenting fluid pressure through centrifugal force. They can be used in both vertical and horizontal wells to a maximum depth of 15,000 feet, both onshore and offshore. Both BHI and GE provide ESPs in the EEA and worldwide.

(12) There are several other types of artificial lifts, including PCP, Gas Lift, Rod lift, Plunger lift, Hydraulic lift which function with different technologies.

(13) While there is some overlap between the capabilities of different artificial lifts (and different systems can be installed in the same well albeit at different stages of its production life8), the market investigation consistently indicated that different types of artificial lift systems have different specifications and address different needs depending on the well's characteristics.9

(14) The Commission considers that ESPs constitute a separate product market for the reasons set out below.

(15) First, from a demand-side perspective, each type of artificial lift is selected according to the specific conditions of the well and the properties that adapt to it. For example, lift requirements and pump rates differ for every pump. Gas lifts and ESPs can cover the largest ranges of depth and flow rate, going until 14,000 ft. deep and 14,000 bbl/d (barrels per day), while rod pumps and PCPs are very limited, only going 8,000 ft. and 4,000 ft. deep each and pumping 2,000bbl/d and 5,000 bbl/d respectively.10 Customers11 and competitors12 who responded to the market investigation confirmed that artificial lift systems cannot be used interchangeably. Temperature, depth and liquid rate are aspects that affect the performance of artificial lift systems. In wells combining high temperature, depth and high liquid rate for instance, an ESP is typically the preferred system because of its enhanced performance as compared to other lifts.13 In general, ESPs are viewed as the most sophisticated and versatile type of lift.

(16) Second, prices also vary greatly depending on the type of artificial lift. ESPs are the most efficient artificial lift system and can be used in complex wells but they tend to be more expensive than other systems, mainly because of the high cost for repairing or replacing the ESP in case of damage.14 A competitor explained: "ESPs are generally the most expensive form of lift because they provide higher horsepower, higher flow rate, and higher pressure due to being at deeper levels and more prolific wells. Rod Lift and PCP are next in line with lower flow rates and lower depths and the systems will be 25-50% less expensive than ESP. Hydraulic Lift is similar. Plunger Lift is the lowest cost form of lift since it uses no external power and consists of only a few components. Gas Lift can vary widely in cost depending on the size of the well."15

(17) Third, from a supply-side perspective, the Commission notes that the set of available suppliers varies by type of artificial lift. The Parties are not active in all systems16 and similarly, competitors do not offer the entire range of artificial lift systems. Competitors also indicated that supplying different types of artificial lift requires different expertise and production facilities.17 The market investigation has confirmed the Notifying Party's view that horizontal pumping systems should be considered as part of the ESP market. An horizontal pumping system is an ESP mounted on a skid that is not installed downhole in a well to lift oil but on the surface to transfer any type of fluids or inject them below the surface. The market investigation indicated that all ESP manufacturers can provide horizontal pumping because the equipment and the knowhow are fairly similar from an engineering perspective.18

(18) In view of the above and in light of the results of the market investigation, the Commission considers that ESPs, including horizontal pumping systems, form a separate product market from other types of artificial lift systems.

4.1.1.2. Onshore and offshore ESPs

(19) The market investigation has revealed that from a technical point of view, the pumps used in ESPs placed offshore follow the same technical principles as those used for onshore.19

(20) However, the ESP systems need to be adapted/modified to cope with the specific conditions present in wells located offshore.20 When deployed offshore, ESPs typically feature higher horsepower to provide increased flow rates in order to work efficiently in deeper wells found offshore. Also, offshore ESP systems need to be more resistant to cope with harsher environmental conditions for a long period of time.21 Offshore equipment imposes higher safety checks and testing requirements by customers.22 The higher requirements of offshore ESPs lead to higher costs, not only related to the price of the ESP system but also for installation and maintenance. Installation costs for ESPs onshore are typically around USD 180,000, while offshore they range between USD 500,000 to USD 1 million.23 The costs of maintenance and repair are also higher offshore than onshore because of the large costs associated with intervening offshore due to higher flow rate, ESP systems requiring additional inspections and enhanced processes as well as the possible need of a rig. Moreover the increased costs of non-productive time24 of offshore wells are also significantly higher given offshore wells have typically higher oil production.25 As explained by a competitor when referring to offshore ESP systems: "This level of sophistication and cost may be considered overkill for the typical onshore well, while for an offshore well, where the consequences of failure are much more serious, customers are likely to demand such higher standards and will be willing to pay accordingly."26

(21) In the EEA, only two providers are active offshore, namely BHI and Schlumberger (SLB). On the contrary, a number of additional suppliers are active onshore, including GE, Canadian Advanced (CAI) and Novomet. While GE has some offshore ESP installations outside the EEA, these installations are located in shallow water where onshore equipment can be used (as they do not require motors as powerful as the ones required to operate in the North Sea). In view of the above and in light of the results of the market investigation, the Commission considers that a segmentation of the ESP market between onshore or offshore is appropriate for the purposes of this decision.

4.1.2.Geographic market definition

(22) The Notifying Party submits that the geographic scope of the market for ESPs is at least EEA-wide, or worldwide in scope, owing to the fact that transport costs are low and prices do not vary depending on geographic location. Differences in regulations also do not play a role in segmenting the market and quality requirements are generally tailored to the well characteristics regardless of geographic location. Finally, the Notifying Party argues that local service teams are not required.27

(23) The Commission considers that the geographic scope cannot be considered wider than the EEA in view notably of the need for the suppliers to be able to send a service team on site in a short timeframe. Suppliers who do not operate a local base may cause customers to incur higher costs, mainly because longer lead times would prolong the non-productive time (NPT) of the well.28 Customers will typically require suppliers to be able to service their ESPs within 24 to 48h in case of failure, and therefore suppliers that are located outside the EEA are typically not considered as viable alternatives.29 ESP suppliers indicated that it is not necessary to have a base in the country where ESPs are provided but at least within the same region.30

(24) The arguments above are valid for both onshore and offshore, with the possible exception of Norway. Norway applies specific standards issued by DNV Norsok that results in higher costs as compared with equipment used in the UK sector of the North Sea. However, given that GE is not active anywhere offshore in the EEA the exact geographic market definition for the EEA offshore market can be left open.

(25) In view of the above and in light of the results of the market investigation, the Commission considers for the purposes of this decision that the geographic scope of the potential onshore market for ESPs is the EEA. For the potential market for offshore ESPs, the market could be narrower than the EEA, potentially segmented into the UK and Norwegian sectors of the North Sea. However, the exact geographic market definition for offshore ESPs can be left open given the proposed Transaction does not give rise to competition concerns under any plausible geographic market definition.

4.2.Inline inspection services

4.2.1.Product market definition

(26) Inline inspection services are a type of pipeline services which seek to identify threats bearing on oil or gas pipelines such as third party pipeline damage, metal loss from internal and external pipeline corrosion, cracks, manufacturing defects and pipeline mechanical damage.

(27) Pipeline inspections are mostly performed by robotic inspection vehicles ("pigs") which, while travelling through the pipeline, will collect data then used to identify the various threats. Around 70% of the pipelines can be inspected with a pig ("piggable pipelines"). Unpiggable pipelines can be assessed through a number of other ways.

(28) The Commission has not previously assessed the market for ILI services. The Notifying Party submits that ILI services should be considered as a single product market without any further segmentation. A narrower product market definition, distinguishing between either different services or between onshore and offshore applications is not warranted. The Notifying Party argues that the suppliers of ILI services are the same across the different segments of the market even though experience might have a larger impact for offshore applications. 31

4.2.1.1.Different types of ILI services

(29) ILI services mainly comprise the four following types of services:

- Metal loss services: detection of corrosion in liquid and gas lines;

- Crack detection services: detection of cracks and axial flaws in liquid and gas lines;

- Geometry and mapping services: measurement of the consistency of the geometry of the pipeline;

- Integrity services: additional and more in-depth analysis of the data obtained from the inspection services, providing information i.a. on the corrosion growth rate or the strain of the equipment concerned.

(30) Both BHI and GE provide all these services in the EEA and worldwide.

(31) The market investigation confirmed that the various ILI services can be considered to be part of a single product market as most of the suppliers offer the full range of services (though some smaller providers may focus on specific services).32

(32) In view of the above and the evidence available from the market investigation, the Commission takes the view that a further segmentation of the ILI services market by type of services provided may not be appropriate. In any event, the precise market definition can be left open as the proposed Transaction would not give rise to competition concerns under any plausible product market definition.

4.2.1.2. Offshore and onshore ILI services

(33) The market investigation yielded mixed results regarding the difference between tools and services for onshore and offshore applications. While some respondents stated that they do not consider the differences between offshore and onshore services to be significant33, as in both settings the tools are placed within a pipeline34, others underscored that for certain offshore applications, specific services and tools were required due to more difficult operating conditions, thicker pipeline walls and flow conditions.35 Further, more stringent certifications are required by some customers for tools used in offshore settings.36

(34) The Commission considers that the precise market definition can be left open as the proposed Transaction does not give rise to competition concerns under any plausible product market definition.

4.2.1.3. MFL vs UT technology

(35) Two different technologies can be used for ILI services, UT and MFL. UT uses acoustic tools to measure directly the diameter of the pipeline37 and MFL tools measure disturbances in an electro-magnetic field.38 Even though both technologies serve the same purpose of identifying threats bearing on the pipeline, each technology has its own advantages and limitations, and there are also some defects that only either of the two can detect (although both technologies can be used to identify most of defects).39

(36) Broadly speaking, UT performs better in term of accuracy and precision.40 It also performs particularly well with smaller diameters and shorter pipelines.41 MFL is more suited for longer lines and larger diameter. 42 UT can only be used with a liquid medium while MFL can be used both in gas and liquid pipelines.43 The majority of customers indicated that they typically procure the two technologies44 through separate tender procedures 45 and for different types of applications.4647 In the tender specifications customers typically indicate the technology (either UT or MFL) that they require. Both technologies will generally not compete in the same tender in view of their specificities. Therefore, demand side substitutability between the two technologies appears to be limited.

(37) Supply-side substitutability however is possible. The market investigation has confirmed that the main actors are able to offer both technologies, both at EEA and worldwide level.48 Although some small suppliers specialise and offer only one of them, according to providers which responded to the market investigation, the decision not to offer the two technologies is rather a strategic direction49 than due to technological limitations.50 It is feasible for an established player providing one of the two technologies to start providing the other.51

(38) In light of the above, and the evidence available from the market investigation, the Commission takes the view that a segmentation of the ILI services market by technology could be plausible. However, the Parties' position in the ILI market does not significantly vary whether it is segmented per technology. In any event, the precise market definition can be left open as the proposed Transaction would not give rise to competition concerns under any plausible product market definition.

4.2.2. Geographic market definition

(39) The Notifying Party submits that the relevant geographic market is at least EEA- wide and possibly global in scope. It argues that the competitive conditions and the main competitors are broadly the same worldwide. Further, local presence is a benefit but is not critical as staff and equipment are readily available across regions. Finally, the Notifying Party indicates that there are no regulatory or other restrictions constraining the provision of services across the world or in the EEA.52

(40) The market investigation suggests that the market for ILI services is at least EEA- wide and possibly worldwide in scope. The vast majority of respondents stated that suppliers operate at worldwide level53 and customers do not restrict tenders to those bidders with a base in the region where the project is located.54 The majority of respondents also confirmed that even if local presence may represent a competitive advantage, it is not essential to compete on the ILI services market.55 This is because staff and equipment can be moved from one region to another without significant difficulties/costs.56 Personnel are only required to be on site when the tools are being deployed in the pipeline. Once the tools are in place, the data analysis can be carried out remotely.57 ILI suppliers generally operate from one single base that serves at least an entire region, if not the world.58

(41) In view of the above and in light of the results of the market investigation, the Commission considers that in the present case, it can be left open whether the geographic market are to be defined worldwide or EEA-wide as the proposed Transaction does not raise competition concerns under any plausible geographic market definition.

4.3.Downstream chemicals

(42) The Parties horizontally overlap in the production and sale of downstream chemicals, i.e. chemicals used by a variety of industries in their production processes. The Parties' activities mainly overlap in the supply of chemicals to refineries and to the petrochemical industry. Contrary to GE, BHI is not active in the supply of equipment for water treatment; hence this area will not be discussed in this decision.

4.3.1. Product market definition

(43) The market for downstream chemicals can be segmented in different ways. First, the market for downstream chemicals can be segmented by product categories, namely water treatment chemicals, process treatment chemicals and fuel additives. Each of the segments could be further segmented by product type, sector or end-use.

4.3.1.1. Segmentation by product category

(44) While there are no precedents discussing this segmentation, in past cases59 the Commission considered water treatment chemicals to be part of a separate market.

(45) The Notifying Party considers that water treatment chemicals, process treatment chemicals and fuel additives should be regarded as constituting separate product markets. 60 The market investigation supported the Notifying Party's view

(46) From the demand-side, all the customers responding to the market investigation indicated that the different product categories cannot be used interchangeably. For example, one customer said that "the products are very application specific" and another customer explained that "the goals and the technological circumstances are different for water treatment, process treatment and fuel additives".61 A customer indicated that although some chemicals in different product categories ultimately perform the same task (for example, corrosion inhibition), "these products are not interchangeable as they have very different properties".62

(47) As regards the supply-side, competitors indicated that there is limited substitutability as the chemicals in different product categories are manufactured with different input components which cannot be easily interchanged in the same production line.63

(48) In light of the above and the results of the market investigation, the Commission considers that each of downstream water treatment chemicals, downstream process treatment chemicals and fuel additives are likely to form separate product markets. However, the precise market definition can be left open as the proposed Transaction would not give rise to competition concerns under any plausible product market definition.

(49) The proposed Transaction does not lead to affected markets as regards fuel additives, therefore they will not be discussed further in this decision.64

4.3.1.2.Segmentation by industry

(50) Chemical compounds are used by a number of different industries in their production processes.

(51) Many manufacturing processes require water of a certain quality to ensure proper equipment functioning and to prevent damage to finished products. Water treatment chemicals have long been used – to varying degrees – in manufacturing applications across the world. The standard practice is to distinguish among the following sectors: petroleum refining; chemical processing, including petrochemical; pulp and paper; textile; and other (such as the food and beverage industry).

(52) Similarly, process treatment chemicals are employed in a number of sectors, albeit predominantly in the hydrocarbon processing industry (HPI) and the chemical processing (CPI) industry. The main sectors in which downstream process chemicals are used are: HPI; CPI, including petrochemical; food and beverage industry; power generation; and, the pulp and paper industry. The Parties' activities overlap in the supply of downstream chemicals to the HPI and CPI industries. The outcome of the market investigation suggests that a segmentation by industry may be appropriate for the following reasons.

(53) First, suppliers indicated that chemicals used in different industries are specific to the industrial sector for which they are manufactured and that depending on the industry there are differences in the characteristics of the chemical product, such as "viscosity, concentration / dosage rate, ph level... etc."65 A competitor said that "there are certain differences in the demand of different industries which might need a special adjustment of the product formulation or a special selection of the raw materials used for the product".66 Second, the majority of the suppliers responding to the market investigation indicated that they are not capable of serving all the industries requiring water treatment chemicals.67 Manufacturers of process treatment chemicals are typically less specialised in some sectors compared to suppliers of water treatment chemicals but nonetheless they rarely serve all industries.

(54) In light of the above and the results of the market investigation, the Commission considers it plausible that each industry within the relevant product categories (water treatment and process treatment chemicals) forms a separate relevant market. In any event, the precise market definition can be left open as the proposed Transaction would not give rise to competition concerns under any plausible product market definition.

4.3.1.3.Segmentation by end-use application

(55) Downstream chemicals have several end-use applications. The primary chemicals used in downstream services include antifoulants, corrosion inhibitors, emulsion breakers, fuel additives, and anti-foaming agents.

(56) The Notifying Party claims that a segmentation by end-use application is not appropriate because of the high degree of supply-side substitutability. 68

(57) According to the Notifying Party, chemicals are produced in batches and the same equipment can be used to produce different chemical compositions. All production lines are configured to allow the manufacturing of multiple products. Thus, although the production of these chemicals requires different raw materials, the same production lines are used and the main adjustments that need to be made are: (a) clean the production line; (b) change raw materials; (c) change the set-up of the production line. All these steps can be done in less than one day and entail limited costs.

(58) The market investigation supported the Notifying Party's view. Suppliers indicated that in general they are able to supply the full range of downstream chemicals in any product category in which they are active.69

(59) The majority of the suppliers also confirmed that the same equipment can be employed to manufacture different types of downstream chemicals. For example, a supplier noted that "the same production line can be technically used to produce all type of downstream chemicals although cleaning of the equipment would be necessary to avoid contamination".70 The outcome of the market investigation suggests that shifting production between different types of chemicals typically takes only a few hours.

(60) In light of the above and the results of the market investigation, the Commission considers that a further segmentation by product or end use is unlikely to be appropriate.

4.3.2.Geographic market definition

(61) The Notifying Party submits that, irrespective of the precise product market definition adopted, the geographic scope of the markets for the supply of downstream chemicals is at least EEA-wide. This is because: (i) suppliers and customers tend to be active in multiple countries; (ii) transport costs are low (below 5%); (iii) there are no trade and regulatory barriers in the EEA; (iv) there is substantial cross-border trade in the EEA; and, (v) the entire EEA region can be served by a few manufacturing facilities, without the need of a local presence. 71

(62) The outcome of the market investigation supports the Notifying Party's view that the geographic market is at least EEA-wide in scope.

(63) First, customers and suppliers consistently indicated that downstream chemicals, irrespective of the product category, can be shipped from afar, and even further than the EEA.72 Some suppliers noted that downstream chemicals can be imported to the EEA from other regions, but this may have a negative impact on the overall price of the chemical.73

(64) Second, while customers typically require suppliers to provide additional services at their premises,74 customers and suppliers responding to the market investigation share the view that a pre-existing local presence in the vicinity of the customers' premises is not necessary to win business. For example, a customer noted that it "invites to tender not only suppliers who already have a local office (or a subsidiary) in the region where the site is located, but also those who do not currently have a presence near the site as long as the suppliers commit to establishing a local presence once the contract is awarded". 75

(65) Third, the market investigation confirmed that regulations and industry requirements are harmonised across the EEA.76

(66) Fourth, all the suppliers responding to the market investigation indicated that they can serve the entire EEA territory and they can either relocate employees in the proximity of the customer's locations or hire new local staff to provide support/service to the customers.77

(67) In light of all the above and the results of the market investigation, and for the purpose of this decision, the Commission considers that the geographic market for downstream chemicals, irrespective of how the product market is defined, is EEA-wide in scope.

4.4.Upstream chemicals

(68) The Parties' activities also overlap in the provision of upstream chemicals. Upstream chemicals include a broad range of chemistries to address flow assurance, asset integrity, and product optimisation challenges in both onshore and offshore oil fields and related applications.78

(69) The market for upstream chemicals could be segmented along similar lines as for downstream chemicals, namely by product categories, industry and application. However, the product as well as the geographic market definition can be left open as the proposed Transaction does not raise any competitive concern even under the narrowest plausible market definition.

4.5.Directional drilling services

4.5.1.Product market definition

(70) Directional drilling (DD) is a form of drilling which enables the drill string to change direction in order to reach a target which is not directly beneath the surface location of the rig. Such wells are called horizontal or deviated wells. The objective of directional drilling is to hit multiple reservoirs from a single rig site and/or to maximise the point of contact within a single reservoir.

(71) DD is always sold with Measurement-While-Drilling (MWD) services, which consists of sensors that measure azimuth and inclination of the drill string thus informing the directional driller about the location and direction of the drill string in real time.

(72) Most of the time, DD/MWD services are provided together with Logging-While- Drilling (LWD) services, which consist of sensors that measure and collect data on the characteristics of the formation surrounding the bore head thus informing the directional driller about the characteristics of the formation through which he is drilling and the nature of the fluids which it contains.

(73) The Notifying Party submits that a distinction can be made between DD/MWD, on the one hand, and LWD services, on the other hand, because DD services will always be provided with MWD services, whereas LWD services are optional.79

(74) However, in a previous decision, the Commission considered DD, MWD and LWD to be part of the same market for directional drilling, because they were part of an integrated system that is often priced and sold together.80

(75) The Commission notes that the markets for DD, MWD and LWD services may further be segmented into onshore and offshore services. O&G companies' requirements with regard to the track record and the portfolio of OFS providers are usually higher for offshore wells than for onshore wells. This is so, because the costs of operating an offshore rig are usually much higher than for an onshore rig. This is also in line with the fact that the markets for offshore services are more concentrated than the markets for onshore services.

(76) However, for the purpose of this decision, the Commission considers that the exact scope of the product market definition can be left open, as the proposed Transaction does not give rise to serious doubts even under the narrowest possible market definition. The notion of 'DD' will subsequently be used to describe the entire scope of DD/MWD/LWD services.

4.5.2.Geographic market definition

(77) In a previous decision the Commission considered that the market for DD services is at least regional in scope, but left the decision open.81 There are indications that the geographic scope of the market for DD services may be EEA- wide or even smaller. In that regard, the Commission notes that the identity of the relevant service providers and their respective market shares are different when looking at the EEA and the worldwide figures and may vary according to different regions within the EEA.

(78) However, for the purpose of this decision, the Commission considers that the exact scope of the geographic market definition can be left open, as the proposed Transaction does not give rise to serious doubts even under the narrowest possible market definition.

4.6.Wireline Logging Services

(79) Wireline logging services describe a range of services which are performed by lowering tools, which are fixed on the end of an electric cable (i.e. the "wireline"), into the borehole. Wireline logging services are generally segmented into open- hole-wireline logging (OHWL) services and cased-hole-wireline-logging (CHWL) services.

(80) The Notifying Party submits that some critical measurements can only be obtained by wireline logging and notes that wireline logging services are usually tendered separately from other oil field services.82 The Notifying Party further submits that a distinction can be made between OHWL and CHWL services. According to the Notifying Party, both services are performed at different stages of the well development. Moreover, OHWL services tend to be more demanding, because they are carried out during the drilling phase in the uncased well, whereas CHWL services are performed after the well has been cased. The Notifying Party also submits that both types of services are often tendered separately.83

4.6.1.Product market definition

4.6.1.1.Distinction between OHWL and CHWL services

(81) The Commission has not previously assessed the markets for wireline services. However, on the basis of the outcome of the market investigation the Commission considers that OHWL services constitute a distinct product market different from CHWL services.

(82) OHWL services are primarily reservoir evaluation services, which are performed during the drilling phase in the uncased (i.e. open) borehole. By contrast, CHWL services are performed after the borehole has been cased.

(83) The main purpose for OHWL services is the characterisation and evaluation of the reservoir in order to determine whether to complete the well for production.84 By contrast, CHWL services are usually performed for a variety of other reasons, only after the initial decision to complete the well for production has been taken.85 CHWL services are generally considered to be less sophisticated and more commoditised than OHWL services.86

(84) A distinction between OHWL and CHWL services is in line with the fact that the competitive landscape differs significantly between the two services. While a few large OFS providers, such as BHI, provide both OHWL and CHWL services, their respective market shares differ significantly between the two types of services. In addition, the market for OHWL services is much more concentrated, because it has higher barriers to entry, whereas the markets for CHWL services are usually characterised by the additional presence of a number of smaller providers some of which have entered this market in the EEA and worldwide in the last five years.87

4.6.1.2. Onshore vs offshore

(85) The Commission further notes that the markets for OHWL and CHWL may further be segmented into onshore and offshore services. O&G companies' requirements with regard to the track record and the portfolio of OFS providers are usually higher for offshore wells than for onshore wells. This is so, because the costs of operating an offshore rig are usually much higher than for an onshore rig. This is in line with the fact that the markets for offshore services are more concentrated than the markets for onshore services.

4.6.1.3.Conclusion

(86) However, for the purpose of this decision, the Commission considers that the exact scope of the product market definition can be left open, as the proposed Transaction does not give rise to serious doubts even under the narrowest possible market definition.

4.6.2.Geographic market definition

(87) There are indications that the geographic scope of the markets for OHWL and CHWL may be EEA-wide in scope, and possibly even smaller. In that regard, the Commission notes that the identity of the relevant service providers and their respective market shares are different when looking at the EEA and the worldwide figures.

(88) However, for the purpose of this decision, the Commission considers that the exact scope of the geographic market definition can be left open, as the proposed Transaction does not give rise to serious doubts even under the narrowest possible market definition.

4.7.OFS Sensors

(89) GE manufactures sensors, which are then purchased by the large integrated OFS providers, such as BHI, or by independent tool manufacturers for their respective drilling tools. The customers integrate these sensors in their tools in order to take a variety of measurements downhole.

(90) The Notifying Party submits that a distinction can be made between gamma sensors, neutron sensors and directional sensors, because they have different product characteristics and perform different types of measurements.88

4.7.1.Product market definitions

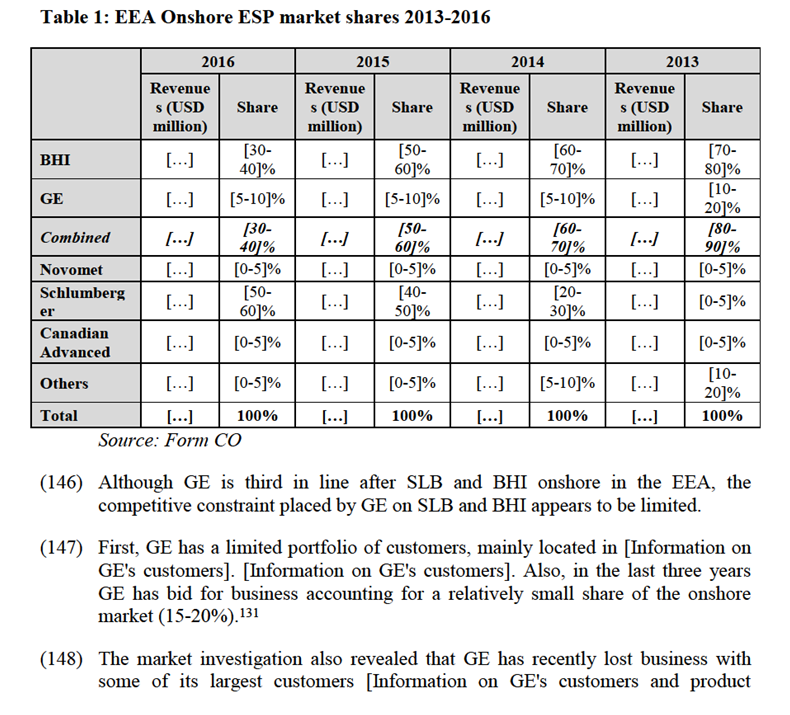

4.7.1.1.OFS Gamma sensors

(91) Gamma sensors are radiation detection devices, which use a crystal to measure mainly the types of rocks and fluids in the borehole, in order to collect data about the presence of hydrocarbons. There are various types of gamma sensors such as gross-counting gamma sensors, which measure primarily the rock type and density gamma sensors which measure primarily fluid types. Customers may use various gamma sensors on the same tool in order to take multiple measurements.

(92) The market investigation suggests that the manufacturing of gamma sensors is essentially an assembly business. Gamma sensors consist of a crystal, a photomultiplier, electronics and a power unit.89 The crystal converts the gamma ray radiation into a light pulse. Gamma sensors usually run sodium iodide (NaI) crystals. The photomultiplier converts the light pulse into an electric signal. The electronics process the data and the power unit provides the required amount of high voltage.90

(93) Some suppliers manufacture one or more of these components in-house. However, all of these components can also be purchased on the open market. For example, crystals can be bought from a variety of crystal growers,91 such as Saint Gobain (USA) or Alpha Spectra (USA).92 Photomultipliers can be bought from companies like Hamamatsu (Japan) or ElectronTubes (UK). Electronics can be bought from companies such as AHV (USA) or Antares (UK).93 In addition, data acquisition software can be bought from companies like Scientific Data Systems (USA).

(94) The added value provided by OFS gamma sensor manufacturers therefore lies in the packaging.94 OFS sensors must often withstand high temperatures as well as shock and vibrations. Specialised manufacturers such as GE and its competitors have the relevant know-how to protect the sensor from these strains while maintaining the functionality of the sensor.

(95) The market investigation confirmed that OFS customers cannot replace gamma sensors with neutron sensors or vice versa, because both types of sensors perform different measurements.95

(96) The market investigation further suggests that a distinction can be made between gamma sensors for DD applications, sensors for OHWL applications and sensors for CHWL applications. This is in line with the fact that each of these applications presents a distinct set of challenges for the respective sensors. The market investigation further suggests that a distinction can be made between gamma sensors for directional drilling applications, sensors for open hole wireline logging (OHWL) applications and sensors for cased-hole-wireline-logging (CHWL) applications. This is in line with the fact that each of these applications presents a distinct set of challenges for the respective sensors.(a) Gamma sensors for DD applications need to be small (i.e. small enough to fit into a pocket on a drill string), vibration resistant (i.e. rugged enough to resist the vibrations from the drilling process) and heat resistant (i.e. resistant enough to withstand the heat from the fluids present downhole).96(b) Gamma sensors for OHWL applications also need to be heat resistant, but they are not exposed to the vibrations of the drilling process, because the OHWL sensors are lowered into the borehole while the drilling process is interrupted. One market player considered OHWL gamma sensors to be the least demanding of the three applications, partly because they can use larger sensors than CHWL applications.97 However, larger crystals may impose their own challenges as regards the 'packaging' of said crystal.98 (c) Gamma sensors for CHWL applications also need to be heat resistant, but they do not need to be particularly vibration resistant, because they are lowered into the borehole only after the drilling has stopped. In addition, they operated in the cased borehole, so that they are shielded from the formation by the cement casing. However, CHWL applications are often smaller than OHWL tools in order to fit into the cased borehole, which puts additional constraints on the size of the gamma sensor.

(97) While the Notifying Party submits that the design of the relevant sensors is essentially the same across these applications, it acknowledges that the size and packaging of the sensors varies between the drilling applications and wireline applications, mostly because OFS gamma sensors for drilling applications need to be smaller, in order to fit into the drill string, as well as more rugged, because they operate close to the drill bit and are thus subject to higher levels of vibration and longer exposure to higher temperatures.99

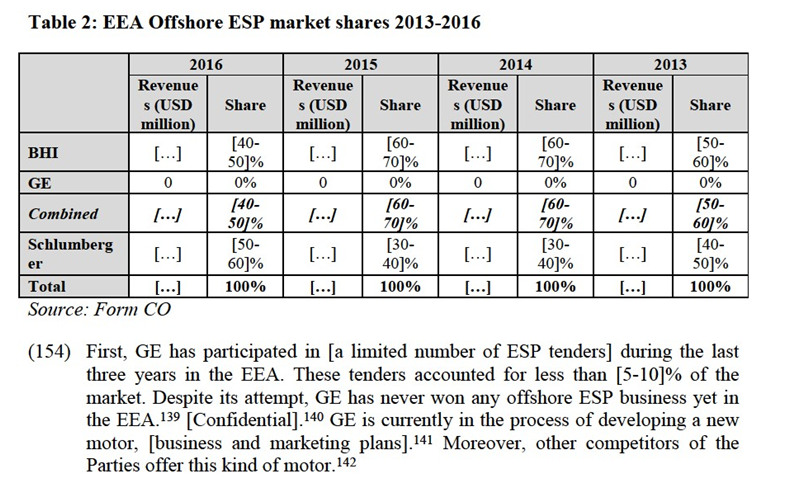

(98) The market investigation indicated that there is only limited demand-side substitution between OFS gamma sensors for different applications.100 While sensors intended for DD applications may in some cases be used for OHWL and CHWL applications, sensors for wireline applications may not be used in DD applications, presumably, because their specifications do not qualify them to withstand the vibration of the drill string (see recital (96)).

(99) The Notifying Party argues that in any case there is significant supply side substitution between sensors for the OFS industry, because the main sensor suppliers can easily customise and move into a different sensor type within a reasonable period of time and without high expenses.101

(100) The market investigation suggests that suppliers of OFS gamma sensors for one application may be able to start supplying OFS gamma sensors for another application in a relatively short timeframe (within 9 to 24 months) depending on the application and at costs of less than EUR 1 million. However, since this may not be sufficiently swift to assume that OFS gamma sensors for the different application belong to the same product market, these aspects will be assessed further in the context of potential entry (see recitals (225) to (232)).

(101) While the downstream markets for DD services, OHWL services and CHWL services may further be segmented in onshore and offshore services, the market investigation indicates that no such distinction can be made with regard to sensors.

(102) For the purpose of this decision, the Commission considers that it can be left open whether the market for gamma sensors should be considered as whole or sub- segmented between DD, OHWL and CHWL applications since the proposed Transaction does not give rise to serious doubts even under the narrowest possible market definition.

4.7.1.2.OFS neutron sensor

(103) Neutron sensors are radiation detection devices, which measure the porosity of the rock formation, in order to collect data about the prospects of extracting the hydrocarbons captured in the formation. Neutron sensors usually operate with He- 3 gas or Li-6 glas. While there may be various gamma sensors on the same tool taking different measurements, there is usually only one neutron sensor on each tool in order to measure porosity.

(104) Neutron sensors are most commonly used in DD or OHWL applications where porosity measurements are important for the drilling process. By contrast, neutron sensors are only rarely used in CHWL applications, because the OFS provider will usually have already gathered porosity measurements before the casing of the well and because it is difficult to make these measurements through the cement layer of the cased well.102

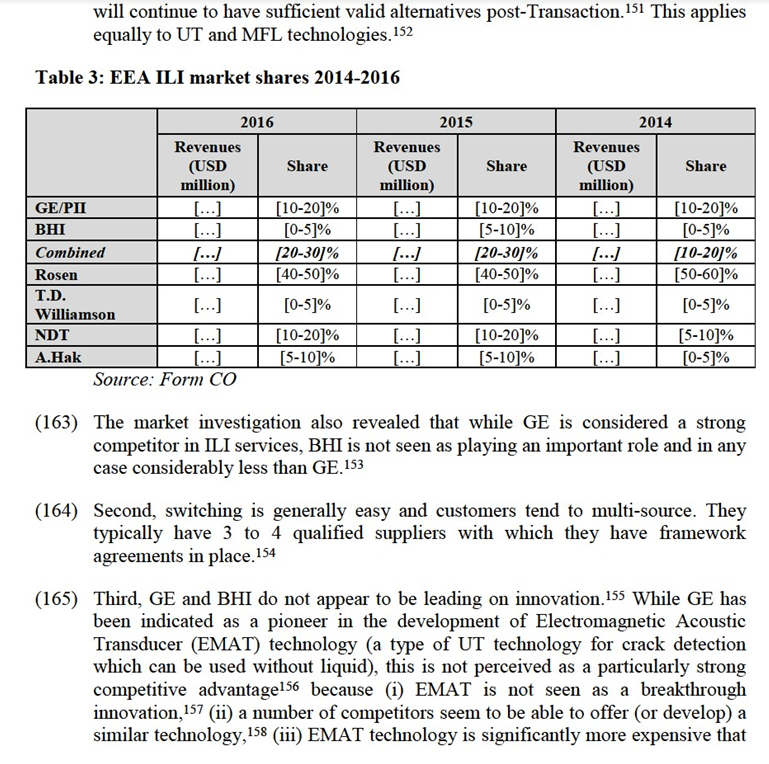

(105) As for gamma sensors, the manufacturing of neutron sensors is essentially an assembly business. Neutron sensors work with two types of technologies, either a Helium-3 filed sealed tube or a Lithium-6 ("Li-6") doped glass scintillator. GE offers both types of neutron sensors. In an Li-6 neutron sensor, neutrons interact with Li-6 doped glass to produce a light pulse. A photomultiplier converts the light pulse into an electric signal. In a He-3 neutron sensor, neutrons interact with the He-3 gas and ionised particles are then captures as pulses on an anode wire that runs through the centre of the tube.103

(106) While some suppliers develop one or more of these components in-house, they can also be purchased on the open market. For instance, Detector Products, a specialised manufacturer of neutron sensors, submitted that they purchase most of the individual components from specialised vendors and then assemble them in- house.104

(107) As mentioned above (see paragraph (96)), the market investigation confirmed that OFS customers cannot replace neutron sensors with gamma sensors because both types of sensors perform different measurements.105 (a) Similarly to gamma sensors, the market investigation suggests that a distinction can be made between neutron sensors for DD applications, for OHWL applications and for CHWL applications as each of these applications presents a distinct set of challenges for the respective sensors. Neutron sensors for DD applications need to be small (i.e. small enough to fit into a pocket on a drill string), vibration resistant (i.e. rugged enough to resist the vibrations from the drilling process) and heat resistant (i.e. resistant enough withstand the heat from the fluids present downhole).106 In addition, with regard to He-3 based neutron sensors, DD applications require the manufacturer to fit a relatively large quantity of He-3 gas in a very small tube, imposing challenges with regard to the sealing of said tube. (b) Neutron sensors for OHWL applications also need to be heat resistant, but they are not exposed to the vibrations of the drilling process, because the OHWL sensors are lowered into the borehole while the drilling process is interrupted. OHWL tools may allow for larger tools, since the uncased hole provides more space than the cased hole. Therefore, neutron sensors on OHWL tools may be larger, which allows for larger He-3 tubes with lower pressure and less strain on the sealing.107(c) Neutron sensors for CHWL applications also need to be heat resistant, but they do not need to be particularly vibration resistant, because they are not used during the drilling process. In addition they operate in the cased borehole, so that they are shielded from the formation by the cement casing. However, CHWL applications are often smaller than OHWL tools in order to fit into the cased borehole, which puts additional constraints on the size of the neutron sensor.108

(108) As for gamma sensors, the market investigation showed that there is only limited demand-side substitution between OFS neutron sensors for different applications.109

(109) The Notifying Party argues that there is significant supply-side substitution between sensors for the OFS industry, because the main sensor suppliers can easily customise and move into a different sensor type within a reasonable period of time and without high expenses.110

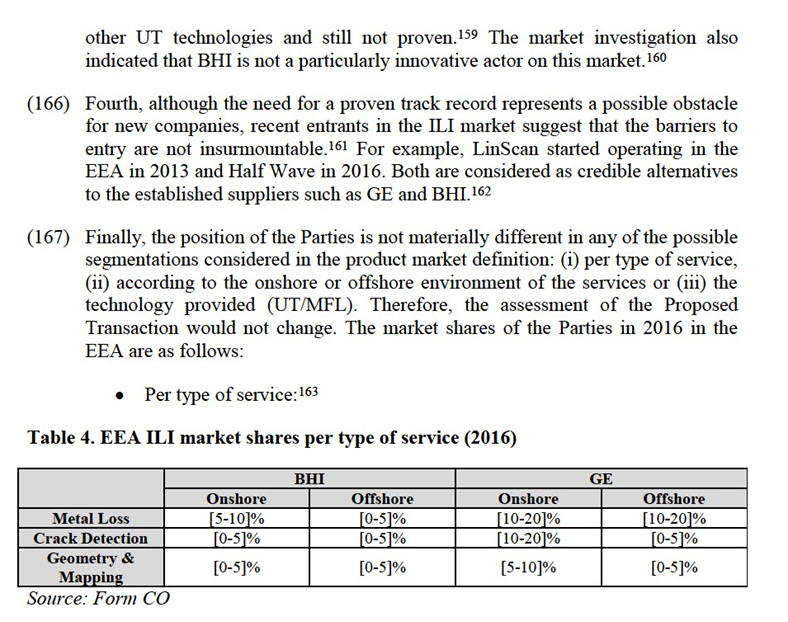

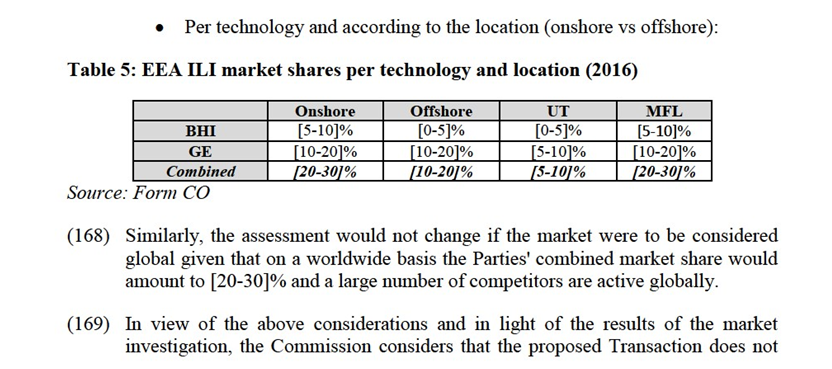

(110) The market investigation suggests that suppliers of OFS neutron sensors for one application may be able to start supplying OFS neutron sensors for another application in a relatively short timeframe (within 2 to 24 months) depending on the application and at costs of less than EUR 1 million. However, since this may not be sufficiently swift to assume that OFS gamma sensors for the different application belong to the same product market, these aspects will be assessed further in the context of potential entry (see recitals (257) to (266)).

(111) While the downstream markets for DD services, OHWL services and CHWL services may further be segmented in onshore and offshore services, the market investigation indicates that no such distinction can be made with regard to sensors.

(112) For the purpose of this decision, the Commission considers that the it can be left open whether the market for neutron sensors should be considered as whole or sub-segmented between DD, OHWL and CHWL applications since the proposed Transaction does not give rise to serious doubts even under the narrowest possible market definition.

4.7.1.3.Directional sensors

(113) Directional sensors describe a group of sensors, which help the OFS provider to locate the downhole tools in space by measuring the position of the drill string or the wireline tool relative to the earth’s magnetic and gravitational fields. Directional sensors are used in drilling and wireline applications. A typical directional sensor consists of 3 single-axis accelerometers and 2 bi-axial magnetometers mounted in a chassis that ensures alignment and orthogonality.111 The assembly also includes electronics to drive the sensors and process their output. A further distinction may therefore be made according to the specific measurements that the directional sensor performs.

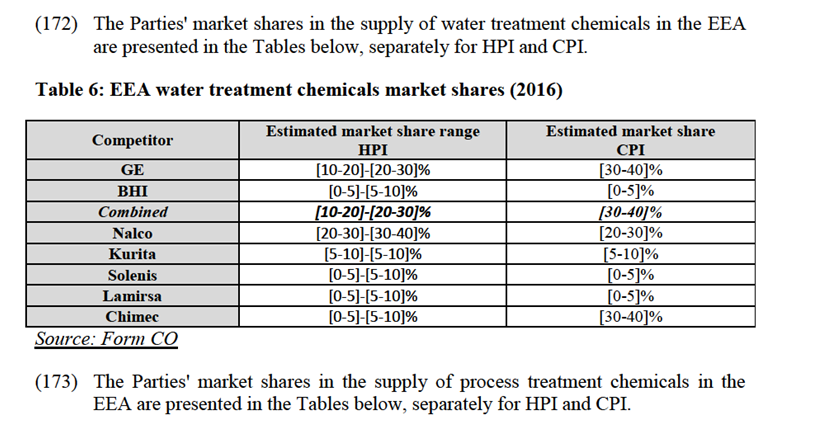

(114) While the downstream markets for DD services, OHWL services and CHWL services may further be segmented in onshore and offshore services, the market investigation indicates that no such distinction can be made with regard to sensors.

(115) However, for the purpose of this decision, the Commission considers that the exact scope of the product market definition can be left open, as the proposed Transaction does not give rise to serious doubts even under the narrowest possible market definition.

4.7.2.Geographic market definitions

(116) The Notifying Party submits that market for OFS gamma, neutron and directional drilling sensors is global in scope, because sensor providers offer their products globally and ship them to the various locations of their customers where they will be incorporated in the relevant drilling tool.

(117) While the U.S. administration may prohibit the sale of sensors to certain countries on sanction lists, the market investigation has confirmed that both customers112 and competitors consider the market to be otherwise global in scale without transport costs or other barriers limiting the supply of sensors to certain areas. Indeed, most sensor providers seem to have only one main manufacturing site from where they supply their customers on a global level.113

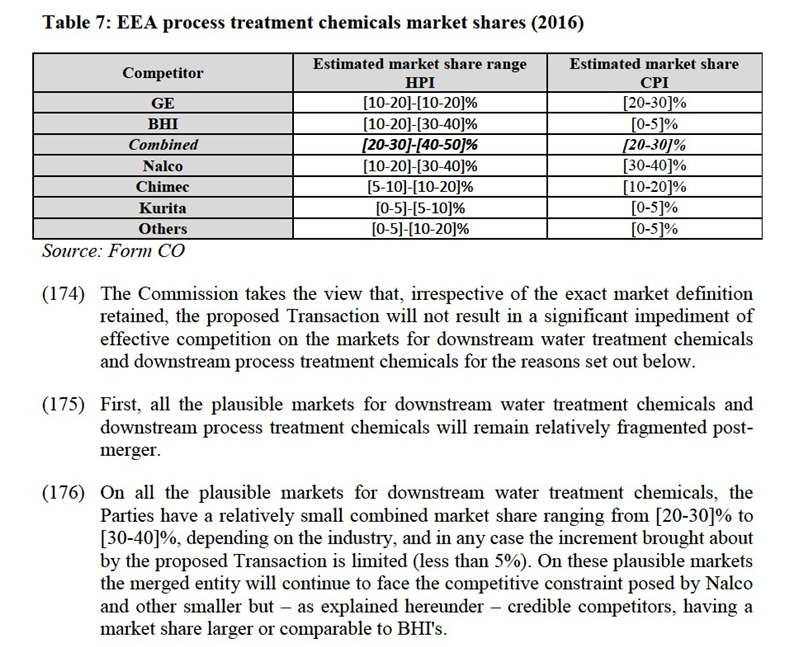

(118) The Commission therefore considers that the markets for the supply of OFS sensors are global in scope.

4.8. Wireline Tools

(119) GE manufactures wireline tools, which are then purchased by the large integrated OFS providers, such as BHI, or by smaller OFS provider for their respective drilling tools. There are two main types of wireline tools, namely OHWL tools and CHWL tools.

(120) The Notifying Party submits that a distinction can be made between OHWL and CHLW tools given that the two types of tools are used at different stages of the well development and are used for different purposes.114

4.8.1.Product market definition

(121) OHWL tools are tools which perform reservoir evaluation services in the uncased ("open") well, while CHWL tools perform a variety of services in the cased well. OHWL tools differ from CHWL tools in many ways.

(122) OHWL tools are lowered into the wellbore during or directly after the drilling process, but always before the borehole has been cased. OHWL tools usually perform reservoir evaluation services. OHWL tools are larger in diameter than CHWL tools and include probes and sensors for measuring rock properties and fluids trapped in the rock formations.115

(123) By contrast, CHWL tools are lowered into the wellbore after the well has been cased. They operate in the relatively protected environment of the cased well and perform a variety of different tasks. CHWL are typically more commoditised tools and often available off-the-shelf.116

(124) However, for the purpose of this decision, the Commission considers that the exact scope of the product market definition can be left open, as the proposed Transaction does not give rise to serious doubts even under the narrowest possible market definition.

4.8.2.Geographic market definition

(125) The Notifying Party submits that the markets for OHWL tools and CHWL are worldwide or at least EEA-wide in scope. The Notifying Party submits that tool manufactures sell their tools globally from a limited number of manufacturing locations.117 While some competitors have regional sales offices, others do not have regional hubs.118 However, for the purpose of this decision, the Commission considers that the exact scope of the geographic market definition can be left open, as the proposed Transaction does not give rise to serious doubts even under the narrowest possible market definition.

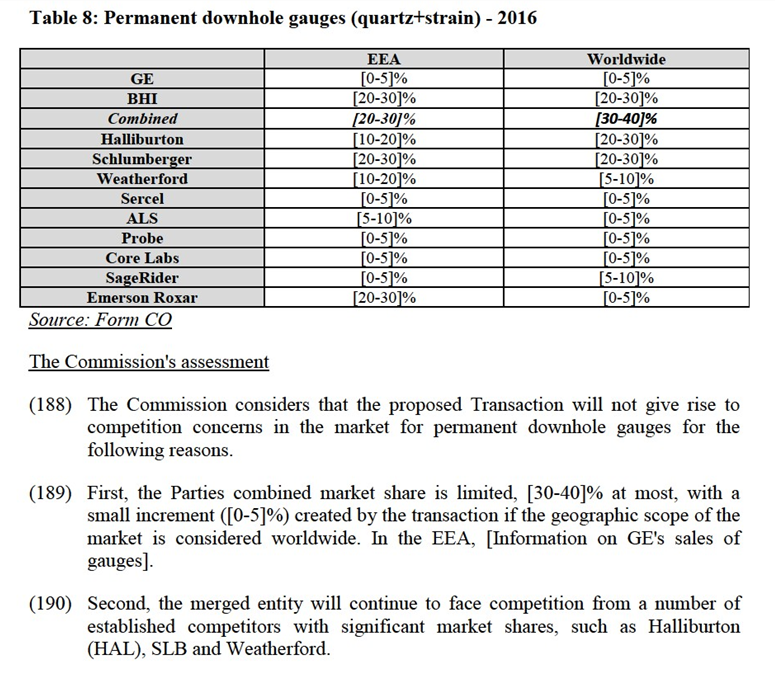

4.9.Permanent downhole gauges

(126) Permanent downhole gauges are sensors used primarily in wells not equipped with artificial lifts or with artificial lift other than ESPs to measure certain data, notably fluid temperature and pressure.

(127) Depending on the transducer technology used to measure physical changes, permanent downhole gauges can be distinguished in: (i) quartz gauges (equipped with quartz transducers) and (ii) strain gauges (equipped with strain transducers).

4.9.1.Product market definition

(128) The Parties submit that permanent downhole gauges are different from ESP sensors notably in light of their different design119, the type of measurement,120 and commercial strategy.121

(129) Customers almost unanimously indicated that the type of measurements performed by the two types of products is different and that they "do not have the same technical capabilities" While some customers indicated that in certain limited situations there is a degree of interchangeability, this appears to be very limited. On this basis the Commission considers that permanent downhole gauges likely constitute a separate product market from ESP sensors.

(130) The Notifying Party also argues that strain permanent downhole gauges and quartz permanent downhole gauges should be regarded as forming part of separate markets because: (i) they are based on different technology, (ii) the quartz technology allows for more accurate data measurement, faster transmission rates, and higher resolution of the information, and greater long term reliability,122 and (iii) quartz gauges are typically three to five times more expensive than strain gauges. 123 The Commission takes the view that a segmentation of the market for permanent downhole gauges by technology, i.e. strain and quartz, is likely to be appropriate as the market investigation indicated that: (a) Customers do not generally consider the two technologies as alternative and would not switch from one to the other in response to a small but significant and non-transitory increase in prices. In the words of a customer: "These gauges have different levels of accuracy and are used in different applications and as such are not interchangeable". (b) Quartz and strain gauges generally serve different applications. Quartz gauges are primarily used in offshore wells and onshore geothermal wells while strain gauges primarily in onshore wells. (c) Prices of strain gauges are significantly lower than prices for quartz gauges (quartz gauges can be up to ten times more expensive than strain gauges).

4.9.2.Geographic market definition

(131) The Notifying Party submits that the geographic scope of the market for permanent downhole gauges is at least EEA-wide, and possibly worldwide in scope owing to the fact that downhole gauges share the same technical characteristics irrespective of the location and are supplied by the same players worldwide. 124

(132) The Commission considers that the precise market definition can be left open as the proposed Transaction does not give rise to competition concerns under any plausible geographic market definition.

4.10.ESP sensors

(133) ESP sensors are specific sensors used to optimize and/or enhance the operation of an ESP. They are installed underneath the downhole ESP motor and powered by the power cable of the motor. ESP sensors aim at optimising reservoir performance and increase the ESP run life by measuring parameters on an ongoing basis. Parameters measured are generally reservoir pressure, fluid temperature, ESP pump intake and discharge pressure, motor temperature, system vibration and current leakage. The vast majority ESPs are offered with the sensor pre-installed, but some customers prefer using ESPs without sensors.

4.10.1.Product market definition

(134) The Notifying Party submits that ESP sensors should be considered as a single product market, distinct from other types of downhole sensors.125 The market investigation confirmed that the type of measurement performed by ESP sensors differs in scope from the data measured by other downhole sensors. Respondents to the market investigation indicated that downhole sensors are usually limited to gather information related to pressure and temperature while ESP sensors offer a wider range of data.126

(135) In view of the above, the Commission considers it likely that ESP sensors constitute a distinct product market.

4.10.2.Geographic market definition

(136) The Notifying Party submits that the geographic scope of the market for ESP sensors is at least EEA-wide, and possibly worldwide in scope owing to the fact that ESP sensors share the same technical characteristics irrespective of the location and are supplied by the same players worldwide.127

(137) The Commission considers that the precise market definition can be left open as the Transaction does not give rise to competition concerns under any plausible geographic market definition.

5.COMPETITIVE ASSESSMENT – HORIZONTAL OVERLAPS

(138) Under Article 2 (2) and (3) of the Merger Regulation, the Commission must assess whether a proposed concentration would significantly impede effective competition in the internal market or in a substantial part of it, in particular through the creation or strengthening of a dominant position.

(139) In this respect, a merger may entail horizontal and/or non-horizontal effects.

(140) As regards horizontal effects, the Commission guidelines on the assessment of horizontal mergers under the Merger Regulation (the "Horizontal Merger Guidelines"128) distinguish between two main ways in which mergers between actual or potential competitors on the same relevant market may significantly impede effective competition, namely non-coordinated and coordinated effects. Non-coordinated effects may significantly impede competition by eliminating important competitive constraints on one or more firms, which consequently would have increased market power, without resorting to coordinated behaviour. In that regard, the Horizontal Merger Guidelines consider not only the direct loss of competition between the merging firms, but also the reduction in competitive pressure on non-merging firms in the same market that could be brought about by the merger.

(141) The Horizontal Merger Guidelines list a number of factors which may influence whether or not significant non-coordinated effects are likely to result from a merger, such as the large market shares of the merging firms, the fact that the merging firms are close competitors, the limited possibilities for customers to switch suppliers, or the fact that a merger would eliminate an important competitive force. That list of factors applies equally if a merger would create or strengthen a dominant position, or would otherwise significantly impede effective competition due to non-coordinated effects.

(142) This decision will analyse whether the proposed Transaction is likely to raise doubts as to its compatibility with the internal market by the creation of non- coordinated effects in those markets on which the Parties' activities lead to horizontal overlaps.

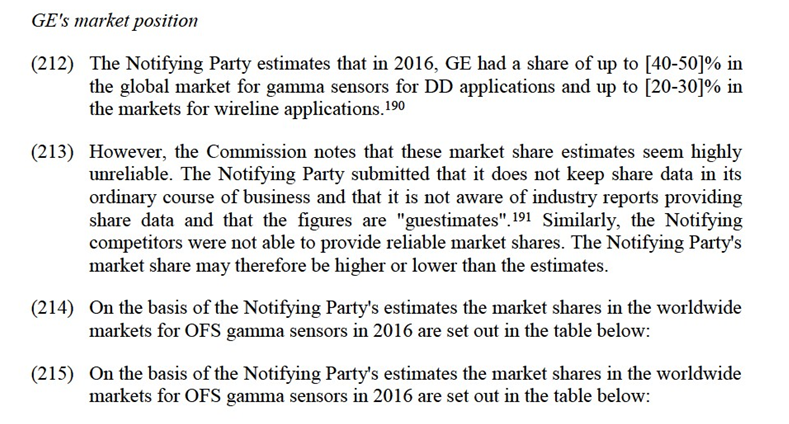

5.1.ESPs

5.1.1.Onshore ESPs

The Notifying Party's view

(143) The Notifying Party submits that the proposed Transaction will not raise competition concerns given GE is a rather small supplier both in the EEA and worldwide. Moreover, the Parties will continue to face competition from the market leader, SLB, as well as from other smaller suppliers active in the EEA such as Borets and Novomet. The Notifying Party also explains that entry is not difficult to provide the type of standard ESP systems GE supplies. 129

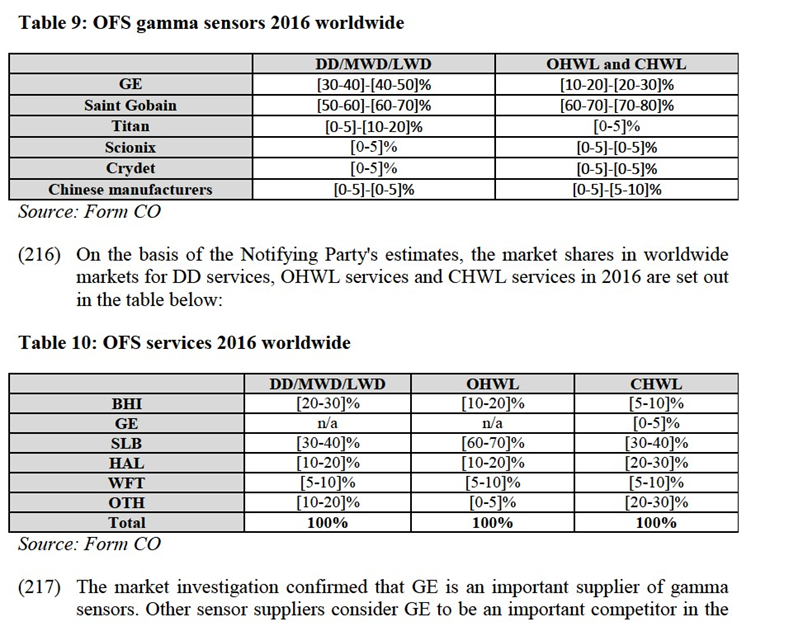

offering].132 As a result, going forward, GE's position would likely be even smaller than suggested by its current market share.

(149) Second, the vast majority of the onshore customers indicated that they have sufficient credible alternatives to which they could switch if need be.133 In particular, SLB, CAI, Borets and Novomet are seen as valid alternatives to the Parties.134

(150) Finally, customers view GE's technology as mainly limited to conventional wells and standard applications, whereas BHI's ESP systems are more sophisticated and can cover a wider range of applications.135 [Information on GE's ESP products].136

(151) On the basis of the above considerations and in light of the results of the market investigation and the evidence available to iy, the Commission considers that GE does not exert a significant competitive constraint on BHI pre-Transaction and that a number of suitable alternative suppliers will remain on the market post- merger. Therefore, the proposed Transaction does not raise serious doubts as to its compatibility with the internal market with respect to the supply of onshore ESPs.

5.1.2.Offshore ESPs

The Notifying Party's view

(152) The Notifying Party submits that the proposed Transaction will not raise competition concerns on the offshore market for ESPs given only BHI is active in the EEA. [Information on GE's sales strategy and R&D plans for ESP in the EEA].137

The Commission's assessment

(153) Only BHI and SLB are active offshore in the EEA with a share of respectively [40-50]% and [50-60]% in 2016. Some concerns have been raised by few market participants indicating that GE has taken part in offshore bids in the EEA, already works offshore outside the EEA and that it is making R&D efforts to upgrade its equipment.138 Nevertheless, the Commission has found that GE is unlikely to enter the offshore market (and to place a significant constraint on BHI and SLB) in a short to medium term for the reasons set out below.

(157) As explained by a competitor: "The industry moves very slowly and GE is suffering from this. For customers to change ESP supplier there needs to be a compelling factor. Price does not qualify as a compelling reason to switch suppliers in the EEA. […], especially offshore, where costs are in any case so high the price of the ESP does not play a major role. Customers would rather select an ESP supplier with a reliable track record and experience than a new supplier they have no experience with providing a cheaper ESP."147

(158) Responses to the market investigation also indicated that other suppliers are in the process of cooperating with customers operating offshore in the EEA to develop alternative solutions.

(159) On the basis of the above considerations and in light of the results of the market investigation , the Commission considers that GE is unlikely to enter the offshore segment given the high barriers to entry in the form of track record and reliability. Therefore, as only BHI and SLB are active suppliers of offshore ESPs, the proposed Transaction does not raise serious doubts as to its compatibility with the internal market with respect to that market (regardless of whether the Norwegian section of the North Sea is included or excluded).

5.2. ILI

The Notifying Party's view

(160) The Notifying Party submits that the proposed Transaction will not raise serious doubts in view of the limited combined position of the Parties and the fact that a significant number of players are active in the market, including Rosen, the market leader by quite some distance.148

The Commission's assessment

(161) The Commission considers that the proposed Transaction will not materially alter the structure of the market in view notably of BHI's small position and the fragmented nature of the market. A market participant raised concerns indicating that the merged entity will have a very broad portfolio that could impact the ability of other suppliers to compete effectively and that both Parties are important innovators, therefore the proposed Transaction could also reduce innovation.149 Nevertheless, the Commission has found those concerns to be unfounded for the reasons set out below.

(162) First, the Parties' combined share is approx. [20-30]% with a [0-5]% increment brought by BHI. The merged entity will be the second largest supplier in the EEA after Rosen, which will remain the market leader post-merger with a share almost twice as large as the combined share of the Parties. The Parties will also face a large number of other established suppliers.150 Customers largely confirmed they

water treatment and process treatment chemicals. These include Nalco, Kurita, Chimec, Solenis, Veolia, Dorf Ketal, Berardinello and Adquimica. For example, a customer noted that, "Generally, post transaction for each product there will always be an alternative supplier to the merged entity",168 that "There are sufficient suppliers in the market with good chemicals and know how" and that the alternative suppliers are credible "[…] independent from product type".169

(180) Customers have also indicated that local/regional suppliers (i.e. suppliers with a more limited geographic footprint than GE, BHI and Nalco) such as Kurita, Chimec and Dorf Ketal are credible alternatives.170 Local/regional suppliers are able to offer products with quality comparable to that of the global players and generally they have a complete product portfolio.171

(181) Fourth, customers responding to the market investigation indicated that switching suppliers is relatively common. Almost all the customers responding to the market investigation switched suppliers in some of their plants in the last five years. Of these switches, in a very limited number of instances, customers replaced GE with BHI or vice versa.172 Also, customers in general consider the cost of switching to be limited. For example, a customer said that "switching is not extremely cumbersome both in terms of cost and time".173

(182) Finally, the market investigation supported the Notifying Party's view that the industry is not capacity constrained. For example, a competitor indicated that it could accommodate an increase in demand up to 50% - 60% more than its current production and that, in addition, it is also looking to expand its blending capacity in the EEA.174

(183) On the basis of the above considerations and in light of the results of the market investigation, the Commission concludes that the proposed Transaction does not raise serious doubts as to its compatibility with the internal market with respect to the supply of downstream water treatment chemicals (whether intended for HPI or CPI) and downstream process treatment chemicals (whether intended for HPI or CPI).

5.4.Upstream chemicals

(184) While BHI has a relatively established position with a share of approx. [20-30]% in the EEA, GE has a negligible presence in the market. GE's share in the EEA (as well as worldwide) is [0-5]% under any plausible segmentation of the upstream

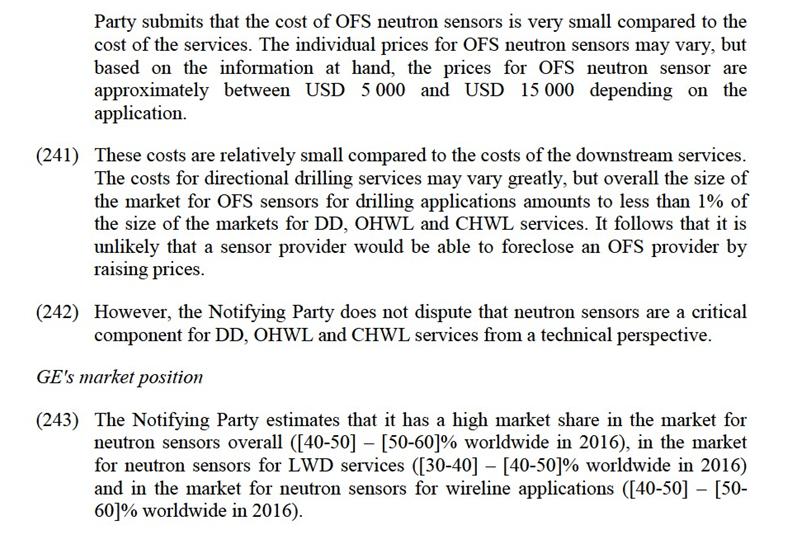

INSERER IMAGE 12+13

(191) Third, the vast majority of customers responding to the market investigation indicated that there are sufficient alternative suppliers to GE and BHI to which they could turn to post-merger.175

(192) Finally, all respondents to the market investigation indicated that the market for permanent downhole gauges is competitive and that the proposed Transaction will have no impact on its functioning and competitiveness.176

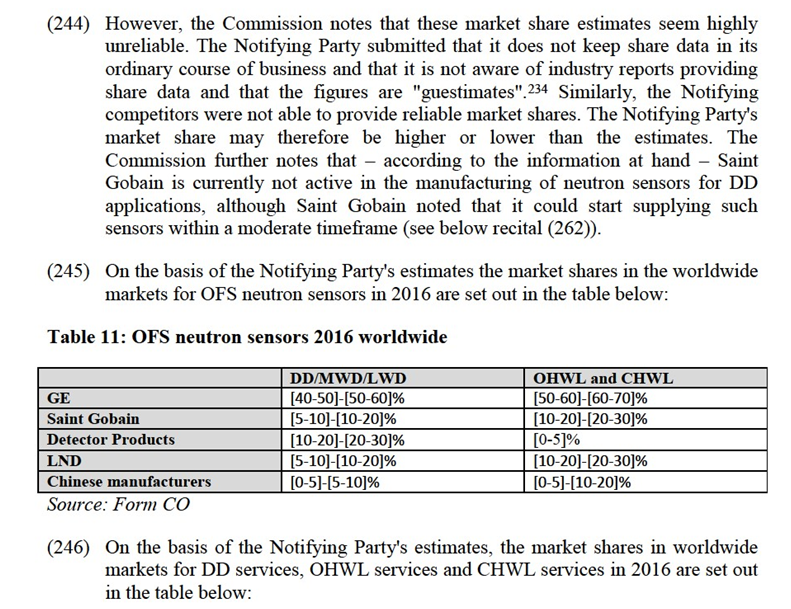

(193) On the basis of the above considerations and in light of the results of the market investigation and having regard to the minor increment created by the proposed Transaction on a worldwide level [Information on GE's sales of gauges in the EEA], the Commission considers that the proposed Transaction does not raise serious doubts as to its compatibility with the internal market on the market for permanent downhole gauges.

5.6.ESP sensors

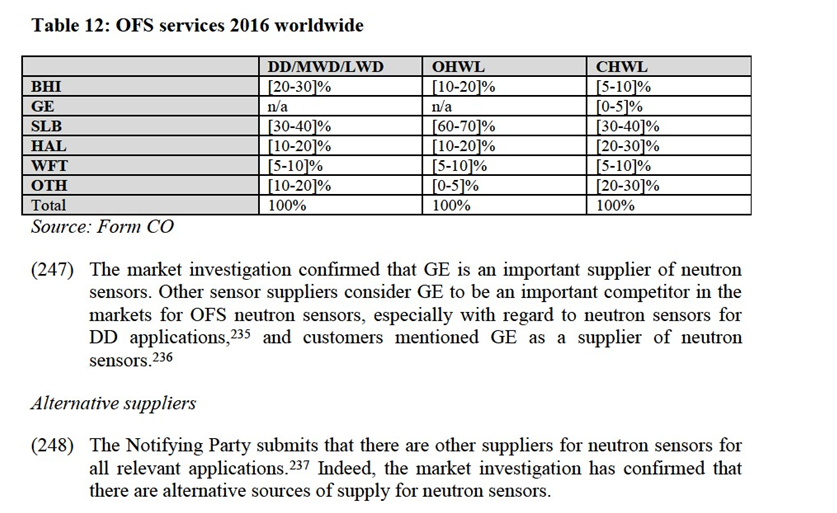

(194) The major ESP suppliers are vertically integrated and have in-house production of ESP sensors. As a result, external sales (ie. sales to third parties) are limited and account for less than one quarter of the total ESP sensor market.177

(195) The Notifying Party submits that the proposed Transaction does not raise competition concerns because (i) [Information on BHI's bidding activities for ESP sensors], (ii) [Information on BHI's sales strategy for ESP sensors], (iii) there are several alternative independent ESP sensor suppliers, and (iv) customers can easily switch between manufacturers because ESP sensors are not specifically engineered for a particular ESP and are essentially "plug and play" pieces of equipment.178

(196) The Commission considers that the proposed Transaction is unlikely to raise concerns in the market for ESP sensors for the reasons set out below.

(197) First, [Information on BHI's sales of ESP sensors in the EEA]. On a worldwide basis the Parties combined share on a worldwide basis is approximately [30- 40]%,179 with a relatively small increment created by the transaction ([5-10]%).

(198) Second, the merged entity will continue to face competition from a number of established ESP sensor manufacturers including: Sercel-GRC ([30-40]%), Elekton ([10-20]%), Oxford Monitoring Solution ([10-20]%) and Triol ([5-10]%).

(199) Third, respondents to the market investigation indicated that the market is rather competitive and that there are valid alternatives to the Parties.180

(200) Based on the above considerations and in light of the results of the market investigation, the Commission concludes that the proposed Transaction does not raise serious doubts as to its compatibility with the internal market for the supply of ESP sensors in the EEA.

6. COMPETITIVE ASSESSMENT – VERTICAL RELATIONS

(201) According to the Non-Horizontal Merger Guidelines,181 non-coordinated effects may significantly impede effective competition as a result of a vertical merger if such merger gives rise to foreclosure.

(202) The Non-Horizontal Merger Guidelines distinguish between two forms of foreclosure. Input foreclosure occurs where the merger is likely to raise the costs of downstream competitors by restricting their access to an important input. Customer foreclosure occurs where the merger is likely to foreclose upstream competitors by restricting their access to a sufficient customer base.

(203) Input foreclosure may raise competition problems only if the upstream product concerns an important input, if the merged entity has significant market power in the market for the provision of this input and if – by reducing access to its own upstream products or services, it could negatively affect the overall availability of these inputs for the downstream market. In its assessment the Commission also considers whether there are effective and timely counter-strategies that rival firms would be likely to deploy such as the possibility of changing their production process to reduce their dependence or the sponsoring of new suppliers in the market for the provision of the input.182Customer foreclosure may raise competition problems if the vertical merger involves a company, which is an important customer with a significant degree of market power in the downstream market. Customer foreclosure can in particular lead to higher input prices if there are significant economies of scale or scope in the input market.183

(204) The competitive assessment as regards potential input or customer foreclosure is not dependant on the downstream geographic market definition since sensors are purchased and sold on a global basis.

(205) Finally, given that the Commission considers that the Notifying Party will have no ability to foreclose its downstream rivals post-Transaction there is no need to assess whether it would have an incentive to do so.

(206) With regard to the proposed Transaction, the Commission has analysed the in particular the following vertical relations:(a) Gamma sensors (upstream market where GE is active), and DD, OHWL and CHWL services (downstream market where BHI is active)184; (b) Neutron sensors (upstream market where GE is active), and DD, OHWL and CHWL services (downstream market where BHI is active)185;

6.1. Gamma Sensors – DD, OHWL and CHWL services

(207) HAL is a large OFS provider and competes with BHI in the provision of OFS services. In its complaint and subsequent submissions, HAL noted that it purchases crystals for gamma sensors from GE and implied concerns in that regard.186 HAL considers that GE is the leading supplier for gamma sensors.187 Moreover, while HAL recognises that there are alternative suppliers such as Hunting-Titan and Saint Gobain, they are considered as less favourable alternatives.188 HAL further submitted that an alternative supplier would need to develop a high degree of specialisation and expertise to meet HAL's needs and that the time and expense for switching suppliers would be significant.189

(208) However, for the reasons set out in the following section the Commission considers it unlikely that the merged entity will have the ability to foreclose downstream competitors from the supply of gamma sensors for DD, OHWL and/or CHWL applications or upstream competitors from access to a significant customer base as a result of the proposed Transaction.

6.1.1.Input foreclosure

No ability to foreclose

Important input

(209) The Notifying Party submits that the cost of the OFS gamma sensors is very small compared to the cost of the services. The individual prices for OFS gamma sensors may vary, but based on the information at hand, the prices for OFS gamma sensor are approximately between USD 5 000 and USD 15 000 depending on the application.

(210) These costs are relatively small compared to the costs of the downstream services. The costs for directional drilling services may vary greatly, but overall the size of the market for OFS sensors for drilling applications amounts to less than 1% of the size of the markets for DD, OHWL and CHWL services. It follows that it is unlikely that a sensor provider would be able to foreclose an OFS provider by raising prices.

(211) Nonetheless, the Notifying Party does not dispute that gamma sensors are a critical component for DD, OHWL and CHWL services from a technical perspective.

markets for OFS gamma sensors192 and customers mentioned GE as an actual or alternative supplier of gamma sensors.193

Alternative suppliers