Commission, April 7, 2017, No M.8354

EUROPEAN COMMISSION

Judgment

FOX / SKY

Subject: Case M.8354 - FOX / SKY

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 3 March 2017, the European Commission received a notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 (3) by which Twenty-First Century Fox, Inc ("21CF" or the "Notifying Party", US) proposes to acquire the remaining shares that it does not currently own in Sky Plc ("Sky", UK, and the "Proposed Transaction"). 21CF and Sky are collectively referred to as the "Parties".

1. THE PARTIES

(2) 21CF (4) is a diversified global media company with operations in three main industry segments: cable network programming, television and filmed entertainment. The activities of 21CF are conducted principally in the United States, the United Kingdom, Continental Europe, Asia and Latin America.

(3) The legal predecessor of 21CF was News Corporation (US). On 21 December 2010, the Commission adopted a decision whereby it […]* unconditionally the proposed acquisition by News Corporation of British Sky Broadcasting ("BskyB") (BSkyB is now known as "Sky" and is the target in the present Proposed Transaction). (5) The NewsCorp/BskyB proposed transaction was ultimately abandoned. At the time of that proposed transaction, BskyB was active in the United Kingdom and Ireland.

(4) On 28 June 2013, the activities of News Corporation (that is, the acquirer in the NewsCorp/BskyB transaction), were separated into two distinct legal entities: (i) 21CF (the acquirer in the present case), which retained News Corporation's cable network programming, TV and filmed entertainment businesses; and (ii) News Corp, which retained the News Corporation's publication business.

(5) On 11 September 2014, the Commission adopted a decision whereby it cleared unconditionally the proposed acquisition by BskyB of Sky Deutschland and Sky Italia from 21CF. (6)

(6) Sky (7) is the holding company of subsidiaries carrying on business in a variety of sectors predominantly in the UK, Ireland, Germany, Austria and Italy (8), including: (i) licensing/acquisition of audio-visual ("AV") programming; (ii) TV channel wholesale supply in the UK and Ireland; (iii) retailing of AV programming to subscribers; (iv) provision of technical platform services to broadcasters on Sky’s direct-to-home ("DTH") platforms in the UK, Ireland, Germany and Austria; (v) sale of TV advertising; (vi) in the UK and Ireland, the provision of fixed-line retail telephony and broadband services.

2. THE OPERATION

(7) The Proposed Transaction relates to the proposed acquisition of control by 21CF over Sky by way of purchase of shares not already owned by it.

(8) On 15 December 2016, 21CF publicly announced pursuant to Rule 2.7 of the UK Takeover Code its firm intention to make an offer to acquire the fully diluted share capital of Sky not already owned by 21CF and its affiliates. This constitutes the announcement of the intention to launch a public bid in terms of Article 4(1) of the EUMR.

(9) As a result of the Proposed Transaction, 21CF will own 100% of the Sky shares and will acquire control of Sky pursuant to Article 3(1)(b) of the Merger Regulation.

(10) The information submitted by the Notifying Party indicates that 21CF's absence of control over Sky remains unchanged compared to the situation assessed by the Commission in case M.5932 – NewsCorp/BskyB.

(11) Like its legal predecessor, News Corporation, 21CF is currently a shareholder in Sky, with a shareholding of 39.14%. The remainder of the shares in Sky are publicly traded and widely held. Indeed, as at 18 January 2017, the only other shareholders with an interest of more than 2% were: (i) Blackrock, Inc – 5.22%; (ii) Franklin Resources – 4.09%; and Invesco – 3.56%.

(12) However, in line with the position adopted in its decision in NewsCorp/BskyB, the Commission considers, for the purposes of the case at hand, that 21CF does not currently control Sky within the meaning of the Merger Regulation, whether on a de jure or on a de facto basis, for the following reasons.

(13) First, 21CF holds a minority shareholding of 39.14% in relation to which, the voting rights that 21CF can exercise at general meetings, are capped at 37.19% pursuant to a voting agreement.9 Therefore, 21CF does not hold the majority of voting rights in Sky.

(14) Second, there are no special rights attached to the shares held by 21CF, which grant it the possibility of exercising control over Sky within the meaning of the Merger Regulation.

(15) Third, as regards voting at shareholder level, 21CF did not hold more than 50% of the total of the present shares that voted at annual general meetings of Sky over the period 2012-2016. The shareholder attendance rate at Sky's annual general meetings during that period was between a minimum level of 82.9% (2014) and a maximum level of 85.55% (2016). (10) 21CF accounted for 43.99% of all votes instructed at Sky’s most recent annual general meeting (13 October 2016), and an average of 44.35% over the period 2012 - 2016.

(16) Strategic decisions (notably those related to the budget and the business plan) in Sky are taken at the level of the Board of Directors on the basis of a majority of votes. 21CF does not have the right to appoint any director to Sky's board of directors. Therefore 21CF cannot impose or block decision making at this level. For completeness, the Board of Directors of Sky is composed of eleven Directors. Three of the eleven directors on Sky's Board of Directors are affiliated to 21CF. One of these directors currently chairs Sky's board. However, the Chairman does not carry a casting vote, and in any event, a majority of members (eight out of eleven) of Sky’s Board have no connection with 21CF.

(17) The information submitted by the Notifying Party indicates therefore that 21CF has no rights in relation to the passing or the blocking of strategic decisions in Sky.

(18) Also for completeness, Sky's directors (and Group CEO (11)) are appointed by the Board of Directors. Board members are then eligible for re-appointment at Sky’s Annual General Assembly with at least 50% of the votes expressed by the participating shareholders. Given its shareholding and voting rights level and the lack of special rights (regarding strategic decisions) attached to its shares, Sky cannot on its own impose, nor can it block decisions, including decisions related to the re-appointment of directors, at the level of the shareholders' meeting. Moreover, as explained above, 21CF held on average 44.35% of the total of the present shares that voted at annual general meetings of Sky over the period 2012-2016. Thus, the information submitted by the Notifying Party indicates that 21CF would not, on its own have the de facto ability to re-appoint board members at the level of the shareholder meeting.

(19) Fourth, the information submitted by the Notifying Party indicates that there are no economic links sufficient to give 21CF control over Sky on the basis of economic dependence.

(20) The Commission's above findings in paragraphs (12) - (19) above are in line with the position of the Commission adopted in its decision in NewsCorp/BskyB in which the Commission assessed the proposed acquisition by 21CF's legal predecessor, News Corporation, over BskyB. On the basis of similar elements to those considered above, in that case the Commission reached the conclusion that News Corporation's 39.14% shareholding did not confer control over Sky (then known BskyB) within the meaning of the Merger Regulation. (12) That position was later confirmed by the Commission in its decision in case M.7332 - BskyB/ Sky Deutschland/ Sky Italia. (13)

(21) The Proposed Transaction therefore constitutes a concentration pursuant to Article 3(1)(b) of the Merger Regulation.

(22) As indicated above, on 28 June 2013, the activities of News Corporation (that is, the acquirer in NewsCorp/BskyB) were separated into two distinct legal entities: (i) 21CF, which retained News Corporation's cable network programming, TV and filmed entertainment businesses; and (ii) News Corp, which retained the News Corporation's publication business.

(23) The Commission notes that The Murdoch Family Trust (the "MFT") is the largest shareholder in both 21CF (the acquirer in the present case) and in the media company, News Corp. (14) Together with minor interests associated with the businessman K. Rupert Murdoch, the MFT holds approximately 38.9% of 21CF’s voting shares and approximately 39.4% of News Corp’s voting shares respectively.

(24) For the purposes of the competition assessment in the present case, the question of whether K. Rupert Murdoch, the MFT or any member of the Murdoch family controls either 21CF or News Corp can be left open given that the outcome of the competitive assessment will not change whether or not K. Rupert Murdoch, the MFT or any member of the Murdoch family controls either 21CF or News Corp. For the purposes of the case at hand, the Commission has therefore undertaken the competitive assessment of the Proposed Transaction as if 21CF and News Corp were under common control.

3. EU DIMENSION

(25) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (15) (21CF: EUR 26 658 million; Sky: EUR 16 006 million; Combined: EUR 42 664 million). Each of them has an EU-wide turnover in excess of EUR 250 million (21CF: EUR […] million; Sky: EUR […] million), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State.

(26) The Proposed Transaction therefore has an EU dimension pursuant to Article 1(2) of the Merger Regulation.

4. RELEVANT MARKETS

(27) The Proposed Transaction relates to all the levels of the TV value chain. Section […]* first provides an overview of the TV value chain and the Parties activities at each level of the chain. Section 4.2 onward then discusses the product and geographic market definition for each level of the TV value chain.

(28) Moreover, as described at paragraph (24), the Commission has undertaken the competitive assessment of the Proposed Transaction as if 21CF and News Corp were under common control. Therefore, the Commission discusses the product and geographic market definition of the advertising market, where 21CF News Corp and Sky are active, in Section 4.5 and the newspaper publishing market, where News Corp is active, at Section 4.6.

4.1. Introduction – the TV value chain and the Parties’ activities

(29) AV content for television (TV content) comprises all products (films, sports, series, shows, live events, documentaries, etc.) that are broadcast via TV (16). In previous decisions, the Commission has identified different activities in the TV value chain, namely: (i) the production and supply of TV content (including the supply of pre-produced TV content and Commissioned TV content); (ii) the wholesale supply of TV channels; and (iii) the retail provision of TV services to end customers (17). As a part of its analysis of the Parties' activities, the Commission also considers: (iv) the sale of advertising on TV channels.

(30) Sections 4.1.1 to 4.1.3 […]** these levels of the TV value chain as well as providing an overview of the Parties' activities at each level in the UK, Ireland, Germany, Austria and Italy.

4.1.1. Production and supply of TV content

(31) This upstream level of the value chain concerns the production of new TV content. TV production companies produce TV content for either: (i) internal use on their own TV channels or retail TV services if they are vertically integrated in the wholesale supply of TV channels and/or in the retail provision of TV services (that is to say, captive TV production); or (ii) supply to third-party customers (that is to say, non-captive TV production).

(32) Third-party customers are typically: (i) TV channel suppliers (TV broadcasters), which then incorporate the TV content into linear TV channels, or (ii) content platform operators, which then retail the TV content to end users on a non-linear basis (that is to say, Pay-Per-View ("PPV") or video on demand ("VOD")), including non-traditional platforms, that is to say internet or so-called Over-The-Top ("OTT") platforms.

(33) TV broadcasters and TV distributors who source TV content for their TV channels or retail TV services generally have a choice between a number of sourcing models, which can be broadly categorised as follows:

(a) Obtaining TV content produced on an ‘ad hoc’ basis (that is to say tailor- made), by:

i. Commissioning TV content from a TV production company (which owns the relevant TV format);

ii. Hiring a TV production company to provide the technical means and deliver the finished TV content based on a format owned by the broadcaster; or

iii. Producing the content themselves by relying on their in-house facilities (captive TV production); or

(b) Acquiring broadcasting rights from TV production companies for pre- produced TV content (pre-produced TV content, sometimes referred to as off-the-shelf or tape sales).

(34) These are discussed further below.

4.1.1.1. Production and supply of commissioned TV production content

(35) In most cases, TV production companies produce TV content tailored to the needs of their customers on the basis of original TV formats (18) that they develop themselves or that they acquire from right holders (commissioned production). However, in some instances, TV production companies are hired by TV broadcasters or content platform operators to simply provide the technical production means and deliver the finished programme based on a TV format owned or acquired by the hiring company (production-for-hire or supply of TV production services).

(36) The production costs are usually borne entirely or almost entirely by the TV broadcasters or content platform operators. As regards ownership of the various rights relating to the TV content (for example, primary TV broadcast rights, ‘catch-up’, VOD, etc.), the extent to which those rights are retained by the production company – as opposed to the acquirer of TV content – may vary based on a number of factors, such as national regulation in the country concerned, the type of broadcasting, the outcome of the commercial negotiations between the parties, etc. Producers or the acquirers of TV content may then achieve secondary revenues by further licensing/distributing the TV content or the TV format to third parties.

(37) It follows that the supply-side of this market comprises TV production companies, while the demand-side comprises third parties that commission the production of TV content or hire TV production services, typically TV broadcasters or content platform operators.

(38) As regards the supply-side of the market:

(a) Sky has some minor activities in the supply of Commissioned TV content through its distribution arm, Sky Vision.

(b) 21CF is active in the supply of commissioned TV content through its JV with Apollo, Endemol Shine Group ("Endemol Shine"). (19)

(39) As regards the demand-side of the market:

(a) Sky acquires some commissioned TV content from third party content owners and distributors to include in its own channels and content platforms.

(b) 21CF does not acquire any commissioned TV content.

4.1.1.2. Licencing of broadcasting rights to pre-produced TV content

(40) This upstream level of the value chain concerns the licensing of broadcasting rights relating to pre-existing TV content – that is to say TV content that has been previously produced and is subsequently made available ‘off-the-shelf’ by the rights holder (so-called pre-produced TV content) – and broadcasting rights relating to sports events.

(41) The broadcasting rights relating to TV content can belong to one or more of the following: (i) the holder of the rights to the TV format; (ii) the production company that produced the TV content; and (iii) the company that commissioned the production of the TV content. In addition, the broadcasting rights can belong to a third-party distributor, to which they were licensed by the original owner, with a right to sub-license.

(42) All of these categories of rights owners, which constitute the supply-side of the market, license broadcasting rights to content aggregators, which constitute the demand-side of the market, namely: (i) TV broadcasters; or (ii) content platform operators.

(43) As regards the supply-side of the market:

(a) Sky licenses small amounts of pre-produced TV content through its distribution arm, Sky Vision.

(b) 21CF licenses pre-produced TV content through 20th Century Fox ("20CF"), Endemol Shine, and Fox Networks Group ("FNG").

(44) As regards the demand-side of the market:

(a) Sky acquires some pre-produced TV content from third party content owners and distributors to include in its own channels and for its content platforms;

(b) 21CF, through FNG, acquires a small amount of Pre-Produced TV content from third party content owners and distributors to include in its own channels.

4.1.2. Wholesale supply of TV channels

(45) TV broadcasters use the TV content that they have acquired or produced in-house in order to package it into linear TV channels. (Linear) TV channels are broadcast to end users either on a free-to-air ("FTA") basis or on a pay-TV basis.

(46) At a very general level, FTA channels are TV channels that are available to viewers free of charge. Pay-TV channels are channels for which the viewer must pay a subscription fee in order to watch. Traditionally, FTA channels finance their operations via advertising revenues (with the exception of the publicly-owned TV channels in a number of Member States which are not allowed to sell advertising space), while pay-TV channels generate revenues through subscription fees.

(47) The Commission notes that TV broadcasters are increasingly complementing their traditional linear TV channel offering with non-linear services such as VOD services. (20)

(48) Some TV broadcasters are vertically integrated as they are also active […]* retail TV operators (TV distributors) in the market for the retail provision of TV services to end users. Other TV broadcasters are not vertically integrated and rely on third party TV distributors to distribute their TV channels at the retail level.

(49) As regards the supply-side of the market:

(a) Sky supplies channels to TV distributors and also holds a 50% stake in channel provider A&E Networks UK, a joint venture with A&E Networks. Sky does not supply channels on a wholesale basis in Italy, and does so only to a limited extent in Germany. (21)

(b) 21CF supplies a range of channels such as FOX, National Geographic, and BabyTV, to TV distributors. 21CF supplies the Fox Sports Channel in the Netherlands and Italy. 21CF also owns Star TV, which distributes a number of special-interest channels targeted at the South Asian community.

(50) As regards the demand-side of the market:

(a) Sky enters into agreements with TV broadcasters for the distribution of TV channels in the UK, Ireland, Germany, Austria and Italy.

(b) 21CF does not acquire TV channels.

4.1.3. Retail provision of TV services to end users

(51) TV distributors either limit themselves to carrying TV channels and making them available to end users, or also act as channel aggregators, which ‘package’ TV channels. The TV services supplied by TV distributors to end users consist of: (i) packages of linear TV channels (which they have either acquired or produced themselves); and (ii) content aggregated in non-linear services, such as VOD, SVOD, TVOD and PPV. TV content can be delivered to end users through a number of technical means including cable, satellite and IPTV.22 OTT players deliver channels and content in both a linear and non-linear fashion through the use of the internet.

(52) The content offered by the TV distributor is presented in an electronic programme guide ("EPG"), which is an application used on television sets to list current and scheduled programmes that are or will be available on each channel and a short summary or commentary for each programme. Each channel broadcast on the TV platform receives an EPG position, which is usually agreed between the TV broadcaster and the TV distributor. Traditional EPGs are not always used with regard to online content platforms and other non-linear methods of supplying content, or may form only part of a TV distributor's customer interface.

(53) In the retail provision of TV services to end users:

(a) Sky offers retail services in the UK, Ireland, Germany, Austria and Italy.

(b) 21CF supplies one FTA channel in the UK.

4.2. Production and supply of TV content

4.2.1. Product market definition

4.2.1.1. Commission precedent

(54) With regard to the market for the supply of TV content, in previous decisions the Commission has concluded that there are separate markets for the: (i) production and supply of commissioned TV content; and (ii) licencing of broadcasting rights for pre-produced TV content. (23)

(55) With regard to the market for licencing of broadcasting rights for TV content, the Commission has considered that it could be subdivided by content type, in particular: (i) films; (ii) sports; and (iii) other TV content (i.e. all non-sport, non-film content); and potential sub-segments within these content types. Ultimately, the Commission left the exact scope of the product market open. (24)

(56) The Commission has also considered further sub-dividing the market for the licensing of broadcasting rights for TV content by exhibition window: (i) subscription video on demand ("SVOD"); (ii) transactional video on demand ("TVOD"); (iii) pay-per-view ("PPV"); (iv) first pay-TV window; (v) second pay-TV window; and (vi) FTA; but left the market definition open. (25)

4.2.1.2. Notifying Party's view

(57) The Notifying Party submits that it is not necessary for the Commission to make a determination on the product market definition for the supply of TV content given the competitive assessment would not change.

(58) The Notifying Party argues that the production and supply of TV content is a heterogeneous activity which makes it difficult to reliably define separate markets. In particular, the Notifying Party does not consider a segmentation of TV content in premium and non-premium content as appropriate. (26)

(59) The Notifying Party further submits that if the Commission were to consider a separate market for sports, it should be a market for the supply of all sports content, which would include the live broadcast of sporting events, as well as sports highlights. (27) Similarly, if the Commission were to consider a market for the supply of film content, the Notifying Party submits that it should encompass all film content, irrespective of origin and across all exhibition windows. Furthermore, in relation to a potential market for other TV content, it submits that it would not be appropriate to further segment this market between pre-produced TV content and commissioned TV production or by type of content (e.g. factual, general entertainment, youth).

(60) Finally, the Notifying Party submits that it would not be appropriate to segment by exhibition window or by type of broadcaster.

4.2.1.3. The Commission's assessment

(61) The results of the market investigation indicate that: (i) commissioned TV content; and (ii) pre-produced TV content; […]* substitutable from either the demand or the supply side. (28) From the demand side, most TV broadcasters note that commissioned TV content is produced especially to meet the taste of the local viewers and that there are significant differences in cost compared to pre-produced TV content. (29) From the supply side, respondents note that significant investment in additional expertise, infrastructure and creative potential would be needed for a company only active in the licensing of pre-produced TV content to start the production of commissioned TV content. (30)

(62) Therefore, it appears that the production of commissioned TV content and the licensing of broadcasting rights for pre-produced TV content are two separate product markets.

(63) With regard to the type of TV content, the market investigation confirms that from the demand side: (i) films; (ii) sport; and (iii) other TV content; are not substitutable and that there are significant differences from a supply side (31). Most of the right holders responding to the market investigation consider that a company which is only active in the production of films or sports content would not be able to start producing TV programmes other than films and sports within a short timeframe and without incurring significant additional costs. (32)

(64) There is also evidence to suggest that these types of TV content should be further sub-divided. With regard to films, most TV broadcasters (from the demand side) and rights holders (from the supply side) indicate that the US films (i.e. films produced by the six 'major' Hollywood studios - Warner, Universal, Disney, 21CF, Paramount and Sony) and other non-US films are not substitutable. Respondents note that major Hollywood studios have a higher budget, are able to attract the mass market and have good international and national reputation. (33)

(65) With regard to other TV content, most TV broadcasters (from the demand side) and rights holders (from the supply side) consider that scripted and unscripted TV content are in general not substitutable with each other due to their differences in the audience, types and genre of content, as well as production process and budget. (34)

(66) The information gathered during market investigation also indicates that premium and non-premium other TV content are not substitutable. These different types of TV content have different costs, target audience and have different competitive and revenue potentials. One respondent noted that the production of premium TV content, especially high end TV series, can be compared with cinema productions in terms of production value. Another respondent highlights that premium and non-premium TV content are in general complementary. (35)

(67) The results of the market investigation suggest that the market for the licensing of pre-produced TV content could be further segmented according to the exhibition window and type of content, in line with the Commission’s previous decisions. (36) With regard to the exhibition window, the market investigation indicates that the majority of the content owners continue to licence their content separately and with different terms with the following windows: (i) SVOD; (ii) TVOD; (iii) PPV; (iv) first pay-TV; (v) second pay-TV; and (vi) FTA. (37)

(68) In any event, for the purpose of this decision, the exact product market definition for production of commissioned TV content and the supply of pre- produced content can be left open, as the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market regardless of whether the market is sub-divided this way or whether these segments are further segmented as described above.

4.2.2.Geographic market definition

4.2.2.1. Commission precedent

(69) In past decisions, the Commission has defined the market for the production and supply of TV content, including production of TV content and the licensing of broadcasting rights for TV content to be either national or regional, based on linguistically homogeneous areas. (38)

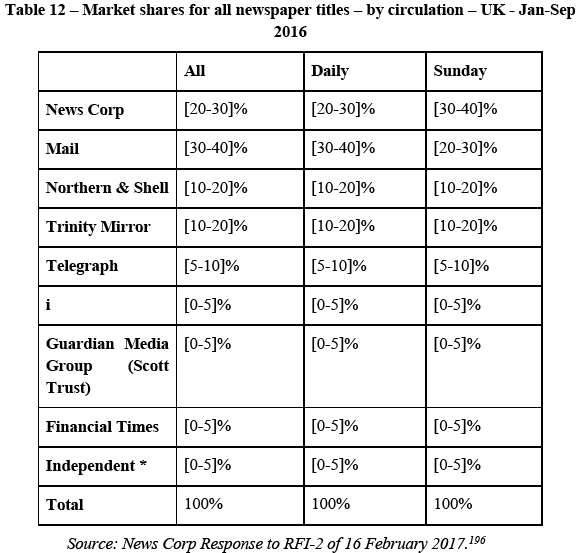

4.2.2.2. Notifying Party's view

(70) The Notifying Party agrees with this market definition and submits that the relevant geographic market for the production and supply of TV content, or any more narrowly defined markets, is either national or regional, based on linguistically-homogeneous areas.

(71) Whether content is licensed on a linguistic region basis primarily depends on the business model of the licensee and the territories where it is active. By contrast, a FTA broadcaster that is only located in one Member State would naturally require a licence for that Member State only.

(72) Ultimately, the Notifying Party submits that the precise geographic scope of the market can be left open in this case.

4.2.2.3. The Commission's assessment

(73) The results of the market investigation suggest that most of the respondents among rights holders and TV broadcasters supply and purchase content nationally or for certain linguistic regions; by way of example, some broadcasters indicate that they buy content for the whole German speaking region since viewing tastes are largely identical. (39)

(74) In any event, for the purpose of this decision, the exact geographic market definition for supply of commissioned TV content and the supply of pre- produced TV content can be left open, as the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market regardless of whether the market is considered to be national or by linguistic region.

4.3. Wholesale supply of TV channels

(75) TV broadcasters package the TV content that they have acquired or produced in-house into linear TV channels. Linear TV channels are broadcast to end users either on a FTA basis or on a pay-TV basis. This wholesale level is an intermediate activity between upstream production and licensing of content, and the downstream retail provision of TV services to customers.

4.3.1. Product market definition

4.3.1.1. Commission precedent

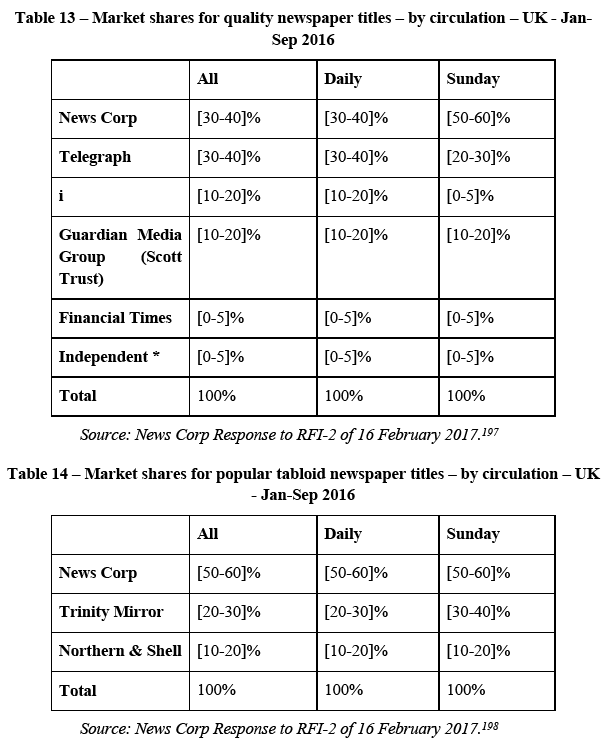

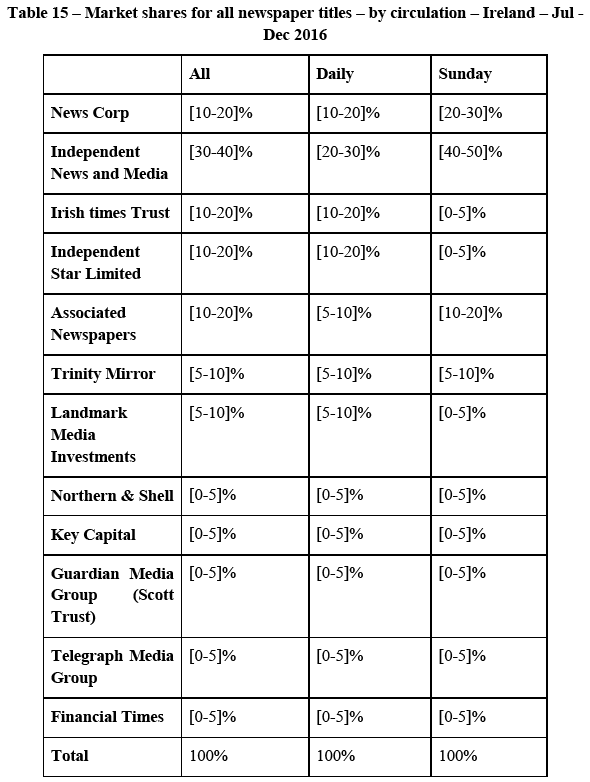

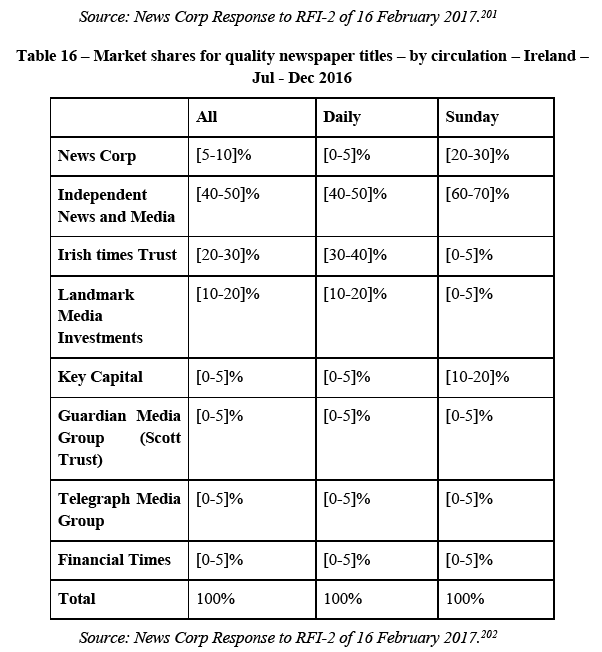

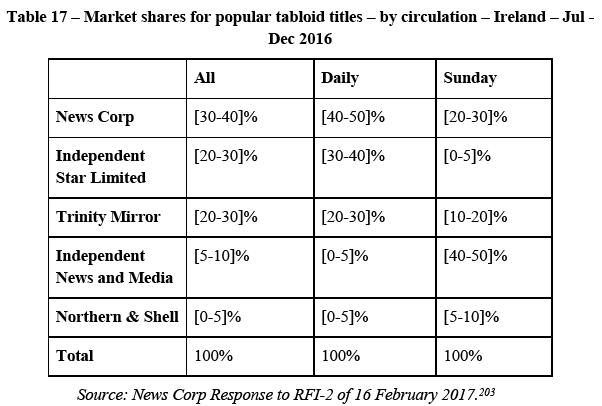

(76) In previous decisions, the Commission has identified a wholesale market for the supply of TV channels. Within that market, the Commission has further identified two separate product markets for: (i) FTA TV channels; and (ii) pay-TV channels (40). The Commission has further concluded that within the pay-TV channel market, there are separate markets for: (i) premium pay-TV channels; and (ii) basic pay-TV channels, conducting the assessment for FTA channels within the market for basic pay-TV channels. (41)

(77) In previous decisions, the Commission also examined a number of other potential segmentations, including: (i) genre or thematic content (such as films, sports, news, youth, and others) (42); (ii) linear channels vs non-linear services (VOD, PPV) (43); and (iii) the different means of infrastructure used for the delivery to the viewer (cable, satellite, terrestrial TV and IPTV). 44 It has ultimately left the market definition open in all these regards.

4.3.1.2. Notifying Party's view

(78) The Notifying Party notes that in its previous decisions the Commission has identified a separate wholesale market for the supply of TV channels and considered a number of other potential segmentations.

(79) The Notifying Party considers that the question of whether the wholesale market for the supply of TV channels must be further segmented according to the type of TV channels or according to the type of platform can be left open.

4.3.1.3. The Commission's assessment

(80) The market investigation indicates that the segmentation between FTA and pay-TV channels continues to be appropriate. Respondents highlight the differences in terms of content, pricing, audience and how broadcast rights are licenced, with price being the key differentiating factor. Most respondents do not consider basic pay-TV specifically and FTA channels to be substitutable (45), citing the significant differences in business models betweenFTA (mainly financed by advertisements and sometimes by public funds) and pay-TV channels (mainly financed by the fees paid by pay-TV retailers). (46)

(81) The results of the market investigation also suggest that a distinction should be made between basic pay-TV and premium pay-TV channels with most respondents considering them not to be substitutable. Several respondents note that premium pay-TV channels typically offer very specific content, e.g. sports, movies or exclusive content which has a particular value to the customer and is not available on basic pay-TV channels. (47)

(82) The results of the market investigation were mixed as to whether the market should be further sub-divided according to genre. Most respondents indicate that channels of a specific genre are only substitutable with channels in the same genre. Several respondents explain that thematic channels are created for specific target audiences. One respondent notes that factual channels are a distinct feature of any pay-TV package and cannot be substituted by channels in another genre. (48)

(83) On the other hand, some respondents indicate that certain genres are substitutable to a certain degree, such as factual channels and general entertainment channels. One respondent notes while TV distributors should offer a complementary ranges of genres, they have flexibility regarding the composition. (49)

(84) With regard to a possible segmentation of TV channels depending on the type of infrastructure used for their transmission, the results of the market investigation did not indicate that there are any differences on either the demand- or supply- side of the market according to the type of infrastructure the TV distributor operates. (50)

(85) In any event, for the purpose of the present decision, the question whether the market for the wholesale supply of TV channels should be further segmented based on the type of infrastructure, among FTA, basic pay-TV and premium pay-TV or by genre could be left open, as the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market under any of these product market definitions.

4.3.2. Geographic market definition

4.3.2.1. Commission precedent

(86) In previous decisions, the Commission found the market for the wholesale supply of TV channels to be either national in scope (51), sub-national (52), or by linguistic region encompassing more than one Member State. (53)

4.3.2.2. Notifying Party's view

(87) The Notifying Party considers […]* national or confined to linguistic region but, in any case, submits that the precise geographic scope of the market can be left open in this case.

4.3.2.3. The Commission's assessment

(88) According to the respondents to market investigation, the majority of agreements between TV broadcasters and retail TV distributors for the wholesale supply of TV channels are negotiated on either a national, sub-national or linguistic basis. (54)

(89) In any event, for the purpose of this decision, the exact geographic market definition for wholesale supply of TV channels can be left open, as the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market regardless of whether the market is considered as national, sub-national or by linguistic region.

4.4. Retail provision of TV services

4.4.1. Product market definition

4.4.1.1. Commission precedent

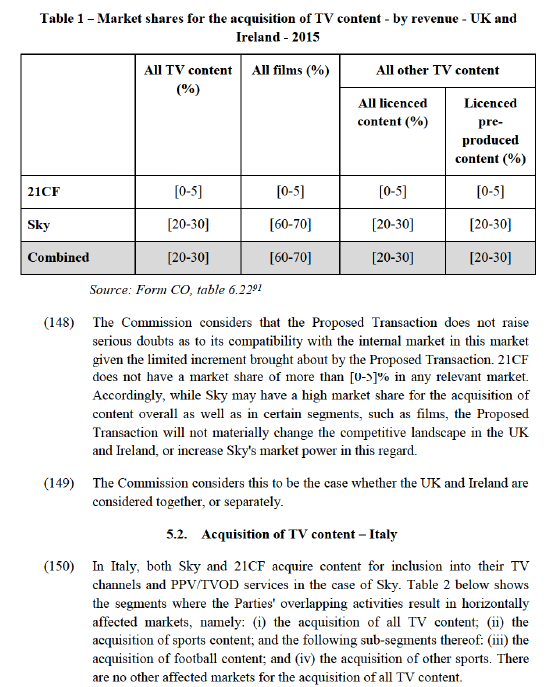

(90) In previous cases the Commission has split the retail supply of television services in two separate markets: (i) FTA and pay-TV . The Commissionalso considered whether pay-TV (55) can be segmented further according to: (ii) linear vs non-linear pay-TV services (56); (iii) according to distribution technologies (e.g. cable, satellite, or terrestrial) (57); and (iv) premium vs basicpay-TV services (58). In recent cases, the Commission has left open the market definition with regard to each of these potential sub-segments.

(91) Notifying Party's view

(92) The Notifying Party submits that the relevant market is the provision of all TV services to end users.

(93) First, the Notifying Party submits that the retail supply of FTA TV and pay- TV should be considered as one market as they are in direct competition for content rights, audiences and advertising revenues.

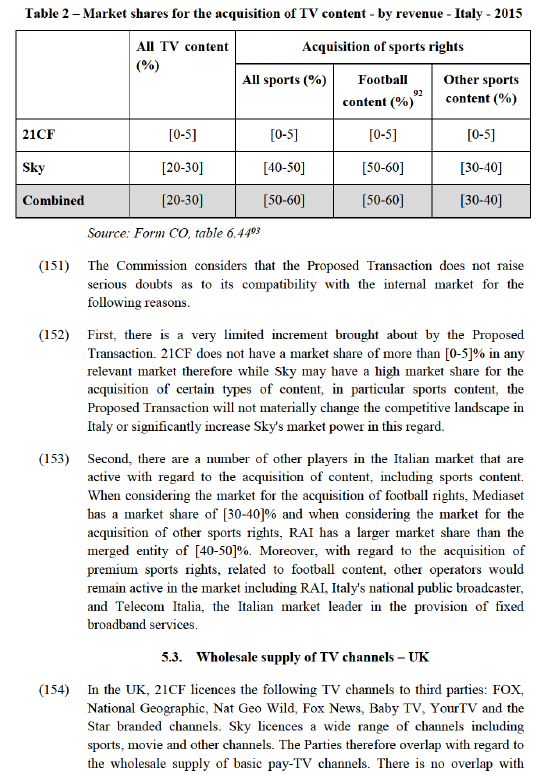

(94) The Notifying Party argues that retail operators typically offer both linear and non-linear services to their customers, and in the case of pay-TV services these are commonly packaged within a single subscription. There is also a huge range of FTA and paid for content that is available on an OTT basis.

(95) The Notifying Party also argues that it is not appropriate to distinguish between different means of television distribution.

(96) Finally, the Notifying Party does not consider it appropriate to distinguish basic pay-TV from premium pay-TV at the retail level.

4.4.1.2. The Commission's assessment

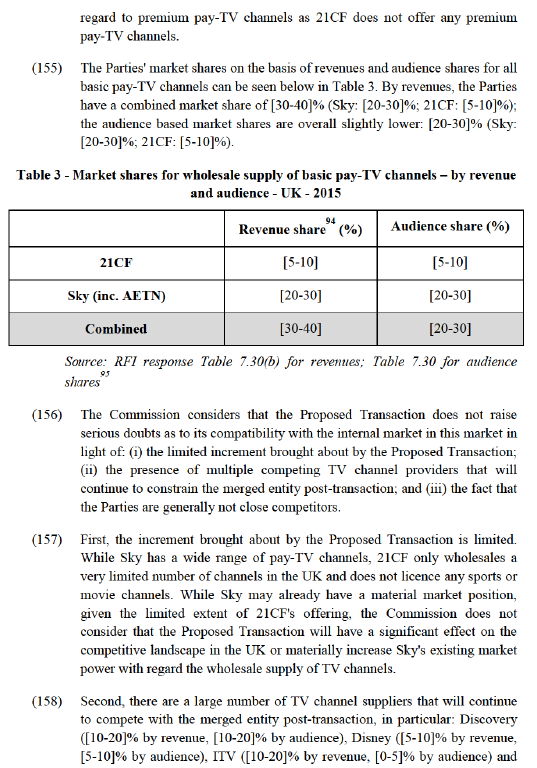

(97) With regard to a potential segmentation of the market for the […]* of TV retail services between FTA and pay-TV, most of the respondents consider that within the market for retail distribution of TV content to viewers, a distinction should be made between the two. Respondents note that there is a clear distinction from consumers' point of view between FTA and pay-TV with the first having a generalist content approach and the latter a more specific one, offering access to premium content such as live sports. (59)

(98) Respondents to the market investigation have mixed views on whether linear TV channels and non-linear services (such as VOD) are substitutable. On the one hand, some respondents indicate that they are substitute since they both compete for viewing time and provide access to identical programming. On the other hand, other retail TV providers consider these services as complements since they have different modes of consumption, different target groups and are not substitutable with each other. (60)

(99) With regard to a possible segmentation of TV channels depending on the type of infrastructure used for their transmission, the results of the market investigation provide mixed results with some respondents arguing that most of the content is available on each technology and it does not matter how it reaches the household while others saying certain services, such as interactivity, are available only for certain infrastructure. (61)

(100) The majority of respondents to market investigation consider that a distinction should be made between basic pay-TV and premium pay-TV services (62). As explained in paragraph (81), the market investigation indicates that basic pay-TV channels and premium pay-TV channels constitute separate product markets; in turn this results in a distinction between […]* includes premium pay-TV channels and a basic pay-TV offering which does not.

(101) In any event, for the purpose of the present decision, the question whether the market for the provision of TV retail services should be further segmented based on the type of infrastructure, among FTA, basic and premium pay-TV could be left open, as the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market under any of these alternative product market definitions.

4.4.2. Geographic market definition

4.4.2.1. Commission precedent

(102) The Commission has previously considered that the market for the retail provision of TV services is either national, or limited to the geographic coverage of a supplier's cable network. (63)

4.4.2.2. Notifying Party's view

(103) The Notifying Party treats the geographic scope of the market as being national but submits that the analysis would not be materially different if the markets were combined into linguistic regions.

(104) Ultimately, the Notifying Party submits that the precise geographic scope of the market can be left open in this case.

4.4.2.3. The Commission's assessment

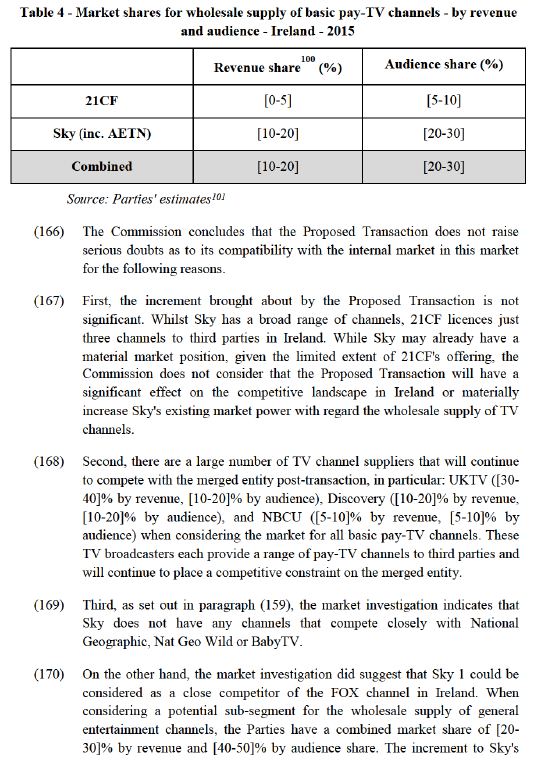

(105) The results of the market investigation suggest that a large majority of distributors make their retail offering available to end customers on a national basis. Some of them also operate on a sub-national level. (64)

(106) In any event, for the purpose of this decision, the exact geographic market definition for the retail provision of TV services can be left open, as the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market whether considered nationally or by linguistic region.

4.5. Advertising

4.5.1. Product market definition

4.5.1.1. Commission precedent

(107) The Commission has previously defined separate product markets for the sale of advertising space in national newspapers and TV broadcasting (65). The Commission has also drawn a distinction between online and offline advertising, due to each channel's specificity and different pricing mechanisms. (66)

(108) Within newspaper advertising, the Commission has considered distinguishing national from local newspapers (67) and daily national newspapers from non-daily national newspapers (68).

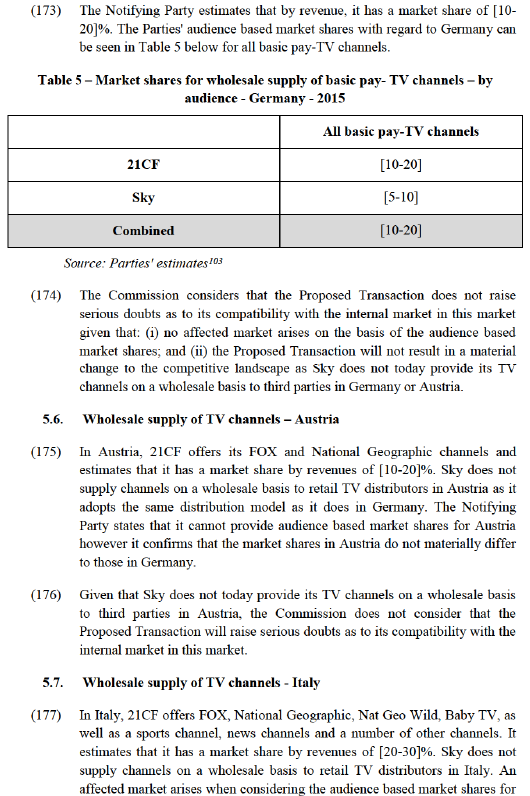

(109) With respect to TV advertising, the Commission has not previously distinguished between advertising space on FTA channels and pay-TV channels (69).

4.5.1.2. Notifying Party's view

(110) The Notifying Party points out that advertisers typically utilise TV advertising to reach a mass audience, while at the same time seeking to reach particular audience demographics that might be delivered by advertising on particular channels or programs. It also argues that online advertising exercises an increasing competitive constraint on TV advertising, but considers that the precise definition of the relevant market can be left open.

4.5.1.3. The Commission's assessment

(111) The results of the market investigation confirm that advertising on TV channels and advertising in print newspapers are separate product markets as these media perform different functions: advertisers can communicate emotionally engaging messages to a broad audience through TV advertising, whereas print ads are rather used to advertise a product in details to a targeted audience.

(112) Concerning advertising in print newspapers, (70) the market investigation confirmed that daily and non-daily newspapers form separate relevant markets. Daily newspapers allow for planning around specific dates and events, whereas this possibility is limited with non-daily newspapers. On the other hand, non- daily newspapers allow for messaging that require more contemplation because readers spend more time on these publications. The market investigation also confirmed that national and local newspapers cannot be substituted as national newspapers offer broader coverage than local newspapers. Advertising in national newspapers thus cannot be readily replaced by advertising in several local newspapers because these have different audiences.

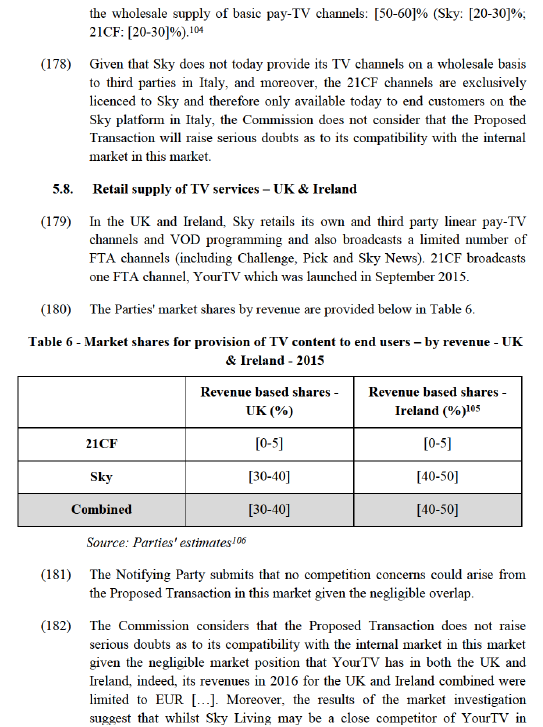

(113) Concerning advertising on TV channels, market participants noted differences between FTA and pay-TV channels in terms of reach, target and costs, with pay-TV channels more adequate to targeted campaigns whereas advertising on FTA TV channels offers a broadest reach.

(114) In line with previous Commission […]* and in the light of the results of the market investigation, the Commission takes the view that TV advertising and newspapers advertising constitute separate markets. As regards the possible segmentations within these markets, for the purposes of the present decision, the exact product market definition can be left open as the Proposed Transaction does not raise any competition concerns under any of the above possible market definitions.

4.5.2. Geographic market definition

4.5.2.1. Commission precedent

(115) In terms of geographic scope, previous Commission decisions have taken the view that the markets for TV and newspaper advertising are national (71).

4.5.2.2. Notifying Party's view

(116) The Notifying Party considers that the precise definition of the relevant market can be left open in this case.

4.5.2.3. The Commission's assessment

(117) The results of the market investigation suggest that the relevant geographic market for advertising remains national and does not comprise both UK and Ireland. Whereas the main buyers and sellers of advertising space as well as the intermediary agencies are similar in the UK and Ireland, prices remain different between the two countries.

(118) In line with previous decisions, the Commission takes the view that the markets for TV and newspapers advertising are national in scope.

4.6. Newspaper publishing

4.6.1. Product market definition

4.6.1.1. Commission precedent

(119) Newspapers are two-sided markets, competing for readership on one side of the market and advertising revenues on the other. Newspaper publishing refers to the market on which newspapers compete for the sale of newspapers and subscriptions to consumers.

(120) In previous decisions, the Commission concluded that written press was separate from other media products (such as TV and radio products).(72)

(121) Furthermore, in News Corp/BskyB the Commission examined whether print newspapers and online news services, whether free or at a fee, constituted separate product markets, but ultimately left that question open.(73)

(122) In News Corp/BskyB the Commission investigated whether news delivery through digital devices such as tablets (e.g. Apple's iPad or Samsung's Galaxy) or e-readers (such as Amazon's Kindle) belong to a separate market or are part of the same market as print, or online, newspapers, but ultimately left the product market definition on this point open.(74)

(123) The Commission has in the past also concluded that the national print newspaper market contains three segments: (i) popular tabloids; (ii) mid-market titles; and (iii) the quality segment. (75)

(124) In the past, the Commission also considered distinguishing between (i) daily and non-daily (i.e. weekly, monthly) newspapers (76) and (ii) national and regional or local newspapers, (77) but ultimately did not reach a conclusion on product market definition

4.6.1.2. Notifying Party and NewsCorp's view

(125) The Notifying Party does not express an opinion on the product market definition for newspaper publishing.

(126) Without expressing an opinion on the exact product market definition, News Corp has submitted that newspaper publishing in the UK and Ireland has been affected by convergence of different forms of media in recent years. (78)

(127) With regard to the segments of “popular tabloid”, “mid-market” and “quality” newspapers News Corp notes that any historic difference between these categories from the reader’s perspective has become increasingly blurred in recent years.

(128) News Corp further submits that online consumers would also have the option of other news sources, such as the branded websites of the BBC and other television broadcasters, in addition to international and specialist news providers. Moreover, dedicated providers of online news would compete with a range of sources not focused solely – or even principally – on the provision of news.

4.6.1.3. The Commission's assessment

(129) With regard to the question whether printed newspapers belong to the same relevant product market as free and paid-for online news services, a majority of newspapers which provided a meaningful response to the market investigation stated that printed newspapers have lost readership or audience to free (79)

and paid-for online editions.(80)

(130) In addition, all respondents to the market investigation have stated that readers consider Internet news portals featuring editorial content on their website and/or online news aggregators and/or informal online sources (such as blogs) to be alternatives to online editions of newspapers.(81)

(131) With regard to the segmentation within the national print newspaper market between popular tabloids, mid-market titles, and quality titles, a majority of newspapers which responded to the market investigation, stated that this segmentation is still pertinent today within the UK and Ireland. (82)

(132) However, the market investigation was inconclusive as to whether the segmentation between national, regional and free print newspapers would still be pertinent within the UK and Ireland. (83) In addition, the market investigation was not conclusive on the relevance of the segmentation between daily and non-daily national print newspapers within the UK and Ireland. (84)

(133) In any event, for the purpose of this decision, the exact product market definition for newspaper publishing can be left open, as the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market under any of the alternative market definitions.

4.6.2. Geographic market definition

4.6.2. Geographic market definition

(134) As regards geographic market definition, in past decisions the Commission concluded that the relevant market for national newspapers is national. (85) This was not put in question by the market investigation in this case.

(135) For the purposes of this decision, the Commission considers that the relevant geographic market for national newspapers is national, in line with Commission precedents

5. COMPETITIVE ASSESSMENT – HORIZONTALLY AFFECTED MARKETS

(136) The Proposed Transaction results in a number of horizontal overlaps at different levels of the distribution chain.

(137) Upstream, the Parties overlap with regard to the supply of TV content. Sky is active with regard to licensing pre-produced and commissioned TV content and sports content. 21CF is active through its wholly owned subsidiary 20CF (movies and other TV content), its Endemol Shine joint venture (other TV content) and, FNG Content Distribution (other TV content, some limited sub- licensing of 20CF films and a small amount of sports content). 21CF also licenses some sports rights through Star TV (principally Indian cricket events). No horizontally affected markets arise in relation to the production or supply of TV content.

(138) The Parties also overlap with regard to the acquisition of TV content which: (i) Sky includes in its TV channels (which are incorporated into its retail TV offering and/or wholesales to third parties) as well as for supply via its PPV/TVOD services; and (ii) 21CF includes in its TV channels which are wholesaled to third parties. This overlap results in a number of horizontally affected markets in the UK, Ireland and Italy which are discussed further below.

(139) Both Parties supply TV channels on a wholesale basis to third parties in a number of Member States. Sky supplies a range of channels including sports, movie and other channels to third parties, in particular those under the Sky brand. 21CF has a more limited number of TV channels, including those under the National Geographic and FOX brands. Horizontally affected markets arise in the UK, Ireland, Germany, and Italy which are discussed further below.

(140) Sky is active as a supplier of TV services in the UK, Ireland, Germany, Austria and Italy. 21CF is active in the UK and Ireland with the overlap resulting in an affected market in these Member States which is discussed further below.

(141) Finally, the Parties also overlap with regard to the supply of TV advertising airtime on their TV channels however no horizontally affected markets arise.

(142) For completeness, the Commission notes that some respondents to the market investigation indicate that the Proposed Transaction increases the merged entity's ability and incentive to foreclose access to premium sports content and channels by increasing Sky's bargaining power (86). For example, (87) it has been mentioned that the merged entity will have greater financial resources to acquire expensive sports rights, and that post-transaction, it will bundle the purchase of certain sports rights in several territories together thereby increasing Sky's bargaining position to the detriment of its competitors.

(143) As regards the acquisition of sports content, (88) the Commission notes that, while Sky purchases sports rights in each of the UK, Ireland, Austria, Germany and Italy (following the acquisition by BskyB of Sky Italia and Sky Deutschland), the only Member State in which 21CF is also present as an acquirer of sport rights is Italy, where the increment in market share brought about by 21CF's acquisition of sport content is between [0-5]% (see paragraphs (150) and (151) below). (89) It is therefore unlikely that the Proposed Transaction changes the bargaining position of Sky as a purchaser of sports rights significantly. Moreover, even if the bargaining power of Sky would be strengthened as a result of the Proposed Transaction, it is unlikely that this would have a significant impact on competition given the very small increment. In particular, in each of the relevant Member States, when bidding for football rights, Sky faces competition from other operators. For example, in the UK, as a result of the bidding by Sky and BT, the cost of the rights to broadcast the premier league football matches in the UK appears to have risen by 70% in each of the last two auctions. (90)

(144) As regards licensing of sport rights, the Commission notes that: (i) 21CF does not license football content (i.e. premium sports content); (ii) 21CF has a market share below [0-5]% in the potential market segment for the licensing of other sports content; and (iii) the Parties' combined market share is below [0-5]% in the potential market segment for the licensing of other sports content. Therefore, the Commission does not consider that the merged entity would have the ability to foreclose rivals' access to sport content. Moreover, with regard to sports channels, the Commission notes that 21CF licenses premium pay TV sports channels only in Italy, where the channels are already exclusively distributed on Sky pre-transaction.

(145) These issues (described in paragraph (142) above) are therefore not discussed further in the present decision.

5.1. Acquisition of TV content – UK & Ireland

(146) In the UK and Ireland, both Sky and 21CF acquire content for inclusion into their TV channels and PPV/TVOD services in the case of Sky. Table 1 below shows the segments where the Parties' overlapping activities result in horizontally affected markets, namely: (i) the acquisition of all TV content; (ii) the acquisition of films; (iii) the acquisition of all licenced content; and the sub-segment of that: (iv) licenced pre-produced content.

(147) There are no affected markets when the market for the acquisition of films is further segmented according to distribution window (e.g. TVOD/PPV or first pay-TV window). There is also no affected market when considering a market for the acquisition of other TV content (Sky: [10-20]%; 21CF: [0- 5]%), only when this market is segmented according to licenced content and the sub-segment of licenced pre-produced content.

UKTV ([10-20]% by revenue, [10-20]% by audience) when considering the market for all basic pay-TV channels. These TV broadcasters each provide a range of pay-TV channels to third parties and will continue to place a competitive constraint on the merged entity.

(159) Third, the results of the market investigation indicate that in the UK, the TV channels that 21CF and Sky wholesale to third parties are not generally close competitors. With regard to 21CF's National Geographic channel and Nat Geo Wild, the results of the market investigation suggest that none of the channels in the Sky portfolio would be considered as close competitors. (96) Equally, the market investigation did not identify any Sky TV channels as being close competitors to Baby TV or the Star branded channels.

(160) On the other hand, some respondents to the market investigation indicate that Sky Atlantic is likely to be the closest competitor to the FOX general entertainment channel. When considering a potential sub-segment for the wholesale supply of general entertainment channels, the Parties have a combined market share of [40-50]% by revenue and [40-50]% by audience share (Sky, including AETN: [30-40]% by revenue, and [20-30]% by audience; 21CF [5-10]% by revenue, and [10-20]% by audience). However, the Commission notes that Sky Atlantic is not currently licenced to third parties. (97)

(161) Moreover, as noted above in recital (158), even if one were to consider a narrow sub-segment for the wholesale supply of general entertainment TV channels, there are a number of competing channel providers that will continue to place a constraint on the merged entity post-transaction, including Universal, Comedy Central and UKTV.

(162) The market investigation indicates that these competing channel providers have a number of general entertainment channels which are also considered to be close competitors to the FOX channel and each have an equivalent market position to FOX today on the potential market for general entertainment channels ([5-10]% by audience share), in particular: Universal ([5-10]% by audience share), Comedy Central ([5-10]% by audience share) and UKTV's W ([5-10]% by audience share) as well as multiple other general entertainment channels. Given the large number of competing channels (both general entertainment channels and basic pay-TV channels in other genres) which exert a competitive pressure on Sky at least equivalent of that exerted by the FOX channel, the Commission does not consider the FOX channel to constitute an important competitive force that has more of an influence on the market than its market share suggests. (98)

(163) With regard to Fox News, the Commission notes that while it potentially competes with the Sky News channels (99), Fox News is currently only licenced to Sky in the UK therefore the Proposed Transaction will not materially change the competitive landscape for the wholesale supply of TV channels to third parties in this regard.

5.4. Wholesale supply of TV channels – Ireland

(164) In Ireland, 21CF licences the following channels to third parties: FOX, National Geographic, Nat Geo Wild and Baby TV. Sky licences a wide range of channels including sports, movie and other channels. The Parties therefore overlap with regard to the wholesale supply of basic pay-TV channels. There is no overlap with regard to premium pay-TV channels as 21CF does not offer any premium pay-TV channels.

(165) The Parties' market shares on the basis of revenues and audience shares for all basic pay-TV channels can be seen below in Table 4. By revenues, the Parties have a combined market share of [10-20]% (Sky: [10-20]%; 21CF: [0-5]%); the audience based market shares are marginally higher: [20-30]% (Sky: [20- 30]%; 21CF: [5-10]%). An affected market only arises when considering the market on the basis of audience shares.

market share (including AETN) ([20-30]% by revenue, [30-40]% by audience) is limited […]* narrower segmentation given 21CF's limited presence (21CF: [0-5]% by revenue, [5-10]% by audience).

(171) As detailed above in paragraph (168) in relation to the UK, even considering this narrow segment for general entertainment TV channels, there are a number of competing channel providers that will continue to place a constraint on the merged entity post-transaction; many of these channels are also active in Ireland. The market investigation indicated that these competing channel providers have a number of channels which are also considered to be close competitors to FOX in Ireland and each have an equivalent or larger market position than FOX today ([5-10]% by audience share) in particular: Universal ([5-10]% by audience share), Comedy Central ([10-20]%) and W ([0-5]% by audience share) when considering the sub-segment of general entertainment channels. Given the large number of competing channels (both general entertainment channels as well as basic pay-TV channels in other genres) which exert a competitive pressure on Sky at least equivalent to that exerted by the FOX channel, the Commission does not consider the FOX channel to constitute an important competitive force that has more of an influence on the market than its market share suggests.

5.5. Wholesale supply of TV channels - Germany

(172) In Germany, 21CF licences the following channels to third parties: FOX, National Geographic Channel, Nat Geo People and Nat Geo Wild. Sky's business model in Germany is a "self-retail" model rather than a wholesale model. In addition to retailing TV channels on its own platform, under its self-retail model cable network and IPTV providers transmit the Sky programme signals to end customers and perform certain marketing and distribution services. Sky however enters into direct contractual relationships with subscribers, controls subscriber data, deploys its own subscriber management system and retains the rights to determine the service packaging and pricing. It therefore submits that it is not active with regard to the wholesale distribution of TV channels and that any revenues it has from such activities in Germany should be considered as retail revenues. (102)

Ireland, there are a number of other channels that also compete closely with it, in particular Discovery's TLC channel, ITVBe, truTV in the UK and Discovery ID and True Crime in Ireland. (107)

6. COMPETITIVE ASSESSMENT – VERTICALLY AFFECTED MARKETS

(183) As noted above: (i) both Parties are active with regard to the supply of TV content; (ii) both Parties supply TV channels on a wholesale basis to third parties; and (iii) Sky is active as a TV distributor for retail TV services in the UK (108), Ireland, Germany, Austria and Italy and 21CF is active in the UK and Ireland. The Proposed Transaction therefore results in a number of vertical relationships (109).

(184) These activities at various levels of the value chain give rise to the following vertically affected markets in various Member States:

(a) 21CF’s and Sky’s upstream activities as suppliers of TV content and their respective downstream activities in the acquisition of TV content;

(b) 21CF’s and Sky’s upstream activities as wholesale suppliers of TV channels and Sky’s downstream activities as an acquirer of channels; and

(c) 21CF’s and Sky’s upstream activities in the supply of TV advertising opportunities on their channels, and Sky Media’s downstream activities as an ad sales house.

(185) Where there are vertically affected markets, two possible forms of foreclosure arise. The first is where the merger is likely to raise the costs of downstream rivals by restricting their access to an important input (input foreclosure). The second is where the merger is likely to foreclose upstream rivals by restricting their access to a sufficient customer base (customer foreclosure).

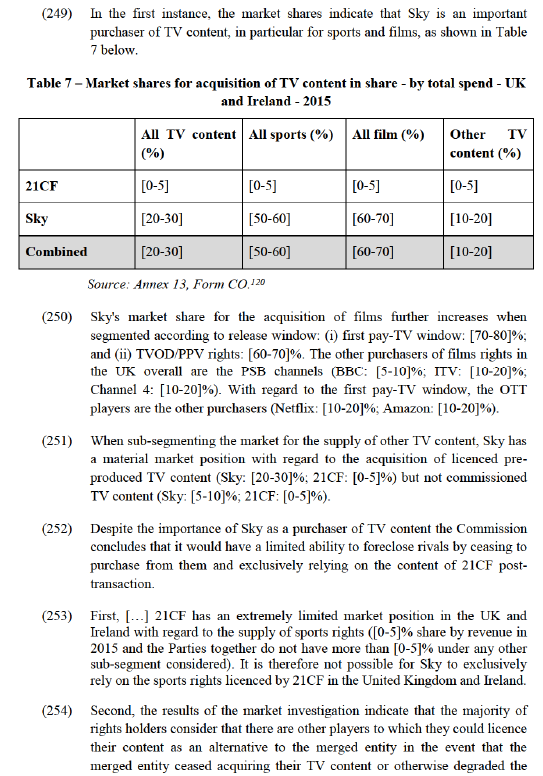

(186) Section 6.1 discusses the possible input foreclosure concerns arising from the Proposed Transaction with regard to TV markets; Section 6.2 discusses the possible customer foreclosure concerns arising from the Proposed Transaction with regard to TV markets; and Section 6.3 discusses both the possible input and customer foreclosure concerns relating to advertising markets.

6.1. Input foreclosure – TV markets

6.1.1. Introduction

(187) The Proposed Transaction will bring about a vertical relationship with regard to the licensing of broadcasting rights. Sky operates as a purchaser of broadcasting rights and TV channels while 21CF is active at the wholesale level as a licensor of TV content (such as films and TV series) and provider of TV channels (such as FOX and National Geographic).

(188) In a merger between companies which operate at different levels of the supply chain, anti-competitive effects may arise when the merged entity's behaviour could limit or eliminate competitors' access to supplies - input foreclosure.

(189) In assessing the likelihood of an anticompetitive input foreclosure scenario, the Commission examines: (i) whether the merged entity would have post- merger the ability to substantially foreclose access to input; (ii) whether the merged entity would have the incentive to do so; and (iii) whether a foreclosure strategy would have a significant detrimental impact on effective competition downstream. (110)

(190) The following sections examine any possible input foreclosure with respect to the supply of TV content and TV channels in the UK, Ireland, Germany, Austria and Italy.

6.1.2. Supply of TV content

6.1.2.1. Views of the Notifying Party

(191) The Notifying Party submits that it would not have the ability to foreclose or partially foreclose downstream broadcasters or distributors because: (i) it does not have upstream market power; (ii) 21CF already licences a large amount of content ([licensing practices of 21CF]) to Sky on an exclusive basis in all five jurisdictions; (iii) with regard to 21CF's other content from Endemol Shine, 21CF would not have the ability to cause the JV to sacrifice supply revenues as Apollo has joint control and has no incentive to allow such a strategy.

(192) The Notifying Party submits that it would not have the incentive to restrict access to either Sky or 21CF content post-transaction given: (i) the high fixed costs and negligible marginal costs in the supply of TV content; (ii) its business model to distribute content as widely as possible which is underpinned by contractual obligations with co-producers and finance companies to maximise the value of its works; and (iii) the fact that revenues lost by 21CF are unlikely to be recuperated by Sky on the downstream wholesale or retail markets as its competitors would still be able to put together attractive packages using content from other providers.

(193) Finally, it submits that even if it were to restrict access to the merged entity's content, it would have no effect as downstream rivals have other potential sources of supply.

6.1.2.2. The Commission's assessment

(a) Ability to engage in input foreclosure

(194) In the UK and Ireland, the merged entity's market share in the upstream market is below [20-30]% in all market segments except for the overall market for the licensing of broadcasting rights for films, where 21CF has a market share of [20-30]% by revenue. Post-transaction the other Hollywood studios have similar market shares: NBC Universal ([20-30]%); Disney ([20- 30]%), Sony ([10-20]%) and Warner Bros ([5-10]%) and will continue to place a competitive constraint on the merged entity post-transaction.

(195) In Germany and Austria, 21CF's market share in the upstream market is below [20-30]% by revenue for all markets except for when the market for the licencing of film rights is segmented according to exhibition window: (i) first pay-TV window: [20-30]%; and (ii) TVOD/PPV: [20-30]%. The other Hollywood studios have similar market shares in these windows and a number have larger market share for the licencing of films overall compared to 21CF ([10-20]%): Disney ([10-20]%); NBC Universal ([20-30]%); and Warner Bros ([10-20]%).

(196) In Italy, 21CF's market share for the licensing of TV content on all segments is below [10-20]% by revenue.

(197) Given the merged entity's limited market position with regard to the licencing of content, the Commission considers that it would not have the ability to foreclose its downstream rivals. In addition, 21CF [licensing practices of 21CF] which would hamper its ability to restrict supply or otherwise degrade the terms on which it supplies content to third parties.

(b) Incentive to engage in input foreclosure

(198) Respondents to the market investigation consider that the merged entity may have the incentive to exclusively supply TV content to Sky and not to other TV channel suppliers/TV services retailers, or to otherwise degrade the terms and conditions to which it provides access. (111)

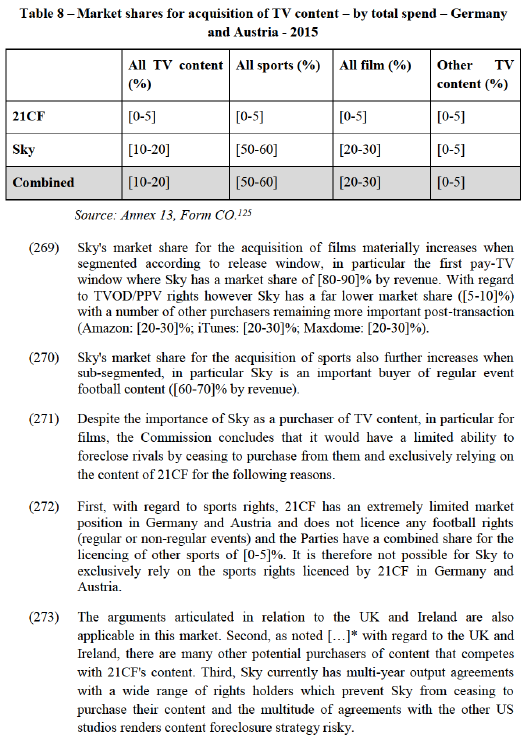

(199) On the other hand, the Commission notes that when 21CF controlled Sky Deutschland (Sky's retail businesses in Germany and Austria) and Sky Italia, (Sky's retail businesses in Italy), (112) 21CF continued to supply its TV content to third parties in those jurisdictions.

(200) Even if the Commission were to assume that, post-Transaction, the merged entity may have the incentive to foreclose TV broadcasters and providers of TV retail services, despite the fact that 21CF's past behaviour does not support such an assumption, the outcome of the assessment would not change given the lack of ability to foreclose and impact on effective competition.

(c) Impact on effective competition

(201) Regardless of whether the merged entity has either the ability or the incentive to foreclose competing downstream rivals with regard to the supply of TV content, the Commission does not consider that such a strategy would have an impact on competition.

(202) First, 21CF already licences its entire output of new films (as well as various library films and TV series) to Sky on an exclusive basis on subscription pay- TV in the UK, Ireland, Germany, Austria and Italy. Therefore, there is no change brought by the Proposed Transaction, in particular for films where 21CF has a market share of more than [20-30]% in some segments.

(203) Second, the market shares presented above indicate that several providers of TV content would remain active in the market in each of the UK, Ireland, Germany, Austria and Italy. This is confirmed by the market investigation which indicates that competing TV channel suppliers and providers of TV retail services would continue to have access to TV content that competes with the content supplied by 21CF today. (113)

(d) Conclusion

(204) In light of the above, the Commission considers that the Proposed Transaction does not give rise to serious doubts with regard to its compatibility with the internal market as a result of input foreclosure effects to the detriment of either competing TV broadcasters or providers of TV retail services in the UK, Ireland, Germany, Austria or Italy.

6.1.3. Wholesale supply of TV channels

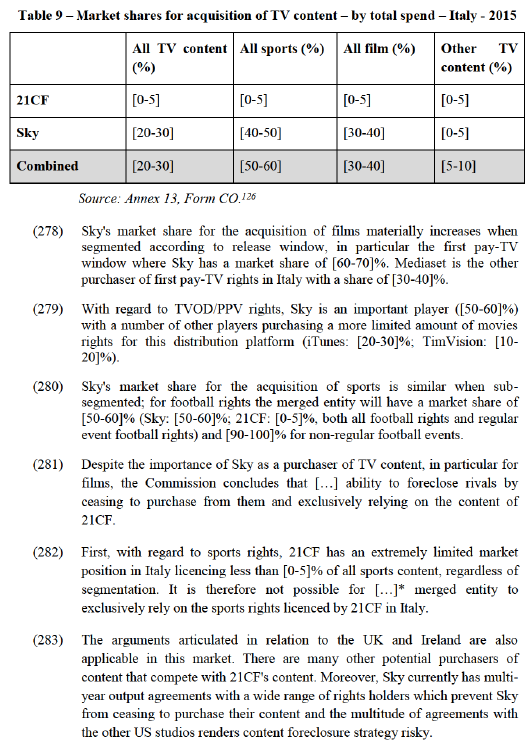

6.1.3.1. Introduction

(205) At the wholesale level, the Proposed Transaction increases Sky's pre-existing vertical integration by adding 21CF's channels to Sky's existing channel portfolio. The Commission has therefore assessed the risk of input foreclosure with regard to TV channels as a result of the Proposed Transaction.

6.1.3.2. Views of the Notifying Party

(206) The Notifying Party submits that the Proposed Transaction does not change the merged entity's ability or incentive to restrict competitors' access to its TV channels in each of the relevant Member States. With regard to the UK and Ireland, the Notifying Party submits that 21CF's [21CF share of viewers] and cannot be considered as an important input. With regard to Germany and Austria, it submits that Sky is not materially active with regard to the wholesale supply of TV channels to third parties and 21CF [21CF market position]. In Italy, it submits that Sky is not active with regard to the wholesale supply of TV channels and 21CF already exclusively supplies its channels to Sky.

(207) Finally, the Notifying Party claims that given the limited audience shares, even if the merged entity were to adopt such a foreclosure strategy, there would be no effect on competition.

6.1.3.3. The Commission's assessment - UK and Ireland

(a) Ability to engage in input foreclosure

(208) As set out above in Table 3, with regard to the wholesale supply of basic pay- TV channels in the UK, the Parties have a combined market share of [30- 40]% by revenue (Sky: [20-30]%; 21CF: [5-10]%) and [20-30]% by audience share (Sky: [20-30]%; 21CF: [5-10]%). As 21CF does not wholesale any premium pay-TV channels there is no overlap in this regard.

(209) As set out above in Table 4, in Ireland, the Parties have a combined market share of [10-20]% by revenue (Sky: [10-20]%; 21CF: [0-5]%) and [20-30]% by audience share (Sky: [20-30]%; 21CF: [5-10]%) with regard to the wholesale supply of basic pay-TV channels. As 21CF does not wholesale any premium pay-TV channels there is no overlap in this regard.

(210) Respondents to the market investigation consider that a number of the Sky channels are "must have" such as Sky Sports and Sky Cinema however there is no strong indication that any of the 21CF channels are "must have". There are multiple close substitutes to 21CF's channels provided by competing TV channel suppliers that will remain in the market post-transaction which have a similar share to 21CF and will continue to place a competitive constraint on the merged entity: Discovery ([10-20]%); Disney ([5-10]%) and ITV ([10- 20]%) (all by revenue).

(211) When considering a potential sub-segment for factual pay-TV channels 21CF's National Geographic has a limited market share of [10-20]% in the UK and [10-20]% in Ireland and Discovery will remain the far larger player in both the UK ([40-50]%) and Ireland ([50-60]%) (by audience)).

(212) With regard to the potential sub-segment for general entertainment pay-TV channels, the Parties' market and audience shares have been presented in paragraph (160) above. In this market segment, alternative competitors with similar audience shares to 21CF's general entertainment channel, FOX, would remain active in the market (UKTV with [10-20]% and [10-20]% in respectively the UK and Ireland).

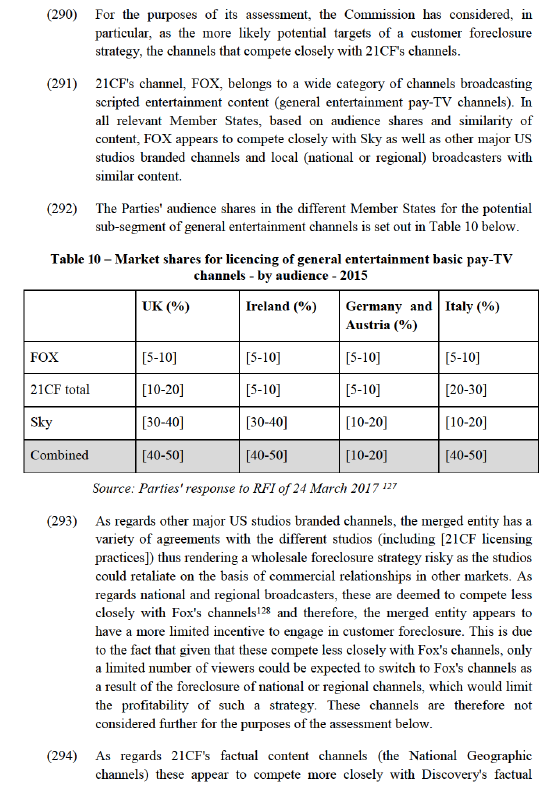

(213) This availability of alternatives is supported by the market investigation which showed that several TV channels are FOX's closest competitor (e.g. Universal, Sky, Alibi). (114) One respondent, for example, notes that the merged entity will face upstream competition from the other main providers of basic pay-TV channels and Channel4 highlights that for some channels there are similar genre services from other major networks (Discovery and UKTV).

(214) Finally, the Parties submit that 21CF's ability to deny or degrade access to National Geographic's TV channels is limited since [internal processes of National Geographic], (115) [internal processes of National Geographic].

(215) Based on the above, the Commission considers that post-transaction the merged entity is unlikely to have the ability to foreclose competing TV distributors in the UK and Ireland.

(b) Incentive to engage in input foreclosure

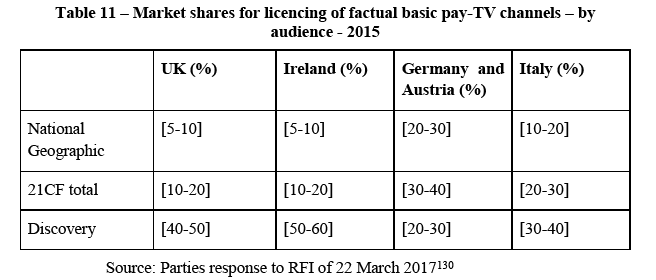

(216) Many respondents to the market investigation consider that post-transaction the merged entity would have the incentive to exclusively supply its channels to Sky and not to other provider of TV retail services, or to degrade the terms and conditions to which it provides access. (116)

(217) Sky is already vertically integrated with regard to the upstream supply of TV channels and the downstream supply of retail TV services; the increment brought about by the Proposed Transaction is therefore limited to the 21CF channels. As noted above, 21CF has a limited market share in the wholesale supply of TV channels, the Commission therefore considers that incentives of the merged entity will not significantly change as a result of the Proposed Transaction.

(218) Moreover, as noted above in paragraph (199), until 2014, 21CF controlled Sky Deutschland and Sky Italia. There is no evidence on the file that 21CF refused to supply its TV channels to third parties in those jurisdictions despite this vertical integration.

(219) Based on the above, the Commission considers that post-transaction the merged entity is unlikely to have the incentive to foreclose competing TV distributors in the UK and Ireland.

(c) Impact on effective competition

(220) Regardless of whether the merged entity has either the ability or the incentive to foreclose competing downstream rivals with regard to the wholesale supply of basic pay-TV channels, the Commission does not consider that such a strategy would have an impact on competition.

(221) As detailed above in paragraphs (208) - (212) […] a number of competing providers of basic pay-TV channels will remain active post-transaction. Therefore even if the merged entity were to adopt a foreclosure strategy, downstream rivals would continue to have access to alternative inputs that compete with the 21CF channels.

(d) Conclusion

(222) In light of the above, the Commission considers that the Proposed Transaction does not give rise to serious doubts with regard to its compatibility with the internal market as a result of input foreclosure effects of TV channels to the detriment of competing retail providers of TV retail services in the UK or Ireland.

6.1.3.4. The Commission's assessment - Germany and Austria

(a) Ability to engage in input foreclosure

(223) As noted above in paragraph (172), Sky is not active with regard to the wholesale supply of non-sports TV channels in Germany as it has adopted a self-retail model. 21CF has a limited portfolio of channels consisting of FOX and the National Geographic channels. As set out in Table 5, when considering the audience shares, the Parties' combined market share is well below [20-30]% (combined: [10-20]%; Sky: [5-10]%; 21CF: [10-20]%).

(224) With regard to Austria, as set out in paragraph (175), Sky has adopted the same self-retail model as it has in Germany and 21CF offers the FOX and National Geographic channels. The Notifying Party states that it cannot provide audience based market shares for Austria however it confirms that the market shares in Austria do not materially differ to those in Germany i.e. below [10-20]%.

(225) Despite its limited TV channel offering, some respondents to the market investigation indicate that 21CF's channels are important input to compete, in particular the National Geographic channels. With regards to other TV channels, some respondents including large downstream operators such as Deutsche Telekom and Telekom Austria consider the FOX branded channels as "must have" because of content and customer awareness. (117)

(226) On the other hand, respondents also note that close substitutes to 21CF's channels would remain in the market both for factual and general entertainment TV channels. With regard to the National Geographic channels, other providers include Discovery (whose ‘Discovery’ and ‘Animal Planet’ channels had an audience share in 2015 of [10-20]% and [0-5]% respectively), AETN/Universal (whose ‘History’ and ‘A&E’ channels had an audience share in 2015 of [10-20]% and [5-10]% respectively) and Spiegel TV/Autentic (with an audience share in 2015 of [10-20]%). (118) Other TV channels providing access to general entertainment content and TV series include: 13th Street, TNT Serie, ProSiebenSat, RTL Crime which compete with the FOX channel.