Commission, July 29, 2019, No M.9294

EUROPEAN COMMISSION

Decision

BMS / CELGENE

Subject: M.9294 – BMS/Celgene

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 24 June 2019, the European Commission received a notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Bristol- Myers Squibb Company (“BMS”, United States) will acquire sole control of Celgene Corporation (“Celgene”, United States). In this Decision, BMS is referred to as the “Notifying Party”. Together, BMS and Celgene are referred to as the “Parties”.

1. THE PARTIES AND THE OPERATION

(2) BMS is a global pharmaceutical company headquartered in the United States. BMS is engaged in the development and commercialisation of innovative medicines in four main therapeutic areas: oncology, autoimmune diseases, cardiovascular diseases, and fibrotic diseases.

(3) Celgene is a global pharmaceutical company headquartered in the United States. Celgene is engaged primarily in the development and commercialisation of innovative therapies in oncology and autoimmune diseases.

(4) On 2 January 2019, the Parties signed a Merger Agreement pursuant to which BMS will acquire Celgene in a cash and stock transaction with an equity value of approximately USD 74 000 million (approximately EUR 62 700 million) (the “Transaction”). Upon closing of the Transaction, BMS will acquire sole control over Celgene.

(5) The Transaction would therefore give rise to a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

2. EU DIMENSION

(6) The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 5 000 million3 in 2018 (BMS: EUR 19 104 million; Celgene: EUR 12 939 million). Each of them has an EU-wide turnover in excess of EUR 250 million in 2018 (BMS: […]; Celgene: […]), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State.

(7) The Transaction therefore has an EU dimension within the meaning of Article 1(2) of the Merger Regulation.

3. FRAMEWORK FOR THE COMMISSION’S COMPETITIVE ASSESSMENT

3.1.General considerations on market definition

3.1.1. Relevant product market

(8) When defining relevant markets in past decisions dealing with finished dose pharmaceutical products,4 the Commission based its assessment on the following general approach.5

(9) The Commission noted that medicines may be subdivided into therapeutic classes by reference to the Anatomical Therapeutic Classification (“ATC”), devised by the European Pharmaceutical Marketing Research Association (“EphMRA”) and maintained by EphMRA and IQVIA, formerly known as Intercontinental Medical Statistics (“IMS”).

(10) The ATC system is a hierarchical and coded four-level system, which classifies medicinal products by class according to their indication, therapeutic use, composition, and mode of action (“MoA”). In the first and broadest level (ATC 1), medicinal products are divided into the 16 anatomical main groups. The second level (ATC 2) is either a pharmacological or therapeutic group. The third level (ATC 3) further groups medicinal products by their specific therapeutic indications. Finally, the ATC 4 level is generally the most detailed one (not available for all ATC 3) and refers for instance to the MoA or any other subdivision of the relevant products.

(11) The Commission has often referred to the third level (ATC 3) as the starting point for defining the relevant product market. However, in a number of cases, the Commission found that the ATC 3 level classification did not yield the appropriate market definition within the meaning of the Commission Notice on the Definition of the Relevant Market.6 In particular, the Commission has considered in previous decisions plausible product markets at the ATC 4 level, at a level of a molecule or a group of molecules that are considered interchangeable so as to exercise competitive pressure on one another.7

(12) The Commission has also envisaged the possibility of defining the market by reference to the disease (and its degree of severity). For instance, in oncology, the Commission took into consideration the type of cancer, its location and whether the cancer is in an initial or an advanced stage.8 Similarly, in autoimmune diseases, the Commission has typically identified relevant product markets by reference to indications.9

(13) In its past decisional practice, the Commission has also considered relevant market segmentations based on (i) the types of treatment (e.g. chemotherapy, targeted therapies and immunotherapies in oncology;10 conventional and biologic treatments in autoimmune diseases),11 (ii) the line of treatment,12 (iii) the MoA,13 and (iv) the mode of delivery (“MoD”, e.g. oral, intravenous, intramuscular, and subcutaneous injections).14

(14) As regards pipeline products, the Commission has in previous decisions considered market definitions based on the indication, the mode of action, and, where relevant, the line of treatment, but ultimately left open the exact delineation of the market.15 The Commission added that when research and development (“R&D”) activities are assessed in terms of importance for future markets, the product market definition can be left open, reflecting the intrinsic uncertainty in analysing products that do not exist yet.16

(15) The Commission will analyse in Section 4 below the relevance of these distinctions for the relevant product market definition in the present case.

3.1.2. Relevant geographic market

(16) The Commission has consistently considered that the markets for FDP products are national in scope, in particular in view of the national regulatory and reimbursement schemes and the fact that competition between pharmaceutical firms still predominantly takes place at a national level.17 For pipeline products, the Commission has considered the geographic scope of the market to be at least EEA- wide.18

(17) The Commission will analyse in Section 4 below the relevance of these precedents for the relevant geographic market definition in the present case.

3.2.General approach to competitive assessment of horizontal effects of the Transaction

(18) Article 2 of the Merger Regulation requires the Commission to examine whether notified concentrations are compatible with the internal market, by assessing whether they would significantly impede effective competition in the internal market or in a substantial part of it, in particular, as a result of the creation or strengthening of a dominant position or the removal of a significant competitive constraint.

(19) In addition, Article 57(1) of the EEA Agreement requires the Commission to examine whether notified concentrations are compatible with the functioning of the EEA Agreement, by assessing whether they would create or strengthen a dominant position as a result of which effective competition would be significantly impeded within the EEA territory or a substantial part of it.

(20) In this framework, “competition” is understood to mean product and price competition (actual or potential), as well as innovation competition, where the Commission assesses in particular potential horizontal non-coordinated effects.19 The Commission considers that a concentration may not only affect competition in existing markets, but also competition in innovation and new product markets.20 This may be the case when a concentration concerns entities currently developing new products or technologies which either may one day replace existing ones or which are being developed for a new intended use and will therefore not replace existing products but create a completely new demand.21

(21) In the pharmaceutical industry, the process of innovation is structured in such a way that it is typically possible at an early stage of clinical trials to identify competing research programmes (or “pipeline” programmes).22 Competing pipeline programmes can be defined as R&D efforts aimed at developing substitutable products and having similar timing. The timing of a research programme should be assessed by reference to the stage of the on-going preclinical or clinical trials.23

(22) In line with the past decisional practice in the pharmaceutical sector24 and the Commission’s decisions in Dow/Dupont and Bayer/Monsanto,25 the Commission has taken into account a four-layer competitive assessment framework, which corresponds to the overlaps between the parties’ activities in terms of:(a) Actual (product and price) competition, assessing the overlaps between the parties' existing (marketed) products;26(b) Potential (product and price) competition, assessing the overlaps (i) between the parties’ existing (marketed) and pipeline products at advanced stages of development and (ii) between the parties’ pipeline products at advanced stages of development. For pharmaceutical products, the Commission in principle considers programmes in Phase II and III clinical trials as being at an advanced stage of development;27(c) Innovation competition in relation to the parties’ ongoing pipeline products, assessing the risk of significant loss of innovation competition resulting from the discontinuation, delay or redirection of the overlapping pipelines (including early stage pipelines); and(d) Innovation competition in relation to the capability to innovate in certain innovation spaces, assessing the risk of a significant loss of innovation competition resulting from a structural reduction of the overall level of innovation.28

(23) The Commission will analyse the overlaps between the activities of the Parties against this framework in Section 4 below.

4. COMPETITIVE ASSESSMENT

(24) BMS and Celgene are both active in the development and commercialisation of pharmaceutical products. The Parties’ activities give rise to limited horizontal overlaps in the EEA in relation to marketed and/or pipeline treatments in autoimmune diseases (Section 4.1), fibrotic diseases (Section 4.2), and oncology (Section 4.3).

4.1.Autoimmune diseases

4.1.1.Introduction

(25) Autoimmune diseases result from a dysfunction of the immune system in which the body attacks its own organs, tissues, and cells. Autoimmune diseases can target almost any part of the body. Autoimmune diseases vary according to the part of the body being targeted by the immune system, and include psoriasis (“PsO”), psoriatic arthritis (“PsA”), inflammatory bowel diseases (“IBD”) including ulcerative colitis (“UC”) and Crohn’s disease (“CD”), and systemic lupus erythematotus (“Lupus” or “SLE”). Autoimmune diseases can range in severity, from mild to severe cases, with the gravity of the disease often increasing over time. They affect approximately 5- 10% of the global population.29

(26) In the autoimmune therapeutic space, the Parties activities overlap with respect to the following indications: PsO (Section 4.1.2), PsA (Section 4.1.3), IBD (Section 4.1.4) and Lupus (Section 4.1.5).

4.1.2.Treatments for Psoriasis

(27) Psoriasis (“PsO”) is a chronic inflammatory disease, which causes an exaggerated reaction of the natural repair and defence mechanisms of the body. This exaggerated reaction causes red, scaly patches of skin to appear.

(28) Patients can suffer from PsO of different gravity, ranging from mild to severe. PsO severity is typically classified with reference30 to the body surface area (“BSA”)31 percentage that is affected by the disease; the Psoriasis area and severity index (“PASI”);32 and the dermatology life quality index (“DLQI”).33

(29) In Europe, it is generally considered that a patient can be considered as suffering from mild PsO when he/she has a BSA of 10% or less; a PASI score of 10 or less; and a DLQI of 10 or higher. A patient is considered as suffering from moderate-to- severe PsO when he/she has a BSA exceeding 10%; a PASI score higher than 10; and a DLQI lower than 10.34

(30) Treatment for moderate-to-severe PsO is typically undertaken in steps through consecutive lines of treatment, matching the severity of the disease and the patient’s symptoms.35 This means that a patient has to first be prescribed with drugs from the earlier line of treatment category and if these do not work, the patient can be moved to a drug from a subsequent line of treatment category.

4.1.2.1. Market definition

(A) Relevant product market

(A.i) Commission’s Precedents

(31) The Commission has not assessed in detail the relevant product market definition for PsO treatments in the past.36(A.ii) The Parties’ view and Commission’s assessment Segmentation by reference to the severity of the disease

(32) The Parties submitted that treatments for moderate-to-severe PsO and treatments for mild PsO belong to separate relevant product markets. In any event, the Parties argued that this question could be left open because the Transaction would not raise competition concerns even under the narrower of the two market segmentations, i.e. treatments for moderate-to-severe PsO.37

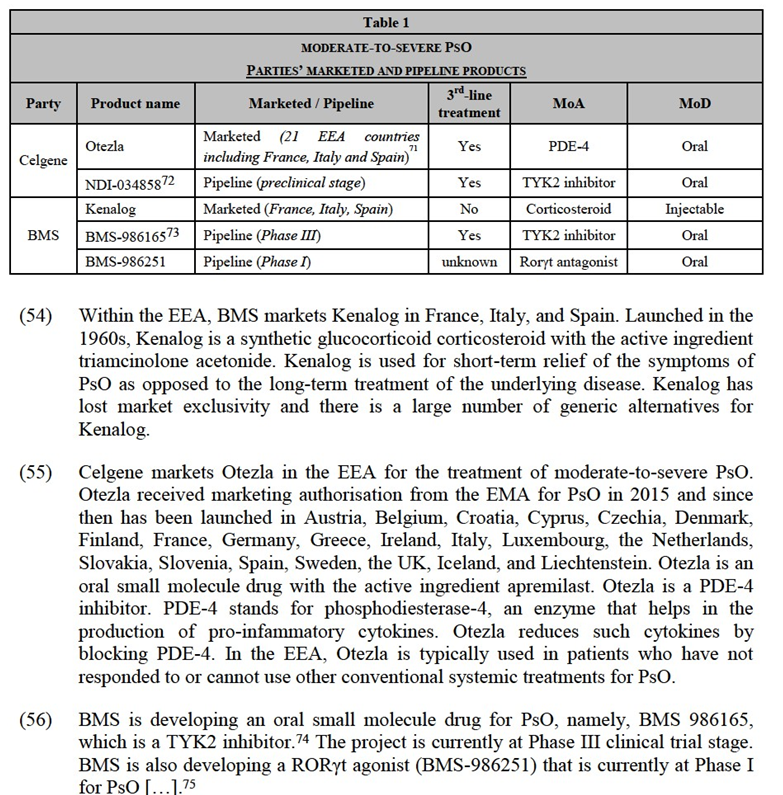

(33) The market investigation suggested that there is a separate relevant product market for treatments for moderate-to-severe PsO. All the competitors and the key opinion leaders (“KOLs”)38 who responded to the market investigation indicated that Celgene’s Otezla and its competing products target the treatment of moderate-to- severe PsO39 and can usually be prescribe for this indication alone. KOLs also recalled that the available guidelines in the EEA specifically concern treatments for moderate-to-severe PsO.40

Segmentation by line of treatment

(34) The Parties submitted that in Europe, lines of treatment for PsO are not as well defined as in other diseases (e.g. in oncology). The Parties added that references to different lines of treatment are rare in clinical guidelines for PsO.41 The Parties suggested that the issue could ultimately be left open because the Transaction would not raise competition concerns even if one looks at moderate-to-severe PsO treatments divided by lines of treatment.42

(35) The majority of competitors who responded to the market investigation acknowledged a three-fold categorisation of moderate-to-severe PsO treatments by line of treatment.43 According to these respondents, (i) first-line treatments for moderate-to-severe PsO include anti-inflammatory drugs, topical treatments, and phototherapies; (ii) second-line treatments include conventional systemic therapies (e.g. methoxetrate or cyclosporine); and (iii) third-line treatments consist of biologics and small-molecule drugs.44 The vast majority of KOLs also agreed45 that the treatment algorithm for PsO is also organised in lines of treatment, which include, after the use of topical treatments, (i) conventional systemic therapies and(ii) biologics and small-molecule drugs. Certain competitors and KOLs noted that the boundaries between the different lines of treatment are blurred,46 however, none of the respondents questioned the fact that biologics and small-molecule drugs are offered as the last line of treatment.

(36) In any event, the exact relevant product market definition can be left open since the Transaction does not give rise to serious doubts as to its compatibility with the internal market and the functioning of the EEA Agreement even if a separate market were defined for the last line (third-line) treatments for moderate-to-severe PsO.

Segmentation by mode of action

(37) The Parties suggested that different treatments for moderate-to-severe PsO compete with each other, regardless of their MoA. The most important factors for a physician choosing a treatment against an autoimmune disease are efficacy and safety. The physician will consider a wide range of MoA taking into account the specific needs of the patient.47 The Parties suggested that the issue could ultimately be left open because the Transaction would not raise competition concerns even if one looks at moderate-to-severe PsO treatments sub-segmented by MoA.

(38) The majority of competitors and KOLs who responded to the market investigation also suggested that treatments for moderate-to-severe PsO compete with each other, regardless of their MoA.48 As one KOL put it, “what matters for doctors when choosing a PsO treatment is the drug’s efficacy as well as its safety. The drug’s mode of action is less important.”49 When asked to compare biologicals and small- molecule drugs, the majority of competitors confirmed that “all available third line treatments compete with one another […] regardless of mode of action”.50 When asked to identify the closest competitor to a product or a pipeline project, the vast majority of competitors indicated products and pipeline projects with different MoA.51

(39) In particular, in light of the Parties’ overlapping products, the Commission investigated whether there is a separate relevant product market for moderate-to- severe PsO treatments with a specific MoA, namely tyrosine kinase 2 (“TYK2”) inhibition. TYK2 is an enzyme involved in the signalling of pro-inflammatory cytokines such as interleukins 12 and 23 and interferon I responses. A TYK2 inhibitor specifically blocks TYK2 and therefore the creation of these pro- inflammatory cytokines, which drive PsO and other autoimmune diseases. TYK2 inhibitors seek to block specifically the TYK2 enzyme and not other kinases, which makes for a safer drug. TYK2 inhibitors are still under development today and none of them has been launched at this stage.

(40) The market investigation suggested that TYK2 inhibitors should not constitute a separate relevant product market. The majority of competitors and KOLs confirmed that TYK2 inhibitors will compete with other treatments for moderate-to-severe PsO, regardless of the MoA.52 For example, most competitors expect that TYK2 inhibitors (if/when launched) would have comparable efficacy and safety to biologics such as interleukin 12/23 (“IL-12/23”) inhibitors.53 Yet, a small minority of competitors stated that TYK2 inhibitors have a unique profile of high efficacy and safety and are bound to disrupt the market of moderate-to-severe PsO treatments when they are marketed.54

(41) In any event, the exact relevant product market definition can be left open since the Transaction does not give rise to serious doubts as to its compatibility with the internal market and the functioning of the EEA Agreement even if a separate market were defined for TYK2 inhibitor treatments for moderate-to-severe PsO.

(42) According to two competitors, which constitutes a small minority of all the respondents, the possible market for TYK2 inhibitor treatments for PsO should be segmented even further. TYK2 inhibition can be achieved with two different mechanisms: an orthosteric mechanism (where the drug docks on the active site of the TYK2 enzyme) and an allosteric mechanism (where the drug docks on the regulatory (non-active) sub-unit of the enzyme). According to the two competitors, allosteric TYK2 inhibitors are a distinct and unique class of treatments for autoimmune diseases because they are particularly selective and this ensures a good safety profile and high efficacy. The market investigation did not support this claim. Indeed, the majority of KOLs stated that allosteric mechanisms are not unique and orthosteric TYK2 inhibitors could possibly achieve comparable levels of efficacy and safety.55 One KOL submitted that “there is no evidence that an allosteric action mechanism leads to any benefits for the patient (in terms of efficacy or safety). Nor is an allosteric mechanism necessary to target a TYK2”,56 while another KOL added: “increased selectivity […] does not necessarily characteri[s]e every inhibitor with an allosteric mechanism”.57 Similarly, a competitor who is currently developing a TYK2 inhibitor stated that “overall, the use of an allosteric or an orthosteric mechanism for TYK 2 inhibition does not make a difference for the patient (i.e. in terms of efficacy or safety). […][A]n allosteric mechanism for TYK 2 inhibition is not necessarily more targeted than an orthosteric mechanism and may give rise to similar side effects.”58 For this reason, the Commission concludes that, at this point in time and on the basis of the elements at its disposal, no separate relevant product market can be defined for allosteric TYK2 inhibitor treatments for moderate-to- severe PsO.

Segmentation by mode of delivery

(43) The Parties also suggested that different treatments for moderate-to-severe PsO compete with each other, regardless of their MoD. The most important factors for a physician choosing a treatment against an autoimmune disease are efficacy and safety. The physician will consider a wide range of MoDs taking into account the specific needs of the patient.59 The Parties suggested that the issue could ultimately be left open because the Transaction would not raise competition concerns even if one looks at moderate-to-severe PsO treatments sub-segmented by MoD.

(44) The market investigation was inconclusive on the question of whether the market for moderate-to-severe PsO treatments should be further sub-segmented based on the MoD, e.g. whether there should be a separate relevant market for oral treatments of moderate-to-severe PsO.

(45) On the one hand, all respondents recognised that efficacy and safety of the treatment60 (not MoD) are the key parameters driving prescription decisions.61 The majority of competitors and KOLs added that oral products compete with injectable drugs (like biologics).62 Many KOLs also indicated that the vast majority of patients is open to an injectable product if it would ensure better results.63 Certain KOLs added that in terms of adherence, oral and injectable treatments for PsO are not significantly different.64 An injectable treatment, e.g. once every 3-4 weeks is comparable in terms of adherence and convenience with an oral drug that the patient needs to take twice per day.65

(46) On the other hand, the majority of competitors confirmed that the MoD plays an important role to determine whether different types of moderate-to-severe PsO treatments compete with each other.66 Some respondents added that oral products have a unique convenience profile and dermatologists prescribe them for special categories of patients, e.g. frequent travellers or patients with needle phobia.67

(47) In any event, the exact relevant product market definition can be left open since the Transaction does not give rise to serious doubts as to its compatibility with the internal market and the functioning of the EEA Agreement even if a separate market were defined for oral third-line treatments for moderate-to-severe PsO.

(B) Relevant geographic market

(B.i) Commission’s Precedents and the Parties’ View

(48) The Commission has consistently defined the geographic markets for marketed products against autoimmune diseases as being national in scope.68 With respect to pipeline products, the Commission has consistently held that the geographic market is either global or at least EEA-wide.69

(49) The Parties submitted that they agree with the Commission’s approach to geographic market definition.70

(B.ii) Commission’s assessment

(50) Nothing in the market investigation suggested that the Commission should depart in the present case from its previous practice concerning the geographic market definition.

(51) For the purpose of this Decision, the geographic market for marketed products for the treatment of moderate-to-severe PsO should be defined at national level.

(52) The exact geographic scope of the market for pipeline treatments for moderate-to- severe PsO can be left open, since the Transaction does not give rise to serious doubts as to its compatibility with the internal market and the functioning of the EEA Agreement even on the basis of the narrowest plausible geographic market definition, i.e. at EEA-wide level.

4.1.2.2.The Parties’ products

(53) Parties’ marketed and pipeline drugs for the treatment of moderate-to-severe PsO are detailed in Table 1 below.

(57) Celgene owns an option to acquire the TYK2 inhibitor programme that is developed by Nimbus, a US biotech company.76 This programme is currently at preclinical trial stage and expected to start the Phase I clinical trials in […]. Nimbus’ programme is […].77

(58) The Transaction gives rise to overlaps between the marketed (existing) products of the Parties and their pipeline products at clinical trial stage in (i) a plausible market for third-line treatments for moderate-to-severe PsO and (ii) a plausible market for oral third-line treatments for moderate-to-severe PsO. Taking into account the Nimbus preclinical asset that Celgene has an option to acquire, the Transaction gives rise to overlaps in the same markets and also in a plausible market for TYK2 inhibitor treatments for moderate-to-severe PsO.78

4.1.2.3. Overlaps involving marketed products and pipeline programmes at clinical trial stage

(A)Parties’ views

(59) The Parties submit that the overlap between Celgene’s marketed drug (Otezla), on the one hand, and BMS’ pipeline products (TYK2 inhibitor and RORγt agonist), on the other hand, would not give rise to competition concerns under any market delineation for the following reasons. First, Otezla has a limited position in EEA markets (with market shares well below 20% in all Member States where it is sold). Second, Otezla and each of BMS’ TYK2 inhibitor and RORγt agonist are differentiated products (with distinct MoA and efficacy/safety profiles). Third, the competitive landscape in moderate-to-severe PsO treatments is crowded, with a large number of marketed products currently available on the market in the EEA and many pipeline projects under development. Fourth, with respect to BMS’ RORγt agonist programme, the Parties argue that, assuming the clinical trials are successful, this Phase I pipeline product would not enter the market for a very long time, by which point Otezla will most likely have lost, or be close to losing, exclusivity. Finally, the Parties claim that, post-Transaction, the merged entity would have no ability and/or no incentive to discontinue (i) the development of BMS’ two pipeline projects or (ii) the supply of Otezla.79

(B) Commission’s assessment

(60) The evidence in the Commission’s file generally confirms the Parties’ claim. It allows the Commission to exclude serious doubts as to the compatibility of the Transaction with the internal market and the functioning of the EEA Agreement resulting from the overlap of the Parties’ activities in third-line moderate-to-severe PsO treatments or (more narrowly) in oral third-line moderate-to-severe PsO treatments.

(61) First, the results of the market investigation show that none of the Parties’ drugs is or is expected to hold a particularly strong position in the moderate-to-severe PsO treatment space:- Otezla. Contrary to the US where it is considered a blockbuster,80 Celgene’s drug has a limited market position in the EEA. In a potential market for third-line treatment for moderate-to-severe PsO, Otezla’s market share remains modest at national level (below 10% in 2018 in all EEA countries where it was sold).81 This is mainly due to the fact that, in the EEA, the S3 Guidelines (and national clinical guidelines) as well as the national reimbursement regimes, restrict the use of Otezla for cost-efficiency reasons.82 Otezla is typically prescribed as third- line treatment (i.e. after conventional systemic therapies have failed or in case of contraindications) and thus competes with other third-line treatments, including biologics and biosimilars. These are all more efficacious than Otezla and physicians in the EEA tend to prefer them. The use of Otezla is even more limited in some EEA countries, where national or regional guidelines recommend Celgene’s drug to be prescribed after biologics have failed or in case of contraindications.83 During the market investigation, all competitors and KOLs consider Otezla’s efficacy to be lower (or much lower) than biologics’.84 Several market participants and KOLs also highlighted potential tolerability problems associated to Otezla, in particular gastrointestinal issues, such as diarrhoea and nausea, and a risk of depression.85 The above considerations explain Otezla’s limited market position in the EEA;86- BMS TYK2 inhibitor pipeline project (BMS-986165). Although BMS TYK2 inhibitor is perceived as a promising drug by several market participants, most respondents to the market investigation indicated that its efficacy and safety profile (i.e. the two key elements in the choice of therapy87) will likely be comparable to or worse than biologics.88 As a KOL put it, “[t]oday in PsO, there are already many efficacious, cost-effective treatments with a proven safety profile and it will be difficult for TYK2 inhibitors to compete with them”.89 BMS internal documents confirm this, citing public authorities in Europe and elsewhere who […];90 - BMS RORγt agonist pipeline project (BMS-986251): given its early stage of development, the exact efficacy and safety profile of this pipeline drug and the line of treatment for which it will be approved are still unknown.91 Assuming it reaches the market and is approved as a third-line treatment, it is likely that more products will have entered the market and Otezla will likely have lost its exclusivity (scheduled to occur around 2028).

(62) That being said, the results of the market investigation suggest that the MoD of the Parties’ drugs (i.e. oral) could constitute a competitive advantage because some patients are reluctant to receive injections and because all the alternative third-line treatments currently available on the market (biologics) are injectable.92 However, this competitive advantage seems limited in practice since (i) in the EEA, the MoD does not drive prescription decisions93 (contrary to the US where the competitive dynamics are very different),94 especially when it comes to third-line treatments where efficacy and safety prevail; (ii) the number of patients reluctant to injections appears to be modest (around 5% of the patient population according to some KOLs)95; and (iii) many competitors are currently developing alternative oral drugs (see below Table 2).

(63) Second, post-Transaction, the combined entity would continue to face strong competitive constraints from a large number of actual and potential competitors.

(68) Third, although some respondents consider that Otezla and BMS TYK2 inhibitor will closely compete because they are both administered orally,108 the market investigation confirmed that the Parties’ drugs are differentiated in terms of (i) MoA, as well as (ii) efficacy and safety profile109 which is the key factor in the choice of the treatment:110- Different MoA. The Parties’ drugs target different enzymes and pathways responsible for PsO. Otezla is a PDE-4 inhibitor, which inhibits the actions of PDE-4, an enzyme which turns cyclic adenosine monophosphate (“cAMP”) to adenosine monophosphate (“AMP”). The inhibition of PDE-4 allows to reduce the production of pro-inflammation cytokines (such as TNF-α) and, thus, inflammation and other PsO symptoms. BMS-986165 is a TYK2 inhibitor, which specifically inhibits the TYK2, in order to target the IL-12 and IL-23 pathways, which are genetically related to PsO.111 BMS-986251 is a RORγt agonist, the way its works remains uncertain but antagonizing RORγt activity with synthetic small molecules seems to inhibit expression of IL-17A.- Different efficacy profile. Otezla significantly reduces the skin area affected by PsO in around one third of patients (PASI 75 response rate112 of 29-33%), while BMS TYK2 inhibitor is expected to be effective in over two thirds of patients (PASI 75 response rate of 67-75% based on the Phase II trial results). This means the efficacy of the BMS TYK2 inhibitor is comparable to the efficacy of biologics, which achieve PASI 75 response rates of approximately 71-91% (as shown in the Graph below). The PASI 90113 scores of patients treated with Otezla, BMS’ TYK2 inhibitor, and biologics corroborate this conclusion.114 This was also confirmed by the vast majority of KOLs and competitors.115- Different safety profiles and monitoring requirements. While the exact safety profile of BMS TYK2 inhibitor will not be known until the completion of the ongoing Phase III trials, it will likely sit between Otezla (which has a very favourable safety profile) and biologics.116 As one KOL put it, “Otezla has a very favourable safety profile and is generally well tolerated by patients with comorbidities. BMS-986165’s safety profile is not likely to be as favourable as Otezla’s since it has immunosuppressant effects (with an increased risk of exposing patients to infections) and will require upfront screening at least for tuberculosis and hepatitis B and C”.117 The fact that Otezla is likely to be safer than BMS TYK2 inhibitor is corroborated by BMS’ internal documents, […].118

(69) The above notwithstanding, some respondents consider that Otezla and BMS TYK2 inhibitor will compete closely because they are both administered orally (as opposed to biologics that are injectable).119 However, during the market investigation, respondents identified many other drugs as closely competing with the Parties. In fact, the majority of respondents consider that all third-line treatments for moderate- to-severe PsO closely compete with each other.120 In addition, as already mentioned, the market investigation confirmed that the MoD is less important than efficacy and safety when a physician chooses treatment for moderate-to-severe PsO.121

(70) Fourth, the Commission considers that, given the modest shares of Otezla in the EEA and the differentiated efficacy/safety profiles of Celgene’s Otezla and BMS TYK2, it is unlikely that the combined entity would have an incentive to cease, repurpose or delay the development of BMS’ pipelines post-Transaction.

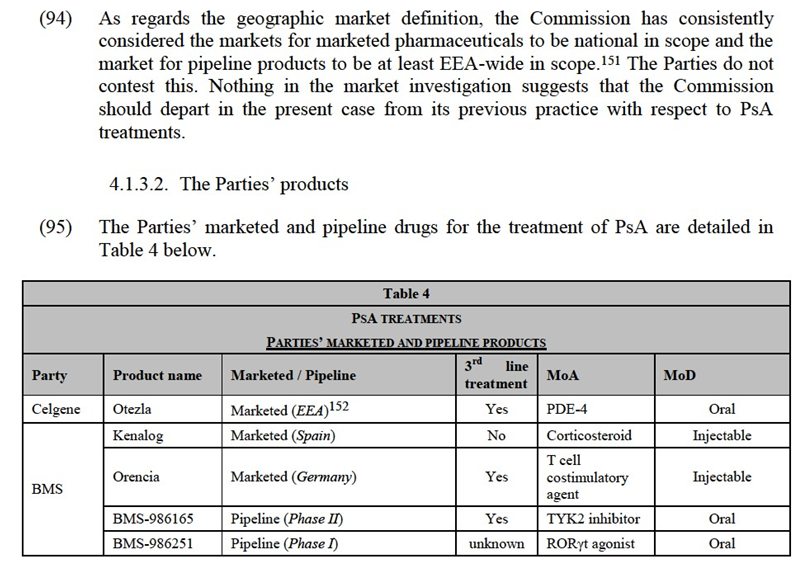

(71) BMS TYK2 inhibitor is expected to be comparable to (injectable) biologics, including in particular the first generation of biologics (i.e. TNF-α inhibitors), in terms of efficacy and safety. The successful introduction of BMS TYK2 inhibitor would likely lead to an overall increase in the number of PsO patients receiving treatment.122 BMS TYK2 inhibitor will also likely claim market share from all competing third-line treatments (including biologics and biosimilars).123 Moreover, BMS’ pipeline project is trialled for a much wider range of indications than merely PsO, for example in CD and Lupus, where there are no or limited overlaps between the activities of the Parties. As a result, discontinuing or delaying the development of BMS TYK2 in an attempt to exclusively commercialise Otezla would result in the delay or loss of revenue streams in PsO and also in other indications. In addition, in BMS’ investor presentations, BMS TYK2 inhibitor is highlighted as one of the six new medicines to be launched by the merged entity in the next two years.124 This shows that BMS is publicly building up expectations amongst its investors that no delay in the development of BMS TYK2 inhibitor will take place.

(72) With respect to BMS RORγt agonist, given the early stage of this pipeline (Phase I) and the fact that Otezla will lose exclusivity in Europe around the time this asset would launch, if successful in trial, it is unlikely that the combined entity would have incentives to stop the development of BMS-986251. Rather, it would make sense for the combined entity to continue the development of the project for life- cycle management purposes.

(73) Fifth, post-Transaction, it is unclear whether the Parties would have the ability and/or incentives to stop supplying or to repurpose Otezla in the EEA. Although one of the Parties’ internal documents125 suggests that, post-Transaction, […], this document seems to relate to the US market, where competitive dynamics are different from the EEA.

(74) In the EEA, for cost-efficiency reasons, the use and reimbursement of Otezla is restricted to patients who have first failed a conventional systemic therapy (or have contraindications). By contrast, in the US, there is no such requirement, which allows Otezla to be used as an earlier stage treatment and for milder cases.126 […]. In fact, today Celgene is seeking to have Otezla approved for mild-to-moderate PsO […] in the US.127 In any event, if the Parties decided to stop the supply of Otezla or to reposition it in the EEA (which remains unclear), the impact on the market would be limited given Otezla’s relatively modest market shares in the EEA (well below 10% in all the EEA countries where Otezla is sold) and the existence of many actual and potential competitors (including oral drugs).128

(C) Conclusion

(75) In view of the above, taking into account the results of the market investigation and all the evidence available to it, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market and with the functioning of the EEA Agreement resulting from the overlap of the Parties’ activities in third-line moderate-to-severe PsO treatments or (more narrowly) in oral third-line moderate-to-severe PsO treatments.

4.1.2.4. Overlap involving a pipeline programme at preclinical trial stage

(76) During the market investigation, two competitors identified an overlap between BMS TYK2 inhibitor pipeline, currently in Phase III trials, and the preclinical TYK2 inhibitor programme developed by Nimbus, in which Celgene has a financial option. According to these competitors, the combination of these two assets under the control of the merged entity could negatively impact competition in the market for moderate-to-severe PsO treatments. The Commission assesses these concerns in the remainder of this section.

(A) The Parties’ view

(77) The Parties submit that the Transaction does not raise serious doubts as a result of the overlap between BMS TYK2 inhibitor pipeline and Celgene’s option in Nimbus’ TYK2 inhibitor programme for two reasons. First, Nimbus’ TYK2 inhibitor project is at preclinical stage of development and has a very low probability of success so that it is wholly uncertain if it will ever reach the (EEA) market. Second, even if successful, Nimbus’ TYK2 inhibitor will be launched in the EEA no earlier than […], that is to say several years after the launch of BMS TYK2 inhibitor. This means that the two pipeline projects do not have “similar timing”129 and should not be considered as competing research programmes.

(B) The Commission’s assessment

(78) The Commission investigated the overlap between BMS TYK2 inhibitor pipeline (Phase III) and Celgene’s option in Nimbus’ TYK2 inhibitor pipeline (preclinical). The market investigation of the Commission showed that the Transaction would not give rise to serious concerns as to its compatibility with the internal market and the functioning of the EEA Agreement resulting from this overlap, irrespective of the relevant market delineation.

(79) In a possible relevant market comprising all third-line treatments for moderate-to- severe PsO, the combined entity would have one marketed product (Celgene’s Otezla) and three pipeline projects (BMS TYK2 inhibitor, Nimbus’ TYK2 inhibitor programme, assuming the relevant option is exercised, and BMS’ Rorγt antagonist in Phase I […]). In this market, the Transaction does not give rise to competition concerns for the reasons explained above regarding the overlap between BMS TYK2 inhibitor and Otezla.130 The addition of Nimbus’ TYK2 inhibitor programme does not change that conclusion because the Parties’ drugs are not expected to exert strong competitive constraints in the market for moderate-to-severe PsO and they would continue to face a large number of actual and potential competitors, including biologics, biosimilars and small molecule drugs.

(80) In a possible relevant market comprising oral third-line treatments for moderate-to- severe PsO, the combined entity would again have one marketed product (Otezla), the two TYK2 inhibitor programmes, and BMS-986251 (a RORγt agonist in Phase I […]). In this market, the Transaction does not give rise to competition concerns for the reasons explained above regarding the overlap between BMS TYK2 inhibitor, Otezla and BMS-986251.131 The addition of Nimbus’ TYK2 inhibitor programme does not change that conclusion because the Parties would continue to face a large number of potential competitors, with several oral drugs at a more advanced stage of development than Nimbus’ TYK2 inhibitor preclinical programme.

(81) In a possible relevant market including only TYK2 inhibitors for the treatment of moderate-to-severe PsO, the combined entity would own BMS TYK2 inhibitor and the financial option to acquire Nimbus’ TYK2 inhibitor preclinical programme. In this segment, the Transaction does not give rise to competition concerns for the reasons explained below.

(82) First, post-Transaction, the combined entity will continue to face strong competitive constraints from several players developing TYK2 inhibitors for moderate-to-severe PsO. Post-Transaction, there will be at least five players developing TYK2 inhibitors as treatments for moderate-to-severe PsO. In addition to the combined entity, these include large pharmaceutical companies (such as Pfizer and AbbVie) and also smaller pharmaceutical companies (such as Nuevolution and Sareum). The pipeline projects of Pfizer and AbbVie are in clinical trial stage (Phase II and Phase I, respectively) which means that they are more advanced than the Nimbus preclinical asset. The pipeline projects of Nuevolution and Sareum have not entered clinical development stage (similar to the Nimbus’ preclinical asset). Therefore, post- Transaction, several competing TYK2 inhibitor research programmes will remain on the market, in addition to the Parties’ programmes.

(83) Second, each of the Parties’ pipeline products appear to compete more closely with competitors’ pipeline products than the Parties' competing ones. BMS TYK2 inhibitor programme is at the most advanced clinical trial stage (Phase III). It is expected to receive approval in the EEA in […] for the treatment of moderate-to- severe PsO. By contrast, Nimbus’ TYK2 inhibitor is still at preclinical trial stage and it is expected to enter Phase I clinical trials in […]. In this sense, BMS TYK2 inhibitor competes more closely with AbbVie’s and Pfizer’s pipelines (both at clinical trial stage) than it does with Nimbus’ programme. These projects have significantly higher chances of success, compared to Nimbus’ pipeline which is still at preclinical trial stage.132 In the market investigation, the vast majority of respondents did not identify Nimbus as a close competitor of BMS TYK2 inhibitor programme. Rather, most of them referred to Pfizer’s TYK2 inhibitor pipeline project (as well as to other treatments with different MoA).133 Nimbus’ TYK2 inhibitor programme competes more closely with other programmes which have not yet entered clinical trial stage, such as Sareum’s and Nuevolution’s projects.

(84) During the market investigation, two competitors flagged that BMS and Nimbus are the only two companies developing allosteric TYK2 inhibitors.134 The two competitors, which constitute a small minority of the respondents, argued that allosteric TYK2 inhibitors have a distinct and unique efficacy and safety profile and that, post-Transaction, all the relevant pipeline projects would be controlled by the combined entity. The market investigation did not support these concerns. The majority of KOLs and market participants indicated that allosteric mechanisms are not unique and orthosteric TYK 2 inhibitors could possibly achieve comparable levels of efficacy and safety.135 In any event, even assuming that allosteric TYK2 inhibitors do have unique characteristics, the market investigation revealed that such drugs are currently under development by companies other than BMS and Nimbus.136

(85) Third, the Commission takes into account the competitive pressure to be exerted on TYK2 inhibitors by alternative treatments for moderate-to-severe PsO (already marketed or under development). The market investigation showed that TYK2 inhibitors will be one of the many drugs in the unconcentrated space of moderate-to- severe PsO treatments. TYK2 inhibitors will face competition from marketed biologics (including TNF-α inhibitors, IL-17 inhibitors, IL-23 inhibitors, and IL- 12/23 inhibitors), their biosimilars, and also a large number of pipeline drugs, including several oral pipelines in Phase II and Phase III.137 A competitor developing a TYK2 inhibitor took the view that its drug will “not just compete with other small molecules (e.g. Otezla or BMS’s TYK2 inhibitor) but also with biologics in the very crowded space of moderate-to-severe PsO treatments”.138

(86) This is also confirmed by the majority of respondents to the market investigation who do not expect TYK2 inhibitors to be more efficacious139 or significantly safer140 than existing treatments. A KOL indicated that “BMS’ TYK2 inhibitor seems to be one of the many pipeline projects that exist today for the treatment of PsO.”141 Another KOL added that “[m]any products currently on the market for PsO have an efficacy and safety profile that is superior to the efficacy and safety profile of the combined BMS/Celgene portfolio. The fact that Celgene purchased an option to acquire the TYK2 inhibitor programme of a US company, Nimbus, does not change this conclusion. There are several companies that develop pipeline projects for PsO”.142

(87) Fourth, it is unlikely that the Transaction will lead to a loss of innovation on the hypothetical market for TYK2 inhibitors PsO treatments. Indeed, Celgene is not developing the Nimbus programme itself. It simply has a financial option to purchase the programme, with a set expiry date.143 Assuming that the combined entity decides not to exercise this option (e.g. because it also owns the BMS TYK2 inhibitor programme), the Nimbus project would not be necessarily discontinued. Nimbus would be free to continue the development of its TYK2 inhibitor programme on its own and/or look for an alternative partner.144 As Nimbus itself put it, “if Celgene does not exercise the option, Nimbus will be free to continue the development of the TYK2 inhibitor programme on its own and/or look for an alternative partner.”145 Nimbus added: “[i]f the merged entity does not exercise the option, other pharmaceutical companies are likely to be interested in acquiring Nimbus’ TYK2 programme. In this respect, Nimbus explained that, before reaching an agreement with Celgene, it had engaged in discussions with several pharmaceutical companies (excluding BMS, precisely because it already had its own TYK2 inhibitor pipeline) and that several of them had expressed interest in its TYK2 inhibitor programme.”146

(88) It is also unlikely that the combined entity would have an incentive to exercise the option, purchase the Nimbus pipeline asset, and then discontinue it. This would involve automatically a significant investment, because the exercise of the option requires an upfront payment of […]147 by the combined entity to Nimbus for an asset whose development and launch on the market remain highly uncertain (5% for small molecule drugs).148

(89) During the market investigation, two competitors, which constitute a small minority of the respondents, also raised the concern that by holding an option over the Nimbus TYK2 inhibitor programme, the combined entity could delay the programme’s development to limit the competitive constraints on the BMS TYK2 inhibitor drug. However, any such delay (e.g. through requests of excessive amounts for information by the combined entity) is unlikely to have a significant impact on the overall timeline of the Nimbus project, which is today more than […] away from the market, and its launch is still uncertain.149 In any event, as explained above,150 before […] (when Nimbus’ TYK2 inhibitor is expected to be launched), other TYK2 inhibitor products more likely to have entered the EEA market and exert competitive constraints on BMS TYK2 inhibitor.

(C) Conclusion

(90) For all these reasons, the Commission concludes that the Transaction would not give rise to serious concerns as to its compatibility with the internal market and the functioning of the EEA Agreement resulting from this overlap, irrespective of the relevant market delineation.

4.1.3. Treatments for Psoriatic Arthritis (“PsA”)

(91) PsA is a chronic, systemic, autoimmune joint disease associated with PsO. It occurs when cells from the immune system move into a patient’s skin and joints, and produce proteins that cause swelling and pain.

(96) Celgene markets Otezla in the EEA as a third-line treatment for PsA. Otezla is a PDE-4 inhibitor with the active ingredient apremilast. It received a marketing authorisation from the EMA for PsA in 2015 and since then has been launched in Austria, Belgium, Croatia, Cyprus, Denmark, Estonia, Finland, France, Germany, Greece, Iceland, Ireland, Italy, Luxembourg, the Netherlands, Slovakia, Slovenia,Spain, Sweden, the UK, and Liechtenstein.153

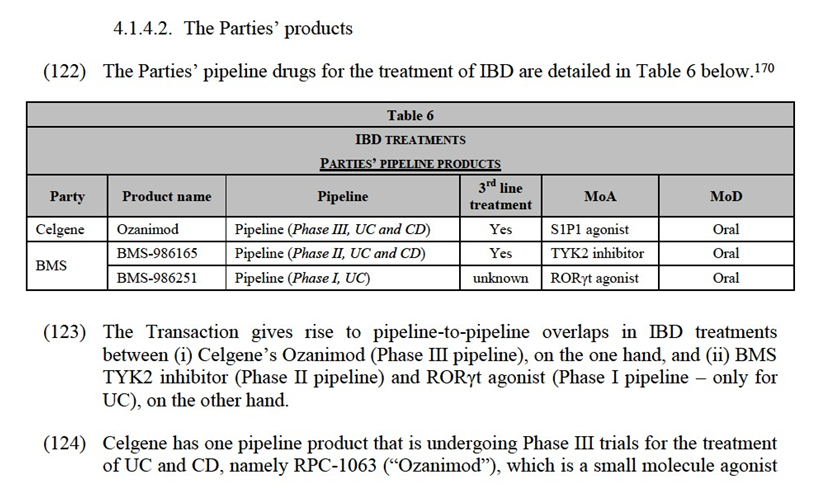

(97) BMS markets Kenalog for the treatment of PsA in Spain. Launched in the 1960s, Kenalog is a synthetic glucocorticoid corticosteroid with the active ingredient triamcinolone acetonide. Kenalog is used for short-term relief of the symptoms of PsO as opposed to the long-term treatment of the underlying disease. Kenalog has lost market exclusivity and there is a large number of generic alternatives for Kenalog.

(98) BMS markets Orencia for the treatment of PsA in Germany. Launched in 2017, Orencia is a T cell costimulatory agent with the active ingredient abatacept.

(99) BMS is developing an oral small molecule drug for PsA, namely BMS-986165, which is a TYK2 inhibitor.154 The project will shortly commence Phase II trials for this indication. It is expected to enter the EEA markets in 2026 as a third-line treatment.

(100) […]. The way it works remains uncertain but antagonizing RORγt activity with synthetic small molecules seems to inhibit expression of IL-17A.

(101) The Transaction gives rise to overlaps between the marketed (existing) products of the Parties and their pipeline products at clinical trial stage in (i) in a plausible market including all treatments for moderate-to-severe PsA,155 (ii) a plausible market for third-line treatments for moderate-to-severe PsA and (ii) a plausible market for oral third-line treatments for moderate-to-severe PsA.

4.1.3.3. Competitive assessment

(102) The Transaction gives rise to marketed-to-pipeline overlaps between (i) Celgene’s Otezla (marketed), on the one hand, and (ii) BMS TYK2 inhibitor (Phase II pipeline) and RORγt agonist (Phase I pipeline), on the other hand.

(103) The Parties argue that no competition concerns arise in the market for PsA treatments or any of its plausible sub-segmentations as (i) Otezla has a limited market share in EEA markets; (ii) Otezla and each of the BMS pipeline projects are differentiated products (with different MoA, projected levels of efficacy, and expected safety profiles); (iii) there is a number of competing products for the treatment of PsA (in the market and under development). The Parties also claim that, post-Transaction, the merged entity would have no ability or incentive to discontinue (i) the development of BMS’ pipeline products or (ii) the supply of Otezla.

(104) The market investigation broadly confirmed the Parties’ arguments regarding PsA treatments and allows the Commission to exclude serious doubts as to the compatibility of the Transaction with the internal market and the functioning of the EEA Agreement.

(105) First, in the market for third-line treatment for PsA in the EEA, Otezla’s market share remains limited at national level. Otezla holds less than 20% in each of the EEA countries where it is marketed.156 Otezla is one of the many drugs available on the market, including biologics and small molecules (JAK inhibitors) but it is less efficacious. One KOL confirmed that “Otezla has a lower efficacy profile than biologics, including TNF inhibitors, and JAK inhibitors. […] Otezla is widely used in the US but is much less popular in Europe (for costs-efficiency reasons)”157 and another explained: “[in PsA] Otezla does not have a strong profile compared to the most effective treatments, which are TNF inhibitors and IL-17 inhibitors”.158

(106) Second, Celgene’s Otezla and BMS TYK2 inhibitor and RORγt agonist are differentiated compounds with (i) different MoA (Otezla is a PDE-4 inhibitor and BMS pipeline drugs are a TYK2 inhibitor and a RORγt agonist); (ii) different expected efficacy profiles (BMS TYK 2 will likely have higher efficacy than Otezla);159 and (iii) different safety profiles and monitoring requirements (Otezla’s safety profile is expected to be higher than BMS TYK2 inhibitor, which could potentially have immunosuppressant effects and require monitoring, similarly to other JAK inhibitors).160 For all these reasons, BMS TYK2 inhibitor is expected to compete more closely with biologics and other JAK inhibitors (such as Pfizer marketed drug Xeljanz (tofacitinib))161 than with Otezla. BMS RORγt agonist will likely compete with other products that are under development for PsA and have a RORγt agonist MoA (e.g. Arrien’s ARN-6039, Akros’ JTE-451, and AstraZeneca’s AZD-0284).162

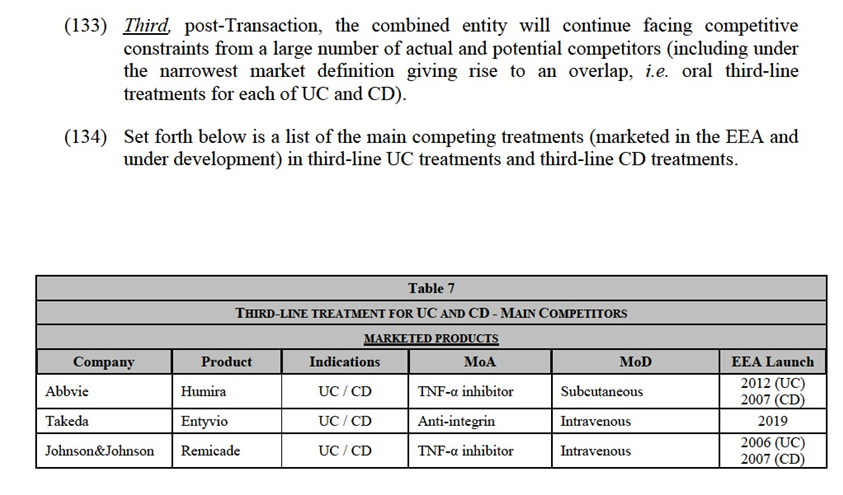

(107) Third, post-Transaction, the combined entity will continue facing competitive constraints from a large number of actual and potential competitors (including under the narrowest market definition giving rise to an overlap, i.e. oral third-line treatments for PsA).

efficacy/safety profiles of the Parties’ products, it is unlikely that the combined entity would have incentives to cease, repurpose or delay the development of BMS’ pipelines post-Transaction.

(112) BMS TYK2 inhibitor is expected to compete more closely with JAK inhibitors and biologics, in terms of efficacy and safety, than with Otezla. Moreover, BMS TYK2 inhibitor pipelines are seeking authorisation for a much wider range of indications than merely PsA. As a result, discontinuing or delaying the development of BMS TYK2 inhibitor in an attempt to exclusively commercialise Otezla would result in the delay or loss of PsA and other indications.

(113) As regards Otezla, if the combined entity decided to stop the supply of the drug or to reposition it in the EEA, the impact on the market would be limited given Otezla’s relatively modest market shares in the EEA (less than 20% at national level).

(114) With respect to BMS RORγt agonist, given the early stage of this pipeline (Phase I) and the fact that Otezla will lose exclusivity in Europe around the time this asset would be launched, if successful in trial, it is unlikely that the combined entity would have incentives to stop the development of BMS-986251.

(115) Fifth, the market investigation did not reveal any substantiated competition concerns in relation to the Transaction in a possible market for third-line PsA treatments or any of its plausible sub-segmentations.

(116) For all these reasons, the Commission concludes that the Transaction does not give rise to serious doubts as to its compatibility with the internal market and the functioning of the EEA Agreement as regards its impact on competition in the possible market for PsA treatments (and its plausible sub-segmentations).

4.1.4. Treatments for inflammatory bowel disease (“IBD”)

(117) IBD typically refers to two conditions: UC and CD, which are inflammatory diseases that affect the digestive system. The main difference between them is that CD can affect any part of the gastroenterology tract, whereas UC is limited to the colon. Similarly, CD affects the full thickness of the intestinal wall whereas the inflammation caused by UC remains within the superficial lining of the intestine.Both diseases are found to have similarly debilitating effects.165

(118) Clinical guidelines, in particular the treatment guidelines issued by the European Crohn’s and Colitis organisation (ECCO), recommend a phased treatment for UC and CD consisting of three lines of treatment. The first-line treatment include aminosalicylates (such as mesalazine or sulfasalazine), which are effective at inducing and maintaining remission. The second line-treatment include corticosteroids and immunosuppressants, which are used for moderate-to-severe cases, although remission cannot be maintained with steroid. The third-line treatment include biologics such as TNF-α inhibitors, anti-integrins and ustekinumab and small molecules.

of sphingosine-1- phosphate receptor 1 (“S1P1”) and sphingosine-1-phosphate receptor 5 (“S1P5”). Ozanimod works by preventing lymphocytes (including T and B cells) from migrating from lymphoid tissues to the sites of inflammation. If successful in Phase III trials, Ozanimod is expected to enter the EEA market in […] (UC) and […] (CD) as a third-line treatment.

(125) BMS is developing an oral small molecule drug for both UC and CD, namely, BMS- 986165, which is a TYK2 inhibitor.171 The projects are undergoing Phase II trials and are expected to enter the EEA market in 2026 as a third-line treatment.

(126) […]. The way it works remains uncertain but antagonizing RORγt activity with synthetic small molecules seems to inhibit expression of IL-17A.

(127) The Transaction gives rise to overlaps between the Parties’ pipeline products at clinical trial stage in (i) plausible markets including all treatments for IBD and each of UC and CD (ii) plausible markets for third-line treatments for IBD and each of UC and CD, and (iii) plausible markets for oral third-line treatments for IBD and each of UC and CD.

4.1.4.3. Competitive assessment

(128) The Parties argues that no competition concerns arise in relation to UC and CD treatments in the EEA, under any plausible market definition, given that (i) the Parties’ pipeline products are at different clinical phases and consequently do not have a “similar timing” 172 as regards their potential market entry, (ii) there is a crowded pipeline for treatments of IBD and, (iii) the Parties’ products have different MoA, different anticipated usage and very different expected safety and efficacy profiles, so that they are unlikely to be close competitors. In addition, BMS-986251 is seeking an indication only for UC.

(129) The market investigation broadly confirmed the Parties’ arguments and allows the Commission to exclude serious doubts as to the compatibility of the Transaction with the internal market and the functioning of the EEA Agreement in relation to UC and CD treatments, under any plausible market definition.

(130) First, the Parties’ compounds and research programmes are very differentiated. Celgene’s Ozanimod is an agonist of the S1P1 and S1P5 receptors, whereas BMS TYK2 is a selective inhibitor of tyrosine kinase 2 and BMS-986251 is a RORγt agonist. The significant differences in Celgene’s Ozanimod as opposed to BMS TYK2 inhibitor are presented in the Figure below, from which it can be seen that S1P1 inhibition targets UC and CD within a completely different stage of the inflammatory process than small molecules belonging to the JAK inhibitor family such as BMS TYK2 inhibitor. According to the Parties, the different MoA in Ozanimod and BMS TYK2 inhibitor suggest that the two products will likely have differentiated efficacy and safety profiles (if and when they reach the market).

(137) Finally, the market investigation did not reveal any substantiated competition concerns in relation to UC and CD treatments in the EEA. Given the differentiated MoA of Celgene’s and BMS’ pipeline projects, the risk of discontinuation or delay for some of them is limited

(138) In light of the above considerations supported by evidence collected over the course of the market investigation, the Commission concludes that the Transaction does not give rise to serious doubts as to its compatibility with the internal market and the functioning of the EEA Agreement as regards its impact on competition in relation to UC and CD treatments, under any plausible market definition.

4.1.5.Treatments for Lupus

(139) Lupus is a long-term systemic autoimmune disease which is difficult to diagnose because it is a very heterogeneous disease (no two cases of Lupus are exactly alike) and its symptoms often mimic those of many other diseases. Lupus can cause inflammation in a wide range of bodily systems, and can involve a wide range of complications depending on which bodily systems are affected. Symptoms include tiredness, mild skin rash or joint pain (in milder cases) and serious inflammation and damage in the skin, lungs, heart, kidneys.

(140) Lupus is a very heterogeneous disease and it is difficult to identify clear lines of treatment.179 Lupus treatments include (i) nonsteroidal anti-inflammatory drugs (such as aspirin and ibuprofen); (ii) antimalarials (such as hydroxychloroquine); (iii) corticosteroids (such as prednisolone); and (iv) immunosuppressant drugs (such as azathioprine and methotrexate). The use of biologics is less common in Lupus than in other autoimmune diseases. There is only one biologic on the market approved for lupus, namely, GSK’s Benlysta (belimumab). Another biologic, Roche’s Rituxan (rituximab), is also now widely used for the treatment of Lupus on an off-label basis.

4.1.5.1. Market definition

(141) The Commission has not previously analysed the relevant product market for Lupus treatments. In J&J/Actelion, whilst the Commission did not define the relevant product market for Lupus treatments, it excluded competition concerns in the Lupus space based of the differentiated MoA, MoD and likely line of treatment of J&J and Actelion’s products.180 The Parties suggested that the relevant product for treatments of Lupus can be left open, as no competition concerns arise under any plausible market delineation (i.e. by line of treatment, by MoA and by MoD). For the purposes of this Decision, it can be left open whether the market for Lupus treatments should be sub-segmented. This is because the Transaction does not give rise to serious doubts as to its compatibility with the internal market and the functioning of the EEA Agreement even under the narrowest market definition giving rise to an overlap between the Parties’ drugs, i.e. oral treatments for Lupus.

of lupus”.184 As shown in Table 9, more than 10 competing pipeline products for the treatment of Lupus are expected to be launched in the EEA by 2023, that is before the most advanced pipeline product of the Parties reaches the EEA market. Many of the competing pipeline projects are based on MoA similar to the MoA of the Parties’ pipeline programmes. For example, Eli Lilly’s baricitinib is a JAK inhibitor, involving a MoA similar to the BMS TYK2 inhibitor. Roche’s fenebrutinib and Merck KGaA’s evobrutinib constitute BTK inhibitors, similar to BMS-986195.

(154) On the narrowest plausible market giving rise to an overlap between the Parties’ pipeline products, which is the market restricted to oral treatments for Lupus, the combined entity will also face strong competitive constraints. Post-Transaction, competing oral treatments will include at least three Phase II projects developed by large pharmaceutical companies, such as Eli Lilly, Merck KGaA, and Roche. If successful, Eli Lilly’s baricitinib is expected to enter the market approximately 3 years earlier than any of the pipeline projects of the Parties.

(155) Third, the market investigation did not reveal any substantiated competition concerns in relation to the Transaction in a possible market for Lupus treatments or any of its plausible sub-segmentations. A KOL added that “[t]he fact that there is still a need for an efficacious lupus treatment makes it unlikely that the combined entity would decide to discontinue one of the pipeline projects that the Parties are developing today”.185

(156) For all these reasons, the Commission concludes that the Transaction does not give rise to serious doubts as to its compatibility with the internal market and the functioning of the EEA Agreement as regards its impact on competition in the possible market for Lupus treatments (and its plausible sub-segmentations).

4.2.Fibrotic diseases

4.2.1.Introduction

(157) Fibrotic diseases include a broad range of diseases (e.g. idiopathic pulmonary fibrosis, non-alcoholic steatohepatitis, advanced liver fibrosis) that involve fibrosis in some part of the body. Fibrosis is the formation of excessive tissue scarring and can occur in different organs, such as the lungs, liver, skin, eyes, heart, and kidneys.

(158) Fibrosis often occurs as a result of sustained injury, which could be caused by, for example, trauma, toxins, inflammation or infection. Normally, an organ or tissue that is affected by an injury undergoes a process of healing through deposition of new collagen fibres, repair of blood vessels, and other activities which restore the integrity of the tissue involved. When these repair processes – specifically the laying down of new collagen fibres – become dysregulated, excessive scarring can form. Excessive scarring in turn can have a very significant impact on the function of the impacted organ.

(159) In fibrotic diseases, the Parties activities overlap with respect to the following indications: Idiopathic Pulmonary Fibrosis (“IPF”) (Section 4.2.2) and Non- alcoholic steatohepatitis (“NASH”) (Section 4.2.3).

4.2.2.Treatments for idiopathic pulmonary fibrosis

(160) Idiopathic pulmonary fibrosis (“IPF”) is a relatively rare chronic progressive disease that affects the lungs. The cause is unknown, and the disease is particularly complex as it is not driven by a single gene or cell type.

(161) IPF is caused by lung tissue becoming thick and stiff and eventually forming scar tissue within the lungs. The scarring, or fibrosis, seems to result from a cycle of damage and healing that occurs in the lungs. Over time, the healing process stops working correctly and scar tissue forms. What causes these changes in the first place is unknown. Symptoms of IPF include: shortness of breath, a dry cough, fatigue, unexplained weight loss, aching muscles and joints, and widening or rounding of the tips of the fingers or toes (clubbing). Disease progression can vary - some patients become ill very quickly and for others the disease progresses over months or years.The mean survival time from diagnosis is 2 to 5 years

(162) There is currently no cure for IPF. The main aim of the two marketed treatments currently available in the EEA (Roche’s pirfenidone and Boehringer Ingelheim’s nintedanib) is to relieve symptoms and to slow progression. As the condition becomes more advanced, palliative care is offered. In addition, lung transplants may be an option for a small subgroup of patients with IPF who meet the necessary criteria.

(163) In 2015, the European Respiratory Society published, jointly with the American Thoracic Society, Japanese Respiratory Society and Latin American Thoracic Association, published guidelines on idiopathic pulmonary fibrosis treatment.186 Only nintedanib and pirfenidone are conditionally recommended by the guidelines.

4.2.2.1. Market definition

(164) The Commission has not previously analysed the relevant product market for IPF treatments. The Parties suggested that the relevant product for treatments of IPF can be left open, as no competition concerns arise under any plausible market delineation (i.e. by line of treatment, by MoA and by MoD). For the purposes of this Decision, it can be left open whether the market for IPF treatment should be sub-segmented. This is because the Transaction does not give rise to serious doubts as to its compatibility with the internal market and the functioning of the EEA Agreement even under the narrowest market definition giving rise to an overlap between the Parties’ drugs (i.e. oral treatments for IPF).

(165) As regards the geographic market definition, the Commission has consistently considered the market for pipeline products to be at least EEA-wide in scope.187 The Parties do not contest this. Nothing in the market investigation suggests that the Commission should depart in the present case from its previous practice with respect to IPF treatments.

NASH. NASH may initially present without fibrosis, but as the condition progresses, fibrosis develops. NASH is generally caused by lifestyle choices (such as poor diet and lack of exercise); however, unlike other fatty liver diseases, it is not caused by alcohol abuse or as a side effect of medication.

(184) The most common symptoms are fatigue and mild pain in the upper right abdomen. As the disease progresses to more advanced stages, more symptoms may become apparent including: bleeding easily, bruising easily, itchy skin, jaundice and fluid accumulation in abdomen.

(185) There are currently no treatments specifically marketed for NASH. Doctors may recommend lifestyle interventions (such as changing diet and losing weight) and treating comorbidities (i.e. one or more additional conditions that occur concomitantly or concurrently with a primary condition). Other options also include bariatric surgery or pharmacotherapy, including treatments with vitamin E, an SGLT2 inhibitor (such as Invokana which is approved as a diabetes medicine in the EEA), or pemafibrate (currently not approved in the EEA).

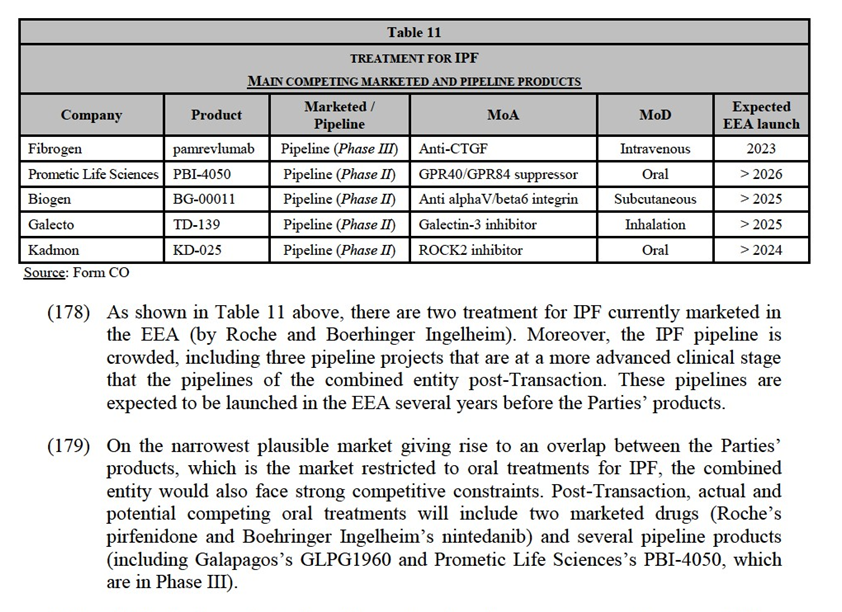

(186) In 2016, the European Association for the Study of the Liver (“EASL”), the European Association for the Study of Diabetes (“EASD”) and the European Association for the Study of Obesity (“EASO”) have published Clinical Practice Guidelines for the management of NAFLD (“NAFLD Guidelines”). The NAFLD Guidelines note that no drug is approved for NASH by regulatory agencies and that no specific therapy can be recommended. The NAFLD Guidelines note that insulin sensitisers, antioxidants (such as vitamin E) and cytoprotective and lipid lowering agents may be helpful. In patients that are unresponsive to lifestyle changes and pharmacotherapy, bariatric surgery may be an option. The NAFLD Guidelines recommend diet and lifestyle changes as an important treatment.

4.2.3.1. Market definition

(187) The Commission has not previously analysed the relevant product market for NASH treatments. The Parties suggested that the relevant product for treatments of NASH can be left open, as no competition concerns arise under any plausible market delineation (i.e. no line of treatment have been identified for the treatment of NASH and the Parties’ pipeline products neither have the same MoA nor the same MoD). For the purposes of this Decision, it can be left open whether the market for NASH treatment should be sub-segmented. This is because the Transaction does not give rise to serious doubts as to its compatibility with the internal market and the functioning of the EEA Agreement even under the narrowest market definition giving rise to an overlap between the Parties’ drugs (i.e. treatments for NASH).

(188) As regards the geographic market definition, the Commission has consistently considered the market for pipeline products to be at least EEA-wide in scope.191 The Parties do not contest this. Nothing in the market investigation suggests that the Commission should depart in the present case from its previous practice with respect to NASH treatments.

(205) The range of treatments for cancer include traditional types of therapies (such as surgery, radiotherapy and chemotherapy) and newer forms of treatment (such as targeted therapies and immunotherapies).

(206) These different types of treatment may be approved as monotherapies or combination therapies. A combination therapy is when two or more drugs (or therapies) are used in parallel for the same indication, which may help to improve the efficacy and safety of the treatment. Each product that is part of the combination treatment is typically marketed by the company controlling the product. and procured by customers on a stand-alone basis.199

(207) The oncology treatments offered by BMS and Celgene include chemotherapies, targeted therapies and immunotherapies. 200

(208) Given the different ways in which they treat cancer, chemotherapies, targeted therapies, and immunotherapies are most often used as complementary treatments:- Chemotherapies involve the use of cytotoxic drugs to kill cancer cells, targeting cells that grow and divide at rapid rates. However, chemotherapies can also attack healthy cells, particularly fast-growing healthy cells, such as red and white blood cells and cells comprising the hair follicles;- Targeted therapies are drugs or other substances that interfere with specific molecules involved in tumour growth and progression. Targeted therapies are designed to specifically ‘target’ and act upon specific mutations, amplifications, molecular aberrations or proteins that are expressed by the form of cancer being targeted. As a result, targeted therapies each have a highly specific MoA;- Immunotherapies are products that utilise a patient’s own immune system to fight cancerous cells. Immunotherapies do not attack cancerous cells directly but are designed to enhance the body’s natural mechanisms to fight cancer, helping the immune system to increase its natural ability to eliminate cancer cells.

(209) In oncology, the Transaction gives rise to limited number of marketed-to-pipeline overlaps and pipeline-to-pipeline overlaps involving early stage pipelines (Phase I or Phase I/II)201, with the same MoA or different MoA. More specifically, the Parties’activities overlaps with respect to BET inhibitors (a targeted therapy) (Section 4.3.2) and various immunotherapies (Section 4.3.3).202

4.3.2. BET Inhibitors

(210) BET inhibitors belong to targeted therapies. Bromodomain and extra-terminal (“BET”) proteins are involved in the expression of several genes controlling activities which are key for cancer development, such as cell proliferation and metastatic spreading. BET inhibitors block the BET proteins, thus preventing the expression of the relevant genes and limiting cancer development.

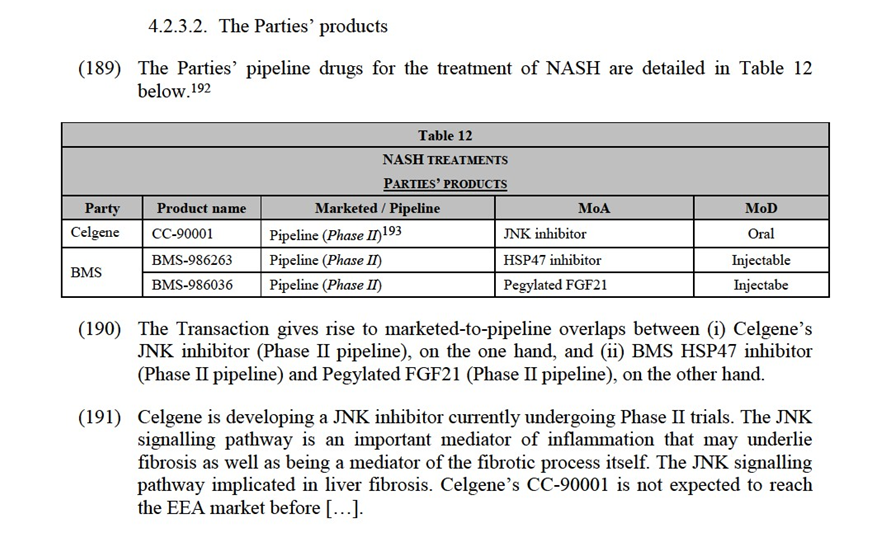

(211) There are currently no marketed BET inhibitors and all BET inhibitors under development are at an early stage (e.g. Phase I or Phase I/II clinical trials). BET inhibitor development covers several possible oncology indications.

4.3.2.1. Market Definition

(212) The Parties submitted that it is not necessary for the Commission to reach a conclusion on precise market definition in this case as no competition concerns arise under any plausible market delineation (i.e. by MoA or by indication).

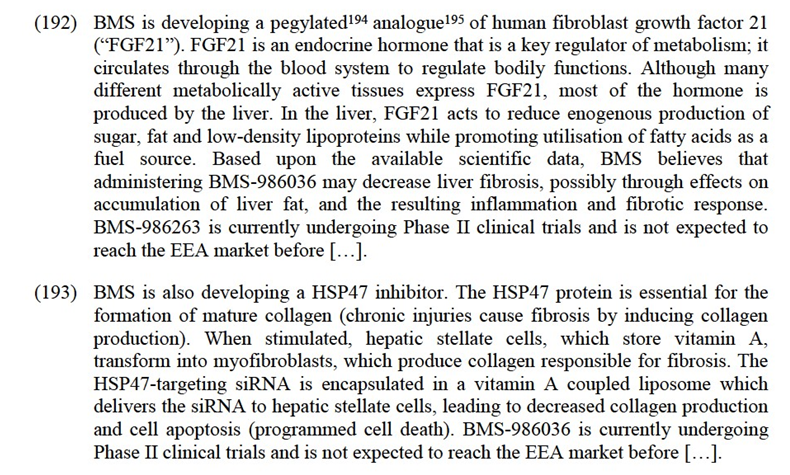

(213) The Commission has discussed relevant product market definition for Phase I/II and Phase II pipeline projects in targeted oncology therapies in GSK/Novartis Oncology. In this case, the Commission found that “the potential for […] clinical research programs to deliver substitutable products should be assessed by reference to the products’ characteristics and intended therapeutic use, in particular by reference to their mechanism of action and to the cancer types for which they are being investigated”.203

(214) In the present case, the market investigation suggested that the relevant product market should be sub-segmented on the basis of the MoA, i.e. as a market for BET inhibitor drugs.204 The market investigation also indicated that the market for BET inhibitor drugs should not be sub-segmented further, i.e. by indication.205 This is due to the fact that all BET inhibitor drugs are still under development today and they are in Phase I or Phase II clinical trial stage. While certain indications may be associated with the pipeline project at that stage, these may be reduced or changed as the trials progress.

(225) As shown in Table 15 above, the BET inhibitor pipeline is crowded, including several pipeline projects that would compete with the pipelines of the combined entity post-Transaction. These projects are at approximately the same stage as the Parties’ BET inhibitor clinical trials.

(226) In a narrower market that includes only BET inhibitors for […],213 the combined entity will still face competitive constraints from several competitors. There is at least one company which continues to develop a BET inhibitor drug specifically for […]. Moreover, all the companies developing BET inhibitors for other indications take the view that it is easy to expand the indications associated with their pipeline programme, for example to cover […].214

(227) Moreover, the market investigation did not reveal any substantiated competition concerns in relation to the Transaction in a possible market for BET inhibitor drugs or specifically in BET inhibitor drugs for […].215

(228) For all these reasons, the Commission concludes that the Transaction does not give rise to serious doubts as to its compatibility with the internal market and the functioning of the EEA Agreement as regards its impact on competition in the possible market for BET inhibitor drugs (and its plausible sub-segmentations).

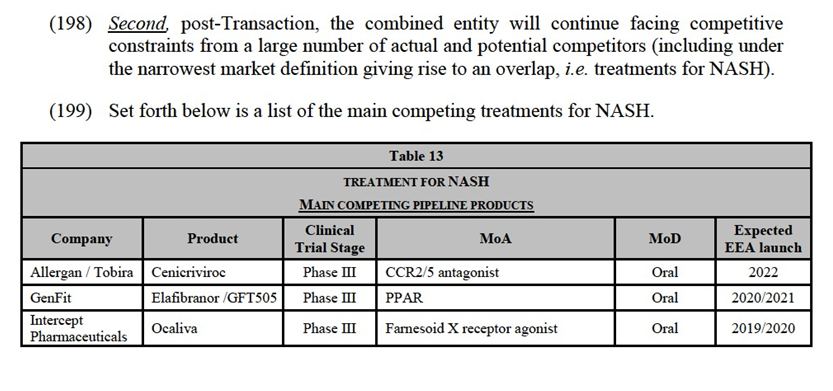

4.3.3.Other Overlaps

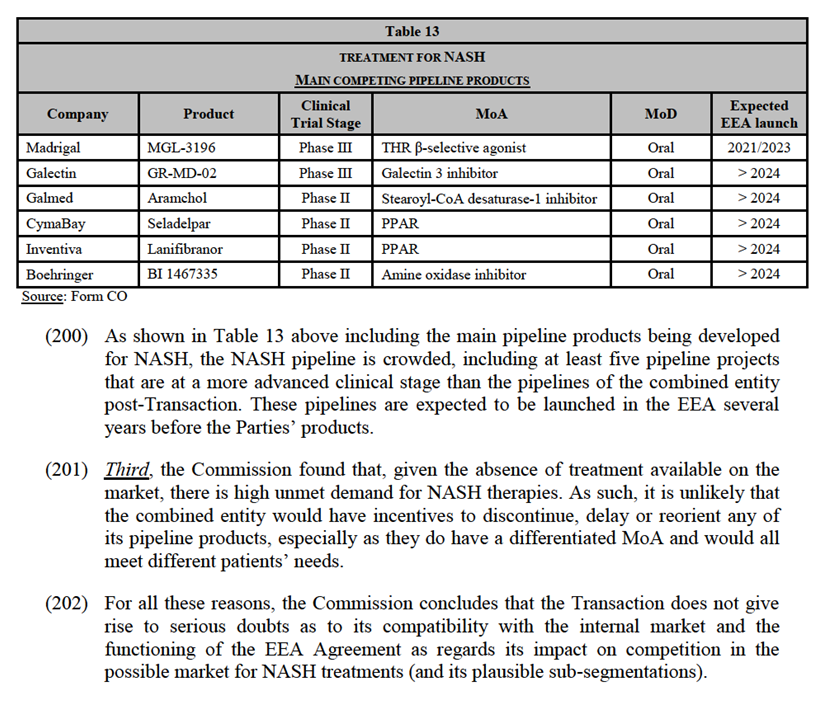

(229) Other areas where the Parties have early stage pipelines with the same indication but a different MoA are:- Immunotherapies for colorectal cancer;- Immunotherapies for head and neck squamous cell cancer ("HNSCC");- Immunotherapies non-small cell lung cancer ("NSCLC");- Immunotherapies small cell lung cancer ("SCLC");- Immunotherapies for ovarian cancer;- Immunotherapies for pancreatic cancer; and- Immunotherapies for multiple myeloma.216

4.3.3.1. Market definition

(230) The Commission has not previously considered the product markets for immunotherapies treating colorectal cancer, HNSCC, NSCLC, SCLC, ovarian cancer, pancreatic cancer, and multiple myeloma.

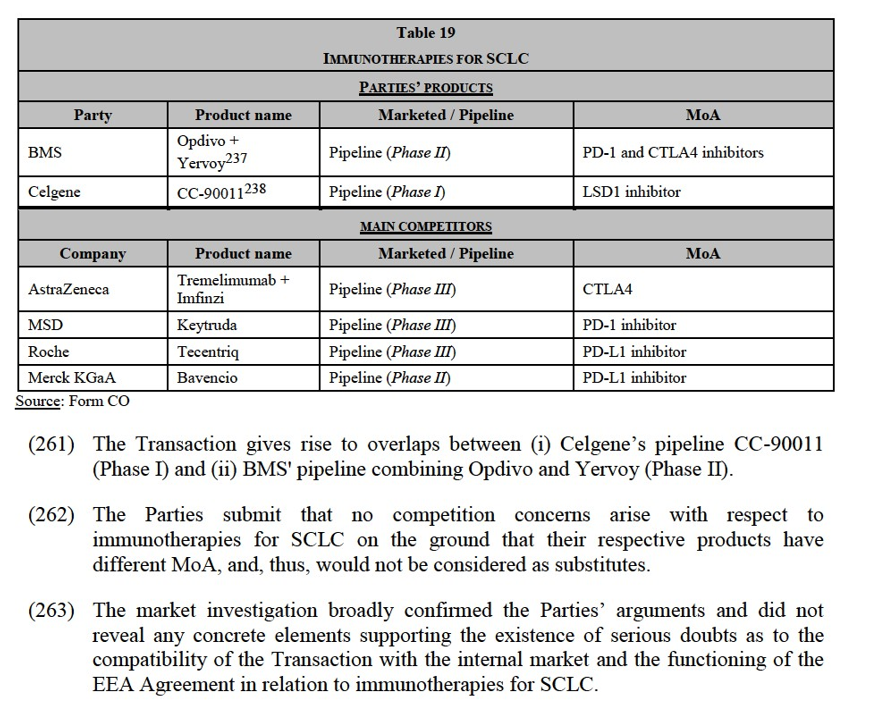

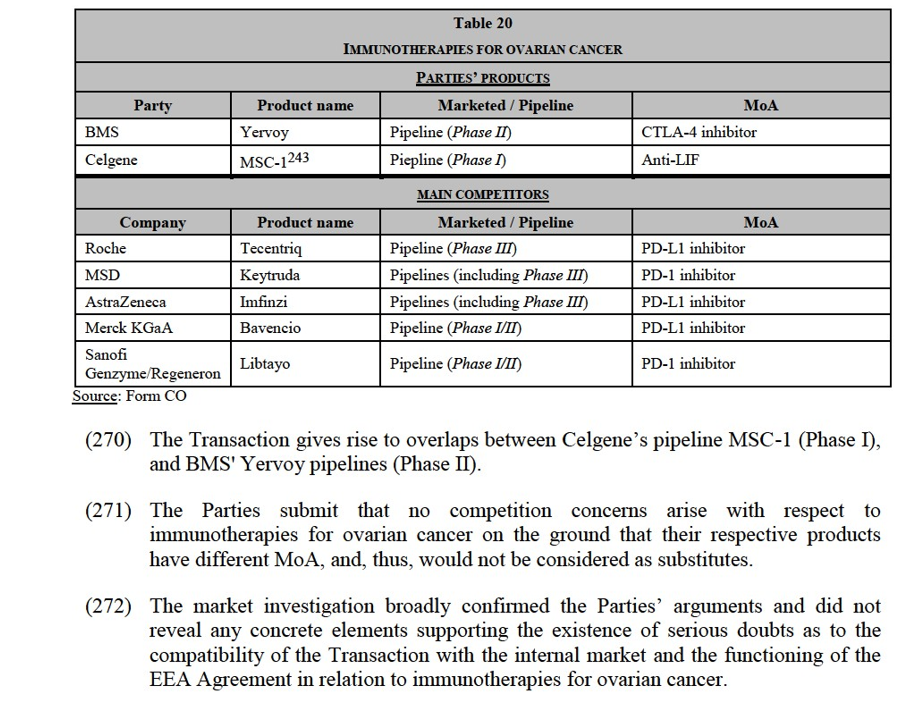

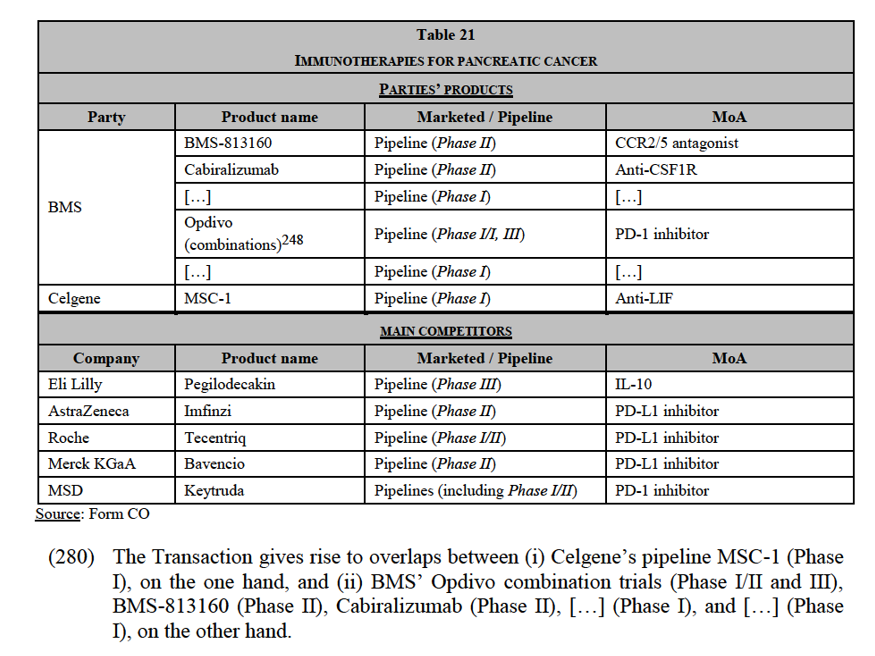

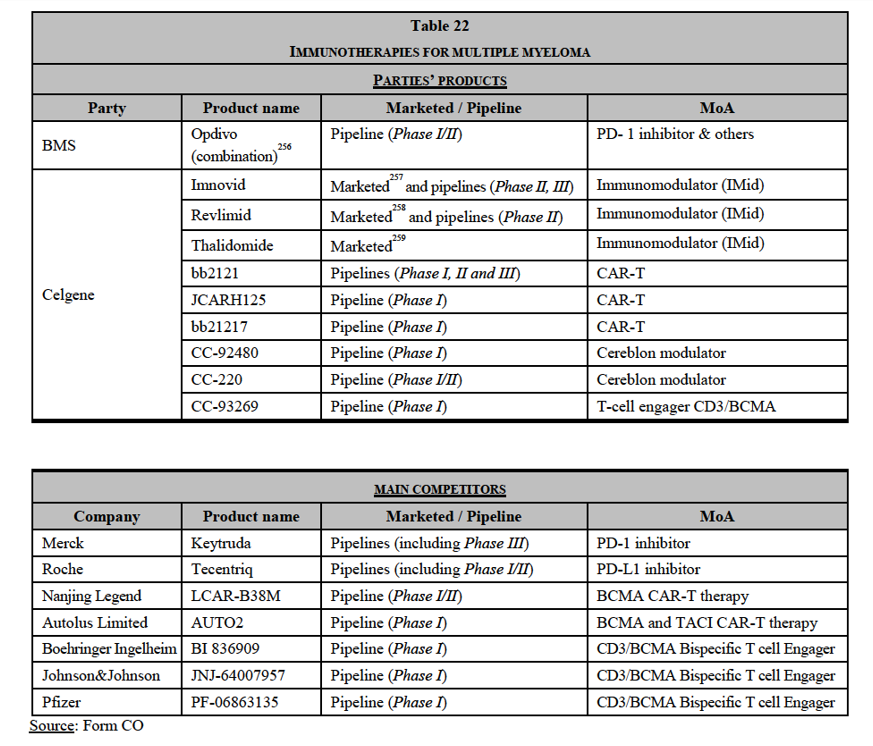

(231) For the purpose of this Decision, it can be left open217 whether the market for (i) immunotherapies for colorectal cancer, (ii) immunotherapies for HNSCC, (iii) immunotherapies for NSCLC, (iv) immunotherapies for SCLC, (v) immunotherapies for ovarian cancer, (vi) pancreatic cancer, and (vii) immunotherapies for multiple myeloma (i.e. by type and stage of the disease, by line of treatment, by MoA and by MoD) as the Transaction does not give rise to serious doubts as to its compatibility with the internal market and the functioning of the EEA Agreement under any plausible market definition.