Commission, February 13, 2019, No M.8941

EUROPEAN COMMISSION

Decision

EQT / WIDEX / JV

Subject: Case M.8941 - EQT / Widex / JV

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 9 January 2019, the European Commission received notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 (the “Merger Regulation”). This notification concerns the creation of a full function joint venture between the following undertakings: Sivantos Pte. Ltd. (“Sivantos”, Singapore), controlled by Equity VI Limited and EQT Fund Management S.à r.l. (together referred to as “EQT”); and Widex A/S (“Widex”, Denmark), controlled by T&W Medical A/S (formerly Widex Holding) (“T&W Medical”, Denmark). T&W Medical and EQT acquire, within the meaning of Article 3(1)(b) and 3(4) of the Merger Regulation, joint control over a newly created entity (the “JV” or the “Merged Entity”), combining the activities of Widex and Sivantos (the “Transaction”). The concentration is accomplished by way of purchase of shares in a newly created company constituting a joint venture. (3) (EQT and T&W Medical are designated hereinafter as the “Notifying Parties” or “Parties”).

1. THE PARTIES

(2) EQT is a private equity company controlling numerous investment funds. The EQT funds’ portfolio companies are active in a variety of industries, including the healthcare, Telecommunications, Media & Technology services, consumer and industrial technology sectors amongst others.

(3) Sivantos is a privately held company controlled by EQT, with headquarters in Singapore, which manufactures hearing aids and complementary accessories and develops fitting software, smartphone apps and diagnostics workflow solutions. Sivantos manufactures and assembles hearing aids both in Europe (in Germany and Poland), as well as at various sites around the world. Sivantos offers hearing aids under the brands Siemens, Signia, Audio Service, Rexton, and A&M. In addition, Sivantos is active in Germany, France and the Netherlands through its online affiliate audibene which refers potential customers to partner audiologists.

(4) Widex is a privately held company controlled by T&W Medical, with headquarters in Denmark. Widex manufactures and assembles hearing aids and complementary accessories, fitting software and smartphone apps. T&W Medical is ultimately jointly controlled by descendants of the two founders of Widex, Christian Tøpholm and Erik Westermann. (4) In Europe, Widex has manufacturing activities in Estonia (subassembly), Poland (refurbishment and repair) and Denmark (chip production, moulding, final assembly and programming), and subassembling activities at various sites around the world. Widex offers hearing aids under the brands Widex and Coselgi.

2. THE OPERATION

(5) On 15 May 2018, the Notifying Parties signed transaction documents including the “Combination Agreement” and the “Shareholders’ Agreement” in which they agreed the implementation conditions, and respectively the management conditions for the JV.

(6) Pursuant to the transaction documents, EQT and T&W Medical will contribute the businesses of Sivantos and Widex to the JV, which will be jointly controlled by the Notifying Parties following several operations, whereby EQT will ultimately own 53% of the JV’s shares and T&W Medical will own the remaining 47%. Post-Transaction, the JV will be the parent company of both Sivantos and Widex.

3. THE CONCENTRATION

(7) The Transaction constitutes a concentration within the meaning of Articles 3(1)(b) and 3(4) of the Merger Regulation.

3.1. Joint control

(8) EQT and T&W Medical will jointly own the JV, EQT owning 53% (through three acquisition vehicles) and T&W Medical owning 47% of the shares issued by the JV.

(9) Pursuant to the Shareholders’ Agreement, EQT and T&W Medical will have equal voting rights in the JV and equal rights to appoint the board of directors in charge of the JV management. Specifically, EQT and T&W Medical will each have the right to separately appoint four (out of eight) members of the board of directors. (5) The board of director decides on matters that are of material importance to the JV.

(10) Pursuant to the transaction documents, the voting procedures grant (negative) control to both T&W Medical and EQT. Decisions of the board of directors are taken by simple majority. (6) The quorum rules applicable to board of directors’ decisions imply the presence (or representation) of at least one director appointed by T&W Medical and one director appointed by EQT. (7) Furthermore, neither EQT nor T&W Medical have a casting vote in case of deadlock.

(11) In addition, a number of strategic matters (8) require the approval of each Party. At board level, strategic matters require the consenting vote of at least one director nominated by T&W Medical and one director nominated by EQT. Similarly, at general meetings of the JV shareholders, decisions on strategic matters require the consenting vote of both T&W Medical and one of the EQT shareholders. As a result, both Parties have veto rights related to such strategic matters, which include the JV’s budget, business plan, and the appointment of senior management. (9)

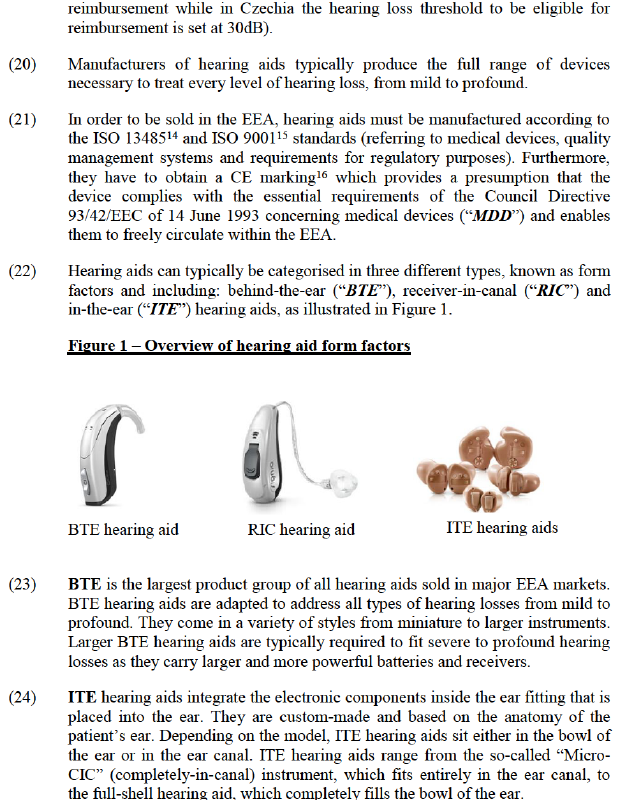

(12) Consequently, the JV will be jointly controlled by the Notifying Parties.

3.2. Full functionality

(13) The JV will combine the existing customer-facing businesses of Sivantos and Widex. The JV will in particular take on the existing manufacturing, wholesale and retail distribution operations of Sivantos and Widex, funding itself from such activities. The JV will have an autonomous presence on the market, benefitting from Sivanto and Widex’s management teams, resources, financing, personnel and tangible and intangible assets. As parent company of Sivantos and Widex, the JV will be in control of these resources. The JV is incorporated for an indefinite period and intended to operate on a long-lasting basis. The Transaction will therefore lead to the creation of a full function joint venture.

4. EU DIMENSION

(14) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (10) (EQT: EUR […] million; T&W Medical: EUR […] million). Each of them has an EU-wide turnover in excess of EUR 250 million (EQT: EUR […] million; T&W Medical: EUR […] million), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State.

(15) The Transaction therefore has an EU dimension pursuant to Article 1(2) of the Merger Regulation.

5. RELEVANT MARKETS

(16) Both Parties are primarily active in the manufacture and wholesale distribution of hearing aids globally.

(17) The Parties are also active in the distribution of audiology diagnostic equipment, including audiometers, otoscopes, and tympanometers. The Parties do not manufacture audiology diagnostic equipment and act as mere resellers. Their activities as distributors of audiology diagnostic equipment do not give rise to any horizontally or vertically affected market in the EEA and will therefore not be further assessed in the present decision. (11)

5.1. Introduction – General characteristics of hearing aids

(18) Hearing aids are medical devices designed to improve a patient’s ability to hear by amplifying acoustic signals. The severity of a hearing loss is specific to every patient and hearing aids are prescribed for addressing the complete range of hearing loss, from mild to profound. (12)

(19) Although there is no minimum threshold of hearing loss required for an individual to start using hearing aids, practitioners typically do not prescribe hearing aids unless the deficit exceeds 30dB. (13) In certain EEA countries, the hearing threshold is a benchmark for determining the entitlement to reimbursement by social security systems of the costs of a hearing aid (for e.g. in Belgium, only patients with a hearing loss of at least 40dB are eligible for

(25) RIC hearing aids are an intermediate solution between BTE and ITE hearing aids. Unlike in traditional BTE hearing aids, the loudspeaker of a RIC model sits inside the ear canal, meaning that fewer components need to fit inside the hearing aid shell that is placed behind the ear.

(26) The manufacturing of hearing aids is based on well-established technologies. The production of most components can easily be outsourced to third-party suppliers. In general, the manufacturing steps differ slightly according to the form factor of the hearing aid, although the majority of electric components contained within the different form factors are identical. Thus, for example, RIC hearing aids (see Figure 2) have the following components: (1) microphones (pick up the sound from the environment), (2) mini-chip (processes the acoustic signal according to the individual hearing needs) (3) receiver (delivers the sound), (4) battery (powers the hearing aid), and (5) program switch / volume control.

(27) By contrast, BTE hearing aids integrate all five components inside the shell which is placed behind the ear and transmits the sound via a sound tube into the ear. While the shell of ITE hearing aids are custom-made in order to fit a patient’s ear, the basic components (including the chip, microphones and some of the electronics) are the same as for BTE and RIC devices.

(28) Hearing aids have significantly evolved over the last couple of decades, with one of the main changes being the move from analogue to digital signal processing. Nowadays, nearly all hearing aids sold on the market are digital. Since this disruptive technological change took place, subsequent improvements have been incremental, focusing in particular on miniaturisation, the introduction of additional features (e.g. connectivity with smartphones, Bluetooth connectivity, directional hearing), improvements to sound quality and the introduction of rechargeable battery solutions.

(29) Irrespective of recent innovations, the basic principle behind every hearing aid remains the same. A microphone picks up the sound signal, a processor converts and treats it, and the receiver plays it back into the ear. A hearing aid can then be outfitted with additional software for extra features (e.g. connectivity, machine learning, rechargeability, etc.). Ultimately, the final price of a hearing aid is primarily linked to its technology level.

(30) Hearing aids must be distinguished from (i) cochlear implants and bone conducting systems, that are surgically implanted to treat hearing impairment, (ii) personal sound amplification products (“PSAPs”), which are wearable electronic devices designed to amplify sounds for non-hearing impaired users (amplification of sounds up to 30dB) and are sold over-the-counter, and (iii) assistive listening devices (“ALDs”), which are devices used to bring distant sound signals directly into the wearer’s ear and to eliminate background noise. Neither of the Parties manufacture cochlear implants, bone conducting systems, PSAP or ALD devices.

(31) The typical route to obtaining a hearing aid (although, this is not the case in every EEA country) involves the patient making an appointment with an ear, nose and throat specialist doctor (“ENT”), who diagnoses their hearing loss and prescribes a hearing aid. The patient then goes to an audiologist to be fitted with a hearing aid device. Audiologists can work either in independent private practices (or as part of a larger chain) or at public clinics and hospitals.

(32) Depending on the EEA country, manufacturers of hearing aids sell their products (either directly or via third-party distributors) to public health services, private retailers or a combination of the two (market for the manufacture and wholesale distribution of hearing aids, see section 5.2.1). In turn, public health authorities and private retailers dispense hearing aids to patients (market for the retail distribution of hearing aids, see section 5.2.2). In some EEA countries, certain hearing aid manufacturers are vertically integrated and also sell hearing aids directly to patients in their retail stores.

(33) On the private part of the wholesale distribution, competition between hearing aid manufacturers focuses on winning business from audiologists such as independent retail stores or large chains. There are significant variations between EEA countries in terms of the downstream retail structure of the hearing aid market, with large multinational chains (and/or optical chains that have expanded into audiology) having a much more significant presence in some EEA countries than others.

(34) On the public part of the wholesale distribution such as in Denmark, Finland, Ireland, Latvia, Malta, Norway, Sweden, or the United Kingdom, competition between hearing aid manufacturers typically arises during tenders for specific product categories, although the precise procurement system largely depends on the national public authorities. Such tenders typically specify a set of technical criteria that hearing aid products must meet. Generally, pricing plays a more significant role in public tenders than on the private wholesale market. (17)

(35) The price of hearing aids significantly varies between EEA countries, both at the wholesale and retail levels. The price charged generally depends on the product itself, its technical features, bilateral negotiations with retailers, tender procedures, as well as other market characteristics in each EEA country (e.g. reimbursement and income levels, presence and size of retail players, etc.). Even if most EEA countries offer some form of financial support to patients for the purchase of hearing aids, the generosity and structure of these reimbursement systems considerably vary between EEA countries. In some countries, the public health system is involved directly (e.g. by sourcing hearing aids through public tenders and distributing them to patients), whilst in others there are private and/or public health insurance providers that offer fixed levels of reimbursement, with the patient usually paying some part of the retail price.

5.2. Product market definition

(36) Manufacturers of hearing aids operate along the hearing aid distribution chain at two levels. At the upstream level, hearing aid manufacturers offer their products at wholesale level to private retailers and public procurement authorities. At the downstream level, manufacturers vertically integrated into retail (along third- party retailers) supply hearing aids and related services directly to end users, i.e. patients suffering from hearing loss. In examining the Transaction, it is appropriate to maintain that distinction.

5.2.1. Upstream: Manufacture and wholesale distribution of hearing aids

(37) Manufacturers of hearing aids generally sell their products (at the wholesale level), either directly or via third-party distributors, to (i) public authorities and/or (ii) private retailers.

5.2.1.1. Precedents

(38) The Commission has not in the past assessed the market for the manufacture and wholesale distribution of hearing aids.

(39) Several national competition authorities examined concentrations in the hearing aids industry in the EEA and consistently identified a single market for the manufacture and wholesale distribution of all types of hearing aids. In particular, in its 2015 decision relating to the acquisition by William Demant of the retailer Audika, the French competition authority identified a market for the manufacture and wholesale commercialisation of hearing aids. (18) In its 2007 decision relating to the planned merger between Phonak (Sonova) and GN, the German competition authority also identified a single product market for the manufacture of hearing aids and their sale to hearing aid retailers, finding in particular that there should be no separate markets depending on the form factors, technology (analogue or digital), or price of hearing aids. (19) Similarly, in its 2016 decision relating to the acquisition by Sonova of the retailer Audionova, the Dutch competition authority identified a market for the manufacture and (wholesale) supply of hearing aids. (20)

5.2.1.2. The Parties’ view

(40) The Parties submit that the overall market for the manufacture and wholesale distribution of hearing aids is the relevant one to assess the Transaction, without the need for further segmentation. In particular, the Parties exclude the existence of separate relevant product markets with respect to the following differentiations: (i) depending on the form factor and/or performance level of hearing aids, (ii) based on the distribution channel, (iii) based on hearing aids’ prices, (iv) between manufacturer-branded products and private label hearing aids, (v) between hearing aids for adults and children, or (vi) between hearing aids and their accessories and services.

5.2.1.3. The Commission’s assessment

(41) Despite providing clear indications that the hearing aid market is highly differentiated, the market investigation generally supported the Parties’ view of a single overall product market encompassing all types of hearing aids as well as related accessories and services. The market investigation also indicated that further segmentations of the hearing aid market is not necessary for the purpose of the present case.

No distinction depending on the form factor, performance level or price of hearing aids

(42) Multiple parameters determine a patient’s requirements when procuring hearing aids. Such parameters include mainly the severity of the hearing loss, as well as the shape of the patient’s ear canal, the patient’s dexterity, or the presence of wax in the ear canal. There are significant overlaps across hearing aids of different form factors to meet each patient’s specific requirements. Most fundamental features of modern hearing aids (software, algorithm, sound processing, amplification etc.) are generally available across all form factors, as these are included in the digital chip that is used by manufacturers across all hearing aid models of a specific generation/platform. In particular, BTE and RIC hearing aids form part of a continuum in terms of performance, with no clear distinction in terms of suitable use for patients. Only a small number of patients cannot use a specific form factor. Most notably, ITE hearing aids are not suitable for patients with profound hearing losses, (21) patients with small or irregularly shaped ear canals, or with excessive amounts of ear wax.

(43) In addition, patients’ awareness about hearing aids, including about form factors, models, prices or brands, is typically very limited, in particular for non- returning patients, which represent the majority of sales. (22) Patients may have some preference between various form factors, designs, or features, in particular for the most discrete models. However, they typically follow the recommendations of ENTs and/or audiologists, which prescribe the most adapted hearing aids to the patient’s requirements. Retailers and ENTs, as trusted professionals, usually act as gatekeepers of the hearing aids market. (23)

(44) The market investigation confirms that retailers of hearing aids typically purchase and offer all types of hearing aids, regardless of their form factor, price or technical performance. (24) They do so in order to offer a full range of hearing aid solutions, which comprises products for all levels of hearing loss severity and addresses patients’ needs and/or preferences. In particular, the market

investigation reveals that the vast majority of customers (retailers, (25) large retail chains, (26) and public procurement authorities (27)) consider it important to dispense a full range of form factors and performance levels of hearing aids, to accommodate all possible patients’ requirements and wishes. Offering a full range of hearing aids even is a legal requirement in some EEA countries, such as Germany. (28)

(45) To reflect demand, most hearing aid manufacturers, in particular every major player, offer hearing aids of all possible form factors, price and performance levels, treating all levels of hearing loss severity, for both adults and children. (29)

No distinction between adults’ and children’ hearing aids

(46) Hearing aids for children are based on the same technology, have the same chip and come in the same variety of form factors as those for adults. However, like all types of hearing aids, solutions for children may integrate specific features due to age-specific requirements. For instance, hearing aids for children typically include a clip and a string to attach the device to a child’s clothes, and a battery door lock to prevent children from swallowing the battery. Consequently, all hearing aid manufactures offer hearing aids for children. A distinction between adult and paediatric hearing aids is thus irrelevant for the purposes of assessing the Transaction.

No separate product markets between manufacturer-branded products and private label hearing aids

(47) The market investigation indicates that branded products and private label products, offered by retailers under their own brand, form part of the same relevant product market. Large retailers, which offer private label products overall confirm that hearing aids do not differ in terms of characteristics and overwhelmingly consider that the negotiation dynamics are similar in both cases. (30) In addition, on the supply side, most hearing aid manufacturers, including all of the primary players offer both branded and private label hearing aids. (31)

No separate product markets between hearing aids and their accessories and services

(48) The market investigation confirms that the wholesale supply of accessories and services should form part of the same relevant product market as the one for hearing aids. The Commission derives from the market investigation that the accessories and services are ancillary to the use of a hearing aid and are typically purchased together with the hearing aid or as replacement sales, and thus consistently linked to the original hearing aid sale. Moreover, according to respondents to the market investigation, the competitive dynamics for the supply of accessories and services are identical to those for the supply of hearing aids which supports the Commission’s conclusion that the market for the wholesale supply of accessories and services is not a separate relevant product market from the one for hearing aids. (32)

Existence of separate product markets between hearing aids distributed through the public system and to retailers on the private segment

(49) The market investigation indicates that the distinction between public and private wholesale distribution channels, in the national markets where it is applicable, gives useful insights for the competitive analysis of the Transaction. (33) Within public schemes, patients acquire their hearing aids from hospitals or health services, typically free of charge. Sales of hearing aids to the public market typically involve the organization of a tender by a public authority, guaranteeing (usually large) sales volumes to the successful bidder(s) over a specific duration, usually reaching or exceeding two years. Specific technical requirements are issued by the relevant public authorities, and the selection process is typically price-driven. All of these factors impact the competitive landscape. (34)

(50) The Commission also investigated whether wholesale distribution of hearing aids to retailers on the private segment should be further segmented between the supply to (i) manufacturer-owned retail outlets, (ii) large retail chains (e.g. Amplifon, Specsavers, etc.), and (iii) supply to other independent retailers. In that respect, the Commission found that all major players in the manufacture and wholesale distribution of hearing aids, including vertically integrated manufacturers supply large chains and/or independent retailers, and compete to increase their sales across all distribution channels. Furthermore, the market

investigation confirms that manufacturer-owned retail outlets often offer products from more than one supplier, even if usually in smaller quantities. (35) Also, some second-tier hearing aid manufacturers such as Audifon and Microson, are owned by retail chains, namely Kind and GAES respectively, who offer a wide portfolio of hearing aid products from different manufacturers besides their own in their retail outlets.

Conclusion

(51) On the basis of the evidence before it, and account taken of the lack of significant differentiations between possible categories of hearing aids from both the demand and supply sides (i) depending on the form factor and/or performance level of hearing aids, (ii) based on hearing aid prices, (iii) for manufacturer-branded products and private label hearing aids, (iv) depending on the patient’s age (i.e. paediatric hearing aids or adult hearing aids), or (v) for accessories and services, the Commission considers that the market for the manufacture and wholesale distribution of hearing aids should not be further segmented according to these distinctions.

(52) However, based on its market investigation the Commission considers that the distinction between the markets for the manufacture and wholesale distribution of hearing aids to the private segment (i.e. to retailers) and, on the other hand, the manufacture and wholesale distribution of hearing aids to the public segment (i.e. to public procurement bodies) may be a relevant factor in the competitive analysis of the Transaction in the EEA countries where public health administrations are directly procuring hearing aids.

(53) For the purpose of the present decision, the Commission considers that the possible segmentation of the product market for the manufacture and wholesale distribution of hearing aids between private and public segments can be left open as the Transaction does not give rise to competition concerns under any such alternative product market definitions.

5.2.2. Downstream: Retail distribution of hearing aids

(54) The market for the retail distribution of hearing aids is downstream from the market for the production and wholesale distribution of hearing aids. (36) Retailers of hearing aids, which include independent shops, large chains (specialized in audiology or not), as well as manufacturer-owned chains, supply patients with hearing aids.

5.2.2.1. Precedents

(55) The Commission has not in the past assessed the markets for the retail distribution of hearing aids.

(56) National competition authorities of the EEA have assessed several transactions related to the retail distribution of hearing aids. In its 2015 decision, the French competition authority identified a single relevant product market for the retail distribution of hearing aids without further segmentations. (37) In its 2016 decision, the Dutch competition authority also identified a product market for the retail distribution of hearing aids and accessories without further segmentations. (38)

5.2.2.2. The Parties’ view

(57) The Parties consider the retail distribution of hearing aids to be the relevant product market, without the need for any further segmentation.

5.2.2.3. The Commission’s assessment

(58) The market investigation did not indicate that any further segmentation of the product market for the retail distribution of hearing aids is justified.

(59) In particular, a distinction between brick-and-mortar and online stores does not appear relevant. Direct online sales of hearing aids are not possible in a number of EEA countries due to hearing aids being medical devices, whose distribution is strictly regulated. While online distribution does exist, it mostly takes the form of an intermediary to traditional brick-and-mortar businesses.

(60) Similarly, a distinction between (i) manufacturer-owned retail outlets, (ii) large retail chains, and (iii) supply to other independent retailers, does not appear relevant. Patients have limited awareness of the hearing aid industry and no marked preference in terms of retail channel. Furthermore, as explained above, retail outlets, including manufacturer-owned outlets, often offer products from more than one manufacturer.

(61) Based on the evidence before it, and account taken of the lack of significant differentiations at the level of the retail distribution of hearing aids, the Commission considers, for the purposes of the present decision, that the market for the retail distribution of hearing aids is the relevant product market. In any event, for the purpose of the present case, the exact scope of the product market definition can be left open with respect to possible further segmentations of the product market for retail distribution of hearing aids as the Transaction does not give rise to competition concerns under any plausible product market definition.

5.3. Geographic market definition

5.3.1. Upstream: Manufacture and wholesale distribution of hearing aids

5.3.1.1. Precedents

(62) In previous cases concerning medical devices, the Commission has considered the geographic scope of the relevant markets as being national in scope. (39)

(63) In its 2015 decision, the French competition authority left the question open whether the geographic dimension of the market was national or supranational in scope. (40) The German competition authority, in its 2007 decision, considered the relevant geographic market to be national in scope due to the significance of national sales systems and local care, buying patterns of purchasers, the diversity of prescription and reimbursement systems across countries, as well as price differences. (41) The 2016 decision of the Dutch competition authority also considered the relevant market to be national in scope. (42)

5.3.1.2. The Parties’ view

(64) The Parties argue that the relevant geographic market for the manufacture and wholesale distribution of hearing aids is national in scope due to the facts that reimbursement regimes, procurement processes and sales organisations of hearing aid manufacturers are national in scope. Moreover, the Parties claim that wholesale price differences between EEA countries indicate national geographic markets for the manufacture and wholesale distribution of hearing aids.

5.3.1.3. The Commission’s assessment

(65) The market investigation broadly confirmed the Parties’ arguments. In particular, the Commission found that the market shares of the major players in the sector substantially vary from one EEA country to another. Furthermore, the market investigation confirmed that the overall market structure is very different from one EEA country to another. The Commission also notes that some second-tier players, such as Audifon, Microson or BHM are only active in certain EEA countries.

(66) As in other medical sectors, the presence of specific reimbursement systems across the EEA has partitioned off the markets at national level. The differences across the various national reimbursement schemes across the EEA contribute to the significant wholesale price variations between EEA countries.

(67) In addition, customers’ profiles (public authorities, larger chains, independent retailers, and/or purchasing groups), as well as purchasing behaviour (tender procedures and/or bilateral negotiations) largely differ from one EEA country to another.

(68) On the private part of the market, while agreements with some key customers, especially for large retail chains such as Specsavers, Amplifon, or Neuroth, may be negotiated across multiple countries, or even at EEA level, most of the competition to supply customers takes place at national level. Only a minority of large retail chains that responded to the market investigation operate in over two countries, (43) and nearly all smaller retailers operate only in one country. (44)

(69) On the public part of the market, where public tenders take place, the design of the tender process and the applicable requirements to qualify differ depending on the public authority. (45) Such tender processes may be particularly complex and in some cases require full time employees with a knowledge of the local tender rules. (46)

(70) However, from a supply-side perspective, a number of factors indicate that the relevant geographic market could also be wider than national, and potentially EEA-wide, in particular due to (i) low regulatory barriers (CE mark); (ii) worldwide production and research and development, (iii) low transport costs; and (iv) the scope of public tenders not being limited to nationally established players.

(71) In conclusion, for the purpose of the present case, the Commission considers that the question of whether the scope of the market for the manufacture and wholesale distribution of hearing aids is national or EEA-wide can be left open, as the Transaction does not give rise to competition concerns under any plausible geographic market definition.

5.3.2. Downstream: Retail distribution of hearing aids

5.3.2.1. Precedents

(72) In its past decisional practice, the Commission has never before assessed the geographic scope of the retail distribution of hearing aids.

(73) In its 2015 decision, the French competition authority analysed the retail market for hearing aids both at national level and within a radius of a 25-minute drive from each of the relevant points of sales as possible alternative relevant geographic market definitions. (47) The 2016 decision of the Dutch competition authority left the exact geographic definition open, but assessed the retail market for hearing aids based on both national and local scope. (48)

5.3.2.2. The Parties’ view

(74) The Parties submit that the relevant geographic market can be considered national in scope, even if hearing aid products are identical globally.

(75) The Parties consider in particular that there is no need to define regional or local markets for the retail distribution of hearing aids.

5.3.2.3. The Commission’s assessment

(76) The market investigation conducted by the Commission indicates that the market for the retail distribution of hearing aids is likely local in scope.

(77) On the demand side, end users typically travel limited distances to their hearing aid retailers. An overwhelming majority of associations for the hearing impaired who responded to the market investigation indicated that patients travelled for around 30 minutes or less (by car or using public transportation) to their audiologist. (49)

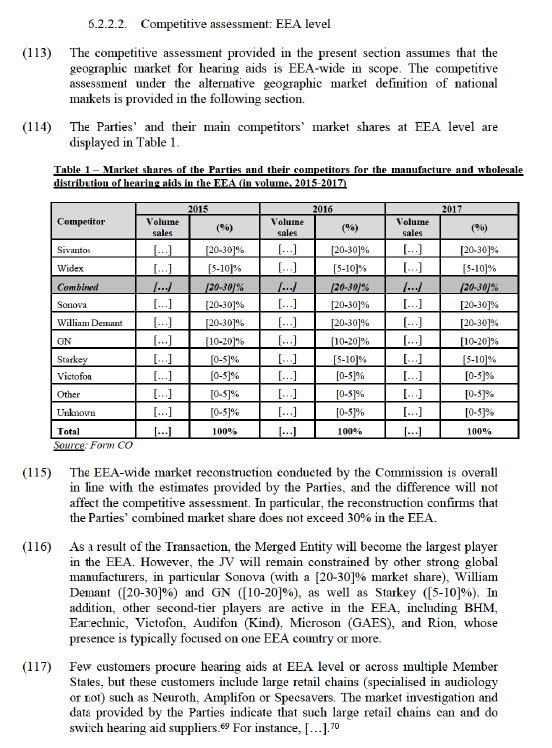

(78) Furthermore, on the supply side, a significant number of retailers only operate a limited number of stores and, as a result, are only present in a specific geographic area. (50) Opening another shop in a distinct catchment area may involve significant investment and time for these retailers.

(79) For the purpose of the present case, the Commission concludes that the question of whether the geographic market for the retail distribution of hearing aids is national or local can be left open as the Transaction does not give rise to competition concerns under any plausible geographic market definition.

6. COMPETITIVE ASSESSMENT

6.1. Data availability: Market reconstruction

(80) From the outset, it should be noted that the market share data provided by the Parties are not entirely reliable in light of methodological challenges and the absence, in many instances, of public information sources. Specifically, difficulties in providing an accurate overview of the market are mainly related to the presence of local smaller-scale competitors and to the need to allocate sales to a specific country in cases where either retailers are active in several countries or manufacturers do not sell their products in the national markets themselves (i.e. in their own points of sale).

(81) During the market investigation, the Commission obtained sales data, both in value and in volume, (51) from the Parties' competitors. This exercise (with all its limitations) did not enable the Commission to fully reconstruct the market, but suggested, together with data from the Parties' own internal documents, that the Parties may have, in several instances, overestimated (at times significantly) their respective market shares, especially as regards value market shares.

(82) In fact, the Commission understands that, due to their various degrees of downstream integration at retail level, hearing aid manufacturers do not use consistent approaches with respect to reporting wholesale prices. Thus, the internal transfer prices at wholesale level do not enable the Commission to consistently compare wholesale value sales data between those manufacturers that are vertically integrated into downstream retail and those that are not. As a result, the Commission considers that (estimated and reconstructed) value market shares constitute unreliable indicators of the respective competitors’ market power. For the purpose of this case, the Commission therefore relies on the Parties’ and their competitors’ market share estimates based on volume data.

(83) Since the volume sales data gathered during the market investigation contains confidential information of third parties, the Decision relies on volume data provided by the Parties in the Form CO and their replies to the Commission’s requests for information, while providing general comments about the accuracy of the Parties’ best estimates.

(84) In any event, and irrespective of the exact market shares, the Commission's assessment in this case is complemented by qualitative elements collected during the market investigation which, taken together, reflect the competitive features of the markets for hearing aids and the Parties' real position on the markets.

6.2. Horizontal non-coordinated effects

6.2.1. Legal framework

(85) Article 2 of the Merger Regulation requires the Commission to examine whether notified concentrations are compatible with the internal market, by assessing whether they would significantly impede effective competition in the internal market or in a substantial part of it.

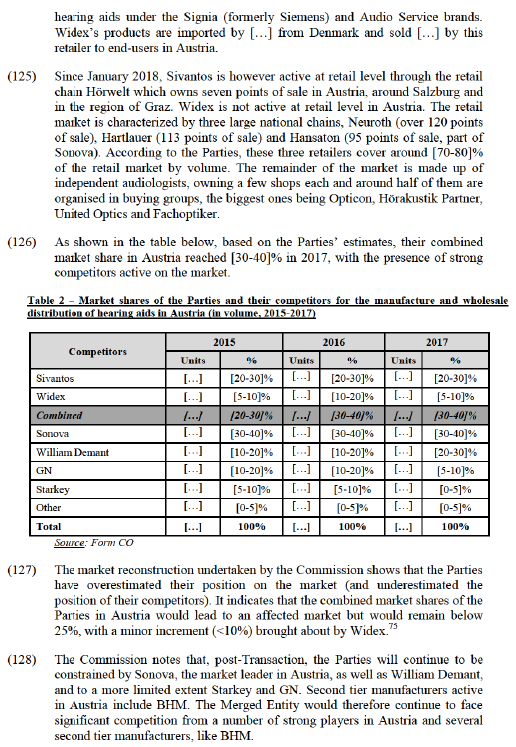

(86) The Commission Guidelines on the assessment of horizontal mergers under the Council Regulation on the control of concentrations between undertakings (52) (the "Horizontal Merger Guidelines") distinguish between two main ways in which mergers between actual or potential competitors on the same relevant market may significantly impede effective competition, namely non-coordinated effects and coordinated effects.

(87) Non-coordinated effects may significantly impede effective competition by eliminating the competitive constraint imposed by each merging party on the other, as a result of which the merged entity would have increased market power without resorting to coordinated behaviour. In this regard, the Horizontal Merger Guidelines consider not only the direct loss of competition between the merging firms, but also the reduction in competitive pressure on non-merging firms in the same market that could be brought about by the merger. (53) According to recital (25) of the preamble of the Merger Regulation, a significant impediment to effective competition can result from the anticompetitive effects of a concentration even if the merged entity would not have a dominant position on the market concerned.

(88) The Horizontal Merger Guidelines list a number of factors which may influence whether or not significant non-coordinated effects are likely to result from a merger, such as the large market shares of the merging firms, the fact that the merging firms are close competitors, the limited possibilities for customers to switch suppliers or the fact that the merger would eliminate an important competitive force. (54) Not all of such factors need to be present for the Commission to exclude that a proposed concentration would not entail significant non-coordinated effects. The list of factors, each of which is not necessarily decisive in its own right, is also not exhaustive.

6.2.2. Upstream market for the manufacture and wholesale distribution of hearing aids

6.2.2.1. Introduction – Competitive features

(89) To the effect of examining the Transaction the Commission considers appropriate to review the following competitive features of the relevant markets identified therewith.

Market players

(90) The market for the manufacture and wholesale distribution of hearing aids is characterised by the presence of several competitors of varying size each with their own strategy.

(91) There are six established manufacturers of hearing aids active globally (in order of size): Sonova (Switzerland), William Demant (Denmark), Sivantos (Singapore), GN (Denmark), Widex (Denmark) and Starkey (US). Each of these manufacturers offers a full range of products, covering the full spectrum of technical capabilities and price points. Together, these players represent approximately [90-100]% of the global production of hearing aids worldwide. (55)

(92) In addition, several second-tier players are present in one or more EEA countries: small manufacturers such as Berl Hörgeräte Manufaktur (“BHM”, Austria), Victofon (Hungary), AcoSound (China), LiSound (China), RION (Japan), NewSound (China) or Ear Technic (Turkey).

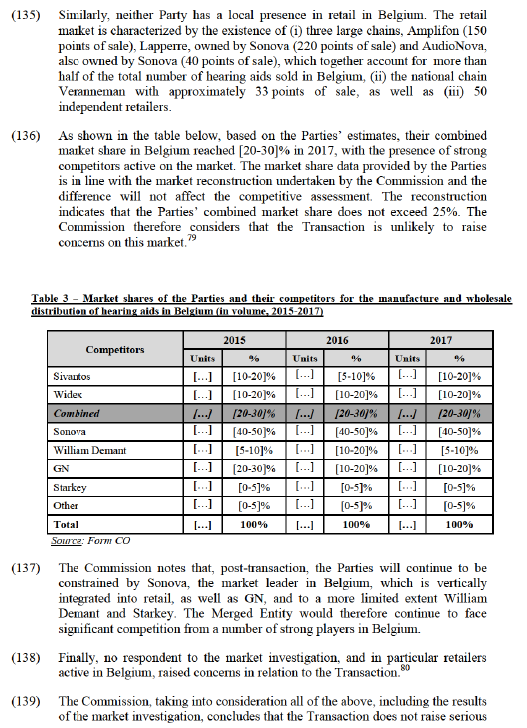

(93) Finally, the market comprises retailers with their own manufacturing capacities, such as Kind (Germany) with the Audifon brand and GAES (Spain) with the Microson brand. These players typically sell their hearing aids through their established network of retail stores.

(94) As a result, the Commission will take into account the diversity of players active on the hearing aid markets in its competitive analysis.

Role of innovation

(95) Hearing aids from different manufacturers are generally comparable in terms of technological features. As explained in recital 26, the manufacturing of hearing aids is based on well-established technologies and most components can be easily outsourced to third-party suppliers. In addition, there is no need to have specific intellectual property rights (“IPR”) in order to manufacture hearing aids.

(96) It is only amongst top-of-the-range products that some differentiation starts to be apparent. Innovation goes from minor refinements to additional features such as connectivity (e.g. with smartphones, direct or indirect connectivity, etc.), and rechargeability. All manufacturers are committed to innovation and devote considerable resources to research and development (around […]% of turnover) in order to facilitate product innovation. The strong level of innovation is reflected in the relatively short product lifecycle of hearing devices (around 18- 30 months).

(97) Although each manufacturer may claim to have a particular strength within one or more areas of innovation, the market investigation revealed that the newest and most sophisticated technologies are gradually integrated by all manufacturers in their product portfolios. Therefore, over time, the advanced technologies generally become a commodity for all manufacturers. It generally takes up to 24 months before a new feature/technology is fully integrated into all major manufacturers’ portfolios. (56) The consequence of this continuous diffusion of innovation is that today's basic performance level is significantly better compared to that of five years ago. Newer hearing aids gradually replace older ones, which are phased out as they become obsolete.

(98) IPR mostly become relevant in the context of premium features, such as Sivantos’ Own Voice Processing technology. These patents are in place to temporarily protect new innovations, but are by no means essential for a new entrant. In fact, these proprietary features vary across the established manufacturers, each one generally choosing to develop their own IPR rather than relying on patents from competitors. In the event that a new entrant chose to design a product with premium innovative features they may similarly decide to protect their new features with a patent.

(99) The Parties’ internal documents indicate that, among the six major hearing aid manufacturers, the Parties are […]. Post-Transaction, the Merged Entity would […]. Similarly, in terms of average R&D investment per hearing aid specific patent, each of the Parties […]. (57)

Purchasing patterns

(100) Hearing aids are distributed (either directly by hearing aid manufacturers or through third-party distributors) through a variety of channels: private retailers including independent stores, multinational audiology chains, optical chains as well as purchasing groups, but also public procurement authorities.

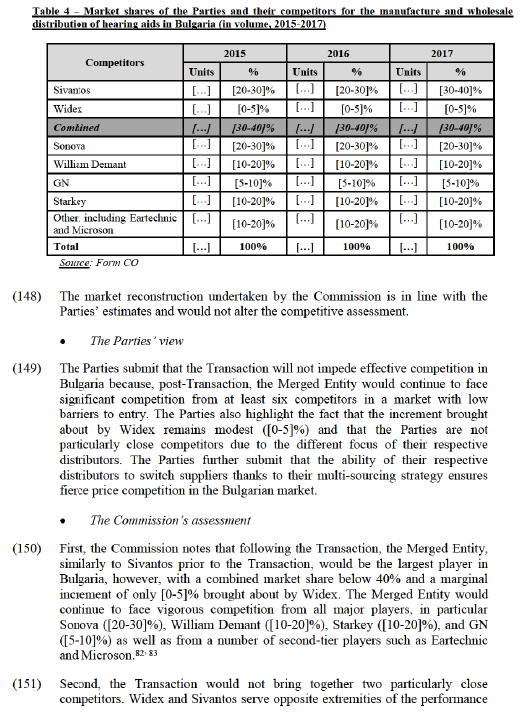

(101) Purchasing processes differ significantly between EEA countries, although some trends may be observed across EEA countries.

(102) First, there is an increasing vertical integration into retail of some of the main hearing aid manufacturers. Most notably, Sonova and William Demant, have adopted vertical integration strategies in several EEA countries, which have typically resulted in a loss of business for manufacturers who previously supplied those retailers while they were still independent. For example, when AudioNova, one of the largest retail chains across several EEA countries, was acquired by Sonova, it essentially stopped procuring hearing aids from the Parties and other competing manufacturers. As a consequence, competition for the remainder of the retail customers has further intensified. While hearing aids are still mainly sold through independent dispensers, this development has resulted in an increased competition to win this important part of the retail market.

(103) Second, there is an increasing presence of large independent national and international audiological and optical chains (such as Amplifon, Specsavers, Neuroth, Fielmann, Optical Center, and Alain Afflelou) on the market. These chains increase competition at retail level and thus create a price pressure on hearing aid manufacturers.

(104) Third, audiologists in most EEA countries tend to pursue a multi-sourcing strategy and stock products from at least three different manufacturers. (58)

(105) As patients typically have very little awareness of the different hearing aid brands available on the market, (59) audiologists are generally able to switch supplier without fear of losing patients. There are no must-have brands or products, (60) and all manufacturers offer a broadly similar product range covering the full spectrum of customer needs, with very few exceptions, (61) and switching can thus easily occur. As a matter of example, in [EEA country] and [EEA country], [name of retailer] stopped carrying Sivantos in favour of […] despite Sivantos having […].

(106) Furthermore, a retailer who starts carrying hearing aids from a new manufacturer will typically require the supply of the manufacturer-specific software and adequate training for the retailer’s audiologists. In most Member States, the manufacturer will bear the majority of these costs. (62) For the retailer, therefore, the main switching cost is the time commitment associated with the training of its employees, including training around the new product’s features, how they need to be fitted and any corresponding software. (63) Depending on the size of the retailer (e.g., a small independent or a large chain) the required training can be completed in as little as one day and possibly some sessions of follow-up training. (64)

Barriers to entry and expansion

(107) The market investigation indicates that there are relatively limited barriers to expansion for existing hearing aid manufacturers. Replies to the market investigation confirmed that all major manufacturers have the capability to regularly develop new hearing aid models, expand their product portfolios and adapt these to the changing needs, demands and technological shifts in the market. (65)

(108) The Parties consider that barriers to entry are equally low for new entrants, and that the rising attractiveness of the hearing aid market is expected to attract entry by new market players active in neighbouring markets.

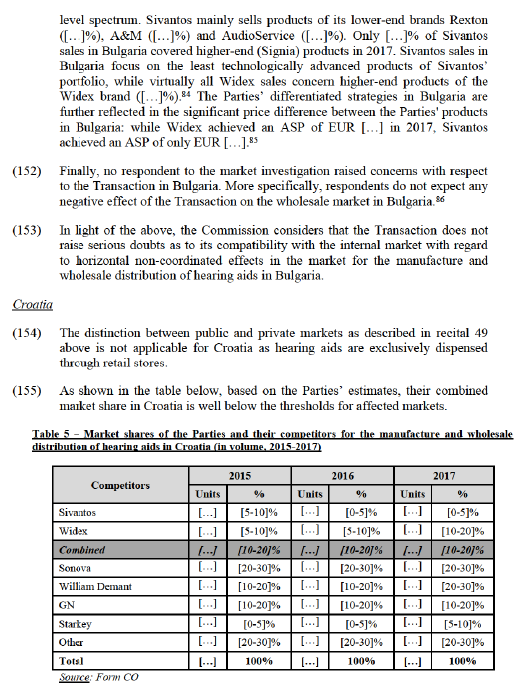

(109) While internal documents of the Parties confirm that players active in neighbouring markets such as Cochlear, Samsung, Bose, Apple or Panasonic individually file a substantial number of patents related to the hearing aid space (sometimes more than each of the Parties), (66) the Commission considers that barriers to entry for a new entrant are significant.

(110) In fact, the Commission considers that, beyond the necessary regulatory approvals and significant initial R&D investments required to set up a complete product portfolio of hearing aids, a new entrant would further need to hire and form a qualified wholesale sales force in order to be able to effectively compete in the industry. Results of the market investigation further confirm that economies of scale are important in order to be able to offer attractive pricing conditions to retailers, which implies that a new entrant manufacturer would need to gain retailers’ loyalty and achieve a minimum efficient scale in order to be competitive on price. (67) Given the fast pace of incremental innovation in the industry, characterised by the introduction of new technological features, a new entrant would similarly need to capture a non-negligible market share before being able to sustainably finance an effective R&D department and be competitive in terms of technological features.

(111) The majority of competitors that participated in the Commission’s market investigation indicated that they do not expect any new hearing aid manufacturer to enter the hearing aid industry in the next three years. (68) Respondents that indicated that they expected new entrants referred exclusively to large manufacturers of consumer electronic goods active in neighbouring markets.

Several of these referred to Bose, that announced in October 2018 that they would enter the over-the-counter hearing aid market in the US.

(112) Conclusively, the Commission considers that possible market entries cannot be expected to happen soon with respect to EEA countries as medical devices cannot currently be sold over-the-counter in the EEA and accordingly this is a relevant factor for the competitive assessment of the Transaction.

(118) The market investigation also confirmed the Parties’ claim that there are no barriers to expansion for existing manufacturers, in particular since virtually all responding hearing manufacturers indicated that they have sufficient capacity to meet an increase in demand of 5-10%. (71)

(119) Due to the limited market shares of the Parties, and the presence of strong competitors at EEA level, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with regard to horizontal non-coordinated effects in the possible market for the production and wholesale of hearing aids at EEA level.

6.2.2.3. Competitive assessment: national level

(120) Based on the Parties’ market share estimates, the Commission finds that with respect to the possible national markets for the manufacture and wholesale distribution of hearing aids, the Transaction would give rise to horizontally affected markets in Austria, Belgium, Bulgaria, Croatia, Czechia, Denmark, France, Germany, Greece, Hungary, Iceland, Ireland, Latvia, Lithuania, Malta, Luxembourg, the Netherlands, Norway, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden and the United Kingdom. (72)

Austria

(121) The distinction between public and private markets as described in recital 49 above is not applicable for Austria as hearing aids are exclusively dispensed through private retail stores (be it independent stores or large chains).

(122) Austria is a well-developed market with around 92 100 units dispensed through around 600 points of sale.

(123) Austria has a reimbursement system where the National Health Insurance subsidises patients from EUR 792 for the purchase of a hearing aid and the fitting (or EUR 1 425 in case of binaural hearing aids) to EUR 2 100 (or EUR 3 780 in case of binaural hearing aids) every six years. (73) To the Parties’ best knowledge, all their hearing aids, as well as their competitors’ products, are eligible for reimbursement. The average sale price (“ASP”) of hearing aids in Austria at wholesale level is EUR 198, which is lower than the EU-wide ASP of EUR 255. The average retail price of the audiologist is comprised between EUR [1 000-1 550]. (74)

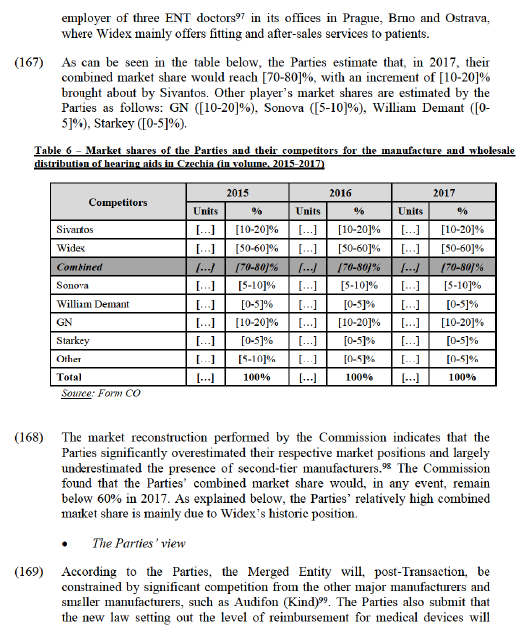

(124) Neither Party has a local presence at wholesale level in Austria. Sivantos is active through its German affiliate, Sivantos GmbH, through which it sells

(129) In addition, no respondent to the market investigation, and in particular retailers active in Austria, raised substantiated concerns in relation to the Transaction. (76) One respondent pointed out that, in general, a large number of hearing aid manufacturers guarantees a greater choice of products for retailers and end- users. However, this respondent also acknowledged that if market conditions were to change, it may consider the possibility of entering into contracts with other potential suppliers, the number of alternative manufacturers on the market post-Transaction being sufficient. (77)

(130) The Commission, taking into consideration all of the above, including the results of the market investigation, concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market in relation to the manufacture and wholesale distribution of hearing aids in Austria.

Belgium

(131) The distinction between public and private markets as described in recital 49 above is not applicable for Belgium as hearing aids are exclusively dispensed through private retail stores (be it independent stores or large multinational chains).

(132) Belgium is a well-developed market with around 103 000 units dispensed through around 680 points of sale. Patients suffering from a hearing loss of at least 40 dB (moderate hearing loss) are eligible for reimbursement from Belgian health insurance of EUR 680 per hearing aid every five years (children receive up to EUR 1 300 per ear every three years). The ASP of hearing aids in Belgium at wholesale level is EUR 348, which is higher than the EU-wide ASP of EUR 255. The average retail price including the fitting fees of the audiologist is comprised between EUR [1 000-1 500]. (78)

(133) Manufacturers who wish to distribute their hearing aids under the public reimbursement system in Belgium need to follow a two-step homologation process: (i) first, in order to sell hearing aids in Belgium, manufacturers need to register the maximum price for their hearing aids with the Ministry of Economic Affairs on a product level, and (ii) second, in order to have hearing aids eligible for reimbursement in Belgium, manufacturers need to request the listing of the hearing aids with RIZIV (part of the Ministry of Health). In practice, the vast majority of hearing aids sold in Belgian are registered with both the Ministry of Economic Affairs and RIZIV.

(134) Neither Party has a local presence at wholesale level in Belgium. Both Parties sell hearing aids to the [a customer] (who resells part of its stock to independent retailers). In addition, Sivantos sells its Signia branded hearing aids to [a customer], and its AudioService branded hearing aids to independent retailers.

doubts as to its compatibility with the internal market in relation to the manufacture and wholesale distribution of hearing aids in Belgium.

Bulgaria

(140) The distinction between public and private markets as described in recital 49 above is not applicable for Bulgaria as hearing aids are exclusively dispensed through retail stores.

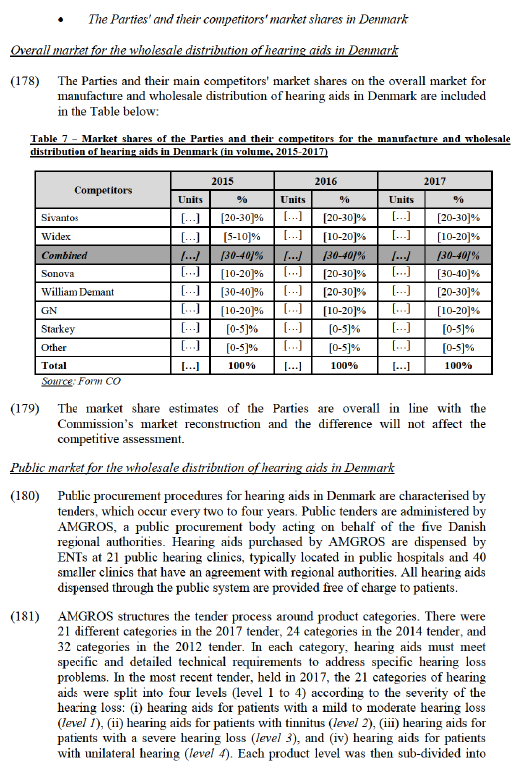

· Regulatory background

(141) While there is a public healthcare financing system in Bulgaria, nearly half of all hearing aids purchased in Bulgaria are not covered by any reimbursement.

(142) The national health insurance scheme provides a flat reimbursement of EUR 200-220 per hearing aid for all adults every 5-6 years (depending on the employment situation). Children benefit from an increased reimbursement rate.

(143) In order to be eligible for reimbursement, a hearing aid must be registered with the Ministry of Health. For this purpose, a hearing aid model has to meet a number of technical requirements. In practice, local distributors are the ones that carry out this registration process.

(144) As of 2018, the Bulgarian government introduced a new reimbursement system relying on vouchers. Under this new scheme, a patient will be allowed to pay with a voucher corresponding to the eligible reimbursement and the retailer (instead of the patient) will have to obtain reimbursement from the national health insurance system.

· The Parties' and their competitors' market shares in Bulgaria

(145) Widex’s hearing aids are […] dispensed by [a customer] who sells the […] and […] other retailers. (81) Sivantos operates in Bulgaria through three third-party distributors, [a distributor], [a distributor] and [a distributor], which are also active at retail level through their respective retail stores.

(146) All the other major manufacturers are active in Bulgaria. While Sonova and Starkey are active in this country through a local wholesale subsidiary, GN and William Demant rely on local third-party distributors, which are typically vertically integrated into the retail market.

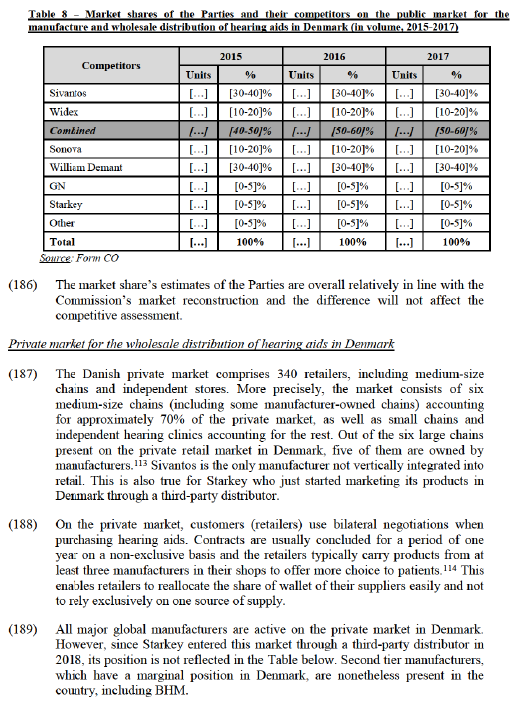

(147) The Parties provided market share estimates for all manufacturers active in Bulgaria from 2015 to 2017.

(156) The market reconstruction undertaken by the Commission slightly differs and indicates that the combined market shares of the Parties in Croatia would lead to an affected market but would remain below 25%, with a minor increment (< 5%) brought about by Sivantos. The Transaction is thus unlikely to raise concerns on this market. (87)

(157) Post-Transaction, the Parties would continue to be constrained by Sonova, the market leader in Croatia, as well as William Demant, and to a more limited extent Starkey and GN, as confirmed by the Commission’s market reconstruction. Second-tier manufacturers active in Croatia include BHM. The Merged Entity would therefore continue to face significant competition from a number of strong players in Croatia.

(158) Finally, no respondent to the market investigation, and in particular retailers active in Croatia, raised concerns in relation to the Transaction. (88)

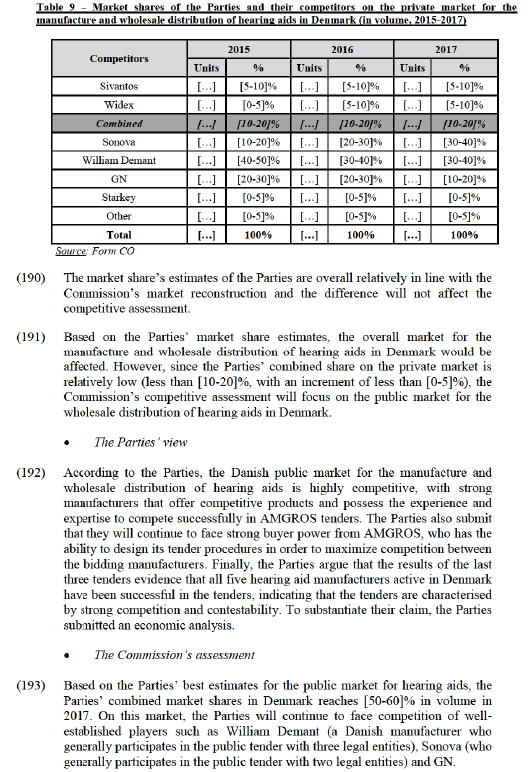

(159) The Commission, taking into consideration all of the above, including the results of the market investigation, concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market in relation to the manufacture and wholesale supply of hearing aids in Croatia.

Czechia

(160) The distinction between public and private markets as described in recital 49 above is not applicable for Czechia as hearing aids in Czechia are exclusively dispensed through authorised ENTs.

(161) All major manufacturers of hearing aids, as well as a number of second-tier players, are active in Czechia. The Parties, GN and Audifon have a direct presence through a local wholesale affiliate. By contrast, Sonova, William Demant, Starkey and other second-tier players are active through third-party distributors.

· Regulatory background

(162) Contrary to the situation in the majority of EEA countries, hearing aids in Czechia can only be dispensed through a regulated number of ENTs (comprised between 135 and 145 authorized ENTs). The price of hearing aids in Czechia is regulated in the sense that prior to being put on the market every device needs to be registered with the public insurance body, at which point in time the price of the device is set and cannot be changed by manufacturers over the device’s lifetime. The maximum mark-up that suppliers (i.e. manufacturers selling hearing aids directly to ENTs and third-party distributors) can apply to the price of registered hearing aids is fixed at 15%. ENTs cannot apply any mark-up to the wholesale price of hearing aids (i.e. the price at which the hearing aid is registered, plus the 15% mark-up of the supplier). ENTs are remunerated for providing fitting services with a flat fee.

(163) Historically, Czechia had been characterized by low reimbursement levels (89) and a low frequency of registration of new products (limited by law to twice per year). Low reimbursement rates translated into few high-end products being sold on the market. Since 1 January 2019, the reimbursement level of hearing aids has been substantially raised, (90) which is expected to shift the market towards higher-end products.

(164) As far as the relationship between hearing aid wholesalers and ENTs is concerned, the regulatory framework governing the sale of hearing aids in Czechia dictates that ENTs are obliged to offer a choice among at least three different manufacturers of hearing aids in order to qualify for reimbursement by the health insurance providers. (91)

(165) In practice, The Commission finds that ENTs typically follow the VZP guidelines and offer hearing aids from at least three different manufacturers for patients to choose from. (92) A majority of dispensers indeed confirmed that “[a]ccording to Czech law, I need to offer different suppliers” (93) or that offering products from a single supplier “is not possible by law”. (94)

· The Parties' and their competitors' market shares in Czechia

(166) All the main manufacturers of hearing aids, as well as a number of second-tier players, are active in Czechia. The Parties, GN and Audifon have a direct presence through a local wholesale affiliate. By contrast, Sonova, William Demant and Starkey are active through third-party distributors. (95) Moreover, Widex has a very small (96) presence at retail level since Widex is the part-time

likely lead to a higher attractiveness of the Czech market and potentially to new market entries and/or increased efforts by established market players. Finally, they argue that the Parties are not close competitors, as Sonova and GN offer a similar range of products to Widex in Czechia and that, in any event, the Transaction would not lead to the elimination of an important competitive force in this country.

· The Commission’s assessment

(170) First, the Commission notes that all major players, some of which having a local presence (like Audifon with both a wholesale and retail presence), are active in Czechia alongside the Parties. Besides the major players, second-tier competitors such as Audifon, BHM, Horentek and NewSound (China) and a couple of local players such as Anticer and Fonika are active in Czechia. (100) The current relatively higher market share of Widex ([50-60]% according to the Parties; lower according to the Commission’s market reconstruction) was explained during the market investigation by respondents as stemming from its historical first-mover advantage. Respondents explain that Widex was the first hearing aid manufacturer to enter the Czech market in the 1990s (101) and thus effectively started its business activity in Czechia with a 100% market share. The erosion of Widex’s market share is illustrated by sales of current competitors active in Czechia. For instance, Sonova’s distributor of hearing aids entered the Czech market 9 years ago (102) and currently holds a market share of more than 8%.

(171) Second, the competitive landscape in Czechia is expected to be reshuffled as a result of the entry into force of a new regulation in January 2019. The increase of the reimbursement level is expected to shift demand to higher-end products, which in turn will render the Czech market more attractive to manufacturers. In addition, suppliers can now register hearing aids on a monthly basis (rather than just twice a year). This likely effect was largely confirmed during the market investigation. (103) ENTs who responded to the market investigation shared their intention to dispense higher-end and more expensive hearing aid products, potentially from alternative manufacturers, as a result of the new regulation. (104)

(172) Third, the fact that ENTs propose hearing aids from at least three suppliers (as imposed by the official VZP guidelines in order for an ENT to qualify for reimbursement by health insurance providers) further guarantees the ability of patients to switch between suppliers. In this respect, respondents to the Commission’s market investigation indicated that price plays a significant role and, should the Merged Entity increase prices post-Transaction, they would have sufficient choice of products by other manufacturers to offer to their patients generally unwilling (or unable) to pay extra amounts. (105) The fact that, ENTs offer products from several suppliers, implies that ENTs who currently offer the two Parties’ products to their patients will likely introduce new manufacturers into their portfolio post-Transaction.

(173) One third-party distributor considers that the Transaction would reinforce the Merged Entity’s capability “to reach out to even more ENTs and allocate significant funds to engage in additional marketing activities (in many cases focused on existing technologies, and neglecting the benefits of new generations of products)” (106) However, such outcome may actually increase the competitive pressure existing in the market. As explained above, the new regulatory system in Czechia is expected to facilitate the introduction of hearing aids including newer technologies. Given that ENTs typically provide products from three different manufacturers, the combination of Widex and Sivantos is likely to lead ENTs who dispense products from both to introduce new manufacturers in their portfolio.

(174) The Commission, taking into consideration all of the above, including the results of the market investigation, concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market in relation to the manufacture and wholesale supply of hearing aids in Czechia.

Denmark

(175) With 158 000 hearing aids sold in 2017, Denmark is the ninth largest market for hearing aids in the EEA. The Danish hearing aid market is around 50% public (sales of hearing aids to a public procurement authority based on tendering procedures) and 50% private (sales of hearing aids to private retail stores based on bilateral negotiations). In line with the market definitions presented in recital 49 above, the Commission assesses the impact of the Transaction on the public and private markets for the manufacture and wholesale distribution of hearing aids separately.

(176) According to the Parties’ best estimates, the ASP of hearing aids at wholesale level in the private sector was EUR 284 per hearing instrument (unit) and EUR 236 per hearing instrument (unit) in the public sector. The average retail price however varies significantly: while hearing aids are provided free of charge on the public market, the price of hearing aids is approximately EUR […] on the private retail market. (107) Patients in the private sector will however receive a reimbursement of EUR 552 for one ear and EUR 870 for both ears, every four years.

(177) All major hearing aid manufacturers except for Starkey are present in Denmark. (108) Widex is active in Denmark with both a wholesale subsidiary and a retail presence. Sivantos only has a wholesale presence in Denmark, through a local subsidiary.

several categories, ranging from A to D, depending on the patients' needs and use of the hearing aids. (109)

(182) As part of its selection process, AMGROS pre-qualifies suppliers whose products meet the technical requirements set for each product category. It then selects the three to five bidders (depending on the category) offering the lowest prices. (110) Suppliers selected by AMGROS are publicly ranked according to the price of their hearing aids (from the cheapest to the most expensive) within each of the tender categories. Once listed, the price of hearing aids is fixed for each category for the duration of the tender. Qualified suppliers may introduce newer versions of their hearing aids (in replacement of older models listed by AMGROS) every 6 months but at the same price as agreed upon in the framework contract.

(183) Contracts resulting from the AMGROS’s tenders typically run for two to four years: an initial period of two years is provided with the possibility for AMGROS of prolonging it by 1+1 years. Therefore, contracts resulting from the latest AMGROS’s tender will run at least until August 2019. According to AMGROS, they are however likely to be extended until August 2021. (111)

(184) ENTs dispense hearing aids from the AMGROS list. In theory, they must prescribe products within the relevant AMGROS category and according to the ranking, unless they can prove that the device does not meet the patient’s needs. In practice, categories are not mutually exclusive and ENTs have a margin of discretion in determining to which category a patient belongs. (112) In addition, ENTs may also dispense hearing aids outside of the AMGROS framework; this situation is rare and typically occurs with returning patients used to a specific brand of hearing aids, or for paediatric hearing aids. This practice is however declining and mostly limited to some niche product categories.

(185) All major global manufacturers participate in AMGROS tender with one or more affiliates, except for Starkey, which is currently not present on the public segment of the Danish market.

(194) As explained above, AMGROS’s tenders are used to select preferred suppliers following a competitive process ultimately based on price competition. As a result of this process, competition on the public market in Denmark first takes place “for the market” (to be listed by AMGROS) and, “in the market”, once listed by AMGROS, in order for manufacturers’ products to be dispensed by ENTs.

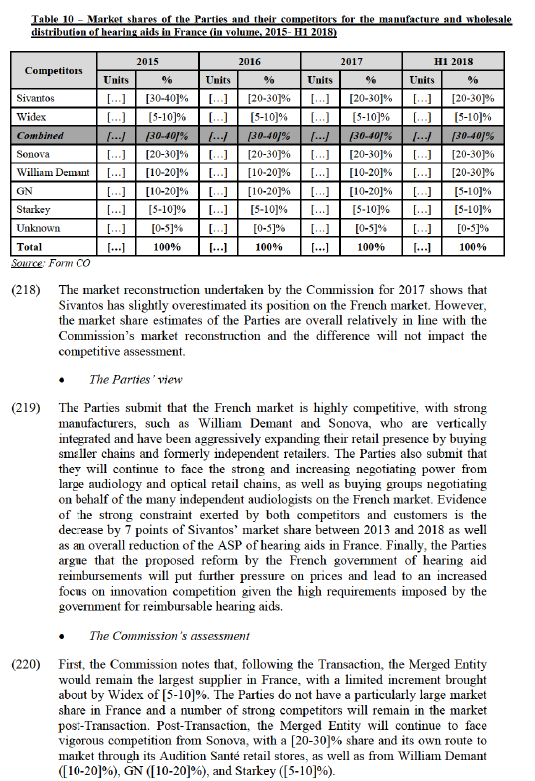

(195) The Commission investigated the extent to which the AMGROS tender makes the Danish public market competitive. To this end, AMGROS provided the Commission with share data for the 12 months preceding the entry into force of the 2017 tender and the 12 months following the entry into force of the 2017 tender. This data enabled the Commission to assess the extent to which AMGROS’s tenders have had an impact of the competitive landscape of the public market in Denmark. It shows that GN, who was ranked in only one tender category in the 2014 tender (category accounting for only [0-5]% of the total number of hearing aids on the public market in Denmark) (115), qualified for 11 out of the 21 tender categories of the 2017 tender (categories accounting for more than [20-30]% of the total number of hearing aids on the public market in Denmark) and increased significantly its market position on the public market within a short period of time. Conversely, while William Demant was selected in 14 tender categories out of 24 tender categories in 2014 (categories accounting for almost [70-80]% of the total number of hearing aids on the public market in Denmark), it was less successful in the 2017 tender and secured position in only four categories (categories accounting for slightly more than half of the total number of hearing aids on the public market in Denmark). This had a direct impact on its market share which decreased in 2018.

(196) These market share fluctuations evidence the importance of being selected by AMGROS in order to be successful on the public market. Securing a position in the AMGROS tender is crucial to increase sales and gain exposure on the public market. Consequently, suppliers have an incentive to bid with a low price; any other strategy would put the supplier at risk of not being listed at all by AMGROS. This is confirmed by the results of the market investigation. In this respect, one participant stressed that the key factor to be successful in AMGROS’s tenders is “to offer low prices”. (116) This is explained by the fact that only the three to five suppliers with the lowest price (potentially the same undertaking as manufacturers are allowed to place several bids through different affiliates or distributors) will be selected.

(197) The volatility of the AMGROS tender results (and as a result of the manufacturers’ market shares) illustrates the contestability of the public market in Denmark: the 2014 and 2017 tender results in particular show that previously successful manufacturers can lose most of their winning positions and previously small players can become important suppliers from one tender to the next. Competition is also strong within each individual tender categories: each tender category generally comprises a sufficient number of alternative suppliers (either actual competitors who have been selected by AMGROS or potential competitors whose bid was not ultimately selected) who will continue to be a significant competitive constraint on the Merged Entity. A less competitive price strategy by the Merged Entity post-Transaction (i.e. in future tenders) would likely translate into an increased risk of losing winning positions, and consequently increase the market shares of other manufacturers.

(198) In that regard, the data provided by the Parties (in line with AMGROS’s data) enabled the Commission to assess the level of competition in the market: while Sivantos was selected in almost all categories of both the 2017 and the 2014 tenders (each time being represented in product categories accounting for virtually all sales on the public market), its market share fluctuated within each tender period. Similarly, respondents to the market investigation pointed out that William Demant recently launched an aggressive marketing campaign to promote its newer products. (117) Thus, despite being listed in fewer categories in 2017 (compared to the 2014 tender) and as a result having lost market share following the entry into force of the 2017 tender, William Demant is expected to re-gain market share in the short term primarily by increasing its share in the categories in which it was selected. ENTs also indicate that, since listed manufacturers are allowed to update their product twice a year within the framework of the AMGROS tenders, manufacturers that introduce newer products, tend to be rewarded by increased prescriptions from ENTs in the categories for which they have been selected. (118)

(199) There are however four tender categories (2C for moderate complexity tinnitus as well as the three categories belonging to the level 4) where the Parties were the only manufacturers selected in the 2017 tender. The Commission first notes that these are ‘niche’ categories characterised by low sales volumes (together accounting for less than 5% of the total sales of hearing aids on the public market in Denmark in 2017). Second, the Commission recalls that it is not possible to change the price of a product during the entire duration of the tender that is in this case likely to run until September 2021. (119)

(200) Finally, as concerns the future tenders, the definition of individual categories regularly evolves with each tender, and AMGROS can design categories ensuring it will receive bids from a sufficient number of manufacturers. Historically, there has been a trend in AMGROS tenders towards a reduction of the number of categories (from 32 in 2012, to 24 in 2014, and 21 in 2017). In future tenders, AMGROS would thus be able to redefine the categories where only the parties were successful in the 2017 tender, with a view to attracting more bidders. Moreover, even if the categories were to remain unchanged, the market investigation indicated that the Merged Entity would continue to be subject to sufficient competitive constraints.

(201) Specifically, as regards category 2C three products have been selected in the current tender, namely products of two affiliates of Sivantos and one affiliate of Widex. However, bidding data shows that several other companies have products responding to the technical requirements of this category and indeed submitted a bid for this category. Although in this specific tender they were not successful, in the future tenders they will exert a competitive constraint on the Merged Entity.

(202) This is also true concerning categories 4A, 4B, and 4D (CROS/Bi-CROS categories) for which three products have been selected in each of these categories in the current tender, namely products of either two affiliates of Sivantos and one affiliate of Widex or two affiliates of Widex and one affiliate of Sivantos. However, the market investigation revealed that Sonova, who was the only manufacturer supplying CROS/Bi-CROS hearing aids to the public market in Denmark prior to the 2017 tender, still enjoys a relatively important market presence due to its reputation on the market (120) and despite not having been listed by AMGROS. (121) Sonova is also expected to exert a strong competitive constraint on the Parties in future tenders. In addition, other manufacturers, such as William Demant offers an alternative solution to traditional CROS/Bi-CROS hearing aids in order to treat unilateral hearing loss; to the best of William Demant’s knowledge, his competing product qualify for CROS/Bi-CROS tender’s categories. (122) Finally, other manufacturers not currently active on the public market in Denmark (e.g. Starkey and second tier manufacturer BHM) have CROS/Bi-CROS products in their portfolios and could participate, either directly or through a third-party distributor, in future tenders. (123)

(203) Finally, respondents to the market investigation did not raise substantiated concerns in relation to the Transaction.

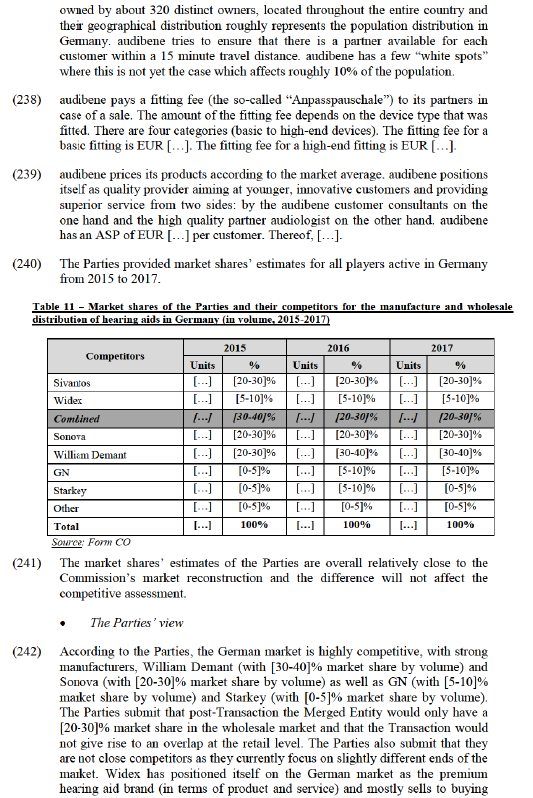

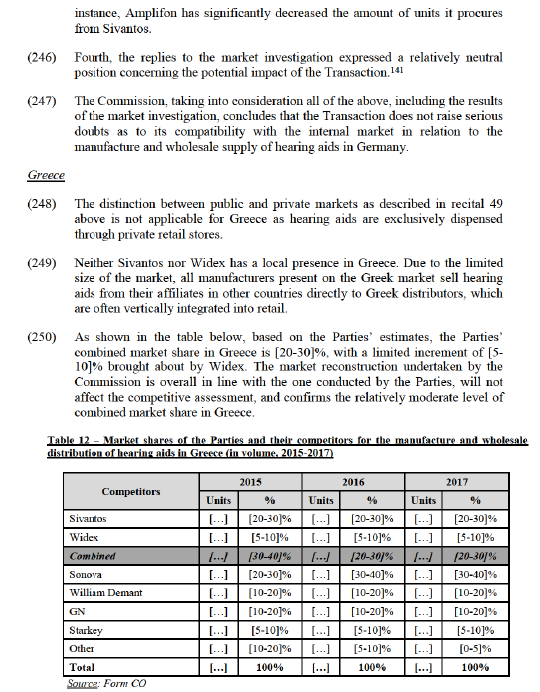

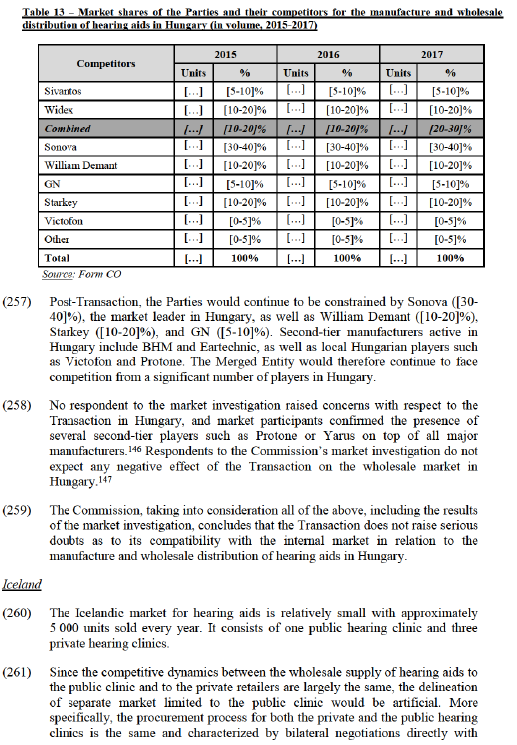

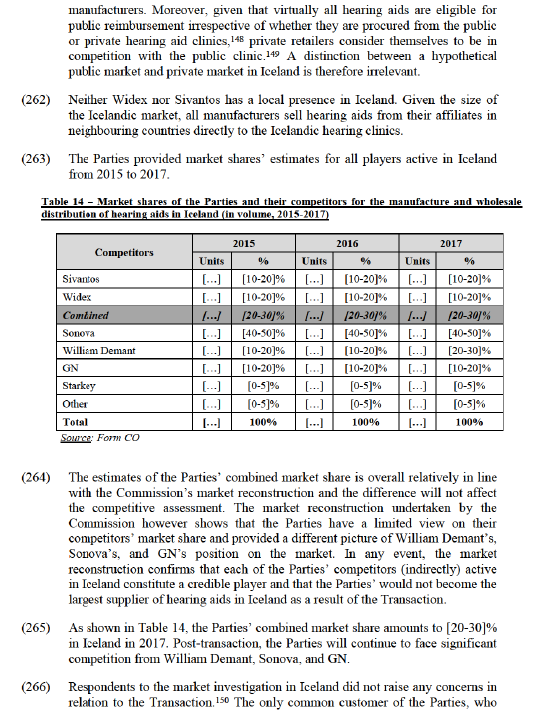

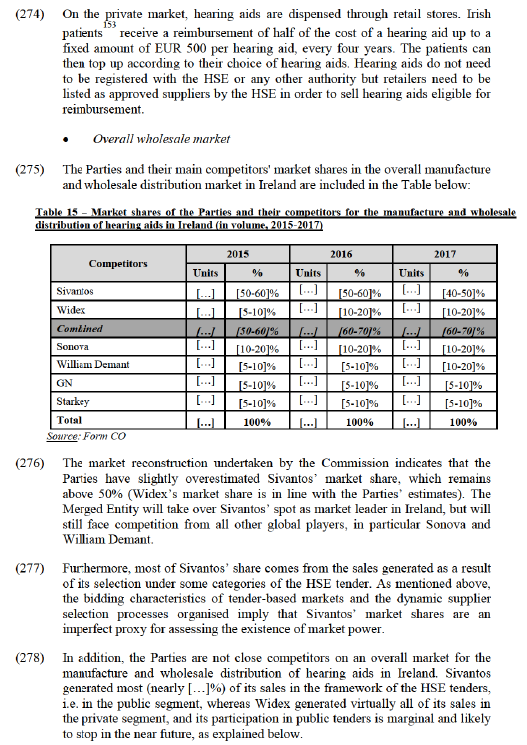

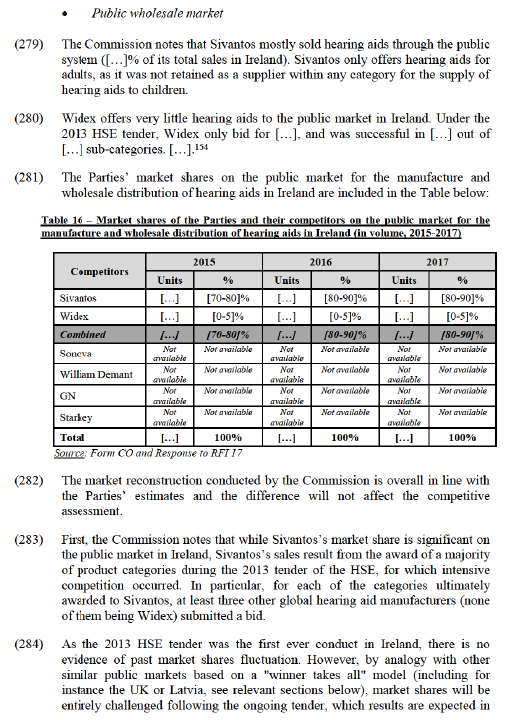

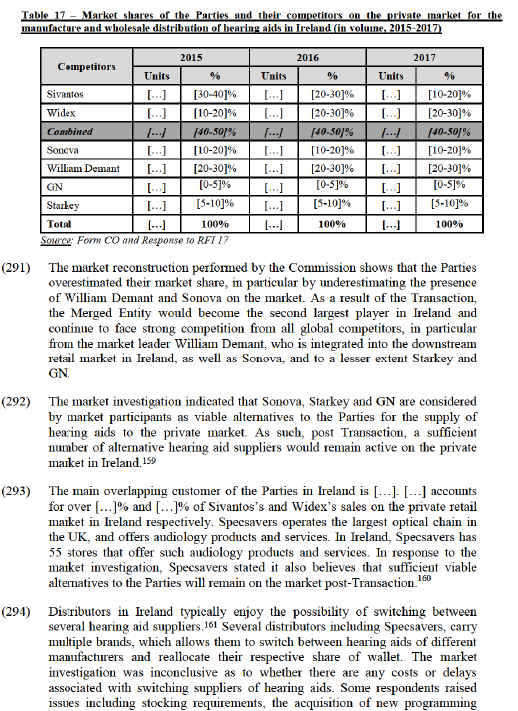

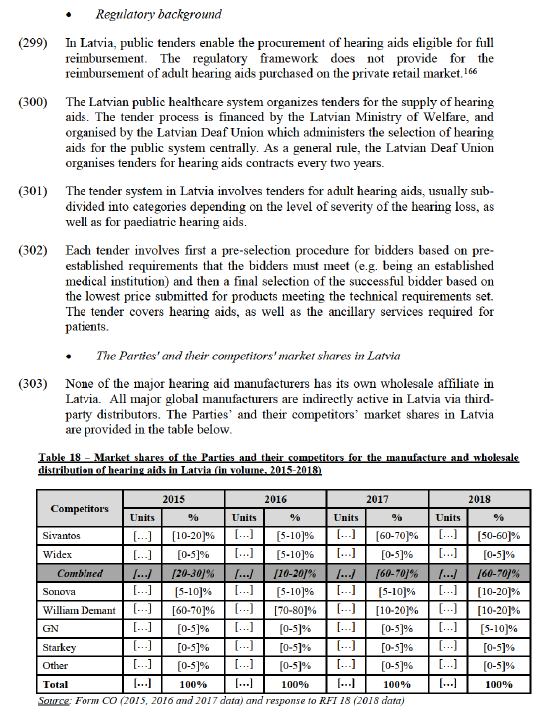

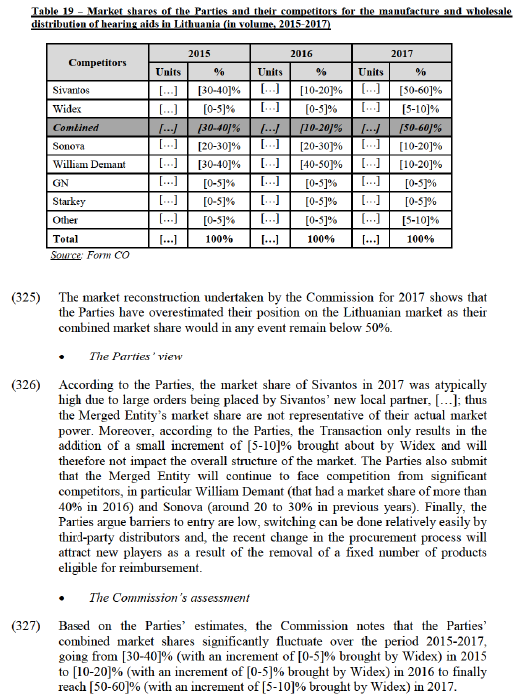

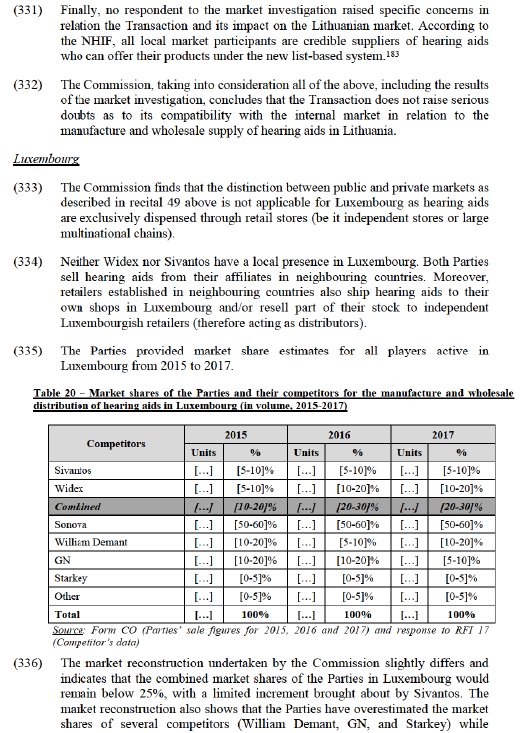

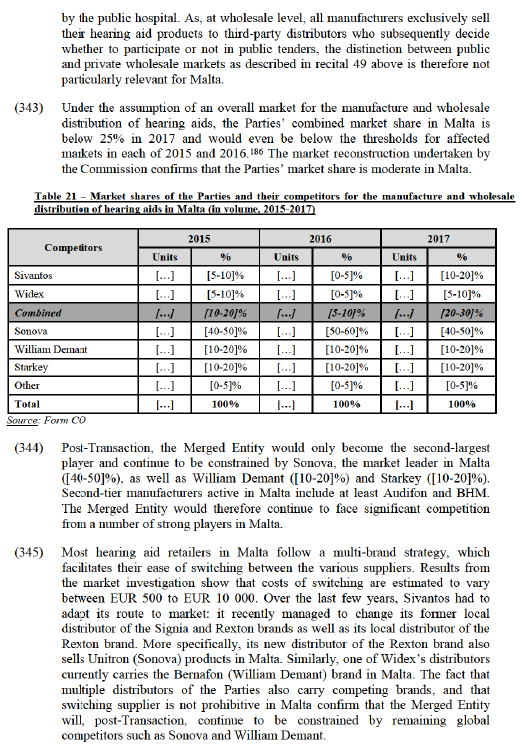

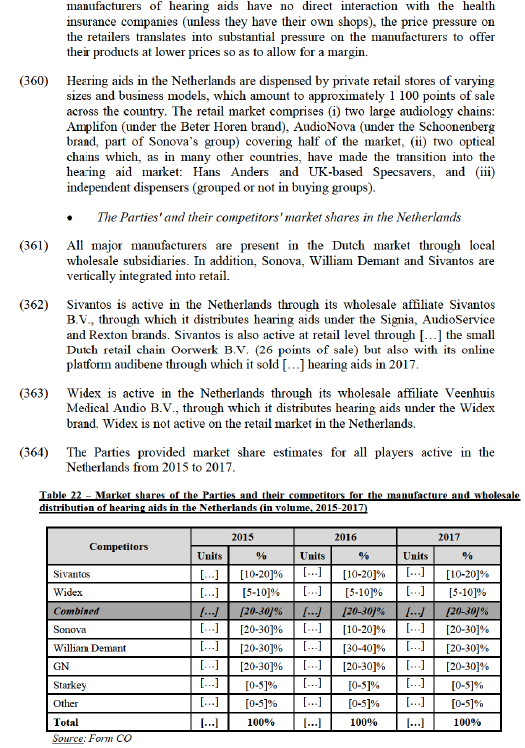

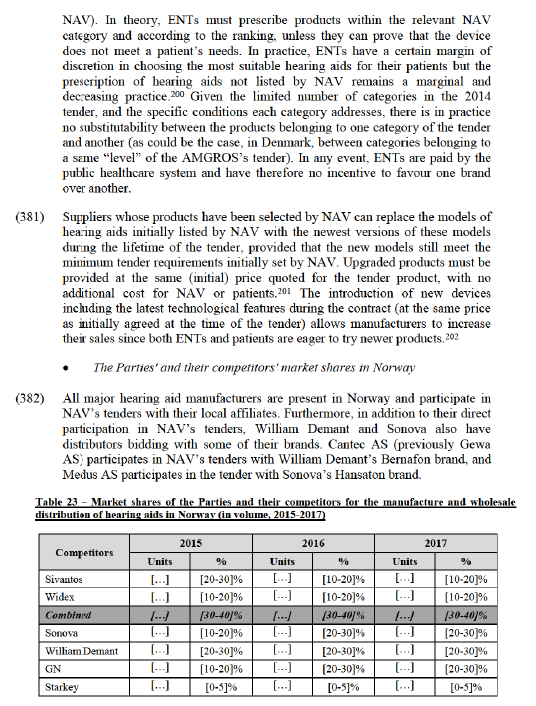

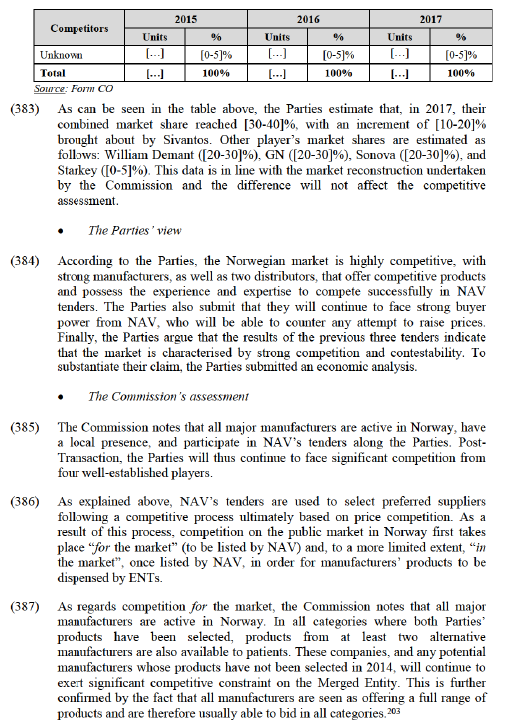

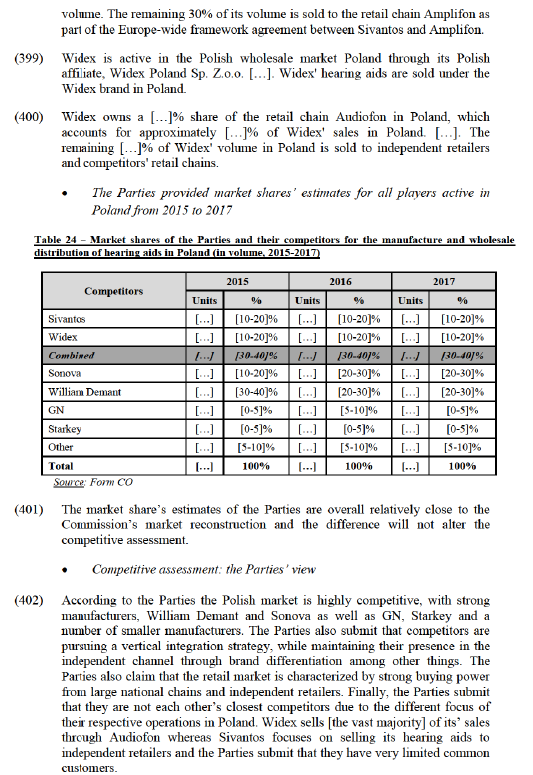

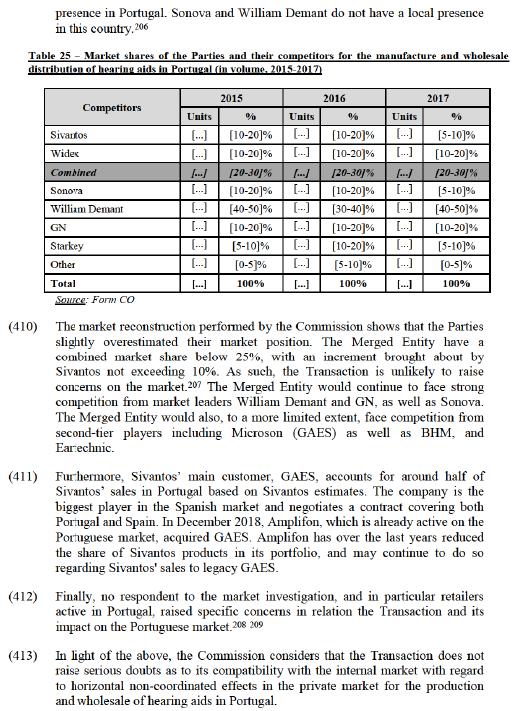

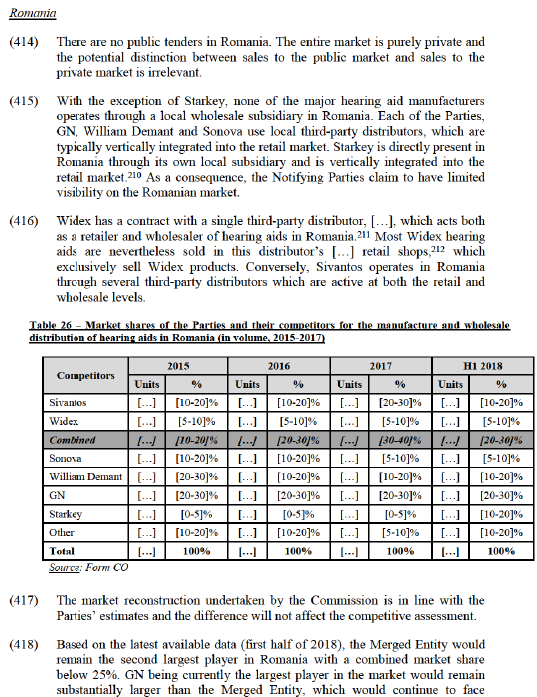

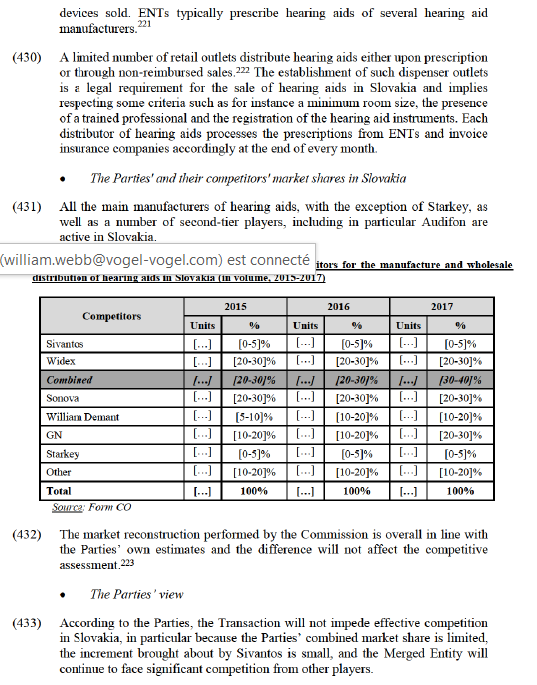

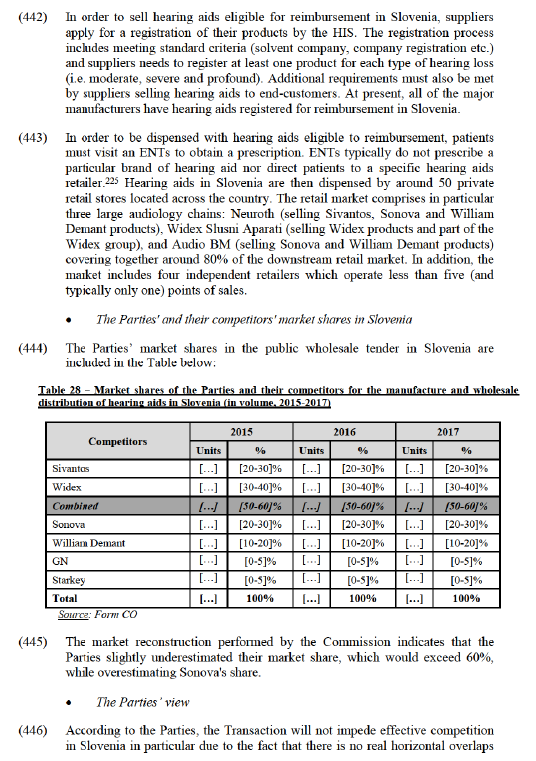

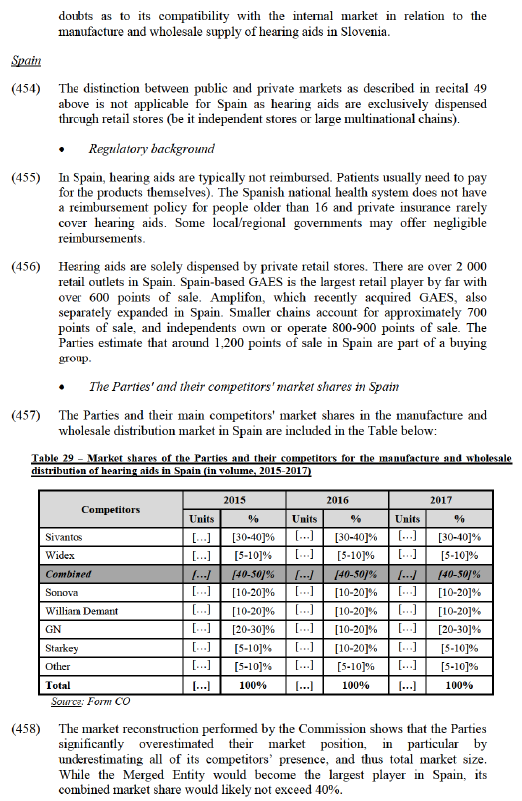

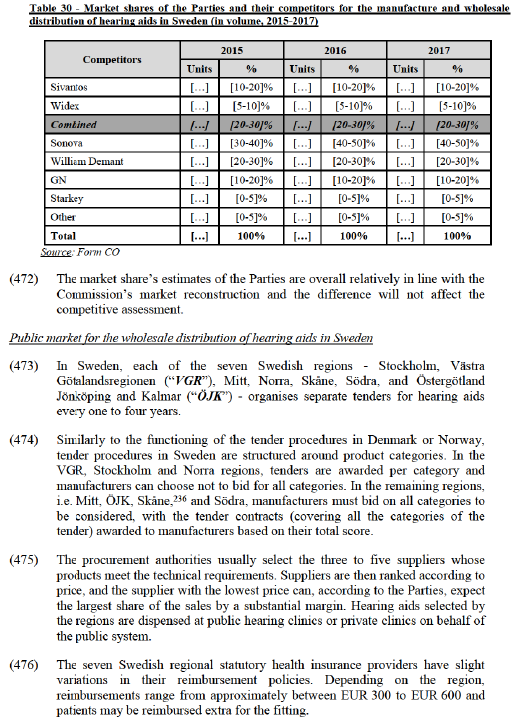

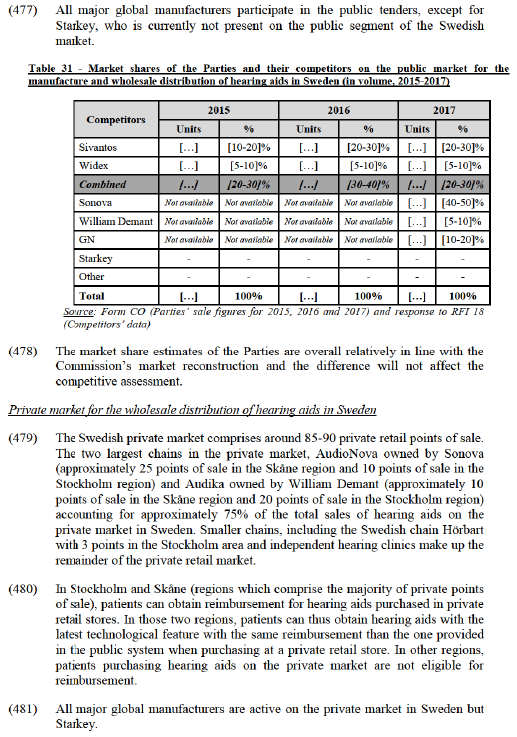

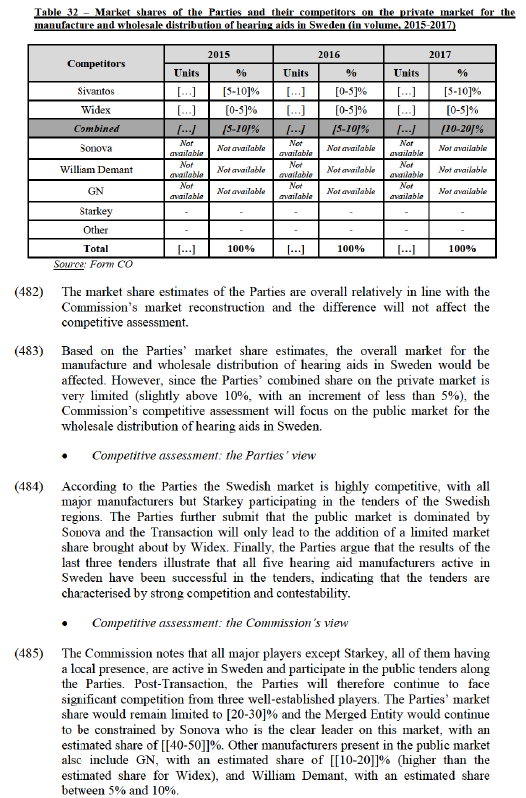

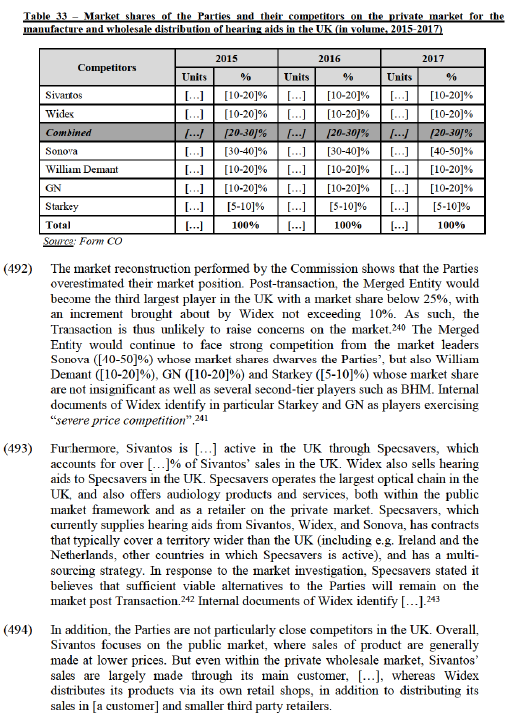

(204) From the point of view of ENTs, which largely determine the commercial success of manufacturers whose products are listed by AMGROS, the market investigation did not point to any manufacturer being more successful in terms of the quality of its products, breadth of its portfolio, services or prices, compared to other players. (124) ENTs are equipped with the fitting software of all manufacturers selected by AMGROS and usually do not have a single preferred supplier. The ENTs having responded to the market investigation considered that all manufacturers active in Denmark constitute credible suppliers of hearing aids on the public market. (125)