Commission, December 9, 2019, No M.9413

EUROPEAN COMMISSION

Decision

LACTALIS / NUOVA CASTELLI

Subject: Case M.9413 – LACTALIS / NUOVA CASTELLI

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir/Madam,

(1) On 4 November 2019 the Commission received a notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 (the 'Merger Regulation') by which Gruppo Lactalis Italia S.r.l. (Italy), belonging to the Groupe Lactalis S.A. (together ‘Lactalis’, France) acquires within the meaning of Article 3(1)(b) of the Merger Regulation of the whole of Nuova Castelli S.p.A. (‘Nuova Castelli’ or the ‘Target’, Italy), a wholly-owned subsidiary of Nuova Castelli Group S.p.A (‘NC Group’, France), in turn controlled by Charterhouse Capital Partners (‘Charterhouse’, United Kingdom) by way of purchase of shares (Lactalis and Nuova Castelli are designated hereinafter together as the ‘Parties’). (3)

1. THE PARTIES

(2) Lactalis produces and supplies cheese such as mozzarella, mascarpone and ricotta, as well as drinking milk, butter, cream and industrial dairy products (milk powder, whey, etc.). Lactalis focuses on branded products, although it also achieves sales in relation to products sold under retailers’ private labels.

(3) Nuova Castelli is a wholly-owned subsidiary of the NC Group, […]. NC produces and sells various Italian cheeses, mostly hard cheeses and soft cheeses (mozzarella, Parmigiano Reggiano, Grana Padano, Pecorino, ricotta, etc.) and has trading activities in relation essentially to mascarpone, Feta and butter. Nuova Castelli specialises in the supply of cheeses to retailers to be resold under private labels.

2. THE OPERATION

(4) The industrial and commercial activities of the NC Group are contained within the Target. Nuova Castelli is currently undergoing a legal reorganisation; however, this does not affect the structure of its ownership. Additionally, prior to the closing of the acquisition, Nuova Castelli will have acquired sole control over ILC La Mediterranea S.p.A. (‘Mandara’). These activities have been taken into account as part of the perimeter of the present Transaction for the purposes of its competitive assessment.

(5) Pursuant to a Sale and Purchase Agreement (‘SPA’) signed on 29.5.2019, Lactalis will acquire all issued and outstanding shares of Nuova Castelli representing 100% of the share capital of the Target. Nuova Castelli will therefore be solely controlled by Lactalis (the ‘Transaction’).

(6) The proposed Transaction therefore constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation. (4)

3. EU DIMENSION

(7) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (5) (Lactalis: […]; Nuova Castelli: […]). Each of them has an EU-wide turnover in excess of EUR 250 million (Lactalis: […]; Nuova Castelli: […]), but each does not achieve more than two-thirds of its aggregate EU- wide turnover within one and the same Member State. The notified operation therefore has an EU dimension.

4. MARKET DEFINITION

4.1. Introduction

(8) Both Parties are active in the production and supply of dairy products. Their activities overlap and give rise to affected markets in (i) the procurement of milk;(ii) the production and sale of cheese (notably the Italian-type cheese and Feta) to retailers (6); (iii) the production and sale of other dairy products (dairy-based desserts) and (iv) the production and sale of butter. (7)

4.2. Procurement of milk

(9) Raw milk refers to milk which has not undergone any treatment (other than cooling) and has a perishable nature. It is produced by dairy farmers, who normally milk cows twice a day. Raw milk is subsequently stored in milk storage cool tanks at the farm which reduces its temperature to 4° C. Raw milk may be kept on the dairy farm for one or two days. It is then delivered to (or collected by) dairy companies like the Parties, where it is pasteurised. Once pasteurised, milk can be freely traded and transported over long distances.

4.2.1. Commission’s precedents

(10) In previous decisions, the Commission considered that the procurement of milk should be divided between conventional milk and organic milk. (8) The Commission left the product market definition open in relation to Germany (9) and Spain (10), and assessed both segments together as a single market in relation to Italy. (11)

(11) The Commission also considered a further segmentation of milk procurement by species (cow, goat and sheep) because of the limited substitutability of the downstream end products, but eventually left the product market definition open. (12)

4.2.2. Notifying Party’s view

(12) According to the Notifying Party, Lactalis procures almost exclusively conventional milk in Italy (13) and that Nuova Castelli has just started collecting limited volumes of organic milk. (14)

(13) The Notifying Party submits that segmenting milk procurement based on conventional or non-organic milk or by species is not relevant, (15) given that the Parties’ activities only overlap in the market for the procurement of conventional cow milk.

(14) The Notifying Party submits that the product market definition may be left open as it has no bearing on the assessment of the Transaction. (16)

4.2.3. Commission’s assessment

(15) As the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to the market for procurement of milk under any plausible product market definition, the question whether the market for the procurement of milk should be further segmented can be left open.

4.3. Supply of Italian-type cheese and Feta

4.3.1. Distinction of Italian-type cheese and Feta by category

(16) The Notifying Party refers to mozzarella, mascarpone and ricotta as Italian fresh cheese; to Gorgonzola as an Italian soft cheese; and Parmigiano Reggiano, Gran Castelli, Grana Padano, Pecorino and Pecorino Romano as Italian-type hard cheeses. (17) Feta is a fresh Greek cheese made from ewe’s and goat’s milk. (18)

(17) The Parties manufacture and trade several cheeses that carry a protected designation of origin label (‘PDO’). Nuova Castelli manufactures and sells: Mozzarella di Bufala Campana, Gorgonzola, Parmigiano Reggiano, and Grana Padano. Nuova Castelli also trades PDO Feta. Lactalis manufactures PDO Gorgonzola and PDO Feta, and it trades Mozzarella di Bufala Campana, Parmigiano Reggiano, and Grana Padano.

4.3.1.1. Commission’s precedents

(18) The Commission has previously distinguished between different categories of cheeses such as “fresh cheese”, “soft cheese”, “semi-hard cheese”, and “hard- cheese” among others. (19)

(19) According to Commission’s precedents, each cheese category could be further segmented by type of cheese due to consumers’ preferences (20) or the unique characteristics of product. (21) In this regard, the Commission assessed in previous decisions whether an Italian-type cheese, mozzarella, might constitute a separate market. The precise market definition was ultimately left open. (22)

(20) In Lactalis/Galbani, the Commission also considered whether each type of cheese could be further sub-segmented by the type of milk used for its production. In particular, the Commission analysed whether cow milk mozzarella and buffalo milk mozzarella might belong to separate product markets, notably due to differences in taste and price. The precise market definition was ultimately left open. (23)

(21) Additionally, in a previous case, the Commission considered further sub- segmentations of blue cheese by specialties; however, it ultimately left the precise market definition for blue cheese open. (24)

(22) In previous cases, the Commission has considered whether segmentation by products protected by designation of origin could be warranted. The Commission noted such segmentation could be justified given that consumers may attach value to the designation of origin, while producers are constrained by specific rules (e.g. origin, ingredients, manufacturing process, etc.). However, the precise market definition was left open. (25)

4.3.1.2. Notifying Party’s view

(23) The Notifying Party argues that the relevant market could be segmented by cheese category, i.e. hard-cheese, fresh cheese, soft cheese; however, it submits that further segmentation by type of cheese does not appear relevant for the supply to retailers of Italian-type branded and private label cheese products. (26)

(24) As regards the supply of branded products to retailers, the Notifying Party argues that a segmentation based on the type of cheese does not always reflect consumer habits; in particular with regard to Italian-type hard cheeses. (27) The Notifying Party claims that, from a demand-side perspective based on consumers’ consumption habits across different European countries except most likely Italy, Italian-type hard cheeses, such as Grana Padano, Parmigiano Reggiano and Pecorino, are substitutable because all cheese types can be used for the same consumption occasion, i.e. in pasta dishes. (28) The Notifying Party also explained that suppliers of Italian-type hard cheeses, such as Parmigiano Reggiano and Grana Padano with the PDO label, produce also their equivalents without the label. (29)

(25) With regard to the supply of private label Italian-type cheese to retailers, the Notifying Party submits that the segmentation by type of cheese does not appear relevant. (30) First, the Notifying Party argues that in the supply of private label Italian-type cheese the relevant factor is the capabilities of suppliers to respond to requirements of the tenders and not consumer preferences. (31) According to the Notifying Party, various types of cheese can be easily manufactured by the same producers and they could belong to the same market. (32) Second, the Notifying Party also submits that some fresh cheese types are sold together to retailers under one contract and the same price (for example, ricotta and mascarpone). (33)

(26) As regards the segmentation of cheese based on the type of milk used to produce that cheese, the Notifying Party submits that, from the point of view of consumers, buffalo milk mozzarella and cow milk mozzarella are substitutable because both products satisfy the same need and there is a correlation between their prices. (34)

(27) Concerning geographical indications, the Notifying Party explains that the labelling of PDO products is subject to stringent rules and requires that the product originates in a specific region and that the ingredients originate and the production takes place in the defined geographic area. Accordingly, only producers located in the specific regions are able to produce PDO cheese.

(28) The manufacturers of Italian-type PDO cheeses are organized in consortia. These consortia require their members to manufacture PDO cheeses from Italian milk produced in specific Italian regions. For example, for Parmigiano Reggiano the milk must come from the provinces of Bologna to the left of Reno river, Mantua to the right of the Po river, Modena, Parma and Reggio nell’Emilia. (35)

(29) However, the Notifying Party argues that segmenting the market based geographical indications such as PDO does not reflect the nature of competition on the market. (36)

(30) The Notifying Party also submits that private label products are substitutable irrespective of the place of where they are manufactured and the origin of milk used. (37) The Notifying Party explains that mentioning the country of origin of the product is voluntary and submits that retailers procure mozzarella, mascarpone and ricotta without giving consideration to the country of origin. (38) As regards the origin of milk, some products carry the indication that milk is of “EU origin”. […]. (39)

4.3.1.3. Commission’s assessment

(31) The market investigation confirmed the previous segmentation of supply of cheese by categories. The majority of responsive customers indicated that the different Italian-type cheese categories (e.g. fresh cheese, soft cheese, semi-hard cheese and hard cheese) were not substitutable among each other. (40)

(32) Moreover, the results of the market investigation also point to a further segmentation between types of cheese within these categories for most of the concerned products (Italian-type cheeses and Feta).

(A) Mozzarella

(33) The vast majority of customers responding to the market investigation considered that mozzarella is not substitutable with any other type of cheese. (41) Customer explained that “[m]ozzarella is too specific and creates a specific market” (42) and that “[i]t is very hard to find the same taste and texture in another product”. (43)

Cow and buffalo milk mozzarella

(34) The results of the market investigation also indicate that, contrary to what the Notifying Party argues, cow and buffalo milk mozzarella are not substitutable.

(35) First, the large majority of customers and competitors that responded to the market investigation indicated that cow milk and buffalo milk mozzarella are not substitutable at all or only partially substitutable in terms of price and product characteristics. (44) As a customer explained: “The quality of the product is superior in buffalo milk. The taste is more pronounced. The price is higher. Many consumers of mozzarella di bufala do not buy mozzarella made of cow milk because they find the product tasteless and unattractive” (45)

(36) Second, the majority of customers and competitors that responded to the market investigation indicated that buffalo milk mozzarella commands a significant price premium (over 30% higher than cow milk mozzarella). (46)

(37) Third, the large majority of customers expressing their views submitted that even if the price of buffalo milk mozzarella increased by 5-10% they would not switch to cow milk mozzarella. (47) The majority of responsive competitors agreed. (48)

(38) Fourth, from a supply-side perspective and according to the market investigation, there is no substitutability between buffalo milk mozzarella and cow milk mozzarella. (49)

PDO and country of origin

(39) First, with regard to buffalo milk mozzarella carrying a PDO label, i.e. Mozzarella di Buffala di Campana, certain customers responsive to the market investigation indicated that PDO carries a certain premium value as it assures quality. (50) However, the large majority of the customers that responded to the market investigation indicated that PDO and non-PDO mozzarella were alternatives in terms of price and product characteristics. (51)

(40) Moreover, the majority of responsive customers indicated that if prices of PDO mozzarella increased by 5-10% end-consumers will switch to non-PDO mozzarella. (52) The responses from competitors were evenly split. (53)

(41) Second, with regard to the country of origin of non-PDO Italian-type cheese products (including country of origin of the milk), the market investigation points at the fact that this is a factor of differentiation recognised by end-consumers particularly in certain countries (e.g. Italy); however, the majority of respondents indicated that retailers do not impose any specifications as regard the origin of the milk of non-PDO Italian-type cheeses. (54)

(42) Third, customers that responded to the market investigation were evenly split between those that considered that mozzarella labelled “made in Italy” was fully or largely substitutable by and mozzarella not labelled as made in Italy and those that considered these products not or only partially substitutable. (55)

Conclusion

(43) In light of the results of the market investigation and for the purpose of this decision, the Commission considers that mozzarella constitutes a distinct product market from other Italian-type fresh cheeses and that it can be further segmented by type of milk species into buffalo milk mozzarella and cow milk mozzarella.

(B) Ricotta

(44) Ricotta and mascarpone are different types of fresh cheese that tend to be used as cooking ingredients. (56) The market investigation confirmed that they belong to separate markets.

(45) First, the results of the market investigation indicate that the large majority of customers consider that there are significant differences between ricotta and mascarpone in terms of consumption occasions and prices. (57)

(46) Second, the vast majority of customers indicated that ricotta is not substitutable at all or only partially substitutable with other type of cheeses in terms of price and product characteristics. (58) Moreover, the majority of competitors that responded to the market investigation indicated that customers do not switch to other products when prices of ricotta increase. (59)

(47) Third, from a supply-side perspective, ricotta is made from whey, a left over from the production of cheese (e.g. mozzarella and mascarpone) and mascarpone is produced from milk fat. (60) The majority of competitors that responded to the market investigation replied that producers of mozzarella could not start producing ricotta without incurring in significant costs and in a short period of time. (61)

(48) Moreover, the majority of the respondents to the market investigation indicated that suppliers active in ricotta could not start producing and selling mascarpone without incurring in significant costs and swiftly. (62)

(49) Fifth, with regard to the country of origin of non-PDO Italian-type cheese products (including country of origin of the milk), as indicated in paragraph (41) above, the majority of responsive customers do not impose any specifications as regard the origin of the milk of non-PDO Italian-type cheese products, including ricotta. (63)

Conclusion

(50) In light of the results of the market investigation and for the purpose of this decision, the Commission considers that ricotta constitutes a separate product market from other Italian-type fresh cheeses.

(C) Mascarpone

(51) As explained in Section (B) above, the market investigation confirmed that mascarpone and ricotta belong to separate markets.

(52) First, the results of the market investigation indicate that the large majority of customers consider that there are significant differences between mascarpone and ricotta in terms of consumption occasions and prices. (64)

(53) Second, the vast majority of customers indicated that mascarpone is not substitutable at all or only partially by other type of cheeses in terms of price and product characteristics. (65) Moreover, the majority of the customers and competitors that responded to the market investigation indicated that customers do not switch to other cheeses when prices of mascarpone increase . (66)

(54) Third, from a supply-side perspective, mascarpone is produced from milk fat and ricotta is made from whey, a left over from the production of cheese (e.g. mozzarella and mascarpone). (67) The majority of competitors that responded to the market investigation replied that producers of mozzarella could not start producing mascarpone without incurring in significant costs and in a short period of time. (68)

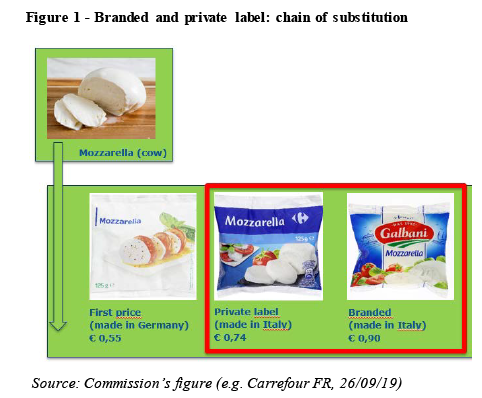

(55) Moreover, the majority of the respondents to the market investigation indicated that suppliers active in mascarpone could not start producing and selling ricotta without incurring in significant costs and swiftly. (69)

(56) Fourth, with regard to the country of origin of non-PDO Italian-type cheese products (including country of origin of the milk), as indicated in paragraph (41) above, the majority of responsive customers do not impose any specifications as regard the origin of the milk of non-PDO Italian-type cheese products, including mascarpone. (70)

Conclusion

(57) In light of the results of the market investigation and for the purpose of this decision, the Commission considers that mascarpone constitutes a separate product markets from other Italian-type fresh cheeses.

(D) Feta

(58) Feta is a fresh Greek cheese made from ewe and goat milk in the mainland Greece and its department of Lesbos bearing a PDO label.

(59) First, the majority of customers expressing views in the market investigation considered that Feta is a distinct product from other fresh cheeses and Feta fulfils different needs. (71)

(60) However, several customers indicated that there are alternatives to Feta for certain uses such as fresh salads. A Belgian customer indicated that “Many alternative products can be substituted for Feta, especially for salad uses”; (72) and French customers pointed out “Feta and mozzarella can be 2 alternatives in many consumption occasions for example in a composition of salad […]” (73) and “Feta is mainly used for salads. It is substitutable with other cheeses”. (74)

(61) Moreover, the majority of competitors that responded to the market investigation indicated that customers would switch to other cheeses if the prices of Feta were to increase. (75)

(62) Second, with regard to Feta carrying PDO labels, the majority of the customers that responded to the market investigation indicated that PDO Feta and non-PDO products were not alternatives in terms of price and product characteristics. (76)

(63) However, the majority of responsive customers and competitors submitted that end-customers would switch from PDO Feta to non-PDO products if the price of the PDO Feta were to increase; (77)

Conclusion

(64) In light of the results of the market investigation and for the purpose of this decision, the precise market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible product market definition.

(E) Gorgonzola

(65) Gorgonzola is a soft blue cheese carrying a PDO label. The production of PDO Gorgonzola follows the rules established by the consortium. Both Lactalis and Nuova Castelli are producers and members of the Consorzio per la Tutela del Formaggio Gorgonzola PDO.

(66) First, the vast majority of customers responding to the market investigation have submitted that Gorgonzola is not substitutable or only partially substitutable with other type of blue cheeses in terms of price and product characteristics (78) A customer explained that “In some way, we could consider other “blue cheese” as “Roquefort”, “Bleu” or “stilton” as substitutes. But, they are stronger than Gorgonzola and can’t fit to all consumers. Gorgonzola is quite unique in terms of taste and texture”. (79)

(67) Second, the majority of competitors that responded to the market investigation submitted that customers would switch to other blue cheeses (in particular roquefort) if the price of Gorgonzola would increase. (80) However, the majority of responsive customers indicated that, if prices of Gorgonzola were to increase, end- consumers would not switch to other blue cheeses. (81)

(68) Third, with regard to Gorgonzola carrying a PDO label, the majority of the customers that responded to the market investigation indicated that PDO and non-PDO Gorgonzola were not alternatives in terms of price and product characteristics. (82)

(69) However, the majority of competitors responsive to the market investigation submitted that end-customers would switch from PDO to non-PDO Gorgonzola if the price of PDO Gorgonzola were to increase; (83) while the majority of responsive customers indicated that if prices of PDO Gorgonzola increased by 5-10% end-consumers will not switch to non-PDO Gorgonzola. (84)

Conclusion

(70) In light of the results of the market investigation and for the purpose of this decision, the precise market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible product market definition.

(F) Italian-type hard cheese

(71) Both Parties sell different Italian-type hard cheeses, with and without PDO label, i.e. Parmigiano Reggiano PDO, Grana Padano PDO, Pecorino PDO, non-PDO Grana Padano-type and Parmigiano-type, as well as other hard cheeses.

(72) The production of Parmigiano Reggiano PDO and Grana Padano PDO is organised by a relevant consortia. Consortia, while not producing or selling the cheese itself, attributes the production quotas and defines the rules that consortia members have to observe in order to use the PDO label and. These rules typically relate to the origin of the milk used (e.g. determined by a specific geographic area), production methods and the packaging. (85) Nuova Castelli is a member of the Consorzio del Formaggio Parmigiano Reggiano and Consorzio Tutela Grana Padano. Lactalis does not produce Parmigiano Reggiano PDO and Grana Padano PDO. (86)

(73) First, the Commission’s market investigation found that the consumption habits of customers may be different across Member States, with the large majority of customers in most countries considering Parmigiano Reggiano and Grana Padano to be substitutable or at least partially substitutable as Italian-type hard cheese for their main intended uses. (87) For example, a customer explained regarding the alternatives for Parmigiano Reggiano: “there is pecorino, grana padano with similar characteristics and a lower price” (88), or as another customer stated: “Substitutable only by Grana Padano or [I]talian Hard Cheese”. (89) Furthermore, some customers considered that, for example Parmigiano Reggiano can be substituted also with other hard cheeses: “could switch to non Italian type hard cheese or Grano Padano”, (90) or as another customer submitted: “Grana Padano could be an alternative. Similarly as other hard cheeses for certain users who grate the cheese […]”. (91)

(74) Second, the majority of customers and competitors expressing their views indicated that if prices of Parmigiano Reggiano or Grana Padano were to increase, end- consumers would switch to other cheeses. (92) The majority of competitors expressing their views indicated that in case of price variation of Grana Padano or Parmigiano Reggiano customers will substitute one with the other. (93) According to the market investigation, while the substitutability was particularly strong between Grana Padano and Parmigiano Reggiano, it was not limited to these Italian-type hard cheeses. (94)

(75) Third, with regard to substitutability between Parmigiano Reggiano and Grana Padano carrying PDO labels, the majority of customers that responded to the market investigation indicated that PDO and non-PDO Parmigiano Reggiano and Grana Padano were not alternatives in terms of price and product characteristics (95) and end-customers would not switch from PDO to non-PDO Parmigiano Reggiano and Grana Padano if the price of the PDO products were to increase. (96)

(76) However, the large majority of competitors expressing their views in the market investigation considered that, in case of a price increase of a PDO-type, the end- customers would switch to the non-PDO equivalent. (97) Moreover, when asked about alternatives for Grana Padano, for example, some customers indicated that it would be substitutable: “With non PDO hard-cheese” (98), or, as another customer explained, if the prices for Grana Padano were to increase: “Some customers could switch to similar cheeses non PDO, with characteristics close to Grana Padano”. (99)

Conclusion

(77) In light of, the results of this market investigation, the information provided by the Parties and for the purpose of this decision, the Commission considers that the relevant market is broader than a singular variety of an Italian-type hard cheese. For the purpose of this Decision, the Commission will carry out the assessment in relation to the plausible market for Italian-hard cheeses.

4.3.2. Possible segmentation of the supply of private label and branded cheese

(78) Both Parties supply branded and private label Italian-type cheeses to retailers. However, for the product markets considered, most of Lactalis’ sales are in branded products, while Nuova Castelli focuses mainly on the supply of private label products.

4.3.2.1. Commission’s precedents

(79) In previous decisions, the Commission considered the distinction between branded and private label products, and in some cases it came to the conclusion that they belong to the same, albeit differentiated market. (100)

4.3.2.2. Notifying Party’s view

(80) The Notifying Party submits that private label products and branded products compete head to head when they are sold to the end consumers; however, when they are sold to retailers, it is necessary to distinguish the supply of private label cheese from the supply of branded cheese. (101)

(81) The Notifying Party argues that private label and branded products are procured separately and differently by retailers. (102) Moreover, the role played by suppliers and retailers in these procedures is different. (103) The Notifying Party explains that retailers procure private label products through separate tender procedures and they have full control over product characteristics (e.g. origin of milk, quality, packaging), as well as volumes, sales and marketing. (104) In contrast, retailers and suppliers negotiate the supply of branded products bilaterally, in over the counter negotiations. These negotiations are done on the basis of product characteristics already determined by the supplier. (105)

4.3.2.3. Commission’s assessment

(82) First, the Commission notes that the results of the market investigation suggest that large majority of customers and competitors consider that branded and private label Italian-type cheeses compete. (106) However, branded products can command a significant price difference even for products of very similar characteristics. (107) As one customer explained: “In terms of texture, taste and smell, the private labels and branded labels are equivalent; the price of branded is generally higher.” (108) Given that the suppliers of branded products usually also supply private label products, the price difference would apply even for products manufactured by the same company.

(83) From a demand side perspective, in the perception of consumers, brand for fresh cheese products is an important and recognised element. The majority of customers expressing their views in the market investigation listed proprietary brands, such as Galbani (Lactalis), Zeta, Casa Azzurra (Granarolo) as the strongest brand for different Italian-type cheeses. (109) Only in few instances a private label was mentioned as the strongest brand. For example, a French customer mentioned that retailer’s private label is the strongest brand for ricotta and Italian-type hard cheeses, or few Italian customers mentioned Italian-type hard cheeses. (110)

(84) Furthermore, the majority of customers expressing their views in the market investigation also considered that at least one of the Parties’ has a “must have brand”. (111) For example, a customer explained: “Galbani is a must for cow milk mozzarella […]. It is also very important for buffalo milk mozzarella, ricotta and mascarpone”; (112) or as another customer submitted: “Galbani Mozzarella (Lactalis) is the market leader in Brands and should be listed in every full-line food retailer”. (113) The internal documents of the Notifying Party also refer to Galbani as the “Italians’ most loved cheese brand” and the “strongest brand in Italian Cheese markets”. (114)

(85) Second, while customer recognition driven by a brand identifies a specific producers and is associated with specific qualitative expectation, which are driven by brand investment, advertising, packaging and indications; the private label products typically carry a retailer brand and are identified as a ‘less costly’ alternative which may be in a somewhat lower price segment. (115)

(86) Third, the private label side of the market is also differentiated, with ‘entry’ products, or white label, carrying an alternative brand denomination and simpler packaging than retailer brands, possibly of lower qualitative specifications and an even lower price. (116)

(87) Fourth, the procurement of branded and private label products is different. The majority of customers expressing views suggested that they have separate procedures for sourcing branded and private label products. (117)

(88) Branded cheese products are procured through bilateral negotiations. Branded cheese products are less substitutable and typically have to feature on shelves, particularly as regards the most recognised brands such as those held by Lactalis. (118) Private label cheese products are usually procured through tendering processes that are organised with concrete specifications. (119) Given that a supplier does not need to invest in brand development and marketing, there are lower barriers to entry. Similarly, given the regular competitive tendering processes based primarily on price as a selection criteria, switching barriers for retailers are likely also lower. (120)

(89) Fifth, despite such differentiation in terms of pricing, brand and characteristics, there is evidence that such a differentiated offer may be a 'continuum' of options available to the customer and for which there would be a chain of substitution. (121)

(90) Sixth, in this context, the different procurement mechanisms may not be sufficient to sustain a finding that pricing dynamics would significantly differ across the different products. Thus, even if, according to precedent, a separate market for procurement of private label products to be supplied under retailer brands may be considered, anti-competitive effects on such market, by affecting the constraint exerted by private label products in on-shelf competition, may eventually also lead to higher overall prices on the spectrum of products available including branded products.

(91) Seventh, consistent with this, the Parties’ internal documents show that they track the market shares for both branded and private label products as competing in the same market. (122) In addition, the Notifying Party’s internal document produced in the regular course of business reads for mascarpone market “Galbani competes with minor brand and PL that are more aggressive in terms of price and distribution” (123). A further example regarding the SWOT (124) analysis for the ricotta market also shows that private label products exert direct competitive constraint on the branded products: Lactalis presents continuously growing private label as a ‘threat’, while Galbani - a leader brand – as a ‘strength’. (125)

(92) Eighth, the Notifying Party explained that it considers private label when making strategic pricing and marketing decisions in order to avoid losing market shares to private label products. (126) Accordingly, if Lactalis takes into account the prices of the competing products, it would indicate that private label exert a competitive constraint on the supply of branded products, too.

(93) Furthermore, the Notifying Party’s internal documents suggest that, as regards specifically the Italian-type cheeses, the share of private label supplies has been increasing over the last years and represents in many geographic markets an important part of the overall market. (127) The Commission notes that the market data submitted by the Notifying Party also indicate that for some Italian-type cheeses in certain countries, the increasing share of private label is achieved at the cost of branded products supplies. (128) This in turn may indicate that retailers gain a stronger negotiation position vis- à -vis branded label suppliers, which have to compete for smaller available shelf space and the risk that it may further shrink because of retailers’ ability to increase volumes in private label segment. As the Notifying Party submits, the retailers decide on the amount of shelf space that they will allocate to branded products and on the amount of shelf space they will allocate to private label products. (129)

(94) Ninth, the Commission also observes that manufacturers of branded products, such as Italian suppliers Casa Azzurra, Lactalis and Nuova Castelli, as well as German suppliers Zott and Goldsteig, also feature on the Notifying Party’s list as the main private label suppliers. (130) The Commission does not have evidence, which would indicate that manufacturers of Italian-type cheese would exclusively produce private label products. Accordingly, as manufacturing facilities for producing private and branded label products are the same, the suppliers would be able to switch from supplying branded to private label products and the other way around.

(95) Tenth, the Notifying Party also explained that for producers focusing on branded cheese supply the private label orders are important “in terms of valuing idle capacities” (131). Accordingly, a shift in the output volumes of private label of the manufacturer focusing on branded products supplies would have an effect on the capacity utilisation and ultimately also on the cost structure and competitiveness of its supplies of branded products.

(96) In light of the findings and the results of the market investigation, the Commission considers that while private label products exert a constraint on branded products, this may not be sufficient to exclude that branded products primarily compete in a different market. In any event, for the purposes of the present case, the exact market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition.

4.4. Production and sale of fresh dairy products

4.4.1. Commission’s precedents

(97) In previous decisions, the Commission held that, within the supply of basic dairy products, a distinction ought to be made between fresh dairy products and long-life dairy products. (132)

(98) With regard to fresh dairy products, these are generally produced from dairy products such as milk and cream, in which, among others, eggs, thickening agents (such as starch), sugar, flavours and/or fruits are added. (133) Within fresh dairy products, the Commission has distinguished different products categories, namely fresh milk, fresh buttermilk or yoghurt. (134)

(99) Concerning fresh dairy desserts, they represent a variety of ready-made sweet dairy desserts including custard, portion packs such as mousse, (rice) puddings, profiteroles, tiramisu and porridges. The Commission considered that fresh custardin gable top, porridge and portion pack dairy desserts constitute separate relevant product markets. (135)

4.4.2. Notifying Party’s view

(100) The Notifying Party submits that, in many cases, consumers consider all types of desserts as substitutable. However, in the absence of any significant overlapping activities, the Notifying Party takes the view that the precise market definition may be left open. (136)

4.4.3. Commission’s assessment

(101) According to the information provided by the Parties, Lactalis manufactures different types of fresh dairy desserts under its brand Galbani, including tiramisu; (137) and that (ii) Nuova Castelli sells in limited volumes one type of fresh dairy desserts, namely tiramisu. (138)

(102) As the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to the production and sale of fresh dairy desserts (including tiramisu) under any plausible product market definition, the Commission considers that the precise market definition may be left open.

4.5. Production and sale of butter

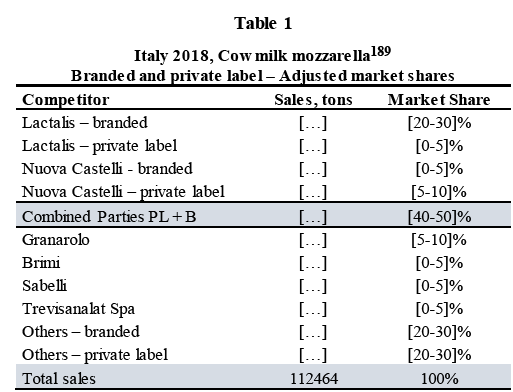

4.5.1. Commission’s precedents

(103) In previous decisions, the Commission held that separate product markets exist for butter sold in bulk and butter sold in packets. (139) Moreover, bulk butter constitutes a separate product market, different from the market for bulk yellow fats including margarine and liquid vegetable oils. (140)

(104) The Commission also came to the conclusion that dairy bulk butter can also be divided into (i) basic butter (with a 82% fat content); (ii) butter oil (or non- fractionated butter oil, i.e., with a 99,8% fat content) and (iii) fractionated butter oil (or fractionated butter). (141)

(105) In addition, the Commission held that vegetable fats (namely, margarine) are not in the packet butter market. (142) The Commission, however, left open the question whether plain packet butter and packet butter with additives constituted separate markets. (143)

4.5.2. Notifying Party’s view

(106) The Notifying Party submits that the Parties are active on the market for the production and sale of butter and that the Parties’ overlap is very limited. (144) Therefore, the Notifying Party takes the view that that the precise market definition may be left open. (145)

4.5.3. Commission’s assessment

(107) As the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to the market for the production and sale of butter under any plausible definition, the precise product market definition may be left open.

4.6. Geographic market definition

4.6.1. Procurement of milk

4.6.1.1. Commission’s precedents

(108) In previous cases, (146) the Commission left open whether the geographic scope of the markets for the procurement of raw milk could be national or narrower, i.e., regional or even local. As regards the Italian market, the Commission left open whether the relevant market for the procurement of raw milk should be defined as narrower than national because raw milk is perishable in nature and the maximum storage duration prior to further processing is limited. (147)

4.6.1.2. Notifying Party’s view

(109) The Notifying Party submits that the markets for the procurement of milk are at least national, if not wider, comprising clusters of countries. (148) The Notifying Party submits that this is particularly the case for Italy due to the fact that (i) procurement of milk may take place throughout Italy; (ii) milk can be easily transported from one region to another; (iii) imports of milk are frequent due to the insufficient level of Italian domestic milk production; and (iv) pricing conditions are broadly consistent throughout Italy. (149)

4.6.1.3. Commission’s assessment

(110) The Parties’ activities only overlap in the procurement of raw cow’s milk in certain regions of Italy. Therefore, the competitive assessment of the Transaction will be carried out at a national level and to a certain extent in narrower areas in Italy.

(111) However, for the purpose of this decision, the precise geographic market definition can be left open the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition.

4.6.2. Supply of Italian-type cheese and Feta to retailers

4.6.2.1. Commission’s precedents

(112) In previous cases, the Commission concluded that the markets for the supply of cheese are national in scope. (150)

4.6.2.2. Notifying Party’s view

(113) In line with the Commission’s precedents, the Notifying Party argues that the markets for the supply of branded cheeses are national due to consumer preferences, price differences between Member States, and to the importance of local brands and strong national trademarks. (151)

(114) However, the Notifying Party argues that the market for the supply of private-label cheese to retailers is wider than national because (i) customers are the retailers, therefore making consumer preferences and brands less relevant; (ii) retailers organise European-wide calls for tenders and some European retailers have regrouped their activities in buying alliances; (iii) suppliers from various Member States have the ability to supply cheeses across Europe; (iv) imports and exports of cheese are significant in the EU; (v) the labelling products does not constraint competition between suppliers from various Member States, and (vi) prices for private-label cheeses are homogenous across various Member States. (152)

4.6.2.3. Commission’s assessment

(115) The market investigation confirms that the markets for the supply of cheese are national.

(116) First, the large majority of customers that responded to the market investigation indicated that they negotiate contracts for the supply of branded and private label cheese at national level.- (153)

(117) Second, the vast majority of responsive customers indicated that the relevant geographic market for the supply of mozzarella, ricotta, mascarpone, hard Italian- type cheeses (Grana Padano, Parmigiano Reggiano) and Feta is national in scope. (154)

(118) Third, seven customers that responded to the market investigation indicated that customers’ demand of Italian-type cheeses is substantially the same across EEA countries, while six customers indicated that it was different. (155) However, the majority of responsive competitors indicated that end-customers’ demand for Italian-type cheeses and Feta are substantially different in terms of brands, customer preferences and product characteristics across EU countries. (156)

(119) Fourth, the majority of customers and competitors that responded to the market investigation indicated that prices of Italian-type cheeses are substantially different across different EEA countries. (157)

(120) For the purpose of this decision, the competitive assessment of the supply of Italian-type cheese and Feta to retailers will be carried out at the narrowest level,

i.e. a national level; however, the precise geographic market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible geographic market definition.

4.6.3. Production and sale of fresh dairy products

4.6.3.1. Commission’s precedents

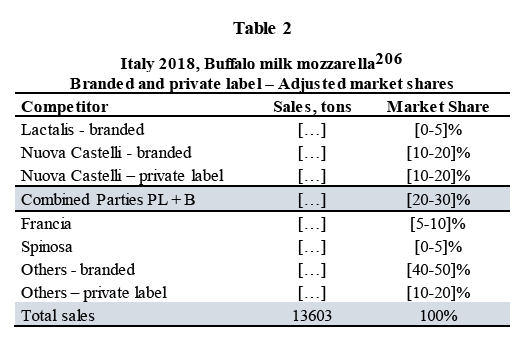

(121) In previous cases, the Commission considered that the relevant market for fresh dairy desserts would be national but the exact market definition was left open. (158)

(122) Regarding portion pack dairy desserts, the Commission considered that it could be wider than national in scope. (159)

4.6.3.2. Notifying Party’s view

(123) The Notifying Party takes the view that, in the absence of any significant overlapping activities, the precise geographic definition may be left open. (160)

4.6.3.3. Commission’s assessment

(124) For the purpose of this decision, the competitive assessment of the Transaction will be carried out at a national level; however, the precise geographic market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible geographic market definition.

4.6.4. Production and sale of butter

4.6.4.1. Commission’s precedents

(125) In previous cases, the Commission considered the geographic market for bulk butter, fractionated butter oil and non-fractionated butter oil to be EEA-wide. (161)

(126) With regard to packet butter, the Commission considered in previous decisions that the relevant geographic market was wider than national and left open whether it was EEA-wide but deemed to be at least regional (i.e. including more than one Member State). (162)

4.6.4.2. Notifying Party’s view

(127) The Notifying Party considers that the markets for butter is EEA-wide, or at least regional. However, in the absence of significant overlapping activities of the Parties on these markets, the Notifying Party submits that this question may be left open. (163)

4.6.4.3. Commission’s assessment

(128) For the purposes of this decision, the competitive assessment of the Transaction will be carried out at the narrowest level possible, i.e. at a national level. However, the precise geographic market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible geographic market definition.

5. COMPETITIVE ASSESSMENT

5.1. Legal framework

(129) Article 2 of the Merger Regulation requires the Commission to examine whether notified concentrations are compatible with the internal market, by assessing whether they would significantly impede effective competition in the internal market or in a substantial part of it.

(130) The Commission Guidelines on the assessment of horizontal mergers under the Merger Regulation (the "Horizontal Merger Guidelines") distinguish two main ways in which mergers between actual or potential competitors on the same relevant market may significantly impede effective competition, namely non- coordinated effects and coordinated effects. (164)

(131) Non-coordinated effects may significantly impede effective competition by eliminating the competitive constraint imposed by one merging party on the other, as a result of which the merged entity would have increased market power without resorting to coordinated behaviour. According to recital (25) of the preamble of the Merger Regulation, a significant impediment to effective competition can result from the anticompetitive effects of a concentration even if the merged entity would not have a dominant position on the market concerned. In this regard, the Horizontal Merger Guidelines consider not only the direct loss of competition between the merging firms, but also the reduction in competitive pressure on non- merging firms in the same market that could be brought about by the merger. (165)

(132) The Horizontal Merger Guidelines list a number of factors, which may influence the rise of substantial non-coordinated effects from a merger, such as: the large market shares of the merging firms; the fact that the merging firms are close competitors; the limited possibilities for customers to switch suppliers; or the fact that the merger would eliminate an important competitive force. The list of factors applies equally if a merger would create or strengthen a dominant position, or would otherwise significantly impede effective competition due to non-coordinated effects. Furthermore, not all of those factors need to be present to make significant non-coordinated effects likely and the list itself is not an exhaustive list. (166)

5.2. Methodology for market shares data

5.2.1. The market shares submitted by the Notifying Party

(133) According to the Horizontal Merger Guidelines and the Non-Horizontal Merger Guidelines, market shares constitute useful first indications of the market structure and of the competitive importance of the market players.

(134) The Notifying Party submitted market shares in volume and value, when available, for each plausible product and geographic market. The market shares were based on the Parties’ actual sales of the Italian-type cheese and Feta-type cheese products as recorded internally at the wholesale level.

(135) The Notifying Party used retail data as a proxy for the total market size. Subject to availability, the market size for volume market shares was based on the Nielsen or IRI panel data providers, who record the total volumes of cheese sold to end- consumers at retail level nationally. Similarly, subject to availability, the market size for value market shares was based on the total value recorded by the panels. (167) (168) For the plausible product markets where panel data for 2018 was unavailable, the Notifying Party used 2016 or 2017 panel data. (169) For the plausible product markets where panel data was not available to the Notifying Party for any years, the Notifying Party used market size estimates based on (i) Nuova Castelli’s estimates recorded in internal documents (170); (ii) Eurostat trade data (171); (iii) per capita consumption approach (172). Finally, for the plausible markets where no estimates for the market size were available, the Notifying Party confirmed that their combined market shares would be below 20% for these markets due to low sales. (173)

(136) The Notifying Party argued that panels tend to underestimate the real size of the market, as they do not cover all outlets active the retail sector and do not capture small sales, and proposed to increase the market size by […] for branded cheese, and branded and private cheese when accounted together (174). This methodology was applied for the market size estimates derived from the panel data. Moreover, the Notifying Party stated that panels tend to underestimate the market size for private label products to a greater extent that for branded products. This is because private label cheese products are also used internally by retailers to sell in their on- premises restaurants or are used as ingredient for the sale of deli foods, such as lasagne, and such sales would not be captured by panels. (175) Therefore, the Notifying Party proposed to amend the market size for the plausible markets of private label products by multiplying the total volume of private label products sold downstream by […] for mozzarella and by […] for mascarpone, ricotta and Gorgonzola due to the fact that such cheeses are more widely used as ingredients in deli dishes than mozzarella. (176) The Commission noted that although multipliers for the market size of private label supply were introduced, the Notifying Party’s market shares are still likely overstated, as in some instances they are larger than 100% and are not in line with the market share estimates of other active players provided by the Notifying Party or the results from the market investigation. (177) The Commission notes that because different multipliers were used to adjust market sizes, the sum of estimated market sizes separately for branded (multiplied by […]) and private label (multiplied by […]or […]) does not fully match the estimated size for branded and private label combined (multiplied by […]). (178)

(137) The Commission examined the methodology and the market shares provided by the Notifying Party, and used the market shares in volume as a primary tool for determining the competitive strength of the Parties. (179) Moreover, in cases of differentiated products, sales in value and their associated market share also reflect the relative position and strength of each supplier. This notion does not apply to private label products, which are not differentiated. However, for branded goods, the Commission used market shares in value to supplement the examination of the Parties’ competitive position in addition to market shares in volume.

5.2.2. Market share analysis developed by the Commission

(138) The Commission has conducted a further quantitative analysis to verify the accurateness of the volume market shares provided by the Notifying Party. Subject to availability, the Commission used the panel sales data as the basis for analysing the market structure and other competitors in the market for the calendar year 2018. (180) Typically, panel data records the sales of various brands and the total volume and value data per type of product in a given year. Although the sales of private label are recorded under one entry and do not specify the wholesale supplier, the sales information on branded goods allows further examination on the Parties’ market share and evaluation of their competitors for the plausible markets of branded goods.

(139) The Commission undertook this approach as the Notifying Party also uses panel data in order to track their own and competitors’ developments in the market in the ordinary course of business. (181) The panel data was provided by Lactalis, which noted that they request granular per-brand data only concerning their largest competitors. As a result, in some instances the sales of Nuova Castelli were included in the total sales captured by the panels, but were not specified under a stand-alone brand due to its insignificant sales share. To address this, the Commission identified such instances where the Parties had internal sales recorded, but no entry for these sales appeared in the panel. Based on the Parties’ internal wholesale sales data (182), the Commission introduced sales of branded products in such instances, scaled down by […]. (183) The Commission did not make any other adjustments to total market size and the sales that were actually recorded by the panels and allocated to various competitors, including Lactalis and Nuova Castelli.

(140) The Commission reconstructed market shares based on the Parties’ sales and total sales recorded by the panel at retail level for branded products.

(141) Moreover, the Commission also used the panel data to determine the Parties’ sales share in the combined markets of branded and private label goods. Given that panel data does not recognize the supplier at wholesale level for private label products, the Commission introduced the actual sales data of the Parties, scaled down by […], and reported the remaining share of private label for other unspecified competitors. This approach follows the same methodology as the one introduced by the Notifying Party for the market shares calculations. In some instances, the adjusted Parties’ sales of private label goods were still larger than the total private label sales recorded by the panels. This confirms the Notifying Party’s allegation that panels tend to underestimate the total market size for private label.

(142) By following this approach, the Commission used third-party data to evaluate the Parties share in the Italian-type cheese and Feta-type cheese products with the adjustments discussed in the paragraphs above.

(143) The Commission finds that the market shares as recomputed (Adjusted market shares) are in principle a more reliable metric of overall market interaction as they rely on all available data, including third party data, adopt a credible approach concerning underlying assumptions, provide results which are consistent with the estimated total size of the market and do not result in shares higher than 100%, and are corroborated by qualitative evidence gathered in the market investigation.

(144) For the above principle, in principle, and subject to data availability, the Commission will use the Adjusted market shares based on panels as the primary and most reliable source of quantitative information to assess the Parties’ position for the plausible markets of branded goods as well as branded and private label combined. When data is not available, reference will be made to shares as submitted by the Notifying Party.

5.3. Horizontal non-coordinated effects

(145) Based on the market share data submitted by the Parties, the concentration would give rise to putative horizontally affected markets in Italy (Section 5.4), France (Section 5.5), Belgium (Section 5.13), Denmark (Section 5.10), Finland (Section 5.12), Germany (Section 5.7), the Netherlands (Section 5.14), Poland (Section 5.8), Portugal (Section 5.11), Spain (Section 5.15), Sweden (Section 5.9), and the United Kingdom (Section 5.6).

5.4. Italy

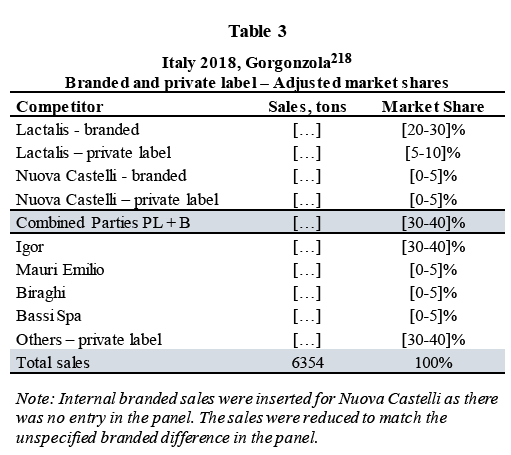

(146) Based on the market share data submitted by the Parties and in light of the methodology used by the Commission (see Section 5.2), the Transaction gives rise to the following horizontally affected markets in Italy: cow milk mozzarella (Section 5.4.1); buffalo milk mozzarella (Section 5.4.2); ricotta (Section 5.4.4) and Gorgonzola (Section 5.4.3);.

5.4.1. Cow milk mozzarella

(147) Both Lactalis and Nuova Castelli supply branded and private label cow milk mozzarella to retailers in Italy. As outlined by the market shares (see Table 1 below), the main overlap between the Parties is in the supply of private label cow milk mozzarella.

(A) Branded cow milk mozzarella

(148) For branded products, based on the Adjusted market shares, the Parties have a combined share of [40-50]% in the supply of branded cow milk mozzarella to retailers in Italy in 2018, with a limited increment of [0-5]%. (184)

(149) First, as regards branded cow milk mozzarella, the Transaction results in an affected market only because of Lactalis’ large market presence with branded products, with strong and widely recognised brands, in particular Galbani, Vallelata, and Invernizzi. (185)

(150) Second, this is consistent with the fact that, in Italy, Nuova Castelli does not enjoy strong brand presence in cow milk mozzarella, but focuses primarily on private label supplies of this product to retailers. Thus, the Transaction will bring a limited increment to Lactalis’ market share of [0-5]%.

(151) Third, several other strong competitors of Lactalis are active in the branded space, for instance Granarolo, Sabelli and Brimi. Overall, the Parties’ competitors in the branded segment have a strong presence with important brands, which account for over [50-60]% of this market segment in Italy.

(152) Fourth, the Adjusted market shares point at a fragmented set of suppliers of branded cow milk mozzarella in Italy, which are as large as or larger than Nuova Castelli.

(153) Moreover, the results of the market investigation reveal that a number of credible competitors can and do offer volumes of branded cow milk mozzarella to retailers in Italy and compete in the negotiations organised by retailers. Data collected from retailers show that a majority of them source from a relatively wide range of suppliers of branded cow milk mozzarella. In particular, the data shows that in 2018 most retailers have sourced from one or more suppliers other than the Parties. (186)

(154) Therefore, the branded segment of cow milk mozzarella will continue having a multitude of credible suppliers with established commercial relations with retailers in Italy.

(155) The Commission has also considered in its assessment the arguments presented in the below section as regards the overall market, and in particular concerning the absence of significant barriers to entry and expansion, the availability of other suppliers, the ability to switch suppliers and the impact of the Transaction that also apply to the assessment of branded cow milk mozzarella.

(156) In conclusion, based on the information available to the Commission and provided by Parties, the Commission finds that the Transaction does not raise serious doubts as to its compatibility with the internal market with regard to the plausible market of branded cow milk mozzarella in Italy.

(B) Private label cow milk mozzarella

(157) For private label, the Parties have a combined share in the supply of private label cow milk mozzarella to retailers in Italy of [20-30]%, with an increment of [10-20]%.

(158) First, in the private label segment, based on the Notifying Party’s estimates, there is a significant number of alternative private label suppliers in Italy: Caseificio Pugliese: [10-20]%; Granarolo: [5-10]%; Centro Latte Bressanone: [5-10]%; Trevisanalat: [5-10]%; Caseificio Villa: [0-5]%; Caseificio Morozzese: [0-5]%; Palazzo SNC [0-5]%; Sabelli: [0-5]%; Sanguedolce: [0-5]%; Ecolat: [0-5]%; Alimenta SpA: [0-5]% and Bustaffa: [0-5]%. (187) These are viable competitors that currently offer volumes of cow milk mozzarella to retailers and will continue to compete with the merged entity in Italy in tenders organised by retailers. This is in line with the data collected from retailers that show that a majority of them source from a relatively wide range of suppliers of cow milk mozzarella. In particular, the data shows that a majority of retailers have sourced from two or more suppliers other than the Parties in 2018. (188)

(159) The Commission has also considered in its assessment of this plausible market the arguments presented in the below section as regards the overall market, and in particular concerning the absence of significant barriers to entry and expansion, the availability of other suppliers, the ability to switch suppliers and the impact of the Transaction that also apply to the assessment of private label cow milk mozzarella.

(160) In conclusion, in light of the above and based on the information available to the Commission and provided by Parties, the Commission finds that the Transaction does not raise serious doubts as to its compatibility with the internal market with regard to the plausible market of private label cow milk mozzarella in Italy.

(C) Overall market for cow milk mozzarella in Italy

(161) On the overall market for the supply of branded and private label cow milk mozzarella to retailers in Italy, based on the Commission’s Adjusted market shares, the Parties have a combined market share in 2018 of [40-50]%, with a moderate increment of [5-10]%.

(162) First, the Transaction will bring a moderate increment to Lactalis’ market shares. This increment mainly relates to the supply of products to be resold under private label by retailers.

(163) Second, the Commission observes the overall market for branded and private label cow milk mozzarella in Italy appears to be extremely fragmented (see Table 1 below) with several active players both in the branded and private label and the production evenly distributed throughout the Italian territory. (190)

(164) Third, as outlined in Section 4.3.2, the market for the supply of cow milk mozzarella to retailers is a differentiated market across sales channels, where suppliers can compete in branded and in private label cheese. Although the presence of suppliers in the same sales channel could be indicative of closeness of competition between them, the pricing of private label products has some effect on the pricing ability in the branded segment of the market.

(165) Beside the considerations concerning the structure and shares of the cow milk mozzarella market, the Commission considers that the Transaction does not raise serious doubts for the following reasons.

(166) First, the Commission finds, based on the results of the market investigation, that barriers to entry are not high for suppliers of cow milk mozzarella in Italy.

(167) Second, as regards barriers to expansion, the results of the market investigation suggest that a number of suppliers active in Italy could increase supply in the short term without incurring in significant cost.

(168) When market conditions are such that competitors have sufficient capacity and find it profitable to expand output sufficiently, the Commission is unlikely to find that the merger would significantly impede effective competition. (191) Conversely, when market conditions are such that the competitors of the merged entity are unlikely to increase their supply significantly should prices increase, the merged entity may have an incentive to reduce output below the combined pre-merger levels thereby raising market prices. (192)

(169) The Notifying Party argues that at the EEA level the production capacity for cow milk mozzarella is almost double than the total EEA supply. (193) The Commission was not able to verify the estimates of the Parties in its market investigation. However, the evidence in the file indicates that several competitors, including non- Italian manufacturers with production assets in the Italian territory, could profitably expand output with their current production assets.

(170) Some competitors have referred to their recent and on-going investments in capacity expansion. (194) Several market respondents indicated that the cost and time required to build additional lines to expand production are not significant. (195) In particular the majority of competitors that expressed a view in the market investigation indicated that they are able to quickly expand production in Italy of Italian-type cheese and, thus, can decide to enter another EEA market for Italian- type cheeses in a relatively short timeframe. (196)

(171) Moreover, the potential expansion of production capacity is not merely hypothetical but corroborated by specific examples relating to the Italian market. In particular, the Commission found that a number of the Parties’ competitors in Italy have expanded their production of cow milk mozzarella in the last 3 years without having to incur into any significant capital investments. (197)

(172) Furthermore, the Commission has assessed whether credible and imminent expansion of the existing production of cow milk mozzarella from the Parties’ rivals would be likely to occur. The market investigation has revealed that more than one of the Parties’ competitors in Italy is planning to expand significantly and structurally their production capability of cow milk mozzarella over the course of the next 3 years and have already mobilised funds to this effect. (198) The Commission, therefore, finds that there are no significant barriers to entry or expansion in cow milk mozzarella in Italy and that alternative suppliers seem to have sufficient capacity and incentives to expand the production volume, should the merged entity increase prices in Italy.

(173) Third, as regards logistics and distribution, competitors and customers in Italy confirmed in the market investigation that distribution on the Italian territory is already fragmented and organised in a way that it is possible to distribute fresh products on the Italian territory without incurring in significant costs, even for smaller manufacturers.

(174) Fourth, with regard to the use of milk from Italy in the production of cow milk mozzarella, this is regarded by many Italian customers as an important element of consumer preference, and it is the object of specific on-label indications. In this regard, however, the competitive constraint exerted by Nuova Castelli is low because the company sources most of the milk used to manufacture mozzarella from outside of Italy. (199)

(175) Fifth, the Italian market is also characterised by low barriers to switching for the products mainly supplied by Nuova Castelli. While the branded position of Lactalis seem to command customer loyalty, the vast majority of the retailers who responded to the Commission’s requests for information stated that it is possible to switch to different suppliers of mozzarella for the type of cow milk mozzarella products supplied by Nuova Castelli. (200) Most of the retailers noted that they have switched to a different supplier of mozzarella over the past 3 years. (201) This suggests that customer switching costs for the supply of cow milk mozzarella in Italy are not significant. This also indicates that there is a dynamic and fragmented range of viable suppliers of cow milk mozzarella in Italy.

(176) Sixth, as regards the impact of the Transaction, the majority of retailers in Italy that expressed a view during the market investigation held that there will be no change post-Transaction with respect to the competitive conditions in relation to the supply of cow-milk mozzarella. (202) Moreover, the majority of responsive retailers in Italy believe that the Transaction will have no impact on the market or on their companies. (203)

(177) Finally, the Commission found that the Transaction does not raise serious doubts as to its compatibility with the internal market on the plausible markets for private label cow milk mozzarella in Italy as well as branded cow milk market mozzarella in Italy.

(178) Based on the above considerations and in the light of the results of the market investigation, the Commission considers that the concentration does not raise serious doubts as to its compatibility with the internal market as regards the overall market for cow milk mozzarella in Italy.

5.4.2. Buffalo milk mozzarella

(179) Lactalis supplies only small volumes of branded buffalo milk mozzarella to retailers in Italy, whereas Nuova Castelli supplies both branded and private label mozzarella.

(180) The Parties’ activities in buffalo milk mozzarella in Italy result in an affected market when considering the supply of branded buffalo milk mozzarella to retailers in Italy, as well as the overall market for buffalo milk mozzarella in Italy.

(A) Branded buffalo milk mozzarella.

(181) For branded products, based on the Commission’s market share analysis, the combined Adjusted market shares for branded buffalo milk mozzarella are [20-30]%, with a moderate increment of [5-10]% due to Lactalis’ moderate branded presence (204) As pointed out by the moderate increment in the market for branded buffalo milk mozzarella, in Italy Lactalis trades limited volumes of branded buffalo milk mozzarella produced by third parties through its brand Galbani (Vallelata). Conversely, in Italy Nuova Castelli enjoys brand presence in relation to buffalo milk mozzarella through its subsidiary Mandara. Additionally, Nuova Castelli supplies private label buffalo milk mozzarella to retailers.

(182) Second, the results of the market investigation point toward a fragmented market. Market participants named a broad number of potential supply options for buffalo milk mozzarella, in particular Fattorie Garofalo, Caseificio Tre Stelle, Spinosa, Cilento, Pettinicchio, Francia Latticini, Caseificio Cirigliana, Diano Casearia, Caseificio Principe and Podere dei Leoni. (205)

(183) This extremely diversified picture is evidenced by the fact that the combined share of the Parties’ competitors in branded buffalo milk mozzarella exceeds [50-60]%, with Francia’s and Spinosa’s shares each approximately equivalent to the increment triggered by the Transaction.

(184) The Commission has also considered in its assessment of this plausible market the arguments presented in the below section as regards the overall market, and in particular concerning the absence of significant barriers to entry and expansion, the availability of other suppliers, the ability to switch suppliers and the impact of the Transaction that also apply to the assessment of branded buffalo milk mozzarella.

(185) In conclusion, in light of the above and based on the information available to the Commission and provided by Parties, the Commission finds that the Transaction does not raise serious doubts as to its compatibility with the internal market with regard to the plausible market of branded buffalo milk mozzarella in Italy.

(B) Overall market for buffalo milk mozzarella in Italy

(186) Based on the Commission’s Adjusted market shares, the Parties’ combined market shares are [20-30]%, with a moderate increment of [0-5]%.

(187) First, the Transaction will bring a moderate increment to Nuova Castelli’ market shares, due to Lactalis moderate branded presence.

(188) Second, the presence of the Parties’ competitors is strong and a significant number of producers are active in the market for buffalo milk mozzarella with access to retailers in Italy, for instance Francia and Spinosa’s shares each approximately equivalent to the increment triggered by the Transaction (see Table 2 above).

(189) The above finding, based on the Parties’ and their competitors’ shares on the overall market for buffalo milk mozzarella, was corroborated in the market investigation, which pointed at multiple supplier options. As an illustration, an Italian retailer indicated that “the market for buffalo milk mozzarella is extremely fragmented.” (207) This was confirmed by the Parties’ competitors, a number of which qualified the market for buffalo milk mozzarella as particularly fragmented. (208)

(190) As indicated in paragraph (182) above, market participants named a broad number of potential supply options for buffalo milk mozzarella, in particular Fattorie Garofalo, Caseificio Tre Stelle, Spinosa, Cilento, Pettinicchio, Francia Latticini, Caseificio Cirigliana, Diano Casearia, Caseificio Principe, Podere dei Leoni. (209) In view of the Parties’ activities, these competitors are closer to Nuova Castelli as manufacturers of their own product, as opposed to Lactalis which does not have manufacturing activities for buffalo milk mozzarella and only trades.

(191) In both branded and private label, the existence of a number of credible competitors offering volumes of buffalo milk mozzarella to retailers in Italy and competing in the negotiations organised by retailers is not only confirmed by qualitative descriptions of market interaction by such customers, but also confirmed by actual sourcing information. Data collected from retailers shows that a majority of them source from a relatively wide range of suppliers of buffalo cow milk mozzarella. In particular, the data shows that most retailers have sourced from one or more suppliers other than the Parties in 2018. (210)

(192) Third, as outlined in Section 4.3.2, the market for the supply of buffalo milk mozzarella to retailers is a differentiated market across sales channels, where suppliers can compete in branded and in private label cheese. Although the presence of suppliers in the same sales channel will be indicative of closeness of competition between them, the pricing of private label products will have some effect on the pricing ability in the branded side of the market.

(193) Beside the considerations concerning the structure and shares of the buffalo milk mozzarella market, the Commission considers that the Transaction does not raise serious doubts for the following reasons.

(194) First, the Commission finds that retailers do not face significant barriers to switching across suppliers in Italy. The vast majority of the retailers who responded to the Commission’s requests for information stated that it is possible to switch to different suppliers of mozzarella. (211) More importantly, most of these retailers noted that they have switched to a different supplier of any type of mozzarella over the past 3 years. (212) This suggests that customer switching costs for private label supply of buffalo milk mozzarella in Italy are not significant. This also indicates that there are little barriers to switching across the fragmented range of viable suppliers of buffalo milk mozzarella in Italy.

(195) Second, as regards barriers to entry, the market investigation suggested that a potential barrier could be the more limited availability of buffalo milk, which is scarcer than cow milk. However, and mainly in view of the range of players already active on the market, this is not regarded as particularly problematic by the Parties’ competitors as well as retailers responding on the issue of barriers to entry or expansion to the market of buffalo milk mozzarella in Italy. (213)