Commission, July 12, 2018, No M.8869

EUROPEAN COMMISSION

Decision

RYANAIR / LAUDAMOTION

Dear Sir or Madam,

Subject: Case M.8869 – Ryanair/LaudaMotion

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

1.INTRODUCTION

(1) On 7 June 2018, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Ryanair Holdings plc ("Ryanair", Ireland) would acquire within the meaning of Article 3(1)(b) of the Merger Regulation control of the whole of LaudaMotion GmbH ("LaudaMotion", Austria), by way of purchase of shares (the "Transaction").3 Ryanair and LaudaMotion are collectively referred to as the "Parties".

2.THE PARTIES

(2) Ryanair is a low-cost point-to-point airline operating throughout Europe. It operates a domestic and international network using a fleet of over 400 Boeing 737-800 aircraft.

(3) LaudaMotion is an Austrian Air Operator Certificate holder owned by the private foundation of Niki Lauda, which has recently started a range of scheduled passenger air transport services primarily from Germany, Austria and Switzerland to Mediterranean and Canary Island leisure destinations. In February 2018, LaudaMotion acquired as a partial take-over certain assets of the former airline NIKI Luftfahrt GmbH ("NIKI"), the leisure subsidiary of insolvent airline Air Berlin, after NIKI had filed for insolvency in Austria and ceased activity as an air carrier on 13 December 2017.4

3.THE CONCENTRATION

(4) On 16 March 2018, the Parties reached agreement on binding Heads of Terms, pursuant to which Ryanair would acquire a 75% shareholding in LaudaMotion in two inter-related stages ("Step One" and "Step Two"). The Transaction was announced on 20 March 2018.5 On 20 April 2018, the Parties executed the corresponding Share Purchase Agreement (the "SPA").

(5) Step One consists in the following:(a) The acquisition by Ryanair of a 24.9% shareholding in LaudaMotion;(b) The provision by Ryanair to LaudaMotion of six aircraft under a wet-lease agreement to LaudaMotion for the Summer 2018 IATA6 Season;(c) The addition by Ryanair of scheduled aircraft capacity of LaudaMotion to its website and the offering of these LaudaMotion seats for sale;(d) The provision by Ryanair of the working capital for LaudaMotion's daily operations and the funding of any losses incurred.

(6) Step Two involves the following:(a) Ryanair will acquire a further 50.1% shareholding in LaudaMotion, subject to LaudaMotion efficiently operating no less than 75% of the former NIKI slots7 at Palma de Mallorca airport;(b) Ryanair will acquire the right to appoint three of the five members of the Board of LaudaMotion;(c) Ryanair will be responsible for growing the fleet of LaudaMotion to at least 30 aircraft over […] years[…];(d) Ryanair will assist LaudaMotion in growing its presence in the scheduled air travel sector in Europe. Ryanair will promote LaudaMotion's services and sales by referring to LaudaMotion as a "partner" airline.

(7) After the Transaction, neither Niki Lauda nor any undertaking other than Ryanair will have any rights that might confer joint control over LaudaMotion. Therefore, by acquiring 75% of LaudaMotion's shareholding and the right to appoint the majority of its Board, Ryanair will acquire sole control over LaudaMotion within the meaning of Article 3(1)(b) of the Merger Regulation.8

(8) In addition, the Commission notes that the acquisition by Ryanair of sole control over LaudaMotion is conditional upon the implementation of the whole of the Heads of Terms, including Steps One and Two. As a consequence, only the implementation of Steps One and Two together would enable Ryanair to acquire control over LaudaMotion. If Step Two would not be implemented, all of Ryanair's obligations, including those related to Step One, would become void.

(9) In view of the unitary nature of Step One and Step Two, as well as the short period of time in which the two steps are to be implemented, and pursuant to paragraphs 38 and 48 of the Commission's Consolidated Jurisdictional Notice,9 the Commission considers that Step One and Step Two constitute a single concentration within the meaning of Article 3 of the Merger Regulation.

(10) The notification of the Transaction follows the adoption by the Commission of two decisions under Article 7(3) of the Merger Regulation.

(11) On 19 March 2018, Ryanair requested a derogation from the suspension obligation provided for in Article 7(1) of the Merger Regulation to implement Step One of the Transaction, as described above.

(12) On 23 March 2018, the Commission granted the first derogation on the basis of Article 7(3) of the Merger Regulation (the "First Derogation Decision").10

(13) On 3 May 2018, Ryanair requested that Step One of the Transaction, as described above, be amended so as to include the following additional measures (the "Additional Measures"): (i) Ryanair would provide between three and eight aircraft under a wet-lease agreement to LaudaMotion for the Summer 2018 IATA Season, in addition to the six aircraft covered by the First Derogation Decision; and (ii) Ryanair would provide operational support to LaudaMotion, including operations control and crew control. In addition, in its second application for a derogation, Ryanair committed itself to notify the Transaction to the Commission without any delay and, in any case, no later than one month from the adoption of the decision on the second derogation request.

(14) Similarly to the measures approved under the First Derogation Decision, the Additional Measures would become void if Step Two of the Transaction would not be implemented.

(15) On 8 May 2018, the Commission granted a second derogation on the basis of Article 7(3) of the Merger Regulation (the "Second Derogation Decision"), subject to Ryanair notifying the Transaction to the Commission pursuant to Article 4 of the Merger Regulation no later than one month from the adoption of the Second Derogation Decision.11

4.EU DIMENSION

(16) The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 5 000 million (Ryanair: c. EUR 6 600 million; LaudaMotion: c. EUR […] million).12 Each of them has an EU-wide turnover in excess of EUR 250 million (Ryanair: c. EUR […] million; LaudaMotion: c. EUR […] million), and they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State.13

(17) The Transaction therefore has an EU dimension within the meaning of Article 1(2) of the Merger Regulation.

5. DESCRIPTION OF LAUDAMOTION'S BUSINESS PLAN AND ACTIVITIES

(18) According to Ryanair, the Transaction arises out of the insolvency of Air Berlin in August 2017. Air Berlin's leisure subsidiary NIKI subsequently went into insolvency and definitively ceased operating as an active air carrier in December 2017. In February 2018, LaudaMotion acquired as a partial take-over certain assets formerly used by insolvent NIKI, including (i) slots at various airports in Germany, Austria, Switzerland, and at holiday destinations in the Mediterranean and Canary Islands, (ii) an expectation to enter into various lease arrangements with Lufthansa Group; and (iii) a 4-bay maintenance hangar in Vienna with up to 86 engineering staff.

(19) At the time of entry into the binding Heads of Terms, LaudaMotion had obtained an Austrian Air Operator Certificate and was planning to commence operating scheduled passenger air transport services in the IATA Summer Season 2018 using slots transferred from NIKI.14;15

(20) Considering that the target of the Transaction is LaudaMotion, not NIKI, it serves no purpose to consider the effects of the Transaction on the markets on which the assets now held by LaudaMotion were formerly used by NIKI (see section 6.1.1.1 below). The effects of the Transaction should rather be assessed on the markets that LaudaMotion had pre-Transaction planned to use the assets transferred from NIKI even though, for the time being and due to the very early stage of its development, it does not exert a significant constraining influence on those markets.

5.1.LaudaMotion's business plan and activities prior to the announcement of the Transaction

LaudaMotion's business plan pre-Transaction

(21) LaudaMotion's original business plan […] the supply of air transport services to four types of customer: (i) individual customers ("B2C"), […];16 (ii) travel agents ("B2B"), including leisure travel agents, online travel agents and dynamic packaging agents; (iii) tour operators ("B2T"), in the form of full charter flights or allotments; and (iv) other airlines ("B2A"), through interline agreements, block space agreements17 and wet-lease agreements.18; 19

(22) According to Ryanair, although LaudaMotion's initial focus was […],20 this approach was adopted only for the short-term purpose of attempting to secure sufficient revenues to operate in the Summer 2018 IATA Season, […].21 As further explained below, LaudaMotion's internal documents substantiate Ryanair's statements […].22 In any case, even if LaudaMotion intended to provide B2A services […], the Transaction would not affect the market for the supply of air transport services to other airlines (see section 6.1.3 below).

(23) In addition, beyond the need to secure revenues, the use of […] sales models by LaudaMotion was aimed at protecting the slots transferred from insolvent NIKI by maximising their use during the Summer 2018 IATA Season.23

(24) Based on the latest four-year fleet plan (from Summer 2018 IATA Season to Winter 2021/2022 IATA Season) available at the date of the Heads of Terms, LaudaMotion was anticipating to operate a 14-aircraft fleet,24 all dry leased from Lufthansa Group and of which (i) 11 were former NIKI aircraft 25 and (ii) three Lufthansa aircraft, not formerly operated by NIKI.26

(25) LaudaMotion's fleet plan also mentioned the temporary use during the Summer 2018 IATA Season of […] wet-leased aircraft from TUIfly, which were to be fully operated by LaudaMotion for TUI.27 However, […] by the time LaudaMotion agreed on the Heads of Terms with Ryanair28 and consequently, LaudaMotion's corrected fleet plan refers to a 14-aircraft fleet only.29 In any case, since the flight capacity (aircraft and crew) would have come from TUI and would have been operated for TUI during one season only, it is the Commission's understanding that LaudaMotion would have mainly provided the slots necessary for the provision of air transport services by TUI on a temporary basis, without delivering other services. Therefore, LaudaMotion's temporary arrangements with TUI would not qualify as LaudaMotion entering the market for the supply of air transport services to tour operators. Likewise, the abandonment of LaudaMotion's temporary arrangements with TUI, even if it were the result of the Transaction (quod non), could not be deemed to have had any structural impact on the market for the supply of air transport services on any specific route.30

LaudaMotion's agreements with Condor and Eurowings prior to the announcement of the Transaction

(26) Before being able to operate autonomously as from 2019, LaudaMotion intended to rely on agreements with two other airlines, Condor and Lufthansa Group, both for the provision of input services and for the sale of its output services. In particular, as further described below, these agreements implied that LaudaMotion's flight capacity would have been almost entirely pre-sold to Condor and Lufthansa Group (B2A), limiting very significantly LaudaMotion's presence on the markets for the wholesale supply of airline seats to tour operators (B2T) and for the retail supply of airline seats to passengers (B2C and B2B).31

(27) Out of the 11 former NIKI aircraft dry-leased from Lufthansa Group,32 (i) five aircraft would be operated by LaudaMotion under a block space agreement with Condor until the end of the Winter 2018/2019 IATA Season (B2A), (ii) five aircraft would be operated by LaudaMotion under a block space agreement with Eurowings until the end of the Summer 2018 IATA Season (B2A), and (iii) one aircraft would be wet-leased back to Lufthansa Group until the end of the Summer 2019 IATA Season. At the expiry of the block space and wet-lease agreements with Condor and Lufthansa Group, it stems from LaudaMotion's fleet scenario that LaudaMotion planned to operate the aircraft at its own risk.33

(28) In addition, the three aircraft dry-leased from Lufthansa Group outside of NIKI's former fleet would be wet-leased back to Lufthansa Group until the end of the Summer 2019 IATA Season. After that date, the aircraft would have been returned to Lufthansa Group.34

(29) At the time of announcement of the Transaction, the block space agreement with Condor had been signed and was binding. Tickets were already on sale. Under the agreement, Condor would purchase 100% of LaudaMotion's capacity on the flights operated by LaudaMotion and identified in the agreement and would bear 100% of the financial and commercial risks of these flights. In particular, Condor would decide on the commercial conditions for the sale of the tickets (including the split between wholesale and retail supply of seats, the pricing policy for tour operators and end-customers, and the distribution channels) and market 100% of the purchased capacity under its own brand.35

(30) The five aircraft covered by the block space agreement with Condor were to be based during the Summer 2018 IATA Season at (i) Duesseldorf airport (two aircraft), serving routes to Ibiza, Malaga and Palma de Mallorca, (ii) at Frankfurt airport (one aircraft), serving routes to Palma de Mallorca, and (iii) at Zurich airport (two aircraft), serving routes to Corfu, Fuerteventura, Heraklion, Ibiza, Lamezia Terme, Lanzarote, Olbia, Palma de Mallorca, and Rhodes. In addition, LaudaMotion had also block-sold to Condor 100% of its capacity on flights on three additional routes: Stuttgart-Palma de Mallorca, Basel-Palma de Mallorca and Basel-Heraklion.36 Plans for the Winter 2018/2019 IATA Season were not finalised yet at the time of announcement of the Transaction.

(31) In addition to the block space agreement, LaudaMotion and Condor had concluded other service agreements, by which Condor would provide operative flight support (e.g. operational control, crew planning and control, ground operations and passenger care) as well as service and infrastructure support (including a website and Internet booking engine) to LaudaMotion for its operations during the Summer 2018 IATA Season. Finally, LaudaMotion and Condor had signed an interline agreement that entitled them to sell each other's flights until the end of the Winter 2018/2019 IATA Season.37

(32) At the time of announcement of the Transaction, LaudaMotion and Lufthansa Group had signed a non-binding term sheet commercial agreement, by which they had agreed on the basic terms for the block space and wet-lease agreements.

(33) Under the block space agreement, Eurowings, a subsidiary of Lufthansa Group, would purchase 90% of LaudaMotion's capacity on the flights operated by LaudaMotion using up to five aircraft and agreed on by the parties.38 Eurowings would bear 90% of the financial and commercial risks on these routes, and would decide on the commercial conditions for the sale of the 90% block-purchased capacity. The 10% remaining capacity would be sold by LaudaMotion at its own risk.39

(34) The five aircraft covered by the block space agreement with Eurowings were to be based during the Summer 2018 IATA Season at Vienna airport (two aircraft), Duesseldorf airport, Cologne airport and Stuttgart airport.40 While negotiations were on-going for the routes to be operated under the block space agreement, the latest version of the schedule development with Eurowings shows the following airport pairs: Basel-Palma de Mallorca, Berlin Tegel-Palma de Mallorca (later replaced by Hannover-Palma de Mallorca),41 Cologne-Palma de Mallorca, Duesseldorf-Palma de Mallorca, Graz-Palma de Mallorca, Innsbruck-Palma de Mallorca, Linz-Palma de Mallorca, Salzburg-Palma de Mallorca, Stuttgart-Palma de Mallorca, Vienna-Brindisi, Vienna-Chania, Vienna-Ibiza, Vienna-Kalamata, Vienna-Malaga, Vienna-Palma de Mallorca, Vienna-Paphos, Vienna-Pisa,Vienna-Santorini, Zurich-Palma de Mallorca.42

(35) Under the wet-lease agreement, Eurowings would purchase the full capacity of the three wet-leased aircraft, would choose the routes on which they would have operated (using Eurowings' slots) and would decide on the key commercial conditions for the sale of tickets. The financial risk for the sale of tickets would have resided with Eurowings, as the lessee.43

Routes to be operated by LaudaMotion prior to the announcement of the Transaction

(36) LaudaMotion published on 16 March 2018 the list of airport pairs for which it would operate flights during the Summer 2018 IATA Season schedule: Basel- Herakleion, Basel-Palma de Mallorca, Berlin Tegel-Palma de Mallorca, Cologne- Palma de Mallorca, Duesseldorf-Ibiza, Duesseldorf-Malaga, Duesseldorf-Palma de Mallorca, Frankfurt-Palma de Mallorca, Graz-Palma de Mallorca, Hannover- Palma de Mallorca, Innsbruck-Palma de Mallorca, Linz-Palma de Mallorca, Salzburg-Palma de Mallorca, Stuttgart-Palma de Mallorca, Vienna-Brindisi, Vienna-Chania, Vienna-Ibiza, Vienna-Kalamata, Vienna-Malaga, Vienna-Palma de Mallorca, Vienna-Paphos, Vienna-Pisa, Vienna-Santorini, Zurich-Corfu, Zurich-Fuerteventura, Zurich-Ibiza, Zurich-Herakleion, Zurich-Lamezia Terme,Zurich-Lanzarote, Zurich-Olbia, Zurich-Palma de Mallorca, Zurich-Rhodes.44

(37) All of these routes correspond to routes for which flights were block-sold to Condor or to be block-sold to Lufthansa Group pursuant to the block seat agreements respectively signed with Condor and under negotiation with Lufthansa Group, with the exception of Berlin Tegel-Palma de Mallorca.45 Therefore, for all of these routes except Berlin Tegel-Palma de Mallorca, LaudaMotion would mainly act as a provider of capacity to Condor and Lufthansa Group (B2A), which in turn would act as wholesalers of seats to tour operators or retailers of seats to passengers.

(38) LaudaMotion would thus only be able to enter the markets for the supply of flight services to tour operators and end-customers with 10% of its capacity on flights to be block-sold to Lufthansa (corresponding to 18-21 seats per flight). Considering the limited available capacity for sale by LaudaMotion and the late finalisation of LaudaMotion's flight schedule (while tour operators tend to purchase capacity in advance), the Commission considers it unlikely that (i) LaudaMotion would be in a position to achieve material sales to tour operators for flights operated during the Summer 2018 IATA Season and would not have entered to any significant extent the wholesale market for passenger air transport services, and (ii) LaudaMotion would not have exerted a significant competitive pressure on the retail market for passenger air transport services.

(39) At the time of announcement of the Transaction, LaudaMotion had neither published nor finalised its flight schedule for the Winter 2018/2019 IATA Season.46

5.2.LaudaMotion's business plan and activities after the announcement of the Transaction

LaudaMotion's business plan post-Transaction

(40) According to the binding Heads of Terms, "[…]."47 Considering that […],48 LaudaMotion's business model post-Transaction is expected to focus on the provision of passenger air transport services to retail customers (B2C).

(41) However, after the signature of the binding Heads of Terms, management at LaudaMotion have been developing a possible business proposal for the next shareholders' meeting of LaudaMotion that […]. […].49 In any case, […], the Transaction would not affect the market for the wholesale supply of passenger air transport services (see section 6.1.2 below).

(42) In addition, according to the binding Heads of Terms, "[i]t is agreed that LM [LaudaMotion] will honour its planned supply agreements with Thomas Cook/Condor, and any block seat agreements with Lufthansa to the extent that these agreements assist LM [LaudaMotion] to protect the scarce slots at the airports listed in clause 6 above."50

(43) However, following announcement of the Transaction, the agreements with Condor were terminated and the negotiations with Lufthansa Group were terminated, both as regards the proposed block space51 and wet-lease arrangements.52 Some of the passengers which had booked tickets from Condor or Eurowings for flights on the block space capacity provided by LaudaMotion to the two airlines have been transferred to LaudaMotion.53 The Commission considers that the termination of the agreements with Condor and the negotiations with Lufthansa result from the Transaction.54

(44) Following the termination of negotiations with Lufthansa Group, LaudaMotion's fleet was reduced to 10 aircraft dry-leased from Lufthansa as former NIKI aircraft.55 The number of operative aircraft for the start of the Summer 2018 IATA Season was further reduced to 8 aircraft, due to factors independent of the Transaction, notably delays in delivery resulting from technical problems.56 As a result of the lack of access to these two aircraft, LaudaMotion will not operate any routes out of Zurich airport,57 nor the Basel-Heraklion route.58 This implies that LaudaMotion will relinquish the summer slots at Zurich airport for which it had obtained NIKI's historic rights.

Measures implemented by Ryanair as part of the Transaction

(45) Following the signature of the binding Heads of Terms, and prior to this Decision, Ryanair was authorised under the First and Second Derogation Decisions to implement part of the Transaction, notably to wet-lease aircraft to LaudaMotion to complete a 19-aircraft flight schedule during the Summer 2018 IATA Season.59 As indicated in the First Derogation Decision (notably paragraph 28) and the Second Derogation Decision (notably paragraph 27), these measures also aim at protecting the most valuable slots held by LaudaMotion.

(46) On 28 March 2018, LaudaMotion published its extended flight schedule for the Summer 2018 IATA Season60 and LaudaMotion and Ryanair started selling tickets for these flights on Ryanair's website. The flight schedule includes (i) flights on the routes already announced by LaudaMotion and operated using the eight aircraft dry-leased by Lufthansa Group to LaudaMotion (including three aircraft based at Duesseldorf airport, two aircraft based at Vienna airport, one aircraft at Cologne airport, one aircraft at Stuttgart airport and one aircraft at Frankfurt airport), as well as (ii) flights on the additional routes to be operated using the aircraft to be wet-leased by Ryanair to LaudaMotion.61

(47) The aircraft wet-leased from Ryanair to LaudaMotion are deployed at Berlin Tegel airport (four aircraft), at Duesseldorf airport (three aircraft), Vienna airport (two aircraft), Munich airport (one aircraft) and Nuremberg (one aircraft). The table below provides an overview of the flights operated by LaudaMotion during the Summer 2018 IATA Season using respectively LaudaMotion's flight capacity and Ryanair's flight capacity made available under the First and Second Derogation Decisions.62

Table 1 - Overview of LaudaMotion's flight schedule

Summer 2018 IATA Season

Flights operated with LaudaMotion's flight capacity | Flights operated with Ryanair's flight capacity |

Basel-Palma de Mallorca | Berlin Tegel-Bari |

Berlin Tegel-Palma de Mallorca | Berlin Tegel-Brindisi |

Cologne-Palma de Mallorca | Berlin Tegel-Corfu |

Duesseldorf-Ibiza* | Berlin Tegel-Faro |

Duesseldorf-Malaga* | Berlin Tegel-Fuerteventuera |

Duesseldorf-Palma de Mallorca* | Berlin Tegel-Girona |

Frankfurt-Palma de Mallorca | Berlin Tegel-Gran Canaria |

Graz-Palma de Mallorca | Berlin Tegel-Heraklion |

Hannover-Palma de Mallorca | Berlin Tegel-Ibiza |

Innsbruck-Palma de Mallorca | Berlin Tegel-Kos |

Linz-Palma de Mallorca | Berlin Tegel-Lanzarote |

Salzburg-Palma de Mallorca | Berlin Tegel-Malaga |

Stuttgart-Palma de Mallorca* | Berlin Tegel-Milan Malpensa |

Vienna-Brindisi | Berlin Tegel-Pula |

Vienna-Chania | Berlin Tegel-Rhodes |

Vienna-Ibiza | Berlin Tegel-Rijeka |

Vienna-Kalamata | Berlin Tegel-Tenerife Sur |

Vienna-Malaga | Duesseldorf-Corfu |

Vienna-Palma de Mallorca* | Duesseldorf-Faro |

Vienna-Paphos | Duesseldorf-Fuerteventura |

Vienna-Pisa | Duesseldorf-Gran Canaria |

Vienna-Santorini | Duesseldorf-Heraklion |

| Duesseldorf-Kos |

| Duesseldorf-Lanzarote |

| Duesseldorf-Rhodes |

| Duesseldorf-Tenerife Sur |

| Hamburg-Palma de Mallorca |

| Munich-Palma de Mallorca |

| Nuremberg- Palma de Mallorca |

| Paderborn/Lippstadt-Palma de Mallorca |

| Rome Fiumicino-Palma de Mallorca |

*: Routes for which certain frequencies are operated using Ryanair's flight capacity

(48) In addition, following the announcement of the Transaction, LaudaMotion also published its flight schedule for the Winter 2018/2019 IATA Season and LaudaMotion and Ryanair started selling tickets for these flights.63 As for the Summer 2018 IATA Season, the flight schedule for the Winter 2018/2019 IATA Season is based on aircraft made available by Lufthansa Group to LaudaMotion independently of the Transaction and aircraft to be made available by Ryanair to LaudaMotion as a result of the Transaction.

(49) Although, prior to the announcement of the Transaction, LaudaMotion had no fixed plans for the Winter 2018/2019 IATA Season, the Commission considers it likely, based on the information provided by LaudaMotion and its original business plan, that LaudaMotion's planned operations on certain routes during the Winter 2018/2019 IATA Season result from the Transaction and would not have been carried out absent the addition of Ryanair's flight capacity to LaudaMotion's own fleet. The table below provides an overview of the flights operated by LaudaMotion during the Winter 2018/2019 IATA Season using respectively LaudaMotion's and Ryanair's flight capacity.64

Table 2 - Overview of LaudaMotion's flight schedule Winter 2018/2019 IATA Season

[…]

(50) In view of the number of frequencies made possible by the operation of LaudaMotion's eight-aircraft fleet during the Summer 2018 IATA Season (see Table 1 above) and of the fact that LaudaMotion will only have one more aircraft in its fleet for the Winter 2018/2019 Season, LaudaMotion may nevertheless not have sufficient capacity to operate all of the routes mentioned in Table 2 and which would be operated with LaudaMotion's own flight capacity. At least, it seems unlikely that LaudaMotion would be able to operate all of the frequencies announced in the Winter 2018/2019 IATA Season flight schedule. The Commission thus considers it likely that, on certain of these Winter 2018/2019 routes, certain flights (frequencies) would be operated using Ryanair's wet-leased aircraft. However, the Commission does not have sufficient information to identify these flights precisely. Therefore, for the purpose of this Decision, the Commission will assume, on a conservative basis, that all flights on sale for the routes listed in this paragraph are to be operated by LaudaMotion using its own nine-aircraft flight capacity.

5.3. Conclusion on the impact of the Transaction on LaudaMotion's business plan and activities

(51) In light of the above, the impact of the Transaction on LaudaMotion's business plan and activities may be summarised as follows.

(52) In terms of retail supply of air transport services to passengers (B2C and B2B), the Transaction results in the addition of LaudaMotion's flights for sale by Ryanair for the Summer 2018 and Winter 2018/2019 IATA Seasons.65

(53) More specifically, for the Summer 2018 IATA Season, as a result of the Transaction and given the cancellation of the arrangements with Condor and Lufthansa Group, the flight capacity that was marketed by Condor (100% of the flight capacity of three aircraft),66 Lufthansa (90% of the capacity of five aircraft) and LaudaMotion (the remaining 10% capacity of five aircraft) pre-Transaction is marketed by the merged entity post-Transaction.67

(54) For the Winter 2018/2019 IATA Season, as a result of the Transaction and given the cancellation of the arrangements with Condor, the flight capacity that was to be marketed by Condor (100% of the flight capacity of five aircraft) and LaudaMotion (100% of the flight capacity of four aircraft) pre-Transaction is marketed by the merged entity post-Transaction.68

(55) In terms of wholesale supply of air transport services to tour operators (B2T), the Transaction may result in LaudaMotion not entering the market, subject to the decision on LaudaMotion's business plan post-Transaction. For the Summer 2018 IATA Season, the Transaction has no impact, since LaudaMotion had not sold and did not plan to sell wholesale seats pre-Transaction.

(56) In terms of the supply or air transport services to other airlines (B2A), the Transaction does not have any structural impact, since LaudaMotion planned to completely cease providing those services at the end of the Summer 2019 IATA Season (see paragraph (28)). The Transaction nevertheless results in LaudaMotion not providing these services to Condor and Lufthansa Group during the next two and three IATA Seasons respectively.69

(57) In section 6.1 below, the Commission will identify the markets relevant for the assessment of the competitive effects of the Transaction based on above- summarised changes brought about by the Transaction on LaudaMotion's business plan and activities.

6. ANALYTICAL FRAMEWORK

(58) Proper examination of the competitive effects of a transaction under the Merger Regulation rests in particular on a sound understanding of (i) the competitive constraints under which the merged entity will operate, and (ii) the specific causal effects of the transaction on the development of competition in the market.

(59) Along those lines, and taking account of the forward-looking nature of merger control and of the changes brought about by the Transaction on the Parties' business plan and activities, the Commission will first identify the markets that may be relevant (section 6.1). Next, the markets identified as relevant will be defined (section 6.2). The Commission will then determine the circumstances likely to prevail on the relevant markets absent the Transaction (the relevant "situation absent the Transaction", section 6.3).

6.1.Identification of the relevant markets

(60) The Transaction relates to air transport services, which both Ryanair and LaudaMotion supply. Ryanair supplies air transport services directly to passengers. LaudaMotion provides air transport services to other airlines and, marginally, to passengers. Considering LaudaMotion's initial business plan described in paragraph (21) above, the Commission will examine whether the provision of air transport services to the three following customer groups constitutes relevant markets: (i) to passengers (section 6.1.1), (ii) to tour operators (section 6.1.2), and (iii) to other airlines (section 6.1.3).

6.1.1.Air transport services to passengers

(61) The Commission has, in its prior decision practice related to air transport, defined the relevant markets for scheduled passenger air transport services on the basis of two approaches: (i) the "point of origin/point of destination" ("O&D") city-pair approach, where the target was an active air carrier;70 and (ii) the "airport-by- airport" approach, when the target included an important slot portfolio.71

(62) Under the O&D approach, every combination of an airport or city of origin to an airport or city of destination is defined as a distinct market. Such a market definition reflects the demand-side perspective whereby passengers consider all possible alternatives of travelling from a city of origin to a city of destination, which they do not consider substitutable for a different city pair. The effects of a transaction on competition are thus assessed for each O&D separately.

(63) Under the airport-by-airport approach, every airport (or substitutable airports) is defined as a distinct market. Such a market definition has notably been adopted to assess the risks of foreclosure entailed by the concentration of slots at certain airports in the hands of a single undertaking. The effects of a transaction on competition are thus assessed for all O&Ds to or from an airport (or substitutable airports) taken together.

6.1.1.1. Relevance of markets defined as O&Ds under the O&D approach

(a) Ryanair's views

(64) Ryanair submits that NIKI ceased its activity as an air carrier on 13 December 2017, grounding all of its aircraft and ceasing to operate on any O&D market. Prior to the partial implementation of the Transaction permitted pursuant to the First and Second Derogation Decisions, LaudaMotion was in the very early stages of recommencing operations using the assets acquired from NIKI and was not an active independent operator. Besides, only in May 2018 did LaudaMotion announce plans to operate certain Winter 2018/2019 IATA Season routes. According to Ryanair, given that the decision to operate these routes was made well after the Transaction was announced, it is strongly arguable that such routes cannot be considered to be competitively affected. Therefore, to the extent that any assessment is made, Ryanair considers that it should focus on the Parties' combined slot holding rather than on O&D pairs.72

(65) For completeness, however, Ryanair also provides information relating to O&D city pair routes on which both Parties are expected to operate in the Summer 2018 and Winter 2018/2019 IATA Seasons.

(b) Commission's assessment

(66) The Transaction involves the acquisition by Ryanair of LaudaMotion, which, at the time of the Transaction, had started providing passenger air transport services on specific city pairs and planned to grow into an active competitor on these routes. Therefore, the Commission considers it appropriate to carry out an assessment of the competitive effects of the Transaction under the O&D approach.

(67) However, such an assessment requires distinguishing between (i) the O&Ds, which LaudaMotion had already started to operate or had decided to operate pre- Transaction (first sub-section below), (ii) the O&Ds, which LaudaMotion could only operate following the early implementation of the Transaction (second sub- section below), and (iii) the routes that NIKI used to operate prior to insolvency (third sub-section). In addition, it is necessary to clarify that non-overlap routes are not relevant for the O&D assessment of the Transaction, since LaudaMotion is not considered as a likely potential competitor on any of these routes (fourth sub-section) and the Transaction has no specific effect on routes exited by Ryanair post-Transaction (fifth sub-section). i) Under the O&D approach, the relevant O&Ds should include the routes operated by LaudaMotion using LaudaMotion's own flight capacity (dry- leased aircraft and crew) pre-Transaction to the extent these overlap with the routes flown by Ryanair

(68) As indicated in paragraphs (53) and (54) above, the Transaction results in the transfer to Ryanair of the eight-aircraft flight capacity to be deployed by LaudaMotion on LaudaMotion's flight schedule published prior to the announcement of the Transaction for the Summer 2018 IATA Season and of the nine-aircraft flight capacity to be deployed by LaudaMotion on LaudaMotion's flight schedule published after the announcement of the Transaction for the Winter 2018/2019 IATA Season.

(69) Since LaudaMotion's flight capacity has been made available to passengers on the retail market independently of the Transaction (by Condor, by Lufthansa and by LaudaMotion, see below), the Commission considers that the O&Ds on which LaudaMotion's flight capacity is deployed should serve to identify the relevant markets under the O&D approach.

(70) More specifically, for the Summer 2018 IATA Season, LaudaMotion's entire eight-aircraft fleet was to be deployed prior to the announcement of the Transaction on flights pre-sold by LaudaMotion to Condor and Lufthansa Group. The corresponding capacity was marketed to passengers by the two airlines at their own risk as well as, to a marginal extent (10% of the capacity of five aircraft), by LaudaMotion at its own risk.73 Post-Transaction, LaudaMotion's entire eight-aircraft flight capacity will be marketed by the merged entity. Therefore, although pre-Transaction LaudaMotion itself was marginally selling seats to passengers on the routes it operated and the number of seats actually sold on routes covered by the block-seat agreements prior to the Transaction is limited,74 the Transaction modifies the competitive constraints under which the merged entity operates on these O&Ds.

(71) Therefore, the following Summer 2018 IATA Season airport pairs, on which LaudaMotion (and previously also via Condor and Lufthansa Group) markets tickets and on which Ryanair is also present (or on substitutable airport pairs) are relevant markets for the O&D assessment: Berlin Tegel-Palma de Mallorca, Cologne-Palma de Mallorca, Duesseldorf-Ibiza, Duesseldorf-Malaga, Duesseldorf-Palma de Mallorca, Frankfurt-Palma de Mallorca, Stuttgart-Palma de Mallorca, Vienna-Malaga, Vienna-Palma de Mallorca and Vienna-Paphos.

(72) For the Winter 2018/2019 IATA Season, it is arguable whether the Transaction modifies the actual conditions of competition on any O&D, considering that the routes on which LaudaMotion's flight capacity would be deployed were neither finalised nor, to the Commission's best knowledge, made public at the time of announcement of the Transaction. Nevertheless, the Commission notes that the flight capacity of five LaudaMotion aircraft during the Winter 2018/2019 IATA Season had already been pre-sold to Condor pre-Transaction, although the corresponding block space flights still had to be defined. In addition, considering that the Winter 2018/2019 IATA Season flight plan was published and put on sale shortly after the agreement on the binding Heads of Terms and the announcement of the Transaction, LaudaMotion can be considered to be a potential competitor pre-Transaction on the routes that it will operate during the Winter 2018/2019 IATA Season using its own nine-aircraft flight capacity.75 Therefore, even if LaudaMotion's flight capacity was considered as not exerting an actual competitive constraint but a potential one only, in accordance with paragraph 58 of the Commission's Horizontal Merger Guidelines76, these routes are relevant for the competitive assessment of the Transaction under the O&D approach, to the extent that Ryanair also plans to operate these routes during the Winter 2018/2019 Season on the basis of its Winter 2018/2019 IATA Season flight schedule.77

(73) As a consequence, the following Winter IATA Season airport pairs, on which both Ryanair and LaudaMotion (using its own flight capacity) plan to operate (or on substitutable airport pairs) are relevant markets under the O&D assessment: Duesseldorf-Alicante, Duesseldorf-Faro, Duesseldorf-Fuerteventura, Duesseldorf- Gran Canaria, Duesseldorf-Lanzarote, Duesseldorf-Malaga, Duesseldorf-Palma de Mallorca, Duesseldorf-Tenerife Sur, Vienna-Larnaca and Vienna-Marrakech. ii) Under the O&D approach, the relevant O&Ds should not include the routes operated using Ryanair's flight capacity (wet-leased aircraft) made available to LaudaMotion as a result of the Transaction

(74) In the easyJet/Certain Air Berlin assets decision, the Commission considered that the traditional O&D approach, under which each O&D city-pair is assessed separately, would fail to capture the structural effects on competition brought about by the concentration, in view of (i) the termination of Air Berlin's operations, hence its exit from all O&D markets, and (ii) the fact that the target consisted mainly of slots (in particular, aircraft and crew were not part of the target).78 Similarly, in the Lufthansa/Certain Air Berlin assets decision, the Commission considered that the traditional O&D approach, under which each O&D city-pair is assessed separately, would fail to capture the structural effects on competition brought about by the concentration, in view of (i) the termination of Air Berlin's (including LGW's79) operations prior to the Transaction, hence its exit from all O&D markets, and (ii) the fact that LGW was used in particular as a vehicle for the transfer of Air Berlin's slots (Lufthansa already had the right to use the aircraft and crew that were part of the target).80

(75) In the case at stake, the Commission also considers that the O&Ds on which LaudaMotion uses or will use Ryanair's flight capacity (wet-leased aircraft) should not be treated as relevant markets, since (i) pre-Transaction, LaudaMotion did not operate and did not plan to operate these routes; the inclusion of these routes in LaudaMotion flight schedules results from the early implementation of the Transaction authorised under the First and Second Derogation Decisions; (ii) LaudaMotion does not hold any of the assets and rights necessary to operate on these routes other than slots and LaudaMotion's involvement is therefore limited to the provision of the slots necessary to operate the routes.81

(76) Consequently, the Transaction cannot be deemed to alter the competitive constraints under which Ryanair operates on these specific O&Ds. Nevertheless, since the merged entity's presence on these routes post-Transaction results from the transfer of LaudaMotion's slots, the effects on competition on these routes, as well as on all other routes to or from the same airports, will be captured under the airport-by-airport assessment.iii) The identification of the relevant markets under the O&D approach should not be based on NIKI's former flight operations

(77) One respondent to the market investigation submits that "the transaction would combine Ryanair and NIKI, the two closest competitors active on the route thus removing an important constraint on Ryanair in terms of pricing. In light of these facts, the Commission should at the very least closely examine routes on which the parties' combined market share (based on NIKI's 2017 shares) would exceed 65%."82 The Commission considers that the approach put forward by this respondent, based on NIKI's former flight operations, is not appropriate for the following reasons.

(78) In the two prior decisions involving assets from insolvent Air Berlin, the Commission did not assess the effects of the Transaction on the basis of the passenger air transport services that Air Berlin used to supply prior to its insolvency, considering notably that Air Berlin had, prior to and independently of the transaction, exited all O&D markets.83

(79) In the present case, the target of the Transaction is LaudaMotion, a newly set-up provider of scheduled air transport services. While LaudaMotion's flight operations build upon the assets transferred from NIKI, in particular the dry-lease agreements with Lufthansa Group for 10 former NIKI aircraft, personnel formerly employed by NIKI84 and a 19-aircraft equivalent slot portfolio formerly held by NIKI, LaudaMotion has to be distinguished from NIKI, as a formerly active air carrier.

(80) First, at the time of transfer of parts of NIKI's former assets to LaudaMotion and even more so at the time of the Transaction, insolvent NIKI had completely and definitively ceased competing as an active air carrier. Therefore, the acquisition of NIKI's former assets by LaudaMotion did not entail any take-over of NIKI's former flight operations nor of the market position on routes that NIKI used to operate before it entered into insolvency proceedings. Attributing NIKI's former market position on routes operated until December 2017 to LaudaMotion would imply a backward looking assessment, contrary to the analytical framework prescribed by the Merger Regulation.

(81) Second, the scope of LaudaMotion's assets is more limited than the scope of the assets formerly held and used by NIKI prior to its insolvency. In particular, LaudaMotion's fleet pre-Transaction consists of 10 leased aircraft (out of which eight are operable during the Summer 2018 IATA Season and nine during the Winter 2018/2019 IATA Season), compared to a 35-aircraft fleet for NIKI prior to its insolvency. In addition, LaudaMotion employs fewer pilots and crew than NIKI prior to its insolvency. Furthermore, LaudaMotion has obtained by transfer from NIKI a portfolio of summer slots, and has already had to handback slots (notably at Zurich airport) for failure to get access to a sufficient number of aircraft. Finally, due to NIKI's insolvency, LaudaMotion did not obatain any customer base nor any sales platforms or operational services from NIKI, thus necessitating the transitional support measures under agreements with Condor and Lufthansa Group during LaudaMotion's start-up phase prior to the Transaction.85

(82) Given the above circumstances, the Commission considers that NIKI's flight operations prior to its insolvency are not relevant for the purpose of the competitive assessment of the Transaction under the O&D approach.iv) Under the O&D approach, the relevant O&Ds should not include any other routes on account of LaudaMotion's potential competition

(83) In prior decisions concerning air carriers, the Commission found that an airline active on a route could be constrained not only by its actual competitors on the route in question but also by potential competitors.86 In this context, the Commission has identified, as relevant O&Ds, non-overlap routes on which one party was found to be a potential competitor of the other party.87

(84) In the present case, the Commission finds that potential competition is not an important parameter of competition between Ryanair and LaudaMotion, in view of LaudaMotion's limited ability to shift and add routes in reaction to changes in the competitive structure of routes.

(85) In particular, the Commission considers that the first condition for establishing loss of potential competition pursuant to paragraph 60 of the Horizontal Merger Guidelines88 is not fulfilled, namely, a potential competitor must already exert a significant constraining influence or there must be a significant likelihood that it would grow into an effective competitive force.

(86) LaudaMotion does not possess all the assets necessary to start operating on routes and has required the operational support of other carriers (Condor and Eurowings pre-Transaction, Ryanair post-Transaction) to operate on any O&D. Furthermore, LaudaMotion does not exert a significant constraint on its competitors on any market for passenger air transport services. It has just established bases for the eight aircraft it is using during the Summer 2018 IATA Season, the largest of which (Vienna and Duesseldorf, which are not Ryanair bases89) would have numbered two aircraft. In addition, due to the scarcity of aircraft and crew in Germany, Austria and Switzerland and to the weak financial resources of LaudaMotion, it is unlikely that LaudaMotion would have significantly expanded its flight capacity in the short or medium term. In fact, LaudaMotion's internal fleet scenarios do not foresee an increase in the number of LaudaMotion's aircraft.90

(87) The Commission acknowledges that (i) the slot portfolio held by LaudaMotion is larger than what the aircraft in its own fleet can operate, and that (ii) the opening of new routes by LaudaMotion would not necessarily require access to new aircraft. LaudaMotion could redeploy aircraft and reduce frequencies on less profitable routes to enter new routes.91 However, the only evidence that the Commission has seen of any pre-Transaction intention by LaudaMotion to re- shuffle capacity relates to only two airport pairs, which are both part of the same route (from Vienna-Paphos to Vienna-Larnaca, see paragraph (179) below). In addition, the flexibility of airlines to adjust capacity and routes so as to react efficiently to demand-side or supply-side evolutions depends on having a sufficiently large fleet to optimise planning.92 In the present case, LaudaMotion lacks sufficient scale to easily shift its frequencies from one route to another and to open, close or change frequencies on routes out of Austria, Germany or Switzerland regularly. Furthermore, LaudaMotion's lack of an established presence at any given airport, which might give it competitive advantages for marketing and advertisement, also constitutes a barrier to entry on new routes.93

(88) In addition, the Commission considers that the second condition for establishing loss of potential competition pursuant to paragraph 60 of the Horizontal Merger Guidelines94 is also not fulfilled. The Commission finds in this Decision that the addition of LaudaMotion's slot portfolio to Ryanair's slot portfolio does not give the merged entity the ability to prevent entry or expansion of the merged entity's competitors at any relevant airport (see section 7.2 below). Strong airlines already well-established on leisure routes out of Germany, Austria and Switzerland, such as the Lufthansa Group, easyJet, Condor or TUI, or which have announced their expansion in these countries, such as IAG, are likely potential competitors which would prevent the merged entity from raising prices on non-overlap routes on which LaudaMotion might have entered.

(89) As a conclusion, the Commission considers that there is no non-overlap route that should be treated as a relevant O&D for the purpose of assessing any loss of potential competition between Ryanair and LaudaMotion. v) Under the O&D approach, the relevant O&Ds should not include the routes exited by Ryanair after the announcement of the Transaction

(90) One respondent to the market investigation points to press reports according to which, as a result of the Transaction, Ryanair would move two aircraft currently based in Greece to Germany. As a consequence, Ryanair would withdraw from a number of Greek domestic routes and would give up its based in Chania (Crete), leading to the end of Ryanair's services on a number of European short-haul routes from and to Chania airport.95 In this context, the respondent submits that the Commission should investigate to what extent Ryanair's withdrawal will lead to a significant impediment of effective competition on the respective routes, for instance by leaving only a single carrier on those routes.96

(91) Ryanair claims that, […]. Therefore, according to Ryanair, there is no Transaction-specific effect on competition on Greek domestic routes or on other routes to or from Chania airport.97 More generally, none of the reductions in the aircraft based at Ryanair's bases between June 2017 and June 2018 related to the Transaction.98

(92) Even if the withdrawal from routes were related to the Transaction, the Commission underlines that, with respect to the determination of affected markets in horizontal mergers, affected markets consist of the relevant markets where the parties to the proposed transaction are engaged in business activities and hence on which the transaction produces merger-specific effects.99 Accordingly, markets where the activities of the parties to the transaction do not overlap are in principle outside the scope of the investigation, as the transaction is not likely to produce merger-specific effects on these markets. Therefore, routes that are only operated by Ryanair and a third party, but not by LaudaMotion, should not, in principle, be considered as relevant markets.

(93) The Commission acknowledges that, in certain prior decisions in the airline sector, it has assessed the effects on competition on such non-overlap markets. This was in particular the case where a factual inquiry indicated that, as a direct result of the merger or as its foreseeable consequence, close links, for instance through a co-operation agreement within the framework of an airline alliance, are likely to be established between one merging party and a close partner of the other merging party.100 In such cases, the incentives to compete in certain routes could indeed be altered as a result of the merger.101

(94) In the present case, the Commission notes in particular that Ryanair is not a member of any airline alliance, nor is it a party to any code-share agreement, block-share agreement, or joint venture.102 As to LaudaMotion, it is not a party to any cooperative agreements other than the short-term agreements with Condor and Lufthansa Group which were terminated as a result of the Transaction.103 Therefore, the Commission considers it unlikely that the Transaction would give rise to any specific coordinated or spill-over effects.

(95) The Commission thus considers that the routes exited by Ryanair, including those on which only one air carrier is left operating, are not relevant markets under the O&D approach.

(c) Conclusion

(96) In light of the above, the Commission concludes that, for the purpose of this Decision, it is appropriate to apply the analytical framework designed to address the loss of O&D competition following the merger between two air carriers only to the routes included in LaudaMotion's Summer 2018 and Winter 2018/2019 IATA Seasons flight schedule and operated by LaudaMotion using its own assets, including aircraft dry-leased from Lufthansa Group.104

(97) Therefore, under the O&D approach, the Commission will only consider as relevant markets the routes operated by LaudaMotion during the Summer 2018 IATA Season using its eight-aircraft flight capacity and the routes to be operated during the Winter 2018/2019 IATA Season by LaudaMotion using its nine- aircraft flight capacity.

6.1.1.2. Relevance of markets defined as airports under the airport-by-airport approach

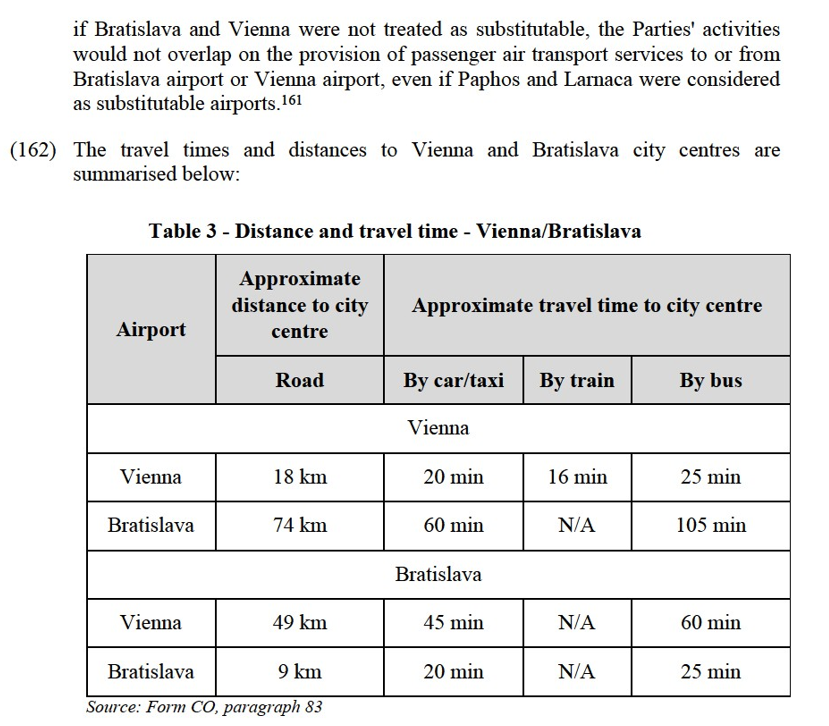

(98) As an introduction, the Commission will describe the relevance of slots as an input for air transport services and the EU rules that govern their allocation at EU airports. The Commission will then determine the extent to which it is appropriate to carry out an airport-by-airport assessment of the competitive effects of the Transaction and identify the markets that are relevant in the context of such an assessment.

(a) Introduction

i) Slots as an input for air transport services

(99) By virtue of the Slot Regulation, slots, i.e. the permission to land and take-off at a specific date and time at congested airports, are essential for airlines' operations. Indeed, only air carriers holding slots are entitled to get access to the airport infrastructure services delivered by airport managers and, consequently, to operate routes to or from those airports.

(100) The Commission has, in its prior decision practice on mergers involving active air carriers, highlighted that the lack of access to slots constitutes a significant barrier to entry or expansion at Europe's busiest airports.105

(101) The Commission has also insisted, in the framework of its airport policy, that "slots are a rare resource" and "access to such resources is of crucial importance for the provision of air transport services and for the maintenance of effective competition."106

(102) In addition, the Slot Regulation recalls that, with the increase of air traffic, there is a continuously growing demand for capacity at congested airports.107 Therefore, the lack of available slots has become a prominent feature of the EU airline industry and is expected to become an even more critical issue for air carriers in the near future.

ii) Rules for the allocation of slots

(103) In the context of the imbalance between demand and supply of airport capacity, the Slot Regulation defines the rules for the allocation of slots at EU airports. It aims to ensure that, where airport capacity is scarce, the latter is used in the fullest and most efficient way and slots are distributed in an equitable, non- discriminatory and transparent way.

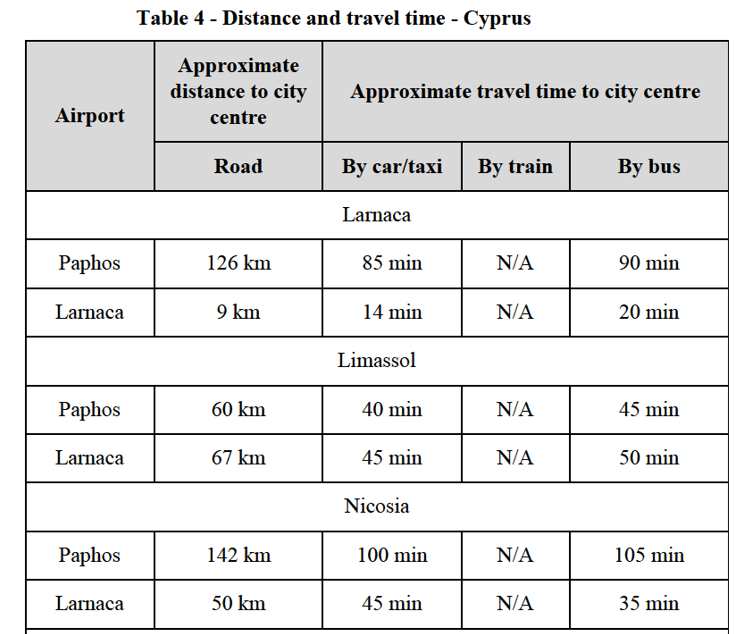

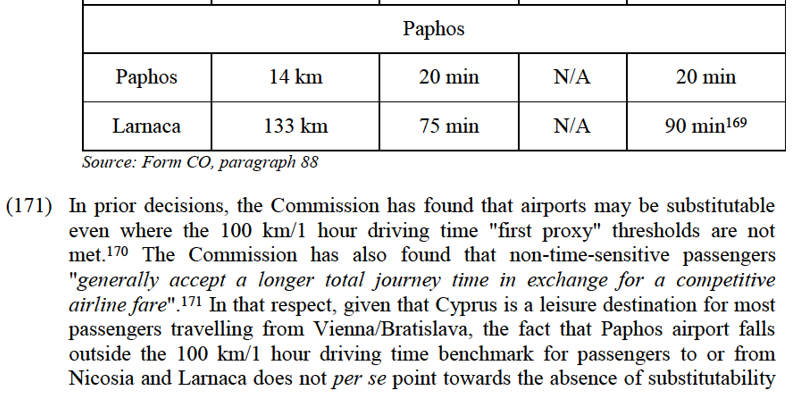

(104) Under the Slot Regulation, the general principle regarding slot allocation is that an air carrier having operated its particular slots for at least 80% during the summer or winter scheduling period is entitled to the same slots in the equivalent scheduling period of the following year (the "grandfather rights").108Consequently, slots which are not sufficiently used by air carriers are reallocated (the "use it or lose it" rule).

(105) The Slot Regulation also provides for the setting up of "pools" containing newly- created time slots, unused slots and slots which have been given up by a carrier or have otherwise become available. 50% of the slots from the slot pool shall first be offered to new entrants. The other 50% of the slots from the slot pool shall be placed at the disposal of other applicant airlines (incumbent airlines). If applications by new entrants amount to less than 50% of the capacity made available through slots from the pool, this remaining capacity shall also be placed at the other applicants' disposal.109

(106) Under the Slot Regulation, slots cannot be traded. They may however be exchanged or transferred between airlines in certain specified circumstances. If the Transaction is consummated, the transfer of slots from LaudaMotion to Ryanair could, subject to the explicit confirmation from the coordinator under the Slot Regulation,110 take place in the framework of this exception.

(b) Ryanair's views

(107) Ryanair submits that "The most significant asset of LaudaMotion is its portfolio of slots".111 Ryanair thus considers that "the competitive effects of the Transaction should be assessed in terms of the Parties' combined slot holdings in relation to the markets for air passenger services to or from particular airports for the IATA Summer Season 2018".112 As regards the Winter 2018/2019 IATA Season, Ryanair submits the Commission's assessment should "focus on the Parties' combined slot holding".113

(c) Commission's assessment

(108) According to the Explanatory Memorandum for the Commission Proposal for a Regulation of the European Parliament and of the Council on common rules for the allocation of slots at European Union airports,114 "the emergence of a strong competitor at a given airport requires it to build up a sustainable slot portfolio to allow it to compete effectively with the dominant carrier (usually the “home” carrier)."

(109) In this context, in a number of prior decisions related to transactions entailing the transfer of slots at certain airports, the Commission has considered the effects of the transaction on the operation of passenger air transport services at a given airport in terms of the slot portfolio held by a carrier at the airport, without distinguishing between the specific routes served to or from that airport.115 Such an approach has notably been adopted to assess the effects of the strengthening of an airline's position at certain airports.116

(110) In this case, the Transaction results in a concentration of slots at certain airports in the hands of a single undertaking. Indeed, through the Transaction, Ryanair will obtain slots currently held by LaudaMotion that can be used for its flight operations which, as explained above, exceed the flight operations that LaudaMotion can perform using its own fleet of eight aircraft for the Summer 2018 IATA Season and nine aircraft for the Winter 2018/2019 IATA Season.117

(111) The Commission has found in two recent decisions involving the transfer of slots formerly held by Air Berlin that the demand for airport infrastructure services at many of the airports concerned by the Transaction is high.118

(112) Therefore, the Commission considers it appropriate to carry out an assessment of the competitive effects of the Transaction under the airport-by-airport approach. For that purpose, and in line with the prior decisions on transactions involving the transfer of slots, the Commission will define two relevant markets: (i) the markets for passenger air transport services to or from the relevant airports, on which the Parties, as slot holders, are both present on the supply side; and (ii) the market for passenger air transport services to or from the relevant airports, on which the Parties are both present on the demand side.119 Indeed, slots relate to air carriers' ability to operate flights to or from the relevant airports, since air carriers, through slots, get access to airport infrastructure, notably to the available runway and terminal capacity, so that the market for airport infrastructure services to airlines is relevant for the assessment of the Transaction under the airport-by-airport approach.

(113) For the purposes of this airport-by-airport assessment, it is necessary to identify the airports where both Ryanair and LaudaMotion hold slots (and historic rights thereto). Indeed, as explained in paragraph (92) above, the Transaction is likely to produce merger-specific effects only at airports, or at substitutable airports, where both Ryanair and LaudaMotion hold slots (and historic rights thereto).

(114) The airports where LaudaMotion holds slots are only a sub-set of the airports where NIKI used to hold slots prior to insolvency.

(115) As explained above, as part of its acquisition of certain NIKI assets in the framework of NIKI's insolvency proceedings in Austria, LaudaMotion only obtained part of the slot portfolio that NIKI held prior to insolvency. Furthermore, LaudaMotion lost access to a number of aircraft formerly used by NIKI and, therefore, had to abandon historic rights over the slots that it could not use anymore. Consequently, the target slot portfolio to be transferred to Ryanair as a result of the Transaction cannot be compared to the portfolio that NIKI used to hold before it ceased operations in December 2017.

(d) Conclusion

(116) In light of the above, the Commission concludes that, for the purpose of this Decision, it is appropriate to apply the analytical framework designed to address the risk of foreclosure from access to airport infrastructure services stemming from the merger between two slot holders, at the airports where both Ryanair and LaudaMotion hold slots for the Summer 2018 and Winter 2018/2019 IATA Seasons.

6.1.2. Air transport services to tour operators

(a) Ryanair's views

(117) Ryanair considers that the Transaction will have a positive impact for tour operators, as it brings more capacity to the market.120

(b) Commission's assessment

(118) Carriers, both charter and scheduled airlines, may sell seats (or entire flights) to tour operators, which then integrate the flights into package holidays or resell seats only to end customers.

(119) In prior decisions, the Commission has regarded the wholesale supply of airline seats to tour operators as a distinct market from the supply of scheduled air transport services to end customers.121 Indeed, from a demand-side perspective, tour operators have different requirements from those of individual passengers (for example, purchase of large seat packages in advance from the start of the season, negotiation of rebates, taking into account passengers' needs in terms of flight times).

(120) As indicated in paragraph (37) above, LaudaMotion was not directly active pre- Transaction on the market for the supply of airline seats to tour operators to any significant extent. Part of its flight capacity was indirectly made available to tour operators by Condor and Eurowings, which acted as wholesalers.122 Nevertheless, according to its business plan, LaudaMotion was planning to enter the wholesale market for the supply of air transport services to tour operations, even if such entry would likely have been limited (see paragraph (37) above).

(121) According to Ryanair, no decision has been taken as to whether LaudaMotion will, post-Transaction, actually sell seat capacity to tour operators.123 In any case, Ryanair is not active on the market for the wholesale of seats to tour operators in Germany, Austria or Switzerland.124 Tour operators may occasionally purchase tickets for groups on Ryanair's scheduled services but Ryanair does not have any framework agreement with tour operators in Germany, Austria and Switzerland.125 Therefore, regardless of LaudaMotion’s intended entry on this market, there is no overlap between the Parties as regards the wholesale supply of seats to tour operators.

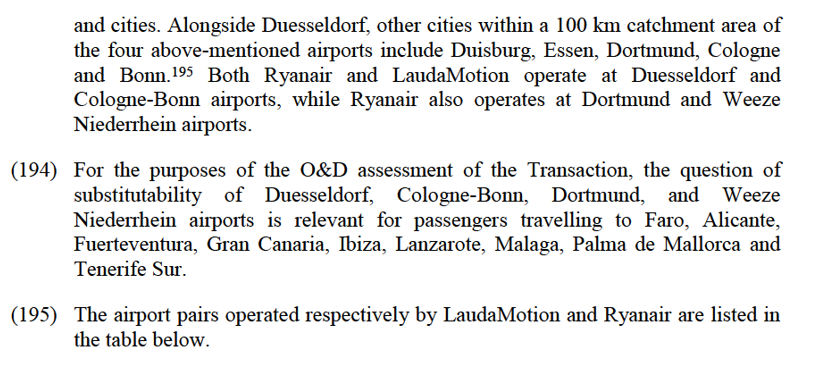

(122) In addition, Ryanair is not active to any material extent on the downstream market for tour operating services in Germany, Austria or Switzerland.126 Therefore, the Transaction does not give rise to any vertical relationship.

(123) One respondent to the market investigation considers that tour operators are the most likely customer group to be affected by the Transaction, since Ryanair's acquisition of LaudaMotion would inevitably lead to Ryanair imposing its single- seat business model on LaudaMotion, thus eliminating a carrier that would have been heavily focused on tour operators absent the Transaction.127 A comparable theory had been evoked in the Ryanair/Aer Lingus III decision.128

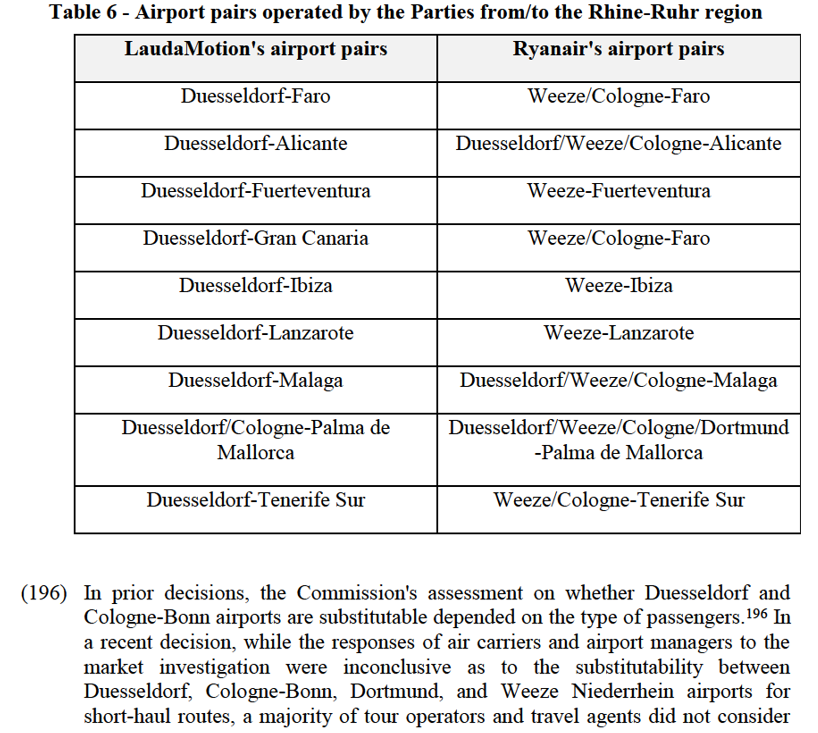

(124) The Commission considers that the concerns expressed by the respondent should be dismissed, for the following reasons.

(125) As a preliminary comment, the Commission notes that it is unclear whether LaudaMotion's plans to enter the wholesale market will be abandoned post- Transaction.

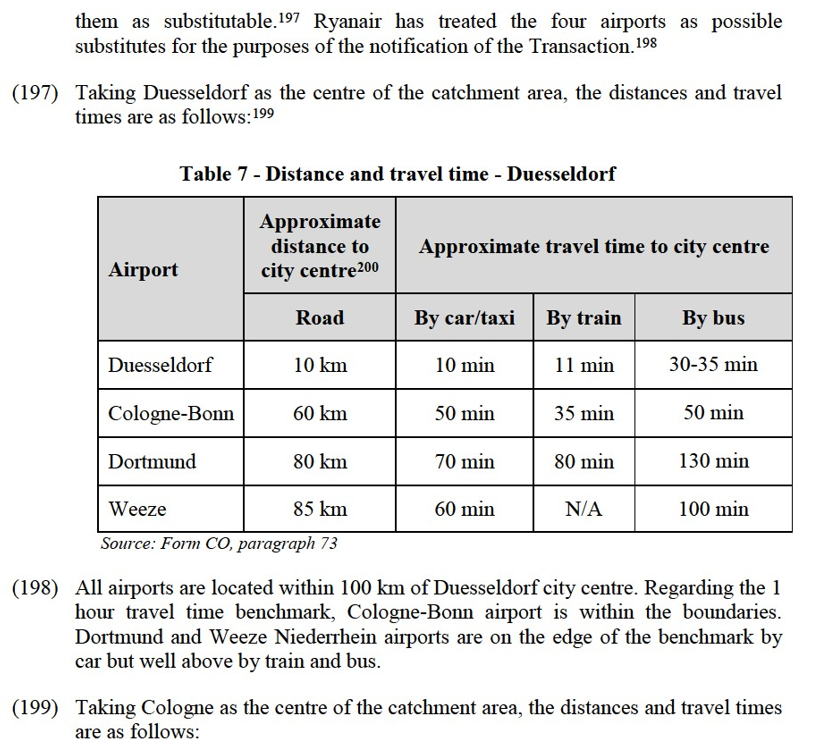

(126) In any case, since Ryanair is not and does not plan to be active on this market, LaudaMotion is neither an actual nor a potential competitor. Therefore, in general and as recalled in paragraph (92) above, the Transaction is unlikely to have any anti-competitive effects on this non-overlap market.

(127) In addition, Ryanair is not active on the downstream market for tour operating services and does not have any cooperative agreement or other links with an airline129 that could benefit from LaudaMotion's departure from its original wholesale-oriented business model.

(128) Either of the above two reasons would thus be sufficient to conclude that the Transaction does not negatively affect tour operators to any significant extent.

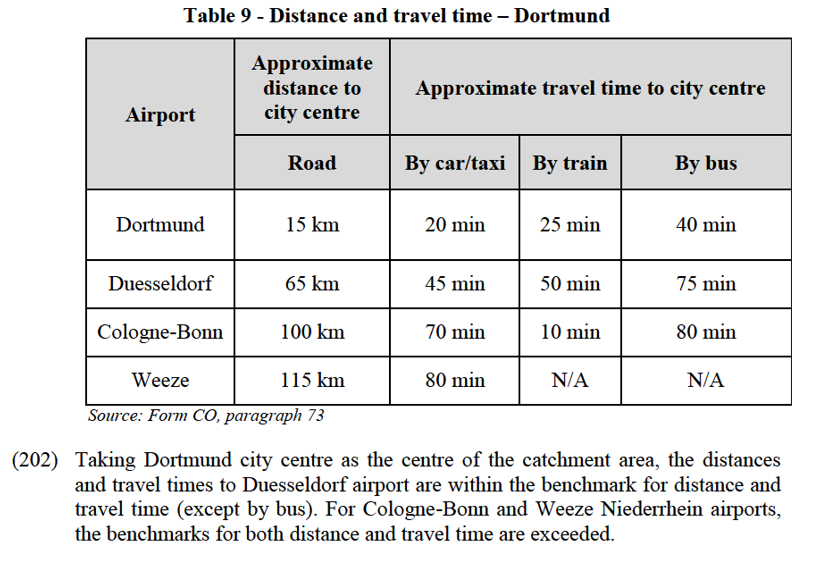

(c) Conclusion

(129) In light of the above, the Commission concludes that, for the purpose of this Decision, the Transaction does not have material specific effects on the market for the wholesale supply of airline seats to tour operators. Therefore, this market is not considered as a relevant market and will not be further assessed in this Decision.

6.1.3.Air transport services to other airlines

(a) Ryanair's views

(130) According to Ryanair, it is inconceivable that the Transaction could have any material adverse effects on other carriers intending to market flights to be operated by LaudaMotion or to wet-lease services from LaudaMotion.130

(b) Commission's assessment

(131) The Commission notes that there are strong indications that the provision by LaudaMotion of air transport services to other airlines was conceived as a short- term solution, and that LaudaMotion did not intend to establish itself as a supplier of flight capacity to other airlines after 2019.131 Therefore, the Transaction cannot be considered as bringing about any structural change in relation to the supply of air transport services to other airlines. Besides, considering that the binding Heads of Terms agreed between LaudaMotion and Ryanair provided for the continuity of the planned supply agreements with Condor and Lufthansa Group,132 it appears that LaudaMotion's exit results in fact from decisions reached together with Condor and Lufthansa Group and not any anti-competitive strategy actively pursued by Ryanair in the framework of the Transaction.

(132) Moreover, given the minimal scale of LaudaMotion's activities provided to Condor133 and to Lufthansa Group,134 the Transaction is unlikely to have any substantial negative impact on the air transport operations of LaudaMotion's customers.

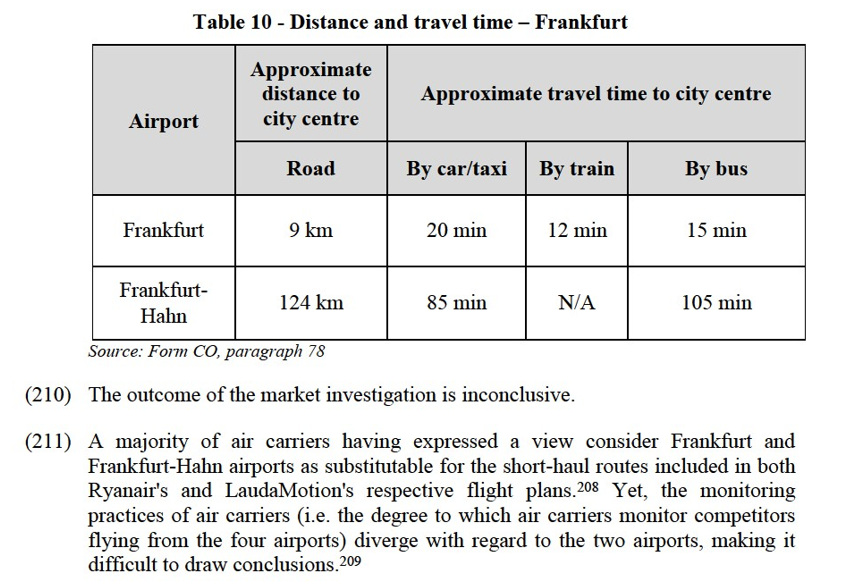

(133) Lastly, Ryanair does not provide any passenger air transport services to other airlines through interline, block space or wet-lease agreements.135 Therefore, in general and as recalled in paragraph (92) above, the Transaction is unlikely to have any anti-competitive effects on this non-overlap market.

(134) Any of the above findings would be sufficient to conclude that the Transaction does not negatively affect other airlines to any significant extent.

(c) Conclusion

(135) In light of the above, the Commission concludes that, for the purpose of this Decision, the Transaction does not have material specific effects on the supply of air transport services to other airlines. Therefore, these services are not considered as constituting a relevant market and will not be further assessed in this Decision.

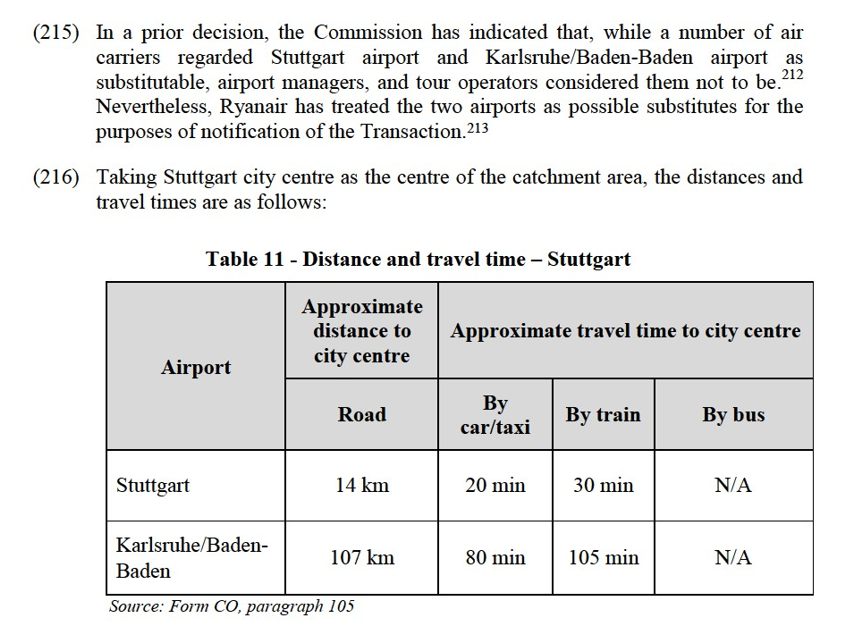

6.2.Definition of the relevant markets under the O&D and airport-by-airport approaches

6.2.1.O&D approach

(136) On the routes listed in paragraphs (71) and (73) above, the Transaction involves the combination of Ryanair's and LaudaMotion's flight capacity currently offered for sale to passengers. The Commission will consider below the possible various delineations of these relevant markets under the O&D approach.

6.2.1.1.Distinction between groups of passengers

(a) Ryanair's views

(137) Ryanair submits that it is not appropriate to define separate markets for different categories of passengers.136

(b) Commission's assessment

(138) The Commission has in its decisional practice (mostly concerning network carriers) considered distinguishing, for a given O&D route, between (i) time sensitive ("TS" or premium) passengers who tend to travel for business purposes, require significant flexibility for their tickets and are willing to pay higher prices for this flexibility, and (ii) non-time sensitive ("NTS" or non-premium) passengers who travel predominantly for leisure purposes, do not require flexibility with their booking and are more price-sensitive than the first category.137

(139) However, in recent decisions, the Commission has considered that the distinction between TS and NTS passengers has become blurred. Passengers are becoming increasingly price-sensitive and more corporate customers apply lowest fare policies. Moreover, on short-haul flights, the distinction between TS and NTS has become somewhat artificial, as the offerings for TS and NTS passengers on these routes has become very similar. The transportation of both categories of passengers usually takes place in the same cabin and further product differentiation (e.g. included meals, newspapers and magazines) are mostly also available to NTS passengers for an upgrade fee.138 In particular, in Ryanair/Aer Lingus III, the Commission found that it was not appropriate on short-haul routes to define separate markets for different categories of passengers, whether according to the distinction between TS and NTS passengers, the distinction between business and leisure passengers, or other approaches such as the "time between booking and departure" approach.139

(140) In this context, the Commission notes that the relevant routes for the purpose of the competitive assessment of the Transaction are all short-haul leisure routes, operated by both Ryanair and LaudaMotion as point-to-point carriers on the basis of an all-economy configuration.

(141) Moreover, the market investigation has not produced evidence indicating that the Commission should depart from the approach it has recently taken in respect of short-haul routes. In particular, respondents have not submitted material comments suggesting that there is any need to define separate markets for the different categories of passengers for the purpose of analysing the Transaction.

(c) Conclusion

(142) In light of the above, the Commission concludes that, for the purposes of the Transaction, it is not appropriate to define separate markets for different categories of passengers, whether according to the distinction between TS and NTS passengers, or any similar distinction.

6.2.1.2. Distinction between direct flights and indirect flights

(a) Ryanair's views

(143) Ryanair submits that indirect flights should not be treated as belonging to the same market as direct flights in respect of the relevant short-haul leisure routes.140

(b) Commission's assessment

(144) On a given O&D pair, passengers can travel either on a direct141 flight between the point of origin and the point of destination or on an "indirect" flight on the same O&D pair but via an intermediate destination. The level of substitutability of indirect flights for direct flights largely depends on the duration of the flight. As a general rule, the longer the flight, the higher the likelihood that indirect flights exert a competitive constraint on direct flights.142

(145) When defining the relevant O&D markets for air transport services, the Commission has considered in prior decisions143 that with respect to short-haul routes (generally below 6 hours flight duration) indirect/one-stop flights do not generally provide a competitive constraint to direct/non-stop flights absent exceptional circumstances (for example when the share of indirect flights in the overall market is significant).144

(146) The market investigation has not produced any evidence indicating that the routes concerned by the Transaction, which are all short-haul routes, present the exceptional features pursuant to which indirect flights could exert a significant constraint on direct flights.

(147) Furthermore, Ryanair does not generally monitor and LaudaMotion does not currently monitor competitors' prices on indirect routes.145 The Commission notes in this regard that Ryanair is unable to quantify the additional capacity corresponding to such indirect flights, thus indicating that Ryanair considers that such flights exert a limited constraint on its direct flights.146

(c) Conclusion

(148) In any case, the question of whether indirect and direct flights would belong to the same market can be left open, as the Transaction would not raise serious doubts as to its compatibility with the internal market under either plausible market definition. Considering that neither Ryanair nor LaudaMotion offer connecting flights to any material extent and connecting traffic is not a matter of business focus for either Party,147 including indirect flights for the purposes of market definition would only dilute the Parties' market position. By excluding indirect flights, the Commission has thus adopted a conservative approach, which, all other things being equal, would tend to underestimate the competition constraints exercised on the Parties in the O&D assessment conducted in Section 7.1.

6.2.1.3. Distinction between charter flights and scheduled flights

(a) Ryanair's views

(149) Ryanair considers, as a general matter, that charter activity exercises a competitive constraint over the scheduled flights offered by Ryanair and LaudaMotion, in particular with regard to leisure passengers.148

(b) Commission's assessment

(150) Charter flights, as opposed to scheduled flights, are usually defined as air transport services that take place outside normal schedules, normally through a hiring arrangement with a particular customer (in particular a tour operator). Charter companies usually operate on a seasonal basis with a relatively low frequency of flights, in response to the requirements of tour operators (for example, once a week on Saturday, only during the summer season).

(151) In prior decisions, the Commission has held that the distinction between scheduled and charter airlines has become blurred, as even full-leisure airlines operate scheduled services149 and has not disputed that Ryanair might be subject to certain competitive constraints from charter airlines on some of its German routes.150

(152) In addition, the market investigation has confirmed that some airlines operate under a mixed business model, offering charter and scheduled services.151

(153) However, the Commission notes that Ryanair is unable to quantify the activity of charter airlines on any of the affected O&Ds, thus indicating that Ryanair considers that such flights exert a limited constraint on its scheduled flights.152

(c) Conclusion

(154) The question of whether charter and scheduled flights belong to the same market can be left open, as the Transaction would not raise serious doubts as to its compatibility with the internal market under either plausible market definition. Considering that Ryanair does not provide and does not plan to provide charter services in Germany, Austria or Switzerland,153 including charter flights for the purposes of market definition would only dilute the Parties' market position. By excluding charter flights from its competitive analysis, the Commission has thus adopted a conservative approach, which, all other things being equal, would tend to underestimate the competition constraints exercised on the Parties in the O&D assessment conducted in Section 7.1.154

6.2.1.4. Airport substitutability

(a) Analytical framework

(155) When defining the relevant O&D markets for passenger air transport services, the Commission has previously found that flights to or from airports with sufficiently overlapping catchment areas can be considered as substitutes in the eyes of passengers (particularly if the airports serve the same main city). In order to correctly capture the competitive constraint that flights to or from two different airports exert on each other, a detailed analysis taking into consideration the specific characteristics of the case at hand is necessary.155

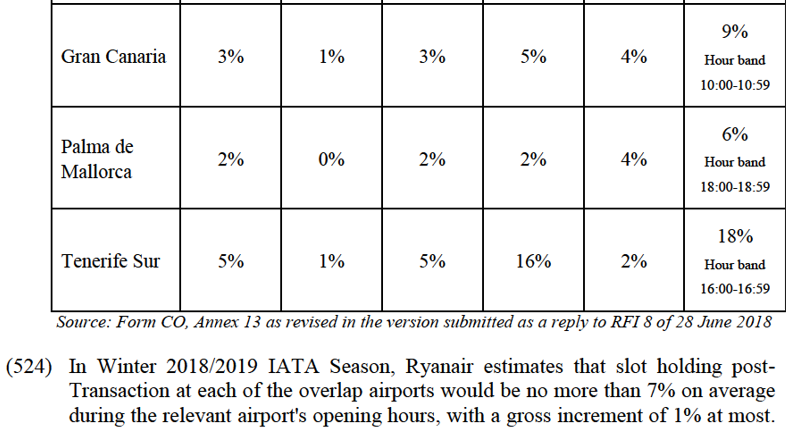

(156) The evidence used to characterise airport substitutability includes inter alia a comparison of actual distances and travelling times to the indicative benchmark of 100 km/1 hour driving time,156 the outcome of the market investigation (views of the airports, the competitors, and other market participants), and the Parties' practices in terms of monitoring.