Commission, June 27, 2019, No M.9205

EUROPEAN COMMISSION

Decision

IBM / RED HAT

Subject: Case M.9205 – IBM / RED HAT

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 20 May 2019, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which International Business Machines Corporation (“IBM” or “Notifying Party”, USA) intends to acquire sole control of Red Hat Inc. (“Red Hat”, USA) (the “Transaction”) (3). IBM and Red Hat are collectively referred to as "Parties".

1. THE PARTIES

(2) IBM is a public company headquartered in Armonk, New York, USA. It is active worldwide in the development, production, and marketing of a wide variety of information technology (“IT”) solutions, namely enterprise IT software and systems (such as servers, storage systems, cloud, and cognitive offerings) and IT implementation services (such as business consulting and IT infrastructure services).

(3) Red Hat is a public company headquartered in Raleigh, North Carolina, USA. It is a global provider of open-source software and support services, using a community-powered approach to develop and offer a wider range of open-source software solutions for enterprise customers, including in hybrid cloud environments.

2. THE TRANSACTION

(4) Under an agreement and plan of merger dated 28 October 2018 (the “Agreement”), IBM will acquire all of Red Hat’s issued and outstanding common shares for a total value of approximately USD 34 billion. Therefore, the Transaction consists of the acquisition of sole control by IBM over Red Hat within the meaning of Article 3(1)(b) of the Merger Regulation.

3. EU DIMENSION

(5) The Parties concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (4) (IBM: EUR 67 392 million; Red Hat: EUR 2 531 million). Each of them has an EU-wide turnover in excess of EUR 250 million (IBM: EUR […]; Red Hat: EUR […]), but they do not achieve more than two- thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension.

4. RELEVANT MARKETS

4.1. Introduction – approach to market definition

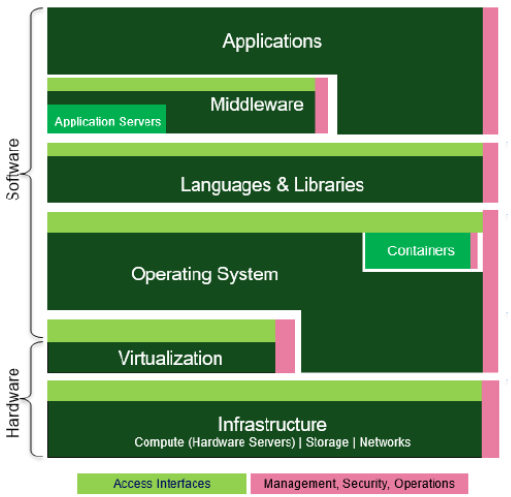

(6) Red Hat and IBM are both active in IT software for enterprise customers across different layers of the IT stack.

(7) The Parties’ activities overlap in a number of plausible markets or market segments at nearly all levels of the IT software stack. The Transaction also creates a large number of non-horizontal relationships.

(8) In determining the relevant markets, where possible, the Notifying Party provided its views on the product and geographic market definitions on the basis of previous Commission decisions. The Notifying Party also relies on the segmentation of the market intelligence companies IDC and/or Gartner, (5) which the Notifying Party submits has been used in previous Commission decisions, in order to identify the narrowest possible product markets on which the Parties are active.

(9) For the purpose of the present decision, the Commission carried out its competitive assessment on the basis of the narrowest possible product market segments identified by the Notifying Party in accordance with IDC and Gartner segmentations for which market share data is available and which were affected on the basis of 2018 market shares data. (6)

(10) In the following Sections, the Commission carries out an assessment on the basis of IDC's primary markets for (i) Application Development and Deployment Software (Section 4.2) and (ii) System Infrastructure Software (Section 4.3).

(11) IDC sub-segments the primary market for Application Development and Deployment Software into the secondary markets for (i) Application Platform Software, (7) (ii) Integration and Orchestration, (8) (iii) Application Development, (9) (iv) Data Management. (10)

(12) IDC sub-segments the primary market for System Infrastructure Software into the secondary markets for (i) Storage, (11) (ii) Physical and Virtual Computing Software, (12) (iii) Network (13) and (iv) Operating Systems (14).

(13) When relevant, the Commission also relied on the Gartner segmentation. (15)

4.2. Application Development and Deployment Software (Middleware)

(14) Middleware is a large and diverse category of software that is used for building and operating large enterprise software applications. Some middleware is provided as prebuilt libraries or components that developers incorporate into applications and components. Middleware simplifies and accelerates development by reducing the need to recreate common functionality required by many applications. Middleware includes several products that could constitute sub- segments such as deployment-centric application platforms, business process management suites, integration software, event-driven middleware, business rules management systems, transaction processing monitors, managed file transfer software, non-relational database management systems, etc.

(15) In Oracle/Sun Microsystems (16), Oracle/BEA (17), and IBM/ILOG (18) the Commission considered whether all types of middleware belong to a single product market or whether it would be necessary to further sub-segment the possible market according to the end use of the product, but ultimately left the precise product market definition open in Oracle/Sun Microsystems and Oracle/BEA. In those decisions, the Commission also relied on IDC and Gartner segmentation in order to identify the possible affected markets.

(16) In Oracle/Sun, the Commission concluded that the relevant geographic market for middleware is worldwide.

4.2.1. Deployment-Centric Application Platforms

(17) Deployment-centric application platforms (“DCAPs”) host applications and provide them with common services that allow the application to operate effectively. DCAPs include application server software platforms (referred to as “application servers” or “app servers”) that provide a common framework for applications to provide services that would need to be duplicated across multiple applications, manage the application runtime environment consistently and at scale, and implement complex functions (e.g. the management of database connections) with high quality and resiliency. (19)

(18) The Parties’ products are: (i) IBM’s WebSphere Application Server (“WAS”) (20) and (ii) Red Hat’s JBoss Enterprise Application Platform (“JBoss”), and JBoss Web Server. Both IBM’s WAS and Red Hat’s JBoss products are Java Enterprise Edition (“Java EE”) compliant products. Java EE extends Java to include a defined list of capabilities that have proven valuable across enterprise applications. These capabilities are typically called Java EE Web Profile and Java EE Full Profile. (21)

(19) Traditional application servers are "heavyweight" and are designed to support large monolithic application architecture. Legacy applications are typically written as monoliths (i.e. all features of the application are contained within that application).

(20) Applications are increasingly built on the principles of integrating many small and dispersed components (a microservices architecture) instead of having to integrate each new application into an existing, large monolithic architecture. These principles allow application components to evolve independently and rapidly, to scale when workloads are unpredictable, and to be reused in a predictable manner. DCAPs supporting these applications have different requirements compared to traditional middleware: they must be lightweight for rapid delivery and startup, use different mechanisms to ensure resilience, focus on integration of dispersed applications rather than on heavy application servers, and address different security risks.

(21) To capture the distinction between architectural needs that process large amounts of data or perform complex processes across multiple systems, IT systems are sometimes placed in the two following categories: (i) system of record and (ii) system of engagement.

· Systems of record are IT systems that focus on managing vast quantities of data. These systems typically interact with databases and manage high volumes of transactions. They have capabilities (also referred to as “back- end capabilities”) focusing on the storing and processing of information. (22)

· System of engagement: systems of engagement are IT systems that focus on interacting with users. Systems of engagement are typically immediate, open, and accessible ad hoc—e.g. software delivered through the cloud and on mobile devices. They have capabilities that focus on interfaces engaging with users (also referred to as “front-end capabilities”), which typically do not require the same degree of data and transactional integrity as systems of record. (23)

(22) On that basis, the Notifying Party has identified three use cases which DCAPs can support: (i) back-end workloads which require extensive capabilities (such as high availability and cluster management, legacy integration, performance and optimization, standards support), (ii) back-end workloads which do not require these capabilities and (iii) front-end workloads.

4.2.1.1. Commission precedents

(23) In Oracle/Sun (24) and Oracle/BEA (25), the Commission considered a possible relevant product market for all application servers without further segmenting according to programming language, operating system compatibility, or proprietary/open source, although it ultimately left the product market definition open.

(24) In Oracle/Sun (26), the Commission concluded that the relevant geographic market for middleware and sub-segments thereof is worldwide.

4.2.1.2. Notifying Party’s views

(25) The Notifying Party submits that the relevant product market for DCAPs should encompass all platforms (i.e. application server software platforms as well as deployment-orientated platforms operating in public and private clouds) that host applications, provide them with common services that would otherwise need to be duplicated across multiple applications, and manage the application runtime environment consistently and at scale. (27)

(26) The Notifying Party argues that DCAPs running monolithic applications and DCAPs running cloud-native microservices belong to the same product market. According to the Notifying Party, there is a continuum of DCAPs spanning from those suitable for heavyweight workloads requiring sophisticated back-end DCAP capabilities in addition to those offered by the Java EE specification to those best- suited for cloud-native applications and front-end workloads, depending on the functionalities of each DCAP. It is therefore difficult to establish clear-cut categories in which to fit each DCAP. (28)

(27) Furthermore, in the Notifying Party’s view, DCAPs vendors have no way of discriminating between customers according to use case, since they have no visibility over how their DCAPs are ultimately used. Therefore, the Notifying Party submits that pursuant to the Market Definition Notice, (29) there are no grounds on which to define a separate product market for DCAPs running monolithic or microservices workloads, as the overlap between these two (hypothetical) groups of customers is necessarily fluid. (30)

(28) The Notifying Party submits that, in line with the Commission decisions listed at paragraphs (23) and (24), the relevant geographic market for DCAPs is global. Nevertheless, the Notifying Party also provided EEA-based market shares for completeness. (31)

4.2.1.3. Commission’s assessment

(29) The Commission considers that the possible market for DCAPs does not need to be further sub-segmented based on programming language, operating system compatibility or use cases / types of applications (e.g. monolithic applications, applications built as a system of microservices) for the following reasons.

(30) First, the results of the market investigation indicated that further segmentation by use cases to which DCAPs can cater is not warranted. A competitor expressed the view that customers do not distinguish between back-end workloads and front- end workloads but “in general customers are looking for an application server platform that supports the Java EE APIs and that is generally applicable to the wide range of workloads found typically in a large organisation”. (32) Another competitor explained that customers are primarily interested in the outcome based on their application needs and “the technical requirements can be met with many application server and architectural options” (33). Customers responding to the market investigation confirm that their DCAPs choice depends on the features required by the various applications and technology decisions. (34)

(31) Therefore, the Commission considers that, from the demand side, customers employ different types of DCAPs which cover a range of use cases and functionalities.

(32) From the supply side, competitors indicated that DCAPs can support a range of different use cases, without making a clear-cut distinction between their functionalities and suitability for specific use cases. (35) These DCAPs include Java EE, other platforms/programming languages, cloud-native application platforms offered by CSPs, serverless programming etc. (36)

(33) Furthermore, with the emergence of new technologies such as Container Infrastructure Software (see Section 4.3.2), any distinction between use cases (back-end and front-end) becomes even more blurred. A competitor explained that “the more modern approach to this class of problems (“how do I run this application”) is to use containers, which wrap up the language together with the application into a container. In that world, the distinctions of front and back end, and compatibility with legacy apps, are very different” (37).

(34) In addition, the market investigation results did not sugest that DCAPs vendors can discriminate between customers using DCAPs for different use cases. (38)

(35) Second, a majority of customers consider that they can switch their traditional (legacy and heavy-weight) application server either to other heavy-weight application servers or to applications built as a system of microservices. (39) Customers responding to the market investigation switched away from WAS to other Java EE DCAPs (e.g. JBoss, Weblogic, Tomcat, Jetty, Pivotal tc Server etc.), or to other platforms e.g. Springboot or .NET. A number of customers indicated that they switched to JBoss mainly due to cost considerations (some mention in addition that they moved to more light-weight options). Even if customers acknowledge that switching entails time, substantial costs and engineering efforts, a large number of customers which responded to the market investigation have migrated at least some existing applications. A small number of customers explained that switching is only likely to happen as part of a wider IT architecture transformations. (40)

(36) In light of the above, the Commission considers that the possible market for DCAPs does not need to be further sub-segmented based on programming language, operating system compatibility or use cases / types of applications (e.g. monolithic applications, applications built as a system of microservices). However, as regards free and unsupported open source DCAPs, the Commission considers that demand-side substitution is most likely too limited to exercise a competitive constraint on DCAPs with commercial support or proprietary DCAPs for the following reasons.

(37) First, customers responding to the market investigation consider free and unsupported open source DCAPs as credible alternatives to proprietary or supported open-source DCAPs only for low-risk use cases. (41) A small number of customers explained that for low-risk use cases, they can self-support open-source software, which requires developing in-house capabilities and relying on the open source community for updates, bug fixes etc. According to some customers, this is an expensive option as compared to procuring commercial support.

(38) Second, for mission-critical applications the majority of customers using open source DCAPs procure commercial support (directly from the vendor or from third parties specialised in providing commercial support for open source software). (42) A number of customers explained that internal companies’ policies and IT startegies would not allow the use of unsupported DCAPs. (43)

(39) Therefore, the Commission does not consider that free and unsupported open source DCAPs belong to the same product market as proprietary or commercially supported DCAPs.

(40) The Commission considers that for the purpose of the present decision, the exact product market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible product market definition.

(41) In line with the Commission decisions listed at paragraph (23), the Commission considers that the relevant geographic market for DCAPs is global. Nevertheless, for completeness, the Commission carried out the competitive assessment in Section 5.2.2 also at the EEA-wide level.

4.2.2. Transaction Processing Monitors

(42) A Transaction Processing Monitor (“TPM”) is a control program that ensures transactions are completed successfully. It primarily handles resource sharing (also referred to as load balancing), as well as ensures optimal use of resources by applications.

(43) IBM offers the following TPM products: (i) IBM CICS is IBM’s main TPM product (44), (ii) IBM TXSeries, (iii) IBM z/OS Connect Enterprise Edition, (iv) IBM z/Transaction Processing Facility, (v) IMS Transaction Manager/Database Manager. Red Hat is not active in TPMs.

4.2.2.1. Commission precedents

(44) In Dell/EMC45 and Oracle/BEA (46), it referred to TPMs as a possible sub-segment of the overall middleware market. In Oracle/Sun (47), the Commission identified TPMs as a product within application server middleware, in accordance with IDC’s classification although it ultimately left the market definition open.

(45) In Oracle/Sun (48), the Commission concluded that the relevant geographic market for middleware and sub-segments thereof is worldwide.

4.2.2.2. Notifying Party's views

(46) The Notifying Party submits that, in accordance with IDC’s taxonomy, TPMs could be viewed as a separate relevant product market. The IDC taxonomy identifies a functional market TPMs, within the secondary market Application Platforms and the primary market Application Development and Deployment Software. IDC does not segment this functional market further. (49)

(47) In the Notifying Party’s view, TPMs have a distinct functionality within enterprise middleware as they mediate and optimize the use of resources (e.g. databases) by applications, balance load of dynamic processes, and monitor and fix processes between the applications and the databases. (50) According to the Notifying Party, the Transaction does not raise any concerns on any of the possible segmentations, and the precise product market definition can be left open. (51)

(48) The Notifying Party submits that, in line with the Commission decisions listed at paragraphs (44)-(45), the relevant geographic market for TPMs is global. Nevertheless, the Notifying Party also provided EEA-based market shares for completeness. (52)

4.2.2.3. Commission’s assessment

(49) In line with Dell/EMC, Oracle/BEA and Oracle/Sun, a possible product market for TPMs can be identified. Nevertheless, the Commission considers that for the purpose of the present decision, the exact product market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under the narrowest possible product market definition identified by IDC for which market shares data is available.

(50) In line with the Commission decisions listed at paragraphs (44)-(45), the Commission considers that the relevant geographic market for TPMs is global. Nevertheless, for completeness, the Commission carried out the competitive assessment in Section 5.3.7.3 also at the EEA-wide level.

4.2.3. Business Process Management Suites

(51) Business process management (“BPM”) Suites provide intuitive, point-and-click environments for non-programmers to model business processes and develop and run simple, process-driven applications based on these models.

(52) In the BPM Suite segment, IBM offers IBM Business Process Manager (“IBM BPM”), including three versions – i.e. BPM Express, BPM, and BPM on Cloud. Red Hat offers Red Hat Process Automation Manager (formerly Red Hat JBoss BPM Suite).

4.2.3.1. Commission precedents

(53) In IBM/ILOG (53) and Oracle/Sun (54) the Commission identified a possible relevant market for “process automation middleware” (which corresponds to model-driven application platforms today). (55) The Commission adopted this segment as the relevant market in IBM/ILOG, but left the product market definition open in Oracle/Sun.

(54) In Oracle/Sun (56), the Commission concluded that the relevant geographic market for middleware and sub-segments thereof is worldwide.

4.2.3.2. Notifying Party's views

(55) The Notifying Party refers to the Commission decisions listed at paragraph (53) and to Gartner's segment for BMP Suites.

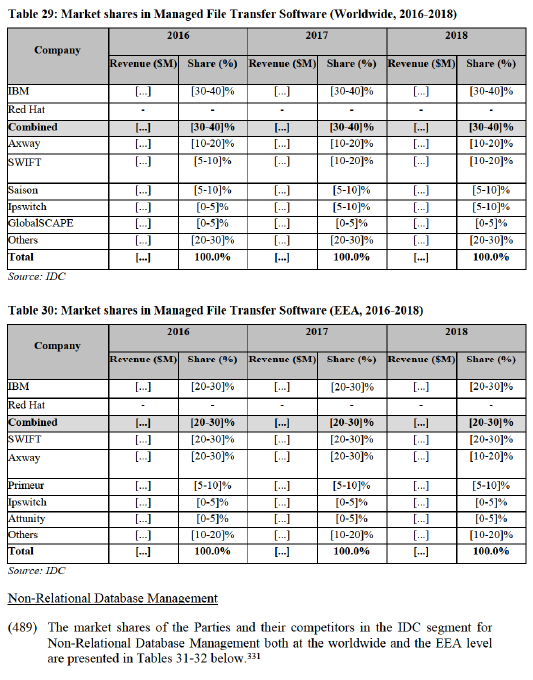

(56) The Notifying Party submits that the term “process automation middleware”, as used in the IBM/ILOG and Oracle/Sun Microsystems decisions, refers to a former IDC segment that has not been included in the IDC Worldwide Software Taxonomy since 2013. The closest segment in IDC’s 2018 taxonomy is the “Model-Driven Application Platforms” (“MDAP”) functional market, which however includes both process-centric and data-centric platforms. As the Parties’ products are both process-centric platforms, and as data-centric platforms typically offer a more limited range of functionality for the design, modelling, and optimization of business processes than process-centric platforms, the Notifying Party submits that the Gartner segment Business Process Management Suites may be an appropriate representation of the relevant product market on a conservative basis.

(57) According to the Notifying Party, the Transaction does not raise any concerns on any of the possible segmentations, and the precise product market definition can be left open. (57)

(58) The Notifying Party submits that, in line with the Commission decisions listed at paragraph (54), the relevant geographic market for BPM Suites is global. Nevertheless, the Notifying Party also provided EEA-based market shares for completeness. (58)

4.2.3.3. Commission’s assessment

(59) In line with IBM/ILOG and Oracle/Sun, the possible product market for BMP Suites can be identified. Nevertheless,the Commission considers that for the purpose of the present decision, the exact product market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under the narrowest product market definition identified by Gartner for which market shares data is available and which leads to the highest combined market shares of the Parties.

(60) In line with the Commission decisions listed at paragraph (54), the Commission considers that the relevant geographic market for BMP Suites is global. Nevertheless, for completeness, the Commission carried out the competitive assessment in Section 5.2.3 also at the EEA-wide level.

4.2.4. Integration Software

(61) Integration Software is server software used to connect two or more separate applications, to coordinate requests from an application’s front end and back-end services, and to connect applications to databases. The Parties’ activities overlap in Integration Software overall, as well as in two types of Integration Software: API management software (59) and integration platforms (60).

(62) As regards API Management Software, IBM offers IBM API Connect, whereas Red Hat offers 3scale API Management. As regards integration platforms, IBM offers IBM App Connect and Red Hat offers Fuse and Fuse Online.

4.2.4.1. Commission precedents

(63) In Oracle/BEA (61), the Commission identified application integration software as a possible relevant market, although it ultimately left the market definition open.

(64) In Oracle/Sun, the Commission concluded that the relevant geographic market for application integration software is worldwide. (62) Similarly, in Oracle/Sun, the Commission concluded that the relevant geographic market for middleware and sub-segments thereof is worldwide. (63)

4.2.4.2. Notifying Party's views

(65) The Notifying Party refers to IDC’s segment for Integration Software which is further sub-segmented into (i) API Management Software, (ii) Integration Platforms, and (iii) Connectivity Adapters And Plug-in Software. The Notifying Party submits that the relevant product market should encompass all Integration Software products without distinguishing between the three categories of products. In the Notifying Party’s view, all these products perform the same function of enabling communication and the exchange of services and data between applications in real time. (64) Nevertheless, the Notifying Party provided market shares data both for Integration Software and the narrowest possible sub- segments as per IDC where both Parties are active, i.e. (i) API Management Software and (ii) Integration Platforms. (65) Only the overall Integration Software segment and its API Management Software sub-segment are affected.

(66) The Notifying Party submits that, in line with the Commission decisions listed at paragraphs (63)-(64), the relevant geographic market for Integration Software (and any possible sub-segment thereof) is global. Nevertheless, the Notifying Party also provided EEA-based market shares for completeness. (66)

4.2.4.3. Commission’s assessment

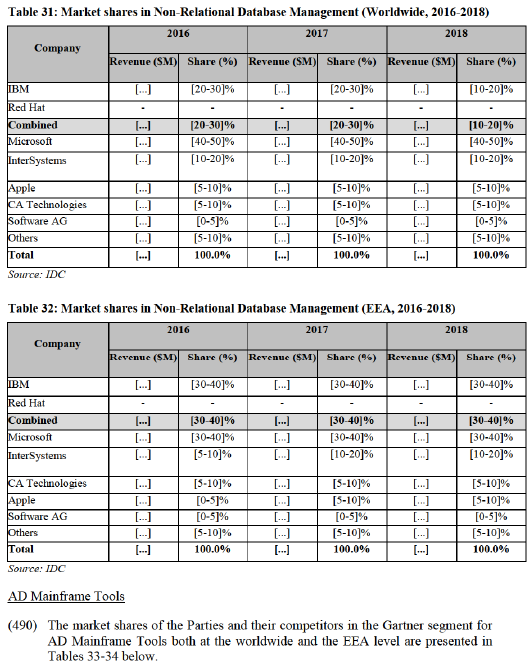

(67) In line with Oracle/BEA and IDC segmentation, the possible product market for Integration Software and its sub-segment for API Management Software can be identified. Nevertheless, the Commission considers that for the purpose of the present decision, the exact product market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under the narrowest possible product market definition identified by IDC for which market shares data is available and which leads to the highest combined market shares of the Parties.

(68) In line with the Commission decisions listed at paragraphs (63)-(64), the Commission considers that the relevant geographic market for Integration Software (and any possible sub-segment thereof) is global. Nevertheless, for completeness, the Commission carried out the competitive assessment in Section 5.2.4 also at the EEA-wide level.

4.2.5. Event-Driven Middleware

(69) Event-Driven Middleware is software that enables program-to-program (or component-to-component) communication—i.e. it facilitates the transfer of information between disparate applications and components across multiple hardware and software platforms that would not otherwise be able to communicate.

(70) IBM offers the following products that fall into Event-Driven Middleware: IBM MQ, IBM Event Streams, and Cloud Functions. Red Hat offers Red Hat AMQ (including Red Hat AMQ Streams).

4.2.5.1. Commission precedents

(71) There is no Commission precedent with regard to Even-Driven Middleware.

(72) In Oracle/Sun (67), the Commission concluded that the relevant geographic market for middleware and sub-segments thereof is worldwide.

4.2.5.2. Notifying Party's views

(73) The Notifying Party refers to IDC’s segment for Event-Driven Middleware which is further sub-segmented into (i) Message-Oriented Middleware, (ii) Streaming Analytics Software, and (iii) Functions Software. (68) IDC does not provide market shares for these sub-segments.

(74) The Notifying Party submits that the relevant product market should encompass all Event-Driven Middleware without distinguishing between the three categories of products. In the Notifying Party’s view, all these products perform the same function: monitoring and detecting events and transmitting the events to relevant applications and systems to execute a response.

(75) According to the Notifying Party, while certain software are more adapted to the transmission of structured messages rather than real-time events, other software combine both capabilities in one product. For example, Red Hat AMQ is equipped to handle traditional messages (including through a centralized message hub) and to carry out real-time event streaming based on Apache Kafka technology. The Notifying Party explains that while certain software may focus on the transmission of events rather than their processing and analysis, other products incorporate all these functions. For example, AWS Kinesis provides customers with the ability to capture continuous real-time data (such as video streams from security cameras), and to process and analyze these volumes of data (for example, to solve traffic problems, prevent crime, or dispatch emergency responders). (69)

(76) The Notifying Party argues that there is also significant substitution of supply, as the main providers of Event-Driven Middleware have all developed offerings suitable for transmitting traditional messages and/or real-time events and products with processing and analytics capabilities.

(77) The Notifying Party submits that, in line with the Commission decision listed at paragraph 72, the relevant geographic market for Even-Driven Middleware is global. Nevertheless, the Notifying Party also provided EEA-based market shares for completeness. (70)

4.2.5.3. Commission’s assessment

(78) The Commission considers that in line with IDC’s segmentation, a possible product market for Event-Driven Middleware can be identified. Based on the Notifying Party’s submission, there are many offerings which can support and combine capabilities for messaging, streaming analytics and functions software. Therefore, the Commission does not consider that it would be justified to further sub-segment the possible market for Event-Driven Middleware.

(79) Nevetheless, the Commission considers that for the purpose of the present decision the product market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market regardless of whether there is an overall market for Event-Driven Middleware or whether there are separate markets for different types of Event-Driven Middleware.

(80) In line with the Commission decisions listed at paragraph 72, the Commission considers that the relevant geographic market for Event-Driven Middleware is global. Nevertheless, for completeness, the Commission carried out the competitive assessment in Section 5.2.5 also at the EEA-wide level.

4.2.6. Managed File Transfer Software

(81) Managed File Transfer Software enables enterprises to transfer files securely and at high speeds over a network, such as the Internet. Managed File Transfer software typically offers a higher-level of security and/or convenience compared to other file transfer options, such as e-mail or external storage devices. They may include additional features such as reporting (i.e. notification of successful file transfers), automation of file transfer-related activities and auditability.

(82) IBM offers the following solutions: IBM Connect:Direct, IBM Aspera, IBM File Gateway, IBM Supply Chain Business Network File Transfer Service, and IBM WebSphere MQ. Each offering provides specific capabilities or deployment models targeting a comprehensive range of use cases. Red Hat is not active in Managed File Transfer Software.

4.2.6.1. Commission precedents

(83) There is no Commission precedent with regard to Managed File Transfer Software.

(84) In Oracle/Sun (71), the Commission concluded that the relevant geographic market for middleware and sub-segments thereof is worldwide.

4.2.6.2. Notifying Party's views

(85) The Notifying Party submits that Managed File Transfer Software (in line with IDC’s taxonomy) constitutes a separate relevant product market. (72) The IDC taxonomy identifies the functional market Managed File Transfer Software within the secondary market for Integration and Orchestration Software and the primary market Application Development and Deployment Software. IDC does not segment this functional market further.

(86) The Notifying Party submits that, in line with the Commission decision listed at paragraph (84), the relevant geographic market for Managed File Transfer Software is global. Nevertheless, the Notifying Party also provided EEA-based market shares for completeness. (73)

4.2.6.3. Commission’s assessment

(87) The Commission considers that in line with IDC’s segmentation, a possible product market for Managed File Transfer Software can be identified. Nevertheless, the Commission considers that for the purpose of the present decision, the exact product market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under the narrowest product market definition identified by IDC for which market shares data is available and which leads to the highest market shares of the Parties.

(88) In line with the Commission decisions listed at paragraph (84), the Commission considers that the relevant geographic market for Managed File Transfer Software is global. Nevertheless, for completeness, the Commission carried out the competitive assessment in Section 5.3.7.3 also at the EEA-wide level.

4.2.7. Business Rules Management Systems

(89) Business rules management systems (“BRMS”) enable business managers to define business rules in a familiar language and manage them in a central repository. Business applications can then be programmed to draw on these rules. This eliminates the need to modify the source code of individual applications each time rules are implemented or updated.

(90) IBM offers IBM Operational Decision Manager (“ODM”) in this market segment, whereas Red Hat offers Red Hat Decision Manager (formerly Red Hat JBoss BRMS).

4.2.7.1. Commission precedents

(91) In IBM/ILOG (74), the Commission identified BRMS as a relevant market.

(92) In Oracle/Sun, the Commission concluded that the relevant geographic market for middleware and sub-segments thereof is worldwide. Similarly, in IBM/ILOG, the Commission concluded that the relevant geographic market for BRMS is worldwide. (75)

4.2.7.2. Notifying Party's views

(93) The Notifying Party submits that relevant product market should be defined as the market for BRMS, as per IDC’s taxonomy. In the Notifying Party's view, BRMS form a separate relevant product market to BPM Suites (see Section 4.2.3). The Notifying Party submits that BPM Suites and BRMS products are often sourced independently of each other, and there is robust demand for standalone BRMS software. (76)

(94) The Notifying Party submits that, in line with the Commission decisions listed at paragraphs (91)-(92), the relevant geographic market for BRMS is global. Nevertheless, the Notifying Party also provided EEA-based market shares for completeness. (77)

4.2.7.3. Commission’s assessment

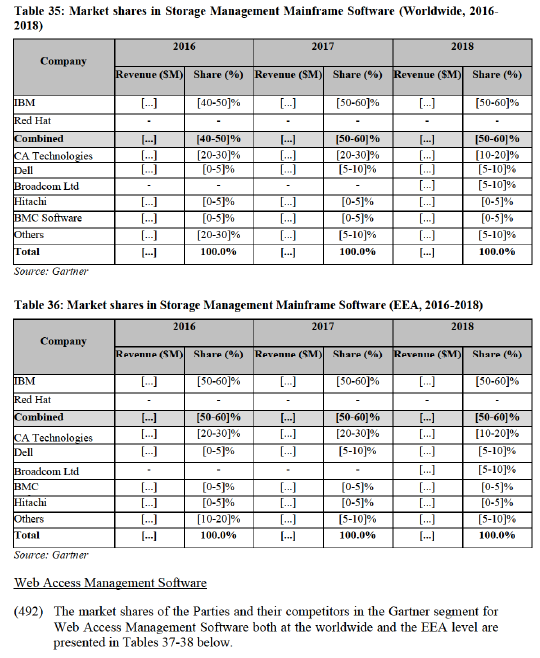

(95) In line with IBM/ILOG, the product market for BRMS can be identified. Nevertheless, the Commission considers that for the purpose of the present decision, the exact product market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under the narrowest possible product market definition for which market shares data is available and which leads to the highest combined market shares of the Parties.

(96) In line with the Commission decisions listed at paragraphs (91)-(92), the Commission considers that the relevant geographic market for BRMS is global. Nevertheless, for completeness, the Commission carried out the competitive assessment in Section 5.2.6 also at the EEA-wide level.

4.2.8. Non-Relational Database Management Systems

(97) According to the Notifying Party, most databases systems today are relational databases that store data in separate tables, instead of placing all data in one large table, and define relationships between these tables. Non-relational database management systems ("DBMS") refer to a residual category of database systems which do not use this system. Non-relational DBMS differ from relational DBMS in programming language and the structure used to organize the data.

(98) IBM offers a non-relational database management system (“DBMS”), called Information Management System. Red Hat is not active in non-relational database management systems.

4.2.8.1. Commission precedents

(99) In IBM/Informix (78), the Commission considered the database market as a whole (without segmentation by relational and non-relational databases), and also considered possible segmentations by “legacy” and distributed environments, operative system and customer requirements, but ultimately left the product market definition open. In Oracle/Sun and SAP/Sybase (79), the Commission segmented the database market between relational and non-relational databases. It also considered further sub-segmentation, but ultimately left the question open. (80)

(100) In Oracle/Sun, SAP/Sybase, and IBM/Informix, the Commission concluded that the relevant geographic market for databases is global.

4.2.8.2. Notifying Party's views

(101) The Notifying Party refers to IDC’s segment for Non-Relational DBMS, which is sub-segmented into four sub-markets: (i) end-user, (ii) navigational, (iii) object- oriented, and (iv) multivalue database management systems. The Notifying Party submits that IDC’s segment for Non-Relational Database Management Software (“DBMS”) constitutes the relevant product market. (81) Nevertheless, the Notifying Party submitted market shares data for the narrowest possible market segmentation including IBM’s product: the Gartner subsegment Prerelational Era DBMS (see Section 5.3.7.3).

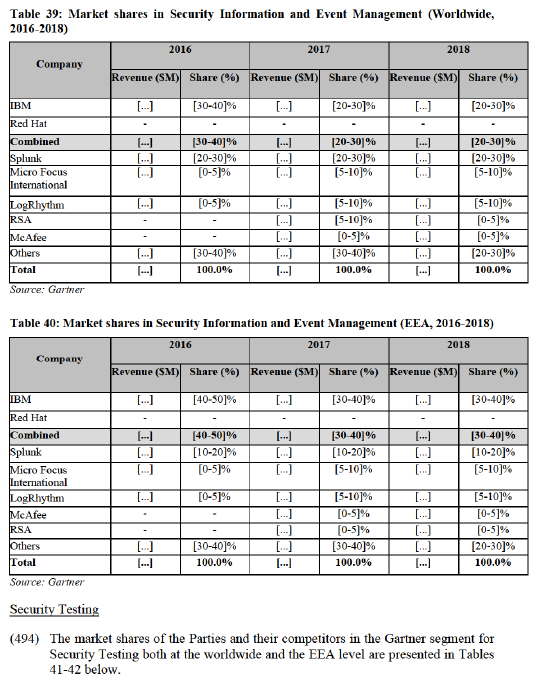

(102) According to the Notifying Party, Non-relational DBMS differ from relational DBMS in programming language and the structure used to organize the data: Non-relational DBMS are not strictly based on the (standard) programming language SQL for data definition and access or on relational theory, i.e. an organization of data in different tables which are formally related to each other.

(103) In the Notifying Party’s view, a large number of competitors are active in Non- Relational DBMS, including Microsoft’s NoSQL on Azure, InterSystems’ Caché, CA Technologies’ Datacomm, and Apple’s FoundationDB, each generating at least USD 100 million in annual worldwide revenues from sales of Non- Relational DBMS. In addition, there is a large range of popular and successful open source offerings, including MongoDB, Redis, Apache Cassandra, HBase, Couchbase and many more. The Notifying Party submits that customers consider these Non-Relational DBMS products substitutable for each other as they all support a multi-value format, in-database computing, intelligent interface services, and emerging data types suited for cloud environment, providing comparable level of support and interoperability. (82)

(104) The Notifying Party submits that, in line with the Commission decisions listed at paragraphs (99)-(100), the relevant geographic market for Non-Relational DBMS is global. Nevertheless, the Notifying Party also provided EEA-based market shares for completeness. (83)

4.2.8.3. Commission’s assessment

(105) In line with Oracle/Sun, SAP/Sybase, and IBM/Informix, the product market for Non-Relational DBMS can be identified. The Commission considers that, for the purpose of the present decision it can be left open whether Non-Relational DBMS constitute a relevant product market and whether it needs to be further sub- segmented as the competitive assessment under Section 5.3.7.3 remains unchanged irrespective of the exact product market definition.

(106) In line with the Commission decisions listed at paragraphs (99)-(100), the Commission considers that the relevant geographic market for Non-Relational DBMS is global. Nevertheless, for completeness, the Commission carried out the competitive assessment in Section 5.3.7.3 also at the EEA-wide level.

4.3. System Infrastructure Software

4.3.1. Software-Defined Storage Controller Software

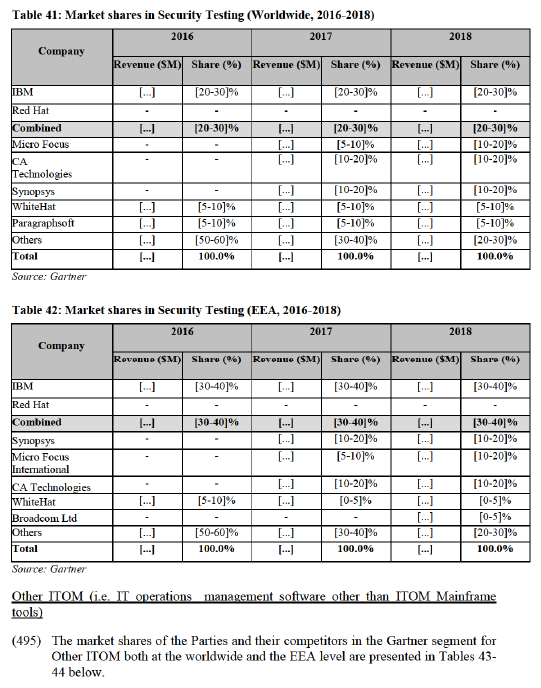

(107) Software-Defined Storage (“SDS”) refers to computer software programs that have been developed to optimize available storage hardware resources by creating a virtualized layer on top of the underlying physical storage hardware and that operates independently of the hardware to enable the efficient management of data storage and the scaling of data capacity, without being reliant on the hardware itself.

(108) IBM’s offering in the Software-Defined Storage Controller space includes: IBM Spectrum Virtualize (for block storage), IBM Spectrum Accelerate (for block storage), IBM Spectrum Scale (for file storage), IBM Spectrum NAS (for file storage), IBM Cloud Object Storage (formerly Cleversafe) (for object storage). Red Hat offers two basic SDS products: (i) Red Hat Ceph Storage and (ii) Red Hat Gluster Storage, based on open source Ceph and Gluster, respectively. These two products form the basis for Red Hat’s other offerings such as Red Hat Storage One, Red Hat Hyperconverged Infrastructure, and Red Hat OpenShift Container Storage.

4.3.1.1. Commission precedents

(109) In Dell/EMC (84), the Commission considered the segment of “storage and virtualization software” but ultimately left the precise product market definition open.

(110) In Symantec/Veritas (85), the Commission considered whether the broader market for storage software was worldwide or at least EEA-wide, but ultimately left the exact scope of the relevant geographic market open.

4.3.1.2. Notifying Party's views

(111) The Notifying Party refers to IDC’s functional market for SDS Controller Software which is further sub-segmented into (i) Block-Based, (ii) File-Based, (iii) Object-Based, and (iv) Hyperconverged Software-Defined Storage Controller Software.

(112) The Notifying Party submits that the relevant product market with regard to the Parties’ activities in the storage level of the IT stack is storage software which encompasses all software that manages, stores and/or ensures the accessibility, availability, and performance of information stored on physical storage media. As the Parties’ activities do not give rise to a horizontally affected market on the overall market for Storage Software, the Notifying Party refers to the narrower possible market for SDS Controller Software. (86)

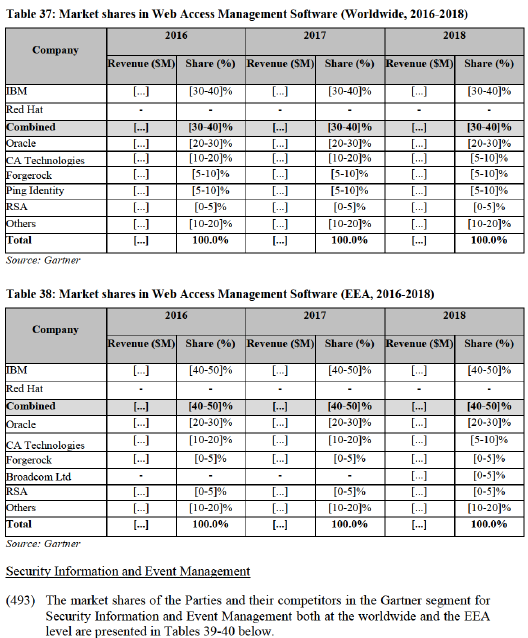

(113) According to the Notifying Party, under IDC’s taxonomy, SDS Controller Software includes and combines block, file, object, and hyperconverged software offerings that enable the creation of a storage system. Most SDS offerings support at least one of the three main types of storage methods: file, block and object storage. (87)

(114) With regard to SDS Controller Software, according to the Notifying Party, the various types of SDS Controller Software are substitutable from a supply perspective. A number of vendors are active with SDS offerings for multiple storage formats. For example, Dell EMC, Hitachi, NetApp, SUSE and Nexenta all offer SDS products for more than one type of storage. (88)

(115) The Notifying Party submits that, in line with the Commission decisions listed at paragraphs (109)-(110), the relevant geographic market for SDS Controller Software is global. Nevertheless, the Notifying Party also provided EEA-based market shares for completeness. (89)

4.3.1.3. Commission’s assessment

(116) The Commission considers that in line with Dell/EMC, a possible product market for SDS Controller Software can be identified. Based on the Notifying Party’s submission, there are a number of SDS Controller Software which support multiple types of storage.

(117) Nevertheless, for the purpose of the present decision the exact product market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market regardless of whether there is an overall market for SDS Controller Software or whether there are separate markets depending on the type of storage (Block-Based, File-Based, Object-Based, and Hyperconverged Software-Defined Storage Controller Software).

(118) In line with the Commission decisions listed at paragraphs (109)-(110), the Commission considers that the relevant geographic market for SDS Storage Controller Software is at least EEA-wide if not global. For the purpose of the present decision, the exact geographic market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible geographic market definition.

4.3.2. Container Infrastructure Software

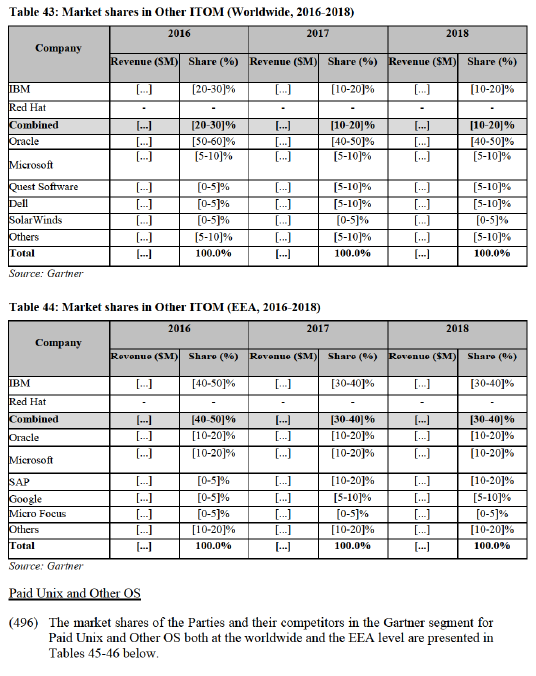

(119) Containers are small, isolated, lightweight virtual workspaces that sit on an operating system and are used to build, host, and deploy an application. Their small footprint compared to other virtual workspaces (like virtual machines) makes containers easily portable between different systems and well-suited to deployment across multiple clouds. Container Infrastructure Software (or “container platforms”) comprises container engines, which instantiate containers, and orchestration software, which facilitate the management of containers and automate tasks such as deployment, workload balancing between containers, and the movement of containers between hosts.

(120) IBM provides Container Infrastructure Software in two products: (i) IBM Cloud Private (“ICP”) and (ii) IBM Cloud Kubernetes Service (i.e. IBM’s public cloud managed Kubernetes service).

(121) ICP is a platform for developing and managing containerised applications. It is an integrated environment for managing containers that includes the container orchestrator (Kubernetes (90)), a private image repository, a management console, and monitoring frameworks. According to the Notifying Party, ICP is focused on […]: it consists of a private cloud that offers open source container platforms focused on using containers to achieve enhanced operational efficiency (targeting […]) and enable new […] technologies. (91)

(122) Red Hat offers several container infrastructure software products as part of the OpenShift family of products. (92) Red Hat OpenShift Container Platform (formerly known as OpenShift Enterprise) provides a platform for deploying both new and existing applications on secure, scalable resources with minimal configuration and management overhead. Enterprises run OpenShift on a wide variety of infrastructure, including public cloud environments, private cloud infrastructure, virtualization software, as well as bare-metal servers or a combination of all or some of the above.

(123) Red Hat OpenShift Container Platform should be distinguished from Red Hat OpenShift Container Engine—both are forms of the paid-for OpenShift product offered by Red Hat, but Red Hat OpenShift Container Engine consists simply of the RHEL or Core OS operating system, a container engine, and Red Hat’s Kubernetes orchestrator, while Red Hat OpenShift Container Platform also includes advanced management capabilities and more detailed development functionality.

4.3.2.1. Commission precedents

(124) In Dell/EMC (93), the Commission considered container technology and virtual machine-based virtualization software as distinct product markets within the broader category of virtualization software, but ultimately left the market definition open.

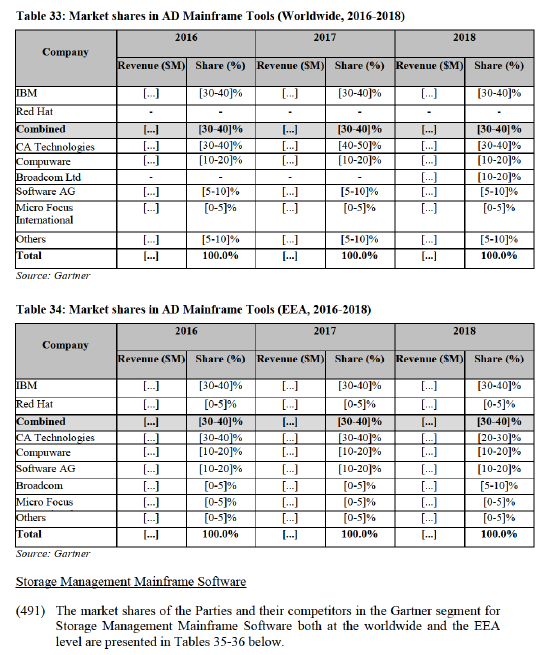

(125) In Dell/EMC (94), the Commission considered whether the market for Container Infrastructure Software was worldwide or at least EEA-wide, but ultimately left the exact scope of the relevant geographic market open.

4.3.2.2. Notifying Party's views

(126) The Notifying Party submits that IDC defines three submarkets within the functional market for Software Defined Compute Software: (i) Container Infrastructure Software, (ii) Virtual Machine Software, and (iii) Cloud System Software. According to the Notifying Party, the Transaction does not raise any concerns on any of the possible segmentations, and the precise product market definition can be left open. (95)

(127) The Notifying Party submits that, in line with the Commission decisions listed at paragraphs (124)-(125), the relevant geographic market for Container Infrastructure Software is global. Nevertheless, the Notifying Party also provided EEA-based market shares for completeness. (96)

4.3.2.3. Commission’s assessment

(128) In line with Dell/EMC and IDC’s segmentation, a possible market for Container Infrastructure Software can be identified. Nevertheless, the Commission considers that for the purpose of the present decision, the exact product market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under the narrowest product market definition identified by IDC for which market shares data is available and which leads to the highest combined market shares of the Parties. As only the subsegment for Container Infrastructure Software is affected, the Commission carried out the competitive assessment in Section 5.2.8 on the basis of the segmentation put forward by the Notifying Party in accordance with IDC’s segment for Container Infrastructure Software.

(129) In line with the Commission decisions listed at paragraphs (124)-(125), the Commission considers that the relevant geographic market for Container Infrastructure Software is at least EEA-wide if not global. For the purpose of the present decision, the exact geographic market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible geographic market definition.

4.3.3. Network Management Software

(130) Network management software is designed to reduce the burden on IT teams by facilitating and automating the network management process. Network management software monitors the devices connected to the network and collects reportable data on these devices. When the software detects a problem on the network (e.g. network faults, performance bottlenecks, or compliance issues), the software will either take any necessary remedial action automatically, or it will present the data to the relevant network administrator which allows the administrator quickly to identify and resolve the problem.

(131) IBM has one offering with network management features, i.e. IBM Netcool Network Management. Red Hat offers Red Hat Ansible Network Automation.

4.3.3.1. Commission precedents

(132) There is no Commission precedent with regard to Network Management Software.

4.3.3.2. Notifying Party's views

(133) The Notifying Party submits that the IDC segment for Network Management Software constitutes the relevant product market. The IDC taxonomy identifies a functional market for Network Management Software and does not segment this functional market further. According to the Notifying Party, the Transaction does not raise any concerns on any of the possible segmentations, and the precise product market definition can be left open. (97)

(134) The Notifying Party submits that, in line with Commission’s previous decisions concerning software, the relevant geographic market for Network Management Software is global. Nevertheless, the Notifying Party also provided EEA-based market shares for completeness. (98)

4.3.3.3. Commission’s assessment

(135) In line with IDC taxonomy, the possible market for Network Management Software can be identified. Nevertheless, the Commission considers that for the purpose of the present decision, the exact product market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under the narrowest product market definition identified by IDC for which market shares data is available and which leads to the highest combined market shares of the Parties.

(136) The Commission considers that the relevant geographic market for Network Management Software is at least EEA-wide, if not global. For the purpose of the present decision, the exact geographic market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible geographic market definition.

4.3.4. Storage Management Mainframe Software

(137) Storage Management Mainframe Software includes tools for storage mainframe implementations, including for archive, backup and recovery, core storage, data replication, and device resource management.

(138) IBM offers DFSMS, which comprises a suite of related data and storage management products for the z/OS operating system focused on managing the life-cycle of data and the devices and media associated with that data. Red Hat is not active in Storage Management Mainframe Software.

4.3.4.1. Commission precedents

(139) In Symantec/Veritas (99), the Commission considered the market definition for storage software more generally and considered that it was not necessary to distinguish the segments backup and archive software according to the OS on which software may run nor according to customer but category and ultimately left the market definition open.

(140) In Symantec/Veritas (100), the Commission considered whether the market for Storage Software was worldwide or at least EEA-wide, but ultimately left the exact scope of the relevant geographic market open.

4.3.4.2. Notifying Party's views

(141) The Notifying Party refers to Gartner’s macromarket for Storage Management Software, which is further divided into nine subsegments, including Storage Management Mainframe Software. (101) The Notifying Party submits that the relevant product market should encompass all software that manages, stores and/or ensures the accessibility, availability, and performance of information stored on physical storage media, and Storage Management Mainframe Software falls within that product market.

(142) In the Notifying Party’s view, vendors of storage software (including Dell EMC, Veritas, NetApp, Microsoft and HPE) are all active across a wide range of storage software and offer products with comparable levels of support and interoperability. The Notifying Party submits that these vendors, together with a number of other vendors and unpaid open source offerings, provide credible alternatives to and exercise a competitive constraint on IBM’s storage software offering. (102)

(143) According to the Notifying Party, the Transaction does not raise any concerns on any of the possible segmentations, and the precise product market definition can be left open. For the purpose of the present decision, the Notifying Party provides information needed to carry out the competitive assessment in Section 5.3.7.3 on the basis of Gartner’s sub-segment for Storage Management Mainframe Software, the only one of the nine sub-segments in which IBM is active. (103)

(144) The Notifying Party submits that, in line with Commission’s previous decisions concerning software, the relevant geographic market for Storage Management Mainframe Software is global. Nevertheless, the Notifying Party also provided EEA-based market shares for completeness. (104)

4.3.4.3. Commission’s assessment

(145) In line with the Commission decision in Symantec/Veritas and Gartner’s segmentation, a possible product market for Storage Management Mainframe Software can be identified. The Commission considers that for the purpose of the present decision the question whether Storage Management Mainframe constitutes a relevant product market and whether it needs to be further sub- segmented into different types of storage depending on their use can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under the narrowest possible product market definition for which market shares data is available. As Gartner’s segment for Storage Management Mainframe Software is the only one affected by the Transaction, the Commission carried out the competitive assessment in Section 5.3.7.3 on the basis of the segmentation put forward by the Notifying Party in accordance with Gartner’s segment for Storage Management Mainframe Software.

(146) The Commission considers that the relevant geographic market for Storage Management Mainframe Software is at least EEA-wide, if not global. For the purpose of the present decision, the exact geographic market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible geographic market definition.

4.3.5. Security Information and Event Management Software

(147) Security information and event management products provide a real-time analysis of the security alerts that have been generated by applications and network hardware. Once security threats (e.g. attacks by a hacker) have been identified, the product alerts the business to the attack and automates the response to such incident.

(148) IBM offers the QRadar family of products which provides an overview visibility of any organization´s security system, since they are able to detect security offences and report them, as well as provide insight that allow teams to respond quickly to reduce the impact of incidents. Red Hat is not active in security information and event management software.

4.3.5.1. Commission precedents

(149) In Intel/McAfee (105), the Commission segmented the market for Security Software following IDC and identified IDC’s functional market Endpoint Security as the relevant product market. It also envisaged further segmentation according to the type of end-customers, but ultimately left the market definition open. (106)

(150) In Intel/McAfee, the Commission considered whether the market for Security Software was worldwide or at least EEA-wide, but ultimately left the exact scope of the relevant geographic market open.

4.3.5.2. Notifying Party's views

(151) The Notifying Party submits that in line with the Commission decision listed at paragraph (149), the relevant market is the IDC segment for Security Analytics, Intelligence, Response, and Orchestration Software. However, as under this IDC segment, a non-horizontally affected market does not arise, the Notifying Party provides information needed to carry out the competitive assessment in Section 5.3.7.3 on the basis of Gartner’s sub-segment for Security Information and Event Management Software. According to the Notifying Party, the Transaction does not raise any concerns on any of the possible segmentations, and the precise product market definition can be left open. (107)

(152) The Notifying Party submits that, in line with line with Commission’s previous decisions concerning software, the relevant geographic market for Security Information and Event Management Software is global. Nevertheless, the Notifying Party also provided EEA-based market shares for completeness. (108)

4.3.5.3. Commission’s assessment

(153) In line with the Commission decision in Intel/McAfee and Gartner’s segmentation, a possible product market for Storage Management Mainframe Software can be identified. Nevertheless, the Commission considers that for the purpose of the present decision, the exact product market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market underunder the narrowest possible product market definition for which market shares data is available. As no IDC segments would be affected by the Transaction, the Commission therefore carried out the competitive assessment in Section 5.3.7.3 on the basis of the segmentation put forward by the Notifying Party in accordance with Gartner’s narrower segment for Security Information and Event Management Software.

(154) The Commission considers that the relevant geographic market for Security Information and Event Management Software is at least EEA-wide, if not global. For the purpose of the present decision, the exact geographic market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible geographic market definition.

4.3.6. Security Testing

(155) Security testing encompasses products aimed at software developers that want to test their web and mobile applications prior to deployment, to detect and fix any security issues. Security testing refers to both dynamic application security testing (“DAST”) (109) and static application security testing (“SAST”) (110).

(156) IBM offers IBM Security AppScan which is a family of web security testing and monitoring tools. Red Hat is not active in Security Testing Software.

4.3.6.1. Commission precedents

(157) In Intel/McAfee (111), the Commission segmented the market for security software following IDC and identified Endpoint Security. It also envisaged further segmentation according to the type of end-customers, which is an IDC functional market, as the relevant product market.

(158) In Intel/McAfee (112), the Commission considered whether the market for Security Software was worldwide or at least EEA-wide, but ultimately left the exact scope of the relevant geographic market open.

4.3.6.2. Notifying Party's views

(159) The Notifying Party submits that the relevant product market with regard to Security Testing is IDC’s functional market for Other Security Software. However, as under this IDC segment, a non-horizontally affected market does not arise, the Notifying Party provides information needed to carry out the competitive assessment in Section 5.3.7.3 on the basis of Gartner’s sub-segment for Security Testing Software (which is narrower than the IDC segment). (113)

(160) The Notifying Party submits that, with line with Commission’s previous decisions concerning software, the relevant geographic market for Security Testing Software is global. Nevertheless, the Notifying Party also provided EEA-based market shares for completeness. (114)

4.3.6.3. Commission’s assessment

(161) In line with the Commission decision in Intel/McAfee and Gartner’s segmentation, a possible product market for Storage Management Mainframe Software can be identified. Nevertheless, the Commission considers that for the purpose of the present decision, the exact product market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under the narrowest possible product market definition for which market shares data is available. As no IDC segments would be affected by the Transaction, the Commission therefore carried out the competitive assessment in Section 5.3.7.3 on the basis of the segmentation put forward by the Notifying Party in accordance with Gartner’s segment for Security Testing Software.

(162) The Commission considers that the relevant geographic market for Security Testing Software is at least EEA-wide, if not global. For the purpose of the present decision, the exact geographic market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible geographic market definition.

4.3.7. Web Access Management Software

(163) Web access management software is a form of identity management that controls access to web resources, by providing authentication management, policy-based authorisations, reporting and auditing services as well as single sign-on convenience.

(164) IBM’s range of products (115) ensures that the relevant people have access to business resources, by providing access controls for web, mobile, cloud and legacy apps, as well as desktops, VPNs, and servers. Red Hat is not active in Web Access Management Software.

4.3.7.1. Commission precedents

(165) In Intel/McAfee (116), the Commission segmented the market for security software following IDC.

(166) In Intel/McAfee (117), the Commission considered whether the market for Security Software was worldwide or at least EEA-wide, but ultimately left the exact scope of the relevant geographic market open.

4.3.7.2. Notifying Party's views

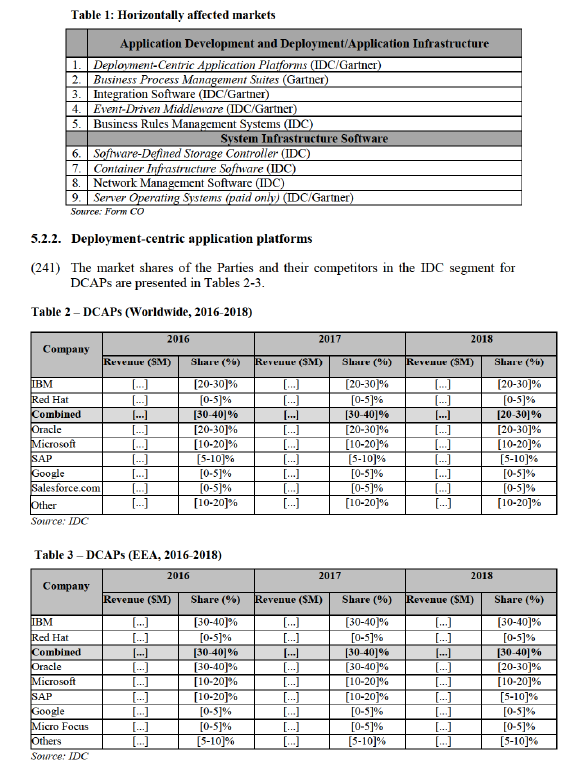

(167) The Notifying Party submits that the relevant product market with regard to its activities in Web Access Management Software is IDC’s segment for Identity And Digital Trust Software. However, as under this IDC segment, a non- horizontally affected market does not arise, the Notifying Party provides information needed to carry out the competitive assessment in Section 5.3.7.3 on the basis of Gartner’s sub-segment for Web Access Management Software (which is narrower than the IDC segment). (118)

(168) The Notifying Party submits that, in line with line with Commission’s previous decisions concerning software, the relevant geographic market for Web Access Management Software is global. Nevertheless, the Notifying Party also provided EEA-based market shares for completeness. (119)

4.3.7.3. Commission assessment

(169) In line with the Commission decision in Intel/McAfee and Gartner’s segmentation, a possible product market for Storage Management Mainframe Software can be identified. Nevertheless,the Commission considers that for the purpose of the present decision, the exact product market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under the narrowest possible product market definition for which market shares data is available. As no IDC segments would be affected by the Transaction, the Commission therefore carried out the competitive assessment in Section 5.3.7.3 on the basis of the segmentation put forward by the Notifying Party in accordance with Gartner’s segment for Web Access Management Software.

(170) The Commission considers that the relevant geographic market for Security Testing Software is at least EEA-wide, if not global. For the purpose of the present decision, the exact geographic market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible geographic market definition.

4.3.8. Other IT Operations Management

(171) Gartner identifies IT Operations Management (“ITOM”) Mainframe Tools as a distinct subsegment within the Gartner macromarket IT Operations Management. Other ITOM is a catch-all category that includes any management tools and/or integrated functionality not specifically covered by one of the other Gartner subsegments within its IT Operations Management macromarket. This includes: output management software used to manage hardware peripherals (such as printers); database administration automation and support tools that automate routine administration of databases; schema development and management; query analyzers; reorganization utilities; space tuners; and bulk data loading/unloading technologies.

(172) IBM's products falling within the category of Other ITOM are: IBM Netcool Operations Insight (120) and IBM Operations Analytics (121). Red Hat is not active in Other ITOM.

4.3.8.1. Commission precedents

(173) There is no Commission precedent with regard to ITOM tools.

4.3.8.2. Notifying Party's views

(174) The Notifying Party submits that the relevant product market with regard to its activities in Other ITOM is IDC’s segment for ITOM software. However, as under this IDC segment, a non-horizontally affected market does not arise, the Notifying Party provides information needed to carry out the competitive assessment in Section 5.3.7.3 on the basis of Gartner’s sub-segment for Other ITOM Tools (which is narrower than the IDC segment). According to the Notifying Party, the Transaction does not raise any concerns on any of the possible segmentations, and the precise product market definition can be left open. (122)

(175) The Notifying Party submits that the relevant geographic market for Other ITOM is global. Nevertheless, the Notifying Party also provided EEA-based market shares for completeness. (123)

4.3.8.3. Commission’s assessment

(176) In line with Gartner’s segmentation, a possible product market for Other ITOM can be identified. Nevertheless, the Commission considers that for the purpose of the present decision, the exact product market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under the narrowest possible product market definition for which market shares data is available. As no IDC segments would be affected by the Transaction, the Commission therefore carried out the competitive assessment in Section 5.3.7.3 on the basis of the segmentation put forward by the Notifying Party in accordance with Gartner’s segment for Other ITOM.

(177) The Commission considers that the relevant geographic market for Other ITOM is at least EEA-wide, if not global. For the purpose of the present decision, the exact geographic market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible geographic market definition.

4.3.9. AD Mainframe Tools

(178) Application Development (“AD”) mainframe tools are used to develop and maintain applications that run on IBM’s proprietary System z mainframes. (124) Red Hat is not active in AD mainframe tools.

4.3.9.1. Commission precedents

(179) There is no Commission precedent with regard to AD Mainframe Tools but the Commission has considered the broader category of application development software in previous decisions. In these decisions, the Commission investigated different types of application development software constitute separate product markets, but ultimately left the market definition open. (125)

(180) In its previous decisions considering application development software, the Commission considered whether the market was worldwide or at least EEA-wide, but ultimately left the exact scope of the relevant geographic market open.

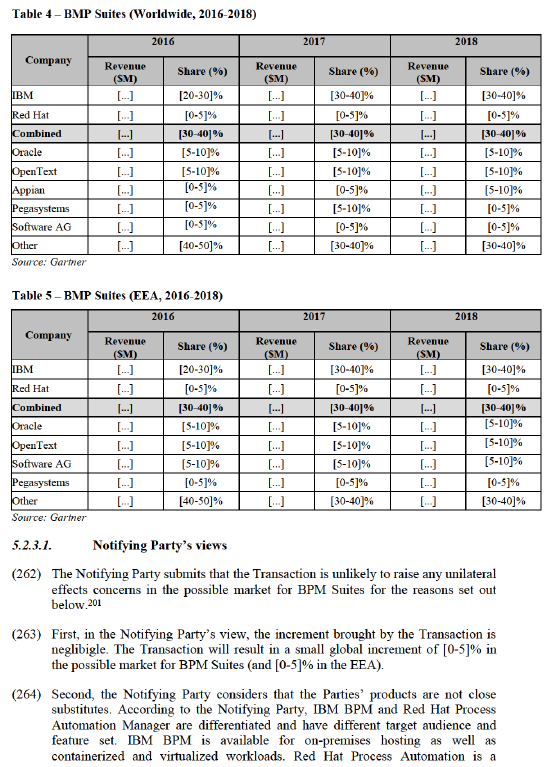

4.3.9.2. Notifying Party's views

(181) The Notifying Party submits that the relevant product market is Gartner’s segment for AD Mainframe Tools, which is not segmented further. IDC does not identify a distinct segment for AD mainframe tools, although they are likely to fall within the IDC secondary market of Application Development Software.

(182) According to the Notifying Party, while application development tools generally include multiple sets of products that enable application discovery, management, development, testing, debugging, DevOps, and performance analysis for application developers, AD Mainframe Tools include specific capabilities to enhance, simplify and automate these activities for developers and operational engineers who are producing and maintaining applications targeting the mainframe. (126)

(183) In line with previous Commission decisions where different types of application development tools have tended to be considered distinct markets (discussed at paragraph (179) above), the Notifying Party considers AD mainframe tools as the relevant product market and provides shares of sales based on Gartner data for this segment.

(184) The Notifying Party submits that the relevant geographic market for AD Mainframe Tools is global. Nevertheless, the Notifying Party also provided EEA- based market shares for completeness. (127)

4.3.9.3. Commission’s assessment

(185) In line with Gartner’s segmentation, a possible product market for AD Mainframe Tools can be identified. Nevertheless, the Commission considers that for the purpose of the present decision, the exact product market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under the narrowest possible product market definition for which market shares data is available. The Commission therefore carried out the competitive assessment in Section 5.3.7.3 on the basis of the segmentation put forward by the Notifying Party in accordance with Gartner’s segment for AD Mainframe Tools.

(186) The Commission considers that the relevant geographic market for AD Mainframe Tools is at least EEA-wide, if not global. For the purpose of the present decision, the exact geographic market definition can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible geographic market definition.

4.3.10. Server Operating Systems

(187) Operating systems manage computer hardware (e.g., processing, memory, and storage) and all other programs in a computer. In the traditional IT stack, operating systems sit above hardware and below middleware and applications. Operating systems save application developers from tailoring their program to the specific hardware in each computer—instead, they write the program for an operating system which provides it with the necessary computer resources to run.

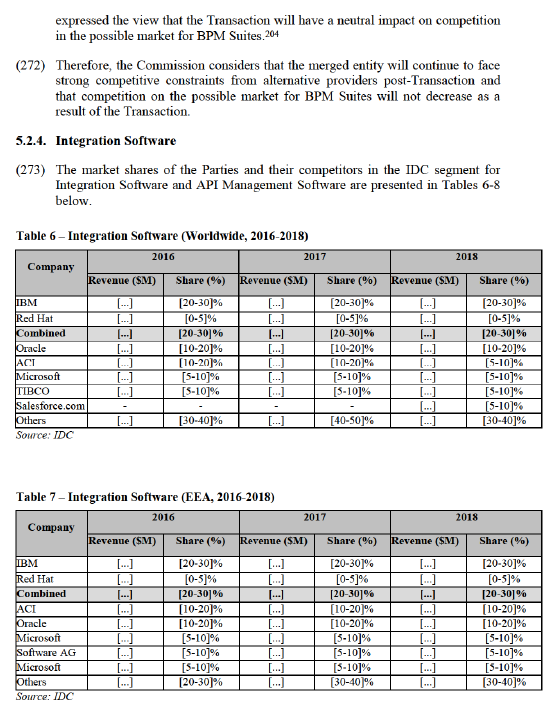

(188) The vast majority of servers today run Windows or Linux operating systems. Windows (128) and Linux are estimated to account for more than [90-100]% of new server operating system deployments and more than [90-100]% of the installed base in 2017. (129) The remainder of deployments are either Unix (130) or other proprietary server operating systems, both of which have significantly declining sales and installed bases. (131)

(189) Linux refers to a range of operating systems built on the Linux kernel, a free, open source operating system core developed by Linus Torvalds in the early 1990s. Because the Linux kernel is open source, it can be modified and tailored to suit different needs. As a result, a range of desktop, mobile, and server Linux distributions have emerged. Linux distributions can be maintained by the open source community, produced commercially—or both. (132)

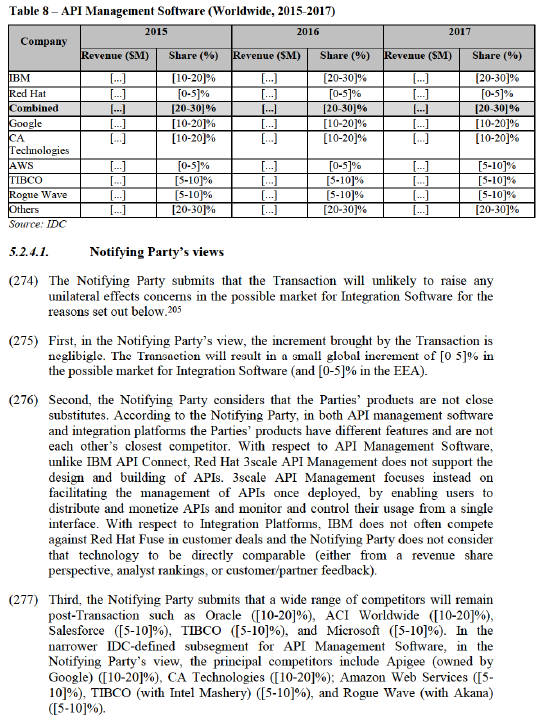

(190) Red Hat offers Red Hat Enterprise Linux (“RHEL”) and IBM’s operating systems are proprietary and based on either Unix or IBM’s own code base: z/OS, zVSE, zTPF, AIX, and IBM i. z/OS, zVSE, and zTPF run exclusively on IBM’s z processors, while AIX and IBM i run exclusively on IBM’s POWER processor architecture.

4.3.10.1. Commission precedents

(191) In Oracle/Sun, the Commission referred to its Microsoft antitrust decision (133) where it had identified a market for work group server operating systems, distinct from other software. (134) It did not segment server operating systems by processor type, or operating system family (i.e., Windows, Linux, or Unix), but ultimately left open the precise product market definition.

(192) In Oracle/Sun, the Commission referred to its Microsoft antitrust decision where it identified a worldwide geographic market for server operating systems.

4.3.10.2. Notifying Party’s view

(193) The Notifying Party considers that the relevant product market for operating systems should encompass all server operating systems, i.e. Windows (server), Linux, Unix, including any “descendants” thereof, such as Solaris, HP-UX and AIX, and other proprietary operating systems, such as IBM i, z/OS, and z/VSE. This product market definition is consistent with the IDC submarket for Core Operating Systems (i.e. server operating systems). It submits that further segmentation of the product market for server operating systems between paid/unpaid or depending on the family (Linux, Windows, etc.) is not warranted. According to the Notifying Party, server operating systems all perform the same basic function, regardless of which “family” they are in. (135)

(194) The Notifying Party submits that, in line with the Commission decisions listed at paragraphs (191)-(192), the relevant geographic market is global. Nevertheless, the Notifying Party also provided EEA-based market shares for completeness. (136)

4.3.10.3. Commission’s assessment

(195) RHEL is the most successful and widely used paid supported Linux distribution. The Commission therefore investigated whether the following categories of server operating systems can be considered part of the same relevant product market as paid supported Linux distributions: (1) free unsupported Linux distributions, (2) other free unsupported open-source operating systems, and (3) other paid supported operating systems from different families (e.g., Microsoft Windows, Unix-based operating systems such as IBM’s AIX, Oracle’s Solaris and HP-UX, and other proprietary operating systems).

(196) As regards free unsupported Linux distributions, the Commission considers that demand-side substitution is most likely too limited to constraint a hypothetical monopolist in paid supported Linux distribution. This is for the following reasons.

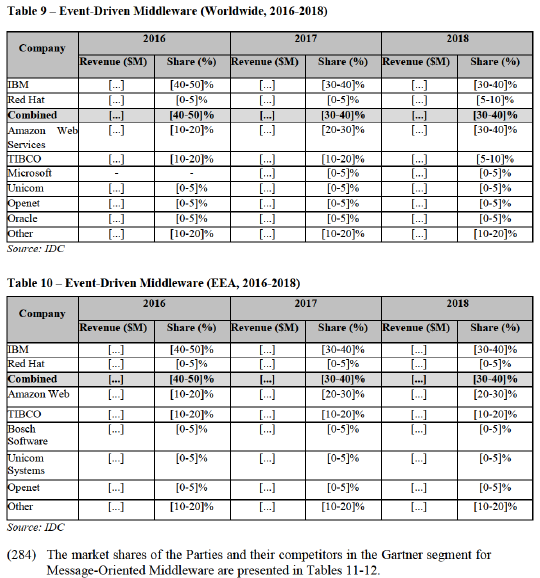

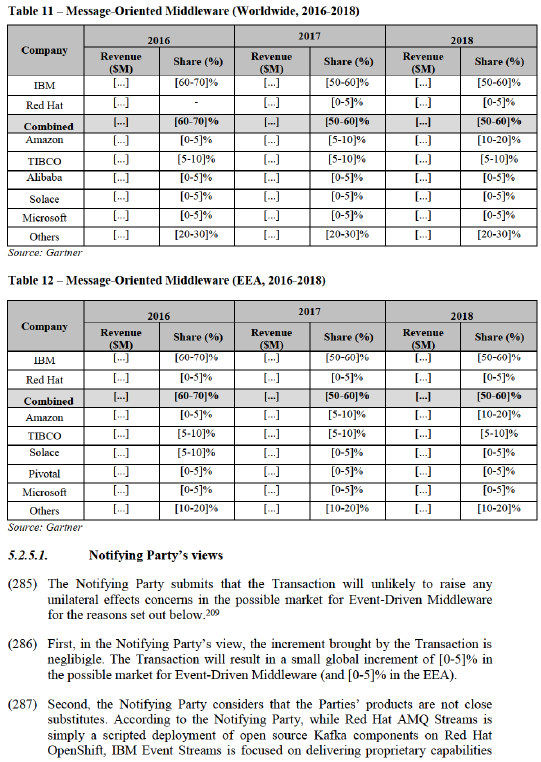

(197) First, a large majority of competitors responding to the market investigation considered that competition between paid Linux distributions and free unsupported Linux distributions was either limited or very limited. Some competitors explained that free unsupported Linux distributions are not considered for mission-critical workloads. Within enterprises, free Linux distributions would mainly be used in testing and development efforts, but not in production. (137) Rival Linux distributors explained that customers who choose to go for a paid Linux distribution do it because they need the support. The Commission therefore considers that customers using paid Linux operating systems would be unlikely to switch to unsupported Linux distributions, at least for mission-critical workloads. (138)

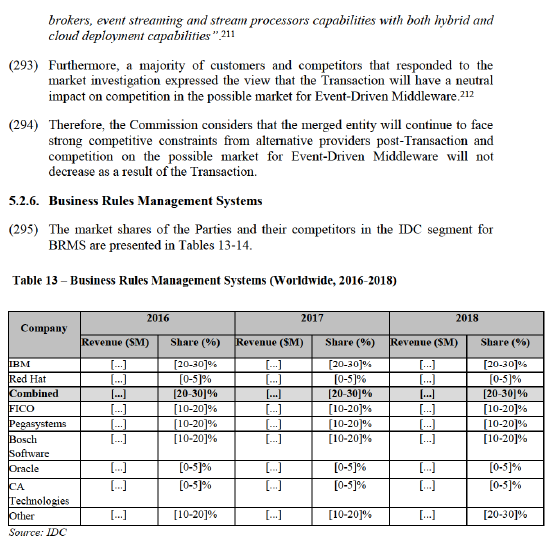

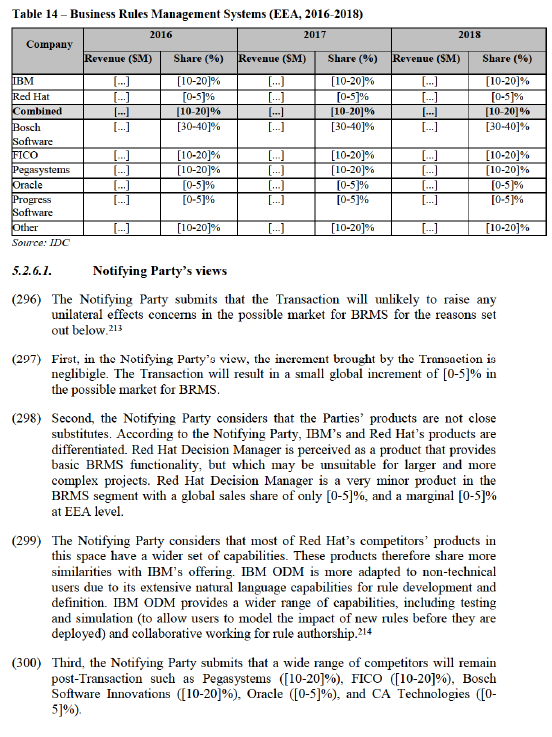

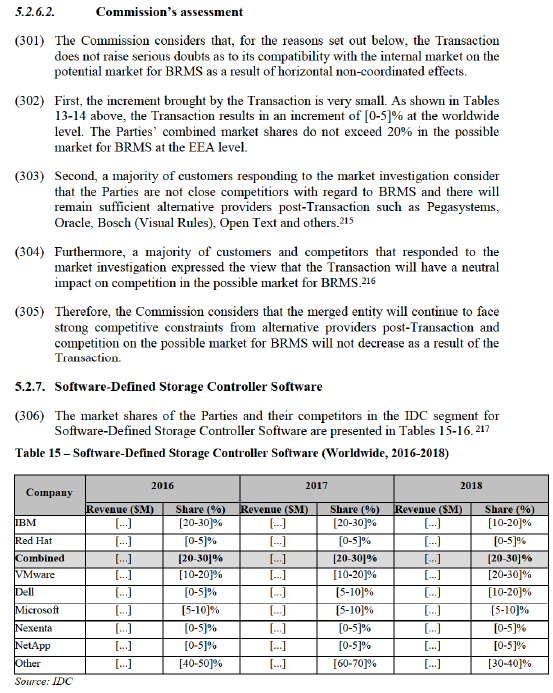

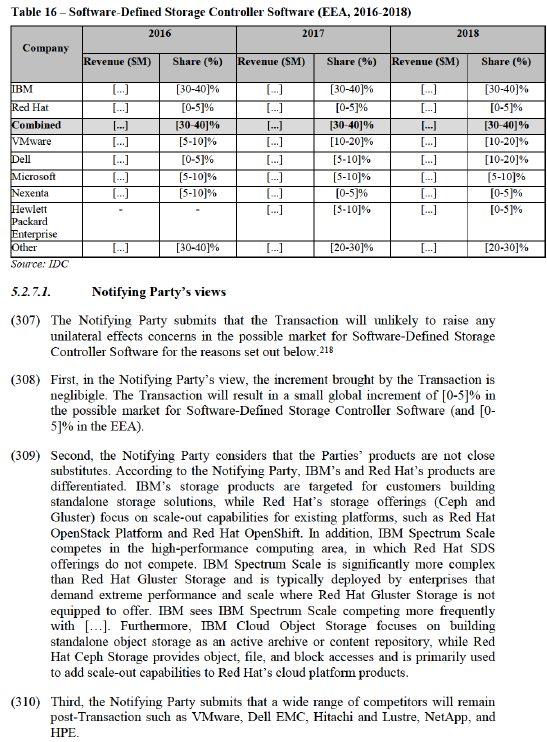

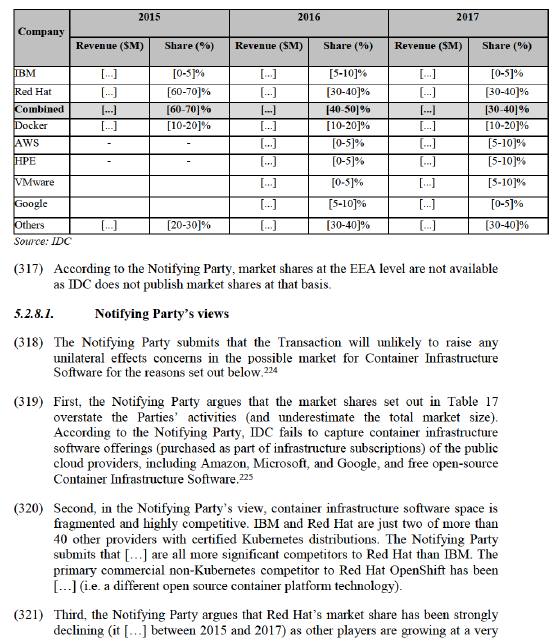

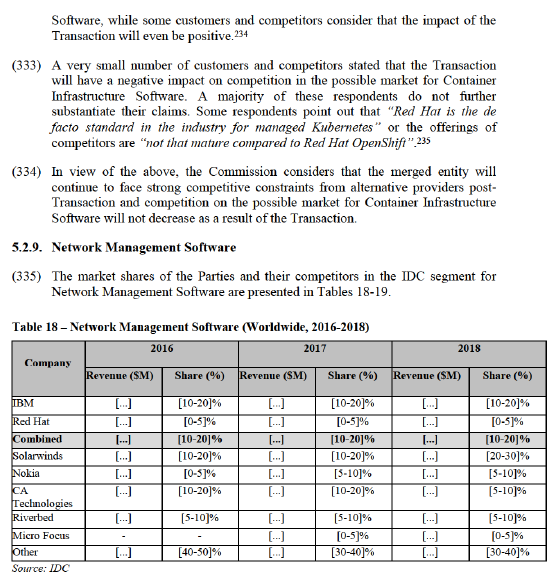

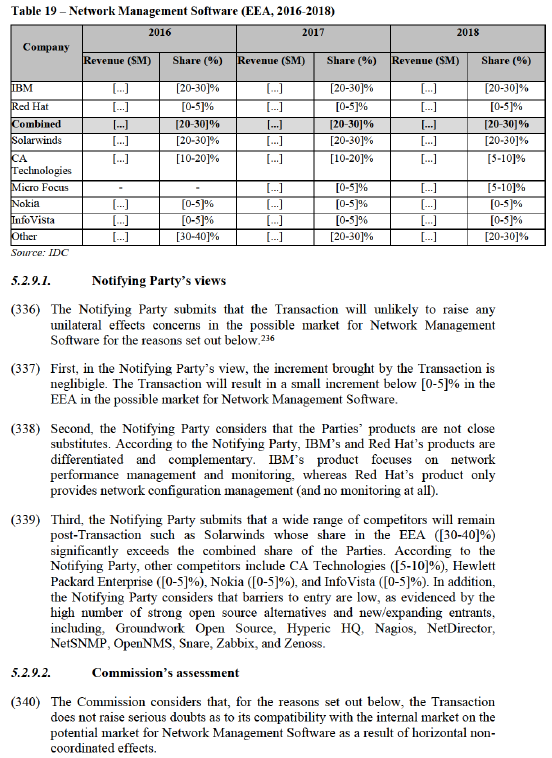

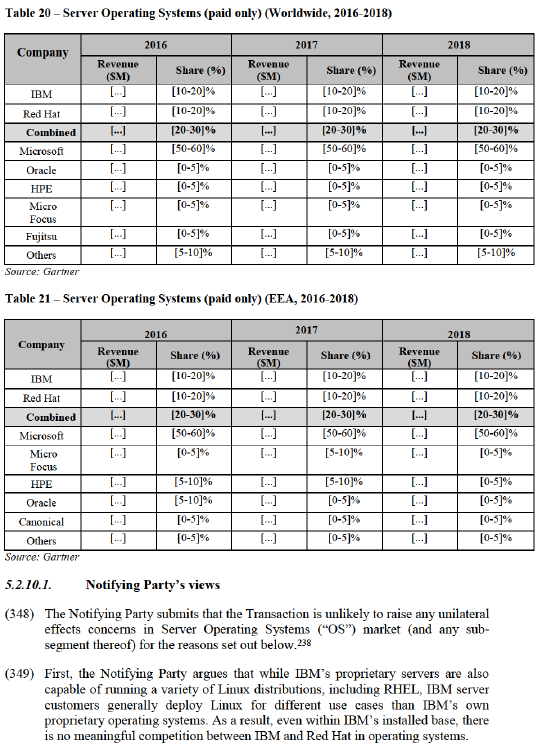

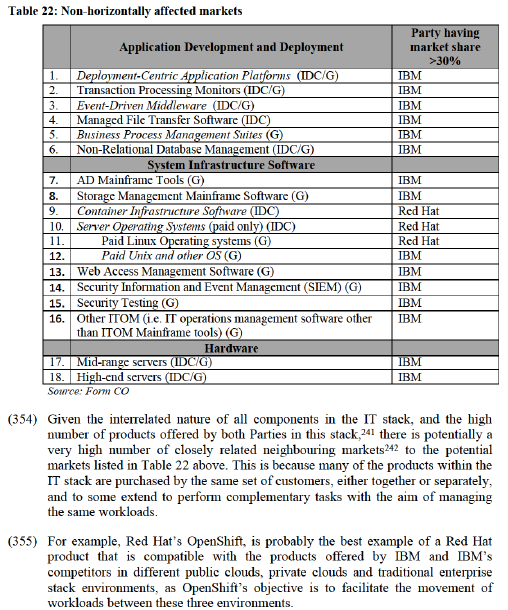

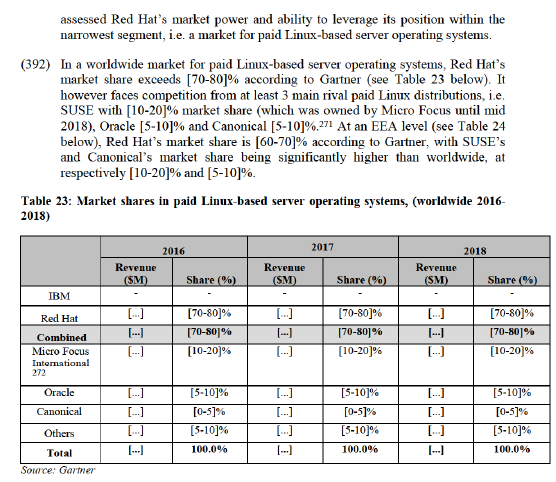

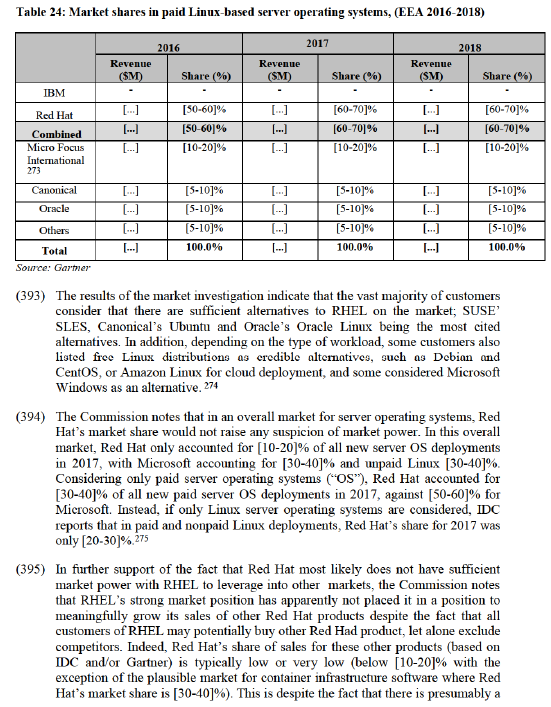

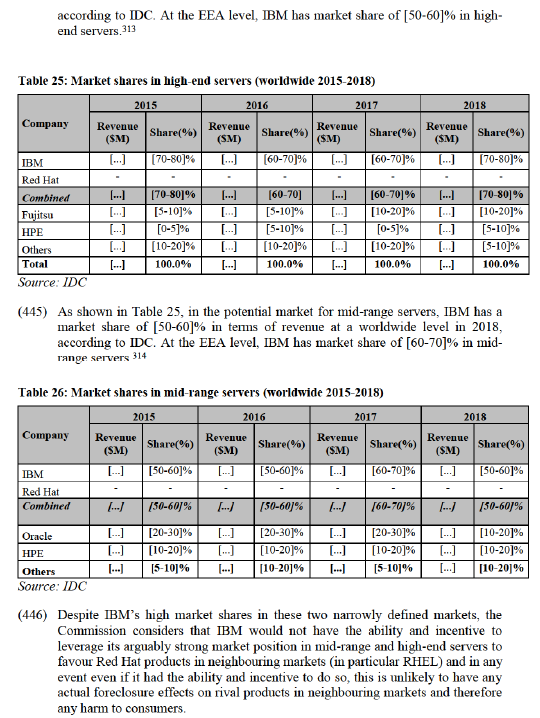

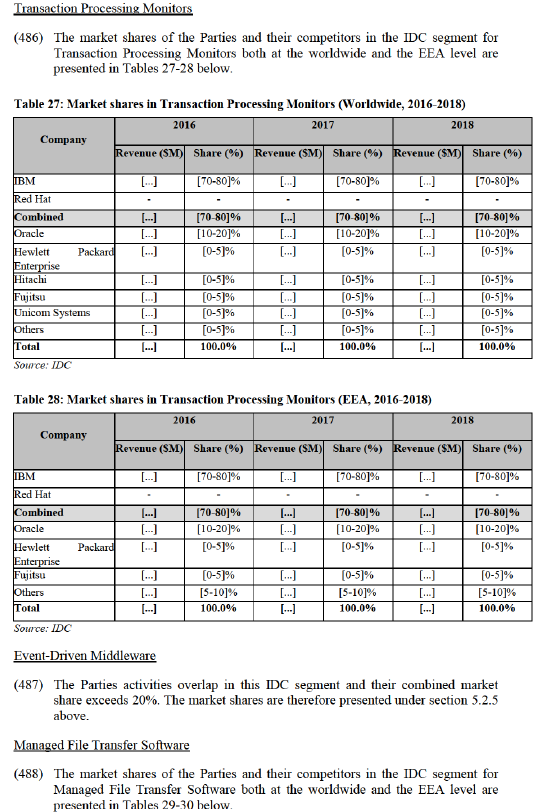

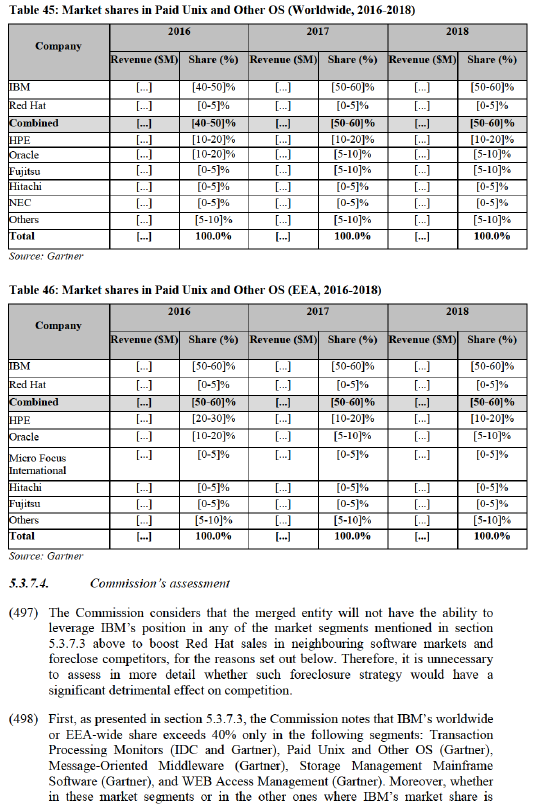

(198) Second, on the customers’ side, a majority of them do not consider free unsupported Linux distributions to be possible alternatives to paid supported Linux distributions. (139) Customers explain that it is generally a company policy to opt for supported distributions, and unsupported alternatives would in any event not be considered.