Commission, July 5, 2017, No M.8449

EUROPEAN COMMISSION

Decision

PEUGEOT / OPEL

Subject: Case M.8449 - PEUGEOT / OPEL

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 30.05.2017, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which the undertaking Peugeot S.A. ("PSA" of France) acquires within the meaning of Article 3(1)(b) of the Merger Regulation sole control over the automotive business of Opel/Vauxhall ("Opel") by way of purchase of shares and assets (hereafter, the "Transaction").3 PSA is designated hereinafter as the "Notifying Party" and together with Opel as the "Parties".

1. THE PARTIES

(1) PSA is active worldwide in manufacturing and supplying passenger cars and light commercial vehicles ("LCVs") under the Peugeot, Citroën and DS brands.Through its subsidiary, Faurecia S.A., it is also active in the manufacturing and supply of interior automotive components.

(2) Opel is currently controlled by General Motors Company ("GM", the USA) and consists of GM's European automotive business under the Opel and Vauxhall brands. Opel manufactures and supplies passenger cars and LCVs.4

2. THE OPERATION

(3) The "Transaction" consists of the acquisition of all assets and shareholdings related to Opel. As a result, PSA will solely control Opel. The Transaction therefore constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

3. EU DIMENSION

(4) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5,000 million.5 Each of them has an EU-wide turnover in excess of EUR 250 million, but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State.

(5) The notified operation therefore has an EU dimension under Article 1(2) of the Merger Regulation.

4. RELEVANT MARKETS

4.1. Manufacturing and supply of passenger cars and LCVs

(6) The Commission has in the past considered separate markets for the manufacturing and supply of passenger cars on the one hand, and of commercial vehicles on the other hand.6 The Notifying Party agrees with this distinction which is retained for the present case.

4.1.1. Product market definition

4.1.1.1. Passenger cars

The Notifying Party's view

(7) The Notifying Party agrees with the Commission's decisional practice7 defining separate product markets for (i) mini cars, (ii) small cars, (iii) medium cars (iv) 2large cars, (v) executive cars, (vi) luxury cars (vii) sport cars, (viii) sport utility vehicles ("SUVs") and (ix) multipurpose vehicles. However, it submits that the boundaries between different vehicle categories are not always clear-cut both in terms of intended use and price.8

(8) With regard to the further sub-segmentation of SUVs based on the size of the car, the Notifying Party submits that given the recent development of the segment it sees no clear distinction between the sub-segments, therefore it considers that analysing the SUV segment as a whole provides a more relevant and accurate picture of the competitive environment.9

(9) Furthermore, the Notifying Party considers that electric vehicles do not constitute a separate product market as electric and hybrid powertrains – as opposed to combustion engines – are available for the majority of the car models, therefore consumers can choose the electric version as an option for the preferred car model.10

(10) As for the geographic scope of these markets, the Notifying Party submits that it is EEA-wide in scope as production of vehicles takes place on an international level and the competitive conditions are largely homogeneous throughout the EEA.11

The Commission's assessment

(11) The Commission's previous segmentation as set out in paragraph (7) was confirmed by the results of the market investigation. Indeed the majority of competitors12 and customers13 indicated that this segmentation is appropriate with regard to passenger cars.

(12) The Commission has previously considered the further sub-segmentation of the SUV segment into (i) small, (ii) medium and (iii) large SUVs but ultimately left the question open.14

(13) The respondents to the market investigation in the present case confirmed that such sub-segmentation is appropriate. However it has to be noted that only a slight majority of competitors15 agreed with this categorization. Others argued that no sub-segmentation is needed as "[t]he differences on price, quality/features and intended use are not significant from one sub-segment to another to justify further segmentation of the SUV segment. A customer could easily substitute all 3 the models comprised within the SUV segment."16 On the other hand, the great majority of customers replied that there are differences – for example with regard to age, lifestyle or income - in the target customers of the SUVs in different sub- segments.17

(14) The Commission investigated in the present case whether electric cars constitute a separate product market and whether this possible market should be further segmented according to (i) technology (electric battery cars and hybrid cars) or(ii) the categories defined for vehicles with combustion engines (see paragraph (7)).

(15) The results of the market investigation are somewhat inconclusive in this regard. While the majority of competitors submitted that electric cars do not constitute a separate product market,18 most of them distinguish between battery electric and hybrid vehicles. However, as a competitor indicated "[s]ome HEVS (Hybrid Electric Cars) are more aligned with BEVs (Battery Electric Vehicles) whilst others are closer to ICE (Internal Combustion Engine). This alignment depends on the actual functions, systems and performance […]"19

(16) As regards hybrid vehicles, several competitors indicated that these – already now– compete directly with combustion engine powered models.20 As for the battery electric models, competitors indicated that they would become an alternative powertrain choice in 2-5 years.21 Customers emphasised the price difference between electric cars and combustion engine powered cars and added that currently the capacity of the batteries and the lack of charging infrastructure limit the use of battery electric cars.22 It was mentioned both by customers and competitors that specific national legislations - such as the tax exemptions in Norway - can significantly influence the competitiveness of electric cars.23

4.1.1.2.LCVs

The Notifying Party's view

(17) The Notifying Party agrees with the Commission's decisional practice24 in distinguishing (i) light, (ii) medium-size and (iii) heavy commercial vehicles.25

(18) The Notifying Party submits that the relevant market encompasses all LCVs under 6 tons but a plausible market segment could be found within this market, comprising vehicles from 0 to 3.5 tons.26

(19) With regard to pick-up trucks, the Notifying Party is of the opinion that they belong to the LCV market rather than to passenger cars.27

(20) The Notifying Party considers that - similar to passenger cars - the LCV market is EEA-wide in scope.28

The Commission's assessment

(21) In previous decisions the Commission has considered but ultimately left open whether to further sub-segment LCVs into vehicles (i) up to 3.5 tons and (ii) between 3.5-6 tons.29

(22) The results of the market investigation were inconclusive as regards the appropriateness of plausible further segmentation of LCVs according to their size. Some market participants in fact indicated that it is an appropriate sub- segmentation,30 while others indicated that they rather consider LCVs as those commercial vehicles only up to 3.5 tons.31

(23) In previous decisions the Commission has ultimately left open whether pick-up trucks can be considered passenger cars given that they can be purchased for private use and can transport both goods and people.32

(24) The results of the market investigation were not entirely conclusive whether pick- up trucks should be considered as a separate product market. Competitors responding to the market investigation indicated that albeit normally registered as commercial vehicles, some customers use pick-up trucks for leisure purposes instead of business purposes. However a large proportion of the respondents to the market investigation in the present case indicated that pick-up trucks are mostly considered as commercial vehicles.33

(25) In previous decisions the Commission has ultimately left open whether the market for manufacturing and supply of passenger cars and LCVs is EEA-wide or national in scope.34 Competitors and customers alike indicated that there are price differences between countries based on list prices35 taking into account the specific competition conditions and the different national tax regimes.36 Customer preferences37 and CO2-emission regulation38 might also differ. Furthermore, retailers export vehicles only to a very limited extent.39 All these factors are pointing towards national markets.

4.1.2.Geographic market definition

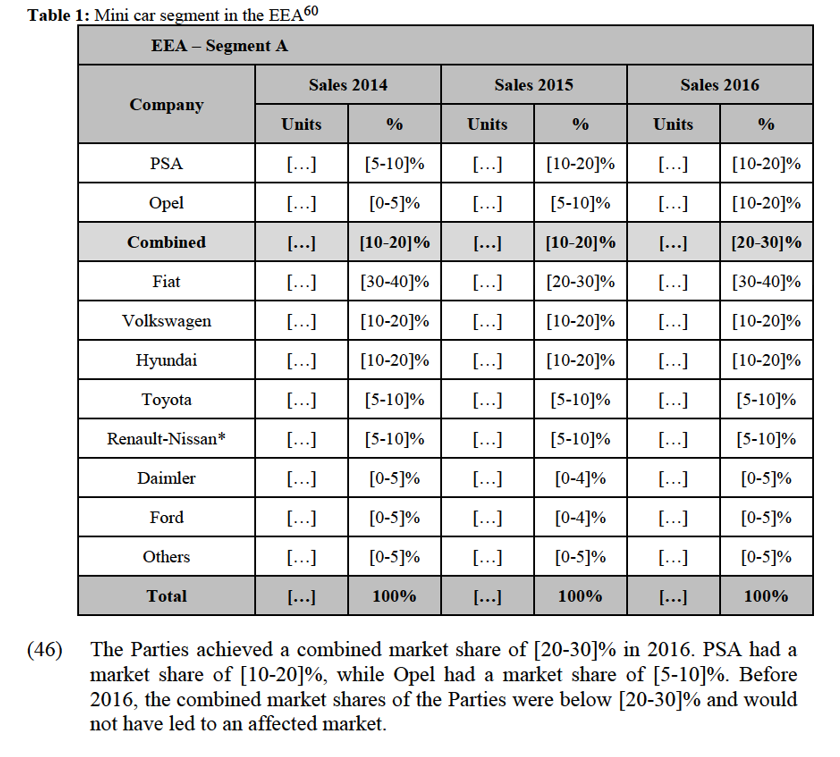

(26) In previous decisions the Commission has ultimately left open whether the geographic scope of the markets for manufacturing and supply of passenger cars and LCVs is EEA-wide or national in scope.40 Competitors and customers alike indicated that there are price differences between countries based on list prices41 set taking into account the specific competition conditions and the different national tax regimes.42 Customer preferences43 ant CO2-emission regulation44 might also differ. Furthermore, retailers sell vehicles outside the country they are located in only to a very limited extent.45 All these factors are pointing towards national markets.

4.1.3.Conclusion

(27) In any event, for the purpose of this decision the Commission considers that the question of the exact product and geographic market definition can be left open, as the Transaction does not give rise to serious doubts as to its compatibility with the internal market even under the narrowest plausible market definition.

4.2.Wholesale distribution of new passenger cars and LCVs

(28) At the wholesale level, distributors or importers distribute vehicles to retailers.46 The wholesale function is often carried out by subsidiaries of the vehicle manufacturers themselves or by independent distributors, although the latter have 6 to ensure consistency with the central marketing strategies developed by the manufacturers.47

The Notifying Party's view

(29) The Notifying Party agrees with the Commission's decisional practice48 and submits that the segmentation of the product market between passenger cars and LCVs is sufficient and any further segmentation, particularly by type of car, is not appropriate.49

(30) As for the geographic scope, the Notifying Party submits that it can be left open, whether the market is EEA-wide or national.50

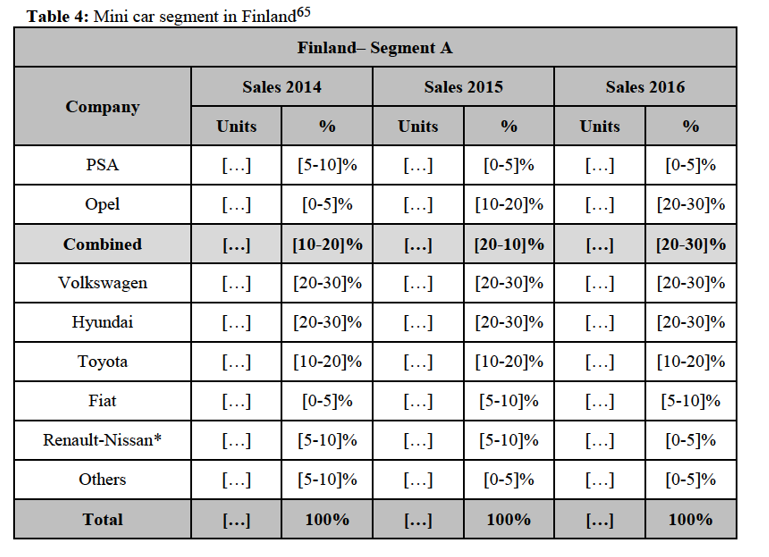

The Commission's assessment

(31) The Commission found that this market should not be further sub-segmented based on "classes" of cars, given that manufacturers normally distribute a model range which covers different market segments under the same distribution channel.51

(32) The Commission has previously considered the wholesale distribution market to be at least national,52 ultimately leaving the question open whether it is EEA-wide or national in scope.53

(33) In any event, for the purpose of this decision the Commission considers that the question of the exact product and geographic market definition can be left open, as the Transaction does not give rise to serious doubts as to its compatibility with the internal market even under the narrowest plausible market definition.

4.3.Retail distribution of new passenger cars and LCVs

(34) At the retail level, vehicles are sold to final customers by independent or vertically integrated retailers.

The Notifying Party's view

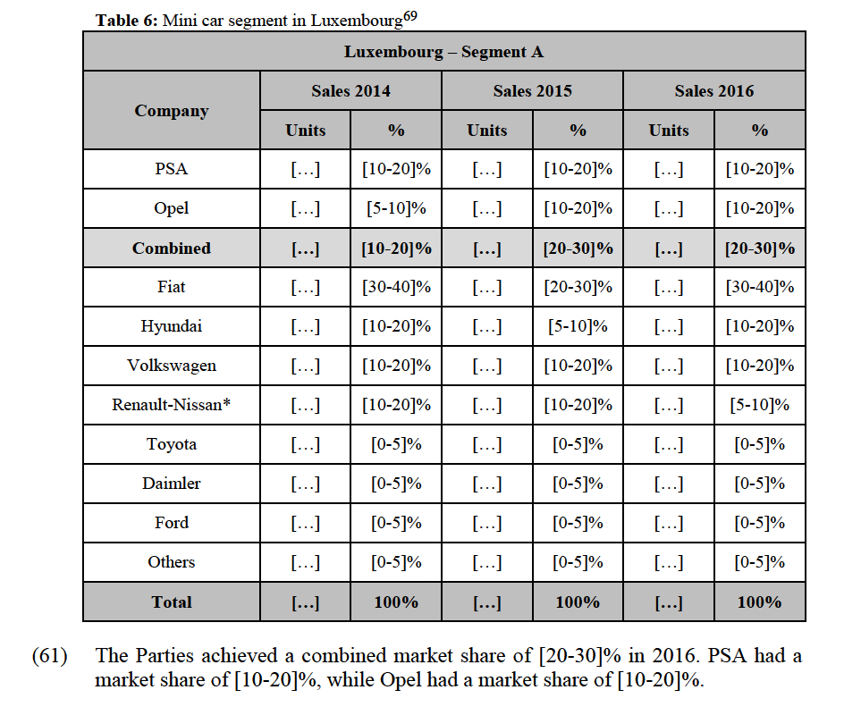

(35) The Notifying Party submits that the exact product and geographic market definition can be left open for the purpose of this decision.54

The Commission's assessment

(36) The Commission has previously considered a distinction between the retail distribution of passenger cars and LCVs.55 Similarly to the wholesale distribution, it found that further sub-segmentation is not appropriate.56

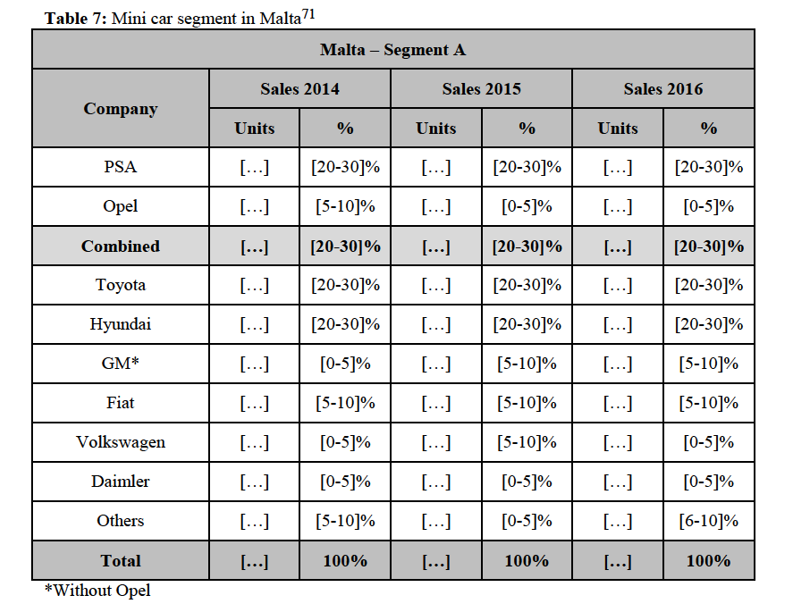

(37) The Commission has so far left open whether the retail distribution markets are EEA-wide, national or local in scope.57

(38) In any event, for the purpose of this decision the Commission considers that the question of the exact product and geographic market definition can be left open, as the Transaction does not give rise to serious doubts as to its compatibility with the internal market even under the narrowest plausible market definition.

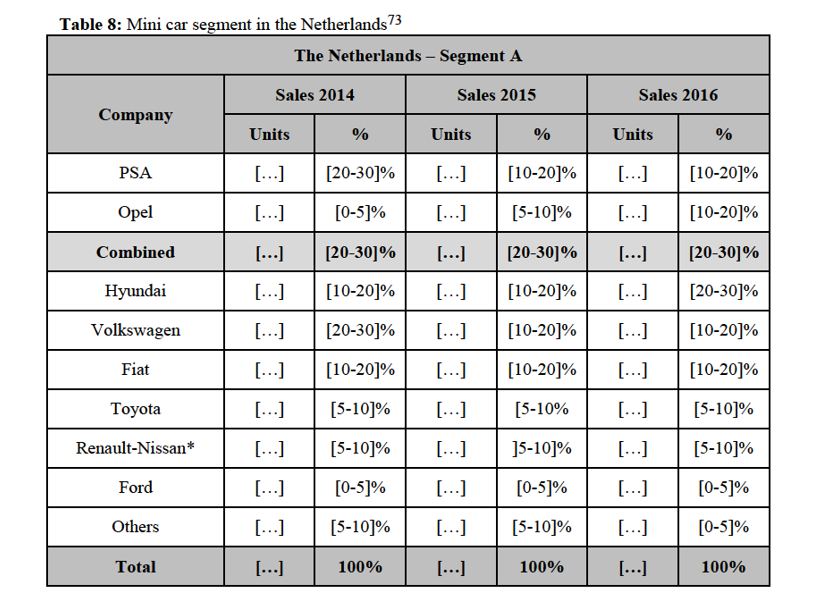

5. COMPETITIVE ASSESSMENT – HORIZONTAL NON-COORDINATED EFFECTS58

5.1.Manufacturing and supply of passenger cars and LCVs

(39) The Transaction gives rise to horizontally affected markets due to the Parties' activities in the following segments: (i) mini cars, (ii) small cars (iii) medium cars, (iv) large cars, (v) SUVs, (vi) multipurpose vehicles, (vii) LCVs and possibly (viii) electric vehicles.

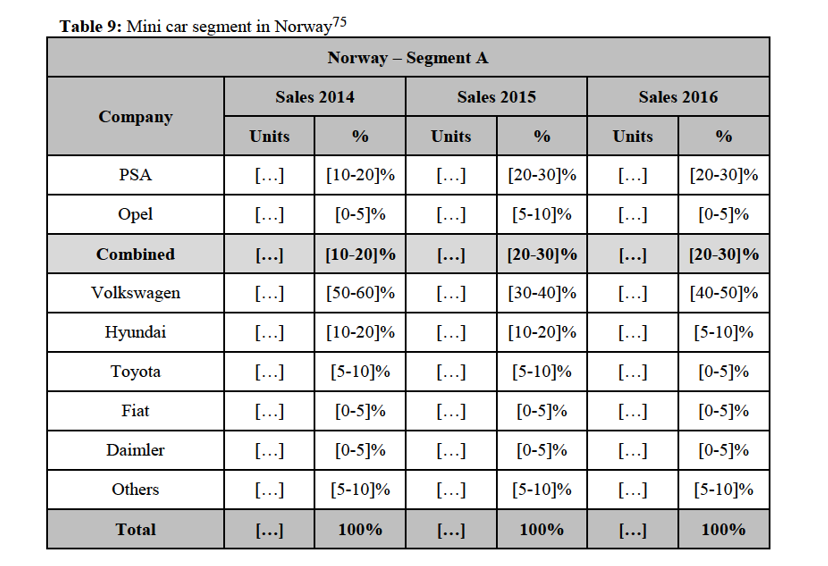

5.1.1.The Notifying Party's view59

(40) The Notifying Party submits that no competition concerns would arise from the Transaction as the Parties combined market shares are relatively low on all plausible markets and the merged entity would be constrained by strong competitors post-Transaction.

(41) Furthermore, given that all vehicle manufacturers are already present across the EEA and that there is an overcapacity in the market, the competitors could counterbalance in a timely manner and without further investments any attempt of the merged entity to increase prices.

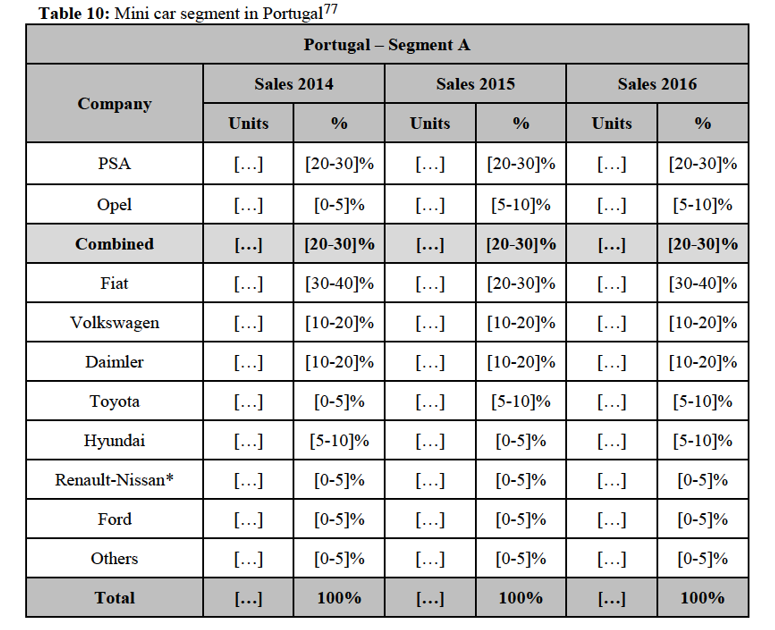

(42) Moreover, the Notifying Party argues that the Parties' brands are not perceived as close alternatives, therefore the Parties cannot be considered as close competitors.

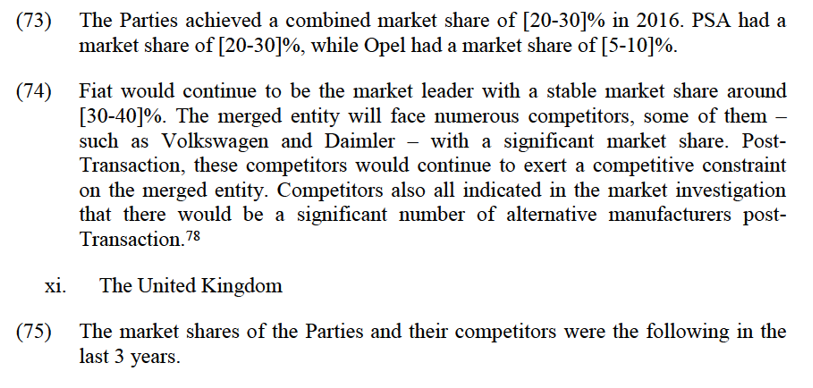

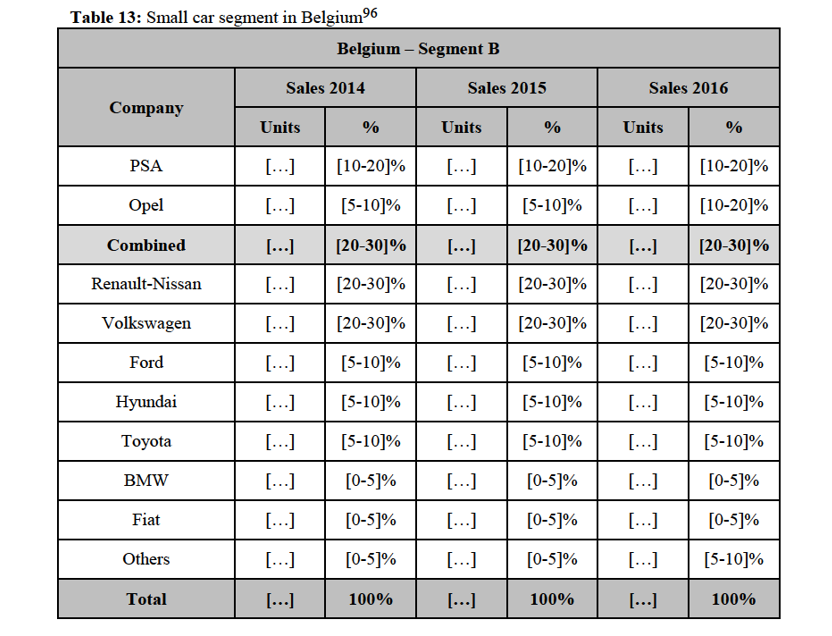

Finland, Luxembourg and Norway, Opel considers that the closest alternative for the Opel Karl is the […]. In France, the closest alternative is the […], while in the Netherlands and in the UK, it is the […] and in Portugal it is the […] from a technical point of view.82

(80) The Commission considers that the Parties are not close competitors to each other with regard to the segment of mini cars.

(81) First, internal documents have further confirmed that […].83

(82) Second, according to the NCBS survey84 the brand substitution […].85

(83) Third, in the market investigation the majority of the retailers replied that end- customers do not see the Parties as close alternatives in the mini car segment.86 Indeed, the majority of the customers asked stated the Transaction will have no impact,87 that the intensity of competition will remain the same,88 that the price level in the different segments will also remain the same89 and that the merged entity will not have a degree of control on the market that would make it difficult for other companies to compete with them.90 The results of the market investigation further indicated that most competitors also do not see the Parties' models as each other's close alternatives in the mini car segment in the affected markets.91 Moreover, competitors of the Parties consider that as a result of the Transaction, the intensity of competition on the affected markets will stay the same.92 Also, competitors stated the merged entity will not have a degree of control on the market that would make it difficult for them to compete with the Parties.93

5.1.2.3. Conclusion

(84) For the reasons mentioned above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to the market for manufacturing and supply of mini cars in the EEA, Belgium, Denmark, Finland, France, Luxembourg, Malta, the Netherlands, Norway, Portugal and the UK.21

5.1.3. Segment B: small cars

(85) PSA is present in these markets with its "Peugeot 208", "Citroën C3", "DS3", "C4 Cactus", "E-Mehari" models,94 while Opel is present through the "Corsa" model.

(86) Based on a market defined as EEA-wide in scope, the Transaction gives rise to an affected market (combined market share of [20-30]%). Based on a market defined at national level, the Transaction gives rise to affected markets in Belgium ([20- 30]%), Croatia ([20-30]%), Denmark ([20-30]%), France ([30-40]%), Greece ([20-30]%), Italy ([20-30]%), Luxembourg ([20-30]%), Malta ([20-30]%), the Netherlands ([20-30]%), Portugal ([20-30]%), Spain ([20-30]%) and the UK ([20- 30]%).

5.1.3.1. Market structure

i. EEA

(87) The market shares of the Parties and their competitors were the following in the last 3 years.

closest alternatives are the […] based on technical characteristics, and the […] from a business point of view.

(128) On the other hand, Opel considers that the closest alternative for the Opel Corsa is the […] based on technical characteristics. From a business point of view however, the closest competing model are different depending on the country. The closest competing models to the Opel Corsa from a business point of view is the […] in Belgium, Luxembourg, Malta and Spain, the […] in Croatia and in the UK, the […] in France, the […] in Greece, the […] in Italy and the […] in Portugal.121

(129) The Commission considers that the Parties are not close competitors to each other with regard to the segment of small cars.

(130) First, internal documents have further confirmed that […].122

(131) Second, according to the NCBS study the brand substitution between Peugeot and Opel […].123

(132) Third, in the market investigation the majority of the retailers replied that end- customers do not see the Parties as close alternatives in the small car segment.124 Indeed, the majority of the customers asked stated that the Transaction will have no impact,125 that the intensity of competition will remain the same,126 that the price level in the different segments will remain the same127 and that the merged entity will not have a degree of control on the market that would make it difficult for other companies to compete with them.128 The results of the market investigation further indicated that most competitors also do not see the Parties' models as each other's close alternatives in the small car segment in the affected markets.129 Moreover, competitors of the Parties consider that as a result of the Transaction, the intensity of competition on the affected markets will stay the same.130 Also, competitors stated the merged entity will not have a degree of control on the market that would make it difficult for them to compete with the Parties.131

5.1.3.3. Conclusion

(133) For the reasons mentioned above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to the market for manufacturing and supply of small cars in the EEA, Belgium, Croatia, Denmark, France, Greece, Italy, Luxembourg, Malta, the Netherlands, Portugal, Spain and the UK.

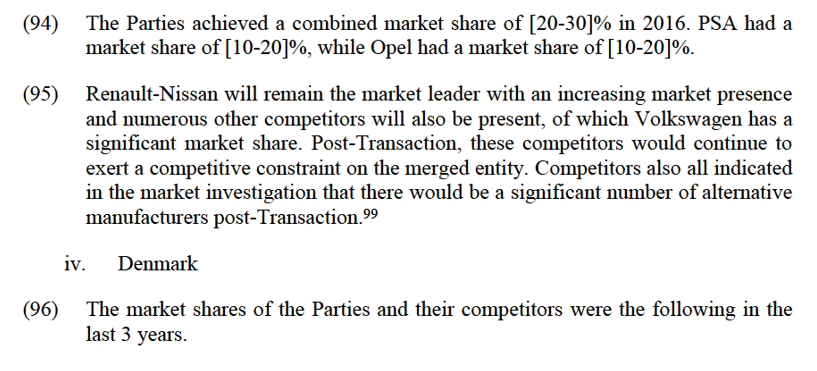

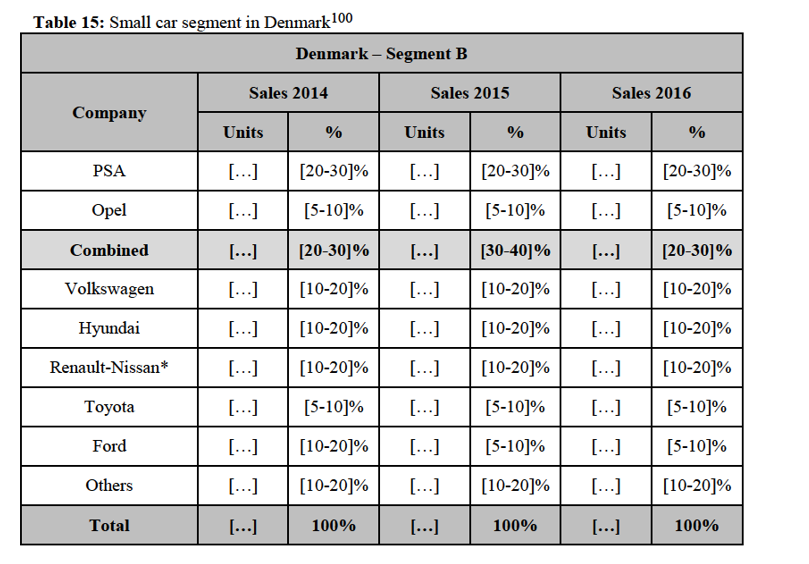

and the Citroën C-Elysée, it is respectively the […] and the […] from both standpoints.

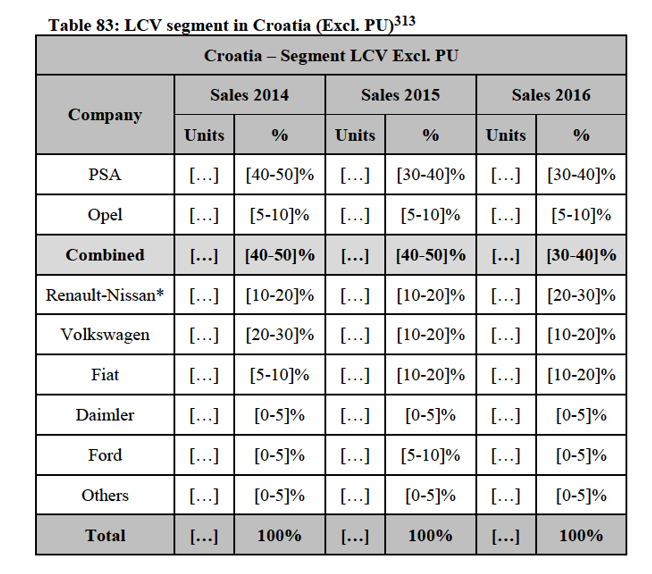

and the Citroën C-Elysée, it is respectively the […] and the […] from both standpoints.

(156) On the other hand, Opel considers the closest alternative for the Opel Cascada to be the […] from a business point of view in all of these countries, except in Spain where it is the […]. In all of these countries, the closest alternative based on technical characteristics is the […] except in the Netherlands where it is the […]. Opel considers that the closest alternative for the Opel Astra145 is the […] in Belgium, Denmark and Spain. In France, the […] is the closest alternative from a technical point of view and the […] is the closest from a business point of view. In Greece, the […] is the closest from a technical point of view, and the […] is the closest from a business point of view.

(157) The Commission considers that the Parties are not close competitors to each other with regard to the segment of medium cars.

(158) First, internal documents have further confirmed that […].146

(159) Second, according to the NCBS study the brand substitution between Peugeot and Opel […].147

(160) Third, in the market investigation the majority of the retailers replied that end- customers do not see the Parties as close alternatives in the medium car segment.148 Indeed, the majority of the customers asked stated that the Transaction will have no impact,149 that the intensity of competition will remain the same,150 that the price level in the different segments will remain the same151 and that the merged entity will not have a degree of control on the market that would make it difficult for other companies to compete with them.152 The results of the market investigation further indicated that most competitors also do not see the Parties' models as each other's close alternatives in the medium car segment in the affected markets.153 Moreover, competitors of the Parties consider that as a result of the Transaction, the intensity of competition on the affected markets will stay the same.154 Also, competitors stated the merged entity will not have a degree of control on the market that would make it difficult for them to compete with the Parties.155

5.1.4.3.Conclusion

(161) For the reasons mentioned above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market wit

(169) There are numerous competitors active on this market, of which Daimler, BMW and Volkswagen achieved a significant market share. Post-Transaction, these competitors would continue to exert competitive constraint on the merged entity. Competitors also all indicated in the market investigation that there would be a significant number of alternative manufacturers post-Transaction.161

5.1.5.2. Closeness of competition

(170) The Parties both target […] with their large car models which all have five seats.[…],162 […].163 164

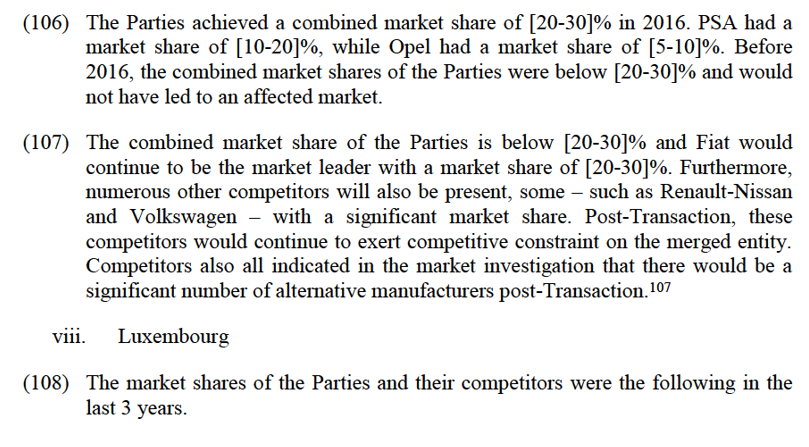

(171) The Notifying Party claims that […]. It submits that it considers that the closest alternative of both Peugeot 508 and Citroën C5 from a technical and business point of view is […] in France and in Malta. The Notifying Party sees the […] as the closest competing model of the DS5 in these countries. Similarly, Opel indicated that […] of Insignia but rather sees […] in France and […] in Malta as the closest competing model.165

(172) The Commission considers that the Parties are not close competitors to each other with regard to the segment of large cars.

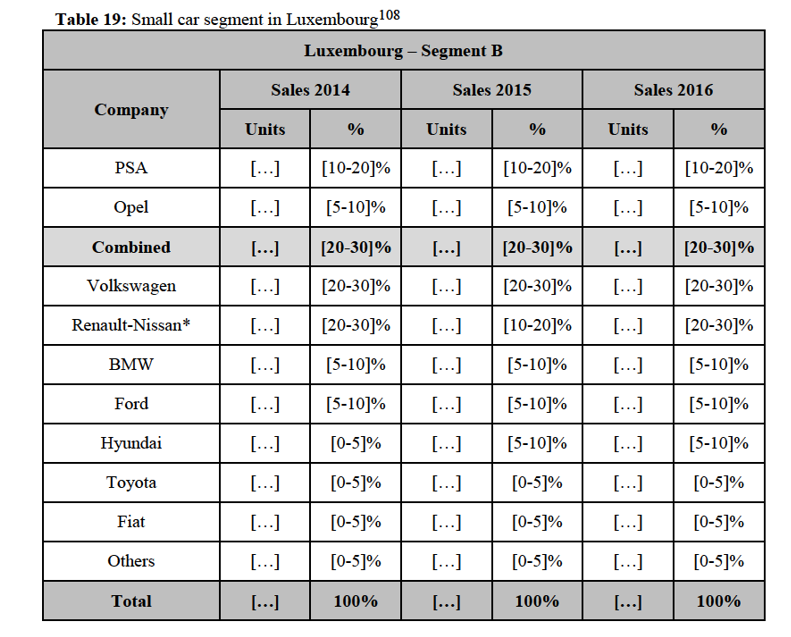

(173) First, internal documents have confirmed […],166[…].167

(174) Second, according to the NCBS study […].168

(175) Third, in the market investigation the majority of the retailers replied that end- customers do not see the Parties as close alternatives in the large car segment.169 Indeed, the majority of the customers asked stated that it does not consider the Parties to be close competitors with regard to price,170 quality/features171 or intended use.172 The results of the market investigation further indicated that most competitors also do not see the Parties' models as each other's close alternatives in the large car segment in France and Malta.173

5.1.5.3. Conclusion

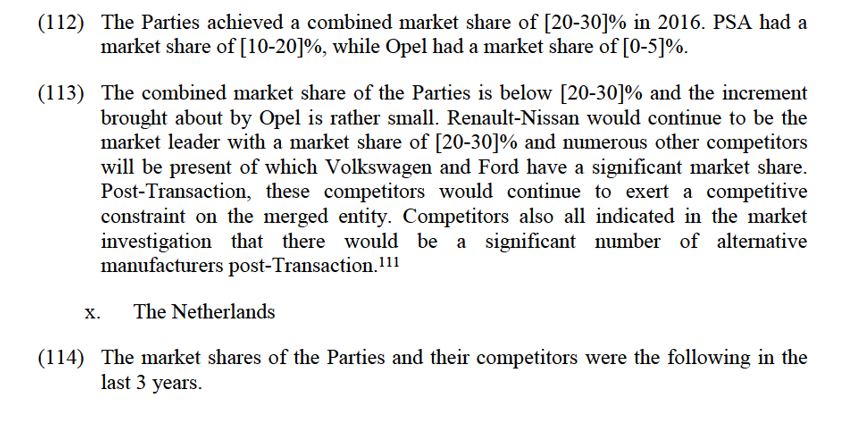

(176) For the reasons mentioned above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to the market for manufacturing and supply of large cars in France and in Malta.

5.1.6.Segment J: SUVs

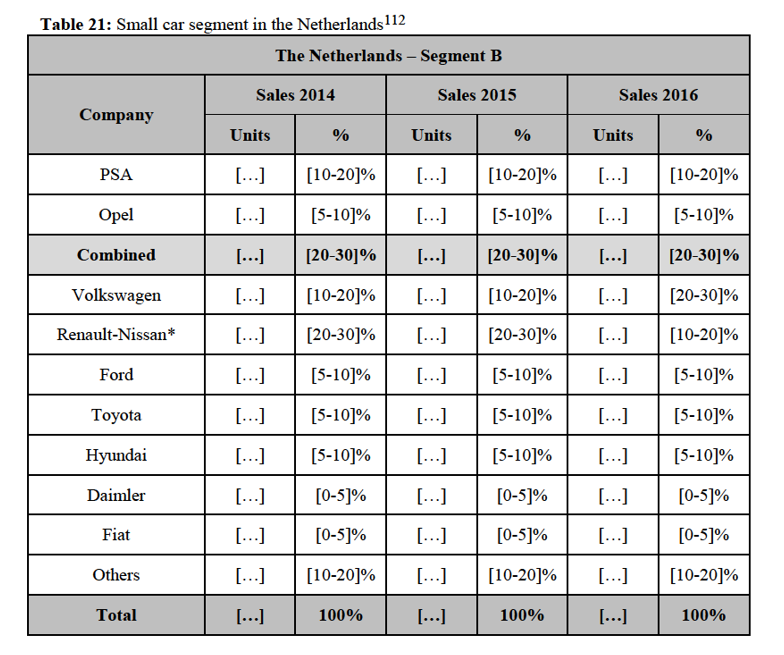

(177) PSA is present in these markets with its "Peugeot 2008" and "Peugeot 3008" models, while Opel is producing "Mokka". The Peugeot 2008 and the Opel Mokka are sub-compact SUVs but the Peugeot 3008 is considered as a compact model which means bigger load space174 and also a higher price.175 176

(178) If the market were to be defined as EEA-wide in scope, the Transaction would not lead to an affected market in this segment (combined market share of [10-20]%). Based on a narrower – national – geographic market definition, the Transaction gives rise to an affected market in France.

(179) If the SUV segment were to be further sub-segmented based on the size of the vehicles, the Transaction gives rise to affected markets with regard to small (sub- compact) SUVs both on an EEA-wide level and on a national level in Austria, Belgium, Croatia, the Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Latvia, Luxembourg, the Netherlands, Norway, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden and the UK.

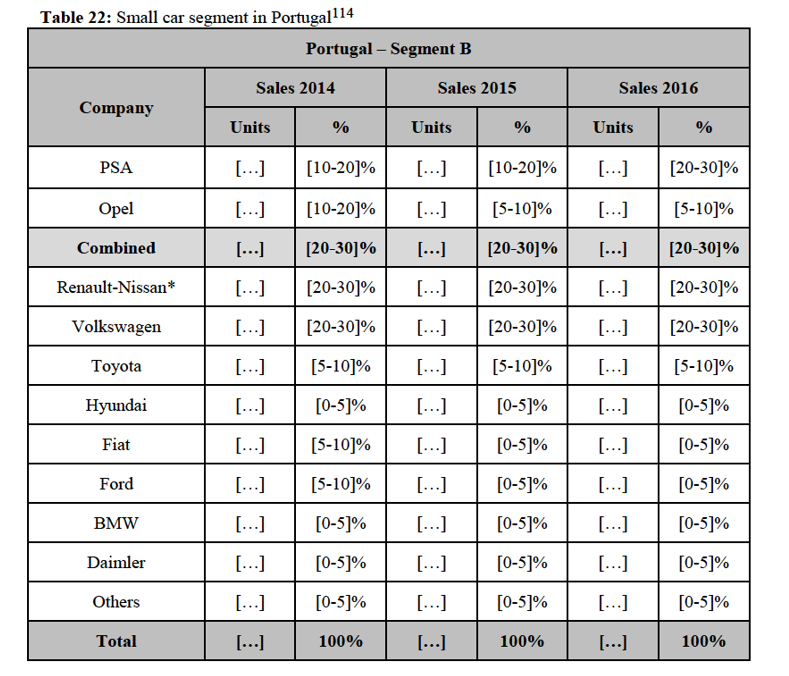

5.1.6.1. Market structure

A. SUVs - France

(180) The market shares of the Parties and their competitors were the following in the last 3 years.

is competing the closest with the Peugeot 3008 in France.231 Similarly, Opel […].232

(257) The Commission considers that the Parties are not close competitors with regard to SUVs.

(258) First, internal documents have confirmed that PSA […]233,[…].234[…]235[…],236[…].237

(259) Second, according to the NCBS study […].238[…].239[…]240[…].241 242

5.1.6.3.Conclusion

(260) Given that the Parties' combined market share is under 40% on all affected markets, the presence of numerous competitors and the fact that the Parties are not close competitors, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to the market for manufacturing and supply of SUVs irrespective of whether the market is defined EEA-wide or national in scope and of whether the SUV segment is further sub-segmented based on the size of the vehicle.

5.1.7. Segment M: multipurpose vehicles

(261) PSA is present in this segment with its "Peugeot 5008", "Citroën C3 Picasso" and "Citroën C4 Picasso" models,243 while Opel is producing the "Zafira Tourer" and the "Meriva".244 245

(262) The Transaction gives rise to affected markets on an EEA-wide level and – based on a narrower, national geographic market definition – in Belgium, Bulgaria,

the price, the Citroën C3 Picasso and the Opel Meriva on the one hand283 and the Peugeot 5008, the Citroën C4 Picasso and the Opel Zafira Tourer on the other hand284 can be considered as closer alternatives. This is also confirmed by the NCBS study (see paragraph (306) and Opel's monitoring practices.285

(303) The Notifying Party submits that […].[…].286 On the other hand, Opel considers the […] as the closest technical alternative of the Opel Meriva, however it indicates […] from a business point of view287 and for the Opel Zafira.288

(304) The Commission considers that PSA and Opel cannot be considered as close competitors with regard to multi-purpose vehicles.

(305) First, internal documents have further confirmed that […],289[…].290

(306) Second, according to the NCBS study the brand substitution between Peugeot and Opel […].291[…].292[…]293[…]294[…]295[…]296[…].

(307) Third, in the market investigation the large majority of the retailers replied that end-customers do not see the Parties as close alternatives in the multipurpose vehicle segment.297 Indeed, the majority of the customers asked stated that it does not consider the Parties to be close competitors with regard to price,298 quality/features299 or intended use.

I

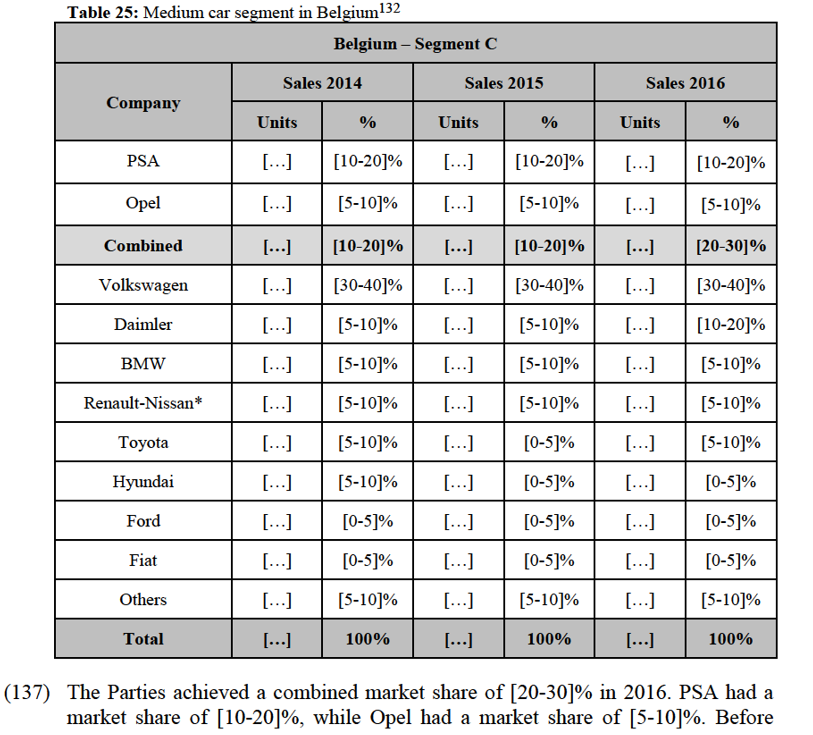

I

average loading capacity of 365 litres, the Partner and Berlingo of 675 litres while the Opel Combo loading capacity ranges between 1000 and 5000 litres.(b) The average towing capacity of PSA's small LCVs, ranging between 600 and 750 Kg, is also smaller compared to that of the Opel Combo which has a towing capacity up to 1 ton.(c) Finally, the Opel combo also has a higher payload capacity – 1.5 tons – compared to PSA's small LCVs which is between 1 and 1.25 tons.

(386) The medium LCVs offered by PSA (the Peugeot Expert and the Citroën Jumpy) have different technical characteristics compared to the Opel Vivaro:(a) First, PSA's medium vans have 3 or 5 seats while the Vivaro has between 2 and 9.(b) The total load space of PSA's medium LCV in 3 497 litres while the total load space of the Opel Vivaro ranges from 1 000 to 8 000 litres.

(387) Finally, large LCVs offered by PSA (the Peugeot Boxer and the Citroën Jumper) have different technical characteristics compared to the Opel Movano:(a) First, the Movano targets […]. PSA's large LCV are intended […]. PSA's medium vans have 3 and 9 eats while the Vivaro has between 2 and 17.(b) The total load space of PSA's large LCV is 8 000 litres while the total load space of the Opel Movano ranges from 1 000 to 17 000 litres, depending on the configuration.(c) Finally, the towing capacity of PSA's large LCVs ranges between 2 and 2.5 tons, while the Movano can support up to 3 tons.

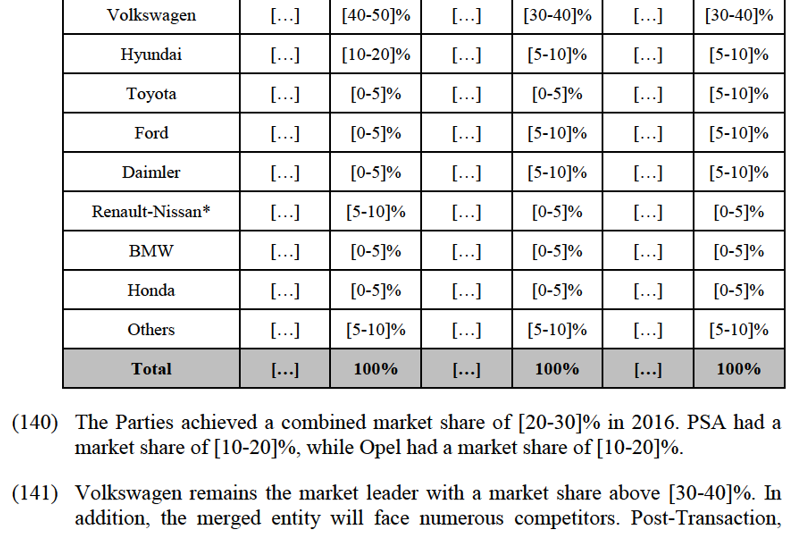

(388) The above conclusions are also supported by the outcome of the market investigation. The majority of customers did not identify the Parties as close competitors to each other, neither in terms of price, of quality or intended use.381

5.1.8.3. ConclusioN

(389) Given (i) the limited increment brought about by Opel in all affected markets, (ii) the presence of numerous strong competitors in each of the affected markets and(iii) the fact that the Parties are not close competitors, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to the market for manufacturing and supply of LCV, irrespective of the product and geographic market definition.

5.1.9. Electric vehicles

(390) Although the results of the market investigation did not indicate clearly that electric vehicles constitute a separate product market (see paragraph (14)), theCommission took a cautious approach and investigated the possible impact of the Transaction based on the narrowest plausible product market definition.

(391) Currently, the Parties' activities do not overlap with regard to electric vehicles. PSA manufactures and supplies five battery electric vehicles382 and three hybrid cars,383 however Opel has no electric vehicle on the market.384

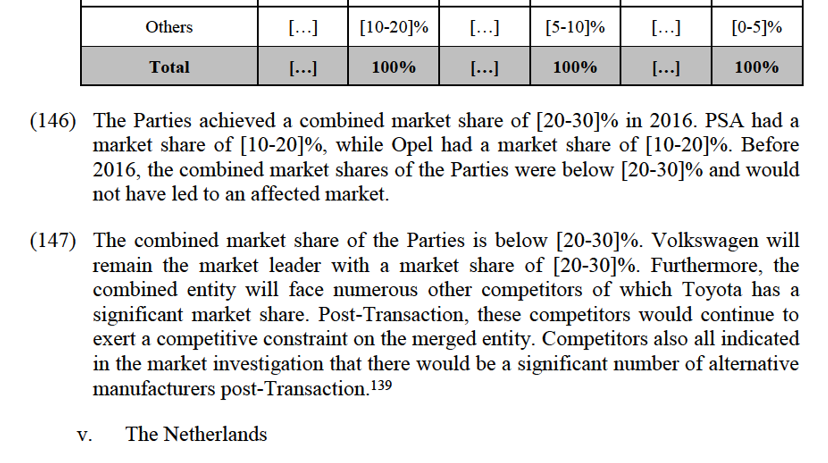

(392) As to future projects, […].385[…]:386- […].387

(393) Therefore, considering the narrowest plausible product market definition based on the size of the vehicles, […].

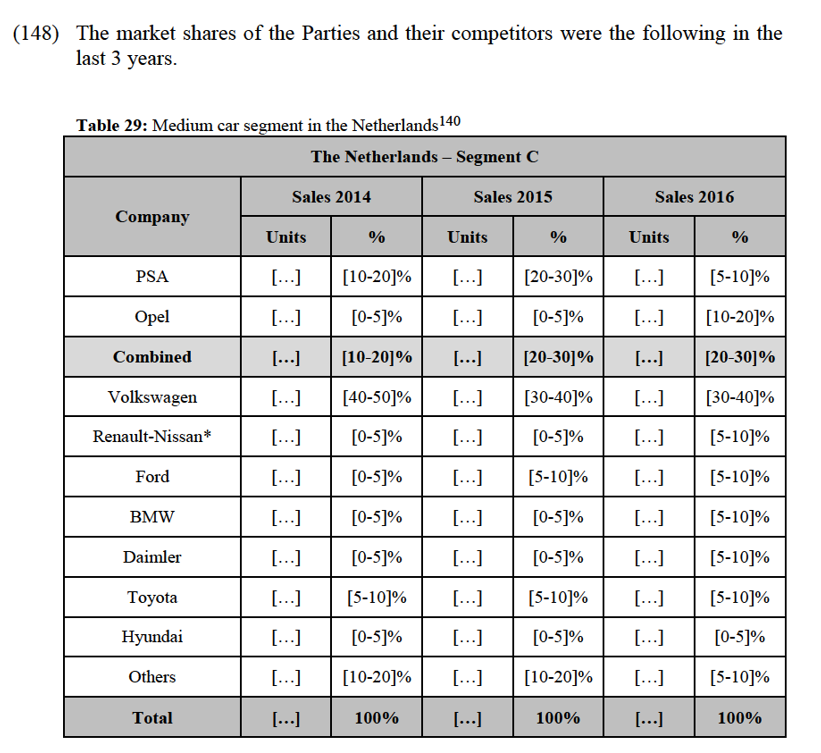

(394) On an EEA-wide battery electric mini car segment PSA achieved a market share of [40-50]% in 2016. This relatively high market share is due to PSA's first-mover advantage.388 However, the merged entity would continue to face competition from numerous competitors such as Volkswagen with a market share of [30- 40]%.389 Furthermore, several competitors have already announced new launches390 or refurbishments391 in this segment.392

(395) On an EEA-wide battery electric small car segment PSA achieved a very limited market share of [0-5]% in 2016.393 In any event, the merged entity would continue to face strong competitors such as Renault-Nissan ([60-70]%) and BMW ([30-40]%).394 Furthermore, several competitors have already announced new launches395 or refurbishments396 in this segment.397

(396) On an EEA-wide battery electric LCV segment PSA achieved a market share of [10-20]% in 2016.398 The merged entity would continue to face competition from strong competitors such as Renault-Nissan ([60-70]%).399 Furthermore, several competitors have already announced new launches400 or refurbishments401 in this segment.402

(397) In view of the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to the market for manufacturing and supply of electric vehicles, irrespective of the product and geographic definition.

5.1.10.Conclusion

(398) In view of the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to the market for manufacturing and supply of passenger cars and LCVs, irrespective of the market definition.

5.2.Wholesale distribution of passenger cars and LCVs

The Notifying Party's view

(399) The Notifying Party submits that no competition concern would arise from the Transaction as the Parties' market shares are relatively low on all plausible markets. Furthermore, both Parties have their own distribution channels, therefore their activities do not overlap with regard to the wholesale distribution of passenger cars and LCVs.

The Commission's assessment

(400) The Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to the market for wholesale distribution of passenger cars and LCVs, irrespective of the market definition, for the following reasons.

(401) First, the combined market shares of the Parties are indeed not high. Given that they do not distribute vehicles of competitors; their market share is closely related to competition at the production level. Therefore, their market share on an EEA- wide or national wholesale distribution markets cannot exceed the figures presented in section 5.1 with regard to passenger cars and LCVs. Furthermore, given that PSA's vehicles are also distributed by independent importers,403 its market share on the wholesale distribution market is allegedly even lower than on the market for manufacturing and supply of passenger cars and LCVs.

(402) Second, the Commission considers that the Transaction would not have an impact on the competitive landscape of this market. The Parties have their own distribution channels which do not overlap, therefore no competition would be lost due to the Transaction.

(403) Third, no market participant expressed concerns in during the market investigation with regard to the market for wholesale distribution of passenger cars and LCVs.

Conclusion

(404) In view of the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to the market for wholesale distribution of passenger cars and LCVs.

5.3.Retail distribution of passenger cars and LCVs

The Notifying Party's view

(405) The Notifying Party submits that the Transaction does not raise any competition concerns on any of the retail distribution markets, as the Parties' combined market shares are relatively low on all plausible markets and both Parties have their own distribution channels. Therefore, the competitive landscape will not change as a result of the Transaction.

The Commission's assessment

(406) The Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to the market for retail distribution of passenger cars and LCVs, irrespective of the market definition, for the following reasons.

(407) Both Parties have their own distribution channels which do not overlap, as both of them are only active in the distribution with respect to their own respective brands. Furthermore, neither pre-Transaction, nor post-Transaction, will competing manufacturers rely on PSA’s or Opel’s distribution channels. Similarly, retailers owned by competing manufacturers do not distribute PSA’s or Opel’s vehicles and will continue to do so post-Transaction.

(408) Given that the Parties distribute only their own vehicles, their market position on these markets is closely related to their market share in the manufacturing and supply of passenger cars and LCVs. Moreover, as the Parties' vehicles are also distributed through independent retailers (dealerships) at the retail level, their market shares are below their market shares at the manufacturing and supply level. Therefore, their market share on an EEA-wide or national retail distribution markets cannot exceed the figures presented in section 5.1 with regard to passenger cars and LCVs.

(409) PSA has […]% of independent dealerships and […]% of owned dealerships. Opel […] does not own any dealership in the EEA with the exception of the UK, where it owns a very limited number of dealerships ([…]).404 Given that Opel's vehicles, with the exception of the […] dealerships located in the UK, are distributed through independent retailers, there is only a minor overlap between the Parties' retail distribution activities within the EEA.

(410) In the UK, […]. Therefore, the Parties’ market share at the retail level should overall be much lower than the Parties’ market shares on the manufacturing and sales market at national level.405

(411) Should the geographic market be considered local, there is only one affected market for LCVs, in the Vickers Lakeside commercial area of responsibility, where the Parties will hold a combined market share of [20-30]%.406 However, this market share is only slightly above [20-30]% and the merged entity will continue to face competition from the independent dealerships of that area.

(412) Finally, no market participant expressed concerns during the market investigation with regard to the market for retail distribution of passenger cars and LCVs.

Conclusion

(413) In view of the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to the market for retail distribution of passenger cars and LCVs, irrespective of the market definition.

6.COMPETITIVE ASSESSMENT – HORIZONTAL COORDINATED EFFECTS

(414) As regards potential horizontal coordinated effects, the Commission considers that the number of competitors active in the market, as well as the nature of the product, make it unlikely that sustainable coordination could be achieved.

(415) First, the competitors of the Parties are numerous and large (Volkswagen, Renault/Nissan, Ford, Fiat Chrysler, Daimler, BMW, Hyundai, Toyota, Honda). They compete fiercely and represent an effective constraint on each other. Following the Transaction, the number of main players will still be around 10.

(416) Second, passenger cars and LCVs are differentiated rather than homogeneous products, even within the same product market (such as mini cars, small cars, medium cars, large cars, multipurpose vehicles, SUVs and LCVs).

(417) For these reasons, it would be difficult for the merged entity and its competitors to reach common terms of coordination.

(418) In view of the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to horizontal coordinated effects in the markets for the manufacturing and supply of passenger cars and LCVs.

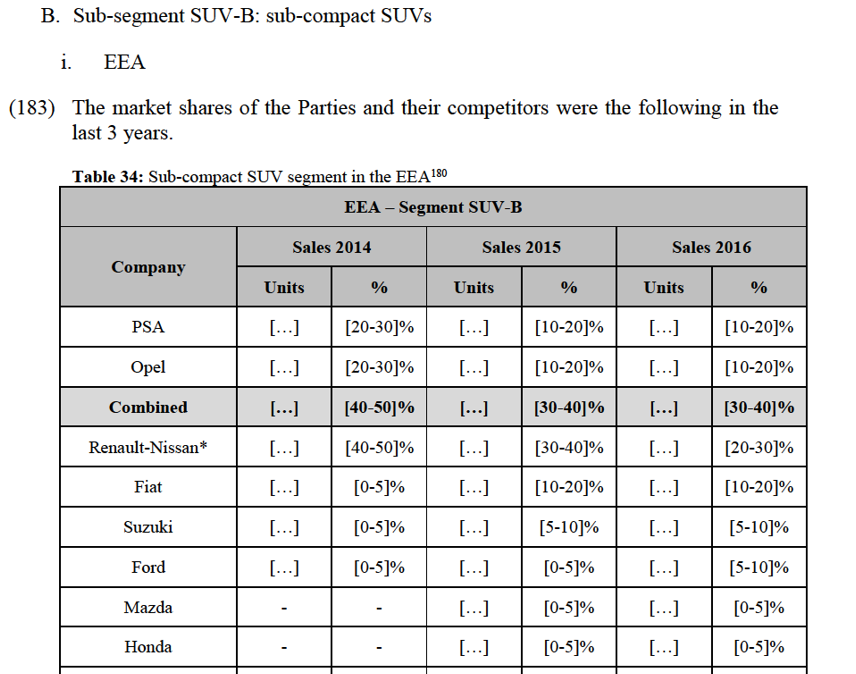

7. COMPETITIVE ASSESSMENT – VERTICAL EFFECTS

7.1.Manufacturing and supply of passenger cars and LCVs (upstream) – wholesale distribution of passenger cars and LCVs (downstream)

(419) The Commission considers that the Transaction would not give rise to serious doubts with regard to the vertical link between the manufacturing and supply (upstream) and wholesale distribution (downstream) of passenger cars and LCVs for the following reasons.

(420) With regard to input foreclosure, the Commission notes that that the market shares of the Parties are not very high on the upstream market. Furthermore, there are numerous established competitors present.

(421) As for customer foreclosure, the Parties' market share is also limited on the downstream market and the competitors do not rely on the Parties' as they operate their own exclusive distribution channels and do not distribute the Parties' vehicles.

7.2.Wholesale (upstream) and retail (downstream) distribution of passenger cars and LCVs

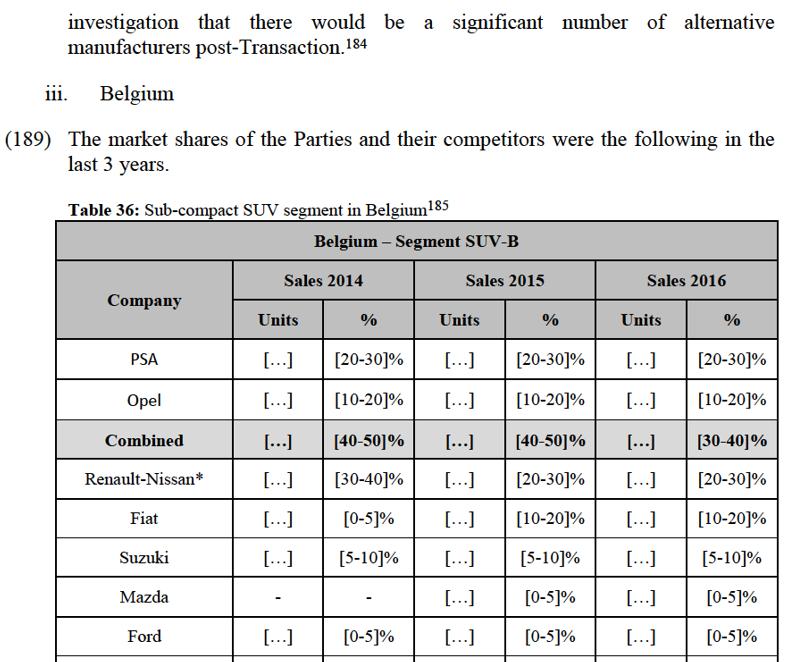

(422) The Commission considers that the Transaction would not give rise to serious doubts with regard to the vertical link between the wholesale (upstream) and the retail (downstream) distribution of passenger cars and LCVs.

(423) First, the Parties' combined market share is rather limited on the upstream market for wholesale distribution, while numerous competitors are also present.

(424) Second, the Parties' market share is also limited on the downstream market and the competitors' retailers do not rely on the Parties' as they operate their own exclusive distribution channels and do not distribute the Parties' vehicles.

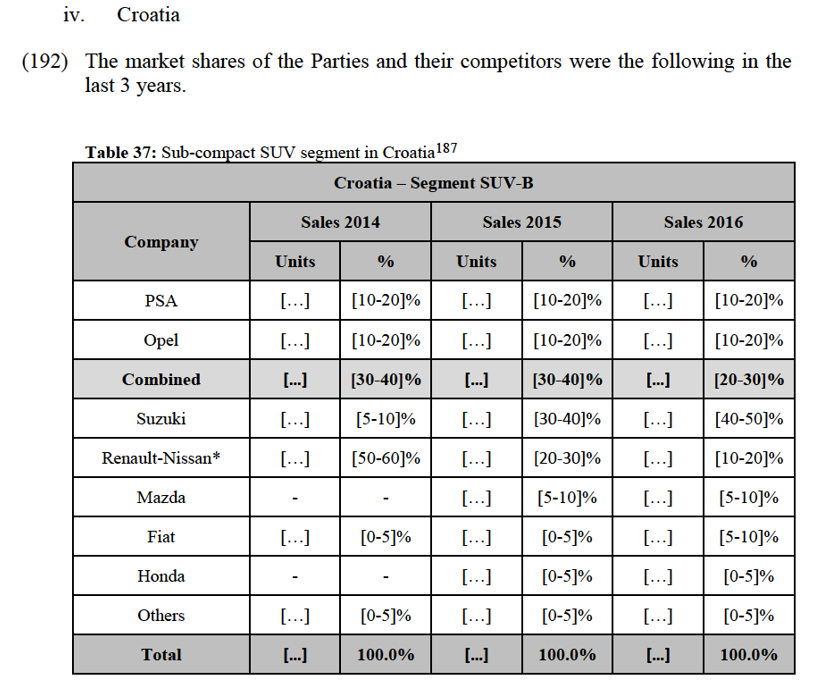

8. CONCLUSION

(425) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

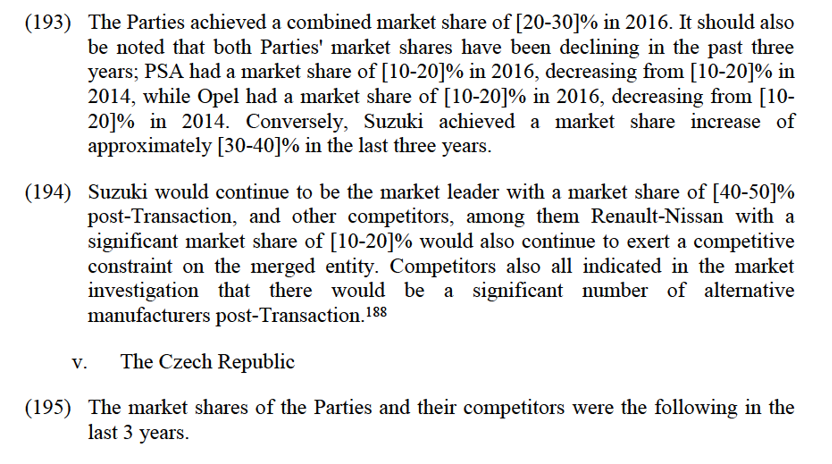

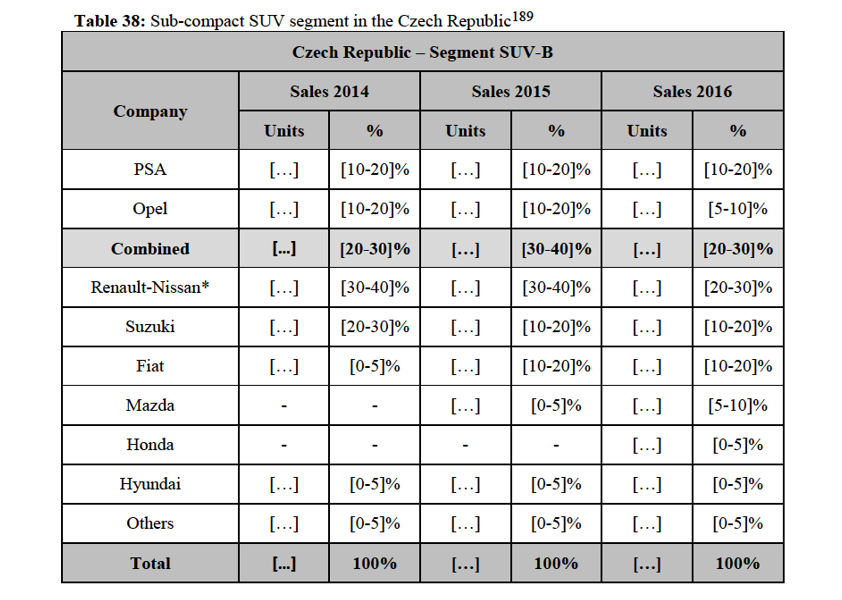

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 Publication in the Official Journal of the European Union No C 179, 07.06.2017, p. 8.

4 Opel operates ten manufacturing facilities (Austria, Germany, Hungary, Poland, Spain, and the UK) and one engineering centre (Germany) in the EEA.

5 Turnover calculated in accordance with Article 5 of the Merger Regulation and the Commission Consolidated Jurisdictional Notice (OJ C 95, 16.4.2008, p. 1).

6 See cases COMP/M.1519 Renault / Nissan (1999); COMP/M. 2832 General Motors / Daewoo (2002); COMP/M.5219 VWAG / OFH / VWGI (2008); COMP/M.5518 Fiat / Chrysler (2009).

7 See cases COMP/M.6403 Volkswagen / KPI Polska / Skoda Auto Polska / VW Bank Polska / VW Leasing Polska (2011); COMP/M.5709 Volkswagen / Mahag (2009); COMP/M.5518 Fiat / Chrysler (2009); COMP/M.5250 Porsche / Volkswagen (2008); COMP/M.5219 VWAG / OFH / VWGI

(2008); COMP/M.2832 General Motors / Daewoo (2002); COMP/M.1847 GM / Saab (2000); IV/M.1452 Ford / Volvo (1999); IV/M.1326 Toyota / Daihatsu (1998); IV/M.1204 Daimler-Benz / Chrysler (1998); IV/M.1036 Chrysler / Distributors (1997).

8 Paragraph 119 of the Form CO.

9 Paragraphs 121 and 122 of the Form CO.

10 Paragraphs 131 and 132 of the Form CO.

11 Paragraph 163 of the Form CO.

12 Non-confidential replies to question 4 of questionnaire Q2 – Competitors and non-confidential minutes of a call with a competitor on 30 May 2017.

13 Non-confidential replies to question 5 of questionnaire Q1 – Customers.

14 See case COMP/M.8099 Nissan / Mitsubishi (2016).

15 Non-confidential replies to question 5 of questionnaire Q2 – Competitors and non-confidential minutes of calls with competitors on 30 May, 7 June, 8 June and 15 June 2017.

16 Non-confidential reply of a competitor to question 5.1 of questionnaire Q2 – Competitors.

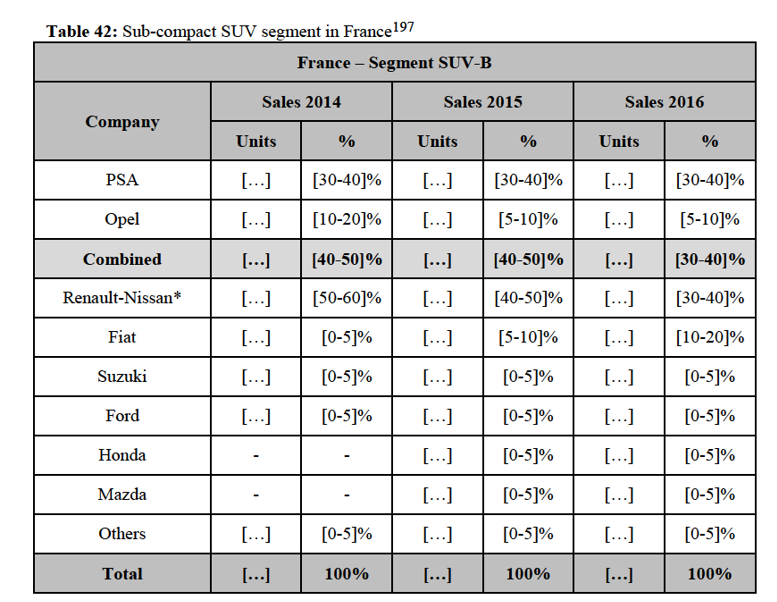

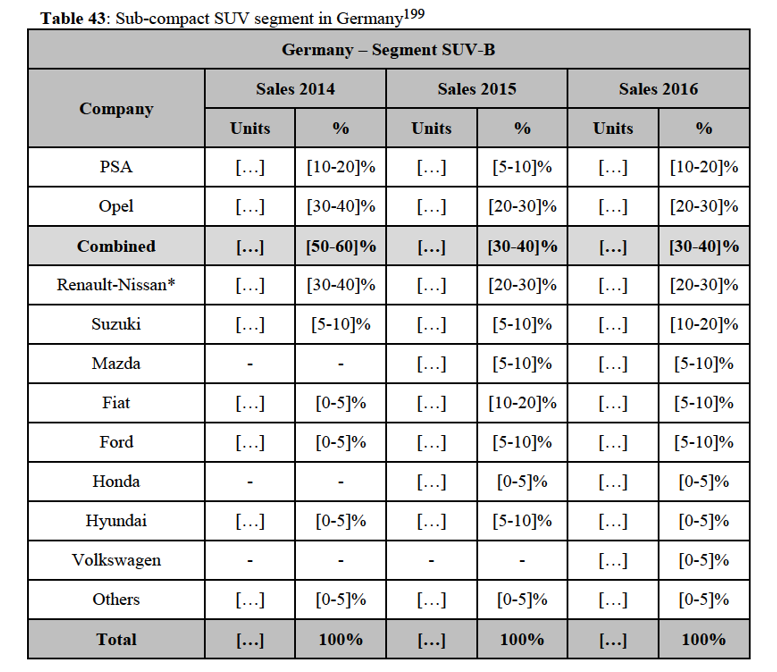

17 Non-confidential replies to question 7 of questionnaire Q1 – Customers.

18 Non-confidential replies to question 7 of questionnaire Q2 – Competitors.

19 Non-confidential reply of a competitor to question 7.1 of questionnaire Q2 – Competitors.

20 Non-confidential replies to question 7.1 of questionnaire Q2 – Competitors and non-confidential minutes of calls with competitors on 7 June, 8 June and 15 June 2017.

21 Non-confidential replies to question 7.1 of questionnaire Q2 – Competitors and non-confidential minutes of calls with competitors on 7 June, 8 June and 15 June 2017.

22 Non-confidential replies to question 8.1 of questionnaire Q1 – Customers.

23 Non-confidential replies to question 7.1 of questionnaire Q2 – Competitors, non-confidential minutes of a call with a competitor on 7 June 2017 and non-confidential replies to question 8.1 of questionnaire Q1 – Customers.

24 See cases COMP/M.6267 Volkswagen / MAN (2011); COMP/M.5157 Volkswagen / Scania (2008); COMP/M.4336 MAN / Scania (2006); COMP/M.2832 General Motors / Daewoo (2002).

25 Paragraph 152 of the Form CO.

26 Paragraph 155 of the Form CO.

27 Paragraph 156 of the Form CO.

28 Paragraph 163 of the Form CO.

29 See cases COMP/M.4785 Russian Machines / Magna (2007), COMP/M.4420 Crédit Agricole / Fiat Auto / FAFS (2006).

30 Non-confidential replies to question 5 of questionnaire Q1 – Customers, non-confidential minutes of a call with a competitor on 30 May 2017.

31 Non-confidential minutes of calls with competitors on 8 June and 15 June 2017.

32 See case COMP/M.8099 Nissan / Mitsubishi (2016).

33 Non-confidential replies to question 5.1 of questionnaire Q1 – Customers, non-confidential replies to question 6 of questionnaire Q2 – Competitors and non-confidential minutes of calls with competitors on 30 May and 8 June 2017.

34 See cases COMP/M.5518 Fiat / Chrysler (2009); COMP/M.5061 Renault / Russian Technologies / Avtovaz (2008).

35 Non-confidential replies to question 11 of questionnaire Q2 – Competitors and non-confidential replies to question 10 of questionnaire Q1 – Customers.

36 Non-confidential replies to question 13 of questionnaire Q2 – Competitors and non-confidential replies to question 12 of questionnaire Q1 – Customers.

37 Non-confidential replies to question 15 of questionnaire Q2 – Competitors.

38 Non-confidential replies to question 14 of questionnaire Q2 – Competitors.

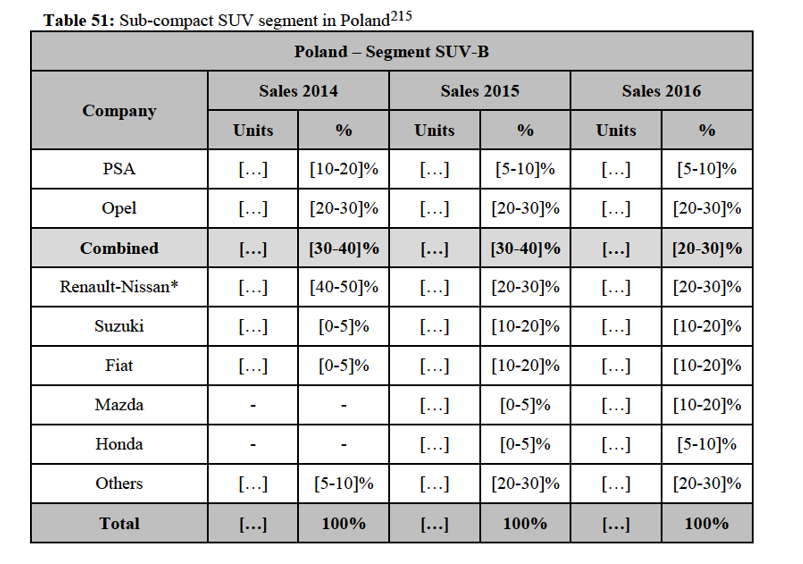

39 Non-confidential replies to question 9 of questionnaire Q1 – Customers.

40 See cases COMP/M.5518 Fiat / Chrysler (2009); COMP/M.5061 Renault / Russian Technologies / Avtovaz (2008).

41 Non-confidential replies to question 11 of questionnaire Q2 – Competitors and non-confidential replies to question 10 of questionnaire Q1 – Customers.

42 Non-confidential replies to question 12 of questionnaire Q2 – Competitors and non-confidential replies to question 11 of questionnaire Q1 – Customers.

43 Non-confidential replies to question 15 of questionnaire Q2 – Competitors.

44 Non-confidential replies to question 14 of questionnaire Q2 – Competitors.

45 Non-confidential replies to question 9 of questionnaire Q1 – Customers.

46 See cases COMP/M.5061 Renault / Russian Technologies / Avtovaz (2008); COMP/M.2832 General Motors / Daewoo (2002).

47 See cases COMP/M.6403 Volkswagen / KPI Polska / Skoda Auto Polska / VW Bank Polska / VW Leasing Polska (2011); COMP/M.5250 Porsche / Volkswagen (2008); COMP/M.2832 General Motors / Daewoo (2002).

48 See cases COMP/M.6958 CD&R / We buy any car (2013); COMP/M.6403 Volkswagen / KPI Polska

/ Skoda Auto Polska / VW Bank Polska / VW Leasing Polska (2011); COMP/M.3388 Ford Motor Company Ltd / Polar Motor Group Ltd (2004).

49 Paragraph 182 of the Form CO.

50 Paragraph 189 of the Form CO.

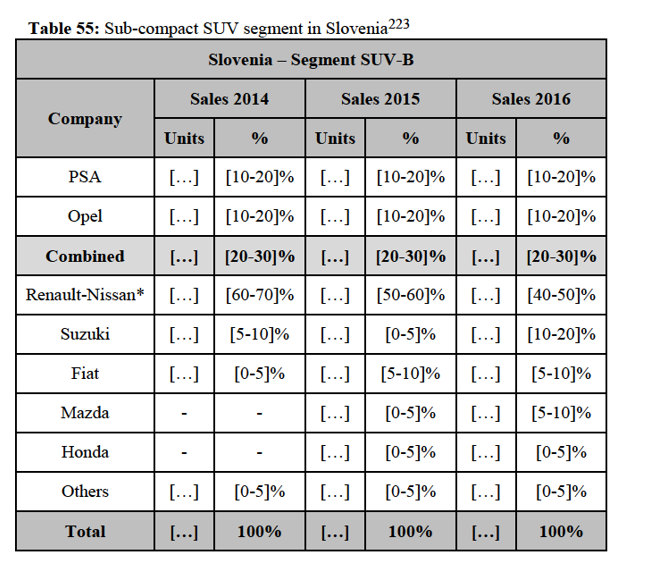

51 See cases COMP/M.6403 Volkswagen / KPI Polska / Skoda Auto Polska / VW Bank Polska / VW Leasing Polska (2011); COMP/M.2832 General Motors / Daewoo (2002); COMP/M.182 Inchape / IEP (1992).

52 See cases COMP/M.6403 Volkswagen / KPI Polska / Skoda Auto Polska / VW Bank Polska / VW Leasing Polska (2011); COMP/M.5709 Volkswagen / Mahag (2009).

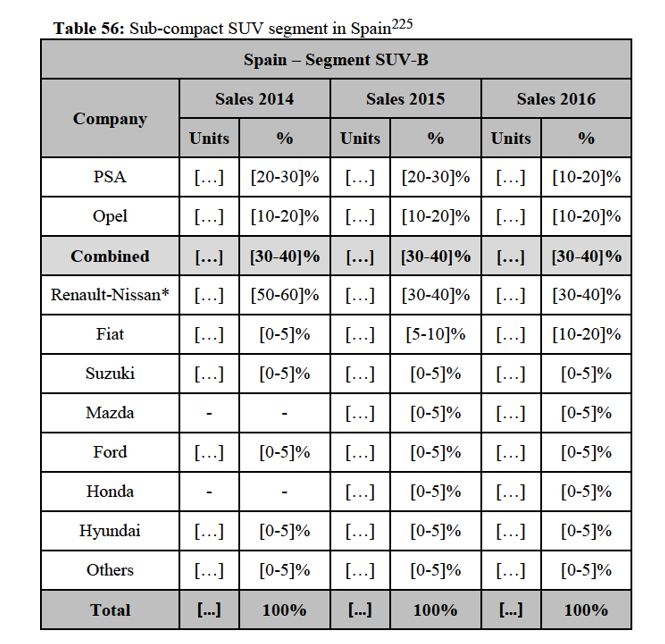

53 See cases COMP/M.6958 CD&R / We buy any car (2013); COMP/M.5250 Porsche / Volkswagen (2008); COMP/M.182 Inchape / IEP (1992).

54 Paragraph 189 of the Form CO.

55 See cases COMP/M.6718 Toyota Tsusho Corporation / CFAO (2012); COMP/M.3388 Ford Motor Company Ltd / Polar Motor Group Ltd (2004).

56 See cases COMP/M.7747 PGA / MSA (2015); COMP/M.6403 Volkswagen / KPI Polska / Skoda Auto Polska / VW Bank Polska / VW Leasing Polska (2011).

57 See cases COMP/M.7747 PGA/MSA (2015); COMP/M.6718 Toyota Tsusho Corporation / CFAO (2012); COMP/M.6403 Volkswagen / KPI Polska / Skoda Auto Polska / VW Bank Polska / VW Leasing Polska (2011); COMP/M. 5709 Volkswagen / Mahag (2009); COMP/M.5250 Porsche / Volkswagen (2008); COMP/M.3388 Ford Motor Company Ltd / Polar Motor Group Ltd (2004); M.3352 VW / Hahn + Lang (2004).

58 On the upstream market for supply of automotive components, based on the information provided by the Notifying Party, Faurecia (PSA) does not achieve more than 30% on any potential component by component market. Therefore, the Transaction does not lead to affected vertical links and negative effects are unlikely to arise.

59 Paragraph 75 of the Form CO.

60 Form CO, Table 82

61 Form CO, Table 90

62 Non-confidential replies to question 19.1 of questionnaire Q2-Competitors.

63 Form CO, Table 112

64 Non-confidential replies to question 19.1 of questionnaire Q2-Competitors.

65 Form CO, Table 120

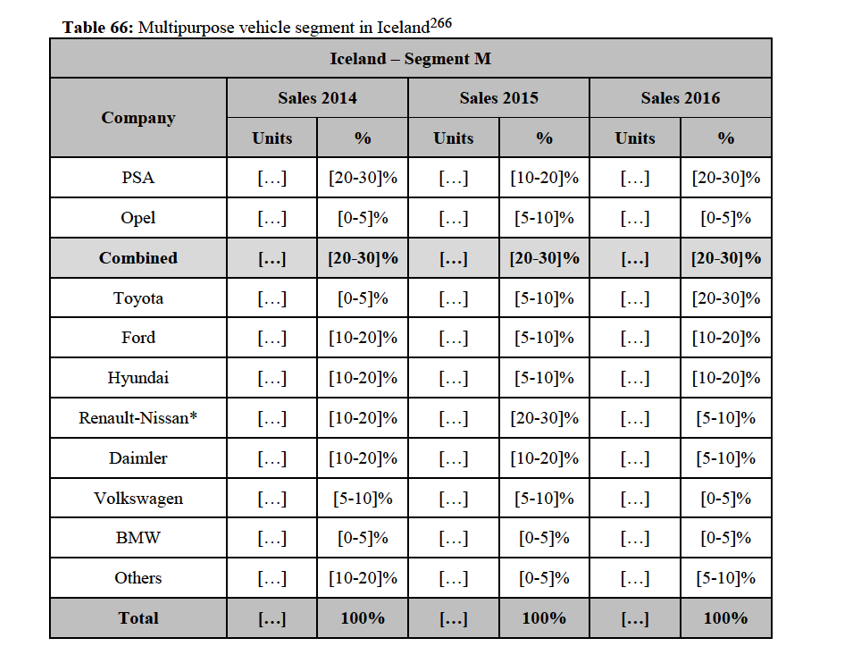

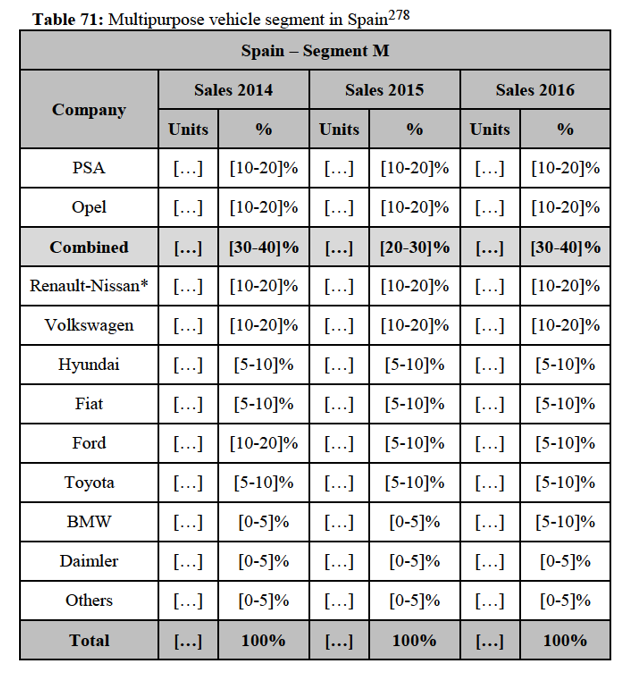

66 Non-confidential replies to question 19.1 of questionnaire Q2-Competitors.

67 Form CO, Table 122

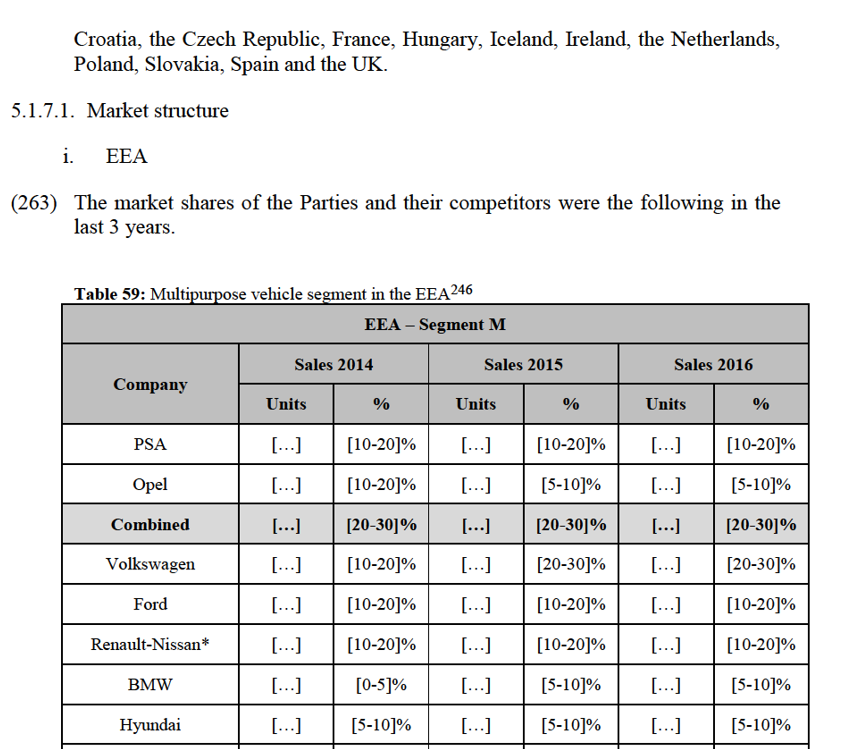

68 Non-confidential replies to question 19.1 of questionnaire Q2-Competitors.

69 Form CO, Table 151

70 Non-confidential replies to question 19.1 of questionnaire Q2-Competitors.

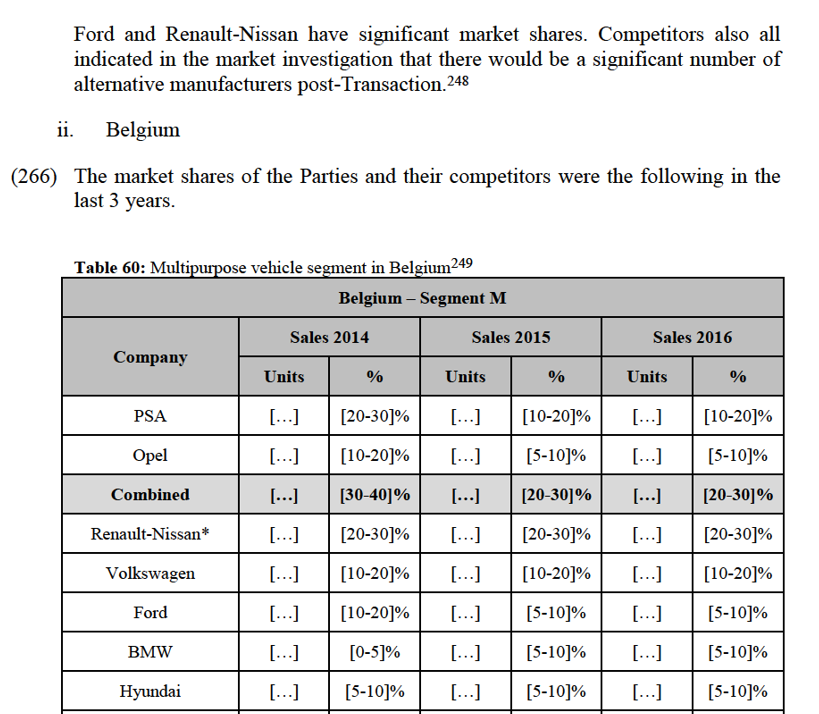

71 Form CO, Table 157

72 Non-confidential replies to question 19.1 of questionnaire Q2-Competitors.

73 Form CO, Table 162

74 Non-confidential replies to question 19.1 of questionnaire Q2-Competitors.

75 Form CO, Table 170

76 Non-confidential replies to question 19.1 of questionnaire Q2-Competitors.

77 Form CO, Table 178

78 Non-confidential replies to question 19.1 of questionnaire Q2-Competitors.

79 Form CO, Table 202

80 Non-confidential replies to question 19.1 of questionnaire Q2-Competitors.

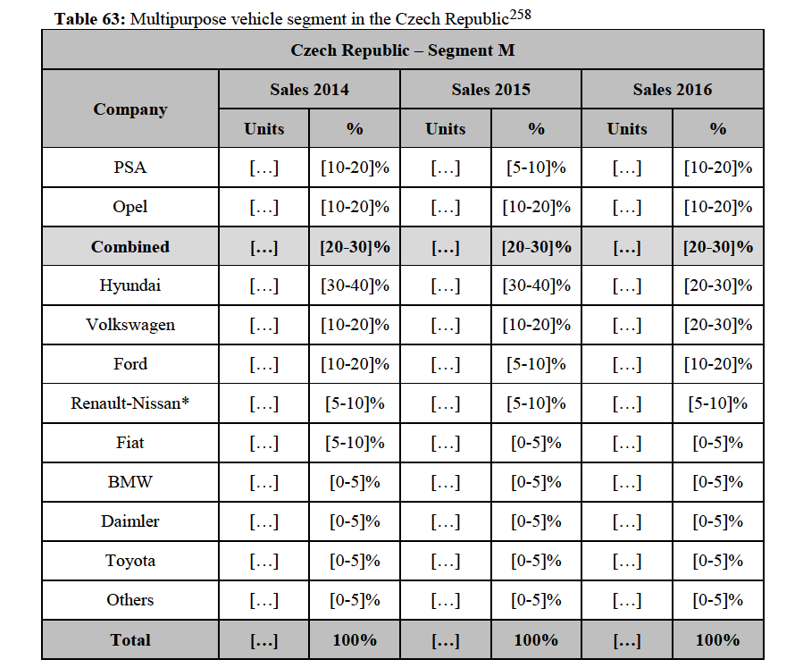

81 This is with the exception of Opel Karl which has 4/5 seats. See reply to question 1 of RFI01 of 2 June 2017.

82 Reply to question 1 of RFI01 of 2 June 2017. To be noted, […].

83 […].

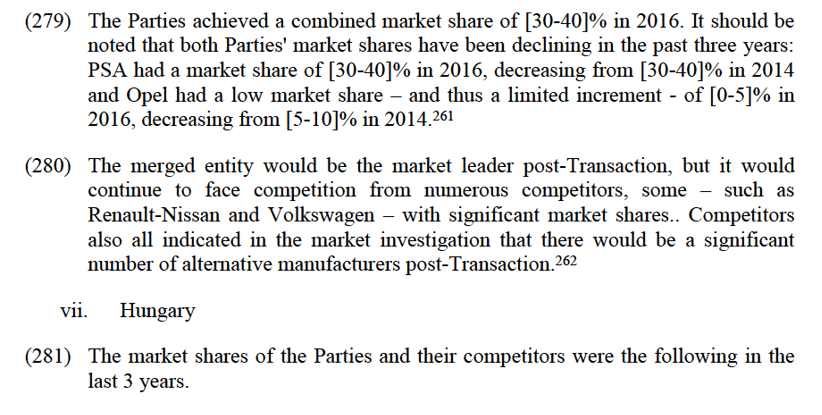

84 The NCBS survey (New Car Buyer Survey) is an annual survey widely used in the automotive sector.

85 Table 65, Table 66, Table 67 and Annex 9 - NCBS data – Closeness of competition of the Form CO.

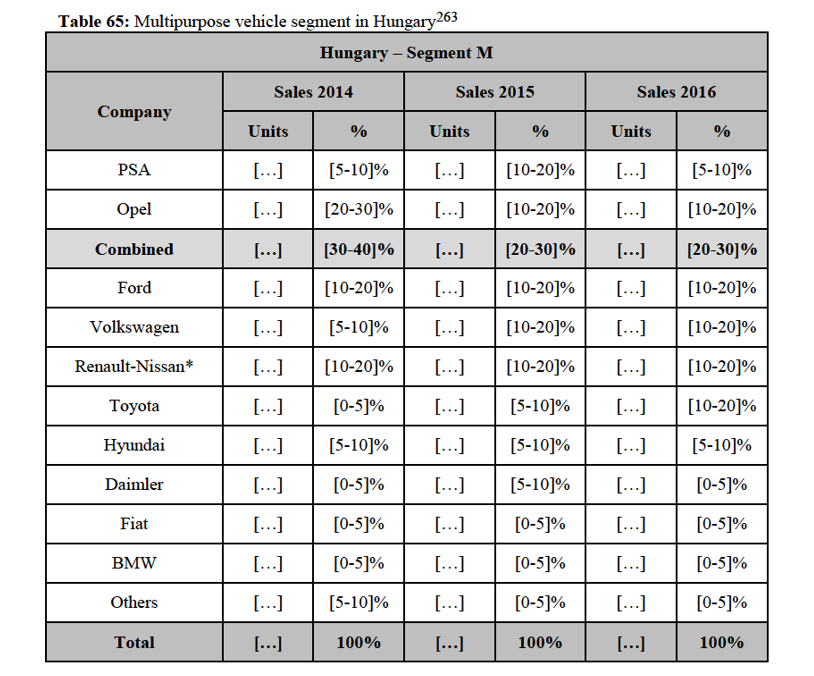

86 Non-confidential replies to question 14.1 of questionnaire Q1 – Customers.

87 Non-confidential replies to question 17 of questionnaire Q1 – Customers.

88 Non-confidential replies to question 18 of questionnaire Q1 – Customers.

89 Non-confidential replies to question 19 of questionnaire Q1 – Customers.

90 Non-confidential replies to question 20 of questionnaire Q1 – Customers.

91 Non-confidential replies to questions 19.1 of questionnaire Q2 – Competitors.

92 Non-confidential replies to questions 21.1 of questionnaire Q2 – Competitors.

93 Non-confidential replies to questions 23 and 23.1 of questionnaire Q2 – Competitors.

94 The production of "Peugeot 206" and "Peugeot 207" has been discontinued.

95 Form CO, Table 83

96 Form CO, Table 91

97 Non-confidential replies to questions 19.2 of questionnaire Q2 – Competitors.

98 Form CO, Table 101

99 Non-confidential replies to questions 19.2 of questionnaire Q2 – Competitors.

100 Form CO, Table 113

101 Non-confidential replies to questions 19.2 of questionnaire Q2 – Competitors.

102 Form CO, Table 123

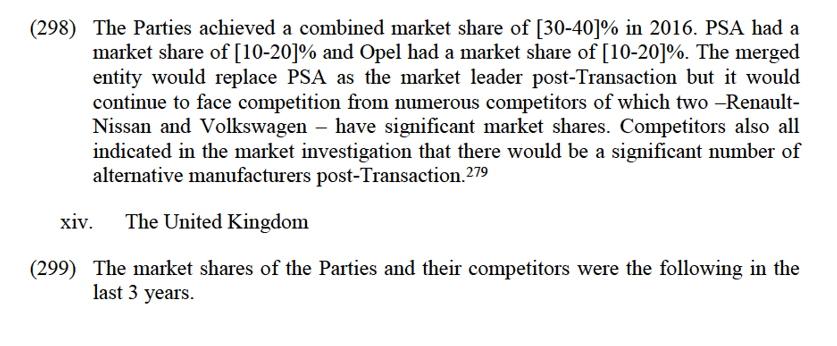

103 Non-confidential replies to questions 19.2 of questionnaire Q2 – Competitors.

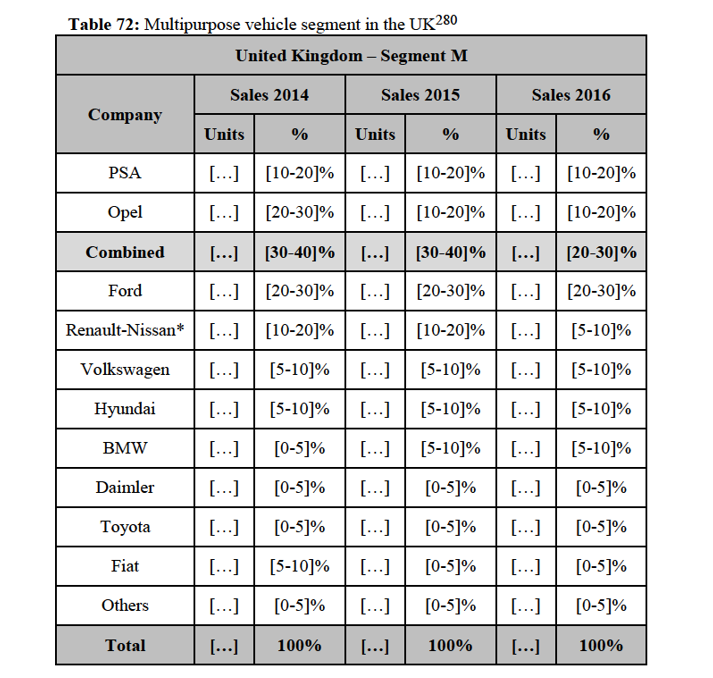

104 Form CO, Table 133

105 Non-confidential replies to questions 19.2 of questionnaire Q2 – Competitors.

106 Form CO, Table 145

107 Non-confidential replies to questions 19.2 of questionnaire Q2 – Competitors.

108 Form CO, Table 152

109 Non-confidential replies to questions 19.2 of questionnaire Q2 – Competitors.

110 Form CO, Table 158

111 Non-confidential replies to questions 19.2 of questionnaire Q2 – Competitors.

112 Form CO, Table 163

113 Non-confidential replies to questions 19.2 of questionnaire Q2 – Competitors.

114 Form CO, Table 179

115 Non-confidential replies to questions 19.2 of questionnaire Q2 – Competitors.

116 Form CO, Table 194

117 Non-confidential replies to questions 19.2 of questionnaire Q2 – Competitors.

118 Form CO, Table 203

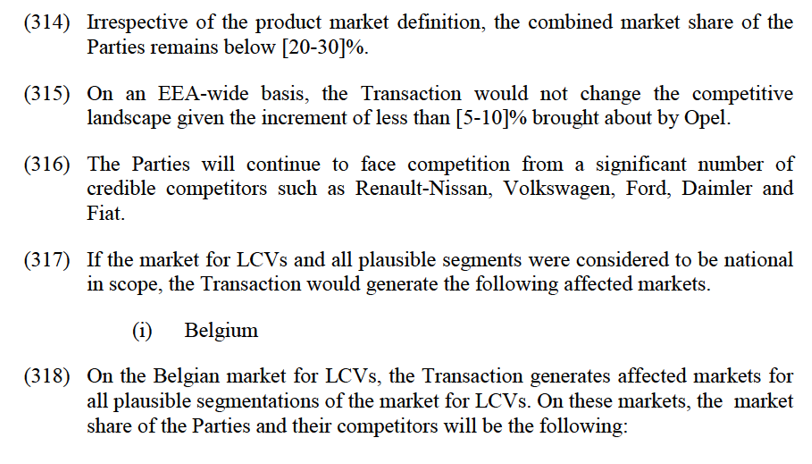

119 Non-confidential replies to questions 19.2 of questionnaire Q2 – Competitors.

120 This is with the exception of Peugeot E.Mehair,which has 4seats. Seet reply to question 1 of RFI01 of 2 june 2017.

121 Reply to question 1 of RFI01 of 2 June 2017. To be noted, Opel […].

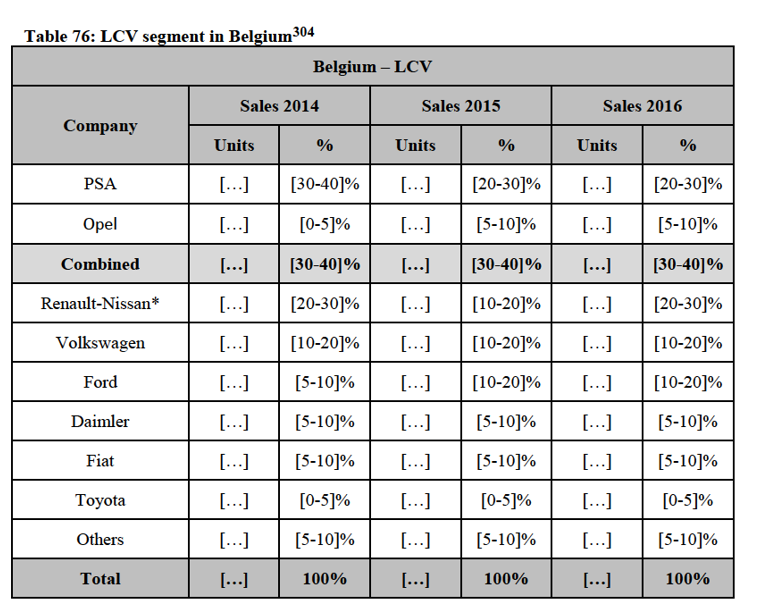

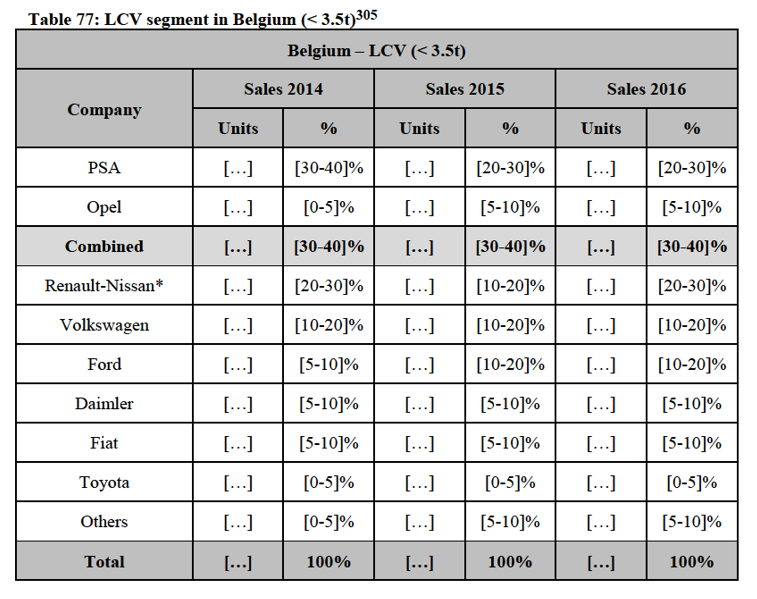

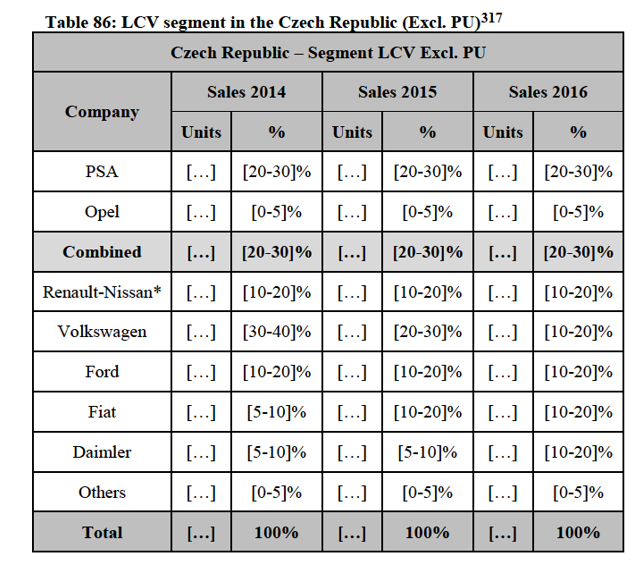

122 [Internal documents].

123 Table 65, Table 66, Table 67 and Annex 9 - NCBS data – Closeness of competition of the Form CO.

124 Non-confidential replies to question 14.2 of questionnaire Q1 – Customers.

125 Non-confidential replies to question 17 of questionnaire Q1 – Customers.

126 Non-confidential replies to question 18 of questionnaire Q1 – Customers.

127 Non-confidential replies to question 19 of questionnaire Q1 – Customers.

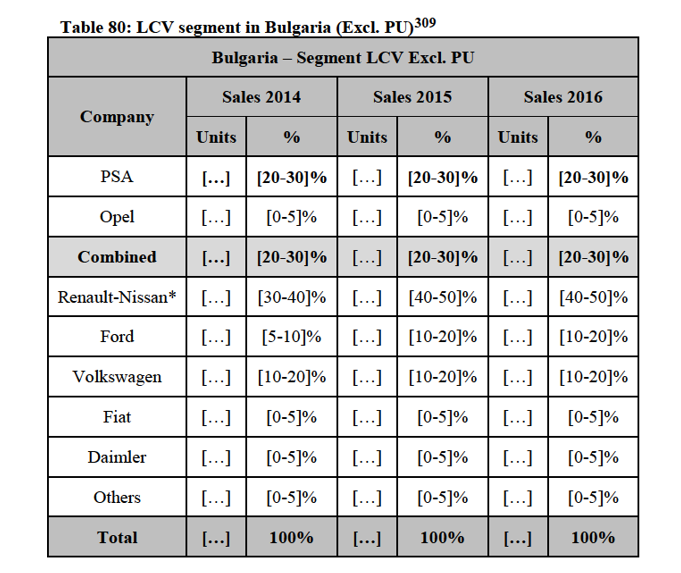

128 Non-confidential replies to question 20 of questionnaire Q1 – Customers.

129 Non-confidential replies to questions 19.2 of questionnaire Q2 – Competitors.

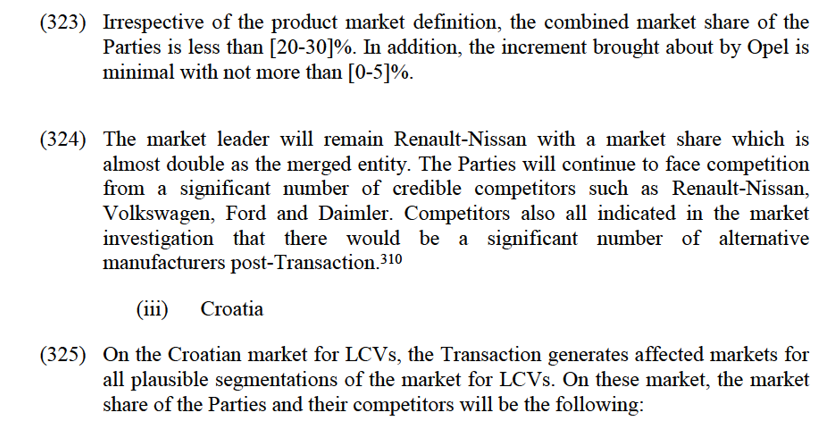

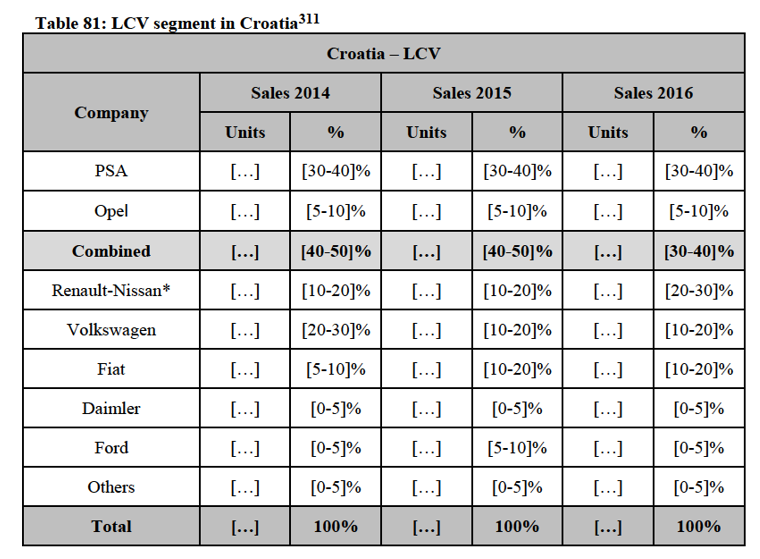

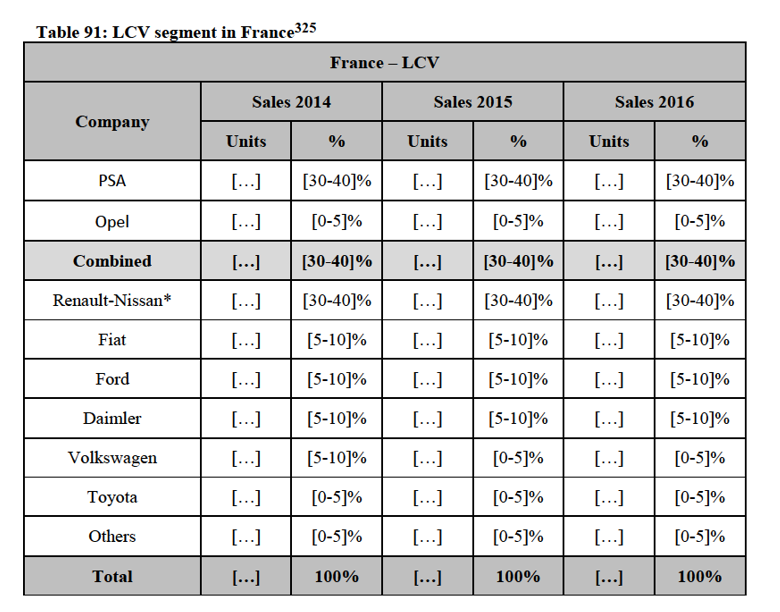

130 Non-confidential replies to questions 21.2 of questionnaire Q2 – Competitors.

131 Non-confidential replies to questions 23 and 23.1 of questionnaire Q2 – Competitors.

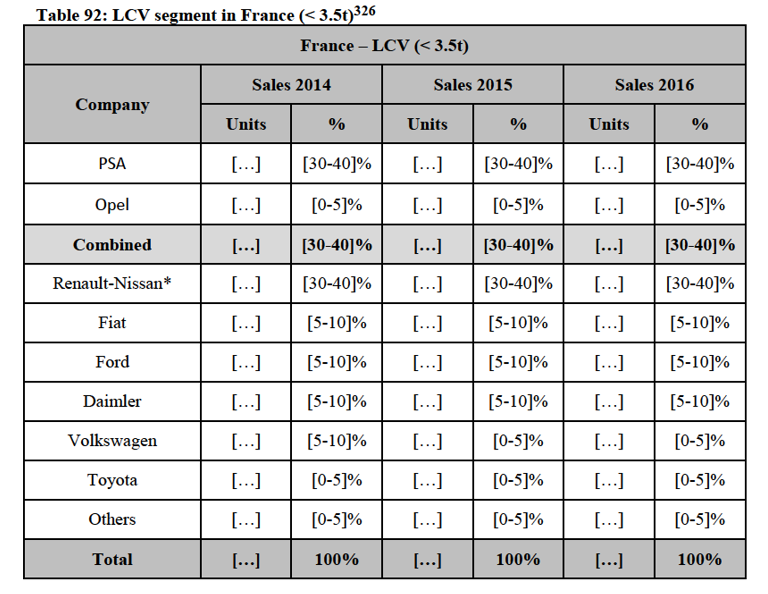

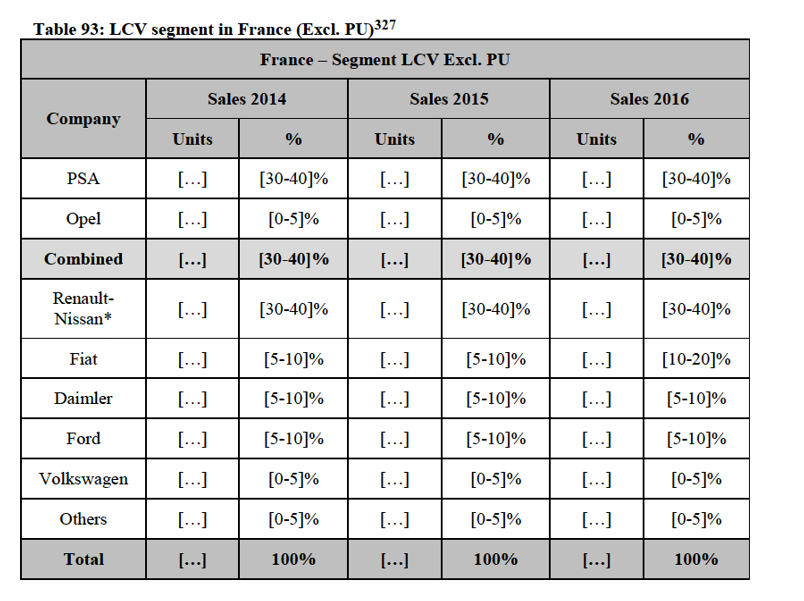

132 Form CO, Table 92

133 Non-confidential replies to question 19.3 of questionnaire Q2 – Customers.

134 Form CO, Table 114

135 Non-confidential replies to question 19.3 of questionnaire Q2 – Customers.

136 Form CO, Table 124

137 Non-confidential replies to question 19.3 of questionnaire Q2 – Customers.

138 Form CO, Table 134

139 Non-confidential replies to question 19.3 of questionnaire Q2 – Customers.

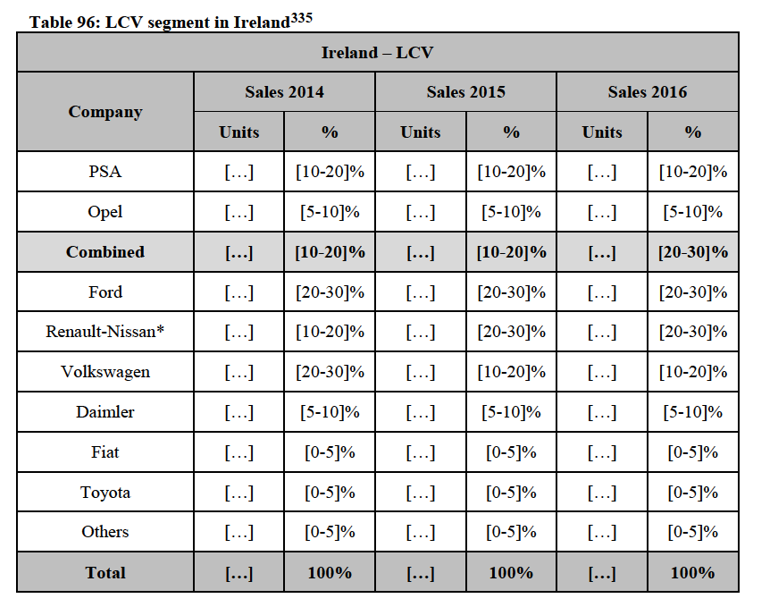

140 Form CO, Table 164

141 Non-confidential replies to question 19.3 of questionnaire Q2 – Customers.

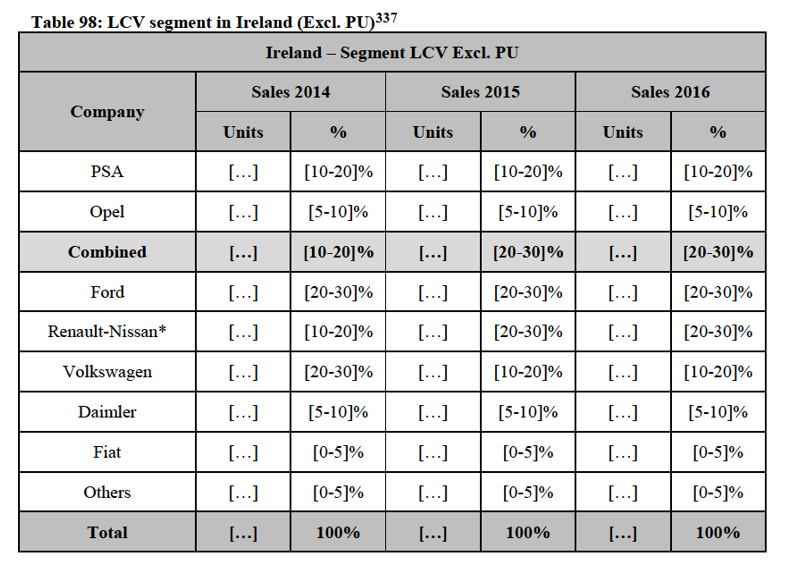

142 Form CO, Table 195

143 Non-confidential replies to question 19.3 of questionnaire Q2 – Customers.

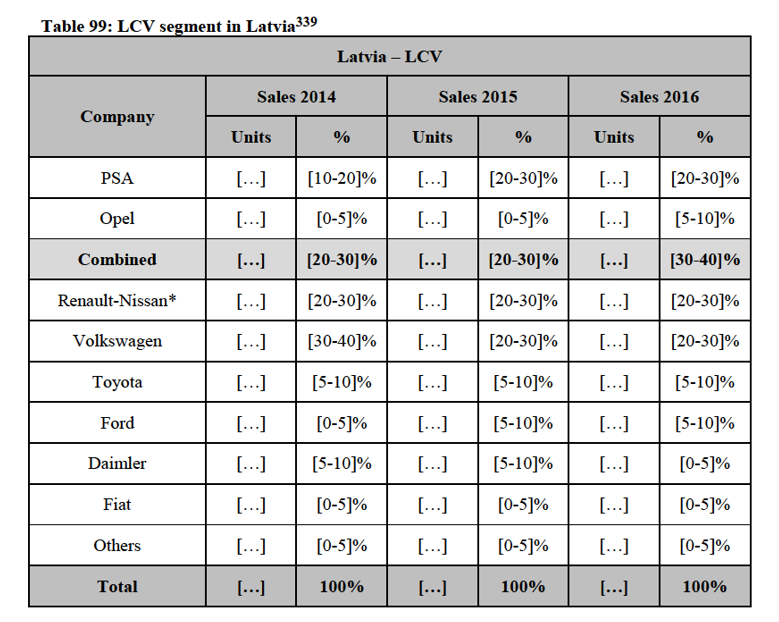

144 This is with the exception of Peugeot E.Mehair,which has 4seats. Seet reply to question 1 of RFI01 of 2 june 2017.

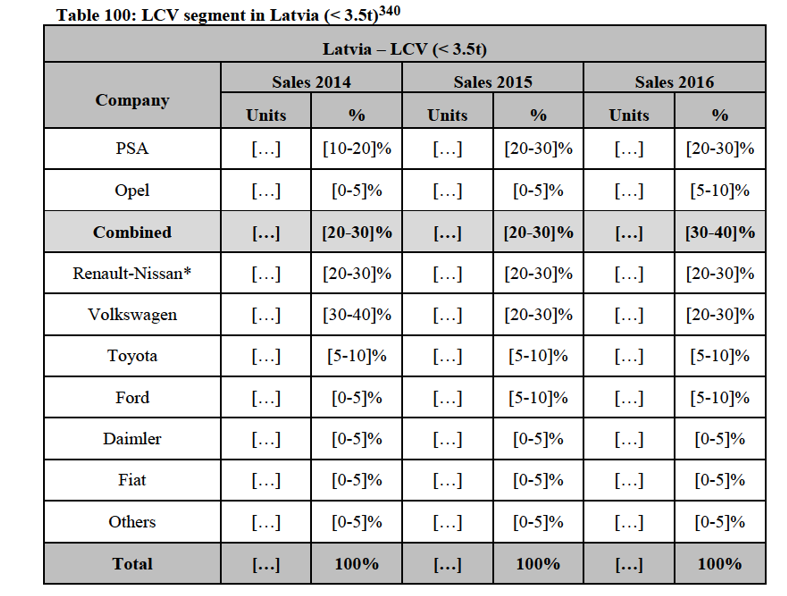

145 Response to question 1 of the RFI01 of 2 June 2017. To be noted, […].

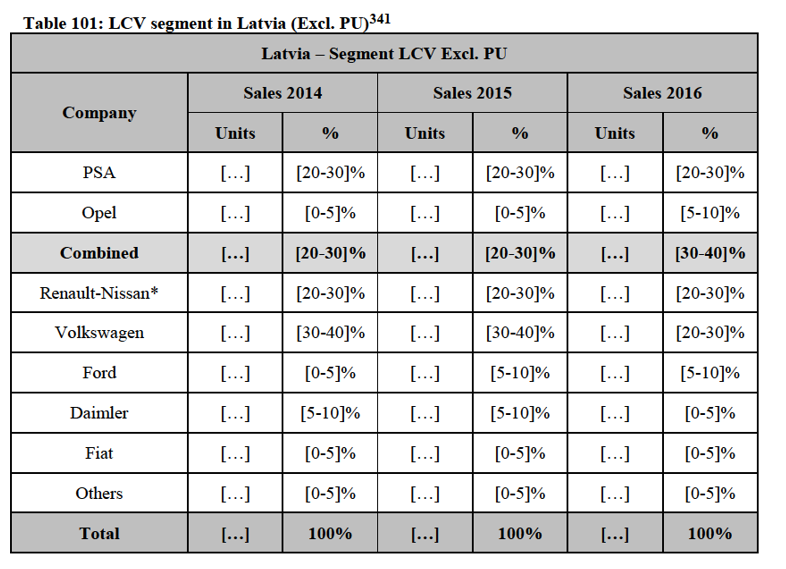

146 [Internal documents].

147 Table 65, Table 66, Table 67 and Annex 9 - NCBS data – Closeness of competition of the Form CO.

148 Non-confidential replies to question 14.3 of questionnaire Q1 – Customers.

149 Non-confidential replies to question 17 of questionnaire Q1 – Customers.

150 Non-confidential replies to question 18 of questionnaire Q1 – Customers.

151 Non-confidential replies to question 19 of questionnaire Q1 – Customers.

152 Non-confidential replies to question 20 of questionnaire Q1 – Customers.

153 Non-confidential replies to questions 19.3 of questionnaire Q2 – Competitors.

154 Non-confidential replies to questions 21.3 of questionnaire Q2 – Competitors.

155 Non-confidential replies to questions 23 and 23.1 of questionnaire Q2 – Competitors.

156 PSA offers the Peugeot 508 and the DS5 also as hybrid cars.

157 Form CO, Table 125

158 The Notifying Party submits that (..)(paragraph 1060 of the Form Co)

159 Non-confidential replies to question 19.4 of questionnaire Q2 – Competitors.

160 Form CO, Table 159

161 Non-confidential replies to question 19.4 of questionnaire Q2 – Competitors.

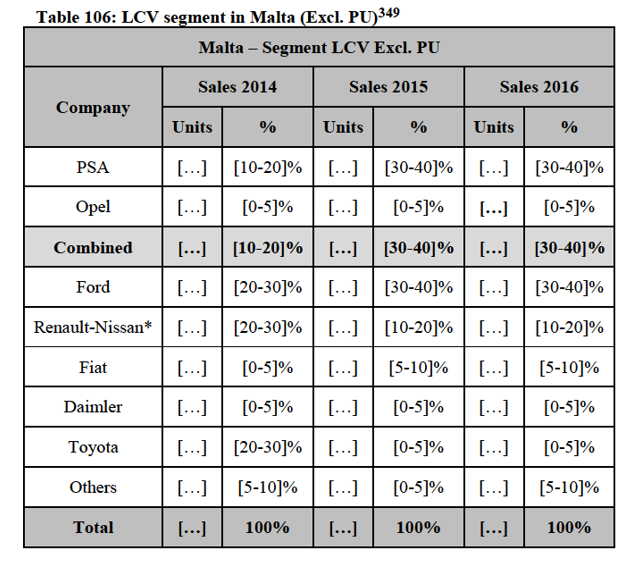

162 France: Peugeot 508 – […], Citroën C5 – […], DS5 – […], Opel Insignia – […]; Malta: Peugeot 508

– […], DS5 – N/A, Opel Insignia – […].

163 France: Peugeot 508 – […], Citroën C5 – […], DS5 – […], Opel Insignia – […]; Malta: Peugeot 508

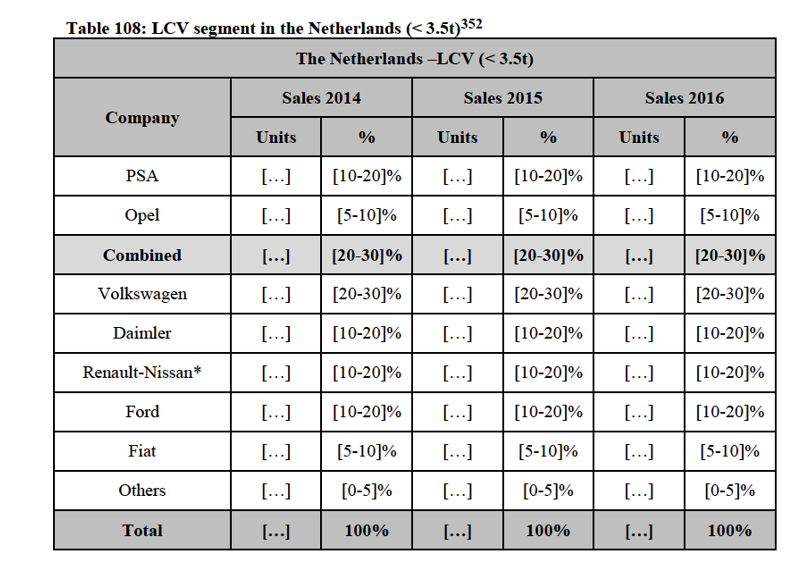

– […], DS5 – N/A, Opel Insignia – […].

164 Reply to question 4-6 of RFI01 of 2 June 2017.

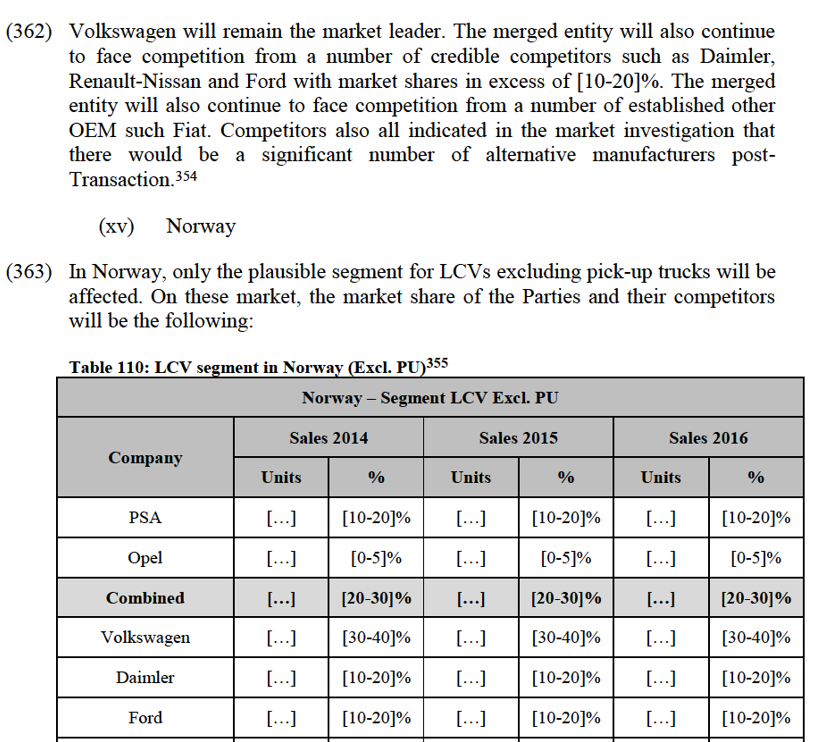

165 Reply to question 4-6 of RFI01 of 2 June 2017.

166 […].

167 [Internal documents].

168 Table 65, Table 66, Table 67 and Annex 9 - NCBS data – Closeness of competition of the Form CO.

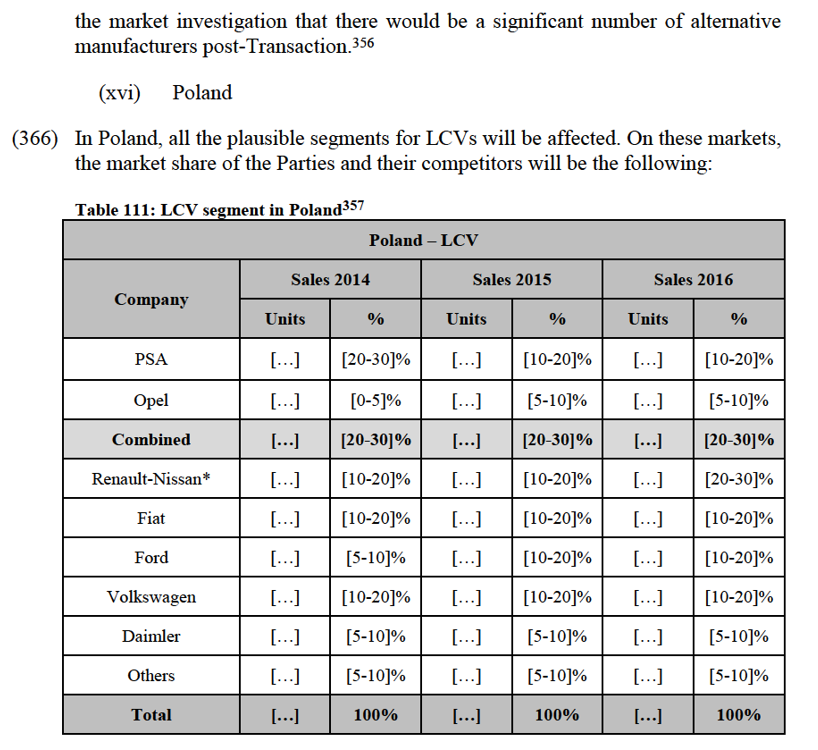

169 Non-confidential replies to question 14.4 of questionnaire Q1 – Customers.

170 Non-confidential replies to question 16.4.1 of questionnaire Q1 – Customers.

171 Non-confidential replies to question 16.4.2 of questionnaire Q1 – Customers.

172 Non-confidential replies to question 16.4.3 of questionnaire Q1 – Customers.

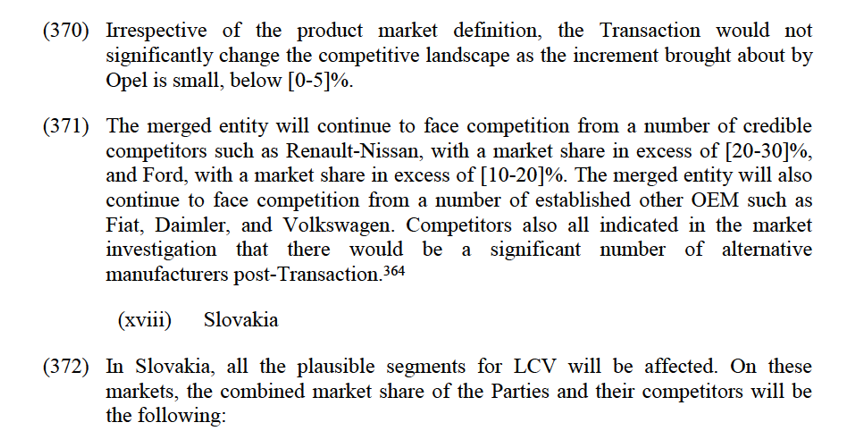

173 Non-confidential replies to questions 20.4.1 and 20.4.2 of questionnaire Q2 – Competitors.

174 Opel Mokka: 356 litres; Peugeot 2008: 410 litres; Peugeot 3008: 520 litres.

175 In France for example, the entry level price of these cars are the following: Peugeot 2008 – […], Opel Mokka – […], Peugeot 3008 – […]. The same difference can be observed with regard to the average price: Peugeot 2008 – […], Opel Mokka – […], Peugeot 3008 – […].

176 Reply to questions 7-9 of RFI01 of 2 June 2017.

177 Form CO, Table 126

178 The Notifying Party submits that PSA's market share decreased due to (..)(paragraph 1072 of the Form Co)

179 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

180 Form CO, Table 84

181 The Notifying Party submits that PSA's market share decreased due to (..)(paragraph 4573 of the Form Co)

182 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

183 Form CO, Table 89

184 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

185 Form CO, Table 93

186 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

187 Form CO, Table 102

188 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

189 Form CO, Table 107

190 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

191 Form CO, Table 115

192 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

193 Form CO, Table 116

194 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

195 Form CO, Table 121

196 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

197 Form CO, Table 127

198 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

199 Form CO, Table 132

200 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

201 Form CO, Table 135

202 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

203 Form CO, Table 140

204 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

205 Form CO, Table 146

206 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

207 Form CO, Table 147

208 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

209 Form CO, Table 153

210 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

211 Form CO, Table 165

212 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

213 Form CO, Table 171

214 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

215 Form CO, Table 173

216 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

217 Form CO, Table 180

218 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

219 Form CO, Table 184

220 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

221 Form CO, Table 185

222 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

223 Form CO, Table 190

224 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

225 Form CO, Table 196

226 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

227 Form CO, Table 201

228 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

229 Form CO, Table 204

230 Non-confidential replies to question 19.5 of questionnaire Q2 – Customers.

231 Reply to questions 7-9 of RFI01 of 2 June 2017 and reply to question 2-3 of RFI02 of 15 June 2017.

232 Opel indicated the following models as the closest alternative of Opel Mokka (if different in the following order: from a technical point of view – from a business point of view): Austria: […]–[…]; Belgium: […]–[…]; Croatia: […]; the Czech Republic: […]–[…]; Denmark: […]–[…]; Finland: […]–[…]; France: […]–[…]; Germany: […]–[…]; Greece: […]–[…]; Ireland: […]–[…]; Italy: […]; Latvia: […]–[…]; Luxembourg: […]–[…]; the Netherlands: […]–[…]; Norway: […]–[…]; Poland: […]–[…]; Portugal: […]; Romania: […]–[…]; Slovakia: […]–[…]; Slovenia: […]–[…]; Spain: […]– […]; Sweden: […]–[…]; the UK: […]–[…] ([…]).

233 […].

234 [Internal documents].

235 [Internal documents].

236 The study examined features such as exterior and interior appearance, interior controls, front seat storage, drives visibility, front row roominess and comfort, rear seat environment, cargo area and value for money.

237 The study examined features such as driver visibility, braking, ride, higher speed handling, driver comfort and roominess, interior quietness, acceleration, low speed manoeuvrability and engine sound.

238 […].

239 […].

240 […].

241 […].

242 Table 65, Table 66, Table 67 and Annex 9 - NCBS data – Closeness of competition of the Form CO.

243 The production of "Peugeot 807" and "Citroën C8" has been discontinued.

244 The production of "Opel Zafira (Family) and "Opel Agila" has been discontinued in 2015.

245 It should be noted however that among the affected markets, PSA does not commercialise the Citroën C3 Picasso in Iceland and Ireland and Opel does not sell the Meriva model in Iceland.

246 Form CO, Table 85

247 According to the Notifying ing Party, Opel's market share has dropped due to (...) (paragraph 586 of the Form Co)

248 Non-confidential replies to question 19.6 of questionnaire Q2 – Customers.

249 Form CO, Table 94

250 PSA submits that its market share has dropped due to (..)(paragraph 692 of the Form CO)

251 Non-confidential replies to question 19.6 of questionnaire Q2 – Customers.

252 Form CO, Table 98

253 The Notifying Party submits that this is due (..) on the hand and (...) on the other hand (..)(paragraph 739 of the Form Co)

254 Non-confidential replies to question 19.6 of questionnaire Q2 – Customers.

255 Form CO, Table 103

256 PSA submits that its market share has dropped due to (..)(paragraph 802 of the Form CO)

257 Non-confidential replies to question 19.6 of questionnaire Q2 – Customers.

258 Form CO, Table 108

259 Non-confidential replies to question 19.6 of questionnaire Q2 – Customers.

260 Form CO, Table 128

261 According to the Notifying ing Party, Opel's market share has dropped due to (...) (paragraph 586 of the Form Co)

262 Non-confidential replies to question 19.6 of questionnaire Q2 – Customers.

263 Form CO, Table 137

264 According to the Notifying ing Party, Opel's market share has dropped due to (...) (paragraph 586 of the Form Co)

265 Non-confidential replies to question 19.6 of questionnaire Q2 – Customers.

266 Form CO, Table 139

267 Non-confidential replies to question 19.6 of questionnaire Q2 – Customers.

268 Form CO, Table 141

269 Non-confidential replies to question 19.6 of questionnaire Q2 – Customers.

270 Form CO, Table 166

271 According to the Notifying ing Party, Opel's market share has dropped due to (...) (paragraph 586 of the Form Co)

272 Non-confidential replies to question 19.6 of questionnaire Q2 – Customers.

273 Form CO, Table 174

274 PSA submits that its market share has dropped due to (..)(paragraph 166 of the Form CO)

275 Non-confidential replies to question 19.6 of questionnaire Q2 – Customers.

276 Form CO, Table 186

277 Non-confidential replies to question 19.6 of questionnaire Q2 – Customers.

278 Form CO, Table 197

279 Non-confidential replies to question 19.6 of questionnaire Q2 – Customers.

280 Form CO, Table 205

281 According to the Notifying ing Party, Opel's market share has dropped due to (...) (paragraph 2019 of the Form Co)

282 Non-confidential replies to question 19.6 of questionnaire Q2 – Customers.

283 Both 5 seaters; load capacity: Citroën C3 Picasso – 385 litres, Opel Meriva – 400 litres; entry level price e.g. in Belgium: Citroën C3 Picasso – […], Opel Meriva – […]; average price e.g. in Belgium: Citroën C3 Picasso – […], Opel Meriva – […].

284 All 5/7 seaters; load capacity: Peugeot 5008 – 679 litres, Citroën C4 Picasso – 537 litres, Opel Zafira Tourer – 650 litres; entry level price e.g. in Belgium: Peugeot 5008 – […], Citroën C4 Picasso – […], Opel Zafira Tourer – […]; average price e.g. in Belgium: Peugeot 5008 – […], Citroën C4 Picasso – EUR […], Opel Zafira Tourer – […].

285 [Internal documents].

286 On all affected markets PSA considers that the closest alternative of the Peugeot 5008 is the […] from a technical point of view and the […] from a business point of view. PSA sees the […] (technical) and the […] (business) as the closest model to the Citroën C3 Picasso. PSA submits that the closest alternative of the Citroën C4 Picasso is the […] both from a technical and a business point of view (reply to questions 10-12 of RFI01 of 2 June 2017).

287 These are […] (reply to questions 10-12 of RFI01 of 2 June 2017).

288 Opel considers the […] to be the closest technical alternative, while sees the […], the […], the […] or the […] as the closest competitor from a business point of view based on the country in question (reply to questions 10-12 of RFI01 of 2 June 2017).

289 […].

290 [Internal documents].

291 […].

292 […].

293 […].

294 […].

295 […].

296 […].

298 Non-confidential replies to question 14.6 of questionnaire Q1 – Customers.

299 Non-confidential replies to question 16.6.1 of questionnaire Q1 – Customers.

300 Non-confidential replies to question 16.6.2 of questionnaire Q1 – Customers.

301 Non-confidential replies to question 16.6.3 of questionnaire Q1 – Customers.

302 .Form CO, Table 87

303 Form CO, Table 88

304 Form CO, Table 95

305 Form CO, Table 96

306 Form CO, Table 97

307 Non-confidential replies to question 19.7 of questionnaire Q2 – Customers.

308 Form CO, Table 99

309 Form CO, Table 100

310 Non-confidential replies to question 19.7 of questionnaire Q2 – Customers.

311 Form CO, Table 104

312 Form CO, Table 105

313 Form CO, Table 106

314 Non-confidential replies to question 19.7 of questionnaire Q2 – Customers.

315 Form CO, Table 109

316 Form CO, Table 110

317 Form CO, Table 111

318 Non-confidential replies to question 19.7 of questionnaire Q2 – Customers.

319 Reply to RFI02 of 15 june 2017, table1

320 Non-confidential replies to question 19.7 of questionnaire Q2 – Customers.

321 Form CO, Table 117

322 Form CO, Table 118

323 Form CO, Table 119

324 Non-confidential replies to question 19.7 of questionnaire Q2 – Customers.

325 Form CO, Table 129

326 Form CO, Table 130

327 Form CO, Table 131

328 Non-confidential replies to question 19.7 of questionnaire Q2 – Customers.

329 As mentioned in paragraph 311 above, the market structure for the segments "LCV excluding PU" and the segment "LCV l.3.5 exclu PU" is not materially different. Therefore the analysis only includes the broader segment but will also apply to the LCV l3.5t exclu PU segment.

330 Form CO, Table 136

331 Non-confidential replies to question 19.7 of questionnaire Q2 – Customers.

332 As mentioned in paragraph 311 above, the market structure for the segments "LCV excluding PU" and the segment "LCV l.3.5 exclu PU" is not materially different. Therefore the analysis only includes the broader segment but will also apply to the LCV l3.5t exclu PU segment.

333 Form CO, Table 138

334 Non-confidential replies to question 19.7 of questionnaire Q2 – Customers.

335 Form CO, Table 142

336 Form CO, Table 143

337 Form CO, Table 144

338 Non-confidential replies to question 19.7 of questionnaire Q2 – Customers.

339 Form CO, Table 148

340 Form CO, Table 149

341 Form CO, Table 150

342 Non-confidential replies to question 19.7 of questionnaire Q2 – Customers.

343 Form CO, Table 154

344 Form CO, Table 155

345 Form CO, Table 156

346 Non-confidential replies to question 19.7 of questionnaire Q2 – Customers.

347 According to IHS, all LCVs sold in Malta are LCVs below 3.5t, therefore an analysis of the plausible market of LCV l3.5t, would be exactly the same to the analysis on all LCVs.

348 Form CO, Table 160

349 Form CO, Table 161

350 Non-confidential replies to question 19.7 of questionnaire Q2 – Customers.

351 Form CO, Table 167

352 Form CO, Table 168

353 Form CO, Table 169

354 Non-confidential replies to question 19.7 of questionnaire Q2 – Customers.

355 Form CO, Table 172

356 Non-confidential replies to question 19.7 of questionnaire Q2 – Customers.

357 Form CO, Table 175

358 Form CO, Table 176

359 Form CO, Table 177

360 Non-confidential replies to question 19.7 of questionnaire Q2 – Customers.

361 Form CO, Table 181

362 Form CO, Table 182

363 Form CO, Table 183

364 Non-confidential replies to question 19.7 of questionnaire Q2 – Customers.

365 Form CO, Table 187

366 Form CO, Table 188

367 Form CO, Table 189

368 Non-confidential replies to question 19.7 of questionnaire Q2 – Customers.

369 Form CO, Table 191

370 Form CO, Table 192

371 Form CO, Table 193

372 Non-confidential replies to question 19.7 of questionnaire Q2 – Customers.

373 Form CO, Table 198

374 Form CO, Table 199

375 Form CO, Table 200

376 Non-confidential replies to question 19.7 of questionnaire Q2 – Customers.

377 Form CO, Table 206

378 Form CO, Table 207

379 Form CO, Table 208

380 Non-confidential replies to question 19.7 of questionnaire Q2 – Customers.

381 Non-confidential replies to question 16.7.4.1.1 to 16.7.4.1.3 and 16.7.4.2.1 to 16.7.4.2.3 of questionnaire Q1 – Customers.

382 Two mini cars: the Peugeot iOn and Citroën CZero; a small car: the Citroën Méhari; and two LCVs: the Peugeot Partner and the Citroën Berlingo (see table 14 of the Form CO).

383 Two large cars: the Peugeot 508 and the DS5; and an SUV, the Peugeot 3008 (see table 14 of the Form CO).

384 Opel used to commercialise a hybrid version of its Ampera (medium) model but the production was stopped in 2015 (see paragraph 138 of the Form CO).

385 Paragraph 139 of the Form CO.

386 […].

387 Paragraph 140 of the Form CO.

388 Paragraph 146 of the Form CO.

389 Paragraph 147 of the Form CO.

390 E.g. Renault-Nissan – "Renault Twingo" – last quarter of 2018; Toyota – "Aygo" – first quarter of 2019; BMW – "Mini" – second quarter of 2019.

391 E.g. Fiat – "500e" – 2019; Volkswagen – "eUp!" – first quarter of 2020; BMW – "i3" – May 2020; Bolloré – "BlueCar" – first quarter of 2023.

392 Table 15 of the Form CO.

393 Paragraph 146 of the Form CO.

394 Paragraph 147 of the Form CO.

395 E.g. Hyundai – "Kona" – first quarter of 2018; Volkswagen – "Audi A1" and "Audi Q2" – last quarter of 2019; Volkswagen – "Polo" – first quarter of 2020; Volkswagen – "Seat Ibiza" – last quarter of 2020; Volkswagen – "Skoda Fabia" – first quarter of 2021; Volkswagen – "Seat Arona" – 2022; Ford

– "Fiesta" – first quarter of 2023.

396 E.g. Renault-Nissan – "Renault Zoe" – last quarter of 2023.

397 Table 15 of the Form CO.

398 Paragraph 146 of the Form CO.

399 Paragraph 147 of the Form CO.

400 E.g. Volkswagen – "Krafter" – third quarter of 2017; Daimler – "Mercedes Vito" – last quarter of 2017; Renault-Nissan – "Renault Master" – last quarter of 2017; Daimler – "Sprinter" – last quarter of 2018; Ford – "Transit Connect" – first quarter of 2019; Fiat – "Doblo" – first quarter of 2019; Daimler

– "Mercedes Citan" – last quarter of 2019; Volkswagen – "Caddy" – first quarter of 2020.

401 E.g. Renault-Nissan – "Kangoo" – first quarter of 2019.

402 Table 15 of the Form CO.

403 Table 17 of the Form CO.

404 Paragraphs 193-194 of the Form CO.

405 Paragraph 207 of the Form CO.

406 Paragraph 222 of the Form CO.