Commission, January 20, 2010, No M.5611

EUROPEAN COMMISSION

Decision

AGILENT/ VARIAN

Dear Sir/Madam,

Subject: Case No COMP/M.5611 – Agilent/ Varian

Notification of 23/11/2009 pursuant to Article 4 of Council Regulation No 139/2004 (1) Publication in the Official Journal of the European Union No. C 289, 28.11.09, p. 26

1. On 23 November 2009 the Commission received a notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 ("EC Merger Regulation") by which the undertaking Agilent technologies Inc ('Agilent', United States of America, hereinafter the 'notifying party') acquires within the meaning of Article 3(1)(b) of the EC Merger Regulation sole control of the whole of Varian Inc ('Varian', United States of America) by way of purchase of shares.

I. THE PARTIES

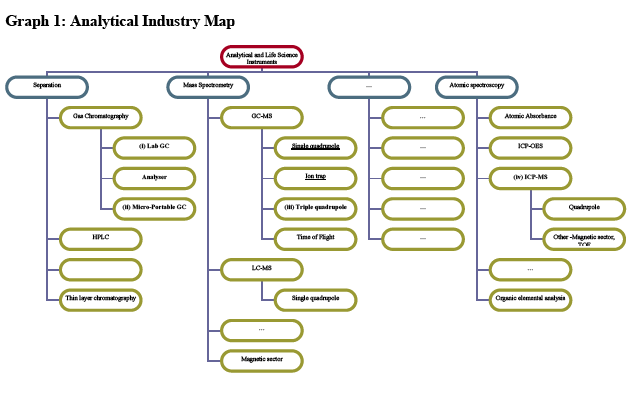

2. Agilent is active in the field of design, development, manufacture and sale of bio-analytical measurement products (including analytical and life science instruments as well as associated services, consumables and software) and electronic measurement products.

3. Varian is active in the design, development, manufacture and sale of bio-analytical measurement products (including analytical and life science instruments as well as associated services, consumables and software) and vacuum products.

II. THE OPERATION AND THE CONCENTRATION

4. On 26 July 2009, Agilent, Varian and Cobalt Acquisition Corp ('Cobalt') (a special purpose vehicle newly established by Agilent) entered into an Agreement and Plan of Merger whereby Cobalt will merge with and into Varian. As a result, Varian will, following the proposed transaction, exist as a wholly-owned subsidiary of Agilent.

5. Agilent will therefore acquire sole control of Varian. The proposed transaction constitutes a concentration within the meaning of Article 3(1)(b) of the EC Merger Regulation.

III. COMMUNITY DIMENSION

6. The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 2 500 million (2) (Agilent: EUR 3 859 million, Varian: EUR 673 million). The combined aggregate turnover of the undertakings concerned is more than EUR 100 million in each of at least three Member States (in the United Kingdom the turnover of Agilent and Varian respectively is […] and […]; in Germany the turnover of Agilent and Varian respectively is […] and […]; in France the turnover of Agilent and Varian respectively is […] and […]). In each of these three Member States, the aggregate turnover of each undertaking concerned is more than EUR 25 million. The aggregate Community-wide turnover of each undertaking concerned is more than EUR 100 million. Neither of the undertakings concerned achieves more than two- thirds of its aggregate Community-wide turnover within one and the same Member State.

7. The notified concentration therefore has a Community dimension pursuant to Article 1(3) of the EC Merger Regulation.

IV. RELEVANT MARKETS

A. General introduction to markets and overlaps/links

8. Agilent and Varian are both active in the analytical and life sciences instrumentation field. This field encompasses the manufacture and sale of instruments as well as associated services, software and consumables used for the analysis of chemicals by customers in a wide variety of applications.

9. From the information submitted by the notifying party and in terms of a report drawn up by the market research analyst, Strategic Developments Inc ('SDI'), (3) it appears possible to identify different sectors within the analytical and life science instrumentation field according to the following nine techniques used for analysis: (i) separations; (ii) life sciences; (iii) mass spectrometry; (iv) molecular spectroscopy; (v) atomic spectroscopy; (vi) surface science; (vi) materials characterisation; (vii) laboratory automation; and (ix) general analytical.

10. Each of these nine sectors may in turn be further segmented on the basis of the respective analytical technique. For example, within the separations sector it is possible to identify sub- segments for instruments based on the gas chromatography ('GC') technique and on the high performance liquid chromatography ('HPLC') technique. Similarly, within the mass spectrometry ('MS') sector it is possible to identify a sub-segment for instruments based on the gas chromatography-mass spectrometry ('GC-MS') technique and on the liquid chromatography-mass spectrometry technique ('LC-MS'). Within the atomic spectroscopy sector it is possible to identify a sub-segment for instruments based on the inductively coupled plasma-mass spectrometry ('ICP-MS') technique.

11. For illustration purposes, a summary chart of the analytical industry segmentation, highlighting the significant horizontal overlaps resulting from the proposed transaction is provided in Graph 1 below.

12. The proposed transaction will result in significant horizontal overlaps and affected markets between Agilent and Varian's activities in the following areas: (i) laboratory GC instruments ('Lab GCs'); (ii) micro/portable gas chromatography instruments ('micro/portable GCs'); (iii) triple quadrupole GC-MS instruments ('triple quad GC-MS instruments'); and (iv) quadrupole

ICP-MS instruments ('quadrupole ICP-MS instruments'). Horizontal overlaps will also arise in relation to certain consumables for each of the GC, Micro-portable, triple quadrupole GC-MS instruments and ICP-MS instruments

13. Furthermore, the proposed transaction will give rise to a number of other minor overlaps, which technically constitute affected markets, but in which one or other of the merging parties has a minor presence. These technically affected markets are: (i) high performance liquid chromatography ('HPLC') instruments; (ii) single quadrupole LC-MS ('single quad LC-MS') instruments; and (iii) single quadrupole GC-MS ('single quad GC-MS') instruments.

14. The proposed transaction will also give rise to a vertical relationship between the merged entity's activities in relation to Lab GC sub-segment and its activities in the GC analyser ('analyser') sub- segment of the GC segment.

B. Relevant product markets

(a) Gas Chromatography (GC)

15. Instruments based on the GC technique are used to separate a complex sample of a thermally stable, volatile substance (that is, a substance which does not disintegrate when heated and which can be vaporised) into its individual components. GC instruments use an inert gas to transport the sample through a chromatographic column which separates the mixture into its individual components prior to detection and quantification. A GC is suitable for use only with known compounds (that is for compounds where the user knows what is being analysed) rather than unknown compounds.

Instruments

16. The notifying party submits that the GC segment can be sub-segmented into three different types of instruments: (i) analysers, that is, highly customised GC instruments which are specially configured to customers' specifications for specialized applications (4); (ii) Micro/portable GC instruments which are smaller, portable instruments which can be used on-site and are based on micro-electromechanical technologies which enable miniaturisation and high speed analysis; and (iii) Lab GCs which are in essence GC instruments not falling within one of the other two categories. (5)

17. In that regard and with respect to the products manufactured by Agilent and Varian, these instruments have very different price points: a Lab GC instrument typically costs in the region of EUR 12,000 to EUR 22,000, whereas an analyser costs in the region from EUR 25,000 to EUR 50,000 or more, and Micro/Portable GC are in the region of EUR 20,000 to EUR 25,000. Moreover, analysers are technologically distinct from Lab GCs insofar as although having a Lab GC as a foundation they are configured to customer specifications for specialised applications, predominantly in the petroleum industry, and tested against those specifications at the manufacturing facility before shipment. An analyser incorporates significant added value to a standard Lab GC, it is estimated that about […] of the additional costs in an analyser are attributable to customisation services performed by the vendor.

18. In contrast to Lab GC, Micro/portable GC (i) can only analyse samples at room temperature, (ii) are generally pre-configured for specific chemical analyses; and (iii) are normally based on specific microelectromechanical technologies which enable miniaturisation and high- speed analysis. Micro/portable GC due to their specific characteristics and design are primarily used in a range of energy sector applications (including, natural gas, fixed gases and refinery gas) where on-site use is critical, as well as in mining, industrial hygiene, landfill gas analysis, selected military uses and fuel cell development.

19. The market investigation has confirmed that given the differences in capabilities, product requirements and the reduced overlap in the areas of analytical application of these GC instruments, customers do not view Lab GC, analysers and Micro/portable GC as interchangeable. In addition, the market investigation has signalled that Micro/portable GCs require a specialised sale force and an alternate distribution channel given the specificity of the product.

20. The market investigation also confirmed that the Lab GC market should not be further segmented according to customer groups into (i) sales to end customers and to value added resellers who lightly customise Lab GCs and (ii) sales to third parties purchasing Lab GCs as inputs for analysers (6). According to the results of the market investigation, pricing and other sales' conditions are similar for both customer groups.

21. Therefore, in light of the above, separate markets are defined for: (i) Lab GCs; (ii) analysers; and (iii) Micro/portable GC instruments.

Software

22. The output of an analytical instrument generally reaches the user through an attached computer data system which allows the user to view and manage the output. In many cases is also important that the user is able to retain and archive that output.

23. The notifying party submits that GC software is commonly sold separately from the instrument itself [5-10]%. Both instrument manufacturers and third party vendors provide similar software systems. Customers can choose between two major types of software to operate their instrument, namely: single instrument, single user GC systems (which are optimised for a single user operating a single GC) (7); and multiple instrument, multiple user software (which allows simultaneous operation of multiple GCs by multiple operators) (8).

24. During the Commission's market investigation, the vast majority of the respondents have confirmed that software is generally integrated and supplied by the same manufacturer of the GC instrument. The vast majority of respondents have also confirmed that they usually purchase the software together with the instrument. Therefore, it is not appropriate to distinguish a product market for GC software which is distinct from the instrument market.

Even assuming that such distinct market existed, the GC instrument supplier share in relation to software would not deviate significantly from the GC instrument share.

Consumables

25. Consumables are products which are necessary to operate analytical instruments, which have a limited lifetime (generally less than one year) and are user-replaceable. Both Agilent and Varian are active in the manufacture and sale of consumables for GC instruments.

26. The notifying party submits that consumables used in relation to GC instruments including Lab GC, Analysers and Micro/portable GC fall into the following main categories: (i) gas management supplies (these supplies allow flow control, pressure regulation and purification of gases supplied to the instrument); (ii) columns and related products (GC columns are used to separate the mixture introduced into the GC system into its individual components prior to detection and quantification); (iii) samples introduction supplies (used to introduce and volatilise a sample); (iv) detector supplies (used to identify and quantify the sample); (v) samples vials/containers (used to contain the sample and solvent prior to introduction into the instrument); and (vi) chemical standard supplies (used for calibration of the instrument).

27. According to the notifying party, customers normally source their consumables from third party suppliers, as well as, or in the alternative, to the instrument manufacturer. Besides manufacturing the product, in many cases, the instrument manufacturer sources it from a third party supplier to re-sell it. The market investigation has confirmed that GC Lab instruments and consumables constitute separate markets as well as the segmentation of consumables submitted by the notifying party. However, for the purposes of this decision, the product market definition as regards consumables used in relation to GC instruments may be left open as the proposed transaction will not give rise to any serious doubts even on the narrow market segmentations used specifically with GC instruments.

(b) High Performance Liquid Chromatography (HPLC)

28. Liquid Chromatography (LC) is a technique involving the separation of soluble chemical compounds in a liquid stream. It differs from GC insofar as it is able to handle non-volatile compounds and thermally unstable molecules.

29. LC technology comes in two forms, which are mainly characterized by the pressure applied to force the liquid stream through the separation device, the chromatographic column. HPLC (High Performance Liquid Chromatography) uses high pressure (several hundred bars), generates very efficient separations and therefore has developed into a standard tool in most analytical laboratories for a variety of different applications. On the other hand LPLC (low pressure liquid chromatography) constitutes a simple methodology, applying only limited pressure to achieve rough separations of chemical and biochemical compounds. It is often used to separate compounds from unwanted sample constituents, for example after a compound has been synthesized or for the analysis of pressure-sensitive biomolecules. The parties' activities do not overlap regarding the LPLC market.

30. It may be possible to sub-segment the HPLC space on the basis of the specific analytical technique of the instruments populating this segment (including, for instance: analytical HPLC, gel permeation/size exclusion HPLC and preparation HPLC). However, the product market definition as regards HPLC instruments may be left open as the proposed transaction will not give rise to any serious doubts in this regard.

(c) Gas Chromatography – Mass Spectrometry (GC-MS)

31. MS is used to identify the chemical composition of a sample on the basis of the mass-to-charge ratio of charged particles. GC-MS instruments combine a GC system with an MS system and are used for the separation and identification of volatile compounds. The critical difference between a GC instrument and a GC-MS instrument is that whereas the former is only suitable for use with known compounds, a GC-MS instrument may be used to identify also unknown compounds. (9)

Instruments

32. There are four existing GC-MS technologies, namely: (i) single quadrupole GC-MS ('single quad GC-MS'); (ii) triple quadrupole ('triple quad GC-MS'); (iii) ion trap GC-MS; and (iv) time of flight ('TOF'). Agilent manufactures and sells single quad and triple quad GC-MS instruments. Varian manufactures and sells single quad, triple quad and ion trap GC-MS instruments. Neither Agilent nor Varian is active in TOF GC-MS instrument space. Therefore, TOF GC-MS instruments are not discussed further in this decision.

33. Single quad GC-MS technology is the most widely used GC-MS technology. It involves passing ions through four rods ('the quadrupole'). By changing the electric field applied, ions of various sizes are permitted to pass through the quadrupole of the detector for detection. Triple quad GC-MS technology also uses the four rod technology described above. However, following passage through the first quadrupole, the ions pass through a collision cell, which breaks them into pieces. These pieces then pass through a further quadrupole. Ion trap GC- MS technology involves the use of a three dimensional electrical field to trap ions which are then ejected selectively for detection. TOF GC-MS technology uses pulses of kinetic energy to push ions towards the detector. The time taken for a particular ion to reach the detector (the time of flight) enables the identification of a particular ion's mass and hence its identity.

34. The notifying party submits that each of these GC-MS technologies is competitively distinct from both a demand side and a supply side perspective and that separate product markets therefore exist for single quad, triple quad, ion trap and TOF GC-MS instruments. The notifying party refers to several factors as the points of distinction between these instruments.

35. In that regard and with respect to the products manufactured by Agilent and Varian, these instruments have very different price points: a single quad GC-MS instrument typically costs EUR 35,000-50,000 whereas an ion trap GC-MS instrument costs EUR 50,000-70,000 and triple quad prices are in the region of EUR 95,000-200,000. Moreover, single quad GC-MS instruments have limited sensitivity in terms of dealing with complex samples (containing a lot of extraneous material) compared to ion trap and especially triple quad instruments. Consequently, they are considered as more robust and reliable for simple matrix-analysis than ion trap or triple quad GC-MS instruments. On the other hand, ion trap and triple quad GC-MS instruments have the ability to undertake multiple iterations of the mass spectrometry testing on a single sample in the same process (MS-MS capability), which greatly enhances identification capabilities. Triple quad GC-MS instruments are mainly used for analysing complex samples containing a lot of constituent parts whereas ion trap GC-MS instruments are mostly used for analysing "cleaner" samples.

36. The market investigation has confirmed that, given these differences in capabilities (and hence end use) of single quad, triple quad, ion trap GC-MS instruments, customers do not view these three types of GC-MS instruments as interchangeable. Moreover, the market investigation has confirmed a lack of supply side substitutability between single quad, triple quad and ion trap GC-MS instruments.

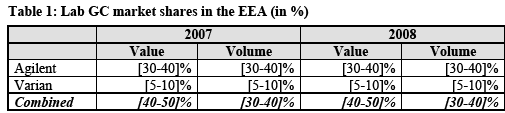

37. Therefore, in light of the above, separate markets are defined for: (i) single quad; (ii) ion trap;

(iii) and triple quad GC-MS instruments.

Software

38. As regards software, the notifying party submits that GC-MS instruments use proprietary, closed access system software which is purchased with the instrument (rather than supplied separately).

39. The market investigation has confirmed that the majority of software used for GC-MS instruments is proprietary and is usually integrated in the instrument and supplied by the instrument manufacturer. For the purposes of this decision, it is therefore concluded that no separate market for software for GC-MS instruments has to be identified.

Consumables

40. As regards consumables, the notifying party submits that consumables used specifically with GC-MS instruments (10) fall into the following main categories: (i) tuning samples (used for calibration of the instrument); (ii) ion source supplies (these are parts of the ion source(11) part of a GC-MS instrument); (iii) detector supplies (used to identify and quantify the sample once separated); and (iv) vacuum consumables (these consumables are parts of the vacuum pump part of a GC-MS instrument). The market investigation has confirmed the segmentation of consumables used specifically with GC-MS instruments in the manner proposed by the notifying party. However, for the purposes of this decision, the product market definition as regards consumables used in relation to GC-MS instruments may be left open, since the proposed transaction will not give rise to any serious doubts even on the narrow market segmentations of consumables used specifically with GC-MS instruments.

(d) Liquid Chromatography – Mass Spectrometry (LC-MS)

41. LC-MS instruments combine an LC system with an MS system in order to perform detailed qualitative analysis on non-volatile compounds and thermally unstable molecules.

42. It may be possible to sub-segment the LC-MS space on the basis of the specific analytical technique of the instruments populating this segment, including, single quad, tandem (Triple quad and ion trap) and time of flight LC-MS instruments. From the information submitted by the notifying party it appears that the proposed transaction will give rise to an affected market only in relation to the parties' single quad LC-MS instrument activities. However, the product market definition as regards LC-MS instruments may be left open as the proposed transaction will not give rise to any serious doubts in this regard.

(e) Inductively Coupled Plasma - Mass Spectrometry (ICP-MS)

43. ICP-MS form part of the Atomic Spectroscopy segment. Atomic spectroscopy allows the user to determine the atomic composition of a sample, i.e. to determine which elements from the periodic table (12) are present in the substance to be analysed. This differs from MS which permits the user to determine which molecular compounds are present in a sample. Within the atomic spectroscopy sector, it is possible to identify the following different sub-segments for instruments which are based on different technologies: (i) the inductively coupled plasma- mass spectrometry ('ICP-MS') technique, (ii) atomic absorbance ('AA'), and (iii) inductively coupled plasma-organic elemental analysis ('ICP-OES'). While Agilent has no presence in the AA and ICP-OES segments, there is a significant horizontal overlap of the parties' activities in the ICP-MS segment.

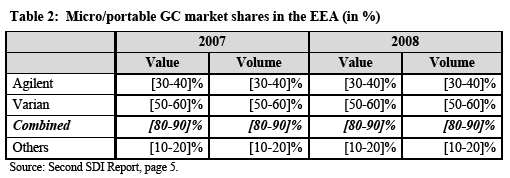

Instruments

44. ICP-MS instruments combine two technologies, namely inductively coupled plasma technology and mass spectrometry technology (13). These instruments are used for the analysis of inorganic materials. While all instruments based on the three above-mentioned techniques are capable of analysing most elements on the periodic table, the notifying party submits that ICP-MS instruments would fall into a separate segment from AA and ICP-OES instruments.

45. Respondents to the Commission's market investigation have unanimously confirmed that ICP- MS is not substitutable with the instruments based on AA and ICP-OES. Main factors of distinction are sensitivity, capabilities and price, ICP-MS being the most sensitive and the most expensive of these three techniques.

46. Within the ICP-MS segment, there are instruments outside the mainstream space which are non-quadrupole products. These high-end instruments use high resolution magnetic sector technology or time of flight technology. The market investigation has shown that these high- end non-quadrupole instruments are not substitutable with quadrupole ICP-MS products, since they are significantly more sensitive and hence used in particular in research and not in routine applications and since their price is significantly higher. Neither Agilent nor Varian is active in this non-quadrupole ICP-MS instrument space. Therefore, non-quadrupole ICP-MS instruments are not discussed further in this decision.

47. In light of the above, a separate market is defined for quadrupole ICP-MS instruments.

Software

48. With regard to ICP-MS system software, the notifying party submits that suppliers' market shares in relation to software follow their ICP-MS instruments shares given that ICP-MS software are usually purchased with the instruments. The market investigation has confirmed that ICP-MS instruments use proprietary, integrated system software which is purchased together with the instrument. For the purposes of this decision, it is therefore concluded that no separate market for software for ICP-MS instruments may be identified.

Consumables

49. As regards consumables, the notifying party submits that ICP-MS consumables fall within the following maim categories: (i) gas management supplies (these supplies allow flow control, pressure regulation and purification of gases supplied to the instrument); (ii) detector supplies (used to identify and quantify the sample once ionised and separated); (iii) samples introduction supplies (used to introduce a sample for analysis); (iv) samples vials/containers (used to contain the sample and solvent prior to introduction into the instrument); and (v) chemical standard supplies (used for calibration of the instrument).

50. The market investigation has confirmed the segmentation of consumables used specifically with ICP-MS instruments in the manner proposed by the notifying party. However, for the purposes of this decision, the further product market definition as regards consumables used in relation to ICP-MS instruments may be left open, since the proposed transaction will not give rise to any serious doubts even on the basis of the narrow market segmentations of consumables used specifically with ICP-MS instruments.

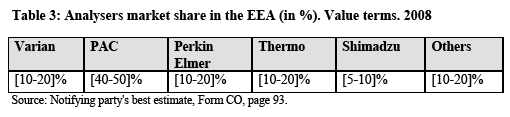

C. Relevant geographic markets

51. The notifying party submits that the geographic scope in respect of the product markets mentioned above is global, or at least EEA-wide since: (i) the parties both manufacture all relevant products from a single site (save in rare cases), and ship from those sites to regional distribution hubs around the world; (ii) transport costs are low as a proportion of total cost of the instrument (up to […] of the cost of the instrument ); (iii) limited regulatory differences apply with respect to the sale of these products between regions of the world; (iv) no technical differences exist between products shipped anywhere in the world; (v) all major manufacturers are present in every geography. In addition, the parties submit to support an EEA-wide market definition that: (i) market positions of competitors are similar throughout the EEA; (ii) prices do not vary significantly between Member States; and (iii) there do not seem to be any barriers to enter a national market in terms of language, distribution or regulatory regimes.

52. The market investigation did not confirm the view of the parties that the geographic scope of the product markets mentioned above is worldwide. Indeed, there is evidence from the market investigation that the competitive conditions are not homogenous between the EEA and the rest of the world. First, most of the customers having responded to the market investigation indicated a preference towards vendor proximity for instrument after sales services and training purposes. Only few customers on the different product markets have indicated within the market investigation that they would be willing to source on global basis if necessary, whereas the majority of customers would stick to suppliers in the EEA.

53. Second, although the parties and their competitors manufacture from a single site, they also operate regional distribution hubs (14) and have subsidiaries in the EEA to sell the products and provide after sales and training services. Third, different pricing lists and to some extent marketing strategies appear to exist for, in particular, the EEA and the USA. Fourth, there are differences regarding the market presence of some competitors: for example on the ICP-MS market, Shimadzu only has a significant business in Asia, its home market.

54. Within the EEA, whilst most customers have indicated a preference for vendor proximity for instrument after sales services and training purposes, the market investigation has confirmed that the main instrument and consumables providers on the different product markets are present in the various EEA states either directly or indirectly via distributors. Customers explained that while they might prefer suppliers which are located in their own country, they generally see no problems in procuring from suppliers on an EEA level should this be necessary.

55. The market investigation has also confirmed that no significant differences in price and market shares of the main players for instruments and consumables exist between EEA states. Since the main players are present in the different countries, the same competitive forces and constraints exist throughout the EEA.

56. Therefore, it is concluded that the geographic scope of the (i) Lab GC instruments; (ii) Analysers; (iii) Micro/portable GC instruments; (iv) triple quad GC-MS instruments; (v) single quad GC-MS instruments; (vi) ICP-MS instruments; and (vii) the hypothetical markets for GC, GC-MS and ICP-MS consumables are EEA-wide in scope.

57. Given the small overlaps which will result from the transaction with regard to HPLC and LC- MS spaces under any plausible alternative market delineation, it can be left open whether these segments are EEA-wide or global.

V. COMPETITIVE ASSESSMENT

(a) Horizontal overlap: Lab GCs

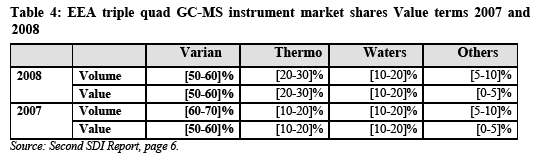

Market share

58. Agilent is the historic market leader in the EEA for Lab GCs. According to the notifying party estimates as shown in table 1 below, in 2008 the merged entity will hold a combined market share of [40-50]% in value terms with a significant increment of [5-10]%, while in volume terms it would hold a combined market share of [30-40]% with an increment of [5-10]%. The market share of the main market participants appear to have been relatively stable over the period 2006-2008. The combined entity will have an appreciably larger market share than the next competitor post-merger.

59. The market investigation has sought to reconstruct the market shares of the main players in the Lab GC market (16). This market reconstruction has revealed significantly higher estimates for the combined market share of the merged entity (approximately [60-70]% in value and [50-60]% in volume for 2008). According to the market reconstruction, the combined entity post-merger would be by far the biggest player with the other remaining competitors, Shimadzu, Thermo and Perkin Elmer having much smaller market shares both in terms of revenue and volume.

60. The notifying party despite the appreciable combined market share of the merged entity achieved as a result of the proposed transaction submits that no serious doubts will arise in the Lab GC market since (i) GC technology has become a commoditised and mature technology; (ii) Intellectual property ('IP') rights, regulation and the need to set up a distribution network do not pose significant barriers to entry; (iii) recent new entry trend by smaller low cost manufacturers and that this trend is likely to continue; (iv) barriers to switching for customers are very low given the simplicity and familiarity of GC technology; and (v) customers are generally able to exercise material purchasing power.

61. During the Commission’s market investigation, the majority of competitors and a significant number of customers (both end-consumers and value-added resellers) expressed concerns that the merged entity would have the capacity to increase prices post-merger. The following factors are relevant in this respect.

62. With regard to actual competition, the market investigation has confirmed that the majority of the customers consider Agilent and Varian to be close competitors in the supply of Lab GC, in particular as participants perceive them to provide instruments with comparable functionalities and that compete in similar application areas. The market investigation has also revealed that Agilent and Varian tend to participate in parallel in open tenders for the supply of Lab GC. The majority of the customers have, in the past, considered the other supplier when purchasing a Lab GC instrument. Varian's transaction level database submitted by the parties showed that Agilent appeared as the most frequently identified competitor in those cases in which Varian finally won a sale.

63. In addition, the market investigation has highlighted that Varian seems to be historically the first undertaking to have started applying a very vigorous discount policy. Some respondents to the market investigation submitted that the merger would thus remove a significant constraint on pricing in the Lab GC market.

64. With regard to potential competition, the market investigation has revealed that although the technology involved in Lab GC has already been available for a relative long period of time, no significant entry in the market has occurred in the last three years and that the main players in Lab GCs tend to maintain their relative market shares over time.

65. The market investigation has also shown that entry of new competitors is unlikely in the foreseeable future due to existence of appreciable barriers to entry in the Lab GC market. In particular, a majority of customers have identified the costs associated with the development and mass production of Lab GC as obstacles to entry. Some respondents have also indicated IP rights, implied R&D expenses and costs associated with the developing and marketing of new technology as further barriers to entry in this market. The results of the market investigation suggest that reputation and brand recognition also play a relevant role in the Lab GC market directly influencing customers' purchases. In this respect, the responses gathered in the market investigation show that customers perceive Agilent and Varian as solid brands exhibiting a strong reputation and customer loyalty in the market.

66. The market investigation revealed that the installed base (i.e. the instruments already being used at the customers' site) is a determinant factor with regards to potential switching. In fact, Lab GCs can be operated in parallel within a laboratory environment or within the same company at different sites. As a result, Lab GCs are subject to learning effects, given that the benefit of each Lab GC instrument to a particular customer increases the more Lab GC instruments of the same brand are purchased. Sticking to just one Lab GC brand has advantages for customers in terms of training, accumulated know how, documentation, software connectivity.

67. In this context, repetitive customers normally stick to one vendor because of the large costs associated to switching and the learning effects mentioned above. Factors such as accumulated know how, service relation with vendors, maintenance of spare parts, required training associated to the use of the instrument make switching highly unlikely. Moreover, given the relevance of obtaining precise measurements, customers show preference for proven products. Accordingly, it is reasonable to conclude that by benefiting post-merger from a very large combined installed base, the combined entity would benefit from a 'lock-in effect' which would make it hard for the other players to reposition in the market and effectively compete with the merged entity.

68. Moreover, the result of the market investigation suggests that in most of the cases the instrument manufacturer is the supplier of the after-sales services of the Lab GC instrument. This factor contributes to strengthen the potential market power achieved through the installed base.

69. In light of the above, it is concluded that the proposed transaction raises serious doubts as to its compatibility with the common market with regard to the EEA market for Lab GCs.

(b) Horizontal overlap: Micro/portable GCs

70. The Micro/portable GC market in the EEA is led by Agilent and Varian. As indicated in table 2 below, the proposed transaction will result in the combined entity holding particularly large market shares for Micro/portable GCs. Varian is the market leader in Micro/portable GCs in the EEA and already enjoys significantly high market shares. The notifying party estimates that as a result of the proposed transaction, the market share of the combined entity would be of [80-90]% in value and [80-90]% in volume. The market shares of the merging parties appear to have been relatively stable over the period 2006-2008.

71. The significantly high market shares to be achieved by the merged entity may in themselves be taken as evidence of the existence of a dominant position on the EEA market for Micro/portable GCs. (17) With such a strong position on the market the merged entity will have the capacity to increase prices post-merger as there would be practically no competition left post-merger in the EEA Micro/portable GC market.

72. In addition to the above mentioned very high market shares, other factors contribute to reinforce the competition concerns arising from the transaction in Micro/portable GC.

73. The market investigation has revealed that a significant number of customers and competitors have a negative perception about the impact of the merger on Micro/portable GCs. The responses obtained highlight that there is already not much competition in Micro/portable GCs and that this limited competition will disappear post-merger given that the market leader is taking over its main competitor.

74. The evidence gathered in the market investigation suggests that the remaining players would not be able to reposition since there are large customers' costs associated to switching, including costs in terms of users' training, adaptation of the production line workflow and rebuilding up the stock of spare parts. Furthermore, the market investigation has revealed that brand recognition, software requirements and installed base effects exert a negative effect on switching for Micro/portable GC customers.

75. The market investigation has revealed large barriers to entry in the EEA Micro/portable GC market. These barriers are linked to the development of required miniaturization technology and to the setting up of a dedicated specialized sales force for Micro/portable GCs. The substantial sunk costs associated with entry in Micro/portable GC reduce the likelihood of entry in the market.

76. For the above mentioned reasons, it is concluded that the transaction raises serious doubts as to its compatibility with the common market in relation to the EEA market for Micro/portable GCs.

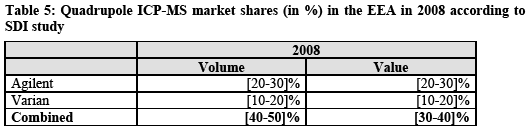

(c) Horizontal overlap: GC consumables

77. As regards the overall market for GC consumables, according to the notifying party estimate, Agilent had a market share of [10-20]% and Varian of [0-5]% ([20-30]%) in 2008. The proposed transaction will therefore lead to a small increment in market share on the markets for consumables used in relation to GC instruments. Moreover, a number of other players (including Sigma Aldrich, Thermo, Merck, Grace, Restek, Shimadzu and Perkin Elmer) sell consumables used in relation to GC instruments in the EEA and may be expected to continue to exercise a competitive constraint on the merged entity.

78. As regards the narrower segmentations of a GC consumables market (the proposed transaction will lead to combined EEA market shares above [10-20]% only in relation to GC columns (Agilent [10-20]%, Varian [20-30]%, combined [30-40]%). The parties have not been in a position to provide market shares of the main other players (Sigma Aldrich, Restek, Phenomenex, Thermo Fisher, SGE and Perkin Elmer) but it transpired from the market investigation that these vendors are present on an EEA market for GC consumables and may be expected to continue to exercise a competitive constraint on the merged entity. Furthermore, the market investigation provided indications that the GC columns from a specific GC manufacturer can be used in the GCs from a different manufacturer, although it may involve the revalidation of the employed analytical method. In addition, as regards the supply of GC columns, customers did not raise any specific competition concerns which would result from the transaction.

79. In light of the above, it is concluded that the proposed transaction will not raise serious doubts as to its compatibility with the common market in relation to GC consumables in the EEA.

(d) Vertical link: Lab GCs (upstream) and Analysers (downstream)

80. Besides its sales of Lab GCs to end customers, Agilent sells Lab GCs as inputs for analysers to nine Analyser Value Added Resellers ('Analyser VARs'). Analyser VARs add features to a standard Lab GC, and then resell it as an analyser as well as offering related services. Varian does not sell Lab GCs as inputs for analysers. Currently, Varian constitutes an integrated undertaking, insofar as it is present both upstream in the Lab GC market and downstream in the Analysers market, whilst Agilent is only present in the upstream Lab GC market. Table 3 below indicates the notifying party's estimate of market shares for Varian and its main competitors on the EEA analyser market.

81. As indicated in Table 1 above, on the upstream market, the proposed transaction will result in the combined entity holding market shares of [40-50]% and [30-40]% in terms of value and volume respectively. Other main Lab GCs suppliers such as Perkin Elmer, Shimadzu and Thermo are all vertically integrated insofar as they manufacture both Lab GCs and analysers.

82. The notifying party submits that the proposed transaction will not result in a risk of input foreclosure with respect to sales of Lab GCs to VARs. In this regard, the notifying party submits that: (i) sales of Lab GCs to Analyser VARs are carried out by virtue of contracts of a short duration ([…]); (ii) other Analyser VARs active on the market besides those currently supplied by Agilent, use Lab GCs supplied by other Lab GC manufacturers; (iii) Analyser VARs could easily switch between suppliers; and (iv) VARs also sell other Agilent products […]. The notifying party also submits that the proposed transaction will not result in a risk of price increase of Varian's Analysers since Varian faces strong competition on the Analyser market and a segment of end- customers has in-house customisation capability.

83. In the market investigation, Analyser's customers have signalled that the underlying Lab GC is the key component for an Analyser, and the Analyser's quality is determined by the quality of the Lab GC. The market investigation revealed that end-customer's source Analysers both from vertically integrated suppliers and from VARs. Most of the Analyser VARs have indicated that they do not consider that the strong presence of Agilent in the Lab GC market and of Varian in the Analyser market could post-merger affect their access to Lab GCs. Indeed, it appears that for a Lab GC manufacturer it is quite important from a business perspective to have a stable supplier relationship with VARs (known as a "channel partner" relationship) because VARs, contrary to end-customers, purchase a large number of instruments and engage in promoting the Original Equipment Manufacturer ('OEM') brand in markets in which the OEM may not be directly present.

84. Even assuming that Agilent would try to impose unsustainable trading conditions to its current VARs and engage in input foreclosure type of behaviour, the other remaining Lab GC suppliers would certainly have the capacity to alternatively supply the VARs given that they are already present in this market at a global scale. In addition, they would also have the incentive to secure such important business relationships and enhance their position in the Lab GC market. Therefore it does not appear that the combined entity would have the required incentives to foreclose access to inputs for VARs.

85. As regards customer foreclosure, the proposed transaction will not result in the integration of an important customer downstream, since Varian is already vertically integrated and self- supplies Lab GCs for the production of analysers. Upstream rivals will continue to have access to the same customer base post-merger. Moreover, Varian's market share in relation to analysers in the EEA is not significant. Therefore, the proposed transaction will not result in any customer foreclosure concerns.

86. Consequently, it is concluded that the vertical link between Lab GCs and Analysers does not lead to serious doubts as regards to its compatibility with the common market. In any event, given that serious doubts have been identified regarding the Lab GC market and remedies have been offered by the parties with the aim of maintaining the pre-merger competitive situation, this proposed solution will also eliminate any new vertical link that may arise as a result of this transaction.

(e) Horizontal overlap: HPLC

87. Both Agilent and Varian are present in the HPLC space and their product activities in this regard overlap in relation to systems based on the following techniques: (i) analytical HPLC; (ii) gel permeation / size exclusion HPLC ('GPC/SEC'); and (ii) preparation HPLC ('Prep HPLC').

88. According to the information submitted by the notifying party, Agilent held a worldwide market share of [10-20]% in 2008 in relation to HPLC instruments, whilst Varian's worldwide market share was only [0-5]% in the same year. The notifying party submits that Agilent and Varian's market shares in the EEA are not materially different from their worldwide shares. Similarly, as regards those possible sub-segments of the HPLC space where the proposed transaction will lead to horizontal overlaps, Agilent appears to be only a minor player worldwide in relation to the GPC/SEC and Prep HPLC sub-segments, whilst Varian appears to be only a minor player worldwide in relation to the analytical HPLC sub- segment. (18) Moreover, a number of competitors such as Waters, Shimadzu, Dionex and Thermo are active in the HPLC space and these market players might be expected to continue to exercise a competitive constraint on the merged entity.

89. In light of the above, it is concluded that the proposed transaction will not raise serious doubts as to its compatibility with the common market in relation to HPLC instruments.

(f) Horizontal overlap: triple quad GC-MS

90. The table below indicates SDI's market share estimates for Varian and its main competitors in relation to the EEA triple quad GC-MS market. Agilent entered the EEA triple quad GC-MS instrument market in 2008. The notifying party submits that no independent comprehensive data has been published since Agilent's entry into the market and therefore the market share data indicated in table 4 below does not include Agilent's market share.

91. The notifying party submits that the triple quad GC-MS instrument market is a highly competitive one and that Agilent and Varian are not each others' closest competitors on this market. Moreover, the notifying party submits that Thermo and Waters will continue to offer strong competition to the merged entity following the proposed transaction and that there is a strong prospect for further entry in this market.

92. The proposed transaction will effectively eliminate competition brought by the very recent entry of Agilent. In 2008 Varian, on its own, already held very large market shares of [50- 60]% and [50-60]% by volume and value respectively on the EEA triple quad GC-MS instrument market, whereas its next two competitors held significantly smaller market shares. Agilent launched its triple quad GC-MS instrument in June 2008 and started generating its first meaningful revenues in this regard in 2009. The market investigation has sought to reconstruct the market shares of the main players in the EEA triple quad GC-MS market. This market reconstruction has revealed lower 2008 market shares for Varian (approximately [40-50]% by volume and approximately [30-40]% by value). There are a number of additional elements indicating that the proposed transaction is likely to raise serious doubts regarding its impact on effective competition by removing a player having brought significant competitive constraint.

93. Agilent's triple quad GC-MS system is the very first such system on the market which has been designed from the ground up as a GC-MS system, rather than being adapted from an LC-MS platform, and therefore purpose-designed for optimal GC-MS capability. (19) Agilent has explained in the notification that its triple quad GC-MS achieves very reliable performances due to an inlet technology which is much better at removing unwanted molecules. Moreover, the collision cell incorporated in Agilent's instruments optimises the accuracy and reliability of results (20). These technological features combine to make the Agilent system a very reliable and robust instrument.

94. Having launched its triple quad GC-MS instrument in June 2008, Agilent's EEA market share in 2008 was almost inexistent. However, given the high capabilities of its product, Agilent has swiftly gained significant influence on the competitive process in the EEA triple quad GC- MS market in 2009 (21) with an estimated market share of [50-60]% in value terms, which shows that its entry has been extremely successful. (22)

95. Indeed, Agilent is seen as having developed a very reliable technology that is welcome by customers and constitutes an immediate competitive force in the market. In this regard, the market investigation has confirmed that, although a recent entrant, Agilent is already considered to exert considerable competitive pressure in the market. Indeed, a significant amount of customers consider that the proposed transaction will have a negative impact on the GC-MS space due to a risk of price increase and decreased innovation. Market participants have indicated that Thermo and Waters would not be in a position to reposition themselves to compensate for this loss of competition and they are therefore similarly concerned that the transaction will result in a limitation of customers' choice.

96. The market investigation has also confirmed that the majority of customers view Agilent and Varian's respective triple quad GC-MS instrument offerings as direct substitutes and that both companies compete directly on the EEA triple quad GC-MS instrument market.

97. Given its strong leading position in the Lab GC market and its significant market presence in neighbouring product areas such as single quad GC-MS and single quad LC-MS and its successful entry in the triple quadrupole LC-MS space (23), Agilent was the main potential candidate for entry into the triple quad GC-MS market. Indeed, Agilent has been the only recent entrant into the EEA triple quad GC-MS market. (24).

98. Although some customers have, in the past, switched GC-MS instrument supplier, revalidation of systems and methodologies, re-training and consumables re-stocking are nonetheless important barriers to switching for customers. Yet, Agilent is viewed by the vast majority of customers as being amongst the best three suppliers for GC-MS instruments in terms of quality, specifications, services/training and price. Therefore, these attributes in combination with its reputation and the reliability of the instrument are serving to enable Agilent to overcome this barrier to successful entry and expansion in the EEA triple quad GC-MS instrument market.

99. Nevertheless, the triple quad GC-MS sub-segment is growing significantly (25) and one could expect that companies active in other GC-MS instrument markets or Lab GC markets might enter the EEA market triple quad GC-MS market. However, for likely entry to be considered as a sufficient competitive constraint on the merging parties, it must be timely and sufficient to deter or defeat any potential anti-competitive effects of the proposed transaction. (26) The market investigation did not show that any potential entry into the EEA triple quad GC-MS market would be timely and sufficient to deter or defeat the potential anti-competitive effects of the proposed transaction.

100. In light of the above, it may be concluded that the proposed transaction is likely to lead to the elimination of an important competitive force on the EEA triple quad GC-MS instrument market (27) and therefore the proposed transaction raises serious doubts with regard to the EEA triple quad GC-MS instruments market.

(g) Horizontal overlap: Single quad GC-MS

101. As regards the EEA single-quad GC-MS market, Agilent held market shares of [60-70]% and [60-70]% by value and volume respectively in 2008. Although it has been present on the single quad GC-MS instrument market for many years (28), Varian has not been able to achieve a significant market share. In fact, it is only a very minor player in this EEA market with a market share below [0-5]% in 2008. (29) Accordingly, the proposed transaction will result in only a very minimal increment in market share for the combined entity.

102. Other market players such as Shimadzu ([10-20]%), Thermo ([10-20]%) and Perkin Elmer ([5-10]%) hold more significant shares in the EEA single-quad GC-MS market than Varian. Consequently, there are a significant number of vendors which exert a stronger competitive constraint on the market leader Agilent. Furthermore, the Commission's market investigation has not revealed any customer concerns in relation to the EEA single quad GC-MS instrument market.

103. Therefore, it is concluded that the proposed transaction does not raise serious doubts as to its compatibility with the common market in relation to the EEA single quad GC-MS market.

(h) Horizontal overlap: GC-MS consumables

104. As regards GC-MS consumables, the proposed transaction will lead to a small increment in market share on a market for all consumables used in relation to GC-MS instruments (Agilent: [20-30]%; Varian: [0-5]%; combined: [20-30]%) (30). Moreover, a number of other players (including Sigma Aldrich, Thermo and Merck) are present on an EEA market for all consumables used in relation to GC-MS instruments and may be expected to continue to exercise a competitive constraint on the merged entity.

105. As regards the narrower segmentations of a GC-MS consumables market the proposed transaction will lead to combined EEA market shares [10-20]% only in relation to GC-MS detector supplies (Agilent: [10-20]%; Varian: [0-5]%, combined [10-20]%) (31) and ion source supplies (Agilent: [10-20]%; Varian: below [0-5]%, combined below [20-30]%). (32) Yet, the combined EEA market shares for the merged entity will remain below [20-30]% in relation to these two categories of consumables.

106. Neither Agilent nor Varian manufactures GC-MS detector supplies; they merely purchase and resell a small number of detector supplies. Moreover, a number of other players (including Shimadzu, Thermo and Perkin Elmer) are present on an EEA market for detector supplies and may be expected to continue to exercise a competitive constraint on the merged entity. Similarly, Varian does not manufacture any ion source supplies but sells filaments and a small number of other consumables in this category. Agilent sells a number of ion source supplies. Moreover, numerous market players (including Shimadzu, SGE and Thermo) are present on an EEA market for ion source supplies and may be expected to continue to exercise a competitive constraint on the merged entity. Furthermore, the market investigation did not reveal any significant concerns in relation to detector supplies and ion source supplies.

107. In light of the above, it is concluded that the proposed transaction will not raise serious doubts as to its compatibility with the common market in relation to GC-MS consumables in the EEA.

(i) Horizontal overlap: LC-MS

108. Both Agilent and Varian are present in the LC-MS space and their product activities in this regard overlap in relation to instruments based on the single quad LC-MS technique.

109. Agilent appears to have held a worldwide market share of [10-20]% in 2007 in relation to LC-MS instruments, whilst Varian's worldwide market share in this regard was only [0-5]% in the same year. (33) As regards the possible single quad LC-MS sub-segment of the LC-MS space, the only sub-segment where the parties' activities overlap, Agilent appears to have held a worldwide market share of [30-40]% in 2007, whilst according to the notifying party's estimates, Varian held a worldwide market share of only [0-5]% in the same year. (34) The notifying party submits that Agilent and Varian's shares in the EEA are not materially different. Therefore, the increment in market share which will result from the proposed transaction will be insignificant both in relation to the LC-MS space in general and, more specifically, as regards single quad LC-MS space. Moreover, a number of competitors are present on the possible single quad sub-segment and might be expected to continue to exercise a competitive constraint on the merged entity post-merger.

110. In light of the above, it is concluded that the proposed transaction will not raise serious doubts as to its compatibility with the common market in relation to LC-MS instruments.

(j) Horizontal overlap: quadrupole ICP-MS

111. The notifying party estimates that the merged entity will hold a combined market share of [40- 50]% in terms of volume and of [30-40]% in terms of value, as indicated in table 5 below. According to the Commission's market reconstruction, the combined entity would have a higher market share in the EEA market for quadrupole ICP-MS (approximately [50-60]% in terms of volume and [60-70]% in terms of value in 2008).

112. On the EEA quadrupole ICP-MS instrument market, the merger would thus lead to a reduction of the number of players active from four to three. The merged entity would have a market share which is higher than those of its remaining rivals Thermo and Perkin Elmer.

113. Despite some technological differences between the instruments offered by Agilent and Varian, a vast majority of respondents to the Commission's market investigation considered Agilent's and Varian's offerings as being in direct competition with each other and as potential alternatives in tenders. Some of these respondents have provided tender data showing that Agilent and Varian compete in general for the same tenders, despite existing differences in ICP technology between these two vendors.

114. Agilent's products are in general perceived as more expensive due to their high capabilities and performance. For example, Agilent is considered by most of the respondents as the best supplier in terms of specifications and service/training. On the other hand, with regard to pricing, most of the respondents on the customer side consider Thermo and Varian as particularly competitive, Varian being "leader in pricing" for some respondents. while Perkin Elmer's development in this field so far has been hindered by the limited resources this company allocated to quadrupole ICP-MS . The proposed transaction would therefore be likely to eliminate a market player which is considered by customers as one of the most competitive in the market.

115. With regard to potential competition, the market investigation has shown that repetitive customers normally stick to one vendor because of the large costs involved with switching (accumulated know how, service relation with vendors, maintenance of spare parts stock, training). Therefore, an "installed base" effect also exists on the EEA quadrupole ICP-MS instrument market. Likewise, building a reputation and a track record of reliability in this high-tech market has been identified by customers as a main barrier to entry and explains the significant customer loyalty to incumbent vendors in this already concentrated market.

116. The notifying party submits that new entry into the EEA quadrupole ICP-MS instrument market could be expected. However, the Commission's market investigation has revealed that potential entry is not expected to occur within the next two years and would thus not be timely. (35)

117. In light of the above, the proposed transaction is likely to give rise to significant non- coordinated effects in the EEA market for the supply of quadrupole ICP-MS instruments and would thus raise serious doubts with regard to its compatibility with the common market.

(k) Horizontal overlap: ICP-MS consumables

118. With regard to ICP-MS consumables, the market shares of the merging parties were as follows in the EEA in 2008: (i) gas management supplies: Agilent [10-20]%, Varian [10- 20]%, combined [20-30]%; (ii) detector supplies: Agilent [20-30]%, Varian below [0-5]%, combined below [20-30]%; (iii) samples introduction supplies: Agilent [10-20]%, Varian below [0-5]%, combined below 19%; (iv) samples vials/containers: Agilent [0-5]%, Varian below [0-5]%, combined below [5-10]%. In particular on the gas management supplies market, other players like Thermo and Perkin Elmer are significant forces.

119. In light of the low increments brought by the transaction and of the presence of significant competitors, it is concluded that the proposed transaction will not raise serious doubts as to its compatibility with the common market in relation to ICP-MS consumables in the EEA.

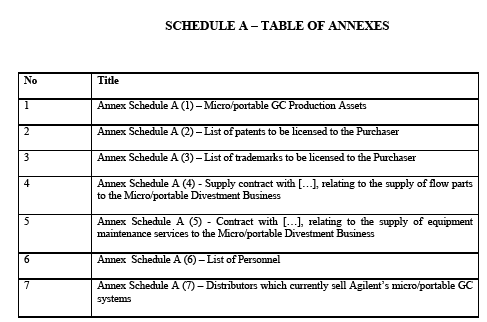

VI. PROPOSED REMEDIES

120. In order to address the serious doubts identified by the Commission, the parties have proposed to divest Agilent's entire global Micro/portable GC business and Varian's entire global Lab GC, triple quad GC-MS and ICP-MS businesses. The parties have committed to divest these four businesses to one or several up-front buyers (36) who will be viable purchasers, independent of and unconnected with the parties and an effective competitor to Agilent/Varian.

a) Lab GCs

121. n order to address the serious doubts identified by the Commission with regard to the EEA Lab GC market, the notifying party has proposed to divest Varian's entire global business located at […] ('Laboratory GC Divestment Business'). The Laboratory GC Divestment Business utilizes approximately […] of the instrument production capacity at Varian’s […] which relates to the manufacture of analytical instruments.

122. The Lab GC Divestment Business consists of:

(i) all Varian-owned assets used in the design, assembly, manufacture and testing of the laboratory GC instruments;

(ii) the relevant know-how and IP (37) rights linked to the design, assembly, testing and operation of Varian’s laboratory GC instruments;

(iii) a licence with a field of use restriction (use only in connection with laboratory instruments) in respect of the software associated with Varian’s laboratory GC instruments, Galaxie, and provision of relevant source codes, as well as a license of any relevant upgrades of Galaxie and technical support for a period of […] from closing;

(iv) up to […] employees dedicated to the research and development, assembly, testing, sale and marketing of Varian’s laboratory GC instruments;

(v) transfer of any agreements between Varian and its customers (excluding service contracts) which relate to the Laboratory GC Divestment Business;

(vi) transfer of any agreements between Varian and its distributors which relate exclusively to the Lab GC Divestment Business (subject to any necessary consents of the counter-party to the relevant agreement) and, to the extent possible, the transfer of the relevant part (being that part relating to the Lab GC Divestment Business) of any agreement between Varian and its distributors which relates to the Lab GC Divestment Business and also to other Varian businesses. Agilent will not distribute its own Lab GC systems through any distributor that currently distributes Varian’s Lab GC system for a time period of […] from Closing;

(vii) transfer of any agreements between Varian and its suppliers which relate exclusively to the Lab GC Divestment Business (subject to any necessary consents of the counter-party to the relevant agreement) and, to the extent possible, the transfer of the relevant part (being that part relating to the Lab GC Divestment Business) of any agreement between Varian and its suppliers which relates to the Lab GC Divestment Business and also to other Varian businesses;

(viii) temporary and transitional supply agreements, under which the Laboratory GC Divestment Business will supply, for a transitional period, laboratory GCs to the retained Varian businesses in single quadrupole GC-MS, ion trap GC-MS and Analysers and to the Triple quad divestment businesses (see below); and

(ix) transitional services to assist with the transfer of the Laboratory GC Divestment Business.

b) Micro/portable GCs

123. In order to address the serious doubts identified by the Commission with regard to the EEA Micro/portable GC market, the notifying party has proposed to divest Agilent's entire Micro/portable GC business ('Micro/portable GC Divestment Business').

124. The Micro/portable GC Divestment Business consists of:

(i) all tangible and intangible assets relating to the design, assembly and testing of the Micro/portable GC instruments at Agilent’s […];

(ii) licenses of the relevant know-how and IP rights linked to the design, assembly and testing of Agilent’s Micro/portable GC unit, with a field of use restriction (for use solely in connection with Micro/portable GC products);

(iii) licenses of Agilent’s marketing materials, manuals, source code for embedded Micro/portable GC-specific software and support documents;

(iv) optionally, up to […] employees dedicated to the design, assembly, testing, and marketing of Agilent’s Micro/portable GC instruments;

(v) optionally, the benefit of some or all of the distribution agreements (and three Value Added Resellers as sales channel support) with some distributors of Agilent's Micro/portable GC systems; subject to their consent (where required), Agilent will either assign the benefit of the relevant part of the relevant distribution agreements, or, if consent is required but is not given, Agilent will make the necessary arrangements for the continued distribution of the products of the Micro/portable GC Divestment Business; Agilent also commits that it will not distribute Varian’s Micro/portable GC system through any of these distributors or VARs for a […];

(vi) unfilled sales orders relating to the Micro/portable GC Divestment Business and other contracts;

(vii) a supply agreement with […], the only dedicated supplier of Agilent’s Micro/portable GC business; as well as a supply agreement whereby Agilent is willing to supply the purchaser with plate manifolds required to assemble the Micro/portable GC products for […]

(viii) a transition Services Agreement relating to other components and services; and

(ix) up […] training on Agilent Micro/portable product specifications and service repair.

c) Triple quad GC-MS

125 In order to address the serious doubts identified by the Commission with regard to the EEA triple quad GC-MS instrument market, the notifying party commits to divest Varian's global triple quad GC-MS business at […] ('triple quad GC-MS divestment business'), which accounts for approximately […] of Varian's manufacturing capacity and resources at the […].

126. The triple quad GC-MS divestment business consists of:

(i) all Varian-owned assets used in the design, assembly, manufacture and testing of the triple quad GC-MS (and those components incorporated therein during the manufacturing process) instruments located in Varian's […];

(ii) transfer of the ownership of all know-how and IP rights exclusively linked to the design, assembly, testing and operation of Varian’s triple quad GC-MS instruments. Those which are not exclusively used in relation to the triple quad GC-MS Divestment Business will be licensed on a royalty-free basis;

(iii) a licence with a field of use restriction (use only in connection with laboratory instruments) in respect of the proprietary software associated with Varian's triple quad GC-MS instruments, MS Workstation and provision of the relevant source codes;

(iv) […] key personnel and at the purchaser’s request, up to a […] employees located within particular business functions within the triple quad GC-MS Divestment Business;

(v) all contracts, commitments and unfilled sales orders and all customers and other records necessary to ensure the viability and competitiveness of the triple quad GC- MS Divestment Business;

(vi) in the same manner as for Lab GCs, transfer of any agreements between Varian and its suppliers which relate to the triple quad GC Divestment Business, including supply by Varian to the Purchaser (at its request) of vacuum rotary and turbo pumps during a transitional period and a supply agreement related to the supply of Lab GCs by Varian to the triple quad GC-MS Divestment Business;

(vii) in the same manner as for Lab GCs, transfer of any agreements between Varian and its distributors which relate to the triple quad GC-MS Divestment Business ; and

(viii) at the request of the purchaser, transitional services pursuant to which the combined entity will offer for a transitional period with the components, know-how and services required for the operation of the triple quad GC-MS Divestment Business.

d) ICP-MS

127. In order to address the serious doubts identified by the Commission with regard to the EEA ICP-MS instrument market, the notifying party proposed to divest Varian's global ICP-MS business at […] ('ICP-MS divestment business').

128. The ICP-MS divestment business consists of:

(i) all Varian-owned assets used in the design, assembly, manufacture and testing of the ICP-MS (and those components incorporated therein during the manufacturing process) instruments located in […];

(ii) transfer of the ownership of all know-how and IP rights exclusively linked to the design, assembly, testing and operation of Varian’s ICP-MS instruments. Those which are not exclusively used in relation to the ICP-MS Divestment Business will be licensed on a royalty-free basis;

(iii) transfer of the proprietary software associated with Varian’s ICP-MS instruments, ICP Expert and provision of relevant source codes;

(iv) all key personnel and personnel dedicated to the research and development, assembly, testing, sale and marketing of Varian's ICP-MS;

(v) all contracts, commitments and unfilled sales orders and all customers and other records necessary to ensure the viability and competitiveness of the ICP-MS Divestment Business;

(vi) in the same manner as for Lab GCs, transfer of any agreements between Varian and its suppliers which relate to the ICP-MS Divestment Business, including supply by Varian to the Purchaser (at its request) of vacuum rotary and turbo pumps during a transitional period;

(vii) in the same manner as for Lab GCs, transfer of any agreements between Varian and its distributors which relate to the ICP-MS Divestment Business; and

(viii) at the request of the purchaser, transitional services pursuant to which the combined entity will offer for a transitional period with the components, know-how and services required for the operation of the ICP-MS Divestment Business.

VII. ASSESSMENT OF THE COMMITMENTS

129. As set out in the Commission Notice on Remedies(38), the Commission assesses the compatibility of a notified concentration with the common market in line with the terms of the Merger Regulation. Where a concentration raises serious doubts which could lead to a significant impediment to effective competition, the Parties may undertake to modify the concentration so as to resolve the serious doubts identified by the Commission with a view to having the transaction approved. In assessing whether or not the remedy will restore effective competition, the Commission considers the type, scale and scope of the remedies by reference to the structure and the particular characteristics of the market in which these serious doubts arise.

130. As concerns the different types of remedy, the most effective way to maintain effective competition is to create the conditions for the emergence of a new competitive entity or for the strengthening of existing competitors via divestiture by the merging parties. The divested activities must consist of a viable business, which if operated by a suitable purchaser, can compete effectively with the merged entity on a lasting basis and which is divested as a going concern.

131. The Commission has concluded that the proposed remedy package as submitted by the notifying party on 19 January 2010 addresses all serious doubts identified during the course of the procedure and adequately deals with concerns identified by market participants in response to the remedy package. As such, the Commission has concluded that the proposed remedy package is effective in removing the serious doubts brought about by the transaction in the relevant markets.

Suitability for removing the serious doubts

a) Lab GCs

132. The remedy proposed as regards Lab GCs completely eliminates the horizontal overlap at global level between the parties. The remedy will restore the market structure which existed pre- merger. The suitable purchaser of the Lab GC Divestment Business will have an initial EEA market share of [5-10]%.

133. The market test of the remedies provoked in general a positive feedback as to the suitability of the remedy in the Lab GC market to address the serious doubts mentioned above. However, some issues have been raised by respondents to the market test, which have been adequately addressed by the parties in their improved remedy proposal submitted on 19 January 2010.

Up-front buyer

134. The Lab GC Divestment Business is not a stand-alone legal entity but includes several tangible and intangible assets, contracts, licenses agreements belonging to or having been concluded by Varian. Some of these assets are currently shared with other product areas where the Commission did not find serious doubts and which are therefore retained by Agilent such as liquid chromatography and analysers.

135. Thus the Lab GC Divestment Business has necessarily to be carved out from the remaining businesses. In such carve-out operations, it is of utmost importance for the viability of the transferred business that it has access to all inputs and other resources such as R&D, distribution networks and intellectual property rights necessary to carry out its operation in full independence. The Commission can only accept commitments which require the carve-out of a business if it can be certain that, when the business is transferred to the Purchaser, the risks for the viability and the competitiveness caused by the carve-out will be reduced to a minimum.

136. In this regard, the transfer of agreements between Varian and its customers (including current Varian's distributors), as well as Agilent's commitment not to distribute its own Lab GC systems through any Varian's distributor for a period of […] have been welcomed by respondents as necessary to facilitate access to customers' base and consequently enhance the viability of the Lab GC carved-out assets.

137. During the market test however, several respondents emphasised that the identity of the purchaser plays an important role for the viability of the Lab GC Divestment Business. It was often expressed that such a purchaser should already have an experience and a proven track record in the Lab GC area for reasons of product and service know-how as well as reputation and brand recognition which influence directly customers' purchases. Given the importance of the installed base as a factor enabling a player to appear as a viable competitive force in the market, expertise in Lab GC appears to be necessary for several respondents.

138. Respondents to the market test who have not indicated that an experience in the GC lab area was essential submitted however that the Purchaser needs to have an established sales and service organization in analytical measurement techniques. In that regard, the Purchaser would need to have specific critical capabilities such as a sales, support and service organization that can sell, train and support customers locally throughout the world and an access to the existing market and customers through a variety of products typically found in the same laboratory as lab GCs.

139. In the light of these comments, and of the fact that the access to such inputs and resources which are necessary to operate viably the Lab GC Divestment Business depends to a large extent on the parties finding a purchaser which meets these requirements or at least may ensure that they are met, the parties have put forward an up-front buyer solution. The parties commit to find a purchaser and not to complete the notified transaction until a binding sale and purchase agreement has been entered with the Purchaser and the Commission has approved both the Purchaser and the terms of sale. In order to be approved by the Commission, it is necessary in particular that such a buyer has the financial resources, proven expertise and incentive to maintain and develop the Divestment Business as a viable and competitive force. The sale of the Lab GC Divestment Business to such a buyer prior to the consummation of the proposed transaction would significantly improve the incentives for the parties to find a suitable Purchaser and enable the Commission to conclude, with the requisite degree of certainty, that the implementation of the remedy will be efficient in restoring effective competition in the EEA Lab GC market.

Software issues and access to some components

140. Several respondents to the market test submitted that the Purchaser should have access to the upgrading of the Galaxie software which supports the functioning of the Varian lab GC. This issue has been considered by these respondents as critical for the success of the Lab GC Divestment Business as updated GC lab software is essential to get best performance of the GC hardware. The parties have addressed this issue by granting a license of Galaxie and technical support for a period of […].

141. Likewise, several respondents highlighted during the market test that access to specific GC labs components such as autosamplers and autoinjectors should be ensured during a longer transitional period before the Purchaser is in a position to source these products from independent suppliers. The parties have agreed to provide autosamplers and autoinjectors for

a longer period ([…] instead of […] in the original remedy proposal, extendable by a further […] at the Purchaser's request).

Conclusion on the Lab GC Divestment Business

142. In the light of the above, the Commission considers the Lab GC Divestment Business as a suitable commitment to remedy the serious doubts identified with regard to the EEA Lab GC market.

b) Micro/portable GCs