Commission, March 20, 2019, No M.8948

EUROPEAN COMMISSION

Decision

SPIRIT / ASCO

Subject: Case M.8948 — Spirit/Asco

Commission decision pursuant to Article 6(1)(b) in conjunction with Article 6(2) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 30 January 2019, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Spirit AeroSystems Holdings, Inc. ("Spirit") would acquire within the meaning of Article 3(1)(b) of the Merger Regulation 100% of the shares of S.R.I.F. NV, which is the holding company of Asco Industries NV, Asco Management NV and Immobilière Asco NV (together, "Asco").3 Spirit and Asco are collectively referred to as the "Parties".

(2) The concentration had already been notified to the Commission on 17 September 2018, but was subsequently withdrawn on 25 October 2018.

1. THE PARTIES

(3) Spirit is a Tier 1 supplier who designs, manufactures and sells aerostructures for commercial and military aircraft. The company is based in the US and its shares are listed on the New York Stock Exchange. Spirit employs ca. 15 500 employees worldwide with a turnover amounting to approximately EUR 6 181 million in 2017, approximately EUR 1 118 million of which were achieved in the EU.

(4) Asco is a Tier 2 specialist in the machining treatment and assembly of hard metal, steel and aluminium alloys, and to a lesser extent, composites. Asco sells components and sub-components for the aerostructures of commercial and military aircraft to OEMs, Tier 1 suppliers and equipment suppliers. The company is based in Belgium and has approximately 1 450 employees. Its annual turnover amounted to approximately EUR 378 million in 2017, approximately EUR […] of which were achieved in the EU.

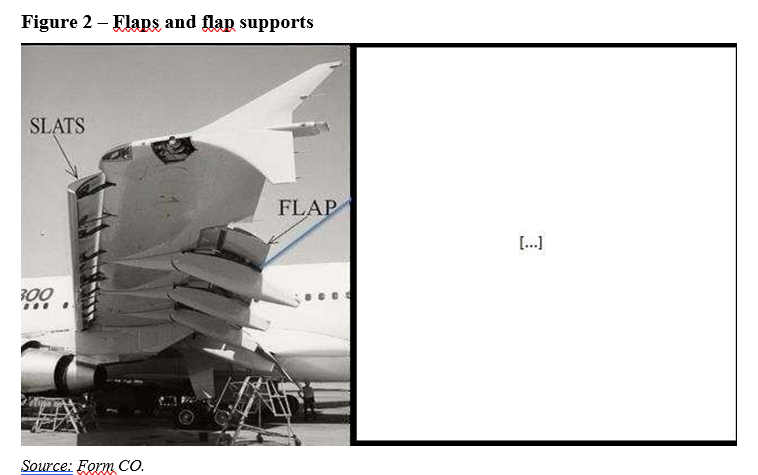

(5) Asco is a shareholder of two joint ventures supplying Airbus:(a) Flabel, formed in 1999, is a joint venture (JV) between Asco, Sonaca, Sabca and Esterline Belgium. The JV acts as a commissionaire (that is in its own name but for the account of its members) through which its parent companies participate in the development and production of flap systems and subcomponents thereof for the Airbus A400M military transport aircraft. Flap systems (or trailing edge assemblies) are wing aerostructures, attached to the rear part of an aircraft wing in order to increase the lift of the wing at a given airspeed during take-off and landing.(b) Belairbus, formed in 1979, is a joint venture between Asco, Sonaca and BMT Eurair. The JV acts as a commissionaire through which its parent companies participate in the development, production and sale of slat systems for all the main commercial Airbus aircraft. Slat systems (or leading edge assemblies) are wing aerostructures, attached to the front part of an aircraft wing (the “fixed leading edge”) in order to increase the lift of the wing at a given airspeed during take-off and landing.

2. THE OPERATION AND CONCENTRATION

(6) The Parties have entered into a binding Agreement for the Sale and Purchase of the shares ("SPA") of S.R.I.F. NV on 1 May 2018. Pursuant to this SPA, Spirit will acquire the entirety of the share capital of S.R.I.F. NV, the holding company of the companies constituting Asco, for a consideration of approximately EUR 556 million ("the Transaction").

(7) Upon completion of the Transaction, Spirit will own 100% of the shares and voting rights in Asco and thus acquire sole control of Asco within the meaning of Article 3(1)(b) of the Merger Regulation.

(8) Therefore, the Transaction constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

3. EU DIMENSION

(9) The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 5 000 million4. Each of them has an EU-wide turnover in excess of EUR 250 million, but each does not achieve more than two-thirds of its aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension.

4. OVERVIEW OF AEROSTRUCTURES

(10) The Transaction concerns the design, engineering, manufacturing and assembly of aerostructures. Aerostructures are components or subsystems of the airframe of an aircraft and generally include the wings, fuselage (or aircraft’s main body) structures, empennages (or tail structure at the rear of an aircraft to provide stability during the flight), nacelles (enclosures on the outside of an aircraft, often attached to the wing, used for housing engines) and other fabricated parts.

(11) The aerostructures industry, with a total estimated value of USD 60.7 billion in 2017,5 is highly fragmented in terms of size and geography, and it is a growing sector. There are a significant number of aerostructure suppliers worldwide.6

(12) OEMs, such as Airbus and Boeing, account for a significant proportion of aerostructure production, with their in-house production accounting for approximately [30-40]% of the total aerostructures market in 2017.7 Whilst Airbus and Boeing account for almost [60-70]% of all large aircraft and [90-100]% of all large commercial aircraft manufactured worldwide in 2017, there are other major aircraft OEMs, such as Bombardier, Embraer, Gulfstream and Dassault.8

(13) OEMs source aerostructures from independent Tier 1 and Tier 2 suppliers, as well as from other aircraft OEMs9. Tier 1 suppliers generally have integration capabilities and provide whole systems and equipment, while Tier 2 suppliers mainly supply components or sub-components to Tier 1 suppliers. However, OEMs may also procure aerostructure components or sub-components directly from Tier 2 suppliers as part of their purchasing strategy10. There is also a current trend towards insourcing aerostructures, with OEMs investing more in in-house manufacturing facilities.11 Nevertheless, the aerostructures market is seen as highly attractive, with a number of new entrants in recent years, including suppliers from Malaysia, China, Taiwan, Indonesia, Thailand, North Africa, India and South Korea.12

5. RELEVANT MARKETS

(14) Spirit is a Tier 1 supplier of aerostructures. Asco is a Tier 2 supplier of components for wing aerostructures, landing gear components and other structural aerostructure components. Asco manufactures and supplies aerostructure components that can be used as an input for (or be sold together with) Spirit’s products. Accordingly, the Transaction gives rise to the following vertical links which, in some cases and depending on the OEM customer’s purchasing strategy, may also appear conglomerate rather than vertical.13

(15) First, Spirit is active in the design, manufacture and assembly of slats and leading edge assemblies (the latter are referred to as “slat systems”). Asco is active upstream from that activity, in the design and manufacture of slat supports and wing structural components.

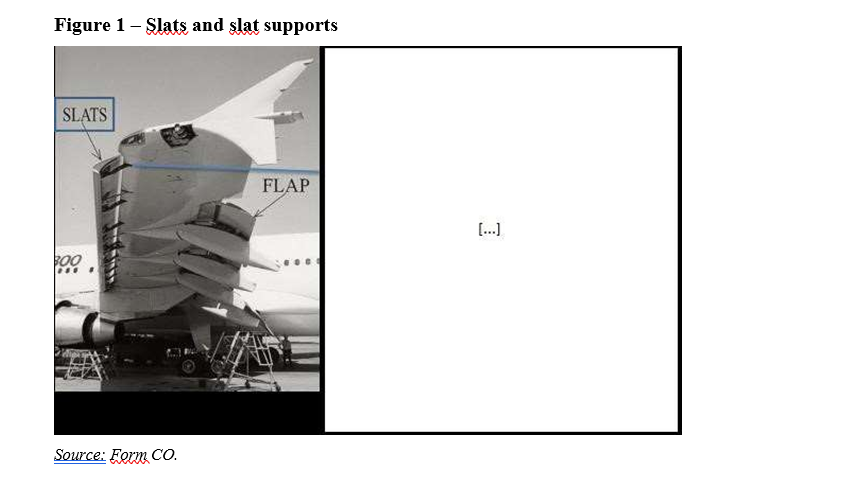

(16) Second, Spirit is active in the design and manufacture of trailing edge assemblies. Asco is active upstream from that activity, in the design and manufacture of flap supports and wing structural components.

(17) Third, Spirit is active in the design and manufacture of the centre section and nose section of the fuselage. Asco is active upstream from that activity, in the design and manufacture of fuselage structural components, including window frames.

(18) Fourth, Spirit is active in the design and manufacture of thrust reversers and pylons. Asco is active upstream from that activity, in the design and manufacture of engine structural components.

5.1.Relevant product market definition

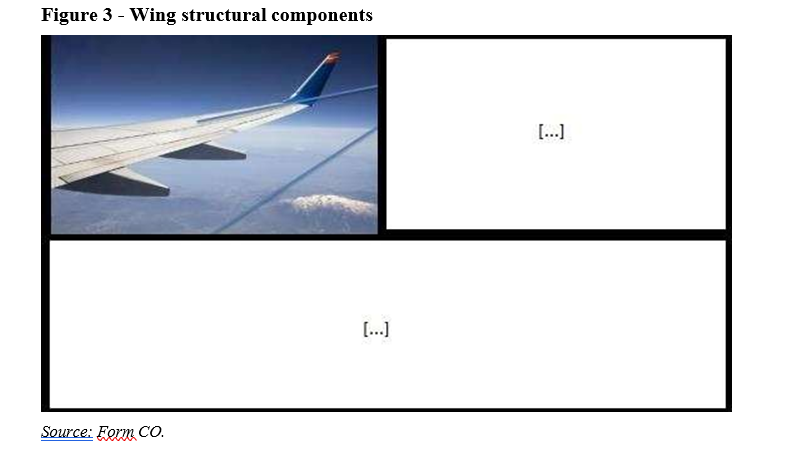

(19) In some previous decisions, the Commission considered that aerostructures can be defined as the metal fabrication aspects of aircraft production, intended to produce products such as wings, fuselages or nacelles. Aerostructures encompass a wide range of products, from final aircraft building to minor components (for example, brackets and cables) through major units (for example, wings and fuselage parts)14. In these cases, the Commission defined the overall market for aerostructures and considered that it was not necessary to further segment the market at the level of individual products (such as wing aerostructures, empennage and other nacelle structures) because no competition concerns would arise under any plausible market definition.15

(20) In other earlier cases16, the Commission adopted a component-by-component approach regarding the manufacturing and sale of components for an aircraft, defining a separate market for nacelle components such as thrust reversers. In Safran/Zodiac Aerospace, the Commission also defined a separate relevant product market for individual sub-components of thrust reversers.17

(21) The Parties take the view that there is a single relevant market for all aerostructures or, more narrowly, for all wing aerostructures, irrespective of the type of aircraft, mainly because of supply-side substitutability.18 The Parties submit that at a component level there is little or no demand-side substitutability (for example, a slat support cannot be substituted for a flap support) and there is little or no demand-side substitution between different aircraft platforms for the same component.19 However, the Parties argue that, from the supply-side perspective, a component-by-component product market definition would not be appropriate because the design and manufacturing capabilities of aerostructure suppliers allow for easy switching between different aerostructures and their components.20

(22) The results of the market investigation confirm that there is no demand-side substitution for the components of wing aerostructures. As regards supply-side substitution, the results of the market investigation are not conclusive. On the one hand, some respondents submitted that aerostructure suppliers have a general expertise that would allow them to manufacture various products, since “what the aerostructure supplier brings to the table is the manufacturing know-how.”21 On the other hand, market participants also indicated that suppliers tend to specialise, for example, in certain wing aerostructure components.22 As one respondent to the market investigation submitted: “In general a slat track or flap track provider is primarily a machining and metal treating center. I would expect such a supplier to remain primarily concerned with complex machining which would be a fairly limited subset of the overall wing structure.”23

(23) The results of the market investigation did not support the view of the Parties that manufacturing expertise is easily and immediately transferrable to manufacture different wing aerostructure components. For example, some market participants indicated that there are many players (independent suppliers and OEMs with in- house manufacturing capabilities) that could supply hard metal machining parts24. However, as regards certain machining components, others indicated that: “Slat supports (i.e. slat tracks) are mainly manufactured from hard metal and therefore require specific machining capabilities that are difficult to replicate. The same applies to other types of wing aerostructure components which also require very specific capabilities (e.g. composite, assembly, etc.).”25 In relation to slats, another component of wing aerostructures, the market participants explained that suppliers of slats are typically capable also to provide other wing movable components (for example, flaps and ailerons),26 but not necessarily “to be able to do all or nearly all of the wing structure”.27 In particular, some slats manufacturers may have broader capabilities; while others may not be able to supply primary structure components for wings such as fixed trailing edge and fixed leading edge (the non-movable part of the wing).28

(24) Furthermore, for products to belong to the same product market, suppliers must be able to switch production to the relevant products and market them in the short term without incurring significant additional costs. The results of the market investigation indicate that this may not be the case for specific wing aerostructure components. As a respondent to the market investigation explained: “To extend these [slat supports manufacturing] capabilities to other wing aerostructure components, a long-term development plan and significant investments would be required from an aerostructure manufacturer.”29 In addition, a company currently not active in hard metal machining parts such as slat supports indicated that the entry into this segment would not be immediate, as it would take some time and investment to produce these components.30

(25) In light of the results of the market investigation, the Commission considers that there are many types of wing structural components and that switching suppliers may not be as easy and immediate as the Parties claim, at least not across all types of aerostructures. The market investigation indicates that the level of supply-side substitution differs depending on the type of component. For example, as already noted in recital (23), certain components require specific capabilities and expertise (for example, slat supports and other complex machining parts), on the one hand; while on the other hand, the same group of suppliers could generally supply all movable wing aerostructure parts. In addition, respondents to the market investigation have indicated that different suppliers are active in design and production of slat supports and other machining parts, on the one hand, and, for example, slat systems, on the other hand.31

(26) For the purposes of this decision, the Commission considers that it is appropriate to assess the effects of the concentration not only in relation to the overall aerostructures market, including the wing aerostructures market, but also to distinguish between the different types of wing aerostructures and possibly between the different components of each type of wing aerostructure. For example, the Commission considers that a slat system or leading edge assembly may need to be distinguished from a flap system or trailing edge assembly, as well as within a slat system, the slat may need to be distinguished from the slat support.32 In particular, the Commission will consider the following likely affected markets within the overall market for aerostructures.

5.1.1. Market for the design, manufacture and supply of slat systems

(27) Slat systems (or leading edge assemblies) are wing aerostructures. Slat systems comprise slats, which are supported by slat supports. Slats are high-lift devices that are attached through the slat supports to the front part of an aircraft wing (the “fixed leading edge”) in order to increase the lift of the wing at a given airspeed during take-off and landing.

(28) The Commission has considered whether within slat systems, separate relevant markets may exist for slat supports, on the one hand, and slats, on the other. However, as this distinction would not have a material impact on the outcome of the competitive assessment, the Commission leaves the relevant market definition for slat systems open.

5.1.2. Other affected markets

(29) The Commission has also analysed the effects of the concentration on the following vertically affected markets. Given that potentially relevant vertically affected markets would only arise at component level, the Commission has analysed the following markets on a component-by-component basis (Sections 6.1.2 to 6.1.4). However, as no competition concerns arise even at such a narrow level, for the purposes of this decision, the Commission considers that the precise market definition for these products may be left open.

(30) Flap systems (or trailing edge assemblies) are wing aerostructures. They comprise flaps, supported by flap supports, and other primary and secondary flight control surfaces (such as ailerons and spoilers). Flap systems are high lift devices attached to the rear part of an aircraft wing (the “fixed trailing edge”) in order to increase the lift of the wing at a given airspeed during take-off and landing.

(31) Design and manufacture of wing structural components. Structural wing components are internal structures of fixed wings, such as spars, stringers, ribs, formers and bulkheads.

(32) Design and manufacture of the fuselage systems. The fuselage is the aircraft’s main body section, to which all other main components attach, such as the wings,vertical and horizontal stabilisers. Fuselage systems may include nose section, forward section, centre section, aft section (section at the back) and tail sections.

(33) Design and manufacture of fuselage structural components. Fuselage construction uses structural components such as beams, frame assemblies, and bulkheads to give shape to the fuselage.

(34) Design and manufacture of thrust reversers. The thrust reverser is a component of engine nacelles. It is located next to the engine and helps the aircraft slow down on the ground by reversing the airflow to produce a retarding backward force. In past decisions, the Commission identified separate product markets for each of the main components of the nacelle, including thrust reversers.33

(35) Design and manufacture of pylons. Pylons are rigid structures used to hold the aircraft engine in place under (or, more rarely, over) an aircraft wing, with minimum interference with the airflow over and under the aircraft wing that is needed for lift and control of the aircraft.

(36) Design and manufacture of engine structural components. Structural engine components, such as engine mounts, serve as the interface attachment between the fuselage and/or fixed wing of the aircraft and the engine. Engine mounts are also used in the nacelle, the surrounding structure of the engine.

5.2.Geographic market definition

(37) In line with the Commission’s decisional practice, the Parties submit that the geographic market for aircraft components, including aerostructures, is worldwide. The Parties submit that they tender on a global basis and compete with suppliers from throughout the world. Prices are quoted on a worldwide basis and do not differ according to a geographic region. Customers purchase civil aircraft components on a worldwide basis. There are significant trade flows for aircraft components across the world and transport costs do not play a significant role.

(38) In its previous decisions34, the Commission found that markets for various aircraft systems and components were worldwide for reasons consistent with those put forward by the Parties. The market investigation in the present case has broadly confirmed that the markets for aerostructures and components are also worldwide in scope.35

6. COMPETITIVE ASSESSMENT

6.1. Non-horizontal non-coordinated effects

(39) Asco manufactures aerostructure components which, depending on the relevant customer's purchasing strategy, can be sold either as an input for aerostructures sold by Spirit (in which case there is a vertical link between them); or in combination with other aerostructure components sold by Spirit (in which case the link is conglomerate). In this section, the Commission assesses the possible non- coordinated effects resulting from these non-horizontal links, including vertical and conglomerate effects.

6.1.1.Legal framework for competitive assessment of non-horizontal non-coordinated effects

6.1.1.1 Vertical mergers

(40) Vertical mergers involve companies operating at different levels of the same supply chain. Pursuant to the Commission Guidelines on the assessment of non-horizontal mergers under the Council Regulation on the control of concentrations between undertakings (the “Non-Horizontal Merger Guidelines”),36 vertical mergers do not entail the loss of direct competition between merging firms in the same relevant market and provide scope for efficiencies. However, there are circumstances in which vertical mergers may significantly impede effective competition. This is in particular the case if they give rise to foreclosure.37

(41) The Non-Horizontal Merger Guidelines distinguish between two forms of foreclosure: input foreclosure, where the merger is likely to raise costs of downstream rivals by restricting their access to an important input, and customer foreclosure, where the merger is likely to foreclose upstream rivals by restricting their access to a sufficient customer base.38

(42) Pursuant to the Non-Horizontal Merger Guidelines, input foreclosure arises where, post-merger, the new entity would be likely to restrict access to its actual or potential rival in the downstream market to the products or services that it would have otherwise supplied absent the merger, thereby raising its downstream rivals' costs by making it harder for them to obtain supplies of the input under similar prices and conditions as absent the merger.39

(43) For input foreclosure to be a concern, the merged entity should have a significant degree of market power in the upstream market. Only when the merged entity has such a significant degree of market power, can it be expected that it will significantly influence the conditions of competition in the upstream market and thus, possibly, the prices and supply conditions in the downstream market.40

(44) Pursuant to the Non-Horizontal Merger Guidelines, customer foreclosure may occur when a supplier integrates with an important customer in the downstream market and because of this downstream presence, the merged entity may foreclose access to a sufficient customer base to its actual or potential rivals in the upstream market (the input market) and reduce their ability or incentive to compete which in turn, may raise downstream rivals' costs by making it harder for them to obtain supplies of the input under similar prices and conditions as absent the merger. This may allow the merged entity profitably to establish higher prices on the downstream market.41

(45) For customer foreclosure to be a concern, a vertical merger must involve a company which is an important customer with a significant degree of market power in the downstream market. If, on the contrary, there is a sufficiently large customer base, at present or in the future, that is likely to turn to independent suppliers, the Commission is unlikely to raise competition concerns on that ground.42

(46) In its assessment, the Commission considers whether it is likely that the merged entity would engage in input or customer foreclosure strategies. In doing so, the Commission in principle analyses the merged entity's ability and incentives to engage in such foreclosure strategies, as well as the possible effects they may have on the relevant markets. Since these factors are intrinsically linked, they are often examined together.43

6.1.1.2 Conglomerate mergers

(47) Pursuant to the Non-Horizontal Merger Guidelines, in most circumstances, conglomerate mergers do not lead to any competition problems. However, foreclosure effects may arise when the combination of products in related markets may confer on the merged entity the ability and incentive to leverage a strong market position from one market to another closely related market by means of tying or bundling or other exclusionary practices.44

(48) The Non-Horizontal Merger Guidelines distinguish between bundling, which usually refers to the way products are offered and priced by the merged entity and tying, usually referring to situations where customers that purchase one good (the tying good) are required to also purchase another good from the producer (the tied good).45

(49) While tying and bundling have often no anticompetitive consequences, in certain circumstances such practices may lead to a reduction in actual or potential competitors' ability or incentive to compete. This may reduce the competitive pressure on the merged entity allowing it to increase prices or deteriorate supply conditions in other ways.46

(50) In assessing the likelihood of such a scenario, the Commission examines, first, whether the merged firm would have the ability to foreclose its rivals, second, whether it would have the economic incentive to do so and, third, whether a foreclosure strategy would have a significant detrimental effect on competition, thus causing harm to consumers.47 In practice, these factors are often examined together as they are closely intertwined.

6.1.2. Market shares

(51) Spirit has significant market shares in a number of downstream markets, for which components manufactured by Asco are potential or actual inputs. Table 1 below sets out the vertical links between the supply of these inputs upstream and the corresponding downstream markets, together with the Parties' market shares in the relevant markets:

Table 1: Asco's upstream market shares and Spirit's downstream market shares, 2017

Upstream market (components manufactured by Asco) | Downstream market (components/products manufactured by Spirit) | ||

Component | Market share48 |

Component/Product |

Market share |

Slat supports |

[90-100]% | Fixed leading edge assembly | [80-90]% |

Slats | [40-50]% | ||

Flap supports | [10-20]% | Fixed trailing edge assembly | [50-60]% |

Structural components for the fuselage |

[0-5]% | Fuselage nose section | [40-50]% |

Fuselage centre section | [30-40]% | ||

Structural components for the engine |

[0-5]% | Nacelles thrust reversers | [30-40]% |

Pylons | [40-50]% | ||

Source: Parties estimates, Form CO.

(52) Asco's upstream market shares are low to moderate in all of these upstream markets, including the market for wing structural components49, except for the market for slat supports. In the market for slat supports Asco had a significant market share of nearly [90-100]% in 2017. According to the Parties' estimates, due to the loss of a significant contract to a new competitor, Kencoa, in 2018, Asco's market share in slat supports is expected to decrease to an estimated [60-70]% in 2019.50 However, even at [60-70]%, Asco would still have a significant market share on the upstream market for slat supports.

(53) Apart from slat supports, the Parties have confirmed that Asco's market shares for all other individual structural components which it manufactures do not exceed 20% on the basis of any plausible (including the narrowest possible) market definition.51

(54) The following non-horizontal non-coordinated effects may potentially arise and will be assessed by the Commission in turn:(a) in respect of both input foreclosure (where Asco manufactures products upstream, which are an actual or a potential input for the downstream markets) and customer foreclosure (where Spirit has a significant market share on the downstream markets, for which Asco supplies structural components), namely:(1) upstream supply of slat supports to downstream markets for (a) slats and (b) slat systems (or "fixed leading edge assembly");(2) upstream supply of flap supports to downstream markets for flap systems (or “fixed trailing edge assembly”);(3) upstream supply of structural components for the fuselage (according to all plausible market definitions) to downstream markets for (a) fuselage nose section and (b) fuselage centre section; and(4) upstream supply of structural components for the engine (according to all plausible market definitions) to downstream markets for (a) nacelles thrust reversers and (b) pylons.

(b) in respect of foreclosure due to tying or bundling.

6.1.3. Potential input foreclosure

6.1.3.1 The Notifying Party's view

(55) The Notifying Party submits that the Transaction will not lead to input foreclosure for the following reasons. First, Asco's products are not a necessary input for Tier 1 suppliers, because these products can be purchased separately by OEMs. Second, for existing contracts, Asco's contractual obligations prevent input foreclosure, since the volumes and prices are set by contracts between Asco and its customers. Third, for future contracts, the merged entity will not be able to foreclose competing Tier 1 suppliers because (i) the merged entity does not possess market power in the upstream market, (ii) OEMs and Tier 1 suppliers can switch easily to a number of alternative upstream suppliers, and (iii) given the significant market power of OEMs, OEMs and Tier 1 suppliers could work around to overcome any attempted foreclosure strategy, e.g. by switching to an alternative supplier.52

(56) The Notifying Party further submits that even if the merged entity were to pursue a successful input foreclosure strategy, competing Tier 1 suppliers would not be marginalised on the market.53

6.1.3.2 The Commission's assessment

(57) As noted in recital (46) above, in its assessment, the Commission considers whether it is likely that the merged entity would engage in input foreclosure strategies, by analysing the merged entity's ability and incentives to engage in such foreclosure strategies, as well as the possible effects these strategies may have on the relevant markets.54

(A) Ability to foreclose access to inputs

(58) As noted in Table 1 and in recital (52) above, Asco has a significant market share in the supply of slat supports worldwide ([90-100]% in 2017, which is expected to decrease to [60-70]% in 2019 due to a loss of a significant contract to a competitor). Asco's market shares in all the other components that it manufactures, on any plausible market definition, is below 20%.55

(59) Input foreclosure may raise competition problems only if it concerns an important input for the downstream product, for example, if it is a critical component without which the downstream product could not be manufactured or effectively sold on the market, or if the cost of switching to alternative inputs is relatively high.56

(60) The results of the market investigation indicate that certain customers do consider the components they procure from Asco as critical. As one OEM customer, describing Asco's products as "complex machining parts" explained: "these are critical parts whose manufacture requires top-end machines and capabilities in the industry with high capex requirements."57 This was echoed by a competitor, who explained that Asco's slat supports "are complicated to machine" and that "Asco has built up a good knowledge of the years".58 The same competitor, however, does not consider that Asco has "any unique non-replicable capabilities", stating that "Asco is not the only supplier capable of supplying these hard metal machining surfaces".59

(61) This view is shared also by another customer, who explains that "Asco has good expertise, infrastructures and a reliable supply chain for machining hard metals, which make it a preferred Tier 2 supplier of components such as slat supports for many Tier 1 suppliers. Although Asco has a strong presence in the market and has occupied a sort of "niche" in hard metals, their capabilities can be replicated by other players".60

(62) Nevertheless, since Tier 2 suppliers such as Asco can and do conclude contracts with and supply OEMs directly (for example, [a significant proportion] of Asco's sales value of slat supports in 2017 was from the supply of slat supports to OEMs directly),61 the components manufactured by Asco do not necessarily represent a necessary or important input for Tier 1 suppliers (despite Asco's high market share in slat supports). This may in part be explained by the fact that, whilst slat supports interface with slats and with the fixed leading edge, slat supports are built directly into the wing at the wing assembly stage at the OEMs' production facilities and not at the time of the manufacture and assembly of the slat or the fixed leading edge.62

(63) Furthermore, a number of factors indicate that the merged entity would not be able to foreclose its downstream rivals post-Transaction, even for the supply of slat supports for which Asco currently has a high market share.

(64) First, a number of alternative suppliers of slat supports and other components manufactured by Asco are available on the market today. These companies are either already supplying or capable of supplying slat supports and these other components. With regard to slat supports specifically, these alternative suppliers include Kencoa ([0-5]% market share in 2017, expected to increase to [20-30]% in 2019),63 GKN ([0-5]% market share in 2017), Triumph ([0-5]% market share in 2017), Sukhoi ([0-5]% market share in 2017), Comac ([0-5]% market share in 2017), Irkut ([0-5]% market share in 2017), SAMCO ([0-5]% market share in 2017, estimated to be [0-5]% in 2018), PCT Group, Figeac, Saab and Mecachrome (the Parties estimated that other suppliers of account for [0-5]% of the global market share for slat supports in 2017).64 With Asco's limited market shares in components other than slat supports, the number of actual and potential alternative suppliers of these components is even greater than those listed above. A number of Asco's customers have indicated that they would be able to source the components they currently source from Asco from alternative suppliers.65

(65) Furthermore, the majority of customers and competitors that expressed a view in the Commission's investigation do not consider there to be any products that Asco sells for which no alternative or only a limited number of suppliers is available.66 The vast majority of customers and competitors that expressed a view in the Commission's investigation also consider that large OEMs would be able to sponsor the market entry of a new supplier of slat supports (the component in which Asco had a market share of [90-100]% in 2017).67

(66) Second, as noted in recital (52) above, one of Asco's customers has recently switched to an alternative supplier of slat supports (Kencoa) in 2018, which shows that switching suppliers is possible and occurs in practice. Kencoa is a new entrant on this market, as it has not previously sold slat supports.68

(67) Third, whilst it may take several months to choose and qualify an alternative supplier, Asco's customers have noted that the current contractual arrangements mean that Asco is bound to continue to supply them for a period of time that is sufficiently long, in their view, for them to either find an alternative supplier or to develop the necessary capabilities in-house if it became necessary.69 The Commission notes that contracts in this industry tend to be typically of a long duration, often exceeding 5 or 10 years, and sometimes extending to the lifetime of the given platform.

(68) Finally, several Tier 1 suppliers and OEMs have indicated that they would also be capable of or are actively exploring the possibility of manufacturing slat supports in-house and may already do this to a certain extent,70 including the majority of competitors and customers that expressed a view in the Commission's investigation.71

(69) In light of the foregoing, the merged entity would not be able to negatively affect the overall availability of inputs (such as slat supports, flap supports and structural components for the fuselage and the engine) for the downstream market in terms of price or quality even if it did reduce access to its own products upstream, and can therefore not be deemed to have the ability to foreclose its downstream competitors.72

(70) For these reasons, the Commission finds that it is unlikely that the merged entity will have the ability to engage in input foreclosure with regard to structural components for the wing, in particular slat supports and flap supports, for the fuselage or for the engine post-Transaction.

(B) Incentive to foreclose access to inputs

(71) In its assessment of the merged entity's incentive to foreclose rivals' access to inputs, the Commission looks at whether the foreclosure would be profitable for the merged entity and the extent to which customers can be diverted away from downstream rivals. The effect is greater where the affected input (in this case structural components for the wing, in particular slat supports and flap supports, for the fuselage and for the engine) represents a significant proportion of downstream rivals' costs or if the affected input represents a critical component of the downstream product.73

(72) As noted in recitals (60) to (61) above, whilst Asco is well-known for its expertise and know-how in slat supports, its capability is not considered by market participants to be non-replicable. Further, slat supports, whilst potentially regarded by some market participants as a critical component for the manufacture of slat systems for the wings,74 can also be manufactured by other suppliers. It is therefore questionable whether the merged entity would have the incentive to engage in an input foreclosure strategy in relation to slat supports. As regards components other than slat supports, the merged entity's incentives to engage in an input foreclosure strategy appear even less probable, given Asco's limited market shares for these components.

(73) For existing platforms under currently valid contracts, Asco is already contracted to supply a set number of slat supports for a set price to a number of Tier 1 suppliers and OEMs and it would not seem profitable for the merged entity post-Transaction to cease supplying these other customers or to attempt to make the conditions of supply less favourable.

(74) First, if it were to attempt to do so, the merged entity risks not only exposing itself to potentially very extensive contractual liability and damages law suits, but also losing the contract (and thereby the income stream) to another existing or potential supplier of slat supports. For example, Asco's contracts with Sonaca are [description of Asco’s contracts with Sonaca].75 Asco's contracts with OEMs are [description of Asco’s contracts with OEMs].76

(75) Second, the trade-off between the profit lost in the upstream market by reducing input sales to competitors and the profit gain from expanding sales downstream77 is not likely to lead to increased profitability for the merged entity. According to market participants, the market for aerostructures is currently a buyer's market,78 with few end-customers (OEMs). These OEMs have already concluded contracts with various suppliers for their existing platforms. OEMs typically follow one of two contractual strategies: OEMs either conclude contracts with Tier 1 and Tier 2 suppliers directly, or OEMs conclude contracts with a Tier 1 supplier, who in turn concludes contracts with Tier 2 suppliers that are qualified by the OEM in question.79 Contracts with Tier 1 suppliers tend to be longer-term than contracts with Tier 2 suppliers (if contracted directly). If the merged entity were to reduce supply of slat supports to its downstream competitors (Tier 1 suppliers), it would not be likely to recoup its lost sales by increasing sales of slats or fixed leading edge assemblies downstream for the following reasons: (i) as described in recitals (64) to (68) the Tier 1 suppliers would be able to find alternative suppliers of slat supports, and (ii) since the contracts between OEMs and Tier 1 suppliers are of a longer-term duration (typically between around 10 years and up to the lifetime of the program), the merged entity would not be able to start supplying slats or fixed leading edge assemblies on the downstream market to the OEM in question in place of the Tier 1 supplier who no longer receives slat supports from the merged entity.

(76) With regard to future platforms, it also does not seem likely that engaging in an input foreclosure strategy would be profitable for the merged entity. As noted in recital (75) above, OEMs being few on the market with a larger number of Tier 1 and Tier 2 suppliers, as well as with increasing capabilities for manufacturing aerostructures in-house, there is ample competition among Tier 1 and Tier 2 suppliers to become the preferred suppliers on future programmes. It would therefore not appear likely that an attempt by the merged entity to foreclose its Tier 1 rivals’ access to slat supports would be profitable.

(C) Overall likely impact on effective competition

(77) The results of the market investigation reveal that a sufficient number of credible downstream competitors who do not depend on the supplies of slat supports from Asco will remain active on the market after the concentration. These downstream competitors should therefore constitute a sufficient constraint on the merged entity and prevent output prices from rising above the pre-concentration levels.

(D) Conclusion on input foreclosure

(78) The Commission also notes that, in the course of the Commission's market investigation, no concerns were raised by any market participants as regards the Transaction's impact on competition in relation to non-coordinated non-horizontal effects as a result of input foreclosure.

(79) In light of the above considerations in Section 6.1.3.2 and based on the results of the market investigation, the Commission finds that the Transaction does not raise serious doubts as to its compatibility with the internal market as regards non-coordinated non-horizontal effects as a result of input foreclosure.

6.1.4. Potential customer foreclosure

6.1.4.1 The Notifying Party's view

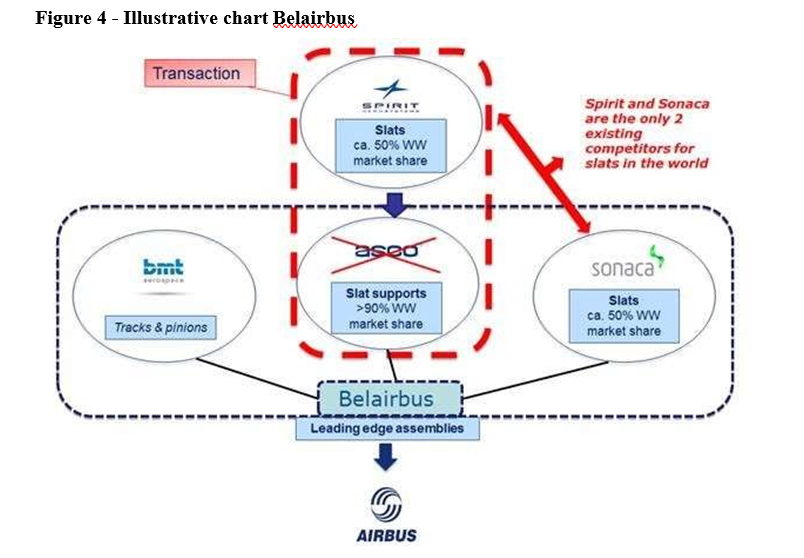

(80) The Notifying Party submits that the merged entity would not be able to foreclose competing Tier 2 suppliers for the following reasons: (i) the merged entity would not possess market power in the relevant downstream markets, and (ii) there are a number of alternative sources of demand for the Tier 2 suppliers' product.80

(81) Moreover, in the Notifying Party's view, even if the merged entity pursued a successful foreclosure strategy, Asco's competitors would not be marginalised on the market.81

6.1.4.2 The Commission's assessment

(82) As noted in recital (46) above, in its assessment, the Commission considers whether it is likely that the merged entity would engage in customer foreclosure strategies, by analysing the merged entity's ability and incentives to engage in such foreclosure strategies, as well as the possible effects these strategies may have on the relevant markets.82

(A) Ability to foreclose access to downstream markets

(83) When assessing the merged entity's ability to foreclose access to downstream markets by reducing its purchases from its upstream rivals, the Commission takes into account whether there are sufficient alternative outlets downstream for upstream competitors to sell their output.83

(84) In the present case, a number of alternative outlets are available for Asco's competitors to sell their products to customers other than Spirit, including other Tier 1 suppliers such as:(a) for slats, Sonaca (with an estimated [50-60]% market share in 2017);84(b) for fixed leading edge assembly, KAL/KAI (with an estimated [5-10]% market share in 2017) and Triumph ([5-10]%),85 with a number of other players having capabilities to supply leading edge assembly, including GKN, Sonaca, TAI, MHI and KHI;86(c) for fixed trailing edge assembly, GKN (with an estimated [20-30]% market share in 2017), KHI ([10-20]%), Boeing ([5-10]%) and RUAG ([0-5]%);87(d) for the fuselage nose section, Aerolia (with an estimated [50-60]% market share in 2017);88(e) for the fuselage centre section, Premium Aerotec (with an estimated [20-30]% market share in 2017), Leonardo ([10-20]%), MHI ([5-10]%);89(f) for the nacelles thrust reversers, UTAS (with an estimated [40-50]% market share in 2017) and Aircelle ([10-20]%);90(g) for pylons, Tier 1 suppliers supplying Airbus platforms ([50-60]%), to the extent that these are not procured by Airbus directly.91

(85) Furthermore, some OEMs contract with Tier 2 suppliers such as Asco directly, since OEMs are increasingly bringing certain elements of assembly in-house92 and must therefore also be considered as an alternative outlet for Asco's competitors to sell their products (e.g. Airbus, with estimated [5-10]% market share for the fuselage centre section in 2017). This may especially be the case for slat supports, since, as noted in recital (62) above, slat supports are built into the wing at the wing assembly stage at the OEMs' production facilities and not into the fixed leading edge assembly by a Tier 1 supplier.93 For example, [a significant proportion] of Asco's sales value of slat supports in 2017 was from the supply of slat supports to OEMs directly.94

(86) Furthermore, OEMs can issue requests for proposals to Tier 1 and Tier 2 suppliers independently,95 meaning that the Tier 2 supplier cannot effectively exercise a choice as to which Tier 1 supplier to supply for the given platform. Even in cases where OEMs have a long-term contract with a Tier 1 supplier which would cover a component supplied by a Tier 2, the Commission’s investigation has shown that OEMs can and do maintain a certain degree of competitive pressure on their supply chain, in relation to the platform covered by that contract and also in relation to possible business for future platforms.96

(87) With regard to slat supports on the upstream market (where Asco had a market share of [90-100]% in 2017) and fixed leading edge assembly (where Spirit had a market share of [80-90]% in 2017) specifically, the Commission also notes that Spirit's existing high market share ([80-90]%) is likely to decrease.

(88) With regards specifically to the Airbus A320 platform, Spirit is not the sole supplier for fixed leading edge assemblies. Furthermore, Spirit’s contract with Airbus stipulates that [description of Spirit’s contracts with Airbus].97

(89) For these reasons, the Commission finds that it is unlikely that the merged entity will have the ability to engage in customer foreclosure with regard to slat supports, flap supports or structural components for the engine or the fuselage post- Transaction.

(B) Incentive to foreclose access to downstream markets

(90) When assessing the merged entity's incentive to foreclose, the Commission assesses whether foreclosing competitors' access to downstream markets would be profitable. The merged entity faces a trade-off between the possible costs associated with not procuring products from upstream rivals and the possible gains from doing so, for example, because it could allow the merged entity to raise price in the upstream or downstream markets.98

(91) The merged entity in the present case is not likely to profit from a customer foreclosure strategy, since it would almost certainly not be able to raise prices in the downstream markets, where any attempted price increase would be resisted by the OEMs.

(92) Given the oligopsonistic nature of the aerostructures market, with a very small number of OEM customers, the merged entity is not likely to engage in customer foreclosure strategies and any attempt to do so is not likely to be profitable.

(C) Overall likely impact on effective competition

(93) In the absence of ability or incentive to engage in customer foreclosure, it does not appear necessary to assess any possible impact on effective competition in this regard.

(94) In any case, as noted above, whilst Spirit is an important customer, a number of alternative customers for Asco's competitors will remain post-Transaction. Therefore, any attempt by the merged entity to foreclose Asco's competitors' access to customers is not likely to be successful in raising Asco's rivals' costs or decreasing their revenues. Furthermore, as noted above, OEMs exercise a sufficient degree of countervailing buyer power, which further diminishes any likelihood for the merged entity to successfully engage in customer foreclosure.

(D) Conclusion on customer foreclosure

(95) The Commission also notes that, in the course of the Commission's market investigation, no concerns were raised by any market participants as regards the Transaction's impact on competition as regards non-coordinated non-horizontal effects as a result of customer foreclosure.

(96) In light of the above considerations and based on the results of the market investigation, the Commission finds that the Transaction does not raise serious doubts as to its compatibility with the internal market as regards non-coordinated non-horizontal effects as a result of customer foreclosure.

6.1.5. Potential foreclosure due to tying or bundling

6.1.5.1 The Notifying Party's view

(97) In addition to the arguments brought in the context of the competitive assessment of potential input foreclosure, the Notifying Party submits that the merged entity will not have the ability or the incentive to make the sale of components currently sold by Asco to Tier 1 customers (and to the OEMs) conditional on them also purchasing products sold by Spirit (or vice versa) through tying and/or bundling in order to foreclose competitors.

(98) First, in the Notifying Party's view, conglomerate effects are not plausible vis-à-vis Tier 1 customers because products sold by Spirit are typically not purchased by other Tier 1 suppliers (instead, these are purchased by OEMs directly).99

(99) Second, the Notifying Party argues that the merged entity will not have market power on any of the markets on which the Parties' current market shares are above 30% (see Table 1 above), since there is a number of alternative current and potential suppliers for each component or product, and in addition OEMs and Tier 1 suppliers are often able to switch to in-house manufacturing.100

(100) Third, the Notifying Party submits that the Transaction does not substantially change the position of Spirit, because Asco's capabilities and components will only be a small addition to Spirit's current portfolio, meaning that the competitive landscape for Tier 1 suppliers will not be impacted as a result of the concentration.101

(101) Finally, the Notifying Party submits that bundles are not currently a feature of the market, with there being very few, if any, instances where tying or bundling takes place, either for Tier 1 suppliers or OEMs, which the Notifying Party views as a strong indication that aerostructures suppliers lack the ability and/or incentive to engage in such conduct. The Notifying Party argues that since the concentration would not result in a substantial change in Spirit's market position, the merged entity would not have the ability or the incentive to engage in a tying and/or bundling strategy.102

(102) In the Notifying Party's view, Tier 1 suppliers and OEMs would be able to withstand any attempt by the merged entity to engage in a tying and/or bundling strategy, since (i) there is a number of alternative actual and potential aerostructures suppliers and (ii) OEMs possess substantial market power and would be able to not only switch to an alternative supplier, but also to punish the merged entity should it attempt to engage in anticompetitive tying or bundling.103

6.1.5.2 The Commission's assessment

(103) As noted in recital (50)(46) above, in its assessment, the Commission considers first, whether the merged firm would have the ability to foreclose its rivals, second, whether it would have the economic incentive to do so and, third, whether a foreclosure strategy would have a significant detrimental effect on competition, thus causing harm to consumers.104

(104) As noted in Table 1 and in recital (52) above, Asco has a significant market share in the supply of slat supports worldwide ([90-100]% in 2017, which is expected to decrease to [60-70]% in 2019 due to a loss of a significant contract to a competitor). On the other upstream markets, however, Asco's market shares are limited and do not exceed 20% on all plausible market definitions. Spirit's market shares in the respective downstream markets for which Asco's products are actual or potential inputs are above 30%, including slats, fixed leading edge assembly, fixed trailing edge assembly, fuselage nose section, fuselage centre section, nacelles thrust reversers and pylons.

(105) However, in light of the considerations in recitals (58) et seq. above regarding the merged entity’s inability to engage in input foreclosure strategies, in combination with the Notifying Party’s arguments set out above in recitals (98)-(102), the Commission has found that the merged entity would also not have the ability to engage in tying or bundling strategies regarding any of the relevant products.

(106) It may be stressed in particular that in spite of its considerable market shares on some potentially relevant components markets (e.g. slats and slat supports), any attempt by the merged entity to engage in tying or bundling would likely be frustrated by the merged entity’s customers. As the Commission’s market investigation has shown, if needed, customers would indeed be able to either switch away their purchases from the merged entity to alternative suppliers or in- source the production of such components.105

(107) Finally, in the absence of the ability to engage in tying or bundling strategies, it does not appear necessary to assess in detail the merged entity’s potential incentive to do so or the possible effects such a strategy may have on the market.

6.2. Horizontal non-coordinated effects

6.2.1. Legal framework for competitive assessment of horizontal non-coordinated effects

(108) The Commission Guidelines on the assessment of horizontal mergers under the Council Regulation on the control of concentrations between undertakings (the "Horizontal Merger Guidelines")106 distinguish between two main ways in which mergers between actual or potential competitors on the same relevant market may significantly impede effective competition, namely non-coordinated and coordinated effects. Coordinated effects will be discussed below in Section 6.3.

(109) Non-coordinated effects may significantly impede effective competition by eliminating important competitive constraints on one or more firms, which consequently would have increased market power, without resorting to coordinated behaviour. In that regard, the Horizontal Merger Guidelines consider not only the direct loss of competition between the merging firms, but also the reduction in competitive pressure on non-merging firms in the same market that could be brought about by the merger.107

(110) The Horizontal Merger Guidelines list a number of factors, which may influence the rise of substantial non-coordinated, effects from a merger, such as: the large market shares of the merging firms; the fact that the merging firms are close competitors; the limited possibilities for customers to switch suppliers; or the fact that the merger would eliminate an important competitive force. That list of factors applies equally if a merger would create or strengthen a dominant position, or would otherwise significantly impede effective competition due to non-coordinated effects. Furthermore, not all of those factors need to be present to make significant non-coordinated effects likely and this is not an exhaustive list.108

6.2.2. The Notifying Party's view

(111) According to the Notifying Party, the concentration does not give rise to horizontal non-coordinated effects, as the combined market shares of the Parties remain moderate and the increments are very small.

6.2.3. The Commission's assessment

(112) The Commission has found that the concentration is unlikely to give rise to anticompetitive horizontal non-coordinated effects.

(113) On the basis of a very broad market definition including all types of aerostructures, the concentration would give rise to an affected worldwide market for the design, manufacture and sale of aerostructures (all types), only if the captive sales of OEMs are excluded from the market. The concentration would also give rise to a possibly relevant horizontally affected market for slat systems (if no distinct markets are defined for each of the system’s components, in particular slats and slat supports). Importantly, based on a component-by-component market definition, the Parties’ activities do not overlap horizontally for any component.

Table 2 - Market shares aerostructures – horizontal overlaps (2017)

Market |

Market size (million €) |

Spirit |

Asco | Combined market share of the Parties |

Aerostructures (all types), incl. captive OEM sales |

52 251 |

[10-20]% |

[0-5]% |

[10-20]% |

Aerostructures (all types), Tier 1 sales only |

30 386 |

[20-30]% |

[0-5]% |

[20-30]% |

Wing aerostructures, incl. captive OEM sales |

17 986 |

[5-10]% |

[0-5]% |

[5-10]% |

Wing aerostructures, Tier 1 sales only |

11 337 |

[10-20]% |

[0-5]% |

[10-20]% |

Slat systems109 | 511 662 | [40-50]% | [0-5]% | [40-50]% |

Source: Form CO.

(114) As the figures in Table 2 above show, on such a broad market for all aerostructures (excluding the OEMs’ captive production of aerostructures), the Parties’ combined market share would remain relatively moderate at [20-30]%, with only a small increment of [0-5]% resulting from the concentration. On the narrower possible market for the production and sale of wing aerostructures only, the combined market share of the Parties would be below 20%. Finally, although on the even narrower possible market for the production and sale of slat systems, the combined market share of the Parties would be close to [50-60]%, the increment would be minimal at [0-5]%.

(115) In addition, the broad overall market for all aerostructures and the narrower market for slat systems would be highly differentiated markets, where Spirit and Asco would likely not be close competitors, for instance because:(a) while Spirit is a Tier 1 supplier of aerostructures, Asco’s profile is that of a Tier 2 components supplier who also offers some Tier 1-type solutions;(b) while Spirit is a large player with a broad portfolio across aerostructures, Asco’s main focus is on high-lift device components (slat supports and flap supports);(c) while Asco’s main strength is the production and sale of slat supports, this is a component that is not in Spirit’s portfolio at all.

(116) Finally, as mentioned above, the Parties’ activities do not overlap at the level of individual components.

(117) Based on the foregoing, the Commission takes the view that the concentration is unlikely to give rise to horizontal non-coordinated effects.

6.3.Horizontal coordinated effects

6.3.1. Legal framework for competitive assessment of horizontal coordinated effects

(118) According to the case law, coordinated effects may arise "as the result of a concentration where, in view of the actual characteristics of the relevant market and of the alteration in its structure that the transaction would entail, the latter would make each member of the dominant oligopoly, as it becomes aware of common interests, consider it possible, economically rational, and hence preferable, to adopt on a lasting basis a common policy on the market with the aim of selling at above competitive prices, without having to enter into an agreement or resort to a concerted practice within the meaning of Article 81 EC."110

(119) According to the Horizontal Merger Guidelines, horizontal mergers may significantly impede effective competition (a) by increasing the likelihood that firms are able to coordinate successfully, or (b) by making existing coordination easier, more stable or more effective, either by making the coordination more robust or by permitting firms to coordinate on even higher prices, for example by facilitating the detection of deviation, limiting the ability and incentives of some market players to deviate and allowing more efficient retaliation.111

(120) Coordination may take various forms, such as setting prices above the competitive level, limiting production or capacity, or dividing the market, for instance by geographic areas or other customer characteristics, or by allocating contracts in bidding markets.112

(121) Coordination is more likely to emerge in markets where it is relatively simple to reach a common understanding on the terms of coordination. This is the case where coordinating firms have similar views regarding which actions would be considered to be in accordance with the aligned behaviour and which actions would not.113 The less complex and the more stable the economic environment (for example, oligopolistic markets), the easier it is for the firms to reach a common understanding on the terms of coordination.114 In addition, firms may find it easier to coordinate if they are relatively symmetric, especially in terms of cost structures, market shares, capacity levels, and levels of vertical integration.115

(122) Coordinating firms may also find ways to overcome problems stemming from complex economic environments for example by establishing a small number of reference pricing points, or a fixed relationship between base prices and a number of other prices. Market transparency through publicly available key information or, for example, by information exchanged through structural links between competitors may further facilitate coordination.116

(123) According to relevant case law, specific emphasis should be placed on the actual economic mechanism according to which tacit coordination is likely to operate.117 The mechanism in question must be consistent with the current market conditions and integrate the industry features prone to induce coordinated behaviour. Furthermore, the ways in which the main actors are likely to reach terms of coordination and, in particular, the parameters that lend themselves to being a focal point of coordination, should be assessed. Finally, a specific focus should be given to whether potential coordination is likely to be sustainable.

(124) In general, three features of the market may provide indications as to whether coordination is likely to be sustainable. First, the coordinating firms should be able to monitor to a sufficient degree whether the terms of coordination are being adhered to. Second, coordinating firms are more likely to adhere to coordinated behaviour if the incentives not to deviate deter them from departing from the coordinated action. Third, the reactions of outsiders, such as current and future competitors not participating in the coordination, as well as customers, should not be able to jeopardise the results expected from the coordination or would be too small to effectively counterbalance the effect of potential coordination on the relevant market.118

(125) In assessing whether it would be possible to reach terms of coordination and whether the coordination is likely to be sustainable, the Commission takes account of all the changes that a transaction is likely to bring about. The reduction of the number of players resulting from the concentration may, in itself, be a factor that facilitates coordination. However, other factors that may increase the likelihood or significance of coordinated effects could also be taken into account.119

6.3.2. The Notifying Party's view

(126) According to the Notifying Party, there is no risk of Spirit and Sonaca coordinating their pricing behaviour through Belairbus. Spirit has argued in this regard that Belairbus is only a platform for negotiation (not manufacturing) and that its activities are limited to existing contracts that have already been attributed to Belairbus. The Notifying Party has also stressed that Spirit would not have any power over the conditions at which Sonaca sells its slats through Belairbus. The Notifying Party has also emphasized that the overall aerostructures market is highly fragmented and that slats specifically are highly differentiated products, rendering coordination more difficult. The Notifying Party has also insisted on the buyer power of OEMs.

6.3.3. The Commission's assessment

(127) The Commission has found that the concentration may give rise to horizontal coordinated effects regarding slat systems as a whole and slats in particular, as a result of the modification the concentration would bring about in the shareholding structure of the Belairbus joint venture.

(128) As mentioned above in recital (5)(b), Belairbus is a joint venture between Asco, Sonaca and BMT Eurair. It acts as a commissionaire through which its parent companies participate in the development, production and sale of slat systems for all the main commercial aircraft platforms of Airbus. When through the concentration Spirit acquires sole control over Asco, in practice it will also take Asco’s place as a shareholder in this JV. In this way, Spirit would become Sonaca's partner in Belairbus, while the latter is an entity dedicated to the development and sale of slat systems for Airbus and while Sonaca and Spirit are currently the only two existing suppliers of slats (and/or slat systems) worldwide, as shown in the market share table below:

Table 3 - Market shares on the worldwide market for slats (2017)

Supplier | Sales (EUR ‘000) | Market share |

Spirit | […] | [40-50]% |

Sonaca | […] | [50-60]% |

Total | 509 849 | 100% |

(129) The change in the composition of Belairbus which the concentration would bring about is illustrated in the chart below:

(130) The Commission’s investigation has shown that Spirit and Sonaca becoming partners in Belairbus, in which context they hold sensitive commercial and technical discussions, risks to significantly reduce the level of competition on the worldwide markets for slat systems in general and slats in particular, in several possible ways. Not only would the concentration increase the transparency between the two sole suppliers of slats in the world, Spirit and Sonaca, it would also increase the likelihood that these competitors could coordinate their behaviour. In addition, in some instances, Spirit may be able to weaken its sole competitor, Sonaca, by using Sonaca’s commercially sensitive information, to which Spirit would not have gained access absent the concentration.

(131) First, in its investigation, the Commission has learned that the shareholders in Belairbus work together closely in the context of the performance of Belairbus's contractual obligations vis-à-vis Airbus. They exchange technical and commercial information between them and need to come to an agreement on the offers Belairbus will make to Airbus. More specifically:(a) very detailed technical information is exchanged through Belairbus on a regular basis because the three components of a slat system (i.e. i) slats, ii) slat supports and iii) racks and pinions) are engineered to operate as an integrated turnkey system for Airbus. Therefore, any issue that may arise during the lifecycle of a Belairbus slat system or any time a Belairbus slat system needs replacing, the shareholders of Belairbus work together;(b) Airbus regularly requests incremental technical improvements on the slat systems it sources through Belairbus. Each time this happens, the shareholders need to work together to find solutions to propose to Airbus. Technical changes generally also have a direct impact on cost as "decisions on incremental improvements are", from Airbus's point of view, "business case driven"120 and "a strong interaction between the technical and commercial processes is required"121;(c) from time to time, Airbus also requests price reductions from Belairbus, in the context of "cost-reduction programmes". The Commission understands that each time this happens, given that Belairbus combines the individual price offers formulated by its shareholders, combines them into a single offer to Airbus and negotiates directly with Airbus, the shareholders need to come to an agreement on how to split the cost implications of Airbus’s request between them122, i.e. which margin reduction each shareholder is willing to accept.

(132) Second, while the scope of Belairbus's activities is indeed limited to existing contracts (i.e. for existing Airbus platforms), the Commission understands that competition for slat systems and slats in fact takes place not only with regard to new platforms, but also for existing platforms, each time Airbus seeks to obtain a cost reduction and/or a technical improvement.

(133) In this regard, it is worth noting that [confidential information relating to commercial dealings]123,124. Thus, Spirit exerts a certain degree of competitive pressure on Belairbus.

(134) Third, Asco and Sonaca cooperate on slat system contracts for other OEMs as well, outside the scope of Belairbus, albeit in a less structural manner. Under those contracts as well, Asco provides slat supports (a component which Sonaca currently does not produce itself) and Sonaca slats. These additional instances of cooperation further enhance the interdependency of interests between Sonaca and what would be the merged entity after the concentration.

(135) Fourth, [Commission referring to indications of possible coordination taking place through Asco]125.

(136) Based on the foregoing, the Commission concludes that in this case, the four criteria for the existence of coordinated effects of a concentration may be met:(a) First, the participation of the two competitors for slats/slat systems for large commercial aircraft in a joint venture in whose framework they discuss sensitive technical and commercial information about bids, may increase the likelihood of reaching terms of coordination;(b) Second, the significantly increased transparency, at least on the side of Spirit, on the technical and commercial terms of bids for Airbus could enable it to monitor deviations;(c) Third, Spirit could be in a position to retaliate on Sonaca on a large stream of its business: (i) through Asco, Spirit would become the […] supplier of one of the key components of the slat systems which Belairbus must deliver to Airbus; (ii) given the significance of Airbus as a customer, Belairbus is an important sales channel for Sonaca’s slats; (iii) through its shareholding in Belairbus, Spirit would have the possibility to block Belairbus decisions; and(iv) Spirit would be Sonaca’s supplier of slat supports on contracts for other OEMs, outside Belairbus;(d) Fourth, the Commission has not been able to identify any other companies that are currently selling turnkey slat systems such as those, which each of Belairbus (combining the inputs of its shareholders) and Spirit delivers. Therefore, it appears unlikely that outsiders would be in a position to react and challenge possible coordinated behaviour between Spirit and Sonaca.

6.3.4.Conclusion

(137) In conclusion, in view of the reasons set out above in paragraphs (127) through (136) regarding the existence of horizontal coordinated effects, the Commission finds that the concentration raises serious doubts as to its compatibility with the internal market regarding slat systems in general and slats in particular.

7. PROPOSED REMEDIES

(138) In order to render the concentration compatible with the internal market, Spirit has modified the notified concentration by submitting commitments to the Commission. The legal framework applicable to the assessment of proposed commitments is set out below in Section 7.1.

(139) Spirit submitted three main sets of commitments. One was submitted on 15 October 2018, before the initial notification was withdrawn (the “First Initial Commitments”). The Commission held a market test to gather the views of market participants on the Initial Commitments (the “first market test”) and Spirit was informed of its outcome. The First Initial Commitments are described below in Section 7.4. After withdrawing its first notification and subsequently submitting its second notification, Spirit formally submitted commitments on 27 February 2019 (the “Second Initial Commitments”), which it formally amended on 8 March 2019 (the “Final Commitments”), following a market test during which the views of market participants were gathered and then shared with Spirit (the “second market test”).

7.1.Legal framework

(140) The following principles from the Remedies Notice126 apply where parties to a merger choose to offer commitments in order to restore effective competition.

(141) Where a concentration raises competition concerns in the sense that it could significantly impede effective competition, in particular as a result of the creation or strengthening of a dominant position, the parties may seek to modify the concentration in order to resolve the competition concerns and thereby gain clearance of their merger.127

(142) The Commission only has power to accept commitments that are capable of rendering the concentration compatible with the internal market in that they will prevent a significant impediment to effective competition in all relevant markets where competition concerns were identified.128 To that end, the commitments have to eliminate the competition concerns entirely129 and have to be comprehensive and effective from all points of view.130

(143) In assessing whether proposed commitments are likely to eliminate its competition concerns, the Commission considers all relevant factors, including inter alia the type, scale and scope of the commitments, judged by reference to the structure and particular characteristics of the market in which those concerns arise, including the position of the parties and other participants on the market.131 Moreover, commitments must be capable of being implemented effectively within a short period of time.132

(144) Where a proposed concentration threatens to significantly impede effective competition, the most effective way to maintain effective competition, apart from prohibition, is to create the conditions for the emergence of a new competitive entity or for the strengthening of existing competitors via divestiture by the merging parties.133

(145) While divestiture commitments are generally the best way to eliminate competition concerns resulting from horizontal overlaps, other structural commitments, such as access remedies, or other non-divestiture remedies may be suitable to resolve concerns if they are equivalent to divestitures in their effects.134

7.2.First Initial Commitments

7.2.1. Description of the Initial Commitments

(146) The Initial Commitments, formally submitted on 15 October 2018 before the Parties withdrew and subsequently refiled their notification, were aimed at: transforming Belairbus:(a) from being the undisclosed agent (“commissionaire”) of its shareholders to being their disclosed agent (“mandataire”);(b) limiting its object to the purposes that can be summarized as:(1) performing the agreements with Airbus, managing invoicing, order processing (but not negotiating prices) and accounting;(2) implementing a factoring agreement and other financial agreements;(3) providing access to the information available within Belairbus to the extent that it does not contain any commercially sensitive information relating to another shareholder;(4) managing surviving rights and obligations resulting from Belairbus’s activities prior to the transformation; (5) performing any activity necessary for performing the commitments;(6) excluding the involvement of Belairbus for any future aircraft.(c) making changes to the corporate bodies and constituent documents of Belairbus so as to:(1) change the composition of the Belairbus Board of Directors and appoint (an) independent director(s) as representative(s) of Asco (with specific criteria for independence such person(s) would have to meet;(2) abolish the Belairbus Board of Managers and Account Managers Board, transferring their functions to each of the shareholders of Belairbus;(3) appoint an independent General Manager of Belairbus;(4) insert into each agency agreement between Belairbus and each shareholder a confidentiality obligation regarding the information of the other shareholders;(5) insert an arbitration clause into the agreements bringing about the commitments;(d) protecting confidential information of Sonaca that is in the possession of Asco by destroying or returning it […] and, for the future, by putting in place firewalls to prevent any such information from being disclosed to any company of the Spirit group (other than Asco).

7.2.2.Assessment of the First Initial Commitments

(147) In view of assessing the appropriateness of the First Initial Commitments, the Commission carried out a market test, which was launched on 16 October 2018 (the “first market test”). Given the specificities of the possible competition concern identified by the Commission, the first market test focused on the companies involved in the Belairbus configuration.

(148) The unanimous view of the market test respondents was that the First Initial Commitments could not remedy the serious doubts identified by the Commission135.

(149) Respondents considered that the proposed transformation of Belairbus would be insufficient to remove the competitive concerns raised by the concentration, while at the same time removing the efficiencies gained from operating through Belairbus.

(150) On 25 October 2018, the Notifying Party withdrew its notification.

7.3.Second Initial Commitments

(151) On 30 January 2019, the Notifying Party re-filed its notification.

(152) The Notifying Party formally submitted the Second Initial Commitments on 27 February 2019.

7.3.1.Description of the Second Initial Commitments

(153) The Second Initial Commitments have two main features:(a) the disaggregation of Belairbus into bilateral contractual supply relationships between each of the shareholders in Belairbus, on the one hand, and Airbus, on the other; and(b) confidentiality arrangements preventing Sonaca's commercially sensitive information from flowing back to or being used by Spirit.