Commission, March 25, 2019, No M.9163

EUROPEAN COMMISSION

Decision

DA AGRAVIS MACHINERY / KONEKESKO EESTI / KONEKESKO LATVIJA / KONEKESKO LIETUVA / KONEKESKO FINNISH AGRIMACHINERY TRADE BUSINESS

Subject: Case M.9163 – DA AGRAVIS MACHINERY HOLDING / KONEKESKO EESTI / KONEKESKO LATVIJA / KONEKESKO LIETUVA / KONEKESKO FINNISH AGRIMACHINERY TRADE BUSINESS

Commission decision pursuant to Article 6(1)(b) in conjunction with Article 6(2) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 4 February 2019, the European Commission (the “Commission”) received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation, by which Danish Agro Group ("Danish Agro") through its subsidiaries DA Agravis Machinery Holding A/S (“DA Agravis”) and Danish Agro Machinery Holding A/S (“Danish Agro Machinery”) (together “the Notifying Parties”), acquires within the meaning of Article 3(1)(b) of the Merger Regulation control of the whole of Konekesko Eesti AS, SIA Konekesko Latvija, UAB Konekesko Lietuva, and assets of Konekesko Oy in Finland, which constitute the whole of Kesko Group’s agrimachinery business (Konekesko Oy). (3) Danish Agro and the Konekesko Oy’s subsidiaries and assets ("Konekesko" or the "Targets") are hereinafter referred to as the “Parties”.

1. THE PARTIES

(2) DA Agravis and Danish Agro Machinery are part of the Danish Agro, a Danish co- operative owned by approximately 10,000 Danish farmers. Danish Agro operates mainly within the sale of animal feedstuff mixes, premix and vitamin mixes, fertilizer, pesticides, seed and agricultural machinery. It also purchases crops from farmers, primarily in Scandinavia, Finland, the Baltic countries, the northern part of Germany, Poland and the Czech Republic.

(3) AS Konekesko Eesti, SIA Konekesko Latvija and UAB Konekesko Lietuva are agricultural machinery trade companies domiciled respectively in Estonia, Latvia and Lithuania. These companies are owned by Konekesko Oy, which ultimately belongs to the Kesko Group, a Finnish retailing conglomerate. The Finnish target comprises the agricultural machinery business of Konekesko Oy in Finland. The Targets primarily focus on the import, sale and after-sales service of agricultural machinery to end-users such as farmers and independent entrepreneurs who offer services to farmers, such as harvesting.

2. THE OPERATION

(4) On 10 February 2017, DA Agravis and Konekesko Oy concluded a framework agreement pursuant to which DA Agravis acquired 45% of the shares of AS Konekesko Eesti, SIA Konekesko Latvija and UAB Konekesko Lietuva, i.e. of each of the three Baltic undertakings. The framework agreement also granted DA Agravis a call option to the remaining 55% shares in each of the three Baltic undertakings. DA Agravis exercised its call option, by a call notice, on 25 May 2018, subject to merger clearance. The full purchase price for 100% of the shares of the three Baltic undertakings is around […]. This transaction is referred to as the “Baltic transaction”.

(5) On 10 February 2017, Danish Agro Machinery and Koneskeko Oy concluded in parallel an agreement pursuant to which Danish Agro Machinery was granted a call option to Konekesko Oy’s Finnish agrimachinery trade business. Danish Agro Machinery exercised its call option, by a call notice, also on 25 May 2018, subject to merger clearance. The purchase price of Konekesko’s Finnish agrimachinery business is around […].

3. CONCENTRATION

(6) The proposed acquisition of the three Baltic undertakings together with the proposed acquisition of Konekesko's Finnish agrimachinery business are to be treated as one and the same concentration arising on the date of the last transaction, according to Article 5(2), sub-paragraph 2 of the Merger Regulation.

(7) Firstly, through each of the proposed transactions, Danish Agro acquires sole control over the three Baltic undertakings and of the Finnish assets, within the meaning of Article 3(1)(b) of the Merger Regulation. Secondly, the transactions will take place within a two-year period between the same undertakings, Danish Agro and Konekesko Oy. The acquisitions of each of the three Baltic undertakings and of the Finnish assets are hereinafter referred to as “the Transaction”.

4. UNION DIMENSION

(8) The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 2 500 million (4) (Danish Agro EUR 4 267 million; Targets EUR 164 million). In each of at least three Member States, the combined aggregate turnover of all the undertakings concerned is more than EUR 100 million. (5) In each of these same Member States, the aggregate turnover of each of at least two of the undertakings concerned is more than EUR 25 million, and the aggregate EU-wide turnover of each of at least two of the undertakings concerned is more than EUR 100 million. (6) None of the undertakings concerned achieves more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The Transaction has therefore a Union dimension pursuant to Article 1(3) EUMR.

5. PROCEDURE

(9) For the assessment of the Transaction, the Commission has made use of the available means of investigation pursuant to Article 11 of the Merger Regulation. In particular, the Commission sent extensive questionnaires to competitors, suppliers (brand manufacturers of agricultural machinery) and customers and held conference calls with brand manufacturers and customers. The Commission also sent a request for information to the national competition authorities of Finland and Estonia, as the Notifying Parties had previously separately notified the proposed acquisition of Konekesko’s Finnish assets and the Estonian agricultural machinery business to each respective authority.

6. RELEVANT MARKETS

6.1. Introduction to the industry and the Parties' activities

6.1.1. Agricultural machinery

(10) Agricultural machinery comprises a number of machines for agricultural use. Both the Notifying Parties and the Targets are active in the distribution and retail sale of tractors, combine harvesters, forage harvesters, balers, grass machines and telescopic handlers:

(a) Tractors are self-propelled machines that can be fitted with different implements and used for a variety of agricultural uses. There are different kinds of tractors, ranging from small narrow-track tractors with up to 100 HP that can operate e.g. between rows in a vineyard or be used in production of vegetables or in orchards ("specialty tractors"), to tractors with normal track width and up to 100 HP for use on grasslands and other terrain where lightweight tractors are more suitable ("small standard tractors") and standard tractors with above 100 HP suitable for use in large fields with heavier implements, e.g. ploughs, harrows or seed drills and ("standard tractors"); (7)

(b) Combine harvesters are self-propelled machines that combine three separate harvesting operations into one single process (reaping, threshing and windrowing) and which are used to harvest a variety of grain (e.g. wheat, oats, rye, barley, corn); (8)

(c) Forage harvesters are self-propelled machines used to make silage by chopping grass and crop into small pieces, passing the chopped material through a blower into a large trailer (which is hauled by a tractor next to the forage harvester); (9)

(d) Balers are machines that are used to compress, cut and rake crop (e.g. hay or silage) into compact balers that are easy to handle, transport and store. Balers are hauled by tractors; (10)

(e) Grass machines are machines used for harvesting (cutting) grass. After the grass is cut by the grass machine, it is dried and can either be baled by a baler or chopped by a forage harvester; (11)

(f) Telescopic handlers are material handling machines that can be fitted with specialist tools (such as buckers, pallet forks or booms) and used inside stables (e.g. for providing feed to the farm animals), outside (e.g. for moving manure) or in the fields (e.g. for loading big hay bales onto trailers, loading grain from silos unto trucks or lifting big bags with seed when filling the seed drills for sowing). (12)

(11) Agricultural machinery is used in the farming industry by farmers and agricultural contractors (the end-users in the value chain). (13) There are a number of manufacturers of agricultural machinery, with both global and regional brands, such as John Deere, AGCO (with the Valtra, Fendt and Massey Fergusson brands), Case IH, New Holland and Claas. (14) At the wholesale level, manufacturers tend to conclude (often exclusive) distribution agreements with independent distributors for specific geographies (typically on a national basis). (15) These distributors are responsible for importing agricultural machines subject to their respective distribution agreements, and at the retail level, for setting up national marketing strategies and engaging with customers, including for the retail sale of agricultural machinery and provision after-sales services. (16)

(12) The Notifying Parties are active in the distribution and retail sale (17) of agricultural machinery (including under the John Deere brand) in Finland and Estonia respectively. In Latvia and Lithuania, DA Agravis has limited imports of trade-in used agricultural machinery, mainly from Denmark. (18) The Targets are active in the distribution and retail sale of agricultural machinery in Finland, Estonia, Latvia and Lithuania. Each of the Targets has concluded exclusive distribution agreements with Claas in each of Estonia, Finland, Latvia and Lithuania. (19)

(13) The Parties are also active in the distribution and retail sale of implements for agricultural machinery. Implements are tractor-compatible not self-propelled tools that can be fitted on a tractor to enable it to perform a variety of tasks for agricultural uses. Implements include sprayers, harrows, manure spreaders, sowing machines (seed drills) and wagons. (20)

(14) The Parties are also active in the distribution and retail sale of spare parts for agricultural machinery. Spare parts are used to replace broken and worn-out spare parts in agricultural machinery. Spare parts can be 'original' (i.e. produced by the same manufacturer that has produced the agricultural machinery in question) or 'non- original' (i.e. manufactured by manufacturers that may not manufacture agricultural machinery themselves). (21)

(15) In addition to their activities in the distribution and retail sale of agricultural machinery, implements and spare parts, the Parties are also active in the provision of after-sales services for agricultural machinery in Estonia and Finland. (22)

6.1.2. Other products

(16) Danish Agro is also active in the sale of animal feedstuff mixes, premix and vitamin mixes, fertilizer, pesticides, seed, energy and the purchase of crops from farmers in Estonia and Latvia. The Targets are not active in any of these activities in either country.

(17) The Targets are active in the distribution of: (i) construction and material handling equipment in Estonia, Finland, Latvia and Lithuania; and (ii) forestry machinery in Estonia, Latvia and Lithuania. Danish Agro is not active in any of these activities in either Finland, Estonia, Latvia or Lithuania.

6.2. Relevant product markets

6.2.1. Retail sale of agricultural machinery

6.2.1.1 Distinction between different types of agricultural machines

(A) The Notifying Parties’ arguments

(18) The Notifying Parties submit that the relevant market should be defined as an overall market for the sale of agricultural machinery, since all brand agreements with global and regional manufacturers oblige the distributors to represent a full product line from the specific brand and all of the global competitors market similar product portfolios. (23) Nevertheless, if necessary, plausible segmentations based on machine type can be made, i.e. (i) standard tractors, (ii) harvesting machines, (iii) telescopic handlers, (iv) balers, (v) forage harvesters and (vi) grass machines. (24)

(B) The Commission's assessment

(19) In previous decisions, the Commission has identified distinct relevant product markets for (i) standard tractors, (ii) specialty tractors, (iii) combine harvesters, (iv) forage harvesters, and (iv) balers at the wholesale level. (25)

(20) The results of the market investigation suggest that the segmentation of the agricultural machinery markets by machine type is warranted in the present case.

(21) First, a large majority of market respondents expressing a view in the market investigation consider that a distinction by type of machinery, and in particular between (i) standard tractors, (ii) specialty tractors, (iii) combine harvesters, (iv) forage harvesters and (v) balers can be observed at retail level. (26)

(22) Second, whereas the majority of responding manufacturers offer their full agricultural product portfolio in each of the countries concerned, a not insignificant number of them do not offer some of the products in some of the countries. (27) As the Notifying Parties themselves state, "global manufacturers such as John Deere, New Holland, Case IH and AGCO do in some countries offer a full range of products including, inter alia, agricultural machinery and different types of implements" (28) and "Claas does not offer a full range of products in any country." (29)

(23) Moreover, whilst the majority of responding competitors consider it "very important", "important" or at least "relevant" that a distributor offer a full range of agricultural machinery, a significant number of competitors stated that this was in fact "not relevant". (30) Also, the majority of customers who responded to the Commission's market investigation deemed the offer of a full range of agricultural machinery to be even less relevant than did some of the competitors. (31)

(24) Third, the end-use of the relevant agricultural machine is considered to be important by market participants. The different categories of agricultural machinery are not substitutable from a demand-side perspective, even with modifications.

(25) For example, when asked whether a self-propelled forage harvester could be used interchangeably with a trailed or mounted harvester (32) in combination with a tractor, a large majority of manufacturers, competitors and customers that responded to the Commission's market investigation stated that this is not the case. (33) As a number of Estonian customers explained, the main advantages of a self-propelled forage harvester are "productivity", which allows "work [to be] done more qualitatively and quicker", ability of " handling large quantities in short period of time" and also the "ability to do more contracting during the season". (34)

(26) Market participants consider self-propelled forage harvesters to be more powerful and efficient, which makes them particularly suitable for larger farms, for which trailed or mounted harvesters are not seen as suitable substitutes. As one Finnish customer explained: "The self-propelled forage harvester is the only viable option for our annual silage harvesting rate (2000ha / year). The power of other methods, and the quality of the feed, do not meet our needs". (35) Self-propelled forage harvesters are also significantly more expensive, and are generally not seen as comparable with trailed or mounted harvesters in terms of quality. As another Finnish customer explained: "Self propelled is lot more efficient, but more expensive, need less workers and forage quality is significantly better/more solid". (36)

(27) By way of a further example, grass machines are also considered to be a separate product, distinct from other types of agricultural machinery. (37) According to the respondents to the Commission's investigation, grass machines tend to be purchased and used by farmers who focus on dairy farming – other farmers do not have a particular need for grass machines. (38) The customer base for this type of machinery is therefore significantly different from other types of agricultural machinery. Furthermore, similar to forage harvesters, grass machines are not considered to be substitutable with other types of agricultural machinery. As one Estonian customer explains: "It is not possible to substitute grass machines with other machines, as other machines do not enable to achieve the same quality of end-product. Substitution may be possible for small farms, but not for large farms, for which time is of essence". (39)

(28) For these reasons, the Commission finds that a distinction based on the type of agricultural machinery is appropriate for the assessment of this Transaction.

6.2.1.2 Distinction between new and used machinery

(A) The Notifying Parties’ arguments

(29) According to the Notifying Parties, almost all customers trade in used machinery to the distributor when buying a new machine, and distributors can then resell used machinery to other customers. The Notifying Parties submit that both new and used machines can fulfil the same overall functions and purpose and can therefore be considered substitutable, even if newer machines may have newer and more efficient technology and there is in many cases a considerable difference in the price of new and used machines. (40)

(B) The Commission's assessment

(30) The results of the market investigation clearly show that there are distinct relevant product markets for new and used agricultural machinery. The vast majority of responding manufacturers, competitors and customers stated that there are clear differences between new and used machinery. (41) Whilst some respondents indicate that the customer base is in general the same, others have pointed to the differences in prices to explain that there are different end-customers for new and used machinery. (42)

(31) Overall, there appear to be different conditions of competition on the markets for new and used machinery. For example, one competitor explained that "Usually used machines market is not interfering with new machines sales". (43) This was echoed by a manufacturer, who stated that "Older machines do usually not compete against new equipment". (44) Furthermore, there is more evidence of cross-border sales of used machinery than of new machinery, (45) as also confirmed by the Notifying Parties: "The import of new machines on retail level is non-existent, wher[e]as some limited import of used machines on retail level does take place." (46)

(32) Furthermore, new agricultural machinery is typically covered by a warranty, typically for the first 12 months following its first exploitation, during which after-sales services can be provided free of charge. (47) Used agricultural machinery is not covered by such a warranty.

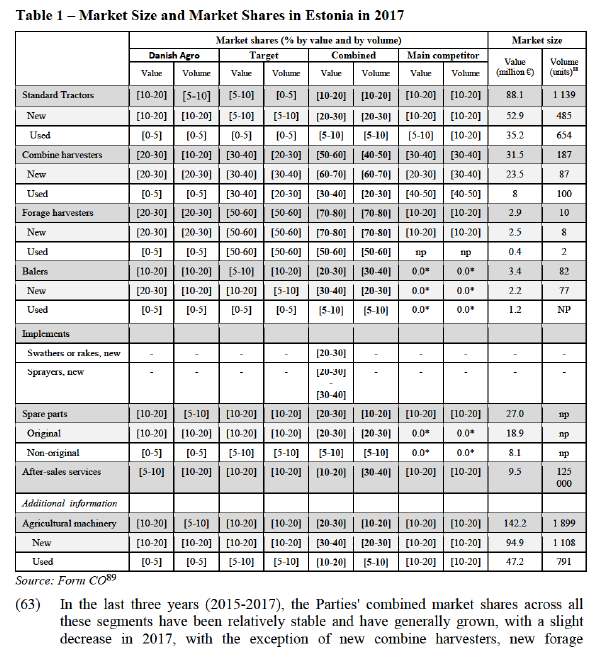

(33) Finally, whilst the distribution agreements between manufacturers and distributors/retailers of agricultural machinery tend to be exclusive with regard to the retail sale of new agricultural machinery, such limitation may not apply with regard to used agricultural machinery. Therefore, distributors/retailers may accept different brands of agricultural machinery as trade ins (and therefore also resell these different brands of used agricultural machinery), whereas their exclusive distribution agreements with particular manufacturers mean that they may only sell those specific brands of new agricultural machinery. (48)

(34) For these reasons, the Commission finds that a distinction between new and used machinery, for each of the types of agricultural machinery at issue in this case, is appropriate for the assessment of this Transaction.

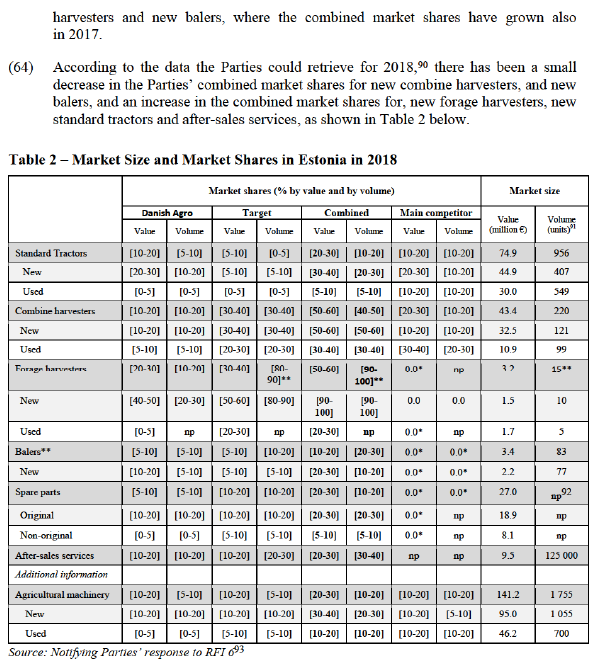

6.2.1.3 Distinction based on size or other parameters

(A) The Notifying Parties’ arguments

(35) The Notifying Parties submit that there is one single market for agricultural machinery, with possible segmentations by type of machinery. Nevertheless, the Notifying Parties also provide detail regarding the different sizes and corresponding uses of tractors, distinguishing between small standard and specialty tractors with up to 100 HP, and large standard tractors with over 100 HP. (49)

(B) The Commission's assessment

(36) Whereas some market participants (in particular manufacturers and competitors) suggested a further segmentation within each type of agricultural machinery based on size or horse power, capacity or performance levels, the majority of the respondents to the Commission's investigation did not think that a further segmentation on the basis of these, or any other factors, is required. (50) A reason given by market participants is that such factors are rather differentiating factors within the different agricultural machinery categories. It appears that customers are prepared to move up or down the horsepower scale, depending on other aspects (e.g. durability, reliability, after-sales servicing, financing, etc.).

(37) In light of the results of the market investigation, the Commission does not deem it necessary in the present case to further segment the relevant product markets for different types of agricultural machinery by size, power, capacity or any other parameters.

6.2.2. Retail supply of implements

6.2.2.1 Distinction between different types of implements

(A) The Notifying Parties’ arguments

(38) The Notifying Parties submit that the market for the retail sale of implements comprises retail sale of all types of implements compatible with tractors, consisting of sprayers, harrows, manure spreaders, sowing machines, semiliquid manure spreaders and wagons. (51)

(39) The Notifying Parties argue that primarily different manufacturers produce implements and agricultural machinery, and that manufacturers of implements are more numerous than manufacturers of agricultural machinery. (52) According to the Notifying Parties, all implements are compatible with and can be fitted to all global brands of tractors regardless of brand. (53) Further, whilst there is generally no substitution between the different types of implements as these have different features and purposes, in the Parties' view, implements are generally regarded as one product group by the end-users, and are offered as one combined portfolio of products by distributors. (54)

(B) The Commission's assessment

(40) Whilst the majority of manufacturers that expressed a view during the Commission's market investigation consider there to be one single product group of implements at retail level, (55) the majority of responding competitors stated that implements should be sub-divided into different categories, since different implements have different end-uses (from grass harvesting to soil preparation and seeding, feeding, transportation etc.) and different end-customers. (56)

(41) Ultimately, the question of whether there are distinct relevant product markets for different types of implements can be left open, as no competition issues arise under any plausible market definition.

6.2.2.2 Distinction between new and used implements

(A) The Notifying Parties’ arguments

(42) The Notifying Parties submit that there is a single overall market for the retail sale of implements, but that a plausible segmentation can be made between new and used implements. (57) In the Notifying Parties’ view, as in the case of agricultural machinery, when buying a new implement many customers trade in used implements, which the distributors then sell on to other customers. (58)

(B) The Commission's assessment

(43) Whilst the majority of manufacturers that responded to the Commission's market investigation consider new and used implements to be part of the same product market at retail level,59 the majority of responding competitors suggested that a distinction should be drawn between new and used implements, since used implements retail at a lower price than new implements and there are customers who would not even consider purchasing one or the other. (60)

(44) Ultimately, the question of whether there are distinct relevant product markets for new and used implements can be left open, as no competition issues arise under any plausible market definition.

6.2.3. Retail supply of spare parts

6.2.3.1 The Notifying Parties’ arguments

(45) The Notifying Parties submit that the market for retail sale of spare parts constitutes a distinct relevant product market, comprising original and non-original spare parts. (61) According to the Notifying Parties, most distributors sell spare parts from various brands, even if they are authorised to sell only one specific brand of agricultural machinery, since spare parts from various brands are required to service the traded-in used machines. (62) Whilst there is no substitution between the various types of spare parts, the Notifying Parties submit that distributors offer spare parts as one combined portfolio and market these as a collective group of products to their customers. (63)

6.2.3.2 The Commission's assessment

(46) The majority of market participants that expressed a view agree that spare parts are generally considered as one product group in the agricultural machinery business. Whilst end-users must normally use original spare parts for repairs within the first 12 months of the lifetime of an agricultural machine for such repairs to fall within the manufacturer's warranty, (64) suitable non-original spare parts may be used for repairs outside the warranty or upon its expiry. The exact relevant product market definition can however be left open, as no competition issues arise under any plausible market definition.

6.2.4. Provision of after-sales services

6.2.4.1 The Notifying Parties’ arguments

(47) The Notifying Parties submit that the market for the provision of after-sales services for agricultural machinery constitutes a separate relevant market, since access to the after-sales services is decisive for the farmers' choice of machinery and since distribution agreements with manufacturers oblige distributors to establish and maintain a network of after-sales locations where agricultural machines of that specific brand can be serviced. (65)

6.2.4.2 The Commission's assessment

(48) Whilst the majority of manufacturers that responded to the Commission's investigation consider that there is a separate product market for the provision of after-sales services, (66) the majority of competitors that expressed a view consider that the provision of after-sales services cannot be separated from the retail sale of agricultural machinery. (67) As one competitor in Finland put it: "All machines will require after-sales services at some point. After sales and sales go hand in hand and cannot be seprated [sic]". (68) This is echoed also by some manufacturers: "It's [after- sales services] connected to sale of new equipment" (69) and "The after sales service is very linked to the new machinery sales, and can not be separated, especially when the new engine emission and safety norms deployed to require substantial technical knowledge to assure the customer satisfaction." (70)

(49) Ultimately, the exact relevant product market definition can be left open, as no competition issues arise under any plausible market definition.

6.2.5. Conclusion on relevant product markets

(50) The Commission finds that for the purposes of the present decision, different types of agricultural machinery constitute separate relevant product markets, namely(i) standard tractors, (ii) specialty tractors, (iii) combine harvesters, (iv) forage harvesters, (v) balers, (vi) grass machines, and (vii) telescopic handlers. The Commission considers that for the purposes of the assessment of the Transaction it is appropriate to further segment these product markets between new and used machinery.

(51) The Commission further considers that for the purpose of assessing the Transaction the distinction between different types of implements as well as between new and used implements can be left open, since no competition issues arise under any plausible market definition. (71) For the same reason, the question whether original and non-original spare parts belong to the same market and whether after-sales services constitute a separate market from the sales of agricultural machinery can also be left open.

6.3. Relevant geographic markets

6.3.1. The Notifying Parties’ arguments

(52) The Notifying Parties submit that the markets for the retail sale of agricultural machinery (including the plausible segments) are national. (72) The Notifying Parties submit that in Finland, Estonia, Latvia and Lithuania, the wholesale and retail structure is integrated, such that the distributors are responsible for the import of agricultural machines, setting up national marketing strategies, conducting retail sales and providing after-sales services. (73)

(53) According to the Notifying Parties, distribution agreements in these countries grant distributors exclusivity within the national borders to market and sell branded agricultural machinery. (74) Moreover, agricultural machinery needs to be serviced and repaired by highly trained personnel with expert knowledge, with the requisite training and education of personnel being to a high degree national and with manuals and instructions being required to be delivered to the customers in the official language of the country where the machinery is placed on the market. (75) Finally, the Notifying Parties note that cross-border retail sales of agricultural machinery are limited (and occur mainly for used machinery). (76)

(54) With regard to the retail sale of implements and spare parts, and for the provision of after-sales services, the Notifying Parties submit that the relevant geographic markets are national, but can be left open, as the Transaction does not significantly affect competition under any plausible market definition. (77) In the Notifying Parties’ view, customers prefer to purchase implements and spare parts and to have their agricultural machinery serviced from distributors and other retailers in proximity to them (since especially during peak periods, it is important for farmers to be able to source spare parts for, and repair, their machinery at short notice) and distribution agreements for implements are organised on a national level (with only minor imports of implements in the countries concerned by the Transaction). (78)

6.3.2. The Commission's assessment

(55) In previous decisions, the Commission has defined the relevant geographic market for agricultural machinery at the retail level as national in scope. (79) In particular, it was found that there are national specifications (e.g. road usage or safety requirements), national customer preferences for certain product configurations, as well as national distribution networks with exclusive distributors and dealers (with a high degree of dealer loyalty among customers) and national preferences for certain brands, primarily as a result of the historic inheritance of local manufacturing presence. (80) Furthermore, access to retailers with local presence and expert knowledge was found to be decisive for customers' choice of agricultural machinery.

(56) The results of the market investigation in the present case confirm the Commission's previous findings and the Notifying Parties’ view that the geographic markets for the retail sale of agricultural machinery, as well as of implements, spare parts and for the provision of after-sales services, are national in scope. A large majority of market participants that responded to the Commission's market investigation confirmed that distributors tend to sell, and customers tend to source, agricultural machinery on a national basis. (81) The results of the market investigation confirm that: (i) customers rely on after-sales services whose proximity and availability are among the key factors for choosing agricultural machinery, (ii) distribution agreements for agricultural machinery in Finland, Estonia, Latvia and Lithuania tend to contain national territorial exclusivity clauses, and (iii) there are only limited cross-border sales (mostly of used machinery) at retail level. (82)

(57) For these reasons, the Commission finds that the markets for the retail sale of different types of agricultural machinery, implements, spare parts and for the provision of after- sales services are national in geographic scope.

6.4. Conclusion on the relevant product and geographic market definition

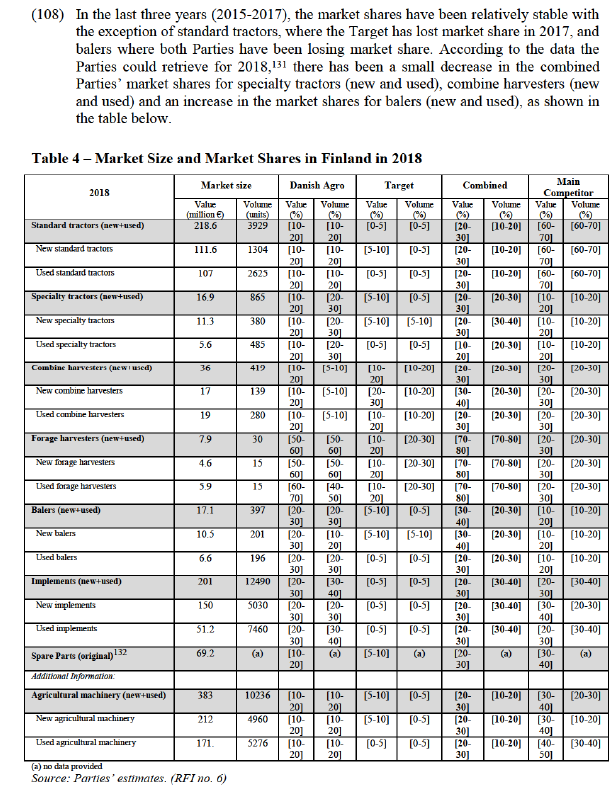

(58) For the purposes of assessing the Transaction, the Commission considers that each type of agricultural machinery is a separate product market, which should be further segmented by new and used machinery. All these product markets are national in scope. On the other hand, for the purpose of assessing the Transaction, the Commission leaves open the precise product market definitions for implements, spare parts and after-sales services. Like the agricultural machinery markets, these markets – independently of further segmentation – are national in scope.

7. COMPETITIVE ASSESSMENT

7.1. Horizontal non-coordinated effects

7.1.1. Analytical framework

(59) The Commission Guidelines on the assessment of horizontal mergers under the Council Regulation on the control of concentrations between undertakings (the "Horizontal Merger Guidelines") (83) distinguish between two main ways in which mergers between actual or potential competitors on the same relevant market may significantly impede effective competition, namely non-coordinated and coordinated effects. (84)

(60) Non-coordinated effects may significantly impede effective competition by eliminating important competitive constraints on one or more firms, which consequently would have increased market power, without resorting to coordinated behaviour. In that regard, the Horizontal Merger Guidelines consider not only the direct loss of competition between the merging firms, but also the reduction in competitive pressure on non-merging firms in the same market that could be brought about by the merger. (85)

(61) The Horizontal Merger Guidelines list a number of factors, which may influence the rise of substantial non-coordinated, effects from a merger, such as: the large market shares of the merging firms; the fact that the merging firms are close competitors; the limited possibilities for customers to switch suppliers; or the fact that the merger would eliminate an important competitive force. That list of factors applies equally if a merger would create or strengthen a dominant position, or would otherwise significantly impede effective competition due to non-coordinated effects. Furthermore, not all of those factors need to be present to make significant non- coordinated effects likely and this is not an exhaustive list. (86)

7.1.2. Estonia

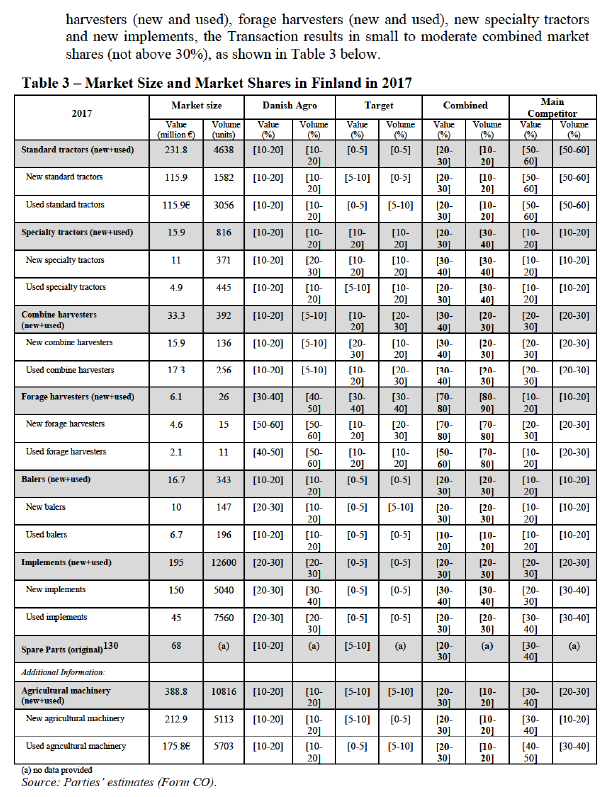

(62) In Estonia, the Transaction gives rise to several affected markets taking into consideration all possible product market segmentations, namely for the retail sale of (i) new standard tractors, (ii) new and used combine harvesters, (iii) new and used forage harvesters and (iv) new balers, as well as for (v) original spare parts and for (vi) the provision of after-sales services. (87) However, with the exception of the markets for new combine harvesters, used combine harvesters, new forage harvesters and new balers, the Transaction results in small to moderate combined market shares (not above around 30%), as shown in Table 1 below.

7.1.2.1 The Notifying Parties’ arguments

(65) The Notifying Parties submit that post-Transaction, no competition concerns would arise despite the high combined market shares, especially in new combine harvesters and new forage harvesters, as the Parties would not be able to affect prices or quality of the goods and would face competition from other distributors of agricultural machinery (e.g. Tatoli AS) with global brands (e.g. New Holland, Case IH, Massey Ferguson, Valtra, Fendt). (94) In particular, with regard to combine harvesters, the Notifying Parties submit that there are a number of players on the market, including long-established companies such as Astla OÜ and Rodnas OÜ, as well as new entrants, such as Intrac Eesti AS, which has recently entered the market with the Massey Ferguson brand. (95) With regard to forage harvesters, the Notifying Parties submit that this is a new product on the Estonian market and that even though only a few competitors are currently active in the retail sale of forage harvesters in Estonia, there are more market players capable of market entry. (96)

(66) The Notifying Parties argue that post-Transaction, their respective activities with regard to the retail sale of Claas and John Deere agricultural machinery (including forage harvesters and combine harvesters) will continue to be conducted independently of, and in competition with, each other, since this is also a requirement of the two manufacturers. Specifically, the Notifying Parties propose that the merged entity create separate divisions for Claas and John Deere agricultural machinery, with separate managing directors and boards of directors, who, along with the employees, IT systems and sales and financial controls, will be independent from the other division. The information as regards the divisions' budgets, sales strategies and sales targets will not be exchanged with the management of the other division, other than in an aggregated and general form, which in the Notifying Parties’ view would prevent specific strategies, sales and targets from being identified. The retail outlets would be separate geographically for each of Claas and John Deere branded agricultural machinery, […]. (97) In the Notifying Parties’ view, if the Parties cease to compete fiercely with each other and underperform in relation to either Claas or John Deere, the respective distribution agreement(s) may be awarded to another distributor and given the importance of these distribution agreements to the Parties (relative to their overall sales), neither Party is prepared to risk losing its respective distribution agreement. (98)

(67) The Notifying Parties also submit that farmers increasingly consolidate into large professional businesses that are price-conscious and demanding customers, often organising tenders for the purchase of agricultural machinery. According to the Notifying Parties, these customers can easily change from one brand or distribution to another, should the latter offer better terms, features or prices. In the Notifying Parties’ view, price and quality prevail over brand loyalty, which the Notifying Parties think is confirmed by the varying market shares of the market participants in different market segments. (99)

7.1.2.2 The Commission's assessment

(68) The Commission notes the Notifying Parties’ arguments with regard to the proposed separation of the John Deere and Claas retail activities within the merged entity post- Transaction, which in the Notifying Parties’ view, would ensure continued fierce competition between the retail sale of John Deere and Claas branded agricultural machinery post-Transaction. In the Commission's view, however, even if followed, the proposed arrangements are not likely to be sufficient in order to dispel competition concerns. The proposed arrangements do not prevent the exchange of all commercially sensitive information as regards the respective brands: even aggregated sales data and sales targets data could give the other division a good idea of its competition and further increase the transparency on the market, especially where, as shown below, the Parties are close competitors who already today have significant market shares, especially in combine harvesters and forage harvesters.

(69) Furthermore, since both proposed divisions (for Claas and John Deere brands) would be under single common ownership post-Transaction, the merged entity would have significant incentives to maximise its revenue by ensuring that both divisions achieve sales targets set by the manufacturers, but not necessarily exceeding any one of these sales targets if doing so would mean that the other sales target would not be achieved. In other words, the merged entity would have the incentives to ensure that each division competes only to the extent that doing so would not risk the other division to underperform.

(70) Overall, therefore, the Commission finds that holding the retail sales activities of the John Deere and Claas branded agricultural machinery separate will not ensure that these retail sales activities will continue to compete post-Transaction in the same way as they do prior to the concentration.

(A) Combine harvesters

(71) The Parties have significant combined market shares in new combine harvesters in Estonia: [60-70]% by value and [60-70]% by volume in 2017 (Danish Agro: [20-30]% by value and [20-30]% by volume, and Target: [30-40]% by value and [30-40]% by volume in 2017). The Parties' combined market shares are estimated to have reduced slightly to [50-60]% by value and [50-60]% by volume in 2018. The Parties had a combined market share of [40-50]% in 2015 and [50-60]% in 2016 by value.

(72) The Parties' combined market shares in used combine harvesters were [30-40]% by value and [20-30]% by volume in 2017, and are estimated to have increased slightly to [30-40]% by value and [30-40]% by volume in 2018. The increment in used combine harvesters is small: [0-5]% by value and [0-5]% by volume in 2017, increased to [5-10]% by value and [5-10]% by volume in 2018.

(73) However, to the extent that trade-ins influence the sales of used machines, the Commission cannot exclude that the merged entity would have more market power in the used segments than its market share suggests.

(74) The Transaction would create the number one distributor/retailer of new combine harvesters in Estonia, with more than twice as large market share as its largest competitor Tatoli AS ([20-30]% by value and [30-40]% by volume in 2017, decreasing to [10-20]% by value and [10-20]% by volume in 2018). The other competitors on the market, Agriland OÜ ([0-5]% by value and [0-5]% by volume in 2017, increasing to [5-10]% by value and [5-10]% by volume in 2018), and Astla OÜ, Intrac Eesti AS and Rodnas OÜ, to which the Notifying Parties collectively attribute a [5-10]% market share by value in 2017 and [20-30]% by value in 2018, (100) are not likely to exert a significant competitive pressure on the merged entity post- Transaction.

(75) The Transaction would therefore result in a significant concentration on the market for new combine harvesters and eliminate an important competitive force in Estonia.

(76) The Commission finds that post-Transaction, the merged entity would be able to successfully raise prices without fear of losing customers to their competitors for the following reasons.

(77) First, the results of the market investigation show that the Parties are close competitors. The majority of customers and competitors that responded to the Commission's market investigation consider that the Parties are close competitors that offer similar prices and similar quality of products and services, and because their networks have a similar reach. (101) Furthermore, the results of the market investigation indicate that the Parties are close competitors specifically in the retail sale of combine harvesters in Estonia. The majority of Estonian customers that responded to the Commission's investigation consider the Parties to be the strongest suppliers of combine harvesters. (102) The other suppliers of combine harvesters in Estonia are considered by customers to either have very little experience with this type of agricultural machine, or to offer combine harvesters of lower quality or of higher price. (103) As one Estonian customer explained: "others have very low presence in Estonia and may have problems with securing the swift supply of spare parts and after-sales services". (104) The availability of spare parts and after-sales services are deemed by customers to be particularly important in their choice of agricultural machinery retailer. (105)

(78) Second, the market investigation has also revealed that customers tend to be brand loyal. (106) When asked what they would do if their preferred brand were to be discontinued, the majority of customers indicated that they would be more likely to look for another dealer that would offer the discontinued brand. (107) This was the view shared also by the majority of competitors that responded to the Commission's market investigation. (108)

(79) Third, customers in Estonia are not likely to exercise a sufficient degree of countervailing buyer power, as they have limited options to source combine harvesters elsewhere. Combine harvesters are large and expensive machines, which are not likely to be sourced by customers abroad. For example, only a couple of Estonian customers responding to the Commission's investigation stated that they could source combine harvesters from abroad, whereas for the majority of Estonian customers this would not be an option. (109) This view is shared also by the responding competitors, the vast majority of whom do not consider imports from abroad as a viable option for customers in Estonia. (110)

(80) Fourth, new market entry is not very likely. The market for the retail sale of combine harvesters in Estonia is relatively small and the machinery is expensive. The brands of both combine harvesters and of the retailers of these machines currently on the market are well known and trusted by customers – building a new brand is difficult and likely to be very time consuming. For example, as several manufacturers explain, finding a new distributor is not easy, as it would require "a lot of time, effort and money", with the manufacturer also having to "invest a lot in training of a new distributor" in addition to ensuring that the new distributor satisfies some of its requirements, including that they be committed to the manufacturer's brand. (111)

(81) Finally, several market participants have expressed concern regarding the impact of the Transaction. Several customers, competitors and manufacturers have indicated that they expect an increase in prices of combine harvesters, and a decrease in choice or quality of service, in Estonia post-Transaction. (112) Some customers and competitors have also expressed concern as regards the impact that the Transaction will have, specifically as a result of bringing the two brands, John Deere and Claas under single ownership. For example, an Estonian competitor stated that the Transaction will have a big impact on its business (and ability to compete) if Danish Agro were to have both these brands. (113)

(82) In circumstances where the customers are brand loyal, view the quality of combine harvesters supplied by other retailers in Estonia as lower, or the quality and reach of the other retailers' networks as more limited than the Parties', and absent a credible source of imports or possible market entry, such customers are more likely to accept a price increase. Moreover, in circumstances where two retailers with two competing brands that are close competitors are placed under single ownership, the merging entity is likely to be able to successfully increase prices on one of the brands, without fear of losing customers, since any lost sales are likely to be captured by the other brand under its ownership.

(83) For these reasons, the Commission finds that the Transaction raises serious doubts as to its compatibility with the internal market as regards its impact on competition for the retail sale of new and used combine harvesters in Estonia due to horizontal non- coordinated effects.

(B) Forage harvesters

(84) The Parties have significant combined market shares in new forage harvesters in Estonia: [70-80]% by value and [70-80]% by volume in 2017 (Danish Agro: [20-30]% by value and [20-30]% by volume, and Target: [50-60]% by value and [50-60]% by volume in 2017).The Parties' combined market shares are estimated to have increased to [90-100]% by value and [90-100]% by volume in 2018. The Parties' combined market shares were relatively stable since the Notifying Parties started supplying new forage harvesters in Estonia in 2016, when the Parties achieved a combined market share of [70-80]% by value. There is no overlap in the retail sale of used forage harvesters, since the Notifying Parties have not made any sales of used forage harvesters in Estonia in either 2017 or 2018.

(85) The Transaction would create the number one distributor/retailer of new forage harvesters in Estonia, with a market share in 2017 more than seven times as large as its largest competitor's, Agriland OÜ ([10-20]% by value and [10-20]% by volume). The only other competitor identified by the Notifying Parties on the Estonian market, Oilseeds Tehnika OÜ, is estimated to have a market share below 10% by value. These competitors are therefore not likely to exert a significant competitive pressure on the merged entity post-Transaction.

(86) Similarly to combine harvesters, to the extent that trade-ins influence the sales of used machines, the Commission cannot exclude that the merged entity would quickly increase its position in the used segment as well.

(87) The Transaction would therefore result in a very significant concentration on the market for new forage harvesters and eliminate an important competitive force in Estonia.

(88) The Commission finds that post-Transaction, the merged entity would be able to successfully raise prices without fear of losing customers to their competitors for the following reasons.

(89) First, as noted above in recital (77) above, the results of the market investigation show that the Parties are close competitors. Furthermore, the results of the market investigation indicate that the Parties are each other’s closest competitors specifically in the retail sale of forage harvesters in Estonia. All of the Estonian customers and the vast majority of competitors that expressed a view in the course of the Commission's investigation consider the Parties to be closest competitors either because they offer similar prices, similar quality (in products and services), or because their networks have a similar reach. (114) The customers in Estonia considered that the other suppliers of self-propelled forage harvesters have very little experience with this machine or are not yet known on the market, are of lower quality or of higher price. (115) As one Estonian customer explained: "others have very low presence in Estonia and may have problems with securing the swift supply of spare parts and after-sales services". (116) As noted in recital (77) above, the availability of spare parts and after- sales services are deemed by customers to be particularly important in their choice of agricultural machinery retailer.

(90) Second, as noted in recital (78) above, the market investigation has also revealed that customers tend to be brand loyal. (117) When asked what they would do if their preferred brand were to be discontinued, the majority of customers indicated that they would be more likely to look for another dealer that would offer the discontinued brand. (118) This was the view shared also by the majority of competitors that responded to the Commission's market investigation. (119)

(91) Third, customers in Estonia are not likely to exercise a sufficient degree of countervailing buyer power, as they have limited options to source forage harvesters elsewhere. Forage harvesters are large and very expensive machines, which are not likely to be sourced by customers abroad. For example, only a couple of customers responding to the Commission's investigation have stated that they could source self- propelled forage harvesters from abroad, whereas for the majority of customers this would not be an option. (120) This view is shared also by the responding competitors, the vast majority of whom do not consider imports from abroad as a viable option for customers in Estonia. (121)

(92) Fourth, new market entry is not very likely. The market for the retail sale of self- propelled forage harvesters in Estonia is small and the machinery is very expensive. The brands of both forage harvesters and of the retailers of these machines currently on the market are well known and trusted by customers – building a new brand is difficult and likely to be very time consuming. For example, as noted above in recital (80), several manufacturers explain that finding a new distributor is not easy, as it would require "a lot of time, effort and money", with the manufacturer also having to "invest a lot in training of a new distributor" in addition to ensuring that the new distributor satisfies some of its requirements, including that they be committed to the manufacturer's brand. (122)

(93) Finally, several market participants have expressed concern regarding the impact of the Transaction. Some customers and competitors have indicated that they expect an increase in prices of forage harvesters, and a decrease in choice or quality of service, in Estonia post-Transaction. (123) Some customers and competitors have also expressed concern as regards the impact that the Transaction will have, specifically as a result of bringing the two brands, John Deere and Claas under single ownership. For example, an Estonian competitor stated that the Transaction will have a big impact on its business (and ability to compete) if Danish Agro were to have both these brands. (124)

(94) In circumstances where the customers are brand loyal, view the quality of forage harvesters supplied by other retailers in Estonia as lower, or the quality and reach of the other retailers' networks as more limited than the Parties', and absent a credible source of imports or possible market entry, such customers are more likely to accept a price increase. Moreover, in circumstances where two retailers with two competing brands that are each other's closest competitors are placed under single ownership, the merging entity is likely to be able to successfully increase prices on one of the brands, without fear of losing customers, since any lost sales are likely to be captured by the other brand under its ownership.

(95) For these reasons, the Commission finds that the Transaction raises serious doubts as to its compatibility with the internal market as regards its impact on competition for the retail sale of new and used forage harvesters in Estonia due to horizontal non-coordinated effects.

(C) New standard tractors

(96) The Parties’ combined market shares in new standard tractors are estimated to be [30-40]% by value and [20-30]% by volume in 2018. The Parties' combined market shares have been quite stable over the last three years: [30-40]% in 2016 and [20-30]% in 2017 by value, and [20-30]% in 2016 and [20-30]% in 2017 by volume.

(97) In Estonia, there are currently a number of other distributors offering new standard tractors, including Tatoli AS with the New Holland brand ([10-20]% by value and [10-20]% by volume), Taure AS with the Valtra brand ([10-20]% by value and [10-20]% by volume), Agriland OÜ with the Fendt brand ([10-20]% by value and [10-20]% by volume) and Dotnuva Baltic AS with the Case IH ([5-10]% by value and [0-5]% by volume). The Notifying Parties attribute the remainder (almost a quarter) of the market to other distributors. Therefore, post-Transaction, several alternative suppliers will remain on the market, including strong suppliers such as Tatoli AS and Taure AS.

(98) For these reasons, the Commission finds that the Transaction does not raise serious doubts as to its compatibility with the internal market as regards its impact on competition for the retail sale of standard tractors in Estonia due to horizontal non- coordinated effects. In any event, the horizontal overlap between the Parties' activities in the retail sale of standard tractors in Estonia is eliminated by the Final Commitments proposed by the Parties, as discussed in Chapter 8.

(D) New balers

(99) The Parties’ combined market shares in new balers were [20-30]% by value and [30-40]% by volume in 2017 and are estimated to have decreased to [20-30]% by value and [10-20]% by volume in 2018. The Transaction would result in a [10-20]% increment in new balers (on the basis of 2017 markets shares, the increments in 2018 are lower). These market shares are relatively modest. Furthermore, a number of alternative suppliers of new balers are available in Estonia, including A.Tammel AS, Agri Partner OÜ, Ala Talutehnika OÜ, Rodnas OÜ and Saare Talutehnika OÜ.

(100) For these reasons, the Commission finds that the Transaction does not raise serious doubts as to its compatibility with the internal market as regards its impact on competition for the retail sale of new balers in Estonia due to horizontal non- coordinated effects. In any event, the horizontal overlap between the Parties' activities in the retail sale of new balers in Estonia is eliminated by the Final Commitments proposed by the Parties, as discussed in Chapter 8.

(E) Implements

(101) According to the Notifying Parties’ estimates, the only affected markets by the Transaction are (i) the retail sale of new swathers and rakes and (ii) the retail sale of new sprayers (125). In these markets, the Parties have a combined value market share of respectively [20-30]% and between 20% to 30%. Hence, under the narrowest market definition, no competition concerns arise as a result of the Transaction. First, the Parties' combined market shares are modest, not exceeding 30%. Second, there are a number of alternative suppliers of implements on the Estonian market, including those that do not also manufacture agricultural machinery. (126) Third, the majority of market participants that expressed a view in the Commission's investigation do not expect an increase in prices or a decrease in choice or quality of implements in Estonia post-Transaction. (127)

(102) For these reasons, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market as regards its impact on competition for the retail sale of implements in Estonia due to horizontal non- coordinated effects. In any event, the horizontal overlap between the Parties' activities in the retail sale of implements in Estonia is eliminated by the Final Commitments proposed by the Parties, as discussed in Chapter 8.

(F) Spare parts

(103) According to the Notifying Parties’ estimates, on the narrowest possible market definition, the Parties' combined market share for the retail sale of original spare parts in Estonia in 2017 was [20-30]% by value and [20-30]% by volume. The Parties' combined market shares for the retail sale of non-original spare parts is less than 10% both by value and by volume. If the retail sale of original and non-original spare parts is considered together, the Parties' combined market share in 2017 was [20-30]% by value and [10-20]% by volume. The Parties' combined market shares are therefore modest and in any event not exceeding 30% even on the narrowest market definition.

(104) Even on the narrowest market definition, no competition concerns arise as a result of the Transaction. First, the Parties' combined market shares are modest, not exceeding 30%. Second, there are a number of alternative suppliers of spare parts on the Estonian market such as A.Tammel AS, Agri Partner OÜ, Ala Talutehnika OÜ, Rodnas OÜ, A ja M Varustus OÜ, Agroparts OÜ, Astla OÜ, Eesti Agritehnika OÜ, Intrac Eesti AS, Leho Kaubandus OÜ, Sike Agri OÜ, Specagra OÜ, Starfield OÜ, Stokker Agri OÜ and Türi Bel-Est OÜ. Third, the majority of market participants that responded to the Commission's investigation expected there to be no change in price or quality as a result of the Transaction. (128)

(105) For these reasons, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market as regards its impact on competition for the retail sale of spare parts in Estonia due to horizontal non- coordinated effects. In any event, the horizontal overlap between the Parties' activities in the retail sale of spare parts in Estonia is eliminated by the Final Commitments proposed by the Parties, as discussed in Chapter 7.

7.1.3. Finland

(106) In Finland, Danish Agro distributes agricultural machinery, implements, spare parts, as well as offers after-sales services, representing several brands, including the global brands John Deere and Krone. The Target also offers agricultural machinery, implements, spare parts, as well as after-sales services, representing several brands, including the global brand Claas.

(107) In Finland, the Transaction gives rise to several affected markets taking into consideration all plausible product market segmentations, namely for the retail sale of (i) new and used standard tractors, (ii) new and used specialty tractors; (iii) new and used combine harvesters, (iv) new and used forage harvesters and (vi) new and used balers, as well as for (vii) new, used and overall new and used implements, (viii) original and overall original and non-original spare parts and for the provision of after-sales services. (129) However, with the exception of the markets for combine

(109) For the majority of the product markets involved, where the combined market share of the Parties is below or equal to 30%, the market share increment brought by the Transaction is also relatively small. In relation to the market for implements (where the combined market share is below 35%), the increment is very small ([0-5]%) given that the Target is hardly present.

(A) Specialty tractors

(110) With regards to new specialty tractors, there has been a decrease in the Parties’ combined market share both in value and in volume from 2017 to 2018: the value market share decrease from [30-40]% to [20-30]% and the volume market share from [30-40]% to [30-40]%. As shown in the tables above, both Danish Agro and the Targets have decreased their sales of new specialty tractors in Finland in the last two years. In Finland, there are currently five other distributors offering specialty tractors (J-Trading, Otto Brandt, Agritek, Hako Ground & Garden and Husqvarna), including products from international brands manufacturers such New Holland, Case IH. (133) Hence, post-Transaction, customers have several alternative suppliers they can switch to in case of a price increase.

(111) With regards to used specialty tractors, the Parties’ presence is even smaller and their sales have also decreased between 2017 and 2018: the value combined market share decreased from [20-30]% to [20-30]% and the volume combined market share from [30-40]% to [20-30]%. Similarly to the new specialty tractors market, there are several other alternative suppliers of used specialty tractors, to which customers could switch in case of a price increase.

(112) For these reasons, the Commission finds that the Transaction does not raise serious doubts as to its compatibility with the internal market as regards its impact on competition for the retail sale of new and used specialty tractors in Finland due to horizontal non-coordinated effects.

(B) Combine harvesters

(113) With the exception of value market shares for new combine harvesters ([30-40]% in 2018 and [30-40]% in 2017), the Parties’ combined market shares for new (volume) and used (value and volume) combine harvesters are moderate. Moreover, the second most important supplier in Finland, Agritek, is not very far from the Parties, with market shares between [20-30]% in both market segments, new and used combine harvesters. Furthermore, in Finland there are currently four other distributers supplying new combine harvesters (AGCO Suomi, Agritek, HCP Finland and Turun Konekeskus), including products from other global brands such as Sampo-Rosenlew, Massey Ferguson and New Holland. (134) In addition, AGCO has recently introduced green-harvesting machinery of another global brand manufacturer in Finland, Fendt, (135) and according to another competitor, “Agco is going to be important player in the future with new models of Fendt and MF combines”. (136) To the extent that trade- ins influence the sale of used combine harvesters, it is reasonable to expect that this competitive dynamic will also have a positive effect in the used combine harvesters market. Hence, post-Transaction there are several alternative suppliers, both in new and used market segments, to which customers can turn to in case of a price increase by the merged entity.

(114) For these reasons, the Commission finds that the Transaction does not raise serious doubts as to its compatibility with the internal market as regards its impact on competition for the retail sale of new and used combine harvesters in Finland due to horizontal non-coordinated effects.

(C) Forage harvesters

(115) As regards the markets for forage harvesters (new and used), the Transaction will not only combine the two main distributors/retailers but will also reduce the supply to two distributors/retailers, the merged entity with very large market shares (70%-80%) and Agritek with a much smaller market share (20%-30%). However, the Parties’ combined market share overstates their market power. For the following reasons, the Commission considers that the merged entity would not be able to profitably increase prices or otherwise exercise market power.

(116) First, and particularly with regard to new forage harvesters, in Finland there has been a concentration of farmland. (137) This not only translates in larger customers with more buying power but also, and in particularly in the case of forage harvesters, it means that farmers are able to use larger machines, instead of the smaller ones. Demand for smaller forage harvesters has kept a few brand manufacturers of larger forage harvesters away from the Finnish market for new forage harvesters. (138) With demand patterns likely to change towards larger machines, expansion of the portfolio of brands already represented in Finland is likely. For example, a competitor expressed its intent to start selling specifically new combine and new forage harvesters. (139)

(117) Second, and particularly with regard to used forage harvesters, customers in Finland also seem to purchase used forage harvesters from abroad. (140) Given that in Finland there are several independent repairers and after-sales service providers capable of servicing these machines, farmers and entrepreneurs also acquire used machines abroad. Contrary to Estonia, in Finland imports of used forage harvesters seem to exert a competitive constraint on the purchase of used forage harvesters. When asked what the reaction would be in case the merged entity were to increase prices, several Finnish customers said they would purchase forage harvesters from abroad. (141) Some competitors and manufacturers also consider customers purchasing from abroad a possible reaction of customers. (142)

(118) Overall, the majority of competitors, (143) customers (144) and all brand manufacturers, (145) who participated in the Commission’s market investigation, expressed no concerns regarding the impact the Transaction would have in Finland. Although a few customers mentioned the possibility of a price increase, the majority consider the Transaction will either not change the competitive environment in terms of price, quality and choice; or will have a positive impact, in particular in the after-sales markets. One customer commented: “[i]n my opinion, the transaction strengthens the aftermarket and maintenance of the brands represented by both heads. The Finnish market is quite small, so there is a need for good after-sales services. Prices are unlikely to have an impact, because the European market is open”. (146) Another customer stated: “I think it is good to become a strong new player investing in Finland, this will affect prices by lowering prices as it increases competition and improves after-sales service”. (147) Moreover, the Finnish customers also consider that the number of distributors, including in forage harvesters, combine harvesters will be sufficient post-transaction to maintain the same level of competition. (148)

(119) For these reasons, the Commission finds that the Transaction does not raise serious doubts as to its compatibility with the internal market as regards its impact on competition for the retail sale of new and used forage harvesters in Finland due to horizontal non-coordinated effects.

7.1.4. Latvia

(120) Danish Agro presence in Latvia is limited to a few internet sales of used tractors and new balers. Danish Agro’s agricultural machinery business has no distribution agreement covering the Latvian territory nor physical presence in Latvia (no sales outlets, no repair shops or repair vehicles). In 2017, Danish Agro’s market share in the used tractors market was [0-5]% and in the new balers, market was [0-5]%.

(121) Koneskesko is the exclusive distributor of Claas machinery in Latvia. Its market share in the used tractors segment is [0-5]%. Konekesko has a market share above 20% only in the following markets: new balers ([40-50]%), new forage harvesters ([50-60]%) and new combine harvesters ([40-50]%). None of the combine and forage harvesters markets are however “affected markets”, since in these cases the Transaction results in a market share transfer from Konekesko to Danish Agro.

(122) The Transaction gives rise to one affected market for new balers. The Parties’ combined value market share is [40-50]%. (149) The increment market share is however very small ([0-5]%). In addition, there are six other distributors offering several branded products, including John Deere products. None of the respondents to the market investigation raised concerns in relation to the horizontal overlaps resulting from the proposed transaction in Latvia.

(123) For these reasons, the Commission finds that the Transaction does not raise serious doubts as to its compatibility with the internal market as regards its impact on competition for the retail sale of new balers in Latvia due to horizontal non- coordinated effects.

7.1.5. Lithuania

(124) Danish Agro presence in Lithuania is limited to a few internet sales of used combine harvesters. Danish Agro’s agricultural machinery business has no distribution agreement covering the Lithuanian territory nor physical presence in Lithuania (no sales outlets, no repair shops or repair vehicles). In 2017, Danish Agro’s value market share in the combine harvesters market was [0-5]%.

(125) Konekesko is the exclusive distributor of Claas machinery in Lithuania. Its value market shares are relatively small in most of all the plausible market segmentations (below 20%), with the exception of the new combine harvesters market ([30-40]%) and the new forage harvesters market ([50-60]%). (150) These markets are however not affected markets, for the Transaction results in a market share transfer from Konekesko to Danish Agro.

(126) The markets where the activities of the Parties overlap are not affected markets under any plausible segmentation. (151) Moreover, in Lithuania there are five other distributors offering several branded products, including John Deere products. In addition, all five distributors offer combine harvesters and at least three of them offer forage harvesters. (152) For these reasons, the Transaction does not raise serious doubts as regards the Parties’ horizontal overlaps in Lithuania due to horizontal non-coordinated effects.

7.2. Conglomerate effects

(127) A competitor of the Parties in Lithuania and Latvia claimed that post-Transaction Danish Agro would have significant market power being the main supplier of both agricultural machinery and agricultural inputs (e.g. seeds, pesticides and fertilizers) as well as a purchaser of crops. According to this competitor, Danish Agro could combine the offer of these products and offer “a reduction of sales prices for agricultural machinery and compensation of this reduction by increased prices for the inputs or reduced grain purchasing prices.” (153) A competitor in Estonia has also approached the Estonian Competition Authority with a similar complaint. (154)

(128) The Commission has therefore assessed any potential conglomerate effects that may arise as a result of the Transaction in the Baltic countries.

7.2.1. Analytical Framework

(129) According to paragraph 92 to the Non-Horizontal Merger Guidelines, “[w]hereas it is acknowledged that conglomerate mergers in the majority of circumstances will not lead to any competition problems, in certain specific cases there may be harm to competition”. For instance, foreclosure effects may arise when the combination of products in related markets may confer on the Merged Entity the ability and incentive to leverage a strong market position from one market to another closely related market by means of tying or bundling or other exclusionary practices. (155)

(130) The Non-Horizontal Merger Guidelines distinguish between bundling, which usually refers to the way products are offered and priced by the Merged Entity and tying, usually referring to situations where customers that purchase one good (the tying good) are required to also purchase another good from the producer (the tied good). (156)

(131) While tying and bundling as such are common practices that often have no anticompetitive consequences (157), in certain circumstances such practices may lead to a reduction in actual or potential competitors' ability or incentive to compete. This may reduce the competitive pressure on the Merged Entity allowing it to increase prices or deteriorate supply conditions in other ways. (158)

(132) In assessing the likelihood of such a scenario, the Commission examines, first, whether the merged firm would have the ability to foreclose its rivals, second, whether it would have the economic incentive to do so and, third, whether a foreclosure strategy would have a significant detrimental effect on competition, thus causing harm to consumers. (159) In practice, these factors are often examined together as they are closely intertwined.

7.2.2. The Notifying Parties’ views

(133) Confronted with the complaints, the Notifying Parties argue that it would not have the ability nor the incentive to adopt such foreclosure strategy for the following reasons. First, the sale of agricultural machines and the sale of agricultural supplies are not complementary businesses. Second, there is no demand for the joint provision of agricultural machinery and agricultural supplies and the demand for each type of product is different. Third, Danish Agro would not have an incentive to combine such businesses since such a combination would not result in additional value nor in a reduction of costs. (160)

7.2.3. The Commission's assessment

(134) Given the nature of the products involved – agricultural machinery on the one hand and seeds, fertilizers, pesticides, or (the purchase of) crops on the other hand -, the merged entity would not be able to leverage its position in one market to foreclose competitors in another by technically tying the products. Given the different times and frequency at which these products are purchased contractual tying also seems very unlikely. If the merged entity were ever to adopt such a foreclosure strategy, it would most likely condition the sales of its products by mixed bundling: where the products are available both separately and jointly but where the sum of the stand-alone price is higher than the bundled price. (161) The Commission hence will focus its analysis on this possibility.

(135) In its assessment, the Commission realised that most of the facts and reasons apply across the different geographic markets mentioned by the complainants. For this reason, the Commission will not present a separate assessment for each geographic market but will highlight the differences whenever necessary.

(136) For the reasons presented below, the Commission considers that the merged entity would not have the ability nor the incentive to foreclose its rivals by combining its sales of agricultural machinery with other agricultural inputs, nor somehow condition those sales on the purchase of crops, in order to foreclose its rivals, causing a detrimental effect on competition.

(137) Firstly, machinery on the one hand and inputs like seeds and fertilizers on the other hand are not complementary products, are purchased for different purposes and, as mentioned above, are purchased at different moments in time and with different frequency (the life cycle of an agricultural machine is between 10 to 15 years; whilst most of the agricultural inputs mentioned above are purchased on a yearly basis). This is even more evident when it comes to conditioning the sale of machinery on the purchase of crops. Moreover, the common customer base for these different products is limited to farmers, as the independent entrepreneurs who offer services to the farmers are not interested in the other products the merged entity has on offer, nor are the potential suppliers of crops. Hence, given the nature of products involved, the merged entity would have difficulties in linking the products together.

(138) Secondly, in order to leverage its position from one market to another, the merged entity has to have market power in the market of the product to which the sale is tied. The merged entity will not have such strong market position in any plausible agricultural machinery market, as explained below.

(139) In Estonia, with the exception of the markets for forage harvesters (whether new and used taken together ([70-80]%), new only ([70-80]%) or used only ([50-60]%)), combine harvesters (whether new and used taken together ([50-60]%), new only ([60-70]%) or used only ([30-40]%)) and new balers ([30-40]% in 2017, reduced to [20-30]% in 2018) the Parties' combined market shares are below 30% in any other agricultural machinery market. (162) Furthermore, as noted above and discussed in more detail in Chapter 8, the Notifying Parties have offered commitments, which would lower the merged entity's market shares and its market power in these markets.