Commission, April 10, 2017, No M.8330

EUROPEAN COMMISSION

Decision

MAERSK LINE / HSDG

Subject: Case M.8330 – MAERSK LINE / HSDG

Commission decision pursuant to Article 6(1)(b) in conjunction with Article 6(2) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 20 February 2017, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which the undertaking Maersk Line A/S ("Maersk", of Denmark), a wholly-owned subsidiary of A.P. Møller - Mærsk A/S (the "Maersk Group"), acquires within the meaning of Article 3(1)(b) of the Merger Regulation control of the whole of Hamburg Südamerikanische Dampfschifffahrts-Gesellschaft KG ("HSDG", of Germany), a wholly-owned subsidiary of Dr. August Oetker KG, by way of purchase of shares (the "Transaction"). (3) Maersk and HSDG are collectively referred to hereinafter as the "Parties".

1. THE PARTIES

(2) Maersk is the subsidiary of the Maersk Group and is governed by Danish law. Maersk is active worldwide in the provision of container liner shipping services operating 611 container vessels, 324 of which are chartered. Maersk markets its services through the Maersk Line, Safmarine, SeaLand (Intra-Americas), MCC Transport (Intra-Asia) and SeaGo Line (Intra-EEA) brands. The Maersk Group also provides (i) container terminal services through its subsidiary APM Terminals ("APMT"), (ii) freight forwarding services, via its subsidiary Damco Distribution Services, (iii) inland transportation, via APMT, (iv) container manufacturing, via its subsidiary Maersk Container Industry, (v) harbour towage services, via its subsidiary Svitzer and (vi) tramp services, via its subsidiary Maersk Tankers.

(3) HSDG is a German subsidiary of Dr. August Oetker KG. It is active worldwide in the provision of container liner shipping services. HSDG operates 130 container vessels, 82 of which are chartered. HSDG markets its services through its global Hamburg Süd brand and its CCNI (Chile) and Aliança (Brazil) brands.

2. THE OPERATION AND THE CONCENTRATION

(4) On 28 October 2016, the Parties entered into a partially binding term sheet that sets out the terms of the Transaction. The Parties intend to enter into a final and fully binding Sales and Purchase Agreement by March 2017. Post-Transaction, HSDG will become a business unit within Maersk operated under the existing Hamburg Süd brand. The acquisition price is approximately EUR […] billion.

(5) The economic and strategic rationale of the Transaction is to bring two complementary container liner shipping businesses. Maersk Line predominantly focusses on East-West trade routes where HSDG has a limited presence. HSDG has a stronger focus on the North-South trades, particularly to and from South America (4). The Parties argue that with the expanded scope of the combined network, customers will have access to the services provided by HSDG in the North-South trades as well as the flexibility and reach provided in Maersk Line’s network (which includes the East-West trades).

(6) The Transaction constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

3. UNION DIMENSION

(7) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (5) (Maersk Group: EUR 35,668 million; HSDG: EUR […] million). Each of them has an EU-wide turnover in excess of EUR 250 million (Maersk Group: EUR […] million, HSDG: EUR […] million). Each of the undertakings concerned does not achieve more than two-thirds of its aggregate Union-wide turnover within one and the same Member State.

(8) The notified operation therefore has an EU dimension pursuant to Article 1(2) of the Merger Regulation.

4. MARKET DEFINITION

(9) The Parties' activities mainly overlap horizontally in deep-sea container liner shipping. To a smaller extent, the Parties' activities also overlap in short-sea container shipping and tramp services (notably on the transport of liquid bulk products in tankers, as there is no overlap between the Parties' activities in drybulk vessels). Furthermore, there are vertically related markets, in particular terminal and harbour towage services but also inland transportation, freight forwarding and container manufacturing.

4.1. Deep-sea container liner shipping services

(10) Deep-sea container liner shipping companies offer regular, scheduled services for the sea transportation of containerised cargo. Deep-sea container liner shipping services are provided as door-to-door or port-to-port services (or any combination thereof). (6)

4.1.1. Relevant product market

(11) In past cases, the Commission has found that the product market for container liner shipping involves the provision of regular, scheduled services for the carriage of cargo by container. This market can be distinguished from non-liner shipping (tramp, specialised transport) because of the regularity and frequency of the service. In addition, the use of container transportation should be distinguished from other non-containerised transport such as bulk cargo. (7)

(12) This product market could be further segmented into the transport of refrigerated goods, which could be limited to refrigerated (reefer) containers only or could include transport in conventional reefer vessels. In past cases, the Commission has looked separately at reefer and non-refrigerated (warm) containers only in the case of legs of trade with a share of reefer containers in relation to all containerised cargo of 10% or more in both directions. (8)

(13) The majority of customers and competitors responding to the Commission's market investigation questionnaires confirmed that the relevant market is that for container liner shipping. (9) Concerning potential sub-segmentations, the majority of customers considered that a distinction between reefer and non-reefer containers would be relevant while the majority of competitors submitted that there is no distinct product market for the transport of refrigerated goods. (10) Moreover, should one consider a market for refrigerated goods only, the majority of competitors consider relevant a segmentation between reefer containers and reefer vessels whereas the majority of customers do not. (11)

(14) In any case, for the purpose of the present decision (the "Decision"), it may be left open whether the deep-sea container liner shipping market could be further segmented into markets for reefer and non-reefer containers as well as for reefer containers and reefer vessels since the competitive assessment of the effects of the Transaction on various markets would not be altered by any such possible segmentation.

4.1.2. Relevant geographic market

(15) Whereas, in prior decisions, the Commission had left open whether the geographic scope should comprise trades, defined as the range of ports which are served at both ends of the service (e.g. Northern Europe – North America) or each individual leg of trade (e.g. westbound and eastbound within a given trade), in its most recent practice (12), the Commission has concluded that container liner shipping services are geographically defined on the basis of the legs of trade (e.g. Northern Europe – North America eastbound).

(16) This is in line with the results of the market investigation as the majority of both customers and competitors responding to the Commission's market investigation questionnaires consider that each leg of trade constitutes a separate geographic market. (13)

(17) The relevant legs of trade for the assessment of the Transaction are those from and to Northern Europe areas and those from and to the Mediterranean in view of the effect of those legs of trade on the internal market. (14) For these legs of trade, the majority of both customers and competitors responding to the Commission's market investigation questionnaires considered that, consistent with precedents, the following ranges of ports constitute a single distinct end of legs: (15)

· Northern Europe ("NE")

· Mediterranean ("MED")

· North America ("NAM")

· East Coast South America ("ECSA")

· West Coast South America ("WCSA")

· Central America/Caribbean ("CAM/CAR")

· Middle East ("MEA")

· Indian Subcontinent ("ISC")

· Far East Asia ("FEA")

· Australia and New Zealand ("AUNZ")

· South Africa ("SAF")

4.2. Short-sea container liner shipping services

4.2.1. Relevant product market

(18) Short-sea container shipping involves the provision of intra-continental (usually costal trade) services for the carriage of cargo by containers liner shipping companies.

(19) In past cases, the Commission has defined a separate product market for short-sea container shipping (i.e. distinct from deep-sea container shipping) involving the provision of regular, scheduled services for the carriage of cargo by container. (16) The Commission has previously considered possible sub segmentations of the market as per the type of cargo carried by containers. In this regard, the Commission has concluded that container shipping is distinct from the transport of bulk cargo (i.e. non-containerised shipping). (17) However, the Commission ultimately left open whether the transport of wheeled cargo (18) should be considered as a different product market. (19). The Commission also left open whether there should be a sub-segmentation between reefer and dry transport (20) as well as whether short-sea shipping should be part of a broader door-to-door multimodal transport services market (21). The Notifying Party considers that no distinction should be made between reefer and dry services. Furthermore, they argue that short-sea shipping is part of a broader market encompassing alternatives modes of transports (including rail, truck and inland barging services). (22)

4.2.2. Relevant geographic market

(20) The Commission previously concluded that the geographic market should be delineated on the basis of single trades, defined by the range of ports which are called at both ends of service. (23) The Commission also considered a further delineation according to legs of trade but ultimately left open this question. (24) The Parties submit that the geographic market should be defined more broadly to encompass all intra-EEA services including those between Northern Europe and Mediterranean based on Container Trade Statistics ("CTS") data. (25)

(21) At the narrowest possible level, the Notifying Party proposes the following delineation in accordance with the its own service offerings (breaking down intra- Europe):

· Northern Europe – North-East Mediterranean (NEM);

· NE – South-East Mediterranean (SEM);

· NE – West Mediterranean (WME);

· Intra-East Mediterranean (EME);

· Intra-Mediterranean; and

· Intra-WME. (26)

4.2.3. Conclusion

(22) However, it is not necessary to conclude on a precise definition of the relevant product and geographic markets as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible definition of the markets for short-sea liner shipping.

4.3. Tramp services

4.3.1. Relevant product market

(23) In past cases (27), the Commission has considered that "the tramp shipping sector relates generally to the transport of a single commodity which fills a single ship.

Unlike the liner sector, tramp shipping markets are unscheduled in the sense that vessels do not sail on advertised, pre-determined routes on particular days."

(24) In its prior decisional practice (28), the Commission considered potential sub segmentations of the product market according to (i) vessel types (ii) types of cargo (iii) vessel sizes and (iv) contract types.

(25) In particular, in Case M.5346 – APMM/Broström, the Commission considered a segmentation between dry and liquid bulk vessels. (29) Moreover, the Commission considered segmentation according to the following DWT (30) ranges: (i) 10 000 – 60 000 DWTs, (ii) 10 000 – 25 000 DWTs and (iii) 25 000 – 60 000 DWTs. A separate market was defined for vessels of less than 10 000 DWT. (31) However, the Commission ultimately left open whether the market should be segmented according to the 25 000 DWTs and 60 000 DWTs dividing lines. (32) The Parties consider that 25 000 DWTs and 60 000 DWTs should be dividing lines. (33)

4.3.2. Relevant geographic market

(26) In its prior decisional practice, the Commission considered the geographic market for tramp services and its possible subsegments to be worldwide. Nevertheless, it considered also a possible narrower geographic scope (regional) for less than 10 000 DWTs tankers, ultimately leaving the exact geographic market definition open. (34) The Parties argue that the geographic market is worldwide. (35) Nevertheless, when inquired about possible narrower geographic markets, the Notifying Party considers that the only plausible regional market would be by reference to a division of the global market between the east of Suez region and the west of Suez region. (36)

4.3.3. Conclusion

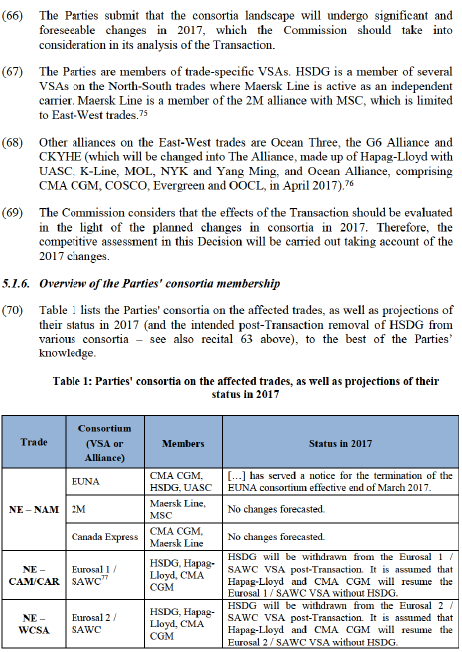

(27) However, it is not necessary to conclude on a precise definition of the relevant product or geographic market as the Transaction would not raise serious doubts as to its compatibility with the internal market under any plausible definition of the markets for tramp services.

4.4. Vertically affected markets

(28) The Transaction creates vertical links between, on the one hand, deep-sea container liner shipping services and, on the other hand, container terminal, inland transportation, freight forwarding and harbour towage services and container manufacturing, which are offered by Maersk Group or its controlled entities.

4.4.1. Container terminal services

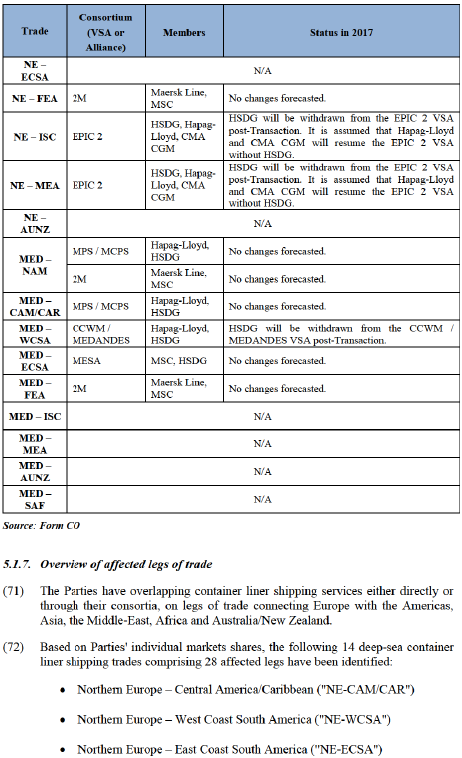

4.4.1.1. Relevant product market

(29) Container terminal services are "input services" to container liner shipping. In previous cases, the Commission defined separate markets for container terminal services for deep-sea container ships, broken down by traffic flows to hinterland traffic and transhipment traffic. (37)

4.4.1.2. Relevant geographic market

(30) In its prior decisional practice, the Commission considered that for container terminal services in deep sea ports, the relevant geographic market is in essence determined by the geographic scope the container terminal generally serves (catchment area). For example, concerning Northern Europe and terminals in Hamburg in particular, the Commission considered that the relevant geographical dimension of stevedoring services is in its broadest scope Northern Europe (for transhipment traffic) and in its narrowest possible scope the catchment area of the ports in the range Hamburg – Antwerp (for hinterland traffic) or possibly even narrower, comprising the German ports only. (38)

(31) The Parties argue that the geographic market should not be defined more narrowly than regional because a national or range of port market definition would be artificial given the international nature of the container liner shipping business and the traffic flows. (39)

4.4.1.3.Conclusion

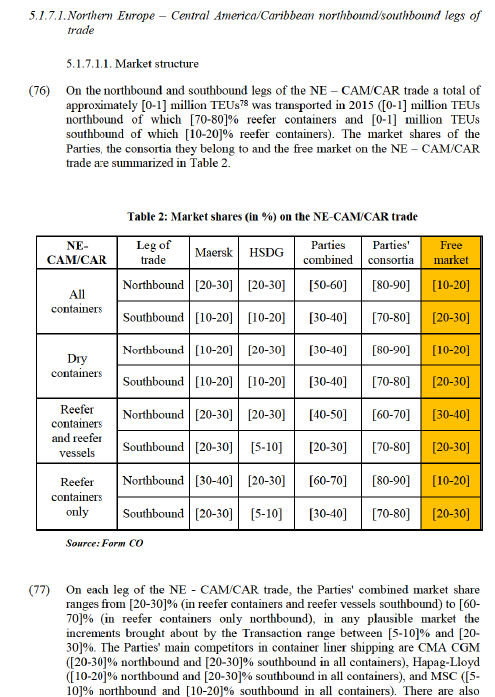

(32) However, it is not necessary to conclude on a precise definition of the relevant product and geographic market since the Transaction would not raise serious doubts as to its compatibility with the internal market under any of the plausible definitions of the markets for container terminal services.

4.4.2. Inland transportation services

(33) If a container liner shipping company provides door-to-door services, it also arranges inland haulage for its customers to and/or from the harbour. Thus, these services are vertically related to container liner shipping.

4.4.2.1. Relevant product market

(34) In accordance with the Commission's previous decisional practice, inland transportation covers the physical movement of goods by using own (i.e. owned or leased) equipment. The Commission also indicated that the various means of inland transport could constitute separate product markets but ultimately left the market definition open.

4.4.2.2. Relevant geographic market

(35) In its prior decisional practice, the Commission considered the geographic scope of the market for inland transportation services as either national or wider. (40) The Parties concur with the Commission's previous decisional practice. (41)

4.4.2.3.Conclusion

(36) However, it is not necessary to conclude on a precise definition of the relevant product or geographic market as the Transaction would not raise serious doubts as to its compatibility with the internal market under any of the plausible definitions of the markets for inland transportation services.

4.4.3. Freight forwarding services

(37) In sea freight forwarding, transportation capacity is provided by container liner shipping companies like Maersk and its competitors. Freight forwarders are thus customers of container liner shipping companies, i.e. freight forwarding is a downstream market to container liner shipping.

4.4.3.1. Relevant product market

(38) In its prior decisional practice, the Commission has defined freight forwarding as "the organisation of transportation of items (possibly including activities such as customs clearance, warehousing, ground services, etc.) on behalf of customers according to their needs". (42) The Commission subdivided the market into domestic and cross-border freight forwarding and into freight forwarding by air, land and sea. (43) (44)

4.4.3.2. Relevant geographic market

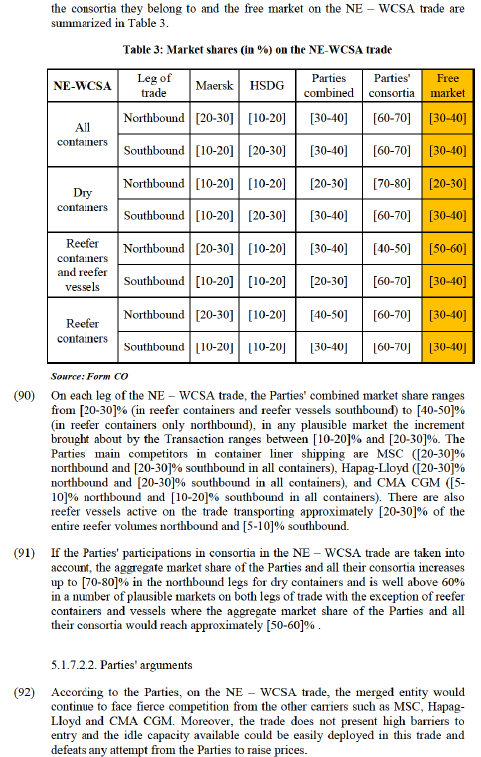

(39) In past decisions, the Commission defined the geographic scope of the market either as national or wider. Specifically for sea freight forwarding, the Commission defined the market as at least national. (45) The Parties did not express any disagreement with this approach. (46)

4.4.3.3.Conclusion

(40) However, it is not necessary to conclude on a precise definition of the relevant product or geographic market as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible definition of the markets for freight forwarding services.

4.4.4. Harbour towage services

4.4.4.1. Relevant product market

(41) Harbour towage services are provided to large vessels (container ships, bulk vessels, cruise ships, etc.) and include precise manoeuvring, positioning assistance, safe berthing, un-berthing and passing narrow gateways. Thus, there is a vertical relationship between container liner shipping activities and harbour towage services.

(42) In previous decisions, the Commission left the exact market definition open. (47) The Notifying Party did not express any disagreement with this approach.

4.4.4.2. Relevant geographic market

(43) In its prior decisional practice, the Commission considered that the narrowest possible geographical market definition was limited to individual ports. (48) The Parties did not express any disagreement with this approach. (49)

4.4.4.3.Conclusion

(44) However, it is not necessary to conclude on a precise definition of the relevant product or geographic markets as the Transaction would not raise serious doubts as to its compatibility with the internal market under any plausible definition of the markets for harbour towage services.

4.4.5. Container manufacturing

(45) Containers constitute an input product for container liner shipping companies. The market for container manufacturing is therefore an upstream market to container liner shipping.

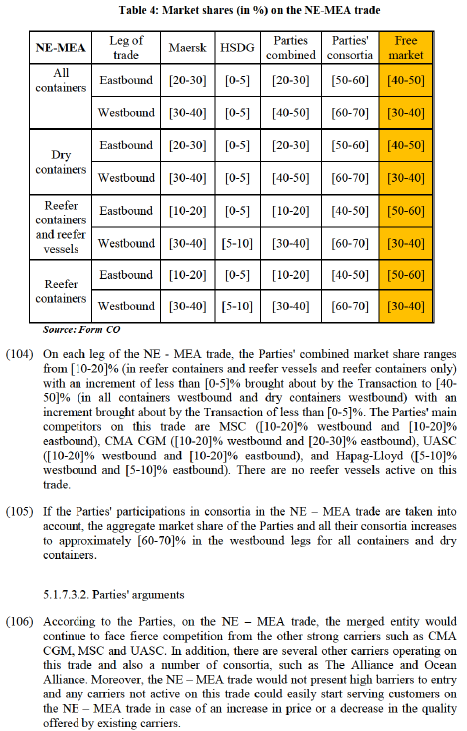

4.4.5.1. Relevant product market

(46) In its prior decisional practice, the Commission ultimately left open whether narrower sub markets regarding the type of container should be defined (i.e. dry freight standard, dry freight special, reefers and tanks). (50) The Parties argue that it would be appropriate to define the container market as comprising all types of containers. (51)

4.4.5.2. Relevant geographic market

(47) In its prior decisional practice (52), the Commission defined the geographic market for container manufacturing as global. The Parties concur with this geographic market definition. (53) In absence of any view to the contrary, the Commission considers that there is no reason to deviate from its prior decisional practice in the case at hand.

4.4.5.3.Conclusion

(48) However, it is not necessary to conclude on a precise definition of the relevant product or geographic market for container manufacturing, as the Transaction would not raise serious doubts as to its compatibility with the internal market under any plausible definition of the markets for container manufacturing.

5. COMPETITIVE ASSESSMENT

5.1. Horizontal overlaps - Deep-sea container liner shipping services

5.1.1. Introduction

(49) Despite a recent consolidation wave (54) the container liner shipping industry is still rather fragmented. Even the largest carriers such as Maersk, MSC, CMA CGM, COSCO and Hapag-Lloyd (55) individually do not have more than around 15% of world's total fleet capacity, and less than 60% combined. (56) Market shares, however, may be substantially higher depending on the trade.

(50) The customers of deep-sea container liner shipping companies can be divided into two major groups: freight forwarders and direct customers. Freight forwarders (e.g., Kühne & Nagel) organise the transportation of goods on behalf of customers according to their needs as intermediaries or freight ‘brokers’. In order to provide these services, freight forwarders purchase deep-sea container liner shipping services (usually port-to-port service, including feeder services where applicable), and inland transportation. Direct customers are typically large manufacturers or distributors of products which in whole or in part require overseas transport (e.g. Ikea or Volkswagen). (57)

5.1.2. Forms of cooperation

(51) Shipping companies provide their services either: (i) individually (i.e. via independent services), (ii) through vessel share agreements ("VSA") or alliances (jointly referred to as "consortia" or iii) by means of slot charter agreements. (58)

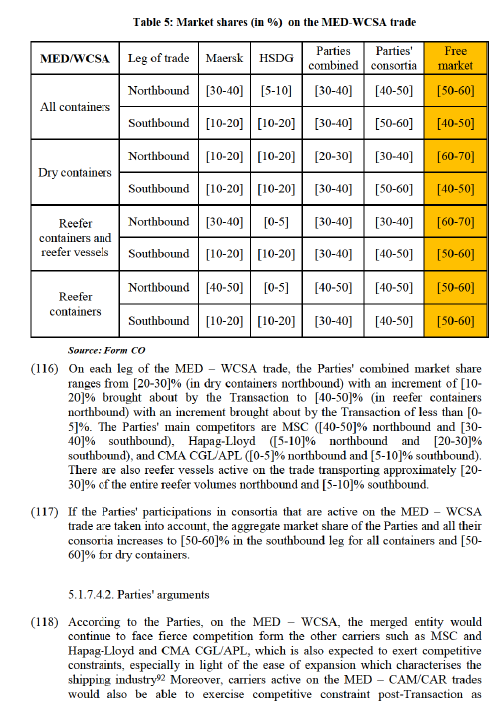

(52) In the case of VSAs, all parties provide some vessels for operating a joint service on an individual trade and in exchange receive a number of slots (allocation) across all vessels in the joint service based on the total vessel capacity that they have each put in. The carriers are not compensated if the slots are not used. (59) Consortium members therefore have a strong incentive to offer their slots at a competitive price to their individual customers in order to make use of their slots as much as possible. The costs for the operation of the vessels are borne by the respective vessel provider. There is no sharing of individual, actual costs or discussions of actual costs between consortium members either. Since every party provides vessel capacity the sailing timetable is decided on jointly. Port terminals are also selected jointly, however, each consortium member typically has separate contracts with the port terminal operators. Apart from these activities, there is no cooperation between the parties. In particular, the majority of VSAs explicitly stipulate that there is no price coordination, no joint marketing, no revenue sharing and typically no joint purchasing.

(53) Consortia cover multiple trades rather than one trade and comprise a matrix of VSAs.

(54) Slot charter agreements are a common means in container liner shipping to offer services to customers on a specific trade without deploying ships or where additional space or port-pairs are required by a carrier. The charterer ‘rents’ a pre- determined number of container slots on a vessel of a different company in exchange for cash (regular slot charter) or slots on its own ships (slot-exchange) with no other form of cooperation between the parties. In particular, there is no joint schedule, joint port terminal services, cost sharing, joint marketing or joint purchasing. Thus, slot charter agreements do not constitute cooperation agreements but agreements for the purchase or exchange of slots.

(55) Although the cooperation of consortium members in jointly operating container liner shipping services is likely to restrict competition, it also enables achieving certain efficiencies, notably by improving the productivity and quality of the available liner shipping services, by enabling the rationalisation of services and economies of scale, by offering greater frequencies, port calls, and, more generally, by promoting technical and economic progress. For customers to benefit from those efficiencies, however, sufficient competition should be maintained in the market. This condition is met, according to the Commission's Block Exemption Regulation ("BER") (60), where the market share of a consortium does not exceed 30% on a given trade (61) and the consortium agreement does not include features likely to significantly restrict competition, such as the fixing of prices, the limitation of capacity, and the allocation of customers or markets. (62)

5.1.3. Assessment framework

(56) In order to offer liner shipping services on a given trade with a regular, usually weekly schedule, a certain minimum volume is required. Therefore, most shipping companies, including the Parties, mainly offer their container liner shipping services in cooperation with other shipping companies through consortia.

(57) According to the Parties, consortium members exercise significant competitive constraints on one another – contrary to the Commission’s views in previous cases. As a result, competition relating to container liner shipping services must be viewed in this context and a consortia market share calculation is therefore not warranted. (63)

(58) In its previous decisional practice, the Commission considered that it was not appropriate to assess the effects of the concentration only on the basis of the Parties' individual market shares. Such an approach would not adequately take into account that a member of a consortium, even by carrying a limited volume, can have a significant influence on the operational decisions of the consortia concerning the characteristics of the service provided, in particular its level of capacity. (64)

(59) The results of the market investigation confirm the Commission's past findings. While the majority of respondents consider that the links created by the Transaction would not necessarily lead to exchange of sensitive information between competing container shipping companies (for example, if the combined entity is active on competing consortia), (65) they emphasized that such links may increase the Parties' ability and incentive to control important parameters of competition such as capacity, prices, frequencies, schedule of services, ports of call, etc. (66)

(60) In line with the Commission's previous decisional practice, the competitive assessment in this Decision will therefore not only be based on the Parties' individual market shares and the market share increment brought about by the Transaction in the different affected markets. (67) It will also take into account the aggregate shares of the Parties' consortia. In so doing, the Commission does not imply that other consortia members are part of the Parties' undertakings but merely takes into account the fact that the Parties' consortium partners exert only a limited competitive constraint on them. (68)

(61) The part of the market that will remain completely independent from the merged entity and its consortia on each market (referred to as the "free market") will also be considered, as it provides a first indication of the level of unfettered competitive constraint that the Parties would continue to face post-Transaction. Similarly, the number and size of the various independent competitors that will continue operating on each trade post-Transaction will be taken into account in the Commission's assessment. Where the number of independent competitors would be limited and their share of the market significantly smaller than that of the Parties or the members of consortia over which the Parties may have influence and in the absence of any other countervailing factors, the Commission will consider this a strong indication that the Transaction raises serious doubts as to its compatibility with the internal market.

5.1.4. Methodology for calculating market shares

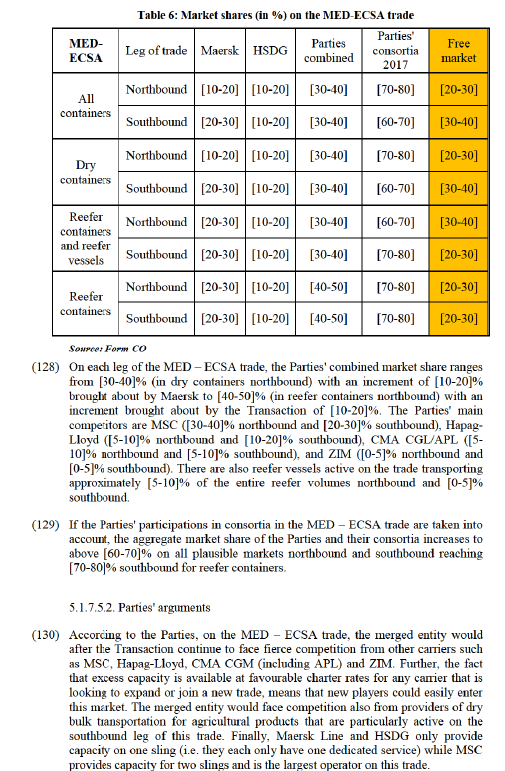

(62) The methodology that the Parties applied for the calculation of market shares follows the approach taken in the three most recent Commission's decisions in the container liner shipping sector. (69) First, the volume and market share data are based on the data obtained from CTS and the Parties' best estimates. Second, the Parties' consortia combined market shares are calculated by summing up the total volumes of all the shipping companies participating in any of the Parties' consortia. (70) Conversely, the free market is calculated by aggregating the market shares of all the container liner shipping companies, active on the respective leg of trade, that are not members of the Parties' consortia.

(63) The Parties' projected 2017 consortia combined market shares and the projected 2017 free market have been calculated based on container liner shipping companies' 2015 market share data and the expected market structure in 2017. (71) More concretely, the Parties assumed that the current consortia will undergo the changes described in Table 1 below.

(64) For the reefer container market, in line with the Commission's previous decisional practice (72) market shares are only taken into account on those legs of trade where the share of transport in reefer containers in relation to all containerised cargo is 10% or more.

5.1.5. The 2017 consortia restructuring

(65) According to the Horizontal Merger Guidelines (73), in assessing the competitive effects of a merger, the Commission compares the competitive conditions that would result from the notified merger with the conditions that would have prevailed without the merger. In most cases, the competitive conditions existing at the time of the merger constitute the relevant comparison for evaluating the effects of a merger. However, in some circumstances, the Commission may take into account future changes to the market that can reasonably be predicted. (74)

· Northern Europe – Far East ("NE-FEA")

· Northern Europe – Indian Subcontinent ("NE-ISC")

· Northern Europe – Middle East ("NE-MEA")

· Northern Europe – Australia/New Zealand ("NE-AUNZ")

· Mediterranean – Central America/Caribbean ("MED-CAM/CAR")

· Mediterranean – West Coast South America ("MED-WCSA")

· Mediterranean – East Coast South America ("MED-ECSA")

· Mediterranean – Indian Subcontinent ("MED-ISC")

· Mediterranean – Middle East ("MED-MEA")

· Mediterranean – Australia/New Zealand ("MED-AUNZ")

· Mediterranean – South Africa ("MED-SAF")

(73) When attributing the Parties' consortia market shares to them, the list of markets, in which the market share of the Parties and their consortia exceed 20% also include the following additional three trades comprising six affected legs:

· Northern Europe – North America ("NE-NAM")

· Mediterranean – North America ("MED-NAM")

· Mediterranean – Far East ("MED-FEA")

(74) The Parties' individual (i.e. without taking into account the consortia) combined market share, reach at most [60-70]% in the northbound leg of the MED-OCE trade; however, in this specific plausible market the increment brought about by the Transaction is only [0-5]%. When the market shares of consortia are also taken into account, the highest combined market shares and the increment increase are above [70-80]% and [20-30]% respectively.

(75) The competitive situation and the market structure pre- and post-Transaction for the affected legs of trades referred to in recitals 72 and 73 are described and assessed in the following sections of the Decision. In Sections 5.1.7.1., 5.1.7.2, 5.1.7.3., 5.1.7.4, 5.1.7.5, the competitive assessment of the following legs of trades is presented: (i) NE - CAM/CAR northbound and southbound, (ii) NE - WCSA northbound and southbound, (iii) NE - MEA eastbound and westbound, (iv) MED - WCSA northbound and southbound, and (v) MED - ECSA, and Section 5.1.7.6. contains the competitive assessment of all other relevant legs of trade including (i) MED - CAM/CAR, (ii) MED - FEA, (iii) MED - NAM, (iv) MED - ISC, (v) NE - FEA, (vi) NE - ISC, (vii) NE - NAM, (viii) NE - AUNZ, (ix) NE - ECSA, (x) MED - AUNZ, (xi) MED – SAF and (xii) MED – MEA.

reefer vessels active on the trade transporting approximately [20-30]% of the entire reefer volumes northbound and [5-10]% southbound.

(78) If the Parties' participations in consortia in the NE – CAM/CAR trade are taken into account, the aggregate market share of the Parties and their consortia increases up to [80-90]% in the northbound legs for reefer containers and [80- 90]% in the northbound leg for all containers.

5.1.7.1.2. Parties' arguments

(79) According to the Parties, on the NE – CAM/CAR trade, the merger entity would after the Transaction continue to face fierce competition from the other carriers such as CMA CGM, Hapag-Lloyd and MSC. Moreover, the trade does not present high barriers to entry and any carriers not active on this trade can easily start serving customers also on the NE – CAM/CAR trade.

5.1.7.1.3. Commission's assessment

(80) On the NE – CAM/CAR trade, while Maersk is not a member of any consortium, HSDG is a member of Eurosal 1/SAWC together with CMA CGM and Hapag- Lloyd.

(81) Pre-Transaction, there are three independent poles of supply customers could choose, namely the Eurosal 1/SAWC consortium of which HSDG is a member, and Maersk and MSC, both operating outside any consortium. After the Transaction, the number of independent suppliers would be reduced to two, as a link between Maersk and the Eurosal 1/SAWC consortium would be created, and customers on the trade would have only two independent poles of supply: the merged entity and Eurosal 1/SAWC on the one hand and MSC on the other hand.

(82) As explained in recitals 52, 58 and 59, members of consortia jointly establish the main criteria for the operation of a trade, including the capacity that will be offered, its allocation among shipping companies, the consortia's schedule and ports of call. Therefore, unfettered competition would only come from those competitors that are unconnected to the Parties and their consortia. On the relevant markets with the highest market shares of the NE – CAM/CAR trade, the northbound legs for reefer containers only and for all containers, the percentage of the free market would after the Transaction correspond to approximately only [10-20]% and [10-20]% respectively. MSC accounts for approximately [60-70]% and [50-60]% respectively of that free market and would remain the main independent player post-Transaction.

(83) As a result, by creating a link between the previously independent Maersk and HSDG's consortium on the NE – CAM/CAR trade, the Transaction would likely reduce competition on this trade. The merged entity would post-Transaction have the ability to influence decisions regarding the level and the allocation of capacity, the setting of ports of call and the services' schedules on a higher share of the market than each of the Parties currently has. Given that these important parameters will be decided jointly by all members of the consortium, the change brought about by the Transaction would impact the level of competition on all plausible markets in respect of the two legs of the NE – CAM/CAR trade.

(84) Respondents to the market investigation questionnaires did not express significant concerns in relation to this trade. (79) However, the majority of the respondents to the market investigation questionnaires consider Maersk the second closest competitor to HSDG and vice versa on the NE–CAM/CAR trade. (80)

(85) The majority of respondents to the market investigation questionnaires also confirmed that links between the Parties and consortia which were previously independent would increase the ability and the incentive of the merged entity to control important parameters of competition (e.g. capacity, prices, frequencies, schedule of the services, ports of call, etc.). (81)

(86) Finally, concerning barriers to entry, the majority of respondents to the market investigation questionnaires submitted that customers could not entice a container shipping company to enter/expand services on a certain leg of trade. (82) Similarly, the majority of competitors indicated that the Transaction would increase barriers to entry. (83)

(87) In view of the above and in particular of the relatively low percentage of the free market in 2017 and the reduction of independent poles of supply for customers from three to two, the Commission considers that the competitive pressure exerted on the merged entity on the NE – CAM/CAR northbound and southbound legs of trade would likely decrease after the Transaction and not be sufficient to effectively constrain the merged entity.

5.1.7.1.4 Conclusion

(88) In light of the above considerations, the Commission concludes that the Transaction would raise serious doubts as to its compatibility with the internal market in respect of the NE – CAM/CAR northbound and southbound legs of trade. However, Maersk has offered Commitments to address the Commission's competition concerns (see section 6).

5.1.7.2. Northern Europe – West Coast South America northbound/southbound legs of trade

5.1.7.2.1 Market structure

(89) On the northbound and southbound legs of the NE – WCSA trade a total of approximately [0-1] million TEUs was transported in 2015 ([0-1] million TEUs northbound of which [60-70]% reefer containers and [0-1] million TEUs southbound of which [5-10]% reefer containers). The market shares of the Parties,

(93) In addition, the Parties claim that Maersk and HSDG are not close competitors on this route since Maersk focuses mainly on providing services from Ecuador, Colombia and Costa Rica with a focus on banana customers and it does not currently offer a direct service from Peru or Chile, while HSDG has a direct service to Peru and Chile, which largely serves producers of cherries, apples, pears, grapes and other fresh fruits.

5.1.7.2.3. Commission's assessment

(94) On the NE – WCSA trade, while Maersk is not a member of any consortium, HSDG is a member of Eurosal 2/SAWC together with CMA CGM and Hapag- Lloyd.

(95) Pre-transaction, customers can choose between three independent poles of supply, namely the Eurosal 2/SAWC consortium, of which HSDG is a member, Maersk and MSC, both operating outside any consortium. After the Transaction, the number of independent suppliers would be reduced to two, as a link between Maersk and the Eurosal 2/SAWC consortium would be created, and customers on the trade would have only 2 independent poles of supply: the merged entity and Eurosal 2/SAWC on the one hand and MSC on the other hand.

(96) As explained in recitals 52, 58, and 59, members of consortia jointly establish the main criteria for the operation of a trade, including the capacity that will be offered, its allocation among shipping companies, the consortia's schedule and ports of call. Therefore, unfettered competition would only come from those competitors that are unconnected to the Parties and their consortia. On the most problematic plausible markets of the NE – WCSA trade, that are the northbound legs for dry containers and the southbound legs for all containers, the percentage of the free market would correspond post-Transaction to approximately [20-30]% and [30-40]% respectively. MSC accounts for approximately [80-90]% and [80- 90]% respectively of that free market and would remain the main independent player post-Transaction.

(97) As a result, by creating a link between the previously independent Maersk and HSDG's consortium on the NE – WCSA trade, the Transaction would likely reduce competition on this trade. The merged entity would post-Transaction have the ability to influence decisions regarding the level and the allocation of capacity, the setting of ports of call and the services' schedules on a higher share of the market than each of the Parties currently has. Given that these important parameters will be decided jointly by all members of the consortium, the change brought about by the Transaction would impact the level of competition on all the plausible markets of the two legs of the NE – WCSA trade.

(98) Respondents to the market investigation questionnaires did not express significant concerns in relation to this trade. (84) However, the majority of respondents to the market investigation questionnaires consider Maersk the second closest competitor to HSDG and vice versa on the NE–WCSA trade.

(99) The majority of respondents to the market investigation questionnaires also confirmed that the links between the Parties and consortia which were previously independent would increase the ability and the incentive of the merged entity to control important parameters of competition (e.g. capacity, prices, frequencies, schedule of the services, ports of call, etc.). (85)

(100) Finally, concerning barriers to entry, the majority of respondents to the market investigation questionnaires submitted that customers could not entice a container shipping company to enter/expand services on a certain leg of trade. (86) Similarly, the majority of competitors indicated that the Transaction would increase barriers to entry. (87)

(101) In view of the above and in particular of the relatively low percentage of the free market in 2017 and the reduction of independent poles of supply for customers, the Commission considers that competitive pressure exerted on the merged entity would likely decrease as a result of the Transaction and not be sufficient to effectively constrain the merged entity.

5.1.7.2.4 Conclusion

(102) In light of the above considerations, the Commission concludes that the Transaction would raise serious doubts as to its compatibility with the internal market in respect of the NE – WCSA northbound and southbound legs of trade. However, Maersk has offered Commitments to address the Commission's competition concerns (see section 6).

5.1.7.3. Northern Europe – Middle East eastbound/westbound legs of trade

5.1.7.3.1. Market structure

(103) On the eastbound and westbound legs of the NE – MEA trade, a total of approximately [1-2] million TEUs was transported in 2015 ([1-2] million TEUs eastbound of which [10-20]% reefer containers and [0-1] million TEUs westbound of which [0-5]% reefer containers). The market shares of the Parties, the consortia they belong to and of the free market on the NE–MEA trade are summarized in the Table 4.

5.1.7.3.3. Commission's assessment

(107) On the NE – MEA trade, while Maersk is not a member of any consortium, HSDG is a member of EPIC 2 together with CMA CGM and Hapag-Lloyd. The increment brought about by the Transaction including links with that consortium would amount to at most [20-30]% on any plausible market. The Transaction would lead to the establishment of links between a consortium and the previously independent Maersk.

(108) As explained in recitals 52, 58 and 59, members of consortia jointly establish the main criteria for the operation of a trade, including the capacity that will be offered, its allocation among shipping companies, the consortia's schedule and ports of call. Therefore, unfettered competition would only come from those competitors that are unconnected to the Parties and their consortia. On the markets of the NE – MEA trade where the Parties would have the highest combined market shares, that is, the westbound legs for all containers and for dry containers, the percentage of the free market would currently correspond to approximately only [30-40]% (increasing to approximately [40-50]% on the eastbound leg). MSC accounts for approximately [10-20]% of that free market and would remain the main independent player post-Transaction.

(109) As a result, by creating a link between the previously independent Maersk and HSDG's consortia on the NE – MEA trade through the participation of the merged entity, the Transaction would likely reduce the intensity of competition on this trade. The merged entity would, post-Transaction, have the ability to influence decisions regarding the level and the allocation of capacity, the setting of ports of call and the services' schedules, and access to information on capacity of a broader range of consortia and competitors than each of the Parties currently has. Given that these important parameters will be decided jointly by all members of the consortium, the change brought about by the Transaction would have a negative impact on the level of competition on the two legs of the NE – MEA trade.

(110) Respondents to the market investigation questionnaires did not express significant concerns in relation to this trade. (88) However, while the majority of customers consider Maersk the second closest competitor to HSDG on the NE–MEA by a narrow margin to the competitor considered closest, CMA CGM/ALP, the majority of competitors consider Maersk as the closest competitor of HSDG. (89)

(111) The majority of respondents also confirmed that the links created by the Transaction could increase the ability and incentive of the merged entity to control important parameters of competition (e.g. capacity, frequencies, schedule of the services, etc.). (90)

(112) Finally, concerning barriers to entry, the majority of respondents to the market investigation questionnaires submitted that customers could not entice a container shipping company to enter/expand services on a certain leg of trade. Similarly, the majority of competitors indicated that the Transaction would increase barriers to entry. (91)

(113) In view of the above and in particular of the relatively low percentage of the free market in 2017, the Commission considers that the competitive pressure exerted on the merged entity on both legs of the NE – MEA trade would likely decrease as a result of the Transaction and not be sufficient to effectively constrain the merged entity.

5.1.7.3.4. Conclusion

(114) In light of the above considerations, the Commission concludes that the Transaction would raise serious doubts as to its compatibility with the internal market on the markets for container liner shipping services in the NE – MEA westbound and eastbound legs of trade. However, Maersk has offered Commitments to address the Commission's competition concerns (see section 6).

5.1.7.4. Mediterranean - West Coast South America northbound/southbound legs of the trade

5.1.7.4.1. Market structure

(115) On the northbound and southbound legs of the MED – WCSA trade a total of approximately [0-1] million TEUs was transported in 2015 ([0-1] million TEUs northbound of which [70-80]% reefer containers and [0-1] million TEUs southbound of which [0-5]% reefer containers). The market shares of the Parties, the consortia they belong to and the free market on the MED–WCSA trade are summarized in the Table 5.

transhipment on this trade via Central America/Caribbean is a feasible alternative to transporting cargo to the South America West Coast trade (93)

5.1.7.4.3. Commission's assessment

(119) On the MED – WCSA, while Maersk is not a member of any consortium, HSDG is a member to the CCWM/MedAndes consortium with Hapag-Lloyd. The Transaction would thus lead to the establishment of links between a consortium and the previously independent Maersk.

(120) As explained in recitals 52, 58, 59, members of consortia jointly establish the main criteria for the operation of a trade, including the capacity that will be offered, its allocation among shipping companies, the consortia's schedule and ports of call. Therefore, unfettered competition would only come from those competitors that are unconnected to the Parties and their consortia. On the potential markets of the MED – WCSA with the highest combined market shares, that is the southbound legs for all containers and for dry containers, the percentage of the free market would currently be slightly below [40-50]%. MSC would remain the main independent player post-Transaction.

(121) As a result, by creating a link between the previously independent Maersk and HSDG's consortia on the MED – WCSA trade through the participation of the merged entity, the Transaction would likely reduce the intensity of competition on this trade. The merged entity would post-Transaction have the ability to influence decisions regarding the level and the allocation of capacity, the setting of ports of call and the services' schedules, and access to information on capacity of a broader range of consortia and competitors than each of the Parties currently has. Given that these important parameters will be decided jointly by all members of the consortium, the change brought about by the Transaction would have a negative impact the level of competition on both legs of the MED – WCSA trade.

(122) Respondents to the market investigation questionnaires did not express significant concerns in relation to this trade. (94) However, the majority of customers and competitors consider Maersk the second closest competitor to HSDG on the MED-WCSA by a narrow margin to the competitor considered closest, CMA CGM/ALP. (95)

(123) In addition, the majority of customers also consider that the links the created by the Transaction could increase the ability and incentive of the merged entity to control important parameters of competition (e.g. capacity, frequencies, schedule of the services etc. (96)

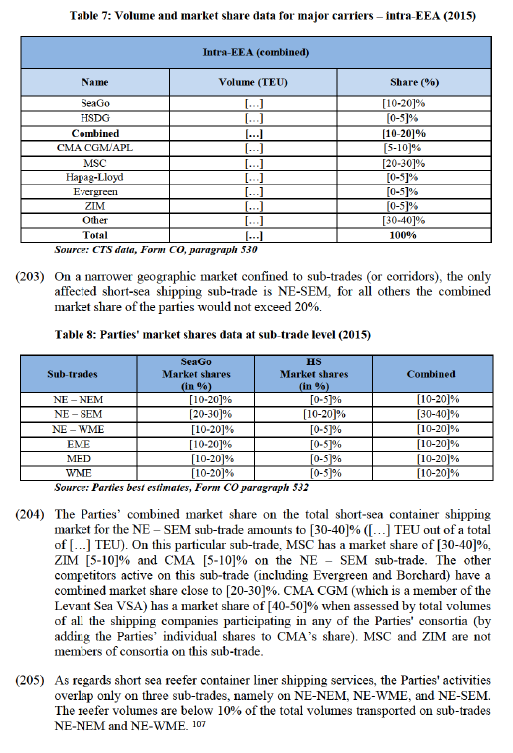

(124) Finally, concerning barriers to entry, the majority of respondents to the market investigation questionnaires submitted that customers could not entice a container shipping company to enter/expand services on a certain leg of trade. In addition, the majority of competitors indicated that the Transaction would increase barriers to entry. (97)

(125) In view of the above and in particular on the relatively low percentage of the free market in 2017, the Commission considers that the competitive pressure exerted on the merged entity on both legs of the MED – WCSA trade would likely decrease after the Transaction and not be sufficient to effectively constrain the merged entity.

5.1.7.4.4. Conclusion

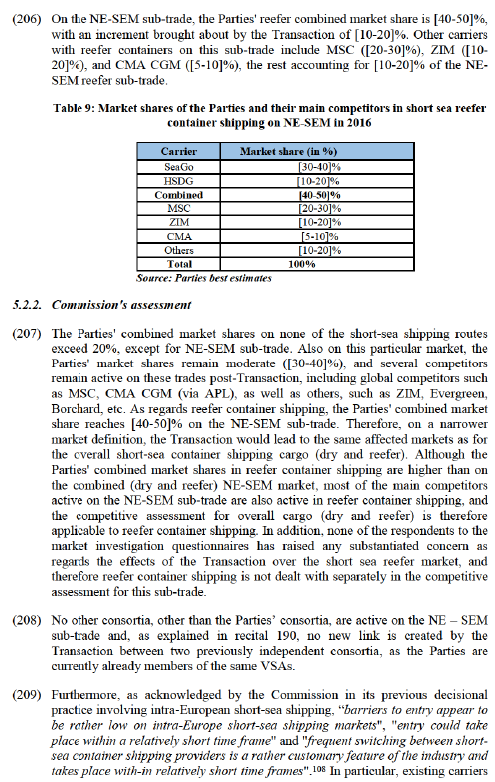

(126) In light of the above considerations, the Commission concludes that the Transaction would raise serious doubts as to its compatibility with the internal market on the markets for container liner shipping services in the MED – WCSA northbound and southbound legs of trade. However, Maersk has offered Commitments to address the Commission's competition concerns (see section 6).

5.1.7.5. Mediterranean – East Coast South America northbound/southbound legs of trade

5.1.7.5.1. Market structure

(127) On the northbound and southbound legs of the MED – ECSA trade, a total of approximately [0-1] million TEUs was transported in 2015 ([0-1] million TEUs northbound of which [30-40]% reefer containers and [0-1] million TEUs southbound of which [5-10]% reefer containers). The market shares of the Parties, the consortia they belong to and the free market on the MED–ECSA trade are summarized in Table 6.

(131) The Parties also submit that Maersk and HSDG are not close competitors on this trade. Maersk does not have a dedicated direct service with its own vessel. Instead, it offers slot chartering on MSC's stand-alone service "Bossa Nova" and the MESA consortium between MSC and HSDG as well as so-called sail-by services. Sail-by means the containers are put on a Maersk vessel coming from Northern Europe heading to ECSA in the outermost harbour of the Mediterranean, Algeciras, and vice versa. This means containers with a destination of all other MED harbours has to be on and offloaded for continuation which is less interesting for customers shipping fresh fruit or valuable goods such as cars, as the intermediate handling increases transit time and risk of delays. HSDG, on the other hand, is part of the MESA consortium which is a dedicated direct service calling on a significant number of MED ports.

5.1.7.5.3 Commission's assessment

(132) The combined market share of the Parties, without taking into account consortia, is around [40-50]%. However, the combined market share increases to very high levels if the MESA consortium HSDG is a member of, is taken into account.

(133) Taking into account the MESA consortium, the increment brought about by the Transaction would range from [20-30]% to [40-50]% on all plausible markets. The Transaction would thus lead to the establishment of links between a consortium and the previously independent Maersk sail-by service.

(134) As explained in recitals 52, 58 and 59, members of consortia jointly establish the main criteria for the operation of a trade, including the capacity that will be offered, its allocation among shipping companies, the consortia's schedule and ports of call. Therefore, unfettered competition would only come from those competitors that are unconnected to the Parties and their consortia. On the potential markets of the MED – ECSA where the Parties' consortia have the highest combined market shares, that is the northbound leg for dry containers and the southbound legs for reefer containers, the percentage of the free market would currently correspond to below 30%. MSC would remain the main independent player post-Transaction.

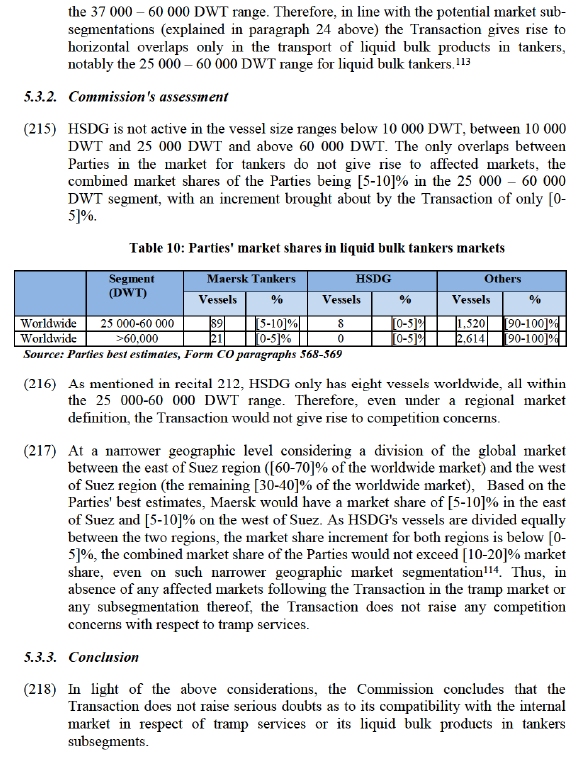

(135) As a result, by creating a link between the previously independent Maersk and HSDG's consortium on the MED – ECSA trade through the participation of the merged entity, the Transaction would likely reduce the intensity of competition on this trade. The merged entity would post-Transaction have the ability to influence decisions regarding the level and the allocation of capacity, the setting of ports of call and the services' schedules, and have access to information on capacity of a broader range of consortia and competitors than each Party currently individually has. Given that these important parameters would be decided jointly by all members of the consortium, the change brought about by the Transaction would have a negative impact on the level of competition on the two legs of the MED – ECSA trade.

(136) Respondents to the market investigation questionnaires did not express significant concerns in relation to this trade. (98) However, concerning the closeness of competition between the Parties, while for the majority of customers, Maersk is the second closest competitor to HSDG by a narrow margin to the competitor considered closest, CMA CGM, the majority of competitors consider Maersk as the closest competitor to HSDG on this trade.99

(137) In addition, the majority of customers also consider that the links created by the Transaction could increase the ability and incentive of the merged entity to control important parameters of competition (e.g. capacity, frequencies, schedule of the services, etc.). (100)

(138) Finally, concerning barriers to entry, the majority of respondents to the market investigation questionnaires submitted that customers could not entice a container shipping company to enter/expand services on a certain leg of trade. Similarly, the majority of competitors indicated that the Transaction would increase barriers to entry. (101)

(139) In view of the above and in particular of the low percentage of the free market in 2017, the Commission considers that the competitive pressure exerted on the merged entity would likely decrease on both legs of the MED – ECSA trade and not be sufficient to effectively constrain the merged entity.

5.1.7.5.4. Conclusion

(140) In light of the above considerations, the Commission concludes that the Transaction would raise serious doubts as to its compatibility with the internal market in respect of container liner shipping services in the MED – ECSA northbound and southbound legs of trade. However, Maersk has offered Commitments to address the Commission's competition concerns (see section 6).

5.1.7.6. Other legs of trade

(141) The market investigation results confirmed that the Transaction would not give rise to competition concerns on any of the affected legs of trade included in this section and assessed more in details in the following paragraphs. The majority of competitors and customers confirmed that there would remain a sufficient number of competing suppliers to prevent the merged entity from raising prices on these trades. (102)

(142) Several competitors responding to the Commission's market investigation questionnaires also indicated that there is spare capacity in the sector. (103) Therefore, should there be an increase in demand on a specific market and in particular in respect of the legs of trade referred to below, one or more container liner shipping companies active on those trades would be able to increase their capacity on the respective leg of trade, notably as result of the low barriers to expansion which characterise this sector.

(143) On the northbound and southbound legs of the Mediterranean - Central America/Caribbean trade a total of [0-1] million TEUs was transported in 2015 ([0-1] million TEUs northbound of which [50-60]% reefer containers and [0-1] million TEUs southbound of which [0-5]% reefer containers). On each leg of trade, the Parties have a combined share of less than [20-30]% under all plausible markets with an increment brought about by the Transaction ranging from less than [0-5]% in northbound reefer containers to [10-20]% in northbound dry containers.

(144) Additional players would remain active on this trade post-Transaction of which CMA CGM/APL is the largest with a market share of [30-40]% for all containers followed by MSC ([20-30]%), Hapag-Lloyd ([10-20]%) and ZIM ([5-10]%).

(145) In terms of the Parties' consortia on the MED - CAM/CAR trade, only HSDG is a member to the MPS/MCPS consortium with Hapag-Lloyd; Maersk Line is not a member of any consortium on this trade. HSDG only provides one out of five vessels to the MPS/MCPS consortium contributing very little in terms of capacity and volumes shipped.

(146) On a consortia basis, the Parties' combined market share on the dry segment of the trade would amount to [30-40]% ([30-40]% northbound and [30-40]% southbound) and marginally above CMA CGM/APL's individual share of [30- 40]%. The free market on this trade would remain above 60%, notably with [60- 70]% of the overall market share of the dry segment ([60-70]% northbound and [60-70]% southbound) belonging to independent competitors outside the Parties' consortia.

(147) Finally, for reefer only, the combined consortia market share amounts to [20- 30]% northbound and [30-40]% southbound remaining below CMA CGM/APL's individual market share on both legs.

(148) In conclusion, on this trade the free market is above 60% in all plausible markets, the Transaction therefore does not raise serious doubts as to its compatibility with the internal market in respect of container liner shipping services in the MED – CAM/CAR northbound and southbound legs of trade.

(149) On the westbound and eastbound legs of the Mediterranean – Far East trade a total of [3-4] million TEUs was transported in 2015 ([1-2] million TEUs eastbound and [2-3] million TEUs westbound). On each leg of trade, the Parties have a combined share of less than 20% under all plausible markets with a marginal increment of approximately [0-5]% due to HSDG's limited presence.

(150) This trade is therefore considered an affected market only when taking into account Maersk Line's participation in the 2M Alliance. HSDG is not a member of any consortium in this trade. The aggregate market share of the Parties and their consortia would be [30-40]% westbound and [20-30]% eastbound.

(151) The Parties' market share is therefore limited compared to the independent market volumes which amount to above 60% on either leg of the MED-FEA trade. Alternative players would remain active on this trade post-Transaction including notably MSC and CMA CGM/APL, which both have market shares in excess of [10-20]% which are comparable to those of the combined entity.

(152) In conclusion, on this trade the free market is above 60% in all plausible markets, the Transaction therefore does not raise serious doubts as to its compatibility with the internal market in respect of container liner shipping services in the MED – FEA westbound and eastbound legs of trade.

(153) On the westbound and eastbound legs of the Mediterranean – North America trade a total of approximately [2-3] million TEUs was transported in 2015 ([0-1] million TEUs eastbound and [1-2] million TEUs westbound). On each leg of trade, the Parties have a combined share of less than 20% under all plausible markets with a marginal increment of less than [0-5]% due to HSDG's limited presence on this trade.

(154) This trade is therefore considered an affected market only when taking into account Maersk Line's participation in the 2M Alliance with MSC and HSDG's participation in the MPS/MCPS consortium with Hapag-Lloyd. The aggregate market share of the Parties and their consortia would be [70-80]% westbound and [60-70]% eastbound.

(155) Alternative players would remain active on this trade post-Transaction such as MSC, ZIM, CMA CGM/APL and Hapag-Lloyd with a market share of [30-40]%, [10-20]%, [5-10]% and [20-30]% respectively.

(156) Despite the high combined market share of the Parties when calculated based on total volumes of all the shipping companies participating in any of the Parties' consortia/alliances, the Transaction is unlikely to lead to serious doubts for the following reasons. Maersk Line's activities on this trade are confined to sailings to the east coast of North America. Therefore, there is no overlap as regards the west coast which is served by HSDG via the MPS/MCPS service with Hapag.

(157) Services to ports on the North American east coast are not close competitors to ports on the west coast, despite the possibility to unload at either coast and to transport the container by rail or road across the continent to its final destination. Customers on the west coast of the United States typically prefer to be served directly through ports on the west coast, and customers on the east coast prefer to be served by services to the east coast ports, as this saves time and in particular money. In this respect, compared to a direct shipment service, Maersk Line estimates the service cost of transporting cargo by rail from the harbour in Houston on the Mexican Gulf coast to Los Angeles or Oakland to be significantly more expensive than a direct sea service into the ports of Los Angeles or Oakland.

(158) Finally, services on the west coast do not actively compete with Great Lakes landings either, given that the physical restrictions of the Great Lakes waterway prevent larger vessels from serving these ports.

(159) On the east coast Maersk is present as part of the 2M alliance while the presence of HSDG is limited ([0-5]% market share); in addition, there are several other carriers operating on this segment and also a number of consortia/alliances, such as The Alliance, Ocean Alliance and MGX.

(160) In conclusion, on this trade, despite high market shares of the Parties and their consortia, for the reasons explained above, the Parties are not close competitors and a number of independent suppliers and consortia, which could easily expand their capacity, will remain active post-Transaction; therefore the Transaction does not raise serious doubts as to its compatibility with the internal market in respect of container liner shipping services in the MED – NAM westbound and eastbound legs of trade.

(161) On the westbound and eastbound legs of the Mediterranean – Indian Subcontinent a total of [1-2] million TEUs was transported in 2015 ([0-1] million TEUs eastbound and [0-1] million TEUs westbound). On each leg of trade, the Parties have a combined share of less than [20-30]%. The increment brought about by the Transaction is less than [0-5]% due to HSDG's limited presence on this trade. (104)

(162) Alternative strong players would remain active on this trade post-Transaction such as MSC, CMA CGM/APL, ZIM, UASC and Hapag-Lloyd with a market share of [20-30]%, [10-20]%, [5-10]% and [5-10]% and [5-10]% respectively.

(163) In conclusion, on this trade the free market is above 60% in all plausible markets, the Transaction therefore does not raise serious doubts as to its compatibility with the internal market in respect of container liner shipping services in the MED – ISC westbound and eastbound legs of trade.

(164) On the westbound and eastbound legs of the Northern Europe – Far East trade a total of [15-20] million TEUs was transported in 2015 ([4-5] million TEUs eastbound and [5-10] million TEUs westbound). On each leg of trade, the Parties have a combined share of less than [20-30]% with a marginal increment of less than [0-5]% due to HSDG's limited presence.

(165) In terms of the Parties' consortia on this trade, only Maersk is a member to the 2M alliance with MSC, while HSDG is not a member of any consortium.

(166) On a consortia basis, the Parties' combined market share would amount to [30- 40]% eastbound and [30-40]% westbound. The free market on this trade would remain above 60%, [60-70]% eastbound and [60-70]% westbound. Alternative players would remain active on this trade post-Transaction including notably CMA CGM/APL and Hapag-Lloyd, as well as Evergreen. The increments are not material ([0-5]% eastbound and [0-5]% westbound).

(167) In conclusion, on this trade the free market is above 60% in all plausible markets, the Transaction therefore does not raise serious doubts as to its compatibility with the internal market in respect of container liner shipping services in the NE – FEA westbound and eastbound legs of trade.

(168) On the westbound and eastbound legs of the Northern Europe – Indian Subcontinent trade a total of [1-2] million TEUs was transported in 2015 ([0-1] million TEUs eastbound and [1-2] million TEUs westbound). The Parties have a combined share of [20-30]% eastbound (Maersk [20-30]%, HSDG [5-10]%) and [30-40]% westbound (Maersk [20-30]%, HSDG [5-10]%).

(169) In terms of the Parties' consortia on this trade, Maersk is not a member of any consortium, while HSDG is a member to the EPIC 2 consortium with Hapag- Lloyd and CMA CGM. The Parties submit that they plan to withdraw HSDG from EPIC 2 post-Transaction, therefore removing any new link created by the Transaction on this trade.

(170) Taking into account the 2017 market structure and even not considering the Parties Commitment to withdraw HSDG from EPIC 2, on a consortia basis, the Parties' combined market share would amount to [20-30]% eastbound and [30- 40]% westbound. The free market on this trade would remain above 60%, [70- 80]% eastbound and [60-70]% westbound. Alternative players would remain active on this trade post-Transaction including notably MSC, CMA CGM/APL and Hapag-Lloyd.

(171) In conclusion, on this trade the free market is above 60% in all plausible markets, the Transaction therefore does not raise serious doubts as to its compatibility with the internal market in respect of container liner shipping services in the NE – ISC westbound and eastbound legs of trade.

(172) On the westbound and eastbound legs of the Northern Europe – North America trade a total of [4-5] million TEUs was transported in 2015 ([1-2] million TEUs eastbound and [2-3] million TEUs westbound). The Parties have a combined share of [10-20]% eastbound (Maersk [5-10]%, HSDG [0-5]) and [10- 20]% westbound (Maersk [10-20]%, HSDG [5-10]%).

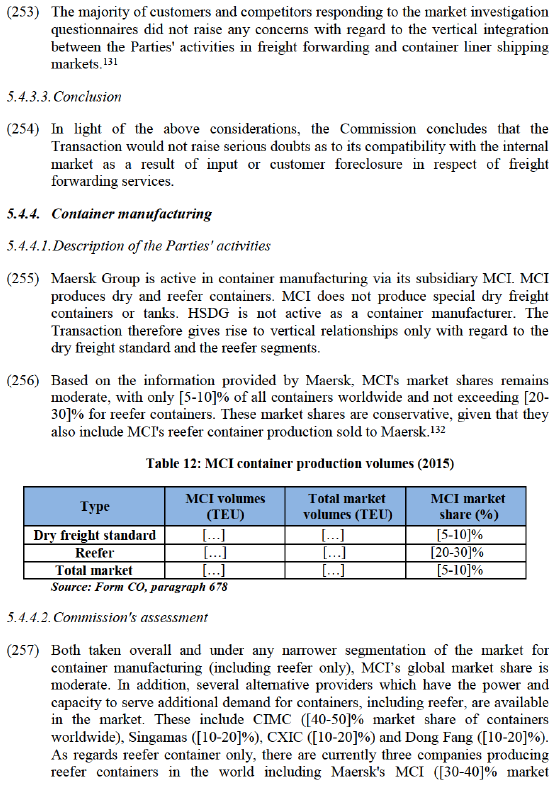

(173) In terms of the Parties' consortia on this trade, Maersk is a member of the 2M Alliance with MSC and also of the Canada Express consortium with CMA CGM, while HSDG is a member to the EUNA consortium with CMA CGM. […] sent a notice of termination for the EUNA consortium on 31 December 2016 and, pursuant to the consortium agreement, the termination is effective as of 31 March 2017; the notice also identifies the date of the last sailing, which commenced on 25 March 2017.

(174) Taking into account the 2017 market structure, on a consortia basis, the Parties' combined market share would amount to [40-50]% eastbound and [50-60]% westbound. The free market on this trade would be close to 60%, notably the trade would have [50-60]% eastbound and [40-50]% westbound of its overall volumes belonging to independent competitors outside the Parties' consortia. Alternative players would remain active on this trade post-Transaction including notably Hapag-Lloyd and OOCL.

(175) In light of the termination of the EUNA consortium, the Transaction does not bring about any new links between previously independent competitors since both Maersk and HSDG are in a consortium with CMA CGM, therefore the Transaction brings about on this trade only the individual market share of HSDG which amounts to [0-5]% northbound and [5-10]% southbound.

(176) In conclusion, on this trade, despite the free market being below 60% in all plausible markets, the Transaction does not create any new link between previously independent consortia and the increment is at most [5-10]%; moreover a number of independent suppliers and consortia, which could easily expand their capacity, will remain active post-Transaction; the Transaction therefore does not raise serious doubts as to its compatibility with the internal market in respect of container liner shipping services in the NE – NAM westbound and eastbound legs of trade.

(177) On the northbound and southbound legs of the Northern Europe – Australia/New Zealand trade a total of [0-1] million TEUs was transported in 2015 ([0-1] million TEUs northbound of which [30-40]% reefer containers and [0-1] million TEUs southbound of which [10-20]% reefer containers). The Parties have a combined share for all containers of [30-40]% northbound (Maersk [30- 40]%, HSDG [5-10]%) and [30-40]% southbound (Maersk [30-40]%, HSDG [0- 5]%). When considering the narrower market for reefer containers, the Parties have a combined share of [50-60]% northbound (Maersk [40-50]%, HSDG [5- 10]%) and [40-50]% southbound (Maersk [30-40]%, HSDG [10-20]%). No reefer vessels are active on this trade.

(178) In terms of the Parties' consortia on this trade, neither Maersk nor HSDG are member to any consortium on the trade, therefore their market shares on a consortia basis are equivalent to the individual market shares of HSDG and Maersk.

(179) On this trade the free market would remain above 60% with the exception of the plausible markets for reefer containers where the free market would not go beyond [40-50]% northbound and [50-60]% southbound. Alternative players would remain active on this trade post-Transaction both in reefer containers as well as in dry containers including notably MSC, CMA CGM and Hapag-Lloyd.

(180) In conclusion, on this trade, in some plausible markets the free market is above 60%, moreover, on all plausible markets the Transaction does not create any new link between previously independent consortia and a number of independent suppliers and consortia will remain active post-Transaction; the Transaction therefore does not raise serious doubts as to its compatibility with the internal market in respect of container liner shipping services in the NE – AUNZ northbound and southbound legs of trade.

(181) On the northbound and southbound legs of the Northern Europe – East Coast South America trade a total of [1-2] million TEUs was transported in 2015 ([0-5] million TEUs northbound of which [30-40]% reefer containers and [0-5] million TEUs southbound of which [10-20]% reefer containers). The Parties have a combined share for all containers of [40-50]% northbound (Maersk [10- 20]%, HSDG [20-30]%) and [40-50]% southbound (Maersk [10-20]%, HSDG [20-30]%). When considering the narrower market for reefer containers, the Parties have a combined share of [40-50]% northbound (Maersk [20-30]%, HSDG [20-30]%) and [50-60]% southbound (Maersk [20-30]%, HSDG [20- 30]%). There are also reefer vessels active on the trade transporting approximately [5-10]% of the entire reefer volumes northbound and [0-5]% southbound.

(182) In terms of the Parties' consortia on this trade, neither Maersk nor HSDG are member to any consortium on the trade, therefore their market shares on a consortia basis are equivalent to the individual market shares of HSDG and Maersk.

(183) On this trade the free market would remain close to 60% ranging between [40- 50]% in the southbound leg for reefer containers and [50-60]% in the northbound leg for all containers. Alternative players would remain active on this trade post- Transaction both in reefer containers as well as in dry containers including notably MSC, CMA CGM and Hapag-Lloyd; moreover reefer vessels are also active on the trade as alternative to reefer containers.

(184) In conclusion, on this trade, in some plausible markets the free market is above 60%, moreover, on all plausible markets the Transaction does not create any new link between previously independent consortia and a number of independent suppliers and consortia, which could easily expand their capacity, will remain active post-Transaction; the Transaction therefore does not raise serious doubts as to its compatibility with the internal market in respect of container liner shipping services in the NE – ECSA northbound and southbound legs of trade.

(185) On the northbound and southbound legs of the Mediterranean – Australia/New Zealand trade a total of [0-1] million TEUs was transported in 2015 ([0-1] million TEUs northbound of which [20-30]% reefer containers and [0-1] million TEUs southbound of which [5-10]% reefer containers). Across the plausible markets the Parties have a combined share ranging between [10-20]% for southbound reefer containers and [60-70]% for northbound reefer containers with an increment brought about by the Transaction reaching at most [0-5]%.

(186) In terms of the Parties' consortia on this trade, neither HSDG nor Maersk are member to any consortium on the trade, therefore their market shares on a consortia basis are equivalent to the individual market shares of HSDG and Maersk.

(187) On this trade the free market would remain close to (or above) 60% with the exception of the plausible markets for reefer containers northbound and for reefer containers and reefer vessels northbound where the free market would not go beyond [30-40]%. Alternative players would remain active on this trade post- Transaction both in reefer containers as well as in dry containers including notably MSC, CMA CGM and Hapag-Lloyd. The increments reach at most [0- 5]%.

(188) In conclusion, on this trade, in some plausible markets the free market is above 60%, moreover, on all plausible markets the Transaction does not create any new link between previously independent consortia, the increment is at most [0-5]% and a number of independent suppliers and consortia, which could easily expand their capacity, will remain active post-Transaction; the Transaction therefore does not raise serious doubts as to its compatibility with the internal market in respect of container liner shipping services in the MED – AUNZ northbound and southbound legs of trade.

(189) On the northbound and southbound legs of the Mediterranean – South Africa trade a total of [0-1] million TEUs was transported in 2015 ([0-1] million TEUs northbound of which [30-40]% reefer containers and [0-1] million TEUs southbound of which [5-10]% reefer containers). Across the plausible markets the Parties have a combined share ranging between [20-30]% for southbound dry containers and [40-50]% for northbound reefer containers only and reefer containers with reefer vessels with an increment brought about by the Transaction reaching at most [0-5]%.

(190) In terms of the Parties' consortia on this trade, neither HSDG nor Maersk are member to any consortium on the trade, therefore their market shares on a consortia basis are equivalent to the individual market shares of HSDG and Maersk.

(191) On this trade the free market would remain close to or above 60% ranging between [50-60]% in respect of the northbound leg for reefer containers only and reefer containers with reefer vessels and [70-80]% in respect of the southbound leg for dry containers. Alternative players would remain active on this trade post- Transaction both in reefer containers as well as in dry containers including notably MSC, DAL, CMA CGM and Messina. Further, the increments are not material, reaching at most [0-5]% in the northbound leg for reefer containers only.

(192) In conclusion, on this trade, in some plausible markets the free market is above 60%, moreover, on all plausible markets the Transaction does not create any new link between previously independent consortia, the increment is at most [0-5]% and a number of independent suppliers will remain active post-Transaction; the Transaction therefore does not raise serious doubts as to its compatibility with the internal market in respect of container liner shipping services in the NE – SAF northbound and southbound legs of trade.

(193) On the westbound and eastbound legs of the Mediterranean – Middle East trade a total of approximately [1-2] million TEUs was transported in 2015 ([1-2] million TEUs eastbound of which [10-20]% reefer containers and [0-1] million TEUs westbound of which [0-5]% reefer containers). On each leg of trade, the Parties have a combined share ranging from approximately [30-40]% for dry containers to [50-60]% for reefer containers. The actual increment brought about by the Transaction is marginal and at most [0-5]% on all plausible markets due to HSDG's limited presence on this trade.

(194) Alternative strong players would remain active on this trade post-Transaction both for all containers such as MSC, UASC and CMA CGM/APL with market shares of [20-30]%, [10-20]% (rising to [10-20]% when attributing Hapag-Lloyd's share to UASC), and [10-20]% respectively as well as reefer containers such as CMA CGL/APL UASC and MSC with market shares of [20-30]%, [10-20]% (rising to [10-20]% if Hapag-Lloyd's volumes are attributed together with UASC) and [10-20]% respectively.