Commission, October 13, 2017, No M.8102

EUROPEAN COMMISSION

Decision

VALEO / FTE GROUP

Dear Sir,

Subject: Case M.8102 – Valeo / FTE Group

Commission decision pursuant to Article 6(1)(b) in conjunction with Article 6(2) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

(1) On 7 September 2017 the Commission received notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 (the "Merger Regulation") by which Valeo Holding GmbH (Germany), controlled by Valeo S.A. ("Valeo" or "the Notifying Party", France), intends to acquire within the meaning of Article 3(1)(b) of the Merger Regulation sole control of the whole of FTE Group Holding GmbH ("FTE" or "the Target", Germany) by way of purchase of shares ("the Proposed Transaction"). (3) Valeo and FTE are collectively designated hereinafter also as "the Parties to the Proposed Transaction" or "the Parties" whilst the undertaking that would result from the Proposed Transaction is referred to as "the new entity".

1 THE PARTIES AND THE OPERATION

(2) Valeo is active in the design, manufacture and sale of automotive equipment, including in particular thermal systems, powertrain systems, comfort and driving assistance systems, and visibility systems.

(3) FTE is active in the design, manufacture and sale of (i) clutch actuation products; (ii) brake actuation products; (iii) electric transmission oil pumps and other components for gearboxes and powertrains based on electro-hydraulic technology. FTE is also active in the remanufacturing of brake calipers. Since 2013, FTE is fully owned by Falcon (BC) Luxco S.C.A. ("Bain Capital").

(4) On 2 June 2016, Valeo entered into an agreement with Bain Capital for the purchase of the whole of the share capital of FTE, which would result in the acquisition by Valeo of sole control over FTE. The Proposed Transaction therefore constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

(5) The Proposed Transaction was initially notified to the European Commission on 10 October 2016. That notification was withdrawn on 29 November 2016 after the Commission informed the Notifying Party following its preliminary investigation that the Transaction would raise serious doubts as to its compatibility with the internal market. On 30 November / 1 December 2016, the Parties entered into an amendment to the sale and purchase agreement intended to extend the drop dead date and allow the Parties to submit a revised notification to the European Commission in order to seek clearance of the Proposed Transaction. This notification was submitted on 7 September 2017.

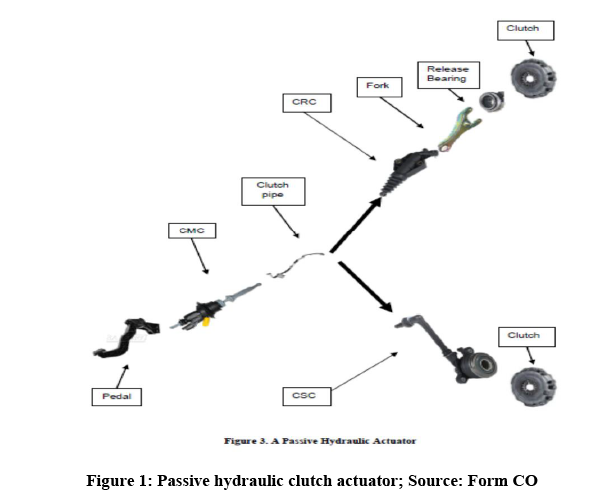

2 UNION DIMENSION

(6) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (Valeo: EUR 16 519 million; FTE: EUR 551.3 million). Each of them has a Union-wide turnover in excess of EUR 250 million (Valeo: EUR […]; FTE EUR: […]), but they do not achieve more than two-thirds of their aggregate Union-wide turnover within one and the same Member State. The notified operation therefore has a Union dimension within the meaning of Article 1(2) of the Merger Regulation.

3 RELEVANT PRODUCT AND GEOGRAPHIC MARKETS

(7) The Parties' activities mainly overlap in the production and sales of passive hydraulic clutch actuator modules and components, both for the original equipment manufacturer market (components to be installed on the vehicle upon first assembly ["OEM"] or intended as original spare parts ["OES"]) and the independent aftermarket ("IAM").

(8) Both Parties are also active on an IAM trading market, on which manufacturers buy and sell their components to other suppliers in order to complete the product range they offer to the IAM customers. Additionally, Valeo sells IAM clutch actuator kits. Depending on the specific kit, these include one or more components of a passive hydraulic actuation system that are manufactured by the Parties.

Clutch actuators

(9) Clutch actuators are part of the transmission system of a vehicle, which is part of a vehicle's powertrain system. The transmission system transfers the power generated by the vehicle's engine to its wheels. Within the transmission system, the actuators are modules used to engage and disengage the clutch in order to change gear.

(10) The technical functioning of actuators is different in manual and automatic transmission systems. In manual transmission systems, a single actuator is used to transfer the pressure exerted by the driver's foot on the clutch pedal to the clutch, allowing the separation of the engine and the transmission. In automatic transmission systems, several actuators, operated by an electronic device called the "transmission control unit", are needed to engage the clutch system, thereby eliminating the need for a clutch pedal and a gear lever. Clutch actuators can therefore be segmented into two main categories:

(1) passive actuators, which are activated by the pressure exerted by the driver's foot and can only be used with manual transmissions; and,

(2) active actuators, which are activated by the power generated by an electric motor and can be used only with automated transmissions.

(11) Within passive clutch actuators a further distinction could be drawn between:

(1) hydraulic actuators, which engage the clutch using hydraulic pressure; and,

(2) mechanical actuators, which use a steel cable that is directly connected to both the pedal and the fork, to transmit the pressure exerted by a driver's foot on the pedal to a fork and a release bearing, which is attached to the clutch.

Passive hydraulic clutch actuators

(12) The Parties' activities overlap as regards the production and sale of passive hydraulic clutch actuators.

(13) As explained above, passive hydraulic clutch actuators are used only in manual transmission and are composed of different elements, as detailed in the picture below:

(14) As shown above, the clutch pedal (operated by the driver) is directly connected by a push rod to a Clutch Master Cylinder ("CMC"). When pushing the clutch pedal, a piston inside the CMC is moved by the push rod and activates a hydraulic pressure, allowing the distribution of a fluid volume. The fluid volume circulates through the clutch pipe, regulated by a damper, and is transmitted either:

(1) to a Concentric Release Cylinder ("CRC"), a piston connected to the clutch pipe, which receives the hydraulic pressure sent by the CMC and applies it on a fork. This fork is then connected to the clutch through a release bearing, allowing it to engage and disengage the clutch (4) (i.e. semi-hydraulic passive hydraulic actuators); or

(2) to a Concentric Slave Cylinder ("CSC"), a cylinder integrating a release bearing that is directly connected to the clutch, which receives the hydraulic pressure sent by the CMC and applies it directly on the clutch (i.e. full-hydraulic passive hydraulic actuators).

3.1 Product market definitions

3.1.1 Automotive components in general

(15) In past decisions on automotive components, the Commission has consistently regarded each component as constituting a distinct product market. (5) The Commission has also previously identified separate relevant product markets depending on the channel into which the components are sold, as well as on the type of vehicle they are intended for.

(16) First, as regards the possible distinction between markets for automotive components according to distribution channels, the Commission concluded in previous decisions that the markets for automotive components are to be further divided into: (i) products for original equipment manufacturers ("OEM"), including products for the original equipment suppliers ("OES"), i.e. replacement parts sold to the OEM manufacturers (throughout this decision the sales to the OEM and the OES are jointly referred to as "OEM"); and (ii) replacement parts sold to the independent aftermarket ("IAM") which consists of independent wholesalers, fast-fitters, centralized purchasing groups and such. (6) The Notifying Party agrees with this market definition, which is retained for the case at hand.

(17) The Parties supply passive hydraulic clutch actuators for both the OEM and the IAM channels.

(18) Second, as regards the segmentation of the relevant product market according to the type of vehicles the components are intended for, the Commission has consistently considered separate relevant product markets for (i) components for passenger cars and light commercial vehicles ("LCV") and (ii) components for heavy duty commercial vehicles, including trucks. (7) The Notifying Party agrees with this segmentation. As Valeo does not produce actuators for heavy vehicles, the Parties' activities only overlap as regards passenger cars and LCVs. Hence, for the purpose of this decision, the relevant market with regard to the type of vehicles the components are intended for is the market for components for passenger cars and LCVs. Passenger cars and LCVs are jointly referred to as "light vehicles" throughout this decision.

3.1.2 OEM passive hydraulic actuator modules and components for light vehicles

3.1.2.1 Active actuators and passive actuators

The Notifying Party's view

(19) As regards the OEM market, the Notifying Party considers different possible segmentations of the product market.

(20) The Notifying Party submits that active actuators and passive actuators belong to different product markets, for the following reasons:

(21) First, active actuators include more sophisticated components which require specific electrical, mechanical and electronics know-how. Passive actuators on the contrary are mostly composed of more basic technology components.

(22) Second, active actuators are significantly more expensive than passive actuators; whereas prices for active actuators range from EUR 100 to EUR 300, prices for passive actuators vary between EUR 10 and EUR 30.

(23) Third, suppliers for passive and active actuators are not necessarily the same.

The Commission's assessment

(24) For the reasons set out below, the Commission takes the view that passive and active clutch actuators form part of distinct product markets.

(25) With reference to demand side considerations, the market investigation indicated that active actuators, which can only be used in automated transmissions, cannot be considered suitable for substituting passive actuators, which can only be used in manual transmissions. (8) According to respondents to the market investigation, this is both because of significant price differences and differences in the intended use of the products.

(26) As regards the technical considerations, OEM customers responding to the market investigation indicated that the underlying technology for active actuators and passive actuators is different. Therefore active and passive actuators cannot be used interchangeably with the same gearbox. (9)

(27) In terms of prices, the market investigation indicated that, as submitted by the Notifying Party, active actuators are significantly more expensive than passive actuators, also as a consequence of the fact that they are technologically more complex products.

(28) As regards the supply side, the market investigation indicated that the production process of active and passive actuators is different and that manufacturers need to employ different production lines.

(29) In light of the foregoing and the results of the market investigation, the Commission takes the view that active clutch actuators and passive clutch actuators constitute separate product markets. As the Parties' activities do not overlap in the production and sale of active actuators, only the market for passive clutch actuators will be further analysed in this decision.

3.1.2.2 Passive hydraulic clutch actuators and mechanical clutch actuators

The Notifying Party's view

(30) The Notifying Party submits that it is appropriate to further segment the market for the production and sale of passive clutch actuators into passive hydraulic actuators and mechanical actuators, because of technology and price differences and limited supply substitutability between them.

(31) Under this market segmentation, the Parties only have overlapping activities in the EEA on the market for passive hydraulic clutch actuators. For that reason, the Notifying Party considers the relevant market to be the OEM market for passive hydraulic actuators for light vehicles.

The Commission's assessment

(32) For the reasons set out below, the Commission takes the view that mechanical actuators and passive hydraulic actuators form part of different product markets.

(33) First, although serving similar purposes, i.e. the operation of manual transmissions, mechanical actuators function according to a different mechanism compared to passive hydraulic actuators. A mechanical actuator more specifically pushes on a component which engages the clutch, whereas a hydraulic actuator applies hydraulic pressure on a component in order to engage the clutch.

(34) More precisely, in a mechanical actuator a steel cable, directly connected to the pedal, transmits the pressure exerted by the driver’s foot on the pedal to a fork and a release bearing attached to the clutch. Mechanical actuators are based on a very simple technology and offer limited comfort to the driver. Mechanical actuators are mainly used in China and emerging markets. In the EEA mechanical actuators have been replaced over time by passive hydraulic actuators and now constitute only 2% of the total actuator market for manual transmissions. (10)

(35) Passive hydraulic clutch actuators function according a different mechanism. As explained above in paragraph 14, passive hydraulic actuators employ hydraulic pressure in order to activate the clutch.

(36) Second, respondents to the market investigation indicated that the manufacturing passive hydraulic clutch actuators is highly complex and requires specific know-how.

(37) Finally the average price of a mechanical actuator is significantly lower than that of a passive hydraulic actuator. According to the information provided by the Notifying Party a passive hydraulic clutch actuator costs on average more than double the average price of a mechanical actuator. (11)

(38) In light of the foregoing and the results of the market investigation, the Commission takes the view that mechanical clutch actuators and passive hydraulic clutch actuators constitute separate product markets. As the Parties' activities do not overlap in the production and sale of mechanical actuators, only the market for passive hydraulic clutch actuators will be further analysed in this decision.

3.1.2.3 Passive hydraulic clutch actuators systems and individual components

The Notifying Party's view

(39) The Notifying Party submits that the relevant product market is the market for passive hydraulic clutch actuators sold as a system and that it would be inappropriate to further segment the product market into the various components of a passive hydraulic clutch actuator system, i.e. Clutch Master Cylinder ("CMC"), Concentric Release Cylinder ("CRC"), Concentric Slave Cylinder ("CSC"), clutch pipe (12), fork (13) and release bearing. (14)

(40) According to the Notifying Party this is so, first, because in almost half of the tender instances, car manufacturers request bids for the full passive hydraulic actuation module or at least two components together.

(41) Second, the Notifying Party submits that such segmentation into components would be inappropriate as the Commission has often considered that the module, and not its individual components, constitutes the relevant product market in the car part sector. (15)

The Commission's assessment

(42) For the reasons set out below, the Commission takes the view that it is appropriate to consider separate product markets both for the passive hydraulic clutch actuators systems as a whole and for each of the components thereof.

(43) The market investigation supports the view that passive hydraulic actuator systems form a separate relevant product market from those for individual components. (16)

(44) From the supply side, the market investigation indicated that manufacturing a complete passive hydraulic actuator system requires specific engineering expertise as knowledge of the entire release system and of adjacent systems is necessary, which a components-only supplier may not have. (17) Indeed, certain suppliers only compete as regards components, and are generally not invited to tenders concerning passive hydraulic actuator modules. A competitor responding to the market investigation indicated that – contrary to the Parties and other competitors – it is only supplying individual components and not the entire passive hydraulic clutch actuator system. This is also confirmed by the analysis of the bidding information relating to tenders in which either of the Parties participated from 2011 to 2017 (the "Bidding Data"). The Bidding Data indicates that in all but 3 tenders for modules only the Parties and LuK competed, whereas fringe competitors such as Aisin and Sachs have been observed only in tenders for individual components.

(45) From a demand side perspective, customers may decide to only purchase certain individual components rather than entire modules or vice-versa, depending on their purchasing strategy and on their ability to assemble and tune the complete release system themselves. This is supported by the analysis of the Bidding Data submitted in the course of the investigation, which shows that the majority of tenders are for individual components or bundles of at least two components ([…] recorded tenders) rather than for the full module ([…] recorded tenders). This observation indicates that there is a distinct and significant demand for individual components alongside that for the modules.

3.1.2.4 Conclusion on the OEM relevant product markets

(46) In light of the foregoing, the Commission considers, on the basis of the market investigation results and the other evidence available to it, that the relevant market is at most as wide as the sale of passive hydraulic clutch actuators systems for light vehicles, although a further segmentation can be considered between the sale of passive hydraulic clutch actuators modules and each of the individual components thereof. However, whether the relevant market constitutes a market which includes all the sales of passive hydraulic actuators systems and individual components or has to be segmented further can be left open for the purpose of this decision, as the Proposed Transaction raises serious doubts as to its compatibility with the internal market in relation to the sales of passive clutch actuators irrespective of the exact product market definition.

3.1.3 IAM passive hydraulic actuator modules and components for light vehicles

The Notifying Party's view

(47) On the IAM, FTE only sells individual components (i.e. CMCs, CRCs and CSCs), whereas Valeo supplies individual components and clutch kits.

(48) Spare parts sold in the IAM can be original equipment ("OE") components developed for the OEM market or so-called adaptable parts, i.e. parts that are developed for the IAM by other suppliers using a similar technology but which do not meet the same durability and quality standards as the OE parts. Adaptable parts are manufactured and sold by both OE suppliers (for car models for which they are not an OEM supplier) and IAM-only suppliers. According to the Notifying Party, it is generally not possible to distinguish OE parts from adaptable parts, as there are no specific markings in catalogues or on the products themselves that would allow distinction between them. Also, adaptable parts are not necessarily sold at a lower price. (18)

(49) Like for the OEM market, the Notifying Party submits that there is a relevant IAM for passive hydraulic actuators, but considers that a narrower market definition for CMCs, CRCs and CSCs sold as stand-alone products on the IAM is plausible. Market share data for these segments has thus been submitted.

The Commission's assessment

(50) The Commission notes that on the IAM segment demand is driven by the need to replace a broken component. Passive hydraulic actuator components can be, and are, replaced separately, without changing the entire module. There is thus specific demand on the IAM for individual components. Indeed, it appears that the entirety of the Parties' IAM sales in the area of passive hydraulic actuators consists of parts sold on a stand-alone basis or, in the case of CSCs, in kits (consisting of a CSC and other parts like a drive plate, cover assembly and DMF) but not of passive hydraulic actuator modules as a whole. (19)

(51) All IAM competitors surveyed in the market investigation indicated that they only sell individual components separately and not entire modules. Furthermore, some IAM suppliers only manufacture and sell certain actuator components: for instance, Metelli only sells CMCs, Donaflex only sells CSCs and Nueva Tecnodelta sells CMCs and CSCs but not CRCs. (20)

(52) Therefore, in light of the results of the market investigation and the evidence available to it, the Commission considers, for the purpose of this decision, that there are separate relevant product markets for individual passive hydraulic actuator components, namely CMCs, CRCs and CSCs, sold on the IAM.

3.1.4 Trading market for passive hydraulic actuator components for light vehicles

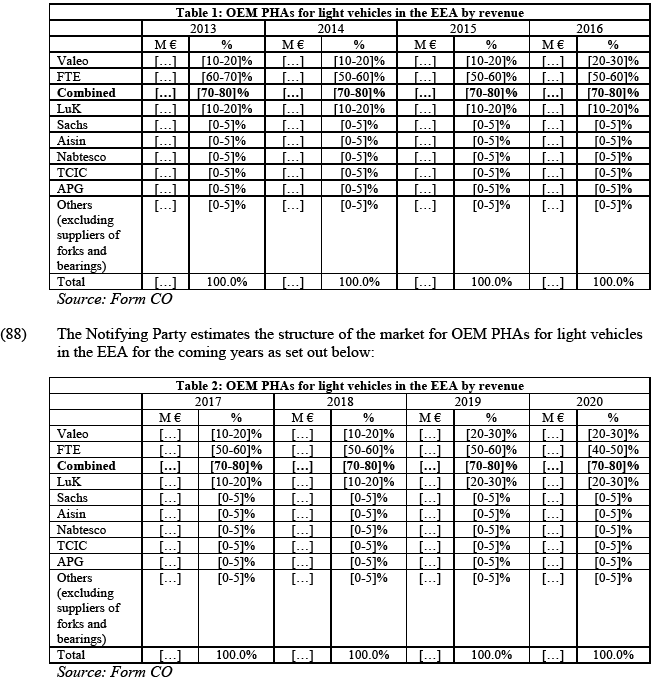

The Notifying Party's view

(53) The Notifying Party submits that there is a trading market for passive hydraulic actuator components, which are intended to be resold to IAM distributors or to be included in clutch kits. On this market, OE suppliers usually distribute their own original spare parts and purchase OE and adaptable spare parts from their competitors, or adaptable parts from IAM-specific suppliers or wholesalers in order to complete their product line and be able to propose a full-range of products to their customers, or in order to integrate them in clutch kits. Parts purchased on this market are then resold under the purchaser's own brand name.

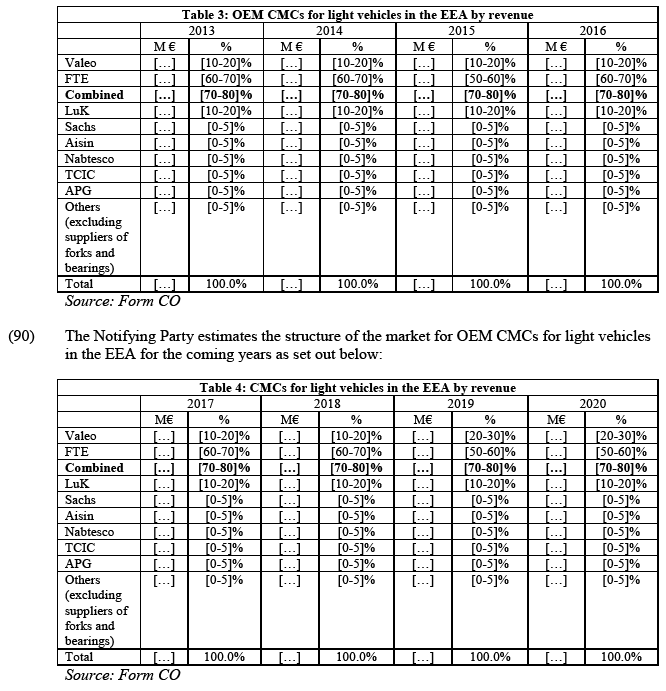

(54) Both Parties are active on this trading market as regards passive hydraulic actuator components.

The Commission's assessment

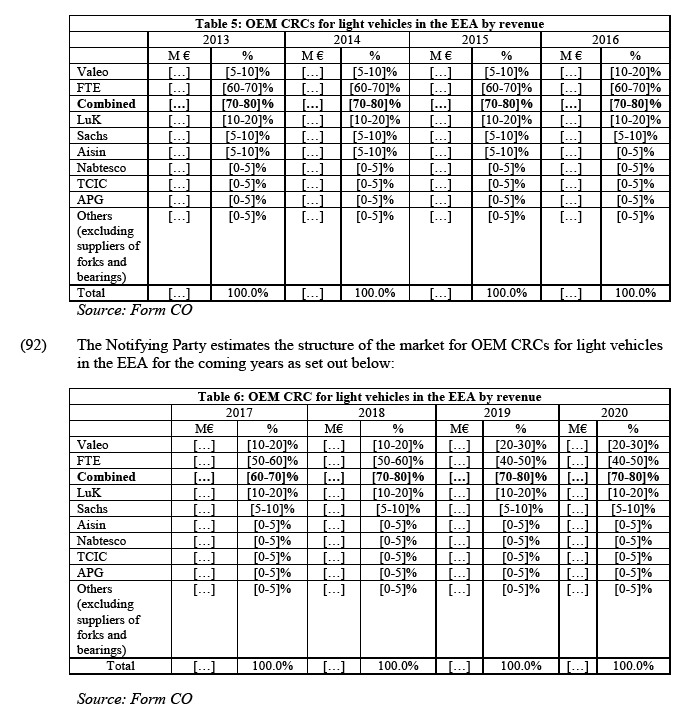

(55) The Commission has not previously considered a trading market for automotive spare parts destined for sale in the IAM. In the present case, the market investigation has confirmed the existence of exchanges of passive hydraulic actuator components between suppliers on a so-called trading market. On this market, OE suppliers and IAM-specific suppliers sell and purchase spare parts to and from each other with the purpose of extending their product range or sourcing inputs for kits. (21)

(56) The Commission considers that the trading of passive hydraulic actuator components could be plausibly considered to constitute a relevant product market separate from, and upstream of, that for the supply of spare parts to IAM wholesale distributors. On this trading market, suppliers face different customer groups than in the IAM: buyers of components are primarily other suppliers of spare parts rather than IAM distributors. These purchase components on the trading market in order to complete their product portfolio and be able to offer a complete offering to their customers (IAM distributors). In addition, these products are sourced on an EEA, rather than national, level (see also section 3.2.3).

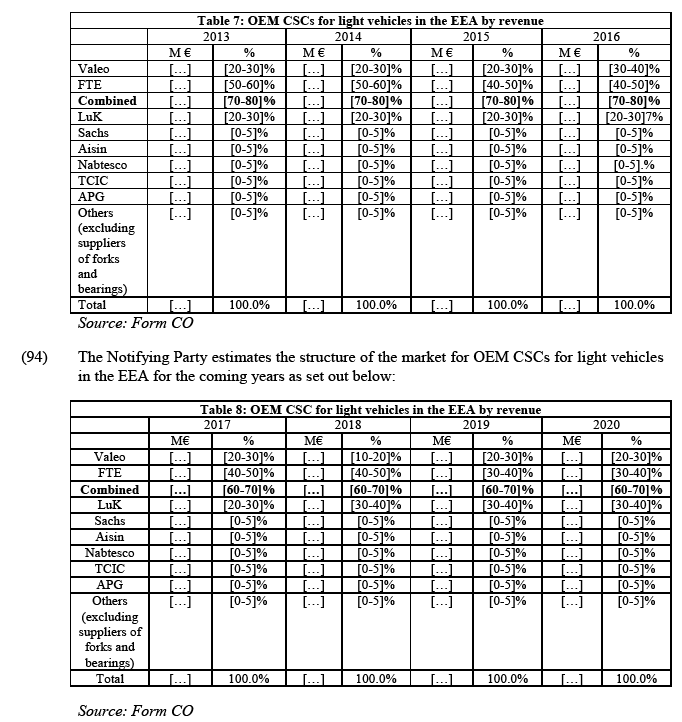

3.1.5 The IAM clutch kits for light vehicles

The Notifying Party's view

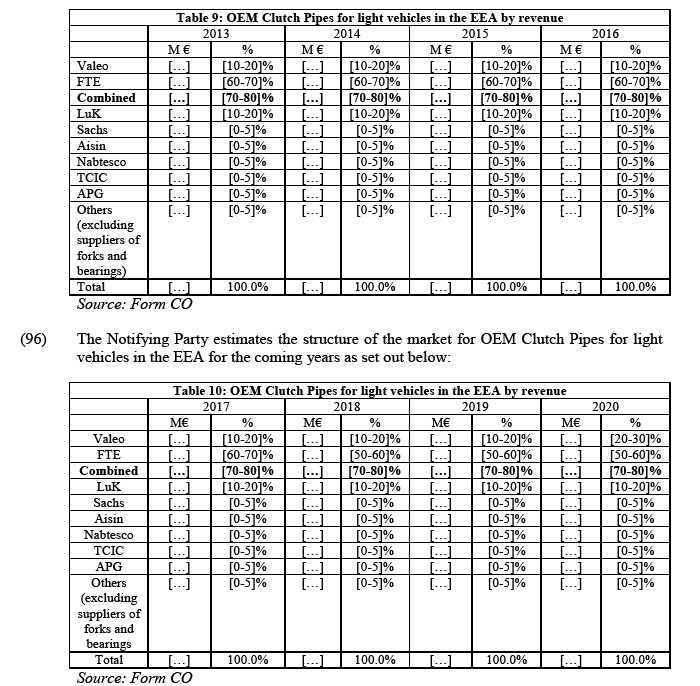

(57) Valeo sells the following types of clutch kits: (i) three-piece kits, composed of a drive plate, a cover assembly and a CSC (for cars equipped with a passive hydraulic actuator) or a release bearing (for cars equipped with a mechanical actuator) (22), (ii) dual-mass flywheel ("DMF") kits, including a drive plate, cover assembly, a DMF and a CSC or release bearing, and (iii) four-piece kits, composed of a drive plate, cover assembly, a CSC or release bearing and rigid flywheel instead of a DMF.

(58) A DMF is a rotating mechanical device used in the clutch system in order to reduce the engine's vibrations, noise and fuel consumption, in particular when the engine runs at low speeds. A rigid flywheel is a device that has the same purpose of reducing the mechanical vibration so as to limit premature wear within the gearbox, but it is based on a different technology than a DMF. (23)

(59) The Notifying Party submits that there is a trend in the IAM towards more sales of kits rather than of individual components: because of the high labour costs involved in replacing individual clutch components, mechanics sometimes recommend changing the entire transmission system at once even if some parts of it are still functioning well, so as to avoid incurring the labour costs of assembling and disassembling the clutch each time a component is broken. (24)

(60) The Notifying Party does not submit a precise definition of the relevant kits market, but appears to consider that there are plausible separate markets for three-piece kits and DMF kits (including rigid flywheel kits, which, according to the Notifying Party, are substitutable from a demand-side perspective with actual DMF kits) and has submitted market share data for these segments.

The Commission's assessment

(61) The market investigation was inconclusive as to whether three-piece kits, DMF kits and rigid flywheel kits constitute distinct relevant markets. However, taking into account that the Parties' activities do not overlap as regards kits and the Proposed Transaction does not raise concerns of a vertical nature, the Commission considers that for the purpose of this decision, the precise market definition with respect to clutch kits can be left open.

3.2 Geographic market definition

3.2.1 OEM passive hydraulic actuator modules and components for light vehicles

The Notifying Party's view

(62) In line with previous Commission decisions in the automotive components industry, (25) the Notifying Party submits that the geographic scope of the OEM market for passive hydraulic actuators is EEA-wide.

(63) According to the Notifying Party, this is because:

(1) transportation costs within the EEA are not significant ([0-5]%);

(2) there are no other obstacles to intra-EEA trade;

(3) prices and delivery conditions are homogeneous within the EEA;

(4) purchasers do not source on a purely national basis but rather on an EEA-wide or global basis;

(5) similar conditions of competition apply throughout the EEA, because there is extensive inter-state trade and because suppliers tend to serve the entire EEA from only a few plants located within the EЕA. (26)

(64) Additionally, the Notifying Party submits elements to substantiate its claim that the geographic scope of the OEM market for passive hydraulic actuators is larger than the EEA. According to the Notifying Party, this is because (i) in the field of passive hydraulic actuators, [80-90]% of the tenders relate to global platforms and are wider than the EEA, (ii) the Parties and other main suppliers of passive hydraulic actuators export significant volumes from the EEA into Asia and South America, and (iii) transportation costs for passive hydraulic actuators are relatively low (about [0-5]% of their selling price within the EEA and [5-10]-[5-10]% between the EEA and South America or Asia). (27)

The Commission's assessment

(65) In line with its past decisional practice on automotive components, (28) the Commission takes the view that the OEM markets for passive hydraulic actuators sold in modules, as well as each of the markets for the components, are EEA-wide in scope.

(66) A large majority of respondents to the Commission's market investigation indicated that they do not purchase OEM passive hydraulic actuator modules or components from suppliers located outside the EEA, (29) nor do they invite them to participate in tenders. (30) The main reason for sourcing within the EEA is the good reputation of the existing EEA- suppliers and the fact that, due to consumer preferences, the demand and supply for manual transmission systems, and thus for passive hydraulic actuators, mainly lies in the EEA, whereas demand and supply outside the EEA rather focusses on automatic transmission systems.

(67) In addition, although the majority of customers indicated that transport costs are not as high as to limit their ability to source passive hydraulic actuators from outside the EEA, the supplier's proximity to their manufacturing plants is an advantage. (31)

(68) Therefore, for the purpose of this decision the Commission considers that the geographic scope of the relevant market for the sale of passive hydraulic modules and components for light vehicles in the OEM market is EEA-wide.

3.2.2 IAM passive hydraulic actuator components for light vehicles

The Notifying Party's view

(69) The Commission has in the past considered the geographic scope of the various IAM markets to be national. (32) The Notifying Party however submits that the relevant geographic market could be wider than national, and possibly EEA-wide, because (i) in the field of passive hydraulic actuators, suppliers are able to deliver spare parts across the EEA, and global and European buying groups represent the major share of the Parties' total sales in the IAM (i.e. around […]% for Valeo and […]% for FTE), (ii) suppliers located outside the EEA are able to and do supply passive hydraulic actuator spare parts in the EEA, (iii) the Parties also export passive hydraulic actuation parts from the EEA to for instance South America, and (iv) the main EU suppliers of passive hydraulic actuators in the IAM are organised not only on the basis of national but also transnational structures. (33)

(70) The Notifying Party has nevertheless submitted market shares on both an EEA and a national basis for each of the IAM product markets affected by the Proposed Transaction.

The Commission's assessment

(71) The evidence submitted by the Parties and collected in the market investigation suggests that on the IAM competition takes place primarily on a national level. Both the Parties and their competitors confirmed that prices are determined at the level of each country, (34) resulting in significant differences between the prices at which passive hydraulic components are sold in each country. (35)

(72) As regards international buying groups, these do not purchase components as such from suppliers, nor are they in charge of negotiating prices on behalf of their members. The Commission in that respect refers to the Notifying Party's explanation that while buying groups may be involved in negotiating certain discounts or rebates, prices are determined in contracts concluded between individual members and suppliers "at the local level, taking into account the market conditions that may exist locally". (36)

(73) Furthermore, the Commission notes that not all suppliers are active in all national markets. (37) As regards the organisation of IAM activities of suppliers active across multiple countries, the majority of participants to the market investigation indicated that their IAM activities are organised on the basis of both national and regional or EEA entities. Only one competitor, which has limited activities on the IAM, indicated that it supplies customers on the basis of regional entities only. (38)

(74) On the demand side, customers indicated that they source passive hydraulic actuators and components both at national and at EEA level. (39)

(75) In light of the results of the market investigation and the evidence available to it, the Commission considers that the geographic scope of IAM markets is likely not wider than national. While there are suppliers that are active across the EEA, and while some customers purchase outside their country, conditions of competition and prices may differ significantly across countries. Therefore, for the purpose of this decision, the Commission takes the view that the relevant geographic market for the manufacture and sale of passive hydraulic actuator components is national in scope.

3.2.3 Trading market for passive hydraulic actuator components for light vehicles

The Notifying Party's view

(76) The Notifying Party submits that the trading market for passive hydraulic actuator components is at least EEA-wide in scope, as suppliers usually source passive hydraulic components at the EEA level. (40)

The Commission's assessment

(77) The Commission has not previously considered a trading market for automotive spare parts destined for sale in the IAM. Based on information submitted by the Parties and that collected in the market investigation, the main suppliers on the trading market for passive hydraulic actuator components primarily are FTE, Valeo, LuK and Sachs, which source from each other on an EEA-wide basis. (41)

(78) The geographic scope of the trading market can therefore be plausibly defined as EEA- wide.

3.2.4 IAM DMF kits and components for light vehicles

The Notifying Party's view

(79) The Notifying Party does not put forth a precise geographic market definition as regards kits.

The Commission's assessment

(80) In line with its decisional practice in the area of manufacturing and supply of spare parts to IAM customers (42) and with its assessment in respect of passive hydraulic actuator components as described in paragraphs (71) to (75), the Commission considers that the relevant geographic market for the manufacture and sale of clutch kits can plausibly be defined as national in scope. The customers and procurement methods are the same as in the case of passive hydraulic actuator components. Suppliers of clutch kits on the IAM are organised on the basis of national entities. (43)

4 COMPETITIVE ASSESSMENT

4.1 Introduction

(81) Under Articles 2(2) and 2(3) of the Merger Regulation, the Commission must assess whether a proposed concentration would significantly impede effective competition inthe internal market or in a substantial part of it, in particular through the creation or strengthening of a dominant position.

(82) As regards the assessment of horizontal overlaps, the Commission guidelines on the assessment of horizontal mergers under the Council Regulation on the control of concentrations between undertakings (44) (the "Horizontal Merger Guidelines") distinguish between two main ways in which mergers between actual or potential competitors on the same relevant market may significantly impede effective competition, namely non- coordinated and coordinated effects. Non-coordinated effects may significantly impede effective competition by eliminating important competitive constraints on one or more firms, which consequently would have increased market power, without resorting to coordinated behaviour. In this regard, the Horizontal Merger Guidelines consider not only the direct loss of competition between the merging firms, but also the reduction in competitive pressure on non-merging firms in the same market that could be brought about by the merger.

(83) The Horizontal Merger Guidelines list a number of factors which may influence whether or not significant non-coordinated effects are likely to result from a merger, such as the large market shares of the merging firms, the fact that the merging firms are close competitors, the limited possibilities for customers to switch suppliers, or the fact that the merger would eliminate an important competitive force. Not all of these factors, indicated in the Horizontal Merger Guidelines as relevant to the analysis of non-coordinated effects, need to be present to make significant non-coordinated effects likely. Also, the list of factors is not exhaustive.

(84) A significant impediment to effective competition can result in particular from the creation or streghtening of a dominant position. Also, according to recital 25 of the Merger Regulation, a significant impediment to effective competition can also be established from anticompetitive effects from the non-coordinated behaviour of undertakings which would not have a dominant position on the market concerned.

(85) On the basis of these elements, the Commission has carried out an extensive competitive assessment of the Proposed Transaction in order to assess whether it raises serious doubts with regard to its compatibility with the internal market and therefore, whether proceedings need to be initiated pursuant to Article 6(1)(c) of the Merger Regulation.

4.2 Non-coordinated horizontal effects

4.2.1 OEM passive hydraulic actuator ('PHAs') modules and components for light vehicles

(86) The Proposed Transaction leads to a further concentration on already highly concentrated markets. It reinforces the dominant market position of the Target by removing an important and close competitor on the markets for OEM passive hydraulic actuator modules and components for light vehicles in the EEA. Switching, barriers to entry and expansion as well as potential competition and countervailing buyer power are not likely to constitute sufficient constraints on the new entity.

4.2.1.1 Market structure

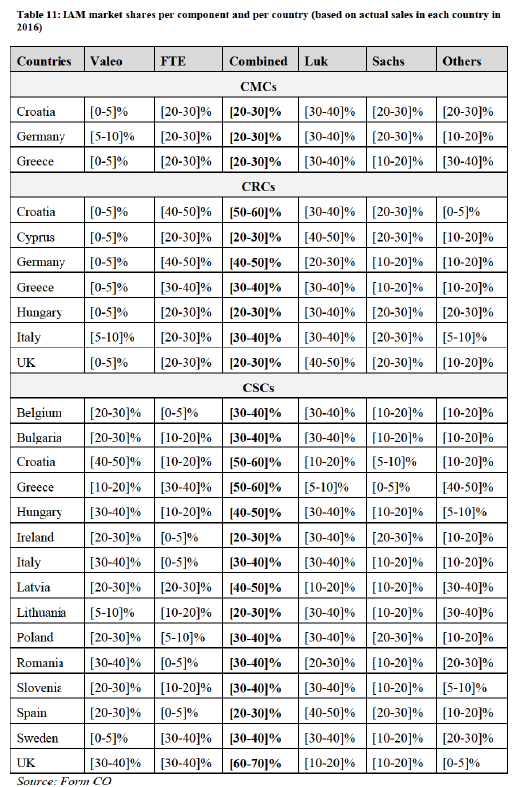

OEM PHAs

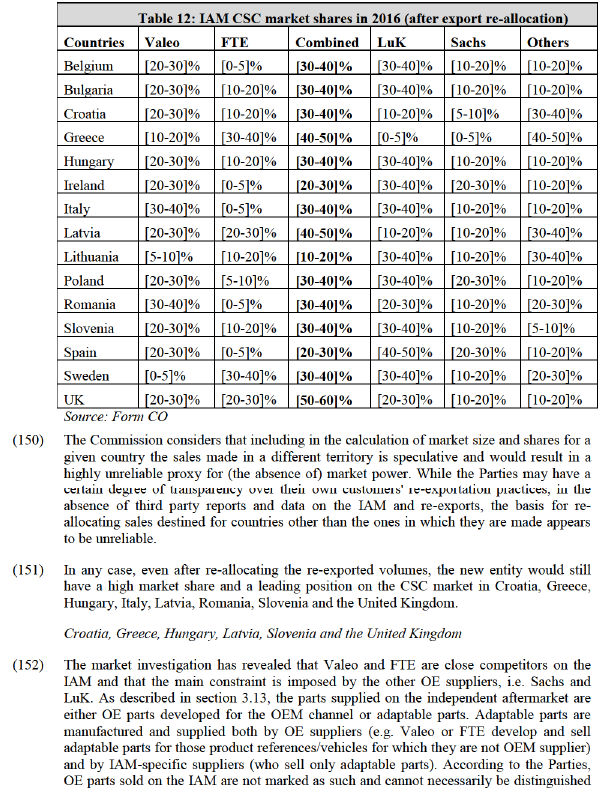

(87) The Notifying Party estimates the structure of the OEM market for PHAs for light vehicles in the EEA over the last years as set out below:

OEM CMCs

(89) The Notifying Party estimates the structure of the market for OEM CMCs for light vehicles in the EEA over the last years as set out below:

OEM CRCs

(91) The Notifying Party estimates the structure of the market for OEM CRCs for light vehicles in the EEA over the last years as set out below:

OEM CSCs

(93) The Notifying Party estimates the structure of the market for OEM CSCs for light vehicles in the EEA over the last years as set out below:

OEM Clutch Pipes

(95) The Notifying Party estimates the structure of the market for OEM Clutch Pipes for light vehicles in the EEA over the last years as set out below:

(97) It follows from the above that the Proposed Transaction would create the largest player on both the market for PHAs sold in modules and on each of the markets for PHA components, with a market share that is often more than four times higher than the market share of the second largest player (LuK).

(98) The Parties' combined market share on the markets for PHAs sold in modules and the markets for individual components has been consistently above [70-80]% over the last years and is expected to remain above this level over the next years. The market share of LuK has been consistently below [20-30]% (except on the market for CSCs) over the last years and is expected not to exceed that level in the following years.

(99) The increment that results from the Proposed Transaction is comparable to the market share of LuK and significantly higher than that of Sachs or Aisin, which are the only other market players with shares above [0-5]%. The HHI index for the overall PHAs market resulting from the Proposed Transaction will be [5900-6000] with a delta of [2200-2300].

(100) The market share estimates for the respective components of PHAs show a similar picture.

(101) In light of the above information, this Decision will examine whether due to the significant market position of the one or both Parties, the Proposed Transaction would lead to anticompetitive effects with regard to the OEM market for PHAs.

4.2.1.2 Closeness of competition The Notifying Party's view

(102) The Notifying Party submits that, following the Proposed Transaction, the new entity will face competition from numerous established suppliers. According to the Notifying Party, these established competitors are LuK, Sachs and Aisin. Moreover, the Notifying Party submits that the Parties are not close competitors, because the Parties' Bidding Data for EEA tenders between 2011 and 2017 shows that FTE and LuK met in the large majority of tenders ([…]), while Valeo participated only in […] tenders, in all of which it met LuK and in most of them also FTE ([…]). (45)

The Commission's assessment

(103) The Commission considers that the Proposed Transaction would reduce the number of significant players in the market for PHA modules and components from three to two. Currently, FTE, Valeo and LuK are the main competitors in this market, while post- Transaction only the new entity and LuK would remain as significant players. The market shares estimates provided by the Notifying Party suggest that currently FTE, Valeo and LuK account for more than [90-100]% of the market while all the remaining players together account for less than [10-20]% of the market.

(104) The results of the market investigation have confirmed that LuK has been competing in tenders with both Parties over the last three years. (46) This is also in line with the Bidding Data provided by the Notifying Party, which shows that both Parties met LuK in almost all the tenders in which they participated.

(105) Contrary to the Notifying Party's submission, the market investigation suggests that Sachs is not competing effectively with the Parties and LuK in the EEA. (47) While it may continue to serve some legacy business relationships, Sachs does not seem to actively compete for market share in this product market any longer. This is also in line with Sachs' low market share (of below [0-5]%) over the last four years and the fact that – according to the Bidding Data provided by the Notifying Party – Sachs participated in only […] of the […] tenders, of which it won only two.

(106) The market investigation further suggests that Aisin is not competing effectively with the Parties and LuK in the EEA. (48) This is in line with the Bidding Data, which shows that none of the Parties met Aisin in any of the tenders in which they participated in the last years. This is also in line with the low market share of Aisin, of below [0-5]% over the last four years. The market investigation suggests that this is the case because Aisin's customers are mostly Asian car manufacturers with a strong focus on cars fitted with automatic transmission systems. Therefore, Aisin does not have a strong focus on manual transmission systems in general and passive hydraulic actuation systems in particular. Although Aisin produces some of these systems, mainly for cars destined for the EEA market, the products are considered less sophisticated than those of the European competitors. Moreover, it should be noted that some car manufacturers may not consider Aisin as an independent supplier, because they are partly owned by Toyota, which holds a 30% stake in this company. (49)

(107) In conclusion, based on the evidence available to it, the Commission finds that the Parties are two of the three main competitors in the EEA market for PHA modules and components, and that the competitive constraint represented by suppliers other than LuK is very limited.

4.2.1.3 Switching

The Notifying Party’s view

(108) The Notifying Party submits that customers could reallocate some of the new entity's volumes to alternative competitors, if they were dissatisfied with its prices, quality or conditions of delivery. (50) While contracts generally last for five years, they are eligible for early termination. Whereas OEMs may need up to two years to reallocate an on-going platform, suppliers can adjust their equipment within several days or weeks if significant changes to the equipment are necessary. The costs on the part of the OEM may range from EUR 0.5 million for adjustments to existing equipment to EUR 2.5 million for a new production line, which includes approximately EUR 1 million for the development phase and up to EUR 1.5 million for the production line. The Notifying Party submits that suppliers can and do switch. In particular, the Notifying Party mentioned the example of Renault / Nissan, which tendered a contract for a platform for 3 years in 2012 and then re- tendered the contract in 2015. (51)

The Commission’s assessment

(109) The Commission considers it unlikely that - by switching suppliers - customers will be able to counterbalance the elimination of the important competitive constraint brought about by the Proposed Transaction.

(110) As shown above, the Proposed Transaction reduces the number of significant suppliers from three to two on the OEM market. Moreover, the Notifying Party itself concedes that OEMs may need up to two years to reallocate an ongoing platform. (52) The Notifying Party further submits that switching costs may deter customers in cases where they tender very small volumes of passive hydraulic actuators or components. (53) In that regard the Commission notes that the Notifying Party considers the market for PHA and components to be in decline. (54) Therefore, the number of contracts limited to smaller volumes is likely to increase over time. Finally, the Notifying Party submits that customers generally extend the contracts for on-going platforms, although the Notifying Party attributes this to suppliers agreeing on requests for cost savings. (55)

(111) The results of the market investigation suggest that supply contracts usually last 5-10 years. While OEMs may switch suppliers after the end of the contract, the market investigation suggests that they almost never switch suppliers for PHAs modules or components before the end of the agreed contract term. Indeed, none of the respondents has done so in the last five years. This can be explained by the fact that switching suppliers during an on-going contract entails significant risks for the OEM, such as delays and additional quality risks. In addition, the Bidding Data suggests that OEMs only very rarely engage in multi-sourcing strategies. This observation has been confirmed by the market investigation, according to which only a small minority of suppliers has engaged in multi- sourcing of PHA modules and components over the last 10 years.

(112) In conclusion, in light of the results of the market investigation and of the evidence available to it, the Commission considers that OEMs face significant barriers to switching to a new supplier, in particular during an ongoing contract.

4.2.1.4 Barriers to entry

The Notifying Party’s view

(113) The Notifying Party submits that new players, which are active in the supply of OEM PHA modules and components outside the EEA, may enter the EEA market for OEM PHA modules and components within the next two to three years, because the technical barriers to entry are low. Firstly, the technology is mature and has already been developed by numerous players outside the EEA. Secondly, the production process does not require complex production tooling. Thirdly, there are no major technical innovations which would prevent competitors from outside the EEA to enter the EEA because most innovations involve only incremental improvements that reduce costs or improve quality. The Notifying Party further suggests that OE customers in the EEA may not require suppliers to provide state-of-the-art products such as full-plastic CSCs and sensors because they may be more interested in the price than in the technology. Finally, the Notifying Party submits that patents in this field essentially protect a new design or process and do not prevent competitors from developing alternatives to the details of this design. The Notifying Party noted in particular that TCIC, a Korean supplier, entered the European market for PHAs five years ago as a supplier of Hyundai. (56)

The Commission’s assessment

(114) The Commission considers that barriers to entry to the market for PHA modules and components are likely to be higher than described by the Notifying Party.

(115) Firstly, with regard to the market entry by TCIC, the Notifying Party itself estimates that TCIC's market share has remained below [0-5]% and is unlikely to increase in the near future. Moreover, there is no other reliable evidence of any other significant entry during the last five years. Neither customers nor competitors are aware of suppliers having entered the EEA market in the last five years. (57) Moreover, neither customers nor competitors expect entry of new suppliers in the coming five years. (58)

(116) Secondly, the market investigation suggests that it takes considerable costs and time to set up a plant for the production of PHA modules and components in the EEA. The Commission understands that entry by a supplier who already has been supplying OEM passive hydraulic actuators modules and components for light vehicles outside the EEA could take more than 2 years, while suppliers active only on the IAM would need significantly more time.

(117) Thirdly, the market investigation suggests that barriers to entry are significant, (59) in particular given the need for suppliers to demonstrate a track record (60) and the fact that customers may require quality certifications, (61) as well as a track record of several years, specifically in the supply of PHA modules and components. (62) This is in line with the fact that market players emphasised that PHAs are a critical product in any vehicle.

(118) Fourthly, the market investigation suggests that there are significant barriers to entry with regard to innovation, IP and know-how. (63) Innovations may relate to Noise Vibration Harshness (NVH), sensor technology, product durability and process and other aspects.

(119) Fifthly, the Notifying Party itself has noted at several instances that the market for PHAs is a declining market in the EEA. (64) The Notifying Party estimates that the total market size will decrease by [5-10]% in value and by [5-10]% in volume from 2015 to 2020. (65)

(120) In light of the results of the market investigation and the evidence available to it, the Commission considers that the barriers to entry into the market for PHA actuator modules and components are significant and that entry is unlikely, in particular when taking into account the limited incentives of a potential entrant to overcome such barriers in order to enter into a declining market. This is in line with the fact that there has been no significant entry in the last 5 years and that neither customers nor competitors expect such entry in the coming 5 years.

4.2.1.5 Countervailing buyer power The Notifying Party's view

(121) The Notifying Party notes that, according to the Horizontal Merger Guidelines, "[e]ven firms with very high market shares may not be in a position, post-merger, to significantly impede effective competition, in particular, by acting to an appreciable extent independently of their customers if the latter possess countervailing buyer power." (66)

(122) In this regard, the Notifying Party submits that the pricing and quality offer for passive hydraulic actuators will be extremely constrained by OEM's countervailing buyer power post-Transaction. (67)

(123) Firstly, the Notifying Party argues that the new entity would face a highly concentrated customer base consisting of a small group of large car manufacturers. (68) In particular, the Notifying Party submits that Valeo is largely dependent on its […], who represent almost all of its total sales in the EEA. Similarly, FTE is largely dependent on its […], which account for [70-80]% of its total sales in the EEA. These customers could reallocate some of the new entity's business to LuK, Sachs, Aisin or any of the alternative suppliers.

(124) Secondly, the Notifying Party argues that that the new entity will be constrained in its pricing and quality offer on passive hydraulic actuators, because customers could leverage the fact that they buy other products from the new entity, which generate far more significant turnover. The Notifying Party submits that passive hydraulic actuators will represent less than […]% of the new entity's global turnover with each individual customer post-Transaction.

(125) Thirdly, the Notifying Party argues that car manufacturers exert significant pressure on suppliers through competitive bidding procedures. In particular, the Notifying Party argues that car manufacturers usually launch worldwide bidding processes, which are open to potential competitors from outside the EEA. Moreover, car manufacturers request target prices. Furthermore, car manufacturers may request annual cost savings contractually at the beginning of the contract or quick-savings or new business award productivity savings, when new contracts are awarded. In that regard, the Notifying Party submits that car manufacturers may exert pressure on suppliers by threatening to put them on "new business on hold" ("NBOH") unless they accept to grant the cost savings. The Notifying Party submitted anecdotal evidence of instances where suppliers put the Parties to the Proposed Transaction on NBOH.

The Commission's assessment

(126) The Commission acknowledges that even firms with very high market shares may not be able to significantly impede competition if the customers possess countervailing buyer power. In that regard, the Horizontal Merger Guidelines make reference to a Commission Decision in the automotive industry, in which the Commission found the existence of significant countervailing buyer power. However, in that case the new entity's combined market share did not surpass [40-50]-[50-60]% and it continued to face competition from at least four alternative suppliers. (69) By contrast, in the case at hand, the new entity would have a combined market share of above [70-80]% and would likely face competition from only one other significant supplier.

(127) Furthermore, the Commission notes that – according to the Horizontal Merger Guidelines

– buyer power should be understood as the bargaining strength that the buyer has vis-a-vis the seller in commercial negotiations due to its size, its commercial significance to the seller and its ability to switch to alternative suppliers. (70) In this regard, the Commission notes the following with respect to the arguments brought forward by the Notifying Party:

(128) Firstly, the Commission recognises that the car manufacturers are large sophisticated customers which operate in a relatively concentrated market. However, the supply side is even more concentrated. Currently, more than a dozen car manufacturers with operations in the EEA face only three suppliers of passive hydraulic actuators with significant operations in the EEA. As a result of the Proposed Transaction, the number of significant suppliers of passive hydraulic actuators would be reduced to only two suppliers, namely LuK and the new entity. The new entity would account for more than [70-80]% of the demand, while LuK would account for less than [20-30]% of the demand. The lack of alternative sources of supply is likely to significantly impair the car manufacturers' ability to credibly threaten to resort to alternative sources of supply. Moreover, the market investigation suggests that customers generally would not consider vertically integrating into the upstream market and only a small minority of customers would consider sponsoring the entry of a new supplier. This may be explained by the fact that other car manufacturers would likely also benefit from the entry of a new supplier, which may lessen the incentives of potential sponsors to make the investment associated with sponsored entry.

(129) Secondly, the Notifying Party implies that car manufactures will be able to leverage the fact that the new entity makes more than [90-100]% of its global turnover with each individual customer with products other than passive hydraulic, which would represent less than [5-10]% of the new entity's global turnover with each individual customer post- Transaction. However, the market investigation suggests that only a small minority of car manufacturers occasionally combine their negotiations for the purchase of passive hydraulic actuators with negotiations for the purchases of other products. The large majority of customers does not align these negotiations. This may be explained by the fact that – according to the market investigation – for the majority of customers, these other products are not purchased at the same time or by the same person within the organisation.

(130) Thirdly, the Notifying Party argues that car manufacturers exert significant pressure on suppliers through competitive global bidding procedures, in which they may request target prices and annual cost savings which they may attempt to enforce by putting suppliers on NBOH. However, the Commission notes that price reductions are common in the automotive industry without necessarily resulting in countervailing buyer power to the degree asserted by the Notifying Party. (71) Moreover, even if such price reductions would indeed be a sign of buyer power, they do not seem to sufficiently countervail the market power of the suppliers in the current market setting. In particular, the market investigation suggests that NBOH is a very exceptional measure which almost exclusively relates to quality problems. This is in line with the fact that the Notifying Party could name only a few instances, in which suppliers put the Parties on NBOH, […]. The majority of the examples for NBOH brought forward by the Notifying Party relate […]. In that regard the Commission considers that it is normal for a supplier to halt its purchases for a product, if the supplier discovers quality problems with regard to this product. The exceptional nature of NBOH was also confirmed by the market investigation, according to which almost none of the respondents to the market investigation put a supplier on NBOH for passive hydraulic actuators or threatened to do so in the last five years. In fact, the market investigation confirms that suppliers are very reluctant to put a supplier on NBOH and only resort to this as a measure of last resort, because it has negative effects on their own purchasing strategy.

(131) Finally, the Commission notes that – in any case – it is not sufficient that buyer power exists prior to the merger, it must also exist and remain effective following the merger. In view of the supply structure post-merger, it seems likely that any degree of countervailing buyer power that may exist in the market at the moment will likely be further reduced as a result of the Proposed Transaction.

(132) In view of the above, the Commission considers it unlikely that car manufacturers will be able to exert enough countervailing buyer power to overcome the increased market power of the new entity post Transaction.

4.2.1.6 Conclusion

(133) In view of the above, the Commission considers that the Proposed Transaction is likely to give rise to anti-competitive non-coordinated effects and, thus, raises serious doubts as to its compatibility with the internal market for PHAs modules and components for light vehicles in the EEA, in particular in view of (i) the very high market shares for the merging entity in the OEM market for sale of PHA modules and components for light vehicle, (ii) the closeness of competition, (iii) the difficulties for customers to switch to a new supplier,

(iv) the unlikelihood of market entry or expansion of other suppliers, and (v) the absence of a high enough level of buyer power capable of countervailing the post-transaction new entity's market power.

4.2.2 IAM passive hydraulic actuator components for light vehicles

(134) The Notifying Party estimates that the market shares of the Parties and their competitors in the affected markets are the following:

(135) In the IAM, the Transaction thus leads to the following affected market segments:

- the market for CMCs in Croatia, Germany and Greece;

- the market for CRCs in Croatia, Cyprus, Germany, Greece, Hungary, Italy and the UK;

- the market for CSCs in Belgium, Bulgaria, Croatia, Greece, Hungary, Ireland, Italy, Latvia, Lithuania, Poland, Romania, Slovenia, Spain, Sweden and the UK.

4.2.2.1 CSCs

The Notifying Party's view

(136) The Notifying Party submits that the Proposed Transaction will not raise concerns in respect of IAM sales of CSCs as the new entity will continue to face strong competition from numerous suppliers in all national markets. In addition to the Parties, a number of OE suppliers such as LuK, Sachs and Aisin are active in the IAM. While their market shares vary across countries, the Notifying Party estimates that LuK and Sachs account for [30- 40]% and [20-30]%, respectively, of overall passive hydraulic actuator component sales in the EEA.72 Like the Parties, these competitors supply both OE parts that they sell on the OEM market and adaptable parts, i.e. components that do not meet the same quality and durability standards as the OE parts but are qualified to be used as spares in the aftermarket. (73)

(137) While the Notifying Party is unable to provide estimate market shares of players other than LuK and Sachs or to even identify the competitors active in each country, it submits that the new entity will also face competition from several European IAM-only suppliers (which manufacture and supply spare parts specifically for the aftermarket, without being active in the OEM market), like Metelli, LPR Brakes, Nuova Tecnodelta and Donaflex, as well as low-cost Asian suppliers that export their products in the EEA. (74)

(138) In addition, the Notifying Party submits that the new entity would face strong competitive pressure from competitors on the segment for CSCs sold in kits (DMF kits or three-piece kits), where the Parties have a small combined market share (highest in the United Kingdom at [10-20]%). (75)

(139) The Notifying Party further points out that several low-cost Asian suppliers have entered or expanded their activities on the IAM in recent years and entry and expansion can easily take place in the future, as there are no significant barriers to entry on this market, which is based on a mature technology. (76)

(140) Finally, the Notifying Party submits that whilst the IAM customer base is more dispersed than on the OEM market, sales to the limited number of international buying groups account for […]% and […]% of FTE's and Valeo's sales, respectively. (77) Furthermore, customers can freely switch suppliers and they can also make arbitrage and source their products from low-cost countries as the level of transport costs is limited. (78) As described above, the Notifying Party submits that significant volumes are subject to re-exportation by customers. (79) For these reasons, the Notifying Party submits that IAM customers yield buyer power which they could use to curtail any attempt on its side to raise prices post- Transaction.

The Commission's assessment

(141) Post-Transaction, the new entity would be the largest player on the market, with a market share above [30-40]% in several EEA countries.

(142) In the United Kingdom the Proposed Transaction would combine the two largest players on the market leading to a market share of [60-70]% for the new entity, with an overlap of [30-40]%. (80) Its two main competitors, LuK and Sachs, have market shares of [10-20]% and [10-20]%, respectively while other, smaller players account for only [0-5]% of sales.

(143) In Croatia, the new entity would have a market share of [50-60]%, with an overlap of [10- 20]% of the market. LuK and Sachs have [10-20]% and [5-10]% of the market, respectively. Smaller IAM players are estimated to have a combined market share of [10- 20]%, although the Parties have not been able to identify them and their market shares.

(144) In Greece, the Parties have a combined market share of [50-60]% with an overlap of [10- 20]%. The remainder of the market is highly fragmented, with LuK and Sachs accounting for [5-10]% of the market each, and other players for the other [40-50]% of the market.

(145) In Hungary, the new entity would also be the market leader with a [40-50]% share of the market. Its main competitors have market shares of [30-40]% (LuK) and [10-20]% (Sachs).

(146) In Latvia, the new entity would have a market share of [40-50]%, with an overlap of [20- 30]% of the market. LuK and Sachs account for [10-20]% of the market each, with smaller IAM-only competitors accounting for the remaining [30-40]% of sales.

(147) In Slovenia, the new entity would have [30-40]% of the market, comparable to that of LuK, and the Parties have an overlap of [10-20]%. Sachs accounts for [10-20]% of sales, and IAM-only players for the other [5-10]%.

(148) In Italy and Romania, the combined market share of the Parties is again of [30-40]%, with a relatively limited overlap of [0-5]%.

(149) The figures in Table 11 above are based on the Parties' actual sales in each country. The Parties state that they have information that some of their large customers which are active in multiple countries purchase components in one country and then re-export them to another country where the sourcing conditions are less favourable. The Notifying Party has thus submitted alternative estimates of market size and shares, in which the volumes re- exported by customers were allocated to the country of destination. The market shares with export re-allocation are presented below:

from adaptable parts. (81) Only adaptable parts sold by IAM-specific suppliers can be recognised as such by virtue of the fact that the suppliers are not active on the OEM market.

(153) Both the Notifying Party and IAM customers state that there is a perceived difference in quality between parts supplied by OE suppliers, be they OE parts or adaptable ones, and parts supplied by low-cost IAM-only suppliers. For instance, the Notifying Party states that "Valeo considers that adaptable products supplied by LuK and Sachs will meet comparable quality and durability standards as OE parts." (82) This view is consistent with that of several IAM customers, who indicated that spare parts manufactured by non-OE suppliers are expected to be of a lower quality. (83) The customers furthermore explained that quality is a very important criterion in their purchasing decision and they have a preference for OE suppliers. When asked whether adaptable parts produced by IAM-specific suppliers are suitable for replacing OE components, over 40% of respondents indicated that they are suitable only sometimes (between 25% and 50% of contracts) or rarely (less than 25% of contracts). (84)

(154) Quality and track record as OEM supplier are thus important elements of competitive differentiation in the IAM, which suggests that OE suppliers compete most closely against each other, while IAM-only suppliers, in particular low-cost Asian suppliers are perceived as providing lower-quality products.

(155) Closeness of competition between OE suppliers in the IAM is also confirmed by the fact that they are selected as "preferred suppliers" by international buying groups. Buying groups, of which a significant share of the Parties' customers are members, (85) select a number of "preferred", "listed" or "associated" suppliers on the basis of their quality, brand reputation, delivery conditions or prices, and encourage their members to source from these suppliers, sometimes even monitoring compliance with these recommendations. (86) The only suppliers holding this status with international buying groups ATR, Temot, Nexus, Groupauto, and AD are the Parties, LuK and Sachs. (87)

(156) For these reasons, the Commission considers that the smaller IAM-only suppliers do not impose a strong competitive constraint on the Parties and that, post-Transaction, the new entity would primarily face competition from LuK and Sachs, which together hold a lower share of the CSCs market in Croatia, Greece, Hungary, Latvia, Romania and the United Kingdom than Valeo and FTE combined.

(157) As regards the Notifying Party's argument that on CSCs sold individually the Parties face competition from CSCs sold in kits, the Commission first notes that there is still significant demand for CSCs sold alone. Even in high-labour cost countries such as Italy, the UK or Sweden, the number of CSCs sold stand-alone is higher than or similar to that of CSCs sold in kits. (88) Furthermore, the Commission is of the view that the Parties' limited share on the market for CSCs sold in kits does not represent evidence of high competitive pressure on the market for CSCs sold stand-alone. As explained by the Parties, kits suppliers typically source CSCs on the trading market in order to integrate them into kits. Indeed, Valeo's main competitors on the kits market, […]: the latter sold […] of CSCs to […] and […] of CSCs to […] in 2015. FTE's market share on the trading market for CSCs is estimated at around [60-70]%. (89) Thus, the extent to which CSCs sold in kits would constrain the Parties with respect to CSCs sold stand-alone depends on kits suppliers' access to CSCs for integration into kits, either through their own production or by sourcing them on the trading market.

(158) The market investigation revealed that customers are not aware of any recent entrants on the IAM market for passive hydraulic actuator components; neither do they expect any entry in the coming 5 years. (90)

(159) While some customers indicated that technical barriers to entry are not high, the majority considered that having manufacturing facilities in the EEA would be necessary for a new entrant to be considered a viable supplier on the IAM. (91) A majority of customers also considered that a track record of several years in the supply of these components outside the EEA is needed. (92)

(160) As acknowledged by the Notifying Party, OE-quality and brand recognition are the main purchasing criteria for customers in the IAM, and are more important in this respect than price. (93) As described above in paragraphs (152) - (155), OE suppliers enjoy a reputational advantage with customers stemming from their perceived superior quality and they are promoted as "preferred" suppliers by international buying groups. For these reasons, existing IAM-only suppliers represent a limited competitive constraint for the Parties and other OE suppliers, and entry or expansion by Asian suppliers is unlikely to take place on a sufficiently large scale, within a sufficiently short timeframe so as to constrain the Parties' market power in certain national markets.

(161) The Commission considers that the customer base on the IAM market, consisting of IAM wholesalers and retail distribution chains, is highly fragmented. While the Notifying Party points out that a high share of the Parties' sales are to international buying groups, it also clarifies that these are not actually in charge of purchasing spare parts on behalf of their members. Rather, buying groups review suppliers and draw up recommendation to their members to purchase from certain "preferred suppliers". Whilst buying groups may negotiate certain commercial conditions such as rebates with these suppliers, the supply contracts are negotiated and concluded by each wholesaler individually. (94)

(162) As regards imports by customers, while in the market investigation some customers indicated that they source passive hydraulic actuator components from other countries within the EEA, this practice does not appear to be widespread enough as to result in significant competitive pressure. As acknowledged by the Parties, price negotiations take place "at local level, taking into account market conditions that may exist locally" (95) and indeed prices differ significantly between countries. (96)

(163) In this context, the Commission considers that IAM customers do not hold a sufficiently high level of buyer power that would countervail the new entity's ability to exercise its market power post-Transaction.

(164) In conclusion, the Proposed Transaction would bring together two of the main competitors on the IAM market for CSCs. In Croatia, Greece, Hungary, Latvia, Slovenia and the United Kingdom, the merger would eliminate a close and significant competitor and turn the new entity into the market leader, with (except in Slovenia) a market share exceeding that of the two other OE-suppliers combined. In light of this and of the limited constraint represented by IAM-only players, of the low likelihood of entry and expansion of other suppliers, and in the absence of a high enough level of buyer power capable of countervailing the post-transaction new entity's market power, the Commission takes the view that the Proposed Transaction raises serious doubts as to its compatibility with the internal market as regards the IAM market for CSCs in Croatia, Greece, Hungary, Latvia, Slovenia and the United Kingdom as a result of non-coordinated horizontal effects.

Belgium, Bulgaria, Ireland, Italy, Lithuania, Poland, Romania, Spain, and Sweden

(165) Although a similar market structure and conditions would characterise the national markets of Italy and Romania post-Transaction, in these two countries FTE is currently a small competitor and thus constitutes a more limited constraint on Valeo. In light of this, the Commission considers that the Proposed Transaction is less likely to result in significant non-coordinated effects and as such, it does not raise serious doubts with respect to the IAM market for CSCs in these two countries. The Commission notes that any potential anticompetitive effects on the Italian and Romanian markets that could occur as a result of the merger would in any event be eliminated given the Notifying Party's Commitments to divest its entire passive hydraulic actuators business.

(166) In the other affected countries, the increment in market share that would be brought about by the Proposed Transaction would be more limited and/or the new entity would face competition from players with a stronger position. In Bulgaria and Poland, the Proposed Transaction entails an increment of [10-20]% and [5-10]%, leading to a combined market share of [30-40]% and [30-40]%, respectively. The new entity would find itself behind LuK (which has a market share of [30-40]% in Bulgaria and [30-40]% in Poland). Sachs would be a significant competitor with [10-20]% and [20-30]% respectively, while smaller IAM-only suppliers account for [10-20]% of sales on each market. In Belgium, the new entity (with a market share of [30-40]%) would also find itself behind LuK ([30-40]%) and the overlap between the Parties is limited to [0-5]%. The increment that would be brought about by the Transaction would also be small ([0-5]% or less) in Ireland, Spain and Sweden, where the new entity would have a share of [20-30]%, [20-30]% and [30-40]%, respectively. In Lithuania, the merger would result in a combined market share of [20- 30]%.

(167) In light of the results of the market investigation and particularly in view of the small or moderate overlap between the Parties and the constraint represented by their main competitors, the Commission considers that the merger is not likely to result in a significant increase in market power and non-coordinated effects in the IAM markets for CSC in Belgium, Bulgaria, Ireland, Lithuania, Poland, Spain, and Sweden.

4.2.2.2 CMCs

(168) In the markets for CMCs in Croatia, Germany and Greece, the Proposed Transaction would lead to a combined market share of less than [30-40]% and a minimal or moderate increment (below [0-5]% in Croatia and Greece, [5-10]% in Germany). LuK is the Parties' main competitor, with a market share of [30-40]% or more, followed by Sachs.

(169) In light of the limited overlap between the Parties and the constraint represented by their main competitors, the Commission considers that the merger is not likely to result in a significant increase in market power and non-coordinated effects in the IAM markets for CMCs in Croatia, Germany and Greece.

4.2.2.3 CRCs

(170) With the exception of Italy, in all affected national markets for CRCs, the Proposed Transaction entails a minimal increment of between [0-5]% and [0-5]%. In Italy, the overlap between the Parties is of [5-10]%, leading to a combined market share of [30- 40]%. The new entity would continue to face competition from LuK ([30-40]%) and Sachs ([20-30]%), as well as smaller players ([5-10]%).

(171) In light of the limited overlap between the Parties and the constraint represented by their main competitors, the Commission considers that the merger is not likely to result in a significant increase in market power and non-coordinated effects in the IAM markets for CRCs in Croatia, Cyprus, Germany, Greece, Hungary, Italy and the UK.

4.3 Non-horizontal effects

(172) According to the Non-Horizontal Merger Guidelines, (97) non-coordinated effects may significantly impede effective competition as a result of a vertical merger if such merger gives rise to foreclosure.

(173) As described in section 3.1.4, an IAM trading market for passive hydraulic actuator components, distinct from the IAM supply of spare parts to wholesale distributors, can be plausibly defined. Under such a definition, the Proposed Transaction gives rise to a vertical relationship between the upstream EEA-wide IAM trading market and the downstream national IAM markets for DMF kits.

(174) On the trading market all IAM manufacturers trade components in order to be able to complete their portfolio by purchasing products of their competitors and then reselling them under their own brand name. Also, suppliers of DMF kits purchase some of the components (such as FTE's CSC) on this market and then incorporate them in the kits they sell under their brand name.

(175) The Notifying Party claims that, even if the entity will theoretically have the ability to engage input foreclosure, it would not have the incentive to do so as: […]. (98) Finally, the Notifying Party claims that even if the new entity was to engage in such behaviour, this would not have an impact on effective competition as […] could resort to alternative IAM suppliers.

(176) For the reasons expressed below, the Commission takes the view that the new entity, albeit potentially having the ability to foreclose downstream competitors, would not have the incentive to do so.

4.3.1 Ability to foreclose

(177) On the EEA IAM trading market, as explained above, the new entity would have a significant market share estimated to circa [50-60]% to [60-70]%. On that market, the new entity would face competition mainly from LuK and Sachs with an estimated share of [20- 30]%-[30-40]% and [5-10]%-[10-20]% respectively. (99)