Commission, June 22, 2017, No M.8348

EUROPEAN COMMISSION

Decision

RAG STIFTUNG / EVONIK INDUSTRIES / HUBER SILICA

Subject: Case M.8348 – RAG STIFTUNG / EVONIK INDUSTRIES / HUBER SILICA

Commission decision pursuant to Article 6(1)(b) in conjunction with Article 6(2) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 27 April 2017, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation and following a referral pursuant to Article 4(5) of the Merger Regulation by which Evonik Industries AG ("Evonik", Germany), controlled by RAG Stiftung (Germany), intends to acquire within the meaning of Article 3(1)(b) of the Merger Regulation sole control of the precipitated silica business ("Huber Silica") of J.M. Huber Corporation ("Huber", US) by way of a purchase of shares and purchase of assets ("the proposed Transaction"). Evonik and Huber are collectively designated hereinafter as "the Parties" and the combination of Evonik and Huber Silica as "the Merged Entity".

1. THE PARTIES

(2) Evonik is headquartered in Germany and listed on the Frankfurt Stock Exchange. In 2016, its world-wide turnover was EUR 12.9 billion (EUR 5.8 billion in the EEA). It is active in the production and marketing of speciality chemicals. Evonik has divided its activities into three business segments: Nutrition and Care, Resource Efficiency and Performanc Materials. Evonik's precipitated silica business is part of Evonik's Business Line Silica within the Resource Efficiency segment.

(3) Huber Silica is part of Huber, a privately owned business headquartered in the US, active in speciality chemicals and minerals, hydrocolloids and engineered woods as well as timber management. In 2016, Huber Silica's world-wide turnover was EUR […] (EUR […] in the EEA). Huber Silica produces precipitated silica with a particular focus on the dental end-user application which accounts for a majority of its sales. In addition, Huber Silica produces sodium silicate which is an input product to precipitated silica.

2. THE OPERATION

(4) On 9 December 2016, the Parties signed a Share and Asset Purchase Agreement for Evonik to acquire four legal entities as well as various assets of Huber, together forming Huber Silica. As a result of the proposed Transaction, Evonik will acquire sole control over Huber Silica.

(5) The notified operation therefore constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

3. REFERRAL REQUEST AND EU DIMENSION

(6) On 23 December 2016, the Commission received a referral request under Article 4(5) of the Merger Regulation with respect to the proposed Transaction, which was capable of being reviewed under the national competition laws of Austria, Germany and the United Kingdom. None of these Member States disagreed with the Parties' referral request.

(7) The notified operation therefore has an EU dimension pursuant to Article 4(5) of the Merger Regulation.

4. RELEVANT MARKETS

4.1. Introduction

(8) In the EEA, both Evonik and Huber Silica are active in the manufacture and supply of precipitated silica (see section 4.2.2), while only Huber Silica is active in the upstream market for sodium silicate (see section 4.2.1). In addition, Evonik is active in the neighbouring markets for organofunctional silanes, fumed silica, and betain (see sections 4.2.3, 4.2.4 and 4.2.5 respectively).

4.2. Relevant product markets

4.2.1. Sodium Silicate

4.2.1.1. Product market definition

(9) Sodium silicate, also known as "liquid glass" or "waterglass", is an inorganic chemical product, combining sodium (Na), silicon (Si) and oxygen (O), that can be supplied in a wide range of grades depending for example on purity, alkalinity (3) or water content and in various forms (aqueous solution or solid as powders, granules or lump blocks).

(10) Sodium silicate is mainly used in the manufacture of detergents, pulp/paper and other industrial applications such as the manufacture of precipitated silica. For the production of precipitated silica, sodium silicate can be either used under (i) liquid form (hydrothermal sodium silicate) or (ii) solid form (obtained from a melting process) which needs to be subsequently dissolved in preparation of the production process.

(11) In previous decisions (4), the Commission considered that the market for sodium silicate constitutes a separate relevant product market without any further subdivision and relied on market findings that "the various product presentations are functional and economic substitutes" (5) although switching between the different forms may incur additional costs.

Notifying Party’s views

(12) While noting that transportation costs for liquid sodium silicate are higher than for solid sodium silicate, the Parties agree with the Commission's previous approach and consider in particular that a segmentation of the market by type of industry supplied is not appropriate. The Parties also consider that switching between the different grades and product forms of sodium silicate is easy.

Commission’s assessment

(13) The Parties' competitors confirm that liquid and solid sodium silicate can be used for the manufacture of precipitated silica, namely "liquid as direct input or solid with preliminary dissolution step". (6) No distinction should be made between powders, granules and/or lump blocks (solid forms) since all of these forms need to be dissolved before use and require particular dissolution equipment. However, results of the market investigation show that a distinction could be made between solid and liquid forms of sodium silicate because of the difference in their transport cost and their respective necessary equipment. Similarly, there are indications that the alkalinity of sodium silicate is a key criterion for the production of precipitated silica.

(14) For the purpose of the present decision, the precise market definition can be left open i.e. whether there is an overall product market for sodium silicate or whether further distinctions need to be made according to solid or liquid forms or according to the alkalinity level since the Transaction does not raise serious doubts as to its compatibility with the internal market under any of the above market segmentations.

4.2.1.2. Geographic market definition

(15) The Commission has previously considered (7) the market for sodium silicate to be EEA-wide in geographic scope.

Notifying Party’s views

(16) The Parties consider the geographic market for sodium silicate to be at least EEA- wide.

Commission’s assessment

(17) The results of the market investigation indicated that the relevant geographic scope of the sodium silicate market is EEA-wide, most notably because most market respondents supply or source (as the case may be) their sodium silicate within 1500km away from the plant where it is produced. (8) Also, most market respondents consider that the sodium silicate market is EEA-wide in geographic scope. (9)

(18) In view of the fact that the Transaction does not raise serious doubts as to its compatibility with the internal market in relation to the sodium silicate market under any plausible market definition, the exact scope of the geographic market can be left open for the purposes of the competitive assessment of the Transaction.

4.2.2. Precipitated silica

4.2.2.1. Product market definition

(19) Silica are specialty chemical products manufactured through the acidification of a sodium silicate solution by a mineral acid (such as sulphuric acid) or by carbon dioxide. Silica can typically be classified according to their production process into: (i) precipitated silica, (ii) silica gels and (iii) colloidal silica. Each of these three types of silica is used for several and separate applications. In a previous decision (10), the Commission therefore considered that they are not substitutable from either the supply or the demand-side perspective and that they therefore belong to separate relevant product markets. For the purpose of the present case however, only precipitated silica is concerned by the proposed Transaction and no further reference will be made to silica gels and colloidal silica.

(20) Precipitated silica are manufactured through a precipitation (11) process during which several parameters (12) can be set up to achieve a large spectrum of different properties, related to the precipitated silica particles' pH value (13), absorption capacity, hardness or abrasiveness. During the manufacturing phases which follow precipitation, namely filtration, drying and potentially milling, granulating and/or coating, other physical properties of the final product can be adjusted to produce various average sizes, average specific surfaces, output shapes (such as powders, micro-pearls or granules), bulk densities, moisture contents, hydrophobic properties, etc.

(21) The various grades of precipitated silica give it specific functionalities that are adapted to the needs of various applications, mainly serving as free-flow agents, anti-caking agents, defoamers, carriers, thickening agents, absorbants, fillers, softeners or abrasive agents.

(22) In its previous decisions (14), the Commission has not assessed whether the overall market for precipitated silica could be further segmented into separate relevant product markets according to the end-use applications.

(23) Within the various potential applications of precipitated silica, a first distinction could be made between rubber applications (majority of EEA or worldwide volume), in which precipitated silica act as re-inforcing fillers, and non-rubber applications, in which precipitated silica can have several different functions. Within rubber applications, a distinction could possibly be made between tyre applications (such as conventional and/or fuel-efficient tyres), silicone rubber, footwear (shoe soles) and other rubber goods. Within non-rubber applications, a distinction may be envisaged between (i) dental, (ii) defoamer, (iii) paints and coatings, (iv) paper, (v) feed additive, (vi) food additive, (vii) battery separators, (viii) matting agents, (ix) agriculture applications and (x) other applications.

(24) Besides the above proposed market segmentation by end-use application, an alternative market segmentation could consist in the distinction of precipitated silica according to their chemical composition into (i) "standard" precipitated silica, (ii) aluminium silicate (involving the addition of aluminium sulfate as input raw material at the precipitation step) and (iii) calcium silicate (involving the addition of calcium chloride as input raw material at precipitation step) as well as according to the precipitated silica's hydrophilic/hydrophobic character into (i) hydrophilic precipitated silica (non-surface treated) and (ii) hydrophobic precipitated silica (surface treated).

Notifying Party’s views

(25) While recognising that precipitated silica are used in a multitude of different end- use applications, the Notifying Party does not consider the different areas of usage to constitute plausible relevant product markets because the precipitated silica for different end-uses is fully substitutable from a supply-side perspective.

(26) In this regard the Notifying Party explains that the precipitated silica supplied is chemically essentially the same across all usage areas and that there are no meaningful barriers to entry into any of the different end-uses. Manufacturers of precipitated silica can therefore switch from producing precipitated silica for one end-use application to another relatively quickly, with low sunk costs. (15) In addition the Notifying Party explains that there are various precipitated silica grades that are used interchangeably between a variety of different end-uses. The Notifying Party also claims that average prices depend primarily on customer specificities and not on the targeted end-use application.

(27) Similarly, while recognizing that aluminium silicate, calcium silicate and "standard" precipitated silica slightly vary from a chemical point of view, the Notifying Party is of the opinion that these products do not constitute separate relevant product markets. Apart from the addition of aluminium sulfate and calcium chloride at the precipitation stage for the production of aluminium and calcium silicate respectively, the Notifying Party explains that the overall production process is identical to the production of "standard" precipitated silica grades, that the same production lines can be used, that there are no materially different costs associated to switching between different "standard" precipitated silica grades, that aluminium and calcium silicate generally fulfil similar functionalities as "standard" precipitated silica and that these products are all supplied to several industries. At the Commission's request, the Notifying Party also provided information on the hypothetical markets for aluminium and calcium silicate, further segmented by end-use applications.

(28) At the Commission's request, the Notifying Party also put forward specific arguments concerning hydrophobic (water-repellent) precipitated silica, which is a surface treated as an additional production step. It consists of standard precipitated silica (hydrophilic) which has been surface-treated with silicone oil. The Notifying Party submits that hydrophobic precipitated silica does not constitute a distinct relevant product market and that hydrophilic and hydrophobic precipitated silica can be used interchangeably as free-flow agents. At the same time the Notifying Party recognises that hydrophobic precipitated silica may show superior effects for instance in defoamer and certain food and feed applications.

Commission's assessment according to the chemical nature of precipitated silica

(29) With regard to the hypothetical segmentation according to the chemical nature of precipitated silica into aluminium silicate, calcium silicate and "standard" precipitated silica, results of the market investigation show that aluminium silicate and calcium silicate are not perceived by customers as constituting substitute products to "standard" precipitated silica (16) and are used for their specific properties.

(30) Contrary to "standard" precipitated silica, and as recognized by the Notifying Party, aluminium and calcium silicate are characterized by higher pH values which make them more suitable for certain applications, such as certain plant protection and coating applications for which acid sensitivity is important (calcium silicate).

(31) Similarly, a majority of competitors agree on the fact that aluminium silicate constitute a separate product market from "standard" precipitated silica because they are "suitable only for certain end-use applications" (17), and because, "from a manufacturing perspective, the production process is different […], the products are not substitutable". (18) More specifically, one competitor is of the opinion that aluminium silicate forms a separate product market for certain applications in paper and paints and coatings, but not for remaining end-use applications within rubber, food, feed "where the aluminium silicate behaves as just another grade of precipitated silica". (19)

(32) Concerning calcium silicate, most competitors did not express any opinion. Only one competitor commented on the matter and considered, as for aluminium silicate, that calcium silicate forms a separate product market since calcium silicate "is suitable only for certain end-use applications". (20)

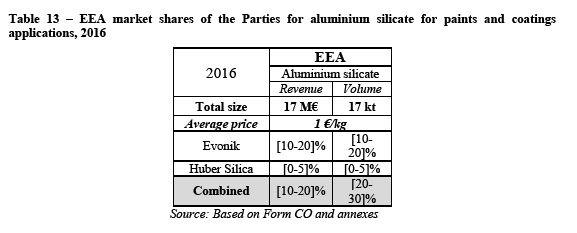

(33) In any event, were separate relevant product markets to be defined for aluminium silicate and/or calcium silicate, the Transaction would only give rise to one affected market in relation to aluminium silicate for paints and coating applications.

(34) In view of the fact that the Transaction does not raise serious doubts as to its compatibility with the internal market in relation to the market for aluminium silicate and calcium silicate, including at the narrower plausible market segmentations per end-use applications, the exact scope of the product market definition for aluminium silicate and calcium silicate can be left open for the purpose of the present case.

Commission's assessment according to the hydrophilic/hydrophobic property

(35) Contrary to standard (hydrophilic) precipitated silica, hydrophobic precipitated silica does "not disperse or mix with water" (21) and "can be made from precipitated silica or fumed silica" (22).

(36) The hydrophobic property of precipitated silica is achieved during the manufacturing process with a specific and final production step through which silicone oil is added at the particles' surface. According to one competitor, this hydrophobisation treatment "create[s] a wholly new manufacturing area with many special requirements, such as VOC (Volatile Organic Compounds), dangerous raw materials, and closed loop or scrubbing emission schemes that complicate production" (23).

(37) As hydrophobisation is performed as a final production step related to the surface treatment, hydrophobisation of particular (hydrophilic) precipitated silica grades can be realised either internally by the precipitated silica manufacturer (ready-to- use hydrophobic precipitated silica) or in situ by the end-user.

(38) Therefore hydrophobic precipitated silica does not constitute a separate end-use application as such but is used for its specific hydrophobic functionality in several end-use applications such as defoamer, paints and coatings and certain food and feed applications.

(39) Concerning the demand-side substitutability of hydrophobic precipitated silica, one competitor explains that, "[i]n most applications the polarity of the precipitated silica is critical. It is not possible to replace one grade for another with a different polarity. The hydrophilic or phobic character of the silica is one of the main contributors to that polarity" (24). Also in light of the results of the market investigation, such observation is confirmed by most customers of hydrophobic precipitated silica who explain that standard (hydrophilic) and hydrophobic precipitated silica grades cannot be used interchangeably because of their different performances (25).

(40) In light of the above, and in particular of the differentiating step in the manufacturing process as well as the absence of demand-side substitutability, the Commission will consider a separate relevant product market for hydrophobic precipitated silica (2% of EEA total market size for precipitated silica in value, 2016). The market for hydrophilic precipitated silica (98% of the total market) will be analysed in more details according to the different end-use applications for precipitated silica.

Commission’s assessment according to different end-use applications for precipitated silica

(41) With regard to the hypothetical segmentation according to end-use applications, the results of the market investigation show that the overall market for precipitated silica must be segmented according to different end-use applications.

(42) First, from a demand-side perspective, a majority of customers consider that there are specific markets for precipitated silica grades, at least for the industry they are active in. (26) For instance a customer indicated that; "[w]e view the precipitated silica market as having several markets due to the fact that the chemistry for each end use is drastically different and not interchangeable. For example, the technology and process needed to produce abrasive oral grades is very different than the process to make for rubber/tire outlets. This is also demonstrated by the fact that suppliers are unable to use tire lines to make the quality for oral care grades." (27)

(43) Another customer explained that "[t]he quality demands required for various markets can be very different. For example, the silica's applied in the Tire industry do not require specifications for heavy metals and dioxin while for Feed Applications, this is a requirement." (28) Accordingly, products target specific end- use applications.

(44) Also, a majority of customers confirmed that there are very different requirements for the performance of precipitated silica depending on their industry. (29) Therefore in the instances in which the base product is the same, or very similar, across end- use applications, customers are typically not aware of it and would not risk disrupting their own production processes by testing grades that are not designed or marketed for them.

(45) Second, from a supply-side perspective, a majority of competitors consider that there are specific markets for precipitated silica grades, which correspond to the following end-use applications; (i) dental, (ii) defoamer, (iii) paints and coatings (iv) paper, (v) rubber, (vi) food additive, (vi) feed additive, (vii) battery separators, (viii) matting agents and (ix) agriculture. (30) Competitors indicate there are different business dynamics in each of these end-use applications. (31)

(46) A majority of competitors consider that there are important price differences between the different end-use applications of precipitated silica products. (32) A customer also explains that "[t]he price mechanisms used can be very different per market." (33)

(47) Most competitors tend to specialize in a limited number of applications. Entering into a different end-use application does not appear feasible in a timely way and without incurring significant costs or risks.

(48) For instance a competitor explains that some markets "[…] have a highly technical know-how or require very specific modified silica grades, with a corresponding high investment cost before production (matting agents, defoamers, battery separators, and all those [where] [competitor name] is present). Though Intellectual Property rights used to be a big hurdle to entry in certain markets the situation has decreased the last ten years, but as indicated above, each market segment requires a specialized know how that cannot be acquired quickly through conventional research. Regulatory approvals and certifications are critical for food, feed, pharma and cosmetics, as well as usually requiring extra investment in the facilities and even some special raw materials." (34)

(49) Competitors also indicated that specific manufacturing equipment is essential for the production of precipitated silica for some end-use applications such as dental, defoamer and paints and / or coatings applications. (35) The Notifying Party also explained that if adaptations to the production facilities are necessary to start producing precipitated silica for a specific end-use application, the installation of new equipment can take up to [period]. (36)

(50) Most customers indicated that they have a qualification process for their suppliers' products which includes steps such as data verification and laboratory testing and can take from one month up to three years. (37) This qualification process can also apply to the production plants where the products are manufactured. (38) Competitors stated that other entities such as local authorities can also carry out qualification processes. (39) The Parties have also provided some information on the regulatory requirements and supplier certification processes per applications. (40) These requirements can vary significantly between applications.

(51) In view of the above the Commission considers that there are separate precipitated silica markets which correspond to the following end-use applications; (i) dental, (ii) defoamer, (iii) paints and coatings, (iv) paper, (v) rubber, (vi) food additive, (vi) feed additive, (vii) battery separators, (viii) matting agents and (ix) agriculture.

(52) Under the market segmentation as analysed above, the Transaction gives rise to the horizontally affected markets in relation to defoamer, dental, paints and coatings, paper, rubber and feed applications. Each of these affected markets is described in more details in the sections below.

The market for precipitated silica for defoamer end-use applications

(53) Certain precipitated silica grades can be used to increase performances of foam control and defoamer agents. Such agents enable to control the formation of foam by reducing the stability of foam films and consequently decompose bubbles.

(54) According to Evonik's technical brochure for "SIPERNAT ® speciality silica and AEROSIL ® fumed silica for defoamer" (41), "foam occurs in many natural and industrial processes as well as everyday life. […] [T]he formation of stable foams causes problems in most industrial processes. Examples are found in the paint and coating, textile, paper, detergent and the chemical industries. Here foam will either affect the quality of the final product directly or impede the manufacturing process, for example, by reducing the carrying capacity of containers or by causing pumping problems".

(55) The Parties do not consider precipitated silica used as defoamer agent to constitute a distinct product market. Furthermore, the Parties do not consider any further segmentation of the defoamer segment into grades with and without hydrophobic treatment to be meaningful because both types of products can be used for the same defoamer applications.

(56) From a supply-side perspective however, results of the market investigation indicated that the market for defoamer applications requires "a highly technical know-how or […] very specific modified silica grades, with a corresponding high investment cost before production" (42). Furthermore, one competitor considers that the defoamer market is "a minor segment in volume, though not in value, with too many obstacles for entry." (43) This observation is confirmed by the fact that average prices for precipitated silica marketed for defoamer applications show significantly higher average prices than in other end-use applications. Based on information provided by the Parties (in particular total market size and market value) (44), precipitated silica for defoamer applications are commercialized at [1.5- 2]€/kg, which is approximately [30-70]% higher than the average price on the hypothetical overall market for precipitated silica ([1.1-1.4]€/kg) (45).

(57) Moreover, as explained in the previous section, hydrophobic precipitated silica can be used in several different end-use applications and does constitute a separate relevant product market under the alternative approach of segmenting the market according to the hydrophilic and hydrophobic character. With respect to a market segmentation by end-use applications, it appears that the hydrophobic property seems to be of particular importance for defoamer applications.

(58) According to Huber's webpage dedicated to hydrophobic precipitated silica (46), "hydrophobic silica is an ideal solution for defoamers and can be used in food products as anti-caking and free-flow agents and in paints and coatings applications." Similarly, Evonik's technical brochure "SIPERNAT ® speciality silica and AEROSIL ® fumed silica for defoamer" (47) indicates that "it is particularly important for the defoaming effectiveness, that the silica has a hydrophobic surface character".

(59) Conversely, Huber's webpage dedicated to precipitated silica for defoamer applications (48), exclusively lists ready-to-use hydrophobic precipitated silica products or hydrophilic precipitated silica for in situ hydrophobisation. (49) And Evonik's technical brochure "SIPERNAT ® speciality silica and AEROSIL ® fumed silica for defoamer" (50) explains that "the use of in situ hydrophobisation in the manufacture of defoamers requires empirical knowledge and comes at high cost in terms of time and equipment. It is often easier to use silica that have already been optimized and hydrophobized for defoaming, like those sold by Evonik."

(60) In light of the above and in particular of the significant price difference of grades for defoamer applications and also of the entry barrier specific to defoamer applications, the Commission will consider the precipitated silica market for defoamer end-use applications to constitute a separate relevant product market.

The market for precipitated silica for dental end-use applications

(61) Precipitated silica has two main applications for dental end-use applications, both as an input for the production of toothpastes. It can be used to control rheology (51) in the manufacturing process and to provide the appropriate aesthetic qualities and stability to the finished toothpaste product (so-called “thickening” characteristics). Precipitated silica can also be used to enhance the cleaning/whitening performance of toothpaste (so-called “abrasive” characteristics).

(62) Some competitors consider that there are significant differences in the production process for each of these functionalities. (52) However most competitors consider that it would be relatively easy for a supplier only active in one of these functionalities to develop another. (53)

(63) The market for precipitated silica for dental end-use applications is described in Evonik's internal analysis as [an important market for silica]" (54)

(64) On the demand-side the market for precipitated silica for dental applications is characterised by the presence of some large customers; Procter and Gamble, GSK, Unilever and Colgate. These customers make up a large part of the overall demand. This is confirmed by Evonik's internal analysis […]. (55)

(65) This can have an impact on entry. As explained by a competitor: "[s]ome of these markets are dominated by a few global customers, where introduction of a new supplier is difficult, such as Dental." (56)

(66) As explained above, there are specific regulatory requirements, including GMP (57) and ISO 9001 requirements which are quite stringent. (58) This is confirmed by Evonik's internal analysis of this market [by referencing various aspects of regulatory requirements]. (59)

(67) Also, R&D and innovation play a significant role in this market. In this regard Evonik's internal analysis refers to innovation [as an important element in the dental market]. (60)

(68) Based on the above evidence, the Commission will consider the overall market for precipitated silica for dental end-use applications for the purposes of the competitive assessment in this case.

The market for precipitated silica for paints and coatings end-use applications

(69) Precipitated silica can be used as additives in emulsion paints (in which they can act as partial substitutes for white pigments) and as rheology modifiers for paint and coating products (in which they enable to fine-tune the proper flowability of the end-product).

(70) At the Commission's request, the Notifying Party identified the following hypothetical sub-applications within the overall market for precipitated silica for paints and coatings applications: (i) decorative paints and coatings (including for wood), (ii) automotive and transportation paints and coatings, (iii) printing inks, and (iv) industrial coatings.

(71) In view of the fact that the Transaction does not raise serious doubts as to its compatibility with the internal market in relation to the markets for paints and coatings applications, including at the narrower possible market definition as considered in the previous paragraph, the exact scope of the product market definition for precipitated silica for paints and coatings applications can be left open for the purpose of the present case.

The market for precipitated silica for paper end-use applications

(72) Within the paper industry, precipitated silica can serve either to increase the paper strength, toughness and resistance to folding (segment of paper pulp preparation / paper mass) or to enhance a paper's ability to absorb ink (61) (segment for surface coating). The intended effect of the latter usage is to achieve an instantly dried surface in order to improve the printed image's quality.

(73) The Transaction gives rise to horizontal overlaps only in the overall segment for paper applications: within the paper industry, Evonik's customers exclusively use Evonik's precipitated silica products for [application 1], while Huber Silica's customers exclusively use Huber Silica's precipitated silica products for [application 2].

(74) In view of the fact that the Transaction does not raise serious doubts as to its compatibility with the internal market in relation to the market for paper applications, the exact scope of the product market definition for precipitated silica for paper applications can be left open for the purpose of the present case.

The market for precipitated silica for rubber end-use applications

(75) Within rubber applications, a distinction can be made between tyre applications, silicone rubber, footwear (typically shoe soles) and other rubber goods.

(76) For tyre applications, precipitated silica are used to improve the performance of the rubber material such as its resistance to abrasion or to heat. Within the particular segment of fuel-efficient tyres, precipitated silica are essential to reduce the rolling resistance and abrasion and to improve the wet traction. In silicone rubber, precipitated silica act as fillers and are designated to mildly support reinforcing effects and provide some tear resistance. In footwear and other rubber goods, precipitated silica are used as reinforcing fillers to improve durability and resilience of the rubber products.

(77) In view of Huber's de minimis presence and the fact that the Transaction does not raise serious doubts as to its compatibility with the internal market, including at the narrower possible market definition as considered in the previous paragraphs, the exact scope of the product market definition for precipitated silica for rubber applications can be left open for the purpose of the present case.

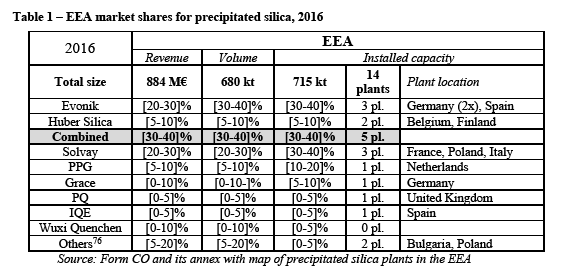

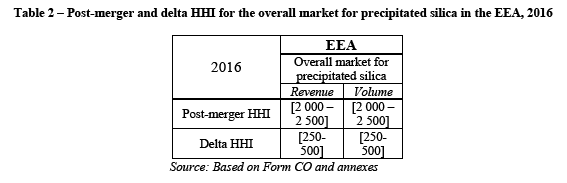

The market for precipitated silica for feed end-use applications

(78) As for food applications (62), precipitated silica are used as additives to improve the flow behaviour for animal feed and nutrition products. Associated effects are the reduction of clumping, of inter-particle interaction and of dust generation. Usage of precipitated silica also enables to improve the final product's storage stability and ability to absorb liquid components.

(79) In view of the fact that the Transaction does not raise serious doubts as to its compatibility with the internal market in relation to the market for feed applications, the exact scope of the product market definition for precipitated silica for feed applications can be left open for the purpose of the present case.

4.2.2.2. Geographic market definition

(80) In a previous case (63), the Commission considered the geographic market for precipitated silica to be at least EEA-wide, but left the precise geographic market definition open.

Notifying Party’s views

(81) The Parties consider the relevant geographic market for precipitated silica to be at least EEA-wide in scope, because it considers that there are no barriers for the trading of precipitated silica within the EEA and that transportation costs within Europe are low. The Parties also submit that the relevant geographic market may be worldwide, given that prices are interrelated on a global level and that some producers are active in Europe (such as Madhu, India) are operating in the EEA based on their intercontinental import capacities without having any production facility in Europe.

(82) The Notifying Party also explains that customers typically purchase internationally, and that large customers sometimes even purchase globally. The Notifying Party adds that due to large overcapacities in China and an erosion of prices in Asia, imports into Europe have been growing over the last years which affected prices in Europe.

Commission’s assessment

(83) The market investigation results indicate that the markets for precipitated silica are EEA-wide in scope.

(84) Although there are some imports from outside the EEA, a majority of customers indicate that they do not import precipitated silica from the US, Asia or from other regions outside Europe to their European facilities. (64) A customer explained that "[w]e do actually not import from outside Europe because of the lower lead times. We would import from outside Europe: - if the price would be lower, providing the required quality - if the manufacturer has a warehouse in Europe to keep a certain quantity in stock." (65)

(85) In parallel, competitors agree that the geographic proximity of suppliers to the customers plays an important role for the precipitated silica business in the EEA. (66) For instance a competitor explains that "[a] plant close to the specific customers could reduce lead-time, save logistics cost, serve customer better and more promptly." (67) Another competitor indicates that "[t]ransport cost contributes to the final price of precipitated silica. Therefore it is easier to be competitive in price with customers close-by." (68)

(86) A majority of competitors indicated that, for 80% of their supplies, the average distance from their production plants to their customers in the EEA is between 1000km and 1500km. (69) Competitors added that this distance does not vary significantly depending on end-use applications. (70)

4.2.3. Organofunctional silanes

(87) Organofunctional silanes are used as binders between inorganic materials such as glass, minerals and metals and organic polymers such as thermoplastics, as surfactants for inorganic and organic materials, and as cross-linking agents for polymers.

(88) In a previous decision (71), the Commission considered that three separate product markets for organofunctional silanes have to be distinguished, namely (i) organofunctional silanes for rubber applications, (ii) organofunctional silanes for non-rubber applications and (iii) alkyl silanes. In a previous decision (72), the Commission considered that the three products markets are at least EEA-wide in scope.

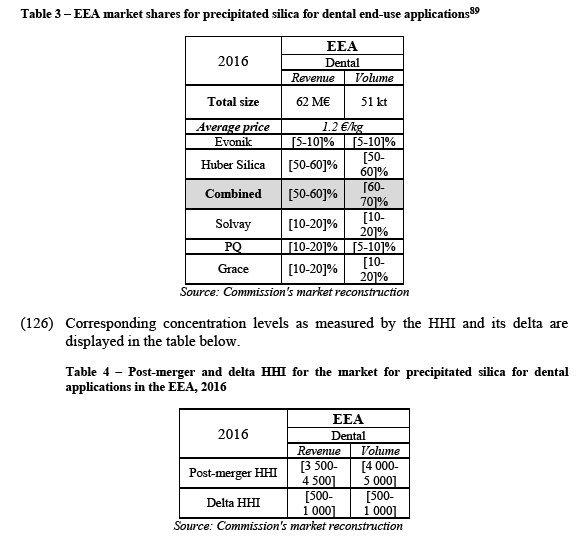

(89) The Notifying Party agrees with such product and geographic market definitions.

(90) For the purpose of the present case, the product and geographic market definitions for organofunctional silanes can be considered as per previous Commission practice. In particular, the question whether the geographic market for organofunctional silanes is EEA-wide or larger can be left open since the Transaction does not raise serious doubts as to its compatibility with the internal market.

4.2.4. Fumed silica

(91) Fumed silica is produced from silicon tetrachloride together with oxygen and hydrogen. The product is used as an additive in a variety of different products. The main areas of use are elastomers (improvement of the mechanical properties of silicone rubber, for example in sealants), thermosetting materials (improving the properties of unsaturated polyesters, epoxy resins and acrylates), and paints and varnishes.

(92) According to the Commission’s past practice (73), fumed silica forms a distinct product market with an EEA-wide geographic scope.

(93) The Notifying Party agrees with this product and geographic market definitions.

(94) For the purpose of the present case, the product and geographic market definitions for fumed silica can be considered as per previous Commission practice.

4.2.5. Betain

(95) Betain is a chemical compound which has application in dish washing liquids, hand disinfectants, oral care, professional car wash, shampoo/bodywash.

(96) There is no previous Commission practice in relation to betain.

(97) The Notifying Party considered a distinct product market for betain with an EEA- wide geographic scope.

(98) For the purpose of this case, the product and geographic market definitions for betain can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market.

5. COMPETITIVE ASSESSMENT

(99) Under Article 2(2) and (3) of the Merger Regulation, the Commission must assess whether a proposed concentration would significantly impede effective competition in the internal market or in a substantial part of it, in particular through the creation or strengthening of a dominant position.

(100) In this respect, a merger may entail horizontal, vertical and/or conglomerate effects.

(101) Within the EEA, the proposed Transaction gives rise to horizontally affected markets (see sections 5.1.2 to 5.1.4) in the markets for precipitated silica delineated (i) according to the precipitated silica's various end-use applications, namely the markets for dental, defoamer, paints and coatings, paper, rubber and feed end-use applications; (ii) according to the precipitated silica's hydrophilic/hydrophobic property, namely the market for hydrophobic precipitated silica; and (iii) according to the precipitated silica's chemical nature, namely the market for aluminium silicate.

(102) The proposed Transaction also gives rise to vertical links (see section 5.2) between the upstream market for sodium silicate (where only Huber Silica is active) and the downstream market for precipitated silica (where both Parties are active).

(103) In addition, potential conglomerate effects will also be examined between the closely related neighbouring markets for: precipitated silica for tyre applications and organofunctional silanes (see section 5.3.3); precipitated silica for paints and coatings and fumed silica (see section 5.3.4); and precipitated silica for dental applications and betain (see section (5.3.5).

5.1. Horizontal assessment

5.1.1 Analytical framework

(104) Horizontal effects are those deriving from a concentration where the undertakings concerned are actual or potential competitors of each other in one or more of the relevant markets concerned. The Commission appraises horizontal effects in accordance with the guidance set out in the relevant notice, that is to say the Horizontal Merger Guidelines.- (74)

(105) The Horizontal Merger Guidelines distinguish between two main ways in which mergers between actual or potential competitors on the same relevant market may significantly impede effective competition, namely non-coordinated and coordinated effects. Non-coordinated effects may significantly impede competition by eliminating important competitive constraints on one or more firms, which consequently would have increased market power, without resorting to coordinated behaviour. In that regard, the Horizontal Merger Guidelines consider not only the direct loss of competition between the merging firms, but also the reduction in competitive pressure on non-merging firms in the same market that could be brought about by the merger.

(106) The Horizontal Merger Guidelines also lists a number of factors which may influence whether or not significant non-coordinated effects are likely to result from a merger, such as the large market shares of the merging firms, the fact that the merging firms are close competitors, the limited possibilities for customers to switch suppliers, or the fact that a merger would eliminate an important competitive force. That list of factors applies equally if a merger would create or strengthen a dominant position, or would otherwise significantly impede effective competition.

(107) This decision will analyse whether the proposed Transaction is likely to raise doubts as to its compatibility with the internal market by the creation of non- coordinated effects in those markets on which the Parties' activities lead to horizontal overlaps and to affected markets, distinguishing between (i) the market segmentation for precipitated silica according to the products end-use applications (section 5.1.2), (ii) the market segmentation for hydrophobic precipitated silica (section 5.1.3) and (iii) the market segmentation for aluminium silicate (section 5.1.4).

5.1.2. Market segmentation of precipitated silica according to the products' end-use applications

5.1.2.1. Description of the hypothetical overall market for precipitated silica

(108) The table below shows the Parties' and their competitors' market shares, as well as the installed capacity in the EEA on the hypothetical market for precipitated silica in 2016. (75)

The Notifying Party's views

(109) The Notifying Party argues that the Transaction will not raise competition concerns on the overall precipitated silica market. In this regard the Notifying Party claims that the Merged Entity will remain subject to strong competition from suppliers active in the EEA as well as from additional suppliers from Asia. Moreover there is increasing overcapacity in the precipitated silica market and the capacity exceeds demand by around 48%. The Notifying Party also explains that competitive pressure increases due to imports from Asia. The Notifying Party indicates that Huber and Evonik have lost market shares in recent years to competitors because of the strong competitive pressure from low-cost producers with spare capacities.

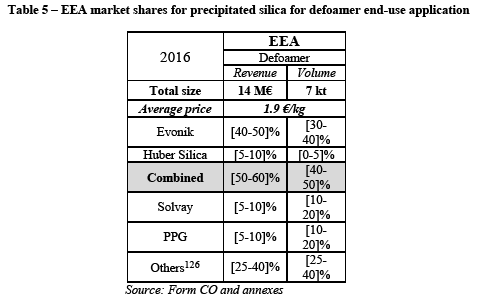

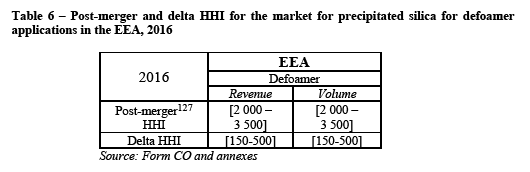

(110) The Notifying Party also argues that the Herfindahl-Hirschman-Index ("HHI") levels (see table above) do not indicate any serious competition concerns and that Evonik and Huber are not close competitors but their products are complementary in terms of product portfolio and geographic footprint. The Notifying Party further argues that customers have strong buyer power, strong leverage in price negotiations and are able to switch suppliers easily. Finally, the Notifying Party claims that there is strong competition in all end-use applications related to the high degree of supply-side substitutability.

(111) For the purposes of general market intelligence, the Notifying Party relied, to some extent, on the industry report realized by Notch Consulting Inc. (the "Notch report"). (77)

(112) Concerning this report, the Parties made the following observations. First, the Notch report does not take into account the sales of Asian suppliers to EEA customers (78). Second, the report inaccurately lists Huber Silica's production facility for precipitated silica in Sweden among active capacities in Europe. (79) Third, it overestimates Huber Silica's total European sales in precipitated silica in 2016 (90M€ (80) instead of [30-60]€).

(113) The Notifying Party adds that the report underestimates the total European market size for 2016 in its last edition of March 2017 at 747M€ (830M$). Indeed, the Notifying Party notes that, in March 2016, the Notch report estimated the EU market size to be 774M€ (860M$) with an expected annual increase of 4-5%, which is in contradiction with its last estimation.

(114) To conclude, the Parties consider the data provided in the Notch report to be broadly reliable in some respects but to be incorrect in others. In particular, the Parties estimate that their own market intelligence and market estimates are in many instances more accurate than the one provided in the Notch report and correctly reflect the actual increase of precipitated silica production and the actual sales of Asian suppliers to EEA customers.

(115) At a narrower level, the Notifying Party is of the opinion that the Notch report [significantly misjudged Evonik's and Huber Silica's sales in this regard].

The Commission's preliminary observations

(116) Table 1 shows that post-Transaction the Merged Entity would be the market leader in the EEA with a market share of [30-40]% in terms of volume and [30- 40]% in terms of revenue with an increment of [5-10]% brought by Huber Silica. Solvay would be the second largest player in the market, with a market share of around [30-40]%. The next competitors would be smaller players, like PPG and Grace.

(117) Regarding the installed production capacity for precipitated silica, the Merged Entity would own more than one third of all 14 plants located within the EEA, representing [30-40]% of the total installed capacity.

(118) The Merged Entity would however still face strong competition, first from Solvay, which has comparable market shares in terms of revenue, volume and installed capacity. Also, most customers consider that Solvay is Evonik's closest or second closest competitor. (81) The Merged Entity would also face other significant players, such as PPG, which has higher market shares than Huber Silica.

(119) In the results of the market investigation, although most customers indicate that suppliers located outside the EEA do not exert significant competitive pressure on EEA-based suppliers (82), some customers nevertheless argue that they do exert some influence. For instance a customer explains that "quality from China and India is on par with European produced material and competitive with EEA produced material." (83)

(120) Almost all competitors with EEA-based capacities indicate in the market investigation to be aware of the Notch report (84) and none of them considers that it provides inaccurate data about the precipitated silica market, market players and their respective market shares. (85) Furthermore none of them identifies significant inaccuracies in the data as reported in the Notch report and raises concerns about any hypothetical lack of transparency in any market. (86)

(121) The Commission notes that the Parties adapted the total amount of EEA sales of precipitated silica provided by the Notch report from 747M€ to 884M€ to reflect its own market intelligence. Similarly, in terms of volumes, the Commission notes that the Parties estimated the total EEA volume of precipitated silica sold in 2016 to be 680kt, which corresponds to the volume sold in Europe as forecasted for 2020 in the Notch report. For 2016, the Notch report estimates the overall demand for precipitated silica to be 557kt in Europe. Such an estimate of the total volume sold in 2016 would lead to a combined market share for the Merged Entity of [40- 50]%.

(122) At a narrower level (i.e. in some markets for precipitated silica for particular end- use applications), the Commission notes that the Parties' best estimates for total market sizes correspond either to market data as provided in the Notch report for 2016 (e.g. markets for precipitated silica for rubber, paper or food applications), or to 2020 forecasts of the Notch report (87) (e.g. market for precipitated silica for dental applications), or to the worldwide demand in 2016 as provided in the Notch report (e.g. market for precipitated silica for defoamer applications). A consequence of the adjustments made by the Notifying Party and compared to the Notch report is an increase in the 'Other' category (88), which the Parties estimate to correspond to 19% of the total estimated volumes sold in the EEA in 2016 (126kt).

(123) In light of the above and as will be detailed below, some market reconstructions have been necessary to have access to an independent estimation of the total market sizes in volume and value for certain of the precipitated silica markets in which the Transaction gives rise to horizontal overlaps.

5.1.2.2. Precipitated silica for dental end-use application

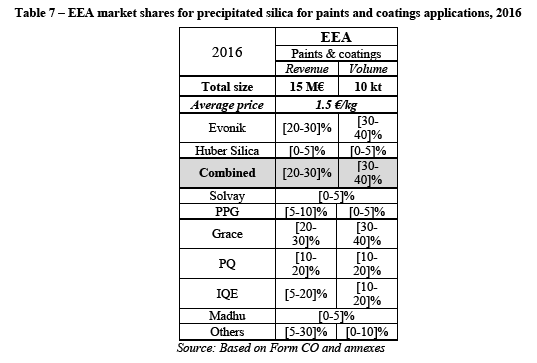

(124) As explained in the previous section, a brief market reconstruction has been necessary to estimate the total market size for precipitated silica for dental applications. In terms of value, the total market size of 60M€ as provided by the Parties has been roughly confirmed and slightly increased while the total market size in volume appears to be in line with the data provided in the Notch report for 2016 (51kt instead of 56kt as forecasted for 2020 and reported by the Parties).

(125) The table below shows the reconstructed market shares in the EEA for Evonik and Huber Silica as well as for their main competitors on the market for precipitated silica for dental end-use applications by value and volume.

The Notifying Party's view

(127) The Notifying Party argues that the Transaction will not raise competition concerns on the market for precipitated silica for dental end-use applications. First, the Notifying Party explains that the Merged Entity will remain subject to strong competition from suppliers such as Solvay and PQ.

(128) Second, the Notifying Party argues that Evonik's sales to dental customers are very limited and have decreased over the last years. Also, according to the Notifying Party Evonik ['s activities in this market are limited].

(129) Third, the Notifying Party submits that there are significant overcapacities in the market due among other things to growing competitive pressure from Asian suppliers.

(130) Fourth, the Notifying Party claims that customers have significant buyer power that will remain unchanged post-merger. The Notifying Party also argues that customers are able to request price decreases and shift orders to have better prices. Moreover, according to the Notifying Party customers can approach any precipitated silica manufacturer and request to start producing grades specifically suited for their use.

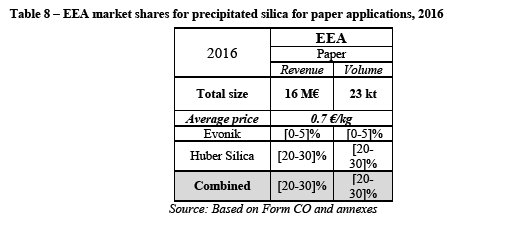

The Commission's assessment

(131) As displayed in Table 3, Huber Silica is the market leader pre-transaction, with a [50-60]% market share (based on revenue and volume data) based on the reconstruction resulting from the market investigation. Such market share levels are indicative of a potential pre-merger dominant position of Huber Silica in the market for precipitated silica for dental applications. With a significant combined market share of [55-70]%, the Merged Entity would enjoy a significantly stronger market position than the three other remaining competitors, with market shares between [5-20]%.

(132) The highly concentrated nature of this market is also reflected in the HHI levels as displayed in Table 4. The Transaction would also involve a significant increment in HHI of [500 – 1 000].

(133) According to Evonik's own internal analysis the "Huber's strong position on the market". (90) This observation has also been confirmed by the market investigation.

(134) First, a majority of customers consider that Huber is an unavoidable supplier for precipitated silica in the EEA. (91) In this regard a customer explains that "the silica qualities of the alternative suppliers works different in our end-use application (toothpaste) or packaging isn't suitable for us". (92) Another customer states that "[w]e cannot substitute the types/grades of one supplier 1:1 to the quality of another supplier, so we have to create "alternative" formulations which a very big effort to handle." (93) A third customer explains that Huber is an unavoidable supplier "[...] because the product are developed with this [Huber's] silicas". (94)

(135) In this regard, similarly to the situation in the overall precipitated silica market, all customers responding to the market investigation indicate that they qualify their suppliers (95). Half of the customers only approve the product, the other half also approve the plant (96). The procedure can take from one month to over a year and sometimes even longer.

(136) A majority of the customers say that it is not easy to switch suppliers (97). For instance a customer explains that switching suppliers "[...] takes a long time - many testing and it may not be in accordance with other raw materials." (98) Another customer indicates that "[s]witching is time consuming and there are significant costs involved. If tests are not made thoroughly there might be problems with our product quality." (99)

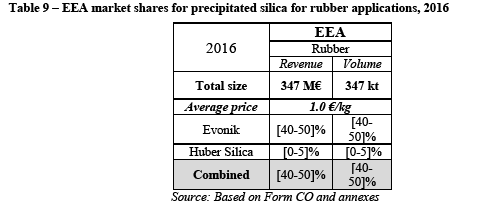

(137) Second, some respondents explain that entry is particularly challenging in this market, for instance a competitor explained that "[w]e did some developments in this area, but we consider this market segment suffers from oversupply so the cost of entry was not supported by good market expectatives [sic]. Also the strong links between each major customer and a precipitated silica supplier is a strong barrier, being limited in the short term to small companies or secondary brands." (100)

(138) Another competitor explains that "[s]ome of these markets are dominated by a few global customers, where introduction of a new supplier is difficult, such as Dental." (101) Indeed, as explained above, the demand on this market is mainly concentrated among four major customers (Colgate, Procter and Gamble, GSK and Unilever). There are indications that smaller suppliers would find it very challenging to supply these customers.

(139) Accordingly, in its internal analysis, Evonik [analyses the challenges to be a successful supplier in this field]. (102)

(140) In this regard, a large customer explains that "[…] its sourcing strategy now emphasizes the need for synergies in its qualification process. In this respect, global suppliers enable [customer name] to simply re-apply identical qualification procedures in several regions throughout the world. Also, [customer name] prefers to be supplied by companies of a certain scale with a global footprint and consistent manufacturing practices. [...] Evonik has the advantage of having a global footprint and could therefore supply [customer name] globally. Solvay, Huber, and Evonik are the only three manufacturers of precipitated silica for oral care to have such global footprint." (103)

(141) Post-merger the market position of Huber's dental business would be further enhanced; with [50-60]% market shares, the Merged Entity would become three times as large as the second largest competitor, Solvay. Three other competitors with shares of [5-20]% would remain active on the market (PQ, Grace and Madhu). Also, most customers confirmed that they do no import precipitated silica for dental end-use applications from outside of the EEA to their EEA facilities.

(142) Despite Evonik's limited activities in the dental segment it is still the fifth largest player in the EEA and has a global presence (104), which is important for the largest customers. Evonik lists [its areas of strengths in an internal document]. (105) Furthermore, Evonik explains in its internal analysis [its areas of strengths]. (106) Reportedly, some of Evonik's products [perform well against those of competitors]. (107)

(143) Evonik's internal analysis also refers to [success with dental customers] (108).(109)

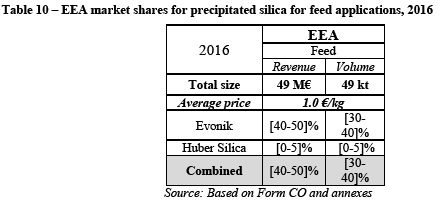

(144) In addition, Evonik explains that [levels of average sales prices to dental customers]. (110)

(145) In view of the above, in its internal analysis Evonik considers that [the advantage to expand in the dental market could outweigh the risks] (111) (112) (113) (114) (115),.

(146) By way of illustration of the opportunities which would be open to Evonik in this market [there is evidence of Evonik being in negotiations with a large toothpaste manufacture] (116) (117)

(147) This would lead to a two to [significant increase in the volumes sold by Evonik while no such decision has yet been reached] (118)

(148) In addition, the market investigation results show that Evonik and Huber are particularly close competitors. Indeed a majority of customers consider that Huber is Evonik's closest or second closest competitor. (119)

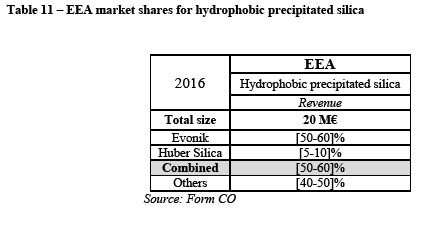

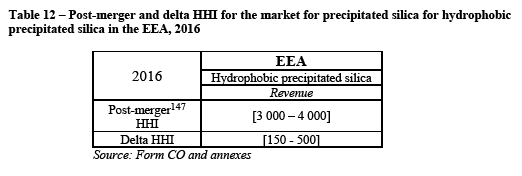

(149) In view of the above the Commission considers that the Transaction could lead to the removal to an important competitive force (Evonik). (120)

(150) As for the impact of the Transaction on customers' choice of suppliers, a customer explains that "[t]here are not sufficient suppliers on EU market as it is now, and there will be even less with this merger." (121) Another customer explains that "[t]oday, there are three global competitors with the capability to offer localized Oral Care capacity. With the merger, this number would be reduced to two. Two key points are 1) very few suppliers deliver good performance silica with a global footprint and 2) longer supply chains across continents often aren't competitive vs. local solutions." (122)

(151) Several customers, of different sizes, are also concerned about a potential price increase post-merger. (123) For instance a customer explains that "[t]here will be less competitors and the ones left will be free to operate the market as they please." (124). Another customer states that "[w]e expect price increase because there will be no direct competition between two suppliers that we know." (125)

(152) In view of the above and of all the evidence available to the Commission, the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the market for precipitated silica for dental end-use applications.

5.1.2.3. Precipitated silica for defoamer applications

(153) The market of precipitated silica for defoamer applications is relatively small in size but constitutes a niche market with one of the highest average price per ton (almost twice as high as in dental).

(154) The table below shows the EEA market shares for Evonik and Huber Silica as well as for the main competitors on the market for precipitated silica for defoamer applications by revenue and volume.

(155) Corresponding concentration levels as measured by the HHI and its delta are displayed in the table below.

The Notifying Party's view

(156) The Notifying Party considers that the Transaction does not give rise to competition concerns in relation to the market for precipitated silica for defoamer applications.

(157) First, The Notifying Party first submits that the Merged Entity will remain subject to strong competition in relation to the defoamer segment. The Notifying Party claims that all products sold to defoamer customers are grades of precipitated silica which can, in identical form, be used in different end-use applications and the vast majority of precipitated silica manufacturers can sell their products to defoamer customers without any need of investment or sunk costs.

(158) Second, the Notifying Party explains that the relatively limited demand for precipitated silica for defoamer applications, only enables opportunistic sales in this particular segment.

(159) Third, the Notifying Party indicates that there is significant overcapacity in the market for precipitated silica because of precipitated silica grades being in identical form.

(160) Fourth, the Notifying Party explains that defoamer customers have significant buyer power and an ability to negotiate favourable terms.

The Commission's assessment

(161) According to the Parties' best estimates for market shares, the Merged Entity would, post-transaction, become leader on the EEA market for precipitated silica for defoamer applications with a combined market share of [40-50]% in volume and [50-60]% in value. Already pre-transaction, Evonik enjoys a strong position in this market with [30-40]% in volume and [40-50]% in value. The increment brought by Huber Silica ranges between [0-5]% in volume and [5-10]% in value. According to the Parties, Solvay and PPG are the only precipitated silica manufacturers to be also active on this market with market shares between [5- 20]%. HHI considerations also highlight a relatively high degree of concentration and increment, in particular for market shares based on revenue considerations.

(162) As already explained, the total EEA market size in volume estimated by the Parties corresponds to the worldwide demand for precipitated silica for defoamer applications, which may lead to a dilution of the Parties' market shares and an increase of the market share attributed to the 'Others' category ([25-40]% according to the Parties). The market investigation sought to reconstruct the market.

(163) For confidentiality reasons, it is not possible to disclose the exact results of the market reconstruction. However, it should be noted that the total size of market in the EEA is significantly lower than the EUR 14 million estimated by the Parties. Consequently, the Parties' combined market share in value is significantly higher than [50-60]% (above [70-80]%).

(164) At the Commission's request, the Parties provided the names of precipitated silica grades of their competitors in the market for precipitated silica for defoamer applications. However, none of these grades are marketed as potential defoamer products on their respective webpages. Furthermore, contrary to the Parties' internet pages (128), none of Solvay's (129) or PPG's (130) webpages provide commercial or technical information with respect to their precipitated silica grades in the context of potential defoamer applications. The Commission observes that the Parties are the only precipitated silica manufacturers to have a targeted marketing strategy towards customers for the defoamer end-use applications. This means that, notwithstanding the relatively small size of the market, the Parties' presence goes well beyond 'opportunistic sales', while the same is not true for their competitors.

(165) As for the Parties' claim regarding overcapacity in the production of precipitated silica, the market investigation provided conflicting evidence of high capacity utilisation by several competitors. For those competitors which have free capacity available, the switch from other grades to defoamer grades is perceived as technically challenging. One competitor explained in the context of the market investigation that the market for defoamer end-use applications requires "a highly technical know-how or […] very specific modified silica grades, with corresponding high investment cost before production". (131)

(166) From a demand-side perspective, concerns are raised in particular by one customer of precipitated silica for defoamer applications who explains that the proposed Transaction would lead to a "monopoly situation". (132) Concerning the alleged buyer power of customers, results of the market investigation show that half of the respondents consider Evonik to be un unavoidable supplier of precipitated silica in the EEA. (133) Furthermore, it should be noted that these respondents include one major customer. It can be concluded that customers have limited ability to switch to alternative suppliers in the EEA.

(167) Some market participants also expressed concerns about potential reduction of competition and potential price increases in the market for precipitated silica for defoamer applications following the proposed Transaction.

(168) In view of the above and of all the evidence available to the Commission, the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the market for precipitated silica for defoamer end-use applications.

5.1.2.4. Precipitated silica for paints and coatings applications

(169) As illustrated in the table below, the market for precipitated silica for paints and coatings applications is affected in 2016, irrespective of the approach for market share calculation based either on value (combined market share of [20-30]%) or on volume (combined market share of [30-40]%).

The Notifying Party's views

(170) The Notifying Party does not put forward any specific arguments for this market. The Commission's assessment

(171) Based on the Parties' market share estimates in the market for precipitated silica for paints and coatings, the combined market shares remains fairly limited when considered per value while becoming [30-40]% when considered in volume. Under both possible approaches, the increment remains modest (below [0-5]%). Furthermore four major competitors would remain active in this segment post- transaction and the Merged Entity would have a similar size to Grace, forming the top two companies active in precipitated silica for paints and coatings applications.

(172) According the Guidelines on the assessment of horizontal mergers ("the Horizontal Merger Guidelines") (134), the Commission is unlikely to identify horizontal competition concerns in a merger with a post-merger HHI between 1 000 and 2 000 and a delta below 250, except where special circumstances are present. (135) At the overall level of precipitated silica for paints and coatings applications, it can also be noted that, under the approach of market share based on value, the post-merger HHI is between 1 000 and 2 000 ([1 500 – 2 000]) and the associated delta is below 250 ([50-150]).

(173) When segmenting the market for precipitated silica for paints and coatings applications into (i) decorative paints and coatings (including for wood), (ii) automotive and transportation paints and coatings, (iii) printing inks, and (iv) industrial coatings, it appears that the Parties' activities only overlap within the narrower segment of decorative paints and coatings (including for wood), which constitutes 73-90% of the total segment for paints and coatings. The Parties' combined market share remains in similar ranges ([20-30]% based on value and [25-40]% based on volume) as for the overall market for paints and coatings.

(174) Market participants did not raise substantiated concerns about the market for precipitated silica for paints and coatings and certain competitors also observed that "[w]ith the possibility of imports and the remaining suppliers there is enough product to avoid a dominance of the market" (136) or that "[t]here does not appear to be much overlap between the end use applications in which Evonik and Huber sell". (137)

(175) In light of the above, the Transaction does not raise serious doubts as to its compatibility with the internal market and concerning the Parties' activities in the market for precipitated silica for paints and coatings applications in the EEA, including at the narrower possible level of decorative paints and coatings (including for wood) applications.

5.1.2.5. Precipitated silica for paper applications

(176) As illustrated in the table below, the market for precipitated silica for paper applications is affected in 2016, irrespective of the approach for market share calculation based either on value (combined market share of [20-30 %]) or on volume (combined market share of [20-30%]).

The Notifying Party's views

(177) The Notifying Party does not put forward any specific arguments for this market, except on the [negligible magnitude of its sales].

The Commission's assessment

(178) Based on the Parties' market share calculations, the combined market share remains fairly limited (up to [20-30]%) and the increment brought by Evonik is de minimis (well below [0-5]%) under both possible approaches of market share calculations based on revenues or volume. Furthermore, several well-established competitors remain active on this market, in particular Grace ([20-30]%), PQ ([10-20]%), PPG ([5-10]%) and OSC ([5-10]%). (138)

(179) Results of the market investigation did not raise particular concerns with respect to the market for precipitated silica for paper applications. One single competitor identified a potential risk of decrease in competition in this market but without substantiating its view on top of the fact that the Merged Entity would enjoy a higher combined market share.

(180) According to the Horizontal Merger Guidelines (139), the Commission is unlikely to identify horizontal competition concerns in a merger with a post-merger HHI between 1 000 and 2 000 and a delta below 250 or in a merger with a post-merger HHI above 2 000 and a delta below 150, except where special circumstances are present. (140) With respect to the market for precipitated silica for paper applications, none of the special circumstances are met and, based on value, the post-merger HHI is between 1 000 and 2 000 ([1 500 – 2 000]) and the associated delta is below 250 ([0-100]), while, based on volume, the post-merger HHI is above 2 000 (2 000 – 3 000) and the associated delta is below 150 ( [0-100]).

(181) As already explained, the Transaction does not lead to any overlap at the narrower possible levels of precipitated silica for paper mass applications and for paper surface coatings applications since Evonik's customers exclusively use Evonik's precipitated silica products for […], while Huber Silica's customers exclusively use […].

(182) In light of the above, the Transaction does not raise serious doubts as to its compatibility with the internal market with regard to the Parties' activities in the market for precipitated silica for paper applications in the EEA, including at the narrower possible level of paper mass applications and paper surface coating applications.

5.1.2.6. Precipitated silica for rubber applications

(183) Among the different precipitated silica markets per end-use applications, the market for rubber applications is by far, the largest in size. According to the Parties' own estimations for 2016, this market alone accounts for 39% of all sales of precipitated silica in the EEA and for 51% of all volume traded in the EEA.

(184) As illustrated in the table below, the market for precipitated silica for rubber applications is affected in 2016, irrespective of the approach for market share calculation based either on value (combined market share of [40-50]%) or on volume (combined market share of [40-50]%).

The Notifying Party's views

(185) The Notifying Party does not put forward any specific arguments for this market. The Commission's assessment

(186) Based on the Parties' market share calculations, the Transaction is characterized by a de minimis increment (below [0-5]%) brought by Huber Silica and under both possible approaches of market share calculations based on revenues or volume. Huber Silica has no focus on this market for precipitated silica and generates almost no sales on it. Several other well-established competitors, including from Asia, are active in this market, in particular Solvay ([30-40]%), PPG ([5-20]%), Wuxi Quenchen (China) ([0-10]%), Grace ([0-5]%), Madhu (India) ([0-5]%) and several other competitors (accounting together for [5- 10]%). (141)

(187) The fact that Huber Silica is almost absent of this market holds true including at narrower possible levels for tyre, silicone rubber, footwear and other rubber applications.

(188) On the overall level of precipitated silica for rubber applications, it can also be noted that the post-merger HHI is above 2 000 ([2 000 – 3 000] in value and [2 000 – 3 000] in volume) and the associated delta is below [0-100] (<1 in value and volume). According to the Horizontal Merger Guidelines (142), the Commission is unlikely to identify horizontal competition concerns in such a situation, except where special circumstances are present. (143) None of these exceptional circumstances are present, in particular the fact that none of the Parties has a pre- merger market share of 50% or more.

(189) In light of the above, the Transaction does not raise serious doubts as to its compatibility with the internal market with regard to the Parties' activities in the market for precipitated silica for rubber applications in the EEA, including at the narrower possible level of tyre, silicone rubber, footwear and other rubber applications.

5.1.2.7. Precipitated silica for feed applications

(190) As illustrated in the table below, the market for precipitated silica for feed applications is affected in 2016, irrespective of the approach for market share calculation based either on value (combined market share of [40-50]%) or volume (combined market share of [30-40]%).

The Notifying Party's views

(191) The Notifying Party does not put forward any specific arguments for this market

The Commission's assessment

(192) Based on the Parties' market share calculations, the Transaction is characterized by a de minimis increment (below [0-5]%) brought by Huber Silica and under both possible approaches of market share calculations based on revenues or volume. Huber Silica has no focus on this market for precipitated silica and generates almost no sales on it. Several other well-established competitors, including from Asia are active in this market, in particular Solvay ([40-50]%), IQE ([5-20]%), Wuxi Quenchen (China) ([5-10]%), PQ ([0-5]%) and several other competitors (accounting together for [10-20]%). (144)

(193) It can also be noted that the post-merger HHI is above 2 000 ([2 000 – 3 000] in value and [2 000 – 3 000] in volume) and the associated delta is below 150 ([0- 50] in value and [0-50] in volume). According to the Horizontal Merger Guidelines (145), the Commission is unlikely to identify horizontal competition concerns in such a situation, except where special circumstances are present. (146) None of these exceptional circumstances are present, in particular the fact that none of the Parties has a pre-merger market share of 50% or more.

(194) In light of the above, the Transaction does not raise serious doubts as to its compatibility with the internal market with regard to the Parties' activities in the market for precipitated silica for feed applications in the EEA.

5.1.3. Market segmentation for hydrophobic precipitated silica

(195) The table below shows the EEA market shares for Evonik and Huber Silica on the market for hydrophobic precipitated silica based on revenue.

(196) Corresponding concentration levels as measured by the HHI and its delta are displayed in the table below.

The Notifying Party's view

(197) The Notifying Party argues that the Transaction will not raise competition concerns in relation to hydrophobic precipitated silica.

(198) First, it argues that Evonik and Huber Silica supply hydrophobic precipitated silica to different customer segments.

(199) Second, the Notifying Party explains that the Transaction will not increase Evonik's capacity as Huber does not produce hydrophobic precipitated silica but has a toll-manufacturing contract with Applied Material Solutions ("AMS") in the US.

(200) Third, sufficient supply alternatives remain to customers post-merger as the Notifying Party claims that several competitors active in the EEA also sell hydrophobic precipitated silica. To the best of the Parties' knowledge, Solvay, Madhu, Torrensil (China), Fuji Silysia (Japan/US), Tulco (US), Elementis (US), AMSI (US) and Hoffman Mineral (Germany) are also active on this market.

(201) Fourth, the Notifying Party adds that the possibility for toll-manufacturing may be more cost efficient for precipitated silica manufacturers than purchasing and operating its own equipment.

The Commission's assessment