Commission, January 23, 2019, No M.9095

EUROPEAN COMMISSION

Decision

UPL / ARYSTA LIFESCIENCE

Subject: Case M.9095 - UPL / Arysta LifeScience

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 7 December 2018, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which United Phosphorus Corporation Ltd. ("UPL Corp"), a wholly owned subsidiary of United Phosphorus Ltd. ("UPL" or the "Notifying Party"), would acquire sole control of Arysta LifeScience Inc. ("Arysta" and, together with UPL, the "Parties") (the "Transaction").

1. THE PARTIES

(2) UPL is active worldwide in the manufacture of products for the protection of plantations, intermediates, specialty chemicals and other industrial chemicals, including insecticides, fungicides, herbicides, fumigants, plant growth regulators ('PGR') and rodenticides.

(3) Arysta is a global provider of innovative crop protection solutions, including bio- solutions and seed treatments. Arysta specialises in the development, formulation, registration, marketing and distribution of differentiated crop protection chemicals for a variety of crops and applications.

2. THE CONCENTRATION

(4) Through the Transaction, UPL would acquire sole control of Arysta from Arysta's current owner Platform Specialty Products Corporation by way of a purchase of shares.

(5) The Transaction would constitute a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

3. UNION DIMENSION

(6) The Transaction does not have a Union dimension within the meaning of Article 1 of the Merger Regulation as it does not meet the thresholds of Article 1(2) or Article 1(3).

(7) However, on 29 August 2018, the Notifying Party informed the Commission by means of a reasoned submission that the concentration would be notifiable in four Member States and would fulfil a number of further criteria for its referral to the Commission. In particular, the referral to the Commission would avoid multiple national filings, thereby increasing administrative efficiency. On that basis, under Article 4(5) of the Merger Regulation, the Notifying Party requested the Commission to examine the Transaction.

(8) The Commission agrees that the referral request meets the legal criteria set out in Article 4(5) of the Merger Regulation in that the Transaction is capable of being reviewed under the national merger control laws of at least three Member States, namely France, Germany, Poland and Spain. In addition, none of the Member States competent to examine the Transaction under the respective national laws expressed their disagreement within 15 working days of receiving the reasoned submission.

(9) Therefore, the concentration is deemed to have a Union dimension pursuant to Article 4(5) of the Merger Regulation.

4. MARKET DEFINITIONS

4.1. Commission precedents

(10) In past cases – notably Dow/DuPont, ChemChina/Syngenta and Bayer/Monsanto – the Commission found that the relevant product markets for formulated crop protection products can be defined on the basis of crop/pest combinations, where each such combination constitutes a separate relevant product market. Moreover, the Commission found that, for herbicides, further distinctions can be made depending on the time of application of the relevant crop protection products. (3)

(11) On this basis, the Commission found that the relevant product markets for selective herbicides can be segmented by crop, weeds targeted and timing of their application. For PGR, it found that the relevant product markets can be segmented by crop. For fungicides, it found that each crop/disease combination constitutes a separate relevant market. Regarding the upstream markets for active ingredients ('AIs'), the Commission found that each AI is a distinct market.

(12) As to the relevant geographic markets for crop protection products, in past cases the Commission found that they are national in scope. For AIs, the Commission found the markets to be at least EEA-wide, if not worldwide.

4.2. Notifying Party's views

(13) In line with the Commission's precedents, the Notifying Party submitted data for formulated products on the basis of national markets segmented by indication, crop and pest (as well as timing of application in the case of herbicides), and on the basis of EEA-wide or global markets for each AI. (4)

4.3. Commission assessment

(14) In light of the elements put forward by the Parties and the results of its investigation, the Commission confirms the conclusions reached in Dow/DuPont, ChemChina/Syngenta and Bayer/Monsanto regarding market definition.

(15) The Commission’s findings in those cases were based on a number of different elements, including:

(a) Farmers buy formulated crop protection products to address specific needs, based on the crop, pest, timing of application they want to target. This implies a narrow relevant product dimension consisting of a crop / pest combination which is not substitutable from the point of view of the farmer with other products that apply to a different crop / pest combination.

(b) Formulated products have labels that typically indicate AIs, formulation, permitted use crops, targeted pests, options for tank mixing, etc.

(c) Discovery and production of a new formulated product involve high costs and a long period, making supply side substitutability very limited.

(16) These elements were broadly confirmed by respondents to the market investigation.

(17) Based on its precedents, and on the results of the market investigation, the Commission thus takes the view that the relevant product markets for selective herbicides can be segmented by crop, weeds targeted and timing of their application. For PGR, the Commission takes the view that the relevant product markets can be segmented by crop. For fungicides, the Commission takes the view that each crop/disease combination constitutes a separate relevant market. Regarding the upstream markets for AIs, the Commission takes the view that each AI is a distinct market.

(18) As to the relevant geographic markets for crop protection products, in its precedents the Commission found that:

(a) Product portfolios are adapted for varying demand of customers in different Member States;

(b) Customer habits, needs and preferences are dependent on geography and differ across EEA countries.

(c) Formulated products are registered at national level;

(d) Design, brand products and prices vary across countries;

(e) At the same time, some characteristics of crop protection products (AI approval, R&D) are determined at the EEA level and impact national competitive dynamics.

(19) These elements were broadly confirmed in the market investigation.

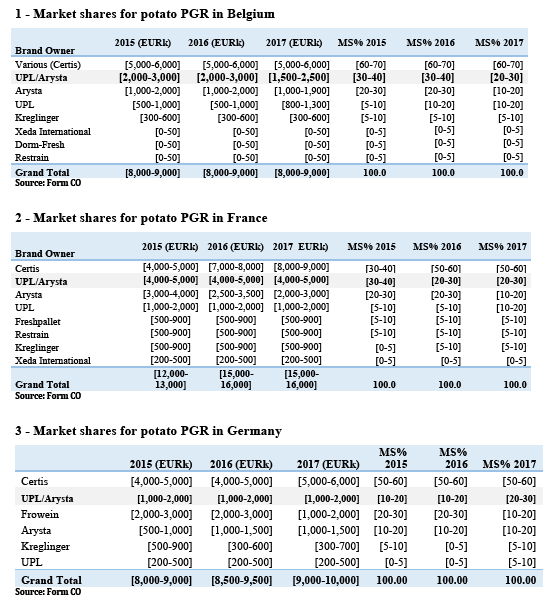

(20) Therefore, based on its precedents and on the results of the market investigation, the Commission takes the view that the relevant markets are national in scope.

(21) As regards AIs which are used in formulated products, the Commission found in its precedents that their relevant geographic market is at least EEA wide, based in particular on the fact that they are registered on a European basis.

(22) For AIs, the Commission therefore takes the view that the markets are at least EEA- wide.

4.4. Conclusion

(23) In light of its precedents and taking into account the results of its investigation, the Commission will assess markets for formulated crop protection products (including, for the avoidance of doubt, PGR) at the national level on the basis of crop/pest combinations – as well as the timing of application for herbicides. For AIs, the Commission will assess each AI as a separate market, at the EEA level or worldwide.

(24) In the present case, the Commission will therefore assess the affected national markets for potato PGR, scab fungicides for pome fruit and post-emergence broadleaf herbicides for sugar beet.

(25) As regards 'broad spectrum fungicides for other fruit', this encompasses different crops but is the narrowest segmentation for which data is available. The Commission will therefore assess the effects of the Transaction on competition in national markets at that level, but will take into account in its assessment competitive dynamics for products targeting the same individual crops within that the cluster.

(26) Finally, the Commission will assess the vertically affected markets regarding the upstream supply of chlorpropham and the downstream markets in which products containing the AI chlorpropham are sold.

5. COMPETITIVE ASSESSMENT

5.1. Overall Framework

(27) Under Article 2(2) and (3) of the Merger Regulation, the Commission must assess whether a proposed concentration would significantly impede effective competition in the internal market or in a substantial part of it, in particular through the creation or strengthening of a dominant position.

(28) The Commission considers below the competitive effects of the Transaction in the areas in which the Parties have overlapping sales giving rise to affected national markets in the EEA: (i) PGR for potatoes (in Belgium, France, Germany, the Netherlands, Spain and the United Kingdom), (ii) broad spectrum fungicides for other fruit (in Greece), (iii) scab fungicides for pome fruit (in France and Greece), and (iv) post-emergence broadleaf herbicides for sugar beet (in Austria, Belgium, France, Italy, the Netherlands and the United Kingdom).

(29) Regarding the supply of AIs to third parties, the only (vertically) affected markets concern products containing chlorpropham. Therefore, no other markets regarding the supply of AIs to third parties will be further discussed in this decision, considering that the Parties are otherwise active only to a limited extent in this business and for each of the AIs that they supply to third parties in the EEA the Parties hold a limited share and there appears to be a significant number of alternative suppliers.

(30) The Parties overlap only to a very limited extent in herbicides and fungicides for other crops, as well as in insecticides and other crop protection indications, without giving rise to any horizontally or vertically affected market other than the ones mentioned above. These activities are, therefore, not further discussed in this decision.

(31) Overall, the Transaction does not give rise to affected markets which are not assessed in this decision.

5.2.Notifying Party's views

(32) The Notifying Party considers that the Transaction would not significantly impede effective competition in the EEA or any substantial part thereof, in essence because in each of the horizontally or vertically affected markets: (i) there are many suppliers and products available, among which growers are able to choose freely to meet their needs; (ii) other suppliers offer products based on the same AIs as those offered by the Parties; (iii) there is also a large number of products based on alternative AIs which are not part of the Parties' offer; (iv) the vast majority of the AIs used in these markets are off-patent, meaning that they are open to generic competition; (v) switching between AIs and formulated products is easy for distributors and growers because the application techniques and needed equipment are the same across the product range; (vi) a number of strong competitors will remain post-Transaction, typically with significantly larger market shares than the merged entity, which would typically have relatively low combined market shares and no market power; (vii) there is significant regulatory pressure on most of the Parties' overlapping products, in particular on chlorpropham, the use of which will therefore likely significantly decrease within a short period of time; (viii) […], such that there is no scope for either customer or input foreclosure in the vertically affected markets. (5)

5.3. Plant growth regulators for potatoes

(33) The main overlap between the Parties' activities in the EEA arises in the area of PGR for potatoes.

(34) PGR are used to inhibit the sprouting of potatoes during storage, which enables longer storage with better product quality. Because potatoes may be stored for months, several treatments are often necessary, either with the same products or by combining different products. In particular, products used in field (based on maleic hydrazide) only prevent sprouting during storage for a limited period of time and typically require the use of additional anti-sprouting treatments.

5.3.1. Activities of the Parties and their competitors

(35) UPL sells products based on chlorpropham (also called 'CIPC') – the traditional and cheapest option for potato anti-sprouting treatments – with EEA sales of approximately EUR [5-9] million in 2017. UPL produces the AI and formulates some of its finished products, but also uses […] as a 'toll formulator' (that is, a contract manufacturer of finished formulated products).

(36) Arysta sells products based on both chlorpropham and maleic hydrazide, another AI, with EEA sales of approximately EUR [8-12] million in 2017. Arysta purchases the chlorpropham AI exclusively from […] – which in turn purchases it […] – and formulates its finished products. Regarding maleic hydrazide products, Arysta procures them from a toll-formulator. Arysta is also in the process of launching a new product based on orange oil.

(37) The Parties' competitors sell products based on a number of AIs.

(38) The Parties’ main competitor is Certis, a fully independent player which is active through the same AI as the Parties' main sales (chlorpropham). Certis is a larger player in EEA markets than the Parties, and the main seller of products based on chlorpropham, as evidenced by the market shares in Tables 1 to 6. Certis procures the AI from a Chinese supplier and holds an approval for the molecule at the EEA level.

(39) Several competitors (Xeda International, DormFresh, Restrain, Freshpallet, Adama) recently launched products based on different new molecules, such as 1,4-dimethylnaphthalene ('1,4-DMN'), ethylene, carvone or mint oil, in response to the severe pressure from regulators and food-chain users regarding the use of chlorpropham.

(40) Products based on chlorpropham such as those sold by the Parties and Certis are used either at the moment of the placement of potatoes into storage, or during storage. By contrast, products based on maleic hydrazide are sprayed in the field, and their anti-sprouting effect is limited in time. Products based on other AIs are typically used during storage only.

5.3.2. Market shares

(41) Tables 1 to 6 show the market shares provided by the Notifying Party for the affected markets in potato PGR in the EEA.

5.3.3. The merged entity would continue to face significant competition, including from players with larger market shares

(42) Tables 1 to 6 show that the Parties' combined market shares remain below [20-30]%, with the exception of the Netherlands where the combined share is […] above [30-40]%.

(43) The main other competitor selling products based on the same AI, Certis, has much larger sales and market shares than the Parties combined in Belgium ([60-70]% compared with [20-30]% for the Parties), France ([50-60]% compared with [20-30]% for the Parties), Germany ([50-60]% compared with [20-30]% for the Parties) and Spain ([70-80]% compared with [20-30]% for the Parties).

(44) In Belgium, as detailed in recital (55), there is strong pressure from the food chain for potato growers and storage operators to use products alternative to those containing chlorpropham.

(45) In Germany, Frowein is another player with a significant market share ([10-20]%) – also based on chlorpropham products. […], it formulates its products independently.

(46) In the Netherlands, as can be seen in Table 4, Certis' market share is comparable to the Parties' combined share ([30-40]% compared with [30-40]% for the Parties), (6) and both DormFresh and Kreglinger have market shares similar to those of each Party (respectively [10-20]% and [10-20]%).

(47) In Spain, BASF is also a significant competitor to the Parties with sales of products based on chlorpropham.

(48) Certis is not only a larger player than the Parties: it is also a close competitor to them as it sells products based on the same AI as many of the Parties' products (chlorpropham) in all Member States except the United Kingdom, and is independent from the Parties as regards the sourcing of this AI.

(49) In the United Kingdom, Arysta only sells maleic hydrazide products. In that market, Aceto […] appears to be the market leading seller of chlorpropham products, ahead of UPL and Certis, and a closer competitor than Arysta.

(50) The merged entity would continue to face significant competition post-Transaction from at least one larger and close competitor active through the same AI in all nationally affected markets – with the possible exception of the United Kingdom, where the Parties do not sell products based on the same AI; as well as the Netherlands, where however the available market share data appears not to be reliable in that regard (see footnote 6) – throughout the EEA.

5.3.4. Products alternative to chlorpropham are likely to capture significant sales and erode its market relevance in view of pressure from the food chain, as is already the case in the two most 'progressive' national markets

(51) Beside the competitive constraint currently exerted by alternative suppliers of formulated products based on the same AI as the Parties (chlorpropham), the merged entity is likely to face significant competition from new products based on alternative AIs.

(52) As evidenced in Tables 4 and 6, in countries where users are more open to new treatments such as the Netherlands and the United Kingdom, alternative products mainly based on maleic hydrazide and 1,4-DMN but also on ethylene or mint oil have already captured significant sales from chlorpropham-based products, in spite of higher prices.

(53) For instance, as shown in Table 4, DormFresh's market share – which are based on 1,4-DMN products – in the Netherlands grew from nil in 2015 to [10-20]% in 2017.

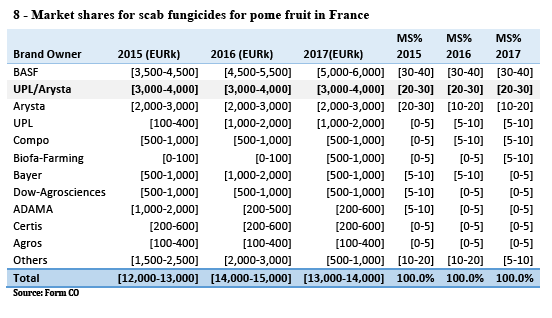

(54) This trend appears to be the result of growing reluctance from the food chain to purchase potatoes treated with chlorpropham, which has been assessed by the European Food Safety Authority ('EFSA') as leaving residues detrimental to human health. (7) This assessment is the basis for the Commission's proposal not to renew the approval of chlorpropham in the EEA, as discussed in Section 5.3.5.

(55) For instance, in Belgium, the Reskia project, an initiative of the potato processing industry, traders and growers, is focused on finding and scaling up alternative products to chlorpropham. Information available on the project’s website concludes that 1,4-DMN, mint oil and ethylene are good alternatives to chlorpropham, with strong support being shown for 1,4-DMN in particular. (8)

(56) Because these serious human health risk considerations apply equally to all countries and consumers in the EEA, it is likely that, moving forward, these alternative products – particularly 1,4-DMN, which appears to be considered the best alternative to chlorpropham – would gradually replace chlorpropham products also in other national markets – as they obtain product authorisations, which are in progress – thereby limiting the scope for effects on competition the Transaction could have. (9)

(57) Such a trend is for the moment visible in the available market data in countries such as the Netherlands and the United Kingdom where new products have been successfully launched, but it can be expected that alternative products will increasingly compete with the products of the Parties based on chlorpropham also in other countries.

(58) For example, 1,4-DMN was only launched during 2017 in other countries, in particular Belgium and France, and has not yet been launched in Spain. Market shares for 2017 do not yet reflect this development for those countries, but the share of supply of alternative products is expected to grow significantly in the coming years.

5.3.5. Chlorpropham is facing regulatory risks, significantly impacting the Parties' positions in potato PGR markets in the EEA

(59) In addition to the other elements detailed in this assessment, on the basis of which the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market and with the EEA Agreement with respect to PGR for potatoes in Belgium, France, Germany, the Netherlands, Spain and the United Kingdom, and in particular the reduced acceptance of products based on chlorpropham due to concerns of customers in the supply chain, the ability of the Parties to compete in the relevant markets is likely to be reduced by the current regulatory pressure on chlorpropham.

(60) In light of the above-referenced EFSA conclusions on serious health risks for consumers, (10) the Commission has already proposed several times to the relevant decision-making body (the Standing Committee on Plants, Animals, Food and Feed – 'SCoPAFF') not to renew chlorpropham's approval. (11) No decision has yet been made at that level, and the Commission reiterates its proposal on the agenda for the next SCoPAFF meeting scheduled for 24-25 January 2019. (12)

(61) Finally, the Rapporteur Member State in charge of chlorpropham's review – the Netherlands, a very significant potato-growing country – has recently taken the official position that, although continued safe uses as a herbicide could in its view be managed, it can in any event no longer support the use of chlorpropham on potatoes, notably in view of EFSA's conclusions on serious health risks for consumers. (13)

(62) In that regard, even assuming that chlorpropham's approval at the EEA level would be renewed, Member States would still individually need to consider user and consumer safety when assessing the ensuing requests for market authorisations for individual finished products to be issued at the Member State level: "[f]ollowing renewal of approval of an active substance, all plant protection products containing that active substance must also undergo a renewal assessment to make sure that products comply with the updated assessment of the active substance and with new scientific and technical knowledge". (14)

(63) In doing so, Member States would thus need to consider EFSA's conclusions regarding serious health risks for consumers, which would likely prevent them from delivering product authorisations for use as potato PGR. In particular, Member States would be free not to deliver authorisations for products containing chlorpropham, even if it would have been approved at the EEA level.

(64) Accordingly, it is likely that the Parties' combined market shares would overestimate their competitive position in the near future.

5.3.6.The Transaction is unlikely to significantly affect competition in potato PGR markets in the EEA

(65) In sum, the Commission's investigation confirmed that while both UPL and Arysta compete in potato PGR through products based on chlorpropham: (15)

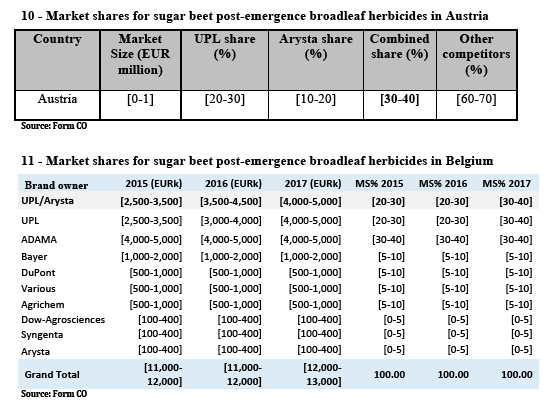

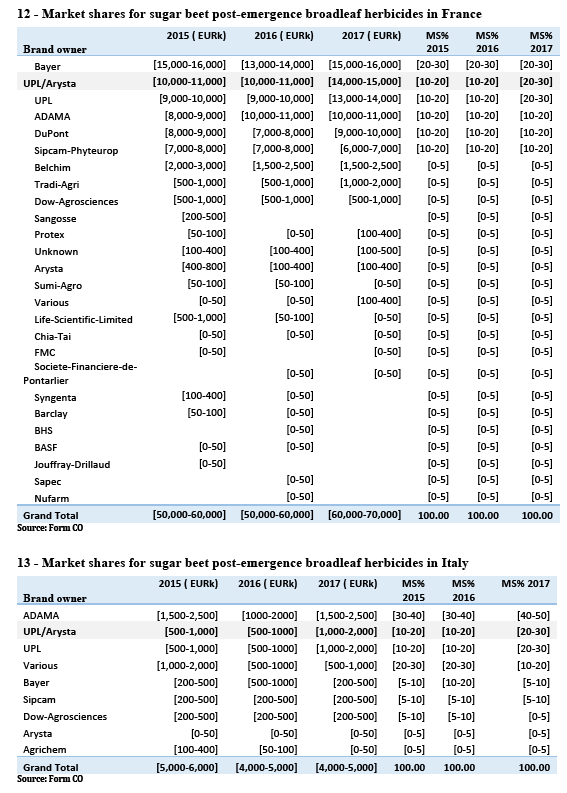

(a) They face close competition from Certis, a larger player marketing products based on the same AI (chlorpropham).

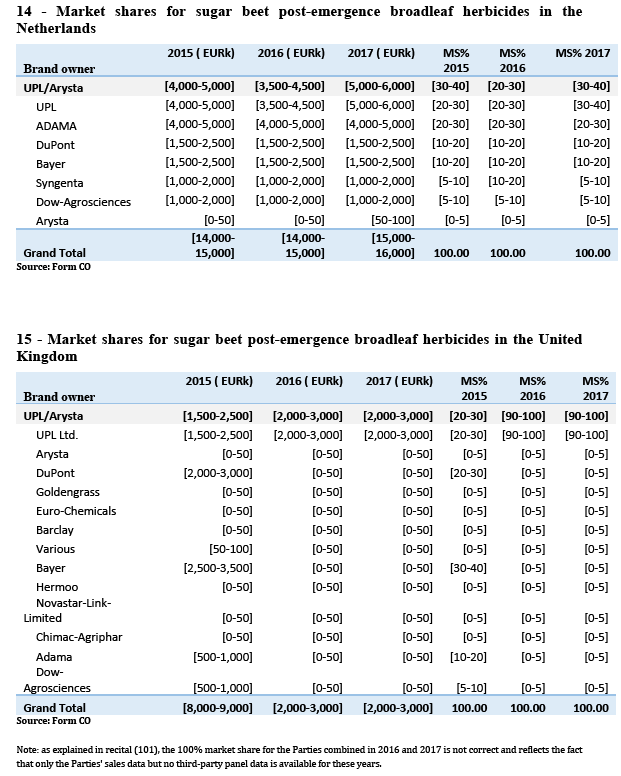

(b) The only markets where Certis is not larger than the Parties combined (the Netherlands and the United Kingdom) are markets where the available information shows that chlorpropham products are being largely replaced by newer and safer options due, among others, to concerns about the residues left by chlorpropham products which may entail dangers for human health. In the Netherlands, for instance, as illustrated by Table 4, the evolution of sales since 2015 shows that as chlorpropham products have lost sales to newer products, this has disproportionately affected more prominent chlorpropham players such as Certis (decreasing from a [40-50]% to a [30-40]% market share), but also UPL (decreasing from [20-30]% to [10-20]%).

(c) There is a reduced likelihood of the Parties being able to significantly compete in the medium term through chlorpropham products due to the same concerns, which have increased regulatory pressure on the molecule, for which the Commission has proposed not to further renew the approval.

(d) In the United Kingdom, Arysta only sells products based on maleic hydrazide, and there is thus no overlap with UPL at the molecule level. The Parties therefore do not compete closely and face competition from different players.

(66) While some customers responding to the Commission’s investigation expressed concerns, most market respondents indicated they do not expect the Transaction to result in anticompetitive effects.

(67) Moreover, even those respondents to the market investigation which expressed some concerns (16) acknowledged that any effect may be short lived due to the significant regulatory and food-chain pressure on the use of chlorpropham, and the fact that market participants anticipate that its authorisation will not be renewed in the very short term.

(68) For instance, a competitor explained that "CIPC , which could be the problem , will probably be banned". Another competitor confirmed that: "YES: they are direct competitors for chloorprofam [sic]. But re-registration (Annex I renewal) of chloorprofam [sic] is uncertain, so this AI may disappear". (17)

(69) A customer similarly explained that the "ban of CIPC will effect [sic] market more than merge [sic] UPL / ARYSTA". (18)

(70) Overall, the respondents to questions on this niche market did not expect the Transaction to significantly affect competition in potato PGR in the EEA. (19)

5.3.7. Conclusion

(71) Based on the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market and with the EEA Agreement with respect to PGR for potatoes in Belgium, France, Germany, the Netherlands, Spain and the United Kingdom.

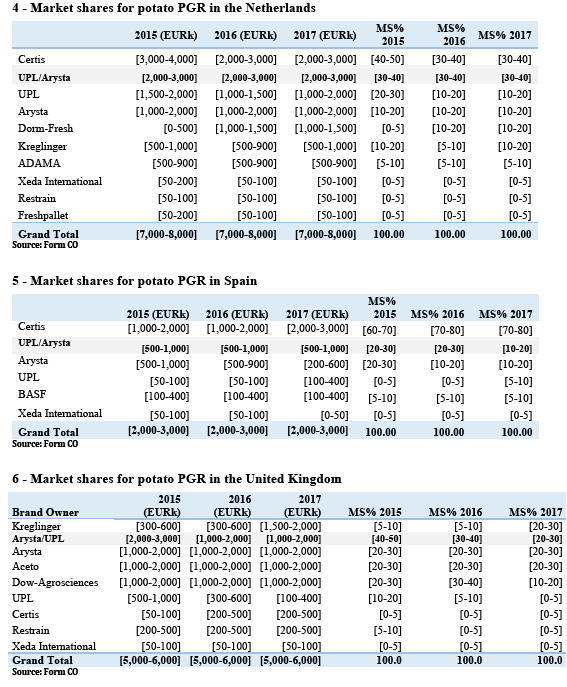

5.4. Broad spectrum fungicides for other fruit (20)

(72) Broad spectrum fungicides for other fruit are products designed to address several diseases (scab, powdery mildew, Monilia, Taphrina, Phytophtora, etc.) in a number of crops – including stone fruit, olives and citrus – rather than for each crop individually.

(73) The competitive dynamics for products addressing diseases in these different crops are likely inaccurately reflected by data at such an aggregate level (namely several crops taken together rather than individually). It is therefore unclear to what extent there would truly be any affected "market" in this case. In any event, Greece would be the only EEA country where there would be possible affected markets in such a hypothetical "market" according to the data provided by the Notifying Party, with a combined share for the Parties of [30-40]%.

(74) On the basis of the information provided by the Notifying Party, the Commission considers that there are no affected markets for individual crop/disease combinations within this aggregation. (21)

(75) Moreover, the Parties overlap only with respect to copper-based products, for which there is a significant number of other possible suppliers (at least eight on the basis of Table 7), (22) be it in the same chemical form as the one sold by the Parties (copper- sulphate) or in other chemical forms (copper-hydroxide, copper-oxychloride) which can also be used.

(76) In addition to the other elements detailed in this assessment, on the basis of which the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market and with the EEA Agreement with respect to broad spectrum fungicides for other fruit in Greece, products sold by the Parties such as copper products as well as mancozeb and captan are under regulatory pressure. Their use is thus being restricted, which may be of concern when it comes to their efficacy such that current sales likely overestimate their competitive relevance in the near future.

(77) On the one hand, the approval for copper salts was recently renewed at EEA level (November 2018) but with a limited maximum dose as the result of eco- toxicological concerns raised during the review process. In consequence, the dose rate per single application and/or the number of sprays to cover the sensitive vegetative period may be too low, particularly for organic growers. For this reason, growers may choose more relevant fungicides to ensure a high level of protection of their orchards.

(78) On the other hand, mancozeb is currently under evaluation by EFSA for renewal. EFSA’s conclusions are not known yet. However, the result of the evaluation carried out by the rapporteur Member State (the UK’s Chemicals Regulation Division - CRD) and the publication of the comments made during the consultation period give a clear indication of the concerns related to the AI. The CRD has stated that mancozeb might be considered as having endocrine disruption properties, which would prevent the notifiers (Mancozeb Task Force composed of Indofil and UPL) from renewing the approval for the AI. Whatever decision is made by the Commission (withdrawal or specific restriction on uses), this may have an immediate effect on mancozeb sales and the Parties’ market shares.

(79) In addition to the EU regulatory drivers, each country implements its own policies on pesticides which can have a very strong influence on market dynamics. Ecological taxes or other incentive/disincentive schemes on certain products with specific “classifications” or profiles can impact prices and growers’ choices.

(80) Conversely, new product launches are planned in the near future, for instance an AI by Agro Kanesho planned for launch in the EEA, possibly also in the sizeable Greek market.

(81) In addition, by contrast with UPL, Arysta does not itself manufacture the main products it sells and only acts as a reseller of products manufactured by a third party (which also supplies other players in that market). Arysta's competitive relevance is therefore likely lower than suggested by its share of sales in Table 7.

(82) Finally, a clear majority of the respondents to the Commission's investigation did not expect that the Transaction would significantly affect competition in broad spectrum fungicides for other fruit. (23)

(83) Based on the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market and with the EEA Agreement with respect to broad spectrum fungicides for other fruit in Greece.

5.5. Scab fungicides for pome fruit

(84) Scab fungicides for pome fruit are products designed to address scab in pome fruit (apples and pears).

(85) As shown in Tables 8 and 9, France and Greece would be the only EEA affected markets according to the data provided by the Notifying Party, with relatively modest combined shares of approximately [20-30]%, far behind the market leader BASF.

(86) Moreover, in France, the Parties do not overlap in the composition of their products, since UPL sells products based on copper and mancozeb whereas Arysta sells products based on pyrimethanil, dodine and captan. The Parties are therefore unlikely to be close competitors in France.

(87) In Greece, the Parties overlap in the composition of their products only with respect to mancozeb and copper-based products, for which there is a significant number of other possible suppliers, be it in the same chemical form as the one sold by the Parties (copper-sulphate) or in other chemical forms (copper-hydroxide, copper- oxychloride) which can also be used.

(88) In addition to the other elements detailed in this assessment, on the basis of which the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market and with the EEA Agreement with respect to scab fungicides for pome fruit in France and Greece, products sold by the Parties such as copper products as well as mancozeb and captan are under regulatory pressure. Their use is thus being restricted, which may be of concern when it comes to their efficacy such that current sales likely overestimate their competitive relevance in the near future.

(89) On the one hand, the approval for copper salts was recently renewed at EEA level (November 2018) but with a limited maximum dose as the result of eco- toxicological concerns raised during the review process. In consequence, the dose rate per single application and/or the number of sprays to cover the sensitive vegetative period may be too low, particularly for organic growers. In France, recent registrations of copper-based products have been granted with very low dose rates on orchards and a limited number of applications (for worker exposure reasons), which may be of concern when it comes to efficacy. For this reason, growers may choose more relevant fungicides to ensure a high level of protection of their orchards. Similarly, other national authorisations of formulated products may also apply restrictions in the forms of dose rates and buffer zones.

(90) On the other hand, mancozeb is currently under evaluation by EFSA for renewal. EFSA’s conclusions are not known yet. However, the result of the evaluation carried out by the rapporteur Member State (the UK’s Chemicals Regulation Division - CRD) and the publication of the comments made during the consultation period give a clear indication of the concerns related to the AI. The CRD has stated that mancozeb might be considered as having endocrine disruption properties, which would prevent the notifiers (Mancozeb Task Force composed of Indofil and UPL) from renewing the approval for the AI.

(91) Indeed, following the request of the CRD, the Mancozeb Task Force removed pome fruits from the list of representatives uses since a safe use was unlikely to be found. This would indicate that pome fruits should not be treated with formulations containing mancozeb and this would force growers to go for other solutions. If for any reason existing registrations on pome fruits can be maintained at country level, the likeliness of getting large buffer zones (50 meters), lower dose rates and/or limited number of sprays, the level of ecotax (in France), the limited possibilities of tank mixes (in France) would render the use of mancozeb on pome fruits less relevant for growers compared to other solutions. Whatever decision is made by the Commission (withdrawal or specific restriction on uses), this may have an immediate effect on mancozeb sales and the Parties’ market shares.

(92) In addition to the EU regulatory drivers, each country implements its own policies on pesticides which can have a very strong influence on market dynamics. Ecological taxes or other incentive/disincentive schemes on certain products with specific “classifications” or profiles can impact on prices and growers’ choices.

(93) France, for example, has increased the level of an already high tax on mancozeb, a key UPL product, which will rapidly and negatively impact UPL’s market share. Specifically, the level of ecotax for mancozeb in France increased on 1 January 2019 from EUR 5.10 per kg of AI to a total tax of EUR 14 per kg of AI, an increase of 175% of the existing level of tax which will likely result in growers shifting to more affordable solution (not or less affected by ecotax).

(94) Conversely, new products have recently been launched in 2017 for instance by Bayer in Greece (for an approximate 2018 market share of 6%) and BASF in France (for an approximate 2018 market share of 1%). Other product launches are planned in the EEA in the near future, for instance AIs by Bayer, Agro Kanesho, Nissan Chemical, Nihon Nohyaku and Nippon Soda. These would in the future likely be launched in the sizeable French and Greek markets for scab in pome fruit.

(95) In addition, by contrast with UPL, Arysta does not itself manufacture the products with the same composition as UPL's products and only acts as a reseller of products manufactured by a third party (which also supplies other players in that market). Arysta's competitive relevance is therefore likely lower than suggested by its share of sales in Tables 8 and 9.

(96) Finally, a clear majority of the respondents to the Commission's investigation did not expect that the Transaction would significantly affect competition in scab fungicides for pome fruit. (24)

(97) Based on the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market and with the EEA Agreement with respect to scab fungicides for pome fruit in France and Greece.

5.6. Post-emergence broadleaf herbicides for sugar beet

(98) Post-emergence broadleaf herbicides for sugar beet are products designed to address broadleaf weeds in already emerged sugar beets.

(99) As shown in Tables 10 to 15, according to the data provided by the Notifying Party the Parties' activities in post-emergence broadleaf herbicides for sugar beet give rise to affected markets in Austria, Belgium, France, Italy, the Netherlands and the United Kingdom.

(100) In each case, the combined market share or increment would be low (inferior to one percentage point). The only exception is Austria, where, however, the available data seems unreliable: in particular, the available data does not split sales by market player (the Parties sales and shares were computed on the basis of their internal data, not the third-party panel market data), and the total market size is small, increasing the effect of possible data inaccuracies.

(101) Similarly, the available panel data for the United Kingdom is incomplete in that it does not include 2016 or 2017 data. Accordingly, only actual sales data for the Parties is available for those years, which explains the 100% market share in Table 15 for the Parties combined in 2016 and 2017, which is obviously incorrect. Based on the 2015 data, UPL held a market share of [20-30]% but there was no overlap between the Parties. While panel data for 2017 is not available, the Parties’ 2017 sales data indicates only a very limited overlap between the Parties (UPL: EUR [2-4] million; Arysta EUR [0-0.5] million).

(102) Moreover, the Parties appear to overlap in the composition of their products only with limited sales of products based on the AI clopyralid, which neither produces and which they both procure from […] (which itself also directly sells products based on that AI).

(103) In addition, there are several other suppliers for each of the Parties' products based on molecules other than clopyralid, in each case typically with larger sales than the Parties. (25)

(104) More generally, the Parties' respective broader herbicide portfolios appear to have different foci: Arysta appears to target grasses in post-emergence, while UPL appears to focus on cross-spectrum/broadleaf products in pre-emergence, and seems to have deliberately developed sugar beet herbicides as a key focus (including with upcoming pipeline products). It is therefore unlikely that the Parties would be close and important competitors even in the relevant affected markets, and consequently that the Transaction would have a significant effect on competition in these markets.

(105) In addition to the other elements detailed in this assessment, on the basis of which the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market and with the EEA Agreement with respect to post-emergence broadleaf herbicides for sugar beet in Austria, Belgium, France, Italy, the Netherlands and the United Kingdom, UPL's products based on desmedipham and phenmedipham – in addition to those based on chlorpropham – are under regulatory pressure. Their approvals expire on 31 July 2019 and their evaluations have highlighted endocrine properties: they are thus likely to be banned or at least heavily restricted. Accordingly, their current sales likely overestimate their competitive relevance in the near future. Specifically, in the most likely scenario where both of the molecules (as well as chlorpropham) could no longer be used in the EEA, UPL would likely lose a total of EUR [20-30] million in sales. Projections provided by the Parties show that their combined market share in the different affected markets would in the most likely scenario either remain relatively similar or decrease. (26)

(106) Conversely, new products have recently been launched for instance by Bayer, Adama, Syngenta, Dow and BASF in 2017 or 2018. Other launches are planned in the near future, for instance products by Bayer, BASF, FMC and others. (27)

(107) Finally, a clear majority of the respondents to the Commission's investigation did not expect that the Transaction would significantly affect competition in post-emergence broadleaf herbicides for sugar beets. (28)

(108) Based on the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market and with the EEA Agreement with respect to post-emergence broadleaf herbicides for sugar beet in Austria, Belgium, France, Italy, the Netherlands and the United Kingdom.

5.7. Vertically affected markets

(109) Under the framework established in the Commission’s guidelines on the assessment of non-horizontal mergers, (29) the Commission assesses so-called vertically affected markets when proposed concentrations concern companies which are respectively active on upstream and downstream markets from each other (that is to say, are in supplier-customer situations). In that context, the Commission mainly considers whether an operation is likely to result in input foreclosure or customer foreclosure.

(110) Regarding possible input foreclosure, on the one hand, UPL is in the EEA a significant seller of chlorpropham as an AI – with an approximate EEA market share of [30-40]% (30) – which is then incorporated in a number of finished herbicides and potato PGR sold on downstream markets.

(111) On the other hand, Arysta makes sales on these downstream markets, notably with products containing chlorpropham.

(112) There is therefore in theory scope for input foreclosure, where the merged entity would attempt to increase its downstream sales by preventing downstream competitors from having access to the necessary upstream input (in this case, the chlorpropham AI).

(113) However, Arysta's (as well as the combined entity's) downstream market shares in markets where Arysta sells products incorporating chlorpropham are typically below 20% (herbicides for other vegetables in France, Poland, the Netherlands and the United Kingdom, and for ornamentals in the Netherlands and the United Kingdom).

(114) For potato PGR, the only Member State for which the market is vertically affected but not horizontally affected – and therefore is not already assessed in Section 5.3 – is Italy, with a [30-40]% market share for Arysta (there is no horizontal overlap because UPL is not active downstream in that country).

(115) Furthermore, these shares relate to the less relevant aggregations at crop level or even aggregations of crops rather than an individual crop/pest combination (for instance herbicides for other crops in Belgium). (31) The information available to the Commission did not reveal that there would be any affected market or any likely effect on competition in individual crops. (32)

(116) In light of these relatively modest market shares, the Commission considers it unlikely that the merged entity could successfully engage in an input foreclosure strategy.

(117) Moreover, only very few market players appear to sell products based on chlorpropham in the relevant downstream markets, and therefore to be potentially relying on UPL as a source of chlorpropham.

(118) In particular, Certis – the main alternative seller of downstream products based on chlorpropham in the EEA – […]. Instead, it appears to be sourcing its chlorpropham from a Chinese supplier.

(119) Regarding other players, in the relevant downstream herbicide markets, the only player aside from Certis and the Parties to sell products containing chlorpropham products is Sipcam. However, its sales in the relevant downstream market (herbicides for other vegetables in France) is very modest ([5-10]%), and in all likelihood only partly attributable to products based on chlorpropham since Sipcam appears to sell products based on a number of AIs in this market.

(120) Similarly, in the relevant downstream potato PGR markets, only few players aside from Certis and the Parties sell products containing chlorpropham: Frowein in Germany, Aceto in the United Kingdom and BASF in Spain. In all cases, as can be seen in Section 5.3, the market share of each player is modest.

(121) Moreover, while UPL's upstream market share in the EEA is significant ([30-40]%), it continues to face two Chinese competitors in the supply of chlorpropham, each with a similar market share and with a significantly higher share combined. The Commission thus considers that, in the hypothetical case where the merged entity would attempt to foreclose access to the chlorpropham AI to some of its downstream competitors, these would likely be able to defeat such a strategy by finding alternative suppliers.

(122) The Transaction would therefore in all likelihood not change the competitive dynamics of the supply of chlorpropham in the EEA.

(123) Regarding possible customer foreclosure, already today […]. The contractual arrangements […] would remain unaffected by the Transaction. The Commission therefore considers that there is no scope for customer foreclosure, whereby […].

(124) In addition to the other elements detailed in this assessment, on the basis of which the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market and with the EEA Agreement with respect to vertically affected markets in the EEA on the basis of products containing chlorpropham, as detailed in Section 5.3.5, chlorpropham at this stage appears unlikely to have its approval renewed in the EEA in the coming months. Any hypothetical effect from the Transaction at this stage thus appears likely to disappear in the very short term.

(125) Accordingly, the Transaction would likely not result in a significant impediment to effective competition in the upstream market for chlorpropham or in any of the vertically affected downstream markets in which Arysta sells formulated products incorporating chlorpropham.

(126) Based on the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market and with the EEA Agreement with respect to vertically affected markets in the EEA on the basis of products containing chlorpropham.

6. CONCLUSION

(127) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 See Commission Decisions in Case M.7932 – Dow/DuPont (2017), notably recitals 319, 332, 657 and 1769; Case M.7962 – ChemChina/Syngenta (2017), notably recitals 102, 117, 138, 166 and 174; Case M.8084 – Bayer/Monsanto (2018), notably recitals 1361 and 2296-2298.

4 Form CO.

5 Form CO, notably paragraphs 9, 11 and 129-131, as well as Annexes PGR Potatoes, Chlorpropham, Herbicides Sugar Beets, Fungicides Pome Fruit and Fungicides Other Fruit; Response to State of Play Meeting.

6 According to the Notifying Party, if products incorrectly allocated to Kreglinger in the market data were correctly allocated to Certis, Certis would be the market leader ahead of the Parties also in the Netherlands (see the Response to State of Play Meeting, footnote 9).

7 EFSA, Peer review of the pesticide risk assessment of the active substance chlorpropham, 18 June 2017, available at: https://efsa.onlinelibrary.wiley.com/doi/epdf/10.2903/j.efsa.2017.4903 ('EFSA risk assessment').

8 https://www flandersfood.com/projecten/reskia.

9 Response to State of Play Meeting.

10 EFSA risk assessment, Table 5.

11 Draft Commission Implementing Regulation concerning the non-renewal of approval of the active substance chlorpropham, in accordance with Regulation (EC) No 1107/2009 of the European Parliament and of the Council concerning the placing of plant protection products on the market, and amending Implementing Regulation (EU) No 540/2011 (5 page(s), in English) Reference: G/TBT/N/EU/565.

12 Agenda for the SCoPAFF meeting of 24-25 January 2019, document sante.ddg2.g.5(2018)7356188, available at: https://ec.europa.eu/food/sites/food/files/plant/docs/sc phyto 20190124 ppl agenda.pdf. In the event that a qualified majority of Member States would then not support its proposal, the Commission can – first – appeal the vote and then, in case it again does not have the needed support at that level, in a second step – provided there is on appeal no qualified majority against its proposal – eventually decide unilaterally.

13 Letter from the Dutch Minister of Agriculture, Nature and Food Quality to the President of the Dutch Parliament, 11 December 2018, Annex 1 to the Response to State of Play Meeting.

14 Quote from https://ec.europa.eu/food/plant/pesticides/authorisation of ppp/application procedure en. More detailed information is available on this Commission website.

15 Q1 – Questionnaire to Competitors, questions 5-15; Q2 – Questionnaire to Customers and Others, questions 5-15.

16 Q1 – Questionnaire to Competitors, questions 5-15; Q2 – Questionnaire to Customers and Others, questions 5-15.

17 Q1 – Questionnaire to Competitors, questions 9.1 and 10.1.

18 Q2 – Questionnaire to Customers and Others, question 14.1.

19 Q1 – Questionnaire to Competitors, question 14; Q2 – Questionnaire to Customers and Others, question 14.

20 For the avoidance of doubt, 'other fruit' in this decision should not be read as meaning 'fruits other than pome fruit' – assessed in Section 5.5 – but rather fruits other than those identified as separate crops in the available market data. These are, in essence, the crops listed in recital (72).

21 See also Form CO, Annex Fungicides Other Fruit, Tables 6 to 28 and paragraph 114-123.

22 See also Form CO, Annex Fungicides Other Fruit, Tables 38 and 49.

23 Q1 – Questionnaire to Competitors, question 26; Q2 – Questionnaire to Customers and Others, question 26.

24 Q1 – Questionnaire to Competitors, question 22; Q2 – Questionnaire to Customers and Others, question 22.

25 See Form CO, Annex Herbicides Sugar Beet, Tables 11, 35, 38, 41, 45 and 48.

26 See Form CO, Annex Herbicides Sugar Beet, paragraphs 37-42 and 92-93, 97-98, 102-103, 111-112 and Tables 20, 24, 28, 32 and 42.

27 See Form CO, Annex Herbicides Sugar Beet, paragraphs 79-80 and Tables 12-13.

28 Q1 – Questionnaire to Competitors, question 19; Q2 – Questionnaire to Customers and Others, question 19.

29 Guidelines on the assessment of non-horizontal mergers under the Council Regulation on the control of concentrations between undertakings, OJ C 265, 18.10.2008, p. 7.

30 See Form CO, paragraph 10.

31 See Form CO, Annex Chlorpropham, Table 7.

32 See Form CO, Annex Chlorpropham, paragraphs 94-95, 113-115, 121-122, 124-125, 127-128 and 130-131.