Commission, March 6, 2020, No M.9674

EUROPEAN COMMISSION

Decision

VODAFONE ITALIA/ TIM/INWIT JV

Subject: Case M.9674 – VODAFONE ITALIA / TIM / INWIT JV

Commission decision pursuant to Article 6(1)(b) in conjunction with Article 6(2) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 17 January 2020, the European Commission (the “Commission”) received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Vodafone Europe B.V. and Telecom Italia S.p.A (“TIM”) will combine into a newly created joint venture their passive mobile telecommunications infrastructure businesses in Italy (the “Transaction”).3

1. THE PARTIES

(2) Vodafone Europe B.V. is part of the Vodafone Group, which operates telecommunications networks and offers telecommunications and other services in a number of countries across the globe. Within the EU, Vodafone is active in ten Member States. In particular, Vodafone Italia S.p.A. (“Vodafone”) provides mobile and fixed telecommunications services to consumers and businesses in Italy.Vodafone Italia also owns its mobile network that consists of approximately 11 000 passive sites and related infrastructure.

(3) TIM provides mobile and fixed telecommunications services to consumers and businesses in Italy. Outside Italy, TIM is mainly active in Brazil. TIM owns the passive infrastructure of its mobile network in Italy through Infrastrutture Wireless Italiane S.p.A. ("INWIT"), a publicly listed, 60.33% owned subsidiary. INWIT operates approximately 11 000 passive infrastructure sites hosting equipment mainly for mobile network operators (“MNOs”) and other providers of electronic communication services.

(4) Vodafone, TIM and INWIT are designated hereinafter as “Parties”.

2. THE TRANSACTION

(5) Pursuant to a Framework Agreement executed on 26 July 2019, the Parties intend to combine their passive infrastructure operations in Italy into a jointly controlled company (hereinafter, the “Joint Venture”, the “JV” or “INWIT”).

(6) For this purpose, Vodafone Italia has created a separate legal entity, Vodafone Towers S.r.l. (“VOD Towers”), to which it has contributed its passive infrastructure operations. INWIT will acquire a minority participation (43.4%) in VOD Towers against the payment of a cash consideration. VOD Towers will then merge into INWIT. As a result, the Parties will each hold shares equal to approximately 37.5% of INWIT’s capital,4 whilst the remaining shares will be free-floating.5 The shareholders of INWIT will then adopt Amended By-Laws and the Parties will execute a Shareholders’ Agreement.

(7) Finally, INWIT will execute with each of TIM and Vodafone Italia a Master Service Agreement (“MSA”) for the provision of hospitality services, for a term of […] years, with tacit renewal clause for an additional […] years. Under the terms of the MSAs:(a) With respect to hospitality services on existing macro-sites6 […]:(i) As result of the Transaction, INWIT will manage around 22 000 existing macro sites. […].(ii) […]. (iii)[…]. (iv)[…].(v) […].7 […].(vi)[…].(b) With respect to hospitality services on new macro sites or small cells8, […]:(i) […].(ii) […], the Parties grant INWIT the status of preferred supplier for the provision of services on new sites, […].(c) […], each of the Parties commit to entrust INWIT the provision of hospitality services on macro sites and small cells, as well as fiber backhaul services, […].(d) […].(e) […]:(i) […].(ii) […].

(8) Thus, the MSAs contain several provisions which afford preferential rights to the Parties to access the sites managed by the Joint Venture. The rationale of these provisions is to ensure that INWIT’s ability to offer hospitality to third parties on any of the sites contributed by the Parties is restricted to the space that the Parties will leave free after the Parties have activated the passive sharing. Thus such provisions are functional to the additional agreements entered into by the Parties described in Section 3.3. And in particular to the agreement related to passive sharing.

(9) The MSAs will be taken into account in the assessment of the effects of the Transaction. On the one hand, these are long-term supply contracts, which arguably go beyond what normally required in a transitory period for the implementation of a transaction. On the other hand, being these binding contracts that will define the rights of the Parties over the assets managed by the Joint Venture, the MSAs will have an influence over the competitive behaviour of the Joint Venture.

3. THE CONCENTRATION

3.1.Joint control

(10) Post-Transaction INWIT will be jointly controlled by Vodafone and TIM within the meaning of Article 3(1)(b) of the Merger Regulation for the following reasons:(a) First, the Parties will each hold 37.5% of INWIT’s capital and thus together hold more than 50%.(b) Second, the Amended By-Laws set out, in particular, the following governance principles:– The Board of Directors will consist of 13 members appointed following a list mechanism. According to this mechanism, if two lists obtain each the votes of at least 25% of INWIT capital (but less than 50% - which would be the case for the lists presented by Vodafone and TIM), such lists appoint each 5 directors. The remaining directors are appointed from the minority lists. Thus the Parties will be able to appoint each 5 directors.– A number of reserved matters, including, among others, the budget and the business plan, the nomination of the CEO and the Chairman, could be decided by the Board only with a supermajority of 9 directors. Thus, in principle, thfavourable vote of directors nominated both by TIM and Vodafone is required.(c) Third, pursuant to the Shareholders’ Agreement, TIM and Vodafone have agreed to appoint each an equal number of member of the Board of Directors of INWIT. For the first term, TIM designates the CEO, while Vodafone designates the Chairman and the CFO. Subsequently, in the absence of agreement, a rotation mechanism for the designation of key managers is applied between Vodafone and TIM. Finally, a three years lock-up period is foreseen on any sale of shares of INWIT.9

3.2. Full-functionality

(11) The Parties submit that the proposed Joint Venture would not be full-function, for the following reasons:(a) the primary purpose of the Joint Venture would not be the formation of an independent tower company active on the Italian market; rather it would be to hold and manage the Parties’ combined passive infrastructure assets for the benefit of the Parties, with third-party sales representing an ancillary element;(b) the Joint Venture’s third party sales are expected to remain below […]% and the Joint Venture is expected to remain economically dependent on sales to its parent companies in the long-term;(c) the governance and contractual rights of the Joint Venture’s parents will significantly limit the Joint Venture’s operational autonomy, in that the Joint Venture will need to prioritise the critical infrastructure needs of TIM and Vodafone over any commercialisation of assets towards third parties;(d) the relationship between the Joint Venture and the parent companies is not “truly commercial” in nature, as the Parties enjoy preferential super anchor tenant rights, which would not be made available on the market by an independent tower company;(e) finally, the fact that the Joint Venture is listed on the Italian Stock Exchange and does have third party minority shareholders does not have any impact on the above-mentioned analysis.

(12) The Commission considers that Post-Transaction INWIT will constitute a full- function Joint Venture within the meaning of Article 3(4) of the Merger Regulation for the following reasons.

3.2.1. Sufficient Resources

First, the Joint Venture will have sufficient resources to operate independently on the hospitality services markets.10 INWIT is an existing company, listed in the Italian stock exchange and after the Transaction about 25% of its share capital will continue to be held by the public and INWIT will thus remain a publicly traded company. INWIT already has and will continue to have a management dedicated to its day-to- day operations with “managerial autonomy” and will continue to have access to sufficient resources (including its own finance, staff and assets) to conduct its business activities independently . In any case, the Parties do not contest this element of the analysis.

3.2.2. Presence on the market

(13) INWIT will not take over one specific function within the parent companies’ business activities and will have its own presence on the market.11

(14) As it will be better explained at following Section 7.2, already today both INWIT and VOD Towers (albeit to a lesser extent) offers telecommunications hospitality services to third parties in Italy and post-Transaction the Joint Venture will continue to be active in the hospitality services markets in Italy, similarly to any other operator on the same markets. The Parties have clearly stated that INWIT will be able to supply third parties on market terms as it sees fit and that it will be better placed to monetise Vodafone’s passive infrastructure by increasing third party tenancies (see below at section 7.5.2).

(15) Concerning the sales by the JV to the parent companies, the essential question is whether the JV will be geared to play an active role on the market and can be considered economically autonomous from an operational viewpoint.12 In case of significant sales of the JV to the parents, a finding of operational autonomy is possible if the relationship between the JV and its parents is truly commercial in character as “the greater the proportion of sales likely to be made to the parents, the greater will be the need for clear evidence of the commercial character of the relationship”.13

(16) Therefore, it is important to consider whether INWIT deals with the Parties at arm’s length. The simple fact that the Parties reserve for themselves a large proportion of the JV’s infrastructure, which is reflected in the high percentage of revenues expected to be realised with the Parties, does not as such exclude that the relationship between the JV and the parents is at arm’s length.

(17) In this respect, in the present case there are strong indications that the Parties will have access to INWIT’s infrastructure at market terms.

(18) While the Parties can reserve for themselves a large part of the JV’s infrastructure, as they have priority access to most of its sites, they still have to pay a market price for that access. Indeed, under the MSAs, to access INWIT’s infrastructure the Parties will […]. The […] fees paid by the Parties appears to be the market remuneration for the preferential super anchor tenant rights that the Parties will enjoy on INWIT’s infrastructure. Nothing in the Commission’s investigation suggests that similar preferential rights could not be granted by independent tower companies to a third- party customer, with a similarly adequate remuneration.

(19) In addition, the fact that the Parties’ access to INWIT’s infrastructure will be subject to market terms is confirmed by the reports of independent experts, who – on the basis of the Italian stock market regulations – were called to evaluate the contractual relations between INWIT and the Parties. Notably, an official report – established on the basis of the evaluation of independent experts – indicates that the economic terms of the MSAs with TIM and Vodafone are in line with market values and would have likely been applied even if the Transaction was concluded with third parties.14

(20) Therefore, it appears that the relationship between the JV and the Parties is truly commercial in character.

(21) For a finding of operational autonomy, it is also relevant that INWIT still has available capacity to offer to third parties and foresees, in addition, to build new sites at the request of third parties.15

(22) In this context, the Commission notes that the capacity reservation on INWIT’s infrastructure appears to be intended to protect the Parties, who need access to INWIT’s key infrastructure, and does not appear to be necessary to allow INWIT to operate on the market (where, as discussed below at Section 7.5.2, there is third parties’ demand for hospitality services on INWIT’s infrastructure). Indeed, before the Transaction INWIT is already operating autonomously on the market, offering a large (and growing) part of its infrastructure to third parties notwithstanding the capacity reservation already enjoyed by TIM.

(23) It thus appears that, on balance, regardless of the amount of sales to the Parties, INWIT is geared to play an active role on the market and can be considered economically autonomous from an operational viewpoint.

3.2.3. Long-lasting nature

(24) Finally, the Joint Venture is intended to operate on a lasting basis.16 INWIT has an indefinite duration and the combined business plans provided by the Parties cover the period up to […], in line with the duration of the MSAs for the provision of hospitality services, which have a term of […] years (with tacit renewal clause for an additional […] years). The Shareholders’ Agreement has a duration of […] years but provide for its possible renewal during a […] period before its expiration.

3.2.4. Conclusion on full-functionality

(25) Therefore, the Commission concludes that the Transaction will lead to the creation of a joint venture performing on a lasting basis all the functions of an autonomous economic entity pursuant to Article 3(4) of the Merger Regulation and thus constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

3.3. Scope of the concentration

(26) Under the Framework Agreement, the Transaction is instrumental to the implementation of a series of other agreements between the Parties:17 (a) A Passive Sharing Agreement, concerning the sharing of sites and passive mobile network equipment between the Parties. It provides for the extension of the existing passive sharing arrangements between the Parties18 on a nationwide basis for a term of […] years, with tacit renewal clause for an additional […] years. Also INWIT will be party to this agreement, as successor of TIM in some of the existing arrangements.(b) An Active Sharing Agreement, concerning the sharing of active mobile network equipment between the Parties. It provides for the implementation of an active sharing of the Parties’ respective existing 2G and 4G networks, as well as the joint roll-out of a 5G network, in municipalities with a population of up to 100 000 inhabitants. The agreement will have the duration of […] years, with tacit renewal clause for an additional […] years.(c) A Backhauling Agreement, setting out the terms and conditions for the supply of backhauling services by the Parties to each other via their existing fiber connections.19 The agreement will have the duration of […] years, with tacit renewal clause for an additional […] years.

(27) According to the Parties, the Transaction and the various agreements mentioned above (together the “Operation”) all serve the rationale of accelerating 5G deployment by the Parties, while creating synergies in terms of CAPEX and OPEX investments.20

(28) The Commission has received third party submissions claiming that the scope of the investigation in the present case under the Merger Regulation should not be limited to the Transaction, but it should extend to entire Operation.

(29) In this respect, the Commission notes that agreements entered into by the parties to a concentration that do not form an integral part of a concentration (because they do not establish control within the meaning of Article 3(2) of the Merger Regulation and do not carry out the main object of the concentration), but still restrict the parties' freedom of action in the market, can be covered by the assessment in a decision declaring the concentration compatible with the common market.21 This is the case if they qualify as ancillary restraints.

(30) For a contractual arrangement to be qualified as an ancillary restraint, it needs to satisfy the following two legal criteria:(a) being directly related to the implementation of the concentration, i.e. economically related to the main transaction and intended to allow a smooth transition to the changed company structure after the concentration, and(b) being necessary to the implementation of the concentration, i.e. in the absence of that agreement, the concentration could not be implemented or could only be implemented under considerably more uncertain conditions, at substantially higher cost, over an appreciably longer period or with considerably greater difficulty.

(31) Pursuant to paragraph 11 and following of the Commission Notice on restrictions directly related and necessary to concentrations, restrictions are not directly related and necessary to the implementation of the concentration simply because the parties regard them as such.22 As clarified by the Court, “[w]here it is not possible to dissociate such a restriction from the main operation or activity without jeopardising its existence and aims, it is necessary to examine the compatibility [with EU competition rules] in conjunction with the compatibility of the main operation”. However, “the fact that that operation is simply more difficult to implement or even less profitable without the restriction concerned cannot be deemed to give that restriction the ‘objective necessity’ required in order for it to be classified as ancillary”.23 As it appears from the examples set out in the Commission Notice on restrictions directly related and necessary to concentrations as well as from the Commission practice,24 ancillary restraints normally consist in agreements in the favour of the joint venture or the target company (such as non-compete clause, supply agreements, etc.), which would enable it to operate in the market in a viable manner especially in a transitory period.

(32) In this context, the Commission considers that it cannot be established that the Passive Sharing Agreement, the Active Sharing Agreement and the Backhauling Agreement constitute ancillary restraints. Indeed, they do not appear to be directly related to the implementation of the Transaction in the sense of paragraph (30)(a), as they regulate relationships between the Parties and the Transaction could be implemented even without them.

(33) Further, it cannot be concluded that the necessity criterion set out in paragraph (30)(b) would be met with respect to the Passive Sharing Agreement, the Active Sharing Agreement and the Backhauling Agreement, as the Transaction could be implemented even in their absence without jeopardising its existence and aims. To the contrary, it appears that it is the Joint Venture that is instrumental to the implementation of the Passive Sharing Agreement and the Active Sharing Agreement: without the Joint Venture it may indeed be more costly or longer to create a common grid of the Parties through the those agreements.

3.4.Conclusion

(34) Therefore, the Transaction constitutes a concentration within the meaning of Articles 3(1)(b) and 3(4) of the Merger Regulation. The scope of the concentration whose effects will be assessed in this Decision will be limited to the agreements bringing out the Transaction, that is to say the Amended By-Laws and the Shareholders’ Agreement, together with the MSAs.25

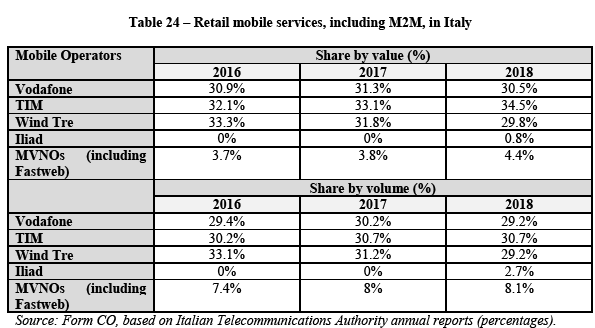

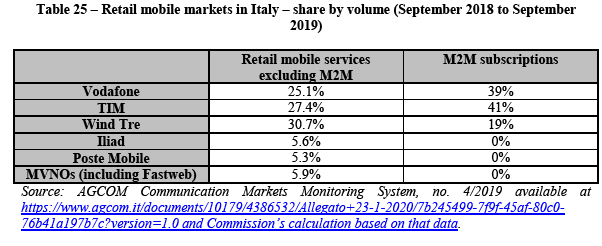

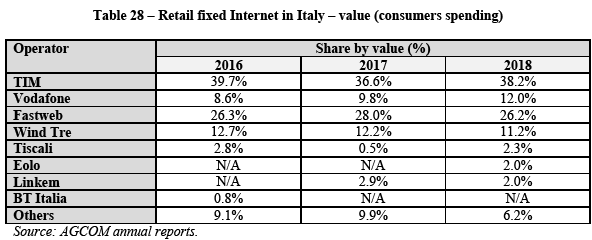

4. EU DIMENSION

(35) The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 5 000 million (Vodafone 50 254 million, TIM 18 934 million).26 Each of Vodafone and TIM has an EU-wide turnover in excess of EUR 250 million (Vodafone […] million, TIM 14 271 million), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has a Union dimension pursuant to Article 1(2) of the Merger Regulation.

5.INDUSTRY OVERVIEW

5.1. Passive network infrastructure

(36) Wireless telecommunications networks are composed of a number of radio access network sites, essentially a mast with an antenna and a radio-frequency system, linked to a core network by backhaul connections.

(37) There are essentially two types of radio access network sites: ground based towers and rooftop towers (together referred to as “macro-sites”). These sites have been originally built for captive use by network operators, but a market for hospitality services on macro-sites has been gradually opened.

(38) Recently, to ensure reliable coverage in buildings or dense urban areas, macro-sites have been supplemented by the use small cells and distributed antenna systems (“DAS”; together, with small cells, “micro-sites”). Micro-sites are expected to be used more prominently in 5G mobile networks and a market for the supply of hospitality services on these sites has started to develop.

(39) Each radio access network site covers a limited area and has a maximum capacity in terms of physical space on which equipment can be housed as well as in terms of electromagnetic fields (“EMF”) limits.

(40) Due to the architectonic configuration of Italian cities, with several historical buildings, often space on sites is limited or the use for telecommunications purposes is restricted.

(41) Further, the legislation on EMF limits in Italy is very stringent. It imposes the same EMF limits (i.e. 20 V/m or 6 V/m depending on the target measurement points stated by law) irrespective of types of uses of antennas. Accordingly, the same EMF limits apply for both broadcasters and telecom operators, as well as for both macro and micro-cells (though the low power and limited coverage of microsites allows for simplified EMF assessments). The Agenzia Regionale per la Protezione dell’Ambiente (“ARPA”) is the Italian regional body tasked with ensuring fulfilment of EMF obligations as well as giving prior authorisation for the installation of additional antennas on a site by an operator after the latter has provided ARPA with the relevant simulation and impact assessment, as prescribed by law. To obtain the prior authorisation from ARPA, current tenants on a site commonly collaborate with, and provide information on their equipment to, prospective tenants on the site, including in respect of the emissions and physical features (e.g. antenna height) of the equipment on the site, so as to enable the potential new tenants to prepare a proper simulation to be submitted to ARPA. The suppliers of hospitality services on the site are usually not involved in these discussions but have an interest in facilitating the process to increase their revenues.27 The challenges for operators to build new sites have been clearly described by the Italian Competition Authority in Segnalazione n. AS1551.

(42) The supply of hospitality services on sites include the rental of the space on the passive infrastructure, for which the customers pay the supplier a hosting fee. Normally the provision of these services is regulated by framework contracts of long duration (between 628 and 15 years) and the possibility of automatic renewal at the first expiration. The framework agreements are then supplemented by specific hosting agreements for relevant sites so that such relationships are governed by both the terms of the relevant overarching framework agreement and the specific hosting agreements pertaining to the relevant sites in question.

(43) A specific type of framework agreements are the “anchor tenant arrangements”. These are usually the result of the outsourcing of the management of previously captive sites to a third party. In this context, in order to keep some degree of control over the key network input constituted by the site, the customer usually reserves some preferential treatment or veto rights over the asset.

5.2. Suppliers of hospitality services on passive network infrastructure

(44) There is a range of providers of hospitality services.

(45) Firstly, sites are owned and managed by MNOs, which use them primarily for their own network purposes but also provide access to third parties. In Italy, there are currently four MNOs managing, operating and, to a different extent, offering access to sites: TIM, Vodafone, Wind Tre S.p.A. (“Wind Tre”) and Iliad Italia S.p.A. (“Iliad”).

(46) As mentioned earlier, TIM operates its 11 000 macro-sites through a separate company, INWIT. The same process of spin-off of the towers operations into a separate company has been recently undertaken by Wind Tre, with the creation of CK Hutchison Networks Italia S.p.A. (“CKHNI”), which manages around 9 000 macro-sites. Vodafone also owns its mobile network that consists of approximately 11 000 macro sites and related infrastructure.

(47) Secondly, sites are owned and managed by independent wireless infrastructure providers, known as "independent TowerCos". In Italy there are three independent TowerCos: Cellnex Telecom, S.A. (“Cellnex”), Ei Tower S.p.A. (“Ei Tower”) and RaiWay S.p.A. (“RaiWay”).

(48) Cellnex started providing hospitality services in Italy in 2015. On 26 March 2015, Cellnex closed the acquisition of 7 377 macro-sites (the “Galata business”) from the mobile operator WIND S.p.A. (“WIND”, today merged into Wind Tre29). WIND retained a 10% non-controlling shareholding over the Galata business. The sale agreement included a tower services agreement for these sites with WIND for period of 15 years, renewable for an additional period of 15 more years, and foresaw the deployment of additional sites that would have allowed WIND to accelerate the offer of new mobile broadband services.30

(49) On 7 May 2019, Iliad (which operates a mobile network not only in Italy but also in France and Ireland) announced that it entered into a series of agreements with Cellnex to form a strategic partnership with respect to Iliad's passive mobile telecom infrastructure in France and Italy.31 In total, Iliad agreed to transfer under the control of Cellnex 7 900 macro-sites (5 700 in France, 2 200 in Italy).32 As part of the contemplated transaction, Iliad entered into long-term service contracts with Cellnex. These agreements comprise the provision of hosting services over mobile telecom infrastructure as well as the construction of new sites through a build-to-suit program encompassing 6 400 macro-sites (4 500 in France and 1 900 in Italy) of which 3 500 committed by Iliad (2 500 in France and 1 000 in Italy).

(50) Ei Towers' activity consists of managing a portfolio of approximately 3 300 infrastructures, of which 2 300 broadcasting sites and approximately 1 000 mobile macro-sites.33 Rai Way is a subsidiary of RAI, Italy's state-owned television and radio broadcaster, and manages over 2 300 macro-sites across Italy.34 Thus, Rai Way and Ei Towers mainly provide coverage and signal for TV and radio broadcasting through broadcasting towers.

5.3.Demand-side of hospitality services on passive network infrastructure

(51) Sites are key inputs for building two types of wireless telecommunications networks: mobile telecommunications networks and fixed-wireless access (“FWA”) networks.

(52) As mentioned, in Italy there are currently four MNOs: TIM, Vodafone, Wind Tre and Iliad. They do not only manage and operate sites, but also use these sites for their supply of telecommunications services.

(53) TIM is the formerly state-owned incumbent and was founded in August 1994 through the merger of five companies: SIP, Iritel, Telespazio, Italcable and Sirm. Based on data published by the Italian telecoms regulator, as of September 2019 TIM was the second largest provider of retail mobile telecommunications services by number of SIM cards (excluding machine to machine (“M2M”) subscriptions; it was the market leader if M2M subscriptions are included).35 TIM also provides mobile virtual network operators (“MVNOs”) with wholesale access to its mobile network. TIM’s mobile network is based on the 2G, 3G and 4G technologies, but it has launched 5G pilots in Rome, Turin and Naples. TIM is also active in the provision of fixed telephony and fixed internet services, both at retail and wholesale level, based on its copper and fiber networks (including recently FWA technology)36 and, based on data published by the Italian telecoms regulator, as of September 2019 it was the market leader in the supply of retail fixed internet services.

(54) Vodafone was formed in 1994 with the name of Omnitel as the first alternative to the market leader TIM. In 2001, Omnitel was acquired by Vodafone Group and in 2003 it changed its name to Vodafone Italia. Based on data published by the Italian telecoms regulator, as of September 2019 Vodafone was the third largest provider of retail mobile telecommunications services by number of SIM cards (excluding M2M subscriptions; it was the second largest if M2M subscriptions are included).37 Vodafone also provides MVNOs with wholesale access to its mobile network. Vodafone’s mobile network is based on the 2G, 3G and 4G technologies, but it has launched 5G pilots in the Milan metropolitan area (including 28 surrounding localities), Rome, Turin, Bologna and Naples. Vodafone also delivers fixed telecommunications services to consumers and businesses without using FWA technology yet and, based on data published by the Italian telecoms regulator, as of September 2019 it was the second largest supplier of retail fixed internet services.

(55) Wind Tre was created in 2016 through a merger between two MNOs previously active in Italy, WIND and H3G S.p.A.38 Since 2018 it is controlled by CK Hutchison Holdings Limited.39 Based on data published by the Italian telecoms regulator, as of September 2019 Wind Tre was the market leader in the supply of retail mobile telecommunications services by number of SIM cards (excluding M2M subscriptions; it was the third largest player if M2M subscriptions are included).40 Wind Tre also provides MVNOs with wholesale access to its mobile network. Wind Tre’s mobile network is currently based on the 2G, 3G and 4G technologies. Wind Tre also delivers fixed telecommunications services to consumers and businesses and, based on data published by the Italian telecoms regulator, as of September 2019 it was the fourth largest supplier of retail fixed internet services.

(56) Iliad entered the Italian market in 2016 as beneficiary of the remedies, whose implementation was condition for the clearance of the merger between Wind and H3G. These remedies consisted of a number of elements designed to allow the entry of a fourth MNO into the Italian market, that is in particular: (1) the transfer of spectrum and the option to acquire/co-locate on macro access sites; (2) an option to enter into a RAN sharing agreement; and (3) a national roaming agreement. Iliad launched its mobile commercial offer on 28 May 2018.

(57) Since 25 July 2019, a fifth MNO is active in Italy, Fastweb S.p.A. (“Fastweb”). Fastweb, an indirect wholly owned subsidiary of Swisscom AG, is active in the Italian mobile market since 2007, originally as MVNO. Following the progressive acquisition of several blocks of high frequency spectrum, in June 2019 Fastweb signed a strategic co-investment with Wind Tre for a joint roll-out of a 5G network starting from 2020. The agreement will lead to the deployment of a shared 5G radio access and backhauling network in Italy, including Wind Tre and Fastweb macro and small cells, connected through dark fiber from Fastweb, to be deployed nationwide, with a targeted coverage of 90% of the population by 2026. Wind Tre will manage the 5G network, while both operators will remain independent in the commercial and operational use of the shared infrastructure. As part of the agreement, Wind Tre will provide Fastweb roaming services on Wind Tre’s existing network (4G and legacy technologies), while Fastweb will provide Wind Tre wholesale access to Fastweb’s fiber network. Indeed, Fastweb is also active in the supply of fixed internet services via its fiber network, as well as via FWA technology. The latter is the result of the acquisition of Fastweb of the FWA branch of Tiscali S.p.A. in July 2018. Based on data published by the Italian telecoms regulator, as of September 2019 Fastweb was the third largest supplier of retail fixed internet services, but it was the second largest, after TIM, in the in the segment for speeds between 10 and 30 Mbps and above 100 Mbps.

(58) Other than Fastweb, there are two large suppliers of FWA services in Italy: Linkem S.p.A. (“Linkem”) and Eolo S.p.A. (“Eolo”).

(59) Linkem is a provider of FWA services to residential and business customers that focuses mainly on metropolitan areas, but also in digital divide areas. Linkem has been awarded 3.4-3.6 GHz frequencies to provide its services until 2029 and currently uses LTE technology to provide last-mile connectivity to end-customers. This may differ from other FWA providers who use proprietary technologies.41 In December 2019 Linkem and Fastweb signed a strategic agreement for the simultaneous deployment of two separate 5G radio access networks (one leveraging Linkem’s spectrum and one leveraging Fastweb’s 26 GHz), and for the reciprocal provision of network slice services. Based on data published by the Italian telecoms regulator, as of September 2019 Linkem was the fifth largest supplier of retail fixed internet services (at distance from the fourth), but it was the second largest, after TIM, in the segment for speeds between 30 and 100 Mbps.

(60) Eolo is provider of FWA services in rural areas and small urban centres (i.e. less than 10 000 inhabitants) with a specific focus on areas with low coverage of fixed access broadband. Eolo operates using both non-licenced frequencies (i.e. 5 GHz) to provide connectivity services at a 30 mbps speed (“EoloWave”) and licenced frequencies (i.e. 28 GHz) that provide connectivity services at 100 mbps (“EoloWave G”). Based on data published by the Italian telecoms regulator, as of September 2019 Eolo was the fourth largest supplier of retail fixed internet services in the segment for speeds between 30 and 100 Mbps.

(61) Based on the results of the market investigation the Commission notes that, irrespective of the type of customers considered from the demand-side, the most important parameter of competition for the supply of hospitality services and driver of customer demand is the location of the specific site the customer is interested in. Indeed, also given the scarcity of sites, customers select the sites based on their radio network planning needs. For MNOs, price is the second driver of customer demand after site location, while for FWA suppliers price and location of the site have the same importance. In relation to MNOs, the same applies for both macro- and micro- sites.42

5.4. Network sharing

(62) MNOs can roll out their network by themselves, independently from other MNOs, or together with other MNOs through a network sharing agreement

(63) In a network sharing agreement, MNOs agree to share some of the network elements in order to reduce costs and improve coverage and capacity. The degree of integration within network sharing agreements varies depending on whether: (i) the MNOs only share their site infrastructure ("passive sharing" or "site sharing");(ii) they also share the RAN equipment at the sites ("active sharing"); (iii) they also share their spectrum ("spectrum sharing"); or (iv) they also rely on the same core network ("full network sharing").

(64) In particular, passive sharing involves sharing the basic infrastructure, such as masts, cabins and sometimes antennas and power supplies ("passive infrastructure"), as well as the cost of the site itself (rent and rates). Active sharing involves also sharing the RAN equipment ("active equipment"), meaning the base transceiver station and the controller nodes (for 2G and 3G), or the base transceiver station (for 4G) in addition to the passive infrastructure. Transmission (backhaul to the MNOs’ core networks) may also be shared under passive or active sharing agreements.

(65) In Italy, all MNOs are engaged in some level of passive sharing or co-location of sites. In particular, since 2007, the Parties have a number of passive sharing arrangements, mainly in municipalities with a population of up to 35 000 inhabitants (and in certain cases up to 50 000 inhabitants). As explained, under the Passive Sharing Agreement the Parties plan to increase their passive sharing arrangements to up to 100% of Italy’s territory. Under the Active Sharing Agreement, they plan to engage in active sharing in cities with less than 100 000 inhabitants.

5.5. Backhauling connections

(66) Backhaul services are the connections between the antenna in an infrastructure and the switches in the core network and are used to ensure the proper functioning of a mobile network. Backhaul are generally wired connections based on either (i) fiber optic cables or (ii) copper cables. However, wireless backhaul can be used in areas where fixed backhaul is not available.

(67) Backhaul providers are primarily fixed operators who are able to provide fiber optic or copper cables from their fixed network. Other than TIM and Fastweb, these are Open Fiber S.p.A. (“Open Fiber”) and Retelit Digital Services (“Retelit”).

(68) Open Fiber is a wholesale-only supplier of fiber connectivity services that started its activity in 2017 after the acquisition of, and subsequent merger with, Metroweb. Open Fiber plans to reach 19 million premises with fiber by 2023. In "black and grey areas", the plan foresees to reach 9.5 million premises of which Open Fiber already reaches over 5.5 million premises. As winner of public tenders for fiber connectivity in "white areas", Open Fiber will also build a public fiber network reaching 9.6 million premises. Almost 15% of the premises in those areas will be served through FWA networks.43

(69) Retelit is a listed company on the Italian stock exchange market and it operates since 2000 a fiber network in Italy that today reaches approximately 12 500 km. Retelit operates under a business-to-business model addressing wholesale and business markets.44

6. MARKET DEFINITION

(70) The Joint Venture will operate the network sites previously operated by the Parties and will offer hospitality services on this infrastructure to the Parties and third parties. Moreover, both Parties are active in Italy in the provision of mobile and fixed telecommunications services to consumers and businesses, for which access to sites is an important input. Finally, TIM and the Joint Venture will be both active in the supply of backhaul connectivity for sites. Therefore, the Transaction may have an impact on a series of telecommunications markets in Italy, which will be examined below.45

6.1. Hospitality services

6.1.1.Product market definition

(71) The Parties submit that the relevant product market is the market for the provision of hospitality services to telecommunication operators, including both macro- and micro-sites, distinct from the market for the provision of hospitality services to TV and radio broadcasting operators. The Parties also submit that supply of hospitality services to MNOs, FWA suppliers and other categories of telecommunications operators (in particular, IoT, but also OTMOs to the extent they are not MNOs or FWA suppliers)46 should be part of the overall market, but in any case the question could be left open, as the Transaction would not raise any competitive concern in that respect.

(72) The Commission has previously identified a market for sites and site infrastructure for digital mobile radio-telecommunications equipment.47 The Commission concluded that the possibility for operators of TV and radio broadcasting sites to satisfy the needs of MNOs were limited. Indeed, although there was a tendency for MNOs to utilise broadcasting structures where they are suitable for the local requirements of the service, generally broadcasting transmission equipment is located on sites affording a much higher level of geographical coverage when compared to the coverage requirements of mobile systems. Consequently, broadcasting sites tend to be tall structures in elevated locations that transmit at high powers in order to achieve optimal population coverage using a limited number of sites. In view of capacity considerations, mobile radio networks are cellular in nature, each site providing sufficient but limited coverage, reducing inter-cell interference and allowing the frequency allocations to be re-used in other areas.48

(73) The vast majority of the participants to the market investigation49 confirmed that suppliers of mobile telecommunications services and suppliers of TV/Radio broadcasting services have different requirements for hospitality services.50 Generally, towers originally designed to serve MNOs would be limited in their ability to offer hospitality services to radio and TV broadcasters. Moreover, TV and radio broadcasters need higher transmission power and need to be located outside of densely populated areas, while MNOs would require capillary distribution of antennas especially in densely populated areas.

(74) With respect to a possible segmentation between different telecommunications operators (MNOs, FWA suppliers), the majority of the respondents to the market investigation submitted that requirements for hospitality services on macro-sites are the same for suppliers of mobile telecommunications services and providers of FWA, at least to a certain extent.51 In general, FWA equipment would be comparable to MNOs’ equipment, although sometimes smaller. Energy requirements could be met within the same infrastructure as MNOs. On the other hand, FWA services would target a customer base living in the less densely populated areas in Italy, where fixed fiber telecommunication services are not as capillary as in the more densely populated areas: in this context FWA suppliers needs a smaller number of sites for their operations (in the range of hundreds sites). On the contrary, MNOs would need capillary distribution in urban and rural areas and have a much greater need for sites (in the range of thousands sites).

(75) Most respondents to the market investigation submitted also that there are other categories of customers that have similar requirements in terms of hospitality services as MNOs, such as in particular IoT providers (public utilities for their smart grids (controllers for meters, smart sensors), security services), but at the moment their demand would be marginal, in terms of space and value, compared to MNOs’ demand.52

(76) With respect to micro-sites, the vast majority of respondents to the market investigation submitted that MNOs using hospitality services on macro-sites would consider hospitality services on micro-sites as a complement and not as an alternative for their network. Micro-cells are used in combination with macro cells to improve coverage and capacity in very densely occupied areas (stadium, shopping malls) or to reach areas where normal infrastructure is insufficient (underground,high buildings). In other terms, while macro-sites are deployed to achieve homogeneous coverage, small cells deployment is instead used to address specific capacity needs within a limited area, often a public venue (outdoor or indoor) or a particularly crowded area. Due to the limited coverage range of a small cell, it will be not feasible, both technically and economically, to plan an extensive coverage only leveraging small cells, since a very high number of small cell sites would be needed to achieve the minimum coverage objective. From a structural point of view, micro-sites would not be suitable to host antenna equipment usually deployed on macro-sites, as antennas hosted on macro-sites are larger and require higher locations. Furthermore, those antennas are characterized by higher output power (and thus electromagnetic emissions) and therefore they cannot be placed on typical micro-cells locations, since these latter are generally at human height.53

(77) As for the possibility for a tower company active in the provision of hospitality services on macro-sites to start offering hospitality services on micro-sites with limited investments and in a reasonable timeframe (and vice versa), the result of the market investigation was mixed.54 In any case, the vast majority of the respondents submitted that framework agreements, which are entered into between MNOs and tower operators to regulate access to a set of locations across the territory under license, generally do not cover both macro- and micro-sites.55

(78) Based on the above, the Commission considers that, in line with its previous decisions, hospitality services to TV and radiobroadcasting operators are not part of the relevant market. Furthermore, the Commission considers that macro-sites and micro-sites are part of separate markets.

(79) With respect to macro-sites, the result of the market investigation has not been conclusive as regards the possible distinction between hospitality services to MNOs and FWA suppliers. Therefore, the Commission leaves this question open and will analyse the impact of the Transaction considering both a general market for hospitality services on macro-sites to customers other than TV and radio broadcasters, and distinct markets for hospitality services on macro-sites to(i) MNOs and (ii) FWA suppliers.

(80) As for the question whether the other categories of customers (excluding TV and radio broadcasters, i.e. in particular IoT providers) form part of a separate market, the Commission considers that this question can also be left open. Indeed, whilst the Commission does not find serious doubts as to the compatibility of the Transaction as a result of horizontal or vertical effects in relation to this customer group, this does not affect the conclusion that serious doubts arise in relation to the overall market for the supply of hospitality services to all customers other than TV and radio broadcasters. This is because the current demand by these customers is marginal compared to the demand by MNOs and FWA suppliers56 and thus does not affect the competitive analysis for the overall market for hospitality services to all customers other than TV and radio broadcasters.

(81) With respect to the market for hospitality services on micro-sites, the Commission notes, based on the market reconstruction57, that this type of sites would be primarily intended to satisfy MNOs’ demand up to 2027, with sales to this customer group representing more than 95% on each year covered by the market reconstruction, by both volume and value. Further, there is no evidence in the file that the effects of the Transaction in relation to the supply of hospitality services on micro-sites to customers other than MNOs would be different. In this context, the Commission considers that, for the purposes of this Decision, the relevant product market would be the overall supply of hospitality services on micro sites, without any further segmentation.

6.1.2. Geographic market definition

(82) The Parties submit that the market for hospitality services is national in scope, because MNOs would purchase hospitality services from a TowerCo so that they can in turn provide services according to the terms of their license, which is typically for the territory of a given Member State. Therefore, MNOs would purchase services from operators that can provide solutions across the entire territory of a Member State. MNOs would not approach TowerCos for a single access purchase at a certain location and they will either rely on TowerCos to manage their networks in its entirety or to provide access to a set of locations across the territory under the license. To address these needs, TowerCos would provide a diversified portfolio of assets conveniently located across the country. These features would explain why there are no local TowerCos for MNOs.

(83) The Commission has in its previous decisions considered that the market for hospitality services for mobile operators is national in scope, because it is driven by nationally licensed operators and the relevant planning rules are guided by national law58 and because all the site hosting activities are subject to a national regulatory environment.59 In addition, national competition authorities have considered in past decisions that the market for hospitality services is national in scope.60

(84) The results of the market investigation generally confirm a national dimension of the market, at least with respect to macro-sites. The majority of the respondents submitted that they normally negotiate framework agreements to obtain/provide access to a set of locations across the territory under license (usually nation-wide) and for the management of the entire national network, in particular for macro- sites.61 Furthermore, the vast majority of the respondents submitted that the main suppliers of hospitality services are the same across Italy, although for micro-sites certain number of respondents did not provide a definite answer, as micro-sites market would still be nascent.62

(85) However, one complainant submitted that in Italy providers of hospitality services would price access to their infrastructure at local level, with access to some sites being much more costly than others.63 This difference in pricing would show the local dynamics of the market, that will depend on:(a) the number of sites available locally, the level of occupation of these sites and their owner;(b) the actual possibility to erect new sites that could be extremely limited in certain area of historic interest;(c) the limits placed by local authorities with regard to the power of the transmission equipment to be placed on the sites;(d) the population reachable via the site concerned.Those persistent price differences would be incompatible with a national dimension of the market, would show that there are significant local barriers to entry and thus would lead to specific local competitive dynamics. The structure of supply would be very different depending on the local area concerned. The Italian Competition Authority would have confirmed the obstacles encountered by tower companies (or MNOs) wishing to extend their presence in certain areas.64

(86) The Commission considers that those observations are not sufficient to put into question the results of the market investigation. First, pricing conditions are just one element among others to be considered in the assessment of the geographic dimension of the market. Other relevant elements to be taken into account are the basic demand characteristics, the significant suppliers’ presence, and the distribution of market shares. In this respect, as explained above at paragraph (84) agreements for hospitality services are generally negotiated at national level to obtain/provide access to a set of locations on the whole national territory and the main suppliers of hospitality services are the same across Italy.

(87) With respect to the distribution of market shares, the same complainant has provided the Parties’ market shares at local level (municipalities), based on the number of sites managed (see below at section 7.2.1.2). Although the Commission has some reservations on the use of this metric to calculate the real market power of tower companies (notably as it would not distinguish between captive sales and sales to third parties, see further below in section 7.2.1.2), the data show that the Parties are generally consistently present on the national territory, with similar market shares.

(88) Furthermore, with regard to the alleged price differences, from the analysis of the agreements in place between tower companies and telecom operators (included the agreement between INWIT and the complainant) it results that the price differences are not directly linked to the geographical location of the sites (in terms of different places in Italy). Sites are generally priced per categories, with sites in urban areas generally more expensive than sites in rural areas and sites in big cities more expensive than sites in towns and smaller cities (other price categories are possible, as touristic places). In general, the pricing categories seem linked to the characteristics of the area served (in terms of coverage and population reachable, as the complainant itself acknowledges) and not to the specific geographic areas. That implies that sites in urban areas are generally more valuable than sites in rural areas. Although it cannot be excluded that in some specific locations there could be specific problems of site scarcity and/or of local authorization processes longer and more difficult than on average (and that this can have an influence on the specific pricing), the Commission considers that this element only cannot justify a market definition al local level, considering that all the other elements point to a national dimension of the market. In any case, the Commission in its analysis will consider a potential distinction between rural and urban areas – also in connection with the existing passive arrangements between the Parties – to take into account this possible difference in the competitive dynamics between rural areas and areas more densely populated, where barriers to entry could be somehow more relevant.

6.2. Retail mobile telecommunications services (“retail mobile markets”)

(89) Mobile telecommunications services to end customers consists of the sale of subscriptions enabling access to public mobile telecommunications networks. Such access allows end users to make voice national and international calls, send and receive messages and use mobile data.65

6.2.1. Product market definition

(90) The Parties submit that, in line with previous Commission decisions, the relevant product market is the overall retail market for mobile telecommunications services. Furthermore, they consider that it is not necessary for the Commission to consider whether any potential segmentation may be appropriate, in the absence of any plausible vertical competition concerns on any basis.

(91) The Commission has considered the retail mobile market in several past decisions, including with specific reference to the Italian market.66 In these decisions, the Commission has considered that there is an overall retail market for mobile telecommunications services constituting a separate market from retail fixed telecommunications services.67 The Commission did not further subdivide the overall retail mobile market based on the type of service (voice calls, SMS, MMS,mobile internet data services), or network technology.68 The Commission considered possible distinctions in the overall retail market for mobile telecommunications services between pre-paid or post-paid services and concluded that these did not constitute separate product markets, but represent rather market segments within an overall retail market.69 In addition, the Commission did not identify separate markets for the provision of mobile telecommunications services to private customers and business customers. This was principally due to supply-side substitutability considerations relevant to the area of overlap between the parties involved in those cases.70 Finally, the Commission ultimately concluded that OTT services do not fall within the same relevant market as mobile telecommunications services, as OTT services rely on mobile telecommunications (data) services and fixed broadband services to function.71 In relation to M2M subscriptions, in recent decisions, the Commission has concluded that these belong to a separate market.72

(92) There are no elements in the Commission's file in the present case that would justify a departure from the position in previous cases.

(93) For the purposes of this Decision, the Commission therefore retains its previous product market definition and considers that there is an overall product market for the retail provision of mobile telecommunications services, excluding M2M subscriptions, and the product market for the retail provision of M2M subscriptions. Since suppliers in each of these markets use the same network is used for the their activities , the vertical analysis of the effects of the Transaction in relation to these retail services will be undertaken jointly and in the following any reference to the “retail mobile markets” should be intended to both the overall product market for the retail provision of mobile telecommunications services, excluding M2M subscriptions, and the product market for the retail provision of M2M subscriptions.

6.2.2. Geographic market definition

(94) The Parties submit that, in line with the Commission's previous decisions, the market for mobile telecommunications services to end customers is national in scope.

(95) In line with previous decisions73 and taking into account that nothing in the Commission's file would justify a departure from the previous position, for the purposes of this Decision, the Commission considers that the geographic scope of the market for mobile telecommunications services is national in scope and corresponds to the territory of Italy.

6.3. Wholesale access and call origination on mobile networks (“wholesale mobile market”)

(96) MNOs provide wholesale access and call origination services which enable operators without their own network, namely MVNOs and Service Providers, to have access to one or more of the MNOs’ networks in order to provide mobile telecommunications services to end customers. “Full” or “thick” MVNOs maintain their own core infrastructure and use MNOs only for access to a radio network. By contrast, “light” or “thin” MVNOs do not have their own infrastructure and rely entirely on the infrastructure of an MNO.74

6.3.1. Product market definition

(97) In line with previous Commission decisions, the Parties submit that there is an overall market for wholesale access and call origination services on mobile networks.

(98) In previous cases, the Commission defined a wholesale market for access and call origination on public mobile networks.75 The services provided by MNOs to non- MNOs were considered as key elements required for non-MNOs to be able to provide retail mobile communication services. Since both services were considered to be generally supplied together, they were seen as being part of a single market.

(99) Nothing in the Commission's file would justify a departure from the previous position.

(100) For the purposes of this Decision, the Commission therefore retains its previous product market definition and considers that there is a distinct wholesale market for access and call origination on public mobile telephone networks.

6.3.2. Geographic market definition

(101) In line with previous Commission decisions, the Parties submit that the relevant geographic scope of the market for wholesale access and call origination on mobile networks is national, that is to say, limited to the territory of Italy.

(102) In previous cases, the Commission considered the wholesale market for access and call origination to be national in scope due to regulatory barriers stemming from the fact that licenses granted to MNOs are generally national in scope.76

(103) In line with previous decisions and taking into account that nothing in the Commission's file would justify a departure from the previous position, for the purposes of this Decision, the Commission considers that the geographic scope of the wholesale market for access and call origination on public mobile networks is national in scope and corresponds to the territory of Italy.

6.4. Retail fixed internet access services (“retail fixed markets”)

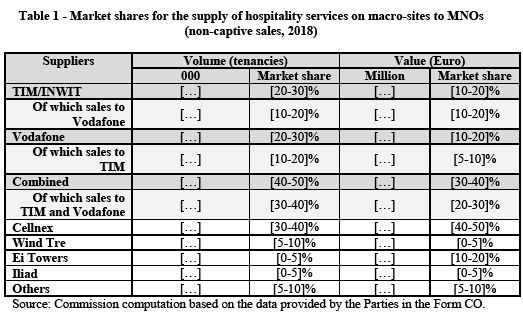

(104) Fixed internet access services at the retail level consist of the provision of subscriptions enabling customers to access the internet through a fixed telecommunications connection.

6.4.1.Product market definition

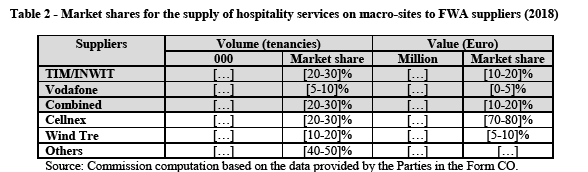

(105) The Parties note that the Italian telecoms regulator (AGCOM) has previously identified a single relevant market for retail broadband access services in Italy, including all the fixed network access technologies available on the market. AGCOM concluded that the relevant market for fixed access included services through copper, mixed copper-fibre, only optical fiber and fixed wireless technologies.77 However, the Parties consider that it is not necessary to conclude on product market definition, and in particular whether a further segmentation between broadband and ultra-broadband would be appropriate in the fixed internet market, in the absence of any competition concern.

(106) In previous decisions, the Commission considered but ultimately left open possible segmentations within the supply of retail fixed internet access services according to(i) product type, distinguishing between narrowband, broadband and dedicated access and (ii) distribution mode, distinguishing between xDSL, fiber, cable, and mobile broadband.78 Conversely, the Commission noted that the retail market for fixed internet access services should not be segmented according to download speed.79 The Commission also considered distinguishing between residential and small business customers, on the one hand, and larger business and public authorities, on the other hand, but ultimately left the question open.80

(107) In a recent case, the Commission considered that the relevant product market was the overall retail market for the provision of fixed internet access services, including all product types, distribution modes and speeds/bandwidths, to residential and small business customers, excluding only the supply of fixed internet services provided through mobile network infrastructure.81

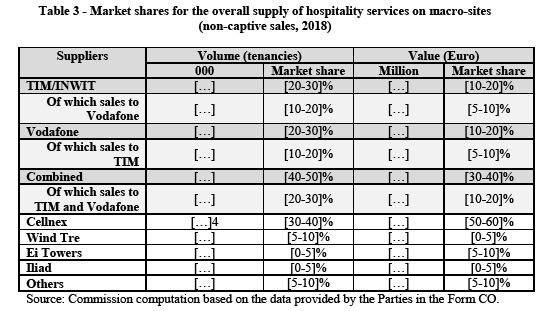

(108) For the purpose of this Decision, the Commission notes that retail fixed services are relevant to the extent a vertical link arises with the supply of hospitality services on macro-sites. From a technological point of view, such link exists only in relation to FWA networks. In this respect, the Commission notes that TIM has recently launched retail fixed services based on FWA technology (to both business and residential customers) and Vodafone […]. In this context, a hypothetical market for the supply of retail fixed services via FWA technology only could be envisaged. Such hypothetical market would be vertically affected by the Transaction and the effects of a potential foreclosure strategy in such market could be more pronounced than in an overall market.82

(109) Further, the Commission notes that, from a network stand-point, the needs of a FWA supplier are likely to be the same, regardless of whether the services are offered to residential and small business customers or to large business customers.

(110) Thus, for the purpose of this Decision, the Commission considers that the relevant product market is either the overall retail market for the provision of fixed Internet access services, including all customer groups, product types, distribution modes and speeds/bandwidths, excluding only the supply of fixed internet services provided through mobile network infrastructure83, or a hypothetical narrower market where services are only supplied based on FWA technology. As the operators in these markets which would be affected by the Transaction are the same, the vertical analysis of the effects of the Transaction in relation to these retail services will be undertaken jointly and in the following any reference to the “retail fixed markets” should be intended to cover both the overall retail market for the provision of fixed internet access services and the hypothetical narrower market where services are only supplied based on FWA technology.

6.4.2. Geographic market definition

(111) The Parties submit that the relevant geographic scope is national.

(112) In previous decisions, the Commission concluded that the retail market for the provision of fixed internet services was national in scope.84 In Liberty Global/BASE Belgium the Commission considered whether the geographic scope of the market should be defined on a regional basis or by reference to the footprint of the operators' networks, but ultimately left the question open.85 In Vodafone/Certain Liberty Global Assets, the Commission considered that the relevant geographic market for the retail provision of fixed internet services was national in scope.86

(113) There are no elements in the Commission's file in the present case that would justify a departure from the position in previous cases.

(114) The Commission therefore concludes that, for the purpose of the present Decision, the relevant geographic market for the retail provision of fixed internet services is national in scope and correspond to the territory of Italy.

6.5.Wholesale fixed internet access services (“wholesale fixed markets”)

(115) Wholesale access to internet services includes different types of access that allow internet service providers to provide services to end consumers. It comprises physical access at a fixed location, non-physical or virtual network access, at a fixed location; and resale of the fixed incumbent's internet offering.

6.5.1. Product market definition

(116) The Parties do not take a view on the exact definition of the market for wholesale fixed access.

(117) In previous decisions87, the Commission defined a separate market for wholesale broadband access and left open the question of whether it should be sub-divided per type of access (LLU, bitstream or resale of the incumbent's offering).

(118) For the purpose of this Decision, the Commission notes that wholesale fixed services are relevant to the extent a vertical link arises with the supply of hospitality services on macro-sites. From a technological point of view, such link exists only in relation to FWA networks. In this respect, the Commission notes that TIM has recently launches FWA wholesale fixed services, whilst […]. In this context, an hypothetical market for the supply of wholesale fixed services via FWA technology only could be envisaged. Such hypothetical market would be vertically affected by the Transaction and the effects of a potential foreclosure strategy in such market could be more pronounced than in an overall market.88

(119) Thus, for the purposes of this Decision, the Commission considers that the relevant product market is either the overall wholesale supply of fixed access, encompassing all technologies, or a hypothetical narrower market where services are only supplied based on FWA technology. As the operators in these markets which would be affected by the Transaction are the same, the vertical analysis of the effects of the Transaction in relation to these wholesale services will be undertaken jointly and in the following any reference to the “wholesale fixed markets” should be intended to cover both the overall wholesale supply of fixed access, encompassing all technologies, or the hypothetical narrower market where services are only supplied based on FWA technology.

6.5.2. Geographic market definition

(120) The Parties do not take a view on the geographic market definition for wholesale Internet access services.

(121) In Carphone Warehouse/Tiscali UK, while there were indications supporting a national scope of the market, the Commission ultimately left open the exact geographic market definition.89 In Liberty Global/BASE Belgium, the Commission considered whether the geographic scope of wholesale access to Internet services should be national or limited to the network footprint of each operator, but ultimately left the product market definition open.90

(122) For the purpose of this Decision, the exact geographic market definition can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to wholesale Internet access services under any alternative geographic market definition.

6.6. Wholesale supply of fixed backhaul services

(123) Backhaul services are the connections between the antennae in an infrastructure and the switches in the core network and are used to ensure the proper functioning of a mobile network. Backhaul networks can be comprised of wireless backhaul (i.e. microwaves) or fixed backhaul. MNOs have typically operated their own microwave backhaul while fixed backhaul has been provided by fixed network operators such as TIM, Open Fiber and Fastweb in Italy. Fixed backhaul services are provided on either (i) fiber optic cables or (ii) copper cables. However, wireless backhaul can be used in areas where fixed backhaul is not available.

6.6.1. Product market definition

(124) The Parties submit that wholesale fixed backhaul forms part of a wider set of fixed telecommunication services, which enable telecommunications providers to connect their own networks to end user sites for the supply of business connectivity services (“wholesale leased lines”). The wholesale market for leased lines could be segmented by trunk and terminating segments as well as between active infrastructure (traditional managed leased lines and Ethernet services with guaranteed bandwidth) and passive infrastructure (dark fiber). Wholesale fixed backhaul would not correspond to any particular segment of wholesale fixed leased lines but rather would comprise different segments of leased lines depending on the particular needs of the relevant telecommunications customer. In any case, the Parties submit the exact product market definition can be left open, as the Transaction would not give rise to any competition concern on any possible basis in this respect.

(125) In previous cases, the Commission has left open the product market definition for backhaul services.91

(126) The vast majority of the respondents to the market investigation submitted that the different transmission means (i.e. wireless, fiber and copper lines) do not satisfy the same backhauling needs (e.g. in terms of capacity and other relevant parameters).92 The different transmission would address different backhauling needs in relation to capacity, stability, time-to-deploy and costs. However, fiber would offer the highest reliability in terms of capacity, throughput, latency, etc. and would be the only option for future 5G backhauling. For example, Iliad notes that fixed copper backhaul is not in use anymore and that wireless backhaul does not provide the same performance. Fastweb further confirms that copper is a legacy technology and that wireless and fixed fiber backhauling are two separate services.

(127) As regard the question whether passive and active infrastructure services satisfy the same backhauling needs (e.g. in terms of capacity and other relevant parameters), the result of the market investigation has been inconclusive: some respondents pointed to a significant substitutability between the two services, others submitted that dark fiber would allow much higher capacity and lower latency with respect to leased lines and Ethernet services.93

(128) Finally, most respondents submitted that suppliers of backhauling connections from the sites to the aggregation point are the same as the suppliers of backhauling connections from the aggregation point to the core network.94

(129) In the present case, the question of the exact product market definition for wholesale services for fixed backhaul can be left open, as the Transaction does not raise competition concerns under any possible product market definition. In any case, thE competitive analysis will focus on fixed fiber backhauling services, irrespective of a segmentation by active or passive infrastructure services, considering that (i) future roll-out would mainly involve fiber connections due to 5G capacity requirements,(ii) MNOs typically self-supply wireless backhaul services.

6.6.2. Geographic market definition

(130) The Parties submit that the geographic market definition for wholesale services for backhaul services is at least national in scope. However, they submit that the exact geographic market definition can be left open, as the Transaction would not give rise to any competition concern on any possible basis.

(131) In a previous case, the Commission has left the exact geographic scope of the possible market for wholesale services for fixed backhaul open.95

(132) Respondents to the market investigation submitted that in general the main suppliers of backhauling services are the same across Italy and offer their services on a national basis. However, some respondents submitted that there are also local suppliers (in particular public infrastructure suppliers).96

(133) For the purposes of this Decision and in line with the result of the market investigation, the Commission considers that the geographic scope of the market for wholesale services for fixed backhaul is national in scope and corresponds to the territory of Italy. A national scope appears to be the most appropriate to assess the Transaction in light of the concerns expressed by some market participants, linked to possible detrimental effects of the Transaction on potential competition at national level.

7. COMPETITIVE ASSESSMENT

7.1.Introduction

(134) The Transaction gives rise to a number of horizontally affected markets in the supply of hospitality services on macro-sites to customers other than TV and radio broadcasters (possibly split by customer type into MNOs and FWA suppliers) in Italy.

(135) Furthermore, both Parties will remain independently active in a series of telecommunications markets in Italy that are downstream from the hospitality service market, notably: (i) the retail mobile markets, (ii) the wholesale mobile market, (iii) the retail fixed markets, and (iv) the wholesale fixed markets. In this respect, the Transaction gives rise to vertically affected markets.

(136) In addition, customers of hospitality services also purchase fixed backhaul services. TIM and the Joint Venture are active in the market for wholesale supply of fixed backhaul services. Thus, the Transaction also gives rise to potential conglomerate effects.

(137) Finally, a risk of cooperative effects from the Transaction arises in relation to (i) the retail mobile markets and (ii) the wholesale mobile market (see footnote 225).

(138) Each of these potential effects is discussed in turn in the following sections. After setting out the market shares in the relevant markets, the Commission will first assess the potential non-coordinated effects stemming from the Transaction (horizontal, vertical and then conglomerate effects). Then the Commission will assess the potential coordinated effects stemming from the Transaction (horizontal and vertical effects). Finally, the Commission will assess the potential cooperative effects of the Transaction.

7.2. Market shares

(139) According to the Horizontal Merger Guidelines and the Non-Horizontal Merger Guidelines,97 in the assessment of the effects of a merger, market shares constitute a useful first indication of the structure of the markets at stake and of the competitive importance of the relevant market players.

7.2.1.Hospitality services on macro-sites

7.2.1.1. Sales market shares

Parties’ submission

(a) Hospitality services on macro-sites to MNOs

(140) Based on the data provided by Parties in the Form CO, the market shares by value and volume for the hypothetical market for the supply of hospitality services on macro-sites to MNOs, at national level and excluding captive sales in 2018, are illustrated in Table 1.

(141) Based on the above Table, the Parties’ combined market share would be [40-50]% by volume and [30-40]% by value. The Joint Venture would thus be, post- Transaction, number one supplier by volume, followed by Cellnex (at [5-10] percentage points distance). Conversely, by value, Cellnex would be the market leader with [40-50]% market share, followed at a distance of almost [20-30] percentage points by the Joint Venture. No other suppliers would have a market share above 10%, by either volume or value, with the exception of Ei Towers by value ([10-20]% market share).

(b) Hospitality services on macro-sites to FWA suppliers

(142) Based on the data provided by Parties in the Form CO, the market shares by value and volume for the hypothetical market for the supply of hospitality services on macro-sites to FWA suppliers, at national level in 2018, are illustrated in Table 2.

(143) Based on the above Table, the Parties’ combined market share would be [20-30]% by volume and [10-20]% by value. The Joint Venture would thus be, post- Transaction, number one supplier by volume, followed by Cellnex (at [0-5] percentage points distance). Conversely, by value, Cellnex would be the clear market leader with [70-80]% market share, followed at a distance of more than [60-70] percentage points by the Joint Venture. The Parties provided only data on Wind Tre as individual alternative supplier, which would have a market share of [10-20]% by volume and [5-10]% by value. For other suppliers, the Parties only provided an aggregated market share by volume, equal to [40-50]%. Importantly, the Parties were not able to provide disaggregated data on sales by Cellnex and Wind Tre to FWA suppliers and others customers. Thus, the above figures are likely to underestimate the Parties’ position in relation to the sales to FWA suppliers.

(c) Hospitality services on macro-sites to customers other than TV and radio broadcasters, MNOs and FWA customers

(144) Based on the dataset provided by the Parties it is not possible to estimate market shares for the hypothetical market for the supply of hospitality services on macro- sites to customers other than TV and radio broadcasters, MNOs and FWA customers, such as providers of IoT services.

(d) Hospitality services on macro-sites to customers other than TV and radio broadcasters

(145) Based on the data provided by Parties in the Form CO, the market shares by value and volume for the hypothetical overall market for the supply of hospitality services on macro-sites to customers other than TV and radio broadcasters, at national level and excluding captive sales in 2018, are illustrated in Table 3.

(146) Based on the above Table, the Parties’ combined market share would be [40-50]% by volume and [30-40]% by value. The Joint Venture would thus be, post- Transaction, number one supplier by volume, followed by Cellnex (at more than [10-20] percentage points distance). Conversely, by value, Cellnex would be the market leader with [50-60]% market share, followed at a distance of more than [20-30] percentage points by the Joint Venture. No other suppliers would have a market share above 10%, by either volume or value.