Commission, November 29, 2018, No M.8951

EUROPEAN COMMISSION

Decision

SUZANO PAPEL E CELULOSE / FIBRIA CELULOSE

Subject: Case M.8951 - SUZANO PAPEL E CELULOSE / FIBRIA CELULOSE

Commission decision pursuant to Article 6(1)(b) in conjunction with Article 6(2) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 9 October 2018, the Commission received notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 (the 'Merger Regulation') (3) by which Suzano Papel e Celulose S.A. ("Suzano") acquires sole control over Fibria Celulose S.A. ("Fibria"). Suzano is hereafter referred to as the "Notifying Party" and together with Fibria as the "Parties".

1. THE PARTIES AND THE TRANSACTION

(2) The Parties are both publicly traded companies registered in Brazil, active in the production of wood pulp from eucalyptus trees. Both are vertically integrated upstream, with limited activities in wood procurement in Brazil, and in the production and supply of eucalyptus pulp. In addition, Suzano is active downstream in the production and supply of paper products.

(3) The controlling shareholders of Suzano entered into a Voting Agreement with Fibria's major shareholders in order to combine Suzano's and Fibria's operations and shareholdings by means of a corporate reorganisation (the "Transaction"). Upon completion of the Transaction, Suzano will own 100% of Fibria's shares and thereby acquire sole control over Fibria. It follows that the Transaction is a concentration pursuant to Article 3(1)(b) of the Merger Regulation.

2. EU DIMENSION

(4) The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 5 000 million. (4) (Suzano: EUR 2 918 million; Fibria: EUR 3 256 million). Each of them has an EU-wide turnover in excess of EUR 250 million (Suzano: EUR […]; Fibria: EUR […]), but they do not achieve more than two- thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension pursuant to Article 1(2) of the Merger Regulation.

3. MARKET DEFINITION

(5) Suzano and Fibria are both mainly active in the manufacture and supply of wood pulp. In addition, Suzano is also active downstream in relation to the manufacture and supply of paper products. (5)

3.1. Manufacture and supply of wood pulp

(6) Wood pulp is a dry fibrous material made from wood, used to manufacture different paper products (tissue, writing paper, paperboard etc.). It can be either used internally by vertically integrated companies for their paper production ("integrated pulp"), or produced to be sold on the merchant market ("market pulp"). For the purpose of this decision, only the latter, market-facing activity will be considered.

(7) Pulp is composed of cellulose fibres, which are either retrieved from wood ("virgin fibres", "virgin fibre pulp") or from recycled paper ("recycled fibres", "recycled fibre pulp"). Virgin fibres are the input to wood pulp; recycled fibres to recycled pulp. In addition, pulp can also be composed of non-wood fibres (obtained from cotton, linen, bamboo, etc.).

(8) Different types of wood pulp exist depending on the production process used for the separation of the fibres ("chemical pulp" or "mechanical pulp"), finish ("bleached pulp" or "unbleached pulp"), fibre length ("hardwood pulp" or "softwood pulp") and type of wood.

(9) Depending on the production process used for the separation of the fibres, wood pulp can be either mechanical or chemical. Mechanical pulp is produced by weakening and separating fibres from wood via mechanical grinding or refining. Mechanical pulp is generally used for lower grade papers, such as newsprint and catalogues, since the fibres' strength and the age resistance of the resulting pulp are lower than that of chemical pulp. Chemical pulp is produced either by using acid to extract the lignin from wood chips in large pressure vessels ("sulphite process") or by being cooked, bleached and dried ("kraft process"). Chemical pulp is more suitable for bleaching as it contains significantly less lignin than mechanical pulp. (6)

(10) Pulp can be bleached or unbleached. The goal of bleaching pulp is to remove all of the residual lignin, which lightens and whitens the pulp. This in turn gives the downstream paper products additional whiteness. Bleaching can be done using a number of molecules or compounds used in a sequence. When hardwood pulp is bleached, it is referred to as BHKP ("Bleached Hardwood Kraft Pulp"), when softwood pulp is bleached it is referred to as BSKP ("Bleached Softwood Kraft Pulp").

(11) There also exist different types of wood pulp in terms of fibre length, namely hardwood pulp and softwood pulp. Hardwood pulp contains short, thick walled fibres and provides softness, smoothness, brightness, opacity and printability properties. Softwood pulp contains long fibres which mainly provide strength.

(12) Hardwood pulp is produced from different flowering trees such as oak, ash, maple, eucalyptus, aspen, beech, birch and acacia. Softwood pulp is made from various conifers such as pine and spruce.

3.1.1. Product market definition

(13) The Parties are active in the manufacture and supply of Bleached Eucalyptus Kraft Pulp ("BEKP"), a hardwood pulp made from eucalyptus trees.

The Notifying Party's view

(14) The Notifying Party submits that chemical wood pulp (including both bleached and unbleached wood pulp, fluff pulp (7), and both softwood and hardwood pulp) constitutes a single relevant product market. (8) The Notifying Party also submits that pulp made from recycled fibres, mechanical pulp and dissolving pulp (9) also exert a competitive constraint on chemical wood pulp while not forming part of the chemical wood pulp market. (10)

(15) The Notifying Party claims that it is not appropriate to (i) further segment the market for chemical wood pulp, and in particular (ii) to segment softwood and hardwood pulp, or (iii) to consider within hardwood pulp a segmentation by individual type of hardwood pulp and thus a market limited to BEKP only, as customers are not reliant on any fibre type, for the following reasons.

(16) First, customers use a mixture of different types of wood pulp in their recipe and can use varying dosages of varying types of wood pulp, depending on their desired outcome. The exact proportion of the types of wood pulp used can be adjusted according to the market conditions.

(17) Second, regardless of the type of pulp used, customers can adjust their production lines through minor investments, such as including additives or modifying the refining process, allowing them to modify the pulp to enhance its properties by refining it according to their own and their respective customers' preferences, and as such, to achieve the desired characteristics with different types of fibres.

(18) Third, pulp customers generally multi-source from a number of different pulp suppliers, and are not technically limited to using one type of market pulp only.

(19) As regards softwood and hardwood pulp specifically, while there are physical differences between hardwood and softwood, the Notifying Party maintains that there are ample technical substitutability possibilities.

(20) From a demand-side perspective, paper manufacturing requires a combination of hardwood and softwood pulp, whereby hardwood provides features such as smoothness and opacity, and softwood provides strength, and customers can allow some variance in their proportions of each product. As such, customers can adjust their hardwood/softwood proportion based on the market conditions.

(21) In terms of prices, softwood and hardwood pulp prices move in parallel for significant periods of time with softwood generally being more expensive, and while they can diverge temporarily, they ultimately move back together.

(22) As regards the supply side, there are pulp mills capable of producing either BHKP or BSKP, so called "flex mills". (11) In addition, the main production equipment is the same.

(23) As for BEKP and other types of hardwood pulp, the Notifying Party submits that substitutability exists both from a demand- and supply-side point of view.

(24) On the demand side, customers are not confronted by technical barriers when switching between BEKP and other hardwood fibres; they only need to adjust their refining process. In addition, since customers determine the exact proportion of the various types of pulp they will purchase on the basis of the applicable market conditions, all customer options are taken into account by pulp suppliers during negotiations.

(25) As regards the supply side, the Notifying Party explains that while it is unlikely that the Parties would produce pulp using another type of wood in the near future, there are no technical obstacles to switching between eucalyptus and other hardwoods.

(26) The Notifying Party further mentions that certifications such as FSC, PEFC and Ecolabel may also influence EEA-customer choices.

The Commission's assessment

(27) In earlier decisions, the Commission has considered a single product market comprising all types of pulp. (12) However, in more recent decisions, the Commission has considered a market for chemical pulp and assessed a potential segmentation between hardwood and softwood pulp, and bleached and unbleached pulp. (13) It has also assessed whether, within hardwood pulp, a separate market for BEKP should be considered. The Commission has however generally left the market definition open.

Virgin fibre vs recycled fibre pulp

(28) As regards the demand-side substitutability between virgin fibre pulp and recycled fibre pulp, the market investigation indicated that recycled fibre pulp has an inferior quality, including a higher risk of impurities and poor absorbency and strength. In addition, it appears that most applications require at least some virgin fibre. (14) As such, substitution appears not possible, or only for certain end- applications. The large majority of those considering the substitutability for certain end-applications also indicated a difference in technical characteristics, price and end-use. (15)

(29) With regard to the supply side, respondents indicated that not only the raw material is different but also the production process, and that machines used for the production of virgin fibre pulp would lose productivity if they are run with recycled fibres, as these fibres are less strong. (16)

(30) In view of the above, the Commission considers that both demand- and supply- side substitutability are limited, supporting the existence of distinct relevant product markets for each of recycled fibre pulp and virgin fibre pulp. Accordingly, and as neither of the Parties is active as regards recycled fibre pulp, the Commission will, for the purpose of this decision, assess the Transaction on a market excluding recycled fibre pulp.

Chemical vs mechanical wood pulp

(31) From a demand-side point of view, the market investigation indicates that substitutability between chemical and mechanical wood pulp is non-existent or limited at most. The majority of all respondents, including both customers and competitors, stated that chemical wood pulp and mechanical wood pulp are not substitutable because of their different characteristics, with mechanical pulp being inferior in terms of resistance, softness, flexibility and printability, and considered less desirable as its higher lignin content causes yellowing of the final product. Of those respondents that indicate that substitution is possible for some end-applications, the vast majority indicated that the technical characteristics of chemical wood pulp and mechanical wood pulp are different, as are their prices. In addition, they also indicated that the level of substitutability is limited, up to 10-15% for printing and writing paper, and not more than 3% for tissue products. (17)

(32) As regards the supply side, the market investigation confirmed the Notifying Party's view, that the manufacturing of chemical pulp and mechanical pulp involves different equipment, technology and manufacturing processes. (18) Notably, while mechanical pulp is made by weakening and separating fibres via a mechanical action, chemical pulp is produced via either the sulphite process, or the kraft process.

(33) In view of the above, the Commission considers that both demand- and supply- side substitutability are limited, indicating – in line with the Notifying Party's view – distinct relevant product markets for each of chemical and mechanical wood pulp. The Commission therefore considers, for the purpose of this decision, that chemical and mechanical pulp belong to separate product markets.

(34) The Commission notes that, in any case, as mechanical wood pulp accounts for less than 10% of the overall merchant market for pulp and neither of the Parties is active as regards mechanical wood pulp, the assessment would not significantly differ irrespective of whether mechanical wood pulp is considered separately or not.

Dissolving pulp vs other types of chemical wood pulp

(35) From a demand-side point of view, respondents to the market investigation indicated that dissolving pulp is mainly used in the textile industry, and not for paper products. (19) A respondent also stated that most of the dissolving pulp goes to China and other growing economies.(20)

(36) As regards the supply side, the market investigation indicated that while the raw material and production equipment is the same to a large extent, the temperature and chemicals used are different, so as to extract more hemicellulose when producing dissolving pulp. Dissolving pulp has a significantly lower hemicellulose content than pulp for paper products. In addition, a respondent mentioned that the chemicals used for the production process of dissolving pulp (the "viscose process") are not used in the EEA anymore. (21)

(37) In view of the above, the Commission considers – in line with the Notifying Party's view – that a separate product market for dissolving pulp should be considered. Accordingly, and as neither of the Parties are active with regard to dissolving pulp, the Commission will, for the purpose of this decision, assess the Transaction considering a market excluding dissolving pulp.

Fluff pulp vs other types of chemical wood pulp

(38) As regards the demand side, the market investigation showed that fluff pulp is mainly used for end-products that require strong absorption qualities such as diapers and feminine care products, but not for paper products. (22)

(39) With regard to the supply side, respondents to the market investigation indicated that the production process of pulp for paper products and fluff pulp is similar, but different in terms of drying (the humidity content of both is different) and manner of packaging, with pulp for paper products being transported in the form of bales and fluff pulp in rolls. (23)

(40) In view of the above, the Commission considers a separate product market for fluff pulp. Accordingly, for the purpose of this decision, the Commission will assess the Transaction considering a market excluding fluff pulp.

Bleached vs unbleached wood pulp

(41) From a demand-side point of view, respondents to the market investigation indicated that bleached and unbleached pulp have different characteristics, and are used for different end-applications.

(42) Generally, unbleached pulp has a brown colour because of the presence of lignin, (24) while bleached pulp is whiter as, through the bleaching process, lignin is extracted. (25) Furthermore, as the Notifying Party acknowledges, (26) bleached pulp is mainly used for white printing and writing paper, tissue products, specialty products and some packaging whereas unbleached pulp is primarily used for packaging, paper bags and envelopes as it is brown in colour. (27)

(43) From a supply side perspective, the Commission notes that the production processes of bleached and unbleached pulp differ only in the sense that for unbleached pulp, the bleaching step (28) is skipped. There is therefore no technical restriction for a producer of bleached pulp to start producing unbleached pulp. However, switching in the opposite direction requires the purchase of chemicals and the addition of a bleaching section to the production line. (29)

(44) The Commission notes that in any case, respondents to the market investigation indicated – in line with the Notifying Party – that the demand for unbleached pulp is very limited. (30) Indeed, only a negligent amount is sold on the merchant market. (31)

(45) In view of the above, it appears that substitutability, especially on the demand- side, is limited, suggesting the existence of distinct product markets for bleached pulp and unbleached pulp. The Commission will therefore consider, for the purpose of this decision, bleached pulp and unbleached pulp as separate product markets. Since the Parties are only active in bleached pulp, unbleached pulp will not be discussed further in this decision.

Hardwood vs softwood pulp

(46) With regard to the demand side, the vast majority of all customers that replied indicated that hardwood and softwood pulp are not, or only to a limited extent, substitutable. For customers located within the EEA, substitutability appears even more limited; a large majority of those customers considers that hardwood and softwood pulp are not at all technically or economically substitutable. (32)

(47) As regards technical substitutability, the market investigation suggests, as the Notifying Party describes, that softwood pulp and hardwood pulp provide an end-product with different properties: softwood provides strength whereas hardwood provides softness, smoothness, opacity, etc. Only a very small minority of customers that replied indicated some characteristics as being similar, with the vast majority perceiving softwood and hardwood pulp as different in terms of opacity, strength, bulk, smoothness, porosity, softness and absorbency. (33)

(48) Customers generally use a mix of both softwood and hardwood pulp, and the exact proportion of each type of pulp that is used will depend on the end- product. (34) While switching between hardwood and softwood pulp is not excluded, any possibility of switching depends on the end-use, and appears in any case only possible to a limited extent. In addition, switching between hardwood and softwood pulp ultimately depends on the requirements of the final customer and takes time because it may require additional testing and validation processes. (35)

(49) When asked about the exact extent to which one could technically substitute hardwood pulp by softwood pulp if at all, the replies to the market investigation were not conclusive with regard to printing and writing, tissue or paperboard products. For specialty papers specifically, however, the possibility to substitute appears very limited or non-existent. (36)

(50) Regarding economic substitutability, the market investigation shows that there is generally a price difference between softwood and hardwood pulp, with hardwood pulp typically being cheaper than softwood pulp. (37) Customers explain that, in view of the price gap between softwood and hardwood, they have been trying to maximise their use of hardwood pulp but have reached their technical limitation of substitution, so that substituting any more would reduce the quality of the end-product or would not be permitted by end customers. (38) Finally, a majority of customers indicated that, in case of a price increase of hardwood pulp by 5% to 10%, they would not switch to using more softwood pulp even if softwood remained readily available at current prices. (39)

(51) As regards the supply side, respondents to the market investigation indicated that, while the machinery needed, as well as the production process of softwood and hardwood pulp, is to a large extent the same, (40) adjustments need to be made to the chemical recipe if one wants to switch from hardwood pulp to producing softwood pulp (or vice versa). The consumption of chemicals is, for example, higher when producing softwood pulp as more extensive refining is needed, which also results in higher energy consumption. (41) In addition, the growth cycle of softwood trees is considerably longer than that of hardwood trees, so that the raw material costs for softwood are higher. (42) Because of the higher energy consumption and raw material costs, the overall production costs of softwood pulp are significantly higher than those of hardwood pulp. Moreover, especially in South America, […]* is grown in large scale plantations, allowing for economies of scale. (43)

(52) A respondent explained that because of this difference in production costs and growth cycles, hardwood pulp mills are generally considerably bigger in size compared to softwood pulp mills, which limits the possibility of switching from producing hardwood to softwood pulp (or vice versa) at a reasonable economic return; a supplier would then either have a pulp mill that is too big for the raw material available, or the mill would be too small to effectively compete. (44)

(53) Furthermore, most pulp producers either produce softwood pulp or hardwood pulp, but not both. This is mainly due to the availability of the raw material; hardwood and softwood generally grow in different parts of the world. (45)

(54) In view of the above, the market investigation in the present case appears to indicate that substitution, both on the demand and supply-side, between softwood and hardwood pulp is limited. The Commission therefore considers softwood pulp and hardwood pulp to form part of distinct product markets for the purpose of this decision.

BEKP vs other types of hardwood pulp

(55) As regards the demand side, respondents to the market investigation indicated that although switching from BEKP to other types of hardwood pulp (e.g. oak, ash, aspen, beech, birch and acacia) is possible both from a technical and economical point of view, this can only be done to a limited extent and depending on the end-application. Some customers specified that they would not be able to switch at all. (46)

(56) Among the various types of hardwood pulp, Bleached Acacia Kraft Pulp ("BAKP") appears to be technically the most similar to BEKP. This pulp, produced from acacia trees, is generally produced in Asia.

(57) However, no sales of BAKP occur in the EEA. This is mainly due to the fact that European customers require pulp to have a certification that guarantees it is produced in a sustainable and environmentally-friendly manner. The most common certifications are the Forest Stewardship Council ("FSC") certification, and the Programme for the Endorsement of Forest Certification ("PEFC") certification. BAKP that is being sold on the merchant market is generally not certified, (47) and European customers only purchase wood pulp that is certified because their customers in turn require such a certification. (48)

(58) Consequently, European customers indicated that they would not switch to non- certified pulp even if the price of certified pulp increased as certification is a prerequisite imposed by their customers. (49)

(59) It follows that BAKP is not considered as an alternative for BEKP by European customers.

(60) Next to BAKP, hardwood pulp can also be produced from, inter alia, oak, ash, maple, aspen, beech and birch. Hardwood pulp can also be the result of a mix of hardwood trees, resulting in the Northern or Southern mixed hardwood pulp (NBHK and SBHK, respectively). Respondents to the market investigation indicated that switching to these types is possible, though only to a limited extent and subject to testing. (50)

(61) Furthermore, irrespective of any switching possibilities, the market investigation pointed out that, in comparison to these different grades of hardwood pulp, BEKP is considered preferable (51) due to technical specifications that cannot be found in other types of hardwood pulp. Indeed, respondents indicated that, although other hardwood trees such as oak, ash, maple, aspen, beech and birch could be used, they negatively impact the quality of the end-product, providing it with less bulkiness, opacity, softness and porosity than if BEKP were used. (52)

(62) In addition, it should be noted that BEKP is the primary type of hardwood pulp; it represents roughly 80% of sales of hardwood pulp in the EEA. The availability of other types of hardwood pulp thus appears to be more limited, also impacting the possibility of switching supply.(53)

(63) With regard to the supply side, while a majority of respondents indicated that different types of hardwood pulp can be produced in the same production facility and even on the same production line, they also noted that the availability of wood species in the area of production constrains suppliers, limiting the switching possibilities. (54)

(64) Furthermore, respondents indicated that, even if machinery and end-uses are often the same, production costs are lower for BEKP than for other types of hardwood pulp. (55) This is mainly due to the fact that eucalyptus trees have a significantly shorter growth cycle than other hardwood trees. (56)

(65) In view of the above, for the purpose of this decision, the Commission considers that the market for BEKP should be considered as the narrowest plausible market, and will assess the Transaction accordingly. Given that the Parties are only active with regard to BEKP, other types of hardwood pulp shall not be further discussed in this decision.

3.1.2. Geographic market definition

The Notifying Party's view

(66) The Notifying Party submits that the chemical wood pulp market is global in scope because (i) pulp is internationally traded and around 90% of the Parties' production is exported, (ii) the price is strongly correlated on a global level, and (iii) there are no logistical barriers to transporting around the world as transport costs represent less than 10% of the total price of the product.

The Commission's assessment

(67) In previous decisions, the Commission found the market for wood pulp to be at least EEA-wide in scope, while ultimately leaving the exact geographic scope open. (57)

(68) The market investigation confirmed that BEKP is supplied on a global scale. Customers indicated that, on average, they source 90% of their BEKP supply from producers located at a distance of 7 000 to 8 000 km. (58) In addition, a majority of respondents, competitors and customers alike, indicated that prices of BEKP are broadly the same worldwide. (59) Transport costs, estimated at 5-20% of the sales price of BEKP, were deemed to be not important by respondents. (60)

(69) However, the results of the market investigation also highlighted certain specificities differentiating the EEA from the global level. First, the two main competitors of the Parties in the EEA are located in the EEA and are only active within the EEA. (61) Furthermore, the market investigation revealed that BEKP must have a certification (FSC or PEFC) in order for EEA customers to consider purchasing it. (62) In this respect, respondents to the market investigation consistently identified certification as a factor limiting the sourcing and supplying of wood pulp. (63) As Asian suppliers generally do not offer certified pulp, given that this feature is not a requirement for Asian customers, (64) no Asian suppliers are present in the EEA. Lastly, it appears that North America is characterised, to a large extent, by local production and vertical integration, so that American producers only play a limited role on the merchant market outside of North America. (65)

(70) In any case, given that the Transaction raises serious doubts as to its compatibility with the internal market irrespective of whether the relevant geographic scope is considered to be at least EEA-wide or global, (66) the precise geographic market definition can be left open.

(71) In view of the above, for the purpose of this decision, the Commission will assess the Transaction based on the narrowest plausible – at least EEA-wide – geographic market definition.

3.2. Manufacture and supply of paper products

(72) Paper products are downstream products manufactured from wood pulp. They are produced in a wide range of qualities and used for various end-applications, such as printing and writing, packaging, personal hygiene and other specialties.

(73) While Fibria is not active with regard to the manufacture and supply of paper products, Suzano is a vertically integrated pulp and paper manufacturer. It operates mills, producing (i) printing and writing paper, and, more specifically, coated and uncoated wood-free paper and (ii) packaging paper, namely paperboard. (67)

3.2.1. Product market definition

Notifying Party's view

(74) Regarding printing and writing paper, the Notifying Party submits that the substitutability between coated and uncoated wood-free paper is rather high, so that producers can relatively easily switch from producing one to another, but that it is in any event not necessary to reach a conclusion on a possible further segmentation of the market also considering its limited sales of printing and writing paper to the EEA.

(75) In relation to packaging, the Notifying Party agrees with the Commission's past decisional practice, considering a separate product market for paperboard, and considers it unnecessary to reach a conclusion as to whether the paperboard market should be further segmented given the lack of competition concerns under any possible segment of the packaging paper market. (68)

Commission's assessment

(76) The Commission has previously considered several separate markets for paper, depending on various aspects such as its category (i.e. printing and writing, packaging, tissue etc.), features and end-usage.

(77) As regards printing and writing paper, the Commission has defined a distinct market for printing and writing paper, and further segmented the market depending on paper features, into wood-containing paper, wood-free coated (WFC) and uncoated paper, magazine paper, newsprint paper and mechanical coated paper. (69) The Commission has also considered separate markets according to whether the paper was supplied in reels or sheets, or depending on the distribution channel, i.e. paper sold directly from the manufacturers or indirectly through merchants, but has ultimately left this open. (70)

(78) For packaging paper, the Commission has defined separate product markets depending on the type of packaging paper involved, namely paperboard (71), sack and kraft paper (72), and corrugated case paper. (73) Within paperboard, the Commission considered a distinction between four main categories of boards, namely (i) solid bleached sulphate (SBS), (ii) coated natural kraft (CNK), (iii) folding box board (FBB) and (iv) white lined chipboard (WLC), but has ultimately left this open. (74)

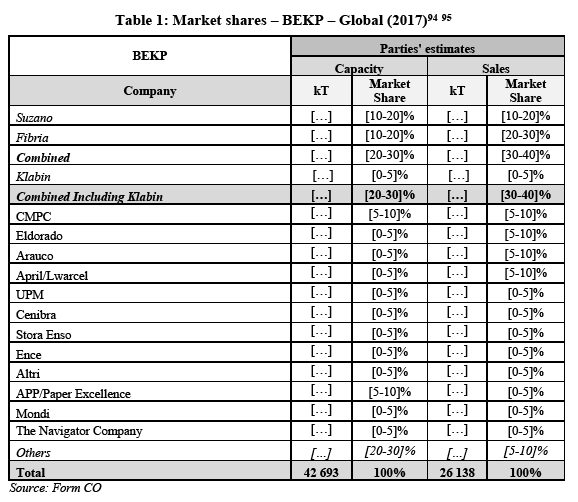

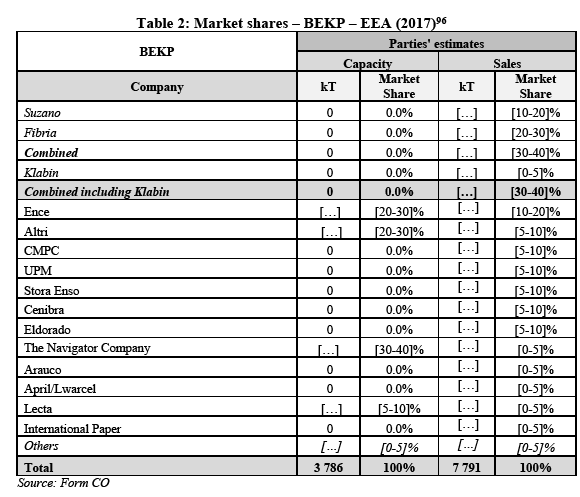

(79) The market investigation in the present case did not provide any indications that would contradict the Commission's previous findings, neither with regard to wood-free coated and uncoated paper, nor in relation to paperboard.

(80) In any event, for the purpose of this decision the exact scope of the product market can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market in this regard, irrespective of the exact market definition.

3.2.2. Geographic market definition

Notifying Party's view

(81) The Notifying Party submits that the geographic market for wood-free coated paper and uncoated paper and paperboard is EEA-wide, in view of the diversity of demand patterns for paper across various regions. (75)

Commission's assessment

(82) In previous decisions, the Commission has considered the relevant geographic market for wood-free coated and uncoated paper is EEA-wide. (76) As to paperboard, the Commission has considered the market to be at least EEA-wide, but ultimately leaving the exact geographic market definition open. (77)

(83) The market investigation did not raise any issues that would contradict the Commission's earlier findings.

(84) In any case, the precise definition of the geographic markets concerning wood- free coated and uncoated paper and paperboard can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market concerning the production of paper products, irrespective of the exact market definition.

4. COMPETITIVE ASSESSMENT

4.1. Analytical framework

(85) Under Article 2(2) and (3) of the Merger Regulation, the Commission must assess whether a proposed concentration would significantly impede effective competition in the internal market or in a substantial part of it, in particular through the creation or strengthening of a dominant position.

(86) In this respect, a merger may entail horizontal and/or non-horizontal effects. Horizontal effects are those deriving from a concentration where the undertakings concerned are actual or potential competitors of each other in one or more of the relevant markets concerned. Non-horizontal effects are those deriving from a concentration where the undertakings concerned are active in different relevant markets.

(87) As regards non-horizontal mergers, two broad types of such mergers can be distinguished: vertical mergers and conglomerate mergers. (78) Vertical mergers involve companies operating at different levels of the supply chain. (79) Conglomerate mergers are mergers between firms that are in a relationship which is neither horizontal (as competitors in the same relevant market) nor vertical (as suppliers or customers). (80)

(88) A case where a merger entails both horizontal and non-horizontal effects may for instance be when the merging firms are not only in a vertical or conglomerate relationship, but are also actual or potential competitors of each other in one or more of the relevant markets concerned. In such a case, the Commission will appraise horizontal, vertical and/or conglomerate effects in accordance with the guidance set out in the relevant notices. (81)

(89) The Commission appraises horizontal effects in accordance with the guidance set out in the relevant notice, that is to say the Horizontal Merger Guidelines. (82) Additionally, the Commission appraises non-horizontal effects in accordance with the guidance set out in the relevant notice, that is to say the Non-Horizontal Merger Guidelines. (83)

4.1.1. Horizontal effects

(90) The Horizontal Merger Guidelines distinguish between two main ways in which mergers between actual or potential competitors on the same relevant market may significantly impede effective competition, namely non-coordinated and coordinated effects.

(91) As regards horizontal non-coordinated effects, under the substantive test set out in Article 2(2) and (3) of the Merger Regulation, mergers that do not lead to the creation or the strengthening of the dominant position of a single firm may still be incompatible with the internal market. Indeed, the Merger Regulation recognises that in oligopolistic markets, it is all the more necessary to maintain effective competition. (84) This is in view of the more significant consequences that mergers may have on such markets. For this reason, the Merger Regulation provides that "under certain circumstances, concentrations involving the elimination of important competitive constraints that the merging parties had exerted upon each other, as well as a reduction of competitive pressure on the remaining competitors, may, even in the absence of a likelihood of coordination between the members of the oligopoly, result in a significant impediment to effective competition". (85)

(92) The Horizontal Merger Guidelines list a number of factors which may influence whether or not significant horizontal non-coordinated effects are likely to result from a merger, such as the large market shares of the merging firms, the fact that the merging firms are close competitors, the limited possibilities for customers to switch suppliers, or the fact that the merger would eliminate an important competitive force. That list of factors applies equally regardless of whether a merger would create or strengthen a dominant position, or would otherwise significantly impede effective competition due to non-coordinated effects. Furthermore, not all of these factors need to be present to make significant non- coordinated effects likely and it is not an exhaustive list. (86) Finally, the Horizontal Merger Guidelines describe a number of factors, which could counteract the harmful effects of a merger on competition, including the likelihood of buyer power, entry and efficiencies.

(93) A merger in a concentrated market may also significantly impede effective competition due to horizontal coordinated effects where, through the creation or the strengthening of a collective dominant position, it increases the likelihood that firms are able to coordinate their behaviour and raise prices, even without entering into an agreement or resorting to a concerted practice within the meaning of Article 101 TFEU. A merger may also make coordination easier, more stable or more effective for firms that were already coordinating before the merger, either by making the coordination more robust or by permitting firms to coordinate on even higher prices. (87)

(94) To assess whether a merger gives rise to horizontal coordinated effects, the Commission should examine, first, whether it would be possible to reach terms of coordination and, second, whether the coordination would be likely to be sustainable. (88)

4.1.2. Vertical effects

(95) A merger is said to result in foreclosure where actual or potential rivals' access to supplies or markets is hampered or eliminated as a result of the merger, thereby reducing these companies' ability and/or incentive to compete. (89) Such foreclosure may discourage entry or expansion of rivals or encourage their exit. Such foreclosure is regarded as anti-competitive where the merged entity — and, possibly, some of its competitors as well — are as a result able to profitably increase the price charged to consumers. (90)

(96) Two forms of vertical foreclosure can be distinguished. The first is where the merger is likely to raise the costs of downstream rivals by restricting their access to an important input (input foreclosure). The second is where the merger is likely to result in foreclosure of upstream rivals by restricting their access to a sufficiently large customer base (customer foreclosure).

4.2. Introduction

(97) Both Parties are active in the manufacture and supply of BEKP. In addition, Suzano is active in the downstream market of the manufacture and supply of paper products.

(98) The Transaction will give rise to a horizontally affected market in the manufacture and supply of BEKP, and a vertically affected relationship as regards the manufacture and supply of BEKP (upstream) and Suzano's activities in relation to the manufacture and supply of paper products (downstream).

4.3. Horizontal non-coordinated effects: Manufacture and supply of BEKP

The Notifying Party's view

(99) The Notifying Party submits that the Transaction will not give rise to a significant impediment to effective competition on the market of BEKP, or under any alternative hypothetical market definition, for the following reasons. (91)

(100) First, both globally and in the EEA, the pulp market is too fragmented for the combined entity to have market power post-Transaction. On the narrowest market segment (BEKP), the Parties' combined market share will be moderate and well below levels that are capable of raising competition concerns.

(101) Second, the Parties' customers will have a wide range of alternatives that they could rely on should their sourcing conditions worsen post-Transaction. In particular, a number of internationally active pulp manufacturers (e.g. International Paper, Asia Pulp and Paper ("APP"), April, UPM, Metsä, Stora Enso and SCA) will remain.

(102) Third, wood pulp customers are large and sophisticated buyers, and many of them can credibly threaten to self-supply and effectively bypass pulp suppliers.

(103) Fourth, vertically integrated paper producers constrain the Parties' pricing. A potential increase in prices would likely make the product of non-integrated customers (which have to heavily rely on supply from third parties) less competitive and lead them to lose market share to integrated rivals. The Parties' sales would fall as a result and this would lower the incentives to raise prices post-Transaction.

(104) Finally, this is a cyclical market where production generally responds to changes in expected demand. Recently, the demand for BEKP has increased and suppliers have already started to increase capacity as a response.

The Commission's assessment

(105) The Transaction will further increase the concentration and allow the merged entity to control the largest capacity on the market for BEKP (combining Suzano, Fibria and Klabin's volumes outside South America, as explained below – see paragraphs (109) to (113)), a market on which the Parties (including Klabin) are close competitors, with capacity constraints and high barriers to entry and expansion, and limited countervailing buyer power of the customers. The Commission considers that the Transaction will likely increase the ability and the incentive of the merged entity to raise prices and maintain high prices of BEKP by keeping capacity on the market tight. The Commission therefore considers that the Transaction raises serious doubts as to its compatibility with the internal market with regard to the manufacture and supply of BEKP as set out below.

Market structure

(106) On the market for BEKP, the Parties are number 1 and 2, in an industry with a long and fragmented tail of competitors.

(107) In terms of sales of the Parties, the combined share would be [30-40]% globally and [30-40]% in the EEA. However, the next strongest competitor will only have approximately a [5-10]% share on a global market (CMPC) and [10-20]% in the EEA (Ence). In terms of capacity, the Parties combine almost [30-40]% of the overall global capacity for BEKP. (92) When excluding integrated capacity, their combined global BEKP capacity share increases to [30-40]% on the merchant market. (93)

(108) Globally, the combined entity is more than 4 times larger than the next competitor in terms of both sales and capacity of BEKP. On an EEA-level, the combined entity is almost 3 times larger than the next competitor in terms of sales of BEKP.

(109) In addition to Suzano and Fibria's capacity, Fibria also has additional volumes of BEKP at its disposal sourced from another Brazilian producer, Klabin, by way of an exclusive offtake agreement (the "Offtake Agreement").

(110) In […], Fibria and Klabin entered into an Offtake Agreement pursuant to which Fibria purchases a minimum of […] tonnes per year of BEKP produced by Klabin to sell outside of South America, including in the EEA. The Offtake Agreement started operating in 2016, and includes an exclusivity clause by which only Fibria can sell Klabin's BEKP outside South America, excluding the possibility for any other competitor, or Klabin itself, from selling it. Given that all sales of Klabin's BEKP outside South America are controlled by Fibria, Klabin was not able to develop a sales force, customer contacts and all the logistics needed to sell outside South America, and was thus effectively foreclosed from entering the EEA market.

(111) The initial term of the Offtake Agreement is […] years ([…]), with the option to renew it. The agreed volumes cover a minimum of […] tonnes of BEKP for […] years and a gradual reduction thereafter. In 2018, after Fibria concluded the qualification process of Klabin's BEKP with European customers, it sold […] tonnes in the EEA (to date).

(112) Klabin is an integrated producer of pulp and paper that is also located in Brazil. It has therefore a similar cost structure to the Parties and is one of the low cost producers of BEKP. In addition, it owns a newly built plant where it produces both BEKP and softwood pulp. (97) Klabin started selling pulp when its mill started operating in 2016 and entered into the Offtake Agreement with Fibria because it did not have, as a new entrant, the capability of serving the global market at that time.

(113) The Transaction therefore accumulates not only Suzano and Fibria's sales, but also Klabin's, in view of the Offtake Agreement in place between Fibria and Klabin.

Closeness of competition

(114) The market investigation has confirmed that the Parties, as well as Klabin, are close competitors. Both Parties and Klabin are based in Brazil and produce the same type of pulp.

(115) The Parties also share a significant number of customers. For example, in the EEA, Suzano's top four customers in 2017 are also customers of Fibria and two of them, […] and […], are among Fibria's top three customers. In addition, out of the top four customers Fibria and Suzano have in common, two of them are supplied by Fibria both with its own pulp as well as Klabin's. Of Suzano's EEA customers, [a significant proportion] of them are also customers of Fibria; [a significant proportion] of Fibria's EEA customers are also customers of Suzano.

(116) In addition, the vast majority of competitors responding to the market investigation have indicated that the Parties are each other's closest competitors in terms of price, quality and volumes. Also customers noted closeness, especially in terms of quality and volumes. (98)

(117) Furthermore, Suzano and Fibria as well as Klabin have a similar cost structure. The Parties acknowledge that there is a high degree of cost asymmetry across countries. In particular, hardwood pulp producers in Brazil, such as the Parties and Klabin, tend to have lower cost structures compared to competitors in Asia, Europe and North America. (99)

Capacity

(118) The market investigation confirmed that production capacity for BEKP is constrained, with suppliers operating at high rates, close to their full capacity. (100) At the same time, prices have been increasing steadily since 2016 in Europe and elsewhere, notably due to growing demand in China. (101)

(119) However, even though demand is on the rise and prices are high, the results of the market investigation revealed that there will be no significant capacity expansions of BEKP producers until 2021. (102) Aside from debottlenecking plans accounting for limited capacity increases, the only significant expansion that is confirmed, concerns a plant to be built by Arauco with a capacity of over 1 500 kT that will start operating in 2021. (103) Beyond 2021 capacity expansions are not confirmed and therefore uncertain.

(120) Expansion prospects for Iberian or other European producers have additional limitations compared to South American producers. First, they cannot benefit from industrial plantations given that land and eucalyptus forests are limited, and the climate in Europe leads to longer growth cycles for trees and thus a lower productivity compared to Brazil. Second, regulatory limitations exist, notably in Portugal, where the amount of land used to grow eucalyptus trees is capped to that which is already in use. (104) As a result, it would not make economic sense for suppliers to build new mills in Portugal.

(121) In addition, integrated players selling part of their production to the merchant market also operate close to full capacity, which would prevent them from starting to sell additional volumes even if prices of BEKP were to increase by 5% to 10%. Neither would they internalise more of their BEKP consumption. (105) Therefore, no integrated producers could increase volumes to counter a potential price increase. This evidence supports the view that, in this case, market shares including integrated capacity do not accurately reflect the volumes of BEKP available for customers and underestimate the market share of the Parties.

Entry

(122) In addition to the existing capacity on the market being constrained, barriers to entry are high, encompassing, inter alia, administrative authorisations and environmental licences, and the costs and time incurred in building a new mill. (106)

(123) In the market investigation, competitors confirmed that the cost of building a mill with an annual production capacity of 1.5 to 2 million tonnes is more than USD 2 billion. (107) Furthermore, according to market investigation respondents, it takes up to two years to obtain the necessary permits and licenses. (108) Moreover, internal documents of the Parties confirm that, even after a new pulp mill is approved, it takes up to three years before volumes hit the market. (109)

(124) Hence, it can be concluded that the vast majority of respondents believe that no entry will take place on the market for the production of BEKP in the next three years. (110) There is also a general view in the industry that the market should be more disciplined so that capacity expansions are controlled in order to prevent price wars and maintain the current high […]* This is also reflected in several internal documents of the Parties, […]. (111)

(125) In addition, the growth cycle of the tree largely depends on the type of tree and the region in which it grows, which benefits production in regions where growth is faster. In particular, it takes eucalyptus trees approximately seven years to grow in Brazil, ten years in Chile and Uruguay and fifteen years in Spain. This facilitates entry as well as expansion of Brazilian producers compared to others as long lead times are necessary before beginning operations, and productivity is lower outside Brazil. (112)

(126) This is compounded by the amount of forest necessary for a mill: approximately 150 000 hectares of planted forests are needed to supply an average mill of a capacity of 1.5 million tonnes. (113) Hence, producers in Brazil, such as the Parties and Klabin, are better placed to expand capacity. The market investigation has confirmed that eucalyptus trees, being the raw material, are not a constraint in Brazil, (114) contrary to other places in the world as explained above (see paragraph (120)).

Buyer power

(127) With regard to the Notifying Party's argument in relation to buyer power, the Commission notes that in addition to the Parties' high margins ([50-60]% for Suzano and [40-50]% for Fibria in 2017), (115) prices have been rising for the past two years, without any decrease or reaction on the demand side, which is evidence that customers have limited bargaining power and cannot counter a price increase.

(128) Customers responding to the market investigation believe that negotiating power will diminish further as a result of the Transaction. They indicated that, in particular, Suzano and Fibria would be able to impose BEKP prices and dominate the market in view of the large capacity that they would control. (116)

(129) The market investigation revealed that customers generally multi-source from various BEKP suppliers in order to secure their supply of BEKP. (117) However, although switching suppliers is not uncommon in the market, (118) it is limited. More specifically, switching suppliers requires a qualification of the pulp by the customers beforehand. (119) This involves trials and testing, which can take up to six months. (120)

Likely effects of the Transaction

(130) As a result, the merger would increase consolidation to a significant extent, considering it combines Suzano and Fibria as well as Klabin's volumes outside of South America, and capacity expansions and entry are unlikely in the next three years. The Transaction is likely to increase the ability of a large player to adjust capacity in order to maintain prices high by controlling a large share of capacity, especially compared to its competitors.

(131) In the long run, the market price for BEKP is determined by the amount of available capacity and by demand. The lower the available capacity, the higher the market price. While all suppliers profit from higher market prices, larger suppliers reap a higher proportion of that benefit. Since the proposed merger increases the largest suppliers' – i.e. the Parties' – market share, the incentive to slow down capacity expansion in order to keep market prices high also increases as a result of the Transaction.

(132) However, even a supplier with a high market share only has a limited incentive to slow down capacity expansions if other suppliers are likely to expand their capacity instead. Since the construction of additional production capacity for BEKP requires a significant investment and takes at least two years, only large competitors would be able to expand in case the merged entity slows down its expansion plans. Therefore, in the absence of clear plans to expand capacity by existing players, the Transaction would significantly increase the incentive for the merged entity to limit its own capacity expansions. This is exacerbated when considering that Klabin, a third important competitor of the Parties with a similar cost structure, is limited in its sales, and thus in its incentives to expand, by way of the Offtake Agreement.

(133) Also, in the short run, prices for BEKP are determined in bilateral negotiations between suppliers and customers. By contrast, prices for some other commodities are determined by the interaction of demand and supply on a commodities exchange. All buyers then pay the same price. In the case of BEKP, larger customers tend to be able to negotiate lower prices than smaller customers. It seems likely that larger suppliers are also able to obtain more favourable results in these negotiations. Moreover, the number of competing suppliers, as well as their cost structure, likely has an effect on the prices for which BEKP customers end up paying.

(134) Therefore, the Transaction eliminates an important low-cost supplier that is also a close competitor to the Notifying Party in terms of prices and quality, and increases the market share of Suzano, not only with the sales of Fibria but also Klabin's. The newly emerging market leader would not only have by far the largest market share but also some of the lowest production costs. The likely result would be that the emerging market leader will be able to negotiate higher prices while also having little incentive to expand its capacity in order to keep these prices high – to the detriment of BEKP customers.

Conclusion on horizontal non-coordinated effects

(135) In view of the above, the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market with regard to the production and supply of BEKP at least in the EEA.

4.4. Horizontal coordinated effects

The Notifying Party's view

(136) The Parties claim that the Transaction will not lead to competitive concerns as a result of coordinated effects, as (i) there are a large number of market players, (ii) prices are not transparent – while price indices and market prices are published, invoice and volume discounts are applied and those are the result of bilateral negotiations, and (iii) contracts are annual, and several negotiations are ongoing simultaneously.

The Commission's assessment

(137) The Commission considers, contrary to the view of a number of market participants, that, as regards potential coordinated effects on the market for the production of BEKP, the Transaction does not raise serious doubts as to its compatibility with the internal market for the reasons set out below.

(138) First, the Commission notes that the number of suppliers and their asymmetries in size renders coordination unlikely. As shown in Tables 1 and 2 above, there is a significant gap between the merged entity and their next competitor, and between the next large producers of BEKP, and a long and fragmented tail of smaller competitors. A strategy of coordination would likely not be successful under those conditions as monitoring deviation would be very difficult.

(139) Second, cost structures of suppliers vary significantly depending on mainly their location, but also their degree of vertical integration. As a result, the incentives to curtail capacity in order to increase prices is not equal among producers, which prevents market players from reaching terms of coordination that would be profitable for all.

(140) Third, considering the high investment costs that characterise the industry, it is likely not economical for producers to cut production but rather to produce at full capacity to amortise investments.

(141) Fourth, even though prices are based on an index, bilateral negotiations take place between suppliers and customers to agree on the discount and the final price to be paid. Those negotiations are confidential and competitors do not have visibility on the final agreed price, which would easily allow for deviation while making retaliation difficult. This was confirmed by the market investigation. (121)

Conclusion on coordinated effects

(142) In view of the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market as regards potential horizontal coordinated effects.

4.5. Vertical non-coordinated effects: Manufacture and supply of BEKP (upstream) and manufacture and supply of wood-free coated and uncoated paper, and paperboard (downstream)

(143) As Suzano is also active downstream, with regard to the manufacture and supply of wood-free coated and uncoated paper as well as paperboard, the Transaction leads to vertical overlaps with regard to these downstream markets.

The Notifying Party's view

(144) The Notifying Party submits that the merged entity will not have the ability nor the incentive to engage in input or customer foreclosure, in view of the minor sales achieved on the various paper markets in the EEA, the number of alternative sources of supply available for paper suppliers, the fact that the merged entity has no spare capacity downstream, as well as the competitive environment in downstream paper markets.

The Commission's assessment

(145) The Commission considers that the Notifying Party will neither have the ability nor the incentive post-Transaction to engage in either input foreclosure or customer foreclosure.

(146) Regarding input foreclosure, the Commission takes the view that, even if the combined entity were to have the ability to foreclose paper producers, by foreclosing them from the supply of BEKP, given that the merged entity has a significant degree of market power on the upstream market (as explained above in Section 4.3), it will not have any incentive to foreclose paper producers.

(147) Given that Suzano's share in the various downstream markets in the EEA is de minimis (122), and that it has no spare capacity on its paper production lines, it would not be able to expand its downstream market share to recoup the losses derived from cutting sales of BEKP upstream.

(148) In any event, the Commission notes that the merged entity will also face competition from a significant number of vertically integrated paper producers that do not rely on the combined entity for BEKP, so that any input foreclosure strategy would have limited effects on them.

(149) Concerning customer foreclosure, Suzano already pre-Transaction does not purchase BEKP for its paper production but uses only pulp produced internally; therefore the Transaction is unlikely to result in customer foreclosure.

(150) Furthermore, no vertical concerns were raised in this regard during the market investigation.

(151) In view of the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market as regards potential vertical non-coordinated effects.

4.6. Conclusion

(152) The Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market with regard to the manufacture and supply of BEKP as a result of non-coordinated horizontal effects.

5. PROPOSED REMEDIES

(153) In order to render the concentration compatible with the internal market, the undertakings concerned have modified the notified concentration by entering into the following commitments, which are annexed to this decision and form an integral part thereof.

5.1. Procedure

(154) On 8 November 2018, the Notifying Party formally submitted commitments in order to alleviate the Commission's concerns with regard to the Transaction ("the Commitments").

(155) The results of the market test were positive in that most respondents agreed that the Commitments would remedy the Commission's serious doubts. (123)

(156) The Commission informed the Notifying Party of the outcome of the market test during a conference call on 16 November 2018.

(157) The Notifying Party submitted the final version of the Commitments on 19 November 2018. (124)

5.2. Description of the Commitments

(158) The Commitments proposed by the Notifying Party consist of (a) Fibria terminating the Offtake Agreement, which it entered into with Klabin in […] and (b) transferring or making available to Klabin, on terms approved by the Commission, all tangible and intangible assets necessary to allow Klabin to independently sell BEKP to any customer in the EEA and in other regions outside South America in a competitive manner ("the Divestment Business").

(159) Through the Commitments, the Offtake Agreement would be terminated, thereby allowing Klabin to sell BEKP worldwide. In addition, with the aim of facilitating the entry of Klabin into the EEA, it will obtain or make use, at cost, of a range of tangible and intangible assets included in the Divestment Business. These include:

a) Personnel;

b) Storage capacity for a transitional period of […];

c) Shipping contracts and thus access to ports for a transitional period of […];

d) Customer, credit and other records;

e) Technical support and assistance in qualification of Klabin BEKP to maintain or obtain acceptance by EEA customers for a transitional period of […] months.

(160) Suzano has made a commitment to not implement the Transaction until it has concluded the agreement to terminate the Offtake Agreement (the "Termination Agreement") with Klabin ("upfront buyer") and it has been approved by the Commission.

(161) The draft Termination Agreement was submitted to the Commission on 13 November 2018. (125) As per the Termination Agreement, which will be subject to approval by the Commission at a later stage, the transfer of (or access to) the assets mentioned above and notably storage will not be limited to the EEA but will be global in scope, in order to enable Klabin to sell globally and become an effective competitor to the Parties, thereby contributing to the viability of the Commitments.

6. ASSESSMENT OF THE PROPOSED REMEDIES

(162) The Commission launched the market test of the Commitments on 9 November 2018. The results of the market test indicated that the Commitments are sufficient to remove the competition concerns raised by the Transaction.

(163) First, the Commitments are in line with paragraph 58 of the Remedies Notice in that it removes "links between the parties and competitors in cases where these links contribute to the competition concerns raised by the merger". (126)

(164) Second, the Commitments eliminate the Commission's concerns both with respect to long-term and short-term effects of the Transaction. The Commitments ensure that Klabin's volumes of BEKP, which are sold by Fibria in the EEA, are no longer under the control of the Parties. At the same time, the remedy facilitates the entry of a new competitor for BEKP with a global presence. This new competitor already operates a newly built pulp mill in Brazil, where the cost of producing BEKP is the lowest. Moreover, Klabin is a large company with the financial shoulders required for further expansion. (127)

(165) The Commitments ensure that Klabin will quickly and easily gain access to markets outside of Brazil and in particular in the EEA. Gaining direct access to BEKP customers in the EEA and across the world increases Klabin's incentives to expand its capacity in the long-run. As a result, the Commitments also reduce the probability that the Parties would slow down expansion plans given that Klabin, a new entrant with low costs and […], will be present in the market. The market test has confirmed that Klabin is considered by customers as an alternative supplier of BEKP from which they would consider purchasing BEKP. (128)

(166) The Commitments allow the entry of a low-cost supplier of BEKP that is a close competitor of the Parties in Brazil, as it has a similar cost structure and would thus be able to sell at similar prices. Moreover, the Commitments reduce the amount of BEKP sold by the Parties, thus reducing their clout in price negotiations. Indeed, in terms of production capacity and sales of BEKP, implementation of the Commitments will result in the merged entity reducing its total capacity and sales outside South America by […] tonnes. (129) As a result, the Commitments also eliminate the Commission's concerns regarding short-term price negotiations, as set out in paragraph (133) above.

(167) As regards the EEA, Fibria's sales of Klabin's BEKP in the EEA increased from […] tonnes in 2017 to approximately […] tonnes in the period January to September 2018, as a result of Klabin's BEKP being qualified by customers, which reinforces the effectiveness and viability of the Commitments.

(168) The Commitments provide for a transitional period of […] months to phase out the Offtake Agreement between Klabin and Fibria. After this phase out, Klabin will be able to independently sell BEKP outside of South America, in particular in the EEA, and will be fully operational as it will have access to all logistical needs and customer contacts. The market test has confirmed that the Divestment Business is viable. (130) No significant risks or uncertainties were identified. (131)

(169) To the contrary, without the remedy the Offtake Agreement would run until […], except if Klabin chose to exercise the change of control clause for its termination at the closing of the Transaction. However, even if the change of control clause was triggered, Klabin would need to set up all the infrastructure, logistics and customer contacts, which would delay its entry significantly.

(170) Furthermore, Klabin has indicated its willingness to increase its sales of BEKP to the EEA. Based on its contacts with customers at this point, it estimates that it will sell approximately […] tonnes in the EEA in 2019.

(171) In terms of capacity, Klabin currently operates one plant in Brazil with a capacity of 1.5 million tonnes, mostly used for the production of BEKP. In addition, it will conduct […]. Klabin also explained that it has the ability and necessary resources to carry out further capacity expansions if it decided to do so. The Commission considers that the Commitments will increase Klabin's incentive to expand given it will gain access to a significantly wider market than it had previously.

(172) In view of the above, it can be concluded that the Commitments will resolve the serious doubts raised by the Transaction as it will enable the entry of a credible competitor into the EEA in the short term, competing on prices with the Parties, and it will also incentivise capacity expansions by Klabin by increasing its sales in the EEA and worldwide, preventing the delay of capacity expansions on the market. This is also supported by respondents to the market test, a majority of which consider that the Commitments will resolve any competition concern the Transaction may have raised. (132)

(173) For the reasons outlined above, the Commitments entered into by the undertakings concerned are sufficient to eliminate the serious doubts as to the compatibility of the Transaction with the internal market.

(174) The Commitments in Section B of the Annex constitute conditions attached to this decision, as only through full compliance therewith can the structural changes in the relevant markets be achieved. The other commitments set out in the Annex constitute obligations, as they concern the implementing steps which are necessary to achieve the modifications sought in a manner compatible with the internal market.

7. CONCLUSION

(175) For the above reasons, the Commission has decided not to oppose the notified operation as modified by the commitments and to declare it compatible with the internal market and with the functioning of the EEA Agreement, subject to full compliance with the conditions in section B of the commitments annexed to the present decision and with the obligations contained in the other sections of the said commitments. This decision is adopted in application of Article 6(1)(b) in conjunction with Article 6(2) of the Merger Regulation and Article 57 of the EEA Agreement.

19 November 2018

Case M.8951 – SUZANO PAPEL E CELULOSE / FIBRIA CELULOSE COMMITMENTS TO THE EUROPEAN COMMISSION

Pursuant to Article 6(2) of Council Regulation (EC) No 139/2004 (the Merger Regulation), Suzano Papel e Celulose S.A. (Suzano) hereby enters into the following Commitments (the Commitments) vis-à-vis the European Commission (the Commission) with a view to rendering Suzano’s acquisition of sole control over Fibria Celulose S.A. (Fibria) (the Concentration) compatible with the internal market and the functioning of the EEA Agreement.

This text shall be interpreted in light of the Commission’s decision pursuant to Article 6(1)(b) of the Merger Regulation to declare the Concentration compatible with the internal market and the functioning of the EEA Agreement (the Decision), in the general framework of European Union law, in particular in light of the Merger Regulation, and by reference to the Commission Notice on remedies acceptable under Council Regulation (EC) No 139/2004 and under Commission Regulation (EC) No 802/2004 (the Remedies Notice).

Section A. Definitions

1. For the purpose of the Commitments, the following terms shall have the following meaning:

Affiliated Undertakings: undertakings controlled by the Parties and/or by the ultimate parents of the Parties, whereby the notion of control shall be interpreted pursuant to Article 3 of the Merger Regulation and in light of the Commission Consolidated Jurisdictional Notice under Council Regulation (EC) No 139/2004 on the control of concentrations between undertakings (the Consolidated Jurisdictional Notice).

Assets: the assets that contribute to the current operation or are necessary to ensure the viability and competitiveness of the Divestment Business as indicated in Section B, paragraph 7 and described more in detail in the Schedule.

BEKP: bleached eucalyptus kraft pulp.

Closing: the transfer of the legal title to the Divestment Business to the Purchaser, and/or to the extent applicable, to make available to the Purchaser the right to use the Assets.

Closing of the Concentration: the period of up to […] calendar days from the Effective Date or any other date agreed between Suzano and the Commission, subject to satisfaction of paragraph 3 below.

Closing Period: the period of up to […] from the approval by the Commission of the terms of the agreement for the transfer of the Divestment Business, or from the Closing of the Concentration, whichever is later.

Confidential Information: any business secrets, know-how, commercial information, or any other information of a proprietary nature that is not in the public domain.

Conflict of Interest: any conflict of interest that impairs the Trustee's objectivity and independence in discharging its duties under the Commitments.

Divestment Business: the business of marketing, selling and distributing Klabin Produced BEKP as more particularly described in Section B and in the Schedule.

Divestiture Period: the period of […] from the Effective Date.

Effective Date: the date of adoption of the Decision.

Fibria: Fibria Celulose S.A., a public-held company organised and existing under the laws of Brazil, with its head office at Fidêncio Ramos Street, No. 302, Edifício Vila Olímpia Corporate, 3rd and 4th floors, Tower B, 04551-010, Vila Olímpia, São Paulo, State of São Paulo, Brazil, and registered with the Brazilian Company Register under number 60643228/0001/21, and its Affiliated Undertakings.

Klabin: Klabin S.A., a public-held company organised and existing under the laws of Brazil, with its head office at AV. Brig. Faria Lima, 3600, 3rd, 4th and 5th floors, São Paulo, State of São Paulo, Brazil, and registered with Brazilian Company Register under number 89637490/0001/45, and its Affiliated Undertakings.

Klabin Commercial Data: information relating to the Klabin Produced BEKP sold by Fibria […].

Klabin Produced BEKP: BEKP produced at Klabin’s production facility located in the city of Ortigueira, Paraná, Brazil.

Monitoring Trustee: one or more natural or legal person(s) who is/are approved by the Commission and appointed by Suzano, and who has/have the duty to monitor Suzano’s compliance with the conditions and obligations attached to the Decision.

Off-take Agreement: the eucalyptus pulp offtake agreement between Fibria International Trade GmbH and Klabin S.A. and Fibria Celulose S.A. as intervening party and guarantor dated 4 May 2015, as amended and provided in Schedule 2.

Parties: Suzano Papel e Celulose S.A. and Fibria Celulose S.A. and their respective Affiliated Undertakings.

Personnel: up to […] of the Parties’ sales personnel located in Europe having experience in selling BEKP in the EEA, […] as further described in the Schedule, in order to maintain the viability and competitiveness of the Divestment Business.

Purchaser: Klabin, as approved by the Commission as acquirer of the Divestment Business.

Relevant Customers: customers to which Fibria has supplied, or is currently supplying Klabin Produced BEKP.

Schedule: the schedule to these Commitments describing in more detail the Divestment Business.

Transitional Period: the period of […] commencing on the first day following the end of the Closing Period.

Trustee: the Monitoring Trustee.

Suzano: Suzano Papel e Celulose S.A., a public-held company organised and existing under the laws of Brazil, with its head office at Av. Professor Magalhães Neto, 1752, 10th floor, CEP 41810-012 Salvador, BA, Brazil, and registered with the Brazilian Company Register under number 16404287/0001/55, and its Affiliated Undertakings.

Section B. The commitment to divest and the Divestment Business

Commitment to divest

2. In order to maintain effective competition, the Parties commit that (a) Fibria will terminate the Off-take Agreement; and (b) the Parties will divest the Divestment Business to Klabin on terms approved by the Commission in accordance with the procedure described in paragraph 17 of these Commitments. To carry out the divestiture, the Parties commit to enter into an agreement with Klabin for the purposes of implementing these Commitments within the Divestiture Period.

3. The Concentration shall not be implemented before the Parties have entered into a final binding agreement for the transfer of the Divestment Business and the Commission has approved the terms of the final and binding agreement referred to in paragraph 17.

4. The Parties shall be deemed to have complied with this commitment if:

a) By the end of the Divestiture Period, the Parties have entered into a final binding agreement with Klabin and the Commission approves the terms of such agreement as being consistent with the Commitments in accordance with the procedure described in paragraph 17; and

b) Closing takes place within the Closing Period.

5. In order to maintain the structural effect of the Commitments, the Parties shall, for a period of 10 years after Closing, not acquire, whether directly or indirectly, the possibility of exercising influence (as defined in paragraph 43 of the Remedies Notice, footnote 3) over the whole or part of the Divestment Business that has been transferred to Klabin, and, subject to paragraphs 10 below, not to […] unless, following the submission of a reasoned request from the Notifying Party showing good cause and accompanied by a report from the Monitoring Trustee (as provided in paragraph 37 of these Commitments), the Commission finds that the structure of the market has changed to such an extent that the absence of influence over the Divestment Business is no longer necessary to render the Concentration compatible with the internal market.

6. The Parties shall not enforce any provision(s) of the Off-take Agreement, to the extent that such provision(s) would contravene compliance with these Commitments.

Structure and definition of the Divestment Business

7. The Divestment Business consists of all tangible and intangible assets, necessary to allow Klabin to independently sell Klabin Produced BEKP to any customer in the EEA, and other regions outside of South America. The object of these Commitments is to ensure that following Closing of the Concentration Klabin is able to act independently of the Parties, and to introduce Klabin as a direct and independent supplier of BEKP in the EEA, and other regions outside of South America, and that the Parties do not directly or indirectly control or influence the supply of Klabin Produced BEKP through any arrangements with, or any practices with respect to, Klabin which are aimed at or have the effect of restricting Klabin’s ability or incentive to compete effectively with the Parties in the supply of BEKP in the EEA and other regions outside of South America. This is, in particular, to improve the overall structure of supply of BEKP in the EEA and in other regions outside of South America. The scope of the Divestment Business is described in the Schedule. The Divestment Business, described in more detail in the Schedule, includes all assets and personnel, that contribute to the current operation or are necessary to ensure the viability and competitiveness of the Divestment Business.