Commission, March 22, 2019, n°M.9196

EUROPEAN COMMISSION

Decision

MARSH & MCLENNAN COMPANIES / JARDINE LLOYD THOMPSON GROUP

Subject: Case M.9196 – MARSH & MCLENNAN COMPANIES / JARDINE LLOYD THOMPSON GROUP

Commission decision pursuant to Article 6(1)(b) in conjunction with Article 6(2) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 1 February 2019, the Commission received notification of a concentration pursuant to Article 4 of the Merger Regulation, which would result from a proposed transaction by which Marsh and McLennan Companies Inc (“MMC”, or “the Notifying Party”) incorporated in the United States intends to acquire sole control, within the meaning of Article 3(1)(b) of the Merger Regulation, over the whole of Jardine Lloyd Thompson plc (“JLT”), incorporated in the United Kingdom (“the Transaction”).3 The concentration is to be achieved by way of public bid announced on 18 September 2018. MMC and JLT are designated hereinafter as “the Parties”. The undertaking that would result from the Transaction is referred to as “the combined entity”.

1. THE PARTIES

(2) MMC is a global professional services firm offering clients advice and solutions in the areas of risk, strategy and people. MMC consists of four key lines of business operated by the following entities (i) Marsh, active in insurance broking and risk management solutions; (ii) Guy Carpenter, active in reinsurance and capital strategies; (iii) Mercer, active in health, wealth and career consulting; and (iv) Oliver Wyman, a strategy, economic and brand consultancy.

(3) JLT is a publicly listed company incorporated in 1997. JLT has two principal business areas: (i) Risk & Insurance, encompassing insurance and reinsurance broking; and (ii) Employee Benefits, comprising advice and services to companies, pension trustees and individuals, including retirement solutions; benefits consulting; wealth and investment management; and technology solutions.

2. THE TRANSACTION

(4) On 18 September 2018, MMC announced its intention to make a public offer under section 2.7 of the City Code on Takeovers and Mergers to acquire the entire issued and to be issued share capital of JLT. The Transaction is intended to be implemented by way of a court-sanctioned scheme of arrangement pursuant to Part 26 of the Companies Act 2006. MMC also has the right to implement the Transaction by way of a takeover offer pursuant to Part 28 of the Companies Act 2006. After completion, MMC will hold directly 100% of the shares in JLT, following which the JLT business will be integrated into MMC’s business. JLT will be delisted from the London Stock Exchange and be re-registered as a private limited company.

(5) The Transaction would therefore result in a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

3. UNION DIMENSION

(6) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million4 (MMC: EUR 12 425.3 million and JLT EUR 1572.8 million). Each of them has an Union-wide turnover in excess of EUR 250 million (MMC EUR […] million; JLT EUR […] million). JLT achieves two- thirds of its aggregate Union-wide turnover in the UK, but Marsh does not.

(7) The concentration has therefore an Union dimension pursuant to Article 1(2) of the Merger Regulation.

4. RELEVANT MARKETS

(8) The Parties are both active primarily in the provision of insurance and reinsurance broking services, as well as in the provision of retirement and employee benefits- related services such as the fiduciary management of pension funds.

(9) The overlap between the Parties’ activities leads to affected markets in the broker services for Aircraft Operators, Aerospace Manufacturing, Energy, Space and FinPro and on the market for fiduciary management services. As the provision of reinsurance (including retrocessional reinsurance) broking services, and the provision of retirement and employee benefits services (with the exception of fiduciary management of pension funds) are not affected markets, they will not be further discussed in this Decision.

(10) In its previous decision Marsh&McLennan / Sedgwick5, the Commission noted that the product markets are likely to be more limited in scope than the distribution of insurance services in general, comprising distribution by direct writers, tied agents and intermediaries such as banks and brokers. The Commission considered a distinction can be made between the distribution of life and non-life insurance, as different providers tend to be involved and the distribution of life insurance in Europe is regulated separately from other types of insurance. The Commission also considered whether non-life insurance distribution could be further segmented based on (a) sales channels, (b) customer size/type, or (c) business sector / risk type. The Commission ultimately left the exact product market definition open6.

4.1. Brokerage and other insurance management alternatives

(11) The Parties operate as insurance brokers servicing large, generally multinational companies with highly technical operations – such as energy companies or airline operators – by placing their risk in the insurance market.

(12) The activities of brokers are different from those of insurers and subject to a different regulatory framework7. The typical broker services provided by the Parties consist in assisting clients in securing suitable and competitive cover to achieve their risk management goals. For that purpose, brokers will scan the insurance market for an insurer or a consortium of insurers capable of carrying the client’s risks. They will typically conduct the negotiation with the insurer(s) on behalf of their clients with the goal of achieving the best possible rates and conditions. In addition to these intermediation services, brokers can also provide advisory services, such as on risk management strategies or policy wording. In the event that the client has to make a policy claim, brokers will typically also handle the process vis-à-vis the insurer. These additional services are equally valued by customers, and clearly separate broking activities from other insurance distribution channels.

(13) According to the Parties, the market for the distribution of commercial non-life insurance for specialty sectors ought to be defined by taking into account all the risk management channels available to its customers: (i) using a broker to place risks on the insurance market; (ii) retaining the risk (including through the use of captive insurers8); (iii) placing the risk directly with an insurer and (iv) accessing alternative forms of capital. In the Parties’ view, these channels are interchangeable and are equally attractive risk management alternatives for customers.

(14) The Commission considers that the relevant product market is limited to the distribution of insurance via brokers, as the market investigation revealed that most customers consider that the other risk management channels are not substitutes for broking services, at least as far as corporate customers are concerned9. The Commission noted in Marsh & McLennan / Sedgwick that corporate customers clearly distinguish between the types of services they can procure from brokers and from insurers10. The results of the present market investigation confirmed that large corporate customers in the specialties concerned consider the activities of brokers as a separate from those of insurers, and that they do not consider insurers to compete directly with brokers in the distribution of insurance for large risks11. Moreover, the vast majority of insurers consulted in the market investigation do not operate their own distribution network which would enable them to compete with brokers directly, and none of them considers it viable to create one12.

(15) Concerning risk retention as a viable alternative to corporate customers, there are different degrees to which this option is relevant depending on the specialty risk considered. For the most part, however, the market investigation revealed that customers would generally retain only small portions of their risk portfolio13, which did not appear to decrease their need for broker services. The decision to set up a captive insurer appears to be a strategic choice for companies, influenced by strategic considerations such as risk appetite, prevailing market prices and the skills available to the company14. Even when customers retain risk, brokers might still provide additional services such as managing the captive insurer where the risk can be placed15. In conclusion, broker services are also distinct from risk retention and belong to separate markets from other insurance management channels.

4.2. Risk broking specialties

(16) Taking the assessment in Section 4.1 into account, wherein the Commission concludes that broking is a separate form of insurance distribution, this Section will focus on the plausible sub-segmentations of the market for brokerage.

(17) The Parties submit that their activities only overlap for large corporates and middle-market corporate clients. For the purpose of this decision, the Commission thus does not further assess the possibility to segment the market of non-life insurance broking based on customer size/type. The Commission also notes that the activities of the Parties are not segmented along the lines of customer-size but based on risk-type or business sector.

(18) In relation to a possible segmentation of the market for insurance broking by business sector / risk type, the Parties submit that such segmentation does not exist and that segmentation varies across brokers. However, the Parties also submit that brokers generally sub-segment the market for non-life insurance broking between broking for property and casualty risks (“P&C”) and broking for a number of specialty risks (“Specialties”). The Parties further submit that it is not appropriate to segment commercial non-life broking into narrower business sector/risk types, since there is significant supply-side substitutability across and within P&C and Specialties. According to the Parties, the basic skills for broking are largely the same across all risk categories and the client relationships and industry expertise resides within small and mobile teams. In their view, expansion into new broking areas is speedy and not very costly, with the threat of new entry constantly exerting constant pressure on incumbents.

(19) However, the Commission considered in a previous decision16 that as regards certain industries as well as certain risk types, distinct markets may be identified by reasons of limited substitutability on both demand and supply-side. Concerning supply-side substitutability, the Commission found that for certain product lines or sectors of the market for the distribution of non-life insurance, a considerable degree of knowledge and specialisation is required in order to compete effectively. The Commission ultimately left the market open.

(20) The results of the market investigation support the Commission’s previous views on the limited scope for demand-side substitutability. Most customers17 indicate that each risk type / business sector requires specific know-how and a good track record. The market investigation also showed that brokers tend to have specialized teams for a business sector / risk type and that the perception of which competitors are stronger varies for each sectors / risk type18. Customers active in a particular industry also do not consider it realistic to switch to a broker that does not have the necessary expertise or proven track-record in that particular industry, indicating a lack of demand-side substitutability at the level of business sector / risk type19.

(21) As regards the potential supply-side substitutability, competitors to the Parties noted during the market investigation that experienced teams with strong technical capabilities are needed to build customer and market relationships20. Also, there are high barriers to entry into sectors / risk types not currently covered by a broker particularly as concerns the requirements for a good track record, ample data, and industry expertise21. These factors appear to indicate that there is little supply-side substitutability between business sector / risk types.

(22) For the purpose of this Decision, the Commission therefore considers that the market for non-life insurance brokerage can be further segmented based on business sector / risk type. The Commission concludes from the market investigation that a segmentation based on business sectors / risk types corresponds with customers’ identification of homogenous risks and competitors’ preference to structure their company based on the different risk types (e.g. a separate division for Energy or Aerospace Manufacturing). The Commission therefore considers that a segmentation of the brokerage market based on business sector / risk type is the most appropriate for the purpose of this Decision.

(23) Following the Commission’s conclusion on the narrowest plausible market segmentation, the Commission notes that the Parties’ activities overlap in the provision of specialised broker services for Aircraft Operators, Aerospace Manufacturing, Energy, Space and FinPro. FinPro is the insurance broking segment that covers the risks associated with the professional indemnity of directors, managers, and employees as well as the financial exposures of a company.

4.2.1.Broker services for Aircraft Operators

(24) Both Parties are active in the broking of commercial insurance for aircraft, jet fleet and rotor fleet operators. This type of insurance predominantly consists of the coverage against damage to the aircraft (“hull coverage”) and general liability to passengers and third parties. Ancillary coverage covering replacement/repair of spare parts and/or coverage against damage or liability arising out of malicious acts (e.g. war or terrorism) is also typically distributed in this business line.

(25) The aircraft insurance industry is characterised by the threat of very low frequency catastrophic events that can trigger very high losses on airline operators. Customers in this segment seek on the one hand good insurance premiums, but they also expect brokers to provide skilful claims handling services should any catastrophic event happen22. Customers purchase such a specific combination of reach, business and technical expertise, and track record that a separate product market might be considered on the basis of customer characteristics alone.

4.2.1.1. Product market Definition

(26) The Parties submit that the relevant product market is that of the distribution of Aircraft Operators insurance, regardless of channel. In their view, brokers compete with third party and captive insurers in the distribution of insurance in this segment.

(27) The Commission has not previously considered the existence of a separate product market for the distribution of commercial aircraft operator insurance. However, it has noted in the past that a distinct market for the distribution of specialty insurance for certain industries – including for aviation – could potentially exist23. The market investigation confirmed that most commercial aircraft respondents identified Aircraft Operators as a distinct market and that they generally contract separate brokers for different types of risks24.

(28) As far as the distribution channel is concerned, as already discussed in section 4.1 the market investigation confirmed that neither dealing directly with third party insurers, nor setting up a captive are considered to be appropriate alternatives in the management of large aviation risks25.

(29) Therefore, based on the reasoning above, the Commission concludes that for the purpose of this Decision, the relevant product market is the broking of commercial Aircraft Operators insurance.

4.2.1.2.Geographic market definition

(30) The Parties submit that the geographic scope for the Aircraft Operators market is at least EEA-wide. The Commission has not previously considered the geographic scope of an Aircraft Operators market.

(31) The market investigation has confirmed that the large majority of customers in this segment purchase broking services at a global level. Most airlines surveyed had operations in territories larger than the EEA, prompting them to purchased insurance brokerage at a global level to ensure consistent coverage for all countries where they operate in. However, there were also indications that the market characteristics at EEA level were different to those at global level, particularly in the number of available competitors, which appeared to be more reduced at EEA than at global level.26

(32) For the purposes of the present analysis, the exact geographic scope of the market for the broking of commercial Aircraft Operator insurance can be left open between EEA and global, since the competitive assessment would remain the same, and serious concerns arise under both possible geographic market definitions.

4.2.2. Broker services for Aerospace Manufacturing

4.2.2.1.Product market definition

(33) The market for the Specialty sector of Aerospace Manufacturing refers to the distribution of commercial insurance to cover risks associated with the manufacturing of aerospace products. Manufacturers of aerospace components purchase cover to insure against damage caused by, or liability arising out of, defects in their products. The most common risk types in this specialty are manufacturers’ hull and liability and aircraft product liability. Other risk types include insurance for airframe, engine part and component manufacturers.

(34) The Parties submit that, if the Commission were to segment the market for the distribution of commercial non-life insurance, the narrowest plausible product market in relation to Aerospace Manufacturing would be the distribution of all commercial Aerospace Manufacturing insurance, regardless of the specific channel (see also recital (13)). The Parties submit that there is significant demand-side substitutability between each of these channels, allowing clients to flex between the various alternatives depending on their attractiveness. However, as described in recital (15) the Commission considers broker services to form a separate market from the other risk management channels.

(35) The Commission has not previously assessed the market for broker services in the Specialty sector of Aerospace Manufacturing. The Commission noted in a previous decision that a distinct market for the distribution of specialty insurance for certain industries – including for aviation – could potentially exist27. However, the product market definition was ultimately left open.

(36) According to the results of the market investigation, nearly all customers in this market consider there is little to no direct competition from insurers28 and that the market for the Specialty sector of Aerospace Manufacturing does not lend itself to using other risk management channels than brokers29.

(37) The insurers responding to the market investigation confirmed the customers’ views, stating that the vast majority of their business in the Aerospace Manufacturing is realised through the intermediation of a broker30. The insurers also confirmed that none of them currently operate their own distribution network in the market for Aerospace Manufacturing31.

(38) Based on the results of the market investigation, the Commission concludes, for the purpose of this Decision, that the relevant product market includes the broking activities in the Specialty sector of Aerospace Manufacturing.

4.2.2.2. Geographic market definition

(39) The Parties submit that the geographic market definition for broking in the Specialty sector of Aerospace Manufacturing is at least EEA-wide. The Parties refer to brokers’ ability to supply their services to clients wherever they are located, travelling to the client as and when necessary. The Parties also submit that Specialist brokers are able to operate using local office licenses, or partner with a local licensed broker.

(40) The Commission has not assessed the market for broker services in the Specialty sector of Aerospace Manufacturing. In Marsh & McLennan / Sedgwick32, the Commission assessed the geographic scope of the overall market for insurance distribution but left open whether the relevant geographic market definition for insurance distribution is larger than national.

(41) According to the results of the market investigation, the majority of customers in the market segment of Aerospace Manufacturing purchase broker services at a global or EEA-wide level33. The results of the market investigation with brokers also suggest that the competition between brokers for specialty risks such as Aerospace Manufacturing takes place on a larger geographic scope such as EEA- wide or global34.

(42) For the purpose of this Decision, the Commission concludes that the geographic scope of the market for broker services in the specialty market of Aerospace Manufacturing is at least EEA-wide.

4.2.3.Broker services for Space

4.2.3.1.Product market definition

(43) The market for broking in the Specialty sector of Space refers to the distribution of commercial insurance to cover risks associated with damage and liability arising out of aircraft in orbit (e.g. satellites) as well as risks that might derail launches of such aircraft. The space industry is characterised by very high financial exposures due to the significant potential for high losses when an insured event occurs.

(44) The Parties submit that if the Commission were to segment the market for the distribution of commercial non-life insurance, the narrowest plausible product market in relation to this specialty would be the distribution of all commercial Space insurance, regardless of the specific channel. According to the Parties, the market thus includes all different channels by which customers can satisfy their Space risk-management needs (see recital (13) for the description of all different channels). The Parties submit that there is significant demand-side substitutability between each of these channels, allowing clients to flex between the various alternatives depending on their attractiveness.

(45) The Commission has not previously defined a separate product market for broking in the Specialty sector of Space. However, the Commission has noted in previous decision that a distinct market for the distribution of specialty insurance for certain industries – including for space – could potentially exist35. However, the product market definition was ultimately left open.

(46) According to the results of the market investigation, nearly all customers in this market consider there is little to no direct competition from insurers36. This view is confirmed by the market investigation with insurers, which revealed that none of the participants in the investigation had developed their own distribution networks to compete with brokers such as the Parties37.

(47) Based on the results of the market investigation, the Commission concludes, for the purpose of this Decision, that the relevant product market is broking in the Specialty sector of Space.

4.2.3.2.Geographic market definition

(48) The Parties submit that the geographic market definition for broking in the Specialty sector of Space is at least EEA-wide and should most appropriately be considered to be global in scope. The Parties refer to brokers’ ability to supply their services to clients wherever they are located, travelling to the client as and when necessary.

(49) The Commission has not assessed the market for broker services in the Specialty sector of Space. In Marsh & McLennan / Sedgwick38, the Commission assessed the geographic scope of the overall market for insurance distribution but left open whether the relevant geographic market definition for insurance distribution is larger than national.

(50) According to the results of the market investigation, the majority of customers in the market segment of Space purchase broker services at a global or EEA-wide level39. The results of the market investigation with brokers also suggest that the competition between brokers for specialty risks such as Space takes place on a larger geographic scope such as EEA-wide or global40.

(51) For the purpose of this Decision, the Commission concludes that the exact geographic scope of the market for broker services in the specialty market of Space is at least EEA-wide.

4.2.4.Broker services for Energy

(52) The specialty of Energy insurance broking refers to the distribution of commercial insurance to cover the risks associated with the complex operations of the production chain for fossil fuels such as coal, oil and natural gas. This includes both upstream (i.e. exploration and extraction) and downstream (i.e. transformation of hydrocarbons into petroleum-based products) activities.

4.2.4.1. Product market definition

(53) The Parties claim that further segmentation of the specialty would not be appropriate, as the skillset required to offer such services is broadly the same for both upstream and downstream processes. In their view, brokers readily compete with third party and captive insurers in the distribution of energy insurance. They conclude by submitting that the relevant product market is that of the distribution of energy insurance, regardless of channel.

(54) The Commission has not previously assessed the existence of a separate market for energy insurance distribution. For the reasons outlined in recitals (14) and (15), the Commission considers that the relevant market is not that of insurance distribution regardless of channel, but instead that of insurance broking in Energy.

(55) The market investigation revealed that most customers identify either an energy market or an upstream/downstream market41, which would confirm the product market definition suggested by the Parties. As far as potential sub-segmentations in this specialty are concerned, the market investigation confirmed that most customers purchase both upstream and downstream insurance broking services from the same brokers when they are active in both markets42. Customers did not express any particularities or significant differences in the competitive landscape of the upstream and downstream energy insurance markets. There were little indications that any other the market sub-divisions would be appropriate or relevant.

(56) In any event, for the purpose of this Decision, it can be left open whether broker activities in the segment of Energy constitute a separate product market from commercial non-life brokerage or whether it should be further segmented, since no doubts as to the compatibility of the notified concentration with the internal market arise under any plausible product market definition.

4.2.4.2.Geographic market definition

(57) The Parties submit that the geographic scope for the Energy market is at least EEA-wide. They claim that oil and gas companies purchase insurance broking services for all of their global activities via a central purchasing function. In their view, adopting a smaller scope than at least EEA-wide would distort the nature of the market.

(58) The Commission has not previously considered the existence or the geographic scope of a market for commercial broking of Energy insurance. The results of the market investigation would suggest that the large majority of customers in the market segment of Energy purchase broker services at a global level43. Those who purchase at a national level do so because their operations are limited to only a few countries. This would appear to be in support of the Parties’ view that the market is at least EEA-wide.

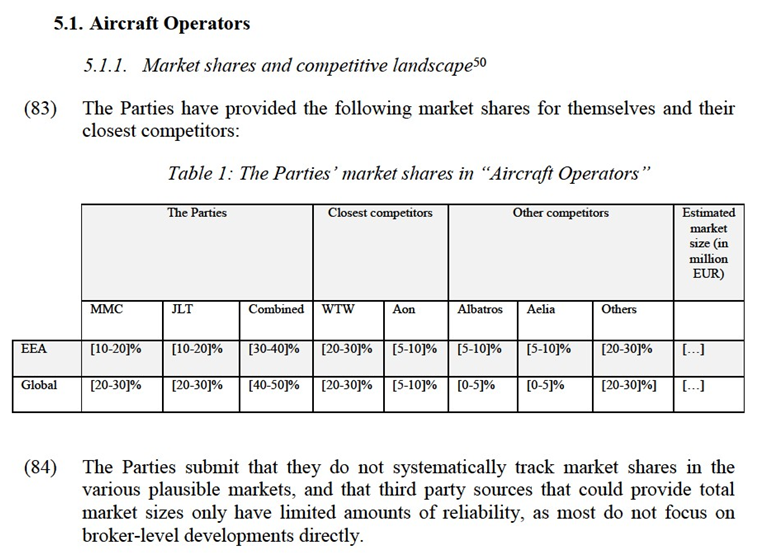

(59) The exact geographic scope of the market of Energy broking can be left open between EEA and global, since no serious doubts as to the compatibility of the notified concentration with the internal market arise under any plausible geographic market definition.

4.2.5. Broker services for FinPro

(60) FinPro is the insurance broking segment that covers the risks associated with the professional indemnity of directors, managers, and employees. It can also cover the financial exposures of a company, such as those borne from M&A transaction or cyber negligence, among others.

4.2.5.1.Product market definition

(61) The Parties submit that the skillset necessary to provide FinPro broking services is broadly similar across all risks, companies and industries. Moreover, they posit that in their FinPro insurance broking activities they compete with the other insurance distribution channels discussed above, namely placing the risk directly with the insurer, retaining risk, or accessing alternative forms of capital. In their view, FinPro insurance distribution should be the narrowest plausible product market.

(62) The Commission notes that the market investigation has not given any reason to challenge the product definition advanced by the Parties as far as the business sector / risk type is concerned. On the other hand, for the reasons outlined in recitals (14) and (15), the Commission considers the relevant product market to be the broking of FinPro insurance, thus excluding all other distribution channels.

(63) In any event, for the purpose of this Decision, it can be left open whether broker activities in the segment of FinPro constitute a separate product market from commercial non-life brokerage, since no doubts as to the compatibility of the notified concentration with the internal market arise under any plausible product market definition.

4.2.5.2. Geographic market definition

(64) The Parties submit that FinPro insurance broking services are purchased by clients active in multiple jurisdictions, while at the same time acknowledging that professional indemnity is largely required by national laws across EU-member states. In their view, the relevant geographic market for FinPro is global or at least EEA-wide.

(65) By contrast, the market investigation revealed that most customers purchase FinPro insurance brokerage at a national level44, and that customers have a preference for brokers with local presence45. These findings would favour an interpretation of the geographic market being national in scope. However, as the concentration in the market for FinPro does not raise serious doubts as to its compatibility with the internal market even under the narrowest possible geographic market definition, the relevant geographic market can be left open.

4.3. Other products (non-broker activities of the Parties)

(66) As stated in recital (8), the Parties are also active the provision of retirement and employee benefits related services, including fiduciary management for pension funds.

4.3.1. Fiduciary management

(67) The Parties’ activities also overlap in the provision of retirement and employee benefits consulting, and more precisely in the provision of fiduciary management to pension scheme trustees. MMC is active predominantly through its Mercer operating company and to a much lesser extent through Marsh. MMC provides these services across the EEA, with the UK being the main market. JLT is substantially smaller and almost exclusively active in the UK.

4.3.1.1.Product market definition

(68) Fiduciary management involves the provision of advice to pension scheme trustees in relation to one or more of the following:1. investment strategy: high level advice on the different types of investment that can be made;2. strategic asset allocation: advice on the mix and proportion of different asset classes to invest in; and 3.asset manager selection: advice on which asset manager to invest funds with.

(69) Fiduciary management also includes the legal delegation of some investment and decision-making powers by the client to the fiduciary manager so that the fiduciary manager can implement the client’s preferred investment strategy.

(70) The Commission has not previously assessed or defined the market for the supply of fiduciary management services to pension schemes.

(71) With respect to the product market definition, the UK Competition and Markets Authority published its Final Report on Investment Consultancy Market Investigation (“UK CMA Final Report”) on 12 December 2018, stating that the supply of fiduciary management services to pension schemes constitutes a distinct market46.

(72) The Parties consider that the supply of fiduciary management services to pension schemes do not constitute a distinct market, but that these services form part of the wider market for the supply of investment management services to pension schemes. However, the Parties also submit that the relevant product market definition can be left open for the purpose of this case.

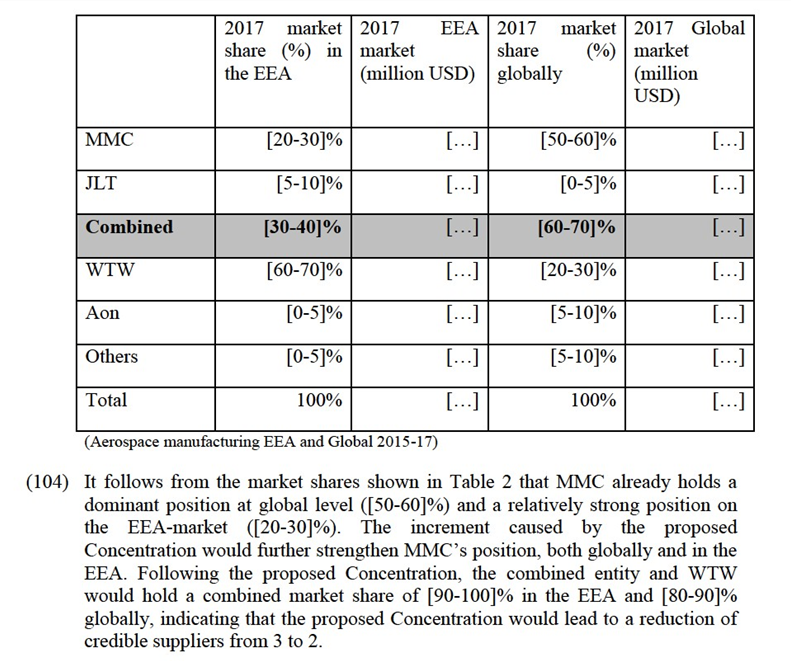

(73) In any event, for the purpose of this Decision, the exact product market definition for fiduciary management services to pension schemes can be left open, since the Transaction does not raise serious doubts as to its compatibility with the internal market, regardless of the product market definition.

4.3.1.2.Geographic market definition

(74) As stated in recital (70), the Commission has not previously assessed the market for the supply of fiduciary management services to pension schemes.

(75) The Parties submit that it is not necessary for the Commission to conclude on the relevant geographic market for the supply of fiduciary management services to pension schemes, as no competition issues arise on the narrowest plausible market.

(76) The UK CMA has considered the relevant geographic market for the supply of fiduciary management services as UK-wide in its recent UK CMA Final Report47.

(77) According to the results of the market investigation, the majority of responding customers purchase fiduciary management services to pension schemes on a national basis48, indicating that the geographic scope could be national.

(78) The exact geographic scope of the market for the supply of fiduciary management services to pension schemes can be left open between national and EEA-wide, since no serious doubts as to the compatibility of the Transaction with the internal market arise, regardless of the geographic scope of the market concerned.

5.COMPETITIVE ASSESSMENT

(79) Article 2 of the Merger Regulation requires the Commission to examine whether notified concentrations are to be declared compatible with the internal market, by assessing whether they would significantly impede effective competition in the internal market or in a substantial part of it.

(80) The Commission Guidelines on the assessment of horizontal mergers under the Council Regulation on the control of concentrations between undertakings49 (the "Horizontal Merger Guidelines") distinguish between two main ways in which mergers between actual or potential competitors on the same relevant market may significantly impede effective competition, namely non-coordinated effects and coordinated effects.

(81) Non-coordinated effects may significantly impede effective competition by eliminating the competitive constraint imposed by each merging party on the other, as a result of which the combined entity would have increased market power without resorting to coordinated behaviour. In this regard, the Horizontal Merger Guidelines consider not only the direct loss of competition between the merging firms, but also the reduction in competitive pressure on non-merging firms in the same market that could be brought about by the merger. According to recital (25) of the preamble of the Merger Regulation, a significant impediment to effective competition can result from the anticompetitive effects of a concentration even if the combined entity would not have a dominant position on the market concerned.

(82) The overlaps between the Parties’ activities give rise to horizontally affected market in the following markets/segments at a geographic level that is at least EEA-wide level: (i) Aircraft operators, (ii) Aerospace Manufacturing, (iii) Energy, (iv) Space, and in two markets/segments that have a national scope: (v) FinPro, in Ireland and (vi) fiduciary management to pension schemes in the UK.

5.1.2.The Commission Assessment

(86) The Parties submit that competition in this segment comes from top competitors such as Aon and Willis Towers Watson (“WTW”) but also from a long tail of smaller and regional brokers. In the Parties’ view, these competitors exert competitive pressure over the Parties, particularly by exerting pressure on the level of premiums.

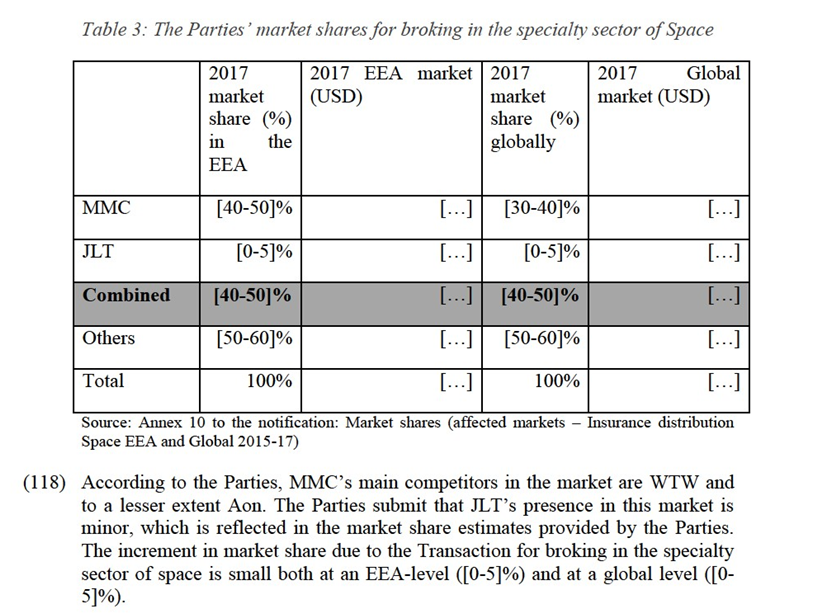

(87) The market investigation revealed that the Aircraft Operators market is concentrated around three or four major brokers, depending on the geographic level (i.e. EEA and global). The Commission has observed that the large majority of customers considered Aon and WTW as the only viable alternatives to the Parties, with other competitors lacking the experience or geographic reach required to service them55. A minority of respondents identified other brokers such as Price Forbes or Gallagher, who appear to have a focus outside of the EEA. Competitors consulted provided on average larger lists of viable competitors, which most customers did not consider suitable to service them.

(88) The Commission noted certain regional differences on the levels of market concentration. While several US-based customers considered Gallagher and Lockton to be viable competitors in Aircraft Operators specialty, no EEA customer did56. Concerning Aon’s market position, most EEA customers did not consider it a viable alternative, or were sceptical of its capacity to handle their business. Respondents noted that Aon had “de-emphasised aviation over the last 10 years”57, that the “technical team and expertise was lost in 2009 when the team moved en-masse to JLT and no capability has been rebuilt” and that they were “not a major player for aviation anymore”58.

(89) The majority of customers, insurers and competitors59 agreed that JLT and Marsh were very close competitors, and that both would be in the top 3 providers of Aircraft Operators insurance broking services.

(90) The Parties submit that the Aircraft Operators market is dynamic, with accounts frequently switching between brokers. As an illustration of this fact, the Parties claim that they win or lose between […]% and […]% of their business every year. The Parties submit that customers possess considerable buyer power, particularly when organised in buying groups able to leverage their concentrated and stronger position vis-à-vis brokers. The Parties characterise customers as very price sensitive, and willing to switch to a different provider who services them at a lower cost.

(91) By contrast, the Commission’s investigation revealed that only 11% of respondents had changed in the Aircraft Operators specialty over the past 5 years, which amounts to an average yearly churn rate of [0-5]%60.

(92) Customers in this segment considered expertise of the broker’s staff and quality of the services provided as the top two selection criteria for potential brokers61. At an aggregate level, worldwide presence, knowledge of local markets and a wide portfolio of services were equally ranked as top selection criteria. While also important for customers, price was not commonly ranked as the most important selection criteria. This suggests that competition in this specialty takes place more in the quality of staff and services provided than in the broker’s prices. The fact that competition takes place on the quality of staff and services represents a significant barrier to entry into the Aircraft Operators insurance broking market, as experienced and knowledgeable staff are scarce in this specialty.

5.1.2.1.Barriers to entry

(93) The Parties submit that entry barriers into broking are low, given that expertise and relationships reside in small and mobile teams of individuals. Given this, entry into a new market could feasibly be achieved by acquiring the necessary human capital – including from competitors – to effectively compete with incumbents.

(94) Despite the Parties’ claims that entry into new markets is easy, most customers62 and insurers63 were only able to identify JLT as a significant new entrant into the Aircraft Operators specialty in the past 5 years. The Parties have claimed that a new wave of potentially disruptive insurers, characterised by their use of technology and data – commonly referred to as “Insurtech” companies – threaten expansion into the distribution of specialty insurance. However, the activities of these companies have focused predominantly on the smaller and simpler risks of private individuals and SMEs, and corporate clients do not consider broker services interchangeable with those provided by insurers. Overall, the competitive landscape does not appear to have significantly evolved during the past 5 years.

(95) Human capital is the most valuable asset in brokerage64. The market investigation results showed that expertise of the broker’s staff was the highest rated consideration for customers in the Aircraft Operators segment65. The fact human capital is scarce in the specialised insurance broking sectors – which can sometimes trigger a “war for talent”66 –increases barriers to entry. Expansion into this market seems to occur only through acquisition of the required talent, supported by the necessary infrastructure. This is indeed how JLT initially entered the Aircraft Operators specialty.

(96) Other barriers to entry are likely to exist in the specialty business line of Aircraft Operators. Firstly, entry into this specialty requires economies of scale and a large upfront investment67. Incumbents, as they control a large share of the market, are capable of handling business costs effectively and compete on price, in addition to possessing staff with the right expertise and contacts. Moreover, the global nature of the operations of customers in this segment requires a global footprint that not many competitors (current or potential) appear to possess68. Though the Parties claim that customers do not require a global, integrated broker, and that customers are equally served by networks of smaller brokers, the large majority of customers expressed a preference for an integrated broker. Customer noted on the one hand the risks of service interruption that broker networks are subject to, and on the other hand the superior communication and efficiency potential of an integrated global broker69.

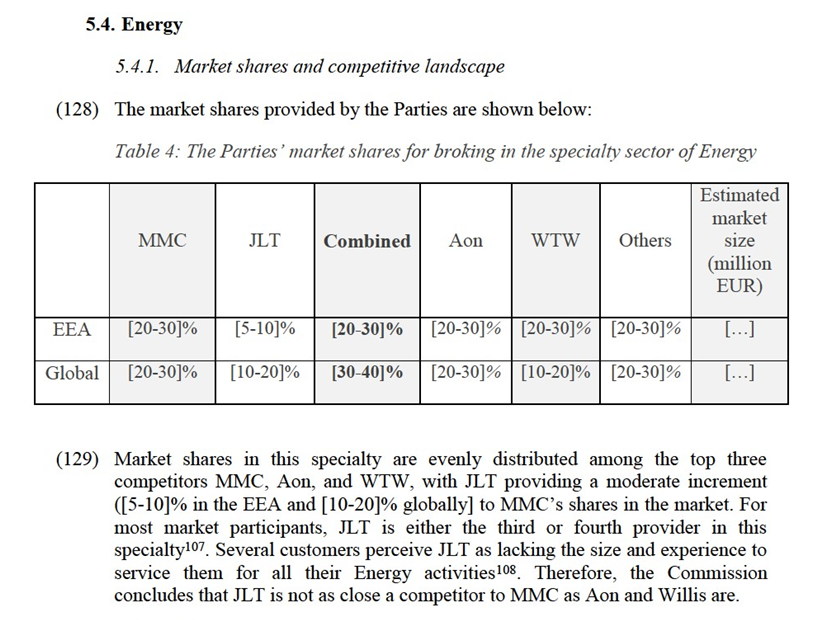

5.1.2.2.Countervailing buyer power

(97) Clients seeking Aircraft Operators broking services generally do so via requests- for-proposal, generally launching a tender every 2-5 years70. Contracts for broker services have a duration of 1 to 3 years, which is on average larger than that of insurance contracts (in most cases 1 year)71. Contracts are often renewed or extended, also without a new tender. The Parties submit that through the tender process, clients create competitive pressure among competitors to ensure that prices and conditions are kept as competitive as possible. The Parties additionally advance that clients may also choose to place two or more brokers for a single risk category (“co-broking”) to maintain competitive pressure even after the tender allocation. They conclude that clients currently have the balance of power in their favour.

(98) The Commission has found that competitive pressure is very high around a small number of large and profitable accounts72. It has also observed that customers tend to have a single broker per risk category, and when they do use co-broking scheme, they do so following a rationale of business continuity and/or of complementing the service capabilities of competitors73. There appears to be bias towards broker retention, as customers believe that switching brokers would be costly and time consuming, particularly due to the wealth of knowledge about the customer’s operations accumulated by the incumbent74.

(99) Customers expressed concerns that the balance of power might shift post- transaction75. With the reduction in viable competitors brought by the Transaction, some customers expressed that if the quality of broker services dropped they would not be able to easily find a replacement. A customer found that brokers would have less incentives to find the best offer on the market due to reduced competition76.

(100) In relation to the observation in recital 88 that the market appears to be more concentrated at EEA level, EEA customers expressed more concerns that non- EEA respondents. In particular, a customer pointed to a risk that prices could “increase dramatically” as broker remuneration increases77. Others expressed concerns that the options in the market might be insufficient78 and that the quality of services offered could deteriorate.

5.1.3. Conclusion

(101) The above observations point to the competitive landscape of Aircraft Operators as being one where only the Parties and WTW are considered to be viable competitors, with no immediate threat or potential disruption in sight. The concentration thus appears to reduce the number of viable competitors from 4 to 3 at a global level and from 3 to 2 in the EEA – an observation which is shared by a number of respondents79

(102) In view of the above considerations and taking account of the results of the market investigation and all of the evidence available to it, the Commission […]* that the concentration raises serious doubts as to its compatibility with the internal market due to its likely horizontal non-coordinated effects in markets for Aircraft Operators at both EEA-wide as well as a global level given the high combined market shares, the concentrated nature of the specialty, the reduced number of competitors and the high barriers to entry.

5.2.Aerospace Manufacturing

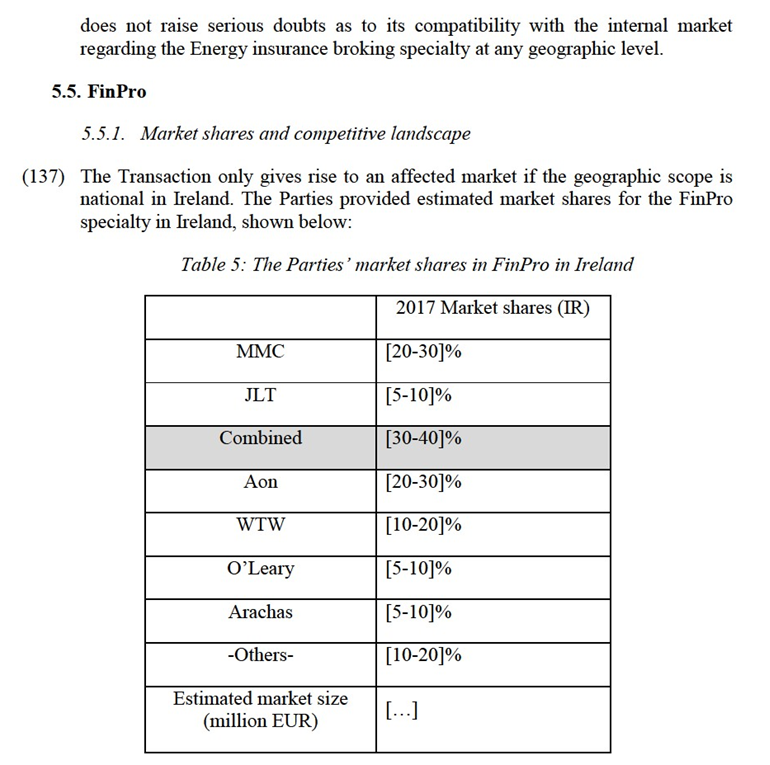

5.2.1. Market shares and competitive landscape

(103) The Parties’ market shares for broking in the specialty sector of Aerospace Manufacturing are presented in the table below

Table 2: The Parties’ market shares for broking in the specialty sector of Aerospace Manufacturing

necessary. The product offerings of the brokers active in this segment are largely similar according to the Parties, with differences mostly relating to the level of service and expertise that a broker can offer. The Parties do however recognise that only MMC, Aon and WTW can offer the size of teams that is required to successfully service the largest customers.

(109) According to the Parties, the barriers to entry in this sector relate to the breadth of knowledge and expertise required to provide the bespoke service demanded by aerospace manufacturing clients. The cost of entry to the segment is considered low by the Partied and would be limited in time (1 year to 1.5 year).

5.2.2. The Commission assessment

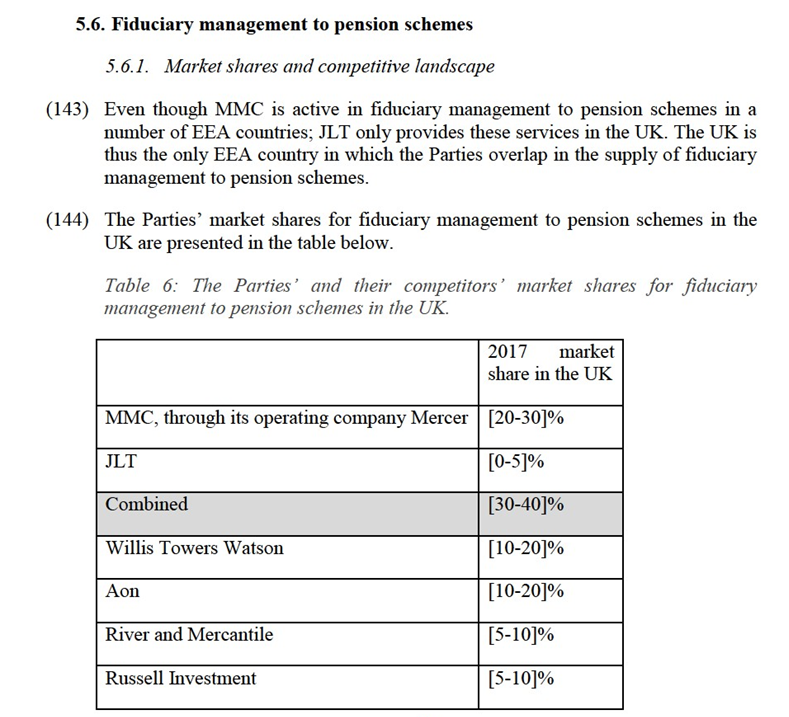

(110) The results of the market investigation with customers provide a mixed picture in relation to the use of tenders to select a broker and average period between market consultations. Customers indicated that the average contract with a broker can be anywhere between one and three years80, but the period between market consultations can be longer (up to 5 years, or evergreen contracts)81. When asked on whether they switched brokers in the last 5 years, the majority of the respondents indicated that they have not switched brokers in the recent past for their activities in Aerospace Manufacturing82. The majority of customers however indicated that it would be possible to switch between brokers, even though it requires an investment in time to educate the broker on the customers’ unique requirements (time estimates range between a couple of weeks to nearly a year)83.

(111) For a customer to switch, a broker must meet specific criteria. When asked to rank the most important criteria, the quality of the service provided, know-how and staff expertise are considered the most important. Price is considered relatively important, but not the most dominant selection criterion84. A broker intending to start servicing customers in the specialty sector of Aerospace Manufacturing must have sufficient know-how, the ability to cover the full geographic footprint of their client’s activities, the ability to comply with regulatory requirements and an overall positive track record85. The geographic footprint could be seen as part of the quality of the service required by customers since customers indicate that a global footprint is required to place their global insurance programs86. The majority of customers also indicate a preference towards brokers that have established their own global network, over brokers that cooperate with local entities through an informal network87.

(112) According to the market investigation, customers consider the Parties to be part of the 4 top providers of broker services in the specialised sector of Aerospace Manufacturing (i.e.MMC, WTW, Aon and JLT)88. This is confirmed by the majority of the Parties’ competitors89.

(113) Customers consider Aon and WTW to be the closest competitors to MMC, while JLT is mentioned as a fourth competitor, but on average not the closest to MMC90. However, the competitors to the Parties consider JLT as the closest competitor to MMC91. When asked to name the closest competitor to JLT, customer identified Marsh as the closest competitor, closely followed by Aon and WTW92. This list of close competitors does not change whether assessed on a global or an EEA-scale.

(114) The market investigation indicated that the majority of customers consider that there will be sufficient alternative suppliers active on the market post-transaction, even though the number of available suppliers seems to be reduced from 4 to 393. The majority does not expect an impact on their business94 or in the EEA95.

(115) The majority of customers do not expect a new entrant on the market, nor have they seen a new entrant in the past five years96, further strengthening the view that the transaction will lead to a reduction of choice. The selection criteria requested by customer (see recital 111), including a global footprint, further strengthen the Commission’s view that new entries into the market are unlikely in the near future.

5.2.3. Conclusion

(116) In view of the above considerations, taking into account the market investigation and all the evidence available to it, the Commission considers that the concentration raises serious doubts as to its compatibility with the internal market with respect to the market for broking in the specialty sector of Aerospace Manufacturing at an EEA-wide geographic scope.

5.3.Space

5.3.1. Market shares and competitive landscape

(117) The Parties’ market shares for broking in the specialty sector of Space are presented in the table below.

5.3.2. The Commission assessment

(122) According to the market investigation, the majority of customers prefers to work with a single broker for a specific risk class97. Customers put brokers in competition with each other for new contracts, making use of either formal tender processes, or through more informal request-for-proposals98. Respondents also indicated that the duration of a contract with a broker can last anywhere between 1 year and 15 years depending on the preference of the customer. However, the majority of customers indicated that contracts are on average limited in duration to 1-2 years99.

(123) Customers indicated that switching between brokers is possible, but all of the respondents indicating that switching is possible stressed that such a switch would require training their new broker and making them familiar with their specific company’s needs. Customers indicate that this process could take several months100. According to the market investigation, the majority of customers has not switched its broker in the specialty sector of Space in the past five years101.

(124) According to the customers responding to the market investigation, no new entrants have emerged over the past 5 years102 and only one customers indicated to be aware of a broker expressing interest in expanding into the sector in the coming years103.

(125) The market investigation with customers indicated that the majority of customers do not consider JLT as a close competitor to MMC. Nearly all of the responding customers indicated that Aon and WTW are the closest competitors to MMC104. When asked for the closest competitors to JLT, the vast majority of customers only mentioned the three main actors on the market (MMC, WTW and Aon).

(126) The vast majority of customers do not expect a negative impact of the Transaction on the market for broking in the specialty sector of Space105. Customers also indicated that there would still be sufficient choice of brokers available on the market post-Transaction106.

5.3.3.Conclusion

(127) In view of the above considerations, taking into account the market investigation and all the evidence available to it, the Commission concludes that the concentration does not raise serious doubts as to its compatibility with the internal market with respect to the market for broking in the specialty sector of Space at an EEA-wide geographic scope.

presence” as one of the least important characteristics that a broker should possess113. All of these elements considered, mid-size competitors appear capable of competing with the top 3 brokers for large accounts in Energy, more so than in any other specialty.

(132) The Parties submit that clients regularly switch between brokers to ensure the best rates and conditions in the market. The market investigation revealed that most customers had not switched providers in the Energy specialty114. However, the large majority of customers also expressed that switching would be easy and would not require significant time or other costs115. There did not appear to be any other significant switching costs.

(133) The Parties claim that in the Energy specialty insurance captives play a larger role as a customer’s potentially viable risk management option than in other segments. Not all customers have the financial strength to set up a captive, but those that do tend to self-insure large portions of their risk116.Although not part of the same market as brokerage, captive insurance is likely to exert some competitive pressure on brokers. Although brokers are generally still involved in the placement of a client’s risk into a captive insurer – by, for instance scanning the market for the best rates and conditions, and benchmarking the captive’s services against them – they receive a fraction of the remuneration that they would receive for other broking services. The use of captives by a significant share of the customer base appears to reduce their dependency on brokers, thus improving their bargaining position.

(134) Lastly, the market investigation returned very few concerns from market participants. Most customers believed that the impact of the Transaction would be limited, and that they would have sufficient amount of choice post-merger117. No impact was expected in the EEA118, as JLT “is not that strong on local level in the EEA”119.

5.4.3.Conclusion

(135) In summary, the market shares of the combined entity in the insurance broking specialty of Energy do not appear to indicate that the combined entity would exert significant market power. The market in this specialty seems sufficiently dynamic, with credible competition coming from mid-size competitors and new entrants. Customers seemingly wield larger amounts of buyer power given their propensity to set up captive insurers, which limit brokers in their potential gains and limit customer’s dependency on brokerage services.

(136) In view of the above, taking into account the market investigation and all the evidence available to it, the Commission concludes that the notified concentration

| 2017 market share in the UK |

Cardano | [5-10]% |

Others | < 5% |

Source: Table 6.18 of the notification

(145) The Parties submit that the market for fiduciary management to pension schemes in the UK has grown significantly over the past 10 years. The Parties submit that there are at least 17 suppliers of fiduciary management services in the UK, split between four larger competitors (WTW, Aon, River and Mercantile and Russel Investment) which will continue to exert significant competitive constraint on the combined entity post-Transaction.

(146) The Parties do not consider each other as close competitors. The Parties further submit that the competitive constraints are enhanced by the growing presence of ringmasters (i.e. companies engaged by pension schemes to scrutinise and challenge the performance of fiduciary managers), pension managers and independent trustee organisations.

5.6.2. Commission assessment

(147) The Parties’ combined market share is above 30% ([30-40]%), with a small increment of [0-5]%. Other competitors in in the market for fiduciary management to pension schemes include brokers such as WTW and Aon, but also advisory and asset management businesses such as Russell Investment and River and Mercantile.

(148) The results of the market investigation indicate that customers do not expect the Transaction to have an impact on the market for fiduciary management123. A small minority of customers indicated that the transaction will lead to a reduction of the number of competitors on the market124, but the vast majority of customers is confident that sufficient alternative suppliers are active and will remain so on the market post-Transaction. The majority of competitors responding to the market investigation confirm the customers’ point of view that the Transaction will not have an impact on the market125.

5.6.3. Conclusion

(149) In view of the above, taking into account the market investigation and all the evidence available to it, the Commission concludes that the concentration does not raise serious doubts as to its compatibility with the internal market regarding fiduciary management to pension schemes in the UK.

5.7. Final conclusion

(150) In light of the considerations in recitals (82) to (149) and in view of the result of the market investigation and all of the evidence available to it, the Commission concludes that the concentration raises serious doubts with respect to the EEA- wide markets for broking in the specialty sectors of Aircraft Operators and Aerospace Manufacturers. The Commission concludes that the concentration does not raise serious doubts with respect to broking in the EEA-wide specialty markets of Space and Energy, nor in the national markets for FinPro in Ireland and fiduciary management to pension schemes in the UK.

6. PROPOSED REMEDIES

(151) In order to render the concentration compatible with the internal market, the undertakings concerned have modified the notified concentration by entering into commitments, submitted to the Commission on 01 March 2019 (the “First Commitments”). The Commission market tested the First Commitments and provided feedback to the Parties. In response to this, the Parties submitted an improved set of Commitments on 18 March 2019 (the “Final Commitments”) which are annexed to this decision and form an integral part thereof.

(152) On 4 March 2019, MMC announced that MMC and JLT entered into an agreement to sell JLT’s aerospace practice, including the transfer of its personnel, to Arthur J. Gallagher & Co (“Gallagher”). This sale is, however, subject to the Commission’s approval and this Decision does not constitute an approval of Gallagher as a suitable purchaser.

6.1. Framework for the assessment of commitments

(153) When a concentration raises competition concerns, the merging parties may seek to modify the concentration in order to resolve those competition concerns and thereby obtain clearance for the concentration.126

(154) The commitments must eliminate the competition concerns entirely and must be comprehensive and effective in all respects. The commitments must also be proportionate to the competition concerns identified.127 Furthermore, the commitments must be capable of being implemented effectively within a short period of time as the conditions of competition on the market will not be maintained until the commitments have been fulfilled.128

(155) Structural commitments proposed by the parties to a concentration will meet that condition only in so far as the Commission is able to conclude, with the requisite degree of certainty, that it will be possible to implement them and that the new commercial structures resulting from them will be sufficiently workable and lasting to ensure that the significant impediment to effective competition which the commitments are intended to prevent, will not be likely to materialise in the relatively near future.129

(156) In assessing whether proposed commitments are likely to eliminate the serious doubts to which the concentration would otherwise give rise, the Commission will consider all relevant factors relating to the proposed remedy itself, including, inter alia, the type, scale and scope of the remedy proposed, judged by reference to the structure and particular characteristics of the market in which the competition concerns arise, including the position of the parties and other players on the market.130

(157) Based on these principles as well on the principles related to the implementation and effectiveness of all types of commitments set out in paragraphs 13 and 14 of the Remedies Notice, the Commission has assessed the commitments put forward by the Parties in the present case.

6.2.Description of the First Commitments

(158) The First Commitments consist of the divestiture to a suitable purchaser of JLT’s Global Aerospace division.

6.2.1.Scope of the First Commitments

(159) The First Commitments include the divestment of JLT’s Global Aerospace division and the transfer of the relevant tangible and intangible assets, licenses permits and authorizations, transitional arrangements and contracts listed below,

(160) The Divestment Business will include the following tangible assets:a. all current customer relationships held by the Divestment Business;b. all records and information held by the Divestment Business relating to current and past customers, including but not limited to customer lists and files, logs of customer support issues, and written correspondence with customers;c. all records and information held by the Divestment Business concerning prospective customers;d. all contracts, records and information held by the Divestment Business concerning insurance companies;e. all marketing and promotional information relating to the Divestment Business; f. all business plans and forecasts relating to the Divestment Business g. technical or other expertise relating to the Divestment Business;h. all research material, data, models, information, analyses and market studies held by the Divestment Business,; and i. credit and other business records currently held by the Divestment Business.

(161) The Divestment Business will include the following intangible assets: a. The brand name for Hayward Aviation; b. The […] client portal software; and c. Other software used by the Divestment Business for its operations (the […] software).

(162) The First Commitments also include:· all licences, permits and authorisations used by the Divestment Business;· all contracts, leases, commitments and customer orders of the Divestment Business;· all customer, credit and other records of the Divestment Business;· the Key Personnel and all Personnel as described in the Commitments;· a best efforts obligation to secure the transfer to the Purchaser of all customer contracts containing a change of control provision or requiring the customer’s consent; and· Transitional services for a period of up to […] after closing, with a possible extension of up to […] and […] are also envisaged in the First Commitments.

(163) The Parties also commit not to solicit the Key Personnel and the Personnel transferred with the Divestment Business for a period of […] after closing. The Parties further commit to retain all liabilities relating to the Divestment Business that are incurred up until closing.

(164) In addition the Parties have entered into related commitments, inter alia regarding the separation of the divested businesses from their retained businesses, the preservation of the viability, marketability and competitiveness of the divested businesses, including the appointment of a monitoring trustee and, if necessary, a divestiture trustee

6.2.2. The purchaser criteria

(165) In order to be approved by the Commission, the purchaser must fulfil the following criteria: a. The Purchaser shall be independent of and unconnected to the Parties and their Affiliated Undertakings b. The Purchaser shall have the financial resources, proven expertise and incentive to maintain and develop the Divestment Business as a viable and active competitive force in competition with the Parties and other competitors.c. The acquisition of the Divestment Business by the Purchaser must neither be likely to create, in light of the information available to the Commission, prima facie competition concerns nor give rise to a risk that the implementation of the Commitments will be delayed. In particular, the Purchaser must reasonably be expected to obtain all necessary approvals from the relevant regulatory authorities for the acquisition of the Divestment Business.d. The Purchaser shall have an existing commercial non-life insurance broking business with a proven track record in serving large customers for complex risks and the geographic reach to integrate and run competitively the Divestment Business.

6.3. Assessment of the proposed remedies

(166) As explained in this Decision, the serious doubts as to the compatibility of the Transaction with the internal market stems from the combination of MMC and JLT’s activities in the broking of commercial insurance for Aircraft Operators and Aerospace Manufacturing markets.

(167) The First Commitments consist in the divestiture to a suitable purchaser of JLT’s Global Aerospace division that includes JLT’s activities in the broking of commercial insurance for Aircraft Operators, Aerospace Manufacturing and Space markets. Therefore, the First Commitments cover all potential markets in respect of which the Commission has serious doubts as regards the compatibility of the Transaction with the internal market.

6.3.1. Aircraft Operators and Aerospace Manufacturing

(168) The Divestment Business includes the entirety of JLT’s Aerospace practice, meaning that there will be no increment to Marsh’s market share in these segments as a result of the Proposed Transaction.

(169) JLT’s Aerospace practice combines all of JLT’s insurance broking activities in Aircraft Operators, Aerospace Manufacturing, and Space, as one combined business division. The Divestment Business includes the divestiture of the entirety of JLT’s Aerospace practice, including Space, although the Commission did not identify competition concerns in relation to broking in the Specialty sector of Space. The inclusion of JLT’s activities in Space in the Divestment Business is, however, necessary to ensure the viability of the Divestment Business and to create an effective competitor in the affected markets.131

(170) The Divestment Business has a diverse client portfolio that includes some of the world’s largest and most complex aerospace risks, and brokers for many of the world’s top major airlines, aerospace manufacturers, airports and related services providers.

(171) There are a number of shared support services within the Aerospace practice that support all of the segments transversally, such as claims management, technical services and contract advisory which are included in the remedy package. The Divestment Business is an integrated, standalone business division that encompasses all necessary assets and personnel, including senior management and all brokers, as well as support services that are dedicated to the Aerospace practice, including marketing and broking, broking and business support, contract advisory, claims management, operations, technical services and insurance brokerage accounts. The market test did not reveal any missing services for the division to operate autonomously.

(172) The Commitments also includes the Divestment Business’s main IT systems: […], a web-based client portal, and […], the system for Hayward Aviation. […], the Divestment Business’s main client-facing IT system, was built and developed by the JLT Aerospace practice and is not linked to other JLT IT systems

(173) The Divestment Business operates globally and will therefore completely remove the overlap both at the EEA and global levels.

(174) The market test confirmed that the Commitments are sufficient to eliminate the serious doubts as to the compatibility of the Transaction with the internal market, as they are feasible, comprehensive and include all necessary assets.

(175) The large majority of competitors, insurers and customers support the view that the commitments offered would remove any possible negative impact in the fields of aerospace manufacturing and aircraft operators.132

(176) Virtually all customers consider that the Commitments allow an existing broker meeting the purchaser criteria purchasing the Divestment Business to effectively compete in the affected markets at a global scale133.

(177) The large majority of respondent to the market test state that the divestment business includes all necessary assets and personnel to operate in the market134, and that a purchaser meeting the established purchaser criteria would likely be able directly compete against the Parties. The market test also confirmed that the purchaser criteria are sufficient.135

(178) The overwhelming majority of customers are of the opinion that the Divestment Business is likely to retain its current customers136 and that the transitional services as described in the Commitments afford adequate safeguards for the viability and competitiveness of the Divestment Business137. Competitors also backed this opinion.138

6.3.2. Final Commitments

(179) While the market test results broadly confirmed the suitability of the commitments, the following changes have been introduced in the Final Commitments in order to strengthen the viability of the Divestment Business.

(180) First, the Final Commitments include transitional services for a period of up to […] after closing, with a possible extension of up to […] and […]. The supply of the […] IT system only shall be for a transitional period of […] after closing, with a possible extension of up to an additional […] at the Purchaser’s request and subject to Commission approval.

(181) Second, the undertaking from the Parties not to solicit the Key Personnel and the Personnel transferred with the Divestment Business for a period of […] after closing is extended to a period of […] after closing. The Parties also commit not to hire, employ or engage, and to procure that Affiliated Undertakings do not hire, employ or engage, the Key Personnel transferred with the Divestment Business for a period of […] after closing.

(182) Finally, the Final Commitments clarify that all electronic records and information relating to current, past and prospective customers of the Divestment Business, as well as all electronic contracts, records and information relating to the Divestment Business concerning insurance companies will be transferred to the Divestment Business. The transfer of physical records, contracts and information will be limited to the last 2 years together with a best efforts obligation from the Parties to the Purchaser to arrange access to all physical business or customer records older than two years that relate to the Divestment Business, at the Purchaser’s request. MMC shall also restrict all retained personnel in practice areas that compete with the Divestment Business from having access to any legacy JLT archive records. All MMC personnel who have access to legacy JLT archive records shall be subject to obligations not to disclose such records to MMC personnel in practice areas that compete with the Divestment Business.

(183) All these changes have been incorporated and form an integral part of the Final Commitments as annexed to this decision.

(184) For the reasons outlined above, the Commission concludes that the Final Commitments entered into by the undertakings concerned and as submitted to the Commission on 18 March 2019 are sufficient to eliminate the serious doubts as to the compatibility of the Transaction with the internal market in respect of aircraft operators and aerospace manufacturing. The full text of the Final Commitments is annexed to this Decision as Annex I and forms an integral part thereof.

7. CONDITIONS AND OBLIGATIONS

(185) Pursuant to the first sentence second subparagraph of Article 6(2) of the Merger Regulation, the Commission may attach to its decision conditions and obligations intended to ensure that the undertakings concerned comply with the commitments they have entered into vis-à-vis the Commission with a view to rendering the concentration compatible with the internal market.

(186) The fulfilment of the measure that gives rise to the structural change of the market is a condition, whereas the implementing steps which are necessary to achieve this result are generally obligations on the Parties.

(187) Where a condition is not fulfilled, the Commission’s decision declaring the concentration compatible with the internal market is no longer applicable. Where the undertakings concerned commit a breach of an obligation, the Commission may revoke the clearance decision in accordance with Article 6(3) (b) of the Merger Regulation. The undertakings concerned may also be subject to fines and periodic penalty payments under Articles 14(2) and 15(1) of the Merger Regulation.

(188) In accordance with the basic distinction between conditions and obligations set out above, this Decision is conditional on full compliance with the requirements set out in Section B paragraph 2 of the Final Commitments, which constitute conditions. The remaining requirements set out in the other Sections of the said commitments are considered to constitute obligations.

8. CONCLUSION

(189) For the above reasons, the Commission has decided not to oppose the notified operation as modified by the commitments and to declare it compatible with the internal market and with the functioning of the EEA Agreement, subject to full compliance with the conditions in Section B paragraph 2 of the commitments annexed to the present Decision and with the obligations contained in the other sections of the said commitments. This Decision is adopted in application of Article 6(1)(b) in conjunction with Article 6(2) of the Merger Regulation and Article 57 of the EEA Agreement.

COMMITMENTS TO THE EUROPEAN COMMISSION

Pursuant to Article 6(2) of Council Regulation (EC) No 139/2004 (the “Merger Regulation”), Marsh & McLennan Companies, Inc. (“MMC”) and Jardine Lloyd Thompson Group plc (“JLT”) hereby enter into the following Commitments (the “Commitments”) vis-à-vis the European Commission (the “Commission”) with a view to rendering the acquisition of JLT by MMC (the “Concentration”) compatible with the internal market and the functioning of the EEA Agreement.This text shall be interpreted in light of the Commission’s decision pursuant to Article 6(1)(b) of the Merger Regulation to declare the Concentration compatible with the internal market and the functioning of the EEA Agreement (the “Decision”), in the general framework of European Union law, in particular in light of the Merger Regulation, and by reference to the Commission Notice on remedies acceptable under Council Regulation (EC) No 139/2004 and under Commission Regulation (EC) No 802/2004 (the “Remedies Notice”).

SECTION A. DEFINITIONS

1. For the purpose of the Commitments, the following terms shall have the following meaning:

Affiliated Undertakings: undertakings controlled by the Parties and/or by the ultimate parents of the Parties, whereby the notion of control shall be interpreted pursuant to Article 3 of the Merger Regulation and in light of the Commission Consolidated Jurisdictional Notice under Council Regulation (EC) No 139/2004 on the control of concentrations between undertakings (the "Consolidated Jurisdictional Notice").

Assets: the assets that contribute to the current operation or are necessary to ensure the viability and competitiveness of the Divestment Business as indicated in Section B, paragraph 5 and described in more in detail in the Schedule.

Closing: the transfer of the legal title to the Divestment Business to the Purchaser.

Closing Period: the period of […] from the approval of the Purchaser and the terms of sale by the Commission.

Confidential Information: any business secrets, know-how, commercial information, or any other information of a proprietary nature that is not in the public domain.

Conflict of Interest: any conflict of interest that impairs the Trustee's objectivity and independence in discharging its duties under the Commitments.

Divestment Business: the business or businesses as defined in Section B and in the Schedule which the Parties commit to divest.

Divestiture Trustee: one or more natural or legal person(s) who is/are approved by the Commission and appointed by the Parties and who has/have received from the Parties the exclusive Trustee Mandate to sell the Divestment Business to a Purchaser at no minimum price.

Effective Date: the date of adoption of the Decision.

First Divestiture Period: the period of […] from the Effective Date.

Hold Separate Manager: the person appointed by the Parties, following approval by the European Commission, for the Divestment Business to manage the day-to-day business under the supervision of the Monitoring Trustee.

Key Personnel: all personnel necessary to maintain the viability and competitiveness of the Divestment Business, as listed in the Schedule, including the Hold Separate Manager.

MMC: Marsh & McLennan Companies, Inc., incorporated under the laws of the United States of America, with its registered office at 1166 Avenue of the Americas, New York, New York 10036 USA, and registered under number US362668272.