Commission, June 27, 2018, No M.8738

EUROPEAN COMMISSION

Decision

RHONE-ZODIAC / FLUIDRA

Subject: Case M.8738 – RHONE-ZODIAC / FLUIDRA

Commission decision pursuant to Article 6(1)(b) in conjunction with Article 6(2) of Council Regulation No 139/2004 and Article 57 of the Agreement on the European Economic Area1

Dear Sir or Madam,

(1) On 3 May 2018, the European Commission ("Commission") received a notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/20042 by which the Rhône Group and Fluidra Founding Families acquire within the meaning of Article 3(1)(b) and 3(4) of the Merger Regulation joint control of Zodiac and Fluidra (the "Transaction"). Zodiac and Fluidra are further collectively referred to as "the Parties", whilst the undertaking that would result from the Transaction is referred to as “the merged entity”.

1. THE OPERATION AND THE CONCENTRATION

(2) The concentration is accomplished by way of purchase of shares in a newly created company constituting a joint venture. The Transaction consists of a statutory merger under Spanish corporate law thereby Zodiac's holding company (Piscine Luxembourg Holding 2 S.À R.L.) will be merged with Fluidra (Fluidra, S.A.). The surviving new entity will bear Fluidra's name. This new entity will be jointly controlled by (a) Rhône Capital L.L.C. (“Rhône”), the current controlling (indirect) shareholder of Zodiac:, and (b) a group of natural persons forming part of the families that founded and currently control Fluidra (the “Fluidra Founding Families”).

(3) Rhône, through Piscine Luxembourg Holding 2 S.À.R.L., will receive 42.43% of the new entity’s share capital in exchange. The Fluidra Founding Families indirect shareholding will, as a result, be reduced to 28.82%. According to the governance rules of the merged entity, each of Fluidra Founding Families and Zodiac will have a veto right over the appointment and removal of all senior management positions. As a result, both Rhône and the Fluidra Founding Families will have joint control over the new Zodiac/Fluidra entity. The remaining shares will remain publicly traded on the Madrid and Barcelona stock exchanges in Spain.

(4) Since the Transaction concerns two existing companies that have market presence in the EU, the entity resulting from the Transaction will have sufficient resources to operate independently on the market and will not have any significant sale/purchase relationship with the parents. The full functionality test is met under Article 3(4) EUMR.

2.UNION DIMENSION

(5) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (in 2016, Rhône: EUR […] million; the Fluidra Founding Families: EUR […] million). Each of them has a Union-wide turnover in excess of EUR 250 million (in 2016, Rhône: EUR […] million; the Fluidra Founding Families: EUR […] million), but they do not achieve more than two-thirds of their aggregate Union-wide turnover within one and the same Member State. The notified operation therefore has a Union dimension pursuant to Article 1(2) of the Merger Regulation.

3. THE PARTIES' ACTIVITIES

(6) Both Parties are active in the manufacture and marketing of swimming pool equipment. Fluidra, through its other subsidiaries, is also active in irrigation and water treatment, industrial and other fluid handling, and engineering of projects in water facilities. The Parties’ activities overlap only with respect to pool equipment.

3.1. Introduction to pool equipment products

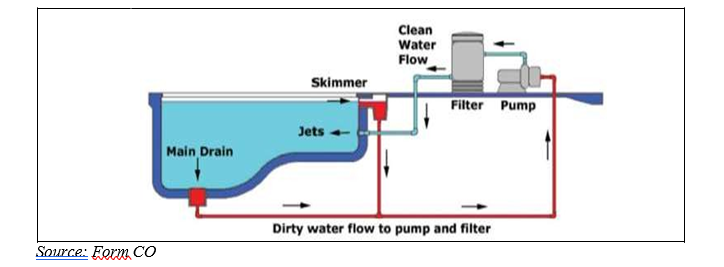

(7) A typical swimming pool consists of a basin and pool equipment. Figure 1 depicts an example of a simple swimming pool set-up.

(8) There are a number of key components without which a swimming pool cannot function properly. These components fall into the category of ‘essential pool equipment’, which encompasses:a. Swimming pool pumps, which are devices that draw water from the pool, pass it through a filter, and return it back to the pool. Pool pumps can be further sub-segmented into single speed, variable speed and booster pumps. The Parties' activities overlap with respect single and variable speed pumps.b. Swimming pool filters, which remove smaller impurities from the water. Generally all filters can be broadly sub-divided by filtration media used: sand filters, cartridge filters, or diatomaceous earth (DE). The Parties' activities overlap with respect to sand filters (in particular, laminated polyester sand filters) and cartridge filters.c. Pool structures: a pool structure is a basin where the water is kept. Pool structures can generally be sub-segmented into above-ground pool structures and in-ground pool structures. In-ground pool structures can be further sub-divided into concrete, vinyl-lined and fibreglass structures. The Parties' activities overlap only with respect to vinyl-lined structures.d. Water treatment products: this category can be split between chemicals and sanitising and dosing equipment used to disinfect the pool water.Sanitising and dosing equipment may be further sub-divided into (i) solid chemical sanitising and dosing equipment such as dispensers and feeders,(ii) liquid chemical sanitising and dosing equipment such as salt water chlorinators (SWCs), pH and ORP regulators and dosing pumps (iii) alternative sanitisers that use ozone, UV or minerals and (iv) testing and measuring equipment.The Parties' activities overlap in (i) liquid chemical sanitising and dosing equipment and (ii) alternative sanitisers.e. Other Essential Equipment: Some other equipment may also be considered essential to the functioning of a swimming pool, including so-called "white goods" (plastic equipment that forms a part of the pool basin itself which will be in contact with the water such as grids, drains, nozzles and skimmers) or piping/tubing. However, Zodiac is not active in this space and, hence, the Parties' activities do not overlap in this respect.

(9) There is also a large number of additional pool equipment that makes the operation of a pool easier, less time consuming and more enjoyable. This is the category of ‘non-essential pool equipment’, and encompasses:a. Pool cleaning equipment: this category of products generally consists of all devices that can be used to clean a pool floor and walls and collect larger debris. Pool cleaners can be broadly sub-divided into (i) basic cleaning equipment (leaf skimmers, brushes and poles), (ii) manual suction cleaners (underwater vacuum cleaners that need to be manually guided to clean a pool), (iii) automatic suction cleaners (vacuum cleaners that do not require manual work and clean the pool surface automatically), (iv) pressure cleaners (automatic cleaning devices that use pressure to clean the pool surface) (v) robotic cleaners (also known as electric cleaners) that are fully automatic and do not use the pool's filtration system, and (vi) in-floor cleaning systems3 (in-built cleaning systems that use pressure to clean the pool floor). The Parties' activities overlap with respect to (i) robotic cleaners and (ii) automatic suction cleaners.b. Pool heating equipment: mostly used in colder climates to artificially heat pool water and, therefore, prolong the effective pool season. Pool heaters can be broadly sub-divided into (i) heat pumps, which function by extracting heat from the surrounding air and transferring it to pool water, and (ii) other heating equipment, which include electric heaters, heat exchangers, solar covers and solar heaters. The Parties' activities overlap with respect to (i) heat pumps and (ii) other heating equipment.c. Pool dehumidifiers: devices that reduce humidity in in-door pools. Both Parties manufacture those products.d. Water features: are decorative pool elements such as waterfalls, water curtains, fountains and jets. Both Parties manufacture those products.e. Pool automation: devices that can remotely control certain elements of a swimming pool such as remotely switch on pump or heat pump. Both Parties manufacture those products.

(10) Fluidra is also active in the wholesale distribution of pool equipment products in certain EEA countries. These activities are carried out through its own traditional branches (warehouses) and its “Cash & Carry” operations. The Cash & Carry operations are self-service outlets targeted at pool professionals (i.e. pool equipment retailers and pool builders/installers of all sizes). Fluidra operates in the wholesale distribution of pool equipment through these Cash & Carry operations in Spain, Portugal, France, Italy and Bulgaria, and through warehouses in the other EEA countries.

(11) The Transaction mainly concerns equipment for residential pools. Sales of commercial equipment represent a small share of the overall sales of the Merging Parties.

(12) Residential pools are smaller pools for single-family homes, which usually have smaller tank capacities and are used less intensively than commercial pools. Commercial pools are usually very large, used for longer periods of time and are accessible to public.

(13) The Parties' activities in pool structures (including under any sub- segmentations), water features and pool automation products do not result in affected markets. These products will, therefore, no longer be discussed in the present decision.

4. RELEVANT MARKETS

(14) With the exception of heat pumps and pool heaters,4 there are no Commission precedents that have analysed pool equipment for which affected markets exist in this case. The Parties' activities result in overlaps for (i) pool cleaning equipment (robotic and automatic suction cleaners); (ii) water treatment products (sanitising and dosing equipment); (iii) pool heating equipment;(iv) pool dehumidifiers; (v) swimming pool pumps; and (vi) swimming pool filters. The Transaction does not result in affected markets with respect to pool structures, water features and pool automation equipment. Therefore, it will not be further analysed in the Decision.

4.1. Relevant Product Markets

4.1.1. Commercial vs residential swimming pool equipment

4.1.1.1. The Parties' view

(15) The Parties consider that it is relevant to distinguish between residential and commercial equipment as commercial pools tend to require particularly robust and reliable, high-capacity equipment, which may form part of more complex engineering solutions compared to residential pools.

4.1.1.2. The Commission's assessment

(16) There is no Commission relevant precedent as regards the distinction between residential and commercial pool equipment. However, in the Zodiac/PSA (2004) case, the French authorities took the view that distinct markets for residential pool heaters and dehumidifiers may be considered.5

(17) Information collected by the Commission through its market investigation and the submission of documents by the Parties support the definition of a product market for residential pool equipment that is separate from commercial pool equipment.

(18) A large majority of competitors, distributors and customers who responded to the market investigation stated that different market conditions apply for residential pool equipment as compared to commercial pool equipment.6

(19) Several respondents highlighted significant differences between the markets for residential pool equipment and commercial pool equipment, in particular with regard to price and sales channels. A French competitor commented: "Price positioning is not the same: the residential pool equipment market is much more competitive; residential and commercial pool equipment do not have exactly the same distribution channel; their requested skills are not the same: the commercial field is much more technical". A Bulgarian distributor noted with regard to switching between residential and commercial equipment: "Prices between residential equipment products and commercial is of significant difference and on the Bulgarian market, being a very price orientated market, this is not possible".7 A German customer noted: "Commercial pool cleaning equipment is too expensive for our customers".8

(20) Some market participants pointed out that commercial and residential pool equipment are governed by different standards and regulations.9 A French competitor mentioned that in France the use of salt water chlorinators is limited to residential pools.10 An Italian competitor commented that in most countries commercial equipment is subject to specific standards "such as DIN, UNI or ÖNorm in Germany, Italy and Austria respectively".11

(21) In addition, internal documents provided by the Parties show that they track commercial and residential pool equipment products separately. For instance, a document from the Fluidra subsidiary Aquatron shows that the company monitors its sales in distinct "residential pool" and "commercial pool" categories.12

(22) The Parties' activities do not overlap with regard to commercial pool equipment with a minor exception in heating equipment and pool humidifiers, which, according to the Parties, is not material.13

4.1.1.3. Conclusion

(23) In the light of the results of the market investigation and taking the other evidence available to it into account, the Commission considers that for the purposes of the present case, residential pool equipment constitutes a distinct relevant product market, the sub-segmentations of which are discussed in the sections below.

4.1.2.Pool cleaning equipment

4.1.2.1. The Parties' view

(24) The Parties are of the view that all pool cleaning equipment form one uniform relevant product market.

(25) According to the Parties, there is a continuum of functionally interchangeable products linked by a chain of substitutability; the prices of one product will overlap with one or more of the other products. For example, basic manual equipment overlaps with and directly constrains the pricing of manual vacuum cleaners, and manual vacuum cleaners will overlap with and directly constrain pricing of suction cleaners (or automatic vacuum cleaners), which in turn are a particularly close substitute to other automatic pool cleaners such as pressure cleaners, electric cleaners, and so forth.14

4.1.2.2. The Commission's assessment

(26) The Commission has not previously assessed the market for pool cleaning equipment.

(27) Previous national precedents, however, considered possible sub-segmentations. In particular, in case Zodiac/PSA15 (2004) the French competition authority considered that all manual cleaning devices have to be considered separately from automatic cleaning devices.

(28) Manual and automatic cleaners are two broad and distinct categories of pool cleaning equipment. Manual cleaners consist of entry level pool cleaning equipment, such as brushes, poles, leaf skimmers and manual suction cleaners. Manual cleaning equipment requires manual labour to clean the pool, while automatic (robotic, suction and pressure) cleaners clean the pool without human intervention. In the present case there is no need to look further at manual and automatic segmentation since overlaps resulting in affected markets arise only with respect to the automatic cleaner category.16

(29) As noted above, all automatic pool cleaning equipment can be further subdivided into robotic cleaners, automatic suction cleaners and pressure cleaners.17

4.1.3. Robotic cleaners

(30) Based on the results of the market investigation the Commission finds that there is a number of demand and supply side substitutability arguments that would justify defining a separate market for robotic cleaners from automatic suction cleaners.

(31) First, these products are inherently different and have different interaction systems with the pool which makes them unlikely substitutes. Automatic suction cleaners have to be connected to the pool's filtration system which requires additional work to install and an additional booster pump to operate.18 On the contrary, robotic cleaners are operated by a power cord and are considered in the industry as plug-and-play items that can be easily operated by the pool owner himself/herself. The market investigation confirmed this view, since the majority of customers, competitors and distributors indicated that main pool cleaning equipment products are in fact different.19

(32) Second, the majority of customers responding to the market investigation confirmed the suitability of the above segmentation. Customers also indicated that there is indeed very limited demand side substitutability, since those products are priced at different price points.20 Convenience of use, especially for larger pools, was cited amongst the factors that distinguish robotic cleaners from all other cleaning equipment.21

(33) Third, competitors confirmed that there is no supply side substitution between automatic suction cleaners and robotic cleaners: competitors manufacturing other cleaners cannot easily and readily switch their production to robotic cleaners.22 The main reason cited was the different technological skill set necessary to produce robotic cleaners.23 As evidenced by the parties' own patent portfolio relating to robotic cleaners, a very significant IP footprint is required in order to produce robotic cleaners.24 This also acts as a barrier to entry which will be further discussed in the competitive assessment. As a result, not all players that are active in automatic suction cleaners are also active in robotic cleaners. With the exception of the Parties, the opposite is also true. For example, while being a significant player in the market for robotic cleaners, Maytronics has no presence in that of automatic suction cleaners.

(34) Fourth, the Parties' internal documents consider those product categories differently. For example, Zodiac's […] management plan clearly differentiates between robotic, pressure and suction cleaners,25 while Fluidra's price determination documents that discuss robotic cleaners do not discuss other types of cleaners.26

4.1.3.1. Conclusion

(35) The Commission therefore considers that for the purposes of the present case, robotic cleaners constitute a separate relevant product market.

4.1.4. Automatic suction cleaners

(36) The Commission investigated whether the automatic suction cleaners (different from robotic cleaners) for which the Parties’ activities overlap, should be further sub-divided into (i) disc rotation automatic cleaning devices (disc rotation cleaners), and (ii) hydro drive train automatic cleaning devices (hydro drive cleaners). The market investigation indicated that there are a number of demand side substitutability arguments to consider all automatic suction cleaners falling under one single relevant product market definition. However, the relevant product market may be left open with respect to automatic suction cleaners since the Transaction will not raise serious doubts under any segmentation for the following reasons.

(37) First, competitors responding to the market investigation confirmed the validity of the segmentation,27 but analogous opinion was not prevalent among customers and distributors.28

(38) Second, there are certain differences between round disc and hydro drive cleaners. For example, disc rotation cleaners are considered to be an old and more entry level technology.29 Also, unlike robotic cleaners, both disc rotation and hydro drive cleaners are connected to the pool system but hydro drive cleaners are generally considered to be more efficient.30 However, the market investigation clearly indicated with respect to the intended use customers and distributors generally find disc rotation and hydro drive cleaners to be close substitutes.31

(39) Third, there is price differentiation among these products (disc rotation devices retail from EUR 60 to EUR 250 RRP, while hydro drive cleaners usually retail for about EUR 250 to EUR 600 RRP).32 Similar to robotic cleaners, price differentiation will be further considered as a closeness of competition argument in the competitive assessment.

4.1.4.1.Conclusion

(40) In the light of the results of the market investigation and taking the other evidence available to it into account, the Commission considers that, for the purposes of the present case, it is not necessary to conclude on the exact scope of the market for automatic suction cleaners, as the Transaction does not raise serious doubts under any plausible alternative market definition.

4.1.5. Water treatment products

4.1.5.1. The Parties' view

(41) The Parties are of the view that all water treatment equipment forms part of a single market. They submit that there is an indivisible continuum made up of a multitude of products from simple dispensers and testing strips at one end, to automatic regulators at the other. They contend that all products meet the same demand and face competition from each other, as well as from the option to manually dispense the chemicals in the pool water, which is the most common method of water treatment in the EEA.33

4.1.5.2. The Commission's assessment

(42) There is no Commission precedent defining the market for this segment. In the Zodiac/PSA (2004) case, the French authorities took the view that “water treatment products” may amount to a relevant market.34

(43) Water treatment equipment covers (i) liquid chemical sanitising and dosing equipment such as salt water chlorinators (SWCs), pH and ORP regulators and dosing pumps, (ii) solid chemical sanitising and dosing equipment such as floating dispensers and in-line feeders, (iii) alternative sanitisers using UV, ozone or minerals and (iv) testing and measuring equipment.

(44) SWCs are liquid chemical sanitising and dosing devices that produce chlorine by electrolysis: salt is added to the pool water and the electrolytic reaction in the SWC’s cell breaks down the salt molecules to generate chlorine. SWCs are an alternative to releasing chlorine directly in the pool water by using a dispenser, feeder, pH/ORP regulator or dosing pump. The main advantage of an SWC, compared to chlorine-releasing devices is that there is no need for the user to store and handle chlorine, which is a potentially hazardous chemical that must be handled with care.

(45) pH regulators are liquid chemical sanitising and dosing devices that are used to keep the pH of the pool water at an optimum level in order to improve the efficiency of the chlorine. These can be combined with SWCs as well as with ORP regulators and dosing pumps.

(46) ORP regulators are liquid chemical sanitising and dosing devices that are used to keep the chlorine content of the pool water at an optimum level. Some ORP regulators are add-on devices that activate the operation of SWCs or dosing pumps, while others are stand-alone devices with an integrated dosing pump.

(47) Dosing pumps are liquid chemical sanitising and dosing devices that are used for injecting chlorine or pH-regulating agents. Some dosing pumps have integrated pH/ORP controls, in which case they are a type of pH/ORP regulators.

(48) Floating dispensers and in-line feeders are solid chemical sanitising and dosing devices that operate through contact between the pool water and with the solid chemical located inside. The water causes the solid chemical to erode and dissolve into the flowing water.

(49) Alternative sanitisers are devices that use non-chemical technology such as UV, ozone or minerals to eliminate organic matter in the pool as a complement to chlorine releasing or producing devices such as pH/ORP regulators or SWCs. Fluidra's alternative sanitisers use UV technology: the pool water runs across a lamp that generates UV-C rays, which eliminate a wide range of organic matter. Zodiac's alternative sanitisers are copper- and silver-based systems that act as a chlorine complement by partially killing specific organic matter and algae.

(50) Testing and measuring equipment such as sensors, photometers, thermometers, comparison test kits, test kits boxes, reagents and testing strips are used to measure the water balance of the pool.

(51) Based on the responses of market participants and on the available evidence, the Commission finds that there are a number of demand and supply side substitutability arguments to support the definition of a relevant product market for all liquid chemical sanitising and dosing devices. This market would comprise salt water chlorinators, pH/ORP regulators and dosing pumps. Based on the results of the market investigation, solid chemical sanitising and dosing devices, alternative sanitisers, and testing and measuring equipment would not be part of such a market.

(52) First, in terms of demand-side substitutability, liquid chemical sanitising and dosing devices perform the same function of automatically producing or releasing liquid chlorine (sodium hypochloride) to the pool water, allowing accurate gauging and control of chlorine levels. pH/ORP regulators and dosing pumps inject liquid chlorine and corrector fluid into the main pool plumbing, disseminating them through the pool. Mineral or salt water chlorinators turn salt or minerals added to the pool water into liquid chlorine, which is then released into the pool water.

(53) Based on the feedback from the market investigation and on information provided by the Parties, the Commission finds that a narrower definition of the market for sanitising equipment is not warranted. A majority of respondents indicated that there is substitutability among all liquid chemical sanitising and dosing devices, i.e. salt or mineral water chlorinators, pH/ORP regulators and dosing pumps.

(54) Despite their differences, those products are considered to provide water sanitation solutions under similar commercial conditions. A Greek distributor commented: "liquid chlorine is substitutable perfectly with salt water electrolysis, hydrolysis or magnesium".35 A Bulgarian distributor stated: "in terms of water sanitizing, salt chlorinators can be substituted with dosing pumps"36 and "pH and ORP controllers can be replaced by dosing pumps"37. A Spanish distributor said that pH and ORP regulators "can be replaced by saline chlorinators".38

(55) In addition, some of the specific advantages associated with SWCs can be replicated by other liquid chemical sanitising systems. A French distributor explained that the milder type of chlorine produced by SWCs is now also available for use with dosing pumps: "Les appareils d'électrolyse de l'eau salée fabriquent, entre autres, de l'hypochlorite de sodium. Cet hypochlorite de sodium existe à l'état liquide à la vente et peut être injecté par des pompes doseuses".39

(56) As regards specific mineral-based chlorinators such as MagnaPool, which is sold by Zodiac, the market investigation indicated that these are very similar to salt-based chlorinators and should be part of the same market. A French competitor explained: "A "mineral water" chlorinator is in fact a "low salt" chlorinator in which an electrolysis cell is dimensioned to produce chlorine with a low concentration (<1g/l or 1000 ppm) of salt (Sodium chloride or Magnesium chloride)."40

(57) Second, as regards the exclusion of solid chemical sanitising and dosing devices from the relevant market for sanitising and dosing equipment, the Commission finds that salt water chlorinators, pH/ORP controllers and dosing pumps are typically more expensive, with average prices above EUR 500, in contrast to average prices well below EUR 500 for solid chemical sanitising and dosing devices such as floating dispensers and in-line feeders.

(58) In addition, solid chemical sanitising and dosing devices use solid chlorine (calcium hypochloride) in granules or tablets that are dissolved or eroded through contact with the pool water, which does not allow control of chlorine levels with the same accuracy as with liquid chemical sanitising and dosing devices.

(59) In this respect, for instance a French water treatment competitor stated that "manual sanitisers are not comparable with automated systems as they have a much lower price, offer much less control over the chlorine content of the water and constantly require the manual addition of chlorine to the dispenser."41

(60) Furthermore, liquid chemical sanitising and dosing systems are devices that are electrically powered and electronically controlled, and are as such technologically very different from solid chemical sanitising and dosing devices, which are simple holding receptacles for chlorine tablets or granules, made by injection moulding.

(61) Third, as regards the exclusion of alternative sanitisers using ozone, UV or minerals from the relevant market for sanitising and dosing equipment, the Commission finds that alternative sanitation systems do not offer valid alternatives to chemical sanitising and dosing systems.

(62) Several respondents to the market investigation and market participants in interviews commented that alternative sanitisers cannot substitute chlorine- based systems as none of them can be used independently. A Greek distributor explained that "no other sanitiser can be considered as an alternative to (electrolysis / hydrolysis / low salt /magnesium) systems 100% because all others either have restrictions in terms of effectiveness or cannot stand alone. They are assistive treatment."42 A competitor explained that alternative sanitisers can merely reduce the overall need for chlorine to some extent but cannot replace the use of chlorine altogether.43 Another competitor commented that as such, sanitisers have no residual effect on the pool water; the pool pump has to operate constantly to ensure sanitation, which is not the case for chemical sanitising and dosing systems. He added that mineral-based sanitisers that use copper and silver have another drawback, in that they release harmful heavy metals in the pool water, and have been known to discolour the hair of pool users.44

(63) As for supply side considerations, mineral/salt water chlorinators, pH/ORP controllers and dosing pumps are devices that either produce or dose the release of liquid chlorine, and are as such technologically very different from alternative sanitisers, which all use non-chlorine-based technologies such as osmosis, mineral ionisation and UV radiation.

(64) The market investigation confirmed that mineral-based sanitisers, which are produced by Zodiac (the Nature2 range), compete with UV-based sanitisers, which are produced by Fluidra.

(65) Fourth, as regards the exclusion of testing equipment from the relevant market for sanitising and dosing equipment, the Commission finds that such products are not used for the same purpose as sanitising and dosing equipment. The market investigation did not show an overall majority among respondents to include testing and measuring devices in the same market. Respondents commented that testing and measuring devices serve a different purpose from sanitising and dosing equipment. A French competitor commented: "Testers are not making any regulation and are not substitutable with any water treatment device."45 Another French competitor explained: "Ils permettent de tester mais pas de corriger".46

4.1.5.3. Conclusion

(66) In light of the above, the Commission therefore considers that for the purposes of the present case, all liquid chemical sanitising and dosing equipment belongs to the same relevant product market, comprising salt water chlorinators, pH/ORP controllers and dosing pumps.

(67) The Commission also considers that there are indications that solid chemical sanitising and dosing equipment, alternative sanitisers and testing and measuring equipment may belong to separate product markets. However, the question may ultimately be left open as the Transaction does not raise serious doubts, irrespective of the specific market definition.

4.1.6. Pool heating equipment

4.1.6.1. The Parties' view

(68) The Parties submit that the relevant product market should include all types of pool heating equipment, as end users weigh the pros and cons (upfront cost, energy consumption, environmental impact, maintenance needs, etc.) of alternative heating options.

4.1.6.2. The Commission's assessment

(69) In a previous case, the Commission observed that pool heating equipment included heat pumps as well as other systems, such as gas and oil-fired burners, solar heaters, electric heaters and heat exchangers.47 The Commission also noted that in the examined Member States (France, Spain and Portugal), heat pumps were the most commonly used method to heat pool water, and represented a high proportion (up to 90%) of the total value of the sales of all pool heating equipment. Ultimately, the Commission left the market definition open and assessed the Transaction on heat pumps alone, as the only product where the Parties’ activities overlapped.

(70) The market investigation in this case provided a number of indications pointing towards heat pumps belonging to a separate product market from other heating equipment.

(71) First, heat pumps present a number of differences affecting how they fulfil their purpose, which may result in different conditions of competition. In particular, distributors of pool equipment observed that, although performing the same function of other pool heating equipment, heat pumps “used less energy than the others and are totally more ecological friendly” and “more effective”.48 Similar views were expressed by competitors and other customers of pool equipment. In this regard, one competitor observed that “heat pumps are more efficient in relation to electricity consumption”;49 and another noted “aunque si que pudieran substituirse como se indica, la bomba de calor reune unas condiciones que las hacen únicas a la hora de calentar el agua de la piscina. Esto dificulta utilizar otros sistemas. Hablo de piscinas residenciales.”50 Finally, one large customer stated “heat pumps are not substitutable with other heating solutions in terms of intended use, price and running costs”51, and another remarked “I don't know any alternative products to heating pumps with the same efficiency, price and running costs.”52

(72) Second, when asked about how their customers may react to a 5-10% price increase of heat pumps, the majority of the competitors who expressed an opinion answered that they believed that their customers would not switch.53 Similar views were provided by general customers, and to a lesser extent by distributors. The competitors answering the Commission’s questionnaire further explained that “in relation to the prices, even if they will increase by 5-10%, efficiency still remains very high”54 and that “heat pumps are very convenient products”.55 One general customer observed that “il n'y a pas de solution alternative au chauffage par pompe à chaleur en termes de performance/ coût de fonctionnement”56 and another that “in case of a higher rate level, heat pumps would be still the most efficient heating method”.57

4.1.6.3.Conclusion

(73) In the light of the results of the market investigation and taking the other evidence available to it, the Commission considers, for the purposes of the present Decision, that the heat pumps for swimming pools form part of a relevant product market separate from other heating equipment.

4.1.7. Pool dehumidifiers

(74) The Parties submit that all dehumidifiers for residential indoor pools form part of a single product market.

(75) They note that the basic functionality and technology used is identical for all pool dehumidifiers, and all leading suppliers of dehumidifiers offer a complete range of consolidated and integrated equipment.

(76) Supply-side substitutability between dehumidifiers of different capacities (measured in litres per hour) is facilitated by the fact that the Parties source key components (such as compressors, fans, evaporators and condensers) from third parties. It is these third-party components that determine the capacity of the dehumidifier. The components are assembled and fitted in the housing and wired up at the Parties’ assembly lines. Such assembly lines are highly flexible and it is easy for a manufacturer to use the same assembly line to manufacture dehumidifiers with different capacities.

(77) The Parties also submit that the market may be even broader than pool dehumidification equipment. Most leading suppliers of pool dehumidifiers in the EEA (such as TEDDINGTON, CLIMEXEL (PROCOPI), FAIRLAND, REXAIR, DANTHERM (CALOREX), MENERGA, and KVS) exploit economies of scale by manufacturing both pool and non-pool dehumidifiers.58 According to the Parties, from a supply-side standpoint, there is no major difference between non-pool and pool applications.

(78) The Commission considers that, for the purpose of present Decision, the exact scope of the product market can be left open, since the Transaction does not give rise to serious doubts about its compatibility with the internal market, even under the hypothetical narrowest market segmentation (residential pool dehumidifiers).

4.1.8. Swimming pool pumps

4.1.8.1. The Parties' view

(79) The Parties claim that all pumps belong to a single relevant product market because of supply side substitution arguments. The Parties' own internal documents59 provide indications that all pumps can be further sub-segmented into single, variable and booster pumps.60

4.1.8.2. The Commission's assessment

(80) The Commission has not previously defined the market for swimming pool pumps.

(81) As noted above, all swimming pool pumps can be sub-segmented into single and variable speed pumps. Single speed pumps operate on a single speed, while variable speed pumps typically have at least two speeds. A variable speed pump is more silent and energy efficient since it operates at lower speed, especially when the pool is not actively used, which is mostly during the night time. Variable speed pumps are also significantly more expensive. The Parties submit that at the moment, the majority of pumps sold in the EEA are single speed pumps.

(82) As illustrated by Figure 2 below, each pump consists of (i) an electric motor, and (ii) a so-called "wet-end" which is a plastic or metal vessel where the water flows in and out of the pump. The market investigation has revealed that the major price difference (variable speed pumps are up to two times more expensive) is due to a more expensive electric motor.61 The Parties submit that electric motors are supplied by third party manufacturers and not manufactured by the Parties themselves.

(83) The Parties claim that the wet-end of both single and variable speed pumps are identical, and that any suppliers which are active in single speed pumps can easily switch to the production of variable speed pumps by simply mounting a different motor.62 However, the market investigation only partly confirmed this view. In particular, major market players indicated that whilst it is technically possible to switch motors, this is almost never done in such a straightforward manner. The key purchasing criteria for variable speed pumps is noise level rather than electricity savings. In particular, variable speed pumps typically have a bigger wet-end since this reduces noise levels. In addition, variable speed pumps can also be beneficial for the filtration system, as lower speed flowing water allows for better filtration. Finally, other parts of the pump, such as the drive shaft (a rod connecting the motor with the pump impeller) are typically different for different types of pumps.63 Therefore, the evidence available tends to suggest a limited demand and supply substitutability between single and variable speed pumps.

4.1.8.3. Conclusion

(84) The Commission considers that, for the purpose of the present Decision, the exact scope of the product market may be left open, since the Transaction does not give rise to serious doubts about its compatibility with the internal market under any plausible relevant market definition.

4.1.9.Swimming pool filters

4.1.9.1. The Parties' view

(85) The Parties claim that all filters belong to a single relevant product market.

4.1.9.2.The Commission's assessment

(86) Generally all filters can be broadly sub-divided by the filtration media they use: sand filters, cartridge filters or diatomaceous earth (DE) filters.64 Cartridge filters are generally more expensive if compared to sand media filters because of the more expensive production process. From a customer perspective, there is also limited demand side substitutability since cartridge filters do not require so- called "backwashing" (or rinsing) of a filter, which saves water. The Parties' overlap with respect to cartridge filters is de minimis.65 Therefore, this overlap is not further analysed.

(87) The Parties' activities principally overlap only with respect to sand media filters, which is the most common type of filter used in the EEA.66 Sand filters in turn can be further sub-segmented into injected, blow-moulded, laminated polyester and bobbin-wound. On the basis of information provided by the Parties67 it is apparent that all those types of filters use different production technologies. The market investigation provided some indications that those different production technologies also allow different positioning of filters. Namely, polyester laminated filters are considered to be in a high range segment, while blow- molded represents low-end segment.68 This differentiation is also supported by the Parties' internal documents.69

4.1.9.3.Conclusion

(88) The Commission considers that, for the purpose of present decision, the exact scope of the product market can be left open since the Transaction does not give rise to serious doubts about its compatibility with the internal market, under any plausible relevant market definition.

4.1.10.Wholesale distribution

(89) As noted above, Fluidra is also active in the wholesale distribution of pool equipment products in certain EEA countries.70

(90) The Parties submit that Fluidra operates at the wholesale distribution level as a pure distributor, i.e. purchasing and reselling under the third party's brand.

(91) The vertical relationship arising from this Transaction is further assessed in Section 5.3 of this decision.

4.2. Relevant Geographic Markets

4.2.1. The Parties' view

(92) The Parties submit that the geographic scope of the pool equipment market is EEA wide. This is because of the substitutability of demand and strong substitutability of supply for those products across the EEA area at the level of trade at which they operate. This substitutability would be driven by the lack of trade or regulatory barriers between Member States, the relative ease of access to local distributors (wholesalers and retailers), and the homogeneity of the demand for products like pumps, filters, cleaners, heaters and water treatment from all pool owners EEA-wide and the presence of significant brands across multiple Member States.

4.2.2. The Commission's assessment

(93) In one precedent concerning heating equipment, the Commission investigation71 pointed at national features of the markets for pool equipment, in particular in view of the presence of different market players, significant price differences and differences in consumption habits.

(94) At the national level, in the Zodiac European Pools/Piscine Services Anjou case, the French Competition Authority considered that the markets of SWC and heat pumps could be national in scope, although the main market players were usually active on a European or worldwide scale.

(95) The investigation in the present case provided indications that the markets might be broader than national, in line with the Parties’ arguments, for example because of the diminution in price differences across countries. For instance, when asked about price differences for pool equipment across European countries, the majority of distributors replied that, on the basis of their knowledge, these prices were similar across countries.72 Similar views were expressed by the general customers and competitors for pool equipment.73 Moreover, as regards sourcing from manufacturers, the majority of the distributors indicated that their most common sourcing pattern of pool equipment was European, i.e. that they buy most of what they need anywhere in Europe.74

(96) However, on balance, there are still elements suggesting a national dimension, which include the existence of different customer preferences and requirements, different distribution channels as well as regulatory and voluntary standards which vary among countries.

(97) First, while distributors purchase on a European level, when it comes to general customers, a sizeable number of customers responding to the market investigation also stated that they buy what they need within their country.75

(98) Second, the strong national differentiation has been confirmed by manufacturers as well. A large majority of pool equipment competitors stated that customer requirements and preferences differ within the EEA and that they do not access the market through the same distribution channels within the EEA.76

(99) Third, market feedback collected during the market investigation indicated the existence of different national preferences and standards for some categories of pool equipment, especially water treatment products. A market participant, for instance, commented that in France there are regulatory and voluntary industry standards which apply to pool equipment products.77 A water treatment competitor said that there is little value in having one standardised product for the entire European market because of the need to comply with different national technical standards and types of usage.78

4.2.3.Conclusion

(100) In the light of the market investigation and taking the other evidence available to it into account, the Commission considers that, for the purposes of the present case, the specific geographic market definition can be left open, as it would have no impact on the competitive assessment.

(101) As regards those markets with respect to which the Transaction does not raise serious doubts, these would not arise even on the basis of an assessment with a narrower national level.

(102) With respect to robotic cleaners, the Transaction does raise serious doubts regarding its compatibility with the internal market, irrespective of whether the market is defined at the EEA or national level.

5. COMPETITIVE ASSESSMENT

5.1. Analytical framework

(103) Under Article 2(2) and 2(3) of the Merger Regulation, the Commission must assess whether a proposed concentration would significantly impede effective competition in the internal market or in a substantial part of it, in particular through the creation or strengthening of a dominant position.

(104) In this respect, a merger may entail horizontal and/or non-horizontal effects. Horizontal effects are those deriving from a concentration where the undertakings concerned are actual or potential competitors of each other in one or more of the relevant markets concerned. Non-horizontal effects are those deriving from a concentration where the undertakings concerned are active in different relevant markets.

(105) As regards non-horizontal mergers, two broad types of such mergers may be distinguished: vertical mergers and conglomerate mergers.79 Vertical mergers involve companies operating at different levels of the supply chain.80 Conglomerate mergers are mergers between firms that are in a relationship which is neither horizontal (as competitors in the same relevant market) nor vertical (as suppliers or customers).81

(106) The Commission appraises horizontal effects in accordance with the guidance set out in the relevant notice, that is to say the Horizontal Merger Guidelines.82 Additionally, the Commission appraises non-horizontal effects in accordance with the guidance set out in the relevant notice, that is to say the Non-Horizontal Merger Guidelines.

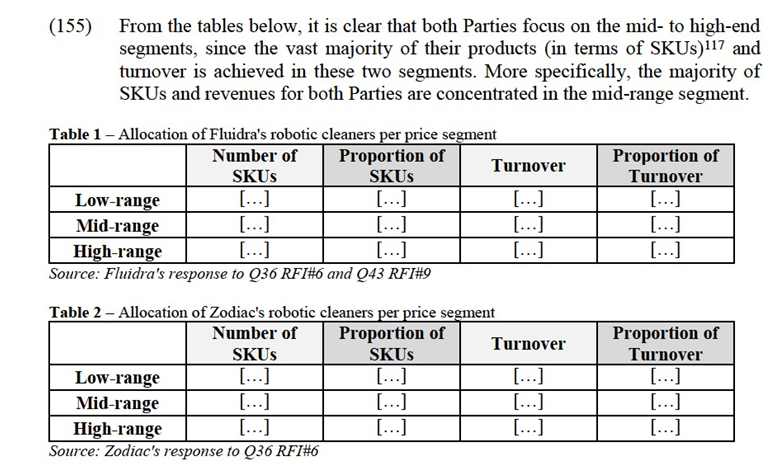

(107) In the present case, the Transaction gives rise to horizontally affected markets in the manufacture and supply of (i) robotic cleaners in the EEA, Sweden, Greece, Spain, Czech Republic, Belgium, Cyprus, Germany, Romania, the Netherlands, Austria, France, Italy, Hungary, Bulgaria, Portugal and Luxembourg,(ii) automatic suction cleaners in the EEA, Portugal, Spain, Belgium, France, Greece, Germany, (iii) sanitising and dosing equipment in the EEA, Spain, France, Portugal, Greece, Italy, Austria, Croatia, Cyprus, Hungary, Poland and the UK, (iv) pool heating equipment, in particular – heat pumps in Spain, Italy, France, Austria, Belgium, Greece and Portugal, (v) pumps in Cyprus, Greece, Spain and the UK, and (vi) laminated polyester filters in Austria, France, Italy, Spain, and the UK.

5.2.Horizontal unilateral effects

5.2.1.Introduction

(108) The Horizontal Merger Guidelines distinguish between two main ways in which mergers between actual or potential competitors on the same relevant market may significantly impede effective competition, namely non-coordinated and coordinated effects.83

(109) Under the substantive test set out in Article 2(2) and 2(3) of the Merger Regulation, mergers that do not lead to the creation or the strengthening of the dominant position of a single firm may also be incompatible with the internal market. Indeed, the Merger Regulation recognises that in oligopolistic markets, it is all the more necessary to maintain effective competition. This is in view of the more significant consequences that mergers may have on such markets. For this reason, the Merger Regulation provides that "under certain circumstances, concentrations involving the elimination of important competitive constraints that the merging parties had exerted upon each other, as well as a reduction of competitive pressure on the remaining competitors, may, even in the absence of a likelihood of coordination between the members of the oligopoly, result in a significant impediment to effective competition".84

(110) The Horizontal Merger Guidelines list a number of factors which may influence whether or not significant horizontal non-coordinated effects are likely to result from a merger, such as the large market shares of the merging firms, the fact that the merging firms are close competitors, the limited possibilities for customers to switch suppliers, or the fact that the merger would eliminate an important competitive force. That list of factors applies equally regardless of whether a merger would create or strengthen a dominant position, or would otherwise significantly impede effective competition due to non-coordinated effects. Furthermore, not all of these factors need to be present to make significant non-coordinated effects likely and it is not an exhaustive list.85

(111) Finally, the Horizontal Merger Guidelines describe a number of factors which could counteract the harmful effects of the merger on competition, including the likelihood of buyer power, entry and efficiencies.

5.2.2.Brief description of pool equipment markets and players

(112) Fluidra is a market leader in pool equipment in Europe. Fluidra is a fully vertically integrated player acting at all levels of trade, namely – manufacturing, distribution and even retail.

(113) There are four global major manufacturers of swimming pool equipment: Fluidra, Hayward, Pentair and Zodiac, known as the "Big Four" competitors in the industry. Those firms are also sometimes referred to as "full line" suppliers since they manufacture and market the entire range of swimming pool equipment that is needed for the installation of a swimming pool. Beside those players, there are a number of smaller competitors referred to as "niche OEMs". Such competitors, such as Maytronics (Israel), do not manufacture the whole range of products but specialize in a particular (usually a high margin) segment such as robotic cleaners.

(114) Finally, there is a high number of small manufacturers both in Europe and in Asia that usually compete on specific products, such as heat pumps. However, they do not as a rule have sufficient brand reputation or portfolio breadth that would allow them to compete efficiently with the "Big Four" or niche OEM manufacturers.

(115) With the exception of Fluidra, all manufacturers of swimming pool equipment rely on distributors to reach their end customers. More specifically, within a certain product category (for example, robotic cleaners) each distributor will typically tend to distribute the products of one specific manufacturer only. The pool owners typically do not make purchasing decisions for swimming pool equipment. They will normally rely on the advice given by a pool builder (also known as a "prescriber") or a retailer, who is in fact considered the end customers in this industry.

(116) The largest pool equipment market in Europe is France, followed by Spain, Italy and Germany. According to the Parties, those markets constitute around 65% of total swimming pool equipment sales within the EEA.

5.2.3. Robotic Cleaners

5.2.3.1. Introduction

(117) The Transaction gives rise to affected markets in robotic cleaners at the EEA level. It also results in 16 affected markets at national level: Sweden, Greece, Spain, Czech Republic, Belgium, Cyprus, Germany, Romania, the Netherlands, Austria, France, Italy, Hungary, Bulgaria, Portugal and Luxembourg.

5.2.3.2. The Parties' view

(118) The Parties submit that the Transaction will not give rise to competition concerns in the EEA-wide market or any national markets for robotic cleaners, because (i) there are a number of credible competitors left on the market post- merger, (ii) the Parties are not close competitors, (iii) robotic cleaners are constrained by other cleaning equipment, (iv) Internet sales channels will strengthen price competition, (v) powerful distributors face no lock-in effects.

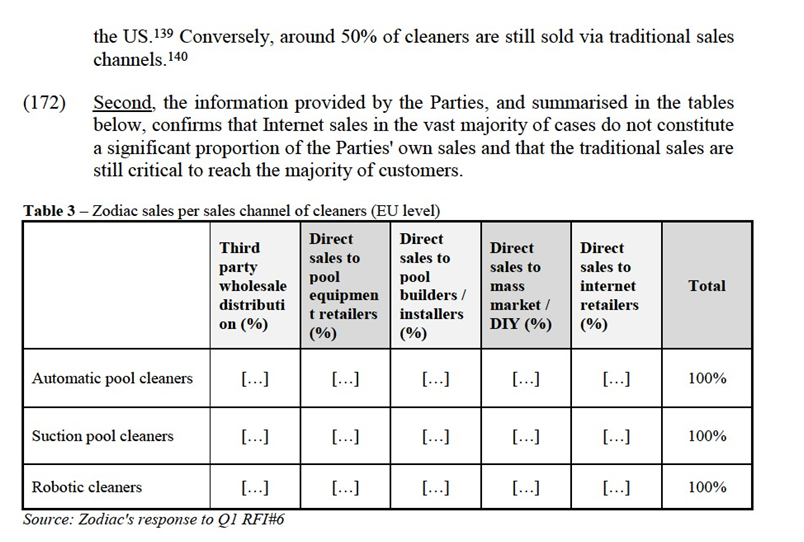

(119) In addition to the arguments raised in the Form CO, the Parties also submitted a report by economic consultants assessing the competitive effect of the Transaction with respect to robotic cleaners ("RBB Report")86 on 13 June 2018. The RBB Report principally claims that the Commission's preliminary concerns are unwarranted because (i) customers will continue to enjoy a large choice of robotic cleaners provided by the Parties' competitors, (ii) Maytronics and Hayward will not have any incentive to follow any price increases, (iii) in case of any hypothetical price increase, customers will revert to automatic suction cleaners, (iv) Hayward and Pentair (a recent entrant) will constrain the Parties,(v) any price increases are likely to incentivize a new entry. Those arguments will be addressed under the relevant sections below.

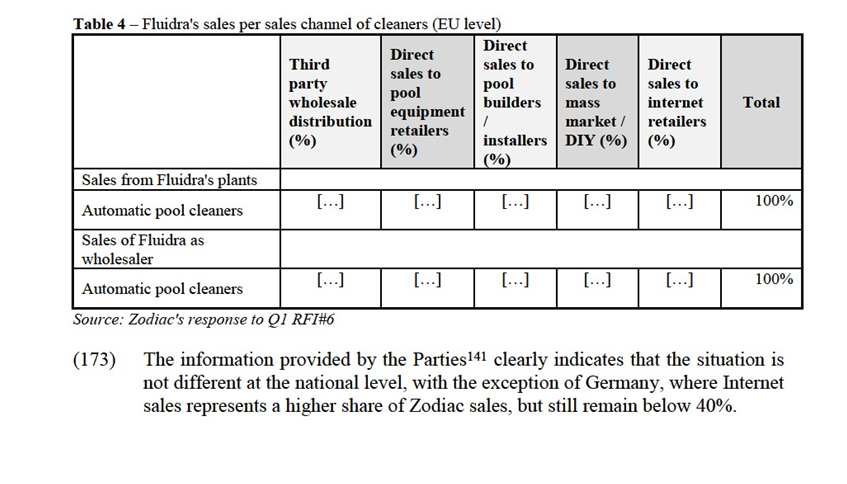

5.2.3.3. The Commission's assessment

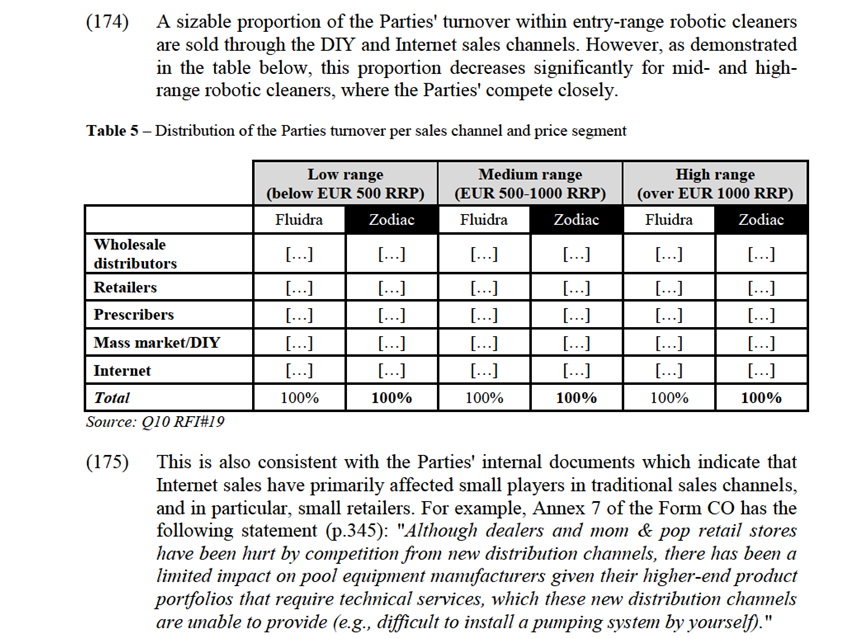

(120) For the reasons set out below, the Transaction raises serious doubts as to its compatibility with the internal market with respect to robotic cleaners, both at the EEA and national levels. Based on the results of its market investigation and on the evidence available to it, the Commission finds that (i) there are few effective competitors in robotic cleaners, (ii) other players have a very limited role in the market for robotic cleaners, (iii) private label players would not be sufficient to constrain the Parties post-Transaction, (iv) the Parties compete closely, (v) the Parties will not be constrained post-merger by other types of automatic cleaners, (vi) distributors do not enjoy countervailing buyer power, (vii) Internet sales are not a sufficient price constraining factor, (viii) significant barriers to entry exist with respect to robotic cleaners, (ix) there will be few alternatives left on the robotic cleaners market.

5.2.3.4. Market structure and market shares

(121) The Parties achieve a significant combined market share in robotic cleaners at both the EEA ([30-40]%) and national levels.

(122) According to the Parties' estimates, the Transaction gives rise to 16 affected markets for robotic cleaners in the EEA (by value), with the highest combined shares in Sweden ([60-70]%), Greece ([60-70]%), Spain ([50-60]%), Czech Republic ([40-50]%), Belgium ([40-50]%), Cyprus ([40-50]%), Germany ([40-50]%), Romania ([40-50]%), the Netherlands ([40-50]%) Austria ([30-40]%), Italy ([30-40]%), France ([30-40]%), Hungary ([30-40]%), Bulgaria ([30-40]%), Portugal ([20-30]%), and Luxembourg ([20-30]%).

(123) The market reconstruction completed in this case largely confirmed the Parties' view. At the EEA level, the market reconstruction demonstrated that Maytronics will maintain its market leader position. Currently, Zodiac is the second largest and Fluidra is the third largest player at the EEA level. The Transaction would therefore create two very similarly sized companies, each holding close to [40-50]% market share with Hayward being a much smaller player [0-10%]. The market structure would be similar also when considering affected markets at the national level.

(124) The description of the competitive dynamics in the EEA as described below largely applies to all Member States where affected markets have been identified, including the importance of other players, closeness of competition and barriers to entry. Below some details are provided with respect to the national situation in the four largest pool equipment markets in the EEA.

Impact in France

(125) In France, the Parties' combined market share is [30-40]% in the market for robotic cleaners (2016 by value) with an increment brought by Fluidra of [10-20]%. The only two other significant players are Maytronics ([40-50]%) and Hayward ([10-20]%). The market reconstruction has largely confirmed the Parties' estimates.

Impact in Spain

(126) In Spain, the Parties' combined market share is [50-60]% in the market for robotic cleaners (2016 by value) with an increment brought by Zodiac of [20-30]%. The only two other significant players are Maytronics ([20-30]%) and Hayward ([10-20]%). The market reconstruction has largely confirmed the Parties' estimates.

Impact in Italy

(127) In Italy, the Parties' combined market share is [30-40]% in the market for robotic cleaners (2016 by value) with an increment brought by Zodiac of [10-20]%. The only two other significant players are Maytronics ([40-50]%) and Hayward ([5-10]%). The market reconstruction has largely confirmed the Parties' estimates.

Impact in Germany

(128) In Germany, the Parties' combined market share is [40-50]% in the market for robotic cleaners (2016 by value) with an increment brought by Fluidra of [5-10]%. The only two other significant players are Maytronics ([40-50]%) and other players ([5-10]%). The market reconstruction has largely confirmed the Parties' estimates.

5.2.3.5. There are only few effective competitors in robotic cleaners

(129) While the Parties claim that there are a number of competitors manufacturing robotic cleaners, the results of the market investigation confirmed that only the Parties, Maytronics and, to a lesser extent, Hayward, can be considered as constraining each other on this market.

(130) The market investigation indicated that the most important drivers when deciding which robotic/automatic suction cleaners to purchase are quality, aftersales, price, and brand for customers, price, quality, warranty and brand according to distributors and quality, price, brand and after-service according to competitors.87

(131) This is also consistent with the Parties' internal documents. Internally, the Parties consider that product quality and availability are the two main commercial decision drivers. Brand is indicated to be associated with reliability and quality from the customers' perspective.88 Market participants also confirmed that any price increase plays a less important role when dealing with more expensive items, such as robotic cleaners or automatic suction cleaners. Distributors and retailers tend to rather sell a more expensive (and more reliable) item than to address any warranty claims or deal with repairs which may reduce the margin they earn.89

(132) Apart from the Parties, the only two other players that can meet those key criteria are Maytronics and Hayward.

(133) Maytronics is the current leader on this market in the EU and will largely retain this position post-merger. While Maytronics is a niche OEM player, it was one of the first companies to introduce robotic cleaners. It is active in all major pool equipment markets in the EU, often holding a major market share.

(134) Next to the Parties and Maytronics, the only other notable player is Hayward. However, as evidenced by market shares and confirmed by the market reconstruction, it is a distant fourth player in this market with its market share in all Member States well below 20%.

(135) The Parties indicated in the Form CO, as well as in other submissions,90 that Pentair has announced the launch of one robotic cleaner in late 2017. From publicly available sources provided by the Parties themselves, it is clear that this product targets the entry-level segment.91 From the Parties' internal documents it is also clear that any of Pentair's products within cleaners are priced at the entry- level.92 Therefore, at this stage, Pentair does not enjoy a strong market presence and portfolio breadth enabling it to act as a significant constraint on the Parties.

5.2.3.6. Other players have a very limited role in the market for robotic cleaners

(136) The Parties claim that other players in robotic cleaners such as smaller European providers (for example, Kwadoo, Ubbink, or Mopper) and Asian players (for example, Kokido) constrain the Parties.

(137) The market investigation does not support the Parties' view that they are constrained by those players.

(138) First, only a very limited number of customers and distributors consider that any of those competitors meet the criteria of quality, aftersales, price, and brand.93

(139) Second, these companies are not viewed by customers or competitors (and only by one distributor) as significant players in the robotic cleaners market.94 In particular, such players are not viewed by customers,95 distributors96 and competitors97 as credible alternatives to the Parties.

(140) Third, even when these players are mentioned, they are said to be active at the lower end of the market.98

(141) Fourth, the fact that such players do not act as a significant constraint is in line with the Parties’ own assessment in their internal documents. More generally, Zodiac's internal documents note that country of origin is directly associated with quality of pool equipment products.99 For example:a. [Excerpt from Rhône’s internal document]100 [excerpt from Rhône’s internal document].101 b. [Excerpt from Rhône’s internal document].102

5.2.3.7. Private label players would not be sufficient to constrain the Parties post-Transaction

(142) The Parties are also engaged in certain private label arrangements with a number of large distributors (for example, [distributor name] European subsidiary) and major DIY European retail chains (such as [distributor names]). Usually the Parties will colour adapt their own products which are exact copies of OEM products sold via traditional sales channels (retailers, distributors and prescribers). According to the Parties' internal documents, Maytronics has similar arrangements (Section 5.2.3.8 below).

(143) The majority of customers, distributors and competitors consider that private label products do not offer a credible alternative to the Parties' products.103

(144) The market investigation provided indications that private label arrangements serve to catch further demand by major manufacturers and as such are indicative of the market strength of such players.104

(145) This is to some degree confirmed by the Parties' internal documents. From the evidence available on file it is clear that at least Zodiac actively manages the sales through such channels. For example, Zodiac's internal document "Product market share analysis" indicates that there is "[excerpt from Zodiac’s internal document]."105

5.2.3.8. The Parties compete closely

(146) The Parties claim that they are not each other's closest competitors because Zodiac offers products in the high-mid range, while Fluidra offers low-mid range robotic cleaners.106 However, this statement is not supported by the evidence collected by the Commission, namely through the Parties' internal documents, the information provided by the Parties in the course of the investigation and the results of the market investigation.

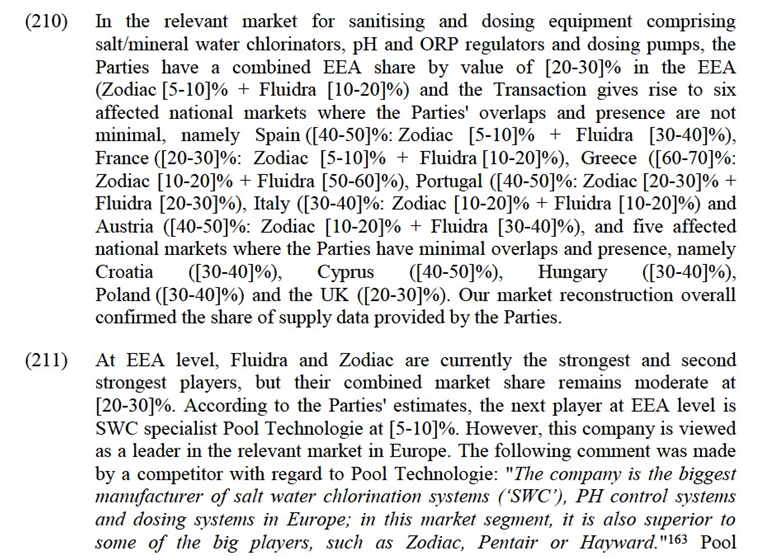

Differentiation by channel and price point

(147) First, the Parties' internal documents107 and the market investigation108 clearly further differentiate robotic cleaners on the basis of their price points. An interview with a competitor indicated that "the key is to position every product at the right price point and to have a sufficiently wide range of products, in order to satisfy every demand".109 The importance of a wide product range is also supported by the Parties' internal documents. For example, the "Product market share analysis" document provided by Zodiac indicates: "[excerpt from Zodiac’s internal document]".110

(148) This is further evidenced by numerous private label arrangements discussed below.111

(149) The main players in this industry differentiate their robotic cleaners in two ways. The first type of differentiation comes from sales channel which usually constitutes different colour adaptations of an identical OEM product.

(150) The RBB Report (Section 2) claims that "Zodiac supplies electric cleaners only under its own brand" and, unlike Fluidra, does not produce under private label arrangements. This claim is neither supported by the information provided in the course of this investigation nor by Zodiac's internal documents. In the course of the investigation, Zodiac explained that it adapts its products in the following ways:112a. [Zodiac’s sales strategy by product].b. [Zodiac’s sales strategy by product].c. [Zodiac’s sales strategy by product].

(151) In the EEA, Fluidra is also active in private label manufacturing and derives a sizable income from such activity.113 This is also supported by arguments developed in the RBB Report (Section 2.1.2).

(156) The market investigation clearly confirmed this view, with several customers and competitors indicating Zodiac as active primarily in mid- to high-range robotic cleaners.118 The same was confirmed for Fluidra.119

(157) Besides the positioning of their products, the market investigation confirmed that the Parties do compete closely. When asked to indicate Zodiac's main competitors, customers, distributors and competitors indicated that Maytronics is Zodiac's closest competitor, immediately followed by Fluidra.120 In most responses Hayward appeared as a third alternative. When asked to indicate Fluidra's competitors, customers, distributors and competitors responded that these included Zodiac and Maytronics. Again, Hayward was mostly indicated to fall behind the Parties and Maytronics.121

(158) This closeness of competition is further demonstrated by the fact that certain large customers delisted the Parties' products because the "price-quality ratio of the cleaning robots of Fluidra and Zodiac are similar. Fluidra's robots do not give an added value".122

(159) Finally, the closeness of competition between the Parties in robotic cleaners is also validated by internal documents. Fluidra's internal documents on pricing determination clearly indicate that first, Fluidra tracks prices only of its main competitors (Zodiac, Maytronics and Hayward),123 and, second, it also shows that in some countries Fluidra's and Zodiac's prices for certain products are very closely aligned:124a. Document "[Fluidra’s internal document]" (p.2), […].b. Document "[Fluidra’s internal document]" (p.3), […].c. Document "[Fluidra’s internal document]" (p.12), […].d. Document "[Fluidra’s internal document]" (p. 7), […].e. Document "[Fluidra’s internal document]" (p.4) […].

(160) In its internal documents, Zodiac also views Fluidra as one of its main competitors.125

5.2.3.9. The Parties will not be constrained post-merger by other types of automatic cleaners

(161) The RBB Report states that consumer demand for robotic cleaners is likely to be elastic, and that customers who choose to buy robotic cleaners also may consider buying other automatic cleaning equipment such as automatic suction cleaners or pressure cleaners.

(162) In this respect, it should be noted that Zodiac has a very significant presence in the remaining two categories of automatic cleaners: suction cleaners and pressure cleaners. According to the Parties' own estimates, Zodiac has an estimated market share of 40-60% in high-end hydro-drive suction cleaners mostly due to its MX product range.126 Hydro drive cleaners due to their positioning can be considered as competing most closely with lower-end robotic cleaners. Zodiac's internal documents also indicate that it holds around [80-90]% market share at the EU level in the pressure cleaner category (which is a non-overlapping product category).127 These are the only product segments that can be considered as potentially competing with lower-end robotic cleaners. Because of Zodiac's high market shares in both pressure and hydro-drive cleaners, the Parties will not be constrained to a sufficient degree by those most closely competing product categories post-merger.

5.2.3.10. Distributors do not enjoy sufficient countervailing buyer power

(163) The Parties argue that, within cleaners, large distributors act as a countervailing buyer power and that the Parties will not be able to raise the prices of automatic residential cleaners post-merger.

(164) As opposed to the U.S., where the distribution level is very concentrated with one major distributor (PoolCorp), in the EU there are no pan-European distribution players that would account for an equally significant share of distribution for the merged entity post-transaction.

(165) PoolCorp is the major distributor of pool equipment worldwide. However, it generates only a very limited turnover within Europe. According to PoolCorp's annual report,128 PoolCorp through its European subsidiaries generated only around 5% of its turnover in 2017 which represents around EUR 120 million.129 In the U.S., PoolCorp is Zodiac's largest customer "[…]").130 However, in the EU Zodiac does not depend on any distributor to the same extent, even in the main pool equipment markets (France, Spain, Italy and Germany).131 The same is applicable for Fluidra.132 Moreover, in the major European pool equipment markets, Fluidra also acts as a major distributor through its wholesale and Cash & Carry outlets.

(166) The fact that distributors do not see themselves as capable of constraining significantly the pricing power of the merged entity post-transaction is also confirmed by the fact that several distributors are amongst those who express concerns about the potential effects of the transaction within the Commission's market investigation.133

(167) Finally, none of the large customers ([…]) are significant enough to constrain the Parties. The Parties' internal documents indicate that the "dealer/retailer" market is fragmented and that even those larger players have no more than 5% ("No player [retailer] has more than 5% market share").134

5.2.3.11. Internet sales are not a sufficient price constraining factor

(168) The Parties claim that the Internet has played a significant role in recent years to increase price competition in cleaners, and robotic cleaners in particular. They further contend that Internet sales are converging with other sales channels and the Parties cannot track their sales online.135

(169) The market investigation has confirmed that to a certain degree, Internet sales have been increasing and play a role within pool equipment sales, especially with respect to cleaners, as they are plug-and-play items that need limited assistance for their use. For example, a competitor indicated that Internet sales may erode manufacturer's margins due to the fact that often products sold online will be sold cheaper than through traditional sales channels (i.e. wholesale distributors, specialized retail shops or pool prescribers).136

(170) However, the information provided by the Parties on their own sales channel split and their internal documents indicate that the actual impact of such sales is still limited, and that companies actively manage any such sales.

(171) First, the penetration of internet sales in Europe is still more limited than in other jurisdictions, and a large part of sales are still made through traditional distribution. The Parties' internal documents137 and market participants138 indicate that around 30% of cleaners will be sold online, as opposed to 60% in

portfolio. This is corroborated by the fact that Zodiac licences out some of its patents even to its competitors.145 Therefore, any new entrant will be faced either with the need to develop its own IP (which is long and costly) or to pay for access through a licence (which makes it dependent on the largest players such as Maytronics, Zodiac or Fluidra).146

(180) [40-50]% of Zodiac's overall patent portfolio relates to robotic cleaners, and this number is even higher for Fluidra ([50-60]%). The Parties also pointed out that they cross-licence each other for a significant amount of their patent portfolio. There is also a history of patent litigation between the Parties, mostly coming from Zodiac as the more innovative player.147 Zodiac also contemplated suing other competitors active in this space, namely – […].148

(181) Second, brand recognition is considered as a key element to entry because robotic cleaners are plug-and-play items.149 As noted above, brands that supply these products in the pool equipment industry are characterised by high quality and reliability.

(182) Third, companies active in the market for robotic cleaners need a sufficient portfolio of products (for all price points)150 in order to catch as much demand as possible. Only the Parties and Maytronics have sufficient breadth of portfolio, whereas a new entrant would face difficulties in bringing to market a sufficiently wide portfolio across price points.151

(183) Fourth, a number of competitors indicated that access to distributors effectively acts as a barrier to entry in this market.152 The main competitors indicated that despite the fact that there are a large number of distributors per Member State, only a few have sufficient client base and scope to offer their products at a large enough scale. Furthermore, while exclusive distribution arrangements are rare, large distributors tend to distribute products of a particular supplier in a given product line (for example, robotic cleaners). This is also confirmed by the Parties' internal documents, which indicate that "while the majority of dealers work with 3+ brands, large dealers focus more on the top 3".153

(184) The RBB Report claims that entry is likely in the space of robotic cleaners. However, this is not supported by the findings of the market investigation. The majority of customers (62%) and competitors (43%) do not consider that new entry is likely.154 In their narrative responses, customers indicated that the following act as barriers to entry; technology, know-how, brands, distribution, high IP costs, and market saturation. Competitors mentioned IP, access to distribution, technology, service structure, reliability, strategy, and expenses to develop and market share of existing suppliers as the main barriers.

5.2.3.13.There will be few alternatives left on the robotic cleaners market

(185) The Parties claim that since robotic cleaners are plug-and-play items, switching is deemed to be comparatively easier than for other pool equipment products.

(186) This view is confirmed by the majority of customers, who indicated switching to be easy.155 However, the feedback from distributors indicated that it is difficult to make customers switch.156 Competitors were also of the same view.157

(187) Irrespective of the ease of switching for robotic cleaners compared to other pool equipment products, after the Transaction, there will only be one large competitor besides the merged entity, with a significant portfolio of products - namely Maytronics, followed by Hayward as a distant third. Therefore, even if switching would be easier than for other pool equipment products, it would not exclude the effects of the Transaction brought about by the significant increase in market concentration post-merger.

5.2.3.14.Conclusion

(188) In light of the above considerations and taking the results of the market investigation into account, the Commission concludes that the Transaction raises serious doubts as to its compatibility with the internal market with respect to market for robotic cleaners, irrespective of whether these are assessed at national level or at EEA level.

5.2.4.Automatic suction cleaners

5.2.4.1. Introduction

(189) The Parties estimate that the Transaction technically gives rise to an affected market with respect automatic suction cleaners at the EEA level, where the Parties' combined market share (by value) in 2016 amounted to [20-30]% with a moderate increment of [0-5]% brought by Fluidra. Moreover, at the national level, the Transaction results in six affected markets for automatic suction cleaners (by value), with the highest combined share in Portugal (combined: [40-50]%; Zodiac: [40-50]% + [0-5]% Fluidra), Spain (combined: [30-40]%; Zodiac [30-40]% + Fluidra [5-10]%), Belgium (combined: [30-40]%; Zodiac [30-40]% + Fluidra [0-5]%), France (combined: [30-40]%; Zodiac [30-40]% + Fluidra [0-5]%),Greece (combined: [30-40]%; Zodiac [30-40]% + Fluidra [0-5]%),Germany (combined: [20-30]%; Zodiac [20-30]% + Fluidra [0-5]%).