Commission, September 22, 2020, No M.9456

EUROPEAN COMMISSION

Decision

SPP / CEZ ESCO / JV

Subject: Case M.9456 – SPP / CEZ ESCO / JV

Commission decision following a reasoned submission pursuant to Article 4(4) of Regulation No 139/20041 for referral of the case to Slovakia and Article 57 of the Agreement on the European Economic Area2.

Date of filing: 24.08.2020

Legal deadline for response of Member States: 15.09.2020

Legal deadline for the Commission decision under Article 4(4): 28.09.2020

Dear Sir or Madam,

1. INTRODUCTION

(1) On 24 August 2020, the Commission received by means of a Reasoned Submission a referral request pursuant to Article 4(4) of the Merger Regulation with respect to the creation of a 50/50 full-function joint venture (the “Joint Venture” or the “JV”) by ČEZ ESCO, a.s. (“ČEZ ESCO“), a Czech joint stock company and a member of the group of companies controlled by ČEZ, a.s. (“ČEZ” and “ČEZ Group”) and a Slovak joint stock company, Slovenský plynárenský priemysel, a.s. (“SPP”) (the “Transaction”). ČEZ ESCO and SPP together referred to as the “Parties”. The Parties request that the operation be examined in its entirety by the competent authorities of Slovakia.(2) According to Article 4(4) of the Merger Regulation, where a certain concentration has a Union dimension, and before a formal notification has been made to the Commission, the parties to a transaction may request that their transaction be referred in whole or in part from the Commission to the Member State where the concentration may significantly affect competition and which present all the characteristics of a distinct market.(3) A copy of this Reasoned Submission was transmitted to all Member States on 25 August 2020.(4) By fax of 27 August 2020, the Antimonopoly Office of Slovakia (“Slovak AMO”) as the competent authority of Slovakia informed the Commission that it agrees with the proposed referral.

2. THE PARTIES

(5) ČEZ ESCO focuses on energy consumption optimization services and related services such as the construction of decentralized energy sources (e.g., co-generation units) and is primarily active in Czechia and to a certain limited extent in other Member States including Slovakia. ČEZ ESCO is a member of the ČEZ Group, whose parent company, ČEZ, a.s. (“ČEZ”), is primarily active in electricity generation in Czechia. ČEZ’s largest shareholder is the Czech State with almost a 70% shareholding, and which exercises its shareholder rights through the Ministry of Finance of Czechia (the “Czech MoF”). In Slovakia, the ČEZ Group is engaged in sales of electricity and to a limited extent in sales of natural gas.3

(6) SPP is primarily active in the retail gas supply sector in Slovakia and is also engaged in retail electricity supply in Slovakia. SPP is wholly owned by the Slovak State, which exercises its shareholder rights through the Ministry of Economy of Slovakia (the “Slovak MoE”).

3.THE OPERATION AND CONCENTRATION

(7) The Transaction will be effected by way of an acquisition by SPP, upon closing of the Transaction, of 50% of the shares of ČEZ ESCO Slovensko, a.s. (“ČEZ ESCO SK”), a subsidiary of ČEZ ESCO, which it created for the purposes of the

Transaction, and to which a number of wholly or partially-owned subsidiaries of ČEZ ESCO will be contributed, as illustrated in the chart below.4

4. EU DIMENSION

(8) The undertakings concerned have a combined aggregated worldwide turnover5 of more than EUR 5 billion (SPP: Worldwide turnover of EUR […] million; ČEZ ESCO: Worldwide turnover of EUR […] million). They have a Community-wide turnover in excess of EUR 250 million (SPP: EU-wide turnover of EUR […] million; ČEZ ESCO: EU-wide turnover of EUR […] million), and the undertakings concerned do not achieve more than two-thirds of their Community-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension within Article 1(2) of the Merger Regulation.

5. ASSESSMENT

(9) For the reasons set out below, the Transaction meets the legal requirements set out in Article 4(4) of the Merger Regulation. The Transaction is a concentration within the meaning of Article 3 of the Merger Regulation, it has an EU dimension (see paragraph (8) above) and it may significantly affect competition mainly due to vertical links relating to the markets in Slovakia for retail gas supply, multi-technical management/maintenance services, provision of district heat, distribution of gas, distribution of electricity, retail electricity supply, and those markets present all the characteristics of distinct markets.

1.1.The JV is a concentration

(10) The JV will be jointly controlled by SPP and ČEZ ESCO. The following table summarises the governance structure of the JV:

JV Body | ČEZ | SPP | Voting |

Board of directors | [Details of the shareholders’ agreement (SHA)] | [Details of the SHA] | [Details of the SHA] |

Supervisory board | [Details of the SHA] | [Details of the SHA] | [Details of the SHA] |

Investment Committee | [Details of the SHA] | [Details of the SHA] | [Details of the SHA] |

General Meeting (shareholders) | [Details of the SHA] | [Details of the SHA] | [Details of the SHA] |

(11) Despite the fact that ČEZ ESCO will have more nominees in the Board of Directors than SPP, the JV will be jointly controlled by SPP and ČEZ ESCO for the following main reasons:a) ČEZ ESCO and SPP will each hold 50% of the shares in the JV. The equal shareholdings is indicative of joint control (although not necessarily conclusive on its own). The Commission Consolidated Jurisdictional Notice (“CJN”)6 starts with an examination of the shareholdings of the parents. When there is an unequal shareholding, or in the event of additional shareholder agreements, the existence of other factors is examined (paragraph 64 of the CJN);b) The parity of representation across the decision-making bodies, which is indicative of the intention that the JV should be run jointly. Each shareholder [details of the SHA – governance structure]. Despite the fact that the Supervisory Board will have no management functions and will only adopt non-binding opinions, [details of the SHA – governance structure] in the Supervisory Board is an element to be taken into account in the overall assessment;c) SPP’s right to nominate the CFO, who will have an instrumental role in the financial matters of the JV, including the preparation of the JV’s annual budgets. [details of the SHA – governance structure/concrete rights];d) SPP’s right to veto [details of the SHA – governance regime] which is one of the strategic documents over which a veto right can confer joint control according to paragraph 70 of the CJN;e) A deadlock resolution mechanism is foreseen in the event of failure to agree on [details of the SHA – deadlock triggers], where either one of the Parties can [details of the SHA – deadlock mechanism]. This goes beyond a minority protection right, given that if a shareholder forces a point it can risk [details of the SHA –deadlock mechanism].

(12) An overall assessment of the elements outlined above indicates that the JV will be jointly controlled by SPP and ČEZ ESCO.

(13) The JV will have a full-function character and it will be active as an autonomous economic entity:a) The JV will not perform one specific function for the Parties but it will be a self-standing entity providing a range of services for third parties. The Parties note that the JV’s business plan anticipates that the vast majority of sales (i.e. significantly exceeding [details of the anticipated sales structure]%) will be derived from sales to third parties. The Parties also note that, in the event that any sales will be made by the JV to the parent companies [details of the anticipated sales structure].b) The JV will have its own dedicated management responsible for its day-to- day operations and will have access to sufficient resources, including finance, staff and assets (tangible and intangible) that will enable it to conduct its business activities on a lasting basis. The Parties note that the key management and vast majority of staff will be employed directly by the JV and/or its subsidiaries [details of the personnel and management employment mechanism].c) Some of the JV’s activities (including design and realisation functions) may be performed by the Parties (in addition to the use of the capacities of the JV and/or external sub-contractors). However, it is anticipated that this will occur primarily within [details of the JV operational structure].d) The JV shall be established for an indefinite period of time [details of the SHA – termination details]

(14) In view of the above, the Transaction constitutes a concentration within the meaning of Article 3(1)(b) in conjunction with Article 3(4) of the EU Merger Regulation.

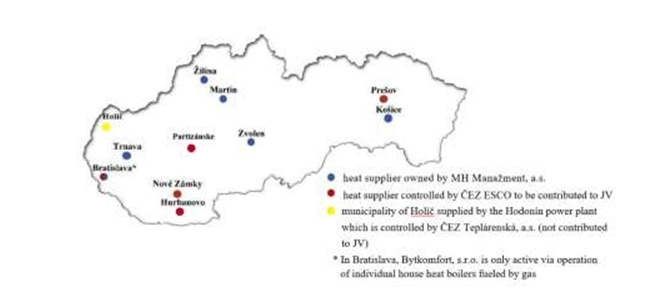

5.2. Activities of the JV

(15) The JV will mainly be active in the provision of specialized energy consumption optimization services aimed at decreasing the energy consumption of its clients in Slovakia (the JV will not provide such services outside Slovakia). Those services will include various project, engineering and implementation works including the construction, operation and maintenance of energy equipment (such as boilers and units for the generation of heat and electricity) and other installations such as heat, ventilation and air-conditioning (HVAC) installations, lighting and the provision of facility management services in Slovakia.

(16) The JV will also be active in the following areas:a) The provision of district heat via heating companies with local heating networks in Slovakia to be contributed to the JV by ČEZ ESCO;b) The construction and operation in Slovakia of local electricity and gas distribution networks that have only a limited local span confined to specific retail or industrial premises;c) Some marginal gas and/or electricity supply activities in Slovakia to customers (not having their own suppliers) connected to the local distribution networks in specific sites (such as industrial or retail parks) that will be constructed and/or operated by the JV, in particular via ČEZ Distribučné sústavy a.s. (“ČEZ DS”).

5.3.Relevant markets – product and geographic market definition

5.3.1. Retail gas supply

5.3.1.1. Product market definition

(17) In previous decisions7 regarding the markets for retail supply of gas (i.e., supply of gas to end customers), the Commission has concluded that the market can be further segmented on the basis of the types of customer and their consumption patterns into retail supply of gas to (i) gas-powered electricity plants; (ii) large industrial customers; (iii) small industrial customers and (iv) household customers. In case M.6984 - EPH/Stredoslovenska Energetika, the Commission had regard to the specifics of the Slovak market and considered the fact raised by the parties in that case that the segment of large industrial customers (i.e., customers with an annual consumption exceeding 60,000 m3) should also include supply of gas to gas-powered electricity production facilities since their annual consumption generally exceeds 60,000 m3. The market segmentation applied in that case included (i) large industrial customers (i.e., with the annual consumption in excess of 60 000 m3 which equals 645.36 MWh8 or 641.4 MWh9); (ii) small industrial customers (i.e., with the annual consumption below 60,000 m3) and (iii) household customers.

(18) The Parties submit that, in general, such segmentation may be appropriate in the context of the Slovak market. Due to the fact that a price regulation as well as other regulatory protection mechanisms apply to a specific category of small enterprises with annual gas consumption of up to 100 MWh under the Slovak RONI Act10, the Parties submit that the segment of small industrial (including commercial) customers (or SMEs) could be further segmented depending on the applicability of price regulation to (i) unregulated SMEs with annual gas consumption between 100 MWh and 60,000 m3 (in appropriate MWh equivalent) and (ii) regulated SMEs with annual gas consumption up 100 MWh.

(19) In the absence of evidence to the contrary, for the purposes of this decision, the Commission will retain the market definitions identified above, that is the retail supply of gas, further sub-segmented between (i) large industrial customers (i.e., with the annual consumption in excess of 60,000 m3 which equals 645.36 MWh or 641.4 MWh); (ii) small industrial customers (i.e., with the annual consumption below 60,000 m3) and (iii) household customers. Within small industrial customers, the Commission will consider a further sub-segmentation between (i) unregulated SMEs with annual gas consumption between 100 MWh and 60,000 m3 (in appropriate MWh equivalent) and (ii) regulated SMEs with annual gas consumption up 100 MWh. These definitions correspond to the Commission’s previous decisional practice and constitute plausible product market definitions.

5.3.1.2. Geographic market definition

(20) The Commission has generally held that the geographic markets for gas supply were national11 in scope, whilst also in some cases considering a narrower regional scope.12

(21) The Parties submit that the market for retail supply of gas should be defined as at least national and not further segmented on regional basis.

(22) In the absence of evidence to the contrary, for the purposes of this decision, the Commission will retain the geographic market definition identified above, that is the market for retail gas supply as being national in scope. This definition corresponds to the Commission’s previous decisional practice and constitutes a plausible product market definition.

5.3.2.The provision of multi-technical management/maintenance services, including energy consumption optimization services

5.3.2.1.Product market definition

(23) In a previous decision,13 the Commission concluded that the relevant product market was the “market for multi-technical management/maintenance services including energy consumption optimization services without the need to identify other distinctions (i.e., without further segmentation)”. The Commission also concluded that the aforementioned overall market included also specific energy consumption optimization services provided on the basis of the so-called “Energy Performance Contracts” (EPC) concerning measurable performance commitments. Further, the Commission came to the conclusion that no segmentation of this market was warranted (e.g., by “customer type”, “building type” or “type of service”).

(24) The Parties are of the view that the characteristics of the market for multi-technical management/maintenance services including energy consumption optimization services in Slovakia coincide with the market characteristics described in the EDF/Dalkia Decision.

(25) In the absence of evidence to the contrary, for the purposes of this decision, the Commission will retain the market definition identified above, that is the market for multi-technical management/maintenance services, including energy consumption optimization services, without further sub-segmentation. This definition corresponds to the Commission’s previous decisional practice and constitutes a plausible product market definition.

5.3.2.2. Geographic market definition

(26) In a previous decision,14 the Commission concluded that the market was national taking into account, in particular, the fact that (i) many undertakings active on the market were able to provide multi-technical management/maintenance services at a national level and (ii) tenders organized by public purchasers for management or multi-technical maintenance services were also advertised at least at national level.

(27) The Parties are of the view that the market conditions in Slovakia are to a considerable extent similar to those described in the EDF/Dalkia decision e.g., due to the existence of a considerable number of players that provide services throughout Slovakia and overall homogeneity of conditions for provision of the services (including licensing and pricing conditions) throughout the whole territory of Slovakia. Therefore, the Parties submit that the geographic dimension of the market for multi-technical management/maintenance services including energy consumption optimization services should be defined as national in scope.

(28) In the absence of evidence to the contrary, for the purposes of this decision, the Commission will retain the geographic market definition identified above, that is the market for multi-technical management/maintenance services, including energy consumption optimization services as being national in scope. This definition corresponds to the Commission’s previous decisional practice and constitutes a plausible product market definition.

5.3.3.The provision of district heat

5.3.3.1.Product market definition

(29) In previous decisions,15 the Commission has considered the provision of district heat as a separate product market comprising production and distribution of steam or hot water to buildings distributed via separate networks owned by the local distributor with different networks usually covering different (non-overlapping) geographic areas.

(30) The Parties submit that both the activities of Spravbytkomfort, Bytkomfort and ČSS (operating a small heat distribution network in the industrial park in Partizánske) that will be contributed to the JV generally correspond to this delineation. The Parties note that this also applies to the activities of the district heat supply companies indirectly controlled by the Slovak MoE via MHM (i.e., BATAS, TEKO, MATAS, TATAS, ZITAS and ZVTP). The Parties also submit that, in case M.7137 - EDF/Dalkia, the Commission also distinguished between (i) direct use of the heating networks by their owner on the one hand and (ii) separate markets for the delegated management of heating and cooling networks which consists of the management of the relevant heating/cooling networks by a third party manager (distinct from the owner of the network) based on various types of contracts including concessions and PPP projects. The Commission has previously left open whether certain elements of this market may form part of the market for multi-technical management/maintenance services. The Parties submit that, although such a distinction is plausible, the question of the exact definition of the product market in this case may be left open since the Transaction does not raise competition concerns irrespective of the market definition. Further, the Parties submit that, although the JV [details of ESCO JV’s potential future business objectives], none of the companies to be contributed to the JV and/or the Parties is actually active on this market in Slovakia.

(31) In the absence of evidence to the contrary, for the purposes of this decision, the Commission will retain the market definition identified above, that is the market for the provision of district heat. This definition corresponds to the Commission’s previous decisional practice and constitutes a plausible product market definition.

5.3.3.2. Geographic market definition

(32) In previous decisions,16 the Commission defined the market for the provision of district heat as local and limited to the relevant network.

(33) The Parties submit that the distribution networks of each of the heating plants to be operated by the JV (Spravbytkomfort, Bytkomfort and a small heating unit operated by ČSS) and/or by companies controlled by the Slovak MoE cover different geographical areas (for more details see the map below) that do not overlap since they are far from each other and cannot be connected. As such, the Parties submit that each such distinct heat supply network in Slovakia constitutes a separate relevant geographic market.

(34) In in the absence of evidence to the contrary, for the purposes of this decision, the Commission will retain the geographic market definition identified above, that is the market for the provision of district heat as being local and limited to the relevant network. This definition corresponds to the Commission’s previous decisional practice and constitutes a plausible product market definition.

5.3.4. Retail supply of electricity

5.3.4.1. Product market definition

(35) In a previous decision relating to Slovakia,17 the Commission has considered a plausible market segmentation based on whether the end-users are connected to the transmission system, on one hand, and to the distribution system, on the other.18 The Commission has further considered a plausible segmentation of the customers connected to the distribution system based on their annual consumption into large industrial customers with yearly consumption above 1 GWh, and customers with yearly consumption below 1 GWh, and whether the latter segment could be further segmented depending on whether or not the Slovak RONI regulated price cap applies to the customer. The Parties generally accept the product market definitions considered by the Commission and submit that in the Slovak context, it may also be possible to distinguish within the regulated segment (i.e. segment to which the price cap regulation set by the Slovak RONI applies) between residential customers (i.e. households) and regulated small and medium sized industrial and commercial customers (SMEs) (i.e. SMEs with yearly consumption below 30 MWh), since some electricity suppliers, including SPP, apply different offerings and tariffs for these two categories of customers.

(36) In the absence of evidence to the contrary, for the purposes of this decision, the Commission will retain the market definition identified above, that is the retail supply of electricity, further sub-segmented between (i) customers connected to the transmission system and (ii) customers connected to the distribution system. Within customers connected to the distribution system, the Commission will retain a further sub-segmentation between (i) regulated (households and SMEs) customers, (ii) unregulated customers with consumption below 1 GWh and (iii) unregulated large customers with consumption above 1 GWh. This definition corresponds to the Commission’s previous decisional practice and constitutes a plausible product market definition.

5.3.4.2. Geographic market definition

(37) In a previous decision relating to Slovakia,19 the Commission has considered the market for retail supply of electricity to end-customers connected to the transmission and the distribution system to be national in scope, encompassing the territory of Slovakia.

(38) The Parties agree with the Commission’s previous conclusions on the geographic delineation of this market, in that the market should be regarded as national and not further segmented on a regional basis.

(39) In the absence of evidence to the contrary, for the purposes of this decision, the Commission will retain the geographic market definition identified above, that is the market for retail supply of electricity as being national in scope. This definition corresponds to the Commission’s previous decisional practice and constitutes a plausible product market definition.

5.3.5. Distribution of electricity

5.3.5.1. Product market definition

(40) Electricity is transported via the transmission network for long distances and via networks with lower voltage level networks at regional and local level. Networks are connected with each other and different voltage levels are connected through transformers.20

(41) The activities of the JV in the field of the operation of local electricity distribution networks in Slovakia encompass the operation and management of lower voltage grids providing electricity transportation services to distributors for the delivery of electricity to final customers.21

(42) In previous decisions, the Commission has identified two separate markets for the transportation of electricity: transmission and distribution.22

(43) In relation to electricity distribution, in previous decisions, the Commission has identified a separate market for the distribution of electricity, namely the operation and management of the lower voltage grids.23

(44) The Parties do not dispute the Commission’s previous decisional practice.

(45) In the absence of evidence to the contrary, for the purposes of this decision, the Commission will retain the market definition identified above, that is the market for electricity distribution via lower voltage networks. This definition corresponds to the Commission’s previous decisional practice and constitutes a plausible product market definition.

5.3.5.2. Geographic market definition

(46) For the distribution of electricity, the Commission has previously considered that the relevant geographic market is the relevant distribution network, as for any given customer distribution through one distribution grid is not substitutable with distribution through another grid.24

(47) The Parties agree with the Commission’s previous decisional practice.

(48) In the absence of evidence to the contrary, for the purposes of this decision, the Commission will retain the geographic market definition identified above, that is the market for the distribution of electricity as being limited to the geographic area of the relevant distribution network. This definition corresponds to the Commission’s previous decisional practice and constitutes a plausible product market definition.

5.3.6. Distribution of gas

5.3.6.1. Product market definition

(49) Gas transmission is the transport of natural gas through a network, which mainly contains high pressure pipelines, with a view to its delivery to (intermediate) customers for distribution. Gas distribution is the transport of natural gas through local or regional pipeline networks with a view its delivery to customers, but not including supply.

(50) The activities of the JV in the field of the operation of local gas distribution networks may be regarded as belonging to the relevant product market for gas distribution.25

(51) In previous decisions, the Commission has generally distinguished between (i) gas transmission (via high pressure systems) and (ii) gas distribution (via medium/low pressure systems).26

(52) The Parties do not dispute the Commission’s previous decisional practice.

(53) In the absence of evidence to the contrary, for the purposes of this decision, the Commission will retain the market definition identified above, that is the market for distribution of gas via medium/low pressure systems. This definition corresponds to the Commission’s previous decisional practice and constitutes a plausible product market definition.

5.3.6.2. Geographic market definition

(54) In previous decisions, the Commission found that the geographic market for distribution of gas is regional within the limits of the area covered by the respective grid, where a Distribution System Operator (“DSO”) operates a natural monopoly with a market share of 100%.27

(55) The Parties agree with the Commission’s previous decisional practice.

(56) In the absence of evidence to the contrary, for the purposes of this decision, the Commission will retain the geographic market definition identified above, that is the market for the distribution of gas as being regional within the limits of the area covered by the respective grid, where a DSO operates. This definition corresponds to the Commission’s previous decisional practice and constitutes a plausible product market definition.

5.4.Assessment of the referral request

5.4.1.Legal requirements

(57) According to the Commission Notice on case referral in respect of concentrations (the “Referral Notice”),28 in order for a referral to be made by the Commission to one or more Member States pursuant to Article 4(4), the following two legal requirements must be fulfilled:a) there must be indications that the concentration may significantly affect competition in a market or markets,29 andb) the market(s) in question must be within a Member State and present all the characteristics of a distinct market.30

(58) Moreover, point 20 of the Referral Notice provides that “Concentrations with a Community dimension which are likely to affect competition in markets that have a national or narrower than national scope, and the effects of which are likely to be confined to, or have their main economic impact in, a single Member State, are the most appropriate candidate cases for referral to that Member State.”

(59) The Transaction gives rise to one horizontally affected market – the market for the retail supply of gas in Slovakia, whether in the overall market for the supply of gas, or in the different plausible sub-segments as described in paragraph (19).a) In the overall market for the retail supply of gas in Slovakia, SPP has a market share of [50-60]%, while ČEZ has a market share of [0-5]%.b) When considering further sub-segmentations of the overall market for the retail supply of gas in Slovakia, the Parties’ market shares are as follows: (i) in the market for the supply of gas to large industrial customers (annual consumption above 60,000 m3) in Slovakia, SPP has a market share of [40- 50]%, while ČEZ has a market share of [0-5]%, (ii) in the market for the supply of gas to unregulated SMEs (annual consumption between 100 MWh and 60,000 m3) in Slovakia, SPP has a market share of [50-60]%, while ČEZ has a market share of [5-10]%; (iii) in the market for the supply of gas to regulated SMEs (annual consumption up to 100 MWh), SPP has a market share of [60-70]%, while ČEZ has a market share of [0-5]%.31 The market share of the JV in the retail supply of gas will be de minimis.32

(60) Given SPP’s pre-existing market position on the retail gas supply markets in Slovakia (see paragraph (59) above) (ČEZ ESCO’s market share (via its Slovak subsidiary, ČEZ Slovensko, s.r.o. (“ČEZ SK”)) is limited), and the “natural monopoly” over the distribution of gas and electricity and the provision of heat over the relevant networks and grids in Slovakia, the Transaction gives rise the following vertically affected markets:a) Retail gas supply in Slovakia (upstream) and multi-technical management/maintenance services, including energy consumption optimization services in Slovakia33 (downstream);34b) Retail gas supply in Slovakia (upstream) and provision of district heat in Slovakia (downstream);c) Distribution of gas in Slovakia (upstream) and retail gas supply in Slovakia (downstream);d) Distribution of electricity in Slovakia (upstream) and retail electricity supply in Slovakia (downstream);35 e) Distribution of electricity in Slovakia (upstream) and multi-technical management/maintenance services, including energy consumption optimization services in Slovakia (downstream);f) Distribution of gas in Slovakia (upstream) and multi-technical management/maintenance services, including energy consumption optimization services in Slovakia (downstream);g) Provision of district heat in Slovakia (upstream) and multi-technical management/maintenance services, including energy consumption optimization services in Slovakia (downstream).

(61) In view of the level of the Parties’ market shares, and in particular SPP’s pre- existing market position on the retail gas supply markets in Slovakia and the vertical links with markets described above, the Transaction is likely to significantly affect competition in these affected markets in Slovakia. According to footnote 21 of the Referral Notice “The existence of ‘affected markets’ within the meaning of Form RS would generally be considered sufficient to meet the requirements of Article 4(4).” Therefore, the first legal requirement set forth in Article 4(4) of the Merger Regulation appears to be met.

(62) Furthermore, the markets in question are limited to Slovakia, some also with local elements, and represent all the characteristics of a distinct market. Therefore, the second legal requirement set forth by article 4(4) of the Merger Regulation also appears to be met. This conclusion is also in line with point 20 of the Referral Notice, as the JV will be active only in Slovakia and thus the effects of the Transaction are likely to be confined to, or have their main economic impact in, a single Member State – Slovakia, and all affected markets are within Slovakia.

5.4.2.Additional factors

(63) In addition to the verification of the legal requirements, point 19 of the Referral Notice provides that it should also be considered whether referral of the case is appropriate, and in particular “whether the competition authority or authorities to which they are contemplating requesting the referral of the case is the most appropriate authority for dealing with the case”.

(64) In addition, point 23 of the Referral Notice states that “Consideration should also, to the extent possible, be given to whether the NCA(s) to which referral of the case is contemplated may possess specific expertise concerning local markets, or be examining, or about to examine, another transaction in the sector concerned”.

(65) Both these considerations appear to apply in this case. First, given that the focus of the competitive effects of the Transaction is confined to Slovakia, the Slovak AMO is well placed to examine the case, since it has experience in assessing the impact of transactions in Slovak gas and electricity markets.36 Second, SPP [details of strategy concerning retail electricity and gas supply markets].37 [Details of strategy concerning retail electricity and gas supply markets].

5.4.3. Conclusion on referral

(66) On the basis of the information provided by the Parties in the Reasoned Submission, the case meets the legal requirements set out in Article 4(4) of the Merger Regulation in that the concentration may significantly affect competition in a market(s) within a Member State which presents all the characteristics of a distinct market.

(67) Moreover, the requested referral would be consistent with points 17-23 of the Referral Notice, in particular because the Slovak AMO appears to be the most appropriate authority to consider the Transaction.

6. CONCLUSION

(68) For the above reasons, and given that the Slovak AMO has expressed its agreement, the Commission has decided to refer the Transaction in its entirety to be examined by the Antimonopoly Office of Slovakia. This decision is adopted in application of Article 4(4) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 In 2017 ČEZ ESCO’s Slovak subsidiary, ČEZ Slovensko, s.r.o. (“ČEZ SK”) exited the household segment in retail supply of electricity and gas in Slovakia.

4 ČEZ ESCO SK is currently and will continue to be 100%-owned by ČEZ ESCO until closing of the Transaction.

5 Turnover calculated in accordance with Article 5(1) of the Merger Regulation and the Commission Consolidated Jurisdictional Notice of 10/07/2007.

6 Official Journal C 95, 16.04.2008, p. 1.

7 Case M.4180 Gaz de France/Suez; case M.3868 Dong/Elsam/Energi; case M.3440 EDP/ENI/GDP.

8 The Parties submit that this is based on [details on SPP´s internal approach to customer segmentation].

9 The Parties submit that this is based on the conversion rate used for the delineation of the tariff rates for gas distribution applied by SPP-D based on the RONI Decision No. 0020/2017/P dated October 31, 2016 available at http://www.urso.gov.sk:8088/CISRES/Agenda.nsf/0/84CC575116A3277DC125805D0021787B/$FILE/0020 2017 P.pdf (“SPP-D Tariff Decision”). The Parties submit that the segmentation using 641.4 MWh as a conversion rate [details on SPP´s internal approach to customer segmentation] (however, the difference between the two approaches to determine the segmentation and/or market data using 645.36 MWh or 641.4 MWh conversion rate is by definition negligible).

10 Act No. 250/2012 Coll., on Regulation of Network Industries, as amended (the “Slovak RONI Act”).

11 COMP/M.6068 ENI/ ACEGASAPS/ JV; COMP/M.5740 Gazprom / A2A / JV; COMP/M.5496 Vattenfall / Nuon Energy; COMP/M.4672 E.on / Endesa Europa / Viesgo; COMP/M. 4110 EON / Endesa; COMP/M.3230 Statoil / BP / Sonatrach / In Salah JV; COMP/M.3007 E.on / TXU Europe Group.

12 COMP/M.5467 RWE Essent; COMP/M.4890 Arcelor / Ferngas.

13 Case M.7137 - EDF/Dalkia.

14 Case M.7137 - EDF/Dalkia.

15 Case M.7137 - EDF/Dalkia and case M.5793 –Dalkia CZ/NWR Energy.

16 Case M.7137 - EDF/Dalkia and case M.5793 –Dalkia CZ/NWR Energy.

17 COMP/M.7927 – EPH/ENEL/SE, para. 17, 18.

18 Electricity is transported via the transmission network for long distances and via networks with lower voltage level networks at regional and local level. Networks are connected with each other and different voltage levels are connected through transformers (see COMP/M.8870 - E.On/Innogy, para. 39, not published yet). According to Articles 2(3) and 2(5) of Directive 2009/72/EC of 13 July 2009 concerning common rules for the internal market in electricity and repealing Directive 2003/54/EC (OJ L 211, 14.8.2009, p. 55–93), “transmission” means the transport of electricity on the extra high-voltage and high-voltage interconnected system with a view to its delivery to final customers or to distributors, but does not include supply, while “distribution” means the transport of electricity on high-voltage, medium-voltage and low-voltage distribution systems with a view to its delivery to customers, but does not include supply.

19 COMP/M.7927 – EPH/ENEL/SE, para. 35.

20 According to Articles 2(3) and 2(5) of Directive 2009/72/EC of 13 July 2009 concerning common rules for the internal market in electricity and repealing Directive 2003/54/EC (OJ L 211, 14.8.2009, p. 55– 93), “transmission” means the transport of electricity on the extra high-voltage and high-voltage interconnected system with a view to its delivery to final customers or to distributors, but does not include supply, while “distribution” means the transport of electricity on high-voltage, medium-voltage and low-voltage distribution systems with a view to its delivery to customers, but does not include supply.

21 Form RS, paragraph 133.

22 COMP/M.7927 – EPH/ENEL/SE, para. 21; COMP/M.5467 – RWE/Essent, para. 179; COMP/M.4238– E.ON/Prazskà plynárenská, para. 18.

23 COMP/M.5827 – Elia/IFM/50Hertz, para. 18; COMP/M.5467 – RWE/Essent, para. 179, 440.

24 COMP/M.5827 – Elia/IFM/50Hertz, para. 23; COMP/M. 5467 -RWE / ESSENT para 21; COMP/M.4238 – E.ON/Prazskà plynárenská, para. 19; COMP/M.3440 – ENID/EDP/GDP, para. 75.

25 Form RS, paragraph 133.

26 COMP/M.7927 – EPH/ENEL/SE, para. 29; COMP/M.7778 – Vattenfall/Engie/Gasag, para. 46; COMP/M.5467 – RWE/Essent, para. 322.

27 COMP/M.7778 – Vattenfall/Engie/Gasag, para. 47.

28 Official Journal C 56, 05.03.2005, p. 2-23.

29 Further developed in point 17 of the Referral Notice.

30 Further developed in point 18 of the Referral Notice.

31 The Parties note that, in the market for the supply of gas to regulated SMEs, the data provided are primarily based on [details of market shares estimation]. Therefore, the estimates provided by SPP differ compared to market shares monitored by the Slovak RONI in its Annual Reports, which are presumably more precise with respect to this segment. According to the data in the 2017-2019 Slovak RONI Annual Reports, the market shares of the Parties and their biggest competitors on this market segment were as follows in 2019: SPP: 75.1%, Innogy: 17.0%, SSE: 3.2.%, Slovakia Energy: 2.3%,others: 2.4%.

32 The the retail supply of gas of ČEZ DS (which will be contributed to the JV) via its local distribution networks in 2019 amounted only to approx. [0-5]% of total sales of gas in Slovakia.

33 In Case M.7137 - EDF/Dalkia, the Commission found that there were no current or potential vertical links between the markets for the retail supply of electricity and those of multi-technical management/maintenance services since the providers of the multi-technical management/maintenance services did not need to provide electricity to be able to provide their multi-technical management/maintenance services (see paragraph 446 of the decision).

34 In the market for multi-technical management/maintenance services in Slovakia, including energy consumption optimization services, the JV’s market share will be below [5-10]%. The Parties note that, in connection with preparation of the business plan of the JV, it was acknowledged that the market size data differed considerably based on the approaches taken to the determination of the market. The main approach to market potential taken into account in relation to the preparation of the business plan of the JV was based on [details of market estimation approach], the JV could possibly reach [20-30]% market share only in [details of market estimation] subject to fulfilment of multiple assumptions the fulfilment of which is inherently uncertain (Form RS, paragraphs 145, 146).

35 In the market for the retail supply of electricity in Slovakia, the Parties’ and the JV’s individual and/or combined market share (including any segmentation) is below [10-20]%.

36 Case No. 2014/FH/3/1/003 (acquisition of sole control of Slovak Ministry of Economy over SPP), Case No. 1051/2017/OK-2017/FH/3/1/032 (VSEH’s acquisition of ČEZ’s household retail electricity and gas business).

37 Form RS, paragraph 13.