Commission, October 15, 2020, No M.9962

EUROPEAN COMMISSION

Decision

MYLAN / ASPEN´S EU THROMBOSIS BUSINESS

Subject: Case M.9962 – MYLAN / ASPEN’S EU THROMBOSIS BUSINESS

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 17 September 2020, the European Commission received notification of a concentration pursuant to Article 4 of the Merger Regulation which would result from a proposed transaction by which Mylan N.V. (“Mylan”, Netherlands), through its subsidiary Mylan Ireland Limited (Ireland) intends to acquire sole control within the meaning of Article 3(1)(b) of the Merger Regulation of the whole of Aspen’s EU Thrombosis Business (“Aspen’s Target Business”, Mauritius), a subset of Aspen Global Incorporated (“AGI”, Mauritius), owned and indirectly controlled by Aspen Pharmacare Holdings Limited (“Aspen”, Mauritius) by way of purchase of assets (‘the Transaction’)3. Mylan is designated hereinafter as the “Notifying Party” and together with Aspen’s Target Business, as the “Parties” to the Transaction. The undertaking that would result from the Transaction is referred to as the ‘merged entity’.

1. THE PARTIES

(2) Mylan is a global pharmaceutical company that develops, licenses, manufactures, markets and distributes generic, branded generic and specialty pharmaceuticals through a vertically integrated global supply chain that includes over 40 manufacturing facilities. Its portfolio includes more than 1 500 products.

(3) Aspen’s Target Business consists of certain intellectual property, assets and rights relating to the unincorporated business of manufacture, distribution and marketing of four AGI antithrombotic products in the EEA, namely Nadroparin (brand names Fraxiparine and Fraxodi), Fondaparinux (brand name Arixtra), Certoparin (brand name Mono Embolex) and Danaparoid (brand name Orgaran). These assets constitute a business with market presence to which a turnover can be clearly attributed.4

2. THE OPERATION AND THE CONCENTRATION

(4) Pursuant to an asset purchase agreement dated 7 September 2020, between Mylan Ireland Limited and AGI, Mylan agreed to acquire sole control of all assets of Aspen’s Target Business and each right attached to these5.

(5) As a result of this Transaction, Mylan will obtain sole control over Aspen’s Target Business within the meaning of Article 3(1)(b) of the Merger Regulation.

3. UNION DIMENSION

(6) The Parties have a combined aggregate worldwide turnover of more than EUR 5 000 million6 (Mylan EUR 10 156 million, Aspen’s Target Business EUR […] million). Each of them has a Union-wide turnover in excess of EUR 250 million (Mylan EUR […] million, Aspen’s Target Business EUR […] million), but they do not achieve more than two-thirds of their aggregate Union-wide turnover within one and the same Member State. The notified operation therefore has a Union dimension pursuant to Article 1(2) of the Merger Regulation.

4. MARKET DEFINITIONS

4.1. Fixed Dose Pharmaceuticals

(7) Mylan and Aspen’s Target Business produce and sell Fixed Dose Pharmaceuticals (“FDPs”). FDPs are pharmaceutical products that have undergone all stages of production, including packaging in the final container and labelling. Production and sale of FDPs is one of the most common activity of pharmaceutical companies.

(8) As regards the product market, the Commission found in a past decision,7 that antithrombotic FDPs falling into ATC4 classes B1B1 (heparin) and B1B2 (antithrombin III), along with those falling into ATC3 class B1X (other antithrombotic agents) that have the same applications as heparins, belong to the same product market as they have the same mode of action (injectable) and range of indications. In a subsequent case,8 the Commission did not specify whether the market should be defined as if each of the above ATC4 classes constitute a different market, or if ATC3 class B1B (of which classes B1B1 and B1B2 are part) also constitutes a market in itself.

(9) The Notifying Party provides market shares for all of those possible product market definitions, including plausible affected markets at molecule level, namely a subset of generic products at ATC4 level that are based on the same molecule.

(10) In any event, for the purposes of this Decision, it is not necessary to conclude on the exact product market definition for antithrombotic FDPs, that is (i) whether classes B1B1 and B1B2 are each a separate product market or if together they constitute a product market (under class B1B), and (ii) whether class B1X is a separate market or it should be considered together with class B1B, as the Transaction does not give rise to serious doubts as to its compatibility with the internal market or the functioning of the EEA agreement under any of those plausible market definitions.

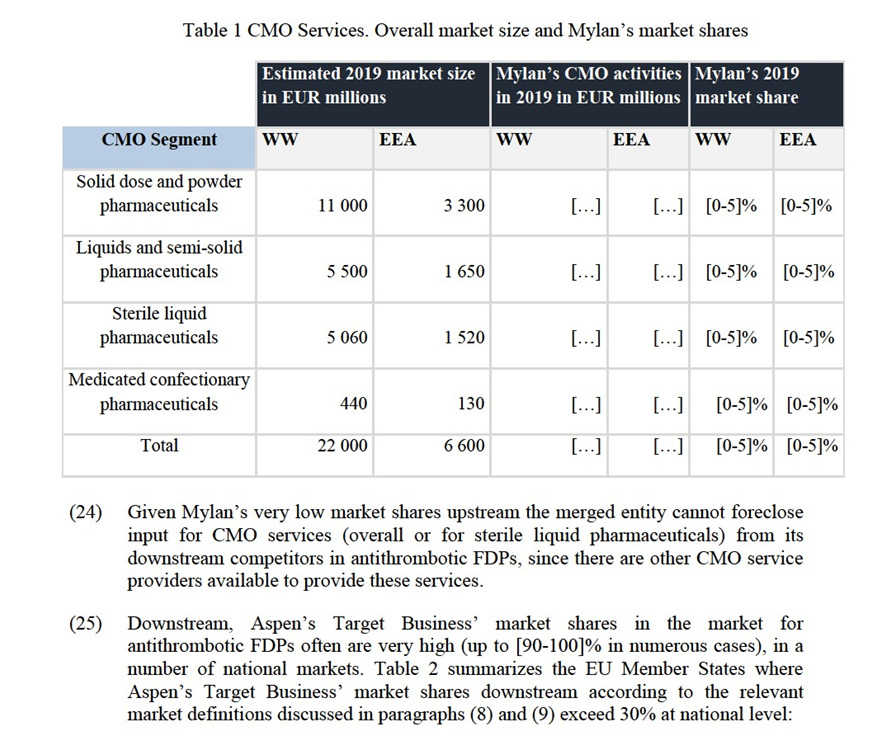

(11) As regards the geographic market, in line with numerous Commission precedents9, the relevant market for antithrombotic FDPs is national.

4.2. Contract manufacturing organisation (“CMO”)

(12) CMO is an arrangement under which a manufacturer provides upstream manufacturing services of FDPs under contract on behalf of third party pharmaceutical companies.

(13) As regards the product market definition, a number of contract manufacturing markets may be defined, corresponding in each case to the pharmaceutical form of the specific product that is manufactured. In some cases, contract-manufacturing markets can be further subdivided by the conditions in which the manufacturing process takes place (types of active pharmaceutical ingredient (“API”) involved in the process, toxicity, sterile environment, etc.).10

(14) In past decisions,11 the Commission left open whether the CMO market should be defined as an overall market, or whether it could be further segmented into four product markets, namely contract manufacturing of: (i) solid dose and powder pharmaceuticals; (ii) liquids and semi-solid pharmaceuticals; (iii) sterile liquid pharmaceuticals; and (iv) medicated confectionary pharmaceuticals.

(15) For the purpose of the assessment of the Transaction, the relevant segment of the upstream CMO product market is the one of sterile liquid pharmaceuticals, as Aspen’s Target Business produces downstream injectable FDPs. In any event, for the purpose of this Decision, the precise product market definition of CMO can be left open as, regardless of the market definition considered (an overall market for CMO, or a market for CMO services for sterile liquid pharmaceuticals), the Transaction does not give rise to serious doubts as to its compatibility with the internal market and the functioning of the EEA Agreement.

(16) With regard to the geographic market, in line with past decisions of the Commission12, the precise market definition for CMO services can be considered to be worldwide, or at least EEA-wide. No further elaboration is necessary, since the transaction does not give rise to serious doubts under either of the above possible geographic market definitions.

5. COMPETITIVE ASSESSMENT

5.1.Analytical Framework

(17) Under Articles 2(2) and 2(3) of the Merger Regulation, the Commission must assess whether a proposed concentration would significantly impede effective competition in the internal market or in a substantial part of it, in particular through the creation or strengthening of a dominant position.

(18) Frequently, a merger can entail horizontal effects. In this respect, in addition to the creation or strengthening of a dominant position, the Commission Guidelines on the assessment of horizontal mergers under the Merger Regulation (“the Horizontal Merger Guidelines”)13 distinguish between two main ways in which mergers between actual or potential competitors on the same relevant market may significantly impede effective competition, namely (a) by eliminating important competitive constraints on one or more firms, which consequently would have increased market power, without resorting to coordinated behaviour (non- coordinated effects); and (b) by changing the nature of competition in such a way that firms that previously were not coordinating their behaviour are now significantly more likely to coordinate and raise prices or otherwise harm effective competition. A merger may also make coordination easier, more stable or more effective for firms which were coordinating prior to the merger (coordinated effects).

(19) Furthermore, a merger can entail vertical effects. The Commission Guidelines on the assessment of non-horizontal mergers under the Merger Regulation (“the non- horizontal Merger Guidelines”)14 also distinguish between two main ways in which non-horizontal mergers may significantly impede effective competition: (a) when they give rise to input and/or customer foreclosure (non-coordinated effects); and (b) when the merger changes the nature of competition in such a way that firms that previously were not coordinating their behaviour, are now more likely to coordinate to raise prices or otherwise harm effective competition (coordinated effects). The non-horizontal Merger Guidelines distinguish two types of foreclosure: (a) where the merger is likely to raise the costs of downstream rivals by restricting their access to an important input (input foreclosure) and (b) where the merger is likely to foreclose upstream rivals by restricting their access to a sufficient customer base (customer foreclosure).

5.2.Competitive assessment

5.2.1. Horizontal Overlap in the market for antithrombotic FDPs.

(20) According to the Notifying Party’s submission, the Parties’ activities horizontally overlap in the FDP market for antithrombotic products only in France. The combined market shares of the Parties post-Transaction would be [10-20]% at most under every possible market definition,15 with very low increment, [0-5]% at most.

(21) In view of the low combined market shares and very limited overlap, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA agreement, as regards this horizontal overlap in the market for antithrombotic FDPs.

5.2.2. Vertical Relationship between Contract Manufacturing Organisation (upstream) and the sale and production of FDPs (downstream)

(22) In the present case, Mylan’s upstream participation in CMO for FDPs in markets where the Target is present downstream with market shares exceeding 30% in several national markets, gives rise to vertically affected markets.16

(23) The Notifying Party agrees to the market definitions drawn from the Commission’s precedence and provides Mylan’s total market share and its market share per segment in the worldwide and EEA-wide market. Mylan’s upstream market shares in the CMO market are [0-5]% at most (see table 1).

Table 2 Market shares of Aspen’s Target Business’ downstream (only if above 30%, “-” means no presence or below 30%)

| B1B (B1B1 + B1B2) | B1B2 | B1X | B1B + B1X |

Austria | - | - | [50-60]% | - |

Bulgaria | [70-80]% | [80-90]% | [90-100]% | [70-80]% |

Belgium | - | - | [90-100]% | - |

Croatia | - | - | [90-100]% | - |

Chechia | [40-50]% | [50-60]% | [90-100]% | [40-50]% |

Estonia | - | - | [90-100]% | - |

Finland | - | - | [90-100]% | - |

France | - | - | [90-100]% | - |

Germany | - | - | [90-100]% | - |

Greece | - | - | [90-100]% | - |

Italy | - | - | [90-100]% | - |

Latvia | [40-50]% | [40-50]% | [90-100]% | [40-50]% |

Lithuania | [70-80]% | [70-80]% | [90-100]% | [70-80]% |

Netherlands | [40-50]% | [40-50]% | [90-100]% | [40-50]% |

Norway | - | - | [90-100]% | - |

Poland | - | - | [70-80]% | - |

Portugal | - | - | [90-100]% | - |

Romania | [40-50]% | [40-50]% | [90-100]% | [50-60]% |

Slovakia | [60-70]% | [70-80]% | [90-100]% | [60-70]% |

Slovenia | [40-50]% | [40-50]% | [90-100]% | [40-50]% |

Spain | - | - | [90-100]% | - |

UK | - | - | [90-100]% | - |

(26) Notwithstanding the high market shares in national markets downstream, customer foreclosure can be excluded, for the following reasons:

(27) Firstly, Aspen’s Target Business’ CMO needs for antithrombotic FDPs pre- Transaction are covered in-house by Aspen.17 Therefore, even if post-Transaction the merged entity were to source all of its CMO needs for antithrombotic FDPs internally, there would be no change to the pre-Transaction situation and no rival CMO supplier would be affected.

(28) Secondly, Aspen’s Target Business’ high market shares in some countries for some injectable FDPs would in any event not give the merged entity sufficient market power to harm rival upstream CMO providers. This is because CMO providers offer the same services for all sterile liquid pharmaceuticals, and do not differentiate if their downstream customers manufacture specific injectable FDPs such as antithrombotic injectables. The potential opportunity for the CMO services linked to Aspen’s Target Business needs for antithrombotic FDPs is only a fraction of around [0-5]% of the market for CMO services for sterile liquid pharmaceuticals in the EEA.18

(29) Consequently, this limited potential demand for CMO services for sterile liquid pharmaceuticals would in any event not allow the merged entity to foreclose Mylan’s rival CMO providers upstream, from accessing downstream markets for injectable FDPs by withholding or reducing Aspen’s Target Business purchases (which are only limited to antithrombotic injectable FDPs).

(30) Thirdly, according to information provided by the Notifying Party, CMO services do not represent a substantial part of the total final costs of injectable antithrombotic FDPs (below [0-5]% on average).19

(31) Finally, the Notifying Party submits that in past Decisions20 the Commission has used as a reference to assess the foreclosure risk, the combined downstream market share of the merged entity and any of its downstream competitors for which the merged entity potentially provides CMO services in order to evaluate the potential harm of similar vertical relationships.

(32) On this basis, the only country in which Mylan provides CMO services to any of Aspen’s Target Business’ downstream competitors is the U.K. More specifically, Mylan provides CMO services for the molecule heparin (B1B1) to [company name], through a production site in [country].21 The combined market share of the Target and [company name] under any possible market definition is below [5-10]%.22 Consequently, the aggregated market shares of the two competitors do not raise competitive concerns as a result of customer foreclosure.

(33) Therefore, the merged entity cannot foreclose its upstream competitors in the provision of CMO services by denying access to the downstream market for antithrombotic FDPs.

(34) In light of the above, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement with regard to the vertical link between the upstream CMO market the downstream market for FDP antithrombotic products.

6. CONCLUSION

(35) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the “Merger Regulation”). With effect from 1 December 2009, the Treaty on the Functioning of the European Union (“TFEU”) has introduced certain changes, such as the replacement of “Community” by “Union” and “common market” by “internal market”. The terminology of the TFEU will be used throughout this decision

2 OJ L 1, 3.1.1994, p. 3 (the “EEA Agreement”).

3 Publication in the Official Journal of the European Union No C 317, 25.9.2020, p. 24.

4 See Commission Consolidated Jurisdictional Notice under Council Regulation (EC) No 139/2004 on the control of concentrations between undertakings, OJ C95 of 16.04.2008, in particular p. 24

5 Including the (i) de-commercialized products (See Form CO footnotes 2 and 4), (ii) Pending Registration Products (See Form CO footnote 5) and (ii) Orgaran New Business Opportunity products (See Form CO, footnote 6), which may be transferred to Mylan at a later date. All of these products have been included in the substantive assessment of the concentration by the Notifying Party.

6 Turnover calculated in accordance with Article 5 of the Merger Regulation

7 Case M. 3354- Sanofi-Synthelabo/Aventis (2004).

8 Case M.5253- Sanofi-Aventis/Zentiva (2009).

9 Case M.5295- Teva/Barr (2008), Case M.5479- Teva/Lonza (2009), Case M.5530- Glaxo Smith Kline/Stiefel Laboratories (2009), Case M.6162- Pfizer/Ferrosan Consumer Healthcare Business (2011).

10 Case M.6613- Watson/Actavis (2012)

11 Case M.5953- Reckitt Benckister/SSL (2010), paragraphs 59 and 62, and Case M.7480- Actavis/Allergan (2015).

12 Cases M.5953- Reckitt Benckiser/SSL (2010) and Case M.6613- Watson/Actavis (2012).

13 Guidelines on the assessment of horizontal mergers under the Council Regulation on the control of concentrations between undertakings, OJ C 31, 5.2.2004 p.5

14 Guidelines on the assessment of non-horizontal mergers under the Council Regulation on the control of concentrations between undertakings, OJ C256, 18.1.2008, p.6.

15 For completeness, the Parties consider alternative market definitions for FDPs for antithrombotic products, based on both the third (ATC3) and the fourth (ATC4) levels of classification. The Parties also provide overall market shares of ATC3 classes B1B and B1X together. In addition to the above, the Parties also consider plausible affected markets at molecule level namely a subset of generic products at ATC4 level that are based on the same molecule.

16 For completeness, the target does not include any CMO contracts or infrastructure.

17 See Form CO, paragraph 88 and footnote 74.

18 See Form CO, paragraph 87

19 See e-mail of 25/09/2020.

20 For instance, see: Case M.5253- Sanofi-Aventis/Zentiva (2009), Case M.5661- Abbott/Solvay Pharmaceuticals (2010), Case M.6278- Takeda/Nycomed (2011) and Case M.6613- Watson/Actavis (2012).

21 Additionally, the Notifying Party submits that [information concerning Mylan’s CMO activities]. See Form CO, footnote 61.

22 See Form CO, paragraph 80.