Commission, June 18, 2020, No M.9815

EUROPEAN COMMISSION

Decision

ADVENT / CINVEN / THYSSENKRUPP ELEVATOR

Subject: Case M.9815 – Advent/Cinven/thyssenkrupp Elevator

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 12 May 2020, the European Commission received notification of a concentration pursuant to Article 4 of the Merger Regulation which would result from a proposed transaction by which Advent International Corporation (US, “Advent”) and Cinven Capital Management (VII) General Partner Limited (UK, “Cinven”) intend to acquire joint control of the whole of thyssenkrupp Elevator AG (Germany, “tkE”). (Advent and Cinven are designated hereinafter as the 'Notifying Parties' and together with tkE as the “Parties”.) (3)

1. THE PARTIES

(2) Advent is an investment company active in the acquisition of equity stakes and the management of investment funds in various sectors, including business and financial services. Advent controls Rubix (4), a distributor of industrial maintenance and repair products and services.

(3) Cinven is an investment company active in the provision of investment management and investment advisory services to a number of investment funds.

(4) tkE is a wholly-owned subsidiary of thyssenkrupp AG, active in the installation and servicing of elevators, escalators, passenger boarding bridges and stairlifts, as well as directly related ancillary activities.

2. THE CONCENTRATION

(5) Pursuant to a share sale and purchase agreement dated 27 February 2020, Advent and Cinven will acquire tkE through a consortium (5) with co-investors (the “Transaction”). tkE will be jointly controlled by Advent and Cinven, in particular by virtue of their veto rights over key strategic matters such as the budget and business plan. Hence, the Transaction qualifies as a concentration within the meaning of Article 3(1)(b) of the EUMR.

3. UNION DIMENSION

(6) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million [Cinven: EUR […], Advent: EUR […]; tkE: EUR […]]. Each of them has a Union-wide turnover in excess of EUR 250 million [Cinven: EUR […], Advent: EUR […]; tkE: EUR […]], but they do not achieve more than two-thirds of their aggregate Union-wide turnover within one and the same Member State. The notified operation therefore has a Union dimension pursuant to Article 1(2) of the Merger Regulation.

4. RELEVANT MARKETS

4.1. Introduction

(7) The Transaction gives rise to a vertical link due to the activities of Advent’s portfolio company Rubix upstream and those of tkE downstream.

(8) In particular, this vertical link relates to the supply by Rubix of bearings used in the repair and maintenance of elevators and escalators.

(9) Bearings are the main item among a number of products and services that tkE procures from Rubix, totalling EUR […] out of less than EUR […]. Each of the other product groups are typically immaterial. The relevant upstream market therefore relates to the wholesale supply of bearings.

(10) As Rubix is a supplier of industrial maintenance, repair and overhaul (“MRO”) products, its bearings are typically not incorporated into new installations of elevators or escalators but are used in the repair or maintenance of elevators and escalators. The relevant downstream markets therefore relate to elevator and escalator repair and maintenance.

4.2. Market Definition

4.2.1.Upstream market: the wholesale supply of bearings

4.2.1.1. Product market definition

(11) Bearings are components that facilitate movement and reduce friction in machines. They have three key functions: (i) guiding motion, by supporting and guiding components that turn relative to one another (e.g. wheels, shafts, pivots), (ii) transmitting forces, and (iii) reducing friction.

(12) Bearings are used in various parts of elevator and escalator installations, such as motors, traction machines, drive wheels, gears and rollers, in order to guide motion and reduce friction. For both production and repair purposes, some of those bearings are procured as a pre-assembled part of an entire unit, while others are procured separately, depending on the manufacturer.

(13) The Parties suggest that the relevant product market is rolling bearings, with possible further sub-segments for ball and roller bearings, possibly also further sub- segmented for industrial use (6).

(14) The Parties submit that there should not be a separate market for bearings used for the elevators and escalators applications, as the bearings used for these products are standard industrial parts (7). Also, the Parties consider that there should be no distinction between original equipment manufacturers (OEM)/original equipment suppliers (OES) and independent aftermarket (IAM) customers, because both types of customers provide maintenance and repair services (8).

(15) A significant proportion of bearings incorporated in elevators and escalators are used in rollers, in particular step rollers, chain rollers, handrail rollers and guide rollers. Such rollers, which consist of a bearing around which a rubber or plastic ring is fitted by injection moulding, are procured as full units for both production and repair purposes. When asked about the use of bearings in escalators, several escalator MRO providers replied in terms of rollers. One escalator MRO provider stated in this respect: “as regards bearings for escalators, the Company understands this term to refer to rollers for chains and steps”. (9) Even though such rollers are components that are closely related to, but separate from, bearings, the Parties state that Rubix does not supply such products. They claim that these components are generally supplied directly by manufacturers such as faigle (rather than distributors such as Rubix) to escalator maintenance providers (10). This was supported by feedback from a bearings manufacturer, who stated: “the Company is not aware of any European manufacturers offering rollers for escalators and considers it unlikely that Rubix has a significant offer of such products”. (11)

(16) The Commission has not previously assessed product markets for bearings used in the maintenance and repair of elevators or escalators specifically. In previous decisions, the Commission considered that there may be separate sub-segments for different types of bearings, including ‘plain’ and ‘rolling’ bearings (12). The Commission has found that ‘rolling’ bearings may include two large sub-categories, namely (i) ball bearings, and (ii) roller bearings, which can be further sub-segmented. (13)

(17) The Commission has also considered that the above markets could be divided into separate markets according to the application for which the bearings are used or the type of customers purchasing those bearings (e.g. automotive vs industrial applications; OEM/OES vs Independent Aftermarket (“IAM”)) (14).

(18) The feedback from market participants confirmed that bearings used in elevator and escalator applications are typically multi-purpose products (15). A bearings manufacturer stated: “the Company manufactures bearings as standard industrial products, and is not aware of special bearings being offered for escalators”. (16)

(19) The Commission’s investigation has indicated that a segmentation between OEM and MRO supply channels may be relevant. Rubix annual reports refer to its market share for bearings in the MRO segment, while a bearings manufacturer distinguished between the MRO and the OEM channel when explaining its competitive relationship with Rubix in the supply of bearings (17).

(20) In any event, for the purpose of this Decision, it can be left open whether the market for the wholesale supply of bearing may be segmented based on the type of bearing, application or customer, as the Transaction does not give rise to serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement regardless of the precise product market definition.

4.2.1.2. Geographic market definition

(21) The Parties submit that the relevant geographic market is at least EEA-wide in scope.

(22) In a previous decision, the Commission considered that the geographic market of bearings sold to independent aftermarket service providers (IAM) in the automotive and industrial sectors is (at least) an EEA–wide in scope but left the relevant geographic market open (18).

(23) Feedback from market participants indicated that bearings may be sourced from China, but that delivery times and quality standards may be an issue, depending on the urgency and type of repair. An escalator MRO provider stated: “spare parts are offered in various standards of quality and most can also be sourced from Chinese suppliers. In general, customers are not against sourcing from China; it is a just a matter of how urgent the repair is, as delivery times from China can run up to 2-3 weeks” (19). A bearings manufacturer stated (20): “the company considers that the escalator business, compared with the elevator business, is less quality-oriented and more often uses bearings from low-cost countries such as China, in particular rollers […] However, European supplies of bearings are used for the more sophisticated parts of escalators such as gears boxes or e-motors”.

(24) In any event, for the purpose of this Decision, the Commission considers the geographic market to be at least EEA-wide in scope, but leaves the precise geographic market definition open, as the Transaction does not give rise to serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement under any of these plausible geographic market definitions.

4.2.2. Downstream market: repair and maintenance of elevators and escalators

4.2.2.1. Product market definition

(25) An elevator is a car that moves in a vertical shaft to carry passengers or freight up and down. Elevators are typically powered by electric motors that drive traction cables and counterweight systems. Elevators have a life span of up to 50 years.

(26) An escalator is made up of a set of interlocking steps, powered by an electric motor. The steps are moved along by a rotating pair of chains, looped around two pairs of gears. Escalators have a life span of up to 50 years.

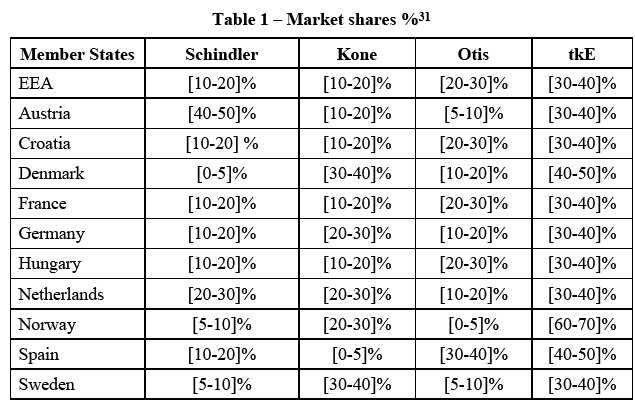

(27) In view of the long life spans of elevators and escalators, a significant proportion of the value chain consists of maintenance and repair which can either be done by the companies installing the equipment, or by alternative maintenance and repair operators.

(28) The Parties consider that there are two plausible alternative product market definitions: (i) a global market for the supply of maintenance services for elevators and escalators (combined); or (ii) two separate markets differentiating between maintenance services for each of (a) elevators; and (b) escalators (21).

(29) In previous decisions, the Commission considered (i) a broad market for elevator installation services comprising elevator installation, modernisation, and repair and maintenance services (22) and (ii) separate markets for (a) the sale and installation of elevators and escalators, (b) maintenance services, and (c) modernisation services. (23)

(30) The Commission has found that maintenance services reflect a separate, broad category including all maintenance and repair services provided with varying content, for instance monitoring and prevention services as well as repair and replacements of spare parts (24).

(31) As regards any potential subsegments within escalator repair and maintenance, feedback from market participants indicates that companies usually provide all the services related to escalators, namely installation, repair, maintenance and modernization. An escalator MRO provider stated: “the Company regards the market for the maintenance of escalators as one overall market as most providers offer the full range of services, from testing to repair, and contracts typically include a wide range of such services” (25).

(32) In light of the feedback from market participants and the information available to it, the Commission concludes that the product market for the repair and maintenance of elevators and escalators could be segmented into (i) repair and maintenance services for elevators and escalators (combined); and (ii) repair and maintenance services for each of: (i) elevators; and (ii) escalators.

(33) In any case, for the purpose of this Decision, it can be left open whether the relevant market for the repair and maintenance of elevators and escalators may be subsegmented based on the number and types of portfolio services, as the Transaction does not give rise to serious doubts as to its compatibility with the internal market regardless of the precise product market definition.

4.2.2.2. Geographic market definition

(34) The Parties agree with the geographic market definition set out in the Commission’s prior decisional practice (26).

(35) In a previous decision, the Commission found the geographic market of maintenance and modernisation services for escalators to be national in scope. (27)

(36) Feedback from market participants indicated that customer preferences and regulations for services provided on escalators vary among countries and that national presence is required. An escalator MRO provider stated: “the Company regards the market for maintenance of escalators as different on a national basis as customer preferences and regulations vary from country to country and market presence in each country is necessary to make the business profitable” (28).

(37) In any event, for the purpose of this Decision, the Commission considers the geographic market for the repair and maintenance of escalators and elevators to be national in scope, but leaves the precise geographic market definition open, as the Transaction does not give rise to serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement under any of these plausible geographic market definitions.

5. COMPETITIVE ASSESSMENT

(38)None of Advent’s or Cinven’s portfolio companies have a direct presence in any of the markets in which tkE operates, namely the installation and servicing of elevators, escalators, passenger boarding bridges and stairlifts, as well as directly related ancillary activities in the EEA. Rubix provides repair and maintenance services, but not for elevators or escalators. The Parties' relationship is therefore only vertical, through Advent’s ownership interest in Rubix.

(39) In view of the vertical links between Rubix and tkE, the Commission will assess in this Section the relation between the upstream wholesale of bearings where Rubix is active and the downstream market for the repair and maintenance of elevators and escalators in which tkE will remain active.

5.1. Market structure in upstream markets

(40) The Parties estimate Rubix’ market share in EEA in bearings sold to elevator and escalator customers at respectively [0-5]%. For the narrower segment of bearings used only for escalator repair and maintenance, Rubix’ market share in EEA is [20-30]% according to the Parties. According to the latest annual reports available from Brammer, the Rubix business unit making up the bulk of the group’s activity in bearings, the company’s market share in bearings sold to the MRO channel was around 10%. The Parties state that they cannot calculate precise market share estimates for Rubix’s competitors in relation to a narrow segment for the supply of bearings for elevator and escalator applications, let alone for an even narrower sub- segment for the supply of bearings for escalator repair and maintenance.

(41) However, the Parties estimate that the largest manufacturers of bearings, in particular SKF (including Cooper), Schaeffler, NTN SNR, NSK and Timken, have larger market shares than Rubix via their direct sales in relation to elevator and escalator applications overall and escalator repair and maintenance specifically. They submit that a wide range of other distributors of bearings are also active throughout the relevant markets in the EEA, including Acorn, BDI, the Bianchi Group, the Blässinger Group and the Descours & Cabaud Group.

(42) Feedback from a bearings supplier (29) shows that the escalators market is not the focus of Rubix’s usual activity: “Rubix distributes around 5000 different products to various industries such as cement and steel plants. The Company does not consider the escalator market to be a usual target area for industrial distributors in general”.

5.2. Market structure in downstream markets

(43) If a global market for the repair and maintenance of both escalators and elevators is considered, tkE’s markets shared would be lower than 30% both EEA-wide and on a national basis and would therefore not give rise to any affected markets.

(44) If a separate market only for repair and maintenance of escalators is considered, a number of national market will be affected, for instance: Austria [30-40]%, Croatia [30-40]%, Denmark [40-50]%, France [30-40]%, Germany [30-40]%, Hungary [30-40]%, Netherlands [30-40]%, Norway [60-70]%, Spain [40-50]% and Sweden [30-40]%, with an EEA-wide market share of around [30-40]% in 2019. These national markets will therefore be considered affected markets.

(45) In the EEA market for escalator repair and maintenance services, the main tkE’s competitors are Kone, Schindler, and Otis. In escalator repair and maintenance on an EEA basis, Otis has a [20-30]% market share, Kone [10-20]%, Schindler [10-20]% and other competitors [10-20]%. These competitors are also tkE’s main rivals in the various Member States in which tkE’s share exceeds 30%, please see Table 1 below. Referring to the national markets for for escalator repair and maintenance services a MRO provider stated: “In smaller countries the big companies do not have the local personnel for installing, repairing and maintaining the escalators, choosing to subcontract such services to smaller companies except for some limited maintenance services. In the markets for services for escalators there several more companies competing with the big players. In the Netherlands there are 6-7 such companies, including Structon and Orona” (30).

5.3. Vertical assessment

5.3.1. Input foreclosure

(46) The Parties submit (32) that even on the wholesale of bearings to escalator repair and maintenance services on a national basis, Rubix’s share of supply is not significant and as such cannot raise any input foreclosure concerns given its lack of market power. This is particularly so as Rubix is a distributor and not a manufacturer of bearings and both direct sales from manufacturers and a variety of other distributors would remain available to customers seeking bearings for elevator and escalator applications following the Transaction. According to the Parties, bearings represent only an insignificant cost factor for elevator and escalator companies, including tkE. tkE estimates that bearings represented approximately […]% of its total purchase volume in FY 2018/2019, and that bearings represent approximately […]% of the total cost of an elevator or escalator. (33)

(47) The outcome of the market investigation shows that the risk of input foreclosure through the notified concentration appears limited. It seems unlikely that, post- merger, Rubix would restrict access to its products by other escalator repair and maintenance providers competing against tkE in any of the EEA countries. The outcome of the investigation indicates that the Transaction in general does not seem to raise any input foreclosure concerns (34): “the Company considers that the transaction will have a positive impact on the market and will be good for tkE. […] Although it anticipates that tkE under new ownership will try to lower the price for Mulder Montage, the company does not consider that the transaction will have a negative impact on its business”. None of the escalator maintenance providers participating to the investigation (in Spain, the Netherlands and Germany) was aware of Rubix as a potential supplier of bearings for their activities: “the Company is not familiar with Rubix/Brammer as a potential supplier of escalator parts” (35).

(48) Rubix’ market share in bearings sold to escalator repair and maintenance companies is not significant, estimated at [20-30]% in the EEA. In addition, the market in which Rubix operates is fragmented, which means that rival escalator repair and maintenance companies would have many alternative sources for the procurement of bearings after the merger. The main source remain the manufacturers of bearings, in particular SKF (including Cooper), Schaeffler, NTN SNR, NSK and Timken, but also other distributors of bearings are also active throughout the relevant markets in the EEA, including Acorn, BDI, the Bianchi Group, the Blässinger Group and the Descours & Cabaud Group.

(49) Furthermore, it appears that bearings are largely commoditised products that can be sourced from a wide range of suppliers. Feedback from market participants has confirmed that manufacturers such as SKF also sell directly (36) to escalator and elevator maintenance companies. A MRO provider indicated in this respect that “the Company buys most of its rollers from Chinese trading companies and occasionally from SKF when required” (37), even though some manufacturers, such as Schaeffler (38), seem to be more focused on the OEM rather than the MRO (Maintenance, Repair and Overhaul) channel. In any case, a wide range of other distributors of bearings seem to be active throughout the relevant markets. Feedback from market participants has indicated that spare parts used in escalator repair and maintenance tend to be more lower-end products compared to elevator repair and maintenance and that bearings for escalator repair and maintenance are often sourced from Chinese suppliers, depending on the urgency of the repair (39). A MRO provider stated that “The Company procures most of its spare parts from Chinese manufacturers and distributors, except when end customers insist on original OEM replacement parts, which the Company then procures from the manufacturers or specialised suppliers. 90%-95% of escalator parts can be bought freely on the market” (40).

(50) In addition, more than […]% of Rubix’ sales of bearings for repair and maintenance for escalators are made with tkE’s competitors. Stopping its sales to those companies and selling exclusively to tkE is likely to lead to reduced sales of Rubix’ products as it seems unlikely that tkE could take over a large part of the sales of its competitors due to such strategy. Moreover, bearings represent a small share of escalator repair and maintenance providers’ costs, estimated at less than 5% (41): “Rollers make up around 5-10 % of all replaced spare parts, and so only 2%-5% of the overall cost” (42); “Bearings are not often replaced in escalators if they are of good quality and they represent less than 5% of overall cost. Bearings are not in the top 5 of spare parts in terms of average cost” (43).

(51) As stated above in paragraph 45, tkE competes downstream with Kone, Schindler, and Otis in each Member State where it exceeds 30% market share in downstream markets, and particularly: Austria [30-40]%, Croatia [30-40]%, Denmark [40-50]%, France [30-40]%, Germany [30-40]%, Hungary [30-40]%, Netherlands [30-40]%, Norway [60-70]%, Spain [40-50]% and Sweden [30-40]%. Therefore, the merged entity would face enough competition pressure post-Transaction and no competition concerns should arise in any of the affected national markets.

(52) In the light of the above considerations and taking the information available to it and the results of the market investigation into account, the Commission considers it is unlikely that Advent would have the ability or the incentive to successfully raise rivals’ costs in relation to the products supplied by Rubix. Therefore, the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement as the Parties will have neither the ability nor the incentive for input foreclosure in relation to the markets for the repair and maintenance services for escalators.

5.3.2. Customer foreclosure

(53) The Parties submits (44) that any customer foreclosure concerns would be negated by the structure of the Transaction - namely, the acquisition of tkE through a consortium. Even if Advent had the incentive to favour Rubix over other suppliers, Cinven would have an incentive for tkE Elevator and Escalator Business to continue sourcing its supply of the products offered by Rubix from whichever suppliers are most competitive (on price, quality, or other factors).

(54) The Commission finds, based on the market investigation, that the risk of customer foreclosure appears to be limited as it seems unlikely that, post-merger, tkE would be able to affect the competitiveness of Rubix’ competitors by foreclosing suppliers of bearings. The outcome of the investigation indicates that the transaction in general does not seem to raise any customer foreclosure concerns (45): “The Company considers that the transaction will have a positive impact on the market and will be good for competition. The Company considers that the industry has seen little innovation for some time and has been very much dominated by the four main players in the market (Otis, tkE, Schindler and Kone). It considers that new owners and new management for tkE may modernise the industry and bring new opportunities also for other market players such as the Company” (46).

(55) As bearings seem to be largely commoditised products with multiple applications, they can be supplied to customers in various industries. If Rubix’ competitors lost potential sales it would be doubtful that this would impact their competitiveness, given that they could keep selling to all alternative customers, not only in escalator repair and maintenance but in all other sectors requiring bearings.

(56) In addition, any customer foreclosure concerns would most likely be mitigated by the transaction structure, namely the fact that Advent would share control over tkE with Cinven. If Advent had any incentive to favour Rubix over other suppliers, Cinven would have an incentive for tkE to continue sourcing its supply of the products offered also by Rubix from the most competitive suppliers in terms of price and quality.

(57) Therefore, it is unlikely that customer foreclosure will arise from the transaction in relation to the markets for the repair and maintenance services for escalators in Austria, Croatia, Denmark, France, Germany, Hungary, Netherlands, Norway, Spain and Sweden.

(58) In light of the considerations in paragraphs (38) to (57) above as well as all evidence available to it, the Commission considers that, the Transaction will not give rise to serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement due to vertical non-coordinated effects under any plausible market definition.

6. CONCLUSION

(59) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This Decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the “Merger Regulation”). With effect from 1 December 2009, the Treaty on the Functioning of the European Union (“TFEU”) has introduced certain changes, such as the replacement of “Community” by “Union” and “common market” by “internal market”. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the “EEA Agreement”).

3 Publication in the Official Journal of the European Union No C174 of 25.5.2020, p. 7.

4 Rubix was previously known as Advent portfolio company IPH/Brammer. The acquisition of IPH by Advent was approved by the European Commission in 2017 (Case M.8524 – Advent International Corporation/Industrial Parts Holding). Advent’s acquisition of Brammer was approved by the European Commission in 2017 (Case M.8316 – Advent/Brammer).

5 […].

6 Form CO, paragraph 81, 84 and 99.

7 Form CO, paragraph 79.

8 Form CO, paragraph 80.

9 Minutes of call with Escalator MRO provider, 14 May 2020.

10 Form CO, paragraph 101, Response of 20 May 2020 to RFI 4, paragraph 2.1.

11 Minutes of call with bearings manufacturer, 15 May 2020.

12 See e.g. Commission decision of 11 October 2011, INA/FAC (M.2608).

13 Commission decision of 27 March 2007, NTN/SNR (M.4346), Commission decision of 19 December 2008, Schaeffler/Continental (M.5294).

14 Commission decision of 11 October 2011, INA/FAC (M.2608), recital 13.

15 Minutes of call with MRO provider, 14 May 2020, paragraph 15; Minutes of call with MRO provider, 19 May 2020, paragraph 13; Minutes of call with Bearings Supplier, 15 May 2020, paragraph 3.

16 Minutes of call with bearings manufacturer, 15 May 2020, paragraph 3.

17 Minutes of call with bearings manufacturer, 15 May 2020.

18 Commission decision of 19 December 2008, Schaeffler/Continental (M.5294).

19 Minutes of call with MRO provider, 19 May 2020, paragraph 11.

20 Minutes of call with Bearings Supplier, 15 May 2020, paragraph 10.

21 Form CO, paragraph 70.

22 Commission decision of 2 December 2010, Triton III Holding 6/Wittur Group (M.5991).

23 Commission decision of 21 February 2007, PO/Elevators and Escalators (COMP/E-1/38.823).

24 Ibidem.

25 Minutes of call with MRO provider, 19 May 2020, paragraphs 2 and 10; Minutes of call with MRO provider, 14 May 2020, paragraph 5.

26 Form CO, paragraphs 57-61.

27 Case COMP/E-1/38.823, PO/Elevators and Escalators.

28 Minutes of call with MRO provider, 14 May 2020, paragraph 7; Minutes of call with MRO provider, 19 May 2020, paragraph 2; Minutes of call with MRO provider, 13 May 2020, paragraph 2.

29 Minutes of call with Bearings Supplier, 15 May 2020, paragraph 8.

30 Minutes of call with MRO provider, 14 May 2020, paragraphs 11 and 12.

31 Form CO, Annex 29.

32 Form CO, paragraph 130.

33 Form CO, paragraph 140.

34 Minutes of call with MRO provider, 19 May 2020, paragraph 17; Minutes of call with MRO provider, 14 May 2020, paragraph 19; Minutes of call with MRO provider, 13 May 2020, paragraph 15; Minutes of call with Bearings Supplier, 15 May 2020, paragraph 13.

35 Minutes of call with MRO provider, 14 May 2020, paragraph 9.

36 Minutes of call with MRO provider, 19 May 2020, paragraph 12; Minutes of call with MRO provider, 13 May 2020, paragraphs 8 and 10.

37 Minutes of call with MRO provider, 14 May 2020, paragraph 18.

38 Minutes of call with Bearings Supplier, 15 May 2020, paragraph 12.

39 Minutes of call with MRO provider, 19 May 2020, paragraph 11; Minutes of call with MRO provider, 13 May 2020, paragraphs 8 and 9.

40 Minutes of call with MRO provider, 14 May 2020, paragraph 14.

41 Minutes of call with MRO provider, 13 May 2020, paragraph 13.

42 Minutes of call with MRO provider, 14 May 2020, paragraph 18.

43 Minutes of call with MRO provider, 19 May 2020, paragraph 15.

44 Form CO, paragraph 142.

45 Minutes of call with MRO provider, 19 May 2020, paragraph 17; Minutes of call with MRO provider, 14 May 2020, paragraph 19; Minutes of call with Bearings Supplier, 15 May 2020, paragraph 13.

46 Minutes of call with MRO provider, 13 May 2020, paragraph15.