Commission, October 6, 2020, No M.9669

EUROPEAN COMMISSION

Decision

PPF GROUP / CENTRAL EUROPEAN MEDIA ENTERPRISES

Subject: Case M.9669 – PPF GROUP / CENTRAL EUROPEAN MEDIA ENTERPRISES

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 1 September 2020, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which PPF Group N.V. ("PPF" or the "Notifying Party", Netherlands) proposes to acquire within the meaning of Article 3(1)(b) of the Merger Regulation sole control of the whole of Central European Media Enterprises Ltd. ("CME", Bermuda) (the “Transaction”).3. PPF and CME are collectively referred to as the "Parties".

1. THE PARTIES

(2) PPF is a multinational finance and investment group focusing on financial services, consumer finance, telecommunications, biotechnology, retail services, real estate and agriculture. Through its subsidiaries (namely, O2 CR and CETIN in Czechia, O2 SK in Slovakia and Telenor in Bulgaria), PPF is active in the audio-visual and telecommunications sectors. Its activities include: (i) the acquisition of broadcasting rights to sport events in Czechia and Slovakia; (ii) the wholesale supply of TV channels in Slovakia; (iii) the retail supply of audio-visual services through IPTV and a video on demand (“VOD”) platform in Czechia and Slovakia; (iv) the sale of TV advertising space in Czechia; (v) the provision of retail fixed internet access services in Czechia and Slovakia; as well as (vi) the provision of retail telecommunications services in Czechia, Slovakia and Bulgaria. PPF is ultimately owned and controlled by Mr. Petr Kellner.

(3) CME is a media and entertainment company active in TV broadcasting and other media sectors, primarily in Bulgaria, Czechia, Slovakia, Romania and Slovenia. In particular, in Czechia, Slovakia and Bulgaria CME is present respectively through TV Nova, Markiza and bTV in various audio-visual markets. CME’s activities include (i) the acquisition of broadcasting rights to pre-produced audio-visual content; (ii) the wholesale supply of free-to-air (“FTA”) and pay TV channels; and (iii) the sale of TV advertising space. CME also is marginally active in the supply of retail audio-visual services via a VOD platform. CME is ultimately controlled by AT&T, Inc., which holds an approximately 75% aggregate beneficial ownership interest in CME through its wholly owned subsidiaries Warner Media, LLC, and Time Warner Media Holdings B.V.

2. THE CONCENTRATION

(4) On 27 October 2019, CME and two of PPF’s affiliates, TV Bidco B.V. and TV Bermuda Ltd, entered into the Agreement and Plan of the Merger (the “Agreement”). Pursuant to the Agreement, TV Bermuda Ltd. will merge with and into CME, with CME continuing as the surviving company in the merger as a wholly-owned subsidiary of TV Bidco B.V.

(5) As a result of the Transaction, PPF will therefore acquire indirect sole control of CME and its subsidiaries within the sense of Article 3(1)(b) of the Merger Regulation.

3. EU DIMENSION

(6) The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 5 000 million (PPF: EUR […]; CME: EUR […]). Each of them has an EU-wide turnover in excess of EUR […] (PPF: EUR […]; CME: EUR […]), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension pursuant to Article 1(2) of the Merger Regulation.

4. RELEVANT MARKETS

4.1. Introduction

(7) As a preliminary remark, the Commission notes that while CME is active in Czechia, Slovakia, Bulgaria, Romania and Slovenia, PPF is not active in any relevant market in Romania and Slovenia. Therefore, the Transaction does not lead to any horizontal or vertical overlaps in these two Member States and they will not be further discussed in this decision.

4.2.The audio-visual value-chain

(8) Audio-visual ("AV") content comprises all products (films, sports, series, shows, live events, documentaries, etc.) that are broadcast via any media. In previous decisions, the Commission has identified different activities in the AV value chain, namely: (i) the production of AV content; (ii) the licensing of broadcasting rights for AV content; (iii) the wholesale supply of TV channels; and (iii) the retail provision of AV services to end customers. In addition, the Transaction relates to: (iv) the sale of TV advertising space; (v) the retail supply of mobile telecommunications services; and (vi) the retail supply of fixed internet access services.

(9) The following sections further describe these levels of the AV value-chain as well as provide an overview of the Parties' activities at each level in Czechia, Slovakia and Bulgaria.

4.3. Market for the licensing of broadcasting rights for pre-produced audio-visual content

4.3.1. Introduction

(10) The upstream level of the value chain concerns the production of new AV content. The parties are not active in this market.

(11) The rights to AV “entertainment products” generally then belong to the creators of the content. These rights-holders license them to (i) TV channel suppliers (TV broadcasters), which then incorporate the AV content into linear TV channels, or (ii) content platform operators, which then retail the AV content to end users on a non- linear basis (that is to say, Pay-Per-View (“PPV”) or VOD), including non- traditional platforms, that is to say internet or so-called Over The Top (“OTT”) platforms.

(12) TV broadcasters and TV distributors who source content for their TV channels or retail TV services generally have a choice between a number of sourcing models, which can be broadly categorised as follows:a. Obtaining TV content produced on an “ad hoc” basis (that is to say tailor- made), by:i. Commissioning TV content from a TV production company (which owns the relevant TV format);ii. Hiring a TV production company to provide the technical means and deliver the finished TV content based on a format owned by the broadcaster; oriii. Producing the content themselves by relying on their in-house facilities (captive TV production); orb. Acquiring broadcasting rights from TV production companies for pre- produced TV content (pre-produced TV content, sometimes referred to as off-the-shelf or tape sales).

(13) As regards pre-produced TV content, this upstream level of the value chain concerns the licensing of broadcasting rights relating to pre-existing TV content – that is to say TV content that has been previously produced and is subsequently made available ‘off-the-shelf’ by the rights holder (so-called pre-produced TV content) – and broadcasting rights relating to sports events.

(14) The broadcasting rights relating to TV content can belong to one or more of the following: (i) the holder of the rights to the TV format; (ii) the production company that produced the TV content; and (iii) the company that commissioned the production of the TV content. In addition, the broadcasting rights can belong to a third-party distributor, to which they were licensed by the original owner, with a right to sub-license.

(15) As regards the supply-side of the market:a. In Czechia, PPF, through its subsidiary O2 CR, creates content for its own O2 TV channels.In Slovakia, O2 CR produces a customized channel for a single customer, Orange a. s. (“Orange”). This channel is produced and distributed under the Orange brand and is built using broadcasting rights for the UEFA Champions League for Slovakia which are owned by O2 CR. O2 CR [information about O2 CR’s production activities].b. CME creates content and licenses the related rights for its own TV channels.In Czechia, CME neither sells nor licenses its content to third parties; it only provides certain input services to third parties, primarily comprising dubbing and subtitling services.In Slovakia, CME licenses TV content to third parties to a very limited extent.4

(16) As regards the demand-side of the market: a. In Czechia, PPF, through O2 CR, purchases broadcasting rights to audio- visual sports related content for its TV channels O2 TV Sport, O2 TV Tenis and O2 TV Fotbal. PPF acquires TV rights to sporting events, such as football, ice hockey, or basketball. The most important sporting events to which PPF acquired broadcasting rights in Czechia are: (i) UEFA Champions League matches for broadcast, (ii) Czech Fortuna Liga (football), (iii) Czech Extraliga (ice hockey), and (iv) WTA.In Slovakia, O2 CR holds the broadcasting rights for UEFA Champions League matches and for the Czech football and ice hockey leagues.b. In Czechia, CME acquires various types of content rights, including sports, foreign movies, domestic movies, series, and other rights. In relation to sporting rights, CME focuses on licensing rights to: (i) the U.S. branded sports, such as NHL (ice hockey), NBA (basketball) or UFC (martial arts),(ii) mainstream European sports, (iii) motorbike MOTO GP, and (iv) emerging sports, such as darts or rugby. In Slovakia, CME acquires various types of content rights, including sports, foreign movies, domestic movies, series, and other rights. In relation to sporting rights, CME focuses on licensing rights to: (i) the U.S. branded sports, such as NHL (ice hockey), NBA (basketball) or UFC (martial arts),(ii) mainstream European sports, (iii) motorbike MOTO GP, and (iv) emerging sports, such as darts or rugby.

4.3.2. Product market definition

4.3.2.1. Commission precedents

(17) With regard to the market for the supply of broadcasting rights, in previous decisions, the Commission has observed that content production companies produce TV content either (i) for internal use through incorporation into their own TV channels or VOD services if they are vertically integrated in the wholesale supply of TV channels and/or in the retail of TV services (i.e. captive TV production); or (ii) for supply to third-party customers (i.e. non-captive TV production).5 However, the Commission has previously found the product market for the production of TV content to be limited to non-captive TV production, thereby excluding captive TV production, as this TV content is not offered on the market.6

(18) With regard to the market for the in-licencing of TV broadcasting rights, the Commission has considered that it may be further subdivided by nature and content type, in particular: (i) premium films; (ii) football events that take place regularly (every year); (iii) football events that are played more intermittently;7 and (iv) other sports.8

(19) The Commission has also considered sub-dividing the market for the licensing of broadcasting rights for TV content into: (i) pay TV / FTA audio visual content; (ii) TV content for linear (TV channels) / non-linear broadcast (VOD), or into the more narrowly defined segment of iii) VOD / PPV / first pay TV window / second pay TV window / FTA TV.9

4.3.2.2. Notifying Party’s view

(20) The Notifying Party submits that the relevant market is the market for the licensing of TV broadcasting rights for (linear) TV channels, with potential further segmentation based on content into the licensing of TV broadcasting rights to (i) football events, and (ii) other sports. The Notifying Party considers that it is irrelevant to consider other market segmentations due to the lack of overlap of Parties activities in these segments and given the substitutability of various rights from the perspective of TV broadcasters.10

4.3.2.3. Commission’s assessment

(21) The results of the market investigation indicate that most content providers and broadcasters consider that the segmentations adopted in prior Commission decisions (by content type and exhibition window as indicated above) remain relevant.11

(22) In any event, for the purpose of this decision, the exact product market definition for the licensing of broadcasting rights can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market regardless of whether the market is segmented on the basis of content type or exhibition window as set out above.

4.3.3. Geographic market definition

4.3.3.1. Commission precedents

(23) The Commission has previously considered the market for the licensing of TV broadcasting rights to be either national or regional, based on linguistically homogeneous areas.12

4.3.3.2. Notifying Party’s view

(24) The Notifying Party submits that the relevant market should be defined as national in scope because, despite the proximity of the territories of Czechia and Slovakia, tender procedures and languages differ in these countries. The Notifying Party submits that in any event the substantive analysis would not be materially different if the markets were combined into a region encompassing both Czechia and Slovakia.13

4.3.3.3. Commission’s assessment

(25) The results of the market investigation show that the majority of the respondents license their content on a national basis. For specific content, the licenses sometimes cover smaller or larger areas.14 Accordingly, most of the respondents among TV broadcasters purchase content nationally or for certain linguistic regions. Broadcasters sometimes also purchase content on an EEA basis.15 The type of rights that this decision addresses, namely sports rights, are usually tendered and acquired at national level.

(26) Therefore, the Commission considers that, for the purpose of this decision, the geographic market definition for the licensing of broadcasting rights is national in scope.

4.4. Market for the wholesale supply of TV channels

4.4.1. Introduction

(27) TV broadcasters package the AV content that they have acquired or produced in- house into linear TV channels. The demand side of this market comprises TV retailers, which aggregate TV channels and provide them to end users via various distribution infrastructures either on a FTA basis or on a pay TV basis.

(28) At a very general level, FTA channels are TV channels that are available to viewers free of charge. Pay TV channels are channels for which the viewer must pay a subscription fee. Traditionally, FTA channels finance their operations via advertising revenues (with the exception of the publicly-owned TV channels in a number of Member States which are subject to advertising limitations), while pay TV channels generate revenues through subscription fees.

(29) The Commission notes that TV broadcasters are increasingly complementing their traditional linear TV channel offering with non-linear services such as VOD services.

(30) Some TV broadcasters are vertically integrated as they are also active as retail TV operators (TV distributors) in the market for the retail provision of TV services to end users. Other TV broadcasters are not vertically integrated and rely on third party TV distributors to distribute their TV channels at the retail level.

(31) As regards the supply-side of the market:a. PPF is not active on the market for the wholesale supply of TV channels in Czechia and Bulgaria. O2 CR incorporates content licensed from third parties as well as its own content into its own O2 TV Sport channels, which it then offers to viewers on its own IPTV platform (O2 TV) in Czechia. O2 CR does not offer these channels to other distributors on the wholesale market.In Slovakia, O2 CR supplies a customized channel to Orange since 2018.16b. CME supplies TV channels on a wholesale basis to cable, satellite, IPTV and other platform distributors in Czechia, Slovakia and Bulgaria through the following subsidiaries:i. TV Nova s.r.o. in Czechia under the brand name “TV Nova”;ii. MARKÍZA-SLOVAKIA spol. s.r.o. in Slovakia under the brand name “Markíza”;iii. bTV Media Group EAD in Bulgaria under the brand name “bTV”.In Czechia, CME offers the following channels: nova, nova 2, nova Gold, nova Cinema, nova Action, nova Sport 1, nova Sport 2 and Nova International.In Slovakia, CME offers the following channels: Markíza, TV Doma, Dajto, nova Sport 1, nova Sport 2 and nova International.In Bulgaria, CME offers the following channels: bTV, bTV Comedy, bTV Cinema, bTV Action, bTV Lady and Ring.

(32) As regards the demand side of the market:a. PPF acquires TV channels for its IPTV platform in Czechia and Slovakia.b. CME is not active on the demand-side of the market.

4.4.2. Product market definition

4.4.2.1. Commission precedents

(33) In previous decisions, the Commission has identified a wholesale market for the supply of TV channels. Within that market, the Commission has identified two separate product markets for: (i) FTA TV channels; and (ii) pay TV channels, pointing to the differences between the financial models of these channels.17 The Commission has further concluded that within the pay TV channel market, there are separate markets for: (i) premium pay TV channels; and (ii) basic pay TV channels.18 The Commission has considered FTA channels to be in the market for basic pay TV channels.19

(34) The question whether this market could be sub-divided by channel genre20, in particular: (i) film; (ii) sport; (iii) news; (iv) youth; and by infrastructure used for transmission21: (i) cable; (ii) satellite; (iii) DTT; (iv) IPTV has been left open in previous decisions. The Commission has considered that individual premium sports channels do not form a separate market even if they show sports content that is particularly interesting to the same group of viewers.22

4.4.2.2. Notifying Party’s view

(35) The Notifying Party submits that the Transaction should be assessed on the basis of the market for the wholesale supply of TV channels. In particular, it considers that it is not relevant to sub-divide the market by channel genre or by infrastructure used for transmission.23

4.4.2.3. Commission’s assessment

(36) The market investigation did not provide a clear indication of the relevance of the distinctions drawn between FTA and pay TV channels as well as between basic and premium pay TV. Although a number of broadcasters and distributors agreed with these distinctions, several respondents found the difference to be negligible because both channels types compete for the same content. Additionally, respondents found that these channels compete for the same audiences as all pay TV subscribers can access FTA channels. Respondents additionally pointed to the fact that the penetration of premium pay TV services is rather limited in Czechia.24

(37) With regard to the distinction between basic pay TV channels and FTA channels, respondents to the market investigation pointed out that in Czechia and in Slovakia basic pay TV mainly shows content that is also available through FTA TV and thus only differs in the infrastructure used for transmission.25

(38) The majority of distributors are of the view that thematic channels are only substitutable with other channels that broadcast the same specific content.26

(39) In any event, for the purpose of this decision, the exact product market definition for the wholesale supply of TV channels can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market regardless of whether the market is segmented on the basis of channel genre or between FTA TV channels and premium/basic pay TV channels.

4.4.3. Geographic market definition

4.4.3.1. Commission precedents

(40) The Commission has previously considered the market for the wholesale supply of TV channels to be either national or regional, based on linguistically homogeneous areas.27

4.4.3.2. The Notifying Party’s view

(41) The Notifying Party submits that the relevant geographic market should be defined as national in scope.28

4.4.3.3. Commission’s assessment

(42) In the present case, the market investigation indicated that the agreements for the wholesale supply of TV channels are, as a general rule, negotiated on a national basis, although they are also sometimes negotiated on a linguistic basis. Exceptionally, agreements are also entered into on a sub-national or EEA basis.29 This is mainly explained by the fact that TV retailers mostly have a national footprint, and that negotiations take place, and prices are set on a national basis.

(43) In light of the above, the Commission considers that the market for the wholesale supply of TV channels is national.

4.5. Market for the retail supply of audio-visual services

4.5.1. Introduction

(44) In the market for the retail supply of TV services, TV distributors provide end users with TV services, which typically consist of: (i) linear TV channels; and (ii) content aggregated in non-linear services, such as Subscription Video on Demand (“SVOD”), Transactional VOD (“TVOD”) and Advertising VOD (“AVOD”).

(45) AV distributors either limit themselves to carrying TV channels and making them available to end users, or also act as content aggregators, which ‘package’ AV channels. The AV services supplied by AV distributors to end users consist of: (i) packages of linear TV channels (which they have either acquired or produced themselves); and (ii) content aggregated in non-linear services, such as VOD, SVOD, TVOD and PPV. AV content can be delivered to end users through a number of technical means including cable, satellite and IPTV. OTT players deliver channels and content in both a linear and non-linear fashion through the use of the internet.

(46) As regards the supply-side of the market:a. In Czechia, PPF (through its subsidiary O2 CR) operates an IPTV platform (O2 TV). Additionally, it operates a VOD platform as a supplementary service.In Slovakia, PPF is marginally active on the AV retail market, via the mobile operator O2 SK’s digital television offers (O2 TV) over mobile and IPTV platforms.In Bulgaria, PPF is active through its subsidiary Telenor Bulgaria, which distributes AT&T’s “HBO GO” VOD service as an add-on to or part of its mobile tariffs.b. CME operates a VOD platform, Voyo, in Czechia, Slovakia and Bulgaria and offers an AVOD service on its website.

4.5.2. Product market definition

4.5.2.1. Commission precedents

(47) In previous decisions, the Commission considered the retail provision of FTA TV and pay TV services as separate markets.30 The Commission also considered whether retail pay TV could be segmented further according to: (i) linear vs non- linear pay TV services31; or (ii) premium vs basic pay TV services32. With regard to the type of distribution technology, the Commission tends to include different technologies within the same product market, but has ultimately left open the precise market definition.33

4.5.2.2. Notifying Party’s view

(48) The Notifying Party submits that the Transaction should be assessed on the basis of the market for the retail supply of pay TV services. In particular, the Notifying Party considers that it is irrelevant to consider other market segmentations due to the lack of overlap in these segments and substitutability of the services from the perspective of TV customers.34

4.5.2.3. Commission’s assessment

(49) The results of the market investigation indicated that all distributors provide both linear and non-linear services.35 However, respondents indicated that broadcasting rights for linear and non-linear services may be acquired separately or together depending on each individual broadcaster.36 A majority of distributors did not consider VOD services offered by OTT providers substitutable to pay TV services.37

(50) In any event, for the purpose of this decision, the exact product market definition for the retail supply of TV services can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market regardless of whether the market is further segmented or not.

4.5.3. Geographic market definition

4.5.3.1. Commission precedents

(51) In its previous decisions, the Commission considered the market for the retail supply of TV services to be national in scope, since suppliers compete on a nationwide basis for the business of end customers, or corresponding to the relevant language area.38 The Commission found that the market can be limited to the geographic coverage of a supplier’s infrastructure.39

4.5.3.2. Notifying Party’s view

(52) The Notifying Party submits that the relevant geographic market should be defined as national in scope.40

4.5.3.3. Commission’s assessment

(53) Nothing in the market investigation contradicts the Commission's previous findings that the market is either national, or corresponds to the relevant language area as the distributors offer their services mainly on a national basis.41 The countries in which the parties are active in retail TV services, namely Czechia, Slovakia, and Bulgaria, also constitute linguistic regions.

(54) The Commission considers, for the purposes of this decision, that the relevant geographic market for the retail provision of TV services is national in scope.

4.6. Market for the sale of TV advertising space

4.6.1. Introduction

(55) TV broadcasters sell advertising space on their TV channels and on their OTT services. The sale of advertising space is an important source of revenues for FTA channels, while pay TV channels in general rely more on fees from retail providers of AV services or from end users.

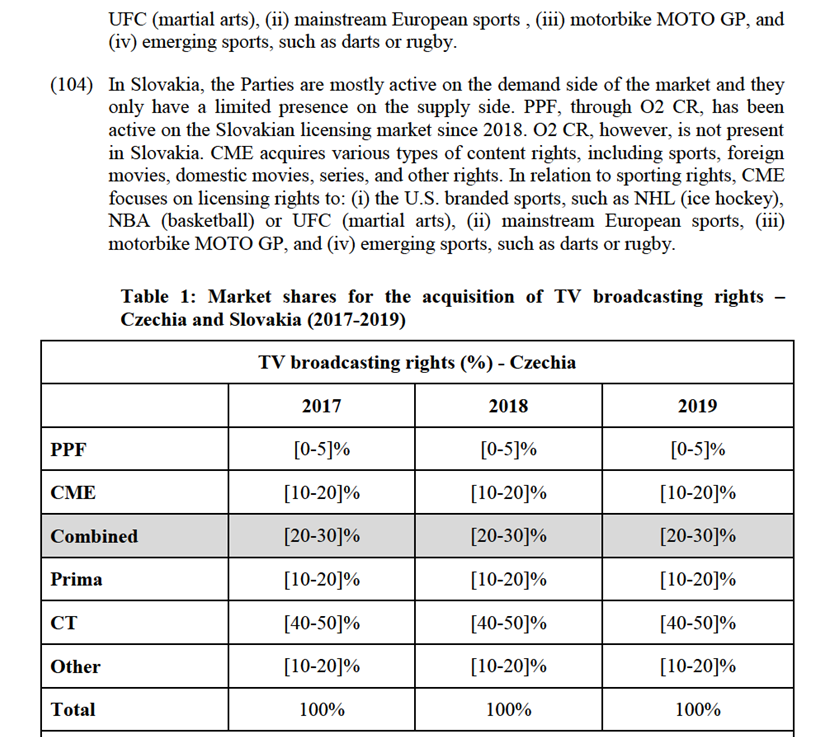

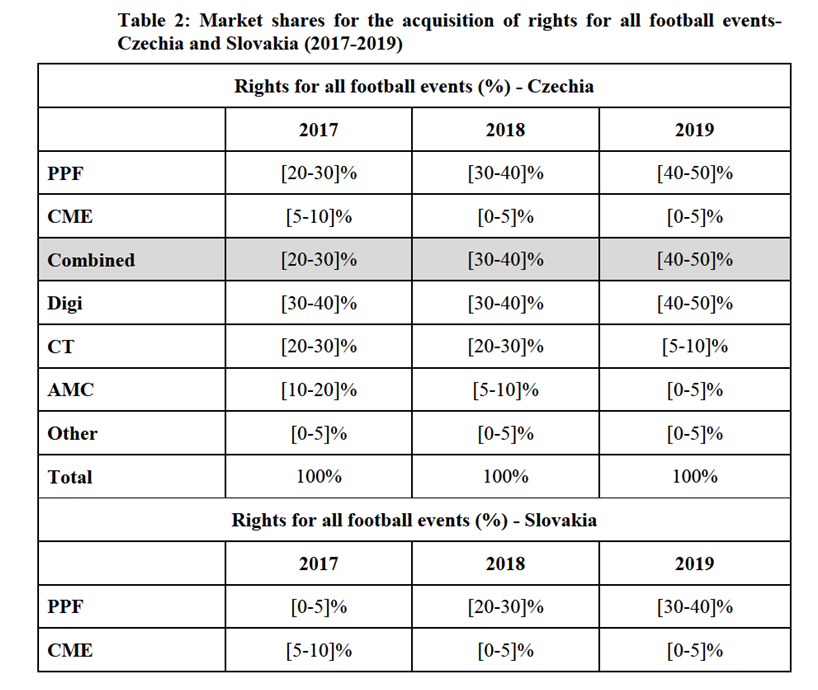

(56) As regards the supply-side of the market:a. PPF, through its subsidiary O2 CR, sells advertising inventory on its channels in Czechia to a minimal extent as the pay TV channels are financed predominantly from subscription fees.It is active on the market in Czechia but not in Slovakia and Bulgaria.b. CME sells advertising inventory on its TV channels in Czechia.In Slovakia and Bulgaria, CME sells advertising inventory on its TV channels and its AVOD service.

(57) As regards the demand-side of the market, PPF is active as it purchases TV advertising inventory in its function as a retailer of AV, mobile telecommunication and fixed internet access services, but also through other subsidiaries which are not active in the AV or telecommunications sectors.

4.6.2. Product market definition

4.6.2.1. Commission precedents

(58) In its previous decisions, the Commission has distinguished between offline and online advertising and classified these two advertising methods as belonging to separate markets.42 The Commission has considered in that respect, that TV advertising, as part of the offline advertising market, constitutes a distinct product market, separate from advertising in other forms of media.43 The Commission has left open the questions, whether in light of the increasing digitization of all media platforms, there is a wider market for sale of advertising space in video format across platforms and whether advertising on pay TV and FTA TV are part of the same market.44

4.6.2.2. Notifying Party’s view

(59) The Notifying Party agrees with the Commission precedent definition and submits that the relevant product market should be defined as the market for the sale of TV advertising space.45

4.6.2.3. Commission’s assessment

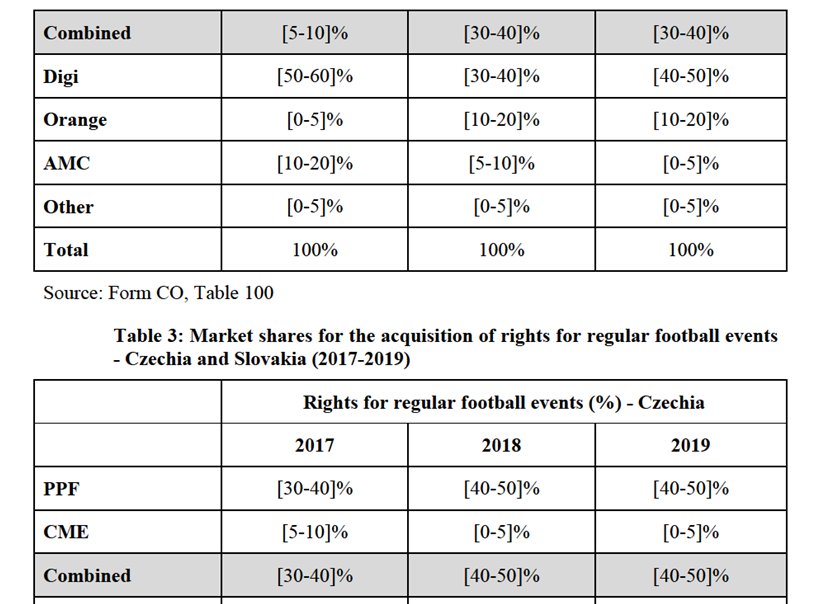

(60) The respondents to the market investigation largely confirm that the market for the supply of advertising space should be segmented by type of media, noting the particular importance of TV advertising due to its wide reach and the frequency of advertising. Nevertheless, several purchasers of advertising space observed that the lines between online and offline advertising is becoming increasingly blurred due to the digitization of all media platforms.46

(61) The majority of the purchasers of advertising space did not consider procuring advertising space on pay TV channels as an alternative to procuring advertising space on FTA channels but they rather view pay TV and FTA channels as complementary. This is because of the much larger audience share of FTA channels and because the financing model of pay TV channels does not allow them to advertise as frequently as on FTA channels.47

(62) Therefore, the Commission considers, for the purpose of this decision, that the sale of TV advertising space is not part of the same relevant product market as the sale of advertising space on other media. For the purpose of this decision, the market for the sale of TV advertising space does not need to be further segmented on the basis of the financing model (FTA or pay TV) because acquirers of advertising space do not view these two different models separately.

4.6.3. Geographic market definition

4.6.3.1. Commission precedents

(63) In its previous decisions, the Commission considered the market for sale of TV advertising space to be national48 in scope or regional, based on linguistically homogeneous areas encompassing several Member States.49

4.6.3.2. Notifying Party’s view

(64) The Notifying Party submits that, in accordance with the Commission practice, the relevant geographic market should be defined as national in scope.50

4.6.3.3. Commission’s assessment

(65) Nothing in the market investigation contradicts the Commission's previous findings that the market is either national, or corresponds to the relevant language area as the purchasers of TV advertising space overwhelmingly procure this advertising inventory on a national basis.51 The countries in which the parties are active in the sale of TV advertising space, namely Czechia, Slovakia, and Bulgaria, also constitute linguistic regions.

(66) Therefore, for the purposes of this decision, the Commission considers the geographic market definition for the retail provision of TV services is national in scope.

4.7. Market for the retail supply of mobile telecommunications services52

4.7.1. Introduction

(67) Mobile telecommunications services for end customers include services for national and international voice calls, SMS (including MMS and other messages), mobile internet with data services, access to content via the mobile network and retail international roaming services.

(68) These services are provided on 2G/GSM, 3G/UMTS and 4G/LTE networks, with the 2G network historically having better coverage and the 3G network being better adapted for larger amounts of data and faster download speeds. 4G/LTE is a mobile technology that increases the speed and capacity of the network and is adapted for improved voice quality and high-speed data transmission from wireless devices, for example, to stream video, Internet TV and to use broadband Internet.

(69) PPF is active on the market for retail mobile telecommunication services in Czechia and in Slovakia, through its portfolio company O2 CR (which wholly owns its subsidiary O2 SK through which O2 CR is active on the market for retail mobile telecommunication services in Slovakia). In Bulgaria, PPF is active on the market through its subsidiary Telenor Bulgaria, which holds a telecommunication license for this territory.

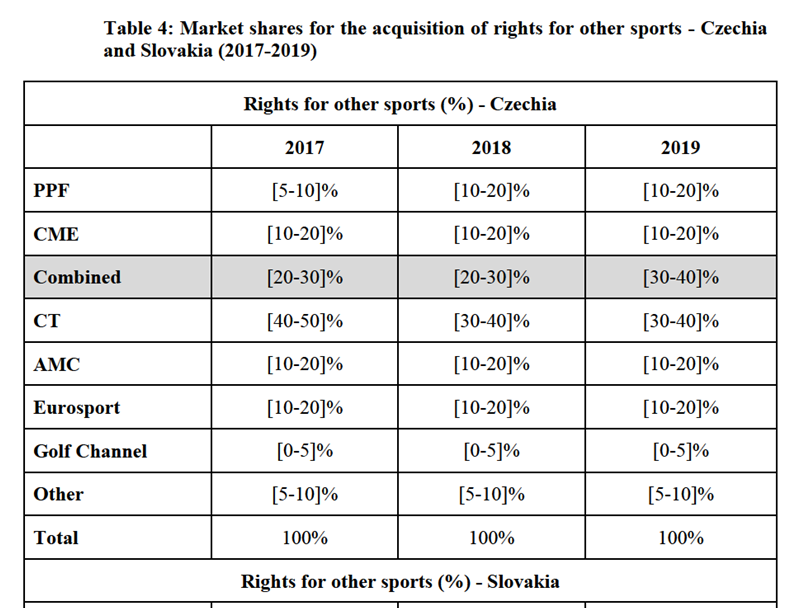

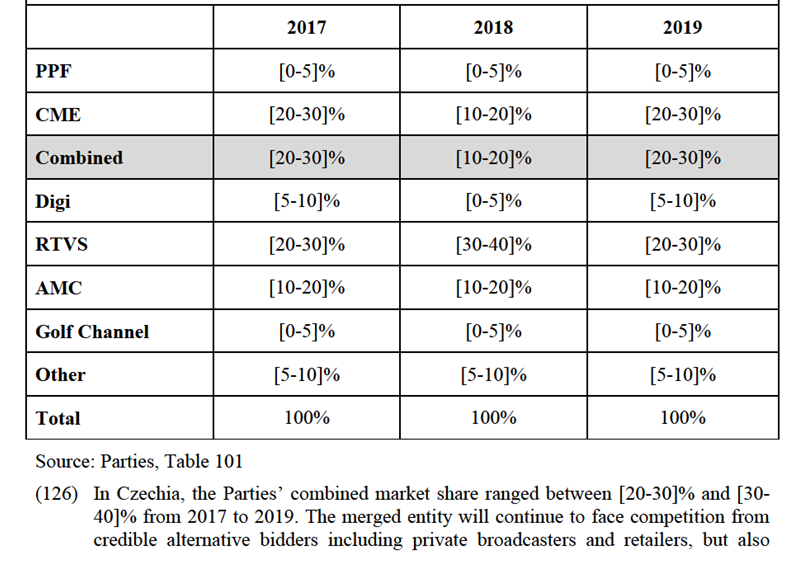

(70) CME is not active on this market.

4.7.2. Product market definition

4.7.2.1. Commission precedents

(71) In previous decisions, the Commission has identified an overall retail market for the mobile telecommunications services constituting a separate market from retail fixed telecommunication services. The Commission examined potential segmentations of the overall retail market for mobile telecommunication services between pre-paid or post-paid services and private customers or business customers as well as based on the type of service or type of network technology, concluding that these did not constitute separate product markets, but rather represent market segments within an overall retail market.53

4.7.2.2. Notifying Party’s view

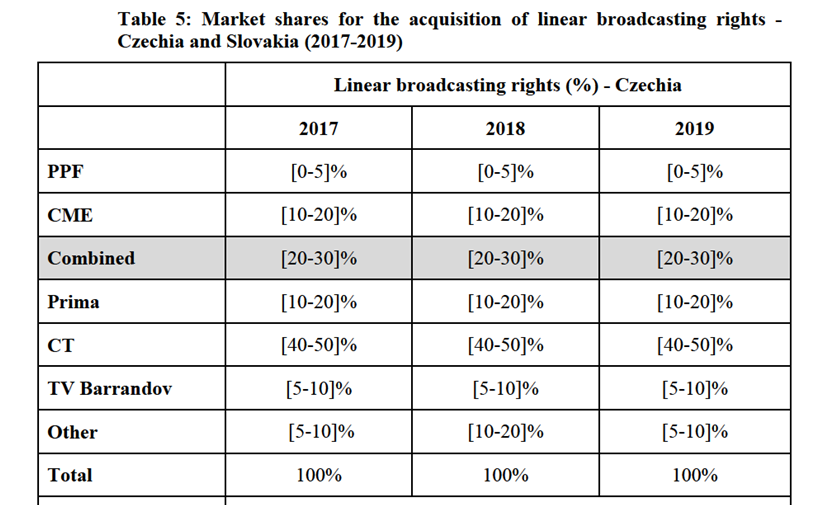

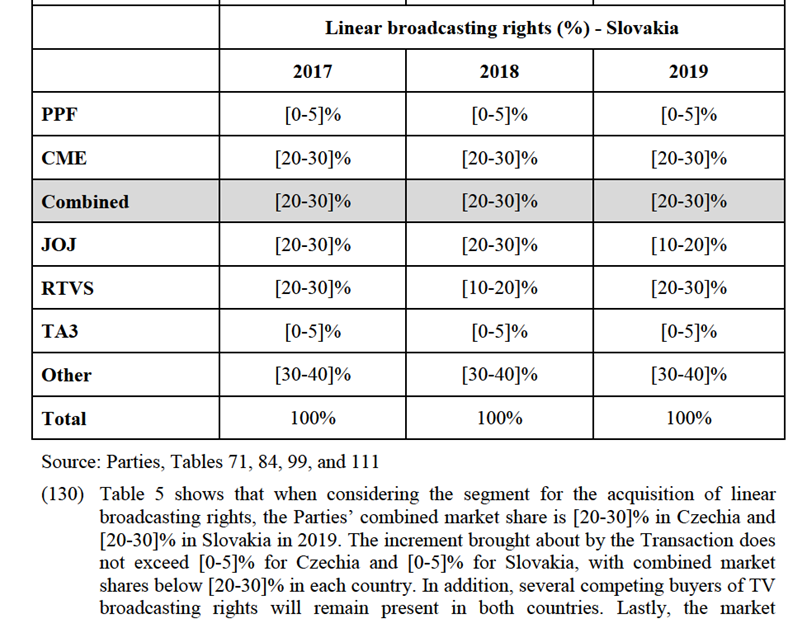

(72) The Notifying Party agrees with this market definition and submits that the relevant product market should be defined as the overall retail market for mobile telecommunication services without further segmentation.54

4.7.2.3. Commission’s assessment

(73) The market investigation in this case has not provided any indication that the Commission should depart from its previous findings. For the purposes of this decision, the Commission will not examine the possible segmentation of the overall market for the retail supply of mobile telecommunication services in relation to the provision of advertising space because the competitive assessment would remain unchanged under all possible segmentations mentioned below in paragraph (74).

(74) Therefore, for the purpose of this decision, the Commission considers that the exact product market definition for the retail supply of mobile telecommunications services can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market irrespective of a further segmentation between pre-paid or post-paid services and private customers or business customers as well as based on the type of service or type of network technology .

4.7.3. Geographic market definition

4.7.3.1. Commission precedents

(75) The Commission has previously considered that the market for the retail provision of mobile telecommunication services is national in scope, due to the existing regulatory barriers and the complete national coverage of the operators.55

4.7.3.2. Notifying Party’s view

(76) The Notifying Party agrees with this market definition.56

4.7.3.3. Commission’s assessment

(77) The market investigation in this case has not provided any indication that the Commission should depart from its previous findings.

(78) Therefore, for the purpose of this decision, the Commission considers that the geographic market for the retail supply of mobile telecommunications services is national in scope.

4.8. Market for the retail supply of fixed internet access services

4.8.1. Introduction

(79) In the market for retail fixed internet access services, customers are provided with access to the internet through a fixed telecommunication connection. These services are provided over a fixed network such as cable, copper or fibre infrastructure.

(80) PPF is active on the market for fixed internet access services in Czechia and in Slovakia, through its portfolio company O2 CR in Czechia (with its subsidiary O2 SK active in Slovakia).

(81) CME is not active on this market.

4.8.2. Product market definition

4.8.2.1. Commission precedents

(82) With regard to the market for the retail supply of fixed internet access services, the Commission has considered a number of potential market segmentation, in particular; segmentation by (i) product type, distinguishing between narrowband, broadband and dedicated access; and (ii) distribution mode, distinguishing between xDSL, fiber, cable, and mobile broadband, but ultimately left the market definition open.57

(83) The Commission has also considered segmentation of that market by type of customer, distinguishing between (i) residential customers and small business customers; and (ii) large business customers, concluding that large business customers form a part of business connectivity services because unlike residential and small business customers, their demands require an individual approach.58 The Commission has further concluded that the market for fixed internet access services should not be segmented according to download speed59 and that fixed internet services provided through mobile network infrastructure should be excluded from its scope.60

4.8.2.2. Notifying Party’s view

(84) The Notifying Party submits that the relevant product market should be defined as the overall retail market for the provision of fixed internet access services, including all product types, distribution modes and speed/bandwidths, to residential and small business customers, excluding services provided through mobile network. In particular, it considers that it is not appropriate to sub-divide the market according to the product type and distribution mode since all these products are substitutable with each other. Nonetheless, the Notifying Party submits that the analysis would not be materially different if the market was divided according to the product type and distribution mode.61

4.8.2.3. Commission’s assessment

(85) The market investigation in this case has not provided any indication that the Commission should depart from its previous findings. For the purposes of this decision, the Commission will not examine the possible segmentation of the overall market for the provision retail fixed internet access services in relation to the provision of advertising space because the competitive analysis would remain unchanged under all possible segmentations mentioned below in paragraph (86).

(86) Therefore, for the purpose of this decision, the Commission considers that the exact product market definition for the retail supply of fixed internet access services can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market irrespective of a possible segmentation of the market by product type, distribution mode or type of customer

4.8.3. Geographic market definition

4.8.3.1. Commission precedents

(87) The Commission has previously considered that the market for the fixed internet access services is national in scope, due to the fact that the supply of upstream wholesale services works on a national basis, and the fact that the pricing policies are mostly national.62

4.8.3.2. Notifying Party’s view

(88) The Notifying Party agrees with this market definition.63

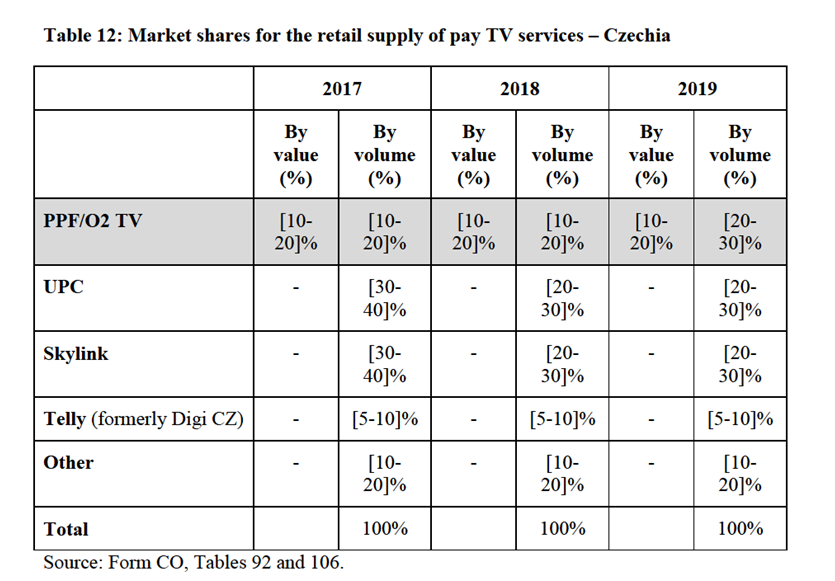

4.8.3.3. Commission’s assessment

(89) The market investigation in this case has not provided any indication that the Commission should depart from its previous findings.

(90) Therefore, for the purpose of this decision, the Commission consider that the geographic market definition for the retail supply of fixed internet access services is national in scope.

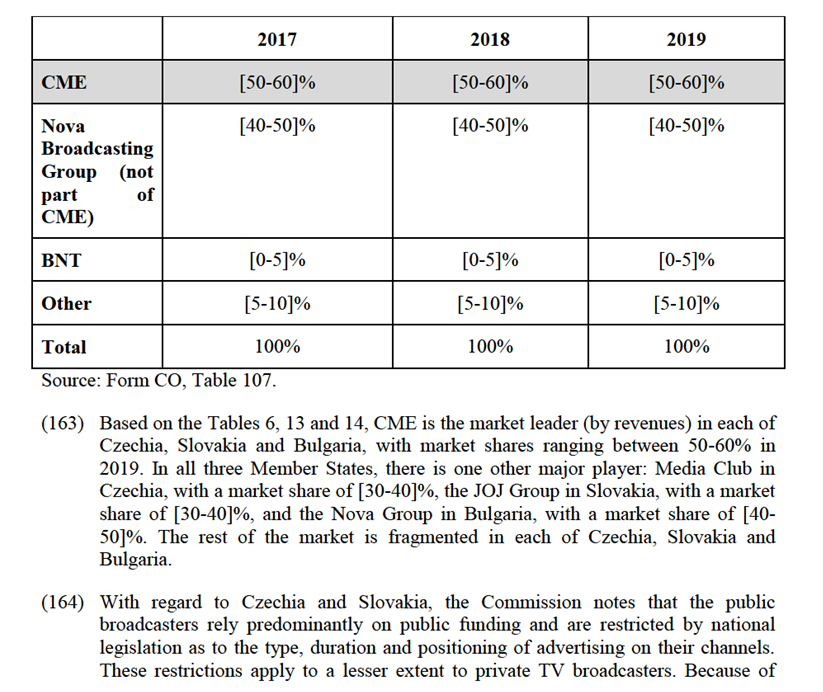

5. COMPETITIVE ASSESSMENT

5.1. Analytical framework

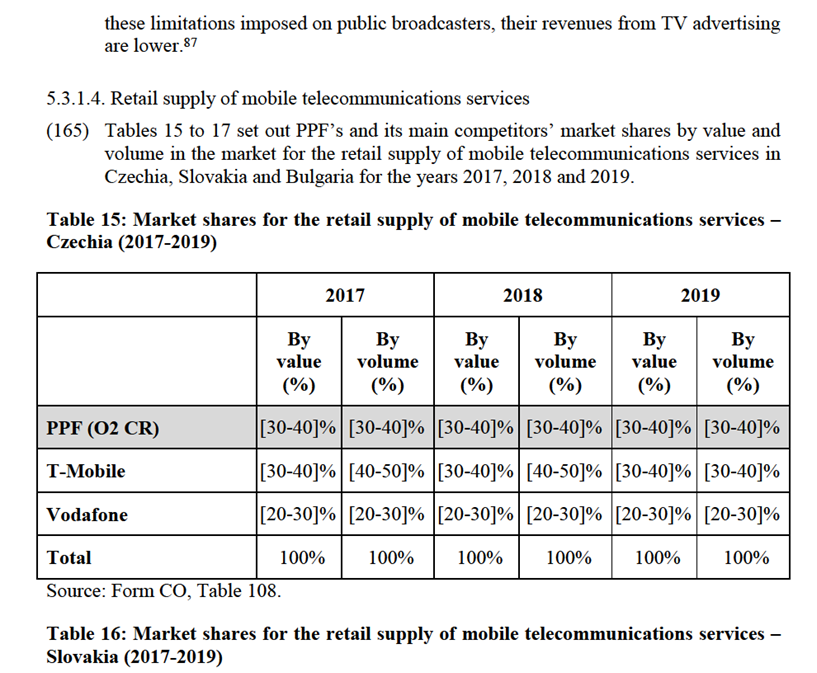

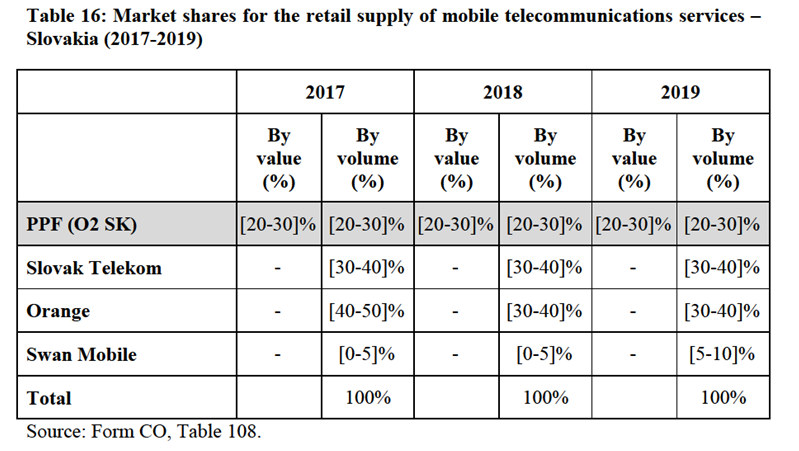

(91) Under Article 2(2) and Article 2(3) of the Merger Regulation, the Commission must assess whether a proposed concentration would significantly impede effective competition in the internal market or in a substantial part of it, in particular through the creation or strengthening of a dominant position.

(92) In this respect, a merger may entail horizontal and/or non-horizontal effects. Horizontal effects are those deriving from a concentration where the undertakings concerned are actual or potential competitors of each other in one or more of the relevant markets concerned. Non-horizontal effects are those deriving from a concentration where the undertakings concerned are active in different relevant markets.

5.1.1. Horizontal non-coordinated effects

(93) The Horizontal Merger Guidelines64 describe horizontal non-coordinated effects as follows: “A merger may significantly impede effective competition in a market by removing important competitive constraints on one or more sellers who consequently have increased market power. The most direct effect of the merger will be the loss of competition between the merging firms. For example, if prior to the merger one of the merging firms had raised its price, it would have lost some sales to the other merging firm. The merger removes this particular constraint. Non-merging firms in the same market can also benefit from the reduction of competitive pressure that results from the merger, since the merging firms’ price increase may switch some demand to the rival firms, which, in turn, may find it profitable to increase their prices. The reduction in these competitive constraints could lead to significant price increases in the relevant market.”65

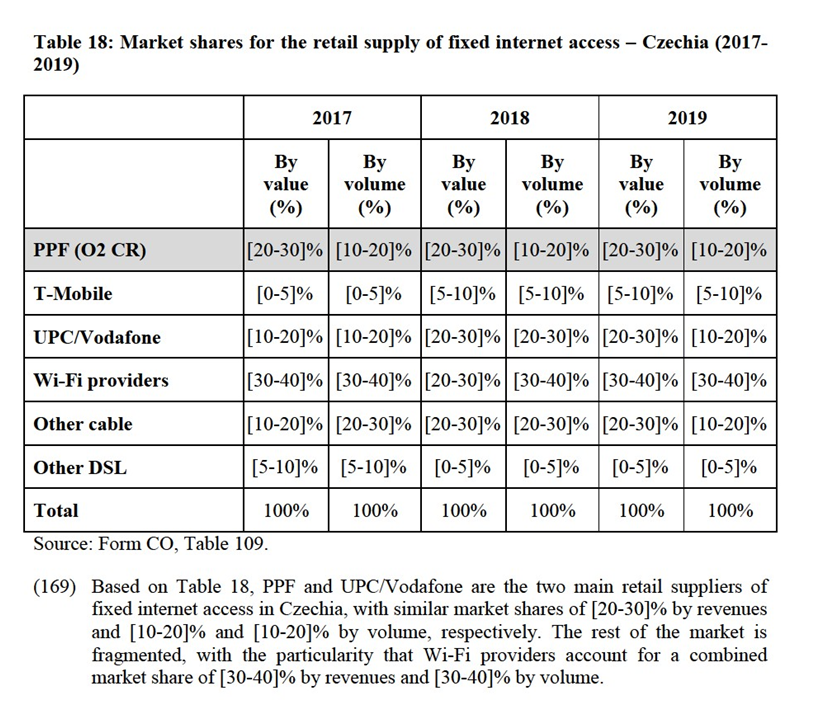

(94) Therefore, a merger giving rise to such non-coordinated effects might significantly impede effective competition by creating or strengthening the dominant position of a single firm, one which, typically, would have an appreciably larger market share than the next competitor post-merger.

(95) The Horizontal Merger Guidelines list a number of factors which may influence whether or not significant horizontal non-coordinated effects are likely to result from a merger, such as the large market shares of the merging firms, the fact that the merging firms are close competitors, the limited possibilities for customers to switch suppliers, or the fact that the merger would eliminate an important competitive force.66 That list of factors applies equally regardless of whether a merger would create or strengthen a dominant position, or would otherwise significantly impede effective competition due to non-coordinated effects. Furthermore, not all of these factors need to be present to make significant non-coordinated effects likely and it is not an exhaustive list.67

(96) Finally, the Horizontal Merger Guidelines describe a number of factors, which could counteract the harmful effects of the merger on competition, including the likelihood of buyer power, entry and efficiencies.

5.1.2. Vertical effects

(97) According to the Non-Horizontal Merger Guidelines, foreclosure occurs when actual or potential rivals’ access to supplies or markets is hampered, thereby reducing those companies’ ability and/or incentive to compete. Such foreclosure may discourage entry or expansion of rivals or encourage their exit.68

(98) The Non-Horizontal Merger Guidelines distinguish between two forms of foreclosure: input foreclosure occurs where the merger is likely to raise the costs of downstream rivals by restricting their access to an important input and customer foreclosure occurs where the merger is likely to foreclose upstream rivals by restricting their access to a sufficient customer base.69

(99) In order for foreclosure to be a concern, three conditions need to be met post- merger: (i) the merged entity needs to have the ability to foreclose its rivals70 ; (ii) the merged entity needs to have the incentive to foreclose its rivals71; and (iii) the foreclosure strategy needs to have a significant detrimental effect on the parameters of competition on the downstream market (input foreclosure)72 or have an adverse impact in the downstream market and harm consumers (customer foreclosure).73 In practice, these factors are often examined together since they are closely intertwined.74

5.2.Horizontally affected markets

(100) The Transaction gives rise to horizontally affected markets in (i) certain segments of the market for the licensing of TV broadcasting rights in Czechia and Slovakia, and(ii) the market for the sale of TV advertising space in Czechia.

5.2.1. Licensing of TV broadcasting rights – Czechia and Slovakia

5.2.1.1. Overall market for the acquisition of broadcasting rights for TV content in Czechia and Slovakia

(101) Both PPF, through its subsidiary O2 Czech Republic, and CME acquire broadcasting rights for AV content for inclusion in their TV channels. Tables 1 to 675 below show the segments where the Parties` overlapping activities result in horizontally affected markets in Czechia and Slovakia, namely: (i) the overall market for the acquisition of TV broadcasting rights, (ii) the acquisition of rights to football events, (iii) the acquisition of rights to football events that occur regularly, (iv) the acquisition of rights to other sports, and (v) the acquisition of rights for linear transmission of AV content.

(102) Both Parties acquire TV content rights for inclusion in their TV channels in Czechia and Slovakia.

(103) In Czechia, PPF purchases broadcasting rights to audiovisual sports-related content for its TV channels O2 TV Sport, O2 TV Tenis and O2 TV Fotbal. CME acquires various types of content rights, including sports, foreign movies, domestic movies, series, and other rights. In relation to sporting rights, CME focuses on licensing rights to: (i) the U.S. branded sports, such as NHL (ice hockey), NBA (basketball) or

AMC | [5-10]% | [0-5]% | [0-5]% |

Other | [0-5]% | [0-5]% | [0-5]% |

Total | 100% | 100% | 100% |

Source: Form CO, Table 11

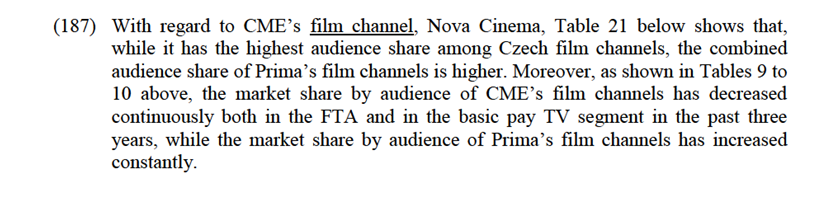

(108) Table 3 shows that when considering a market for the acquisition of rights to football evets that occur regularly the Parties’ combined market share in Czechia amounted to [40-50]% (PPF [40-50]%, CME [0-5]%) and to [30-40]% (PPF [30-40]%, CME [0-5]%) in Slovakia in 2019. In Czechia, CME’s market share has remained stable at [0-5]%- [0-5]% in the period 2017-2019 whereas PPF’s market share increased from [20-30]% in 2017 to [40-50]% in 2019. Digi is the other large player on the market with a market share ranging from [30-40]% to [40-50]% in the period 2017-2019. Other acquirers include CT and AMC. CT had [20-30]% in 2017 which dropped to [5-10]% in 2018 and 2019. AMC represented [0-5]% of the market in 2017.

(109) In Slovakia, CME’s market share was [5-10]% in 2017 and [0-5]% in 2018-2019. PPF’s market share at [30-40]% for 2018-2019. The market leader is Digi with [50- 60]% and [40-50]% for 2017 and 2018-2019 respectively, followed by RTVS ([20- 30]% in 2017, [5-10]% in 2018-2019), Orange (which had no market share in 2017 but increased its presence to [10-20]% of the market in 2018-2019), and AMC (which represented [5-10]% of the market in 2017 but had a negligible share in 2018-2019).

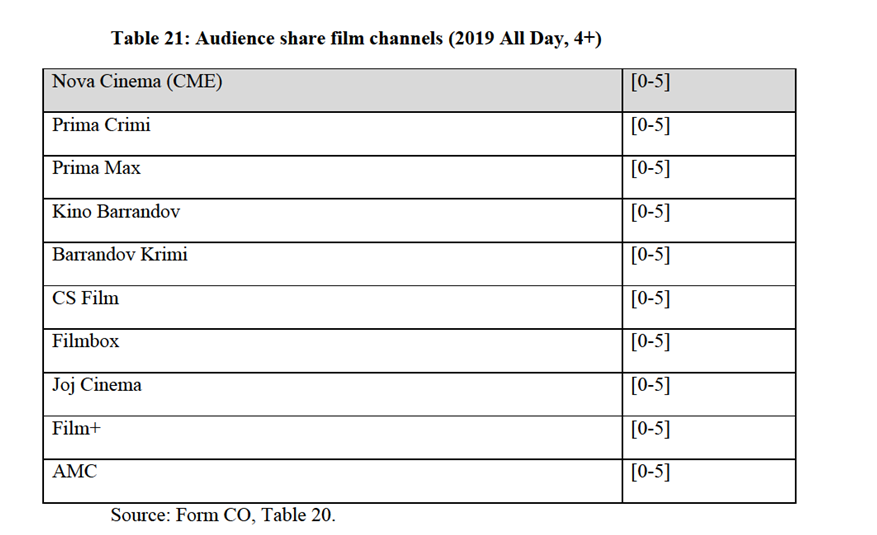

5.2.1.2.1. Notifying Party’s view

(110) The Notifying Party submits that the Transaction will only bring about an immaterial increase to PPF’s market share given the limited market share increment both in Czechia and Slovakia. Further, the Notifying Party explains that CME and PPF are not close competitors, while Digi remains PPF’s closest competitor in Czechia and Slovakia. In addition, PPF will be constrained post-transaction by strong existing competitors such as CT, AMC, Arena, and Eurosport in Czechia, and RTVS, Orange, AMC, Arena and Eurosport in Slovakia. Lastly, the Notifying Party explains that the merged entity’s market share may decrease significantly for the coming seasons given that sports broadcasting rights are tendered in transparent procedures where many strong bidders participate each time.

5.2.1.2.2. Commission’s assessment

(A) Czechia

(111) The results of the market investigation are largely neutral vis-à-vis the Transaction. Overall, the large majority of rightsholders consider that the Transaction will have a neutral impact both on the market for the acquisition of football rights and on their own business.76 They consider that the merged entity will not be in a position to impose less favourable terms when negotiating the acquisition of rights77 and that competitors will remain able to credibly participate in tenders opposite the merged entity.78 From the demand-side, however, two competitors take the view that PPF generally has a decisive advantage in tenders due to the financial strength of the entire PPF group.79 These competitors consider that pre-transaction PPF has been leveraging its strong financial position, which increases overtime, in order to win tenders.

(112) In particular, a competitor considered that the Transaction would induce significant horizontal effects on the market for the acquisition of broadcasting rights for football events in Czechia. According to its submission, PPF’s particularly strong financial position enables it to outbid any other participant to a tender.

(113) However, the Commission considers that the Transaction will not materially affect the market for the acquisition of broadcasting rights for football events that occur regularly in Czechia.

(114) First, the Commission notes that the increment brought about by the Transaction is limited. In Czechia, CME’s market share has not exceeded [5-10]% in the period 2017-2019. The addition of this increment will not materially change PPF’s position on the segment for the acquisition of rights to football events that occur regularly.

(115) Second, the Parties are not competing to acquire the same sports rights. PPF and CME pursue different strategies, particularly with respect to the distribution of their sports channels, and specialize in different sports. They acquire different content and their channels attract different viewers. In particular, CME holds none of the main Czech football rights (holding only second pick and other rights for the UEFA Europe League 2019/2020) or the national ice hockey championship rights80 and a very limited set of other rights. As explained in paragraph (103), CME rather focuses on licensing rights to U.S. branded sports, mainstream European sports (e.g., the French Football League, motorbike, and emerging sports, such as darts). CT holds the majority of football rights (both for national and UEFA/Europa leagues as explained below in paragraph (118) (b)) and Digi Sport holds virtually all of the internationally attractive football league rights. Further, the majority of non-football rights are held by CT, Eurosport or Sport 1.

(116) As a result, PPF and CME generally do not meet in tenders for the various sports rights they acquire. Based on bidding data submitted by the Parties PPF and CME [confidential bidding data].

(117) While PPF increased its market share over the period 2017-2019 by successfully competing for the acquisition of attractive football rights, possibly as a result of superior financial capabilities, its very limited competitive interaction with CME pre-merger shows that the Transaction is not likely to materially impact PPF’s ability to win tenders post-transaction.

(118) Third, other companies that closely compete with PPF will remain active on the market post-transaction:(a) Digi CZ, which holds the broadcasting rights for the English Premier league, German Bundesliga, as well as the Spanish and Italian football leagues, and the ATP (until 2021, after which the ATP rights will be held by Eurosport). The Notifying Party estimates that Digi CZ’s market share on the Czech market for the licensing of broadcasting rights for football events ranged between [30-40]% and [40-50]% (from 2017/2018 season to 2019/2020 season).(b) CT, the Czech public broadcaster, which holds the broadcasting rights for a portion of the UEFA Champions League (highlights and final), Czech football league (4th pick) and Europa League (1st pick) packages, UEFA Euro 2020, including qualifiers of the Czech team, and ice hockey, including the Hockey World Championships, the Olympics, Euro Hockey Tour, certain Czech national team hockey matches, and certain matches of the Czech National Hockey League. The Notifying Party estimates that CT’s market share on the Czech market for the licensing of broadcasting rights for football events ranged between [5-10]% and [20-30]% (from the 2017/2018 season to the 2019/2020 season).(c) AMC Networks Entertainment LLC (Sport 1 and Sport 2 channels), which holds the broadcasting rights to one live match of the Slovak National Hockey League (Tipsport liga), rights for the football qualifiers for the Euro 2020 and the FIFA World Cup 2022 (for all matches excluding the Czech national team), the Portuguese and Turkish football leagues, all Formula One races, NFL and boxing. The Notifying Party estimates that the market share of AMC on the Czech market for the licensing of broadcasting rights for football events ranged between [0-5]% and [10-20]% (from the 2017/2018 season to the 2019/2020 season).(d) Arena Sport, which holds the broadcasting rights for the Dutch football league.(e) Discovery’s Eurosport channels, which held rights to Major League Soccer USA. Eurosports channels also feature a range of other sports rights, including non-exclusive broadcasting rights to all Alpine and Nordic Ski events (Alpine ski races, Biathlon, Ski jumping/Ski flying, Nordic events), the Olympic Games 2020 and 2022, and the main ATP and WTA tennis tournaments (1000 series and 500 series), and non-exclusive rights for the Tour de France relevant for the Czech market).

(B) Slovakia

(119) The results of the market investigation have been largely neutral vis-à-vis the Transaction. Rightholders consider that the merged entity will not be in a position to impose less favourable terms when negotiating the acquisition of rights81 and take the view that other entities will be able to credibly participate in tenders opposite the merged entity. Form the demand-side, the majority of broadcasters consider that negotiations are ordinary and on equal footing and are not concerned with the Transaction.82 Accordingly, the Commission considers that the Transaction will not materially affect the market for the acquisition of broadcasting rights for football events that occur regularly in Slovakia.

(120) First, the Commission notes that the increment brought about by the Transaction is very limited. In Slovakia, CME’s market share has not exceeded [0-5]% in the period 2018-2019. The addition of this market share will therefore not materially change PPF’s position on the segment for the acquisition of rights to football events that occur regularly.

(121) Second, PPF, through O2 CR, has been active as an acquirer of sports rights on the Slovakian market since 2018. However, O2 CR does not broadcast its O2 TV Sport channels in Slovakia. In order to use the sports content that it acquired – which are often tendered together with broadcasting rights for the Czech market – O2 CR produces a customized channel for Orange, its sole customer in Slovakia. This channel is produced and distributed under the Orange brand and is built around O2 CR rights for the UEFA Champions League and other content owned by Orange.

(122) Third, other companies that closely compete with PPF will remain active on the market post-transaction(a) Digi SK (a subsidiary of Slovak Telekom/Deutsche Telekom), which holds the broadcasting rights for the English Premier league, German Bundesliga, as well as the Spanish and Italian first league football leagues. The Notifying Party estimates that Digi SK’s market share on the Slovak market for the licensing of broadcasting rights for football events ranged between [30-40]% and [50-60]% (from the 2017/2018 season to the 2019/2020 season).(b) RTVS, the Slovak public broadcaster, which holds the broadcasting rights for the annual Hockey World Championships, games of the national Hockey team (Euro Hockey Challenge), the European Football Championship 2020, the next three years’ Slovak National Football Team qualifiers (including UEFA Nations League, the Euro 2020 and the World Cup 2022) on an exclusive basis, and the Olympic Games in 2020. Additionally, RTVS has non-exclusive broadcasting rights for all stages of the Tour de France and Tour de Suisse, and exclusive broadcasting rights for the U21 and U23 Hockey youth team qualifiers. The Notifying Party estimates that the market share of RTVS on the Slovak market for the licensing of broadcasting rights for football events ranged between [5-10]% and [20-30]% (from the 2017/2018 season to the 2019/2020 season).(c) Orange, which among other rights holds the broadcasting rights for Slovak football league (1st pick, Fortuna liga). The Notifying Party estimates that the market share of Orange on the Slovak market for the licensing of broadcasting rights for football events amount to [10-20]% and [10-20]% in the 2018/2019 and 2019/2020 season, respectively.(d) AMC Networks Entertainment LLC (Sport 1 and Sport 2), which holds the broadcasting rights to one live match of the Slovak National Hockey League (Tipsport liga), rights for the football qualifiers for the Euro 2020 and the FIFA World Cup 2022, Portuguese and Turkish football leagues, Formula One, NFL and boxing. The Notifying Party estimates that the market share of AMC on the Slovak market for the licensing of broadcasting rights for football events ranged between [0-5]% and [10-20]% (from 2017/2018 season to 2019/2020 season).(e) Arena Sport, which holds the broadcasting rights for the Dutch football league.(f) Discovery’s Eurosport channels, which held the broadcasting rights to Major League Soccer USA. These channels also feature a range of other sports, including non-exclusive broadcasting rights to Alpine and Nordic Ski events, the Olympic Games 2020 and 2022, and the main ATP and WTA tennis tournaments, as well as non-exclusive rights for the Tour de France relevant for the Slovak market.

(123) Consequently, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with regard to the markets for the acquisition of broadcasting rights for football events and for football events that take place regularly, in Czechia and Slovakia.

5.2.1.3.Market for the acquisition of (i) other sports content and (ii) linear broadcasting rights in Czechia and Slovakia

(124) The Parties overlap in the acquisition of other sports, meaning all sports other than football events. They Parties also overlap in the acquisition of linear broadcasting rights, meaning rights for content that is transmitted via linear broadcasting.

(125) First, with respect to the market for the acquisition of rights for other sports, the Parties’ and their main competitors’ market shares are the following.

state-operated broadcasters, who are particularly strong in this segment. In particular, Parties will be constrained by CT, which represented between [30-40]% and [40- 50]% of the market between 2017 and 2019, AMC (between [10-20]% and [10-20]%between 2017 and 2019), and Discovery (between [10-20]% and [10-20]% between 2017 and 2019). Lastly, the market investigation did not point to any particular concerns in relation to the segment of other sports in Czechia.

(127) In Slovakia, the increment brought about by the Transaction does not exceed [0-5]%, leading to a combined market share below 25%. Several credible competing buyers or sports rights will remain present in both countries. PPF is a recent entrant, having entered the market in 2018, mainly due to the fact that broadcasting rights are often tendered together for Czechia and Slovakia. Furthermore, PPF’s presence in Slovakia is limited to the production of a customized channel for Orange, as described above in paragraph 122. Lastly, the market investigation did not point to any particular concerns in relation to the segment of other sports in Slovakia.

(128) Consequently, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with regard to the segment for the acquisition of rights for other sports in Czechia and Slovakia.

(129) Second, with respect to the market for the acquisition of linear broadcasting rights, the Parties’ and their main competitors’ market shares are the following.

has a market share of approximately [50-60]%. PPF’s market share is negligible. Media Club83 follows with [30-40]% and CT with [5-10]%.

5.2.2.1. Notifying Party’s view

(135) The Notifying Party submits that PPF’s market share is below [0-5]%. As the Transaction will not lead to a material market share increment, it will not have a material impact on CME’s competitive position.

5.2.2.2. Commission’s assessment

(136) The Commission considers that the Transaction will not materially affect the market for the sale of TV advertising space in Czechia.

(137) First, the increment brought about by the Transaction is limited as while CME has a market share of approximately [50-60]%, PPF’s share is below [0-5]%. The Parties’ position would be similar on the segment for the sale of TV advertising space on linear channels.

(138) Second, whilst CME has a large share for the sale of TV advertising space in Czechia, the Transaction does not materially change the competitive landscape in this market and is unlikely to significantly increase CME's market power because of the limited increment that it generates.

(139) Third, alternative players will remain present in the market for sale of TV advertising space, including Media Club and CT.

(140) Fourth, the market investigation did not point to any horizontal concerns with regard to the combination of the Parties’ activities as regards the sale of TV advertising space.

(141) Consequently, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with regard to the sale of TV advertising space, including the sale of TV advertising space on linear channels.

5.2.2.3.Conclusion

(142) In light of the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with regard to the market for the acquisition of TV advertising space in Czechia and Slovakia.

5.3.Vertically affected markets

(143) The Parties’ activities at different levels of the AV value chain and in some telecommunications markets give rise to the following vertically affected markets in Czechia, Slovakia and Bulgaria:

Total | 100% | 100% |

Source: Form CO, Tables 30 and 31.

(157) As noted above, PPF produces three sport channels that it does not offer at a wholesale level, but exclusively distributes via its own pay TV platform. The Commission therefore considers that PPF’s sports channels are not part of the market for the wholesale supply of TV channels. Nevertheless, the Parties have provided estimates of PPF’s market shares on the possible segment for the wholesale supply of pay TV sports channels if captive channels were to be included. Based on these estimates, PPF would have a market share of [5-10]% by revenues and [0-5]% by audience for the possible segment for the wholesale supply of pay TV sports channels in Czechia in 201984. If PPF’s, Digi’s and Premier captive sports channels were included in the potential segment for the wholesale supply of sports TV channels, the revenue-based combined market share of the Parties would be approximately [20-30]%.85

(158) The segment for the wholesale supply of sports TV channels is not vertically affected since the Parties’ individual and combined market shares remain below 30% in this segment, as well as any potential segmentations thereof. In particular, the Commission notes that neither Party supplies its channels FTA in Czechia. On the potential pay TV segment, the Parties’ individual and combined market shares remain below 30% even when including PPF’s captive channels. Within the pay TV segment, PPF’s channels would qualify as premium pay TV channels, while CME only supplies sports channels as part of its basic pay TV offering. The Parties have not provided estimates of their market shares in the segment for premium pay TV sports channels, since CME does not have premium pay TV sports channels and PPF does not offer its channels on the market. As for the segment for basic pay TV sports channels, as shown in Table 11, CME’s market shares remain below 30% both by revenues and by audience.

(159) However, several market participants have pointed to the importance of CME’s sports channels for their retail AV services offerings and expressed concerns that PPF would no longer make them available on the wholesale market post- Transaction. The Commission will therefore assess the likelihood of input foreclosure of CME’s sports channels under Section 5.3.2.2 below.

5.3.1.2. Retail supply of AV services

(160) Table 12 sets out PPF’s and its main competitors’ market shares in the segment for the retail supply of pay TV services in Czechia86 by value (revenues) and by volume (number of connected households) for the years 2017, 2018 and 2019.

– partially foreclose downstream competitors by degrading the terms and conditions of the acquisition of TV channels, for example through worse terms and conditions or materially higher carriage fees.

(172) No respondent to the market investigation considered it likely that the merged entity would stop licensing all of its TV channels to competing suppliers of AV services.90 However, several respondents were concerned that the merged entity may stop licensing some of its TV channels, and in particular its sports channels, to third parties post-Transaction.91 Moreover, all of the respondents to the market investigation considered it likely that the merged entity would degrade the terms and conditions when licensing all or some of its TV channels to third parties.92

(173) The Commission has therefore assessed specifically whether the merged entity would have the ability and incentive to stop licensing its sports channels or degrade the terms and conditions of all or some of its TV channels when licensing them to competing suppliers of retail AV services.

5.3.2.1. The Notifying Party’s view

(174) The Notifying Party submits that the merged entity would lack the ability to engage in input foreclosure. It argues that none of CME's channels can be considered to constitute important inputs to downstream competitors. It argues that, in any event, most of CME’s channels are part of standard retail TV packages and do not offer unique content.93 The Notifying Party also indicates that there will remain a sufficient number of wholesale competitors for downstream rivals to have access to alternative inputs, namely the commercial TV broadcasters Prima and Barrandov, as well as the public broadcaster CT.94

(175) In addition, the Notifying Party submits that the merged entity would lack the incentive to engage in total input foreclosure. It argues that [confidential data regarding revenues] of CME’s revenues in 2019 were generated by television advertising, not by carriage fees. Therefore, CME has an incentive to maximise its reach and not to foreclose downstream distributors. Moreover, the Notifying Party argues that any potential profits that could be generated by a foreclosure strategy could not offset the greater reductions in CME’s advertising revenues.95

(176) With regard to partial input foreclosure, the Notifying Party argues that CME’s bargaining position when negotiating carriage fees will not materially change post- Transaction. This is because CME relies on the broad availability of its channels through all TV retailers and its continued supply over DTT. Due to PPF’s limited position on the overall market for the retail supply of AV services, CME’s incentives to broadly supply its channels will likely not change post-Transaction.96

(177) Finally, the Notifying Party argues that any total or partial input foreclosure strategy would have a very limited impact on retail TV prices, given the number of alternative providers of TV channels, and therefore any potential impact on competition would be immaterial.97

5.3.2.2. The Commission’s assessment

(178) For the reasons set out below, the Commission considers that the merged entity will not have the ability and incentive to foreclose competing suppliers of retail AV services by engaging in input foreclosure, e.g. by stopping to supply all or some of CME’s channels to PPF’s downstream rivals or by increasing the prices or degrading the quality of the channels. Furthermore, even if the merged entity were to engage in input foreclosure, such a strategy would not have a significant detrimental effect on competition.

(A) Ability to engage in input foreclosure

(179) CME holds a [30-40]% audience share in the general entertainment segment, [30- 40]% audience share in the FTA general entertainment sub-segment, [30-40]% audience share in the basic pay TV general entertainment sub-segment and [30-40]% audience share in the FTA film channels sub-segment in Czechia.

(180) The Commission notes that in the overall market for the wholesale supply of TV channels and all other plausible segments, CME’s audience share remains below 30%. In particular, in the segment for pay TV sports channels, CME has a market share of [10-20]% by revenues and [5-10]% by audience. Even if PPF’s captive sports channels were included, the Parties combined market share would remain below 30% both by revenues ([20-30]%) and by audience ([5-10]%). As for the sub- segment for basic pay TV sports channels, CME has a market share of [20-30]% by revenues and [5-10]% by audience.

(181) In respect of the merged entity’s ability to engage in input foreclosure, respondents to the market investigation consider that CME holds a leading market position and “must have” channels, which are important inputs to compete.98 This is particularly true with respect to Nova, which is a general entertainment channel and the channel generating the most audience out of CME’s portfolio, with a [20-30]% audience share among all FTA and basic pay TV channels.

(182) Additionally, several respondents considered CME’s sports channels, Nova Sport 1 and Nova Sport 2, as important inputs to compete, in particular for suppliers of retail pay TV services. They submitted that, due to the importance of FTA distribution in Czechia, pay TV distributors rely on content, and in particular sports channels, to attract customers and distinguish themselves from competitors.99

(183) Moreover, most respondents to the market investigation submitted that they had no alternatives to CME’s channels. For CME’s main channel, Nova, this is due to the level of its audience share; for CME’s sports channels, respondents consider that there would be no alternatives with a similar quality of content.100 Therefore, most respondents to the market investigation considered their bargaining position to be low when licensing TV channels from CME.101

(184) In order to assess whether Nova on the one hand, and Nova Sport 1 and Nova Sport 2 on the other, should be considered as particularly important for distributors of AV services, more than their audience share would suggest, the Commission requested the Parties to provide viewer shares based on different parameters.102 Table 19 summarizes such information in relation to the total viewing, continuous viewing and prime time viewing of CME's channels and their closest competitors in Czechia.

Table 19: Viewership data of FTA/basic pay TV channels in Czechia (2019, 4+)

| All Day Total time 30 min. | N | All Day Total time 180 min. | N | All Day Continuous time 30 min. | N | All Day Continuous tome 180 min. | N | Prime time Continuous time 30 min. | N | Prime time Continuous time 180 min. | N |

CME | […] | 1 | […] | 1 | […] | 1 | […] | 2 | […] | 1 | […] | 1 |

CT | […] | 2 | […] | 2 | […] | 2 | […] | 1 | […] | 2 | […] | 2 |

Prima | […] | 3 | […] | 3 | […] | 3 | […] | 3 | […] | 3 | […] | 3 |

Barrandov | […] | 4 | […] | 4 | […] | 4 | […] | 4 | […] | 4 | […] | 4 |

AMC | […] | 5 | […] | 5 | […] | 5 | […] | 5 | […] | 5 | […] | 5 |

Stanice O

(Očko Music Channels) | […] | 6 | […] | 6 | […] | 6 | […] | 6 | […] | 6 | […] | 6 |

Source: Form CO, Table 124.

(185) The Commission notes that despite CME’s strong 2019 all day audience share position for FTA/basic pay TV channels, different viewership metrics described in Table 19 show that CME’s position remains comparable to those of CT’s and Prima’s channels, which rank second and third.

(186) With regard to the general entertainment channels, the data provided by the Parties confirms that CME’s general entertainment channels account together for [20-30] of the total audience share, while CT’s general entertainment channels account for [20- 30] and Prima’s channels for [10-20] of the total audience share. Moreover, CME’s

(193) In addition, one competitor indicates that PPF currently does not sub-licence its TV channels to other distributors, which raises concerns that this practice will continue post-transaction and will extend to CME.

(194) The Notifying Party argues that it will lack the incentive to foreclose competing pay TV operators from CME’s TV channels in general, and sports channels in particular. It has submitted economic studies assessing the risk of (i) total and (ii) partial foreclosure of CME’s channels in general, as well as (iii) CME’s sports channels in particular.106

(195) As concerns the total foreclosure of CME’s Nova channels,107 the study assesses whether the merged entity would have an incentive to stop distributing CME’s Nova channels on rival pay TV platforms. The study assesses different scenarios (foreclosure of individual pay TV retailers; foreclosure of all pay TV retailers combined, foreclosure of both DTT and rival pay TV platforms) and finds that, under any conceivable strategy, additional retail profits would not suffice to offset carriage and advertising losses. This is because CME’s profitability relies significantly on advertising revenues. Therefore, CME has a strong economic incentive to maximize the reach of its channels, an incentive which will not change post-Transaction. If the merged entity would engage in total input foreclosure, it would thus lose a significant amount of advertising revenues and carriage fees, due to O2’s limited downstream footprint. On the other hand, the merged entity’s increase in retail profit would be limited due to the fact that not all customers would switch distributors, and even those who would all not switch to O2.108

(196) In respect of partial foreclosure of CME’s Nova channels109 in the form of higher carriage fees or generally degraded commercial conditions imposed on competing TV retailers, the study posits that the merged entity may internalise the possibility that a blackout of CME’s channels on rival TV platforms resulting from a refusal of the merged entity’s proposed terms would have a profit-enhancing effect on O2’s retail TV business, thus making such blackouts less costly for the merged entity. However, despite the merged entity’s improved ability to threaten blackouts, the study finds that, due to O2’s limited downstream footprint and the limited number of expected diversion in favour of O2 following a blackout of CME’s channels110, the merged entity’s bargaining position would not materially improve post-Transaction.

(197) Finally, in relation to CME’s sports channels,111 the study finds that, in light of those channels’ low audience shares, end-customers could not be expected to switch distributors following a blackout. As a result, the merged entity would expect to lose carriage fees without any significant gains to be expected on the retail side. As for partial foreclosure, the study found that CME’s bargaining position would not materially change post-Transaction and that in any event, the effects on retail prices would be even lower than in the case of a partial foreclosure of all of CME’s channels.

(198) With regard to CME’s sports channels in particular, the Notifying Party also submitted that “the Nova sport channels do not hold highly attractive rights and are, therefore not valuable as captive production alongside the more valuable sports content O2 already broadcasts on its O2 sports channels”.112

(199) A number of PPF’s internal documents support the Notifying Party’s claim that the merged entity would have no incentive to engage in input foreclosure. In particular, in a presentation for financing banks regarding the Transaction from September 2019113 and a lender presentation regarding the loan for the Transaction from October 2019114, PPF has consistently presented long-term plans to its lenders that are based on a wide distribution of CME’s channels. PPF’s long term planning relies on the growth of CME’s advertising revenues and carriage fees revenues in the coming five years.115 PPF’s financial forecasts therefore assume that the merged entity will continue to ensure a broad distribution of CME’s main channel Nova, which accounts for most of CME’s advertising revenues, as well as of Nova’s sports channels, which accounted for [confidential data regarding revenues] of CME’s carriage revenues in Czechia in 2019.

(200) With regard to the increase in carriage fees in particular, the Commission notes that given the low audience shares of CME’s sports channels and the type of content they broadcast, any increase in carriage fees is unlikely without a service in return (such as an increase in quality and/or the offer of ancillary rights). Therefore, absent other evidence, the Commission considers that any increase in carriage fees would not result from the implementation of a foreclosure strategy.

(C) Impact on effective competition of input foreclosure

(201) Regardless of whether the merged entity has either the ability or the incentive to foreclose competing downstream rivals with regard to the supply of TV channels, the Commission does not consider that such a strategy would have an impact on competition.

(202) As detailed above in paragraphs (144) to (158), there are several providers of FTA and basic pay TV channels that compete with CME’s channels and will remain active post-Transaction. In particular with regard to CME’s sports channels, even if the merged entity were to adopt a foreclosure strategy, downstream rivals would continue to have access to sufficient alternative sports channels.

(203) As for a partial foreclosure strategy, the Commission notes that CME’s carriage fees represent a small amount of the overall carriage fees payed by TV distributors. Moreover, carriage fees payed by TV retailers are relatively small when compared to the level of retail TV fees. Even if the merged entity would decide to increase carriage fees, it is unlikely that downstream rivals would be significantly impacted and unable to compete effectively post-merger.

5.3.2.3.Conclusion

(204) In light of the above, the Commission considers that the Transaction does not give rise to serious doubts with regard to its compatibility with the internal market as a result of input foreclosure effects to the detriment of competing providers of retail AV services in Czechia.

5.3.3. Customer foreclosure relating to the wholesale supply of TV channels and the retail supply of AV services in Czechia

(205) The Transaction combines CME’s activities as a TV broadcaster with PPF’s downstream activities as a pay TV retailer in Czechia.

(206) According to the Non-Horizontal Merger Guidelines, a downstream firm being part of a vertical merger may refuse to buy inputs from its rival input suppliers as a result of the Transaction. This incentive to foreclose access to customers downstream may result from the vertical integration of an upstream supplier with an important customer downstream. Due to its downstream presence, the merged entity may foreclose its upstream rivals’ access to an important customer base. In turn, this can inhibit upstream rivals to effectively compete.116