Commission, January 19, 2021, No M.10028

EUROPEAN COMMISSION

Decision

BLACK DIAMOND CAPITAL MANAGEMENT / INVESTINDUSTRIAL GROUP / PHENOLIC SPECIALTY RESINS BUSINESS OF HEXION

Subject: Case M.10028 – BLACK DIAMOND CAPITAL MANAGEMENT / INVESTINDUSTRIAL GROUP / PHENOLIC SPECIALTY RESINS BUSINESS OF HEXION

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 2 and Article 57 of the Agreement on the European Economic Area3

Dear Sir or Madam,

(1) On 4.12.2020, the European Commission received a notification of a proposed concentration (the ‘Transaction’) pursuant to Article 4 of the Merger Regulation by which Black Diamond Capital Management LLC (‘Black Diamond’, the United States of America) and Investindustrial S.A. (‘Investindustrial’, Luxembourg) through its subsidiary Fusion Investment S.a.r.l. (‘FI’, Luxembourg), acquire within the meaning of Article 3(1)(b) of the Merger Regulation joint control of the Phenolic Specialty Resins Business of Hexion (‘Target’), belonging to Hexion Inc (‘Hexion’, the United States of America).4 Black Diamond and Investindustrial are designated hereinafter as the ‘Notifying Parties’, while the Notifying Parties together with the Target are referred to as the ‘Parties’.

1. THE PARTIES

(2) Black Diamond is an investment advisory firm with a focus on four investment areas: (i) control distressed/private equity funds; (ii) hedge funds; (iii) non-control stress/distressed closed end funds; and (iv) collateralised loan obligations.

(3) Investindustrial is a group of independently managed investment, holding and financial advisory companies. Independently managed subsidiaries of funds managed by companies of Investindustrial invest predominantly in medium-sized enterprises active in industry sectors such as consumer and leisure; healthcare and services; and industrial manufacturing.

(4) Hexion produces thermosetting resins, or thermosets, and adhesive and structural resins and coatings. The Target is mainly a producer of phenolic specialty resins, which are used in applications that require extreme heat resistance and strength, such as after-market automotive and OEM truck brake pads, filtration, aircraft components and foundry resins.

2. THE OPERATION

(5) The Transaction is structured as a purchase of assets, pursuant to a Purchase Agreement and a Framework Agreement, both signed on 27 September 2020. According to the Purchase Agreement, Fusion UK Holding Ltd., a subsidiary indirectly controlled by Investindustrial, will acquire the Target through wholly owned acquisition vehicles set up for the purposes of the Transaction. Upon closing of the Transaction, Black Diamond and Investindustrial will each indirectly hold equal equity interests in Fusion UK Holding Ltd. and therefore the Target.

(6) As such, following completion of the Transaction, the Target will be jointly owned and controlled by Black Diamond and Investindustrial. The Transaction therefore qualifies as a concentration pursuant to Article 3(1)(b) of the Merger Regulation.

3. UNION DIMENSION

(7) The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 5 000 million (Black Diamond: EUR […]; Investindustrial: EUR […]; Target: EUR […]). Each of them has a Union-wide turnover in excess of EUR 250 million (Black Diamond: EUR […]; Investindustrial: EUR […]; Target: EUR […]), but they do not achieve more than two-thirds of their aggregate Union-wide turnover within one and the same Member State.

(8) As a result, the Transaction has a Union dimension pursuant to Article 1(2) of the Merger Regulation.

4. MARKET DEFINITION

(9) The main products relevant to the merger control assessment of the Transaction are

(i) the liquid polymer known as unsaturated polyester resins (‘UPR’), and

(ii) thermoset moulding compounds5 which use UPR as their input (‘UPR-based thermoset compounds’), namely bulk and sheet moulding compounds (‘BMCs’ and ‘SMCs’), as well as dry granular thermoset moulding compounds (‘DGMCs’).

(10) Polynt-Reichhold, a portfolio company controlled by Black Diamond and Investindustrial, is an integrated manufacturer of composites, coatings, resins and intermediate and specialty chemical polymers, UPR, as well as UPR-based bulk and sheet moulding compounds (BMCs, SMCs). The Target is active in the production and supply of DGMCs which use various polymers as inputs, including UPR-based DGMCs.

(11) The Notifying Parties explain that UPRs are produced by the polycondensation of saturated and unsaturated dicarboxylic acids with glycols.6 UPRs form highly durable structures and coatings when they are cross-linked with a vinylic reactive monomer, most commonly styrene (‘pure UPR’ or “non-reinforced UPR’). Because on their own UPRs have only limited structural integrity, they are often combined with fiberglass or mineral fillers (‘reinforced UPR’) before cross-linking to enhance their mechanical strength. Reinforced UPRs are mostly used in construction, as well as marine and land transportation industries, while non-reinforced UPRs are used to make cultured marble and solid surface counter tops, gelcoats, automotive repair putty and filler, and other products, such as bowling balls and buttons.

(12) As for thermoset moulding compounds (which include, among others, BMCs, SMCs and DGMCs), they are produced using thermosetting polymeric matrices, the most common ones being, phenolic (‘PF’), melamine/phenolic (‘MF’), unsaturated polyester, vinylester and epoxy (‘EP’) resins. The end uses of thermoset compounds typically relate to transportation, electrical, or construction services.7

4.1 Product market definition

Unsaturated polyester resins (UPRs)

4.1.1.1 The Commission’s precedents

(13) In its past decisions, the Commission found that UPR could constitute a separate product market as it is not substitutable with other resins or chemical compounds intended for the same use.8

(14) Moreover, in previous cases, the Commission found that UPR is not a homogenous product, as it can be supplied in two forms: pure UPR or reinforced UPR. As opposed to pure UPR with a standard formulation, reinforced UPR combines UPR with different additives in certain quantities to match the specific requirements and needs of each customer.9 However, although for each end-use application (industry) it is necessary to have a special formulation of UPR, suppliers that are focused on customers from certain industries can easily adapt their production to start supplying UPR for use in other industries as well.10

(15) Thus, due to an extensive supply-side substitutability with regard to the manufacturing of UPR for different end-uses, the Commission considered the market for UPR as a single, differentiated product market.11

4.1.1.2 The Notifying Parties’ view

(16) The Notifying Parties submit that there is a relevant product market for UPR, which relates to the production and supply of pure UPR,12 which is generally styrene based, and not reinforced UPR. In particular, they recall arguments made by the parties in M.7359 - PCCR USA/ TOTAL'S CCP COMPOSITE BUSINESS that suppliers produce only pure UPR, with customers themselves, if needed, producing reinforced UPR13 at a later stage.14

4.1.1.3 The Commission’s assessment

(17) The results of the Commission’s market investigation confirm the findings from M.8059 – Investindustrial / Black Diamond / Polynt/ Reichhold. In particular, while many suppliers indeed produce UPR in its pure form only, others offer both pure and reinforced UPR.15

(18) Thus, in line with its past decisional practice, the Commission considers that the production and supply of UPR in any of its forms (pure or reinforced) constitutes one relevant product market without any warranted segmentations.

Bulk moulding compounds, sheet moulding compounds and dry granular thermoset moulding compounds (BMCs, SMCs and DGMCs)

4.1.2.1 The Commission’s precedents

(19) In its only precedent defining the market for BMCs and SMCs,16 the Commission considered these two compounds to be competing in the same market, due to their demand- and supply-side substitutability, but it left the exact market definition open.

(20) The Commission has not previously examined market definition in relation to DGMCs.

4.1.2.2 The Notifying Parties’ view

(21) The Notifying Parties submit that BMCs and SMCs are not substitutable with DGMCs, arguing that the compounds are distinct in terms of composition, manufacturing, processing, final production and type of application.17

(22) As for the supply-side perspective, the Notifying Parties argue that the production of DGMCs differs in manufacturing technologies used from that of BMCs and SMCs. Moreover, for the production of the former various polymers can be used as an input (i.e. reinforced UPR, PF, MF or EP resins), whilst the production of the latter requires pure UPR as an input.

(23) Regarding the demand side, the Notifying Parties submit that SMCs and BMCs are liquid/semi-liquid resins, composed of long fibres and suitable for compression moulding, whilst DGMCs are dry granular raw materials, suitable for injection moulding. Moreover, the Notifying Parties claim that SMCs and BMCs are heavier and cheaper compared to DGMCs. Although all three compounds are generally used in similar industries (i.e. automotive, electrical engineering and electrical components industries), the Notifying Parties argue that their application differs due to their distinct product characteristics.

(24) For example, DGMCs may be used in household appliances and tight tolerance/high performance parts in automotive under-the-hood applications, such as pistons, pulleys, valve blocks and pump parts, due to their better dimensional stability, higher heat resistance high viscosity flow, high mechanical properties and insulating properties, whilst SMCs and BMCs’ typical applications include more demanding electrical applications, corrosion resistant needs, and structural components due to their mechanical strength.

4.1.2.3 The Commission’s assessment

(25) The majority of the respondents to the Commission’s market investigation supported the Notifying Parties’ view on the absence of supply-side substitutability, confirming that different technologies are required for the production of DGMCs on the one hand and of SMCs/BMCs on the other hand.18

(26) Moreover, some of the respondents further agreed with the distinction between DGMCs and SMCs/BMCs made by the Notifying Parties due to the absence of demand-side substitutability.19

(27) However, other respondents expressed a contrary view, outlining a number of similarities between DGMCs and SMCs/BMCs. More specifically, these respondents indicated that when it comes to processing of these three compounds, similar technologies can be used. For instance, one respondent stated that ‘DGMCs can also be compression moulded’20 using the ‘same press equipment’.21 In addition, the compounds’ weight was considered to often be comparable depending on its composition.22 More specifically, the length of the fibres of DGMCs ‘can be increased’,23 and their density can ‘range between 1.35 and 2.1 g/cm3’.24 Similarly, depending on the type of DGMC (i.e. EP-, PF-based), the three compounds ‘can be at the same price level or be cheaper’25 and there is therefore, ‘no clear line between prices’.26 Finally, as regards the compounds’ properties, ‘specific DGMCs will outperform SMCs/BMCs in mechanical strength’.27

(28) The participants’ responses to the market investigation also suggest that, while the properties of DGMCs can vary according to the polymer used as an input (UPR, EP, PF, MF),28 since DGMCs based on different inputs share some similar properties, they are also to some degree substitutable with each other. More specifically, according to the respondents, customers can substitute different DGMCs because of (i) the similarity of their ‘strong points’29 (i.e. properties), which is sufficient according to the customers’ technical requirements,30 (ii) the price of each compound,31 and (iii) other reasons (i.e. certain changes in regulatory requirements due to, among others, some thermoset moulding compounds being considered as environmentally unfriendly).32 None of the participants’ responses to the market investigation suggested that DGMCs should constitute separate product markets based on their input.

(29) On that note, market participants suggested that thermoset moulding compounds are easily substitutable between one another, depending on the technical requirements of their customers.33 More specifically, market participants suggest that in some fields of application, DGMCs can be substituted by SMC/BMCs, and vice versa, whilst other fields of application ‘can only be covered by one of the two product classes; and that ‘this strongly depends on the individual [end-] product properties’.34 Other market participants suggested that the substitutability between DGMCs and SMCs/BMCs is possible only in ‘small industrial niches where two different material groups can cross’.35

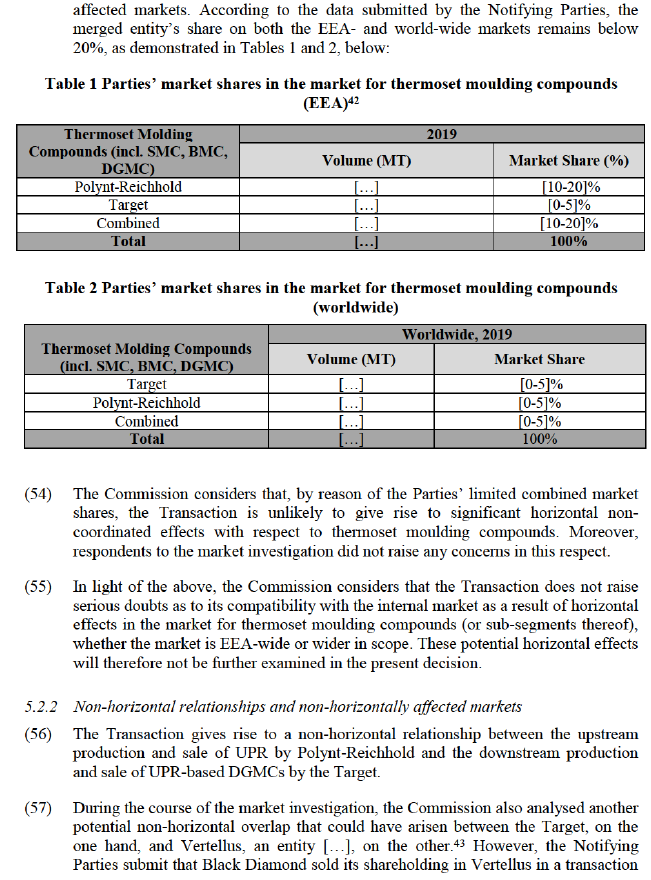

(30) Overall, the responses to the market investigation suggest that, from a demand-side perspective, DGMCs, SMCs and BMCs are to some degree substitutable. Although some responses to the market investigation distinguish the various thermoset moulding compounds according to the polymer used as their input (i.e. UPR, EP, PF, MP),36 none of the responses support the fact that thermoset moulding compounds belong to separate product markets based on their input.

(31) Therefore, the Commission considers that BMCs/SMCs and DGMCs could belong to a broader, differentiated market for thermoset moulding compounds of various polymers (e.g. pure/reinforced UPR, PF, MP and EP resins).

(32) Whether or not a distinction should be drawn between (i) SMCs/BMCs and (ii) DGMCs can be left open, since the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition.

Conclusion on product market definition

(33) On the basis of the above, the Commission finds that:

i) UPR constitutes a separate relevant product market;

ii) Thermoset moulding compounds (i.e. BMCs, SMCs and DGMCs) of different polymers (e.g. pure/reinforced UPR, phenolic, melamine/phenolic and epoxy resins) could constitute a relevant product market or, alternatively, (i) SMCs/BMCs and (ii) DGMCs could constitute separate relevant product markets. This question can be left open.

4.2 Geographic market definition

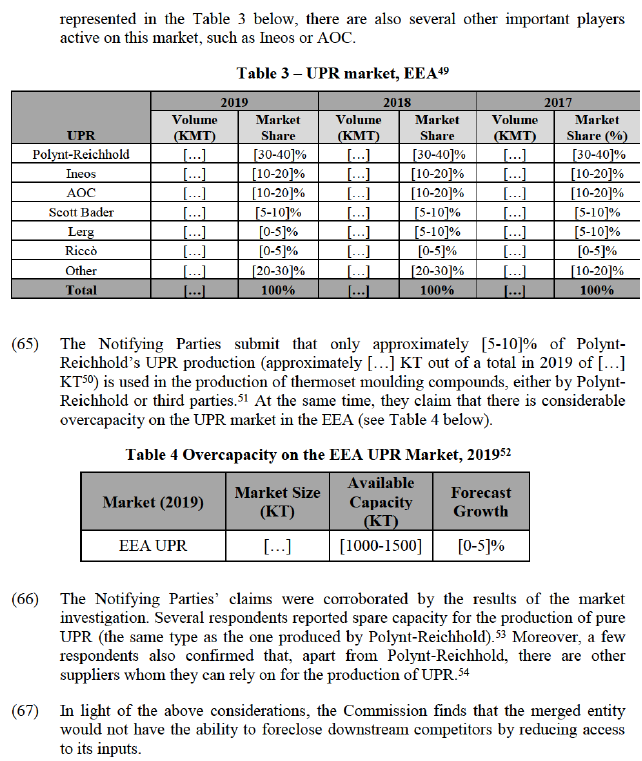

Unsaturated polyester resins (UPRs)

4.2.1.1 The Commission’s precedents

(34) In previous decisions, the Commission considered the geographic market definition for production and sale of UPR to be EEA-wide.37 In fact, despite moderate transport costs, some product characteristics, in particular product stability and temperature conditions, impede UPR from being transported over long distances. As a result, European customers’ plants are mainly sourced within Europe.

4.2.1.2 The Notifying Parties’ view

(35) The Notifying Parties submit that, for the purposes of the assessment of the Transaction, it is not necessary to determine whether the geographic scope of the UPR market is EEA-wide or worldwide in scope, since they consider that the Transaction does not raise any competition concerns under any possible geographic market definition.

4.2.1.3 The Commission’s assessment

(36) The Commission’s market investigation did not provide any elements that would warrant a departure from its past decisional practice. Thus, the Commission finds that the relevant geographic market for the production and sale of UPR is EEA-wide in scope.

4.2.2 Bulk moulding compounds, sheet moulding compounds and dry granular thermoset moulding compounds (BMCs, SMCs and DGMCs)

4.2.2.1 The Commission’s precedents

(37) As for BMCs and SMCs, in M.8059 – Investindustrial / Black Diamond / Polynt/ Reichhold, the Commission found the relevant geographic market to be EEA-wide, due to product supplies taking place across the EEA, relatively low transport costs and the fact that customers explained that sourcing outside the EEA was not considered a suitable option. In the absence of competition concerns, the exact scope of the geographic market was left open.38

(38) The Commission has not previously defined a geographic market for DGMCs.

4.2.2.2 The Notifying Parties’ view

(39) The Notifying Parties submit that DGMCs are not substitutable with, and constitute a separate product market from SMCs and BMCs. As a result, they consider that SMCs and BMCs are not relevant to the Transaction and therefore, do not submit their view on the relevant geographic market for SMCs/BMCs.

(40) They nevertheless suggest that the relevant geographic market for DGMCs is at least EEA-wide in scope, in light of product supplies taking place across the EEA and relatively low transport costs, resulting from the fact that DGMCs are dry, non- hazardous products that can be stored for very long periods of time (6-12 months). To support their view, the Notifying Parties submit that the Target produces DGMCs only in Germany, but sells them worldwide.

4.2.2.3 The Commission’s assessment

(41) In line with its past decisional practice for SMCs and BMCs, the Commission finds, for the purposes of the assessment of the Transaction, the geographic market for thermoset moulding compounds (and sub-segments thereof) to be at least EEA-wide.

(42) However, the precise definition of the relevant geographic market, i.e. whether it is EEA-wide or wider (e.g. worldwide) in scope, can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition.

Conclusion on geographic market definitions

(43) On the basis of the above, the Commission finds that for

i) UPR the relevant geographic market is EEA-wide in scope;

ii) Thermoset moulding compounds (and possible segments thereof) the relevant geographic market is EEA-wide or wider (e.g. worldwide) in scope but the exact market definition can be left open.

5. COMPETITIVE ASSESSMENT

5.1 Legal framework

(44) Under Article 2(2) and (3) of the Merger Regulation, the Commission must assess whether a proposed concentration would significantly impede effective competition in the internal market or in a substantial part of it, in particular through the creation or strengthening of a dominant position. In this respect, a merger can entail horizontal and/or non-horizontal effects.

5.1.1 Horizontal effects

(45) Horizontal effects are those deriving from a concentration where the undertakings concerned are actual or potential competitors of each other in one or more of the relevant markets concerned. The Commission appraises horizontal effects in accordance with the Horizontal Merger Guidelines.39 Horizontal effects may be non- coordinated or coordinated.

(46) As regards horizontal non-coordinated effects, according to paragraph 26 of the Horizontal Merger Guidelines, a number of factors (the list of which is non-exhaustive) may be taken into account in order to determine whether significant non- coordinated effects are likely to result from a concentration.

(47) In assessing the likelihood of coordinated effects, the Commission takes into account all available relevant information on the characteristics of the markets concerned, including both structural features and the past behaviour of firms.40

5.1.2 Non-horizontal effects

(48) Non-horizontal effects mainly relate to the foreclosure of competitors that can arise from vertical or conglomerate integration. In general, vertical integration is the consequence of the combination of products, services or businesses across different levels of the same supply chain. Conglomerate integration relates to the combination of complementary products or services that are generally purchased by the same set of customers.

(49) Pursuant to the Non-Horizontal Merger Guidelines,41 vertical integration may result in two forms of foreclosure: input foreclosure, where the concentration is likely to raise costs of downstream rivals by restricting access to an important input or deteriorating supply conditions, and customer foreclosure, where the concentration is likely to foreclose upstream rivals by restricting their access to a sufficient customer base.

(50) In assessing the likelihood of foreclosure scenarios, the Commission examines, first, whether the merged firm would have the ability to foreclose its rivals, second, whether it would have the economic incentive to do so and, third, whether a foreclosure strategy would have a significant detrimental effect on competition, thus causing harm to consumers. In practice, these factors are often examined together as they are closely intertwined.

5.2 Market structure

5.2.1 Horizontal relationships and horizontally affected markets

(51) The Transaction give rise to a horizontal relationship in the overall market for thermoset moulding compounds between the production and sale of UPR-based bulk and sheet moulding compounds (BMCs and SMCs) by Polynt-Reichhold, a portfolio company controlled by Black Diamond and Investindustrial, and the production and sale of dry granular thermoset moulding compounds (DGMCs) by the Target.

(52) Under the narrowest plausible market definition, that is to say the production and sale of DGMCs, on the one hand, and of BMCs and SMCs, on the other hand, the Transaction does not result in any horizontal overlaps (and thus there are also no horizontally affected markets).

(53) As for the horizontal overlap between the Parties’ activities on the wider market for production and sale of thermoset moulding compounds (BMCs, SMCs and DGMCs) in the EEA and world-wide, the Transaction does not lead to any horizontally

that closed in December 2020. On that basis, this potential non-horizontal relationship will not be further discussed in the present decision.44

(58) As regards the vertical link between the upstream production and sale of UPR by Polynt-Reichhold and the downstream production and sale of UPR-based DGMCs by the Target, the Transaction gives rise to affected markets both upstream and downstream.

(59) Indeed, first, Polynt-Reichhold’s share of the upstream market for UPR production and sale in the EEA amounted to [30-40]% in 2019.45

(60) Second, as for the downstream activities, in 2019, the Parties held [10-20]% and [0- 5]% of the market for production and sale of thermoset moulding compounds (including SMCs, BMCs and DGMCs) respectively in the EEA and worldwide (see paragraph (53) above). The Target’s shares of the market for DGMCs amounted in 2019 in the EEA to [30-40]%46 and worldwide to [0-5]%.47

5.3 Non-horizontal effects

5.3.1The Notifying Party’s view

(61) The Notifying Parties argue that there is no actual or potential vertical link between the UPR produced by Polynt-Reichhold and UPR-based DGMCs produced by the Target.48

(62) In particular, they submit that for its production of UPR-based DGMCs, the Target purchases exclusively UPR resins in their reinforced form, while Polynt-Reichhold only produces pure UPR (based on styrene).

(63) Moreover, according to the Notifying Parties, Polynt-Reichhold would not be able to produce reinforced UPR without very substantial cost and time investments, whilst the Target would not be able to use pure UPR due to i) a specific granular form of its DGMCs that requires a use of reinforced UPR, ii) the inability to process pure UPR by its manufacturing assets and finally iii) the flammable character of styrene contained in pure UPR, which would require the establishment of an explosive- protection zone in its production operations.

5.3.2 The Commission’s assessment

5.3.2.1 Input foreclosure

Ability to foreclose

(64) The Notifying Parties submit that Polynt-Reichhold’s share per volume in the market for the production and supply of UPR in 2019 in the EEA was [30-40]%. As

Incentives to foreclose

(68) According to the Notifying Parties’ submissions recalled in paragraph (62), Polynt- Reichhold produces only pure UPR based on styrene, while the Target, for its UPR- based DGMCs production, purchases exclusively UPR in its reinforced form and would not be able to rely on pure UPR instead. Thus, the merged entity would not be able to source UPR for its downstream production of DGMCs internally, which makes the recuperation of losses generated by a potential input foreclosure strategy upstream via its downstream activities in the production and sale of DGMCs unlikely.

(69) Moreover, the results of the market investigation did not suggest that an input foreclosure strategy could be profitable.

Overall effects on competition

(70) In light of the lack of ability and incentives for the merged entity to engage in input foreclosure, the Commission finds that any such strategy would be unlikely to have any detrimental effect on overall competition. This assessment is further supported by the results of the market investigation, as the respondents did not raise any substantial concerns in this regard.

Conclusion on input foreclosure

(71) On the basis of the above, the Commission considers that the Transaction does not raise any competition concerns related to input foreclosure.

5.3.2.2 Customer foreclosure

Ability to foreclose

(72) As stated in paragraph (62), the Notifying Parties submit that Polynt-Reichhold produces only pure UPR, while the Target, for its UPR-based DGMCs production, purchases exclusively UPR resins in their reinforced form. Thus, post-Transaction, the merged entity would not have an ability to engage in customer foreclosure by resorting to self-supply.

(73) Moreover, as stated in paragraph (60), the Target’s share of the market for DGMCs amounted in 2019 in the EEA and worldwide to [30-40]% and [0-5]% respectively, which, even in the event of a customer foreclosure strategy, would leave more than [60-70]% of the EEA demand available to other UPR suppliers.

(74) Moreover, the respondents to the market investigation did not raise any concerns related to the merged entity’s ability to engage in customer foreclosure. On the contrary, one of the respondents who supplies UPR to the Target stated that any foreclosure behaviour of the merged entity ‘wouldn´t cause any impact on our company resp. our profitability, since this would only affect a quite small part of our whole sales’.55 Another UPR supplier that has a commercial relationship with the Target did not reply to the market investigation.

(75) In light of the above considerations, the Commission finds that the merged entity would not have the ability to foreclose upstream competitors by reducing access to customers.

Incentives to foreclose

(76) The aforementioned inability of the Target to use UPR produced by Polynt- Reichhold for its DGMCs production results in a lack of incentives to engage in customer foreclosure.

(77) Furthermore, any potential incentives would in any case be reduced by important switching costs. The Notifying Parties claim that to be able to start producing reinforced UPR, the merged entity would need to incur substantial costs and invest significant time.

(78) Thus, post-Transaction, the merged entity would have no incentives to engage in customer foreclosure.

Overall effects on competition

(79) In light of the lack of ability and incentives for the merged entity to engage in customer foreclosure, the Commission finds that any such strategy would be unlikely to have any detrimental effect on overall competition. This assessment is further supported by the results of the market investigation, as the respondents did not raise any substantial concerns in this regard.

Conclusion on customer foreclosure

(80) On the basis of the above, the Commission considers that the Transaction does not raise any competition concerns related to customer foreclosure.

5.3.3 Conclusion on non-horizontal effects

(81) On the basis of all of the above considerations and in view of the results of the market investigation, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market as a result of non- horizontal effects.

6. CONCLUSION

(82) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the ‘Merger Regulation’). With effect from 1 December 2009, the Treaty on the Functioning of the European Union (‘TFEU’) has introduced certain changes, such as the replacement of ‘Community’ by ‘Union’ and ‘common market’ by ‘internal market’. The terminology of the TFEU will be used throughout this decision.

2 For the purposes of this Decision, although the United Kingdom withdrew from the European Union as of 1 February 2020, according to Article 92 of the Agreement on the withdrawal of the United Kingdom of Great Britain and Northern Ireland from the European Union and the European Atomic Energy Community (OJ L 29, 31.1.2020, p. 7), the Commission continues to be competent to apply Union law as bregards the United Kingdom for administrative procedures which were initiated before the end of the transition period.

3 OJ L 1, 3.1.1994, p. 3 (the ‘EEA Agreement’).

4 Publication in the Official Journal of the European Union No C 435, 16.12.2020, p. 5–6.

5 ‘Based on their response to temperature, plastic materials may be classified into two main categories: thermoplastics and thermosets. A thermoplastic behaves like a fluid above certain temperature level, but the heating of a thermoset leads to its degradation without its going through a fluid state. […] This classification is not restricted to plastic material but may also be extended to the behavior of coatings, adhesives and several other categories’. Source: Jean-Pierre Pascault, Henry Sautereau, Jaques Verdu, Roberto J.J. Williams, Thermosetting Polymers (CRC Press, 2002) 1.

6 Form CO, paras. 6.39-6.41.

7 Form CO, paras 6.3 ff and Annex 6.1.b.

8 Case COMP/M.7359 – PCCR USA/Total’s CCP Composite Business, 27 October 2014, para. 17.

9 Case COMP/M.8059 – Investindustrial / Black Diamond / Polynt/ Reichhold, 12 May 2017, para. 30

10 Case COMP/M.7359 – PCCR USA/Total’s CCP Composite Business, 27 October 2014, paras 16-19.

11 Ibid, paras 31-34.

12 In the Form CO, the Notifying Parties use the terms ‘liquid’, ‘virgin’ and ‘non-reinforced’ to refer to ‘pure’ UPR. In reply to request for information 8 of 15.01.2021, the Notifying Parties confirmed that the terms ‘non-reinforced’, ‘liquid’ and ‘virgin’ used in the Form CO, refer to the format of UPR referred to as ‘pure’ by the Commission in Case COMP/M.8059 – Investindustrial / Black Diamond / Polynt/ Reichhold, 12 May 2017.

13 In the Form CO, the Notifying Parties also use the terms ‘dry’ or ‘solid’ to refer to ‘reinforced’ UPR. In reply to request for information 8 of 15.01.2021, the Notifying Parties confirmed that the terms ‘dry’ and ‘solid’ used in the Form CO, refer to the format of UPR referred to as ‘reinforced’ by the Commission in Case COMP/M.8059 – Investindustrial / Black Diamond / Polynt/ Reichhold, 12 May 2017.

14 Form CO, paras 6.44-6.53.

15 Reply to the Commission’s market investigation received on 11.12.2020.

16 Case COMP/M.8059 – Investindustrial / Black Diamond / Polynt/ Reichhold, 12 May 2017, para. 88.

17 Form CO paras 6.3-6.35 and Table 2.

18 Replies to the Commission’s market investigation received on 08.12.2020 and 14.12.2020 (1). One reply to the Commission’s market investigation received on 11.12.2020 suggested that the materials can be substituted from a supply-side perspective ‘depend[ing] on the market, technical requests on products, laws’.

19 Reply to the Commission’s market investigation received on 14.12.2020 (2).

20 Reply to the Commission’s market investigation received on 11.12.2020.

21 Reply to the Commission’s market investigation received on 14.12.2020 (1).

22 Reply to the Commission’s market investigation received on 14.12.2020 (3).

23 Reply to the Commission’s market investigation received on 11.12.2020.

24 Reply to the Commission’s market investigation received on 14.12.2020 (1).

25 ibid.

26 Reply to the Commission’s market investigation received on 14.12.2020 (3).

27 Reply to the Commission’s market investigation received on 14.12.2020 (1).

28 Replies to the Commission’s market investigation received on 11.12.2020 and 14.12.2020 (2).

29 Reply to the Commission’s market investigation received on 14.12.2020 (2).

30 Reply to the Commission’s market investigation received on 14.12.2020 (2) points out some of the similarities between DGMCs of various inputs. The respondent suggests that, among others, (i) UPR-, MP- and EP- based DGMCs, all have good electrical properties, (ii) UPR- and PF- based DGMCs both have dimensional stability MP- and EP-based DGMCs both have copper adhesion, etc.

31 Reply to the Commission’s market investigation received on 11.12.2020.

32 ibid.

33 Reply to the Commission’s market investigation received on 11.12.2020.

34 Reply to the Commission’s market investigation received on 08.12.2020.

35 Reply to the Commission’s market investigation received on 14.12.2020 (2).

36 Replies to the Commission’s market investigation received on 08.12.2020, 11.12.2020 and 14.12.2020 (2).

37 Case COMP/M.7359 - PCCR USA/Total’s CCP Composite Business, 27 October 2014, paras. 21 and 23; Case COMP/M.8059 – Investindustrial / Black Diamond / Polynt/ Reichhold, 12 May 2017, para. 44.

38 Case COMP/M.8059 – Investindustrial / Black Diamond / Polynt/ Reichhold, 12 May 2017, paras 80-90.

39 Guidelines on the assessment of horizontal mergers under the Council Regulation on the control of concentrations between undertakings (‘Horizontal Merger Guidelines’), OJ C 31, 5.2.2014.

40 Horizontal Merger Guidelines, paragraph 43.

41 Guidelines on the assessment of non-horizontal mergers under the Council Regulation on the control of concentrations between undertakings. OJ C 265, 18.10.2008, p. 6.

42 Reply to the request for information 3 of 17.12.2020.

43 Form CO, paras 6.85 ff.

44 Reply to the request for information 6 of 11.01.2021. For the press release issued by Vertellus see https://vertellus.com/pritzker-private-capital-acquires-vertellus/.

45 Form CO, Table 9.

46 Form CO, Table 11.

47 Form CO, Table 10.

48 Form CO, paras 6.78 ff.

49 Form CO. Table 9.

50 Reply to the request for information 6 of 11.01.2021: "The value of [...] KMT in Table 9 of the Form CO [Table 3 of this decision) refers to volumes sold. The value of approximately [...] KT in response to question 1 of EC RFI 3 [request for information 3] refers to volumes produced. [...] both KT and KMT are the same unit and refer to Kilo (Metric) Tons.

51 Reply to the request for information 3 of 17.12.2020. The Notifying Party futher submits that whien measured by value, the percentage would be similar, taking into account Polynt-Reichhold's total 2019 UPR supply of approximately EUR [...] million.

52 Form CO. Table 20.

53 Replies to the market investigation of 11.12.2020, 12.12.2020 and 17.12.2020.

54 Replies to the market investigation of 11.12.2020 and 14.12.2020.