Commission, February 18, 2020, No M.9802

EUROPEAN COMMISSION

Decision

LIBERTY GLOBAL / DPG MEDIA / JV

Subject: Case M.9802 – Liberty Global / DPG Media / JV

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 7 July 2020, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Liberty Global plc (‘Liberty Global’, United Kingdom) and DPG Media NV (‘DPG Media’, Belgium) acquire within the meaning of Articles 3(1)(b) and 3(4) of the Merger Regulation joint control of a newly created joint venture (‘JV’, Belgium) (the “Transaction”).3 Liberty Global and DPG Media are designated hereinafter as the “Notifying Parties” and each individually as “Notifying Party”. The Notifying Parties together with the JV are designated hereinafter as the “Parties”.

1. THE PARTIES

(2) Liberty Global, through its subsidiary Telenet, is a cable and mobile network operator in Belgium and parts of Luxembourg. Telenet supplies broadband internet, fixed telephony services and cable television (“TV”) primarily in Flanders and parts of Brussels, as well as mobile telecommunications services in the whole of Belgium. In addition, Telenet operates (i) Dutch-language pay TV channels and video-on- demand services (Play, Play More and Play Sports), free-to-air TV channels (Vier, Vijf, Zes), and a radio station (NRJ Vlaanderen), (ii) the advertising sales house SBS Sales Belgium, and (iii) the production company Woestijnvis.

(3) DPG Media belongs to DPG Media Group, which operates media companies in Belgium, the Netherlands and Denmark. The activities of DPG Media are, in Belgium: (i) the supply of Dutch-language daily newspapers (Het Laatste Nieuws, De Morgen) and magazines (e.g. Dag Allemaal, Goed Gevoel, Humo), (ii) the operation of TV channels (VTM, Q2, Vitaya, CAZ, and VTM Kids), an advertising- based video on demand service (VTM Go) and radio stations (Q-music and Joe), and (iii) the operation of a telecom mobile virtual network (Mobile Vikings).

(4) The JV will provide a subscription video on demand (“SVOD”) service in Belgium under a new and independent brand focused on Dutch-speaking consumers (i) directly to customers in Belgium via an over the top (“OTT”) platform (including website and smart phone app) and (ii) on an exclusive wholesale basis to Telenet, for distribution by Telenet through its cable platform (integrated in Telenet’s channel packages and/or set top box interface). The JV will acquire content from the Notifying Parties, third parties, and will also commission new original content for its SVOD service. The JV’s offering will primarily consist of local and international films and series. It will neither include (i) sports or adult content, nor (ii) linear channels (of Telenet and/or DPG Media and/or of third parties)4 and ancillary services linked thereto (e.g. catch up services).

2. THE OPERATION AND THE CONCENTRATION

(5) The Transaction will take place pursuant to a binding Memorandum of Understanding (“MoU”) concluded by DPG Media and Telenet on 12 February 2020.

2.1. Joint control

(6) Telenet and DPG Media will each own 50% of the shares of the JV, and have the ability to exercise decisive influence over the JV. In particular, the Notifying Parties will each appoint an equal number of directors. An independent (non-executive) chairman of the board will be appointed by unanimity. The board will decide by simple majority, except for specific items for which approval of each shareholder/director is required (but not of the independent chairman). These include inter alia [Details of the JV agreement].5

(7) Therefore, as a result of the Transaction, Liberty Global and DPG Media will jointly control the JV within the meaning of Article 3(1)(b) of the Merger Regulation.

2.2. Full-functionality

(8) The JV will be fully functional. First, the JV will employ its own management dedicated to its day-to-day operations, and have access to sufficient resources, including finance, staff and assets that will enable it to operate independently on the market for the retail supply of audiovisual (“AV”) services, performing the functions normally carried out by undertakings operating on the same market. In particular, both Parties will contribute to the JV certain content agreements and staff so as to allow the JV to be (both financially and operationally) self-sustaining (through the revenues deriving from its operations with third parties and its own borrowing capacity on the market).

(9) Second, the JV is intended to operate as an autonomous entity and will have its own, independent access to and presence on the markets for (wholesale and retail) supply of SVOD services. Its activities will not be limited to the distribution or sale of its parent companies' products, as the JV will supply its own SVOD offering to end customers, as a fully independent company with its own personnel (20-25 employees). In addition, the JV has negotiated and/or will negotiate agreements with its parents (e.g. a wholesale agreement and IT/back-end services agreement with Telenet; and a long-form video platform agreement with DPG Media) on an arm’s length basis, reflecting the normal market conditions it practices with third parties.

(10) Third, the JV and will not only purchase from and/or supply to its own parents. It will have direct contractual relationships with third party licensors and will not be reliant on its parents for licensing relationships. It will also commission original productions from TV production studios, the majority of which will be sourced from third party TV production studios. In addition, the JV will source additional and new SVOD licenses to content mainly from third party content providers.6

(11) Finally, the JV is intended to operate on a lasting basis. Due to applicable corporate law restrictions, the shareholders agreement currently has a duration of [Details of the JV shareholder agreement].

(12) Therefore, the Transaction will lead to the creation of a full-function joint venture within the meaning of Article 3(4) of the Merger Regulation.

3. EU DIMENSION

(13) The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 5 000 million (Liberty Global: EUR 12,277 million; DPG Media: EUR 1,601 million; combined: EUR 13,878 million). Each of them has an EU-wide turnover in excess of EUR 250 million (Liberty Global: EUR 11,082 million; DPG Media: EUR 1,601 million), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State.

(14) The Transaction therefore has a Union dimension pursuant to Article 1(2) of the Merger Regulation.

4. RELEVANT MARKETS

4.1. Introduction

(15) The Transaction concerns all the levels of the AV value chain, namely: (i) the production of AV content; (ii) the licensing of broadcasting rights for individual AV content; (iii) the wholesale supply of TV channels; and (iv) the retail supply of AV services.

(16) Providers of retail AV services offer end users packages of linear and/or non-linear AV services. Linear services are services that broadcast scheduled programs, not streamed by a specific user. Non-linear services, or video-on-demand (“VOD”) services, are services provided for the viewing of programmes at the moment chosen by the users and at their individual request, on the basis of a catalogue of programmes. AV services may be offered either on a free-to-air (“FTA”) or pay-TV basis. Providers of retail AV services deliver their content to end customers via a number of technical means: (i) traditional networks, such as cable, satellite (“direct- to-home” or “DTH”), internet protocol television (“IPTV”), and to a lesser extent, digital terrestrial TV (“DTT”) and/or (ii) the “Over-The-Top” (“OTT”) distribution technology which allows AV content to be delivered through the use of open internet.

(17) In addition, the Transaction concerns: (v) the retail supply of fixed internet access services; (vi) the retail supply of mobile telecommunications services; (vii) the retail supply of multiple play services; and (viii) the sale of advertising space.

4.2. The AV value chain

(18) In previous cases, the Commission set out the different levels of the AV value chain as follows: (i) the (upstream) markets for the production and the licensing of AV content, (ii) the (intermediate) market for the wholesale supply of TV channels, and (iii) the (downstream) market for the retail supply of AV services.7

(19) The market investigation confirmed that this three-layer classification with regard to the chain of supply of AV content is still applicable today.8

4.3. Market for the production of AV content

(20) This part of the value chain concerns the production of new AV content. The supply side of the market comprises AV production companies while the demand side comprises companies (TV broadcasters or content platform operators) that can commission the production of AV content or hire AV production services.9

(21) The Parties’ activities and those of the JV overlap on the demand side of the market only. On the supply side, while Telenet is active in the production of content through its subsidiary Woestijnvis, and DPG Media is active but exclusively for captive use. DPG Media has no plans to enter the merchant market for the production of TV content in the near future. The JV will not produce any AV content.

4.3.1. Product market definition

4.3.1.1. Previous Commission decisions

(22) The Commission has consistently considered that the production of AV content should be distinguished from the licensing of broadcasting rights for AV content.10 The Commission has also found the product market for the production of TV content to be limited to non-captive TV production, thereby excluding content produced by TV broadcasters for use on their own channels.11

(23) In addition, in its 2015 case Liberty Global/Corelio/W&W/De Vijver Media, the Commission considered that the market for the production of TV content could be further segmented depending on the type of TV content (that is films, sports or other) or exhibition window (namely SVOD, transaction-based VOD (“TVOD”), Pay Per View (“PPV”), Fist pay TV window, Second pay TV window, FTA), but ultimately left those possible segmentations open.12 In subsequent cases, the Commission either did not consider further segmentations or left open the question whether the market for the production of AV content should be further segmented. In particular, the question was left open whether the market for production of general entertainment TV content should be further segmented: (i) by genre; (ii) between scripted and non-scripted content; and (iii) between commissioned TV production or TV production for-hire.13

4.3.1.2. Notifying Parties’ view

(24) The Notifying Parties submit, in accordance with the Commission’s position in case Liberty Global/Corelio/W&W/De Vijver Media, that the precise product market definition for the production of AV content can be left open.14

4.3.1.3. Commission’s assessment

(25) A majority of respondents to the market investigation indicated that, in Belgium, the distinction between the market for the production of AV content on the one hand, and the market for the licensing of broadcasting rights for pre-existing individual AV content on the other hand is at present appropriate.15 In addition, nothing in the Commission’s file gives reasons to depart from the previous approach of considering that the product market for the production of AV content is limited to non-captive AV production. Further, the results of the market investigation were mixed as to whether the market for the production of AV content needs to be subdivided by content type16 or exhibition window.17 Last, nothing in the Commission’s file gives reasons to depart from the previous approach that the question whether the market should be further segmented (i) between scripted and non-scripted content; and (ii) between commissioned AV production or AV production for-hire is to be left open.

(26) In light of the above, the Commission concludes that, for the purpose of this decision and in line with its previous practice, it is appropriate to consider as relevant the market for the non-captive production of AV content, while the question whether that relevant product marked needs to be further sub-segmented on the basis of content type or exhibition windows, or between scripted and non-scripted content, and between commissioned AV production or AV production for-hire can be left open, since the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement under any such plausible product market definitions.

4.3.2. Geographic market definition

4.3.2.1. Previous Commission decisions

(27) In previous cases, the Commission considered that the question whether the geographic scope of the market for the production of TV content was national or regional (the Flemish Region or the combination of the Flemish Region and the Brussels Capital Region) could be left open.18 The Belgian Competition Authority (“BCA”) has either previously considered that the geographic market for the production of Dutch-language TV content was (i) national,19 or (ii) Telenet’s footprint,20 or (iii) left the exact geographic scope of the market open.21

4.3.2.2. Notifying Parties’ view

(28) The Notifying Parties submit, in accordance with the Commission’s position in case Liberty Global/Corelio/W&W/De Vijver Media, that the precise geographic market definition can be left open.22

4.3.2.3. Commission’s assessment

(29) The results of the market investigation were mixed as to whether the geographic scope of the market for the production of AV content is national or by linguistic area.23

(30) In light of the above, the Commission considers that, for the purpose of this decision and in line with its previous practice, the question whether the relevant geographic market for the production of AV content, including all the possible sub-segments, is national or by linguistic area (the Dutch-speaking areas of Belgium), can be left open, since the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement under any such plausible geographic market definitions.

4.4. Market for the licensing of broadcasting rights of pre-existing individual AV content

(31) The Notifying Parties’ activities overlap on both the demand and supply side of the market. The JV will be active on the demand side, and have minimal activities on the supply side of the market.24

4.4.1. Product market definition

(32) This part of the value chain concerns the licensing of (i) broadcasting rights relating to pre-existing individual AV content, which is made available ‘off-the-shelf’ by the rights holder, and (ii) broadcasting rights for sports events. The broadcasting rights can belong to either (or a combination of) the rights holder to the AV format, the production company that produced the content, the company that commissioned the production of the content, or a third party distributor to which the rights were licensed by the original owner. The rights holders license rights to AV broadcasters, or content platform operators which retail the content to end-users on a non-linear basis (e.g., SVOD service providers).

4.4.1.1. Previous Commission decisions

(33) In its 2015 case Liberty Global/Corelio/W&W/De Vijver Media, the Commission considered that the market for the licensing of broadcasting rights to TV content could be further segmented depending on the type of TV content or exhibition window, but ultimately left the question open.25 In subsequent cases, the Commission again considered a further segmentation of the market according to (i) content type (films, sports, other AV content),26 and (ii) exhibition window,27 and left the exact market definition open. The question whether AV content could be further sub-divided by distinguishing premium and non-premium content, or scripted and non-scripted content was also left open.28

4.4.1.2. Notifying Parties’ view

(34) The Notifying Parties submit that the question whether the market for the licensing of individual AV content should be sub-segmented by exhibition window can be left open. However, they submit that this market should be sub-segmented (i) by content type, distinguishing between at least sports rights and other types of content, given - inter alia - the different competitive dynamics of the sale of sports rights, and (ii) according to premium vs. non-premium, given that premium and non-premium content have different economic values and that these types of content are generally offered and negotiated separately by licensors. As to the distinction between scripted and non-scripted content, they submit that it can be left open, in particular since the JV will primarily focus on scripted content.29

4.4.1.3. Commission’s assessment

(35) The results of the market investigation were mixed as to whether the market for the licensing of broadcasting rights for pre-existing individual AV content needs to be subdivided by content type (films, sports, other),30 or exhibition windows.31 In addition, nothing in the Commission’s file provided reasons to depart from its previous approach as to whether the market should be further segmented: (i) between scripted and non-scripted content; and (ii) between premium and non-premium content.

(36) In light of the above, the Commission considers that, for the purpose of this decision and in line with the previous practice, a relevant market for the licensing of broadcasting rights for pre-existing individual AV content has to be considered, while the question whether this relevant product marked needs to be further sub- segmented on the basis of content type or exhibition windows, or between scripted and non-scripted content, and between premium and non-premium content can be left open, since the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement under any such plausible product market definitions.

4.4.2. Geographic market definition

4.4.2.1. Previous Commission decisions

(37) In previous cases, the Commission left open the question whether the geographic scope of the market for the licensing of broadcasting rights for TV content was national or regional (the Flemish Region or the combination of the Flemish Region and the Brussels Capital Region) left open.32

(38) The BCA has either previously (i) decided that the markets for the licensing of premium film or sports content in Belgium had to be divided by language group,33 (ii) decided that this market was national,34 or (iii) delineated the geographic market to the footprint of Telenet.35

4.4.2.2. Notifying Parties’ view

(39) The Notifying Parties submit that the precise scope of the geographic market can be left open.36

4.4.2.3. Commission’s assessment

(40) According to a majority of respondents to the market investigation, the geographic scope of agreements for the licensing of individual broadcasting rights for AV content is either national or by linguistic area.37

(41) In light of the above, the Commission considers that, for the purpose of this decision and in line with its precedents, the question whether the relevant geographic market for the licensing of individual broadcasting rights for AV content, including all the possible sub-segments, is national or by linguistic area (the Dutch-speaking areas of Belgium), can be left open, since the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement under any such plausible geographic market definitions.

4.5. Wholesale supply of TV channels

(42) The Notifying Parties both supply TV channels. Telenet and DPG Media (through its retail OTT service Stievie, which will be discontinued as of 1 September 202038) are also purchasers of TV channels for their activities on the market for the retail supply of AV services.39 The JV will not offer or purchase TV channels.

4.5.1. Product market definition

(43) TV broadcasters package the AV content and broadcasting rights for AV content that they have produced in-house or acquired into linear TV channels, which are broadcast to end users either on a FTA basis or on a pay TV basis. Ancillary services have gradually been associated to TV channels in order to complement the TV offering and enhance the viewer experience of traditional linear TV channels.

4.5.1.1. Previous Commission decisions

(44) In its past decisional practice, the Commission identified a wholesale market for the supply of TV channels. Within that market, in certain decisions, the Commission further identified two separate product markets for (i) FTA TV channels, and (ii) pay TV channels.40 The Commission further stated that within the pay TV channels market, there could be different segments for (i) basic pay TV channels; and (ii) premium pay TV channels,41 for which end customers pay a premium in addition to their basic subscription fee.

(45) In other decisions, the Commission concluded that at the level of the wholesale supply of TV channels there were two separate product markets, one consisting of the wholesale supply of premium pay TV channels and one consisting of the wholesale supply of FTA and basic pay TV channels.42 In its decision of 24 February 2015 in case M.7194 – Liberty Global/Corelio/W&W/De Vijver Media, the Commission has considered that, given that (i) FTA channels were mostly supplied together with basic pay TV channels, and (ii) the competitive assessment would remain the same even if FTA channels were regarded as belonging to a separate product market from that of basic pay TV, it was not necessary to make a distinction between FTA and basic pay TV channels on the market for wholesale supply of TV channels in that case.

(46) In addition, in previous decisions including its recent decision of 12 November 2019 in case M.9064 – Telia Company/Bonnier Broadcasting Holding, the Commission considered that there was no need to draw a distinction between linear TV channels and their ancillary services, which are licensed by TV broadcasters to TV distributors along with, or in addition to those linear TV channels.43

(47) Further, in previous decisions, the Commission examined a number of other potential additional segmentations, including genre or thematic content (such as sports, films, general entertainment, news, youth, and others), and ultimately left the market definition open, in these regards.44

(48) Last, in its recent decision of 12 November 2019 in case M.9064 – Telia Company/Bonnier Broadcasting Holding, the Commission considered that the market for wholesale supply of TV channels, and any other possible segmentation, should not be further segmented according to the type of infrastructure used for the delivery to the viewer (cable, satellite, terrestrial TV and IPTV).45

4.5.1.2. Notifying Parties’ view

(49) The Notifying Parties submit that the precise product market definition can be left open, since the JV will not be active in the wholesale supply of TV channels.46

4.5.1.3. Commission’s assessment

(50) A majority of respondents to the market investigation indicated that it remains appropriate to segment the wholesale supply of TV channels between FTA and basic pay TV channels on the one hand, and premium pay TV channels on the other hand in Belgium.47

(51) In addition, the results of the market investigation indicated that the wholesale supply of pay TV channels could be further divided according to genre (e.g., films, sports, youth, general entertainment, news).48 Indeed, most respondents stressed that distributors would seek to offer a variety of genres to end-customers.

(52) With regard to a possible distinction between linear TV channels and their ancillary services, the results of the market investigation did not provide reasons to depart from the Commission's previous approach, as the results of the market investigation indicated that ancillary services (e.g., TVE, catch-up, PVR, etc.) are associated to TV channels in Belgium in order to complement the TV offering and enhance the viewer experience of traditional linear channels.49

(53) With regard to distribution technologies, a majority of respondents to the market investigation considered that the market for the wholesale supply of TV channels should not be further segmented according to distribution forms.50

(54) In light of the above, the Commission concludes that, for the purpose of this decision and in line with its precdents, the wholesale supply of FTA/basic pay TV channels, and of premium pay TV channels should be considered as constituting two separate product markets, each including its ancillary services. The Commission also considers that each of these markets should not be further segmented based on the distribution technology of the channel in question. In that respect, the question whether these markets can be further segmented by genre can be left open, since the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement under any such plausible product market definitions.

4.5.2. Geographic market definition

4.5.2.1. Previous Commission decisions

(55) The Commission recently considered that the geographic market for the wholesale supply of TV channels might remain the footprint of Telenet's cable network as in the 2015 case Liberty Global/Corelio/W&W/De Vijver Media, but that it also might be enlarged to a regional or national scope. The exact geographic delineation of the market (i.e. whether it corresponds to Telenet's footprint, is regional or national) was left open.51

4.5.2.2. Notifying Parties’ view

(56) The Notifying Parties submit that the geographic market for the wholesale supply of TV channels could be Telenet’s footprint, or alternatively regional or national in scope, and that the precise geographic market definition can be left open, since the JV will not be active in the wholesale supply of TV channels.52

4.5.2.3. Commission’s assessment

(57) The results of the market investigation indicated that it is still relevant to consider that the relevant geographic markets for both (i) the wholesale supply of FTA/basic pay TV channels, and (ii) the wholesale supply of premium pay TV channels might be Telenet's footprint, or enlarged to a regional or national scope.53

(58) In light of the above, the Commission concludes that, for the purpose of this decision and in light of its previous practice, the relevant geographic market for the wholesale supply of TV channels, including all the possible sub-segments, is either the local footprint of Telenet's cable network, or its enlarged regional or national scopes. In that respect, the Commission considers that the exact geographic market definition (i.e. whether it corresponds to Telenet's footprint, is regional or national) can be left open, since the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement under any such plausible geographic market definitions.

4.6. Retail supply of AV services

(59) The Notifying Parties and the JV supply AV services to end customers.

4.6.1. Product market definition

(60) Retail providers of AV services offer packages of linear AV services and/or non- linear AV services to end customers. Such linear and non-linear AV services can be augmented with ancillary services, such as catch-up TV or TV everywhere. Retail AV services can be delivered to end-users though a number of technical means including cable, satellite, IPTV and OTT.

4.6.1.1. Previous Commission decisions

(61) In its past decisional practice, the Commission considered the retail supply of FTA TV and pay TV as separate markets, but ultimately left open the product market definition.54 The Commission also considered whether pay TV could be segmented further according to: (i) linear vs non-linear pay TV services;55 (ii) premium vs basic pay TV services.56 However, the Commission left open the market definition with regard to each of these potential sub-segments.

(62) In addition, the Commission considered a possible segmentation of the market for the retail supply of AV services according to distribution technology (for example, cable, OTT, satellite, IPTV or terrestrial). In its decisions of 12 November 2019 in case M.9064 – Telia Company/Bonnier Broadcasting Holding, and of 30 May 2018 in case M.7000 – Liberty Global/Ziggo, the Commission considered that all the different distribution technologies were part of the same product market,57 while leaving the exact product market definition open in a number of other decisions.58

4.6.1.2. Notifying Parties’ view

(63) The Notifying Parties submit that the relevant product market should include all distribution technologies including OTT.59 In addition, they submit that the question whether the relevant product market should (i) be further segmented between the retail supply of basic pay and premium pay TV channels, and (ii) include non-linear services, can be left open.60 The Notifying Parties also submit that if linear and non- linear AV services are not regarded as part of the same market, non-linear offers do at least exert some competitive pressure on more traditional AV offers.61

4.6.1.3. Commission’s assessment

(64) A majority of respondents to the market investigation indicated that the retail provision of FTA/basic pay AV services currently constitutes a market separate from the retail provision of premium pay AV services in Belgium.62

(65) The results of the market investigation were mixed as regards a possible segmentation between linear and non-linear pay AV services.63 Indeed, some respondents indicated that the market for the retail supply of AV services should be further segmented between linear services (namely TV channels) and non-linear services, such as SVOD, as pure OTT non-linear offers are an alternative to linear offers for a limited, bespoke group of customers only, and the SVOD success is more likely to become an alternative to premium pay AV service while complementing basic pay AV services. One other respondent claimed that linear and non-linear services are part of the same markets given that both types of services provide access to identical programming, and compete for viewing time.

(66) As regards distribution technologies, a majority of respondents to the market investigation considered that end customers perceive the distribution forms (e.g. cable, IPTV, satellite, terrestrial, or OTT) through which they access AV content in Belgium as alternative to each other.64

(67) In light of the foregoing, the Commission concludes that, for the purpose of this decision and in light of its previous practice, the relevant product market at retail level is to be considered the market for the retail supply of AV services encompassing all distribution technologies. Moreover, the Commission considers that, in any case, the question whether the retail supply of AV services should be further segmented between (i) FTA and pay AV services can be left open, as well as also the question whether in turn the retail supply of pay AV services should be segmented according to (ii) linear and non-linear pay AV services, and (iii) premium and basic pay AV services can be left open, since the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement under any such plausible product market definitions.

4.6.2. Geographic market definition

4.6.2.1. Previous Commission decisions

(68) In previous decisions, the Commission considered that the relevant geographic market for the retail provision of TV services to end users was the footprint of Telenet’s cable network.65

4.6.2.2. Notifying Parties’ view

(69) The Notifying Parties consider that there are strong indicators for a national geographic market, since cable operators such as Telenet compete with retail AV providers such as Proximus and Orange, which are active nationally and apply uniform pricing across all regions of Belgium.66

4.6.2.3. Commission’s assessment

(70) The results of the market investigation indicated that it is still relevant to consider that the relevant geographic market for the retail supply of AV services to end users is Telenet's footprint.67

(71) In light of the foregoing, the Commission concludes that, for the purpose of this decision and account taken of its previous decisional practice, the relevant geographic market for the retail supply of AV services, including all possible sub- segments, is the one encompassing Telenet’s footprint.

4.7. Retail supply of fixed internet access services

(72) Only Telenet is active as a retail supplier of fixed internet access services.

4.7.1. Product market definition

4.7.1.1. Previous Commission decisions

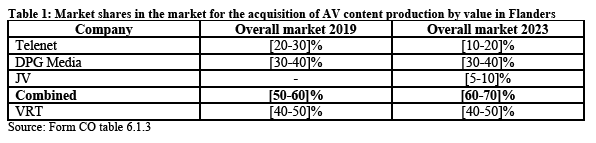

(73) In recent cases, the Commission considered but ultimately left open possible segmentations according to (i) product type (distinguishing narrowband, broadband, and dedicated access), and (ii) distribution technology (distinguishing xDSL, fibre, cable). Moreover, the Commission acknowledged that the retail market for fixed internet access services should not be divided according to download speed.68

(74) The Commission also considered, but ultimately left open, possible segmentations as to customer type, distinguishing between residential and small business customers, on the one hand, and larger business and public authorities, on the other hand.69

4.7.1.2. Notifying Party’s view

(75) The Notifying Parties do not provide any views as to the relevant product market definition.

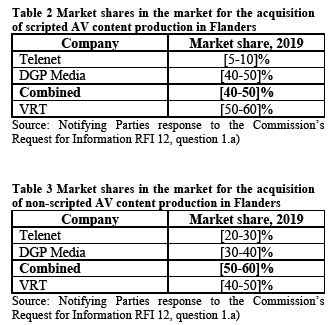

4.7.1.3. Commission’s assessment

(76) With regard to a possible segmentation of the market for the retail provision of fixed internet access services according to product and customer type or according to distribution technology (that is to say, xDSL, cable or fibre), nothing in the Commission’s file provided reason to depart from its approach in previous cases.

(77) In light of the foregoing, the Commission does not depart from its previous assessment, and concludes, for the purposes of this Decision, that the exact scope of the product market definition in relation to the provision of retail fixed internet access services can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement under any plausible product market definition.

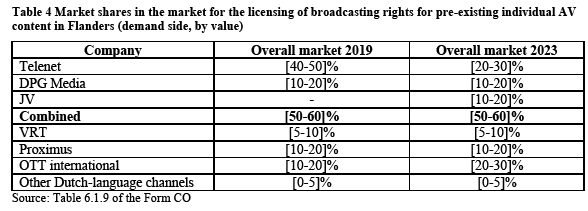

4.7.2. Geographic market definition

4.7.2.1. Previous Commission decisions

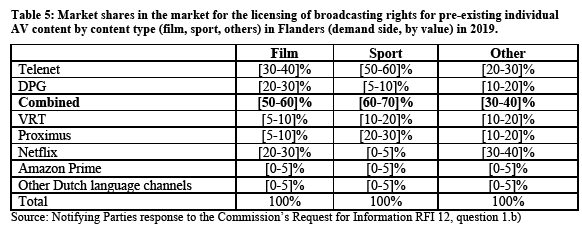

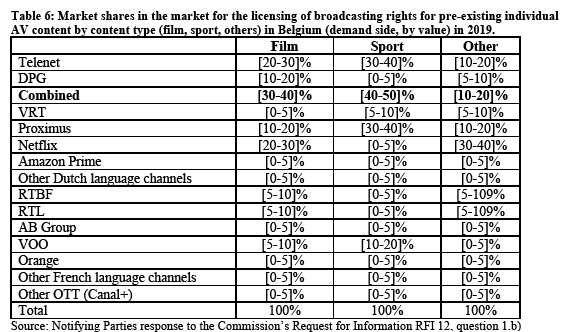

(78) In its previous decisions, the Commission concluded that the retail market for the provision of fixed internet services was national in scope.70

4.7.2.2. Notifying Party’s view

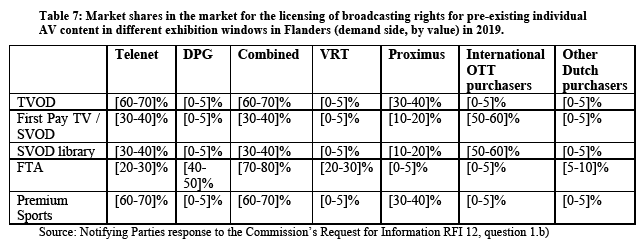

(79) The Notifying Parties submit that the market for the retail supply of fixed internet access services should be regarded as national.71

4.7.2.3. Commission’s assessment

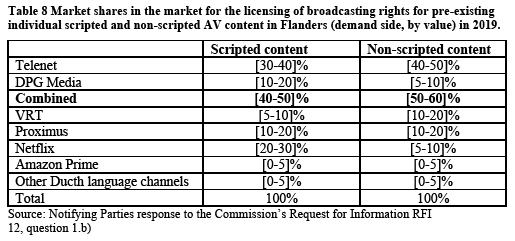

(80) The market investigation did not provide any indication that the Commission should depart from its findings in previous cases, according to which the geographic market should be national.

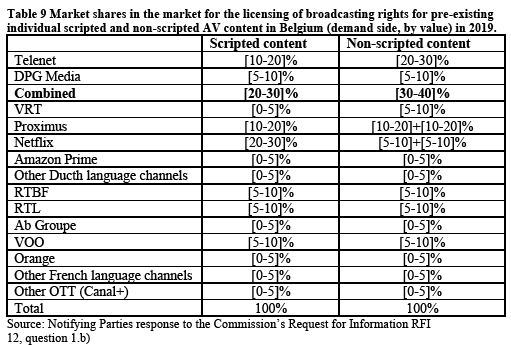

(81) In light of the foregoing, the Commission concludes that it is appropriate not to depart from its previous practice, and considers that, for the purpose of this decision, the relevant market for the provision of fixed internet services is national in scope.

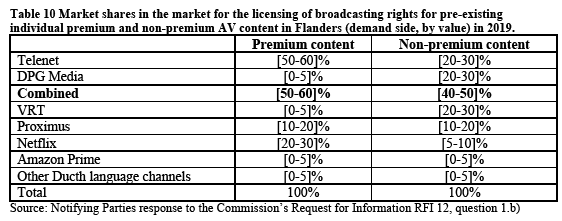

4.8. Retail supply of mobile telecommunication services

(82) Both Telenet and DPG Media are active as suppliers of retail mobile telecommunication services. Telenet operates a mobile telecommunication network covering the entire territory of Belgium, and DPG Media operates as a Mobile Virtual Network Operator (“MVNO”) under the brand Mobile Vikings. MVNOs are operators without their own network, which require access to a network of a Mobile Network Operator (“MNO”) in order to provide retail mobile services to end customers.

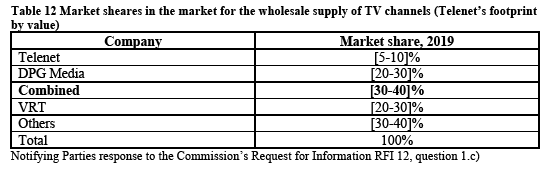

4.8.1. Product market definition

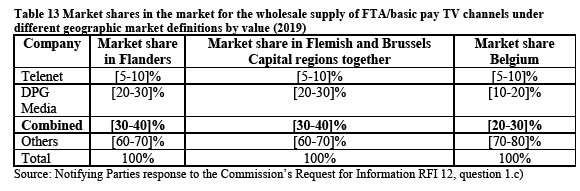

4.8.1.1. Previous Commission decisions

(83) The Commission has previously considered that there is an overall retail market for mobile telecommunications services constituting a separate market from retail fixed telecommunication services.72 The Commission did not further segment the overall retail mobile market based on the type of service (voice calls, SMS, MMS, mobile internet data services), or the type of network technology (for example, 2G/3G/4G). The Commission considered distinctions within the overall retail market for mobile telecommunication services between pre-paid or post-paid services and private customers or business customers, concluding that these did not constitute separate product markets but represent rather market segments within an overall retail market.73

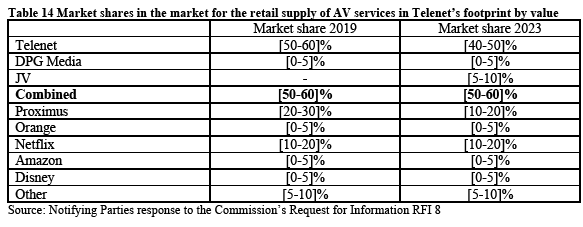

4.8.1.2. Notifying Parties’ view

(84) The Notifying Parties do not provide any views as to the relevant product market definition.

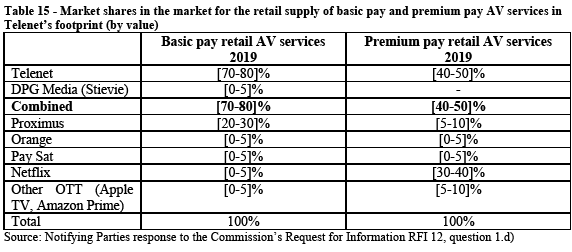

4.8.1.3. Commission’s assessment

(85) Nothing in the Commission's file indicated that the market for retail supply of mobile telecommunications services should be further segmented according to the type of services, the type of customers or the network technology used.

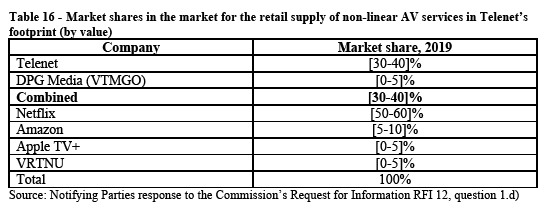

(86) In light of the foregoing, the Commission concludes that it is appropriate to not depart from its previous practice, and considers that, for the purpose of this decision, the relevant product market is the overall retail market for mobile telecommunications services without any further segmentations.

4.8.2. Geographic market definition

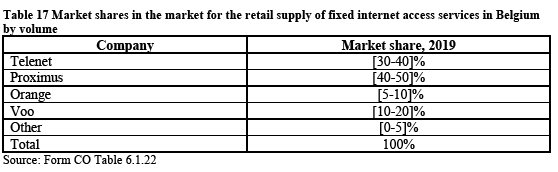

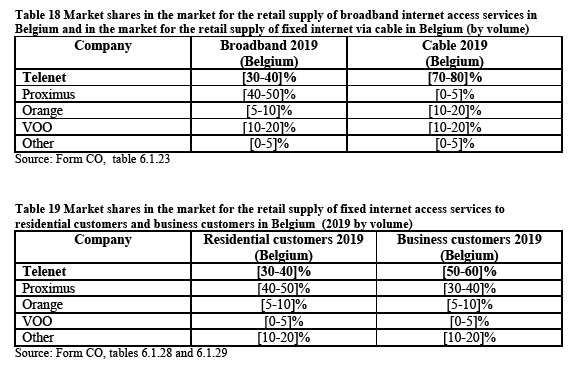

4.8.2.1. Previous Commission decisions

(87) In its previous decisions, the Commission concluded that the retail market for the provision of mobile telecommunications services was national in scope.74

4.8.2.2. Notifying Parties’ view

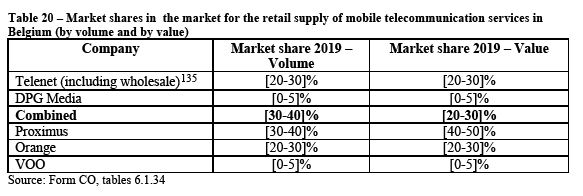

(88) The Notifying Parties do not provide any views as to the relevant geographic market definition.

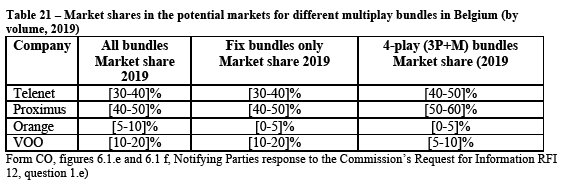

4.8.2.3. Commission’s assessment

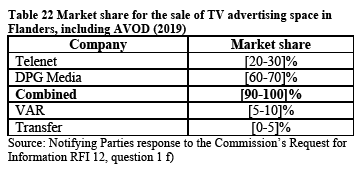

(89) The market investigation in the present case did not provide any indication that the Commission should depart from its previous findings.

(90) In light of the foregoing, the Commission concludes that it is appropriate to not depart from its previous practice, and considers that, for the purpose of this decision, the relevant market for the retail provision of mobile telecommunications services is national in scope.

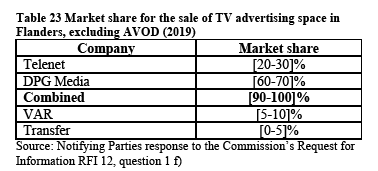

4.9. Retail supply of multiple play bundles

(91) Only Telenet is active as a provider of multiple play bundles.

4.9.1. Product market definition

(92) The term "multiple play" relates to offers comprising two or more of the following services provided to retail consumers: mobile telecommunication services, fixed telephony, fixed internet access and TV services. Multiple play comprising two, three or four of these services is referred to as dual play ("2P"), triple play ("3P") and quadruple play ("4P") respectively.

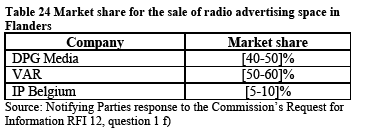

4.9.1.1. Previous Commission decisions

(93) In previous decisions, the Commission has considered but ultimately left open the question as to whether there exist one or more multiple play markets, which are distinct from each of the underlying individual telecommunication services.75 Moreover, in previous decisions, the Commission has noted that due to different services, delivered over different infrastructures (fixed for dual play and triple play or fixed and mobile for quadruple play), that are included in the different multiple play bundles, instead of one possible market for multiple play, there could be several possible multiple play markets: a market for fixed bundles (dual play, and triple play) and another separate market for fixed-mobile convergence bundles. The Commission has also noted that the possibility for several mobile subscriptions to be included in a quadruple play bundle further complicates the picture.76

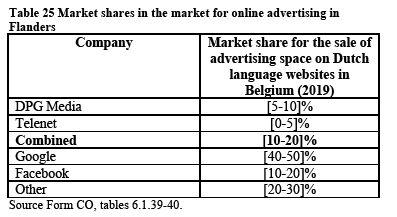

4.9.1.2. Notifying Parties’ view

(94) The Notifying Parties submit that the question whether a separate market for multiple play bundles including retail TV services exists can be left open, as (i) the JV will not be active on any possible multiple play markets, and (ii) with a few exceptions,77 Telenet does not include SVOD services in its multiple play bundles with a TV component in Belgium, and has no immediate plans to change the bundle line up.78

4.9.1.3. Commission’s assessment

(95) The market investigation in the case at hand provided no clear evidence as to the substitutability between multiple play services on the one hand and combinations of standalone services on the other hand.

(96) In light of the foregoing, the Commission concludes that it is appropriate not to depart from its previous decisional practice, and considers that, for the purpose of this decision, the question as to whether there exist one or more multiple play markets which are distinct from each of the underlying individual telecommunications services can be left open, since the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement under any such plausible product market definitions.

4.9.2. Geographic market definition

4.9.2.1. Previous Commission decisions

(97) In previous decisions, the Commission considered that the geographic scope of any possible retail market for multiple play services would be national since the components of the multiple play offers are offered individually at a national level, and the bundling of the services would not change the geographic scope of the components.79

4.9.2.2. Notifying Parties’ view

(98) The Notifying Parties submit that the question whether a separate market for multiple play bundles including retail TV services exists in Belgium can be left open.80

4.9.2.3. Commission’s assessment

(99) The market investigation in the present case did not provide any indication that the Commission should depart from its findings in previous cases.

(100) In light of the foregoing, the Commission concludes that it is appropriate not to depart from its previous decisional practice, and considers that, for the purpose of this decision, any possible market for the retail supply of multiple play services would be national in scope.

4.10. Supply of advertising: (i) TV advertising, (ii) radio advertising and (iii) online advertising

(101) The Notifying Parties are both active in the supply of TV advertising on the Dutch- language TV channels in Flanders. Both Telenet and DPG Media sell advertising space on their own FTA TV channels (Vier, Vijf, Zes for Telenet and VTM, Q2, Vitaya, CAZ, CAZ 2 and VTM Kids for DPG Media). Both of them act as sales representatives for third party TV channels. Both parties are active in the selling of online advertising space, namely on websites related to their TV channels and publications. In addition, DPG Media is active in the supply of radio advertising space. It sells advertising space on its own traditional radio channels (mainly Qmusic and Joe, and, to a more limited extent, on the digital radio channels it operates). The Notifying Parties and the JV will also be active as purchasers of such advertising space.

4.10.1. Product market definitions

4.10.1.1. Previous Commission decisions

(102) The Commission has previously defined the sale of advertising space on TV, the sale of advertising space on radio and the sale of advertising space on websites as distinct product markets, rather than forming part of a wider advertising market (incorporating, among others, also print advertising).81

(103) With respect to the market for TV advertising, the Commission has also considered whether sales of advertising space on pay TV and FTA TV channels are part of the same market, and whether the sale of advertising space on AVOD services is part of the same market as the sale of advertising space on TV channels. It ultimately left this question open.82

(104) The BCA has previously defined a separate market for the sale of advertising space on national TV channels and a separate market for the sale of advertising space on national radio channels, i.e. covering the entire Belgian territory. In these decisions, it also limited the markets to Dutch-language advertisements.83 In 2018, the BCA also found strong indications to conclude that a separate market for online adverisements may exist and conducted its analysis on that basis.84

4.10.1.2. Notifying Parties’ view

(105) The Notifying Parties submit that the fact that the Commission has defined radio advertising and TV advertising as separate product markets does not mean that they are not subject to competitive pressures from advertising on other media, notably online advertising.85 They consider that the market has evolved significantly towards online advertising (leading to an erosion of the importance of traditional media for advertising), and that a separate market for the sale of online advertising space should be determined.86

(106) In addition, the Notifying Parties consider that the market for TV advertising should not be further segmented between the sale of advertising space on Pay and FTA TV channels. Furthermore, the Parties believe that the sale of advertising space on AVOD services should be considered as part of the online advertising market (for sale of advertising space on Dutch-language websites).87

4.10.1.3.Commission’s assessment

(107) The market investigation in the present case did not provide any indication that the Commission should depart from its findings in previous cases. The majority of respondents responding to this question indicated that these findings (distinction of online vs. offline advertising and segmentation of advertising market by media channel) are still accurate in Belgium today.88

(108) In light of the foregoing, the Commission concludes that, for the purpose of this decision and to follow its previous decisional practice, the market for TV advertising, the market for radio advertising and the market for online advertising constitute separate markets. The Commission also concludes that the question whether the market for TV advertising includes both Pay and FTA TV channels and/or AVOD services or whether it can be divided into those two segments can be left open, since the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement under any such plausible product market definitions.

4.10.2. Geographic market definitions

4.10.2.1.Previous Commission decisions

(109) The Commission previously considered that the geographic markets for (i) TV advertising, (ii) radio advertising and (iii) online advertising are either national or regional (along linguistic lines; in Belgium concerning the Flemish region, potentially including the Brussels-capital region).89 The BCA has previously determined the geographic scope of the TV and radio advertising markets as comprising the Flemish Community (and left open the exact geographic scope of the online advertising market).90

4.10.2.2.Notifying Parties’ view

(110) The Notifying Parties did not provide any views on the geographic scope of these advertising markets.

4.10.2.3. Commission’s assessment

(111) The majority of respondents responding to the question indicated that they sell/purchase advertising on the basis of the linguistic region.91 One market respondent indicated that “in practice suppliers of advertising space generally focuss on respectively the Dutch speaking market or the French speaking market”, while another responded that “[l]anguage is the first criteria when choosing a media channel.”92 One other market respondent stated that “[t]his is the most logical approach to try to get the broadest advertising reach.”93

(112) In light of the foregoing, the Commission concludes that, for the purpose of this decision, the relevant market for TV, radio and online advertising, including all the possible sub-segments, is regional in scope encompassing the Flemish region and possibly also the Brussels-capital region.

(113) Consequently, the Commission considers it appropriate to assess the possible effects of the Transaction on the markets for the sale of advertising spaces on (i) Dutch language TV channels, (ii) Dutch language radio channels and (iii) Dutch language websites in Belgium, which correspond to the two regional delinations indicated above (Flemish region or the Flemish region and the Brussels-capital region).

5. COMPETITIVE ASSESSMENT

(114) As explained in paragraph 4, the only activity of the JV will be to provide a SVOD service in Belgium.

(115) In order to provide its SVOD service, the JV will acquire content from [JV’s commercial strategy]. The JV will not acquire linear channels and ancillary services of the Notifying Parties and/or of third parties.

(116) In order to market its SVOD service, the JV will acquire advertising space from a series of suppliers, [JV’s commercial strategy]. The JV’s SVOD service will not carry advertising.

(117) The stated rationale of the transaction is to create a local SVOD player that can locally compete with international established players like Netflix and Amazon as well as with future entrants in the SVOD market like Disney and HBO.94

5.1. Identification of the affected markets

(118) The Transaction gives rise to the following horizontally affected markets:

i. the market for the production of AV content in Flanders (demand side)95 and possibly more narrowly defined markets;96

ii. the market for the licensing of broadcasting rights for pre-existing individual AV content in Flanders (demand side)97 and possibly more narrowly defined markets;98 and

iii. the market for the retail supply of AV services (including SVOD services) in Telenet’s footprint and possibly more narrowly defined markets.99

(119) The markets under i) and ii), including the possible narrower markets, would also be affected if the geographic market was defined as a) Flanders and the Brussels Capital Region together or as b) Telenet’s footprint, both of which largely correspond to the Dutch-speaking part of Belgium. In addition, some of the narrower product markets under ii) would also be affected if the geographic market was defined as c) the whole of Belgium.100

(120) In each of these horizontally affected markets, the Notifying Parties will also remain active independently.

(121) The Transaction also gives rise to the following non-horizontally affected markets:

i. The upstream market for AV content production in Flanders (supply side), and possible narrower markets,101 where Telenet is active, due to the combined share of both Notifying Parties and the JV on the downstream market for AV content production in Flanders (demand side) and possible narrower markets102 (customer foreclosure). The upstream product markets, including the potential narrower markets, would also be affected if the geographic scope of the downstream markets were defined as a) Flanders and the Brussels Capital Region together or as b) Telenet’s footprint, both of which largely correspond to the Dutch-speaking part of Belgium.103

ii. The upstream market for the licensing of broadcasting rights for pre-existing individual AV content in Flanders (supply side), and possibly more narrowly defined markets,104 where both Notifying Parties are active, due to the individual or combined share of the Notifying Parties and the JV on the downstream market for the licensing of broadcasting rights for pre-existing individual AV content in Flanders (demand side), or possibly more narrowly defined markets105 (customer foreclosure). The upstream product markets, including the potential narrower markets, would also be affected if the geographic scope of the downstream markets were defined as a) Flanders and the Brussels Capital Region together or as b) Telenet’s footprint, both of which largely correspond to the Dutch-speaking part of Belgium. If the geographic scope of the downstream markets were defined as c) the whole of Belgium, only some of the more narrowly defined upstream markets106 would be affected.107

iii. The downstream market for the retail supply of AV services (including SVOD services) in Telenet’s footprint, and possibly more narrowly defined markets,108 (where both the JV and the Notifying Parties will be active), due to the the Notifying Parties’ upstream activities on the market for wholesale supply of FTA/basic pay TV channels, and possible narrower markets,109 in Telenet’s footprint (input foreclosure). The downstream product markets, including the potential narrower markets, would also be affected if the geographic scope of the upstream market were defined as a) Flanders and the Brussels Capital Region together, as b) Flanders or as c) the whole of Belgium.

iv. The market for the retail supply of mobile telecommunication, fixed internet and multiple play services in Belgium, and possibly more narrowly defined markets,110 where Telenet is active, due to the Parties’ strong presence in the market for the retail supply of AV services (including SVOD services) in Telenet’s footprint, and possible narrower markets111 (conglomerate effects).

v. The market for the the retail supply of AV services (including SVOD services) in Telenet’s footprint, and possibly more narrowly defined markets,112 where Telenet and the JV are active, due to Telenet’s strong presence in the retail supply of mobile telecommunication, fixed internet access and multiple play services, and possible narrower markets.113 (conglomerate effects)

vi. The downstream market for the retail supply of AV services (including SVOD services) in Telenet’s footprint, and possibly more narrowly defined markets,114 where the JV and both Notifying Parties are active, due to the Notifying Parties’ upstream activities on the market for the sale of TV advertising space on TV channels in Flanders, as well as the possibly more narrowly defined markets,115 and DPG Media’s upstream activities on the market for the sale of radio advertising space in Flanders (input foreclosure). The downstream product markets, including the potential narrower markets, would also be affected if the geographic scope of the upstream markets were defined as Flanders and the Brussels Capital Region together, given that in both cases the geographic market corresponds to the Dutch linguistic area in Belgium.

(122) None of these vertical links is newly created by the Transaction since the Notifying Parties are autonomously active in the downstream markets where the JV will be active. The JV will merely give rise to an increase of the combined market share downstream.

(123) The Notifying Parties will remain independently active in a number of the same markets as the JV, notably: (i) the production of AV content (demand side)116, in particular in the segment for production for hire; (ii) the licensing of individual AV content (supply and demand side), in particular in the first PayTV and library SVOD exhibition window segments; and (iii) the retail supply of AV services, in particular in the non-linear segments. The Notifying Parties will also remain independently active in a number of markets closely related to the activities of the JV, notably: (i) the licensing of individual AV content (supply and demand side), in particular in the FTA, TVOD, Premium Sports and series SVOD segments; (ii) the retail supply of AV services, in particular in the linear segments117; (iii) the sale of advertising space on Dutch language TV channels and websites; (iv) the wholesale supply of TV channels; and (v) the retail supply of mobile communications services.

(124) Each of these potential effects is separately discussed in the following sections. After setting out the market shares in the relevant markets and possible sub-segments (section 5.2), the Commission will first assess the potential horizontal non- coordinated effects stemming from the Transaction (section 5.3). Then the Commission will assess the potential non-horizontal effects stemming from the Transaction (section 5.4). Finally, the Commission will assess the potential cooperative effects of the Transaction (section 5.5).

5.2. Market shares

(125) According to the Horizontal Merger Guidelines and the Non-Horizontal Merger Guidelines,118 in the assessment of the effects of a merger, market shares constitute a useful first indication of the structure of the markets at stake and of the competitive importance of the relevant market players.

5.2.1. Production of AV content (demand side)119

5.2.1.1. Overall market in Flanders

(126) The Parties’ and their main competitors’ shares in the market for the acquisition of Dutch-language AV content production in Flanders are summarised in Table 1 below.120 The Commission notes that the Parties have a significant presence in Belgium with combined market shares by value, exceeding [50-60]%. The Parties submit that the JV will have modest activities on the demand side, which will represent a market share of [5-10]% in 2023. This is also indicated in Table 1.

5.2.1.2. Alternative market definitions

(127) If the product market is unchanged but the geographic scope of the market was defined as a) Flanders and Brussels Capital Region together or b) as Telenet’s footprint, the market shares indicated in Table 1 would not change materially. 121

(128) If the product market was defined more narrowly and separate markets were defined based on the distinction by exhibition window (TVOD window, SVOD/first pay TV window, SVOD library window, FTA window and premiums sports window), the market shares would be very similar to those in Table 1.122 This is because the party purchasing original AV content generally purchases the rights for all exhibition windows at the time of the production agreement.

(129) Likewise, market shares would be similar if separate markets were defined based on the distinction between commissioned AV production and AV production for hire, as purchasers are estimated to acquire these types of contents in similar proportions. 123 The only difference to Table 1 is that the JV will not be active in the market for the production of AV content for hire, i.e. it will not purchase such content.

(130) If the market was defined more narrowly and separate markets were defined based on the distinction between scripted and non-scripted AV production, the relevant market shares are indicated in Tables 2 and 3.

(131) Exact shares are not available for separate markets by content type (i.e. separate markets for the production of film content, sport content and other content – demand side). However, given the concentrated nature of the market the combined share of the Notifying Parties are well in excess of 30% in Flanders.124 Likewise combined market share of the Notifying Parties would be in excess of 30% for any combination of the these segmentations.125

(132) In the case of all the alternative product market definitions, the market shares would not change materially if the geographic market was defined as a) Flanders and Brussels Capital Region together or b) as Telenet’s footprint.126

5.2.2. Licensing of broadcasting rights for pre-existing individual AV content (demand side)

5.2.2.1. Overall market in Flanders

(133) The Parties’ and their main competitors’ shares in the market for the acquisition of individual AV content in Flanders are summarised in Table 4 below. The Commission notes that the Parties have a significant presence in Belgium, with combined shares, by value, exceeding [50-60]%. The Parties submit that the JV will have a share of around [10-20]% in 2023.

5.2.2.2. Alternative market definitions

(134) If the product market is unchanged but the geographic scope of the market was defined as a) Flanders and Brussels Capital Region together or b) as Telenet’s footprint, the market shares indicated in Table 1 would not change materially. 127

(135) If the product market was defined more narrowly and separate markets were defined based on the distinction by content type (film, sport, other), the resulting market shares are indicated in Table 5. As indicated, market shares would exceed 30 % in all markets defined this way and would be particulary high in films and sports.

(136) The market shares in Table 5 would not change materially if the geographic market was defined as a) Flanders and the Brussels Capital Region together or as b) Telenet’s footprint, both of which largely correspond to the Dutch-speaking part of Belgium. The market shares under a geographic scope corresponding to the whole of Belgium are indicated in Table 6. As indicated by Table 6, the market for film licensing (demand side) and the market for sport licensing (demand side) would still be horizontally affected and the corresponding upstream licensing markets (supply side) would be vertically affected. The market for the licensing of broadcast rights for “other” content would cease to be affected horizontally and the corresponding upstream supply side would also not be affected.

(137) If the product market was defined more narrowly and separate markets were defined based on the distinction by exhibition window (TVOD window, SVOD/first pay TV window, SVOD library window, FTA window and premiums sports window), the resulting market shares are indicated in Table 7. As indicated in Section 5.1, under such definitions only the market for the licensing of broadcasting rights for AV content in the FTA window would be affected horizontally. However, also as indicated Section 5.1, on the supply side the TVOD, First Pay TV/SVOD, SVOD library, FTA and premium sports windows would all be vertically affected (customer foreclosure).

(138) The market shares in Table 7 would not change materially if the geographic market was defined as a) Flanders and the Brussels Capital Region together or as b) Telenet’s footprint, both of which largely correspond to the Dutch-speaking part of Belgium. As indicated in Section 5.1. if the scope of the geographic market was Belgium, only the market for licensing AV content in the FTA window would be horizontally affected on the demand side and only the corresponding TVOD, FTA and premium sports licensing markets on the supply side would be vertically affected.

(139) If the product market was defined more narrowly and separate markets were defined based on the distinction between scripted and non-scripted content, the resulting market shares are indicated in Table 8.

(140) The market shares in Table 8 would not change materially if the geographic market was defined as a) Flanders and the Brussels Capital Region together or as b) Telenet’s footprint, both of which largely correspond to the Dutch-speaking part of Belgium. The market shares under a geographic scope corresponding to the whole of Belgium are indicated in Table 9. As indicated in Section 5.1. under this geographic market definition, both of these markets would still be horizontally affected. However, under this geographic market definition only the upstream market for the licensing of broadcasting rights for pre-existing individual non-scripted AV content (supply side) would still be vertically affected (customer foreclosure).

(141) If the product market was defined more narrowly and separate markets were defined based on the distinction between premium and non-premium content, the resulting market shares are indicated in Table 10.

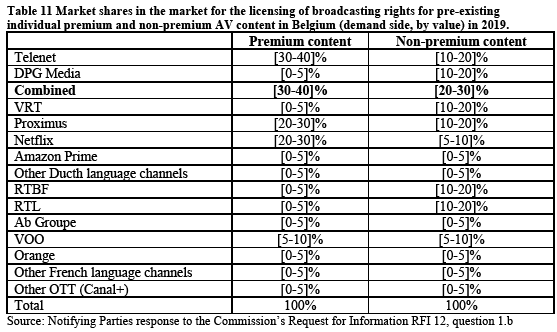

(142) The market shares in Table 10 would not change materially if the geographic market was defined as a) Flanders and the Brussels Capital Region together or as b) Telenet’s footprint, both of which largely correspond to the Dutch-speaking part of Belgium. The market shares under a geographic scope corresponding to the whole of Belgium are indicated in Table 11. As indicated in Section 5.1, under this geographic market definition both of these markets would still be horizontally affected. However, under this geographic market definition only the upstream market for the licensing of broadcasting rights for pre-existing individual premium AV content (supply side) would still be vertically affected (customer foreclosure).

5.2.3. Wholesale supply of FTA/basic pay TV channels

5.2.3.1. Overall market in Telenet’s footprint

(143) The Parties’ and their main competitors’ shares for the wholesale supply of FTA/basic pay TV channels by value in Telenet’s footprint are summarised in Table 12 below. The Commission notes that the Parties have a market strong position with combined shares of [30-40]%, by value. The only other significant competitor is the public broadcaster VRT.

5.2.3.2. Alternative market definitions

(144) Table 13 summarises the relevant market shares if the product market is unchanged but the geographic scope of the market was defined differently. As shown by Table 13, the market shares would not change materially relative to Telenet’s footprint if the geographic market is defined as a) Flanders or b) Flanders and Brussels Capital Region together and all. The combined shares would be significantly lower if the geographic market share was defined as c) Belgium.

(145) If the market was defined more narrowly and separate markets were defined based on genre, the market shares in the general entertainment genre (i.e. in the market for the wholesale supply of FTA/basic pay general entertainment TV channels) would not be materially different from those indicated in Table 12 (for Telenet’s footprint) and Table 13 (for Flanders, the Flemish and Brussels Capital regions together and Belgium). This is because the Notifying Parties are either not present in other genres (news, sports or the residual “other” genres128) or have minimal viewership/presence (youth/kids genre).129

5.2.4. Retail supply of AV services

5.2.4.1. Overall market

(146) The Parties’ and their main competitors’ shares in the overall market for the retail supply of AV services in Telenet’s footprint are included in Table 14 below. Based on the Parties’ business plan, in 2023 the JV is expected to have a share of around [5-10]% by value, which is also indicated in Table 14.

5.2.4.2. Alternative market definitions

(147) If the market was defined more narrowly and separate markets were defined based on FTA AV and pay AV services, the Parties would only be active in the market for the retail supply of pay AV services. Their market share on this market would not be materially different from those indicated in Table 14 as only the French language public broadcaster supplies AV services on an FTA basis130 and its share in the Telenet’s footprint (which largely corresponds to the Dutch speaking parts of Belgium) is necessarily modest.

(148) If the market for the retail supply of pay AV services was further segmented and separate markets were defined for basic pay AV and premium pay AV services, the resulting market shares for both markets are included in Table 15 below.

(149) The Commission notes that currently DPG Media’s presence in basic pay retail AV services (and indeed in any retail AV services) is limited to Stievie, an OTT platform with very limited viewership, which will be discontinued as of 1 September 2020.131 Thus, the horizontal overlap results entirely from the JV, which is not indicated in Table 15 in the absence of a forecast taking these narrower markets as a basis. The Commission also notes that the market shares assume that Netflix’s SVOD service is part of the premium pay retail AV services market, although this is not entirely clear on the basis of the market investigation as some respondents consider SVOD services as a substitute for even basic pay retail AV services.132 The same applies to the JV’s SVOD service.

(150) If the market for the retail supply of pay AV services was further segmented and separate markets were defined for linear and non-linear (e.g.SVOD) retail AV services, the market shares in the market for the retail supply of linear AV services would be similar to the shares in basic pay retail AV services in Table 15.133 The Commission notes again that this assumes that non-linear SVOD services do not compete with basic pay retail AV services, which is not certain. The market for the retail supply of non-linear AV services in Telenet’s footprint is indicated in Table 16 below.

(151) As regards Table 16, the Commission notes that the JV will add to the Parties’ market shares by 2023, even though this is not indicated in the table due to the absence of a forecast taking this hypothetical market as a basis. However, given that the size of this market is much smaller than the overall retail AV services market (in Telenet’s footprint), the increment brought about by the JV is will be significantly more than [5-10]% by 2023 if the business plan is realized.

5.2.5. Retail supply of fixed internet services

5.2.5.1. Overall market

(152) The Parties’ and their main competitors’ shares in the overall market for the retail supply of fixed internat services in Belgium is indicated in Table 17 below. These are volume shares (i.e. share of subscribers) but the Parties estimate that the value based market shares (i.e. market shares based on revenues) for the retail supply of fixed internet access in Belgium are similar to the market shares based on subscribers134

5.2.5.2. Alternative market definitions

(153) As discussed in Section 4.7., in the case of retail supply of fixed internet services, potentially separate markets could be distinguished based on product type (narrowband, broadband, dedicated line), distribution technology (xDSL, cable or fibre) and customer types (residential, small businesses, large businesses, public authorities).

(154) Of these potential narrower markets, the Notifying Parties have only been able to submit market shares for the broadband segment (product type), the cable segment (distribution technology), and the residential and business customer segments (customer type). These market shares are indicated in Tables 18 and 19 below.

5.2.6. Retail supply of mobile telecommunication services

(155) The Parties’ and their main competitors’ shares in the overall market for the retail supply of mobile telecommunications services in Belgium is indicated in Table 20 below.

5.2.7. Retail supply of multiple play bundles

(156) Table 21 below contains the market shares, in Belgium, in the potential markets for i) all multiplay bundles ii) only fix bundles (i.e. double-play and triple play bundles together) and iii) fixed-mobile convergence bundles (quad-play bundles).

5.2.8. Supply of advertising (TV, radio and online advertising markets)

5.2.8.1. TV advertising

Overall market

(157) The Parties’ and their main competitors’ shares in the overall market for the sale of TV advertising space in Flanders is indicated in Table 22 below. This overall market includes the sale of advertsing space from AVOD services.

Alternative market definitions

(158) If the product market is unchanged but but the geographic scope of the market was defined as a) Flanders and Brussels Capital Region together, the market shares indicated in Table 22 would not change materially as in both cases the market would roughly correspond to the Dutch linguistic area and advertising on Dutch language TV channels.

(159) If the product market is defined more narrowly such that the sale of advertising space on AVOD services is excluded, the resulting market shares are included in Table 23. As shown by Table 23, the market shares do not change materially relative to the overall market.

(160) The product market could also be further segmented on the basis of FTA or pay TV channels, i.e. separate markets could be defined for the sale of TV advertising space on FTA channels and for the sale of advertising space on pay TV channels. If this segmentation is applied, the market for the sale of advertising space on pay TV channels is not significant as the content is financed mainly by subscription/license fees.136 For example the Parties submitted that gross spending on advertsing space on pay TV channels amount to less than [Parties’ advertising spend] compared to the total spend on FTA advertising channels.137 By contrast FTA channels are mainly financed through advertising and thus advertisement spent on these channels is much greater. It follows that the market shares on the market for the sale of TV advertising space on FTA channels is not materially different from the shares included in Table 23 (excuding AVOD) and in Table 22 (including AVOD).

(161) The market shares on the alternative product markets would not change materially if the geographic scope of the market was Flanders and the Brussels Capital Region together138 as in both cases the market would roughly correspond to the Dutch linguistic area and advertising on Dutch language TV channels.

(162) Thus under all possible market definitions the Parties’ combined market share is very high.

5.2.8.2. Radio advertising

(163) Table 24 below presents the market shares on the market for the sale of radio advertising in Flanders.

(164) If the product market is unchanged but but the geographic scope of the market was defined as a) Flanders and Brussels Capital Region together, the market shares indicated in Table 24 would not change materially as in both cases the market would roughly correspond to the Dutch linguistic area in Belgum and advertising on Dutch language radio channels.

5.2.8.3. Online advertising

(165) Table 25 below presents the market shares on the market for the sale of online advertising in Flanders.

(166) If the product market is unchanged but the geographic scope of the market was defined as a) Flanders and Brussels Capital Region together, the market shares indicated in Table 25 would not change materially as in both cases the market would roughly correspond to the Dutch linguistic area in Belgium and advertising on Dutch language websites.

5.3. Horizontal assessment

5.3.1. Introduction

(167) Article 2 of the Merger Regulation requires the Commission to examine whether notified concentrations are compatible with the internal market, by assessing whether they would significantly impede effective competition in the internal market or in a substantial part of it, in particular through the creation or strengthening of a dominant position.

(168) The Commission Guidelines on the assessment of horizontal mergers under the Merger Regulation (the "Horizontal Merger Guidelines") distinguish between two main ways in which mergers between actual or potential competitors on the same relevant market may significantly impede effective competition, namely non- coordinated effects and coordinated effects.

(169) Non-coordinated effects may significantly impede effective competition by eliminating the competitive constraint imposed by each merging party on the other, as a result of which the Integrated Company would have increased market power without resorting to coordinated behaviour. The Horizontal Merger Guidelines list a number of factors139 which may influence whether or not significant non- coordinated effects are likely to result from a merger, such as the large market shares of the merging firms, the fact that the merging firms are close competitors, the limited possibilities for customers to switch suppliers, or the fact that the merger would eliminate an important competitive force. Not all of these factors need to be present for significant non-coordinated effects to be likely. The list of factors, any one of which is not necessarily decisive, is also not an exhaustive list.

5.3.2. Horizontal non-coordinated effects in the production of AV content (demand side)140

(170) The Notifying Parties’ activities and those of the JV significantly overlap on the demand side of the market. The Parties have a 2019 combined market share by value of [50-60]% (Liberty Global: [20-30]%; DPG Media: [30-40]%), and expect to have a in 2023 combined market share by value of [60-70]% (Liberty Global: [10-20]%; DPG Media: [30-40]%; JV: [5-10]%), in the acquisition of Dutch-language AV content production in Belgium.

5.3.2.1. Notifying Parties’ view

(171) The Notifying Parties submit that the Transaction does not raise horizontal competition concerns on the basis of any plausible definition of the relevant product and geographic market for the reasons set out below.141

(172) First, the Notifying Parties submit that the JV will have modest activities on the demand side of the AV content production market. Its market share would amount to approximately [5-10]% in 2023. Therefore, the scope of the agreements put in place regarding collaboration between the JV and each of its parents regarding AV content production would also be necessarily limited. In addition, [JV’s commercial strategy].

(173) Second, the Notifying Parties claim that Telenet and DPG Media’s activities on the AV content production market will continue to take place outside of the JV post- Transaction, and that they will continue to be active as independent purchasers of AV content production services.

(174) Third, the Notifying Parties submit that there will continue to be strong buyers on the demand side of the market, such as VRT, Proximus and international providers like Netflix.

5.3.2.2. Commission’s assessment

(175) The Commission considers that the Transaction does not give rise to serious doubts as to its compatibility with the internal market as a result of horizontal effects on the market for the production of AV content (demand side), or any possible narrower affected markets, regardless of precise market definition, for the following reasons.

(176) First, the JV will be a new additional purchaser of AV content production. In 2023, it will only represent [5-10]% of the demand (by value) in the market for the production of Dutch-language AV content in Belgium. Therefore, the merger specific change brought about by the Transaction will be limited.142