Commission, August 7, 2020, No M.9771

EUROPEAN COMMISSION

Decision

HITACHI / HONDA / HIAMS / KEIHIN / SHOWA / NISSIN KOGYO

Subject: Case M.9771 — Hitachi/Honda/HIAMS/Keihin/Showa/Nissin Kogyo Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 7 July 2020, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Hitachi, Ltd. (“HTL”, Japan) and Honda Motor Co., Ltd. (“Honda”, Japan) acquire within the meaning of Article 3(1)(b) and 3(4) of the Merger Regulation joint control of the whole of Hitachi Automotive Systems, Ltd (“HIAMS”, Japan), Keihin Corporation (“Keihin”, Japan), Showa Corporation (“Showa”, Japan) and Nissin Kogyo Co., Ltd (“Nissin Kogyo”, Japan)3. Honda and HTL are designated hereinafter as the “Notifying Parties” or “Parties to the proposed transaction”. HIAMS, Keihin, Showa and Nissin Kogyo are designated hereinafter as the “Targets”.

1. THE PARTIES

(2) HTL is a multinational conglomerate company and is the ultimate parent company of the Hitachi group of companies. HTL is a highly diversified company, mainly active in the manufacture and sale of products and services in the IT, energy, industry, mobility and smart life sectors.

(3) Honda is the parent company of the Honda group of companies, and is active in the production and distribution of automobiles, motorcycles and power products.

(4) HIAMS is active in the production and supply of automotive products and technologies. HIAMS is wholly owned by HTL.

(5) Keihin is active in the manufacture and supply of electrification systems for hybrid and electric vehicles, engine management systems for gasoline and natural gas vehicles, and products for fuel cells. As at 31 March 2019, Honda owned 41.35% of the voting rights in Keihin and was Keihin’s major shareholder, albeit it did not exert control over Keihin.4 The remainder of Keihin’s shares are widely held. Keihin is currently not controlled by any company or person for the purpose of the Merger Regulation.5

(6) Showa is active in the manufacture and supply of components for automobiles, motorcycles and outboard motors. As at 31 March 2019, Honda owned 33.5% of the voting rights in Showa and was Showa’s major shareholder, albeit it did not exert control over Showa.6 The remainder of Showa’s shares are widely held. Showa is currently not controlled by any company or person for the purpose of the Merger Regulation.7

(7) Nissin Kogyo is active in the manufacture and supply of integrated braking systems for vehicles. As at 31 March 2019, Honda owned 34.86% of the voting rights in Nissin Kogyo and was Nissin Kogyo’s major shareholder, albeit it did not exert control over Nissin Kogyo.8 The remainder of Nissin Kogyo’s shares are widely held. Nissin Kogyo is currently not controlled by any company or person for the purpose of the Merger Regulation.9

(8) Although prior to the concentration Honda did not exercise control over Keihin, Showa and Nissin Kogyo, it had a strong purchase relationship with them and was a major customer for most of the products giving rise to an affected market.

2. THE CONCENTRATION

2.1. Interrelated transactions

(9) The concentration is accomplished by way of purchase of shares. Pursuant to a single agreement entered into between the Parties on 30 October 2019 (the Management Integration Agreement),10 Honda will conduct tender offers for the shares it does not already own in Keihin, Showa and Nissin Kogyo (the “First Step”). Thereafter, each of Keihin, Nissin Kogyo and Showa will be amalgamated into HIAMS (“the Absorption Merger”) to form one company (the “Integrated Company”). In consideration, common shares representing 33.4% of the voting rights in the Integrated Company will be allotted to Honda (“the Second Step”). .11

(10) Both the First Step and the Second Step have been agreed upfront by the Parties simultaneously, in a single agreement and are economically mutually dependent, in that as a matter of commercial reality the First Step would not occur absent the Second Step.12 Pursuant to Article 7.1.1 of the Management Integration Agreement, the Parties have agreed that the Second Step will occur promptly after the First Step. In this regard, pursuant to the Commission Consolidated Jurisdictional Notice under Council Regulation (EC) No 139/2004 on the control of concentrations between undertakings13 (“Consolidated Jurisdictional Notice” or “CJN”), indications of interdependence of transactions may be statements of the parties (such as those referenced in the press release relating to the proposed transaction)14 and simultaneous entry into the relevant agreements.15

(11) The First Step will not therefore bring about a change of control on a lasting basis for the purpose of Article 3(1) of the Merger Regulation. Accordingly, the proposed transaction (comprising the First Step and the Second Step) constitute a single concentration for the purpose of the Merger Regulation.16

2.2. Full-function

(12) The Integrated Company will operate as a full-function joint venture in that it will play an active role on the market and will be economically autonomous from HTL and Honda from an operational viewpoint:17

(a) The Integrated Company will consist of four entities that already operate autonomously on the market, with access to sufficient resources including finance, staff, and assets (tangible and intangible) to conduct their business activities on a lasting basis. The Integrated Company will continue to have its own sales team, R&D resources, and production facilities to manufacture and supply its products to the market. In addition, the Integrated Company will have a management dedicated to its day-to-day operations. […] the Integrated Company will establish […] as the deliberative and decision- making body for important managerial issues of the Integrated Company, and the members […] will include […] appointed by […].

(b) The Integrated Company will continue to operate as a market-facing business, providing automotive components to third party customers, and so it is not the case that the Integrated Company's activities will be limited to carrying out a specific function for HTL or Honda.

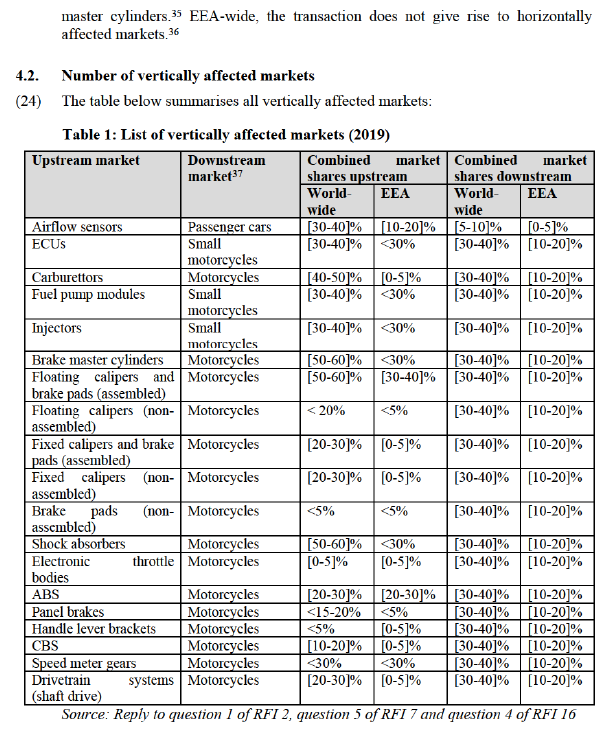

(c) The Integrated Company will consist of entities that already have a track record of operating autonomously on the market, with their own customer base. The Parties' intention is that the Integrated Company will continue to be reliant on third party sales. Reflective of this, it is not the intention that the Integrated Company will be heavily reliant on sales to Honda. For example, Honda currently accounts for [Percentage of HIAMS’ sales of component parts accounted for by Honda]% of HIAMS’ total sales of component parts and, on a weighted average basis, the Targets’ combined total sales to the Parents account for approximately [Percentage of Parents’ sales of component parts accounted for by the Targets]% of their total sales.18 Furthermore, sales between the Targets and their Parents will be at arm’s length, on normal commercial conditions:19 as confirmed by the Notifying Parties, [Details of supply and purchase arrangements of the Parties], therefore, Honda will be supplied by the Targets on the same terms as other third parties.20

(d) The Integrated Company will be formed by the amalgamation of four pre- existing entities that already operate on the market and the Parties' intention is that the Integrated Company will continue to operate on the market on a lasting basis.

2.3. Joint control

(13) Pursuant to an agreement entered into between HTL and Honda on 30 October 2019 (the “Subsidiary Integration Agreement”),21 HTL will own 66.6% and Honda will own 33.4% of the voting rights of the Integrated Company.

(14) The Subsidiary Integration Agreement provides that HTL will have the right to appoint the majority of directors to the board of directors of the Integrated Company (the “Integrated Company Board”): the Integrated Company Board shall have six directors in total, of which HTL may nominate four and Honda may nominate two. [Description of provisions in the agreement entered into between HTL and Honda].22

(15) [Description of provisions in the agreement entered into between HTL and Honda].23

(16) The Notifying Parties note that similar procedures for the approval of the annual business plan and budget were used in a previous joint venture between HIAMS and Honda in Case COMP/M.8485 – Hitachi Group / Honda / JV. In that case, the Commission concluded that the joint venture in question was jointly controlled by HIAMS and Honda […]. On that basis, the joint venture fell within the jurisdiction of the Merger Regulation, and was notified to and approved by the Commission.24 The Notifying Parties have confirmed that [Description of provisions in the agreement entered into between HTL and Honda].25

(17) Pursuant to the CJN and the Commission’s decisional practice, joint control can be exercised on a de facto basis, where as a matter of practice the shareholders must reach a common understanding in determining the commercial policy of the joint venture.26 According to the CJN, “[…] collective action can occur on a de facto basis where strong common interests exist between the minority shareholders to the effect that they would not act against each other in exercising their rights in relation to the joint venture”27 and “[i]ndicative for such a commonality of interests is a high degree of mutual dependency as between the parent companies to reach the strategic objectives of the joint venture. This is in particular the case when each parent company provides a contribution to the joint venture which is vital for its operation (e.g. specific technologies, local know-how or supply agreements)”.28 Pursuant to the CJN, de facto joint control may also arise as a result of decision making procedures – such as those envisaged under [Description of provisions in the agreement entered into between HTL and Honda] – which are “tailored in such a way as to allow the parent companies to exercise joint control even in the absence of explicit agreements granting veto rights”.29

(18) In the case of the Integrated Company there will be a strong commonality of interests between the shareholders, consistent with the arrangements in relation to the proposed transaction requiring that [Description of provisions in the agreement entered into between HTL and Honda].30 This commonality of interests is reflected in the following elements:

(a) Importance of Honda as a customer of the Integrated Company: while the specific products and volumes that the Integrated Company will supply to Honda has still to be determined, the Parties consider that the proportion of their total sales of component parts that Honda currently accounts for provides a reasonable proxy for the expected importance of Honda as a customer of the Integrated Company. Honda accounts for approximately [Percentage of HIAMS' sales of component parts accounted for by Honda]% of HIAMS' total sales of component parts. However, for each of Showa, Keihin and Nissin Kogyo the proportion of sales that Honda accounts for is significantly higher:

– Keihin: Honda accounts for approximately [Percentage of total sales of component parts accounted for by Honda]% of its total sales of component parts;

– Showa: Honda accounts for approximately [Percentage of total sales of component parts accounted for by Honda]% of its total sales of component parts;

– Nissin Kogyo: Honda accounts for approximately [Percentage of total sales of component parts accounted for by Honda]% of its total sales of component parts.

(b) Importance of the IP licensed by Honda to the Integrated Company:[Licensing practices of Honda].31 [Licensing practices of Honda]:

– Keihin: [Licensing practices of Honda].

– Showa: [Licensing practices of Honda].

– Nissin Kogyo: [Licensing practices of Honda].

(c) Importance of the corporate functions provided by Honda to the Integrated Company: [Description of future corporate functions and supply arrangement between Honda and the Integrated Company].

(d) Importance of the Honda personnel transferred to the Integrated Company. [Details of employment arrangements with Honda]:

– Keihin: [Details of employment arrangements with Honda].

– Showa: [Details of employment arrangements with Honda].

– Nissin Kogyo: [Details of employment arrangements with Honda].

(19) Because of the strong commonality of interests between Honda and the Integrated Company, Honda will exercise de facto joint control over the Integrated Company together with HTL [Description of commercial arrangement between HTL and Honda].

(20) As a result of the proposed concentration, the Integrated Company will be jointly controlled by HTL and Honda.

3. EU DIMENSION

(21) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (HTL: EUR […] million; Honda: EUR […] million; Keihin: EUR […] million; Showa: EUR […] million; Nissin Kogyo: EUR […] million).32 At least two of them has an EU-wide turnover in excess of EUR 250 million (Hitachi: EUR […] million33; Honda: EUR […] million; Keihin: EUR […] million; Showa: EUR […] million; Nissin Kogyo: EUR […] million), but not each of the undertakings concerned achieves more than two-thirds of its aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension within the meaning of Article 1(2) of the Merger Regulation.

4. COMPETITIVE ASSESSMENT

(22) The concentration gives rise to affected markets only in the original equipment manufacturers (OEM) segment. Therefore, the affected markets cited in this decision refer only to the OEM segment.34

4.1. Number of horizontally affected markets

(23) Worldwide, the activities of the Notifying Parties and the Targets result in two horizontally affected markets in relation to the following components for use in motorcycles: floating calipers and brake pads (as an assembled product), and brake

(25) In the EEA, the activities of the Parties and the Targets result in vertically affected markets due to market shares exceeding 30% in an upstream component market in relation to floating calipers and brake pads (as an assembled product) for use in motorcycles.

(26) Worldwide, the activities of the Parties and the Targets result in vertically affected markets due to market shares exceeding 30% in an upstream component market in relation to airflow sensors for use in passenger cars, and the following components for use in motorcycles: engine control units “ECUs”, carburettors, fuel pump modules, injectors, brake master cylinders, floating calipers and brake pads (as an assembled product), and shock absorbers.

(27) Given Honda’s market share of [30-40]% in the downstream market for motorcycles at worldwide level, the following markets are also vertically affected.

i. In the EEA and worldwide additional vertically affected markets are:

- Electronic throttle bodies (upstream) – motorcycles (downstream)

- Anti-lock braking systems (“ABS”) (upstream) – motorcycles (downstream)

- Brake pads (as a non-assembled component) (upstream) – motorcycles (downstream)

- Floating calipers (non-assembled) (upstream) – motorcycles (downstream)

- Panel brakes (upstream) – motorcycles (downstream)

ii. Additional vertically affected markets at worldwide level only:

- Combined brake systems “CBS” (upstream) – motorcycles (downstream)

- Fixed calipers and brake pads (assembled) (upstream) – motorcycles (downstream)

- Fixed calipers (as a non-assembled component) (upstream) – motorcycles (downstream)

- Drivetrain systems (shaft drive) (upstream) – motorcycles (downstream)

- Handle lever brackets (upstream) – motorcycles (downstream)

- Speed meter gears (upstream) – motorcycles (downstream)

4.3. Market definition

(28) The Targets are active in the manufacture and sale of motorcycle and automotive components such as engine management and injection systems (airflow sensors, ECUs, carburettors, fuel pump modules, injectors and electronic throttle bodies), braking systems (brake master cylinders, calipers and brake pads, ABS, CBS, panel brakes) and anti-vibration systems (shock absorbers) and others (drivetrain systems, speed meter gears and handle lever brackets for motorcycles).

(29) Some components are only used in motorcycles, some only in passenger cars, and some in both: airflow sensors are only used in cars, whereas carburettors, panel brakes, handle lever brackets, CBS, speed meter gears and drivetrain systems are only used in motorcycles. All other components are parts of passenger cars and motorcycles, although the Parties do not produce all these components for passenger cars and motorcycles (the second column of Table 1 shows which products the Parties produce for passenger cars, which for motorcycles and which for both).

(30) In the market for automotive parts and components, the transaction gives rise to one vertically affected market, namely airflow sensors.

(31) In the market for motorcycle parts and components, the transaction gives rise to two horizontally affected and 19 vertically affected markets for the sale of components (see paragraphs (24) and (27)). Below the Commission provides an analysis of the market definition for those products where market shares at upstream level exceed 30%.

4.3.1. Automotive and motorcycle parts and components overall

4.3.1.1. Product market

(A)The Commission’s decisional practice

(32) The Commission has consistently defined the relevant product market for the manufacture and supply of automotive components on a product-by-product basis,38 and has left open whether there may be a wider market comprising automotive components, modules and systems, or separate markets for “components” and “modules”.39 Within the market for automotive parts and components, the Commission has also further made the following segmentations:40 (a) depending on the type of vehicles for which the product is supplied (Light Vehicles and Heavy Commercial Vehicles);41 and (b) depending on the distribution channel to which the product is supplied (OEMs and independent aftermarket (IAM)42).

(33) The Commission has not specifically addressed the product market for the manufacture and sale of motorcycle components.

(B) The Notifying Parties’ views

(34) The Notifying Parties do not contest the product market definition for automotive components described in the Commission’s precedents cited above.43

(35) The Targets produce components both for small motorcycles (with an engine size below 250cc) and for large motorcycles (with an engine size above 250cc). However, the Notifying Parties submit that components for use in motorcycles of all sizes should be considered to belong to the same product market. This is because, from the demand side perspective, components for use in all sizes of motorcycles are substitutable, due to the fact that the structure, size and shape of such components are the same, regardless of the size of motorcycle that they are used in. From the supply side, suppliers are easily able to switch production between manufacturing components for different sizes of motorcycles, within a short time frame and without requiring a large amount of capital investment, as the production processes for all components (regardless of size of motorbike for end use) is very similar.44

(36) The Notifying Parties note that for components used in both passenger cars and motorcycles, supply-substitutability suggests that a broader market definition might be considered. The Notifying Parties submit that such substitutability applies for brake master cylinders, floating calipers, fixed calipers, brake pads, ECUs, fuel pump modules, injectors and electronic throttle bodies.45 On the other hand, the Notifying Parties submit that there is no supply side substitutability for ABS for passenger cars and for motorcycles, and for shock absorbers for passenger cars and for motorcycles.46 Finally, the Notifying Parties submit that airflow sensors are only supplied for passenger cars, while carburettors, panel brakes, CBS, speed meter gears and drive train systems are only supplied for motorcycles.47

(C) The Commission’s assessment

(37) The Commission considers that for the purpose of the present case, its decisional practice related to automotive components, as outlined in paragraph (32) can be maintained. In its market investigation, the Commission tested whether this practice can be applied to the motorcycle components it investigated in a similar way. The results of the market investigation showed that whereas from a demand-side perspective some markets can be further segmented into types of each components, the same companies usually produce all different types of these products.48

(38) The Commission also investigated the argument of the Parties that no sub- segmentation between components for small motorcycles and components for large motorcycles should be made. A majority49 of customers and competitors considers that components for small motorcycles are not the same as components for large motorcycles.50 Several respondents and a majority of competitors noted that all components being investigated differ between small and large motorcycles in performance and size and are therefore not substitutable, for instance “large motorcycles have different suspensions and brakes due to different performances and mass. In case of ECUs, smaller bikes have simpler engines and less electronic functionalities. […] In terms of contribution margin, large motorcycles are more likely to use more expensive [components]”51 However, there appears to be supply-side substitutability as the market investigation confirmed that the same companies manufacture components for both small and large motorcycles.52 A customer summarised that “in general all components for large 2wheelers are also used for small 2wheelers but size, function and characteristics can differ”.53

(39) The Commission also investigated the argument of the Parties that no sub- segmentation between components for motorcycles and components for passenger cars should be made. The market investigation was inconclusive as to whether the component markets should be divided by passenger car and motorcycle component. In particular, a majority of respondents in the market investigation confirmed that components for passenger cars differ from components for use in motorcycles.54 As a customer explained, “The principle and general functionality of the listed components are comparable for 2wheeler and 4wheeler but you cannot use the same ECU, Fuel pump... for both vehicle types”.55 Competitors confirmed this as well: “Technical and functional characteristics, performances and liabilities of automotive components for passenger cars are generally different from components for motorcycles.”56

(40) However, there appears to be a high degree of supply-side substitutability between automotive and motorcycle components. A majority of respondents in the market investigation confirmed that the same companies that produce the motorcycle components in question also produce these components for passenger cars (ECUs, fuel pump modules, injectors, brake master cylinders, floating calipers and shock absorbers).57 As a competitor confirmed, “Normally, production technologies of car and motorcycle parts are the same.”58

(41) In conclusion, the Commission will leave open whether one product market exists for automotive and motorcycle components. As for automotive components (i.e. not used in motorcycles), the Commission will retain the product market definition provided in its past decisional practice as described in paragraph (32). For components that are also, or exclusively used in motorcycles, it can be left open whether a distinction should be made between components for large and for small motorcycles.59

4.3.1.2. Geographic market

(A) The Commission’s decisional practice

(42) In previous decisions, the Commission has found that the geographic markets for the manufacture and supply of OEM automotive components are at least EEA-wide, and possibly worldwide, but has left open the precise definition.60 In a recent case, the existence of at least EEA-wide markets was justified as follows: i) the Parties operated worldwide; ii) OEMs increasingly source products at worldwide level; iii) within the EEA, transport costs are not significant; iv) product regulation and safety standards are set at EEA level; v) there are no obstacles to intra-EEA trade and vi) prices are similar throughout the EEA.61

(43) The Commission has not specifically addressed the geographic market for the manufacture and sale of motorcycle components.

(B) The Notifying Parties’ views

(44) The Notifying Parties consider the markets for the manufacture and supply of all automotive and motorcycle components discussed in this Decision to be worldwide in scope. According to the Notifying Parties, this worldwide market definition follows from the fact that transport costs are low: in many cases, the Notifying Parties estimate that transport costs per unit amount to [Percentage of the price of the component comprised of transport costs]% of the price of the component. In addition, the Notifying Parties submit that there are no specific trade barriers and these products are traded globally.62

(C) The Commission’s assessment

(45) The market investigation confirmed that the market for the manufacture and sale of OEM automotive and motorcycle components is at least EEA-wide, if not worldwide. A vast majority of customers purchase original automotive and motorcycle components at a worldwide level.63 Specifically for motorcycle components, a majority of customers confirmed that motorcycle components are usually shipped globally and that transport costs are low.64 Even though some European motorcycle manufacturers purchase a large proportion of components in the EEA, they nevertheless make their purchase decisions based on comparisons with suppliers worldwide, as a competitor explained: “[company name] in general purchases motorcycles components mostly (circa 75%) in Europe; however the driver for the choice is also the know-how and quality and competitiveness of the components thus various suppliers are located outside Europe”.65

(46) For the purposes of this decision, the Commission therefore considers that it can be left open whether the geographic market for manufacture and sale of the automotive and motorcycle components under investigation is defined as EEA-wide or worldwide, as the proposed transaction does not raise any competition concerns, irrespective of the exact market definition adopted.

4.3.2. Automotive airflow sensors

(47) Airflow sensors are one of the key components of an electronic fuel injection system and measure the amount of air entering the car engine. They are not currently used in motorcycles.66

4.3.2.1. Product market

(A) The Commission’s decisional practice

(48) The Commission has not previously considered a separate product market for manufacture and sale of airflow sensors for automobiles. However, in previous cases involving other sensors for automobiles, it considered each type of automotive sensor to constitute a separate product market based on its area of employment. This concerned, for example, temperature sensors, pressure sensors, fluidity level sensors, speed sensors and acceleration sensors. The Commission found that as each of these sensors has a different function, namely to measure specific information for the vehicle, they are not substitutable from a demand-side perspective. Also, producers of sensors cannot easily switch their production from one type of sensor to the other, which is why separate product markets per sensor function are justified also from a supply-side perspective.67

(B) The Notifying Parties’ view

(49) The Notifying Parties submit that the product market for automotive airflow sensors is the narrowest relevant segmentation.68 They note that given the high degree of supply-side substitutability, no further sub-segmentation by different variations of airflow sensors is necessary. For instance, the equipment required to manufacture airflow sensors for gasoline and diesel passenger cars is the same. Therefore, manufacturers are able to produce such components without any additional investment or time delay.69

(50) In relation to single/standalone mass airflow sensors and airflow sensors with integrated additional features with pressure/humidity,70 manufacturers are able to produce these components without significant investments. The Parties estimate that it would take [Parties’ estimate of switching costs] to start production of airflow sensors with integrated additional features with pressure/humidity.71

(C) The Commission’s assessment

(51) In line with its previous practice, the Commission considers that each automotive sensor fulfilling a different function constitutes a separate product market, and the results of the market investigation did not contest this. As for the possibility of a further sub-segmentation of airflow sensors, in the market investigation, a competitor mentioned the following possible segments of airflow sensors for automobiles, confirming that it produces “all different types of air flow sensors with customer specific programmable output” and that the different types are “relatively easy to produce”:

– Gasoline and diesel airflow sensors.

– Single/standalone mass airflow sensors and airflow sensors with integrated additional features with pressure/humidity.72

(52) While there are different types of airflow sensors, the different types are easy to produce, so there is supply-wide substitutability. As automotive airflow sensors all fulfil the same function, namely measuring the amount of air flowing into the engine, demand-side substitutability was also confirmed in the market investigation.73 As a respondent in the market investigation explained, “In case of sensors, different technologies might be used in order to make the same kind of measurement.”74

(53) Therefore, the Commission concludes that the relevant product market is the market for manufacture and sale of automotive airflow sensors.75

(54) In any event, for the purpose of the present decision, the exact product market definition can ultimately be left open76 as the proposed transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition.

4.3.2.2. Geographic market

(A) The Commission’s decisional practice

(55) The Commission has not previously analysed the market for of airflow sensors for passenger cars. In previous cases where the Commission analysed the market for automotive sensors, it defined the market as at least EEA-wide.77

(B) The Notifying Parties’ view

(56) As outlined in paragraph (44), the Notifying Parties consider that all markets for engine management and injection systems, including the market for airflow sensors, should be analysed at a worldwide level for the purpose of this Decision.78

(C) The Commission’s assessment

(57) In line with its decisional practice and the findings of the market investigation outlined in paragraph (45), for the purposes of this Decision it can be left open whether the geographic market is defined as EEA-wide or worldwide, as the proposed transaction does not raise any serious doubts as to its compatibility with the internal market under any plausible market definition adopted.

4.3.3. ECUs and electronic throttle bodies

(58) Like airflow sensors, ECUs and electronic throttle bodies are key components of the engine management system.79

(59) An electronic throttle body is a mechanism that supplies air to the engine, controlled by an ECU.80

(60) Based on information from sensors, an ECU controls the amount and timing of fuel flowing through the fuel injectors into the combustion chamber, the amount of air passing through the throttle body and the timing of the ignition spark which ignites the fuel in engines. ECUs are used in a variety of engines (including diesel and gasoline-powered engines for automobiles, motorcycles and general purpose engines, such as small ships or power generators).

4.3.3.1. Product market

(A) The Commission’s decisional practice

(61) The Commission has previously identified potential separate markets for the supply of ECUs and electronic throttle bodies. The Commission also previously concluded that each ECU used in a different area of employment constitutes a separate market. For instance, in Continental / Siemens VDO, the Commission found separate markets for (i) gasoline ECUs, (ii) diesel ECUs for passenger cars and light vehicles and (iii) diesel ECUs for heavy vehicles.81

(B) The Notifying Parties’ view

(62) The Notifying Parties agree that ECUs and electronic throttle bodies each constitute separate product markets and that, within ECUs, a distinction may be drawn between ECUs used in gasoline and diesel-powered engines.82 However, the Notifying Parties submit that there is no need to conclude on such a distinction in this case as no competition concerns arise even on a the narrowest plausible market.83

(63) The Notifying Parties consider that it would be appropriate to define a single market for the supply of ECUs for use in both motorcycles and passenger cars, in view of the supply side substitutability between these products. The same should apply to electronic throttle bodies.84 Suppliers are easily able to switch production between these components for use in motorcycles and passenger cars, within a short time frame and without requiring a large amount of capital investment, as the production processes for these components is very similar.85

(64) As outlined in paragraph (35), the Notifying Parties consider that a sub-segmentation between ECUs for small and large motorcycles, or electronic throttle bodies for use in small large motorcycles, is not justified.

(65) The Notifying Parties submit that no segmentation is required with regard to different types of ECUs, as manufacturers would be able to produce such variations without significant additional investment or time delay.86

(C) The Commission’s assessment

(66) The Commission considers that the previous practice to distinguish between diesel and gasoline ECUs, and within diesel ECUs for light and heavy vehicles can be maintained for the purposes of the present decision.87 It should be noted that these distinctions are relevant for ECUs for use in passenger cars, whereas the results of the market investigation suggest that different distinctions might be relevant for ECUs used in motorcycles. Distinctions mentioned by respondents are the following:

- ECUs capable of e-gas and not capable of e-gas,88

- Fuel powered and electric powered ECUs,89

- Single cylinder and multi cylinder ECUs, 90

(67) A majority of respondents confirmed that there is no demand-side substitutability, neither between ECUs for passenger cars and for motorcycles,91 nor between small and large motorcycles.92 However, the market investigation confirmed supply-side substitutability between ECUs for passenger cars and for motorcycles, as manufacturers usually produce all types of ECUs,93 and a majority of respondents replied that the same suppliers produce all types of ECUs, both for passenger cars and motorcycles.94 A competitor explained that “ECU in general are engine/customer specific components”. This indicates that ECUs are bespoke products (i.e. suppliers manufacture a slightly different type of ECU not only for each OEM but for each vehicle model) and therefore a single market for manufacture and sale of all ECUs, including ECUs for small/large motorcycles, motorcycles/passenger cars and different types as mentioned in the market investigation, might be warranted.95

(68) The market investigation did not find the need for a further segmentation of the market for supply of electronic throttle bodies.96 Therefore, the Commission will retain its practice to define a separate market for the manufacture and sale of electronic throttle bodies.

(69) In any event, for the purpose of the present decision, the exact product market definition can ultimately be left open97 as the proposed transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition.

4.3.3.2.Geographic market

(A) The Commission’s decisional practice

(70) In previous cases, the Commission considered the geographic market for the manufacture and sale of ECUs to be at least EEA-wide, if not worldwide.98

(B) The Notifying Parties’ view

(71) The Notifying Parties submit that the appropriate geographic market for the supply of component parts for all engine management and injection systems, the product category including ECUs and electronic throttle bodies, is worldwide. Transport costs are low: in many cases, the Notifying Parties estimate that transport costs per unit amount to [Percentage of the price of the component comprised of transport costs]% of the price of the component part. In addition, there are no specific trade barriers and these products are traded globally. In fact, Keihin does not manufacture component parts for engine management and injection systems in the EEA and all its sales are achieved through import.99

(72) In any event, the Notifying Parties submit that the geographic market definition can be left open as the proposed transaction will not raise any competition concerns, irrespective of the exact market definition.100

(C) The Commission’s assessment

(73) The market investigation did not find that the geographic market for the manufacture and sale of ECUs and electronic throttle bodies diverges from the general finding that the geographic market for automotive and motorcycle components at least EEA- wide.101

(74) In line with its decisional practice and the findings of the market investigation outlined in paragraph (45), for the purposes of this Decision it can be left open whether the geographic market is defined as EEA-wide or worldwide, as the proposed transaction does not raise any serious doubts as to its compatibility with the internal market under any plausible market definition adopted.

4.3.4. Carburettors

(75) A carburettor is a mechanical apparatus used to premix vaporised fuel and air in proper proportions and supplying the mixture to a motorcycle internal combustion engine.102

4.3.4.1. Product market

(A)The Commission’s decisional practice

(76) The Commission has not previously considered a product market for the supply of carburettors. In cases concerning other components of internal combustion engines, the Commission has found that each component constitutes a different product market, with a further subdivision based on the size of the engine (as the cases concerned the automotive market, the distinction was drawn between components for light duty applications and components for heavy duty applications).103

(B) The Notifying Parties’ view

(77) The Notifying Parties submit that the overall market for the manufacture and sale of carburettors is the narrowest relevant segmentation.104 The Parties submit that carburettors are only used for motorcycles, not any more for passenger cars, and that, for the purposes of this Decision, the relevant product market should be the market for the manufacture and sale of carburettors for motorcycles.105

(78) As outlined in paragraph (35), the Notifying Parties consider that a sub-segmentation between carburettors for small and large motorcycles is not justified.

(C) The Commission’s assessment

(79) The Commission considers that, in line with its previous decisional practice, the relevant market is carburettors for motorcycles, and a further possible distinction between carburettors for small and for large motorcycles. This was confirmed by the market investigation which found that carburettors for small motorcycles are different from carburettors for large motorcycles.106

(80) However, the market investigation also confirmed that there is a high degree of supply-wide substitutability between carburettors for small and for large motorcycles, as the same suppliers usually produce all types of carburettors.107

(81) In any event, for the purpose of the present decision, the exact product market definition can ultimately be left open108 as the proposed transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition.

4.3.4.2. Geographic market

(A) The Commission’s decisional practice

(82) The Commission has not previously analysed the market for the supply of carburettors, or other motorcycle components. For automotive components, the Commission found that the geographic markets for the manufacture and supply of OEM automotive components are at least EEA-wide, and possibly worldwide, but has left open the precise definition (see paragraph (42)).

(B) The Notifying Parties’ view

(83) The Notifying Parties submit that the appropriate geographic market for the supply of component parts for engine management and injection systems, the product category including carburettors, is worldwide, as explained in paragraph (71).

(C) The Commission’s assessment

(84) In line with its decisional practice and the findings of the market investigation outlined in paragraph (45), for the purposes of this Decision it can be left open whether the geographic market is defined as EEA-wide or worldwide, as the proposed transaction does not raise any serious doubts as to its compatibility with the internal market under any plausible market definition adopted.

4.3.5. Fuel pump modules

(85) A fuel pump module filters fuel from the fuel tank and uses a pump to retrieve fuel from the tank and pressurise it. The module features a built-in pressure regulator to maintain constant pressure for supply to the injectors.109

4.3.5.1. Product market

(A) The Commission’s decisional practice

(86) The Commission has not previously considered a product market for the supply of fuel pump modules. In cases concerning other components of internal combustion engines, the Commission has found that each component constitutes a different product market, with a further subdivision based on the size of the engine (as the cases concerned the automotive market, the distinction was drawn between components for light duty applications and components for heavy duty applications).110

(B) The Notifying Parties’ view

(87) The Notifying Parties submit that the relevant product market is the market for the supply of fuel pump modules without any further segmentation per type.111 With regard to fuel pump modules for motorcycles with different tank shapes and sizes, top-mount/bottom-mount, mounted inside/outside fuel tank, the Notifying Parties submit that manufacturers would be able to produce such variations without significant additional investment or time delay.112

(88) The Notifying Parties consider that it would be appropriate to define a single market for the supply of fuel pump modules for use in both motorcycles and passenger cars, in view of the supply side substitutability between these products. 113 Suppliers are easily able to switch production between components for use in motorcycles and passenger cars, within a short time frame and without requiring a large amount of capital investment, as the production processes for these components are very similar.114

(89) As outlined in paragraph (35), the Notifying Parties consider that a sub-segmentation between fuel pump modules for small and large motorcycles is not justified.

(C) The Commission’s assessment

(90) In the market investigation, some respondents mentioned the following possible segments of fuel pump modules:

- Fuel pump modules for different tank shapes and sizes, top-mount/bottom- mount, mounted inside/outside fuel tank

- Low and high flow rate115

(91) A majority of respondents in the market investigation confirmed that there is no demand-side substitutability, neither between fuel pump modules for passenger cars and for motorcycles, nor between these inputs for small and large motorcycles,116 The reason is that fuel pump modules for motorcycles have “different flow and pressure requirements, different geometry”117 than fuel pump modules used in passenger cars, so that they are not substitutable. However, as fuel pump modules are less complex than most other products discussed in the market investigation, such as brake components, they “need less effort to interchange”.118

(92) The market investigation confirmed supply-side substitutability as a majority of respondent replied that the same suppliers produce all types of fuel pump modules, both for passenger cars and for motorcycles.119

(93) In any event, for the purpose of the present decision, the exact product market definition can ultimately be left open120 as the proposed transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition.

4.3.5.2. Geographic market

(A) The Commission’s decisional practice

(94) The Commission has not previously analysed the market for the supply of fuel pump modules. For automotive components, the Commission generally found that the geographic markets for the manufacture and supply of OEM automotive components are at least EEA-wide, and possibly worldwide, but has left open the precise definition (see paragraph (42)).

(B) The Notifying Parties’ view

(95) The Notifying Parties submit that the appropriate geographic market for the supply of component parts for engine management and injection systems, the product category including fuel pump modules, is worldwide, as explained in paragraph (71).

(C) The Commission’s assessment

(96) In line with its decisional practice and the findings of the market investigation outlined in paragraph (45), for the purposes of this Decision it can be left open whether the geographic market is defined as EEA-wide or worldwide, as the proposed transaction does not raise any serious doubts as to its compatibility with the internal market under any plausible market definition adopted.

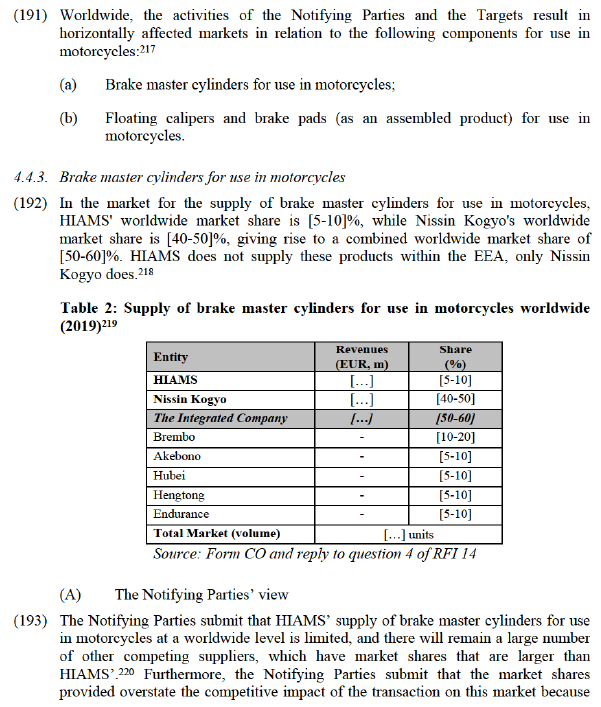

4.3.6. Injectors

(97) Fuel injectors are a part of the fuel injection system (a system which mixes fuel with air) which, when signalled by an ECU, open up to spray pressurised fuel into the engine.121

4.3.6.1. Product market

(A) The Commission’s decisional practice

(98) The Commission has previously identified a potential separate product market for diesel injectors, with a potential sub-segmentation for use in light vehicles as opposed to heavy vehicles.122

(B) The Notifying Parties’ view

(99) The Notifying Parties consider that engines are distinguished by the location of the injector that injects fuel (direct-injection and port injection).123

(100) Direct-injection engines use a method in which the injector directly injects the fuel into the combustion chamber of the engine. On the other hand, port-injection engines use a method in which fuel is injected into the inlet port that supplies air to the engine.124

(101) Therefore, the Notifying Parties submit that the Commission should distinguish between injectors used in (i) direct injection engines or port injection engines (ii) hydrogen fuel cell vehicles or natural gas vehicles,125 (iii) motorcycles and passenger cars126 or other applications (such as outboard engines127).

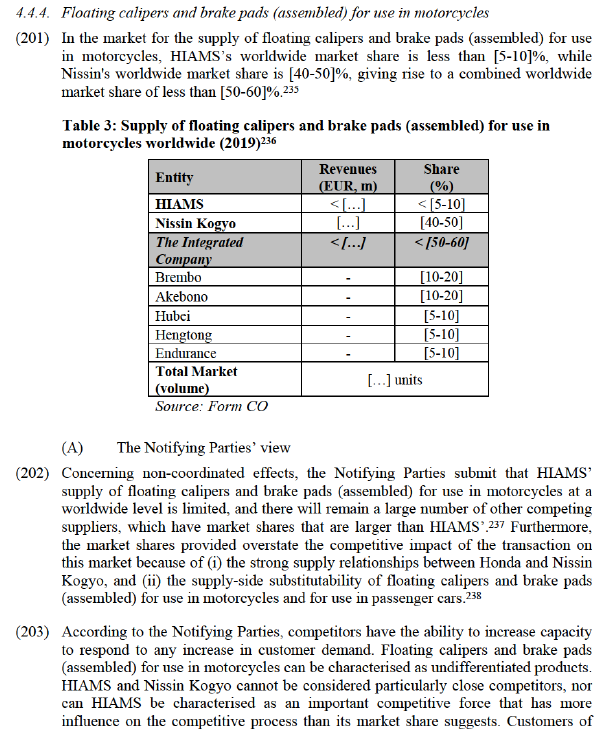

(102) With regard to injectors for motorcycles with different types of engines, variations in spray pattern requirements, the length of the injector body or fixation methods, the Notifying Parties submit that manufacturers would be able to produce such variations without significant additional investment or time delay.128

(103) The Notifying Parties consider that it would be appropriate to define a single market for the supply of injectors for use in both motorcycles and passenger cars, in view of the supply side substitutability between these products.129 Suppliers are easily able to switch production between components for use in motorcycles and passenger cars, within a short time frame and without requiring a large amount of capital investment, as the production processes for these components is very similar.130

(104) As outlined in paragraph (35), the Notifying Parties consider that a sub-segmentation between injectors for small and large motorcycles is not justified.131

(C) The Commission’s assessment

(105) The Commission considers that its previous market definition for diesel injectors can be maintained for the purposes of the present case.132 In the market investigation, some respondents mentioned the following variations of injectors:

- Injectors depending on the type of engine, variations in spray pattern requirements, length of injector body and fixation method.133

(106) A vast majority of both competitors and customers confirmed that the same companies produce injectors for passenger cars and motorcycles.134 In this case, it appears that indeed injectors are the same for motorcycles and cars,135 as well as for small and large motorcycles, as a majority of competitors confirmed,136 as they “need less effort to interchange due to less complexity” and therefore “to some extent, there is a carry-over from car to MC possible”.137

(107) In any event, for the purpose of the present decision, the exact product market definition can ultimately be left open138 as the proposed transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition.

4.3.6.2. Geographic market

(A) The Commission’s decisional practice

(108) The Commission found the market for diesel injectors to be at least EEA-wide, if not worldwide.139

(B) The Notifying Parties’ view

(109) The Notifying Parties consider the market for the supply of all component parts for engine management and injection systems, the product category including injectors, as worldwide, as explained in paragraph (71).

(C) The Commission’s assessment

(110) In line with its decisional practice and the findings of the market investigation outlined in paragraph (45), for the purposes of this Decision it can be left open whether the geographic market is defined as EEA-wide or worldwide, as the proposed transaction does not raise any serious doubts as to its compatibility with the internal market under any plausible market definition adopted.

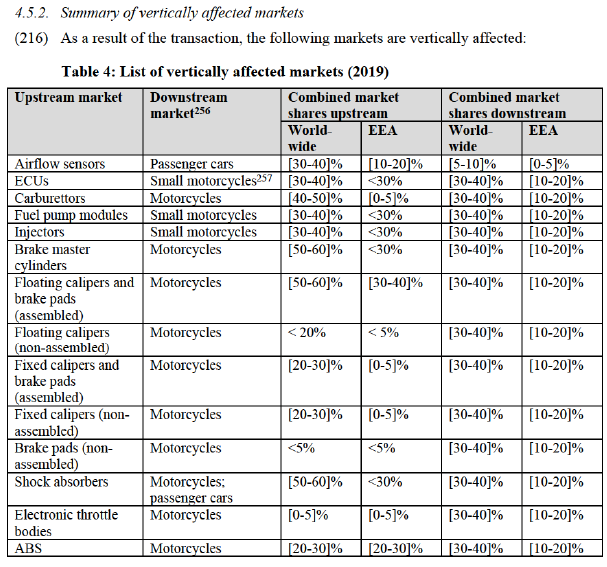

4.3.7. Brake master cylinders

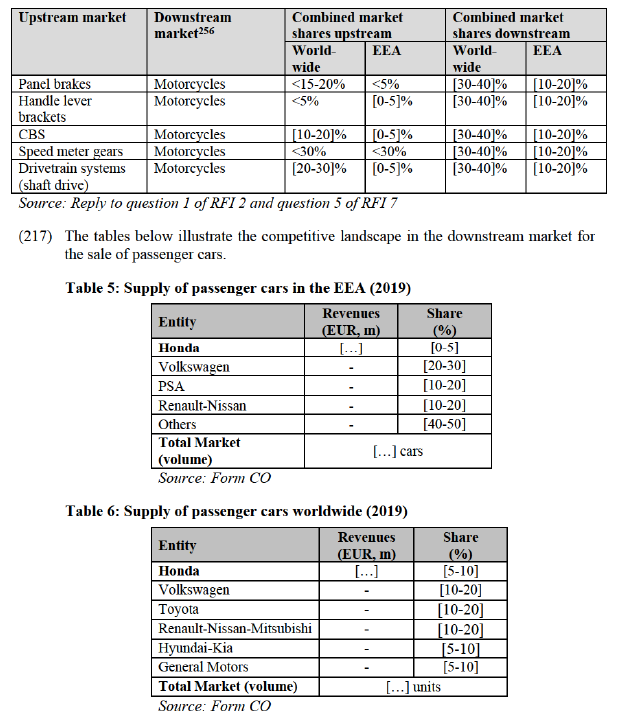

(111) A brake master cylinder is a component of a hydraulic braking system that converts the force exerted on the brake pedal into hydraulic pressure to apply the brakes by establishing a liquid linkage between the master cylinder's pistons and the calipers and wheel cylinders.140

4.3.7.1. Product market

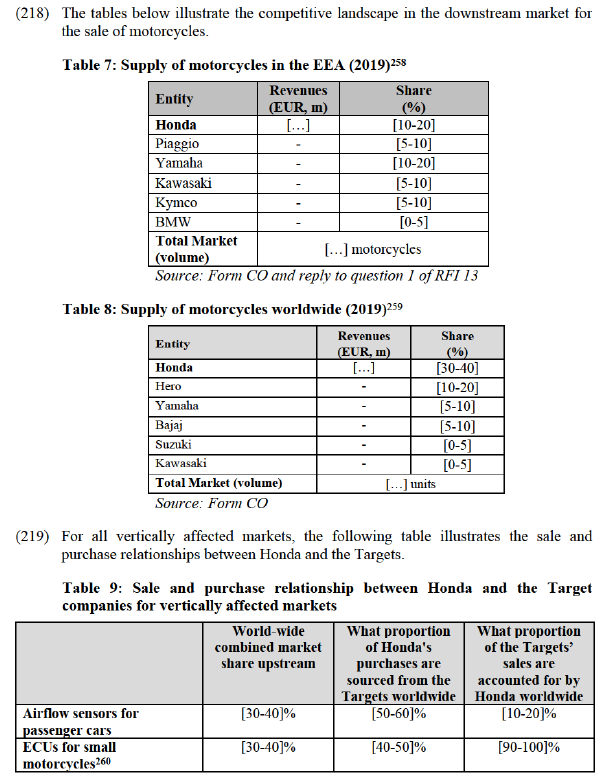

(A) The Commission’s decisional practice

(112) With regard to braking systems for automobiles,141 in a previous decision the Commission distinguished between pneumatic and hydraulic brakes. Moreover, due to the essential technical and commercial differences, the Commission considered that hydraulic braking systems for lighter vehicles and commercial vehicle brakes for heavy vehicles are two separate markets. The Commission has not previously considered a separate product market for brake master cylinders for motorcycles, but analysed them as parts of hydraulic braking systems without further defining the market.142 For pneumatic braking systems, the Commission distinguished between: (a) air supply/actuation systems, and therein further between (i) air compressors, (ii) air dryers and (iii) other parts of actuation systems; (b) foundation brakes, and therein further (i) drum brakes and (ii) disc brakes; and (c) brake and chassis control and therein further between (i) anti-lock braking systems (ABS), (ii) traction control system (TCS, also known as ASR) and (iii) electronic braking systems (EBS). 143

(B) The Notifying Parties’ view

(113) The Notifying Parties consider that it would be appropriate to define a single market for the supply of brake master cylinders for use in both motorcycles and passenger cars, in view of the supply side substitutability between these products.144 Suppliers can switch between manufacturing brake master cylinders for use in passenger cars and motorcycles without particular difficulty. The Parties estimate that any switch would require [Parties’ estimate of switching costs].145

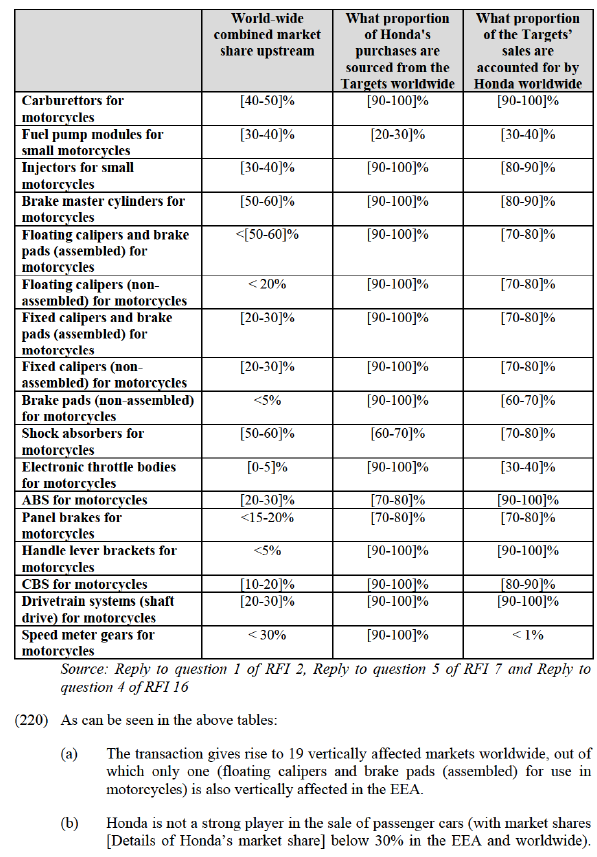

(114) As outlined in paragraph (35), the Notifying Parties consider that a sub-segmentation between brake master cylinders for small and large motorcycles is not justified.

(C) The Commission’s assessment

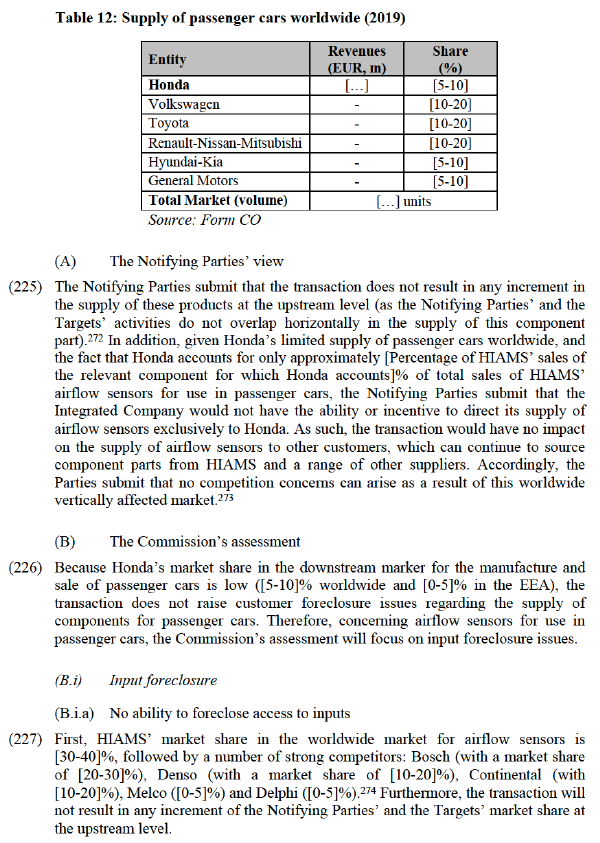

(115) While precedents have not dealt with brake master cylinders for motorcycles but as part of hydraulic brake systems, based on its decisional practice to define a separate product market for each component of pneumatic braking systems (see paragraph (112)), the Commission considers that the relevant product market is brake master cylinders. The market investigation indicated that a further sub- segmentation between brake master cylinders for (i) passenger cars and (ii) brake master cylinders for motorcycles and between small and large motorcycles cannot be excluded.

(116) A majority of respondents in the market investigation confirmed that there is no demand-side substitutability, neither between brake master cylinders for passenger cars and for motorcycles, nor between small and large motorcycles. “Brake and suspension parts for motorcycles are very special. They do not fit into cars.”146 The reason, as respondents explained is that motorcycles require fewer connections than automobiles, the differences in weight and sizing restrictions for motorcycles require different dimensions. Finally, motorcycles are more exposed to water and dirt.147

(117) However, the market investigation confirmed supply-side substitutability as a majority of respondents replied that the same suppliers produce all types of brake master cylinders, both for passenger cars and for motorcycles.148

(118) In the market investigation, some respondents mentioned the following possible segments: radial and tangential brake master cylinders.149

(119) In any event, for the purpose of the present decision, the exact product market definition can ultimately be left open150 as the proposed transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition.

4.3.7.2. Geographic market

(A) The Commission’s decisional practice

(120) The Commission has not previously analysed a geographic market for brake master cylinders. In relation to the supply of components parts for braking systems, the Commission has considered (but ultimately left open) that (a) the geographic market for supply of these products to the OEM channel customers may be EEA-wide in scope, if not worldwide. 151

(B) The Notifying Parties’ view

(121) The Notifying Parties submit that the appropriate geographic market for the supply of components of braking systems, the product category including brake master cylinders, is worldwide. Transport costs are low: in many cases, the Notifying Parties estimate that transport costs per unit amount to [Percentage of the price of the component comprised of transport costs]% of the price of the component. In addition, there are no specific trade barriers and these products are traded globally.152

(C) The Commission’s assessment

(122) In line with its decisional practice and the findings of the market investigation outlined in paragraph (45), for the purposes of this Decision it can be left open whether the geographic market is defined as EEA-wide or worldwide, as the proposed transaction does not raise any serious doubts as to its compatibility with the internal market under any plausible market definition adopted.

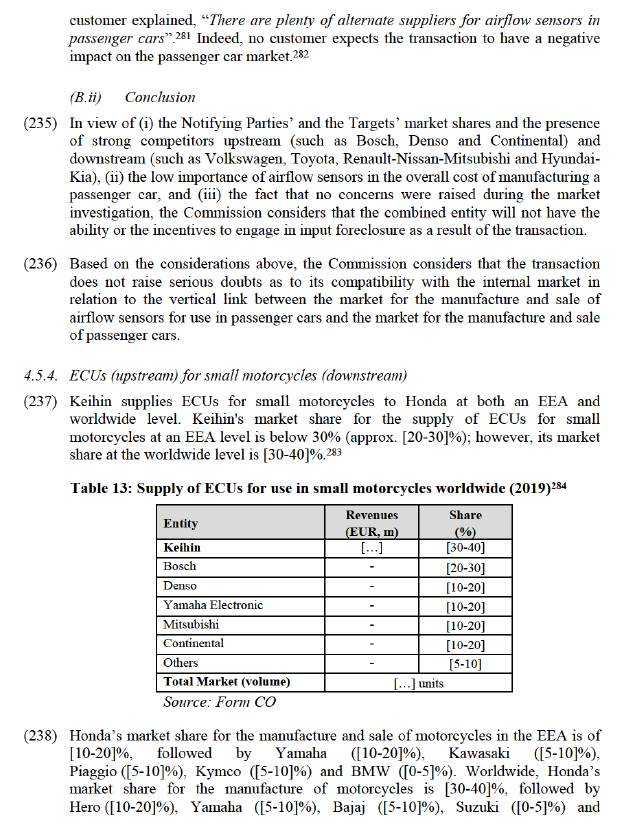

4.3.8. Calipers and brake pads

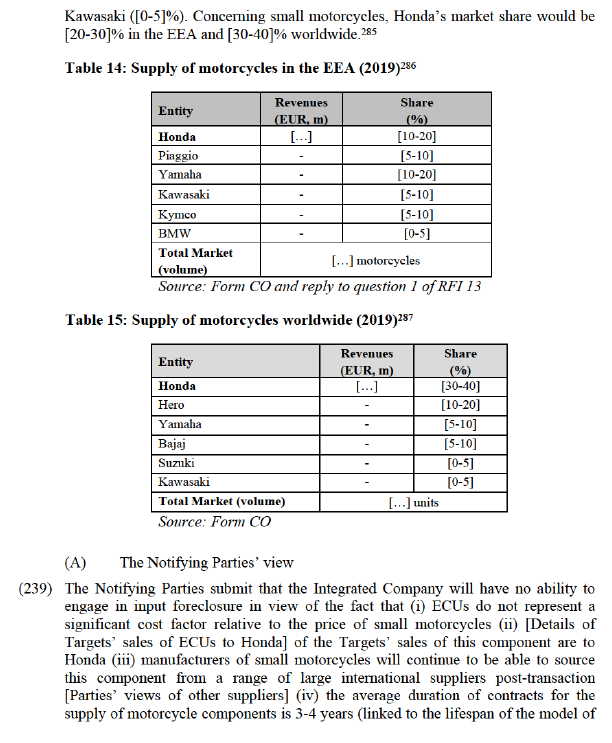

(123) Calipers and brake pads are two of the three component parts of disc brakes (the other being the brake disc/rotor). A disc brake is a brake system that controls the rotation of a wheel by pressing a friction material (brake pad) from both sides of a brake rotor that rotates along with the wheel.153

(124) There are two principal types of calipers: floating calipers and fixed calipers. Floating calipers are those that move relative to the brake disc and have one or two pistons. Fixed calipers do not move relative to the brake disc and have more than two pistons. Each is typically also combined with a different type of brake discs.154

(125) Brake pads are pieces of friction-generating material which are fitted to either side of the caliper. As the operator applies the brakes, the pressure stored by the brake fluid pushes a piston against the caliper. This causes the caliper to squeeze the brake pads against the brake disc, which in turn slows down the spinning wheel by restricting its ability to move freely. When this process happens simultaneously on all wheels of a vehicle, it will slow vehicle down in a controlled manner and will eventually bring the vehicle to a stop.155

4.3.8.1. Product market

(A) The Commission’s decisional practice

(126) Within disc brakes, the Commission distinguished between (a) calipers and, therein, further between (i) floating calipers and (ii) fixed calipers; and (b) the friction materials that form inputs to disc brakes, namely brake pads.156 This resulted from the fact that calipers differ in size, performance, quality and price. Fixed calipers have more than two pistons and are made from aluminium, whereas floating calipers have one or two pistons and are made from cast iron or cast iron/aluminium. Accordingly, the (foundry and machining) equipment used for the production of fixed calipers is different from the equipment of floating calipers. From a demand side, floating calipers and fixed calipers are used with different types of brake discs, for different types of vehicles.157 The Commission has also previously identified different markets for each different component of a braking system, e.g. brake pads.158

(B) The Notifying Parties’ view

(127) The Notifying Parties note that calipers and brake pads are often supplied to OEM customers together as an assembled product. OEM customers usually then attach the brake discs themselves, to create the fully assembled disc brake. Alternatively, calipers and brake pads can each be supplied separately as standalone components. Further, components for calipers can also be supplied separately.159

(128) The Notifying Parties consider that it would be appropriate to define a single market for the supply of floating calipers and brake pads (assembled) for use in both motorcycles and passenger cars, in view of the supply side substitutability between these products.160 Suppliers can switch between manufacturing floating calipers and brake pads (assembled) for use in passenger cars and motorcycles [Parties’ estimate of switching costs].161

(129) As outlined in paragraph (35), the Notifying Parties consider that a sub-segmentation between calipers and brake pads for small and large motorcycles is not justified.

(C) The Commission’s assessment

(130) The Commission considers that for the purposes of the present case, its previous decisional practice can be maintained. The market investigation did not raise further sub segmentations in addition to those the Commission previously identified.

(131) Competitors for this product also confirmed the argument of the Parties that floating calipers and brake pads are usually supplied to OEMs as an assembled product, as a competing producer of this product confirmed: (“[name of competitor] manufacture calipers internally and procure pads from suppliers, pads are then assembled into the calipers. So for us it is common practice to obtain pads separately and assemble them in calipers. […] To our knowledge this is the common practice among motorcycle brake manufacturers.”)162

(132) In the market investigation, a majority of respondents confirmed that there is no demand-side substitutability, neither between calipers for passenger cars and for motorcycles, nor between small and large motorcycles. However, the market investigation confirmed supply-side substitutability as a majority of respondents replied that the same suppliers produce all types of calipers, both for passenger cars and for motorcycles.163

(133) For the purposes of this Decision, the Commission will consider all plausible markets, including market for assembled and non-assembled products:

- floating calipers and brake pads (as an assembled product)

- floating calipers (as a non-assembled product)

- brake pads (as a non-assembled product)

- fixed calipers and brake pads (as an assembled product)

- fixed calipers (as a non-assembled product).

(134) In any event, for the purpose of the present decision, the exact product market definition can ultimately be left open164 as the proposed transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition.

4.3.8.2. Geographic market

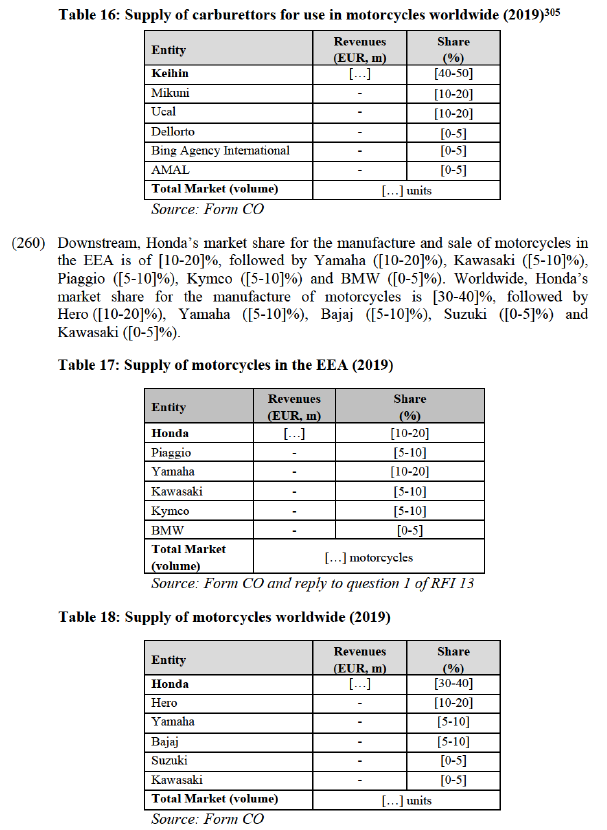

(A) The Commission’s decisional practice

(135) In relation to the supply of components parts for braking systems, the Commission has considered (but ultimately left open) that the geographic market for supply of calipers to the OEM channel customers may be EEA-wide in scope, if not worldwide.165

(B) The Notifying Parties’ view

(136) The Notifying Parties submit that the appropriate geographic market for the supply of components of braking systems, the product category including calipers and brake pads, can be left open between EEA-wide and worldwide, as outlined in paragraph (121).

(C) The Commission’s assessment

(137) In line with its decisional practice and the findings of the market investigation outlined in paragraph (45), for the purposes of this Decision it can be left open whether the geographic market is defined as EEA-wide or worldwide, as the proposed transaction does not raise any serious doubts as to its compatibility with the internal market under any plausible market definition adopted.

4.3.9. Anti-lock braking systems (ABS)

(138) ABS are parts of electronic braking systems which optimise braking pressure across wheels and assist in steering stability while braking.166

4.3.9.1. Product market

(A) The Commission’s decisional practice

(139) In previous decisions, the Commission has defined a market for electronic brake systems but left open whether a segmentation between ABS and Electronic Stability Control (ESC) is necessary.167 This potential segmentation was based on the finding that, as a result of the different technical designs of air pressure brakes and hydraulic brakes, the ABS and the components of the system are also different. The ABS and the components of the system are adapted to the respective mode of braking power generation and transmission and are closely related to the braking system. It is not possible to replace the ABS for hydraulic brakes with that for air pressure brakes.168

(B) The Notifying Parties’ view

(140) The Notifying Parties submit that the market for electronic braking systems is the relevant product market, and that it is not necessary to further segment between ABS and ESC.169 They submit that there is no supply-side substitutability between ABS for motorcycles and ABS for passenger cars.

(141) As outlined in paragraph (35), the Notifying Parties consider that a sub-segmentation between ABS for small and large motorcycles is not justified.

(C) The Commission’s assessment

(142) The Commission considers that the distinction between ABS and ESC can be maintained for the purposes of the present case, as no affected markets arise for ESC as a component used in heavy duty applications, as outlined in paragraph (112).170 As the Parties are only selling ABS for motorcycles, the Commission will analyse this narrower market, while leaving open whether a distinction should be made between ABS for passenger cars and ABS for motorcycles.

(143) In any event, for the purpose of the present decision, the exact product market definition can ultimately be left open171 as the proposed transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition.

4.3.9.2. Geographic market

(A) The Commission’s decisional practice

(144) In Bosch/Allied Signal, the Commission defined the market for ABS as EEA-wide, as it found that most OEMs in the EEA were purchasing ABS from suppliers established in the EEA. For reasons of security of supply and their close cooperation in the development and production of ABS, vehicle manufacturers expect their suppliers to produce in proximity to their factories. In competition for supply contracts, the supplier has a decisive advantage which can make the parts available at the vehicle manufacturers’ manufacturing sites in a timely and demand-driven manner. For this reason, almost all suppliers of vehicle manufacturers in the EEA had set up production facilities in Europe.172

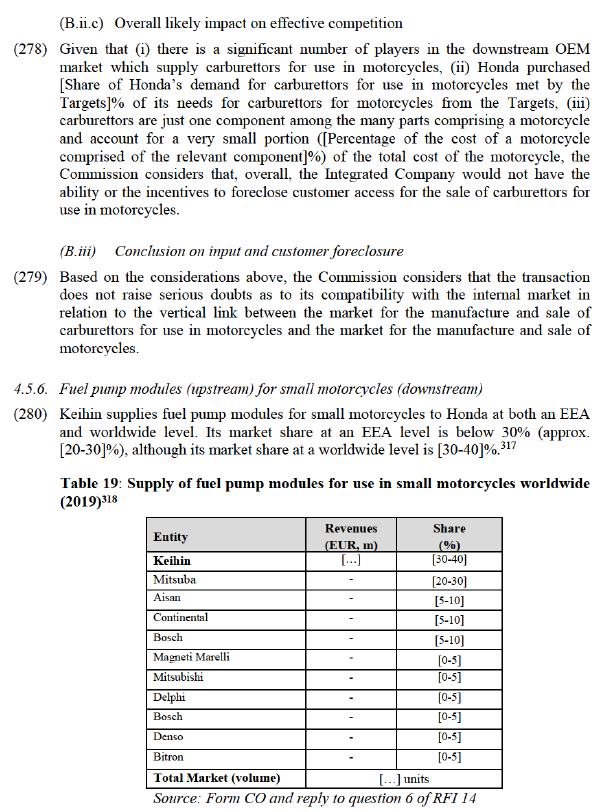

(B) The Notifying Parties’ view

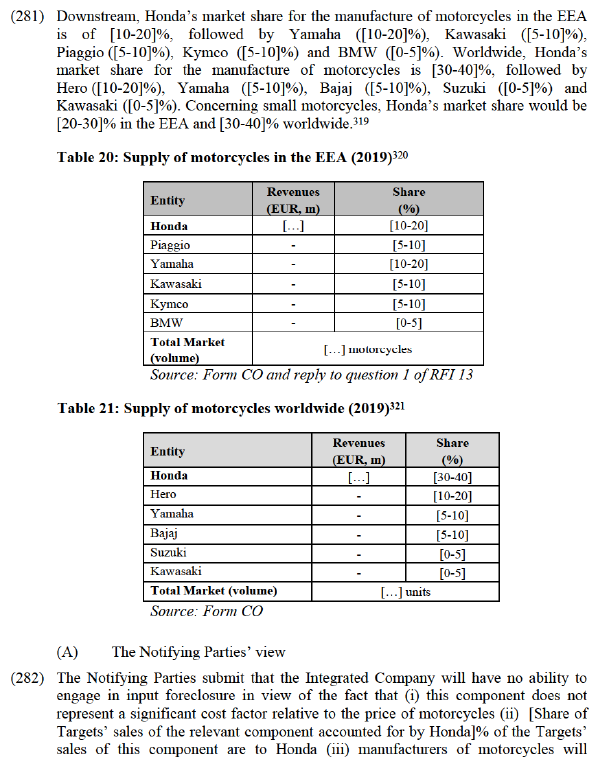

(145) The Notifying Parties submit that the appropriate geographic market for the supply of components of braking systems, the product category including ABS, is worldwide. The Notifying Parties submit that transport costs are low: in many cases, the Notifying Parties estimate that transport costs per unit amount to [Percentage of the price of the component comprised of transport costs]% of the price of the component. In addition, there are no specific trade barriers and these products are traded globally.173

(C) The Commission’s assessment

(146) The Commission notes that since its assessment of the ABS market in Bosch/Allied Signal (in 1996), it is likely that supply chains have become more global, as the results of the market investigation, outlined in paragraph (37), as well as the more recent automotive component cases cited in this Decision show. In any case, for the purposes of this Decision, it can be left open whether the geographic market is defined as EEA-wide or worldwide, as the proposed transaction does not raise any serious doubts as to its compatibility with the internal market under any plausible market definition adopted.

4.3.10. Shock absorbers

(147) Shock absorbers (also known as dampers) form part of a vehicle’s suspension system, and are used to control the impact and rebound movement of a vehicle’s spring and suspension. Typically, dampers are oil, hydraulic liquid or gas-filled piston cylinders which act to curb unnecessary vibrations in the suspension by absorbing force through the resistance that occurs when the oil or hydraulic liquid passes through fine holes that penetrate the piston inside the damper (the force that occurs due to this resistance is called ‘damping force’). As such, dampers absorb the vibrations and impacts transmitted from the road to the wheels, in order to ensure the wheels maintain contact with the road surface, and that the vehicle does not move excessively.174

4.3.10.1. Product market

(A) The Commission’s decisional practice

(148) The Commission has previously looked at the market for all shock absorbers, considering that it constitutes a separate product market. The Commission left open (a) whether a distinction could be drawn between different types of shock absorber, namely: assembled suspension struts, shock absorbers (i.e., dampers) and suspension springs (i.e., coil springs) and (b) whether shock absorbers may form part of larger modules such as corner modules or complete axles.175

(B) The Notifying Parties’ view

(149) The Notifying Parties agree that there is likely a distinction between conventional and electronically-controlled dampers as the latter is typically much more sophisticated and costly.176 However, there is supply side substitutability as it is possible for manufacturers to switch their production without incurring significant costs.177

(150) The Notifying Parties further consider that front forks with conventional damping shock absorbers, front forks with active damping shock absorbers, shock absorbers with conventional damping, rear shock with active damping shock absorbers and steering dampers form part of an overall product market for shock absorbers.178 In addition, with regard to front forks and rear cushions, although common technologies are used, switching production would require a certain amount of time and investment. Nevertheless, in most cases, motorcycle manufacturers purchase front forks and rear cushions as a set from a single supplier, and the competition status is similar in terms of market share and competitors.179

(151) In view of the time and expenses for manufacturers to switch manufacturing lines for shock absorbers for use in passenger cars to those for use in motorcycles (or vice versa), the Parties do not consider that there is supply side substitutability between the supply of shock absorbers to motorcycles and passenger cars.180

(152) As outlined in paragraph (35), the Notifying Parties consider that a sub-segmentation between shock absorbers for small and large motorcycles is not justified.

(C) The Commission’s assessment

(153) The Commission notes that the precedent which analysed shock absorbers related to these components for heavy duty vehicles and that for motorcycles, additional categories appear to be relevant.

(154) In the market investigation, one respondent mentioned the following variations of shock absorbers, as “these products are not substitutable by the customer due to different design and functionality”:181

- Front fork with conventional damping182

- Front fork with active damping183

- Shock absorber with conventional damping184

- Rear shock with active damping185

- Steering damper186

(155) Moreover, a majority of respondents in the market investigation confirmed that there is no demand-side substitutability, neither between shock absorbers for passenger cars and for motorcycles, nor between small and large motorcycles.187

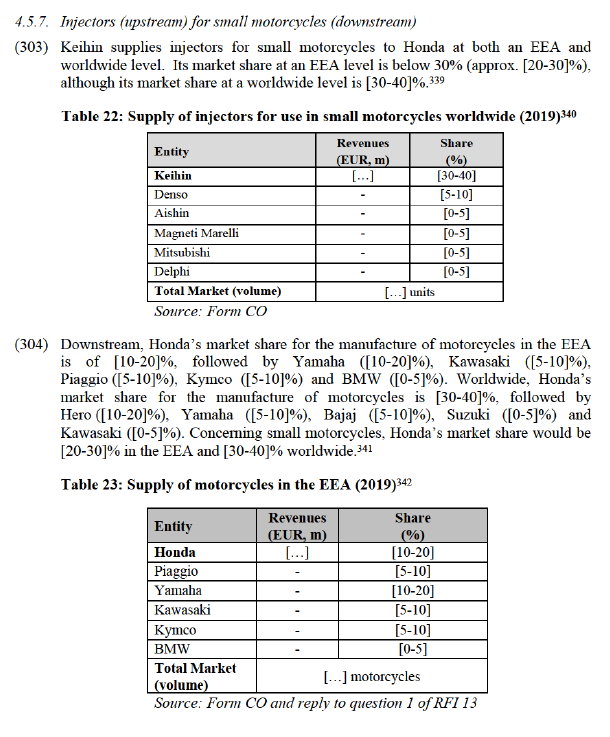

(156) However, the market investigation, contrary to the statement of the Parties, pointed to supply-side substitutability as a majority of respondents replied that the same suppliers produce all types of shock absorbers, both for passenger cars and for motorcycles.188 Competitors explained that “With respect to some types of shock absorbers, the technology used in passenger car and motorcycle applications may be similar, but the products will not be the same in terms of price, performance characteristics or intended use” and “Technical and functional characteristics of Shock Absorbers are the same, but the structure is different and not interchangeable.”189

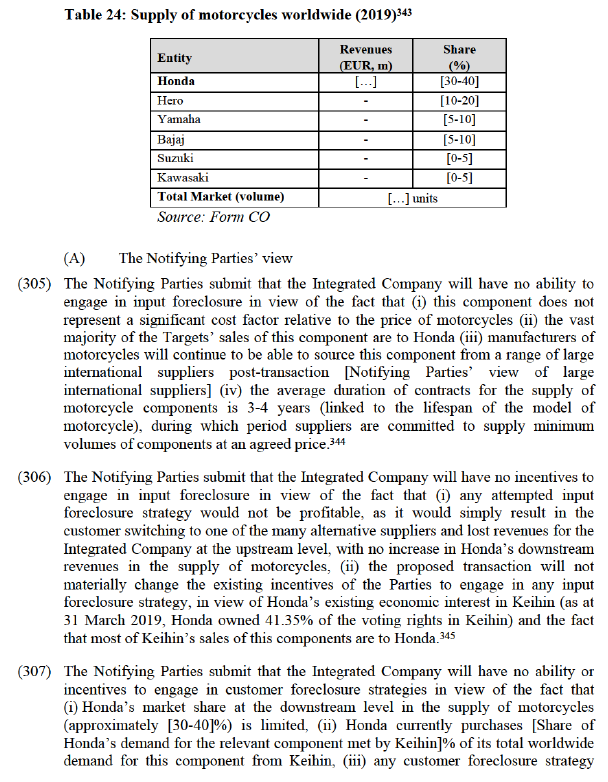

(157) In any event, for the purpose of the present decision, the exact product market definition can ultimately be left open190 as the proposed transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition.

4.3.10.2. Geographic market

(A) The Commission’s decisional practice

(158) In relation to the supply of shock absorbers, the Commission has considered (but ultimately left open) that the geographic market for supply of these products may be EEA-wide in scope, if not worldwide.191

(B) The Notifying Parties’ view

(159) The Notifying Parties submit that the appropriate geographic market for shock absorbers is worldwide: transport costs are low, there are no specific trade barriers and these products are traded globally. For example, Showa does not manufacture component parts for anti-vibration systems in the EEA and all its sales are achieved through imports. HIAMS manufactures shock absorbers within the EEA for sale in the EEA.192

(C) The Commission’s assessment

(160) In line with its decisional practice and the findings of the market investigation outlined in paragraph (45), for the purposes of this Decision it can be left open whether the geographic market is defined as EEA-wide or worldwide, as the proposed transaction does not raise any serious doubts as to its compatibility with the internal market under any plausible market definition adopted.

4.3.11. Other motorcycle components

(161) The Transaction also gives rise to vertically affected markets in relation to the following motorcycle components (not used in passenger cars). Nevertheless, in those motorcycle component markets, the Parties’ combined market share remains below 20%193 and no competition concerns arise in any of these product markets, as also confirmed by the market investigation.

(162) A handle lever bracket is an aluminium clamp for securing the handlebars of a motorcycle to the body.194

(163) A panel brake is a drum brake for motorcycles (i.e. a brake system in which a friction material is pressed from inside the drum to generate braking force).195A CBS is a system combining the front and rear brakes of a motorcycle whereby the rider's braking action of depressing one of the levers is applied to both the front and rear brakes.196

(164) A speed meter gear is attached to the wheel accelerator of a motorcycle to measure speed by detecting the rotation speed of the wheel.197

(165) Drivetrain systems are power transmission devices. They play a role in transferring to the rear wheel the rotational force generated by the engine and the acceleration and deceleration adjustments in revolutions per minute (RPM). Motorcycles use either a chain, a belt or a shaft drive to transmit power from the engine to the wheels. The driving force generated by an engine is transmitted through the side gear (bevel gear), the drive shaft and the final gear (bevel gear). These gears play an important role with regard to changes in the rotational force generated by the engine and the acceleration and deceleration adjustments in RPM. The side gear assembly turns the force of the output shaft of the engine by 90°, and transmits the power to the final gear assembly through a drive shaft. The final gear assembly transfers the power of the engine into the rotation of the rear wheel. 198

4.3.11.1. Product market

(A) The Commission’s decisional practice

(166) The Commission has not previously analysed any of the motorcycle components identified above. However, the Commission has in past cases identified different markets for each different automotive component. 199

(B) The Notifying Parties’ view

(167) The Parties submit that none of the markets mentioned above (handle lever brackets, panel brakes, CBS, speed meter gears and drivetrain systems (shaft drive)) should be further sub-segmented.200

(C) The Commission’s assessment

(168) The Commission considers that based on its practice to distinguish between each distinct automotive component, the relevant product markets for the purpose of the present decision are the markets for the supply of handle lever brackets, panel brakes, speed meter gears, CBS, and shaft drive drivetrain systems. The market investigation did not raise concerns or potential sub-segmentations for these markets.

(169) In any event, the precise product market definition for these components can be left open201, as the proposed transaction does not raise serious doubts as to its compatibility with the internal market for any of these products.

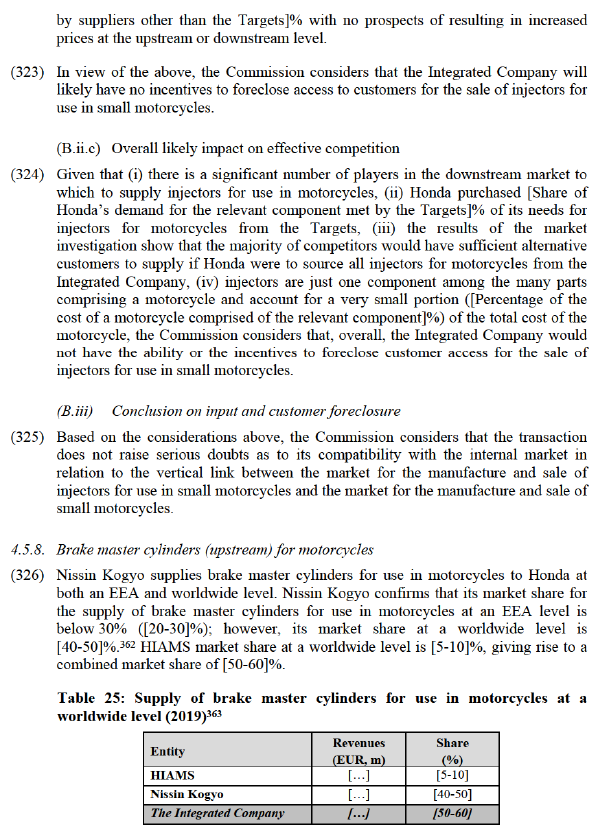

4.3.11.2. Geographic market

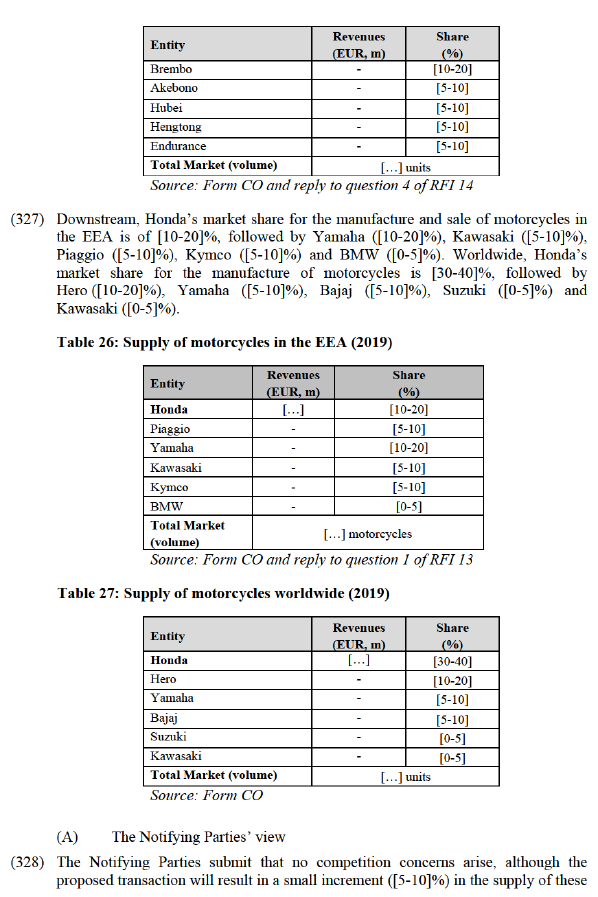

(A)The Commission’s decisional practice

(170) The Commission has not previously analysed the market for the supply of any motorcycle components. In recent cases in which the Commission analysed the markets for supply of automotive components parts, the Commission considered (but left open) that the geographic market may be EEA-wide in scope, if not worldwide.202

(B) The Notifying Parties’ view

(171) The Notifying Parties submit that the appropriate geographic market for the supply of automotive and motorcycle components is worldwide. Transport costs are low: in many cases, the Notifying Parties estimate that transport costs per unit amount to [Percentage of the price of the component comprised of transport costs]% of the price of the component. In addition, there are no specific trade barriers and these products are traded globally.203

(C) The Commission’s assessment

(172) In line with its decisional practice and the findings of the market investigation outlined in paragraph (37), for the purposes of this Decision the Commission considers that the geographic market for these products can be left open between EEA-wide and worldwide.

4.3.12. Passenger cars

4.3.12.1. Product market

(A) The Commission’s decisional practice

(173) In previous cases where the Commission assessed automotive markets, it left open whether the product market includes all passenger cars or should be segmented by type of passenger car (into (i) mini cars, (ii) small cars, (iii) medium cars (iv) large cars, (v) executive cars, (vi) luxury cars (vii) sport cars, (viii) sport utility vehicles ("SUVs") and (ix) multipurpose vehicles).204 The Commission has previously considered the further sub-segmentation of the SUV segment into (i) small, (ii) medium and (iii) large SUVs but left this question open.205

(174) In Peugeot/Opel, the Commission investigated whether electric cars constitute a separate product market and whether this possible market should be further segmented according to (i) technology (electric battery cars and hybrid cars) or (ii) the categories defined for vehicles with combustion engines.206

(B) The Notifying Parties’ view

(175) The Notifying Parties agree that the relevant downstream market should be the market for passenger cars, but submit that it is not necessary to conclude on market definition, as market shares in any potential upstream and downstream markets are not indicative of foreclosure concerns.207

(C) The Commission’s assessment

(176) Therefore, the Commission will retain the product market definition provided in its past decisional practice as described in paragraph (173).

4.3.12.2. Geographic market

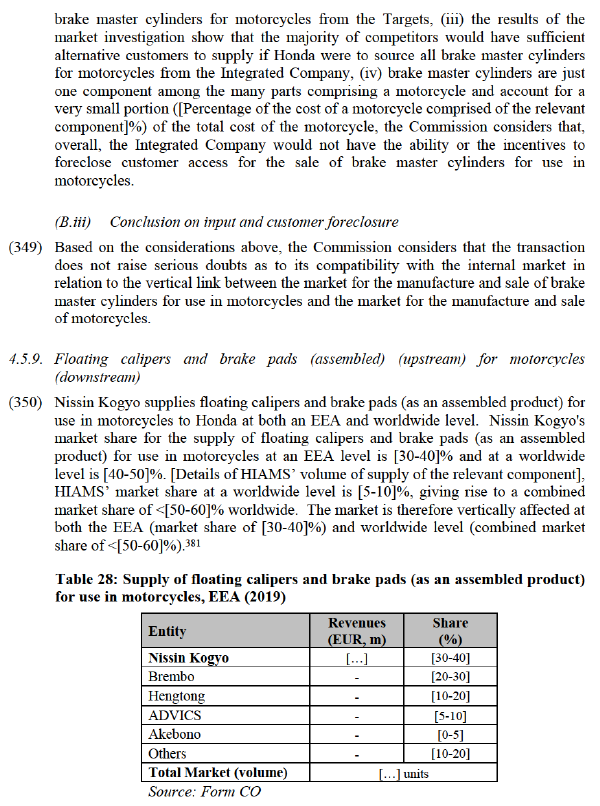

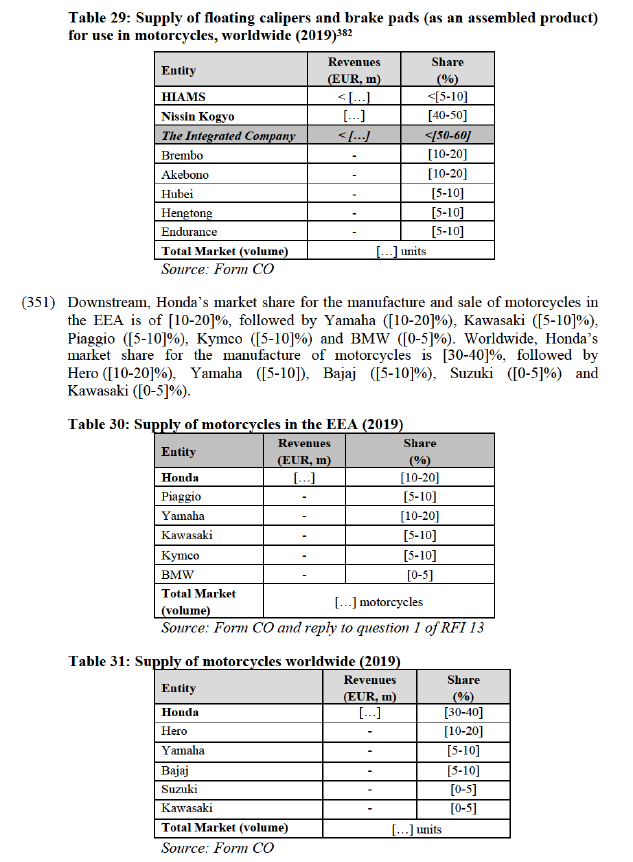

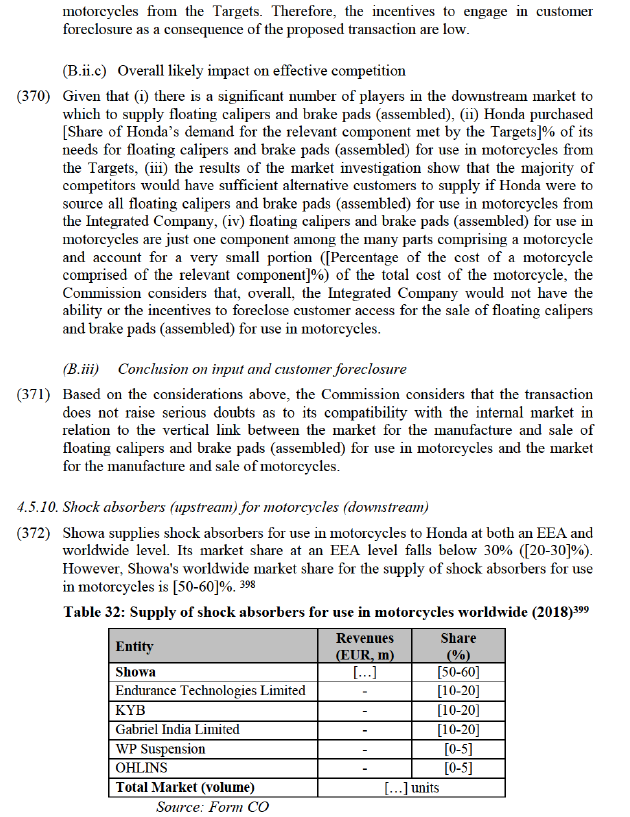

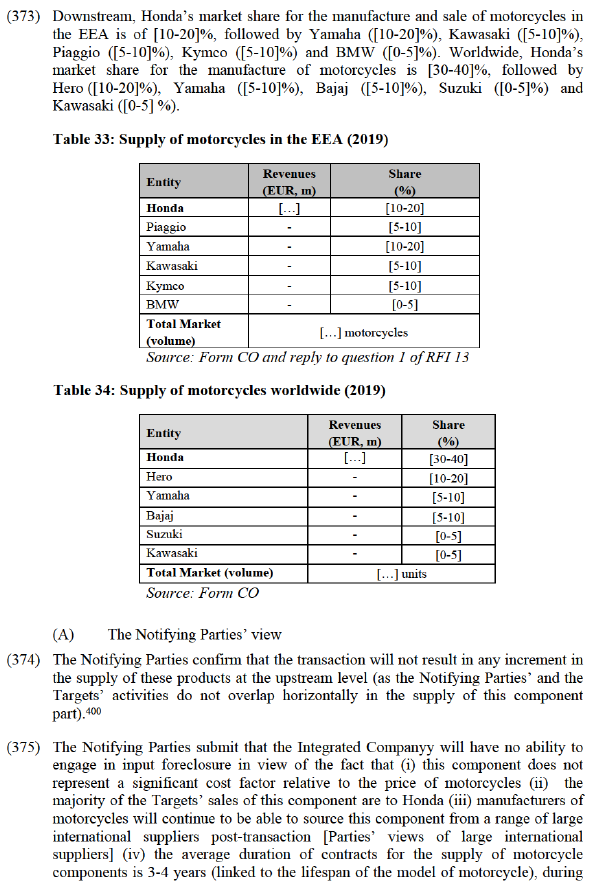

(A) The Commission’s decisional practice