Commission, April 3, 2020, No M.9546

EUROPEAN COMMISSION

Decision

GATEGROUP / LSG EUROPEAN BUSINESS

Subject: Case M.9546 – GATEGROUP / LSG EUROPEAN BUSINESS

Commission decision pursuant to Article 6(1)(b) in conjunction with Article 6(2) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 14 February 2020, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Gategroup Holding AG (“Gategroup”) intends to acquire within the meaning of Article 3(1)(b) of the Merger Regulation sole control over parts of the European business of LSG Lufthansa Services Holding AG (“LSG”) by way of a purchase of shares and selected assets (the “Transaction”). The target of the Transaction, the European business of LSG, is referred to as “LSG EU”.

(2) Gategroup is referred to as the “Notifying Party”. Gategroup (and its controlling parents) and LSG EU are collectively referred to as the “Parties”.

1. THE PARTIES

1.1. Gategroup

(3) Gategroup is headquartered in Switzerland and provides airline catering, retail on- board, equipment services and hospitality products and services to its customers globally.

(4) In the EEA, Gategroup is mainly active in aviation-related services. Through its brands Gate Gourmet and Servair, Gategroup provides in-flight catering services, which accounted for […] % of its turnover in the EEA in 2018.3 Gategroup also provides inter alia (i) on-board services through its brands Gateretail and Dutyfly, (ii) packaged food solutions, (iii) equipment services (including the manufacturing) to airlines and foodservice providers through its subsidiary deSter and (iv) lounge management services in Paris Charles de Gaulle, Frankfurt airport and London Heathrow. These activities respectively accounted for […]% of its EEA turnover in 2018.4

(5) Gategroup is ultimately jointly controlled by Temasek Holdings Limited (Singapore) and RRJ Capital (Hong Kong).5 Temasek is an investment company that owns a majority shareholding in Singapore Airlines, which operates passenger flights to/from certain European airports, in particular in France, Germany, Italy and the Netherlands.6

1.2. LSG EU

(6) LSG is headquartered in Germany and is a wholly-owned subsidiary of Deutsche Lufthansa AG (“DLH”). DLH is the holding company of Lufthansa Group, an aviation group which notably operates Lufthansa, Austrian, Swiss, Eurowings and Brussels Airlines.

(7) LSG EU comprises the European airline and train catering business of LSG, the global lounge business of LSG, the European frozen food production of LSG (operated through the brand Evertaste), the equipment business of LSG (through the brand Spiriant) and airport retail services in Germany (through the retail store chain Ringeltaube).7 However, they do not include LSG’s airline catering business at UK airports,8 nor its retail on-board business (provided under the brand Retail-in- Motion).

(8) In-flight catering services represents the largest part of LSG EU’s revenues.9 In 2018, the Lufthansa Group was the main client of LSG EU, representing approximately EUR […] of revenues.10

2. THE CONCENTRATION

(9) On 7 December 2019, the Parties entered into a share and asset purchase agreement (the “SPA”), pursuant to which Gategroup agreed to acquire all of the shares of the entities composing LSG EU.

(10) In addition, pursuant to the SPA,11 Gategroup and DLH will establish a joint venture with respect to the in-flight catering operations at Lufthansa Airline’s hub airports Frankfurt and Munich. Gategroup and DLH will respectively hold […]% and […]% of the share capital. According to the term sheet for the proposed shareholders’ agreement (the “Term Sheet”),12 Gategroup will have sole control over the joint- venture company (the “JVC”). More specifically, [description of the governance structure in relation to the adoption of strategic decisions].

(11) In light of the above, the Transaction consists in the acquisition of sole control by Gategroup over LSG EU within the meaning of Article 3(1)(b) of the Merger Regulation.

(12) As an inherent part of the proposed Transaction, the Parties have agreed to enter into a long-term framework agreement for catering services, through which DLH will appoint Gategroup as its catering supplier for Lufthansa Airline’s hubs Munich and Frankfurt and outlying airports in Germany (the Framework Agreement for Catering Services or “LHCC”)13 for a duration of […] years.14

(13) DLH Group and LSG EU have also entered into a long-term strategic partnership on [date] under which DLH Group will [details on supply sources] source inter alia [details on supply sources].15

3. EU DIMENSION

(14) The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 5 000 million16 in 2018 [Gategroup: […], LSG EU: […]]. The EU-wide turnover of each of the undertakings concerned is more than EUR 250 million [Gategroup: […], LSG EU: […]]. The Parties do not achieve more than two-thirds of their aggregate EU-wide turnover within the same Member State.17 The notified operation therefore has an EU dimension pursuant to Article 1(2) of the Merger Regulation.

4. RELEVANT MARKETS

4.1. In-flight catering services

4.1.1. Product market definition

(15) In-flight catering services comprise the provision and delivery of food and beverage solutions to airlines, which will be served to passengers on an aircraft during the flight.

4.1.1.1. Past decisional practice

(16) In previous decisions, the Commission concluded that there exists a separate market for in-flight catering services,18 which comprise the provision of the entire range of meals for all travel classes (economy/business/first class) for all types of flights (short haul/long haul).19

(17) The Commission also decided in its previous practice20 to leave open the question whether a distinction should be made between the provision of in-flight catering services by type of suppliers, namely between the so-called “traditional” and “non- traditional” suppliers.21

4.1.1.2. The Notifying Party’s view

(18) The Notifying Party agrees with the Commission’s decisional practice that the product market includes all in-flight catering services for all types of flights (short-haul/long-haul) and that a segmentation between flight classes (i.e., economy/business/first class) is not warranted.22

(19) In addition, the Notifying Party considers that the market for in-flight catering services should not be segmented by type of supplier.23

4.1.1.3. Commission’s assessment

(20) Although the majority of competitors and customers indicated that customers have different requirements for in-flight catering depending on the type of flight,24 the majority of customers indicated that they do not purchase in-flight catering services for short/medium haul flight separately from in-flight catering services for long haul flights.25 The majority of in-flight catering providers consider that in-flight caterers can generally provide services on both short/medium haul and long haul flights. In that respect, a competitor explained, “in the production process there is no big difference between service short/mid haul and long haul. The only difference is the hot kitchen which becomes necessary for a long haul carrier flying with first class”.26

(21) The Commission notes that airline requirements with respect to in-flight catering services may differ depending on the type of flight. The Commission further observes that the provision of in-flight catering services on long haul flights may require additional infrastructure investments in comparison to the supply of such services on short/medium haul flights. However, in view of the results of the market investigation and in line with its past decisional practice, the Commission considers that a segmentation of in-flight catering services by type of flights (short/medium haul vs long haul) is not warranted.

(22) With respect to the possible segmentation of in-flight catering services by type of travel class, the majority of customers having replied to the market investigation indicated that their requirements for in-flight catering differ depending on the travel class (economy/business/first class).27 However, all airlines having responded to the market investigation purchase catering services for the different travel classes from one single supplier.28 In that respect, an airline explained, “All classes have a different product proposition with regards to equipment, menu and spend. However, a single supplier is able to meet our requirements for all travel classes (providing it has hot and cold kitchens)”.29 Some airlines indicated that sourcing from one single supplier is “the most efficient and cost saving” way, in particular because it allows to “avoid multiple visits to aircraft and potential departure delays”.30 The majority of competitors also indicated that while requirements differ between travel classes, this does not prevent customers from usually contracting with one single supplier.31

(23) In view of the results of the market investigation and in line with its past decisional practice, the Commission considers that a segmentation of in-flight catering services by travel class (economy/business/first class) is not warranted.

(24) With regard to a possible segmentation of in-flight catering services by type of supplier, the market investigation yielded mixed results among competitors as well as customers.32 The market investigation indicates that the substitutability of traditional and non-traditional suppliers would depend on the requirements of airlines.33 A customer considers that “non-traditional caterers are able to provide many of the services offered by traditional caterers. However where the catering includes hot food, often logistics firms will partner with traditional caterers so that they can provide a seamless end-to-end service”.34 Some customers and competitors explained that non-traditional suppliers would not be a viable alternative for certain travel classes (business/first class) or for long haul flights, because “long haul business and first class are typically more complex and therefore that market is dominated by traditional catering service providers.”35 By contrast, the distinction between traditional and non-traditional suppliers would not be warranted when the airline service proposition consists in frozen meals and snacks.36

(25) For the purpose of this decision, it is not necessary to conclude whether the market for in-flight catering services should be segmented by type of supplier, because the competitive assessment would remain unchanged since no non-traditional suppliers are currently active at the airports where the Parties’ activities overlap and where the Transaction creates vertical links.37

(26) In view of the above considerations and in line with its decisional practice, the Commission concludes that the market for the provision of in-flight catering services comprises the entire range of meals for all travel classes (economy/business/first class) and for all types of flights (short-haul/long-haul). Furthermore, in view of the above considerations and in line with its decisional practice, the Commission considers that, for the purpose of this decision, the question whether in-flight catering services should be segmented by type of supplier (“traditional” and “non- traditional” suppliers) can be left open, as this would not change the outcome of the competitive assessment.38

4.1.2. Geographic market definition

4.1.2.1. Past decisional practice

(27) The Commission has considered in previous decisions that the geographic market for in-flight catering services is the relevant airport39 or at most an area comprising several airports located in close proximity to each other.40

4.1.2.2. The Notifying Party’s view

(28) The Notifying Party considers that that the relevant geographic area to assess competition for in-flight catering services may be either the airport level or an area comprising several airports.41 In that regard, with respect Germany, the Notifying Party considers a catchment area of up to 450 km around a given airport or a travel time of up to 10 hours (in a chilled truck) could be considered as the relevant geographic market for the provision of in-flight catering services.42 Therefore, the Notifying Party submits that the following geographic markets would comprise several airports: (i) Frankfurt, Dusseldorf and Cologne-Bonn airports; (ii) Hamburg and Hannover airports; (iii) Berlin Tegel, Berlin Schönefeld and Leipzig airports.43

4.1.2.3. Commission’s assessment

(29) The majority of customers indicated that they generally source in-flight catering services on an airport-by-airport basis.44 The majority of customers and competitors consider it important that the supplier of in-flight catering services has production facilities in the catchment area of the relevant airport.45 An airline indicated that “the supplier’s proximity to the airport is extremely important to [name of the customer] for flexibility, food safety, operational complexity, and service”.46 Another customer explained, “Aircraft turnaround and loading time is limited. Caterer needs to have facilities and proximity [sic] to the airport apron area in order to be able to cater aircraft within time limits”.47 Furthermore, the majority of airlines have negotiated the possibility to place last-minute orders up to 60 minutes before the flight departure.48 Consequently, the majority of airlines having expressed a view indicated that they would accept a transport time of up to one hour between the airport and the facility of the caterer.49

(30) On the other hand, the majority of airlines that responded to the market investigation indicated that they do purchase in-flight catering services from caterers with a remote facility located outside of the airport catchment area or at a neighbouring airport. In addition, the majority of competitors supply or would supply in-flight catering from a remote facility.50 However, some customers explained that they prefer to have a supplier with a facility within the catchment area of the relevant airport but they might be forced to accept remote catering because of the absence of alternative, for example, when the supplier closes its production facility.51 Some competitors consider that catering from a remote facility is possible, but this would be a “Far from optimal set-up but possible with some constraints” and “it gives you a bit more stress where there are traffic jams or something is wrong”. 52

(31) Considering that that the outcome of the competitive assessment would remain unchanged under any of the plausible geographic market definitions,53 the Commission considers that it is not necessary to decide whether the geographic scope of in-flight catering services is a given airport or a geographic area encompassing several neighbouring airports.54

(32) In view of the above considerations and in line with its previous decisional practice,55 the Commission considers that, for the purpose of this decision, the geographic market for the provision of in-flight catering services is either the airport’s catchment area or at most a geographic area encompassing several neighbouring airports, namely (i) Frankfurt, Dusseldorf and Cologne-Bonn airports, (ii) Hamburg and Hannover airports, (iii) Berlin Tegel, Berlin Schönefeld and Leipzig airports, where the Notifying Party argues that the geographic market is broader than the airport’s catchment area. Therefore, the Commission will assess the effects of the Transaction on the narrowest plausible geographic market definition (i.e. the airport’s immediate catchment area) and on the plausible broader geographic areas where the Notifying Party claims that the geographic market definition is broader than the airport’s catchment area.

4.1.3. Conclusion

(33) In view of the above considerations and in line with its past decisional practice, the Commission concludes for the purpose of this decision that the relevant product market for in-flight catering services comprises the entire range of meals for all travel classes (economy/business/first class) for all types of flights (short-haul/long-haul) and that the question whether the market for in-flight catering services should be segmented by type of supplier can be left open. For the purpose of this decision, the Commission leaves open the question whether the relevant geographic market is limited to the airport’s catchment area or encompasses several neighbouring airports with respect to the following geographic areas that may comprise several airports (i) Frankfurt, Dusseldorf and Cologne-Bonn airports, (ii) Hamburg and Hannover airports, (iii) Berlin Tegel, Berlin Schönefeld and Leipzig airports, as this would not change the outcome of the competitive assessment.

4.2. In-flight equipment services

(34) In-flight equipment services comprise the provision of custom-made concepts of a range of serving products used on aircraft (such as cutlery, cardboard containers, tray settings, tray dressings, bespoke beverage solutions, casseroles, tableware) and on- board comfort articles (such as sleepwear, amenities and textiles). In-flight equipment providers have different business models, some focusing more on service aspects (design, consulting, management etc.) without having their own production facilities, while others design and manufacture the items in-house.56

4.2.1. Product market definition

4.2.1.1. Past decisional practice

(35) In some previous decisions, the Commission suggested that the provision of in-flight equipment services was ancillary to an overall market for in-flight catering services and has not distinguished further between these product markets.57 In the case EQT/Smurfit Munksjö, the Commission has nevertheless considered a separate market for the provision of custom-made concepts of serving products and comfort items for airline passengers consisting in the “provision of various concepts of serving products and comfort items for airline passengers, such as plastic serving trays, plastic glasses, pillows, blankets, tablecloths, porcelain cups”.58

4.2.1.2. The Notifying Party’s view

(36) The Notifying Party considers that there is no separate market for the provision of in-flight equipment services, but that it should rather be considered as ancillary to the provision of in-flight catering services.59 The Notifying Party argues that in- flight equipment products are often “nominated” and supplied by airlines as part of the in-flight catering service agreement.60 Moreover, the Notifying Party claims that in-flight catering equipment is always purchased with a direct link to the in-flight catering business.61 In addition, the Notifying Party reasons that most in-flight caterers have in-flight equipment activities ancillary to their core business.62

(37) The Notifying Party further submits that should equipment services nonetheless be considered a separate market by the Commission, the relevant product market would encompass all equipment services for the travel/foodservice industries and not just for the in-flight catering industry. According to the Notifying Party, all providers of in-flight equipment services (including the Parties) also supply equipment services to non-aviation customers, as there is little differentiation between equipment products for airlines and non-aviation customers. Moreover, the Notifying Party submits that competitors generally supply the full range of equipment and from a customer’s perspective, there is no need to source from specialised suppliers.63

4.2.1.3. Commission’s assessment

(38) First, the Commission notes that airlines generally purchase in-flight equipment services separately from in-flight catering services. In that respect, the Notifying Party itself submits that in-flight equipment services are generally not tendered by airlines together with in-flight catering services “but generally tendered separately and independent of in-flight catering services contracts”. The airlines tend to purchase in-flight equipment services centrally64 and then make the in-flight equipment products available to the in-flight caterer that “will be in charge of handling the equipment” and bring it on-board.65 The Notifying Party’s submission was confirmed by the majority of customers during the market investigation. The majority of airline customers purchase the in-flight equipment services themselves and subsequently make the equipment products available to their in-flight caterer.66 The majority of airline-customers that purchase other services than in-flight catering (such as in-flight equipment services) do not typically purchase in-flight catering services and other services together from one single supplier. Often, even different components of equipment services are tendered individually.67 The majority of customers also indicated that they have no problem with purchasing in-flight catering services separately from other services such as in-flight equipment services, citing flexibility, greater choice, better prices as well as quality of products offered as the main reason for sourcing these other services separately from in-flight catering.68

(39) Second, contrary to the Notifying Party’s claim,69 the majority of in-flight caterers do not provide in-flight equipment services as ancillary services to their core business, or only to a very limited extent.70 None of the Parties’ in-flight catering services competitors are among their main competitors with regards to the provision of in-flight equipment services.71

(40) In view of the above considerations, for the purpose of this decision, the Commission considers that equipment services are not ancillary to in-flight catering services and constitute a relevant separate market. The question whether equipment services should be segmented by type of customers can be left open, as the Transaction is unlikely to raise competition concerns with respect to the market for equipment services, even on a plausible narrower market for in-flight equipment services.

4.2.2. Geographic market definition

4.2.2.1. Past decisional practice

(41) The Commission has not previously defined the exact geographic scope of in-flight equipment services. In the case EQT/Smurfit Munksjö, the Commission had considered the market for custom-made concepts of serving products and comfort items for airlines passengers to be either EEA or worldwide in scope, but ultimately left the question open in this case.72

4.2.2.2. The Notifying Party’s view

(42) The Notifying Party submits that the geographic market for equipment services and the narrower market for in-flight equipment services would be worldwide in scope, as the main providers of equipment services and in-flight equipment services are active globally and there are no barriers to cross-border supply of equipment, as airlines tend to procure equipment centrally and comprehensively and even regional customisations73 can be provided by suppliers located in other regions.74

4.2.2.3. Commission’s assessment

(43) The Commission considers the geographic scope for a market for in-flight equipment services to be either EEA- or worldwide for the following reasons: the main providers of in-flight equipment services are active globally and airlines tend to procure equipment centrally and comprehensively.75

(44) For the purpose of this Decision, the Commission considers that the geographic market definition can be left open as the Transaction would not raise serious doubts as to its compatibility with the internal market under any plausible geographic market definition, including the narrowest plausible geographic market definition, which is EEA-wide.

4.2.3. Conclusion

(45) In light of the above and the results of the market investigation, the Commission finds the market for the provision of equipment services to be separate from the market from in-flight catering services. The question whether in-flight equipment services constitute a separate market can be left open, as the Transaction is unlikely to raise serious doubts as to its compatibility with the internal market under any plausible market definition. For the purpose of this decision, the Commission will assess the effects of the Transaction on a plausible narrower product market for in- flight equipment services. The Commission will also leave open the question whether the geographic market is EEA-wide or worldwide and will assess the effects of the Transaction under each of the two plausible geographic market definitions.

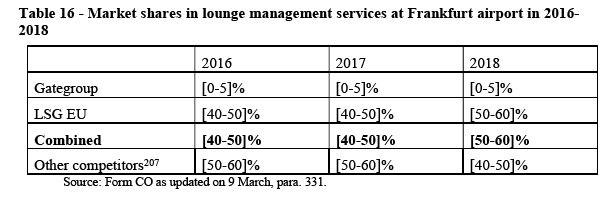

4.3. Lounge management services

(46) Lounge services comprise the provision of a rest area in an airport, typically accompanied by additional food, beverage, rest and shower facilities. Lounges may be provided by airports, airlines and third-party service providers, and entry is typically based on payment of a fee, purchase of a business or first class airline ticket or inclusion in a travel membership programme.76 Consequently, lounge management services are provided to an airport or to an airline or airline alliance.

4.3.1. Product market definition

(47) While the Commission concluded in previous decisions that the provision of lounge services is part of an overall market for ground handling services, the Commission suggested in its two latest decisions that lounge services constitute a separate product market.77

(48) The Notifying Party considers that lounge services are part of an overall market for ground handling services.78

(49) A horizontally affected market arises only under the narrowest plausible market definition comprising a separate market for lounge services at a certain airport.79

(50) For the purpose of the Decision, the question of whether the relevant product market comprises only lounge management services or whether lounge management services are part of an overall market for ground handling services can be left open, as the Transaction would not raise serious doubts as to its compatibility with the internal market under the narrowest plausible market definition.

4.3.2. Geographic market definition

(51) The Commission has not previously considered the geographic scope of a separate market for lounge management services.

(52) For the overall market for ground handling services, the Commission considered that this market is local and does not extend beyond a single airport or possibly two or more neighbouring airports.80 The Notifying Party agrees with the Commission’s geographic market definition.81

(53) For the purpose of this Decision, the Commission considers that the geographic market definition can be left open as the Transaction would not raise serious doubts as to its compatibility with the internal market under the narrowest plausible geographic market definition (i.e. the catchment area of a single airport).

4.3.3. Conclusion

(54) In view of the above considerations, the Commission leaves the question open whether there is a separate market for lounge management services or whether lounge management services belong to the market for ground handling services, as the Transaction is unlikely to raise serious doubts as to its compatibility with the internal market, under the narrowest plausible product and geographic market definition of lounge management services.

4.4. Ready-made food products

(55) Ready-made food products to the commercial foodservice sector comprise ready- made food products (such as fresh pre-packed sandwiches, snacks, frozen meals, etc.) that are supplied, among others, to airlines. In the in-flight catering sector, the supply of ready-made food products is sometimes referred to as the supply of “convenience products”.82

4.4.1. Product market definition

(56) In previous decisions, the Commission found a separate market for ready-made food products. It has further considered a possible sub-division of this market by customers into the retail sector (supermarkets, open markets and speciality stores) and the commercial foodservice sector, the latter of which could further be subdivided between commercial (restaurants, snack-bars, hotels, fast-food chains, leisure sector) and social (public institutions such as canteens, schools and hospitals) segments.83 The question whether within the retail sector and both the commercial and social segments of the food service sector, the markets for ready-made foods can be further subdivided into frozen foods, chilled foods and fresh foods was left open.84

(57) The Notifying Party does not disagree with the Commission’s decisional practice.85

(58) In line with its past decisional practice, the Commission considers that, for the purpose of this decision, the relevant market is the supply of ready-made food products to the commercial foodservice sector. The question whether the market for ready-made food products to the commercial foodservice sector should be further subdivided by type of products (frozen foods, chilled foods and fresh foods) can be left open, as the Transaction would not raise serious doubts as to its compatibility with the internal market under any such plausible market definition.86

4.4.2. Geographic market definition

(59) In previous decisions, the Commission has left open whether the geographic market definition of ready-made food products was national or EEA-wide.87

(60) The Notifying Party considers that the geographic scope of the market for ready- made food products is likely EEA-wide.88

(61) Considering that the Transaction is unlikely to raise serious doubts as to its compatibility with the internal market under either geographic market definition, the Commission considers that the question whether the market for ready-made food products to the commercial foodservice sector is national or EEA-wide can be left open for the purpose of this decision.89

4.4.3. Conclusion

(62) In view of the above considerations and in line with its past decisional practice, the Commission concludes that, for the purpose of this decision, the relevant market will be considered as the market for ready-made food products to the commercial foodservice sector. It can be left open whether the market should be further subdivided by type of products (frozen foods, chilled foods and fresh foods) as well as whether the geographical scope is national or EEA-wide, as the Transaction would not raise serious doubts as to its compatibility with the internal market under any plausible market definition.

4.5. Retail on-board services

(63) Retail on-board services comprise the provision of shopping services during the flight, such as snacks and duty-free goods.

4.5.1. Product market definition

(64) In previous decisions, the Commission left open the question whether the market for retail on-board services should be segmented by type of product, namely snacking products and duty-free products.90

(65) The Notifying Party agrees with the previous decisional practice of the Commission and considers that the exact product market definition can be left open.91

(66) In line with the Commission’s past decisional practice, the Commission considers that, for the purpose of this decision, the question whether the market for retail on-board services should be segmented by type of product (i.e. between snacking and duty-free products) can be left open, as the Transaction would not raise serious doubts as to its compatibility with the internal market under any plausible market definition mentioned above.92

4.5.2. Geographic market definition

(67) In previous decisions, the Commission concluded that the market for retail on-board services was at least EEA-wide and left open whether the relevant geographic market was global.93

(68) The Notifying Party agrees with the previous decisional practice of the Commission and considers that the geographic scope of retail on-board services is at least EEA- wide.94

(69) Considering that the Transaction is unlikely to raise serious doubts as to its compatibility with the internal market under any of the plausible geographic market definitions above and in line with its past decisional practice, the Commission considers that the question whether the market for retail on-board services is EEA- wide or worldwide can be left open for the purpose of this decision.95

4.5.3. Conclusion

(70) In view of the above considerations and in line with its past decisional practice, the Commission concludes that, for the purpose of this decision, it can be left open whether retail on-board services should be segmented by type of product (snacking and duty-free products) and whether the geographic market is EEA-wide or worldwide, as the Transaction would not raise serious doubts as to its compatibility with the internal market under any plausible market definition.

4.6. Passenger air transport services

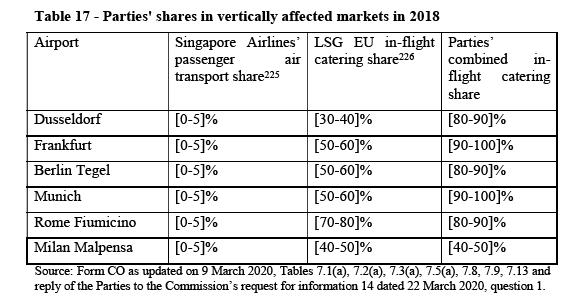

(71) Gategroup is co-controlled by Temasek, which holds a majority shareholding in Singapore Airlines, active in passenger air transport services.96

4.6.1. Product market definition

(72) In previous decisions, when assessing vertical relationships,97 the Commission considered that there is an overall market for passenger air transport services, but left open whether this market might be further sub-segmented into scheduled and charter flights or into “time-sensitive” and “non-time-sensitive passengers.98

(73) The Notifying Party agrees with the previous decisional practice of the Commission and considers that the for the purpose of assessing vertical relationships, there is no need to distinguish between time-sensitive and non-time-sensitive passengers or between charter and scheduled flights because an airline’s demand for in-flight catering or retail-on-board products is a function of total passenger numbers, irrespective of the time-sensitivity of those passengers.99

(74) In line with its past decisional practice, Commission considers that, for the purpose of this decision and the assessment of the vertical relationship between the Parties’ activities in in-flight catering and passenger air transport, the relevant market is an overall market for passenger air transport services. The question whether the market for passenger air transport services should be segmented into charter and scheduled flights or “time-sensitive” and “non-time-sensitive” passengers can be left open, as the Transaction would not raise serious doubts as to its compatibility with the internal market under any such plausible market definitions.100

4.6.2. Geographic market definition

(75) In previous cases involving a vertical relationship between in-flight catering and retail on-board services on the one hand and passenger air transport services on the other hand, the Commission found that airlines procure in-flight catering and retail on-board services on an airport-by-airport basis and not on a route-by-route basis. Therefore, it was considered necessary to look at the market share of the particular airline into the total demand for in-flight catering services at the relevant airport (i.e. for every route to or from the relevant airport) instead of making a route-by-route assessment.101

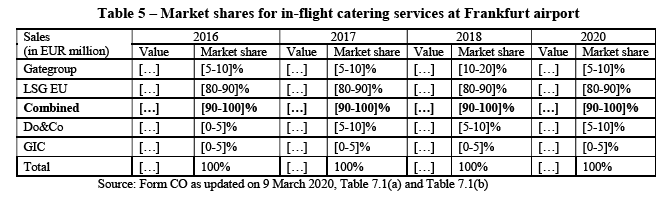

(76) The Notifying Party agrees with the Commission’s decisional practice and submits that the relevant geographic market for the assessment of the vertical relationship between Singapore Airlines’ passenger air transport services and the provision of in- flight catering is an airport-by-airport approach (i.e. every route to or from a given airport).102

(77) In line with its past decisional practice, the Commission considers that, for the purpose of this decision and the assessment of the vertical relationship between the Parties’ activities in in-flight catering and passenger air transport, the geographic market for the provision of passenger air transport services comprises every route to or from a given airport. The Commission will therefore assess the vertical effects of the Transaction on an airport-by-airport approach.

4.6.3. Conclusion

(78) In view of the above considerations and in line with its past decisional practice, the Commission concludes that, for the purpose of this decision, the relevant market is an overall market for passenger air transport services to or from a given airport. The question whether the product market should be further segmented into charter and scheduled flights or “time-sensitive” and “non-time-sensitive” passengers can be left open, as the Transaction would not raise serious doubts as to its compatibility with the internal market under any plausible market definition.103

5. COMPETITIVE ASSESSMENT

5.1. Horizontal non-coordinated effects104

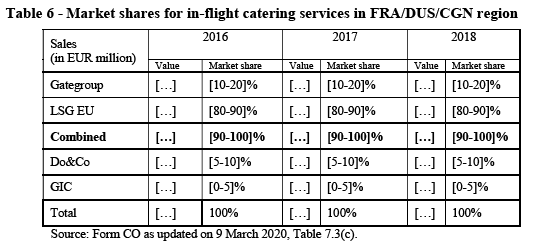

5.1.1. Framework for the competitive assessment

(79) Effective competition brings benefits to consumers, such as low prices, high quality products, a wide selection of goods and services, and innovation. Through its control of mergers, the Commission prevents mergers that would be likely to deprive customers of those benefits by significantly increasing the market power of firms.105

(80) Under Article 2(2) and (3) of the Merger Regulation, the Commission must assess whether a proposed concentration would significantly impede effective competition in the internal market or in a substantial part of it, in particular as a result of the creation or strengthening of a dominant position. The notion of "significant impediment to effective competition" must be interpreted as extending, beyond the concept of dominance, to the anticompetitive effects of a concentration resulting from the non-coordinated behaviours of undertakings which do not have a dominant position on the market concerned.106

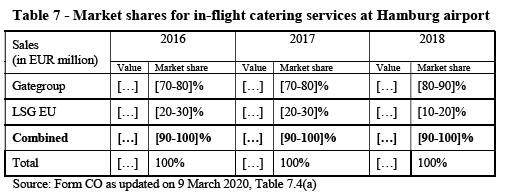

(81) As regards its non-coordinated effects, a merger presenting horizontal overlaps may significantly impede effective competition in a market, even if it does not result in the creation or strengthening of a dominant position, by removing important competitive constraints and influencing parameters of competition.107

(82) The Horizontal Merger Guidelines list a number of factors which may influence whether or not significant non-coordinated effects are likely to result from a merger, such as the large market shares of the merging firms, the fact that merging firms are close competitors, the limited possibilities for customers to access to the services provided by the parties and their competitors and the fact that the merger would eliminate an important competitive force.108

(83) It is in light of the principles set out above that the Commission must analyse whether and to what extent the Transaction may raise serious doubts as to its compatibility with the internal market due to its horizontal non-coordinated effects.

5.1.2. In-flight catering services

5.1.2.1. Introduction

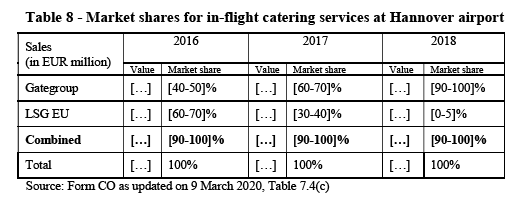

(84) The Notifying Party submits that the competitive concerns that might arise due to the Transaction are being mitigated by (i) the bidding nature of the market, (ii) the presence of strong competitors on the markets, (iii) the ease of switching between in- flight catering suppliers and (iv) the evolution of airline catering needs.

(A) Market shares are a reliable indicator in in-flight catering bidding market

(85) The Parties submit that the in-flight catering services market is a bidding market, as nearly all in-flight catering products are awarded through competitive tenders, issued on a regular basis by airlines. The parties argue that, in line with previous Commission decisions, “in bidding markets, market shares are an imperfect proxy for establishing the effective market strength of parties”, due to quick shifts in large volumes of business.109 According to the Parties, the mere aggregation of market shares would overstate the strength of the combined entity.110

(86) While the results of the market investigation show that most airlines launch tender processes for in-flight catering contracts, airlines also do negotiate contracts with suppliers bilaterally.111 More importantly, several airlines indicated that launching a tender is sometimes futile because there is only one (viable) caterer active at the particular airport.112 In that respect, the bidding data submitted by the Parties shows that caterers not yet present at the airport generally do not bid on contracts covering that airport.113 It thus cannot be argued that competitors not yet active at a given airport are potential bidders that would exert a competitive pressure on the Parties post-Transaction.

(87) Therefore, in view of the above considerations, the Commission considers that market shares are a reliable indicator of the actual market position of the Parties at the relevant airports over the past years.

(88) With respect to German airports, the Parties have submitted their market share estimates for each airport or certain geographic areas which, in the Parties’ view, comprise several airports, in two versions: including and excluding captive sales. Prior to the merger, all sales of LSG to the Lufthansa Group were internal, i.e. captive sales. As explained in paragraph (12) above, Gategroup will enter into a long-term supply contract with Lufthansa for the hub airports Frankfurt and Munich, as well as outlying German airports. In the absence of this long-term agreement, the demand of the Lufthansa Group airlines could have been part of the contestable market. Therefore, the Commission will take account of the formerly captive sales between LSG and the Lufthansa Group airlines in the calculation of the merged entity’s share at German airports or broader geographic areas comprising several airports. However, the competitive assessment will remain unchanged, should formerly captive sales be excluded from the calculation of the merged entity’s market share post-Transaction, notably since the merged entity shares without (formerly) captive sales would remain high at these airports or in these broader geographic areas and the merged entity would not face sufficient competition constraint post-Transaction. With respect to the Amsterdam airport, where the Parties’ activities in in-flight catering services overlap, the Commission assessment will exclude the captive sales between KCS and the KLM group which are not part of the contestable market, as these sales between KCS and the KLM group were captive sales pre-Transaction and will remain captive post-Transaction.

(B) Barriers to entry

(89) According to the Parties, barriers to entry in the in-flight catering business are low.114

(90) The market investigation has shown however that significant barriers to entry exist regarding the market for in-flight catering services. Replies were mixed amongst competitors regarding the question how difficult it is for a company already providing in-flight catering services at certain airports to enter an airport at which it does not operate,115 whereas the majority stated that it would be relatively or very difficult for a company not already active in in-flight catering services to start doing so.116

(91) According to respondents, depending on which airport a company intends to start providing catering services at, a relatively high degree of assets or knowledge are necessary to start doing so. These include e.g. available spaces and/or facilities for a catering unit close to the airport, experience and knowledge in the catering industry, experienced staff, high-loaders & trucks, specific IT-infrastructure as well as kitchen equipment, some of which are scarce resources or require a relatively high upfront investment.117 In addition, entering a new airport will only be viable if a critical number of customers will award the new supplier a contract from day one of operation.118

(92) Competitors further stated that depending on whether entering a hub- or non-hub airport, it would take between six months and two years to set up a business at a new airport and even longer if the company was not previously active in the provision of in-flight catering services.119 The complexity and timeframe of entry is further exacerbated by the fact that many airlines have multi-airport-contracts with in-flight caterers, which for a new entrant might require simultaneous entry at several airports.120 The geographic footprint (i.e. prior presence of the supplier at the relevant airport) as well as the (size of the) existing network of the supplier were both named as important criteria for airlines when selecting an in-flight catering services supplier.121 Prior presence at an airport is therefore a major advantage to a supplier of in-flight catering services and lack thereof constitutes a significant barrier to entry. Correspondingly, analysing the Parties’ recent tendering data, it can be observed that competitors generally do not bid at airports where they are not already active.122 The majority of customers that replied to the market investigation also did not expect new entries in the coming five years into the market for the supply of in- flight catering services in the EEA.123

(C) Switching suppliers

(93) According to the Parties, switching suppliers in the in-flight catering services market is easy. The Parties state that airlines usually make no purchase commitment and can often terminate the contract with little notice and at no significant cost. Moreover, the Parties submit that barriers to entry are low and that airlines are able and willing to introduce and sponsor new entrants for in-flight catering services to an airport. In addition, the Parties claim that airlines could further exercise significant constraints on in-flight caterers due to the possibility of switching back to in-house sourcing or switching to return-catering (meaning aircraft are catered and loaded at a given airport with sufficient catering to last for several flight legs), the latter of which would allow airlines to not use any caterer at a particular airport and supply their aircraft with catering from their central hub instead.124

(94) The parties provide recent examples of airlines switching their in-flight caterers, such as British Airways’ and Iberia’s switch to Do&Co for their hubs in London and Madrid, [customer]’s switch from LSG to Gategroup at Rome Fiumicino Airport and [customer] switching from Gategroup to LSG at Amsterdam Schiphol Airport.125 Indeed, the majority of customers responding to the Commission’s market investigation confirmed that they have switched their in-flight catering services supplier in the last five years. However, some airlines point towards the exit of their previous supplier, leaving them no choice but to switch despite higher prices.126

(95) Although in past decisions, the Commission indicated that switching suppliers in the in-flight catering market was relatively easy,127 the market investigation has revealed that this is no longer the case. In fact, the majority of customers responding to the Commission’s market investigation expressed the view that it was relatively or very difficult for an airline to switch to a different supplier. The reasons for this ranged from a lack of alternative suppliers and capacity constraints in some markets to the time and additional investments needed by the airline to switch suppliers.128

(96) Furthermore, the case of Do & Co in Heathrow and Madrid cannot be seen as a normal switching, as it is a case of sponsoring entry at a hub airport by the hub carrier, therefore guaranteeing a high volume. Similarly, the case of [customer]’s switch from LSG to Gategroup at Rome Fiumicino Airport is special, as [customer] owns the kitchen and other infrastructure, which it lets to the caterer. Therefore, these examples of switching work only in hub airports for the hub carrier, and cannot be cited as a general possibility at all airports.

(97) The majority of customers also stated that it was impossible or difficult for an airline to switch to source in-flight catering services in-house, citing the lack of experience and infrastructure, high investment-costs as well as different business models as the main reasons129. The majority of customers responding to the market investigation have also not switched to in-house catering services in the past130. In fact, only one airline, Finnair, has done this for their entire in-flight catering needs in the EEA according to the market-investigation.131

(98) Similarly, while responses by customers as to whether it would be feasible for an airline to sponsor the entry of a supplier of in-flight catering services in the EEA at which it does not operate yet were mixed,132 the majority of airlines was not aware of any airline doing so in the past other than IAG and many airlines expressed the view that they have never considered this as an option.133 The majority of customers also currently does not deem it feasible to switch to return-catering for long-haul flights.134

(D) Competitors on the market

(99) According to the Parties, they face strong competition regarding the provision of in- flight catering services from several large and internationally active operators such as Newrest, Do&Co and dnata. All of them provide a wide range of in-flight catering services. In addition, competitors do not only rely on their own infrastructure and presence at particular airports, but frequently enter into joint venture agreements (such as Newrest and Servair in Belgium). The Parties moreover argue that they face additional pressure from non-traditional suppliers.135

(100) The Commission considers companies such as Newrest, Do&Co and Dnata as viable competitors with regards to the provision in-flight catering services in the EEA. Considering that the geographic scope of in-flight catering services is local (i.e. the catchment area of an airport or an area comprising several neighbouring airports), the Commission will assess the competitive constraint exerted by competitors on the relevant geographic market, taking account of potential entry.

(E) Negotiation power of customers

(101) The market investigation has shown that contrary to the Parties’ assertion, depending on the airport in question, the negotiation power of customers vis-à-vis in-flight caterers is limited. In particular, if there is no alternative supplier present at a given airport, airlines would only have two options: threatening them that they would switch to in-house catering, as explained in paragraph (97) above, or to return- catering (see paragraph (93)). In particular, resorting to return-catering in a destination airport (or several) is not likely to be an option because, by switching to return-catering in those airports, the airline would lose the efficiencies and economies of scale linked to the purchase of in-flight catering services for the numerous flights departing from its hub/base airport. In addition, the majority of customers responding to the market investigation having expressed a view stated that the merged entity will have the ability and incentive to foreclose competitors by inciting an airline to conclude multi-airport contracts post-Transaction by leveraging its position at the overlap airports where the merged entity’s position will be strengthened.

(F) Conclusion

(102) The Commission will assess the horizontal effects of the Transaction in the market for in-flight catering on the relevant geographic markets, taking account of the general characteristics of in-flight catering services in the EEA described in the sections above.

5.1.2.2. Berlin Tegel

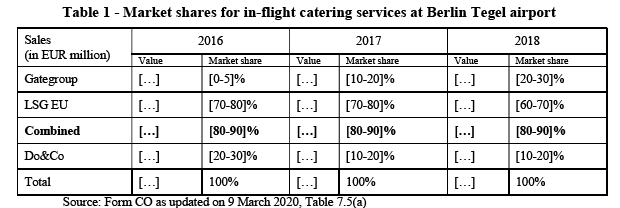

(103) The Transaction leads to a horizontal overlap between the Parties’ activities in in- flight catering at Berlin Tegel airport. The evolution of the market shares of the Parties and their competitor at Berlin Tegel airport during the period from 2016 to 2018 is set out in the table below.

(104) As shown in the table above, the proposed Transaction would lead to a combined market share of [80-90]% in the provision of in-flight catering services at Berlin Tegel airport.

(105) The Commission considers that post-Transaction, the merged entity would face limited competition at Berlin Tegel airport, because Do&Co will be the only remaining competitor with a market share of [10-20]%. The respondents to the market investigation gave mixed replies as to whether the merged entity would have the ability to restrict the expansion or the entry of competitors post-Transaction at Berlin Tegel airport.136

(106) The majority of competitors having expressed a view consider that the Transaction will have a negative impact on the market for in-flight catering services at Berlin Tegel airport.137 However, the views of customers as to whether the Transaction would have a negative impact on in-flight catering services at Berlin Tegel are mixed.138 A customer indicated that the proposed transaction “would likely have a negative impact on cost and service quality levels, particularly at the following airports stations in the EEA: Berlin (TXL)”.139 Respondents that consider that the impact of the Transaction would not be negative did not further substantiate their reply.

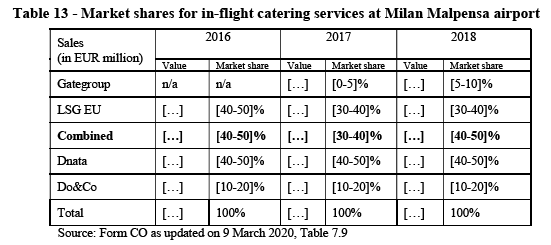

(107) Furthermore, the majority of respondents to the market investigation indicated that they are not aware of any recent or potential entry at Berlin Tegel airport.140 More specifically, a customer explained that “An incumbent (or purchaser) in limited size markets can impact competitors primarily due to volume (i.e. if there is not enough volume, competitors may be reluctant to enter the market)”.141 The Commission therefore notes the lack of entry projects that would defeat or deter the anticompetitive effects of the Transaction on the market for in-flight catering services at Berlin Tegel airport.

(108) In view of the above considerations and all evidence available to it, the Commission concludes that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the horizontal effects in the market for in-flight catering services at Berlin Tegel airport, since the Transaction would create a dominant position for Gategroup.

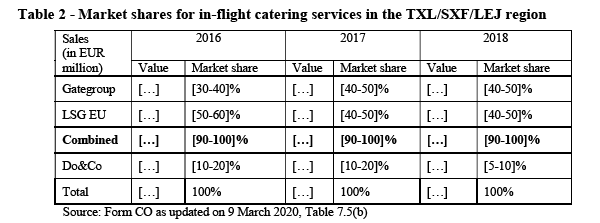

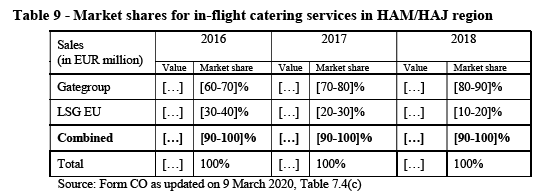

5.1.2.3. Berlin Tegel/Berlin Schönefeld/Leipzig

(109) The Transaction also leads to a horizontal overlap between the Parties’ activities in in-flight catering on a geographic market encompassing Berlin Tegel/Berlin Schönefeld and Leipzig airports since Gategroup is active in Berlin Tegel, Berlin Schönefeld and Leipzig airport and LSG EU is active in Berlin Tegel. The evolution of the market shares of the Parties in this geographic market during the period from 2016-2018 is set out in the table below.

(110) As shown in the table above, the Transaction would lead to a combined share of more than [90-100]% in a broader geographic market encompassing Berlin Tegel/Berlin Schönefeld and Leipzig airports. The merged entity would face limited competition from the only other in-flight caterer Do&Co with a [5-10]% market share.

(111) In view of the merged entity's high market share and of the considerations set out in Section 5.1.1.2 above, the Commission concludes that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the horizontal effects in the market for in-flight catering services in a geographic area encompassing Berlin Tegel/Berlin Schönefeld and Leipzig airports since it would create a dominant position for Gategroup in a geographic area comprising Berlin Tegel/Berlin Schönefeld and Leipzig airports.

5.1.2.4. Cologne-Bonn

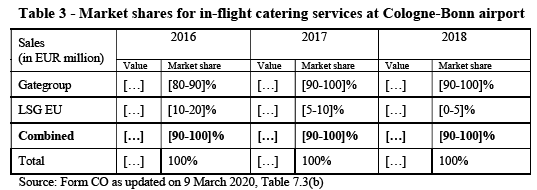

(112) The Transaction leads to a horizontal overlap between the Parties’ activities in in- flight catering at Cologne-Bonn airport. The evolution of the market shares of the Parties at Cologne-Bonn airport during the period from 2016 to 2018 is set out in the table below.

(113) Gategroup and LSG EU were the only providers of in-flight catering services at Cologne-Bonn airport in the past years. The proposed Transaction would therefore lead to a monopoly situation at Cologne-Bonn airport.

(114) The majority of respondents to the market investigation having expressed a view consider that the Transaction will have a negative impact on the market for in-flight catering services at Cologne-Bonn airport.142 An airline indicated “if GG becomes sole source, we anticipate increased costs in the future”.143 Another customer explained that “we have seen in airports today […] where Gate Group is the only supplier that the cost is substantially higher than on other airports as well as they deliver lower quality and higher degree of errors and we have higher percentage of flight delays due to catering than in other airports”.144

(115) Furthermore, the majority of respondents to the market investigation indicated that they are not aware of any recent or potential entry at Cologne-Bonn airport.145 The Commission therefore notes the lack of entry projects that would defeat or deter the anticompetitive effects of the Transaction on the market for in-flight catering services at Cologne-Bonn airport.

(116) In view of the above considerations and all evidence available to it, the Commission concludes that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the horizontal effects in the market for in-flight catering services at Cologne-Bonn airport since it would create or strengthen a dominant position for Gategroup.

5.1.2.5. Dusseldorf

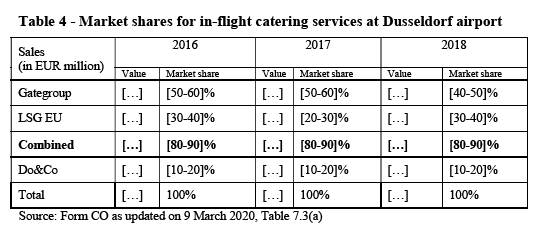

(117) The Transaction leads to a horizontal overlap between the Parties’ activities in in- flight catering at Dusseldorf airport. The evolution of the market shares of the Parties and their only competitor at Dusseldorf airport during the period from 2016 to 2018 is set out in the table below.

(118) As shown in the table above, the proposed Transaction would lead to a combined market share of [80-90]% in the provision of in-flight catering services at Dusseldorf airport.

(119) The Commission considers that post-Transaction, the merged entity would face limited competition at Dusseldorf airport, because Do&Co will be the only remaining competitor with a market share of [10-20]%. The majority of respondents to the market investigation having expressed a view consider that the merged entity would have the ability to restrict the expansion or the entry of competitors post-Transaction at Dusseldorf airport.146

(120) In addition, the majority of respondents to the market investigation having expressed a view consider that the Transaction will have a negative impact on the market for in-flight catering services at Dusseldorf airport.147 A customer indicated that the proposed transaction “would likely have a negative impact on cost and service quality levels, particularly at the following airports stations in the EEA: […] Duesseldorf (DUS)”.148

(121) Furthermore, the majority of respondents to the market investigation indicated that they are not aware of any recent or potential entry at Dusseldorf airport.149 The Commission therefore notes the lack of entry projects that would defeat or deter the anticompetitive effects of the Transaction on the market for in-flight catering services at Dusseldorf airport.

(122) In view of the above considerations and all evidence available to it, the Commission concludes that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the horizontal effects in the market for in-flight catering services at Dusseldorf airport since the Transaction would create a dominant position for Gategroup.

5.1.2.6. Frankfurt

(123) The Transaction leads to a horizontal overlap between the Parties’ activities in in- flight catering at Frankfurt airport. The evolution of the market shares of the Parties and their competitors at Frankfurt airport during the period from 2016 to 2018, as well as the estimates for 2020,150 are set out in the table below.

(124) As shown in the table above, the proposed Transaction would lead to a combined market share of [90-100]% in the provision of in-flight catering services at Frankfurt airport.

(125) The Commission considers that post-Transaction, the merged entity would face limited competition at Frankfurt airport because Do&Co and GIC would respectively have a market share of [5-10]% and [0-5]%. The respondents to the market investigation gave mixed replies as to whether the merged entity would have the ability to restrict the expansion or the entry of competitors post-Transaction.151

(126) However, the majority of respondents to the market investigation having expressed a view consider that the Transaction will have a negative impact on the market for in- flight catering services at Frankfurt airport.152 An airline indicated that “less competition results in higher catering costs and lower quality […]. From a passenger point of view, there is also a high risk of less innovation and variation in inflight catering concepts with less supplier competition in the market”.153 A competitor considers that the merged entity “will drive the prices too high because they have the major client base in FRA. Opportunities to bid for business will reduce as more customers will automatically transfer to the new entity”.154

(127) Furthermore, the majority of respondents to the market investigation indicated that they are not aware of any recent or potential entry in Frankfurt.155 The Commission therefore notes the lack of entry projects that would defeat or deter the anticompetitive effects of the Transaction on the market for in-flight catering services at Frankfurt airport.

(128) In view of the above considerations and all evidence available to it, the Commission concludes that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the horizontal effects in the market for in-flight catering services at Frankfurt airport, since it would create a dominant position for Gategroup.

5.1.2.7. Frankfurt/Dusseldorf/Cologne-Bonn

(129) The Transaction also leads to a horizontal overlap between the Parties’ activities in in-flight catering on a geographic market encompassing Frankfurt, Dusseldorf and Cologne-Bonn airports since both Gategroup and LSG EU are active in Frankfurt, Dusseldorf and Cologne-Bonn. The evolution of the market shares of the Parties in this geographic market during the period from 2016-2018 is set out in the table below.

(130) As shown in the table above, the Transaction would lead to a combined share of more than [90-100]% in a broader geographic market encompassing Frankfurt, Dusseldorf and Cologne-Bonn airports. The merged entity would face limited competition from Do&Co and GIC, with a market share of respectively [5-10]% and [0-5]%.

(131) In view of the merged entity high market share and of the considerations set out in Sections 5.1.1.4 to 5.1.1.6 above, the Commission concludes that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the horizontal effects in the market for in-flight catering services in a geographic area encompassing Frankfurt, Dusseldorf and Cologne-Bonn airports, since it would create a dominant position for Gategroup.

5.1.2.8. Hamburg

(132) The Transaction leads to a horizontal overlap between the Parties’ activities in in- flight catering at Hamburg airport. The evolution of the market shares of the Parties at Hamburg airport during the period from 2016 to 2018 is set out in the table below.

(133) Gategroup and LSG EU were the only providers of in-flight catering services at Hamburg airport in the past years. The proposed Transaction would therefore lead to a monopoly situation at Hamburg airport.

(134) The majority of respondents to the market investigation having expressed a view consider that the Transaction will have a negative impact on the market for in-flight catering services at Hamburg airport.156 An airline indicated “If a monopoly or dominant position, this would mean increased prices.”157

(135) Furthermore, the majority of respondents to the market investigation indicated that they are not aware of any recent or potential entry at Hamburg airport.158 The Commission therefore notes the lack of entry projects that would defeat or deter the anticompetitive effects of the Transaction on the market for in-flight catering services at Hamburg airport.

(136) In view of the above considerations and all evidence available to it, the Commission concludes that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the horizontal effects in the market for in-flight catering services at Hamburg airport, since it would create or strengthen a dominant position for Gategroup.

5.1.2.9. Hannover

(137) The Transaction leads to a horizontal overlap between the Parties’ activities in in- flight catering at Hannover airport. The evolution of the market shares of the Parties at Hannover airport during the period from 2016 to 2018 is set out in the table below.

(138) Gategroup and LSG EU were the only providers of in-flight catering services at Hamburg airport in the past years. The proposed Transaction would therefore lead to a monopoly situation at Hannover airport.

(139) The majority of respondents to the market investigation having expressed a view consider that the Transaction will have a negative impact on the market for in-flight catering services at Hannover airport.159 An airline indicated “We are worried that monopoly and oligopoly will lose cost competitiveness”160 while another explained “There is the possibility that the cost of service may increase slightly as Gate has tended to be more expensive than LSG when we have tendered our contracts.”161

(140) Furthermore, the majority of respondents to the market investigation indicated that they are not aware of any recent or potential entry at Hannover airport.162 The Commission therefore notes the lack of entry projects that would defeat or deter the anticompetitive effects of the Transaction on the market for in-flight catering services at Hannover airport.

(141) In view of the above considerations and all evidence available to it, the Commission concludes that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the horizontal effects in the market for in-flight catering services at Hannover airport, since it would create or strengthen a dominant position for Gategroup.

5.1.2.10.Hamburg/Hannover

(142) The Transaction also leads to a horizontal overlap between the Parties’ activities in in-flight catering on a geographic market encompassing Hamburg and Hannover airports since both Gategroup and LSG EU are active in Hamburg and Hannover. The evolution of the market shares of the Parties in this geographic market during the period from 2016-2018 is set out in the table below.

(143) As shown in the table above, the Transaction would lead to a monopoly in a broader geographic market encompassing Hamburg and Hannover airports.

(144) In view of the merged entity high market share and of the considerations set out in Sections 5.1.1.8 and 5.1.1.9 above, the Commission concludes that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the horizontal effects in the market for in-flight catering services in a geographic area encompassing Hamburg and Hannover airports since it would create or strengthen a dominant position for Gategroup.

5.1.2.11.Munich

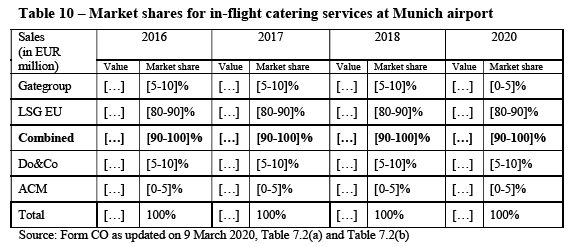

(145) The Transaction leads to a horizontal overlap between the Parties’ activities in in- flight catering at Munich airport. The evolution of the market shares of the Parties and their competitors at Munich airport during the period from 2016 to 2018, as well as the estimates for 2020,163 are set out in the table below.

(146) As shown in the table above, the proposed Transaction would lead to a combined market share of [90-100]% in the provision of in-flight catering services at Munich airport.

(147) The Commission considers that post-Transaction, the merged entity would face limited competition at Munich airport because Do&Co and ACM would respectively have a market share of [5-10]% and [0-5]%. In fact, the takeover would leave airlines with only one accredited alternative, Do & Co, and a niche player, ACM. The respondents to the market investigation gave mixed replies as to whether the merged entity would have the ability to restrict the expansion or the entry of competitors post-Transaction at Munich airport.164

(148) However, the majority of respondents to the market investigation having expressed a view consider that the Transaction will have a negative impact on the market for in- flight catering services at Munich airport.165 An airline considers that “In case LSG and Gate Gourmet are present at the same station, an impact on the competitive landscape is expected, particularly a potential increase in prices and potentially less choice. This also of course depends highly on the amount and position of remaining competitors. It is important to have a choice in supplier in case of quality reduction or operational issues”.166 A competitor considers that the proposed Transaction “will create a powerful Giant”.167

(149) Furthermore, the majority of respondents to the market investigation indicated that they are not aware of any recent or potential entry at Munich airport.168 The Commission therefore notes the lack of entry projects that would defeat or deter the anticompetitive effects of the Transaction on the market for in-flight catering services at Munich airport.

(150) In view of the above considerations and all evidence available to it, the Commission concludes that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the horizontal effects in the market for in-flight catering services at Munich airport, since it would create a dominant position for Gategroup.

5.1.2.12.Brussels

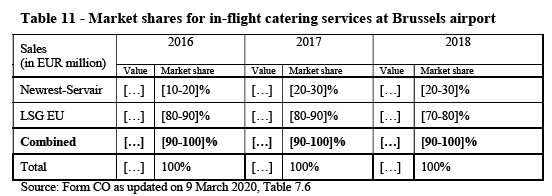

(151) LSG EU is active in the provision of in-flight catering services at Brussels airport. Gategroup holds a […]% interest in Newrest Servair Belgium SPRL (the “Newrest- Servair JV”), a joint venture between Newrest Group Holdings S.A. and Servair Investissements Aéroportuaires (“Servair”) created in 2014. Servair is controlled by Gategroup.169

(152) The Notifying Party submits that it does not have control over the Newrest-Servair JV.170 More specifically, [description of the governance structure in relation to the adoption of strategic decisions].171

(153) However, the Commission notes that [description of the governance structure in relation to the adoption of decisions]. […]172 […]173. The Commission therefore considers that Gategroup has at least the possibility to exercise decisive influence, if not actual decisive influence, over the commercial strategy of the Newrest-Servair JV.

(154) Therefore, in view of the above considerations and the evidence available to it, the Commission considers on balance that Gategroup has joint control over the Newrest- Servair JV within the meaning of Article 3(2) of the Merger Regulation.

(155) The Transaction therefore leads to a horizontal overlap between the Parties’ activities in in-flight catering services at Brussels airport. The evolution of the market shares of the Parties and their competitor at Brussels airport during the period from 2016 to 2018 is set out in the table below.

(156) The Transaction would therefore lead to a monopoly situation.

(157) The Commission considers that the entry of new competitors at Brussels airport is unlikely until at least October 2025 because the number of catering transport licences at Brussels Airport is limited to two by Royal Decree of 6 November 2010.174 As a result, competitors cannot enter into the market for in-flight catering services at Brussels airport, unless they subcontract the last-mile services (i.e. the loading on board of aircraft) to either LSG EU or Newrest-Servair. The Commission therefore considers that there would not be sufficient competition at Brussels airport to deter or defeat any anticompetitive effects of the Transaction.

(158) In view of the above considerations and all evidence available to it, the Commission concludes that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the horizontal effects in the market for in-flight catering services at Brussels airport, since it would create or strengthen a dominant position for Gategroup.

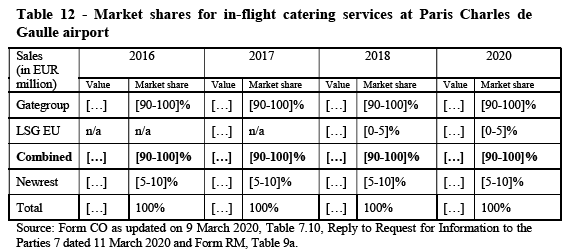

5.1.2.13. Paris Charles de Gaulle

(159) Gategroup provides in-flight catering services at Paris Charles de Gaulle airport, through its subsidiary Servair, which used to be Air France’s in-house in-flight catering supplier.175 LSG EU currently serves only one airline, [customer], since 2018, for a relatively small volume. However, LSG EU bid unsuccessfully for several tenders at Paris Charles de Gaulle airport since 2018.176 For that reason, several airlines considered in their replies to the market investigation LSG EU as an alternative supplier.

(160) The Transaction therefore leads to a horizontal overlap between the Parties’ activities in in-flight catering at Paris Charles de Gaulle airport.

(161) The evolution of the market shares of the Parties and their competitor at Paris Charles de Gaulle airport during the period from 2016 to 2018 is set out in the table below, as well as the Parties’ estimates for 2020.

(162) As shown in the table above, the proposed Transaction would lead to a combined market share of [90-100]% in the provision of in-flight catering services at Paris Charles de Gaulle airport. The takeover of LSG would remove at least a potential alternative source for airlines, given that LSG has in the recent past participated in tenders. The second player pre-Transaction, Newrest, is a relatively small supplier.

(163) The Commission considers that post-Transaction, the merged entity would face limited competition at Paris Charles de Gaulle airport, because Newrest will be the only remaining competitor with a market share of less than [5-10]%. The respondents to the market investigation gave mixed replies as to whether the merged entity would have the ability to restrict the expansion or the entry of competitors post-Transaction at Paris Charles de Gaulle airport.177 In that respect, a customer explained “Paris – less competition and the new merged company will become a large player. Still competition from Newrest but will become a duopoly”.178 Respondents who consider that the merged entity would not have the ability to restrict competition did not further substantiate their views.

(164) The market investigation also yielded mixed results as to whether the Transaction would have a negative impact on the market for in-flight catering services at Paris Charles de Gaulle.179 No respondent considers that the Transaction would have a positive impact on price or quality of service.180 By contrast, some customers and competitors consider that the Transaction would likely result in higher prices and in a decrease in quality of service.181 A customer indicated “when competition at specific locations is limited […] prices tend to be higher and the caterer leverages this position. Quality can also suffer because of limited competition. Caterers’ incentives to invest in assets such as new trucks, facilities, technology, people, and process improvements will generally be directed to locations where there is healthy competition and where the caterer has to maintain certain quality levels to win business.”182

(165) Furthermore, the majority of respondents to the market investigation indicated that they are not aware of any recent or potential entry at Paris Charles de Gaulle airport.183 The Commission therefore notes the lack of entry projects that would defeat or deter the anticompetitive effects of the Transaction on the market for in- flight catering services at Paris Charles de Gaulle airport.

(166) In view of the above considerations and all evidence available to it, the Commission concludes that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the horizontal effects in the market for in-flight catering services at Paris Charles de Gaulle airport, since it would create or strengthen a dominant position for Gategroup.

5.1.2.14. Milan Malpensa

(167) The Transaction leads to a horizontal overlap between the Parties’ activities in in- flight catering at Milan Malpensa airport. The evolution of the market shares of the Parties and their competitors at Milan Malpensa airport during the period from 2016 to 2018 is set out in the table below.

(168) As shown in the table above, the proposed Transaction would lead to a combined market share of [40-50]% in the provision of in-flight catering services at Milan Malpensa airport.

(169) While the majority of competitors having expressed a view consider that the merged entity will not have the ability to restrict the expansion or the entry of competitors at Milan Malpensa airport, the customers gave mixed replies as to whether the Transaction would result in a lessening of competition.184 In addition, the market investigation yielded mixed results as to the impact of the Transaction on the market for in-flight catering at Milan Malpensa airport.185 A customer indicated that in Milan Malpensa “DNATA could stay and expand with other airlines”,186 while another explained “The merger will reduce competition in the market, reducing customer choice.”187

(170) The Commission considers that post-Transaction, the merged entity will continue facing significant competition from established in-flight caterer Dnata, with a [40- 50]% market share. Do&Co will also be an alternative supplier with a [10-20]% market share.

(171) In view of the above considerations and all evidence available to it, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to the horizontal effects in the market for in- flight catering services at Milan Malpensa airport.

5.1.2.15. Rome Fiumicino