Commission, August 17, 2020, No M.9744

EUROPEAN COMMISSION

Decision

MASTERCARD / NETS

Subject: Case M.9744 – MASTERCARD / NETS

Commission decision pursuant to Article 6(1)(b) in conjunction with Article 6(2) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

1. On 26 June 2020, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation and following a referral pursuant to Article 22 of Merger Regulation by which MasterCard Incorporated (“Mastercard” or the “Notifying Party”, United States) acquires sole control of Nets’ A/S (“Nets”, Denmark) account-to-account payment business (the “Target”) (the “Transaction”).3 Mastercard and the Target are together referred to as the “Parties”.

2. The Transaction was referred to the Commission by the Danish competition authority pursuant to Article 22 of the Merger Regulation (the “Referral Request”). The Referral Request was subsequently joined by the national competition authorities of Austria, Finland, Norway, Sweden, and the UK. The Commission acquired jurisdiction to examine the Transaction on 2 April 2020.

1. THE PARTIES AND THE OPERATION

3. Mastercard is a US-based technology company operating in the global payments industry. Mastercard’s main activities include ownership and operation of payment card schemes and provision of switching services for card transactions. Mastercard is also active in alternative payment solutions through its subsidiary VocaLink Holding Limited (“Vocalink”). In particular, Vocalink provides account-to-account (“A2A”) core infrastructure services (“CIS”) for interbank payment schemes (also known as “A2A CIS”). A2A payment schemes allow for payments directly from one bank account to another, with no need for a card.

4. The Target is currently a business unit within Nets, a payment solution provider headquartered in Denmark. The Target operates as a global payments business providing payment services and technology solutions, mainly in the Nordic region, as well as in the Single Euro Payments Area (“SEPA”). The Target’s activities focus on the provision of (i) A2A CIS, (ii) A2A payment and ancillary services and (iii) open banking services.

5. On 6 August 2019, Mastercard and Nets entered into a sale and purchase agreement pursuant to which Mastercard agreed to purchase all the shares of three newly incorporated wholly owned indirect subsidiaries of Nets, which hold the assets comprising the Target’s business. Therefore, the Transaction consists in the acquisition of sole control by Mastercard of the Target and gives rise to a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

2. UNION DIMENSION

6. The Transaction does not meet the turnover thresholds set out in Articles 1(2) or 1(3) of the Merger Regulation. As a result, the Transaction does not have a Union dimension within the meaning of Article 1 of the Merger Regulation.

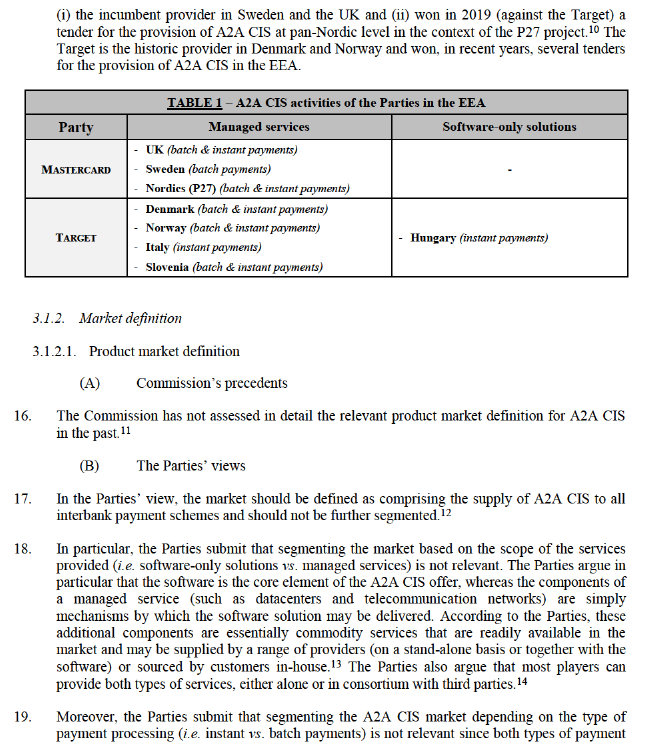

7. The Transaction was referred to the Commission by the Danish national competition authority on the basis of Article 22 of the Merger Regulation on 27 February 2020. The Referral Request was subsequently joined by the national competition authorities of Austria, Finland, Norway, Sweden and the UK (together with Denmark the “Referring States”) within the legal deadline of Article 22(2) of the Merger Regulation.

8. On 2 April 2020, the Commission adopted six decisions pursuant to Article 22(3) of the Merger Regulation accepting the requests of the Referring States.4 On this basis, the Commission acquired jurisdiction to examine the Transaction with regard to the Referring States.

3. COMPETITIVE ASSESSMENT

9. The Parties’ activities overlap horizontally mainly with respect to the provision of (i) A2A CIS and (ii) A2A payment services.5

3.1. A2A CIS

3.1.1. Overview of the market and the Parties’ activities

10. A2A CIS consist in providing interbank payment scheme operators6 with the core infrastructure and related services required for the processing of payments directly from the payer’s bank account to the payee’s bank account, without requiring the use of a card (“A2A payments”).

11. More specifically, suppliers of A2A CIS provide the core infrastructure/technology required to authorise, clear7 and initiate the settlement (i.e. the completion of the transaction through the transfer of funds) of A2A payments. The Parties are active in the clearing process but do not conduct the settlement process, which is carried out by distinct providers (which are typically central banks). In other words, A2A CIS entail all the clearing processes that precede the transfer of funds, such as verifying that there are funds or credit available on individual accounts, authorising the transactions, bookkeeping, forecasting and liquidity management.8

12. Depending on the requirements of the interbank payment scheme operator, suppliers of A2A CIS may provide (i) batch payment processing (i.e. processing together payment orders at discrete intervals of time), (ii) instant (or real-time) payment processing (i.e. processing of payments on a transaction-by-transaction basis in real time) or (iii) both. Historically, A2A core infrastructures only processed batch payments. However, with the emergence of instant payments in the last decade, the market is progressively migrating from batch payments to instant payments.

13. A2A CIS can be provided either as:

- a software solution including only the provision of a licence for the software allowing the processing of A2A payments (“software-only solution”); or

- a managed solution consisting in the provision of A2A core infrastructure (including the software, together with the hardware and the telecommunication networks and processes), as well as its management and operation in accordance with the rules set out by the scheme operator (“managed services”).

14. The markets for the provision of A2A CIS are essentially bidding markets. Suppliers of A2A CIS (as software-only solutions or managed services) compete in tenders for contracts with interbank payment scheme operators. A2A CIS contracts are long-term contracts, the duration of which can exceed 10 years, which may be periodically tacitly renewed to ensure continuity of the infrastructure without switching A2A CIS provider.

15. Mastercard and the Target both provide software-only solutions and managed services. Their respective offering also includes both batch and instant payment processing. The Parties participate in A2A CIS tenders across the EEA (and beyond).9 As detailed in Table 1 below, in the EEA, the Parties currently provide A2A CIS in several countries. In particular, Mastercard is processing (i) co-exist in most cases (e.g. it is common for A2A CIS tenders to cover both batch and instant payments); (ii) are characterised by the same competitive landscape and (iii) rely to a very large extent on the same core technology and standards. In this respect, the Parties indicate that the vast majority of requirements in A2A CIS tenders are identical, notwithstanding whether the tenders relate to instant or batch payment processing.15

(C) The Commission’s assessment

(C.i) Potential segmentation based on the scope of the services provided

20. The results of the market investigation indicates that software-only solutions and managed services are likely to constitute distinct product markets for the following reasons.

21. First, most competitors and a significant share of customers consider that A2A CIS providers do not typically have the capabilities to provide both software solutions and managed services. In particular, market participants stressed the fact that the “business model for [managed] services and [software] products is quite different” and that providing managed services “implies much wider responsibilities and different type of expertise than just delivering a [software] product”.16 The Commission notes that this contradicts the argument made by the Parties, according to which managed services are simply mechanisms by which the software solution may be delivered.

22. Moreover, several market participants disputed the Parties’ claim that, apart from the software, the components required to provide managed services are commodity products readily available on the market, indicating that some of these components are “proprietary or complex components” (such as core gateways),17 which are difficult to find on the market.18 In addition, a competitor stressed that “select[ing], specify[ing] and arrang[ing] these components to work effectively with the [software]” is “essential” to be able to provide managed services and require specific “knowledge”.19

23. Second, competitors generally consider that the provision of managed services and software- only solutions are characterized by different competitive dynamics and landscape.20 A large number of respondents to the market investigation explained that, although some A2A CIS providers (such as the Parties) offer both types of solutions, most players provide either only managed services or only software solutions. A competitor expressly indicated that “in most cases, providers are specialized to offer only one type of solution”. Similarly, a customer stated that A2A CIS provider “normally offer one or another kind of solutions, but not both”.21 For example, STET indicated that it “only offers the managed service but do not sell the products i.e. not the software”.22 This is also reflected in the Parties’ internal documents, which qualify two competitors, namely […] and […], as “software vendor”.23 The Parties do not contest the above and expressly acknowledged that a large number of A2A CIS providers do not offer both managed and software solutions which, in their view, “may be due to competitors’ capabilities” or to “a deliberate strategic choice based on each competitor’s preferred business model”.24

(C.ii) Potential segmentation based on the type of payment processing

24. The results of the market investigation suggest that distinguishing instant and batch payment processing would not be warranted.

25. First, the Commission found that instant payments are progressively replacing batch payments, but that the migration of the entire market may take a long time depending on the specificities of each country; for this reason, batch payments are expected to continue to exist for many years.25 As a result, both types of payment processing are currently coexisting in the EEA, where it is not uncommon to have A2A CIS tenders requiring solutions covering both batch and instant payments. The Parties provided several recent examples of such tenders (including e.g. in the Nordics (P27), the UK, Austria, Bulgaria and Slovenia).26 This is also corroborated by the feedback received from the market. For example, a competitor stated that “requirements in A2A CIS tenders tend to encompass both batch and real-time solutions”.27

26. Second, a majority of competitors consider that the processing of batch and instant payment relies, to a large extent, on the same core technology. For example, a rival of the Parties indicated that “the approach to processing A2A instant payments and A2A batch payments follow very similar patterns”. Although some market participants took the opposite view, they did not deny the existence of similarities between batch and instant payments, but gave a more nuanced picture stating that the “underlying technology could be different” or that “while the underlying processes can be very similar and the software deployed can also be very similar, there are significant differences on how the underlying systems behave”.28

27. Third, most competitors and customers consider that A2A CIS providers typically have the capabilities to process both types of payment. A respondent explained that “traditionally A2A CIS players provided batch payment solutions but […] have developed instant payment solutions to respond to demand”, which has evolved over time. Several respondent also stressed that A2A CIS providers, which do not have yet the capabilities to process instant payments, “will complete sooner or later the necessary steps to develop and implement A2A instant payment solutions”.29

28. Finally, competitors generally took the view that the batch and instant payment processing should not be considered as separate markets as they present similar competitive dynamics and landscape.30

(D) Conclusion

29. Based on the results of the market investigation and for the purpose of this decision, the Commission concludes that the provision of A2A core infrastructure managed services and software-only solutions constitute distinct product markets. A further differentiation based on the type of payment processing is not warranted.

3.1.2.2. Geographic market definition

(A) Commission’s precedents

30. As previously indicated, the Commission has not assessed in detail the relevant market definition for A2A CIS in the past. However, in 2016, in case M.8149 - Mastercard/VocaLink, the Commission concluded (in line with the view expressed by Mastercard in that case) that the provision of A2A CIS presents the characteristics of national markets. This conclusion was based on the fact that the Commission has consistently considered that the markets for payments processing services are national in scope (due to the existence of various national characteristics) and that the core infrastructures in this case were designed according to the specific characteristics of the payment schemes in the UK.31

(B) The Parties’ views

31. In the present case, Mastercard and the Target submit that the market is global in scope for several reasons.32 First, they claim that the provision of A2A CIS is highly standardised worldwide, with the increasing adoption of the ISO 20022 messaging standard at global level33 and that there is no material difference between the requirements set by the tendering authorities around the world. Second, the Parties consider that the emergence of supra-national tenders (such as the P27 Layer 1 tender in the Nordics) demonstrates that demand from tendering authorities is wider than national. Third, the Parties argue that A2A CIS providers compete across the globe (with non-EEA players bidding in the EEA and EEA players bidding outside of the EEA) and that participating in A2A CIS tenders does not involve significant costs and risks, or any other significant technical or legal barriers for foreign bidders.

32. In any event, the Parties conclude that the geographic scope of the market can be left open in the present case since the Transaction does not raise competition concerns under any plausible geographic market definition.

(C) The Commission’s assessment

33. The market investigation was not fully conclusive with respect to the geographic scope of the A2A CIS markets: while the Commission found that these markets are unlikely to be worldwide, their exact geographic scope in the EEA is unclear.

(C.i) A2A CIS markets are unlikely to be global in scope

34. As explained below, the market investigation strongly suggests that, contrary to the Parties’ claim, the A2A CIS markets are unlikely to be global in scope.

35. First, the market investigation contradicted the Parties’ claim that the market is highly standardized across the globe. Although market participants acknowledged “a trend towards the ISO20022 standard which provides for a common minimum standard”, they generally stressed the fact that this standard “has not been implemented in many countries yet (especially outside of Europe)” and that global standardization is “still to be achieved” and “will take many years.”34

36. For example, a competitor indicated that “there are still material differences depending on the geography, because jurisdictions have different approaches towards A2A, both in terms of the underlying technology, or standards used”.35 Another player noted that “outside Europe, market conditions are not uniform, (e.g. the ISO 20022 messaging standard is not uniformly adopted across the globe) and vary from country-to-country with different standards and regulations”.36 Similarly, customers indicated that “at global level there are differences in terms of standardization due to different regulations and customer behaviours” and that “the ISO20022 is not yet globally used everywhere”.37

37. It follows that both customers and competitors consider that the level of standardization at global level is still rather low.38

38. Second, the Commission found that market conditions are not homogeneous across the globe. A large majority of respondents (including both customers and competitors) consider that, as a result of the above lack of standardization, the competitive dynamics and landscape differ depending on the geographies.39 For instance, a market participant explained that “the competitive landscape is generally different in Europe and in Asia because in each specific market, a supplier needs to have proven experience and references, taking into consideration the market features and the specific regulations”.40

39. In this respect, the Commission notes that, while the elements in the Commission’s file confirm that A2A CIS providers compete, to some extent, across the globe, they also suggest that participating in tenders involves significant costs and technical or legal barriers for non-EEA bidders and may take up several years. For example, according to a competitor, “albeit non- European players […] may participate in EEA/UK tenders and could potentially enter the EEA/UK market for A2A CIS, they currently exert limited competitive constraints in the EEA/UK because (i) they lack local knowledge and footprint, which are paramount, and (ii) they offer A2A CIS solutions that are not SEPA compliant.”41 Other players indicated that “the process of participating in a tender is in itself highly complex, expensive and time consuming”.42

40. Contrary to what the Parties argue, the mere participation of non-EEA players in the RFI phase of EEA tenders for the provision of A2A CIS does not disprove the above.43 Indeed, according to the Parties themselves “it is the RFP process […] that is the time-consuming element”.44 , The RFP phase is also much more costly: according to Annex 6.57 to the Form CO, the costs incurred by the Target for the participation of the RFP phase can be up to […] higher than the costs incurred for the RFI phase.45 This is confirmed by a competitor, which explained that “the investment required for the RFI phase is rather low, contrary to the RFP phase, which requires significant investments and the constitution of a dedicated team”.46 The Parties also admit that “tender processes have become more complex over time and hence newer process are more costly” and Mastercard indicates that the participation in a single tender can cost […]. Moreover, the bidding data submitted by the Parties shows that non- EEA players are rarely shortlisted (i.e. invited to the RFP phase) in EEA tenders and that, conversely, EEA players have a very limited track record outside of the EEA.47

(C.ii) The exact geographic of the A2A CIS markets in the EEA is unclear

41. The results of the market investigation are not conclusive as regards the exact geographic scope of the A2A CIS markets in the EEA.

42. On the one hand, several elements suggest that the A2A CIS are no longer national in scope and could be potentially regional (e.g. pan-Nordic) or EEA-wide.

43. First, in recent years, the provision of A2A CIS in the EEA has been increasingly governed by international standards (e.g. the messaging standard ISO 20022). In particular, respondents emphasized the role of the SEPA48 and the European Payment Council (“EPC”)’s payment schemes49 in the increasing standardisation and competition in the EEA. It follows that customers and competitors generally consider that the provision of A2A CIS is relatively standardized at EEA level.50

44. Second, some recent tenders for the provision of A2A CIS took place at supranational level, such as the pan-Nordic level Layer 1 tender issued by P27 in 2018 and the pan-European tender organised by EBA Clearing in 2015.51

45. Third, EEA customers do not always require A2A CIS providers to have a local presence at national level. For instance, […]. An EEA customer also explained that datacentres are not always needed at national level but should be “at least located in the EEA for regulatory reasons and technical limitations (having data centres located too far away could undermine the processing of instant payments)”.52

46. Fourth, the main EEA providers of A2A CIS, including the Parties, compete across the EEA.53

47. Finally, customers consider that competitive dynamics are rather homogenous across the EEA. While competitors disagree with this statement, they share the customers’ views that competition for the provision of A2A CIS is homogeneous in the Nordic region (due notably to the P27 project).54

48. On the other hand, other elements in the file also suggest that the geographic market could still be national.

49. First, although the level of standardization in the EEA is higher than in other geographies, several competitors and customers stressed the “lack of interoperability across Europe” which, according to them, reveals “a lack of standardization (even in Europe)”. Another market participant explained that “in EEA, SEPA has achieved a high level of standardization, but even here there are differences in implementation due to different interpretation of SEPA Implementation Guidelines or because some aspects of processing are left open to the market”. As a result, competitors generally expressed the view that competition is not homogeneous in the EEA.55

50. Second, many market participants stressed the importance of having a local footprint due to the existence of national specificities and the need to tailor the A2A core infrastructures to meet specific customer needs and local requirements/specificities. For example, a competitor explained that “even in Europe, [A2A] core infrastructure solutions are highly customised to local market dynamics”.56 Similarly, another player stressed the “existence of local specificities/requirements (e.g. legal requirement for payments data to be held in data centres located in the same country/region)” and the fact that “consumers’ habits remain very different from one country to another (including in the EEA). As a result of the above, it is important to have local presence/footprint and, depending on the region/country, the competitive dynamics/conditions may differ (including in the EEA)”.57

51. In this respect, some elements in the file suggest that the local footprint may be more important for managed services than for software services. For instance, according to a competitor, the local footprint is “of paramount importance, especially for managed services (providers being usually required to operate the system locally notably for data privacy constraints)” and that “local presence is, to some extent, less relevant for the provision of software-only solution”.58

52. Finally, the Commission notes that the Parties themselves acknowledged that it is an “inherent part of any A2A CIS providers’ business model to understand the particularities of local markets, obtaining regulatory approval and building up working relationships with the local national bank”,59 which is also corroborated by their internal documents.60

(D) Conclusion

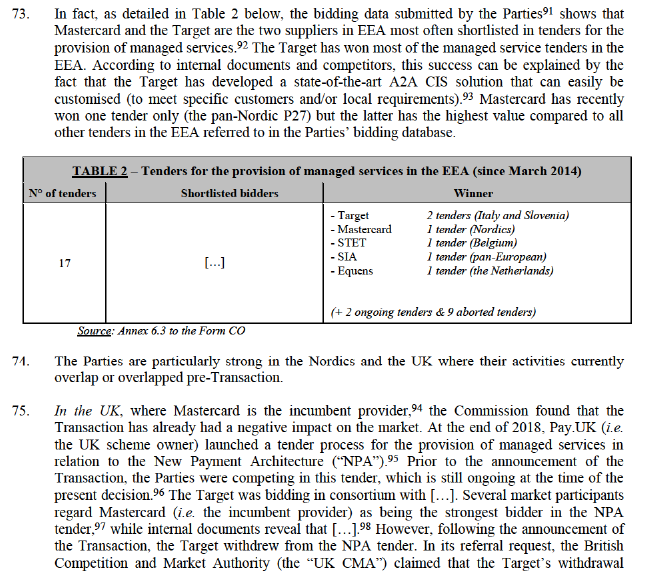

53. Based on the results of the market investigation and for the purpose of this decision, the Commission considers that it can be left open whether the A2A CIS markets are national, regional within the EEA or EEA-wide in scope as these alternative geographic market delineations do not affect the Commission’s conclusions regarding the compatibility of the Transaction with the internal market.

3.1.3. Competitive assessment

3.1.3.1. The Parties’ views

54. The Parties submit that the Transaction does not give rise to competition concerns regardless of the exact scope of the A2A CIS market. Their main arguments are summarized below.

55. First, the Parties submit that, post-Transaction, the new entity would face significant competition in the EEA from a wide range of competitors with relevant capabilities across both managed services and software-only solutions. In particular, over the period 2014-2019, the Parties have identified 21 competitors having participated in EEA tenders for the provision of A2A CIS. The Parties note that several of these rivals have been shortlisted and have won at least once.61

56. Second, the Parties argue that the growing trend towards the constitution of bidding partnerships (or consortia) by A2A CIS providers favours competition. Consortia allow A2A CIS providers (i) to participate in tenders for projects that they would not be able to run on their own or (ii) to improve their offer and, thus, their chances to win (by e.g. partnering with a local partner). The Parties also note that sometimes the creation of consortia is even encouraged by A2A CIS customers.62 In this context, the Parties submit that, when assessing the number of credible players currently active on the market, the Commission should not only consider players able to bid on their own but should also take into consideration consortia. They also submit that bidding in consortia allows providers unable to bid on their own to progressively gain expertise and build a track record.

57. Third, the Parties consider that they are not each other’s closest competitors in the market for the provision of A2A CIS. This, according to them, is corroborated by the bidding data. In terms of offerings, the Parties observe that their products are largely complementary: [Parties views on how their products compare to each other].63

58. Fourth, the Parties consider that A2A CIS customers play a critical role in ensuring an adequate level of competition within the market. These sophisticated customers have the relevant expertise to design competitive tender processes and generally extend the invitation to a large number of providers, including the possibility to participate in consortia. In addition, the Parties submit that customers’ capability to develop A2A CI solutions in-house further exerts significant competitive pressure on A2A CIS providers.64

59. Finally, the Parties consider that the market for A2A CIS is characterised by relatively low barriers to entry and to switching. In particular, they note that customers often impose transitional arrangements on incumbent providers to facilitate the switching to new providers. They also observe that increasing standardization facilitates market access.65

3.1.3.2. The Commission’s assessment

(A) Preliminary remarks

60. As a preliminary remark, the results of the market investigation, do not materially differ depending on the EEA country or region concerned.66 Although national or regional specificities exist (with e.g. different incumbent providers and specific local requirements), the main characteristics of supply and demand in the A2A CIS markets can be described along the same set of dimensions across the EEA. Therefore, unless otherwise specified, the findings of Section 3.1.3.2 (regarding e.g. competitive landscape, closeness of competition, barriers to entry and switching) do not materially differ depending on the geographic market at stake.

61. In addition, as explained in Section 3.1.1 above, A2A CIS markets are essentially bidding markets where competition primarily takes place during the tender processes for the award of contracts with payment scheme operators. Moreover, the latter typically award their contracts to a single successful bidder (“winner-takes-all” principle). In this context, the Commission considers, in this case, that the number of credible competitors is a better metric of market power than market shares (at a given date), because momentary market share figures are unlikely to give reliable indications as to how competition will unfold when a new tender comes up).67 The above is not disputed by the Parties.68 In this context, the Commission’s assessment will focus on the number of alternative credible competitors remaining active on the A2A CIS markets post-Transaction.

(B) Market for the provision of managed services

62. For the reasons set out below, the Commission finds that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the provision of managed services in the EEA under all plausible market definition.

63. First, the number of credible players able to bid on their own for the provision of managed services in the EEA is limited. In this market, the elements in the Commission’s file, including the feedback received from the market investigation, as well as the Parties’ internal documents and bidding data, revealed that the Transaction would lead to the reduction in the number of credible competitors from five to four, the Parties’ main and only credible competitors in the EEA being Equens, SIA69 and STET.70

64. In fact, many of the players mentioned in the Form CO (i) do not consider themselves as competitors of the Parties71 and (ii) are perceived by market participants as being neither credible72 nor competitive73 providers of managed services in the EEA. Several respondents also stressed that the “number of managed service providers [is] more restricted” than for software- only solutions and that “very few providers offer Managed Services”.74

65. This is also corroborated by the Parties’ internal documents, which suggest that several players mentioned in the Form CO are not active or credible in managed services. For example, the Parties’ internal documents (i) qualify […] as “software vendor”;75 and state that (ii) […];76 that (iii) […];77 and that (iv) […].78

66. Similarly, the bidding data submitted by the Parties79 shows that, while many players are participating in the RFI phase of tenders for the provision of managed services,80 very few have been shortlisted at least once (namely […]81) and (ii) only three of them (i.e. Equens, STET and SIA) have won at least one tender82 (see Table 2 below).

67. Second, although the market investigation confirmed that it is common to bid in consortia when participating in tenders for the provision of managed services, it also revealed that the competitive constraints exerted by consortia in A2A CIS tenders are more limited than suggested by the Parties.

68. On the one hand, the results of the market investigation suggest that such consortia allow competitors that would not have the capabilities to run a project on their own to leverage the footprint or the specialized capabilities of third parties to submit credible bids.83 Some respondents also confirmed that consortia may compete on an equal level with providers bidding on their own.84

69. However, on the other hand, the Commission found that setting up consortia may be difficult since some of the components required to provide managed capabilities are “proprietary or complex” and, thus, hard to find on the market.85 The market investigation also suggests that consortia are not relevant for all tenders and mainly concern large and complex projects, which are less common. For smaller and less sophisticated tenders, consortia are primarily justified by the need to acquire the required local footprint, rather than the need to acquire capabilities that are missing in-house.86 Moreover, several respondents stressed that consortia may be riskier and more complex, which can affect the competitiveness of the bid. For example, a customer explained that an A2A CIS provider bidding on its own “offers “one-stop-shopping”: avoiding the need to run multiple procurement processes, enabling less complexity in the contractual constructions without back-to-back agreements and multi-vendor governance, and a more stable and secure delivery of procured services.” Similarly, another customer stated that a “consortium is less competitive, due to the division of tasks and responsibilities between companies and because of the mixing of different technologies.” Similarly, another competitor stated that “it is not easy to set up a consortium to participate in an A2A CIS tender (and be successful)” and that a “fully integrated solution is inherently lower risk than a partnership”.87 The Commission also observes that, albeit bidding in consortia might facilitate, over time, the emergence of new credible stand-alone providers of managed services in the EEA (by allowing players unable to bid on their own to progressively gain expertise and build a track record), this would necessarily take time and depend on the ability of these players to develop the missing managed service capabilities in-house.

70. In view of the foregoing, the Commission considers that the existence of consortia is not sufficient to compensate the limited number of credible competitors currently able to bid on their own for the provision of managed services in the EEA.

71. Third, the Commission found that the Parties are strong competitors in the EEA. Market participants perceive Mastercard as the most competitive player in the EEA, while the Target’s competitiveness is similar to or slightly better than the other main players (i.e. Equens, SIA and SET).88

72. This is also supported by the Parties’ internal documents. For example, an internal presentation of the Target reads: […].89 Similarly, another internal presentation refers to […] and to the fact that […].90

weakened […], which had to find an alternative partner (namely […]), at short notice in the middle of the tender process.99 The Parties challenge this view, which is however corroborated by their internal documents. For instance, […].100

76. In the Nordics, the Target is the incumbent provider of the existing domestic A2A core infrastructures in Norway and Denmark, whereas Mastercard won in 2019 the P27 Layer 1 tender for the future provision of managed services at pan-Nordic level. The market participants […] confirm that the market in the Nordics is expected to migrate within a few years from existing domestic A2A core infrastructures (including the ones operated by the Target) to the new P27 pan-Nordic A2A core infrastructure,101 which is expected to be more innovative and cheaper (owning to economies of scale). In this respect, the Commission notes that the above tender has been awarded prior the Transaction and that the progressive phasing out of the domestic A2A core infrastructures currently managed by the Target largely reflects the “winner- takes-all” feature of the A2A CIS markets, and that there is thus no merger specificity in this respect. That being said, the Commission also notes that (i) there is an intrinsic degree of uncertainty as to whether the P27 project, which is not operational yet, will go forward for the entire Nordic region, including Norway and that (ii) the launch of P27 is subject to a merger filing and clearing licence approval. In this context, the Commission considers that the reduction in the number of credible providers of managed services for future A2A CIS tenders in the EEA could potentially affect the Nordics region.

77. Fourth, albeit the market investigation suggests a certain complementarity between the Parties’ activities (Mastercard is characterised by a large geographic footprint and a rather dated technology, while the Target is perceived by the market as an innovative and regional player),102 market participants consider that the Parties are close competitors (and potentially each other’s closest competitors according to their rivals).103 This conclusion is also supported by the Parties’ (i) internal documents, where Mastercard and the Target are identified as […],104 and (ii) bidding data (see Table 2 above).

78. Fifth, the elements in the Commission’s file suggest that one of the three credible competitors active in the EEA, namely STET, exerts limited competitive constraints on the market. This is notably illustrated by […].105 Several competitors share the above view, submitting that STET “focuses its activities in France and Belgium and is reluctant to bid in other EEA/UK countries”.106 One competitor even indicated that it “does not consider STET […] as [a] real competitor[]” since the latter “does not show a strong appetite to compete outside of French speaking countries”.107 The above does not mean that STET never participates in tenders outside of France and Belgium ([…]) but that its participation in A2A CIS tender across the EEA is much more limited than the Parties, SIA and Equens.

79. Sixth, the market investigation largely confirmed that barriers to entry are high for the provision of managed services, requiring “capabilities (expertise, track record, security…) that cannot be acquired either easily or in the short-term”.108 In addition to the track record and expertise, the main barriers to entry appear to be the need to have local or regional footprint depending on the tenders’ requirements (e.g. some tenders require to have datacenters at national, others at regional level), the investments required and the duration of the contracts.109 Moreover, although customers may impose transitional arrangements in their contracts, switching A2A CIS provider remains difficult. In fact, virtually all competitors and customers consider that switching is either difficult or very difficult and very few customers have switched suppliers in the last 10 years (including as a result of a new tender).110

80. Seventh, the market investigation did not support the Parties’ claim that A2A CIS customers have significant countervailing buying power. In particular, a large majority of customers indicated that they are not able to develop A2A CIS solutions in house.111

81. Finally, many competitors expressed competition concerns regarding the impact of the Transaction in the EEA, especially in the Nordics where most of them anticipate a negative impact of the Transaction.112

82. Competitors are notably concerned by the fact that the market is “already, pre-Transaction, quite concentrated with a limited number of providers and that the Transaction would further reduce the number of players in the EEA”.113 One of them also stressed that “the Transaction already had a negative impact on the market, distorting competition in Europe”, in particular in the UK as a result of the Target’s withdrawal from the ongoing NPA tender (see paragraph 75 above).114

83. In addition to the above, several players raised a risk of foreclosure explaining that the combination of Mastercard’s financial strength and card payment activities with the Target’ state of the art A2A solution (see footnote 93 above), and the Parties’ respective track records, will significantly strengthen the leading player (Mastercard) and that “post-Transaction, it might be difficult for the rival […] to be as competitive as the Parties”.115

84. In particular, one competitor stressed that, post-Transaction, it will very difficult to “successfully bid […] especially in the Nordics”, where “the combination of the Target’s A2A payment activities and Mastercard’s card payment activities would enable the new entity to control the whole financial infrastructure in the Nordics and, thus, to potentially foreclose its competitors.” This respondent considers that the Transaction constitutes a “dangerous move for the market” on the ground that, post-Transaction, “Mastercard might offer price below cost in the A2A space, by using its card payment revenues to cross-subsidize its A2A activities”, which would allow the Notifying Party to “end up dominating both the card-based and A2A payment systems”. In other words, according to this player, Mastercard has the ability and incentive to leverage its strong market position on the card payment markets to expand its activities in the A2A space. According to this player, this is notably illustrated by the fact that, already pre-Transaction, “Mastercard is very aggressive in the A2A payment space, acquiring A2A companies (such as Vocalinks and the Target) at a very high price (above market price) and bidding at very low price (and potentially below costs) ([…]) to gain strong market positions” in the A2A payment space in order to “preempt the decline of card payments”.116 In this respect, the Commission notes that […].117

85. Although most customers did not complain about the Transaction, some of them share the competitors’ views. In particular, one customer stated that (i) apart from the Parties, “the other suppliers that participated in [its] tendering process [for managed services] do not offer a suitable alternative” and that (ii) Mastercard’s expansion into the A2A space could be detrimental for competition, suggesting that Mastercard could potentially “give priority” to cards over instant payments, “making the latter less attractive as the method for displacing cash”. 118

86. In view of the above considerations, the Commission concludes that the Transaction raises serious doubts as to its compatibility with the internal market and the functioning of the EEA Agreement with respect to the overlaps between the Parties’ activities in the market for the provision of A2A CI managed services under any plausible geographic markets (i.e. national, regional or EEA-wide).

(C) Market for the provision of software-only solutions

87. Albeit some of the findings described in the previous section also apply to the provision of software-only solutions (i.e. the Parties are strong players and perceived as close competitors also in the provision of software-only solutions), the results of the market investigation revealed that the provision of such solutions presents different features allowing the Commission to exclude serious doubts on this potential market.

88. First, the market investigation confirmed that a sufficient number of credible providers of software-only solutions would remain active in the EEA post-Transaction. Indeed, the Commission found that the number of players in the software-only market is higher than in the market for managed services. The differences in the competitive landscape are confirmed by the market investigation results, in which the majority of competitors indicated that A2A CIS providers do not have typically the ability to provide both managed services and software-only solutions.119 One customer mentioned that “based on [its] experience […], very few providers offer Managed Services while all of them have software-only solutions available”,120 explaining that “during [its] tender process [for the provision of managed services], big majority of participating tenderers only had the capability of Software-only solutions”.121 Another customer confirmed that “there are more providers in the software-only solutions market segment than in the managed services market”.122 In the software market, the Parties face several credible players, including Equens, SIA/EBA Clearing, but also players that are not active (or not perceived as credible) in the market for managed services, such as Montran, ACI and, to a more limited extent, IBM.123 For instance, according to the Parties’ bidding data, which underestimate the winning rates of some competitors,124 IBM and Montran were able to win tenders for software-only solutions in, respectively, Spain and Portugal (IBM) and Bulgaria and Romania (Montran). In addition to these players, other providers (such as ACI)125 have the capability to offer software-only solutions in the EEA and are perceived by market participants as being credible. As a result of the above, the competitive landscape for A2A CI software-only solutions appears more dynamic than for managed services, with a sufficient number of competitors remaining post-Transaction.126

89. Second, the market investigation revealed that barriers to entry are lower in software-only solutions. Market participants explained that providing software-only solutions requires less expertise and responsibilities. In comparison with providing managed service solutions and referring to the provision of software-only solutions, one competitor mentioned that “managing a service implies much wider responsibilities and different type of expertise than just delivering a product”.127 The need for a local (national or regional) footprint also appears to be less prominent, having a local footprint being not considered essential for a credible bid in tenders for software-only solutions.128 For instance, a competitor explained that there was no requirements for a local footprint in the recent Bulgarian tender for the provision of software- only solution.129 Another competitor added that “it is easier to supply software-only solution as track-record and experience in managing the solution will not be a factor in the tender.130” Moreover, A2A CIS providers generally indicated that their respective software solutions could be easily customized to be adapted to different geographies and requirements. Therefore, barriers to entry in this market appear lower than in the market for managed services, allowing more players to present credible offers and, eventually, win tenders for the provision of software-only solutions.

90. The higher number of current credible players for A2A CI software-only solutions and the lower barriers to entry render this market more dynamic and competitive compared to the market for managed services.

91. In view of the above considerations, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market and the functioning of the EEA Agreement with respect to the overlaps between the Parties’ activities in the market for the provision of A2A CI software-only solutions in the EEA, under any plausible geographic market definition (i.e. national, regional and/or EEA-wide).

3.1.3.3. Conclusion

92. In view of the above considerations, taking into account the market investigation and all the evidence available, the Commission concludes that the Transaction raises serious doubts as to its compatibility with the internal market and functioning of the EEA Agreement with respect to overlaps between the Parties’ activities in the EEA market(s) for the provision of A2A CI managed solutions in the EEA under any plausible geographic market definition (i.e. national, regional and/or EEA-wide).. The Commission notes that, in relation to the market for the provision of A2A CI software-only solutions, due to the presence of a sufficient number of competitors post-Transaction and the lower barriers to entry, no serious doubts arise. In any event, the final commitments offered by the Parties fully address the competition concerns identified in the decision in relation to the provision of A2A CI managed services in the EEA (see Section 4 below).

3.2. A2A Payment Services

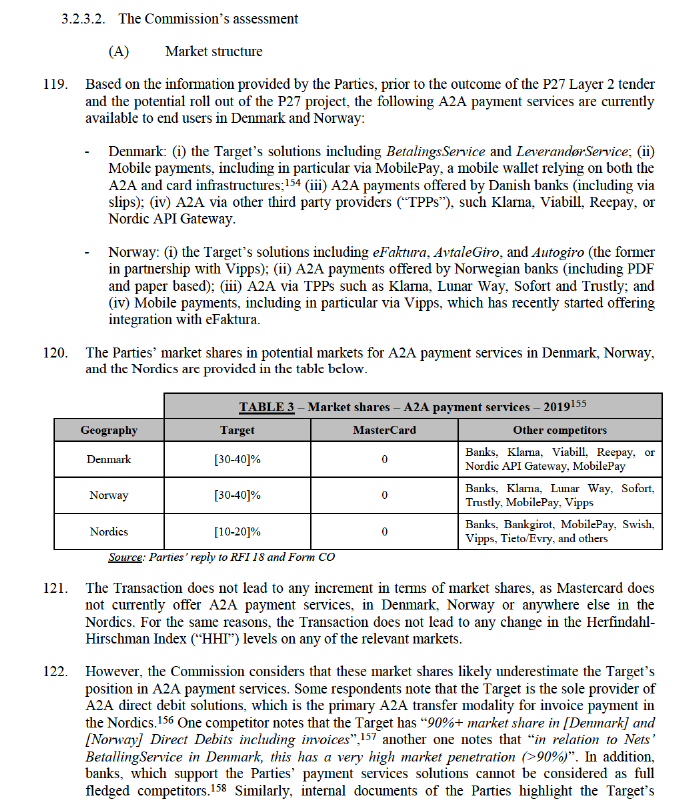

3.2.1. Overview of the market and the Parties’ activities

93. A2A payment services are end-user services/applications, using an A2A core infrastructure, to transfer money from one bank account to another.131 A2A payments are typically made from consumers to businesses ("C2B") or between businesses ("B2B"). A2A payment services are mainly used for payments that are recurring (e.g. monthly utilities bill) but can also be used for the payment of one-off invoices.132

94. In this area, the Target offers several A2A payments solutions:

- in Denmark it offers solutions including (i) BetalingsService, a direct debit payments solution designed for one-off and recurring invoice payments from consumers to businesses (C2B); (ii) LeverandørService, a direct debit payments solution designed for one-off and recurring payments from business debtors (B2B); as well as ancillary services, and

- in Norway it offers solutions including (i) eFaktura, a corporate e-billing service (i.e. designed to receive and pay bills electronically) covering both B2C and B2B transactions (in partnership with Vipps, a Norwegian mobile payment application); (ii) AvtaleGiro, a consumer bill payment and direct debit payments solution; (iii) Autogiro, a corporate bill payment and direct debit payment solution for B2B; as well as ancillary services.

95. In these countries, the Target is the incumbent player, having provided the dominant A2A payment services solutions for over 40 years in Denmark and over 30 years in Norway. In addition, the Target offers OmniBilling, an e-billing solution for end-customers both on the creditor and debtor side, […].

96. Mastercard does not currently offer A2A payments services in Denmark, Norway or more generally in the Nordics. However, Mastercard does offer certain A2A payment

97. The Parties are currently competing for the ongoing P27 tender for A2A payment services in the Nordics (the “P27 Layer 2 tender”). The P27 project currently aims at covering Denmark, Finland and Sweden. Norwegian banks were also initially part of the project but withdrew from it in 2018. However, the Parties still expect that […].133 The P27 Layer 2 tender intends to capture use cases currently covered by the different (national) bill payment legacy solutions throughout the Nordics (including A2A payment solutions such as BetalingsService in Denmark), such as direct debit payments for B2B and C2B transactions. It also aims at covering additional payment scenarios such as: (i) invoices currently not processed through an end-to-end bank-served solution; (ii) recurring payments processed via card-on-file solutions (e.g. online subscriptions); and (iii) one-off e-commerce and Point-of-Sale (“POS”) payments currently addressed primarily by card payment services providers (merchant acquirers). […] The tender process was put on hold in June 2020 and the RFP may be sent out in the late autumn of 2020.

3.2.2. Market definition

3.2.2.1. Product market definition

(A) Commission’s precedents

98. The Commission has not specifically assessed the relevant product market definition for A2A payment services in the past. However, in case M.2567 – Nordbanken/Postgirot, the Commission assessed a market for “services provided by payment systems”, including A2A domestic payment services, by way of so-called “giro payment systems services” in Sweden. The Commission considered the market for such services as potentially distinct from bilateral bank transactions.134

(B) The Parties’ views

99. In the absence of Commission precedents, the Parties submit that, under the narrowest possible market delineation, A2A payment services would be part of the market for invoice payment services (i.e. services enabling remote payments of invoices), including both A2A payment services and recurring card payments, as they are both used interchangeably by individuals and businesses to pay bills.135

100. Recurring card payments cover both withdrawals at regular intervals and payments that recur when the customer decides to use the relevant service, and are used for periodic payments or subscriptions, for instance towards telecom operators, transport companies and streaming services providers. Such services are usually provided by merchant acquirers (such as Adyen, Worldpay, Worldline, or Nets).136

(C) The Commission’s assessment

101. The market investigation did not fully support the Parties’ claims that recurring card-based payment services and A2A payment services form part of a single product market for invoice payment services. Competitors and customers expressed differing views on this part. To the contrary, some elements of the market investigation clearly suggest that A2A payment services form part of a distinct product market from recurring card payment services.

102. While responding competitors indicated that A2A payment services and recurring card-based payment services are interchangeable for EEA customers (financial institutions or end users), this was contradicted by a large majority of responding customers.137 One customer notes, for instance, that “cards are rarely used for payment of invoices (e.g. monthly utilities) - A2A payment instruments (SCT and SDD) are the preferred methods”. 138

103. A significant share of responding customers highlight that competitive dynamics are different between A2A and recurring card-based payment services, in particular due to differences in terms of technologies, prices and the role of international card schemes.139 Only a minority of responding competitors indicate competitive dynamics differ between these segments, and one of them notes there is increased convergence across segments, stating that “dynamics are different today, but with the increasing demand and availability of instant payments, open banking and mobile payments solutions, they are becoming more blurred”.140

104. Regulatory requirements may also vary between recurring card-based payment services and A2A payment services, in particular in terms of fees regulation. For instance, one competitor notes that “providers of A2A-based IPS (such as direct debit solutions, payment slips) are allowed to apply a surcharge freely, which is not the case for card-based IPS for which the application of surcharge is banned”.141 Another competitor notes that “some A2A payments are today subject to deeper checks like sanction screening and transaction monitoring”.142

105. The market investigation also indicated that a segmentation based on the type of transactions concerned (B2B, C2B, or C2C) or A2A payment methods (direct debit, payment slips, account- to-account payments provided by banks, and mobile payment solutions) could be relevant. Indeed, the feedback received from the market and the review of the Parties’ internal documents suggest that the competitive landscape and dynamics for the provision of A2A payment services differ significantly depending on the type of transactions concerned or A2A payment method.143

(D) Conclusion

106. For the purpose of this decision, the exact product market definition for the provision of A2A payment services and the question of whether they are part of a wider market for invoice payment services including recurring card-based payments, or segmented based on the types and methods of A2A transactions concerned can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition.

3.2.2.2. Geographic market definition

(A) Commission’s precedents

107. The Commission has not specifically assessed the relevant geographic market definition for A2A payment services in the past.

108. In its past decisional practice relating to services provided by payment systems, the Commission has consistently considered markets to be national or wider in scope, but ultimately left the decision open.144

(B) The Parties’ views

109. In the present case, the Parties argue that the market for invoice payment services is no longer national but regional, covering the entire Nordic region (where the Parties’ A2A payment service activities overlap). In particular, the Parties submit that the Nordic region is increasingly integrated with the progressive removal of national regulatory and technical barriers and increasing cross-border activities, as illustrated by the P27 project.145

(C) The Commission’s assessment

110. The market investigation did not fully support the Parties’ claims that the markets for A2A payment services were regional in scope. In fact, the market investigation indicated that markets for A2A payment services (regardless of the type of transaction or A2A payment method concerned) are likely national in scope.

111. The market investigation indicated that there is a relatively low level of standardisation of invoice payment services at supra-national level, both in the EEA and in the Nordic region.146 The typical geographic scope of invoice payment services is national according to a large majority of respondents, meaning such solutions can only be used in a given country.147 Providers of payment solutions indicate that their solutions are largely standardised, but require local customisation. This may require providers of invoice payment solutions to work together with local financial services institutions such as banks. One provider of such services in the Nordic stated for instance that “[their] A2A solution has been developed specifically and requires an initial collaboration with banks operating in the country where [they] offer [their] services […].”148

112. Trans-border competition is perceived by most market participants (customers and competitors alike) as limited, including competition from neighbouring countries.149 As a result, the markets are unlikely to be EEA-wide in scope. Some respondents note that the situation may be different in the Nordics. One competitor notes that “[i]n large economies, there is little competition across invoice payment services. In smaller nations, such as the Nordics and Central Eastern Europe, there is more competition across national boundaries”, another one that “[t]he Nordics are more harmonized as a region”. However, cross-border transactions are considered as more complex, in particular among different currencies,150 and all Nordic countries currently use different currencies. Going forward, the pan-Nordic scope of the P27 project, which will include A2A payment services in its scope, may indicate that A2A payment services in the Nordics will become increasingly regional in scope.

113. For card-based invoice payment services specifically, the market investigation indicates that competitive dynamics are usually more homogenous at supranational level, as they follow the rules set by international card schemes, such as Mastercard or Visa. One competitor notes for instance that “[e]nd user UX [User Experience] seems more standardised with card based payments”, a customer states that “the level of standardisation is higher on a cross country level for card based payments services, as these services are regulated by one common set of rules set by the scheme”, and another one that “[c]ard payments are very standardized and users can rely on the fact that they will be able to make a payment with their card regardless of the country they are in and country where the card was issued”.151

(D) Conclusion

114. For the purpose of this decision, the exact geographic market definition for the provision of A2A payment services can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition (national or regional at the Nordic level).

3.2.3. Competitive assessment

115. The Transaction gives rise to affected markets for invoice payment services and A2A payment services in the Nordics where horizontal overlaps arise.

116. As none of the Parties is active in recurring card-based payments, the Commission’s assessment will primarily focus on the narrower markets for A2A payment services.

- In Denmark, where the Target is the incumbent provider of A2A payment services, in particular with its BetalingsService and Leverandørservice solutions. Moreover, both the Target and Mastercard submitted a bid for the ongoing P27 Layer 2 tender.

- In Norway, where the Target is the incumbent provider of A2A payment services, in particular with its eFaktura, AvtaleGiro, and Autogiro solutions. Moreover, both the Target and Mastercard submitted a bid for the ongoing P27 Layer 2 tender, […].

- In the Nordic region, including Denmark, Norway, Sweden and Finland (all at least potentially included within the scope of the P27 project) due to the Target’s incumbent position in Denmark and Norway, and the Parties’ bids for the P27 Layer 2 tender. At Nordic level, the Target’s market share is currently below 20%, i.e. technically below the affected market threshold. However, the competitive assessment will consider the Nordic region in light of the P27 Layer 2 tender.

3.2.3.1. The Parties’ views

117. The Parties indicate that Mastercard does not currently compete in the Nordics in the area of invoice payment services, and there is therefore no overlap between the Parties’ activities. The Parties also consider that the Transaction would not give rise to significant anti-competitive effects on the invoice payment services markets, even if Mastercard was to be considered as a (potential) competitor to the Target in invoice payment services. The Parties argue in particular that (i) competitors, including providers of A2A payment transfers such as banks, will maintain sufficient competition on the merged entity post Transaction; (ii) […]; (iii) […].152

118. In a supplementary submission focusing specifically on the impact of the Transaction in Denmark,153 the Parties further argue that (i) […], and that (ii) […].

market share of [70-80]% and [50-60]% in Denmark and Norway respectively for A2A payment services for C2B transactions.159

(B) A2A payment services markets present some characteristic of natural monopolies

123. Markets for A2A payment services are largely “winner-takes-all” markets. In addition to the payment services offered directly by the banks or new services, such as mobile payments, offered by fintech providers (which currently concern a much more limited number of transactions in the Nordics), there is typically one dominating provider of A2A payment services per EEA country, besides banks that provide A2A transfer services. The Target is the incumbent provider for such services in Denmark and Norway, where it is currently the only market player offering specific transfer modalities such as direct debi

124. A2A payment solutions are two-sided in nature, connecting creditors and debtors. As a result, individuals and businesses favour using the solutions with the widest target base, which complicates the development of multiple similar solutions in parallel. The market investigation, as well as the Parties’ own submissions, confirm that A2A payment services are characterized by strong network effects.160

125. In that respect, bank support and integration has proven important historically to the development and adoption of successful A2A payment services. A2A payment services sponsored by banks typically expand quickly to become the de facto standard. For instance, MobilePay exited the Norwegian market after the launch of Vipps, which was supported by Norwegian banks and gained more traction in the country.161 Similarly, the Target’s successful position in Denmark results from its cooperation with local banks. In 2014, Nets entered into a cooperation agreement with around 21 Danish and foreign banks under which Nets committed to […]. These same banks are largely expected to support the P27 initiative, and some of them are even driving the project.

126. Markets are also tender-driven, with procedures typically involving RFIs and RFPs to multiple service providers as the standard procurement modalities according to the majority of respondents to the market investigation. However, vendors may be selected based on long-term vendor relationships.162 The markets also involve long product lifecycles, as the retained solution becomes a de facto standard for A2A payment services. One competitor notes for instance that it is “[d]ifficult to replace something which is already accepted and all kind of interfaces are already in place (e.g. ERP system)”, another one qualifies A2A payment services as “bid-driven market with long selling lifecycle”.163 This implies that, similarly as for A2A CIS, competition for A2A payment services largely takes place for the market, as opposed to in the market (even if some competition takes place at the latter level, primarily with bank and fintech players).

127. These characteristics of A2A markets explain why the markets, including in Denmark, Norway and the Nordics are not perceived by a significant number of competitors as involving a sufficient number of suppliers or a large degree of competition,164 and characterized by important barriers to entry or expansion.165

(C) The Parties are competitors on the market as evidenced by their participation in the P27 Layer 2 tender

128. Contrary to the Parties’ claim, Mastercard cannot be considered only as a potential competitor of the Target. The Parties both currently compete in the P27 Layer 2 tender. As mentioned above, A2A payment services markets are largely characterized by markets with competition for the market. As a result, Mastercard and the Target should be considered as actual competitors for the provision of A2A services in the Nordics (including Denmark and potentially Norway).

129. Mastercard is not perceived as one of the top players in the A2A payment services field by customers. Locally, the main market players mentioned include (i) the Target, Tieto/Evry and Bankgirot in the Nordics, (ii) the Target and MobilePay in Denmark, as well as (iii) the Target, Tieto/Every and Vipps in Norway. Mastercard is not mentioned by any customer as a national or regional player in the Nordic.166 However a significant number of competitors see Mastercard as a top supplier of A2A payment services at EEA level, and a material number of competitors (who participated in the P27 Layer 2 tender) consider the company to be an important player in either Denmark, Norway or the Nordics more broadly.167

130. The market investigation indicated that the Parties are perceived as having different commercial profiles. While the perceived key strength of Mastercard is its global card presence and related brand recognition, the key strengths of the Target include primarily its strong presence in A2A solutions in Denmark and Norway.168 However, Mastercard and the Target are perceived as particularly close competitors, in particular by competing A2A players, primarily as a result of the head-to-head competition between the Parties in the context of the P27 Layer 2 tender, in which both Parties are particularly credible bidders.169

(D) The competitive landscape is expected to change drastically following the award of the P27 Layer 2 tender

131. The P27 A2A payment services solution is expected to benefit from the network effects described above, potentially even more so than national solutions due to its wider geographic reach. Adoption of the P27 A2A payment services solution will necessarily take place to the detriment of national solutions, including the Target’s in Denmark (and potentially Norway).

132. […]. An overwhelming majority of respondents to the market investigation indicate that providing A2A CIS is an advantage to succeed in a tender for A2A payment services by the same tender authority. Reasons cited include primarily the ease of integration into the A2A CIS platform as well as “keep[ing] the contractual relationship simple”, or “cost, functionality and operations”.170 […].171 Internal documents also indicate that A2A CIS and A2A payment services form part of the same ecosystem and are closely linked products, both technically and commercially.172 […]173 […]174 Mastercard’s internal documents also estimate that […],175 […]. Furthermore, […].176 Considering […], it further evidences Mastercard’s position as a frontrunner for the provision of A2A payment services in the Nordics.

133. […]. The Target would indeed be able to facilitate (or hinder) the transition from the national A2A payment services (in particular in Denmark) to the pan-Nordic ones following the tender. Internal documents of the Parties reveal that […].177

134. As explained below, while competition between the Parties exists, the Transaction does not appear to restrict effective competition significantly on the relevant markets for A2A payment services, due to the lack of merger-specificity in relation to the tender, and in light of the number of participants involved in the process, as mentioned in Section 3.2.3.2(E) below.

135. The award of the P27 Layer 2 tender to Mastercard […], would lead the Transaction to combine the legacy incumbent player for A2A payment services in Denmark ([…]) and the new solution provider at pan-Nordic level. Both the Parties and respondents to the market investigation expect the pan-Nordic A2A services to be offered following the P27 Layer 2 tender to compete with the domestic A2A payment solutions currently available in the Nordic region, such as the Target’s BetalingsService solution in Denmark.178

136. While competition between the P27 Layer 2 laureate (potentially Mastercard) and the Target’s solutions in Denmark ([…]) may occur, such competition would only take place for a limited period of time, and would unavoidably be resolved in favour of the P27 Layer 2 laureate. While respondents to the market investigation indicate that the precise impact of the P27 Layer 2 tender on the market for payment services remains uncertain at this stage,179 the market features (characterized by strong network effects) and statements by various players indicate that P27 will become the preferred solution for market participants in the Nordics. All respondents to the market investigation expect the P27 Layer 2 services to compete effectively with the A2A payment solutions currently available in the Nordic region (including BetalingsService in Denmark) and in fine replace them.180 This also seems to be the intent of the banks involved in the P27 tender, according to […].181 The same banks currently support the use of BetalingsService in Denmark. This is particularly relevant in light of the importance of network effects and bank support for the provision of successful A2A payment services as detailed in paragraphs 123 to 127 above.

137. In addition, a material number of respondents to the market investigation indicate that Nets’ technology in A2A payment services is dated and that the company is not a strong innovator.182 BetalingsService itself is over 40 years old. Based on the information on the Commission’s file it is likely that customers would switch to the new P27 solutions which is expected to be cheaper (in particular due to economies of scale), more innovative, and include additional features, compared to the legacy Target solutions,183 to the extent that they will remain available.

138. In any event, with regard to Denmark specifically, […]. Internal documents of the Target indeed state that, […]184 […]185 As market dynamics are largely similar in both countries, the same scenario would most likely materialise in Norway should the P27 project cover the Norwegian market.

Figure 1 – Market share projections – P27 and domestic schemes

[…]

Source: Annex 124 to Form CO

139. In that respect, the Commission notes that the award of the P27 Layer 2 to Mastercard, […] would also potentially generate synergies, as it would facilitate operational and technical integration between the different A2A layers (A2A CIS and A2A payment services respectively), which is particularly attractive to financial institutions relying on the platform.186 Furthermore, in that scenario, the Transaction would also generate efficiencies in the sense that it would likely facilitate migration from the legacy national solutions, at least in Denmark (and potentially Norway). Internal documents of the Parties indicate that the Target […].187

(E) There are multiple competitors for A2A payment services in the Nordics

140. There are multiple competitors to the Parties active on the A2A payment services segment.

141. This includes in particular competition for the market, as outlined by the P27 Layer 2 tender process. P27 indicated that this tender is “very competitive” with many credible bidders.188 In addition to the Parties, several other bidders were […] by the tendering authority, and can thus be considered as credible competitors. There is therefore a significant pool of credible players competing against the Parties in the P27 Layer 2 tender.

142. In addition to the core competition for the market for A2A payment services, by way of participation in tenders to operate the main national service, some more limited degree of competition will remain in the market. Such competition results from the activities of fintech players and banks, which are expected to continue offering A2A payment solutions competing with the Target’s in Denmark and Norway, as well as P27’s in the Nordics should it materialise. This is for instance the case of MobilePay in Denmark or Vipps in Norway. Regardless of the P27 Layer 2 tender outcome, more generally, EEA markets for invoice payment services are considered dynamic. The market investigation confirms that there has been recent entry, in particular by fintech players including in the Nordics (with MobilePay in Denmark and Finland, Vipps and Klarana in Norway Swish in Sweden, and Nordic API Gateway in all these jurisdictions).189 Open banking and the implementation of the Directive (EU) 2015/2366 on payment services (so-called “PSD2”) will likely further facilitate entry in this segment. The PSD2 regulatory technical standards, which came into force on 14 September 2019, set out the terms on which financial institutions must provide third parties access to information based on customer payment accounts for a defined set of services (also known as open banking), which should lead to the emergence of additional payment methods and market players.

143. All respondents to the market investigation expect the A2A payment service market to significantly evolve in the next five years, including in terms of competitive landscape and the technology used, in particular due to the expected growth of the markets,190 which may attract additional players to compete at the margin with the merged entity.

(F) Limited concerns expressed by market participants

144. Most respondents to the market investigation expect the Transaction to have a neutral or positive impact on competition for A2A payment services.

145. A material number of competitors expect a negative impact of the Transaction, but these concerns are either not substantiated or do not appear to be merger-specific.191

- Out of the competitors expecting a negative impact in A2A payment services, one considers that the Transaction “may discourage new solutions to establish in Denmark, Norway - as Mastercard will be a huge and very strong competitor”. However, the Commission notes that the network effects identified in the relevant market, and the outcome of the P27 Layer 2 tender necessarily entail that market players will be discouraged from establishing a competing A2A payment service in the Nordics, and that competition is currently primarily taking place for the market.

- Another competitor notes that “[w]ith wider client base, the Target will be providing further standardised services that are easier to exploit by innovators within the ecosystem, reducing cost rather than having to create country and group specific solutions”, which appears to be a concern relating to potential synergies and efficiencies brought about by the Transaction.

- Lastly, another one mentions it is “unable to provide a clear answer to this question [on the impact of the Transaction] as this will depend on the plans that Mastercard has for Nets, and the results of the P-27 overlay services tender in the Nordics”. However, as mentioned above, even in the case Mastercard were to be awarded the P27 Layer 2 tender, the Transaction would give rise to a certain number of synergies and efficiencies.

146. In contrast, customers who responded to the market investigation unanimously consider that the Transaction will have a neutral or positive impact in the Nordic region, as well as in Denmark and Norway.192 Responding customers unanimously consider that there will remain sufficient alternative suppliers of invoice payment services to obtain competitive offers at Nordics level, as well as in Denmark and Norway.193

3.2.4. Conclusion

147. Based on the above considerations, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market in relation to the potential market for the provision of A2A payment services (or the wider market for invoice payment services) in Denmark and Norway or the wider Nordic region.

4. COMMITMENTS

4.1. Framework for the assessment of the Commitments

148. Where a concentration raises serious doubts as regards its compatibility with the internal market, the parties may undertake to modify the concentration to remove the grounds for the serious doubts identified by the Commission. Pursuant to Article 6(2) of the Merger Regulation, where the Commission finds that, following modification by the undertakings concerned, a notified concentration no longer raises serious doubts, it shall declare the concentration compatible with the internal market pursuant to Article 6(1)(b) of the Merger Regulation.

149. As set out in the Commission’s Remedies Notice,194 the commitments have to eliminate the competition concerns entirely, and have to be comprehensive and effective from all points of view.195

150. In assessing whether commitments will maintain effective competition, the Commission considers all relevant factors, including the type, scale and scope of the proposed commitments, with reference to the structure and particular characteristics of the market in which the transaction is likely to significantly impede effective competition, including the position of the parties and other participants on the market.196

151. In order for the commitments to comply with those principles, they must be capable of being implemented effectively within a short period of time. Concerning the form of acceptable commitments, the Merger Regulation gives discretion to the Commission as long as the commitments meet the requisite standard. Structural commitments will meet the conditions set out above only in so far as the Commission is able to conclude with the requisite degree of certainty, at the time of its decision, that it will be possible to implement them, and that it will be likely that the new commercial structures resulting from them will be sufficiently workable and lasting to ensure that the serious doubts are removed.197 Divestiture commitments are normally the best way to eliminate competition concerns resulting from horizontal overlaps.

4.2. Proposed Commitments