Commission, February 6, 2019, No M.9221

EUROPEAN COMMISSION

Decision

CMA CGM / CEVA

Subject: Case M.9221 - CMA CGM / CEVA

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 21 December 2018, the Commission received notification of a concentration pursuant to Article 4 of the Merger Regulation which would result from a proposed transaction by which CMA CGM S.A. ("CMA CGM", France) intends to acquire, within the meaning of Article 3(1)(b) of the Merger Regulation, sole control of the whole of CEVA Logistics AG ("CEVA", Switzerland) by way of public bid announced on 26 November 2018 (‘the Transaction’).3 In this Decision, CMA CGM and CEVA are collectively referred hereinafter as “the Parties”. The undertaking that would result from the Transaction is referred to as “the merged entity”.

1. THE PARTIES

(2) CMA CGM is the parent company, governed by the laws of France, of an international group of companies involved in container liner shipping, port terminal services and, to a much smaller extent, freight forwarding services through its subsidiary CMA CGM Logistics (“CC Log”).

(3) CEVA is a Switzerland-based company that offers a range of services in two severable lines of business: (i) freight forwarding – including air and ocean freight, ground transportation, customs brokerage and other value-added services – and (ii) contract logistics – including warehousing services, transportation, inbound logistics and manufacturing support.

2. THE TRANSACTION

(4) At the time of adoption of this Decision, CMA CGM holds a non-controlling participation of 32.99% in CEVA’s share. CMA CGM intends to have sole control of CEVA by acquiring 100% of CEVA’s outstanding shares by way of public bid. This bid comes as a counter offer to a bid by DSV from Denmark, a close competitor of CEVA, which was rejected by CEVA.

(5) On 24 October 2018, CMA CGM concluded with CEVA a Transaction Agreement, which lays down the main terms and conditions of the transaction. Pursuant to the terms of the Transaction Agreement, on 25 October 2018 CMA CGM disclosed its intention to launch a public tender offer (“PTO”) for CEVA. On 26 November 2018, pursuant to a commitment made in the Transaction Agreement and in accordance with applicable Swiss regulations, CMA CGM made a pre-announcement of the PTO. This pre-announcement is binding insofar as it compels CMA CGM to subsequently launch the PTO.

(6) The Transaction would therefore result in a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

3. UNION DIMENSION

(7) The Parties have a combined aggregate worldwide turnover of more than EUR 5 000 million4 [CMA CGM EUR […] million; CEVA EUR 6 188 million]. The aggregate Union-wide turnover of each of the Parties is more than EUR 250 million [CMA CGM EUR […] million; CEVA EUR […] million], but neither of the Parties achieves more than two-thirds of their aggregate Union-wide turnover within one and the same Member State.

(8) The concentration therefore has a Union dimension within the meaning of Article 1(2) of the Merger Regulation.

4. MARKET DEFINITION

(9) CEVA is active in freight forwarding services and contract logistics services. CMA CGM is also active in freight forwarding services through its subsidiary CC Log. In addition, CMA CGM provides container liner shipping services, which are inputs to freight forwarding services.

4.1. Freight forwarding services

4.1.1. Relevant product market

(10) In previous decisions, the Commission defined freight forwarding as "the organisation of transportation of items (possibly including activities such as customs clearance, warehousing, ground services, etc.) on behalf of customers according to their needs".5

(11) In previous decisions, the Commission also considered possible sub- segmentations of the freight forwarding product market, namely (i) between domestic freight forwarding and cross-border freight forwarding, and, (ii) depending on the modes of transport, by air, land, and sea.6

(12) The Parties do not necessarily agree with these further possible sub-segmentations of the freight forwarding services market.7 They have nonetheless provided the Commission with the information necessary to assess the effects of the Transaction under any plausible market definition.

(13) Given that the Transaction would not raise serious doubts as to its compatibility with the internal market even under the narrowest product market definition, the Commission will leave open the exact product market definition and in particular the questions whether that market should be further segmented by distinguishing between domestic and cross-border freight forwarding or different modes of transport.

4.1.2. Relevant geographic market

(14) In past decisions, the Commission left open whether the geographic scope of the freight forwarding services market – including sea freight forwarding services – is national or wider than national.8

(15) The Parties submit that the relevant geographic market cannot be narrower than national or domestic in scope.9

(16) Given that the Transaction would not raise serious doubts as to its compatibility with the internal market even under the narrowest plausible geographic market definition, the exact geographic delineation of this market can be left open.

4.1.3. Conclusion

(17) The precise product and geographic definition can be left open as the Transaction does not raise serious doubts on any plausible market definition, including the narrowest markets:

(a) Product markets: the freight forwarding services markets by reference to: the (i) type of operations, whether domestic or cross-border; and the (ii) means of transportation, whether by air, land and sea;

(b) Geographic markets: the national markets.

4.2. Contract logistics services

4.2.1. Relevant product market

(18) Contract logistics services is the part of the supply chain process that plans, implements and controls the efficient, effective flow and storage of goods, services and related information from the point of origin to the point of consumption in order to meet customers’ requirements.10 This part of the supply chain has the provision of warehousing and management of the flow of goods for customers as its focal point.11

(19) In Deutsche Post/Exel and Norbert Dentrassangle/Laxey Logistics,12 the Commission considered whether the contract logistics market should be segmented “i) into cross-border and domestic logistics, ii) by reference to the type of good handled or the industry serviced or iii) into lead logistics providers (“LLPs”) and traditional logistics providers (“3PLs”)”. In the end, however, the Commission decided to leave the precise scope of the relevant product market open.13

(20) The Parties do not necessarily agree with the above possible sub-segmentations of the market for contract logistics services. They have nonetheless provided the Commission with the information necessary to assess the effects of the Transaction under any plausible market definition.

(21) Given that the Transaction would not raise serious doubts as to its compatibility with the internal market even under the narrowest product market definition, the Commission will leave open the exact product market definition.

4.2.2. Relevant geographic market

(22) Concerning the geographic scope of the market, the Commission previously found that the contract logistics market is European, allowing a possible segmentation into national markets.14

(23) The Parties submit that the market for contract logistics services is usually regarded as national in scope, as contract logistics tenders are usually launched at national scales and for national needs.15

(24) Given that the Transaction would not raise serious doubts as to its compatibility with the internal market even under the narrowest geographic market definition, the Commission will leave open the exact geographic market definition.

4.2.3. Conclusion

(25) As the Transaction would not raise serious doubts as to its compatibility with the internal market under any plausible market definition, the Commission concludes that, for the purpose of this Decision, the precise product and geographic market definitions for contract logistics services can be left open.

4.3. Container liner shipping services

(26) In past cases, the Commission found that the product market for container liner shipping involves the provision of regular, scheduled services for the carriage of cargo by container. This market can be distinguished from non-liner shipping (tramp, specialised transport) because of regularity and frequency of the service. In addition, the use of container transportation separates it from other non- containerised transport such as bulk cargo.16

(27) The Commission has defined a separate product market for short-sea container shipping, distinct from deep-sea container shipping.17 Unlike deep-sea container liner shipping, short-sea container liner shipping involves the provision of intra- continental (usually coastal trade) services.18

4.3.1. Deep-sea container liner shipping services

4.3.1.1. Relevant product market

(28) Deep-sea container liner shipping services involves the offer of regular, scheduled services for the sea transportation of containerised cargo.19

(29) A possible narrower product market for deep-sea container liner shipping services is that for the transport of refrigerated goods, which could be limited to refrigerated (reefer) containers only or could include transport in conventional reefer vessels. In past cases, the Commission has looked separately at the plausible narrower markets for reefer containers and non-refrigerated (warm) containers only when the share of reefer containers in relation to all containerised cargo is 10% or more on both legs of a trade.20

(30) The Parties do not necessarily agree with these possible delineations, especially with the existence of a market for short-sea shipping services distinct from the market for deep-sea shipping, and with the distinction between reefer container liner shipping services and dry container liner shipping services. The Parties have nonetheless provided the Commission with the information necessary to assess the effects of the Transaction based on those narrower markets.

(31) Given that the Transaction would not raise serious doubts as to its compatibility with the internal market even under the narrowest product market definition, the Commission will leave open the exact product market definition.

4.3.1.2. Relevant geographic market

(32) Whereas, in prior decisions, the Commission had left open whether the geographic scope should comprise trades, defined as the range of ports which are served at both ends of the service (e.g. Northern Europe – North America) or each individual leg of trade (e.g. westbound and eastbound within a given trade), in its most recent practice,21 the Commission concluded that container liner shipping services are geographically defined on the basis of the legs of trade (e.g. Northern Europe – North America eastbound and Northern Europe – North America westbound separately).

(33) The Parties do not contest this approach and submit that the following ranges of ports constitute distinct ends of legs of trade:22

· Northern Europe;

· Mediterranean;

· North America;

· Central America/Caribbean;

· East Coast of South America;

· East Coast of South America;

· Middle East;

· Indian Subcontinent;

· Far East Asia;

· Australia and New Zealand;

· East Coast of Africa;

· West Coast of Africa; and

· South Coast of Africa.

(34) In the present case, in line with the Commission’s prior decisional practice, the geographic market for deep-sea container liner shipping services is defined on the basis of legs of trades.

4.3.1.3. Conclusion

(35) As the Transaction would not raise serious doubts as to its compatibility with the internal market under any plausible product market, it is not necessary to conclude whether a separate market for the transport of refrigerated (reefer) goods could be identified in the market for deep-sea container liner shipping services and whether the market for refrigerated (reefer) goods could be limited to refrigerated containers only or could include transport in conventional reefer vessels. The geographic scope of deep-sea container liner shipping services is defined on the basis of legs of trades.

(36) The Commission will assess the effects of the Transaction on the following markets:

(a) Product markets: market for (i) deep-sea container liner shipping services and (ii) the plausible reefer container liner shipping sub-segment;

(b) Geographic markets: legs of trade whose distinct ends have been set out above.

4.3.2. Short-sea container liner shipping services

4.3.2.1. Relevant product market

(37) Short-sea container liner shipping involves the provision of regular, scheduled intra-continental (usually costal trade) services for the carriage of cargo by container liner shipping companies.

(38) In its prior decisional practice related to container liner shipping services, the Commission defined a separate product market for short-sea container liner shipping, i.e. distinct from deep-sea container shipping and short-sea non-liner shipping.23

(39) In its prior decisional practice related to short-sea shipping services, the Commission concluded, as regards the type of cargo transported, that short-sea container shipping services should be distinguished from non-containerised shipping, such as bulk shipping,24 but it has ultimately left open whether the transport of wheeled cargo25 and short-sea container shipping services should be considered as belonging to the same product market.26

(40) The Commission also left open whether there should be a sub-segmentation between reefer (refrigerated) and dry (non-refrigerated) container shipping services.27

(41) The Parties do not necessarily agree with these possible delineations. In line with the Commission’s prior decisional practice, they have nonetheless provided the Commission with the information necessary to assess the effects of the Transaction under any plausible market definition.

(42) Given that the Transaction would not raise serious doubts as to its compatibility with the internal market even under the narrowest product market definition, the Commission will leave open the exact product market definition.

4.3.2.2. Relevant geographic market

(43) In its prior decision practice, the Commission considered that the relevant geographic market for short-sea container liner shipping services should be defined on the basis of (i) either single trades or corridors, defined by the range of ports which are served at both ends of the service;28 (ii) or single legs of trade.29

(44) The Parties do not contest these possible delineations and have provided the Commission with the information necessary to assess the effects of the Transaction under any plausible market definition.

(45) Given that the Transaction would not raise serious doubts as to its compatibility with the internal market even under the narrowest geographic market definition, the Commission will leave open the exact geographic market definition and in particular the question whether this market should be defined on the basis of single trades or corridors or single legs of trade.

4.3.2.3. Conclusion

(46) For the purposes of this Decision, it can be left open whether the product market for short-sea container liner shipping services forms part of (i) a broader market encompassing the transport of wheeled cargo or (ii) an overall market for intra- European door-to-door multimodal transport services, as the Transaction would not raise serious doubts as to its compatibility with the internal market under either of these definitions. For the same reason, it is also not necessary to conclude whether the market for short-sea container liner shipping services should be segmented between reefer and dry services. With respect to the geographic market for short-sea container liner shipping services, it may be left open whether short-sea container liner shipping services should be defined on the basis of single trades or corridors, or single legs of trade.

(47) The Commission will assess the effects of the Transaction on the following markets:

(a) Product markets: (i) the market for short-sea container liner shipping services, as well as (ii) the plausible narrower market for short-sea reefer container liner shipping services;30

(b) Geographic markets: the narrowest plausible geographic market, that is to say legs of trade.

5. COMPETITIVE ASSESSMENT

(48) CMA CGM is active in the markets for container liner shipping services and freight forwarding, while CEVA is active in the markets for freight forwarding services and contract logistics services.

(49) Therefore, the Transaction creates horizontal overlap between the Parties’ activities in the market for freight forwarding services.

(50) Moreover, he Parties’ activities are vertically related, as CMA CGM is active in the upstream market for (i) container liner shipping services, namely in both deep-sea container liner shipping services and short-sea container liner shipping services,31 while CEVA is active in the downstream markets for (iii) freight forwarding services.

(51) CEVA is also active in the market for contract logistics services, which is not directly linked to any of CMA CGM’s activities. However, the Commission will assess whether the Transaction could give rise to conglomerate effects.32

5.1. Horizontal overlaps in relation to freight forwarding services

(52) The Parties’ activities in freight forwarding overlap in the EEA as a whole and in a few EEA countries, namely Belgium, Czech Republic, France, Germany, Italy, the Netherlands, Poland, Spain and the United Kingdom.

(53) The Parties’ combined market share post-Transaction will be below [0-5]% at EEA level and below [0-5]% in each of the overlap countries, with a negligible increment brought about by the Transaction.33

(54) Under any plausible product34 and geographic market delineation as defined in paragraph 17, the Parties’ combined market share will not exceed 15% at national and wider-than-national levels. Therefore, the Transaction does not give rise to any affected market.

(55) In addition, the Commission notes that the markets for freight forwarding services are highly fragmented and encompass major global players such as Deutsche Post DHL, DB Schenker, Damco or Kühne + Nagel.

(56) Based on the above considerations and in light of all the evidence available to it, the Commission considers that the Transaction would not raise any serious doubts as to its compatibility with the internal market with respect to freight forwarding services.

5.2. Vertical links in relation to container liner shipping services

(57) CEVA is active in the downstream market for freight forwarding services, while CMA CGM is active in the upstream market for container liner shipping services

5.2.1. Legal framework

(58) According to the Non-Horizontal Merger Guidelines,35 foreclosure occurs when actual or potential rivals' access to markets is hampered, thereby reducing those companies' ability and/or incentive to compete.36 Such foreclosure can take two forms: (i) input foreclosure, when access of downstream rivals to supplies is hampered;37 and (ii) customer foreclosure, when access of upstream rivals to a sufficient customer base is hampered.38

(59) For input or customer foreclosure to be a concern three conditions need to be met post-Transaction: (i) the merged entity needs to have the ability to foreclose its rivals; (ii) the merged entity needs to have the incentive to foreclose its rivals; and (iii) the foreclosure strategy needs to have a significant detrimental effect on competition on the downstream market (input foreclosure) or on consumers (customer foreclosure).39 In practice, these factors are often examined together since they are closely intertwined.

5.2.2. Analytical framework

(60) In its prior decisions relating to container liner shipping services, the Commission considered that shipping companies that are members of alliances/consortia (the latter are also called vessel sharing agreements, “VSAs”) jointly agree on the capacity that will be offered by the service, on its schedule and ports of call. Generally, each party provides a number of vessels for operating the joint service and in exchange receives a number of container slots across all vessels deployed in the joint service based on the total vessel capacity that it contributes. The allocation of container slots is usually predetermined and shipping companies are not compensated if the slots attributed to them are not used. The costs for the operation of the service are generally borne by the vessel providers individually so that there is limited to no sharing costs between the participants in a VSA.40

(61) In previous cases, the Commission also considered that it is not appropriate to assess the effects of the concentration only on the basis of the Parties' individual market shares. Such an approach would not adequately take into account the fact that a member of an alliance/VSA can have a significant influence on operational decisions determining service characteristics. This influence can have a dampening effect on competition on the trade/s served by the alliance/VSA in question. Hence, the competitive assessment should also be based on the aggregate shares of the Parties' alliances/VSAs.41

(62) In line with its prior decisional practice, the Commission will assess the effects of the Transaction on the above-mentioned trades and legs of trade by taking into account the aggregate market shares of CMA CGM and of its partners in the respective alliances/VSAs.

5.2.3. Overview of the vertically affected markets

(63) Related markets in which CMA CGM holds a market share of at least 30% in the upstream markets and/or CEVA and CC Log hold an individual or combined market share of at least 30% in the downstream markets are considered to be vertically affected by the Transaction.

(64) As regards the upstream markets for container liner services,42 post- Transaction:

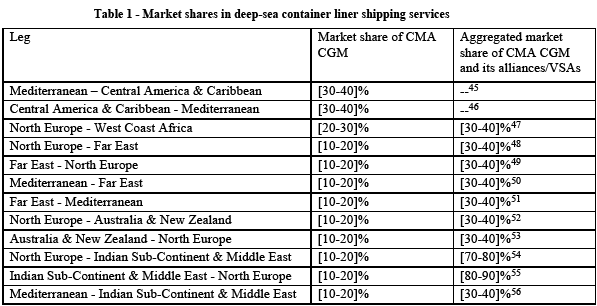

· CMA CGM’s market shares in the market for deep-sea container liner shipping services would exceed 30% on two legs of trade, namely (i) Mediterranean to Central America & Caribbean ([30-40]%) and (ii) Central America & Caribbean to Mediterranean ([30-40]%).43

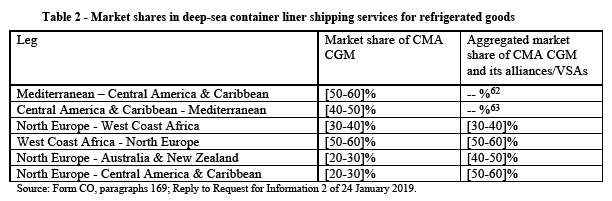

· CMA CGM’s market shares in the market for deep-sea container liner shipping services for refrigerated goods would exceed 30% on four legs of trade, namely (i) Mediterranean to Central America & Caribbean ([50-60]%), (ii) Central America & Caribbean to Mediterranean ([40-50]%), (iii) North Europe to West Coast Africa ([30-40]%) and (iv) West Coast Africa to North Europe ([50-60]%).44

· When attributing CMA CGM’s alliances/VSAs market shares to CMA CGM, CMA CGM’s market shares in the market for deep-sea container liner shipping services would exceed 30% on 17 legs of trade listed in the table below.

· When attributing CMA CGM’s alliances/VSAs market shares to CMA CGM, CMA CGM’s market shares in the market for deep-sea container liner shipping services for refrigerated goods would exceed 30% on six (6) legs of trade listed in the table below.

· CMA CGM’s market shares in the market for short-sea container liner shipping services would exceed 30% on four legs of trade: (i) British Isles to Russia ([70-80]%), (ii) Russia to British Isles ([70-80]%), (iii) Poland to British Isles ([40-50]%) and (iv) Baltic States to British Isles ([40-50]%).64 CMA CGM is not part to any alliances/consortia on these legs of trade.

· CMA CGM’s market shares in the market for short-sea container liner shipping services for refrigerated goods would not exceed 30% on any leg of trade in the EEA where reefer accounts for 10% or more of transported cargo on both legs of a trade.65

· With respect to short-sea container liner shipping services, CMA CGM is part of a very limited number of alliances/consortia. Attributing the market shares of these alliances/consortia to CMA CGM would not give rise to any additional affected market.66

(65) With respect to the downstream markets for freight forwarding services, the merged entity’s activities do not give rise to any affected market.

5.2.4. Assessment of the vertically affected markets in relation to container liner shipping companies services

(66) The Commission will assess in this Section whether the Transaction could lead to (i) input foreclosure, pursuant to which CMA CGM would foreclose CEVA’s competitors by restricting access to or deteriorating the quality of the container liner shipping services that it provides to CEVA’s competitors in the countries where it is active; or (ii) customer foreclosure, pursuant to which CEVA would foreclose CMA CGM’s competitors by sourcing its container liner shipping services requirements mostly or exclusively from CMA CGM.

5.2.4.1. Input foreclosure

The Parties’ views

(67) With respect to the risk that CMA CGM’s restricts access of CEVA’s competitors to its container liner shipping services, the Parties submit that CMA CGM will have neither the ability nor the incentive to engage in an input foreclosure strategy.67

The Commission’s assessment Ability to foreclose

(68) For input foreclosure to be a concern, the vertically integrated firm resulting from the merger must have a significant degree of power in the upstream market and thus, possibly, on prices and supply conditions in the downstream market.68

(69) The Commission notes that CMA CGM, along with its partners in alliances/VSAs, holds market shares above 50% and up to a maximum of [80- 90]% only on 11 legs of trades (five in the market for deep-sea container liner shipping services,69 four in the market for deep-sea container liner shipping services for refrigerated goods70 and two in the market for short-sea container liner shipping services71) to engage in an input foreclosure strategy towards third- party freight-forwarders on the downstream market.

(70) First, CMA CGM lacks market power on the upstream market as significant and long-established competing carriers provide container liner shipping services on the above-mentioned legs of trade independently from CMA CGM and its consortia partners.72 On all but two legs, those independent carriers account for around half of the market and are not capacity constrained. Therefore, in case CMA CGM were to decide to limit or stop supplying third party freight forwarders, third-party freight-forwarders will continue to have access to equivalent services provided by competing carriers which do not face any capacity constraints.73 On the route to and from India, CMA CGM’s individual market shares remain well below 30% (they are indeed equal to [10-20]% on the outbound leg and [10-20]% on the inbound leg). Moreover, there is available capacity on that trade, given that the Parties’ consortia market share in terms of capacity is below 30%, which means that 70% of the capacity on that trade is provided by independent carriers.74

(71) Second, any foreclosure attempts by CMA CGM would only benefit its subsidiary CEVA, but not its consortia partners. The divergent interests of CMA CGM’s consortia partners on all these routes would lead these partners not to follow such a strategy.

(72) Third, third-party freight forwarders are not captive since they do not face any switching costs when they decide to switch carriers, even until the very last minute. Furthermore, most of the freight-forwarders show no brand loyalty and do multi-source their needs in container liner shipping services among different sea carriers.75

(73) In light of the above, the Commission considers that CMA CGM would likely not have the ability to implement any successful input foreclosure strategy post- Transaction.

Incentive to foreclose

(74) The incentive to foreclose depends on the degree to which foreclosure would be profitable. The vertically integrated firm will take into account how its supplies of inputs to competitors downstream will affect not only the profits of its upstream activities, but also of its downstream activities. Essentially, the merged entity faces a trade-off between the profit lost in the upstream market due to a reduction of input sales to (actual or potential) rivals and the profit gain, in the short or longer term, from expanding sales downstream or, as the case may be, being able to raise prices to consumers.76

(75) The Commission notes that CEVA’s demand for deep-sea container liner services is negligible on any of the affected legs of trade and is even more negligible for short-sea container liner services. CEVA’s global demand for container liner shipping services accounted for less than [0-5]% of CMA CGM’s container liner shipping activities in 2017.77 CEVA’s demand for short-sea container liner shipping services represents less than [0-5]% of CMA CGM’s short-sea activities.78 By engaging in an input foreclosure strategy, CMA CGM would therefore face the risk of jeopardising its commercial relationship with third-party freight-forwarders downstream, which represent its primary source of activities and revenue. Indeed, freight forwarders other than CEVA (and CC Log) represent close to […]% of CMA CGM’s revenues in container liner shipping.79

(76) As a result, even if post-Transaction CMA CGM decided to stop or limit its supply of container liner shipping services to other freight forwards, this would likely be unprofitable since CEVA’s activity in freight forwarding would not compensate the losses incurred in the upstream market.

(77) In light of the above, the Commission considers that CMA CGM will likely not have an incentive to engage in an input foreclosure strategy post-Transaction.

Overall effect of input foreclosure

(78) In general, a merger will raise competition concerns because of input foreclosure when it would lead to increased prices in the downstream market thereby significantly impeding effective competition.80

(79) If there remain sufficient credible downstream competitors whose costs are not likely to be raised, for example because they are themselves vertically integrated or they are capable of switching to adequate alternative inputs, competition from those firms may constitute a sufficient constraint on the merged entity and therefore prevent output prices from rising above pre-merger levels.81

(80) In that respect, the Commission notes that many other carriers provide container liner shipping services in the EEA and compete fiercely for customers such as freight-forwarders, which represent a significant part of their revenues. Therefore, even if CMA CGM were to engage in an input foreclosure strategy by limiting its supply only to CEVA and CC Log, other carriers would immediately start providing container liner shipping services to the other freight-forwarders on the downstream market.

(81) The fierce competition at play on the upstream market combined with low barriers to entry would therefore be sufficient to prevent the prices for output on the downstream market (i.e. freight-forwarding services) from rising. Therefore, the Commission considers that CEVA’s competitors in the downstream market for freight-forwarding services will likely be unaffected by the Transaction.

(82) Consequently, the Commission considers that an input foreclosure strategy post- Transaction by CMA CGM would be unlikely to have a negative effect on competition.

Conclusion

(83) Based on the above considerations and all evidence available to it, the Commission concludes that an input foreclosure strategy post-Transaction by CMA CGM in order to exclude CEVA’s competitors purchasing container liner shipping services in any of the affected legs of trade is unlikely.

5.2.4.2. Customer foreclosure

The Parties’ views

(84) CMA CGM submits that the merged entity will not have the ability or the incentive to engage into any customer foreclosure strategy by sourcing most or all of its needs in container liner shipping services from CMA CGM in the EEA, in particular in view of CEVA’s minimal shares in freight forwarding downstream.82

The Commission’s assessment Ability to foreclose

(85) For customer foreclosure to be a concern, it must be the case that the vertical merger involves a company which is an important customer with a significant degree of market power in the downstream market. If, on the contrary, there is a sufficiently large customer base, at present or in the future, that is likely to turn to independent suppliers, the Commission is unlikely to raise competition concerns on that ground.83

(86) First, the Commission notes that the merged entity’s shares in the downstream markets for freight forwarding services are limited (less than [0-5]% in the overall market for freight forwarding in the EEA, no more [0-5]% at national level). Even when looking at further product market delineations, the merged entity’s share will remain significantly below 20%. More specifically, CEVA’s demand in container liner shipping services is small ([…]), as compared to a total market of container liner shipping services of more than 47 million TEUs. Therefore, CEVA cannot be considered as an important customer with a significant degree of market power.

(87) Second, the market for freight forwarding is segmented and includes major players. In sea freight forwarding, the main competitors are Kühne + Nagel, Sinotrans and DHL Global Forwarding.84 Should CEVA contract exclusively with CMA CGM, CMA CGM’s competitors in container liner shipping services would have access to a sufficient customer base.

(88) In light of the above, the Commission considers that, post-Transaction, the merged entity will not likely have the ability to engage in a customer foreclosure strategy in the EEA and in the countries where CEVA is active.85

Incentive to foreclose

(89) The incentive to foreclose depends on the degree to which it is profitable. The merged entity faces a trade-off between the possible costs associated with not procuring products from upstream rivals and the possible gains from doing so, for instance, because it allows the merged entity to raise price in the upstream or downstream markets.86

(90) Given CEVA’s small demand for container liner shipping services in the EEA, the merged entity would have limited benefits on the upstream markets for container liner shipping services.

(91) In addition, it seems that no freight forwarder can afford, in order to address its clients’ needs, to procure all of its needs in container liner shipping services from a single sea carrier, such as CMA CGM. The fact that CMA CGM’s subsidiary CC Log only sources […]% to […]% of its needs from CMA CGM carriers supports this observation.87

(92) Therefore, should CEVA decide to stop procuring container liner shipping services from CMA CGM’s competitors post-Transaction, it is likely that the merged entity would incur losses in the downstream market for freight forwarding, with no prospect of increasing volumes and revenues in the upstream markets for container liner shipping services.

(93) In light of the above, the Commission considers that, post-Transaction, the merged entity will not likely have the incentive to engage in a customer foreclosure strategy in the EEA and in the countries where CEVA is active.88

Overall effect of customer foreclosure

(94) It is only when a sufficiently large fraction of upstream output is affected by the revenue decreases resulting from the vertical merger that the merger may significantly impede effective competition on the upstream market. If there remain a number of upstream competitors that are not affected, competition from those firms may be sufficient to prevent prices from rising in the upstream market and, consequently, in the downstream market.89

(95) The Commission considers that even if CEVA’s demand for container liner shipping services was sourced exclusively from CMA CGM, this would have a limited impact on the markets for container liner shipping services. Indeed, CEVA’s demand ([…]) represents less than […]% of the total demand in the EEA (47 million TEUs).

(96) Moreover, the Commission notes that CEVA already purchases […]% of its needs in container liner shipping services in the EEA from CMA CGM. Consequently, the pre-existing situation subdues the effect of a diversion of CEVA’s demand on the upstream market for container liner shipping services towards CMA CGM.

(97) Therefore, the Commission considers that CMA CGM’s competitors in the upstream market for container liner shipping services will likely be unaffected by the Transaction.

(98) In light of the above, the Commission considers that, post-Transaction, the implementation of a customer foreclosure strategy by the merged entity would have likely no overall negative impact of effective competition in the EEA and in the countries where CEVA is active.90

Conclusion

(99) Based on the above considerations and in light of all the evidence available to it, the Commission concludes that a customer foreclosure strategy post-Transaction by the merged entity in order to exclude CMA CGM’s competitors selling container liner shipping services in the EEA and in the countries where CEVA is active is unlikely.

5.2.5. Conclusion on the vertical effects

(100) Based on the above considerations and in light of all the evidence available to it, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market due to vertical effects.

5.3. Conglomerate effects in relation to contract logistics services

(101) The Transaction may have a conglomerate dimension, as it involves services that belong to related markets (i.e. container liner shipping services and contract logistics services), that is, products that are purchased by a significant set of consumers for a similar end use (either together in a bundle or separately). The main concern in the context of conglomerate mergers is that of foreclosure. The combination of products in related markets may confer on the merged entity the ability and incentive to leverage a strong market position from one market to another by means of tying of bundling. Those practices are common and often have no anticompetitive consequences. Companies engage in tying and bundling in order to provide their customers with better products or offerings in cost- effective ways.91

The Parties’ views

(102) The Parties submit that the Transaction will not lead to any conglomerate anticompetitive effects. Through the Transaction, CMA CGM will enlarge its contract logistics offering by creating synergies between its transportation activities and CEVA’s logistics activities.92

The Commission’s assessment

(103) Whereas it is acknowledged that conglomerate mergers in the majority of circumstances will not lead to any competition problems, in certain specific cases there may be harm to competition.93 In order to assess the likelihood of such anticompetitive foreclosure strategy, the Commission will examine whether the merged entity has (i) the ability to foreclose and (ii) the incentives to foreclose. Lastly, the Commission will assess whether such practices may have a significant negative impact on competition and consumers.94

(104) The Commission considers that CMA CGM will not gain any ability, post- Transaction, to engage in a strategy of tying or bundling its contract logistics services with its container liner shipping services. First, the merged entity will lack the market power on any of the markets concerned to engage in such a strategy. CMA CGM is not active on the market for contract logistics whereas CEVA has only a very limited share in contract logistics ([0-5]% at EEA level). Second, the Commission notes that competing container liner shipping services and contract logistics services will remain available on a stand-alone basis from other sea carriers and logistics providers.

(105) The incentive to foreclose rivals through bundling or tying depends on the degree to which this strategy is profitable.95 The Commission considers that CMA CGM would have no incentive post-Transaction to favour any tied or bundled offers to the detriment of its core container liner shipping activities. Indeed, CEVA’s share in contract logistics services is small while CMA CGM is the fourth largest container liner company.96 Consequently, CMA CGM intends to continue to offer such services separately.97 Second, the market structures of shipping services and logistics services differ, which makes bundling difficult. While contract logistics services are customer-demand driven and tailor made, container liner shipping services and freight forwarding services are mostly off-the-shelf services.

(106) Should the merged entity decide to increase the price of standalone contract logistics services or container liner shipping services, the Commission considers that the incentive to do so would be mitigated by the existence of alternative shipping services providers and contract logistics services providers. The Commission considers that the Transaction is unlikely to have an overall negative impact on effective competition in the markets for contract logistics services and container liner shipping services, as any bundling or tying strategy is unlikely to reduce the ability and incentives to compete of the significant competing providers that are active in the EEA. Customers will continue to have immediate access to competitive container liner shipping services and contract logistics services on a standalone basis. Overall, the Commission is of the view that the effects of any hypothetical tying or bundling strategy is unlikely to have an overall negative impact on prices and choice.

(107) Based on the above considerations and in light of all the evidence available to it, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market in relation to hypothetical conglomerate effects.

6. CONCLUSION

(108) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 Publication in the Official Journal of the European Union No C 009, 10.01.2019, p. 10.

4 Turnover calculated in accordance with Article 5 of the Merger Regulation and the Commission Consolidated Jurisdictional Notice (OJ C 95, 16.4.2008, p. 1).

5 Cases M.8594 – COSCO SHIPPING/OOIL, paragraph 23; M.8120 – Hapag-Lloyd/United Arab Shipping Company, paragraph 26; M.7268 – CSAV/HGV/Kühne Maritime/Hapag-Lloyd, paragraph 3; M.6059 – Norbert Dentressangle/Laxey Logistics, paragraph 17.

6 Cases M.8594 – COSCO SHIPPING/OOIL, paragraph 23; M.8330 – Maersk Line/HSDG, paragraph 38; M.8120 – Hapag-Lloyd/United Arab Shipping Company, paragraphs 26-27, M.7630 – FEDEX/TNT EXPRESS, paragraphs 24-25; M.6059 – Norbert Dentressangle/Laxey Logistics, paragraph 18.

7 Form CO, paragraph 110.

8 Cases M.8594 – COSCO SHIPPING/OOIL, paragraph 24; M.8330 – Maersk Line/HSDG, paragraph 39; M.8120 – Hapag-Lloyd/United Arab Shipping Company, paragraphs 26-27; M.7630 – FEDEX/TNT EXPRESS, paragraphs 24-25; M.6059 – Norbert Dentressangle/Laxey Logistics, paragraphs 20 and 22; M.5480 – Deutsche Bahn/PCC Logistics, paragraphs 12-17; M.5450 – Kühne/HGV/TUI/Hapag-Lloyd, paragraph 18.

9 Form CO, paragraph 120.

10 Case M.6059 – Norbert Dentressangle/Laxey Logistics, paragraphs 9-16.

11 Case M.1895 – Ocean Group/Exel (NFC), paragraphs 7-11.

12 Cases M.6059 – Norbert Dentrassangle/Laxey Logistics, paragraphs 10-13; M.3971 – Deutsche Post/Exel, paragraphs 15-19.

13 Cases M.6570 – UPS/TNT, paragraph 32; M.3971 – Deutsche Post/Exel, paragraph 20.

14 Cases M.6570 – UPS/TNT, paragraph 33; M.6059 – Norbert Dentrassangle/Laxey Logistics, paragraph 15; M.3971 – Deutsche Post/Exel, paragraphs 28-29.

15 Form CO, paragraph 122.

16 Cases M.8594 – COSCO Shipping/OOIL, paragraph 11; M.8120 – Hapag-Lloyd/United Arab Shipping Company, paragraph 10; M.7908 – CMA CGM/NOL, paragraph 8; M.7268 – CSAV/HGV/Kühne Maritime/Hapag-Lloyd AG, paragraph 16; M.5450 – Kühne/HGV/TUI/Hapag-Lloyd, paragraph 13.

17 Cases M.8330 – Maersk Line/HSDG, paragraph 19; M.7523 – CMA CGM/OPDR, paragraph 50.

18 Case M.8330 – Maersk Line/HSDG, paragraph 18.

19 Case M.8330 – Maersk Line/HSDG, paragraph 10.

20 Cases M. 8594 – COSCO Shipping/OOIL, paragraph 13; M.8120 – Hapag-Lloyd/United Arab Shipping Company, paragraph 11; M.7908 – CMA CGM/NOL, paragraph 9; M.7268 – CSAV/HGV/Kühne Maritime/Hapag-Lloyd AG, paragraph 18; M.3829 – Maersk/PONL, paragraph 10.

21 Cases M. 8594 – COSCO Shipping/OOIL, paragraph 14; M.8330 – Maersk Line/HSDG, paragraph 15; M.8120 – Hapag-Lloyd/United Arab Shipping Company, paragraph 19; M.7908 – CMA CGM/NOL, paragraph 15.

22 Form CO, paragraph 37.

23 E.g. tramp or specialised transport.

24 Cases M.8330 – Maersk Line/HSDG, paragraph 19; M.7523 – CMA CGM/OPDR, paragraph 49.

25 Roll on-roll off ("Ro-Ro") shipping corresponds to the transport of wheeled cargo (lorries, cars, etc.) on ships.

26 Cases M.8330 – Maersk Line/HSDG, paragraph 19; M.7523 – CMA CGM/OPDR, paragraph 50.

27 Cases M.8330 – Maersk Line/HSDG, paragraph 19; M.7523 – CMA CGM/OPDR, paragraph 48.

28 Cases M.8330 – Maersk Line/HSDG, paragraph 20; M.7523 – CMA CGM/OPDR, paragraph 59.

29 Cases M.8330 – Maersk Line/HSDG, paragraph 20; M.7523 – CMA CGM/OPDR, paragraph 60.

30 The Commission will not assess the effects of the Transaction on (i) a broader market encompassing short-sea wheeled cargo shipping and short-sea container shipping or (ii) an overall market for door- to-door intermodal transport services, since the market shares of the Parties on these broader markets will be diluted.

31 In its prior decisions, the Commission has consistently considered container liner shipping services as an upstream market to the provision of freight forwarding services (see for example M.8594 – COSCO SHIPPING/OOIL, paragraph 61; M.8330 – Maersk Line/HSDG, paragraph 249; M.8120 – Hapag- Lloyd/United Arab Shipping Company, paragraph 137; M.7523 – CMA CGM/OPDR, paragraph 144).

32 The Commission has not identified significant conglomerate effects in the present case. According to CMA CGM, post-Transaction, (i) CMA CGM will not have the ability to tie or bundle such logistics services to its container liner shipping services; (ii) CMA CGM would also have no incentive to engage in a tying/bundling foreclosure strategy as this would be detrimental to its core shipping activities; (iii) CMA CGM’s customers would in any event continue to have access to competitive sea shipping services and logistics services on a stand-alone basis, including from other sea carriers and logistics providers (Form CO, paragraphs 184-187).

33 Form CO, paragraphs 140-150.

34 i.e. freight forwarding by air, sea and land on the one hand; domestic and cross-border freight forwarding on the other hand.

35 Guidelines on the assessment of non-horizontal mergers under the Council Regulation on the control of concentrations between undertakings, OJ C 265, 18.10.2008, p. 7.

36 Non-Horizontal Merger Guidelines, paragraphs 20-29.

37 Non-Horizontal Merger Guidelines, paragraph 31.

38 Non-Horizontal Merger Guidelines, paragraph 58.

39 Non-Horizontal Merger Guidelines, paragraphs 32 and 59.

40 Cases M.8594 – COSCO SHIPPING/OOIL, paragraphs 28-29. Consortia are operational agreements between shipping companies established on individual trades for the provision of a joint service. Alliances are matrices of vessel sharing agreements that cover multiple trades rather than one trade, as opposed to consortia. Expanding cooperation across multiple trades increases the ability of the container liner shipping companies to deploy assets in the most appropriate and cost efficient way.

41 Cases M.8594 – COSCO SHIPPING/OOIL, paragraphs 32-33; M.8330 – Maersk Line/HSDG, paragraph 60; M.7523 – CMA CGM/OPDR, paragraph 33.

42 The source of market share in deep-sea container liner shipping is CTS. When relevant, the Parties have indicated that some alliance/consortium members do not contribute to CTS.

43 Form CO, paragraph 167.

44 Form CO, paragraph 169 and Reply to Request for Information 1a of 9 January 2019.

45 CMA CGM is part of a VSA with Marfret, which does not contribute to CTS. Therefore, its volumes are not available. However, the Parties note that Marfret is a small player whose market share is unlikely to have a significant impact on the aggregate market share.

46 CMA CGM is part of a VSA with Marfret, which does not contribute to CTS. Therefore, its volumes are not available. However, the Parties note that Marfret is a small player whose market share is unlikely to have a significant impact on the aggregate market share.

47 CMA CGM is part of one VSA, namely EURAF 5 with Nile Dutch.

48 CMA CGM is in alliance with COSCO, OOCL, and EMC.

49 Ibid.

50 CMA CGM is in alliance with COSCO, OOCL, and EMC.

51 Ibid.

52 CMA CGM is part of two separate VSAs with Marfret and Hapag-Lloyd.

53 Ibid.

54 CMA CGM is part of two VSAs, namely, EPIC 1 with MSC and Hapag-Lloyd, and EPIC 2 with COSCO, Hapag-Lloyd and ONE. CMA CGM submits that ONE does not contribute to CTS its volumes are not available to CMA CGM. However, the Parties note that ONE is a small player whose market share is unlikely to have a significant impact on the aggregate market share.

55 Ibid.

56 CMA CGM is part of three VSAs, namely, MEDEX with COSCO and Hapag-Lloyd, MEGEM with COSCO and Hapag-Lloyd, and INDIAMED with COSCO.

57 CMA CGM is part of two VSAs, namely, ECS with Hapag-Lloyd and NEFGUI with Marfret.

58 CMA CGM is part of a VSA, namely EUROSAL XL (with COSCO and Hapag-Lloyd).

59 Ibid.

60 CMA CGM is part of two VSAs, namely, MED AMERICAS with Hapag-Lloyd, and SIRIUS with Maersk.

61 Ibid.

62 CMA CGM is part of a VSA with Marfret, which does not contribute to CTS. Therefore, its volumes are not available. However, the Parties note that Marfret is a small player whose market share is unlikely to have a significant impact on the aggregate market share.

63 CMA CGM is part of a VSA with Marfret, which does not contribute to CTS. Therefore, its volumes are not available. However, the Parties note that Marfret is a small player whose market share is unlikely to have a significant impact on the aggregate market share.

64 Form CO, paragraph 181. For the purpose of this Decision and in the absence of competition concerns, the market shares were calculated in terms of capacity deployed instead of volumes because the Parties could not provide any reliable market share data in terms of volumes.

65 Form CO, paragraph 182.

66 Form CO, paragraph 182 and reply to Request for Information 3 of 25 January 2019.

67 Form CO, paragraph 159.

68 Non-Horizontal Merger Guidelines, paragraph 35.

69 North Europe to Indian Sub-Continent & Middle East ([70-80]%); Indian Sub-Continent & Middle East to North Europe ([80-90]%); North Europe to Central America & Caribbean ([50-60]%); Mediterranean to South America West Coast ([50-60]%) and South America West Coast to Mediterranean ([50-60]%).

70 Mediterranean to Central America & Caribbean ([50-60]%); West Coast Africa to North Europe ([50- 60]%); West Coast Africa to North Europe ([50-60]%); North Europe to Central America & Caribbean ([50-60]%).

71 British Isles to Russia ([70-80]%) and Russia to British Isles ([70-80]%).

72 Regarding the market for deep-sea container liner shipping services, on most of the affected legs of trade, CMA CGM’s faces competitive constraints from the largest container liner shipping companies, such as MSC, Maersk and Hapag Lloyd (Form CO, paragraphs 168-169 and 174-175). Regarding the market for short-sea container liner shipping services, CMA CGM’s major competitors are Transfennica, Finnlines, Maersk, Unifeeder and Mann Lines (Form CO, paragraph 181).

73 More than 50% of the capacity on the affected legs of trade is deployed by competitors of CMA CGM and its alliances/VSAs (Form CO, paragraphs 172-175 and 179 and 182; Reply to Request for Information 1 of 7 January 2019). Furthermore, the Parties submit that barriers to entry are low in the upstream market for container liner shipping services; therefore, competitors could easily deploy additional capacities (Form CO, paragraphs 212, 215 and 223).

74 Reply to Request for Information 1a of 9 January 2019.

75 Form CO, paragraphs 198-199.

76 Non-Horizontal Merger Guidelines, paragraph 40.

77 Form CO, paragraph 161.

78 Form CO, paragraph 162.

79 Form CO, paragraph 159.

80 Non-Horizontal Merger Guidelines, paragraph 47.

81 Non-Horizontal Merger Guidelines, paragraph 50.

82 Form CO, paragraph 155.

83 Non-Horizontal Merger Guidelines, paragraph 61.

84 Form CO, paragraph 151.

85 Namely Austria, Belgium, Czech Republic, Finland, France, Germany, Hungary, Ireland, Italy, the Netherlands, Poland, Portugal, Romania, Slovakia, Spain, Sweden and the United Kingdom (Form CO, paragraph 142).

86 Non-Horizontal Merger Guidelines, paragraph 68.

87 Form CO, paragraph 158.

88 Namely Austria, Belgium, Czech Republic, Finland, France, Germany, Hungary, Ireland, Italy, the Netherlands, Poland, Portugal, Romania, Slovakia, Spain, Sweden and the United Kingdom (Form CO, paragraph 142).

89 Non-Horizontal Merger Guidelines, paragraph 74.

90 Namely Austria, Belgium, Czech Republic, Finland, France, Germany, Hungary, Ireland, Italy, the Netherlands, Poland, Portugal, Romania, Slovakia, Spain, Sweden and the United Kingdom (Form CO, paragraph 142).

91 Non-Horizontal Merger Guidelines, paragraph 93.

92 Form CO, paragraph 184.

93 Non-Horizontal Merger Guidelines, paragraph 92.

94 Non-Horizontal Merger Guidelines, paragraph 94.

95 Non-Horizontal Merger Guidelines, paragraph 105.

96 Form CO, paragraph 93.

97 Form CO, paragraph 184.