Commission, July 18, 2019, No 39711

EUROPEAN COMMISSION

Decision

Qualcomm (predation)

COMMISSION DECISION of 18.7.2019

relating to a proceeding under Article 102 of the Treaty on the Functioning of the European Union and Article 54 of the EEA Agreement

Case AT.39711 – Qualcomm (predation)

(Text with EEA relevance) (Only the English text is authentic)

THE EUROPEAN COMMISSION,

Having regard to the Treaty on the Functioning of the European Union ("Treaty"),1 Having regard to the Agreement on the European Economic Area ("EEA Agreement"),

Having regard to Council Regulation (EC) No 1/2003 of 16 December 2002 on the implementation of the rules on competition laid down in Articles 81 and 82 of the Treaty,2 and in particular Article 7 and Article 23(2) thereof,

Having regard to the complaint lodged by Icera Inc. on 30 June 2009, as updated and revised on 8 April 2010 and supplemented by submissions of Nvidia Inc. of 1 May, 17 May and 31 July 2012, alleging infringements of Article 102 of the Treaty and Article 54 of the EEA Agreement by Qualcomm Inc. and requesting the Commission to put an end to those infringements,

Having regard to the Commission decision of 16 July 2015 to initiate proceedings in this case,

Having given the undertaking concerned the opportunity to make known its views on the objections raised by the Commission pursuant to Article 27(1) of Council Regulation No 1/2003 and Article 12 of Commission Regulation (EC) No 773/2004 of 7 April 2004 relating to the conduct of proceedings by the Commission pursuant to Articles 81 and 82 of the Treaty,3

After consulting the Advisory Committee on Restrictive Practices and Dominant Positions, Having regard to the final report of the Hearing Officer in this case,

Whereas:

1. INTRODUCTION

(1) This Decision establishes that Qualcomm Inc. ("Qualcomm") infringed Article 102 of the Treaty and Article 54 of the Agreement on the European Economic Area by supplying, between 1 July 2009 until 30 June 2011, certain quantities of three of its UMTS compliant chipsets (the MDM8200, MDM6200 and MDM8200A based chipsets) to two of its key customers, Huawei and ZTE, below cost, with the intention of eliminating Icera, its main competitor at that point in time in the market segment offering advanced data rate performance ("leading edge segment"). By containing Icera's growth at the two key customers in this segment, which consisted at the time almost exclusively of chipsets used in mobile broadband devices, Qualcomm intended to prevent Icera, a small and financially constrained start-up, from gaining the reputation and scale necessary to challenge Qualcomm's dominance in the market for UMTS baseband chipsets, in particular in view of the expected growth potential of the leading edge segment due to the global take-up of smart mobile devices, thus depriving original equipment manufacturers in this segment from access to an alternative source of chipsets for their mobile phones and reducing consumer choice.

2. THE PARTIES CONCERNED

2.1.Qualcomm

(2) The addressee of this Decision is Qualcomm, a leading developer of wireless technology products and services headquartered in San Diego, California (USA). Qualcomm holds essential intellectual property rights ("IPRs") in a number of mobile telephony standards including the third generation UMTS and the fourth generation LTE standards. It is the leading supplier of chips and chipsets used in mobile handsets and other mobile devices.

(3) Qualcomm has a number of wholly-owned subsidiaries worldwide, among which two are of particular relevance for the conduct under investigation, since they were also involved in discussions with Huawei and ZTE: Qualcomm Europe Inc., ("Qualcomm Europe") and Qualcomm China Inc. ("Qualcomm China").

(4) Qualcomm conducts business primarily through its business units Qualcomm CDMA Technologies ("QCT") and Qualcomm Technology Licensing ("QTL"), which are operated by Qualcomm and its direct and indirect subsidiaries.4

2.2. The complainant

(5) Icera Inc. ("Icera") was the initial complainant in this case. Founded in 2002 by four European semiconductor executives, Icera was established as a Delaware corporation but with its headquarters in Bristol, UK. Icera developed chipsets for devices providing mobile communications based on the UMTS standard, including data- cards (for example, USB sticks), laptops, netbooks, tablets and e-book readers.

(6) In May 2011, Icera was acquired by Nvidia Inc. ("Nvidia") and became a wholly owned subsidiary of Nvidia. Nvidia consequently assumed Icera's position as a complainant.5

(7) Nvidia is a technology company based in Santa Clara, California. Nvidia's core business focus is on graphics processing units. More recently, Nvidia has moved into the mobile computing market, where it produces Tegra processors used in phones and tablets, as well as auto infotainment systems.6

(8) In September 2012, Nvidia took the decision to cease supplying chipsets for USB sticks.7 In May 2015, Nvidia announced that it would wind down its modem operations (i.e. Icera's baseband chipset business).8

2.3. Interested Third Persons

(9) On 22 April 2016, […] requested to be admitted to the proceedings as an interested third person.9 […] is a multi-national telecommunications company providing mobile and fixed telecommunication services to consumers and businesses.

(10) On 24 May 2016, the Hearing Officer admitted […] to the proceedings as an interested third party pursuant to Article 27(3) of Council Regulation No 1/2003 and Article 13 of Commission Regulation No 773/2004. On 8 July 2016, in accordance with Article 13(1) of Commission Regulation No 773/2004, […] was informed in writing of the nature and subject matter of the proceedings by means of a summary version of the Statement of Objections adopted on 8 December 2015.10 On 9 August 2016, […] confirmed that it did not have any comments on the document.11 Since then, […] has not exercised any of its rights as an interested third person.

3. PROCEDURE

(11) On 30 June 2009, the Commission received a complaint under Article 7 of Council Regulation No 1/2003, lodged by Icera against Qualcomm ("initial Complaint"). On 8 April 2010, an updated and revised version of the initial Complaint was lodged ("Complaint"), specifying that it replaced the initial Complaint. The Commission started its investigation in this case on the basis of the allegations made in that updated and revised version of the initial complaint.

(12) On 26 July 2010, Qualcomm submitted its observations with respect to the Complaint.

(13) By submissions of 1 May, 17 May and 31 July 2012, Nvidia, which had acquired Icera in May 2011, supplied further information, supplementing and bringing to the fore allegations concerning predatory pricing.

(14) On 16 July 2015, the Commission decided to initiate proceedings within the meaning of Article 2(1) of Commission Regulation No 773/2004.

(15) On 3 September 2015, a State of Play meeting with Qualcomm was held.

(16) On 8 December 2015, the Commission adopted a Statement of Objections ("SO") addressed to Qualcomm.12

(17) On 21 December 2015, Qualcomm was granted access to the file.

(18) On 15 August 2016, Qualcomm submitted a response to the SO ("SO Response") contesting the Commission's preliminary findings.13

(19) On 10 November 2016, an Oral Hearing took place.

(20) On 13 June 2017, Qualcomm lodged an application for the annulment of a Commission decision of 31 March 2017 requesting information from Qualcomm pursuant to Article 18(3) of Council Regulation No 1/2003 ("Article 18(3) Decision") with the General Court.14 On the same date, Qualcomm also introduced an application under Articles 278 and 279 of the Treaty, seeking the suspension of the Article 18(3) Decision of 31 March 2017 or, in the alternative, the adoption of interim measures in this respect. By order of 12 July 2017, the President of the General Court dismissed the application for interim measures.15 By judgment of 9 April 2019, the General Court dismissed the application for the annulment of the Article 18(3) Decision of 31 March 2017.16 On 18 June 2019, Qualcomm lodged an appeal for the annulment of the General Court’s judgment of 9 April 2019.17

(21) On 18 July 2018, a State of Play meeting with Qualcomm was held.

(22) On 19 July 2018, the Commission adopted a Supplementary Statement of Objections ("SSO") addressed to Qualcomm.18

(23) On 31 July 2018, Qualcomm was granted access to the documents registered on the Commission's file after the adoption of the SO on 8 December 2015.

(24) On 22 October 2018, Qualcomm submitted a response to the SSO ("SSO Response") contesting the Commission's preliminary findings as set out in the SO and supplemented by the SSO.

(25) On 10 January 2019, an Oral Hearing took place.

(26) On 5 February 2019, the Commission sent a request for information pursuant to Article 18(2) of Council Regulation No 1/2003 to Qualcomm.19

(27) On 8 February 2019, the Commission sent an Article 18(2) request for information to ZTE.20

(28) On 19 February 2019, the services of the Directorate General of Competition met with Qualcomm in order to provide it with an update on the status of the Commission's assessment of the arguments raised by Qualcomm in its SSO Response and at the Oral Hearing.

(29) On 22 February 2019, the Commission sent Qualcomm a letter ("Letter of Facts") to

(i) provide it with clarifications regarding certain elements set out in the SSO with which Qualcomm had taken issue in its SSO Response; (ii) inform it about pre- existing evidence that was not expressly relied on in the SO and SSO but which, on further analysis of the file, might have been relevant to support the preliminary conclusions reached in the SO as supplemented by the SSO; and (iii) bring to its attention limited updates to the SSO's price-cost analysis, which did not have an appreciable impact on the results.21

(30) On 24 March 2019, Qualcomm submitted its comments on the Letter of Facts ("Comments on the Letter of Facts").22

(31) On 25 April 2019, Qualcomm provided the Commission with a follow-up submission to the Oral Hearing of 10 January 2019.23 The arguments contained in the submission mirror to a large extent those already made in Qualcomm's SO Response and SSO Response.24

(32) On 3 July 2019, a State of Play meeting with Qualcomm was held.

4.QUALCOMM’S CLAIMS OF PROCEDURAL IRREGULARITIES

(33) Qualcomm claims that the Commission has infringed Qualcomm's rights of defence due to a number of elements that it considers to constitute procedural irregularities.

(34) First, Qualcomm claims that the Commission failed to conduct a proper and timely investigation, which affected Qualcomm's ability to exercise its rights of defence.25 Relatedly, Qualcomm claims that the passage of time has also affected Huawei's and ZTE's ability to respond to the Commission's questions, resulting in the Commission's analysis relying on partial and selective information.26 These claims are incorrect for the following reasons.

(35) In the first place, the Commission has made at all times utmost efforts to proceed with the investigation as swiftly as possible, while duly complying with its obligation to carefully and impartially examine all relevant evidence,27 including the arguments raised by Qualcomm in the course of the investigation.28

(36) In the second place, the duration of the investigation reflects the complexity of the predatory pricing allegations made by Icera/Nvidia, which the Commission has been actively investigating only as of 2012 following additional submissions made by Nvidia (see recital (13) above).29 In particular, the assessment that the Commission had to carry out in this case included, in addition to a comprehensive qualitative analysis of the contemporaneous evidence on the file, a particularly cumbersome analysis of a large amount of quantitative evidence for the purpose of establishing the prices effectively paid by Huawei and ZTE, as well as an appropriate cost measure for the application of the price-cost test. The fact that the investigation in this case concerns composite products made the required analyses of large amounts of data, most of which can be accessed only by the investigated party, particularly complex.30

(37) In the third place, the duration of the investigation reflects the extent to which Qualcomm has been willing to cooperate with the Commission. In fact, throughout the investigation, Qualcomm has shown a certain reluctance to provide the Commission with the information that the Commission considered necessary, notably for establishing an appropriate cost measure in relation to the products under investigation. In particular, when requested to provide specific information on cost items incremental to the products under investigation, Qualcomm failed to provide meaningful information in this respect, limiting itself instead to criticising the Commission's efforts to establish a sound cost measure.31 This made it necessary for the Commission to engage in a time-consuming exploration of potential alternative approaches. As a result, in the SO adopted in December 2015 (i.e. after three and a half years of investigating Icera's predatory pricing related allegations, see recital

(36) above), the Commission relied on Qualcomm's average yearly expenditure on R&D as a proxy for the purposes of its price-cost test.32 This cost measure was revised in the SSO issued in July 2018 in reaction to the arguments made by Qualcomm in its SO Response and at the Oral Hearing.

(38) Moreover, when the Commission requested on 30 January 2017 certain data and information necessary to assess some of the arguments raised by Qualcomm in its SO Response and at the Oral Hearing, Qualcomm failed to provide the requested information, thereby requiring the Commission to seek that data and information by means of an Article 18(3) Decision adopted on 31 March 2017.33 After having sought an extension of the time limit to respond to that information request until 28 July 201734 and later until 31 August 2017,35 Qualcomm submitted its reply on 16 and 30 June 2017, following limited deadline extensions granted by the case team36 and by the Hearing Officer,37 i.e. around 3 months after the adoption of the Article 18(3) Decision and around 5 months after the Commission's Article 18(2) information request of 30 January 2017. The appropriateness of the time period granted to Qualcomm for providing the requested information was confirmed by the General Court.38

(39) In the fourth place, the duration of the investigation was impacted by the choices made by Qualcomm in the context of its defence strategy against the preliminary objections raised by the Commission in the SO. For example, following the adoption of the SO, Qualcomm chose to engage in an extensive exchange of correspondence39 with the Commission with regard to a total of 449 alleged access to file related issues40 and a number of alleged "referencing issues in the SO".41 The time needed to clarify these issues resulted in Qualcomm's SO Response eventually reaching the Commission only on 15 August 2016, i.e. more than eight months after the adoption of the SO.

(40) In the fifth place, the duration of the investigation cannot have impacted Qualcomm's rights of defence since Qualcomm has been aware of the Commission's investigatiosince at least June 201042 and was therefore under a duty, at least as from that date, to act with greater diligence and to take all appropriate measures in order to preserve evidence relevant to the investigation.43 Given that exculpatory evidence (i.e. Qualcomm internal documents disproving the existence of a predatory strategy) can only stem from Qualcomm itself, the inability of third parties to provide information on their perception of Qualcomm's intentions due to the relevant employees having since left the company or relevant documents having been deleted or lost cannot affect Qualcomm's rights of defence.

(41) Second, Qualcomm claims that it has not been given sufficient time to respond to the SO and to the SSO.44 Both claims are unfounded.

(42) As regards the SO, the time period of four months initially granted to Qualcomm for responding to the Commission's objections was, despite the limited length of the SO (119 pages), already longer than usual45 to take account of the size of the file and the nature of the objections as well as of the fact that the Commission had addressed a second Statement of Objections to Qualcomm in another case on the same day.46 This time period was subsequently extended upon Qualcomm's request to an overall period of around 8 months. Considering notably the length of Qualcomm's SO Response (335 pages excluding annexes, as compared to the SO of 119 pages), there are no indications that the time period eventually available to Qualcomm was insufficient for it to be able to exercise its rights of defence in relation to the SO.

(43) As regards the SSO, the Commission notes that the objections set out in the SSO were (except for the reduced duration of the conduct) identical to the objections set out in the SO. The SSO essentially consisted of a revised price-cost test and a more extensive analysis of the documentary evidence in the file in reaction to the arguments made by Qualcomm in its SO Response and at the Oral Hearing. Despite Qualcomm therefore already having been familiar with subject matter of the SSO, the time limit of eight weeks initially granted to Qualcomm for responding to the SSO was extended twice to almost 12 weeks, i.e. almost three times the minimum period and almost five weeks more than the time period normally granted in more complex cases.47 Considering notably the length of Qualcomm's SSO Response (379 pages excluding annexes, as compared to the SSO of 287 pages), there are no indications that the time period eventually available to Qualcomm was insufficient for it to exercise its rights of defence in relation to the SS

(44) Third, Qualcomm claims that it has not been granted adequate access to the file following the adoption of both the SO and the SSO.48 These claims are unfounded.

(45) As regards the SO, Qualcomm itself acknowledged that any access to file related issues it had raised were resolved well before it submitted its SO Response.49 Any such issues cannot therefore have affected its rights of defence in relation to the SO.

(46) As regards the SSO, Qualcomm was granted access to the file on 31 July 2018.50 Upon request and as a matter of courtesy, on 6 August 2018, Qualcomm was provided with the working spreadsheets underlying the price-cost test carried out in the SSO.51 The Commission also promptly reacted to Qualcomm's subsequent access to file related requests,52 amongst other by providing revised non-confidential versions of a total of 18 documents53 as well as certain explanations and clarifications on other issues raised by Qualcomm in this context.54 The absence of any prejudice to Qualcomm's rights of defence from the access to the file granted to Qualcomm following the adoption of the SSO is corroborated by the fact that Qualcomm did not make use of the opportunity offered by the Commission to complement its SSO Response after having been provided with revised non- confidential versions of certain documents55 which Qualcomm had previously labelled as "most relevant to Qualcomm's defence".56

5. STANDARDS, STANDARD-SETTING ORGANISATIONS AND STANDARD ESSENTIAL PATENTS

5.1. Standards

(47) Standards ensure compatibility and interoperability between related products. This has many benefits.57 Standards can encourage innovation and lower costs by increasing the volume of manufactured products. Standards can strengthen competition by enabling consumers to switch more easily between products from different manufacturers. Standards may also further the Treaty objective of achieving the integration of national markets through the establishment of an internal market. The European Union has accordingly promoted standardisation as a tool for European competitiveness.58

5.2.Standard-setting organisations

(48) Standard-setting organisations are organisations whose primary activity is to develop and maintain standards by bringing together industry participants and interested stakeholders to evaluate competing technologies for inclusion in standards.

(49) Standard-setting organisations also seek to ensure that participants contribute technology that will create valuable standards and that these standards are widely adopted. The broader the implementation of a standard, the greater the interoperability benefits.

(50) Participants in a standard-setting process can obtain significant benefits if their technology becomes part of a standard. These include potential royalties from licensees, a large base of licensees, increased demand for their products and improved compatibility with other products using the standard.

(51) The European Union and the European Free Trade Association (EFTA) have recognised three standard-setting organisations as official European standardisation bodies:59 the European Committee for Standardisation (CEN), the European Committee for Electrotechnical Standardisation (CENELEC) and the European Telecommunications Standards Institute (ETSI).60

5.3.Standard essential patents

(52) Standards frequently make reference to technologies that are protected by patents, especially in industries such as telecommunications. Hundreds or even thousands of patents may read on a single standard. Thus, when a user of a standard (also known as an "implementer") manufactures standard-compliant products, it cannot avoid that its products use technologies that are covered by such patents.

(53) Patents that are essential to a standard are those that cover technology to which a standard makes reference and that implementers of the standard cannot avoid using in standard-compliant products. These patents are known as standard-essential patents ("SEPs"). SEPs are different from patents that are not essential to a standard ("non-SEPs"). This is because it is generally technically possible for an implementer to design around a non-SEP to comply with a standard. By contrast, an implementer has to use the technology protected by a SEP when manufacturing a standard- compliant product.

(54) The major standard-setting organisations in the field of wireless communications, namely ETSI, the Institute of Electrical and Electronics Engineers ("IEEE") and the International Telecommunications Union ("ITU") require their members to license their SEPs on (fair,) reasonable and non-discriminatory ("(F)RAND") terms.

6. THE TECHNOLOGY AND PRODUCTS CONCERNED BY THE DECISION

(55) This Decision concerns baseband chipsets that implement and comply with the UMTS standard of cellular communication technology.

(56) Cellular communication technology allows communication by means of a cellular network, which is a radio network distributed over land through cells, where each cell includes a fixed location transceiver known as a base station. These cells together provide radio coverage over larger geographical areas. Cellular user equipment, such as mobile phones, is therefore able to communicate even if the equipment is moving through those cells during transmission.

(57) In this Decision, the following definitions apply:

(a) "UMTS(-compliant) chipsets" means baseband chipsets that implement and comply with the UMTS cellular communications standard;

(b) "GSM chipsets" means baseband chipsets that comply with the GSM standard but not with the UMTS and LTE standards.

6.1. The evolution of cellular communication standards

6.1.1. GSM

(58) Global System for Mobile Communications ("GSM") is a standard developed by ETSI to describe technologies for second generation ("2G") digital cellular networks. Developed as a replacement for first generation ("1G") analogue cellular networks, the GSM standard originally described a network optimized for voice telephony. The standard was expanded over time to include packet data transport via General Packet Radio Services ("GPRS") and Enhanced Data rates for GSM Evolution ("EDGE"). Later technology generations build on the principles established by this standard.

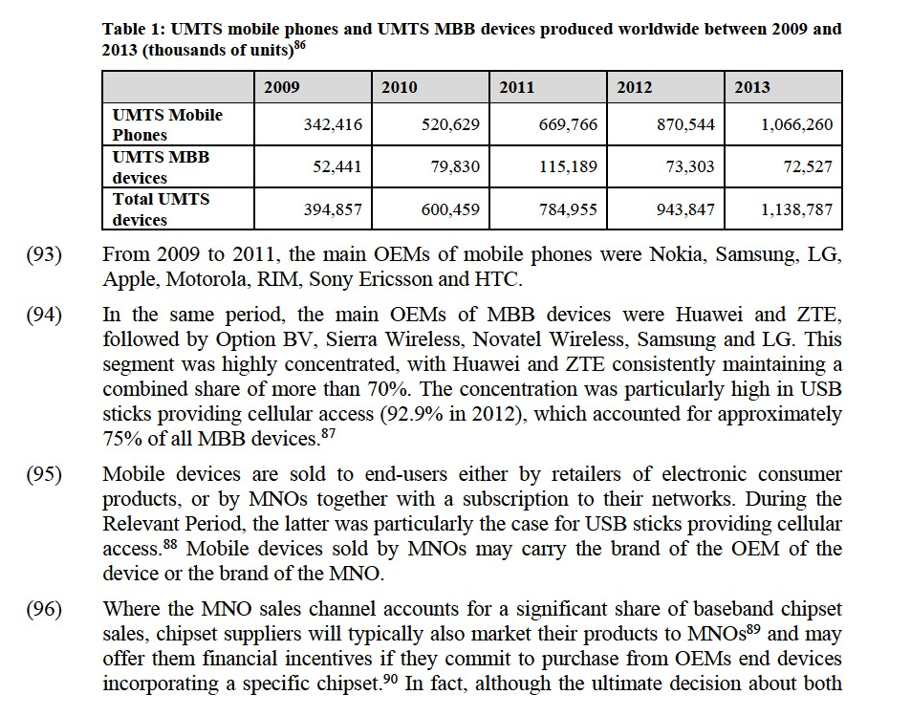

(59) In this Decision, references to GSM include GPRS and EDGE.

6.1.2. UMTS

(60) Universal Mobile Telecommunications System ("UMTS") is a third generation ("3G") wireless and mobile communications standard capable of supporting multimedia services beyond the capability of 2G systems such as GSM.

(61) The beginning of the UMTS standard setting process dates back to the early 1990s when the concept of UMTS emerged from European research programmes. In 1992, ETSI established a technical working group61 specifically to investigate the UMTS concept. By January 1998, the decision was made to adopt two alternative technologies, Wideband-Code Division Multiple Access ("W-CDMA") and Time Division-(Synchronous) Code Division Multiple Access ("TD-(S)CDMA")62 as options for the radio part of the UMTS standard.

(62) In December 1998, following a decision of the ETSI General Assembly, the work on UMTS was moved to a new group which included delegations from the US, South Korea and Japan as full members. It became known as the 3rd Generation Partnership Project or "3GPP". The aim of 3GPP was to create a globally applicable 3G mobile phone system standard.

(63) In December 1999, 3GPP completed what was known as "Release 99". This marked the first iteration of the UMTS standard. Release 99 was then transposed by ETSI into formal European standards throughout 2000. In line with the requirements of Decision 128/1999/EC,63 the UMTS standard was implemented in most Member States during the following years.

(64) 3GPP has further evolved the W-CDMA variant of UMTS in order to provide improved characteristics, including higher data rates. Notable evolutions of W- CDMA include High Speed Packet Access ("HSPA"),64 Evolved High Speed Packet Access ("HSPA+")65 and Dual Carrier HSPA ("DC-HSPA").66 These evolutions formed part of subsequent 3GPP Releases (see section 6.2.2 below).

(65) In this Decision the term UMTS will be used to describe only the W-CDMA variant of the radio interface as well as its evolutions, i.e. HS(D/U)PA, HSPA+, DC-HSPA. These technologies are also known as UMTS Frequency Division Duplexing ("UMTS-FDD"), as opposed to the alternative technology UMTS-TDD (see recital

(61) above and section 10.2.5. below).

6.1.3. LTE

(66) Long Term Evolution ("LTE") is based on the GSM and UMTS standards, increasing the capacity and speed using a different radio interface together with core network improvements. This standard was also developed by 3GPP.

(67) LTE is commonly referred to as a fourth generation ("4G") standard, although strictly speaking the requirements set for 4G are satisfied only by its later iterations (known as LTE-Advanced or LTE-A).

(68) In this Decision, the term LTE will be used to refer to LTE, LTE-A, and further iterations of the LTE technology.

6.1.4. Other cellular and wireless communication standards

(69) In addition to GSM, UMTS and LTE, there are other cellular communication standards such as Code Division Multiple Access ("CDMA").67 Moreover, there are standards for wireless communication which do not make use of cellular technology, such as Worldwide Interoperability for Microwave Access ("WiMAX") and Wireless Local Area Network ("WLAN"), also commonly called WiFi.

(70) These standards are standardised by standard-setting organisations like the Third Generation Partnership Project 2 ("3GPP2")68 and the IEEE.

6.2. Baseband chipsets

6.2.1. Functions

(71) Mobile devices such as smartphones, tablets, portable PCs and e-book readers require mobile broadband69 connectivity to the internet through cellular mobile telecommunication networks ("mobile networks"; see recital (56) above).

(72) The core component providing mobile connectivity in a device is the baseband processor. Its main task is to perform the signal processing functionality according to communication protocols described by cellular standards. Baseband processors can be embedded directly in mobile devices, or in external modules (e.g. a USB stick), which are in turn plugged into a device.

(73) A baseband processor typically consists of both hardware and software. It is made of semiconductor material ("silicon die") and packaged into a chip using ceramic or plastic material. That chip is referred to as a "baseband chip".

(74) In addition to the baseband processor, certain types of mobile devices require an application processor, used for running the operating system and applications (like messaging, internet browsing, imaging and games). This application processor can be provided as a standalone product, packaged into a separate chip or can be integrated with the baseband processor into the same silicon die and packaged into the same chip.

(75) Based on the above distinction, baseband chips can be divided into two categories:

(a) Standalone baseband chips, where no application processor is included; and

(b) Integrated baseband chips, where the baseband processor has been integrated with an application processor, usually into a single silicon die, and is packaged in the same chip.

(76) Regardless of the presence of an application processor, a baseband processor is typically paired with two additional components to complete its functionality, namely the Radio Frequency ("RF") integrated circuit, also known as RF transceiver,70 and the Power Management ("PM") integrated circuit.71 All three functionalities (baseband processor, RF transceiver and PM circuitry) are necessary for mobile connectivity and their resulting combination is called a "baseband chipset".72 The three components of baseband chipsets are usually purchased from the same supplier, either as a bundle or separately.73

(77) In this Decision, the term "integrated baseband chipset(s)" or simply "integrated chipset(s)" will be used for chipsets that include an integrated baseband chip. The term "standalone baseband chipset(s)", "slim baseband chipset(s)" or "slim modem(s)" will be used for chipsets that include a baseband chip but not an application processor.

(78) Baseband chipsets, whether standalone or integrated, implement one or multiple wireless standards, from the same or from different technology families and generations. For example, a baseband chipset might implement only the GSM standard, or it might implement a combination of the GSM, UMTS and LTE standards.

6.2.2. Technological evolution of UMTS compliant chipsets74

(79) The UMTS compliant chipset technology evolution is driven to a significant extent by the UMTS standardisation process. New market requirements trigger the development of new iterations of UMTS and other standards from the same family, namely GSM and LTE.75

(80) In turn, the adoption of new standards spurs product development, both for mobile network infrastructure and for mobile devices. Since the baseband chipset is the device component responsible for connectivity to the mobile network, the compliance with standards is a key feature of baseband chipsets. Developments of both network infrastructure and devices are appropriately coordinated, with all suppliers engaging in extensive testing to ensure interoperability. For technical reasons, readiness of mobile infrastructure usually precedes readiness of devices.

(81) The standardisation process is driven by contributions from the industry. These contributions are typically based on research and development activities undertaken by the companies involved well before a standard is discussed and adopted. It follows that companies which have significantly contributed to a standard are better placed to develop products compliant with that standard, enjoying a head-start compared to their competitors.

(82) The major breakthroughs in the evolution of UMTS compliant chipsets are related to the support of increasingly high data rates of mobile broadband connectivity: before HSPA technology, UMTS was supporting data rates up to 0.384 Mbps. These data rates were inadequate to support typical broadband applications like full internet browsing and video streaming. HSPA technology (3GPP Release 4 and 3GPP Release 5) enabled data rates up to 14 Mbps providing true broadband connectivity. Subsequent iterations of HSPA+ in 3GPP Releases 7 and 8 increased the data rates even further to 28 Mbps and 42 Mbps, respectively (see also recitals (340) and (352) below).

(83) UMTS compliant chipsets typically also provide support for GSM/EDGE (2G).76 This support is indispensable in the case of mobile phones, as for most mobile network operators ("MNOs") GSM is still important for voice in terms of coverage and capacity. GSM/EDGE may also be useful for mobile broadband ("MBB") devices (see section 6.2.4 below), although it does not provide broadband connectivity. Via its basic connectivity support, however, GSM can ensure service continuity in case of gaps in UMTS network coverage.

(84) With the development of the LTE standard (first release adopted in December 2008), LTE baseband chipsets started to emerge. The initial LTE chipsets were compliant exclusively with LTE (so-called "single-mode" LTE chipsets), which limited their practical use due to the limited deployment of LTE networks. Gradually, the major baseband suppliers developed chipsets supporting both UMTS and LTE, with the first such products becoming commercially available in 2011-2012. The UMTS and LTE technologies were developed in parallel by 3GPP, for improved performance and interoperability.

6.2.3. UMTS chipset development and production

(85) Baseband chipset suppliers typically design and develop their products themselves.77 The majority however do not fabricate them in their own facilities. Instead, they outsource fabrication to specialised manufacturers called foundries which aggregate demand from multiple semiconductor suppliers. The baseband chipset suppliers that outsource the production of chipsets are called "fabless suppliers".78

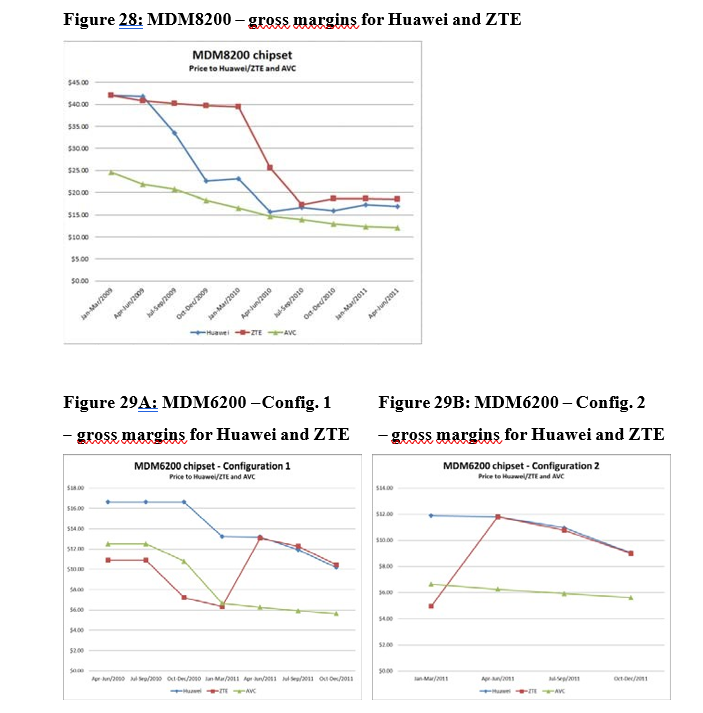

(86) A further development for UMTS compliant chipsets has been the introduction of slim modems (see recital (77) above). As further explained at recitals (374)-(375) below, Icera entered the UMTS chipset market with sales of the first slim modem in 2006, targeting the MBB segment (see section 6.2.4 below). Shortly thereafter, Qualcomm followed Icera in the development and launch of slim modems. Other companies like Intel/Infineon, Mediatek and HiSilicon have later also developed slim modems, in parallel to their integrated chipsets.

(87) Slim modems have eventually prevailed in MBB devices such as data cards (see recitals (102)-(104) below). They are however also widely used in smartphones and tablets, when an OEM prefers to have the baseband processor and the application processor residing in different chips (a concept known as "two-chip" architecture; see recital (99) below).

6.2.4. Customers and applications

(88) Baseband chipsets are typically sold to original equipment manufacturers ("OEMs"), which incorporate them into devices that make use of mobile connectivity. OEMs include Apple, HTC Corporation ("HTC"), Huawei Technologies Co. Ltd. ("Huawei"), LG Corp ("LG"), Nokia Corporation ("Nokia"),79 Samsung Group ("Samsung"), and ZTE Corporation ("ZTE").

(89) OEMs incorporate baseband chipsets into a variety of mobile devices, which could be grouped in two broad categories during the period from 2009 to 2011 ("Relevant Period"):

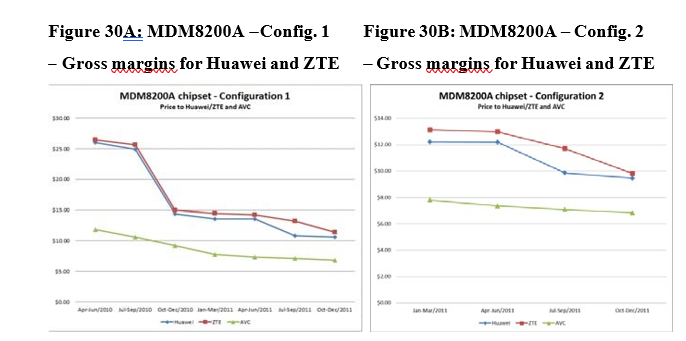

(a) Mobile phones (also called handsets), usually further classified into

(1) Basic phones (phones providing only basic functionality like voice and messaging);

(2) Feature phones (phones providing more advanced functionality, like multimedia applications and internet connectivity);

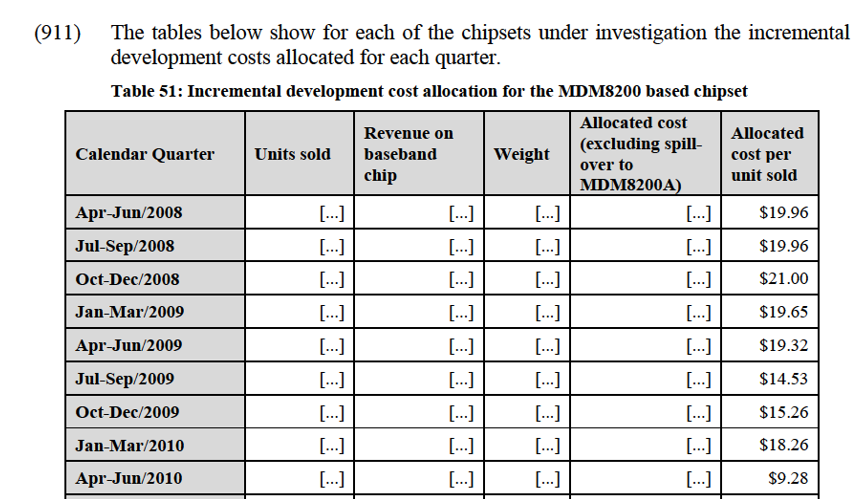

(3) Smartphones (phones providing advanced functionality, comparable to the functionality provided by a personal computer).

(b) MBB devices,80 which cover devices with mobile connectivity, other than mobile phones, and include in particular:

(1) Tablets with cellular access;81

(2) Data cards with cellular access, typically in the form of USB sticks (also called "dongles");

(3) Wireless routers that rely on cellular networks to act as WiFi hotspots (also called "MiFi" devices);

(4) Other devices (e.g. laptops) using embedded modules with cellular access.

(90) The main purpose of cellular access in MBB devices is broadband data connectivity, based on UMTS or LTE technology.82 Typically, these devices do not provide traditional voice telephony (also called "circuit switched"83 voice), or do so only exceptionally.84

(91) By contrast, for mobile phones, voice telephony is an absolute requirement. Mobile phones typically use a number of interoperable technologies, in order to provide a seamless voice experience to users. During the Relevant Period, this refers for most European mobile networks to the capability to use both GSM and UMTS technologies for traditional voice telephony.85

(92) The mobile phone market is considerably bigger than the MBB device market (in particular for UMTS enabled devices). It has also been growing considerably faster. The Commission has estimated the size of these markets (in terms of volume) as follows:

the design of a particular device and the selection of the appropriate chipset ordinarily resides with the OEM, the needs of MNOs heavily influence this decision.91

6.2.5. Baseband chipset selection by OEMs

(97) OEMs typically judge the combination of a baseband chip, RF transceiver and PM circuitry as proposed by the chipset supplier as a whole chipset package92 in order to choose the chipset that best suits their requirements among the various competing solutions offered by chipset suppliers.93 Therefore, even though chipset suppliers typically sell each of the components of a chipset individually94 and customers are free to "mix-and-match" as they see fit,95 competition between chipset suppliers takes place at the chipset level.

(98) The choice of the most appropriate baseband chipset by an OEM is driven by the desired technical characteristics of the device, including supported standards, features and targeted price segment. In fact, in their responses to Article 18(2) requests for information,96 OEMs have mentioned inter alia the following characteristics as most important for their baseband chipset selection: supported architecture (slim/integrated), price, supported standards and performance, size, power consumption, the supplier's reliability, the supplier's ability to offer and provide support, certainty of supply, IPR coverage and protection against IPR related legal risks. Sections 6.2.5.1 to 6.2.5.3 below provide an overview of some of themost important considerations OEMs undertake when choosing the most appropriate baseband chipset for a certain device.

6.2.5.1. The choice between integrated and standalone baseband chipsets

(99) Devices that interact with users (such as mobile phones and tablets) require both a baseband processing and an application processing functionality. For such devices manufacturers face two choices:

(a) to use an integrated chipset (see recital (77) above) providing both functionalities. This is referred to as "one chip (or one chipset) architecture"; or

(b) to combine a separate baseband processor (see recital (77) above) with a separate application processor. This is referred to as a "two chip (or two chipset) architecture".

(100) As explained by a number of OEMs, the use of an integrated chipset is preferred for devices that require both baseband and application processing due to:97

(a) The savings in time and effort for the integration of the two functionalities by the OEM, as they come pre-integrated;

(b) The reduced space used by the integrated chipset in the device;

(c) The reduced cost of the integrated chipset compared to the price of the two separate products.

(101) However, if the desired characteristics (either on the application processing or on the baseband processing side) cannot be met by any available integrated chipset, the OEM may opt for a two chip architecture combining separate components, possibly from different suppliers. This also applies if the OEM is vertically integrated (i.e. is a supplier of either application processors or baseband chipsets)98 and may therefore prefer its own supply over the merchant market supply for one of the two components.

(102) There are also mobile devices that do not require any application processing functionality because this is provided to the user by another device. A number of MBB devices require only connectivity and thus fall into this category,99 with data cards (such as USB sticks) being the most typical example.100

(103) Therefore, in cases where either a two chip architecture has been chosen, or only connectivity is required, the preferred type of baseband chipset is the standalone baseband chipset (slim modem). This is primarily for reasons of cost optimisation, as slim modems use less silicon and are therefore less expensive than integrated chipsets with equivalent baseband characteristics (see also recital (382) below).101 Other reasons include reduced size and power consumption.

(104) However, there have also been devices where an integrated chipset was used to provide only connectivity, without making any use of its application processing capabilities.102 This choice was made either before the introduction of slim modems or due to specific desired characteristics that were not available in slim modems at the time. In some of these implementations, the application processing functionality of the baseband chipset was technically disabled. In other implementations, there was no technical disabling, but there was a contractual provision or a commercial incentive restricting the use of the application processor.103

6.2.5.2. The choice on the basis of performance considerations

(105) Certain OEMs have different performance requirements for baseband chipsets, depending on the device and its target market. Therefore, different device groups or even different tiers within the same device group might require different baseband chipsets.

(106) […] for example has stated that "[c]ompared with handset product, BCs [baseband chipsets] for MBB product must provide better performance (i.e. they must keep up with the wireless standard's development, and high communication rate)."104

(107) For […], "customers' request plays a critical role in our company's determination on BCs [baseband chipsets]. Some customer/operator requests device supporting advanced standards regardless the higher price; some requests device supporting less advanced standards with lower cost."105

6.2.5.3. Intellectual Property Rights considerations

(108) A number of OEMs have stressed the importance of IPR in their chipset sourcing decisions. In particular, they stated a preference for chipset suppliers that (in addition to products) can provide the widest possible coverage of IPR related to the chipset technology, including patent licenses, non-assertion provisions and indemnification.106

7. QUALCOMM'S BASEBAND CHIPSET BUSINESS

7.1. Qualcomm's products

(109) Qualcomm has a broad product portfolio ranging from low and mid-cost baseband chipsets for the mass-market to leading edge baseband chipsets implementing the latest standards.107 Being active also in the development of application processors, it offers both standalone and integrated chipsets.

(110) Qualcomm has marketed its baseband chips (and by extension chipsets) mainly under the following product family names:108

(a) The MDM (Mobile Data Modem) product family, which includes standalone baseband chips, namely chips that mainly provide baseband processing (connectivity);

(b) The MSM (Mobile Station Modem) product family, which includes integrated baseband chips, namely chips that provide both application processing and baseband processing (connectivity);

(c) The QSC (Qualcomm Single Chip) product family, which includes integrated baseband chips. QSC products incorporate the RF and PM functionalities in the same chip, in addition to the baseband and application processors;109 and

(d) The QSD (Qualcomm SnapDragon) product family, which includes a specific range of integrated chips, featuring a "Snapdragon" application processor. The QSD designation was withdrawn in 2010 and replaced by MSM.

7.2. Qualcomm's patent portfolio

(111) Qualcomm is the largest IPR holder active in the supply of baseband chipsets. As of 6 August 2015, it owned more than 100,000 distinct patents.110 Between 1 January 2008 and 27 February 2014, Qualcomm made disclosures with respect to approximately 500 amended patent families as potentially essential to UMTS and 809 amended patent families as potentially essential to LTE.111

7.3. Qualcomm's product creation process

(112) The process for creating Qualcomm's chips involves four main phases: (i) […]; (ii) […]; (iii) […]; and (iv) […]. So-called […] take place between the […] and […] stages (i.e. the […], which generally corresponds to the […] and between the […] and […] stages (i.e. the […], which generally corresponds to the […]).112

(113) […]113

(114) […]114 […]115 […]116

(115) […]117 […]118 […]119

(116) […]120 […]121

(117) […]122 […]123

(118) […]124

(119) The following figure provides an overview of Qualcomm's product creation process.

Figure 1: "[…]"125

[…]

7.4.Qualcomm's price setting process

(120) Qualcomm typically sells […]. […], when communicating its prices and price proposals (so-called "price indications") to its customers and comparing the competitiveness of its products vis-à-vis other chipset suppliers, Qualcomm […].126 The pricing of the […].127

(121) Qualcomm sells chips pursuant to negotiated terms and conditions […]. The terms and conditions applicable to Qualcomm's sales are governed by […] between Qualcomm and each of its customers. Qualcomm's […].128

(122) Qualcomm's pricing decisions, including any price reductions or other financial incentives, have to be approved by Qualcomm's […].129 […]130 […].131

(123) […].132 […].133 […].134 […].135 […].136 The flow of Qualcomm's decision making process for chip and chipset related pricing is illustrated in Figure 2 below.

Figure 2: Qualcomm's pricing decision making process137 […]

(124) […].138

(125) […].139 […].140

(126) Subsequently, […] price approvals are reflected in a formal agreement setting forth the terms and conditions of the approved incentive, signed by both parties.141 During the Relevant Period, such formal agreements were […].142 In fact, as explained by Qualcomm, it is not uncommon that agreements are […].143

8. PRODUCTS CONCERNED BY THE INVESTIGATION

(127) The investigation concerns Qualcomm's UMTS chipsets that are based on Qualcomm's MDM8200, MDM6200 and MDM8200A baseband chips ("the MDM8200/6200/8200A based chipsets") which competed with Icera's UMTS chipsets that are based on Icera's ICE8040, ICE8042 and ICE8060 baseband chips ("the ICE8040/8042/8060 based chipsets") during the Relevant Period. These Qualcomm and Icera products are standalone baseband chipsets144 supporting data connectivity at maximum downlink data rates145 of 7.2146/14.4 Mbps147 up to 28 Mbps during the Relevant Period. These chipsets are compliant with the W-CDMA variant of UMTS (so-called UMTS-FDD; see recital (65) above) and support GSM/EDGE. A more detailed description of each of Qualcomm's and Icera's chipsets is provided in sections 8.1.1 to 8.1.3 and sections 8.2.1 to 8.2.3 respectively.

(128) In the following, any references that do not explicitly mention the chipset (e.g. "the MDM8200") are to be understood as references to the relevant baseband chip, as defined in recital (73) above.

8.1. Qualcomm's chipset offering in the leading edge segment during the Relevant Period

8.1.1. Qualcomm's MDM8200 based chipset

(129) The MDM8200 based chipset was Qualcomm's first standalone chipset conceived and designed as a modem-centric chipset suitable for use in MBB devices.148 It combined Qualcomm's MDM8200, its RTR6285 RF chip and its PM7540 PM chip.149 It supported HSPA+150 and downlink rates of up to 28 Mbps.151

(130) The product development started on 6 June 2007 […]152 to launch the development phase of the MDM8200153 which was meant to "deliver HSPA+ Technology for early 2009 commercial deployment" and to "[m]aintain [m]odem [l]eadership" for Qualcomm.154 The commercial release155 of the MDM8200 took place in May 2009 and the first end devices incorporating the MDM8200 based chipset were launched on the market at the beginning of June 2009.156 In 2010, sales of the MDM8200 were gradually replaced by sales of the MDM8200A, an improved version of the MDM8200. Nevertheless, sales of the MDM8200 continued into 2011, with the MDM8200 eventually being moved into the End of Life stage on 30 March 2011.157

(131) The MDM8200 was developed in cooperation with the […] network carrier […] who wanted to become the first carrier in the world to deploy infrastructure and devices implementing the HSPA+ protocol.158 To help […] achieve this goal, Qualcomm also collaborated closely with […].159

(132) The commercial launch of an HSPA+ device achieving data rates of 21 Mbps was, at the time, a technological "leapfrog".160 In order to allow […] to be "first to market", the MDM8200 was initially launched without handover capability from GSM infrastructure to W-CDMA infrastructure, and inferior power consumption and thermal performance than one might expect in a cutting-edge chip.161 […] first endevice incorporating the MDM8200 based chipset (the […]) was launched at the Mobile World Conference in Barcelona in February 2009.162

(133) […], Qualcomm advertised the MDM8200 based chipset as its "New Leading Edge Data Card Chipset" with "[s]ignificant modem performance improvement over all known commercial and pre-commercial chipsets".163 However, the commercial success of the MDM8200 based chipset was limited. On the one hand, the MDM8200's power and heat issues (as well as the missing support for wireless voice functionality) made the MDM8200 ill-suited for use in mobile phones,164 restricting its target market to MBB devices like data cards.165 On the other hand, the slow uptake of demand for chipsets supporting HSPA+ exposed the MDM8200 based chipset to competition from Icera. Although Icera's ICE8040 based chipset did not initially support downlink speeds as high as the MDM8200 based chipset, it was able to better capture the market demand at the time due to its ability to software upgrade to higher downlink speeds and its lower price (see recital (410) below).

8.1.2.Qualcomm's MDM6200 based chipset

(134) The MDM6200 is a standalone baseband chip featuring an integrated RF circuit in the same chip, which was combined with Qualcomm's PM8028 or PM8015 PM chip during the Relevant Period to form the MDM6200 based chipset.166 It supports downlink speeds of up to 14.4 Mbps and voice functionality without modification.167 It was developed in tandem with the MDM6600, from which it distinguishes itself mainly due to the fact that it is only compatible with the UMTS (HSPA+) standard, whereas the MDM6600 is both compatible with CDMA2000168 and UMTS (HSPA+).169 Like the MDM8200 and the MDM8200A, the MDM6200 was also intended primarily for data-only applications.170

(135) The MDM6200 is a derivative of the QSC6295 integrated baseband chip (similarly, the MDM6600 is a variation of the QSC6695).171 The launch of its development phase was approved […].172 The originally envisaged date for the commercial launchof the MDM6200 was December 2009, but the development of the MDM6200 […].173 Therefore, only limited quantities of the MDM6200 were shipped to customers as of the second quarter of 2010 […]. Only as of 2011 was the MDM6200 sold in higher quantities.174 […].175

(136) The MDM6200 based chipset was intended to be Qualcomm's response to the growing competitive pressure it was experiencing in particular from Icera, which was addressing the market demand for chipsets supporting data rates of up to 14.4 Mbps with its ICE8040 based chipset during 2009 (see, e.g., recital (466) below). However, as towards the end of 2009 Icera's ICE8040 based chipset was reported to be able to "be software upgraded to support 21 Mbps" with a "single chipset pricing for all data rates (3.6 HDPA to 31M) at around $10 starting from Jan. 2010",176 the market attention for the MDM6200 based chipset faded. This limited the commercial success of the MDM6200 based chipset during the Relevant Period (see, e.g., recital

(535) below).

8.1.3. Qualcomm's MDM8200A based chipset

(137) The MDM8200A baseband chip was a "shrinked" (from 65 to 45 nanometres)177 […] which supported HSPA+178 and downlink speeds of up to 28 Mbps.179 It relied on the same processor technology as the MDM8200.180 Like the MDM8200, it was primarily intended for data-only applications,181 but capable of supporting wireless voice functionality, subject to a minor software and hardware amendment.182 It was typically combined with Qualcomm's RTR6285 RF chip and the PM8028 or PM8015 PM chip to form the MDM8200A based chipset.183

(138) The product development started on 21 April 2009.184 Although the originally envisaged date for the commercial launch of the MDM8200A was March 2010,185 it was first made commercially available only in May 2010.186 Shipments of significant numbers of the MDM8200A to Huawei and ZTE took place as of the third quarter of 2010.187

(139) Qualcomm's decision to start the development of the MDM8200A was, amongst other things, taken in view of the fact that Qualcomm was anticipating "strong price competition" in the HSPA+ data card market at the time.188 Whereas Qualcomm considered that the MDM8200 was "not cost competitive", it expected the cost structure of the MDM8200A to be around […] USD lower, thus allowing "Qualcomm to maintain margin and share at key accounts".189 The […] for the MDM8200A which provided the basis for Qualcomm's decision to launch the product development shows Qualcomm's intention of "[a]ggressively [p]rotecting the [d]ata [c]ard [m]arket", a market which Qualcomm considered as "rapidly growing" and "easier to enter". The MDM8200A was therefore meant to "[d]eny beach-head entry to new players" by preventing them from having the "opportunity to prove their technology before going after higher volume hand-set market".190

8.2. Icera's chipset offering competing with Qualcomm's chipset offering in the leading edge segment during the Relevant Period

8.2.1. Icera's ICE8040 based chipset

(140) The ICE8040 based chipset, also referred to as Espresso-300 ("E300") chipset,191 was Icera's second generation UMTS chipset.192 The chipset consisted of an ICE8040 standalone baseband chip, combined with an ICE8215 RF chip and an ICE8145 PM chip.193 The commercial launch of the ICE8040 based chipset took place in October 2008.194

(141) The ICE8040 based chipset initially supported a maximum downlink speed of 10 Mbps.195 It was a so-called "soft" modem chipset, meaning that most of its baseband processing functionality was implemented in software running on a custom processor, as opposed to the conventional approach of designing and implementing these functions in silicon using a series of fixed function silicon blocks.196 Iceraadvertised this soft-modem architecture as one of the main distinctive characteristics of the ICE8040 based chipset, as it would enable the chipset to benefit from further performance upgrades and enhancements delivered in the form of software upgrades.197 This meant that the ICE8040 based chipset could be enabled to support higher data rates by simple software update and therefore adapt to the future rollout of HSPA+ networks (see notably evidence quoted in recital (382) below). Chipset customers were attracted by this possibility and therefore started viewing the ICE8040 based chipset as an alternative to Qualcomm's higher-priced MDM8200 based chipset, despite the fact that the initial throughput capability of Icera's chipset was inferior to 14.4 Mbps and only gradually increased to 21 Mbps during the Relevant Period.198

(142) Apart from the ability to scale up its capability in terms of support for higher downlink speeds, the ICE8040 based chipset also benefited from efficiencies achieved by a reduction of the size of the silicon die required for the baseband chip. With a die size of 18.2 mm2, compared to the size of 109 mm2 of Qualcomm's MDM8200 based chipset, Icera's ICE8040 based chipset had a lower bill of materials (i.e. list of components required to manufacture a product) than Qualcomm's MDM8200 based chipset.199 This allowed Icera to offer the ICE8040 based chipset at particularly competitive prices (see recital (382) below).

8.2.2. Icera's ICE8042 based chipset

(143) The ICE8042 based chipset, also referred to as Espresso-302 ("E302") chipset,200 was a variant of the ICE8040 based chipset which benefited from certain improvements with regard to power consumption and radio performance.201 The chipset consisted of an ICE8042 standalone baseband chip, combined with an ICE8260 RF chip and an ICE8145 PM chip.202 The commercial launch of the ICE8042 based chipset took place in December 2009.203

(144) At the time of its commercial launch, the ICE8042 based chipset supported downlink speeds of up to 14.4 Mbps. In March 2010, software updates increased the downlink speed supported by the ICE8042 based chipset to 21 Mbps.204 Icera also launched a variant of the Espresso-302 chipset called Espresso-302-1 ("E302-1") chipset in a design that was exclusive to ZTE, incorporating a fuse to ensure it could not deliver downlink speeds greater than 7.2 Mbps. The Espresso-302-1 chipset was therefore a downgraded version of the ICE8042 based chipset which was not able to compete with Qualcomm's leading edge chipsets during the Relevant Period.205

8.2.3. Icera's ICE8060 based chipset

(145) The ICE8060 based chipset, also referred to as Espresso-400 ("E400") chipset,206 was Icera's new generation chipset announced in October 2010.207 The chipset consisted of an ICE8060 standalone baseband chip, combined with an IC8260 RF chip and a third party PM chip. Like the ICE8040 and ICE8042 based chipsets, also the ICE8060 based chipset was a soft modem chipset, thus benefitting from Icera's software-defined modem architecture. It supported downlink speeds of up to 28 Mbps.208 Compared with the ICE8040 and ICE8042 based chipsets, the ICE8060 based chipset offered improvements with regard to power consumption and benefited from bill of materials savings.209 Similarly to the E302-1 chipset, the E400 based chipset was also offered in a downgraded variant called E400-1 chipset, which was capable of reaching a maximum downlink speed of 7.2 Mbps and therefore not able to compete with Qualcomm's leading edge chipsets during the Relevant Period.210

9. OTHER SUPPLIERS OF UMTS COMPLIANT CHIPSETS

(146) A number of other baseband chipset suppliers were also supplying UMTS compliant chipsets during the Relevant Period. The following recitals provide a brief description of the main market players during that period.

9.1. Infineon/Intel

(147) Infineon Technologies AG ("Infineon"), is a Germany based company active in a broad range of semiconductor solutions.

(148) […].211 […]. However, in terms of data rates, Infineon's products did not have the same performance compared to the UMTS chipset offerings of Qualcomm and Icera during the Relevant Period. Its first chipset supporting data rates of 21 Mbps was the

XMM6260 based standalone chipset, which was first shipped to key customers only in February 2011.212 […].213

(149) As of 2011 Qualcomm became […] supplier of UMTS compliant chipsets,214 but Infineon continued to supply other smartphone manufacturers like […]. Its presence in the MBB segment was marginal.215

(150) On 29 August 2010, Intel Corporation ("Intel"), a U.S. based multinational, announced the acquisition of the Wireless Solution business of Infineon,216 which included its baseband chipsets.217 The acquisition was completed on 31 January 2011. Since then, Intel has taken over and developed the business of Infineon in the baseband chipset space.

9.2. ST-Ericsson

(151) ST-Ericsson NV ("ST-Ericsson") was a multinational manufacturer of wireless products and semiconductors headquartered in Geneva, Switzerland, and established on 3 February 2009 as a 50/50 joint venture between Ericsson ("Ericsson") and ST Microelectronics N.V. ("ST Microelectronics"). ST-Ericsson supplied its baseband chipsets to OEMs such as […], […], […] and […].

(152) ST-Ericsson was supplying both integrated and standalone UMTS compliant chipsets. With its M570 chipset supporting data rates of up to 21 Mbps,218 ST- Ericsson intended to offer […]219 and thus to potentially address the same market demand as Qualcomm's and Icera's chipsets described in section 8 above. However, during the Relevant Period this chipset did not appear to have gained significant market traction, […] (see evidence quoted in recital (387) below).

(153) The ST-Ericsson Joint Venture was dissolved on 2 August 2013,220 with its baseband assets being transferred to Ericsson. Eventually, on 14 September 2014, Ericsson decided to exit the baseband chipset market completely.221

9.3. MediaTek

(154) MediaTek Inc. ("MediaTek") is a fabless semiconductor company for wireless communications and digital multimedia solutions headquartered in Taiwan.

(155) During the Relevant Period, […].222 It started to produce UMTS-compliant baseband chipsets in 2010. Due to their lower speed performance and architecture characteristics, MediaTek's initial UMTS compliant chipsets were much more successful in the low and mid-range smartphone segment than in MBB devices.

9.4. Marvell

(156) Marvell Technology Group, Ltd. ("Marvell") is a U.S. based fabless semiconductor supplier. Its product portfolio has been mostly comprised of integrated baseband chipsets, including UMTS compliant chipsets. During the Relevant Period, the company […], without however providing leading edge UMTS compliant chipsets.

9.5. HiSilicon

(157) HiSilicon Technologies Co. Ltd ("HiSilicon") is a China based fabless semiconductor supplier223 and a subsidiary of the Chinese device manufacturer Huawei. […] during the Relevant Period.224

(158) HiSilicon started production of UMTS compliant chipsets in 2009, for use in Huawei's MBB devices (mainly USB sticks) with low to mid-level performance (see evidence quoted in recital (387) below).225 […].

9.6. Nokia

(159) Nokia Corporation ("Nokia"), a multinational company based in Finland, […].

(160) Gradually, however, Nokia moved away from self-supply and relied on merchant market chipsets.226

(161) In July 2010, Nokia stopped completely the development of new UMTS compliant chipsets, selling its baseband assets to Renesas.227 […].

9.7. Renesas

(162) Renesas Mobile Corporation was a wholly-owned subsidiary of Renesas Electronics Corporation ("Renesas"), headquartered in Japan. It was active in the design and development of platforms for mobile phones and other mobile devices. It mainly supplied Japanese phone manufacturers such as Fujitsu, Sharp, NEC, Sony and Panasonic.228

(163) In 2010, Renesas expanded its activities in baseband chipsets by acquiring Nokia's baseband assets.229

(164) The company never succeeded in gaining significant market traction outside Japan and eventually exited the market in 2013, transferring its baseband assets to Broadcom.230

9.8. Broadcom

(165) Broadcom Corporation ("Broadcom") was a U.S. based fabless semiconductor company that designed solutions for a broad range of wired and wireless communications markets. The company developed a number of integrated UMTS compliant chipsets, […].231

(166) In 2013, Broadcom acquired the baseband assets of Renesas.

(167) In July 2014, the company announced the wind-down of its baseband business.232

(168) In February 2016, Broadcom was acquired by the semiconductor company Avago Technologies Ltd. The new merged entity is called Broadcom Limited.

9.9. Samsung/LSI

(169) Samsung Systems LSI ("LSI") is a South Korean-based foundry semiconductor company that designs and manufactures baseband chipsets to be incorporated in mobile devices such as smartphones and tablets.

(170) LSI is a […].233

10. MARKET DEFINITION

10.1.Principles

(171) The definition of the relevant market is carried out, in the context of the application of Article 102 of the Treaty, in order to define the boundaries within which it must be assessed whether a given undertaking is able to behave to an appreciable extent independently of its competitors and its customers.234

(172) The concept of the relevant market implies that there can be effective competition between the products or services which form part of it and this presupposes that there is a sufficient degree of interchangeability between all the products or services forming part of the same market in so far as a specific use of such products or services is concerned.235

(173) An examination to that end cannot be limited solely to the objective characteristics of the relevant products and services, but the competitive conditions and the structure of supply and demand on the market must also be taken into consideration.236

(174) The definition of the relevant market does not require the Commission to follow a rigid hierarchy of different sources of information or types of evidence. Rather, the Commission must make an overall assessment and can take account of a range of tools for the purposes of that assessment.237

10.2. Relevant Product Market

10.2.1. Principles relating to product market definition

(175) The identification of the relevant product market by the Commission derives from the existence of competitive constraints. Undertakings are subject to three main sources of competitive constraints, namely demand-side substitution, supply-side substitution and potential competition.238 From an economic point of view, for the definition of the relevant market, demand-side substitution constitutes the most immediate and effective disciplinary force on the suppliers of a given product.239

(176) Supply-side substitution may also be taken into account when defining markets in those situations in which its effects are equivalent to those of demand-side substitution in terms of effectiveness and immediacy. There is supply-side substitution when suppliers are able to switch production to the relevant products and market them in the short term without incurring significant additional costs or risks in response to small and permanent changes in relative prices. When these conditions are met, the additional production that is put on the market will have a disciplinary effect on the competitive behaviour of the companies involved.240

(177) Supply-side substitution is, however, not taken into account for the definition of a relevant market each time it would entail the need to adjust significantly existing tangible and intangible assets, additional investments, strategic decisions or time delays.24

10.2.2. Application to this case

(178) The Commission concludes that the relevant product market in this case is comprised of slim and integrated chipsets that are compliant with different iterations of the UMTS standard and limited to the merchant market. It will be referred to as the UMTS (baseband) chipset market in the following.242

(179) The Commission has reached this conclusion based on the following factors:

(a) Baseband chipsets that comply with any technology other than UMTS, such as GSM, CDMA, TD-SCDMA (UMTS-TDD), WiFi and WiMAX do not exert a competitive constraint on UMTS chipsets (see sections 10.2.3 to 10.2.6 below);

(b) Baseband chipsets that comply with certain iterations of UMTS exert a competitive constraint on chipsets compliant with other iterations of UMTS (see section 10.2.7 below);

(c) Integrated baseband chipsets exert a competitive constraint on standalone baseband chipsets (slim modems) (see section 10.2.8 below); and

(d) Captive production of baseband chipsets does not exert a competitive constraint on merchant market sales of UMTS chipsets (see section 10.2.9 below).

(180) Contrary to Qualcomm's claims,243 the Commission is able to reach these conclusions without having to carry out a SSNIP (small but significant non-transitory increase in price) test (see section 9.2.10 below).

10.2.3. The substitutability of GSM chipsets and UMTS chipsets

(181) During the Relevant Period, GSM chipsets represented a relatively large proportion of total sales of baseband chipsets. For example, in 2010, GSM chipsets represented more than half of worldwide shipments of all baseband chipsets.244

(182) The Commission concludes that GSM chipsets that are not compliant with UMTS are not substitutable for UMTS chipsets. This is for the following reasons:

(183) First, data rates achieved by GSM chipsets are inadequate for data-transfer intensive applications like video streaming. For an operator or mobile OEM wishing to enable these services, GSM chipsets with a data rate limit of approximately 100 kbps are not a viable alternative. This is confirmed by several replies of baseband chipset customers to requests for information, for example:

(a) According to […], "[i]n most markets with widespread 3G adoption (including the EEA), neither MNOs [Mobile Network Operators] nor end consumers would be likely to accept devices limited to GSM as alternatives to devices supporting more modern mobile standards. In addition, OEMs (including […]) tend to market the smallest number of devices possible which could serve the majority of the markets in which they are present."245

(b) According to […], "[a]s for technology, GSM does not offer the same data rates as UMTS, and hence the theoretical user of a GSM-only device cannot use as many applications that depend on higher data rates. Some would argue that EDGE, which is an evolution of GSM, provides for higher data rates.

However, these EDGE rates are not as high as UMTS and its evolution."246

(184) Second, UMTS chipsets are more efficient in the use of spectrum, both for data and for voice.247 According to […], "UMTS provides higher user capacity than GSM. This enables operators using UMTS over GSM to serve more customers in a given area with fewer base stations or cells and at a higher data rate."248

(185) Third, suppliers of GSM chipsets are unable to switch to the supply of UMTS chipsets in a short time frame and without incurring significant additional investments or risks.249 For example:

(a) According to […], "GSM chipsets do not allow easy transition to UMTS. Indeed, a number of BC [baseband chipset] suppliers have attempted unsuccessfully to make this switch - for example, […]".250

(b) According to […], "[i]n order to switch from supplying GSM chipsets to chipsets supporting GSM/UMTS, a supplier must undertake significant additional investments, because little of the original GSM investment can be leveraged into UMTS development. As much as […] of the GSM/UMTS chipset is specific to UMTS, […]. Further, the UMTS standard also requires the use of many additional components as compared to GSM hardware. Accordingly, […] estimates the total time needed for such a switch as approximately between three and five years."251

(186) The Commission's conclusion is not put into question by Qualcomm's argument that chipsets supporting late iterations of the GSM standard (such as EDGE) were substitutable for chipsets supporting early iterations of UMTS.252 This is for the following reasons.

(187) First, to the Commission's best knowledge the data rates allegedly achieved by EDGE according to Qualcomm (1.3 Mbps) have never been supported by networks or commercial products. Qualcomm has not provided any evidence to the contrary.

(188) Second, in the same reply to an information request by […] adduced by Qualcomm in support of its claims, […] itself noted that […]. Moreover, […] referred to other factors due to which GSM chipsets do not represent a viable substitute for UMTS chipsets, such as carrier requirements, coverage and power as well as capacity restrictions.253

(189) Third, barriers for chipset suppliers to switching between different standards (such as from GSM/EDGE to an early iteration of UMTS) are higher than barriers for chip suppliers to switching between different iterations of a certain standard (see recital

(207) below).

(190) Fourth, in any case, even if there were a limited overlap in terms of performance between chipsets at the edge of the transition from one standard to another, this would not be sufficient to conclude on the overall substitutability between chipsets implementing different standards (see recitals (182)-(185) above).

10.2.4. The substitutability of chipsets supporting UMTS and chipsets that support CDMA but not UMTS

(191) The Commission concludes that CDMA chipsets that do not support UMTS are not substitutable for UMTS chipsets.

(192) First, a large number of replies of UMTS chipset customers to requests for information indicated that they would not find it technically or commercially feasible to switch to CDMA chipsets that do not support UMTS.254 This is because the majority of mobile networks and 3G-enabled devices in the EEA use UMTS technology and CDMA compliant devices are not compatible with UMTS networks. For example:

(a) According to […], "[t]he requirement for which standard is supported by the product is driven by the individual carrier". Moreover, "CDMA is only used by a limited number of carriers in the world".255

(b) According to […], it "does not consider CDMA BCs [baseband chipsets] to be technically and commercially potential substitutes for UMTS/LTE BCs [baseband chipsets]. Technically, CDMA BCs [baseband chipsets] cannot operate on the UMTS/LTE network. […] The cellular networks (operated by the regional telecom operators) define what wireless standard is required and in most regions (except […]) the CDMA standard is not supported by the networks."256

(c) According to […], "[c]ustomers want products that support UMTS/LTE. If […] were to switch to using chipsets supporting only CDMA or other non-3GPP wireless standards (e.g. WiMax, WiFi, etc), its devices would no longer match customers' requirements."257

(193) Second, suppliers of CDMA baseband chipsets that do not support UMTS cannot switch or expand their supply to UMTS baseband chipsets in a short time frame and without incurring significant additional investments or risks.258

(194) While Qualcomm appears to claim that CDMA chipsets that do not support UMTS and chipsets that support UMTS form part of the same market,259 it has not submitted any evidence to support this claim.

10.2.5. The substitutability of chipsets supporting UMTS-FDD and chipsets supporting UMTS-TDD but not UMTS-FDD

(195) The Commission concludes that UMTS-TDD chipsets that do not support UMTS- FDD are not substitutable for chipsets that support UMTS-FDD.

(196) First, a large number of replies of baseband chipset customers to requests for information indicated that the majority of mobile networks and 3G enabled devices in the EEA use UMTS-FDD technology.260 Only limited frequencies have been assigned in some Member States to UMTS-TDD technology261 and UMTS-TDD compliant devices are not compatible with UMTS-FDD networks. For example:

(a) According to […], "UMTS-TDD is only used in […]. UMTS-FDD is required by Telecom Operators outside of […]. Chipsets supporting only UMTS-TDD, therefore, would not satisfy the requirements of Telecom Operators outside of […], making them commercially unfeasible."262

(b) According to […], "UMTS-TDD is only used in […]. […] It is not commercially feasible for our company to replace the BCs [baseband chipsets] supporting UMTS-FDD with BCs [baseband chipsets] supporting UMTS-TDD if UMTS-TDD is not supported by local carrier."263

(197) Second, a majority of the replies of baseband chipset suppliers to requests for information indicated that suppliers of UMTS-TDD baseband chipsets that do not support UMTS-FDD cannot switch or expand their supply to UMTS-FDD baseband chipsets in a short time frame and without incurring significant additional investments or risks.264 For example:

(a) According to […], "[a] switch from the supply of UMTS-TDD chipsets to chipsets supporting UMTS-FDD requires the development of technology under the new standard. This requires a very significant investment in R&D, including […]. Such switch will require a multi-year development phase."265

(b) According to […], "[a]lthough the actual time and expense involved will vary, we believe that it is extremely unlikely that a supplier of a chipset supporting one standard could switch to the supply of a chipset supporting another standard in less than two years (in fact, we believe that two years would be an unusually rapid development timeframe), and for a total expenditure of […]"266

(198) While Qualcomm appears to suggest that UMTS-TDD chipsets that do not support UMTS-FDD and UMTS chipsets that support UMTS-FDD form part of the same market,267 it has submitted no evidence to support this claim.

10.2.6. The substitutability of UMTS baseband chipsets and baseband chipsets supporting WiFi and WiMAX but not UMTS

(199) For the reasons set out below, the Commission concludes that chipsets supporting WLAN (commonly known as WiFi) but not UMTS and chipsets supporting WiMAX but not UMTS are not substitutable for UMTS chipsets.

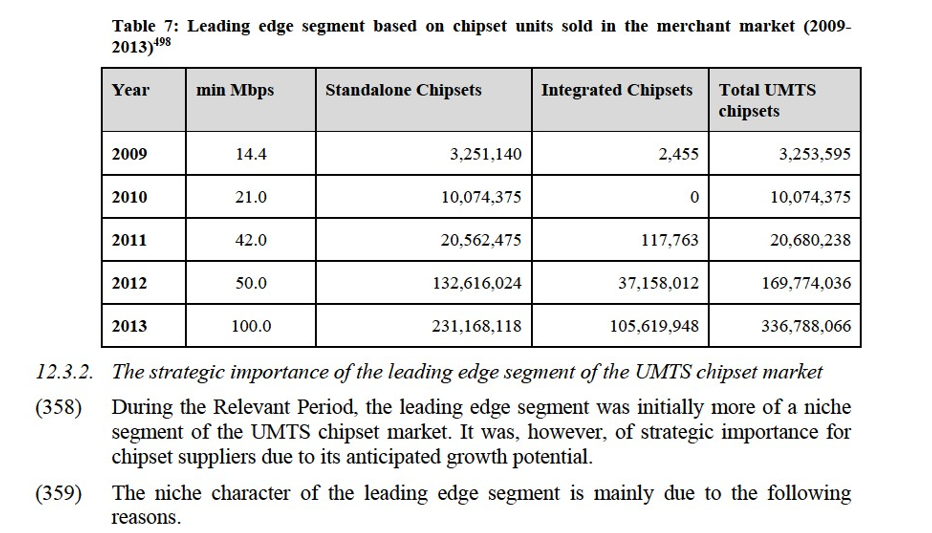

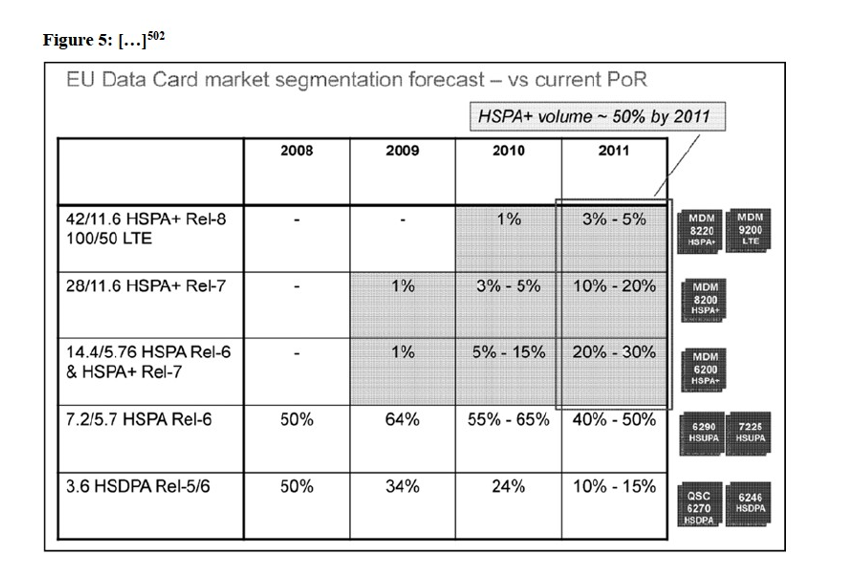

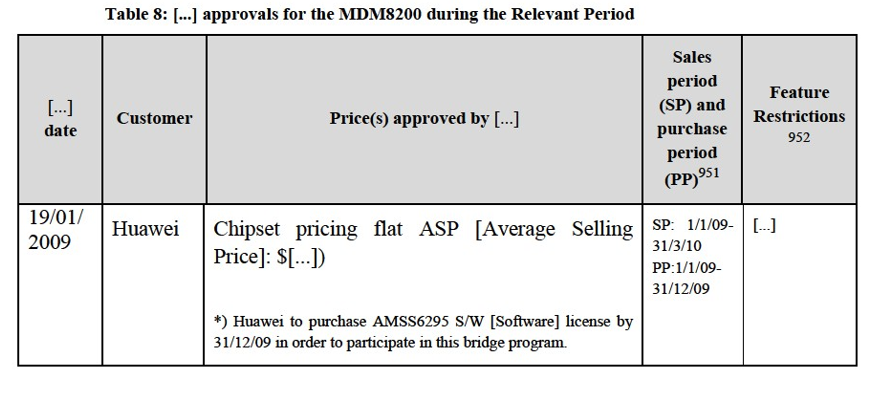

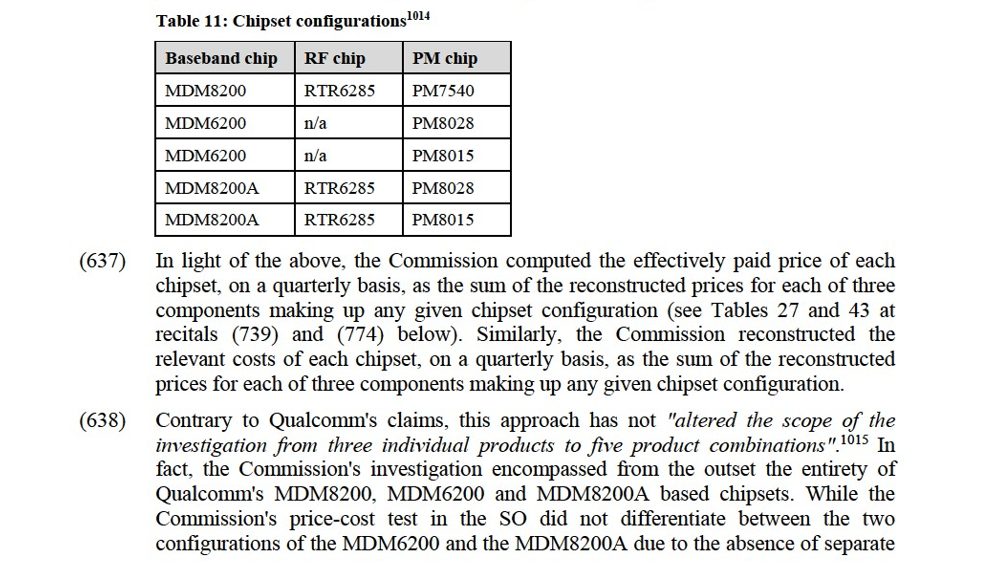

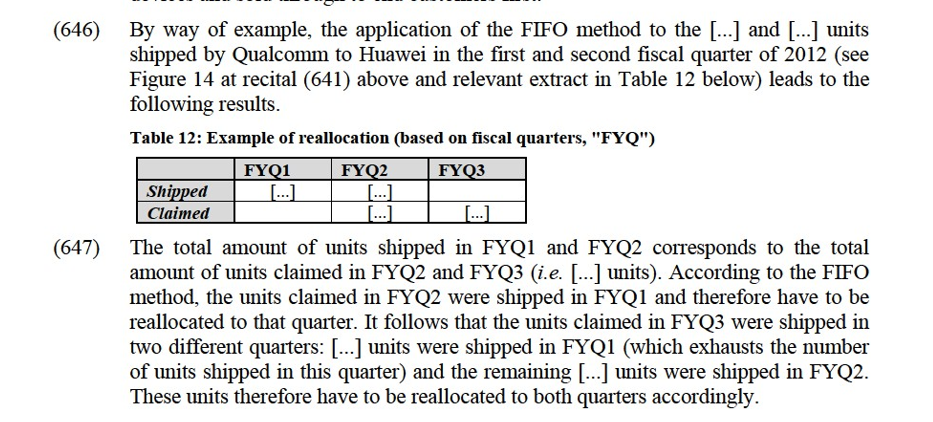

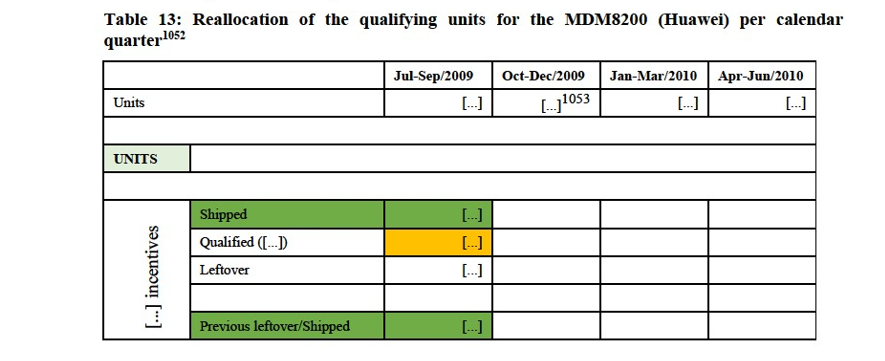

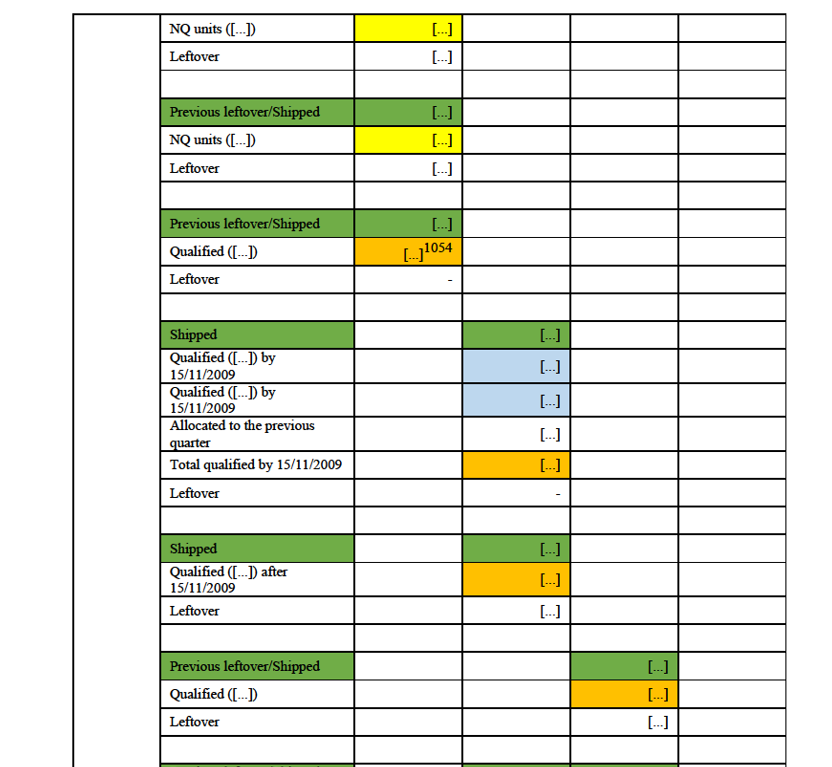

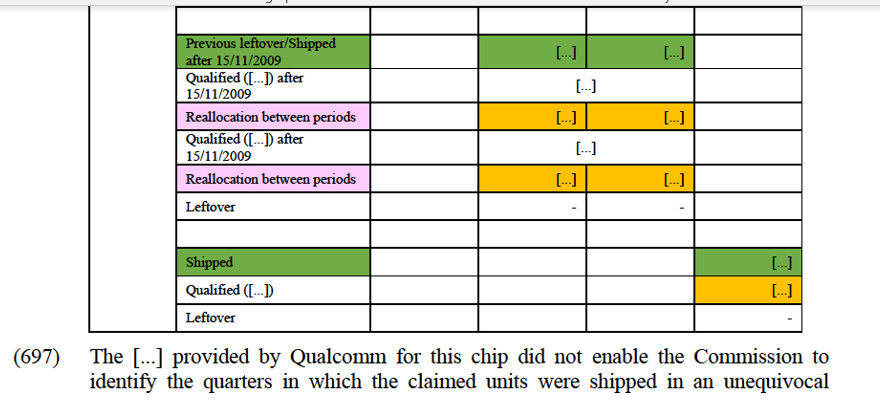

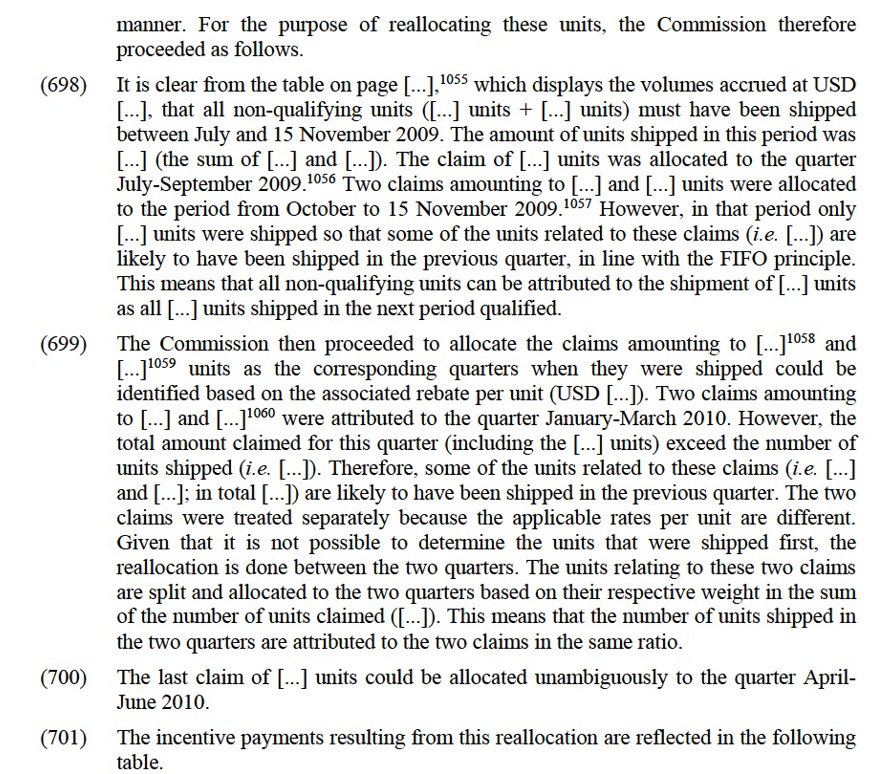

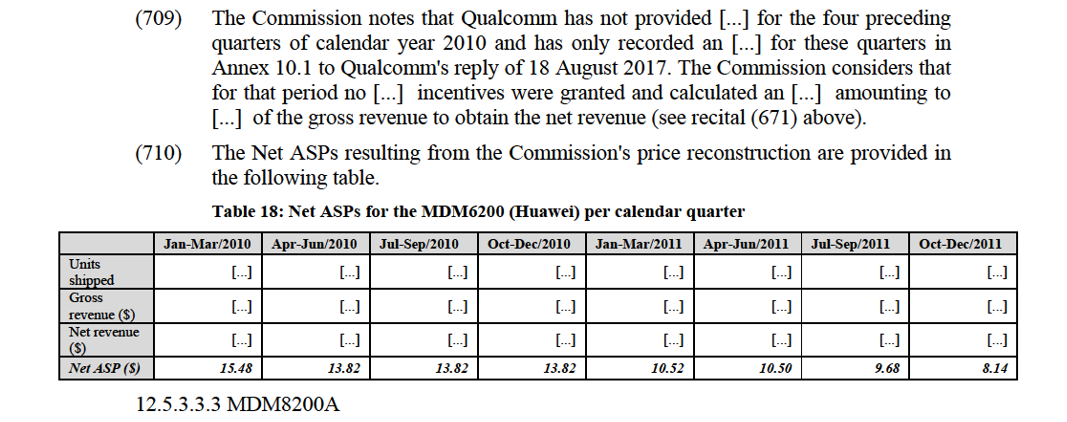

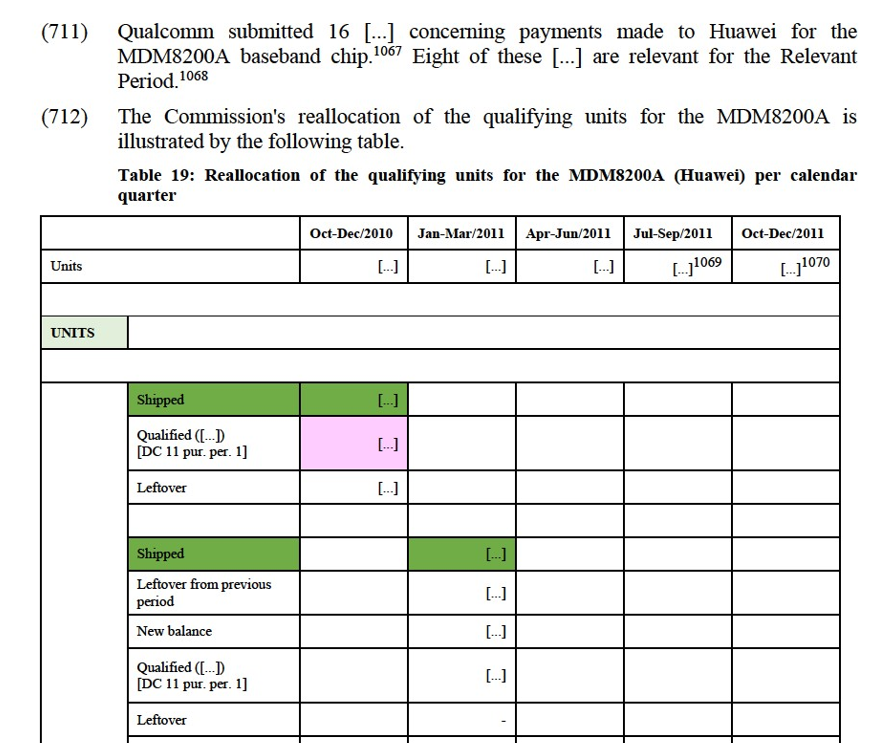

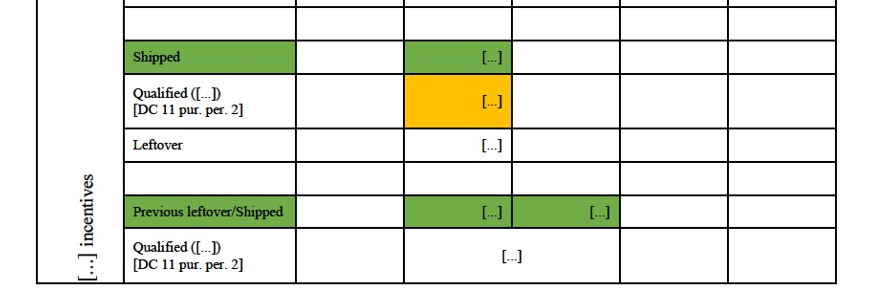

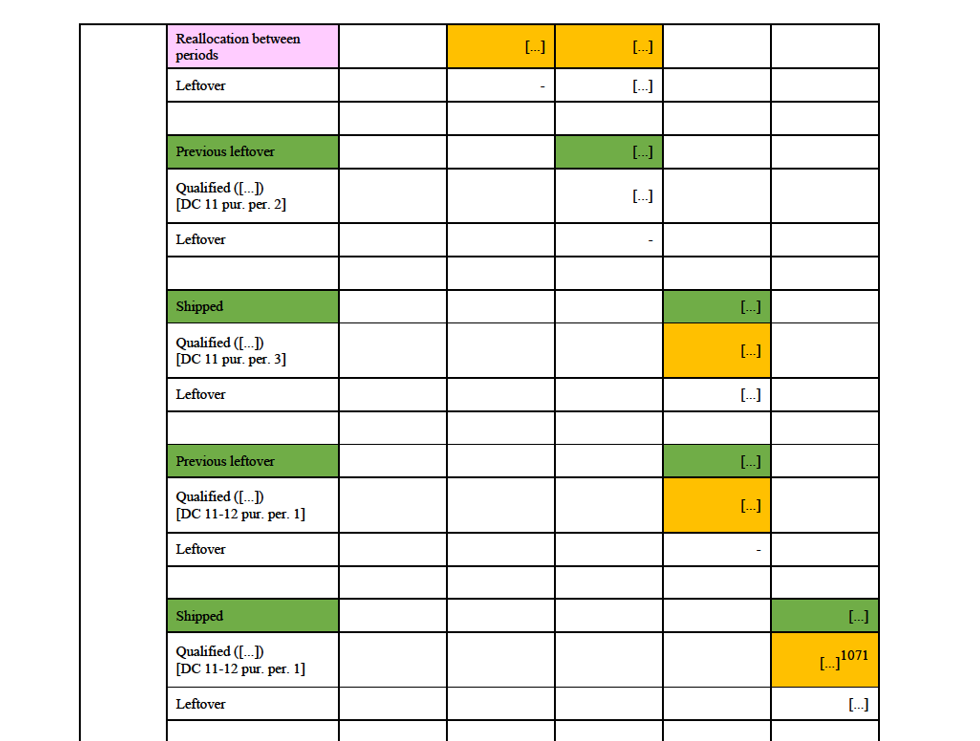

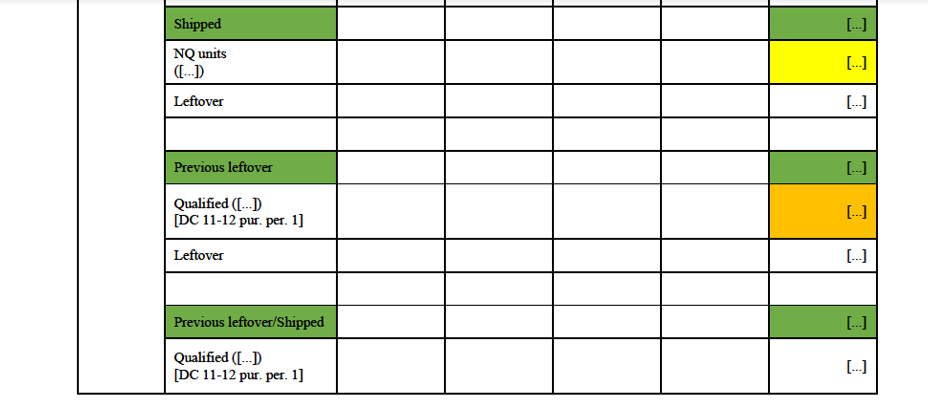

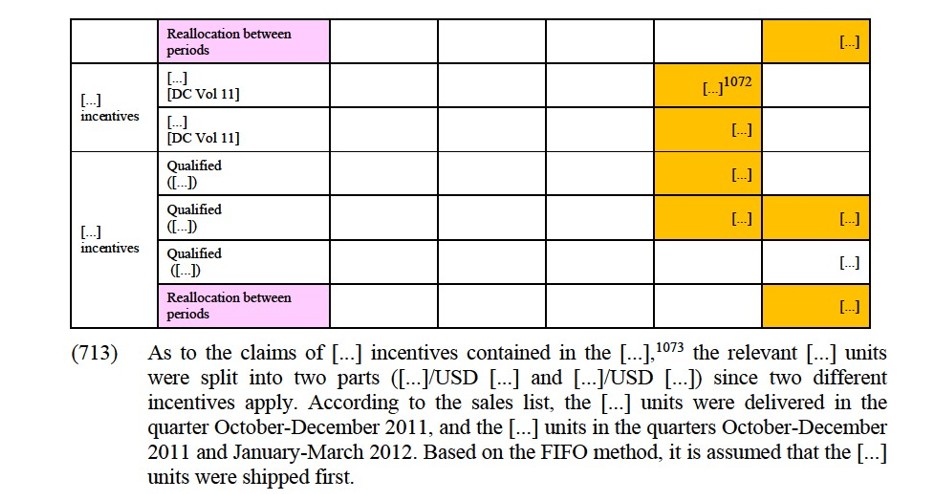

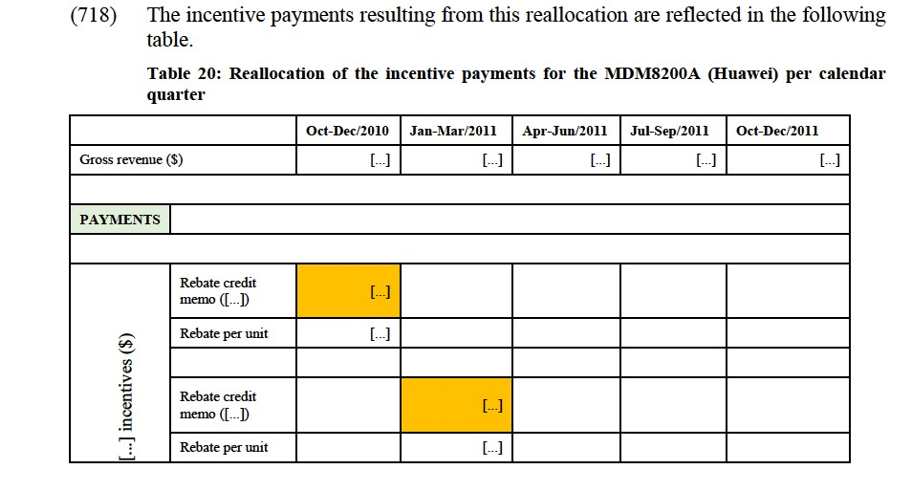

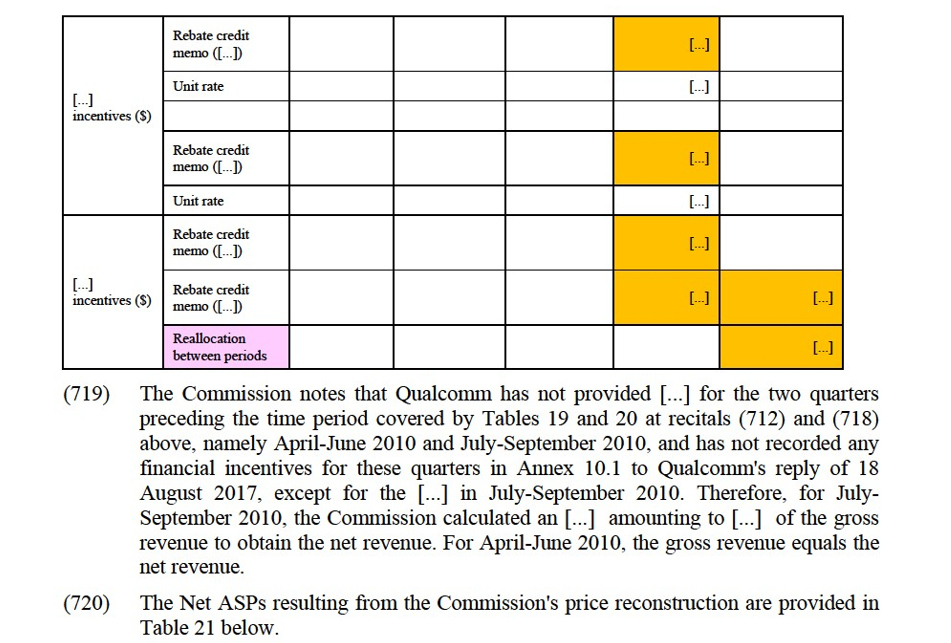

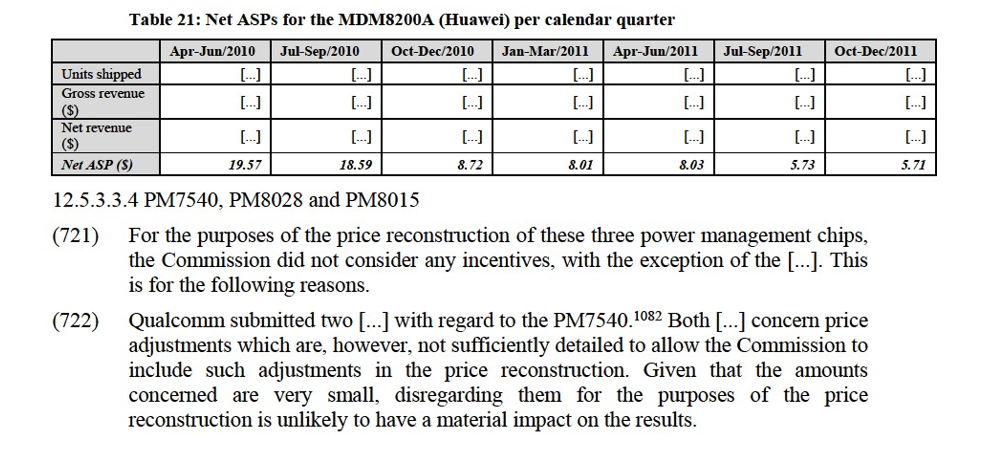

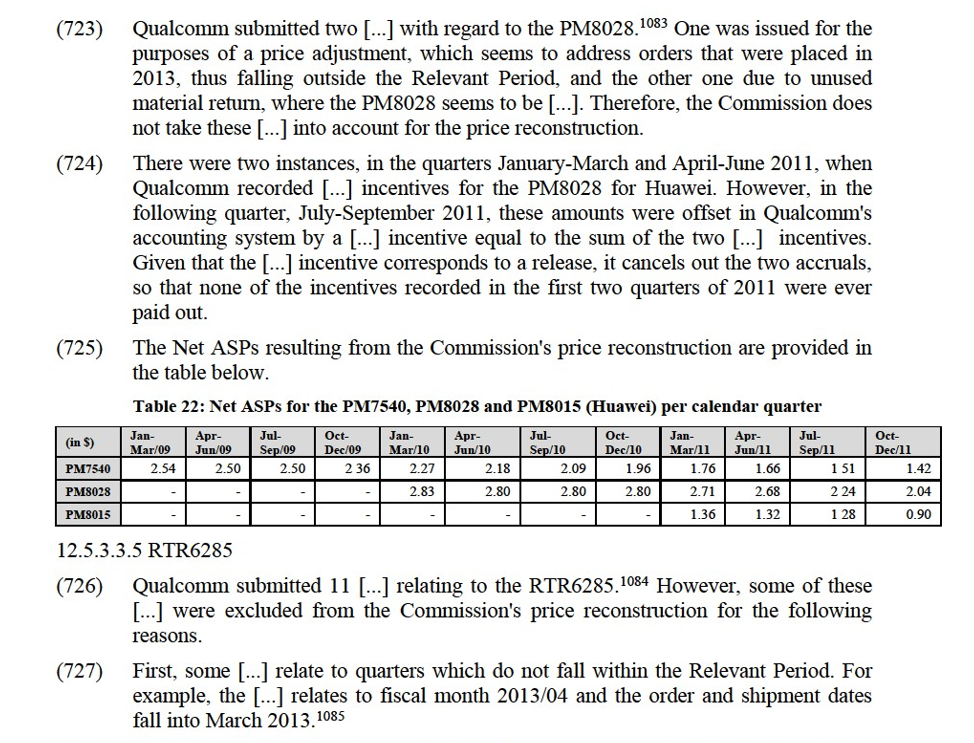

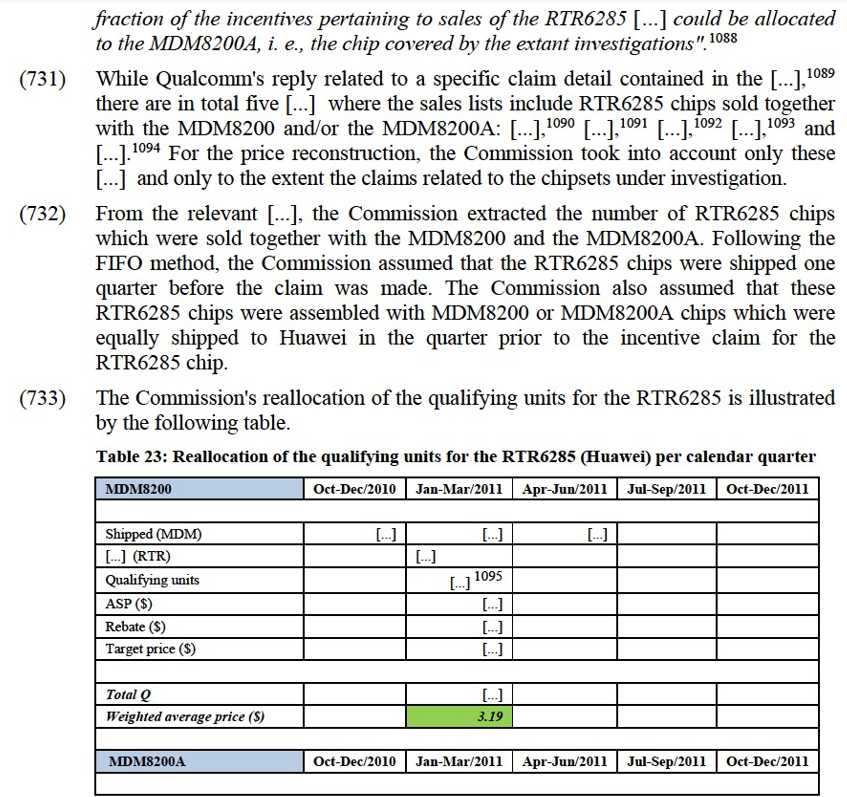

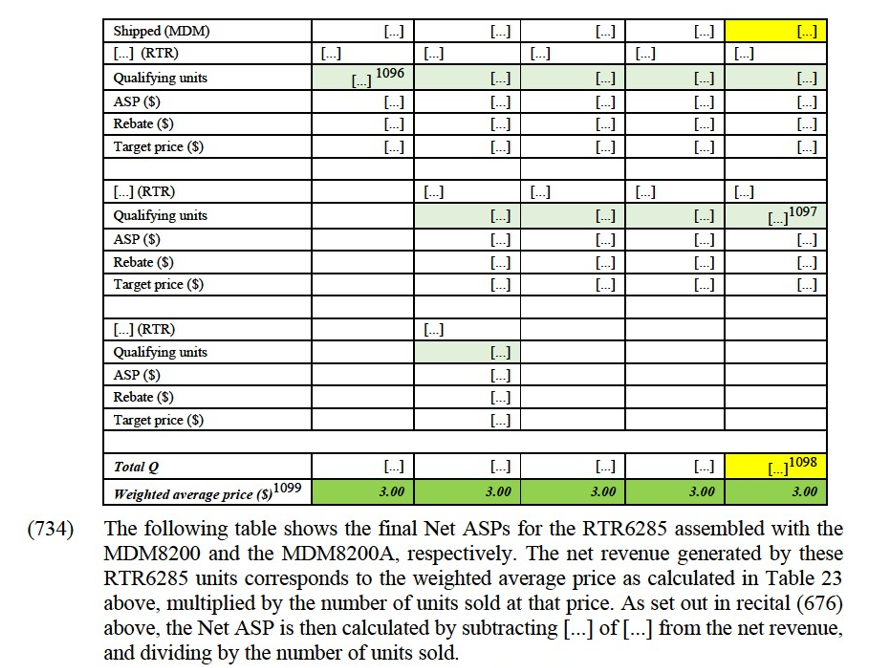

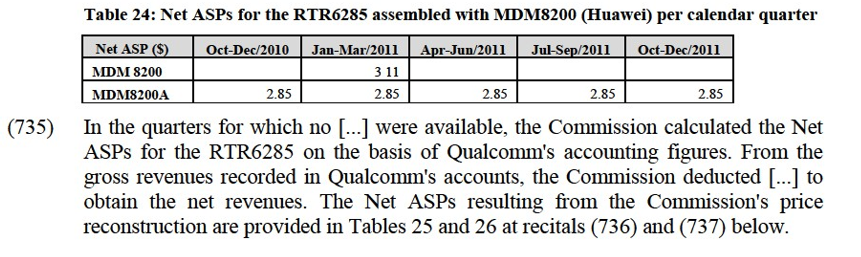

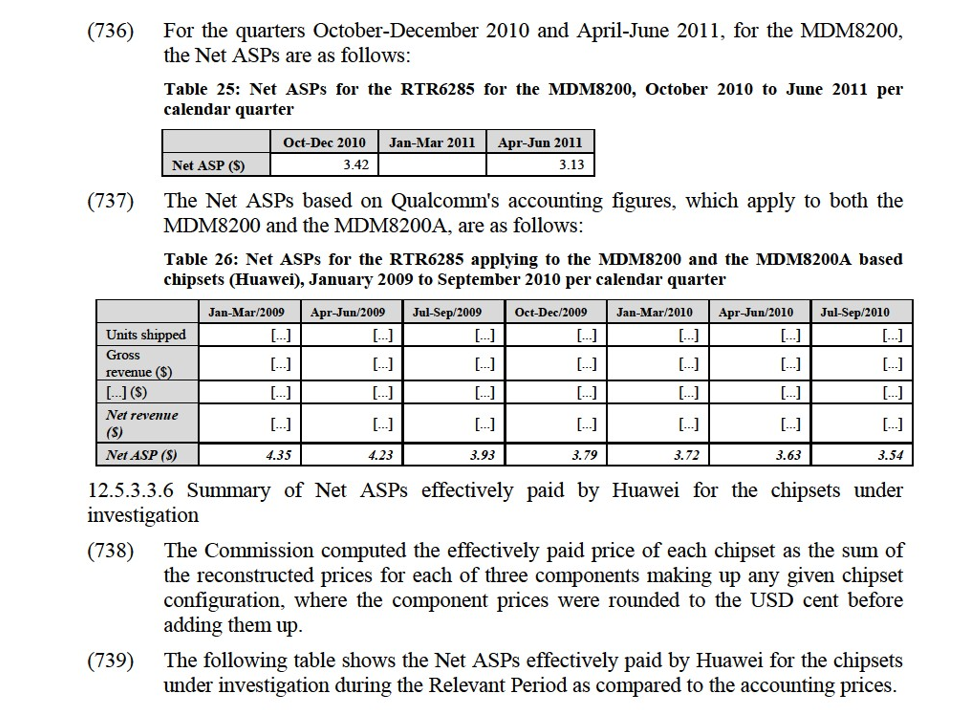

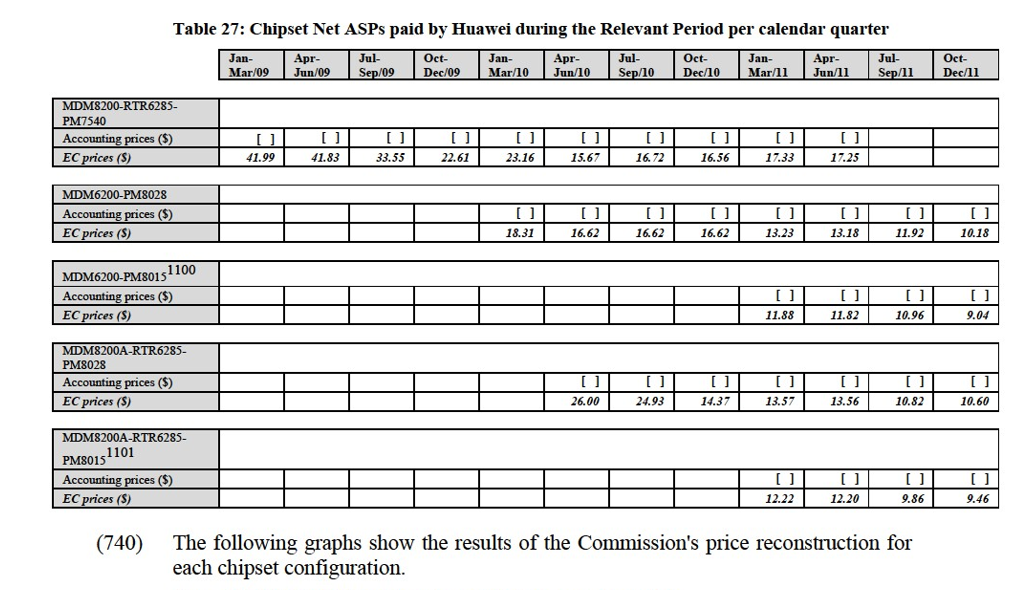

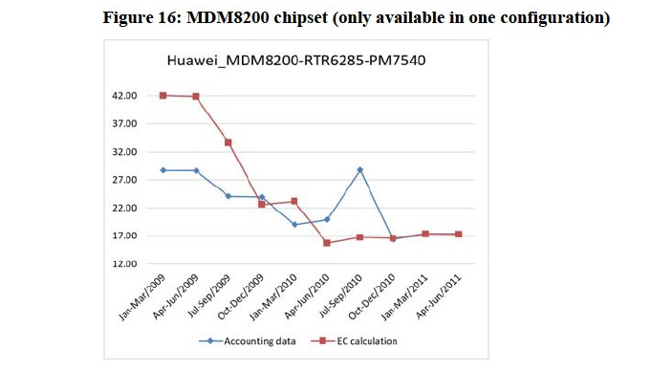

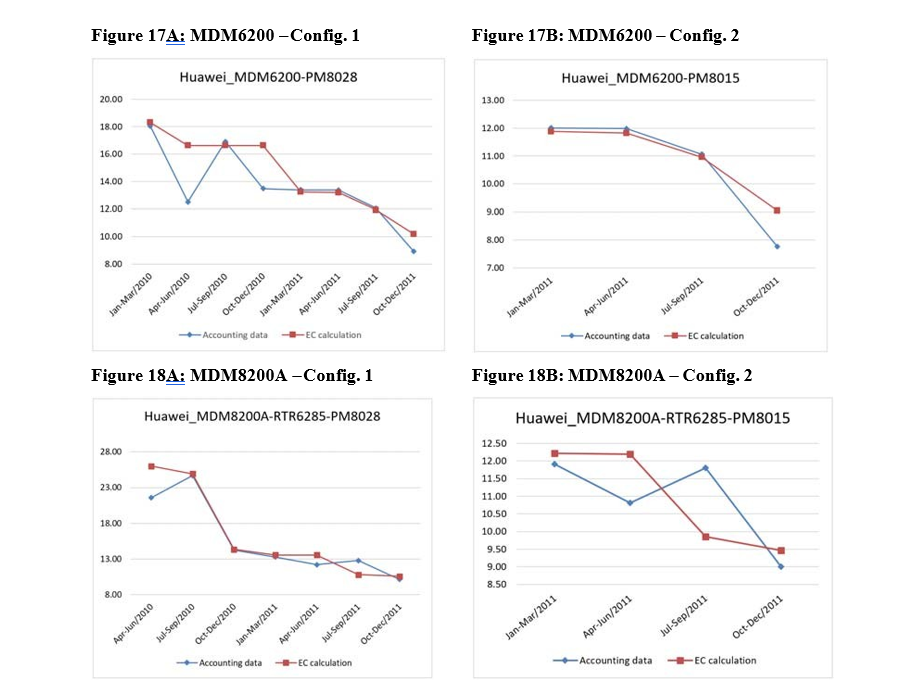

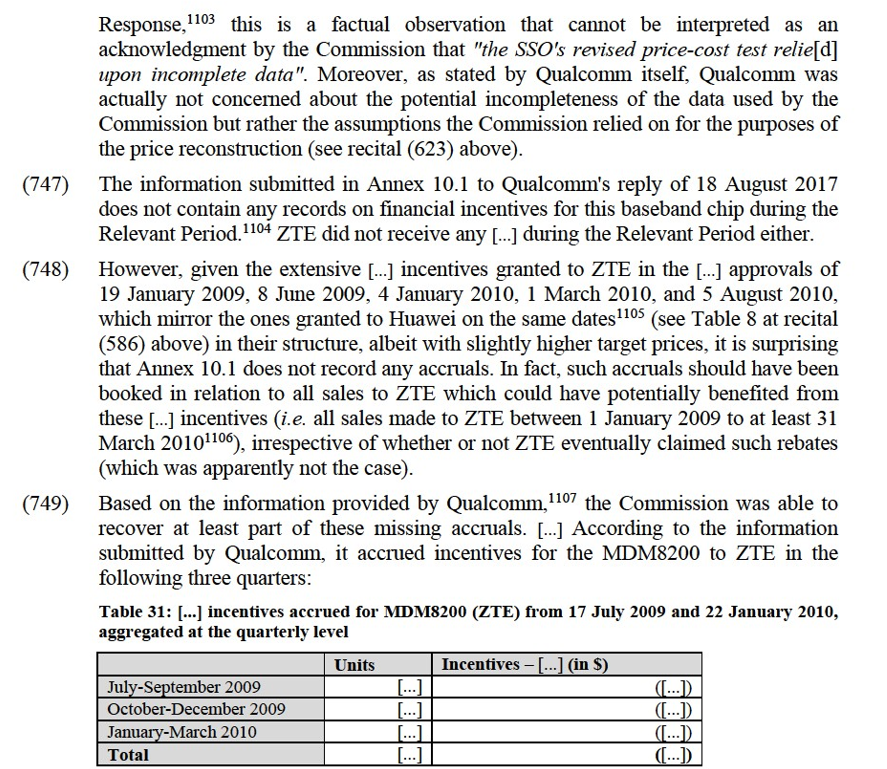

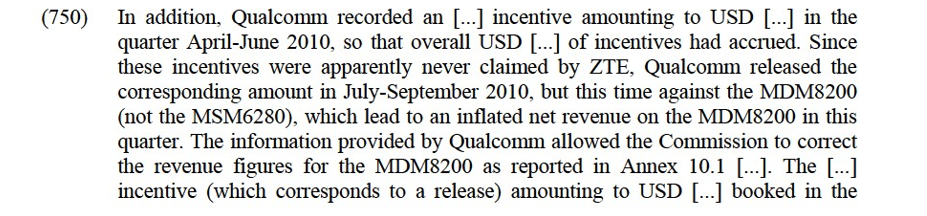

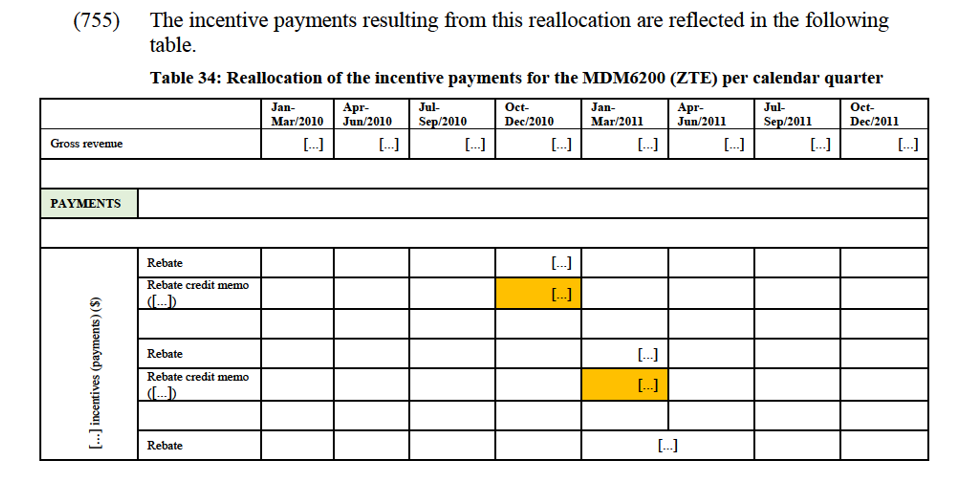

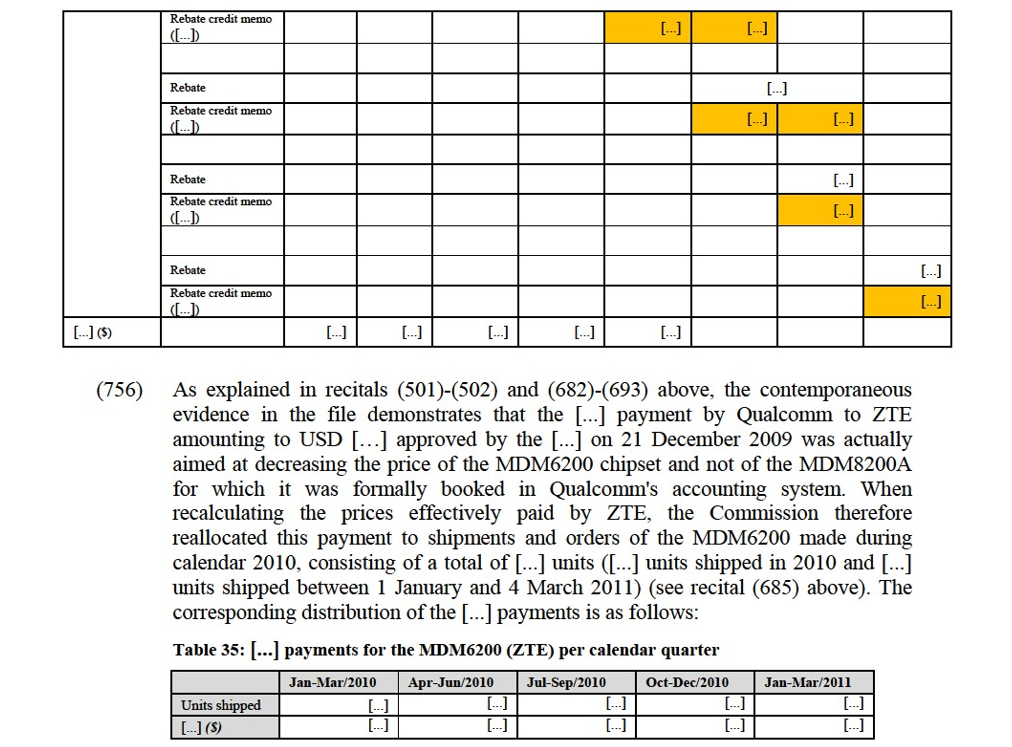

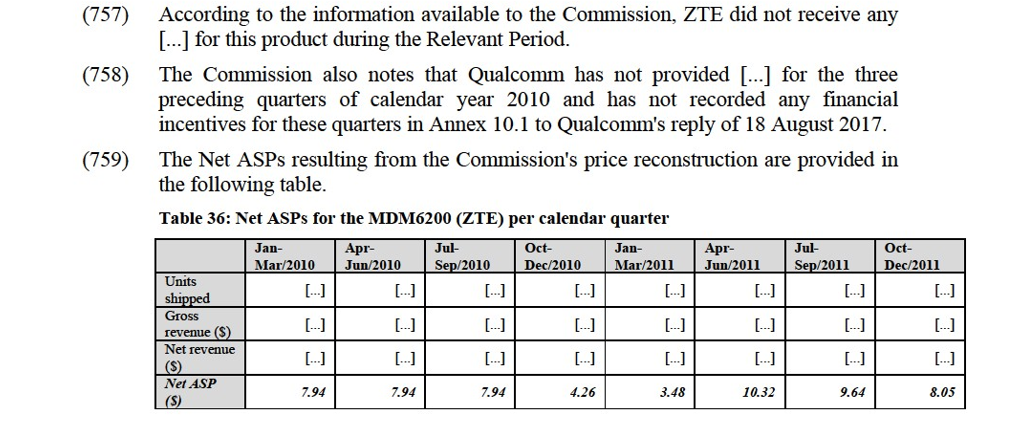

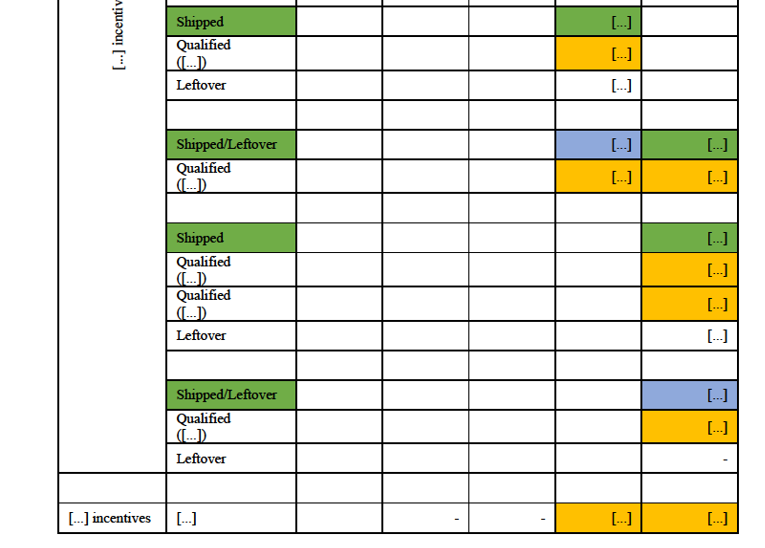

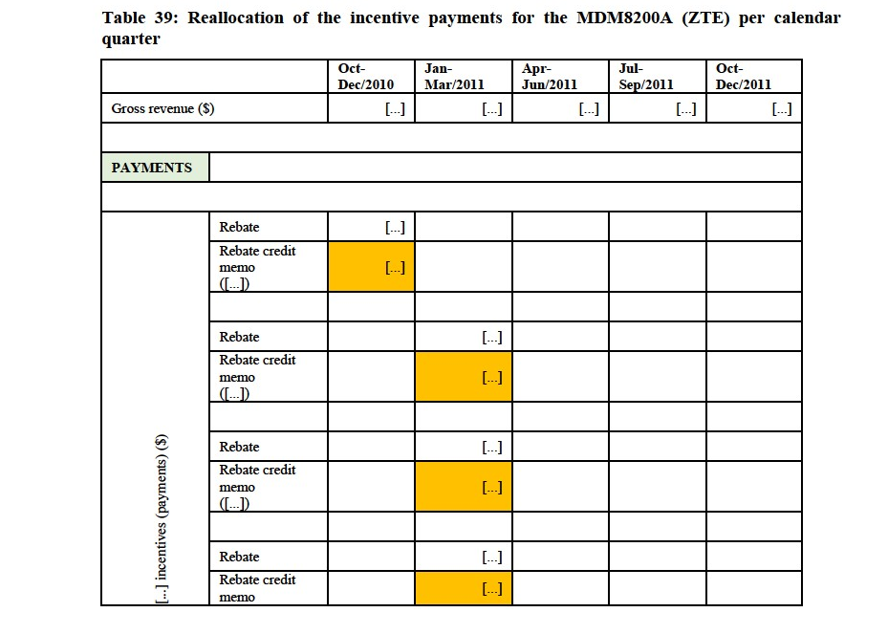

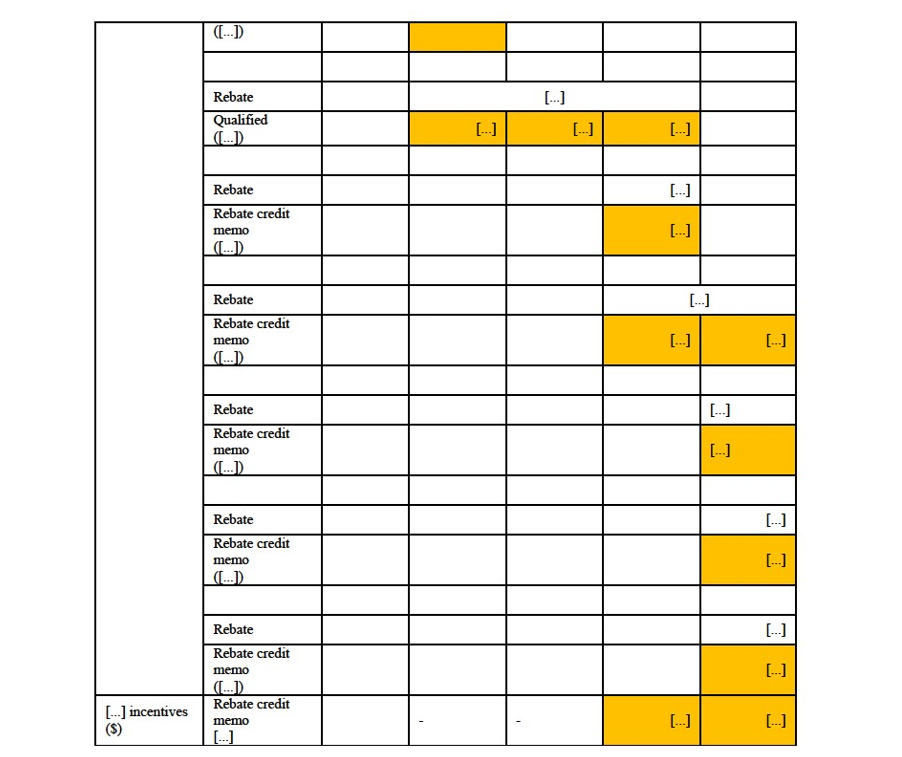

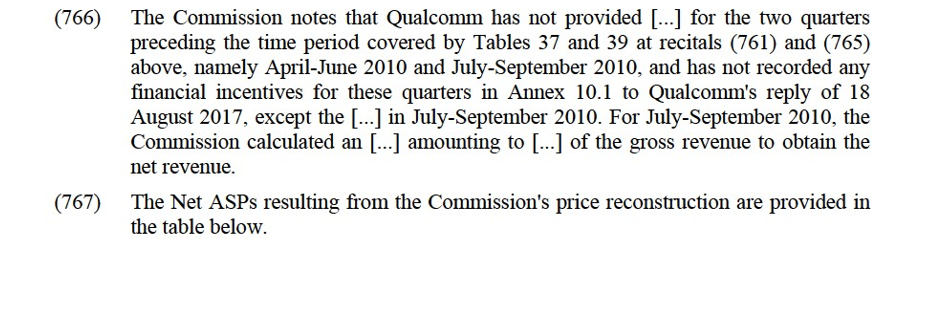

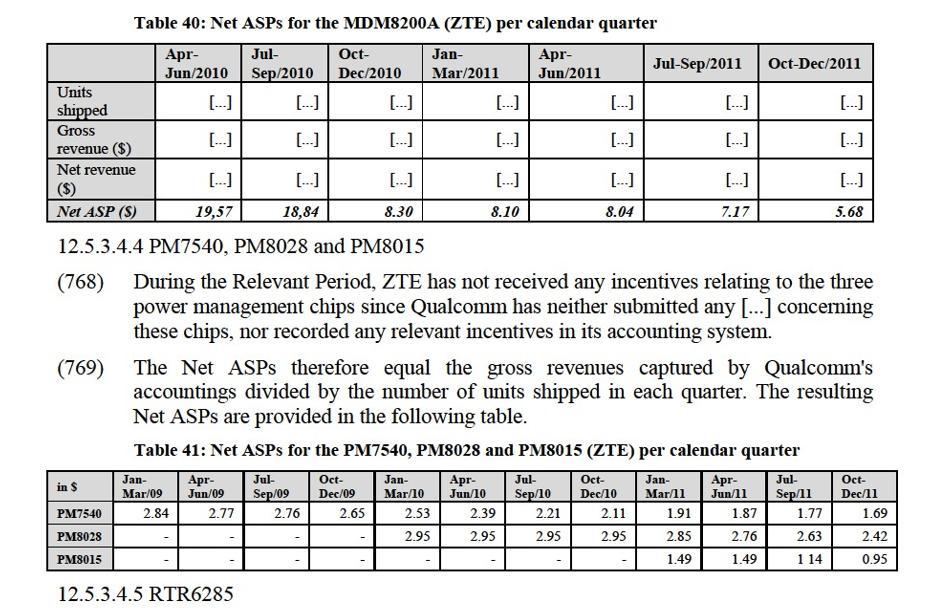

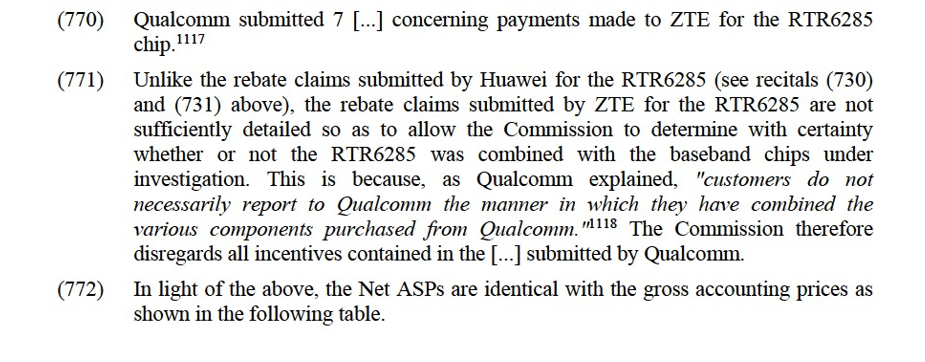

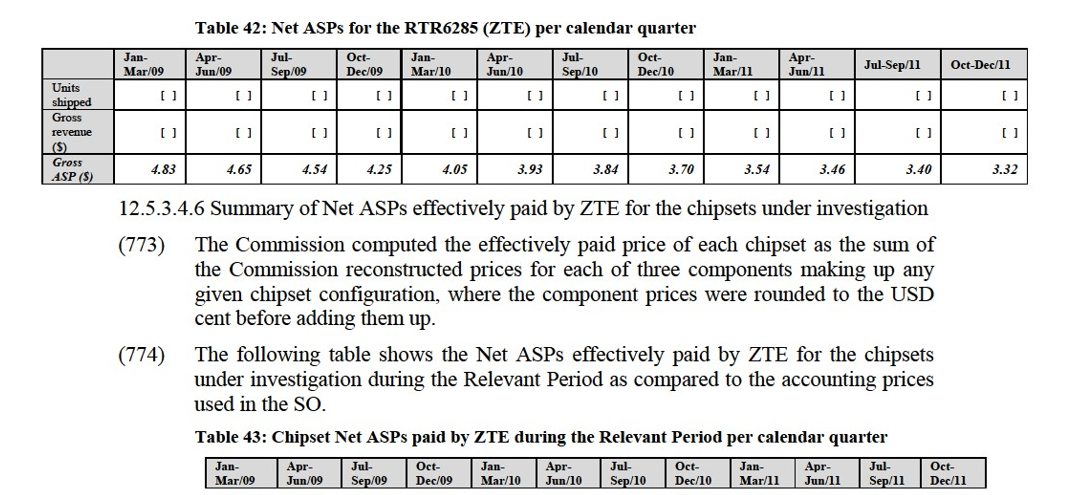

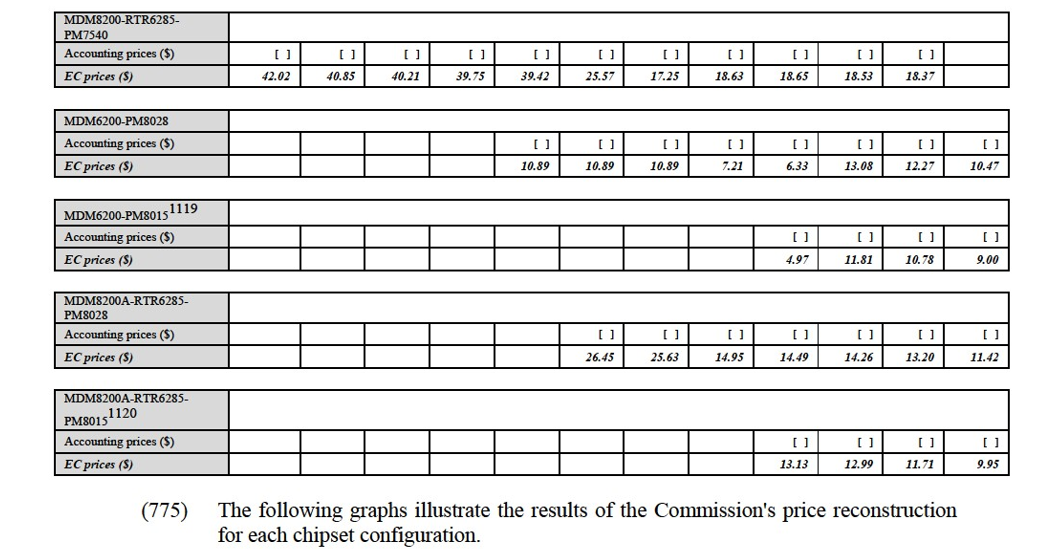

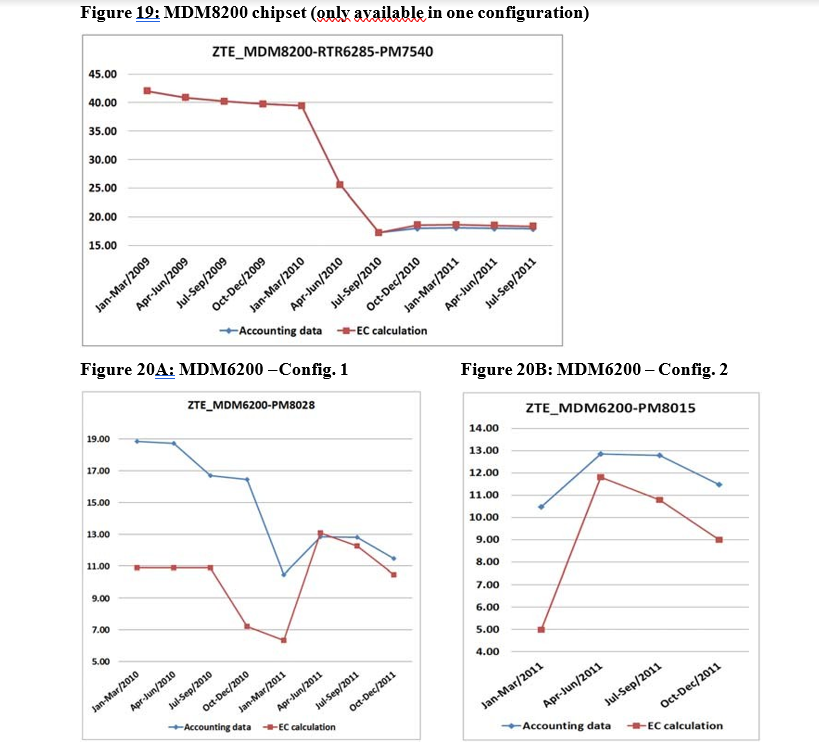

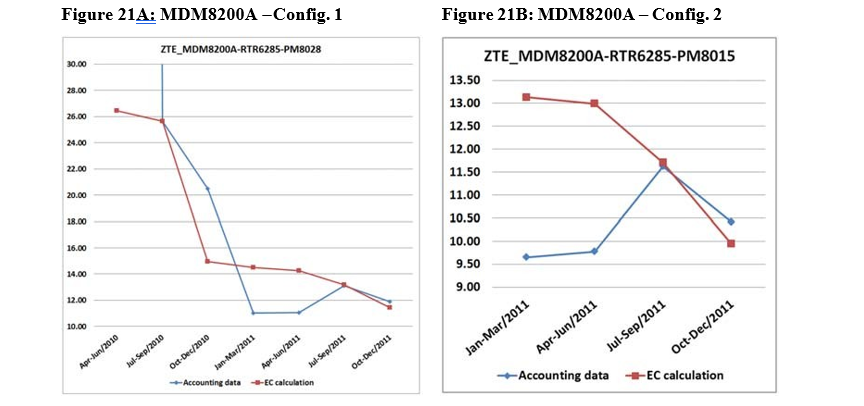

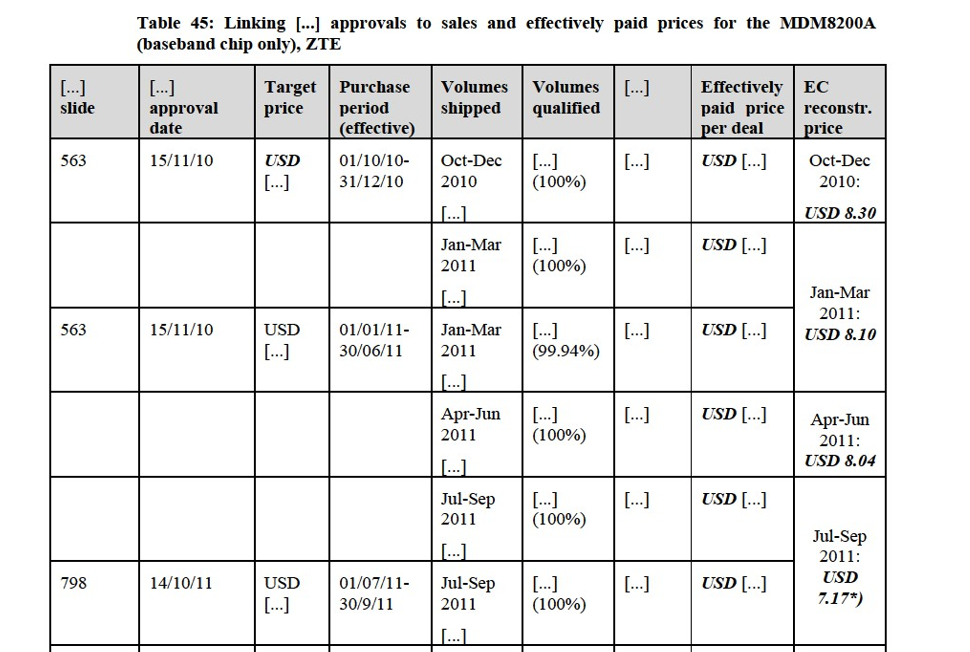

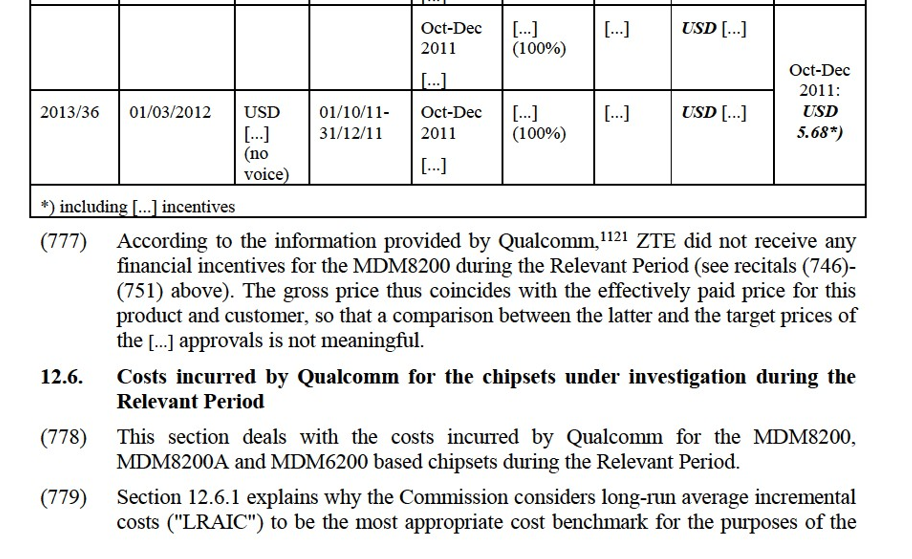

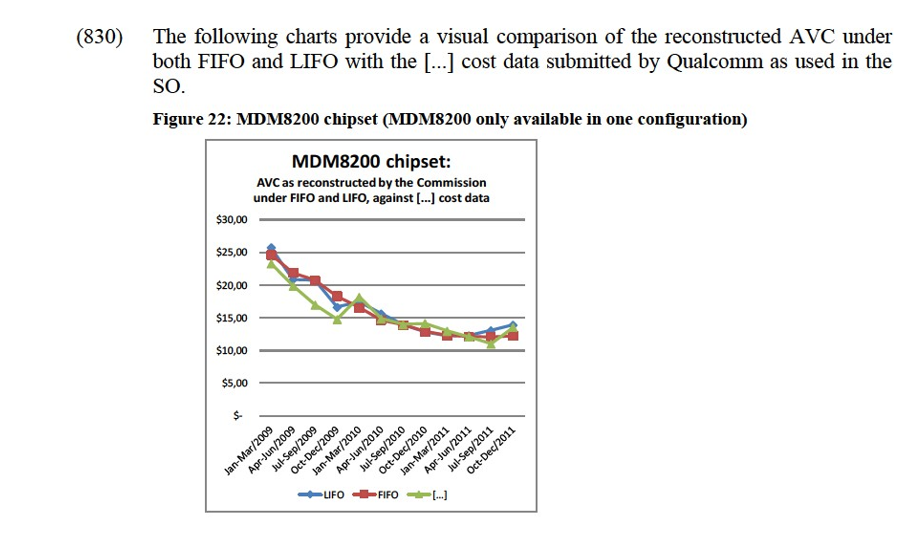

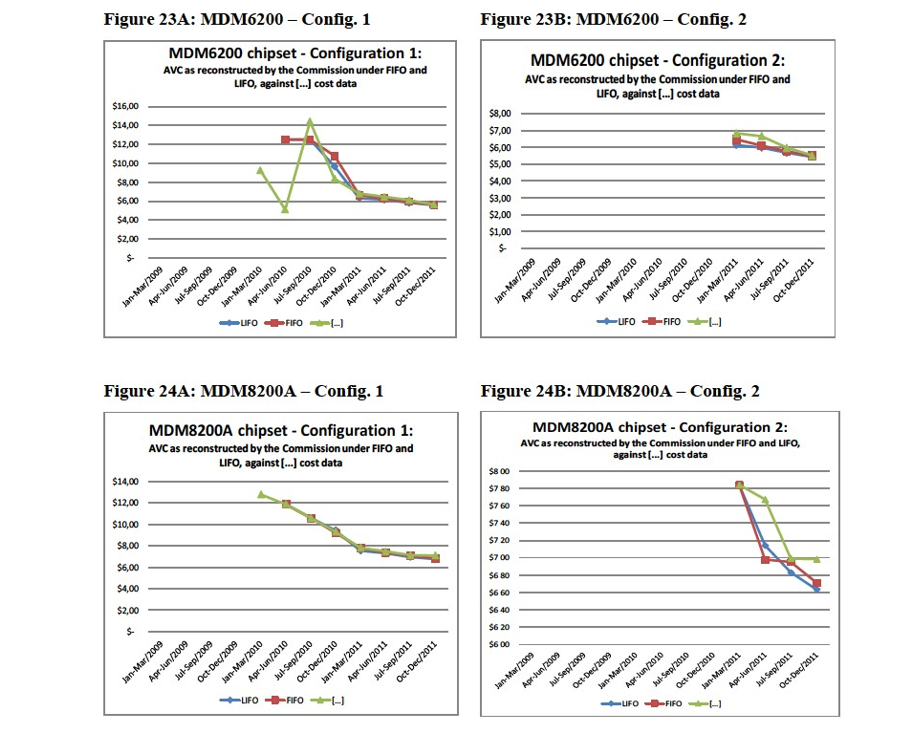

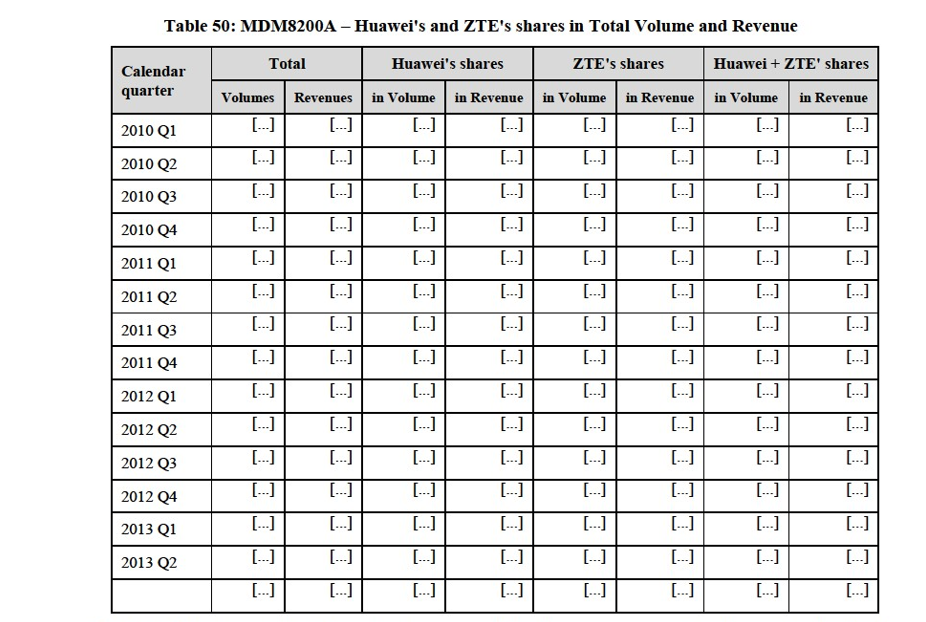

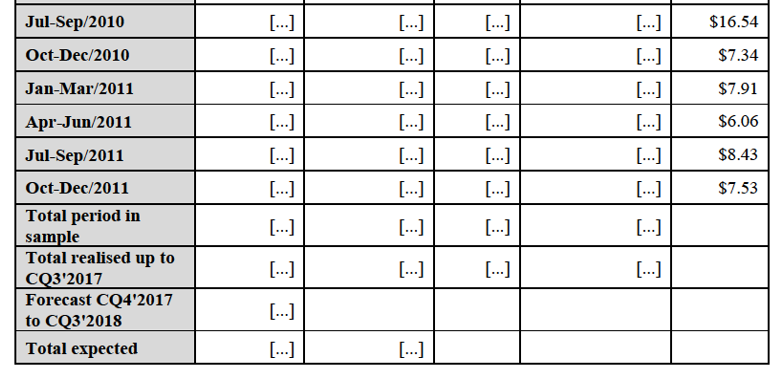

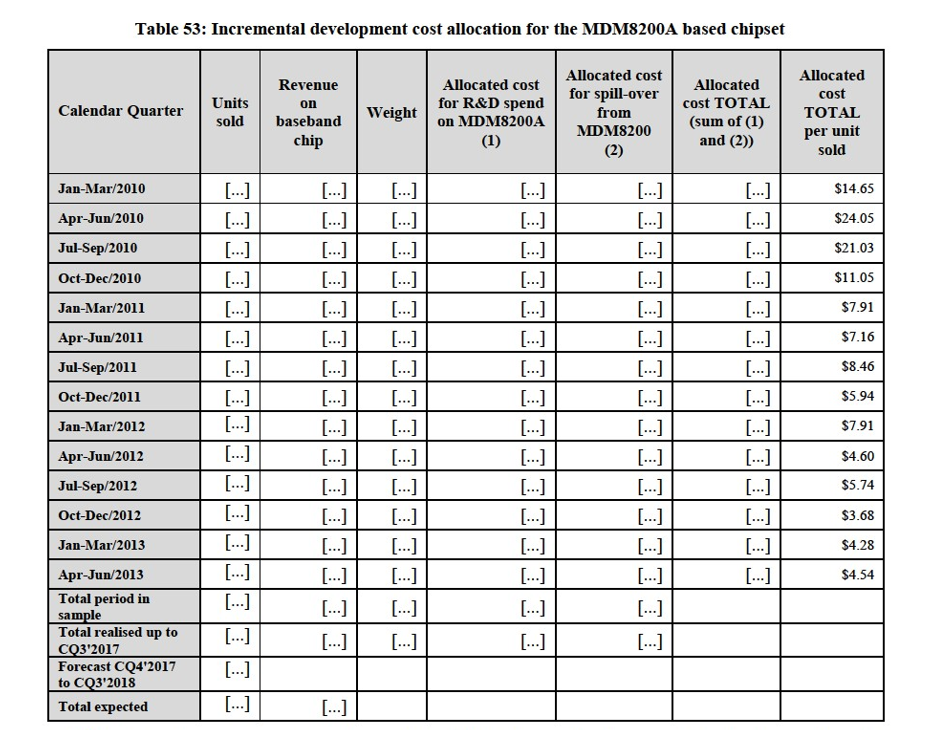

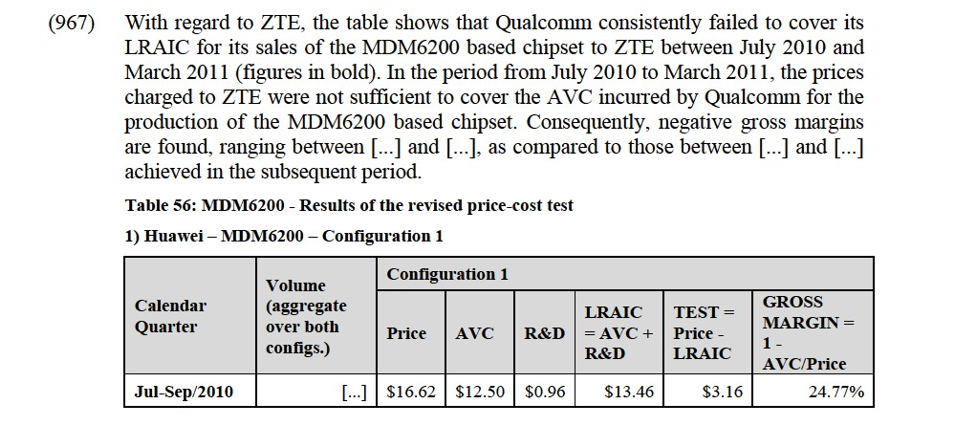

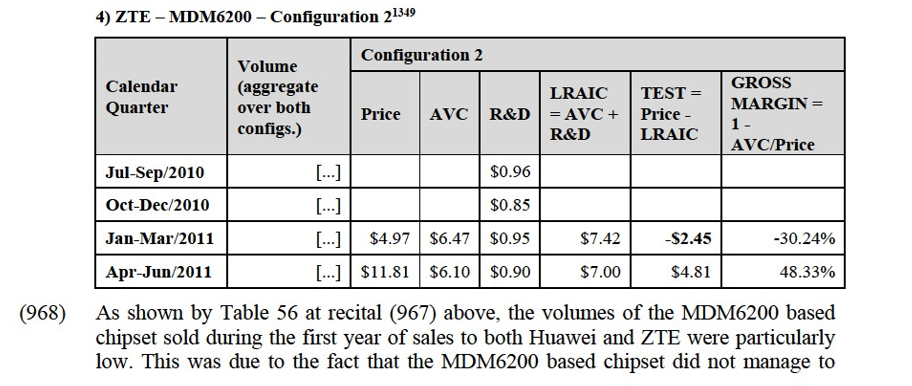

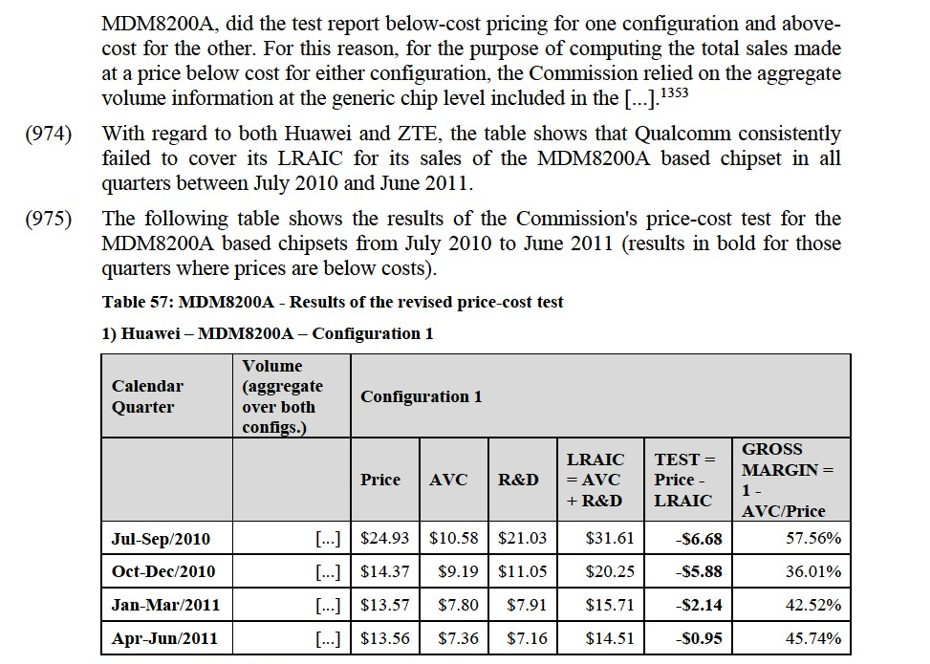

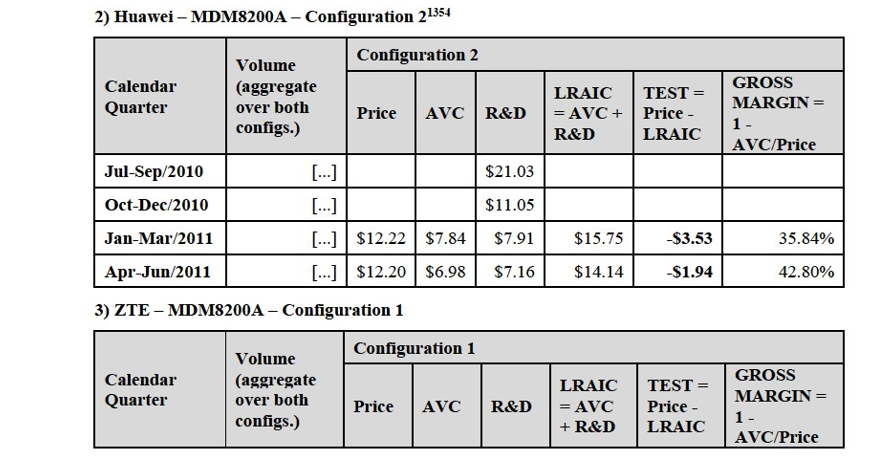

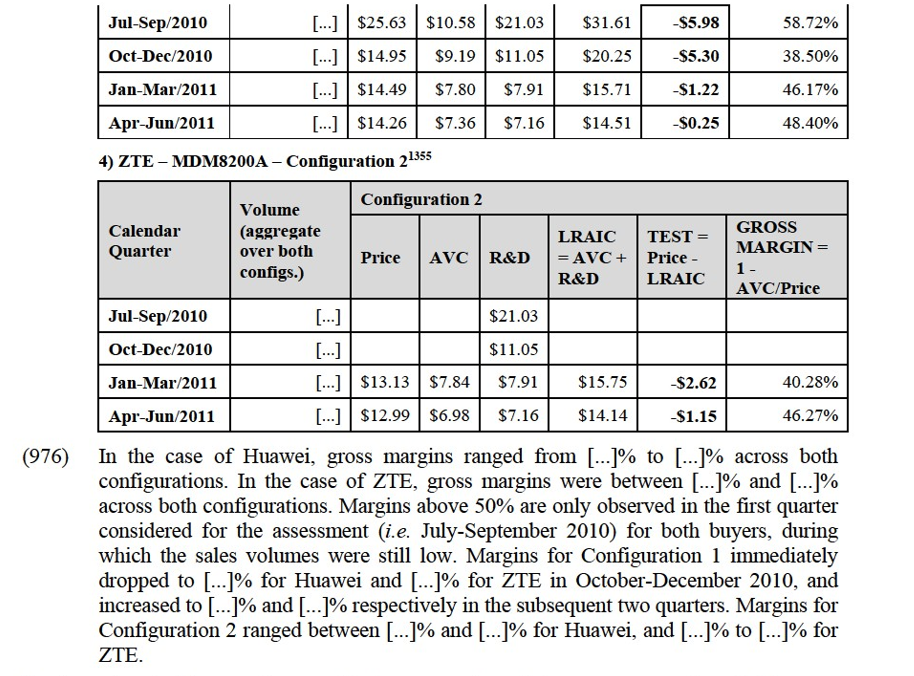

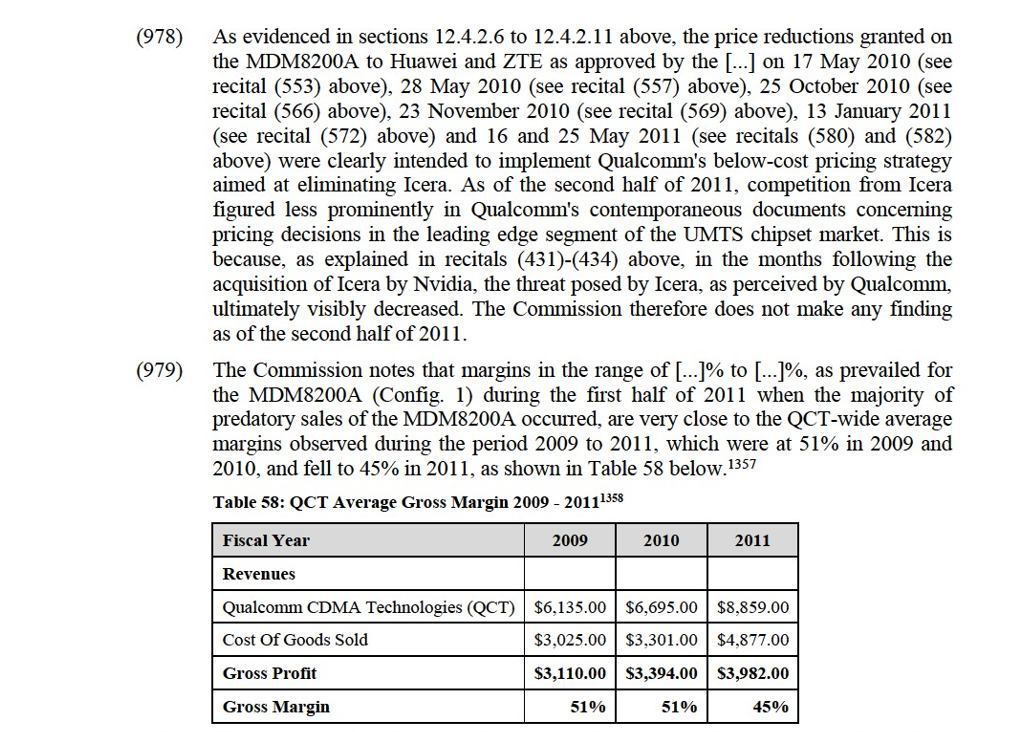

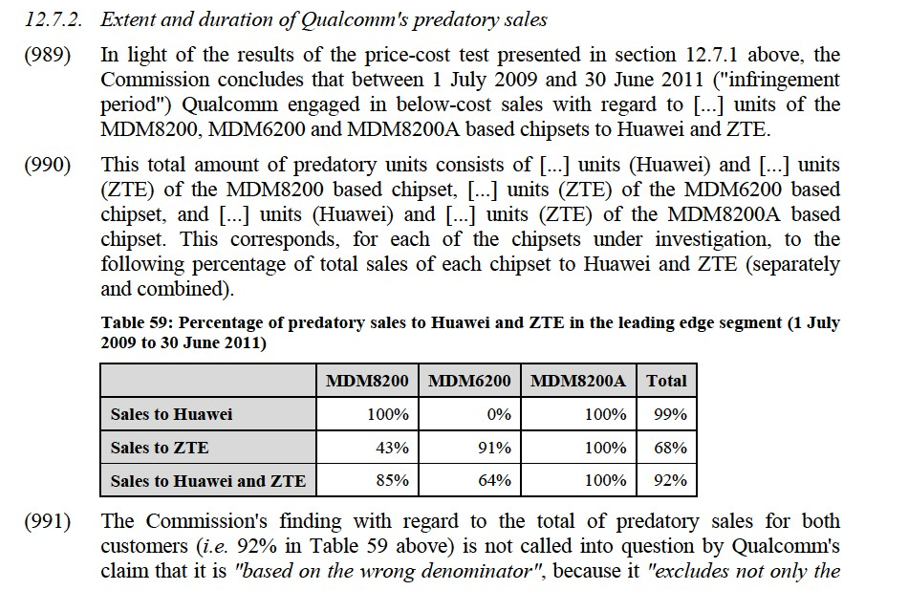

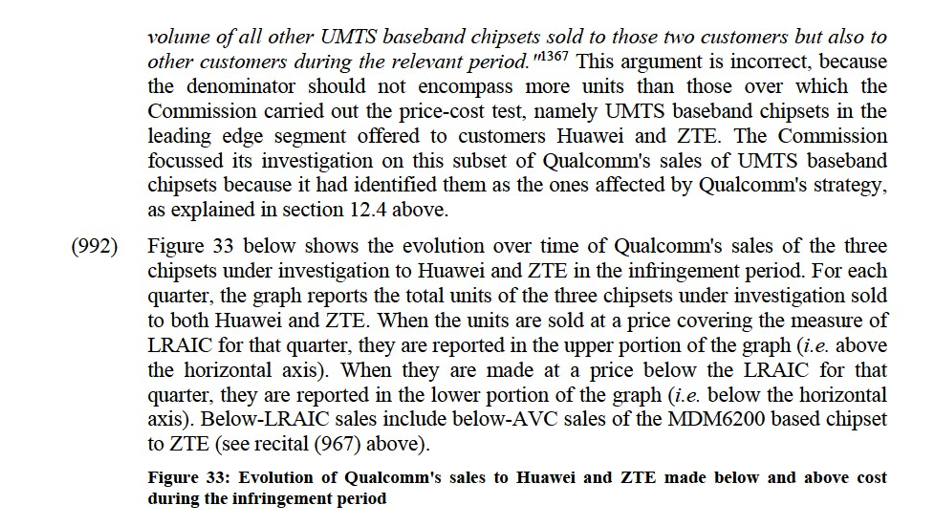

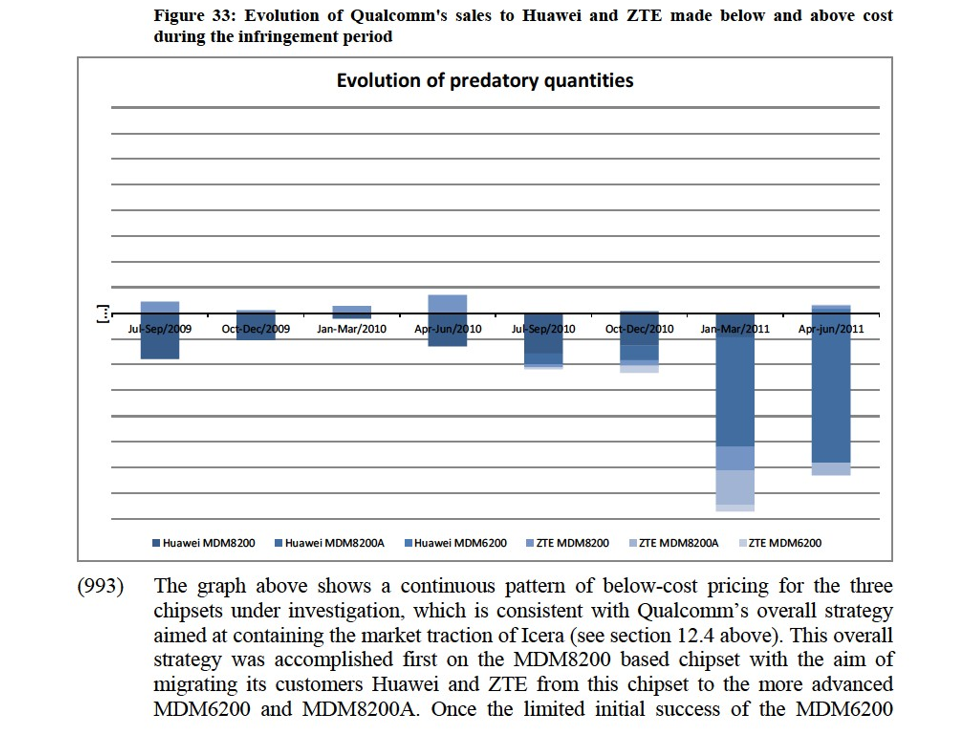

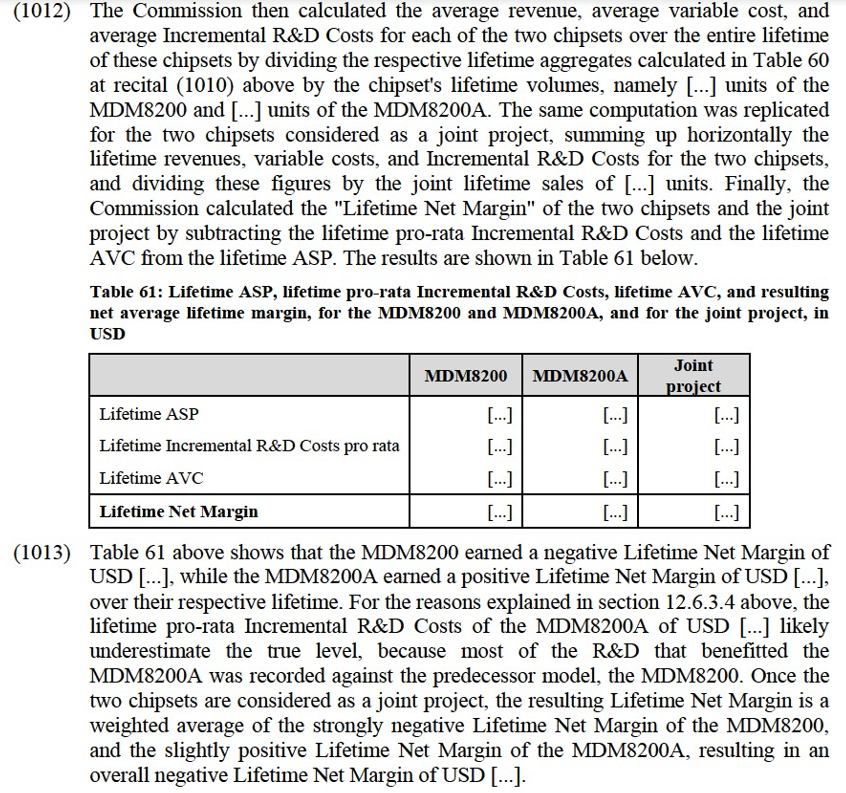

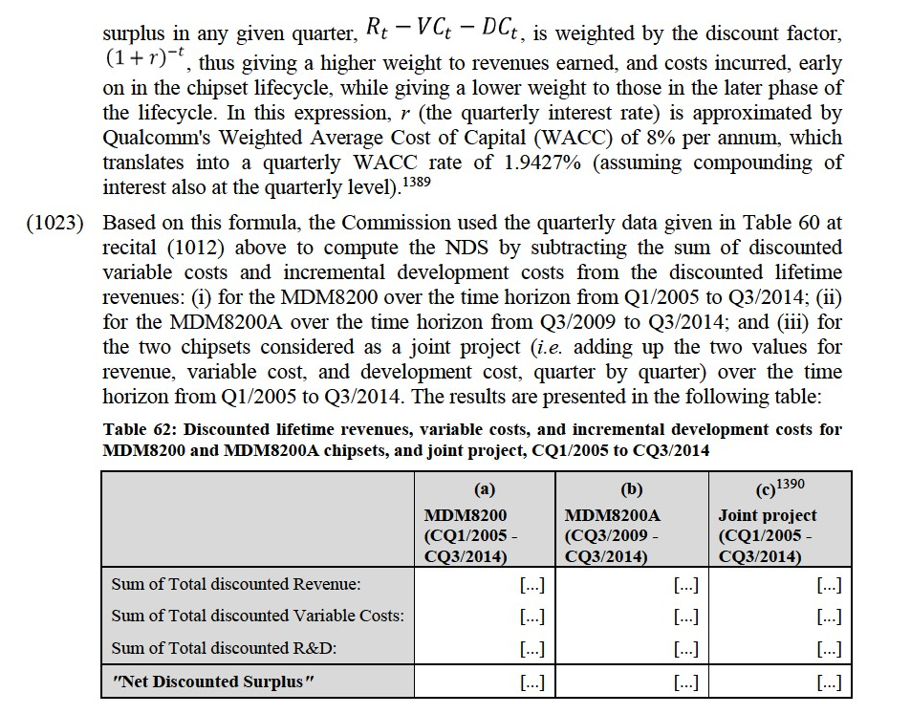

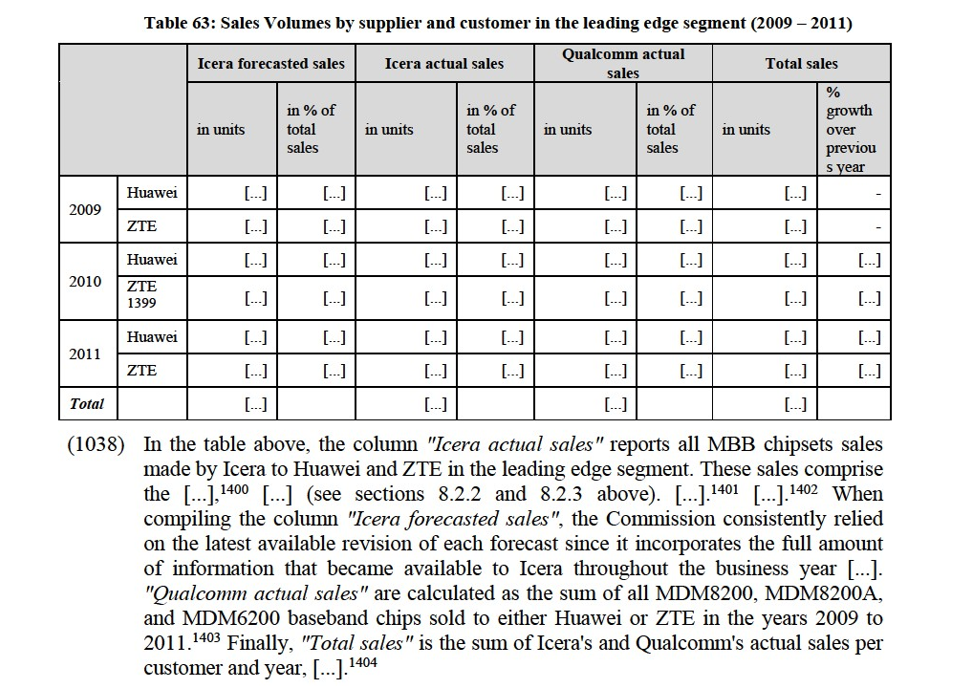

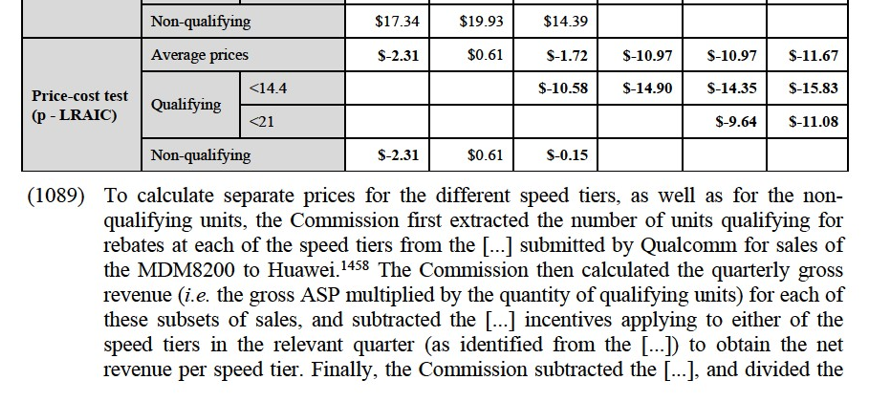

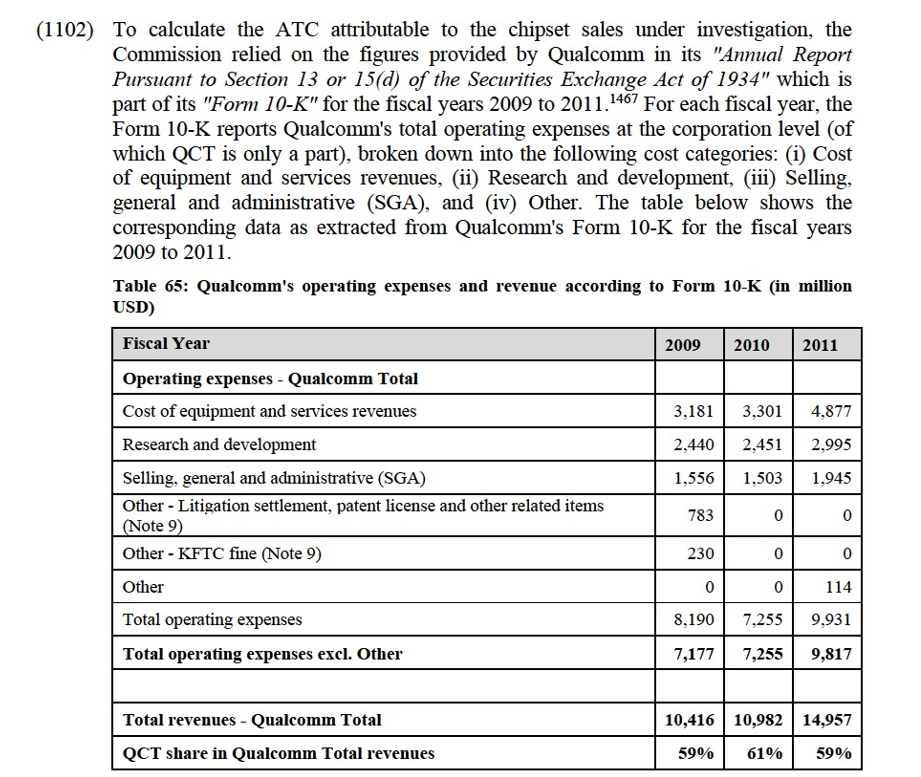

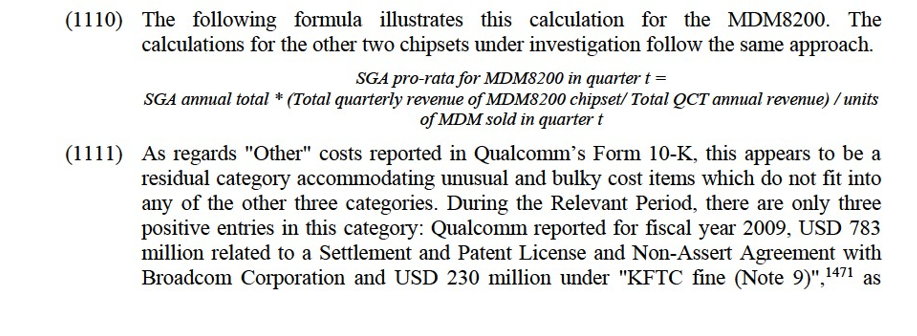

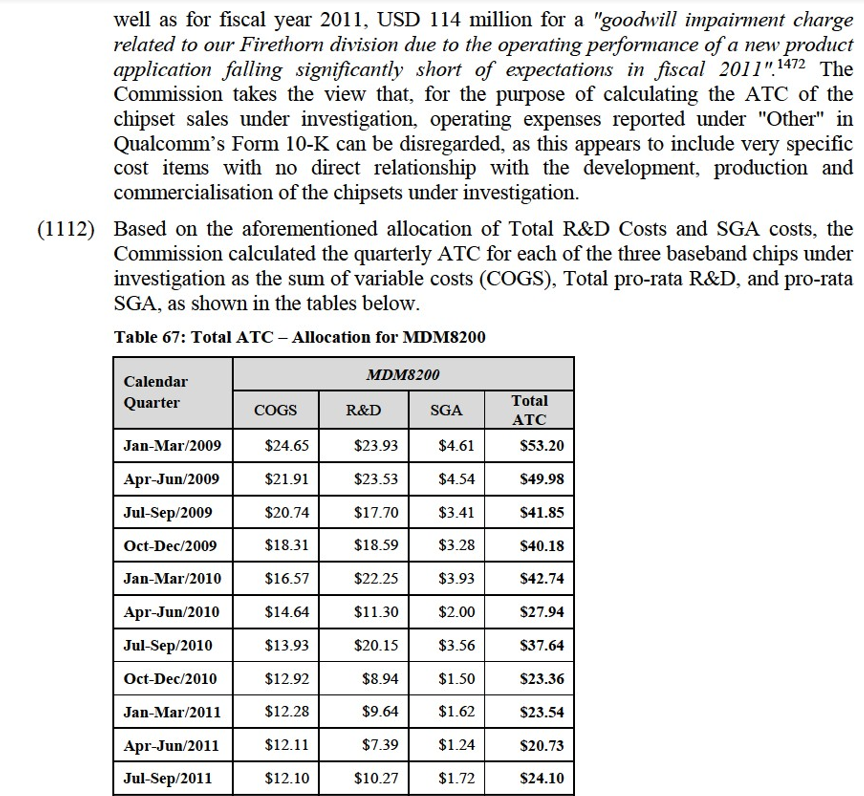

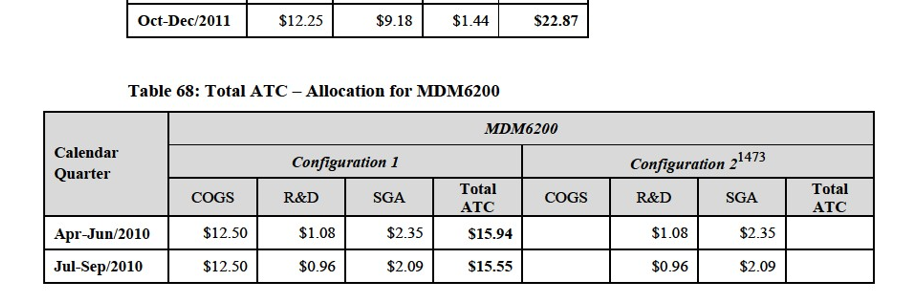

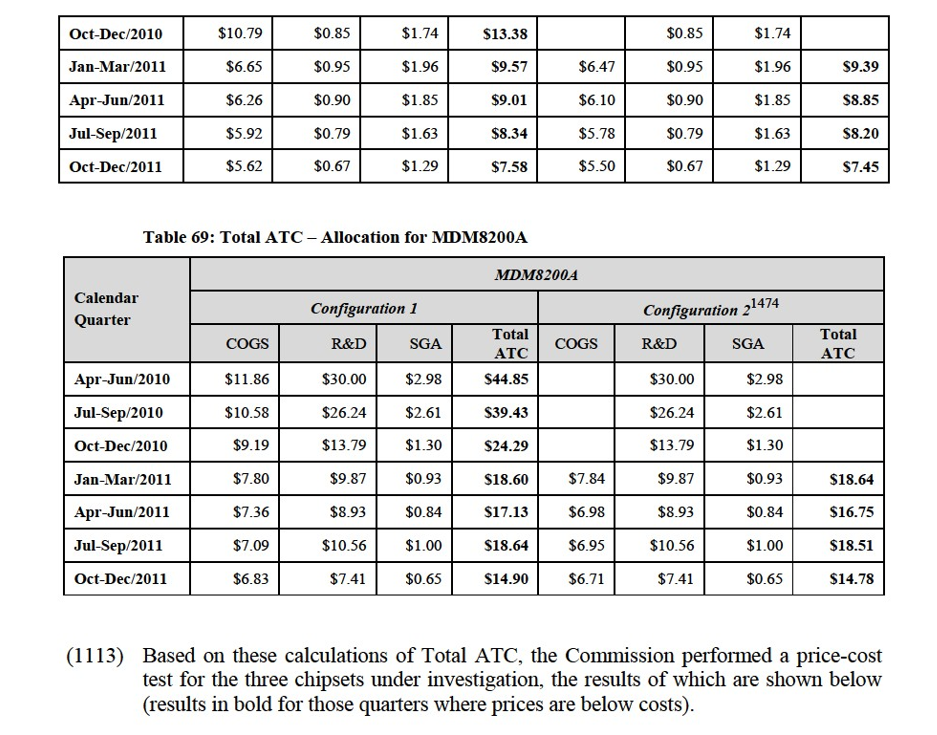

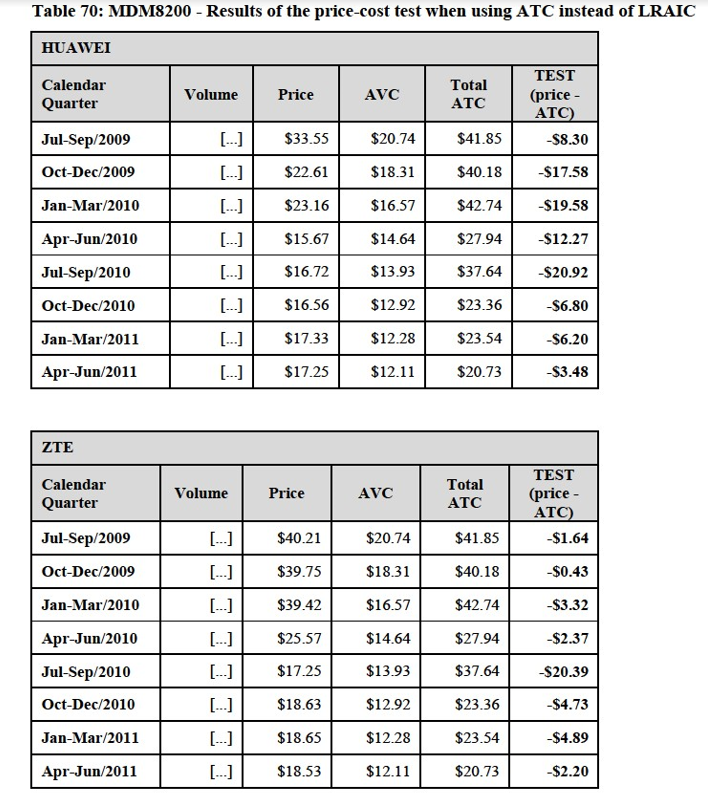

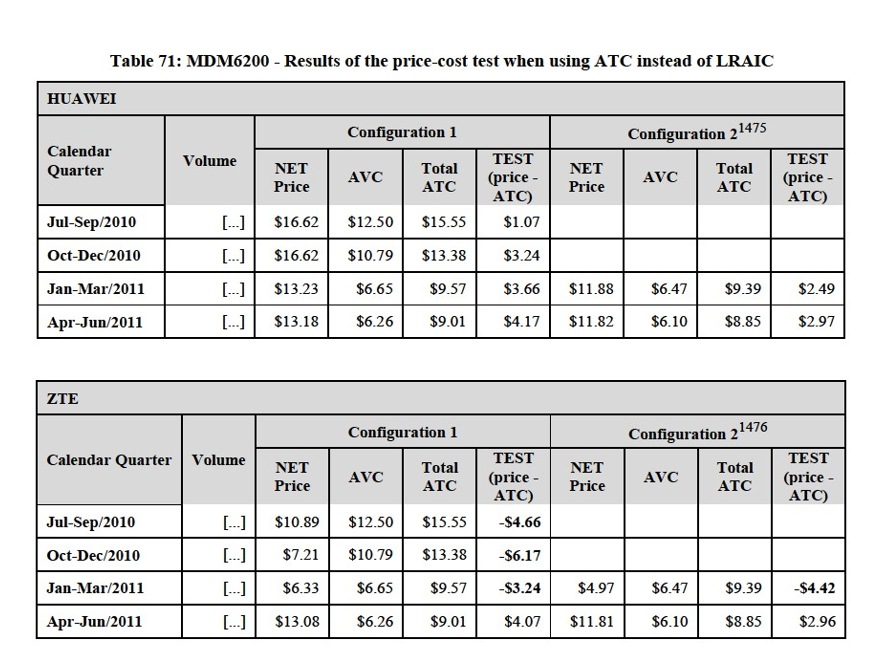

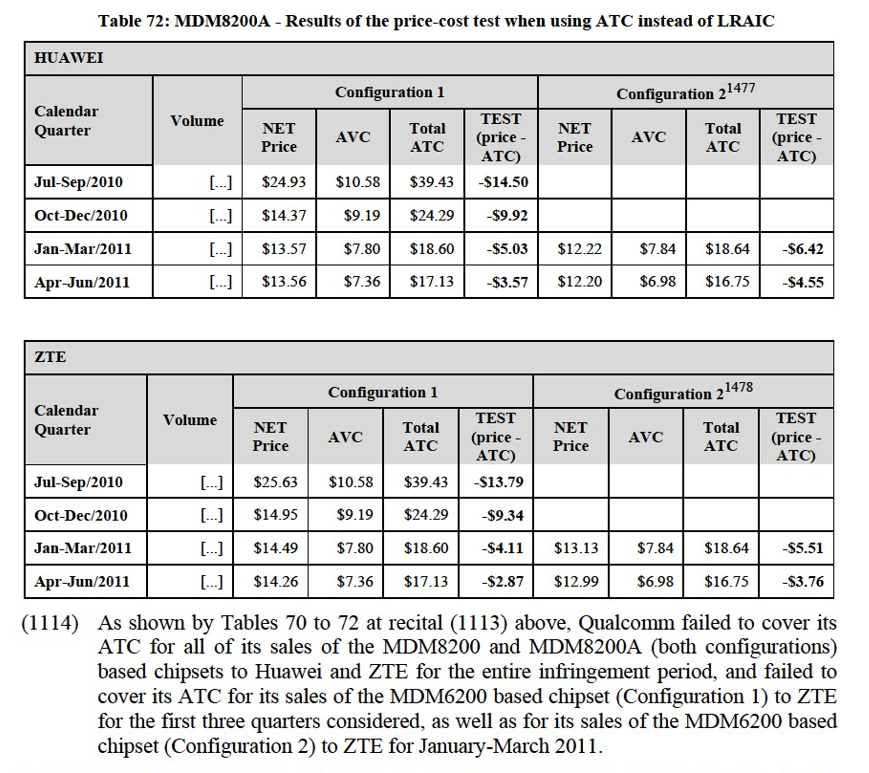

(200) First, neither WiFi nor WiMAX offers mobile connectivity like UMTS. This is because user access is restricted to a limited number of venues, typically including their home, place of work and selected public venues.