Commission, November 12, 2019, No M.9064

EUROPEAN COMMISSION

Decision

TELIA COMPANY/ BONNIER BROADCASTING HOLDING

COMMISSION DECISION of 12.11.2019

declaring a concentration to be compatible with the internal market and the EEA agreement

(Case M.9064 – Telia Company / Bonnier Broadcasting Holding)

(Only the English text is authentic)

THE EUROPEAN COMMISSION,

Having regard to the Treaty on the Functioning of the European Union,

Having regard to the Agreement on the European Economic Area, and in particular Article 57 thereof,

Having regard to Council Regulation (EC) No 139/2004 of 20 January 2004 on the control of concentrations between undertakings1, and in particular Article 8(2) thereof,

Having regard to the Commission's decision of 10 May 2019 to initiate proceedings in this case, Having regard to the opinion of the Advisory Committee on Concentrations2,

Having regard to the final report of the Hearing Officer in this case, Whereas:

1. INTRODUCTION

(1) On 15 March 2019, the Commission received notification of a proposed concentration pursuant to Article 4 of Regulation (EC) No 139/2004 (“the Merger Regulation”) by which Telia Company AB (“Telia”, or “Notifying Party”), Sweden would acquire within the meaning of Article 3(1)(b) of the Merger Regulation sole control of the whole of Bonnier Broadcasting Holding AB (“Bonnier Broadcasting”), Sweden (the “Transaction”). The concentration would take place by way of purchase of shares3. Telia and Bonnier Broadcasting are hereinafter collectively referred to as the “Parties” and each individually as a "Party".

(2) This Decision is structured as follows. Section 2 describes the Parties. Section 3 explains why the Transaction constitutes a concentration and the relationships between the Swedish State and each of Telia and SVT. Section 4 explains why the concentration brought about by the Transaction has a Union dimension. Section 5 describes the procedure followed in this case. Section 6 describes the investigation undertaken by the Commission into the Transaction. Section 7 defines the relevant product and geographic markets. Section 8 sets out the Commission's assessment of whether the Transaction is likely to significantly impede effective competition. Section 9 sets out the Commission's assessment of the efficiencies claims of the Notifying Party. Section 10 contains the Commission’s assessment of the commitments. Section 11 contains the Commission's conclusions.

2. THE PARTIES

(3) Telia is a Swedish telecommunication operator and the parent company of the Telia group, which has approximately 20 000 employees. The Telia group provides mobile and fixed telecommunications services as well as broadband and television services in Denmark, Estonia, Finland, Lithuania, Norway and Sweden. It provides mobile telecommunications services in Latvia4 and wholesale network access (carrier services) worldwide. Telia is a publicly listed company. Telia’s largest shareholder is the Swedish state.

(4) Bonnier Broadcasting is a Swedish based media company with approximately [...] employees engaged primarily in the television (“TV”) broadcasting business, in Sweden and Finland, but also to a more limited extent in Denmark and Norway. Bonnier Broadcasting's activities are conducted through the subsidiaries TV4 AB, C More Entertainment AB, and MTV Oy. Furthermore, Bonnier Broadcasting owns the captive Finnish production company Mediahub. Finally, Bonnier Broadcasting also produces news and other journalism content in Sweden and Finland. Bonnier Broadcasting is a wholly owned subsidiary of Bonnier Euro Holding AB. Bonnier Euro Holding AB is a wholly owned subsidiary of Bonnier AB and ultimately controlled by Albert Bonnier AB.

3. THE OPERATION AND THE CONCENTRATION

3.1. As to whether the Transaction constitutes a concentration

(5) On 20 July 2018, Telia and Bonnier Euro Holding AB (a wholly owned subsidiary of Bonnier AB) entered into a share purchase agreement under which Bonnier Euro Holding AB (and indirectly Bonnier AB) has agreed to sell and transfer all of the shares in Bonnier Broadcasting to Telia. Following the Transaction, Telia will own 100% of the shares in Bonnier Broadcasting.

(6) Therefore, the Transaction consists of the acquisition of sole control by Telia over Bonnier Broadcasting within the meaning of Article 3(1)(b) of the Merger Regulation.

3.2. As to whether Telia and Sveriges Television AB are economic units with an independent power of decision

3.2.1. Introduction

(7) Certain market participants have argued that the Swedish state controls both Telia and the public service broadcaster Sveriges Television AB (“SVT”)5 and that, as a result, the Swedish state could influence the programming decisions of both Telia and SVT. Those claims are based on the fact that the Swedish state, which owns 38.4% (37.3% at the time of notification of the Transaction) of the shares in Telia, is Telia’s largest shareholder.6 It is also argued that the Swedish state owns SVT.7

(8) In the Form CO (“initial submission”) and in its written comments on the Decision pursuant to Article 6(1)(c) of the Merger Regulation (“Article 6(1)(c) Decision”) on 24 May 2019 (the “Response to the Article 6(1)(c) Decision”), the Notifying Party submits that no legal or natural person, including its largest shareholder the Swedish state, has de jure or de facto control over Telia. In any event, according to the Notifying Party, the Swedish state does not control any (other) undertaking active within any relevant market related to the Transaction, including the public broadcaster SVT.8 The Notifying Party further submits that even if the Swedish state were regarded as the owner of both Telia and SVT, they constitute two separate economic units without any legal or practical possibilities of coordination and have to be assessed as separate entities.

(9) In order to analyse these claims, pursuant to Articles 3(1) and 5(4) of the Merger Regulation, read in conjunction with Recital 22 of that Regulation and the Consolidated Jurisdictional Notice9, the Commission has assessed whether Telia and SVT have a power of decision independent from the Swedish state. In addition, the Commission has assessed whether the Swedish state is able to coordinate the commercial conduct of Telia and SVT. In principle, the outcome of that assessment might indeed affect the scope of the substantive assessment of the Transaction.

(10) In determining whether an undertaking could be considered as having an independent power of decision regardless of the fact that the state owns it or is a majority shareholder, it is relevant to assess whether the undertaking sets its business plan, budget and strategy by itself, in its own commercial interests and independently from the state. The lack of interlocking directorships between undertakings and the existence of adequate safeguards ensuring that commercially sensitive information is not shared between such undertakings are two relevant factors that may be taken into account in the assessment of whether the state can, directly or indirectly, impose or facilitate coordination between any of the other undertakings owned by the same state entity, but are not exhaustive.10

(11) In its analysis, and in line with precedents,11 the Commission has focused on Telia’s and SVT’s ability to adopt decisions independently from the Swedish state to decide on their own strategy, business plan and budget, and the possibility for the Swedish state to coordinate the commercial conduct of Telia and SVT.

3.2.2. Relationship between the Swedish state and Telia

(12) The Commission has assessed whether the Swedish state's 38.4% (37.3% at the time of notification of the Transaction) ownership in Telia12 allows it to decide on Telia’s strategy, business plan and budget.

(13) Article 3(2) of the Merger Regulation provides that control is constituted by rights, contracts or any other means which confer the possibility of exercising decisive influence on an undertaking. According to the Consolidated Jurisdictional Notice13 sole control is normally acquired on a legal basis where an undertaking acquires a majority of the voting rights of a company, or, in the case of a minority shareholding, in situations where specific rights are attached to this shareholding.14 A minority shareholder may also be deemed to have sole control on a de facto basis, in particular where the shareholder is highly likely to achieve a majority at the shareholders' meetings, given the level of its shareholding and the evidence resulting from the presence of shareholders in the shareholders' meetings in previous years.15 Moreover, according to the Consolidated Jurisdictional Notice, the Commission may assess the position of other shareholders and their role16 taking into account criteria such as whether the remaining shares are widely dispersed, whether other important shareholders have structural, economic or family links with the large minority shareholder or whether other shareholders have a strategic or a purely financial interest in the target company. Where, on the basis of its shareholding, the historic voting pattern at the shareholders' meeting and the position of other shareholders, a minority shareholder is likely to have a stable majority of the votes at the shareholders' meeting, then that large minority shareholder is taken to have sole control.

(14) In its initial submission and in its Response to the Article 6(1)(c) Decision, the Notifying Party submits that the Swedish state does not have de jure control over Telia given: (i) the minority shareholding interest of the Swedish state; (ii) the absence of any shareholders’ agreement granting the Swedish state the right to veto strategic decisions; (iii) the lack of any representative of the Swedish state on Telia’s board; (iv) the lack of any specific rights attached to the Swedish state’s shareholding; (v) the absence of a particular organisational structure granting the Swedish state the right to manage activities of Telia and to determine its business policy; and, (vi) the absence of a situation of negative sole control.

(15) The Notifying Party also considers in its initial submission and in its Response to the Article 6(1)(c) Decision that the Swedish state does not have de facto control over Telia given that: (i) despite having had the majority of voting rights at Telia’s shareholders’ meetings, the Swedish state does not have a representative on Telia’s board of directors, which is the body that takes the strategic decisions, such as the removal of the CEO of Telia; (ii) the Swedish state only has one representative on the five-person nominating committee that manages the recruitment to the board of Telia; (iii) the Swedish state has not set out any economic goals or assignment goals for Telia; and, (iv) the Swedish state does not have the power to reappoint the board of directors at Telia, which is a decision that can only be taken through a decision at a shareholders’ meeting.17

(16) The Commission has investigated the Notifying Party’s claims and considers that the Swedish state does not appear to have de jure control over Telia for the following reasons. First, the Swedish state does not hold the majority of the voting rights in Telia but has a 38.4% (37.3% at the time of notification of the Transaction) shareholding. There is no shareholders’ agreement granting the Swedish state (solely or jointly) a veto over strategic decisions in Telia.18 Second, the Swedish state does not have any special rights, such as preferential shares, attached to its shareholding in Telia. Third, there is no particular organisational structure granting sole control to the Swedish state.19 Fourth, given the Swedish state’s minority shareholding there does not appear to be a situation of negative sole control.

(17) As to the question whether the Swedish state has de facto control over Telia, the Commission considers that Telia does not appear to have autonomy from the Swedish state in deciding on its own strategy, business plan and budget for the reasons set out in recitals (18) to (29).

(18) First, during Telia’s shareholders’ meetings in the period 2014 to 2018 the Swedish state, acting through the Ministry of Enterprise and Innovation, held a majority of the total participating shares and votes.20 Based on the current shareholding, the Swedish state is therefore likely to achieve a majority at Telia's shareholders' meetings in the coming years.

(19) The members of Telia’s board of directors21 are elected by the shareholders at the Annual General Meeting (“AGM”) and for all elections that take place at an AGM (for example, election of board members and auditors), the candidate that receives the most votes is elected.22 The Swedish state’s shareholding therefore allows it to elect and reappoint the members of Telia’s board of directors23, which is the body that takes the strategic decisions in Telia, and thus confers upon it the power to exercise decisive influence on the commercial policy of Telia. 24

(20) The Notifying Party submits that, should the Swedish state attempt to take control over the board of directors by appointing its “own” representatives, the private shareholders (representing 62.7% of the shares and votes at the time of notification of the Transaction) would likely unite to create a majority at the shareholders’ meeting to oppose such an attempt.25

(21) However, the Commission considers that any wide-ranging coalition against the vote of the Swedish state is unlikely for the reasons set out in recitals (22) to (25).

(22) In the first place, the remaining shares in Telia are widely dispersed. The shareholdings of all 472 489 holders of the 4 209 540 375 shares in Telia26 in order of magnitude are shown below:

· Swedish state: 38.4% ;

· Blackrock: 3.0% ;

· Vanguard: 1.8% ;

· Swedbank Robur Funds: 1.7% ;

· Telia: 1.4% ;

· AMF Insurance and Funds: 0.9% ;

· Mondrian Investment Partners Ltd: 0.9% ;

· AFA Insurance: 0.9% ;

· Other shareholders: 48.8%.

(23) Therefore, the second largest shareholder of Telia is Blackrock, which has a 3.0% shareholding. The remaining shares are widely dispersed, with the third largest shareholder, Vanguard, having a shareholding of 1.8%.

(24) In the second place, Telia’s largest shareholders are major international and Swedish investors, including Blackrock, Vanguard, Swedbank Robur Funds and AMF Insurance and Funds, which suggests that these shareholders have a purely financial interest in Telia.

(25) In the third place, shareholders holding 0.9% or more (Blackrock; Vanguard; Swedbank Robur Funds; Telia; AMF Insurance and Funds; Mondrian Investment Partners Ltd; AFA Insurance) represent only 12.8% of shares.

(26) Therefore, the Commission considers that, contrary to the Notifying Party’s claim, if the Swedish state decided to appoint its representatives to the board of directors, the remaining shareholders would be unlikely to manage to form a majority capable of opposing the Swedish state’s decisions. In any event, there is no evidence in the file that there has been any such wide-ranging coalition in the past. The Notifying Party has put forward examples of shareholders’ voting patterns in previous Telia AGMs.27 The examples provided refer to only two proposals that were voted upon by Telia’s AGM during the past ten years where: (i) other minority shareholders together representing between 9.9% and 10.9% (in the period 2016-2018) of the shares represented at those meetings voted in a manner different to that of the Swedish state28; and (ii) approximately 25% of the shares (in 2009) and 15 large shareholders (in 2010) made a reservation against a Swedish state’s proposal.29 That in itself is not sufficient to reach a finding that there exists a strong commonality of interests amongst minority shareholders that would lead to the de facto forming of a coalition. In particular, in this case the veto powers that minority shareholders have over certain resolutions at Telia’s general meetings, seem30 not to go beyond the veto rights normally accorded to minority shareholders to protect their investment in Telia.31 Therefore, the examples relied on cannot be considered as conclusive evidence of the existence of any wide-ranging coalition of Telia’s other shareholders.

(27) Second, for the same reason, the Commission cannot agree with the Notifying Party’s argument that the Swedish state has not set out any economic goals or assignment goals for Telia. Given that the Swedish state’s shareholding allows it to elect the members of Telia’s board of directors, which is the body that takes the strategic decisions in Telia, the Commission considers that the Swedish state has the possibility to exercise decisive influence on the commercial policy of Telia.

(28) Third, as to the argument that the Swedish state only has one representative on Telia’s nominating committee, the Commission notes that the nomination committee is a preparatory body for the shareholders’ meetings, with the task to prepare proposals for the AGM in respect of, among others, elections (including members of the board of directors), fees to the board of directors and the auditor.32 The nomination committee only nominates candidate board members, while it is the AGM which appoints the board of directors through an election.33 Furthermore, the AGM is not limited by the proposals of the nomination committee.34 In addition, if the Swedish state, acting through its representative in the nomination committee, seeks to nominate state representatives for election to the board of directors and if such proposal fails to reach unanimity in the nomination committee, the proposal can be presented as an individual proposal by the Swedish state's nomination committee representative.35 The Commission concludes on this basis that a failure to reach unanimity in the nomination committee is not an impediment to proposing a board member to the AGM.

(29) In this case the Commission has also considered whether there are other elements ensuring that Telia has a power of decision independent from that of the Swedish state, in spite of the fact that the Swedish state’s stake in Telia allows it to elect and reappoint the members of the board. In this regard, the Notifying Party has stated that under Telia’s decision-making structure there is no special reconciliation with the Swedish state, that Telia is a public company and that the Swedish government has indicated that it opposes the Transaction.36 For this reason, the Commission has examined whether any safeguards exist that would prevent the Swedish state from exercising its ability to exercise decisive influence over Telia’s activities. However, the Commission has not identified any evidence in the file of the existence of any holding arrangements, special provisions or other safeguards that ensure that the commercial activities of Telia are handled independently from the Swedish state.

(30) Based on the arguments set out above, the Commission, in the Article 6(1)(c) Decision, reached the preliminary conclusion that Telia does not have an independent power of decision from the Swedish state.

(31) In its Response to the Article 6(1)(c) Decision, the Notifying Party additionally submits that, as a publicly listed company, Telia is subject to capital market regulations requiring its board members to be independent of both its owners and its senior management. However, the Commission notes that even if board members are required to be independent from the owners and senior management, the Swedish state nevertheless has the power to elect and reappoint the members of Telia’s board of directors, the body that takes the strategic decisions in Telia, which confers upon it the power to exercise decisive influence on the commercial policy of Telia.

(32) In any event, it is not necessary for the Commission to reach a definitive conclusion on the independence of Telia from the Swedish state as the Swedish state does not control any (other) undertaking active within any relevant market concerned by the Transaction. In particular, as explained in section 3.2.3, the Commission concludes that the public broadcaster SVT has an independent power of decision from the Swedish state. That finding was not contested by the Notifying Party in the Response to the Article 6(1)(c) Decision.

3.2.3. Relationship between the Swedish state and SVT

(33) In this case, since the Commission concludes that Telia does not have an independent power of decision from the Swedish state, it is necessary to investigate whether SVT, another undertaking active on the same markets where the merged entity will operate, has an independent power of decision from the Swedish state. 37

(34) During the investigation, market participants raised the concern that the merger would lead to a significant concentration among wholesale suppliers of TV channels leading to competition being eliminated between the merged entity and SVT since it is claimed38 that both Telia and SVT are controlled by the Swedish state. An additional concern raised by market participants is that competition between the merged entity and SVT for the acquisition of broadcasting rights for audio-visual (“AV”) content will be adversely affected.39

(35) The Notifying Party submits in its initial submission that the Swedish state cannot be considered to exercise decisive influence on SVT. According to the Notifying Party, the following mechanisms ensure independence between SVT and the Swedish state:(i) the fact that SVT is not owned by the Swedish state but by the foundation Förvaltningsstiftelsen för Sveriges Radio AB, Sveriges Television AB och Sveriges Utbildningsradio AB (the “Foundation”) which, as all other foundations under Swedish law, does not have any owners or owner (and is therefore not owned by the Swedish state); (ii) the structure of the Foundation’s board (including the process for the appointment of its members and the limitations on who can become a board member); (iii) the Foundation’s financing; (iv) the Foundation’s limited influence over SVT as its powers as owner of SVT are restricted; (v) the process for appointment of SVT’s board members and their limited influence over its core activities; (vi) the system through which SVT is financed; and, (vii) the provisions of the Swedish Fundamental Law on Freedom of Expression preventing the Swedish state from imposing obligations on SVT’s content.40 In any event, the Notifying Party considers that even if the Swedish state were regarded as the owner of both Telia and SVT, Telia and SVT would have to be assessed as separate entities as they do not belong to the same economic unit because, as far as SVT is concerned, (i) there are mechanisms ensuring SVT's independence in relation to the Swedish state with regard to decisions concerning commercial activity; (ii) there are no formal and informal links between Telia and SVT, as there are no overlapping board assignments or senior positions between individuals and the Swedish state’s ownership role in Telia is pursued by the Ministry of Enterprise and Innovation, while SVT is owned by the Foundation; and (iii) the State has never intervened to coordinate the actions of Telia and SVT.

(36) The Commission considers that for the reasons set out in recitals (37) to (44) SVT likely has an independent power of decision from the Swedish state.

(37) In this case, the Swedish state does not own either SVT or SVT’s owner, the Foundation. There is therefore no formal link of ownership between the Swedish state and SVT. SVT is owned by the Foundation, which was established by a decision adopted by the Riksdag (Swedish parliament) in accordance with a Swedish government proposal in 1997. The Foundation is, however, not owned by any person or undertaking in accordance with Swedish Law.41 According to SVT, the Foundation “was created to promote the independence of public service radio and television”. 42 When the Foundation was created a specific sum of capital was dedicated to the Foundation. The Foundation exercises sole control over that capital and the Foundation’s administration is funded exclusively by the returns from that capital.43

(38) Since there is no formal link of ownership between the Swedish state and SVT, the Commission has assessed whether there exists an indirect link between the Swedish state and SVT, through the appointment of the board of the Foundation. The Swedish state appoints the members of the board of the Foundation, acting through the Swedish government, namely the Ministry of Culture.44 In turn, the board of the Foundation appoints the board of SVT. However, there are certain restrictions on who can be a member of the board of the Foundation.45 In addition, the members of the board of the Foundation are nominated for relatively long periods of time: the chairperson has a term of office of four years, while the twelve ordinary members have eight-year terms. Furthermore, neither the Swedish state nor any public authority have a direct role in the nomination and selection process of the board of SVT and the management of SVT.

(39) The aim of the Foundation is to own and manage the shares in its subsidiaries, inter alia SVT, and to exercise the tasks which that entails. Accordingly, one of the Foundation’s main tasks is the appointment of the board of directors of SVT, and the boards of the two other subsidiaries wholly owned by the Foundation. The board of the Foundation meets with the board of SVT once a year in order to inform itself about SVT’s work and development.46

(40) The board of directors of SVT is composed of one chairperson, six ordinary directors, two employee representatives and two deputy employee representatives.47 The board of the Foundation appoints the board of directors of SVT (not including the employee representatives48) at SVT’s annual shareholders’ meeting.49

(41) The tasks of SVT’s board of directors50 include taking the following decisions51: appointing and dismissing the CEO, laying down strategies, long-term goals and operational plans for SVT, the overall orientation of the programming activities based on the company's broadcasting licence, financial planning and major investments. However, the board does not have any influence over the production or purchasing of content or SVT’s other ongoing activities. In addition, while the board decides which part of the budget should be allocated to programme making, it does not decide how the budget should be allocated between different genres or programmes. 52

(42) SVT’s CEO is appointed and can be dismissed by the directors of the board.53 The CEO is in charge of coordinating SVT’s operations and is assisted by the management group.

(43) SVT’s management group consists of ten individuals (including the CEO).54 The CEO is responsible for appointing the remaining members of the management group, including the publishers.55 Neither the Swedish state nor any public authority has any role in the nomination and selection process. 56 There is no fixed duration for membership of the management group, including the CEO.57

(44) The role of the management group is to take the decisions concerning the range of programmes and activities of SVT. According to SVT, this includes setting the content strategy, deciding on the content plan for the upcoming years. It is during this process that almost all of SVT’s content is defined and ordered.58 The Swedish state, the Foundation and the board of SVT have no powers in relation to the decisions taken by the management group.59

(45) The findings set out in recitals (37) to (44) above, which the Commission set out as preliminary conclusion in the Article (6)(1)(c) Decision, were not contested by the Notifying Party in the Response to the Article 6(1)(c) Decision.

(46) Based on the above, the Commission considers for the purposes of this Decision that there are sufficient elements likely conferring on SVT an independent power of decision from the Swedish state.

3.2.4. As to whether the Swedish state is able to coordinate the commercial conduct of SVT and Telia

(47) The Commission considers that coordination between the commercial conduct of Telia and that of SVT could not be imposed or facilitated by the Swedish state, for the reasons set out in recitals (48) to (53).

(48) In accordance with the provisions of the current Swedish Radio and TV Act60, the Swedish government grants the broadcasting permit (“the Charter”) for SVT. The Swedish Radio and TV Act contains an exhaustive list of the conditions that can be attached to the Charter.61 The current Radio and TV Act and the Charter do not allow the Swedish state to interfere in the nature of the programmes broadcast by SVT.62 The Charter provides that the activities of SVT must be independent from the Swedish state and various economic, political and other interests in society. 63 The Charter’s conditions that relate to content64 include an obligation on SVT to broadcast a “varied programming”. Specifically with regard to news activities, the Charter provides that SVT must ensure diversity in news selection, analysis and commentary. The current Charter is valid until the end of 2019. It is currently under review so it is technically possible that the Swedish government might adapt those conditions for the next period.65 Under the current Radio and TV Act, the Swedish government could theoretically lift the obligation for SVT to broadcast a “varied programming” thus giving more flexibility to SVT to focus on specific programming, but the Swedish government could not, in the Charter, dictate which programming SVT should focus on. Furthermore, since the list of conditions set out in the Radio and TV Act is exhaustive, the Swedish government cannot impose a negative obligation on SVT to not focus on certain programming. The Charter that is set to enter into force in 2020 will be adopted by the Swedish government in December 2019 and will cover the period 2020–2029. Ahead of the review, the Swedish parliament’s public service committee issued a report from the Parliamentary Commission of Inquiry (SOU 2018:50). The report includes the committee’s proposal as to how the public service mandate should be formulated, including that its remit continues to be broadly formulated as regards content and no changes from the current conditions on varied programming are proposed in this respect. Therefore, the committee does not propose that SVT’s content should be narrower in the future.

(49) There are constitutional safeguards in place preventing public authorities and public bodies’ from examining the content of the public broadcasters.66 The Foundation has no legal ground to examine the content broadcast by SVT and to follow-up on whether SVT has fulfilled its public service tasks. The Swedish Broadcasting Commission, an independent review committee, is the only body that follows up whether SVT has exercised its broadcasting rights in accordance with the conditions set out in the Charter.67 Their examination looks into whether or not the conditions of the Charter have been met, thus safeguarding varied programming, diversity in news selection etc. However, the examination does not relate to how the conditions have been met.68 The examination therefore does not concern the content or specific programmes.69 This provides a safeguard for ensuring that the content broadcast by SVT is not subject to examination by any public body.

(50) As to SVT’s funding conditions, as of 1 January 2019, as part of the adoption of the new Public Service Act70 Sweden has introduced a public service fee that all taxable persons above 18 years of age with a taxable income will pay (instead of a TV licence that was to be paid by whoever had a TV). The tax authority collects this public service fee from everyone. The fee is run via accounts controlled by the Legal, Financial and Administrative Services Agency (Kammarkollegiet), an agency under the Justice Ministry. The public service broadcaster SVT is therefore not financed through the state budget.71 Decisions on the allocation of funding are taken by the Swedish government in accordance with a “guideline decision” taken by the Swedish parliament. The funding allocation decision will run in parallel to the Charter term of 8 years. The funds are earmarked to be only used for the financing of public service broadcasting (SVT being one of the three public service companies being financed). The extent to which the Swedish state is able to intervene and influence the amount of funds transferred to SVT during the 8-year funding period therefore appears to be very limited. The provisions that relate to SVT’s news activities under the current funding conditions (valid until the end of 2019) provide an additional safeguard against possible coordination between Telia and SVT, through the Swedish state. The Commission further notes that one of the stated reasons why it was necessary to adopt the new Public Service Act was to improve further the independence of public service in Sweden.72 Ahead of the new Charter that will be adopted by the Swedish government in December 2019 for the period 2020–2029, the Swedish parliament’s public service committee issued a report from the Parliamentary Commission of Inquiry (SOU 2018:50). The report includes the committee’s proposal for how the public service mandate should be formulated. The committee does not foresee any material changes to SVT’s funding conditions in the future.

(51) In addition, there are legal constraints that prevent the Swedish state and other public authorities from interfering in the production of content of SVT. In particular, regulatory provisions set out in the Fundamental Law on Freedom of Expression and the Radio and TV Act further prohibit interference in the production of content.73

(52) Furthermore, none of the members of the board of the Foundation or of SVT are members of the board of Telia and vice versa.

(53) Finally, the Commission considers that the board members of Telia are bound by regulation as well as governance principles applicable to listed companies relating to confidentiality as regards commercially sensitive information. The board of Telia is thus legally restricted from sharing such information with the owner.74

(54) The findings set out in recitals (48) to (53), which the Commission set out as preliminary conclusions in the Article (6)(1)(c) Decision, were not contested by the Notifying Party in the Response to the Article 6(1)(c) Decision.

(55) The Commission therefore considers for the purposes of this Decision that the commercial activities of Telia and SVT cannot be coordinated through the intervention of the Swedish state.

3.2.5. Conclusion

(56) On the basis of the above, the Commission considers that, for the purposes of this Decision, SVT should be considered to constitute an economic unit with independent power of decision. In the competitive assessment, Telia and SVT should therefore be considered as independent from one another.

4. UNION DIMENSION

(57) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million75 (Telia: EUR […] million; Bonnier Broadcasting: EUR […] million; combined: EUR […] million; in 2017). Each of them has a Union- wide turnover in excess of EUR 250 million (Telia: EUR […] million; Bonnier Broadcasting: EUR […] million; in 2017), but they do not achieve more than two- thirds of their aggregate Union-wide turnover within one and the same Member State.

(58) The Transaction therefore has a Union dimension pursuant to Article 1(2) of the Merger Regulation.

5. PROCEDURE

(59) The Transaction was notified to the Commission on 15 March 2019.

(60) After a preliminary examination of the notification and based on the first phase (“Phase I”) market investigation, the Commission raised serious doubts as to the compatibility of the Transaction with the internal market and adopted a decision to initiate proceedings (“Phase II”) pursuant to Article 6(1)(c) of the Merger Regulation on 10 May 2019.

(61) The Parties submitted their written comments on the Article 6(1)(c) Decision on 24 May 2019.

(62) On 29 May 2019, a state of play meeting took place between the Parties and the Commission.

(63) On 4 June 2019, the Commission adopted a decision pursuant to Article 11(3) of the Merger Regulation, addressed to Telia, following Telia’s failure to provide complete information in response to a request for information ("RFI") from the Commission (the "Telia Article 11(3) Decision”). On the same day, the Commission adopted a second decision pursuant to Article 11(3) of the Merger Regulation, addressed to Bonnier Broadcasting following Bonnier Broadcasting’s failure to provide complete information in response to a RFI from the Commission (the "Bonnier Broadcasting Article 11(3) Decision”). Both the Telia Article 11(3) Decision and the Bonnier Broadcasting Article 11(3) Decision compelled their addressees to submit a complete response to the RFIs originally sent by the Commission and suspended the time limits referred to in the first subparagraph of Article 10(3) of the Merger Regulation until the receipt of complete and correct information required by the two decisions. Telia complied with the Telia Article 11(3) Decision on 4 July 2019 and Bonnier Broadcasting complied with the Bonnier Broadcasting Article 11(3) Decision on 4 July 2019. Thus, the suspension of the time limits expired at the end of 4 July 2019.

(64) On 4 July 2019, the Notifying Party requested an extension of the time period for the Commission’s investigation by 20 working days under the second subparagraph of Article 10(3) of the Merger Regulation.

(65) On 12 August 2019, the Notifying Party submitted commitments pursuant to Article 8(2) of the Merger Regulation in order to address the competition concerns identified by the Commission. On 13 August 2019, the Commission launched a market test of the commitments submitted by the Notifying Party on 12 August 2019.

(66) The Commission gave the Parties detailed feedback on the outcome of the market test during calls on 28 August 2019, 30 August 2019 and 2 September 2019.

(67) On 2 September 2019, the Notifying Party submitted revised commitments pursuant to Article 8(2) of the Merger Regulation.

(68) The Advisory Committee discussed a draft of this Decision on 24 October 2019 and issued a favourable opinion.

6. THE COMMISSION'S INVESTIGATION

(69) This Decision contains the Commission's findings on the basis of the investigation it carried out: prior to the notification of the Transaction; in the first phase; and in the second phase of the investigation.

(70) Prior to the notification of the Transaction, the Commission sent thirteen RFIs to the Parties, responses to which were included in the notification.

(71) During the Phase I investigation, the Commission sent thirteen RFIs to the Parties, as well as 8 RFIs and 12 questionnaires to TV distributors, TV broadcasters, right holders, consumers and housing associations in Sweden, Finland, Norway and Denmark. The Commission also conducted multiple interviews with market participants, such as large TV distributors and broadcasters, as well as with the national competition authorities, namely the Swedish and Finnish competition authorities.

(72) During the Phase II investigation, the Commission sent 35 RFIs to the Parties, as well as 14 RFIs and 7 questionnaires in addition to numerous requests for information and data to TV distributors, TV broadcasters, advertisers, and Open City networks in Sweden and Finland. The Commission also had technical meetings with the Parties, and meetings and/or calls with certain market participants, such as large TV distributors and new OTT service providers. The Commission had further contacts with the national competition authorities and national regulators in Finland and Sweden. The Commission also reviewed internal documents submitted by the Parties in response to RFIs from the Commission. In total, the Parties have provided more than 770 000 documents to the Commission (Telia around 290 000 and Bonnier Broadcasting around 480 000).

7. RELEVANT MARKETS

7.1. Markets concerned by the Transaction

(73) The Transaction relates to all the levels of the AV value chain (the structure of which is presented at section 7.2), namely: (i) the production of AV content; (ii) the licensing of broadcasting rights for AV content (together at section 7.3); (iii) the wholesale supply of TV channels (section 7.4); and (iv) the retail supply of AV services (section 7.5). In addition, the Transaction relates to: (v) the retail supply of fixed telephony services (section 7.6), (vi) the retail supply of fixed internet access services (section 7.7); (vii) the retail supply of mobile telecommunications services (section 7.8); (viii) the retail supply of multiple play services (section 7.9); and (ix) the sale of advertising space on AV services (section 7.10).

(74) For each of these types of products, the remainder of this section provides an overview of the Parties’ activities. Sections 7.3 – 7.10 then examine the product and geographic market definition for each level of the AV value chain and the other markets where the Parties are active. Section 7.11 concludes.

7.1.1. Production of AV content

(75) Upstream of the value chain is the production of new AV content. AV production companies produce AV content either (a) for internal use on their own AV services if they are vertically integrated in the wholesale supply of TV channels and/or in the retail provision of AV services (that is to say, “captive AV production”), or (b) for supply to third-party customers (that is to say, “non-captive AV production”). Third- party customers are typically: (i) TV broadcasters, which then incorporate the AV content into linear TV channels, that is to say, services provided for simultaneous viewing of programmes on the basis of a programme schedule,76 and ancillary services, that is to say, services that TV broadcasters add to their TV channels in order to enhance the viewer experience (such as Catch-Up TV and Start-Over);77 or(ii) etail providers of AV services, which then retail the AV content to end users.

(76) Wholesale or retail providers who seek AV content for their TV channels or AV services generally have a choice between a number of sourcing models, which can be broadly categorised as follows: (a) acquiring broadcasting rights from AV production companies for pre-produced AV content (sometimes referred to as ‘off-the-shelf’ or ‘tape sales’); (b) obtaining AV content produced on an ‘ad hoc’ basis (that is to say tailor-made).

(77) The supply-side of the market for the production of AV content thus comprises AV production companies, while the demand-side comprises third parties that commission the production of AV content or hire AV production services, typically TV broadcasters or retail providers of AV services.

(78) As regards the supply-side of the market, neither Party is active as a supplier to third parties. In particular, AV content produced by TV4 AB in Sweden, and Mediahub in Finland, which are part of Bonnier Broadcasting, is fully captive.78

(79) As regards the demand-side of the market: (a) Bonnier Broadcasting commissions AV content in Sweden and Finland from various external production companies and format owners;79 (b) Telia is not active in Sweden and has been active in Finland only since August 2018, as it has commissioned production of content related to the Finnish ice hockey league (“Liiga”).80

7.1.2. Licensing of broadcasting rights for AV content

(80) This part of the AV value chain concerns the licensing of broadcasting rights for pre- existing AV content – that is to say AV content that has been previously produced and is subsequently made available ‘off-the-shelf’ by the rights holder – and broadcasting rights for sports events.

(81) The broadcasting rights for pre-produced AV content can belong to one or more of the following: (i) the holder of the rights to the AV format, (ii) the production company that produced the AV content, or (iii) the company that commissioned the production of the AV content. In addition, the broadcasting rights can belong to (iv) a third-party, to which they were licensed by the original owner, along with a right to sub-license.

(82) All of these categories of rights owners, which constitute the supply-side of the market, license broadcasting rights to content aggregators, which constitute the demand-side of the market, namely: (a) TV broadcasters; or (b) retail providers of AV services.

(83) As regards the supply-side of the market: (a) Bonnier Broadcasting occasionally licenses rights to external buyers in Sweden, Finland and Denmark (for example, when unable to fully exploit the acquired content licence or upon request of a foreign TV broadcaster).81 In Norway, besides the occasional licensing of broadcasting rights for TV shows primarily produced for the Swedish audience, Bonnier Broadcasting has entered into a sub-licensing agreement with [Identity of the sub-licensee and scope of the sub-licensing agreement]. This sub-licensing agreement will expire on[…];82 (b) Telia sub-licenses broadcasting rights for certain Liiga ice hockey games in Finland [Terms and conditions in Telia Company’s licensing agreement].83

(84) As regards the demand-side of the market: (a) in Sweden, Bonnier Broadcasting acquires broadcasting rights for specific AV content (sports events, films or TV shows) for purposes of incorporating them into its TV channels or streaming services.84 In Finland, Bonnier Broadcasting has acquired the rights to broadcast the FIA Formula One World Championship (“Formula 1”) for the 2019-2021 seasons, as well as some foreign AV content for purposes of incorporating them into its TV channels or streaming services.85 In Denmark, Bonnier Broadcasting acquires broadcasting rights for some Danish-language scripted AV content for purposes of including it in its streaming services.86 In addition, the broadcasting rights for international AV content that Bonnier Broadcasting acquires for its Swedish and/or Finnish activities normally also cover Denmark and Norway;87 (b) Telia is only active in Finland where it acquired the rights to broadcast Liiga ice hockey games for six seasons, from the season 2018/2019 to the season 2023/2024, as well as some minor broadcasting rights, such as [Content of Telia Company’s agreements].88

7.1.3. Wholesale supply of TV channels

(85) TV broadcasters use the AV content and broadcasting rights for AV content that they have acquired or produced in-house in order to package it into TV channels. TV channels are linear services, broadcast to end users either on a free-to-air (“FTA”) basis or on a pay TV basis. TV channels are wholesaled by TV broadcasters to retail providers of AV services.

(86) The viewer experience is evolving and shifting from traditional linear viewing to non-linear viewing. The development of new forms of AV consumption as a result of new technology has made it possible to distinguish between rights for conventional (‘linear’) TV and those for ‘non-linear’ AV services (see section 7.1.4).

(87) In the specific context of linear television, viewers must watch TV content at the established time it is broadcast, and on the channel on which it is presented, according to the specific schedule defined by the broadcaster, with no possibility to interact with it or change the time.

(88) In addition, ancillary services to TV channels ("ancillary services") have gradually been integrated in traditional TV channels to enhance the viewer experience. Such services allow a more enriched viewing experience by enabling the viewer to interact with TV programming and choose the time and manner of watching content according to tailored needs and demands. TV broadcasters thus can offer viewers a vast array of functions and services as part of the experience of the TV channels. For instance, Catch-Up TV is a service that makes the content of a channel available for a certain period to the viewer, who can choose when to view it.

(89) The main ancillary services, which could be both linear and non-linear, are currently the following:

– Personal Video Recorder (“PVR”), which allows viewers to record selected contents that are offered on the TV channels, and made available to viewers on an on-demand basis;

– Network Personal Video Recorder (“NPVR”), which allows viewers to record selected contents that are offered on the TV channels, and made available to viewers on an on-demand basis on a platform owned or operated by a TV distributor;

– Catch-Up TV, which allows viewers to access selected contents that are offered on the TV channels on an on-demand basis for a limited period of time following their first linear transmission;

– TV Everywhere (“TVE”), which allows viewers to watch the TV channels on multiple devices, such as tablets and smartphones;

– Start-Over, which allows viewers to restart a program on the TV channel at any time during its linear broadcast exhibition;

– Dual Entry, which allows end users to view concurrent content (in an application or site that is made available to them) which, irrespective of whether the content is transmitted in a linear fashion, is offered as part of the retail subscription.

(90) As regards the supply-side of the market: (a) Bonnier Broadcasting wholesales TV channels in Sweden through TV4 AB (“TV4”) and C More, and in Finland through MTV and C More.89 In Denmark, Bonnier Broadcasting wholesales a limited number of C More TV channels, namely C More film and series TV channels.90 In Norway, Bonnier Broadcasting is currently not active as a supplier to retailers, as it has sublicensed C More film and series TV channels to the Norwegian broadcaster TV2;91 (b) Telia is not active.92

(91) As regards the demand-side of the market: (a) Bonnier Broadcasting is not active;93(b) Telia provides retail AV services to end customers in Sweden, Finland, Denmark, as well as Norway, since the acquisition of the Norwegian operator GET AS (“GET”) in 2018.94

7.1.4. Retail supply of AV services

(92) Retail providers of AV services offer packages of linear AV services and/or non- linear AV services to end customers.

(93) As explained in section 7.1.3, linear services are services that broadcast scheduled programs, conventionally over the air or through satellite/cable, not streamed to a specific user. Nearly all broadcast television services count as linear services.

(94) Non-linear services, or video-on-demand (“VOD”) services, are services provided for the viewing of programmes at the moment chosen by the user and at the user’s individual request on the basis of a catalogue of programmes selected by the service provider.95 Non-linear services can be further differentiated into the following types:

– Advertising Video On Demand (“AVOD”), which consists of on-demand access to a catalogue of films, series, sports and other AV content free of charge to consumers and funded by advertising;

– Subscription Video On Demand (“SVOD”), which consists of on-demand access to a catalogue of films, series, sports and other AV content for a subscription fee;

– Transactional Video-On-Demand (“TVOD”), which consists of purchase and/or rental of AV content on an “a la carte” basis (meaning that the end- customer pays for individual AV content that can be viewed at any time);

– Pay-per-view (“PPV”), which designates a service whereby the end user makes a payment to watch a single title that is being broadcast at a specific time, which is the same for all viewers.

(95) The above described linear and non-linear pay AV services can be augmented with ancillary services, such as Catch-Up TV, PVR, TVE, Start-Over or Dual Entry.

(96) To provide their linear and non-linear services to end-customers, retail providers of AV services use (i) traditional networks, such as cable, xDSL and fibre, internet protocol television, “IPTV”, satellite and, to a lesser extent, digital terrestrial TV (“DTT”), and/or (ii) the “Over-The-Top” (“OTT”) distribution technology, which allows AV content to be delivered through the use of the open internet. AV services that are supplied via the OTT distribution technology are hereinafter referred to as “OTT-based AV services” or as “OTT services”. In some cases, OTT services are sold to end customers on a standalone basis, that is to say without being associated with a subscription for non-OTT based AV retail services or for retail telecommunications services (hereinafter, “standalone OTT services”).

(97) TV distributors, such as Telia, are a sub-set of retail suppliers of AV services, who usually act as TV channel aggregators, i.e. they license TV channels and ancillary services from different broadcasters and make them available to end users as a package(s). The AV services supplied by TV distributors to end users consist of: (i) packages of linear TV channels (which they have either acquired or created themselves); and (ii) content aggregated in non-linear services, such as VOD, SVOD, TVOD and PPV. TV content can be delivered to end users through a number of technical means including cable, satellite and IPTV.

(98) OTT players are a sub-set of retail suppliers of AV services, who deliver TV channels and AV content in both a linear and non-linear fashion through the use of the internet. The main global OTT players, such as Netflix and Amazon, deliver content exclusively in a non-linear fashion. Local OTT players, such as Bonnier Broadcasting and NENT offer to their customers non-linear AV content but also the possibility to watch their TV channels linearly through the use of the internet. In order to provider OTT services, OTT players acquire OTT rights for channels and ancillary services from broadcasters, and OTT rights for AV content from suppliers of AV content or of broadcasting rights for AV content. OTT players that, similarly to TV distributors, act as TV channels aggregators are hereinafter referred as "OTT channels aggregators"

(99) Operator OTT services are a sub-set of OTT services enabling a company, usually providers of telecommunications services, to grant OTT access to their subscribers, even to those who do not have traditional TV subscriptions, as long as they are existing customers of other services (for example, as subscriber of fixed internet or mobile services). In order to provide Operator OTT services, OTT players acquire Operator OTT rights.

(100) OTT services that are purchased on a standalone basis without any other service are hereinafter referred as "standalone OTT services". In order to provide standalone OTT services, OTT players acquire standalone OTT rights.

(101) TV distributors also deliver TV channels and AV content in both a linear and non- linear fashion through the use of the open internet as an ancillary service to the main cable, satellite or IPTV subscription, namely TVE. TVE enables end customers to watch the TV channels or AV content linked to their cable, satellite or IPTV subscription through the open internet, on multiple devices, such as tablets and smartphones. In order to provider TVE services, TV distributors acquire TVE rights from broadcasters.

(102) Therefore, while both TVE and OTT are services delivered over the open internet, TVE is an ancillary service to the traditional subscription to retail AV services (i.e. cable, satellite, DTT, DTH or IPTV AV service), while OTT service could also be purchased on a standalone basis without any other service (i.e. standalone OTT service).

(103) In the retail provision of AV services to end users, (a) Bonnier Broadcasting provides standalone OTT services in Sweden (AVOD service “TV4 Play” and SVOD service “C More”) and Finland (AVOD service “MTV” and SVOD service “C More”).96 In Denmark and Norway, Bonnier Broadcasting provides OTT services through C More;97 (b) Telia provides AV services in Sweden through IPTV, cable and OTT98 as well as an ancillary service via TVE service.99 In Finland, Telia provides AV services through IPTV, cable, as well as a standalone OTT service (streaming service “Telia TV” and related TVOD services).100 In Denmark, Telia provides AV services though IPTV by using the fixed network of national incumbent TDC, as well as an ancillary OTT service (“Telia TV”).101 In Norway, following the acquisition of GET in 2018, Telia provides AV services through cable and IPTV, as well as an ancillary service via OTT.102

7.1.5. Retail supply of fixed telephony, fixed internet, mobile telecommunications and multiple play services

(104) Fixed telephony services comprise the provision of connection services at a fixed location or access to the public telephone network, for the purpose of making and/or receiving calls and related services.

(105) Fixed internet access services at the retail level consist of the provision of a fixed telecommunications link enabling end customers to access the internet.

(106) Mobile telecommunications services to end customers (also referred to as "retail mobile services") include services for national and international voice calls, SMS (including MMS and other messages), mobile internet with data services, access to content via the mobile network and retail international roaming services.

(107) The term "multiple play" relates to offers comprising two or more of the following services provided to retail consumers: mobile telecommunication services, fixed telephony, fixed internet access and TV services. Multiple play comprising two, three or four of these services is referred to as dual play ("2P"), triple play ("3P") and quadruple play ("4P") respectively.

(108) Three of the four services mentioned above, namely fixed telephony, TV services and fixed internet access, are “fixed” services as they are provided over a fixed network such as cable, copper or fibre infrastructure. Multiple play comprising any combination of two or more of these fixed services without a mobile component is referred to as "fixed multiple play". Multiple play comprising one or more of these fixed services in combination with a mobile component (including either voice or data, or both together) is referred to as "fixed-mobile multiple play" or “fixed-mobile convergence” (“FMC”). Fixed-mobile multiple play may involve a single mobile subscription (SIM card) or more than one mobile subscription combined with the fixed services.

(109) In the retail provision of mobile, fixed telephony and fixed internet access and multiple play telecommunications services to end users: (a) Telia provides retail fixed telephony, retail fixed internet access, retail mobile telecommunications and retail multiple play services103 in Sweden, Finland, Norway and Denmark;(b) Bonnier Broadcasting is not active.

7.1.6. Sale of advertising space on AV services

(110) TV broadcasters sell advertising space on their TV channels and on their OTT services. The sale of advertising space is an important source of revenues for FTA channels, while pay TV channels in general rely more on fees from retail providers of AV services or from end users.

(111) As regards the supply-side of the market: (a) Bonnier Broadcasting sells advertising space in Sweden - on its TV4 TV channels and AVOD service, on some of its C More TV channels, and on certain online media properties (e.g., websites) -, and in Finland - on its MTV TV channels and AVOD service, on some of its C More TV channels, and on certain online media properties;104 (b) Telia has entered into advertisement and sponsorship agreements in Finland in connection with the broadcasting of Liiga ice hockey games.105

(112) As regards the demand-side of the market: (a) Bonnier Broadcasting purchases advertising space on different media channels, such as online and TV in Sweden, Finland and Denmark. These purchases are mainly captive (i.e., purchases made on its own media properties, such as space on Bonnier Broadcasting's TV channels);106(b) Telia purchases advertising space in different media channels in Sweden, Finland and Denmark.107

7.2. Structure of the AV value chain

(113) In previous cases, the Commission set out the different levels of the TV value chain as follows: (i) the (upstream) markets for the production and the licensing of AV content, (ii) the (intermediate) market for the wholesale supply of TV channels, and(iii) the (downstream) market for the retail supply of TV services.108 The market investigation confirmed that this three-layer classification remains accurate with regard to AV content. Some market respondents note that companies active in the downstream market for the retail supply of TV services also acquire AV content directly (i.e., without the intermediation of companies active in the market for the wholesale supply of TV channels) from companies active in the upstream market for the production and the licensing of AV content.109

7.3. Production and licensing of broadcasting rights for AV content

(114) In previous decisions,110 the Commission has concluded that there are separate markets for: (i) production of commissioned TV content; and (ii) licensing of broadcasting rights for pre-produced TV content, which constitute alternative ways through which TV broadcasters and retail providers of AV services may source AV content.

(115) For the purpose of the market definition and for the sake of simplicity given that the Transaction raises similar issues in both markets, in the following section the Commission analyses the two separate markets for the production and the licensing of AV content together.

7.3.1. Product market definition

7.3.1.1. Previous Commission decisions

(116) With regard to the production of TV content, the Commission has found the product market for the production of TV content to be limited to non-captive TV production, thereby excluding captive TV production (TV content produced by TV broadcasters for use on their own channels), as this TV content is not offered on the market.111

(117) With regard to the market for the licensing of broadcasting rights for pre-produced TV content, the Commission has considered that this market may be subdivided by content type, in particular: (i) films, (ii) sports,112 and (iii) other TV content; and potential sub-segments within these content types, but ultimately left the market definition open.113 The Commission has also considered further sub-dividing the market for the licensing of broadcasting rights for TV content by exhibition window:(i) SVOD, (ii) TVOD, (iii) PPV, (iv) first pay TV window, (v) second pay TV window, and (vi) FTA.114

7.3.1.2. Notifying Party’s view

(118) In its initial submission, the Notifying Party considers that it is not necessary to take a firm view on whether, on the one hand, the production and supply of TV content and, on the other hand the licensing of broadcasting rights for pre-produced TV content constitute separate product market since the Transaction cannot be deemed to lead to a significant impediment to effective competition in either case.115

(119) With regard to the production of TV content, the Notifying Party submits that it would be neither appropriate, nor necessary to subdivide the market into different segments, as the Transaction would not give rise to any overlaps or affected markets under any market segmentation.116

(120) With regard to the licensing of broadcasting rights for pre-produced TV content, the Notifying Party submits that it would be neither appropriate, nor necessary to subdivide the market into different segments, as the Transaction would (i) not give rise to any overlaps between the Parties on the licensing side or acquisition side of the market in Sweden and Denmark, and (ii) give rise to minor overlaps on the licensing side and the acquisition side of the market in Finland.117

7.3.1.3. Commission’s assessment

(121) The information gathered during the Phase I market investigation118 did not give reason to depart from the distinction between the market for the production of AV content on the one hand, and the market for the licensing of broadcasting rights for pre-produced AV content on the other hand.119

(122) With regard to the market for the licensing of broadcasting rights for AV content, a majority of the respondents considered that the product market could be further segmented on the basis of the type of content. The results of the Phase I market investigation, however, showed that a further segmentation on the basis of the type of exhibition windows would not necessarily be relevant, given that such a segmentation at this level of the value chain is becoming increasingly blurred due to the uptake of non-linear services.120

(123) In the Article 6(1)(c) Decision, the Commission reached the preliminary conclusion that the production of AV content on the one hand and the licensing of broadcasting rights for TV content on the other hand were two separate product markets, and that, in any event, the question whether the market for the licensing of broadcasting rights for AV content could be further segmented depending on the type of AV content or exhibition window could be left open, as the effects of the Transaction were unlikely to differ irrespective of the scope of the product market.

(124) In its Response to the Article 6(1)(c) Decision, the Notifying Party did not contest the preliminary assessment of the Commission. No further elements emerged during the Phase II investigation.

(125) In light of the foregoing, the Commission does not depart from its previous assessment, and concludes, for the purpose of this Decision, that (i) the production of AV content and the licensing of broadcasting rights for AV content constitute two separate product markets, and (ii) the question whether the market for the licensing of broadcasting rights for AV content can be further segmented depending on the type of AV content or exhibition window can be left open, as this would not change the outcome of the competitive assessment in the present case.

7.3.2. Geographic market definition

7.3.2.1. Previous Commission decisions

(126) The Commission has previously considered the geographic markets for both the production of TV content and the licensing of broadcasting rights for TV content to be national in scope or encompassing a linguistically homogeneous area.121

7.3.2.2. Notifying Party’s view

(127) In its initial submission, the Notifying Party submits that the exact definition of the geographic markets for the production of TV content and the licensing of broadcasting rights for TV content can be left open, as the Transaction would not raise competitive concerns under any alternative market definition.122

7.3.2.3. Commission’s assessment

(128) According to a majority of respondents to the Phase I market investigation, the geographic scope of agreements for the licensing of broadcasting rights for AV content is either national, by linguistic area, or regional, that is to say, encompassing the Nordic region.123

(129) In the Article 6(1)(c) Decision, the Commission reached the preliminary conclusion that, in any event, the exact geographic market definition for the production of TV content and the licensing of broadcasting rights for AV content could be left open, as the effects of the Transaction were unlikely to differ depending on the geographic scope of the market.

(130) In its Response to the Article 6(1)(c) Decision, the Notifying Party did not contest the preliminary assessment of the Commission. No further elements emerged during the Phase II investigation.

(131) In light of the foregoing, the Commission does not depart from its previous assessment, and concludes, for the purpose of this Decision, that the geographic markets for the production of AV content and the licensing of broadcasting rights for AV content are either national, by linguistic area, or regional, that is to say, encompassing the Nordic region, but that the exact geographic market definition can be left open, as this would not change the outcome of the competitive assessment in the present case.

7.4. Wholesale supply of TV channels

(132) As explained in Section 7.1.3 above, TV broadcasters package the AV content and broadcasting rights for AV content that they have acquired or produced in-house into linear TV channels, which are supplied to retail providers of AV content, and then broadcast to end users either on a FTA basis or on a pay TV basis. Ancillary services have gradually been associated to TV channels in order to complement the TV offering and enhance the viewer experience of traditional linear channels.

(133) The wholesale supply of TV channels is an intermediate layer between (i) the upstream production and licensing of content, and (ii) the downstream retail provision of AV services to end customers.

7.4.1. Product market definition

7.4.1.1. Previous Commission decisions

(134) In previous decisions, the Commission identified a wholesale market for the supply of TV channels. Within that market, in certain decisions, the Commission has further identified two separate product markets for: (i) FTA TV channels, and (ii) pay TV channels.124 The Commission has further stated that within the pay TV channels market, there could be different segments for: (i) basic pay TV channels, and (ii) premium pay TV channels,125 for which end customers pay a premium in addition to their basic subscription fee.

(135) In its decision of 24 February 2015 in case M.7194 – Liberty Global/Corelio/W&W/De Vijver Media, the Commission has concluded that at the level of the wholesale supply of TV channels there were two separate product markets, one consisting of the wholesale supply of premium pay TV channels and one consisting of the wholesale supply of basic pay TV/FTA channels. Given that(i) FTA channels were mostly supplied together with basic pay TV channels and(ii) competitive assessment would remain the same even if FTA channels were regarded as belonging to a separate product market from that of basic pay TV, the Commission has considered that it was not necessary to make a distinction between FTA and basic pay TV channels on the market for wholesale supply of TV channels in that case.126

(136) In that case, the Commission also considered that there was no need to draw a distinction between linear TV channels and their ancillary services, which are licensed by TV broadcasters to TV distributors along with, or in addition to, those linear TV channels.127

(137) In addition, in previous decisions, the Commission also examined a number of other potential segmentations, including: (i) genre or thematic content (such as films, sports, news, youth, and others)128; and (ii) the different means of infrastructure used for the delivery to the viewer (cable, satellite, terrestrial TV and IPTV).129 It has ultimately left the market definition open in all these regards.

7.4.1.2. Notifying Party’s view

(138) Both in its initial submission and in its Response to the Article 6(1)(c) Decision, the Notifying Party considers that there is no need to make any segmentation on the market for wholesale supply of TV channels.130

(139) In particular, the Notifying Party considers in its initial submission that it is not relevant to segment (i) the market for wholesale supply of TV channels between FTA TV channels and pay TV channels, (ii) the market for wholesale supply of pay TV channels between basic pay TV channels and premium pay TV channels, (iii) the market for wholesale supply of premium pay TV channels between premium pay TV sports channels and premium pay TV film channels, and (iv) the market for wholesale supply of TV channels between general interest TV channels and thematic TV channels.131 In addition, the Notifying Party considers that it is not necessary to segment the market for wholesale supply of TV channels (i) according to the type of infrastructure used for their transmission, or (ii) between linear and ancillary non- linear services.

(140) Ultimately, the Notifying Party submits that the question whether the wholesale market for the supply of TV channels must be further segmented can be left open.132

7.4.1.3. Commission’s assessment

(141) A majority of respondents to the Phase I market investigation across the four relevant geographies indicated that the segmentation between FTA and pay TV channels continues to be appropriate.133

(142) However, a number of well-substantiated responses to the Phase I market investigation suggested that this segmentation is not clear-cut for the following reasons.

(143) First, from a supply-side perspective, some respondents indicated that, in the countries at stake, it might be relevant to consider FTA and pay TV channels together. In that respect, some respondents which are active across the Nordics (NENT, The Walt Disney Company, HBO Nordic) stressed that broadcasters of pay TV channels and broadcasters of FTA TV channels often compete for the same content and ultimately compete for the same viewer base.134 While not considering that there exists distinct product markets for wholesale supply of FTA and pay TV channels, NENT further noted that if one were to segment the market for wholesale supply of TV channels, a distinction should be made between non-commercial FTA TV channels on the one hand, and commercial FTA TV channels and pay TV channels on the other hand, as the business model of non-commercial FTA TV channels differs significantly from the business model of commercial FTA TV channels or pay TV channels.

(144) Second, the Swedish retail provider Tele2 and the Finnish retail provider Elisa considered that it would be more accurate to segment the market for wholesale supply of TV channels between FTA and basic pay TV channels on the one hand, and premium pay TV channels on the other hand, notably given similarities between FTA and basic pay TV channels.135 In that respect, Tele2 submitted that FTA and basic pay TV channels shared the following features: a broad offering, the prominence of advertising revenues (with regard to commercial FTA only), and the fact that all basic pay TV packages include the FTA channels.

(145) Last, some market participants stressed the specificity of the Finnish market, where there is a minor offer of basic pay TV channels in view of the national legislative framework, which prevents housing companies from collecting basic TV fees from households.136

(146) The results of the Phase I market investigation were also mixed as to whether a distinction should be made between (i) basic pay TV channels, and (ii) premium pay TV channels, for which end customers pay a premium in addition to their basic subscription fee.137

(147) Some respondents to the Phase I market investigation considered this distinction to be blurred, given notably that several retail providers are introducing point based optional packages, where subscribers may use points to select between a range of channels and services that include both basic and premium pay TV channels.138 However, most respondents stressed the premium nature of the pay TV channels that offer such valuable content that end-customers are willing to pay more to view it. This held in particular true with regard to premium pay TV sports channels.139 In that respect, for instance, Sanoma considered that “In Finland premium sports is still a big, if not the biggest driver of consumer paid TV content”.

(148) The results of the Phase I market investigation indicated that the wholesale supply of pay TV channels could be further sub-divided according to genre (e.g. films, sports, youth, general entertainment, news).140 Indeed, most respondents stressed that distributors would seek to offer a variety of genres to end-customers. Channels of different genres would thus be complementary. In this respect, one respondent considered that “a pay-TV package with a wide appeal within a household should contain genres that appeal to men (e.g. sports, which are considerably more expensive to acquire than the other channels), women (e.g. films) and kids (e.g. youth, entertainment)”.141 In particular, some retail providers of AV services stressed the specific place of sports channels within their retail offers.142

(149) In that respect, the Finnish retail provider DNA considered that “especially premium sports channels are to be distinguished as a separate market from other thematic pay-TV channels due to the audience not being willing to switch to premium sports to any other genre”.143 DNA also evidenced this distinction by stressing (i) the fact that premium sports are broadcast live, and (ii) the significant price difference between premium sports channels and other pay TV channels. In addition, another Finnish retail provider, Elisa, stated that “[a] retail distributor cannot substitute or supply as an alternative particularly premium sports, such as Formula 1 and national ice hockey league (Liiga), with any other genre of content or even with a lesser sports content” and that “[t]here is also a clear difference in the customers willingness to pay for content between different genre”.144

(150) With regard to a possible segmentation of TV channels depending on the type of infrastructure used for their transmission, the results of the Phase I market investigation did not provide reasons to conclude that different means of infrastructure used for the delivery to the viewer (cable, satellite, terrestrial TV and IPTV) could constitute different product markets.

(151) With regard to a possible distinction between linear TV channels and their ancillary non-linear services, the results of the Phase I market investigation did not provide reasons to depart from the Commission’s previous approach.145

(152) In the Article 6(1)(c) Decision, the Commission reached the preliminary conclusion that the relevant product markets were, irrespective of whether a segmentation by type of transmission infrastructure would be relevant, as follows:

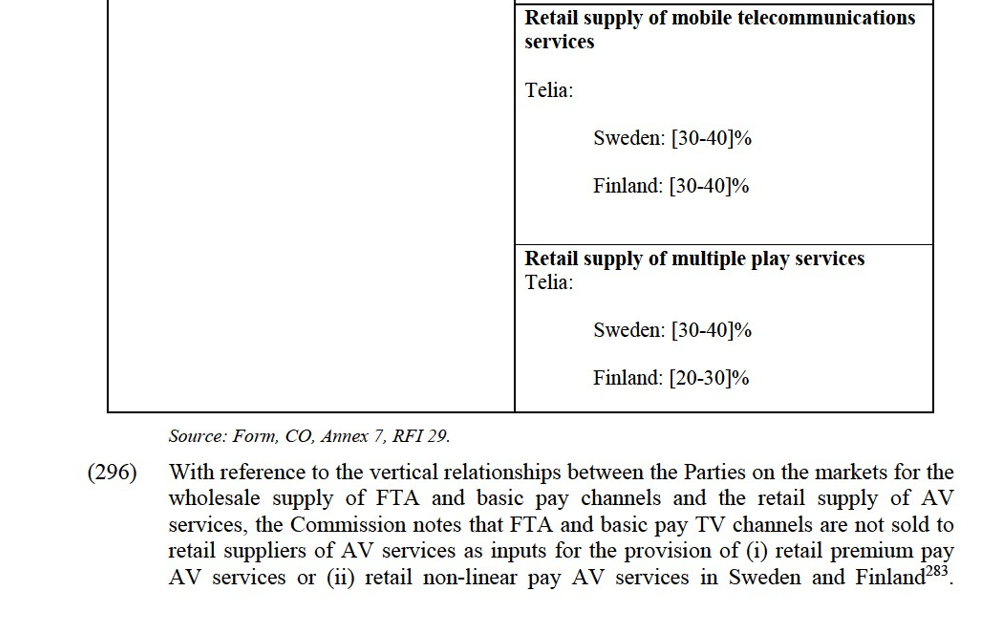

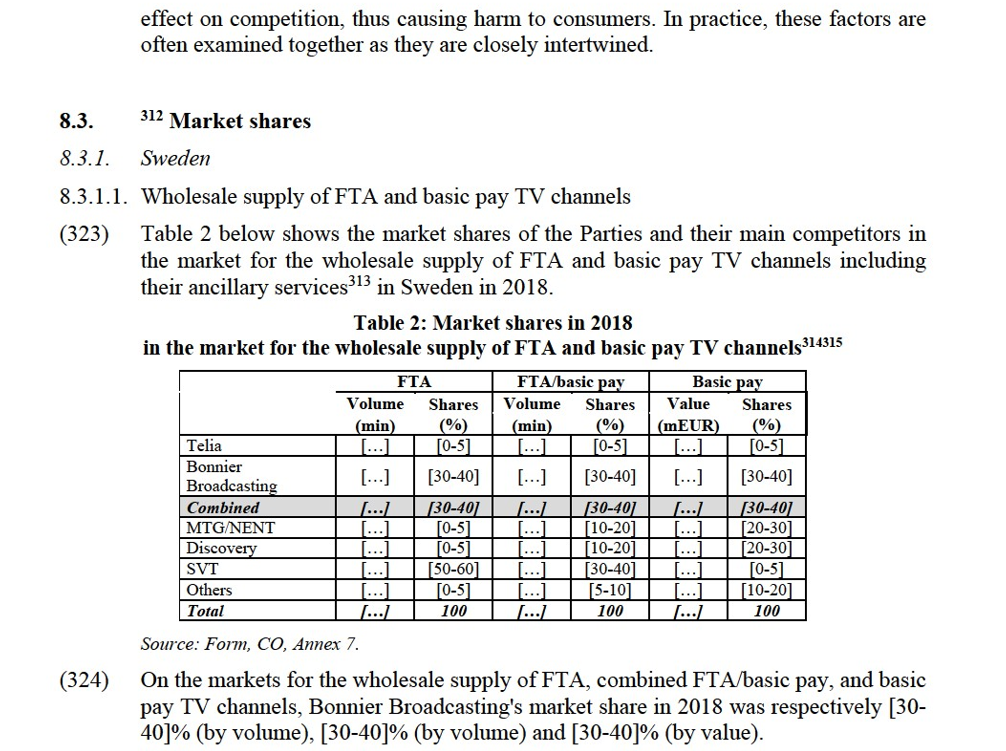

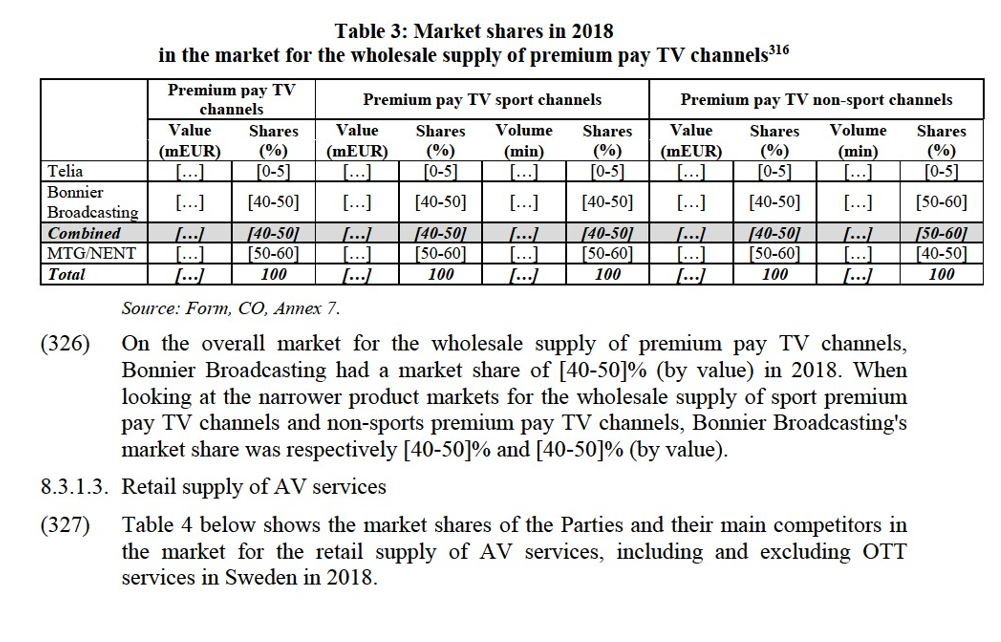

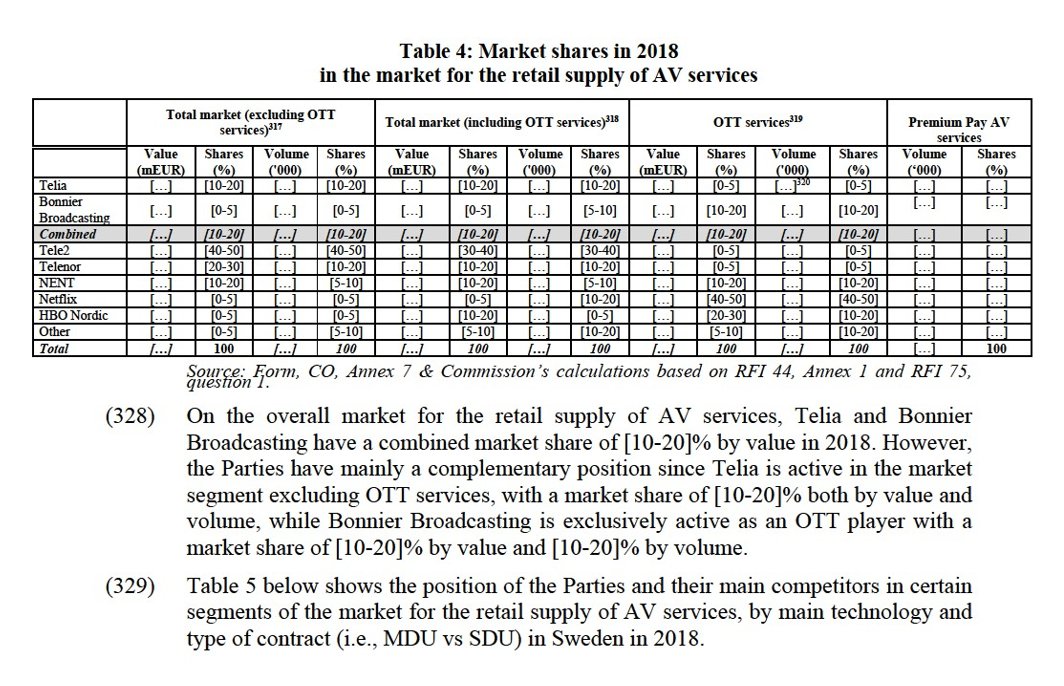

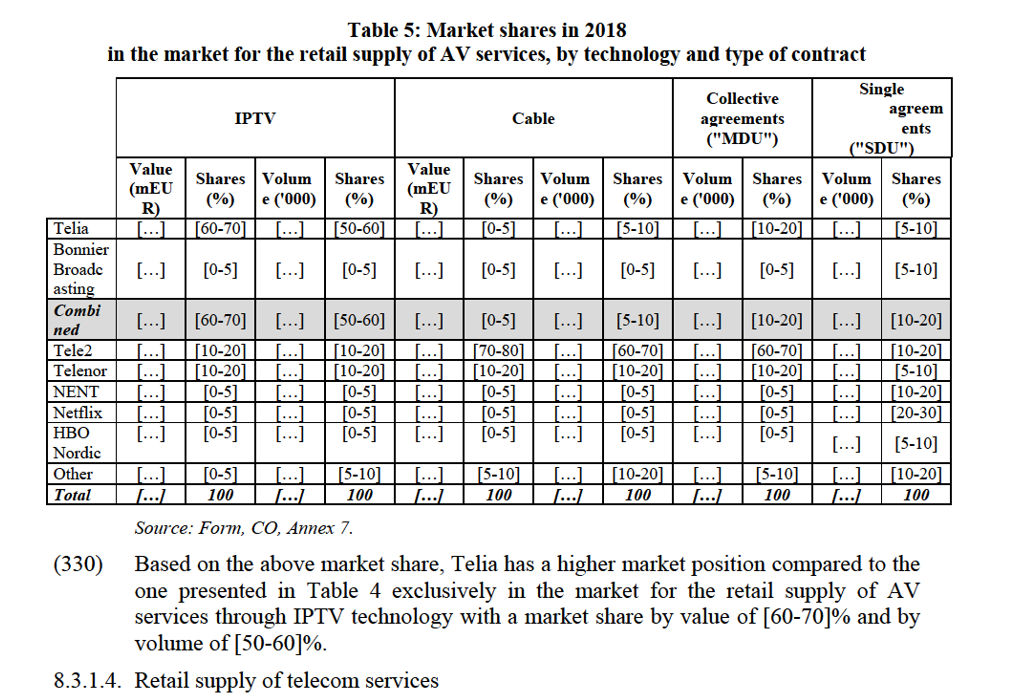

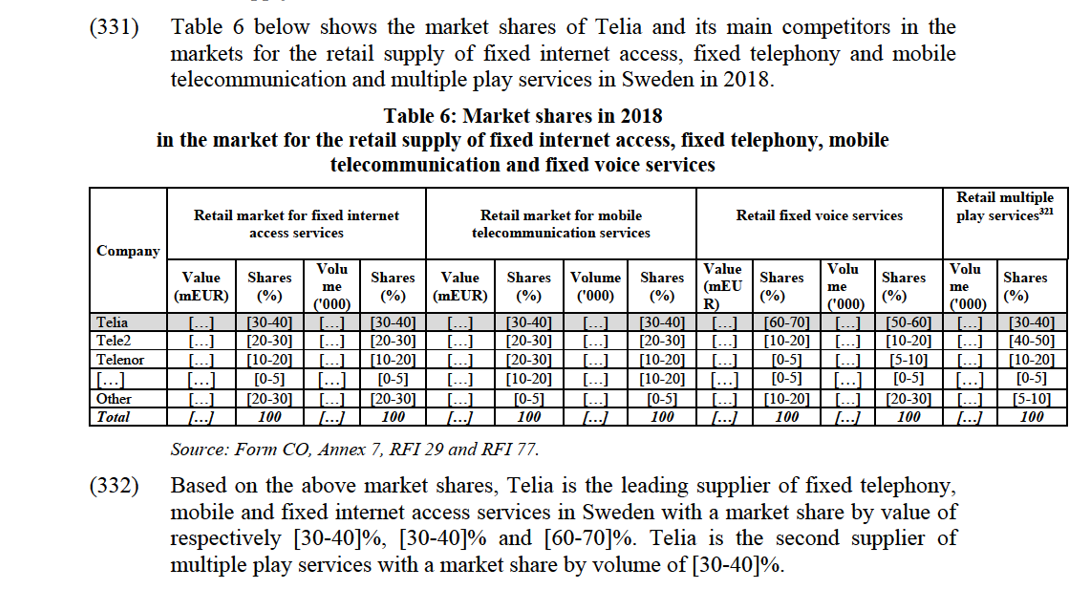

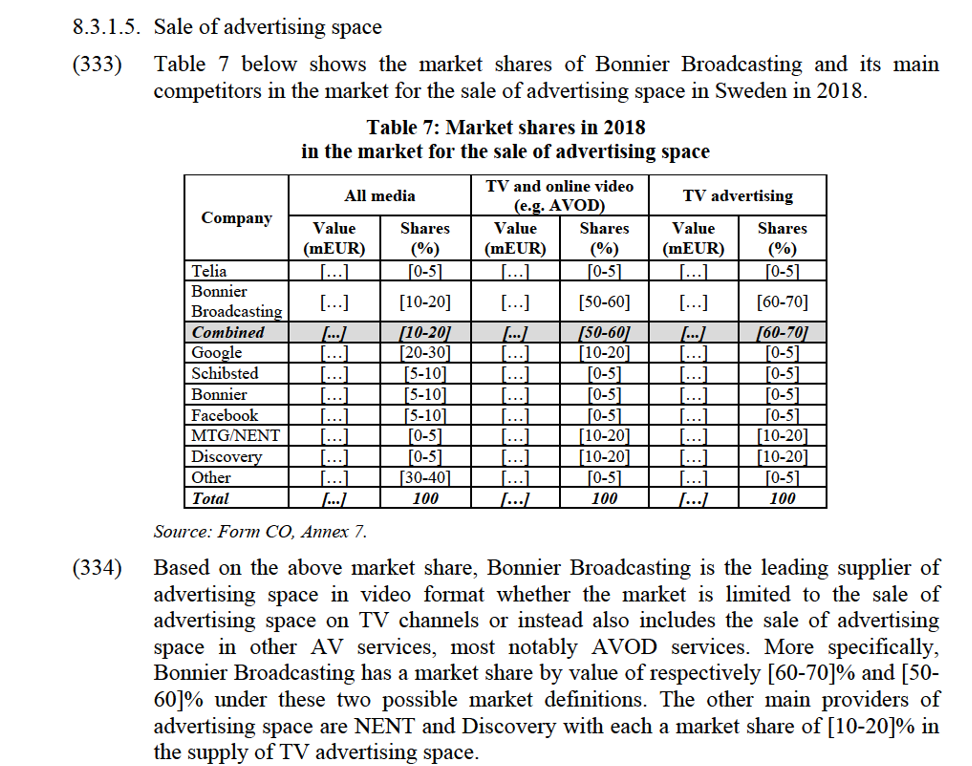

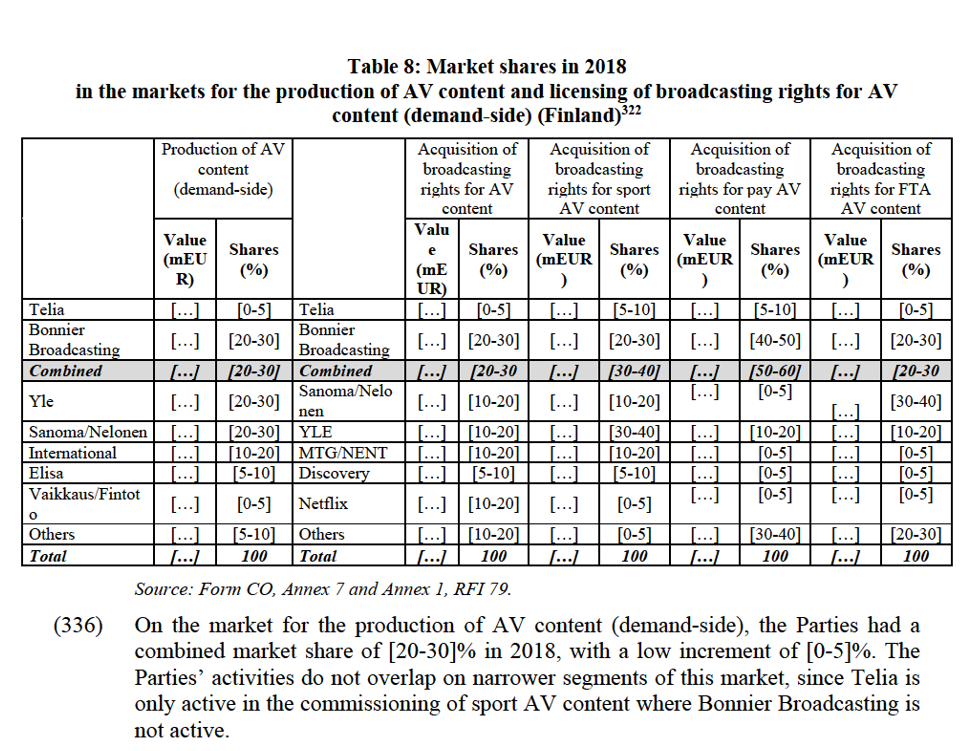

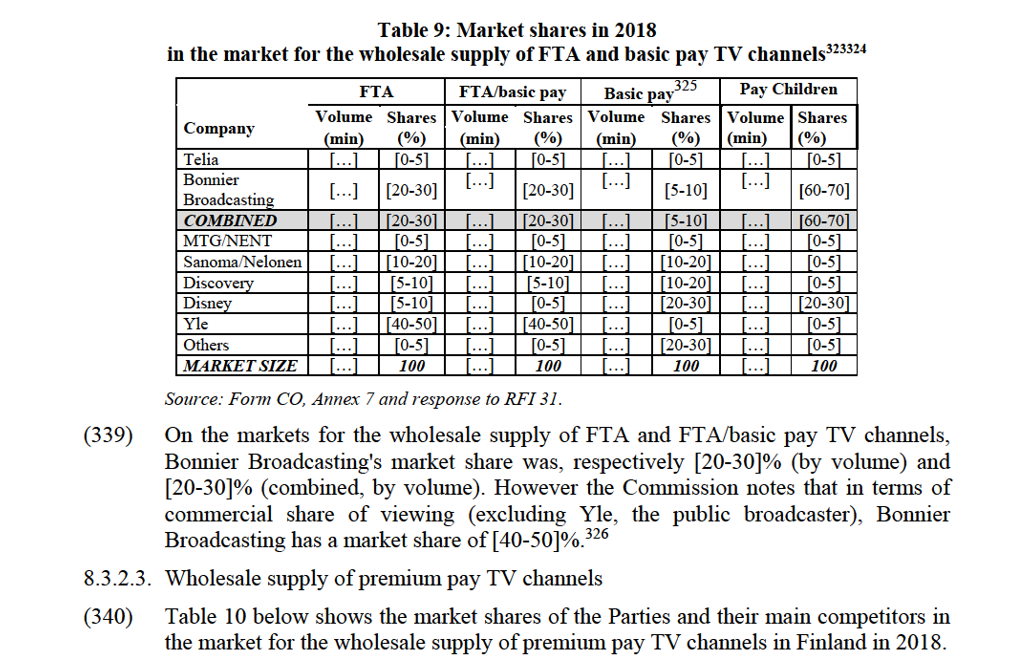

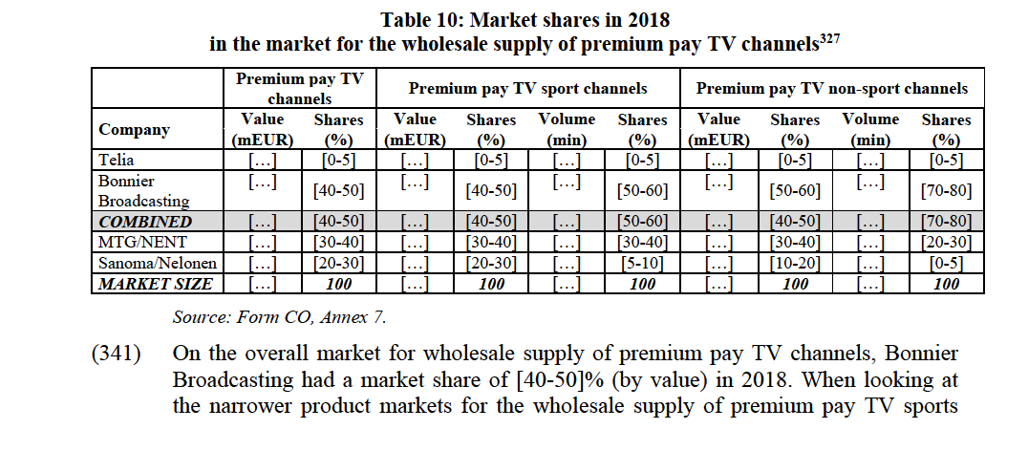

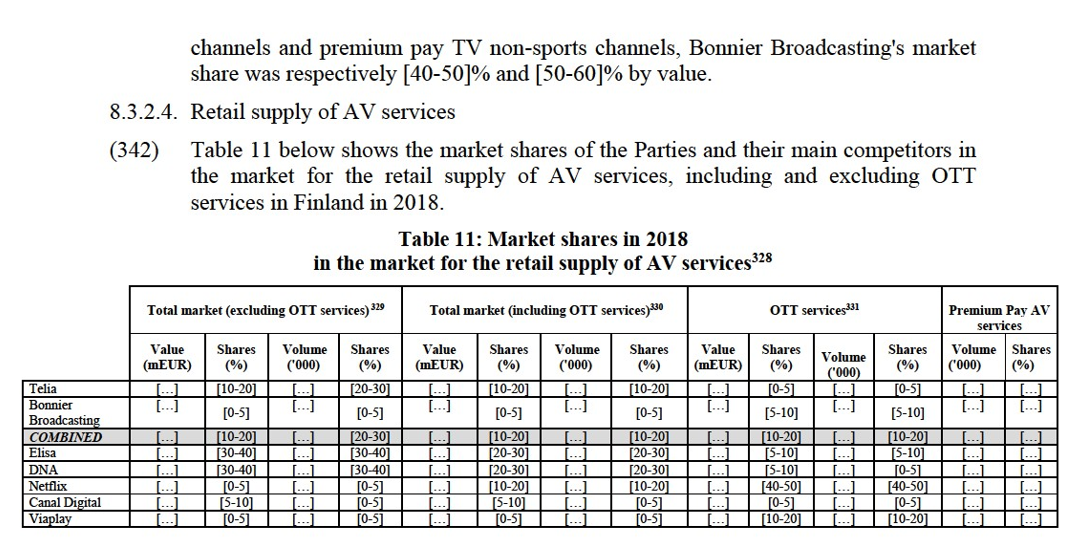

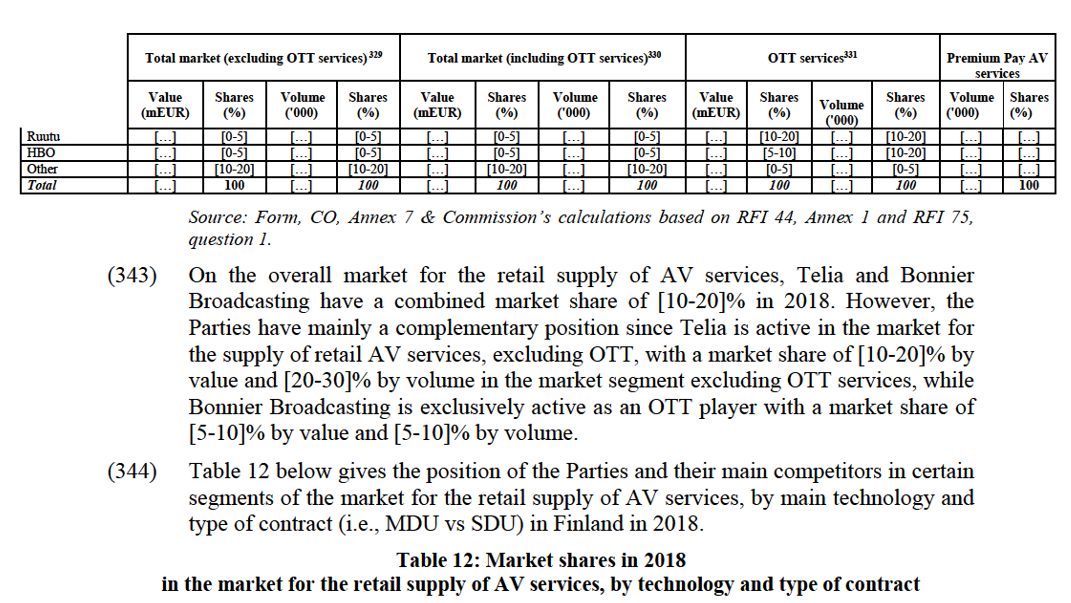

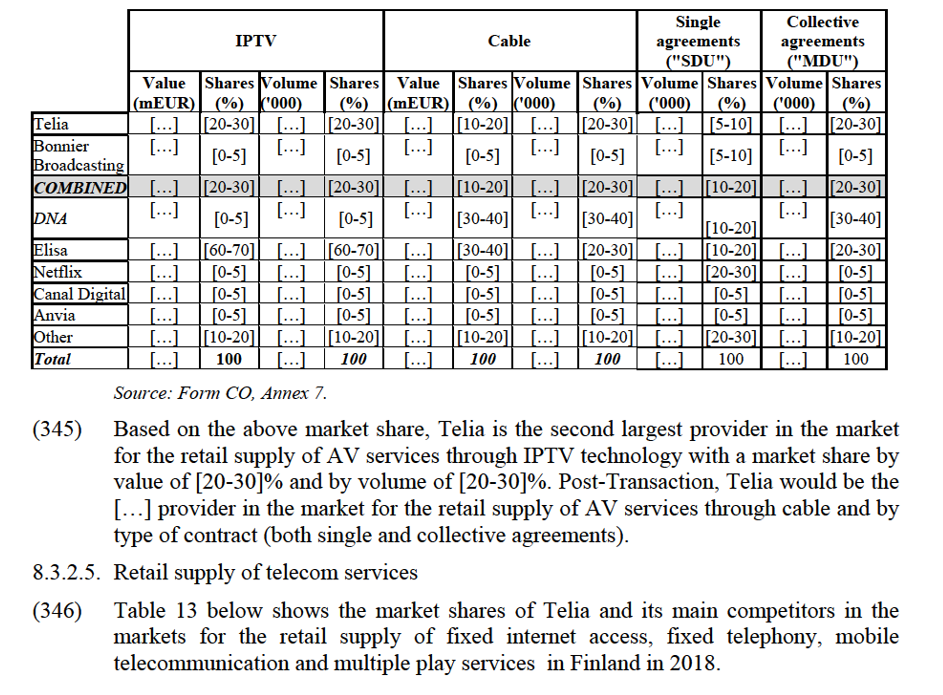

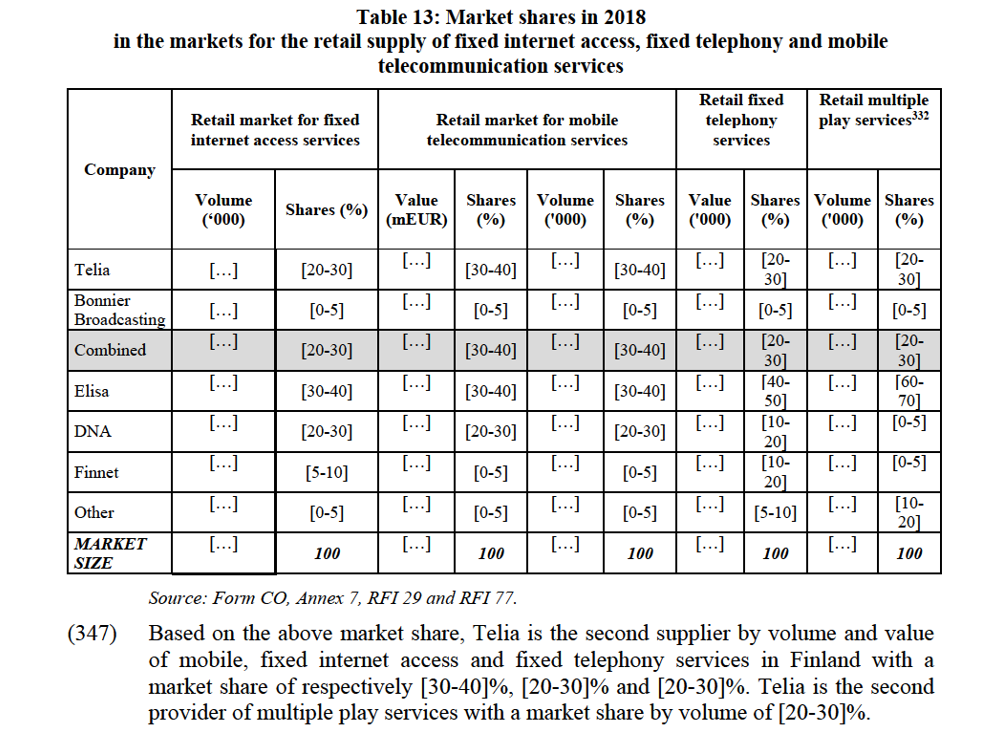

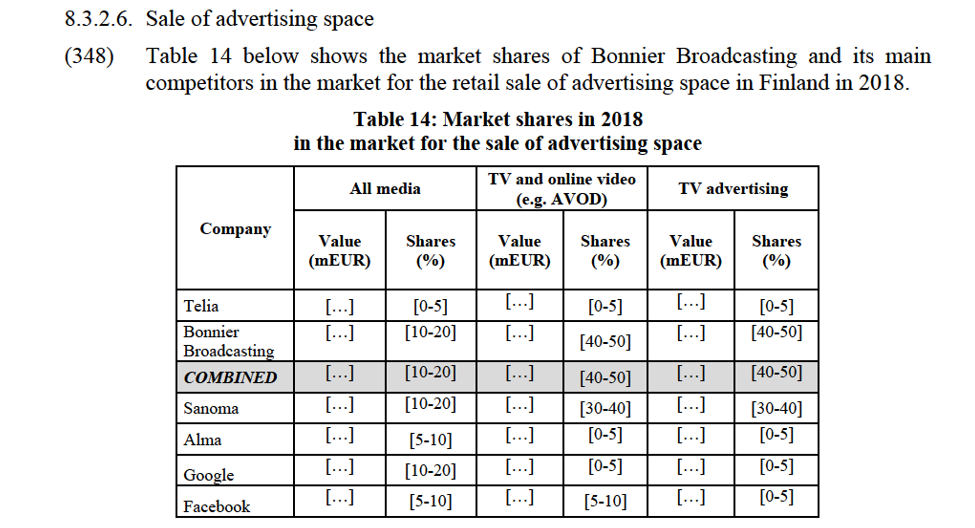

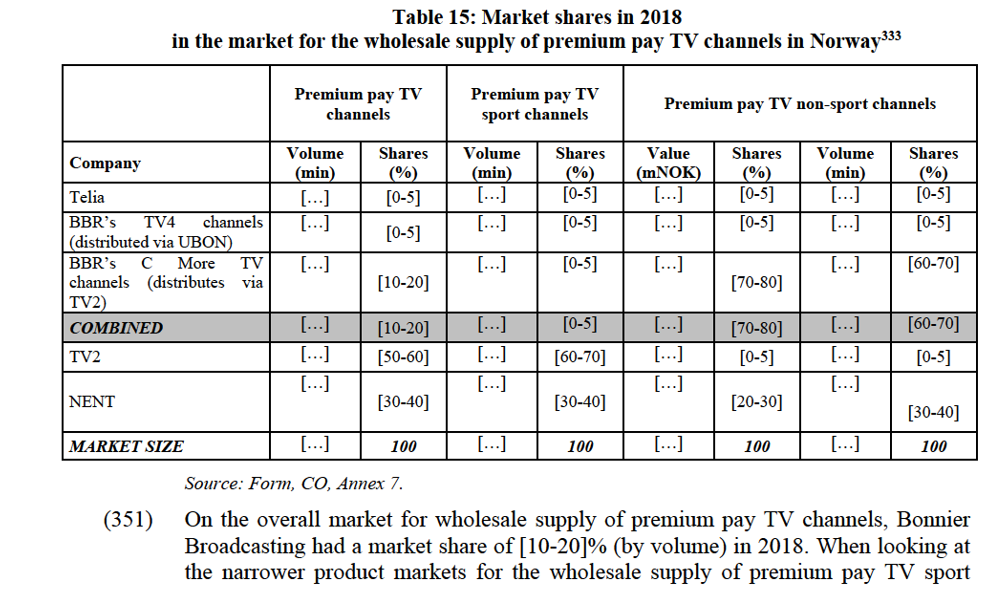

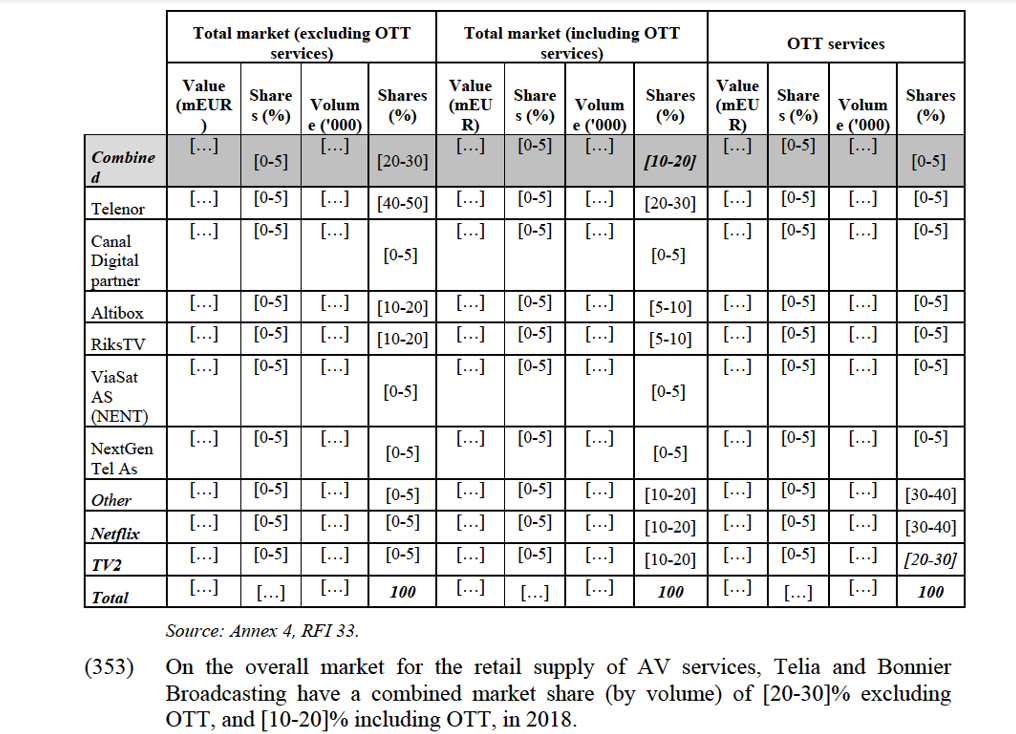

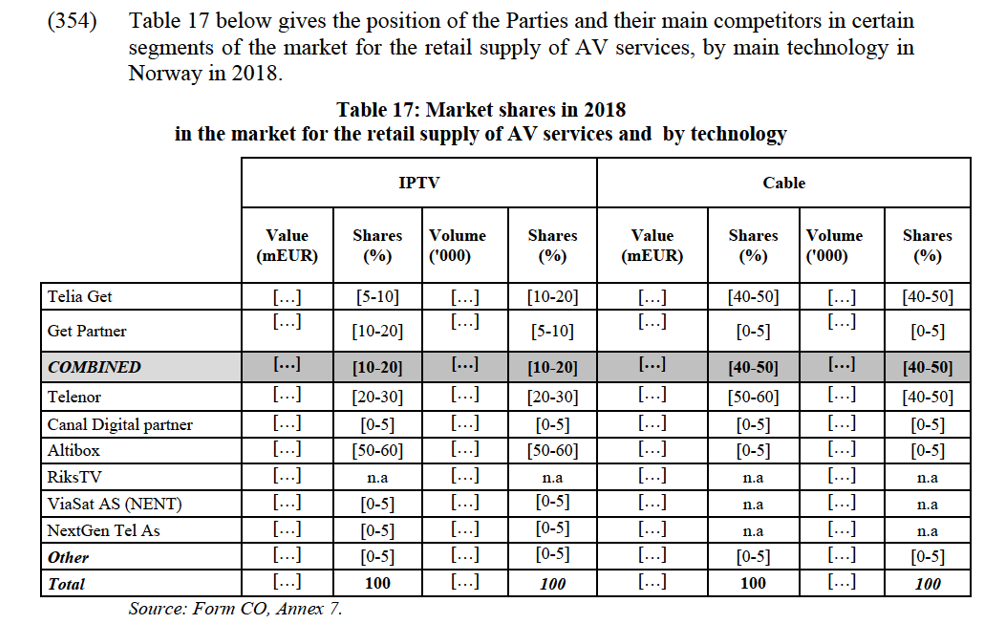

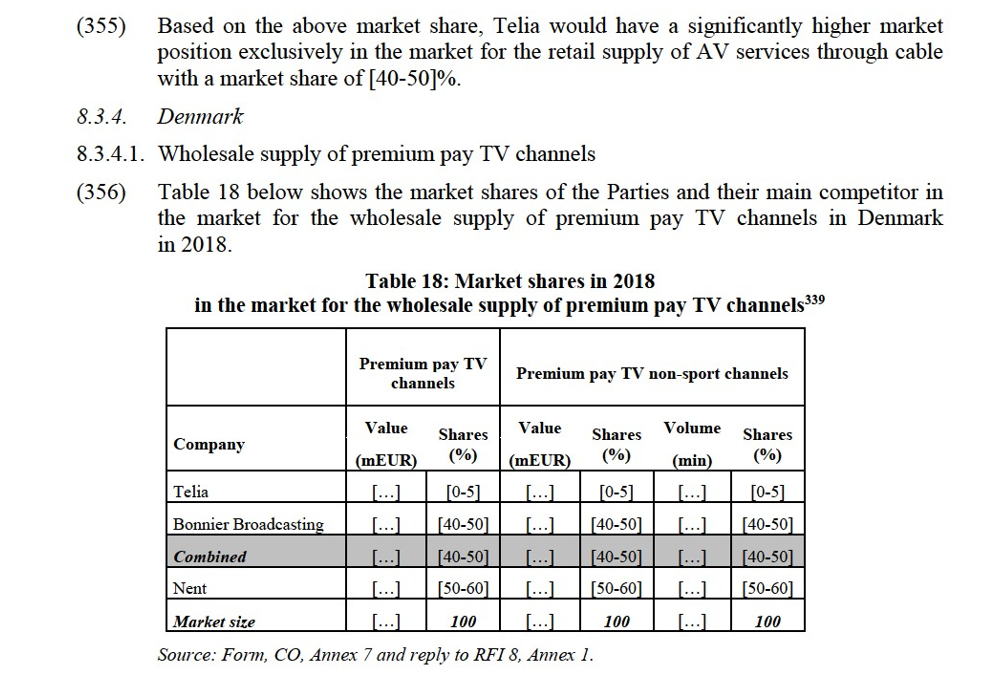

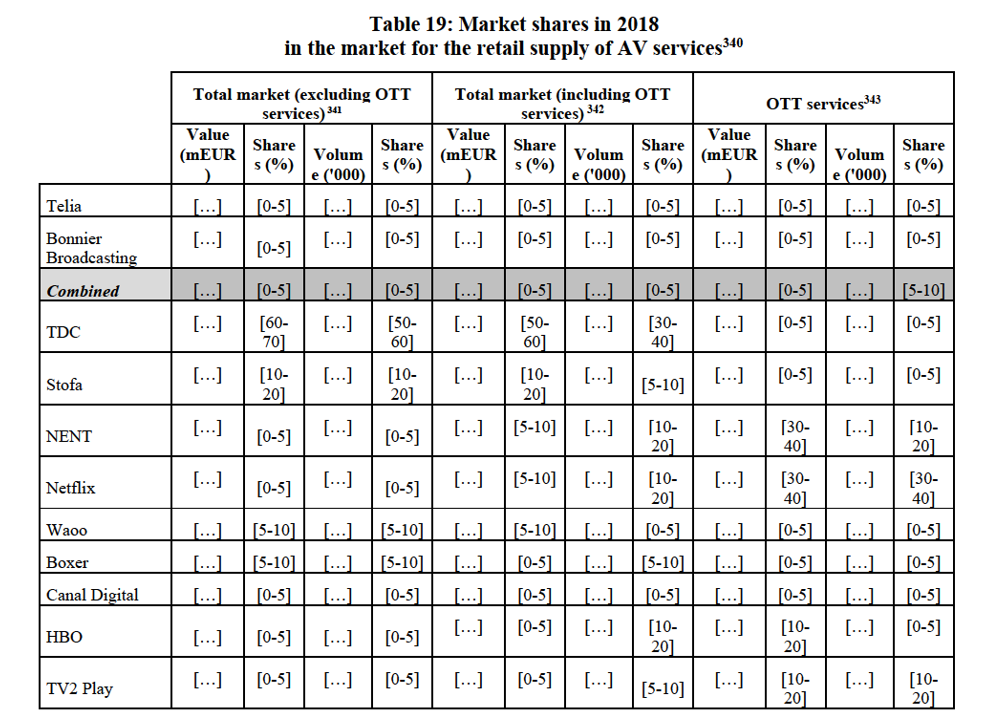

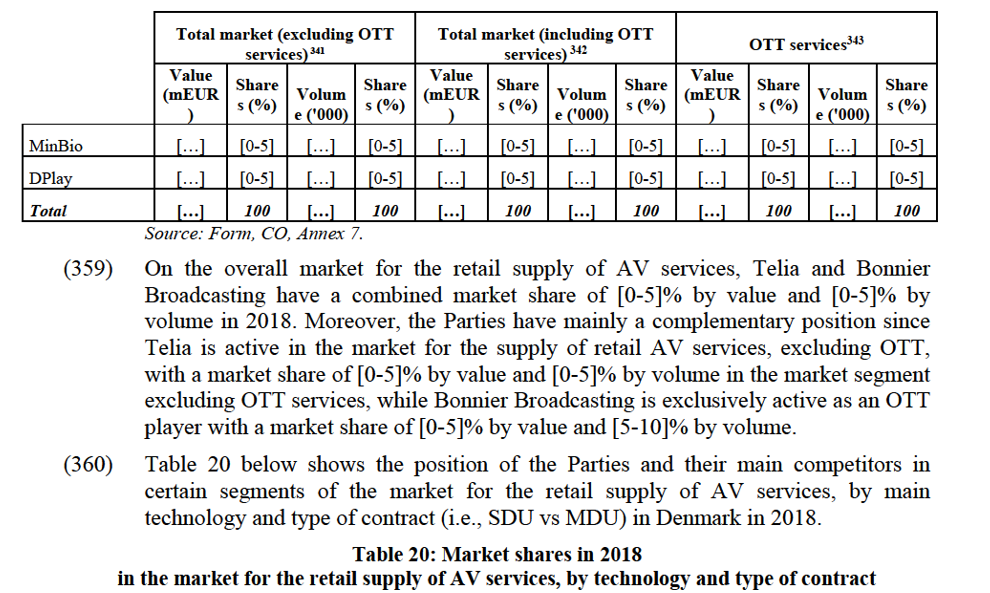

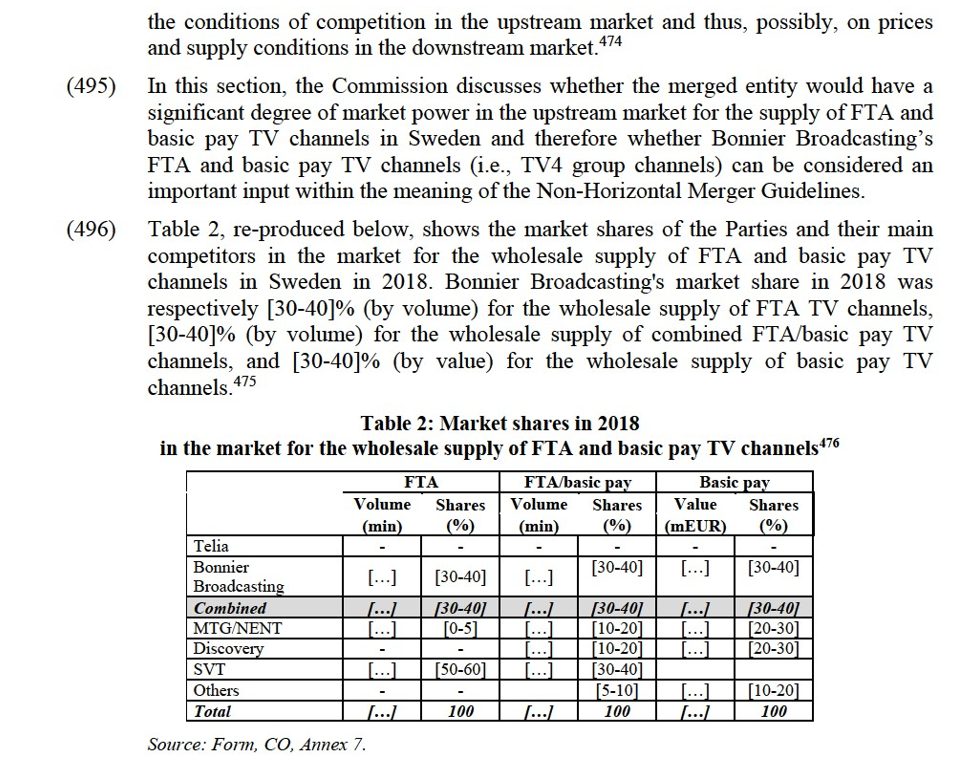

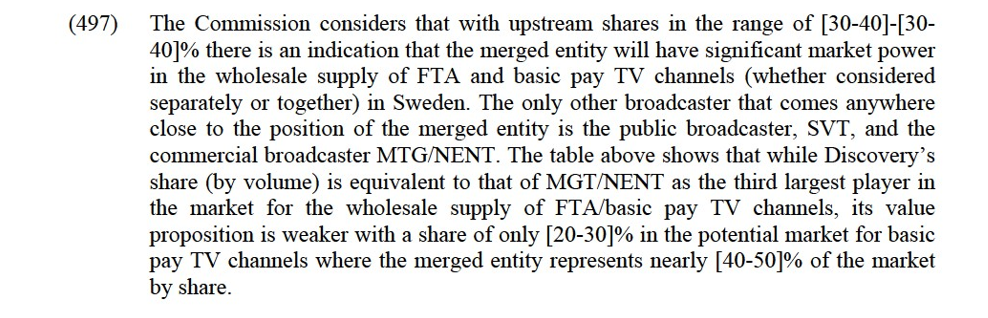

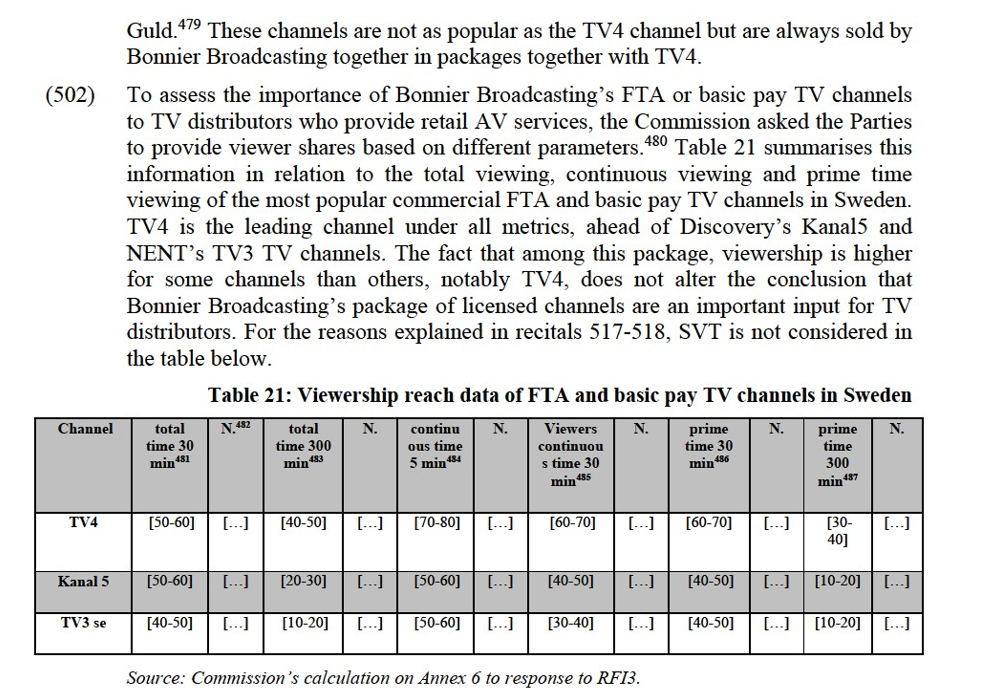

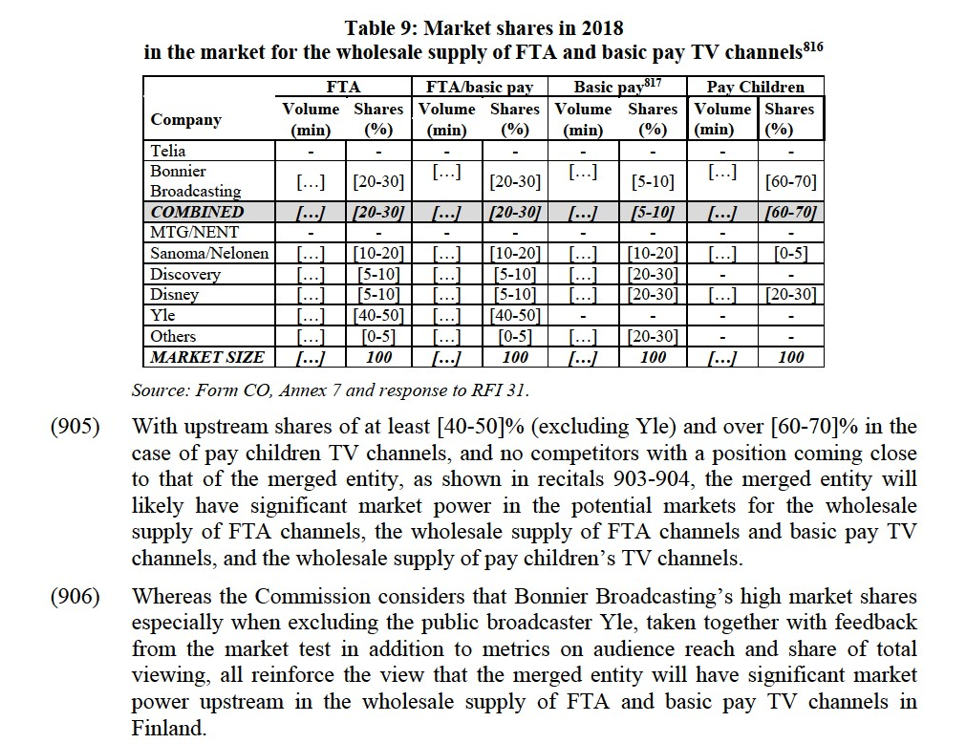

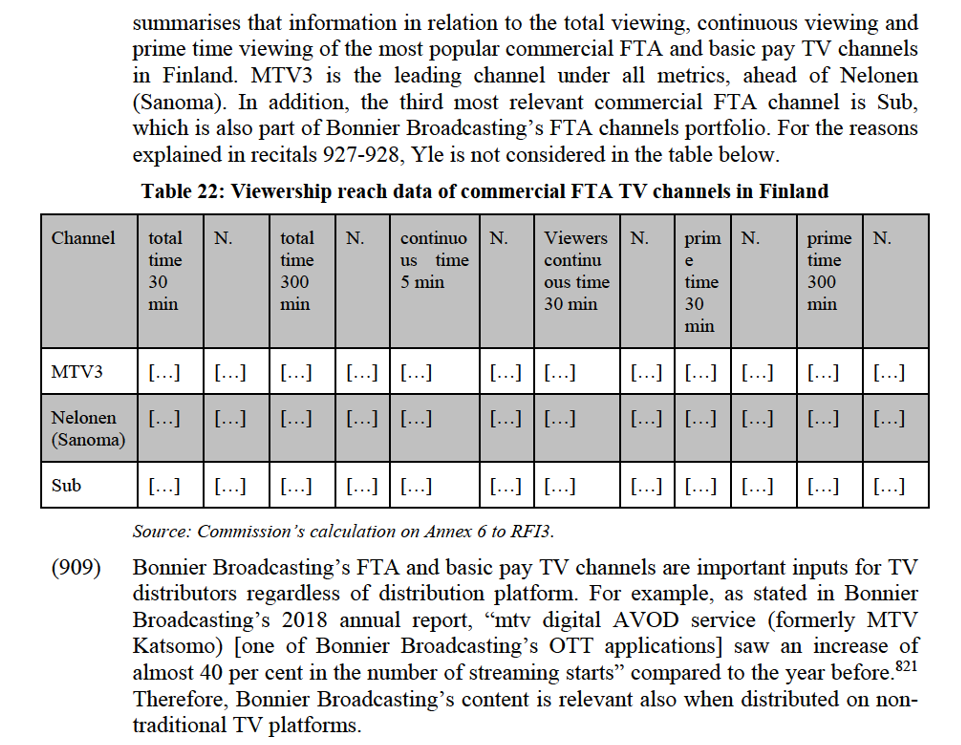

– the market for wholesale supply of FTA and basic pay TV channels, including their ancillary services. The question whether this product market can be further segmented between FTA and basic pay TV channels or by genre could be left open, as the Transaction would raise serious doubts as to its compatibility with the internal market regardless of the precise product market definition;