Commission, March 19, 2021, No M.10118

EUROPEAN COMMISSION

Decision

INVESTINDUSTRIAL / GUALA CLOSURES

Subject: Case M.10118 – Investindustrial/Guala Closures

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 17 February 2021, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Special Packaging Solutions Investments S.à.r.l. (‘SPSI’ or the ‘Notifying Party’, Luxembourg), controlled by Investindustrial S.A. (‘Investindustrial’, Luxembourg), acquires within the meaning of Article 3(1)(b) of the Merger Regulation sole control over Guala Closures S.p.A. (‘Guala’, Italy) (the ‘Transaction’).3 SPSI and Guala are referred to hereinafter as the ‘Parties’.

1. THE PARTIES

(2) SPSI is an independently managed investment subsidiary of Investindustrial. Investindustrial is active in the management of investment, holding and financial advisory companies mainly operating in the following sectors: consumer and leisure, healthcare and services and industrial manufacturing. Amongst Investindustrial’s portfolio companies, Benvic SAS (‘Benvic’) develops, produces and markets PVC-based thermoplastic solutions in the form of powders and compounds that are used across a wide range of end-applications, including the production of PVC liners for bottle closures.

(3) Guala is active in the production of bottle closures made from different materials, such as metal, aluminium, plastic and recyclable materials and for a variety of end- uses, including for spirits, wine, oil and vinegar, water and other beverages.

2. THE CONCENTRATION

(4) The Transaction is realised through a series of acquisitions of shares taking place in and outside the stock market and a public bid on Guala’s ordinary shares, which will lead to Investindustrial acquiring all outstanding Guala shares.

(5) Investindustrial is in the process of acquiring Guala’s shares with the goal of reaching just under 30% of the voting rights in Guala, the level at which Italian law requires the launch of a mandatory tender offer. Moreover, Investindustrial has entered into various agreements to purchase further shares in Guala that would bring it to hold 40.8% of the voting rights in Guala (and 45.5% of Guala’s share capital). The acquisition of these further shares would likely lead to Investindustrial having de facto control over Guala because, based on the attendance level to Guala’s recent shareholders meetings, Investindustrial would have the majority of the voting rights at such meetings. The acquisition of these additional shares has not been completed and is subject to several conditions, including clearance by the European Commission. Once Investindustrial would hold at least 30% of the voting rights in Guala,4 it will launch a public tender offer to acquire the remaining outstanding share capital in Guala.

3. UNION DIMENSION

(6) The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 5 000 million5 (Investindustrial: EUR […] million; Guala: EUR 605.5 million). Each of the undertakings concerned has an EU-wide turnover in excess of EUR 250 million (Investindustrial: EUR […] million; Guala: EUR […] million) and they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The Transaction therefore has an EU dimension.

4. RELEVANT MARKETS

(7) The Transaction does not give rise to horizontal overlaps.

(8) There is a vertical link in the EEA between the upstream activities of one of Investindustrial’s portfolio companies, Benvic, which is active in the manufacture and supply of suspension PVC (‘S-PVC’) compounds, and Guala’s downstream activities in the manufacture and supply of aluminium closures.6

4.1. Relevant product markets

4.1.1. Manufacture and supply of S-PVC compounds (upstream)

(9) Investindustrial is active in the manufacture and supply of gelled and dry blend S- PVC compounds that are used to produce PVC liners. These are obtained by blending additives (such as pigments, stabilisers or plasticisers) with S-PVC and are further processed to produce PVC end-products. In particular, S-PVC compounds are sourced by Guala as an input in the production of PVC liners, which are used to manufacture some of Guala’s aluminium closures. Guala uses PVC liners to avoid any contact between the liquid and the bottle cap, which ensures the preservation and protection of the liquid contained in the bottle and prevents oxygenation.

4.1.1.1. The Notifying Party’s view

(10) The Notifying Party submits that it is possible to identify a single market for the manufacture and supply of S-PVC compounds, without distinguishing between gelled and dry blend S-PVC compounds. However, given the very limited vertical relation between the Parties, the Notifying Party submits that it is not necessary to define the exact scope of the market for the purpose of the Transaction.7

4.1.1.2. Previous cases and Commission’s assessment

(11) In past decisions, the Commission defined a separate market for the manufacture and supply of S-PVC compounds.8 The Commission left open a possible segmentation of this market into dry blend compounds and gelled compounds.9

(12) Because the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible product market definition, it can be left open for the purpose of this case whether the market for the manufacture and supply of S-PVC compounds constitutes a single market or whether distinct markets should be identified for dry blend compounds and gelled compounds.

4.1.2. Manufacture and supply of closures (downstream)

(13) Guala is active in the manufacture and supply of closures for beverages and food. In particular, Guala produces aluminium closures for wine and other beverages that use PVC liners produced with gelled and dry blend S-PVC compounds. Guala is moreover active in the manufacture and supply of non-refillable closures that use valves or internal devices to make difficult the counterfeiting of beverages. Figure 1– Example of Guala’s roll-on aluminium closures for wine bottlesshows an example of Guala’s aluminium closures for wine bottles.

4.1.2.1. The Notifying Party’s view

(14) The Notifying Party submits that all closures belong to the same product market without the need for further segmentations based on their material (metal, aluminium, plastic, etc.), intended use (food and beverages, cosmetics and fragrances, pharma, etc.) or degree of sophistication (safety closures and regular closures).10

4.1.2.2. Previous cases and Commission’s assessment

(15) In past decisions, the Commission distinguished separate product markets depending on the closures’ (i) material; and (ii) end-use. In particular, concerning the closures’ material, the Commission previously found a separate market for metal crown closures, on the one hand, and aluminium and threaded plastic crowns, on the other hand.11 It also considered, although ultimately left open, a further segmentation of the latter market into aluminium closures, on the one hand, and plastic closures, on the other hand.12 With regard to the closures’ end-use, the Commission’s precedents also concluded that closures for beverages constitute a separate market and left open further segmentations for other end-uses.13 Some Commission precedents also considered that separate markets may exist based on a combination of the closures’ material and end-use (e.g., plastic beverage closures or aluminium beverage closures).14

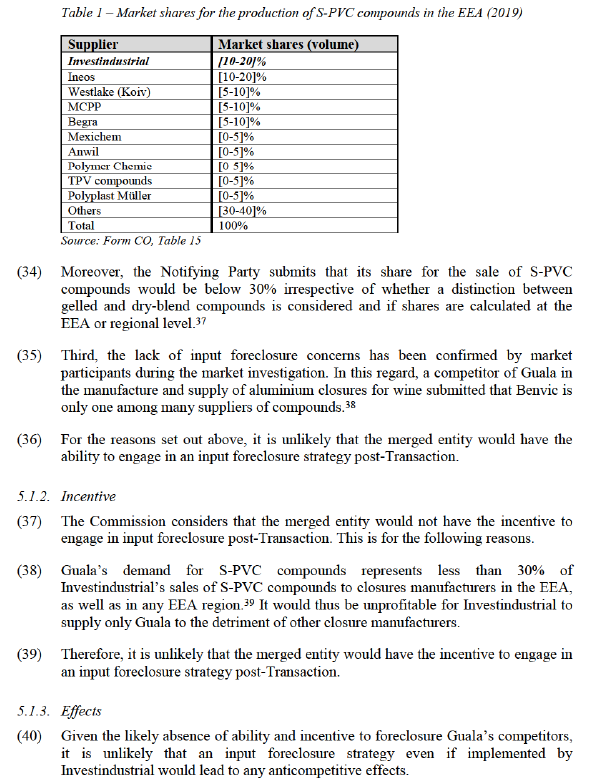

(16) In the present case, the market investigation suggests that it may be appropriate to distinguish closures made from different materials and, in particular, that aluminium and plastic closures may belong to separate markets. Several market participants have indicated that closures made of plastic, on the one hand, and aluminium, on the other, are not in direct competition with one another and that different production lines are normally used to manufacture them.15

(17) Concerning the segmentation of the closures’ market per end-use, the market investigation suggests that, as regards aluminium closures, there is a strong supply side substitutability and aluminium closures made for different end-uses are generally all manufactured on the same production lines. The main differentiating factor among aluminium closures is the measurement of the bottleneck in which the closure will be inserted. In this regard, production lines may, easily and in a short period of time, be adapted to produce closures of different height and width such as narrower and longer aluminium closures for wine bottles or wider and shorter

aluminium closures for spirits.16 This has also been confirmed by Guala, […].17 On the contrary, one manufacturer of cork closures has suggested the existence of a separate market for closures for wine bottles since, in its view, all closures for wine bottles compete for the same bottlenecks, irrespective of the material they are made of.18

(18) In any event, because the Transaction does not raise serious doubts as to its compatibility with the internal market under all plausible market definitions, it can be left open for the purpose of this case whether the market for the manufacture and supply of aluminium closures constitutes a separate market from other types of closures. It can moreover be left open whether it is appropriate to consider a segmentation of closures on the basis of their end-use.

4.2. Relevant geographic markets

4.2.1. Manufacture and supply of S-PVC compounds (upstream)

(19) The Notifying Party submits that, while there is no need to define the exact scope of the market in this case, the geographic dimension of the market is at least EEA-wide.

(20) In previous decisions, the Commission considered, although ultimately left open, whether the market is EEA-wide or regional in scope.19

(21) Nothing in the market investigation has called into question the Commission’s previous decision-making practice as regards the geographic definition of the relevant market. Because the Transaction does not raise serious doubts as to its compatibility with the internal market under all plausible market definitions, it can be left open for the purpose of this case whether the geographic scope of this market is EEA-wide or regional.

4.2.2. Manufacture and supply of closures (downstream)

(22) The Notifying Party agrees with the previous Commission decisions20 finding that the market for the production and supply of closures is at least EEA-wide if not worldwide.21

(23) This definition is supported by the market investigation, which suggests that the market for the manufacture and supply of closures is at least EEA-wide.22 This is particularly the case for aluminium closures, which are generally sold across the EEA.23

(24) Because the Transaction does not raise serious doubts as to its compatibility with the internal market under all plausible market definitions, it can be left open for the purpose of this case whether the geographic scope of this market is EEA-wide or broader.

5. COMPETITIVE ASSESSMENT

(25) The activities of Guala and those of Investindustrial do not give rise to any horizontal overlap. However, the Transaction gives rise to a vertical link in the EEA between: (i) the activities of one of Investindustrial’s portfolio companies, Benvic, which is active upstream in the manufacture and supply of gelled and dry blend S- PVC compounds; and (ii) Guala’s downstream activities in the manufacture and supply of aluminium closures. In particular, as mentioned above, Guala purchases gelled and dry blend S-PVC compounds24 and […] process them into PVC liners. The resulting PVC liners are then used by Guala in the production of some of its aluminium closures for beverages, including beers, wines and, in some cases, spirits.25

(26) Investindustrial’s shares for the manufacture and supply of S-PVC compounds are well below 30% under all plausible market definitions. Likewise Guala’s shares are below 30% for the production of aluminium closures (across all end-uses) as well as for the production of closures for specific end-uses (across all materials). Therefore, on this basis, the Transaction does not give rise to vertically affected markets.

(27) The Transaction would give rise to vertically affected markets only if the segment of aluminium closures for wine bottles is considered, because in this segment Guala would hold a share of [30-40]%26 in the EEA in 2019.27

(28) The Notifying Party submits that the vertical relationship between S-PVC compounds and aluminium closures does not raise competition problems for the following reasons: (i) Investindustrial’s S-PVC compounds are only indirectly in a vertical relationship with aluminium closures; (ii) Investindustrial’s S-PVC compounds are not an important input for the closures market, since the use of PVC in the food sector is declining, to the benefit of liners made from other materials; (iii) Guala is a very small customer of S-PVC compounds; and (iv) Investindustrial is not an important supplier of S-PVC compounds for the production of closures, which constitute a […].28

(29) According to the Non-Horizontal Merger Guidelines, foreclosure occurs when actual or potential rivals’ access to supplies or markets is hampered, thereby reducing those companies’ ability and/or incentive to compete. Such foreclosure may discourage entry or expansion of rivals or encourage their exit.29 The Non-Horizontal Merger Guidelines distinguish between two forms of foreclosure: input foreclosure occurs where the merger is likely to raise the costs of downstream rivals by restricting their access to an important input, while customer foreclosure occurs where the merger is likely to foreclose upstream rivals by restricting their access to a sufficient customer base.30

(30) Three conditions need to be met post-merger in order for concerns about potential foreclosure to arise: (i) the merged entity needs to have the ability to foreclose its rivals;31 (ii) the merged entity needs to have the incentive to foreclose its rivals;32 and (iii) the foreclosure strategy needs to have a significant detrimental effect on the parameters of competition on the downstream market (input foreclosure)33 or have an adverse impact in the downstream market and harm consumers (customer foreclosure).34 In practice, these factors are often examined together since they are closely intertwined.

5.1. Input foreclosure

5.1.1. Ability

(31) The Commission considers that the merged entity would not have the ability to engage in input foreclosure post-Transaction. This is for the following reasons.

(32) First, Investindustrial […]. Investindustrial […].35

(33) Second, as shown in Table 1 below, Investindustrial holds at the EEA-level a share of approximately [10-20]% in the production of overall S-PVC compounds and faces competition from a number of sizeable competitors (including Ineos, Westlake, MCPP, Begra, Mexichem and Anvil).36 Therefore, should Investindustrial engage in an input foreclosure strategy, a high number of potential suppliers of S-PVC compounds would remain, to which Guala’s competitors could resort.

5.2. Customer foreclosure

(41) It appears unlikely that post-Transaction the merged entity would have the ability to foreclose access to downstream markets. In this regard, Guala represents only […] of the total demand for S-PVC compounds in the EEA40 and, as such, there would be sufficient alternative customers for suppliers of S-PVC compounds to sell their products. It follows that a customer foreclosure strategy, if implemented post- Transaction, would not have an appreciable effect on Investindustrial’s competitors for the supply of S-PVC compounds. This appears all the more true considering that pre-Transaction Guala was already purchasing […]% of its demand for S-PVC compounds from Investindustrial.41

(42) As a consequence, the Commission considers that the merged entity is unlikely to engage in a customer foreclosure strategy post-Transaction.

5.3. Conclusion on vertical effects

(43) For the reasons set out above and in light of the results of the market investigation and of all the evidence available, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market as regards the vertical relationship between the upstream manufacture and supply of S-PVC compounds and the downstream manufacture and supply of closures.

6. CONCLUSION

(44) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the ‘Merger Regulation’). With effect from 1 December 2009, the Treaty on the Functioning of the European Union (‘TFEU’) has introduced certain changes, such as the replacement of ‘Community’ by ‘Union’ and ‘common market’ by ‘internal market’. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the ‘EEA Agreement’).

3 Publication in the Official Journal of the European Union No C 65, 25.2.2021, p. 14–15.

4 Currently, Investindustrial holds approximately […]% of Guala’s voting rights.

5 Turnover calculated in accordance with Article 5 of the Merger Regulation and the Commission Consolidated Jurisdictional Notice (OJ C 95, 16.4.2008, p. 1).

6 Investindustrial is also marginally active in the manufacture and supply of thermo plastic elastomers (‘TPE’) compounds which are an input used in certain closures. Guala uses […] TPE compounds in the production of […] closures. In 2020, Guala’s purchases of TPE for use in the EEA amounted to […]. Moreover, Investindustrial has only recently become active in the production of TPE and estimates its share to be below [0-5]% at EEA, regional and national level. Therefore, the potential vertical relationship between TPE and […] closures will not be further discussed in this decision. Investindustrial and Guala are also active in two markets that are to some extent related. Namely, Investindustrial, through its subsidiary Della Toffola, is active in the manufacture of capping machines used to fix closures onto beverage bottles. Della Toffola has de minimis sales of capping machines in the EEA (EUR […] million) and holds an estimated share well below [0-5]% at the EEA level under all plausible market definitions. Therefore, the potential relationship between capping machines and closures will not be further discussed in this decision.

7 Form CO, para. 106.

8 See Cases M.4734 - Ineos/Kerling, para. 41; M.6218 - Ineos/Tessenderlo Group S-PVC Assets, para. 73; M.7132 - Ineos/Doeflex, para. 10; and M.7572 - Og Capital/Kem- One Innovative Vinyls, para. 15.

9 See Cases M.4734 - Ineos/Kerling, paras. 40-41; M.6218 - Ineos/Tessenderlo Group S-PVC Assets, para. 73; M.7132 - Ineos/Doeflex, paras. 10-15; and M.7572 - Og Capital/Kem- One Innovative Vinyls, paras. 15-17.

10 Form CO, paras. 111 and 113.

11 See Cases M.2843 - Amcor/Schmalbachlubeca, para. 24, M.6665 - Sun Capital/Rexam Personal and Home Care Packaging Business, paras. 21-23, M.603, Crown Cork & Seal/CarnaudMetalbox, paras. 32-36.

12 See Cases M.2843 - Amcor/Schmalbachlubeca, para. 24, M.6665 - Sun Capital/Rexam Personal and Home Care Packaging Business, paras. 21-23, M.603, Crown Cork & Seal/CarnaudMetalbox, paras. 32-36.

13 See Case M.603, Crown Cork & Seal/CarnaudMetalbox, paras. 32-36; M.6665 - Sun Capital/Rexam Personal and Home Care Packaging Business, paras. 23-24.

14 See Case M.603, Crown Cork & Seal/CarnaudMetalbox, paras. 34-36.

15 See minutes of the calls with global competitors of Guala of 25 February 2021 (para. 4) and 4 March 2021 (para. 7).

16 See minutes of the calls with global competitors of Guala of 24 February 2021 (para. 7) and 4 March 2021 (para. 9).

17 See response to RFI 2 to Guala, question 2.

18 See minutes of the call with a global competitor of Guala of 24 February 2021 (para. 6).

19 See Cases M.4734 - Ineos/Kerling, para. 153; M.6218 - Ineos/Tessenderlo Group S-PVC Assets, paras. 23-26; M.7132 - Ineos/Doeflex, paras. 16-21; M.7572 - Og Capital/Kem One Innovative Vinyls, paras. 18-22.

20 See Cases M.2843 - Amcor/Schmalbachlubeca, paras. 31-32, M.6665 - Sun Capital/Rexam Personal and Home Care Packaging Business, para. 47, M.603, Crown Cork & Seal/CarnaudMetalbox, para. 50.

21 Form CO, para. 115.

22 See minutes of the calls with global competitors of Guala of 24 February 2021 (para. 9) and 4 March 2021 (para. 10).

23 See minutes of the calls with global competitors of Guala of 25 February 2021 (para. 7) and 4 March 2021 (para. 10).

24 Guala […] purchases gelled S-PVC compounds. The Parties however were not in a position to provide estimated shares for the market of gelled S-PVC compounds.

25 Response to RFI 2 to Guala, question 2.

26 Guala would hold a share of [30-40]% in an EEA market including the UK.

27 Form CO, Table 22 and response to RFI 2 to SPSI, Table 3.2.

28 Form CO, paras. 169 to 172.

29 Guidelines on the assessment of non-horizontal mergers under the Council Regulation on the control of concentrations between undertakings (‘Non-Horizontal Merger Guidelines’), OJ C 265/6, 18.10.2008, para. 29.

30 Non-Horizontal Merger Guidelines, para. 30.

31 Non-Horizontal Merger Guidelines, paras. 33 to 39 and 60 to 67.

32 Non-Horizontal Merger Guidelines, paras. 40 to 46 and 68 to 71.

33 Non-Horizontal Merger Guidelines, paras. 47 to 57.

34 Non-Horizontal Merger Guidelines, paras. 72 to 77.

35 Form CO, para. 97.

36 Form CO, Table 15.

37 Response to RF1, Table No. RF1-1 and Form CO, para 147 and Response to RFI2 to SPSI, question 2.

38 Non-confidential email from an EEA competitor of Guala of 3 March 2021.

39 Form CO, paras, 101 and 102.

40 Form CO, Table 24 and response to RFI 2 to SPSI, question 3.

41 Response to RFI 1 to Guala, question 1.