Commission, April 30, 2021, No M.10173

EUROPEAN COMMISSION

Decision

LUMINUS / ESSENT BELGIUM

Subject: Case M.10173 – Luminus/Essent Belgium

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 23 March 2021, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Luminus S.A. (‘Luminus’, Belgium) acquires within the meaning of Article 3(1)(b) of the Merger Regulation sole control of the whole of Essent Belgium NV (‘Essent Belgium’, Belgium)3. (Luminus and Essent Belgium are designated hereinafter as the ‘parties’ to the proposed transaction.)

1. THE PARTIES

(2) Luminus is controlled by EDF S.A. (‘EDF’, France). It is active in Belgium in the markets for generation and supply of electricity, gas trading on hubs, supply of gas to dealers as well as the retail supply of electricity and gas to large industrial and commercial (‘I&C’) customers, small I&C customers and household customers. Luminus also provides various energy-related services in Belgium for both household and I&C customers, including heating, ventilation, and air conditioning solutions, photovoltaic panels, e-mobility solutions, and energy performance contracts.

(3) Essent Belgium is active in the retail supply of electricity and gas to small I&C customers and household customers and in the supply, installation and maintenance of photovoltaic panels in Belgium.

2. THE TRANSACTION

(4) The proposed transaction consists of the acquisition by Luminus of 100% of the shares of Essent Belgium. Upon completion of the Transaction, Luminus will exercise sole control over Essent Belgium.

3. UNION DIMENSION

(5) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million [EDF: EUR 71,317 million; Essent Belgium: EUR 497 million]4. Each of them has a Union-wide turnover in excess of EUR 250 million [EDF: EUR […]; Essent Belgium: EUR […])], and they do not achieve more than two-thirds of their aggregate Union-wide turnover within one and the same Member State. The Transaction therefore has a Union dimension within the meaning of Article 1(2) of the Merger Regulation.

4. COMPETITIVE ASSESSMENT

(6) The Parties’ activities overlap horizontally as regards the retail supply of electricity and high-calorific gas (‘H-gas’) and low-calorific gas (‘L-gas’) to small I&C customers and household customers in Belgium. There are also horizontal overlaps in the supply, installation and maintenance of photovoltaic panels, trading of Guarantee of Origin certificates (‘GoOs’)5 and, marginally, in other activities in Belgium,6 none of which gives rise to an affected market under any plausible product or geographic market definition.

(7) The Transaction also gives rise to the following vertical links: (i) between the generation and supply of electricity in Belgium (upstream) where Luminus is present, and the retail supply of electricity to small I&C customers and household customers (downstream) in Belgium where both Luminus and Essent Belgium are present; and (ii) between gas trading on hubs and the supply of H-gas and L-gas to dealers in Belgium (upstream) where Luminus is present, and the retail supply of H- gas and L-gas to small I&C customers and household customers (downstream) in Belgium, where both Luminus and Essent Belgium are present. These overlaps do not give rise to any vertically affected market under any plausible product and geographic market definition.

(8) The present Decision will therefore focus on the impact of the proposed transaction on the retail supply of electricity, H-gas and L-gas to small I&C customers and to household customers in Belgium.

4.1. Markets for the retail supply of electricity to small I&C and household customers

4.1.1. Relevant markets

4.1.1.1. Product market definition

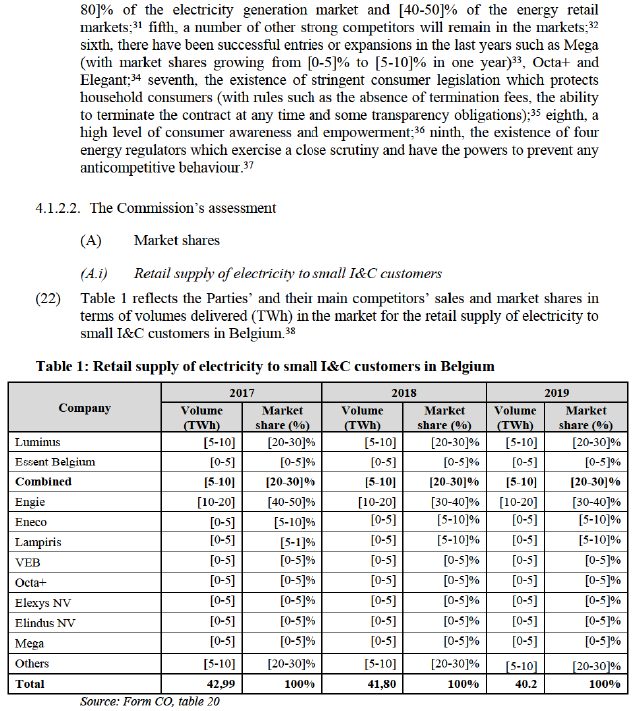

(A) Distinction by type of customers

(9) In the past the Commission distinguished, within the retail supply of electricity in Belgium, three separate product markets for the supply of electricity to: (i) large I&C customers connected to the transmission network (at above 70 kilovolts (kV)); (ii) small I&C customers connected to the distribution networks (below 70 kV); and (iii) household customers.7 These definitions, which are not contested by the Parties and have been confirmed by the market investigation8, are to be retained for the purposes of this Decision. The Parties’ activities only overlap with respect to the latter two.

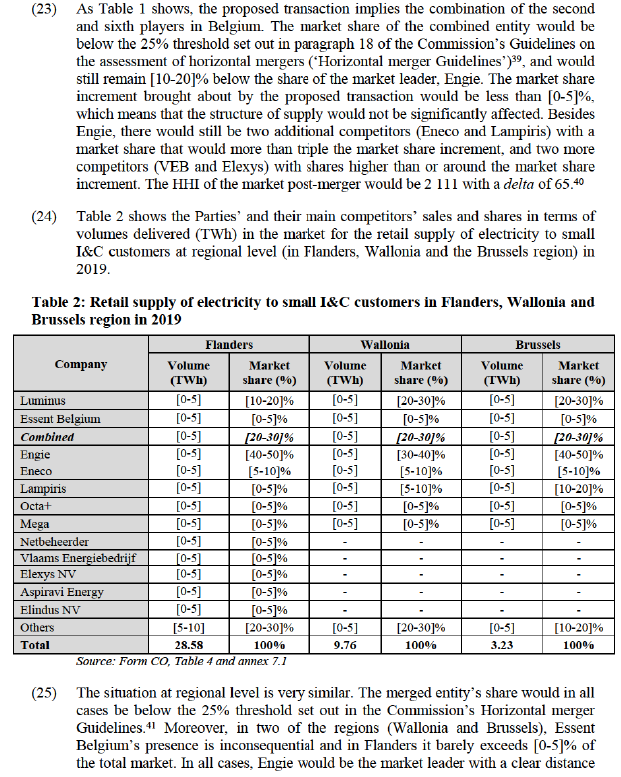

(B) Retail supply of “green” electricity

(10) The Commission considered whether a separate product market for the retail supply of electricity energy generated from renewable sources (‘green electricity’) to small I&C and household customers should be defined.9

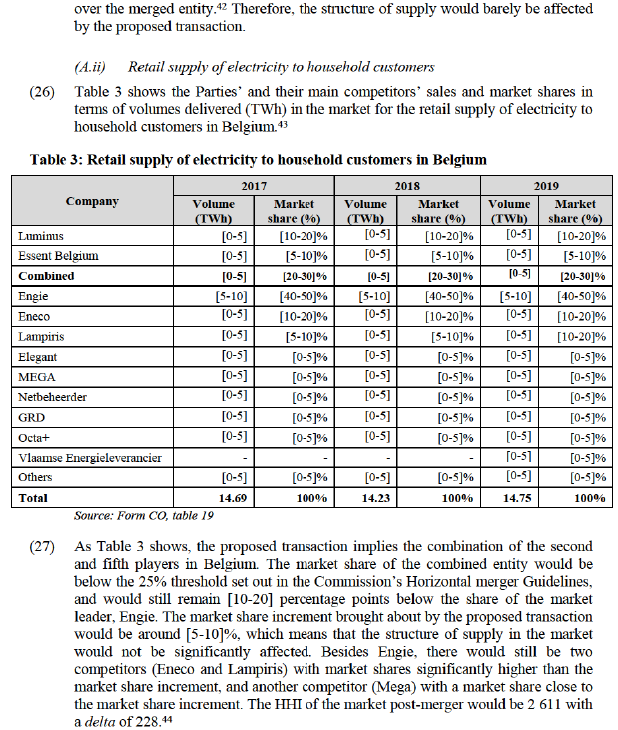

(11) The Parties considered that there are no separate markets for the supply of green electricity for several reasons.10 First, green energy is supplied under very similar tariffs to non-green energy. In addition, the Parties stress that price remains the main selection criterion of consumers and that ultimately whether energy is green or not only has a minor influence on customers’ choice. Moreover, GoOs and green gas certificates systems are designed in such a way that all suppliers can offer green energy. Furthermore, the parties underline that launching a “green tariff” is straightforward and only requires slight tweaks in the procurement strategy. Lastly, the parties emphasise that all suppliers currently offer “green energy products”.

(12) The Commission agrees that, at the present stage, narrower markets for the retail supply of green electricity are not warranted in Belgium, for the following reasons.

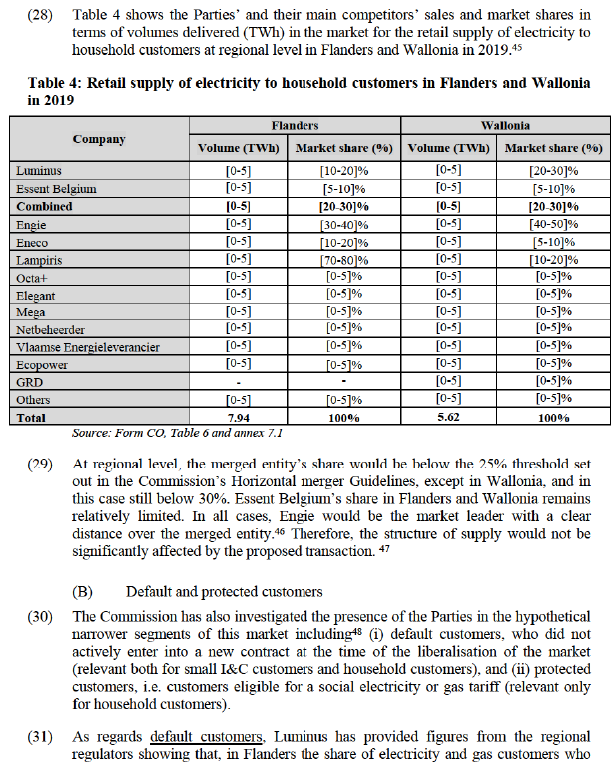

(13) The Belgian federal energy regulator, the Commission for Electricity and Gas Regulation (‘CREG’), told the Commission that it considers green energy to be an element of competition rather than a separate market and that it has not seen a particular increase in the number of green electricity contracts being offered.11

(14) From the demand side, six of the 12 small I&C customers responding to the Commission’s market investigation12 replied that green electricity should be considered a separate segment of the market, with five of those respondents stating that they are ready to pay a higher price for green electricity.13 However, most of the competitors and customers who responded to the questionnaires confirmed that price is the most important factor by which customers select their electricity supplier, and only two of the customers ranked the type of electricity (green) amongst the two most important factors and none of the competitors did so.14

(15) From the supply-side, all competitors responding to the market investigation indicated that the supply of green energy should not be considered a separate segment of the retail market, with two competitors commenting that “[g]reen energy is likely to be another element of competition rather than a separate market” and “[g]reen electricity is an additional product attribute a supplier can offer to its customers, but doesn’t justify to be a separate segment per se”.15 All respondents to the market investigation have indicated that they already supply at least some green electricity.16 This can be done either by producing green electricity themselves or by purchasing GoOs. GoOs allow for the traceability of the electricity that is purchased by a supplier on the wholesale market and offer the guarantee that a quantity of electricity equivalent to the certificate has been produced using a renewable energy source.17 The prices of such certificates are reflected on the invoice sent to the customer but only represent a limited proportion of the final price of electricity. In Belgium, in 2020, the increase was of 0.70 EUR/MWh. By way of illustration, the average yearly electricity consumption of an average household is 3.5 MWh.18 Its impact in the final price is thus insignificant. This means, on the one hand, that customers that opt for “green electricity” contracts do not necessarily need to pay a significantly higher price than customers that choose non-green contracts, and second, that suppliers can start offering green electricity or expanding their current offer without the need to adjust any production or distribution assets, make additional investments (other than the cost of purchasing of GoOs) or incur in any time delays.

(16) Therefore, even if for some customers green and “non-green” electricity were not completely substitutable, the effects of supply-side substitutability could be seen as equivalent to those of demand substitution in terms of effectiveness and immediacy, since suppliers are able to switch to the relevant products and market them in the short term.19

(C) Default customers and protected customers

(17) In the past the Commission has considered that in Germany basic or default supply tariffs, i.e. those applicable to disengaged customers who remain with their historical incumbent, are not materially constrained by competitive tariffs and, as a result, the two types of contracts constitute two separate relevant product markets.20 For this reason, the Commission has considered whether within the retail supply market to household customers in Belgium a separate market should be considered for the supply to default customers, i.e. passive customers who did not change supplier since the liberalisation of the market.21

(18) In the case of Belgium a market segmentation for the supply to default customers may not be warranted as in Belgium such customers are supplied under regular tariffs and these contracts are not specifically regulated,22 which means there is no indication of any substantial price difference between the prices and other conditions applied to default and non-default customers. Moreover, the majority of respondents to the market investigation did not support such a sub-segmentation.23 In any event, the question whether a separate market exists for the supply of electricity to default customers can be left open as the proposed transaction does not raise serious doubts as to its compatibility with the internal market under any plausible product market definition.

(19) The Commission has also considered whether narrower product markets should be considered including only the supply of electricity to protected household customers eligible for a social tariff, which applies to around 15% of the household customers in Belgium.24 The Parties contend that a market segmentation for supply to protected customers is not warranted because there is no active competition between energy suppliers for protected customers, who pay the same social tariff irrespective of the supplier they have.25 A small majority of respondents to the market investigation supported such a sub-segmentation.26 In any event, the question whether a separate market exists for the supply of electricity to protected customers can be left open as the proposed transaction does not raise serious doubts as to its compatibility with the internal market under any plausible product market definitions.

4.1.1.2. Geographic market definition

(20) In the past the Commission considered that the geographic scope of the electricity retail supply markets in Belgium was not wider than national but left open whether these markets should be considered national or regional (Flanders, Wallonia and Brussels region) in scope.27 The Parties contend that the retail markets are national in scope. A slight majority of the responses to the market investigation suggested that the market is national. In any case, the question whether the electricity retail supply markets in Belgium should be considered national or regional in scope can be left open as the proposed transaction does not raise serious doubts as to its compatibility with the internal market under any plausible geographic market definition.

4.1.2. Horizontal non coordinated effects

4.1.2.1. The Notifying Party’s views

(21) The Notifying Party submits that the proposed Transaction will not give rise to concerns in the markets for the retail supply of electricity and gas28 to small I&C and household customers for the following reasons: first, the combined entity’s market shares will be limited; second, the share increment will be low;29 third, the energy markets in Belgium are very competitive with switching rates among the highest in Europe;30 fourth, markets are dominated by the incumbent Engie, with almost [70-

had not yet actively signed up with a supplier and were therefore still supplied by the default supplier was already equal to 0%. In Wallonia, the number of “passive customers”, i.e. those who did not chose a supplier at the time of the liberalisation, in 2019 amounted to a 7% for household electricity customers and 6% for non- household customers, 4% for household gas customers, and 5% for non-household gas customers. In Brussels, the share of these customers at the end of 2019 was 10% for all electricity customers (both household and non-household) and 9% for all gas customers.49 In all cases, the figures provided show that the number and percentage of these default customers have been decreasing intensely in the last decade.50 In any case, according the Parties’ best estimates, their combined share among these customers would be below [5-10]% at national level and in the Wallonia/Brussels regions combined, both for household and for small I&C customers.

(32) As regards protected customers, Luminus explains that once a customer qualifies for the social tariff, the customer is automatically transferred to the more favourable social tariff price level while remaining with the same supplier.51 Therefore, protected customers are automatically assigned to their current supplier and, as social tariffs are fixed and determined by public authorities, suppliers cannot compete with more attractive prices for these customers. For these reasons, Luminus submits that shares among protected customers generally reflect the market shares for the supply of electricity and gas to household customers and therefore estimates that the Parties’ shares at national level would be approximately [20-30]% (for Luminus) and [5-10]% (for Essent Belgium) both for gas and electricity.

(C) Other elements

(33) On the supply-side, in addition to the moderate market share levels of the Parties, the Commission notes that there are more than eight other market players that supply electricity to small I&C and household customers and there seem to be no apparent obstacles for these suppliers to expand their sales in the market as a response to a price increase by the Parties’ post-merger. The market investigation has indeed confirmed this. In fact, a majority of respondents to the market investigation have indicated (i) that the Parties do not have any competitive advantage vis-à-vis other entities which already offer electricity retail supply services in Belgium,52 and (ii) that following the proposed transaction electricity prices would remain essentially unaltered since sufficient competition would remain post-merger.53 Moreover, the responses to the market investigation do not support that the Parties could be considered particularly close competitors.54

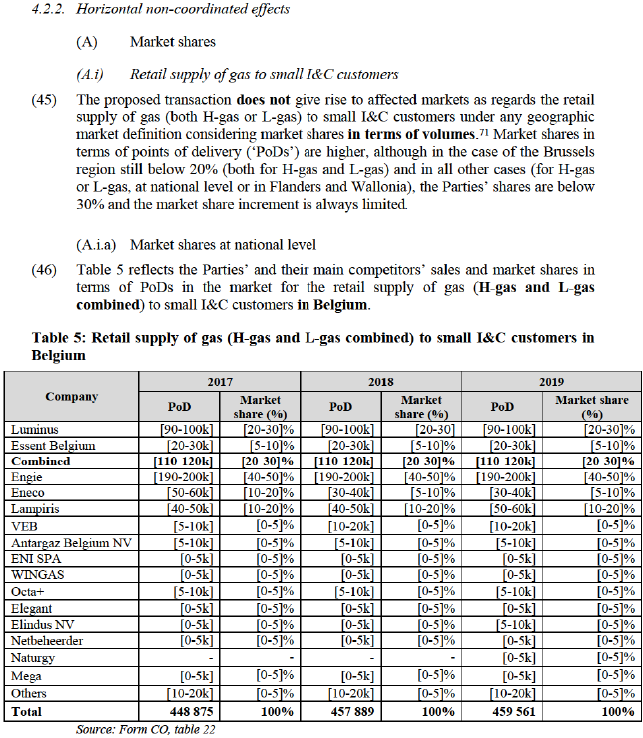

(34) Some competitors voiced some concerns in relation to the vertical integration of the combined entity and to the alleged duopolistic structure of the market55 (which are addressed in Section 4.3below) although one of them at the same time admitted that commodity prices in the market are currently low,56 and one referred generically to the size of the merged entity as a possible competitive advantage. However, of those competitors, only one indicated that the proposed transaction could have a negative impact of the retail supply markets of electricity, whereas one said – like the majority of competitors – that it would have no impact on the market and the third one was of the view that the proposed transaction would have a positive impact in the market. Moreover, all competitors (i.e. also those which expressed some concerns) considered that (i) were the merged entity to increase prices, there would be alternative suppliers for customers to turn to, and that (ii) the proposed transaction will have no impact on prices in the market. Besides the impact on prices, none of the Parties’ competitors identified any other possible effects that the proposed transaction could have in the market.

(35) From the demand side, most small I&C customers responding to the market investigation explained that they organise tenders for their electricity contracts, for which they receive at least three offers.57 And – like competitors – most of them were of the view that if the merged entity were to increase prices, there would be alternative suppliers, in addition to Engie, to turn to.58 Some I&C customers even indicated that they receive offers to switch suppliers several times per month, and others replied that the market is open and competitive and that there are enough alternative suppliers.59 Finally, most I&C customers declared to have switched electricity supplier in the last five years and all customers considered it relatively easy or very easy to switch supplier,60 which would be consistent with the high switching rate in the Belgian market.61

(D) Conclusion

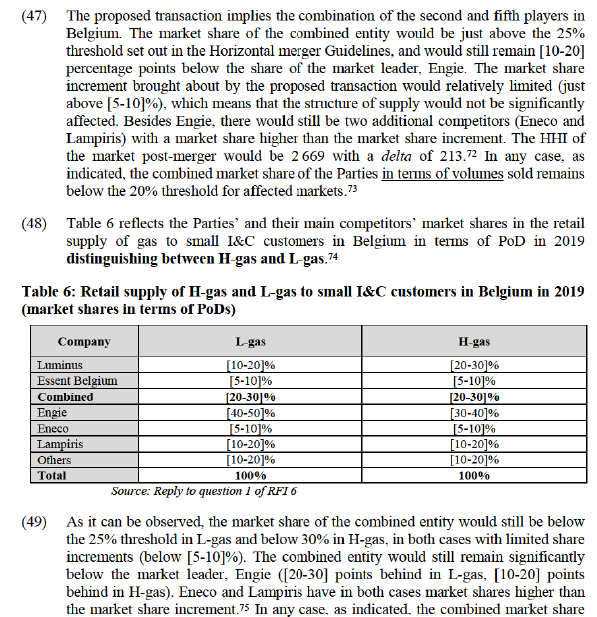

(36) In view of the (i) moderate market shares that the combined entity would have post- merger; (ii) the very limited market share increase brought about by the proposed transaction; (iii) the distance behind the market leader (Engie); (iv) the existence of other competitors with market shares higher or equivalent than the market share increase; (v) the majority opinion by market respondents that the Parties have no particular competitive advantages, that there are sufficient alternatives (other than Engie) in the market, that it is very easy to switch suppliers, and that the proposed transaction will have no impact on prices or on other aspects of competition, the Commission takes the view that the proposed transaction does not raise serious doubts as to its compatibility with the internal market as regards the markets for the retail supply of electricity to small I&C customers and to household customers in Belgium.

4.2. Markets for the retail supply of H-gas and L-gas to small I&C and household customers

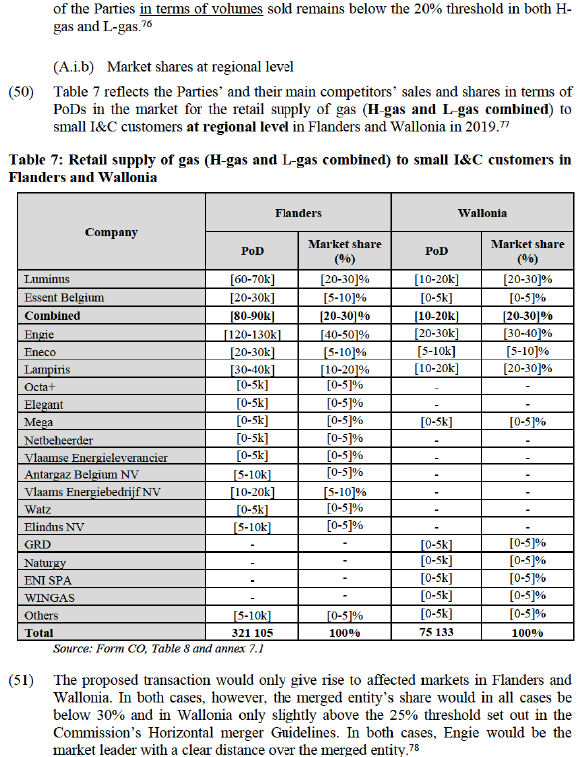

4.2.1. Relevant markets

4.2.1.1. Product market definition

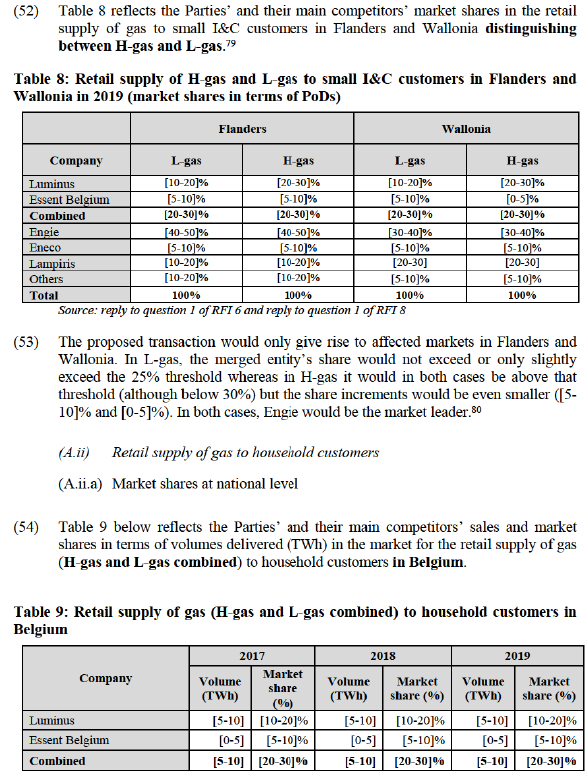

(A) Distinction by type of customers

(37) In the past the Commission distinguished three separate product markets in Belgium for the retail supply of gas to: (i) large I&C customers; (ii) small I&C customers; and (iii) household customers.62 Those definitions, which are not contested by the Parties63 and have been confirmed by the market investigation64, are to be retained for the purposes of this Decision. The Parties’ activities only overlap with respect to the latter two.

(B) Distinction by type of gas

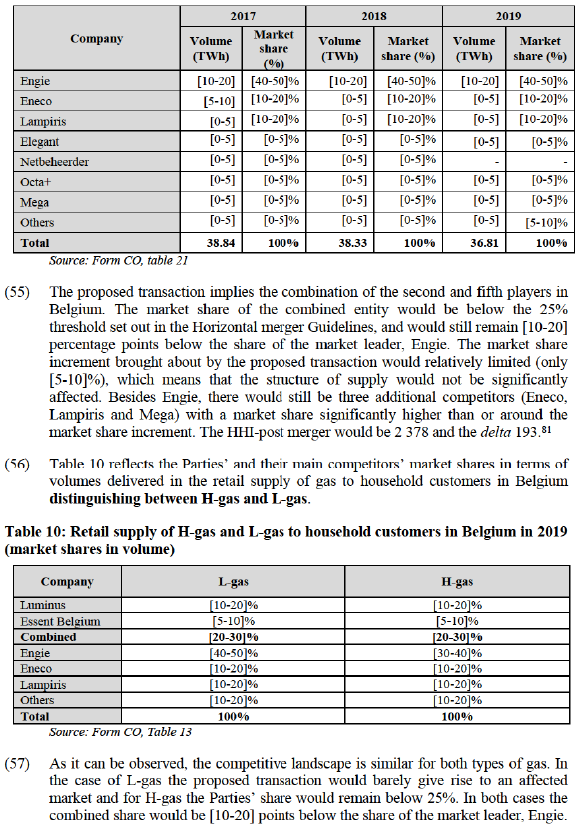

(38) Within each of these markets, the Commission has distinguished in the past separate product markets for the supply of H-gas and for the supply of L-gas.65

(39) The Parties consider that distinction is no longer warranted given that customers must use the type of gas of the network to which they are connected, there are no significant price differences, and it easy for all suppliers to procure both types of gas.66

(40) The responses to the market investigation were mixed, with a slight majority of competitors responding that the supply of L-gas and H-gas should not be considered as being separate markets.67 Nearly half of the small I&C customers who responded did not know which type of gas they are supplied.68

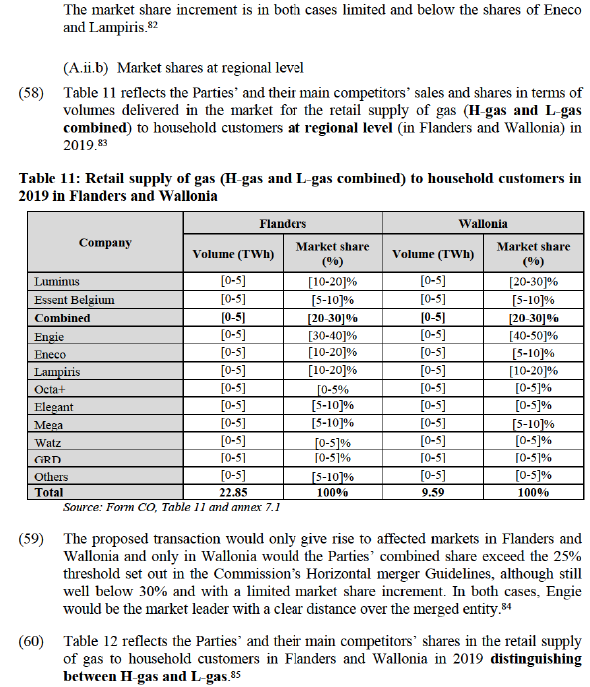

(41) In any event, the question whether separate markets exists for the retail supply of H- gas and L-gas can be left open as the proposed transaction does not raise serious doubts as to its compatibility with the internal market under any plausible product market definitions.

(C) Default customers and protected customers

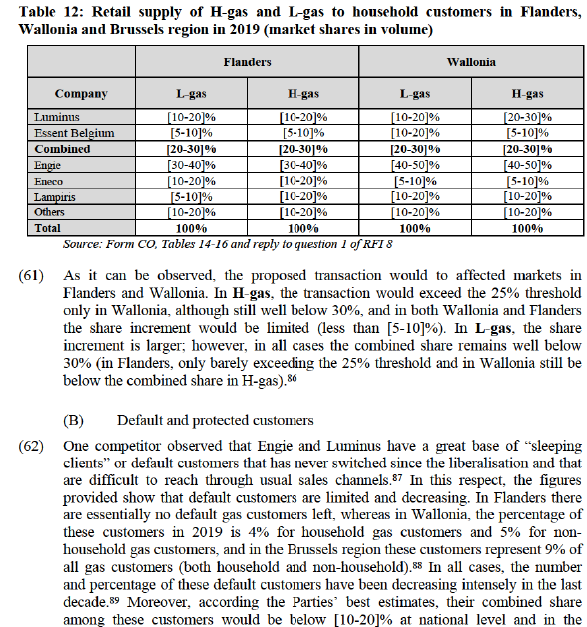

(42) As done for electricity in Section 4.1.1.1(C), the Commission considered whether within the market for the retail supply of gas to household customers in Belgium separate product markets should be considered for the supply to (i) default customers, i.e. customers who did not change supplier since the liberalisation of the market, and (ii) protected household customers eligible for a social tariff. The analysis for gas is the same as presented above for electricity. Therefore the question whether separate markets exist for the retail supply of gas to default and protected customers can be left open as the proposed transaction does not raise serious doubts as to its compatibility with the internal market under any plausible product market definitions.

4.2.1.2. Geographic market definition

(43) The Commission has previously held that the markets for the retail supply of gas in Belgium to I&C customers are national in scope, but for the retail supply to household customers it left open whether it should be considered national or regional (Flanders, Wallonia, Brussels region) in scope.69 The Parties consider that the markets for the retail supply of gas in Belgium should be defined as national for all customers. The responses to the market investigation were mixed and inconclusive.70

(44) In any case, the question whether the gas retail supply markets in Belgium should be considered national or regional (Flanders, Wallonia, Brussels region) in scope can be left open as the proposed transaction does not raise serious doubts as to its compatibility with the internal market under any plausible geographic market definition.

Wallonia/Brussels regions combined, both for household and for small I&C customers.

(63) As regards protected customers, the Commission refers to the assessment in Section 4.1.1.1(C). The Parties’ shares at national level for the retail supply of gas to protected customers would be in line with those for the general market, i.e. approximately [20-30]% (for Luminus) and [5-10]% (for Essent Belgium).

(C) Other elements

(64) On the supply-side, in addition to the moderate market share levels of the Parties, the Commission notes that there are at least eight other market players that supply gas to small I&C and household customers and there seem to be no apparent obstacles for these suppliers to expand their sales in the market as a response to a price increase by the Parties’ post-merger. The market investigation has indeed confirmed this. In fact, as in the case of electricity markets, a majority of respondents to the market investigation have indicated (i) that the Parties do not have any competitive advantage vis-à-vis other entities which already offer H-gas or L-gas retail supply services in Belgium,90 and (ii) that following the proposed transaction H-gas and L- gas prices would remain essentially unaltered since sufficient competition would remain post-merger.91 Moreover, the responses to the market investigation do not support that the Parties could be considered particularly close competitors, neither in H-gas nor in L-gas.92 Finally, a majority of competitors considered that they could increase significantly the amount of H-gas or L-gas that they currently supply to retail customers.93

(65) One competitor voiced some concerns in relation to the alleged duopolistic structure of the market94 (which are addressed in Section 4.3 below) although at the same time admitting that commodity prices in the market are currently low,95 and another referred generically to the size of the merged entity as a possible advantage. However, both of them also indicated that prices in the gas market would not increase in the short or medium term as a result of the proposed transaction In fact, all competitors considered that (i) were the merged entity to increase prices, there would be alternative suppliers for customers to turn to, and that (ii) the proposed transaction will have no impact on prices in the market. None of the Parties’ competitors identified any other possible effects that the proposed transaction could have in the market.

(66) From the demand side, most small I&C customers responding to the market investigation explained that they organise tenders for their gas contracts, for which they receive at least three offers.96 And – like competitors – most of them were of the view that if the merged entity were to increase prices, there would be alternative suppliers, in addition to Engie, to turn to.97

(D) Conclusion

(67) In view of the (i) moderate market shares that the combined entity would have post- merger (in the case of market shares in terms of volume in the supply to small I&C even insufficient to give rise to affected markets); (ii) the limited market share increase brought about by the proposed transaction; (iii) the distance behind the market leader (Engie); (iv) the existence of other competitors with market shares higher or equivalent than the market share increase; (v) the majority opinion by market respondents that the Parties have no particular competitive advantages in H- gas or L-gas, that there are sufficient alternatives (other than Engie) in the market, that there is scope for competitors to expand their sales of H-gas or L-gas to retail customers, and that the proposed transaction will have no impact on prices or on other aspects of competition, the Commission takes the view that the proposed transaction does not raise serious doubts as to its compatibility with the internal market as regards the markets for the retail supply of H-gas and L-gas to small I&C customers and to household customers in Belgium.

4.3. Vertical and coordinated effects

(68) One competitor raised concerns that, due to the combined market share of Luminus and Engie post-merger in the electricity generation and retail markets, the market could evolve towards a “duopoly of vertically integrated companies” that may enable coordinated effects leading to less competition and possibly higher prices in the long term.98 Another competitor mentioned that suppliers with electricity generation capacity have in general a significant advantage99 although it also considered that the proposed transaction would not have a negative impact on the market or would lead to higher prices.100

(69) As regards the Parties’ vertical integration, the Commission observes, first, that the proposed transaction does not lead to any vertically affected markets. Second, since Essent Belgium is not present in the electricity generation market, the proposed transaction does not “create” a vertical integration (Luminus’ vertical integration is not merger-specific) but simply adds some market share to the downstream market. Third, Luminus has provided data showing […],101.

(70) In relation to any possible coordinated effects, the Commission notes, first, that the asymmetry between Engie and Luminous remains significant after the proposed transaction ([30-40]% vs [20-30]% in supply to small I&C and [40-50]% vs [20- 30]% for household customers).102 Second, as explained in Section 4.1.2.2(A), the structure of supply will remain essentially unaffected by the proposed transaction given the very limited share of Essent Belgium in retail supply to household customers (barely above [5-10]%) and its negligible presence in the supply to I&C customers (not present in the supply to large customers and [0-5]% share to small customers). In fact, the delta HHI of the proposed transaction in the retail supply of electricity to small I&C customers in Belgium would only be 65 in electricity and 50 in gas (H-gas and L-gas combined).103 Therefore, the proposed transaction does not seem to change in a significant way any incentives of Luminus and Engie to engage in any coordination. Third, there is consensus in the market that the proposed transaction will not give rise to an increase in prices.104 Fourth, the same competitor that raised concerns about the duopolistic structure of the market admits that commodity prices are currently low.105

(71) In view of the above, the Commission considers that the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market as a result of any vertical or coordinated effects.

5. CONCLUSION

(72) For the above reasons, the Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the ’Merger Regulation’). With effect from 1 December 2009, the Treaty on the Functioning of the European Union (‘TFEU’) has introduced certain changes, such as the replacement of ‘Community’ by ‘Union’ and ‘common market’ by ‘internal market’. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the ‘EEA Agreement’).

3 Publication in the Official Journal of the European Union No C 113, 31.3.2021, p. 14.

4 Turnover calculated in accordance with Article 5 of the Merger Regulation.

5 See footnote 101 of the form CO.

6 Namely, the supply and installation of smart home services, the maintenance of gas boilers for household customers, and the supply of electric vehicle charging stations in Belgium.

7 In relation to Belgium, see Cases COMP/M.9587 Engie / EDP Renovaveis / EDPR Offshore Espana (25/02/2020), paragraphs 21-24, 27-28; COMP/M.8855 Otary / Eneco / Electrabel / JV (05/07/2018), paras. 26-28; COMP/M.5549 EDF/Segebel (12/11/2009), paragraphs 131-133, 138; COMP/M.4180 Gaz de France/Suez (14/11/2006), paragraphs. 689-695, 738-743.

8 See replies to question 3-5 of Questionnaire Q1 – Questionnaire to Customers in the retail supply of gas and electricity and to question 3-5 of Questionnaire Q2 – Questionnaire to Competitors in the retail supply of gas and electricity.

9 See Decision 21-DCC-18 of the French competition authority (29 January 2021) concerning Dijon Métropole, Storengy and Rougeot, paragraphs 66–73, where ultimately the question of whether there should be a new retail segmentation for the supply of green electricity in France was left open. (https://www.autoritedelaconcurrence fr/fr/decision-de-controle-des-concentrations/relative-la-prise-de- controle-conjoint-de-la-societe-dijon).

10 Paragraph 156 of the form CO.

11 See paragraph 6 of the Minutes of the call between DG COMP and CREG of 24 February 2021.

12 In relation to customers of the Parties, for its market investigation the Commission engaged with some of their small I&C customers but not with any household customers as it was impractical to do so. It seems reasonable to suppose that the comments of small I&C customers would reflect similar views of household customers. In any case, the Commission did engage with competitors active in the supply to household customers and, in addition, it also engaged with CREG and the views of the regulator cover, among other things, the household markets.

13 See replies to questions 6 and 7 of Questionnaire Q1 – Questionnaire to Customers in the retail supply of gas and electricity.

14 See replies to question 19 of Questionnaire Q1 – Questionnaire to Customers in the retail supply of gas and electricity and replies to question 29 of Questionnaire Q2 – Questionnaire to Competitors in the retail supply of gas and electricity.

15 See replies to question 9 of Questionnaire Q2 – Questionnaire to Competitors in the retail supply of gas and electricity.

16 See replies to question 7 of Questionnaire Q2 – Questionnaire to Competitors in the retail supply of gas and electricity.

17 In practice, the GoO system guarantees that, at the EU level, for every MWh of green electricity that is sold, one MWh of green electricity has effectively been produced. The Parties are present in the market for the trading of GoOs but this does not constitute an affected market for the purposes of this Decision (see recital (6)).

18 See paragraph 150 of the form CO.

19 See Commission Notice on the definition of relevant market for the purposes of Community competition law (97/C 372/03), paragraph 20-21.

20 See Case COMP/M.8870 E.ON / Innogy (17/09/2019), paragraphs 47-62.

21 The gas and electricity retail supply markets in Belgium were fully liberalised in Flanders on 1 July 2003, and in Brussels and Wallonia for business customers on 1 July 2004 and fully on 1 January 2007. Customers who had not actively entered into a new contract were assigned to the supplier selected (after a public tender) as default supplier for the corresponding distribution system operator (‘DSO’). No such customers still exist in Flanders. In 2019, such customers represented 4-7% of gas and electricity customers in Wallonia and 9-10% of customers in Brussels (paragraphs 218-223 of the form CO).

22 See paragraphs 218-223 of the form CO.

23 See replies to question 14 of Questionnaire Q2 – Questionnaire to Competitors in the retail supply of gas and electricity.

24 Customers in Belgium may be eligible for a regulated social electricity and gas tariff if they meet some specific conditions. The social tariff levels are determined by CREG. The social tariff levels, which are determined quarterly, are lower than the price level of all other supply contracts because they are based on the lowest price that is offered, at that moment, by suppliers.

25 Paragraphs 227 and 228 of the form CO.

26 See replies to question 15 of Questionnaire Q2 – Questionnaire to Competitors in the retail supply of gas and electricity.

27 Cases COMP/M.9587 Engie / EDP Renovaveis / EDPR Offshore Espana (2020), paragraph 28; COMP/M.8855 Otary / Eneco / Electrabel / JV (2018), paragraph 31; COMP/M.5549 EDF / Segebel (2009), paragraph 137; COMP/M.4180 Gaz de France / Suez (2006), paragraphs 739, 740, 742.

28 The Parties’ provide the same arguments in relation to the electricity and gas markets.

29 Paragraph 368 et seq. of the form CO.

30 Footnote 297 of the form CO.

31 Paragraph 393 of the form CO.

32 Paragraph 386 of the form CO.

33 Paragraph 407 of the form CO.

34 Paragraph 409 of the form CO.

35 Paragraph 415 of the form CO.

36 Paragraph 417 et seq. of the form CO.

37 Paragraph 427 et seq. of the form CO.

38 Luminus has also provided market shares in terms of points of delivery ("PODs', i.e. access points to the transmission or distribution network), which do not change substantially the competitive picture with respect to the shares in volumes.

39 Guidelines on the assessment of horizontal mergers under the Council Regulation on the control of concentrations between undertakings, OJ C 31, 05.02.2004, p. 5.

40 Calculated excluding the category "others", which amounts to [10-20]% of the market.

41 In terms of PODs, the retail supply of electricity to small I&C customers in the Brussels region would not even be an affected market, since the combined market share would only be [10-20]%.

42 Engie had in 2019 a [40-50]% share in Flanders,[30-40]% in Wallonia and [40-50]% in Brussels.

43 Market shares in terms of PODs are very similar to those in terms of volumes.

44 Calculated excluding the category "others", which amounts to (0-5]% of the market.

45 In the Brussels region the market shares would be below 20%.

46 Engie had in 2019 a (30-40]% share in Flanders, (40-50]% in Wallonia and (60-70]% in Brussels.

47 In Flanders, the HHI of the market post-merger would be 2 300 with a delta of 237. In Wallonia, 2 930 and 294, respectively.

48 The markets excluding these customers would not have a significantly different competitive analysis either because of the relatively small number of such customers and/or because of their similarities to other customers.

49 See paragraphs 221 et seq. of the form CO. Luminus additionally notes that, according to the Walloon regional regulator, active and passive household customers have been charged tariffs that are on average significantly equivalent.

50 In Wallonia, the number of passive customers has decreased from more than 700,000 in 2007 (right after the liberalisation) to slightly above 100,000 in 2019 for household customers, and from around 90,000 to 13,000 for non-households. In Brussels, passive customers have decreased from 85% of the total number of customers in 2007 to 10% in 2019 for all customers. The figures provided show that the decrease has continued, albeit at a less pronounced pace, also in the more recent years. See Luminus’ reply to question 2 of RFI 5 of 9 April 2021.

51 Paragraphs 227 et seq. of the form CO. In 2021 there were an estimated 1.4 million customers benefitting from social tariffs in Belgium (870,000 PODs for electricity and 529,000 for gas).

52 See replies to question 33 of Questionnaire Q1 – Questionnaire to Customers in the retail supply of gas and electricity and replies to question 22 of Questionnaire Q2 – Questionnaire to Competitors in the retail supply of gas and electricity.

53 See replies to question 25 of Questionnaire Q1 – Questionnaire to Customers in the retail supply of gas and electricity.

54 All customers and competitors consider Engie as Luminus’ closest competitor. Competitors consider Essent to be Luminus’ fourth competitor (Lampiris and Eneco being second and third). By contrast, customers place Essent as the second closest at the same level as Eneco. Competitors and customers consider that Engie, Luminus and Eneco to be similarly close competitors to Essent. See replies to question 20 and 21 of Questionnaire Q1 – Questionnaire to Customers in the retail supply of gas and electricity and replies to question 30 and 31 of Questionnaire Q2 – Questionnaire to Competitors in the retail supply of gas and electricity.

55 See replies to question 33 of Questionnaire Q2 – Questionnaire to Competitors in the retail supply of gas and electricity.

56 See replies to question 42 of Questionnaire Q2 – Questionnaire to Competitors in the retail supply of gas and electricity.

57 See replies to question 24 and 24.1 of Questionnaire Q1 – Questionnaire to Customers in the retail supply of gas and electricity.

58 See replies to question 25 of Questionnaire Q1 – Questionnaire to Customers in the retail supply of gas and electricity.

59 See replies to question 25.1 of Questionnaire Q1 – Questionnaire to Customers in the retail supply of gas and electricity.

60 See replies to question 33 and 34 of Questionnaire Q1 – Questionnaire to Customers in the retail supply of gas and electricity.

61 See recital (21).

62 Case COMP/M.4180 Gaz de France / Suez (2006), paragraphs 78-81.

63 The criteria used to delineate the border between large and small I&C customers is either (i) whether the customer is connected to the transmission or distribution networks or (ii) a threshold of annual consumption (which the Parties suggest should be 10 GWh). In this decision, the analysis is based on the distinction between connection to the transmission or to the distribution network, but in any case the information provided shows that using the consumption threshold would not have any impact on the assessment (paragraphs 204-210 of the form CO).

64 See replies to questions 8-10 of Questionnaire Q1 – Questionnaire to Customers in the retail supply of gas and electricity and replies to question 16-18 of Questionnaire Q2 – Questionnaire to Competitors in the retail supply of gas and electricity.

65 For cases relating to Belgium, see COMP/M.4180 Gaz de France/Suez (2006) and COMP/M.5467 RWE/Essent (2009).

66 See paragraphs 172-186 of the form CO. The Notifying Party further mentions that with Dutch L-gas fields rapidly depleting, and in the absence of appropriate alternative sources for L-gas imports in Belgium, the Belgian government is preparing to transition from L-gas to H-gas entirely by 2029.

67 See replies to question 21 of Questionnaire Q2 – Questionnaire to Competitors in the retail supply of gas and electricity.

68 See replies to question 11 of Questionnaire Q1 – Questionnaire to Customers in the retail supply of gas and electricity.

69 Cases COMP/M.5549 EDF / Segebel (2009), paragraph 184; COMP/M.4180 Gaz de France / Suez (2006), paragraph 105.

70 See replies to questions 16-18 of Questionnaire Q1 – Questionnaire to Customers in the retail supply of gas and electricity and replies to questions 26-28 of Questionnaire Q2 – Questionnaire to Competitors in the retail supply of gas and electricity.

71 The Parties combined market share in 2019 based on volumes for L-gas and H-gas combined would be [10-20]% (10-20]% Luminus: [0-5]% Essent Belgium) at national level, [10-20]% in Flanders ([10-20% and (0-5]%), [10-20]% in Wallonia ([10-20]% and (0-5]%), and [10-20]% in Brussels ([10-20]% and (05]%). For L-gas: [10-20]% at national level, in Flanders and in Brussels region, and (5-10]% in Wallonia. For H-gas: (10-20]% at national level and in Flanders, (10-20]% in Wallonia and (0-5]% in Brussels region (see tables 13-16 in the form CO).

72 Calculated excluding the category "others", which amounts to less than [0-5]% of the market. These figures are calculated taking into account shares in terms of PoDs. With the shares in terms of volumes the concentration levels would be substantially lower (HHI post-merger of 1 876 and delta of 50).

73 See recital (45).

74 The Notifying Party submits that to the Parties' knowledge, there is no publically available data distinguishing between the retail supply of H-gas and the retail supply of L-gas for household customers and small I&C customers, at national level and per region. The Parties therefore estimated their market shares in terms of volume under the assumption that L-gas accounts for 23% of the total gas volumes supplied to household customers and small I&C customers in 2019 at national level, 35% in Flanders, 5% in Wallonia, and 95% in Brussels (see paragraphs. 347 et seq. of the Form CO). The HHI post-merger in L-gas would be of 2 896 with a delta of 187. In H-gas, it would be 2 536 and 226.

75 These figures are calculated on the basis of market shares in terms of PoDs; with the shares in terms of volumes the concentration levels would be substantially lower.

76 See recital (45).

77 In the Brussels region the market shares would be below 20% also in terms of PoDs (see recital (45)).

78 The HHI post-merger in Flanders would be 2579, with a delta of 273 (excluding the category "others" with less than 50-51% share). In Wallonia, it would be 2 534 and 138 (excluding a[0-5]% of the market). In all cases calculated on the basis of shares in terms of PoDs; with the shares in terms of volumes the concentration levels would be substantially lower.

79 In the Brussels region the market shares would be below 20% also in terms of PoDs (see recital (45)).

80 The HHI post-merger and delta would be as follows: Flanders L-gas, 2 549 and 279; Flanders H-gas, 2 557 and 265; Wallonia L-gas, 2 524 and 284; Wallonia H-gas, 2526 and 126. In Flanders, excluding approximately (10-20]% of the market, in Wallonia [5-10]%. In all cases calculated on the basis of shares in terms of PoDs, with the shares in terms of volumes the concentration levels would be substantially lower.

81 Calculated excluding the category "others", which amounts to [5-10]% of the market.

82 The HHI post-merger in L-gas would be of 2 552 with a delta of 174. In H-gas, it would be 2 251 and 200.

83 In the Brussels region the market shares would be below 20%.

84 The HHI post-merger in Flanders would be 2117, with a delta of 225 (excluding the category "others" with approximately [5-10]% share). In Wallonia, it would be 2 648 and 252 (excluding a [0-53% of the market).

85 In the Brussels region the market shares would be below 20%.

86 The HHI post-merger and delta would be as follows: Flanders L-gas, 2 092 and 297; Flanders H-gas, 2 059 and 182: Wallonia L-gas, 2 600 and 331; Wallonia H-gas, 2 603 and 236. In Flanders, excluding approximately (10-20% of the market, in Wallonia (10-20)%

87 See replies to question 32.1 of Questionnaire Q2 - Questionnaire to Competitors in the retail supply of gas and electricity. At the same time, this competitor considers that the proposed transaction will not give rise to an increase in prices in the gas retail markets.

88 See paragraphs 221 et seq. of the form CO. Luminus additionally notes that, according to the Walloon regional regulator, active and passive household customers have been charged tariffs on average significantly equivalent.

89 In Wallonia, the number of passive customers has decreased from more than 700,000 in 2007 (right after the liberalisation) to slightly above 100,000 in 2019 for household customers, an 13.000 for non-households. In Brussels, passive customers have decreased from 85% of the total number of customers in 2007 to 10% in 2019 for all customers. The figures provided show that the decrease has continued, albeit at a less pronounced pace, also in the more recent years. See Luminus' reply to question 2 of RFI 5 of 9 April 2021.

90 See replies to questions 29 and 30 of Questionnaire Q1 – Questionnaire to Customers in the retail supply of gas and electricity and replies to question 38 of Questionnaire Q2 – Questionnaire to Competitors in the retail supply of gas and electricity. One competitor raised concerns about possible coordination effects between Engie and Luminus; these are addressed in Section 4.3.

91 See replies to question 39 of Questionnaire Q1 – Questionnaire to Customers in the retail supply of gas and electricity.

92 All customers and competitors consider Engie as Luminus’ closest competitor. Competitors consider Essent to be Luminus’ third or fourth competitor (at similar levels as Lampiris and Eneco). Customers place Essent as the second closest at the same level as Eneco. Competitors and customers consider that Engie and Luminus are similarly close competitors to Essent, with Eneco and Lampiris following closely. Competitors do not see any differences in closeness depending in the type of gas (H-gas or L-gas). See replies to questions 27 and 28 of Questionnaire Q1 – Questionnaire to Customers in the retail supply of gas and electricity and replies to questions 36 and 37 of Questionnaire Q2 – Questionnaire to Competitors in the retail supply of gas and electricity.

93 See replies to question 22 of Questionnaire Q2 – Questionnaire to Competitors in the retail supply of gas and electricity.

94 See replies to question 41.1 of Questionnaire Q2 – Questionnaire to Competitors in the retail supply of gas and electricity.

95 See replies to question 43 of Questionnaire Q2 – Questionnaire to Competitors in the retail supply of gas and electricity.

96 See replies to questions 31 and 31.1 of Questionnaire Q1 – Questionnaire to Customers in the retail supply of gas and electricity.

97 See replies to questions 32 of Questionnaire Q1 – Questionnaire to Customers in the retail supply of gas and electricity.

98 See replies to questions 41 and 42 of Questionnaire Q2 – Questionnaire to Competitors in the retail supply of gas and electricity.

99 See replies to question 33 of Questionnaire Q2 – Questionnaire to Competitors in the retail supply of gas and electricity.

100 See replies to questions 41 and 42 of Questionnaire Q2 – Questionnaire to Competitors in the retail supply of gas and electricity.

101 See paragraph 461 et seq.of the form CO. […].

102 See Commission Horizontal merger Guidelines, paragraph 48.

103 See Commission Horizontal merger Guidelines, paragraph 20. In the case of retail supply of gas to small I&C customers the proposed transaction would not even give rise to affected markets if markets shares in terms of volumes are considered.

104 See Section 4.1.2.2(C).

105 See replies to questions 42 and 43 of Questionnaire Q2 – Questionnaire to Competitors in the retail supply of gas and electricity.

24