Commission, March 30, 2021, No M.10061

EUROPEAN COMMISSION

Decision

COCA-COLA HELLENIC BOTTLING COMPANY / HEINEKEN / STOCKDAY

Subject: Case M.10061 - COCA-COLA HELLENIC BOTTLING COMPANY / HEINEKEN / STOCKDAY

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 24 February 2021, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Coca-Cola HBC Romania ('CCH Romania') intends to acquire joint control over Stockday S.R.L. ('Stockday') together with Heineken Romania S.A. ('Heineken Romania' and, together with CCH Romania and Stockday, the 'Parties') (the 'Transaction').3 Currently, Stockday is solely controlled by Heineken Romania.

1. THE PARTIES

(2) CCH Romania is a wholly owned subsidiary of Coca-Cola HBC AG ('CCH'), an authorized bottler of The Coca-Cola Company ('TCCC'). CCH Romania is active in the production and distribution of beverages bearing the TCCC brand as well as other beverages. In Romania, CCH Romania offers non-alcoholic beverages and spirits.

(3) Heineken Romania is a wholly owned subsidiary of Heineken N.V. ('Heineken'). Heineken Romania supplies a range of Heineken’s local and international brands of beer and cider in Romania.

(4) Stockday is an online distribution platform established by Heineken in 2017 that operates as an intermediary between producers of beverages and retailers.

2. THE OPERATION

(5) On 3 November 2020, the Parties entered into a shares purchase agreement by means of which CCH Romania will acquire 50% of the shares of Stockday. Heineken Romania will retain the remaining 50% of Stockday’s shares. Post-Transaction, CCH Romania and Heineken Romania will have the same number of voting rights in the shareholders’ meeting and in the governing board of Stockday. All decisions relating to the strategic commercial behaviour of Stockday, including the appointment of senior management at Stockday and the approval of Stockday’s business plan and budget, will require the agreement of both CCH Romania and Heineken Romania.

(6) Moreover, post-Transaction Stockday will operate as an autonomous entity with independent market access to and presence in the wholesale distribution of beverages and will have: (i) sufficient resources to operate independently on the market; (ii) activities beyond one specific function for its parents; (iii) sales or purchase relations with its parents at arms' length basis;4 and (iv) a lasting basis nature.

(7) On the basis of the above, the Transaction constitutes an acquisition of joint control over a full-function undertaking, within the meaning of Articles 3(1)(b) and 3(4) of the Merger Regulation.

3. UNION DIMENSION

(8) The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 5 000 million5 in 2019 (CCH: EUR 7 026 million; Heineken: EUR 23 894 million; Stockday: [individual turnover]) and the aggregate Union-wide turnover of each of at least two of the undertakings concerned is more than EUR 250 million ([individual turnovers]). The undertakings concerned do not achieve more than two- thirds of their Union-wide turnover within the same Member State.

(9) Therefore, the Transaction has a Union dimension pursuant to Article 1(2) of the Merger Regulation.

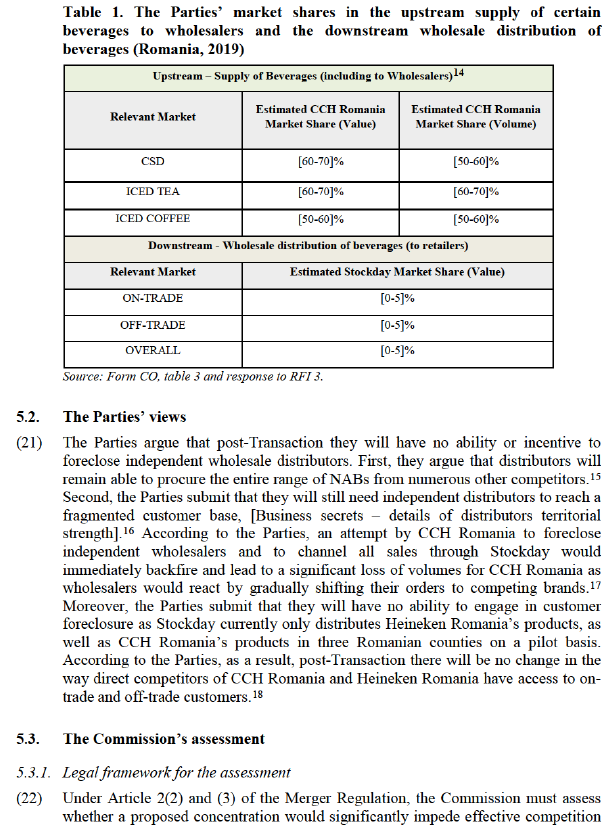

4. MARKET DEFINITION

4.1. Product market definition

(10) In past decisions regarding the production and supply of beverages,6 the Commission has distinguished between alcoholic beverages ('ABs') and non- alcoholic beverages ('NABs'). As to ABs, in the past the Commission has identified separate product markets for the production and distribution of (i) beer and (ii) cider. With regard to spirits, the Commission has concluded in previous decisions that spirits should be distinguished from other beverages and that the spirit market should be segmented by spirit type. As to NABs, the Commission has previously considered that the production and bottling of carbonated soft drinks ('CSDs') and non- carbonated soft drinks ('NCSDs') constitute two separate product markets. Within CSDs, the Commission has in the past established that there was a separate product market for cola-flavoured CSDs and left open whether other CSDs formed a single product market or should be further subdivided by flavour groups. Within NCSDs, the Commission has distinguished between packaged/bottled water, iced/ready-to- drink tea, iced/ready-to-drink coffee, coffee, juices and energy drinks, but ultimately left the segmentation open. In addition, the Commission has considered distinguishing the market for plant-based milk from the market from dairy-based milk, while it ultimately left this question open.

(11) In the past, the Commission has identified7 a separate product market for the wholesale distribution of beverages including ABs and NABs, which is downstream from production. Moreover, the Commission has considered, but ultimately left open, a potential distinction of the market for the wholesale distribution of beverages depending on whether beverages are sold to retail outlets ('off trade' channel) or to points of sale for direct consumption, e.g. restaurants or hotels ('on trade' channel).

(12) The market investigation conducted in the present case confirmed the Commission’s findings in previous cases that (the production of): (i) CSDs; (ii) iced/ready-to-drink tea; (iii) iced/ready-to-drink coffee; (iv) packaged/bottled water; (v) energy drinks; (vi) juices; (vii) coffee; (viii) spirits; (ix) plant-based beverages/milk; (x) beer; and (xi) cider can be distinguished,8 since they ‘[address] different customer needs’.9

(13) Regarding wholesale distribution, although each distributor follows a somewhat different distribution model, the majority of distributors sell a range of products both in the beverages and non-beverages category. It follows that from a supply perspective, the split by beverage type that is appropriate in the upstream production of beverages is not appropriate downstream for wholesale distribution.

(14) Because the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible product market definition, the exact product market definition can be left open for the purpose of this case. For the purpose of this Decision, the Commission will consider the markets for the production and supply (to wholesalers) of: (i) CSDs (including cola and non-cola flavoured CSDs); (ii) iced/ready-to-drink tea; (iii) iced/ready-to-drink coffee; (iv) packaged/bottled water; (v) energy drinks; (vi) juices; (vii) coffee; (viii) spirits; (ix) plant-based beverages/milk; (x) beer; and (xi) cider, where either CCH Romania or Heineken Romania is active; as well as the markets for the on trade and off trade wholesale distribution of beverages, where Stockday is active.

(15) In line with past Commission’s decisions,10 a segmentation of the markets for the production and supply of beverages between sales to retailers and wholesalers by producers does not seem to be justified, since producers compete for the overall supply of beverages in Romania.

4.2. Geographic market definition

(16) In past cases, the Commission has concluded that the relevant geographic markets for the production and supply of NABs (including CSDs and NCSDs) and ABs (including spirits, beer and cider) are national in scope. Moreover, the Commission has considered the market for the wholesale distribution of beverages to be national in scope.11

(17) The market investigation generally confirmed that the market for the wholesale distribution of beverages is national in scope. The majority of market participants who expressed an opinion shares this view.12

(18) For the purpose of the present case, the Commission will look at the wholesale distribution of beverages in Romania.

5. COMPETITIVE ASSESSMENT

5.1. Introduction

(19) On the basis of the market definition described above, CCH Romania is active in the Romanian markets for the production and supply of: (i) CSDs; (ii) packaged/bottled water, (iii) iced/ready-to-drink tea, (iv) iced/ready-to-drink coffee, (v) coffee, (vi) energy drinks, (vii) juices, (viii) spirits, and (ix) plant-based beverages/milk. Heineken Romania is active in the Romanian markets for the production and supply of beer and cider. Stockday is active as on-trade and off-trade distributor of NABs (CSDs, packaged/bottled water, iced/ready-to-drink tea, etc.), beer and cider with plans to expand its portfolio [to other products] in the course of [Business secrets – details on timing to expand portfolio]. CCH Romania’s and Heineken Romania’s portfolios are complementary, therefore there are no horizontal overlaps between their activities. In addition, CCH Romania and Heineken Romania do not compete with Stockday, as they are not active on the market for the on trade or off trade wholesale distribution of beverages in Romania.

(20) The Transaction gives rise to vertically affected markets between, on the upstream level, CCH Romania’s production and supply of (i) CSDs, (ii) iced/ready-to-drink tea, and (iii) iced/ready-to-drink coffee; and, on the downstream level, Stockday’s wholesale on-trade and off-trade distribution of beverages.13

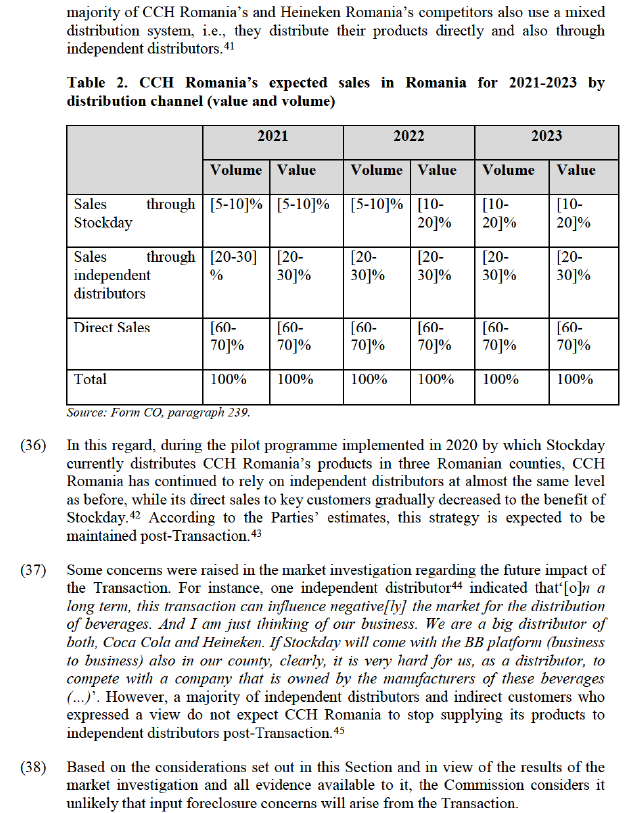

in the internal market or in a substantial part of it, in particular through the creation or strengthening of a dominant position. In this respect, a merger can entail horizontal and/or non-horizontal effects.

(23) As regards non-horizontal effects, the Commission Non-Horizontal Merger Guidelines19 distinguish between the effects of vertical mergers, which involve companies operating at different levels of the supply chain, and of conglomerate mergers, which involve companies that are active in closely related markets.

(24) According to paragraph 29 of the Non-Horizontal Merger Guidelines, a vertical merger is said to result in foreclosure where actual or potential rivals' access to supplies or markets is hampered or eliminated as a result of the merger, thereby reducing these companies' ability and/or incentive to compete.

(25) Paragraph 30 of the Non-Horizontal Merger Guidelines distinguishes two forms of foreclosure. The first is where the merger is likely to raise the costs of downstream rivals by restricting their access to an important input (input foreclosure). The second is where the merger is likely to foreclose upstream rivals by restricting their access to a sufficient customer base (customer foreclosure).

(26) The present Section 5.3 assesses whether the Transaction is likely to raise vertical effects on the affected markets identified in Section 5.1.

5.3.2. Input foreclosure

(27) The Commission considers that, post-Transaction, the Parties are unlikely to have the ability or the incentive to engage in an input foreclosure strategy by restricting competitors’ access to an important input. Moreover, any hypothetical input foreclosure strategy from the Parties would be unlikely to have an impact on competition. This is for the following reasons.

(28) First, even though CCH Romania’s upstream market shares are above 50% for the affected markets identified (i.e. CSD, iced/ready-to-drink tea and iced/ready-to-drink coffee), CCH Romania would not have the ability to restrict independent distributors’ access to an important input as CCH Romania’s products are only a relatively small percentage of the portfolio of its distributors. In particular, according to the Parties, the CCH Romania portfolio weighs on average for about […]% of the total sales of its independent distributors.20 A majority of independent distributors and indirect customers that expressed a view indicated that less than 20% of their revenues corresponds to sales from CCH Romania’s and Heineken Romania’s products.21 Therefore, independent distributors active in the downstream wholesale distribution of beverages (both on trade and off trade) have alternative sources for their portfolio.

(29) In this regard, although CCH Romania’s and, to a lesser extent, Heineken Romania’s products are considered a “must-have”,22 market participants have indicated that they could procure the categories of products supplied by CCH Romania (including CSD, iced/ready-to-drink tea and iced/ready-to-drink coffee) from numerous other competitors.23 In addition, most distributors purchase a wide range of beverages in terms of brands and categories covered.24

(30) Second, CCH Romania would not have the ability or incentive to foreclose independent distributors by exclusively supplying Stockday, as Stockday is currently active in only 15 out of 41 Romanian counties. Therefore, it cannot fully replace CCH Romania’s existing independent distribution network, which includes independent distributors that operate across all Romanian counties. In this regard, several of CCH Romania’s independent distributors indicated that, although Stockday could expand the geographic scope of its activities, they do not consider Stockday’s digital platform as an appropriate distribution channel outside of Romania’s main cities, because in rural areas customers still prefer in person interaction and are more reluctant to use digital platforms.25 This applies indistinctly for on trade and off trade supplies of CSD, iced/ready-to-drink tea and iced/ready-to- drink coffee; and is consistent with the Parties’ view that Stockday’s operations would be complementary to their existing indirect sales distribution via independent wholesale distributors

(31) In addition, during the market investigation respondents highlighted26 some limitations of Stockday’s online platform to reach all customers, including ‘(…) time consuming operations (ordering process) transferred from suppliers to customer, less interactions with trained sales/distribution professionals, more rigid supply chain (…)’ and that ‘it will be difficult for some customers to place orders’. In addition, one competitor explained that ‘the order shall be paid before delivery’.27 On the other hand, the use of Stockday has positive effects such as ‘(…) price transparency, the easy tracking of orders, payments, returns and recycled packaging such as bottles’.

(32) Moreover, Stockday currently contracts logistic and delivery services from independent partners as it does not currently own any logistics assets (trucks or warehouses).28 Therefore, Stockday would not have the capabilities to replace its distributors post-Transaction and, according to the information provided by the Parties, it is not planning to develop such capabilities.29

(33) Third, Stockday’s market share in the on-trade and off-trade wholesale distribution of beverages in Romania is very limited, [0-5]% and [0-5]% respectively (2019).30 Such market share is expected to increase in the coming years and to stabilize at a relatively low level. In fact, the expected market share for Stockday for the on-trade and off-trade beverages segments in Romania is expected to be only [0-5]% by 2023.31 Therefore, it appears unlikely that it will replace CCH Romania’s independent distribution network. Moreover, post-Transaction, Stockday will continue to be constrained by strong competitors such as Interbrands, Aquila Part Prod Com, Luzan Logistic, Macromex and Punctual Comimpex.32

(34) Fourth, a majority of the independent distributors who expressed a view consider that the Transaction may have negative or mixed impact on their business due to the loss of turnover and clients.33 However, CCH Romania and Heineken Romania submit that their sales through Stockday will remain limited ([10-20]% by 2023 in the case of Heineken Romania34 and [10-20]% by 2023 in the case of CCH Romania)35 and that they will continue to strongly rely on independent distributors.36 In addition, when asked about the past impact on their business of the launch of Stockday, a majority of independent distributors that expressed a view on this point said that they did not experience any negative impact.37 In particular, in the three counties (Arges, Cluj and Dambovita) where CCH Romania implemented a pilot programme with Stockday for the sale of its products, the majority of distributors, indirect customers and competitors active in these counties that expressed a view did not experience any impact after the launch of this pilot programme.38 It is worth noting that the majority of indirect customers of Heineken Romania’s products who expressed a view experienced no impact or a positive impact from the establishment of Stockday in 2017.39 Indeed, until 2023 CCH Romania's sales through independent distributors are expected to remain substantially stable (and to go from EUR […] million in 2019 to EUR […] million in 2023) whereas CCH Romania's direct sales are expected to materially decrease (from EUR […] million in 2019 to EUR […] million in 2023).40

(35) Stockday will mainly take over some of CCH Romania’s direct sales to end customers and indirect sales distribution via independent distributors ('ISD') will continue to play an important role in CCH Romania’s distribution system. CCH Romania is expected to continue to use ISD via independent distributors in parallel to Stockday. CCH Romania’s sales through Stockday are expected to be relatively limited and to have a low growth after the launch phase. The need for CCH Romania and Heineken Romania to continue to rely on independent distributors seems to be in line with the nature of the wholesale distribution market in Romania. Namely, the

5.3.3. Customer foreclosure

(39) The Commission considers that, post-Transaction, the Parties are unlikely to have the ability or the incentive to engage in a customer foreclosure strategy. Moreover, any hypothetical customer foreclosure strategy from the Parties would be unlikely to have an impact on competition. This is for the following reasons.

(40) First, despite CCH Romania’s market shares above 50% in the supply of CSD, iced/ready-to-drink tea and iced/ready-to-drink coffee, given Stockday’s limited market shares46 downstream ([0-5] % for on-trade and [0-5] % for off-trade distribution), it is highly unlikely that the Parties would have the ability to foreclose competitors by restricting access to a sufficient customer base in Romania post- Transaction. As already mentioned, such market share is expected to increase in the coming years but to stabilize at a relatively low level (to only [0-5]% in Romania in 2023).47

(41) Second, Stockday operates in a highly competitive market, where numerous independent distributors compete for sales to a fragmented customer base of small retailers (e.g. grocery shops, convenience shops) and Horeca outlets. The competitors of CCH Romania and Heineken Romania will have access to wholesale distributors like Aquila, Luzan, Macromex, Punctual and Interbrands which distribute all the major consumer goods brands like Danone, Nestle’, Mars, Procter & Gamble, Henkel, Barilla in both the on-trade and off-trade channel.48

(42) Third, according to the information provided by the Parties, Stockday plans to expand its distribution to third-party products [Business secrets – details on timing to expand portfolio] and to start distributing also beverages from other suppliers [Business secrets – details on timing to expand portfolio].49

(43) In view of the considerations in paragraphs (39) to (42) above and all evidence available to it, the Commission considers that it is unlikely that customer foreclosure concerns will arise from the Transaction.

5.3.4. Other concerns raised during the market investigation

(44) During the market investigation, one competitor50 raised the risk of ‘a possible leveraging strategy based on the data that the platform would provide to the owners’ post-Transaction. However, as most independent distributors offer a wide range of beverage products, the Commission considers that they could equally collect and leverage information on customers’ purchase patterns or share it with the Parties' competitors. Therefore, the Commission considers that it is unlikely that the Transaction would negatively affect competition in this regard.

5.3.5. Conclusion of the Commission’s assessment

(45) In light of the above and all evidence available to it, the Commission considers that the Transaction does not give rise to serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement due to vertical non- coordinated effects under any plausible market definition.

6. CONCLUSION

(46) For the above reasons, the Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 Publication in the Official Journal of the European Union No C 74, 3.3.2021, p. 8.

4 The Parties submit that, post-Transaction, both CCH Romania and Heineken Romania will set the transfer prices in line with the prices set for wholesale customers. In addition, according to the Parties, under the current estimations, Stockday will generate approximately […]% of its turnover from the distribution of its parents' products in 2021. As third party brands are added to the portfolio, this percentage is expected to decrease to less than [Business secrets – expected percentages by year until 2026].

5 Turnover calculated in accordance with Article 5 of the Merger Regulation.

6 See Cases M.2268 – Pernod Ricard/Diageo/Seagram Spirits, paragraph 17, M.2276 – The Coca-Cola Company/Nestlé/JV, paragraphs 17 to 21, M.2504 – Cadbury Schweppes/Pernod Ricard, paragraphs 7 and 8, M.3182 – Scottish & Newcastle/Hp Bulmer, paragraphs 8 to 14, M.5114 – Pernod Ricard/V&S, paragraph 8, M.7292 – Demb/Mondelez/Charger Opco, paragraphs 43 to 45, M.8150 – Danone/The Whitewave Foods Company, paragraph 50 and M.9369 - Pai Partners/Wessanen, paragraphs 116 and 117.

7 See Case M.5560 – Carlsberg Deutschland/Nordmann/JV Nordic Getränke, paragraph 10.

8 Questionnaire to distributors, question 6; questionnaire to indirect customers, question 5; and questionnaire to competitors, question 4.

9 Questionnaire to indirect customers, question 5.1.

10 Case M.7220 – Chiquita Brands International/Fyffes, paragraphs 95-98.

11 See Cases M.2276 – The Coca-Cola Company/Nestlé/JV, paragraph 23, M.3182 – Scottish & Newcastle/Hp Bulmer, paragraphs 15 to 16, M.5114 – Pernod Ricard/V&S, paragraph 43, M.7292 – Demb/Mondelez/Charger Opco, paragraph 157, M.8150 – Danone/The Whitewave Foods Company paragraph 51 and M.9369 - Pai Partners / Wessanen, paragraphs 116 and 117.

12 Questionnaire to distributors, question 8, questionnaire to competitors, question 6 and questionnaire to indirect customers, question 6.

13 Form CO, paragraph 216.

14 Including direct sales by CCH Romania.

15 Form CO, paragraph 218.

16 Form CO, paragraph 211,218 and 219.

17 Form CO, paragraph 242.

18 Form CO, paragraph 210.

19 Guidelines on the assessment of non-horizontal mergers under the Council Regulation on the control of concentrations between undertakings (‘Non-Horizontal Merger Guidelines’) (2008/C 265/07).

20 Form CO, paragraph 224.

21 Questionnaire to direct distributors, question 4.1.

22 Questionnaire to distributors, questions 10 and 11.

23 Questionnaire to distributors, question 5, questionnaire to competitors, question 8. The following suppliers seem to remain available to independent distributors in Romania: (i) for CSDs: Pepsico, European Dreanks, Romaqua Group, Alconor and Gama & Gama; (ii) for iced/ready-to-drink tea: Pepsico, Maspex, San Benedetto, Phanner and Rauch; (iii) for iced/ready-to-drink coffee: Nestle, Hell, Molkerei, Allois Muller, Illy, Arlafoods; (iv) for bottled water: Romaqua Group, Borsec, Carpathian Springs, European Drinks, Maspex, San Benedetto, Perla Harghitei and Apemin tusnad; (v) for juices: Tymbark, Maspex, Pepsico, Pfanner, Romaqua Group, Eckes-Granini Group and European Drinks ; and (vi) for beer Asahi/Ursus, Bergenbier/Molson Coors, Tuborg URB and Carlsberg.

24 Form CO, paragraph 342.

25 Minutes from 11.03.2021 from a call with a distributor, questionnaire to distributors, questions 19.2 and 20.1.

26 Questionnaire to indirect customers, question 8.2.1.

27 Questionnaire to competitors, question 19.1.

28 Form CO, paragraph 332.

29 Form CO, paragraphs 7 and 52.

30 Form CO, paragraph 207, Table 3.

31 Form CO, paragraph 306.

32 Form CO, paragraph 192.

33 Questionnaire to distributors, questions 15 and 15.1.

34 Form CO, paragraph 265.

35 Form CO, paragraph 239.

36 Form CO, paragraphs 242 and 265.

37 Questionnaire to distributors, question 12.2.

38 Questionnaire to distributors, question 14, questionnaire to indirect customers, question 10 and questionnaire to competitors, question 15.

39 Questionnaire to indirect customers, question 12.

40 Form CO, paragraph 240.

41 Questionnaire to competitors, question 11.

42 Form CO, paragraph 235.

43 Form CO, paragraph 239.

44 Questionnaire to distributors, question 16.1.

45 Questionnaire to distributors, question 20, questionnaire to indirect customers, question 15.

46 Form CO, paragraph 207, Table 3.

47 Form CO, paragraph 306.

48 Form CO, paragraph 278.

49 Form CO, paragraphs 10 and 333, Annex 7 to the Form CO.

50 Questionnaire to competitors, question 19.1.