Commission, March 31, 2021, No M.9926

EUROPEAN COMMISSION

Decision

ADI / MAXIM

Subject: Case M.9926 – ADI/Maxim

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 24 February 2021, the Commission received notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 by which Analog Devices, Inc. (“ADI”) intends to acquire within the meaning of Article 3(1)(b) of the Merger Regulation sole control of the whole of Maxim Integrated Products, Inc. (“Maxim”) (the “Transaction”)3. ADI is referred to as the “Notifying Party”, ADI and Maxim together as the “Parties”.

1. THE PARTIES

(2) ADI is a public global technology company headquartered in the USA. It designs, manufactures and markets a broad portfolio of solutions, including integrated circuits (“ICs”), algorithms, software and subsystems that use analog, mixed-signal and digital signal processing technologies. ADI’s products serve customers across the globe in a number of sectors, including the industrial, communications, automotive and consumer sectors.

(3) Maxim is a public global technology company headquartered in the USA. It designs, develops, manufactures and markets a broad range of analog, mixed-signal and digital ICs. Its products serve customers in diverse geographic locations in the automotive, communications and data centre, computing, consumer and industrial sectors.

2. THE OPERATION

(4) The notified transaction concerns the acquisition by ADI of the global activities of […]* (the “Transaction”). It will be implemented in accordance with the Agreement and Plan of Merger between ADI, Maxim and Magneto Corp. (a wholly-owned subsidiary of ADI), dated and executed on 12 July 2020 (the “Merger Agreement”). Pursuant to the Merger Agreement, Magneto will be merged with and into Maxim, with Maxim surviving the merger and continuing as a wholly-owned subsidiary of ADI.

(5) Therefore, the Transaction constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

3. UNION DIMENSION

(6) The notified operation has a Union dimension pursuant to Article 1(2) of the Merger Regulation. In their last completed financial year, the combined worldwide turnover of the Parties exceeded EUR 5 000 million (ADI: EUR 5,353 million, Maxim: EUR 2,062 million, combined: EUR 7,415 million) and each of ADI and Maxim had turnover of more than EUR 250 million in the EU (ADI: EUR […] million, Maxim: EUR […] million). The Parties did not achieve more than two thirds of their respective EU turnover in one and the same Member State during the same period.

4. RELEVANT MARKETS

4.1. Introduction

(7) The Transaction concerns the semiconductor industry, and more specifically analog ICs.

(8) Semiconductors are materials, such as silicon, which act as an insulator, but are also capable of conducting electricity. By combining conductive material, semiconductor material and insulators in a predetermined pattern, the movement of electricity through a device can be precisely controlled. Semiconductors are at the heart of devices such as diodes, transistors and other electronic components, and can be found in virtually every electronic device today.

(9) Semiconductors are rarely bought by end-products by consumers. They are mainly bought by equipment manufacturers in virtually all sectors within the electronic equipment industry.

4.2. Overview of the semiconductor industry

(10) In previous decisions, the Commission has divided the market for semiconductors by

(i) category of semiconductor; and (ii) end-use application:4

i. Category: the Commission considered that there are four distinct categories of semiconductors: (i) ICs; (ii) discretes; (iii) optical semiconductors;and (iv) sensors and actuators.5

ii.End-use application: the Commission has also considered that there are six main application-specific semiconductor types: (i) consumer; (ii) data processing; (iii) communications; (iv) automotive; (v) industrial; and (vi) military, aerospace and defence (“ASD”). The Commission has made this distinction on the basis that semiconductors manufactured for each application differ in their function and are not substitutable from one application to another.6

(11) As regards ICs, the Commission found in previous decisions that digital ICs and analog ICs should be considered as separate markets, since this differentiation reflects the structure of customer purchasing categories and is in line with the standard definition provided by World Semiconductor Trade Statistics (“WSTS”).7

(12) The Commission also found that analog ICs can be further sub-segmented between general purpose analog ICs and application-specific analog ICs, the latter being tailored to specific functions or specific devices.8

(13) The results of the market investigation in the present case9 confirmed the general categorization of semiconductors10, as well as the distinctions between digital and

analog ICs and the distinction between general purpose analog ICs and application- specific analog ICs11. Within application-specific analog ICs, it appears that a distinction could be made by product category.12

(14) The Parties only have tangential activities in digital ICs and only have overlapping activities in the supply of microcontrollers (“MCUs”). The Parties’ combined worldwide market share in the overall market for MCUs for 2019 is [0-5]%.13

(15) As regards the other categories of semiconductors, the Transaction also does not give rise to significant overlaps between the Parties. There is no overlap in the market for discretes where only Maxim is present14 and there are only minimal overlaps between the Parties in sensors and actuators where the Parties have a combined worldwide market share of [0-5]%. The Parties’ strongest presence in sensors and actuators is in a segment for temperature sensors, where combined their market share does not exceed [5-10]%.15

(16) It follows that the Parties' activities mainly overlap in analog ICs. For the purpose of this decision the other categories of semiconductors are not discussed further.

4.3. Product market definition

4.3.1. General purpose analog ICs

(17) An IC is a semiconductor device composed of diodes, transistors and electronic components, combined with conductive interconnect material, which controls the current and voltage of electricity running through it. Analog ICs are used to process real-world signals, using electronic voltage patterns that represent the original signal. Real-world signal inputs include sound, light, video, radio waves, temperature and other physical, chemical or biological properties.

(18) As mentioned in paragraph (13) above, the Commission previously found that analog ICs can be further sub-segmented between general purpose analog ICs and application-specific analog ICs. The Commission has not in previous decisions considered in detail whether the broader product market for general purpose analog ICs should be further segmented.

4.3.1.1. Notifying Party’s view

(19) The Notifying Party submits that, based on the Commission’s previous decisions, general purpose analog ICs can be regarded as a relevant product market and that it is not necessary to conclude on a narrower product market definition.

(20) In particular, the Notifying Party submits that IC manufacturers tend to supply a broad range of general purpose analog ICs and that it is relatively easy to adjust test and assembly plants to produce different types of ICs. […]. Finally, the Notifying Party submits that customers tend to purchase a wide range of general purpose analog ICs and it is relatively easy for customers to switch between technologies if required.

(21) Should the Commission consider to further segment the market for general purpose analog ICs, then the Notifying Party submits that, on the basis of the WSTS 2019 standard product classification, a distinction could be made in terms of functionality as follows: (i) amplifiers/comparators; (ii) data/signal conversion; (iii) interface/isolators; and (iv) power management.

(22) The Notifying Party submits however that the exact definition of the relevant product market can be left open in the present case, as the Transaction would not raise serious doubts as to its compatibility with the internal market under any of the plausible market definitions.

4.3.1.2. The Commission’s assessment

(23) The market investigation confirmed the existence of a separate relevant product market for general purpose analog ICs (as compared to application-specific analog ICs), as the majority of customers and competitors indicated that such a segmentation is warranted.16

(24) A further sub-segmentation of the market for general purpose analog ICs in (i) amplifiers & comparator ICs (also referred to as signal conditioning ICs), (ii) nal conversion ICs, (iii) interface and isolation ICs, and (iv) power management ICs is also appropriate according to a majority of the respondents, due to the fact that these type of analog ICs have different functions.17 From the supply side, competitors confirmed the absence of scope for substitution.18

(25) Moreover, the results of the market investigation confirm that a further distinction between (i) linear regulators, (ii) switching regulators, (iii) voltage references, (iv) supervisors, sequencing and control, (v) battery charging and management and (vi) other power management could also be made within a potential market for analog power management ICs.19 According to the results of the market investigation, these components are not compatible and switching products would require big efforts.20 Also from the supply side, competitors confirmed the absence of scope for substitution.21

4.3.1.3. Conclusion on product market definition

(26) The Commission considers that, for the purposes of this decision, the exact product market definition with regard to general purpose analog ICs can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market irrespective of whether the market of general purpose analog ICs is further segmented in (i) amplifiers & comparator ICs (also referred to as signal conditioning ICs), (ii) signal conversion ICs, (iii) interface and isolation ICs, and (iv) power management ICs, or possible sub-segmentations of the analog power management ICs market.

4.3.2. Application-specific analog ICs

(27) Further to the description of analog ICs in paragraph (17) above and contrary to general purpose analog ICs, application-specific analog ICs are being tailored to specific functions or specific devices.22

4.3.2.1. Notifying Party’s view

(28) The Notifying Party submits that in previous decisions, the Commission further segmented on the basis of the following product categories: (i) consumer; (ii) data processing (including computing and storage functions); (iii) communications (sub- divided into wired communications and wireless communications); (iv) automotive; (v) industrial; and (vi) ASD.23

(29) The Notifying Party observes that these product categories are closely aligned with the application-specific ICs identified by WSTS, being automotive, consumer, industrial (including ASD), communications and computer. ADI […] whilst Maxim generates only minimal revenues. Further, the Transaction also does not lead to an overlap in relation to ASD analog ICs as Maxim has no activities in this area. Therefore, the Notifying Party submits that, given the absence of an overlap, there is no need to further segment these markets.

(30) As regards automotive application-specific standard products (“ASSPs”), the Commission previously considered but ultimately left open a distinction between automotive power and non-power analog ICs.24 The Notifying Party submits that it is not necessary or appropriate to conclude on the scope of the market for automotive ASSPs, as the Transaction does not lead to a significant impediment on effective competition on any basis. However, the Notifying Party provided an assessment of the market for application-specific analog IC used in automotive applications, distinguishing infotainment ASSPs from other automotive ASSPs. The Notifying Party further provided an assessment of the Parties’ overlap within Battery Management Systems (“BMS”), which could be considered as a further segmentation of a potential market for other automotive ASSPs. However, the Notifying Party maintains that ultimately the definition of the market for application- specific analog IC used in automotive applications can be left open.

(31) As regards the market for application-specific analog ICs for consumer applications, the Commission has not yet considered in detail any narrower segments should be identified. The Notifying Party submits that this would not be appropriate or necessary as the Transaction does not raise competition concerns.

(32) In previous decisions, the Commission has not yet considered whether the market for application-specific analog ICs for industrial applications should be further segmented. The Notifying Party observes that WSTS makes the following distinction regarding industrial ASSPS: (i) RFID transponders; (ii) industrial healthcare; and (iii) other industrial. However, the Parties consider that following these segmentations is unnecessary, as the Transaction does not raise competition concerns.

(33) Finally, the market for application-specific analog ICs used in communications applications comprises ICs that are designed specifically for and used in non- military data communications, equipment and infrastructure. This covers both wired and wireless communications. The Notifying Party agrees with the approach previously considered by the Commission to further segment the market into wired and wireless technologies.25

4.3.2.2. The Commission’s assessment

(34) As mentioned, the market investigation confirmed the existence of a separate relevant product market for application-specific analog ICs (as compared to general purpose analog ICs).26 In NXP/Freescale, the Commission previously found that this market could be further segmented into: (i) consumer; (ii) data processing (including computing and storage functions); (iii) communications (sub-divided into wired communications and wireless communications); (iv) automotive; (v) industrial; and (vi) military/aerospace.27 The majority of the respondents agree with this segmentation.28

(35) The Commission also investigated whether any further sub-segmentation of these markets should be made. As regards application-specific analog ICs used in automotive applications, the majority of the responding consumers agree that a distinction could be made between infotainment ASSPs and other ASSPs mainly because infotainment ASSPs are used within a vehicle’s cabin where they are not exposed to the temperature ranges that ICs in motor control are exposed to.29 The responses from competitors were however inconclusive, indicating that other sub segmentations might also be relevant.

(36) Further to a specific concern raised by a respondent during the market investigation, the Commission specifically considered whether competition issues would arise on a separate product market for BMS ICs. However, there are indications that BMS ICs would not constitute a separate market, because BMS ICs are used in a wide range of industries albeit with different specifications. Ultimately, the Commission considers that the precise market definition can be left open.

(37) The Commission’s investigation also focused on the question whether with regard to application-specific analog ICs used in consumer applications. Different product markets could be considered for specific applications. On this basis, the Commission verified whether a distinction should be made in the following areas: (i) Audio/Video; (ii) DSC/Camcorder; and (iii) other consumer products. The majority of the respondents to the market investigation agreed with this distinction because quality and features are key. From a supply-side, competitors moreover confirmed the absence of scope for substitution. However, some respondents submit that within other consumer products a distinction could still be made between for example PC, handheld, gaming, smart home and wearables.30

(38) Further, the Commission investigated whether, with regard to application-specific analog ICs used in industrial applications, different product markets should be considered for specific applications. On this basis, the Notifying Party submitted that a distinction could be made for industrial analog ICs used in the following areas: (i) RFID transponders; (ii) healthcare; and (iii) other industrial. This was confirmed by the majority of the competitors that responded to the market investigation, although some respondents suggest further possible distinctions within the segment other industrial applications (such as factory automation).31 From the supply side, competitors confirmed the absence of scope for substitution. Some of the customers responding to the market investigation indicated that they do not agree with the aforementioned distinction, without proposing alternative distinctions.32

(39) The Commission finally investigated whether application-specific analog ICs used in communications applications could be sub-segmented as follows: (i) cellular phones, (ii) wireless infrastructure, (iii) wireless communication – short range, (iv) other wireless communication, and (v) wired communications and infrastructure. The majority of the respondents to the market investigation confirmed that this segmentation was relevant.33 Moreover, from the supply side, competitors confirmed the absence of scope for substitution.34

4.3.2.3. Conclusion on product market definition

(40) The Commission considers that, in light of the findings of the market investigation, it appears that application-specific analog ICs can be further distinguished between: (i) consumer; (ii) data processing (including computing and storage functions); (iii) communications (sub-divided into wired communications and wireless communications); (iv) automotive; (v) industrial; and (vi) military/aerospace.

(41) While the market investigation confirms that for each of these segments a further sub-segmentation could be considered, the Commission concludes that for the purpose of this decision the precise market definition can be left open, as the proposed Transaction does not raise serious doubts as to its compatibility with the internal market with regard to application-specific analog ICs and any relevant sub- segments therein, under any alternative product market definition.

4.3.3. Semiconductors by specific end-use application

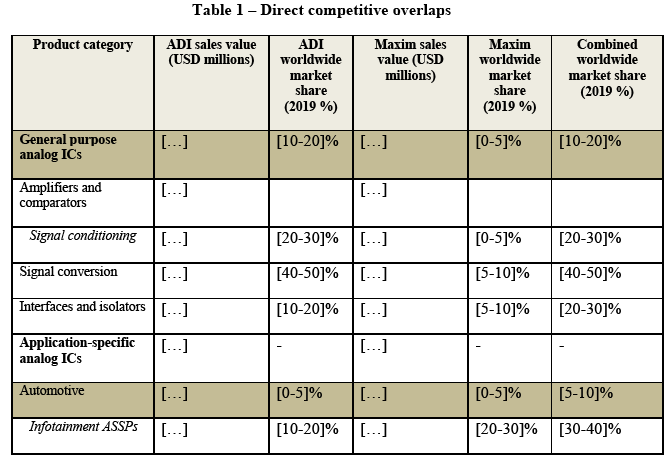

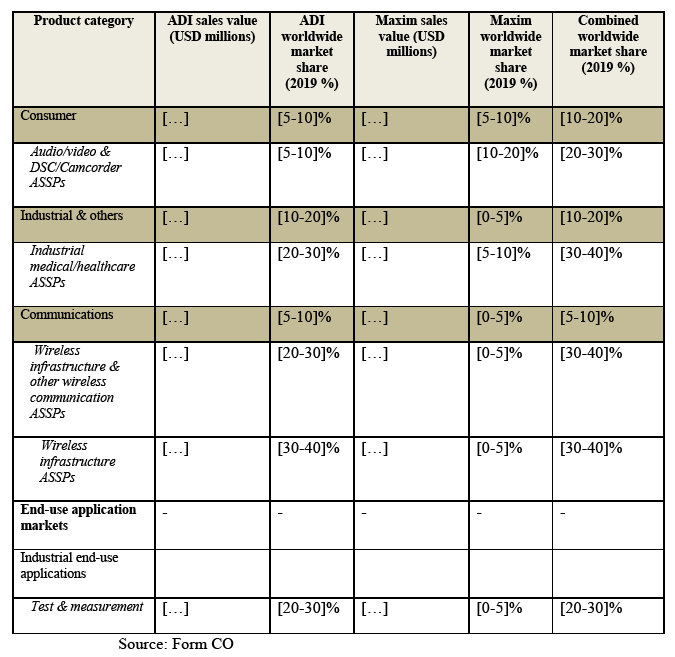

4.3.3.1. Notifying Party’s view

(42) The Notifying Party submits that, in Qualcomm/NXP, the Commission previously considered a distinction of the semiconductors market by end-use application. In this decision, the Commission considered whether a further segmentation should be made in semiconductors for automotive applications, semiconductors for Internet of Things (“IoT”) applications and semiconductors for mobile devices.35

(43) According to the Notifying Party, any segmentation by end-use application of the semiconductors market could comprise a number of different technologies (e.g. both digital and analog ICs) that could be used interchangeably to fulfil any given function from a customer’s perspective. The Notifying Party submits that the Parties’ products are sold primarily on a standalone basis, and only exceptionally as part of a “kit” or “solution”. As such, contrary to the situation in Qualcomm/NXP, competition happens based on the function of the standalone IC rather than the end- use of a consolidated solution. Therefore, the Notifying Party submits that the Transaction should be assessed on the basis of function / technology types.

(44) For automotive end-use applications, the Commission previously considered a distinction between the following function blocks: (i) powertrain; (ii) chassis; (iii) safety; (iv) body and comfort; (v) infotainment; and (vi) security.36 The Notifying Party submits that the Parties only have a reasonable presence in powertrain and infotainment and considers that no further segmentation is appropriate or necessary as the Transaction does not raise any competition concerns on these markets.

(45) For IoT end-use applications, the Notifying Party submits that this market is generally standardized and that many of the ICs purchased from the Parties for IoT applications come from their general purpose catalogues. Moreover, there is also supply-side substitutability across different function blocks within IoT applications, meaning that IC suppliers can shift their production resources between different technologies. Therefore, the Notifying Party submits that no further segmentation is required.

(46) The Commission did not yet previously consider a specific semiconductors market for industrial end-use applications. The Notifying Party submits that no further segmentation of this market would be appropriate, because: (i) customers may choose to put ICs in different industrial application types as the technologies used are similar and substitutable; the market for the sale is the same regardless of application type; and (iii) there is supply-side substitutability as most suppliers produce a range of ICs that can be used for industrial applications.

(47) Should the Commission consider segmenting the relevant market according to industrial end-use applications, then the Notifying Party refers to the categorization used in the reports by Omdia: (i) medical electronics; (ii) automation; (iii) test and measurement; (iv) security and video surveillance; (v) power and energy; and (vi) other industrial.

(48) Further, the Commission has previously considered whether semiconductor devices could be assessed by reference to their end-use application in relation to consumer, communications and ASD. The Commission has not previously analyzed consumer and ASD end-use applications and the Notifying Party submits that no further segmentation of these markets is required as the Transaction does not raise any competition concerns.

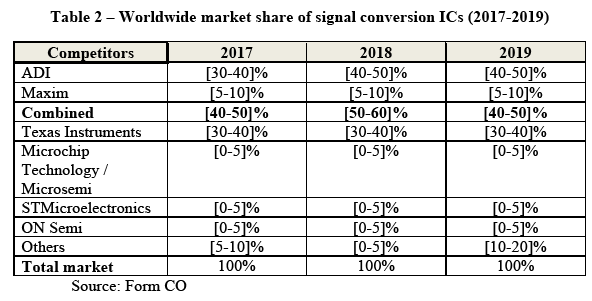

(49) Finally, as regards communications end-use applications, the Commission previously made a distinction between chipsets that are inserted in wireless electronic equipment and those that are inserted in electronic equipment used in wired communications systems.37 The Notifying Party considers that it is not necessary to segment this market more narrowly given that the Parties do not overlap in the specific segments previously identified by the Commission and the Parties’ market shares in this end-use market are very low.

4.3.3.2. The Commission’s assessment

(50) In previous decisions, the Commission considered whether the semiconductors market could be categorized on the basis of end-use application.38

(51) The results of the market investigation confirm that distinct semiconductors markets can be identified on the basis of end-use application, namely: (i) communication, (ii) consumer, (iii) computer, (iv) military (ASD), (v) industrial, (vi) automotive, and (vi) Internet of Things (IoT). This is because components are not compatible, quality requirements are different between sub-segments and switching would require significant efforts for running projects.39 Some responding consumers point out that IoT is however a vague and transversal market segment, that includes industrial, consumer and communication products.40

4.3.3.3. Conclusion on product market definition

(52) The Commission considers that, in light of the findings of the market investigation, it appears that the semiconductors market can be further distinguished by end-use application. However, the results of the market investigation suggest that at least one of the potential sub-segments, IoT, is a vague and transversal market segment, that includes industrial, consumer and communication products. In any event, the Commission considers that for this decision, and in the context of this Transaction, the exact product market definition with regard to the end-use applications on the semiconductors market can be left open as the proposed Transaction does not raise serious doubts as to its compatibility with the internal market, under any plausible market definition.

4.4. Geographic market definition

4.4.1.1. Notifying Party’s view

(53) In line with the Commission’s previous decisions, the Notifying Party considers that the geographic market for semiconductors and sub-segments, including general purpose analog ICs and application-specific analog ICs, is worldwide, in particular because: (i) manufacturing of ICs is performed on a global basis; (ii) competition between suppliers takes place globally for both existing and pipeline products; there are no regulatory barriers for supplying semiconductor devices internationally and transportation costs are below 1% of the product value; and (v) average price levels for semiconductor devices are similar globally.

4.4.1.2. The Commission’s assessment

(54) In NXP/Freescale, the Commission found that the geographic scope of the semiconductor markets was likely worldwide in scope, as competition between suppliers is worldwide, transport costs are very low, and price differences among regions are small. The exact market definition was, however ultimately left open.41

(55) In Qualcomm/NXP, the Commission concluded that the geographic scope of the semiconductor product markets at issue in that case, including semiconductors for automotive applications, was likely worldwide.42 In Infineon/Cypress, the Commission similarly concluded that the geographic scope of the semiconductor product markets relevant in that case was likely worldwide.43

(56) The results of the market investigation in the present case confirm that the geographic scope of the semiconductor markets is worldwide. The vast majority of respondents replied in particular that they sell and purchase their products at global scale, that a local presence of a supplier close to the location of a customer is not required, and that no specific barriers to trade exist in respect of the products in question.44

4.4.1.3. Conclusion on geographic market definition

(57) For the purposes of this decision, the Commission therefore concludes that the geographic scope of the semiconductor product markets relevant in this case, notably general purpose analog ICs and application-specific analog ICs (and their respective sub-segments) as well as any relevant market identified by end-use application, are worldwide.

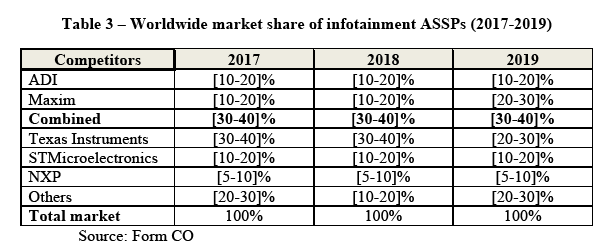

5. COMPETITIVE ASSESSMENT

5.1. Analytical Framework

(58) The Guidelines on the assessment of horizontal mergers (“Horizontal Merger Guidelines”)45 describe two main ways in which horizontal mergers may significantly impede effective competition, in particular by creating or strengthening a dominant position: (i) by eliminating important competitive constraints on one or more firms, which consequently would have increased market power, without resorting to coordinated behaviour (non-coordinated effects); and (ii) by changing the nature of competition in such a way that firms that previously were not coordinating their behaviour, are significantly more likely to coordinate and raise prices or otherwise harm effective competition (coordinated effects46) as a result of the proposed concentration.

(59) A merger giving rise to horizontal non-coordinated effects might significantly impede effective competition by creating or strengthening the dominant position of a single firm, one which, typically, would have an appreciably larger market share than the next competitor post-merger. Moreover, also mergers that do not lead to the creation of or the strengthening of a single firm’s dominant position may create competition concerns under the substantive test set out in Article 2(2) and Article 2(3) of the Merger Regulation. Regarding mergers in oligopolistic markets, the Merger Regulation clarifies that “under certain circumstances, concentrations involving the elimination of important competitive constraints that the merging parties exerted upon each other, as well as a reduction of competitive pressure on the remaining competitors, may, even in the absence of a likelihood of coordination between the members of the oligopoly, result in a significant impediment to effective competition”.47

(60) The Horizontal Merger Guidelines list a number of factors which may influence whether or not significant horizontal non-coordinated effects are likely to result from a merger, such as the large market shares of the merging firms, the fact that the merging firms are close competitors, the limited possibilities for customers to switch suppliers, or the fact that the merger would eliminate an important competitive force. Not all those factors need to be present to make significant non-coordinated effects likely and it is not an exhaustive list.48

(61) Further, in some markets, a merger may give rise to coordinated effects where the structure is such that firms would consider it possible, economically rational, and hence preferable, to adopt on a sustainable basis a course of action on the market aimed at selling at increased prices.49 According to the Horizontal Merger Guidelines, coordination is more likely where it is relatively simple to reach a common understanding on the terms of coordination. Moreover, three conditions need to be met for coordination to be sustainable: (i) the coordinating firms must be able to monitor to a sufficient degree whether the terms of the coordination are being adhered to; (ii) there must be some form of credible deterrent mechanism that can be activated if deviation is detected; and (iii) the reactions of outsiders as well as customers should not be able to jeopardise the results expected from the coordination.50

(62) The Commission has assessed whether the overlaps between the Parties’ activities within various relevant segments and sub-segments of general purpose analog ICs, application-specific analog ICs and the semiconductors market (further segmented by end-use application) would give rise to horizontal non-coordinated and coordinated effects in Section 5.2.

(63) Lastly, the Guidelines on the assessment of non-horizontal mergers (“Non- Horizontal Merger Guidelines”) focus, besides vertical mergers, on conglomerate mergers consisting of mergers between companies that are active in closely related markets, for instance suppliers of complementary products or of products which belong to a range of products that are generally purchased by the same set of customers for the same end use.51

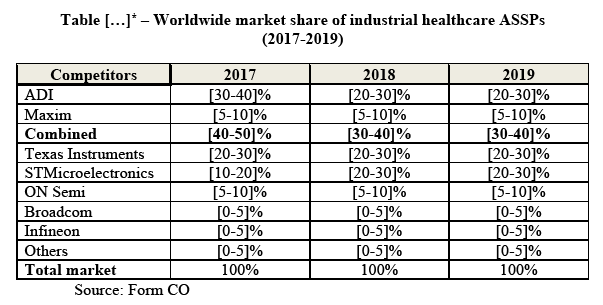

(64) In the majority of circumstances, conglomerate mergers do not lead to any competition concerns but in certain specific cases there may be harm to competition.52 The main concern in the context of conglomerate effects is that of foreclosure.53 Conglomerate mergers may allow the merger entity to combine products in related markets and this may confer on the merged entity the ability and incentive to leverage a strong market position from one market to another by means of tying or bundling, or other exclusionary practices.54

(65) In assessing the likelihood of conglomerate effects, the Commission examines, first, whether the merged firm would have the ability to foreclose its rivals, second, whether it would have the economic incentive to do so and, third, whether a foreclosure strategy would have a significant detrimental effect on competition, thus causing harm to consumers. In practice, these factors are often examined together as they are closely intertwined.55

(66) The Commission has assessed whether the proposed Transaction gives rise to conglomerate effects in […]*

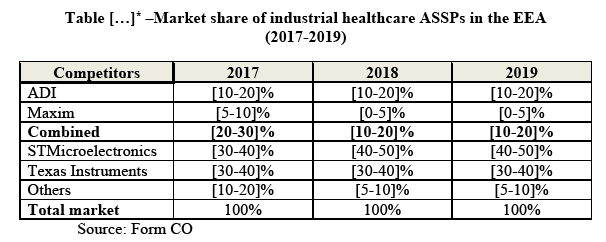

5.2. Potential horizontal non-coordinated and coordinated effects

(67) According to the Notifying Party, the Parties are mainly active in the manufacture and supply of analog ICs where their activities are complementary. As regards application-specific analog ICs, ADI’s […], while Maxim’s portfolio would focus on ICs for different types of industrial, consumer and automotive applications. […].

(68) The following table summarizes competitive overlaps in the different segments within general purpose analog ICs and application-specific analog ICs where the Parties’ activities hold worldwide combined market shares amounting to [20-30]% or more:

(69) The Commission notes that the market share data provided above is based on third party industry reports from WSTS and Omdia. As mentioned above in section 4, the Parties’ activities overlap particularly within general purpose analog ICs and application-specific analog ICs. However, the proposed Transaction does not give rise to any horizontally affected markets in the market for general purpose analog ICs, or in any of the subcategories of the market for application-specific analog ICs (automotive, industrial, consumer, communications).

(70) The Commission has further assessed the overlaps between the Parties’ activities within various narrower relevant segments and sub-segments of both general purpose analog ICs and application-specific analog ICs as well as specific end-use applications on the semiconductors market.

(71) On the sub-segments within general purpose analog ICs for signal conditioning and interfaces and isolators, the Parties’ combined market shares do not exceed [30-40]% and competition concerns can be excluded given the Parties’ limited competition position and the existence of major alternative competitors post-Transaction (including Texas Instruments, ON Semi, Microchip / Microsemi and NXP). In the segment for application-specific analog ICs - Audio/Video & DSC/Camcorder ASSPs, the Parties’ equally do not exceed [30-40]% and competition concerns can be excluded given the Parties’ limited competition position and the presence of major competitors including Cirrus Logic, Rohm, Texas Instruments and NXP. On a market for test & measurement end use applications, combined market share for the Parties also remains below [30-40]%. On this market, competition concerns can also be excluded given the presence of major alternative competitors post-Transaction (including Texas Instruments, Infineon and STMicroelectronics) and given the fact that the Transaction would cause a market share increment of less than [0-5]%.

(72) The Parties’ combined market share exceeds [30-40]% in the following possible markets, which the Commission will assess in more detail in sections 5.2.1 to 5.2.3 below:

· General purpose analog ICs: signal conversion;

· Application-specific analog ICs: Automotive – Infotainment ASSPs; and

· Application-specific analog ICs: Industrial – Medical/Healthcare.

(73) Following concerns expressed during the market investigation, the Commission has further assessed in section 5.2.4 whether the Transaction would raise any serious doubts with regard to its compatibility with the internal market as a result of possible horizontal effects regarding the manufacture and supply of BMS.

5.2.1. General purpose analog ICs: signal conversion

5.2.1.1. The Notifying Party’s view

(74) The Notifying Party submits that the Transaction would not have any negative effect on a market for general purpose analog ICs and in particular for signal conversion ICs. They consider that their combined market share overstate the importance of competition between the Parties on the market because the Parties face competition from other suppliers that exercise an effective competitive constraint. The Parties further explain that they are not close competitors. Finally, the Notifying Party considers that customers exert a significant power over suppliers.

5.2.1.2. The Commission’s assessment

(75) As reported in Table 1 above, in 2019 ADI had a market share of [10-20]% on the market for general purpose analog ICs and Maxim had a market share of [0-5]%. Combined, the Parties would have a market share of [10-20]%. The Transaction therefore does not give rise to a horizontally affected market. However, in the signal conversion ICs sub segment, the Parties have a combined market share of [40-50]%, with ADI having a market share of [40-50]% and Maxim having a market share of [5-10]%.

(76) Table 2 below provides an overview of the Parties’ (and their main competitors’) market shares in the global supply of signal conversion ICs in the period 2017-2019.

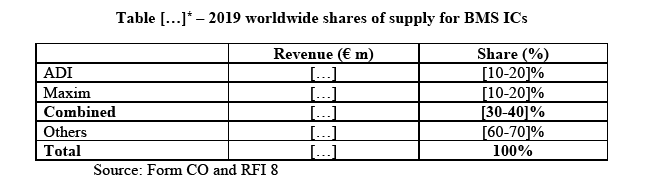

(77) Table 2 confirms that ADI and Texas Instruments are each other’s biggest competitors in the sub-segment of signal conversion ICs, while Maxim represents a smaller portion of the market, along with several other smaller competitors.

(78) The results of the market investigation confirm that, after the acquisition, there will be sufficient suppliers of signal conversion IC left to exercise an effective competitive constraint on the merged entity.56 One customer observed that Texas Instruments has been the strongest player and that the proposed Transaction will allow ADI to finally catch up: “With TI's acquisition of National Semiconductor in 2011, the dominance of TI has been high, so ADI caught up with the acquisition of Linear Technology and now with Maxim. Plus, there will be other suppliers like ON with a vested interest in this market. Not to forget Microchip which has grown into a viable competitor, too.”57 Another consumer echoes that sufficient alternative suppliers of analog semiconductors remain on the market post-Transaction: “There are many players in the analog semiconductor market, and we think that this transaction will not change the market structure in a non-competitive state.”58 Finally, one of the responding competitors signals that other suppliers of analog ICs have the know-how required to compete on a market for signal conversion ICs: “Concerning signal conversion ICs and Voltage reference ICs, part of the market and competition may be found in Analog specific market developing equivalent products, even if products are not classified in the same way, the know-how is available in other companies.”59

(79) Moreover, the majority of respondents indicate that ADI and Maxim are not engaged in head-to-head competition, submitting for example that while the Parties’ portfolios overlap to a certain degree, ADI’s products […] and Maxim’s products rather middle-end products.60 Overall, no consumers or competitors expect that the Transaction will have a negative impact on the market for signal conversion ICs while several respondents expect that the acquisition will have a positive impact.61

(80) Finally, the Commission considered whether the Transaction might make coordination on the market for general purpose analog ICs or on a potential market for signal conversion ICs more likely. The Court of Justice of the European Union has defined coordination as follows: “[…] the relationship of interdependence existing between the parties to a tight oligopoly within which, on a market with the appropriate characteristics in particular in terms of market concentration, transparency and product homogeneity, those parties are in a position to anticipate one another’s behaviour and are therefore strongly encouraged to align their conduct on the market in such a way as to maximise their joint profits by increasing prices […]. In such a context, each operator is aware that highly competitive action on its part [i.e. cheating] would provoke a reaction on the part of the others [i.e. punishment], so that it would derive no benefit from its initiative.”62

(81) Coordination is more likely to emerge in markets where it is relatively simple to reach a common understanding on the terms of coordination.63 While the potential market for signal conversion ICs is concentrated and would be more concentrated following the Transaction, the Commission considers that the market is not transparent. […], there are many smaller suppliers remaining. Furthermore, one respondent to the market investigation also stated that other suppliers of analog ICs have the know-how required to compete on a potential market for signal conversion ICs: “Concerning signal conversion ICs and Voltage reference ICs, part of the market and competition may be found in Analog specific market developing equivalent products, even if products are not classified in the same way, the know- how is available in other companies.”64 Therefore, the Commission considers that coordination on a potential market for signal conversion ICs or a market for general purpose analog ICs is likely not to be feasible.

(82) The Horizontal Merger Guidelines, after referring to the transparency of the market as a condition to reach the terms of the coordination, set out three specific conditions that are required for coordination to be sustainable: (i) the ability to monitor; (ii) a credible deterrence mechanism; and (iii) the impact of reactions by outsiders.65 As regards the first condition, the Commission considers that because of the presence of other suppliers of signal conversion ICs and others suppliers of analog ICs with the know-how required to compete on this potential market, it would generally be difficult to achieve coordination and to monitor any coordinated behaviour on the market. As to the third condition, any form of collusion might be broken by any of these suppliers.

(83) Finally, the Commission considers that coordination on a potential market for signal conversion ICs would not be more likely as a result of the proposed Transaction. The market shares from 2017-2019 in Table 2 above indicate that the market is currently already concentrated and that Maxim will only contribute with a [5-10]% market share (2019) to the combined entity. Thus, the pre-merger concentration levels would not fundamentally change following the Transaction. Moreover, […]

(84) The results of the market investigation also confirm that no consumers or competitors expect that the Transaction will have a negative impact on the market for signal conversion ICs, while several respondents expect that the acquisition will have a positive impact.66 In this regard, the Commission also notes that there is no evidence of past collusive behaviour on this potential market.

(85) In light of the above, the Commission concludes that the Transaction does not give rise to serious doubts with regard to its compatibility with the internal market as a result of possible horizontal effects on a potential market for signal conversion ICs.

5.2.2. Infotainment ASSPs used in automotive applications

5.2.2.1. The Notifying Party’s view

(86) The Notifying Party observes that, based on the Commission’s previous decisions, the market for semiconductors may be divided by (i) category of semiconductor; and (ii) end-use application. As regards the distinction by category, the Notifying Party submits that the Transaction does not have any negative impact on the market for application-specific analog ICs used in automotive applications as the Parties’ combined market share is only [5-10]%.

(87) When the market is assessed on the basis of the end-use application, the Notifying Party submits that there is a horizontal overlap on a potential market for Infotainment ASSPs, the Notifying Party states that this does not lead to competition concerns.

(88) In particular, the Notifying Party argues that the Parties would face competition from other suppliers and they would not be close competitors. Moreover, the Notifying Party submits that customers exert buyer power on a potential market for Infotainment ASSPs.

5.2.2.2. The Commission’s assessment

(89) On the basis of the results of the market investigation and the information provided by the Notifying Party, the Commission considers that the proposed Transaction does not raise serious doubts as to its compatibility with the internal market as regards application-specific analog ICs used in automotive applications or as regards infotainment ASSPs for the following reasons.

(90) First, the market investigation makes clear that neither competitors nor consumers perceive either ADI or Maxim as the leading market player in infotainment ASSPs. Rather, the majority of competitors and customers indicates that […].67

(91) […], which provides an overview of the Parties’ (and their main competitors’) market shares in the global supply of infotainment ASSPs in the period 2017-2019.

(92) […] quantitatively, it is consistent with the results of the market investigation as it does show that the Parties face competition from several other important suppliers in a potential market for infotainment ASSPs. This is confirmed by the market investigation, where a majority of competitors and consumers indicates that there will be sufficient manufacturers left on the market after the Transaction to exercise an effective constraint on the merged entity.68

(93) Second, the majority of the respondents to the market investigation indicate that ADI and Maxim are competing head to head for infotainment ASSPs. According to the Notifying Party however, the product portfolios of the Parties only overlap in two product areas within infotainment ASSPs: (i) connectivity; and (ii) infotainment power products. With regard to the former, Maxim focusses primarily on […], a high-speed connectivity solution), whereas ADI focusses primarily on […]. As to infotainment power products, Maxim’s products are mainly used for […], whereas ADI’s products are mainly used for […].

(94) Third, as regards the buyer power of customers, the Notifying Party submitted that most customers are sophisticated, globally active and they look for a number of suppliers to meet their infotainment needs. The Commission’s market investigation confirms that infotainment ASSP products are particularly customised to fulfil demanding requirements of customers and suit end-products.69 Customers often organise tenders for new designs at the “design in” stage. During this process, manufacturers often cooperate with customers in order to agree on specific technical and packaging requirements.70. Moreover, Customers have also generally confirmed that an adequate number of alternative suppliers will remain on the market post- Transaction.71 As a result, a majority of customers expects the impact of the Transaction to be neutral.72

(95) Fourth, the results of the market investigation show that also the majority of the competitors expect that the Transaction will have a neutral impact on the market, while no competitors fear a negative impact.73

(96) In light of the above, the Commission considers that the proposed Transaction does not raise serious doubts as to its compatibility with the internal market in relation to the potential market for application-specific analog ICs used in automotive applications, as well as in the potential market for infotainment ASSPs, in light of the fact that the Parties have a small combined market share on the former potential market and the fact that sufficient alternative market players will remain active following the Transaction.

5.2.3. Application-specific analog ICs: Industrial – Medical/healthcare

5.2.3.1. The Notifying Party’s view

(97) The Notifying Party submits that the Transaction would not have any negative effect on a market for application-specific analog ICs used in industrial applications as the combined market share of the Parties does not exceed [20-30]%. While the Commission did not distinguish a further segmentation for these type of ICs in prior decisions, the Notifying Party submits that even on a potential market for industrial healthcare ASSPs, the Transaction does not raise serious concerns for competition as the combined market share of the Parties overstates the level and importance of competition between the Parties on the market.

(98) The Notifying Party submits in particular that the Parties would face competition from other suppliers and that the Parties would not be close competitors. Lastly, customers would exert buyer power in a potential market for industrial healthcare ASSPs.

5.2.3.2. The Commission’s assessment

(99) Table 1 above shows that on a market for application-specific analog ICs used in industrial applications the combined market share of the Parties does not exceed [20-30]%. Moreover, the market share increment resulting from the merger on this market would only be [0-5]%. On a potential market for healthcare ASSPs however, there is a horizontal overlap between the Parties.

(100) Table […]* below provides an overview of the Parties’ (and their main competitors’) market shares in the global supply of industrial healthcare ASSPs in the period 2017-2019.

(101) The market shares in Table […]* above indicate that […]. According to the Notifying Party, this […] coincides with general market growth as medical applications are one of the fastest growing segments of the market for industrial semiconductors.74

(102) […]. The combined market share of the Parties in the EEA does not exceed [20-30]%, while the market share increment resulting from the merger on an EEA- wide market would only be [0-5]%. Table […]* below shows the Parties’ (and their main competitors’) market shares in the global supply of industrial healthcare ASSPs in the period 2017-2019.

(103) On the basis of the above, the Commission considers that the Parties face significant competition from larger competitors on a potential narrow market for industrial healthcare ASSPs, particularly within the EEA.

(104) Lastly, the Commission assessed whether customers are able to exert buyer power on a potential market for industrial healthcare ASSPs. The Notifying Party submits that competition generally takes place at the ‘design in’ stage of product development, on a socket by socket basis, meaning that customers choose a preferred supplier for each relevant socket/design. Since customers may require a number of sockets/components, it would be common for customers to multi-source. Furthermore, […].

(105) The results from the market investigation are however not conclusive as regards the possibility for customers to switch to other products. While a majority of competitors responded that customers can easily switch between different providers for analog ICs in general, the majority of customers (including […]) indicated that this would not be the case.75

(106) However, regardless of the question whether customers will be able to exert buyer power, the Commission considers that market share information above confirms that other suppliers will exercise sufficient competitive constraints on the Parties after the proposed Transaction. In any event, the market investigation confirmed that a majority of the respondents considers that the Transaction will have a positive or neutral impact on the market for application-specific analog ICs in industrial applications. No competitor or consumer expects that the proposed Transaction will have a negative impact on the market.76

(107) In light of the above, the Commission considers that the proposed Transaction does not raise serious doubts as to its compatibility with the internal market in relation to the potential market for application-specific analog ICs used in industrial applications, as well as in the narrower potential market for industrial healthcare ASSPs.

5.2.4. Application-specific analog ICs: Automotive (BMS)

(108) As mentioned above in paragraph (36), a competition concern was expressed in the course of the market investigation by a competitor regarding the Parties’ [...] in the supply of BMS ICs.

(109) BMS encompass various ICs (including microcontrollers, battery cell controllers, detectors/sensors, resistors etc.) and are used to manage the energy levels of battery cells by monitoring their state and report that to a central system. Within BMS ICs, battery cell controllers are components that specifically measure the battery’s state of health or state of charge. While BMS can be used in many different end-use applications, they are increasingly in demand in the automotive industry to monitor energy levels of batteries in electric and hybrid vehicles.

(110) The Parties do not manufacture whole battery packs or all ICs that are part of a BMS. Rather, both ADI and Maxim manufacture the battery controllers and the ICs that bridge these battery cell controllers to the microcontrollers to take appropriate action on what is sensed in the battery (e.g. the levels of remaining energy).

(111) According to a respondent to the market investigation, […].77

5.2.4.1. The Notifying Party’s view

(112) The Notifying Party submits that it is not necessary or appropriate to identify a separate market for BMS ICs for automotive applications, or even more narrowly a market for battery controllers, because they are used in a wide range of industries albeit with different specifications. Even on these narrow markets however, the Transaction would not lead to competition concerns in the Notifying Party’s view, because the Parties would face competition from several alternative suppliers, the Parties would not be close competitors and customers exert buyer power.

(113) On potential wider markets including BMS ICs, such as other automotive ASSPs or application-specific analog ICs used in automotive applications, the combined market share of the Parties does not exceed [20-30]% (2019) and the Notifying Party therefore submits that that the Transaction would not raise competition concerns on these markets, also because several alternative suppliers remain on these markets post-Transaction.

5.2.4.2. The Commission’s assessment

(114) On the basis of the information in Table 1 above, the Commission concludes that the proposed Transaction does not lead to any competition concerns on a market for application-specific analog ICs used in automotive applications, as the combined market share of the Parties does not exceed [20-30]% for 2019. Therefore, the Commission focussed its assessment on potential narrower markets.

(115) As indicated in paragraph (30), previously, the Commission considered whether within the market for application-specific analog ICs used in automotive applications a further distinction may be drawn between power and non-power analog ICs.78 However, ultimately the Commission concluded that the precise product market definition could be left open.

(116) On the basis of this distinction, both BMS ICs for automotive applications and even more narrowly, battery cell controllers would fall within a potential market for power analog ICs, with among others smart power ICs and discrete power devices. The combined market shares of the Parties on this potential market for power analog ICs would however be only [5-10]% (2019).79 The proposed Transaction would therefore not raise any concerns on a potential market for power analog ICs.

(117) The Notifying Party further submits that a distinction could be made between infotainment ASSPs and other automotive ASSPs, in accordance with the methodology used by the WSTS. On the latter potential market for other automotive ASSPs, the combined worldwide market share of the Parties would only amount to [0-5]% (2019).80 On this market, the proposed Transaction therefore does not raise a competition concern.

(118) Lastly, the Commission considered whether the proposed Transaction raises competition concerns on a separate market for BMS and more narrowly a market for battery cell controllers.

(119) The Notifying Party submits that WSTS does not report data regarding either BMS or battery cell controllers. Therefore, the Notifying Party provided other third party market information relating to product segments for BMS ICs used in hybrid-electric and electric vehicles, as well as BMS ICs used in start-stop systems (no specific market share data at the granularity of battery cell controllers is available). This information is included in Table […]* below.

(120) The Notifying Party further submitted that the Parties have […]. Moreover, the worldwide shares of supply above would most likely overstate the Parties’ actual position on the market. Notably, the success of BMS ICs depends on the success of the platform within the vehicle for which they are used. BMS ICs are typically sourced for the lifetime of a platform, which is usually around four to five years. Therefore, competition for BMS ICs takes place in the context of calls for tenders. As a result of […], the Notifying Party submits that their revenues […].

(121) In addition to ADI and Maxim, there are several other suppliers of BMS ICs that will be able to compete following the acquisition. On the basis of the Notifying Party’s best estimate, these competitors include NXP ([10-30]%), Texas Instruments ([10-20]%), Infineon ([5-20]%), Panasonic/Nuvoton ([5-20]%), Denso ([5-20]%), STMicroelectronics ([0-10]%) and Renesas/Intersil ([0-10]%).81 As no market data is available regarding battery cell controllers, the Notifying Party further submits that the competitive landscape for battery cell controllers from its perspective does not look materially different. […].82

(122) On the basis of the above, the Commission considers that, on a potential market for BMS ICs, sufficient competition will remain following the proposed Transaction. Finally, the Commission assessed whether customers may exert buyer power on a potential market for BMS ICs. Moreover, customers on the market for BMS ICs are sophisticated purchasers. Competition between BMS IC suppliers mainly takes place at the ‘design in’ stage, where on a socket by socket basis, customers choose a preferred supplier. In this regard, customers of BMS ICs tend to multisource and switch between suppliers as also demonstrated by the examples in paragraph (120) above. As regards battery cell controllers, the Commission concludes that there seems to […]* market information available at this level of granularity. However, it has not found any information that would support a conclusion that its market assessment would be substantially different from its assessment of the potential competitive impact on a potential market for BMS ICs.

(123) Taking into account all of the above, the Commission concludes that even on a narrow potential market for BMS ICs, the proposed Transaction does not raise serious competition concerns.

5.2.5. Conclusion on potential horizontal effects

(124) For the reasons set out in sections 5.2, and in light of the evidence made available during the investigation, the Commission considers that the Transaction does not give rise to serious doubts with regard to its compatibility with the internal market as a result of possible horizontal non-coordinated effects, either through the creation of strengthening of a dominant position or otherwise significantly impeding effective competition, in any of the above analysed markets (i.e. markets for signal conversion ICs, application-specific analog ICs used in automotive applications, infotainment ASSPs, application-specific analog ICs used in industrial applications, industrial healthcare ASSPs, power analog ICs, other automotive ASSPs and BMS ICs ).

5.3. Potential conglomerate effects in analog IC markets

5.3.1. Introduction

(125) The Notifying Party submitted that one of the key economic and strategic rationales of the proposed Transaction is to combine the Parties’ portfolios, which are largely complementary. […]. The Notifying Party also submits that the Parties’ combined annual R&D budget will allow the merged entity to better serve customer needs and compete more effectively with other industry participants.

5.3.2. The Notifying Party’s view

(126) The Notifying Party submits that the proposed Transaction would not give rise to any conglomerate concerns.

(127) First, the Notifying Party argues that the Parties would not have the ability to foreclose competitors because none of the products offered by the merged entity are “must have” products. It explains that several significant competitors offer comparable products on a global basis and that these competitors will continue to exert pressure on the merged entity.

(128) Furthermore, the Notifying Party submits that the combination of the Parties’ product portfolios would not create opportunities for technical tying or commercial bundling of any products. Moreover, it argues that even if the Parties were to engage in bundling strategies, the Parties’ competitors would be able to replicate the Parties’ potential bundles and to compete effectively.

(129) Second, the Notifying Party argues that the merged entity would not have an incentive to engage in a foreclosure strategy. The Notifying Party submits that the Parties have a modest market share across the majority of their respective and combined portfolios. In affected markets, it considers that there will remain a sufficient number of competitors to exercise an effective constraint. Furthermore, customers in this sector are generally sophisticated market players that closely evaluate and would make use of other supply options if any market player were to attempt to tie or bundle ICs. Lastly, ADI argues that it already has many of the Parties’ product types in its current product portfolio and yet does not currently bundle or integrate these products technically or commercially. It considers that the proposed Transaction would not change its incentives to do so.

(130) Third, in the absence of the ability or incentive to engage in a foreclosure strategy, the Notifying Party submits that any anticompetitive impact is improbable.

5.3.3. The Commission’s assessment

5.3.3.1. Ability to foreclose

(131) In order to have the ability to foreclose rivals, the merged entity must have a significant degree of market power in at least one of the markets concerned. That is, at least one of the Parties’ products must be viewed by many customers as particularly important and there must be few relevant alternatives for that product.83

(132) In this respect, the Commission notes that the merged entity will represent [40-50]% of the market for general purpose analog ICs - signal conversion. Moreover, there is at least one significant competitor with a comparable market position (Texas Instruments) and several smaller players in the market. Therefore, in light of the structure of the market for general purpose analog ICs – signal conversion and the merged entity’s position in that market, it is unlikely that after the Transaction the merged entity will have the ability to leverage its position into other neighbouring markets after the Transaction. Moreover, the Parties’ combined market share in general purpose analog ICs as well as in other sub-segments in the general purpose analog market will remain below [30-40]%.

(133) The Commission also notes that the merged entity would have a market share of [30-40]% in the market for application-specific analog ICs – infotainment automotive ASSPs. There is at least one significant competitor with a comparable market position (Texas Instruments), another strong competitor (STMicroelectronics) and several smaller players in the market. The Commission is therefore of the view that based on its position in the market for application-specific analog ICs – infotainment automotive ASSPs, it is unlikely that after the Transaction the merged entity will have the ability to leverage its position into other neighbouring markets.

(134) The Commission also notes that the merged entity would have a market share of [30-40]% in the market for application-specific analog ICs – industrial medical/healthcare ASSPs. There are at least two significant competitors with a comparable or material market position (Texas Instruments and STMicroelectronics), and several smaller players in the market. The Commission is therefore of the view that based on its position in the market for application-specific analog ICs – industrial medical/healthcare ASSPs, it is unlikely that after the Transaction the merged entity will have the ability to leverage its position into other neighbouring markets.

(135) Moreover, the Parties’ combined market share in any of the product categories within the market for application-specific analog ICs will remain below [30-40]%. There are, however, two sub-segments where the combined market shares of the Parties will be equal to or exceed [30-40]%. These sub-segments are: wireless infrastructure & other wireless communication ASSPs [30-40]% and one of its further potential sub-segmentations, wireless infrastructure ASSPs [30-40]%. However, the increment brought about by the Transaction would be less than [0-5]% in each of these potential markets. For this reason, the Transaction cannot be deemed to consolidate a situation of market power such that the merged entity will have the ability to leverage its position into other neighbouring markets.

(136) The Notifying Party has also provided the Parties’ and competitors’ market shares for the rest of the semiconductor products indicated in paragraph (68). According to those market data, the merged entity’s estimated market shares for semiconductor markets other than the aforementioned markets, will not exceed [30-40]% and several significant competitors will remain active in each market.

(137) The results of the market investigation confirm that, in principle, the Parties do not sell any product that would be difficult to source from alternative suppliers. Both customers and competitors agree that that the merged entity would have neither an advantage over its main competitors nor the ability to leverage its position on the market.84 Most of the competitors indicated that alternative suppliers would remain on the market for each product in the respective Parties’ portfolio, such that competitors would have the capability to supply equivalent or similar products

(138) Some customers took the view that, even though switching to alternative suppliers would be possible, such switching would not be likely considered during the implementation of a specific project relying on the relevant ICs, but would be possible from one project to the other. This is because the ICs that manufacturers produce are often dependent on customer requirements and end-designs. According to a customer “semiconductor manufacturers do not completely develop the final product themselves, but rather decide which component functionality would be suitable for the customer’s end product and then develop solutions accordingly, taking into account technical feasibility. Afterwards, customers evaluate the semiconductor products and select a design, which is the most suitable for their final product”.85 Nevertheless, the Commission observes that competition between

suppliers largely happens before a project is implemented by a given customer, such that the scope of switching would be sufficient to constrain de merged entity.86

5.3.3.2. Incentive to foreclose

(139) The Commission has also assessed whether the merged entity will have an incentive to engage in bundling of different semiconductors, in order to foreclose rivals from effectively competing for customers who purchase different products.

(140) The merged entity will continue to face several credible competitors, many of which are able to offer the same range of products (as single solutions or bundles) as the Parties. These suppliers will therefore be able to respond to the merged entity bundling strategies by offering equally attractive solutions. Accordingly, the market investigation confirms that, after the Transactions, by integrating their respective product portfolios, the Parties will not gain a competitive advantage on their main competitors, but rather achieve the same breadth of offer.87

(141) Possible bundled sales by the merged entity would therefore unlikely lead to the marginalisation of competitors, who will be able to replicate the offers and/or to propose different discounts on other bundles.

(142) Consistently with this view, the majority of the participants to the market investigation submitted that the merged entity, through the offering of bundles including different products would not have the incentive to foreclose competing operators in any of the aforementioned markets.. This was also confirmed by preliminary contacts with the Parties’ customers and competitors.88

(143) Based on the above, the Commission considers that the merged entity is unlikely to have the incentive to foreclose competitors in semiconductors markets by bundling different products post-Transaction.

5.3.3.3. Impact on effective competition

(144) Regardless of whether the merged entity has either the ability or the incentive to foreclose rivals in the semiconductors markets by bundling different products, the Commission considers that such strategy would not have an appreciable impact on competition.

(145) Any potential impact of such bundling strategy would be mitigated by the ability of competitors to react to such strategy by offering similar or other bundles based on their portfolio. This could be particularly the case with respect to the Parties’ main competitors (e.g. Texas Instruments, STMicroelectronics, NXP, ONSemi), that have a similar market presence and comparable […]* portfolios. Furthermore, customers tend to acquire separate ICs from various suppliers, depending on their end-solution and technical requirements. For these reasons, bundling is not a common practice in the semiconductor market.89

(146) The results of the market investigation confirm the limited effect of the Transaction. Notably the vast majority of the participants to the market investigation submitted that the Transaction would not affect the markets for general purpose signal conversion ICs, general purpose amplifier & comparator ICs, general purpose power management – voltage reference ICs, automotive infotainment ASSPs, general purpose interfaces and isolator ICs, general purpose power management ICs, switching regulator ICs, supervision, sequencing and control and other power management ICs, application-specific ICs: communication, application-specific ICs: consumer, application-specific ICs: industrial and others, end-use specific ICs: industrial - test and measurement.90

(147) Similarly, the vast majority of respondents submitted that the Transaction would have an either positive or neutral impact on their activity.91

5.3.3.4. Conclusion on conglomerate effects

(148) In light of the above, the Commission considers that […]* does not raise serious doubts as to its compatibility with the internal market as a result of conglomerate effects, which could create or strengthen a dominant position or otherwise impede effective competition in the semiconductors markets.

6. CONCLUSION

(149) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the ’Merger Regulation’). With effect from 1 December 2009, the Treaty on the Functioning of the European Union (‘TFEU’) has introduced certain changes, such as the replacement of ‘Community’ by ‘Union’ and ‘common market’ by ‘internal market’. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the ‘EEA Agreement’).

3 Publication in the Official Journal of the European Union No C 76, 05.03.2021, p. 21

4 Commission decision of 16 October 2019 in case M.9466 - Infineon/Cypress, paragraph 10.

5 Commission decision of 17 September 2015 in case M.7585 - NXP Semiconductors/Freescale Semiconductor, paragraph 14; Commission decision of 18 January 2018 in case M.8306 - Qualcomm/NXP Semiconductors, paragraph 33; Commission decision of 16 October 2019 in case M.9466 - Infineon/Cypress, paragraphs 10-11.

6 Commission decision of 24 June 2002 in case M.2820 - STMicroelectronics/Alcatel Microelectronics, paragraph 11; Commission decision of 17 September 2015 in case M.7585 - NXP Semiconductors/Freescale Semiconductor, paragraphs 44-45; and Commission decision of 16 October 2019 in case M.9466 - Infineon/Cypress, paragraph 10.

7 Commission decision of 17 September 2015 in case M.7585 - NXP Semiconductors/Freescale Semiconductor, paragraph 14; Commission decision of 18 January 2018 in case M.8306 - Qualcomm/NXP Semiconductors, paragraph 33; and Commission decision of 16 October 2019 in case M.9466 - Infineon/Cypress, paragraph 14.

8 Commission decision of 17 September 2015 in case M.7585 - NXP Semiconductors/Freescale Semiconductor, paragraph 48; Commission decision of 23 November 2015 in case M.7686 - Avago / Broadcom, paragraph 14.

9 Throughout this decision, when the Commission refers to the (number of) respondents in relation to a given question of the market investigation, this excludes all respondents that have not provided an answer to that question or replied “I don’t know”, unless stated otherwise. For example, “a majority of respondents” means “a majority of respondents having replied to a given question and not having ticked “I don’t know””.

10 Replies to Commission questionnaire 1 to customers and Commission questionnaire 2 to competitors, question 3.

11 Replies to Commission questionnaire 1 to customers and Commission questionnaire 2 to competitors, question 5.

12 Commission decision of 17 September 2015 in case M.7585 - NXP Semiconductors/Freescale Semiconductor, paragraphs 49 and 51. The distinction by product category was confirmed by the market investigation (Replies to Commission questionnaire 1 to customers and Commission questionnaire 2 to competitors, question 8).

13 Section 6.H of the Form CO.

14 Section 6.E of the Form CO.

15 Section 6.I of the Form CO.

16 Replies to Commission questionnaire 1 to customers and Commission questionnaire 2 to competitors, question 5.

17 Replies to Commission questionnaire 1 to customers and Commission questionnaire 2 to competitors, question 6.

18 Replies to Commission questionnaire 2 to competitors, question 6.2.

19 Replies to Commission questionnaire 1 to customers and Commission questionnaire 2 to competitors, question 7.

20 Replies to Commission questionnaire 1 to customers, question 7.1.

21 Replies to Commission questionnaire 2 to competitors, question 7.2.

22 Commission decision of 17 September 2015 in case M.7585 - NXP Semiconductors/Freescale Semiconductor, paragraph 48; Commission decision of 23 November 2015 in case M.7686 - Avago / Broadcom, paragraph 15.

23 Commission decision of 17 September 2015 in case M.7585 - NXP Semiconductors/Freescale Semiconductor, paragraph 49.

24 Commission decision of 17 September 2015 in case M.7585 - NXP Semiconductors/Freescale Semiconductor, paragraph 48-52.

25 Commission decision of 17 September 2015 in case M.7585 - NXP Semiconductors/Freescale Semiconductor, paragraph 49.

26 Replies to Commission questionnaire 1 to customers and Commission questionnaire 2 to competitors, question 5.

27 Commission decision of 17 September 2015 in case M.7585 - NXP Semiconductors/Freescale Semiconductor, paragraph 49.

28 Replies to Commission questionnaire 1 to customers and Commission questionnaire 2 to competitors, question 8.

29 Replies to Commission questionnaire 1 to customers, question 9.

30 Replies to Commission questionnaire 1 to customers and Commission questionnaire 2 to competitors, question 10.

31 Replies to Commission questionnaire 2 to competitors, question 11.

32 Replies to Commission questionnaire 1 to customers, question 11.

33 Replies to Commission questionnaire 1 to customers and Commission questionnaire 2 to competitors, question 12.

34 Replies to Commission questionnaire 2 to competitors, question 12.2.

35 Commission decision of 18 January 2018 in case M.8306 - Qualcomm/NXP Semiconductors, paragraph 24.

36 Commission decision of 18 January 2018 in case M.8306 - Qualcomm/NXP Semiconductors, paragraphs 33-45.

37 Commission decision of 24 June 2002 in case M.2820 - STMicroelectronics/Alcatel Microelectronics, paragraph 14.

38 Commission decision of 18 January 2018 in case M.8306 - Qualcomm/NXP Semiconductors, paragraph 24.

39 Replies to Commission questionnaire 1 to customers and Commission questionnaire 2 to competitors, question 13.

40 Replies to Commission questionnaire 1 to customers, question 13.1.

41 Commission decision of 17 September 2015 in case M.7585 - NXP Semiconductors/Freescale Semiconductor, paragraph 58.

42 Commission decision of 18 January 2018 in case M.8306 - Qualcomm/NXP Semiconductors, paragraph 242.

43 Commission decision of 16 October 2019 in case M.9466 - Infineon/Cypress, paragraph 38.

44 Replies to Commission questionnaire 1 to customers and Commission questionnaire 2 to competitors, questions 14-17.

45 Guidelines on the assessment of horizontal mergers under the Council Regulation on the control of concentrations between undertakings (“Horizontal Merger Guidelines”), OJ C 31, 05.02.2004, paragraph 22.

46 A merger may also make coordination easier, more stable or more effective for firms which were coordinating prior to the merger.

47 Merger Regulation, recital 25. Similar wording is also found in paragraph 25 of the Horizontal Merger Guidelines.

48 Horizontal Merger Guidelines, paragraph 26.

49 Horizontal Merger Guidelines, paragraph 39.

50 Horizontal Merger Guidelines, paragraph 41.

51 Guidelines on the assessment of non-horizontal mergers under the Council Regulation on the control of concentrations between undertakings (“Non-Horizontal Merger Guidelines”), OJ C 265, 18.10.2008, paragraph 91.

52 Non-Horizontal Merger Guidelines, paragraph 92.

53 Non-Horizontal Merger Guidelines, paragraph 93.

54 Non-Horizontal Merger Guidelines, paragraph 93.

55 Non-Horizontal Merger Guidelines, paragraph 94.

* Should read: “Section 5.3.”.

56 Replies to Commission questionnaire 1 to customers and Commission questionnaire 2 to competitors, question 20.

57 Replies to Commission questionnaire 1 to customers, question 21.4.

58 Replies to Commission questionnaire 1 to customers, question 21.4.

59 Replies to Commission questionnaire 2 to competitors, question 21.4.