Commission, December 7, 2020, No M.9677

EUROPEAN COMMISSION

Decision

DIC / BASF COLORS & EFFECTS

Subject: Case M.9677 — DIC/BASF Colors & Effects

Commission decision pursuant to Article 6(1)(b) in conjunction with Article 6(2) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Madam or Sir,

(1) On 16.10.2020, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which the DIC Corporation (together with the entities it directly or indirectly controls referred to as “DIC”) acquires within the meaning of Article 3(1)(b) of the Merger Regulation sole control of the whole of BASF SE’s (“BASF”, Germany) BASF Colors & Effects (together with the entities it directly or indirectly controls referred to as “BCE”), (“the Transaction”).3 DIC is designated hereinafter as the “Notifying Party” and, together with BCE, as the “Parties”.

1. THE PARTIES

(2) DIC is a publicly listed company headquartered in Japan, active in the production and sale of printing inks, organic pigments and synthetic resins. As regards pigments and other colourants, DIC is mainly active through its wholly-owned subsidiary SunChemical Corporation (“SunChemical”, US).

(3) BCE’s business includes the manufacture and sale of pigments and other colourants. BASF is a publicly listed international chemical and industrial company headquartered in Ludwigshafen am Rhein, Germany. BCE represented less than [small percentage] of BASF’s worldwide turnover in 2018.

2. THE OPERATION

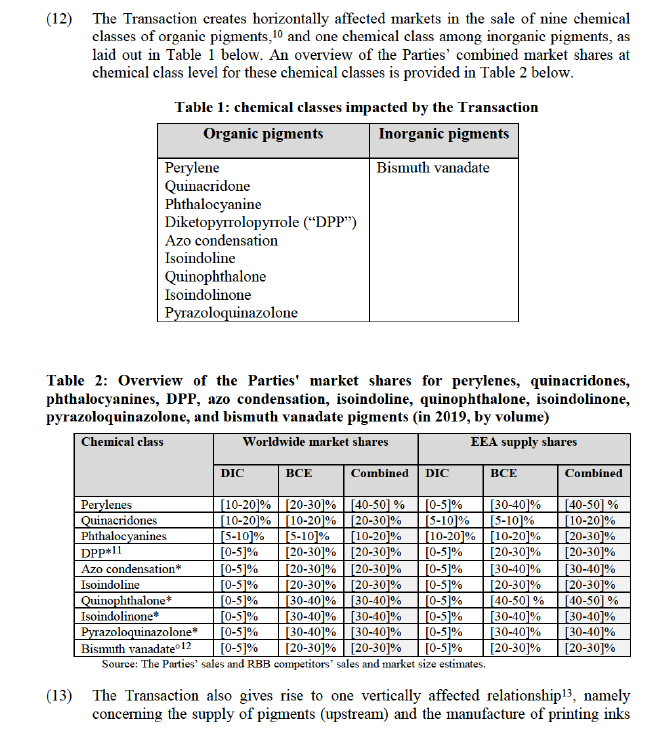

(4) In August 2019, DIC Corporation and BASF concluded a Sale and purchase Agreement setting out the terms of the Transaction, by which DIC will acquire the entirety of the shares of 19 individual entities as well as certain assets, jointly constituting BCE, from BASF. Following completion of the Transaction, DIC will thus acquire sole control of BCE. The Transaction is therefore a concentration within the meaning of Article 3(1)(b) of the EU Merger Regulation.

3. UNION DIMENSION

(5) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (DIC: EUR [...], BCE: EUR [...]).4 Each of them has an EU- wide turnover in excess of EUR 250 million (DIC: EUR [...], BCE: EUR [...]), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension.

4. THE PROCEDURE

(6) The Transaction was previously notified on 15.05.2020 and subsequently withdrawn on 23.06.2020. It was notified again on 16.10.2020.

(7) As a consequence, the Commission’s market investigation was twofold, with one set of questionnaires sent on 15.05.2020, and an additional, more targeted, set of questionnaires sent on 16.10.2020. The Commission considers that both sets of questionnaires constitute informative and relevant information for the purpose of assessing the present Transaction. As a result, both sets of questionnaires will be referred to in the present Decision, and both will be referred to under the terms “the Commission’s market investigation” or “the market investigation”.

5. COMPETITIVE ASSESSMENT

5.1. Analytical framework

(8) Under Articles 2(2) and 2(3) of the Merger Regulation, the Commission must assess whether a proposed concentration would significantly impede effective competition in the internal market or in a substantial part of it, in particular through the creation or strengthening of a dominant position.

(9) A merger can entail horizontal effects. In this respect, the Commission Guidelines on the assessment of horizontal mergers under the Merger Regulation (“the Horizontal Merger Guidelines”)5 distinguish between two main ways in which mergers between actual or potential competitors on the same relevant market may significantly impede effective competition, namely (a) by eliminating important competitive constraints on one or more firms, which consequently would have increased market power, without resorting to coordinated behaviour (non-coordinated effects); and (b) by changing the nature of competition in such a way that firms that previously were not coordinating their behaviour are now significantly more likely to coordinate and raise prices or otherwise harm effective competition. A merger may also make coordination easier, more stable or more effective for firms which were coordinating prior to the merger (coordinated effects).6

(10) In addition, a merger can also entail vertical effects when it involves companies operating at different levels of the same supply chain. Pursuant to the Commission Guidelines on the assessment of non-horizontal mergers under the Council Regulation on the control of concentrations between undertakings (the “Non-Horizontal Merger Guidelines”),7 vertical mergers do not entail the loss of direct competition between merging firms in the same relevant market and provide scope for efficiencies. However, there are circumstances in which vertical mergers may significantly impede effective competition. This is in particular the case if they give rise to foreclosure.8 The Non-Horizontal Merger Guidelines distinguish between two forms of foreclosure: input foreclosure, where the merger is likely to raise costs of downstream rivals by restricting their access to an important input, and customer foreclosure, where the merger is likely to foreclose upstream rivals by restricting their access to a sufficiently large customer base.9

5.2. Overview of affected markets

(11) The Transaction combines the activities of two global suppliers of (primarily organic) pigments. The focus of the Transaction is on combining the parties’ capabilities in the supply of certain types of pigments. Pigments are compounds that provide colour to a given material either by covering its surface (paints, coatings, printing inks) or by mixing with it (plastic applications). Pigments are distinct from dyes, which engage in chemical reactions with the material they are supposed to colour.

(downstream). This relationship is affected within the meaning of EU merger control14 because upstream the Parties’ market shares would exceed 30% in the sales of certain pigment chemistries which are used to produce printing inks. Moreover, the relationship is also affected because DIC’s market share for the manufacture of printing inks downstream exceeds 30% in one potential sub-segment, namely the manufacture of gravure liquid inks in the EEA.

(downstream). This relationship is affected within the meaning of EU merger control14 because upstream the Parties’ market shares would exceed 30% in the sales of certain pigment chemistries which are used to produce printing inks. Moreover, the relationship is also affected because DIC’s market share for the manufacture of printing inks downstream exceeds 30% in one potential sub-segment, namely the manufacture of gravure liquid inks in the EEA.

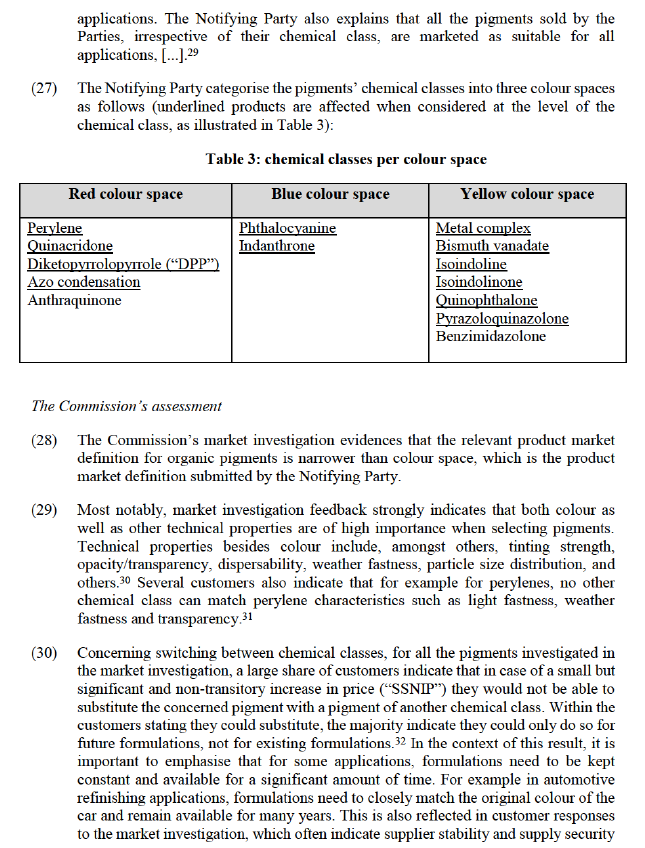

5.3. Market definitions

5.3.1. Pigments

(14) As explained above, a distinction can be drawn between organic pigments, whose chemical formula contain carbon atoms in covalent bonding, and inorganic pigments. Aside from these, effect pigments can be considered as forming a category of their own, in the sense that their main function is not to provide a given colour, but rather an effect (such as a metallic or a pearlescent effect).

(15) As shown above in Table 1, the main overlaps between the Parties’ activities relate to organic pigments. There are around 20 chemical classes of organic pigments, covering a range of colour shades. Each chemical class of pigments requires a different manufacturing process and often requires dedicated equipment. Within a chemical class, there are typically several different pigments, with different chemical composition, providing different colours and shades. For instance, the perylene class contains red, maroon, violet and black pigments. These individual pigments are usually referred to using their so-called colour index (for instance Pigment Red 179 – abbreviated PR179 – refers to a specific red shade within perylene pigments). However, some chemical classes, such as quinophthalone, only contain one colour index. Pigments can be mixed together (irrespective of their chemical class) to obtain even more colours.

5.3.1.1. Product market definition

Commission’s precedents

(16) In Clariant/Hoechst,15 the Commission considered organic and inorganic pigments as distinct product markets. In BASF/CIBA,16 the Commission considered a further potential sub-segmentation of organic and inorganic pigments by chemical class, and considered a potential further sub-segmentation into the following categories of pigment applications: (i) coatings, (ii) plastics and (iii) others, with the coatings category potentially split further into: (i) automotive, (ii) industrial and (iii) decorative coatings, ultimately leaving both questions open.

(17) As regards pigments other than organic pigments, in BASF/CIBA,17 the Commission treated bismuth vanadate and pearlescent effect pigments as separate chemical classes, and the potential segmentations by application described in paragraph (15) were also applied to them.

(18) In more recent pigment-related cases (Huntsman/Equity Interests18 and Tronox/Cristal19), the Commission suggested further sub-segmentations of each of the three categories of pigment applications (coatings, plastics and others). More particularly, with respect to TiO2,20 the Commission also considered potential segmentation by crystalline form (rutile vs anatase), as well as production process (sulphate-based vs chloride-based). However, both these cases analysed the market for TiO2, which is a white inorganic pigment, and which significantly differs from the broader range of primarily organic pigments being combined as a result of the Transaction in present case.

The Notifying Party’s view

(19) The Notifying Party submits that the appropriate market definition is by colour space, and that all red pigments, all blue pigments and all yellow pigments form three distinct relevant product markets. The Notifying Party considers that pigments within these classes exhibit similar properties, and can be substituted without changing the final product’s features.21

(20) First, the Notifying Party argues that it is colour rather than the chemical composition of the pigment that is most important to customers, and that, with this respect, manufacturers can rely on different chemistries to meet the customers’ colour and property requirements.22 The Notifying Party submits that the chemical classes can be categorised in colour spaces as indicated in Table 3 below and that the pigments categorised to each colour space have similar physical properties.

(21) Second, the Notifying Party stresses that switching pigments/formulation while conserving the final product’s precise colour and characteristics has become increasingly easy thanks to the recent improvements of colour matching software.23

(22) Third, the Notifying Party exhibits several examples of colour points that can be attained through different alternative formulations, using pigments from different chemical classes, as well as a few examples of products (in automotive coating or consumer goods) for which the precise colour can be matched exactly using alternative pigments formulations, all approved by their owner company (for example the automotive manufacturer who sells the vehicle).24 The Notifying Party also provides some examples of customers of the Parties switching between pigments belonging to different chemistries for the same application/need.25

(23) With respect to the possibility of finding alternatives in different chemical class for a given pigment, the Notifying Party provides the specific example of lead chromate pigments, a class of yellow pigments that was progressively removed from the market from 2010 onwards, due to its toxicity. The Notifying Party explains that several alternatives/substitutes/replacement solutions for lead chromate pigments, based on different chemistries. While presenting these elements, the Notifying Party however acknowledges that finding alternatives for lead chromates had been difficult and technically challenging due to these products’ high quality and cost-effectiveness.26

(24) Fourth, the Notifying Party further explains that pigment finder tools on pigment manufacturer’s websites usually allow customers to filter the searches by colour and applications, but not by chemical class. The Notifying Party submits that these tools are designed to reflect the customer’s expectations and criteria.27

(25) Fifth, in relation to a potential sub-segmentation of each chemical class by colour index (see above paragraph (14)), the Notifying Party argues that there is enough supply-side substitution, within each chemical class, between different colour indices, for them to be considered as forming part of the same product market, and that, despite requiring extensive washing of the production pipes, switching between colour indices is feasible, [...].28

(26) Finally, with respect to potential substitution across applications, the Notifying Party considers that pigments within each chemical class exhibit similar properties that make them suitable for use across applications, and that they are priced [...] across

as important criteria.33 Therefore, in case of a SSNIP, only a small minority of customers would be able to substitute a pigment of another chemical class in a short period of time.

(31) Moreover, the majority of customers indicated that within chemical classes they cannot easily switch between pigment products within the same colour index, with the majority claiming that it is either not possible or possible only for some applications, and indicating that testing and requalification would be required.34 Some customers point out, that different products, even within the same colour index, can have different qualities and characteristics.35 One customer points out that generally, “the more demanding the application, the harder it is to switch / qualify a new supplier” for a given colour index.36

(32) A majority of customers indicate they have used colour-matching software in the past five years. While many indicate that it can be helpful when selecting pigments or even replacing a pigment in an existing formulation, some say it is just a start as it only matches the colour. Significant qualification and testing processes may therefore still be required to confirm whether other technical specifications are met.37 One pigment competitor specifically mentioned that colour matching is not particularly relevant for high-performance pigments.38

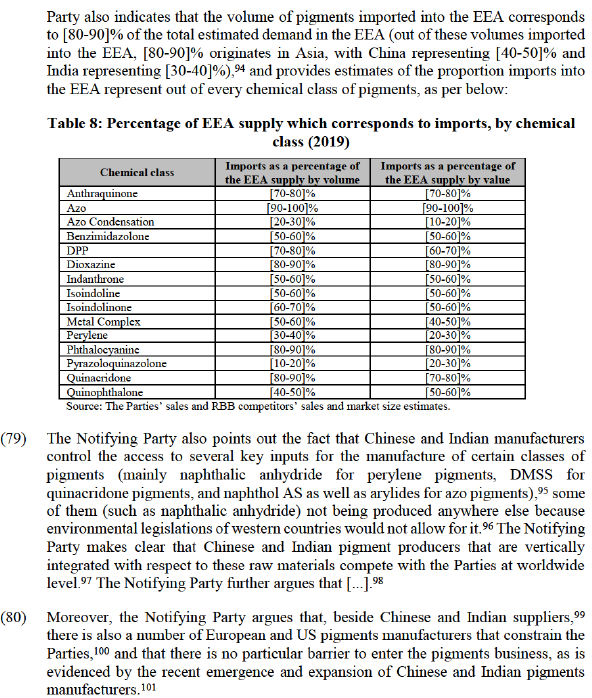

(33) The same argument applies to pigment finder tools on supplier websites. While these may give a general indication of colour and performance characteristics, it is not conclusive on whether a pigment meets a customer’s needs – particularly for demanding applications.

(34) In summary, the market investigation provides evidence that there is only very limited demand-side substitutability between chemical classes, and even between different products within a colour index. In situations where substitution is possible, it is often a time-consuming and costly process.39

(35) On the supply side, there appears to be very limited substitutability between chemical classes and even between colour indices within a chemical class. A competitor indicates that each chemical class has dedicated production lines. As different process steps are involved for each chemical class, switching will entail significant delays and investments and so it is not typically possible within the short period of time required to consider them to belong to the same relevant market from a supply side perspective.40 41

(36) With regard to supply side substitutability between colour indices within a chemical class, the Notifying Party argues this is possible and [...] for certain colour indices within quinacridones and phthalocyanines. However, the results of the market investigation gave clear indications that supply side substitutability is only possible for some chemical classes, and within these chemical classes for some colour indices only. For perylenes, all competitors indicate that switching production from one colour index to another within the chemical class costs considerable time and effort and constitutes a strategic decision.42 When asked for an example of such a switch for perylenes, one competitor notes: “I have not seen a switch in colour index as it does not make business sense.”43 For quinacridones and phthalocyanines, the vast majority of competitors indicate that switching production from one colour index to another within the chemical class costs considerable time and effort and constitutes a strategic decision.44 With regard to quinacridones, a competitor states: “Quinacridones are manufactured via two different technologies, namely Acidic ring closure (PPA route) and Thermal ring closure (Solvent route). We can switch CI [colour index] from one to another if the technology used to make the final CI is the same.” As for phthalocyanines, a competitor explains that while it is possible to switch between blues (i.e. various types of blue), it is not possible to switch between a blue and a green.

(37) A product market definition by application, as has been considered in Commission precedents, appears to be less appropriate and to yield a less clear market definition than a product market definition by chemical composition.

(38) First, pigments can be used for multiple applications. While the more high performance chemical classes are typically used for more demanding applications, none of the chemical classes is only used for specific applications.45 Within the chemical class, while some products are particularly suited to a specific application, individual products may also be suitable for multiple applications and are marketed as such.46 In the market investigation, customers explained that they used all chemical classes in a variety of applications.47 The majority of customers also agreed that some applications may use the same pigments.48

(39) Second, average price by application [...].49

(40) In summary, the Commission considers it likely that the specific application matters less than the specific customer’s need in terms of product quality and characteristics (e.g. in terms of light fastness, weather fastness and other characteristics). While a correlation between specific applications (e.g. automotive) and specific product characteristics (e.g. light and weather fastness) can be observed, this does not mean that the market should necessarily be distinguished by application, rather than the characteristics of the pigment. Indeed, pigments are distinguishable by chemical class or even within class by narrower colour indices. Expensive and high performance chemical classes, such as perylenes, will typically be used for a variety of demanding applications. For the purposes of this decision, the Commission will therefore assess the markets […]*the level of chemical class and colour index.

(41) In light of the above, the Commission considers that, for the purposes of the present decision, the appropriate definition of the relevant product market for pigments corresponds to at least the level of chemical class, and possibly to the narrower level of the colour index within each chemical class.

(42) However, even within colour indices, products differ in their characteristics and are not easy to substitute. Therefore, the Commission considers that certain segmentations within colour indices should be retained for the purposes of the competitive analysis, as there may be significant product differentiations.

(43) Ultimately, the question whether the product market definition is by chemical class or colour index can be left open for the purposes of the present decision, as it does not materially affect the Commission’s assessment since serious doubts arise as to the compatibility of the Transaction with the internal market due to horizontal effects in perylene and quinacridone pigments under any plausible product market definition relating to colour index level and no serious doubts arise as to the compatibility of the Transaction with the internal market as a result of non-horizontal effects or horizontal effects in chemical classes of pigments other than perylene and quinacridone under any plausible product market definition relating to colour index level.

5.3.1.2. Geographic market definition

Commission’s precedents

(44) The Commission has previously considered that the relevant geographic market for pigments is at least EEA-wide and possibly worldwide in scope.

(45) In case M.5355 – BASF / CIBA, the Commission’s market investigation showed that customers in the EEA were supplied from plants outside the EEA for pigments such as perylenes, suggesting a worldwide market.50 For some other pigments, such as bismuth vanadate, the Commission found that differences in regulation and prices suggested an EEA-wide market. Ultimately, the question was left open.

The Notifying Party’s view

(46) The Notifying Party submits that the geographic scope of the pigment sector is global.51

(47) Firstly, the Notifying Party argues that the Parties and their competitors supply their customers globally from a limited number of production locations. For example, DIC produces perylene pigments [...] in its Bushy Park (South Carolina, US) plant, and sells it globally.52

(48) Secondly, the Notifying Party submits that the pigment sector is characterised by significant global trade flows, particularly from China and India into the Western hemisphere.53 By way of illustration, the Notifying Party indicates that the volume of pigments imported into the EEA correspond to [80-90]% of the total estimated demand in the EEA. Out of these volumes imported into the EEA, [80-90]% originates in Asia, with China representing [40-50]% and India representing [30-40]%.54 Finally, the Parties stress that Chinese and Indian producers continue to expand production capacities and build distribution and warehousing facilities in the EEA to facilitate export and sales.55

(49) Finally, the Notifying Party argues that the pigments sector is not subject to significant transportation costs and not subject […]*significant regulatory barriers. As an indication, the Parties submit that transportation and related costs, such as packaging and freight, represent well below [small percentage] of total costs.56 In terms of regulation, the Notifying Party indicates that pigments are subject to the EU-wide REACH regulation.57 According to this regulation, manufacturers and importers of chemicals, including pigments, are obliged to register substances they produce and market. The Notifying Party considers that this does not form a barrier for non-EEA companies, evidenced by the significant amount of REACH registrations made by non-EU companies. The Notifying Party illustrates this further by supplying multiple examples of Chinese and Indian pigment suppliers showcasing their REACH compliance.58

The Commission’s assessment

(50) The Commission’s market investigation gave sufficient evidence to conclude that the market for pigments is global.

(51) First, the market investigation confirmed the Notifying Party’s claim that pigments are non-hazardous and easy to transport materials, and that transports costs are low compared to pigments cost per unit of weight.59

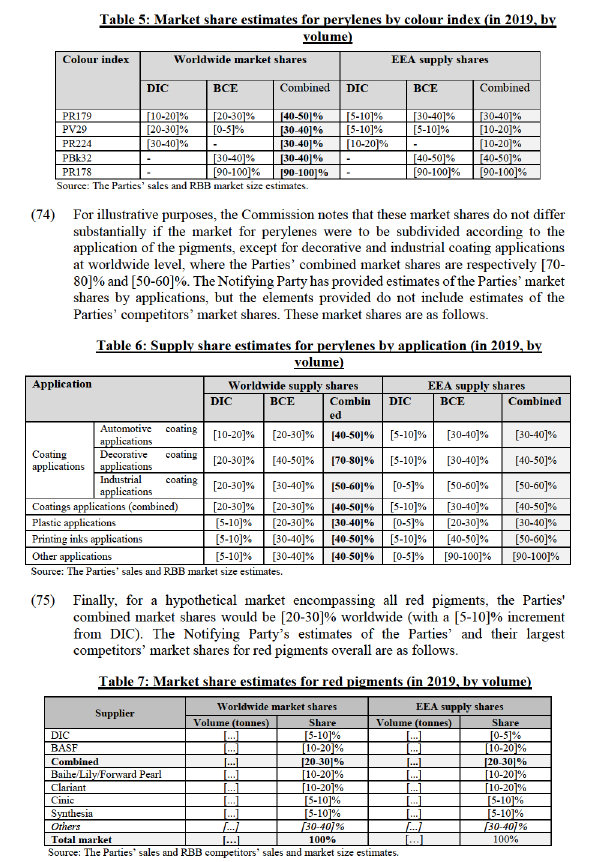

(52) Second, a majority of pigments manufacturers either already supply their EEA customers from plants outside the EEA or consider that plants outside the EEA could credibly do so,60 and a majority of customers either already purchase their pigments globally or would consider doing so in case of a SSNIP within the EEA.61 As such, it does not appear important for customers that their supplier’s factory be close to their production plants.62

(53) Third, a majority of customers consider non-EEA manufacturers to be credible alternatives for EEA customers.63 This last element should however be considered in light of the mixed feedback from customers regarding the ability of Chinese and Indian suppliers to meet their requirements for high quality pigments or to match the Parties’ products in terms of quality and consistency; especially for perylene pigments, as set out in section 5.4.1 below.

(54) In light of the above, the Commission considers that, to the effect of the present decision, the relevant geographic market for pigments is worldwide, however with a geographic differentiation between Chinese and Indian suppliers and the rest of the world, in particular as regards perylene and quinacridone. Accordingly, the Commission considers that the assessment of the Transaction would not change under a possible relevant geographic market definition as EEA-wide.

5.3.2. Printing inks

(55) Printing inks are mixtures of colourants (pigments, preparations or dyes), binders, solvents and additives for use in printing processes. Printing inks have numerous applications, such as print media products, packaging products, newspaper and books.

5.3.2.1. Product market definition

Commission’s precedents

(56) In previous decisions, the Commission considered segmentations of printing inks both on the demand side, into publication and packaging inks as well as on the supply side, into paste and liquid inks. The Commission noted that the majority of publication inks are paste inks and most packaging inks are liquid inks. The Commission found that on the demand side, there is limited substitutability between liquid and paste inks and that on the supply side, different equipment is required for manufacturing of liquid inks and paste inks.64

(57) The Commission has additionally considered a further segmentation of paste inks into heatset ink, coldset ink and sheetfed ink, and of liquid inks into gravure and flexographic inks.65

(58) The Commission concluded that a segmentation based on physical characteristics, i.e. liquid inks and paste inks, provides a clearer market delineation than a segmentation based on application. However, finally it left the question open.66

The Notifying Party’s view

(59) The Notifying Party submits that a segmentation based on the physical characteristics of the ink, i.e. liquid and paste inks, is sufficient and no further segmentation would be appropriate.67

(60) The Notifying Party argues that there is a high degree of supply-side substitutability among different types of liquid and paste inks. It further argues that the main difference between paste and liquid inks is the pigment load, with paste inks having a higher proportion of pigments.68 Despite the differences in pigment loads, the Notifying Party submits that same results can be achieved with liquid inks and paste inks and that the only difference is the amount of ink required. As paste inks contains more pigment, a thinner layer will achieve the same result as a thicker layer of liquid ink.69 The Notifying Party finally submits that paste and liquid inks do not require different chemistries of pigments; all pigments are suited for use in all types of printing inks.70

(61) However, if a subdivision of printing inks based on their physical characteristics (liquid or paste) and their type (between heatset ink, coldset ink and sheetfed ink within paste inks, and between gravure and flexographic inks within liquid inks) was to be applied, the Notifying Party submits that DIC produces a third type of liquid inks that was not examined under any Commission precedent, which is jet inks.71

The Commission’s assessment

(62) From a demand-side perspective, the market investigation did not provide any indications suggesting that the Commission should depart from its past decisional practice.

(63) From the supply-side, while the market investigation provided strong indications that switching between paste and liquid ink constitutes a major strategic decision, involving considerable costs and efforts,72 it was inconclusive as to whether printing inks manufacturers had the ability to switch easily and in a timely manner between heatset, coldset and sheetfed inks within paste inks.73 In a similar fashion, the feedback received from the market investigation did not allow the Commission to form a conclusion as to whether there would be a sufficient degree of supply-side substitutability between gravure, flexographic and jet inks within liquid inks to consider these three types of liquid inks as forming a single product market.74

(64) In any event, the Commission considers that, for the purpose of the present case, the exact scope of the product market definition for printing inks can be left open, since no serious doubts as to the compatibility of the Transaction with the internal market arise under any plausible product market definition (i.e. segmented between liquid and paste inks or further segmented between heatset, coldset and sheetfed inks within paste inks and between gravure, flexographic and jet inks within liquid inks).

5.3.2.2. Geographic market definition

Commission’s precedents

(65) The Commission has previously defined the market for printing inks as EEA-wide. The Commission found that transport costs are comparatively low, there is a significant level of cross-border trade and all major competitors have a multinational presence. Considering the minimal level of imports into the EEA, the Commission excluded a global market.75

The Notifying Party’s view

(66) The Notifying Party submits that the liquid and paste ink markets are global. It argues that the Commission established in its previous decisions that transportation costs are low, price levels in different continents are comparable, major competitors have multinational presence and local production is not a prerequisite to compete and that those characteristics are indicative of a global market.76

The Commission’s assessment

(67) From a demand-side perspective, the market investigation did not provide any indications suggesting that the Commission should depart from its past decisional practice.

(68) From the supply-side, while the vast majority of printing inks manufacturers indicated that suppliers from outside the EEA could credibly supply customers within the EEA,77 the market investigation proved inconclusive as to whether the respondents themselves would have the ability to supply customers within the EEA from plants outside the EEA without incurring additional costs and efforts.78 Some respondents, though a minority, even suggested that they primarily supplied their customers from manufacturing facilities close to their customer’s plant in South-West Europe or the Mediterranean area.79 Some respondents also suggested that the geographic market could be wider for paste inks than for liquid inks, since liquid inks are more voluminous and transport costs per unit of value would are more important.80

(69) In any event, the Commission considers that, for the purpose of the present case, the exact scope of the geographic market definition for printing inks can be left open, since the Transaction does not raise serious doubts as to its compatibility with the internal market, regardless of the precise geographic market definition (i.e. EEA-wide or worldwide).

The Notifying Party’s view

(76) The Notifying Party’s arguments are twofold: the Notifying Party first presents general arguments that apply to all categories of pigments under review, and then moves on to presenting arguments which are specific to each of the three colour spaces, which it submits should be considered as separate relevant product markets. In this section the Notifying Party’s general arguments will be presented first, followed by the arguments that apply more specifically to perylene pigments. In the following sections, the Commission lays down the specific arguments relating to each specific chemical class.

General considerations on all chemical classes

(77) With respect to all categories of pigments, the Notifying Party first explains that the Parties as well as their western competitors face increased competitive pressure from Chinese and Indian pigment manufacturers, who have progressively acquired sufficient know-how over the course of the years to be presently in a situation to supply pigments belonging to all chemical classes at very competitive rates thanks to cheap labour and lower investment in R&D, and with a quality that matches customers’ requirements.82 The Notifying Party argues that, doing so, Chinese and Indian pigments manufacturers have benefitted from the expertise of former employees from western pigment manufacturers,83 as well as government support,84 allowing them to enter these markets without incurring the significant developments costs that were necessary to develop the specifications used to manufacture the pigments, as well as the industrial production of these pigments,85 and to progressively commoditise all chemical classes of pigments, including high performance pigments.86 As an illustration, the Notifying Party indicates that after the expiration of the relevant patent in 2014, the average selling price of DPP pigments fell from EUR [...] / kg in 2005 to EUR [...] / kg as of today.87 The Notifying Party also provides extracts from communications made by Chinese and Indian suppliers on their strategy to expand their pigment portfolio from low-end markets and commodity pigments to specialised markets and speciality pigments, and to develop their footprint in western countries88, [...].89

(78) The Notifying Party also emphasises the fact that Chinese and Indian manufacturers take advantage of their better cost position to increase their production capacity and capacity shares, to the effect that the market is currently characterised by over-capacity at worldwide level,90 and that these manufacturers expand in western markets.91 In support of this statement, the Notifying Party provides [...],92 [...].93 The Notifying

(81) The Notifying Party also explains that the Parties’ customers [...],102 [...].103 [...].104 [...].105

(82) Regarding closeness of competition, the Notifying Party explains that the Parties are not close competitors, given that for most chemical classes, either only BCE manufactures this product (DIC [...]) or the increment brought by the Transaction is small.106 The Notifying Party also explains that research and development is of limited importance for pigments.107

(83) In a paper regarding the impact of COVID-19 on the competitive assessment of the Proposed Transaction, the Notifying Party also explains that the COVID-19 pandemic has drastically reduced the demand for pigments,108 mainly from coating manufacturers active in the automotive industry, because the production of cars was stopped in many plants throughout the world, and sales of cars have collapsed in particular in the EEA,109 as well as in the printing industry, because advertising materials represent 40% of all printing products in Europe and companies have cut their advertising expenses because of the crisis.110 The Notifying Party further explains that as a result of this situation, [...],111 [...],112 [...],113 while Chinese pigments manufacturers have resumed operations thanks to the earlier improvement of the sanitary situation in China, and have taken advantage of this situation to further expand their operations.114

(84) Finally, in a paper on buyer power of the Parties’ customers annexed to the Form CO, the Notifying Party provides additional argumentation on why buyer power would make attempted price increases unsuccessful. The Paper on Buyer Power describes that for perylene and quinacridone, [...].115[...].116 [...].117 [...].118

Considerations specific to the perylene chemical class

(85) More specifically with respect to perylene pigments, the Notifying Party argues that the Parties are facing increasingly aggressive competition119 from a number of strong Chinese and Indian suppliers, such as LianGang, HongGang, Gaoyou, Pidilite, Trust Chem, Union Colours, Anshan Hifi, as well as others,120 including in the most demanding applications such as automotive coating applications121 and that Chinese manufacturers are able to match the quality offered by western producers.122 The Notifying Party explains that both Liaoning Lian Gang’s and Liaoning Hong Gang’s production capacity for perylene pigments [...], and will continue to increase in the future due to planned capacity expansions. Due to these capacity expansions, the Parties’ global capacity share for perylene pigments decreased [...], from [40-50]% to [30-40]%.123

(86) In addition, the Notifying Party provides a list of recent entries in the perylene market, mainly from the two Chinese manufacturers: Riwa (who claims to export 80% of its pigment production) and Anshan Hifi, both vertically integrated with respect to naphthalic anhydride (see paragraph (87) below), as well as the Czech manufacturer Synthesia.124 The Notifying Party submits that Chinese companies that entered into the perylene market benefitted in doing so from the support of Chinese governmental bodies such as the Shenyang Institute of Chemical Engineering and the Tianjin University Chemical Engineering Institute.125

(87) In order to illustrate the aggressiveness of Chinese competition with respect to [...],126 [...].127 [...]. Finally, the Notifying Party explains that DPP pigments, for which prices have decreased sharply over the past years (see paragraph (61) above) represent a very attractive alternative to perylenes and quinacridones pigments.128

(88) The Notifying Party also emphasises the importance of naphthalic anhydride as an input for the production of perylene pigments (see paragraph (63) above), a product which is only produced in China, for which some of the Parties’ largest Chinese competitors for perylene products (Liaoning Lian Gang, Liaoning Hong Gang and Anshan Hifi) are vertically integrated, and in relation to which the 25% import tariffs imposed by the American administration on several products imported from China puts DIC at a further [...] disadvantage compared to its Chinese competitors.129

(89) The Notifying Party also points out that [...]. [...].130 The Notifying Party explains that this provides its customers with countervailing buying power, [...].

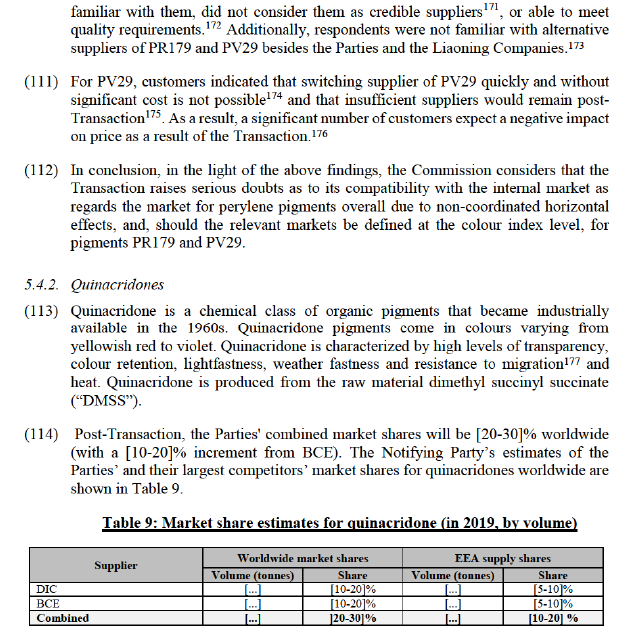

(90) Finally, in the Notifying Party’s paper regarding the impact of COVID-19, [...].131

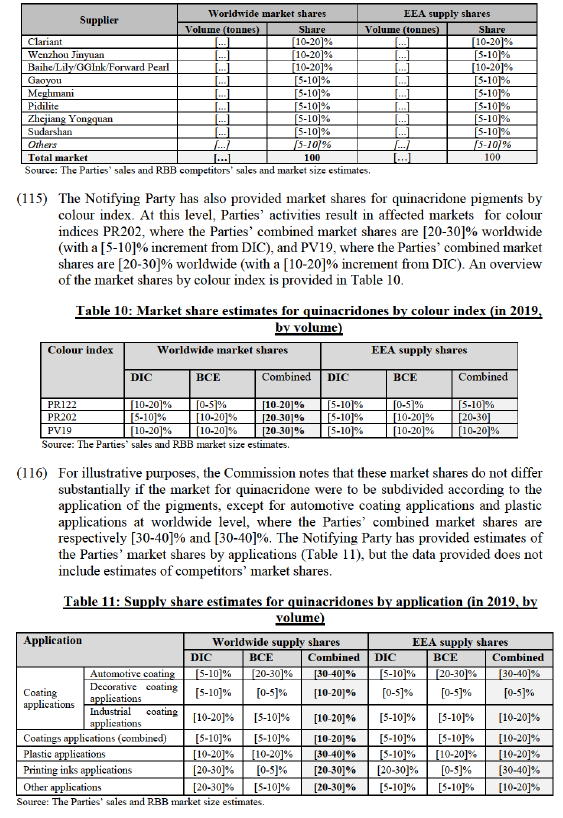

The Commission’s assessment

(91) For the reasons set out in this section, the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market with respect to perylene pigments. The Commission considers that serious doubts would also arise if the product market were instead considered at colour index level, as set out below.

(92) First, as regards the Notifying Party’s claim that Chinese and Indian competitors represent a significant competitive pressure on the Parties’ activities, while this argument was partly confirmed by the market investigation with respect to several other chemical classes, it was strongly contradicted by the results of the market investigation with respect to perylene pigments. In particular, despite the fact that a small majority of EEA customers would consider switching to a non-EEA supplier in case of a price increase for perylenes in the EEA,132 less than half of the EEA customers that expressed a view consider that Chinese and Indian suppliers are credible for the supply of perylene pigments to EEA customers.133 Moreover, a majority of customers procure their perylene pigments exclusively from inside the EEA.134 When asked to rate perylene manufacturers according to their competitive strength for the supply of perylene pigments in the EEA, customers respond in such a way that no Indian or Chinese manufacturer ranks among the top 5 suppliers.135 When asked to perform the same exercise for the supply of perylene pigments worldwide, only one Chinese or Indian perylene pigments manufacturer ranks among the top 5 suppliers worldwide, as number 5.136 These elements should be read in conjunction with the fact that virtually all customers consider that there are less than 5 credible suppliers for perylenes overall,137 and, based on customers’ comments, it is likely that there is in fact an even more limited number of close competitors to the Parties for perylenes, at least for the highest quality grades.138

(93) Beyond the average rating received by each competitors, the Commission also considered the number of times they were rated. Since customers only rated competitors they are aware of, have looked into in the past, or have considered as potential suppliers in the past, this is also a good indication of the degree of information customers have regarding the existence of various perylene suppliers, from around the world. While DIC, BCE and Clariant all get above 45 ratings, the number four supplier, Synthesia, gets rated 27 times, and the number one Chinese supplier, Liaoning LianGang, only 24 times.139

(94) The fact that a majority of perylene suppliers that the Commission asked customers to rate (based on a list of top perylene competitors provided by the Parties, a majority of which were Chinese suppliers) were unknown to customers is also reflected in the customers’ comments. As one customer explains, “As a customer it is very intransparent whether the a.m. suppliers are really producers.” Another top customer of the Parties states that “[Customer] is generally aware that Clariant has limited participation in perylenes, but does not purchase perylene from Clariant and is not in a position to comment on its competitive strength. [Customer] does not have information on the competitive strength of any of the other suppliers listed and does not purchase perylene from any of them.” A Japan-based top customer of the Parties also mentions that “we don't know about such many suppliers mentioned above besides BCE, Clariant and DIC, we don't hear so much about reputation or evaluation about such non-traditional suppliers in our Japanese market.”140

(95) It should also be noted, in addition, that while the volume of pigments imported into the EEA corresponds to [80-90]% of the total estimated demand in the EEA (with Chinese and Indian suppliers representing [80-90]% of these imports – see also paragraph (77) above), this proportion is significantly lower for perylene pigments, namely around [30-40]% in volume and [20-30]% in value. Perylene is in fact, with azo condensation and pyrazoloquinazolone, among the chemical classes for which imports into the EEA represent the smallest fraction of EEA consumption of all organic pigments. Given the apparent lack of obstacles to trade pigments around the world, as well as the fact that [80-90]% of all pigment imports to the EEA are from Asia, this would seem to indicate that a substantial proportion of non-EEA competition for perylenes is considered a less credible source of supply by EEA customers. As such, these elements indicate that there is a degree of geographic differentiation in the market, where Chinese and Indian pigments manufacturers are more distant competitors that do not exert a strong competitive pressure on the Parties’ perylene activities.

(96) Second, with respect to the Parties’ arguments that their perylene customers can and do switch [...]141 [...] while the result of the market investigation clearly evidenced the fact that the most demanding applications for perylene are automotive coating applications, and in particular automotive refinish applications, which are mainly driven by western customers.142 This distinction is important inasmuch as the Commission considers this to be a heterogeneous product market, where the specific demands of customers will dictate the characteristics of products supplied and the proximity of suppliers in competitive terms. [...]143 [...].144

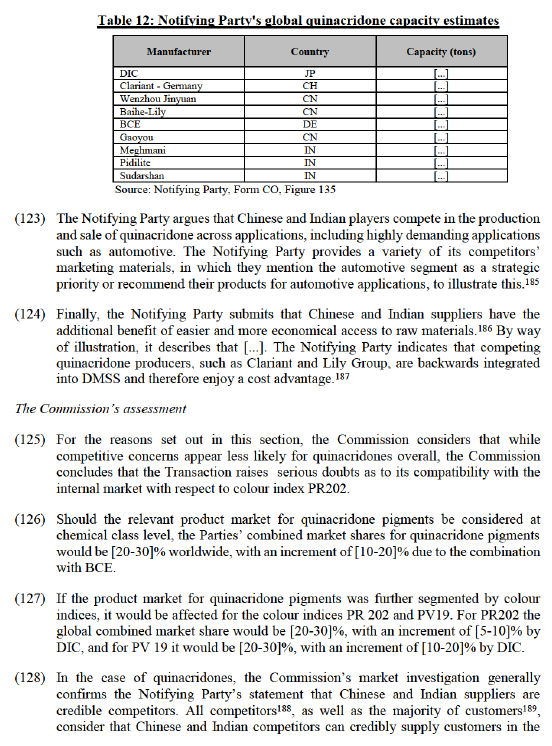

(97) The fact that the Notifying Party was not in a position to provide multiple and meaningful examples of EEA customers switching away their perylene business to Chinese or Indian pigments manufacturers is suggestive of the fact that perylene products manufactured by suppliers other than the Parties are not considered either close or as credible alternatives as the Parties’ own perylene products.

(98) In addition, while the Commission acknowledges that [...]145 [...]146. [...] results of the market investigation, evidencing that a majority of perylene customers consider that prices have increased by 5% or more in the last 5 years relative to the raw materials used for their production.147 Observing a [...] and increase in sales price suggests that while some of the Parties’ less demanding customers, accounting for roughly [...]% of the Parties’ sales, were able to switch away from them, the vast majority of the Parties’ customers had no choice [...] over the period. This is supported by results of the market investigation, evidencing the fact that virtually none of the Parties’ customers have qualified a new supplier for their perylene pigments over the past three years,148 as well as the fact virtually none of the Parties’ customers have switched supplier for their perylene pigments over the past three years.149

(99) Third, as regards the Notifying Party’s arguments that the perylene market is characterised by overcapacity, the Commission acknowledges the fact that the figures provided by the Notifying Party can indeed be considered as indicative of a situation of over-supply for perylene pigments overall. However, according to the information provided by the Notifying Party, the vast majority of this overcapacity is due to capacity expansions by Chinese perylene pigments manufacturers,150 which cannot be considered close competitors to the Parties. As a result, such over-capacity is likely to have little bearing on the Parties’ activities and competitive interactions.

(100) Fourth, with respects to the Notifying Party’s arguments on the importance of naphthalic anhydride, which is only produced in China by some of the Parties’ largest perylene competitors, as an input for the production of perylene pigments, the Commission notes that the fact that one of the major inputs for perylene production is controlled by Chinese competitors of the Parties does not appear to put the Parties, or their EEA competitors, at a disadvantage compared to other perylene manufacturers. As mentioned above in paragraph (91), when asked to rate perylene manufacturers according to their competitive strength for the supply of perylene pigments in the EEA, customers respond in such a way that no Indian or Chinese manufacturer ranks among the top 5 suppliers in terms of average rate;151 and when asked to perform the same exercise for the supply of perylene pigments worldwide, only one Chinese or Indian perylene pigments manufacturer ranks among the top 5 suppliers worldwide, as number 5.152 Moreover, [...] data [...]153 [...]. It therefore appears quite clearly that, even assuming that the current supply situation with respects to naphthalic anhydride is putting the Parties at a [...] disadvantage compared to their Chinese competitors, the Parties’ position, as well as the performance and uniqueness of the products they manufacture, [...].

(101) Fifth, as regards the constraints posed to the Parties by EU and US manufacturers, the Commission notes that when asked to rate perylene manufacturers according to their competitive strength for the supply of perylene pigments either in the EEA, or worldwide, customers respond in such a way that BCE and DIC are consistently ranked number one and number two respectively.154 A competitors also comments in this respect that “BCE and DIC are the leaders, others like Clariant are distant seconds.”155 This conclusion would apply to competition from both EEA and non- EEA perylene pigments manufacturers.

(102) Sixth, as regards the Parties’ arguments regarding the absence of barriers to enter the perylene market, the Commission notes that the manufacturing process described by the Notifying Party for the synthesis of perylene pigments from naphthalic anhydride involves seven different steps, and the Notifying Party acknowledges that the production process is “comparably complex”.156 Moreover, the vast majority of customers and competitors were unable to name perylene manufacturers who had recently entered (in the past 5 years)157 or were intending to enter (in the next 2 years) the market for perylenes.158 Therefore, contrary to what the Notifying Party submits, barriers to enter the perylene market appear to exist.

(103) Seventh, as regards the Parties’ argument [...] customers, who enjoy significant bargaining power, this argument was largely contradicted by the market investigation, that evidenced that the majority of customers consider that they have either little or very little bargaining power compared to the strongest suppliers for perylenes.159 [...].160 [...]161 [...].

(104) Eighth, as regards the Notifying Party’s arguments that they are not close competitors in perylene pigments, when asked specifically to name who DIC’s top competitors are on the one side, and who BCE’s top competitors are on the other side, while other EEA competitors such as Clariant and DCC are mentioned a number of times, the Parties are by far more often mentioned to be each other’s closest competitors.162 Moreover, in relation to the potential impact of the Transaction, several customers suggest that the perylene market is already, as of today, rather concentrated, with very few alternative suppliers. One customer states: “Actual number of EEA suppliers are reduced, so additional reduction will bring to even less competition”.163 Another comments: “The choice was already limited”.164 A third one explains: “Not enough serious competitioners (sic) for BCE/DIC left in the market, just 1 or 2”.165 In summary, as a customer of the Parties puts it, “Alternative suppliers with a quality level of BASF and DIC/Sun are very rare.”166 These elements support the conclusion that, contrary to what the Notifying Party claims, DIC and BCE are closely competing in the perylene market.

(105) Ninth, as regards the impact of the COVID-19, the Commission acknowledges the scale and importance of the very serious disruptions the COVID crisis created in the automotive industry as well as the printing industry, and estimates that in all likelihood this crisis may indeed have lasting consequences in these industries, thus affecting the demand for pigments in general, and perylene pigments in particular in the short and even medium terms. Nevertheless, in its assessment, the Commission also needs to take into account the fact that a merger creates a structural changes in a market, which are likely to have long-lasting consequences. In addition, the Commission’s initial market investigation was carried out between May-June 2020 and the market investigation following re-notification in October-November 2020, at a time when the COVID-19 and its potential consequences were already known to all market players. The Commission therefore considers that the impact of this crisis taken into account by respondents, in particular when answering questions about the effects of the Transaction and its impact on prices, quality, choice of products and innovation.

(106) Finally, and consistent with all of the above, the results of the market investigation showed that customers were concerned about the impact of the Transaction. While a small majority of customers considered that there would remain a sufficient number of suppliers post-Transaction,167 a significant majority considered that either slight or significant price increases were likely.168 Moreover, close to half of the customers that expressed a view expected either a small or a large decrease in the choice of products available to them.169 This is indicative of the fact that a majority of perylene customers expect a significant negative impact of the Transaction.

(107) In conclusion, based on the above findings, the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market in respect of perylene pigments.

(108) If the relevant product market were instead considered to be at colour index level, only two colour indices would be affected at worldwide level, namely PR179 and PV29. The findings set out above in paragraphs (90) to (106) hold true for PR179 and PV29 individually as well.

(109) In the first market investigation, the majority of concerns voiced by respondents that were specific to a single colour index pertained to PR179. PV29, which is a smaller product market in terms of volume, was mentioned less frequently. Therefore, following the second notification of the Transaction, the Commission performed a targeted market investigation on, among others, perylene colour index PV29. This targeted market investigation further confirmed that the findings for perylene apply to PV29 as well. In particular, the lack of credible alternative suppliers for perylene pigments would appear to be even more critical for PV29 (in addition to PR179).

(110) The main competitors for PR179 and PV29 identified by the Parties are Chinese companies Liaoning Hong Gang and Liaoning Liang Gang, which in fact appear to belong to the same group, Liaoning Companies according to some respondents. The large majority of respondents to the market investigation indicated that they are not familiar with either of the Liaoning Companies. 170 Those that did indicate to be

(117) As mentioned above in section 5.4.1, the Notifying Party argues that all red pigments with similar physical properties form a single product market. Quinacridone pigments would be part of this hypothetical combined market. In this combined market, the Parties’ combined market shares amounts to [20-30]% worldwide (with a [5-10]% increment from DIC).The Notifying Party’s estimates of the Parties’ and their largest competitors’ market shares for red pigments overall worldwide are as laid out above in Table 7.

The Notifying Party’s view

(118) As described in section 5.4.1, the Notifying Party presents arguments in its competitive assessment that apply broadly to all pigments, as well as arguments specific to quinacridone. Arguments that apply to all pigments have been laid out in section 5.4.1; arguments specific to quinacridones are presented in this section.

(119) The Notifying Party submits that quinacridone customers have significant countervailing buyer power. To evidence this, [...].178 The Notifying Party also submits that customers have plenty of credible alternative suppliers of quinacridone they can switch to, as will be detailed below.

(120) The Notifying Party indicates that [...].179 [...].180

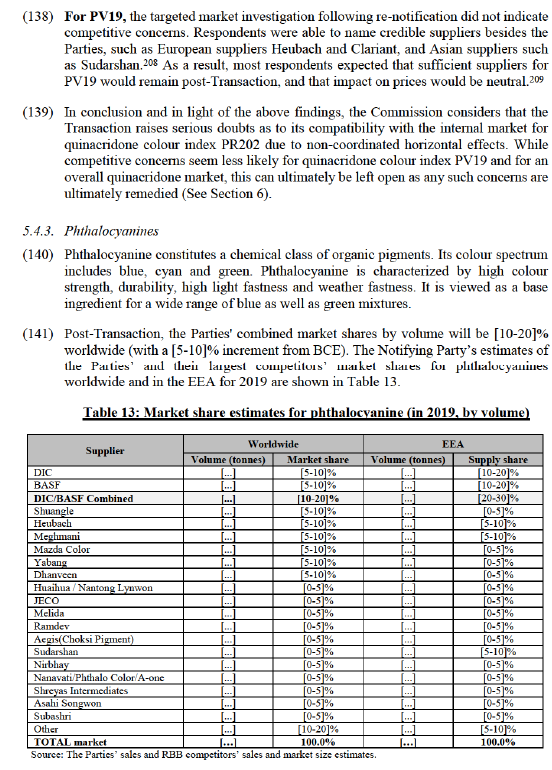

(121) As described in paragraphs (76) and (77), the Notifying Party argues that the Parties experience significant competition, particularly from Chinese and Indian entrants for all pigments. For quinacridones specifically, the Notifying Party submits that the Parties’ global capacity shares are falling due to capacity expansions of competitors, from [20-30]% in 2017 to [20-30]% in 2020. By way of illustration, the Notifying Party mentions a capacity expansion [...] by Pidlite [...], as well as capacity expansions [...] by Ami Pigments [...], [...] by Gharda [...] and [...] by Sudarshan [...].181 The Notifying Party’s estimates of global quinacridone production capacities are provided in Table 12, and show that according to the Notifying Party, six out of the top manufacturers are from China or India.182

(122) The Notifying Party indicates that because of the capacity expansions, global production capacities exceeded demand by [more than 20]% in 2018, putting pressure on prices.183 Additionally, it indicates that DPP, since its patent expiry, has become a lower-cost alternative to quinacridone, putting further downward pressure on prices.184

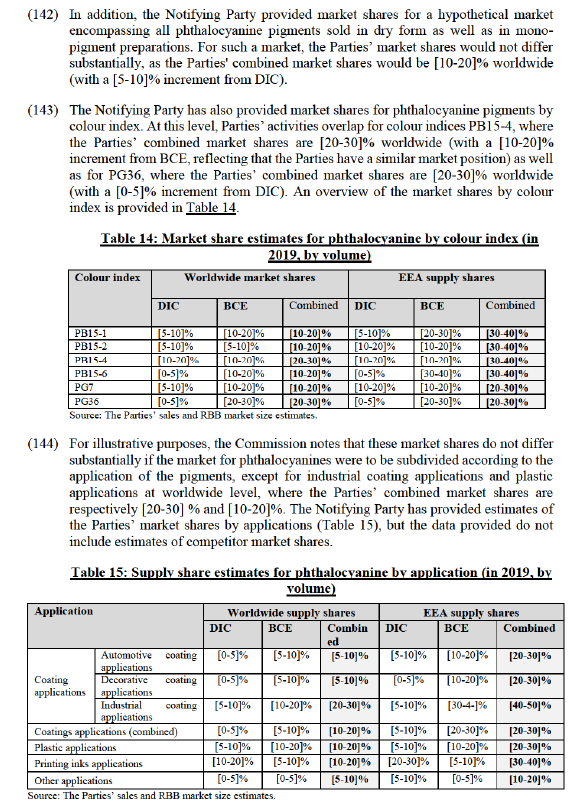

EEA. A small majority of customers indicate that they already source part of their quinacridones from Chinese and Indian suppliers today.190

EEA. A small majority of customers indicate that they already source part of their quinacridones from Chinese and Indian suppliers today.190

(129) Despite these results, a majority of customers indicated there are barriers for suppliers from outside the EEA to supply EEA customers. One of the barriers named most frequently are regulatory barriers, notably REACH certification.191 However, as the Notifying Party indicates, a significant number of non-EEA pigments suppliers have obtained REACH certification.192 These non-EEA suppliers include Chinese and Indian suppliers of quinacridone pigments.193

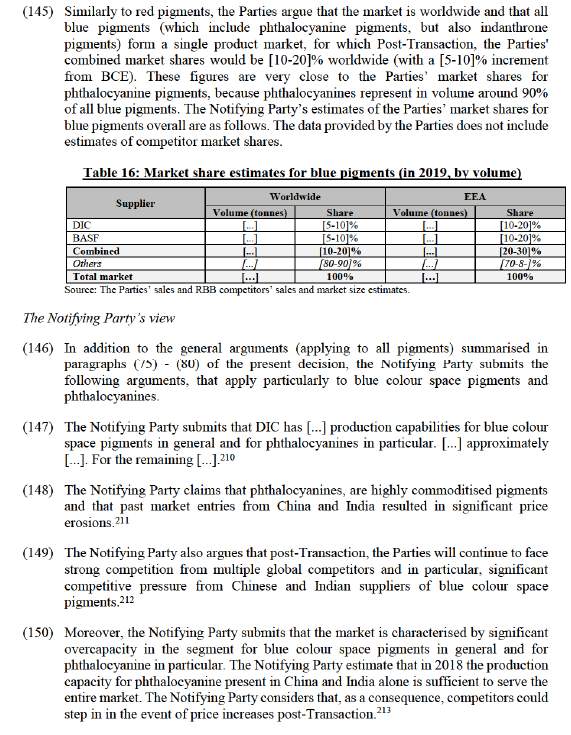

(130) Nevertheless, overall, a majority of customers and competitors expect no impact on their business with respect to quinacridones in general as a result of the Transaction. Some mention that if the merged entity rationalises its product portfolio post- Transaction, this may lead to requalification cost and effort.194 Notably, one customer states: “The situation with [q]uinacridones is much better than with the perylenes. Especially because Clariant remains as second market leader and there are already existing alternative capacities in Asia.”195

(131) However, with regard to specific colour indices within quinacridone, some customers mention that competition is less credible for specific colour indices because competitors to the Parties do not meet the required quality standards. Notably, one large customer states: “PR 202 in suitable qualities is currently only offered by the two parties, a Chinese manufacturer is currently developing an alternative product, PR 122 today available qualities from Chinese and Indian suppliers can substitute the products of the parties, for PV 019 substitution is difficult as each product vary in its content of beta- and gamma crystal phase which leads to different technical performance”.196

(132) Contrary to the Notifying Party’s claim that customers exercise significant countervailing buyer power, the majority of customers indicate that they experience their buyer power as equal or lower than that of the Parties. This includes large customers, one of which indicates that bargaining power is specifically low for colour indices for which there are few or no alternatives to the Parties, such as PR 202: “For P R 122 bargaining power is significant. For P R 202 and For P V 019 lower bargaining power.” Another customer points to the difficulty to substitute pigments: “Main reason for low negotiation power rate is the difficulty to substitute a pigment by an other one from a competitor. We often are in a kind of "captive" commercial situation.” 197

(133) Both customers and competitors consider Clariant as the strongest player in quinacridone pigments. The Parties are considered as the second and third strongest, followed by Sudarshan of India.198 However, one competitor indicates the picture is different for some colour indices, indicating that PR202 is only supplied by the Parties.199

(134) Finally, the large majority of customers consider that sufficient suppliers of quinacridone pigments in general remain post-Transaction.200 A small majority of customers expect a small increase in price, while most expect quality and innovation to be unaffected. Results on product choice are inconclusive, with no strong majority for any option.201 The majority of competitors expect no impact on price, quality or product innovation and a slight decrease in choice.202 However, some customers mention that too few alternative suppliers would remain for colour index PR202.203

(135) Because of the mixed feedback on quinacridone colour indices PR202 and PV19 in the initial market investigation, the Commission focused, among others, specifically on these two colour indices in its targeted market investigation following re- notification of the Transaction.

(136) For PR202, the only competitors identified by the Notifying Party, are Wenzhou Jinyuan and Zhejiang Yongquan of China. The majority of the respondents to the targeted market investigation following re-notification indicated not to be familiar with either of those competitors. The large majority of those that were familiar with them, indicated not to consider either of them as a credible PR202 supplier that is able to meet quality requirements. 204 Additionally, respondents were not familiar with alternative suppliers of PR202 besides the Parties, Wenzhou Jinyuan and Zhejiang Yongquan.205

(137) Customers indicated it is difficult to switch from PR202 to an alternative supplier of PR202 quickly and without significant cost.206 As a result, the majority of customers consider that insufficient suppliers remain post-Transaction and that the Transaction will have a negative impact on price.207

(151) The Notifying Party argues that the Parties’ customers [...] have countervailing buyer power [...].214

The Commission’s assessment

(152) For the reasons set out in this section, the Commission considers that serious doubts can be excluded for phthalocyanine pigments (in case of a product market definition by chemical class, with product differentiation within the product market) as well as for colour indices within the phthalocyanines chemical class (in case of a product market definition by colour index).

(153) If the product market for phthalocyanine pigments was considered at chemical class level, the Parties’ combined market shares for phthalocyanine pigments would be [10- 20]% worldwide, well below the 20% threshold for a market to be considered as affected.

(154) If the product market for phthalocyanine pigments was further segmented by colour indices, it would be affected only for the colour indices PB15-4 and PG36.

(155) For PG36, the increment from the Transaction would remain marginal ([0-5]%) with a HHI increment of <150. Therefore, in the absence of any additional specific motive for concern (see also paragraph (136) below), the Commission considers that the Transaction does not raise competition concerns in relation to the market for PG36.

(156) For PB15-4, the Parties’ combined market shares are [20-30]% worldwide, with a [10- 20]% increment from BCE and an HHI increment of [390-400]. However, the market investigation didn’t reveal any general concerns with respect to phthalocyanine pigments, nor did it reveal any specific concern with respect to the PB15-4 colour index.

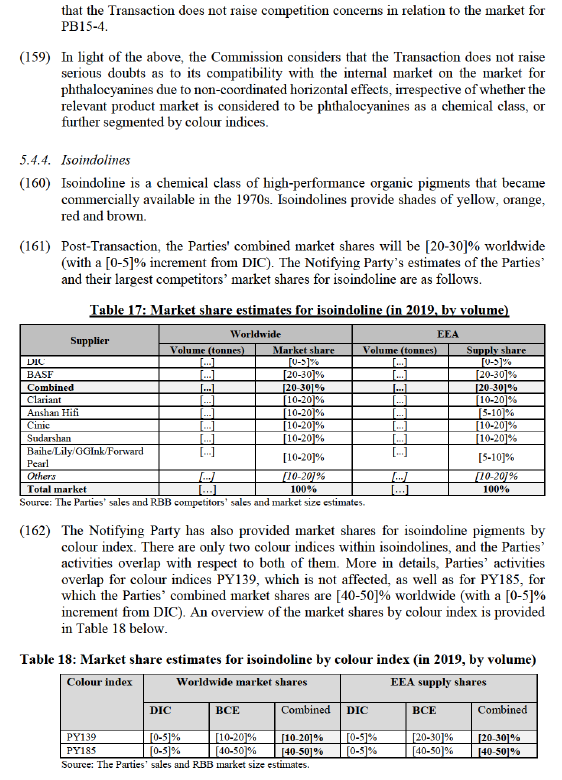

(157) With respect to phthalocyanine pigments overall, which is not an affected market, the market investigation confirmed the Notifying Parties’ claim that the phthalocyanine pigments are a commoditised class of pigments, with a competitive market as well as strong and credible competitors. A vast majority of respondents consider that there will remain a sufficient choice of credible phthalocyanine suppliers post-Transaction at both EEA and worldwide level,215 and the majority of customers expected either no impact or a decrease in the price of phthalocyanine pigments as a result of the Transaction at both worldwide and EEA level.216

(158) PB 15-4 specifically is mentioned on very few occasions by either customers or competitors. While a number of customers emphasised for instance the very specific tint and properties of PB15-1 and PB15-6,217 this was not the case for PB15-4. One of the very few occasions where PB15-4 are mentioned explicitly is to emphasise the ability of switching supplier for this particular colour index: “Changing the supplier for PB15:4 gave remarkable savings”218 For these reasons, the Commission considers

The Notifying Party’s view

(163) In addition to the general arguments (applying to all pigments) summarised in paragraphs (75) - (80) of the present decision, the Notifying Party submits that the increment brought by the Transaction is minimal,219 that the Parties are facing the competition of several strong suppliers, including Chinese and Indian suppliers, such as Clariant, Anshan Hifi, Cinic, Sudarshan, Baihe/Lily,220 but also Vijay and Trust Chem,221 and that, as a result of the fierce competition in the isoindoline market, [...].222

(164) The Notifying Party also emphasises the importance of o-phthalodinitrile, gaseous ammonia, solvents, diiminoisoindoline, methylene compounds and acids that are used as inputs for the production of isoindoline pigments. The Notifying Party claims that these products are controlled by Chinese manufacturers, including some of the Parties’ Chinese competitors for isoindoline products.223

(165) The Notifying Party also points out that both Parties’ customer bases for isoindoline pigments [...]. [...].224 The Notifying Party explains that this provides its customers with countervailing buying power, [...].225

The Commission’s assessment

(166) For the reasons set out in this section, the Commission considers that serious doubts can be excluded for isoindoline pigments (in case of a product market definition by chemical class, with product differentiation within the product market) as well as for colour indices within the isoindolines chemical class (in case of a product market definition by colour index).

(167) If the product market for isoindoline pigments were considered at chemical class level, the Parties’ combined market shares for isoindoline pigments would be [20-30]% worldwide, just over the 20% threshold for a market to be considered as affected. The increment from DIC would be marginal, at [0-5]%, with a HHI increment of less than 150.

(168) If the product market for isoindoline pigments were to be further segmented by colour indices, it would be affected only for the colour index PY185, for which the Parties’ combined market shares are [40-50]% worldwide (with a [0-5]% increment from DIC). It should be noted that the other colour index within isoindolines, PY139, represents [high percentage] of all isoindoline pigments, and is not affected. As for PY185, the Commission notes that the increment from DIC would be marginal, at [0- 5]%, with a HHI increment of less than 150.

The Notifying Party’s view

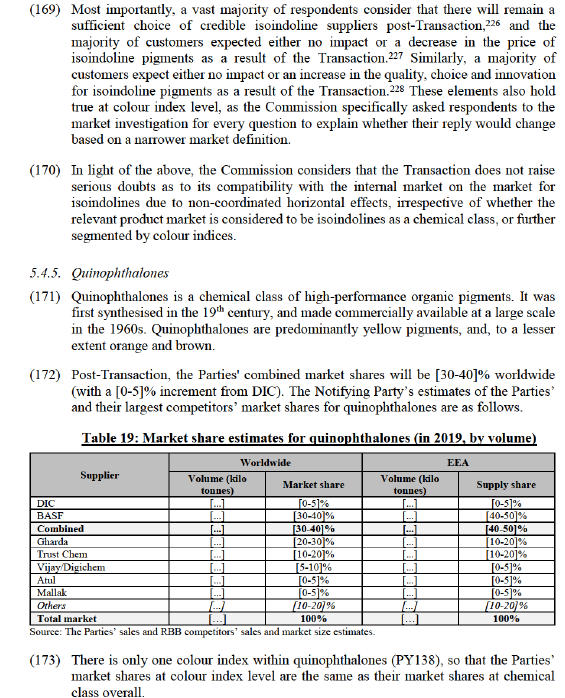

(174) In addition to the general arguments (applying to all pigments) summarised in paragraphs (75) - (80) of the present decision, the Notifying Party submits that the increment brought by the Transaction is minimal,229 that the Parties are facing the competition of several strong Chinese and Indian suppliers, such Gharda, Trust Chem, Vijay-Digichem, Atul and Mallak,230 and that, as a result of the fierce competition in the quinophthalone market, [...].231

(175) In addition, the Notifying Party stresses the fact that [...].232

(176) The Notifying Party also points out that part of the competition it faces results from recent entries on the quinophthalone market, such as the entry of Vijay in 2015,233 and that the quinophthalone market is nowadays characterised by overcapacity.234

The Commission’s assessment

(177) For the reasons set out in this section, the Commission considers that serious doubts can be excluded for quinophthalone pigments (in case of a product market definition by chemical class, with product differentiation within the product market) as well as for colour indices within the quinophthalone chemical class (in case of a product market definition by colour index).

(178) If the product market for isoindoline pigments was considered at chemical class level, the Parties’ combined market shares for quinophthalone pigments would be [30-40]% worldwide, with only a small increment from DIC ([0-5]%). Moreover, account should be taken of the fact that [...]. The same argument also holds true if the product market for quinophthalone pigments was further segmented by colour indices, considering that there is only one colour index within quinophthalones (PY138).

(179) Most importantly, a vast majority of respondents consider that there will remain a sufficient choice of credible quinophthalone suppliers post-Transaction,235 and the majority of customers expected either no impact or a decrease in the price of quinophthalone pigments as a result of the Transaction.236 Similarly, a majority of customers expect either no impact or an increase in the quality, choice and innovation for quinophthalone pigments as a result of the Transaction.237 These elements also hold true at colour index level, as the Commission specifically asked respondents to the market investigation for every question to explain whether their reply would change based on a narrower market definition.

(180) In light of the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market on the market for quinophthalones due to non-coordinated horizontal effects, irrespective of whether the

(see paragraph (78) above).245 In addition the Notifying Party explains that [...],246 that BCE is facing significant competitive pressure, noticeably from Anshan, […],247 [...].248

(186) For isoindolinone, the Notifying Party submits that isoindolinone is among the products [...],249 that [...],250 and that the isoindolinone market is characterised by overcapacity.251

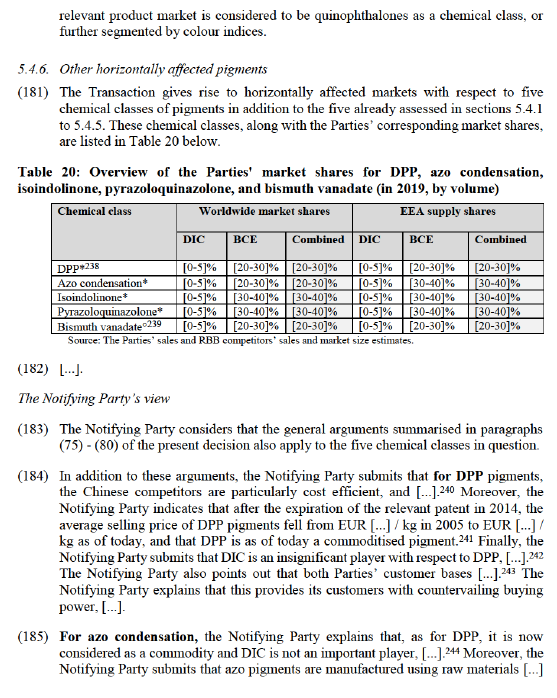

(187) For pyrazoloquinazolone, the Notifying Party does not mention any other argument, either as an addition or as a complement, to the ones summarised in paragraphs (75) - (80) of the present decision, beside the fact that [...] and that the isoindolinone market is characterised by overcapacity.252

(188) For bismuth vanadate pigments, the Notifying Party submits that that [...].253 Moreover, the Notifying Party explains that [...], to such an extent that these would now be qualified as commoditised pigments.254

The Commission’s assessment

(189) For all five chemical classes considered under section 5.4.6, market shares estimates of the Parties, as well as their competitors, allowed the Commission to compute HHI as well as HHI increment estimates in support of its assessment.

(190) For DPP, at worldwide level, the Parties’ combined market share in the overall market for DPP in 2019 was [20-30]%, with a small increment of [0-5]% from DIC, and a HHI increment of less than 150. The Parties’ shares in each of the potential sub- segments are also modest. Moreover, the Commission’s assessment should take into account the fact that [...]. Finally, no material concerns were raised in the course of the market investigation regarding the Parties’ horizontal overlap in DPP. In light of the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market due to non-coordinated horizontal effects in relation to the market for DPP.

(191) For azo condensation, at worldwide level, the Parties’ combined market share in the overall market for azo condensation in 2019 was [20-30]%, with a negligible increment of [0-5]% from DIC, and a HHI increment of less than 150. The Parties’ shares in each of the potential sub-segments are also modest. Moreover, the Commission’s assessment should take into account the fact that [...]. Finally, no material concerns were raised in the course of the market investigation regarding the Parties’ horizontal overlap in azo condensation. In light of the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market due to non-coordinated horizontal effects in relation to the market for azo condensation.

(192) For isoindolinone, at worldwide level, the Parties’ combined market share in the overall market for isoindolinone in 2019 was [30-40]%, with a small increment of [0- 5]% from DIC, and a HHI increment of less than 150. The Parties’ shares in each of the potential sub-segments are also modest. Moreover, the Commission’s assessment should take into account the fact that [...]. Finally, no material concerns were raised in the course of the market investigation regarding the Parties’ horizontal overlap in isoindolinone. In light of the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market due to non-coordinated horizontal effects in relation to the market for isoindolinone.

(193) For pyrazoloquinazolone, at worldwide level, the Parties’ combined market share in the overall market for pyrazoloquinazolone in 2019 was [30-40]%, with a small increment of [0-5]% from DIC, and a HHI increment just above 150 ([150-160]). The Parties’ shares in each of the potential sub-segments are also modest. Moreover, the Commission’s assessment should take into account the fact that [...], DIC is likely to have a market power even lower than suggested by its (already modest) market shares. Finally, no material concerns were raised in the course of the market investigation regarding the Parties’ horizontal overlap in pyrazoloquinazolone. In light of the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market due to non-coordinated horizontal effects in relation to the market for pyrazoloquinazolone.

(194) For bismuth vanadate pigments, at worldwide level, the Parties’ combined market share in the overall market for bismuth vanadate pigments in 2019 was [20-30]%, with a negligible increment of [0-5]% from DIC, and a HHI increment of less than 150. At EEA level, the Parties’ combined market share in the overall market for bismuth vanadate pigments in 2019 was [20-30]%, with a negligible increment of [0-5]% from DIC, and a HHI increment of less than 150. The Parties’ shares in each of the potential sub-segments are also modest. Moreover, the Commission’s assessment should take into account the fact that [...], DIC is likely to have a market power even lower than suggested by its (already modest) market shares at both EEA and worldwide level. Finally, no material concerns were raised in the course of the market investigation regarding the Parties’ horizontal overlap in bismuth vanadate pigments. In light of the above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market due to non-coordinated horizontal effects in relation to the market for bismuth vanadate pigments.

5.5. Competitive assessment of the vertical relationships

5.5.1. Pigments (upstream) with printing inks (downstream)

(195) Both Parties are active in the manufacture of pigments. Only DIC is active in the manufacture of printing inks. The link is vertically affected because the Parties’ combined market shares in the sales of certain pigments (namely perylenes, quinacridones, pyrazoloquinazolone, isoindolinone, quinophthalone, azo condensation, bismuth vanadate and DPP) and certain colour indexes are above 30% (see Section 5.4 above).

(199) The Notifying Party also submits that there is no risk of customer foreclosure given DIC’s reasonable market shares downstream (except in gravure liquid inks), as well as the fact that colourants have multiple uses other than the manufacture of printing inks, so that colourant manufacturers have multiple customers outside the printing industry.260

The Commission’s assessment

(200) As regards a potential input foreclosure strategy, the Commission first notes that the Parties’ ability to put in place such an input foreclosure strategy should be put into perspective in light of the significance of resales between pigments competitors in the industry, as is evidenced by the significant number of purchases, resales and even contractual relationships among pigment manufacturers.261 This is also evidenced by the fact that for five classes of pigments among the ten chemical classes that are affected as a result of the Transaction, [...] (see Table 20 above). The relatively high number of pigment distributors active on the market262 further enriches the picture, to such an extent that customers are often not aware of whether the pigment they purchase from a given supplier was actually manufactured by that supplier or not. As an illustration, only a small minority of customers that responded to questions regarding quinophthalones were aware of the fact that [...].263 For all these reasons, it appears unlikely that the Parties would have the ability to put in place a foreclosure strategy that would enable them to target printing ink manufacturers specifically, because any product they sell to a distributor or a competitor, as a result of a supply agreement for instance, might end up eventually being sold to any end-customer, including printing ink manufacturers.

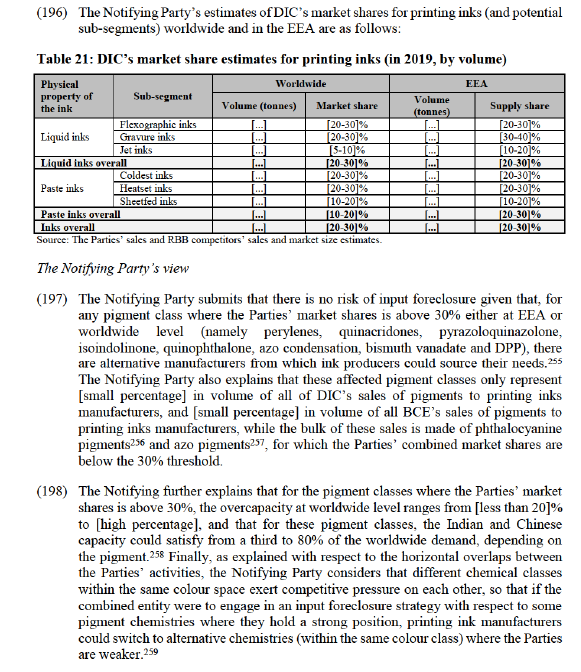

(201) Moreover, the Commission notes that given the worldwide nature of the market for pigments, the Parties would most likely lack the ability to put in place such an input foreclosure strategy for any pigment for which their combined market share worldwide is lower than 30%. This leaves only perylenes, quinophthalones, isoindolinones and pyrazoloquinazolone, as well as some colour indices within these chemical classes, as potential candidates for input foreclosure. These represent only four chemical classes out of over twenty, and, as the Notifying Party sets out, less than [small percentage] in volume of all of DIC’s sales of pigments to printing inks manufacturers, and [small percentage] in volume of all BCE’s sales of pigments to printing inks manufacturers (see paragraph (195) above). As such, the Parties would therefore assuredly lack the ability to foreclose access to all pigments that are used as an input for the manufacture of printing inks.

(202) Most importantly, even for pigment classes where the Parties’ combined market share level is above 30% at worldwide level, a majority of printing inks manufacturers that expressed a view consider that there would remain sufficient sources of pigments for them to manufacture printing inks if the combined entity decided to stop supplying this input product to them.264

(203) For the reasons set out above, the Commission concludes that the Parties would lack the ability to foreclose access to pigments as an input for the manufacture of printing inks.

(204) As regards incentive and effects of a potential input foreclosure strategy, it is not necessary for the Commission to conclude on whether the Parties would have an incentive to engage in a potential input foreclosure strategy aiming at foreclosing access to pigments or whether such a foreclosure strategy would have effects, as the lack of ability would already prevent the Parties to engage in such a potential foreclosure strategy in the first place.