Commission, April 29, 2021, No M.10164

EUROPEAN COMMISSION

Decision

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

PARTIES

Demandeur :

CVC

Défendeur :

STARK GROUP

(1) On 23 March 2021, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which CVC Capital Partners SICAV-FIS S.A. ('CVC', Luxembourg) intends to acquire within the meaning of Article 3(1)(b) of the Merger Regulation sole control of STARK Group A/S ('Stark', Denmark) (the 'Transaction'). 3 CVC and Stark are designated hereinafter as the 'Parties'

1. THE PARTIES

(2) CVC and its subsidiaries manage investment funds and platforms. In particular, CVC owns Ahlsell AB (“Ahlsell”), which is active as a retailer and distributor of installation products for heating, ventilation and air-conditioning (“HVAC”), electrical equipment, tools and supplies, as well as building materials. Ahlsell has an approximate turnover of EUR [2 500 - 3 000] million. Ahlsell is active in Denmark, Finland, Norway and Sweden (“the 'Nordics”).

(3) Stark is mainly active as a retailer and distributor of heavy building materials, such as timber products, bricks, insulation, plasterboards, doors, windows and cement. Stark also offers a limited range of installation products and tools and supplies. Stark is active in the Nordics and in Germany.

2. THE CONCENTRATION

(4) On 8 January 2021, CVC agreed to acquire Stark via certain, indirectly wholly owned, special purpose vehicles under a sale and purchase agreement. Following the Transaction, Stark would be fully owned and solely controlled by CVC.

(5) As a result, the Transaction constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

3. UNION DIMENSION

(6) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million4 (CVC: EUR […] million (2019); Stark: EUR […] million (2019)). Each of them has a Union-wide turnover in excess of EUR 250 million (CVC: EUR […] million (2019); Stark: EUR […] million (2019)), and they do not achieve more than two thirds of their aggregate Union-wide turnover within one and the same Member State.

(7) The Transaction therefore has a Union dimension within the meaning of Article 1(2) of the Merger Regulation.

4. MARKET DEFINITION

(8) The Parties are both active in the distribution of building materials. Whereas Ahlsell is a specialist builder's merchant, Stark is a generalist builder's merchant. Ahlsell specialises in the distribution of installation products in the segments HVAC and electrical, as well as tools and supplies. Stark is active as distributor of general building materials. Ahsell is present both at wholesale and retail levels whereas Stark is only present at the retail level.

4.1. Relevant Product Market

4.1.1. The Commission's Previous Decisions

(9) Within the overall market of distribution of building materials, the Commission has previously defined a market for the distribution of building products in general, but it has left open whether this market can be further divided into: (i) wholesale to retailers, (ii) retail sale to professional customers, and (iii) retail sale to consumers ('non-professional customers') primarily through (DIY) stores.5

(10) In respect to (i), wholesale to retailers, the Commission has further considered a distinction by product category.

(11) In respect to (ii) and (iii), retail sale to professional customers and consumers, the Commission has also noted that a distinction may exist between generalist builder's merchants and specialist builder's merchants6. Within specialist builder's merchants, the Commission also considered whether separate product markets exist for the distribution of individual product categories, for example insulation, installation products.7 However, such potential segmentations have been ultimately left open.

(12) Against this matrix whereby the markets for the distribution of building materials are defined by sales channel, distinction between generalist and specialist merchants, and product categories, the Commission has considered that the distribution of (i) installation products8 and (ii) tools and supplies9 to constitute separate markets from the market for the distribution of building materials.

(13) In relation to the distribution of installation products, the Commission has considered a distinction between the following sales channels: (i) wholesale to retailers, (ii) retail sale to professional customers, and (iii) retail sale to non- professional customers.10 The Commission has also considered further segmentations by individual product categories, in particular it has considered (i) the wholesale distribution of heating, ventilation, air conditioning (HVAC) and (ii) the wholesale or retail distribution of electrical products.11 These further segmentations have been ultimately left open.

(14) Similarly in regard to the distribution of tools and supplies, the Commission has previously considered a distinction by sales channel: (i) wholesale to retailers, (ii) retail sale to professional customers, and (iii) retail sale to non-professional customers. The Commission also considered a further segmentation by product category whereby, the distribution of workwear and personal protective equipment would constitute a separate market.12 However, the Commission '' but it ultimately left this issue open.13

4.1.2. The Parties' Arguments

(15) The Parties agree with the segmentation by sales channels. At the wholesale level, the Parties agree with the distinction of installation products and tools and supplies but argue that a further distinction by product category is not necessary as the majority of suppliers offer a broad portfolio within each of these two categories. At the retail level, the Parties agree with the distinction between generalist and specialist merchant markets and with the further segmentation of specialists' merchant markets by the broader categories regarding installation products and tools and supplies. However, they argue that each of these two markets should not be further segmented by product category.

(16) In conclusion, the Parties submit that at the wholesale level there are two relevant product markets: the wholesale market for the distribution of installation products and for the wholesale market for the distribution of tools and supplies. At the retail level, the Parties submit there is a generalist market for building materials, which can be further segmented by type of customer (professional and non-professional), and two specialist markets: one for installation products and another for tools of supplies further segmented by type of customer but not by product category.

4.1.3. Assessment

(17) In respect to the wholesale markets, the majority of the respondents to the market investigation confirmed that there are two distinct markets: one for the wholesale of installation products; and another for the wholesale distribution of tools and supplies. However, the majority of respondents that expressed a view do not agree with a further segmentation of each of these two markets by product categories.14

(18) The alternative segmentation of the wholesale installation products into HVAC in one hand, and electrical products, on the other does not affect the outcome of the competitive assessment of the Transaction, therefore the Commission concludes that exact product definition of the wholesale installation product market maybe left open.

(19) Similarly, the further distinction of workwear and PPE from the overall tools and supplies market does not affect the outcome of the competitive assessment of the Transaction, therefore the Commission concludes that exact product definition of the wholesale market for tools and supplies maybe left open.

(20) In respect to the retail markets, the majority of the respondents have also confirmed that the following are distinct markets: (i) generalist building materials, (ii) retail distribution for installation products, as well as (iii) retail distribution for tools and supplies. The majority of respondents that expressed a view also agree with a further segmentation of each of these three markets by customer type, and into retail sales to professionals and retail sales to non-professionals.15 However, the majority of respondents do not consider it necessary to further segment the retail market for installation products into HVAC products and electrical products. The majority of respondents that expressed a view also do not consider it necessary to further distinguish the workwear and PPE from the tools and supplies market.16.

(21) The alternative segmentation of the retail buildings materials market by customer type, into retail sales to professionals and retail sales to non-professionals does not affect the outcome of the competitive assessment of the Transaction, therefore the Commission concludes that exact product definition of the retail markets for building materials may be left open.

(22) The alternative sub-segmentation by product category of the retail markets for installation products into HVAC products and electrical products does not affect the outcome of the competitive assessment of the Transaction. Similarly the alternative sub-segmentation by customer type, into retail sales to professionals and retail sales to non-professionals also does not affect the competitive assessment of the Transaction, therefore the Commission concludes that exact product definition of the retail markets for installation products may be left open.

(23) The alternative sub-segmentation by product category of the retail markets for tools and supplies into work-wear and PPE does not affect the outcome of the competitive assessment of the Transaction. Similarly, the alternative segmentation by customer type, into retail sales to professionals and retail sales to non-professionals also does not affect the competitive assessment of the Transaction, therefore the Commission concludes that exact product definition of the retail markets for tools and supplies may be left open.

(24) Based on the above, for the purpose of assessment of the Transaction the Commission will consider the following markets and segmentations:

(a) Wholesale market of installation products with a possible segmentation by product categories into HVAC products and electrical products.

(b) Wholesale market of tools and supplies with a possible distinction of workwear and PPE products.

(c) Retail distribution market for building materials with a possible segmentation by customer type into professional and non-professional customers, and between generalist builder's merchants and specialist builder's merchants.

(d) Retail distribution market for installation products, as a possible segment of the retail specialist building materials market, with a possible further segmentation by customer type into professional and non-professional customers, as well as by product category into HVAC products and electrical products

(e) Retail of tools and supplies, as a possible segment of the retail specialist building materials market, with a possible further segmentation by customer type into professional and non-professional customers, as well as with a possible distinction of the product category workwear and PPE.

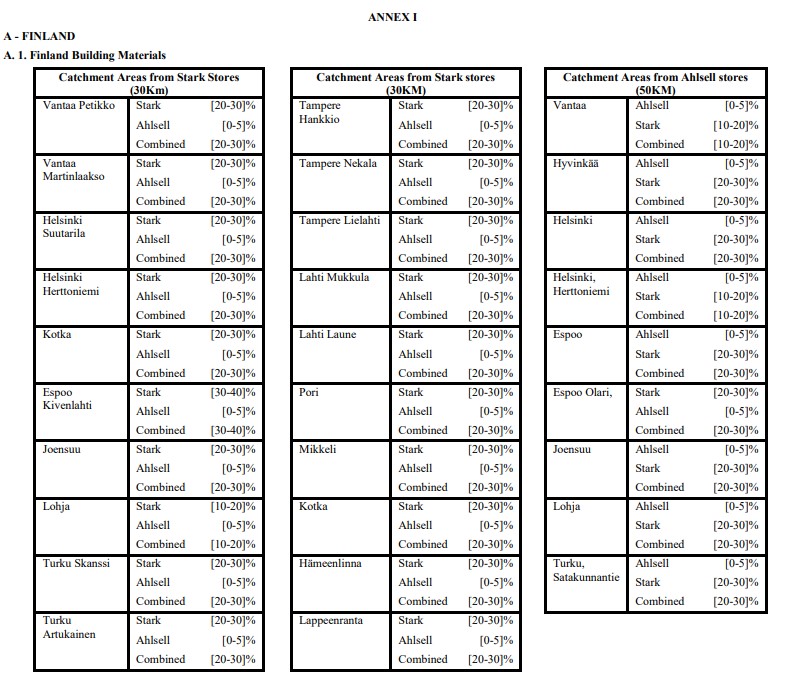

4.2. Relevant Geographic Market

4.2.1. The Commission's Previous Decisions

(25) In relation to wholesale markets for installation materials, including the alternative segmentations into HVAC and electrical products, the Commission has considered the relevant geographic market to be at least national but ultimately left the exact definition open. 17 Similarly, the Commission also considered the wholesale markets of tools and supplies, including the workwear and PPE to be at least national but ultimately left the exact market definition open18

(26) In relation to the retail distribution markets for building materials, installation products (including further product segmentations), tools and supplies (including workwear and PPE) the Commission has previously found the relevant geographic markets to be national or potentially narrower (local). The question has been ultimately been left open.19 The alternative of national or local markets applies to both retail sales to professional customers and retail to professional customers.

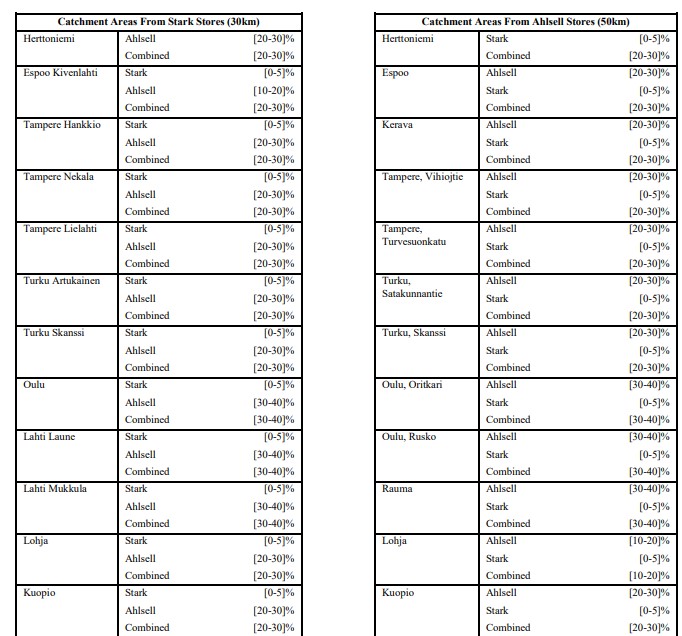

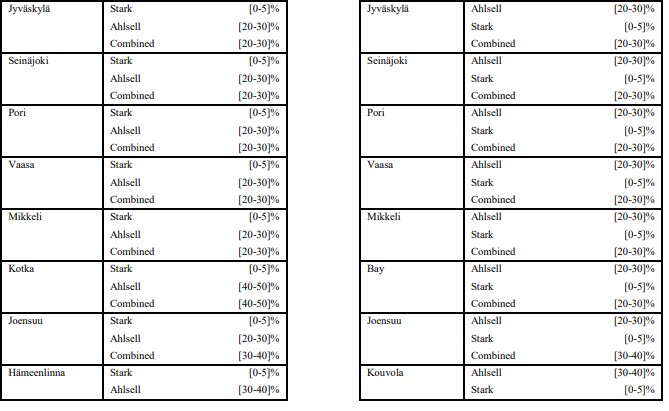

(27) The retail local markets have been defined by catchment areas of 30 km radius from generalist builder's merchant stores and by catchment areas of 50 km from specialist builder's merchant stores, which includes the installation products and the tools and supplies products.20

4.2.2. The Parties' Arguments

(28) The Parties submit that each wholesale market for installation products (including the HVAC and electrical products segmentations), as well as the wholesale market for tools and supplies (including workwear and PPE segment) are national in scope.

(29) The Parties submit that each of the retail markets for distribution of building materials, installation products and tools and supplies are national in scope because all of their main competitors operate at the national level and their price lists are set nationally. Moreover, the Parties argue that customers also order online and by phone and have their purchases delivered directly to them either from the retailers' warehouses, or from the manufacturers' sites. For example, […]. Nonetheless, the Parties have provided data for catchment areas within a 30 km radius of Stark's stores and for catchment areas within a 50 km radius of Ahlsell's stores.

4.2.3. Assessment

(30) The majority of respondents to the market definition considers that the retail markets of (i) building materials, (ii) installation products and (iii) tools and supplies are local (i.e. based on catchment areas within a 30 km radius from the store for generalist builder’s stores or 50 km radius from the store for specialist builder’s stores) whereas wholesale markets for installation products and tools and supplies are national.21

(31) In line with past decisional practice, the Commission considers the wholesale markets for (i) installation products and (ii) tools and supplies are at least national in scope for the purposes of this Decision.

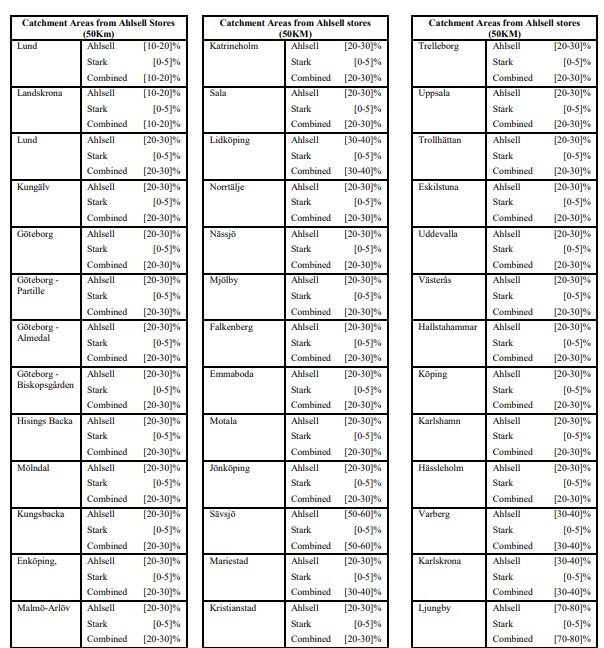

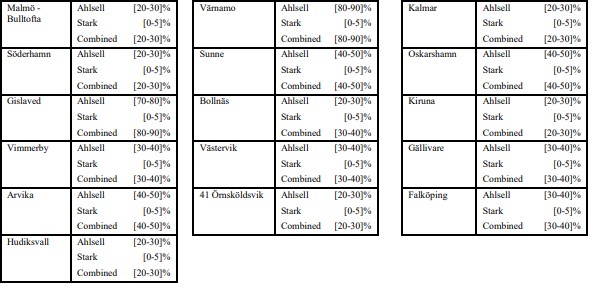

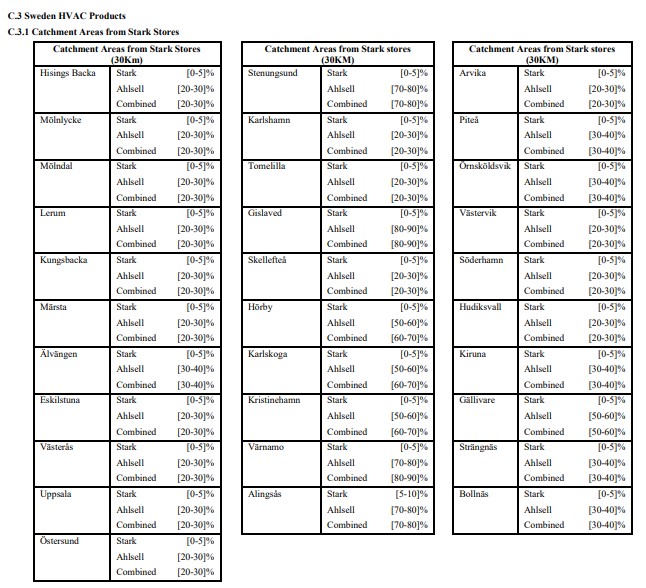

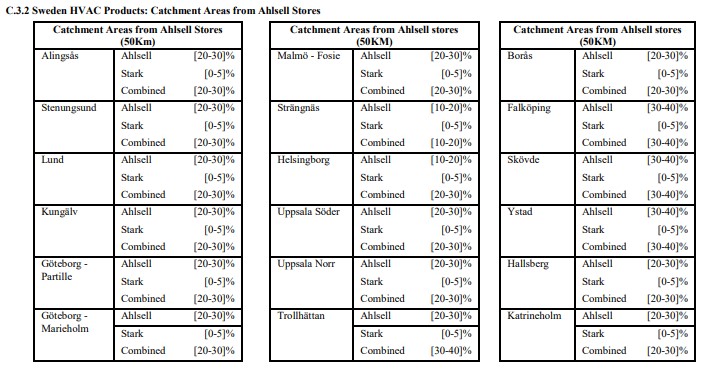

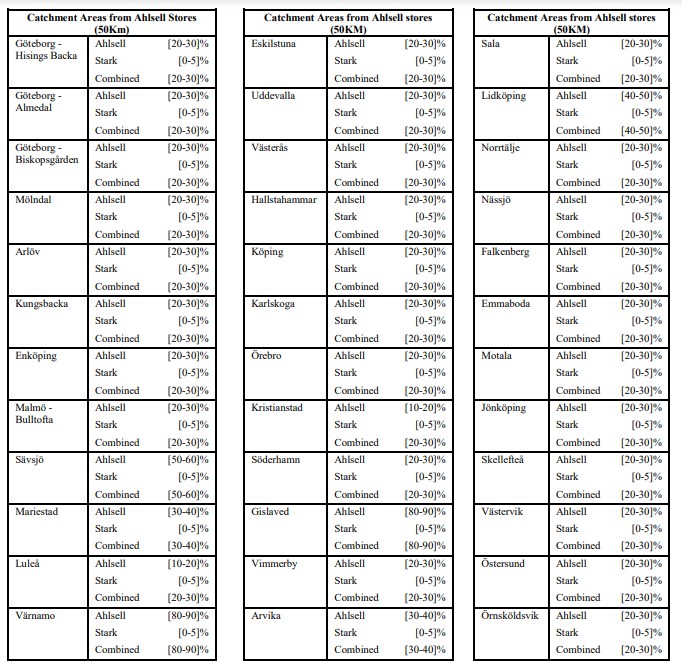

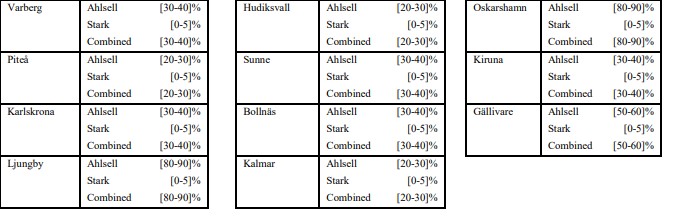

(32) In respect to the retail markets of building materials, installation products (including HVAC and electrical products), tools and supplies (including workwear and PPE) the geographic relevant markets are national or local. The exact geographic market definition can be left open, as the outcome of the competitive assessment does not change under either of these two alternatives.

5. COMPETITIVE ASSESSMENT

5.1. Analytical framework

(33) Under Article 2(2) and (3) of the Merger Regulation,22 the Commission must assess whether a proposed concentration would significantly impede effective competition in the internal market or in a substantial part of it, in particular through the creation or strengthening of a dominant position. Depending on the position of the parties in the supply chain, a concentration may entail horizontal and/or non-horizontal effects.

(34) Horizontal effects arise when the parties to a concentration are actual or potential competitors in one or more of the relevant markets concerned. The Commission appraises horizontal effects in accordance with the guidance set out in the Horizontal Merger Guidelines.23

(35) Non-horizontal effects arise when the parties to a concentration operate in different levels of the supply chain in certain relevant markets (vertical effects). The Commission appraises non-horizontal effects in accordance with the guidance set out in the Non-Horizontal Merger Guidelines.24

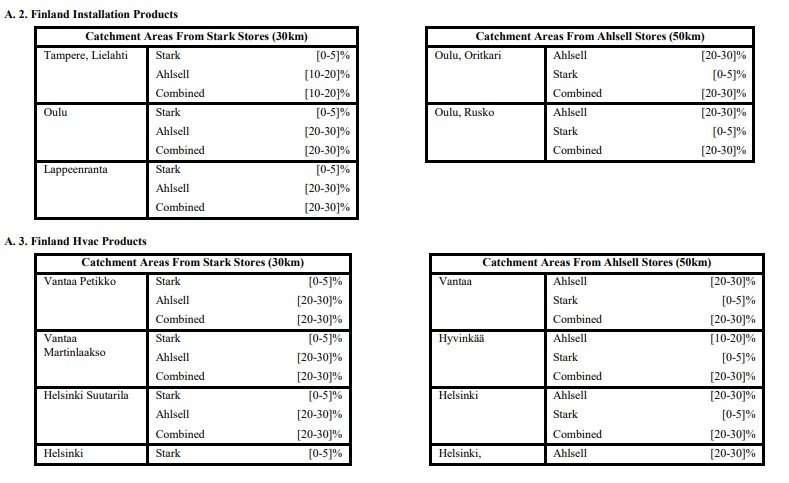

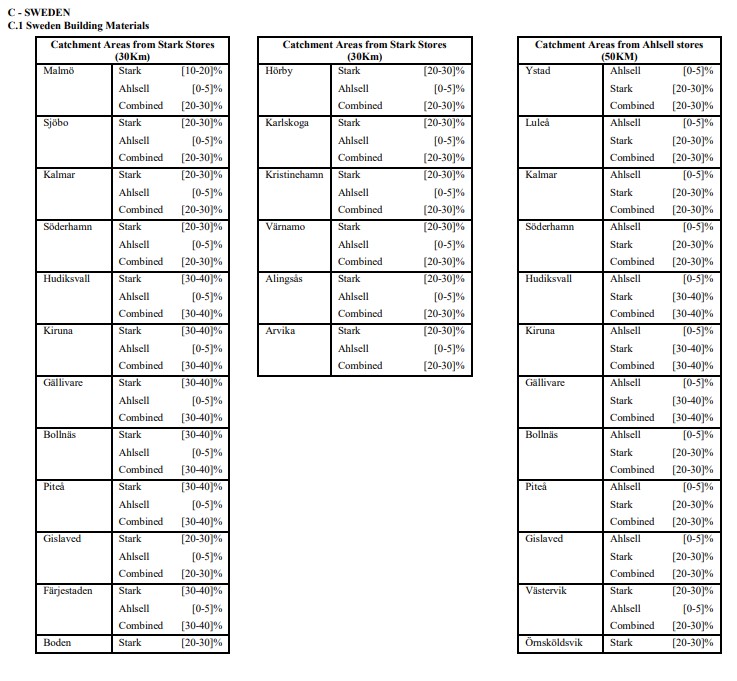

(36) Both the Horizontal and Non-Horizontal Merger Guidelines distinguish between two main ways in which mergers between actual or potential competitors on the same relevant market may significantly impede effective competition, namely non-coordinated and coordinated effects.

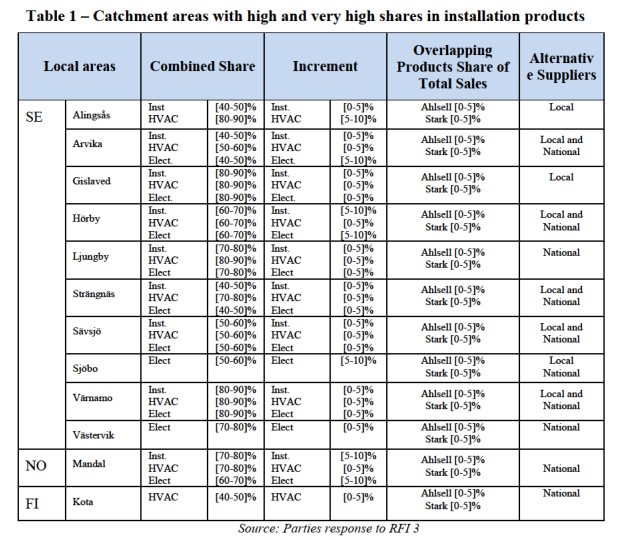

(37) In horizontal mergers, non-coordinated effects may significantly impede effective competition by eliminating the competitive constraint imposed by each party to the merger on the other, as a result of which the merged entity would have increased market power, without resorting to coordinated behaviour. In that regard, the Horizontal Merger Guidelines consider not only the direct loss of competition between the merging firms, but also the reduction in competitive pressure on non- merging firms in the same market that could be brought about by the merger.25

(38) The Horizontal Merger Guidelines list a number of factors, which may influence whether or not significant non-coordinated effects are likely to result from a merger. In particular, the Horizontal Merger Guidelines refer the large market shares of the merging firms, the fact that the merging firms are close competitors, the limited possibilities for customers to switch suppliers or the fact that the merger would eliminate an important competitive force.26 Not all these factors need to be present for significant non-coordinated effects to be likely. The list of factors is also not exhaustive.

(39) In non-horizontal mergers, non-coordinated effects may arise when the concentration gives rise to foreclosure. In vertical mergers, foreclosure can take the form of input foreclosure, where the merger is likely to raise costs of downstream rivals by restricting their access to an important input; and/or the form of customer foreclosure, where the merger is likely to foreclose upstream rivals by restricting their access to a sufficient customer base.27

(40) In assessing the likelihood of an anticompetitive foreclosure scenario, the Commission examines whether the merged entity would have post-transaction the ability to foreclose access to either inputs or customers, whether the merged entity would have the incentives to do so and whether such foreclosure strategy would have a detrimental effect on competition.28

5.2. Horizontally affected markets

(41) Both Parties are active in the Nordics. Sweden is the largest market for Ahlsell where approximately [60-70] % of its revenue is generated, followed by Norway with [10-20] %, Finland with [10-20] % and Denmark with [0-5] %. Denmark is the largest market in Nordics for Stark. Approximately [50-60] % of the Stark's revenue is generated in the Nordics (the remaining [40-50] % in Germany). Stark's sales in the Nordics are split between Denmark ([40-50] %), Sweden ([20-30] %), Finland ([20-30] %) and Norway ([5-10] %).

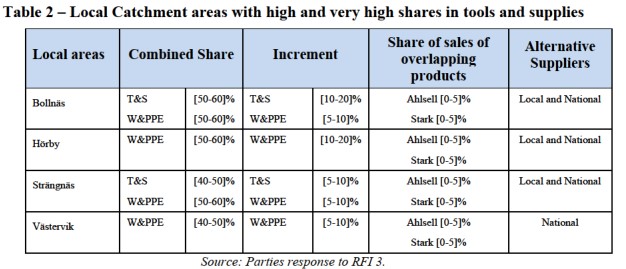

(42) The Parties' activities overlap in the retail markets for building materials in Sweden, Finland and Norway. The Parties' activities also overlap in the retail of installation products, including in the HVAC and electrical products segments in these countries and in Denmark as regards HVAC segment. Finally, the Parties' activities overlap in the retail of tools and supplies, including in work wear and PPE in Sweden, Norway and Finland. Although Ahlsell almost exclusively serves professional customers, there is an overlap in both sales channels to professional and non-professional customers in respect to each of the retail markets: for building materials, installation products and the HVAC and electrical products segments, tools and supplies, including workwear and PPE.

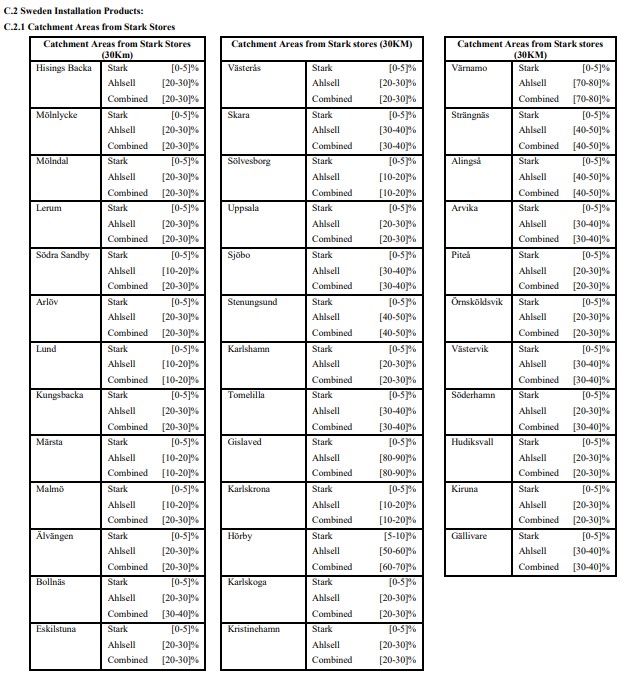

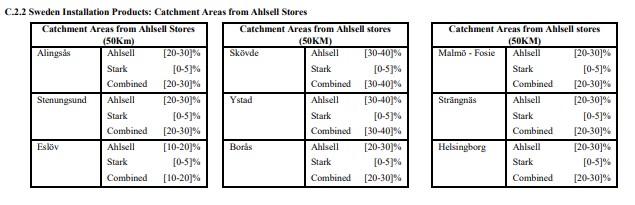

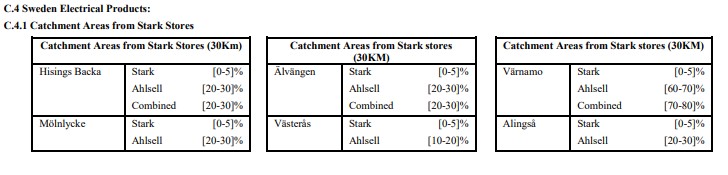

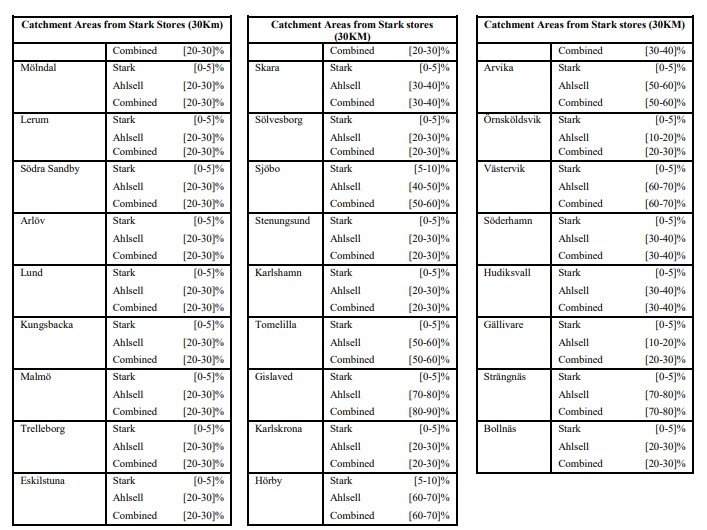

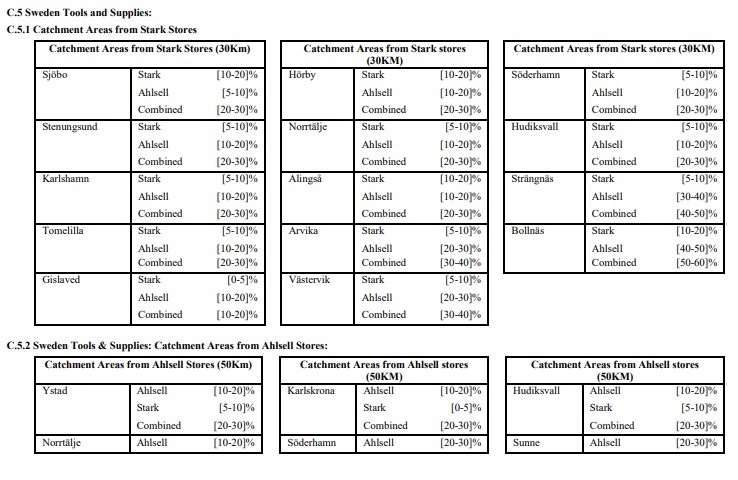

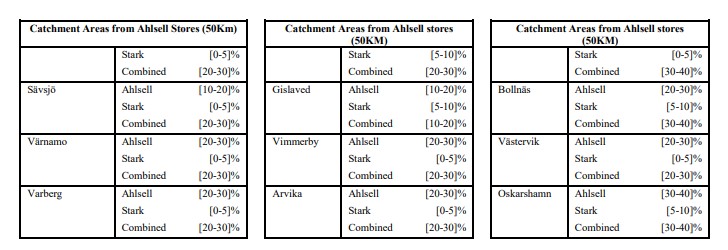

(43) While not all overlaps give rise to affected markets, the Transaction gives rise to the following horizontally affected markets (on the basis of value market shares) under all plausible market segmentations in terms of product and geography (national or local pursuant to catchment areas with 30 km or 50 km):

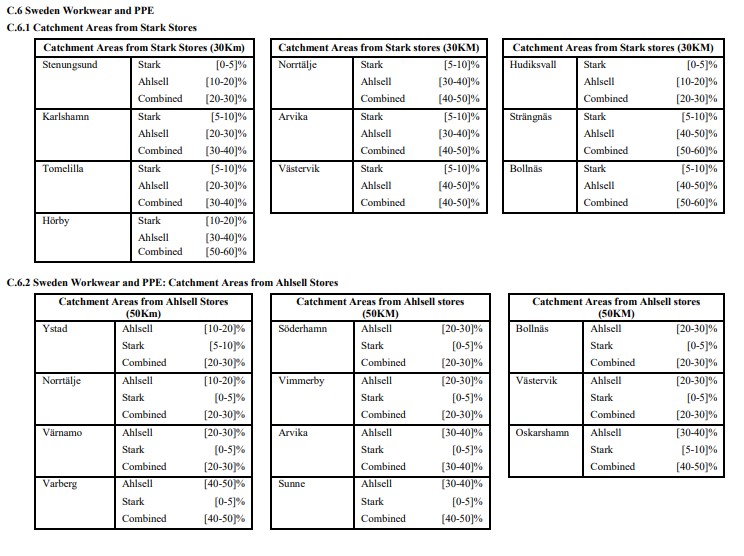

(a) Retail sale of building materials to professional customers at national level in Finland and at local level in Finland, Sweden and Norway ;

(b) Retail sale of installation products to professional customers at national level in Sweden and at local level in Finland, Sweden and Norway ;

(c) Retail sales of HVAC to professional customers at national level in Sweden and at local level in Finland, Sweden and Norway ;

(d) Retail sale of electrical products to professional customers at national level in Sweden and at local level in Sweden and Norway ;

(e) Retail sale of tools and supplies to professional customers at national level and at local level in Sweden ;

(f) Retail sale of professional work wear and PPE to professional customers at national level in Finland and Sweden and at local level in Sweden.

5.2.1. Retail sale of building materials to professional customers

(44) As mentioned in paragraph (8), Stark is a general builders merchant. It therefore has a larger offering of building products than Ahlsell who specialises in the distribution of installation products and tools and supplies. In fact, an analysis of the Parties’ internal documents shows that they do not see each other as competitors. This is reflected in the market positions that each Party has in the retail markets for building materials, both at national and local levels. Within all possible affected markets, Stark's highest market share is at [30-40] % (at local level in Sweden), whereas Ahlsell's highest market share is at [0-5] % (at local level in Sweden).

(45) At national level, one affected market arises in the retail distribution of building materials to professional customers in Finland. The Parties have a combined market share of [20-30] % and the increment brought about by the Transaction is negligible. Stark has a market share of [20-30] % whereas that of Ahlsell is merely [0-5] %. This is consistent with Stark being primarily focused on building materials while Ahlsell is only present in this market to a limited extent. In addition, there are several other competitors present at a national level, such as Kesko, Hartman, RTV, and Puumerkki. Kesko, which is considered by respondents to the market investigation to be a very close competitor to Stark, has a market share of [20-30] %. Hartman, RTV, and Puumerkki have market shares of [5-10] %, [5-10] % and [5-10] %, respectively.

(46) Based on a local market definition, additional affected markets arise in catchment areas in Finland, Norway and Sweden. In Finland, there are 20 affected catchment areas with a 30 km radius from Stark's stores ('Stark catchment areas) and nine catchment areas with a 50 km radius from Ahlsell's stores ('Ahlsell catchment areas'). The Parties' combined shares are in the range of 20-30 % and the increment brought about by Ahlsell is consistently below [0-5] %.29 In Norway, […]* two affected catchment areas, one with a 30 km radius from a Stark' store and another of 50 km from Ahlsell's store, where the Parties have a combined share of [20-30] % and [20-30] % and the increment brought about by Ahlsell is up to [0-5] %.30 In Sweden there are 18 affected catchment areas with a 30 […]** radius from Stark stores and catchment areas with a 50 km radius from Ahlsell […]***. In these catchment areas the Parties' combined market shares range from 20-39 %; however the increment brought about by the Transaction is consistently low, within a range from [0-5] %.31With regard to building materials, the Parties do not appear to be close competitors. The Parties have argued and the market investigation confirmed32 that Ahlsell focuses on light products (e.g. plumbing, electrical products) whereas Stark focuses on heavy products (e.g. timber, bricks). While, light and heavy products form part of the same overall retail building materials market, as there is some overlap between what can be described as a light and a heavy product, and in particular since suppliers tend to stock both types of products to some extent; the market is nevertheless very differentiated as the suppliers offer a wide range of products. Ahlsell's sales of light building materials are in fact peripheral to its installation business and Ahlsell only sells heavy building materials in a few locations in Sweden.33 On its end, Stark as a generalist builder offers both light and heavy materials but with an emphasis on the so-called heavy materials. Indeed, for the most part, the Parties' portfolios of products are not in direct competition but rather complement one another. In the market investigation, the majority of respondents that expressed a view consider that the Parties have mainly complementary offerings.34

(47) The Parties also target different customer groups. Whereas Ahlsell focuses on installers, in particular, plumbers and electricians, Stark focuses on builders, in particular masons and carpenters. In fact, the majority of customers and competitors that expressed a view consider that Parties target the same customers to a limited extent. Moreover, considering the limited product overlap between the Parties, the same type of customer does not necessarily look for the same item in Ahlsell's and Stark's offerings.

(48) The majority of respondents that expressed a view does not consider Ahlsell and Stark to be very close or close competitors. The majority of respondents that expressed a view consider Dahl to be a very close competitor to Ahlsell, followed by Onninen and Rexel. Similarly, the majority of respondents that expressed a view consider Kesko and XL Bygg to be very close competitors to Stark.

*Should read “there are”

** Should read “km”

*** Should read “stores”

(49) The majority of respondents that expressed a view also consider that the Transaction will have no impact on prices, quality and choice in the markets for retail of building materials to professional customers.35

(50) In light of the above, particularly in view of the results of the market investigation, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement in relation the retail distribution of building materials to professional customers, both at national and local levels.

5.2.2. Retail sale of installation products to professional customers

(51) In the retail sale of installation products, Ahlsell, as a specialist builder merchant, has a stronger position than Stark.

(52) At the national level, one affected market arises in the retail sale of installation products to professional customers in Sweden. The Parties have a combined share of [30-40] % and the increment brought about by the Transaction is below [0-5] %, as Stark has a very small presence on this market and its possible segments. Once again, these shares reflect the different focus and nature of the Parties product portfolios. Other suppliers in Sweden are Dahl with [10-20] % market share, followed by Sonepar with [10-20] %, Rexel with [10-20] % and Solar with [5-10] %.

(53) If a narrower market definition were adopted, the Transaction would also give rise to two other nationally affected markets in Sweden: the retail sale of HVAC products to professional customers and the retail sale of electrical products to professional customers. Similarly to the overall installation products market, the increment brought about by the Transaction is very limited and below [0-5] % as the Target does not have a significant presence for the retail distribution of these products. In the retail sale of HVAC, the Parties have a combined share of [30-40] %. The market leader is Dahl ([30-40] % share); other suppliers are Solar ([5-10] %), Lundagrossisten ([5-10] % share). In the retail sale of electrical products, the Parties have a combined market share of [20-30] %. Other suppliers are Sonepar ([20-30] % share), Rexel ([20-30] % share), and Solar ([10-20] % share).

(54) The market investigation suggests that the Parties are not close competitors in relation to installation products. A majority of customers and competitors that expressed a view consider that the Parties have a different or very different product assortment regarding HVAC, one of the categories of installation products where they overlap. The majority of respondents to the market investigation that expressed a view also consider that the Parties' electrical product assortments are different. Only in relation to work wear and PPE, the majority of the respondents that expressed a view consider the product assortment to be similar. However, Ahlsell's workwear and PPE is ancillary to its installation business, while Stark's is ancillary to its heavy building materials business and thus they target different customer groups.

(55) The majority of respondents that expressed a view also consider that the Transaction will have no impact on prices, quality and choice in the national markets for retail of installation products to professional customers, nor in the narrower markets of HVAC and electrical products at national level.36

(56) At the local level, there are a several affected catchment areas not only in Sweden, but also in Norway and Finland.

(57) In Sweden in respect to the retail sales of installation products there are 37 affected Stark catchment areas and 64 affected Ahlsell catchment areas. In the vast majority of these catchment areas the Parties’ combined market shares in the installation markets are between 20-30 % with an increment of up to [0-5] %. There are also a number of catchment areas where the Parties have a combined share between 30-50 % and the increment is up to [0-5] %. Finally, there are a few areas where the combined share is between 50-80 % where the increment is up to [5-10] % and two catchment areas where the Parties have a combined share between [80-90] % and the increment is up to [0-5] %.37 The catchment areas where the Parties have combined market share of [50-60] % and above are further discussed in paragraph (66).

(58) In respect to narrow market of HVAC there are 31 affected Stark catchment areas and 65 affected Ahlsell catchment areas in Sweden. In the majority of these areas the Parties have a combined market share between 20-30 % with an increment of up to [0-5] %.There are also a number of areas where the Parties have a combined market share between 30-50 % with an increment up to [0-5] %. However, there are a few areas where the combined share is between 50-80 % and where the increment is up to [5-10] %; and two catchment areas where the Parties have a combined share between 80-89 % and the increment is up to [0-5] %.38 The catchment areas where the Parties have a combined share below [40-50] % do not appear to raise concerns given that the increment is below [0-5] % and given the lack of closeness of the Parties. The catchment areas where the Parties have combined market share of [50-60] % and above will be further discussed in paragraph (66) below.

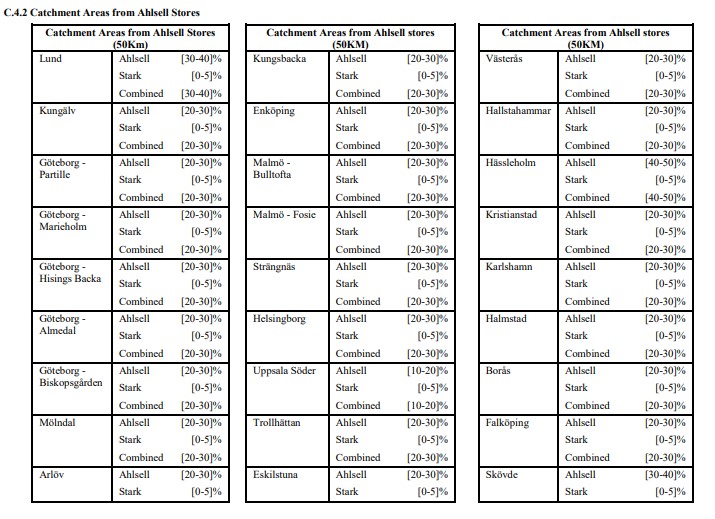

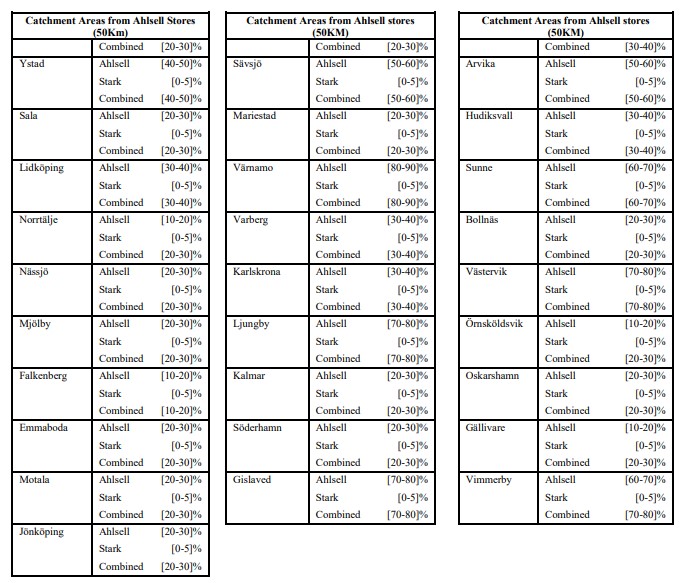

(59) In respect to the narrow local markets of electrical products, there are 32 affected Stark catchment areas and 55 affected Ahlsell catchment areas in Sweden. In the majority of these areas the Parties have a combined market share between 20-30 % with an increment of up to [0-5] %.There are also a number of areas where the Parties have a combined market share between 30-50 % with an increment up to [0-5] %. Finally, there are a few areas where the combined share is between 50-70 % with an increment is up to [5-10] %; three catchment areas where the combined market share is between 70-80 % and the increment up to [0-5] % and two catchment areas where the Parties have a combined share between [80-90] % and the increment is up to [0-5] %.39 The catchment areas where the Parties have a combined share below [40-50] % do not appear to raise concerns given that the increment is only up to [0-5] % and given the lack of closeness of the Parties. The catchment areas where the Parties have combined market share of [50-60] % and above are further discussed in paragraph (66).

(60) In Norway, there are five affected Stark catchment areas and four affected Ahlsell catchment areas in respect to the installation products market. Except for one catchment area where the Parties have a combined share of [70-80] % and an increment of [5-10] %, in all other catchment areas the Parties have a combined share between [20-30] % with an increment below [0-5] %.40 Given the low combined shares and increment of less than [0-5] %, the vast majority of catchment areas do not appear to raise concerns. The catchment area where the Parties have a combined share of [70-80] % is further discussed in paragraph (66).

(61) In respect to the HVAC products segment, there are six affected Stark catchment areas and five affected Ahlsell catchment areas in Norway. Except for one catchment area where the Parties have a combined share of [70-80] % and an increment of [0-5] %, in all other catchment areas the Parties have a combined share between 20-30 % with an increment below [0-5] %.41 Given the low combined shares and increment of less than [0-5] %, the vast majority of catchment areas do not appear to raise concerns. The catchment area where the Parties have a combined share of [70-80] % is further discussed in paragraph (66).

(62) In respect to the electrical products segment, there are eight affected Stark catchment areas and three affected Ahlsell catchment areas in Norway. The Parties have combined shares between 20-30 % with an increment below [0-5] % in all areas except for one where the combined share is [30-40] % and the increment [0-5] %, and another where the combined share is [60-70] % and the increment [5-10] %.42 Given the low combined shares and increment of less than [0-5] %, the vast majority of catchment areas do not appear to raise concerns. The catchment area where the combined share is [60-70] % and the increment [5-10] % is further discussed in paragraph (66).

(63) In Finland there are three affected Stark catchment areas and two affected Ahlsell catchment areas in respect to the retail sale of installation products. In these catchment areas the Parties' combined market share range between [20-30] % and the increment is below [0-5] %.43

(64) In respect to the HVAC segment, there are 24 affected Stark catchment areas and 24 affected Ahlsell catchment areas in Finland. In the vast majority of catchment areas the Parties have a combined share of 20-30 % with an increment below [0-5] %. There are few catchment areas where the Parties have a combined share of 30-40 % with an increment up to [0-5] %. There is one catchment area where the Parties' combined share is [40-50] % and the increment below [0-5].44 The catchment areas where the Parties have a combined share below [40-50] % do not appear to raise concerns given that the increment is below [0-5] % and the Parties’ lack of closeness. The catchment areas where the Parties have a combined share of [40-50] % is further discussed in paragraph (66).

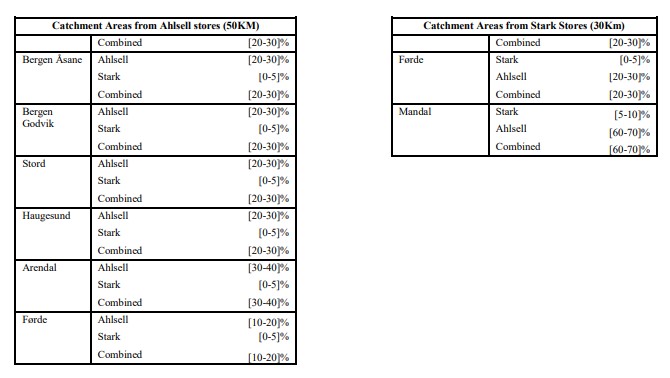

(65) Table I lists the catchment areos wheie the Parties have hipb and veiy high morket shares.

(66) Even in these catchment areas the Transaction does not raise serious doubts. First, the Parties ore not close competitors : the sales of the overlapping products account for a very small percentage of each of Ahlsell end Stark sales, which shows how differentiated the Parties’ offerings are. Second, there are alternative supplies present in these areas end the customers can olso turn to online or over-the-phone orders.45 Third, since catchment areas are overlapping, there is a certain number of clients that have the choice to go to stores located in the other catchment area and therefore, the Parties’ market power seems to be less than what the market shares would indicate. For example, within 30 km from Hörby is Eslov where the Parties have a combined share of [20-30]% in installation products. With 30 km from Mandal is Kristiansand where the Parties have a combined share below [10-20]% in installation products market as well as in the HVAC end electrical segments. In fact, the majority of the market respondents that expressed a view does not expect a price increase or a quality or choice decreased as a result of the Transaction at local level,

in particular in the catchment areas identified in Table 1.46

(67) In light of the above, particularly in view of the results of the market investigation, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement in relation to the retail distribution of installation products to professional customers, both at national and local levels.

5.2.3. Retail sale of tools and supplies to professional customers

(68) At the national level, the Transaction gives rise to an affected market in the retail sale of tools and supplies to professional customers in Sweden, where the Parties have a combined share of [30-40] %. The increment brought about by the Transaction is minimal at [0-5] %. Ahlsell has a share of [30-40] % whereas Stark has a share of [0-5] %. This is consistent with Ahlsell's activities primarily being focused on installation products and tools and supplies; whereas Stark is more focused on building materials. There are a number of alternative suppliers such as Momentum ([10-20] % market share), Procurator ([5-10] % market share), and Würth ([5-10] % market share).

(69) If a narrower market definition is adopted where workwear and PPE are a part of a separate market from other tools and supplies, the Transaction would give rise to affected national markets in Sweden and in Finland. In Sweden, the Parties have a combined market share of [20-30] %. However, the increment is low ([0-5] %). Ahlsell has a [20-30] % share and Stark has a [0-5] % share. Ahlsell's main competitors in the segment are Momentum ([10-20] % share), Procurator ([5-10] % share) and Würth ([5-10] % market share). In Finland, the Parties have a combined market share of [20-30] %. However, the increment is small and just over [0-5] %: Ahlsell has a [20-30] % share and Stark has a [0-5] % share. Ahlsell's main competitors in the segment are Würth ([20-30] % share), Etra ([10-20] % share), IHK ([10-20] % share) and Linström ([5-10] % share) amongst others.

(70) At the local level, additional affected markets arise for the retail to professional customers of tools and supplies, and for workwear and PEE in Sweden.

(71) The Transaction gives rise to 14 affected Stark catchment areas and 15 affected Ahlsell catchment areas for the market for tools and supplies (excluding PPE/workwear) in Sweden. In the vast majority of these affected catchment areas, the Parties' combined market shares in these locally affected markets are in the region of 20-30 %. There are two Stark catchment areas and three Ahlsell catchment areas where the market shares are between 30-40 % and there a small number of areas where the combined market share is above [40-50] % (detailed in Table 2 below). In all affected catchment areas, the increments brought about by the Transaction range from [0-20] %.47

(72) In relation to workwear/PPE, the Transaction gives rise to 10 affected Stark catchment areas and 11 affected Ahlsell catchment areas in Sweden. In the majority

(73) However, in a small number of catchment areas they reach 40-60 % as can be seen from Table 2 below. Similarly to installation product markets, the sales of overlapping products account for a small percentage of the overall sales of Ahlsell and Stark and post-Transaction several competitors would remain as shown in Table 2.

(74) The majority of the market respondents that expressed a view consider that the Transaction will not lead to a decrease of choice or quality either at a notional or local level for tools end supplies or its narrower sub-segments. Equally, a majority of respondents who expressed a view consider the Transaction will not lend to price increases either notionally or locally, including in the local areas with higher shares 49

(75) In light of the above, particularly in view of the results of the market investigation which on balance suggests the Transaction does not lead to competition concerns, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement in relation to the retail distribution of tools end supplies, as well as workwear end PPE to professional customers on any considered geographic market definition.

(76) The Commission therefore concludes that the Transaction does not give rise to serious doubts as to its compatibility with the internal market in relation to any of the horizontally effected markets for retail distribution of (i) building materials, (ii) installation products or (iii) tools and supplies, including for any relevant potential sub-segments of these markets.

5.3. Vertically affected markets

(77) As Ahlsell is active in the wholesale of installation products, as well as the wholesale of tools and supplies in all Nordic countries, and Stark is active in the wholesale of building materials in Finland, the Transaction also creates vertical links with the Parties' retail distribution businesses. Not all vertical links give however rise to vertically affected markets. Mainly due to the Parties' positions in the retail markets the following vertically affected markets arise (on the basis of value market shares):

(a) Wholesale of installation products (national) and retail of these products to professional customers at national and local levels in Sweden and at local level in Norway and Finland.

(b) Wholesale of HVAC products (national) and retail of these products to professional customers at national and local levels in Sweden and at local level in Norway and Finland.

(c) Wholesale of electrical products (national) and retail of these products to professional customers at local level in Sweden, Norway.

(d) Wholesale of tools and supplies and retail of these products to professional customers at national and local levels in Sweden.

(78) Ahlsell is active in the wholesale of installation products in Sweden, Finland and Norway however, its presence is relatively limited, since it has a market share up to [5-10] % in Sweden, up to [5-10] % in Finland and up to [0-5] % in Norway, including in the HVAC and electrical products segments. The wholesale markets are vertical affected markets, due to the Parties' position in the retail markets for these products, in particular Ahlsell's position.

5.3.1. Wholesale and retail distribution of installation products

(78) Ahlsell is active in the wholesale of installation products in Sweden, Finland and Norway however, its presence is relatively limited, since it has a market share up to [5-10] % in Sweden, up to [5-10] % in Finland and up to [0-5] % in Norway, including in the HVAC and electrical products segments. The wholesale markets are vertical affected markets, due to the Parties' position in the retail markets for these products, in particular Ahlsell's position.

(79) At the national level, the Transaction gives rise to affected markets in Sweden for the retail (downstream) and wholesale distribution (upstream) of installation products. If a narrower market definition is adopted, the wholesale and retail markets for HVAC products are also affected. In the wholesale markets, Ahlsell has a market share of [5-10] % in the overall installation products market and of [0-5] % in the HVAC products market. In the respective retail markets, Parties have a combined share of [30-40] % in the overall installation product and [30-40] % in the HVAC products market. Stark brings an increment of less than [0-5] % in both installation products and in the HVAC sub-segment.

(80) At the local level, there are a several vertically affected catchment areas in Sweden not only regarding the downstream retail sale of installation products and the HVAC segment and the respective upstream national wholesale markets, but also regarding the downstream retail sale of electrical products market and the respective upstream national wholesale market. In Sweden, Ahlsell has also a market share of [5-10] % in the wholesale of electrical products.

(81) Likewise, in Norway the Transaction gives rise to vertically affected markets in the upstream wholesale and the downstream retail of installation products, HVAC and electrical products due to the Parties' combined position in downstream markets. The position of Ahlsell at the upstream wholesale is however limited ([0-5] % market share).

(82) Similarly, due to the Parties' position at the downstream retail local markets, in particular Ahlsell's, the Transaction gives raise to vertically affected markets for the upstream wholesale and downstream retail of HVAC products in Finland. In Finland, Ahlsell has a small share of [5-10] % in the upstream wholesale of HVAC products.

(83) Both looking at the national and local markets in the three countries, the merged entity will have no ability to adopt an input foreclosure strategy. First, as explained above Ahlsell has a very limited presence in the upstream wholesale markets and therefore lacks the necessary degree of market power. There are a number of competitors active at the wholesale level in each country, which provide alternative sources of supply to builders merchants. Second, Ahlsell's supplies are not sufficiently important inputs for Stark and other general builder's merchants as their focus is the distribution of building materials. Third, Ahlsell is already present in the downstream retail installation product markets and the increment brought by the Transaction is small.

(84) In addition, the merged entity will also not have the incentive to adopt an input foreclosure strategy, First, Ahlsell's main wholesale customers are not close competitors of Stark, therefore it would not compensate to lose sales at the wholesale level, by refusing to sell or increase the wholesale prices, when these losses cannot be compensated for at the retail level, by selling more retail products via Stark. Second, Ahlsell is already making some wholesale sales to Stark, while it is also present at the retail level, which means that the sales to Stark are not a threat to its retail business for the companies do not directly compete. Supplying only to Stark would also not be profitable, as Stark cannot absorb all the wholesale supplies of Ahlsell.

(85) Similarly, the merged entity would not have the ability to adopt a customer foreclosure strategy. First Ahlsell is already vertically integrated in the installation markets and the increment brought at the retail level is small. Second, Stark has a small share of the retail markets for HVAC products in Sweden, Finland and Norway, both at national (below [0-5] %) and local levels (up to [5-10] %). Stark is therefore not an important customer of HVAC wholesale distributors. Third, there are sufficient alternatives to Stark to whom Ahlsell's wholesale competitors can sell their output.

(86) In addition, the merged entity will also have no incentives to adopt a customer foreclosure strategy. Stark has a small presence in the retail markets of HVAC products, therefore the possibility to enjoy increased margins downstream by virtue of a price increase at the wholesale level is very unlikely.

(87) Indeed, the majority of competitors that expressed a view considers that the Transaction will have no impact on their ability to source, installation products, nor on their ability to access retailers.50

(88) In light of above, and in view of the results of the market investigation, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market in relation to the vertical link between the wholesale and the retail distribution of installation products.

5.3.2. Wholesale and retail distribution of tools and supplies

(89) Ahlsell is a wholesale supplier of tools and supplies in Sweden, but it has a very limited presence with a less than [0-5] % market share. Due to the Parties' presence in the retail markets, in particular Ahlsell's, the Transaction gives rise to vertical affected markets both at the national level (combined share of [30-40] %) and local level (combined shares between 30-60 %).

(90) The merged entity will have no ability to adopt an input foreclosure strategy. First, Ahlsell has less than [0-5] % share of the wholesale market. Second, Ahsell supplies are not significant inputs for Stark and its close competitors, as they focus on building materials. The merged entity will also have no incentive to adopt such strategy. Being already present today in the retail market, where the increment brought by the Transaction is small, the merged entity will have no ability to adopt an input foreclosure strategy both at the national and local levels. Likewise, the arguments made regarding the relevance of Ahlsell supplies and the relevance of Stark as a wholesale customer for the installation markets also apply to tool and supplies markets.

(91) Indeed, the majority of competitors that expressed a view considers that the Transaction will have no impact on their ability to source, tools and supplies, nor on their ability to access retailers.51

(92) In light of above, and in view of the results of the market investigation, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement in relation to the vertical link between the wholesale and the retail distribution of tools and supplies.

(93) The Commission therefore concludes that the Transaction does not give rise to serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement in relation to any vertical links.

6. CONCLUSION

(94) For the above reasons, the European Commission decides not to oppose the Transaction and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

For the Commission

(Signed)

Margrethe VESTAGER

Executive Vice-President

ANNEXE

NOTES

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union (the 'TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 Publication in the Official Journal of the European Union No C 113, 31.3.2021, p. 12.

4 Turnover calculated in accordance with Article 5 of the Merger Regulation.

5 See, for example, Case COMP/M.7703 – PontMeyer/DBS, paragraphs 11–12; Case COMP/M.3407 – Saint Gobain/Dahl, paragraphs 12 and 16; Case COMP/M.3142 – CVC/Danske Traelast, paragraphs 11– 13; Case M.8733 – Lone Star/Stark, paragraph 25; and Case COMP/M.9406 – Lone Star - Stark Group / Saint Gobain BDD, paragraph 19

6 Case COMP/M.3943 – Saint-Gobain/BPB, paragraph 15. Case COMP/M. 9790 – Blackstone/KP1, paragraph 22 and 23.

7 Case COMP/M.3407 – Saint Gobain/Dahl, paragraph 15 and Case COMP/M.3943 – Saint-Gobain/BPB, paragraphs 17-19. Case COMP/M.4050 – Goldman Sachs/Cinven/Ahlsell, paragraphs 8–13

8 Case M.7910 – Kesko/Onninen, paragraph 21

9 Case COMP/M.9644 – Nordstjernan/Momentum Group, paragraphs 13-21.

10 Case COMP/M.4050 – Goldman Sachs/Cinven/Ahlsell, paragraphs 8–13.

11 Case COMP/M.7457 – CVC/Paroc, paragraphs 23-25.

12 Case COMP/M.9644 – Nordstjernan/Momentum Group, paragraphs 13-21.

13 Case COMP/M.9644 – Nordstjernan/Momentum Group, paragraphs 13-21.

14 Responses to Q1 – Questionnaire to customers, question 8; and Q2 – Questionnaire to competitors, question 6.

15 Responses to Q1 – Questionnaire to customers, question 6; and Q2 – Questionnaire to competitors, question 4.

16 Responses to Q1 – Questionnaire to customers, question 9; and Q2 – Questionnaire to competitors, question 7.

17 Case COMP/M.7457 – CVC/ Paroc, paragraphs 26-28

18 Case COMP/M.7457 – CVC/ Paroc, paragraphs 26-28.

19 Case COMP/M.9644 – Nordstjernan/Momentum Group, paragraph 16.

20 Case COMP/M.3142 – CVC/Danske Traelast, paragraphs 14-16.

21 Case COMP/M.7703 - Pontmeyer/DBS, paragraph 21; Case COMP/M.7107 – Cordes & Graefe Case COMP/M.3184 - Wolseley / Pinault Bois & Materiaux, paragraphs 19–22.

22 As regards the assessment in relation to the EEA, see also Annex XIV to the EEA Agreement.

23 Guidelines on the assessment of horizontal mergers under the Council Regulation on the control of concentrations between undertakings (OJ C 31, 5.2,2014, p. 5).

24 Guidelines on the assessment of non-horizontal mergers under the Council Regulation on the control of concentrations between undertakings (OJ C 265, 18.10.2008, p. 6).

25 Horizontal Merger Guidelines, paragraph 24.

26 Horizontal Merger Guidelines, paragraph 26.

27 Non-Horizontal Merger Guidelines, para 30

28 Non-Horizontal Merger Guidelines, para 30

29 See Annex I, section A.1.

30 See Annex I, section B.1.

31 S Annex I, section C.1.

32 Responses to Q1 – Questionnaire to customers, question 12; and Q2 – Questionnaire to competitors, question 11.

33 Form CO, paragraph 71 and Parties' response to RFI no.3, question 1.

34 Responses to Q1 – Questionnaire to customers, question 11; and Q2 – Questionnaire to competitors, question 10.

35 Responses to Q1 – Questionnaire to customers, question 22; and Q2 – Questionnaire to competitors, question 29.

36 Responses to Q1 Responses to Q1 – Questionnaire to customers, question 22; and Q2 – Questionnaire to competitors, question 29.

37 See Annex I, sections C.2.1 and C.2.2.

38 See Annex I, sections C.3.1 and C.3.2.

39 See Annex I, sections C.4.1 and C.4.2.

40 See Annex I, section B.2.

41 See Annex I, section B.3.

42 See Annex I, section B.4.

43 See Annex I, section A.2.

44 See Annex I, section A.3.

45 Response to RFI n° 5.

46 Responses to Q1 Responses to Q1 – Questionnaire to customers, questions 23.1 and 23.2; and Q2 – Questionnaire to competitors, questions 29.3 and 29.4

47 See Annex I, sections C.5.1 and C.5.2

48 See Annex I, sections C.6.1 and C.6.2

49 Response to QI Responses to QI – Questionnaire to customers, questions 24 and 24.2; and Q2 – Questionnaire to competitors, questions 29.5 and 29.6

50 Responses to Q2 – Questionnaire to competitors, questions 22 and 23.

51 Responses to Q2 – Questionnaire to competitors, questions 22 and 23.