Commission, July 9, 2021, No M.10154

EUROPEAN COMMISSION

Decision

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

PARTIES

Demandeur :

BME Group Holding

Défendeur :

Saint-Gobain Distribution the Netherland

(1) On 4 June 2021, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which BME Group Holding B.V. (‘BME’ or the ‘Notifying Party’, the Netherlands) intends to acquire within the meaning of Article 3(1)(b) of the Merger Regulation sole control over Saint-Gobain Distribution the Netherlands B.V. (‘SGDN’, the Netherlands). The acquisition is accomplished by way of purchase of shares (‘the Transaction’).3 BME and SGDN are designated hereinafter as the ‘Parties’.

1. THE PARTIES

(2) BME is a Netherlands-based company indirectly controlled by The Blackstone Group Inc. (‘Blackstone’). BME is active in the distribution of building materials via general builders’ merchant (‘GBM’), specialist builders’ merchant (‘SBM’) and do-it-yourself (‘DIY’) stores in Austria, Belgium, France, Germany, the Netherlands, Portugal,4 Spain5 and Switzerland.

(3) In the Netherlands, BME operates 72 GBM stores under the BMN brand, 6 SBM stores specialised in interior finishing products under the BMN Wijcks brand, 2 SBM stores specialised in ironmongery under the BMN IJzerwaren brand and 17 cash-and-carry stores as a franchisee under the Bouwmaat brand.6

(4) SGDN is active in the Netherlands as a distributor of building materials via GBM and SBM stores. Moreover, it is active in the wholesale of ceramic tiles and of sanitary, heating and plumbing (‘SHAP’) products.

(5) SGDN operates in the Netherlands 35 GBM stores under the Raab Karcher (32 stores) and De Jager Tolhoek (3 stores) brands and one SBM store in interior finishing products under the Van Keulen brand.

2. THE CONCENTRATION

(6) On 1 April 2021, BME, via its fully owned subsidiary BMN Bouwmaterialenhandel

B.V. (‘BMN’), entered into a share purchase agreement (‘SPA’) to acquire 100% of the shares of SGDN. As a result of the Transaction, SGDN will be solely controlled by BME.

(7) The Transaction is therefore a concentration pursuant to Article 3(1)(b) of the Merger Regulation.

3. UNION DIMENSION

(8) The undertakings concerned have a combined aggregate worldwide turnover in 2019 of more than EUR 5 000 million (Blackstone: EUR […] million; SGDN: EUR […] million).7 Each of them has a Union-wide turnover in 2019 in excess of EUR 250 million, (Blackstone: EUR […] million; SGDN: EUR […] million) but they do not achieve more than two-thirds of their aggregate Union-wide turnover within one and the same Member State.

(9) The Transaction has therefore a Union dimension pursuant to Article 1(2) of the Merger Regulation.

4. RELEVANT MARKETS

4.1. Relevant Product Markets

(10) The Parties’ activities overlap in the retail distribution of building products via GBM stores and in the retail distribution of interior finishing products via SBM stores. In addition, there is a vertical link between SGDN’s activities in the wholesale distribution of ceramic tiles and SHAP products and BME’s activity as a GBM retail distributor.

(11) The Commission has previously defined a market for the distribution of building products in general, and has considered but left open whether this market can be further divided into: (i) wholesale to retailers; (ii) retail sale to professional customers, primarily via GBM and SBM stores; and (iii) retail sale to non- professional customers, primarily through DIY stores.8

4.1.1. Wholesale distribution of building products

(12) In relation to the wholesale distribution of building materials to retailers, the Commission has considered potential markets for particular types of building products.9

(13) In light of this distinction by product category, the Notifying Party submits that there are two distinct relevant product markets: (i) the wholesale supply of tiles and (ii) the wholesale supply of SHAP Products.

(14) According to the Notifying Party there is no need to further segment the wholesale supply of tiles market according to the type of material (e.g. ceramic, stone or concrete). Nonetheless, because SGDN only supplies ceramic tiles, the Notifying Party has provided market shares data on this narrower plausible segment. In addition, the Notifying Party submits that given supply-side substitution, there is no need to further segment the ceramic tiles market according to the end use, i.e. tiles for floors, on one hand, and tiles for walls, on the other.10

(15) Similarly, the Notifying Party claims there is no need to further segment the wholesale supply of SHAP market, by subcategories of products, such as sanitary ware. However, as SGDN mainly supplies sanitary ware, the Notifying Party has provided market share data also for this segment.11

(16) Market participants who expressed a view support a distinction per product category within the market for the wholesale distribution of building products.12 They maintain that, for instance, each type of building product (e.g. SHAP) serves the needs of a different type of customer (e.g. plumbers) and that the supply chains of certain products (e.g. concrete) are different from those of other building materials.13

(17) For the purpose of this Decision, the Commission will assess the effects of the Transaction on the market for the wholesale supply of ceramic tiles and on the market for the wholesale supply of SHAP. Because the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible narrower market definition, it can be left open for the purpose of this Decision whether it is appropriate to further segment each of these two markets.

4.1.2. Retail sale of building materials

(18) As mentioned in paragraph (11), the Commission has considered, although ultimately left open, a further segmentation of the market for the retail sale of building products based on the type of customer, i.e. professional and non- professional customers. The Commission has also previously considered whether the retail sale to professional customers could be further divided between GBMs and SBMs.14

(19) Within SBMs, the Commission has also considered whether separate product markets exist for the distribution of individual product categories.15 In particular, the Commission has considered specialist retailers in relation to 'fitting-out' or interior finishing products, including plaster-based products, suspended ceilings and associated products, but has left the market definition open.16.

(20) The Notifying Party considers that there is an overall market for retail sales of building products, without further distinction between professional or non- professional customers,17 given that there are a number of retailers on the Dutch market which are present on both segments and target both professional and non- professional customers.18

(21) The market investigation however supports the distinction between retail sales to professional and to non-professional customers. Namely, the ample majority of market participants who expressed a view19 consider such distinction per type of customer justified based on, inter alia, the differences in: (i) sales approach and service levels; (ii) pricing; (iii) packaging sizes; (iv) quality of products; and/or (v) delivery and transport.20 Notwithstanding, a number of market participants21 note that the distinction between professional and non-professional customers, while still relevant, is becoming increasingly blurry and outdated: “one-person building companies buy indistinctively from general building merchants and DIY stores, blurring the distinction between B2B and B2C.”22

(22) Although the Notifying Party also disagrees with the distinction between GBMs and SBMs stores, it has nonetheless provided information on the retail sale of interior finishing products via SBM stores, including for the dry finishing products segment, as this is the only product sub-category where the Parties’ activities overlap.

(23) The market investigation has also supported the distinction between retail sales to professional customers via GBM stores and SBM stores, namely, retailers specialised in interior finishing products. Such distinction is particularly relevant from the point of view of customers who expressed a view, in light of the different kinds of products, prices and services offered by SBM and GBM stores.23 Although to a lesser extent, competitors who expressed a view also support this distinction, claiming, inter alia, that: “the knowhow of the sales person plays an important role” in the SBM segment.24 However, also in this case some market participants indicate that the distinction between both types of stores is becoming more and more unclear.25

(24) In any event, because the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition, the exact market definition of the retail sales of building products can be left open for the purpose of this Decision. The Commission will assess the impact of the Transaction taking account of the following narrower plausible market definition that give rise to an affected market, i.e. retail distribution of building materials to professional customers via GMB stores and retail distribution of interior finishing products, including dry finishing products, via SBM stores.

4.2. Relevant Geographic Markets

4.2.1. Wholesale distribution of building products

(25) The Commission has previously found that the relevant wholesale markets are likely to be at least national in scope (and possibly wider).26

(26) The Notifying Party shares this view,27 which has also been widely confirmed by market participants who expressed a view due to, inter alia, the high transport costs and the homogeneous prices at national level.28

(27) Hence, for the purpose of the present decision, the Commission will examine the market for the wholesale distribution of building products in the Netherlands.

4.2.2. Retail sale of building products

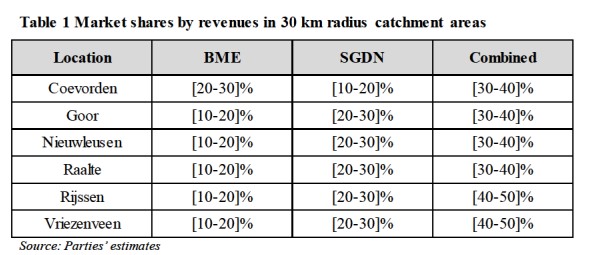

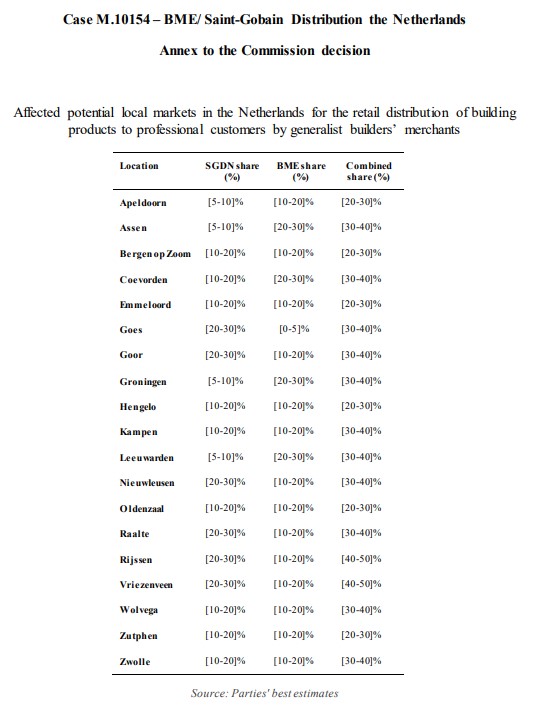

(28) In past decisions, the Commission has considered national29 or local30 geographic market dimensions for the retail distribution of building products, although the question has ultimately been left open. At local level, catchment areas with a 30-km radius around GBM stores and catchment areas with a 50-km radius around SBM stores have been considered.31

(29) The Notifying Party submits that the market for the retail distribution of building products to professional customers is national in scope in the Netherlands.32 It emphasises the importance of centrally placed orders and direct deliveries from central warehouses, which they claim reduces the significance of local stores.33

(30) With regard to the retail sale of building products to professional customers via GBM stores, the market investigation was inconclusive as to whether the market is national or local (i.e., within a 30 km radius from the store) in scope. While a narrow majority of competitors who expressed a view considers the market to be national in scope, a narrow majority of customers who expressed a view sees the market as local.34 Concerning the retail sale of building products to professional customers by SBM stores, the majority of market participants who expressed a view support the definition of the market as national in scope.35

(31) Because the Transaction does not raise serious doubts as to its compatibility with the internal market even under the narrowest segment, it can be left open for the purpose of this Decision whether the geographic scope of the market for the retail sale of building products, possibly segmented by customer type (between retail sale to professional and to non-professional customers) and further segmented by sales channel (into GBM or SMB stores), is local or national.

5. COMPETITIVE ASSESSMENT

5.1. Analytical Framework

(32) Under Article 2(2) and (3) of the Merger Regulation,36 the Commission must assess whether a proposed concentration would significantly impede effective competition in the internal market or in a substantial part of it, in particular through the creation or strengthening of a dominant position. Depending on the position of the parties in the supply chain, a concentration may entail horizontal and/or non-horizontal effects.

(33) Horizontal effects arise when the parties to a concentration are actual or potential competitors in one or more of the relevant markets concerned. The Commission appraises horizontal effects in accordance with the guidance set out in the Horizontal Merger Guidelines.37

(34) Non-horizontal effects arise when the parties to a concentration operate in different levels of the supply chain in certain relevant markets (vertical effects). The Commission appraises non-horizontal effects in accordance with the guidance set out in the Non-Horizontal Merger Guidelines.38

(35) Both the Horizontal and Non-Horizontal Merger Guidelines distinguish between two main ways in which mergers between actual or potential competitors on the same relevant market may significantly impede effective competition, namely non-coordinated and coordinated effects.

(36) In horizontal mergers, non-coordinated effects may significantly impede effective competition by eliminating the competitive constraint imposed by each party to the merger on the other, as a result of which the merged entity would have increased market power, without resorting to coordinated behaviour. In that regard, the Horizontal Merger Guidelines consider not only the direct loss of competition between the merging firms, but also the reduction in competitive pressure on non- merging firms in the same market that could be brought about by the merger.39

(37) The Horizontal Merger Guidelines list a number of factors, which may influence whether or not significant non-coordinated effects are likely to result from a merger. In particular, the Horizontal Merger Guidelines refer to the large market shares of the merging firms, the fact that the merging firms are close competitors, the limited possibilities for customers to switch suppliers or the fact that the merger would eliminate an important competitive force.40 Not all these factors need to be present for significant non-coordinated effects to be likely. The list of factors is also not exhaustive.

(38) Concentrations which, by reason of the limited market share of the undertakings concerned, are not liable to impede effective competition may be presumed to be compatible with the internal market. An indication to this effect exists, in particular, where the market share of the undertakings concerned does not exceed 25% either in the internal market or in a substantial part of it.41

(39) In non-horizontal mergers, non-coordinated effects may arise when the concentration gives rise to foreclosure. In vertical mergers, foreclosure can take the form of input foreclosure, where the merger is likely to raise costs of downstream rivals by restricting their access to an important input; and/or the form of customer foreclosure, where the merger is likely to foreclose upstream rivals by restricting their access to a sufficient customer base.42

(40) In assessing the likelihood of an anticompetitive foreclosure scenario, the Commission examines whether the merged entity would have post-transaction the ability to foreclose access to either inputs or customers, whether the merged entity would have the incentives to do so and whether such foreclosure strategy would have a detrimental effect on competition.43

5.2. Horizontally Affected Markets

(41) The Transaction gives rise to potentially relevant horizontally affected markets with regard to (i) the retail distribution of building materials to professional customers by GBM stores in the Netherlands, and (ii) the retail distribution of interior finishing products to professional customers by SBM stores in the Netherlands.

5.2.1. Retail distribution of building materials to professional customers via General Builders’ Merchants

(42) In the retail distribution of building materials to professional customers via GBMs, BME is active with GBM and cash-and-carry formats (the latter as a franchisee), whereas SGDN is active with only GBM formats under two brands (Raab Karcher and De Jager Tolhoek).

(43) The Notifying Party submits that the Transaction will not give rise to a significant impediment of effective competition (SIEC) and puts forward a number of arguments to that effect. First, the market shares are small to moderate. Second, the Parties are not close competitors because they offer different product ranges, target different customer groups and focus on different channels to market. Third, the Parties face strong competitors with similar networks of stores. Fourth, customers multisource. Fifth, the majority of retail competitors have access to the same manufacturers. Sixth, the Parties also face competition from manufacturers who sell directly to builders.

(44) Considering both GBM and cash-and-carry formats, the Parties have a combined value share of [20-30]% (and a combined volume share of [20-30]%) at national level. Post-Transaction several other GBMs will remain in the market, including national brands with a footprint of stores across the Netherlands. They include among others: TABS with two brands and circa 100 stores; Bouwcenter, a marketing and purchasing group that includes several brands and has approximately 82 branches; 4Plus, a marketing and purchasing group of builders' merchants with 65 affiliated members and circa 72 stores; De Stiho Groep with 23 stores; Sakol, a GBM purchasing group with 8 members and 26 branches, amongst others.

(45) A couple of larger customers expressed the concern that Post-Transaction the Parties’ competitors would not have the same ability to address their needs with regard to very large projects.44 However, several findings suggest that this concern 12 others; in Raalte, 15 others; in Rijsen, 13 others; and in Vriezenveen, 15 others. The alternative competitors include other GBM networks and independent GBMs.

(46) Concerning smaller customers, although loyalty could play a significant role, possibly making switching less likely, the vast majority of customers seem to multisource from more than 3 suppliers.46 More importantly, the vast majority of customers, including smaller customers, either does not expect the Transaction to have on effect on their business, or expects a positive effect.47

(47) At local level, the Parties would have a combined value share between 20% and 30% in six catchment areas (based on volume shares, the catchment areas would increase to 26), and between 30% and 40% in 13 catchment areas (based on volume shares the number of catchment areas would decrease to one).4 In the latter group, the Parties’ combined share are around 40% in six catchment areas (based on volume shares there is no catchment area with a market share equal or above 35%). The local markets with the highest combined shares are listed in Table I below.

(48) As the figures in Table I above show, the Parties’ market shares in these six catchment areas are relatively high. However, these market shares seem to overestimate the Parties’ market power for the following reasons. First, many several alternative GBMs will remain post-Transaction. In Coevorden, there are 10 other competitors active; in Goor there are 11 other competitors; in Nieuwleusen 12 others; in Raalte, 15 others; in Rijsen, 13 others; and in Vriezenveen, 15 others. The alternative competitors include other GBM networks and independent GBMs.

(49) Second, both customers and competitors consider that most of these alternative GBMs are also close or very close competitors to the Parties. These competitors are TABS, Concordia, 4Plus, and Sakol. In addition, some of the independent GBMs present in these six catchment areas have a similar product offering to the Parties. In Coevorden, 3 independent GBMs offer a similar product assortment; in Goor, 2 independent GBMs; in Nieuwleusen, 1; in Raalte, 3; in Rijsen, 4; and in Vriezenveen, 4 independent GBMs.49

(50) Third, in each of these six catchment areas the majority of sales come from ‘project sales’, i.e., sales invoiced by the GBM but delivered directly from the manufacturers to the building sites.50 In these types of sales, characteristic of large and medium customers, the Parties feel also the constraint imposed by manufacturers that sell directly to larger and medium customers. Moreover, the direct access to the manufacturers gives these customers bargaining power vis-à-vis the Parties.

(51) Fourth, the customer overlap between the Parties in each of these catchment areas is relatively small, which shows that already today the vast majority of the Parties’ customers source from other competitors. In Coevorden, [10-20]% of the SGDN's customers are also BME customers, whereas only [10-20]% of the BME customers are also SGDN customers. This shows that more than [80-90]% of SGDN customers and nearly [90-100]% of BMN's customers are able to get their supplies from other GBMs. In Goor, [10-20]% of the SGDN's customers are also BME customers, whereas [10-20]% of the BME customers are also SGDN customers. This shows that more than [80-90]% of the SGDN's and BMN's customers are able to get their supplies from other GBMs. In Niewleusen, [10-20]% of the SGDN's customers are also BME customers, whereas only [10-20]% of BME customers are also SGDN customers. This shows that around [80-90]% of the each of the Parties' customers are able to get their supplies from other GBMs. In Raalte, [10-20]% of the SGDN's customers are also BME customers, whereas [10-20]% of the BME customers are also SGDN customers. This shows that around [80-90]% of SGDN customers and around [80-90]% of BMN's customers are able to get their supplies from other GBMs. In Rijsen and in Vriezenvenn, [10-20]% of the SGDN's customers are also BME customers, whereas [10-20]% of the BME customers are also SGDN customers. This shows that almost [80-90]% of SGDN customers and more than [80-90]% of BMN's customers are able to get their supplies from other GBMs.51

(52) Finally, concerning both national and local levels, the majority of respondents to the market investigation do not expect that the proposed Transaction will have an effect on prices, quality or choice.52 Moreover, no stakeholder has raised concerns that can be confirmed on the basis of the available evidence.

(53) In light of the above, the Commission concludes that the proposed Transaction does not raise serious doubts as to its compatibility with the internal market in relation to the retail distribution of building materials to professional customers via GBM stores in the Netherlands, be it at the national or at the local level.

5.2.2. Retail distribution of interior finishing products to professional customers

(54) The Parties are also active in the retail distribution of interior finishing products to professional customers by SBM stores. This overlap does not give rise to an affected market on the basis of a 50-km radius catchment area as considered in the precedents.53 A horizontally affected local market arises only if a catchment area with a 30 km radius is considered from SGDN’s only SBM store Van Keulen in Amsterdam. Even in such a hypothetical scenario, narrower than the precedent and not supported by the market investigation, the Parties would have relatively low combined market shares ([20-30]% in value and [30-40]% in volume) and at least three credible competitors would remain present, such as SIG ([20-30]% in volume),

DSG ([20-30]% in volume), and Baustoff Metal ([10-20]% in volume).54

(55) At national level, the Transaction would only give rise to a horizontally affected market if a hypothetical market for the retail of dry finishing products via SBMs and GBMs was considered. On such hypothetical market – not supported by the Commission’s past decisions, nor by the market investigation results – the Parties would have a combined value share of [20-30]%. In such a scenario, a number of competitors would remain active. More specifically, the merged entity would compete for the sale of these products with all SBMs and all GBMs active in the Netherlands. If only SBMs were considered to be part of the relevant market, the Parties would have a combined share of [10-20]% at the national level.55

(56) In addition, in the market investigation, no concerns were raised regarding the retail of interior finishing products.

(57) In light of the above, the Commission concludes that the proposed Transaction does not raise serious doubts as to its compatibility with the internal market in relation to the market for retail distribution of interior finishing products to professional customers via SBM, be it at the national or at the local level.

5.3. Vertically affected Markets

(58) SGDN is also active in the wholesale of ceramic tiles (under its TGN and Galvano brands) and SHAP products (under its Galvano brand). The Transaction gives rise to affected markets with regard to the vertical relation between SGDN’s wholesale activities for these products in the Netherlands (upstream) and BME’s activities in the retail distribution of building products as a GBM in several local markets in the Netherlands (downstream).

5.3.1. Wholesale of ceramic tiles in the Netherlands

(59) SGDN is the market leader in the wholesale of ceramic tiles in the Netherlands, with an estimated market share of [30-40]%. However, considering that a significant part of wholesale tiles is sold directly by manufacturers to retailers, this figure may overestimate SGDN’s market power. At the retail level, as discussed above in sections 5.2.1 to 5.2.2, the Parties have a combined market share of [20-30]% in the GBM format nationally, and a market share above 30% in 13 catchment areas, in particular market shares of around 40% in five catchment areas.

(60) With regard to input foreclosure, the Notifying Party argues that the merged entity has no ability or incentives to adopt an input foreclosure strategy either at national or at local level, based on a number of arguments. First, SGDN makes limited sales to GBMs, as it supplies mostly specialist retailers. Second, the majority of brands SGDN carries are non-exclusive and therefore available for purchase from other wholesalers. Third, none of SGDN’s private label or exclusive brands are must-have brands for retailers. Fourth, there are several other alternative wholesale distributors of ceramic tiles. Fifth, already today SGDN supplies its GBM brand to Raab Karcher and a few other GBMs.

(61) The Commission finds that the merged entity would most likely not have the ability nor the incentive to enter into an input foreclosure strategy. First, post-Transaction, GBMs would be able to source from alternative tile wholesalers and tile manufacturers. Second, given the Parties’ combined shares in the retail market for tiles ([20-30]% in both GBM and SBM stores), the merged entity would most likely not be able to recover the loss of wholesales at the retail level. Third, today BME sources mostly from tiles manufacturers directly. In addition, in the market investigation, most respondents stated that they did not consider that the merged entity would have both the ability and the incentive to engage in input foreclosure strategies. A large majority of competitors of the Parties indicated that they did not expect the Transaction to have any impact on their sourcing of ceramic tiles.56

(62) With regard to customer foreclosure, the Notifying Party argues that they have no ability to adopt a customer foreclosure strategy. First, they claim that BMN is not an important route to market for wholesale distributors of ceramic tiles. In 2019, BME’s purchases of ceramic tiles accounted for [0-5]% of the total wholesale market revenues. Second, they contend that following the Transaction, SGDN’s competitors will continue to have access to several specialist retailers and other GBMs. The Commission’s investigation confirms that competing wholesalers do not expect that the merged entity would have the ability or the incentive to negatively impact their ability to sell to customers.

(63) The Commission finds that the merged entity would most likely not have the ability nor the incentive to enter into a customer foreclosure strategy. As mentioned above, today BME sources the vast majority of its tile offering from manufacturers directly. Therefore, BME is not an important customer for wholesale competitors of SGDN. In the market investigation, the majority of respondents stated that they did not consider that the merged entity would have both the ability and the incentive to engage in customer foreclosure strategies. None of the responding competitors of the

Parties expect the Transaction to have any impact on their ability to sell tiles to retailers.57

(64) In light of the above, the Commission concludes that the proposed Transaction does not raise serious doubts as to its compatibility with the internal market in relation to the wholesale distribution of ceramic tiles in the Netherlands.

5.3.2. Wholesale of SHAP products in the Netherlands

(65) SGDN has a small presence in the wholesale market of SHAP products, with a market share of [0-5]%. Hence, vertically affected markets arise only due to the Parties’ combined market share on the downstream GBM retail market in 13 catchment areas.

(66) The Notifying Party argues that in view of SGDN’s very limited presence upstream in the SHAP wholesale market, the merged entity would not have the ability or incentives to adopt an input or a customer foreclosure strategy.

(67) The market investigation has widely confirmed that the merged entity would not have the ability nor the incentive to engage in input or customer foreclosure. A large majority of respondents expects the merger to have no impact on their ability to sell or source SHAP products in the Netherlands.58

(68) In light of the above, the Commission concludes that the proposed Transaction does not raise serious doubts as to its compatibility with the internal market in relation to the wholesale distribution of SHAP products in the Netherlands.

6. CONCLUSION

(69) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

For the Commission

(Signed)

Margrethe VESTAGER Executive Vice-President

ANNEXE

NOTES

1 OJ L 24, 29.1.2004, p. 1 (the ’Merger Regulation’). With effect from 1 December 2009, the Treaty on the Functioning of the European Union (‘TFEU’) has introduced certain changes, such as the replacement of ‘Community’ by ‘Union’ and ‘common market’ by ‘internal market’. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the ‘EEA Agreement’).

3 Publication in the Official Journal of the European Union No C 234, 17.6.2021, p. 10–11.

4 BME Group has announced that it has reached an agreement to acquire the remaining 50% of the share capital in Portuguese retailer Maxmat from Sonae MC; the transaction is expected to be completed in Q3 of 2021.

5 BME’s acquisition of Grupo BMV, a supplier of interior finishing building products with 36 distribution centres across Spain, closed on 2 June 2021.

6 BME owns and operates […] Bouwmaat cash-and-carry franchise stores (which are […]% owned) and partly owns and operates […] Bouwmaat franchise stores (which are owned on a […] basis with its joint venture partner, Ter Steege Handel). BME also has a […]% interest in […] Bouwmaat franchise store which is managed by Ter Steege Handel ([…]). For completeness, BME is also active in the sale of bricks and roof tiles in the Netherlands through Kooy Baksteencentrum B.V. and V.O.F. De Amstel […].

7 Turnover calculated in accordance with Article 5 of the Merger Regulation

8 See, for example, Case COMP/M.7703 – PontMeyer/DBS, paragraphs 11–12; Case COMP/M.3407 – Saint Gobain/Dahl, paragraphs 12 and 16; Case COMP/M.3142 – CVC/Danske Traelast, paragraphs 11-13; Case COMP/M.8733 – Lone Star/Stark , paragraph 25; and Case COMP/M.9406 – Lone Star - Stark Group/ Saint Gobain BDD, paragraph 19.

9 Case COMP/M.9406 – Lone Star - Stark Group/Saint Gobain BDD, paragraphs 27 to 49; Case COMP/M.8733 – Lone Star/Stark , paragraphs 10 to 24; and Case COMP/M. 9790 – Blackstone/KP1, paragraphs 15 to 17.

10 Form CO, paragraphs 86 and 87.

11 Form CO, paragraph 90.

12 Questionnaire Q2 to competitors, question 4.

13 Questionnaire Q2 to competitors, question 4.1.

14 Case COMP/M.3943 – Saint-Gobain/BPB, paragraph 15.

15 Case COMP/M.3407 – Saint Gobain/Dahl, paragraph 14 and 15, Case COMP/M.3943 – Saint-Gobain/ BPB, paragraphs 17-19 and Case COMP/M.9790 – Blackstone/KP1, paragraph 23.

16 Case COMP/M.3943 – Saint-Gobain/BPB, paragraph 114.

17 Form CO, paragraph 92.

18 Form CO, paragraph 92.

19 Questionnaire Q2 to competitors, question 5 and Questionnaire Q1 to customers, question 7.

20 Questionnaire Q2 to competitors, question 5 and Questionnaire Q1 to customers, questio n 7.

21 Questionnaire Q2 to competitors, question 5 and Questionnaire Q1 to customers, question 7.

22 Minutes of the call with a competitor on 4 March 2021, paragraph 6.

23 Questionnaire Q2 to competitors, question 6 and Questionnaire Q1 to customers, question 8.

24 Minutes of the call with a competitor on 4 March 2021, paragraph 16.

25 Questionnaire Q2 to competitors, question 6 and Questionnaire Q1 to customers, question 8.

26 Case COMP/M.7703 – Pontmeyer/DBS, paragraph 17; COMP/M.3142 – CVC/Danske Traelast,

27 paragraph 14.

28 Form CO, paragraphs 99 and 100.

29 Case COMP/M.3142 – CVC/Danske Traelast, paragraphs 14 to 16.

30 Case COMP/M.7703 – Pontmeyer/DBS, paragraphs 21 and 22; Case COMP/M.3943 – Saint-Gobain/ BPB, paragraphs 20 to 22.

31 Case COMP/M.7703 – Pontmeyer/DBS, paragraph 21; Case COMP/M.7107 – Cordes & Graefe/ POMPAC/COMAFRANC paragraph 19; Case COMP/M.3184 – Wolseley/Pinault Bois & Materiaux, paragraphs 19–22.

32 Form CO, paragraph 104.

33 Form CO, paragraph 104.

34 Questionnaire Q2 to competitors, question 8 and Questionnaire Q1 to customers, question 9.

35 Questionnaire Q2 to competitors, question 9 and Questionnaire Q1 to customers, question 10.

36 As regards the assessment in relation to the EEA, see also Annex XIV to the EEA Agreement.

37 Guidelines on the assessment of horizontal mergers under the Council Regulation on the control of concentrations between undertakings (OJ C 31, 5.2,2014, p. 5).

38 Guidelines on the assessment of non-horizontal mergers under the Council Regulation on the control of concentrations between undertakings (OJ C 265, 18.10.2008, p. 6).

39 Horizontal Merger Guidelines, paragraph 24.

40 Horizontal Merger Guidelines, paragraph 26.

41 Horizontal Merger Guidelines, para 18.

42 Non-Horizontal Merger Guidelines, para 30.

43 Non-Horizontal Merger Guidelines, para 30.

44 Agreed Minutes of a call with a Customer on 11 March 2021 and agreed minutes of a call with a Customer on 12 March 2021.

45 Form CO, Annex 13.22, page 4

46 QI – Questionnaire to customers, question 25.

47 Q2 – Questionnaire to customers, question 27.

48 Annex to the present Decision : potentially affected local markets on the basis of value market shares.

49 Form CO, Annex 24.B, Annex 24.D, Annex 24.I, Annex 24.K, Annex 24.L, Annex 24.N.

50 Form CO, Annex 24.B, Annex 24.D, Annex 24.I, Annex 24.K, Annex 24.L, Annex 24.N.

51 Form CO, Annex 24.B, Annex 24.D, Annex 24.I, Annex 24.K, Annex 24.L, Annex 24.N.

52 Q1- Questionnaire to Customers, questions 28 and 29; and Q2 – Questionnaire to Competitors, questions 33 and 34.

53 Case COMP/M.7703 – Pontmeyer/DBS, paragraph 21; Case COMP/M.7107 – Cordes & Graefe/ POMPAC/COMAFRANC, paragraph 19; Case COMP/M.3184 – Wolseley/Pinault Bois & Materiaux, paragraphs 19–22.

54 Form CO, Table 22. The Parties were not able to provide value market shares for their competitors.

55 Form CO, Table 21.

56 Q2 – Questionnaire to Competitors, question 10 and question 12.