Commission, July 16, 2021, No M.10263

EUROPEAN COMMISSION

Decision

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area

PARTIES

Demandeur :

Ardian France (SA)

Défendeur :

Deli Home

(1) On 16 June 2021, the European Commission (‘the Commission’) received notification of a concentration pursuant to Article 4 of Regulation (EC) No 139/2004 (‘the Merger Regulation’), which would result from a proposed transaction by which Ardian France SA (‘Ardian’ or ‘the Notifying Party’) intends to acquire sole control, within the meaning of Article 3(1)(b) of the Merger Regulation, over the whole of Deli Home Holding B.V. (‘Deli Home’ or ‘the Target’) by way of a purchase of shares (‘the Transaction’). In this Decision, Ardian and Deli Home are referred to as ‘the Parties'. The undertaking that would result from the Transaction is referred to as ‘the merged entity’.

1. THE PARTIES

(2) Ardian, headquartered in Paris, France, is an international private equity asset management company that is fully owned by the Ardian Group (formerly known as AXA Private Equity Group).

(3) Deli Home, headquartered in Gorinchem, the Netherlands, supplies timber-based home improvement products to retailers, builders’ merchants and online markets. Deli Home has production facilities in the Netherlands, Poland and Czechia. Deli Home is active in 20 countries with over 1 250 employees.

2. THE CONCENTRATION

(4) On 2 April 2021, the Parties entered into a share purchase agreement by which Ardian is to acquire sole control over Deli Home, which is, at present, solely controlled by NPM Capital, a private equity fund indirectly controlled by SHV. The purchase price amounts to an equity value of EUR […] million.

(5) After the Transaction, Ardian will hold […] % of Deli Home’s shares while Deli Home’s management will hold the remaining […] %. The minority shares that management will hold after the Transaction will not lead to any control rights, and only entitle management to typical minority protection rights. Therefore, after the Transaction, Ardian will have sole control over Deli Home.

(6) It follows that the Transaction would result in a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

3. UNION DIMENSION

(7) The Parties have a combined aggregate worldwide turnover of more than EUR 5 000 million (Ardian: EUR […] billion and Deli Home: EUR […] million). Each of them has a Union-wide turnover in excess of EUR 250 million (Ardian EUR […] billion and Deli Home EUR […] million). Neither of the Parties achieves more than two- thirds of their aggregate Union-wide turnover within one and the same Member State.

(8) The concentration has, therefore, a EU dimension within the meaning of Article 1(2) of the Merger Regulation.

4. MARKET DEFINITION

4.1. Activities of the Parties

(9) The Transaction does not give rise to any horizontal overlap, as Ardian and Deli Home are not active in the same markets.

(10) Ardian jointly controls – together with Goldentree Asset Management LP – the Maxeda Group (‘Maxeda’). Maxeda is active on the downstream markets for the retail sales of do-it-yourself (‘DIY’) products3 to non-professional customers (i.e. consumers) via its DIY stores. Maxeda operates under the brands ‘Brico’ and ‘Brico Planit’ in Belgium and Luxemburg, and under the brand ‘Praxis’ in the Netherlands. Maxeda has 345 DIY stores in Belgium, Luxembourg and the Netherlands.

(11) Deli Home is active in the supply of wood-based products to retailers (including DIY stores in Belgium and in the Netherlands) and to wholesale customers including general builders’ merchants and to a limited extent construction and renovation companies.4 Deli Home is, therefore, active in a number of upstream markets in respect of which Ardian is – through Maxeda – active downstream.

(12) Accordingly, the Transaction does give rise to vertical relationships in Belgium and in the Netherlands between the activities of Deli Home and those of Maxeda.

4.2. Product market definition

4.2.1. Introduction

(13) Section 4.2.2 will outline the product market definitions linked to the step of the DIY value chain that relates to the production level (namely the upstream markets), where manufacturers produce building materials and DIY products, which are sold to wholesalers and/or retailers. Deli Home both produces and wholesales certain DIY products, namely: (i) floors and flooring materials, (ii) timber construction materials, (iii) doors, (iv) storage furniture, and (v) insect screens.

(14) Section 4.2.3 will outline the product market definition linked to the step in the value chain, namely the retail level where DIY retailers sell DIY products to end customers (that is downstream markets). Maxeda is active in the downstream market for the retail sale of DIY products to non-professional customers.

4.2.2. Wholesale sales to retailers (upstream markets)

(15) Deli Home is active in the upstream markets for the supply to retailers (including DIY retailers such as Maxeda) of (i) floors and flooring materials, (ii) timber construction materials, (iii) doors, (iv) storage furniture, and (v) insect screens.

4.2.2.1. The Commission’s past practice

(16) In CVC/Dankse Traelast, the Commission considered the segmentation of the wholesale distribution of building materials by product category, such as, for example, timber, insulation, watering equipment, pipes and fittings, plumbing products etc.5 In Sonae Industria/Hornitex, 6 the Commission considered specifically markets in the wood-based industry.

(17) With respect to floors and flooring materials, in previous decisions the Commission considered that flooring and flooring materials constitute a distinct market from other building materials.7 The Commission also considered a further distinction by the type of floor (e.g. laminate, wood, PVC, etc.) and potential sub-segmentations thereof (e.g. laminate used for private or for commercial buildings), but it ultimately left open the exact definition of this product market.8

(18) With respect to timber construction materials, in previous decisions,9 the Commission considered that timber materials such as plywood, hardboard, raw particleboards and coated particleboards, decorative laminates and wood-based panel components for the furniture and construction industry are likely to belong to separate product markets. Ultimately, the Commission left open the exact definition of this product market.

(19) In Mohawk Industries/International Flooring Systems, the Commission considered in details wood products made from compressed wood fibres (also known as fibreboards) and identified a number of possible sub-segmentations, including for example the distinction between Medium Density Fibreboard (‘MDF’) and High Density Fibreboard (‘HDF’), and between different sizes of MDF. Ultimately, the Commission left the exact definition of the product markets open.

(20) With respect to doors, storage furniture, and insect screens no meaningful Commission’s decision is available.

4.2.2.2. The Notifying Party’s view (21) The Notifying Party submits that the relevant product markets are to be defined according to product categories of (i) floors and flooring materials, (ii) timber construction materials, (iii) doors, (iv) storage furniture, and (v) insect screens, without any further distinction of narrower segments due to the high degree of demand-side and supply-side substitutability. 10

(22) For floors, timber construction materials and doors, however, the Notifying Party distinguishes further hypothetical segmentations as follows:

(a) for floors and flooring materials: (i) wooden floors, (ii) laminate floors and (iii) vinyl (PVC) floors;11

(b) for timber construction materials: (i) wood-based boards, (ii) wood-based panel components for the furniture and construction industry and (iii) other wood/timber construction materials. With respect to wood-based boards and panels, a further sub-segmentation is considered, according to: particleboard, MDF and HDF, OSB, e. Hardboard; f. Softboard; and g. Sawn soft wood.12

4.2.2.3. The Commission’s assessment (23) The Commission agrees with the Notifying Party that, in line with the Commission’s past practice, each of the product categories referred to in Section 4.2.2 likely constitutes separate product markets.

(24) Moreover, the results of the market investigation suggest that further segmentations might be relevant for the present case. Further distinctions, as indicated by certain market participants, may be based on (i) the intended use of the product (for example, for doors, the distinction is between external or internal use); (ii) the material used; (iii) the sale channel (i.e. if it is intended to be sold through DIY stores or through builders’ merchants); and (iv) whether the products are sold branded or unbranded.13

(25) The relevance of the segmentations outlined in paragraph 24 seems to be further corroborated by an internal document of Deli Home, produced in its ordinary course of business.14 For each of the product category that it sells, Deli Home distinguishes between sale channels (that is to say if it is sold to DIY retailers, to builder merchants, or directly to professional customers) and if the product is sold as branded or as unbranded. While distinctions among intended uses and material used are also adopted, these segmentations would typically depend on each product category. By way of an example, doors are sub-divided into internal and external, but no distinction is made according to the material used to manufacture them. Conversely, floors and flooring materials are distinguished by material, but not by intended use.

(26) In any event, based on the results of the market investigation, the Commission considers that alternative segmentations of the markets for wholesale sales to retailers does not affect the outcome of the competitive assessment of the Transaction. Therefore, for the purposes of this Decision, the exact product definition of this market may be left open.

4.2.3. Retail sale to non-professional customers through DIY stores (downstream markets)

4.2.3.1. The Commission’s past practice (27) In previous decisions,15 the Commission considered that the downstream markets for the retail sale of building materials can be distinguished according to the sale channel through which products are sold, namely: (i) retail sales to professional customers (primarily through builders’ merchants); and (ii) retail sale to non-professional customers (primarily through DIY stores).

(28) First, with respect to (i), the Commission considered in previous decisions a further segmentation between specialist and generalist retailers.16

(29) Second, with respect to (ii), the Commission considered in previous decisions the markets for the distribution of DIY and home improvement products to non-professional customers, and identified sub-segmentation by product groups, including the specific product group of building materials. 17

(30) With particular regard to building materials, the Commission previously considered that, while most building materials are sold by generalists and DIY stores, each product serves a specific purpose and is not substitutable with other building materials.18 Therefore, while leaving the exact definition open, the Commission considered plausible relevant markets according to the product categories of building materials.

(31) The Commission also previously considered a segmentation according to distinct sale channels and types of stores, namely: (i) large DIY stores; (ii) large food stores; (iii) retailers specialised in one type of products; and (iv) convenience stores.19

4.2.3.2. The Notifying Party’s view

(32) The Notifying Party submits that, contrarily to the Commission’s past practice, the relevant product market should be limited to the retail sales of building materials and DIY products and that no further segmentations of that market would be relevant or necessary.20

(33) More particularly, the Notifying Party argues that, for example, a distinction by product type or material is not relevant because from a demand-side perspective most customers purchase a variety of DIY products and, from a supply-side perspective, most retailers offer a variety of DIY products. The Notifying Party also argues that a distinction by sale channels (i.e. sales to non-professional customers via DIY stores and sales to professional customers via builders’ merchants) would not be appropriate because there is an ongoing convergence of traditional retailers and wholesalers to sell to both professional and non-professional customers. Ultimately, the Notifying Party considers that if segmentations were to be considered, the narrowest relevant market would be the market for retail sales of DIY products to non-professional customers via DIY stores.

4.2.3.3. The Commission’s assessment (34) The Commission considers that, consistently with its past practice, plausible relevant product markets should be defined according to sale channels (namely by distinguishing between sales made through DIY stores and those made through builders’ merchants). Furthermore, within the market for retail sales to non-professional customers through DIY stores, a further distinction according to product categories might be relevant.

(35) First, the results of the market investigation largely supports the distinction between retail sales to professional customers (primarily through builders’ merchants) and retail sales to non-profession customers (primarily through DIY shops and online sales).21 The Notifying Party has not provided, in this respect, any evidence that current market conditions should differ compared to the market conditions prevailing at the time of the Commission’s decisions described in Section 4.2.3.1. Further, the Notifying Party has not provided market shares aggregated for both DIY stores and builders merchants. This suggests that, in their ordinary course of business, the Parties consider the distinction between sale channels to be relevant.

(36) Second, regarding a possible segmentation by product categories, the market investigation confirmed that certain distinctions by categories and, within each category, by intended use, material used, etc. might be relevant in the present case.22 Furthermore, and as a matter of reasoning, the Commission recalls that according to the Commission’s Notice on the definition of relevant markets,23 supply-side substitutability implies that “suppliers are able to switch production to the relevant products and market them in the short term without incurring significant costs or risks in response to small and permanent changes in relative prices”. Therefore, contrarily to what the Notifying Party argues, the mere fact that most DIY stores offer a wide range of products does not necessarily imply supply-side substitutability to the extent that all the products they sell belong to the same product market.

(37) In any event, based on the results of the market investigation, the Commission considers that alternative segmentations of the markets for retail sale to non-professional customers through DIY stores does not affect the outcome of the competitive assessment of the Transaction. Therefore, for the purposes of this Decision, the exact product definition of this market may be left open.

4.3. Geographic market definition

4.3.1. Wholesale sales to retailers (upstream markets)

4.3.1.1. The Commission’s past practice

(38) In Pontmeyer/DBS, the Commission considered that the upstream market for wholesale sales to retailers are predominantly national.24 In CVC/Fankse Traelast, the Commission has also considered the wholesale of building materials (for all products) to be at least national but possibly wider, including certain neighbouring countries.25 (39) With respect to the supply of floors and flooring materials to retailers, the Commission considered the relevant geographic market for all types of flooring to be at least EEA-wide in scope, but left open the exact definition of the market.26

(40) With respect to the supply of timber construction materials to retailers, the Commission considered that the geographic markets for the various timber construction materials were wider than national and at least cross-border regional. Regional markets that the Commission previously considered were circular catchment areas drawn with a radius of at least 500 km around a production facility.27 Other regional markets were considered for a travel range of 500 and 1,000 km from a facility.28 Ultimately, the Commission left the exact definition of the relevant geographic markets open.

(41) With respect to the supply of doors, storage furniture, and insect screens to retailers, no meaningful Commission’s decision is available.

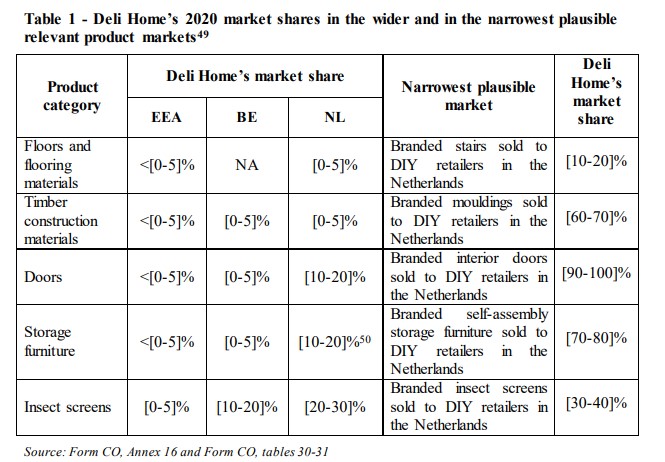

4.3.1.2. The Notifying Party’s view

(42) The Notifying Party submits that for the supply of various products to retailers the geographic scope of the market is wider than national.29

(43) With respect to the supply of floors and flooring materials to retailers, the Notifying Party submits that the relevant market is at least EEA-wide in scope.30

(44) With respect to the supply of timber construction materials to retailers, the Notifying Party submits that the relevant market is at least EEA-wide in scope.31

(45) With respect to the supply of doors,32 storage furniture,33 and insect screens34 to retailers, the Parties submit that the relevant markets are at least EEA-wide in scope.

4.3.1.3. The Commission’s assessment

(46) With respect to the supply of floors and flooring materials to retailers, while a number of respondents to the market investigation indicated that the markets are national or global in scope, the majority of respondents considers that the markets are EEA-wide in scope.35

(47) With respect to the supply of timber construction materials to retailers, while a number of respondents to the market investigation indicated that the markets are national or global in scope, the majority of respondents considers that the markets are EEA-wide in scope.36 (48) With respect to the supply of doors to retailers, while a number of respondents to the market investigation indicated that the markets are in scope, the majority of respondents considers that the markets are national in scope for both interior and exterior doors.37 This reflects the national character of trade standards for the installation of doors, which has consistently emerged over the course of the market investigation.38

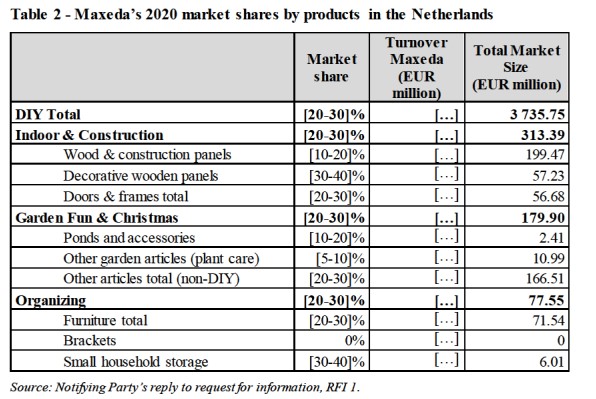

(49) With respect to the supply of storage furniture to retailers, while the majority of Deli Home’s customers who responded to the market investigation stated that the markets are EEA-wide in scope, the majority of competitors indicates that they mostly sell their products in the country of manufacture.39

(50) With respect to the supply of insect screens to retailers, while a number of respondents to the market investigation indicated that the markets are national or global in scope, the majority of respondents considers that the markets are EEA-wide in scope.40

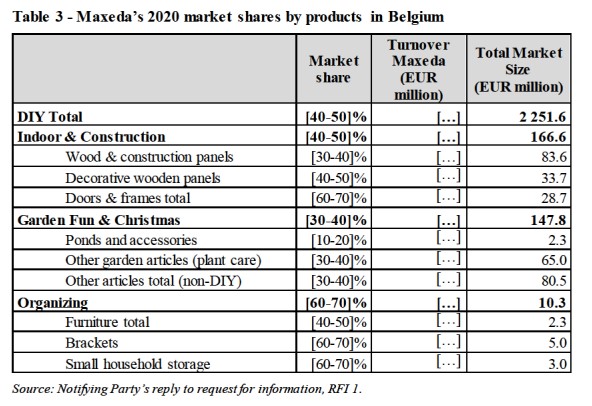

(51) In any event, based on the results of the market investigation, the Commission considers that the exact geographic market definition of the markets for wholesale sales to retailers do not affect the outcome of the competitive assessment of the Transaction. Therefore, for the purposes of this Decision, the exact geographic definition of these markets may be left open.

4.3.2. Retail sale to non-professional customers through DIY stores (downstream markets)

4.3.2.1. The Commission’s past practice

(52) In Wolseley/Pinault Bois & Materiaux, the Commission considered local markets for the retail distribution of DIY products via DIY stores .41

(53) In particular, in Pontmeyer/DBS, the Commission considered local markets as corresponding to the catchment area with a radius of 30 km from a store’s location.42

4.3.2.2. The Notifying Party’s view

(54) The Notifying Party submits that the geographic scope of the relevant downstream markets for the retail sale to retailers (such as DIY stores) or to wholesalers should be national for the following reasons:43 (i) lack of horizontal overlaps between the activities of Deli Home and those of Maxeda; (ii) various catchment areas work as a chain of substitution from a supply side perspective; (iii) presence of central procurement, pricing and offers among DIY retailers like Maxeda; and (iv) franchisees are subject to central procurement and pricing.

4.3.2.3. The Commission’s assessment (55) With respect to the retail sale to non-professional customers through DIY stores, a number of respondents submit that these markets are local in scope (namely, with a 30 km radius from the store), whereas others consider them to be national.44

(56) In any event, based on the results of the market investigation, the Commission considers that the exact geographic market definition for the markets for retail sale to non-professional customers through DIY stores do not affect the outcome of the competitive assessment of the Transaction. Therefore, for the purposes of this Decision, the exact geographic definition of these markets may be left open.

4.4. Conclusions on relevant markets

(57) In conclusion, the Commission considers that, for the purposes of this Decision, it is appropriate to assess the following markets:

(a) For the upstream markets: the markets for the wholesale sales to retailers of each of: (i) floors and flooring materials, (ii) timber construction materials, (iii) doors, (iv) storage furniture, and (v) insect screens. Each of these plausible product markets might be further segmented according to: (i) the intended use of the product (for example, for doors, the distinction is between external or internal use); (ii) the material used; (iii) the sale channel (i.e. if it is intended to be sold through DIY stores or through builders’ merchants); and (iv) whether the products are sold branded or unbranded. The plausible geographic scope for each of these product markets is likely national or EEA-wide.

(b) For the downstream markets: the market for the retail sale to non-professional customers through DIY stores, which can be further segmented according to the product categories. The plausible geographic scope for each of these product markets is likely national or local with a catchment area’s radius of 30 km from a store’s location.

5. COMPETITIVE ASSESSMENT

5.1. Legal framework of the assessment

(58) Pursuant to Article 2(2) and (3) of the Merger Regulation, the Commission must assess whether a proposed concentration would significantly impede effective competition in the internal market or in a substantial part of it, in particular through the creation or strengthening of a dominant position. In this respect, a merger can entail horizontal and/or non-horizontal effects.

(59) As explained in paragraphs (10)-(11), the Transaction gives rise to a vertical relation between Deli Home’s supply and Ardian’s sales – through Maxeda – of (i) floors and flooring materials, (ii) timber construction materials, (iii) doors, (iv) storage furniture, and (v) insect screens. For this reason, in the context of the competitive assessment of the Transaction, the Commission has to analyse potential non- horizontal effects.

(60) Non-horizontal effects arise when the parties to a concentration operate in different levels of the supply chain in certain relevant markets (vertical effects). The Commission appraises non-horizontal effects in accordance with the guidance set out in the Non-Horizontal Merger Guidelines.45

(61) The Non-Horizontal Merger Guidelines distinguishes between two main ways in which mergers between actual or potential competitors on the same relevant market may significantly impede effective competition, namely non-coordinated and coordinated effects.

(62) In non-horizontal mergers, non-coordinated effects may arise when the concentration gives rise to foreclosure. In vertical mergers, foreclosure can take the form of input foreclosure, where the merger is likely to raise costs of downstream rivals by restricting their access to an important input; and/or the form of customer foreclosure, where the merger is likely to foreclose upstream rivals by restricting their access to a sufficient customer base.46

(63) In assessing the likelihood of an anticompetitive foreclosure scenario, the Commission examines whether the merged entity would have post-transaction the ability to foreclose access to either inputs or customers, whether the merged entity would have the incentives to do so and whether such foreclosure strategy would have a detrimental effect on competition.47

(64) Based thereupon, the Commission will analyse the vertical relationship arising from the Transaction in order to assess whether the merged entity would have the ability and the incentives to engage in the input foreclosure strategy, and if such a foreclosure strategy would impede effective competition in the EEA or parts thereof.

5.2. The Parties’ market shares are low to moderate, with the exception of certain market segments 5.2.1. Deli Home’s market shares (upstream)

(65) The Notifying Party provided estimates of Deli Home’s market shares of the plausible relevant markets.48 Table 1 reports Deli Home’s market shares for the wider (namely at the level of product category for the EEA, for Belgium and for the Netherlands) and for the narrowest plausible relevant markets (where market shares are the highest).

(66) Table 1 indicates that for flooring and flooring materials, Deli Home’s market shares are well below 30 % for any plausible market definition. More specifically, under the narrowest market definition, its market share would be [10-20] %.

(67) With respect to timber construction materials, Deli Home’s market shares are below [0-5] % at EEA-level, [0-5] % in Belgium and [0-5] % in the Netherlands. In the narrow market definition for which Deli Home’s market share is the highest, namely the market for branded mouldings sold to DIY retailers in the Netherlands, its market share is [60-70] %.

(68) With respect to doors, Deli Home’s market shares are below [0-5] % at EEA-level, [0-5] % in Belgium and [10-20] % in the Netherlands. In the narrow market definition for which Deli Home’s market share is the highest, namely the market for branded interior doors sold to DIY retailers in the Netherlands, its market share is [80-90] %.

(69) With respect to storage furniture, Deli Home’s market shares are below [0-5] % at EEA-level, [0-5] % in Belgium and [10-20] % in the Netherlands. In the narrow market definition for which Deli Home’s market share is the highest, namely the market for branded self-assembly storage furniture sold to DIY retailers in the Netherlands, its market share is [70-80] %.

(70) With respect to insect screens, Deli Home’s market shares are [0-5] % at EEA-level, [10-20] % in Belgium and [20-40] % in the Netherlands. In the narrow market definition for which Deli Home’s market share is the highest, namely the market for branded insect screens sold to DIY retailers in the Netherlands, its market share is [30-40] %.

5.2.2. Maxeda’s market shares (downstream)

(71) With respect to the market for retail of DIY products through DIY stores (with no distinction of individual products), Maxeda’s 2020 market share in the Netherlands is [20-30] % and in Belgium [40-50] %.51

(72) For both Belgium and the Netherlands, the Parties were unable to estimate Maxeda’s market shares at the level of catchment areas of 30 km radius but submit that they would be above 30 % in several local markets.52 As explained in paragraph (90), Maxeda’s market shares are relevant to assess, among other things, Maxeda’s ability to foreclose Deli Home’s competitors. As this ability relates to the total volume supplied by Deli Home’s competitors to Maxeda (as opposed to the volume supplied in individual catchment areas), the exact values of market shares at the level of individual catchment areas, are less relevant for the case at hand. Therefore, the estimate provided by the Notifying Party appear to be sufficient for assessing Maxeda’s market power in the case at hand.

(73) With regard to a distinction by product category, the Notifying Party provided market shares according to the classification used by the market analyst GfK, which reflects Maxeda’s classification used in its ordinary course of business (Table 2 and Table 3). Maxeda’s market shares in individual categories broadly reflect its market shares at DIY retail level.

(74) Specifically for the Netherlands, Maxeda’s market share remain below [20-30 %] % (which is the national market share at DIY retail level) for all the various product categories, with the exception of two: (i) “decorative wooden panels”, for which market share is [30-40] % and (ii) “small household storage”, where market share is [30-40] %. However, it is to be noted that, with respect to the last product category, the market size of this segment is relatively small, namely EUR 6 million, which is less than 0.2 % of the market for retail of DIY products through DIY stores in the Netherlands.

(75) With respect to Belgium, market shares at the level of individual product categories are similar to those at DIY retail level (which is [40-50] %) with the exception of : (i) “Wood & construction panels” for which market share is [10-20] % and (ii) the products categorized under “organising”, “Furniture total”, “Brackets”, “Small household storage”, which are, respectively : [40-50] %, [60-70] % and [60-70] %. It is to be noted, however, txt these product categories have relatively small market sizes as the total sales of the category “organizing” amount to EUR 10.3 million, which represents less than 0.5 % of the overall market for retail of DIY products through DIY stores in Belgium Table 2 - Maxeda’s 2020 market shares by products in the Netherlands Table 3 - Maxeda’s 2020 market shares by products in Belgium

(76) The Notifying Party also estimated that if the market for retail of DIY products through DIY stores is segmented according to the product category used by Deli Home (which is a different classification than that used by Maxeda), Maxeda’s market shares would remain at a similar level than those reported in Tables 2 and 3.

5.3. No competition concerns with respect to vertical relationships

5.3.1. The Transaction is not likely to lead to input foreclosure

5.3.1.1. Post-Transaction, the Parties would likely not have the ability nor the incentive to foreclose Maxeda’s competitors.

(77) First, the market shares of Deli Home aggregated at the level of product category (i.e. doors, storage, timber construction products, floorings and steps, and insect screens) are small (i.e., well below 20 %) both at EEA and national level. Deli Home’s market shares are larger only for narrow market segments at the national level, in particular in the Netherlands (i.e., [50-60] % for branded doors, [60- 70] % for branded doors for external use, [80-90] % for branded doors for internal use, [70-80] % for branded self-assembly closets, [60-70] % for branded mouldings, [70-80] % for non-branded mouldings, [50-60] % for branded panels and [30-40] % for branded insect screens). (78) The high market shares in these narrow market segments, however, are not indicative of a market power that enables input foreclosure. In certain cases, in addition to the suppliers already active in the Netherlands, suppliers active in neighbouring countries such as Germany or France would be able to enter the Dutch market.53

(79) Second, after the Transaction, Deli Home’s customers would continue to have credible alternative suppliers. A large majority of Deli Home’s customers that replied to the market investigation indicated that for the products they source from Deli Home can be acquired from other suppliers, 54 and that, in case Deli Home increases prices or reduces supplies, they would be able to switch to other suppliers.55 Furthermore, a large majority of Deli Home’s customers that replied to the market investigation indicated that they would likely switch from Deli Home to another supplier in case of price increase or of degradation of commercial conditions.56

(80) Third, Deli Home sells a number of products for which its market shares are relatively small, but – taken together – they contribute substantially to Deli Home’s overall sales. For example, taking 30 % market share as a reference, and considering Belgium and the Netherlands (which are the countries where Deli Home is mostly active) all the products sold to DIY retailers and for which its market shares are below this value generate revenues for approximately EUR […] million annually. 57 These sales represent approximately […] % of Deli Home’s sales to DIY retailers in these two countries.58. As most of retailers that purchase these products also purchase those products where Deli Home’s market shares are high, these sales would be at risk in case Deli Home attempted to foreclose its customers in those products for which its market shares are high.

(81) Therefore, the potential benefit of an input foreclosure in selected products such as branded internal doors, branded mouldings sold to DIY retailers in the Netherlands, etc. would likely put at risk revenues deriving from other products supplied by Deli Home.

(82) Fourth, a majority of Deli Home’s customers that replied to the market investigation consider that after the Transaction, Deli Home would not have the ability or the incentive to increase prices or to reduce supply of its products.59

5.3.1.2. The effects of an input foreclosure strategy would likely be negligible

(83) First, as explained in Section 5.2.1, in the broader product categories Deli Home’s market shares are small or moderate. Therefore, an input foreclosure strategy, if implemented by Deli Home, would have limited effects.

(84) Second, after the Transaction, Deli Home’s customers would continue to have credible alternative suppliers.

(85) Third, the majority of Maxeda’s competitors does not appear to be concerned of a potential input foreclosure strategy by Deli Home.60 On the contrary, some of them indicated that they are already switching to other suppliers in view of the Transaction. As a large majority of Maxeda’s customers considers that switching away from Maxeda would not reduce their competitiveness,61 an attempted input foreclosure strategy from Deli Home would have limited or no impact on its customers and consequently on the downstream market.

(86) Furthermore, when explicitly asked about the expected impact of the Transaction on price, on quality and on the choices for the end-customers, a majority of Deli Home’s customers replied that do not expect significant changes after the Transaction.62

5.3.2. The Transaction is not likely to lead to customer foreclosure

5.3.2.1. The Parties would likely not have the ability nor the incentives to foreclose Maxeda’s suppliers (87) Post-Transaction, the Parties would likely not have the ability and incentives to foreclose Maxeda’s suppliers for the reasons outlined below.

(88) First, as indicated by the market investigation, 63 those manufacturers that supply their products to Maxeda typically supply them also to Maxeda’s competitors. Therefore, if Maxeda attempts to foreclose Deli Home’s competitors, these would be able to continue selling to Maxeda’s competitors, as also confirmed in the market investigation.64

(89) This is also corroborated by Maxeda’s market shares. At DIY retail level, Maxeda’s market share in Belgium is [40-50] % and in the Netherlands is [20-30] %, which means that Deli Home’s competitors would be able to continue supplying [50-60] % of the Belgian market and [70-80] % of the Dutch market. In particular, in Belgium Hubo has a market share of [10-20]-[20-30] % and independent DIY retailers have a market share of [30-40]-[40-50] %. In the Netherlands, Intergamma has a market share of [40-50] % and Hornbach a market share of [10-20] %.65

(90) While, for certain individual product categories, in Belgium Maxeda has high market shares (see Table 3), these market shares do not confer Maxeda with the ability and incentive to foreclose Deli Home’s competitors. This is the case because Deli Home’s competitors typically produce different products and types of products and therefore these competitors would continue supplying large customers with other products.

(91) Furthermore, while Maxeda likely has higher shares in certain catchment areas, this would not provide Maxeda with the ability and incentive to foreclose Deli Home’s competitors because the upstream markets are likely national, if not wider, and therefore manufacturers would be able to continue supplying in other catchment areas and/or countries.

(92) Second, Deli Home’s competitors would continue to have access to large number of customers active in other sale channels. This is the case because Maxeda is active only in the downstream retail sale of DIY products to non-professional customers, while Deli Home’s competitors also supply customers active in other sale channels (as for example builders’ merchants). .

(93) Third, Deli Home’s competitors that replied to the market investigation consider that Maxeda does not have the ability and the incentive required for foreclosing Deli Home’s competitors.66

5.3.2.2. The effects of a hypothetical customer foreclosure would likely be negligible

(94) First, as explained in Section 5.3.2.1, if Deli Home's competitors were to be foreclosed from making sales to Maxeda, they would have sufficient alternative customers in Belgium, in the Netherlands and, more broadly, in the EEA.

(95) Second, a large majority of Deli Home’s competitors that replied to the market investigation consider that the Transaction would not have an impact on their business,67 and do not consider that their competitiveness would be affected if Maxeda stops sourcing certain products from them after the Transaction.68

(96) Third, certain competitors of Maxeda indicated that they are not concerned about the Transaction, as it will be possible to find other suppliers for all products currently supplied by Deli Home.69 It could, therefore, be argued that, as a result of the Transaction, business opportunities may open up for Deli Home’s competitors.

5.3.3. [details of internal documents]

(97) [Details of internal documents].

(98) [...] certain market participants, which consider it unlikely that post-Transaction Ardian will seek to integrate the activities of Maxeda with those of Deli Home.70

5.3.4. Conclusion on non-horizontal effects

(99) In conclusion, in light of the above, the Commission considers that the merged entity would not have the ability nor the incentive to engage in a foreclosure strategy and that, in any event, a foreclosure strategy would not have a significant impact of effective competition.

5.4. Conclusion on competitive assessment (100) Based on the considerations included in Sections 5.1-5.35.3.4 and in light of the results of the market investigation and of all the evidence available to it the Commission concluded that the notified concentration does not give rise to serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement because of vertical non-coordinated effects in the markets for the wholesale sales to retailers of each of: (i) floors and flooring materials, (ii) timber construction materials, (iii) doors, (iv) storage furniture, and (v) insect screens under any plausible market definition, as well as in the market for the retail sale to non-professional customers through DIY stores under any plausible market definition.

6. CONCLUSION

(101) For the above reasons, the Commission has decided not to oppose the notified concentration and to declare it compatible with the internal market and with the EEA Agreement. This Decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

For the Commission (Signed)

Margrethe VESTAGER

Executive Vice-President

NOTES

1 OJ L 24, 29.1.2004, p. 1. With effect from 1 December 2009, the Treaty on the Functioning of the European Union (“TFEU”) introduced certain changes, such as the replacement of “Community” by “Union” and “common market” by “internal market”. The terminology of the TFEU will be used throughout this Decision.

2 OJ L 1, 3.1.1994, p. 3 (the “EEA Agreement”).

3 DIY products include, e.g., products for home and garden, including ironware and tools, decorative products, electrical goods and lighting, sanitary equipment, tools, building material, carpentry and gardening products.

4 Deli Home has also limited number of online sales to downstream customers. In 2020, these sales amounted to approximately [0-10] % of Deli Home’s revenues (see Form CO, paragraph 85).

5 M.3142 – CVC/DANKSE TRAELAST.

6 M.4165 – Sonae Industria/Hornitex, paragraph 6.

7 See for example: M.2051 – Nordic Capital/HIAG/Nybron/Bauwerk; M.4048 – Sonae Indústria/Tarkett/JV; M.7529 – Mohawk Industries/International Flooring Systems .

8 M.1253 – Paribas/JDC Sarl/GERFLOR; M.2051 – Nordic Capital/HIAG/Nybron/Bauwerk; M.7529 – Mohawk Industries/International Flooring Systems .

9 M.4165 – Sonae Industria/Hornitex; M.7529 – Mohawk Industries/International Flooring Systems .

10 Form CO, paragraphs 130, 146, 163, 174, 197 and 210.

11 Form CO, paragraph 147.

12 Form CO, paragraphs 168-169.

13 Replies to Q2 - questionnaire to competitors, questions 6-6.2.

14 Form CO, Annex 16.

15 See for example, M.9406 – Lone Star – Stark Group/Saint-Gobain BDD; M.7703 – PontMeyer/DBS; M.3943 Saint Gobain/BPB; M.3407 – Saint Gobain/Dahl; and M.3142 – CVC/Danske Traelast.

16 Case COMP/M.7703 – Pontmeyer/DBS, Commission decision of 20 August 2015, paragraph 9.

17 M.7283 – Kingfisher/Mr Bricolage, paragraphs 13-14; M.2898 – Leroy Merlin/Brico, paragraph 9.

18 See for example: M.3943 Saint Gobain/BPB, paragraph 17; M.8733 Lone Star/Stark, Section 4.2.5;

19 M.7283 Kingfisher/Mr Bricolage, paragraph 14. Translated from French language. The original text reads: (i) grandes surfaces de bricolage (« GSB »), (ii) grandes surfaces alimentaires (« GSA »), (iii) magasins spécialisés dans un seul type de produit, et (iv) magasins de proximité ».

20 Form CO, paragraph 131.

21 Replies to Q1 - questionnaire to customers, question 7; Replies to Q2 - questionnaire to competitors, question 7.

22 Replies to Q1 - questionnaire to customers, question 6.

23 Commission Notice on the definition of relevant market for the purposes of Community competition law, paragraph 20.

24 M.7703 – Pontmeyer/DBS, paragraphs 17 – 22.

25 M.3142 – CVC/Dankse Traelast, paragraphs 14-15.

26 M.4525 – Kronospan/Constantia, paragraphs 36-37; M.6871 – Mohawk Industries/Spano Invest, paragraphs 49–50; M.4048 Sonae Industria/Tarkett/JV, paragraphs 17 – 18.

27 M.7529 – Mohawk Industries/International Flooring Systems, paras. 61 – 65.

28 M.4165 – Sonae Industria/Hornitex, paragraphs 6 – 11.

29 Form CO, paragraph 130.

30 Form CO, paragraph 148. 31 Form CO, paragraph 170.

32 Form CO, paragraph 185.

33 Form CO, paragraph 200.

34 Form CO, paragraph 212.

35 Replies to Q1 - questionnaire to customers, questions 8 and 8.1; Replies to Q2 - questionnaire to competitors, questions 9 and 9.1.

36 Replies to Q1 - questionnaire to customers, questions 8 and 8.1; Replies to Q2 - questionnaire to competitors, questions 9 and 9.1.

37 Replies to Q1 - questionnaire to customers, questions 8 and 8.1; Replies to Q2 - questionnaire to competitors, questions 9 and 9.1.

38 Non-confidential minutes of a call with a market participant, 10 June 2021; Non-confidential minutes of a call with a market participant, 26 May 2021.

39 Replies to Q1 - questionnaire to customers, questions 8 and 8.1; Replies to Q2 - questionnaire to competitors, questions 9 and 9.1.

40 Replies to Q1 - questionnaire to customers, questions 8 and 8.1; Replies to Q2 - questionnaire to competitors, questions 9 and 9.1.

41 M.3184 – Wolseley/Pinault Bois & Materiaux, paragraph 22.

42 M.7703 – Pontmeyer/DBS, paragraph 21.

43 Form CO, paragraph 133.

44 Replies to Q1 - questionnaire to customers, questions 10 and 11; Replies to Q2 - questionnaire to competitors, questions 10 and 11.

45 Guidelines on the assessment of non-horizontal mergers under the Council Regulation on the control of concentrations between undertakings (OJ C 265, 18.10.2008, p. 6).

46 Non-Horizontal Merger Guidelines, para 30.

47 Non-Horizontal Merger Guidelines, para 30.

48 Form CO, Annex 16.

49 Market shares relating to the year 2020 can be considered representative of market power in the last 3 years. The market dynamics have not changed substantially because the number of suppliers remained stable, and so did their share of supply with their largest accounts. Refer, for example, to the minutes of a call with Maxeda's competitor, 25 May 2021, para. 13.

50 This market share refers to the sale channel to retailers because the Notifying Party did not provide a more aggregated figure.

51 Form CO, paragraphs 359 and 361.

52 Form CO, paragraphs 360 and 362.

53 See for example the minutes with a competitor of Maxeda on 15 June 2021, paragraph 17.

54 Replies to Q1 – Questionnaire to retailers, questions 13 and 14.

55 Replies to Q1 – Questionnaire to retailers, questions 15 and 16.

56 Replies to Q1 – Questionnaire to retailers, question 17.

57 Form CO, Annex 16.

58 Form CO, Annex 16.

59 Replies to Q1 – Questionnaire to retailers, question 12.

60 Replies to Q1 – Questionnaire to retailers, question 18, minutes of a call with a competitor of Maxeda on 25 May 2021, paragraph 10; minutes of a call with a competitor of Maxeda on 15 June 2021, paragraphs 23-24.

61 Replies to Q1 – Questionnaire to retailers, question 19.

62 Replies to Q1 – Questionnaire to retailers, questions 20 and 20.1.

63 Replies to Q2 – Questionnaire to competitors, questions 13-14.1.

64 Replies to Q2 – Questionnaire to competitors, question 15-16.1.

65 Form CO, tables 34-35.

66 Replies to Q2 – Questionnaire to competitors, question 12.

67 Replies to Q2 – Questionnaire to competitors, question 18.

68 Replies to Q2 – Questionnaire to competitors, question 19.

69 See, for example, minutes with a competitor of Maxeda on 15 June 2021, paragraph 24. 70 See for example Minutes with a competitor of Maxeda on 15 June 2021, paragraph 19.