Commission, 20 juillet 2021, n° M.10158

COMMISSION EUROPÉENNE

Décision

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

PARTIES

Demandeur :

IHS Markit Ltd

Défendeur :

CME Group Inc.

Dear Sir or Madam,

(1) On 15 June 2021, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which IHS Markit Ltd. (‘IHSM’, UK) and CME Group Inc. (‘CME’, USA) will contribute IHSM’s over-the-counter (‘OTC’) derivatives and foreign exchange (‘FX’) trade processing business (MarkitSERV) and CME’s trade processing and optimization businesses (Traiana, TriOptima, Reset) to a joint venture called Parthenon Ltd (‘JV’, UK), which they will jointly control (IHSM and CME are referred to hereinafter as the ‘Notifying Parties’ and IHSM, CME and the JV are referred to hereinafter as the ‘Parties’).3 The creation of the JV and the contribution of the aforementioned businesses is referred to as the ‘Transaction’.

1. THE PARTIES

(2) IHSM is an international provider of information, analytics, expertise, and solutions to major industries, financial markets, and governments globally. IHSM provides pricing and reference data, financial indices, security identifiers, valuation and trading services, and data feeds/data management solutions.

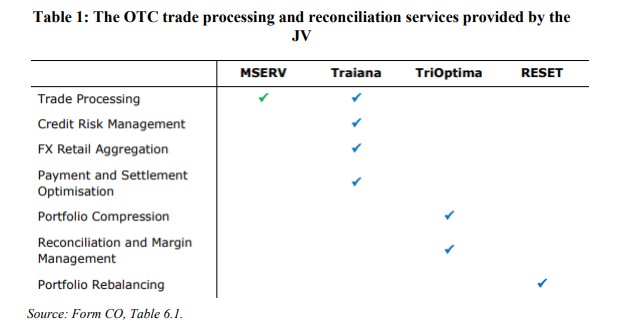

(3) CME is a US based global risk management firm. CME owns and operates several exchanges (Chicago Mercantile Exchange, Chicago Board of Trade (CBOT), New York Mercantile Exchange (NYMEX) and the Commodity Exchange (COMEX)) and provides other trading and clearing services across a range of asset classes, including commodities, equity indices, foreign currency (FX) products4, interest rate derivatives (IRDs)5 and cryptocurrencies.

(4) The JV will be active in trade processing and trade/portfolio optimization services in a number of asset classes.

2. THE CONCENTRATION

(5) On 12 January 2021 IHSM and CME signed a Transaction Agreement pursuant to which IHSM will transfer the shares of the entities carrying out the MarkitSERV businesses6 and CME will transfer the shares of the Traiana, TriOptima and Reset businesses7 to the JV.

(6) Pursuant to the Transaction Agreement, IHSM, through its indirectly wholly owned subsidiary IHS Equity, will hold 50% of the shares of the JV and CME, through its wholly owned subsidiary CME NEX, will hold 50% of the shares of the JV. Pursuant to the Shareholders Agreement that the Notifying Parties will execute upon closing, IHSM and CME will have the right to appoint an equal number of Directors to the Board. A quorum requires at least one CME and one IHSM director to be present. All board matters will be determined by simple majority, including approval for the budget, business plan and management team. Accordingly, the positive consent of CME and IHSM is required to approval all strategic matters; therefore, the JV will be jointly controlled by IHSM and CME.

(7) The JV would perform all the functions of an autonomous economic entity on a lasting basis. The JV would have sufficient own staff, financial resources and dedicated management for its operation and for the management of its business interests. Furthermore, the JV would consist of pre-existing businesses and it would not be limited to exercising a specific function for its parents. It would have an independent market presence and would not have significant sale or purchase relationships with its parents. Finally, the JV would be set up for an indefinite period and thus intended to operate on a lasting basis. Therefore, the JV would be a full- functional joint venture.

(8) The Transaction thus constitutes a concentration within the meaning of Articles 3(1)(b) and 3(4) of the Merger Regulation.

3. UNION DIMENSION

(9) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million8. Each of them has a Union-wide turnover in excess of EUR 250 million, but they do not achieve more than two-thirds of their aggregate Union- wide turnover within one and the same Member State. The Transaction therefore has a Union dimension pursuant to Article 1(2) of the Merger Regulation.

4. MARKET DEFINITION

4.1. Overview of Parties’ activities

(10) The contributed businesses to the JV provide trade processing services and trade optimization services.

(11) IHSM contributes MarkitSERV to the JV. MarkitSERV provides trade processing services in relation to OTC derivatives, namely credit default swaps9 (‘CDS’), equity derivatives10, IRDs, as well as FX spot and derivatives, with a focus on IRDs and CDS. Its core service sends and receives details of executed trades to (i) the trading parties; (ii) the execution venue, if any; (iii) the central counterparty (‘CCP’); and (iv) the trade repository.

(12) CME contributes Traiana, TriOptima and Reset to the JV. Traiana is a market infrastructure technology provider that offers pre-trade risk monitoring and automated post-trade processing services. TriOptima consists of three core services: compression, portfolio reconciliation and margin optimization. Reset is a multilateral basis risk mitigation service based on interbank offered rates (IBORs) for interest rates, FX non-deliverable forwards (‘NDFs’), FX options and inflation derivatives.

(13) The below overview shows the activities of the businesses across different services:

Source: Form CO, Table 6.1.

4.2. Over-the-counter ‘OTC’ derivatives (14) Derivatives are financial products (including options, futures and swaps) designed to transfer various types of economic risks between the parties to a trade. They do not transfer ownership of underlying financial assets but derive their value from such assets. Financial derivatives enable a transfer of risk between two counterparties without needing to invest in the underlying financial assets. There are different types of financial derivatives based on the underlying asset class, such as equity derivatives, CDS, FX derivatives, and IRDs.

(15) In broad terms, derivatives may either be traded OTC or on an exchange (i.e. exchange-traded-derivatives (‘ETDs’). In 2019, OTC derivatives accounted for 92% of the outstanding notional amount of the EU derivatives market, with ETDs accounting for the remaining 8%.

(16) Exchange trading (as opposed to OTC trading) means that the agreement to trade securities or derivatives takes place on an exchange or ‘regulated market’11, which is subject to different regulation and supervision than OTC trading (venues). While trading on exchange is normally anonymous, i.e. the trading parties do not know the identity of their counterparty, OTC trading is generally more “relationship-based” and counterparties know who they are trading with, (though trading protocols ensuring anonymity do exist, e.g. on dealer-to-dealer venues). The reason for this is, that financial instruments traded on exchange are standardized and fungible, while OTC traded products are bespoke (e.g. derivatives) or not standardized (e.g. bonds).

(17) In OTC trading, counterparties need to negotiate and agree on the price and other terms of the trade. This often takes place on a regulated trading venue (such as a Multilateral Trading Facility (‘MTF’) or organised trading facility (‘OTF’), or a regulated venue in another jurisdiction); alternatively, the OTC trades are negotiated bilaterally between the counterparties to the trade.

(18) Most OTC derivatives are traded on a bilateral basis (i.e. the contract is between two parties, the dealer trader and the buyside trader (so-called ‘dealer-to-client’ or ‘D2C’) or a dealer trader and another dealer trader (so-called ‘dealer-to-dealer’ or ‘D2D’).

(19) Given that the Transaction does not lead to any horizontal or vertical links relating to exchange trading or exchange-traded products, the Commission does not further assess the market for exchange trading.

4.3. Derivatives trading services

4.3.1. Introduction and Parties’ services (20) CME owns and operates several exchanges (Chicago Mercantile Exchange, Chicago Board of Trade, New York Mercantile Exchange and the Commodity Exchange) and an electronic trading venue for derivative products across all asset classes (called CME Globex), an electronic trading venue for fixed income cash products (called BrokerTec) and an FX trading platform (called EBS).

(21) IHSM does not operate any trading venues and does not offer any services with respect to exchange traded products. There are no vertical relationships between CME’s Futures & Options trading and clearing offering (CME Globex) and MarkitSERV.12 The only trading service leading to a vertical relationship with the JV (FX NOE messaging and FX CCP connectivity) is the offering of CME’s FX trading venue EBS. EBS offers trading of FX spot contracts as well as FX derivatives (non- deliverable forwards, forwards and FX swaps).

4.3.2. Relevant product market definition

4.3.2.1. Commission’s previous decisions

(22) In past decisions, the Commission considered that the provision of trading services for derivative contracts can be distinguished based on underlying asset classes, execution environment, types of contracts and currency pairs.13

(23) First, regarding the type of underlying variable or asset, the Commission considered that trading services for derivatives can be categorised into trading services for equity derivatives (single stock or index based), IRDs, currency derivatives, commodity derivatives, credit derivatives, and FX derivatives.14

(24) Second, the Commission previously identified separate relevant product markets for the provision of trading services for derivatives on exchanges (i.e. exchange-traded derivatives or ‘ETDs’) and the trading of derivatives over-the-counter (i.e. ‘OTC’ derivatives) in view, in particular, of their different characteristics15 and different applicable legal framework.16

(25) Third, the Commission previously segmented the provision of trading services for derivatives according to the types of contracts and considered that trading services for swaps17 are part of a distinct product market from trading services for options18 and futures/forwards,19 although it left open whether trading services for futures and for options comprise separate markets as well.20

(26) Fourth, the Commission has previously considered potential segmentations by currency pair, but ultimately left open the product market definition.21

4.3.2.2. Notifying Parties’ view

(27) The Notifying Parties agree that separate markets should be defined by reference to execution method (ETD versus OTC). In addition, the Notifying Parties are of the view that it is not appropriate to segment the market with respect to FX spot and derivative products since competitors and customers in this space are the same.

4.3.2.3. Commission’s assessment

(28) With respect to the distinction by asset class, the Commission’s market investigation did not provide any evidence that would justify departing from the approach followed in previous decisions. For the purposes of this decision, therefore, the Commission identifies separate derivative trading services markets based on asset class. The only relevant asset class for derivatives trading services markets in this case is FX. CME does not offer derivative trading services in equity derivatives, IRDs or CDS. Hence, derivative trading services in relation to other asset classes than FX are not relevant in the context of the Transaction and are not assessed further in this decision.

(29) The Commission further investigated distinctions by execution environment (ETD versus OTC), trading channel (electronic versus bilateral/voice execution) and types of contracts or currencies.

(30) With respect to the distinction between ETD and OTC execution methods, the Commission’s market investigation did not provide any evidence that would justify departing from the approach followed in previous decisions. For the purposes of this decision, therefore, the Commission identifies separate markets based on execution method (i.e. ETD versus OTC). MarkitSERV is not present in, nor does it provide any services for, ETDs. Hence, ETD-based markets are not relevant in the context of the Transaction and are not assessed further in this decision.

(31) As detailed below, in the context of FX trading services, the Commission investigated whether separate markets should be defined as between: (i) FX spot and FX derivative trading services; (ii) electronic and bilateral trading (also referred to as “voice”); (iii) anonymous (dealer-to-dealer) and disclosed (dealer-to-client) trading services; and (iv) different types of contracts.

(32) All FX trading venue competitors responding to the Commission’s investigation provide trading services for FX spot and FX derivatives22, suggesting that no distinction is warranted at this level from a supply-side perspective. However, the question whether FX spot and FX derivatives constitute separate markets can be left open for the purposes of this decision, as a conclusion on this issue does not affect the outcome of the Commission’s assessment in the present case.

(33) Regarding a distinction by trading channel, based on the replies to the market investigation, most FX trading venue competitors (60%) consider that separate markets exist for electronic FX trading services on the one hand, and bilateral/voice FX trading services on the other.23 One competitor states: “(…) While the market continues to become more electronic, the rate of adoption has slowed substantially, suggesting that some form of voice trading will continue to be the preferred execution method for a segment of the client market. Those customers are effectively not in scope for electronic FX trading venues/services.”24 (34) Other respondents consider that an overall market exists covering both electronic FX trading services and bilateral/voice FX trading services, since market participants regularly trade in both ways, electronically and via voice, depending on the trade. Respondents also indicated that preferences are also dependent on particular products or currencies. For example, non-standardized products and “non-G10 currencies” tend to be traded via voice.25

(35) The Commission considers that the question whether electronic FX trading services and bilateral/voice FX trading services constitute separate markets can be left open for the purposes of this decision, as a conclusion on this issue does not affect the outcome of the Commission’s assessment in the present case.

(36) The Commission considered further whether “anonymous” versus “disclosed” FX trading constitute separate markets. Anonymous trading (also referred to as dealer-to- dealer trading) refers to trading protocols that keep the identity of the trading counterparty confidential before the trade. Disclosed trading (also referred to as dealer-to-client trading) means that trading counterparties on the respective platform know who they are trading with. One competitor noted that “there is generally no requirement for particular clients to use one over the other, therefore clients can (and some do) use both anonymous and disclosed liquidity sources. Therefore, these two types of trading venue do compete for business.”26 (37) The Commission considers, however, that the question of whether “anonymous” and “disclosed” FX trading constitute separate markets can be left open for the purposes of this decision, as a conclusion on this issue does not affect the outcome of the Commission’s assessment in the present case.

(38) The market investigation provided some evidence that it might be appropriate to define separate markets by type of contract or currency (see recital (34). Some customers consider these distinctions to be relevant in relation to the question via which channel to trade. For example, FX trading venue competitors mention specifically non-deliverable forwards, forwards, swaps and options when asked about which trading services they offer.27 This suggests that the mentioned products may be relevant distinctions in their service offering. One competitor mentions: “Clients can access liquidity in more than 300 currency pairs for FX spot and up to 70 currency pairs for FX derivatives.”28 This indicates that the coverage of certain currency pairs may be a distinguishing factor in the offer of FX trading services.

(39) The Commission considers that the question whether different types of contracts and currencies in FX trading constitute separate markets can be left open for the purposes of this decision, as a conclusion on this issue does not affect the outcome of the Commission’s assessment in the present case.

4.3.2.4. Conclusion (40) In view of the above, the Commission considers that separate FX trading services markets exist for exchange traded and OTC traded FX products. Possible further distinctions may exist with respect to (i) trading channel (electronic, voice/bilateral), (ii) pre-trade transparency (anonymous or disclosed trading), and (iii) by type of contract and currency. However, concerning these additional possible distinctions, the relevant product market definition can be left open as the Transaction does not give rise to serious doubts as to its compatibility with the internal market even on the narrowest plausible market.

4.3.3. Relevant geographic market definition

4.3.3.1. Commission’s previous decisions (41) The Commission has previously considered the relevant geographic market definition for derivative trading markets, in particular exchange traded European interest rate, equity index and single stock options and futures29, as well as for OTC FX trading services. The relevant geographic market definitions in those instances were considered to be EEA-wide or global.

4.3.3.2. Notifying Parties’ view

(42) The Notifying Parties did not provide any explicit views on the relevant geographic market for the supply of OTC FX trading services, or the potentially narrower markets, but provided market shares of EBS and its competitors in a global market.

4.3.3.3. Commission’s assessment

(43) Responses to the market investigation varied regarding the question of the geographic level of competition. Nevertheless, a majority of competitors indicate that they offer FX trading services to customers at a worldwide level, sets fees for FX trading at a worldwide level and consider that their competitors are active at a worldwide level.30 The competitors who responded include those operating some of the biggest electronic FX trading venues globally31 and hence cover a large proportion of global FX trading. Approximately 30% of FX trading takes place bilaterally and not on electronic trading venues and hence in this part of the market, it cannot be excluded that market participants could have a more regional focus. From a demand-side perspective, the market investigation in a previous case revealed that the majority of customers trade OTC FX products on worldwide venues.32

(44) Regarding a plausible EEA-wide market, the Commission notes that less than [5- 10]% of EBS' trading volumes (and less than [0-5]% of EBS' revenues) are accounted for by EEA customers.33 Hence, the Commission considers that the question regarding the geographic scope of the market for OTC FX trading services can be left open for the purposes of this decision, as a conclusion on this issue does not affect the outcome of the Commission’s assessment in the present case.

4.3.3.4. Conclusion

(45) In view of the above, the Commission considers, in line with previous decisions, that the relevant geographic market for OTC FX trading and potential narrower markets is likely global and at least EEA-wide. However, the exact geographic market definition (i.e. EEA-wide or global) can be left open for the purposes of this decision, as a conclusion on this issue does not affect the outcome of the Commission’s assessment in the present case.

4.4. Derivatives clearing

4.4.1. Introduction and Parties’ services

(46) Clearing refers to all activities occurring between the time of trading (i.e. when a trade has been agreed between the buyer and the seller) and the moment in which commitments are fulfilled, or “settled” (i.e. the seller has delivered the rights to the financial asset to the buyer and the buyer has paid the agreed amount to the seller). The main function of clearing is to insure each party to a trade against non-fulfilment of the commitments agreed to by the other party. This is commonly referred to as insuring “counterparty risk”. Where the clearing service is performed centrally by a third party, this third party is referred to as the central counterparty (“CCP”) or clearing house. In addition to its principal function of managing counterparty risk, the CCP can also perform other ancillary activities such as the registration and verification of the trade and its counterparties and the transmission of the details of the trade to the relevant settlement body.34 (47) CME offers clearing and settlement services across asset classes for exchange-traded and OTC derivatives through its clearinghouse, CME Clearing.

4.4.2. Relevant product market definition

4.4.2.1. Commission’s previous decisions

(48) The Commission has previously considered separate product markets for the clearing of derivatives by underlying asset class (e.g. IRDs), execution environment (exchange-traded and OTC), type of customer and type of contract (defining swaps as separate from futures and options, while leaving open whether futures and options or separate currencies constitute separate markets in terms of clearing).35

4.4.2.2. Notifying Parties’ view

(49) The Notifying Parties submit that OTC and ETD derivatives clearing are separate relevant product markets. The Notifying Parties submit that it may be appropriate to further distinguish between relevant product markets for derivatives clearing services by asset class because the underlying financial instruments are used by different customer bases for different purposes. They argue that this is also supported by the supply-side focus of CCPs. In particular, they point to the fact that CME’s market position varies considerably by asset class (c.[5-10]% for OTC IRD clearing worldwide, less than [0-5]% for OTC FX clearing worldwide) and the fact it is no longer active in some asset classes (e.g. CDS). Moreover, certain CCPs are split by asset class. For example, LCH Swap Clear specialises in clearing swaps, LCH Forex Clear specialises in clearing FX, and ICE Clear Credit specialises in clearing credit.36

4.4.2.3. Commission’s assessment

(50) The results of the market investigation did not provide any indication that it would be appropriate to depart from the Commission’s previous assessment of derivatives clearing markets.37 In relation to whether clearing services for different asset classes should be within the same or separate product markets, the market investigation indicated that there is limited supply-side substitutability for clearing services across different asset classes. Respondents indicated that expanding into new clearing services requires significant investment and a long time period to implement the relevant technology solutions, obtain regulatory approvals and build a client base.38

4.4.2.4. Conclusion

(51) In view of the above, the Commission concludes, in line with its previous decisional practice, that there are separate product markets for the clearing of derivatives by underlying asset class. The Commission also considers, in line with its previous decisional practice, that there are separate product markets for the clearing of derivatives by execution environment, type of customer and type of contract. However, for the purposes of this decision, the distinction by type of customer and contract does not appear relevant. The Transaction gives rise to a vertical link between MarkitSERV’s OTC FX and IRD CCP connectivity service (upstream) and CME’s OTC FX and IRD clearing services (downstream). MarkitSERV’s service is provided without any differentiation across all customer and contract types, and the market investigation did not give rise to any suggestion that the impact of the Transaction or dynamics of this vertical link would differ by customer and contract types. Therefore, the Commission’s assessment focuses on the relevant markets for OTC FX clearing and OTC IRD clearing services without further distinguishing between customer or contract types.

4.4.3. Relevant geographic market definition

4.4.3.1. Commission’s previous decisions

(52) The Commission has previously considered the relevant market for clearing services (for OTC traded interest rate derivatives) to be at least EEA-wide in scope. In particular, the Commission noted that third country CCPs often have a different geographic focus and not all customers in the EEA consider them as viable alternatives to which they could switch within a short time.39

4.4.3.2. Notifying Parties’ view

(53) The Notifying Parties did not provide any explicit views on the relevant geographic market for the supply of clearing services, but provided market shares on the basis of a global market. The Notifying Parties confirmed that these market shares (which are less than 10% on any plausible basis at worldwide level) would be even lower on an EEA-wide market.40

4.4.3.3. Commission’s assessment

(54) The market investigation indicated that most CCPs provide clearing services at the worldwide level41 and none of the responses to the Commission’s market investigation indicated that it would be appropriate to depart from the Commission’s previous assessment of the relevant geographic market for clearing services as at least EEA-wide.

4.4.3.4. Conclusion

(55) In view of the above, the Commission considers, in line with previous decisions, that the relevant geographic market for clearing services is at least EEA-wide. However, the exact geographic market definition (i.e. EEA-wide or global) can be left open for the purposes of this decision, as a conclusion on this issue does not affect the outcome of the Commission’s assessment in the present case.

4.5. Trade processing services

4.5.1. Introduction and Parties’ services (56) Once the terms of a trade are agreed, the trade is submitted for post trade processing by the execution/trading venue, or by the parties themselves, if traded off-venue. This includes the transmission of messages between different parties to the trade, affirmation/confirmation of the trade, and sending the trade to the relevant CCP (if applicable) and reporting it to the relevant trade repositories/regulatory bodies (as applicable).

(57) MarkitSERV provides trade processing services in relation to OTC derivatives covering the following asset classes: CDS, equities, OTC FX products and IRD, with a focus on IRD and CDS. Its core service sends and receives details of executed

trades to: (i) the trading parties; (ii) the execution venue, if any; (iii) the CCP; and (iv) the trade repository.

(58) CME is active in trade processing services through Traiana. Traiana is a market infrastructure technology provider that offers credit limit monitoring and automated post-trade processing services for FX, equities and exchange traded derivatives. Credit limit monitoring is a service provided to prime brokers, executing brokers and buy-side clients and consists in credit checks to ensure that the counterparty of a trade has sufficient credit to enter into a transaction (see Section 4.9 for more details).

4.5.2. Relevant product market definition

4.5.2.1. Commission’s previous decisions (59) The Commission has not previously considered trade processing services directly. In past decisions, the Commission has considered that the provision of trading services for derivative contracts can be distinguished based on underlying asset classes, execution environment, and types of contracts (see Section 4.3.2 above).42

4.5.2.2. Notifying Parties’ view (60) According to the Notifying Parties, trade processing services are separate markets based on the following criteria: (a) asset class, e.g. IRDs, equity derivatives or FX derivatives; (b) type of trade, i.e. bilateral or prime broker (also known as ‘tri-party’); and (c) service type, e.g. notice of execution messaging or CCP connectivity. The Notifying Parties support their views on the basis of the following elements:

(61) Distinction by asset class. The most common underlying assets for derivatives are interest rates, credit (e.g. debt or fixed-income instruments), currencies (FX), commodities, and equities. Trade processing software and services for different asset classes are likely to constitute separate markets, because the functionality and the regulatory requirements vary between asset classes. There is no demand-side substitutability because customers require trade processing services specific to the asset class they are trading and the individuals responsible for different asset classes within an organisation also typically vary. There is also limited supply-side substitutability, since to expand into a new asset class it would be necessary to invest in new systems and to recruit individuals with the requisite knowledge of the new products and workflows, as well as to build relationships with new individuals at customer organisations.

(62) Distinction by trade type. Buy-side firms trade with multiple firms directly and can either manage their transactions with those firms throughout the life of the trades (i.e. on a bilateral basis) or they can use a prime broker. Prime brokerage services comprise a bundle of services provided by a bank (such as BNP, Citibank, Deutsche Bank, HSBC, JP Morgan, Morgan Stanley and UBS) to hedge funds, asset managers, small banks and other clients. Prime brokerage services allow a wide variety of smaller clients to trade with dealers while maintaining a credit relationship, placing collateral and settling with a single entity (the prime broker). In practice, the prime broker steps in to enter two offsetting trades: one with the client and one with the executing broker. In this way, the prime broker takes over the trade and effectively becomes the guarantor of the buy-side client for the trade. Typically, prime broker customers choose this structure as they do not have the credit required to engage in bilateral trades. Thus, the vast majority of prime broker customers using trade processing services would not consider bilateral trades (and related trade processing services) to be a substitute for them. Prime brokerage is most prevalent in FX markets. As the prime broker sits between the two executing parties, these trades are often referred to as "tri-party", and the suite of trade processing services that are involved in supporting prime brokerage trades are different from those involved in a bilateral trade.

(63) Distinction by service type. Trade processing services can also be distinguished by the service type (i.e. services relating to different stages of the trade life cycle) including: (i) credit risk management (pre- and post-trade) (ii) notice of execution (NOE) messaging, and (iii) CCP connectivity. There is no demand-side substitutability because customers use these services for different purposes, e.g. messaging services involve the transmission of messages from a broker/venue/liquidity provider to clients who have just executed a trade to feed their internal risk management systems. This service cannot be substituted with another trade processing service like CCP connectivity, which consist in sending details of trades executed on a trading venue or bilaterally to CCPs for clearing. There is also limited supply-side substitutability as different services require different input and technical connections to different market participants. In addition, different trade processing services are typically procured by different divisions, desks and individuals within the same organisation, making it necessary to build new relationships in order to expand into new service types.

4.5.2.3. Commission’s assessment (64) While the Commission has not previously considered trade processing services directly, the results of the market investigation indicate that trade processing service markets are separate markets in similar ways to trading services (e.g. by asset class), as proposed by the Notifying Parties.

(65) Regarding a distinction by asset class, a customer explains that “different products have different requirements and different system integrations”.43 Even though customers do not necessarily source different trade processing services from the same provider, 44% say they do procure some products together, but only within the same asset class.44 Customers often seem to be organised internally by asset class. One customer states: “Within each asset class we try to align the negotiation of products / contracts.”45 One market participant notes: “(…)customers themselves operate in very different ways across asset classes and procure products separately (e.g. the FX trading desk of a major bank will not align with the fixed income desk).”46

(66) On the supply side, there would seem to be some substitutability across asset classes. For example, one market participant states: “From a supply side perspective, thetechnical requirements to offer services are the same/similar across asset classes.”47 However, generally suppliers start providing trade processing services by focusing on one asset class at first. For example, “Traiana started in FX and has expanded to cover other asset classes” notes one customer.48 One market participant observes that “[FX] is much simpler as an asset class than fixed income. Fixed income is even more complex because different types of fixed income instruments trade in different ways, and trade differently in Europe/US/Japan. Therefore would not be easy to expand from FX to fixed income, as it requires a lot of work.” 49

(67) One competitor notes: “For asset class, there are differences in requirements in terms of trade source, trade matching and enrichment criteria and potential workflows. For FX specifically, trade source could be from risk management systems or trading platforms which tend to be asset class specific. The matching and enrichment requirements for FX also vary from other derivatives and those of equity or fixed income along with different market standards and governing regulations.”50

(68) Also, some market participants contacted during pre-notification, considered that they do not compete with the Parties because their services, while equivalent to the Parties’, related to a different asset class, in which the Parties were not active.51

(69) Based on the above, the Commission considers that trade processing services for different asset classes constitute separate markets.

(70) As regards a distinction by trade type (bilateral, tri-party), a customer who is active as a prime broker as well as an executing broker notes: “We run bilateral and PB at arms length as they have different requirements.”52 Several customers answering the market investigation answered in a similar fashion, e.g. “Segregation required between Prime and Franchise activity.”53 A competitor in this space confirms this view: “Often there are information barriers and physical separation between the PB and other desks within sell-side participants.”54 These quotes from both customers and competitors indicate that customers distinguish in their operations between bilateral and tri-party FX trading, if they do both, and tend to keep these operations separate.

(71) Equally, from a supply-side perspective, competitors in other related trade processing services markets underline the different purposes and focus of the Parties’ services, particularly in terms of trade type. One market participant exemplifies the view of the majority by noting that they “do not see much overlap nor complementarity between Traiana and Markitserv, the former being PB focused and the latter being sell-side market making focused.”55 Responses from competitors also support the Notifying Parties’ view that MarkitSERV and Traiana serve different customer groups and types of transactions56, and that services generally differ for bilateral and tri-party transactions.

(72) Based on the above, the Commission considers that trade processing services for different trade types constitute separate markets.

(73) With respect to a distinction by service type, on the demand side, the results of the market investigation indicate that customers do not consider trade processing services to be substitutable: “We utilise different services for different needs.”57 Some customers consider that links/connectivity between services lead them to procure from the same provider: “From a pricing and technology integration perspective it often makes sense to procure products from the same supplier – particularly from a connectivity perspective.”58 The majority of customers (77%) purchase some products together59, though the possibility to purchase services together does not seem to be a major factor in the decision from whom to procure.60 One customer states: “We consider each component individually based on our needs, weighed with convenience of using same provider.”61

(74) One competitor notes that the market is “segmented based on the service type required by the client, for example there are different dynamics between products that provide for the monitoring of trades in front office (such as credit limit checking) compared with products that control trades that are received for middle and back offices. There could be thus a distinction between purely ‘technical’ services and more ‘value added’ business services.”62

(75) Both customers and competitors seem to view different trade processing services separately, though there may be certain product combinations that are purchased together. For example, when asked which services customers procure together, many answer that they buy several products from each Party.63 However, no clear pattern emerges from the answers as to which combinations are more prevalent than others. Also, most respondents state that they negotiate the procurement of different products separately, noting that “these services are typically procured separately” and they are “separate contracts”.64

(76) From a supply-side perspective, there may be a certain level of substitutability of general capabilities across services, as evidenced by the fact that Traiana is active in several trade processing services. However, the landscape of providers is fragmented and diverse.65 Since trade processing services are ancillary to the trading and clearing of trades, the market participants active in these services are in some cases also trading venues (e.g. FX trading venues provide NOE messaging as part of trading services) or CCPs themselves, or other ancillary services providers (providers of order management systems or risk management systems). However, the providers of order management systems or risk management systems do not seem to compete closely with the Parties for most services as evidenced by responses to the market investigation.66 In any case, offering a new service from the perspective of an already active provider of trade processing services is not necessarily an easy undertaking. For example, a market participant notes with respect to IHSM: “(…) in 2013-4, Markit attempted to enter the credit limit checking space, but today (…) is not aware of any significant competition to Traiana.”67

(77) In summary, the answers from market participants indicate that while customers may buy several trade processing products from the same supplier, the decisions are made independently for each particular service, based, first and foremost, on service quality.68 The least important criterion when choosing trade processing service providers was whether the provider also offered other related services.69 Competitors agreed that separate trade processing services markets exist by service type.70 Considering that customers procure these services separately and competitors offer them standalone, the Commission considers that trade processing services are separate product markets by service type.

(78) In addition, a distinction by type of customer is conceivable regarding some trade processing services. One competitor states: “Competitors may also vary based on target market as the requirements for the likes of asset managers, hedge funds and banks significantly differ based on functionality specifics. For example, some buy side clients may require support for master/sleeve account structures which would not be as applicable to banks.”71

(79) The Commission considers, in line with its previous decisional practice in related markets (e.g. derivatives clearing, see Section 4.4.2), that it is possible that there may be separate product markets for trade processing services by type of customer. However, for the purposes of this case, the distinction by type of customer does not appear relevant. The Transaction gives rise to a horizontal overlap in FX NOE messaging services and FX PB give-up management services, as well as a vertical relationship between CME’s OTC FX trading services (upstream) and MarkitSERV’s OTC FX CCP connectivity service (downstream). All those services are provided without any differentiation across customer types, and the market investigation did not give rise to any suggestion that the impact of the Transaction or dynamics of these relationships would differ by customer types. Therefore, the Commission’s assessment focuses on the relevant markets for FX NOE messaging, FX PB give-up management, OTC FX CCP connectivity services and OTC FX trading services without further distinguishing between customer types.

4.5.2.4. Conclusion

(80) In view of the above, the Commission considers that trade processing services consist of separate markets (i) by asset class, (ii) by trade type (bilateral, tri-party) and (iii) by service type (at least into NOE messaging, PB give-up management, CCP connectivity). A separate market by customer type may exist though a conclusion on this distinction is not necessary as it is not relevant in the markets affected by the Transaction.

(81) The relevant distinct trade processing services markets in which the Parties overlap horizontally or vertically (JV with the parent or within the JV) are covered in Sections 4.6 to 4.10, namely FX PB give-up management, FX NOE messaging, CCP connectivity, credit limit management for OTC derivatives and trade confirmation.

4.6. Prime broker (PB) give-up management

4.6.1. Introduction and Parties’ services

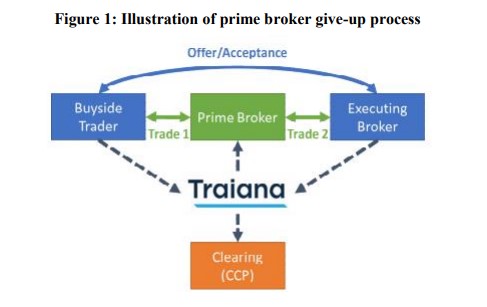

(82) When a prime brokerage trade is agreed between the two trading parties (the buy-side trader and the executing broker), they submit a message via a PB give-up management services provider’s “message interface” and a prime broker can then agree to step in, with the parties being notified through the message interface. The prime broker then enters into two offsetting trades: one between its client (the buy- side trader) and the prime broker; and one between the executing broker and the prime broker. The client, prime broker and executing broker must communicate with each other throughout this process. PB give-up messaging services facilitate this trilateral communication, including confirmation that a broker has agreed to step in between the parties, allocations and confirmations. The below Figure provides a graphic visualization of the process to which PB give-up management services relate.

Figure 1: Illustration of prime broker give-up process

Source: Form CO, Table 6.3.

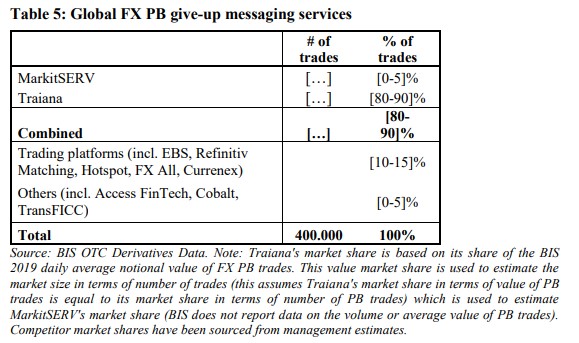

(83) Traiana is active in PB give-up management services for FX, equity, IRD and exchange-traded derivatives trades across several asset classes (though not for FX).72 PB give-up management services comprise the following sub-services: PB give-up messaging services, processing give-up agreements, tri-party documentation management, credit limit management and aggregation.

(84) MarkitSERV provides a sub-set of PB give-up management services for a very small volume of FX prime brokerage trades for a limited number of customers. Concretely, MarkitSERV has […] customers who use FX NOE messaging services for both bilateral and prime broker trades. In addition […], a small number of customers use MarkitSERV’s TradeSTP service for FX PB give-up messaging. MarkitSERV does not provide any other FX PB give-up management services mentioned in the previous recital.

4.6.2. Relevant product market definition

4.6.2.1. Commission’s previous decisions

(85) The Commission has not previously considered the prime broker (PB) give-up management services market. However, the Commission has considered the related market of trading services for derivative contracts and considered in past decisions that the market can be distinguished based on underlying asset classes, execution environment, and types of contracts.73

4.6.2.2. Notifying Parties’ view (86) The Notifying Parties’ views with respect to the general distinguishing criteria in trade processing services markets (by asset class and trade type) applies also to PB give-up management services (see Section 4.5.2).

(87) The Notifying Parties note that FX is the only asset class with a significant volume of prime broker trades. In addition, on the demand side, different divisions, desks and individuals are responsible for services by asset class in customers’ organisations.

(88) The Notifying Parties consider that FX PB give-up management services constitute one relevant product market which should not be further distinguished by service type. Traiana offers different, distinguishable FX PB-give-up management services that are all available to be purchased individually. Some customers purchase only one service, while others purchase several. However, the Notifying Parties submit that it is not necessary to conclude on whether FX PB give-up management services should be further distinguished by service type, as it does not affect the competitive assessment.

4.6.2.3. Commission’s assessment

(89) The results of the market investigation indicate that it is appropriate to consider PB give-up management services as a separate product market from other trade processing services. Furthermore, the market investigation supports the conclusion that there are separate PB give-up management services markets by asset class and trade type.

(90) Regarding distinctions based on type of contract and execution environment, there may be separate markets with respect to PB give-up management services in other asset classes or trade types. However, in the present case, affected markets only arise with respect to FX PB give-up management, and within FX a further separation by type of contract or execution environment is not relevant.

(91) Regarding distinctions by service type or trading channel, the market definition can be left open as no serious doubts as to the Transaction’s compatibility with the internal market arise regardless of whether a broader market (including all FX PB give-up management services, i.e FX PB give-up messaging services, processing give-up agreements, tri-party documentation management, credit limit management and aggregation for trades executed electronically and bilaterally/via voice) or separate markets are assessed. The below sets out in more detail the Commission’s considerations.

(92) In terms of a distinction on an asset class basis, the majority of respondents to the market investigation considered that, from a demand-side perspective, a distinction between PB give-up management services by asset class is relevant.74 The respondents refer in particular to FX as a relevant asset class. This may be related to the fact that FX is the only asset class with significant volumes of prime broker trades.75

(93) From a supply-side perspective, the question does not arise in a meaningful way, as no other asset class except FX has significant volume of primer broker trades.76 The Commission considers that the PB give-up management services market is separated by asset class. Hence, the Commission considers for the purposes of this decision, that FX PB give-up management services constitute a separate market.

(94) In terms of execution environment, the distinction of whether a trade is executed on exchange or OTC is not relevant for the markets in the present case, as FX PB trades are all executed OTC and not on exchanges.77 Hence, a distinction by execution environment is not relevant for the assessment of the overlap the Transaction leads to in FX PB give-up management services. This distinction is therefore not further assessed for the purposes of this decision.

(95) In terms of type of contract, FX PB give-up management services do not provide for any distinction by type of contract. The market investigation did not reveal any such distinction as being relevant in FX PB give-up management services. Traiana and its competitors provide FX PB give-up management services for all contract types for FX and no distinction is made with respect to the services by type of contract.78 Hence, a distinction by type of contract is not relevant for the assessment of the overlap the Transaction leads to in FX PB give-up management services. This distinction is therefore not further assessed for the purposes of this decision.

(96) In terms of a distinction by service type within FX PB give-up management services, the Commission notes that such a distinction may exist, given that products are available standalone and in combination, and customers seem to buy one or several products depending on their needs and hence, there seems to be no “fixed bundle” constituting FX PB give-up management services.79 The majority of Traiana’s customers buy the FX PB give-up messaging service ([…] clients of FX PB give-up management services overall), indicating the importance of this service within FX PB give-up management services.

(97) In the market investigation, the Commission asked whether customers considered that they could use other service types to replace their current FX PB give-up management provider. Responses were mixed with a minority answering “yes” and a majority answering “it depends” or “no”. When asked to explain, the general tenor was that certain parts of FX PB give-up management can be replaced by in-house self-supply or other providers while other parts, like the messaging service, rely on the “network” which only Traiana currently seems to provide.80

(98) In addition, evidence available to the Commission suggests that entry in the market of FX PB give-up management is not easy in the sense that suppliers in adjacent markets are not able to switch quickly to provide FX PB give-up management services and market them in the short term.81 This is supported by the fact that MarkitSERV entered the market 10 years ago but has not gained significant traction, even though it already competed in adjacent trade processing services markets.

(99) While a distinction by service type cannot be excluded based on the evidence available, a conclusion on this point is not relevant, as the competitive assessment would not change based on a narrower market definition distinguishing FX PB give- up management services further.

(100) In terms of trading channel, prime brokers use Traiana’s FX PB give-up messaging services regardless of how a trade was executed (electronically or bilaterally), so from a demand-side perspective, customers do not distinguish between those channels when purchasing this service.82

4.6.2.4. Conclusion

(101) Based on the results of the market investigation and the evidence available to it, the Commission considers that PB give-up management services are a separate relevant product market from other trade processing services and that it is appropriate to distinguish the market for PB give-up management services by asset class and trade type.

(102) While separate markets based on the execution environment and types of contracts may exist with respect to other asset classes, these distinctions are not relevant for the present case, as the Parties’ activities only present a link with respect to FX. In FX PB give-up management services, these distinctions are not relevant.

(103) Potentially narrower separate markets by service type and trading channel within FX PB give-up management may exist, though these can be left open, as the Transaction does not give rise to serious doubts as to its compatibility with the internal market irrespective of such a distinction. Concretely, the Transaction leads to a horizontal overlap in FX PB give-up messaging services (see Section 5.5) and possible conglomerate effects with respect to FX PB give-up management services (see Section 5.9), the assessment of which does not change depending on the above further plausible distinction.

4.6.3. Relevant geographic market definition

4.6.3.1. Commission’s previous decisions

(104) The Commission has not previously considered the relevant geographic market definition for FX PB give-up management services. However, relevant geographic market definitions in related markets like derivative trading and clearing have generally been at least EEA-wide or global.83

4.6.3.2. Notifying Parties’ view

(105) The Notifying Parties submit that the relevant geographic market for the supply of trade processing services is global, given that the Parties and their competitors provide their services to customers across the world. The Notifying Parties did not submit a specific view with respect to FX PB give-up management services.

4.6.3.3. Commission’s assessment

(106) The Commission asked customers of FX PB give-up management services in the market investigation whether they compare offers of service providers at worldwide, EEA, national or other geographic level and whether the same suppliers are active on these levels. In both cases, customers answered practically unanimously that they compared offers at worldwide level and that suppliers are active worldwide.84

(107) Suppliers of FX PB give-up management offer their services to customers worldwide and there are no physical barriers to the provision of services.

4.6.3.4. Conclusion (108) In light of the foregoing, for the purposes of this decision, the Commission considers the geographic market of FX PB give-up management services to be worldwide.

4.7. NOE messaging services

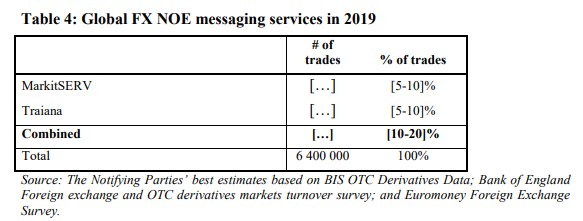

4.7.1. Introduction and Parties’ services (109) Notice of execution (‘NOE’) messaging services involve sending NOEs from brokers or venues to customers to feed customers internal risk management systems. A notice of execution message is an electronic message sent by brokers or liquidity providers to their clients to notify them of the fact that a trade has been executed and of the terms of that trade. It enables counterparties to check the terms of the trade and (for bilateral trades) to enter it in their risk management system. MarkitSERV provides bilateral NOE messaging services for trades in several asset classes (credit, equities, FX and interest rate derivatives). Traiana provides bilateral NOE messaging in FX, cash equities and exchange traded derivatives. Hence, a horizontal overlap arises in bilateral FX NOE messaging services. In addition, MarkitSERV and Traiana provide tri-party NOE messaging services. While for Traiana this service is an integral part of its PB give-up management services offering, MarkitSERV is only active as a marginal player in tri-party FX NOE messaging.

4.7.2. Relevant product market definition

4.7.2.1. Commission’s previous decisions

(110) The Commission has not previously considered the NOE messaging services market. However, the Commission has considered the related market of trading services for derivative contracts and considered in past decisions that the market can be segmented based on underlying asset classes, execution environment, and types of contracts.85

4.7.2.2. Notifying Parties’ view

(111) The Notifying Parties’ views with respect to the general segmentation in trade processing services markets (by asset class and trade type) applies also to NOE messaging services (see chapter 4.5.2.2).

(112) The Notifying Parties consider that FX NOE messaging services can be distinguished by trade type (bilateral, tri-party). While the Notifying Parties agree that there is some supply-side substitutability between bilateral FX NOE messaging and tri-party FX PB give-up messaging from a technical perspective, they consider that there are other barriers that make it difficult to expand from being a provider of FX NOE messaging services to FX PB give-up messaging and vice versa. A provider would have to build new workflows and new relationships with individuals in customers’ organizations, since different divisions in customers’ organizations handle FX NOE messaging and FX PB give-up messaging.

(113) The Notifying Parties do not consider that there are separate markets for FX NOE messaging by type of contract (e.g. non-deliverable forwards, options, etc.). According to the Notifying Parties, there is supply-side substitution, as NOE messaging is substantially the same across different types of derivatives with only limited differences in the data fields.86 However, there is no demand-side substitution between different types of contracts.

(114) Regarding independent provision versus a captive provision of FX NOE messaging services, the Notifying Parties consider this not to be a plausible distinction. The Notifying Parties consider that suppliers that provide FX NOE messaging services in an ancillary capacity (captive providers) compete with suppliers that provide FX NOE messaging services as their core service and without being vertically integrated (independent providers). These other providers are for example risk management system providers (Murex, OpenLink, Finastra), post-trade messaging vendors such as Refinitiv or Broadridge or trading platforms like EBS, Refinitiv Matching, Hotspot (CBOE), FX all and Currenex. While the Notifying Parties recognise that there are some trading venues that only provide FX NOE messaging in relation to trades executed on their venue, there is competition with respect to FX NOE messaging even for those trades. Third party providers (such as Refinitiv and MarkitSERV) are commonly used for FX NOE messaging services and hence, trades on these venues cannot be considered captive.

4.7.2.3. Commission’s assessment

(115) The results of the market investigation indicate that it is appropriate to consider NOE messaging services as a separate product market from other trade processing services. Furthermore, the market investigation supports the conclusion that there are separate NOE messaging markets by asset class and trade type.

(116) Regarding distinctions based on type of contract and execution environment, it is possible that there may be separate markets with respect to NOE messaging services in other asset classes or trade types. However, in the present case, affected markets only arise with respect to FX NOE messaging, and within FX a further separation by type of contract or execution environment is not relevant.

(117) Regarding distinctions based on trading channel (electronic or bilateral/voice execution) and independent versus captive provision of services, the market definition can be left open as no serious doubts as to the Transaction’s compatibility with the internal market arise regardless of whether a broader market (including both) or separate markets are concerned. The below sets out in more detail the Commission’s considerations.

(118) Regarding a distinction by asset class, the Commission’s market investigation provided no evidence that NOE messaging services are contracted across asset classes. Respondents procure trade processing services together, where it makes technical and commercial sense, though a majority indicates that this is often the case within the same asset class.87 Clients of trade processing services are organized internally by asset class and often source these services accordingly. One customer explains: “This is negotiated at the FX business level.”88

(119) From a supply-side perspective, there may be some substitutability across asset classes. However, it would not seem to be the case that suppliers are easily able to switch their messaging product to other asset classes89, as this requires connections to different venues and brokers (which operate segmented by asset class too). Hence, separate markets by asset class seem to be plausible.

(120) With respect to the trade type, there is some supply-side substitutability in NOE messaging services across bilateral and tri-party trade flows, as evidenced by the fact that MarkitSERV and Traiana offer both types of messaging services. However, the mere presence of the Parties in the respective markets alone does not indicate that the messaging market is one market across bilateral and tri-party messaging services. From a demand-side perspective, customers do not consider Traiana and MarkitSERV as potential substitutes in FX NOE messaging.90 One customer notes: “The FXPB business does not procure FX NOE messaging services from MarkitSERV. The FX Options business procures FX NOE messaging services from MarkitSERV.”91 While MarkitSERV is considered a competitor to Traiana in FX NOE messaging92, the closer competitor to Traiana’s offering (which is broader than messaging) is considered to be a recent entrant, Cobalt.93

(121) Asked whether customers consider it important that their FX NOE messaging provider is also able to provide other messaging services (FX PB give-up messaging services), answers are mixed.94 One customer that is active as a prime broker and as an executing broker (and hence has bilateral and tri-party trade flows) comments: “We do not consider there to be obvious efficiencies to be gained across these types of messaging products.”95 Another customer in the same situation mentioned the following: “As we are a PB we require access to NOE messages, Traiana is the largest provider and therefore it is critical we can access as a PB and EB.”96 A third customer mentions: “Harmony [Traiana’s trade processing services suite] is not used in the bilateral FX space, where SWIFT and CLS are the main providers.”97

(122) While there seems to be some supply-side substitutability between bilateral and tri- party messaging services, the majority of responding market participants do not consider the Parties’ activities to be substitutable.98 This is not surprising as messaging services are only a part of the suite of products that are included in PB give-up management services. When asked about competitors in FX PB give-up management services that provide these services as a core offering, the only two companies consistently mentioned are Traiana and Cobalt, not MarkitSERV.99

(123) The Parties provide, and some customers use, the messaging services of one Party for both bilateral and tri-party messaging (see recital (109)). However, given that only very few customers use the services of the Parties interchangeably indicates that for the large majority of customers they do not seem to be alternatives or there is no perceived benefit in sourcing the services from the same provider. Another aspect to consider is that bilateral NOE messages are sent from brokers or venues to customers “pre-risk”, i.e. before the trade is entered into the customers risk management systems. The messages therefore need to be sent in real time to be of use for customers. PB give-up management services are, however, provided “post-risk”, i.e. after the trade is entered into the customers risk management system. For this use case, the speed does not matter as much as it does for “pre-risk” messages.100

(124) In conclusion, there seem to be different views on whether there is a benefit in procuring bilateral and tri-party FX NOE messaging services from the same or different providers, depending on the customer’s business activities. However, even where customers are active as a prime broker and an executing broker, this does not necessarily mean they source related trade processing services from the same provider (see quotes in recitals (120) and (121)).

(125) In terms of execution environment (exchange-traded versus OTC execution), the distinction between whether a trade is executed on exchange or OTC is not relevant for the markets in the present case, as the Parties only offer trade processing services in the affected markets for OTC derivatives.101 Hence, this distinction is not further assessed for the purposes of this decision.

(126) In terms of type of contract, FX NOE messaging services do not provide for any distinction by type of contract.102 The market investigation did not reveal any such distinction as being relevant in FX NOE messaging services. NOE messaging is substantially the same across different types of derivatives with only limited differences in the data fields. MarkitSERV, for example, charges the same fee for NOE messaging irrespective of the type of derivative. While some types of contracts may require several NOE messages for different “legs” of the contract (and therefore, they are more expensive from a NOE messaging cost perspective than others), this is unlikely to be a meaningful distinguishing factor for either demand or supply side, given that the overall cost of NOE messaging services compared to other trading costs is very small.103 The Commission therefore considers that there is no need to conclude on such a distinction as this is not relevant for the purposes of the present decision.

(127) As regards a distinction by trading channel (electronic versus bilateral/voice execution), trades are submitted to the NOE messaging provider either by the electronic trading venue when the trade is executed electronically, or by the parties to the trade themselves, when the trade is executed bilaterally, e.g. by phone. In FX markets in particular, the majority of trading has moved to electronic venues in recent years, though ca. 30% of trading volume is still executed bilaterally/via voice.104 Most electronic FX trading venue competitors were of the opinion that the market is split into electronic FX trading and bilateral/voice trading.105 However, this may be different from a demand-side perspective. In any case, there is no need to conclude on whether there are separate FX NOE messaging services markets for trades executed on electronic venues or bilaterally/via voice, as the distinction would not change the Commission’s assessment in the present case.

(128) In addition, the Commission considered whether there could be separate FX NOE messaging services markets based on an independent provision of services (“independent”) versus a vertically integrated provision of services (“captive”). This is a plausible distinction given that trading venues and brokers (as well as other providers), offer messaging services as an ancillary part of their trading/intermediation services, i.e. they provide trade messaging for the trades executed on their venues/through their intermediation. However, for example MarkitSERV also processes trades executed on various third party trading platforms, which may have their own captive messaging services that they provide to their clients.

(129) First, the line between independent and captive providers is somewhat blurred. While MarkitSERV and Traiana’s messaging services are considered independent of any trading venue106, some FX trading venue providers also provide NOE messaging services to third party venues. In particular, Refinitiv, which operates an FX trading platform and is according to the Notifying Parties the largest provider of FX NOE messaging services, is active as an independent provider to third party venues, in that its customers can use messaging services for trades executed on the Refinitiv trade platform or on other, third party trade platforms.

(130) Second, one competitor is of the view that customers prefer a provider that connects to several venues for efficiency reasons: “The benefit of using IHSM or Traiana’s service, as opposed to a drop copy from a trading venue for example, is operational efficiency – clients do not need to use multiple different messaging systems across their trading platforms and so can avoid the development time and effort needed to make their systems work with different platform’s messaging services.”107 However, this contrasts with other evidence available to the Commission. The market investigation indicated that in most cases customers consider independent and captive providers’ services to be substitutable. Historically, switching is not common among customers,108 which one customer explained was because “[w]hile it is not difficult to change provider…, there would need to be a good reason to justify the cost and time involved”, noting that its current providers’ offering has worked well and so it has not had reason to consider changing.109 However, customers’ replies to the market investigation suggested that should a need to switch arise, captive providers (which can be trading venues, brokers or risk management system providers) would be an alternative to independent ones. Even though it could be argued that captive providers only ever provide a partial replacement for an independent provider that connects to several venues, it is conceivable that those providers would be able to develop a wider solution (like Refinitiv). In particular, large customers could sponsor such entry as has been demonstrated in past cases110. In any case, a large majority of customers (70%) indicated that they would be able to fully or at least partially replace the FX NOE messaging service they currently procure with an alternative service.111 One customer notes: “We could direct connect to platforms.”112

(131) The ability to switch by customers is further confirmed by win-loss analyses of both Parties’ FX NOE messaging services between 2016 and 2021. During the last 5 years, MarkitSERV lost […] clients, […] of which replaced MarkitSERV’s services with an in-house solution and […] of which changed to a competitor.113 The Commission notes that in this context an ‘in-house solution’ likely refers to a solution whereby the customer switches to the messaging services offered by trading venues (i.e. the customer conducts internal development so as to build a solution that enables it to effectively use these services of trading venues). Traiana’s bilateral FX NOE messaging service lost […] clients during the same time, […] of which no longer needed the service, […] of which built in-house connectivity and […] of which possibly moved to a competitor (no names known), while […] provided no reason.114

(132) Third, the market investigation revealed that customers consider captive providers to have similar competitive strength in the market for FX NOE messaging115 as the main independent suppliers (MarkitSERV, Traiana and Refinitiv). The fact that several captive providers are considered to have similar competitive strength as the main independent suppliers further indicates that customers consider these providers to offer substitutable services. In addition, some captive providers, like credit monitoring vendors and order management system providers (as well as FX aggregators) market connectivity to multiple trading venues for the purpose of execution and can and do provide multi-venue NOE messaging to their clients.116

(133) Fourth, certain providers have a “hybrid” model. Both Traiana and Refinitiv act as “independent” provider, i.e. offering services to competing trading venues, but also as a “captive” provider, given that they both own (or their respective parent company also owns) FX trading venues (Traiana’s parent CME owns FX trading venue EBS and Refinitiv owns FX all and Matching, two FX trading venues). Furthermore, an independent provider like MarkitSERV provides FX NOE messaging services to a number of customers trading on Refinitiv’s venues, even though Refinitiv has its own FX NOE messaging service, further illustrating MarkitSERV and Refinitiv’s products would be substitutable.

(134) In summary, the market investigation confirms that customers generally consider that the FX NOE messaging services provided by independent and captive providers would be substitutable to a large extent, with captive providers being considered possible substitutes of independent providers. Furthermore, most “independent” providers including Traiana are not actually independent in the sense that they are owned by parents that also own FX trading venues. In any case, the Commission considers that a conclusion on the question whether there are separate markets for independent provision of FX NOE messaging services and captive provision of FX NOE messaging services (including a narrower definition of captive provision of FX NOE messaging services for each venue) or one market including both is not necessary, as the Transaction does not give rise to serious doubts as to its compatibility with the internal market on the basis of either market definition.

4.7.2.4. Conclusion

(135) Based on the results of the market investigation and the evidence available to it, the Commission considers that NOE messaging services are a separate relevant product market from other trade processing services, and that it is appropriate to distinguish the market for NOE messaging services by asset class and trade type. A further distinction by type of contract and execution environment is not relevant in the present case, where overlaps exist only with respect to FX NOE messaging. The conclusion on whether electronic vs. bilateral/voice execution channels and independent versus captive service provision are separate markets can be left open, as the Transaction does not give rise to serious doubts as to its compatibility with the internal market irrespective of such a distinction. Concretely, the Transaction leads to a horizontal overlap with respect to bilateral FX NOE messaging (see Section 5.4), the assessment of which does not change depending on the above further plausible distinctions.

4.7.3. Relevant geographic market definition

4.7.3.1. Commission’s previous decisions

(136) The Commission has not previously considered the relevant geographic market definition for bilateral FX NOE messaging services. However, relevant geographic market definitions in related markets like derivative trading and clearing have generally been at least EEA-wide or global.117

4.7.3.2. Notifying Parties’ view

(137) The Notifying Parties submit that the relevant geographic market for the supply of trade processing services, including bilateral FX NOE messaging services, is global, given that the Parties and their competitors provide their services to customers across the world.

4.7.3.3. Commission’s assessment

(138) The Commission asked customers of bilateral FX NOE messaging services in the market investigation whether they compare offers of service providers at worldwide, EEA, national or any other geographic level and whether the same suppliers are active on these levels. In both cases, customers answered practically unanimously that they compared offers at worldwide level and that suppliers are active worldwide.118

(139) Competitors in this space did not mention any geographically narrower basis on which they compete.119

4.7.3.4. Conclusion (140) Therefore, for the purposes of this decision, the Commission considers the geographic market of bilateral FX NOE messaging services to be worldwide.

4.8. CCP connectivity

4.8.1. Introduction and Parties’ services (141) CCP connectivity services consist in sending details of trades executed on a venue or bilaterally to a central counterparty (‘CCP’) for clearing. CCP connectivity services are also referred to as ‘middleware’ and are closely linked to derivatives trading services (as it can be a source of trades to be sent to clearing) and clearing services (the destination of the trade).

(142) MarkitSERV provides CCP connectivity for CDS, FX and IRDs.

(143) Traiana is mainly active in the provision of CCP connectivity in the equities asset class, which represents the vast majority ([80-90]%) of its CCP connectivity revenues. Traiana is also active, to a much lesser extent, in the FX and IRD asset classes for CCP connectivity.120

4.8.2. Relevant product market definition

4.8.2.1. Commission’s previous decisions (144) The Commission has not previously considered the relevant product market for CCP connectivity services. However, the Commission has considered the related market of trading services for derivative contracts and considered in past decisions that there are separate relevant product markets based on the underlying asset classes, execution environment, and types of contracts.121 Similarly, the Commission has previously assessed the relevant product market for the clearing of derivatives, and considered separate product markets for the clearing of derivatives by underlying asset class, execution environment, type of customer and type of contract.122

4.8.2.2. Notifying Parties’ view (145) The Notifying Parties’ views with respect to the general approach to market definition in trade processing services markets (namely that there are separate product markets by asset class and trade type, see Section 4.5.2) apply also to CCP connectivity services, although the Notifying Parties did not detail why they considered this would be the case.

(146) The Notifying Parties further submit that there is limited supply-side substitutability between the different asset classes for CCP connectivity. This is due to the different functionality and impact of regulatory requirements for trade processing services (such as CCP connectivity) in different asset classes, and the fact that in customer organisations different divisions, desks and individuals are responsible for procuring trade processing services, such as CCP connectivity. Therefore, the Notifying Parties submit that expanding a CCP connectivity service from one asset class to another would require investment in new systems, knowledge of new products and workflows, and to build new client relationships.123

4.8.2.3. Commission’s assessment

(147) The results of the market investigation indicate that it is appropriate to consider CCP connectivity as a separate product market from other trade processing services and are consistent with the Notifying Parties’ submissions that there is limited supply- side substitutability between different asset classes.