Commission, May 20, 2021, No M.10059

EUROPEAN COMMISSION

Decision

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

PARTIES

Demandeur :

SK Hynix Inc.

Défendeur :

Intel’s NAND, SSD business

Dear Sir or Madam,

(1) On 13 April 2021, the European Commission received notification of a proposed concentration (the “Transaction”) pursuant to Article 4 of the Merger Regulation by which SK Hynix Inc. (“SK hynix", South Korea) acquires within the meaning of Article 3(1)(b) of the Merger Regulation sole control of the NAND and solid-state drive business of Intel (the “Target Business”)3. SK hynix is designated hereinafter as the “Notifying Party”, SK hynix and the Target Business together as the “Parties”.

1. THE PARTIES

(2) SK hynix is active in the manufacturing and marketing of semiconductor products. SK hynix is headquartered in the Republic of Korea and originally founded its semiconductor business in 1983 as Hyundai Electronic Industrial Co., Ltd. Today, SK hynix primarily designs and manufactures memory storage devices such as Dynamic Random Access Memory (“DRAM”), NAND (meaning “not AND”) flash memory and NAND-based Solid-State Drives (“SSDs”), as well as system semiconductors such as Complementary Metal-Oxide-Semiconductor (“CMOS”) image sensors.

(3) The Target Business is active in developing, designing, manufacturing, assembling, testing, marketing and selling products utilizing the NAND flash memory technology. The Target Business is also active in developing, designing, manufacturing, assembling, testing, marketing and selling SSDs that utilize NAND flash memory technology.

2. THE OPERATION

(4) The notified Transaction concerns the acquisition by SK hynix of the NAND and SSD business of Intel. It will be implemented by means of a Master Purchase Agreement (the “MPA”) entered into on 19 October 2020 by the Parties and will be completed in two steps. At the first closing, SK hynix will acquire Intel’s NAND Fabrication (“Fab”) Assets through a wholly-owned subsidiary to be organized in China (“FabCo”) and, through another wholly-owned subsidiary (“SSDCo”), it will acquire Intel’s SSD Business Assets. Intel’s remaining NAND operations will be transferred to one or more wholly-owned subsidiaries of Intel (“OpCo”). At the second closing, SK hynix will acquire all of Intel’s remaining NAND Business Assets by way of an acquisition of the equity interests in OpCo from Intel.

(5) Therefore, the Transaction constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

3. UNION DIMENSION

(6) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 2 500 million (Parties: […])4. In each of at least three Member States, the combined aggregate turnover of the Parties is more than EUR 100 million ([…]). The aggregate turnover of each Party is more than EUR 25 million in each of the Czechia ([…]), the Netherlands ([…]) and Poland ([…]). Each of the Parties has a Union-wide turnover in excess of EUR 100 million ([…]), but they do not achieve more than two- thirds of their aggregate Union-wide turnover within one and the same Member State. The notified operation therefore has a Union dimension pursuant to Article 1(3) of the Merger Regulation.

4. RELEVANT MARKETS

4.1. Introduction to flash memory and data storage solutions

(7) The Transaction relates to flash memory and data storage solutions. Data storage solutions allow for the creation, management and preservation of digital content. They are used in a variety of information technology (“IT”) devices and applications, such as personal computers, servers, and other business storage systems as well as in industrial and consumer electronic applications, such as digital video recorders, gaming devices and automotive applications. Data storage solutions used in these devices and applications include SSDs, Hard Disk Drives ("HDDs"), memory cards, USB flash drives and embedded flash storage.

(8) Data storage solutions require computer memory, i.e. components and recording media, to retain digital data. There are two types of computer memory: volatile and non-volatile memory. Volatile memory (such as random access memory, "RAM"), retains the stored information only while powered. By contrast, non-volatile memory can retain information after having been power cycled (i.e., turned on and off). Volatile memory comes in two main types: Static Random Access Memory ("SRAM") and DRAM.

(9) Flash memory is a type of non-volatile storage technology that stores data in transistors and that does not require power to retain data. Flash memory uses two different technologies to map and store data, NAND and NOR. The names refer to the type of logic gate used in each memory cell ("Not AND" and "Not OR"). Contents of NOR memory can be read more rapidly than the contents of NAND, while data can be written to NAND more rapidly than to NOR.

(10) An SSD is a storage solution that uses NAND flash memory to store digital data.5 The NAND flash memory is a key input for SSDs. The other main components of an SSD are the controller and the interface. The controller is a chip that directs memory reading, writing, and certain other functions (in other words, it manages how and where data is stored on the memory chips within the SSDs). The interface is the connection between the storage unit and the computer or system where it is inserted. It consists of a physical layer, the physical interconnector, and a logical layer, the protocol used to structure the communication.

(11) The notified Transaction concerns the following three types of data storage that are used in the value chain described above: (a) DRAM: a type of non-volatile memory, that can retain memory after having been power cycled, used in data and graphic processing applications in data centres as well as in a wide array of IT devices for consumer applications – where only SK hynix is active;

(b) NAND: flash memory (a type of non-volatile semiconductor media) used for data storage in consumer devices, enterprise systems, and industrial applications – where both SK hynix and the Target Business are active; and

(c) SSDs: a type of storage solution used in IT devices and applications, which are based on flash memory – where both SK hynix and the Target Business are active.

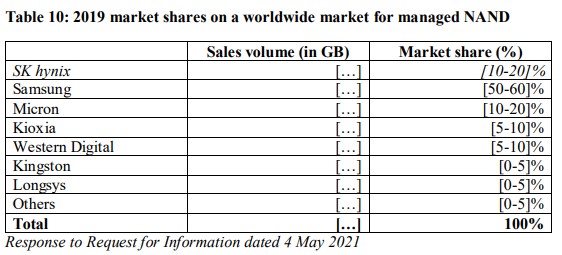

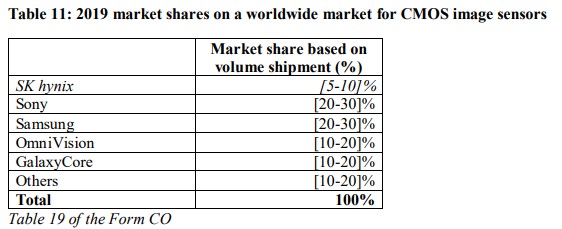

(12) In addition to the activities set out above, SK hynix also designs “CMOS” image sensors and managed NAND.

(13) CMOS image sensors are non-memory semiconductors that serve the role of digital film in many IT devices. They are found in several types of electronic components, including microprocessors, batteries, and digital camera image sensors, and are mainly used in digital cameras, smartphones and miniature medical imaging systems. The Target Business is not active in this field or in markets that are upstream or downstream of CMOS image sensors.

(14) Managed NAND is a product that combines NAND and a controller, or both a controller and DRAM. Managed NAND is commonly used in mobile phones, and to a lesser extent in tablets and low-grade laptops (the primary form of storage in laptops and PCs is hard drives and SSDs). It is available in different types:

(a) Embedded MultiMedia Card ("eMMC") is a small storage device that incorporates NAND flash memory and a simple storage controller on a single integrated circuit. It is commonly used in portable devices, such as tablets and mobile phones, as a low-cost method of providing primary internal storage. eMMC can also be used in on-board vehicle entertainment and navigation systems. The next generation of eMMC is Universal Flash Storage ("UFS"). It is a high performing integrated circuit with higher memory capacity and optimized performance for multithreaded applications. As a result, it is currently used in high-end smartphones only.

(b) Embedded Multi-Chip Memory ("eMCP") is Multi-Chip-Package comprising eMMC and DRAM. It is typically used in basic smartphones or non- smartphones/utility phones given its lower cost. uMCP is a new solution comprising UFS and DRAM and expects to utilize UFS's fast speed and MCP's advantages in occupying a smaller foothold area in printed circuit boards and in reducing phone makers’ effort in system design.

(15) The Target Business is not active in managed NAND. In addition, as explained further in Section 5.5, even though NAND is an input for managed NAND products, the Target Business' NAND cannot be integrated into SK hynix's current managed NAND products.

4.2. Product market definition

4.2.1. DRAM

4.2.1.1. Previous Commission decisions

(16) In past decisions, the Commission examined whether it was necessary to differentiate between the different types of DRAMs. In particular, the Commission considered whether commodity DRAMs, used as components for personal computers, and high- speed DRAMs, used in high-performance servers and workstations, are separate product markets but ultimately left the market definition question open.6

(17) In JV.44 Hitachi/NEC — Dram/JV, the Commission considered that DRAMs could be differentiated according to the memory size (e.g. the quantity of data that can be stored on the chips), their intended application (FPM-DRAM, EDO-DRAM, SDRAM, or RDRAM) or the type of the final product where they are installed: servers, PCs, mobiles, games, network devices, PC peripherals, and others. However, it was not necessary to further delineate the relevant product markets in the context of that case.7

(18) From the demand-side, the Commission found that the same type of DRAMs is available to customers as DRAMs are commodity products with standardized specifications.8 From the supply side, the Commission considered that manufacturers are able to switch between different functional types of DRAM due to similar production technologies, but that switching between different generations of DRAM required significant technology investment costs and important production ramp-up time.9

4.2.1.2. Notifying Party’s view

(19) The Parties agree with the Commission’s past practice that DRAMs are commodity products with standardized specifications, and that DRAM manufacturers are able to switch between different functional types of DRAM due to similar production technologies. However, the Parties submit that the precise product market definition can be left open in this case given that the proposed Transaction will not raise competition concerns irrespective of the precise product market definition.10

4.2.1.3. The Commission’s assessment

(20) The market investigation confirmed that commodity DRAMs, used as components for personal computers, and high-speed DRAMs, used in high-performance servers and workstations, are separate product markets.11

(21) As regards further segmentations, the results were not clear for a segmentation according to the memory size as the majority of the respondents did not have sufficient information to assess whether this market segmentation would be possible.12 In addition, the majority of respondents to the market investigation took the view that DRAM should not be further segmented into distinct product markets on the basis of its intended application into: (i) FPM-DRAM, (ii) EDO-DRAM, (iii) SDRAM, and (iv) RDRAM.13 On the contrary, the respondents to the market investigation confirmed that the DRAM market should rather be further segmented on the basis of the type of final product where it is installed into (i.e. (i) servers, (ii) PCs, (iii) mobiles, (iv) games, (v) network devices, (vi) PC peripherals, and others).14

4.2.1.4. Conclusion on product market definition

(22) For the purpose of this decision and in light of the results of the market investigation, the Commission will assess the overall product market for DRAM as including all possible narrower markets, i.e. the market for commodity DRAMs, and the DRAM markets for (i) servers, (ii) PCs, (iii) mobiles, (iv) games, (v) network devices, (vi) PC peripherals, and others. In any event, the market definition can be left open as the above market segmentations do not impact the outcome of the competitive assessment of the Transaction.

4.2.2. NAND flash memory

4.2.2.1. Previous Commission decisions

(23) The Commission previously considered a separate market for NOR and NAND.15 The Commission found that NOR and NAND should be distinguished due to low supply- side substitutability between the types of flash memory. Many suppliers were not active in the whole flash memory spectrum and would incur significant costs and risks switching from one memory type to another. On the demand-side, the Commission noted the different end-applications of NOR and NAND and the significant switching cost for consumers.16 In its most recent decision concerning NAND, the Commission took the view that NAND formed a distinct product market, on the basis that NAND and NOR flash memory have different characteristics and are used in different applications.17

(24) The Commission has also previously considered whether NAND should be further distinguished by 2D and 3D NAND and ultimately left the product market definition open.18 The differences between 2D NAND and 3D NAND in terms of technology, price and capacity were not considered sufficient to conclude that they constitute two separate product markets.

4.2.2.2. Notifying Party’s view

(25) The Notifying Party considers19 that 2D NAND is being increasingly displaced by 3D NAND for many applications, due to the constant effort to reduce the size of chips and the need to increase storage capacity. Moreover, today the cost per GB of 2D NAND is several times higher than that of 3D NAND. 2D NAND flash memory today accounts for a very limited portion of NAND flash memory and has virtually been displaced by 3D NAND flash memory. Competition between NAND suppliers is focused on 3D NAND, and 2D NAND production remains only for niche applications to fulfill product warranty requirements. This displacement is illustrated by the evolution of NAND in smartphones. Until 2016, all smartphones used 2D NAND; since 2017, both 2D and 3D NAND devices have been used on smartphones. Today's Samsung Galaxy and Apple's iPhone utilize only 3D NAND. As such, suppliers have already, or are in the process of phasing out 2D NAND.

(26) The Notifying Party submits that the Transaction will not result in any competition concerns, irrespective of whether 2D NAND and 3D NAND are considered part of the same or separate product markets. The Target Business is no longer active in 2D NAND, while the Parties' combined position in 3D NAND is very similar to their combined position in the overall NAND segment.

4.2.2.3. The Commission’s assessment

(27) The market investigation confirmed the existence of separate markets for each of NOR and NAND.20

(28) As regards the existence of separate markets between 2D and 3D NAND, the market investigation was inconclusive. From a demand-side perspective, the majority of the respondents explained that 2D and 3D NAND are substitutable.21 However, from a supply-side perspective, the majority of the respondents confirmed that a supplier could not rapidly switch manufacturing and supplying between 2D NAND and 3D NAND without incurring significant investment.22 The market investigation confirmed that 2D NAND is an older, legacy technology that is being used decreasingly because it has capacity limitations. 3D NAND technology on the other hand allows stacking which increases capacity and reduces cost. Lastly, the market investigation confirmed that there are no other relevant segmentations within the overall NAND market.23

4.2.2.4. Conclusion on product market definition

(29) For the purpose of this decision and in light of the results of the market investigation, the Commission will assess the overall product market for NAND as including the possible markets for 2D and 3D NAND. In any event the market segmentation into 2D and 3D NAND does not impact the outcome of the competitive assessment of the Transaction and the market definition can be left open.

4.2.3. Storage – segmentation based on technology (HDDs vs. SSDs)

4.2.3.1. Previous Commission decisions

(30) With regard to storage solutions, in its decisional practice, the Commission has analyzed potential segmentations based on technology (HDDs vs. SSDs), on intended use (enterprise vs. client storage), on interface (SATA, SAS, PCI). Each of these potential segmentations are discussed in detail below.

(31) The Commission has also found in its previous decisions that HDDs and SSDs did not belong to the same relevant product markets, neither for enterprise use nor for client use24 due to the significant price difference between the two technologies and the limited storage capacity of SSDs relative to HDDs.25 The Commission, however, noted that SSDs and HDDs could be substitutes for some enterprise applications, for instance in the case of low-performance SSDs which could be substitutable with high-performance HDDs.26 In its most recent decision on HDDs and SDDs, the Commission noted the long term trend whereby HDDs are being displaced by SSDs and left open the question as to whether HDDs and SSDs belong to the same product market with respect to client applications. It however concluded, albeit for the sole purpose of that decision, that HDDs and SSDs belonged to separate product markets with respect to enterprise applications.27

4.2.3.2. Notifying Party’s view

(32) The Notifying Party considers that, since the adoption of the most recent Commission decision regarding these product areas (Western Digital/SanDisk in 2016), SSDs have rapidly expanded in both client and enterprise applications, at the expense of HDDs. Although HDDs still offer a cost advantage per GB, SSDs benefit from better performance, speed, lower power consumption and increased durability, which ultimately leads to several cases where the total lifetime cost of using an SSD is in fact comparable or lower than that of using an HDD. SSDs have also grown in storage capacity. For example, […].28

4.2.3.3. The Commission’s assessment

(33) The market investigation confirmed the segmentation by technology into HDD and SSD.29 In particular, from the demand-side, the majority of market participants takes the view that SSD and HDDs are not substitutable, as HDD customers seek large capacity storage at the lowest per GB price and SSD is used in lower capacity storage with higher performance. According to the results of the market investigation, if substitution occurred between HDDs and SSDs, it would go primarily in the direction of SSDs replacing HDDs.30

(34) From the supply-side, it is considered that suppliers cannot switch manufacturing and supplying between HDDs and SSDs rapidly and without incurring significant investment as the production process for HDDs is different from that of SSDs and they cannot be produced on the same production lines.31

4.2.3.4. Conclusion on product market definition

(35) For the purpose of this decision and in light of the results of the market investigation, the Commission will assess the product markets for SSDs and HDDs32 separately. In any event the market the market definition can be left open as the segmentation into SSDs and HDDs does not impact the outcome of the competitive assessment of the Transaction.

4.2.4. Storage – segmentation based on intended use (enterprise vs. client storage)

4.2.4.1. Previous Commission decisions

(36) Previously, the Commission found a distinction between enterprise and client storage because enterprise storage generally requires higher performance and superior endurance, compared to client storage.33 The Commission has however noted that in some cases, client SSDs can be used for enterprise applications that do not require a high workload.34

4.2.4.2. Notifying Party’s view

(37) The Notifying party takes the view that enterprise SSDs are generally used in high workload environments, such as servers and corporate datacenters, while client SSDs are deployed in consumer devices (including tablets, smartphones) or systems (such as desktop PCs, notebooks, gaming consoles).

(38) The main customers of enterprise SSDs include OEMs (e.g. producers of enterprise computers or storage systems such as Dell and Oracle) and ODMs (original design manufacturers, which produce computer or storage systems on behalf of OEMs and hyperscalers); end user customers that often purchase SSDs directly from manufacturers for use in "hyperscale" distributed computing environments, such as Facebook, Google, Amazon Web Services, Microsoft, Baidu, Alibaba and Tencent, as well as other large end-users; and distributors that serve smaller OEMs.

(39) Client SSD customers include OEMs such as Apple, Sony, Dell, Lenovo, HP and others, which incorporate SSDs into consumer products (PCs, tablets, storage devices); ODMs such as Quanta, Compal, Wistron and others; end consumers, who purchase client SSDs from client SSD suppliers or from standard electronics hardware stores; and distributors.

4.2.4.3. The Commission’s assessment

(40) The market investigation confirmed that the market for storage products should be segmented by intended use into: (i) enterprise (eSSDs) and (ii) client (cSSDs).35

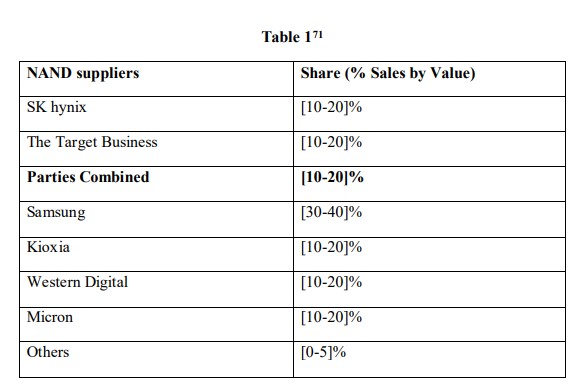

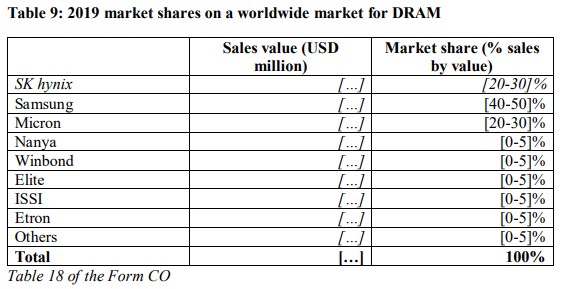

(41) From the demand-side, client storage and enterprise storage are not substitutable. Client storage products do not typically have the same price point, components, form factor, or performance specification as enterprise products.36 From the supply-side, the respondents indicated that it would be relatively easy for a supplier to switch manufacturing between client storage and enterprise storage and start supplying eSSDs or cSSDs rapidly and without incurring significant investment.37

4.2.4.4. Conclusion on product market definition

(42) For the purpose of this decision and in light of the results of the market investigation, the Commission will assess the product markets for enterprise and client SSDs as separate markets. In any event the market definition can be left open as the segmentation into enterprise and client SSDs does not impact the outcome of the competitive assessment of the Transaction.

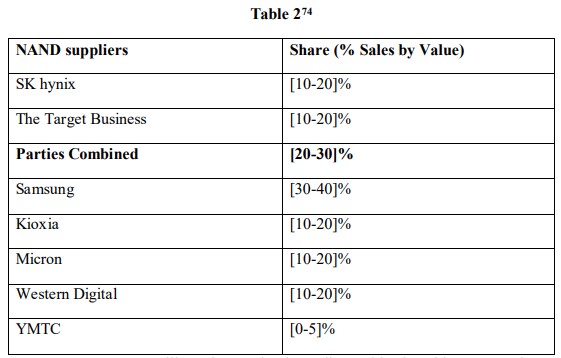

4.2.5. Enterprise storage – segmentation based on interface (SATA vs. SAS vs. PCIe)

4.2.5.1. Previous Commission decisions (43) In its most recent decision regarding SSDs, the Commission found that enterprise SSDs with different interfaces have different endurance, reliability, latency and price, and are used for different end uses and applications. Ultimately, the Commission left open the question of whether enterprise SSDs should be further segmented by interface.38 In its previous decisions regarding HDDs, the Commission considered the different interfaces of HDDs to be relevant in the definition of the relevant product markets.

4.2.5.2. Notifying Party’s view

(44) The Notifying Party submits that in recent years, Peripheral Component Interconnect Express (“PCIe”) eSSDs have been increasingly outperforming and replacing Serial Advanced Technology Attachment (“SATA”) eSSDs for enterprise applications. This trend is mainly driven by a decrease in price of NAND flash memory, which has resulted in lower prices for better performing PCIe eSSDs, as well as in an increase in the performance of PCIe eSSDs, which are gradually exceeding the maximum throughput of SATA and Serial-Attached SCSI (“SAS”) eSSDs (except for newer versions of SAS). Moreover, due to their scalability, PCIe eSSDs can be used for both lower-cost, mainstream performance purposes, as well as for higher-cost, higher- performance purposes. Thus, in recent years, PCIe eSSDs are replacing both SATA and a portion of SAS eSSDs, especially among customers looking to purchase new systems (for whom potential interface incompatibility issues have no real significance).

(45) The Notifying Party submits that there are several competitors in the overall SSD market and not all of them are active in all three categories mentioned above. Indicatively, the biggest players are active in all three, while the Parties are only active in eSSD SATA and eSSD PCIe.

(46) Ultimately the decision to use PCIe eSSDs, SAS eSSDs or SATA eSSDs primarily depends on the performance requirements of the individual customer, and will be attenuated by their degree of price sensitivity, and their willingness to incur the cost of switching. For example, a more cost-sensitive enterprise customer might be willing to sacrifice higher speeds and reliability for a cheaper price and would therefore purchase SATA eSSDs over PCIe eSSDs (the former is cheaper and slower, relative to PCIe eSSDs).

4.2.5.3. The Commission’s assessment

(47) The results of the market investigation are not clear as to whether the market for eSSDs should be segmented by interface into (i) SATA, (ii) SAS and (iii) PCIe.39

(48) From the demand-side, the different interfaces for eSSDs were in general not considered to be substitutable. Some respondents take the view that customers show strong interface preferences in the eSSDs they buy and systems designed for a specific interface would need to be modified to switch to another interface of eSSDs. Based on this, it can be deemed that there is limited scope for substitution of eSSDs with different interfaces. Nevertheless, other respondents took the view that all eSSDs could be considered interchangeable with respect to the fact that they perform the same general function. However, they recognized that differences in performance based on interface exist (e.g., for example PCIe is faster than SATA). The possibilities for substitution depend on the specific server or storage device that requires eSSDs, as there is a need to have matching interface connectors on the motherboards of such systems in order for them to match with the specification of the eSSD.40

4.2.5.4. From the supply-side, the replies of the respondents were mixed as regards the ability of a supplier to switch manufacturing and supplying between the different interfaces for eSSDs rapidly and without incurring significant investment. In particular, the responses to the market investigation indicate that if a supplier has developed eSSDs with different interfaces, switching between manufacturing one interface eSSD and another generally does not require significant effort or expense as different interface SSDs are easy to develop. This is because the components used for eSSDs are common across interfaces. In particular, the NAND flash memory chip component is common and once the supply of NAND is secured, the other components in an eSSD such as controllers and firmware are available from third parties or can be designed and manufactured in-house.41 Conclusion on product market definition

(49) For the purpose of this decision and in light of the results of the market investigation, the Commission will assess the product markets for PCIe eSSDs, SAS eSSDs or SATA eSSDs as separate markets. In any event, the market definition can be left open as the segmentation into enterprise and client SSDs does not impact the outcome of the competitive assessment of the Transaction.

4.3. Geographic market definition 4.3.1. DRAM

4.3.1.1. Previous Commission decisions

(50) In its previous decisions concerning the markets for DRAMs and flash memories, the Commission took the view that the geographic scope of all possible products markets is worldwide.42

4.3.1.2. Notifying Party’s view (51) The Notifying party has not taken a view regarding the geographic scope of the DRAM market.

4.3.1.3. The Commission’s assessment

(52) The market investigation has confirmed that the market for DRAMs and all its possible segmentations is worldwide.43

4.3.1.4. Conclusion on geographic market definition

(53) In light of the results of the market investigation, the Commission will assess the worldwidemarket for DRAM including all its possible narrower markets, i.e. the market for commodity DRAM,.and DRAM on the basis of the type of final product where it is installed into: (i) servers, (ii) PCs, (iii) mobiles, (iv) games, (v) network devices, (vi) PC peripherals and others.

4.3.2. NAND flash memory

4.3.2.1. Previous Commission decisions (54) The Commission has previously concluded that the geographic market for NAND flash memory is global in scope.44

4.3.2.2. Notifying Party’s view (55) The Notifying Party submits that the geographic market for NAND, 2D NAND and 3D NAND is worldwide in scope.45

4.3.2.3. The Commission’s assessment (56) The market investigation confirmed that the geographic market for NAND (and also 2D and 3D NAND) is worldwide in scope.46

4.3.2.4. Conclusion on geographic market definition (57) In light of the results of the market investigation, the Commission will assess the overall worldwide market for NAND, including 2D and 3D NAND.

4.3.3. Storage – segmentation based on technology (HDDs vs. SSDs), segmentation based on intended use (enterprise vs. client storage), segmentation based on interface (SATA vs. SAT vs. PCIe)

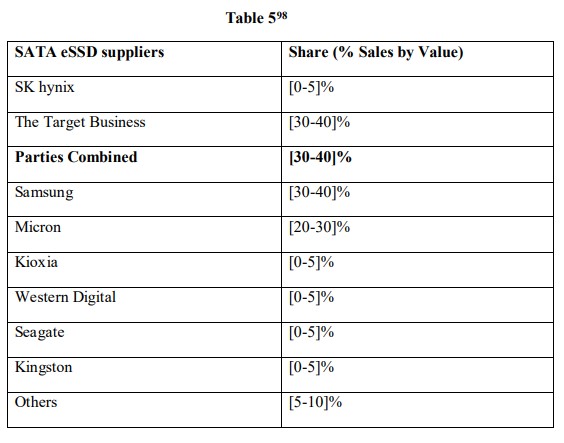

4.3.3.1. Previous Commission decisions

(58) In the Commission's previous decisions, the geographic market for SSDs (including any putative narrower markets thereunder) was considered to be worldwide in scope, because (i) transport costs do not play a significant role and amount to less than 1 % of total product cost; (ii) there are no significant barriers to trade; (iii) prices do not typically differ by region; (iv) products and product features do not differ by region; (v) manufacturers are active on a global basis (thus competitors tend to be the same regardless of the regions taken into consideration); and (vi) the market players decide their strategy on a global level.47

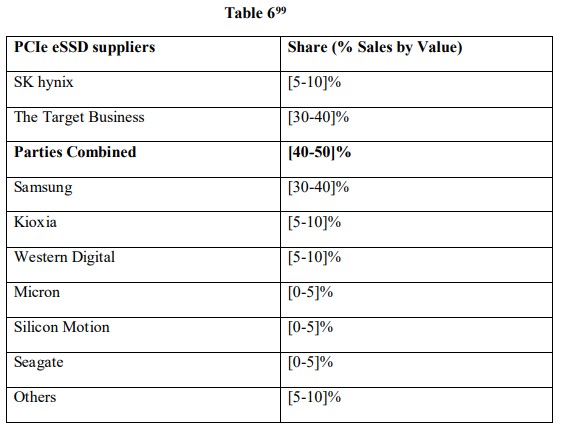

4.3.3.2. Notifying Party’s view (59) The Notifying Party agrees with the Commission’s previous decisions that the market for SSDs is worldwide.

4.3.3.3. The Commission’s assessment

(60) The market investigation confirms that the market for SSDs and all its possible segmentations is worldwide.48

4.3.3.4. Conclusion on geographic market definition

(61) In light of the results of the market investigation, the Commission will assess the worldwide market for SSDs and all its possible segmentations.

5. COMPETITIVE ASSESSMENT

5.1. Analytical framework (62) The Guidelines on the assessment of horizontal mergers (“Horizontal Merger Guidelines”)49 describe two main ways in which horizontal mergers may significantly impede effective competition, in particular by creating or strengthening a dominant position: (i) by eliminating important competitive constraints on one or more firms, which consequently would have increased market power, without resorting to coordinated behaviour (non-coordinated effects); and (ii) by changing the nature of competition in such a way that firms that previously were not coordinating their behaviour, are significantly more likely to coordinate and raise prices or otherwise harm effective competition (coordinated effects50) as a result of the proposed concentration.

(63) A merger giving rise to horizontal non-coordinated effects might significantly impede effective competition by creating or strengthening the dominant position of a single firm, one which, typically, would have an appreciably larger market share than the next competitor post-merger. Moreover, also mergers that do not lead to the creation of or the strengthening of a single firm’s dominant position may create competition concerns under the substantive test set out in Article 2(2) and Article 2(3) of the Merger Regulation. Regarding mergers in oligopolistic markets, the Merger Regulation clarifies that “under certain circumstances, concentrations involving the elimination of important competitive constraints that the merging parties exerted upon each other, as well as a reduction of competitive pressure on the remaining competitors, may, even in the absence of a likelihood of coordination between the members of the oligopoly, result in a significant impediment to effective competition”.51

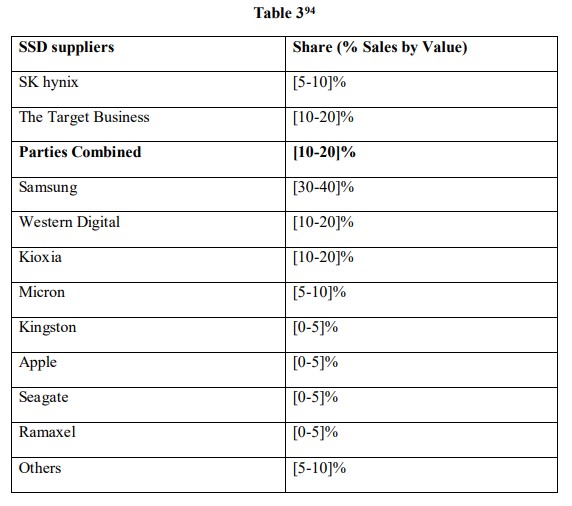

(64) The Horizontal Merger Guidelines list a number of factors which may influence whether or not significant horizontal non-coordinated effects are likely to result from a merger, such as the large market shares of the merging firms, the fact that the merging firms are close competitors, the limited possibilities for customers to switch suppliers, or the fact that the merger would eliminate an important competitive force. Not all those factors need to be present to make significant non-coordinated effects likely and it is not an exhaustive list.52

(65) Further, in some markets, a merger may give rise to coordinated effects where the structure is such that firms would consider it possible, economically rational, and hence preferable, to adopt on a sustainable basis a course of action on the market aimed at selling at increased prices.53 According to the Horizontal Merger Guidelines, coordination is more likely where it is relatively simple to reach a common understanding on the terms of coordination. Moreover, three conditions need to be met for coordination to be sustainable: (i) the coordinating firms must be able to monitor to a sufficient degree whether the terms of the coordination are being adhered to; (ii) there must be some form of credible deterrent mechanism that can be activated if deviation is detected; and (iii) the reactions of outsiders as well as customers should not be able to jeopardise the results expected from the coordination.54

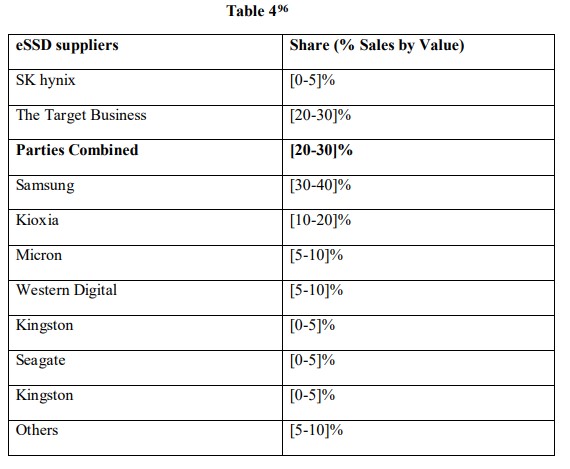

(66) Next to horizontal effects, the Guidelines on the assessment of non-horizontal mergers (“Non-Horizontal Merger Guidelines”) sets out that there are also two broad types of non-horizontal mergers that can be distinguished: vertical mergers and conglomerate mergers.55

(67) Vertical mergers involve companies at different levels of the supply chain. According to the Non-Horizontal Merger Guidelines, non-coordinated effects may significantly impede effective competition as a result of a vertical merger if such merger gives rise to foreclosure. Foreclosure occurs where actual or potential rivals’ access to supplies or markets is hampered or eliminated as a result of the merger, thereby reducing these companies’ ability and/or incentive to compete.56 Such foreclosure may discourage entry or expansion of rivals or encourage their exit.57 There are two forms of foreclosure: input foreclosure occurs where the merger is likely to raise the costs of downstream rivals by restricting their access to an important input, and customer foreclosure occurs where the merger is likely to foreclose upstream rivals by restricting their access to a sufficient customer base.58 A vertical merger could also lead to other non-coordinated effects, for instance where the merged entity may, by vertically integrating, gain access to commercially sensitive information regarding the upstream or downstream activities of rivals.59 Finally, a vertical merger may also give rise to coordinated effects.

(68) Lastly, the Non-Horizontal Merger Guidelines focus, besides vertical mergers, on conglomerate mergers consisting of mergers between companies that are active in closely related markets, for instance suppliers of complementary products or of products which belong to a range of products that are generally purchased by the same set of customers for the same end use.60

(69) In the majority of circumstances, conglomerate mergers do not lead to any competition concerns but in certain specific cases there may be harm to competition.61 The main concern in the context of conglomerate effects is that of foreclosure.62 Conglomerate mergers may allow the merged entity to combine products in related markets and this may confer on the merged entity the ability and incentive to leverage a strong market position from one market to another by means of tying or bundling, or other exclusionary practices.63

(70) In assessing the likelihood of conglomerate effects, the Commission examines, first, whether the merged entity would have the ability to foreclose its rivals, second, whether it would have the economic incentive to do so and, third, whether a foreclosure strategy would have a significant detrimental effect on competition, thus causing harm to consumers. In practice, these factors are often examined together as they are closely intertwined.64

5.2. Horizontal non-coordinated effects (71) The Commission has investigated and assessed whether the Transaction is likely to give rise to a significant impediment to effective competition as a result of non- coordinated effects in the markets for (i) 3D NAND65 and (ii) SSDs and the possible narrower markets therein

5.2.1. NAND

5.2.1.1. Notifying Party’s view (72) The Notifying Party takes the view that within NAND, the Parties' activities overlap only in 3D NAND.66 The Parties provided a competitive assessment under all relevant NAND segmentations to show that the proposed Transaction will not raise horizontal concerns under any such segmentations.

(73) The Parties combined market share in the NAND martet (approximately [20-30] %) would still be smaller than Samsung’s market share and it would be very closely followed by the third competitor, Kioxia.

(74) The Notifying Party submits that the Parties are not close competitors. They serve to a great extent different customers/applications in the NAND segment. More specifically, [60-70] % of SK hynix's NAND revenues are derived from NAND flash memory mobile phone applications, an area where the Target Business is not active.[…].67

(75) According to the Notifying Party, the Parties face a number of strong, well-resourced competitors and new entries are occurring as indicated above in paragraph (75) above. Chinese competitor YMTC is in the process of implementing significant expansion plans and is expected to account for about [5-10] % of global NAND flash memory output in 2021, and expand further beyond that to become a leading player in NAND.68

(76) Moreover, the Notifying Party submits that there is significant and constant innovation in NAND flash memory. In order to remain competitive, NAND flash memory vendors must continue to innovate and scale the number of stacks.69

(77) The Notifying Party submits that Parties and their competitors have different costs structures, different technological capabilities in terms of increasing the number of layers and number of bits per cell, different production capacities. . At the same time, each of the Parties' rivals have ample financial resources and R&D capabilities to be able to exert significant competitive pressure on the Parties and will continue to do so post-Transaction.70

5.2.1.2. The Commission’s assessment

(78) For the purposes of this decision, the Commission will assess the overall market for NAND including the markets for 2D NAND and 3D NAND. The Commission’s market investigation results also concern the overall NAND market and the 3D NAND market. The Target Business is no longer active in 2D NAND, while the Parties' combined position in 3D NAND is very similar to their combined position in the overall NAND segment. (i) Market shares for the global NAND market

(79) The Parties and their main competitors’ market shares in the global NAND market for 2019 are as follows:

(80) The Target Business is the sixth player and holds a single digit share ([5-10] %) on the overall NAND market. SK hynix is the fifth player with a share of [10-20] %. Aside from the Parties, there are at least four other NAND suppliers active on a global basis whose NAND sales are larger than those of the Parties, namely Samsung ([30-40] %), Kioxia ([10-20] %), Western Digital ([10-20] %) and Micron ([10-20] %). In addition, there is a number of well-resourced smaller players, as well as a new entry, while competitors are expanding capacity.72

(81) Samsung will remain the leader in this market, with a approximate [30-40] % share that is almost double the Parties' combined share. Kioxia (approximately [10-20] %), Western Digital (approximately [10-20] %), Micron (approximately [10-20] %) are also major players fiercely competing in this segment. In all, there will be five suppliers with double-digit shares post-Transaction.73

(i) Market shares for the global 3D NAND market

(82) The Parties and their main competitors’ market shares in the global 3D NAND market for 2019 are as follows:

(83) Post-merger Samsung will continue to be the undisputed leader with an approximate [30-40] % share, followed by the merged entity (approximately [20-30] %), Kioxia (approximately [10-20] %), Micron (approximately [10-20] %) and Western Digital (approximately [10-20] %), all strong competitors with double-digit shares. YMTC has started making its way in this market with significant technological achievements and capacity expansion plans.

(ii) Supply for NAND

(84) Customers usually have a variety of options when choosing a supplier. The results of the market investigation indicate that suppliers of NAND sell their products through requests for quotations and long-term agreements with their customers.75 Respondents to the market investigation described purchasing NAND either on the basis of long term agreements or on the basis of individual orders. In the latter case, this is done after collecting quotations from various suppliers .76 Pricing tends to be reasonably similar between suppliers and independent market consultant reports can be used to evaluate whether pricing is competitive.77 This means that suppliers need to maintain a competitive portfolio, both in terms of price and quality, to effectively compete in the market.

(85) Post-transaction, there will continue to be several players in the market, maintaining a high level of competition. Consistent with the Parties and their main competitors’ market shares, respondents to the market investigation identified Western Digital, Samsung and Kioxia as top NAND suppliers.78 They also confirm that the level of competition in the market for 3D NAND is high, and the market is intensely competitive. As a result, at least six entities currently develop and manufacture NAND, including Samsung, SK hynix, Micron, Intel, Kioxia, Western Digital, and YMTC. These companies invest in R&D and manufacturing process technologies. 79

(86) Although the Parties are significant 3D NAND players, as they both provide 3D NAND, which (in contrast to 2D NAND) accounts for the majority of NAND product offerings in today’s market,80 they compete closely with Samsung, Kioxia, Western Digital andMicron. This was confirmed by the respondents to the market investigation. The Parties and the aforementioned players are globally competing, covering all major applications for NAND flash memory, such as smartphone/cSSDs/ eSSDs/ others. These players are active in all the markets where the Parties are active. YMTC, for its part, is active primarily in Chinese market at this moment.81

(87) From the supply-side, suppliers experience pressure from (potential) new market entrants in the supply of 3D NAND.Moreover, as a result of the existing players and potential new entrants, the supply of 3D NAND is readily available. When the supply of 3D NAND is readily available, there is a constraint imposed on suppliers which results in a reduction in pricing. YMTC, for example, is a new entrant in the supply of 3D NAND, its entry will increase the level of supply in the market and thus lead to a reduction in pricing. Additionally, suppliers also experience pressure from the fact that customers multisource, as indicated below. 82

(iii) Demand for NAND

(88) From the demand-side, the Transaction is not likely to provide the Parties with exclusive customers. It is common for customers to source from various suppliers which means that switching suppliers would not be difficult. Respondents to the market investigation confirm that it is easy for a customer to switch between suppliers of 3D NAND83 as customers usually multisource the product from different suppliers and therefore, do not depend on a single supplier.84 For this reason, they are also able to easily increase or decrease the amount of their purchases from a given supplier.85

(89) However, customers would not have the ability to credibly threaten producers of 3D NAND by starting to source their needs for 3D NAND in-house as the capital expenditure required to produce their own NAND is cost-prohibitive for customers. Production requires dedicated manufacturing fabs and decades of knowledge to maintain the pace on lithography transitions.86

(iv) Innovation and financial capacity in the NAND market

(90) The ability of a supplier of 3D NAND to innovate also plays a significant role in remaining competitive on the market for 3D NAND. 3D NAND is quantified by the number of layers stacked in a device. As more layers are added, the bit density increases. Generally, suppliers are scaling 3D NAND roughly one technology generation every year. It is crucial for each player to quickly introduce advanced technologies to gain (or retain) competitiveness. 87

(91) The market investigation results indicate that suppliers or potential suppliers of 3D NAND have a financial strength comparable to that of SK hynix and the Target Business. In particular, respondents to the market investigation take the view that all the competitors are generally of equal size to SK Hynix and the Target Business and make similar CAPEX investment. The exception to this is Samsung, which is larger and its CAPEX greater than that of other competitors.88 As a result, the Parties do not appear to have a particular advantage in terms of financial capacity.

(92) The Transaction is viewed by the market players as a transaction that will increase the competition in the market.89 Moreover, market participants take the view that the Transaction will improve competition as well as the quality and the range offering of products.90 In fact, according to market participants, the transaction will create a “memory house” able to compete with Samsung. (v) Competition in the NAND market

(93) While the market investigation results point to an increased market share of the merged entity in 3D NAND post-Transaction, and while the Transaction will lead to a reduction in the number of large suppliers of 3D NAND from seven to six, this does not raise competition concerns for the majority of the respondents. The merged entity will continue to face significant competitive constraints from the remaining players, such that the increase in the merged entity’s market share will not lead to the acquisition of market power.91

Conclusion

(94) In light of the above, and in particular in view of the moderate combined market share of the Parties as well as the important number of competitors of varying size that will remain active post-merger, the Commission considers that the Transaction does not give rise to serious doubts as to its compatibility with the internal market with respect to the possible markets for NAND.

5.2.2. SSD

(95) The Parties are both active in SSDs, including eSSDs and cSSDs. SK hynix has historically focused on cSSDs, whereas the Target Business has focused on eSSDs. (96) Within enterprise SSDs, the Parties’ activities only overlap in SSDs with PCIe and SATA interfaces. Neither party sells SAS SSDs. Intel […] does not itself compete in SAS SSDs.

5.2.2.1. Notifying Party’s view

(97) According to the Notifying Party, the market for SSDs is highly competitive. Samsung is by far the largest player. Western Digital, Kioxia, Micron and Kingston are also major SSD competitors, while YMTC's entry/expansion92 will introduce another major competitor. Other emerging players include Seagate (a leading HDD manufacturer) and Ramaxel. SK hynix is the sixth biggest player with a market share of approximately [5-10] %, with only one percentage point separating it from the seventh player, Kingston. Post-Transaction, the merged entity would have a market share of approximately [20-30] % ([10-20 % according to Forward Insights; [20-30] % according to Omdia).

(98) The Notifying Party submits that the Parties are not close competitors in SSD. The Target Business primarily focuses on enterprise SSD. Enterprise SSD represents approximately […] % of the Target Business' total 2019 SSD revenues. Conversely, SK hynix focuses more on client SSD. Client SSD represents approximately […] % of SK hynix's total 2019 SSD revenues. Within the enterprise segment, the Parties have differentiated offerings, with the Target Business addressing the requirements of both OEMs and cloud customers, while SK hynix is focused predominantly on cloud customers, with most of its revenues coming from a single customer to which it sells a customized offering ([…]).

(99) The Notifying Party notes that the SSD market is highly competitive not only because of the existence of several competitors but also due to its quality as a dynamic market, in which innovation plays an important part.

(100) In light of the above, the Notifying Party takes the view that the proposed Transaction would not give rise to any anti-competitive concerns in the overall market for SSDs. The Notifying Party further submits that the same conclusion would apply to possible segmentations of the SSD market.

(A) Enterprise SSDs

(101) The Notifying Party submits that if the proposed Transaction was assessed under the narrower enterprise SSDs and client SSDs segments, it would likewise not be problematic.

(102) The proposed Transaction will not change the competitive landscape in the enterprise SSD space. SK hynix is only the sixth player in enterprise SSDs, with a market share by revenue of approximately [0-5] %, and approximately […] % of SK hynix's enterprise SSDs sales are derived from […].

(103) Post-transaction, Samsung will remain the leader with a share of approximately [30-40] % followed by the merged entity with a share of approximately [20-30] % (and a share increment of approximately [0-5] % %). The Parties' major competitors in the enterprise SSDs segment include, besides Samsung, Kioxia, Micron, Western Digital and Seagate. Kioxia (approximately [10-20] %), Micron (approximately [5-10] %) and Western Digital (approximately [5-10] %) are approximately three to four times larger than SK hynix, while Seagate (approximately [0-5] %) has a comparable position to SK hynix.

(104) According to the Notifying Party, yperscale customers have developed and produced their own enterprise SSDs for in-house use in their data centers. Huawei, Google and Amazon also manufacture their own enterprise SSDs. Customers that already produce their own enterprise SSDs can threaten to shift more of their enterprise SSD consumption to their own internal production, and customers that do not already produce their own enterprise SSDs can threaten to do so. Enterprise SSD segmentation by interface

(105) According to the Notifying party, even assuming the enterprise SSD segment were to be further divided by interface, no competition concerns would arise in the resulting subsegments.

(B) SAS Enterprise SSDs

(106) The Notifying Party submits that neither Party sells SAS enterprise SSDs ("SAS eSSDs").

SATA Enterprise SSDs

(107) According to the Notifying Party, as regards SATA enterprise SSDs ("SATA eSSDs"), the merged entity would have a combined market share of approximately [30-40] %. SK hynix has a market share of approximately [0-5] %, thus the proposed Transaction would result in a de minimis market share increment. […].

(108) The Notifying Party submits that the Target Business’s market share has lost [10-20] percentage points between 2015 and 2019 (from approximately [40-50] % in 2015 to approximately [30-40] % in 2019) and its sales have also declined significantly in absolute terms from USD […] in 2017 to USD […] in 2019 given its focus on PCIe. In view of the fact that in recent years PCIe SSDs have been increasingly outperforming and replacing SATA SSDs for enterprise applications, […]. Samsung (approximately [30-40] %) would have a comparable position to the merged entity, followed by Micron (approximately [20-30] %). Further, a number of smaller competitors including, Kioxia (approximately [0-5] %), Western Digital (approximately [0-5] %) and others will continue to compete in this market.

(C) PCIe Enterprise SSDs

(109) In the possible market for PCIe enterprise SSDs ("PCIe eSSDs"), the Parties’ combined market share is approximately [40-50] % (Target Business approximately [30-40] % and SK Hynix approximately [5-10] %). Western Digital (approximately [5-10] %)93 and Kioxia (approximately [510] %) have comparable positions to SK hynix, while Micron (approximately [0-5] %) is rapidly catching up (between 2017 and 2019 Micron more than doubled its share). The factors discussed above illustrating the highly competitive nature of the overall segment for enterprise SSDs likewise apply in the narrower markets of SATA eSSDs and PCIe eSSDs.

(110) The Notifying Party submits that the proposed Transaction will not result in any competition concerns in the areas of enterprise SSDs. In the overall enterprise SSD market, SK hynix is the sixth player with a revenue share of approximately [0-5] %, and behind Samsung, Kioxia, Micron, Western Digital, as well as the Target Business, and only half a percentage point ahead of Seagate. Cloud customers, in particular, exercise significant negotiating leverage due to the large size of their purchases and demonstrated ability to manufacture their own SSDs.

(111) The Notifying Party submits that this conclusion would be similar on an SSD interface basis. The Parties are not active in SAS, and SK hynix only has a market share of approximately [0-5] % in SATA. In PCIe, […] % of SK hynix's 2019 global PCIe eSSD sales were to […].

(D) Client SSDs (112) The Notifying Party considers that the segment for client SSDs is highly competitive. Numerous companies compete in the client SSD segment, in which the Parties' combined share is approximately [10-20] %. Samsung will continue to be the leading supplier with a market share of approximately [30-40] %, while Western Digital (approximately [10-20] %), Kioxia (approximately [10-20] %), Kingston (approximately [5-10] %) and Micron (approximately [5-10] %) are all strong and well- established global players, who will exert competitive pressure on the merged entity.

(113) First, a number of emerging and expanding players, including Seagate and Ramaxel, also participate in the segment. Seagate's history as a major hard drive manufacturer gives it an edge as it expands its SSD business, as it has established relationships with OEMs, which are the major purchasers of client SSDs.

(114) Second, YMTC's entry announced in 2020, provides additional evidence of the highly competitive nature of this segment. Industry analysts suggest that YMTC’s recently released products appear to have comparable performance to Samsung's client SSDs.

(115) Third, some potential large clients are currently covering their demand for client SSDs in-house. For example, Apple captures approximately [0-5] % of the total demand.

5.2.2.2. The Commission’s assessment (116) The market investigation confirmed the Notifying Party’s claims.. Even though the Parties are considered significant market players in the SSD market, the Commission considers that the Transaction is not likely to give rise to anti-competitive effects for the reasons mentioned below.

(i) Market shares for the global SSD market

(117) The Parties’ and their main competitors’ market shares in the global SSD market for 2019 are as follows:

(118) Post-transaction Samsung will remain the leading SSD supplier, with a share of approximately [30-40] %, far exceeding the combined share of the merged entity. Western Digital (approximately [10-20] %), Kioxia (approximately [10-20] %), Micron (approximately [5-10] %) are also suppliers in SSDs with shares above 5 %, and a number of smaller competitors such as Kingston ([0-5] %), Seagate ([0-5] %) and Ramaxel ([0-5] %) have also gained share in recent years. Kingston has increased sales significantly in 2019, capturing now approximately [0-5] % of the SSD supply. Seagate is a new entrant in the SSD market but a leading manufacturer of HDD.95

(i) Market shares for the global Enterprise SSD (eSSD) market

(119) The Parties’ and their main competitors’ market shares in the global eSSD market for 2019 are as follows:

(120) Post-transaction, Samsung will remain the leader with a share of approximately [30-40] % followed by the merged entity with a share of approximately [20-30] % (and a share increment of approximately [0-5] %). The Parties' major competitors in the enterprise SSDs segment include, besides Samsung, Kioxia, Micron, Western Digital, Kingston and Seagate. Kioxia (approximately [10-20] %), Micron (approximately [5-10] %) and Western Digital (approximately [5-10] %) are approximately three to four times larger than SK hynix, while Seagate (approximately [0-5] %) has a comparable position to SK hynix. It is noteworthy that SK hynix relies on […] for most of its sales.97 (i) Market shares for the global SATA eSSD market.

(121) The Parties’ and their main competitors’ market shares in the global SATA eSSD market for 2019 are as follows:

(122) Samsung (approximately [30-40] %) would have a comparable position to the merged entity, followed by Micron (approximately [20-30] %). Further, a number of smaller competitors including, Kioxia (approximately [0-5] %), Western Digital (approximately [0-5] %) and others will continue to compete in this subsegment.

(123) The Target Business has lost [10-20] percentage points in share between 2015 and 2019 (from approximately [40-50] % in 2015 to approximately [30-40] % in 2019) and its sales have also declined significantly in absolute terms from USD […] in 2017 to USD […] in 2019 given its focus on PCIe (as described below). In view of the fact that in recent years PCIe SSDs have been increasingly outperforming and replacing SATA SSDs for enterprise applications, […]. (i)Market shares for the global PCIe eSSD market

(124) The Parties’ and their main competitors’ market shares in the global PCIe eSSD market for 2019 are as follows:

(125) Samsung will be the largest competitor after the merged entity (approximately [30-40] %). Western Digital (approximately [5-10] %) and Kioxia (approximately [5-10] %) have comparable positions to SK hynix, while Micron (approximately [0-5] %) is rapidly catching up (between 2017 and 2019 Micron more than doubled its share).

(126) Despite the Parties’ combined market shares in the PCIe eSSD market, in light of the assessment below and in particular of the indications provided by the results of the market investigation that a sufficient number of alternative suppliers will remain active in PCIe eSSDs, the Commission considers that the Transaction does not give rise to serious doubts as to its compatibility with the internal market with respect to the possible market for PCIe eSSDs. (i) Market shares for the global Client SSD (cSSD) market

(127) The Parties’ and their main competitors’ market shares in the global cSSD market for 2019 are as follows:

(128) Post-transaction the merged entity will have a share of approximately [10-20] %, which means that the market for cSSDs is not affected. Samsung will continue to be the leading supplier with an approximately [30-40] % share, while Western Digital (approximately [10-20] %), Kioxia (approximately [10-20] %), Kingston (approximately [5-10] %) and Micron (approximately [5-10] %) are all strong and well- established global players, who will exert competitive pressure on the merged entity. Assessment on the global market for SSDs

(129) The Commission’s assessment applies to the global SSD market as well as all its potential narrower markets. (130) As regards the global SSD market, according to the Horizontal Merger Guidelines, in a concentration where the market share of the undertakings concerned is low, the concentration is presumed to be compatible with the internal market. An indication to this effect exists, in particular, when the market share of the undertakings does not

100 Form CO, para. 6.145. exceed 25 % either in the common market or in a substantial part of it, the concentration.101 The above apply to the global SSD market, where the combined market share of the undertakings concerned is ([10-20] %). First, the market investigation results show that the overall SSD market is highly competitive. According to the majority of respondents, competition is equally high for the eSSDs market further divided into the SATA eSSDs and PCIe eSSDs markets.102 The market for cSSDs is not considered to be an affected market since the Parties’ combined market share is less than 20 %.

(131) The high level of competition is reflected by the existence of other players that compete closely with the Parties in terms of product portfolio similarity, performance, quality and price in the overall market for SSDs and its potential narrower markets (SATA eSSDs, PCIe eSSDs).103 Samsung will remain the leading SSD supplier, with several other players in the market (i.e. Western Digital, Kioxia, Micron) that are also established suppliers in SSD occupying considerable market shares. The only market in which Samsung will be the second biggest player, is the market for PCIe eSSDs. A number of smaller competitors such as Kingston, Silicon Motion, Seagate and Ramaxel have also gained share in recent years. In addition, YMTC's recent entry provides additional evidence of the existence of significant competitive constraints in the SSD segment.

(ii) Demand for SSDs

(132) Second, from the demand-side, the market investigation participants take the view that it is easy for a customer to switch between suppliers of SSDs, cSSDs and eSSD (including the markets for SATA eSSDs, PCIe eSSDs). Customers typically multi- source and compare the price offered by each supplier.104 Customers are also able to easily increase or decrease the amount of their purchases for the above products from a given supplier.105

(133) In addition to multi-sourcing, vertical integration is not something that can affect demand in the SSD market. In-house sourcing of SSDs is possible for customers as SSDs can be produced even by suppliers that do not make their own NAND, since they can procure NAND separately from existing suppliers on the market.106 For the eSSD segment in particular, Google, Amazon and Huawei manufacture their own eeSSDs. Microsoft is already developing eeSSDs by procuring NAND and working with ODMs (e.g., Quanta, Wistron), to develop solutions for its own data centres. The ability of customers to successfully produce their own eSSDs gives them leverage in negotiating with eeSSD suppliers. This means that customers may resort in producing their own eSSDs if that proves to be more cost-efficient than procuring it from suppliers. As the vertical integration continues, they are also less likely to depend on suppliers in the future.. (iii) Supply for SSDs

(134) Third, from the supply-side, the market investigation indicated that current suppliers experience pressure from (potential) new market entrants in the markets of SSDs and in the markets of all its possible markets.107 Suppliers sell in a variety of different ways, including responding to requests for quotations, long-term agreements and sales through distributors and retailers.108 The ability to innovate plays an important role for the suppliers who want to remain competitive in the market for SSDs, including all its potential segmentations. The respondents to the market investigation confirm that the SSD market is dynamic and characterized by significant leapfrog innovation. Competitors seek to differentiate their offerings through the development and release of new products and technologies in this space. This rapid pace of technological innovation in SSDs is driving significant growth in demand, which incentivizes all competitors to compete aggressively to capture a larger share of the growing market. It is, therefore, important for suppliers to keep up with the most recent changes in interface and performance. Competition in the SSD market is further intensified by the fact that, similarly to NAND, SSD is a rapidly growing market.109

(135) Fourth, contracts in the market for SSDs and of all its sub-markets are typically negotiated bilaterally. Suppliers usually provide a production description and sample products to the customer. Following customer product qualification, the supplier and the customer will extensively negotiate the supply agreement. Enterprise SSD customers typically qualify more than one supplier and multi-source not only for security of supply purposes but also to obtain a stronger bargaining leverage.110 (iv) Competition in the SSD market

(136) Furthermore, the increased market power of the merged entity is unlikely to lead to competition concerns. First, the Parties will still have to live up to the pace of a very dynamic market. The new requirements, as well as the new entrants that appear in the market, will result in the market maintaining its competitiveness. Second, Samsung will still hold the largest market share and will continue to be the market leader. The transaction will create a strong competitor with a portfolio consisting of different types of memory that will be able to challenge Samsung and thus, increase competition in the market. Samsung is a powerful “memory house” able to supply different types of memory to different customers and the merged entity is expected to be able to do the same post-Transaction.

(137) In sum, the market investigation results confirm that the increase in market share brought about by the Transaction will not lead to competition concerns. The increase of the merged entity’s market share will be outweighed by the fact that the SSD market is highly dynamic, with the Parties facing significant competitive constraints from established suppliers. In addition, post-Transaction, the merged entity will remain smaller than Samsung, the market leader. Certain market participants even took the view that the acquisition of Intel’s SSD business by SK hynix will enable the merger entity to better compete with Samsung. This is because the Parties will form another supplier with both SSD and DRAM offerings, improving the overall competition in the market. becoming a viable competitor to an otherwise dominant player, Samsung.111

Conclusion

(138) In light of the above, and in particular in view of the moderate combined market share of the Parties as well as the important number of competitors of varying size that will remain active post-merger, the Commission considers that the Transaction does not give rise to serious doubts as to its compatibility with the internal market with respect to the possible markets for SSDs and all possible narrower markets.

5.3. Horizontal coordinated effects

(139) The Commission has investigated and assessed whether the Transaction is likely to give rise to a significant impediment to effective competition as a result of coordinated effects in the markets for (i) 3D NAND112 and (ii) SSDs and the possible narrower markets therein.

5.3.1. The Notifying Party’s view

(140) The Notifying Party submits that there is no plausible basis to conclude that the Transaction could lead to a significant impediment of effective competition stemming from coordinated effects.113

5.3.1.1. Ability to reach terms of coordination

(A) NAND/3D NAND

(141) First, the Notifying Party explains that the Transaction does not lead to a material increase in concentration as the NAND/3D NAND market is already fragmented, SK hynix and the Target Business are only number 5 and 6 players, and their combined market share is very limited both in NAND and 3D NAND.

(142) Second, NAND/3D NAND is a highly competitive segment under rapid growth where demand and supply conditions cannot be characterized as leading to a stable economic environment. Flash memory storage has become a key component in smartphones and, as a result, NAND/3D NAND demand has grown - and continues to grow - rapidly, driven by the growth in the use of smartphones and of their average capacity. Other consumer products, such as tablets and cameras, along with industrial equipment and sensors, automotive systems and medical devices, also rely upon flash memory. Industry NAND/3D NAND supply has continued to grow alongside this rapidly expanding demand and is projected to continue to do so.

(143) Third, market conditions in NAND/3D NAND are not stable. Capacity and production are expanding rapidly to keep up with increased demand, while cost and prices are falling. The Notifying Party considers that the rapidly increasing demand means that it is unlikely for NAND/3D NAND competitors to reach a common understanding on the terms of a potential coordination.

(144) Fourth, the Notifying Party submits that asymmetric positions and diverging priorities will remain post-transaction. Samsung will remain the largest supplier with a market share (approx. [30-40] % in NAND and [30-40] % in 3D NAND) significantly higher than the remaining players. Kioxia (approximately [10-20] % in both NAND and 3D NAND), Western Digital (approximately [10-20] % in both NAND and 3D NAND) and Micron (approximately [10-20] % in NAND and in [10-20] % 3D NAND) are also major suppliers and their market shares have fluctuated over time, reflecting the fierce competition between all players.

(145) Fifth, the Notifying Party observes that there are recent entry and expansion efforts in NAND/3D NAND, in particular by YMTC, which is being reported to be increasing its capacity.

(146) Sixth, the Notifying Party explains that NAND (and 3D NAND in particular) is a technologically evolving hi-tech component making coordination difficult and thus highly unlikely. NAND differentiation results from continuous R&D, which is tied to capacity, cost, layer count and bit density. These factors affect the 3D NAND performance, durability, reliability and price. (147) Last, the Notifying Party notes that sales of NAND/3D NAND are lumpy with suppliers typically concluding framework sales contracts with customers. Customers then make purchase undertakings, where volumes and prices are negotiated within such framework sales contracts. Opportunities for NAND/3D NAND suppliers to compete for sales contracts are relatively infrequent, while purchase undertakings are typically large, which makes coordination unlikely.

(B) SSD

(148) First, the Notifying Party considers that, in light of the number of players and the position of SK hynix in SSD114 and the possible markets thereof, the Transaction does not lead to a material increase in concentration.

(149) Second, the Notifying Party submits that SSD is complex and highly competitive with rapid growth where demand and supply conditions cannot be characterized as stable. Demand for enterprise SSD in recent years has been driven by expansion of data center servers in an increasingly connected cloud environment. New and/or improved enterprise SSD products tend to be released in a cycle of approximately 18 months.

(150) Third, the Notifying Party observes that, post-Transaction there will remain many strong competitors with asymmetric and fluctuating shares, different costs and capacity, and diverging priorities. In addition, smaller but vigorous competitors and dynamic new entrants contribute to share asymmetry.

(151) Fourth, the Notifying Party considers that the asymmetric nature of upstream and downstream vertical integration in the SSD industry results in different production costs and would make a hypothetical coordination even more difficult. SSD suppliers have adopted different make/buy strategies regarding the key SSD components, i.e, NAND, controllers and firmware, including in-house production, outsourcing, or a combination of the two.

(152) Fifth, the Notifying Party notes that SSDs are a heterogeneous product and differ in terms of characteristics such as performance, endurance and reliability and, to a lesser extent, other features (such as power consumption). SSDs are customized to meet customer specific performance and endurance requirements and undergo customer qualification processes to ensure they meet the specifications of the customer's system or device.

(153) Sixth, the Notifying Party submits that constant innovation in SSD would undermine coordination as competitors constantly attempt to differentiate their offerings through the development and release of new products and technologies in this space.

(154) Last, the Notifying Party observes that sales of SSDs are lumpy with suppliers typically concluding framework sales contracts with customers. Customers then make purchase undertakings, where volumes and prices are negotiated within such framework sales contracts. Opportunities for SSDs suppliers to compete for sales contracts are relatively infrequent, while purchase undertakings are typically large, which makes coordination unlikely.

5.3.1.2. Sustainability of coordination (A) Ability to monitor deviations (155) The Notifying Party submits that for both NAND/3D NAND and SSDs the market is not transparent. The supply contracts in NAND and SSD are typically based on non- transparent, confidential bilateral negotiations between customers and suppliers. As a result, NAND and SSD prices and other commercial terms are highly opaque. There is no public price reporting on individual contracts. Market intelligence firms report only on historic aggregated data that they receive by each supplier, and they also have no way of verifying the accuracy of each supplier's transmitted data.

(156) Monitoring (and enforcing) a hypothetical agreement to slow down on NAND and SSD R&D/innovations (e.g., delaying the introduction of 100+ layer NAND) would be equally difficult, as there is no transparency whatsoever regarding R&D activities of competitors, and suppliers can only detect deviations with a delay (i.e., when a "cheating" supplier launches a new product). It would take time for other suppliers to catch up and punish the "cheater", while at the same they would be incurring significant losses from falling behind technologically vis-à-vis the cheater

(B) Ability to establish a credible deterrent mechanism

(157) The Notifying Party submits that the lack of market transparency in NAND and SSD would not allow for a credible deterrent mechanism to be established. In addition to prices being opaque, customers can create strong incentives for aggressive price competition. In order to remain competitive, NAND suppliers must continue to innovate and scale the number of stacks - generally suppliers are scaling 3D NAND roughly by one technology generation every year. In view of the short technological cycle of the NAND and SSD products, the gains from deviation from a hypothetical coordination would be significant due to the expected profits made with next generation products. (C) Reaction of outsiders

(158) The Notifying Party considers that the presence of a significant number of competitors with asymmetric and fluctuating capacity and market positions makes coordination very difficult. Both markets are also characterized by new entry and expansion, which would destabilize any coordination attempt. Customers can create strong incentives for aggressive price competition while, in particular with regard to eSSDs, hyperscale customers have developed and produced their own enterprise SSDs for in-house use in their data centres, which gives them an important leverage not only in negotiating with enterprise SSD suppliers but also in neutralizing any coordination attempt.

5.3.1.3. SK hynix’s shareholding in Kioxia (159) The Notifying Party submits that SK hynix' existing passive interest in Kioxia has no impact on the risk of potential coordinated effects from the Transaction. (160) First, the Notifying Party notes that this interest exists pre-merger and the Transaction does not modify the competitive dynamics in the NAND and SSD markets. The Transaction does not lead to any material increase in concentration; it brings together two companies with largely complementary product portfolios, overlapping only in a few markets where they are not close competitors and with moderate combined market shares. There is no indication of past coordination or softened competition in NAND or SSD

(161) Second, to the extent that structural links may increase the risk of coordinated effects, the Notifying Party argues that this is typically the case where they involve or lead to the exchange of confidential or competitively sensitive information. SK hynix' interest in Kioxia […]. Therefore, this link does not in any way increase the level of transparency in the industry. The Transaction does not in any way change this reality.

5.3.2. The Commission’s assessment

(162) The Commission considers that the Transaction will not create conditions that will enable or sustain coordination.

5.3.2.1. Ability to reach terms of coordination

(163) The Commission considers that suppliers of NAND and SSD will not be able to reach terms of coordination as a result of the Transaction.

(A) NAND

(164) Overall, the market investigation confirmed that the risk of coordination will remain low post-Transaction.115 NAND/3D NAND is expected to remain competitive because there will remain six suppliers competing for business. Currently NAND suppliers do not coordinate their behaviour and the continued strength of competition between suppliers post-Transaction means that the Transaction will not in any way impact this lack of coordination.116

(165) The Commission, considers that the Transaction is unlikely to enable suppliers of NAND to reach terms of coordination.

(166) First, the Transaction will not significantly increase concentration on the market as there will remain several NAND/3D NAND suppliers on the market. In NAND, market leader Samsung, Kioxia, Western Digital, and Micron, along with Windbond and Powerchip will remain on the market. Similarly, in 3D NAND Samsung, Kioxia, Micron, Western Digital and YMTC will remain active.